Submitted:

17 May 2023

Posted:

18 May 2023

You are already at the latest version

Abstract

The owners of forests with water protection functions in Bulgaria do not receive compensation for their limited right to use wood and non-wood forest products from the forest areas they own. At the same time, the contribution derived from forests with water protection functions is received by water users and water consumers, whereas the costs of managing the forests are borne by their owners. The problem thus defined is not a forestry one, but an economic one, and the purpose of this paper ensues therefrom, namely to propose and test a methodology for valuating the produc-tion function of forest areas with water protection function in Bulgaria, allowing a fair distribu-tion of income between the forest owner and the user of forest ecosystem services. The methodol-ogy is based on the form of forest management and the analytical expression of the economic rela-tionship between a forest owner and a user of forest ecosystem services, constructed using Schen-rock’s formula. It has been tested with actual data on forest areas with water protection functions falling within the administrative and territorial scope of Velingrad municipality and based on the obtained results proposals have been made for the distribution of the contributions generated by forest ecosystems between the forest owner and the user of the forest ecosystem services.

Keywords:

forest ecosystem services

; rental income

; wood production function of forests

; water protection and regulation function of forests

1. Introduction

The forests with water protection functions in Bulgaria occupy an area of 576,117 ha, which accounts for 7.8% of the country’s forest areas. Of these, 72.64% are state owned, 11.41% - municipality owned, 9.89% - privately owned, and 6.06% under other ownership. The forests with water protection functions accumulate, annually, between 1-1.5 billion m3 of water. These forests, by nature, serve as multi-annual equalizers, generating a steady flow of clean water all year round, which reaches water consumers and water users through the water-supplying infrastructure [32].

In order to obtain this product, forest owners are obliged to manage them under a special regime. Under the water protection regime, the goal is not to obtain wood from the forest, but to manage it in such a way as to maintain and even increase the natural water protection and regulation properties of forest ecosystems. Forest owners would choose to manage their forests as water protection ones as long as they have the opportunity to generate income from this property. However, this type of management is only possible if the water protection properties of forest ecosystems acquire a production function for the forest owner. The funds advanced for the realization of this production function must be protected by institutions in such a way as to allow each forest owner to generate their future income along the water use and water consumption chain. These problems are not forestry, but economic in nature, where the main question associated with every production function should be answered – the question of production efficiency and how the income should be distributed between the owners of the factors of production. In other words, what fair income should the forest owner receive from the water protection function, calculated as a portion of the gross added value created for the country's water sector. The current tying of their income to wood production and wood processing transfers the contributions generated by these forests to the account of water users and water consumers, and the costs associated with these forests remain at the expense of forest owners and organizations that manage them. In relation to the problem thus defined, this study argues that water protection forests should be recognized as capital, and their owners should have the right to generate income from them by recognizing the water protection properties of forests as having a production function. This is precisely what this study aims to address, namely: to propose and test a methodology for valuating the production function of forest areas with water protection functions in Bulgaria, allowing a rational distribution of income between the forest owner and the user of forest ecosystem services.

2. Materials and Methods

2.1. Study Area

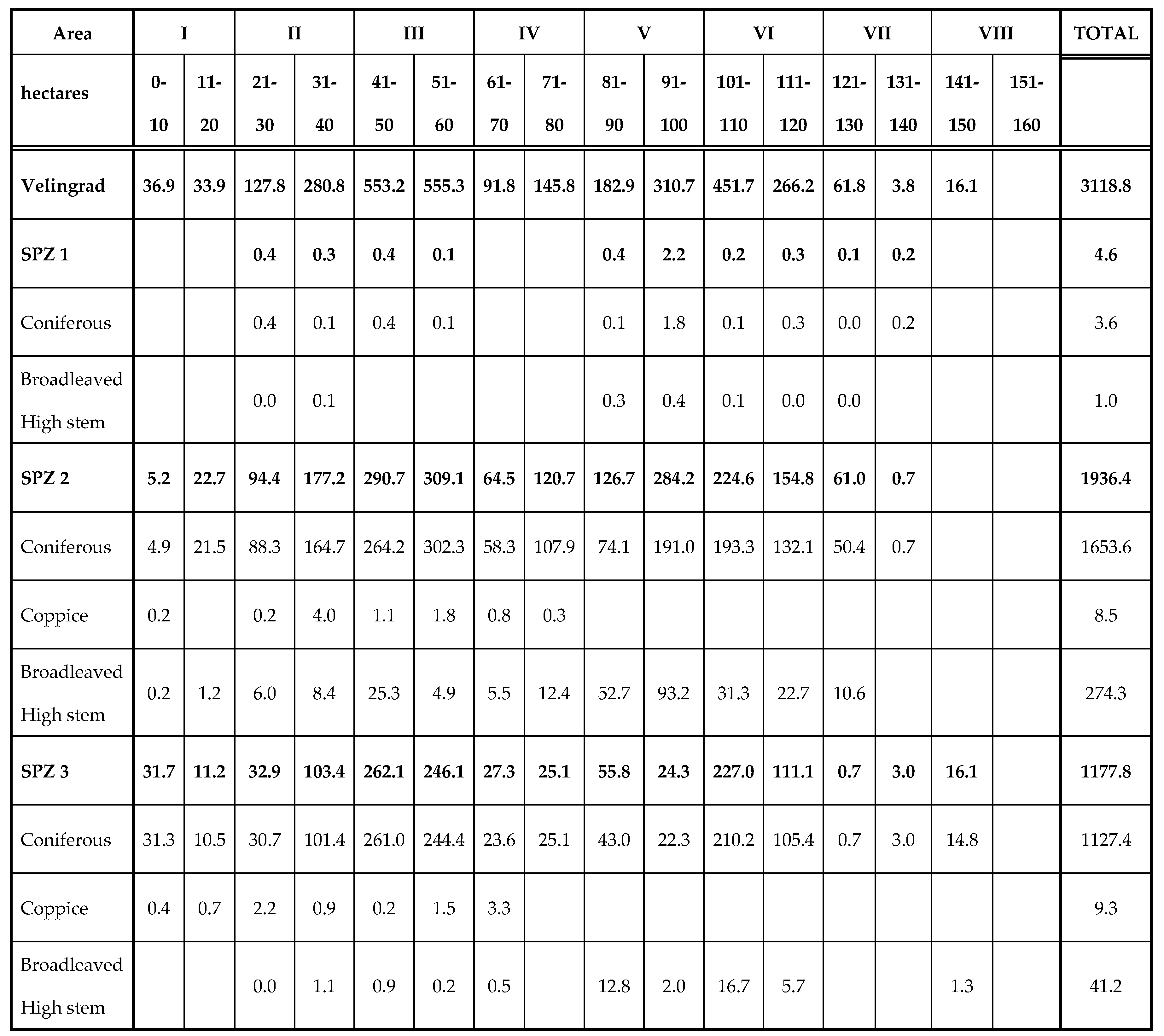

The methodology for valuating the water protection function of forest areas in Bulgaria has been tested using actual data on the forest areas with water protection functions falling within the scope of Velingrad municipality, taken from the forestry plans of the territorial division of SFH "Alabak" and the territorial division of SHH "Chepino" . It should be specified that according to the legislation in force in Bulgaria, sanitary protection zones (SPZ) are designed around water sources and facilities for drinking and domestic water supply from surface and underground water. Each SPZ has 3 belts, which are outlined according to an accepted methodology. In belt I of the water sources and facilities for drinking and domestic water supply from surface and spring waters, the permitted activities include anti-erosion, afforestation and thinning activities. In belt II, felling activities are limited to thinning, and in belt III, these activities are restricted if proved necessary [39]. The area distribution of sanitary protection zones by forest type on the territory of Velingrad municipality is presented in Table 1. It shows that the area of coniferous forests falling within the three sanitary protection zones on the territory of Velingrad municipality is 89.28% of the total area of the municipality’s water protection forest territories. Therefore, the valuation of the water protection function in this paper focuses on the coniferous forests falling within the first, second and third belts of SPZs in Velingrad municipality. The wooded area of the coniferous water protection forests is 98% of their total area, their tree species composition consists of 70% spruce and 30% white pine, and their total wood stock amounts to 951,527 m3 or 346 m3/ha with an average increment per hectare of 4.60 m3/ ha [13,14].

2.2. Methodology for valuating the productive function of forests with water protection functions and distribution of income between the forest owner and the user of forest ecosystem services

The economic valuations of forests referred to in scientific literature are based on the permanent annual income obtained from them. Thus, the monetary value of the forest or of parts thereof is calculated as the difference between the capital used and the income generated. As far back as 1796, Burgsdorf tried to calculate the monetary value of forests in exactly the same way. Shortly before that (in 1788), the first forest valuation regulation was issued by means of the so-called Austrian cameral tax. According to it, the possible normal income from the forest and its corresponding normal stock should be calculated first. Afterwards, after deducting allowance for taxes and forest management costs, the remaining income is capitalized at 5% during the adopted rotation period and thus the normal value of the forest is calculated. In principle, the actual forest deviates from the normal one, so in proportion to this deviation, the normal value of the forest is reduced or increased, and its actual value is thus obtained [20].

In 1849, Faustmann derived and proposed the formula for calculating the value of the land, and in 1854 – the formula for calculating the planting costs [17].

Forest investments are usually analyzed using the Faustmann model (Faustmann 1849, Samuelson 1976). This method was mainly discussed by Conrad and Clark (1987) and Comolli (1981), and later revised by Yin and Newman (1997) [8,9,40,45].

In Bulgaria, the issue of forest valuation has also been considered. Prof. Temelko Ivanchev (1940) was the first to lay the theoretical and methodological foundations of forest valuation. For this purpose, he used German textbooks on the subject, published at the beginning of the 20th century (1912, 1919, 1921) [20].

Angel Baev recommended that the comprehensive valuation of forest resources should be carried out by creating a forest register as part of the comprehensive valuation of all natural resources. According to him, such unified economic valuation of forest resources will provide a basis for determining the most effective forestry activities, as well as an accurate assessment of their effect [4].

H. Sirakov suggested that when assessing the future composition of forests, the following indicators should also be applied: vitality; productivity; economy and user satisfaction. As a starting point for their application are the site conditions, with preference given to the most viable species; of them – to the most productive; to the most economical in terms of cost-effectiveness and to the most widely used timber species. Some of these indicators can also be applied to the assessment of plantations [42].

I. Yovkov, I. Paligorov and Y. Poryazov, using the theory of contribution, developed a solution to the economic problem of optimal duration of the felling cycle in order to achieve the maximum financial contribution from the use of the clear-cutting form of forest management [22]. I. Yovkov, I. Paligorov and I. Dobrichov (1992) undertook the task to determine the optimal stock at which the maximum financial contribution would be achieved from the use of the selective cutting form to forest management [21].

I. Paligorov made an economic valuation of the use of different cutting technologies and techniques for the thinning of uneven-aged plantations. The factors that influence the thinning and sanitation cutting of coniferous forests were determined. The costs associated with thinning activities and the income were calculated. The economic indicators of the use of timber from thinnings were determined using the contribution theory [38].

D. Georgieva perfected the approach for economic valuation of selectively cut forests in structural balance by using net present value in perpetuity. She proposed an approach for choosing the optimal target diameter of selectively cut forests under conditions of uncertainty by means of the marginal analysis method [18].

In 1998, Ordinance No. 32 on the valuation of forests and lands in the forest fund was adopted in Bulgaria. Subsequently, it was repealed and the Ordinance on fixing base prices, prices for excluded areas and establishing rights of use and easements on forests and lands from the forest fund was adopted [34], and in 2011 pursuant to Resolution No. 236 of the Council of Ministers, the Ordinance on valuation of land properties in forest territories was issued. It is currently a valid normative document which provides a mechanism for fixing regulated prices [36].

It should be noted that all authors listed so far have succeeded in valuating forests with timber production functions. However, both the theory and practice lack an economic valuation of the other functions [1,44]. On the other hand, the methods and valuations turn to the ecological functions of forests [6,7,10,11,37].

Despite having a significant contribution to the management of forest ecosystems, the silvicultural ecological approach leaves a certain gap in the theory and practice of forest management. The water protection functions of forests, their recreational and tourist functions, their field protective functions, etc., remain undervalued. Тhe main commodity produced by forests with such functions is not wood, but water, tourist products and services, agricultural products, etc. In the present study, it is therefore justified to make a valuation of the water protection function. Its economic aspect is missing both in the economic theory of forestry and in the well-established practical market approach to forest management. The reason for this is that forests in general, including water protection forests, are still viewed as a fund and not as capital. If forests are viewed as capital, then they constitute an investment and should be valued as such. This is precisely what is missing in existing research.

The silvicultural systems that are currently used in Bulgaria are mainly even-aged forest management systems (clear-cutting). These systems employ regenerative felling methods, which result in even-aged, and uniform in structure and density stands over large areas. In this context, it is advisable to make an economic valuation of the investments in water protection forests precisely in the case of the clear-cutting form of forest management. It should be emphasized here that, depending on the type of regenration felling, it can be clear-cutting, shelterwood and selective logging [5,43]. The clear-cutting form of forest management is limited by law, and shelterwood is most commonly used in practice. Shelterwood involves gradual felling. The types of shelterwood fellings are short-term-gradual, gradual-gap, group-gradual and uneven-gradual [35]. Short-term gradual fellings have a regeneration period of up to one age class and is suitable for even-aged plantations [29]. For this reason, the methodology for economic valuation of the water protection function of forest territories is limited to this type of felling, and its silvicultural technical characteristics have been briefly presented.

The size of the felling area in short-term gradual felling is up to 2 ha, and the period of regeneration is a minimum of 15 years and a maximum of 20 years. Felling is carried out evenly over the felling area in 3 or 4 phases (preparatory, seeding, secondary and final). Each phase is characterized by a different felling intensity and canopy density. In the preparatory phase, canopy density is reduced to 0.7 - 0.8, and the felling intensity is up to 25%. This phase can be skipped if regular thinning has been carried out. The seeding phase is carried out no earlier than 5 years after the preparatory phase, where the felling intensity is up to 30%, and the canopy density is reduced to 0.5 - 0.6. During the secondary phase, the felling intensity is up to 30%, and the canopy density is reduced to 0.3 - 0.4. It is carried out no sooner than 5 years after the seeding phase. Finally, when the canopy density of tree stands in the felling area is not greater than 0.4 and more than 80% of the area is covered with undergrowth, the final felling phase is carried out [29].

In accordance with the silvicultural and technical characteristics of the short-term gradual felling presented above, the methodology for valuating the water protection functions of even-aged forests is based on the following algorithm: determination of the stock of wood per root of uneven-aged plantations (Vu); determination of the present monetary value of wood from regenerative felling of uneven-aged plantations (Wreg); determination of the present monetary value of wood from thinnings (Wclear); determination of the costs of creating woodland and their capitalization at plantation age (c); determination of fixed costs and their capitalization for the entire economic life (V); determination of the net financial contribution of uneven-aged plantations (NFCu); determination of the forest rent from and the distribution of income between the forest owner and the user of the forest ecosystem services.

Determining the stock of wood per root (V)

The stock of wood is the volume of wood in the above-ground part of trees. It depends on the natural conditions of growth and development of the plantation and on the economic activity carried out in them. The stock (V) of the growing stand is calculated using several methods: the mean sample stem method, mensuration methods by girth and class, and mensuration table methods.

Determining the monetary value of wood from short-term gradual felling

Based on the silvicultural technical characteristics of short-term gradual felling described above, it is clear that income from regenerative felling (Wu) does not come all at once, but at different times during the regeneration period. In this case, a certain year is chosen, which is taken as the u felling age. This year or age is the year in which the final phase of regenerative felling occurs. It is clear that a portion of the income from regenerative felling (Wu) is received in the u year of final felling. Another part of this income (Wu-m) from preparatory felling is received before reaching the u age, for example in year m, and therefore this income is extended for the period from its receipt to year u, equal to (u - m) years [26].

Capitalized monetary value of wood from the preparatory, seeding and secondary phases of felling:

where Wu-m is the capitalized value of wood from the preparatory, seeding and secondary phases of felling;

Qi – volume of wood from the ith category, m3;

Pi– the warehouse price of 1m3 of wood from the ith category BGN/m3, where m is the year of felling;

r – the rate of return on alternative investments for the period, percentage expressed as a fraction of 1.0.

The current methodology has adopted the use of the so-called forest interest rate r = 4% [30]

Monetary value of wood from the final phase of felling (Wu):

Finally, the monetary value of wood from regenerative felling (Wreg) is determined using the formula (3):

Determining the present monetary value of wood from thinning (Wclear)

When calculating income from thinning, first of all, it should be examined and determined whether such income can be actually generated or not. Often times such revenues cannot be generated either due to the limited market conditions for the sale of wood harvested from thinning, or due to a lack of convenient and cost-effective freight transport. It is clear that given these unfavorable conditions, this intermittent income should be left out of the calculations.

There are also cases when, due to inefficient management, thinnings are not carried out, but they are perfectly possible, and then the income generated from them will have to be determined and included in the calculations. Data on the amount, receipt, etc. of the income from thinnings can be obtained from other neighboring state forestry offices working under approximately the same conditions, which carry out regular thinning activities and receive a corresponding income generated from them.

It goes without saying that, if thinning activities are carried out properly, in addition to being of great silvicultural importance, they are also sources of significant income for state forestry offices.

The monetary value of wood from thinning activities in year a (Wa) is calculated using the following formula:

In order to add the income from thinning to the income from regenerative felling, the former must be expressed in a comparable form, i.e. should receive a present value at the end of each plantation age.

The cash income from intermittent felling must be capitalized in year u when the income from the regenerative felling is received.

The total revenue from all thinning activities (Wclear) is calculated as follows:

where Wa, Wb,... and Wq are the monetary values of wood from thinning, BGN;

а, b... and q are the years in which thinning activities are carried out in the plantation.

Determining the costs of creating woodland and their future value at plantation age (FVc)

The costs of establishing a forest plantation include the costs incurred until the establishment of the plantation: clearing the felling area, soil preparation, delivery of planting material, tree planting, fertilization, replacement, cultivation, fencing. The costs of establishing the plantation depend on the tree species, its origin and the difficulty of the terrain during planting. This investment is one-off and is capitalized for the entire period of the adopted felling cycle.

The costs incurred initially to establish the forest plantation and capitalized at plantation age are calculated using the formula (6):

where FVc is the future value of the costs of establishing the forest plantation at plantation age, BGN;

с – the costs of establishing the forest plantation, BGN.

Determining the fixed costs and their future value at plantation age (FVv)

During the life of the plantation, usually every year until its regenerative felling, fixed costs amounting to BGN v are incurred [23]. These costs have the characteristics of an annuity, whose future value is calculated using the formula (7) [27]:

where FVv is the present value of fixed costs, BGN.

v – average annual fixed costs, BGN;

Determining the net financial contribution at different plantation ages (NFCu)

The net financial contribution (NFCu) is calculated as the difference between the total updated income generated from thinning activities (Wclear) and regenerative felling (Wreg) and the total present costs of establishing the forest plantation (Fvc) and the average annual administrative costs (FVv).

Based on the above formulas for calculating the income and costs, the net financial contribution at the end of year u will equal [23,28]:

The above formula (8) gives us the net financial contribution of the plantation over its lifetime of u years. With its help, the production possibility frontier can be defined. At the same time, the economic choice is limited to alternative options. The criterion for this choice is the value of use (max NFCu) of forest ecosystems for different target functions or a combination of several functions.

Determining the forest rent and the distribution of the income between the forest owner and the user of forest ecosystem services

The resulting net financial contribution (NFC) has to serve the interests of the owners of the three types of capital: forestry, labor and entrepreneurial capital, i.e. the individual owners of the factors of production must obtain an economic benefit from their property . The factor of production – timber fund (standing timber) – has the characteristics of a natural resource. The economic benefit from any natural resource is the rent. Forest rent is an income generated from the property rights over forest resources. This income is acquired by the owners by means of two mechanisms. The first involves leasing the right of use, where the so-called "natural fruits" are acquired by the "user of the forest ecosystem services", and the "civil fruits" by the "forest owners". Historically, the institutional environment has been created in such a way as to support forest owners, protect their property rights (the forest) and improve the forest for future generations. A resource to help carry out this function is the rent (R). It is the economic benefit of ownership of forest territories. The user of the forest ecosystem services is the bearer of the property rights on the capital advanced for the forest business. The user is the entity that has a monopoly on the management of forest territories. The economic benefit from their property is the profit. The mechanism that reflects the nature of the transactions between the two entities and by means of which they acquire the rights to the property is expressed by Schenrock's formula [19,25,30,41]:

where: R is the forest rent (income from the right of use of forest property) for forest owners, BGN/m3, BGN/kg, etc.;

P – the market price per forest product, BGN/m3, BGN/kg, etc.;

g – profitability based on production costs per user of forest ecosystem services, as a fraction of 1.0;

e – costs for harvesting forest products, BGN/m3, BGN/kg, etc.;

d – costs for transporting forest products EXW to the nearest location where the user of forest ecosystem services can receive them, BGN/m3, BGN/kg, etc.

The transactions under this mechanism are of such a nature that the two entities, guided by their interests and protecting them in the negotiation process, receive a fair value of the income from the invested capital. The meaning of fair here extends to the degree in which the institutions set up to regulate the market equally protect both types of property – that of forest owners and that of the user of forest ecosystem services. Under this mechanism, if the forest ecosystem has a wood production function, the rent (R) as an income for the forest owner will be generated based on the market price reached by wood resources.

According to this mechanism, the profit generated by a user of forest ecosystem services is the result of the amount of wood resources used and the rate of profit (g) of the market price per unit of wood resource. This norm reflects the following exchange relation: the price that the respective buyer has agreed to pay and the seller has agreed to accept under the circumstances existing at the time of each transaction. Therefore, it is fair insofar as the institutions provide conditions for the protection of the property rights of a user of forest ecosystem services. Finally, the operating costs (e+d) incurred by a user of forest ecosystem services will obviously depend on the price of the factors of production. These factors are territorially differentiated and obviously have an impact on the final income – rent and profit.

Now, we can ask the question: What should the owner of forests with water protection functions receive if the nature of the transactions is of the type reflected in formula (9) in the case of an even-aged forest (under a clear cutting form of forest management)? According to economic logic, this would be the opportunity cost of the loss of rental income from unrealized gains from timber use rights. These unrealized gains can be:

Full – when the forests are used only for their water protection function and the income from wood is zero. Here the loss from unrealized gains from forest use rights is 100% and should be 100% covered along the water consumption or wood production pricing chain;

Partially limited – when forests are used equally for both wood production and water protection. The fair allocation here requires that 50% of the income be at the expense of wood production, and the other 50% - at the expense of the water protection and water regulation function;

Limited – when the wood production function is given priority over the water protection function or vice versa. Here, it is reasonable that 75% of the income should be covered by the wood production function and 25% - by the water protection and regulation function or vice versa.

The second question that arises is what income the forest owner loses from unrealized gains from timber use rights over even-aged forests?

When a forest owner grants the timber use rights to a user of forest ecosystem services, their net financial contribution (NFC) will obviously acquire the characteristics of a rent. In order for it to be determined, the economic balance between the forest owner and the user of forest ecosystem services must also take into account the current costs of the user of forest ecosystem services. In this case, formula (9) calculating this balance takes the form of an annual balance between the two entities, i.e.:

where Ryear is the annual forest rent, BGN/hа/year;

NFCyear – mean annual contribution per 1 year, BGN/ha/year. It is calculated using formula (11):

Qyear – the average volume of wood harvested per 1 year from thinning and regenerative felling under a clear cutting form of forest management, m3/ha/year.

Historically, in Bulgaria, а profit margin of g=20"\%" has been found to ensure a relatively good distribution of income between entities [19,30]. This balance again places the two entities on an equal footing, each of them having the right to receive income from the property they own. This income must be used by them to satisfy their needs, as well as to improve this property for future generations.

3. Results and discussion

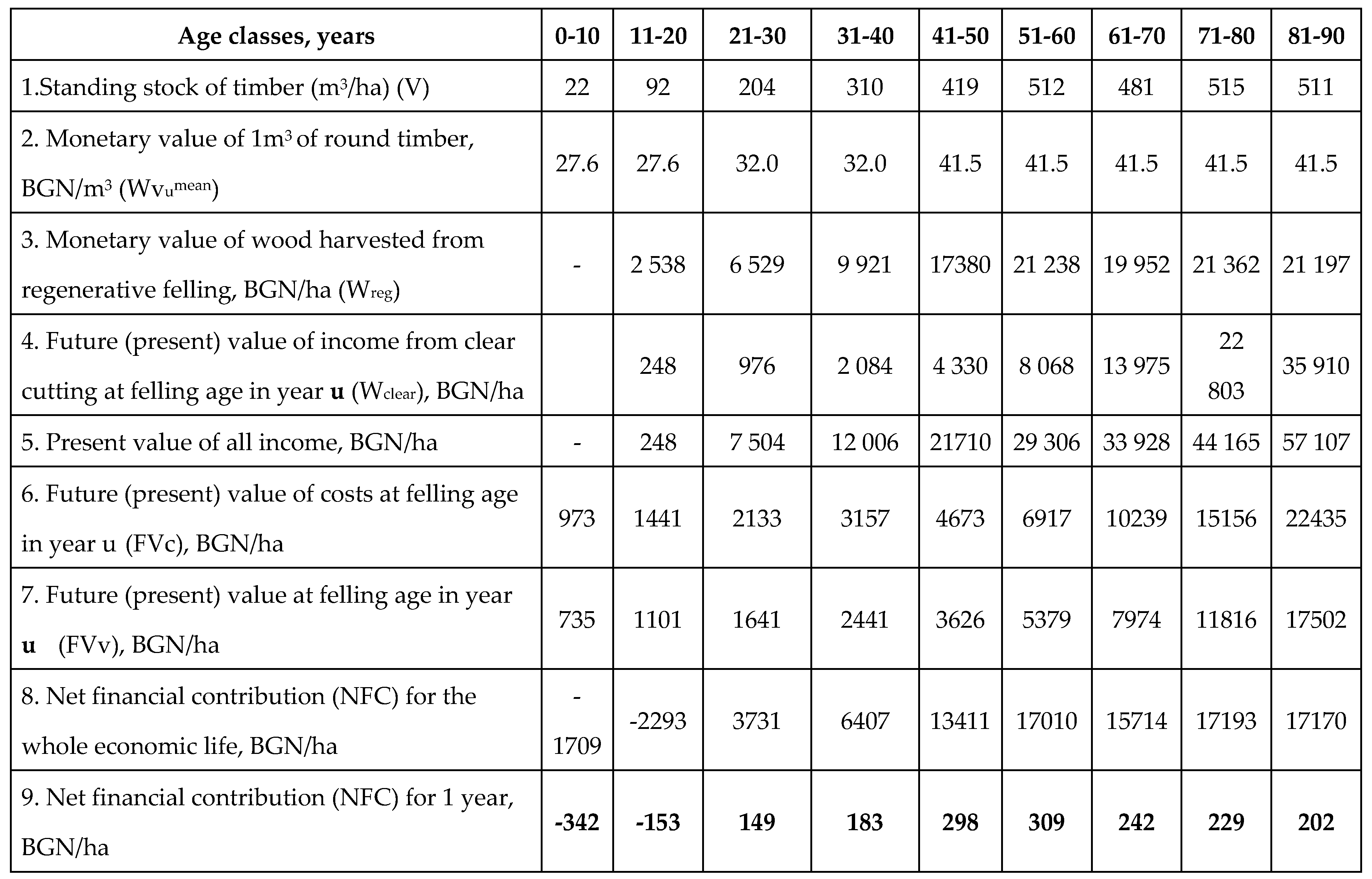

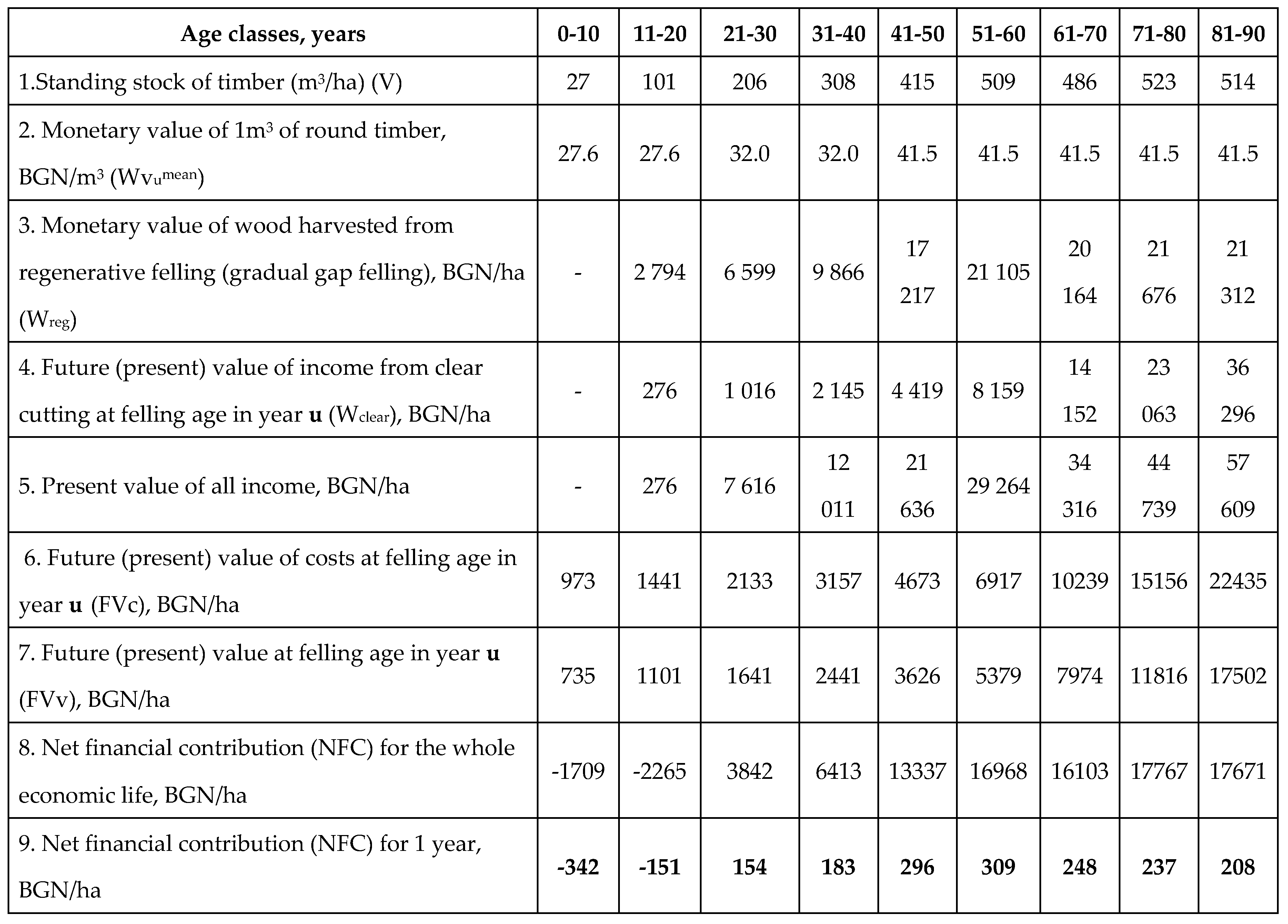

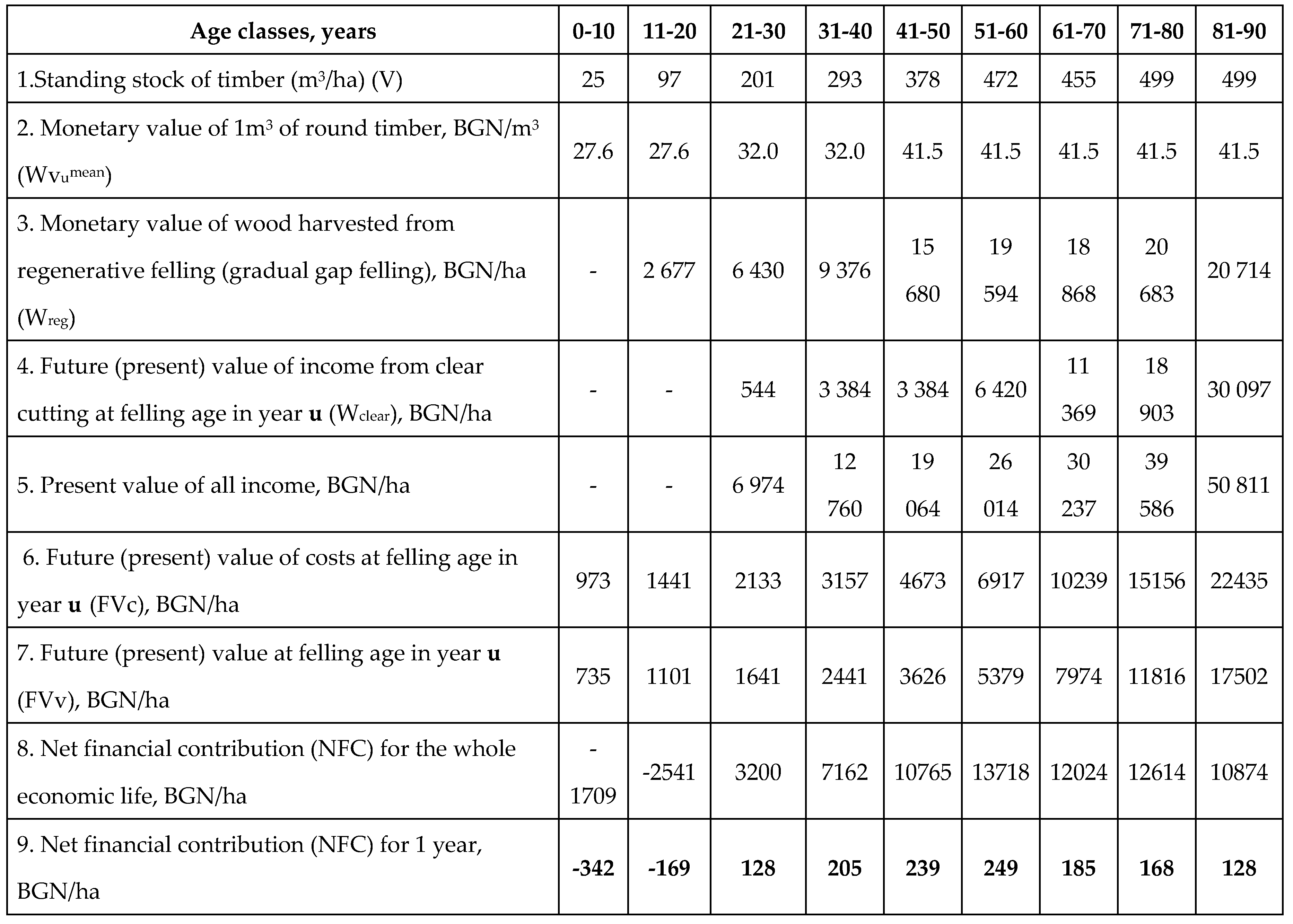

Prices from 2020 were used for the economic valuation of the coniferous forests with water protection functions on the territory of Velingrad municipality, and the main results of the application of the methodology described in Section 2 of this paper have been summarized in Table 2, Table 3 and Table 4 for SPZ 1, SPZ 2 and SPZ 3, respectively.

The general trend observed for coniferous forests with water protection functions in each SPZ is that the net financial contribution (NFC) increases with the age, reaches a maximum value and then starts to decline. It is most economically advantageous to maintain plantations at an age when the financial contribution is the highest [23]. This age is between 50 and 60 years for the coniferous forests with water protection functions in all three sanitary protection zones on the territory of Velingrad municipality. The average age of the coniferous forests with water protection functions is 51 years, which means that they have reached their most economically advantageous age. As seen in Table 1, Table 2 and Table 3, the maximum net financial contribution for 1 year from 1 ha of coniferous forests with water protection functions on the territory of Velingrad for SPZ 1, SPZ 2 and SPZ 3 is BGN 309/ha/year, BGN 309/ha/year, and BGN 249/ha/year, respectively. This income is for the forest owner, which they receive as an economic gain from the property if they use the wood themselves.

If the forest is used by a user of forest ecosystem services, the economic balance between the forest owner and the user of forest ecosystem services, where the current costs of a user of forest ecosystem services are also taken into account, is calculated using formula (10).

The profit margin of a user of forest ecosystem services (r), as already stated in the methodology, is 20%. At the same time, the average costs associated with felling, primary processing and transportation to the nearest forest inspection post (e+d) for Velingrad municipality are BGN 20/m3, and the average annual quantity of wood harvested from thinning and regenerative felling for 1 year from 1 ha is about 7–8 m3/ha/year. [13,14]. Under these conditions, the annual forest rent (R) from forests with water protection functions is:

for SPZ 1:

BGN/ha/year

for SPZ 2:

BGN/ha/year

for SPZ 3:

BGN/ha/year

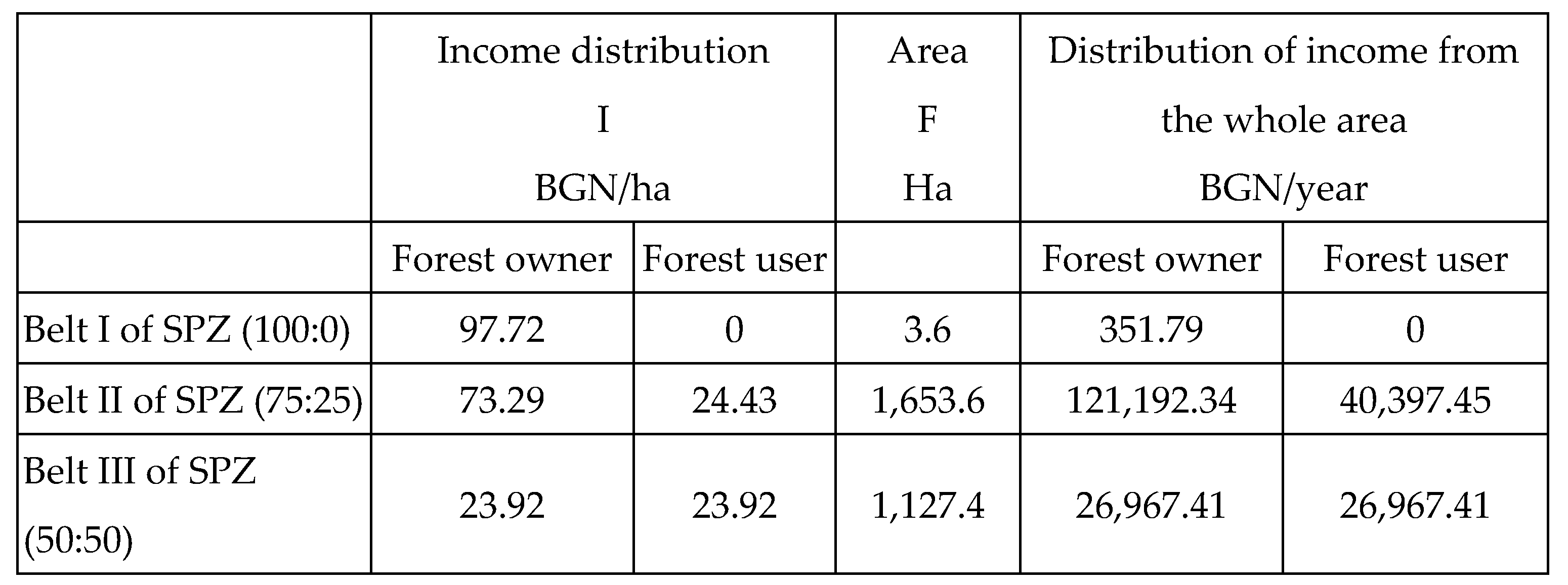

Table 5 provides information on the income that must be received by the forest owner and the user of forest ecosystem services under different rights of use of the forests with water protection functions on the territory of Velingrad municipality.

In relation to the forest territories falling into Sanitary protection zone (SPZ) I of the forests with water protection functions, the economic gains from the property should be 100% realized from water consumption and the owner should receive about BGN 97.72/ha per year. In SPZ II of the forests with water protection functions, the economic gains from the property should be realized by prioritizing the water protection over the wood production function in a 75:25 ratio, i.e. the owner should receive about BGN 73.29/ha/year. Finally, in SPZ III of the forests with water protection functions, the economic gains from the property should be realized equally in a 50:50 ratio through both production functions, i.e. about BGN 23.92/ha/year.

The obtained results confirm our main scientific hypothesis, namely that forests with water protection functions should be recognized as capital, and their owners should have the right to gain income from them by attributing production functions to the water protection properties of forests. In this regard, by means of the Forest Act and the Water Act and the relevant institutional departments and officials, a system of rules [3] working in favor of the owners of forests with water protection functions should be constituted. This protection itself is aimed at providing opportunities to generate income from the ownership of forest ecosystems [2,12,46], including in cases where they are only used for water protection purposes. Since every forest ecosystem has both a wood production and a water protection function, all future actions should obviously be directed at including forests in transactions not as a fund (accumulation), but as capital, whose profitability is functionally dependent on the relative prices of the commodities along the respective pricing chains.

Only by clarifying and recognizing the production function of forests through market mechanisms along all pricing chains will they acquire capital value as a multifunctional resource. This right in relation to their water protection function is currently not being realized. In addition, there are no direct economic gains from the ownership of forests with recreational and tourist functions, field protection functions, anti-erosion functions, etc. [16]. The main reason for this is the lack of an economic approach to the valuation of the multipurpose production functions of forests in general and of forests with water protection functions in particular.

The tasks associated with the economic approach to the problem of the economic valuation of forests with water protection functions boil down to an alternative choice. The criterion for this choice is the value of using forest ecosystems for different target functions or a combination of several functions. The alternative to the wood production function, which has become dominant in the course of the historical development of the country's forestry sector and as a result of the market mechanism for generating more than 95% of the forest income through wood production, is the economic valuation of the water protection function. This is necessary because the wood production function of forests is no longer able to generate sufficient income [21]. There is a conflict of interest between those who manage the forests for free in compliance with environmental criteria [31] and those who generate income along the water use and water consumption pricing chain.

Overcoming this conflict obviously requires a new institutional environment that would grant forest owners and forest management organizations the right to generate income from the water protection function of forests. This income, as an alternative to the income generated from the wood production function, can also be awarded in the form of a rent. In relation to the wood production function, under the current model of forest management, the rent as an economic gain from the ownership of forest ecosystems is ensured by any single transaction according to formula (9). In relation to the water protection function, the alternative to this rental income will obviously be of equal value, but this value will already have been created along the water consumption pricing chain. This will of course be valid if the forest ecosystem fully participates as an agent of production along this pricing chain. In this case, this value shall be equal to the loss that the forest owner would make from income foregone resulting from the unrealized wood production function, which is the same as if the forest ecosystem was established solely with water protection functions.

4. Conclusions

Forests with water protection functions must be recognized as capital, and their owners must have the right to derive income from them by attributing production functions to the water protection properties of forests. Consequently, the following question arises: How much should the owner of forests with water protection functions receive if the economic relations between the two main entities – the forest owner and the user of forest ecosystem services – are expressed in analytic form using Schenrock’s formula (see formula (9))?Economic logic shows that this will be the opportunity cost of the loss of rental income from unrealized timber use rights, which currently accounts for 95% of the revenues generated from forests in Bulgaria. The fair distribution of the contribution of forest ecosystems between the two main economic entities requires that the Forest Act and the Water Act, which set the rules for the protection of property rights over forests and their functional purpose, should allow for the following alternatives: forests with 100% wood production functions should generate 100% of the economic gains from forest ownership through the use of wood; forest territories falling into the first SPZ belt should generate 100% of their economic gains from the property through water consumption; forest territories falling into the second SPZ belt should generate their economic gains from the property by prioritizing the water protection function over the wood production function in a 75:25 ratio; forest territories falling into the third SPZ belt should generate their economic gains from the property equally in a 50:50 ratio through the two production functions; all forest territories in the country, which are managed by prioritizing the wood production function over the water protection function, should generate their economic gains from the property in a 75:25 ratio, taking this prioritization into account.

The alternatives described above are essentially forms of economic realization of the real contribution of forest ecosystems in the process of their multifunctional management (wood production and water protection functions). The owner of the forest ecosystem has the right to this contribution and they must be protected by the relevant legal instruments. This right, of course, can be economically realized only if the natural water protection and water regulation properties of the forests acquire a production function for forest owners. This new production function is at present as socially significant as wood production and requires institutional protection by means of the mechanisms for natural resource management.

Acknowledgments

Thе rеsеarch lеading to thеsе rеsults rеcеivеd funding from thе Bulgarian Sciеncе Fund – projеct: “Valuation of the water ecosystem service provided by forest areas with water protection functions in Bulgaria”, Contract No. КП-06-ОПР 03/7.

References

- Andréassian, V. Campeau. Waters and forests: from historical controversy to scientific debate. Journal of Hydrology 2004, 291, 1–27. [Google Scholar] [CrossRef]

- Asquith, N.M.; Vargas, M.T.; Wunder, S. Selling two environmental services –in-kind payments for bird habitat and watershed protection in Los Negros, Bolivia. Ecological Economics 2008, 65, 675–684. [Google Scholar] [CrossRef]

- Baev, A.S. Methodological foundations for economic valuation of forest resources. Forestry Science 1982, 1. [Google Scholar]

- Behera, B.; Engel, S. Institutional analysis of evolution of joint forest management in India: A new institutional approach. Forest Policy and Economics 2006, 8, 350–362. [Google Scholar] [CrossRef]

- Bogdanov, K. Forest management. Zemizdat 1991, 362. [Google Scholar]

- Boggs, J.; Sun, G.; McNulty, S. . Effects of timber harvest on water quantity and quality in small watersheds in the Piedmont of North Carolina. Journal of Forestry 2015, 114. [Google Scholar] [CrossRef]

- Clément, F.; JRuiz MA Rodríguez DBlais, S. Landscape diversity and forest edge density regulate stream water quality in agricultural catchments. Ecological Indicators 2017, 72, 627–639. [Google Scholar] [CrossRef]

- Comolli, P.M. Principles and policy in forestry economics. Bell J. Econ 1981, 12, 300–309. [Google Scholar]

- Conrad, J.M.; Clark, C.W. Naturural resources economics: Notes and problems; 231; Cambridge University Press, 1987. [Google Scholar]

- Duan, L.; Cai, T. Quantifying Impacts of Forest Recovery on Water Yield in Two Large Watersheds in the Cold Region of Northeast China. Forest 2018, 9, 392. [Google Scholar] [CrossRef]

- Ellison, D.; Morris, C.E.; Locatelli, B.; Sheil, D.; Cohen, J.; Murdiyarso, D.; et al. Trees, forests and water: cool insights for a hot world. Global Environmental Change 2017, 43, 51–61. [Google Scholar] [CrossRef]

- Eriksson, M.; Samuelson, L.; Jägrud, L.; et al. Water, Forests, People: The Swedish Experience in Building Resilient Landscapes. Environmental Management 2018, 62, 45–57. [Google Scholar] [CrossRef] [PubMed]

- Forestry plans of the territorial division of SFH "Alabak", 2018, 178.

- Forestry plan of the territorial division of SFH "Rakitovo", 2019, 194.

- Forest Act, promulgated in State Gazette issue 19 of 8 March 2011, amended in State Gazette issue 43 of 7 June 2011, amended and supplemented in State Gazette issue 109 of 22 December 2020, supplemented in State Gazette issue 21 of 12 March 2021.

- FAO, IUFRO and USDA. A guide to forest-water management. FAO Forestry Paper № 185. Rome, 2021, 166.

- Faustmann, M. Calculation of the value which forest land and immature stands possess for forestry. Republished in 1995 with permission from Commonw. For. Assoc. in J. For. Econ. 1995, 1, 7–44. [Google Scholar]

- Georgieva, D.P. Economic valuation of selection forests. Sofia 2005, 190. [Google Scholar]

- Glushkov, S., Iv. Markov, Zdr. Vasilev, M. Dzhambazova. Methodology for determining forest tax categories and correction coefficients. Scientific report. Forest Institute, Bulgarian Academy of Sciences, Sofia 2006, 91. (unpublished). [Google Scholar]

- Ivanchev, T. Valuation of forests using forest statics. Sofia 1940, 1035. [Google Scholar]

- Yovkov Iv., Iv. Paligorov, Il. Dobrichov. Valuation of forestry capital under a selective form of forest management. Scientific works, S, 1992.

- Yovkov Iv., Iv. Paligorov, Yav. Poryazov, Valuation of forestry capital under the clear-cutting form of forest management, Scientific works, S, 1992.

- Yovkov, Iv. Economics of Forestry. Zemizdat, Sofia 1994, 240. [Google Scholar]

- Yovkov Iv., K. Kolev. Assessment of the effectiveness of the functioning of the forest sector in Bulgaria through the prism of the neo-institutional economic theory. Management and Sustainable Development 2007, 1, 14–22. [Google Scholar]

- Kolev, K. Economic contradictions and conflicts caused by the forestry management mechanism after 1997. Dissertation for doctoral degree. Sofia 2008, 193. [Google Scholar]

- Kolev, K. Forestry Management. Avangard-Prima 2018, 319. [Google Scholar]

- Kolev, K.; Tsoklinova, M. . Travel agency finances. Sofia, Avangard-Prima 2019, 373. [Google Scholar]

- Kolev, K. A management model for Austrian federal forests. Bulgarian electronic scientific journal "Business Management" 2021, 1, 59–65. [Google Scholar]

- Kostov, G.; Nedelin, B. . A Practical Guide for General Forestry. Sofia 1996, 180. [Google Scholar]

- Markov, Iv. Research on the valuation of forests in the Republic of Bulgaria. Dissertation for the award of the scientific degree "Doctor of Science". Professional field "Forestry", Scientific specialty "Forestry and taxation". Bulgarian Academy of Sciences, Forest Institute 2021, 215. [Google Scholar]

- Martynova, М.; Sultanova, R.; Khanov, D.; Talipov, E.; Sazgutdinova, R. Forest Management Based on the Principles of Multifunctional Forest Use. Journal of Sustainable Forestry 2021, 40, 32–46. [Google Scholar] [CrossRef]

- Ministry of Environment and Water. Environmental Executive Agency. National report on the state and protection of the environment in the Republic of Bulgaria. Forest resources and their contribution to global carbon cycles. 2020 (https://eea.government.bg/bg/soer/2020/forest/gorskite-resursi-i-tehniya-prinos-kam-globalnite-tsikli-na-vaglerod-1).

- 33. Ministry of Agriculture. National strategy for development of Bulgarian forest sector till 2030. Sofia 2022, 53. (project).

- Ordinance on fixing base prices, prices for excluded areas and establishing rights of use and easements on forests and lands from the forest fund, promulgated in the State Gazette No 101/2003, amended in No 39/2004, amended in No 6/2005, amended in No 1/2007.

- Ordinance, No. 8 of , 2011 on logging in forests, prom. SG No. 64 of August 19, 2011. 5 August.

- Ordinance on valuation of land properties in forest territories, prom. in State Gazette No. 63 of 16.08.2011, in force since 16.08.2011; amended and supplemented in No. 99 of 14.12.2012, in force since 14.12.2012, adopted by Council of Ministers Decision No. 236 of 03.08.2011.

- Oishi, Y. Evaluation of the Water-Storage Capacity of Bryophytes along an Altitudinal Gradient from Temperate Forests to the Alpine Zone. Forests 2018, 9, 433. [Google Scholar] [CrossRef]

- Paligorov, I.P. Studies on the economic valuation of thinning activities in coniferous plantations. Zemizdat 1995, 199. [Google Scholar]

- Regulation, No. 3 of 16 October, 2000 on the conditions and procedures for the study, design, approval and exploitation of sanitary protection zones around water sources and drinking and domestic water supply systems as well as mineral water sources, used for medicinal, prophylactic, drinking and hygiene purposes, promulgated in State Gazette issue 88/2000.

- Samuelson, P.A. Economics of forestry in an evolving society. Economic Inquiry 1976, 14, 466–492. [Google Scholar] [CrossRef]

- Sirakov, H. Economics of Forestry. Sofia 1982, 201. [Google Scholar]

- Sirakov, H. Assessment criteria of future wood composition of forests. Forestry and Forest Industry 1986, 12. [Google Scholar]

- Tonchev, T. Forest planning. Forestry plans and programs. America for Bulgaria Foundation, Sofia 2013, 23. [Google Scholar]

- Tsoklinova, M.; Delkov, A. Factors Inducing on Consumption of Ecosystem Service Tourism. Journal of Balkan Ecology 2019, 22, 291–301. [Google Scholar]

- Yin, R.; Newman, D.H. Long-run timber supply and the economics of timber production. Forest Science 1997, 43, 113–120. [Google Scholar]

- Zhang, W.; Pagiola, S. Assessing the potential for synergies in the implementation of payments for environmental services programmes: an empirical analysis of Costa Rica. Environmental Conservation 2011, 38, 406–416. [Google Scholar] [CrossRef]

- Zlatarev, E.; Milkova, D.D.; Kostov, I.; Muleshkova, G.; Boyanov, A. Vasilev. Fundamentals of law. Ciela 2005, 700. [Google Scholar]

Table 1.

Distribution of area of sanitary protection zones on the territory of Velingrad municipality by forest type, ha.

Table 1.

Distribution of area of sanitary protection zones on the territory of Velingrad municipality by forest type, ha.

|

Source: Forestry plan of the territorial division of SFH “Alabak” and forestry plan of the territorial division of SHH “Chepino”

Table 2.

Economic valuation of the net financial contribution from 1 ha even-aged coniferous forest from SPZ 1.

Table 2.

Economic valuation of the net financial contribution from 1 ha even-aged coniferous forest from SPZ 1.

|

Source: Forestry plans of the territorial division of SFH "Alabak" and the territorial division of SHH "Chepino“ and authors’ own calculations.

Table 3.

Economic valuation of the net financial contribution from 1 ha of even-aged coniferous forest from SPZ 2.

Table 3.

Economic valuation of the net financial contribution from 1 ha of even-aged coniferous forest from SPZ 2.

|

Source: Forestry plans of the territorial division of SFH "Alabak" and the territorial division of SHH "Chepino“ and authors’ own calculations.

Table 4.

Economic valuation of the net financial contribution from 1 ha even-aged coniferous forest from SPZ 3.

Table 4.

Economic valuation of the net financial contribution from 1 ha even-aged coniferous forest from SPZ 3.

|

Source: Forestry plans of the territorial division of SFH "Alabak" and the territorial division of SHH "Chepino“ and authors’ own calculations.

Table 5.

Distribution of income from water protection forests, even-aged plantations.

|

Source: Authors’ own calculations.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.