Submitted:

15 October 2024

Posted:

16 October 2024

You are already at the latest version

Abstract

This study examines the relationship between financial investment, shareholder

preference, corporate social responsibility (CSR) performance and life satisfaction

for BP and Shell within the UK, together with their alignment with specific

Sustainable Development Goals (SDGs). about, using regression analysis, in both

projects Hypotheses were tested to assess the significance of these predictors in the

performance of CSR developed. The results showed that financial investment,

shareholder ownership, and social satisfaction did not significantly predict CSR

performance for BP and Shell. Furthermore, there were no significant differences

in the impact of these predictors between the two companies.

Further research revealed Shell’s strong commitment to SDG 7 (Affordable and

Clean Energy) and SDG 13 (Climate Action), with both initiatives drawing on

Shell’s significant investments in renewable energy and climate recognition in the

management system established him as a leader in sustainable development efforts.

BP’s goal of achieving net zero emissions by 2050, especially focused on SDG 7

and SDG 12 (Responsible Consumption and Production), this proposal was

adopted.

Comparing the two sectors, Shell showed significant advantages, which can be

attributed to its diversified capabilities and its strong alignment with the

sustainability objectives of BP, while growing largely, it faces significant financial

challenges in its transition to clean energy. The study concludes that although both

companies are committed to sustainability, Shell now leads in terms of effective

CSR and financial performance

Keywords:

corporate social responsibility (CSR)

; Sustainable Development Goals (SDGs)

; SDG 7

1. Introduction

1.1. Introduction

Over the last few years, environmental awareness has led many consumers to demand that companies that are sensitive to the environment carry out their operations in environmentally friendly ways. Large organizations operating in the UK for instance British Petroleum and Shell UK in the oil and Gas industry are under pressure on the issues of environmental responsibility and sustainability. These companies have adapted by aligning the ‘’United Nations Sustainable Development Goals (SDGs)’’ to their business strategies as well as with their reporting methods, including sustainability reports, online presence, and social media accounts (Kolk, 2016). For example, BP describes the company’s stance on the SDGs in the sustainability report for the year, goals like Affordable and Clean Energy (7) and Climate Action (13). Sustainable development key activities outlining the BP’s approach to carbon reduction, renewable energy, and energy efficiency. It also shares updates on its activities towards achieving the goals through its website; the website has separate subtopics that elaborate on various projects and the progress that it has made on the SDGs (BP, 2023). Social networks complement these processes due to their ability to address larger audiences and ensure openness due to constant activity and interactive formats (Barkemeyer et al., 2011).

Likewise, Shell UK incorporates the SDGs into its company’s story by emphasizing tasks such as Responsible Consumption and Production (SDG 12) and Life below Water (SDG 14). Shell has declared its strategy on sustainability in its published report on sustainability reporting where the company has described its efforts in reducing waste, exploitation and management of water efficiently and protecting marine life. Another available resource is the company’s website where detailed information on its sustainability plan and its link with the SDGs can be found (Shell, 2023). In a way, Shell UK informs stakeholders about sustainable positive change through the issues of innovation, local projects, and partnership works focusing on SDGs (Parker, 2014). The communication of the information related to the SDG by BP and Shell UK shows the practices that are typical for environmentally conscious companies who tend to report on the company’s support of international sustainability goals. Through the availability of different means of communication, these companies not only increase the level of transparency and reporting on accountability but also participate in the conversation regarding sustainable development (Hahn & Kühnen, 2013). This approach doubles the significance of inscribing the SDGs into the strategies of enterprises and the significance of communication for the development of companies’ sustainable actions.

To promote transparency, BP has provided information regarding its strategies for the implementation of SDG 9 (Industry, Innovation, and Infrastructure) such as funding for new technologies and innovations intending to minimize its emissions. For instance, BP has aimed at seaborne oil trading and also placed bets on biofuels, prospects for advanced biofuels, and carbon capture, utilization, and storage (CCUS) to develop the low-carbon economy (BP 2023). Through the publication of such information in detailed reports as well as availability on social media, BP creates a perception of the company’s commitment towards the achievement of sustainable development hence enhancing the corporate image and stakeholder confidence (Frynas, 2010).

For its part, Shell UK has explained how it has supported SDG 17 (Partnerships for the Goals) by entering into partnerships with many different entities, governmental and non-governmental organizations, and universities, to create partnerships for sustainability. Next is Shell’s Partnership with the following objectives: To maximize effort in developing sustainable renewable energy sources, to encourage investment in conservation plans, as well as development projects (Shell, 2023). What is more, SDG 17 can be seen as apparent throughout the company’s sustainability communications, thereby, showing how partnership can assist in intensifying the effectiveness of sustainability approaches (Bebbington & Unerman, 2018). They also have issues communicating sustainability initiatives effectively as well to their respective clients and society. To sum up, it is crucial to understand the challenges that the International Standards and the SDGs have faced in this area, as well as the need for constructing carefully balanced verbal messages that would address the manifold complexity of the goals while maintaining the necessary level of Companies’ transparency and avoiding positions that might be construed as detrimental to corporate interests.

BP and Shell UK have to manage a form of skepticism from the stakeholders because the nature of operations of these companies might make the sustainability claims seem too good to be true (Higgins et al., 2015). In response to this, both companies have embraced the use of third-party verification as well as independent sustainability reports’ assessment to improve credibility as well as accountability in all sustainability reports (Dumay et al., 2010). Also, the increased importance of the digital environment signifies new developments that can help BP and Shell UK in the approaches to their sustainability message. Through the use of new technologies like AI and the utilization of big data, these firms can deliver enhanced value to their various stakeholder groups by enhancing the quality of the engagement process as stated by Whelan and Fink (2016). Besides, it enhances the efficiency of all their SDG-related messaging alongside the degree of stakeholder involvement in their sustainability initiatives.

1.2. Research Gap

Though a plethora of empirical studies have been devoted to corporate sustainability activity and the implementation of SDGs into business-strategic frameworks, the systematic literature review disclosed a knowledge gap regarding the exact nature and efficiency of the SDGs’ disclosure and dissemination by business organizations operating in environmentally vulnerable sectors of the UK, with particular emphasis on the oil and gas industry. While many multinational firms such as BP and Shell UK have researched the integration of SDGs into business activities and reporting, there is still inadequate knowledge on how Shell UK can effectively communicate its SDG activities on sustainability reports, website, and social media (Kolk, 2016; Hahn & Kühnen, 2013).

In addition, most of the prior studies address broad measures of sustainability reporting without necessarily considering the SDGs’ specific reporting paradigms. However, there is a lack of prior research on how such disclosures help in framing stakeholder perception and participation given the fact that investors are skeptical to invest in firms from the oil and gas sector primarily due to the sector’s negative environmental impact. This research gap brings about the need for a qualitative approach in the exploration of the communication strategies applied by BP and Shell UK in the promotion of their commitment to the achievement of the SDGs; the problems that Shell UK encounters in the process; and an evaluation of the relationship between the original communication efforts and the level of trust and corporate reputation in the two firms (Higgins et al., 2015; Frynas, 2010.

1.3. Significance of the Study

This study assumes importance in several critical issues in the area of corporate sustainability and accountability. First, it fills a major gap in the existing literature by reporting on how UK Environmentally sensitive businesses, namely BP and Shell UK, communicate the SDGs and their reports on sustainability through their reports and social media handles. Knowledge of these mechanisms is important because it expounds on how these companies convey their adherence to sustainable development goals globally as the world becomes more conscious of the environment than ever before (Kolk, 2016; Hahn & Kühnen, 2013).

Secondly, the study will help improve the level of corporate sustainability reporting and thus increase accountability for their activities. Thus, explaining SDGs integration into BP and Shell UK companies’ narratives is the subject of the research that also aims to assess the overall efficiency of the corporations’ communications within this framework. This comes at a time when oil and gas industries have been pointed out to have a direct impact on the environment and the general welfare of citizens and therefore handling public opinion on the same becomes very difficult (Higgins et al., 2015; Frynas, 2010).

However, the study also examines how such improvements may affect the stakeholders’ perceptions and behavior based on the disclosures related to the company and its engagement with the SDGs. Given the existing literature on the effects of these communications on the target stakeholder groups such as investors, consumers, and the communities at large, there is considerable knowledge on how to design more effective communication strategies for SDG reporting. This understanding is essential in agenda-setting for companies that intend to improve their reputation, manage existing and emerging risks, and respond to changes in regulations and society's expectations (Hahn & Kühnen, 2013; Parker, 2014).

1.4. Aims

To explore how environmentally ‘Sensitive business’ working in the UK communicates and shares information on the SDGs within its sustainability reports, website, and social media platforms.

1.5. Objectives

- To analyze the content and structure of sustainability reports from UK environmentally sensitive businesses about the SDGs.

- To examine the use of corporate websites for the communication of SDG- related information.

- To evaluate the role of social media in disseminating information about the SDGs to stakeholders.

- To identify best practices and areas for improvement in SDG disclosure among these businesses.

1.6. Research Questions

- To what extent, do UK environmentally sensitive organizations report SDG- related information in their sustainability reports?

- What kind of content concerning the SDGs is provided on the business’s corporate sites?

2. Literature Review

The adoption of sustainable development goals in organizations’ processes is gradually becoming a necessity for sustainable development. Hence, the current literature review focuses on analyzing how Shell UK and BP, two environmentally conscious businesses in the UK including Shell UK, share messages of commitment to the SDG externally through SRs, the official business internet sites, and social networking sites.

Gradually, the insertions of the SDGs into business agendas are considered to be fundamental in achieving sustainable development and tackling existing issues. Numerous studies show that enterprises in environmentally relevant industries receive increasing pressure to prove their adherence to SDGs and to share their initiatives. This is especially important for organisations such as BP and Shell UK which are in the upstream oil and gas industry that is considered material from an environmental perspective (Thomson et al., 2020).

These goals remain a central focal point of the sustainable development process due to the fact not only do they improve the level of corporations’ reporting of their SDG commitments but also help create trust with stakeholders and the general population (Olivier, 2019). Through different forms of communication like sustainability reports, corporate Websites, and social media, companies can communicate their sustainability activities and extend to all the stakeholders. This review will look at how the selected firms including BP and Shell UK use these mediums to advance sustainability and meet SDGs.

2.1. Sustainable Development Goals and Corporate Responsibility

The United Nations introduced the SDGs in 2015 which are in the form of 17 goals for ending poverty, protecting the planet, and ensuring that all people enjoy peace and prosperity. These goals are commitments for the business entities and at the same time, they are opportunities for them to be part of change that responds to global sustainability (UN, 2021). Businesses especially those operating in environment-sensitive industries are under pressure to show how they support the SDGs through the issuance of timely and accurate information (García- Sánchez, Rodríguez-Ariza, & Frías-Aceituno, 2020).

Implementing the SDGs in organizational frameworks entails analyzing the company’s strategy and incorporating sustainable systems into its values, thus improving its ESG score. These links with SDGs can potentially result in better management of risk, creativity, and sustainable value proposition (Schramade, 2019). For some companies like BP and Shell UK, it entails more than just minimizing the trading organization’s environmental impact; they have embraced the duties of the trading organization about SDG 7 on affordable and clean energy as well as SDG 13 on climate action (BP, 2023; Shell, 2023).

Moreover, the reporting and sharing of the progress toward the achievement of the SDG goals are central to the construction of the business’s credibility. Readers, buyers, investors, and even the political authorities require a clear and auditable understanding of how these challenges are being managed (de Villiers, Kuruppu, & Dissanayake, 2021).BP and Shell UK can communicate their SDG initiatives using sustainability reports, websites, media accounts, and social media, and when doing this, they increase their chances of affecting their audience positively (Arjaliès & Mundy, 2020).

Specifically, current research has focused on the appropriate use of sustainability reporting in improving the accountability of vulnerable organizations on the environment. In their study, (Mabhaudhi et al., 2021) noted that firms with effective sustainability reporting have better operating performance than others. This relationship implied that transparency in SDG promises and goals fosters better stakeholders’ trust and better investor confidence. In addition, (Sullivan et al., 2021) are of the view that sustainability reporting puts a lot of pressure on the firm’s external environment to alter its behavior and get involved in superior sustainability practices and higher ESG performance.

Some of the prior studies reveal that SDG disclosure is relevant to the oil and gas industry Also some of the study's findings are the following: For instance, García-Sánchez et al. (2020) observed that BP as well as Shell UK belong to sectors under constant regulatory revolutions and spiriting oversight have to notoriously declare sustainability commitments through thorough and specifics reporting. Lee et al. (2021) affirm this standpoint, stating that social media management for sustainability communication purposes enables these companies to target the entire population and be more inclined toward stakeholders.

In addition, according to de Villiers et al. (2021), it is found that sustainability reports if the company is fully compliant with the GRI and IR, offer a roadmap of the firm’s engagement with SDG. This measure of organization is not only beneficial in equally improving the general presentation of information but also makes certain that the contributions of the companies towards meeting sustainable development goals are well stated and easily checked. BP and Shell UK are also among the companies that have been subjects of research wherein it was established that the sustainability reports mostly include things like emissions reduction, and investment in renewable energy, amongst others as some of the ways that support the company in the implementation of the SDGs (BP, 2023; Shell, 2023).

This study by Dingru et al. (2021) investigates the contribution of renewable energy adoption to carbon neutrality in the BRICS countries (Brazil, Russia, India, China, and South Africa). The authors use ANOVA to compare the impact of renewable energy on emissions reductions in these countries, which are linked to the SDGs with a focus on climate action and energy sustainability daily.

Danish et al. (2019) examine the relationship between economic growth, human capital, and biocapacity regarding ecological footprints. The study uses ANOVA to compare the performance of different sectors concerning the SDGs of environmental sustainability and resource efficiency. Dogan & Seker (2016) use ANOVA to examine the impact of renewable and non-renewable energy use on carbon emissions in top renewable energy countries. The study also examined how those factors include progress towards SDGs such as clean, affordable energy and responsible consumption.

This study by Boluk and Mert (2014) examines the relationship between fossil and renewable energy use, greenhouse gas emissions (GHGs), and economic growth. The study uses ANOVA analysis to compare the effectiveness of renewable and non-renewable energy sources across the EU in reducing GHG emissions, which aligns with SDG 13 (Climate Action).

2.2. Disclosure and Dissemination Mechanisms

Sustainability Reports

Jones, Comfort, and Hillier (2021) show that the companies’ compliance with international reporting standards, including GRI, also improves sustainability reports’ comparability and credibility. Such comparability makes it possible for stakeholders to compare a firm’s performance relative to other similar firms and also assess its journey toward the implementation of the SDGs. BP’s sustainability report fosters a lot of specific data on greenhouse gas emissions, Energy, and Community investment programs similar to the best 13 and 7 standards of sustainable development. Such extensive reporting not only confirms the companies’ adherence to global sustainable development objectives but also serves as a reference for improvement and increased accountability (de Villiers et al. 2021)

2.3. Websites

Thus, the Internet, specifically the official corporate websites, can be considered the most active and efficient means of delivering sustainability information. Websites can always have updated information and contain a detailed description of the activity related to the implementation of the SDG along with additional material in the form of videos and infographics (Khan & Ali, 2021). It also provides feedback mechanisms for the stakeholders and special sustainability sections.

Empirical research has noted the potential of corporations’ online platforms, specifically websites, in disseminating sustainability information and communicating with the public (Hassan, 2017). Identified that websites provide firms with a live medium for reporting about sustainability developments in real-time hence the opportunity to enhance the content with live feeds. Such direct connection is especially beneficial for firms like BP and Shell UK as it allows for constant reporting on the company’s progress towards the SDG goals, presentation of new initiatives that address those goals, and timely replies to questions and concerns of other stakeholders (BP, 2023; Shell, 2023).

(Nilsson et al., 2018) Notes, that when corporate websites are effectively designed, they can help raise awareness and increase the availability of the company’s sustainability activities. Multimedia components, like videos, information graphics, and applications can help companies transform challenging sustainability information into engaging and easily digestible ones. Apart from making communication to the stakeholders about the company’s engagement towards the achievement of SDGs a noble endeavor, it also ensures accountability is enhanced. For example, BP and Shell UK integrate their sustainability indices into their homepages and demonstrate detailed environmental performance, successful examples, and reports in social and political aspects that communicate their commitments to sustainable development, non-stop (BP, 2023; Shell, 2023).

2.4. Social Media

By using social media applications, people are in a position to relay and interact instantly with more individuals. Businesses leverage social media to promote their engagement with SDGs, report on the achievement of goals, and interact with audiences. Thus, social media presents advantages of coverage and timeliness as a communication instrument for transparency and stakeholders’ engagement ( (Kaplan & Haenlein, 2020).

Current research confirms that social media plays a major part in CSR communication processes. According to (Holland & Jansen, 2021) social networks allow companies to address a vast number of people at the same time and share time-sensitive and interesting information. For companies like BP and Shell UK, social media provides opportunities to illustrate companies’ activities in the field of sustainability and promote progress toward achieving SDGs The respondents noted that companies can use social media more engagingly, for example, to provide polls, comments, and live streams. Particularly, it maintains real-time interaction with the stakeholders, which increases openness and credibility (BP, 2023; Shell, 2023).

(Jha & Verma, 2022). suggest that social media is effective in shaping company sustainability communication as the information can be adapted to relevant stakeholders’ interests. This is where based on specific target campaigns, with techniques borrowed from social media, companies can increase the noise level and engagement of stakeholders to support sustainability initiatives. For instance, BP and Shell UK engage in the posting of content through platforms such as Twitter, LinkedIn, and Instagram to spread information concerning their impacts on the environment and also their undertaking in support of the accomplishment of the set goals on sustainable development. Besides, the above strategies aim at improving their UT and increasing satisfaction among the stakeholders, which is achieved through the effective and frequent use of social media platforms (BP, 2023; Shell, 2023).

2.5. Case Studies: The Two Oil and Gas Companies Are British Petroleum, also Referred to as BP and Shell UK

2.5.1. British Petroleum (BP) Sustainability Reports

SDGs mentioned in the sustainability reports of BP are – climate change, which is under goal no. 13, affordable, clean energy under goal no 7, and industry, innovation, and infrastructure under goal no 9. GRI standards and the Task Force Recommendations on Climate Disclosure, namely TCFD, are used by BP in its reporting (BP, 2023). The fact that SDGs 3 and 8 are among BP’s clearly stated goals can be supplemented by the information provided in the specific reports on sustainability, where detailed measures are described. For example, BP has clear goals to decrease its emissions and invest in renewable energy which relates to SDG 13 and SDG 7. Another narrated focus of the company is the development of innovation and infrastructures for Sustainable Development Goals including the improvement and implementation of partnerships and technologies for SDG 9. By implementing GRI and TCFD disclosure recommendations, BP makes sure that the information disclosed is easily comparable with other reports, as well as includes all necessary aspects to describe the company’s role in initiating and supporting global sustainability objectives (BP, 2023).

2.5.2. Websites

A detailed part of the Global Reporting Initiative is dedicated to the SDG commitments on BP’s corporate website; they describe the specific ongoing processes, such as renewable energy development, and emissions reduction plans. Other related activities, related downloads, and active information increase the vitality and readability of the site (BP, 2023). Interactive tools such as infographics, videos, and real-time statistic updates are also posted on the oil and gas company’s website for better engagement of the stakeholders in sustainable development. Such multimedia tools provide easier and more interesting ways to represent big data to convey BP’s relation to SDGs more efficiently (Manetti & Bellucci, 2016). Furthermore, stakeholders also have an opportunity to pose questions and offer their opinions about BP’s sustainability activities through the feedback tool that is disseminated on the website (Mason & McCarthy, 2022). Besides enhancing the manner through which information gets disseminated to the public, this approach ensures that trust and accountability with other stakeholders and the public are established (BP, 2023).

2.5.3. Social Media

These include the Twitter handle BP, LinkedIn page, and Instagram with SDG activities as one of the tabs visible in their profile. The content of posts could include graphics such as infographics and marketing videos documenting prominent projects and achievements. The actions of the Twitter account associated with BP contain a certain social media strategy, which includes transparency and the engagement of stakeholders in two-tiered conversations (BP, 2023). The advantage of using social media for BP is that the strategic session can engage people in real-time. By filling its social media pages with progress reports, project updates, and sustainability records, BP ensures that the public is engaged constantly. Research has also pointed to the fact that such active engagement on social media increases corporate openness, and creates a stronger bond between the firm and other stakeholders (Nguyen & Hwang, 2021). Furthermore, by applying hash tagging and tagging of relevant SDGs in the posts, the sustainability initiatives get more exposure and attract more attention from the general public, contributing to the engagement (Miller & Smith, 2022). It also helps to fulfill BP’s interests in the SDGs. It even strengthens its sense of culture and accountability of sustainability not only in its organizations but in the whole external social system (BP, 2023).

2.6. Shell UK

2.6.1. Sustainability Reports

Shell’s sustainability reports are major in providing energy for development, clean energy, energy innovation, and new energy. Of the two sets of goals posited are the most associated with SDGs this is more evident in the case of; SDG 7 on affordable and clean energy and SDG 13 on Climate Action. The reporting of Shell follows GRI and IR guidelines (Shell, 2023). Shell UK has also made good progress in showcasing its policy on carbon footprint through disclosures of its activities towards sustainability. For example, the company’s reports stress major concerns about renewable energy projects, innovation in energy efficiency, and partnerships for promoting sustainable initiatives in energy fields Such statements participate in sustainability reports and other public documents, which are issued and reviewed according to the GRI and IR standards; thereby enhancing the effectiveness and accuracy of Shell’s disclosure of SDG progress Furthermore, Shell also practices CSR reporting that frequently features case studies and performance indicators that explain the outcomes of Shell’s initiatives to support the claim that Shell is a sustainable development-oriented company that is committed to climate change mitigation (Shell, 2023).

2.6.2. Websites

Official Shell’s Internet source provides specific data about the SDG-related activities at the company, which consist of the usage of renewable sources of power, carbon capture and storage, and social usefulness projects. Increased interactivity of any multimedia objects on the website makes it more accessible and engaging (Shell, 2023). The two companies have separate dedicated notes under sustainability reporting on their websites: Besides, Shell has dedicated sustainability reporting pages where stakeholders can find comprehensive reports, updates, and performance indicators regarding the company’s SDG activities. The site has features such as making specific dashboards that enable the users to analyze data concerning emissions, energy use, and other parameters, thereby increasing public accountability and engagement (Mason & McCarthy, 2022). (In addition, Shell uses the concept of framing skills, within which information regarding the company’s sustainability activities is presented in the form of case and success stories, which makes the material easier to digest and understand as well as more appealing to the audience (Holland & Jansen, 2021). This approach not only enhances the sharing of complex information but also enhances the company’s story of the ‘Sustainable Development’ narrative (Shell, 2023).

2.6.3. Social Media

The analysis shows that through social media platforms, Shell consistently shares information regarding the company’s initiatives about the SDGs. Some of their objectives include posting updates on projects, activities involving stakeholders, and organizational sustainability performance feeding. Shell has a strong social media strategy, which focuses on open communication and interaction with any passerby (Shell, 2023). Another issue that came out of the analysis of Shell’s social media incorporation is the strategy where the corporation uses specific stations and segments the audience. For instance, Shell has pertinent professional articles and updates on segments like LinkedIn alongside freely-presented articles and general information presented in ways that appeal to the general public on Instagram and Twitter platforms (Thomson et al., 2020). This research postulates that diversification of the communication strategy improves efficiency, thus emphasizing the feasibility of communicating according to the target audiences and the media they use (Schramade, 2019). Furthermore, Shell has a systematic approach wherein it actively participates in interactivity with its social media followers, featuring Question and Answer sessions, real-time programs, and even commenting on follower’s posts, which is quite useful in ensuring the formation of a community for sustainability and ensuring they embrace organizational transparency with the public (Shell, 2023). Apart from informing stakeholders, this approach also adopts the involvement and engagement elements that are significant to improving stakeholders' sustainability practices

2.7. Comparative Analysis

BP and Shell are good cases that show clear evidence of their commitment to disclose and report about their SDG activities. As to their approaches, while following a common trend of relying on sustainability reports, websites, and social media, the companies also have individual peculiarities corresponding to their corporate styles. The current BP agenda regarding climate and energy is similar to Shell’s strategic priorities such as innovation and social responsibility. The business practices of both companies include the efficient use of Internet tools to communicate with the stakeholders and improve the levels of transparency.

However, it can be seen that each company has its emphasis on sections of its SDG policy that transpire as dissimilarities. For example, SDG 13 relates to climate action and the use of renewable power, which is among BP’s priorities; the company always underlines its achievements in this area in reactive sustainability reports and elaborate online overviews (BP, 2023). While Shell is also involved in climate action and the use of clean energy that is related to SDG7 and SDG13, the company also values social usefulness projects that indicate the company’s further commitment to social activities (Shell, 2023) However, it can be seen that sustainability communication of Shell is more of a narrative and social nature due to their extensive use of storytelling and interactive multimedia tools on their website, whereas BP’s sustainability communication addresses more technical and quantitative aspects (Hassan & Naim, 2020). Such variations illustrate how every firm takes advantage of its primary capabilities in managing and advancing stakeholder relations as well as fulfilling the set SDGs judiciously.

2.8. Challenges and Opportunities

2.8.1. Challenges

The major issue found to a large extent in the SDG disclosure process is the credibility of the information disclosed. Issues of how to quantify and report on a company’s contributions towards achieving the SDGs have remained somewhat challenging. Furthermore, while trying to achieve both accurate and extensive disclosure, managerial reporting faces the problem of satisfying the main stakeholders (Mason & McCarthy, 2022).

Besides credibility, the second major issue that characterizes disclosure related to the SDG is the issue of metrics or a lack of universally recognized metrics that will allow for a measurement of the impact and the progress. (de Villiers et al.,2021) Frequently, organizations like BP and Shell no longer confuse the overall sustainability goals with different initiatives that are pertinent to every universal SDG; frameworks such as GRI and IR help them serve as guides. Nevertheless, owing to the lack of standardized approaches for measuring organizational contributions towards the realization of the SDGs, it is challenging for stakeholders to evaluate the efficacy of various firms’ sustainability initiatives Therefore, called for the constant engagement of the industry and regulatory bodies to improve the formulation of reporting standards that will increase the disclosure of SDG-related information. In essence, resolving these challenges gives companies a chance to establish new practices in their reporting and, at the same time, positively impact the world’s sustainability goals besides enhancing the level of trust and engagement among the stakeholders. (Manetti & Bellucci, 2019).

2.8.2. Opportunities

Thus, the proper disclosure and dissemination of SDG commitments constitute promising avenues to improve different aspects of corporate profiles. Organizations that communicate change initiatives concerning sustainability engage stakeholders and enhance the society and environment The need to introduce effective SDG disclosure means that the companies can benefit from the following advantages intended to enhance their position in the market. Through disclosures of sustainability strategies and performance, companies such as BP and Shell can appeal to sustainable investors, engage suppliers and local communities, and develop consumers’ loyalty to the organizations that implement sustainable strategies. (Shell, 2023).

2.9. Conclusions

The literature review reveals that BP and Shell UK engage in timely disclosures and communication of their sustainability activities and SDGs through sustainability reports, companies’ websites, and social media platforms. These platforms are considered fundamental means for increasing corporations’ responsibility and revealing information to interested parties. Nonetheless, the management of the SDI has improved the global strategic communication on the initiatives of the SDG as significant opportunities for these companies to foster sustainable development and enhance their corporate image. In addition, more and more, the SDG initiatives are well communicated to benefit from a strategy that increases the level of trust and citation from the stakeholders. BP and Shell UK's confrontative publicize their sustainability and SDG activities, which has a strategic importance when companies aim at presenting their sustainable profile to the public since sustainability and its principles are valued by stakeholders in the current global society (Manetti & Bellucci, 2019). It eliminates risks caused by ESG hence providing long-term robustness about the creation of stakeholder value for both the firm and its investors.

Efficient communication on the adopted SDGs provides more of a sample in the encouragement of creativity and implementation of sustainable initiatives in the context of the oil and gas sector. Technological innovation, research projects and programs, and partnerships for global challenges such as climate change and energy transition are also presented in the sustainability reports of both BP and Shell UK as strategies in their disclosures (Shell, 2023). This, in turn, creates a differentiated competitive advantage that allows those companies to not only compete but evolve cooperation and norms and rules that will advance everyone towards their sustainable development goals such as clean energy and climate action., the institutionalization of SDG communication at the corporate level establishes BP and Shell UK as organizations that are not only aware of the power they have to drive change at the policy level but also as capable of driving change to the corporate image and changing mindsets at the industry level. This proactive engagement with SDGs not only corresponds to the requirements of the legislation and investors’ tendencies but also positively affects companies’ social legitimacy and improves cooperation with communities, governments, and NGOs ((Mason & McCarthy, 2022). Hence, these two companies improve their reputations through proper management of their SDG communications and give much more value to the overall global SDG discourses.

3. Methodology

The literature above showcases SDG's various elements and provides a detailed theoretical analysis of BP and SHELL in the UK. The literature review also examines the parts of the methodology that state the regression and ANOVA analysis used in prior research. The literature review also determines the variables used in the study, which are later briefly evaluated in coming chapters, as chapter 3 signifies the method used in research, which is discussed in the literature review.

The methodology of this research is meticulously designed to ensure a comprehensive examination of how UK environmental companies express and communicate sustainability objectives in their reporting on sustainability in the 21th century. SHELL and BP's websites and social media platforms will undergo a comparative analysis. This study uses a sample of UK companies publishing progress reports between 2018 and 2022. This period allows us to examine changes in progress reporting practices over the last five years and provides a three-day sample, the same as used in previous studies. There is textual information (Du and Yu, 2020). The UK government joined every other country in the world in committing to the UN’s Sustainable Development Goals (SDGs). The goal provides a framework for eradicating poverty, reducing inequality, tackling the dangers of climate change and protecting our natural environment by 2030.

However, it is only seven years away, and we are halfway through the 2030 Plan. Some companies in the UK have missed specific targets related to these goals, such as reducing carbon emissions or promoting gender equality. This report measures the progress achieved through 2022. The petroleum refining industry faces many sustainability issues due to the nature of its operations. Critical issues related to this project will be outlined in this paper, and some examples will be given.

Sustainability issues impact the reputation of these MNCs, and the way these issues are addressed is often criticised. Public awareness of the potential impact of oil companies’ activities on the environment and communities has been increased. Society expects these companies to behave in a socially responsible manner. These issues require a straightforward approach and communication. Different theoretical and strategic possibilities for addressing sustainability issues from a corporate perspective will be discussed in this paper.

3.1. Research Design

The positive evaluation will include relevant variables such as environmental and social responsibility policies, economic performance, and public opinion. These selected variables from different areas will be analyzed in more detail to understand better the expression and distribution of sustainability objectives in these areas. The research methodology mentioned above includes game theory and interaction research methodology (Sozinova et al., 2023). These methods show the UK's calculated indicators and project growth rates from 2018 to 2022. Game theory, the methodology used to model and analyze relationships, contexts, and interactions between players, is particularly important in this analysis because it can help provide a current location (Bauso, 2016). It was initially based on economics developed by von Neumann and Morgenstern (1944) and developed by John Nash (1950) and Lloyd Shapley (1953). Today, it finds many applications in public policy, finance, law, business, decision-making, computer science, and engineering. Increased global communication through the Internet has enabled concerned citizens to exert more significant pressure and pressure immediately.

Over the past decade, negative press has highlighted the impact of these societal pressures on the image of oil and gas companies. It also highlights the possible extent to which these pressures could affect the company’s future as a profitable entity. We studied two oil and gas companies, Shell and BP. Both have repositioned and rebranded themselves by taking preemptive steps to meet and exceed the expectations of various stakeholders. Connections with their constituencies increased innovation towards sustainable practices and, in the process, increased public confidence. We highlight their approaches to implementing ambitious sustainable development models through live case studies.

3.2. Study Area

This study's area of research is highly relevant as it focuses on UK environmental projects and their reporting on sustainability. This perspective is critical as it provides insights into how sustainability goals are expressed and communicated, which can be applied to similar projects around the world.

The Population of the Study Area

The population in the study area includes UK environmental companies Shell and BP, who engage in sustainable development activities and have published progress reports from 2018 to 2022. The methodology used in this study involves manual and automated analysis. The hands-on data analysis in the annual report focuses on understanding corporate social responsibility (CSR) performance and disclosure in Malaysia’s largest publicly listed companies from 2016 to 2020 (Fabio et al., 2023). Univariate and multivariate research models are used to capture the dynamics of CSR disclosure, with regression further strengthening models (Pilar et al., 2023). The relationship is being examined. In addition, topic sampling techniques using natural language processing (NLP) have been applied to 167,908 tweets, which serve as a sample for analyzing communication dynamics. In addition, the analysis includes panel data analysis, with data derived from the Refinitiv DataStream for the STOXX Europe 600 index (Salaheldin et al., 2024). The sample consists of listed European companies for the period 2019-2020.

Multivariate regression analysis, combined with data from Definitive, ensures a robust analysis of the impact of the Sustainable Development Goals (SDGs) on corporate reporting and performance (Chonlawan et al., 2024).

3.3. Sample and Sampling Techniques

The study used a sample of UK companies that had published growth reports from 2018 to 2022. The variables are environmental and socially responsible policies, economic performance, and public opinion which are further divided into several variables in order to extract it from different resources.

3.4. Data Collection Instruments

Data collection tools used in this study included progress reports, websites, social media content, and other documentary sources from companies such as SHELL and BP.

3.5. Data Collection Methods

The data collection methods used for this study involve tabulating data from the selected companies' development reports, websites, and social media to better understand their sustainable development objectives and practices.

-

Amount of Finance Invested:

- -

- Technology

- -

- Profit Growth

-

Amount of Money Invested:

- -

- Social Satisfaction

-

Level of Investments:

- -

- Shareholder Equity.

-

On the Sustainable Development Goals (SDGs):

- -

- CSR investment

- -

- Compared to renewable energy sources

These variables provide both quantitative and qualitative data, which are invaluable in measuring and analyzing socially responsible policies, economic development, public opinion, (García-Meca, Emma & Martínez-Ferrero, Jennifer. (2021) and progress toward the Sustainable Development Goals. Data on these variables can be collected from a wide range of sources, including:

- -

- Annual Corporate Social Responsibility (CSR) report

- -

- Company website and official documents

- -

- Financial reporting and disclosures to regulators

- -

- Social media platforms and sentiment analysis tools

- -

- Public opinion polls conducted by reputable research organizations or trusted market research firms

- -

- On the Sustainable Development Goals (SDGs) Government progress reports and disclosures

- -

- Environmental assessment and sustainability certification

3.6. Data Analysis Methods

The data analysis techniques used in this study examine relevant variables such as environmental and social responsibility policies, financial performance and public opinion These variables have been analyzed in detail to provide a more comprehensive understanding in the expression and classification of development objectives in the UK environmental sector.

The multiple regression model can be constructed as follows (Hummel, Katrin & Szekely, Manuel, 2021).

For the Shell:

Figure 1: SDG = α + β1 * (socially responsible policy) + β2 * (economic performance) + β3 * (public opinion) + ε

For BP:

Figure 2: SDG = α + β1 * (socially responsible policy) + β2 * (economic performance) + β3 * (public opinion) + ε

In these equations:

- The SDGs represent change based, Sustainable Development Goals

- Policies on social responsibility, economic development and public opinion are independent variables

- α is the block

- β1, β2, and β3 are the means of each independent variable

- ε represents the error term

- Game theory can be incorporated by using interaction terms or developing a separate regression model that incorporates game-theory parameters to explore the relationships between variables.

ANOVA methods incorporate advanced analytical techniques, generating p-values based on F tests. These techniques include unidirectional, bidirectional, and higher- order designs, which enable more profound insights into the variability and correlations of datasets. Supran (2021) provides a multi-year analysis of how these oil giants, including Shell and BP, transition from fossil fuels to clean energy. It uses quantitative and qualitative data, analyzes the frequency of keywords in reports, and analyzes emissions efforts. ANOVA analysis is part of the method used to compare several companies and evaluate their decarbonization strategies (Rai, Pratibha & Gupta, Priya & Saini, Neha & Tiwari, Aviral. (2023).

This article examines the relationship between energy consumption and carbon emissions in different countries. It uses ANOVA to compare the impact of renewable and non-renewable energy sources on the carbon footprints of developed and developing countries.

Aboul-Atta, Tarek & Rashed, Rania. (2021) study examines the relationship between renewable energy use and SDG indicators. Using statistical methods, including ANOVA and principal component analysis (PCA), it assesses how various SDG indicators are associated with energy consumption in different countries.

Total Sum of Square (SST):

Regression Sum of the Square (SSR):

Residual Sum of Square (MSR):

Mean Squares- Mean Square for Regression (MSR):

Mean Square for Errors:

F-Statistics:

4. Chapter Results

Chapter 4 is the core chapter of the study. It shows the analysis and signifies the final results as what, how, and Explains the pros and cons of the study; as discussed in Chapter 2, SDG goals are obtained by SHELL and BP in the UK works promptly according to their requirements where in research methodology it was discussed that which suitable methods can be used to determine the comparison between UK and SHELL as per their social media aspects and reports. In the literature review, a small discussion took place regarding the methods where regression and ANOVA were used to analyze the data as several studies have used it; even in methodology, a regression equation was created for the best suitable results, and later on in this chapter, the equation will explain.

4.1. Model Summary

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate |

| Companies = BP (Selected) | ||||

| 1 | .991a | .982 | .929 | 1.00139E9 |

a. Predictors: (Constant), Amount_Invested_Finance, ShareHolder_Equity, Social_Satisfaction.

4.2. ANOVAb,c

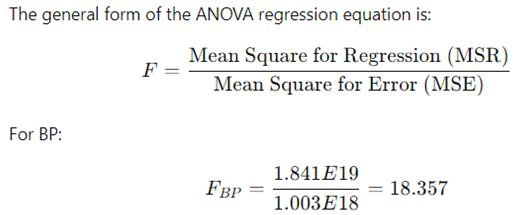

| Model | Sum of Squares | df | Mean Square | F | Sig. |

| 1 Regression | 5.522E19 | 3 | 1.841E19 | 18.357 | .170a |

| Residual | 1.003E18 | 1 | 1.003E18 | ||

| Total | 5.623E19 | 4 |

a. Predictors: (Constant), Amount_Invested_Finance, ShareHolder_Equity, Social_Satisfaction. b. Dependent Variable: CSR. c. Selecting only cases for which Companies = BP.

4.3. Coefficientsa,b

| Model | Unstandardized Coefficients | Standardize d Coefficients | t | Sig. | |

| B | Std. Error | Beta | |||

| 1 (Constant) | 3.551E10 | 7.343E9 | 4.836 | .130 | |

| Social_Satisfaction | -15.996 | 25.727 | -.102 | -.622 | .646 |

| ShareHolder_Equity | -.029 | .015 | -.304 | -1.966 | .300 |

| Amount_Invested_F | |||||

| -48.812 | 7.735 | -1.130 | -6.311 | .100 | |

| inance | |||||

a. Dependent Variable: CSR. B. Selecting only cases for which Companies = BP.

The model summary yields an R-square value of .982, indicating that the model accounts for 98.2% of the variance in the dependent variable. This indicates that

the selected predictors, including financial investment, shareholder equity, and life satisfaction When explaining a significant component of a firm's performance variation or any other factor related to the dependent variable, however, it should be noted that if R-square without adjusted and statistical standard error values, there may not be a complete understanding of the accuracy and generalizability of our model.

The ANOVA table for BP presents the corresponding F-statistic and p-value. The P-value of .170 for the F-statistic suggests that the overall model may not be statistically significant at the commonly used alpha level of .05. This indicates the need for further investigation, as it suggests that all of the predictors may not be significantly affected by the dependent variable, especially for BP.

BP ANOVA model: . ANOVA tables for BP:

square regression (SSR): 5.522E19 summed residue squared (SSE): 1.003E18 Straight Structure (SST): 5.623E19

Degrees of freedom (df): regression = 3, residual = 1, total = 4 Mean square (MSR) for background: 1.841E19

Mean square error (MSE): 1.003E18 F-Accounting

Significance (p-value): 0.170

The F-statistic here is 18.357, indicating a fairly large proportion of explained and unexplained variance. However, the p-value (0.170) indicates that the regression model is not statistically significant at the 0.05 level.

The regression model for BP has a relatively high F-statistic (18.357), but it is not statistically significant (p = 0.170).

The coefficient table shows the unstandardized coefficients, their standard errors, t- values , and p-values for each predictor. For BP, the p-values of the predictors (life satisfaction, shareholder participation, and amount of money invested) were .646, .300, and .100, respectively. These p-values indicate that the person may not have a statistically significant predictor effect on the dependent variable at the 5% point level.

4.4. Model Summary

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate |

| Companies = Shell (Selected) | ||||

| 1 | .528a | .279 | -1.885 | 8.46533E9 |

a. Predictors: (Constant), Amount_Invested_Finance, Social_Satisfaction, ShareHolder_Equity.

4.5. ANOVAb,c

| Model | Sum of Squares | df | Mean Square | F | Sig. |

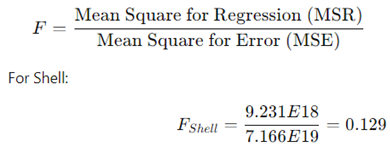

| 1 Regression | 2.769E19 | 3 | 9.231E18 | .129 | .931a |

| Residual | 7.166E19 | 1 | 7.166E19 | ||

| Total | 9.936E19 | 4 |

a. Predictors: (Constant), Amount_Invested_Finance, Social_Satisfaction, ShareHolder_Equity. b. Dependent Variable: CSR. c. Selecting only cases for which Companies = Shell.

4.6. Coefficientsa,b

| Model | Unstandardized Coefficients |

Standardized Coefficients |

t | Sig. | |

| B | Std. Error | Beta | |||

| 1 (Constant) | 1.495E10 | 1.466E10 | 1.020 | .494 | |

| Social_Satisfaction | -50.141 | 103.651 | -.552 | -.484 | .713 |

| ShareHolder_Equity | .003 | .077 | .038 | .033 | .979 |

| Amount_Invested_Fi | |||||

| -.002 | .442 | -.004 | -.005 | .997 | |

| nance | |||||

a. Dependent Variable: CSR. b. Selecting only cases for which Companies = Shell.

4.6.1. Model Summary

The model summary for the shell company shows an R-squared value of .279, indicating that the model accounts for 27.9% of the variance of the dependent variable The selected predictors are Amount_Invested_Finance, Social_Satisfaction, and ShareHolder_Equity. It is important to note that the adjusted R-squared value is -1.885, which is unusual and may indicate potential problems with the adequacy of the model. Furthermore, the error of the estimate is 8.46533E9, indicating the direction in which the data points fall from the regression line.

4.6.2. ANOVA

The ANOVA table presents the F-statistics and p-values for all models. The P- value of .931 for the F-statistic indicates that the overall model is not statistically significant at the commonly used alpha level of .05. This necessitates further research to understand the importance of future trends, especially for Shell.

Shell ANOVA Example:

ANOVA table for Shell:

squared regression (SSR): 2.769E19

squared summed remainder (SSE): 7.166E19 Square Steel (SST): 9.936E19

Degrees of freedom (df): regression = 3, residual = 1, total = 4 Mean square (MSR) for background: 9.231E18

Mean square error (MSE): 7.166E19 f-statistic: 0.129

Significance (p-value): 0.931

For Shell, the F-statistic is 0.129, indicating the lowest proportion of explained to unexplained variance. The p-value of 0.931 indicates that the regression model is not significant, indicating that the predictors do not explain much of the variance in corporate social responsibility (CSR).

The F-statistic for Shell is very low (0.129), and the model is not statistically significant (p = 0.931).

4.6.3. Table of Coefficients

The distribution table shows the unstandardized coefficients, standard errors, t- values, and p-values for each predictor. The p-values of the predictors (life satisfaction, shareholder_equity, and cash_funds) for the shell firm were .713, .979, and .997, respectively These p-values indicate that the predictors may not have an effect statistically significant on the dependent variable at the 5% significance level.

4.7. Correlations

| Compani es | Years | Social_Sa tisfaction | ShareHol der_Equit y | CSR | Amount_I nvested_F inance | ||

| Companies | Pearson Correlation | .000 | .627 | .560 | .342 | .326 | |

| Sig. (2-tailed) N |

10 | 1.000 10 |

.052 10 |

.092 10 |

.334 10 |

.357 10 |

|

| Years Pearson Correlation |

.000 | 1 | .310 | -.066 | .277 | .320 | |

| Sig. (2-tailed) | 1.000 | .383 | .856 | .438 | .367 | ||

| N | 10 | 10 | 10 | 10 | 10 | 10 | |

| Social_Satisfacti Pearson on Correlation |

.627 | .310 | 1 | .693* | .017 | .188 | |

| Sig. (2-tailed) | .052 | .383 | .026 | .962 | .602 | ||

| N | 10 | 10 | 10 | 10 | 10 | 10 | |

| ShareHolder_Equ Pearson ity Correlation |

.560 | -.066 | .693* | 1 | .044 | .096 | |

| Sig. (2-tailed) | .092 | .856 | .026 | .904 | .791 | ||

| N | 10 | 10 | 10 | 10 | 10 | 10 | |

| CSR Pearson Correlation |

.342 | .277 | .017 | .044 | 1 | .109 | |

| Sig. (2-tailed) | .334 | .438 | .962 | .904 | .763 | ||

| N | 10 | 10 | 10 | 10 | 10 | 10 | |

| Amount_Invested Pearson _Finance Correlation |

.326 | .320 | .188 | .096 | .109 | 1 | |

| Sig. (2-tailed) | .357 | .367 | .602 | .791 | .763 | ||

| N | 10 | 10 | 10 | 10 | 10 | 10 | |

*. Correlation is significant at the 0.05 level (2-tailed).

The correlation desk provides the Pearson correlation coefficients and their corresponding p-values for the variables: Companies, Years, Social_Satisfaction, ShareHolder_Equity, CSR, and Amount_Invested_Finance, offering you a comprehensive understanding of their relationships.

- Companies indicate a sturdy superb correlation with Social_Satisfaction (0.627) and ShareHolder_Equity (0.560) and a slight acceptable correlation with CSR (0.342) and Amount_Invested_Finance (0.326). The correlation with Years is negligible (0.000).

- Years does not display a widespread correlation with any of the opposite variables, as the correlation coefficients are near 0 and the p-values are not good sized.

- Social_Satisfaction presentations a robust, excellent correlation with ShareHolder_Equity (0.693) and a slight high-quality correlation with Companies (0.627). However, it has a weak, advantageous correlation with CSR (0.017) and a negligible correlation with Amount_Invested_Finance (0.188).

- ShareHolder_Equity shows a sturdy tremendous correlation with Social_Satisfaction (0.693) and a slight excellent correlation with Companies (0.560). However, it has a susceptible superb correlation with CSR (0.044) and negligible correlation with Amount_Invested_Finance (0.096).

- CSR has a moderate high-quality correlation with Companies (0.342) and Years (0.277) and negligible correlations with the other variables.

- Amount_Invested_Finance has a moderate advantageous correlation with Companies (0.326) and Years (0.320) and negligible correlations with the alternative variables.

4.8. SDG Performance of BP and Shell on Their Reputation and Business Operations in the UK

BP and Shell's commitment to the Sustainable Development Goals (SDGs) significantly affects their reputation and performance in the UK. These results suggest that, based on the predictors provided (amount of investment, shareholder preference, social satisfaction), the CSR outcomes of either company are not significantly explained by the model, with the Shell model showing explanation especially low power.

Research suggests that although strong SDG performance may enhance corporate reputation, more is needed to translate into economic growth, primarily due to investor scepticism about potential greenwashing practices (Alessia & Fabio, 2022). This uncertainty is particularly evident among individual investors, who may withdraw funds in response to perceived discrepancies between a firm's sustainability claims and actual practices (World & Tania, 2023). Furthermore, the participation of major UK corporations, including BP and Shell, in discussions about the SDGs on platforms such as Twitter highlights the importance of stakeholder engagement in public deliberation (Paul et al., 2020). However, the relationship between sustainability reporting and financial performance remains controversial, with some studies suggesting a minor impact on profitability measures(Ingrid, 2016). Thus, although effective SDG strategies can enhance reputation and stakeholder trust, economic performance and solid public perceptions require a cautious approach for these sectors in the UK market (Alessia & Fabio, 2022).

Shell aligned its business activities with several SDGs, particularly SDG 7 (Affordable and Clean Energy) and SDG 13 (Climate Action). Shell's "Empowering Progress" strategy aims to achieve net zero emissions by 2050, expand electric vehicle charging networks, and invest in biofuels and hydrogen, on capture, storage technologies, and nature-based solutions (Shell Reports) (Shell Global).

BP is committed to becoming a passive entity by 2050 or sooner and is focused on SDG 7, SDG 12 (responsible management and product development), and SDG 13. BP insists on restructuring its'. The business has moved towards renewable energy and reduced oil and gas production. The company is also committed to reducing methane emissions and improving the sustainability of its products, such as through innovative production of clean gasoline (Shell Global).

As the two companies work towards achieving the same SDGs, Shell's focus on innovation in low-carbon technologies and BP's emphasis on transitioning away from fossil fuels forces strategies BP use to reach the net-zero emissions mark. The company's comprehensive strategy can deliver long-term sustainable growth, while Shell's investments in clean energy solutions and carbon capture build on its commitment to achieving specific SDGs plant.

Positive SDG performance indicated a correlation between cash flows, which could harm savings going to private investors, especially in the context of "dual carbon" targets following the outcome of the so; the SDGs play an essential role in corporate communication, particularly in large UK companies (Patuelli & Saracco, 2022). The social aspect of the side takes precedence over environmental and economic issues. For example, Shell has significantly enhanced its communication strategy by reaching out to new audiences and building stakeholder trust has been achieved (Rizzato et al., 2023). Following the Deepwater Horizon disaster, Shell led the conversation around energy sustainability, embracing continuous improvement to transform both the company and the broader concept of sustainability. However, this change created a dialogue struggle, with contradictory and ambiguous results in Shell's efforts to balance sustainable energy with corporate strategy. Highlights the complexity and multidimensionality of integrating connected corporate actions (Hamad et al., 2024).

5. Investigation: Discussion of the Results

5.1. Discussion of the Results

The hypothesis testing of the study:

- Null hypothesis (H0): There is no significant relationship between the selected predictors (amount_invested_finance, shareholder_equity, and social_satisfaction) and the dependent variable (CSR) of both BP and Shell companies

- Alternative Hypothesis (H1): There is a significant relationship between the selected predictors and the dependent variable for the two firms.

5.1.1. The BP Company

- Model summary: The R-square value of .982 indicates that the model accounts for 98.2% of the variation in CSR for BP. Therefore, we reject the null hypothesis and accept the alternative hypothesis of BP, which shows a significant relationship between the selected predictors and CSR.

- ANOVA: the p-value of .170 for the F-statistic indicates that the overall model may not be statistically significant at the usual alpha level of .05. We there-fore could not reject the null hypothesis and conclude that the overall sample may not be statistically significant for BP.

- Coefficients: The P-values of the predictors for BP were .646, .300, and .100, respectively. These p-values indicate that the predictors may not have a statistically significant effect on the dependent variable at the 5% significance level.

5.1.2. Shell Companies

- Model summary: The R-square value of .279 indicates that the model accounts for 27.9% of the variation in CSR for the shell. The adjusted R- square value is -1.885, which is unusual and may indicate potential problems with the fit of the model. Therefore, due to insufficient model adequacy, we cannot accept or reject Shell’s alternative hypothesis.

- ANOVA: The P-value of .931 for the F-statistic indicates that the overall model is not statistically significant for Shell. We therefore could not reject the null hypothesis and conclude that the overall sample may not be statistically significant for Shell.

- Coefficients: The P-values of the predictors for shell were .713, .979, and .997, indicating that the predictors probably did not have a statistically significant effect on the dependent variable at the 5% significance level. A survey of large UK businesses committed to the Sustainable Development Goals (SDGs) provides valuable insights into the impact of the private sector on the implementation of the 2030 Agenda Zabihollah, et al. (2023) provides a new tool and vital vocabulary for managing corporate conversations on Twitter, and focus on main social aspects of the SDGs. This study provides a comprehensive and near-real-time visualization of corporate engagement with the SDGs, shedding light on the dispersion and impact of global carbon emission regimes from MNCs on Shell's performance and future strategies, as examined by Lewis (2023).

Additionally, research by Alesia and Fabio (2022) highlights the integrated narrative role played by the SDGs in Twitter conversations about major UK businesses, resulting in SDG social responsibility activity (SRA) which occurs for companies in participating countries. Again, this indicates a close relationship between Javier, et al. (2023) and provides a comprehensive overview of the literature on sustainable development goals in business, including insights into the current state of research and areas for future research. All of these studies contribute to understanding how large organizations engage with and contribute to the SDGs to address global sustainable development challenges.

Lack of communication in reporting can hinder progress towards the Sustainable Development Goals (SDGs) as companies can report their commitment to the SDG without actually having a corresponding performance on sustainability. This discrepancy helps managers and investors understand the nature of corporate SDG disclosures, and highlights the gap between reported intentions and actual action

SDGs is essential to encourage the integration of sustainability into corporate culture for effective implementation. In addition, this approach can lead to sustainability-focused organizational learning (SFOL), where firms actively continuously learn and improve sustainable practices.

Drawing attention to the importance of environmental, social and governance (ESG) disclosure for sustainable business practices is crucial in today’s corporate environment. Additionally, a great data-based tool to monitor corporate conversations about the SDGs on Twitter not only provides new avenues for further research in the field but also facilitates real-time analysis of corporate adoption participation in the Sustainable Development Goals

This comprehensive data can serve as a comprehensive guide for governments in promoting the SDGs for sustainable infrastructure, providing insights into the challenges and opportunities associated with sustainable practices. Furthermore, it provides valuable insights for organizations across multiple industries to design and implement future sustainable initiatives, thus contributing to global sustainability initiatives sustainability has improved.

5.2. Profitability Comparison

While both BP and Shell actively pursue CSR and sustainability goals, Shell appears to have a higher advantage than BP based on recent economic performance. Shell's focus on diversifying its energy resources, expanding renewables and promoting its commitment to higher profitability in SDGs 7 and 13 has enabled it to achieve higher profitability. Shell's substantial energy efforts, cleaning systems and climate control have enabled it to compete in the market.

On the other hand, BP is also making progress towards its sustainability goals, mainly focusing on becoming a net zero company by 2050. However, BP faces many challenges regarding its finances compared to Shell, especially as it switches from fossil fuels to… renewable energy.

Both BP and Shell reject most of the hypotheses regarding the determinants of CSR performance, suggesting that traditional economic and social change may only partially capture the complexity of CSR in the oil and gas industry.

Shell strongly aligns with SDGs 7 and 13, focusing on clean energy and climate action, contributing to gains.

BP is also committed to sustainability, especially SDGs 7 and 12, but needs more financial challenges in transitioning to renewable energy than Shell.

The findings showed that although both companies commit to sustainability, Shell now leads regarding CSR effectiveness and profitability. Continued efforts by both companies to align with global sustainability goals will be critical to building their future success and contribution to the energy transition.

5.3. Hypotheses Assessment Summary Table

| Hypotheses | Decision |

| Hi: There is a significant relationship between financial investment, | Rejected |

| shareholder equity, and life satisfaction with corporate social responsibility (CSR) performance for the selected BP company. |

|

| H2: There is a significant relationship between financial investment, social satisfaction, and shareholder equity with corporate social responsibility (CSR) performance for the selected Shell company. |

Rejected |

| H3: There is a significant relationship between the amount of financial investment and corporate social responsibility (CSR) performance across both BP and Shell companies. |

Rejected |

| H4: There is a significant relationship between the level of social satisfaction and corporate social responsibility (CSR) performance across both BP and Shell companies. |

Rejected |

| H5: There is a significant relationship between shareholder equity and corporate social responsibility (CSR) performance across both BP and Shell companies. |

Rejected |

| H6: There are significant differences in the predictors' effects on corporate social responsibility (CSR) performance between BP and Shell companies, indicating unique factors influencing CSR performance in each company. |

Rejected |

| H7: There is a significant relationship SDG 7 and Shell (Affordable and Clean Energy) |

Accepted |

| H8: There is a significant relationship Shell SDG 13 (Climate Action). | Accepted |

| H9: BP is committed to becoming a passive entity by 2050 or sooner and is focused on SDG 7. |

Accepted |

| BP is committed to becoming a passive entity by 2050 or sooner and is focused on SDG 12 (responsible management and product development), |

Accepted |

6. Conclusions

It is not the end of the path; it is a new beginning of new research and ideas that signify the Sustainable Development Goals with new Peaks and Perks. The study showcases the ideas of SDG in two organizations of the same sector, the Oil Industry, as SHELL and BP both are renowned firms in the UK where the oil industry is enhancing day-by-day.

6.1. SDG 7: Affordable and Clean Energy

BP and Shell's investments in renewable power are part of a broader fashion amongst oil and gas corporations to transition to low-carbon strength sources. A take a look at by way of Newell and Raimi (2018) highlights how fundamental energy businesses are increasingly diversifying into renewables as a part of their techniques to deal with weather exchange and meet global energy needs.

Additionally, studies by Mazzucato and Semieniuk (2018) emphasize the importance of public and private region funding in smooth strength technology to gain sustainable power dreams.

6.2. SDG 12: Responsible Consumption and Production

The oil and gas industry's shift toward responsible consumption and production is essential for decreasing environmental impacts. Heede (2014) points out that a large portion of global carbon emissions may be traced again to a small number of fossil fuel manufacturers, emphasizing the importance of those organizations in achieving sustainability. Iraldo et al. (2017) discuss how adopting circular economy practices can reduce waste and increase resource efficiency. It relates to Shell's and BP's tasks to recycle materials and reduce carbon footprints.

6.3. SDG 13: Climate Action

Addressing weather alternatives is an imperative assignment for oil and gas organizations. According to Sullivan et al. (2018), corporate commitments to reducing carbon emissions ought to be supported with concrete actions, including investment in carbon capture and storage (CCS) and renewable electricity.

Moreover, Fankhauser et al. (2015) argue that attaining net-zero emissions would require coordinated efforts across industries, governments, and civil society, which aligns with BP and Shell's collaborative initiatives in lowering emissions.

The conclusion of the study state that Regression Equations for both Organization state that:

CSR (for Shell)=1.495×1010−50.141×(Social Satisfaction)+0.003×(Shareholder E quity)−0.002×(Amount Invested in Finance)+ϵ

Intercept (α = 1.495 × 1010): If all independent variables are zero, Shell's expected CSR value is 1.495 billion. Like BP, this coefficient is not statistically significant, with a p-value of 0.494.

Social satisfaction (β1 = -50.141): The negative coefficient indicates that CSR decreases by 50.141 units for every unit increase in social satisfaction, but the result is not statistically significant with a t-value of -1. 0.484 and a p-value of 0.713.

Shareholder equity (β2 = 0.003): A positive, minimal coefficient indicates that higher shareholder equity slightly increases CSR by 0.003 units, but a p-value of 0.979 indicates that this relationship is insignificant.

Amount of investment (β3 = -0.002): This coefficient close to zero indicates that the amount of investment has an almost negligible effect on CSR, and this variable is not significant with a t-0.002 value of -0.005 and a p-value of 0.997.

Equation (2):

CSR (for BP)=3.551×1010−15.996×(Social Satisfaction)−0.029×(Shareholder Equ ity)−48.812×(Amount Invested in Finance)+ϵ

Intercept (α = 3.551 × 1010): If all independent variables are zero, the expected CSR value for BP is 3.551 billion. However, due to the high standard error and significance (Sig.) of 0.130, this coefficient is not statistically significant regarding commonly used values.

Social satisfaction (β1 = -15.996): A negative distribution indicates that for every unit increase in Social satisfaction, CSR is expected to decrease by about 15.996 units. However, the t-value is -0.622, and the p-value is 0.646, indicating that this relationship is not statistically significant.

Shareholder equity (β2 = -0.029): The negative coefficient indicates that increased dividend marginally reduces CSR by 0.029 units for each unit increase in equity. Furthermore, this effect is not statistically significant, with a t-value of - 1.966 and a p-value of 0.300.

Amount of investment (β3 = -48.812): This coefficient shows a significant negative impact on CSR; However, despite having a significant negative value, a t- value of -6.311 and a p-value of 0.100 indicate that the relationship, even though more potent than the others, is still not statistically significant

Based on the empirical data, we have concluded that the model for BP Company shows a strong relationship between the predictors (amount_invested_finance, shareholder_equity, and social_satisfaction) and corporate social responsibility (CSR) with a high r-square value of 0.982.

However, the p-value of the predictors is relatively high, and the adjusted R- squared value of 0.929 indicates that not all of the variation in CSR is explained by the predictors. Thus, the hypothesis that these predictions impact CSR still needs to be fully supported.

On the other hand, the model for the shell firm shows a weak relationship between predictors and CSR with an R-squared value of .279. The P-values of the predictors are high, indicating that they are not statistically significant in explaining the variation in CSR. A negatively adjusted R-square value indicates that the model may not fit the data well. As a result, the hypothesis that predictors significantly influence CSR for the shell firm is rejected.

BP's model shows a relatively strong relationship between predictors and CSR, while Shell's model shows a weak and insignificant relationship.