Submitted:

06 October 2025

Posted:

07 October 2025

You are already at the latest version

Abstract

As global efforts to decarbonize intensify, hydrogen produced via renewable electricity has emerged as a pivotal energy vector for a sustainable industrial future. This commentary offers a critical analysis of the current state of the hydrogen economy within Europe, detailing the core principles, operational mechanisms, and industrial progress of four primary water electrolysis technologies: alkaline (ALK), proton exchange membrane (PEM), solid oxide (SOEC), and anion exchange membrane (AEM). Furthermore, it explores the significant socio-political challenges inherent in producing green hydrogen in non-EU nations for subsequent import into the European market.

Keywords:

green hydrogen

; water electrolysis

; European projects

; socio-political challenges

1. Introduction

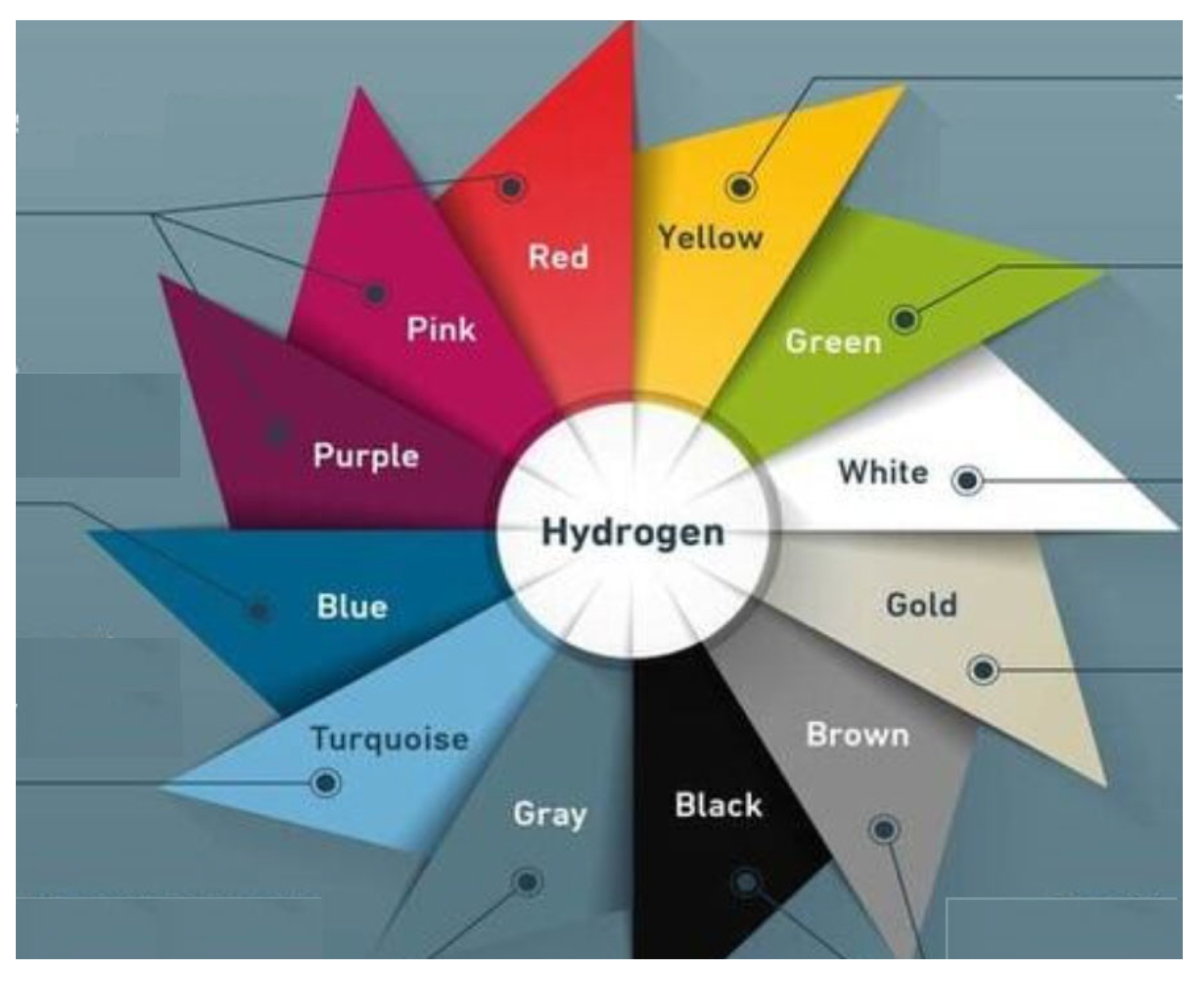

Hydrogen is conventionally classified on a spectrum of colors that denote the carbon intensity of its production process. For instance, black or brown hydrogen is derived from gasified coal, while the most common form, gray hydrogen, is produced from natural gas via steam methane reforming (SMR), a process that emits roughly 12 kg of CO₂ per kilogram of H₂ (Table 1, entry 1). Blue hydrogen represents a lower-carbon variant, as it combines SMR with carbon capture and storage (CCS) to sequester a large portion of the CO₂ emissions, reducing its footprint to an estimated 1-10 kg CO₂ per kg H₂ (Table 1, entry 2).

Beyond these fossil-based methods, hydrogen can be found naturally in the Earth's crust, where it is referred to as white or gold hydrogen. However, the commercial extraction of geological hydrogen is not yet a proven endeavor, with current estimates suggesting a carbon footprint starting from 0.4 kg CO₂ per kg H₂, which can increase if other gases like methane are present [1].

When hydrogen is produced by splitting water using electrolysis, its designation depends on the source of the electricity. If powered by renewables like wind or solar, it is termed green hydrogen, boasting a very low carbon footprint of around 0.3 kg CO₂ per kg H₂ [1]. Currently, hydrogen produced using wind power is often considered to have a slightly better environmental profile than solar-based production due to lower embodied energy in manufacturing and more consistent maximum output [5]. When nuclear power fuels the electrolysis, the resulting hydrogen is labeled pink, purple, or red (Figure 1).

In Table 1 carbon footprint and production costs of the main types of hydrogen mentioned above are reported. While white hydrogen is not yet commercially developed, green hydrogen with the lowest expected/ estimated carbon footprint (0.3 kg CO2 kg-1 H2 as reported in Table 1) is often viewed by policymakers, climate activists and the energy sector as the ‘holy grail’

A significant reduction in the cost of renewable energy is projected by 2050, driven primarily by economies of scale and ongoing technological improvements [1,7]. This trend is critically important for green hydrogen, as electricity expenses can account for as much as 75% of its final production cost.

The global policy landscape for decarbonization is divergent. In the United States, the administration of Donald Trump moved in early 2025 to cancel a number of government-supported decarbonization initiatives. Concurrently, significant debate ensued regarding the distribution of funding among various climate-related strategies, with green hydrogen being a key topic. This period also saw major energy corporations, including Air Products, Shell, and BP, recalibrating their business approaches by scaling back the priority of decarbonization projects.

In stark contrast to the American stance, the European Commission unveiled its Clean Industrial Deal on 26 February 2025, a strategy explicitly designed to propel decarbonization and re-industrialization efforts [8]. President Ursula von der Leyen emphasized the continent's dual identity, stating, “Europe is not only a continent of industrial innovation, but also a continent of industrial production. However, the demand for clean products has slowed down, and some investments have moved to other regions. We know that too many obstacles still stand in the way of our European companies from high energy prices to excessive regulatory burden. The Clean Industrial Deal is to cut the ties that still hold our companies back and make a clear business case for Europe.” [9]. Central to this plan are renewable energies and low-carbon hydrogen technologies, especially green hydrogen, with many recent European investments aligning within this strategic context.

Tangible commitments are already materializing across the continent. For instance, a $169 million grant was approved by the French prime minister in mid-April to fund a new water electrolysis facility in the Le Havre port area of Normandy [10]. Scheduled for commissioning in 2029, this plant is expected to yield 34 metric tons of hydrogen daily. Its strategic location near chemical manufacturers like Yara International provides a ready customer base seeking low-carbon hydrogen for their own decarbonization. Further European initiatives underscore this momentum. The producer Hy2gen, for example, runs a German plant generating 2.5 tonnes of green hydrogen per day for transport and is advancing projects in Norway for green ammonia and in France for sustainable aviation fuel (SAF) [10]. Similarly, as part of its own sustainability transition, the Austrian petrochemical company OMV has commissioned a 10 MW green hydrogen plant with an approximate daily output of 4 tonnes [10].

This commentary provides an examination of contemporary advancements in green hydrogen. It begins by detailing the principal electrolyzer technologies used in its production and showcasing specific European projects. Subsequently, the analysis broadens to consider the wider evolution of the hydrogen economy, featuring a comparative evaluation of the cost-competitiveness between green and blue hydrogen, alongside the pivotal socio-political factors that will influence its future trajectory.

2. The Steps Toward a Green Hydrogen Economy in Europe

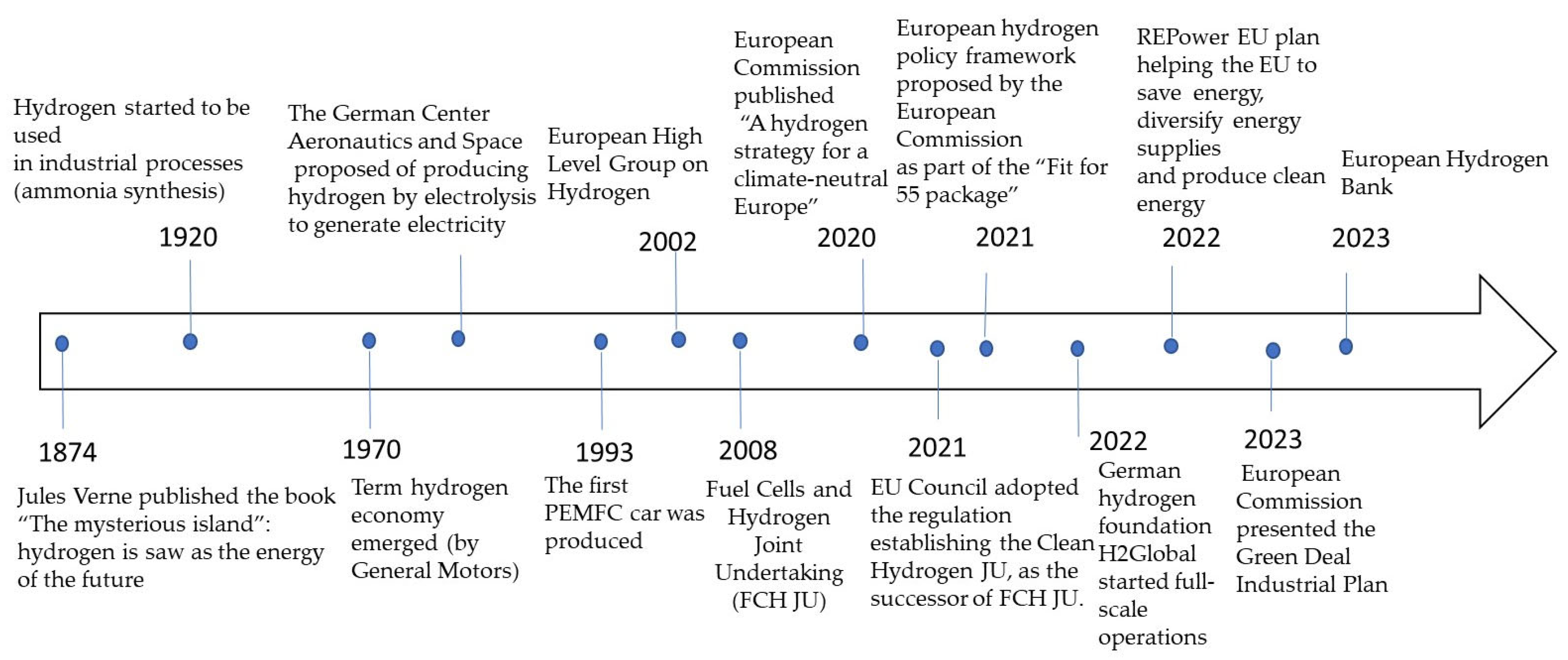

The conceptual foundation for a hydrogen-based energy system was laid as early as 1874 by the French author Jules Verne in his novel “The Mysterious Island,” which depicted a future transition from the then-dominant coal economy to one powered by hydrogen derived from water electrolysis.

While this vision was initially a distant prospect, it has progressively moved toward reality over the subsequent decades (Figure 2).

The practical application of hydrogen began in the 1920s with its use in industrial ammonia synthesis, and it later became a critical component of NASA's space program starting in 1958. The specific term "hydrogen economy" first entered the lexicon during the 1970s, a period defined by oil crises and a burgeoning global consciousness about environmental challenges [11]. During this era, the German Center for Aeronautics and Space (DLR) put forward a proposal to utilize diverse primary energy sources for electricity generation, with subsequent hydrogen production via electrolysis [12].

A significant automotive milestone was reached in 1993 with the development of the first proton-exchange membrane fuel cell for cars [11].

Institutional momentum in Europe grew with the formation of the European High Level Group on Hydrogen in 2002, an informal advisory body [13]. This group was instrumental in advocating for the establishment of the European Hydrogen and Fuel Cell Technology Platform (HFP), which operated from 2004 to 2007 and highlighted the pivotal role of these technologies in Europe's transition to innovative and clean energy. This effort culminated in the creation of the Fuel Cells and Hydrogen Joint Undertaking (FCH JU), a public-private partnership. The FCH JU was founded under the European Community's 7th Framework Programme (FP7) (2007-2013), uniting the European Commission with industrial and research organizations to accelerate development.

This initial phase, which concluded in 2020, was financed through a collaborative trio comprising the European Commission, Hydrogen Europe (representing industry), and Hydrogen Europe Research (representing the research community). Their joint efforts were instrumental in fostering high-visibility initiatives and securing the EU's position as a global leader in electrolyzer technology and hydrogen refueling infrastructure. Subsequently, in 2021, the EU Council formally adopted a regulation to establish the Clean Hydrogen Joint Undertaking (JU) as the successor to the FCH JU, with a mandate to support the development of a sustainable, decarbonized, and fully integrated energy system for the EU.

A pivotal policy document, the communication “A hydrogen strategy for a climate-neutral Europe” [14], was released by the European Commission in July 2020. It underscored the vital role of hydrogen in displacing fossil fuels within carbon-intensive industries like steel and chemicals. The strategy outlined an ambitious EU industrial plan to achieve 40 GW of electrolyzer capacity domestically and a further 40 GW in neighboring regions for export to the EU by 2030, with interim targets of at least 6 GW by 2024. The Communication delineated a three-phase rollout. The initial phase (2020-2024) focused on installing a minimum of 6 GW of renewable hydrogen electrolyzers and producing up to one million tonnes of renewable hydrogen to decarbonize existing production, necessitating the scaling of large-scale electrolyzers up to 100 MW. During this stage, various forms of low-carbon hydrogen were expected to contribute to market growth.

The second phase (2025-2030) aimed for at least 40 GW of electrolyzer capacity and the production of up to 10 million tonnes of renewable hydrogen within the EU, with the expectation that it would become cost-competitive with other production methods. This period was also anticipated to see the emergence of integrated local ecosystems, known as “Hydrogen Valleys,” leveraging decentralized renewable energy for local production and consumption with minimal transport. In the third and final phase (2030-2050), renewable hydrogen technologies were projected to achieve full maturity and large-scale deployment, with an estimated quarter of the EU's renewable electricity potentially dedicated to its production by 2050.

The European hydrogen policy framework was first proposed in 2021 as a component of the “Fit for 55 package,” a comprehensive legislative suite targeting a minimum 55% reduction in EU greenhouse gas emissions by 2030 and climate neutrality by 2050 [15]. Concurrently, Germany's H2Global foundation, established in mid-2021, commenced full operations in 2022 to facilitate future imports of hydrogen from outside the EU for German industry.

The geopolitical landscape further accelerated these efforts with the launch of the REPowerEU plan in May 2022 [16], a direct response to Russia's invasion of Ukraine aimed at energy saving, supply diversification, and clean energy production. This strategy set explicit targets of 10 million tonnes for both domestic green hydrogen production and imports by 2030. Key measures included a Hydrogen Accelerator, a goal to ramp up electrolyzer manufacturing capacity to 40 GW by 2030, and the initiation of major collaborative projects like the IPCEI Hy2Tech to build out the hydrogen value chain. According to the European Commission, green hydrogen is central to decarbonizing heavy industry and transport, while also enhancing grid flexibility for renewable integration.

Further consolidating this direction, the European Commission presented the Green Deal Industrial Plan on 1 February 2023, aligning with the broader objectives of the 2019 European Green Deal [8,9]. This plan sought to create a more supportive regulatory and institutional environment to expand the EU's production capacity for clean technologies and zero-emission products. This intent was concretized on 16 March 2023 with the proposal of a new Critical Raw Materials Act and a Net-Zero Industry Act.

Simultaneously, the Communication on the European Hydrogen Bank [17] detailed the structure of this new financing instrument around four pillars: domestic, international, transparency and information coordination, and support instrument coordination. The domestic pillar is designed to stimulate the hydrogen production market within the European Economic Area (EEA) and link renewable hydrogen supply with demand. The international pillar focuses on creating a mechanism to attract green hydrogen imports into the EU via joint European auctions. Operationalizing this framework, the European Commission launched a market-based Hydrogen mechanism in July 2025 to bolster the development of renewable and low-carbon hydrogen and its derivatives, including ammonia, methanol, and Sustainable Aviation Fuel (SAF).

3. Types of Electrolyzers: Theoretical Background and Relevant Projects

As previously noted, the strategic roadmap laid out by the European Commission in its 2020 document “A hydrogen strategy for a climate-neutral Europe” targets the installation of a minimum of 6 GW of green hydrogen electrolyzers within the EU by 2024, with a significant expansion to 40 GW planned for 2030 [14]. A key short-term goal for the 2020-2024 period is the deployment of these 6 GW of renewable hydrogen electrolyzers, coupled with the production of up to one million tonnes of renewable hydrogen, primarily aimed at decarbonizing the existing hydrogen supply.

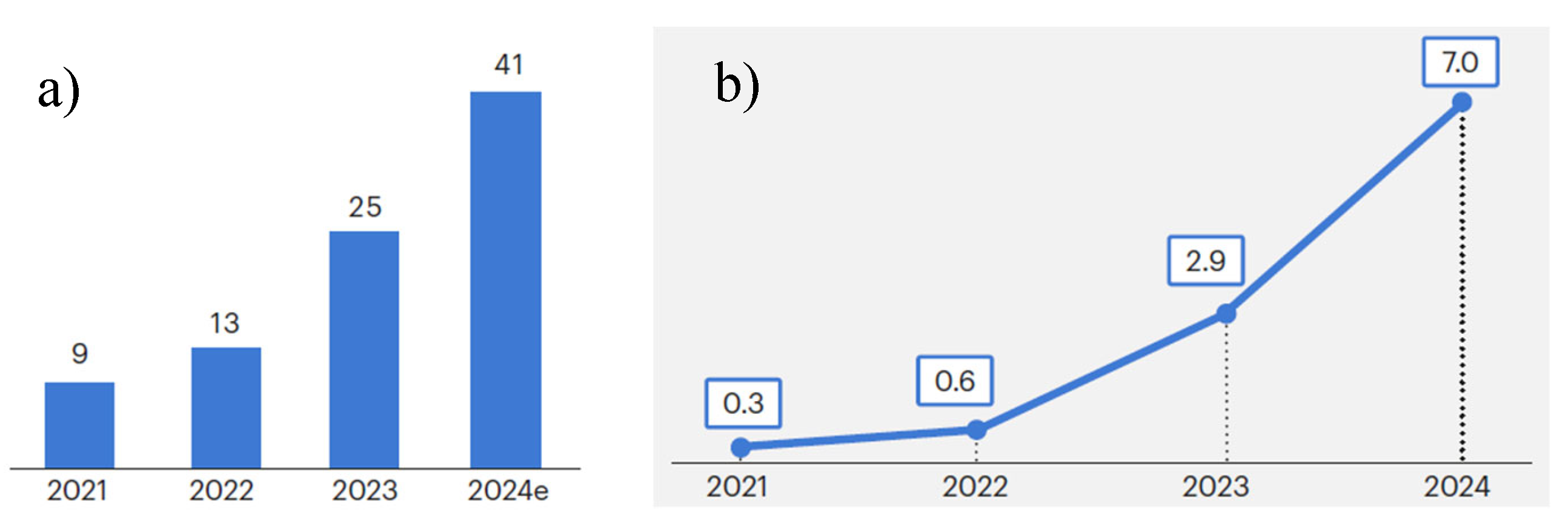

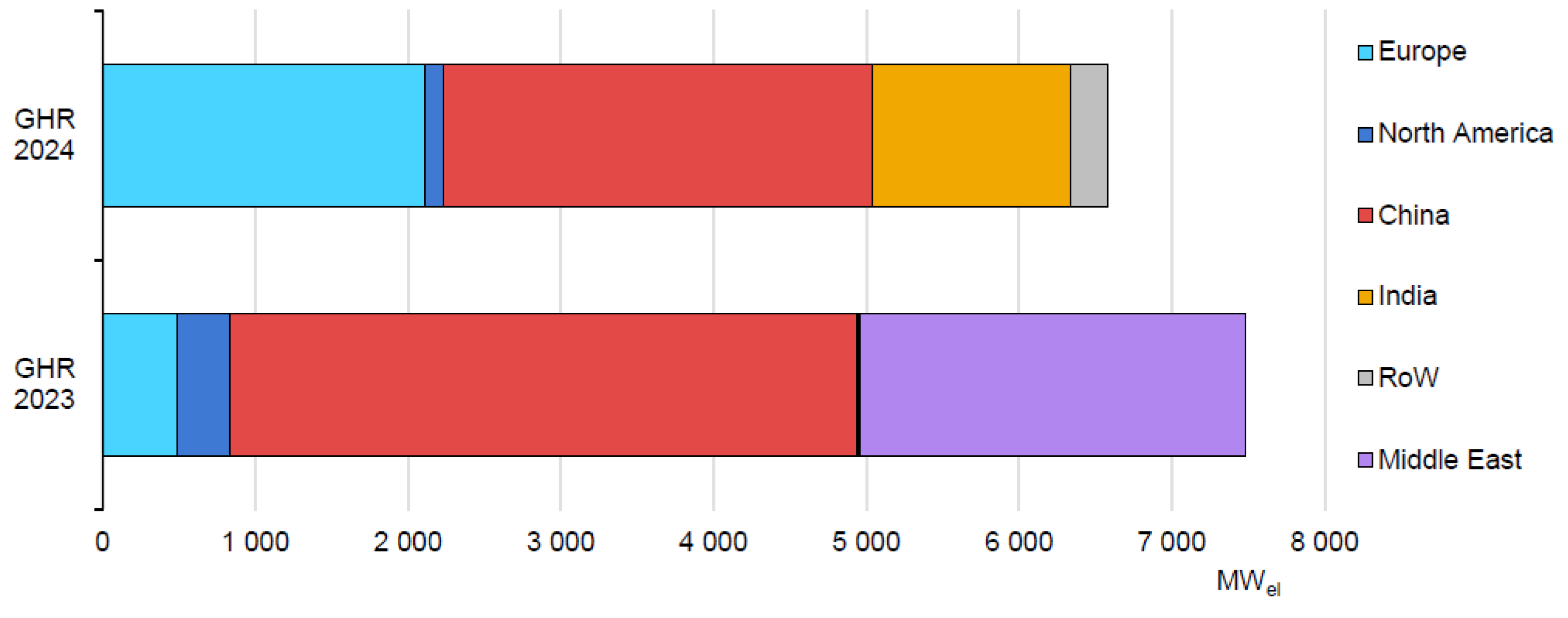

Examining the global context reveals a rapidly evolving landscape. While decarbonized hydrogen accounted for less than 1 million tonnes (Mt) of the 97 Mt global hydrogen demand in 2023—a market still dominated by carbon-intensive black, brown, and gray hydrogen—the sector is poised for transformative growth. Production of low-emission hydrogen via electrolysis is on a strong upward trajectory (Figure 3), with projections suggesting it could achieve 49 Mt per annum by 2030, supported by announced electrolysis capacity that totals nearly 520 GW [7].

The pace of project development in Europe has accelerated markedly, with Final Investment Decisions (FIDs) for electrolysis installations increasing fourfold in a single year to surpass 2 GW of capacity. Concurrently, India has positioned itself as a major contender in the global market, largely due to a single, substantial FID amounting to 1.3 GW (Figure 4). Meanwhile, China's dominance in the manufacturing sector, where it accounts for 60% of the world's electrolyzer production (Figure 4), is anticipated to significantly reduce technology costs, mirroring its previous impact on the solar PV and battery industries [18].

The electrolysis process facilitates the non-spontaneous splitting of water (H₂O) into its constituent elements through the application of an electric current. This current flows between two electrodes—a cathode and an anode—which are immersed in an electrolyte and separated by a membrane. Within the cell, the electrical energy drives two distinct half-reactions: at the cathode, water molecules are reduced to form hydrogen gas (H₂), while at the anode, they are oxidized to produce oxygen gas (O₂).

H2O → H2 + ½ O2

G= +237 kJ/mol

The landscape of water electrolysis is defined by four principal technological pathways, each distinguished by a unique combination of operational characteristics, performance specifications, and functional mechanisms.

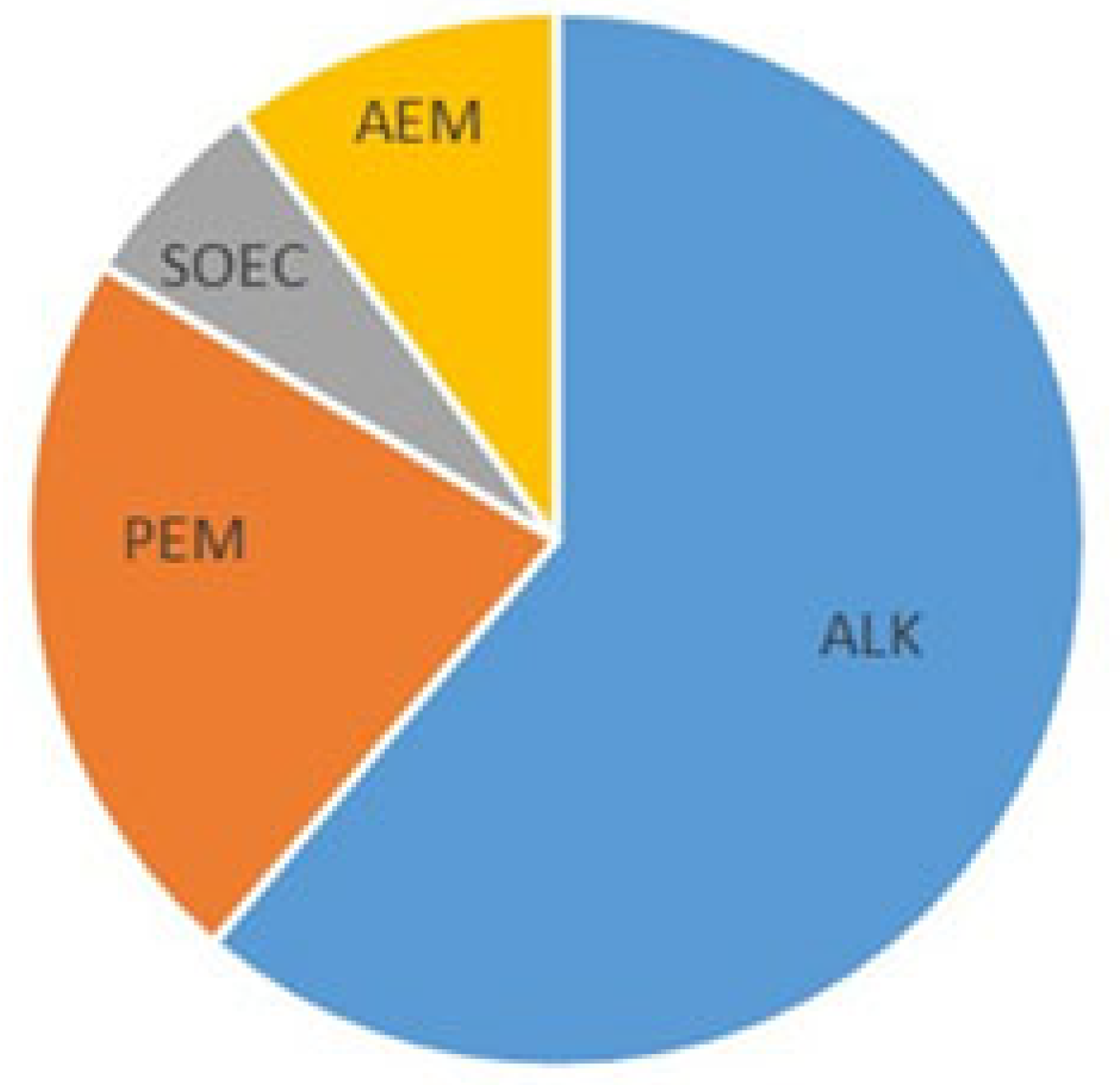

Current market distribution, as reported by the International Energy Agency (IEA) [7], shows alkaline electrolysis (ALK) as the dominant force, representing over 60% of installed global capacity, with the bulk of this deployment located in China (Figure 5). Accounting for 22% of the 2023 installed capacity, Proton Exchange Membrane (PEM) electrolysis holds the second-largest share. Its projected growth, nearly half of the 43 GW/year anticipated by 2030, is concentrated primarily in Europe, followed by North America and India. Solid oxide electrolyzers (SOEC) currently constitute a niche segment of approximately 6% (Figure 5), a proportion expected to remain stable through 2030 due to the technology's ongoing pre-commercial status for large-scale hydrogen manufacturing. In contrast, while Anion Exchange Membrane (AEM) technology commands a minimal share of today's manufacturing output, its market presence is forecast to exceed 10% by the end of the decade (Figure 5). The commercial viability of AEM is demonstrated by manufacturers like the German-Italian firm Enapter, a pioneer and leading producer in this space, which reported an approximate fourfold increase in sales between the final quarters of 2022 and 2023, underscoring growing interest from developers of smaller-scale projects.

Selecting an appropriate electrolyzer technology is a decision dictated by the particular demands and intended scale of the hydrogen production initiative. ALK systems, prized for their robustness and longevity, are optimally deployed in large-scale installations functioning under consistent operational loads. The compact design and high efficiency of PEM electrolyzers make them well-suited for smaller-scale applications powered by more variable energy sources, such as renewables. AEM technology was conceived to integrate the most beneficial aspects of both ALK and PEM systems but has yet to achieve widespread industrial scaling. SOECs promise superior efficiency and have the added capability for syngas production, positioning them as a strong candidate for industrial-scale uses; however, these advantages must be conclusively validated upon full commercialization [19]. A significant hurdle for SOEC adoption is its presently higher overall cost and challenges related to achieving a long operational lifespan.

A general downward trend in capital expenditure across all electrolyzer technologies is anticipated leading up to 2030, with ALK consistently regarded as the most economically advantageous option [20].

The following sections provide a concise overview of the operational principles behind ALK, PEM, SOEC, and AEM technologies, alongside examples of relevant European projects where they are being implemented.

3.1. Alkaline Electrolysis

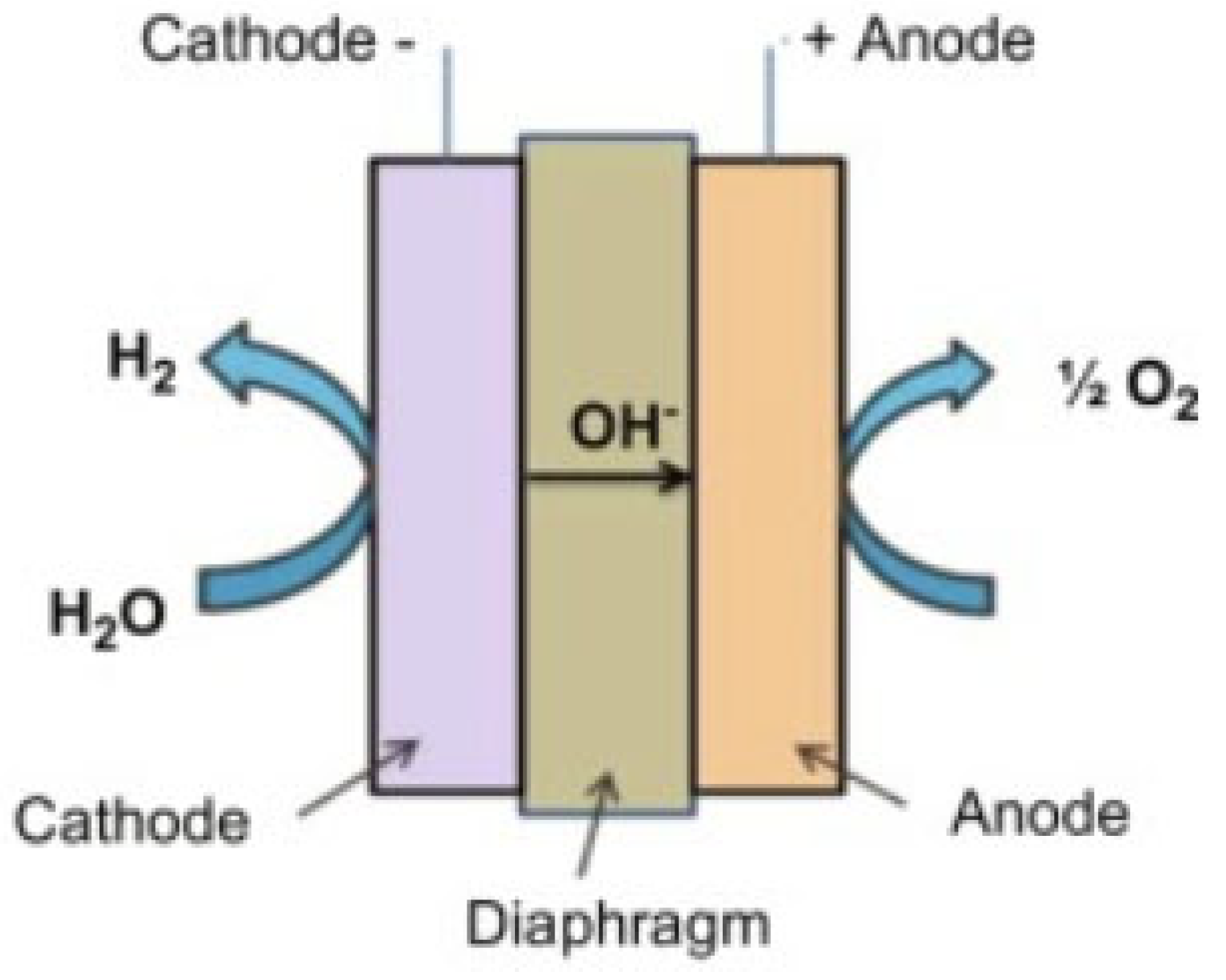

Alkaline electrolysis (ALK) is a long-standing technological approach with a history of industrial application dating back to the 1920s, originally deployed within the chlor-alkali sector for substantial hydrogen generation. The fundamental operating mechanism involves two electrodes submerged in a liquid alkaline electrolyte, typically a solution of potassium hydroxide (KOH) or sodium hydroxide (NaOH). A critical component, a porous diaphragm, physically separates these electrodes. This diaphragm functions as an ionic conductor, permitting the transit of hydroxide ions (OH⁻) from the cathode compartment—where hydrogen gas is produced via the Hydrogen Evolution Reaction (HER) (Eq. 2) – to the anode compartment, where the Oxygen Evolution Reaction (OER) takes place (Eq. 3), as illustrated in Figure 6.

2H2O + 2e- → H2 + 2OH-

2OH- → ½ O2 + H2O + 2e-

ALK systems typically function within a operational temperature window of 50 to 80 °C. A key feature is their ability to deliver hydrogen at output pressures from 10 to 200 bar, enhancing their versatility for different downstream uses. This technology benefits from the use of inexpensive, non-precious metal catalysts—such as cobalt, nickel, or iron—on its electrodes, contributing to a lower capital cost. Furthermore, these electrolyzers are recognized for their extended operational lifespan and the high purity of the hydrogen gas they produce [21].

A significant limitation of conventional alkaline systems, however, is their requirement to operate at comparatively low current densities, generally between 0.05 and 0.7 A/cm². This constraint is primarily due to the properties of the porous diaphragm, which must effectively prevent gas crossover while allowing ion transport [22]. Their performance is also less optimal with variable power inputs, as they are not well-suited to unstable or highly fluctuating loads. Rapid shifts in current can diminish overall system efficiency, hasten the degradation of the diaphragm, and lead to a reduction in gas purity. Despite these drawbacks, the surging global interest in alkaline electrolysis is catalyzing renewed research and development efforts from both academic and industrial sectors. A primary focus of this innovation is the advancement of more efficient, low-cost, and durable electrocatalysts to overcome existing limitations [22].

The state-of-the-art performances of ALK and near-future performance envisioned by FCH JU, predecessor of Clean Hydrogen JU mentioned above, is summarized in Table 2.

The global alkaline electrolyzer industry has been significantly shaped by the contributions of several European manufacturers, including prominent players like Green Hydrogen, McPhy, Sagim S.A., and Accagen. A detailed comparison of the technical specifications and performance metrics for various models offered by these and other companies is provided in Table 3.

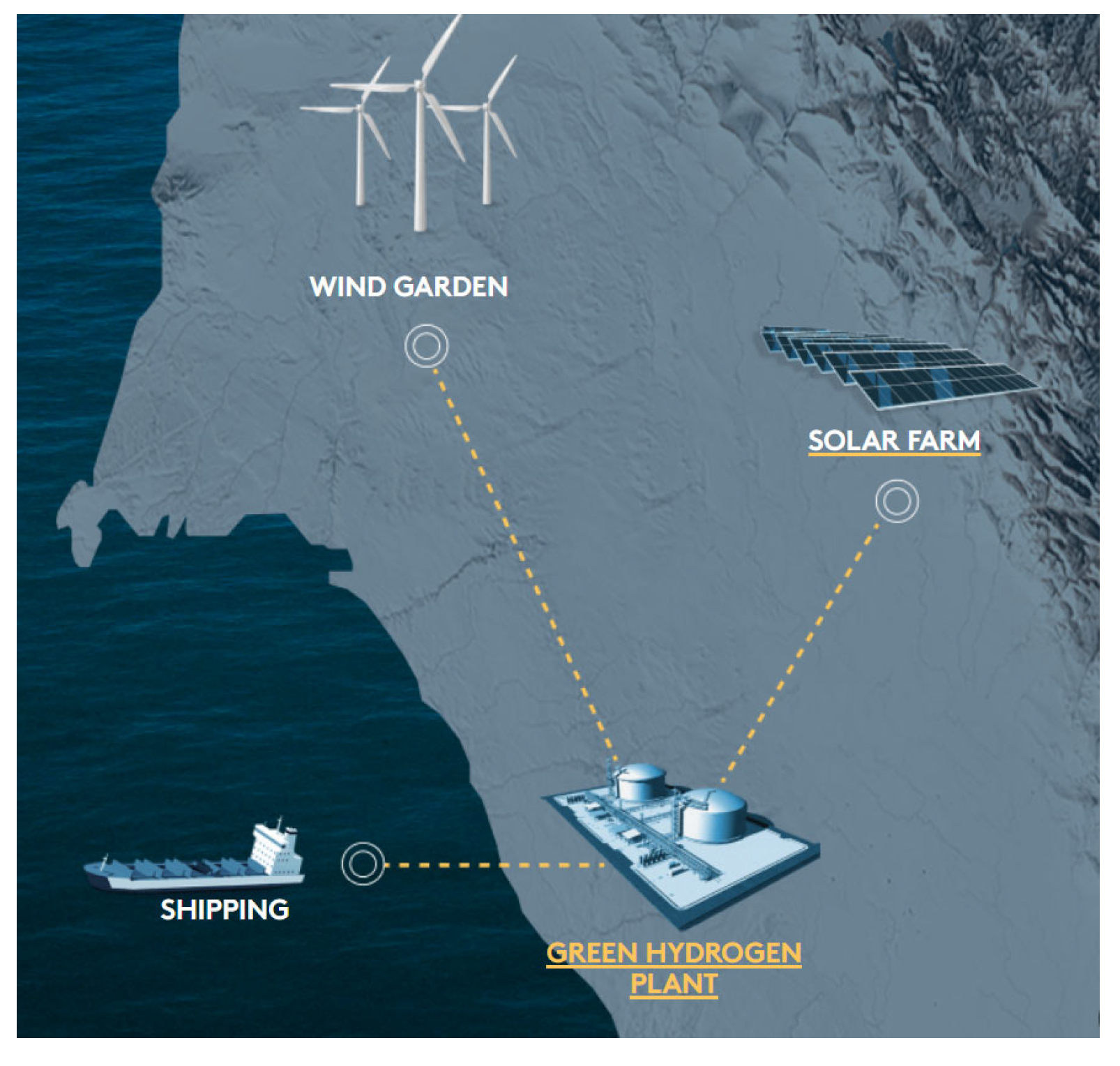

The deployment of alkaline electrolyzer systems has accelerated recently, with numerous projects achieving operational status. A major catalyst for this momentum is the Final Investment Decision (FID) for the NEOM Green Hydrogen Project in Saudi Arabia. This initiative represents the world's largest electrolyzer project to reach this stage, featuring 2.2 GW of alkaline units supplied by the German firm Thyssenkrupp Nucera. Central to Saudi Arabia's Vision 2030 for economic diversification, this facility is designed to yield up to 600 tonnes of carbon-free hydrogen daily, which will be converted into green ammonia for global distribution to the transportation and industrial sectors (Figure 7). The project's dedicated 4 GW renewable energy generation complex is slated for commissioning by mid-2026, with the first shipments of green ammonia anticipated in 2027 [25]. Air Products holds exclusive rights to market the output, which will be exported globally via a dedicated loading jetty operated by the Neom Green Hydrogen Company (NGHC).

European investment in hydrogen infrastructure saw remarkable growth, with Final Investment Decisions (FIDs) for over 2 GW of electrolyzer capacity finalized between September 2023 and August 2024—a fourfold increase compared to the preceding year.

A landmark initiative in this wave is the GreenH2Atlantic project in Sines, Portugal. Spearheaded by GALP, a major Portuguese energy supplier, the project will deploy 100 MW of McPhy alkaline electrolyzers (Table 3) to produce approximately 15,000 tonnes of renewable hydrogen annually for diverse applications. A key objective is to integrate this output into the Sines refinery, displacing around 20% of its current gray hydrogen consumption and potentially reducing greenhouse gas emissions by 110,000 tonnes per year [26]. Construction commenced in April 2024, with operations scheduled to begin by mid-2026 [27].

Complementing this production effort, Portugal is advancing its transport infrastructure through two pivotal projects announced in November 2023: ‘H2Med/CelZa’ and the ‘Portuguese Hydrogen Backbone’. These initiatives form the foundation of the Green Energy Corridor, a planned network to connect the Iberian Peninsula with Central Europe. The 'H2Med/CelZa' project, managed by gas transmission operator REN-Gasodutos, involves building a 242 km pipeline, with 162 km located within Portugal. The related ‘Portuguese Hydrogen Backbone’ project will similarly adapt the national gas grid, creating critical enabling conditions for green hydrogen production and integration in the country's central interior region [28].

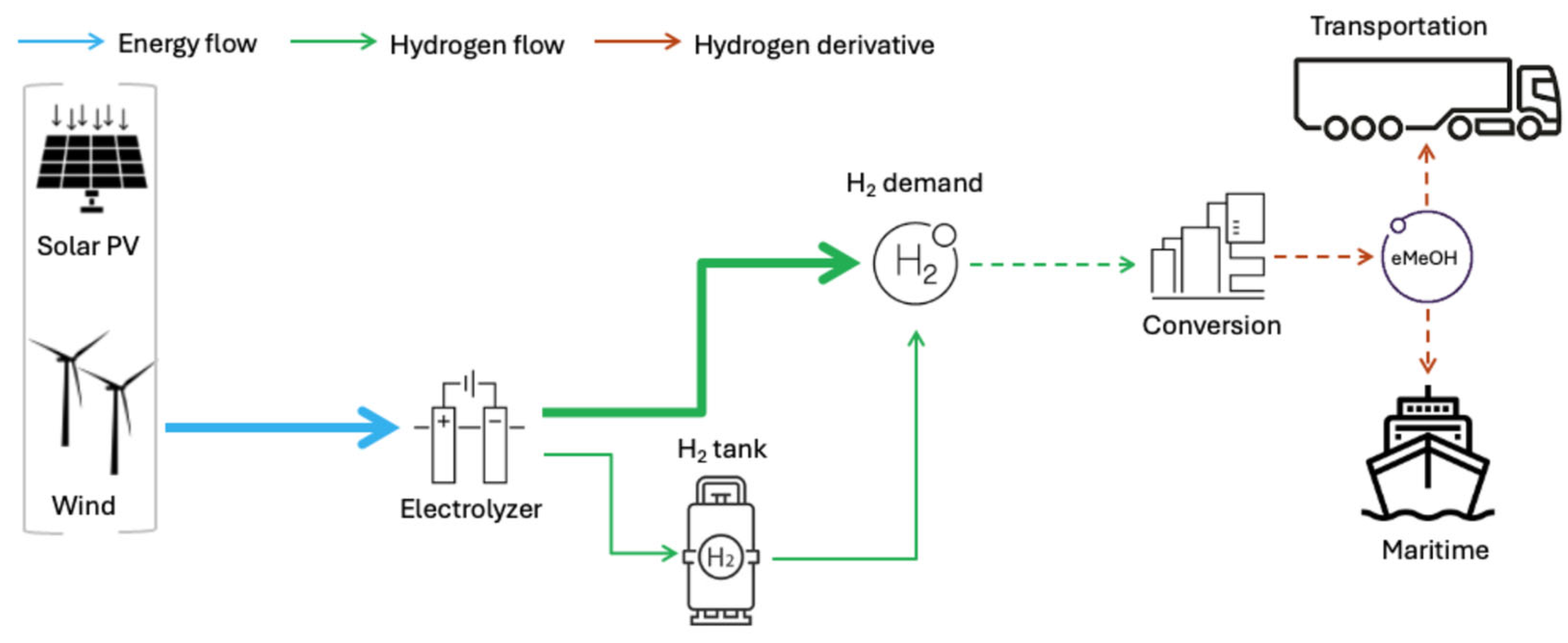

Beyond the Iberian Peninsula, Denmark's GreenLab Skive represents a different model—a circular industrial park in Northern Jutland dedicated to piloting the green industrial transition. It functions as a live testing ground for integrated energy systems, notably hosting a Power-to-X (PtX) plant for generating green hydrogen and methanol (Figure 8). This facility is central to the EU-funded GreenHyScale project (2021-2026). A significant milestone was reached in 2023 with the delivery of the first 6 MW electrolysis module from Green Hydrogen Systems. The core technology is the company's X-Series prototype, a modular, pressurized alkaline electrolyzer designed for multi-stacking (Table 3). The deployment and testing of this unit at GreenLab Skive is a crucial step in the GreenHyScale project, validating the technology's progression toward commercial viability [29].

Today, Germany has a total electrolyser capacity of approximately 120 MW accounting for around 40% of Northwestern Europe’s operational electrolytic hydrogen production capacity. Projects that have reached FID and/or are under construction could add close to 1.3 GW of low-emissions electrolytic hydrogen capacity by 2030. The Clean Hydrogen Coastline project by EWE in Emden includes a 320 MW alkaline electrolyzer. The project which aims to integrate hydrogen production, storage, transport, and utilization on a large scale, is part of the IPCEI (Important Projects of Common European Interest) program, receiving significant funding from the German government and the state of Lower Saxony.

Another key hydrogen project in Germany is RWE’s GET H2 Nukleus, which involves developing 300 MW of electrolysis capacity in Emsland in three expansion stages by 2027. In 2024 RWE has commissioned the German electrolyzer specialist Sunfire (Table 3) to supply 100-megawatt alkaline electrolyser for 3rd Nukleus construction phase in Lingen. The electrolyzer will thus contribute one-third of the total production capacity of RWE's 300 MW plant. The plant will produce up to two tons of green hydrogen per hour, primarily for industrial customers in Lower Saxony and North Rhine-Westphalia.

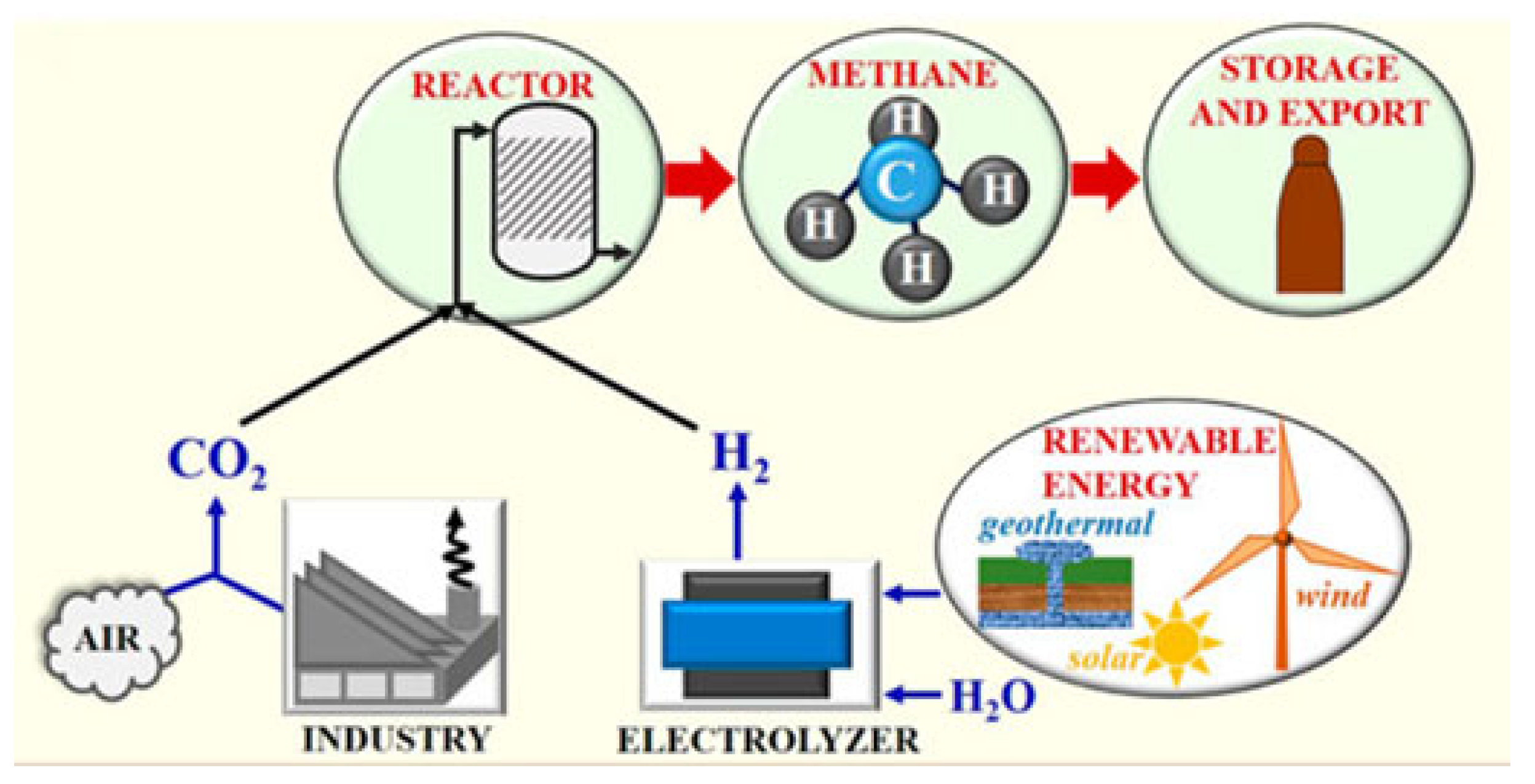

Finland has a unique opportunity to take a leading role in the development and production of green hydrogen and its derivatives. Not only from a climate and environmental perspective but also from the viewpoint of security of supply, competitiveness, and geopolitical strategy. In March 2025 the Finland’s first industrial scale green hydrogen production in Harjalvalta was inaugurated. A key component of the plant is Sunfire’s 20 MW alkaline electrolyzers. The plant is relevant because it is also preparing to begin the production of renewable syntetic methane (e-methane), which is produced by combining hydrogen made with renewable energy and carbon dioxide (Figure 9), within the EU mandating that at least 1% of transport fuels must consist of Renewable Fuels of Non Biological Origin (RFNBO) by 2030.

A separate Finnish initiative is poised to address the rising European need for e-methane, a demand largely propelled by EU regulations targeting the heavy-duty transport and maritime industries. Spearheaded by the Norwegian energy firm Freija, plans are advancing to construct a major e-methane production plant in Nokia, which would rank among Europe's largest [31]. The project, which will utilize alkaline electrolyzers, is structured for development in three distinct stages. Freija is targeting a Final Investment Decision (FID) in 2026, with the initial production phase scheduled to become operational in 2029.

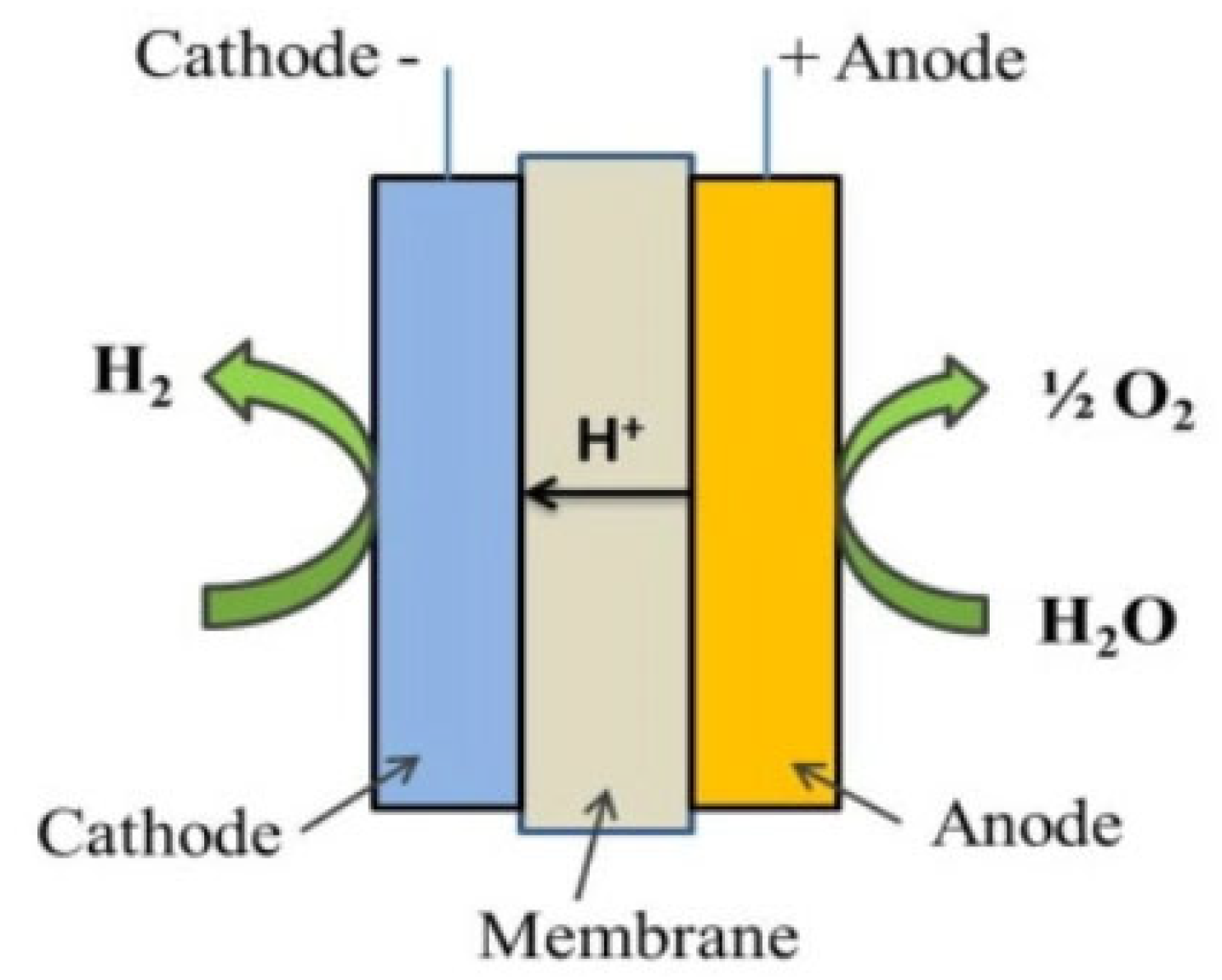

3.2. Proton Exchange Membrane

In PEM technology, proton (H+) is transported through a polymer electrolyte membrane (Figure 10). Electrocatalysts promote the HER and OER as reported in Eqs. 4 and 5:

2H+ + 2e-→ H2

H2O→½ O2 + 2H+ +2e-

PEM electrolyzers run at ideal temperatures of 60 °C to 80 °C.

The state-of-the-art performances of PEM envisioned by FCH JU is given in Table 4.

The deployment of Proton Exchange Membrane (PEM) electrolyzers gained substantial momentum across Europe in 2024, with several projects becoming operational and others advancing through development pipelines. A notable example is the commissioning of a 10 MW PEM plant by Plug Power at the Szazhalombatta refinery in Hungary early in the year [32]. The same company is also providing a much larger 280 MW PEM system for Arcadia eFuels' facility in Vordingborg, Denmark, where the green hydrogen will be used to synthesize Sustainable Aviation Fuel (SAF) [33]. Plug Power's collaboration with Galp on a 100 MW PEM installation in Portugal further underscores this growth trend [34].

In Norway, Yara commenced operations of the initial phase of its Porsgrunn project, which integrates a 24 MW PEM electrolyzer from ITM Power for renewable ammonia synthesis [35]. The choice of ammonia is strategic, leveraging its established, cost-effective global transport infrastructure. The facility has already yielded its first batches of fertilizers produced from this green ammonia, signaling a strategic shift for Yara toward a product portfolio increasingly based on low-carbon ammonia, including that derived from processes incorporating carbon capture and storage (CCS) [36].

Further solidifying this trend, Shell made a Final Investment Decision (FID) in 2024 on the REFHYNE II project, a 100 MW PEM electrolyzer at its Rheinland Energy and Chemicals Park in Germany, with operations scheduled for 2027 [37]. Shortly thereafter, in March 2025, Germany's largest PEM electrolyzer to date—a 54 MW system—began operation at BASF's Ludwigshafen complex after a two-year construction period [38]. The installation, comprising 72 individual stacks, will supply hydrogen both as a chemical feedstock and for fuel cell mobility applications in the Rhine-Neckar Metropolitan Region, supporting the creation of a local hydrogen economy [38].

In the UK, the Aberdeen Hydrogen Hub project also reached FID in 2024. This joint venture between BP and Aberdeen City Council will feature a containerized 2.5 MW PEM electrolyzer supplied by Norwegian manufacturer Nel [39]. Nel brings a deep historical pedigree to the project, having commissioned the world's first large-scale hydropower-driven electrolysis plant at Rjukan, Norway in 1940, followed by a similar facility in Glomfjord for ammonia production in 1953 [40]. For the Aberdeen hub, Hydrasun has been selected to design and construct the refueling station and associated infrastructure, which will be supplied by Nel's on-site electrolyzer [41].

3.3. Solid Oxide Electrolysers

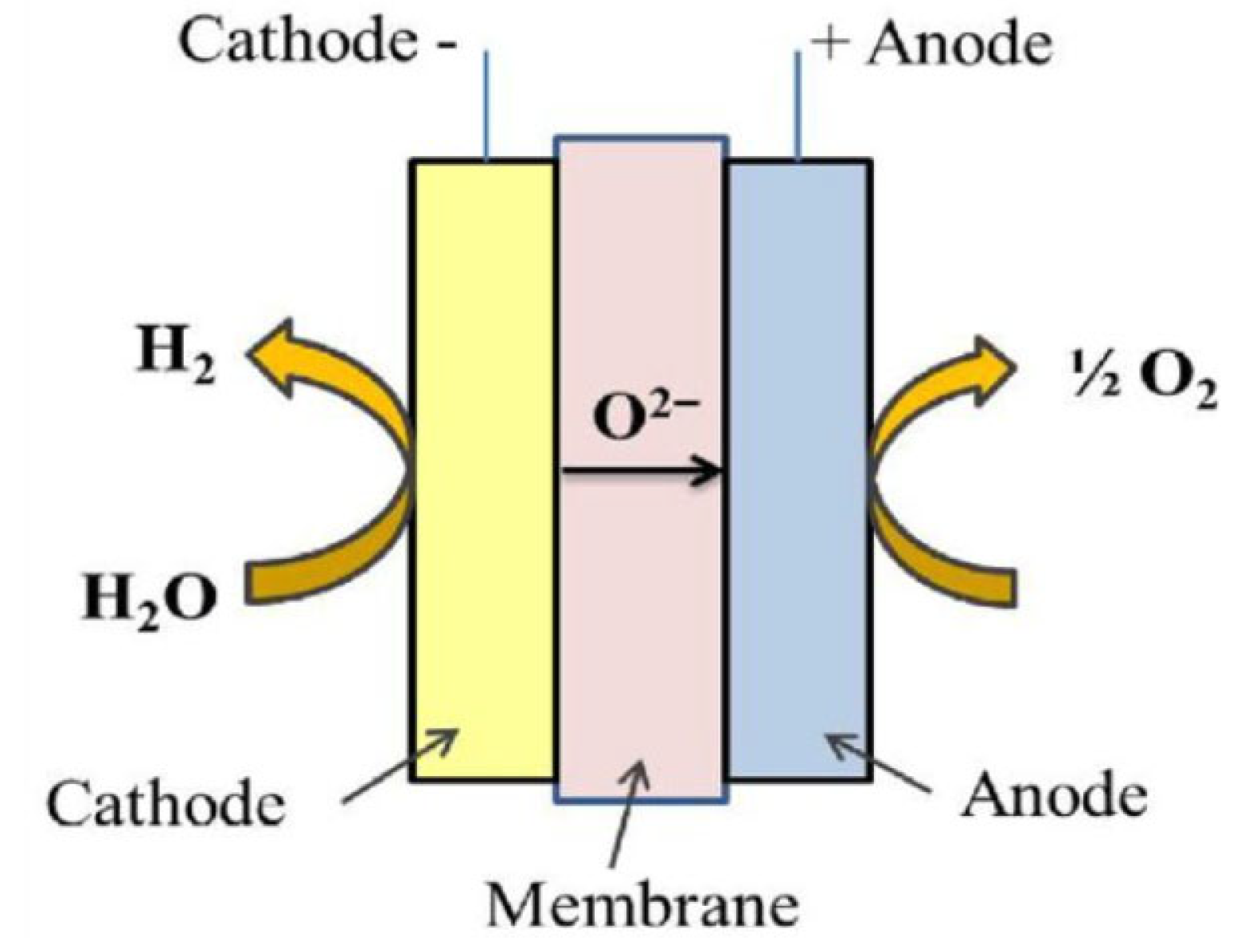

In SOECs for water electrolysis the electrolyte materials are proton conducting ceramic membranes with a working temperature to >700 °C [42]. Oxygen ions (O2−) requires a water supply to the hydrogen electrode (cathode) (Figure 11) and involves distinct HER and OER expressions:

H2O + 2e- → H2 + O2-

O2- → ½ O2 + 2e-

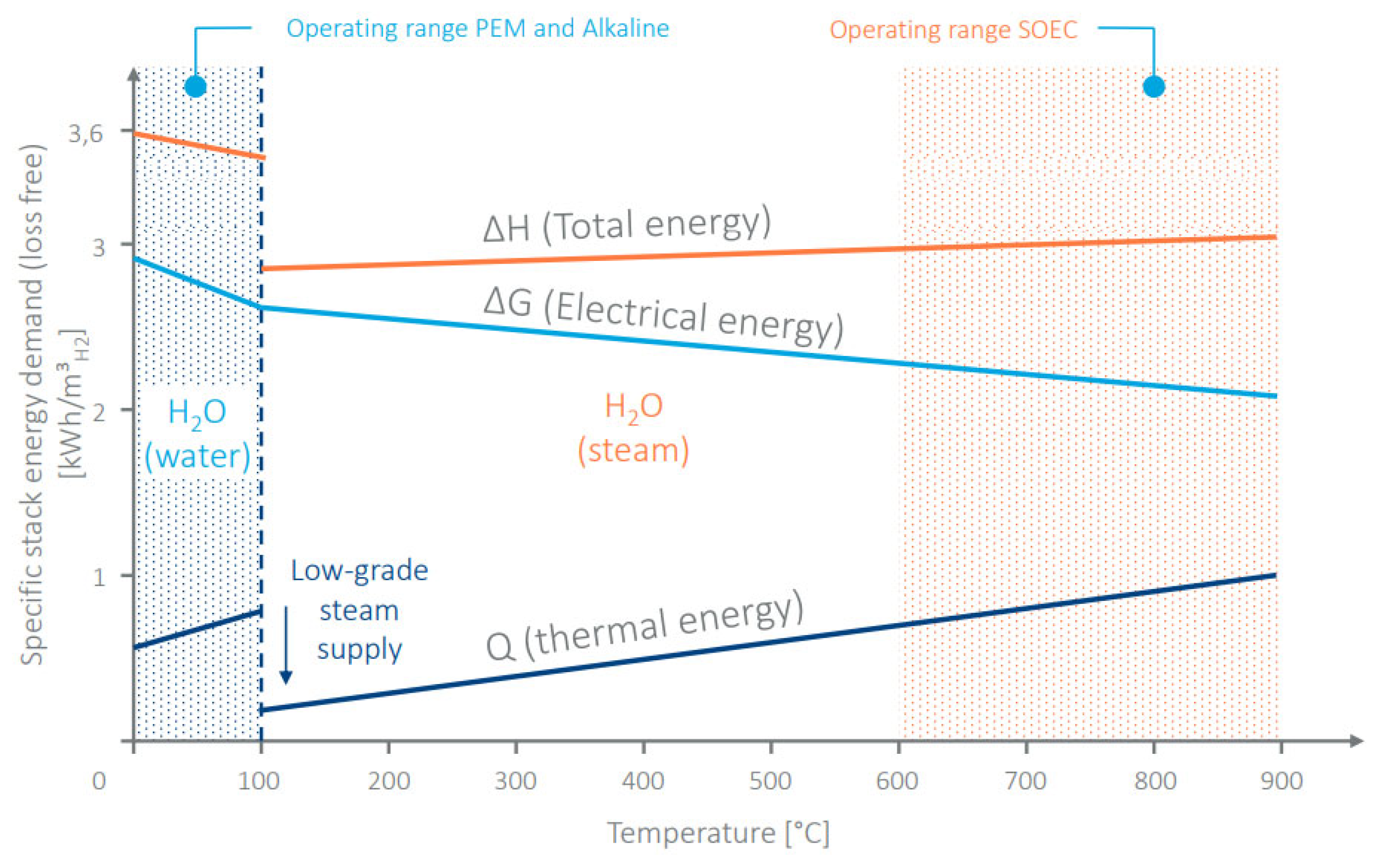

Compared to ALK and PEM electrolyzers SOEC shows lower ohmic losses as well as advantageous kinetics and thermodynamics due to the high operating temperatures. As for practical application, SOEC meet remarkable challenges as concerns the thermal stability of materials, gas mixture and sealing issues. However, due to the dissociation of steam, SOECs require less energy compared to liquid water (Figure 12).

In particular in Europe there have been notable recent developments in the field.

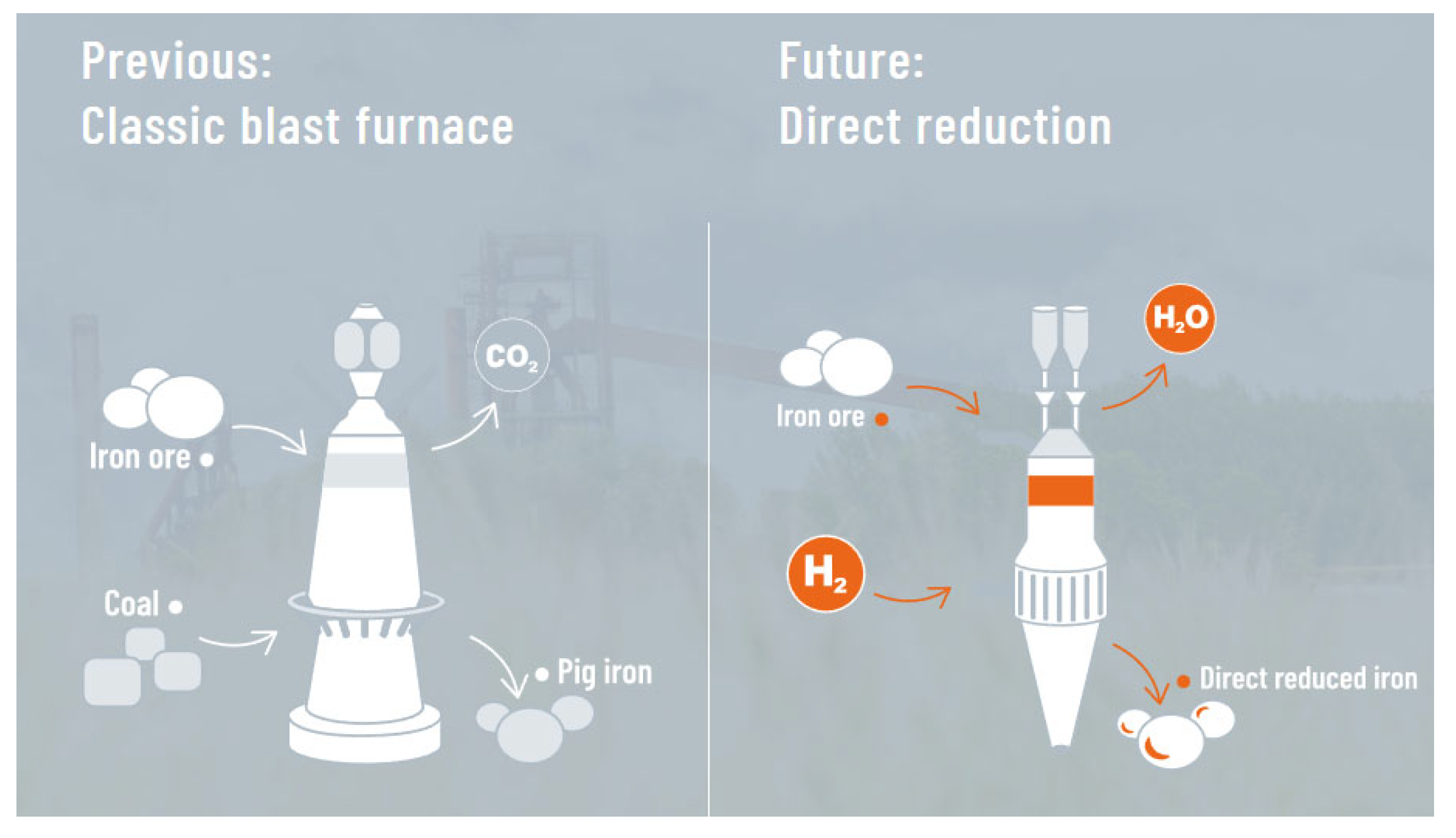

A primary advantage of SOEC technology is its capacity for integration with high-temperature industrial waste heat, such as the excess thermal energy generated in steel manufacturing. This synergistic coupling can lower the system's electrical consumption by an estimated 20% to 30% relative to low-temperature electrolyzers [43]. The steel sector itself is a key arena for this application, exemplified by the SALCOS® (Salzgitter Low CO₂ Steelmaking) initiative [44]. This program's strategy centers on using renewable electricity to power Sunfire's SOEC electrolyzers for on-site green hydrogen production. This hydrogen is pivotal for a process shift, displacing coal currently used in traditional blast furnaces. The method involves direct reduction plants, where iron ore is converted into iron in a solid state using hydrogen, bypassing the coke-based reduction that releases CO₂. This transition allows for a potential reduction in carbon emissions exceeding 95%. The SALCOS roadmap involves a phased replacement of existing blast furnaces with these direct reduction facilities, as depicted in Figure 13.

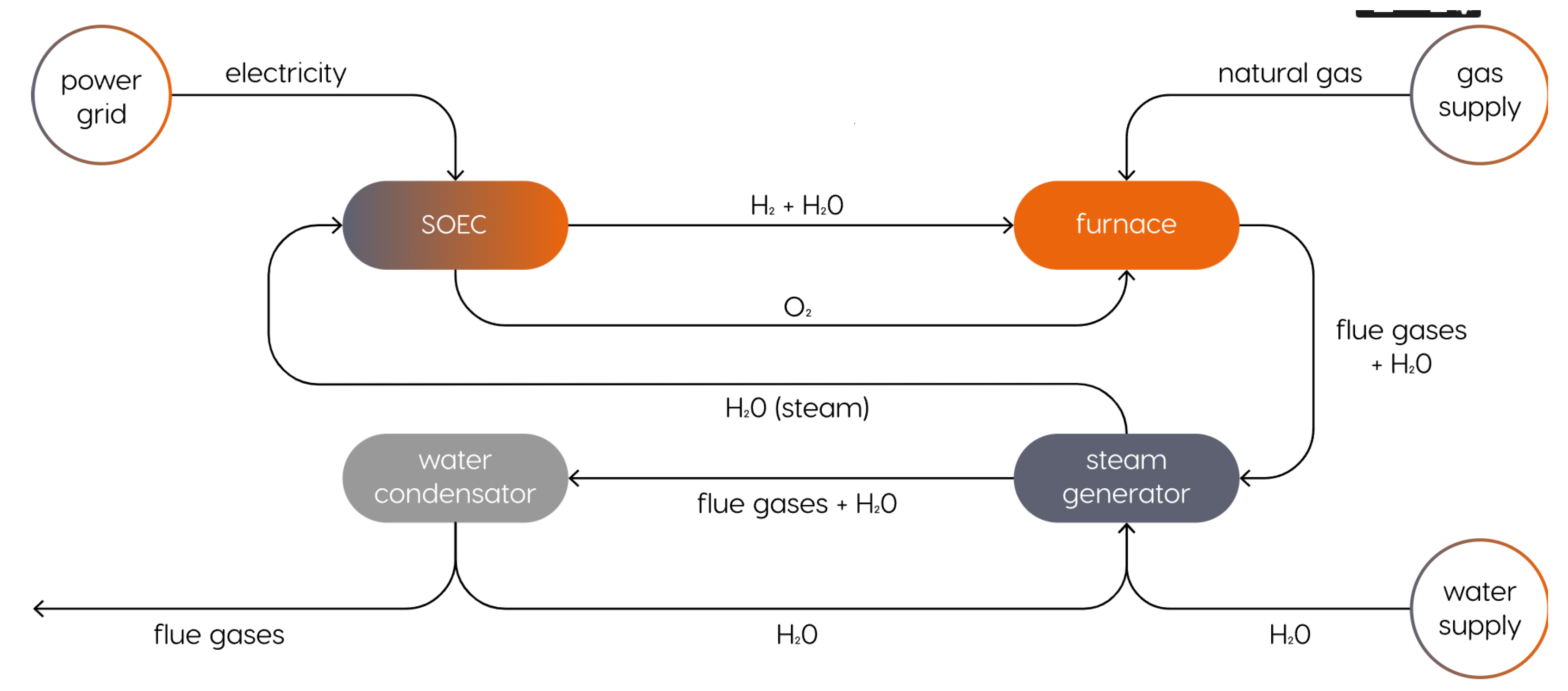

A second significant pilot initiative is the SYRIUS project, formally titled "SOE Hydrogen Integration and Circular Use in Steel-Making Process" [45]. Launched on January 1, 2025, the project receives backing from the Clean Hydrogen Partnership and co-financing from the European Union. Its core objective is the seamless incorporation of a 4.2 MW SOEC system, capable of generating 100 kg of green hydrogen per hour, into a fully operational Electric Arc Furnace steel plant. The project design includes a slab reheating furnace and incorporates comprehensive heat and water recovery systems with integrated steam generation (Figure 14). Anticipated outcomes from SYRIUS include a substantial boost in energy efficiency through the recovery of 25 TWh per year of useful heat and annual CO₂ emission reductions exceeding 10.9 million tonnes. The Estonian SOEC manufacturer Elcogen, which has also secured funding from the EU's NextGenerationEU plan, will supply the SOEC stacks for both the initial demonstrator and the subsequent final system. The operational industrial environment for integration will be provided by the Italian steelmaker Acciai Speciali Terni (AST).

The integration of SOEC with exisisting ammonia production plants is another opportunity offered for decarbonization by reducing the consumption of natural gas as a feedstock and fuel.

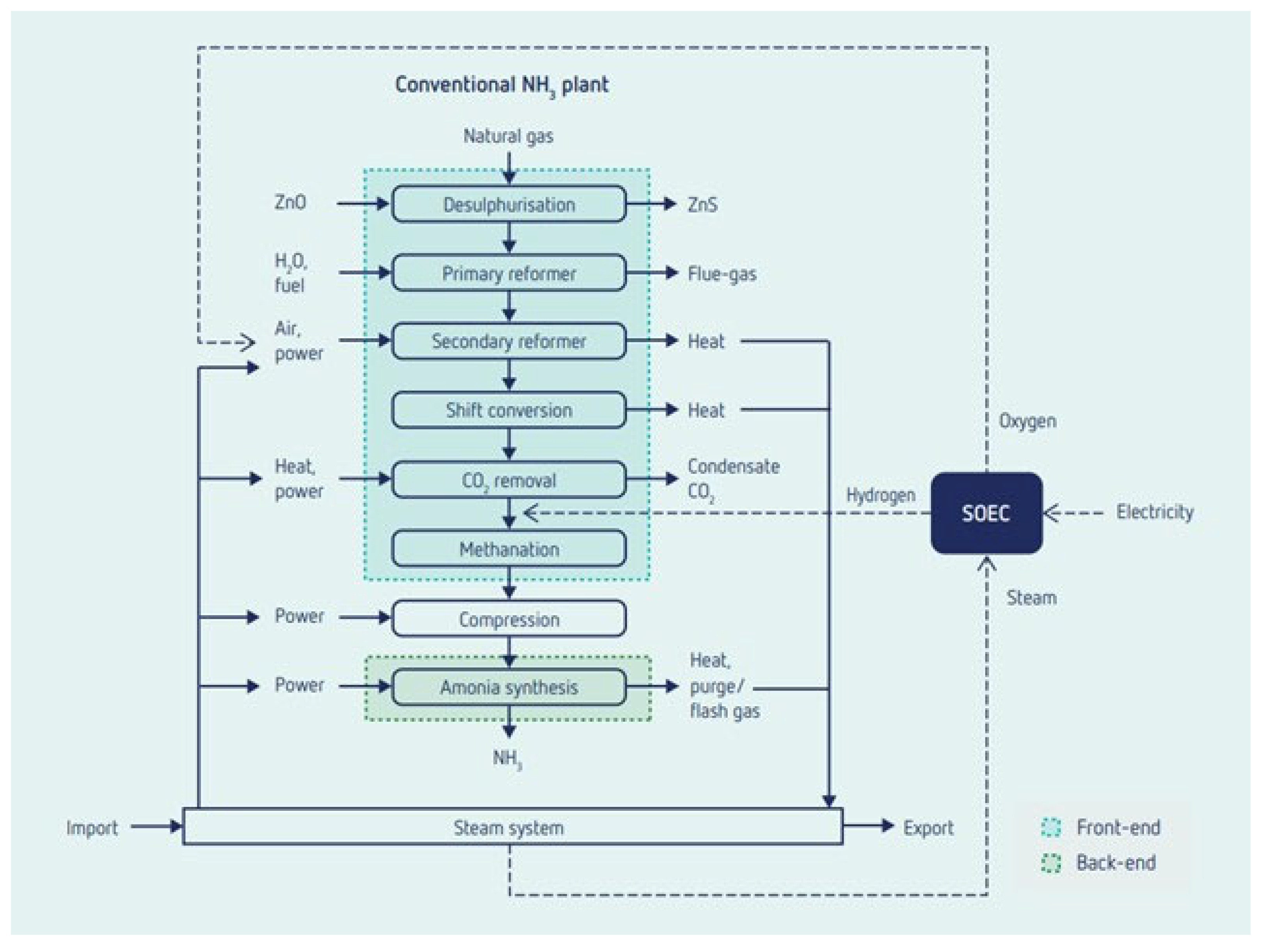

In the Next Level SOE project, the Institute for Sustainable Process Technology (ISPT) and the Netherland Organisation for Applied Scientific Research (TNO) have performed a feasibility study on SOEC for the production of hydrogen in an ammonia plant at OCI Chamelot site in the Netherlands [46]. As known ammonia synthesis occurs through the Haber-Bosch reaction:

N2 + 3H2 ⇆ 2NH3

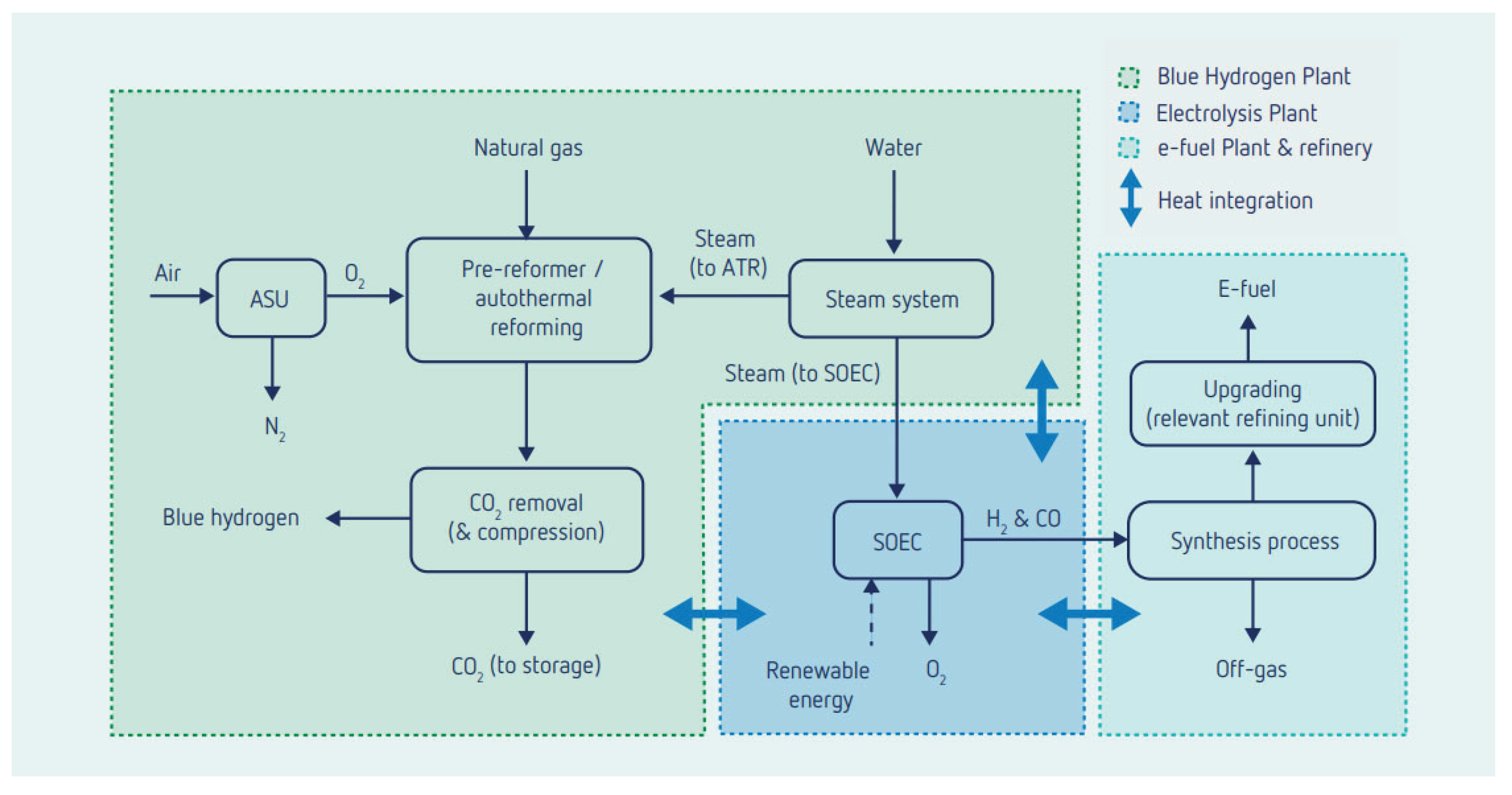

Within an ammonia production facility, the green hydrogen generated by a Solid Oxide Electrolyzer Cell (SOEC) system can be blended with hydrogen derived from conventional synthesis gas prior to the ammonia synthesis loop (Figure 15). A further benefit is the potential use of the co-produced oxygen to enhance the efficiency of the steam reforming process, while waste heat from the plant can be utilized to support the high-temperature operations of the SOEC. The commercial viability of this specific application is gaining significant traction, as evidenced by the Danish company First Ammonia's plans to deploy a 500 MW SOEC electrolyzer, supplied by the Danish firm Topsoe, at its Herning facility. This large-scale project is scheduled to commence operations within the next few years, serving as a critical demonstration before planned future expansion [47].

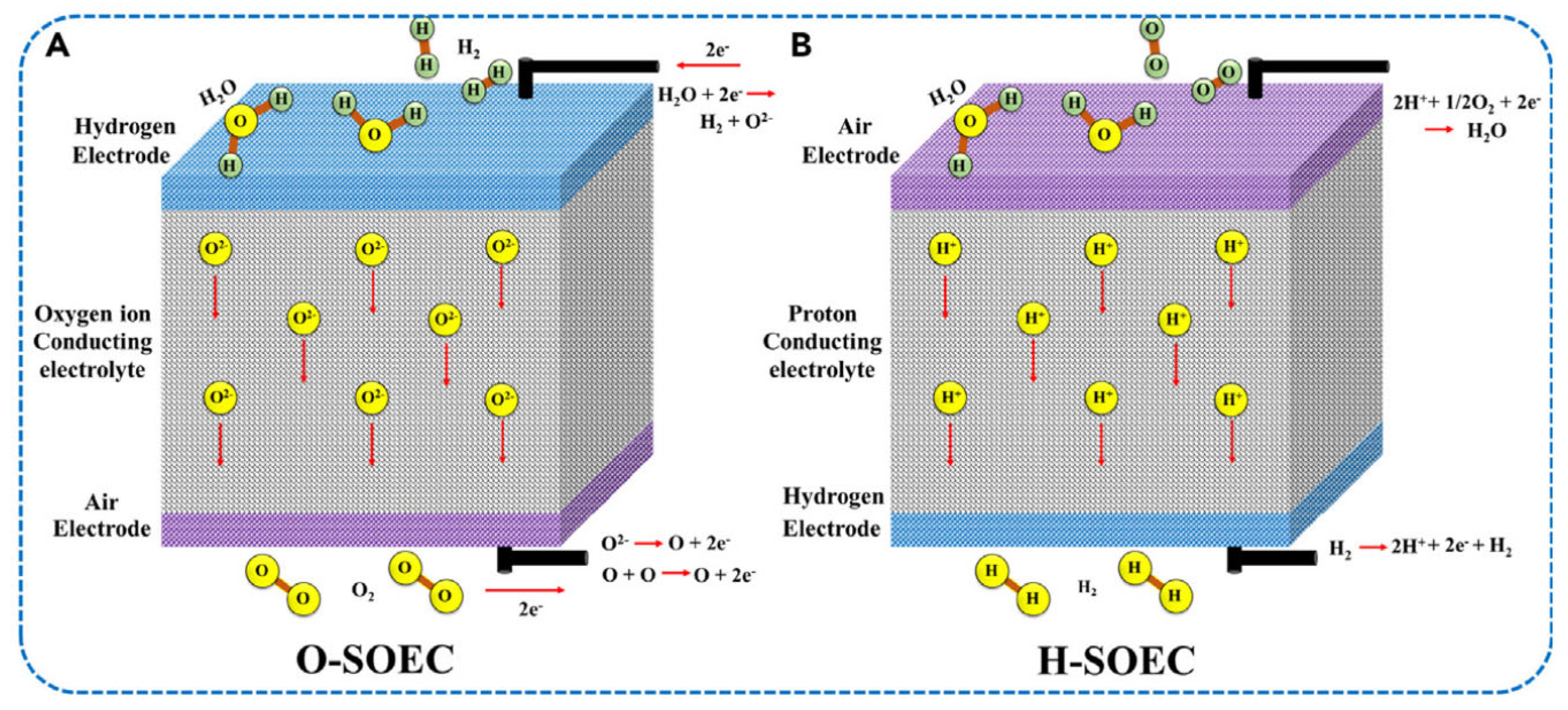

Solid Oxide Electrolysis Cell (SOEC) technology offers a distinct advantage in the field of carbon dioxide (CO₂) valorization. Electrochemical CO₂ reduction is currently pursued through two primary pathways: low-temperature conversion (operating between -20°C and 200°C) using Alkaline (ALK) or Proton Exchange Membrane (PEM) electrolyzers, and high-temperature conversion (operating between 600°C and 1000°C) utilizing SOECs. The high-temperature approach inherent to SOECs demonstrates superior performance metrics, including enhanced current density, greater energy efficiency, and improved operational stability. Research in this area focuses on two main SOEC configurations: those employing oxygen ion-conducting electrolytes (O-SOEC) and those based on proton-conducting electrolytes (H-SOEC), as depicted in Figure 16. These two systems facilitate different electrochemical reactions at the cathode and anode during the high-temperature CO₂ electrolysis process.

The underlying electrochemical mechanisms differ significantly between the two SOEC configurations. In an oxygen ion-conducting electrolyte (O-SOEC), carbon dioxide molecules at the cathode gain electrons, resulting in the formation of carbon monoxide and oxygen ions (Equation 11). These oxygen ions then migrate through the electrolyte membrane to the anode, where they release electrons to form oxygen gas (Equation 12).

Conversely, in a system with a proton-conducting electrolyte (H-SOEC), the CO₂ conversion process is coupled with water electrolysis. When powered by renewable energy, this co-electrolysis simultaneously generates green hydrogen. The process initiates at the anode, where water molecules are oxidized, producing oxygen gas and protons (Equation 13). These protons then diffuse through the electrolyte to the cathode. Upon arrival, they acquire electrons and subsequently react with CO₂ molecules, facilitating their reduction into valuable products like carbon monoxide or other hydrocarbons (Equations 14–17).

CO2 + 2e-→CO + O2-

O2-→1/2O2 + 2e-

H2O →2H+ + 1/2O2 +2e-

2H+ + 2e-→H2

CO2 + 2H+ + 2e-→CO + H2O

CO2+ 8H+ + 8e-→CH4 +2H2O

CO2 +6H+ + 6e-→CH3OH + H2O

The chemical outputs derived from CO₂ electrolysis are broadly classified as either single-carbon (C1) or multi-carbon (C2+) molecules [49]. C1 products are generally simpler to produce and frequently act as essential building blocks for synthesizing more complex C2+ compounds [50]. Among the most significant green C1 products are methane (CH₄) and methanol (CH₃OH), generated via Equations 16 and 17, respectively. These substances are highly valued for their roles in chemical manufacturing and energy. Methane is a promising, infrastructure-compatible substitute for fossil fuels, attracting growing attention [51]. Methanol sees extensive use in fuel cells, syngas processing, and as a precursor for synthesizing longer-chain chemicals [52].

The application of SOECs for CO₂ electrolysis has historical roots in 1960s space programs, where it was studied for oxygen production from the Martian atmosphere [53]. Recently, this technology has experienced a resurgence due to its potential to address pressing environmental and energy challenges [51]. This process offers a dual benefit: it utilizes industrial CO₂ as a feedstock, thereby helping to mitigate climate change, and it co-produces sustainable synthesis gas alongside green hydrogen. This creates a unique value proposition with significant potential for the energy transition, enabling the production of sustainable chemical feedstocks and electrofuels (e-fuels), as illustrated in Figure 17.

After half a century of development, great progresses have been made, however, there are still many challenges remained for CO2 electrolysis with high conversion and efficiency.

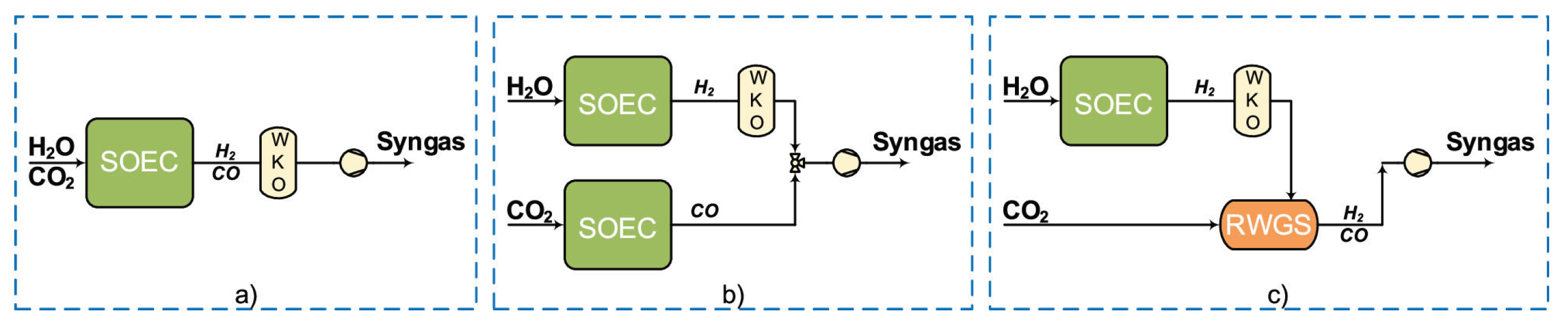

Three routes for syngas production using high-temperature SOCs have been investigated (Figure 18) [54].

In the first route reduction of steam and carbon dioxide occur simultaneously, i.e. so-called coelectrolysis (Figure 18a).

In the second route, steam and carbon dioxide are reduced within two separate electrolyzers, and the produced hydrogen and carbon monoxide are mixed downstream to produce syngas (Figure 18b). The third route involves SOEC only for steam reduction. A reverse water gas shift reactor (RWGS) is used to produce syngas (Figure 18c). This route has the advantage of combining SOEC, which has a low technology readiness level (TRL), with a relatively higher TRL technology, i.e, RWGS.

A comparative assessment of the three syngas production routes reveals that co-electrolysis (Route 1) and the separate electrolysis of steam and CO₂ (Route 2) attain comparable levels of system efficiency. In contrast, the pathway combining steam electrolysis with a reverse water-gas shift reactor (Route 3) was determined to be slightly less efficient, exhibiting a 2-7% lower performance [54].

Beyond efficiency, scaling up SOEC technology presents its own challenges, particularly in manufacturing larger cell areas. These technical and economic factors require careful evaluation by the chemical industry when formulating both near-term and long-term hydrogen and decarbonization strategies. A significant step toward overcoming these hurdles was the inauguration of the first dedicated SOEC pilot production plant on 27 May 2025 in Arnstadt, Thuringia. This facility, a joint venture between the German firm Thyssenkrupp Nucera and the Fraunhofer IKTS research institute, represents a critical milestone in the journey toward the large-scale industrial application of SOEC for decarbonizing key sectors [56].

3.4. Anion Exchange Membrane

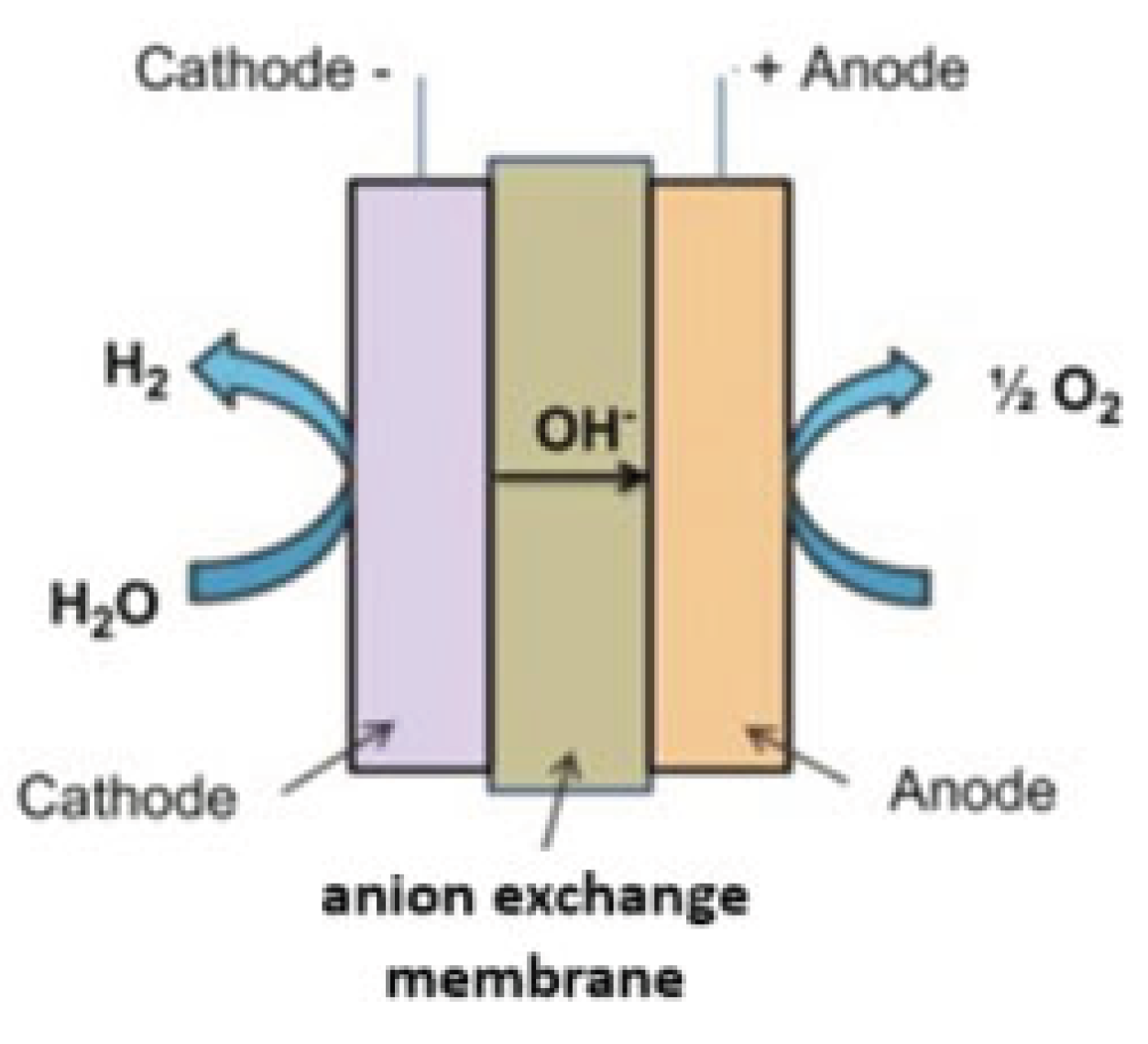

Anion Exchange Membrane (AEM) electrolysis, like Alkaline (ALK) and Proton Exchange Membrane (PEM) systems, is a low-temperature water-splitting technology. Its fundamental distinction from traditional ALK lies in the separator's design. In ALK, a porous diaphragm achieves conductivity by being saturated with a liquid KOH electrolyte, whereas the AEM utilizes a solid, non-porous polymer membrane with inherent anionic conductivity (Figure 19). Research indicates that AEM technology already demonstrates higher efficiency than conventional ALK and can function in high-pH conditions without requiring critical raw materials (CRMs) like platinum and iridium for its oxygen and hydrogen evolution catalysts [57,58,59,60,61].

This architecture confers several key benefits over ALK systems, including operation at elevated current densities due to reduced electrical resistance, the capability for electrochemical hydrogen compression, and enhanced operational safety from the solid, non-porous membrane. Compared to PEM electrolysis, AEM's advantages include a diminished reliance on CRMs across the entire bill of materials and a lower overall environmental footprint throughout the product lifecycle. A significant differentiator is AEM's avoidance of fluorinated polymers, which the European Commission is moving to restrict, thereby mitigating future regulatory risk [62,63].

Despite these promising advantages, AEM remains an emerging technology confronting significant developmental challenges, particularly concerning long-term operational stability and the need for further efficiency improvements.

Significant public and private initiatives are actively working to advance AEM technology. The EU-backed HYScale project (2023-2027) is focused on scaling AEM electrolysis to the megawatt level and beyond to facilitate large-volume green hydrogen generation [64]. A central aim is to optimize and scale up the manufacturing of core components—membranes, ionomers, electrodes, and stacks—to the 100 kW level. The final integrated system will undergo industrial testing and validation at Technology Readiness Level (TRL) 5 to hasten its path to market. By forgoing critical raw materials and implementing innovative designs, the project targets a 50% cost reduction to 400 €/kW, aiming for a hydrogen production cost under 3 €/kg, thereby accelerating its use for energy storage and decarbonization.

Another key effort is the AEM-HUB, a cluster of three projects (Anione, Channel, Newely) funded by the Fuel Cells and Hydrogen Joint Undertaking (FCH JU) with the shared objective of progressing AEM technology [65]. The Anione project seeks to validate a 2 kW AEM electrolyzer with an output of roughly 0.4 Nm³/h. The Channel project is dedicated to constructing a cost-effective 2 kW unit optimized for dynamic operation with renewables. The Newely project aims to build and test a 2 kW, 5-cell AEM stack prototype using hydraulic compression and novel components designed for enhanced performance and durability.

In the commercial sphere, Enapter's AEM Nexus project has launched the world's first megawatt-scale AEM electrolyzer [66]. A prototype is currently operational in Saerbeck, Germany, where its operating concept is being refined. Enapter will supply four of these units (totaling 4 MW) for the Falconara Hydrogen project in Italy, a significant venture for the country's energy transition and local economic development [67]. This project, managed by the joint venture Opificio Idrogeno Marche, plans to convert dormant industrial areas into a thriving 'Hydrogen Valley'. A subsequent phase will involve a 30 MW agrivoltaics plant, supported by a dedicated 7.8 MWp solar array, to power the electrolyzers for clean mobility applications.

Furthermore, the IANUS project, led by Ansaldo Green Tech, is concentrated on the development and industrial manufacturing of innovative AEM electrolyzers, involving an expansion of its research laboratories in Genova [68]. As part of a larger European IPCEI, this project seeks to accelerate the energy transition by establishing hydrogen as a cornerstone of a sustainable future through expanded R&D, modular electrolyzer development, and a new production line.

4. Socio-Political Challenges

The REPowerEU strategy establishes ambitious goals not only for domestic green hydrogen output but also for its importation, targeting 10 million tonnes from each source by 2030 [69]. A key instrument for achieving the import target is the European Hydrogen Bank, designed to facilitate market entry for external suppliers. This raises a critical question regarding the origins of this imported hydrogen. North African nations are frequently identified as potential suppliers, yet these regions grapple with inherent challenges, including severe water scarcity and electricity grids that remain heavily dependent on fossil fuels [70,71]. Consequently, a foundational prerequisite for these countries should be the decarbonization of their own power sectors before embarking on large-scale hydrogen production for European export.

While the technical and economic prospects for green hydrogen are considerable, its swift rollout—especially via export-oriented projects in the Global South—introduces profound socio-political risks that could compromise the core tenets of a just energy transition. These concerns are effectively analyzed through the framework of energy justice, which integrates distributive, procedural, and recognition-based dimensions [72,73].

A primary concern is the potential reinforcement of neo-colonial patterns in resource extraction. The EU's import-driven strategy, while enhancing its own energy security and industrial decarbonization [69], risks replicating historical dynamics where raw materials from the Global South are primarily developed for the benefit of the Global North [74,75]. Agreements such as those between Germany and Namibia have faced accusations of "green colonialism," critiqued for prioritizing external market supply over tangible local socio-economic advancement in the producer country [75].

This imbalance directly undermines distributive justice, which focuses on the fair allocation of costs and benefits. A clear manifestation of this is the global disparity in technological ownership and value creation. The entire electrolyzer manufacturing industry is concentrated in the Global North (e.g., France, Germany, USA) [76,77], while the optimal locations for low-cost renewable energy and hydrogen production are often in the less industrialized Global South. This fosters a relationship of technological dependence, potentially confining producer nations to the role of mere raw material exporters without fostering local industrial capacity or skilled job markets, thereby hindering equitable development [78,79].

Large-scale green hydrogen production is inherently resource-intensive, requiring massive inputs of water, renewable energy (which could be directed toward local electrification), and land. The electrolysis process itself consumes an estimated 9 to 35 litres of pure water per kilogram of hydrogen [80,81]. In water-scarce prospective export hubs like Morocco or Namibia, diverting precious freshwater or expensive desalinated water for hydrogen destined for Europe presents a serious ethical dilemma. When local communities lack secure water access, prioritizing its use for export can intensify existing inequities and violate distributive justice by depriving populations of a vital resource [82,83].

Furthermore, many nations on the EU's list of potential suppliers have not yet significantly decarbonized their own economies. For instance, renewable sources contributed less than 1% of electricity in most Gulf states in 2022 (with the UAE at 4.5% being an exception). As highlighted by Algerian researchers, it seems more logical and equitable for these countries to prioritize their own domestic energy transitions rather than exporting green hydrogen while continuing to rely on fossil fuels at home [84]. This perspective is echoed by over 500 African civil society groups, which in a 2023 declaration rejected green hydrogen as a "false solution" for similar reasons.

The extensive land requirements for renewable energy projects to power electrolysis can also lead to community displacement and human rights abuses. Such projects frequently fail to meet the standards of procedural justice, which mandates the fair and meaningful involvement of all stakeholders in decision-making [85,86]. A telling example from within Europe is the failed UK proposal for a hydrogen-heating trial in Whitby. The project was cancelled after residents opposed what they perceived as a top-down, non-transparent decision that treated them like "lab rats" [87,88,89]. This case demonstrates that community resistance can arise anywhere if engagement is inadequate.

This procedural failure is often more acute in the Global South, where indigenous and local communities are routinely marginalized in negotiations. In Namibia, the Nama people have protested a German company's planned port expansion on a sacred site, viewing it as a modern form of colonization [90]. In Colombia's La Guajira region, a key area for wind en ergy development, the indigenous Wayuu people—who suffer the nation's highest poverty rates [91,92]—have seen plans for dozens of wind farms on their ancestral lands proceed without their free, prior, and informed consent. This has triggered widespread protests and the suspension of projects like Enel's Windpeshi [93,94], representing a clear failure of recognition justice. This principle demands respect for the rights, cultures, and identities of all peoples and protection from exploitation [95,96].

The ethical landscape is further complicated in contested territories. A portion of Morocco's projected green hydrogen potential is located in the disputed Western Sahara [97]. Development projects there, such as a power plant in Laayoune, advance without the consent of the Sahrawi people who seek independence, thereby disregarding both procedural and recognition justice and using green projects to legitimize control over the territory.

5. To What Extent Can Low Carbon Hydrogen Complement Green Hydrogen?

The European Commission's strategic vision, outlined in "A hydrogen strategy for a climate-neutral Europe" [14], originally targeted 80 GW of electrolyzer capacity by 2030, split evenly between the EU and its neighboring export regions. However, Germany, the bloc's industrial leader and largest emitter, is encountering significant headwinds despite its ambitious national hydrogen strategy backed by substantial subsidies. Industry executives have recently voiced concerns that the current cost of green hydrogen remains prohibitively high compared to conventional fuels, casting doubt on a central element of the nation's decarbonization plan. This economic reality is pressuring major companies; for instance, Thyssenkrupp has indicated that unless renewable hydrogen becomes more affordable, it may be forced to use fossil fuels at its intended flagship green steel plant in Duisburg [98].

Anticipating such medium-term challenges, the European Commission has formally recognized the necessity of other low-carbon hydrogen sources to facilitate the broader adoption of renewable hydrogen in the future, as noted in its communications [14]. Subsequent policy frameworks, including the REPowerEU plan [16] and the Hydrogen and Gas Market Directive adopted in May 2024, explicitly incorporate provisions for low-carbon hydrogen to act as a transitional bridge [99]. A prominent example of this category is blue hydrogen, produced from natural gas with carbon capture and storage (CCS) [100].

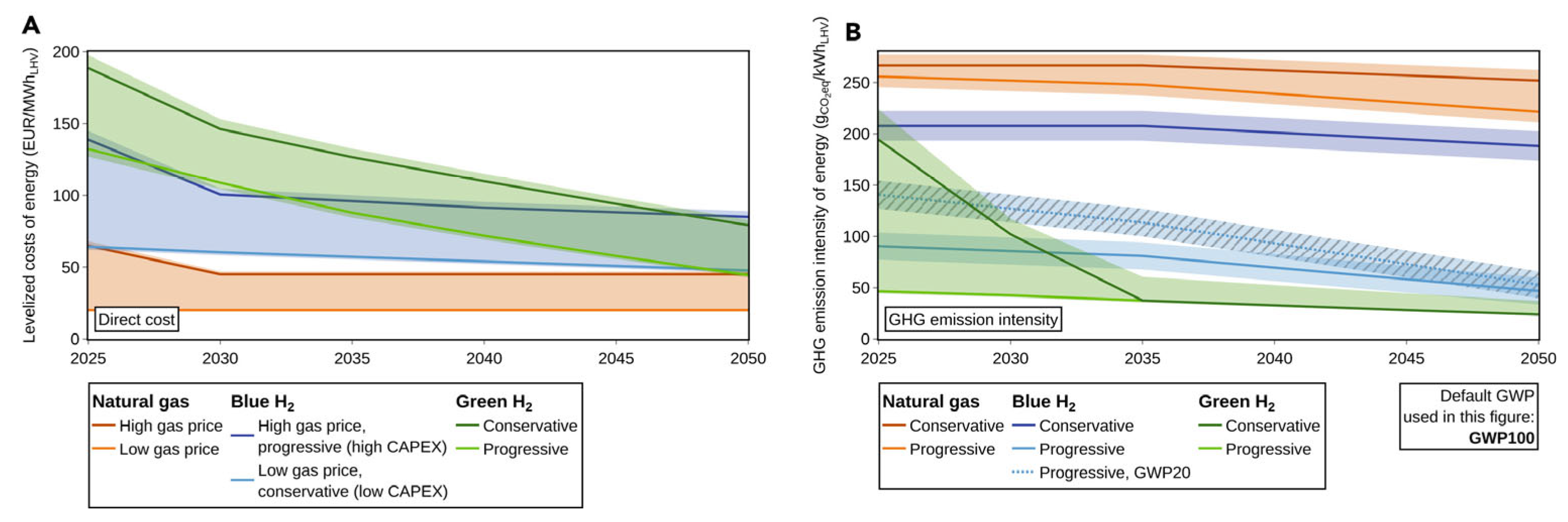

A 2022 case study by George et al. [101] examined the competitiveness of grid-connected green hydrogen produced in Germany against blue hydrogen. The analysis concluded that, under pre-crisis conditions with low gas prices and without fully accounting for methane emissions, blue hydrogen represented the most viable medium-term low-carbon alternative.

A more recent analysis by Ueckerdt et al. [102] highlights a shifting economic landscape. While green hydrogen was significantly more expensive than blue hydrogen before the 2021/22 energy crisis, the subsequent surge in natural gas prices—which are expected to remain elevated in import-dependent Europe—has narrowed this cost differential. As illustrated in Figure 20A, the production cost of blue hydrogen is predominantly dictated by volatile natural gas prices, whereas the cost of green hydrogen is largely a function of its renewable electricity source, specifically whether the electrolyzer is connected to the general grid or directly to a dedicated renewable asset [102]. The greenhouse gas emission profile of blue hydrogen (Figure 20B) is highly variable, influenced by the CO₂ capture rate, methane leakage across the supply chain, and the selected global warming potential (GWP) timeframe [102].

Within their modelling of an advanced blue hydrogen scenario, Ueckerdt and colleagues [102] based their projections on the premise that autothermal reforming (ATR) would achieve widespread commercial deployment. This specific technological pathway is frequently identified in literature as the most appropriate for attaining high net rates of carbon dioxide capture [103,104,105,106].

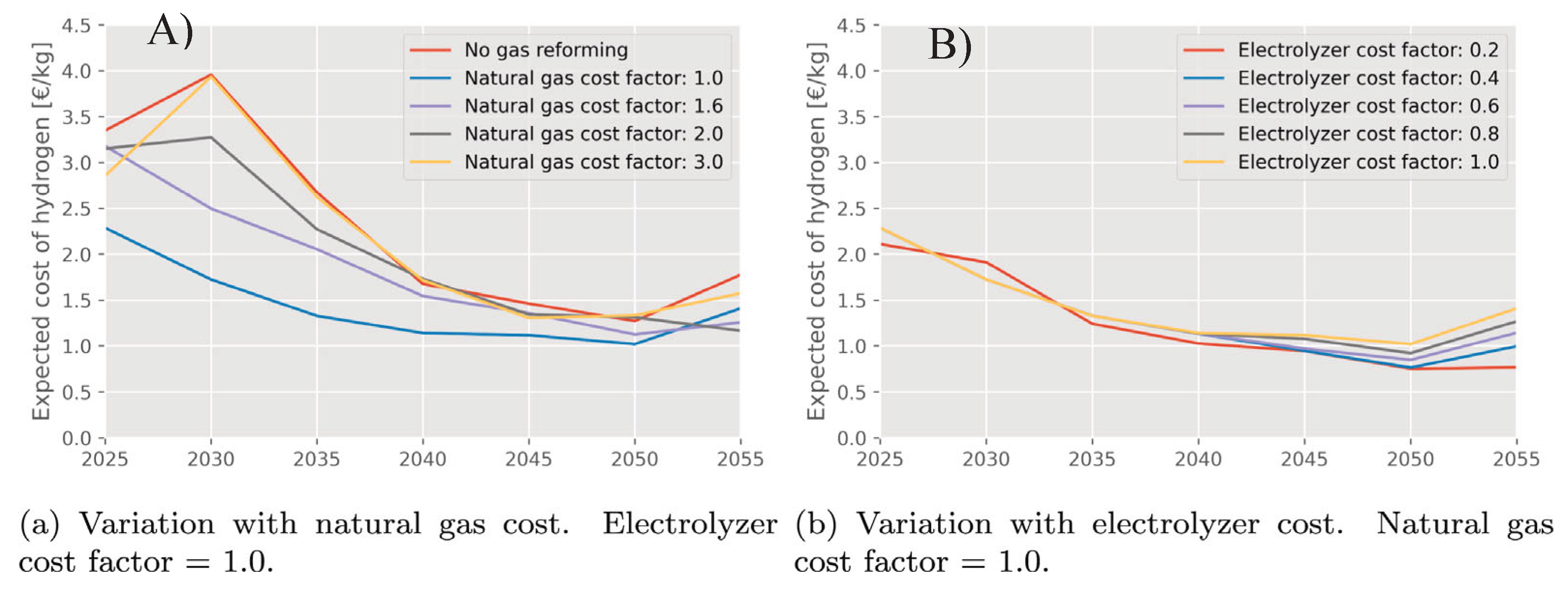

Separate research conducted by Durakovic et al. [107] illustrated the projected trajectory of natural gas pricing within Europe, analysing various potential cost factors for both natural gas and electrolysers (Figure 21 a,b). The study demonstrated that the price of hydrogen is dramatically influenced by the underlying cost of natural gas, as depicted in Figure 21a.

Furthermore, the data in Figure 21b indicates that a substantial reduction in electrolyser costs—approximately 80% from the initial baseline scenario—would be a necessary condition for green hydrogen to emerge as a major supply source within the overall hydrogen market.

6. Conclusions and Outlook

The significant environmental advantages of green hydrogen make it a particularly compelling energy vector. Despite this promise, its widespread potential remains constrained, primarily due to the substantial costs involved. Consequently, numerous European nations, alongside the European Union as a collective entity, are actively evaluating strategies for importing green hydrogen from countries outside the EU.

To facilitate this shift, certain member states like Germany are allocating financial resources to modernise infrastructure, thereby enabling a more seamless transition towards a sustainable energy model. Nonetheless, formidable obstacles extend beyond just production at scale, encompassing the parallel development of efficient storage systems and comprehensive distribution networks.

Within this strategic context, several recent EU-level actions warrant attention. The year 2025 saw the formal establishment of the European Network of Network Operators for Hydrogen (ENNOH). Founded under the EU Hydrogen and Decarbonised Gas Package, this body coordinates collaboration among the EU's Hydrogen Transmission Network Operators (HTNOs). ENNOH's mandate is to concentrate efforts on constructing a dedicated hydrogen infrastructure within the Union and to enable the efficient cross-border transportation of hydrogen [108].

Furthermore, in July 2025, the EU enacted the act “Clarity to hydrogen sector with new EU methodology for low-carbon hydrogen and fuels” [109]. This regulation acknowledges that low-carbon hydrogen, including blue hydrogen, is essential for decarbonising sectors where direct electrification is not currently feasible, such as aviation, maritime shipping, and specific heavy industrial processes. The initiative is designed to support the achievement of the EU's 2050 climate neutrality goal while simultaneously preserving the competitive edge and leadership of the European hydrogen and industrial sectors. Looking forward, the European Commission plans to evaluate how these alternative energy pathways affect the overall energy system and emission reductions, and will consider the necessity of ensuring fair competition with hydrogen sourced from fully renewable electricity. A public consultation on a draft methodology concerning the use of Power Purchase Agreements (PPAs) for nuclear energy is scheduled for 2026, which aims to provide clearer guidelines for producing low-carbon hydrogen using direct nuclear power [109].

References

- Ballentine, CJ; Karolytė, R. ; Cheng, A.; Lollar, B.S.; Gluyas, G.; Daly, M.C. Natural hydrogen resource accumulation in the continental crust. Nature Reviews Earth & Environment 2025, 6, 342–356. [Google Scholar]

- Klein, F.; Tarnas, J.D.; Bach, W. Abiotic sources of molecular hydrogen on Earth, Elements 2020, 16, 19–24.

- https://www.oxfordenergy.org/wpcms/wp-content/uploads/2024/09/ET38-Natural-geologic-hydrogen-and-its-potential-role-in-a-net-zero-carbon-future.pdf accessed on 13 September 2025.

- https://www.wired.com/story/gold-hydrogen/. (accessed on 13 September 2025).

- https://climate.mit.edu/ask-mit/how-clean-green-hydrogen. (accessed on 8 September 2025).

- Alabbadi, A.A.; AlZahrani, A.A. Nuclear hydrogen production using PEM electrolysis integrated with APR1400 power plant. Int J Hydrogen Energy 2024, 60, 241–260. [Google Scholar] [CrossRef]

- Global Hydrogen review, 2024 available at: www.iea.org.

- The Clean Industrial Deal: A joint roadmap for competitiveness and decarbonization. Available online at https://commission.europa.eu/document/download/9db1c5c8-9e82-467b-ab6a-905feeb4b6b0_en. (accessed on 03 March 2025).

- A Clean Industrial Deal for competitiveness and decarbonisation in the EU. Available online at https://ec.europa.eu/commission/presscorner/detail/en/ip_25_550. (accessed on 03 March 2025).

- Bettenhausen, C. Green hydrogen is still making gains. Chemical & Engineering News, 8 May 2025.

- Ajanovic, A.; Sayer, M.; Haas, R. On the future relevance of green hydrogen in Europe. Applied Energy 2024, 358, 122586. [Google Scholar] [CrossRef]

- Groll, M. Can climate change be avoided? Vision of a hydrogen-electricity energy economy. Energy 2023, 264, 126029. [Google Scholar] [CrossRef]

- https://www.clean-hydrogen.europa.eu/about-us/our-story_en#:~:text=2002%20%2D%202004,on%20the%20clean%20energy%20map. (accessed on 09 September 2025).

- https://energy.ec.europa.eu/system/files/2020-07/hydrogen_strategy_0.pdf. (accessed on 09 September 2025).

- https://energy.ec.europa.eu/topics/eus-energy-system/hydrogen_en. (accessed on 09 September 2025).

- https://commission.europa.eu/topics/energy/repowereu_en. (accessed on 09 September 2025).

- [17] https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52023DC0156&qid=1682349760946. (accessed on 09 September 2025).

- Buonomenna, MG. Inorganic thin-film solar cells: Challenges at the terawatt-scale. Symmetry 2023, 159, 1718. [Google Scholar] [CrossRef]

- Danish Energy Agency, Energinet. Technology data for renewable fuels. Tech. rep., 2023, available online at http://www.ens.dk/teknologikatalog.

- Proost, J. State-of-the art CAPEX data for water electrolysers, and their impact on renewable hydrogen price settings. Int. J. Hydrog. Energy 2019, 44, 4406–4413. [Google Scholar] [CrossRef]

- Guillet, N. , Millet, P. Alkaline Water Electrolysis. In Hydrogen Production; Wiley-VCH 2015; pp 117−166, ISBN: 9783527333424.

- Tüysüz, H. Alkaline Water Electrolysis for Green Hydrogen Production Acc. Chem. Res. 2024, 57, 558–567.

- Santoro, C.; Lavacchi, A.; Mustarelli, P.; Di Noto, V.; Elbaz, L.; Dekel, D.R.; Jaouen, F. What is Next in Anion-Exchange Membrane Water Electrolyzers? Bottlenecks, Benefits, and Future. ChemSusChem 2022, 15, e202200027. [Google Scholar] [CrossRef]

- Hassan, A.; Abdel-Rahim, O.; Bajaj, M.; Zaitsev, I. Power electronics for green hydrogen generation with focus on methods, topologies, and comparative analysis. Scientific Reports 2024, 14, 24767. [Google Scholar] [CrossRef]

- [25] a) https://www.offshore-energy.biz/worlds-largest-green-hydrogen-plant-construction-reaches-80-completion/ accessed on 09 September 2025. b) https://nghc.com/.

- https://www.energiser.pt/en/forward/2023-10-04-Green-hydrogen-picks-up-pace-in-Portugal-28614f9a#:~:text=Galp%20has%20been%20increasingly%20involved,to%20commence%20operations%20in%202025 accessed on 09 September 2025.

- https://www.aman-alliance.org/Home/ContentDetail/87785. (accessed on 09 September 2025).

- https://www.portugal.gov.pt/en/gc23/communication/news-item?i=portuguese-green-energy-corridor-projects-have-a-european-seal-of-common-interest. (accessed on 09 September 2025).

- a) https://greenhyscale.eu/wp-content/uploads/2023/04/UK_Denmarks-first-large-scale-electrolyser-module-delivered.pdf.(accessed on 09 September 2025). b) Andreae, E.; Fan, Y.F.; Petersen, M.; You, S.; Bindner, H.W.; Jacobson. M. Z. Green hydrogen production pathways: Comparative insights from Denmark, the U.S., and China. Energy Conversion and Management 2025, 342, 120065.

- [30] Biswas, S.; Kulkarni, A.P.; Giddey, S.; Bhattacharya, S. A Review on Synthesis of Methane as a Pathway for Renewable Energy Storage With a Focus on Solid Oxide Electrolytic Cell-Based Processes. Frontiers in Energy Research 2020, 8, 570112. [Google Scholar] [CrossRef]

- https://fuelcellsworks.com/2025/01/23/fuel-cells/freija-unveils-plan-for-one-of-europe-s-largest-major-green-hydrogen-based-e-methane-facility-in-nokia-norway. (accessed on 09 September 2025).

- https://www.offshore-energy.biz/mol-group-opens-10-mw-green-hydrogen-plant-in-hungary/. (accessed on 09 September 2025).

- https://arcadiaefuels.com/arcadia-efuels-taps-plug-power-for-280-mw-electrolyzer-system/. (accessed on 09 September 2025).

- https://fuelcellsworks.com/news/galp-announces-launch-of-a-major-100-mw-electrolysis-plant-in-portugal. (accessed on 09 September 2025).

- https://www.spglobal.com/commodity-insights/en/news-research/latest-news/energy-transition/061024-yara-starts-up-europes-largest-green-hydrogen-plant-in-norway. (accessed on 09 September 2025).

- https://www.yara.com/corporate-releases/yara-opens-renewable-hydrogen-plant-a-major-milestone/. (accessed on 09 September 2025).

- https://www.shell.com/what-we-do/hydrogen/latest-news-from-shell-hydrogen/shell-to-build-100-megawatt-renewable-hydrogen-electrolyser-in-germany.html. (accessed on 9 September 2025).

- https://www.basf.com/global/en/media/news-releases/2025/03/p-25-046. (accessed on 9 September 2025).

- https://bebeez.eu/2025/03/20/nel-asa-receives-purchase-order-for-one-mc500-containerized-pem-electrolyser/. (accessed on 09 September 2025).

- https://nelhydrogen.com/wp-content/uploads/2020/03/Renewable-hydrogen-made-cost-competitive.pdf. (accessed on 9 September 2025).

- https://www.h2-view.com/story/hydrasun-selects-2-5mw-nel-electrolyser-for-aberdeen-hydrogen-hub/2123272.article/. (accessed on 9 September 2025).

- Buonomenna, MG. Proton-Conducting Ceramic Membranes for the Production of Hydrogen via Decarbonized Heat: Overview and Prospects. Hydrogen 2023, 4, 807–830. [Google Scholar] [CrossRef]

- a) https://multiplhy-project.eu/Documents/Workshop%20on%20Advanced%20PtG%20and%20PtL%20Technologies%20High-Temperature%20Electrolysis_Posdziech.pdf (accessed on 14 September 2025). b) Wu, C.; Zhu, Q.; Dou, B.; Fu, Z.; Wang, J.; Mao, S. Thermodynamic analysis of a solid oxide electrolysis cell system in thermoneutral mode integrated with industrial waste heat for hydrogen production. Energy 2024, 301, 131678.

- https://salcos.salzgitter-ag.com/en/index.html. (accessed on 09 September 2025).

- https://syrius-project.eu/project/. (accessed on 09 September 2025).

- Next level Solid Oxide electrolysis by Institute for Sustainable Process Technology available at https://ispt.eu/media/20230508-FINAL-SOE-public-report-ISPT.pdf. (accessed on 9 September 2025).

- https://www.topsoe.com/press-releases/topsoe-and-first-ammonia. (accessed on 09 September 2025).

- Hanif, M.B.; Rauf, S.; Abadeen,Z. ; Khan, K.; Tayyab, Z.; Qayyum,S.; Mosiałek, M.; Shao, Z.; Li, C.X.; Motola, M. Proton-conducting solid oxide electrolysis cells: Relationship of composition-structure-property,their challenges, and prospects. Matter 2023, 6, 1782–1830. [Google Scholar] [CrossRef]

- Choi, W.; Choi, Y.; Choi, E.; Yun, H.; Jung, W.; Lee, W.H.; Oh, H.-S.; Won, D.H.; Na, J.; Hwang, Y.J. ; Microenvironments of Cu catalysts in zero-gap membrane electrode assembly for efficient CO2 electrolysis to C2+ products. J. Mater. Chem. A 2022, 10, 10363–10372. [Google Scholar] [CrossRef]

- Cheon, H.; Kim, J.H.; Kim, J.S.; Park, J.-B. Valorization of single-carbon chemicals by using carboligases as key enzymes. Curr. Opin. Biotechnol. 2024, 85, 103047. [Google Scholar] [CrossRef] [PubMed]

- Berberich, M.E.; Beaulieu, J.J.; Hamilton, T.L.; Waldo, S.; Buffam, I. Spatial variability of sediment methane production and methanogen communities within a eutrophic reservoir: Importance of organic matter source and quantity. Limnol. Oceanogr. 2023, 65(6), 1–23. [Google Scholar] [CrossRef] [PubMed]

- Bube, S.; Sens, L.; Drawer, C.; Kaltschmitt, M. Power and biogas to methanol – A techno-economic analysis of carbon-maximized green methanol production via two reforming approaches. Energy Convers. Manag. 2024, 304, 118220. [Google Scholar] [CrossRef]

- Cheon, H.; Kim, J.H.; Kim, J.-S.; Park, J.-. BValorization of single-carbon chemicals by using carboligases as key enzymes. Curr. Opin. Biotechnol. 2024, 85, 103047. [Google Scholar] [CrossRef]

- Gupta, S.; Riegraf, M.; Costa, R.; Heddrich, M.P.; Friedrich, K.A. Solid Oxide Electrolysis Cell-Based Syngas Production and Tailoring: A Comparative Assessment of Coelectrolysis, Separate Steam, CO2 Electrolysis, and Steam Electrolysis. Ind. Eng. Chem. Res. 2024, 63, 8705–8712. [Google Scholar] [CrossRef]

- Strategic Research And Innovation Agenda 2021−2027, Clean Hydrogen Joint Undertaking; 2022 available at https://www.clean-hydrogen.europa.eu/system/files/2022-02/Clean%20Hydrogen%20JU%20SRIA%20-%20approved%20by%20GB%20-%20clean%20for%20publication%20%28ID%2013246486%29.pdf. (accessed on 09 September 2025).

- https://www.thyssenkrupp-nucera.com/thyssenkrupp-nucera-and-fraunhofer-ikts-open-first-soec-pilot-production-plant-for-stacks-for-the-production-of-green-hydrogen/. (accessed on 09 September 2025).

- Serov, A.; Kovnir, K.; Shatruk, M.; Kolen’ko, Y.V. Critical Review of Platinum Group Metal-Free Materials for Water Electrolysis: Transition from the Laboratory to the Market. Johnson Matthey Technol. Rev. 2021, 65, 207–226. [Google Scholar] [CrossRef]

- Jin, H.; Ruqia, B.; Park, Y.; Kim, H.J.; Oh, H.-S.; Choi, S.-I.; Lee, K. Nanocatalyst Design for Long-Term Operation of Proton/Anion Exchange Membrane Water Electrolysis. Adv. Energy Mater. 2021, 11, 2003188. [Google Scholar] [CrossRef]

- Ďurovič, M.; Hnat, J.; Bouzek, K. Electrocatalysts for the hydrogen evolution reaction in alkaline and neutral media. A comparative review. J. Power Sources 2021, 493, 229708. [Google Scholar] [CrossRef]

- Mahmood, N.; Yao, Y.; Zhang, J.-W.; Pan, L.; Zhang, X.; Zou, J.-J. Electrocatalysts for Hydrogen Evolution in Alkaline Electrolytes: Mechanisms, Challenges, and Prospective Solutions. Adv. Sci. 2018, 5, 1700464. [Google Scholar] [CrossRef]

- Baek, D.S.; Lee, J.; Lim, J.S.; Joo, S.H. Nanoscale electrocatalyst design for alkaline hydrogen evolution reaction through activity descriptor identification. Mater. Chem. Front. 2021, 5, 4042–4058. [Google Scholar] [CrossRef]

- https://cen.acs.org/environment/persistent-pollutants/say-goodbye-PFAS/97/i46. (accessed on 14 September 2025).

- Cousins, I.T.; Goldenman, G.; Herzke, D.; Lohmann, R.; Miller, M.; Ng, C.A.; Patton, S.; Scheringer, M.; Trier, X.; Vierke, L.; Wang, Z.; DeWittl, J.C. The concept of essential use for determining when uses of PFASs can be phased out. Environ. Sci. Process. Impacts 2019, 21, 1803–1815. [Google Scholar] [CrossRef]

- https://cordis.europa.eu/project/id/101112055/reporting#:~:text=The%20HYScale%20project%20is%20a,hydrogen%20technology%20innovation%20and%20deployment. (accessed on 14 September 2025).

- https://www.sintef.no/projectweb/channel-fch/aem-hub/#:~:text=The%20AEM%2DHUB%20is%20a%20cluster%20of%20three,water%20electrolysers%20(AEMEL)%20for%20green%20hydrogen%20production. (accessed on 14 September 2025).

- https://enapter.com/en/product/aem-nexus/. (accessed on 14 September 2025).

- https://fuelcellsworks.com/2025/03/13/electrolyzer/fallback-thursday-enapter-to-supply-aem-nexus-electrolysers-for-falconara-hydrogen-project-in-italy. (accessed on 14 September 2025).

- https://www.hydrogeninsight.com/innovation/italy-grants-317m-to-state-owned-company-to-build-aem-hydrogen-electrolysers/2-1-1784205. (accessed on 14 September 2025).

- European Commission. REPowerEU. Available from: https://commission.europa.eu/topics/energy/repowereu_en. (accessed on 14 September 2025).

- European Investment Bank. A pipeline to better lives Available from: https://www.eib.org/en/stories/morocco-water-scarcity. (accessed on 14 September 2025).

- Voice of America. Morocco expands freshwater efforts, but needs more energy. Available from: https://learningenglish.voanews.com/a/morocco-expands-freshwater-efforts-but-needs-more-energy/6844012.html. (accessed on 14 September 2025).

- Jenkins, K.; McCauley, D.; Heffron, R.; Stephan, H.; Rehner, R. Energy justice: A conceptual framework. Energy Res Soc Sci 2021, 75, 101–112. [Google Scholar]

- Muller, M.; et al. Hydrogen and justice: A framework for assessing the social impacts of hydrogen production. Energy Res Soc Sci 2023, 90, 102–115. [Google Scholar]

- Corporate Europe Observatory. Hydrogen from North Africa – a neo-colonial resource grab. Available from: https://corporateeurope.org/en/2022/05/hydrogen-north-africa-neocolonial-resource-grab (accessed on 14 September 202).

- Skládalová, D. Unmasking green colonialism in EU-Namibia hydrogen deal. Available from: https://www.ejiltalk.org/unmasking-green-colonialism-in-eu-namibia-hydrogen-deal/. (accessed on 14 September 2025).

- CIC energiGUNE. Electrolyzers: A manufacturing industry that everyone wants to lead [Online]. Available from: https://cicenergigune.com/en/blog/electrolyzers-manufacturing-industry-everyone-lead; (Accessed on 14 September 2025).

- Blackridge Research and Consulting. Global top 20 hydrogen electrolyzer manufacturers . Available from: https://www.blackridgeresearch.com/blog/list-of-global-top-hydrogen-electrolyzer-manufacturers-companies-makers-suppliers-in-the-world (Accessed on 14 September 2025).

- Dillman, K.J.; Heinonen, J. A ‘just’ hydrogen economy: a normative energy justice assessment of the hydrogen economy. Renew Sustain Energy Rev 2022, 167, 112648. [Google Scholar] [CrossRef]

- Dembi, V. Ensuring energy justice in transition to green hydrogen. Available from: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4015169 Accessed on 14 September 2025.

- Europe Hydrogen. Hydrogen production & water consumption [Online]. Available from: https://hydrogeneurope.eu/wp-content/uploads/2022/02/Hydrogen-production-water-consumption_fin.pdf (Accessed on 14 September 2025).

- International PtX Hub. A first look at water demand for green hydrogen and concerns and opportunities with desalination. Available from: https://ptx-hub.org/a-first-look-at-water-demand-for-green-hydrogen-and-concerns-and-opportunities-with-desalination/ (Accessed on 14 September 2025).

- Ourya, I.; Nabil, N.; Abderafi, S.; Boutammachte, N.; Rachidi, S. Assessment of green hydrogen production in Morocco, using hybrid renewable sources (PV and wind). Int J Hydrogen Energy 2023, 48, 37428–37442. [Google Scholar] [CrossRef]

- EU’s clean hydrogen plan raises dirty doubts Available from: https://www.politico.eu/article/eu-clean-hydrogen-plan-doubts/ (Accessed on 14 September 2025).

- Walker, G. Beyond distribution and proximity: Exploring the multiple spatialities of environmental justice. Antipode 2009, 41, 614–634. [Google Scholar] [CrossRef]

- Schlosberg, D. The justice of environmental justice: Reconciling equity, recognition, and participation in a political movement. In: Light A, De-Shalit A, editors. Moral and political reasoning in environmental practice. London, UK: MIT Press; 2003. p. 125–156.

- BBC. Hydrogen heating trial treats us like guinea pigs – residents. Available from: https://www.bbc.com/news/science-environment-64028510 (Accessed on 14 September 2025).

- ‘We’ve got no choice’: Locals fear life as lab rats in UK hydrogen heating pilot Available from: https://www.theguardian.com/environment/2022/nov/21/no-choice-hydrogen-heating-pilot-whitby-ellesmere-port-lab-rats (Accessed on 14 September 2025).

- Energy Institute. UK government rejects Whitby hydrogen village trial. Available from: https://knowledge.energyinst.org/new-energy-world/article?id=138075 (Accessed on 14 September 2025).

- Voice of America. Namibia’s Nama community rejects green-hydrogen port expansion. Available from: https://www.voanews.com/a/namibia-s-nama-community-rejects-green-hydrogen-port-expansion-/7574111.html (Accessed on 14 September 2025).

- Future Power Technology. La Guajira: The renewable centre tearing itself apart over wind. Available from: https://power.nridigital.com/future_power_technology_aug23/guajira-colombia-development-wayuu-enel-wind (Accessed on 14 September 2025).

- Latina Pensa. Colombian Government to solve vulnerabilities in La Guajira. Available from: https://www.plenglish.com/news/2023/06/24/colombian-government-to-solve-vulnerabilities-in-la-guajira/ (Accessed on 14 September 2025).

- Wind energy and Wayuu Indigenous communities: Challenges in La Guajira. Available from: https://www.sei.org/features/wind-energu-wayuu-la-guajira/ (Accessed on 14 September 2025).

- ReCharge. ‘This hurts us’. Enel suspends Colombia wind farm build as years of protests take toll. Available from: https://www.rechargenews.com/wind/this-hurts-us-enel-suspends-colombia-wind-farm-build-as-years-of-protests-take-toll/2-1-1456238 (Accessed on 14 September 2025).

- Bullard RD. Environmental justice in the 221st century. In: Dryzek J, Schlosburg D, editors. Debating the earth. Oxford, UK: Oxford University Press; 2005. p. 322–356.

- Davies, A. Environmental justice as subtext or omission: Examining discourses of anti-incineration campaigning in Ireland. Geoforum 2006, 37, 708–724. [Google Scholar] [CrossRef]

- McSheffrey, E. Northwest first nations join forces to pursue renewable energy in B.C. Available from: https://globalnews.ca/news/10076258/first-nations-renewable-energy-bc/ (Accessed on 09 September 2025).

- WSRW. Greenwashing occupation. Available from: https://vest-sahara.s3.amazonaws.com/wsrw/feature-images/File/405/616014d0c1f1d_Greenwashing-occupation_web.pdf (Accessed on 09 September 2025).

- Expensive ‘green’ hydrogen jeopardises German industrial energy transition Available from https://www.ft.com/content/bc4e49d6-ac89-4835-80dd-87663de0cfd1 (Accessed on 09 September 2025).

- https://energy.ec.europa.eu/topics/markets-and-consumers/hydrogen-and-decarbonised-gas-market_en (Accessed on 09 September 2025).

- https://ec.europa.eu/commission/presscorner/detail/en/ip_25_1743 (Accessed on 09 September 2025).

- George, J.F.; Muller, V.P.; Winkler, J.; Ragwitz, M. Is blue hydrogen a bridging technology? - the limits of a CO2 price and the role of state-induced price components for green hydrogen production in Germany. Energy Policy 2022, 167, 113072. [Google Scholar] [CrossRef]

- Ueckerdt, F.; Verpoort, P.C.; Anantharaman, R.; Bauer, C.; Beck, F.; Longden, T.; Roussanaly, S. On the cost competitiveness of blue and green hydrogen. Joule 2024, 8, 104–128. [Google Scholar] [CrossRef]

- Bauer, C.; Treyer, K.; Antonini, C.; Bergerson, J.; Gazzani, M.; Gencer, E.; Gibbins, J.; Mazzotti, M.; McCoy, S.T.; McKenna, R.; et al. On the climate impacts of blue hydrogen production. Sustainable Energy Fuels 2021, 6, 66–75. [Google Scholar] [CrossRef]

- Oni, A.O.; Anaya, K.; Giwa, T.; Di Lullo, G.; Kumar, A. Comparative assessment of blue hydrogen from steam methane reforming, autothermal reforming, and natural gas decomposition technologies for natural gasproducing regions. Energy Convers. Manag. 2022, 254, 115245. [Google Scholar] [CrossRef]

- Antonini, C.; Treyer, K.; Streb, A.; van der Spek, M.; Bauer, C.; Mazzotti, M. Hydrogen production from natural gas and biomethane with carbon capture and storage—A techno-environmental analysis. Sustainable Energy Fuels 2020, 4, 2967–2986. [Google Scholar] [CrossRef]

- Global hydrogen review 2022. Available from https://www.iea.org/reports/global-hydrogen-review-2022 (Accessed on 09 September 2025).

- Durakovic, G.; Crespo del Granado, P.; Tomasgard, A. Are green and blue hydrogen competitive or complementary? Insights from a decarbonized European power system analysis. Energy 2023, 282, 128282. [Google Scholar] [CrossRef]

- https://energy.ec.europa.eu/news/important-step-towards-establishing-european-network-network-operators-hydrogen-2025-05-16_en (Accessed on 14 September 2025).

- https://ec.europa.eu/commission/presscorner/detail/en/ip_25_1743 (Accessed on 14 September 2025).

Figure 1.

The various colors of hydrogen.

Figure 2.

The main milestones towards green hydrogen economy in Europe.

Figure 4.

Electrolyser capacity to reach FID by region [7].

Figure 4.

Electrolyser capacity to reach FID by region [7].

Figure 5.

Expected manufacturing capacity of various types of electrolyzers by the year 2030. On the basis of data reported in [7].

Figure 5.

Expected manufacturing capacity of various types of electrolyzers by the year 2030. On the basis of data reported in [7].

Figure 6.

Schematization of Alkaline Electrolysis.

Figure 7.

NEOM Hydrogen project in Saudi Arabia [25].

Figure 7.

NEOM Hydrogen project in Saudi Arabia [25].