Submitted:

13 June 2023

Posted:

14 June 2023

You are already at the latest version

Abstract

This study proposes a framework to integrate Sustainability within Management Systems Standards and subsequently implement and disclose Sustainable Development goals and results. Moreover, it investigates the SD goals (SDGs) and results (SDRs) that Portuguese organizations with Integrated Management Systems (IMSs) disclose to their interest parties. The study, supported by content analysis, highlights that the four more frequently disclosed SDGs are “life on land“(50.0%), “industry, innovation, and infrastructure” (47.1%), “responsible consumption and production” (47.1%), and “partnerships for the goals” (47.1%). Conversely, the four SDRs most frequently disclosed are “employment” (82.4%), “economic performance” (79.4%), “anti-corruption” (64.7%), and “occupational health and safety” (61.8%). Hence, SDGs disclosure emphasizes the environmental dimension, while SDRs disclosure highlights the social dimension (economic dimension present in both SDGs and SDRs). Finally, the disclosure of SDGs and SDRs in institutional reports presents a positive and strong correlation that is statistically significant. Overall, the contributions of this research are twofold. First, it supports the integration of the SDGs within organizations, and second, it stimulates the demonstration of their impacts on the SDGs (the SDRs).

Keywords:

Strategic CSR

; Sustainable development goals

; sustainable development results

; integrated management systems standards

; sustainability reports

; institutional reports

; content analysis

1. Introduction

Reports such as "The Limits to Growth―A Report for The Club of Rome's Project on the Predicament of Mankind" [1] and "Our Common Future―Report of the World Commission on Environment and Development" (World Commission on Environment and Development [2], [3], identified systemic sustainability problems and were essential to support the concept of Sustainable Development (SD) worldwide.

Holistically, humanity can adopt a global development strategy based on the concept of SD―that is, ''development that meets the needs of the present without compromising the ability of future generations to meet their own needs'' [2] [3]. In this context, the concept of SD implies a focus on the Planet and People [4] [5]. According to Isaksson [5], ''People and Planet could be defined as the primary stakeholders" (p. 489). Hence, the concept of SD is fully aligned with the economic, environmental, and social dimensions (see [6], [7], [8]). Furthermore, SD is not only an issue for world nations but also for organizations [9]. Consequently, at the organizational level, the concept of SD is generally approached by several authors as Corporate Sustainability (CS) and Corporate Social Responsibility (CSR) [10] [11] [12]. Strategic CS (or Strategic CSR) requires organization to engage in socially and environmentally responsible activities that are economically sound for their financial performance usually in response to the businesses’ stakeholders’ expectations and demands [13] [14].

CSR can generate value for shareholders, customers, workers, partners, and society [15]. Amongst the CSR-reported benefits are risk reduction, staff recruitment and retention, cost savings, and good stakeholder relationships [16]. Hence, while supporting the organizations legitimacy, CSR can also foster competitive advantage by facilitating the access to capital and support from different stakeholders [17].

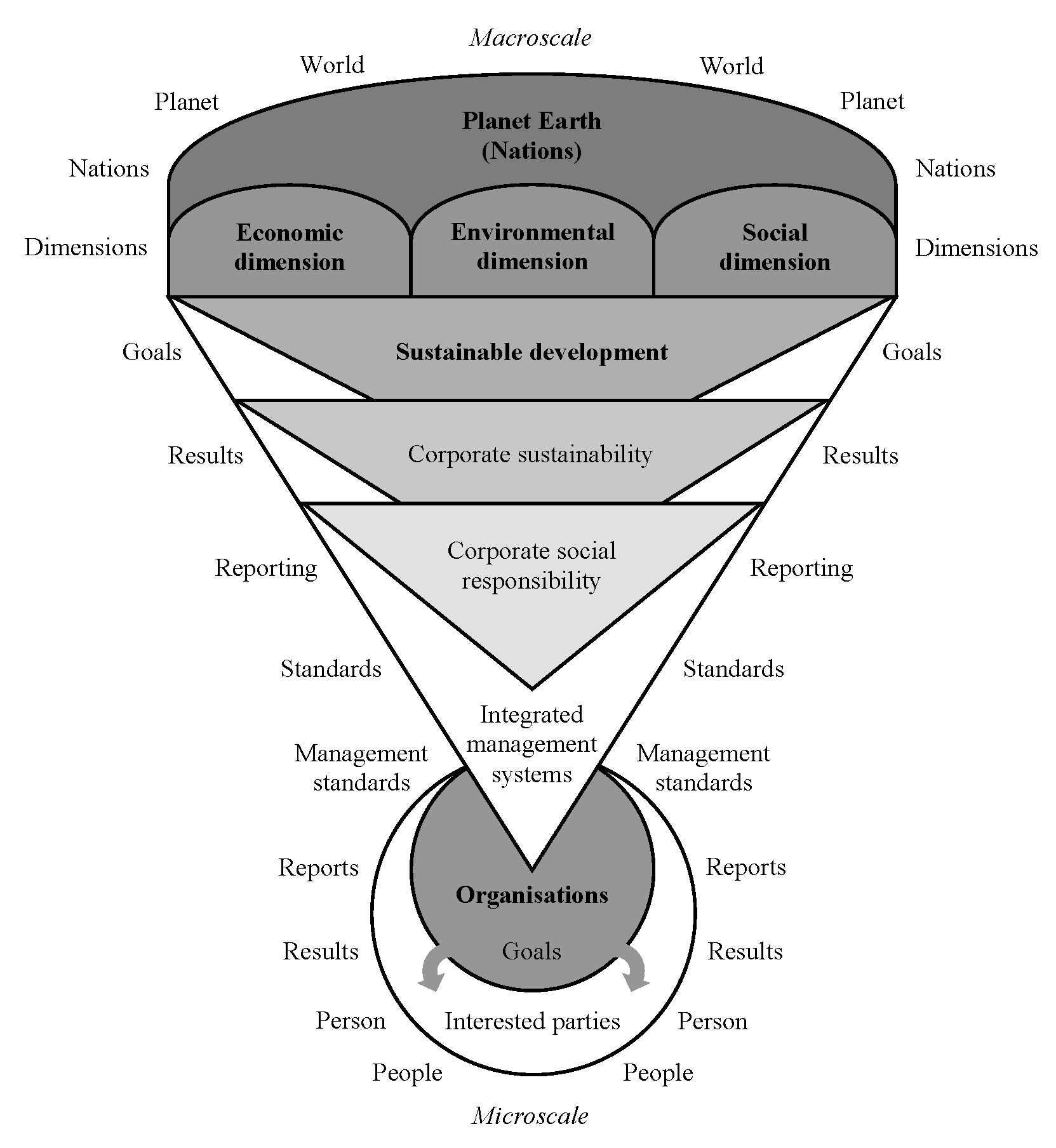

Figure 1 shows the holistic process of the evolution of the concept of SD from the macro-level (macroscale―planet and its nations) to the micro-level (microscale―organizations and their interested parties), as already advocated by many authors (e.g., [18], [19]). The interested parties (i.e., natural, or legal persons who relate to organizations) represent humanity and society at large. Interested parties (i.e., stakeholders) are "any group or individual who can affect or is affected by the achievement of the organization’s objectives" [20].

In an approach to SD, the term "goals" means "what it seeks to achieve" [23]. In turn, "results" is generally a synonym for "metrics, information, measures, indicators, outcomes, and outputs [24]. Thus, effective communication of the organisations' Sustainable Development Goals (SDGs) and Sustainable Development Results (SDRs) to their interested parties is essential for promoting the concept of SD, as well as for promoting the organisations' achievements [25]. To support these aims, frameworks, guidelines, indices, and standards are fundamental for organisations to achieve their SDGs and communicate the intended SDRs [26]. The relevance of companies disclosing their contributions to SD is also highlighted by Directive 2014/95/EU of the European Parliament and of the Council of October 22, 2014" and it represents one of the main innovations introduced by the European Commission to encourage large companies to disclose their contribution to SD" [27].

The level and the content of sustainability information on company reports are increasing worldwide [28]. From a theoretical perspective, Stakeholder, Resource Based View, and Institutional theories support the communication of the SDG and SDRs [29] [30]. The success of an organisation depends on its collaboration with multiple stakeholders [20], and Stakeholder Theory integrates business and social issues [31]. Furthermore, the Resource Based View theory [32] [33] suggests that an organisation's resources are essential to superior firm performance, competitive advantage, and strategic success. Hence, the adoption of strategies and actions towards SD can develop rare, valuable, inimitable, and non-substitutable resources and capabilities that can help an organisation integrate with stakeholders (a unique resource) and respond to their demands, and ultimately achieve superior performance, as advanced by Stakeholder Theory.

In addition, the Institutional theory posits that organisations, to achieve legitimacy and support, align their social values systems with those expected by society and are pursued by the best organisations to increase the likelihood of survival [34]. Moreover, academics such as Camilleri [35] consider that "CSR communications and stakeholder engagement may bring shared value to business and society by engaging with key stakeholders to address societal, environmental, governance and economic deficits" and support managers to improve their organisational stewardship and to reinforce their legitimacy with institutions and other stakeholders in society [36].

Hummel and Szekely [37] advance that the ambition to achieve the SDGs must be the responsibility of the governments of all the 193 member states (nations) of the UN and the top management of all organisations and "depends on the joint efforts of all individuals, organisations, and governments" [38]. However, barriers such as resource limitation, the COVID-19 pandemic [39], and the war in Ukraine [40] have negatively impacted the SDGs fulfilment with adverse outcomes for humankind and the planet. Moreover, the SDGs were developed by and for the government, and some organisations might need help understanding them [41]. Hence, supporting organisations to comprehend, integrate and contribute to the SDGs is critical. Moreover, business leaders must adopt sustainable business models and operate more ethically [42].

The growth of global supply chains fostered the adoption of voluntary management systems standards (MSS) as regulatory mechanisms to respond to stakeholder concerns [43]. These MSSs can be audited and certified by independent external certification bodies (CBs) that, by performing a third-party audit, assess whether the applicable MSS complies with the international reference and achieves the intended results [12]. Several MSSs, namely those published by the International Organization for Standardization (ISO), can support organisations addressing several potential issues inherent to the SD economic, environmental, and social dimensions. Since MSSs certified organisations should comply with international validated requirements and the corresponding certification bodies are subject to the accreditation schemes, the accredited certification is an assurance that all certified organisations, regardless of the country of origin or company size and industry, comply with the same requirements and achieve the intended standards results. Therefore, contributing to the generalisation of the research results to similar certified organisations worldwide.

Furthermore, entities such as the Social Accountability International (SAI), the British Standards Institution (BSI), and the Portuguese Institute for Quality (IPQ, "Instituto Português da Qualidade"), also published MSSs with an SD scope ([19] [21] [44] [45] [49]).

ISO MSSs share common concepts, core text, and high-level structure to facilitate the harmonisation and unity of the several MSSs [46] and academic research posits formal standards are perceived by stakeholders to positively contribute to achieving the SDGs [47]. Moreover, ISO and GRI promote their alignment with the UN SDGs and CBs work to effectively support that aim [21].

Table 1 presents four main MSS disciplines of MSSs that contribute to an integral approach to SD at the organisational level and supports achieving their goals and intended results [48] [49] [50] [51] [52].

In the last three decades, the implementation and certification of Quality, Environmental, Occupational Health and Safety, and Social Responsibility (QEOH&S&SR) MSs have increased worldwide and specifically in Portugal [56] [57] [58] [59] and the strategies for adopting multiple MSs certified are well reported in the literature [60].

The organisations that strategically adopt MSSs in the various disciplines and implement their integration based on the PDCA (Plan–Do–Check–Act) cycle promote SD and communication with the interested parties [11] [18]. Consequently, the integration of MSSs (Integrated Management Systems (IMSs) allows the development of ''conceptual models" that show the mechanism for the disclosure of SD goals and results to interested parties (e.g., [11] [18] [45] [60] [61].

Table 2 shows the relationship between the three dimensions of the SD, the potential issues associated with the SD, and the main MSSs currently adopted by Portuguese organisations.

Corporate sustainability (CS) reports have become the instrument of companies to communicate sustainability issues with their stakeholders and move forward to the balance of the Triple Bottom Line [62]. However, SDGs and SDRs reporting still have many issues that deserve research [27] [63] [64]. Presently, the institutional website of organisations with certified MSSs is considered an effective communication channel for disclosing institutional reports and information on SD [11] [18]. Recent academic research addresses the existing corporate reporting concerning SDGs [9] [65]. Moreover, [78] [19] propose an evaluation framework to identify the amount of disclosure topics from CSR/sustainability reports regarding SDGs. Furthermore, Izzo et al. [66] investigated the information disclosure in European companies integrating reporting (IR) guidance used to cover issues concerning SDGs.

Holistically, the object of study of this investigation aims to propose a framework to integrate Sustainability within Management Systems Standards and subsequently implement and disclose Sustainable Development goals and results and answer the following three ‘Research Questions’ (RQ):

RQ1: What are the main SDGs disclosed in institutional reports by Portuguese organisations with multiple certified MSs (QEOH&S&SR)?

RQ2: What are the main SDRs disclosed in institutional reports by Portuguese organisations with multiple certified MSs (QEOH&S&SR)?

RQ3: How the disclosure of SDGs and SDRs in institutional reports is correlated?

This paper contributes to the literature on SDGs in several ways. First, most of the available academic research has provided theoretical reflections on the SDGs [67]. Further research should address how sustainability can be better understood and managed at an organisational and local level [68]. By integrating GRI and MSs and fostering SDGs and SDRs communication, this study can support organisations to comprehend, integrate and contribute to the SDGs. Hence, the contributions of this research are twofold. First, it supports the integration of the SDGs within organisations, and second, it stimulates the demonstration of their impacts on the SDGs (the SDRs).

The remaining of the article is organised into the following sections: Section 2 addresses the Literature review; Section 3 presents the Materials and Methods; Section 4 exposes the Results; Section 5 shows the Discussion; and Section 6 reveals and highlights the Conclusions of the study and presents the mains limitations, restrictions, and recommendations for further research. By integrating GRI and MSs and fostering SDGs and SDRs communication, this study can support organisations to comprehend, integrate and contribute to the SDGs.

2. Literature review

2.1. Communication on sustainable development

In 2015, the General Assembly of the United Nations (UN) formally adopted "The 2030 Agenda for Sustainable Development" [69] and agreed upon the 17 Sustainable Development Goals (SDGs). The "SDGs can indicate and measure the progress towards SD and represent a shared expression of global stakeholder needs, balancing economic, social, and environmental development" [70].

SD reports are " public reports by companies to provide internal and external stakeholders with a picture of the corporate position and activities on economic, environmental, and social dimensions" [71]. These reports are also called institutional reports [65] [72].

Consequently, at the organizational level, internal and external communication is essential for promoting the concept of SD and the organizations’ achievements [25]. According to Heemskerk et al. [71], the communication on SD through SD reports promotes several internal and external benefits at the organizational level, such as: “'transparency to stakeholders”; “maintaining a license to operate”; “creating financial value”; “attracting long-term capital and favorable financing conditions”; “raising awareness, motivating and aligning staff, and attracting talent”; “improving MSs”; “risk awareness”; “encouraging innovation”; “enhancing reputation”; and “continuous improvement” (p. 15).

The Global Reporting Initiative (GRI) is one of the most preferred frameworks for SD reporting [73]. In the past two decades, GRI published several versions of guidelines and standards that have helped organizations to report the SDRs in three dimensions—that is, economic, environmental, and social [74] [75] [76]. GRI Standards report publicly corporate economic, environmental, and social impacts, including positive or negative contributions of companies to SD and comprehend a set of interrelated standards: GRI 100: Universal Standards; GRI 200: Economic, GRI 300: Environmental and GRI 400: Social [76]. Moreover, the SDG Compass establishes the interlinkage between GRI disclosures, the 17 SDGs, and their targets [77]. According to Tsalis et al. [78], the "GRI Standards serve as a communication channel for organizations with interested parties providing a holistic picture of the CS management and the organization’s contribution to SD".

The various versions of the GRI Guidelines and the current version of the GRI Standards incorporate the theoretical basis of the concepts of Triple Bottom Line (TBL) and Triple P (Profit, Planet, and People), proposed by Elkington [79] [80], within an integrated approach to the three dimensions of the SD at the organizational level (e.g., [75] [21] [81]).

Nowadays, a sustainability report can be defined as a global report published by organizations to report the impact of their activities in economic, environmental, and social terms [63,76]. In other words, sustainability reporting can be defined as the practice of disclosing an organization’s economic, environmental, and social impacts publicly ([63] [65] [9]).

2.2. Sustainable development goals

The UN 17 Sustainable Development Goals (SDGs) and 169 targets are integrated and indivisible, and thus demonstrate the holistic vision of this new universal 2030 Agenda for Sustainable Development and align with the three dimensions of the SD ([65] [70] [9] [78] [69] [82]), see Table 3. According to the UN (2015), the SDGs and targets set will stimulate action by 2030 in areas of critical importance for humanity and the planet—that is, “People”, “Planet”, “Prosperity”, “Peace”, and “Partnership” [69].

In recent years, a growing number of organizations have implemented or are currently implementing reporting on the SDGs [37]. Sustainable Development Goal (SDG) reporting can be defined as "the practice of reporting publicly on how an organization addresses the SDGs" ([66] [9]). In other words, "SDG reporting is the practice of companies publicly disclosing their commitment to fulfil the 2030 Agenda demands" [84]. However, "the SDGs are not a corporate reporting tool; they do not provide any reporting guidelines or corporate indicators” [85]. Thus, GRI standards can aid organizations in reporting their SDGs [84]. Furthermore, the sustainability reports (e.g., GRI) contribute to the disclosure of the SDGs [86].

Fonseca and Carvalho [65] found that the communication of SDGs is more prominent in Portuguese organizations certified in Quality, Environment, and Occupational Health and Safety (QEOH&S) that disclose their sustainability reports (GRI) on their website. In recent years, the UN SDGs have been approached together with the main MSs (see, e.g., Fonseca & Carvalho [65], as well as with the ISO standards and other standards (see, e.g., [21] [82] [83]). Table 3 shows the relationship between the UN SDGs, the primary ISO MSSs, and others.

2.3. Sustainable development through management systems: a proposed framework

Quality Management Systems (such as those based on ISO 9001) contribute to the economic dimension of the SD, mainly by providing products and services effectively, therefore, aiming to ensure the satisfaction of the customers and other interested parties ([12] [51] [53] [87]). In turn, the internalization of quality management (e.g., based on the ISO 9001 standard) also contributes to the performance of the other dimensions of the SD [88] [89] [90].

Environmental Management Systems (e.g., based on ISO 14001) contribute to the environmental dimension of the SD, mainly by protecting the environment by preventing or mitigating adverse environmental impacts (e.g., operational efficiencies through better utilization of resources and waste management systems) and reinforcing business license to operate and legitimacy with stakeholders ([93] [94,12] [21] [50]).

Occupational Health and Safety Management Systems (OH&SMS), such as those based on ISO 45001 or BS OHSAS 18001, contribute to the social dimension of the SD, mainly by preventing work-related injury and ill health to workers and providing safe and healthy workplaces ([52] [54] [95] [96] [97]).

The International Standard SA 8000:2014 Social Accountability [98] is one of the primary worldwide standards to implement and certify an SRMS ([99] [100]). The Portuguese Standard (NP, Norma Portuguesa) entitled NP 4469:2019 Social Responsibility Management System—Requirements and Guidelines for its Usage [49] is the national reference to implement and certify an SRMS [49]. Overall, the SRMS (SA 8000 or NP 4469) contributes to the social dimension of the SD, mainly by providing ethical and transparent behavior towards all the interested parties that structure the global society ([49] [100] [101]). According to Castka et al. [102], the requirements and principles of the SRMS are integrated into the ISO MSs.

BSI [48] defines the Integrated Management System (IMS) as “MS that integrates multiple aspects of an organization’s systems and processes to one complete framework, enabling an organization to meet the requirements of more than one MSS” (p. 2). Integrated management systems support corporate responses to sustainable development ([103].

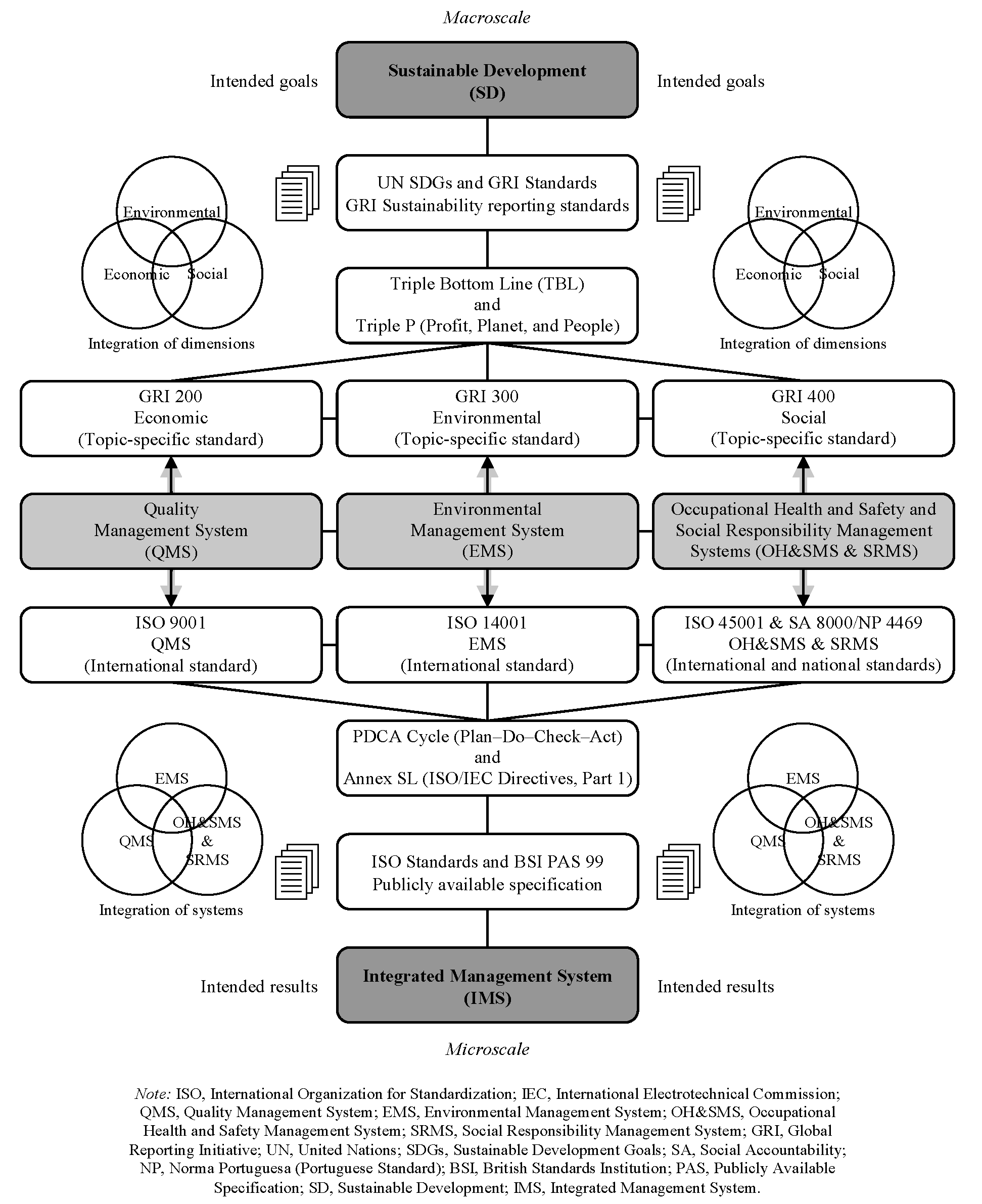

The IMS (QEOH&S&SR) based in the PDCA cycle and the Annex SL of the ISO standards of MSs is aligned with the UN SDGs and the GRI standards and supports the concept and application of SD ([44] [104]). Furthermore, the SD positively impacts the IMS [105]. Hence, UN SDGs, ISO standards, GRI standards, and other standards (e.g., SAI and IPQ) contribute to the global approach to SD and IMS ([21] [26] [57] [61] 109]). In sum, the concepts of SD (i.e., macroscale view) and IMS (i.e., microscale view) are aligned (see, e.g., [18] [65] [72]). Figure 2 presents a framework for implementing and disclosing Sustainable Development goals and results through MSSs. The proposed framework is framed by the relationship between SD and IMS concepts supported by various MSSs.

2.4. Communication through management systems & institutional reports

According to Derqui [107], “communication is central for the success of any sustainability strategy” (p. 2714). Consequently, organizational communication (internal and external) is relevant and essential for good interaction with all stakeholders [107]. Thus, internal, and external communication is present in several requirements of the MSSs (e.g., ISO 9001, ISO 14001, ISO 45001, SA 8000, and NP 4469), as well as in other standards and specifications relevant to the IMSs (e.g., ISO 26000 and PAS 99), see Table 4. In this context, several frameworks, and standards (e.g., GRI, ISO 9001, ISO 14001, ISO 45001, SA 8000, and others) aim to sustain reporting in the SD's scope ([26] [83]).

At the organizational level, internal and external communication supported in institutional reports is crucial to disclose to the interested parties the goals and results achieved under the SD ([106] [107]). In this context, the institutional reports published by organisations that disclose information on SD to interested parties can present different types ([29] [78] [84] [109]). In line with this, “such reports attempt to describe the company’s contribution toward SD” [71]). Academic studies addressing the disclosure of SDGs and SDRs comprehend the following types of institutional reports (e.g., see [65] [106]): Sustainability reports; social responsibility reports; environmental reports; occupational health and safety reports; management reports; accounts reports; accounts and management reports; financial reports; corporate governance reports; and integrated reports.

3. Materials and Methods

3.1. Research sample

The current study encompasses 34 organizations comprehending all the Portuguese organizations with multiple certified MSs (QEOH&S&SR) at the end of 2017, which cumulatively satisfied the following two conditions (see Table 5):

- Made an institutional website accessible on the Internet on July 31, 2019 (i.e., the final date of the exploratory analysis).

- Disclosed at least one of their institutional reports on the website in the past four years (i.e., published from 2015 to 2018).

The research was not extended into 2020 and beyond to avoid the contextual influence of the COVID-19 pandemic.

The organizations in the research sample belong to various sectors of economic activities and represent 69.4% of the total organizations with multiple certified MSs (QEOH&S&SR) at the end of 2017. The sector of economic activity called ‘water collection, treatment, and supply’ is the most representative of the sample, comprising 7 (20.6%) organizations. In turn, three other sectors of economic activity designated as “‘construction”, “other service activities”, and “sewerage and waste management” are also commonplace in the sample (11.8%). In addition, the research sample integrates 19 (55.9%) organizations that belong to the private business sector and 15 (44.1%) organizations that belong to the public business sector (i.e., public sector or business sector of the State). Finally, the organizations included in the research sample have headquarters in several Portugal districts, with the district of Lisbon (i.e., Lisboa) accounting for more than half of the organizations included in the sample (52.9%). In turn, the district of Oporto (i.e., Porto) is the second district most representative of the sample (11.8%).

3.2. Research method

The content analysis method has been used frequently in many types of research, whose object of study is the exploratory analysis of themes on SD that are published and disclosed in institutional reports by organizations around the world ([38] [78] [83] [109)]. Therefore, the content analysis method supports this research. According to Maier (2017a), "content analysis is a quantitative process for analyzing communicative messages that follow a specific process" (p. 243). In other words, "content analysis is a systematic, quantitative process of analyzing communication messages by determining the frequency of message characteristics" (Maier, 2017b, p. 239).

The first activity of the content analysis process (i.e., the definition of the objectives and theoretical reference framework) is described and grounded in Section 1 and Section 2 (see Introduction and Literature review). The corpus of analysis (i.e., the set of all the documents for analysis) selected was constituted by institutional reports that are published and disclosed on the institutional website of the organizations under study (e.g., [65] [106] [113]). The categories of analysis defined were supported by the economic, environmental, and social dimensions of the SD (e.g., Carvalho et al., 2019; [65]). In this sense, the categories of analysis that sustain the SDGs (e.g., Fonseca & Carvalho [65]) and the SDRs (e.g., Carvalho, 2019) are aligned with the three dimensions of the SD. In turn, the categories of analysis are based on 'GRI Standards' (GRI, 2016)—that is, economic (GRI 200), environmental (GRI 300), and social (GRI 400).

The subcategories of analysis defined in the study of the disclosure of SDGs were supported in seventeen items (i.e., UN SDGs items), as used in the past in other research (e.g., [37] [65] [66] [110]). In turn, the subcategories of analysis defined to the study of the disclosure of SDRs were supported by the various reporting items that constitute the “GRI Standards” in the 2016 version [76], as previously used in other studies (e.g., Carvalho, 2019; [81,73] [78]; Vieira et al., 2021). In this case, the subcategories of analysis were based on thirty-six items (i.e., GRI items), include on “Universal Standards” (GRI 103) and “Topic-specific Standards” (GRI 200; GRI 300, and GRI 400), as proposed by the “GRI Standards” [76].

The units of analysis defined were based on concepts (i.e., themes, words, and phrases) as used in previous research (e.g., [18] [65] [72] [83]). Thus, the units of analysis used allowed for quantifying the occurrence of the disclosure de SDGs (e.g., Fonseca & Carvalho [65]; Rashed et al. [83]) and SDRs (Carvalho [106]) in institutional reports.

The quantification activity was based on the analysis of the “presence” or “absence” of specific contents in the communication disclosed (Abbott & Monsen [111]; Carvalho et al. [72])—that is, identify of the 'presence' or 'absence' of units of analysis related to the various subcategories of analysis in the content of the institutional reports published. For this reason, the content of the institutional reports was analyzed in a dichotomous or binary way (i.e., 0 or 1).

Additionally, the global quantification was based on two Disclosure Indexes (IDs), whose mathematical formulation is based on the literature (e.g., Carvalho [106]; Carvalho et al. [72]; Fonseca & Carvalho [65]; Gerged et al. [108])—that is, the Sustainable Development Goals Disclosure Index (SDGsDI), expressed by Equation 1 (De Iorio et al. [109]; Fonseca & Carvalho [65]), as well as the Sustainable Development Results Disclosure Index (SDRsDI), expressed by Equation 2 (Carvalho [106]).

In equation 1, the DI expresses the level of the disclosure of SDGs for an organization (j). Consequently, in the numerator, the sum (i.e., ∑ from 1 to nj) of the SDGij represents the SDGs (i.e., UN SDGs items) that an organization discloses; thus, SDG is equal to 1 if the SDG item (i-th) is disclosed by the organization (j-th), and 0 otherwise. On the other hand, in the denominator, the nj represents the SDGs expected in total, that is, all the SDGs items that an organization (j) may disclose (i.e., nj is equal to 17 items). Therefore, if SDGsDI equals 0, the organization (j-th) does not disclose any SDG item. In turn, if SDGsDI equals 1, the organization (j-th) discloses all the SDGs items.

In equation 2, the DI expresses the SDRs' disclosure level for an organization (j). Consequently, in the numerator, the sum (i.e., ∑ from 1 to nj) of the SDRij represents the SDRs (i.e., GRI items) that an organization discloses; thus, SDR is equal to 1 if the SDR item (i-th) is disclosed by the organization (j-th), and 0 otherwise. On the other hand, in the denominator, the nj represents the SDRs expected in total, that is, all the SDRs items that an organization (j) may disclose (i.e., nj is equal to 36 items). Therefore, if SDRsDI equals 0, the organization (j-th) does not disclose any SDR item. In turn, if SDRsDI equals 1, the organization (j-th) discloses all the SDRs items.

So, we have two IDs that are both quantitative variables (i.e., continuous) that may take values in the range between 0 and 1 or [0; 1]—that is, 0 ≤ SDGsDI ≤ 1 and 0 ≤ SDRsDI ≤ 1. Consequently, the SDGsDI and SDRsDI variables are used to verify whether the disclosure of SDGs and SDRs in institutional reports has a significant statistical correlation. According to Schober et al. (2018), correlation “is a measure of an association between variables” (p. 1763). In other words, “correlation is a measure of a monotonic association between 2 variables” (Schober et al. [112]) and a “correlation coefficient” measures the relationship between two variables [112].

Recently, the correlation was used in research as a measure of association to study the relationship between variables in the scope of the SDGs (e.g., [70]) and the SDRs (e.g., [113]). Table 5 shows the correlation levels classification according to the literature ([65] [112]).

Lastly, the following sections and subsections present the research data collection procedure and the interpretation of the results obtained (i.e., the sixth and last activity of the content analysis process).

3.3. Research data

This study developed research data collection and analysis in two distinct phases. In the first phase, which occurred between May and June 2019, several computer files in PDF (Portable Document Format) of the institutional reports (the latest available version) were downloaded from the institutional websites of the organizations. Subsequently, the contents of the institutional reports were analyzed and classified based on the content analysis method. In the second phase, which occurred in July 2019, the research data collected and analyzed were all validated in terms of the classification initially assigned.

Consequently, all research data collected and analyzed (in both phases) were recorded in a research database (i.e., a computer application developed in the software Microsoft® Office® Excel® 2019 version). This way, the research database recorded the research data dichotomously (i.e., in binary form). Therefore, whenever the content of the institutional reports in terms of concepts (i.e., themes, words, and phrases) is relevant to demonstrate the disclosure of SDGs (i.e., UN SDGs items) and SDRs (i.e., GRI items) in the scope of the various subcategories of analysis studied, it is assigned to the item (i-th) the code or value of 'one' (1)—that is, the case of presence or, otherwise, it is assigned to the item (i-th) the code or value of 'zero' (0)—that is, the case of absence (see, e.g., [65] [106]).

Lastly, the research data were treated and analysed statistically using the software IBM® SPSS® Statistics 26 version (International Business Machines—Statistical Package for the Social Sciences) and the macro KALPHA 3.1 version (Krippendorff's Alpha). Subsequently, the measurement of research data reliability obtained through the content analysis method (by comparing the research data obtained in both phases) was determined based on Krippendorff's alpha (α) coefficient. Thus, Krippendorff's alpha reliability estimate obtained for the research data of the disclosure of SDGs and SDRs resulted in alpha (α) values of 0.953 and 0.930, respectively.

According to Krippendorff [114], the data reliability is considered acceptable for values of alpha (α) ≥ 0.800 when the research data is obtained through the content analysis method.

4. Results

4.1. Descriptive statistics analysis

The exploratory analysis of the institutional reports disseminated on the institutional website by the Portuguese organizations with multiple certified MSs (QEOH&S&SR) shows that the accounts report (33.0%) and the sustainability report (32.1%) are the institutional reports most frequently disclosed among the various institutional reports published annually by the organizations. Author(s) such as Camilleri [91] report an increase in the number of stakeholders, including contractors, non-governmental organizations (NGOs) and research firms who scrutinize businesses’ environmental, social and governance (ESG) behaviors. Moreover, the application of the content analysis method was based on the latest available version of the institutional reports published and disclosed by each of the 34 organizations (QEOH&S&SR). Table 6 shows the 77 institutional reports classified by the analyzed type. Thus, 23 (67.6%) and 22 (64.7%) organizations published and disclosed the accounts and sustainability reports.

Consequently, the content analysis process adopted in the research allowed for qualifying and quantifying the occurrence of SDGs and SDRs disclosed in institutional reports by the organizations (QEOH&S&SR). Table 7 presents the SDGs disclosed by the organizations under study according to the categories and subcategories of analysis adopted in the research.

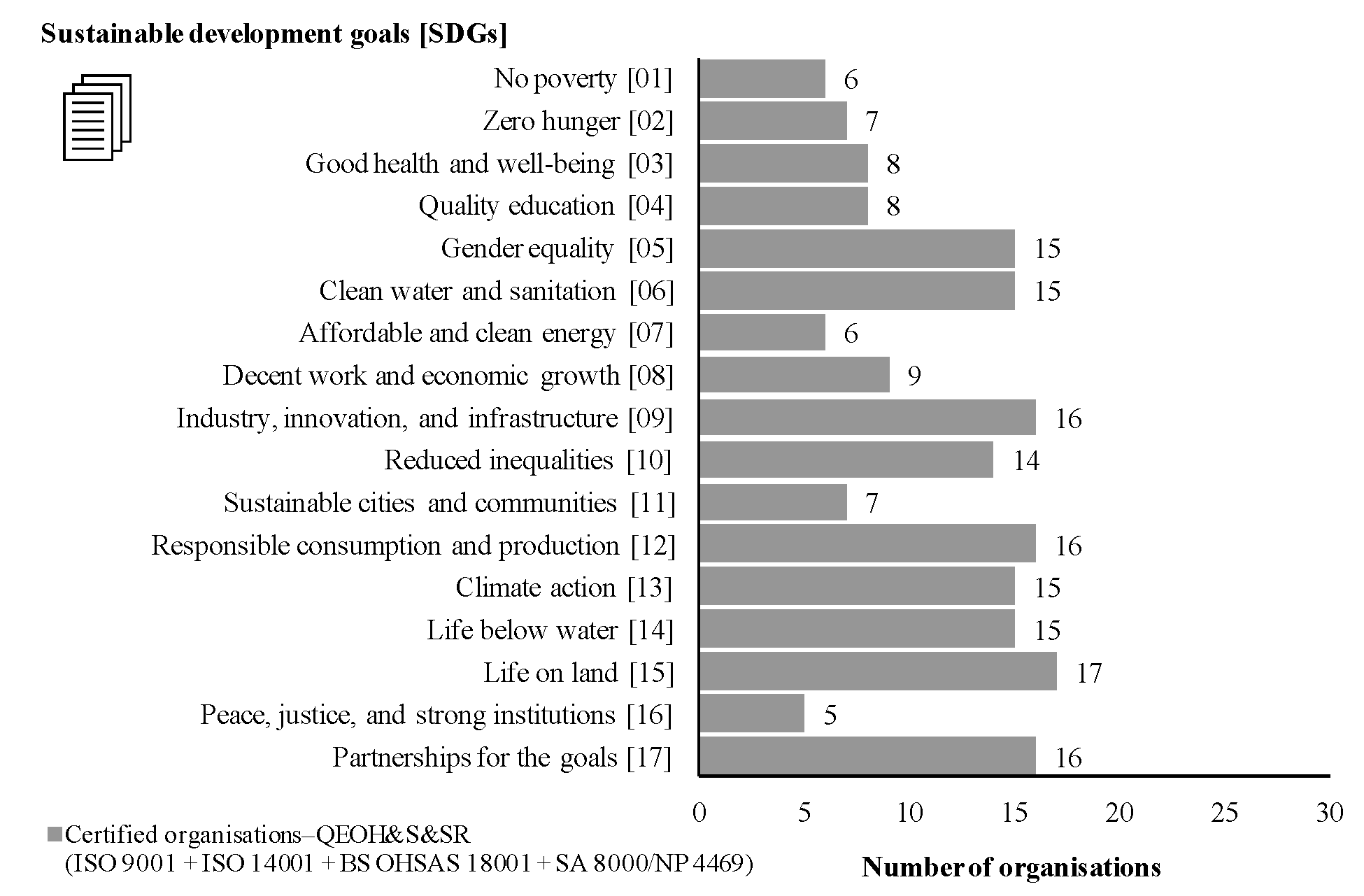

The results highlight the occurrence (number and percentage) of the disclosure of SDGs by the organizations (QEOH&S&SR), with four subcategories of analysis (i.e., UN SDGs items) presenting a more significant occurrence in the disclosure of SDGs (in descending order): "life on land" (SDG 15), disclosed by 17 (50.0%) organizations; "industry, innovation, and infrastructure" (SDG 09), disclosed by 16 (47.1%) organizations; "responsible consumption and production" (SDG 12), disclosed by 16 (47.1%) organizations; and "partnerships for the goals" (SDG 17), disclosed by 16 (47.1%) organizations.

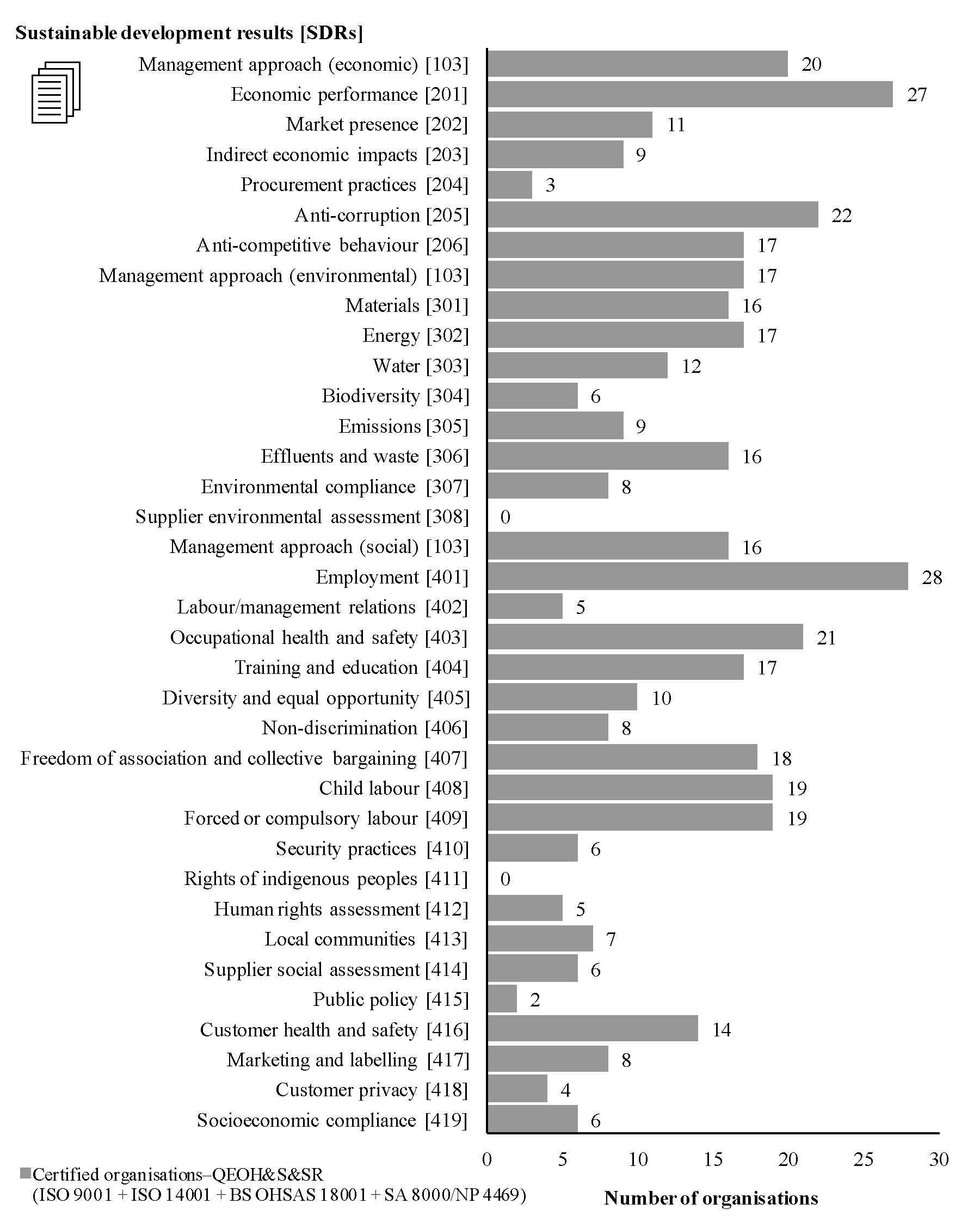

Additionally, Figure 3 shows the relationship of all the SDGs obtained by approaching the several subcategories of analysis (UN SDGs items and Figure 4 presents the relationship of all the SDRs obtained by approaching the several subcategories of analysis (GRI items). In this sense, the results show a large discrepancy between the values of the thirty-six subcategories analyzed—the disclosed SDRs and between the values of the seventeen subcategories analyzed—the disclosed SDGs.

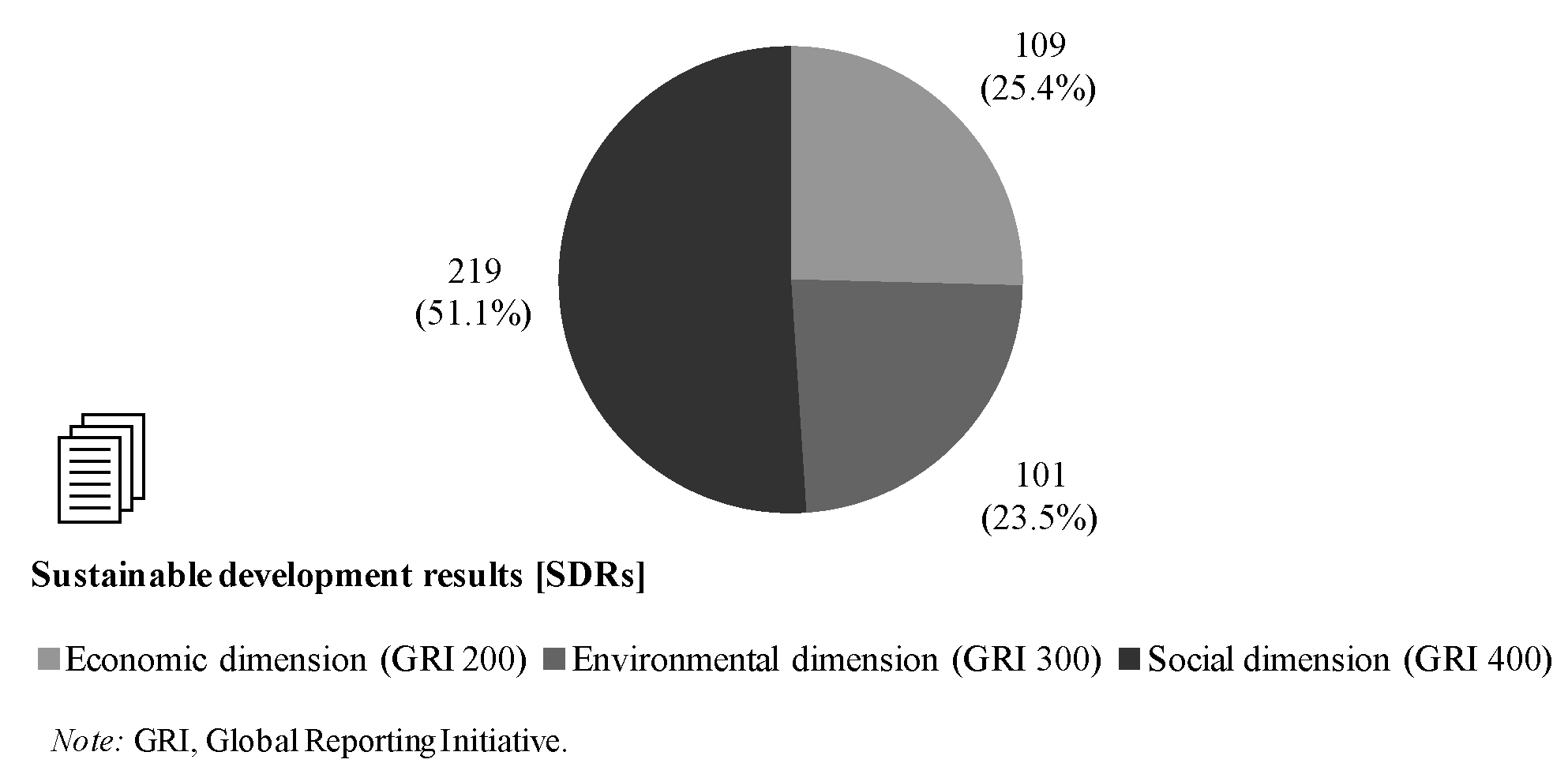

Figure 5 summarizes the SDRs' disclosure results by categories of analysis (by all organizations), with 429 SDRs accounted for approaching the three categories of analysis. Thus, the economic dimension (GRI 200) disclosed 109 (25.4%) items, the environmental dimension (GRI 300) disclosed 101 (23.5%) items, and the social dimension (GRI 400) disclosed 219 (51.1%) items.

4.2. Bivariate correlation analysis

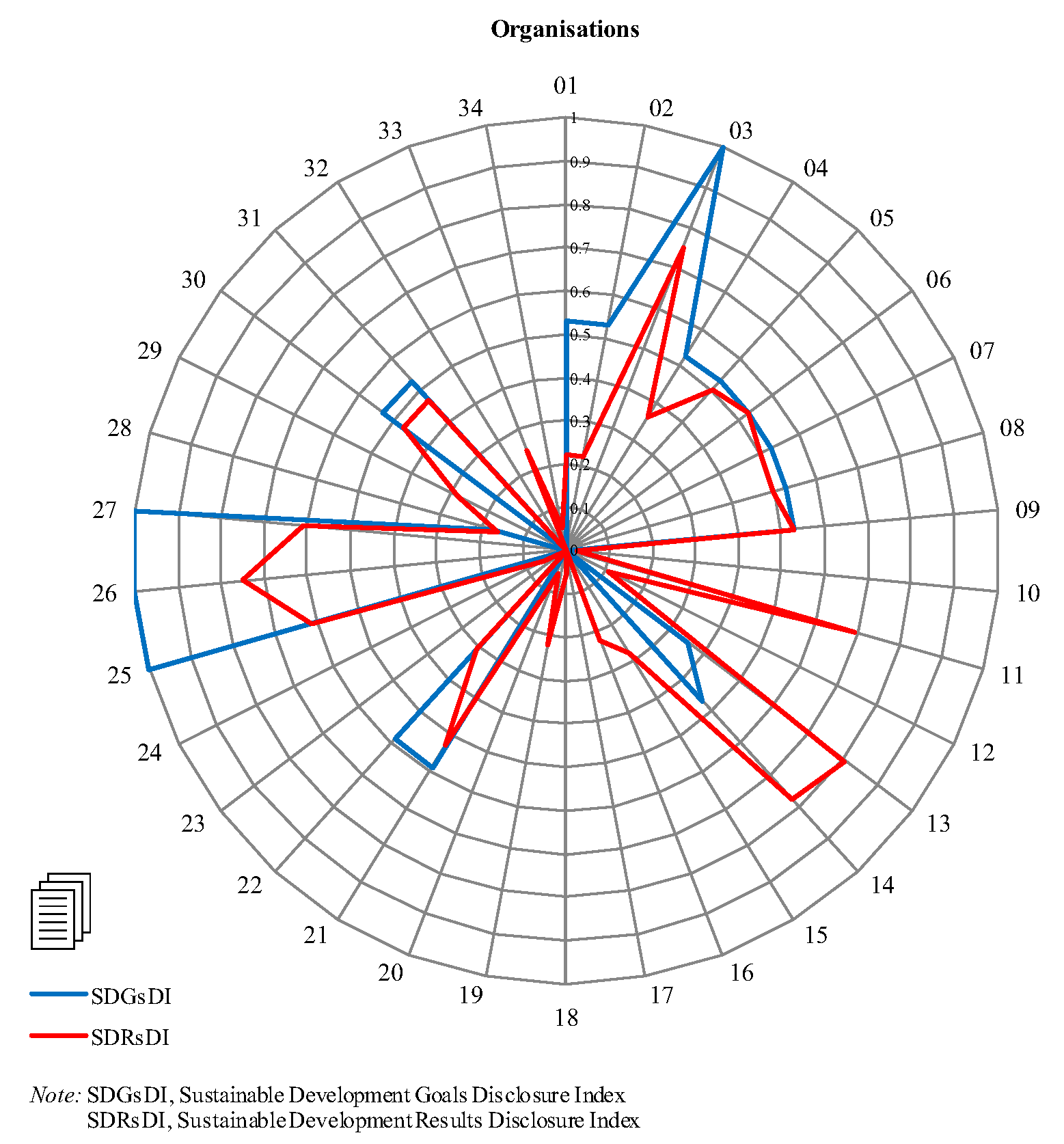

The study of the correlation between the disclosure of SDGs and SDRs was based on the relationship between the SDGsDI and SDRsDI variables, both quantitative. Thus, the study of the bivariate correlation aimed to verify the existence of a statistically significant linear association between the SDGsDI and SDRsDI variables. Table 13 shows the results obtained from the SDGsDI and SDRsDI variables for each sample organization and other sample characterization parameters.

The results show that disclosing SDGs and SDRs in institutional reports is a reality for 19 (55.9%) organizations and 31 (91.2%) organizations, respectively. In turn, 19 (55.9%) organizations jointly disclose the SDGs and SDRs. In contrast, only 3 (8.8%) organizations do not disclose the SDGs and SDRs.

Additionally, it is essential to remember that both variables (SDGsDI and SDRsDI) are continuous and assume values between 0 and 1. Table 9 shows the results of the descriptive statistics that characterize both variables, such as the obtained values for minimum, maximum, and mean.

The correlation (i.e., association) between the variables (SDGsDI and SDRsDI) was statistically tested using the Pearson correlation coefficient (parametric test) and the Spearman correlation coefficient (nonparametric test). Table 10 shows the results of applying Pearson's and Spearman's correlation to SDGsDI and SDRsDI variables. Additionally, it is essential to recall that the "correlation coefficients describe the strength and direction of an association between variables" (Schober et al. , [112]).

The value of the Pearson correlation coefficient (r) is 0.733 (p-value ≈ 0.000), and the value of the Spearman correlation coefficient (ρ) is 0.697 (p-value ≈ 0.000), both positive coefficients. In turn, the significance values of the correlation coefficients are lower than 0.05, which shows that both coefficients are statistically significant (p-value < 0.01). A correlation coefficient that takes values from 0.7 to 0.9 is classified as a "strong positive correlation" (Fonseca et al. [70]). Consequently, since the significance level is 0.05 (i.e., a confidence level of 95%), the statistical results obtained by both correlation coefficients demonstrate, with significant statistical evidence (p-value < 0.05), that the correlation between the two variables (SDGsDI and SDRsDI) is positive and strong.

Additionally, Figure 6 shows the association between the two variables (SDGsDI and SDRsDI) at the level of each of the 34 organizations in the research sample graphically. Therefore, a holistic graph view can support the validation of the Model for SD implementation trough MSSs and shows both variables' correlation (i.e., association). Generally, a high value in the disclosure of SDGs corresponds to a high value in the disclosure of SDRs, and vice versa.

5. Discussion

This research results show that the accounts and sustainability reports are the most frequently disclosed among the several institutional reports published and disclosed annually on the institutional website by Portuguese organizations with multiple certified MSs. Thus, our results align with other previously published studies (e.g., [11] [72] [106]).

Consequently, the four main SDGs (i.e., UN SDGs items) disclosed in institutional reports by certified Portuguese organizations (QEOH&S&SR) are the following (in descending order): "life on land" (SDG 15); "industry, innovation, and infrastructure" (SDG 09); "responsible consumption and production" (SDG 12); and "partnerships for the goals" (SDG 17), these last three in ex aequo in terms of ranking. Therefore, in this research, SDG 15 is highlighted as the goal most disclosed of all the SDGs—the main SDG disclosed in institutional reports. However, recent research shows that SDG 15 usually does not occupy a rank among the top five of the SDGs most disclosed in institutional reports (e.g., [37] [65] [66] [86] [106] [109]). Additionally, some recent studies identify SDG 15 among the least attention and priority SDGs for organizations (e.g., [28] [37] [66]). Consequently, in our case, we believe that the result obtained for SDG 15 may be related to the characteristics of the research sample—that is, Portuguese organizations with multiple certified MSs (QEOH&S&SR) that are aligned with the principles of the SD.

Overall, the results obtained for the items SDG 09, SDG 12, and SDG 17 are in line with other research (e.g., Fonseca & Carvalho [65])—that is, the SDG 09, SDG 12, and SDG 17 are among the top five SDGs disclosed in institutional reports by certified Portuguese organizations. However, other recent studies show that only SDG 9 and SDG 12 are among the top five SDGs disclosed in institutional reports (e.g., Hummel & Szekely [37]; Izzo et al. [66]; Manes-Rossi & Nicolò [29]). On the other hand, however, we found in other research that only SDG 12 is among the three, four or five SDGs most disclosed in institutional reports (e.g., Gunawan et al. [110]; Heras-Saizarbitoria et al. [115]; Ionașcu et al. [38], Ivic et al. [86]; PwC [28]; Silva [59]).

Additionally, the four main SDRs (i.e., GRI items) disclosed in institutional reports by certified Portuguese organizations (QEOH&S&SR) are the following (in descending order): 'employment' (GRI 401); 'economic performance' (GRI 201); 'anti-corruption' (GRI 205); and 'occupational health and safety' (GRI 403). In our case, the GRI 401 is the most disclosed SDR in institutional reports. In turn, Bastas and Liyanage [116] argue that the GRI 201; GRI 205, and GRI 403 are all sustainability items (i.e., SDRs) priorities as per the voice of the stakeholder's analysis.

Overall, the results obtained for the items GRI 201, GRI 401, and GRI 403 are in line with other research (e.g., Carvalho [106])—that is, the GRI 201, GRI 401, and GRI 403 are among the four main SDRs disclosed in institutional reports by certified Portuguese organisations. In addition, other research shows that the theme of GRI 201, GRI 401, and GRI 403 are in the top ten SDRs disclosed in institutional reports (e.g., Lambrechts et al. [117]).

According to Pacheco et al. [81], items GRI 201 and GRI 401 are among the most disclosed in institutional reports (a specific case of the universities). On the other hand, Yang et al. (2020) shows that item GRI 201 is the sub-topic (i.e., GRI item) most disclosed in the economic dimension for the specific case in the airline industry. Conversely, Saber and Weber [73] argue that the items GRI 401 and GRI 403 are among the most disclosed in institutional reports (a specific case of grocery retailing).

Holistically, our results show that more than half of the SDRs (i.e., GRI items) disclosed in institutional reports belong to the social dimension (GRI 400). On the other hand, the SDRs disclosed referring to the economic (GRI 200), and environmental (GRI 300) dimensions are similar. Therefore, this study's results align with other previously published research (e.g., Kolsi et al. [118]).

Recently, in the literature, the integrated approach to SDGs (based on UN SDGs items) and SDRs (based on GRI standards items) disclosed in the institutional reports of the organizations is showing the first results (e.g., [63] [78] [84]). However, Diaz-Sarachaga [63] argue that "the correlation between the SDGs and CS reporting systems has barely been studied" (p. 1299), for example, the correlation between the SDGs and the GRI standards. In this context, our research's results demonstrated statistically that the disclosure of SDGs (i.e., UN SDGs items) and SDRs (i.e., GRI items) in institutional reports present a strong positive correlation.

5. Conclusions

According to the literature, the implementation and certification by the organizations of multiple MSs (QEOH&S&SR) allow demonstrating to stakeholders a responsible commitment in favor of the SD. In Portugal, the number of organizations with multiple certified MSs (QEOH&S&SR) is a reality that has grown in recent years. Usually, the Portuguese organizations with multiple certified MSs (QEOH&S&SR) publish annually various institutional reports on the institutional website (on the Internet) to disclose contents on SD to stakeholders. In turn, the accounts and sustainability reports are the institutional reports most frequently used to disclose the SDGs (i.e., UN SDGs items) and the SDRs (i.e., GRI items) to interested parties. Therefore, holistically, the object of study of this investigation was achieved with the proposal of a framework to integrate Sustainability within Management Systems Standards and subsequently implement and disclose Sustainable Development goals and results and the answer to the three "Research Questions" (RQ) initially proposed.

In answer to RQ1: What are the main SDGs disclosed in institutional reports by Portuguese organizations with multiple certified MSs (QEOH&S&SR)? We found that the four main SDGs disclosed in institutional reports by certified Portuguese organizations (QEOH&S&SR) are the following (in descending order): "life on land" (SDG 15); "industry, innovation, and infrastructure" (SDG 09); "responsible consumption and production" (SDG 12); and "partnerships for the goals" (SDG 17), these last three in ex aequo in terms of ranking. Thus, SDG 15 is the goal most disclosed of all the SDGs in institutional reports. Overall, SDG 15 ('life on land') focuses on People and Planet.

In response to RQ2: What are the main SDRs disclosed in institutional reports by Portuguese organizations with multiple certified MSs (QEOH&S&SR)? We found that the four main SDRs disclosed in institutional reports by certified Portuguese organizations (QEOH&S&SR) are the following (in descending order): 'employment' (GRI 401); 'economic performance' (GRI 201); 'anti-corruption' (GRI 205); and 'occupational health and safety' (GRI 403). Consequently, the GRI 401 is the result most disclosed of all the SDRs—the main SDR disclosed in institutional reports. Overall, the GRI 401 ("'employment") focuses on People.

In reply to RQ3: How the disclosure of SDGs and SDRs in institutional reports is correlated? We found that the SDGs and the SDRs disclosed in institutional reports by certified Portuguese organizations (QEOH&S&SR) are statistically significantly correlated. Accordingly, our research statistically demonstrated that the disclosure of SDGs and SDRs in institutional reports has a strong positive correlation. Moreover, there is an emphasis on the environmental dimension within SDGs disclosure and on the social dimension for SDRs disclosure, with the economic dimension present in both SDGs and SDRs. Overall, the contributions of this research are twofold. First, it supports the integration of the SDGs within organizations and proposes a model for SD implementation through MSSs. Second, it stimulates the demonstration of organizations impacts on the SDGs (the SDRs). Hence, these findings contribute to the state of the art of knowledge in this study area, as the research on the relationship between the disclosure of SDGs and SDRs is still at an early stage. Moreover, it can support organizations to comprehend, integrate and contribute to the SDGs, by adopting MSSs.

The research sample size and the limited number of institutional reports analyzed are limitations and restrictions that affected the present investigation. However, since MSSs certified organizations should comply with international validated requirements and the corresponding certification bodies are subject to the accreditation schemes, ensuring confidence and the compliance with the applicable MSs requirements, the study results can be generalized to similar certified organizations worldwide.

Finally, we propose as possible future developments of this investigation the realization of similar studies with post COVID 19 data and with certified organizations from other countries to assess different countries’ patterns and the possible generalization of this research results.

A Business Model supports organizations in creating, delivering, and capturing value, and Business Excellence Models have been proposed to integrate the SDGs while delivering outstanding results and promoting transformation [119]. Nevertheless, frameworks are needed to support the many certified MSSs organizations worldwide to achieve those aims. By integrating Sustainability within Management Systems Standards and subsequently implementing and disclosing Sustainable Development goals and results, the proposed framework can align and integrate Sustainability with the organizations' strategy, processes and key performance indicators and results. This contribution raises the awareness of SD goals and results publications within organizations with certified Management Systems Standards. It answers the calls for more emphasis on the SDGs and the support of MSSs for that aim [120] [121] [122]. It can support academics and decision-makers (focusing on business leaders and organization managers) to comprehend, integrate and contribute to the SDGs. Moreover, it can motivate other researchers to replicate this study in different contexts.

Author Contributions

The authors confirm their contributions to this paper as follows: Conceptualization, LF, FC and GS; Data curation, FC; Formal analysis, FC and LF; Investigation, FC, LF and GS; Methodology, LF, FC and GS; Writing – original draft, LF and FC; Writing – review & editing, LF, FC and GS.

Funding

The work of the author Luis Fonseca is supported by national funds, through the FCT— Portuguese Foundation for Science and Technology under the project - UIDB/50022/2020 (LAETA Base Funding).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Meadows, D. H., Meadows, D. L., Randers, J., & Behrens III, W. W. (1972). The limits to growth: A report for the club of Rome’s project on the predicament of mankind. Universe Books.

- World Commission on Environment and Development. (1987a). Our common future. Oxford University Press.

- World Commission on Environment and Development. (1987b). The report of the world commission on environment and development: Our common future (UN General Assembly No. A/42/427). United Nations (UN). http://www.un.org/ga/search/view_doc.asp?symbol=A/42/427&Lang=E.

- Cöster, M., Dahlin, G., & Isaksson, R. (2020). Are they reporting the right thing and are they doing it right?—A measurement maturity grid for evaluation of sustainability reports. Sustainability, 12(24), Article 10393. https://doi.org/10.3390/su122410393. [CrossRef]

- Isaksson, R. (2021). Excellence for sustainability – Maintaining the license to operate. Total Quality Management & Business Excellence, 32(5-6), 489–500. https://doi.org/10.1080/14783363.2019.1593044. [CrossRef]

- Bansal, P. (2005). Evolving sustainably: A longitudinal study of corporate sustainable development. Strategic Management Journal, 26(3), 197–218. https://doi.org/10.1002/smj.441. [CrossRef]

- Lozano, R. (2008). Envisioning sustainability three-dimensionally. Journal of Cleaner Production, 16(17), 1838–1846. https://doi.org/10.1016/j.jclepro.2008.02.008. [CrossRef]

- Strezov, V., Evans, A., & Evans, T. J. (2017). Assessment of the economic, social and environmental dimensions of the indicators for sustainable development. Sustainable Development, 25(3), 242–253. https://doi.org/10.1002/sd.1649. [CrossRef]

- Rosati, F., & Faria, L. G. D. (2019). Addressing the SDGs in sustainability reports: The relationship with institutional factors. Journal of Cleaner Production, 215, 1312–1326. https://doi.org/10.1016/j.jclepro.2018.12.107. [CrossRef]

- Steurer, R., Langer, M. E., Konrad, A., & Martinuzzi, A. (2005). Corporations, stakeholders and sustainable development I: A theoretical exploration of business–society relations. Journal of Business Ethics, 61(3), 263–281. https://doi.org/10.1007/s10551-005-7054-0. [CrossRef]

- Carvalho, F., Santos, G., & Gonçalves, J. (2018). The disclosure of information on sustainable development on the corporate website of the certified Portuguese organizations. International Journal for Quality Research, 12(1), 253–276. https://doi.org/10.18421/IJQR12.01-14. [CrossRef]

- Fonseca, L., Silva, V., Sá, J. C., Lima, V., Santos, G., & Silva, R. (2022). B Corp versus ISO 9001 and 14001 certifications: Aligned, or alternative paths, towards sustainable development?. Corporate Social Responsibility and Environmental Management, 29(3), 496–508. https://doi.org/10.1002/csr.2214. [CrossRef]

- Freeman, R. E., Phillips, R., & Sisodia, R. (2020). Tensions in stakeholder theory. Business & Society, 59(2), 213-231. [CrossRef]

- Siltaloppi, J., Rajala, R., & Hietala, H. (2021). Integrating CSR with business strategy: a tension management perspective. Journal of Business Ethics, 174(3), 507-527. [CrossRef]

- Fonseca, L., Ramos, A., Rosa, A., Braga, A.C. and Sampaio, P. (2016). Stakeholders satisfaction and sustainable success, Int. J. Ind. Syst. Eng., vol. 24, no. 2, pp. 144–157, 2016. [CrossRef]

- Welford, R. & Frost, S. (2006). Corporate Social Responsibility in Asian Supply Chains. Corporate Social Responsibility and Environmental Management.13, 166–176 (2006). https://doi.org/10.1002/csr.121. [CrossRef]

- hou, Yinyoung, Manisha Singal, e Yoon Koh. 2016. “CSR and Financial Performance: The Role of CSR Awareness in the Restaurant Industry”. International Journal of Hospitality Management 57: 30–39. https://doi.org/10.1016/j.ijhm.2016.05.007P. [CrossRef]

- Carvalho, F., Santos, G., & Gonçalves, J. (2020). Critical analysis of information about integrated management systems and environmental policy on the Portuguese firms’ website, towards sustainable development. Corporate Social Responsibility and Environmental Management, 27(2), 1069–1088. https://doi.org/10.1002/csr.1866. [CrossRef]

- Tsalis, T. A., Malamateniou, K. E., Koulouriotis, D., & Nikolaou, I. E. (2020). New challenges for corporate sustainability reporting: United Nations’ 2030 Agenda for sustainable development and the sustainable development goals. Corporate Social Responsibility and Environmental Management, 27(4), 1617–1629. https://doi.org/10.1002/csr.1910. [CrossRef]

- Freeman, R. E. (1984). Strategic management: A stakeholder approach. Pitman Publishing.

- Ikram, M., Zhang, Q., Sroufe, R., & Ferasso, M. (2021). Contribution of certification bodies and sustainability standards to sustainable development goals: An integrated grey systems approach. Sustainable Production and Consumption, 28, 326–345. https://doi.org/10.1016/j.spc.2021.05.019. [CrossRef]

- Van Marrewijk, M. (2003). Concepts and definitions of CSR and corporate sustainability: Between agency and communion. Journal of Business Ethics, 44(2-3), 95–105. https://doi.org/10.1023/A:1023331212247. [CrossRef]

- Robert, K. W., Parris, T. M., & Leiserowitz, A. A. (2005). What is sustainable development? Goals, indicators, values, and practice. Environment: Science and Policy for Sustainable Development, 47(3), 8–21. https://doi.org/10.1080/00139157.2005.10524444. [CrossRef]

- Pojasek, R. B. (2003). Scoring sustainability results. Environmental Quality Management, 13(1), 91–98. https://doi.org/10.1002/tqem.10100. [CrossRef]

- Azapagic, A. (2003). Systems approach to corporate sustainability: A general management framework. Process Safety and Environmental Protection, 81(5), 303–316. https://doi.org/10.1205/095758203770224342. [CrossRef]

- Siew, R. Y. J. (2015). A review of corporate sustainability reporting tools (SRTs). Journal of Environmental Management, 164, 180–195. https://doi.org/10.1016/j.jenvman.2015.09.010. [CrossRef]

- Pizzi, S., Del Baldo, M., Caputo, F., & Venturelli, A. (2022). Voluntary disclosure of sustainable development goals in mandatory non- financial reports: The moderating role of cultural dimension. Journal of International Financial Management & Accounting, 33(1), 83–106. https://doi.org/10.1111/jifm.12139. [CrossRef]

- PricewaterhouseCoopers International. (2019). SDG Challenge 2019: Creating a strategy for a better world (PwC Report No. SDG Challenge 2019). https://www.pwc.com/gx/en/services/sustainability/sustainable-development-goals/sdg-challenge-2019.html.

- Manes-Rossi, F., & Nicolo', G. (2022). Exploring sustainable development goals reporting practices:From symbolic to substantive approaches—Evidence from theenergy sector. Corporate Social Responsibility and Environmental Management,29(5), 1799–1815.https://doi.org/10.1002/csr. [CrossRef]

- Silva, S. (2021). Corporate contributions to the sustainable development goals: An empirical analysis informed by legitimacy theory. Journal of Cleaner Production, 292, Article 125962. https://doi.org/10.1016/j.jclepro.2021.125962. [CrossRef]

- Crane, A., & Ruebottom, T. (2011). Stakeholder theory and social identity: Rethinking stakeholder identification. Journal of Business Ethics, 102(S1), 77–87. https://doi.org/10.1007/s10551-011-1191-4. [CrossRef]

- Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17b(1), 99–120. https://doi.org/10.1177/014920639101700108. [CrossRef]

- Barney, J. B. (2001). Resource-based theories of competitive advantage: A ten-year retrospective on the resource-based view. Journal of Management, 27(6), 643–650. https://doi.org/10.1177/014920630102700602. [CrossRef]

- DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147–160. https://doi.org/10.2307/2095101. [CrossRef]

- Camilleri, M. A. (2015). Valuing stakeholder engagement and sustainability reporting. Corporate Reputation Review, 18(3), 210–222. https://doi.org/10.1057/crr.2015.9. [CrossRef]

- Camilleri, M. A. (2021). The market for socially responsible investing: a review of the developments. Social Responsibility Journal, 17(3), 412–428. https://doi.org/10.1108/SRJ-06-2019-0194. [CrossRef]

- Hummel, K., & Szekely, M. (2022). Disclosure on the sustainable development goals – Evidence from Europe. Accounting in Europe, 19(1), 152–189. https://doi.org/10.1080/17449480.2021.1894347. [CrossRef]

- Ionașcu, E., Mironiuc, M., Anghel, I., & Huian, M. C. (2020). The involvement of real estate companies in sustainable development—An analysis from the SDGs reporting perspective. Sustainability, 12(3), Article 798. https://doi.org/10.3390/su12030798. [CrossRef]

- Leal Filho, W., Vidal, D. G., Chen, C., Petrova, M., Dinis, M. A. P., Yang, P., Rogers, S., Álvarez-Castañón, L. d. C., Djekic, I., Sharifi, A., & Neiva, S. (2022). An assessment of requirements in investments, new technologies and infrastructures to achieve the SDGs. Environmental Sciences Europe, 34, 1-17. https://doi.org/10.1186/s12302-022-00629-9. [CrossRef]

- Lim, W. M., Chin, M. W. C., Ee, Y. S., Fung, C. Y., Giang, C. S., Heng, K. S., Kong, M. L. F., Lim, A. S. S., Lim, B. C. Y., Lim, R. T. H., Lim, T. Y., Ling, C. C., Mandrinos, S., Nwobodo, S., Phang, C. S. C., She, L., Sim, C. H., Su, S. I., Wee, G. W. E., & Weissmann, M. A. (2022). What is at stake in a war? A prospective evaluation of the Ukraine and Russia conflict for business and society. Global Business and Organizational Excellence, 23-36. https://doi.org/10.1002/joe.22162. [CrossRef]

- Lozano, R., & Barreiro-Gen, M. (2022). Organisations' contributions to sustainability. An analysis of impacts on the Sustainable Development Goals. Business Strategy and the Environment, 1–12. https://doi.org/10.1002/bse.3305. [CrossRef]

- Welford, R. (Ed.). (1997). Hijacking Environmentalism: Corporate Responses to Sustainable Development (1st ed.). Routledge. https://doi.org/10.4324/9781315070889. [CrossRef]

- Büthe, T., & Mattli, W. (2011). The New Global Rulers: The Privatization of Regulation in the World Economy. Princeton University Press.

- Nunhes, T. V., Espuny, M., Lau áReis Campos, T., Santos, G., Bernardo, M., & Oliveira, O. J.(2022). Guidelines to build the bridge between sustainability and integrated management systems: A way to increase stakeholder engagement toward sustainable development. Corporate Social Responsibility and Environmental Management,29(5), 1617–1635.https://doi.org/10.1002/csr.2308. [CrossRef]

- Rebelo, M. F., Santos, G., & Silva, R. (2016). Integration of management systems: Towards a sustained success and development of organizations. Journal of Cleaner Production, 127, 96–111. https://doi.org/10.1016/j.jclepro.2016.04.011. [CrossRef]

- International Organization for Standardization & International Electrotechnical Commission. (2021). ISO/IEC Directives, Part 1: Consolidated ISO Supplement—Procedures for the technical work—Procedures specific to ISO (ISO/IEC Standard No. ISO/IEC Directives, Part 1). https://www.iso.org/sites/directives/current/consolidated/index.xhtml.

- Blind, K, & Heß, P. (2023).Stakeholder perceptions of the role of standards for addressing the sustainable development goals, Sustainable Production and Consumption, 37, 2023, 180-190, https://doi.org/10.1016/j.spc.2023.02.016. [CrossRef]

- British Standards Institution. (2012). Specification of common management system requirements as a framework for integration (BSI Standard No. PAS 99:2012). https://shop.bsigroup.com/ProductDetail?pid=000000000030254209.

- Instituto Português da Qualidade. (2019). Sistema de gestão da responsabilidade social—Requisitos e linhas de orientação para a sua utilização [Social responsibility management system—Requirements and guidelines for its usage] (IPQ Standard No. NP 4469:2019). https://lojanormas.ipq.pt/product/np-4469-2019/.

- International Organization for Standardization. (2015a). Environmental management systems—Requirements with guidance for use (ISO Standard No. ISO 14001:2015). https://www.iso.org/standard/60857.html.

- International Organization for Standardization. (2015b). Quality management systems—Requirements (ISO Standard No. ISO 9001:2015). https://www.iso.org/standard/62085.html.

- International Organization for Standardization. (2018b). Occupational health and safety management systems—Requirements with guidance for use (ISO Standard No. ISO 45001:2018). https://www.iso.org/standard/63787.html.

- International Organization for Standardization. (2015c). Quality management systems—Fundamentals and vocabulary (ISO Standard No. ISO 9000:2015). https://www.iso.org/standard/45481.html.

- British Standards Institution. (2007). Occupational health and safety management systems—Requirements (BSI Standard No. BS OHSAS 18001:2007). https://shop.bsigroup.com/ProductDetail/?pid=000000000030148086.

- International Organization for Standardization. (2010). Guidance on social responsibility (ISO Standard No. ISO 26000:2010). https://www.iso.org/standard/42546.html.

- Fonseca, L.M., Domingues, J.P., Machado, P.B. and Calderón, M. (2017). Management System Certification Benefits: Where Do We Stand? Journal of Industrial Engineering and Management (JIEM), 10(3), pp. 476-494; DOI: http://dx.doi.org/10.3926/jiem.2350. [CrossRef]

- Ikram, M., Zhang, Q., & Sroufe, R. (2020a). Developing integrated management systems using an AHP-Fuzzy VIKOR approach. Business Strategy and the Environment, 29(6), 2265–2283. https://doi.org/10.1002/bse.2501. [CrossRef]

- Santos, G., Mendes, F., & Barbosa, J. (2011). Certification and integration of management systems: The experience of Portuguese small and medium enterprises. Journal of Cleaner Production, 19(17-18), 1965–1974. https://doi.org/10.1016/j.jclepro.2011.06.017. [CrossRef]

- Silva, C., Magano, J., Moskalenko, A., Nogueira, T., Dinis, M. A. P., & Sousa, H. F. P. (2020). Sustainable management systems standards (SMSS): Structures, roles, and practices in corporate sustainability. Sustainability, 12(15), Article 5892. https://doi.org/10.3390/su12155892. [CrossRef]

- Hernandez-Vivanco, A., Domingues, P., Sampaio, P., Bernardo, M., & Cruz-Cázares, C. (2019). Do multiple certifications leverage firm performance? A dynamic approach. International Journal of Production Economics, 218, 386–399. https://doi.org/10.1016/j.ijpe.2019.07.016. [CrossRef]

- Ikram, M., Zhang, Q., Sroufe, R., & Ferasso, M. (2020b). The social dimensions of corporate sustainability: An integrative framework including COVID-19 insights. Sustainability, 12(20), Article 8747. https://doi.org/10.3390/su12208747. [CrossRef]

- Freundlieb, M., & Teuteberg, F. (2013). Corporate social responsibility reporting – A transnational analysis of online corporate social responsibility reports by market-listed companies: Contents and their evolution. International Journal of Innovation and Sustainable Development, 7 (1), 1–26. [CrossRef]

- Diaz-Sarachaga, J. M. (2021). Shortcomings in reporting contributions towards the sustainable development goals. Corporate Social Responsibility and Environmental Management, 28(4), 1299–1312. https://doi.org/10.1002/csr.2129. [CrossRef]

- Erin, O. A., & Bamigboye, O. A. (2022). Evaluation and analysis of SDG reporting: evidence from Africa. Journal of Accounting & Organizational Change, 18(3), 369–396. https://doi.org/10.1108/JAOC-02-2020-0025. [CrossRef]

- Fonseca, L., & Carvalho, F. (2019). The reporting of SDGs by quality, environmental, and occupational health and safety-certified organizations. Sustainability, 11(20), Article 5797. https://doi.org/10.3390/su11205797. [CrossRef]

- Izzo, M. F., Ciaburri, M., & Tiscini, R. (2020). The challenge of sustainable development goal reporting: The first evidence from Italian listed companies. Sustainability, 12(8), Article 3494. https://doi.org/10.3390/su12083494. [CrossRef]

- Guarini, E., Mori, E., & Zuffada, E. (2022). Localizing the sustainable development goals: A managerial perspective. Journal of Public Budgeting, Accounting & Financial Management, 34(5), 583–601.

- Leal, W., Azeiteiro, U., Alves, F., Pace, P., Mifsud, M., Brandli, L., et al. (2018). Reinvigorating the sustainable development research agenda: The role of the sustainable development goals (SDG). International Journal of Sustainable Development & World Ecology, 25(2), 131–142. [CrossRef]

- United Nations. (2015). Transforming our world: The 2030 agenda for sustainable development (UN General Assembly Resolution No. A/RES/70/1). https://undocs.org/A/RES/70/1.

- Fonseca, L. M., Domingues, J. P., & Dima, A. M. (2020). Mapping the sustainable development goals relationships. Sustainability, 12(8), Article 3359. https://doi.org/10.3390/su12083359. [CrossRef]

- Heemskerk, B., Pistorio, P., & Scicluna, M. (2002). Sustainable development reporting: Striking the balance. World Business Council for Sustainable Development. https://www.wbcsd.org/Programs/Redefining-Value/External-Disclosure/Reporting-matters/Resources/Sustainable-Development-Reporting-Striking-the-balance.

- Carvalho, F., Domingues, P., & Sampaio, P. (2019). Communication of commitment towards sustainable development of certified Portuguese organisations: Quality, environment and occupational health and safety. International Journal of Quality & Reliability Management, 36(4), 458–484. https://doi.org/10.1108/IJQRM-04-2018-0099. [CrossRef]

- Saber, M., & Weber, A. (2019). Sustainable grocery retailing: Myth or reality?—A content analysis. Business and Society Review, 124(4), 479–496. https://doi.org/10.1111/basr.12187. [CrossRef]

- Chowdhury, E. H., Rambaree, B. B., & Macassa, G. (2021). CSR reporting of stakeholders’ health: Proposal for a new perspective. Sustainability, 13(3), Article 1133. https://doi.org/10.3390/su13031133. [CrossRef]

- Girella, L., Zambon, S., & Rossi, P. (2019). Reporting on sustainable development: A comparison of three Italian small and medium-sized enterprises. Corporate Social Responsibility and Environmental Management, 26(4), 981–996. https://doi.org/10.1002/csr.1738. [CrossRef]

- Global Reporting Initiative. (2020). Consolidated set of GRI sustainability reporting standards 2020 (GRI Standards No. GRI 2020). https://www.globalreporting.org/standards/gri-standards-download-center/.

- SDG Compass. (2020). The guide for business action on the SDGs. Retrieved from https://sdgcompass.org.

- Tsalis, T. A., Malamateniou, K. E., Koulouriotis, D., & Nikolaou, I. E. (2020). New challenges for corporate sustainability reporting: United Nations’ 2030 Agenda for sustainable development and the sustainable development goals. Corporate Social Responsibility and Environmental Management, 27(4), 1617–1629. https://doi.org/10.1002/csr.1910. [CrossRef]

- Elkington, J. (1997). Cannibals with forks: The triple bottom line of 21st century business. Capstone Publishing Limited.

- Elkington, J. (2004). Enter the triple bottom line. In A. Henriques & J. Richardson (Eds.), The triple bottom line: Does it all add up? (pp. 1–16). Earthscan.

- Pacheco, J. A. B., Teijeiro-Álvarez, M. M., & García-Álvarez, M. T. (2020). Sustainable development in the economic, environmental, and social fields of Ecuadorian universities. Sustainability, 12(18), Article 7384. https://doi.org/10.3390/su12187384. [CrossRef]

- Zhao, X., Castka, P., & Searcy, C. (2020). ISO standards: A platform for achieving sustainable development goal 2. Sustainability, 12(2), Article 9332. https://doi.org/10.3390/su12229332. [CrossRef]

- Rashed, A. H., Rashdan, S. A., & Ali-Mohamed, A. Y. (2022). Towards effective environmental sustainability reporting in the large industrial sector of Bahrain. Sustainability, 14(1), Article 219. https://doi.org/10.3390/su14010219. [CrossRef]

- Calabrese, A., Costa, R., Gastaldi, M., Ghiron, N. L., & Montalvan, R. A. V. (2021). Implications for sustainable development goals: A framework to assess company disclosure in sustainability reporting. Journal of Cleaner Production, 319, Article 128624. https://doi.org/10.1016/j.jclepro.2021.128624. [CrossRef]

- Elalfy, A., Weber, O., & Geobey, S. (2021). The sustainable development goals (SDGs): A rising tide lifts all boats? Global reporting implications in a post SDGs world. Journal of Applied Accounting Research, 22(3), 557–575. https://doi.org/10.1108/JAAR-06-2020-0116. [CrossRef]

- Ivic, A., Saviolidis, N. M., & Johannsdottir, L. (2021). Drivers of sustainability practices and contributions to sustainable development evident in sustainability reports of European mining companies. Discover Sustainability, 2(17), 1–20. https://doi.org/10.1007/s43621-021-00025-y. [CrossRef]

- Siva, V., Gremyr, I., Bergquist, B., Garvare, R., Zobel, T., & Isaksson, R. (2016). The support of quality management to sustainable development: A literature review. Journal of Cleaner Production, 138, 148–157. https://doi.org/10.1016/j.jclepro.2016.01.020. [CrossRef]

- Alsawafi, A., Lemke, F., & Yang, Y. (2021). The impacts of internal quality management relations on the triple bottom line: A dynamic capability perspective. International Journal of Production Economics, 232, Article 107927. https://doi.org/10.1016/j.ijpe.2020.107927. [CrossRef]

- Chavez, R., Yu, W., Jajja, M. S. S., Lecuna, A., & Fynes, B. (2020). Can entrepreneurial orientation improve sustainable development through leveraging internal lean practices?. Business Strategy and the Environment, 29(6), 2211–2225. https://doi.org/10.1002/bse.2496. [CrossRef]

- Tarí, J. J., Molina-Azorín, J. F., López-Gamero, M. D., & Pereira-Moliner, J. (2021). The association between environmental sustainable development and internalization of a quality standard. Business Strategy and the Environment, 30(5), 2587–2599. https://doi.org/10.1002/bse.2765. [CrossRef]

- Camilleri, M. A. (2018). Theoretical insights on integrated reporting: The inclusion of non-financial capitals in corporate disclosures. Corporate Communications: An International Journal, 23(4), 567–581. https://doi.org/10.1108/CCIJ-01-2018-0016. [CrossRef]

- Camilleri, M. A. (2021). The market for socially responsible investing: a review of the developments. Social Responsibility Journal, 17(3), 412–428. https://doi.org/10.1108/SRJ-06-2019-0194. [CrossRef]

- Camilleri, M. A. (2022). The rationale for ISO 14001 certification: A systematic review and a cost–benefit analysis. Corporate Social Responsibility and Environmental Management, 29(4), 1067–1083. https://doi.org/10.1002/csr.2254. [CrossRef]

- Fonseca, L. M. C. M. (2015). ISO 14001:2015: An improved tool for sustainability. Journal of Industrial Engineering and Management, 8(1), 37–50. http://dx.doi.org/10.3926/jiem.1298. [CrossRef]

- Chen, Q. (2004). Sustainable development of occupational health and safety management system − Active upgrading of corporate safety culture. International Journal on Architectural Science, 5(4), 108–113. http://www.bse.polyu.edu.hk/researchCentre/Fire_Engineering/summary_of_output/journal/IJAS/V5/p.108-113.pdf.

- Jilcha, K., & Kitaw, D. (2017). Industrial occupational safety and health innovation for sustainable development. Engineering Science and Technology, an International Journal, 20(1), 372–380. https://doi.org/10.1016/j.jestch.2016.10.011. [CrossRef]

- Marhavilas, P., Koulouriotis, D., Nikolaou, I., & Tsotoulidou, S. (2018). International occupational health and safety management-systems standards as a frame for the sustainability: Mapping the territory. Sustainability, 10(10), Article 3663. https://doi.org/10.3390/su10103663. [CrossRef]

- 98. Social Accountability International. (2014). Social accountability 8000 (SAI Standard No. SA 8000:2014). https://sa-intl.org/resources/sa8000-standard/.

- Murmura, F., & Bravi, L. (2020). Developing a corporate social responsibility strategy in India using the SA 8000 standard. Sustainability, 12(8), Article 3481. https://doi.org/10.3390/su12083481. [CrossRef]

- Santos, G., Murmura, F., & Bravi, L. (2018). SA 8000 as a tool for a sustainable development strategy. Corporate Social Responsibility and Environmental Management, 25(1), 95–105. https://doi.org/10.1002/csr.1442. [CrossRef]

- Jonkutė, G., Staniškis, J. K., & Dukauskaitė, D. (2011). Social responsibility as a tool to achieve sustainable development in SMEs. Environmental Research, Engineering and Management, 57(3), 67–81. https://erem.ktu.lt/index.php/erem/article/view/465.

- Castka, P., Bamber, C. J., Bamber, D. J., & Sharp, J. M. (2004). Integrating corporate social responsibility (CSR) into ISO management systems – In search of a feasible CSR management system framework. The TQM Magazine, 16(3), 216–224. https://doi.org/10.1108/09544780410532954. [CrossRef]

- Oskarsson, K., & Von Malmborg, F. (2005). Integrated management systems as a corporate response to sustainable development. Corporate Social Responsibility and Environmental Management, 12(3), 121–128. https://doi.org/10.1002/csr.78. [CrossRef]

- Nadae, J., Carvalho, M. M., & Vieira, D. R. (2021). Integrated management systems as a driver of sustainability performance: Exploring evidence from multiple-case studies. International Journal of Quality & Reliability Management, 38(3), 800–821. https://doi.org/10.1108/IJQRM-12-2019-0386. [CrossRef]

- Barbosa, A. S., Silva, L. B., Souza, V. F., & Morioka, S. N. (2022). Integrated management systems: Their organizational impacts. Total Quality Management & Business Excellence, 33(7-8), 794–817. https://doi.org/10.1080/14783363.2021.1893685. [CrossRef]

- Carvalho, F. J. F. (2019). A comunicação de resultados sobre desenvolvimento sustentável nas organizações portuguesas certificadas em qualidade, ambiente e segurança [The communication of results on sustainable development in the certified Portuguese organisations in quality, environment, and safety] [Master’s thesis, Instituto Superior de Engenharia do Porto – Instituto Politécnico do Porto]. Repositório Científico do Instituto Politécnico do Porto. http://hdl.handle.net/10400.22/14980.

- Derqui, B. (2020). Towards sustainable development: Evolution of corporate sustainability in multinational firms. Corporate Social Responsibility and Environmental Management, 27(6), 2712–2723. https://doi.org/10.1002/csr.1995. [CrossRef]

- Gerged, A. M., Cowton, C. J., & Beddewela, E. S. (2018). Towards sustainable development in the Arab Middle East and North Africa region: A longitudinal analysis of environmental disclosure in corporate annual reports. Business Strategy and the Environment, 27(4), 572–587. https://doi.org/10.1002/bse.2021. [CrossRef]

- De Iorio, S., Zampone, G., & Piccolo, A. (2022). Determinant factors of SDG disclosure in the university context. Administrative Sciences, 12(1), Article 21. https://doi.org/10.3390/admsci12010021. [CrossRef]

- Gunawan, J., Permatasari, P., & Tilt, C. (2020). Sustainable development goal disclosures: Do they support responsible consumption and production?. Journal of Cleaner Production, 246, Article 118989. https://doi.org/10.1016/j.jclepro.2019.118989. [CrossRef]

- Abbott, W. F., & Monsen, R. J. (1979). On the measurement of corporate social responsibility: Self-reported disclosures as a method of measuring corporate social involvement. Academy of Management Journal, 22(3), 501–515. https://doi.org/10.5465/255740. [CrossRef]

- Schober, P., Boer, C., & Schwarte, L. A. (2018). Correlation coefficients: Appropriate use and interpretation. Anesthesia & Analgesia, 126(5), 1763–1768. https://doi.org/10.1213/ANE.0000000000002864. [CrossRef]

- Ching, H. Y., & Gerab, F. (2017). Sustainability reports in Brazil through the lens of signaling, legitimacy and stakeholder theories. Social Responsibility Journal, 13(1), 95–110. https://doi.org/10.1108/SRJ-10-2015-0147. [CrossRef]

- Krippendorff, K. (2018). Content analysis: An introduction to its methodology (4th ed.). Sage Publications.

- Heras-Saizarbitoria, I., Urbieta, L., & Boiral, O. (2022). Organizations’ engagement with sustainable development goals: From cherry-picking to SDG-washing?. Corporate Social Responsibility and Environmental Management, 29(2), 316–328. https://doi.org/10.1002/csr.2202. [CrossRef]

- Bastas, A., & Liyanage, K. (2018). ISO 9001 and supply chain integration principles based sustainable development: A delphi study. Sustainability, 10(12), Article 4569. https://doi.org/10.3390/su10124569. [CrossRef]

- Lambrechts, W., Son-Turan, S., Reis, L., & Semeijn, J. (2019). Lean, green and clean? Sustainability reporting in the logistics sector. Logistics, 3(1), Article 3. https://doi.org/10.3390/logistics3010003. [CrossRef]

- Kolsi, M. C., Ananzeh, M., & Awawdeh, A. (2021). Compliance with the global reporting initiative standards in Jordan: Case study of hikma pharmaceuticals. International Journal of Sustainable Engineering, 14(6), 1572–1586. https://doi.org/10.1080/19397038.2021.1970273. [CrossRef]