Submitted:

22 March 2025

Posted:

24 March 2025

You are already at the latest version

Abstract

This study points significant and specific attention to strategy. Structured, and semi structured questionnaires and interview materials were applied in data collection from randomly drawn participants and respondents from the population. The population sampled consists of up to 275 responses captured in Roma. Brand reputation - investment risks, and Brand equity - investment risks from ‘SEM showed statistical significances at the 5% level of significances. From the results, ‘p – value (>0.05) indicates a statistical significance, implying the assumption of the relationship existing and connecting two different groups on their perceptions of activism against the state on climate change shown as analyzed and captured from data in this poll and experimental survey.

Keywords:

climate change

; CSR

; litigation trends

; stakeholder theory

; competing vs. complementary interests

; environment

; investment risks & sustainability

1. Introduction

Climate changes have brought about drastic changes on the environment from different forms of business activities, and events in a vast changing scenario.

Despite this circumstances, evidence on the impacts of climate change litigation is still mostly found anecdotal (Setzer & Vanhala, 2019), sceptically doubtful and seems not realistically true and reliable enough. The extant dynamics and terrains have been constantly changing and rapidly evolving around ‘climate change associated with economic activities.

Human rights activism, and advertisements related to gender equality and ethics have emerged. Strong activism and advocate for channelling resources on community related activities, welfare state and societal development has grown in magnitude and tremendously.

Topics, and discourse, such as child labour, gender equality and ethics in advertising have been defined in academic literature (Crane & Kazmi, 2010; Martin-Ortega & Wallace, 2013).

Existing literature emphasized the significant role of corporate social responsibility (CSR) role in respecting human rights and their direct relationship to advocate and canvas or push for children’s right, interests and respect (Crane and Kazmi, 2010; Krstić, 2017; Zadek, 2004). In this sense, CSR is defined as a management principle embedding four areas of activities drawn from: the economic – driven towards accomplishment of economic goals of the company, the legal – pointing to the obligation in complying to legal statutes, the moral – entailing the moral obligation or expectations in demands and expected to be discharged towards all stakeholders and the philanthropic – about investment of own resources with the objective of fulfilling higher purposes in the community or society (Carroll, 1991; Ivanović-Đukić, 2011).

Obviously, CSR has assumed a ‘multi – dimensional perspective in recent times following its emergence dated to the 1950s.

Matten and Moon (2008) identified and stressed on the ‘multidimensional perspective of ‘CSR.

The ‘multidimensionality of ‘CSR can be strategically defined. The literatures have enumerated the strategic perspectives of ‘CSR, and some key components from ‘stakeholder’s theory and stakeholder management, prominent among them (Heikkurinen, 2018; Kim et al., 2018; Sekulic & Pavlovic 2018).

Other authors also pointed to other key, crucial and essential aspects of ‘CSR, stakeholder and management, such as social development (Frynas & Yamahaki, 2016; Heikkurinen., & Mäkinen, 2016; Heikkurinen,2018), firm value creation and shareholder, and ‘CSR as a strategic means of achieving a competitive advantage (Camilleri 2017; Godfrey, 2005; Godfrey et al., 2009; Porter & Kramer, 2006, 2011; Turker, 2009).

What could be considered to be a ‘dangerous’ level of climate change, and second to determine what levels of greenhouse gas stabilization are consistent with avoiding said climate changes (Schneider; 2005; Smith; 2009, Knutti,2008) and anticipated severities or unforeseen circumstances.

This study and research sought to highlight the key and pertinent issues associated with the socio – economic impacts of activities of companies and corporations and seek for a potential and practical redress, specifically on the environment, ‘climate change related issues.

Finally, this study points to the significance and crucial need or essence for striking and achieving a balance from the point of “competing vs. complimentary” interests so as to extrapolate and project beyond economic interests and motives triggered and prompted by economic gains and motives or purpose for doing business.

The stakeholder aspect and philanthropy can be embraced and from the standpoint of a strategic framework of a novel business model built around strategy, shared value creation transcending to equity and building a platform and template for investment risks towards mitigation and amelioration, while addressing key environmental issues, ‘climate changes occurrence, averting ligation cases and activism, then meeting social needs and climate change mitigation demands, amelioration and expectations for sustainability.

2. Methodology

This research is based on quantitative methods, making vivid qualitative analysis and quantitative treatments from inferential statistical method.

The assumptions of the normal distribution and symmetry at the significance level and confidence bound interval for the set limit criterion and threshold of significant level - α. The β’s is estimated from the ‘SEM: structural equation modelling between response and explanatory variables.

Design

Structured questionnaires and semi structured interview materials would be applied in data collection from randomly drawn participants and respondents from the population across organizations and consumers. The population sampled consists of 175 responses captured in Roma, including a minimum of 20 interviews to support the previous data of 100 responses from semi structured questionnaires and analyses from previous studies. The total estimated data size available is 295.

Convergent validity criterion transmits, and reflects actuality of the measures. This is affirmed by average variance extracted (AVE) (Ahmad S. et al., 2019). The AVE value should be larger or greater than 0.5, according to Fornell and Larcker (1981).

The items of CSR are adopted based on the literature and similar to those from López-González et al. (2019). All items of CSR assessed were measured and scaled using 5-points Likert-Scale (1 “strongly disagree” and 5 “strongly agree”). The alpha of CSR. brand & image * 0.84906. The results indicate that the AVE reflecting convergence based on the factor loading of each item is more than the standard value (0.60). Hence, measures were considered adequate. The factor loading of each item is mentioned in Table 2.1.

The items of BE are adopted in resemblance from previous studies Çifci et al. (2016). For the measurement of brand equity, the 5-point Likert-Scale was applied as rated: (1“strongly disagree” and 5 “strongly agree”). The alpha of BE was 0.927, which is appropriate. The results are strongly valid indicating that the convergent validity criterion for each item is more than the standard value (0.60) based on the AVE. The alpha values met the threshold criteria. The AVE based on the factor loading of each item is mentioned in Table 2.1.

The items of CSR, brand & reputation were modified to reflect those of CR that were adopted by Suki and Suki (2019). All items attached to CR were measured and based on a 5-point Likert-Scale (1 “strongly disagree” and 5 “strongly agree”). The alpha of CSR, brand & reputation was 0.97820. The reliability of each item is guaranteed as the values are more than the standard value (0.70), and for AVE (0.6).

Also, measures and the items resembled those developed by Tzempelikos and Gounaris (2017). These items are based on a 5-points Likert-Scale (1“strongly disagree” and 5 “strongly agree”). The alpha of Sustainability was 0.882245, and that of Investments risks & CSR was 0.8824, which is acceptable. The results indicate convergence that the AVE based on the factor loading of each item is more than the standard value (0.60). Also, the alpha values met the threshold criteria. The AVE based on the factor loading of each item is shown in Table 2.1.

Table 2.1.

Cronbach Alpha of the Variables.

| ‘Cronbach alpha | |

|---|---|

| Brand awareness | 0.78947 |

| Investments risks & CSR | 0.8824 |

| Brand preferences & culture | 0.88725 |

| Perceptions | 0.88235 |

| Brand image | 0.9245 |

| Brand reputation | 0.83768 |

| Brand communication | 0.92308 |

| Brand equity | 0.917 |

| Sustainability | 0.882245 |

‘Source: ‘Present study draft & author’s draft as adapted from previous study, 2022, 2023 & 2024.

3. Background Literature

Friedman in his ideology on ‘CSR around the classical economic view wrote his first paper in 1970.

Carroll (1979, 19991, 2008, 2011, 2015) outlined motives for pursuing ‘CSR, around ‘3 – 4 key pillars comprising; “economic, legal, philanthropy and ethics”.

The main goal of business, motives and purposes in the classical sense and context is the economic gains. The revolutionist ‘Thatcher – Regan pushed strongly in favour of tax cut exemptions and subsidies for profit – making firms and corporations for pulling their countries out of recession and addressing inflation and persistent rising costs prevalent in the 1980s. This conception aligns with the Friedman’s perspective around economic reasons and motives of doing business in penchant for wealth creation and accumulation in meeting the shareholder’s expectations.

The ‘Urgenda led to another regime and beginning of an era when activist groups rise against the government and institutions against actions that negate the environment or of negative bearing and consequences, II, III.

Subsequently, the trends in state activism and calls for actions due to cases emerging demands attentions.

A suit case presented by 10 families from Portugal, Germany, France, Italy, Romania, Kenya, Fiji and Sáminuorra, the Swedish Saami Youth Association was rejected and struck-out by the court. The case was declared dismissed and the jury stated there was no sufficient evidence that the group directly affected by EU policies to challenge these in court. However, the fact was acknowledged that “every individual could be affected or impacted, and influenced by climate change” in various ways.

Unsatisfied by the court proceeding, outcome and decision, and unsatisfactory rulings; the plaintiffs planned to appeal before 15 July 2019 to seek a redress again. III ‘**

The multidisciplinary origin of CSR (Aguascalientes & Medero Gómez, 2016; Correa, 2007) has a great and significant bearing. As a result, companies that have strategic conversations between different interested parties, have great possibilities of experiencing fewer gaps in the perceptions of their mission and values (Miles et al., 2006).

However, it is severely risky that stakeholder actions erode CSR over time, thus unsustainable (Strand et al., 2015). Ultimately, the sustainability of management approaches, such as CSR depends on its position in society (Steurer et al., 2005).

A coherent relationship between the company and its stakeholders have a positive impact on the worth, positioning and net value derived by the company (Ifada et al., 2021).

Companies have to define strategies that reflect and allow them to adapt to changing realities enabling a sustainable differentiation from other competitors (Orviz Martínez et al., 2021; Ullah et al., 2021).

The success of companies depends on the implementation of business models based on corporate social responsibility (CSR) activities, translating to better financial performance (Khediri, 2021; Lee et al., 2018). CSR plays a fundamental role, and has encompassed an increasingly broader panorama and scope (Morejón & Lorenzo, 2020).

Prediction from the classic theoretical argument of Friedman (2007) shows a negative relationship between CSR and financial performance due to the costs implications associated with CSR-related activities. Stakeholder theory, on the contrast as proposed by Freeman (Gholami et al., 2022) suggests a positive relationship between CSR performance, stakeholder relationships, available and existing market opportunities or shares (Aouadi & Marsat, 2018) and reduced transaction costs (Jones, 1995).

Previous studies led to conflicting findings regarding CSR performance and financial performance (Brooks & Oikonomou, 2018; Khan, 2022l; Zhou et al, 2022).

Friedman (2007) views CSR performance as an agency issue whereby managers misallocate corporate resources to CSR-related activities that damage a firm’s competitive advantages.

Freeman (1984), outlined that stakeholder theory posits that a firm becomes more financially, the better it manages its relationship with different stakeholders with vested interest and stake or claim in the firm.

Based on the instrumental stakeholder theory proposed by Jones (1995), a firm is a nexus of contracts that can improve its competitive advantage by reducing contracting costs (Jensen, & Meckling, 1976).

This results from building and establishing trust among stakeholders (Jensen, & Meckling, 1976; Berman et al., 1999).

Firm engagement in CSR-related activities is a fundamental mechanism for establishing and improving stakeholder relationships. Gavana et al. (2022) present empirical evidence indicating a noteworthy moderating effect of ESG performance on earnings management and improving corporate-disclosure behaviour.

Jones (1995) notes that certain types of CSR performance manifest the firm’s efforts to establish trust and cooperative stakeholder association, leading to positive impact on firm’s financial performance. A firm with solid CSR performance might be attractive enough and have easier access to desirable employees (Greening & Turban, 2000).

According to Crane et al. (2008), “corporate social responsibility should be conceptualized as a strategic investment tool, means and device in deriving and sustaining the corporate reputation.” This indicates that direct and indirect execution of CSR of a company are viewed from a resource-based view (RBV) lens and perspective when these types of leads, executions and exercises culminate to advantages for the firms.

The manageable upper hand can be collected from these immaterial resources on the basis that they are off chance, uncommon, important, and supreme (Shin and Thai, 2015). RBV fills in as a valuable tool and apparatus in comprehending and understanding or discerning why firms, participate in socially mindful exercises (Branco & Rodrigues, 2006).

The success of companies depends on the implementation of corporate social responsibility (CSR) activities and practices fused in their business models, which guarantee better and enhanced financial performance (Khediri, 2021; Lee et al., 2018). CSR plays a fundamental role, and has evolved and encompassed an increasingly broader panorama and dimensions (Morejón & Lorenzo, 2020).

Stakeholders must receive relevant, timely and understandable information about their activities from corporate reports for companies to meet their obligations under the ethics of responsibility (Clayton et al., 2015). Most companies recognize legal obligations and commitments to employees, customers, suppliers, managers, and the government. The state should remain involved in business dynamics in terms of CSR (Popkova et al., 2021) and favor its institutionalization in all companies.

Studies confirm divergences between companies (Salvini et al., 2018). In fact, small companies engage more with interested parties compared to medium-sized companies (Ocampo López et al., 2016).

3.1. Theoretical Framework

- Investment risks, climate change & strategy:

The significance of strategic steps towards ‘CSR to address the situation from present dynamics and emerging trends of events have grown of an increased importance and need.

- Research Question(s) and Hypotheses

1. Can organizations enhance their financial performances by engaging ‘CSR?

2. Can we establish a connection and relationship between ‘CSR activities of corporations and their financial outputs or returns?

3. How can firms gain competitive advantage from a strategic point of view?

3.2. Propositions & Frame work for Hypothesis:

Newburry et al. (2019) define CR as a collective perception of the past activities or existing traditions and beliefs of the firm regarding its future activities and prospects. Also, Gotsi and Wilson (2001) demonstrate that CR is the future marketing direction that will impact the internal and external stockholders of the organization. Jeffrey et al. (2019) supported the fact that CR is a reputation that establish trust and loyalty between consumers and vendors. This brings employee development, and retention.

CR refers to extent of a firm being considered and positioned in great regard for perceptions of its partners (Newburry et al., 2019). It also summarizes all perceptions of the stakeholders towards a firm regarding how it will fulfill and meet or exceed anticipations and all expectations (Rettab and Mellahi, 2019; Hameed et al., 2021). Also, the reputation of a firm is determined and assessed by the indicators of the marketplace regarding its behavior, as understood by stakeholders (Jeffrey et al., 2019).

The environment, and stakeholders. CSR initiatives can include philanthropy, ethical practices, environmental sustainability, and community engagement (McWilliams, A.; Siegel, 2001; Brooks, C.; Oikonomou, 2018).

The equity market has also shown a vested and keen interest in social efforts for improved CSR performance. These endeavours are due to increased need and societal expectations (Jain et al., 2016; Ng, 2020; Gong et al., 2018).

As unveiled, corporate commitment to CSR positively influences the level of sustainable performance of companies (Mallah & Jaaron, 2021). The role played by employees is potentially vital in addressing the new challenges faced and encountered by companies when carrying out initiatives within the framework of corporate sustainability (Revuelta-Taboada et al., 2021).

Employee engagement plays a mediating role in high-performance work systems, which allow the organization to retain and satisfy its employees, and also positively influencing sustainability indicators (Alafeshat & Tanova, 2019). Leaders who advocate for CSR, support and do not resist changes, are able to get the best out of their followers, by increasing intrinsic motivation, psychological empowerment (Khusanova et al., 2019).

The subjective value of CSR strategies shown or expressed from feelings by the employee in readiness and their willingness to overcome possible problems by negotiation and maintain a sustainable long-term employment relationship (Clipa et al., 2019). However, job insecurity is negatively related to health and job satisfaction (Giunchi et al., 2019). The perceived CSR of an organization can lead to a sense of trust among employees leading to the construction of corporate reputation (Yadav et al., 2018). Prosperity at work is a psychological state, occurring when employees experience a sense of vitality (Abid et al., 2018). Despite efforts, potential dark sides have been largely ignored, as expressed in, even though the literature has explored the positive effects of socially responsible management of employees (Shao et al., 2019).

3.3. Formulations & Hypothesis:

3.3.1. Hypotheses:

- Corporations can achieve optimal utilization of resources by engaging n ‘CSR, and embracing as an investment risks against wasteful expenditures, such as seeking legal redress against ligations, activism and motivations against careless activities from climate change events.

- As an investment risks and the manner being embedded into the ‘CSR strategy of an organization, a reputable brand can be built and translate to a brand equity.

- A sustainable business model can be achieved by adopting ‘CSR as a strategic tool from investment risks and a derivative of operational efficiency, effective organizational and financial performances.

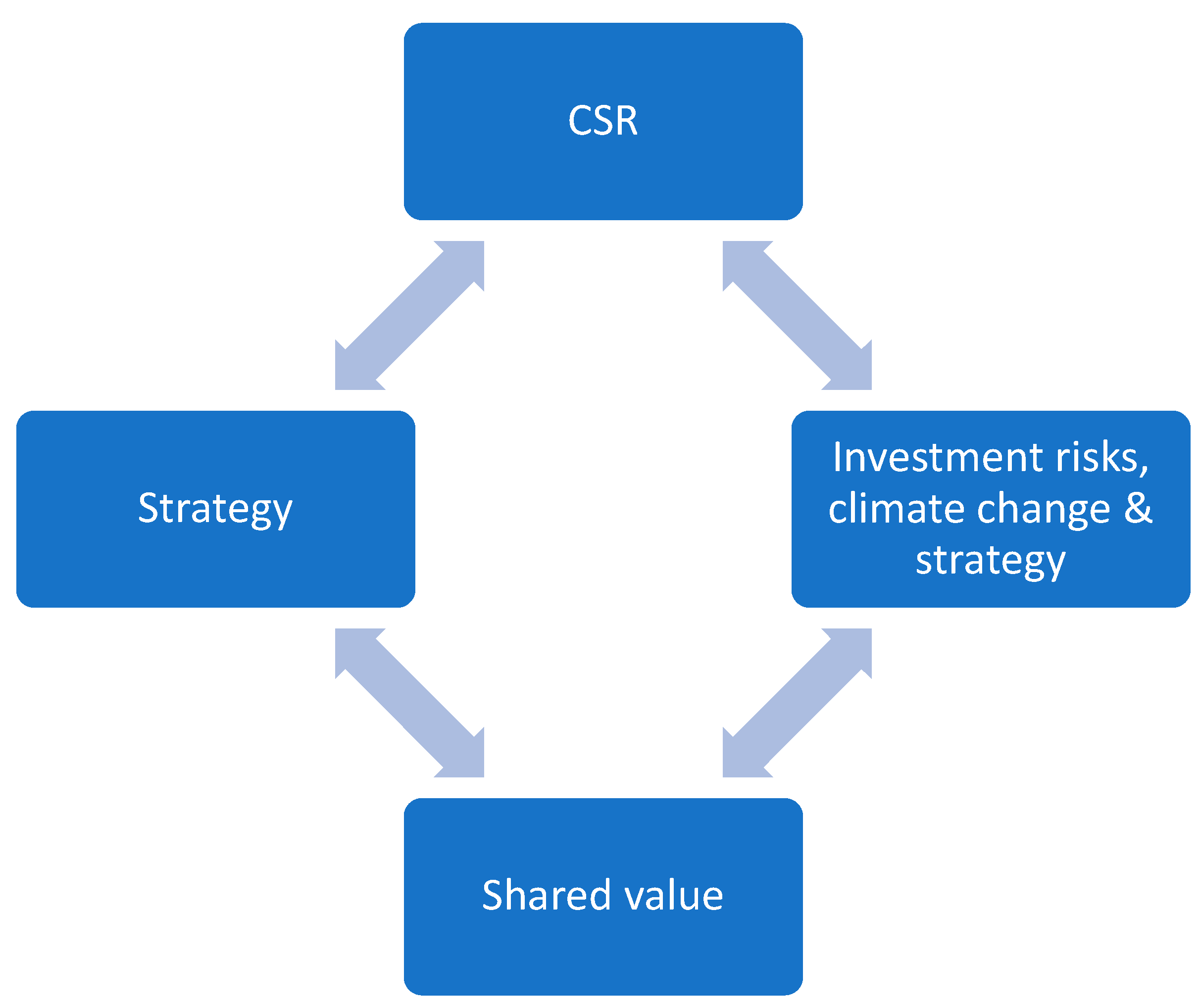

One step towards this is by “investment & incorporating climate change risks” into the business model strategy, ‘CSR strategy and investments templates as embedded in the framework from Figure 1.

Figure 1.

Framework around ‘CSR based on strategy from investment risks towards climate change mitigation. ‘Source: ‘Author’s draft from present study, 2024.

Figure 1.

Framework around ‘CSR based on strategy from investment risks towards climate change mitigation. ‘Source: ‘Author’s draft from present study, 2024.

4. Data Analysis

4.1. Reliability Test & Validity

The reliability test and validity assessment are carried out by making use of the ‘Cronbach; alpha to assess these measures as presented in the following table.

As shown in the table above; from Table 2.1, the ‘Cronbach alphas lies between 0.78947 and 0.92308, which far exceeds the threshold, and relatively high, hence justifying reliability of the variables and parameters or measures or assessment.

Table 2.1 b) shows that the “composite reliability (>0.60), Cronbach alpha (>0.70), and AVE (>0.50). Hence, based on the values shown and obtained, each construct falls within the acceptable range, which shows that the tool used for checking the hypothesis is reliable (Chatfield, 2018; Ahmed et al., 2020).

Source: ‘Author’s draft from recent study, 2023

Table 2.1.

(b) ‘Cronbach Alpha of the Variables, Composite Reliability (CR) & ‘AVE:.

| ‘Cronbach alpha | ‘Composite reliability | ‘AVE | ‘Factorial loadings ‘** | |

|---|---|---|---|---|

| Brand awareness | 0.78947 | 0.87200 | 0.623 | 0.7893 |

| Images & brand reputation | 0.83768 | 0.84100 | 0.640 | 0.790 0.825 |

| CSR. brand & image | 0.84906 | 0.88100 | 0.79725 | 0.8928 |

| Image, preferences & brand | 0.92308 | 0.93500 | 0.78325 | 0.8850 |

| ‘investment risks, CSR & brand * | 0.88720 | 0.95600 | 0.84375 | 0.9185 |

| ‘brand preferences & perceptions | 0.98640 | 0.96700 | 0.8785 |

0.93728 |

| Investment asks from litigation | 0.8225 | 0.88825 | 0.8821 | 0.9250 0.8982 0.9224 0.9224 |

| Operational efficiency | 0.9978 | 0.9988 | 0.8823 | 0.8900 |

| Financial stability & performances | 0.8978 | 0.8254 | 0.7224 | 0.8490 0.8882 |

| CSR, brand & reputation | 0.97820 | 0.9824 | 0.8825 | 0.9801 0.9394 |

| CSR, Image & brand reputation | 0.92245 | 0.92556 | 0.8254 | 0.9225 0.9085 0.8908 |

| Consumer preferences & brand image | 0.84906 | 0.8524 | 0.7234 | 0.8505 |

| Image & brand communication | 0.8225 | 0.89724 | 0.75524 | 0.8690 |

| ‘Brand, inclinations, media & culture | 0.89640 | 0.938 | 0.7900 | 0.8888 0.8824 |

| ‘Brand, lifestyles, culture & interactions | 0.92310 | 0.94000 | 0.79225 | 0.8001 0.825 0.8824 |

| Communication, brand, preferences & culture | 0.82502 | 0.8725 | 0.79234 | 0.8901 |

‘Source: ‘Author’s draft from present study, 2024.

Table 3.0.

Table of Estimates & SEM.

| ‘Parameter or variables | ‘Indicators | ‘Estimate | ‘T value |

|---|---|---|---|

| - perception of consumers and employees from reputation - perception from awareness, communication & message - perception of effectiveness from experiences & activities or engagement - perception of image - perception from association, culture & link or lifestyles |

P1 P2 P3 P4 P5 |

0.770 0.728 0.625 0.725 0.885 |

4.225 5.225 3.602 9.772 6.825 |

| - investment risks from climate changes \& events - investment risks from litigation - investment risks & incentives - investment risks, resources & incentives |

R. 1 R 2 R. 3 R. 4 |

0.326 0.424 0.238 0.221 |

4.880 6.824 6.200 2.594 |

| - sustainability and performances - operational efficiency and performances - operational efficiency, performances & effectiveness - enhanced financial performances - future growth and sustainability |

S 1 S 2 S 3 S4 S5 |

0.384 0.644 0.625 0.724 0.86 |

9.224 8.225 12.829 6.24 7.24 |

| Brand reputation - investment risks | 0.224 | 12.40 | |

| Brand equity - investment risks | 0.625 | 8.25 |

‘Source: ‘Author’s draft & present study.

Brand reputation - investment risks, and Brand equity - investment risks from ‘SEM showed statistical significances at the 5% level of significances. Hence, investment risks when adopted and fused in the business model can raise the reputation and translate to a brand equity, and shared value creation as consumers get to trust the company and organization more, thus they propagate such brands, and enhance the reputation.

4.2. Climate Change, Mitigation, Models, Projections and Litigation

4.2.1. Climate Change: ’Combating Climate Changes, Stabilization & Mitigation Efforts! ‘*

The focus on atmospheric stabilization is historically driven, rooted and traced to the text of Article 2 of the United Nations Framework Convention on Climate Change (UNFCCC), in which is written:

The ultimate or prime objective of this Convention … is to achieve … stabilization of greenhouse gas concentrations in the atmosphere at a level that would prevent dangerous anthropogenic or man-made interference with the climate system and manifestations that could be seen.(UNFCCC (UN Report, 1992)

Towards this goal and aim or agenda, a considerable body of literature has evolved and emerged to attempt to primarily and fundamentally quantify what could be considered to be a ‘dangerous’ level of climate change, and second to determine what levels of greenhouse gas stabilization are consistent with in avoiding said climate changes (Schneider, 2005, Smith, 2009, Knutti,2008) and anticipated severities or unforeseen.

The lower the desired stabilization level being sought or anticipated and expected, the sooner global GHG emissions must peak and decline or subside (Fisher et al, 2007). Based on observations, trends and the present state; GHG concentrations are unlikely to stabilize this century or anytime sooner without major key policy changes (Rogner et al., 2007) or instruments I ……………….and aggressive policy measures by “stakeholders, parties and concerned” entities.

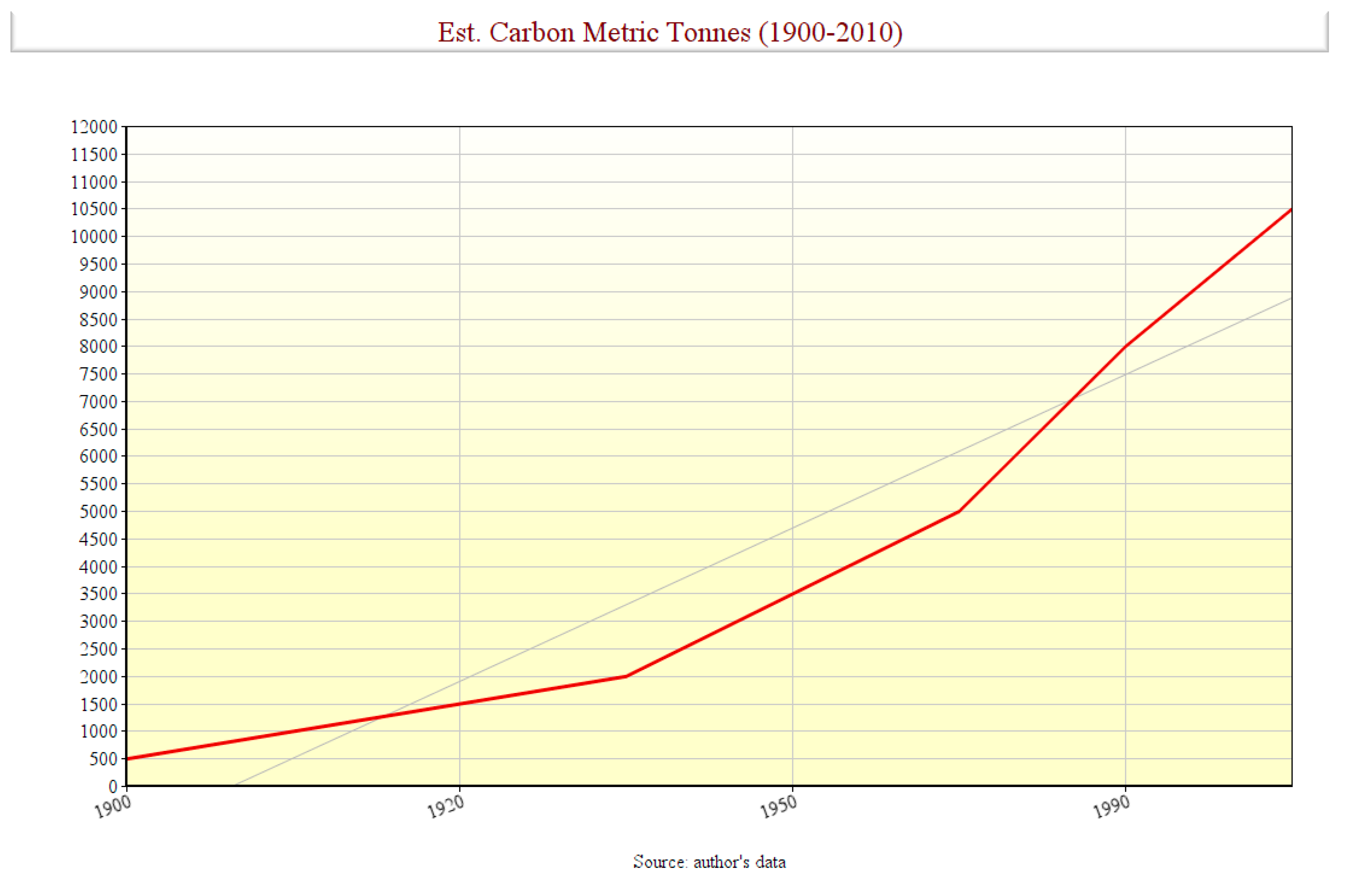

Figure 2.

Global Green House Emissions.

Figure 3.

Estimate from our Model starting 1900 beyond 2000. ‘Source: ‘Author’s draft & extraction from published study, 2023. Ref & Source Citation: ADEWOLE O.O et al., 2018 from the Literature;

Figure 3.

Estimate from our Model starting 1900 beyond 2000. ‘Source: ‘Author’s draft & extraction from published study, 2023. Ref & Source Citation: ADEWOLE O.O et al., 2018 from the Literature;

4.3. Qualitative Results on Consumer’s Perception: ‘Themes & Analysis:

- ‘Responses:

‘Association with brands that pursue ‘CSR 88-93%

‘CSR & environment: 78-93%

Optimal use of resources: 78-94%

‘Climate change, risks, CSR and investments: 88-94%

Redress ligation & state activism: 78-93%

- Themes:

Based on the observation poll, and interview responses from this study and the previous section the following themes are deduced:

Brand engagement: CSR can be adopted as a tool of brand engagement

‘ESG: The rating of disclosure from transparency and symmetry can be improved and reflects on the ESG

Resource optimization: Resource optimization be achieved using ‘CSR as a tool

Hedge: A hedge or insurance against risks can be generated

Trust: Redressing litigation can result from trust, and in turn lessen activism against the state

‘Source: ‘Author’s draft & present study

A strong correlation exists between the brand, reputation and ‘CSR engagements as an alignment exists between the perceptions of 2 groups on activism against the state.

This shows and implies a strong tie and connection if the p -value is high (>0.05) and further elaborated as presented and statistically built and developed subsequently and shown in more details in the appendix section (Tables A1a) & A1b)).

From the ‘themes, and specifically, C, the fact of convergence is established between findings of the qualitative and quantitative data. From the results, a ‘p – value (>0.05) implies the assumption of the composite relationship existing and connecting the two groups on their perceptions perception shown and demonstrated by the people as analyzed and captured from data in this poll and experimental survey.

Furthermore, in addition to the quantitative data from the poll and experimental survey, the qualitative analysis and data show and indicates there is a strong bearing on the brand and essentially in connection with ‘CSR from theme C reflective, and as emerged in Figures 1 & A1 from the (appendix section) (Adewole, 2024). This also enhances the results on the traditional tools of brand communication based on the 3rd component and layer or strata carved around; ‘CSR & images captured. In fact, the point of convergence, or triangulation is a key point and crucial fact in mixed methods research approaches as justified.

Limitation(s) or Further Restraint & Experience(s): ‘A major restraint or limitation of this research work again is funding and limited funds as this project is presently carried out with personal funds.

Another major difficulty in the acquisition of the primary data is due to some few ignorant individuals who never responded to the survey.

6. Conclusions

From the results, ‘p – value (>0.05) implies the assumption of the composite relationship existing and connecting the two groups on their perceptions from investment risks based on resource conservation against state activism and perception on litigation being redressed as shown (appendix section from Table A1.1 b) and demonstrated by the people, comprising organizations and consumers as analyzed based on the data captured in this study from the poll and experimental survey.

Adapting and carving ‘CSR models into business, and from a strategic point should emphasize value-based creation that turns products that give maximum satisfaction anticipated by customers or consumers and also environmental friendly as potential tool towards a redress and abating the present situation from realities being met and seen considering the rising prominences and incidences in litigation, jury and pending legal cases.

Abbreviations

| CSR: | Corporate social responsibility |

| ‘BE: | Brand equity |

| ‘BR: | Brand relationship |

| ‘CR: | Corporate responsibility or reputation |

| ‘ESG: | Environment, society & governance |

| ‘EU: | European Union |

| ‘UNFCCC: | United Nations Framework Convention on Climate Change |

| ‘IPCC: | Intergovernmental Panel on Climate Change |

| ‘WOM: | Wood of mouth |

| CV: | Coefficient of variance or variations |

| z – tabulated: | tab) and z – calculated: cal) |

| t-cal: | calculated t-test statistics from formula or expression |

| tc: | critical value from the t-test |

| μ: | mean or sample mean |

| μ0: | hypothesized or drawn population mean |

| ‘AVE: | Average Variance Extracted |

| S.D: | Standard deviation |

| SEM: | Structural equation modeling |

Appendix A

Appendix A.1.1 Observations and Ratings: ‘Based on Likert Ratings (1 – 5)

The ratings from two observation groups are employed based on the ‘LKERT ratings and scale:

- ‘N.B:

Group 1: ‘perception of corporations on activism and resource conservation

Group 2: ‘perceptions of consumers on corporations that shield against ligations

Table A.1.

(a): Summary. (b) ANOVA Summary & Statistics.

| (a) Summary and Statistics | |||||

| N | Mean | Std. dev., | Std. err | ||

| Group 1 | 50 | 4.758 | 0.825 | 0.1069 | |

| Group 2 | 75 | 4.895 | 0.423 | 0.0724 | |

| ‘Source: ‘Author’s draft from present study, 2024. | |||||

| (b): ANOVA Summary & Statistics | |||||

| ‘Source | ‘Df | SS | MS | F | P |

| Between Groups | 1 | 0.075 | 0.075 | 0.6001 | 0.445 |

| Within Groups | 124 | 3.4995 | 0.125 | ||

| Total | 125 | 3.5745 | |||

| p -value: 0.445. F: 0.6001. ‘Source: ‘Author’s draft from present study, 2024 | |||||

A connecting of the two groups has been developed based on their perceptions

as shown as analyzed and captured from data in this poll and experimental survey.

A correlation existing between the two groups presented people shows and implies a strong tie and connection as seen based on the p -value from the above table, as elaborated and presented and statistically, built and developed.

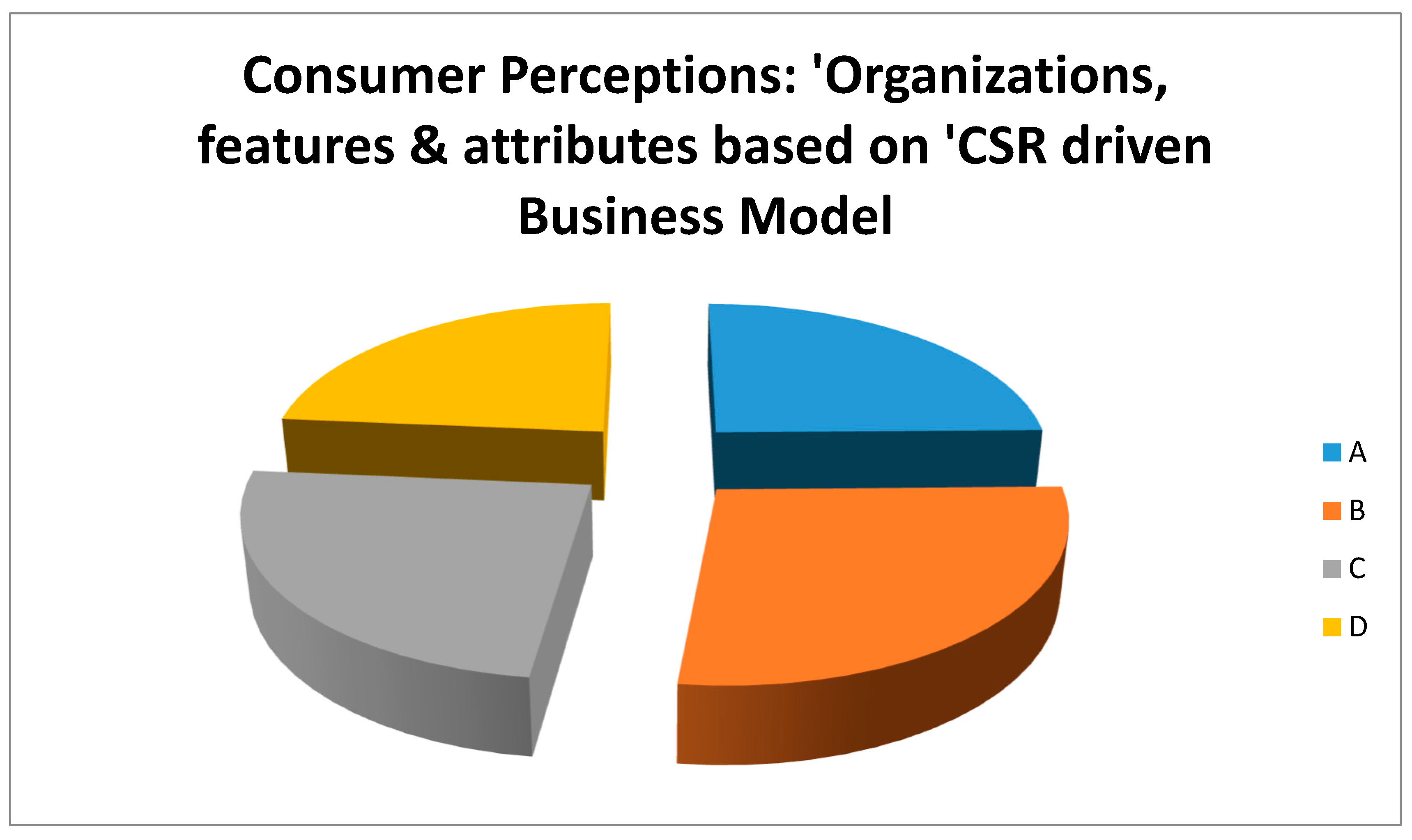

Appendix A.1.2 Extrapolated/Simulation: ‘A Simulated/Extrapolated Responses and Illustrations of Consumers Responses based on Perceptions of Organizations– Business Models Attributes from ‘CSR & Features from the Research Questions, Interview and Survey

It is extrapolated, projected and assumed from the responses captured from the interviews, survey and questionnaires in arriving at the ‘themes from the analyses and codes:

A: I associate with companies, organizations and brands showing care for welfare needs, environmental related courses and societal needs. enjoy working in a diverse environment or workplace: 78-93%

B: Effective & integrated strategic mix from business models based on ‘CSR and would enhance sustainable marketing and drive the path to ‘climate change mitigation from a socially responsible perspective: 89–99%

C: A ‘CSR based business model tied to cultural and lifestyles of the people from brand context would foster effectiveness and efficiency in the operational modules as well as impact on financial performance: 75–85% or over

D: A ‘CSR based business model and structure can enhance change transitions from short term to long term goals, drive to sustainability, localized stabilization and ‘sustainable domains: 85%

‘Consumer Perceptions from Organizational Structure, Business Model & ‘CSR driven

Attributes: A simulated/extrapolated responses and illustrations of the research questions with the codes or short phrases and labelled categories; ‘A, B, C & D.

Figure A1.

A simulated/extrapolated responses and illustrations of the research questions. Source: Author’s Extraction & Analysis, published 2024 ‘*

Figure A1.

A simulated/extrapolated responses and illustrations of the research questions. Source: Author’s Extraction & Analysis, published 2024 ‘*

From these categories as stated from A, B, C, & D, the following themes emerge as; “brand reputation, brand equity, ‘sustainability/investment risks – climate change mitigation, and efficiency, effectiveness & enhanced performances” as presented in Figure A 1. These align with the research findings, research questions as presented and the scope of the investigation and research.

Notes

- I.

- Shanks & Roegner. (2007). Aquatic Climate Change Adaptation Services Program-Pacific ……publications.gc.ca>collection_2016>mpo-df0>Fs97-4-3049-eng

- II.

- III.

- ‘https://www.ejiltalk.org/a-new-classic change in climate-change-litigation: the –dutch-supreme court-decision—in-the-urgenda-case/

References

- Adewole, O. Translating brand reputation into equity from the stakeholder’s theory: an approach to value creation based on consumer’s perception & interactions. International Journal of Corporate Social Responsibility. 2024, 9, 1. [Google Scholar]

- Ahmed, R. R. , Vveinhardt, J., Warraich, U. A., Hasan, S. S. U., & Baloch A. Customer Satisfaction & Loyalty and Organizational Complaint Handling: Economic Aspects of Business Operation of Airline Industry. Inzinerine Ekonomik–Engineering Economics. 2020, 31, 114–125. [Google Scholar] [CrossRef]

- Ahmed, R. R. , Hussain, S., Pahi, M. H., Usas, A., & Jasinskas, E. Social Media Handling and Extended Technology Acceptance Model (ETAM): Evidence from SEM-Based Multivariate Approach. Transformation in Business & Economics. 2019, 18, 246–271. [Google Scholar]

- Alafeshat, R. , & Tanova, C. Servant leadership style and high-performance work system practices: Pathway to a sustainable jordanian airline industry. Sustainability. 2019, 11, 6191. [Google Scholar] [CrossRef]

- Abid, G. , Sajjad, I., Elahi, N. S., Farooqi, S., & Nisar, A. The influence of prosocial motivation and civility on work engagement:The mediating role of thriving at work. Cogent Business and Management. 2018, 5, 1–19. [Google Scholar]

- Adewole O, Fajemiroye J.A and Esholomo J.O. “An Assessment and Model for Dynamic Behaviour and Climate Change Mitigation Action Plan” Published in International Journal of Trend in Research and Development (IJTRD) 2018, 5. http://www.ijtrd.com/papers/IJTRD16758.pdf.

- Aguilera, R. , Rupp, D., Williams, C. and Ganapathi, J. ‘Putting the S back in corporate social responsibility: A multilevel theory of social change in organizations.’ Academy of Management Review. 2007, 32, 36–863. [Google Scholar]

- Aguinis, H. and Glavas, A. ‘What we know and don’t know about corporate social responsibility: A review and research agenda.’ Journal of Management. 2012, 38, 932–968. [Google Scholar]

- Armstrong, Gary, and Philip Kotler (2008). Principles of Marketing, 12th ed., Upper Saddle River, NJ, Pearson Educational Inc.

- Brooks, C.; Oikonomou, I. The effects of environmental, social and governance disclosures and performance on firm value: A review of the literature in accounting and finance. Br. Account. Rev. 2018, 50, 1–15. [Google Scholar]

- Branco, M. C. , and Rodrigues, L.L. Corporate social responsibility and resource-based perspectives. J. Bus. Ethics. 2006, 69, 111–132. [Google Scholar] [CrossRef]

- Bendell, J. In whose Name? The Accountability of Corporate Social Responsibility: Development in Practice. 2005, 15, 362–374. [Google Scholar]

- Bendixen, M. , & Abratt, R. Corporate identity, ethics and reputation in supplier-buyer relationships. Journal of Business Ethics. 2007, 76, 69–82. [Google Scholar]

- Berenbeim, R. E. Business ethics and corporate social responsibility: Defining an organization’s ethics brand. Vital Speeches of the Day. 2006, 72, 501–503. [Google Scholar]

- Berkhout, T. Corporate gains: Corporate social responsibility can be the strategic engine for long-term corporate profits and responsible social development. Alternatives Journal 2005, 31, 15–18. [Google Scholar]

- Bryson, J. What to do when stakeholders matter. Public Management Review 2005, 6, 21–53. [Google Scholar] [CrossRef]

- Berman, S.L.; Wicks, A.C.; Kotha, S.; Jones, T.M. Does stakeholder orientation matter? The relationship between stakeholder management models and firm financial performance. Acad. Manag. J. 1999, 42, 488–506. [Google Scholar]

- Clipa, A.-M. , Clipa, C.-I., Danilet, M., & Andrei, A. G. Enhancing sustainable employment relationships: An empirical investigation of the influence of trust in employer and subjective value in employment contract negotiations. Sustainability. 2019, 11, 4995. [Google Scholar] [CrossRef]

- Chatfield, C. (2018). Introduction to Multivariate Analysis. London: Routledge.

- Camilleri, M.A. Corporate sustainability and responsibility: creating value for business, society and the environment, Asian Journal of Sustainability and Social Responsibility (AJSSR), ISSN 2365-6417, Springer, Cham 2017, 2, p. 59-74. [CrossRef]

- Çifci, S. , Ekinci, Y., Whyatt, G., Japutra, A., Molinillo, S., and Siala, H. A cross validation of consumer-based brand equity models: driving customer equity in retail brands. J. Bus. Res. 2016, 69, 3740–3747. [Google Scholar] [CrossRef]

- Clayton, A. F. , Rogerson, J.M., & Rampedi, I. Integrated reporting vs. sustainability reporting for corporate responsibility in South Africa. Bulletin of Geography. 2015, 29, 7–17. [Google Scholar] [CrossRef]

- Carroll, A. B. Corporate social responsibility: The centerpiece of competing and complementary frameworks. Organizational Dynamics 2015, 44, 87–96. [Google Scholar] [CrossRef]

- Carroll, A. B/. & Buchholtz, A.K. (2011). Business and society: Ethics and stakeholder management. Australia: Thomson South-Western.

- Crane, A. & Kazmi, B.A. Business and Children: Mapping Impacts, Managing Responsibilities. Journal of Business Ethics. 2010, 91, 567–586. [Google Scholar] [CrossRef]

- Carroll, A. B. (2008). A history of corporate social responsibility: concepts and practices. In A. M. Andrew Crane, D. Matten, J. Moon, & D. Siegel (Eds.), The Oxford handbook of corporate social responsibility (pp. 19–46). New York: Oxford University Press.

- Carroll, A. B. (1991). The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Business Horizons, 39-48.

- Carroll, A.B. A three dimensional conceptual model of corporate performance. Academy of Management Review. 1979, 4, 497–505. [Google Scholar]

- Crane, A. , McWilliams, A., Matten, D., Moon, J., and Siegel, D. S. (2008). “The corporate social responsibility agenda,” in The Oxford Handbook of Corporate Social Responsibility, eds A. McWilliams, D. E. Rupp, and D. S. Seigel (Oxford: Oxford University Press). [CrossRef]

- FATMAWATI1, I. , & FAUZAN2 N. Building Customer Trust through Corporate Social Responsibility: The Effects of Corporate Reputation and Word of Mouth Journal of Asian Finance, Economics and Business. 2021, 8, 0793–0805, Print ISSN: 2288-4637 / Online ISSN 2288-4645. [Google Scholar] [CrossRef]

- Friedman, M. The social responsibility of business is to increase its profits. In Corporate Ethics and Corporate Governance; Zimmerli, W.C., Holzinger, M., Richter, K., Eds.; Springer: Berlin/Heidelberg, Germany, 2007; pp. 173–178. [Google Scholar]

- Frynas, J.G. , & Yamahaki, C. Corporate social responsibility: review and roadmap of theoretical perspectives. Business Ethics, the environment & responsibility. 2016, 25, 285. [Google Scholar]

- Feldstein, M. (2013). The Reagan-Thatcher revolution. https://www.dw.com/en/the-reagan-thatcher-revolution/a-16732731. Accessed 9 Nov 2018.

- Ferrell, O.C. , and Michael D. Hartline. (2011). Marketing Strategy. Msason, OH: South – Western Cengage Learning.

- Friedman, M. The social responsibility of business is to increase its profits. In Corporate Ethics and Corporate Governance; Zimmerli, W.C., Holzinger, M., Richter, K., Eds.; Springer: Berlin/Heidelberg, Germany, 2007; pp. 173–178. [Google Scholar]

- Fisher, B.S; et al. (2007). “Issues related to mitigation in the long term context”. In B. Metz et al. eds., Climate change, 2007: Multi - guide Contribution of Workshop Group 111 to the Forum. Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press. Retrieved, 20 May, 2007.

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Cambridge, UK, 1984. [Google Scholar]

- Fornell, C. , and Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Friedman M (1970) The social responsibility of business is to increase its profits. New York Times Magazine (September 13), 32–33.

- Gavana, G.; Gottardo, P.; Moisello, A.M. Related party transactions and earnings management: The moderating effect of esg performance. Sustainability 2022, 14, 5823. [Google Scholar] [CrossRef]

- Giunchi, M. , Vonthron, A.-M., & Ghislieri, C. Perceived job insecurity and sustainable wellbeing: Do coping strategies help? Sustainability. 2019, 11, 784. [Google Scholar] [CrossRef]

- Godfrey, P. C, Merrill C.B, Hansen J.M. The relationship between corporate social responsibility and shareholder value: an empirical test of the risk management hypothesis. Strateg Manag J. 2009, 30, 425–445. [Google Scholar]

- Godfrey, P.C. The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. Acad. Management Rev. 2005, 30, 777–798. [Google Scholar]

- Glavas, A. and Piderit, S.K. ‘How does doing good matter? Effects of corporate citizenship on employees.’ The Journal of Corporate Citizenship. 2009, 36, 51–70. [Google Scholar]

- Greening, D.W.; Turban, D.B. Corporate social performance as a competitive advantage in attracting a quality workforce. Bus. Soc. 2000, 39, 254–280. [Google Scholar]

- Gotsi, M. , and Wilson, A.M. Corporate reputation: seeking a definition. Corp. Commun. Int. J. 2001, 6, 24–30. [Google Scholar] [CrossRef]

- Hameed, K. , Arshed, N., Yazdani, N., and Munir, M. Motivating business towards innovation: a panel data study using dynamic capability framework. Technol. Soc. 2021, 65, 101581. [Google Scholar] [CrossRef]

- Heikkurinen, P. “Strategic corporate responsibility: a theory review and synthesis”, Journal of Global Responsibility 2018, 9, 388–414. [CrossRef]

- Ifada, L. M. , Ghozali, I., & Faisal. Corporate social responsibility, normative pressure and firm value: Evidence from companies listed on Indonesia stock exchange. Advances in Intelligent Systems and Computing. 2021, 1194, 390–397. [Google Scholar]

- Ivanović-Đukić, M. Podsticanje društveno odgovornog poslovanja preduzeća u funkciji pridruživanja Srbije EU. Ekonomske teme 2011, 49, 45–58. [Google Scholar]

- Jeffrey, S. , Rosenberg, S., and McCabe, B. Corporate social responsibility behaviors and corporate reputation. Soc. Responsib. J. 2019, 15, 395–408. [Google Scholar] [CrossRef]

- Jain, A.; Jain, P.K.; Rezaee, Z. Value-relevance of corporate social responsibility: Evidence from short selling. J. Manag. Account. Res. 2016, 28, 29–52. [Google Scholar] [CrossRef]

- Jamali, D. and Neville, B. ‘Convergence vs divergence in CSR in developing countries: An embedded multi-layered institutional lens.’ Journal of Business Ethics. 2011, 102, 599–621. [Google Scholar]

- Jones, T.M. Instrumental stakeholder theory: A synthesis of ethics and economics. Acad. Manag. Rev. 1995, 20, 404–437. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Khan, M.A. ESG disclosure and Firm performance: A bibliometric and meta analysis. Res. Int. Bus. Finance. 2022, 61, 101668. [Google Scholar] [CrossRef]

- Khediri, K. B. CSR and investment efficiency in Western European countries. Corporate Social Responsibility and Environmental Management 2021, 28, 1769–1784. [Google Scholar] [CrossRef]

- Khusanova, R. , Choi, S.B., & Kang, S.-W. Sustainable workplace: The moderating role of office design on the relationship between psychological empowerment and organizational citizenship behaviour in Uzbekistan. Sustainability. 2019, 11, 7024. [Google Scholar] [CrossRef]

- Kim, C. , Kim, J., Mmarshall, R., & Afzali, H. Stakeholder influence, institutional duality, and csr involvement of mnc subsidiaries. journal of business research. 2018, 91, 40–47. [Google Scholar] [CrossRef]

- Krstic, N. Primena Principa poslovanja i prava dece u strategiji društveno odgovornog poslovanja preduzeća u Srbiji. Sociologija 2017, 59, 351–363. [Google Scholar] [CrossRef]

- Knutti, R. & Hegerl, G. The equilibrium sensitivity of the earth’s temperature to radiation changes. Nat. Geosci. 2008, 1, 735–743. [Google Scholar]

- López-González, E. , Martínez-Ferrero, J., and García-Meca, E. Corporate social responsibility in family firms: a contingency approach. J. Clean. Prod. 2019, 211, 1044–1064. [Google Scholar] [CrossRef]

- Liu, M. , and Lu, W. Corporate social responsibility, firm performance, and firm risk: the role of firm reputation. Asia Pacific J. Account. Econ. 2019, 27, 2991–3005. [Google Scholar] [CrossRef]

- Li, Y.; Gong, M.; Zhang, X.-Y.; Koh, L. The impact of environmental, social, and governance disclosure on firm value: The role of CEO power. Br. Account. Rev. 2018, 50, 60–75. [Google Scholar]

- Lee, J. , Graves, S.B., & Waddock, S. Doing good does not preclude doing well: Corporate responsibility and financial performance. Social Responsibility Journal. 2018, 14, 764–781. [Google Scholar]

- Morejón, B. R. G. , & Lorenzo, A.F. Responsabilidad social empresarial y competitividad en las clínicas de salud privadas de Quito, Ecuador. Cooperativismo y Desarrollo. 2020, 8, 315–328. [Google Scholar]

- McAvoy, John, and Tom Butler. “A Critical Realist Method for Applied Business Research.” Journal of Critical Realism. 2018, 17, 160–175. [CrossRef]

- Morgeson, F. P. , Aguinis, H., Waldman, D. A. and Siegel, D. S. ‘Extending corporate social responsibility research to the human resource management and organizational behavior domains: A look to the future.’ Personnel Psychology. 2013, 66, 805–824. [Google Scholar]

- Mallah, M. F. , & Jaaron, A.A. M. An investigation of the interrelationship between corporate social responsibility and sustainability in manufacturing organisations: An empirical study. International Journal of Business Performance Management. 2021, 22, 15–43. [Google Scholar]

- Martin-Ortega, O. , & Wallace, R. Business, Human Rights and Children: The Developing International Agenda. Denning Law Journal 2013, 105-128.

- Morsing, M. and Perrini, F. ‘CSR in SMEs: do SMEs matter for the CSR agenda?’. Business Ethics: A European Review. 2009, 18, 1–6. [Google Scholar]

- Matten, D. , & Moon J. ‘‘Implicit’ and ‘Explicit’ CSR: A conceptual framework for a comparative understanding of corporate social responsibility’. Academy of Management Review. 2008, 33, 404–424. [Google Scholar]

- Maignan, I. , & Ferrell, O.C. Corporate citizenship: Cultural antecedents and human benefits. Journal of the Academy Management Science. 2005, 27, 455–469. [Google Scholar]

- Maignan, I. & Ferrell, O.C, & Ferrell, L. A Stakeholder Model for Implementing Social Responsibility in Marketing. European Journal of Marketing. 2005, 39, 956–977. [Google Scholar]

- Maignan, I. and Ferrell O.C. ‘Corporate social responsibility and marketing: An integrative framework’. Journal of the Academy of Marketing Science. 2004, 32, 3–19. [Google Scholar]

- Michelon, G. , Boesso, G. & Kumar, K. Examining the link between strategic corporate social responsibility and corporate performance: An analysis of the best corporate citizens. Corporate Social Responsibility and Environmental Management. 2013, 20, 81–94. [Google Scholar]

- McWilliams, A. & Siegel, D. Corporate social responsibility and financial performance: Correlation or misspecification? Strateg. Manag. J. 2000, 21, 603–609. [Google Scholar]

- Miles, M. P. , Munilla, L.S., & Darroch, J. The role of strategic conversations with stakeholders in the formation of corporate social responsibility strategy. Journal of Business Ethics. 2006, 69, 195–205. [Google Scholar] [CrossRef]

- Morsing, M. and Perrini, F. ‘CSR in SMEs: do SMEs matter for the CSR agenda?’. Business Ethics: A European Review. 2009, 18, 1–6. [Google Scholar]

- Ng, A.C.; Rezaee, Z. Business sustainability factors and stock price informativeness. J. Corp. Financ. 2020, 64, 101688. [Google Scholar]

- Newburry, W. , Deephouse, D. L., and Gardberg, N. A. (2019). “Global aspects of reputation and strategic management,” in Global Aspects of Reputation and Strategic Management, eds D. Deephouse, N. Gardberg, and W. Newburry (Bingley: Emerald Publishing Limited). [CrossRef]

- Orviz Martínez, N. , Cuervo Carabel, T., & Arce García, S. Review of scientific research in ISO 9001 and ISO 14001: A bibliometric analysis. Cuadernos de Gestión. 2021, 21, 29–45. [Google Scholar] [CrossRef]

- Ocampo López, O. , Vargas Barrera, L.., & Suárez Giraldo, K. Determinación de brechas estructurales en la integración de la responsabilidad social en empresas del sector textil-confección de la región Centro-Sur de Caldas. Revista Ciencias Estratégicas. 2016, 24, 137–154. [Google Scholar]

- Orlitzky, M. , Siegel, D.S. and Waldman, D. A. ‘Strategic corporate social responsibility and environmental sustainability.’ Business and Society. 2011, 50, 6–27. [Google Scholar]

- Orlitzky, M. and Swanson, D. 2006. ‘Socially responsible human resource management: Charting new territory.’ In J. Deckop (Ed.), Human Resource Management Ethics: 3-25. Greenwich: IAP.

- Popkova, E. , Delo, P., & Segi, B. S. Corporate social responsibility amid social distancing during the COVID-19 crisis: BRICS vs. OECD countries. Research in International Business and Finance. 2021, 55, 101315. [Google Scholar]

- Porter, M. E. , & Kramer, M. R. (2011). Creating shared value. Harvard Business Review, 1 – 17 (Accessed January-February, 2011).

- Porter, M.E. ; & Kramer, M.R. Strategy and society: The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar]

- Porter, M.E.; Kramer, M.R. The competitive advantage of corporate philanthropy. Harv. Bus. Rev. 2002, 80, 56–68. [Google Scholar]

- Revuelto-Taboada, L. , Canet Giner, M.T., & Balbastre-Benavent, F. High-commitment work practices and the social responsibility issue: Interaction and benefits. Ustainability. 2021, 13, 1–25. [Google Scholar]

- Rettab, B. , and Mellahi, K. (2019). “CSR and corporate performance with special reference to the middle east,” in Practising CSR in the Middle East, eds B. Rettab and K. Mellahi (Berlin: Springer), 101–118. [CrossRef]

- Robbins, R. , (2011). Does Corporate Social Responsibility Increase Profits? Retrieved from http://www.environmentalleader.com/2011/05/26/does-corporate-social-responsibility-increase-profits/.

- Suki, N. M. , and Suki, N. M. (2019). “Correlations between awareness of green marketing, corporate social responsibility, product image, corporate reputation, and consumer purchase intention,” in Corporate Social Responsibility: Concepts, Methodologies, Tools, and Applications, eds Management Association and Information Resources (Pennsylvania: IGI Global), 143–154. [CrossRef]

- Setzer., & Vanhala, (2019). Climate change litigation: A review of research on courts and litigants in climate governance. Wiley Online (https://onlinelibrary.wiley.com/doi/abs/10.1002/wcc.580).

- Shao, D. , Zhou, E., Gao, P., Long, L., & Xiong, J. Double-edged effects of socially responsible human resource management on employee task performance and organizational citizenship behavior: Mediating by role ambiguity and moderating by prosocial motivation. Sustainability. 2019, 11, 2271. [Google Scholar] [CrossRef]

- Sekulić, V. , & Pavlović, M. Corporate social responsibility in relations with social community: Determinants, development, management aspects. Ekonomika. 2018, 64, 59–69. [Google Scholar]

- Salvini, G. , Dentoni, D., Ligtenberg, A., Herold, M., & Bregt, A. K. Roles and drivers of agribusiness shaping climate-smart landscapes: A review. Sustainable Development. 2018, 26, 533–543. [Google Scholar] [CrossRef]

- Shin, Y. , and Thai, V.V. The impact of corporate social responsibility on customer satisfaction, relationship maintenance and loyalty in the shipping industry. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 381–392. [Google Scholar] [CrossRef]

- Strand, R. , Freeman, R.E., & Hockerts, K. Corporate social responsibility and sustainability in Scandinavia: An overview. Journal of Business Ethics. 2015, 127, 1–15. [Google Scholar] [CrossRef]

- Spitzer, Randy. Is Social Responsibility Good? Journal for Quality& Participation. 2010, 3, 13–17.

- Smith, J.; et al. Assessing dangerous climate change through an update of the Intergovernmental Panel on Climate Change (IPCC) ‘reasons for concern’. Proc. Natl Acad. Sci. USA, 2009; 106, 4133–4137. [Google Scholar]

- Steurer, R. , Langer, M.E., Konrad, A., & Martinuzzi, A. Corporations, stakeholders and sustainable development I: A theoretical exploration of business-society relations. Journal of Business Ethics. 2005, 61, 263–281. [Google Scholar] [CrossRef]

- Schneider, S. H. & Mastrandrea, M.D. (2005) Probabilistic assessment of ‘dangerous’ climate change and emissions pathways. Proc. Natl Acad. Sci. USA. 2005, 102, 15-728–15-735. [Google Scholar]

- Simmons, J. Managing in the post-managerialist era: Towards socially responsible corporate governance. Management Decision 2004, 42, 601–611. [Google Scholar]

- Tzempelikos, N. , and Gounaris, S. (2017). “A conceptual and empirical examination of key account management orientation and its implications–the role of trust,” in The Customer is NOT Always Right? Marketing Orientationsin a Dynamic Business World, ed C. L. Campbell Berlin: Springer. [CrossRef]

- Turker, D. Measuring corporate social responsibility: A scale development study. Journal of Business Ethics 2009, 85, 411–427. [Google Scholar] [CrossRef]

- Ullah, Z. , Arslan, A., & Puhakka, V. Corporate social responsibility strategy, sustainableproduct attributes, and export performance. Corporate Social Responsibility and Environmental Management. 2021, 28, 1–14. [Google Scholar] [CrossRef]

- United Nations: 1992. Framework Convention on Climate Change, United Nations Conf. on Environment and Development, Rio de Janeiro, Brazil.

- UNFCCC (9 May 1992). United Nations Framework Convection on Climate Change, New York, archived from the original on 14 April 2005.

- UNFCC (25 October 2005). Sixth Compilation and Synthesis of initial national common actions from parties not included in Annex 1to the convention note by the Secretariat Executive Summary. Document code FCCC/SBI/2005/18, Geneva Switzerland: United Nations Office.

- UNFCCC. (2009). Copenhagen Accord (United Nations Framework Convention on Climate Change). See http://unfccc.int/resource/docs/2009/cop15/eng/l07.pdf.

- Yadav, R. S. , Dash, S.S., Chakraborty, S., & Kumar, M. Perceived CSR and corporate reputation: The mediating role of employee trust. Vikalpa. 2018, 43, 139–151. [Google Scholar]

- Zhou, G.; Liu, L.; Luo, S. Sustainable development, ESG performance and company market value: Mediating effect of financial performance. Bus. Strategy Environ. 2022, 31, 3371–3387. [Google Scholar] [CrossRef]

- Zadek, S. The Path to Corporate Responsibility. Harvard Business Review. 2004, 82, 125–132. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.