Submitted:

21 July 2025

Posted:

22 July 2025

You are already at the latest version

Abstract

We investigate the key factors that shape the dynamic evolution of Day-Ahead spot prices of seven European interconnected electricity markets of the Core Capacity Calculation Region, Core CCR (Austria AT, Hungary HU, Slovenia SI, Romania RO), the Southeast CCR (Bulgaria BG, Greece GR) and the Greece-Italy CCR , GRITR (Italy), with emphasis on price surges and discrepancies observed in SEE CCR markets, during the period 2022-2024. The high differences in the prices of the two groups, has generated political reactions from the countries that ‘suffer’ from these price discrepancies, as shown by the intense reactions of the governments of the affected countries and other institutions, as the sending of letters of Prime Ministers European Commission President). By applying Machine Learning (ML) approaches, as Markov Blanket (MB) and Local, causal structures learning (LCSL), we are able of ‘revealing’ the entire path of volatility spillover of spot price as well as the Cross-Border Transfer Availabilities (CBTA) between the countries involved, from north to south, thus uncovering i.e. ‘lifting the blanket’, to discover the ‘true’ structure’ of the path of causalities, responsible for the price disparity. The above methods are supported by the ‘mainstream’ approach of computing the correlation of the spot price and CBTA’s volatility curves of all markets, to detect volatility spillover effects across markets. The main findings of this hybrid approach are: a) the volatility of Austrian market’s spot price and its CBTAs with DE, CZ, and SI, ‘uncovered’ to be a pivotal market, behaving as a ‘transmitter’ of spot price and cross-border activity volatility, over its entire connection path with SEE CCR markets, which finally ‘receive’ the volatility disturbances, causing their price surge, b) the combination of weather and geopolitical factors with the limited interconnectivity of SEE markets, seem to have exacerbated the impact of the Flow-based Market coupling method (FBMC) used in the Core CCRs, on the prices of SEE CCR’s countries that rely on the Net Transfer Capacity -NTC- mechanism, by inducing non-intuitive flows, thus challenging the reliability of European Target’s model (based on FBMC) in protecting SEE markets from ‘unexpected-unfair-irrational’ price surge.

Keywords:

Electricity wholesale electricity prices surge in SEE

; Local causality structure

; Markov blanket

; Bayesian tool

; wholesale Electricity prices

; spot price volatility spillover

1. Introduction

1.1. Price Disparity in Electricity Markets of Southeastern Europe (SEE) and Political Reactions

In this paper we present a ML approach in detecting the most critical and causal factors responsible for causing an unprecedented electricity spot prices surge, a phenomenon also called ‘European regional electricity crisis’, appeared mainly in Bulgaria (BG), Greece (GR), by analyzing the entire path of their interconnections with the ‘core’ countries of Austria, AT, Hungary (HU), Slovenia (SI) and Romania (RO), as well as the Greece- Italy interconnection. We note here that AT, HU, SI and RO are members of the Core CCR (Core Capacity Calculation Region) while BG and GR constitute the Southeast European SEE CCR (regions in which specific methodologies are used to compute cross-zonal capacities, see Section 3).

The ‘huge’ price disparity mainly in Bulgaria and Greece, and in Romania against the rest of the Core countries, challenges the capacity and success of the European electricity Target model, as we will see below. There are a variety of the factors that are behind this disparity, both ‘apparent and hidden’, as climatic, geopolitical and structural (generation mix, networks, interconnections), described in Section 3. The above countries that have been strongly affected took several initiatives to ease the pressure this disparity has imposed on their electricity Day-ahead prices. Among other reactions, they have prepared a proposal for the formation of a permanent intervention mechanism that would be triggered any time electricity prices turn extremely high in their markets, especially in cases where their region is disconnected from the rest of the core energy markets. A characteristic example of such reactions, is the letter of the Greek Prime Minister sent to European Commission President, to propose a set of measures [1]. Similar reactions were recently reported, as in Romania and in North Macedonia in which also an examination has initiated of the reasons for the huge price disparity. Another characteristic reaction is that of the Romanian Minister of Energy who sated that the country would ask the EU for compensation for this high price difference, but however listing several problems related to geopolitics (due to war in Ukraine), weather, power generation mix, and interconnections of his country with AT and other Core CCRs. Also at ministerial level, Greece, Bulgaria and Romania sat at the same table on 11th September 2024, with the three countries agreeing on the diagnosis of the problem. The three energy ministries drafted a text that was sent to the Commission, asking for flexibility from the relevant EU Directive for the implementation of a claw-back mechanism against high deviations in electricity prices. According to their draft text, this mechanism could be activated occasionally, for the imposition of a cap on the compensation of power plants and the recovery of excess revenues per technology, just as was done during the 2022 energy crisis. We point out here, however, that this mechanism (the request), in practice, cancels in practice the result of the Day-Ahead (DA) market price clearing methodology (the cornerstone of the European Target model), i.e. cancels the system's marginal price, which pays all units under this model, to contain large discrepancies. However, this objective seems to be very ambitious, as any modification on the core structure of the target model is a very crucial issue, and it needs the agreement of all involved markets’ ‘shareholders. As the Greek Prime minister said [1], ‘I do not expect that there will be immediate solutions to the problem, but at least let someone seriously deal with it, to highlight it, so that we can make sure that we do not have such distortions again in the future’.

1.2 Relating SEE CCR’s Price Discrepancies with Europe’s Target Model (TM). Is Its Algorithm an Incomprehensible Black Box?

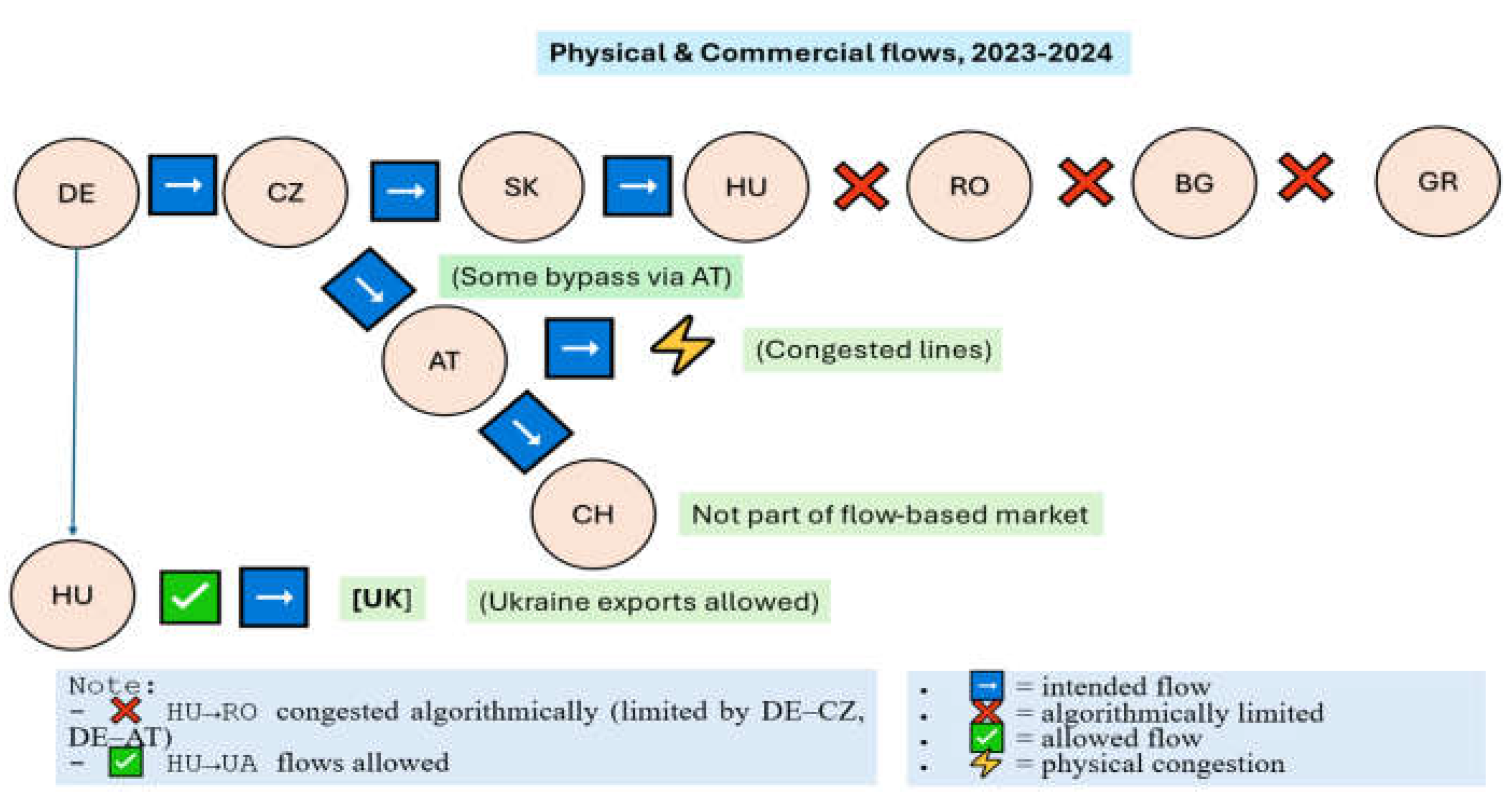

After detecting the underlying crucial factors that have caused the discrepancies mentioned, it would be extremely interesting to examine whether these factors relate to the structural characteristics of the European Target model and more importantly, how this model has been performed in the case of the price surge mentioned. In fact, there are criticisms against the operational algorithm of the model, because at times, it seems that the algorithm has disconnected SEE countries from the rest of the European markets, turning the region into an energy island! The algorithm is based on the current mode of operation of electricity markets, which is different in Core CCRs and SEE CCRs, in respect of the way the available capacities in the zonal bidding-zones are calculated. More specifically, SEE CCR countries trade according to the net transfer capacity (NTC) mechanism, while the Core CCRs countries use the flow-based market coupling (FBMC) system (ACER 2024 report, [2]). A description of the above two mechanisms, the critical role they play in the formation of price surge in the SEE CCR, is given in Section 3 and Section 3.1. A notable ‘malfunction’ of the application of FBMC, as described in Section 3.1, is the production of counterintuitive power flows, that have drastically limited imports into high-demand regions like HU and RO, starting a price spike diffusion to ‘downstream’ BG and GR countries, a phenomenon challenging strongly the robustness of Europe’s ambitious TM, aiming at ensuring a fair and ‘homogeneous’ price landscape.

1.3. Characteristic Events in SEE CCR’s Markets, Core and Regional Structural Distortions

We give some critical events indicating the suffering of the SEE & RO electricity markets from extremely high prices. Due to exports to the North, in the evening (20:00) of 12 September 2024 in Greece, the maximum price was 485.60 euros per megawatt hour, while in Bulgaria 558.09 euros/MWh, in Romania 678.5 euros/MWh and in Hungary 667.75 euros/MWh (see Supplementary material C (table C3) for the maximum prices in the evening, hour 20:00, of 12th September 2024). For comparison, in the same period, in the Czech Republic the maximum price reached 242.87 euros/MWh and in Austria (a self-sufficient and net exporter market due to RES), at 256.15 euros/MWh. Thus, a price discrepancy (difference) of 161% against Hungary is observed which is not a conjunctural spread but rather seems to be a permanent phenomenon, not accepted in an environment of coupled markets. It is as if Greece and Bulgaria, two neighboring coupled market, have a price difference of more than 100 euros per megawatt hour, an unacceptable fact that challenges the way the Target Model operates in this region. Thus, intensive skepticism is diffused among the members of the SEE CCRs, based on such critical events as above, that the Core CCR countries, using a variety of ‘mechanisms’ in the Target Model’s FBMC approach can inhibit the normal energy outflows from their borders, reducing the capacity of cross-border transfer availability (CBTA). This occurred in the case of Hungary (HU), leaving the corridor between GR, BG and RO to meet Kiev's increased needs. This view is shared by the Greek and other governments in the region, as well as by other institutions as the president of the Greek Union of Industrial Consumers. It is broadly accepted that the ‘typical’ European electricity market is known to have some structural deficiencies-distortions that affect severely the competitiveness of EU’s member states (due to ‘systemically’ higher energy cost) [3], however due to the Ukraine crisis these distortions became more pronounced. Even at the borders of member states, for short distances, there exist price differences of 200, 300 or even 500 euros/MWh. The ‘mechanisms’ mentioned above refer to the advantages of the FBMC method in comparison to the Net Transfer Capacity (NTC) approach (in which cross-border transactions must cover at least 70% of interconnection capacity), followed by the SSE CCR countries (Section 3). The ‘mechanisms’ are considered responsible for the reduction or even zeroing, via a specific mathematical algorithm (characterized by the politicians as a black-box), of the capacity of cross-border interconnections. Besides the ‘core’ structural distortions emerging from the TM’s application on the region of the suffering markets, there are also other ones having regional effects. For example, in the interconnection of Greek and Italian electricity markets a ‘mechanism’ seems to exist, making almost systematically the Greek spot price to increase during the hours of peak demand. For example, in the evenings, constant electricity exports to Greece take place, making the cross-border transfer capacity between the two countries relatively ‘inadequate’ since the installed cable of 500 MW (at the time this report is written) becomes congested, and consequently disconnected from the system. Even more strange, the traditionally more expensive Italian wholesale market becomes cheaper than the Greek one. As an example, on 12thSeptember, at hour 20:00, the maximum price in the Italian energy exchange was 155.8 Euros/MWh, while the corresponding price in the Greek one reached at 485.60, a deviation of 212%!!

The rest of the paper is structured as follows: in Section 2 we provide a short literature review on the Markov Blanket-based causal feature selection accompanied by a description of Bayesian Analysis and Causality Structure Learning (CSL) approaches in electricity markets (extra information is also provided in Section 5). The crucial role of the power cross-border transfer availability between the markets analyzed, and especially its calculation method in Core CCR and SEE CCR counties, is discussed adequately in Section 3. The description of data sets used, their summary statistics and correlation analysis of the market’s variables, is given in Section 4. An extensive methodology of the MB and LCSL tools is provided in Section 5, which also contains practical issues in applying these methods in the field of electricity market analysis. The approach of rolling volatility of the crucial factors (extracted by the above tools) in causing the spot price surge as well as the volatility spillover effects in SEE markets, is described in Section 6. Section 7 provides the empirical results of both CSL and rolling volatility methods, with extensive comments, and finally in Section 8 we include a discussion, the conclusions and policy recommendations.

2. Literature Review on Markov Blanket-Based Causal Feature Selection

From our intensive literature review, we manage to locate a few specific research papers that apply Markov Blanket-based causal feature selection directly to energy market analysis. First, we have found several foundational works that discuss, in general, the use of Markov Blankets in causal discovery and feature selection, while in Section 2.2 we provide how MB has been adapted to energy market studies.

In the work of [4], the authors demonstrate how a generic feature-selection algorithm that returns strongly relevant variables can be transformed into a causal structure-learning algorithm. The authors prove this under the Faithfulness assumption for the data distribution. [5], provide a comprehensive review of feature selection and causal discovery research, summarizing theoretical results and presenting methods to enhance the scalability of discovery algorithms. A paper that discusses the use of Markov blankets in Bayesian networks for feature selection, addressing challenges when data distributions violate the faithful condition, and in which the authors propose the concept of representative sets to improve feature selection robustness, is the work by [6]. The study of [7] introduces a causal feature selection method based on an extended Markov blanket, aiming to reduce the number of features while retaining key ones. Experimental results demonstrate the method's effectiveness. The article of [8] explores the intersection of causal inference and feature selection, emphasizing the role of Markov blanket discovery algorithms in both fields. It discusses methods to enhance the efficiency of these algorithms. [9] summarize research on feature selection via the induction of Markov blankets over the past decade, providing insights into various algorithms and their applications. These papers mentioned above do not specifically address energy market analysis, however their methodologies have been adapted to study causal relationships and feature selection within that domain (see below). Applying Markov Blanket-based methods, in combination with LCSL methods to energy market data could help identify key factors influencing market dynamics, such as the dynamics of SEE price surges, by focusing on the most relevant variables and their causal interdependencies. Some areas on which MB has been successfully applied, are : a) healthcare: in predicting a disease, the Markov Blanket can identify the strongest causal factors (e.g., symptoms, genetic markers, lifestyle factors) while excluding irrelevant variables, b) in finance: for predicting stock prices, it can reveal key economic indicators, market trends, and company performance metrics that directly influence price movements, c) in marketing: in customer churn prediction, it can highlight the most influential factors (e.g., satisfaction scores, service usage patterns) while excluding noise.

Application of Bayesian Analysis and Causality Structure Learning Approaches in Electricity Markets

However, to the best of our knowledge, only a few papers dealing with the application of MB on analyzing energy markets were found in our literature review. [10] used a causality-based FS approach for data-driven dynamic security assessment of power systems. Their work describes how a probabilistic graphical model (of DAG type), tree augmented naïve bays structures, and an approximate MB, are used in building an online dynamic security assessment (DSA) framework. [11] have built an alternative approach to predictive modeling for energy demands, based on learning causality structure using demand date from an Argentinian electricity company. An improved, non-causal, feature selection algorithm of electricity price forecasting, using Support Vector Machine (SVM), is introduced by [12]. In their paper, the FS algorithm consists of threshold based mutual information (MI) (see Section 5.2), together with inequality correlations of symmetrical uncertainty and pairwise evaluation methods, to perform electricity price forecasting.

In [13] the authors have presented a Bayesian inference approach to unveil supply curves in electricity markets. In their study they introduced this approach, for revealing the aggregate supply curve in a day-ahead electricity market. Their proposed algorithm relies on Markov Chain Monte Carlo and Sequential Monte Carlo methods, and they argue that the major advantage of this approach is that it provides a complete model of the uncertainty of the aggregate supply curve, through an estimate of its posterior distribution. The authors have shown, in a small case study, that it is possible to reveal accurately the aggregate supply curve with no prior information on rival participants, information that can be used by a price-maker producer to devise an optimal bidding strategy.

In [14], the authors have applied Bayesian Belief Networks in the modelling of wholesale electricity price formation, specifically in power systems with a high penetration of non-firm renewable generation. Their work links the mathematical Bayesian representation to established statistical and computational approaches using a functional supply-side wholesale electricity market pricing model and introduces a novel validation method employing volatility analysis to assess the case study’s performance. Their work is valuable in examining the transition of electricity generation from firm to non-firm renewable generation, a factor that creates changes in wholesale electricity price dynamics, therefore challenging existing modeling approaches due to the stochastic nature of wind and solar as the primary energy source. They showed that constructing robust pricing models essential for optimizing financial performance in today’s electricity markets, can be greatly facilitated by using their Bayesian Belief Networks approach.

The aim of the paper in [15], is the study of Bayesian forecasting of electricity prices traded on the German continuous intraday market which fully incorporates parameter uncertainty. Their target variable was the IDFull price index, and the model’s forecasts were provided in terms of posterior predictive distributions. They validated the results, using the exceedingly volatile electricity prices of 2022. The IDFull index is the weighted average price of all continuous trades executed during the full trading session of any EPEX SPOT continuous contract. This index includes the entire market liquidity and thus represents the obvious continuous market price references for each contract.

In [16] researchers have used Bayesian networks for analysis and prediction, to understand the causal relationships between variables such as consumption, greenhouse emissions, investment in renewables and investment in fossil fuels, towards making a reliable energy policy focusing mainly on renewable energy sector, and not only by observing energy scenarios in various economic or social conditions. In their paper have presented expert models using the capabilities of Bayesian networks in the renewable energy sector, considering renewables in Germany and Italy, using the tool BayesiaLab (a powerful desktop application-Windows/Mac/Unix- for knowledge management, data mining, analytics, predictive modeling and simulation, all based on the paradigm of Bayesian networks), with supervised learning, on a data set consisted of the consumption rate of geothermal and hydro energy sectors. They have found that, as oil prices grow, greenhouse emissions will decrease, and that the precision of the expert model is no less than 90%.

In the paper [17], the authors have provided for the first time a complete literature review in the application of Bayesian networks in renewable energy systems, for which the implementation of conventional methods does not solve the problems associated with the complexities of these systems. According to the authors, recently, Artificial Intelligence techniques such as Artificial Neural Networks, Fuzzy Logic and Genetic Algorithms, have been widely used to deal with these problems in the field of Renewable Energy. However, the degree of uncertainty that is involved in these methods needs Bayesian Networks since this is one of the most effective theories to face them. In their work, they present the state of art of the applications of Bayesian Networks in Renewable Energy, such as, solar thermal, photovoltaic, wind, geothermal, hydroelectric energies and biomass, including related topics such as energy storage, smart grids and energy assessment. They have found that the main applications were in forecasting, fault diagnosis, maintenance, operation, planning, sizing and risk management, and they argue that Bayesian Networks constitute a powerful and versatile tool for the field of Renewable Energy.

With the rapid development of the economy, fully leveraging the priority role of electricity is of great significance for accelerating the modernization of electricity, continuously meeting the growing demand for electricity and social production and consumption and promoting socio-economic development. Among them, the role of electricity marketing is becoming increasingly prominent. How to fully mine and utilize the large amount of power marketing data accumulated by electric power enterprises over the years, to provide reliable support for the analysis and research of power marketing decisions. Bayesian network is a graphical pattern used to represent the continuous probability distribution of a set of variables, which provides causal information to discover potential relationships between data, and because of these characteristics, it is widely used in data mining.

In the work of [18], researchers apply Bayesian network to the analysis and research of power marketing decisions and establishes a Bayesian network suitable for power marketing decision-making for customer value evaluation, providing reliable support for marketing decision-making. They emphasized the ability of Bayesian network of making good decision models, based on their feature of making graphical patterns used to represent the continuous probability distribution of a set of variables, which provides causal information to discover potential relationships between data.

3. Power Cross-Border Transfer Availability in Core and Southeast Europe Capacity Calculation Regions (CCRs) and Its Impact on the SEE Markets Spot in Prices

Between 2022 and 2024, cross-border electricity transfer availability in Central Eastern and Southeastern Europe (CEE and SEE) significantly influenced wholesale electricity prices, particularly in the SEE region. Cross zonal trading opportunities are critical in curbing Day-Ahead or spot price volatilities. Due to insufficient cross-border transfer availability in year 2023, an explosion in negative DA prices (see Figure 5 and Table 4, Table 5 and Table 6 in this paper) occurred, because a low electricity demand coincided with an increased renewable supply in each bidding zone1. According to Figure 1 of ACER’s 2024 report [2] , Greece (GR) exhibited zero occurrences of spot negative prices, BG 11, RO 32, HU 74, AT 111, SI 96 and IT-South zero negative prices, emphasizing the need for the markets with negative prices, for local flexibility and the criticality of the cross-zonal transmission capacity (measured by CBTAs in our data set). Another crucial parameter as well as a proxy for the level of implementation of a ‘really successful’ integration of the EU power systems, related to the cross-border capacity, is the price convergence of bidding zones within Capacity Calculation Regions (CCR), in the wholesale market. During 2023, GR-IT CCR the price convergence (% of hours) was moderate2 (16%) and full (28%), while in 2022 the values were 8% and 28% respectively [2]. According to the same report, the most crucial factors explaining the price convergence are the differences in the generation mixes, the way the implicit market coupling in DA markets is implemented and finally, and most important for the targets of our study, the level of transmission capacity available for cross-zonal trade (our CBTA variable). Thus, detecting the most crucial factors shaping the price surge and discrepancy between Core markets (AT, SI, HU and RO) and the SEE markets of BG and GR, is strongly linked to the above crucial factors in explaining price convergence, between the Core Capacity Calculation Region (Core CCR) of the core markets and the SEE CCR markets, two CC regions using different capacity calculation methods3, the Flow-Based (FB) in Core CCR and Coordinated Net Transfer Capacity (CNTC), in the SEE CCR (the CBTAs in our data set are calculated by the CNTC methods, used by the TSO of the specific region). Table 1 (our elaboration based on data from [2]) informs about the implementation status of the Regional Capacity Calculation methodologies, for the markets analyzed in the present work. In 2023, the level of cross-zonal capacity offered, on average, in the biding zone borders of Core, GRIT and SEE CCRs, for the spot market is: 2100 MW Core, 2090 GRIT and 1200 MW SEE.

We now give some information, based also on [2], about the yearly evolution of transmission capacities available for cross zonal trade in the Day-Ahead market, that we consider to be very related to this analysis. More specifically, the level of interconnectivity of Member States calculated as the yearly average offered import capacity of every Member State as a percentage of peak electricity demand, and the yearly average offered export capacity of every Member State as a percentage of peak generation. Table 2 provides such information, from which we observe that the markets of Core CCRs show significantly larger levels of connectivity than the SEE CCRs and the GRIT CCR. This important information shows that the Core CCR markets included in flow-based market coupling in 2024 (also in 2022 and 2023) exhibit a considerable increase in their levels of interconnectivity, as measured by the above two measures. In general, as we have already mentioned, FB market coupling generally offers more exchange possibilities than NTC calculation, because it incorporates the modelling of the underlying electricity network in the allocation of cross-zonal capacities. The maximum import and export capacities in FB regions on a given bidding zone border are dependent on other exchanges in the region, which is not the case for NTC values, which are simultaneously feasible on all bidding zone borders. FB optimization-oriented approach leads to available capacities on specific network elements being allocated where they generate most socio-economic welfare.

Table 1.

Implementation status of the Regional Capacity Calculation methodologies, for the markets analyzed in this report (Based on data in [2]).

Table 1.

Implementation status of the Regional Capacity Calculation methodologies, for the markets analyzed in this report (Based on data in [2]).

|

Capacity Calculation Region (CCR) |

Calculation approach |

Day Ahead | |

| Regulation* | Implementation Status | ||

| Core: AT, HU, SI, RO | FB Coupling | Capacity Allocation and Congestion Management (CACM) |

Mostly |

| GRIT: GR, IT | Coordinated net Transfer capacity CNTC |

Capacity Allocation and Congestion Management (CACM) |

Mostly |

| SEE: BG, GR | Coordinated net Transfer capacity CNTC |

Capacity Allocation and Congestion Management (CACM) |

Mostly |

| *Note: Article 34 of regulation (EU), 2015/1222 | |||

To ensure that cross-zone capacity offered to the market is always efficiently allocated, all EU bidding zones borders, are now included in the Single DA-Coupling (SDAC) and the Single Intraday Coupling (SIDC), a very significant progress. In 2029, the EU Electricity Regulation [54], has ‘forced’ TSOs to offer the market a minimum level of cross-zonal capacity (CZC), considering however each TSO’s operational security limits. In 2020 a 70% minimum was imposed for implementing the requirement, without risking system security, allowing also the TSOs to opt for a transitional period. In this research paper, we assume that the way each TSO in the above CCRs (Core and SEE) have reacted to this 70% minimum of cross-zonal capacity has affected the dynamic evolution of the CBTAs of each market analyzed and consequently the spot price discrepancy between Core and SEE CCRs.

Table 2.

Level of interconnectivity of Member States in the day-ahead market measured as the average yearly import capacity as a percentage of peak demand and peak generation, in 2024.

Table 2.

Level of interconnectivity of Member States in the day-ahead market measured as the average yearly import capacity as a percentage of peak demand and peak generation, in 2024.

| Capacity Calculation. Region (CCR) |

As % of peak demand (2024) |

As % of peak Generation (2024) |

|---|---|---|

| Core: AT, HU, SI, RO | 75, 102, 224, 47 | 53, 129, 273, 34 |

| GRIT: GR, IT | 11, 13 | 11, 4 |

| SEE: BG, GR | 32, 11 | 29, 11 |

Limited Cross-Border Capacity and Market Fragmentation

The minimum 70% requirement translates in practice into the margin made available for cross-zonal trade MACZT), which is so a proxy for the level of integration of EU national day-ahead electricity markets. MACZT corresponds to the portion of capacity of a given CNEC that is made available for cross-zonal trade by the TSOs. The current level of optimization of the cross-zonal electricity transmission infrastructure across European spot markets, as well as the degree of the 70% implementation requirement is assessed by a MACZT monitoring report. However, despite EU regulations mandating that at least 70% of cross-border transmission capacity be available for electricity trading by the end of 2025, many regions in both Core CCR and SEE CCR, fell short. For example, based on the ACER’s report 2024 [2], during 2023, from the Core regions, only SI has achieved a value 97% of MACZT , (i.e. the % of hours when the minimum hourly MACZT was above 70% ), while the values of this index for other markets, in the same period, were: for AT 20% MACZT<50%, for HU only 6% for MACZT > 70 and 61% in the range 50% MACZT<70%, and RO 95% in the range 20% MACZT<50%.

Regarding the SEE CCR, encompassing the bidding zone borders Romania-Bulgaria and Bulgaria-Greece, in which the CNTC method is applied, the percentage of hours when the relative MACZT was above the minimum 70% requirement or within predefined ranges, in 2023, are as follows (ACER, 2024) : a) Bulgaria : for BG>GR and GR>BG no limiting element in the Member State, b) Greece: for BG>GR, 44% in range MACZT , 43% in range 20% MACZT<50%, while for GR>BG, 75% in range MACZT and 14% in range 50% MACZT<70% , and finally c) Romania: for BG>RO only 9% in MACZT , 53% in 20% MACZT<50% and 21% in MACZT<20%, while for RO>BG only 18% in MACZT 20% MACZT<50%, 21 % in range 50% MACZT<70% and finally 14% in MACZT<20%. The above-mentioned report also presents the percentage of hours when the limiting CNEC was, from the perspective of every Member State, located in the neighboring Member State, and therefore the TSO had no limiting CNEC to report. The report shows that this was particularly evident in the case of Bulgaria, for which the limiting CNEC on the Bulgaria–Greece and Bulgaria–Romania borders is often located in Greece and Romania, respectively. It is worth mentioning that in 2020, the SEE CCR achieved this 70% minimum target only 8% of the time, indicating substantial underutilization of interconnectors.

While the above information shows the extent to which Member States in the SEE region offered a minimum of 70% MACZT on its limiting CNECs in 2023, it does not include any information regarding the reasons for deviating below 70%. During the capacity validation period, reductions of capacity may be sent by either TSO on each bidding zone. During 2023 most limitations in the SEE CCR have been requested by the Bulgarian TSO, affecting so the MACZT results of the Greek and Romanian TSOs. A very important finding from comparing the Core and SEE CCRs adaptation in the 70% requirement is that the capacity calculation methodology implemented in the latter region does not have any specific provision in order the calculated capacities to adjust accordingly to comply with the minimum cross-zonal capacity requirements, Of course, such a provision must consider the remedial action potential in each market of the region. Due to this, a relatively poorer performance is observed in the SEE CCR in 2023. According to ACER’s 2024 report, Greece has requested a derogation in applying the requirement. Specifically, the derogation requested by the Greek TSO does not include a commitment on the levels of MACZT offered but sets a minimum value of 15% of the MCCC, a commitment that in Greece has been largely met in 2023. The same cannot be said about Romania’s action plan linear trajectory value of 43% of the MACZT in 2023.

For the Greece-Italy CCR, the Percentage of hours when the minimum hourly MACZT was above 70% or within predefined ranges in the GRIT CCR for each Member State and oriented bidding zone border – 2023 (% of hours) are as follows: a) for GR: 78% in range MACZT , for both GR>IT-South and IT-South>GR, while for b)Italy, 76% in range MACZT , for IT-South>GR. We note here that the GRIT CCR contains the internal Italian bidding zone borders and the DC bidding zone border with Greece, thus the impact of exchanges with third countries is considered limited. Additionally, thanks to the grid structural specifications, the impact of exchanges across other borders within the region is considered negligible (ACER, 2024).

From the above we conclude that SEE CCR’s limited capacity may have hindered electricity imports during periods of high demand, contributing to price spikes. Furthermore, the SEE region's reliance on the Net Transfer Capacity (NTC) mechanism, as opposed to the Flow-Based Market Coupling (FBMC) used in Central and Western Europe, exacerbated market fragmentation. FBMC's complex algorithms (a critical feature of the Target model) sometimes resulted in counterintuitive power flows, limiting imports into high-demand regions like Hungary and Romania, and leading to significant price disparities.

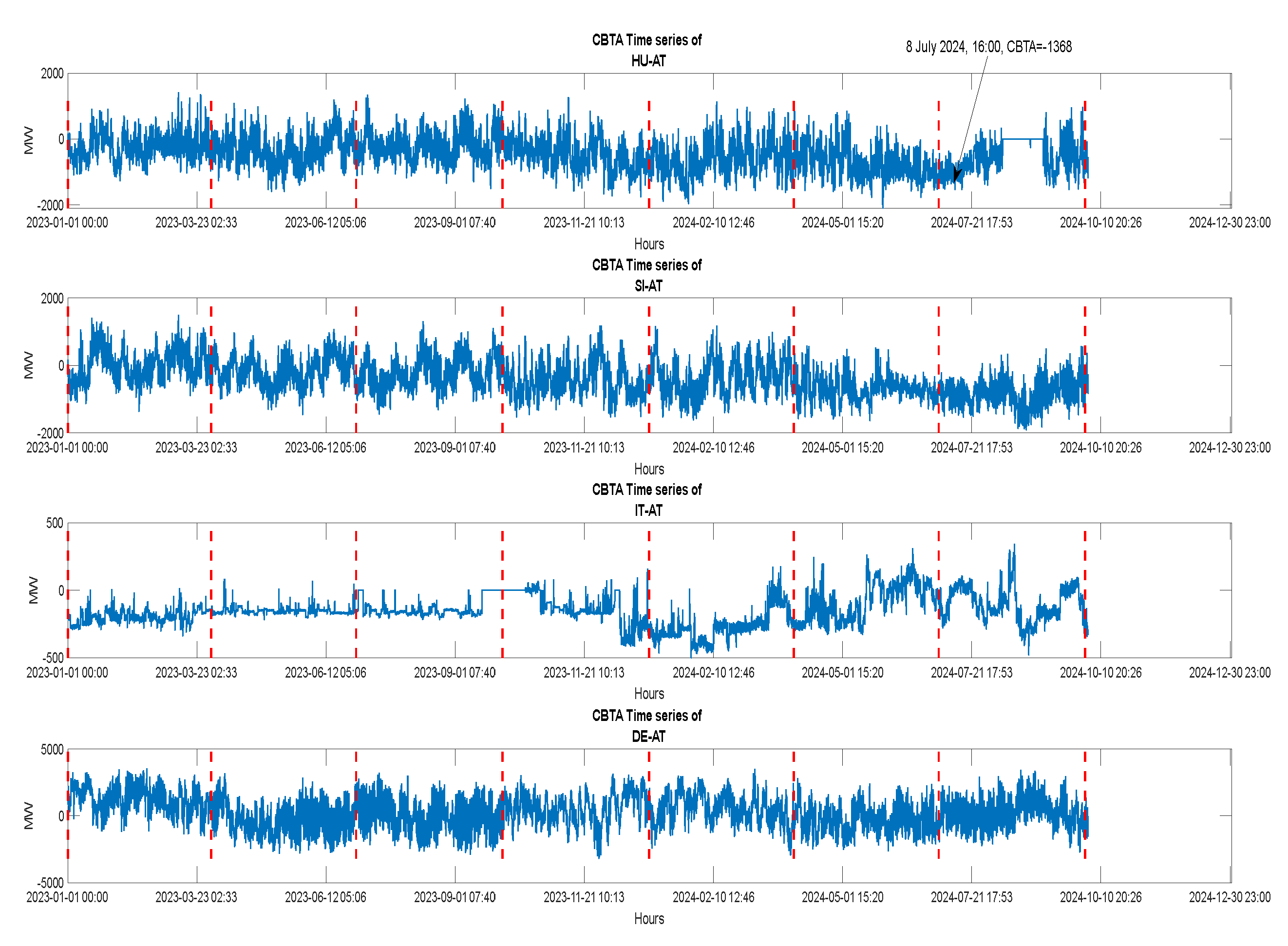

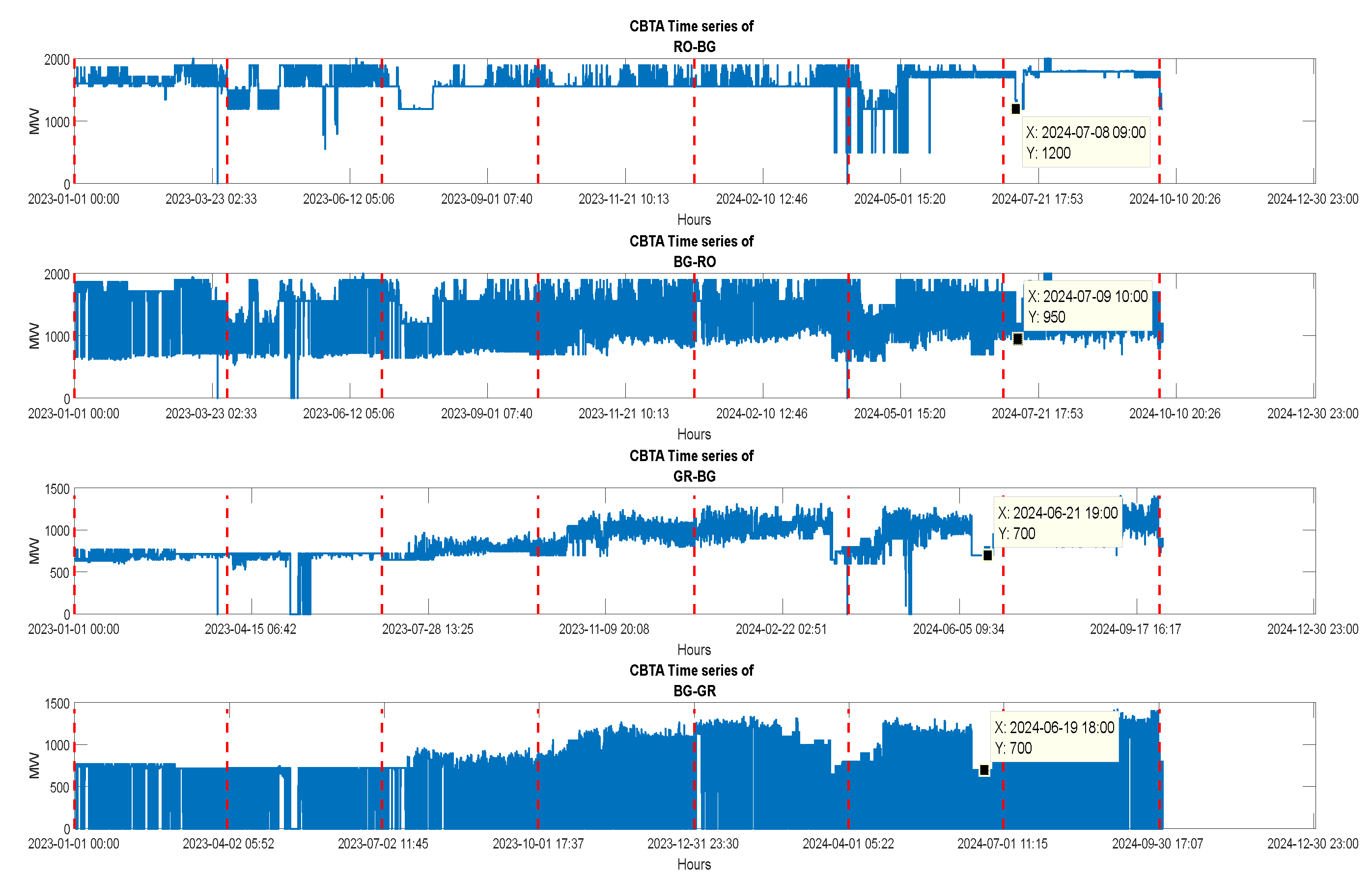

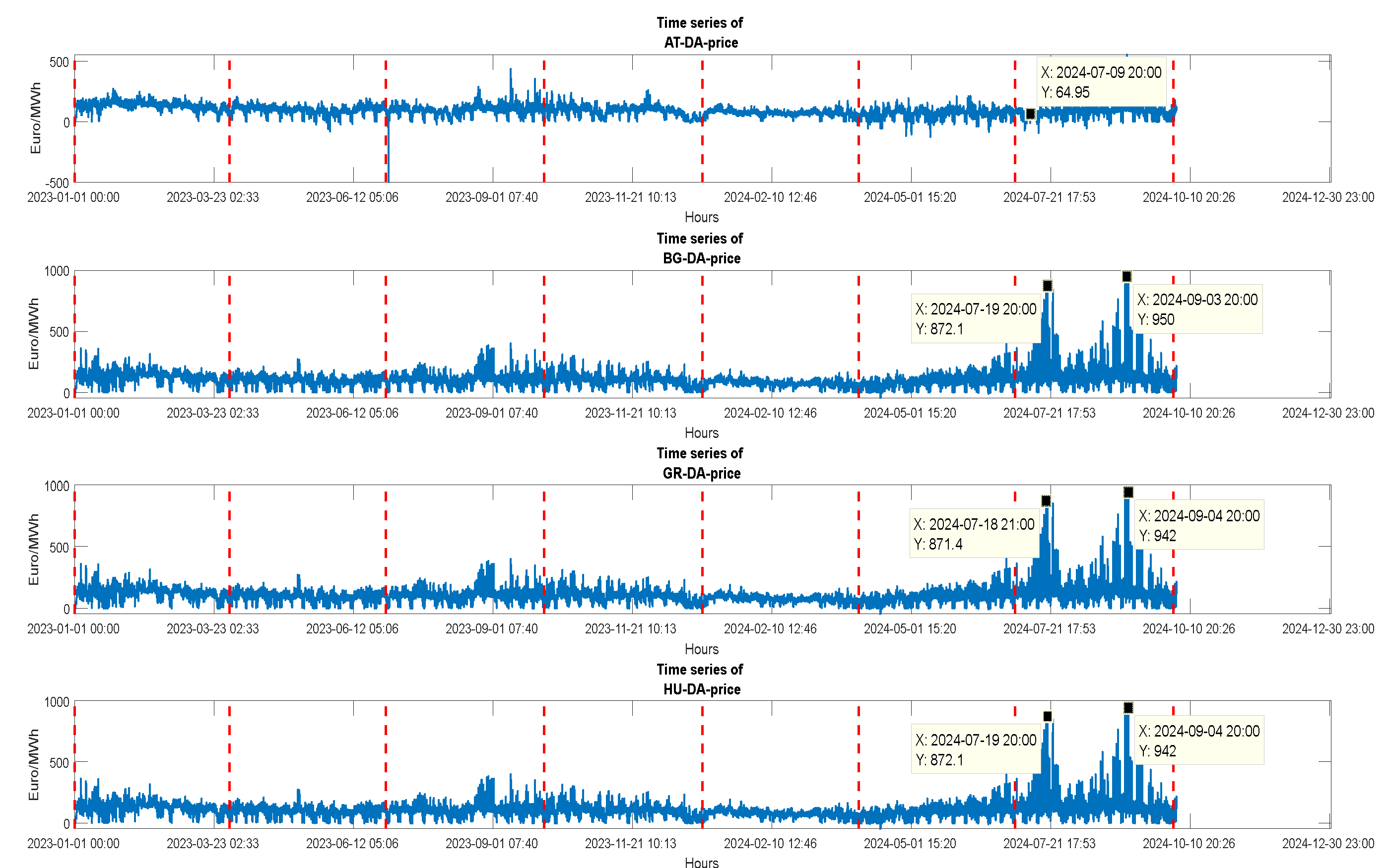

Figure 1 and Figure 2 show the time series of CBTAs of Austria’s CBTAs with Hungary, Slovenia, Italy and Germany-Luxembourg, and between Romania and Bulgaria (RO-BG, BG-RO), Greece and Bulgaria (GR-BG, BG-GR), respectively. In Figure 3 we show the DA prices of the markets involved in the previous cross-border transactions, for a visual inspection of how these prices have been affected by CBTAs. In July 2024 (see Figure 1), reduced imports to Hungary occurred, a notable event highlighting FBMC's shortcomings. More specifically, after July 8, FBMC allocations from Western Europe to Hungary decreased by approximately 1,200–1,300 MW during peak evening hours (19:00–24:00). This reduction was not due to maintenance or physical grid constraints but stemmed from FBMC's algorithmic decisions. Consequently, Hungary's HUPX market (Hungarian Power exchange, https://hupx.hu) experienced price surges up to €940/MWh, while neighboring Austria's prices remained around €61/MWh, illustrating a stark disparity across an internal EU border (see Figure 3). Almost concurrently, counterintuitive flows to Romania happened (see Figure 2). Romania faced reduced imports from Bulgaria due to maintenance on the BG>RO interconnector, decreasing capacity from 1,700 MW to 1,200 MW. To compensate, FBMC facilitated increased imports from Hungary. However, this led to situations where Romania's OPCOM market (the Romanian Electricity and Gas Market Operator) had prices up to €250/MWh lower than Hungary's HUPX, despite importing electricity from Hungary. Such non-intuitive flows strained Hungary's market further and underscored FBMC's limitations in addressing regional demand effectively.

Figure 1.

The cross-border transfer availabilities (CBTAs) between HU and AT, SI and AT, IT and AT, and DE and AT. (All countries are in the Core CCR). Total flows, i.e. (+) from HU to AT and (-) from AT to HU.

Figure 1.

The cross-border transfer availabilities (CBTAs) between HU and AT, SI and AT, IT and AT, and DE and AT. (All countries are in the Core CCR). Total flows, i.e. (+) from HU to AT and (-) from AT to HU.

Figure 2.

The cross-border transfer availability (CBTA) between RO and BG, and between GR and BG countries. (RO is in the Core CCR, and GR and BG in the SEE CCR).

Figure 2.

The cross-border transfer availability (CBTA) between RO and BG, and between GR and BG countries. (RO is in the Core CCR, and GR and BG in the SEE CCR).

Figure 3.

DA-prices of AT, HU (Core CCR), and BG, GR (SEE CCR) markets.

Several external factors have also enhanced the impact of limited cross-border capacity. More specifically, climate events such as record-high temperatures and droughts in SEE regions have reduced hydropower output and increased electricity demand for cooling, stressing the already constrained grid. Additionally, geopolitical tensions as the Russia-Ukraine conflict, disrupted energy supplies, with Ukraine, as we already mentioned, transitioning from an electricity exporter to an importer, increasing demand on neighboring countries' grids. Finally, infrastructure limitations, as delays in returning key power plants, like Bulgaria's Kozloduy nuclear plant, to full operation, reduced available generation capacity (the plant disrupted one of its two reactors, for a period until November 30, 2024, with the consequence the regional system to have 1 GW less). These factors have contributed to unprecedented wholesale electricity price spikes in the SEE region. Based on Figure 3, in August 2024, Greece's electricity prices more than doubled from €60 to €130 per megawatt-hour (MWh). Hungary (HU) experienced prices as high as €940/MWh during peak hours, while neighboring Austria (AT) saw prices around €61/MWh, highlighting severe regional disparities. Romania (RO) and Bulgaria (BG) also faced significant price increases, with day-ahead market prices reaching €700/MWh and €500/MWh, respectively. The findings above have stressed the importance of the interactions of volatilities of spot prices and CBTAs, that are enhanced further by the combined influences of external factors, geopolitical tensions and infrastructure limitations (as the limited interconnectivity of SEE countries, emerging from their reliance on the Net Transfer Capacity (NTC) mechanism, contrasting with FBMC's application in Central Europe, a critical discrepancy that hinders seamless integration and efficient electricity distribution). All these findings challenge the status of the current policy, an issue discussed in Section 8.

4. Data Sets, Preprocessing, Summary (Descriptive) Statistics, Correlation Analysis and Cross-Border Transfer Availability

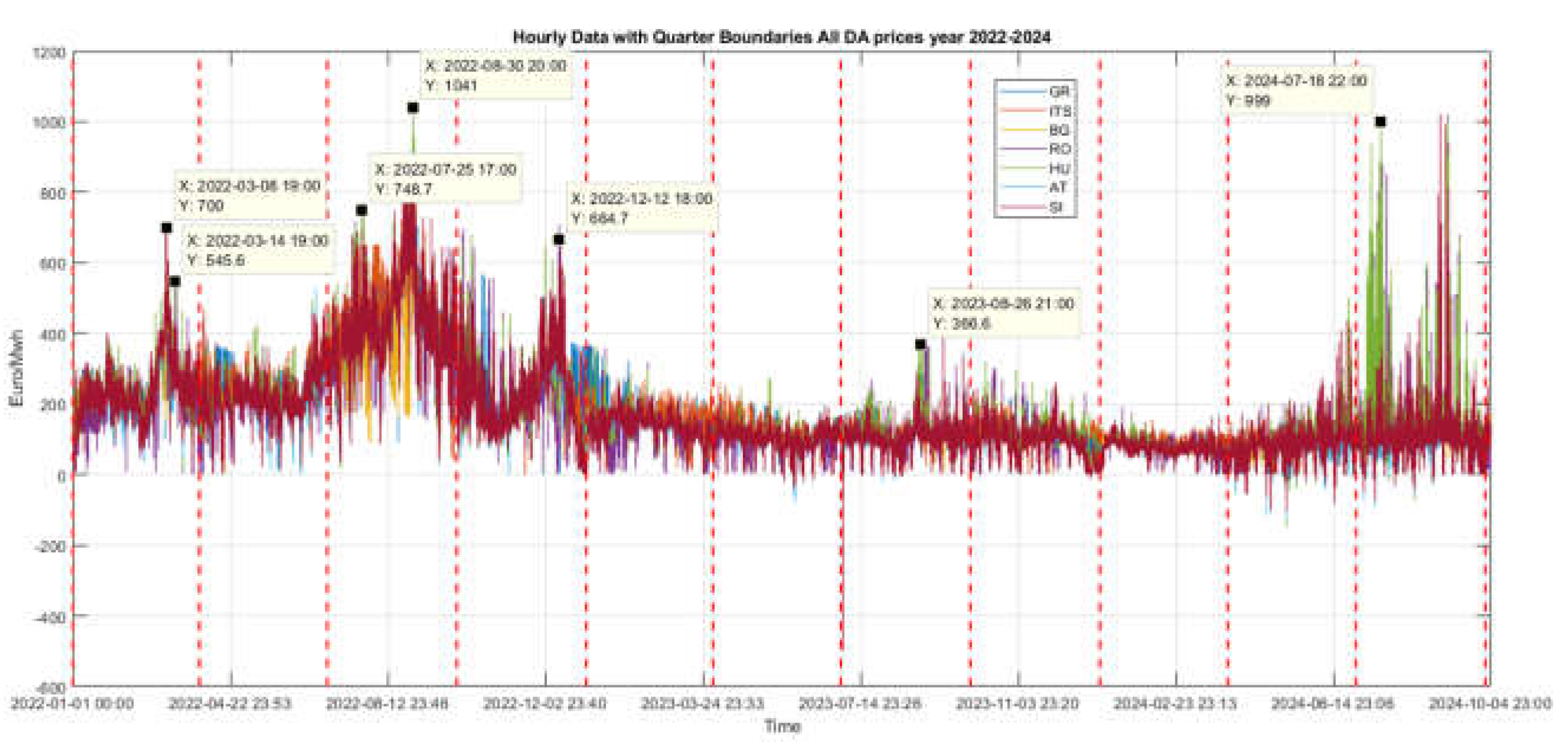

We use data downloaded from ENTSO-E Transparency platform (transparency@entsoe.eu), for our set of seven electricity markets, including Austria (AT), Bulgaria (BG), Romania (RO), Slovenia (SI), Greece (GR), Hungary (HU), and Italy (South bidding zone) (ITsouth), from January 2022 to October 4, 2024. We analyze hourly wholesale price data expressed in in Euro/Mwh. The countries under analysis are shown in Figure 4, which also depicts the borders where the calculation of the Capacity from the interfaces changes from Net Transfer Capacity (NTC) to Flow Based (FB) [2]. The dataset covers the period from 1.1.2022 to 4.10.2024, their missing values have been filled appropriately, with frequency converted from originally 15 minutes to hourly data. Thus, the size of dataset is 24194. Figure 5 shows the time series of hourly spot prices of all markets for the period of 1st January 2022 to 4 October 2024, and Figure 6 the time series of Greek DA hourly spot prices. Two distinct periods of high spot prices and volatility, in all markets of our analysis, are observed in Figure 5. The first is from early spring (March) of 2022 to December 2022, with a pronounced upward and downward price oscillations, and a peak price occurring on 30th of July (1041 Euro/MWh). The second period covers the summer of 2024, ending approximately at the end of August 2024. We describe shortly at this point the main drivers that seem to be the prevailing factors in shaping the price dynamics shown in Figure 5. For the 2022 price surge the main drivers are : a) gas crisis from Russia’s Invasion of Ukraine, since Russian pipeline gas flows into Europe plummeted, TTF gas prices spiked over €300/MWh in late August 2022, and finally power prices in gas-dependent regions soared as gas-fired generation costs increased dramatically, b) high CO₂ Prices, EU ETS prices sustained levels above €70–€90/tonne, resulting to elevated variable costs for gas, coal, and lignite units, c) low Hydro and Renewables output, due to severe drought conditions reduced hydro output in parts of the Balkans, also low renewables increased reliance on thermal generation, d) nuclear and thermal Outages, since extensive nuclear outages in France reduced regional supply, and as a consequence raising cross-border demand into the SEE region, e) strong market interconnections, i.e. tight markets in Italy, Austria, and Germany that quickly impacted neighboring SEE countries via cross-border flows, and finally f) risk premiums and volatility, since market uncertainty drove elevated forward prices and risk premiums, spilling over into day-ahead markets. Thus, in the March-April 2022 period, these drivers are responsible for spot prices in the region to frequently exceed €300–€400/MWh, while in peak hours during crisis events, sometimes surpassed €500–€800/MWh.

Similarly, for the second period, in 2024, of high spot price volatility, the main drivers are: 1) Stabilized but Elevated Gas Prices : TTF gas prices ranged ~€25–€35/MWh in 2024, far below 2022 peaks but above historical norms, and LNG markets remained tight due to global competition, 2) Extreme heatwaves : repeated heatwaves across Southern and Eastern Europe, increased cooling demand, and lower river levels affected hydro generation and thermal plant cooling capacity, 3) Reduced nuclear and hydro generation : France’s nuclear fleet partially recovered but still faced outages, and Balkan hydro production again stressed by droughts, 4) Transmission Constraints: cross-border congestion, particularly toward Italy, constrained SEE import potential, 5) Sustained CO₂ Prices, EU ETS prices in the range of €65–€85/tCO₂, and finally 6) High Solar Penetration: major solar capacity expansions in Italy, Greece, Bulgaria, and Romania, depressed midday prices but triggered steep evening ramps.

Figure 4.

Left: definition of the bidding zone review regions as per Article 3 (2) of the BZR Methodology (Adopted from ACER 2024, [2]) and Right: ENTSO-E, 2025, Interconnections Grid. The left picture shows the Core and SEE CC regions and the right their interconnection lines.

Figure 4.

Left: definition of the bidding zone review regions as per Article 3 (2) of the BZR Methodology (Adopted from ACER 2024, [2]) and Right: ENTSO-E, 2025, Interconnections Grid. The left picture shows the Core and SEE CC regions and the right their interconnection lines.

Figure 5.

Time series of hourly spot prices of all markets for the period of 1st January 2022 to 4 October 2024, with quarter boundaries, and values of price spikes at specific dates.

Figure 5.

Time series of hourly spot prices of all markets for the period of 1st January 2022 to 4 October 2024, with quarter boundaries, and values of price spikes at specific dates.

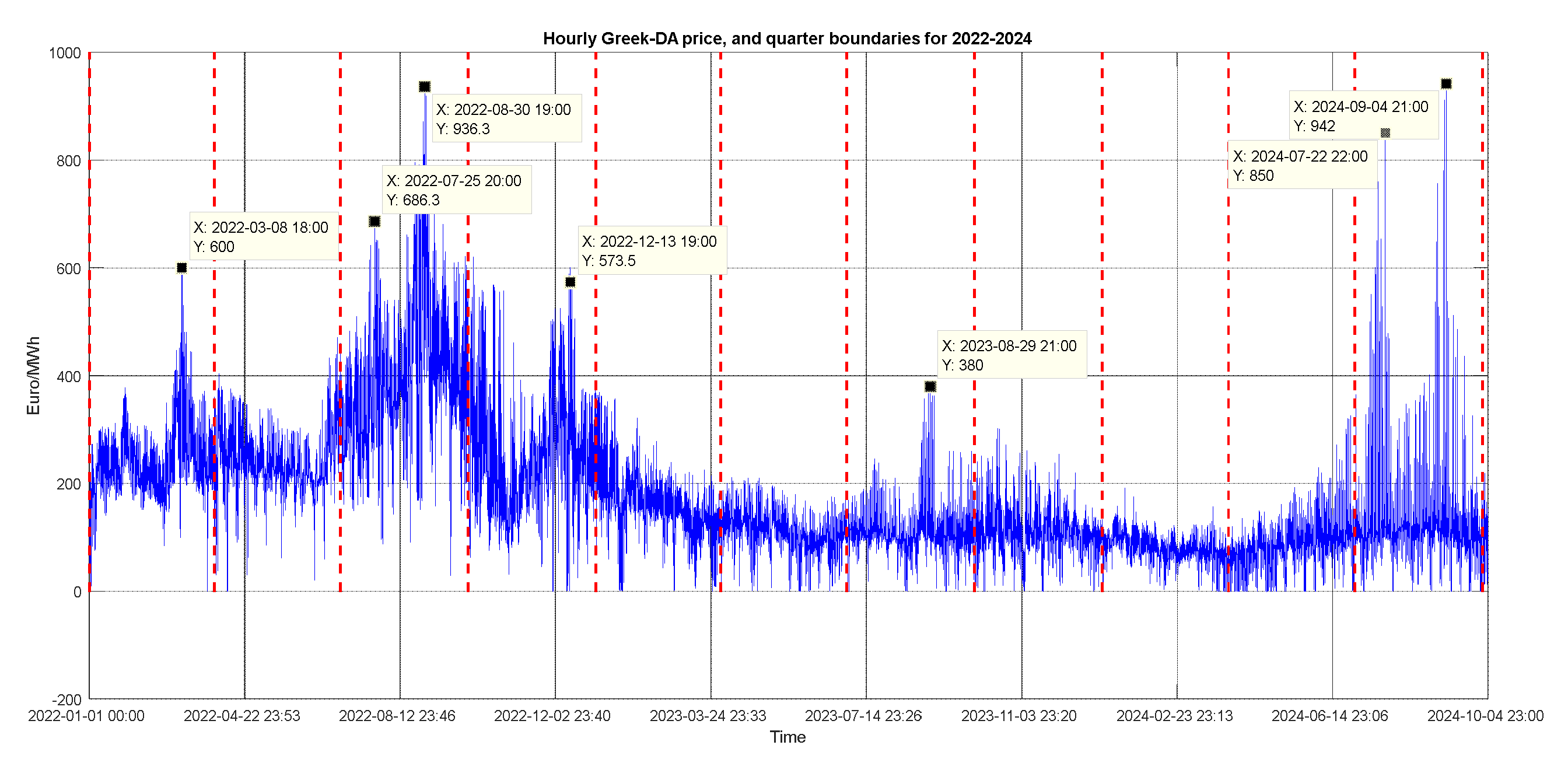

Figure 6.

Time series of Greek DA hourly spot prices for the entire period of 1st January 2022 to 4 October 2024, with quarter boundaries, and values of price spikes at specific dates. On 4th September 2024, at 21:00, the electricity spot hourly Greek price reached 942 Euro/Mwh.

Figure 6.

Time series of Greek DA hourly spot prices for the entire period of 1st January 2022 to 4 October 2024, with quarter boundaries, and values of price spikes at specific dates. On 4th September 2024, at 21:00, the electricity spot hourly Greek price reached 942 Euro/Mwh.

Table 3.

Shows the data set of all fundamental variables considered in our work, collected for each of the seven electricity markets. Descriptive statistics for the hourly spot prices, for each market, are given in Table 4, Table 5, Table 6, and Table 7 (for each separate year and for the entire period 2022-24, respectively). List of all sixty-seven (67) fundamental variables considered in our work, for all electricity markets. In bold letters, the DA spot prices of the markets under analysis.

Table 3.

Shows the data set of all fundamental variables considered in our work, collected for each of the seven electricity markets. Descriptive statistics for the hourly spot prices, for each market, are given in Table 4, Table 5, Table 6, and Table 7 (for each separate year and for the entire period 2022-24, respectively). List of all sixty-seven (67) fundamental variables considered in our work, for all electricity markets. In bold letters, the DA spot prices of the markets under analysis.

| Node (Variable) | Name | Description | Unit |

|---|---|---|---|

| 1 | AT_DA_price | DA Electricity price, Austria | Euro/MWh |

| 2 | AT_actTotal_Load | Actual Total Load, Austria | MW |

| 3 | AT_foreTotal_Load | Forecasted Total Load, Austria | MW |

| 4 | AT_actGas | Gas power production, Austria | MW |

| 5 | AT_Solar_Fct | Solar forecst. Power product. , Austria | MW |

| 6 | AT_Hydro_Actual | Hydro Power Forecasted, Austria | MW |

| 7 | BG_DA_price | DA Electricity price, Bulgaria | Euro/MWh |

| 8 | BG_actTotal_Load | Actual Total Load, Bulgaria | MW |

| 9 | BG_foreTotal_Load | Forecasted Total Load, Bulgaria | MW |

| 10 | BG_actGas | Gas power production, Bulgaria | MW |

| 11 | BG_Wind_Fct | Wind forecast generated power, Bulgaria | MW |

| 12 | BG_Solar_Fct | Solar forecast. Power product., Bulgaria | MW |

| 13 | BG_Hydro_Actual | Hydro Power production, actual, Bulgaria | MW |

| 14 | BG_actual_Lignite | Lignite act power production, Bulgaria | MW |

| 15 | GR_DA_price | DA Electricity price, Greece | Euro/MWh |

| 16 | GR_actTotal_Load | Actual Total Load, Greece | MW |

| 17 | GR_foreTotal_Load | Forecasted Total Load, Greece | MW |

| 18 | GR_actGas | Gas power production, Greece | MW |

| 19 | GR_Wind_Fct | Wind forecast generated power, Greece | MW |

| 20 | GR_Solar_Fct | Solar forecast. Power product., Greece | MW |

| 21 | GR_Hydro_Actual | Hydro Power production, actual, Greece | MW |

| 22 | GR_Hydro_Storage_Actual | Hydro Power act consumption, Greece | MW |

| 23 | GR_actual_Lignite | Lignite act power production, Greece | MW |

| 24 | HU_DA_price | DA Electricity price, Hungary | Euro/MWh |

| 25 | HU_actTotal_Load | Actual Total Load, Hungary | MW |

| 26 | HU_foreTotal_Load | Forecasted Total Load, Hungary | MW |

| 27 | HU_actGas | Gas act.power production, Hungary | MW |

| 28 | HU_Wind_Fct | Wind forecast generated power, Hungary | MW |

| 29 | HU_Solar_Fct | Solar forecast. Power product., Hungary | MW |

| 30 | HU_Hydro_Actual | Hydro Power production, actual, Hungary | MW |

| 31 | HU_actual_Lignite | Lignite act power production, Hungary | MW |

| 32 | ITS_DA_price | DA Electricity price, Italy (South) | Euro/MWh |

| 33 | IT_actTotal_Load | Actual Total Load, Italy | MW |

| 34 | IT_foreTotal_Load | Forecasted Total Load, Italy | MW |

| 35 | IT_actGas | Gas power production, Italy | MW |

| 36 | IT_Wind_Fct | Wind forecast generated power, Italia | MW |

| 37 | IT_Solar_Fct | Solar forecast. Power production., Italia | MW |

| 38 | IT_Hydro_Actual | Hydro Power production, actual, Italia | MW |

| 39 | RO_DA_price | DA Electricity price, Romania | Euro/MWh |

| 40 | RO_actTotal_Load | Actual Total Load, Romania | MW |

| 41 | RO_foreTotal_Load | Forecasted Total Load, Romania | MW |

| 42 | RO_actGas | Gas power production, Romania | MW |

| 43 | RO_Wind_Fct | Wind forecast generated power, Romania | MW |

| 44 | RO_Solar_Fct | Solar forecast. Power product., Romania | MW |

| 45 | RO_Hydro_Actual | Hydro Power production, actual, Romania | MW |

| 46 | RO_actual_Lignite | Lignite act. power production, Romania | MW |

| 47 | SI_DA_price | DA Electricity price, Slovenia | Euro/MWh |

| 48 | SI_actTotal_Load | Actual Total Load, Slovenia | MW |

| 49 | SI_foreTotal_Load | Forecasted Total Load, Slovenia | MW |

| 50 | SI_actGas | Gas power production, Slovenia | MW |

| 51 | SI_Solar_Fct | Solar forecast. Power product., Slovenia | MW |

| 52 | SI_Hydro_Actual | Hydro Power production, actual, Slovenia | MW |

| 53 | SI_actual_Lignite | Lignite act power production, Slovenia | MW |

| 54 | GR_BG | Cross Border Transfer, GR-BG | MW |

| 55 | BG_GR | Cross Border Transfer, BG-GR | MW |

| 56 | IT_GR | Cross Border Transfer, IT-GR | MW |

| 57 | GR_IT | Cross Border Transfer, GR-IT | MW |

| 58 | RO_BG | Cross Border Transfer, RO-BG | MW |

| 59 | BG_RO | Cross Border Transfer, BG-RO | MW |

| 60 | SI_IT | Cross Border Transfer, SI-IT | MW |

| 61 | IT_SI | Cross Border Transfer, IT-SI | MW |

| 62 | AT-CH | Cross Border Transfer, AT-CH | MW |

| 63 | AT-CZ | Cross Border Transfer, AT-CZ | MW |

| 64 | AT-DELU | Cross Border Transfer, AT-DELU (Austria to Germany-Luxembourg) | MW |

| 65 | AT-ITNorth | Cross Border Transfer, AT-ITNorth | MW |

| 66 | AT-SI | Cross Border Transfer, AT-SI | MW |

| 67 | AT-HU | Cross Border Transfer, AT-HU | MW |

Table 4.

Descriptive statistics of hourly spot prices, for all markets, 2022-4th October 2024.

| 2022-Oct.2024 | |||||||

|---|---|---|---|---|---|---|---|

| Statistics | HU | RO | BG | GR | ITSouth | SI | AT |

| min | -500.0 | -106.30 | -45.00 | -1.02 | 0.00 | -500.00 | -500.00 |

| max | 1047.10 | 1021.60 | 950.00 | 942.00 | 870.00 | 1023.00 | 919.60 |

| mean | 161.89 | 159.40 | 154.75 | 170.61 | 180.85 | 159.71 | 151.06 |

| median | 120.96 | 119.74 | 119.28 | 130.63 | 134.06 | 117.90 | 111.30 |

| mode | 0.0 | 0.0 | 0.0 | 100 | 100 | 0.0 | 0.0 |

| Std | 128.53 | 128.13 | 119.10 | 117.57 | 120.71 | 126.31 | 122.89 |

| prctile25 | 84.18 | 83.13 | 83.09 | 92.77 | 104.08 | 82.86 | 78.46 |

| prctile75 | 204.15 | 200.63 | 197.51 | 223.07 | 220.00 | 203.50 | 189.10 |

| iqr | 119.97 | 117.50 | 114.42 | 130.30 | 115.92 | 120.64 | 110.64 |

Table 5.

Descriptive statistics of hourly spot prices, for all markets, 2022.

| 2022 | |||||||

|---|---|---|---|---|---|---|---|

| Statistics | HU | RO | BG | GR | ITSouth | SI | AT |

| min | 0.0 | 0.0 | 0.0 | -0.01 | 0.0 | 0.0 | 0.0 |

| max | 1047.10 | 964.20 | 936.30 | 936.30 | 870.00 | 879.30 | 919.60 |

| mean | 271.62 | 265.26 | 253.20 | 279.86 | 295.77 | 274.43 | 261.36 |

| median | 237.20 | 232.58 | 225.08 | 249.28 | 257.23 | 240.01 | 224.00 |

| mode | 138.41 | 138.41 | 138.41 | 200.00 | 650.00 | 220.00 | 190.00 |

| Std | 139.88 | 142.95 | 131.20 | 116.10 | 131.03 | 137.00 | 138.47 |

| prctile25 | 178.25 | 165.31 | 163.27 | 206.89 | 206.43 | 185.03 | 169.09 |

| prctile75 | 345.26 | 342.15 | 320.14 | 339.31 | 370.00 | 343.24 | 336.98 |

| iqr | 167.00 | 176.84 | 156.86 | 132.42 | 163.56 | 164.20 | 167.88 |

Table 6.

Descriptive statistics of hourly spot prices, for all markets, 2023.

| 2023 | |||||||

|---|---|---|---|---|---|---|---|

| Statistics | HU | RO | BG | GR | ITSouth | SI | AT |

| min | -500.0 | -23.18 | -1.10 | 0.0 | 0.0 | -500.0 | -500.0 |

| max | 437.47 |

436.89 | 400.00 | 383.82 | 298.20 | 426.18 | 437.47 |

| mean | 106.79 | 103.71 | 103.82 | 119.09 | 125.03 | 104.30 | 102.11 |

| median | 104.48 |

102.72 | 102.74 | 112.47 | 120.94 | 103.38 | 101.91 |

| mode | 0.0 | 122 | 122 | 100 | 100 | 120 | 0.0 |

| Std | 48.43 | 50.78 | 50.33 | 50.18 | 37.69 | 45.33 | 44.40 |

| prctile25 | 83.75 | 79.26 | 79.20 | 93.00 | 103.47 | 83.21 | 82.09 |

| prctile75 | 133.56 | 132.56 | 132.54 | 141.33 | 145.30 | 130.95 | 128.84 |

| iqr | 49.81 | 53.30 | 53.34 | 48.33 |

41.83 | 47.74 | 46.75 |

Table 7.

Descriptive statistics of hourly spot prices, for all markets, 01-01-2024 to 4th October 2024.

Table 7.

Descriptive statistics of hourly spot prices, for all markets, 01-01-2024 to 4th October 2024.

| 2024 (up to 4th October) | |||||||

|---|---|---|---|---|---|---|---|

| Statistics | HU | RO | BG | GR | ITSouth | SI | AT |

| min | -149.98 | -106.36 | -45.00 | -1.02 | 0.0 | -105.88 | -426.42 |

| max | 999.0 | 1021.6 | 950.00 | 942.0 | 252.1 | 1022.3 | 555.7 |

| mean | 90.15 | 93.53 | 92.37 | 94.79 | 103.24 | 81.85 | 70.48 |

| median | 81.85 | 85.00 | 85.00 | 88.67 | 102.84 | 79.72 | 74.21 |

| mode | 0.0 | 0.0 | 0.0 | 0.04 | 100.0 | 0.0 | 0.0 |

| Std | 78.91 | 78.66 | 74.06 | 64.93 | 31.22 | 56.02 | 37.19 |

| prctile25 | 60.49 | 61.65 | 61.42 | 69.53 | 88.84 | 58.90 | 55.13 |

| prctile75 | 104.98 | 108.01 | 107.49 | 108.11 | 115.59 | 101.82 | 91.20 |

| iqr | 44.49 | 46.35 | 46.06 | 38.58 | 26.75 | 42.91 | 36.07 |

4.1. Boxplots, Aggregated and Hourly-Wised Summary Statistics of Spot Prices

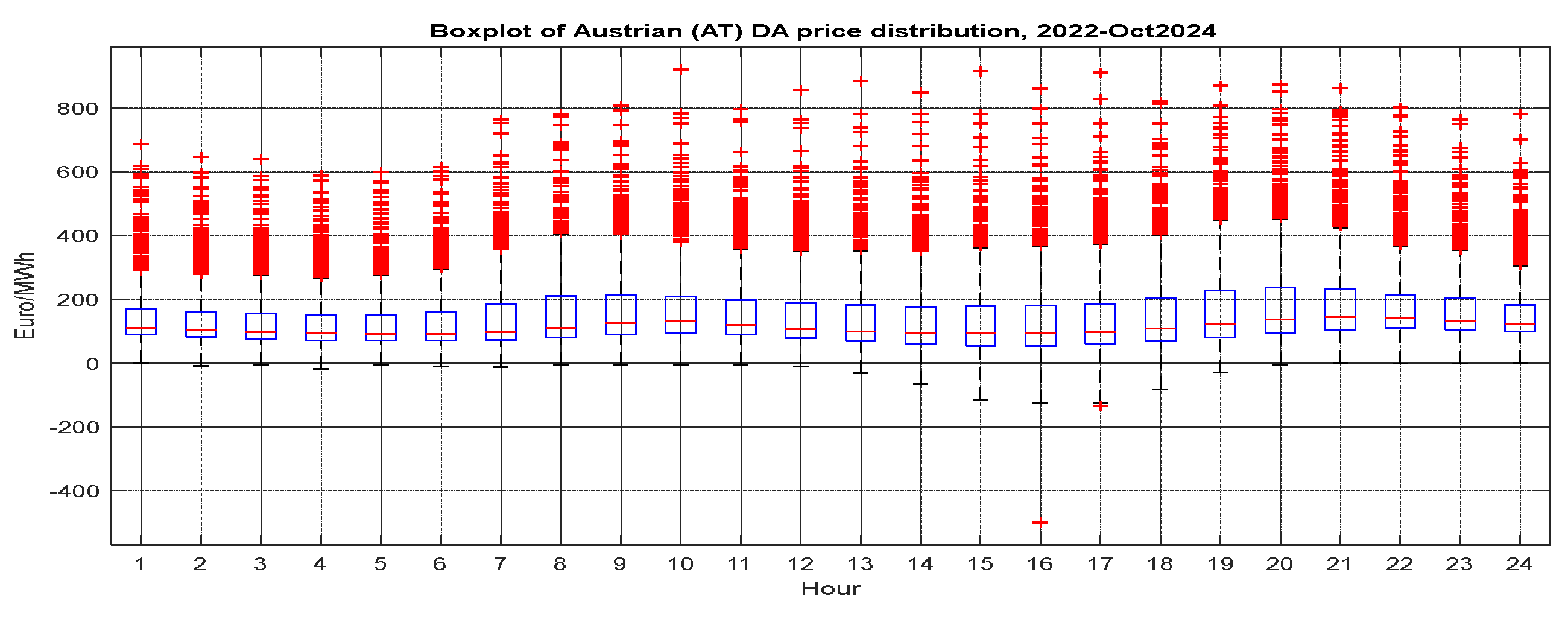

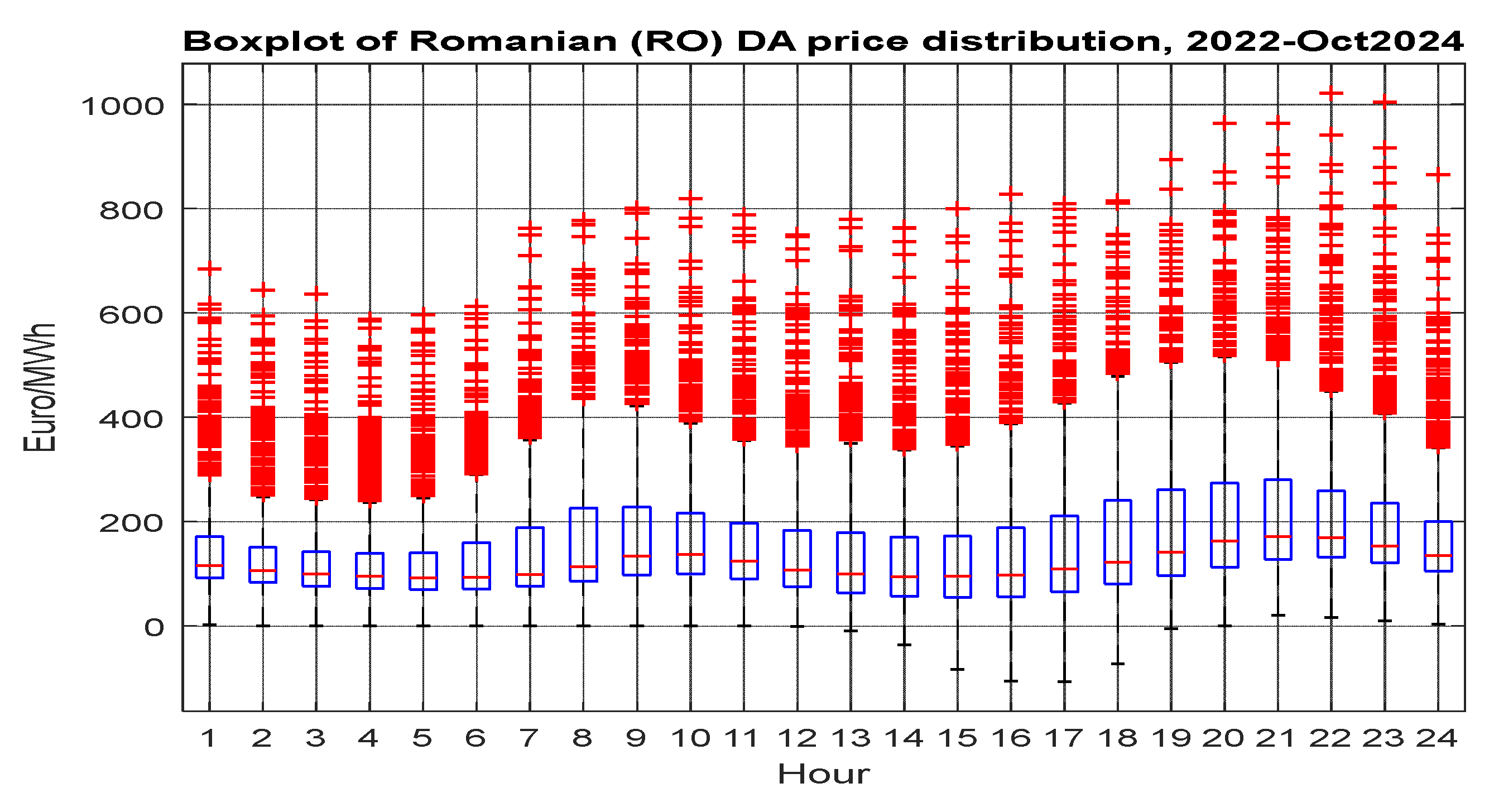

The boxplot comparison of hourly electricity prices across the seven markets reveals notable differences in both price levels and variability. Figure 7 and Figure 8 show, for comparison purposes, the boxplots of the distribution of AT and RO DA prices, hourly-wise i.e. for each separate hour H1 to H24. The boxplots of the rest of the markets are given in Supplementary material D. The same information, quantitatively, as well as other descriptive statistics, is provided in Table A1, Table A2, Table A3, Table A4, Table A5, Table A6 and Table A7, of Supplementary material A. From the figures we see that, for the price levels, Romania (RO) shows consistently higher spot prices than Austria (AT) across almost all hours. The median prices in Romania are around 200–300 EUR/MWh, while Austria's median prices mostly range between 100–200 EUR/MWh. Regarding volatility and outliers, Romania exhibits greater price volatility, indicated by wider interquartile ranges (IQRs), a larger number of extreme outliers (red pluses), often surpassing 800–1000 EUR/MWh, while Austria also shows outliers but with lower frequency and magnitude compared to Romania. For the daily hourly trends, AT’s prices are relatively stable throughout the day, and slight increases in the morning (8–11) and evening (18–21) hours, reflecting typical demand patterns, and finally price distribution is narrower, suggesting a more stable market. RO’s prices tend to spike during evening hours (19–22), both in terms of median and outliers. Morning hours (7–10) also show noticeable increases in median price and spread, and prices are lowest and least volatile between 1–5 AM, consistent with low demand. Now, regarding negative prices, Austria exhibits occasional negative prices, especially in the afternoon hours (13–17), a fact that could be due to high renewable (e.g., solar) generation exceeding demand, grid constraints or export limitations. Romania, in contrast, does not display negative prices, suggesting tighter supply conditions or less flexible generation mix, and possibly lower penetration of renewables or less dynamic market adjustments. Table 8 below gives a summary of the comments above.

Table 9 presents summary statistics across the entire datasets (not just by hour) (we have computed mean, median, standard deviation (St.dev.), interquartile range (IQR) etc., per market, aggregating all 24 hours. This gives us a general picture of volatility and price level without the hourly resolution. The indicators (statistics) (average daily price, standard deviation, average daily peak-of-peak spread, skewness and kurtosis and frequency of extreme prices, e.g. > 90th percentile) help us rank the markets more broadly, without dissecting hour-by-hour details (which are, however. shown in Figure 4, Figure 5, Figure 6, Figure 7, Figure 8, Figure 9 and Figure 10 and Table A1, Table A2, Table A3, Table A4, Table A5, Table A6 and Table A7 of Supplement A). The note at the bottom of Table 7 explains the indicators shown.

Thus, based on Table 9, the Italian and Greek markets (ITS and GR) exhibit the highest mean and median prices, suggesting a generally more expensive electricity supply, while Slovenian and Austrian markets (SI and AT) have the lowest medians (117.9 and 111.3 respectively), indicating more affordable rates. Greek market displays the wider interquartile range (IQR=120.6), reflecting greater variability in hourly prices and potentially higher market volatility (even though has the lowest aggregated st.dev). In contrast, AT and BG markets have a relatively narrow IQR, pointing to more stable and predictable pricing. Romanian and Bulgarian markets have the largest Peak-Off-Peak (PoP) spreads (95.3 and 94.1) followed by Hungarian and Greek markets (86.1 and 76.43). The largest CV (coefficient of variation, a volatility measure) is presented by TA and RO markets, followed by HU and GR markets. Additionally, skewed distributions in markets TA, BG, HU, ITS and RO hint at asymmetric pricing behavior, showing a tendency for upward price spikes. The table shows no differences between the markets for the frequency of extreme points, and HU exhibits the highest price, followed by SI and RO markets. From Table 10 we observe that the Greek and Italian markets have the highest total number of hourly price outliers.

4.2. Correlation Analysis of All Raw DATA, 2022-Oct2024.

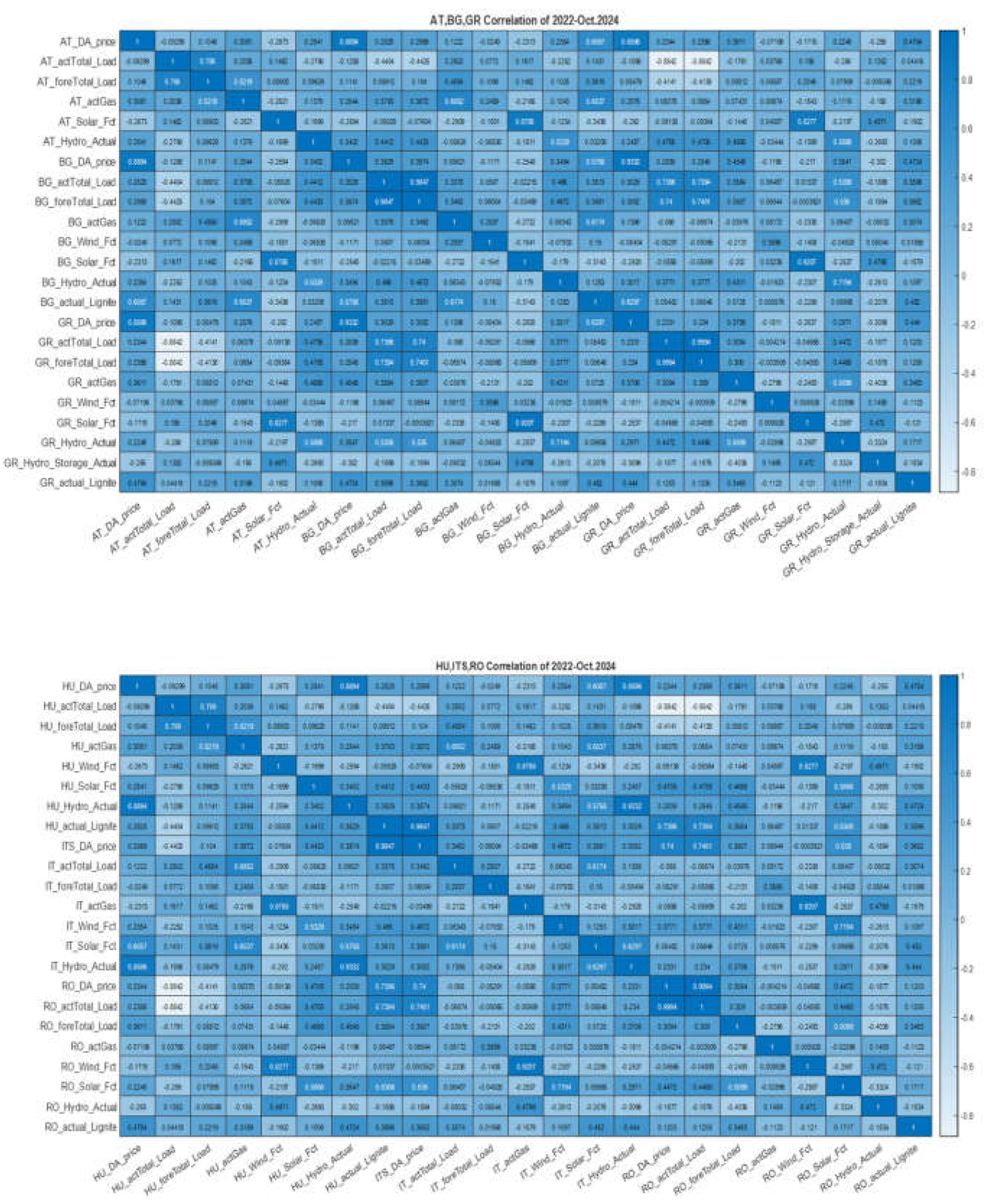

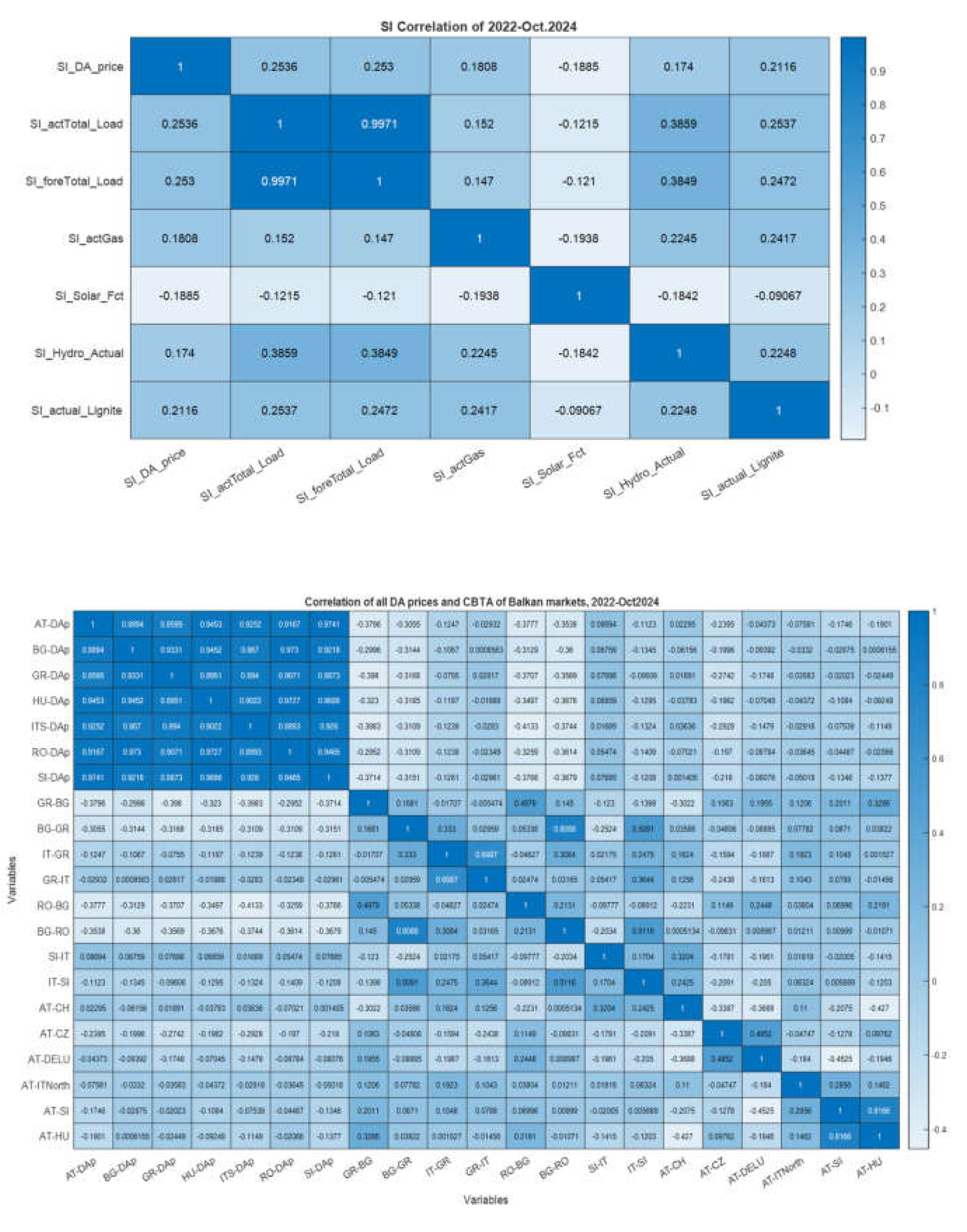

Even though correlation analysis is not capable of revealing any causalities, profound or hidden, its result can serve as a useful, albeit rough guide of the ‘interactions’ between the variables involved. We use correlation analysis (Figure 9a–d) to ‘detect’: a) strong regional spot price interactions, b) price-fuel correlations, c) North-South correlation gradient (strength), d) cluster of markets and finally e) the role of local fuels. High correlations between neighboring countries' Day-Ahead (DA) prices (e.g., AT-DA-price, HU-DA-price, SI-DA-price) suggest significant market coupling or shared supply-demand fundamentals. These strong correlations may reflect cross-border electricity trade, similar weather conditions or economic patterns, and coordinated market operations within the EU internal electricity market. Regarding price-fuel correlations, we observe that GR-Gas, AT-Gas, HU-Gas, and SL-Gas have medium to small positive correlations with DA prices in their respective countries, while this fact is not observed in BG, IT and RO markets. This results in natural gas being a relatively marginal fuel, especially during price-setting hours, highlighting the influence, to some degree, of gas prices on electricity pricing in these markets. Now, as far as the strength or gradient of correlations, from north to south markets, we observe a decrease in correlation strength between prices from Core CCR (AT, HU, SI, RO) to SEE CCR markets (GR, IT). For example, the average spot prices correlation between AT and HU, SI and RO markets, is higher than in AT and GR, BG markets (0.94 and 0.86 respectively). The same is observed between the mean correlation of prices of HU, SL and RO markets, with the mean value between HU and GR markets (0.965 and 0.915). This could indicate transmission bottlenecks, different generation mixes (e.g., higher renewable share in some markets), or regulatory or market structure differences. The figures show also clustered Markets countries like AT, HU, SI, and RO that form a highly correlated cluster, indicating a tightly interconnected sub-region, while GR and IT are more loosely connected, possibly due to their geographical positioning and more, in general, isolated grid conditions. For the role of local fuels play, we observe that hydro and lignite generation in BG and GR markets are only locally correlated with their own DA prices, which implies a local dependency on these two fuels for power generation. The two markets show similar local dependency of their own prices on their RES (wind and solar generations).

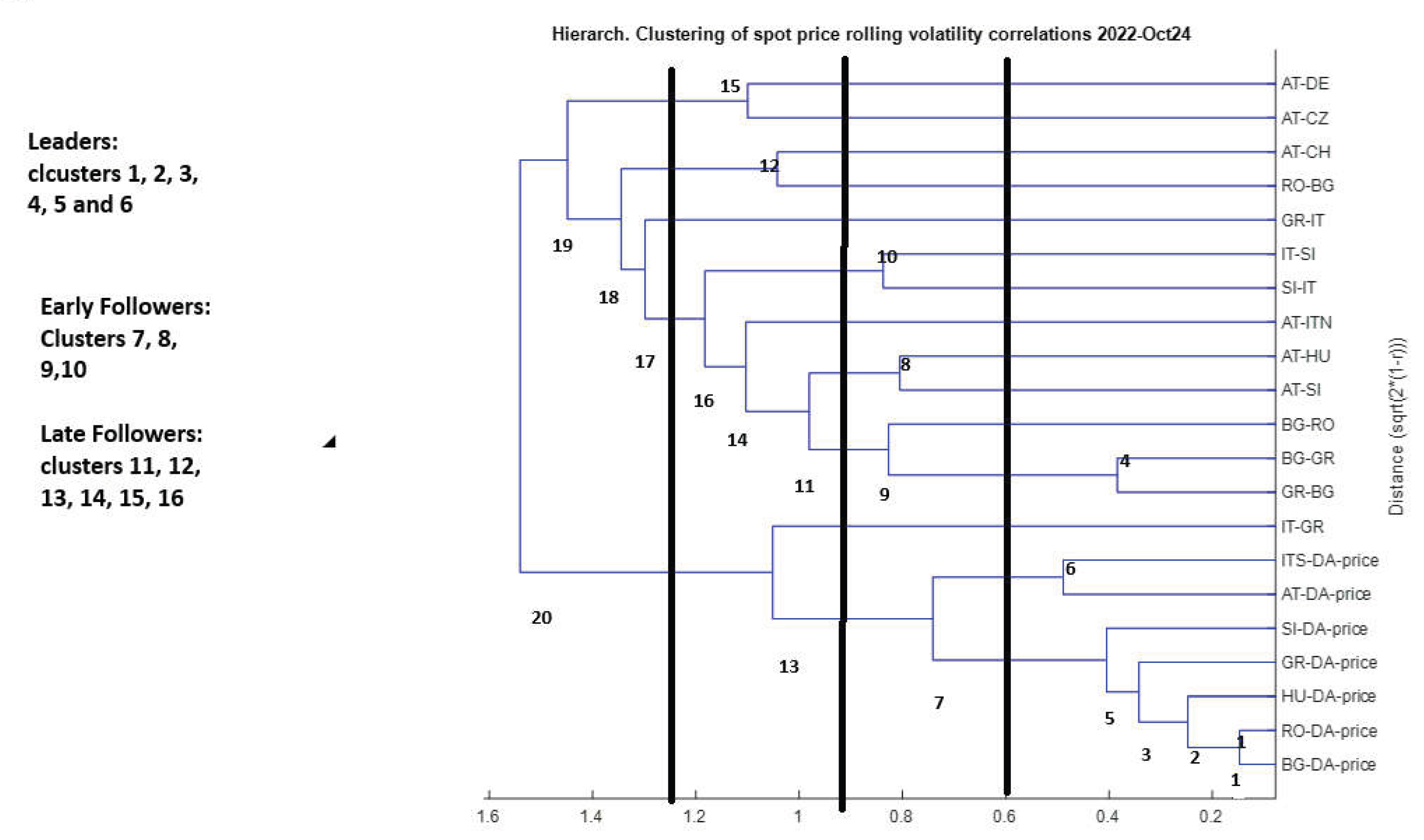

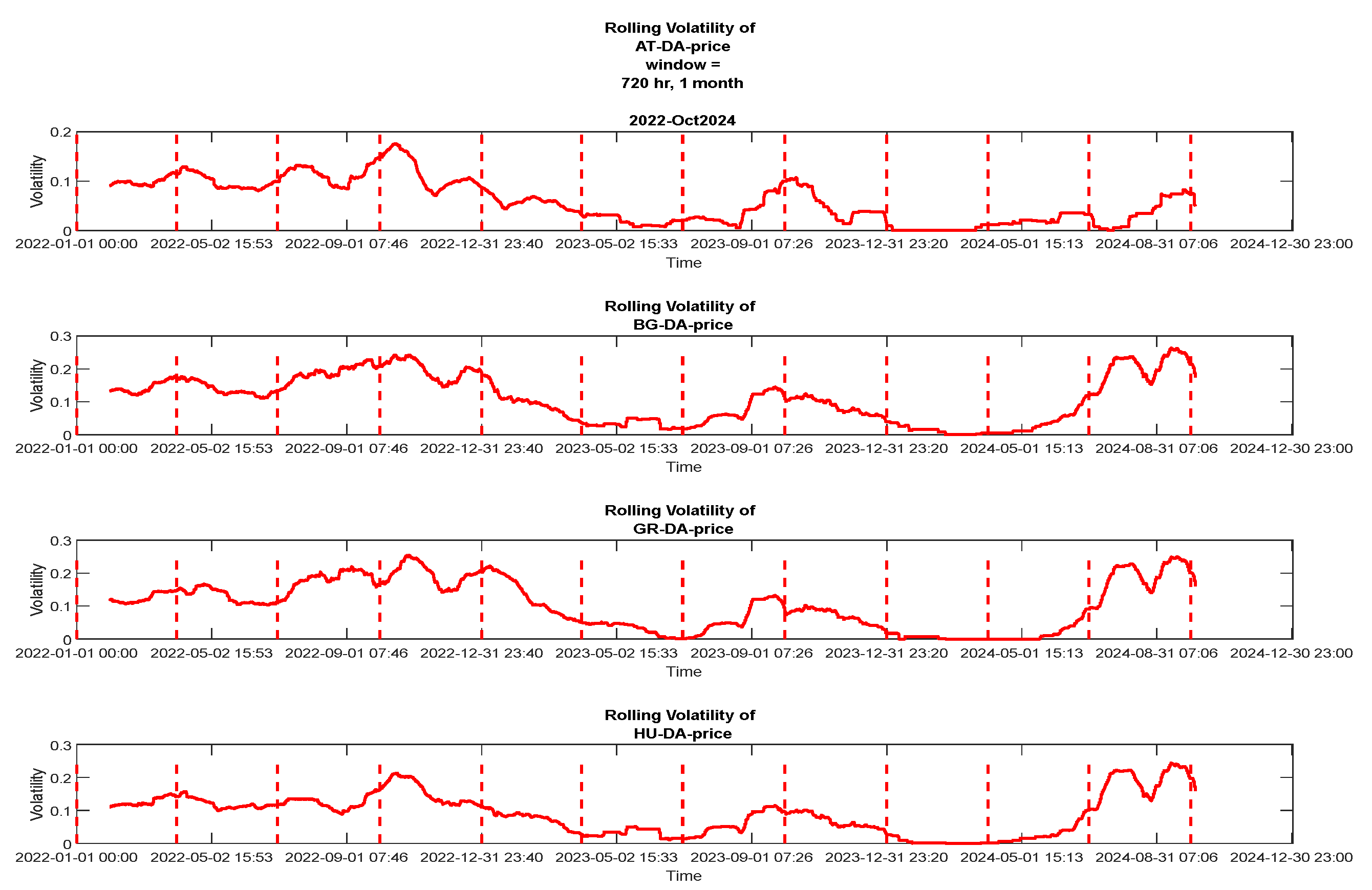

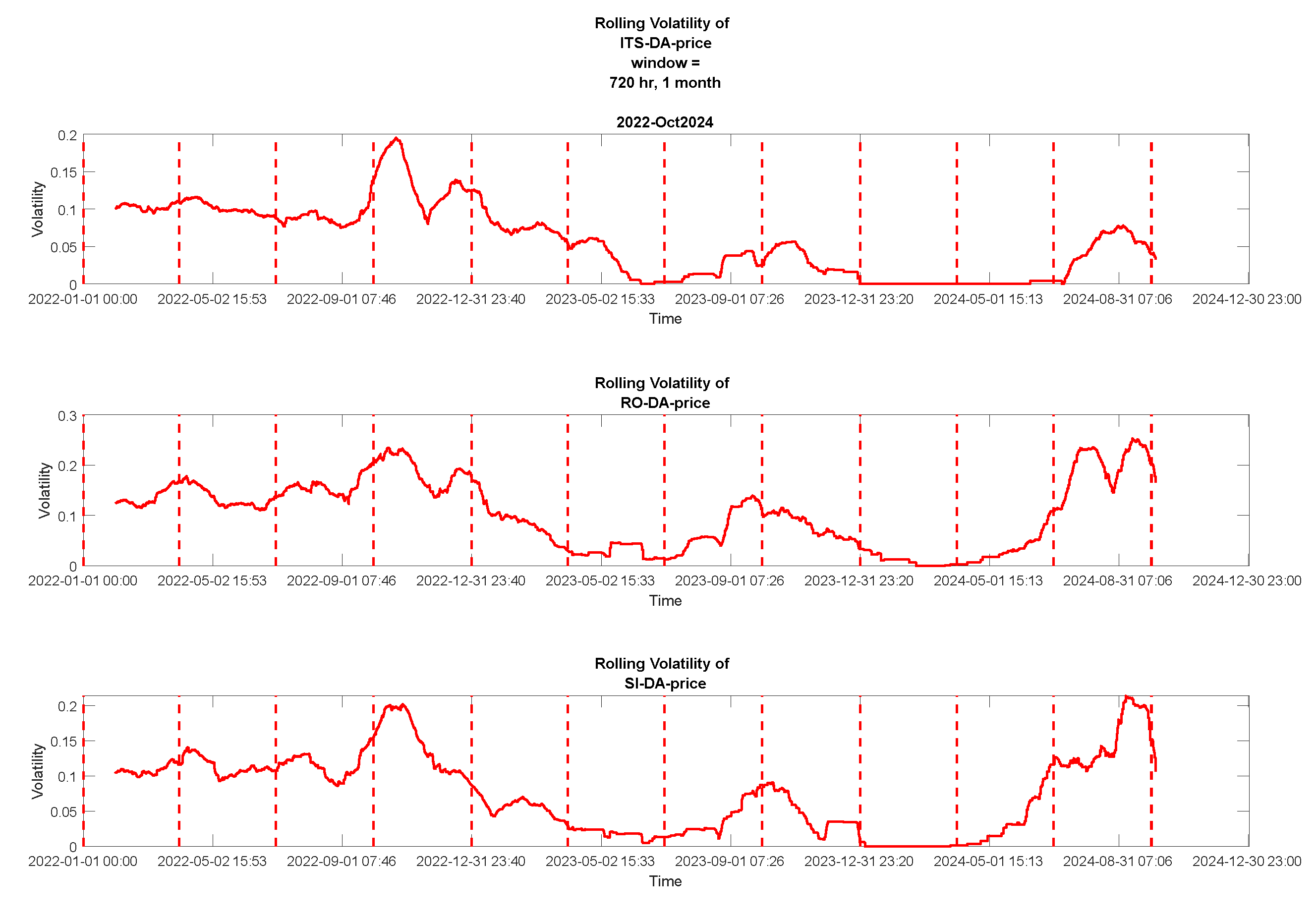

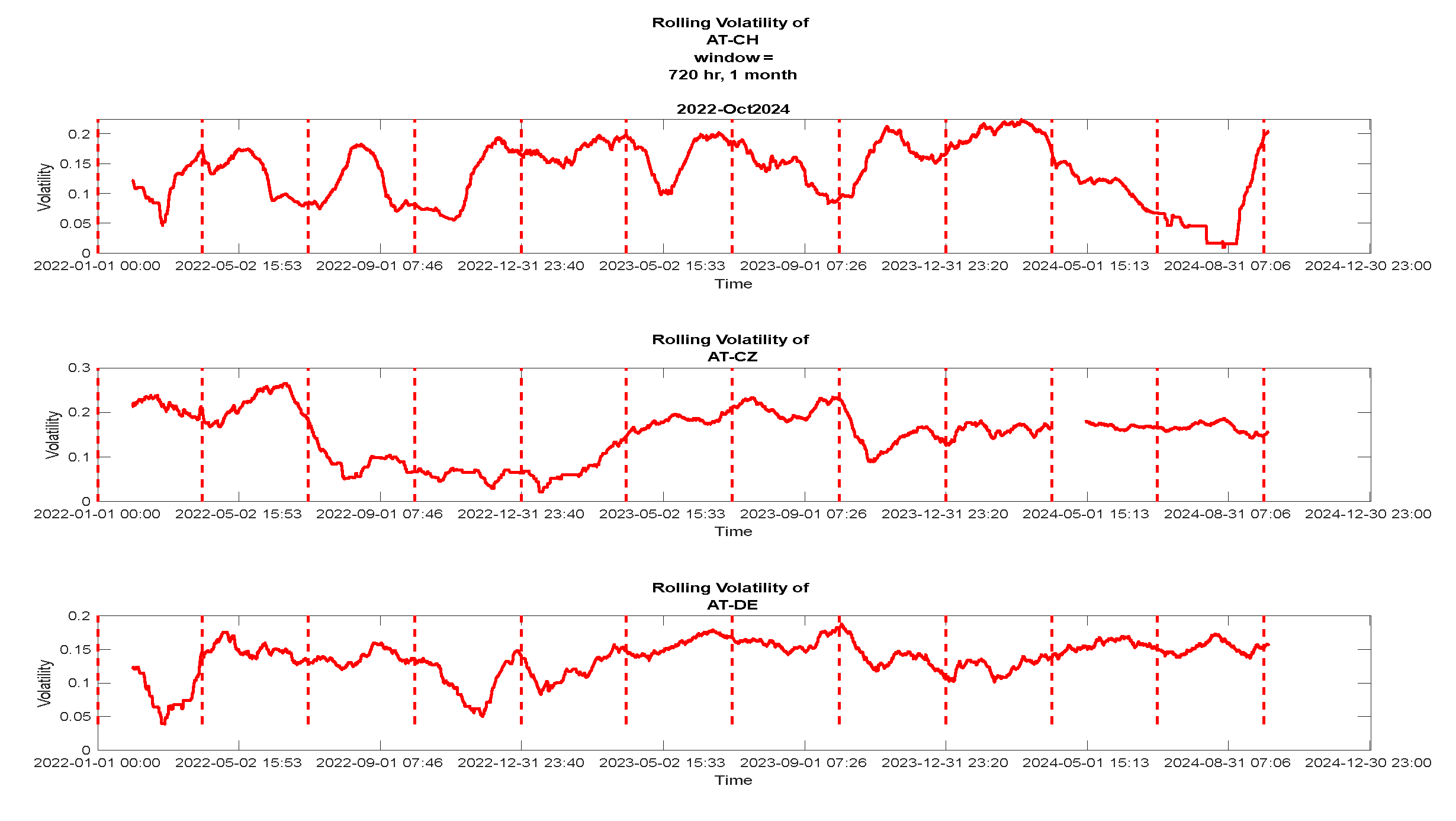

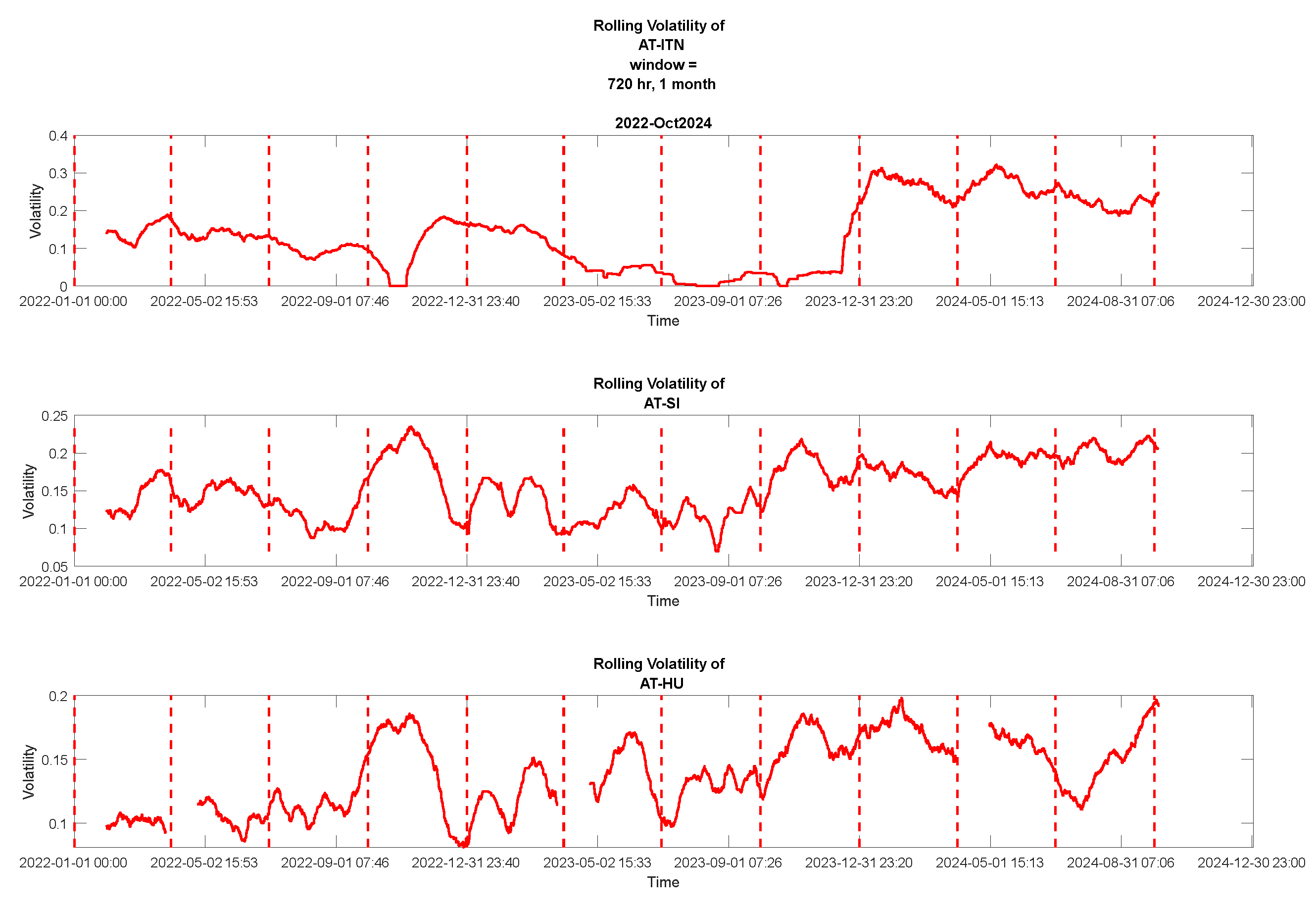

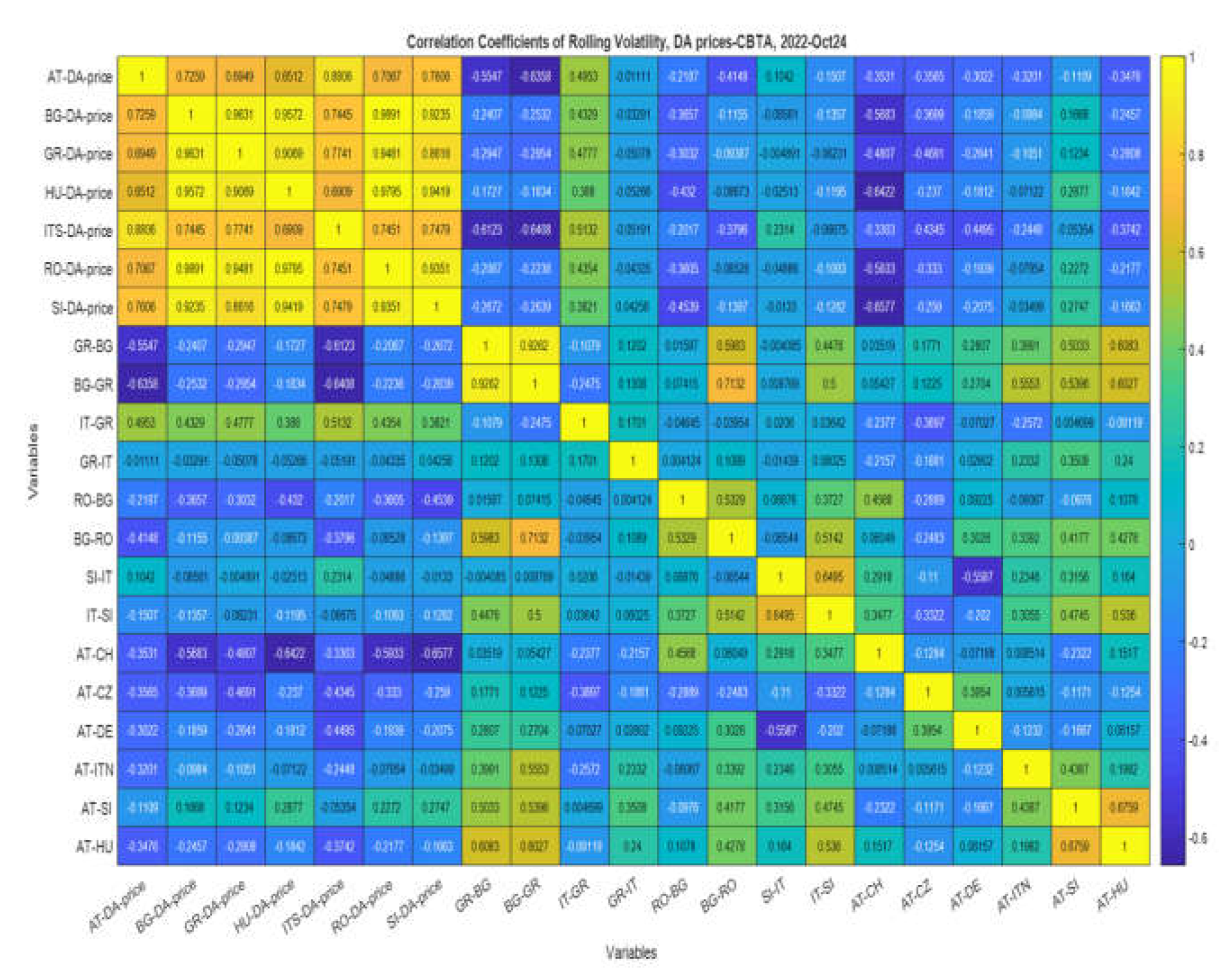

We observe also that the cross-border transfer availabilities (CBTAs) RO-BG (between Romania and Bulgaria), BG-RO, GR-BG, and BG-GR exhibit the largest, negative correlations with the spot prices. Instead of trying to explain these findings, we refer to Section 7.3 where we present the results of rolling volatility spillover of spot prices and CBTAs, between all pairs of markets. More specifically, we have computed the correlations of the rolling volatility curves of both spot prices and CBTAs, of all markets, and have analyzed their volatility spillover from one market to another, thus enhancing further the causality structure learning findings of Section 7.1 (MB and LCSL results).

Figure 9.

a: Heat map of all possible correlations between pairs of AT, BG, GR markets’ fundamental parameters, excluding CBTA. b: Heat map of all correlations between pairs of HU, ITS, RO markets’ fundamental parameters, excluding CBTA. c: Heat map of all correlations between pairs of SI market’s fundamental parameters, excluding CBTA. d: Heat map of correlations between pairs of all DA prices and Cross Border Transfer (CBT) availability.

Figure 9.

a: Heat map of all possible correlations between pairs of AT, BG, GR markets’ fundamental parameters, excluding CBTA. b: Heat map of all correlations between pairs of HU, ITS, RO markets’ fundamental parameters, excluding CBTA. c: Heat map of all correlations between pairs of SI market’s fundamental parameters, excluding CBTA. d: Heat map of correlations between pairs of all DA prices and Cross Border Transfer (CBT) availability.

5. Methodology

In Section 5.1 we provide a short review for Global, Local Causal structure learning, and Markov Blanket learning, emphasizing their differences and the fields they are applied, although we do not use Global causal structure learning in the present work. Section 5.2–5.4 then present the necessary mathematical background (definitions and key propositions without proofs), with emphasis on Markov Blanket learning, and finally Section 5.5–5.8 provide information on the practical aspects of the applied algorithms.

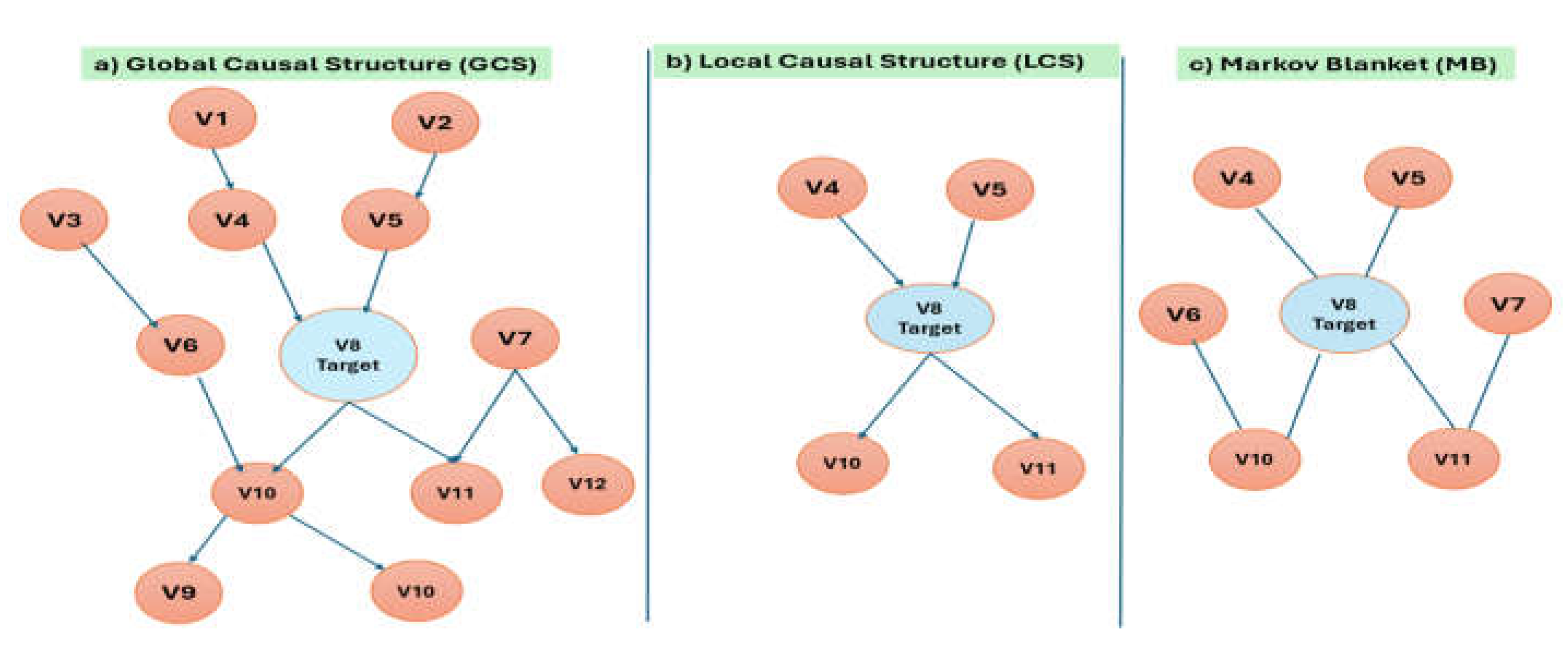

5.1. The Difference Between Global, Local Causal Structure Learning, and Markov Blanket Learning

Causal structure learning involves discovering the causal relationships among variables in a dataset. The three main approaches—Global Causal Structure Learning (GCSL), Local Causal Structure Learning (LCSL), and Markov Blanket Learning (MBL) differ in their scope and methodology. In the GCSL, the goal is to learn the entire causal graph over all variables in the dataset, using various approaches such as constraint-based, score-based, or hybrid methods to infer the global causal structure. Constraint-based method uses conditional independence tests (e.g., Parent Child -PC- algorithm, FCI), while the score-based one optimizes a scoring function (e.g., BIC, Bayesian scores) over possible graphs (e.g., GES). Finally, the hybrid method combines both approaches (e.g., Max-Min Hill-Climbing, MMHC). The advantages of GCLS are the fact that it provides a complete causal structure (it provides ‘the big picture’ of the problem under analysis, and it can infer direct and indirect causal effects. However, it is computationally expensive, especially for high-dimensional data, and it requires strong assumptions (e.g., causal sufficiency, faithfulness). This is the reason (as well as the advantages of LCSL listed below) we do not use this method in this work. The transition from local to global learning plays an essential role in Bayesian network (BN) structure learning. Mainstream algorithms for this type of learning were based on first constructing the skeleton of a DAG (directed acyclic graph) by learning the MB (Markov blanket) or PC (parents and children) of each variable in a data set and then orienting edges in the skeleton. Since it requires expensive computational resources (especially with a large-sized BN, resulting in inefficient local-to-global learning algorithms), [6] developed an efficient local-to-global learning approach using feature selection, using the well-known Minimum-Redundancy and Maximum-Relevance (MRMR) feature selection approach for learning a PC set of a variable, and proposed the efficient F2SL (feature selection-based structure learning) approach to local-to-global BN structure learning, the algorithm adopted in our preset work.

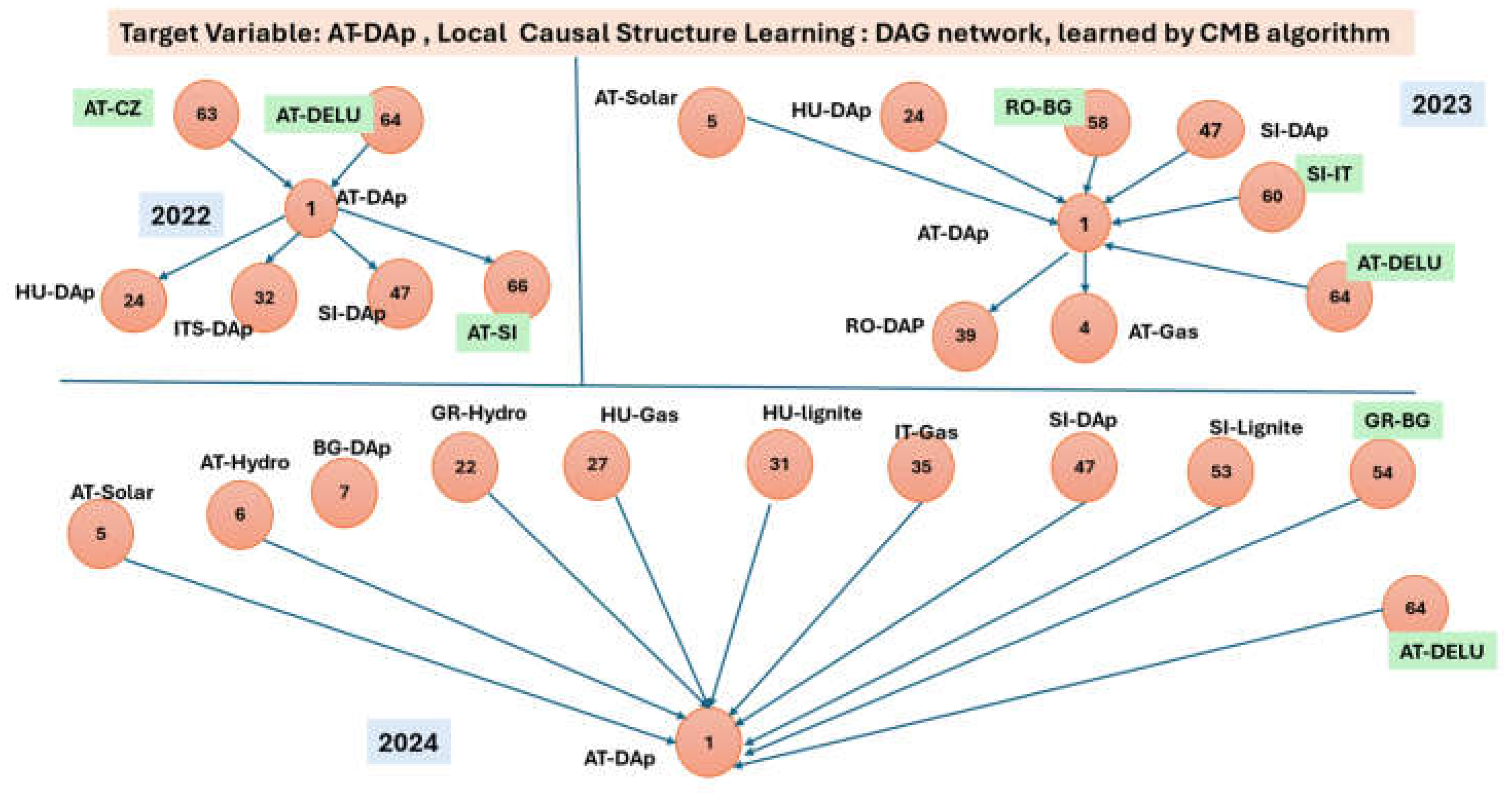

One the opposite, in LCSL the goal is to learn causal relationships for a subset of variables (e.g., the most crucial variable around a target variable). We focused on this method, since our main target is to detect the most relevant factors that shape the dynamics (especially the surge) of spot prices target variables. The most crucial variables coincide with the set of members detected in the MB. LCSL identifies MB’s members direct causes and effects without reconstructing the entire causal graph, using methods as local constraint-based methods (e.g., HITON, Grow-Shrink, see Table 11), and local score-based methods. Advantages of this learning method include that it is more scalable than global learning, and focuses on relevant variables, therefore reducing noise. However, LCSL does not capture the full causal structure (across all European interconnected markets) and may miss indirect causal effects, however avoiding both these ‘defects’, is beyond the purpose of our analysis.

We applied Local causal structure learning (LCSL) in our dataset to discover and distinguish the direct causes and direct effects of all seven DA spot prices, the chosen target variables. Since the mainstream LCSL algorithms need to perform an exhaustive subset search within the currently selected variables for PC (i.e., parents and children) discovery, to speed up and make the process more efficient, several algorithms have been developed. Examples are the work of [19], proposing the LCS FS model and the Causal Markov Blanket, CMB [18] is the algorithm adopted in our study.

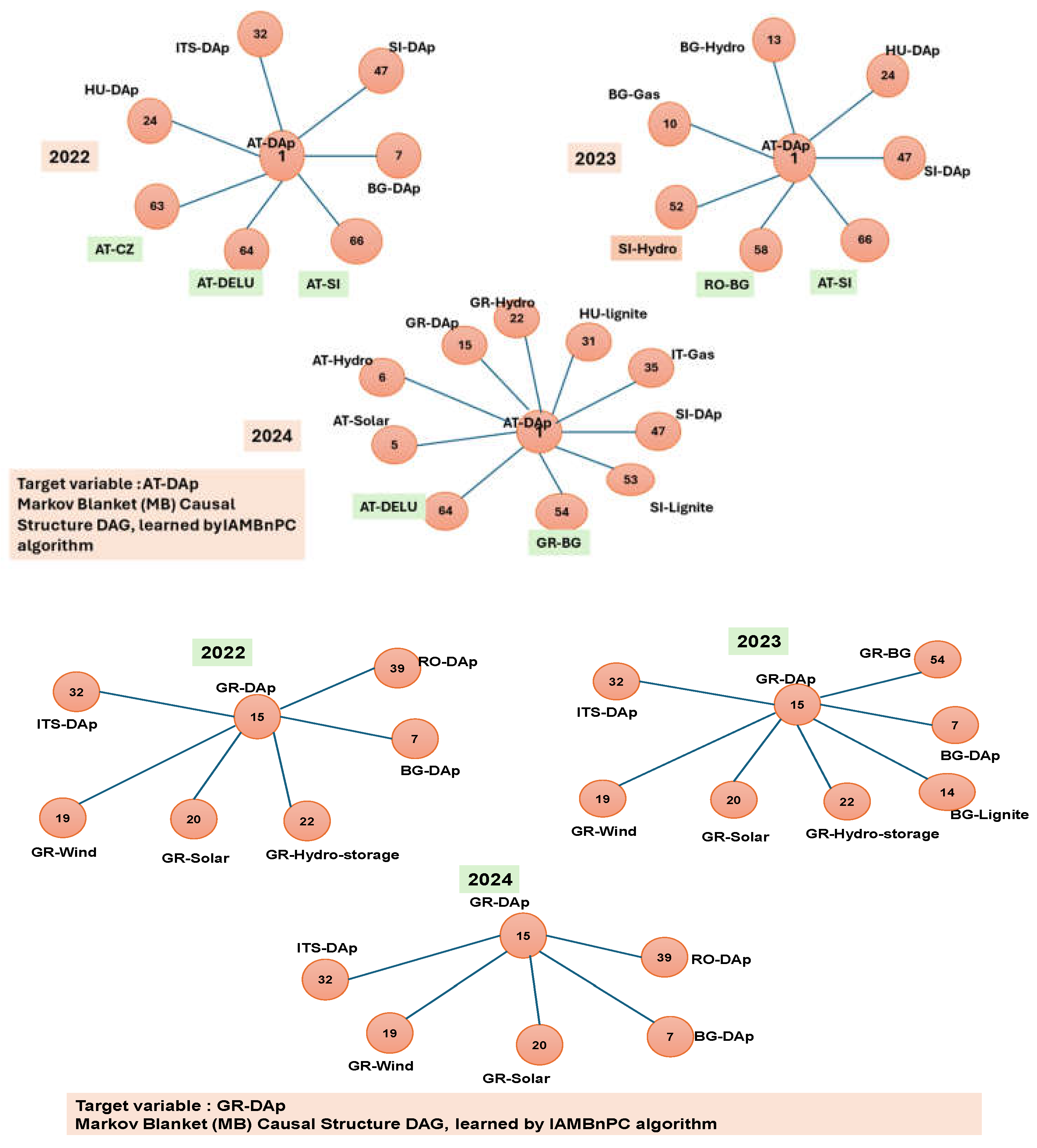

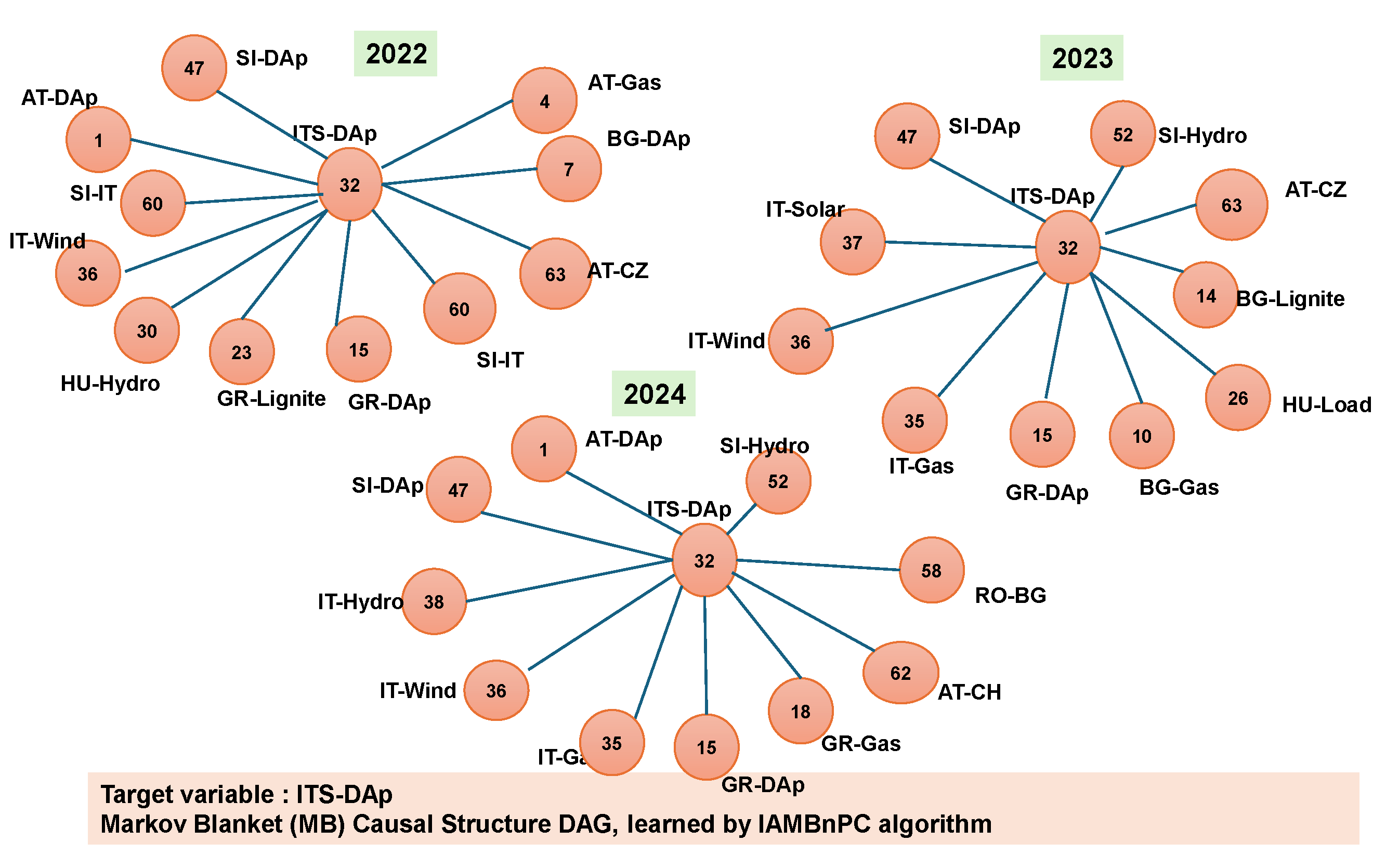

In the MB learning, the goal is to identify the Markov Blanket of a target variable, which consists of Parents (direct causes), Children (direct effects), and Spouses (other parents of the target’s children). It uses conditional independence tests or local structure learning to identify the minimal set of variables that render the target variable conditionally independent from all others. A plethora of methods exist, such as HITON-MB, IAMB, Fast-IAMB, PCMB, InterIAMBnPC (see also Table 8). This learning approach is efficient for feature selection and reduces dimensionality while preserving relevant information. However, it does not provide a full causal graph and is sensitive to sample size and independence test accuracy. Therefore, we can use Global Learning when the entire causal structure is needed (e.g., causal discovery), Local Learning when only a subset of causal relationships is relevant and Markov Blanket Learning when feature selection is needed (e.g., as in machine learning, predictive modeling). In our present work we have adopted the combination of MB and LCSL and the InterIAMBnPC algorithm [32] for MB learning.

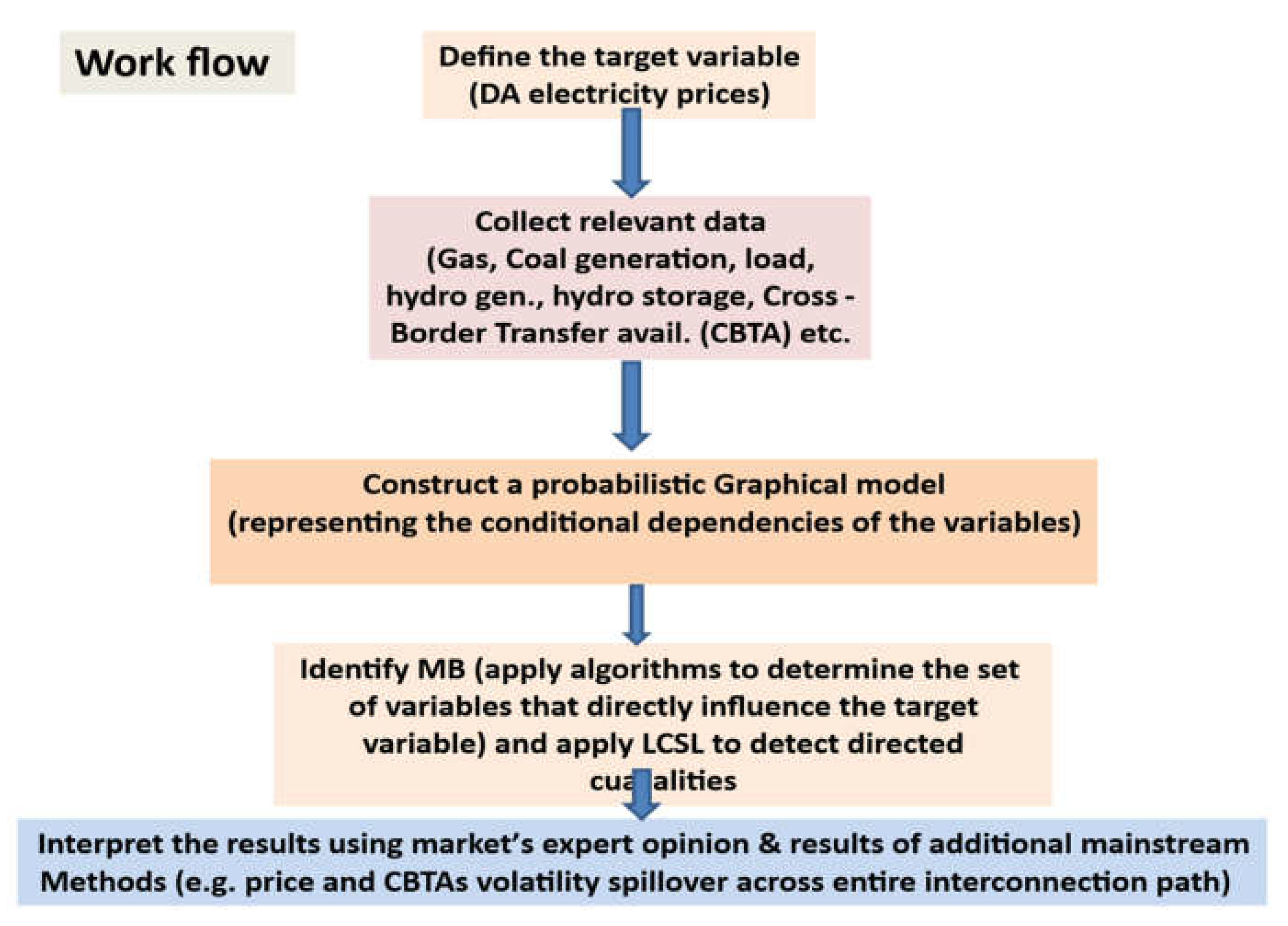

In the application of Markov Blanket Learning in detecting causalities in electricity markets the main goal, as already mentioned, is the ‘revealing’ of a subset of variables, i.e. Markov Blanket of a target variable (e.g., electricity price in a specific market) consisting of the direct causes (parents) → Fundamental drivers (e.g., demand, supply, weather, fuel prices, interconnector flows, i.e. CBTAs), direct effects (children) → Downstream impacts (e.g., price fluctuations in neighboring markets), and finally spouses (other parents of the target’s children) → Variables that influence price through shared dependencies. Therefore, by identifying the MB of a spot price, we can determine the most relevant factors affecting price fluctuations while filtering out irrelevant variables. MB is particularly useful for feature selection (reducing dimensionality), predictive modeling (improving forecasting), and identifying key influences of price changes (this is the case in our paper). We stress here that MB learning alone does not establish causal direction beyond identifying relevant variables. The challenges with using only MB learning are: a) no explicit causal structure as the learning tell us which variables are important but not necessarily the cause-effect relationships, b) it does not capture indirect effects, since some causes may influence price via intermediate variables, which MB learning might miss, and c) the method does not consider temporal causality, since spot prices are dynamic and evolve over time, and MB learning typically works on static datasets. To overcome these problems and properly discover causal relationships, as we have pointed out, we combine MBL with LCSL and mainstream time series analysis, as the rolling volatility of spot prices and CBTAs, to capture the volatility spillover effects due to interaction of the markets. The steps of our workflow are described as follows:

Step 1: MB Learning (Feature Selection). We used the algorithm IAMB, to identify the most relevant fundamental variables affecting DA electricity prices, thus reducing further the dimensionality of the dataset and focusing only on key drivers.

Step 2: Causal Discovery on the MB Selected Variables, we applied LCSL (CMB algorithm) to the wholesale DA price variables to determine direct causal relationships.

Step 3: We validated the results by using the results of volatility spillover as well as consulting experts in the electricity markets field working in the Greek TSO and other European institutions (see affiliations of authors), to ensure that our findings align with real energy market dynamics (domain knowledge).

5.2. A Short Mathematical Background in Bayesian network (BN), Markov blanket (MB) and Causal Feature Selection (CFS)

We provide here the necessary, short background theoretical information (notation and definitions etc.), based on the works of [6,20] which describe in a rigorous mathematical approach all the theoretical basis (all related theorems and their proofs).

We symbolize with C our Target Variable (TV) (or Class attribute, CA) of interest. Let φ represent the distinct TV values (or labels), as c={ , and the set of all distinct features. Let also that D is a training dataset, D=, with the number of instances, the i-th instance i.e. a n-dimensional vector defined on F, and a label of the TV associated with . To facilitate our presentation, let the set of all variables under consideration in our analysis, where and C . Let V \ indicate the set V \{ }, that is, all features excluding , ∀∈V. To consider conditionality, let use ╨ |S are conditionally independent given S, and , and the expression (not ╨) |S, to denote that is conditionally dependent on given S.

Definition 1 (Conditional Independence). Two distinct variables ∈V are said to be conditionally independent given a subset of variables S ⊆V \ { } (i.e., ╨ |S), if and only if P (|S) = P( |S)P( |S). Otherwise, are conditionally dependent given S, (not ╨) |S.

5.3. Bayesian Network, Markov Blanket, and Causal Feature Selection

We provide basic knowledge at this point associated with causal feature selection (CFS), including the basics of BN, MB, and why we choose causal feature selection. Suppose that P (V) is the joint probability distribution over the set of all variables V, and G = (V, E) represents a directed acyclic graph (DAG) having nodes V and edges E, where an edge represents the direct dependence relationship between two variables.

In a DAG, symbolizes that is a parent of and is a child of .

Definition 2 [20]. The triplet V, G, P(V)is called a BN, if the Markov condition as defined below (definition 3) is valid:

Definition 3 (Markov Condition) [20]. For a DAG G, the Markov condition holds in G, if and only if, every node of G is independent of any subset of its non-descendants conditioned on its parents. Thus, the joint probability over a set of variables V is encoded by a BN which decomposes P (V) into the product of the conditional probability distributions of the variables given their parents in G.

Let () be the set of parents of in G. Then, P(V) can be written as

In this paper, we consider a CBN, a BN in which an edge indicates that is a direct cause of [20,21]. In the definition 4 below, we give the key concepts and assumptions associated with BNs and MBs.

Definition 4 (Faithfulness) [20]. Suppose that a BN <V, G, P (V)>, then G is faithful to P(V) if and only if every conditional independence present in P is entailed by G and the Markov condition. P(V) is faithful if and only if G is faithful to P (V).

Definition 5 (Causal Sufficiency) [20]. Causal sufficiency assumes that any common cause of two or more variables in V is also in V.

Definition 6 (d-Separation) [20]. In a path πof a DAG G, and are said to be blocked by a set of nodes S ⊂V, if and only if: (a) π contains a chain

or a fork

such that the middle node is in S, or (b) the path π contains a v-structure

such that S holds and no descendants of are in S. A set S is said to d-separatefrom if and only if S blocks every path from

Theorem 1 [20,21]. Given a BN <V,G, P (V )>, under the faithfulness assumption, d-separation captures all conditional independence relations that are encoded in G, which implies that and in G are d-separated by S ⊂V \{, }, if and only if and are conditionally independent given S in P(V). The theorem concludes the equivalence of conditional independence in data distribution and d-separation in the corresponding DAG, under the assumption of faithfulness.

Definition 7 Markov Blanket (MB). [20]. The Markov Blanket (MB) of a variable in a BN is unique and consists of its parents (direct causes), children (direct effects), and spouses (other parents of the variable’s children), provided that the faithfulness assumption is valid.

The relation between PC in a BN, and how to identify spouses are given by proposition 1 and 2 respectively and are the basis of designing CFS algorithms.

Proposition 1 [21]. In a BN, there is an edge between the pair of nodes and , if and only if they are dependent (i.e. (not ╨) |S), for all S ⊆V \ { , }.

Proposition 2 [21]. In a BN, assuming that is adjacent to , is adjacent to , and is not adjacent to (e.g., → ←), if ∀S ⊆V \ { , }, ╨ |S) and (not ╨) |S∪{ is a spouse of .

The cornerstone of causal and non-causal feature selection is the concept of Mutual Information (MI), introduced initially in machine learning by [22] and later by [23,24], and used then as an additional concept in explaining feature relevance, in non-causal FS [25]. The conditional MI between X and Y given another feature Z is given by:

It is based on the concept of Sannon’s entropy:

of a variable X, and on the conditional entropy of X after observing the values of Y

In equations (3) ana (4), P(x) is the prior probability of X=x (the value x that the variable X takes) and similarly P(Y) is the posterior probability of Y=y, in the context of Bayes Rule, so the MI between X and Y is

Using (2), then in the context of non-causal FS, a feature is strongly relevant to C if and only if I(.

5.4. The Objective Function of Optimal Feature Selection Problem, Based on the MI Concept

The problem of finding a subset , given a dataset D containing C and F, in a feature selection context is formulated as follows

i.e. try to find a subset of features that maximizes the conditional probability of C. Equation (6), using equation (2) is written finally as

It is shown, in the literature provided, that the feature set S∗ defined in Equation (7) is the set of features that leads to the minimal Bayes error rate. Recently, [26] has shown that for a given classification problem, the minimum classification error attainable, by any classifier, is called its Bayes error rate. In this work we adopt the approach of [25] in choosing the Bayes error rate for justifying Equation (7) since, according to the associated literature, this error is the tightest possible classifier-independent lower-bound, since it depends only on the predictor features and the Target variable (class attribute). In setting the lower and upper bounds on the Bayes error rate, [27,28,29] have finally made the connection of the Shannon conditional entropy [30] to the Bayes error rate, a crucial step in rigorously formulating CFS approach in ML.

In general, Feature selection (FS) is used in model building as well as data understanding and is a process of identifying a subset of features (predictor variables) from the original set of features. FS is more pressing now, in the era of big data, since the handling of ‘inherently ubiquitous’ high-dimensional datasets is very difficult. FS has become the cornerstone behind any efficient classification model. There is a plethora of FS methods that fall into three categories: a) Filter, b) Wrapper and c) embedded methods. The two last methods are classifier dependent while filter methods are classifier or prediction model independent.