Submitted:

15 January 2026

Posted:

16 January 2026

You are already at the latest version

Abstract

Quantum computing has been rapidly evolving as a field, with innovations driven by industry, academia, and government institutions. The technology has the potential to accelerate computation for solving complex problems across multiple industrial sectors. Finance and economics, with many problems exhibiting computationally heavy requirements, is a high-profile sector where quantum computing could have a significant impact. Therefore, it is important to identify and understand to what extent the technology could find utility in the sector. This technical review is written for quantum applications researchers, quantitative analysts in finance and economics, and researchers in related mathematical sciences. It is divided into two parts: (i) a survey of quantum algorithms pertinent to problems in finance and economics, and (ii) mapping of several use cases in the sector to the potential quantum algorithms presented in part (i). We discuss some challenges on the pathway to achieving quantum advantage. Ultimately, this review aims to be a catalyst for interdisciplinary research that will accelerate the advent of the practical advantages of quantum technologies to solve complex problems in this sector.

Keywords:

quantum computing

; quantum algorithms

; fintech

; finance

; economics

1. Introduction

Quantum computing was first theorised in the 1970s [1], and the new research field gained more momentum after Feynman’s seminal talk [2]. At its core, quantum computing leverages the principles of quantum physics to process information. For problems that are intractable for classical computing, like simulation of complex quantum many-body systems, quantum computing is expected to solve them efficiently in a time frame that scales linearly with the system size [2,3]. In contrast, classical methods for such problems have computational times to solution that scale exponentially with system size. Furthermore, it was theorised that quantum computing could speed up computations for classically tractable problems like searching [4]. The landscape of proposed quantum algorithms that have speed-ups over their classical counterparts ranges from quadratic [4,5] to exponential [6,7]. Such theoretical discoveries, along with the rapid development of quantum hardware [8], have led many researchers to believe that quantum computing will have a significant impact across many disciplines and industry sectors.

In particular, in finance and economics, where complex calculations, large datasets, and optimisation problems are ubiquitous, quantum computing has the potential to improve computational efficiency for specific problem cases, provided certain conditions are met, such as efficient data loading and quantum error-correction [9]. For example, intricate models in finance for risk assessment, portfolio optimisation, fraud detection, and high-frequency trading, which generally require substantial use of high-performance computing, can potentially benefit from quantum computing. Similarly, economic modelling and simulation (particularly in macroeconomic forecasting, game theory, and market equilibrium analysis) could benefit from the integration of quantum processors in the computational pipeline. The expected gains with quantum computing methods are twofold: (i) large-scale, high-dimensional problems can be handled efficiently without resorting to many approximations and truncation as typically needed for classical computing approaches; and (ii) the computational time to solution can be significantly reduced, and accuracy improved for some categories of problems [10]. However, there are a few current bottlenecks in realising these potential gains, which include the challenge of efficiently loading and reading out data from a quantum computer [11,12].

This review explores some of the promising use cases in finance and economics where quantum computing could have a significant impact. We discuss the theoretical foundations of pertinent quantum algorithms, recent proof-of-concept implementations, and potential future implications. By examining these specific use cases, such as option pricing and risk management, this review highlights both the opportunities and limitations of quantum computing in the context of the aforementioned sectors. We aim to provide an objective analysis, providing a technical review of key quantum algorithms, corresponding use cases, and the overall state-of-the-art of quantum computing for finance and economics.

1.1. Motivation and Contributions

This review seeks to provide a bridge between use cases, as encountered by practitioners in finance and economics, and their potential solutions using quantum computing. This survey contributes towards stimulating interdisciplinary research to accelerate the development and demonstration of quantum computing advantage for applications in these sectors.

What is meant by advantage in quantum computing is often debated, since there is currently no unique definition for it. There are generally three terms commonly used in association with quantum advantage:

- Computational Advantage - also referred to as Quantum Supremacy [13], is a point where quantum computers can efficiently perform a task that is intractable for a classical computer. The task does not have to be directly useful for real-world applications, such as efficient random sampling from a particular probability distribution [14,15,16,17].

- Quantum Utility - a point when quantum computers can solve a problem more efficiently than classical brute force methods. This definition was first introduced by IBM Quantum in association with their work in simulating spin systems [18].

- Practical Quantum Advantage - a point where quantum computers can solve a problem more efficiently than the most advanced classical methods. In this case, the problem/task in question has real-world practical application(s) and impact in areas such as logistics, healthcare, finance, and economics.

Therefore, most researchers consider Practical Quantum Advantage (PQA) a monumental milestone that will unlock the benefits of quantum computing to the growth of the economy and society at large. Oxford Economics has quantified these benefits as an economy-wide productivity boost, which is projected to be up to 8.3% by 2055 in the UK, with initial gains from as early as 2034 [19]. Under reasonable assumptions, this is equivalent to each worker in the UK producing an extra one and a half weeks’ worth of output annually, without putting in any additional hours [19]. Furthermore, the report estimates that by 2055, the quantum computing industry will contribute between £5.9 billion and £12.9 billion in total gross value added to the UK’s GDP [19]. Globally, McKinsey [20] has projected that applications of quantum technologies in finance will contribute a total value of $622 billion by the year 2035. Hence, some analysts have predicted that the financial services sector will be one of the first industries to reap the benefits of quantum technologies [21].

Since the general expectation is that quantum computing will generate a lot of value both in the UK and globally, the key question is what is a viable path towards PQA? What are the hardware engineering and software algorithmic hurdles to overcome to achieve PQA? And what could accelerate the collaborative effort towards that common goal? This review seeks to contribute towards answering these questions by providing:

- 1.

- A survey of state-of-the-art quantum algorithms with potential applications in finance and economics.

- 2.

- A mathematical outline of use cases in the aforementioned sectors and viable quantum approaches towards an efficient solution. Note that this review is among the first to extend the scope of such a survey to cover use cases in economics.

- 3.

- A discussion of the technical challenges towards realising PQA of quantum computing applications in these sectors.

The following subsections outline how our contribution adds to previously published related survey reports and the benefits of the structure of this review.

1.2. Related Survey Reports

The interest in quantum computing use cases in finance is evident in the rapidly growing number of publications and investments in the field. The total number of papers, articles, and theses written on quantum computing for finance has grown from under 2,000 in 2014 to over 10,000 in recent years [22]. Commensurate with the growth of the field, regular survey reports of quantum computing in finance progressed from general overviews in the years 2019 to 2020, to specialised applications in Quantum Machine Learning and financial modelling in the years 2021 to 2024. This is a reflection of the field shifting toward practical implementations, with increasing focus on derivatives pricing, risk assessment, and quantum-enhanced financial strategies. Table 1 presents a sample list of related survey reports of quantum computing applications in finance from 2019 to 2025.

Each of the survey reports above is written for a specific audience, as reflected in the depth of technical details covered and the emphasis on either quantum algorithms or financial use cases. In this review, our approach is to present the technical depth of the key quantum algorithms and the mathematical formulation of the use cases in finance and economics. We hope this approach will spur interdisciplinary collaboration that will accelerate the advent of PQA for industrial applications.

1.3. Structure of the Review

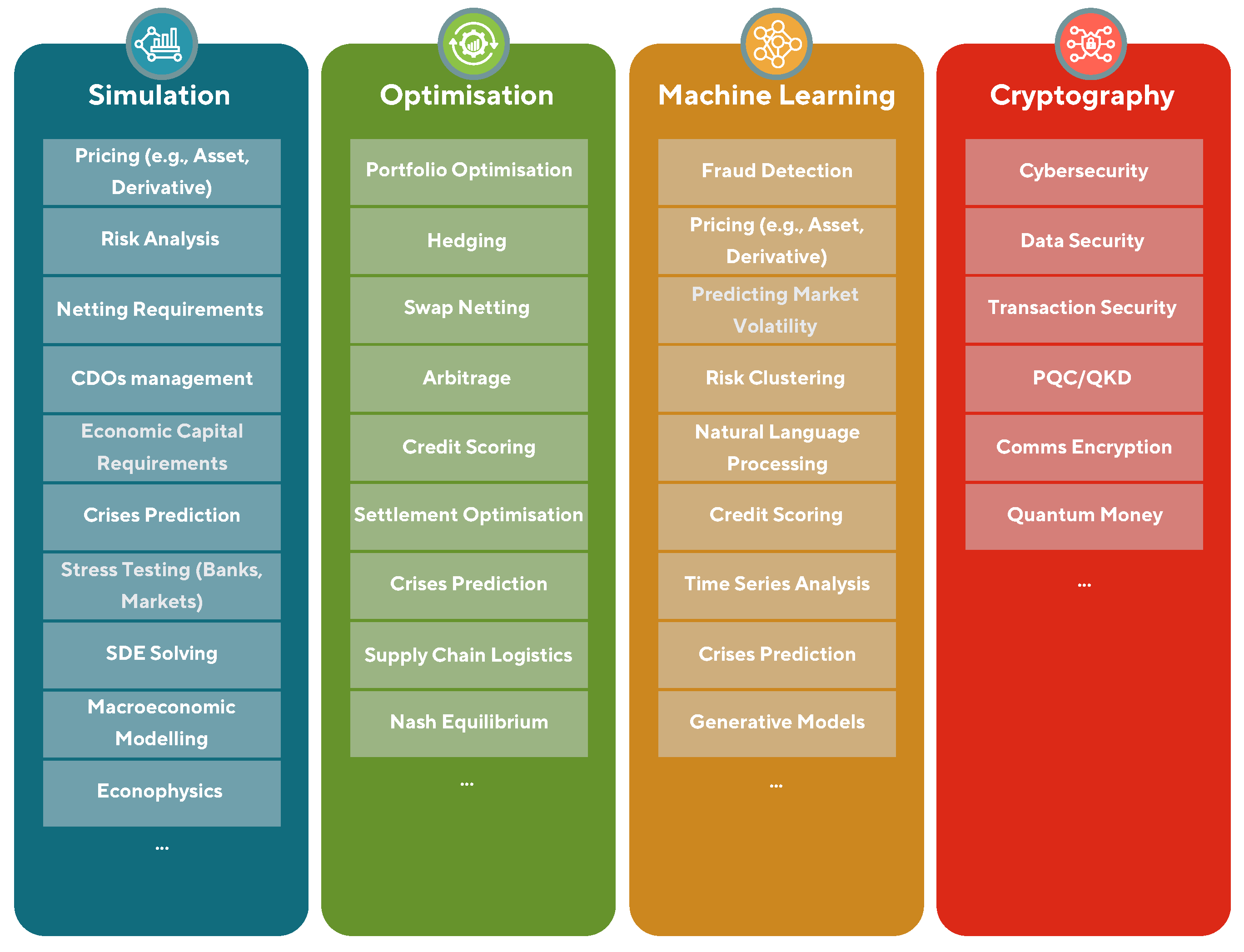

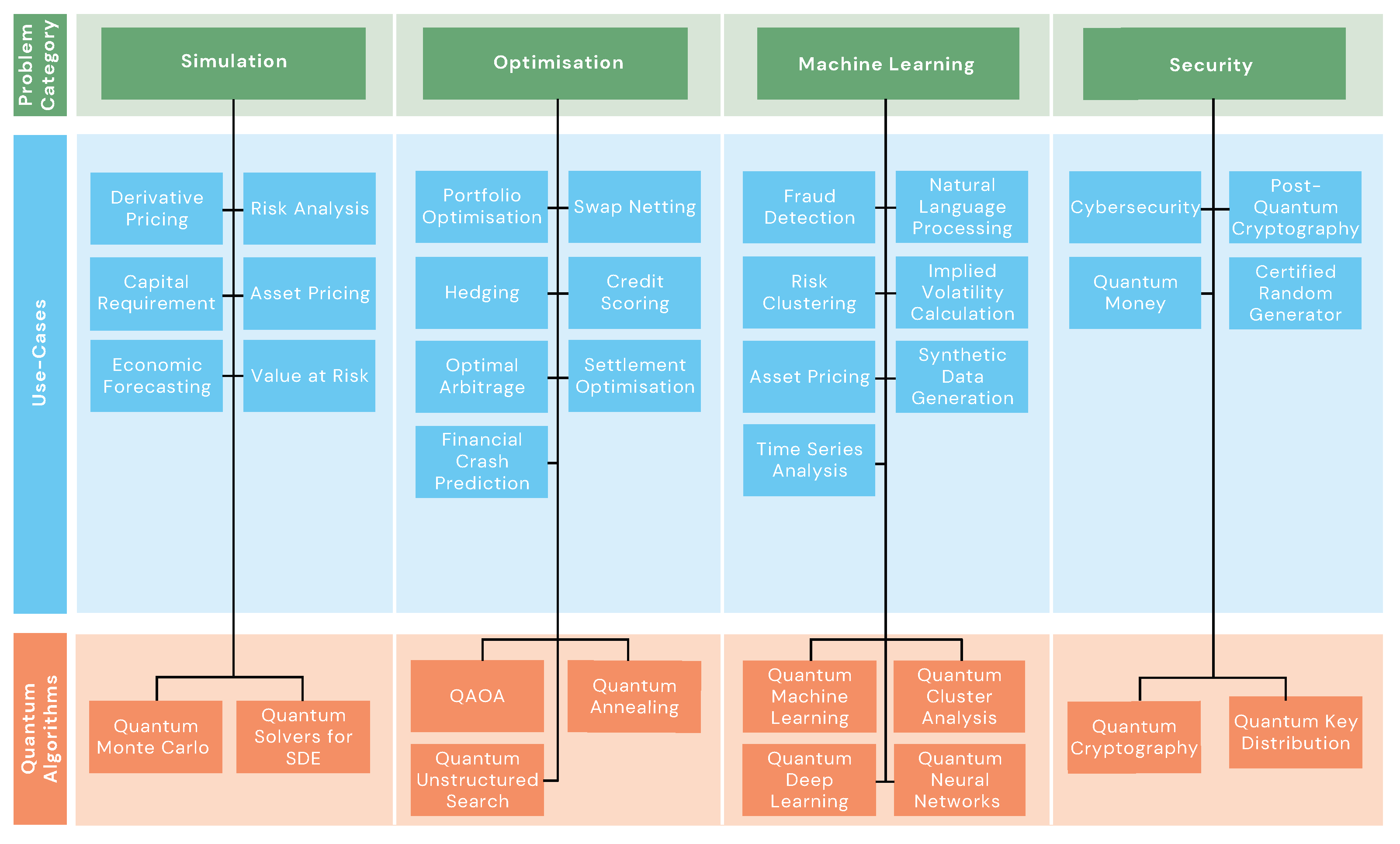

The structure of the review resembles the mapping between use cases and problem domains shown in Figure 1.

Thus, we have divided this report into three parts:

- Part I:

-

Quantum algorithms - a review of the key quantum algorithms with potential PQA in finance and economics. These are grouped into four problem domains:

- (a)

- Simulation algorithms are presented in section (2.2), including Quantum Monte Carlo Integration and quantum solvers for Stochastic Differential Equation.

- (b)

- Optimisation algorithms are presented in section (2.3), particularly for combinatorial and convex optimisation problems with state-of-the-art examples.

- (c)

- Quantum Machine Learning algorithms are presented in section (2.4), which are quantum extensions of classical Machine Learning techniques for supervised, unsupervised, and reinforcement learning.

- (d)

- Quantum cryptography methods are presented in section (2.5), including a discussion of future expected threats to cybersecurity posed by quantum computers once the technology reaches full maturity, and some quantum-safe protocols for data encryption and communication.

The pertinent primitive algorithms that feature as subroutines to quantum algorithms in the above problem domains are outlined in section (2.1). - Part II:

-

Use cases in finance and economics - a review of the mathematical formulations of potential use cases of quantum computing in finance and economics. These are grouped into three parts:

- (a)

- Banking and Investment - presented in section (3.1), we identify some of the computational bottlenecks for classical methods in banking and investment problems, and use cases where quantum computing can potentially have an advantage. These include pricing assets and derivatives, portfolio optimisation, hedging, and arbitrage.

- (b)

- Risk Management and Cybersecurity - presented in section (3.2), we identify some of the simulation and security challenges in risk management and cybersecurity, respectively. Similar to banking and investment, we present the technical formulations of use cases of quantum computing in this category. This includes quantum approaches for risk analysis (Value-at-Risk, credit scoring, etc.) and fraud detection.

- (c)

- Economics - presented in section (3.3), the mathematical formulation of potential use cases of quantum technologies for problems arising in economics is outlined. These include quantum money and macroeconomic forecasting.

- Part III:

- Summary and outlook - of this report is presented in section (4), in which we reiterate the benefits to financial organisations in working towards quantum readiness, and provide an outlook of one possible route towards PQA.

Note: This review is not a comprehensive review of all quantum algorithms nor use cases in finance and economics. We have selected a subset of use cases that represent areas of potential high impact with some current published research activity in the form of proof-of-concept proposals and/or demonstrations. Similarly, we have chosen to give technical details for simpler formulations of quantum algorithms for a problem domain and mention more complex approaches in passing. Furthermore, this review is also not intended as a primer on quantum computing or quantum information theory. In the quantum-specific sections, we assume a level of familiarity with quantum mechanics and related terminology, which other sources will be able to provide in more detail. In the next section, we will summarise some of the notation used in this review for the reader’s convenience. Finally, we hope that financial organisations interested in incorporating quantum technologies can work with quantum applications engineers to develop relevant solutions using this survey and others as a starting point.

1.4. Notation

In this section, we summarise some of the key notation used in this review for clarity. This is not an exhaustive list, and some of the notation can be overloaded when the meaning is clear in the context. For example, in some parts of the text, the Hamiltonian may be denoted as H, and it should not be confused with the Hadamard gate. Similarly, the Big-O notation may be denoted as or , which both mean the same thing. Table 2 gives a sample of common notation in quantum computing and analysis of quantum algorithms that are used in this review. Since this review is not an introductory text in the field, a reader who is unfamiliar with these notations can refer to Ref. [44] for more information.

2. Quantum Algorithms

2.1. Primitive Quantum Algorithms

This section offers an introduction to a set of quantum algorithms, here referred to as primitive algorithms, that are used as the basis or fundamental building blocks from which more complex quantum algorithms, models, or frameworks are constructed [47]. As primitive algorithms do not directly solve an end-to-end problem, groups of these fundamental algorithms (also called subroutines) are needed to create a wide range of high-end quantum applications [48].

2.1.1. Quantum Phase Estimation

One of the earliest quantum algorithms to be discovered is the Quantum Phase Estimation (QPE), which was first formalised in 1995 by Kitaev1 [50]. This subroutine has been widely used by many other algorithms, including Shor’s quantum algorithm for factoring large numbers [49,51], Hamiltonian diagonalisation [52], and solving systems of linear equations [6].

QPE serves as a key building block for quantum algorithms, of which some have a potential quantum speed-up that is exponential due to it. The objective of the algorithm is the following [44]: given a unitary operator U, estimate the phase in the representation

Here is an eigenvector and is the corresponding eigenvalue. To implement the QPE, the quantum system needs to be separated into registers: the state register that contains and the phase register that contains the encoded estimate of the phase . The QPE subroutine is constructed as follows:

- 1.

- Setup: initialise the state register with the state . The additional set of n qubits that form the phase register is set in state . After initialisation, the global state of the system will be:

- 2.

- Superposition: an n-bit Hadamard gate is applied on the phase register, leaving the global state as:

- 3.

-

Controlled Unitary Operations: consider a controlled unitary that applies the unitary operator U on the target register (i.e., the phase register) only if its corresponding control qubit is [44]. Since U is a unitary operator with eigenvector such that , it follows that:Applying all the n-controlled operations with , and using the relation , leads to the global state:where k denotes the integer representation of n-bit binary numbers.

- 4.

- Inverse Fourier Transform: The Quantum Fourier Transform (QFT) maps an n-qubit input state into:The expression of the global state is the result of applying QFT on the global expression of Step 2. Therefore, to recover the state , an inverse Fourier transform is applied on the phase register [53]. Doing so, it is found that

- 5.

- Measurement: the above expression peaks near . For the case when is an integer, measuring in the computational basis gives the phase in the phase register with high probability, as the global state now is:For the case when is not an integer, it can be shown that the above expression still peaks near with probability at least [44].

Algorithm (1) summarises the key steps of the QPE subroutine which scales as , for desired additive error [50]. The standard QPE circuit requires controlled- operations, which can be a resource challenge for current Noisy Intermediate-Scale Quantum (NISQ) hardware. Hence, QPE is considered a Universal Fault-Tolerant (UFT) quantum algorithm which requires Quantum Error Correction (QEC) to obtain highly accurate phase estimates. In the NISQ era, practitioners often employ approximate versions of QPE with reduced circuit depth and error mitigation methods to suppress effects of noise. These variants of QPE include the Iterative Quantum Phase Estimation (IQPE), which uses a single control qubit repeatedly and employs classical post-processing to update estimates of [54]. IQPE typically has the same asymptotic error scaling but requires fewer qubits [54], making it more suitable for near-term quantum devices. There have also been proposals for alternatives to QPE such as the quantum eigenvalue estimation via time series analysis [55] and the phase estimation of local Hamiltonians [56]. These methods used expectation values of the evolution operator for various times to estimate the eigenvalues of a Hamiltonian, which makes them more feasible to implement on NISQ hardware.

| Algorithm 1 Quantum Phase Estimation |

|

Initialising. Initialise the quantum system. There exist two qubit registers, the phase register initialised in state , and the state register initialised in .

Superposing. Apply Hadamard gates on the phase register.

Applying the unitary. Apply the controlled unitary operation as shown in the third step of the mathematical analysis.

Inverse QFT. Apply the inverse quantum Fourier transform to decode the state of the phase register.

Measure. Measure the phase register to get an approximation of the desired phase, .

|

2.1.2. Quantum Amplitude Algorithms

Another set of widely used quantum subroutines introduced by Brassard et al. [57] are the Quantum Amplitude Amplification (QAA) and Quantum Amplitude Estimation (QAE). These algorithms are an extension of the principles of Grover’s search algorithm [4] to a broader range of applications.

Quantum Amplitude Amplification

The first amplitude subroutine, QAA, also used within Grover’s search algorithm [4], enhances the probability amplitude of desired outcomes within a quantum algorithm. The QAA generalizes Grover’s unordered search to any algorithm with a known success probability [58], enabling a potential quadratic speed-up over classical repetition strategies [57].

Consider a quantum algorithm that produces a state

where is the `good’ subspace (desired states), a the probability of measuring a `good’ state, and the `bad’ subspace. The amplification process is done using the Grover-like operator , which acts as a rotation and is defined to be [57]

where

The operator reflects about the initial state, which flips the sign of the amplitudes of the good states if and only if . The operator reflects about the good state which flips the sign of if and only if . This implies that [57]

The probability amplitude of the good state is where , with , and the optimal m number of iterations is . Applying Q iteratively to , the state evolves such that after m applications, the state is

Thus, Q rotates the state in the plane per each iteration. If a is known, QAA achieves a quadratic speed-up with applications of and . For unknown a, quantum search algorithms like one outlined in Section (2.1.3) use exponentially increasing numbers of iterations to find a good solution. This approach is also expected to use same applications and if [57]. Algorithm (2) summarises the QAA subroutine using the operator Q and a general algorithm.

| Algorithm 2 Quantum Amplitude Amplification |

|

Initialise: Apply a quantum algorithm to to prepare the state:

Amplify: Define the amplification operator and apply it to m number of iterations to rotate the state:

Measure: Measure the final state to obtain a good state.

Repeat: If a is unknown, use exponentially increasing m until a good state is found.

|

An extension of QAA, called the variable time amplitude amplification, which can be decomposed into multiple steps with different stopping times [59], has been applied as a subroutine that improves the complexity of Harrow et al. [6] Quantum Linear Systems Solver. Improvements to the QAA subroutine have been proposed, such as the oblivious amplitude amplification [60] which handles the issue that occurs when it is not possible to perform the required reflection about the state . Another version of QAA is the fixed-point amplitude amplification [61] that ensures amplitude amplification happens regardless of an unknown amplitude. These improved versions of QAA are subroutines for Quantum Singular Value Transformation (QSVT) methods [62] and have been recently compared in the Hamiltonian simulation problem [63].

Quantum Amplitude Estimation

The second amplitude subroutine, QAE algorithm first proposed by [57], is closely related to QAA and seeks to estimate the probability amplitude of a specific outcome with high precision. It is a key subroutine for a broad class of Monte Carlo-like estimation tasks [64] and offers a potential quadratic quantum speed-up [5].

The QAE can be described similarly as QAA. Consider an algorithm that outputs a state given by Equation (2), the QAE seeks to produce an estimate for the amplitude a of the good state , where . Using the operator Q given by Equation (3), QAE estimates the value of a by using QPE to find the eigenvalues of Q [57]. Hence, both QAA and QAE use the operator Q, but the former boosts a for measurement of , while the latter quantifies a itself.

The key idea is to assign the value of a to an angle so that the estimate of to a given precision using QPE gives us the estimate of a. This is done by setting and then applying QPE to the controlled-Q operations, since Q acts as a rotation in with eigenvalues . The estimate with M evaluations has errors bounds given by [57]

with probability at least for , and higher for . Algorithm (3) summarises the QAE that utilises QPE.

| Algorithm 3 Quantum Amplitude Estimation |

|

Initialise: Apply a quantum algorithm to to prepare the state: (same as QAA).

Define: Define the amplification operator Q given by Equation (3). The eigenvalues of Q are where for .

Estimate: First apply a total of M controlled-Q operations on state such that

Let , then apply QPE to estimate the eigenphase which we use to recover the amplitude

|

This version of the QAE algorithm is relatively resource-expensive due to the use of QPE, which uses many ancilla qubits for a good estimate, multiple controlled-Q operations, and the inverse QFT. Hence, this results in deep circuits which are not feasible to run on near-term devices. Some variants of QAE that do not make use of QPE include the Maximum Likelihood Amplitude Estimation [65], Faster Amplitude Estimation [66], Iterative QAE [67], Variational QAE [68], and low depth algorithms for QAE [64] which are more feasible on near-term devices. An important application of QAE to finance is to perform Monte Carlo integration, which will be discussed in more detail in Section (2.2.1). Other applications of QAE include general numerical integration [69], estimating the probability of success of a quantum algorithm [70], and approximate counting [71].

2.1.3. Quantum Unstructured Search (Grover’s Algorithm)

First proposed in 1996 by Lov Grover [4], the Quantum Unstructured Search (QUS)2 algorithm utilises the QAA subroutine to potentially obtain a quadratic quantum speed-up over classical methods for searching an item in an unstructured dataset.

In this section, we describe the key idea behind the QUS algorithm. For a database of entries, let be the set of items in an array, and w the marked item (i.e., the item the routine searches for). Let f be a function such that if and only if and otherwise. The quantum states can be encoded as binary strings . One can then define the oracle acting on a quantum state, , as

Thus, the oracle does nothing to the unmarked quantum states and negates the phase of the marked state . Geometrically, the unitary matrix of this oracle corresponds to a reflection about the origin for the marked item in an N-dimensional vector space.

The QAA subroutine provides the quadratic speed-up of QUS by amplifying the amplitude (and thus, the probability) of the target quantum state, making it more likely to appear after measurement. This procedure is summarised in Algorithm (4) and has been shown to have a query complexity of , which is a quadratic speed-up over classical brute force methods of [4].

| Algorithm 4 Quantum Unstructured Search (Grover’s Algorithm) |

|

Initialisation: Start with , apply Hadamard gates to create a uniform superposition:

Each state has amplitude .

Oracle Application: Apply the oracle , which flips the phase of solution states, such that for one solution , the state becomes:

This marks solutions by changing their sign.

Diffusion Operator: Apply the diffusion operator , where I is the identity. This reflects the state over , amplifying solution amplitudes:

The action of the Grover operator is to amplify the amplitude of the solution state.

Iteration: Repeat the Grover operator k times and then measure to find highest probability state . The optimal k receptions to maximise the probability of finding the target state(s) is approximately:

|

Grover’s algorithm has been applied as a subroutine for various applications, including speeding up nested search of structured problems [72], stochastic pure adaptive search for unconstrained global optimization [73], high-energy physics data at the Large Hadron Collider [74], image pattern matching [75], and homomorphic encryption schemes [76]. The QUS algorithm as described here is considered a fault-tolerant quantum algorithm due to the deep circuits (required to reach optimal k iterations) which are infeasible to run successfully on current NISQ hardware. Hence, similarly to the other primitives reviewed here, improvements have been suggested to the QUS to make it amenable to run on near-term quantum hardware. These include the divide-and-conquer strategy and partial diffusion operators to reduce circuit depth and error accumulation [77,78], as well as variational approaches [79,80].

2.1.4. Quantum Walks

Random walks have long served as a foundational model in the study of stochastic processes, with applications spanning physics, computer science, biology, and finance. In its classical form, a random walk describes the trajectory of a particle that takes successive steps in random directions, typically governed by a Markov process [81]. Random walks have also been generalised to graphs [82], in which case they can be viewed as finite-state Markov chains over the set of vertices [83]. A simple example is the one-dimensional symmetric random walk, where a particle at position moves to or with equal probability at each time step. In finance, the Geometric Brownian Motion (GBM) is a widely used random walk for modelling market stochastic quantities like asset prices [84,85].

The quantum analogue of random walks, known as quantum walks, emerged in the early 1990s as a framework for modelling quantum dynamics and as a potential basis for quantum algorithms [86]. Unlike classical random walks, quantum walks evolve according to unitary transformations, preserving coherence and allowing for interference between paths. This leads to fundamentally different behaviour, including faster spreading and potential algorithmic advantages [87].

Two main formulations of quantum walks exist: discrete-time and continuous-time. The Discrete-time Quantum Walk (DTQW) was first formalised by Aharonov et al. [86], incorporating a coin space to account for internal degrees of freedom. In contrast, the Continuous-time Quantum Walk (CTQW), introduced by Farhi and Gutmann [88], operates directly on the graph structure without an explicit coin. In this section, we will review the key ideas behind quantum walks, beginning with their mathematical foundations and then exploring their distinctive dynamical properties, algorithmic formulations, bottlenecks, and applications.

Discrete-Time Quantum Walks

Consider a walker on a 1D line, flipping a quantum coin to decide whether to turn left or right at each step. This represents one of the simplest quantum walks, also referred to as a qubit walk on a finite cycle (with N states) in discrete time [89]. This quantum walk can be described by repeated application of a unitary evolution operator U which acts on the Hilbert space composed of the coin qubit (C) with basis and state space (S) with basis for , respectively. The unitary U is defined as [89]:

where S is the conditional shift operator given by [90]

The operator moves the walker one step to the right, increasing its position, and to the left, decreasing its position. The quantum coin operator C is can be chosen to the Hadamard gate H, such that

We note that although this coin is unbiased3, the quantum walk from this coin operator () will be asymmetric with bias towards rightward paths. This is because the leftwards path () undergoes more destructive quantum interference, whereas the rightwards path undergoes more constructive quantum interference [91]. This phenomenon has no classical analogue and makes quantum walks more expressive than classical random walks [86,87]. The coin represented by the Hadamard operator alongside a step operator causes the probability amplitude to become distributed over an increasing space in discrete jumps [92]. This asymmetry can be overcome by choosing a balanced coin operator [87], for example

which treats both and the same, independent of the initial coin state.

Intuitively, in each step, the qubit first ’splits’ into two paths (C puts it in a superposition) and then one ’half’ steps leftwards, while the other steps rightwards. This process, when repeated with T-steps, produces a probability distribution that is ballistic with standard deviation , whereas the classical random walk has a diffusive distribution with standard deviation [87]. This implies the quantum walk propagates quadratically faster than classical walks [87], which means they can explore more of a graph in fewer steps than classical random walks [93].

Generally, quantum walks in discrete time can be viewed as a Markov chain over the edges of a graph and consist of a series of interleaved reflection operators [94,95]. This formulation of quantum walks generalises the QAA and Grover’s algorithm discussed in Sections (Section 2.1.2.1) and (Section 2.1.3), respectively [96,97]. The bipartite character of the graph introduces the modularity property of quantum walks (similarly to classical random walks), which is that after an even (odd) number of steps, the probability to find the walker on odd (even) positions is always zero [98]. This property allows for simplified analysis of the performance of quantum walks, in particular, to two important metrics: the mixing time and hitting time of random walks on graphs. The mixing time of a graph is the time it takes for a random walk on the graph to become close to the stationary distribution; that is, the point where the walk "forgets" where it started and behaves as if it started from a random node [99]. The hitting time from node u to node v is the expected number of steps a random walk starting at u takes to reach v for the first time [81]. Quantum walks are shown to potentially have a polynomial quantum speed-up in mixing times [89,93,100] and hitting times for Markov-chain-based search algorithms [94,95,101,102,103,104,105] than their classical random walks counterpart. There have been several proof-of-concept implementations of DTQW on NISQ hardware, which include a Hadamard-based on the 4-cycle and 8-cycle [106] and extensions to multi-qubit systems [107,108].

Continuous-Time Quantum Walks

Consider an undirected graph , where V is the set of its vertices and E the set of its edges. In classical mechanics, a diffusion equation can be used, which allows probability to leak to or from neighbouring vertices. The number of neighbouring nodes equals the degree of the node j, or . This diffusion operation can be expressed as

where t is an arbitrary continuous time parameter, is a function that describes the probabilistic exchange between node j and its neighbouring nodes. The operator L is symmetric and Hermitian, called the Laplacian of G, given by

Thus, since L is a Hermitian matrix, it can play the role of a Hamiltonian in Schrödinger’s equation as

where, for simplicity it can be assumed that and is the state of the system at arbitrary time t. First introduced by Farhi and Gutmann in [88], Equation (14) represents the Continuous-time Quantum Walk (CTQW). As evident from the above formulation, the CTQW does not need a quantum coin that drives the evolution, unlike the DTQW. This makes CTQW a construct that shares dynamics with the DTQW, but exhibits different behaviour. In contrast to the quantum coin tossing example described in Section (2.1.4.1), the walker now moves smoothly (or continuously), guided by an evolution rule (which is driven by the Hamiltonian, typically the graph Laplacian L). This evolution follows the Schrödinger Equation (14) and the walk is continuous without distinct steps. Therefore, we can summarise the fundamental differences between the two quantum walks as:

- State space: CTQWs require only the vertex space, while DTQWs models need an auxiliary coin space for evolving. As described in Section (2.1.4.1), the coin operator drives the symmetry or asymmetry of the quantum walk.

- Dynamics: CTQWs have continuous Schrödinger evolution (via Hamiltonians), whereas discrete-time walks rely on alternating coin and shift operators per time step.

In addition, the various mixing operators used in Quantum Approximate Optimisation Algorithm, described in Section (2.3.1.4), can be viewed as CTQW connecting the feasible solutions [109]. Similarly to DTQWs, the CTQWs can showcase a quadratic advantage in terms of accelerating diffusion (i.e., spreading) compared to classical continuous-time random walks [110]. For some oracular graph problems, the CTQW can theoretically achieve exponential advantage over classical methods [111].

It was shown by Childs that CTQW can be regarded as a universal computational primitive, with any quantum computation encoded in some graph [112]. Later, Lovett et al. [113] showed that the DTQW can also achieve universal quantum computation. Hence, there have been multiple proposed unifications of quantum walks in continuous and discrete time [114,115], something that is true for the classical versions [116]. For a comprehensive review of quantum walks, see the survey in [115]; and for an overview and a discussion of connections between the various quantum-walk-based search algorithms, see the work by [103].

Quantum walks have since found applications in a variety of areas, including quantum search algorithms [97], modelling transport in biological systems [117], and many others [110]. Their utility stems from the combination of quantum superposition and interference, which enable new algorithmic paradigms not feasible in classical settings. Current research into quantum walks faces many challenges. As in any other quantum algorithm, a significant issue is implementation on NISQ devices where noise can disrupt the coherent evolution required for quantum walks. Efforts to mitigate these decoherence effects have been explored in various studies, such as [118], which simulate quantum walks of interacting particles and demonstrate topological protection against noise. However, achieving scalable quantum walks on large graphs, or lattices, remains a challenging task [110], as current hardware limitations restrict the size and duration of coherent quantum evolutions.

2.1.5. Quantum Linear System Solver

Linear systems of equations are ubiquitous in science, engineering, and mathematical fields. There are several numerical methods developed over the years for solving them efficiently on classical computers [119,120,121]. The general Linear Systems Problem (LSP) can be formally defines as:

Definition 1

(LSP). Given a matrix and a vector , find a vector s.t. , or indicate that the system has no solution.

In other words, Definition (1) describes a matrix-inversion problem since the solution is given by . The Quantum Linear Systems Problem (QLSP) is quantum version of the LSP, and is defined as:

Definition 2

(QLSP). Given a matrix and and a vector , prepare the state on a quantum computer with qubits such that

where ϵ is the desired precision. The target quantum state with

where are the component of vector b.

One of the key differences between the LSP and QLSP is that the former outputs the full solution vector x whilst the latter outputs a normalized vector proportional to the solution . Table 3 shows the time complexity of the best known classical algorithm for solving the LSP, with A matrix sparse [122] and dense [123], compared with a few quantum algorithms for solving the QLSP.

HHL Algorithm In this section, we will consider the Harrow-Hassidim-Lloyd (HHL) algorithm [6] which is the first quantum algorithm for solving the QLSP. As mentioned earlier, it does not provide the whole solution vector, but a quantum state proportional to the solution, which we can sample from with relatively low additional error. Given that the coefficient matrix A is sparse and well-conditioned, the quantum algorithm can potentially achieve an exponential quantum speed-up in the dimension of the matrix N compared to the best known classical algorithm [6]. However, there are caveats for this speed-up to be possible, which include [6,11] the following conditions:

- 1.

- Matrix A must be sparse or can be efficiently decomposed into a sparse form.

- 2.

- The condition number of A must be small and scale as .

- 3.

- The elements of A can be efficiently utilized via black-box oracle calls as needed.

- 4.

- The final output is the case where one does not need to know the solution itself, but rather an approximation of the expectation value of some operator associated with , e.g., for some matrix M.

It may seem that these constraints, alongside other challenges in quantum computation restricts the possibility of having a PQA as noted by Aaronson [11]. Ongoing research [133] and improved versions of HHL, such as shown in Table 3, are promising to deliver PQA.

The main steps of the algorithm are (i) phase estimation, followed by (ii) a controlled rotation, (iii) uncomputation, and, finally, (iv) measurement and post-selection [133]. A summary of the HHL algorithm is provided below, and for more information, the reader is referred to [6,133]. Consider the matrix A that is s-sparse and Hermitian, then its spectral decomposition is given

where is the eigenvector of A with respective eigenvalue . In this decomposition, the matrix inversion of A is then given by

We can express in the eigenbasis of A as

where we already have an implicit normalisation constant since we are talking about a quantum state. The goal of the HHL is to exit the algorithm with the readout register in the state approximately , which can also be expressed in the eigenbasis of A as

Therefore, the HHL algorithm encodes A into a unitary U given by

Thus, by applying QPE, one can implement the mapping

where is the binary representation of up to a tolerated precision. Following this, the implementation of a controlled rotation takes place conditioned on . This requires an ancilla register, S, which is added to the system initialised in state . The controlled rotation is of the form of a -rotation (i.e., a rotation around the y-axis or quantisation axis) and produces a normalised state of the form.

where c is a normalisation constant. This can be achieved through the application of the quantum operator

where . Thus, enacting the procedure described above in the latter superposition, it is derived that

Finally, the first register is uncomputed, giving

Following the uncomputation, we see that the state of the system (including all the quantum registers) is , or in other words, it exists in a state that is close to the solution . The state can be reconstructed within the clock register, C, by measuring the ancilla register, S, and post-selecting on the outcome 1 modulo the constant factor of normalisation, c. The success probability of the final step can be boosted using QAA. This procedure is summarised in Algorithm (5).

| Algorithm 5 Harrow-Hassidim-Lloyd algorithm for QLSP |

|

Input. Encode the state vector and the matrix A with oracular access to its elements. Define , and as the desired precision.

Initialise. Prepare the input state , where .

Hamiltonian. Apply the conditional Hamiltonian evolution following the input state.

Apply QFT to the register C, denoting the new basis states , for . Define .

Controlled rotation. Append the ancilla register, namely S, and apply a controlled rotation on S with C as the control register, mapping states . The state is defined in such a way that it produces an output which denotes whether an inversion has occurred and if that inversion is well-conditioned or not [133].

Uncomputation. Uncompute the register C.

Measurement. Measure the register S.

Repeat. Perform rounds of QAA on the HHL algorithm.

Output. Result is the state s.t.

|

The HHL algorithm was the first QLSS and, as shown in Table 3, there have been many improvements on it up to the recent ones with optimal scaling in and [131,132]. It is worth noting these state-of-the-art quantum algorithms for the QLSS with optimal scaling for the case when A is sparse, and there have been a few proposals for the case when A is dense. For the latter case, Wossing et al. [126] utilised the Quantum Singular Value Estimation (QSVE) algorithm of [134] to achieve a polynomial speed-up over the best known classical algorithm based on powers of tensors with subcubic complexity [123]. However, as noted in [126], the classical algorithm with subcubic complexity [123] is difficult to achieve in practise hence, for the dense matrix case, the Cholesky decomposition with complexity [135] is often used. This implies that for problems with non-sparse A matrix, such as kernel methods and neural networks in machine learning [136], the potential exponential quantum advantage of HHL-type quantum algorithms is lost.

Following this, Kerenedis and Prakash generalised the QSVE-based linear systems solver to handle both sparse and dense matrices and introduced a technique for spectral norm estimation [137]. Another general framework for solving the QLSP is the Quantum Singular Value Transformation (QSVT) [138], which uses an iterative least square algorithm and has been proposed [139,140]. Although this algorithm does not have optimal scaling with and , it is general in the sense that it does not assume that A is invertible nor that it is a square matrix, but uses the Moore-Penrose pseudoinverse [141] such that the output is achieved efficiently [48,139,140]. Furthermore, the QSVT also provides a general framework that unifies [62] a variety of quantum algorithms, such as linear algebraic subroutines like singular-value-threshold projectors [134,138] and matrix-vector multiplication [139]. An outline of QSVT is presented in Algorithm (6).

| Algorithm 6 Quantum Singular Value Transformation |

|

Input: A block-encoding of matrix A, i.e. ; a definite-parity polynomial of degree d; and a phase sequence from polynomial synthesis.

Construct QSVT sequence: Let , and define

This yields a block-encoding of with the corresponding odd/even forms.

Linear combination: Using that implements , define

Output: that is a block-encoding of .

|

While solving the QLSP does not provide classical access to the solution vector, this can still be done by utilising methods for vector-state tomography with a cost of samples [142]. Applying tomography would no longer allow for an exponential speed-up in the system size N [11]. However, polynomial speed-ups with tomography for some linear algebra-based algorithms are still possible for certain types of problems [48]. In addition, without classical access to the solution, certain statistics, such as the expectation of an observable with respect to the solution state, can still be obtained without losing the exponential speed-up in N [6,143]. Another current bottleneck for QLSS is loading the data of A and b into quantum gates and states, respectively [11]. In theory, this can be dealt with by using one of the two main quantum models for data access [48,139]: (i) the sparse-data access model and (ii) the quantum-accessible data structure. The sparse-data access model provides efficient quantum access to the nonzero elements of a sparse matrix. The quantum-accessible data structure, suitable for fixed-sized, non-sparse inputs, is a classical data structure stored in a quantum memory (e.g., Quantum Random Access Memory (QRAM)) and provides efficient quantum queries to its elements [139]. Considering the cost of QRAM with QEC overheads [144], the potential quantum advantage of QLSS may be reduced to polynomial at best [48] or none in the worse-case [11].

Lastly, for LSPs that involve only low-rank matrices, classical Monte Carlo methods for numerical linear algebra (e.g., the FKV algorithm [145]) can be used. These techniques have been used to produce classical algorithms that have an asymptotic exponential speed-up in dimension for various problems involving low-rank linear algebra (e.g., some machine learning problems) [146,147]. These classical quantum-inspired (dequantised) algorithms seem to have robustness issues [148], making QLSS potentially advantageous for certain cases. In addition, since these results do not apply to sparse linear systems, there is still the potential for provable speed-ups for problems involving sparse, high-rank matrices [48].

2.1.6. Variational Quantum Algorithms

Classical variational method is a well-established technique in quantum mechanics [149] for finding the ground state(s) of a quantum system based on the variational principle. The methods involve:

- 1.

- Ansatz - specifying some trial parametrised wavefunction where are the set of variational parameters.

- 2.

- Variation - minimising the expected energyby varying the parameters .

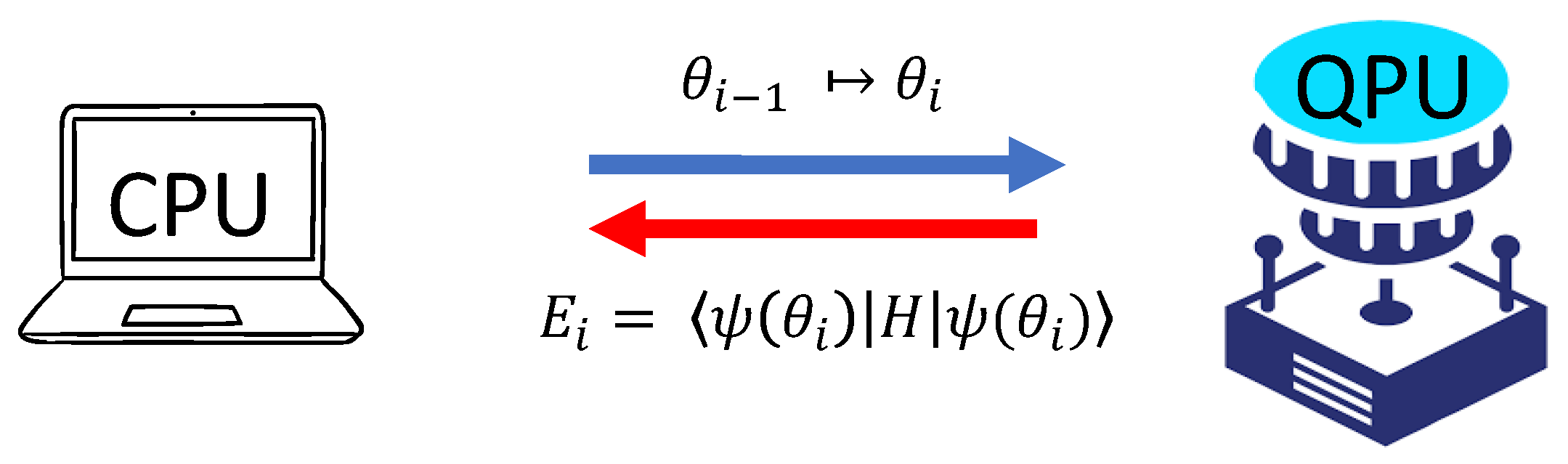

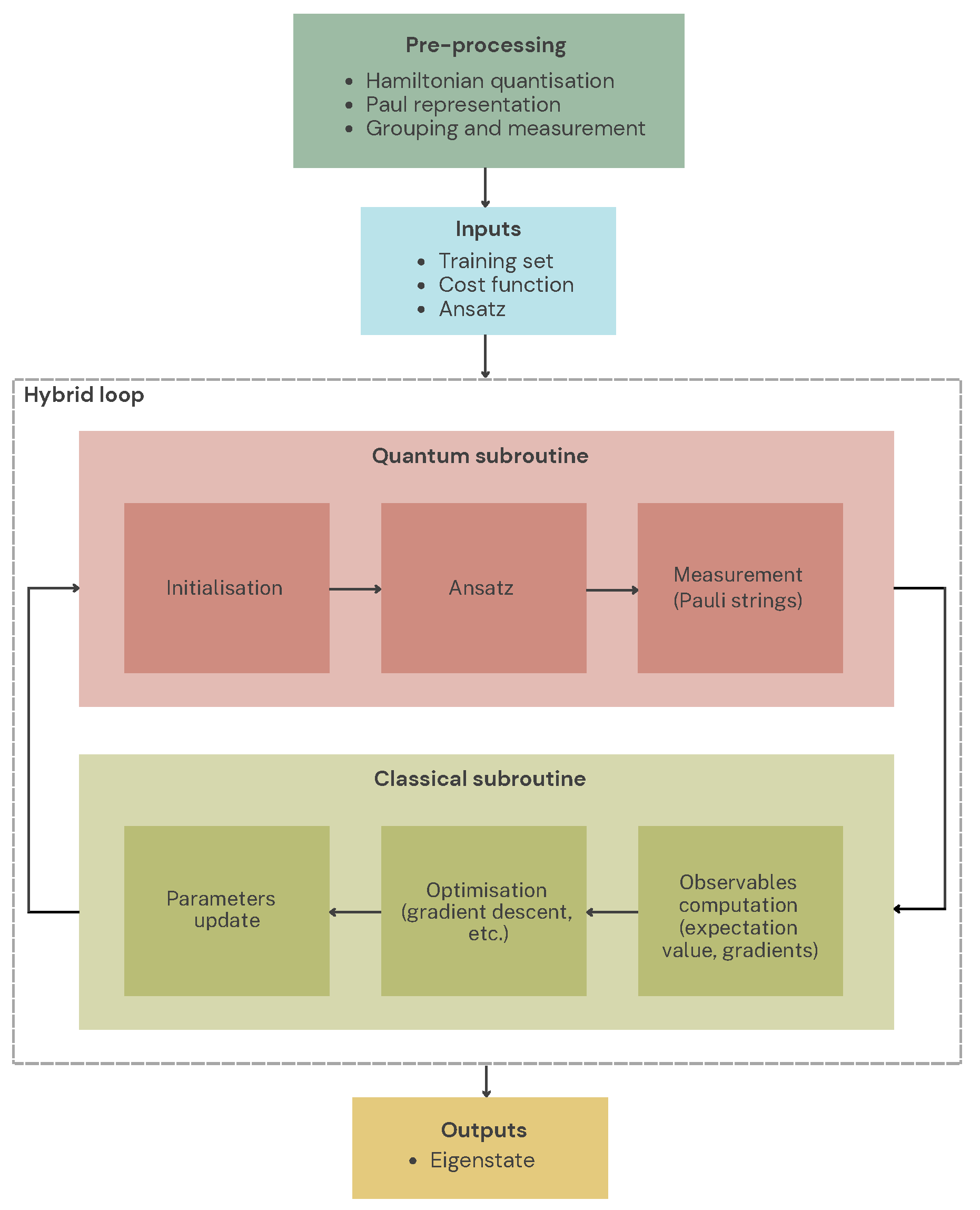

Here, is the Hamiltonian for the system, and by the variational principle, the energy E after each variation will always be bound below by the true ground state energy [149]. Hence, the set of parameters that minimizes Equation (23) results in a good approximation of the true ground-state energy . In practice, there may be factors preventing the true ground state from being found, such as a failed optimisation, or an inappropriate ansatz that does not include the support basis vectors of the true ground-state [149]. In general, this task is computationally expensive for a complex many-body system with a Hilbert space that grows exponentially with system size. Hence, leveraging the high-dimensional capabilities of quantum computers to reduce the complexity of this method leads to the Variational Quantum Eigensolver (VQE) [150]. Figure 2 gives a sketch of the roles the classical and quantum computer plays in the VQE algorithm. Essentially, since the computation of the expectation value of Equation (23) is prohibitive classically, it is assigned to the Quantum Processing Unit (QPU) and the task of finding optimal parameters is assigned to the CPU [150].

The choice of the VQE ansatz can have a significant effect on both the speed and quality of the solution. For example, the ansatz may be chosen to reflect a certain symmetry in the problem set up, or such that it rules out or focuses on a particular region of the Hilbert space, reflecting constraints on possible solutions [151]. Apart from the guideline of symmetry and expressiveness of the ansatz, there is no known general rule for picking the `best’ ansatz as it seems to be problem specific [152]. Another factor that impacts the quality of the solution is the performance of the classical optimiser. One common problem encountered when implementing variational algorithms is that of barren plateau [153], referring to solution landscapes that have exponentially vanishing gradients as a function of the number of qubits. This results in the optimiser being unable to efficiently find the optimal solution or being stuck in a local minimum. A lot of research has been done on the problem [154], but there is not yet a consensus on how to consistently identify or mitigate the issue [154,155,156].

The VQE algorithm can be considered a special cased of general Variational Quantum Algorithms (VQAs) with parametrized quantum circuits (denoted by the unitary ) and a cost function given by [152]

Here, is some set of functions with properties defined in [152], are input states from a training set, and are set of observables. The goal is to find an optimal set of parameters

by using a QPU to estimate the cost function (or its gradient) while leveraging the efficiency of a classical optimizer to train the parameters . This framework naturally applies to quantum algorithms for optimisation problems [48,152,157] (see section (2.3) for more details). There have been numerous proposed applications of VQA which includes solving the QLSP [158,159]), PDEs) [160,161], and QML problems (section (2.4)) [162]. Although quantum computers are efficient in estimating the cost function, the general training VQAs (i.e., finding the optimal ansatz parameters) is an NP-hard non-convex optimisation problem [163,164]. Furthermore, these algorithms are heuristic with no yet provable quantum advantage in complexity of the algorithm [152], but they have empirical proof-of-concept implementations in NISQ era [48] and might obtain PQA with Mega-QuOps4 QPUs [165].

2.1.7. Quantum Annealing

The Quantum Annealing (QAnn) algorithm [166,167] is an approach to quantum computing based on Adiabatic Quantum Computing (AQC) [168], which is an alternative to gate-based models of which all previous algorithms outlined in this section are derived from. While gate-based algorithms represent any computation as a series of gates, employing the concept of universality [44], AQC is an analogue approach that is suitable for a specific set of optimisation problems [168]. Primarily, the Quadratic Unconstrained Binary Optimisation (QUBO) problems (further discussed in section (2.3)), form the basis for a wide variety of NP-hard combinatorial optimisation problems tackled by QAnn [169].

Annealing relies on the adiabatic quantum theorem [168], which states that if the system starts in the nth eigenstate of a time-dependent Hamiltonian , and this Hamiltonian evolves slowly enough, the system will remain in the instantaneous nth eigenstate during the evolution. More specifically, during the time evolution, the parameters are changed sufficiently slowly that the system adapts to the new parameter configuration quasi-instantaneously. The length of time required for the evolution to succeed depends on the spectral properties of the Hamiltonian path and, in particular, on the minimum spectral gap [168]. For example, the change from to can be achieved by the Hamiltonian:

where is the the scheduling function and is the annealing parameter. The scheduling function is chosen such that at , the system is governed by some initial Hamiltonian , and at the final dynamics are governed by the problem Hamiltonian . This implies that must be strictly increasing and the simplest choice gives the vanilla AQC. If the system starts in the ground state (eigenstate with minimal energy) of and slowly evolves, then according to the adiabatic theorem, it will remain the ground state throughout its evolution until it rests in the ground state of [168]. This means that, to find the unknown ground state of a Hamiltonian for a hard-to-solve problem , one can start from an easy-to-solve Hamiltonian with a known ground state and apply the QAnn algorithm.

Typically, the Hamiltonian has the form with ground state being the equal superposition of all bit strings [166]. On the other hand, is described by the canonical Ising model

where the biases and couplings are determined by the problem [166]. In practice, it is very difficult to fulfil the conditions to achieve adiabaticity, mainly due to unwanted noise on NISQ hardware. Therefore, annealers forego some of the stringent theoretical conditions and heuristically repeat the annealing procedure many times, collecting several samples from which the configuration with the lowest energy can be selected as the optimal solution, but with no strict guarantee that the optimal solution will be in this sample set [48,170].

One key issue affecting annealing is the requirement that the problem is reformulated in the correct format (as it is believed the transverse-field Ising Hamiltonian is not universal [57]. For problems which have a native structure (including many graph-based problems, for example), annealing is particularly suitable [170]. For non-native problems, this reformulation may introduce a significant overhead, or such strenuous constraints, that annealing might fail consistently, or any potential quantum advantage might be lost [170]. There exist classes of time-dependent Hamiltonians that, through adiabatic evolution, can approximate arbitrary unitary operators applied to qubits [168,171]. Thus AQC can also realise universal quantum computation for such a class of problems. However, by polynomial equivalence to the circuit model, gate-based devices can also efficiently simulate these problems [168,170].

The main reason behind the interest in QAnn is that it provides a non-classical heuristic, tunnelling, that is potentially helpful for escaping from local minima [168]. Its closest classical analogue is simulated annealing [172], a Markov chain Monte Carlo method that was inspired by classical thermodynamics and uses temperature as a heuristic to escape from local minima. So far QAnn has demonstrated usefulness for solving QUBOs with tall yet narrow peaks in the cost function [173,174]. The overall benefit of QAnn is still a topic of ongoing research [48,170,173]. Furthermore, commercially available quantum machines that implement QAnn, from providers such as D-Wave [175], have allowed for various near-term exploration [176,177,178,179].

2.2. Quantum Simulation

While quantum simulation was originally envisioned as a tool for modelling quantum mechanical systems [2,3], recent advances have demonstrated its broader potential to address classical problems whose dimensional complexity renders them inefficiently solvable when tackled with conventional methods [180]. This is the case in the domain of quantitative finance, where the numerical solutions of Stochastic Differential Equations (SDEs) play a central role in modelling financial products such as pricing options [84,85]. These problems, while inherently classical, often involve high-dimensional integration and probabilistic dynamics that render them computationally intensive [181]. Quantum simulation techniques, including those adapted for solving linear systems and sampling probability distributions, provide promising pathways to address these challenges [9,31]. In the classical regime, SDEs such as those arising in the pricing of financial derivatives under the Black-Scholes-Merton or Heston models, require discretisation techniques like finite differences or Monte Carlo simulations [182]. However, the computational cost grows rapidly with the number of risk factors or underlying assets - a manifestation of the so-called curse of dimensionality. Quantum computing offers a potential remedy through quantum algorithms, which can achieve polynomial [5] or even exponential speed-ups over classical counterparts for problems with certain structures [183]. In this review, we will consider quantum algorithms that speed up Monte Carlo Integration (MCI) and quantum solvers for SDEs.

2.2.1. Quantum Monte Carlo

Monte Carlo methods are very commonly used to approximate solutions to equations that are difficult to solve analytically or when numerical methods scale poorly with the dimension of the problem. These include inference [184], optimisation [185], numerical integration [186], and stochastic expectation values [182]. For the latter, MCI is ubiquitously used in finance for problems such as asset pricing and risk analyses of complex investment portfolios (see use cases in sections (3.1)-(3.3)). The major advantage of MCI methods is that their scaling depends on the number of samples and not the dimension of the problem [182]. However, their downside is that they have a slow convergence since their estimation error decays as , where is the number of sample paths taken [5]. Routine finance problems such as risk analysis or pricing options often require large amounts of samples to achieve a desired precision [9]. Thus, there is value in exploring and understanding any potential benefits that quantum computing could bring in this space.

QMCI Algorithm

The typical use of MCI in finance is to estimate the expected value of an unknown financial quantity (e.g., price of a financial derivative), which is a function of other nondeterministic variables (e.g., market state) [9]. The methodology, described in more detail in Section (3.1.2), generally starts with choosing a stochastic model for the underlying random variables from which samples, denoted as , are taken. Then the corresponding value of the target quantity, denoted as 5, is computed based on the samples drawn. The weighted average of all obtained values of the target quantity is given by the expectation [182]

where is the probability distribution. Note that the random variable is sampled from a space that could be multi-dimensional. The Quantum Monte Carlo Integration (QMCI) [5] is the quantum formulation of the MCI method. Outlined in Algorithm (7), the QMCI utilises the Quantum Amplitude Estimation subroutine to compute the expectation given in Equation (28) and can potentially achieve a quadratic speed-up over classical MCI [5]. This is because the estimation error for QMCI decays as , where is the number of queries made to a quantum oracle that computes . This is comparable to the complexity in terms of the number of samples for MCI which has an error that scales as . Thus, if samples are considered as classical queries, the QMCI requires quadratically fewer queries than classical MCI to achieve the same desired error.

| Algorithm 7 Quantum Monte Carlo Integration |

|

Define: Let be the set of potential sample paths of a stochastic process that is distributed according to some probability , and is a real-valued function on , where is bounded.

Construct: A unitary operator to load a discretised and truncated version of . The probability value translates to the amplitude of the quantum state representing the discrete sample path . In mathematical form, it is

Normalise: The function f into , and construct a unitary that computes and loads the value onto the amplitude of . The resultant state after applying and is

Perform: The QAE with unitary and an oracle that marks states with the last qubit being . See Section (2.1.2.2) for details.

Result: Will be an approximation to

This value can be estimated to a desired error utilising evaluations of U and its inverse [5].

Rescale: The output to the original bounded range (A) to obtain .

|

Challenges for Quantum Advantage

At the time of this manuscript, no demonstration of quantum advantage with QMCI has been made, primarily due to the limitations of current quantum hardware and algorithmic challenges in key subroutines [12]. The former hardware limitations are due to:

- 1.

- Clock speed: As noted in [187], to achieve a Practical Quantum Advantage using QMCI over classical MCI, the quantum device would need to be able execute about layers of T-gates6 per second. This implies a required logical clock rate of about 50MHz to be competitive with current classical MCI methods. Recent methods [188] have reduced this requirement to 45MHz, which is still beyond the capabilities of current hardware.

- 2.

- Fault-tolerant: The code distance for fault-tolerant implementations needs to be large enough to support error-free logical operations [187]. In addition, quantum algorithms with a proposed quadratic speed-up need to tackle significantly high-dimensional problems to potentially realise some advantage [46], which further complicates fault-tolerant implementations.

- 3.

- Resource: The estimates are high for fault-tolerant resources needed to achieve competitive performance for finance problems that are challenging for classical methods. The latest estimates for derivative pricing [188] based on Quantum Signal Processing are logical qubits, T-depth, and T-count. These requirements are beyond currently available quantum hardware, and seem to be significantly higher in comparison to classical MCI, which requires samples and about 10 seconds to achieve the same accuracy [48].

On the other hand, the latter algorithmic challenges are due to:

- 1.

- Loading distribution: The state-preparation of an arbitrary probability distribution requires exponentially large circuits in terms of the number of qubits [189], which affects the potential quantum speed-up of QMCI. The improved state-preparation algorithm by Grover–Rudolph [190] is insufficient to achieve a quantum speed-up [191]. However, for certain distributions, a quadratic speed-up is possible [95,192,193]. It is noteworthy that various non-unitary methods exist for efficient state preparation for large circuits [194,195]. However, these methods are usually incompatible with QAE because of the non-invertibility of the operations involved. Furthermore, other alternative methods have been proposed, such as Quantum Generative Adversarial Networks (QGAN) [196] and tensor networks [197].

- 2.

- 3.

- Estimation: The first proposed QAE algorithm employed QPE which has a resource requirement beyond the capabilities of NISQ devices (see Section 2.1.1). However, non-QPE implementations of QAE have been proposed which can enable near-term implementations of QMCI (see Section 2.1.2.2).

As noted in [193], many other factors will drive the adoption of quantum computing in finance beyond exceeding classical performance. Some of these factors will be technical, such as ease of incorporation of QPU in a computational pipeline in finance, and others may be business and/or regulatory-related. In any case, it is important to have a well-defined framework [199] to evaluate the goal of achieving Practical Quantum Advantage. In this review, we will consider several use cases for QMCI in finance and economics, which are good candidates for obtaining a PQA in the long-run as the quantum technology matures.

2.2.2. Quantum Solvers for Stochastic PDEs

Stochastic Differential Equations (SDEs) have become fundamental tools for modelling a wide array of phenomena within finance and economics [200]. The dynamic and often unpredictable nature of financial quantities, such as asset prices, interest rates, and their derivatives, aligns naturally with the framework provided by SDEs, which explicitly incorporates stochastic elements into their structure. Unlike deterministic models based on ordinary differential equations, which yield a unique solution for a given initial condition, SDEs describe the evolution of continuous-time stochastic processes, reflecting the inherent uncertainties present in financial systems. The necessity of employing SDEs in finance arises from the fact that many financial variables exhibit diffusive dynamics, a characteristic well-captured by stochastic processes [200]. For instance, the Heath-Jarrow-Morton model [201], a cornerstone in interest rate modelling, is formulated as an SDEs. Similarly, the Heston [202] model for pricing of options under conditions of stochastic volatility, where the volatility itself is modelled as a random process, leads to a set of coupled SDEs7.

Despite the power and versatility of SDEs in capturing the complexities of financial markets, obtaining analytical solutions to these equations is often a formidable challenge for realistic models [200,203]. This is due to various factors, which include nonlinearities in models that complicate integration and inherent high-dimensionality from multiple underlying variables [204]. There are various numerical methods for solving SDE with diverse approaches; however, in this review, we will only consider the approach of employing the Feynman-Kac formula, which gives the expectation value8 to Equation (28) as a solution to a parabolic PDE. This will make it easier to compare with the QMCI algorithms described above.

Feynman-Kac Formula

Originally conceived within the framework of quantum mechanics by Feynman through his path integral formulation [205] and later rigorously formulated in a probabilistic context by Kac [206], this formula provides an alternative perspective for solving the expectation value given by Equation (28). Its original usage had the reverse objective to what we use it for here; that is, to solve a complex PDE with high dimensionality or non-constant coefficients by computing the expected value of a carefully constructed stochastic process [200]. However, since quantum computing is more suited to handle serious dimensional problems, it makes sense to convert expected values of stochastic processes into parabolic PDEs.

The Feynman-Kac formula [200,205,206,207] establishes a profound connection between parabolic partial PDEs and the expected values of certain stochastic processes. This relationship provides a conversion between the two, which can be a powerful tool for analysis and computation.

Mathematical Formulation Consider a parabolic PDE for the unknown variable of the form:

with a terminal condition , where is the terminal payoff function. Here the known functions: is a vector-valued function representing the drift, is an matrix representing the diffusion coefficient, is a scalar potential function, and is a source term. The operators: is the gradient of u, is the Hessian matrix of u, and Tr denotes the trace of a matrix. The Feynman-Kac theorem [200,207] states that the solution to the PDE in Equation (31) can be expressed as the conditional expectation:

where the function is given by

The stochastic variable is the solution to the following SDE [200]:

with the initial condition , and is a d-dimensional standard Brownian motion under a probability measure Q. The expectation is taken with respect to this probability measure, conditional on the initial state . Intuitively, the Feynman-Kac formula suggests [207] that the value of the function at a point can be seen as the expected future value, discounted by the potential V, of a stochastic process X that starts at x at time t and evolves according to the SDE in Equation (34). The terminal condition contributes at the final time T, and the source term contributes along the path of the process. The function acts as a stochastic discount factor, accounting for the accumulated effect of the potential along the random path.

Example BSM Model A classic example is the Black-Scholes-Merton (BSM) model for the vanilla European option9, where Equation (31) can be formulated as [31]

where is the option expected value with the terminal condition

Here is the payoff function, r is the risk-free rate, and is the volatility of the stochastic underlying asset . At the PDE of the form of Equation (35) can be solved by using quantum algorithms outlined in the ensuing sections.

Finite Difference Method

A widely used class of numerical techniques is Finite Difference Method (FDM) [208] that approximate the derivatives appearing in differential equations using differences between the values of the unknown function at discrete points in time and space. When applied to SDEs, the FDMs involves discretising both the spatial and temporal domains into a grid and replacing the continuous derivatives with their finite difference approximations [200]. Various finite difference schemes exist, including explicit and implicit methods, each exhibiting different characteristics in terms of stability and computational requirements [208]. For instance, explicit schemes are generally simpler to implement but may have stricter stability conditions, while implicit schemes, such as the Crank-Nicolson method, are known for their numerical stability, particularly for parabolic PDEs common in finance [208,209]. In situations where the financial model exhibits convection-dominated behaviour, upwind schemes are often employed to ensure numerical stability and accuracy [210].

Algorithm (8) outlines a general scheme of the FDM for solving SDEs via the Feynman-Kac formula. For every time step , the problem boils down to solving a linear system of equations with dimension N that depends on the discretisation in the stochastic variable x. Therefore, assuming the matrix A in Equation (38) is well conditioned, we can employ the Quantum Linear Systems Solver discussed in Section (2.1.5) to potentially obtain an exponential speed-up [131,132]. For arbitrary cases, A is not guaranteed to be well-conditioned, and the condition number may scale as a polynomial with the dimension: . In such cases, both classical and quantum methods can make use of preconditioners to reduce before running the linear system solver algorithm. The use of preconditioners for QLSSs has been explored [183,211,212,213] and has shown promising results. For example, authors in [183] used a wavelet basis as an auxiliary system of coordinates in which the condition number of associated matrices is independent of N by a simple diagonal preconditioner.

| Algorithm 8 Finite Difference Method for solving SDEs |

|

A crucial aspect of employing FDMs for SDEs is the analysis of their stability and convergence in the presence of stochastic terms [200]. Stability ensures that any numerical errors introduced during the computation do not grow uncontrollably as the simulation progresses. Convergence analysis, on the other hand, aims to determine whether the numerical solution obtained through the FDM approaches the true solution of the SDE as the discretization step sizes in time and space are refined. In general, the convergence of numerical schemes can be characterized in two ways [208,209]: strong convergence, which focuses on the pathwise accuracy of the approximation, and weak convergence, which concerns the accuracy of the moments of the solution. These concepts of strong and weak convergence are extended to the numerical analysis of SDEs as well [200]. Therefore, it is still an active area of research [215,216] to determine how noise from quantum computing affects the stability and convergence analysis of SDEs.

Hamiltonian Simulation

The natural language of quantum computing is in terms of Hamiltonian representation [149], thus an interesting approach to solving a PDE of the form of Equation (31) is to convert it into a Schrödinger or Schrödinger-like equation. For example, in Ref. [217] showed that for the BSM model given by Equation (35), one can perform a change of variables for and reversal of time to reformulate Equation (35) into a Schrödinger-like equation:

where is a non-Hermitian Hamiltonian given by

Here, in the momentum operator. Since the associated propagator is non-unitary, the approach of [217] is to decompose into a sum of Hermitian and anti-Hermitian part, , with

Since, the two parts of commutes with each other , then via the Baker-Campbell-Hausdoff formula [218] the evolution operator can be written as . The non-unitary is then embedding it into an enlarged Hilbert space requiring one additional ancillary qubit, such that the corresponding unitary evolution is given by

A proof-of-concept implementation using 8 qubits on a simulator got results in good agreement with analytical solutions for the BSM model[217].

The major drawback with the approach of [217] is that the embedding technique doubles the size of the problem. An alternative Hamiltonian simulation is to make an additional change of variables [216,219]:

where are constants given by the BSM model. This allows for the mapping of Equation (35) into the heat equation of the form [216,219]:

A Wick rotation is performed on the time variable , which then can be mapped to a Schrödinger-like equation in imaginary time:

where the operator is given by

This simulation can be performed using the Quantum Imaginary Time Evolution (QITE), which was first proposed for quantum chemistry problems [220] but has also been applied to other quantum simulation problems [221]. State-of-the-art methods for QITE include accelerated approaches using random measurements [222], and an alternative approach that uses orthogonal basis states to efficiently express the propagated state [223]. The Schrödingerisation method of [219] can be applied to general linear differential equations, including the Fokker–Planck equation [224], which describes the time evolution of the probability density function of the velocity of a particle under the influence of drag forces and random forces. Hence, methods of solving SDE via the Fokker–Planck formulation can also be handled by the aforementioned quantum algorithm [216].

Other Approaches It is worth mentioning other quantum approaches to solving SDEs, in particular the the variational algorithm of Ref. [161]. In this approach, they first approximate the target SDE by a trinomial tree structure with discretisation to obtain a linear differential equation describing the probability distribution of SDE solutions. The resulting differential equation is then solved by formulating it as the time-evolution of a quantum state embedding the probability distributions of the SDE variables. This approach utilises the Fokker–Planck equation [224], which also gives the time evolution of the probability distributions of SDE solutions. A proof-of-concept implementation of this approach was shown to be in close agreement with classical methods [161], but the reported scaling of this method does not seem promising for achieving Practical Quantum Advantage for industrial-scale problems.

2.3. Quantum Optimisation

Broadly speaking, optimisation is the act of modifying a process to extremise some property, which might be the occurrence of favourable outcomes, the profit of some business model, expected returns of a portfolio, or any number of other things [225,226]. Performing an optimisation requires us to make some assumptions about the real world. For example, an investor who wishes to optimise their portfolio to maximise returns or minimise risk could begin by stating assumptions about present and future market conditions, such as risk or volatility, and comparative returns [204,227]. Since there is no way to accurately calculate these in real-time, the proper estimation of these values is vital [181,204].

In the financial sector, optimisation is the process of making a financial system more effective by adjusting the variables used for technical analysis, which might involve, for example, reducing certain transaction costs, risks, or targeting assets with greater expected returns [228]. Depending on the underlying assumptions or the target of the optimisation, there may be multiple potential optimisation procedures. The success of the chosen procedure will depend on how well one has estimated or quantified the risks, costs, and potential payouts.

Optimisation problems are, therefore, almost ubiquitous, but often very time-consuming or computationally expensive to solve given the number of variables involved [229]. Their high impact, combined with the existence and relative maturity of many quantum algorithms for solving them [150,157,230,231,232], means there is a lot of potential value in exploring commercially relevant applications on NISQ hardware [150,157]. Furthermore, improvements in hardware mean that the prospect of thorough and reliable benchmarking of various quantum algorithms is closer to reality. A recent paper [233] presented ten optimisation problem classes, as well as a Quantum Optimisation Benchmark Library for recording problem instances and solution track records, with standardised reporting and comparisons to the classical state of the art. This and similar efforts allow more rigorous comparison of different quantum optimisation algorithms, clarifying competing claims of suitability or performance, and enabling laypersons to more confidently explore and implement solutions.

This section discusses how such quantum algorithms may be used to solve two types of optimisation problems [152]: (i) combinatorial optimisation and (ii) convex optimisation. The former is a discrete optimisation problem, consisting of finding the optimal combination of values for some cost function, while the latter is a continuous optimisation problem involving optimising some convex cost function.