Submitted:

05 November 2025

Posted:

07 November 2025

You are already at the latest version

Abstract

Canonical market microstructure theories, validated in liquid financial markets, are often misapplied to illiquid power futures. This study introduces the Impact-Inventory Parity (IIP) parameter Ψ, bridging the Kyle (information-based) and Ho-Stoll (inventory-based) models, and uses agent-based simulations to test its validity in thin markets. We uncover a critical asymmetry: while competition consistently pushes markets towards inventory dominance, the countervailing effect of non-linear inventory costs systematically weakens as markets thin due to lower inventory variance. This creates a structural bias toward inventory dominance Ψ=1 that persists despite strong convex penalties. Adaptive behaviour revealed a stability paradox, causing severe parity breakdown that was amplified by liquidity, not thinness. Parameter space analysis showed market stability rests equally on three structural pillars: participation, liquidity, and information quality. Among stable markets, information quality dominates regime outcomes, while adaptative behaviour acts as a critical threshold where small changes can trigger immediate market collapse. Across the physically plausible parameter space, inventory-dominated regimes comprise the vast majority (73%) of configurations, while the balanced-risk conditions predicted by classical theory are rare (8%), confirming parity as a narrow, fragile equilibrium. The framework proves robust in thin, fragmented markets—precisely where canonical models fail, while becoming unreliable in the liquid, centralized venues where those models were validated.

Keywords:

market microstructure

; power futures markets

; market maker

; agent-based modeling

; liquidity provision

; Kyle model

; inventory risk

; thin markets

; electricity trading

1. Introduction

1.1. The Liquidity Challenge in Power Futures Markets

Power futures markets often exhibit low liquidity. Despite billions in annual trading volumes— concentrated primarily in near-term contracts —bid-ask spreads in electricity futures often exceed comparable financial markets by an order of magnitude [1,2]. This illiquidity imposes severe economic costs precisely when these markets are most needed. The global energy transition depends on efficient price discovery and risk management tools for renewable energy investments [3]. Yet the very markets designed to provide these functions can suffer from chronic illiquidity, particularly for contracts extending beyond one year.

The consequences cascade throughout the energy system. Wide spreads increase transaction costs for hedging. Volatile prices complicate investment planning [4]. Limited market depth restricts large participants from managing portfolio risks effectively. Most critically, inadequate liquidity creates barriers to capital formation for clean energy infrastructure. Renewable developers struggle to secure long-term revenue certainty, while utilities cannot efficiently hedge variable generation exposure [5,6]. Industrial consumers face elevated costs for managing price risk.

Market makers represent the standard financial solution to these liquidity challenges. By continuously quoting two-sided markets and absorbing temporary order imbalances, they typically reduce spreads, increase volumes, and improve price efficiency. Recognizing this potential, regulators worldwide are actively developing market maker programs for power futures markets [7]. The Agency for the Cooperation of Energy Regulators (ACER), national authorities across Europe, and the U.S. Commodity Futures Trading Commission are all exploring mechanisms to enhance liquidity. However, these initiatives often import program designs and theoretical frameworks directly from liquid financial markets. This paper addresses this gap by analyzing the effectiveness of standard market maker models in an environment characterized not by information asymmetry, but by structural illiquidity and inventory risk. We ask: under what conditions can market maker programs succeed when their foundational assumptions of competitive pressure and deep order flow are absent?

1.2. Canonical Models of Market Making

The Kyle [8] model provides the foundational framework for analyzing market maker effectiveness under information asymmetry. This cornerstone of market microstructure theory elegantly captures how adverse selection affects liquidity provision. Crucially, the model assumes market makers are perfectly competitive (or operate under a market-clearing mandate), leading to a zero-expected-profit condition in steady state. This zero-profit assumption, however, is unlikely to hold in illiquid markets where the lack of competition allows market makers to wield significant pricing power. The focus is squarely on how they process private information signals embedded in order flow. The model derives closed-form solutions for optimal market maker pricing when facing potentially informed traders. Kyle’s lambda parameter precisely quantifies market depth as the price impact per unit of order flow.

Kyle’s theoretical predictions have received extensive empirical validation across liquid, anonymous financial markets. Studies confirm the predicted relationships between order flow and price changes [9]. Research documents the inverse correlation between informed trading intensity and market depth. The model’s insights about spread determinants and volume patterns consistently match observed market behaviour. This empirical success has established Kyle’s framework as the standard benchmark for analyzing liquidity provision and market maker programs [10,11]. This empirical success, however, is confined to the very markets that power futures are not: deep, anonymous, and information-rich. The structural features of energy markets call the direct applicability of these findings into question.

Analytical work in market microstructure has also explored other drivers of liquidity provision. The model of Ho and Stoll [12] represents a foundational framework focusing on inventory risk as a primary driver of market maker behaviour (see also Amihud and Mendelson [13]). In contrast to the Kyle framework, Ho-Stoll features a market maker acting as a risk manager rather than an information processor; quotes are influenced by the need to manage an unbalanced portfolio. A market maker holding excess inventory will lower its quotes to attract buyers and deter sellers, and vice versa. This introduces a distinct motivation for quoting behaviour and provides a richer, though still highly stylized, model of liquidity provision. Together, the Kyle and Ho-Stoll models represent the canonical benchmarks for information-based and inventory-based market making, respectively.

Beyond these two canonical models, our analysis also draws on related streams of market microstructure theory. The framework of Glosten and Milgrom [14] refines the modeling of adverse selection in sequential trade, while research by Easley and O’Hara [15] highlights the information content revealed by trade size, a critical factor in thin markets. More directly, recent work by Pena and Rodríguez [16] provides the first empirical examination of market maker programs in European electricity futures. Our paper builds on this by providing a theoretical foundation for their findings and exploring the strategic behaviour of market makers, a topic previously analyzed in other thin commodity markets by Antón and Bushnell [17] and Kumar and Seppi [18].

1.3. The Mismatch Between Theory and Power Market Reality

Power markets violate the assumptions of these canonical models in fundamental ways. These disconnects span two critical dimensions—– physical characteristics and market structure –—that challenge the frameworks’ applicability, particularly in thin markets, defined here as markets with a finite number of buyers and sellers.

First, electricity’s physical characteristics differ radically from financial assets [19,20]. Unlike storable commodities, electricity cannot be easily inventoried, which profoundly shapes hedging needs and prevents market makers from managing positions through a physical spot market. The grid itself imposes structural constraints: transmission bottlenecks fragment the market into location-specific prices, while generation faces hard capacity and ramping limits that restrict supply elasticity [21]. The trading structure also departs from financial archetypes; while futures trade continuously, their pricing is inextricably linked to discrete, high-volume daily auctions in the underlying physical market, creating a distinct informational heartbeat.

Second, the behavioural and informational assumptions of canonical models fail. The assumption of anonymity is frequently violated; participants are registered entities with known generation or load obligations, allowing for reputation-based behaviours that are absent from anonymous markets. Instead of a single informed trader facing a sea of uninformed noise traders, the market consists of strategic, oligopolistic generators with known market power [22,23] and load-serving entities with highly predictable hedging needs. Crucially, information often arrives through public channels, such as weather forecasts or grid condition reports, rather than the private signals central to Kyle’s framework. This public information structure and non-anonymous, strategic environment fundamentally alters the nature of liquidity provision.

The systematic violation of these assumptions renders traditional equilibrium analysis inadequate for power markets. In thin markets, participants recognize their impact on prices and adapt their behaviour accordingly, moving away from the price-taking behaviour assumed in competitive equilibrium models. Analytical models achieve tractability only by eliminating these defining features: strategic interaction, non-storability, and imperfect competition. Relaxing these assumptions simultaneously destroys closed-form solutions.

1.4. The Role of Agent-Based Modeling

Agent-based models (ABMs) offer a promising methodological approach to address these analytical challenges [24,25]. ABMs allow heterogeneous agents to embody distinct operational characteristics, information sets, and realistic behavioural rules, including adaptive heuristics and strategic behaviours that are difficult to model analytically. While this departs from the strict assumption of idealized payoff maximization used in equilibrium analysis, it allows us to model the complex interactions and emergent market dynamics characteristic of real-world power trading [26]. This flexibility is essential for exploring environments where traditional assumptions are violated and equilibrium analysis becomes intractable [27].

1.5. A Methodological Bridge: Validation Through Analytical Benchmarks

The methodological approach adopted in this paper—– establishing rigorous analytical benchmarks before advancing to complex simulations –—reflects a fundamental principle from mature computational sciences, yet one that remains underutilized in economics. This creates a tension. On one side, analytical microstructure models provide elegant closed-form solutions that have been extensively validated in liquid financial markets. On the other, agent-based simulations can capture the complexity of thin, strategic power markets but are often viewed skeptically by mainstream economists as difficult to verify or connect back to established theory. The question is not which approach is superior, but rather how to bridge them in a methodologically rigorous way.

This bridging problem has been confronted—– and largely solved –—in fields with long histories of numerical computation. In computational physics, fluid dynamics, astrophysics, and related disciplines, analytical solutions are not viewed as competitors to simulation but as essential validation instruments [28,29]. A numerical model earns credibility only after demonstrating it can accurately reproduce known closed-form solutions in simplified regimes where such solutions exist. Only then is the model trusted to explore complex, nonlinear phenomena beyond analytical reach. The simulation extends the theory rather than replacing it; deviations from analytical predictions in complex regimes become quantifiable measurements of the impact of nonlinearities, boundary effects, or emergent collective behaviour that the simplified theory cannot capture.

This validation tradition has deep roots, and it is worth consdiering in detail some illustrative examples across the computational sciences:

Partial Differential Equations

Finite difference and finite element codes are systematically validated using the Method of Manufactured Solutions [28], where analytical solutions to simplified PDEs are constructed by design. Codes must demonstrate proper convergence rates before being trusted for production simulations.

Computational Fluid Dynamics

Numerical hydrodynamics codes are routinely validated against the Riemann problem, particularly the Sod shock tube test [30], which provides an exact analytical solution for shock propagation that any reliable code must reproduce.

Plasma Physics

Particle-in-cell (PIC) and Vlasov simulation codes must accurately reproduce Landau damping [31]—– the analytical prediction for collisionless damping of plasma oscillations—before being considered reliable for turbulent plasma simulations where no analytical solutions exist.

Astrophysical Structure Formation

Before modeling nonlinear gravitational collapse, N-body cosmological codes are benchmarked against the Zel’dovich approximation [32], which provides closed-form predictions for density perturbations in the linear regime of structure formation.

General Relativity and Black Holes

Perhaps the most striking example comes from gravitational physics. Analytical solutions to Einstein’s field equations—– the Schwarzschild solution for non-rotating black holes [33] and the Kerr solution for rotating black holes [34] –—were derived in the early-to-mid 20th century. However, numerical relativity faced a decades-long struggle to reproduce even these known solutions in computational simulations. The field experienced a crisis when codes systematically failed to remain stable long enough to simulate black hole mergers [35]. The breakthrough came only in 2005, when Pretorius [35] developed numerical methods that could finally reproduce the analytical predictions and remain stable through merger events. This more-than 40-year gap between analytical solution and numerical validation underscores a critical lesson: without the analytical benchmarks, the field would have had no way to diagnose whether simulation failures reflected physical insight or computational error. The Schwarzschild and Kerr solutions served as validation instruments that eventually enabled reliable predictions for phenomena far beyond analytical reach, such as gravitational wave signals from binary black hole mergers [36].

ABMs in Economics

Economics has begun to recognize the value of this validation paradigm. Windrum et al. [37] document the validation challenge facing agent-based modeling in economics and call for more systematic approaches to grounding complex simulations. More recently, Axtell and Farmer [25] emphasized that as computational tools become more sophisticated, the need for rigorous validation protocols becomes more acute, not less. However, the gap between analytical benchmarks and computational validation remains wider in economics than in the physical sciences.

This paper aims to narrow that gap for market microstructure research. We treat canonical analytical models not as theories to be confirmed or rejected, but as measurement instruments. By deriving a generalized framework that extends classical models to incorporate realistic market features, we create a diagnostic tool for quantifying how thin market structure systematically deviates from idealized conditions. The agent-based simulation is not validated by whether it matches the analytical prediction. We expect it will not, precisely because power markets violate the simplifying assumption. But by whether the deviations are economically interpretable and empirically meaningful. A failure to match the benchmark becomes a measurement rather than a failure: it quantifies the impact of competition, nonlinear costs, or adaptation. This approach provides a methodologically rigorous path for moving from the elegant simplicity of closed-form microstructure theory to the complex reality of thin power futures markets, while maintaining theoretical discipline throughout.

1.6. The Roadmap of this Paper

This paper is structured as a systematic progression from classical analytical theory to complex computational simulation. Each section serves a distinct methodological function, and understanding their interconnections is essential for interpreting the results.

We present this as a deliberate sequence: first establishing theoretical benchmarks, then constructing a computational laboratory, validating measurement procedures through controlled experiments, and finally exploring the full parameter space. The narrative arc mirrors the validation hierarchy standard in computational sciences: simple cases with known solutions precede complex cases where emergent behaviour dominates.

Section 2: An Analytical Toolkit

In realistic markets, both the Kyle and Ho-Stoll mechanisms will be at play simultaneously. We begin by proposing a diagnostic parameter— the Parity Index —that measures the relative strength of the two fundamental forces in market maker pricing. These are: the information-based price impact from order flow (the Kyle mechanism) and the inventory-based price adjustment from position management (the Ho-Stoll mechanism).

Under the idealized conditions assumed in classical microstructure theory, i.e., perfectly competitive or market-clearing dealers, linear inventory costs, and time-invariant behaviours, the two canonical models predict this balance should equal unity: . However, thin power markets systematically violate these classical assumptions. We therefore derive a generalized Impact-Inventory Parity (IIP) parameter that extends the baseline models to incorporate three realistic departures from theory: liquidity fragmentation through imperfect competition, non-linear inventory constraints that penalize large positions, and adaptive behaviour where dealers adjust their information extraction based on current inventory exposure.

For each extension, the framework yields precise theoretical predictions. Note that these predictions are not presented as claims about how real markets behave. They are the known analytical solutions against which we will validate our computational model. This section establishes what we should measure if the simulation correctly implements the economic mechanisms we intend to study— the benchmarks that will enable us to interpret subsequent deviations as meaningful measurements rather than simulation artifacts.

Section 3: The Computational Laboratory

We next construct agent-based simulations that will serve as our experimental environment. The model specifies heterogeneous agents (informed traders, liquidity providers, risk-averse market makers), their behavioural rules derived from microstructure theory aligned with the assumptions of the classical market maker models, and the market-clearing mechanisms.

Critically, this section also defines the rigorous econometric measurement protocol we will apply to simulation output: ordinary least squares regressions for the Kyle and Ho-Stoll relationships, cointegration testing via the Augmented Dickey-Fuller test to verify that theoretically predicted long-run relationships emerge in the data, and Rubin’s Rules for aggregating results across stochastic simulation runs. These statistical procedures constitute the validation standard by which we judge whether the simulation produces economically coherent dynamics. The ABM is the laboratory; the econometric protocol is the measurement apparatus.

Section 4: Controlled Experiments and Validation

With both the analytical benchmark and the computational laboratory established, we systematically test whether the simulation can reproduce known theoretical predictions before asking it to explore unknown territory. Section 4.1 validates the baseline: under idealized conditions (monopolistic dealership, linear costs, time-invariant behaviours), the measured Parity Index achieves with precision limited only by finite-sample econometric noise. This confirms the simulation correctly implements the intended economic mechanisms. We also validate this result follows the expected result for non-monopolistic markets.

Section 4.2–Section 4.4 then introduce complexities one at a time through controlled experiments. Section 4.2 validates the kurtosis effect and reveals how market thickness moderates non-linear inventory costs. Section 4.4 demonstrates the breakdown of static parity predictions under state-dependent adaptive behaviour. Each experiment isolates a single mechanism while holding others constant, enabling precise causal attribution.

Section 4.5 provides a critical meta-validation: we demonstrate that the linear approximations underlying our analytical framework remain empirically tight even in the presence of non-linear simulation dynamics, with high regression values across all parameter configurations. This section validates not merely that the simulation works, but that our measurement framework remains reliable for quantifying deviations from classical theory.

Section 5: Global Sensitivity Analysis

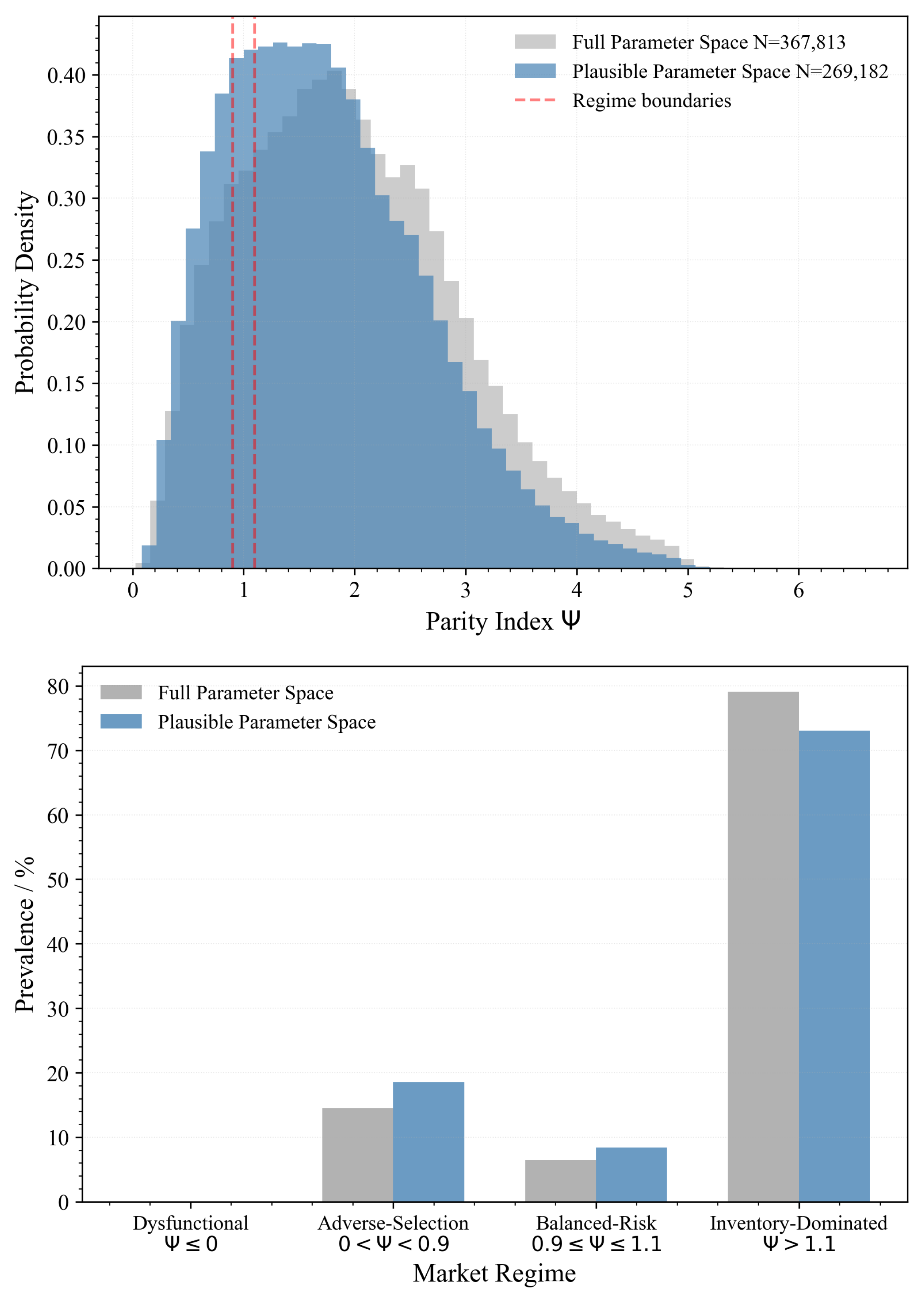

Having validated the methodology, we now deploy the full computational model across the entire six-dimensional parameter space, calibrated to thin power market conditions. Using variance-based Sobol decomposition, we address questions that cannot be answered through controlled experiments. For example, which parameters determine whether markets achieve basic stability versus collapse entirely? Among stable markets, which structural features determine regime outcomes? What is the prevalence of balanced-risk conditions versus inventory-dominated or adverse-selection-dominated regimes across the physically plausible parameter space?

This global analysis reveals that market stability depends equally on three structural pillars (participation, liquidity, information quality), that information quality dominates conditional regime determination, and that the balanced-risk equilibrium predicted by classical theory represents a narrow knife-edge (8% of configurations) rather than a robust attractor. These findings emerge from simulation but are interpretable precisely because we established analytical benchmarks: we can quantify that 73% of realistic parameter combinations produce inventory-dominated outcomes , a systematic deviation from the classical prediction whose magnitude and prevalence have direct policy implications.

Interpreting the Results

The linear analytical models presented in Section 2 should not be read as claims about how real thin markets behave. They are baseline measurement standards–— the null hypotheses against which we detect and quantify complexity. When simulation results deviate from , this is not a failure of either the analytical model or the simulation. It is a successful measurement of the impact of market structure on pricing dynamics.

For example, a competition effect pushing in fragmented markets quantifies how liquidity provision differs from the idealized benchmark. A kurtosis effect suppressing under strong non-linear costs measures the practical impact of inventory constraints. A collapse to under adaptive behaviours reveals where static assumptions break down entirely. The value of this paper lies not in confirming or rejecting classical microstructure theory, but in providing a theoretically grounded, empirically rigorous method for quantifying how far thin power markets deviate from that theory, which mechanisms drive those deviations, and what those deviations imply for market maker program design. The analytical benchmarks make the simulation results interpretable; the simulation makes the analytical deviations quantifiable and policy-relevant.

2. Theoretical Framework: Impact-Inventory Parity (IIP)

This section develops the analytical framework that bridges the two canonical models of market microstructure: the information-based model of Kyle [8] and the inventory-based model of Ho and Stoll [12]. We derive a theoretical relationship— the Impact-Inventory Parity (IIP) —that predicts how the forces of adverse selection and inventory risk management interact.

We begin by defining the two fundamental relationships that capture market maker behaviour, and establish a benchmark parity condition under idealized assumptions. We then generalize the framework to account for realistic market features like fragmented dealership and non-linear costs. The section continues with an interpretation of market regimes through the lens of the IIP, and derivation of plausible parameter ranges. Finally, we ground IIP in the context of secondary financial power markets and discuss its relevance to the unique characteristics that power markets present.

2.1. The Duality of Information and Inventory

A market maker’s pricing decisions can be viewed through two complementary lenses, each captured by a distinct regression plot:

- 1.

- The Kyle Plot is a regression of price changes with the signed order flow . The resulting slope measures market depth, or the price impact of a trade. A higher indicates lower liquidity, as the market maker must adjust prices more significantly to protect against informed trading. This is a reactive response to the informational content of order flow.

- 2.

- The Ho-Stoll Plot is a regression of the deviation of the mid-price from its fundamental value with the market maker’s lagged inventory . The slope measures inventory aversion. A more negative indicates that the market maker aggressively skews quotes to offload inventory risk. This is a proactive apporach to manage the cost of holding an unbalanced position.

The central diagnostic of our framework is the Parity Index defined as the ratio of the proactive inventory sensitivity to the reactive flow sensitivity

This index quantifies the balance between the two primary risks a market maker faces. A value of suggests a balanced market where informational risk and inventory risk are managed in balance. Deviations from unity signal that one risk management dominates the other, defining distinct market regimes which we will explore later.

2.2. The Classical Parity Condition

Under the idealized conditions assumed in classical microstructure theory, a perfect duality exists between the informational impact of order flow and the price pressure from inventory management. We formalize this relationship by establishing a benchmark where competition is perfect and inventory costs are linear. In this special case, the Parity Index equals unity. This result is established through two complementary theorems.

Theorem 1

(Kyle on the Ho-Stoll plot). In a pure information-based market (no inventory tilt ) with a monopolistic market maker and linear costs, if price discovery follows the linear impact rule , the implied slope of the Ho-Stoll plot is .

Proof.

Iterating the price update gives . The cumulative order flow is thus when . Combining these yields , a linear relationship with slope . □

Theorem 2

(Ho-Stoll on the Kyle plot). In a pure inventory-based market (no information impact ) with a monopolistic market maker and linear costs, if the market maker sets prices according to a linear inventory tilt , the implied slope of the Kyle plot is .

Proof.

The price change is . Since the inventory update is , this yields , a linear relationship with slope . □

These theorems demonstrate that under idealized, single-factor conditions, the informational price impact and the inventory price pressure are perfectly symmetric. An information-only model generates an apparent inventory slope, while an inventory-only model generates an apparent informational slope. In a combined model where both effects are present, and , their impacts are additive. The slopes become

This leads to the parity condition and thus . This benchmark provides a sharp, parameter-free prediction that serves as a null hypothesis for testing the impact of more realistic market features.

2.3. The Generalized Parity Index

We now relax the classical assumptions to account for two critical features of real-world markets: fragmented dealership and non-linear inventory costs. We introduce two parameters to capture these effects:

- 1.

- Liquidity Fragmentation: We define as the fraction of the total net order flow captured by the market maker. A value of represents a competitive environment where the market maker does not intermediate all trades.

- 2.

- Convex Inventory Costs: We model non-linear costs using a symmetric cubic penalty term . This captures the escalating risk of holding large inventory positions, which requires more aggressive price adjustments.

These generalizations modify the model dynamics. The market maker updates their belief about the fundamental value V based on the total order flow, but their inventory changes only by the captured flow

The pricing rule is updated to include the non-linear cost term

We use odd-ordered polynomial terms () to model symmetric, mean-reverting costs. An even-ordered term like would be non-reverting, incorrectly pushing the price in the same direction for both long and short positions.

Under these generalized dynamics, we can derive the estimators for the Ho-Stoll and Kyle slopes. First, we establish a relationship between the market maker’s belief and their inventory. Since inventory accumulates only a fraction of the flow that drives belief updates, the perceived price deviation for a given inventory level is amplified by

Using this relationship, we can now derive the explicit forms for the generalized Ho-Stoll and Kyle slopes.

The Ho-Stoll slope is the OLS estimator from the regression of price deviation on lagged inventory . We begin by expressing the price deviation entirely in terms of inventory. We substitute the belief-inventory relationship Equation 5 into the pricing rule Equation 4,

The OLS estimator is defined as . Substituting our expression for the price deviation yields

Using the properties of covariance, this becomes

Assuming the inventory process is stationary with a mean of zero, we have and . The equation simplifies to

We recognize that this is a linear approximation of a non-linear process. The validity and tightness of this approximation will be empirically tested in Section 4.5.

By definition, the kurtosis is . Substituting this in gives the final exact expression for the generalized Ho-Stoll slope under our assumptions

The Kyle slope is the OLS estimator from the regression of price changes on order flow . We first derive the price change

To handle the cubic term, we substitute and expand

Substituting this back gives the full expression for the price change

This reveals that the relationship between and is non-linear when . To find the linear regression coefficient , we must approximate this relationship. We do so under two standard assumptions: (1) that the net order flow is independent of the market maker’s lagged inventory , and (2) that we can neglect the impact of higher-order terms of order flow () on the linear projection. These higher order terms will typcially be neglible if the order flow distribution is symmetric about zero. The OLS estimator then isolates the expected value of the coefficient on the term linear in

Recognizing that , we arrive at the approximated generalized Kyle slope

2.4. Analysis of the Generalized Framework

The generalized form of the Impact-Inventory Parity reveals a fundamental tension between the effects of competition and non-linear costs. To clarify the interpretation, we can factorize Equation 16:

This factorization isolates two distinct mechanisms that drive deviations from the classical parity of .

The first term represents a competition effect. This factor captures the impact of liquidity fragmentation. As competition increases ( decreases), the market maker’s belief about the fundamental value is still updated by the total market order flow, but their inventory changes by a smaller, captured fraction of that flow. This creates a disconnect: the market maker’s inventory becomes a weaker proxy for the cumulative order flow that has informed their price. As shown in Equation 5, the relationship between belief deviation and inventory is amplified by . This inflates the magnitude of the measured Ho-Stoll slope relative to the Kyle slope, pushing the Parity Index upwards. In the absence of non-linear costs , the second term equals one, and we recover the simple prediction that .

The second term represents a kurtosis effect. This factor captures the impact of non-linear inventory costs. Convex costs strongly penalize large inventory positions, inducing aggressive mean-reversion in the market maker’s behaviour. This constrains the inventory distribution, leading to thinner tails than a standard Gaussian distribution, i.e., platykurtosis where . Because the inventory kurtosis K appears in the numerator while the Gaussian benchmark of appears in the denominator’s coefficient, a platykurtic distribution causes the numerator to be smaller than the denominator. This pushes the value of the second term below unity, thereby pushing the Parity Index downwards.

The IIP framework therefore reveals a core conflict: competition tends to increase , while non-linear costs tend to decrease it. The observed market state depends on the relative strength of these opposing forces and the emergent response of the inventory statistics to the underlying market structure.

2.5. Breakdown of Parity: The Covariation Remainder

The IIP framework derived thus far relies on a critical assumption: that the market maker’s behavioural parameters () remain constant regardless of market conditions. However, this assumption breaks down in thin power markets characterized by adaptive oligopolistic participants. Consider a concrete scenario: a market maker holding a large long position in power futures faces an incoming buy order. If they process this order using their standard information extraction , they risk accumulating an even larger long position, potentially approaching physical delivery obligations they cannot fulfill. A rational response is to become more cautious, extracting information more aggressively (higher effective ) to avoid further exposure. Conversely, when holding negligible inventory, the same market maker might process orders more passively.

This state-dependent behaviour is not merely a theoretical possibility but a practical necessity in power markets. Large players— generation companies, utilities —observe market makers’ quote patterns and can infer inventory positions. When they perceive vulnerability (large inventory imbalance), they may trade more aggressively to exploit it. The market maker, anticipating this, adjusts their response dynamically. Unlike anonymous equity markets where such adaptation is difficult to implement, the concentrated structure of power futures makes state-dependent behaviours both observable and important.

To quantify the magnitude of such dynamic behaviour, we consolidate all sources of linear price impact into a single, time-varying effective price impact coefficient . This coefficient captures the baseline informational impact , the inventory-hedging pressure , and any additional adjustments made in response to current market state

where represents price moves not caused by order flow. Summing these price changes gives the cumulative deviation from the fundamental value

To connect this cumulative impact to the current inventory , we apply summation by parts (the discrete equivalent of integration by parts). This decomposes the relationship into the standard parity term and a new term that explicitly accounts for changes in the impact coefficient over time:

This identity reveals when and how the static IIP framework breaks down (for example, as a result of dealers becoming more cautious as they approach potentially unmanageable physical delivery obligations). If the price impact remains constant (), the Covariation Remainder vanishes, and we recover the static parity relationship scaled by . However, when market makers adapt their information extraction based on inventory exposure, the Covariation Remainder becomes non-zero and systematically alters the measured Ho-Stoll slope.

The economic interpretation is straightforward: the term quantifies the correlation between changes in price impact and past inventory positions . When a market maker increases their price impact precisely when holding large inventory ( large), the Covariation Remainder accumulates systematically, breaking the classical parity prediction.

The Parity Index therefore serves dual purposes: measuring static market structure () under time-invariant behaviour, and detecting dynamic, state-dependent adaptation when that assumption fails. In Section 4.4, we test this breakdown empirically through controlled simulations.

2.6. Defining Market Regimes

The theoretical framework developed thus far provides a powerful tool for diagnosing market dynamics, but its value lies in its connection to observable economic behaviour. While the condition of perfect parity serves as a theoretical benchmark, understanding the implications of deviations from this ideal is essential. In this section we classify the economic meaning of different values of into distinct market regimes; and establish physically grounded bounds on the underlying regression coefficients to ensure our analysis remains anchored in economic reality.

The Parity Index can be interpreted as a descriptor of the market maker’s dominant risk-management stance. By analyzing its value, we can move beyond a binary test of parity and classify the market into one of four primary regimes:

2.6.1. Regime 1: Inventory-Dominated Market

In this regime, the market maker’s pricing is more sensitive to their own inventory imbalance than to the informational content of incoming order flow . The dominant perceived risk is the cost of holding a large position. This is characteristic of a market with a high proportion of noise or liquidity trading, where the market maker acts as a classic inventory-balancing dealer, aggressively skewing quotes to offload risk.

2.6.2. Regime 2: Balanced-Risk Market

This regime represents the theoretical ideal of Impact-Inventory Parity . Here, the price impact from a trade (a reactive measure against adverse selection) is perfectly offset by the price adjustment made to manage the resulting inventory (a proactive measure). This corresponds to a well-functioning, efficient dealership market where both primary risks are managed in equilibrium. We define this regime as a relatively tight band around unity .

2.6.3. Regime 3: Adverse-Selection-Dominated Market

When is less than one, the market maker’s pricing is more sensitive to the informational content of order flow than to their inventory position . The dominant risk is adverse selection. The market maker acts more like an information processor, reacting strongly to each trade while tolerating larger short-term inventory imbalances to avoid losses to better-informed traders. This regime is characteristic of a market with a high proportion of informed trading.

2.6.4. Regime 4: Dysfunctional Non-Dealership Market

A negative value for signifies a breakdown of the rational dealership model. Assuming a positive price impact , a negative implies that . This would mean that the market maker raises their quote midpoint in response to accumulating a long inventory— an economically irrational behaviour. Such a result suggests that the emergent market dynamics do not conform to a dealership structure, perhaps because intense competition has decoupled the designated market maker’s inventory from the market’s overall price formation process.

An even more pathological scenario leading to occurs if price impact becomes negative while inventory management is also destabilizing . A negative would imply a complete reversal of price discovery: the market maker lowers the price in response to net buying and raises it in response to net selling, effectively paying traders to take liquidity. Simultaneously, a positive means the market maker raises prices when long and lowers them when short, actively working to worsen their inventory imbalance. While highly irrational, this combination represents a total failure of both the information-processing and inventory-management functions of a market maker.

In either case, a measured does not imply a flaw in the measurement itself, but rather signals that the emergent market dynamics do not conform to any rational dealership structure.

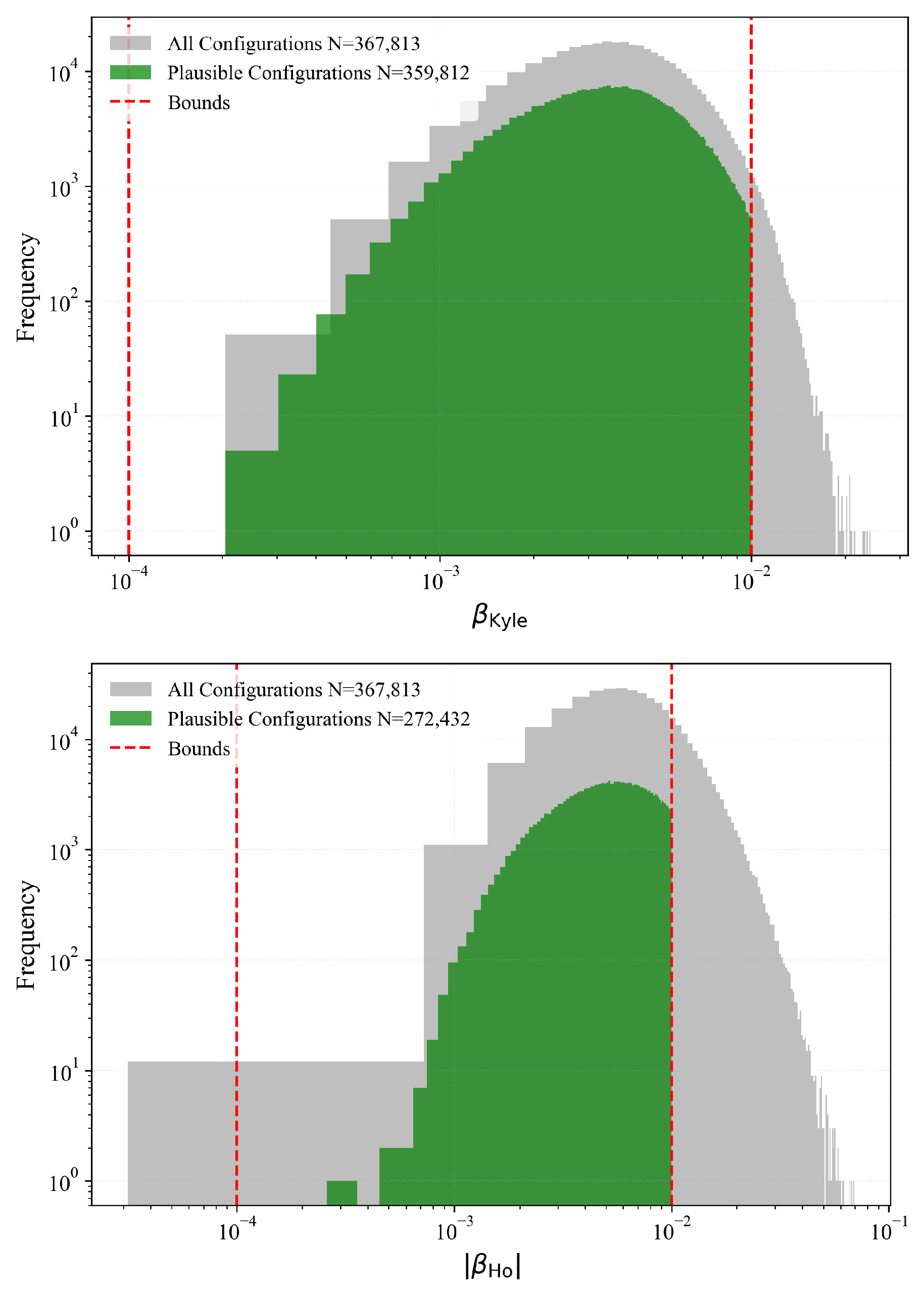

2.7. Plausible Order-of-Magnitude Parameter Bounds

To ensure our analytical predictions apply to economically realistic markets, we establish physically grounded bounds for the two key regression coefficients and . These are derived from a dimensional analysis based on observable market characteristics: typical tick sizes , meaningful order sizes , and standard inventory positions . This anchoring in empirical scales identifies the relevant parameter space for testing the IIP predictions. Given the wide variation in these characteristics across markets, our goal is not spurious precision but the identification of a conservative, order-of-magnitude range for plausible market dynamics.

The Kyle coefficient is dimensionally the ratio of a characteristic price change to the order size that causes it

A representative tick size of units is common in many futures and equity markets. Secondly, we define a characteristic order flow as a meaningful, liquidity-demanding order, ranging from 10 to 100 contracts or lots. Finally, we assume the resulting price change will be a small number of ticks in a liquid market (e.g., 1-10 ticks) but a larger number in an illiquid one (e.g., 10-100 ticks). This yields a range

The Ho-Stoll coefficient is dimensionally the ratio of a characteristic price skew to the inventory imbalance that necessitates it

Here, the characteristic inventory represents a position large enough to require active management, which we assume to be in the range of 10 to 100 contracts. The price skew is the amount in ticks that a market maker adjusts their quotes to attract offsetting flow. This might be a few ticks (e.g., 1-10) for moderate inventory pressure but could become much larger (e.g., 10-100 ticks) under severe constraints. This gives the range for its absolute value

This independent analysis yields a similar range for as for . This is a notable finding, as it ensures that the condition of parity is physically achievable across the full spectrum of plausible market conditions. At the lower end, values near for both and represent highly liquid markets where both price impact from large orders and price skewing for large inventories are minimal. The upper end approaching corresponds to illiquid markets where prices are highly sensitive to both order flow and inventory imbalances, while the intermediate band of captures the dynamics of typical electronic markets.

2.8. Relevance of the IIP Framework for Power Markets

While the IIP framework is a general theory of market making, its individual components are particularly suited to address the specific structural challenges inherent in secondary financial power markets. The core assumptions of classical models often fail in this environment, whereas the generalizations we have introduced directly map to the defining features of electricity trading.

2.8.1. Acute Inventory Risk and Non-Storability

A particular characteristic of electricity as an asset is its non-storability. For a market maker in power futures, inventory risk is not merely a financial concern about price fluctuations; as a contract nears expiry, it becomes a risk of physical delivery obligation. Unlike a market maker in equities who can hold a position indefinitely, a power market maker accumulating a large short or long position faces the tangible prospect of having to source or deliver physical power— a specialized activity for which they are likely ill-equipped. This reality makes the inventory aversion parameters and especially the non-linear costs critically important. We can hypothesize that the fear of unmanageable physical positions will lead to strong, non-linear quote shading, making the kurtosis effect a dominant force in price formation.

2.8.2. Thin Markets and Limited Competition

Power futures markets are often thin, characterized by a small number of active participants and designated market makers. This stands in stark contrast to deep equity markets with dozens of competing liquidity providers. Consequently, the assumption of perfect competition is particularly inappropriate. The liquidity fragmentation parameter is central to modeling this environment, where it is the norm for any single market maker to capture only a fraction of the total order flow. The competition effect, which pushes upwards, is therefore expected to be a primary and persistent feature of these markets.

2.8.3. Adaptive Behaviour of Large Players

The participants in power markets are not anonymous noise traders. They are often large entities (e.g., generation companies, utilities) with significant market power and sophisticated knowledge of the underlying physical system. These players are capable of recognizing when a market maker may be vulnerable due to a large inventory imbalance. This creates the potential for strategic trading, where agents might increase their trade sizes or aggression precisely to exploit the market maker’s position. Such state-dependent behaviour is exactly what the Covariation Remainder is designed to capture. It is not merely a theoretical curiosity, but a necessary tool for detecting the impact of adaptive interactions that break the static assumptions of classical models.

In summary, the IIP framework provides a precise vocabulary to analyze the fundamental tension in power markets. It allows us to quantify the balance between a market maker’s fear of adverse selection from traders with superiour forecasts and their more pressing fear of accumulating untenable physical delivery obligations (). It provides the tools to measure how this balance is distorted by limited competition and exploited by adaptive agents . This framework is therefore essential for moving beyond transplanted financial models to a theory of market making genuinely tailored to the unique physics and economics of power.

3. Methodology: Agent-Based Simulation and Econometrics

Having established the Impact-Inventory Parity as our theoretical framework, we now turn to the methodology used to test its predictions through simulations unconstrained by direct implementation of those predictions: the IIP relationships must arise emergent from micro-level agent interactions.

Testing the theory on real-world power markets is challenging. Empirical data is scarce, and the high concentration of participants makes it difficult to isolate the causal effects of competition or adaptive behaviour. Analytical models require simplifying assumptions— perfect competition, linear costs, and time-invariant behaviours— that are precisely the conditions our framework seeks to relax. This section details our use of Agent-Based Modeling (ABM) as a computational laboratory to bridge this gap. We outline the simulation design, the agent architecture, and the econometric protocol used to measure emergent market dynamics.

3.1. Rationale for Agent-Based Modeling in Power Markets

Agent-Based Modeling (ABM) provides a bottom-up approach to studying complex economic systems where traditional methods fall short. An ABM constructs a simulated market from the micro-level interactions of heterogeneous agents, each with specific objectives and behavioural rules. This methodology is particularly well-suited for testing the IIP framework in power markets for three key reasons:

- 1.

- Controlled experimentation. The ABM environment allows us to surgically introduce and isolate the mechanisms that our theory predicts are important. We can precisely control the level of competition , the degree of non-linear inventory costs , or introduce specific adaptive behaviours . This enables us to test the causal impact of each factor on the Parity Index in a way that is impossible with observational data.

- 2.

- Perfect observability. Unlike real markets, the internal states of our agents are fully observable. We can track the market maker’s belief about the fundamental value , their inventory position , and the true fundamental value V itself. This allows us to directly estimate all components of the IIP framework, including the Ho-Stoll slope , which requires knowledge of the fundamental value— a quantity that is unobservable in real markets.

- 3.

- Emergent macro-outcomes from programmed micro-behaviour. This separation between micro-level programming and macro-level outcomes is the methodological foundation of our test. We program agents with competitive behavioural rules derived from classical microstructure theory: informed traders exploit private signals according to the Kyle framework, market makers adjust quotes based on inventory following Ho-Stoll principles, noise traders submit random orders. Critically, we implement only the implicit assumptions of these canonical models at the agent level. We do not program the predicted market-level parity relationships. The key regression coefficients and must emerge from the collective interaction of agents over thousands of trading periods. Whether these emergent, statistically measured coefficients align with our theoretical predictions–— whether micro-level assumptions generate macro-level parity –—constitutes the empirical test of the IIP framework.

This methodology allows us to rigorously explore the conditions under which canonical microstructure theories hold and, critically, to identify and quantify the mechanisms through which they break down in the environment of thin power markets.

3.2. Simulation Environment and Agents

Our ABM is designed as a minimal yet robust representation of a continuous limit order market that combines the core mechanics of both information-based and inventory-based microstructure theories. The simulation proceeds in discrete time steps , within which a cast of heterogeneous agents interact around a single traded asset with a fixed fundamental value V.

3.2.1. The Market Maker (MM)

At the heart of the simulation is a single, risk-averse market maker who must simultaneously manage two distinct risks. At the beginning of each period t, the MM posts a mid-price according to the pricing rule

where is the MM’s current belief about the fundamental value, is their inventory position from the previous period, is the linear inventory aversion parameter, and is the non-linear (cubic) inventory cost parameter. This pricing rule implements the Ho-Stoll framework: the MM proactively skews quotes away from the fundamental value to attract offsetting order flow and manage inventory risk. After observing the aggregate order flow in period t, the MM updates their belief about the fundamental value according to

where is the price impact coefficient. This belief update implements the Kyle framework: the MM learns from order flow, treating net buying pressure as a signal that informed traders perceive the asset to be undervalued.

In the baseline configuration, is constant and equal to , representing a fixed informational price impact. In some experiments we explore an simple adaptive price impact mechanism

where is a state-dependence parameter. This captures the possibility that the MM becomes more cautious when holding large inventory positions, increasing their price impact response to order flow precisely when they are most vulnerable. This state-dependent behaviour is the mechanism underlying the Covariation Remainder derived in Section 2.3. The MM’s inventory evolves according to

where represents the fraction of total order flow captured by the MM. When , the MM intermediates all trades (monopolistic dealership). When , the MM faces competition from other liquidity providers who absorb a portion of the order flow.

3.2.2. Informed Traders

The simulation features M informed traders who represent market participants with superior analytical capabilities. We adopt a differential information framework: at the start of the simulation, each trader receives a unique, noisy private signal about the true fundamental value

This setup avoids the unrealistic assumption of a single, perfectly informed insider and better reflects a power market environment where participants (e.g., generation firms, weather forecasting specialists) form proprietary, imperfect views on future prices based on private analysis and data. In each period t, each informed trader submits a market order proportional to the difference between their signal and the current mid-price

where is the aggressiveness parameter that governs how much capital they deploy per unit of perceived mispricing. The aggregate informed order flow is thus . Informed traders do not update their signals during the simulation, maintaining their initial differential information throughout.

3.2.3. Liquidity Traders

To represent hedgers and other non-speculative participants, liquidity trades arrive stochastically according to a Poisson process with arrival rate . In each period t, the number of arrivals is drawn as . Each arriving liquidity trade is a market order to buy (+1 unit) or sell ( unit) with equal probability. The aggregate liquidity order flow is thus

These traders’ inelastic demand serves two essential functions: it creates the inventory risk that the market maker must manage, and it provides noise (camouflage) for the informed traders’ activity, making the market maker’s information-processing problem non-trivial.

3.2.4. Timing and Market Clearing

Within each period t, the sequence of events is

- 1.

- The MM posts the mid-price based on their current belief and inventory .

- 2.

- Informed traders observe and submit orders based on their signals.

- 3.

- Liquidity traders arrive and submit random orders.

- 4.

- The total order flow is executed against the MM’s quotes.

- 5.

- The MM updates inventory: .

- 6.

- The MM updates belief: .

The simulation runs for periods. The first periods allow the system to reach a statistical steady state, after which we collect data for periods for econometric analysis. All agents begin with zero inventory, and the MM’s initial belief is set to the true value .

3.3. Econometric Measurements

Let’s take stock of the mechanics of the simulation we are dealing with. The agent-based model generates a time series of market activity. At each period t, informed traders submit orders based on their private signals, liquidity traders arrive stochastically, and the market maker posts quotes reflecting their current belief about the fundamental value and inventory position . Trades execute, the market maker updates their inventory and their belief based on observed order flow , and a new mid-price forms. After running the simulation for periods, we observe complete time series: . At this point our data analysis can begin.

The central econometric question is: do these emergent price dynamics exhibit the Kyle relationship and the Ho-Stoll relationship predicted by theory? More precisely, can we reliably measure the regression coefficients and , and do they satisfy the parity prediction under idealized conditions?

To measure the emergent properties of the simulated market and test the IIP predictions, we employed a three-stage econometric statistical analysis. Unlike a deterministic model with closed-form solutions, our ABM is stochastic: random arrivals of liquidity traders, random signals for informed traders, and random order flow mean that each simulation run produces a different market trajectory. A single run could be misleading due to chance. Moreover, even within a single run, we estimate relationships from finite time-series data, introducing estimation error. Our analysis addressed both sources of uncertainty: we ran many independent simulations (addressing simulation variability), and we used appropriate time-series methods for each run (addressing estimation error). Finally, we pooled results across runs using statistical theory designed for multiple imperfect measurements. This ensures that our conclusions about the IIP framework are not artifacts of a lucky (or unlucky) random draw, but reflect the true emergent properties of the model.

3.3.1. Stability Filtering

Before any econometric analysis, we monitored each simulation for numerical stability. The model includes hard constraints to prevent explosive, uncontrolled growth that would indicate ill-conditioned dynamics rather than economically meaningful equilibrium behaviour. Specifically, we terminated and excluded any run where

- Inventory position grew faster than the scaling expected from a random walk, indicating the MM had lost control of their position.

- Price deviation exceeded a multiple of the fundamental value, indicating the market had detached from rational pricing.

These filters ensured that we analyzed only simulations exhibiting stable, economically interpretable dynamics. The proportion of runs that fail this test is not an indication of errors. Rather, the failure rate is a key diagnostic of market fragility that will be analyzed as a primary result in Section 4.5.

3.3.2. Steady State Verification and Burn-in Period

Before collecting measurement data, we verified that the system had reached statistical steady state. We ran extended diagnostic simulations of 5000 periods and monitored rolling window statistics (window size = 100 periods) for key state variables: inventory position , belief error , and price deviation . Steady state was confirmed when the coefficient of variation of these rolling statistics fell below 2% and remained stable. Across all parameter configurations, we found that steady state was achieved within 500 periods. We therefore set for all experiments and discarded this initial transient period before econometric analysis.

3.3.3. Stage 1: Coefficient Estimation

For each stable simulation run, we collected periods of data after discarding the initial burn-in period of periods. We estimated the two primary coefficients using Ordinary Least Squares (OLS) regression. The Kyle Coefficient measures the price impact of order flow

This forward-looking specification captures how order flow in period t affects the subsequent price , consistent with the MM’s belief-update mechanism. Both the price change and order flow are stationary by construction, making standard OLS appropriate. We computed Newey-West (HAC) standard errors with automatic lag selection to account for potential autocorrelation and heteroskedasticity in the residuals.

The Ho-Stoll Coefficient measures inventory sensitivity

Here we faced a more delicate statistical problem. Under the IIP framework’s dynamics, both inventory and price deviation are non-stationary: they accumulate past shocks rather than reverting to stable means (both are integrated of order one processes). Regressing one non-stationary series on another without establishing cointegration risks producing a spurious regression: a statistically significant relationship that is merely an artifact of trending variables rather than a genuine economic connection.

However, the economic mechanism shared by both the Kyle and Ho-Stoll models predicts these variables should be cointegrated. Both inventory and price deviation are driven by the same underlying process—– cumulative order flow. Inventory accumulates captured order flow ; while price deviation accumulates the information extracted from that same order flow . Because they share a common stochastic driver, the theory predicts a stable long-run linear relationship between them, even as both variables wander individually.

To test whether this theoretical prediction holds in the simulated data, we applied the Augmented Dickey-Fuller (ADF) test to the regression residuals . If the test rejected the null hypothesis of a unit root in the residuals at the 5% level, this confirmed the residuals are stationary and verified the cointegrating relationship predicted by theory. We then reported with HAC standard errors as a valid estimate of inventory sensitivity.

If cointegration failed— that is, if the ADF null hypothesis was not rejected at the 5% level —we discarded that run from further analysis. This failure was not merely a statistical technicality; it indicates that the simulation was ill-conditioned. The market may have failed to reach a steady state, exhibited explosive dynamics that escaped the stability filters, or produced economically incoherent behaviour that violated the IIP framework’s structural assumptions.

3.3.4. Stage 2: Parity Index Calculation

For runs which passed all filters and cointegration tests, we computed the Parity Index

To perform hypothesis tests on , we calculated its standard error using the Delta method, which propagates the estimation uncertainty from the two underlying regressions, assuming asymptotic independence

3.3.5. Stage 3: Aggregation Across Runs

A single simulation represents one stochastic realization of the model. To obtain robust estimates that properly account for simulation variability, we performed independent simulations for each parameter configuration, each initialized with a different random seed. Point estimates and standard errors from valid runs (those passing stability checks and cointegration tests) were pooled using Rubin’s Rules, the established statistical method for combining multiple imperfect measurements.

Rubin’s Rules correctly combines within-run variance (estimation uncertainty from finite time-series data) and between-run variance (simulation uncertainty from stochastic agent behaviour). For any parameter , such as , , or ,

where is the number of runs passing all validity checks. The pooled estimate is with standard error . Confidence intervals were constructed using the t-distribution with degrees of freedom calculated via the Barnard-Rubin approximation, which accounts for the finite number of simulations and the relative magnitudes of within-run and between-run uncertainty. This rigorous protocol ensured that our reported estimates of the Parity Index and its components are statistically sound, reflecting the true emergent behaviour of the model rather than sampling noise or unstable simulation artifacts.

4. Results: Testing the IIP Framework

This section presents results from numerical experiments designed to test the core predictions of the Impact-Inventory Parity (IIP) framework. We systematically examine the effects of liquidity fragmentation, non-linear inventory costs, and adaptive behaviour on market maker pricing. Simulations were conducted using the Agent-Based Model (ABM) architecture described in Section 3.

The baseline parameters for the simulation environment and calibrated agent behaviours are summarized in Table 1. The environmental parameters represent a moderately thin market structure characteristic of illiquid power futures contracts: a limited number of informed traders , sparse liquidity provision arrivals per period, and meaningful signal noise reflecting the difficulty of forecasting power prices even with sophisticated analysis. These values generate order flow patterns and inventory dynamics consistent with the thin market conditions motivating the IIP framework.

The behavioural parameters , , and were calibrated such that the classical parity condition holds under idealized conditions of monopolistic dealership and linear costs . This calibration ensures that deviations from parity observed in subsequent experiments reflect the mechanisms under investigation (competition, non-linear costs, adaptive behaviour) rather than arbitrary parameter choices. The calibrated values also satisfy the dimensional consistency bounds established in Section 2.7, producing regression coefficients consistent with empirically observed price impacts in commodity futures markets.

4.1. Validation of Classical Parity and Competition Effect

We began by validating the model under the idealized conditions assumed by canonical microstructure theory: monopolistic dealership , linear inventory costs , and time-invariant response . Under these conditions, the IIP framework predicts perfect parity with . The simulation confirmed this benchmark with high precision: (SE, ) for the baseline market environment given in Table 1. This validated both the ABM implementation and the econometric measurement protocol.

The competition effect, which predicts under linear cost conditions , demonstrated equally precise agreement with theory. We varied the flow capture rate from 0.3 to 1.0 in eight steps, measuring the emergent Parity Index at each level. Linear regression of measured against yielded

This alignment validated the theoretical mechanism derived in Section 2.3: when , the market maker observes total order flow for belief updates but accumulates inventory based only on captured flow . This structural disconnect creates a systematic amplification factor of in the relationship between inventory position and price deviation in Equation. 5. The market maker’s inventory becomes a progressively weaker proxy for the cumulative order flow informing their price as competition increases, inflating the measured Ho-Stoll slope relative to the Kyle slope .

To assess robustness, we tested whether the competition effect persists across different market environments. We replicated the sweep in thin market configurations (; ) representing severely illiquid conditions. Despite these substantial changes in market structure and parameter values, the competition effect remained robust. Linear regression of measured against again yielded with a slope indistinguishable from unity. This confirms that the relationship is a structural feature of fragmented dealership that operates independently of market thickness, liquidity levels, or the specific calibration of behavioural parameters. The mechanism–— inventory decoupling from total order flow when –—proves universal across the thin market spectrum.

4.2. The Kurtosis Effect: Non-Linear Inventory Costs

Having validated the classical predictions under idealized conditions, we now examine the first mechanism that produces systematic deviations from parity: non-linear inventory costs. The theory predicts that convex costs induce platykurtosis in the inventory distribution, suppressing the Parity Index below unity. The mechanism operates through the generalized IIP given in Equation 17: non-linear terms contribute differently to the Kyle and Ho-Stoll slopes based on the inventory distribution’s higher moments, with the effect scaling with inventory variance .

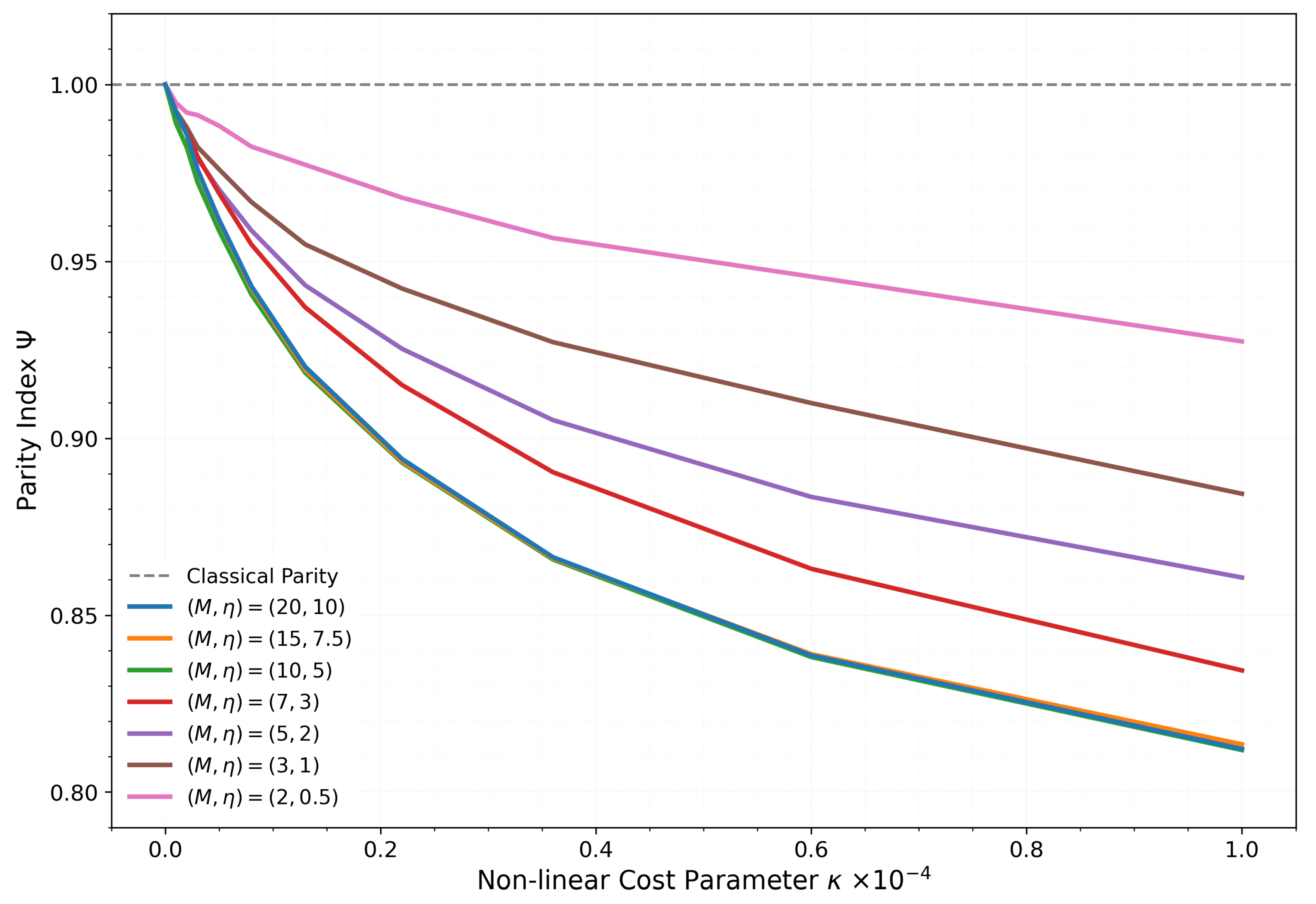

We tested this prediction by varying the non-linear cost parameter from 0 to across 11 steps, while maintaining monopolistic conditions and non-adaptive behaviour . The market maker’s pricing rule becomes , where the cubic term penalizes large inventory positions with escalating severity. To assess how market thickness moderates this effect, we conducted experiments across seven market environments spanning a liquidity gradient from very liquid to very thin . Figure 1 presents the results.

The results confirm the theoretical prediction across all market environments and reveal a consistent pattern. Starting from the validated classical parity at , all markets exhibit monotonic suppression of the Parity Index as non-linear costs increase. However, the magnitude of this suppression is strongly moderated by market thickness, producing a clear stratification visible in Figure 1.

In the most liquid market , the kurtosis effect is most pronounced. The Parity Index falls from at to at , representing an 18.8% deviation from classical parity and a transition into the Adverse-Selection-Dominated regime (Regime 3, ). At this extreme, the market maker’s pricing becomes substantially more sensitive to order flow information than to inventory pressure.

As market thickness decreases, the suppression effect attenuates systematically. The baseline market shows at maximum , while moderately thin markets reach . In the thinnest environment , the effect is most muted: falls only to at , representing a 7.3% deviation— less than half the magnitude observed in liquid markets.

This stratification pattern is precisely predicted by the theoretical framework. The generalized IIP given in Equation 17 shows that the influence of scales with inventory variance . In thinner markets, reduced trading activity (lower and fewer informed traders M) leads to smaller absolute inventory swings, lowering . With smaller inventory variance, the non-linear terms and in the numerator and denominator become smaller relative to the linear terms and , weakening the overall suppression of . The market maker in a thin environment still employs the same convex cost structure, but accumulates smaller positions, reducing the practical impact of the non-linearity.

This finding has important implications for applying the IIP framework to illiquid power markets. While the kurtosis effect operates universally as theory predicts, its magnitude depends on the market’s trading intensity. Market makers in highly illiquid environments face elevated informational risk (reflected in higher equilibrium ) but accumulate smaller inventory positions, naturally limiting the severity of non-linear inventory costs. Even in the thinnest simulated market, however, strong convexity produces economically significant deviations from classical parity— the effect is attenuated but not eliminated. This suggests that inventory cost structures matter across the full spectrum of market conditions, though their relative importance declines as markets become thinner.

4.3. Joint Effects and Market Regime Boundaries

Having isolated the competition and kurtosis effects independently, we now examine their interaction by varying both parameters simultaneously across multiple market environments. This analysis maps the full landscape of market regimes that can emerge from the fundamental tension between these opposing forces and reveals how market thickness moderates their interaction.

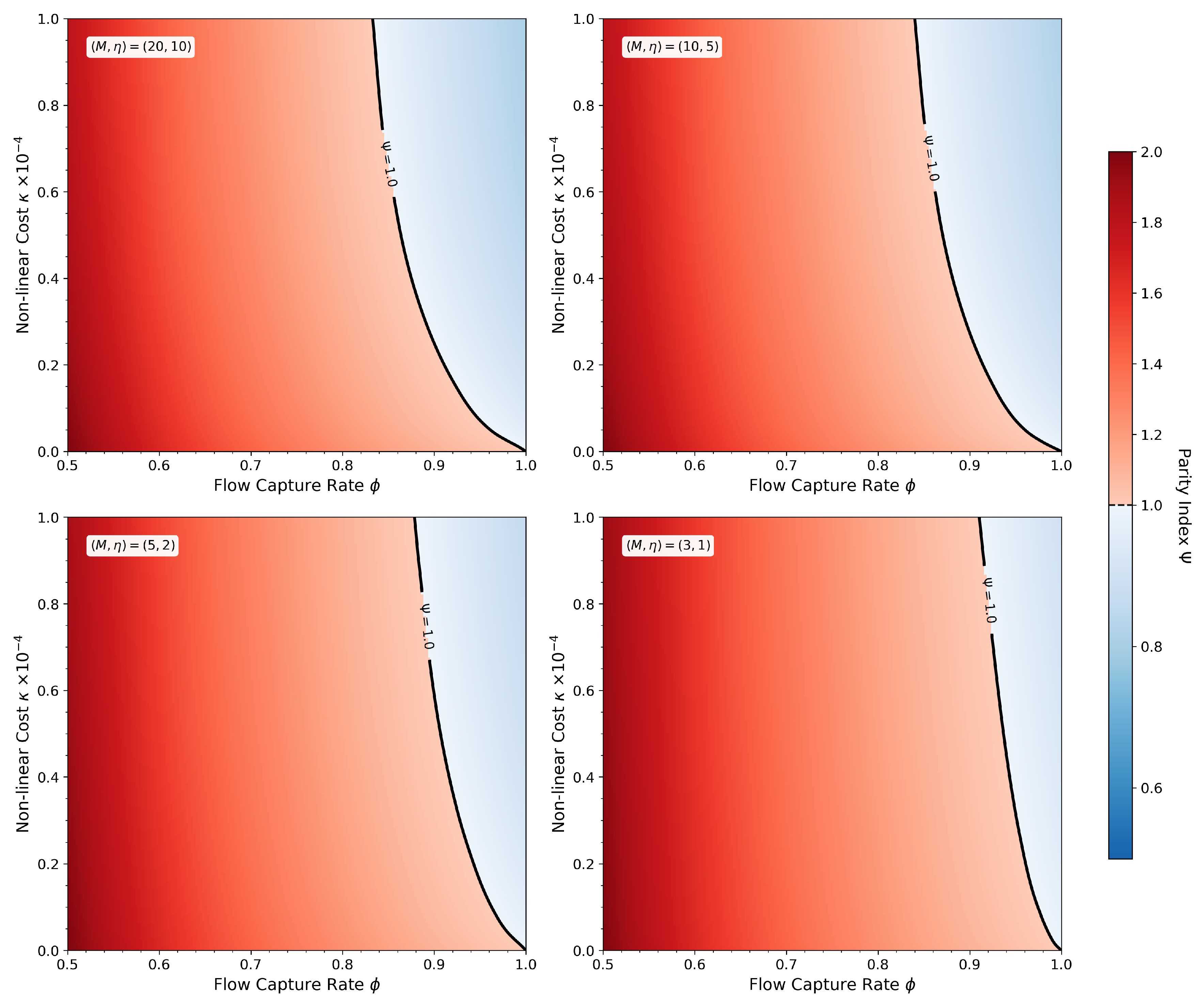

We conducted two-dimensional parameter sweeps varying the flow capture rate from 0.5 to 1.0 across six levels and the non-linear cost parameter from 0 to across six levels, yielding 36 parameter configurations. All configurations maintained non-adaptive behaviour . We replicated this grid across four market environments spanning the liquidity gradient: very liquid , baseline , illiquid , and thin . Figure 2 presents the results as heatmaps of the measured Parity Index across the parameter space for each market environment.

The heatmaps reveal consistent structural patterns across all market environments, with systematic variations in magnitude. In all four panels, three key features emerge:

- 1.

- Competition dominance at low . The left edge of each heatmap (low , low ) exhibits elevated values, consistent with the isolated competition effect. Markets with show ranging from approximately 1.8 to 2.1 across the four environments (with linear costs ), placing them firmly in the Inventory-Dominated regime (Regime 1). This demonstrates that liquidity fragmentation systematically elevates inventory sensitivity relative to price impact, independent of market thickness.

- 2.

- Kurtosis dominance at high . The upper-right region (high , high ) in all panels shows suppressed values below unity. Markets approaching monopolistic structure with strong convex costs exhibit , entering the Adverse-Selection-Dominated regime (Regime 3). This confirms that non-linear inventory costs can overcome the baseline parity condition through the kurtosis mechanism, again independent of market environment.

- 3.

- Third, non-linear interaction and curved regime boundaries. Notably, the contour (black line) curves through the parameter space in all panels, demonstrating that the two effects do not combine linearly. As competition increases (lower ), progressively stronger non-linear costs are required to maintain balanced-risk conditions. A monopolistic market maker () achieves parity with linear costs , but introducing modest competition to requires to restore balance. At severe fragmentation , the required to achieve parity exceeds the tested range in all environments.

However, market thickness introduces quantitative moderation. Comparing across the four panels reveals systematic compression of the range as markets thin. In the very liquid market , the Parity Index spans approximately 0.75 to 2.1, a range of 1.35. This range compresses progressively as market thickness decreases: the baseline market exhibits a range of 1.20 (from 0.80 to 2.0), the illiquid market shows a range of 1.05 (from 0.85 to 1.9), and the thin market displays the most compressed range of 0.97 (from 0.88 to 1.85). This near-monotonic compression represents a 28% reduction in the parameter space’s dynamic range when moving from the most liquid to the thinnest market environment.

This compression reflects the attenuated kurtosis effect documented in Section 4.2: thinner markets accumulate smaller inventory positions, reducing the impact of non-linear costs. Consequently, the blue region (Adverse-Selection-Dominated) shrinks in thinner markets, while the overall topology of the parameter space remains structurally similar.

The contour also shifts systematically. In the very liquid market, the balanced-risk boundary reaches lower into the parameter space (allowing higher values before exiting the balanced regime). In thin markets, the contour is pushed toward lower values, indicating that even modest non-linear costs can be sufficient to offset competition effects when inventory variance is low.

These findings reveal fundamental constraints on market design in thin, competitive environments. The structural force pushing toward inventory dominance (the competition effect) operates at full strength regardless of market thickness, while the countervailing kurtosis effect weakens in thin markets. This asymmetry suggests that severely fragmented thin markets may be inherently difficult to maintain in a balanced-risk state through inventory cost adjustments alone. For market maker programs in illiquid power futures, this implies that regulatory interventions to increase effective (by consolidating liquidity or providing exclusivity arrangements) may be more effective than relying on market makers to manage the imbalance through sophisticated inventory risk management.

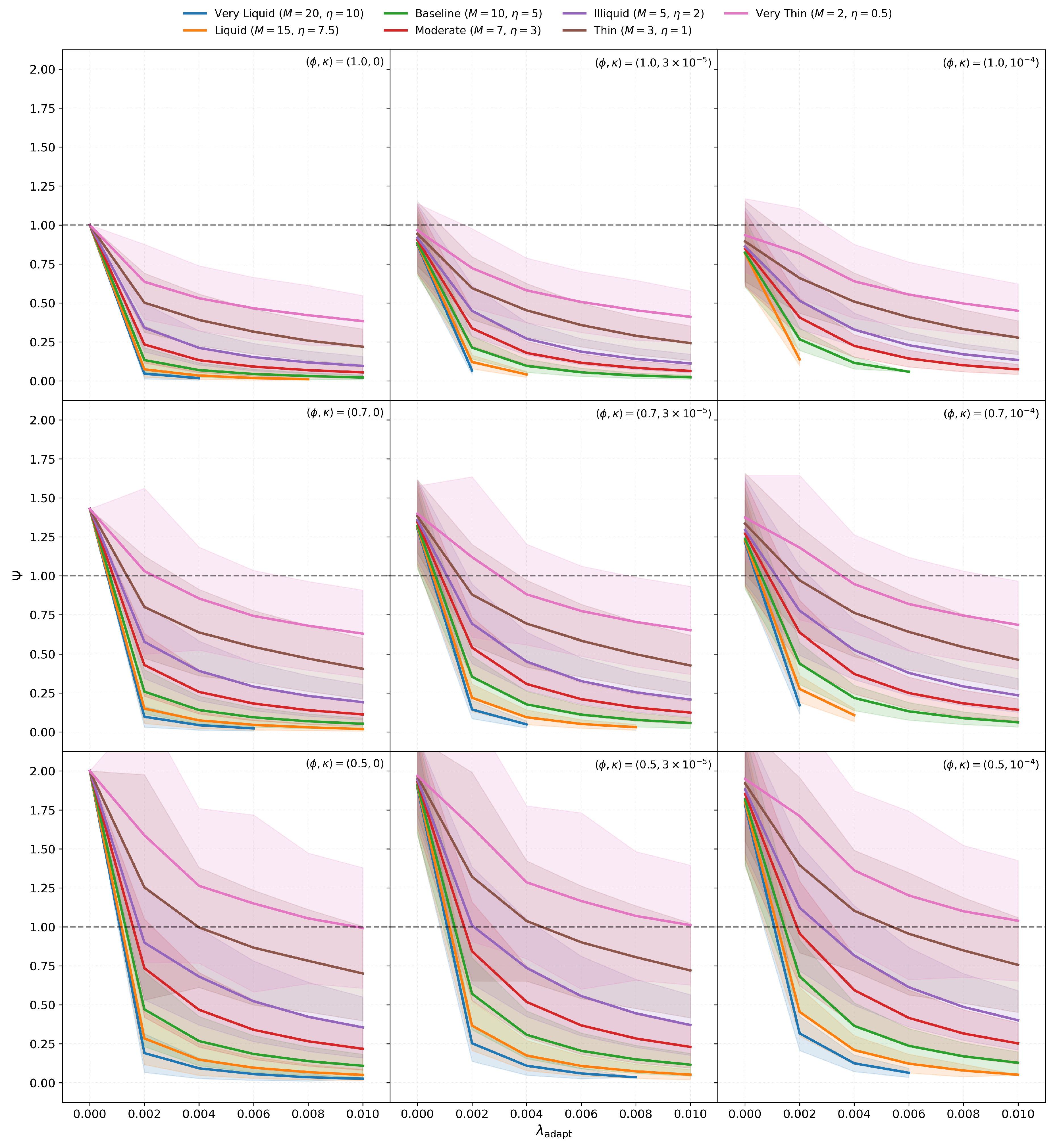

4.4. Adaptive Behaviour and Parity Breakdown

The preceding experiments examined structural market features (competition, cost structure) that produce systematic but bounded deviations from classical parity. We now turn to a more fundamental question: under what conditions does the IIP framework itself break down?

Section 2.3 derived the Covariation Remainder, which quantifies how time-varying information processing causes deviations from the static parity relationship. To test this mechanism, we introduced a parsimonious parameterization where the market maker’s belief-updating intensity responds to inventory exposure,

This specification is not intended to represent an empirically measurable behavioural parameter. Rather, it serves as a minimal model to operationalize state-dependent information processing: the market maker extracts information more aggressively from order flow when inventory risk is elevated. The parameter controls the intensity of this state-dependence, where recovers the static Kyle model.

We tested the robustness of the IIP framework by varying from 0 to 0.01 under controlled baseline conditions. The covariation remainder theory from Equation 20 predicts this adaptation should primarily affect the Kyle regression. When varies systematically with inventory, the measured Kyle slope becomes

capturing both the baseline informational sensitivity and the covariation between inventory exposure and order flow. In contrast, the Ho-Stoll regression measures the long-run cointegrating relationship between price deviation and inventory position, which should be less sensitive to the state-dependence of belief updating.

To test this mechanism comprehensively, we conducted a three-dimensional parameter sweep: varying from 0 to 0.01 across six levels, market structure through three combinations representing different competitive and cost environments, and market thickness through seven configurations ranging from very liquid to very thin markets. This yields distinct market configurations, and for each configuration. Figure 3 presents nine panels, one for each combination, with each panel showing the response of all seven market environments.

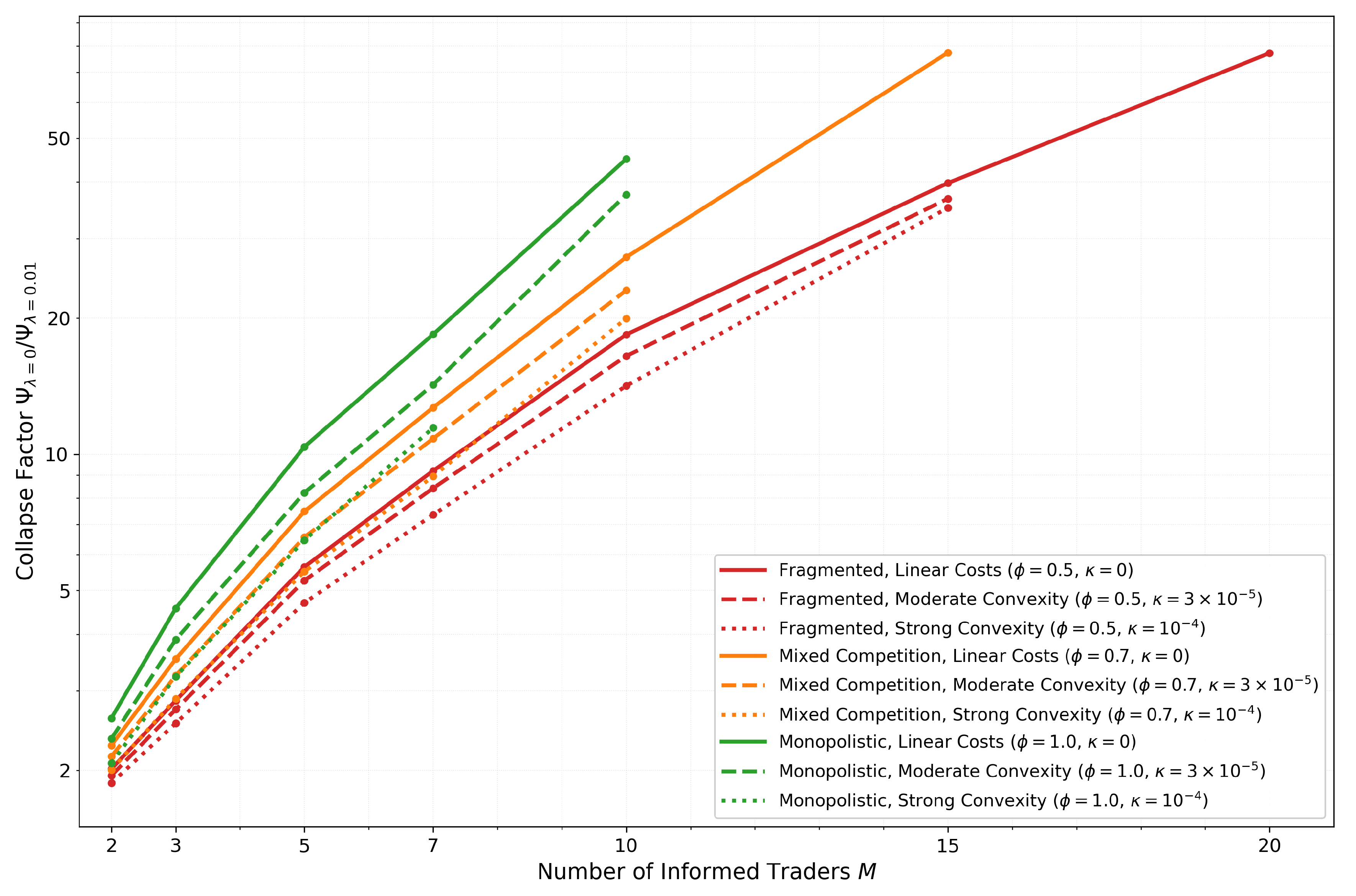

The multi-panel results reveal three systematic patterns. First, liquidity amplifies collapse rather than providing stability. In monopolistic markets with linear costs (, ), very liquid markets (, ) declined from to approximately at — a nearly 20-fold decrease. Meanwhile, very thin markets (, ) declined only to under identical adaptation parameters. This systematic fan pattern is visible across all nine parameter combinations, with liquid markets (blue lines) always collapsing fastest and thin markets (pink lines) showing the greatest resilience.