Submitted:

30 December 2025

Posted:

01 January 2026

You are already at the latest version

Abstract

This paper examines the short-run transmission of monetary policy shocks to bank credit granted to the non-financial corporate sector in Morocco, a bank-based emerging economy. While conventional monetary theory emphasizes the interest rate channel, growing empirical evidence suggests that monetary transmission is increasingly conditioned by banks’ balance-sheet constraints and credit risk considerations. The central question addressed is whether policy-rate shocks translate into short-run credit expansion or are instead absorbed through alternative banking adjustment mechanisms. The empirical analysis relies on monthly macro-financial data over the period 2014–2024 and employs a reduced-form Vector Autoregressive (VAR) framework. Impulse response functions, forecast error variance decompositions, and Granger causality tests are used to assess the dy-namic interactions between the policy rate, non-financial corporate credit, banks’ sovereign asset holdings, and credit risk conditions.The results show that monetary policy shocks generate weak, short-lived, and economically negligible responses in non-financial corporate credit, with no evidence of sustained credit expansion following policy-rate changes. By contrast, monetary impulses are associated with systematic balance-sheet reallocation toward sovereign assets and with more pronounced, though transitory, movements in credit risk indicators. Variance decompositions further reveal that short-run credit dynamics are overwhelmingly driven by internal banking and risk-related factors, while monetary policy shocks explain only a marginal share of credit fluctuations. Overall, the findings indicate that short-run monetary transmission in Morocco operates predominantly through risk-sensitive balance-sheet adjustments rather than through direct quantity-based credit responses, thereby reframing the interpretation of weak credit reactions to monetary policy in bank-based emerging economies.

Keywords:

monetary policy

; short-run monetary transmission

; credit risk

; bank balance sheets

; VAR analysis

; emerging economy

; non-financial corporate

1. Introduction

The transmission of monetary policy to the real economy has long been a central issue in modern macroeconomics and financial economics. More specifically, understanding how policy rate changes affect investment, credit, and economic activity is particularly important in emerging economies, where financial systems remain predominantly bank-based and alternative financing channels are limited. Despite the widespread reliance on interest rate instruments, a growing body of empirical evidence suggests that monetary transmission is neither automatic nor uniform across institutional environments.

From a theoretical perspective, this debate originates in the longstanding tension between Keynesian and monetarist traditions. On the one hand, since the seminal contribution of Keynes (1936), the relationship between interest rates, investment, and economic activity has been viewed as inherently unstable, shaped by expectations, confidence, and uncertainty. On the other hand, the monetarist view advanced by Friedman (1968) emphasizes disciplined control of monetary aggregates and short-term interest rates as a mechanism for ensuring a relatively predictable transmission of monetary policy to real outcomes. This theoretical divide remains highly relevant, particularly in bank-dominated financial systems where credit allocation decisions depend critically on banks’ balance-sheet positions and risk perceptions.

In such economies, monetary transmission is commonly assumed to operate through the bank credit channel. However, the link between policy rates and credit volumes is far from mechanical. Credit rationing theory, formalized by Stiglitz and Weiss (1981), demonstrates that banks may restrict lending independently of interest rates when information asymmetries and credit risk considerations dominate. Consequently, an accommodative monetary stance does not necessarily translate into an expansion of private-sector credit, especially when banks prioritize balance-sheet preservation and risk management over volume-based lending adjustments.

These mechanisms are particularly salient in the Moroccan context. Since 2014, Bank Al-Maghrib has implemented broadly accommodative monetary policies aimed at supporting economic activity and private-sector financing. Nevertheless, bank credit growth has remained moderate, while asset quality has deteriorated and banks’ holdings of sovereign securities have increased. The coexistence of low interest rates, rising credit risk, and sustained portfolio reallocation toward public debt suggests that monetary impulses may be absorbed through balance-sheet adjustments rather than transmitted directly to private-sector lending.

Consistent with this interpretation, recent empirical literature highlights that, under conditions of heightened uncertainty and binding prudential constraints, monetary transmission operates primarily through indirect channels related to banks’ balance-sheet management and risk considerations, rather than through a simple pass-through from policy rates to lending rates (Tenreyro & Thwaites, 2016; De Leo et al., 2022). In this framework, monetary policy tends to influence banks’ asset allocation decisions more strongly than short-run movements in aggregate credit volumes.

Despite these advances, important gaps remain in the literature. Integrated dynamic analyses that jointly examine monetary policy, bank credit, portfolio allocation, and credit risk remain scarce, particularly in bank-based emerging economies. Moreover, credit risk is often treated as an ex post outcome rather than as a conditioning factor shaping banks’ lending and balance-sheet decisions. In the Moroccan case, dynamic macro-financial evidence remains limited despite significant monetary and prudential reforms implemented over the past decade (Eddani, 2024; Lakhchen, 2025).

Against this background, the central research question of this study is the following: does the weak short-run response of bank credit to monetary policy shocks reflect an inefficiency of monetary policy itself, or does it rather signal an endogenous reallocation of the transmission mechanism toward balance-sheet and risk-adjustment channels within a constrained banking system?

In this context, the objective of this study is to examine the short-run transmission of monetary policy in Morocco by focusing on the joint dynamics of non-financial private-sector bank credit, banks’ holdings of sovereign securities, and credit risk conditions. Relying on monthly data spanning the period 2014–2024 and a reduced-form Vector Autoregressive (VAR) framework, the analysis investigates whether monetary policy shocks translate into observable short-term changes in non-financial corporate sector credit or whether they primarily induce balance-sheet and portfolio adjustments.

This paper does not merely document a weak short-run response of bank credit to monetary policy shocks. It contributes by showing that, within a monthly horizon and a bank-based emerging economy, monetary impulses are predominantly absorbed through balance-sheet reoptimization and risk-sensitive adjustments rather than through quantity-based lending responses. By jointly modeling credit volumes, sovereign asset holdings, and credit risk within a unified VAR framework, the study clarifies why short-run monetary transmission appears weak without implying monetary policy irrelevance.

Overall, the empirical findings indicate that monetary policy shocks generate weak and transitory responses in bank credit, while balance-sheet reallocation and credit risk dynamics play a more prominent role. These results suggest that, in a bank-based emerging economy, the conventional interest rate channel has limited short-run traction and that monetary transmission is largely mediated by risk-sensitive balance-sheet adjustments.

The remainder of the paper is organized as follows. Section 2 reviews the related literature Section 3 outlines the conceptual framework. Section 4 presents the data and empirical methodology. Section 5reports and discusses the empirical results. Section 6 concludes and discusses the policy implications of the findings

2. Literature Review

Debates over the effectiveness of monetary policy stem from the longstanding theoretical tension between the monetarist and Keynesian traditions. From a monetarist perspective, as articulated by Friedman (1968), macroeconomic stability can be achieved through disciplined control of monetary aggregates and short-term interest rates, under the assumption of relatively stable transmission mechanisms and predictable behavioral responses. Within this framework, monetary policy is expected to influence real economic activity primarily through price-based adjustments, notably via interest rate movements that affect borrowing costs and investment decisions.

By contrast, the Keynesian perspective places uncertainty at the center of economic decision-making. As emphasized by Keynes (1936), investment and financing choices depend not only on the cost of capital but also on expectations, confidence, and perceptions of risk. Consequently, the effectiveness of interest rate adjustments is inherently contingent on the broader macro-financial environment and on economic agents’ willingness to respond to price signals. This theoretical divergence becomes particularly salient during periods of economic and financial stress, when heightened uncertainty alters behavior across firms, households, and financial intermediaries.

In such contexts, precautionary motives intensify, balance-sheet constraints become more binding, and risk-management considerations gain prominence. As a result, standard interest-rate-based transmission mechanisms tend to weaken, as monetary impulses are absorbed less through price adjustments and more through indirect channels related to expectations, financial conditions, and balance-sheet dynamics. Monetary policy transmission thus becomes less mechanical and increasingly dependent on the state of the financial system.

Consistent with these theoretical insights, a growing body of empirical evidence shows that the effectiveness of monetary policy shocks tends to diminish during recessionary phases. Tenreyro and Thwaites (2016) demonstrate that monetary policy’s capacity to stimulate real economic activity weakens significantly during economic downturns, particularly when heightened uncertainty affects firms’ and banks’ expectations and induces precautionary behavior. Under such conditions, transmission mechanisms based solely on interest rate adjustments lose traction.

Early cross-country evidence further questions the centrality of the bank credit channel in monetary transmission. Using VAR models for the United States, Japan, and Germany, Barran et al. (1995) find that credit volumes respond only weakly to changes in policy rates, even in advanced financial systems. Taken together, these results suggest that monetary impulses are subject to substantial transmission leakages beyond interest rate movements, indicating that credit is not systematically the primary conduit through which monetary policy affects the real economy.

The attenuation of monetary transmission is further amplified when crises directly affect bank balance sheets. Zentefis (2020) provides evidence that financial shocks simultaneously depress asset values and increase default risk, prompting banks to tighten lending standards and restrict credit supply. The COVID-19 crisis provides a particularly clear illustration of this mechanism. For instance, Kolotioloman (2024) shows that, in WAEMU countries, long-term bank credit contracted despite accommodative monetary policies, reflecting a disruption of the credit channel under heightened macro-financial stress.

At the same time, additional evidence highlights the state-dependent and time-varying nature of monetary transmission in unstable environments. Focusing on the Turkish economy, Gayaker and Yalcin (2025) demonstrate that the response of bank credit to monetary impulses varies substantially across periods, thereby casting doubt on the empirical relevance of linear and time-invariant transmission models during episodes of pronounced macro-financial volatility.

These international findings are largely corroborated in the Moroccan context. Najab et al. (2022) show that, despite policy rate cuts during the health crisis, firms continued to face significant financing constraints, as banks adopted a cautious lending stance amid elevated perceived risk. At the microeconomic level, Boutfssi and Quamar (2024) identify three forms of credit rationing total, partial, and self-rationing and highlight the central role of information asymmetry and borrowers’ expectations of loan rejection in shaping access to bank financing. From a macroeconomic perspective, El Hassani and Ouali (2023) conclude that Moroccan monetary policy primarily influences inflation dynamics, while its impact on real activity and bank credit remains limited, suggesting persistent structural rigidities in the monetary transmission mechanism.

Beyond these macro-level considerations, classical monetary theory assigns a central role to the policy rate in the transmission of monetary impulses. In the standard framework, reductions in interest rates are expected to lower borrowing costs, stimulate investment, and expand bank credit (Bernanke & Gertler, 1995; Mishkin, 1996). Implicit in this mechanism is the assumption of a smooth and relatively symmetric pass-through of policy rates into the financing conditions faced by firms and households.

However, a substantial body of empirical work increasingly challenges this assumption in emerging and bank-based economies. Institutional rigidities, risk-based pricing practices, and balance-sheet constraints often weaken the transmission from policy rates to lending conditions, thereby limiting the effectiveness of the interest rate channel. In Morocco, Bank Al-Maghrib (2023,2024) reports indicate that, over the period 2022–2024, successive policy rate cuts were only partially reflected in lending conditions applied to the private sector, pointing to persistent frictions in credit pricing and allocation.

Micro-level evidence reinforces this interpretation. Najab et al. (2022) show that lending rates charged to firms particularly those perceived as riskier—responded weakly to episodes of monetary easing. This asymmetric adjustment suggests that banks internalize policy rate reductions primarily through balance-sheet management and risk considerations rather than through uniform price adjustments. As a result, monetary easing affects financing conditions unevenly across firms and does not translate mechanically into lower effective borrowing costs or broad-based credit expansion.

Several studies attribute this inertia to deeper structural and informational frictions. Aït Hmadouch (2023) emphasizes that institutional weaknesses and information asymmetries common to developing economies constrain monetary transmission beyond what standard interest rate models predict. Consistently, Moussaoui and Benyacoub (2024) confirm, using an ARDL framework, that the pass-through from the policy rate to lending rates in Morocco is both slow and incomplete, particularly during periods of heightened macroeconomic uncertainty. At the same time, De Leo et al. (2022) show that short-run movements in risk premia may diverge substantially from policy rates, thereby neutralizing the expected expansionary effects of accommodative monetary policy.

More recent contributions further emphasize the heterogeneity and state dependence of monetary transmission. Ottonello and Winberry (2020) and Cloyne et al. (2023) demonstrate that firms’ financial structures and exposure to credit constraints critically shape their responses to monetary shocks. In emerging economies, Pamungkas et al. (2025) document a segmented bank credit channel across loan categories and regions, while Checo et al. (2024) find that monetary shocks primarily affect financial conditions rather than aggregate credit volumes. Taken together, this evidence suggests that the interest rate channel operates in a fragmented and indirect manner, with balance-sheet and risk-related mechanisms playing a dominant role in shaping short-run credit outcomes.

Prudential regulation further reinforces these dynamics. Under the Basel II and Basel III frameworks, banks are required to hold regulatory capital proportional to their risk-weighted assets, directly linking credit expansion to balance-sheet constraints and risk assessments. While accommodative monetary conditions may reduce funding costs, they do not automatically relax capital constraints, thereby limiting the scope for credit expansion. Fraisse and Mésonnier (2023) show that monetary easing can support lending to low-risk borrowers, but that tighter prudential requirements tend to restrain aggregate credit supply when banks face binding capital constraints.

Empirical evidence confirms that banks’ responses to monetary impulses depend critically on balance-sheet strength. Albertazzi et al. (2021) and Imbierowicz et al. (2021) demonstrate that capitalization levels, asset quality, and funding stability shape lending behavior following monetary shocks. In this context, banks often respond to accommodative monetary conditions by reallocating their portfolios toward low-risk assets most notably sovereign securities rather than expanding private-sector lending. In Morocco, Bank Al-Maghrib (2024) reports that rising non-performing loans have constrained banks’ capacity to expand credit portfolios, even in a prolonged low-interest-rate environment.

Moreover, prudential regulation does not uniformly ease credit conditions across firms. Quamar et al. (2020) show that regulatory frameworks do not necessarily reduce capital requirements across all borrower categories, limiting banks’ incentives to lend to riskier firms. Extending this perspective, Boutfssi and Zizi (2025) provide evidence that access to bank financing reflects a complex interaction between macroeconomic factors monetary policy and prudential regulation and micro-institutional determinants related to internal risk assessment processes. Their findings indicate that credit risk perception and regulatory constraints dominate the direct effects of monetary impulses.

Recent evidence from African banking systems further corroborates these conclusions. Musamu et al. (2025) confirm that effective credit risk management is essential for financial stability but may simultaneously restrict credit supply when banks prioritize capital preservation. At the micro level, Ogundele and Nzama (2025) show that credit risk and risk disclosure practices significantly shape banks’ financial outcomes, reinforcing the central role of asset quality and balance-sheet considerations in banks’ behavior.

Finally, Hazra et al. (2023) show that tighter Basel III capital and liquidity requirements increased interest rate spreads and reduced private-sector lending in the short run in Bangladesh. This evidence closely mirrors the mechanisms highlighted in the Moroccan context, where accommodative monetary policy fails to generate sustained credit expansion due to balance-sheet and prudential constraints. In both cases, regulation acts as a structural filter that weakens the credit channel and shifts banks’ behavior toward balance-sheet consolidation rather than lending.

3. Conceptual Framework and Research Hypotheses

The conceptual framework of this study builds on established insights from the literature on monetary policy transmission in bank-based financial systems and provides a structured foundation for the empirical analysis of the Moroccan case. In such systems, monetary impulses are not transmitted solely through the conventional interest rate channel but are mediated by banks’ balance-sheet conditions, risk perceptions, and regulatory constraints.

Within this framework, banks’ lending decisions are inherently conditional on asset quality, capitalization, and portfolio allocation strategies, which jointly determine their responsiveness to monetary policy shocks. Rather than mechanically adjusting credit volumes following policy rate changes, banks actively arbitrate between private-sector lending and low-risk assets most notably sovereign securities particularly in environments characterized by heightened uncertainty and binding prudential requirements. As a result, balance-sheet optimization and risk management considerations constitute the primary margins of adjustment in the short run.

The Moroccan economy offers a particularly relevant context in which to examine these mechanisms. Over the past decade, periods of accommodative monetary policy have coincided with moderate private-sector credit growth, rising non-performing loans, and a sustained increase in banks’ exposure to public debt. This configuration suggests that monetary impulses interact closely with banks’ balance-sheet adjustments and credit risk dynamics, rather than translating directly into broad-based credit expansion.

The analytical framework is developed over a sample period encompassing both relatively conventional monetary conditions and exceptional episodes of public intervention, most notably during the Covid-19 crisis. These episodes are not modeled as distinct regimes but are treated as exogenous shocks that temporarily altered standard transmission mechanisms. Their inclusion reinforces the relevance of an approach focused on short- to medium-term balance-sheet and risk-driven dynamics, rather than on long-run equilibrium relationships.

Accordingly, the framework conceptualizes monetary transmission as an indirect and state-dependent process. Monetary policy shocks primarily affect banks’ balance sheets and portfolio allocation decisions, which, in turn, interact with prevailing credit risk conditions and prudential constraints. These interactions generate limited and transitory short-run adjustments in private-sector lending, even under accommodative monetary conditions. In this setting, weak credit responses do not indicate monetary policy ineffectiveness but reflect an endogenous reallocation of the transmission mechanism toward balance-sheet and risk-sensitive channels.

This conceptual perspective directly informs the formulation of the research hypotheses and underpins the empirical strategy adopted in the study, which relies on a reduced-form VAR framework designed to capture short-run dynamic interactions among monetary policy, bank balance sheets, credit risk, and private-sector credit.

Finally, this perspective directly informs the formulation of the research hypotheses and underpins the empirical strategy, which is based on a reduced-form VAR analysis.

H1

. Monetary policy shocks are associated with weak and short-lived short-run responses of bank lending to the non-financial corporate sector.

H2.

Monetary policy shocks are more strongly reflected in banks’ balance-sheet adjustments and portfolio reallocations particularly between private-sector credit and sovereign securities than in sustained changes in non-financial private-sector credit.

H3.

Credit risk conditions significantly condition the short-run response of non-financial corporate sector credit to monetary and financial shocks

4. Methodology and Econometric Strategy

4.1. General Methodological Framework

The objective of this study is to examine the mechanisms by which monetary policy is transmitted to non-financial corporate sector bank lending in a bank-based emerging economy, with particular emphasis on the roles of credit risk dynamics and banks’ balance-sheet adjustments. In this regard, the analysis focuses on the short-run interactions among key macro-financial variables, which are inherently dynamic, endogenous, and mutually interdependent.

To properly account for these features, the empirical strategy relies on the estimation of a Vector Autoregressive (VAR) model, building on the seminal approach introduced by Sims (1980) and the methodological framework outlined by Lütkepohl (2005). Specifically, the VAR methodology is well suited to capturing the joint evolution of monetary policy indicators, private-sector bank credit, banks’ holdings of sovereign securities, and credit risk measures, while avoiding the imposition of restrictive a priori assumptions regarding causal ordering or structural transmission channels.

This empirical approach is particularly appropriate in the context of emerging economies, where monetary transmission mechanisms are often incomplete, unstable, and shaped by institutional frictions, prudential regulation, and fiscal considerations. Accordingly, rather than assuming a well-defined and stable interest rate channel, the VAR framework allows monetary transmission to emerge endogenously from the data through observed dynamic interactions. As such, it provides a flexible and internally consistent framework for assessing how monetary policy shocks are absorbed, propagated, or attenuated through bank balance sheets and credit risk conditions.

4.2. Data and Variables

4.2.1. Data Selection

The empirical analysis relies on monthly macro-financial data spanning January 2014 to December 2024, yielding a total of 131 observations. This sample size reflects the maximum consistent and continuous data coverage that could be reliably constructed from official institutional sources, primarily the publications of Bank Al-Maghrib. The choice of this period is therefore not arbitrary, but constrained by data availability, methodological consistency, and the need to ensure homogeneity across all macro-financial variables included in the analysis.

The use of monthly data is particularly appropriate for the objectives of the study. Monetary policy decisions, liquidity management, portfolio reallocations, and credit risk adjustments are implemented and observed at relatively high frequencies within the banking system. Monthly observations allow the analysis to capture short-run dynamics and adjustment delays in banks’ balance sheets and lending behavior following monetary policy impulses, which would be obscured in lower-frequency (quarterly or annual) data.

The sample period includes 2020–2021, corresponding to an exceptional macro-financial episode marked by large-scale public intervention and unconventional policy measures in response to the COVID-19 shock. However, the empirical strategy does not explicitly segment the sample into pre-, during-, and post-COVID subperiods. This methodological choice is motivated by two considerations. First, given the monthly frequency, isolating the COVID episode would yield a limited number of observations, rendering separate dynamic estimations statistically fragile. Second, the primary objective of the study is not to evaluate crisis-specific policy measures, but rather to identify persistent and underlying mechanisms of monetary transmission and bank balance-sheet adjustment over the full sample period.

Accordingly, the COVID episode is treated as a transitory macro-financial disturbance embedded in the stochastic structure of the VAR model. Its effects are absorbed through the system’s average dynamics, without compromising the interpretation of short-run relationships or the validity of impulse response and forecast error variance decomposition analyses.

4.2.2. Variable Selection

Within this framework, the VAR model includes four key variables that capture the core dimensions of monetary transmission in a bank-based financial system.

First, bank credit to the non-financial corporate sector (CREDIT-NFCSₜ) is used as a proxy for credit allocated to the real economy. Focusing explicitly on the non-financial private sector allows the analysis to isolate productive lending activity and avoid confounding effects associated with interbank credit, financial institutions, or purely financial transactions. This choice is particularly important in the Moroccan context, where bank balance sheets contain significant financial-sector exposures that do not directly reflect real economic financing.

Second, banks’ holdings of Treasury securities (TBILLSₜ) capture portfolio allocation decisions and asset–liability management behavior. This variable reflects banks’ arbitrage between non-financial corporate sector lending and low-risk sovereign assets, a mechanism frequently emphasized in the literature on balance-sheet and portfolio channels of monetary transmission in emerging economies.

Third, the central bank policy rate (PRₜ) represents the conventional monetary policy instrument and serves as the primary indicator of monetary policy shocks within the VAR system.

Finally, the non-performing loan ratio (NPLRₜ) is introduced as an indicator of credit risk and asset quality. Including credit risk explicitly allows the analysis to account for the fact that lending decisions are conditioned not only by monetary policy signals, but also by banks’ perceptions of borrower risk and balance-sheet vulnerability.

Taken together, this variable selection ensures a coherent empirical representation of monetary policy, credit supply, portfolio allocation, and risk conditions, thereby allowing a comprehensive assessment of short-run monetary transmission mechanisms in a bank-based emerging economy

4.3. Time-Series Properties and Stationarity

The numerical series employed in this study exhibit heterogeneous statistical properties, which, in turn, necessitates differentiated transformations to ensure stationarity while at the same time preserving economic interpretability. Accordingly, this approach follows standard time-series econometric practice aimed at avoiding spurious regressions and ensuring valid inference in VAR models (Granger & Newbold, 1974; Sims, 1980; Hamilton, 1994; Lütkepohl, 2005).

In particular, the volume variables bank credit to non-financial corporate sector ((CREDIT-NFCSₜ) and banks’ holdings of Treasury securities (TBILLSₜ) are expressed in nominal levels and display strong persistence and stochastic trends, which is a common feature of macro-financial aggregates observed at monthly frequency. Therefore, to eliminate non-stationarity and stabilize conditional variance, both series are transformed into logarithmic first differences, which can be interpreted as growth rates:

As a result, these transformations remove unit roots while preserving economically meaningful information on short-run dynamics and proportional changes in credit volumes and portfolio allocations. In this sense, interpreting the series in growth rates is particularly appropriate in the context of monetary transmission analysis, since the focus lies on short-term adjustments rather than on long-run levels.

By contrast, variables expressed in rates namely the central bank policy rate (PRₜ) and the non-performing loan ratio (NPLRₜ) exhibit different stochastic properties. Although bounded by definition, these series display persistence at monthly frequency and are therefore transformed by first differencing in order to capture short-run adjustments and deviations from trend:

This treatment ensures that all variables included in the VAR system are stationary, thereby satisfying the key assumptions required for consistent estimation, valid impulse response analysis, and reliable forecast error variance decomposition.

Overall, the combination of logarithmic differencing for volume variables and first differencing for rate variables provides a coherent and parsimonious transformation strategy. In doing so, it allows the VAR model to focus on short-run monetary transmission mechanisms, balance-sheet adjustments, and credit risk dynamics, while simultaneously avoiding distortions associated with non-stationary data.

4.4. Stationarity Tests

Prior to any dynamic estimation, the stationarity of the transformed series is systematically assessed using two complementary unit root tests. First, the Augmented Dickey–Fuller (ADF) test is implemented with an intercept and lag length selected according to the Schwarz Information Criterion (SIC). Second, the Phillips–Perron (PP) test is employed as a robustness check, as it is resilient to heteroskedasticity and serial correlation through a Newey–West heteroskedasticity and autocorrelation consistent (HAC) correction.

4.5. VAR Model Specification

Given the homogeneous stationarity of the transformed variables, the empirical analysis relies on a Vector Autoregressive (VAR) framework specified in stationary form. The VAR approach provides a flexible representation of the joint dynamics among macro-financial variables, allowing for feedback effects and endogenous interactions without imposing a priori structural restrictions on causal relationships.

The vector of endogenous variables is defined as:

With

- -

- : Measures the growth rate of bank credit to the non-financial corporate sector. This variable captures short-run adjustments in credit supply and represents the main indicator of how bank lending responds to monetary and financial shocks.

- -

- : Represents the growth rate of banks’ holdings of Treasury bills. It reflects banks’ portfolio allocation decisions, particularly the arbitrage between lending to the private sector and investment in low-risk sovereign assets.

- -

- : Denotes the change in the central bank policy rate and captures the monetary policy shock transmitted to the banking system.

- -

- : Measures the change in the non-performing loan ratio, serving as an indicator of credit risk conditions and asset quality, which may influence lending behavior independently of interest rate movements.

The general VAR model of order is given by:

where denotes a vector of intercepts, are coefficient matrices to be estimated, and is a vector of reduced-form innovations assumed to be serially uncorrelated with constant variance.

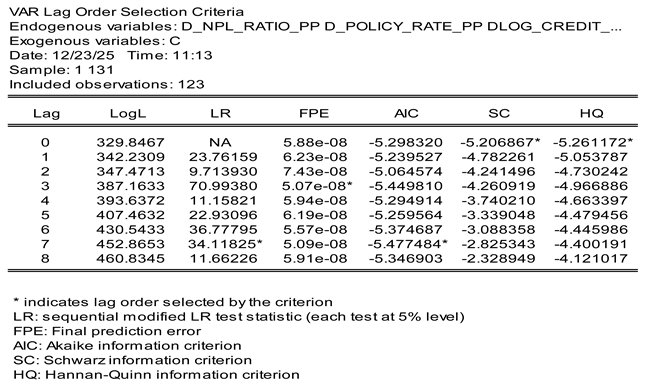

4.6. Lag Length Selection

The optimal lag length is selected based on a set of standard information criteria, including the Akaike Information Criterion (AIC), the Schwarz Information Criterion (SC), and the Hannan–Quinn Criterion (HQ), and is further complemented by the sequential likelihood ratio (LR) test. These criteria are jointly evaluated while explicitly accounting for the monthly frequency of the data and the finite sample size, in order to balance model fit and parsimony.

The results indicate some divergence across the criteria. On the one hand, the Schwarz and Hannan–Quinn criteria favor a specification without lag, reflecting primarily contemporaneous interactions once stationarity is ensured. On the other hand, the Akaike criterion and the LR test point to a richer dynamic structure. In this context, a VAR(1) specification is retained as the baseline model, as it represents the minimal dynamic structure compatible with both statistical robustness and economic plausibility.

Beyond purely econometric considerations, this choice is grounded in the institutional and operational characteristics of monetary transmission in bank-based financial systems. In practice, banks’ lending and portfolio decisions do not adjust instantaneously following changes in monetary policy. Credit allocation typically involves internal decision-making processes such as credit committee deliberations, risk assessments, and balance-sheet optimization—that introduce short but economically meaningful adjustment delays. At a monthly frequency, these institutional frictions justify the inclusion of at least one lag to capture short-run transmission dynamics.

Moreover, banks’ asset and liability management decisions, particularly the arbitrage between private-sector loans and sovereign securities, are generally implemented over monthly horizons. These decisions reflect liquidity management cycles, regulatory reporting schedules, and internal risk-monitoring practices. Consequently, monetary policy shocks are expected to affect bank balance sheets with a short delay, even in the absence of strong autoregressive persistence.

From an econometric perspective, maintaining a minimal dynamic structure is also necessary to ensure model admissibility, enable standard diagnostic testing, and allow for meaningful impulse response and forecast error variance decomposition analyses (Hamilton, 1994; Lütkepohl, 2005). In line with methodological recommendations for small and medium-sized samples, the VAR(1) specification offers a parsimonious representation that preserves interpretability while avoiding overparameterization (Stock & Watson, 2001; Canova, 2007).

Accordingly, the VAR(1) model is interpreted as capturing short-run adjustment dynamics rather than persistent autoregressive behavior. As such, it is particularly well suited to analyzing monetary policy transmission when the focus lies on the timing and magnitude of banks’ immediate responses to policy impulses, rather than on long-term equilibrium relationships.

4.7. Diagnostic Tests of the VAR Model

Diagnostic tests are treated as integral components of the empirical strategy rather than as post-estimation formalities. Accordingly, a set of standard diagnostic checks is conducted to assess the econometric adequacy of the VAR specification prior to dynamic analysis, in line with established practices in applied macroeconometrics (Sims, 1980; Hamilton, 1994; Lütkepohl, 2005).

The stability of the VAR system is first examined by verifying that all eigenvalues of the companion matrix lie strictly within the unit circle. This condition ensures that the VAR is dynamically well behaved and that its moving-average representation exists, which is a necessary requirement for impulse response functions (IRFs) and forecast error variance decompositions (FEVDs) to be well defined and interpretable (Sims, 1980; Lütkepohl, 2005).

Residual autocorrelation tests are then employed to evaluate whether the selected lag structure adequately captures short-run dynamics at a monthly frequency. The absence of serial correlation in the residuals indicates that the model successfully absorbs the temporal dependence present in the data and that no systematic dynamics remain unmodeled (Box & Pierce, 1970; Lütkepohl, 2005).

Tests for heteroskedasticity and normality are also conducted as part of the diagnostic assessment. In macro-financial VAR applications, departures from Gaussian residuals are common and typically reflect fat-tailed distributions and infrequent large shocks rather than structural misspecification (Hamilton, 1994; Kilian, 1998). As a result, statistical inference for IRFs and FEVDs is based on Monte Carlo simulation techniques, which provide more reliable confidence intervals under non-normal innovations and finite-sample conditions (Sims & Zha, 1999; Kilian & Lütkepohl, 2017).

Overall, the diagnostic analysis validates the admissibility of the reduced-form VAR framework and delineates the scope of inference, ensuring that subsequent results are interpreted as short-run dynamic relationships rather than long-run structural effects.

4.8. Dynamic Analysis

Impulse response functions (IRFs) are employed to analyze the dynamic effects of an exogenous one-unit shock to the variables included in the VAR system. Starting from the moving-average representation of the estimated VAR model, IRFs trace the time path of each endogenous variable following an innovation to one element of the reduced-form disturbance vector. This framework has become standard in empirical macroeconomics and monetary analysis, as it allows researchers to assess the timing, magnitude, and persistence of dynamic adjustments to structural shocks (Sims, 1980; Christiano et al., 2005).

4.8.1. Identification Strategy: Cholesky Decomposition

Given the reduced-form nature of the VAR model, identifying economically interpretable shocks requires an orthogonalization of the residuals. In this study, innovations are identified using a recursive Cholesky decomposition of the variance–covariance matrix of reduced-form residuals. This approach imposes a contemporaneous causal ordering among variables that is consistent with conventional monetary transmission mechanisms, whereby monetary policy and financial market variables are assumed to be predetermined within the period, while bank credit responds with a delay due to contractual rigidities, information frictions, and internal risk assessment procedures.

The Cholesky identification scheme is widely used in the empirical monetary policy literature because it offers a transparent and parsimonious structure in settings where strong external instruments or credible sign restrictions are unavailable (Sims, 1980). Christiano, et al 2005) demonstrate that recursive identification provides reliable estimates of monetary policy effects when the ordering is theoretically grounded and robust to reasonable permutations. In bank-based financial systems, where credit aggregates display high persistence and sluggish contemporaneous adjustment, the recursive assumption is particularly appropriate (Eddani, 2024).

Moreover, alternative structural identification strategies such as long-run restrictions or fully specified SVARs often require stronger assumptions that are difficult to justify empirically in emerging economies with limited data availability. By contrast, the Cholesky approach avoids over-identification risks and allows for a coherent interpretation of both impulse responses and variance decompositions within a reduced-form framework (Stock & Watson, 2001; Lütkepohl, 2005).

4.8.2. Forecast Error Variance Decomposition (FEVD)

To complement the IRF analysis, forecast error variance decomposition (FEVD) is employed to quantify the relative importance of each orthogonalized shock in explaining the forecast error variance of bank credit at different horizons. Formally, the FEVD decomposes the h-step-ahead forecast error variance of an endogenous variable into components attributable to each structural innovation derived from the Cholesky factorization of the residual variance–covariance matrix (Lütkepohl, 2005).

The FEVD provides a synthetic and intuitive measure of shock dominance within the system, allowing for a hierarchical assessment of monetary policy shocks, financial market disturbances, credit risk innovations, and credit-specific dynamics. In the context of monetary transmission, FEVDs are particularly useful for evaluating whether policy rate shocks play a quantitatively meaningful role relative to balance-sheet and risk channels (Bernanke et al., 1999; Cloyne et al., 2023).

4.8.3. Inference: Monte Carlo Confidence Intervals (10,000 Replications)

Inference on impulse responses and variance decompositions is conducted using Monte Carlo confidence intervals based on 10,000 replications. The reliance on simulation-based inference is strongly motivated by the econometric literature. As shown by Sims and Zha (1999) and Kilian (1998), asymptotic approximations for IRFs and FEVDs can be misleading in small and medium samples, especially when variables are persistent or when residuals deviate from normality features commonly observed in macro-financial data.

Monte Carlo simulations approximate the finite-sample distribution of nonlinear VAR statistics by repeatedly drawing from the estimated residual distribution and re-estimating the model. This approach allows for more accurate confidence bands than analytical methods, particularly when the VAR includes highly autocorrelated series or when the sample size is limited (Lütkepohl, 2005; Kilian & Lütkepohl, 2017).

The choice of 10,000 replications reflects a trade-off between computational feasibility and numerical precision. The econometric literature suggests that a large number of replications is necessary to ensure smooth and stable confidence intervals and to minimize simulation error (Doan, 2019; Kilian & Lütkepohl, 2017). Accordingly, the use of 10,000 replications aligns with best practices in recent high-quality empirical studies and enhances the robustness and credibility of the dynamic inference.

4.8.4. Granger Causality as a Complementary Diagnostic

As an additional robustness check, Granger causality tests are conducted following the dynamic analysis. While IRFs and FEVDs focus on dynamic propagation and shock importance, Granger causality tests assess predictive relationships based on lagged information. Consistent with the reduced-form VAR framework, Granger causality is not interpreted as evidence of structural causation but rather as a complementary diagnostic tool capturing short-run lead–lag relationships (Granger, 1969; Hamilton, 1994).

Accordingly, the core empirical conclusions of the study are derived from impulse response functions and forecast error variance decompositions, with Granger causality results playing a secondary, confirmatory role in supporting the interpretation of short-run monetary transmission dynamics.

5. Results

5.1. Unit Root and Stationarity Tests

The unit root properties of the variables are examined using both the Augmented Dickey–Fuller (ADF) and Phillips–Perron (PP) tests. The results, reported in Table 1, indicate that all variables become stationary after appropriate transformations.

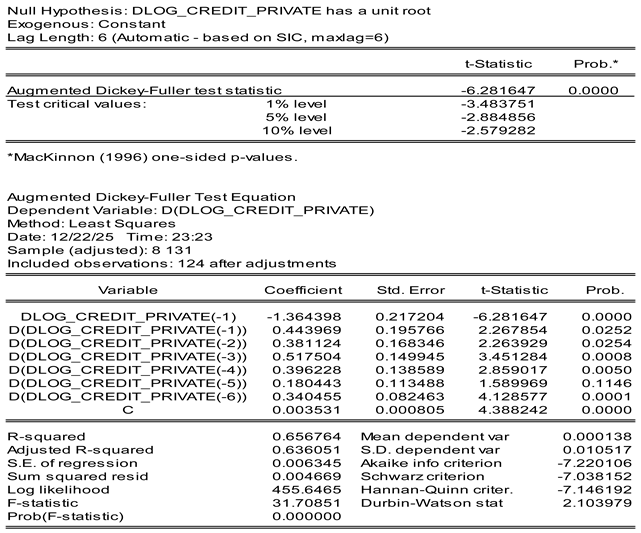

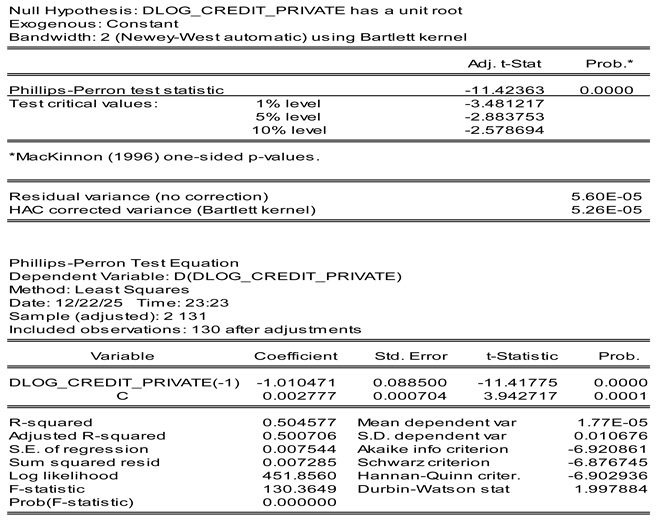

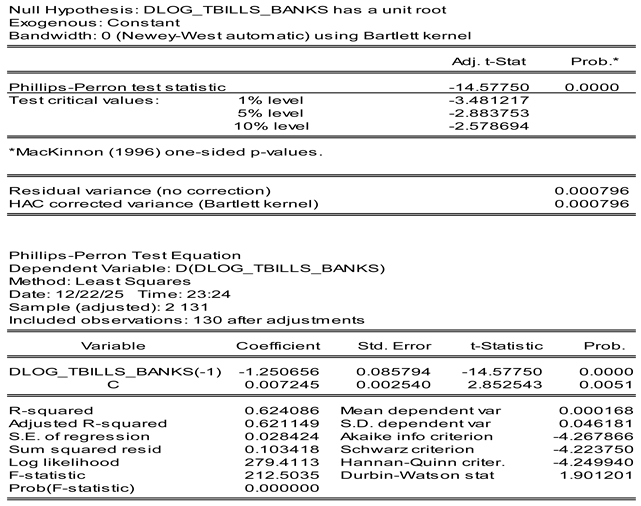

For volume variables namely bank credit to the private sector and Treasury securities held by banks stationarity is achieved after first differencing in logarithms. The ADF statistics for Δlog(CREDIT) and Δlog(TBILLS_BANKS) are −6.28 and −14.58, respectively, while the corresponding PP statistics equal −11.42 and −14.58. In both cases, the null hypothesis of a unit root is strongly rejected at the 1% significance level.

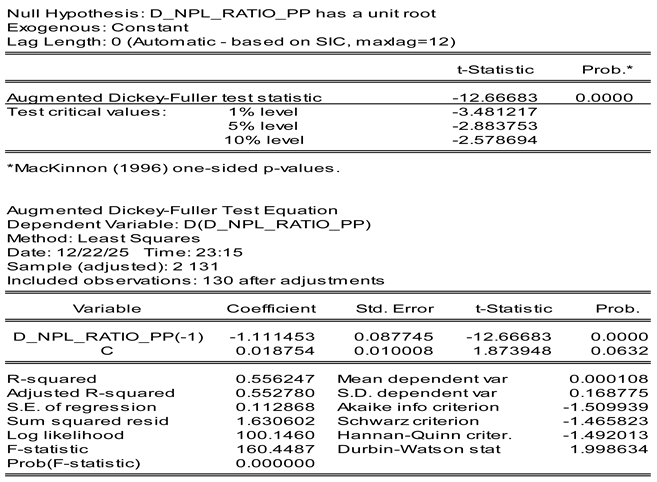

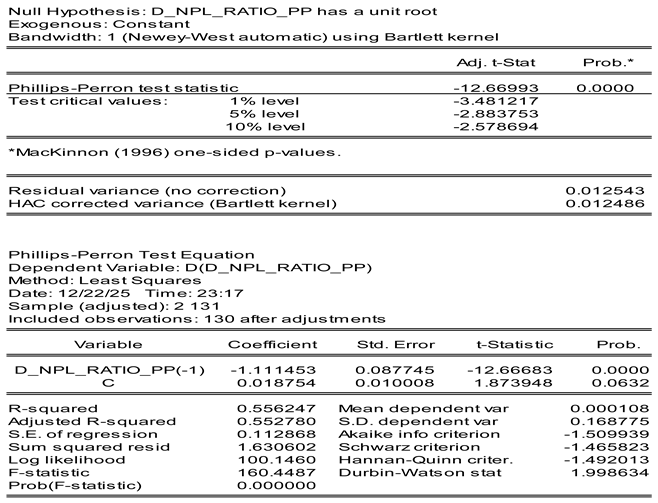

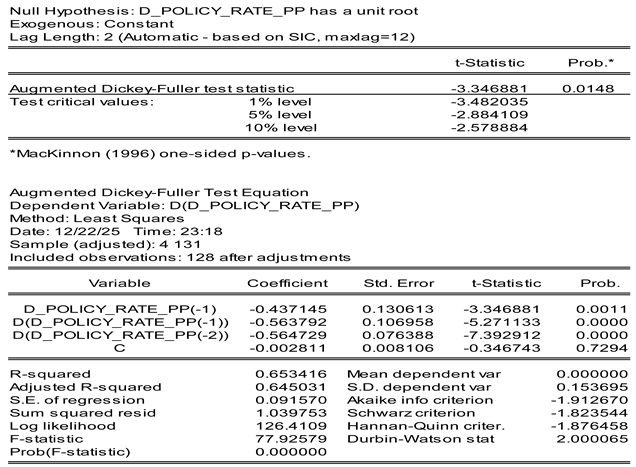

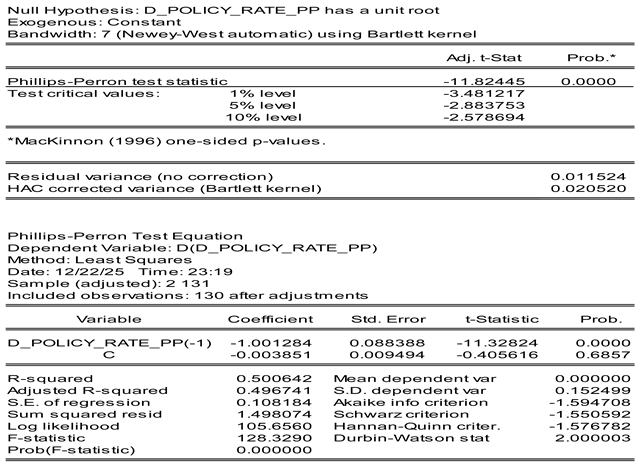

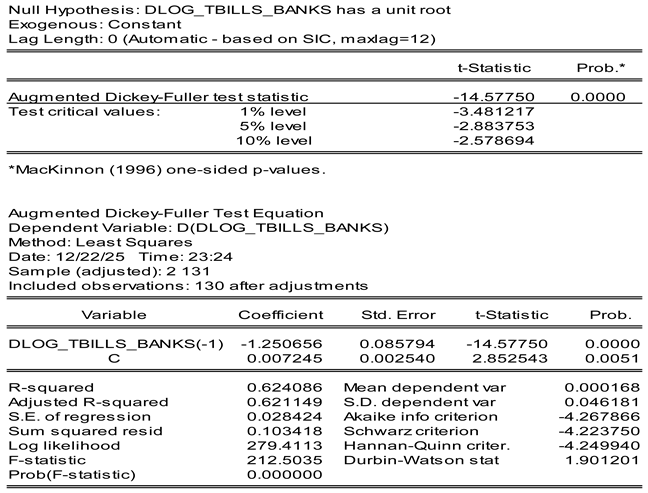

Variables expressed in rates, including the policy rate and the non-performing loan (NPL) ratio, become stationary after first differencing in levels. The policy rate exhibits ADF and PP statistics of −12.67, both significant at the 1% level. For the NPL ratio, the ADF statistic equals −3.35 (p = 0.015), while the PP statistic reaches −11.82 (p < 0.001). Although the ADF statistic is smaller in absolute value, the joint evidence from both tests confirms stationarity after transformation.

Across all variables, the consistency between ADF and PP test results supports the robustness of the stationarity assessment. All transformed series are therefore classified as I(0), ruling out concerns related to spurious regression and eliminating the need for cointegration-based specifications. This result provides a sound econometric basis for estimating the VAR model in stationary form and ensures that subsequent impulse response and variance decomposition analyses capture short-run dynamic interactions rather than long-run equilibrium relationships.

Note: Δlog denotes the first difference of the logarithm, while Δ denotes first differencing in levels. The null hypothesis of a unit root is rejected at least at the 5% significance level for all transformed series.

5.2. VAR Model Specification

5.2.1. Lag Length Selection and Model Estimation

Lag length selection results reported in Table 2 indicate a divergence across standard information criteria. The Schwarz Information Criterion (SC) and the Hannan–Quinn Criterion (HQ) both reach their minimum at lag zero, thereby favoring a highly parsimonious contemporaneous specification. In contrast, the Akaike Information Criterion (AIC) and the sequential likelihood ratio (LR) test point toward richer dynamic structures, with the AIC attaining its minimum at lag seven and the LR test remaining significant at higher lag orders.

Such divergence across criteria is common in multivariate VAR models estimated on finite samples, particularly at a monthly frequency. While the AIC and LR test are designed to capture additional short-run dynamics, they also impose weaker penalties on model complexity. Conversely, the SC and HQ criteria place greater weight on parsimony and consistency, thereby favoring more compact specifications.

In this context, a VAR(1) specification is retained as the baseline model. This choice reflects a deliberate compromise between statistical parsimony and the need to capture short-run dynamics. From an econometric standpoint, the inclusion of at least one lag is required to ensure model admissibility and to allow the computation of impulse response functions and forecast error variance decompositions. From an economic standpoint, monetary policy transmission through banking systems is unlikely to be fully contemporaneous, even at a monthly frequency, given the presence of short adjustment delays in balance-sheet and portfolio decisions.

Accordingly, the VAR(1) model is interpreted as capturing minimal short-run adjustment dynamics rather than persistent autoregressive behavior. This specification preserves degrees of freedom, avoids over-parameterization, and remains well suited for the analysis of short-horizon monetary transmission mechanisms.

5.2.2. VAR Estimation Results and Short-Term Interactions

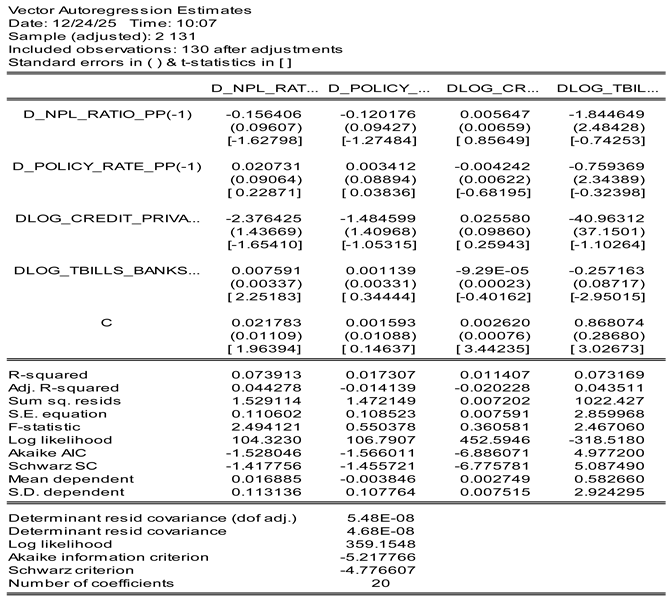

Once stationarity is ensured, the VAR(1) estimation provides insights into short-run dynamic interactions among monetary policy, bank balance-sheet variables, credit risk, and non-financial corporate sector credit. As expected in a short-horizon VAR estimated on differenced monthly data, most individual lagged coefficients exhibit limited statistical significance.

In the credit equation, none of the lagged explanatory variables is statistically significant. In particular, lagged changes in the policy rate (β = −0.004; t = −0.68) and in banks’ holdings of Treasury securities (β = 0; t = −0.40) do not exert a measurable delayed effect on non-financial corporate sector credit growth. This result indicates that, at a monthly frequency, aggregate credit volumes do not respond through linear lagged adjustments to monetary or balance-sheet shocks within the VAR framework.

By contrast, balance-sheet and risk-related variables display more pronounced short-run dynamics. Lagged changes in banks’ holdings of Treasury securities exert a positive and statistically significant effect on the non-performing loan ratio (β = 0.007; t = 2.25), pointing to short-run co-movements between portfolio reallocations and observed credit-risk conditions. In addition, Treasury-bill growth exhibits a significant negative own-lag coefficient (β = −0.257; t = −2.95), consistent with short-term mean-reverting dynamics and active balance-sheet management.

Overall, the relatively low R2 values, which are typical of VAR models estimated in first differences at a monthly frequency, suggest that short-run interdependence is not primarily captured by individual lagged coefficients. Instead, dynamic interactions are expected to materialize through the joint propagation of shocks, which is examined in the subsequent impulse response and variance decomposition analyses.

|

Explanatory variable (t−1) |

ΔNPLRₜ | ΔPRₜ | Δlog(CREDIT-NFCS)ₜ | Δlog(TBILLS)ₜ |

| ΔNPLRₜ₋1 | −0.156(0.096) | −0.120(0.094) | 0.006 (0.007) | −1.844 (2.484) |

| [−1.63] | [−1.27] | [0.86] | [−0.74] | |

| ΔPRₜ₋1 | 0.021 (0.091) | 0.003 (0.089) | −0.004 (0.006) | −0.759 (2.344) |

| [0.23] | [0.04] | [−0.68] | [−0.32] | |

| Δlog(CREDIT-NFCS)ₜ₋1 | −2.376 (1.437) | −1.485 (1.410) | 0.026 (0.099) | −40.963 (37.150) |

| [−1.65] | [−1.05] | [0.26] | [−1.10] | |

| Δlog(TBILLS)ₜ₋1 | 0.008 (0.003) | 0.001 (0.003) | −0.0001(0.0002) | −0.257 (0.087) |

| [2.25] | [0.34] | [−0.40] | [−2.95] | |

| Constant | 0.022 (0.011) | 0.002 (0.011) | 0.003 (0.001) | 0.868 (0.287) |

| [1.96] | [0.15] | [3.44] | [3.03] | |

| R2 | 0.074 | 0.017 | 0.011 | 0.073 |

| Observations | 130 | 130 | 130 | 130 |

Source: Authors’ calculations based on Bank Al-Maghrib data.

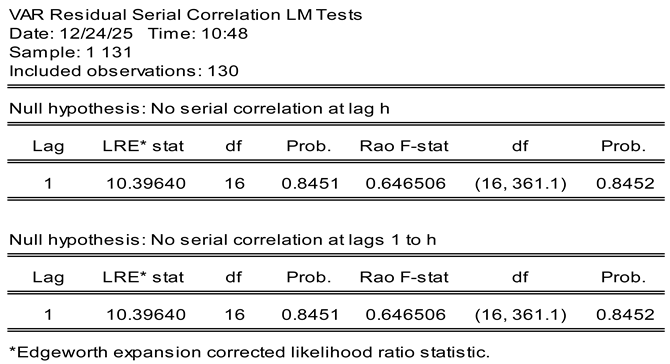

5.2.3. Residual Serial Correlation and VAR Model Admissibility

The presence of residual serial correlation is examined using the multivariate Lagrange Multiplier (LM) test. The results reported in Table 4 indicate that the null hypothesis of no residual autocorrelation cannot be rejected at lag 1. Specifically, the likelihood ratio statistic (LR = 10.396, p = 0.845) and the Rao F-statistic (F = 0.647, p = 0.845) both display high p-values, well above conventional significance thresholds.

These findings indicate that the VAR(1) specification adequately accounts for short-run serial dependence in the data and that no significant residual autocorrelation remains. As a result, the model satisfies a key admissibility condition for multivariate time-series analysis.

The absence of residual serial correlation ensures that the impulse response functions and forecast error variance decompositions derived from the VAR model are statistically well defined and are not distorted by omitted lag dynamics. This diagnostic result supports the use of the selected VAR specification for subsequent short-run dynamic analysis.

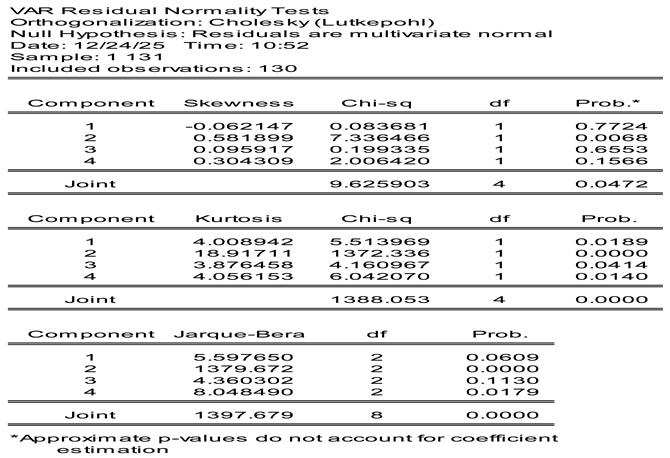

5.2.4. Residual Diagnostics and Robustness of Statistical Inference

The distributional properties of the VAR residuals are examined using multivariate normality tests. The results reported in Table 5 indicate a clear rejection of the null hypothesis of Gaussian residuals at the system level. The joint skewness statistic is statistically significant at the 5% level (χ2 = 9.626, p = 0.047), suggesting the presence of moderate asymmetry in the residual distribution. However, skewness remains relatively limited across most individual components.

Deviations from normality are primarily driven by excess kurtosis. The joint kurtosis statistic is overwhelmingly significant (χ2 = 1388.053, p = 0.000), revealing pronounced fat-tailed behavior in the residuals. This result is largely attributable to one component of the system, which exhibits extremely high kurtosis values, reflecting the presence of infrequent but large macro-financial shocks. Such features are well documented in macro-financial time series, particularly in monthly data subject to crisis episodes and policy interventions.

As a consequence, the joint Jarque–Bera statistic strongly rejects multivariate normality (JB = 1397.679, p = 0.000). Importantly, this rejection should not be interpreted as evidence of model misspecification. Non-Gaussian innovations are a common characteristic of VAR models applied to financial and macroeconomic variables and do not invalidate the consistency of parameter estimates, provided that residual serial correlation is absent and the stability condition is satisfied.

Nevertheless, departures from normality may affect standard asymptotic inference. To address this issue and to ensure robust statistical inference in the presence of fat-tailed shocks and finite-sample uncertainty, impulse response functions and forecast error variance decompositions are computed using Monte Carlo simulation methods. This approach allows the construction of confidence intervals that are robust to non-Gaussian residuals and is consistent with best practices in applied macroeconometric analysis.

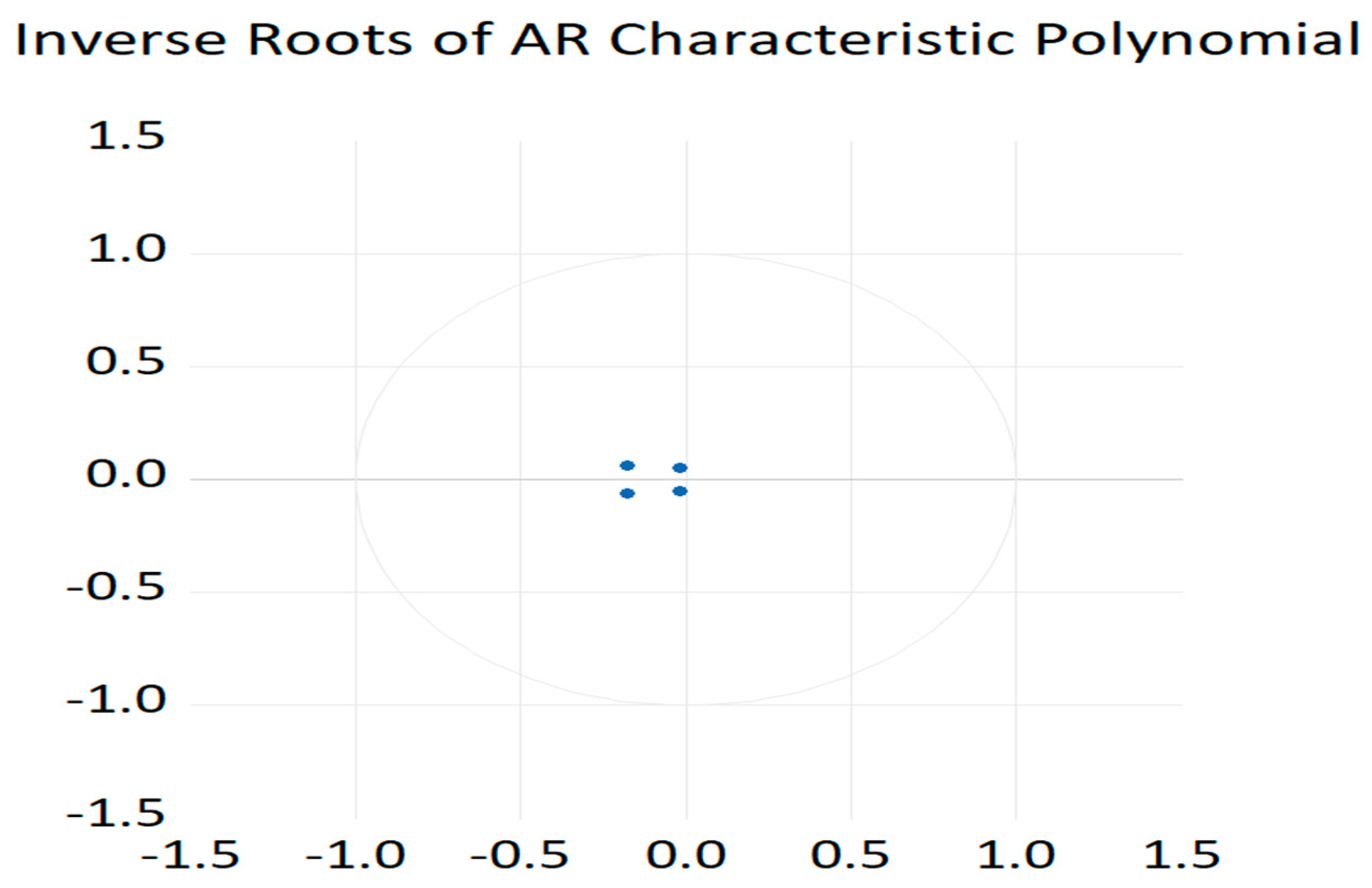

5.2.5. Stability Test of the VAR(1) Model

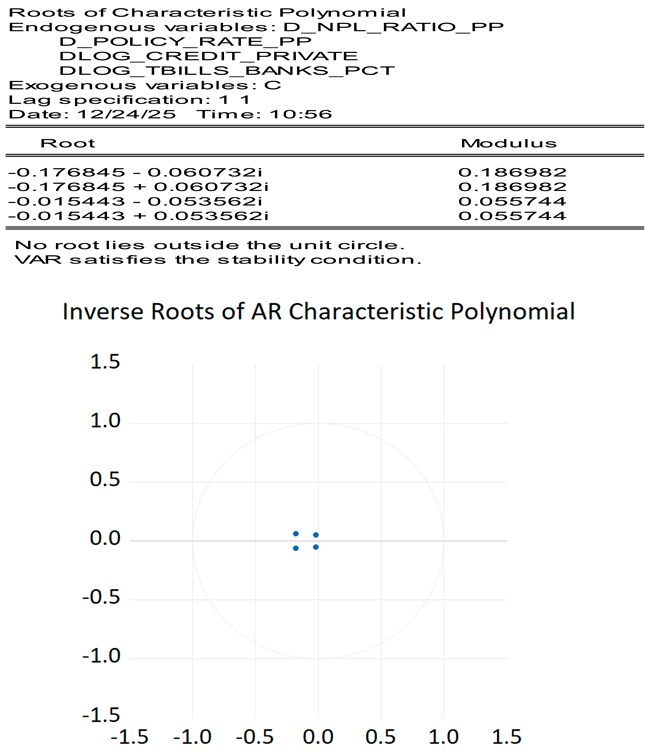

The stability of the estimated VAR(1) model is assessed by examining the roots of the characteristic polynomial. As reported in Table 6, all roots lie strictly within the unit circle, with moduli ranging from 0.0557 to 0.1870. The largest modulus (0.1870) remains well below unity, thereby confirming that the VAR system satisfies the stability condition.

This result indicates that the estimated VAR represents a stationary and dynamically stable system, in which the effects of shocks decay over time rather than generating explosive or non-convergent dynamics. The stability condition ensures that impulse response functions and forecast error variance decompositions derived from the model are well defined and can be meaningfully interpreted.

Importantly, the confirmation of stability supports the econometric admissibility of the selected VAR(1) specification, despite the limited lag dependence suggested by some information criteria. A minimal dynamic structure is therefore sufficient to capture short-run interactions without introducing spurious persistence or over-parameterization.

Overall, the stability diagnostics indicate that the estimated VAR provides a coherent and reliable framework for analyzing short-run dynamic interactions among monetary policy, bank balance-sheet variables, and credit risk within the scope of the empirical analysis.

Figure 1displays the inverse roots of the autoregressive characteristic polynomial. All roots lie well within the unit circle, confirming the dynamic stability of the estimated VAR(1) model.

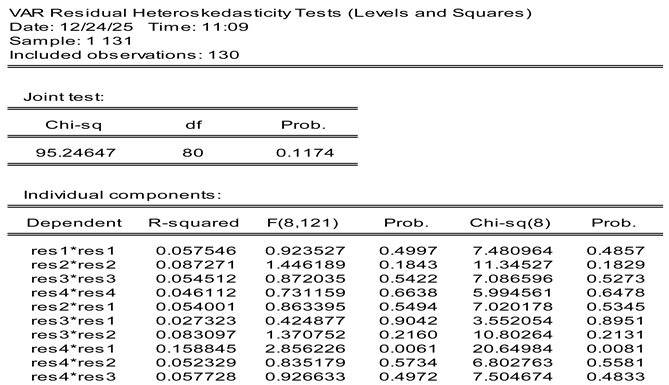

5.2.6. White Test for Residual Heteroskedasticity in the VAR Model

Residual heteroskedasticity in the VAR(1) model is examined using the multivariate White test. At the system level (Panel A), the joint test statistic yields a χ2 value of 95.246 with 80 degrees of freedom and a corresponding p-value of 0.117. As this p-value exceeds conventional significance thresholds, the null hypothesis of homoskedastic residuals cannot be rejected. This result indicates the absence of pervasive variance instability jointly affecting the VAR system.

Panel B reports equation-specific residual components and cross-product terms. Consistent with the system-wide result, the majority of individual variance terms and interaction effects are statistically insignificant. In particular, the squared residuals associated with the policy rate, non-financial private-sector credit growth, Treasury bill holdings, and the non-performing loan ratio display p-values well above 0.10 under both F-statistics and χ2 tests, suggesting no systematic variance instability at the equation level.

Regarding cross-product terms, most interactions between monetary, credit, and portfolio variables remain statistically insignificant, indicating limited evidence of generalized volatility spillovers across equations. One exception arises for the interaction between changes in the non-performing loan ratio and the policy rate, which is statistically significant. This result points to a localized variance interaction between credit risk conditions and monetary policy movements. However, as this effect is isolated and does not extend across other residual components, it does not overturn the system-level conclusion of homoskedasticity. Such localized significance is commonly observed in macro-financial VAR applications and typically reflects episodic volatility clustering rather than structural misspecification.

Overall, the combined evidence from the system-wide and equation-specific tests supports the conclusion that the VAR(1) model does not exhibit pervasive residual heteroskedasticity. Consequently, coefficient estimates remain reliable, while inference based on standard asymptotic assumptions may be affected by residual non-normality. For this reason, Monte- Carlo based confidence intervals are employed for impulse response functions and forecast error variance decompositions to ensure robust inference in finite samples.

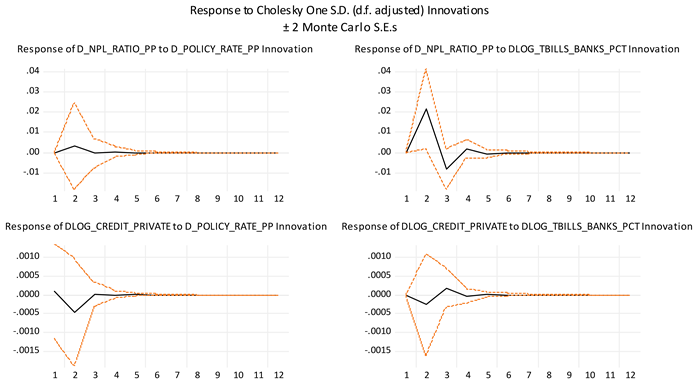

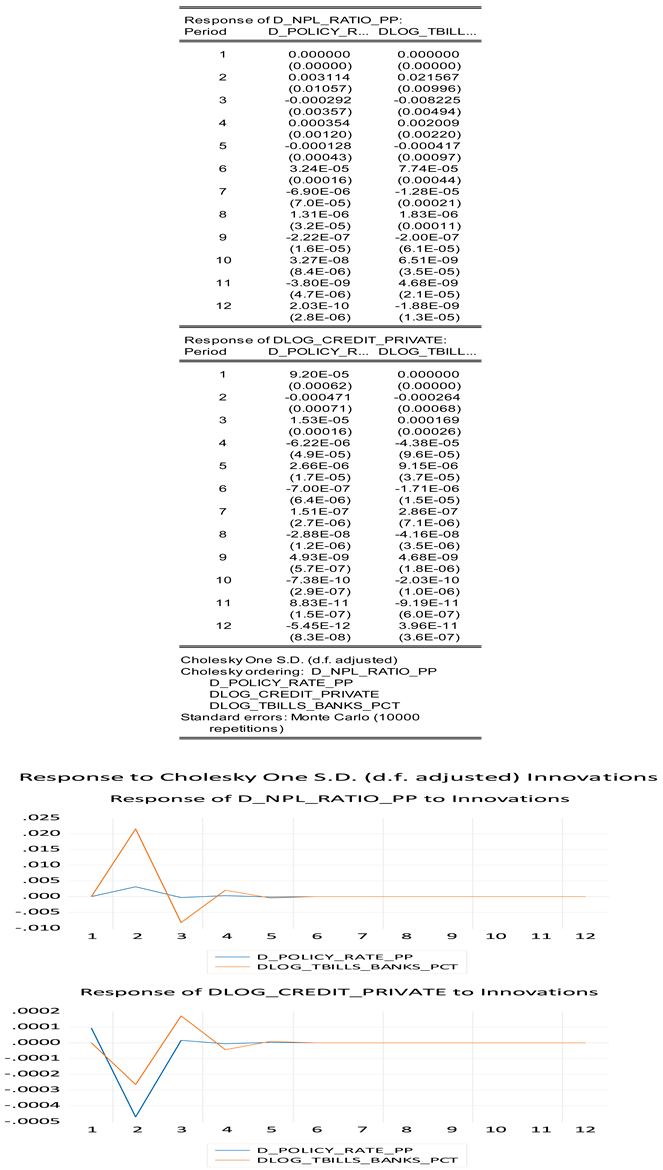

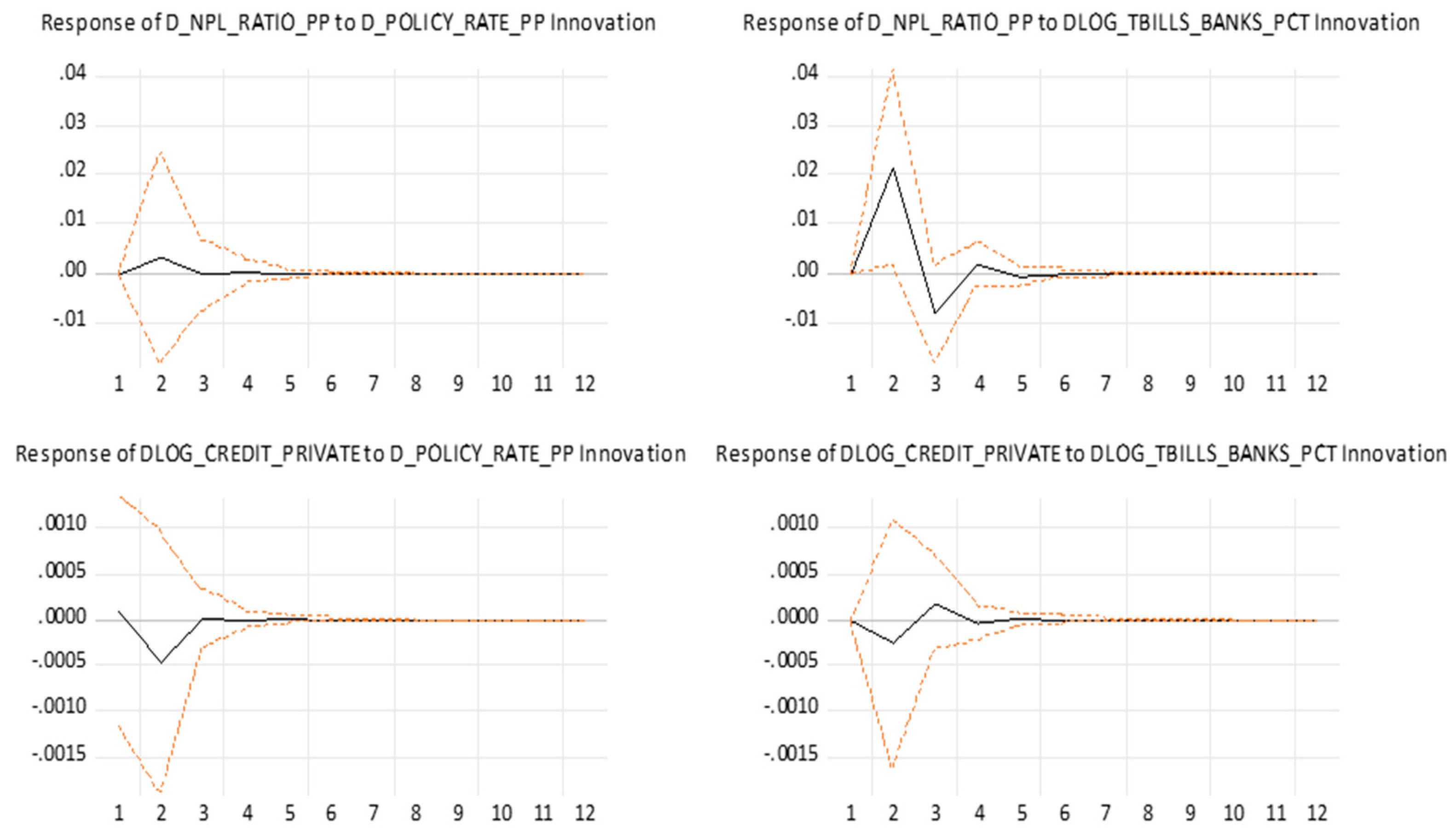

5.3. Impulse Response Functions

Impulse response functions are used to examine the short-run dynamic effects of monetary policy and balance-sheet shocks within the VAR(1) system. All responses are reported for a one-standard-deviation innovation and are evaluated over a short horizon.

Following a policy-rate shock, the non-performing loan (NPL) ratio exhibits a modest and short-lived response. The reaction reaches a small positive peak at the second period (approximately 0.0031), turns slightly negative in the subsequent period, and rapidly converges toward zero. By the fifth period, the response becomes economically negligible. No evidence of persistent effects on credit risk is observed.

In comparison, shocks to banks’ holdings of Treasury bills generate a quantitatively larger response in the NPL ratio. The response peaks at the second period at approximately 0.0216, before reversing sharply and dissipating over subsequent periods. Despite its larger magnitude, this response also remains transitory and converges toward zero within a few periods.

The responses of non-financial private-sector credit growth to both monetary policy shocks and Treasury-bill shocks are uniformly weak across all horizons. Following a policy-rate innovation, the maximum response occurs at the second period and does not exceed −0.00047, after which it quickly attenuates. Similarly, a Treasury-bill shock generates a very small positive response, peaking at approximately 0.00026, followed by negligible oscillations. In all cases, the magnitude of the credit responses remains economically insignificant and exhibits no persistence.

Overall, the impulse response analysis indicates that short-run dynamic adjustments following monetary and balance-sheet shocks are concentrated primarily in risk and portfolio-related variables, while aggregate private-sector credit volumes display minimal short-run responsiveness.

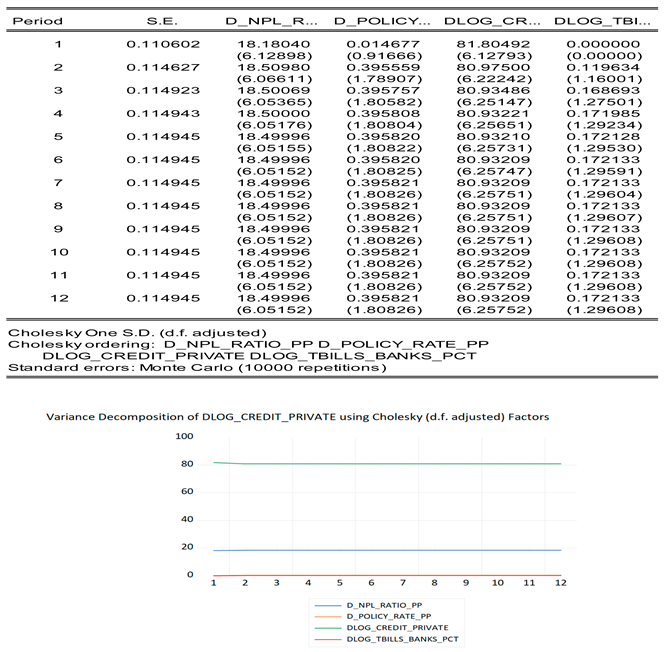

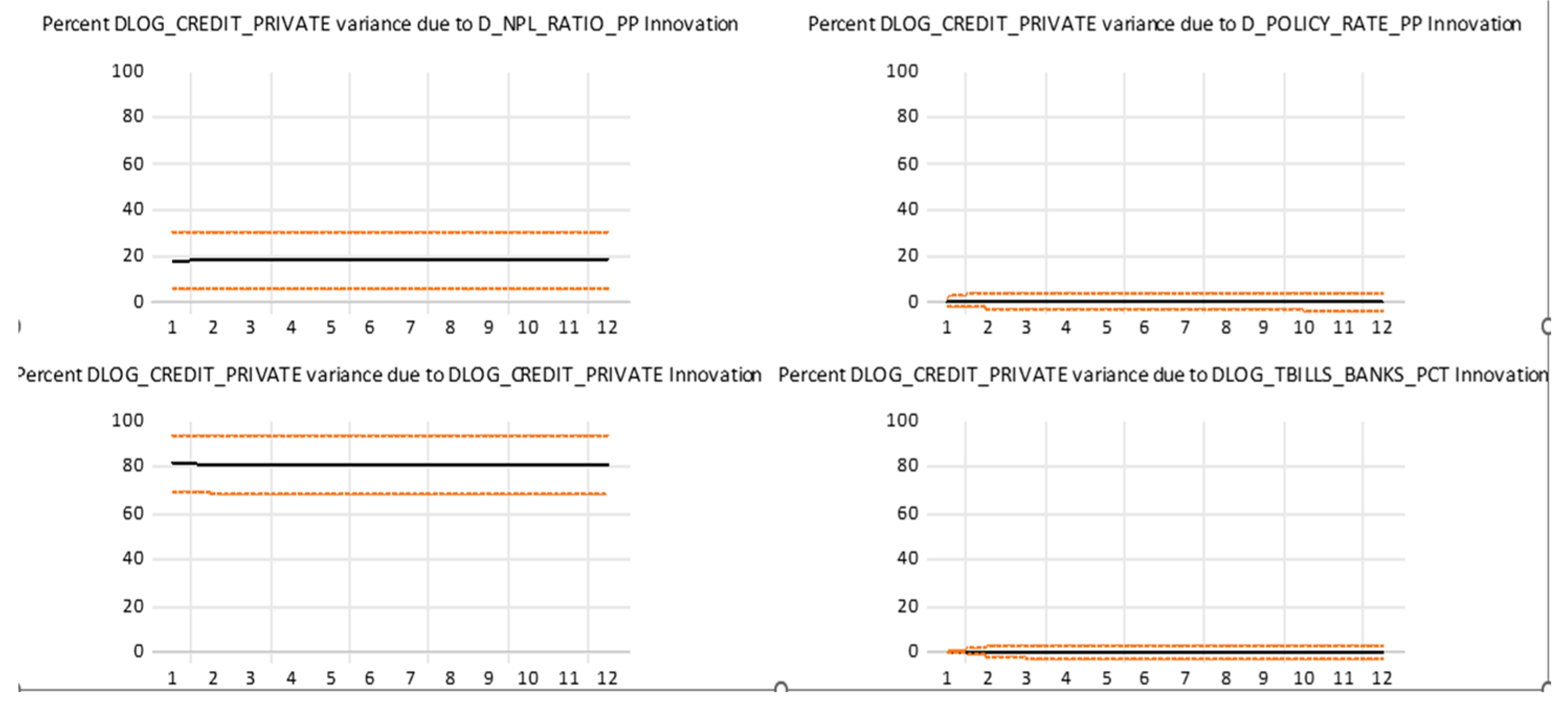

5.4. Forecast Error Variance Decomposition Results

To complement the impulse response analysis, a forecast error variance decomposition (FEVD) of non-financial private-sector credit growth is conducted based on the reduced-form VAR identified through a Cholesky decomposition. The FEVD evaluates the relative contribution of shocks to monetary policy, credit risk conditions, banks’ sovereign exposure, and credit’s own innovations in explaining fluctuations in Δlog(CREDIT-NFCS) over a 12-period horizon.

The results indicate a pronounced dominance of own-credit shocks. Across all forecast horizons, innovations specific to Δlog(CREDIT-NFCS) account for approximately 78–82% of the total forecast error variance. This contribution remains remarkably stable over time, indicating that credit dynamics are largely driven by shocks intrinsic to the credit process itself.

Credit risk shocks, proxied by changes in the non-performing loan ratio, constitute the second most important source of variation. These shocks explain approximately 16–18% of the forecast error variance of private-sector credit, with their contribution exhibiting a slight increase at medium horizons.

By contrast, monetary policy shocks, captured by innovations in the policy rate, contribute only marginally to fluctuations in private-sector credit growth. Their share of explained variance remains consistently below 2% throughout the forecast horizon. Similarly, shocks related to banks’ holdings of Treasury bills account for only a small fraction of credit variance.

Overall, the FEVD results highlight a clear hierarchy in the sources of short- to medium-term fluctuations in private-sector credit growth, with dominant contributions from own-credit innovations, followed by credit risk shocks, and only limited contributions from monetary policy and portfolio-related shocks.

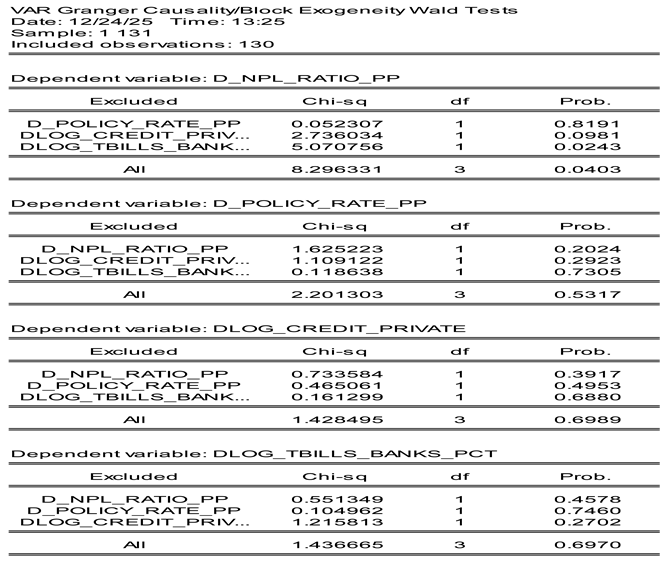

5.5. Granger Causality Results

Granger causality tests are conducted to examine short-run predictive relationships among monetary policy, bank balance-sheet variables, credit risk, and private-sector credit within the VAR(1) framework. The results are reported in Table 9.

The analysis indicates that changes in banks’ holdings of Treasury bills Granger-cause variations in the non-performing loan ratio. The null hypothesis of non-causality is rejected at the 5% significance level (χ2 = 5.071, p = 0.024), suggesting that past movements in sovereign portfolio positions contain predictive information for subsequent changes in observed credit risk.

In addition, the joint block exogeneity test confirms that the set of explanatory variables taken together Granger-causes the non-performing loan ratio (χ2 = 8.296, p = 0.040). This result indicates that credit risk dynamics are influenced by information jointly embedded in monetary conditions, portfolio allocation, and credit-related variables.

By contrast, no evidence of Granger causality is found from the policy rate to any of the endogenous variables in the system. Across all specifications, the null hypothesis of non-causality cannot be rejected, with p-values remaining well above conventional significance thresholds.

Similarly, no statistically significant Granger causality is detected toward private-sector credit growth. Neither individual variables nor their joint block tests exhibit predictive power for Δlog(CREDIT_PRIVATE) over the short-run horizon captured by the VAR(1).

Overall, the Granger causality results indicate that short-run predictive relationships are concentrated in risk-related dynamics, particularly those associated with banks’ balance-sheet variables, while private-sector credit growth and policy-rate innovations exhibit limited short-run predictive linkages.

| Dependent variable | Excluded variable | Chi-square | df | p-value |

| 0.052 | 1 | 0.819 | ||

| 2.736 | 1 | 0.098 | ||

| 5.071 | 1 | 0.024 | ||

| All excluded variables (joint test) | 8.296 | 3 | 0.040 | |

| 1.625 | 1 | 0.202 | ||

| 1.109 | 1 | 0.292 | ||

| 0.119 | 1 | 0.731 | ||

| All excluded variables (joint test) | 2.201 | 3 | 0.532 | |

| 0.734 | 1 | 0.392 | ||

| 0.465 | 1 | 0.495 | ||

| 0.161 | 1 | 0.688 | ||

| All excluded variables (joint test) | 1.428 | 3 | 0.699 | |

| 0.551 | 1 | 0.458 | ||

| 0.105 | 1 | 0.746 | ||

| 1.216 | 1 | 0.270 | ||

| All excluded variables (joint test) | 1.437 | 3 | 0.697 |

Source: Authors’ calculations based on Bank Al-Maghrib data.

6. Discussion

The effectiveness of monetary policy transmission remains theoretically contested, particularly in bank-based financial systems where credit intermediation is dominated by commercial banks. In the Keynesian tradition, monetary policy is expected to influence real activity and credit primarily through the interest rate channel and liquidity conditions shaping investment decisions (Keynes, 1936). By contrast, the monetarist perspective emphasizes the role of money, expectations, and broader monetary aggregates, arguing that policy transmission does not necessarily rely on a stable or immediate relationship between interest rates and credit quantities (Friedman & Schwartz, 1963; Friedman, 1968).

In modern banking systems, however, this debate is further complicated by institutional and financial frictions. Asymmetric information, risk-based lending rules, and prudential regulation imply that banks do not mechanically adjust credit volumes following policy-rate changes. Consequently, the central issue is not whether monetary policy affects the banking system, but whether policy-rate shocks translate into economically meaningful short-run adjustments in credit quantities, or whether they are endogenously absorbed through banks’ balance-sheet management and risk optimization mechanisms.

The empirical evidence presented in this study provides a clear and internally consistent answer. Across impulse response functions, forecast error variance decompositions, and Granger causality tests, policy-rate shocks generate weak, short-lived, and economically negligible responses in private-sector credit growth, as well as limited and transitory effects on credit risk indicators. The impulse responses display rapid mean reversion, the FEVD assigns only a marginal share of credit variance to monetary policy innovations, and Granger causality tests fail to detect predictive precedence of the policy rate over either credit or risk variables. Taken together, these results indicate that the short-run interest rate–credit channel is empirically weak over the monthly horizon considered.

Importantly, this finding should not be interpreted as evidence of monetary policy ineffectiveness. Rather, it suggests that monetary impulses are primarily absorbed through non-quantity margins of adjustment, consistent with a transmission mechanism operating via balance-sheet reoptimization, portfolio allocation, and risk management rather than through immediate changes in lending volumes. This interpretation is fully consistent with the monetarist view that monetary policy may exert influence through indirect, delayed, or expectation-driven channels not captured by short-run VAR dynamics (Friedman, 1968). It also aligns with empirical evidence from bank-based economies where balance-sheet constraints and regulatory capital requirements dominate lending behavior (Kashyap & Stein, 2000; Cloyne et al., 2023).

In the Moroccan context, these findings refine and extend existing evidence of incomplete and state-dependent monetary transmission. While earlier VAR studies document statistically significant pass-through from the policy rate to lending rates, particularly in the short run (Mossadak, 2017), this pricing channel does not translate mechanically into credit volume adjustments. More recent VAR and SVAR analyses identify dynamic links between monetary policy and selected macroeconomic aggregates under specific identification schemes (Eddani, 2024), without establishing a robust or persistent transmission to bank credit quantities. Structural analyses further emphasize institutional rigidities such as limited interest rate sensitivity, partial financial inclusion, and weakly anchored expectations that dampen the effectiveness of monetary impulses (Nazih & Hefnaoui, 2025). Within a short-run monthly horizon and a macro-financial framework explicitly focused on credit volumes and risk indicators, the present study contributes by demonstrating that balance-sheet reoptimization and risk interactions dominate observed transmission patterns, while sustained quantity-based credit responses remain empirically weak.

In contrast to the muted response of credit volumes, the results reveal more pronounced short-run interactions between banks’ sovereign portfolio adjustments and credit risk dynamics. Shocks to Treasury bill holdings generate larger, albeit transitory, responses in the non-performing loan ratio, and Granger causality tests indicate that changes in sovereign exposures precede observed movements in credit risk. These findings are consistent with the sovereign–bank nexus literature, which highlights the role of regulatory treatment, liquidity considerations, and risk-weight incentives in shaping banks’ portfolio allocation decisions (Acharya & Steffen, 2015; Gennaioli, Shleifer & Vishny, 2018). The absence of persistence in these responses suggests that such adjustments reflect short-run balance-sheet reoptimization rather than self-reinforcing credit risk cycles.

The near absence of significant responses of private-sector credit volumes to both monetary and portfolio shocks underscores the relevance of non-price adjustment mechanisms in credit markets. Under conditions of asymmetric information, banks may optimally respond to changing macro-financial conditions by tightening lending standards, intensifying screening, and reallocating credit internally rather than expanding aggregate lending volumes, even under accommodative monetary conditions. This mechanism lies at the core of the credit rationing model developed by Stiglitz and Weiss (1981). From this perspective, the weak quantitative responses observed in the impulse responses and the dominance of own-credit shocks in the FEVD indicate that the binding margin of adjustment operates through risk assessment and internal credit allocation rather than through aggregate credit quantities.

Theoretical Implications

The analysis yields three main theoretical implications.

First, monetary transmission is filtered through banks’ balance-sheet constraints and risk management practices, consistent with the financial accelerator framework). Second, sovereign exposure emerges as a relevant state variable for short-run credit risk dynamics, in line with sovereign–bank nexus theories. Third, the dominance of credit persistence and the weakness of quantity-based responses are consistent with credit rationing models under asymmetric information.

Practical Implications for Banks

From a banking perspective, the results underscore the importance of integrated balance-sheet management. Asset–liability decisions, sovereign exposure, and credit risk monitoring are closely interconnected, and short-run portfolio reallocations toward sovereign assets may contain early information about changes in credit risk, even when lending volumes remain stable.

Policy Implications

From a policy perspective, the results suggest that policy rate adjustments alone are unlikely to stimulate lending to the private sector in the short term when risk constraints and credit rationing mechanisms are tight. Complementary instruments, such as targeted refinancing facilities and macroprudential calibration, appear necessary to enhance the effectiveness of monetary transmission. Furthermore, coordination between monetary policy and sovereign debt management is relevant, given the influence of sovereign asset treatment on banks' portfolio incentives and balance sheet decisions.

7. Conclusion

This study investigates the short-run transmission of monetary policy to non-financial corporate sector bank credit in Morocco, with a particular focus on banks’ balance-sheet adjustments and credit risk dynamics in a bank-based emerging economy. Relying on a reduced-form VAR framework estimated on monthly macro-financial data over the period 2014–2024, and combining impulse response functions, forecast error variance decompositions, and Granger causality tests, the analysis provides a coherent assessment of short-run monetary transmission beyond the conventional interest rate channel.

The empirical evidence leads to a clear and circumscribed conclusion. Within the short-run monthly horizon considered, policy-rate shocks generate weak, rapidly dissipating, and economically negligible responses in private-sector credit volumes. Across all dynamic tools employed, responses converge quickly toward zero, and monetary policy innovations explain only a marginal share of short-horizon forecast error variance. These results indicate that, in the short run, the conventional interest rate–credit channel operates in a highly attenuated manner in the Moroccan banking system.

By contrast, balance-sheet and portfolio dynamics play a more prominent role in shaping short-term credit risk behavior. Shocks associated with banks’ sovereign asset holdings are followed by more visible though still transitory movements in credit risk indicators. This asymmetry suggests that banks primarily absorb monetary and financial shocks through immediate portfolio rebalancing, internal risk reassessment, and screening mechanisms, rather than through short-term adjustments in aggregate lending volumes.

Taken together, the findings demonstrate that short-run monetary transmission in a bank-based emerging economy is dominated by balance-sheet reoptimization and risk interactions, while quantity-based credit adjustments remain limited over the horizon examined. Importantly, this result should not be interpreted as evidence of monetary policy irrelevance. Rather, it highlights that monetary impulses are primarily absorbed through non-quantity margins of adjustment in the short run, with potential effects materializing only beyond the immediate adjustment window captured by the model.

The study contributes to the literature by reframing the interpretation of weak short-run credit responses. Instead of viewing them as a failure of monetary transmission, the analysis shows that they reflect an endogenous reallocation mechanism operating through banks’ balance sheets and risk management practices. By jointly modeling credit volumes, sovereign asset holdings, and credit risk within a unified dynamic framework, the paper clarifies why short-run monetary transmission appears weak without implying the absence of monetary influence.

Several limitations should be acknowledged. First, the analysis is explicitly confined to short-run dynamics and does not address medium- or long-term transmission mechanisms related to investment behavior, expectations formation, or structural change. Second, the use of aggregate macro-financial data limits the ability to capture heterogeneity across banks, sectors, and firm sizes. Third, the reduced-form identification strategy does not disentangle deeper structural channels or policy regime shifts that may shape transmission over longer horizons.

Accordingly, future research could extend this framework in several directions. Medium- and long-term models may help assess whether monetary policy effects materialize with longer delays. Bank-level or loan-level data would allow for a more granular analysis of credit supply behavior and risk-taking across institutions and borrower types. Finally, regime-dependent and nonlinear approaches could shed further light on state-contingent transmission mechanisms that remain unobservable within a short-run linear VAR framework.

Author Contributions

Conceptualization, A.B.; Methodology, A.B., and T.Q.; Software, A.B.; Formal analysis, A.B., Data curation, ,A.B., and T.Q.; Writing—original draft, A.B.; Writing—review & editing, A.B and T.Q.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix

The empirical results are presented in the form of screenshots because the Student Version of EViews 12 does not permit the direct export or downloading of estimation outputs in editable formats (such as Excel, or Word tables). As a result, it is not technically possible to transfer the original output tables directly from the software into the manuscript.

Accordingly, all reported tables in the paper were carefully reconstructed and formatted based on the original EViews output displayed in the screenshots. Each coefficient, test statistic, and p-value was transcribed faithfully from the software results, ensuring full consistency between the presented tables and the underlying estimations. The screenshots are provided for transparency and verification purposes, allowing readers and reviewers to cross-check the reported values against the original software output.