Submitted:

13 February 2025

Posted:

14 February 2025

You are already at the latest version

Abstract

Corporate Social Responsibility (CSR) and Sustainability have proliferated the corporate boardroom agenda and companies’ leadership teams are trying to find ways to improve their social and environmental performance and enhance their corporate governance management systems. This paper investigates the main CSR and sustainability-related standards that modern corporations use. To do so, it uses a sample of the 60 companies listed in ATHEX ESG Index. Firstly, a content analysis of those companies’ sustainability reports is conducted. The 60 companies are categorized in sectors according to the Global Industry Classification Standard (GICS). The sustainability standards used by each sector are grouped into four categories namely environmental; social; governance and reporting. Furthermore, an attempt is made to establish a link between the standards used and both the sectors they belong to and the material topics of each sector as they emerge from each company’s materiality analysis. Our research shows that our sample companies predominantly utilize reporting standards regardless of their sector. We did not establish a definitive relation between the prioritized material topics and the relative standards employed by the companies. We may have recognized certain pairings such as environmental material topics with relative environmental management systems, but not in a rigid manner or across all material topic categories.

Keywords:

CSR standards

; Sustainability standards

; ESG standards

; ATHEX ESG Index

; Sustainability reporting

; materiality

; GICS

1. Introduction

With the expansion of globalization, companies progressively adopted management standards established by the International Organization for Standardization (ISO) as a response to customer expectations [1]. The main incentive for standards implementation is increased demand for sustainably produced goods and services through Global Value Chains and export markets, new domestic markets and public procurement [2].

There is a proliferation of rival and uncoordinated voluntary sustainability standards developed mainly by NGOs and private companies, which expedite serving as catalysts enabling the implementation of sustainability policies [3]. These standards often compete against each other for market shares and legitimacy despite the fact that they coevolve and appear to promote each other. Using the coffee industry, a study highlights the spread of voluntary sustainability standards and recognizes a tension between the shared objective of promoting sustainability and the competition among standards organizations [4].

CSR standards assess a company’s sustainability and its internal management’s efficacy and ethical principles [5]. A hotel industry study stated that hotels require internal motivators to assimilate a quality system, as external factors alone do not adequately elucidate the process of quality internalization [6]. A study highlighted the need for evolved ESG reporting standards that have to include at a bare minimum the following: validation procedures for the reported KPIs; data timeliness; management of intangible assets; and standard procedures for qualitative data and descriptive information [7].

The development of ESG reporting standards improves transparency, accountability, trust, and innovation, hence facilitating informed decision-making for investors. At the same time, the organizations that adopt these reporting standards aim to promote sustainability efforts and enhance trust among stakeholders [8]. The more socially and environmentally conscious all stakeholders become, compliance with robust ESG standards may provide a competitive advantage, improving a company’s reputation and strengthening its market position [9]. The implementation of robust ESG standards can enhance the ESG performance of organizations [10].

When organizations adopt voluntary management systems, namely, those published by the International Organization for Standardization (ISO), they can address several potential issues related to sustainable development [11]. ISO itself published a relative edition where it pairs ISO Standards with the United Nations Sustainable Development Goals [12]. Fonseca and Carvalho [13] discovered that the communication of United Nations Sustainable Development Goals (SDGs) is more pronounced in Portuguese firms accredited in Quality, Environment, and Occupational Health and Safety that publish their sustainability reports (GRI) on their websites. A study highlighted an interlinkage between ISO standards and United Nations Sustainable Development Goal 2: Zero hunger—End hunger, achieve food security and improved nutrition, and promote sustainable agriculture [14]. ISO standards have the potential to contribute especially to two SDG 2 sub-targets, namely targets 2.3 and 2.4 (ibid).

The proliferation of standards and the differentiation of Key Performance Indicators (KPIs) used created a vague benchmark environment where comparison among companies’ sustainable performance was difficult to achieve. Although some frameworks were successfully developed e.g., by Krajnc & Glavič, 2005 [15], the direct comparison even between two companies of the same size and sector using the same sustainability reporting standards is not a straightforward task. ESG indicators lack universally standardized criteria, and rating agencies globally employ diverse frameworks and metrics to assess the ESG performance of corporations [16].

The fact that companies adopt management standards does not necessarily guarantee a change in culture and/or corporate behavior. The internalization of quality management standards entails embedding these standards into everyday business practices and always pursuing enhancement. This process is evaluated by constructs such as everyday practices and continuous improvement [17].

Recognizing and isolating CSR and sustainability-related standards is not a straightforward, simple task, as CSR has a holistic, strategic character and crosses the whole of an organization vertically and horizontally. Glavic & Lukman [18] gathered and analyzed 51 sustainability-related terms and their definitions and tried to establish their interconnection between terms based on semantic similarities and differences. Under this context, it is important to understand that all quality management systems form an interconnected system towards a better sustainable performance and may help the companies to become better on an everyday basis, which is the whole meaning of corporate responsibility in the first place. Thus, besides the reporting sustainability standards, which belong a priori to the sustainability category, all other management standards could fall under sustainability categories such as environment, social, and governance.

This research paper uses the case of 60 listed companies in the ATHEX ESG Index in Greece. It analyzes the content of the sustainability, ESG, and corporate social responsibility reports of these companies, focusing on their management standards. At first, an identification of the standards used is performed. Then, those management standards are manually categorized in four categories: environment, social, governance, and reporting. In addition, the standards used by each company are analyzed in relation to the prioritized sustainability material topics for each respective company.

The ATHEX ESG Index is a sustainability index established by the Athens Stock Exchange (ATHEX) to advance the concepts of ESG (Environmental, Social, Governance) within Greek corporations. It was inaugurated in August 2021, originally comprised of 35 firms, chosen for their environmental, social, and governance (ESG) performance, and reached its goal of 60 companies as of June 2023. The index comprises companies that have published ethical business practices and adhere to rigorous sustainability standards. The index offers an assessment of organizations’ dedication to sustainable development by analyzing their environmental, social, and governance performance. According to the ATHEX ESG announcements, involvement in the Index necessitates compliance with principles of transparency and information disclosure, allowing investors to recognize companies that incorporate ESG values into their strategies and operations [19].

This paper provides valuable localized insights into ESG mapping in the specific geographical location, namely Greece, and at the same time offers general insights into the sustainability standards market, possibly suggesting new research fields. It enriches the academic and practical discourse around ESG by providing empirical evidence from a European listed market. It may act as a model for other markets and allow cross-country research comparisons. The identification and categorization of management standards into environmental, social, governance, and reporting categories enables clear benchmarking. Moreover, the connection between standards used and materiality offers the opportunity to sustainability scholars to enhance sustainability strategies and understand possible gaps in sustainability management approaches. Additionally, the content analysis of the sustainability reports gives a comprehensive understanding of reporting practices in a European listed market and offers valuable insights both for sustainability reporting status quo and for the management approaches of ESG topics. Furthermore, the manual classification of standards in the four different categories may act as a model that can be benchmarked against other countries and recognizes trends and practices that can inform stakeholders and policymakers.

2. Materials and Methods

The first step of the content analysis was to familiarize ourselves with the ATHEX ESG Index. In November 2024 we found the 60 listed companies that shape the Index and visited their corporate websites. Then we downloaded the latest sustainability reports. 59 companies had already published their sustainability report for the reporting period 2023, while one did not publish a report for 2023, and so we relied on the report for 2022. This way we created a database of 60 sustainability reports.

The next step was to categorize the companies according to the Global Industry Classification Standard (GICS). We relied solely on the companies’ primary business activity and did not take into account the secondary and tertiary business activities. We chose GICS because is a well-established taxonomy employed to categorize and arrange organizations into industrial groupings and sectors according to their principal business activity. GICS offers a uniform framework for the global comparison of enterprises and industries. It guarantees that enterprises are methodically categorized, facilitating analysis and comparison for investors internationally.

Then, we examined the sustainability reports and found useful data for our research that we placed in an Excel file. The main Excel tab consisted of the following columns: Company’s name; GICS company’s sector; standards used; other certifications; management systems; year of publication; reporting standard; prioritized material topics. Each line presented data for the relative company.

Next, we classified the standards used by the companies of each sector according to the four categories: environment, social, governance, and reporting standards. In addition, we created another tab with all sustainability-prioritized topics for each company as derived from its materiality analysis exercise. Finally, we created another Excel tab where we put data regarding the material ESG topics for each company and grouped the companies and topics per sector. We arranged material topics that belonged in the same category and had similar names or descriptions. For example, we treated “climate change adaption” and “climate change action” as the same topic under the name: climate change. Then, we investigated whether the sector and/or the material topics influence the management standards that each company uses.

3. Results

Sixty (60) companies that are included in the ATHEX ESG Index were surveyed and each was categorized into one of the 11 GICS sectors based on the core business activity that they engage in (Table 1). The secondary and tertiary business activities were not taken into account during this categorization. For example, METLEN’s core business activity is metallurgy, but has expanded into energy production, however since energy production is currently a secondary activity it has been categorized under the Materials sector for the purposed of this paper.

Overall, three companies (HELLENiQ ENERGY and Motor Oil, DEI) belong in the Energy sector, twelve companies (FLEXOPACK, METLEN, TITAN CEMENT INTERNATIONAL, VIOHALCO, AKRITAS, Alumil, Elastron, ElVAHALCOR, IKTINOS HELLAS, THRACE PLASTICS Co S.A., Plastika Kritis, SIDMA S.A.) belong in the Materials sector, mostly in the Metals, Construction Materials and Packaging industries, eight companies (CENERGY HOLDINGS, INTRAKAT, AVAX, AEGEAN, ELLAKTOR, Eltongroup, ThPA S.A., P.P.A. S.A.) belong in the Industrials sector, mostly in the Construction and Engineering and Transportation industries, nine companies (Autohellas, FOURLIS, JUMBO, QUEST, Elinoil, Motodynamics, OPAP, Petropoulos, REVOIL) belong in the Consumer Discretionary sector, five companies (COCA-COLA HBC AG, LOULIS FOOD INGREDIENTS, Gr. Sarantis S.A., Kri, Papoutsanis) belong in the Consumer Staples sector, mostly in the Beverages, Food Products and Personal Care Products industries, two companies (LAVIPHARM, Athens Medical Group) belong in the Health Care sector, nine companies (ALPHA TRUST HOLDINGS, ALPHA TRUST ANROMEDA, Alpha Services and Holdings, EUROBANK ERGASIAS, IDEAL HOLDINGS, National Bank of Greece, Athens Exchange Group, Interlife, PIRAEUS FINANCIAL HOLDINGS) belong in the Financials sector, two companies (SPACE HELLAS, Intracom) belong in the Information Technology sector, one company (OTE) belongs in the Communication Services sector, five companies (ADMIE Holding, GEK TERNA, EYDAP, EYATH S.A.) belong in the Utilities sector and four companies (BRIQ PROPERTIES, DIMAND, LAMDA DEVELOPMENT, Premia Properties REIC) belong in the Real Estate sector based on their key business activities.

3.1. ESG Standards Used per Sector

This section presents data and analysis of the standards used by every sector of the ATHEX ESG Index divided in 4 categories namely environment; social; governance; reporting.

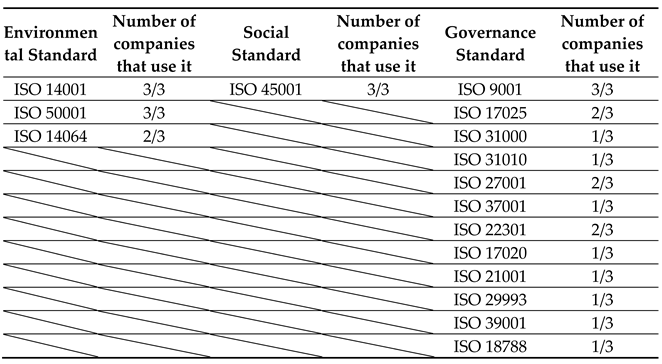

Table 2 presents the Environmental, Social and Governance Standards, while Table 3 presents the Reporting Standards used in the Energy Sector.

The Energy sector favors reporting standards with every company using GRI, UNGC, ATHEX ESG Index, Greek Sustainability Code and AA1000AP.

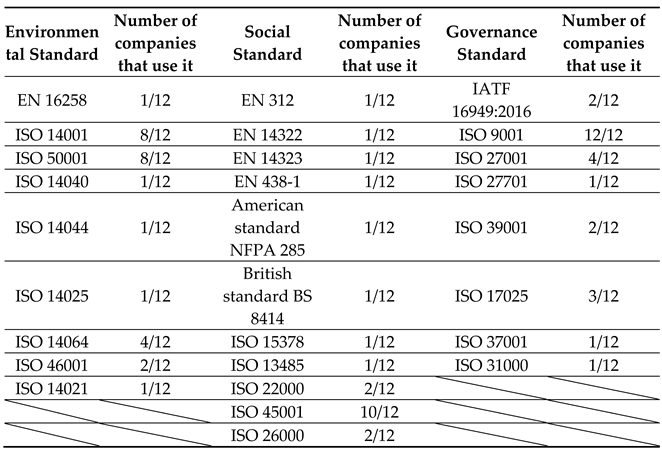

Table 4 presents the Environmental, Social and Governance Standards, while Table 5 presents the Reporting Standards used in the Materials Sector.

The Materials sector favors reporting standards. The overwhelming majority of companies (11/12) utilize the GRI Standards and a significant majority (9/12) uses UNGC and ATHEX ESG Index, whereas a significant minority (5/12) uses SASB. GRI is the only standard that is sometimes used on its own, whereas all others are used in conjunction with each other.

This sector also favors various management standards, with an overwhelming preference for ISO management standards.

In the social sphere, this sector favors several product quality standards that benefit the end user such as E312 for the quality of particle boards, ΕΝ 14322 for the quality of decorative melamine faced boards for interior use, ΕΝ 14323 for the quality of wood-based products, ΕΝ 438-1 for the quality of high-pressure decorative laminates, ISO 15378:2017 for the quality of primary packaging materials for medicinal products, ISO 13485:2016 for the quality management for medical devices.

Regarding environment the emphasis is on environmental management (ISO 14001), GHG management (ISO 14064), energy management (ISO 50001) and environmental management through LCA (ISO 14040, ISO 14044, ISO 14025).

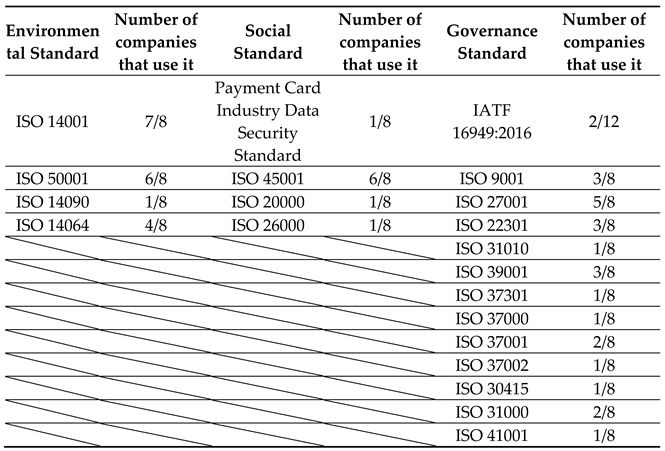

Table 6 presents the Environmental, Social and Governance Standards, while Table 7 presents the Reporting Standards used in the Industrials Sector.

The Industrials sector favors reporting standards, with UNGC and the ATHEX ESG Index being the most prevalent. GRI is also widely used with ESRS being mostly used for materiality purposes as for the reporting period we performed research, they were not yet obliged by the CSRD.

This sector also favors exclusively ISO management standards, with an emphasis on Governance standards. In the environmental sphere the emphasis is on environmental management (ISO 14001), with 7/8 companies of this sector adhering to this standard and energy management, with 6/8 companies using ISO 50001.

Table 8 presents the Environmental, Social and Governance Standards, while Table 9 presents the Reporting Standards used in the Consumer Discretionary Sector.

The Consumer Discretionary sector favors reporting standards, with the ATHEX ESG Index being the most prevalent followed by GRI and UNGC.

This sector also favors management standards, mostly ISO standards, however in this sector 2/9 companies don’t utilize ISO at all. The emphasis on this sector is on Governance standards.

Table 10 presents the Environmental, Social and Governance Standards, while Table 11 presents the Reporting Standards used in the Consumer Staples Sector.

This sector emphasizes reporting standards. All companies utilize the GRI Standards and a significant majority uses the ATHEX ESG Index. SASB and ESRS are used mostly for materiality purposes.

Table 12 presents the Environmental, Social and Governance Standards, while Table 13 presents the Reporting Standards used in the Health Care Sector.

The two companies of the health care sector apply reporting standards. Both companies use GRI and UNGC Standards. This sector also favors various management standards, with an overwhelming preference for ISO management standards.

In the social sphere, product quality standards that benefit the end user such as ISO 13485 for the quality management for medical devices are being used.

Regarding the environment the only standards used are for environmental management (ISO 14001) and GHG management (ISO 14064).

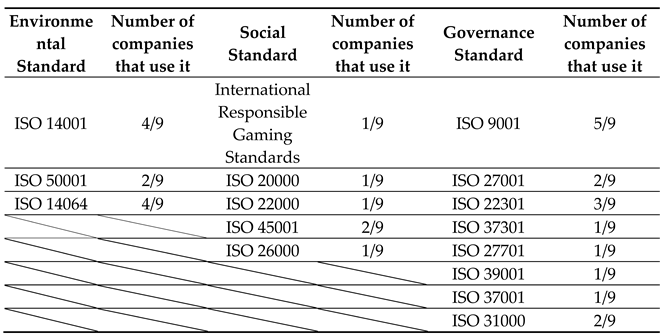

Table 14 presents the Environmental, Social and Governance Standards, while Table 15 presents the Reporting Standards used in the Financials Sector.

The governance and the reporting standards prevail in the Financials sector. We identify 10 different governance standards used with one of them mentioned by 6 out of 9 companies and at the same time all 9 companies report on their ESG performance.

Table 16 presents the Environmental, Social and Governance Standards, while Table 17 presents the Reporting Standards used in the Information Technology Sector.

One company shows a preference in using standards. Both companies in this sector use the same reporting standards in conjunction with each other.

Table 18 presents the Environmental, Social and Governance Standards, while Table 19 presents the Reporting Standards used in the Communication Services Sector.

A single company was included in the ATHEX ESG Index in this sector so no sector benchmarking can be presented.

Table 20 presents the Environmental, Social and Governance Standards, while Table 21 presents the Reporting Standards used in the Utilities Sector.

The Utilities sector showcases an increased action on environmental standards as most of the companies apply such standards. Nevertheless, social, governance and reporting standards are not left behind.

Table 22 presents the Environmental, Social and Governance Standards, while Table 23 presents the Reporting Standards used in the Real Estate Sector.

In this sector we find various governance and reporting standards but only one and two social and environmental standards respectively.

3.2. Sector ESG Materiality

The Energy sector has identified climate, energy, resource management as material topics related to the environment (Table 24). That is also reflected in the use of standards related to the environment, such as the ISO standards for Environmental Management (ISO 14001), Energy Management (ISO 50001) and GHG Management (ISO 14064). The material topics included in the climate concerns in the Energy sector include climate change, climate change mitigation, climate adaptation, resilience, and transition. The energy concerns are mostly stated as promotion of Renewable Energy Sources (RES) & energy management, energy access and availability. However, when it comes to waste or water management no specific standard seems to be used.

In the social scope material topics have been identified, such as concerns about human rights, the quality of employment, the local stakeholders and customer relations and satisfaction. However, this is not ultimately reflected in the standards used, since the only area that has both been identified as a material issue and a related standard has been utilized is that of the health and safety of employees (ISO 45001).

The material topics related to governance are varied and include regulatory compliance, business ethics and continuity, creation of economic value, data privacy and mobility. These priorities are also reflected in the standards used. We observed the use of standards relating to risk management (ISO 31000, ISO 31010), information security management (ISO 27000), business continuity (ISO 22301), road safety (ISO 39001) Nevertheless we also observed the use of standards that did not relate to any topics that were mentioned as material by any of the companies in this Sector, such as the ISO 37001 (anti-bribery management systems).

The Materials sector has identified climate, energy, resource management and biodiversity as material topics related to the environment (Table 25). That is also reflected in the use of standards related to the environment, such as the ISO standards for Environmental Management (ISO 14001, ISO 14040, ISO 14044), Energy Management (ISO 50001) and GHG Management (ISO 14064), Water efficiency management (ISO 46001). The material topics included in the climate concerns in the Materials sector include climate change, climate change mitigation, climate adaptation. The energy concerns are mostly stated as energy, responsible energy management, energy consumption, energy efficiency and renewable sources, energy management. However, when it comes to waste or raw material management no specific standard seems to be used.

Within the social context several material topics have been identified, such as concerns about human rights, the quality of employment, the local stakeholders, customer relations and satisfaction, product innovation and safety. This sector seems to focus on standards relating to product quality. However, the rest of the social material topics identified are not necessarily reflected in the standards used, since the areas that have both been identified as a material issue and a related standard has been utilized are those of the health and safety of employees (ISO 45001) and of social responsibility (ISO 26000).

The material topics related to governance are varied and include regulatory compliance, business ethics and continuity, anti-corruption, creation of economic growth, data privacy and infrastructure. These priorities are also reflected in the standards used. We observed the use of standards relating to risk management (ISO 31000), information security management (ISO 27000, ISO 27701), anti-bribery management (ISO 37001). However, we also observed that some material topics are not reflected in the standards used, such as the issue of business continuity.

The Industrials sector has identified climate, energy, resource management and biodiversity as material topics related to the environment (Table 26). That is also reflected in the use of standards related to the environment, such as the ISO standards for Environmental Management (ISO 14001), Energy Management (ISO 50001) and GHG Management (ISO 14064), Adaptation to climate change (ISO 14090). The material topics included in the climate concerns in the Industrials sector include climate change, and climate change mitigation and adaptation. The energy concerns are mostly stated simply as energy, energy transition, energy management. Nonetheless, when it comes to waste or water management no specific standard seems to be used.

In the social domain various material topics have been identified, such as concerns about human rights, the quality of employment, the local stakeholders, customer relations and satisfaction, product innovation and safety. This sector seems to have used only one standard relating to product quality. Nevertheless, the rest of the material topics identified in the social sphere are not necessarily reflected in the standards used, since the areas that have both been identified as a material issue and a related standard has been utilized are those of the health and safety of employees (ISO 45001) and of social responsibility (ISO 26000).

The material topics related to governance are varied and include business ethics and continuity, anti-corruption, creation of economic growth, data privacy and infrastructure. These priorities are also reflected in the standards used. We observed the use of standards relating to risk management (ISO 31000), business continuity (ISO 22301), information security management (ISO 27000), anti-bribery management (ISO 37001, ISO 37002).

The Consumer Discretionary sector has identified climate, energy and resource management as material topics related to the environment (Table 27). That is also reflected in the use of standards related to the environment, such as the ISO standards for Environmental Management (ISO 14001), Energy Management (ISO 50001) and GHG Management (ISO 14064). The material topics included in the climate concerns in the sector include climate change, climate stability. The energy concerns are stated as energy, energy transition, energy management, and investing in renewable energy sources. However, when it comes to waste, water or resource management no specific standard seems to be used.

Regarding the social dimension many material topics have been identified, such as concerns about human rights, the quality of employment, the local stakeholders, customer relations and satisfaction, product innovation and safety. This sector seems to use standards relating to product quality, health and safety of employees (ISO 45001) and of social responsibility (ISO 26000).

The material topics related to governance are varied and include business ethics and continuity, anti-corruption, creation of economic growth, data privacy and infrastructure. These priorities are also reflected in the standards used. We observed the use of standards relating to risk management (ISO 31000), business continuity (ISO 22301) and information security management (ISO 27000). However, we also observed that some material topics are not reflected in the standards used, such as the issue of anti-bribery.

The Consumer Staples sector has identified climate, energy, resource management and biodiversity as material topics related to the environment (Table 28). That is also reflected in the use of standards related to the environment, such as the ISO standards for Environmental Management (ISO 14001), Energy Management (ISO 50001) and GHG Management (ISO 14064). However, when it comes to waste, water or resource management no specific standard seems to be used.

In the social sphere many material topics have been identified, such as concerns about human rights, the quality of employment, the local stakeholders, customer relations and satisfaction, product innovation and safety. However, most material topics do not seem to be reflected in the standards used by this sector, but for health and safety of employees (ISO 45001).

The material topics related to governance are varied and include business ethics and governance, creation of economic growth, data privacy and infrastructure. The issue of data privacy is also reflected in the standards used These priorities are also reflected in the standards used (ISO 27000), but the rest of the material topics are not necessarily reflected by the use of a standard.

The Health Care sector has identified climate, energy and resource management as material topics related to the environment (Table 29). That is also reflected in the use of standards related to the environment, such as the ISO standards for Environmental Management (ISO 14001) and GHG Management (ISO 14064). However, when it comes to waste, water or energy management no specific standard seems to be used.

In the social domain material topics have been identified, such as concerns about human rights, the quality of employment, the local stakeholders, customer relations and satisfaction, product innovation and safety. This sector seems to use standards relating to product quality relating to health.

The material topics related to governance are varied and include business ethics, data privacy and infrastructure. These priorities are not necessarily reflected in the standards used.

The Financials sector has identified climate, energy, resource management and biodiversity as material topics related to the environment (Table 30). That is also reflected in the use of standards related to the environment, such standards for Environmental Management (ISO 14001), Energy Management (ISO 50001) and GHG Management (ISO 14064, GHG Protocol Corporate Accounting and Reporting Standard, Global GHG Accounting and Reporting Standard for the Financial Industry). The material topics included in the climate concerns in the Financials sector include climate change, climate stability, climate change mitigation and adaptation. The energy concerns are mostly stated simply as energy, energy conservation, energy consumption, financing energy transition increased use of renewable energy sources. However, when it comes to waste, water or resource management no specific standard seems to be used.

In the social sphere many material topics have been identified, such as concerns about human rights, the quality of employment, the local stakeholders, customer relations and satisfaction, product innovation and safety. This sector seems to use standards relating to product quality, health and safety of employees (ISO 45001) and of social responsibility (ISO 26000).

The material topics related to governance are varied and include business ethics and continuity, anti-corruption, creation of economic growth, data privacy and infrastructure. These priorities are also reflected in the standards used. We observed the use of standards relating to risk management (ISO 31000), business continuity (ISO 22301), information security (ISO 27000, ISO 27017, ISO 27018), anti-bribery and whistle-blowing (ISO 37001, ISO 37002).

The Information Technology sector has identified climate, energy and resource management as material topics related to the environment (Table 31). That is also reflected in the use of standards related to the environment, such as the ISO standards for Environmental Management (ISO 14001) and GHG Management (ISO 14064). However, when it comes to waste, water or energy management no specific standard seems to be used.

Within the social framework various material topics have been identified, such as concerns about human rights, the quality of employment, the local stakeholders, customer relations and satisfaction, product innovation and safety. However, only one standard from the ones that have been used fall under the social category, that of health and safety of employees (ISO 45001).

The material topics related to governance are varied and include business ethics and continuity, anti-corruption, creation of economic growth, data privacy and infrastructure. Not all these priorities seem to be reflected in the standards used. We observed the use of standards relating to business continuity (ISO 22301), information security and security techniques (ISO 27000, ISO 27701).

The Communication Services sector has identified climate, energy and emissions as material topics related to the environment (Table 32). That is also reflected in the use of standards related to the environment, such as the ISO standards for Environmental Management (ISO 14001) and Energy Management (ISO 50001).

In the social domain many material topics have been identified, such as concerns about the health and safety of employees, customer relations and satisfaction, product innovation and safety. However, only on social standard is being used, that of health and safety of employees (ISO 45001).

The material topics related to governance are varied and include business ethics and continuity, risk management data privacy and infrastructure. These priorities are also reflected in the standards used. We observed the use of standards relating to risk management (ISO 31000), business continuity (ISO 22301), information security (ISO 27001, ISO 27002). However, we also observe the use of standards that do not correspond to any of the material topics mentioned such as anti-bribery and whistle-blowing (ISO 37001, ISO 37002).

The Utilities sector has identified climate, energy, resource management and biodiversity as material topics related to the environment (Table 33). That is also reflected in the use of standards related to the environment, such standards for Environmental Management (ISO 14001), Energy Management (ISO 50001) and GHG Management (ISO 14064, GHG Protocol Corporate Accounting and Reporting Standard). However, when it comes to waste, water or resource management no specific standard seems to be used.

Within the social context material topics have been identified, such as concerns about the quality of employment, the local stakeholders, customer relations and satisfaction, product innovation and safety. However most material topics don’t seem to be reflected in the standards used, with the only exception being the health and safety of employees (ISO 45001).

The material topics related to governance are varied and include business ethics and continuity, anti-corruption, creation of economic growth and data privacy. Some of priorities are also reflected in the standards used. We observed the use of standards relating to risk management (ISO 31000), business continuity (ISO 22301), information security (ISO 27001).

The Real Estate sector has identified climate, energy, resource management and biodiversity as material topics related to the environment (Table 34). Only some of these priorities are also reflected in the use of standards related to the environment, such standards for Environmental Management (ISO 14001), and GHG Management (ISO 14064,).

In the social sphere many material topics have been identified, such as concerns about human rights, the quality of employment, the local stakeholders, customer relations and satisfaction, product innovation and safety. However most material topics don’t seem to be reflected in the standards used, with the only exception being the health and safety of employees (ISO 45001).

The material topics related to governance are varied and include risk management, creation of economic growth and data privacy. Some of priorities are also reflected in the standards used. We observed the use of standards relating to risk management (ISO 31000) and information security (ISO 27001).

4. Discussion

This paper examined the CSR and sustainability standards utilized by contemporary organizations. It employed a sample of 60 companies from the ATHEX ESG Index. A content analysis of the sustainability reports of the indexed companies was performed. The 60 companies were classified into sectors based on the Global Industry Classification Standard (GICS). The sustainability standards employed by the companies were classified into four categories: environmental, social, governance, and reporting. Additionally, the paper tried to link the standards used with their respective industries and see if a sector pattern exists. Also, the material issues of each organization as identified in their materiality study were linked to the identified sectors in to find any connection.

The primary management standards employed by firms are the reporting ones, irrespective of the sector they belong to. This can be multiple explained. Firstly, all sample companies are listed in the specific ESG Index, which requires the companies to have an ESG report. In the same context, ATHEX provides to companies its own reporting guidelines, namely ATHEX ESG. In addition, some of those companies have a legal obligation to publish a sustainability report because of NFRD, and thus, they had to follow a reporting standard of their choice. Furthermore, the prevalence of reporting standards can be justified by the heightened pressure across the value chain for companies to report on their ESG and overall performance exerted by their business partners.

Our research did not find an absolute linkage between the prioritized material topics and relative standards used by the companies. We may identify some pairings, but not in a strict form neither in all material topic categories. Most pairings appear in the environmental domain, where material topics and relative standards used have the strongest connection. This might be interpreted based on the increased pressure throughout the supply chain for environmental management systems that preceded the pressure for social and governance standards. Nevertheless, even in the environmental section some topics were not covered specifically through a relative environmental management standard.

Another point that we want to take into consideration is that in most of the cases management systems preexisted any materiality analysis or even any ESG – sustainability report. Thus, we don’t have the knowledge of the strategic planning and business motivations behind the implementation of a management standards. Hence, we do not imply nor suggest that material ESG topics should have already had enforced particular management standards. This highlights the need for future research in the same sample to identify any new standards implementation that might be an outcome of strategic ESG decision to manage impacts in a holistic way.

Our research, grounded in content analysis, provided useful insights into the sustainability standards used in Greece. It may serve as a foundation for more discourse and research. Initially, it can be directly implemented on another market’s ESG index to compare the outcomes. Furthermore, a crucial study path would involve conducting in-depth interviews with the 60 quality; CSR and sustainability managers of the studied organizations to gain insight into the motivations and strategic planning underlying the management standards employed. We believe that comprehensive qualitative research in this field is needed to better understand the interconnection between materiality and standards used and to highlight the motives behind the implementation of a management standard.

Author Contributions

“Conceptualization, T.P and G.F.; methodology, T.P and G.F.; formal analysis, T.P.; investigation, T.P.; resources, T.P.; data curation, T.P.; writing—original draft preparation, T.P. and G.F.; writing—review and editing, T.P. and G.F.; visualization, T.P. and G.F. All authors have read and agreed to the published version of the manuscript.” Please turn to the CRediT taxonomy for the term explanation. Authorship must be limited to those who have contributed substantially to the work reported.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Su, H., Dhanorkar, S., & Linderman, K. (2015). A competitive advantage from the implementation timing of ISO management standards. Journal of Operations Management, 37(1), 31–44. [CrossRef]

- Sommer, C.S. (2017). Drivers and constraints for adopting sustainability standards in small and medium-sized enterprises (SMEs).

- Lambin, E. F., & Thorlakson, T. (2018). Sustainability standards: interactions between private actors, civil society, and governments. Annual Review of Environment and Resources, 43(1), 369–393. [CrossRef]

- Reinecke, J., Manning, S., & Von Hagen, O. (2012). The emergence of a standards market: Multiplicity of sustainability standards in the global coffee industry. Organization studies, 33(5-6), 791-814.

- Aurora, A., & Sharma, D. (2022). Do environmental, social and governance (ESG) performance scores reduce the cost of debt? Evidence from Indian firms. Australasian Accounting, Business and Finance Journal, 16(4).

- Tarí, J. J., Molina-Azorín, J. F., Pereira-Moliner, J., & López-Gamero, M. D. (2019). Internalization of Quality Management Standards: A Literature Review. Engineering Management Journal, 32(1), 46–60. [CrossRef]

- Cort, T., & Esty, D. (2020). ESG standards: Looming challenges and pathways forward. Organization & Environment. [CrossRef]

- Elidrisy, A. (2024). Comparative review of ESG reporting standards: ESRS European sustainability reporting standards versus ISSB international sustainability standards board (Comparative analysis of ESG reporting standards). International Multilingual Journal of Science and Technology (IMJST), 9(3). ISSN: 2528-9810.

- Zeng, L., Li, H., Lin, L., Hu, D. J. J., & Liu, H. (2024). ESG Standards in China: Bibliometric Analysis, Development Status Research, and Future Research Directions. Sustainability, 16(16), 7134. [CrossRef]

- DasGupta, R., & Roy, A. (2023). Firm environmental, social, governance, and financial performance relationship contradictions: Insights from institutional environment mediation. Technological Forecasting and Social Change, 189, 122341. [CrossRef]

- Fonseca, L., Carvalho, F., & Santos, G. (2023). Strategic CSR: Framework for Sustainability through Management Systems Standards—Implementing and Disclosing Sustainable Development Goals and Results. Sustainability, 15(15), 11904. [CrossRef]

- International Organization for Standardization. (2018). Contributing to the UN Sustainable Development Goals with ISO standards. Retrieved from https://www.iso.org/publication/PUB100429.html.

- Fonseca, L., & Carvalho, F. (2019). The reporting of SDGs by quality, environmental, and occupational health and safety-certified organizations. Sustainability, 11(5797). [CrossRef]

- Zhao, X., Castka, P., & Searcy, C. (2020). ISO Standards: A Platform for Achieving Sustainable Development Goal 2. Sustainability, 12(22), 9332. [CrossRef]

- Krajnc, D., & Glavič, P. (2005). How to compare companies on relevant dimensions of sustainability. Ecological Economics, 55(4), 51563. [CrossRef]

- Huiping, G., Teck, T. S., & Nellikunnel, S. (2024). Navigating the Complexities of ESG Integration: Challenges, Opportunities and Path to Sustainable Corporate Development. Journal of Business and Social Sciences, 2024.

- Tarí, J. J., Pereira-Moliner, J., Molina-Azorín, J. F., & López-Gamero, M. D. (2019). Heterogeneous adoption of quality standards in the hotel industry: Drivers and effects. International Journal of Contemporary Hospitality Management, 31(3), 1122–1140. [CrossRef]

- Glavič, P., & Lukman, R. (2007). Review of sustainability terms and their definitions. Journal of Cleaner Production, 15(18), 1875–1885. [CrossRef]

- ATHEX ESG. (2024). Presentation of ATHEX ESG Index. Retrieved from https://www.athexgroup.gr/el/athex-esg.

Table 1.

Companies surveyed categorized into the GICS sectors.

| GICS Sector | Number of Companies |

|---|---|

| Energy | 3 |

| Materials | 12 |

| Industrials | 8 |

| Consumer Discretionary | 9 |

| Consumer Staples | 5 |

| Health Care | 2 |

| Financials | 9 |

| Information Technology | 2 |

| Communication Services | 1 |

| Utilities | 5 |

| Real Estate | 4 |

Table 2.

Environmental Standards used in the Energy Sector.

Table 3.

Reporting Standards used in the Energy Sector.

| Standard | Number of companies that use it |

|---|---|

| SASB | 2/3 |

| CDSB | 1/3 |

| TCFD | 2/3 |

| SBTi | 1/3 |

| GRI | 3/3 |

| UNGC | 3/3 |

| ATHEX ESG Index | 3/3 |

| Greek Sustainability Code | 3/3 |

| AA1000AP | 3/3 |

| ESRS | 2/3 |

Table 4.

Environmental, Social and Governance Standards used in the Materials Sector.

Table 5.

Reporting Standards used in the Materials Sector.

| Standard | Number of companies that use it |

|---|---|

| GRI | 11/12 |

| UNGC | 9/12 |

| ATHEX ESG Index | 9/12 |

| Greek Sustainability Code | 1/12 |

| AA1000AP | 3/12 |

| ESRS | 3/12 |

| SASB | 5/12 |

| SMETA /SEDEX | 1/12 |

| TCFD | 2/12 |

| ASI Performance Standard | 2/12 |

| ASI Chain of Custody Standard AS9100D | 2/12 |

| REACH | 1/12 |

| AccountAbility 1000 Stakeholder Engagement Standard | 1/12 |

Table 6.

Environmental, Social and Governance Standards used in the Industrials Sector.

Table 7.

Reporting Standards used in the Industrials Sector.

| Standard | Number of companies that use it |

|---|---|

| GRI | 5/8 |

| UNGC | 6/8 |

| ATHEX ESG Index | 6/8 |

| Greek Sustainability Code | 1/8 |

| AA1000AP | 2/8 |

| ESRS | 4/8 |

| SASB | 5/8 |

Table 8.

Environmental, Social and Governance Standards used in the Consumer Discretionary Sector.

Table 9.

Reporting Standards used in the Consumer Discretionary Sector.

| Standard | Number of companies that use it |

|---|---|

| GRI | 8/9 |

| UNGC | 5/9 |

| ATHEX ESG Index | 9/9 |

| AA1000AP | 1/9 |

| ESRS | 2/9 |

| SASB | 3/9 |

| TCFD | 1/9 |

| IFRS | 1/9 |

Table 10.

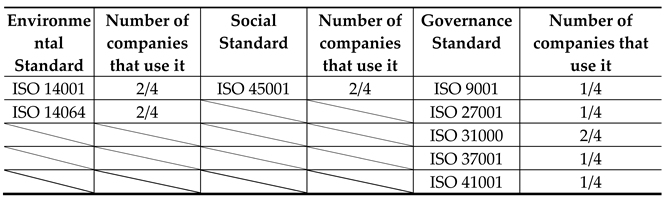

Environmental, Social and Governance Standards used in the Consumer Staples Sector.

| Environmental Standard | Number of companies that use it | Social Standard |

Number of companies that use it | Governance Standard | Number of companies that use it |

|---|---|---|---|---|---|

| ISO 14001 | 3/5 | IFS | 2/5 | ISO 9001 | 4/5 |

| ISO 50001 | 1/5 | ISO 22000 | 2/5 | ISO 27001 | 2/5 |

| ISO 14064 | 4/5 | ISO 45001 | 2/5 | ISO 22716 | 1/5 |

Table 11.

Reporting Standards used in the Consumer Staples Sector.

| Standard | Number of companies that use it |

|---|---|

| GRI | 5/5 |

| UNGC | 2/5 |

| ATHEX ESG Index | 4/5 |

| ESRS | 1/5 |

| SASB | 1/5 |

| TCFD | 1/5 |

Table 12.

Environmental, Social and Governance Standards used in the Health Care Sector.

Table 13.

Reporting Standards used in the Health Care Sector.

| Standard | Number of companies that use it |

|---|---|

| GRI | 2/2 |

| UNGC | 2/2 |

| ATHEX ESG Index | 1/2 |

| SASB | 1/2 |

Table 14.

Environmental, Social and Governance Standards used in the Financials Sector.

Table 15.

Reporting Standards used in the Financials Sector.

| Standard | Number of companies that use it |

|---|---|

| GRI | 9/9 |

| UNGC | 6/9 |

| ATHEX ESG Index | 6/9 |

| ESRS | 1/9 |

| SASB | 3/9 |

| TCFD | 4/9 |

| AA1000 | 1/9 |

Table 16.

Environmental, Social and Governance Standards used in the Information Technology Sector.

Table 17.

Reporting Standards used in the Information Technology Sector.

| Standard | Number of companies that use it |

|---|---|

| GRI | 2/2 |

| UNGC | 2/2 |

| ATHEX ESG Index | 2/2 |

| SASB | 2/2 |

Table 18.

Environmental, Social and Governance Standards used in the Communication Services Sector.

Table 19.

Reporting Standards used in the Communication Services Sector.

| Standard | Number of companies that use it |

|---|---|

| GRI | 1/1 |

| ATHEX ESG Index | 1/1 |

| TCFD | 1/1 |

| SASB | 1/1 |

| AA1000 | 1/1 |

| IFRS | 1/1 |

| Greek Sustainability Code | 1/1 |

| ESRS | 1/1 |

Table 20.

Environmental, Social and Governance Standards used in the Utilities Sector.

Table 21.

Reporting Standards used in the Utilities Sector.

| Standard | Number of companies that use it |

|---|---|

| GRI | 5/5 |

| UNGC | 2/5 |

| ATHEX ESG Index | 5/5 |

| SASB | 5/5 |

| ESRS | 2/5 |

| GHG Protocol | 1/5 |

Table 22.

Environmental, Social and Governance Standards used in the Real Estate Sector.

Table 23.

Reporting Standards used in the Real Estate Sector.

| Standard | Number of companies that use it |

|---|---|

| GRI | 4/4 |

| UNGC | 3/4 |

| ATHEX ESG Index | 4/4 |

| SASB | 1/4 |

| ESRS | 1/4 |

| AA1000AP | 1/4 |

Table 24.

Material topics identified in the Energy sector with ESG categorization.

| Material issue | Environmental | Social | Governance |

|---|---|---|---|

| Climate concerns | x | ||

| Biodiversity | x | ||

| Decarbonization | x | ||

| Energy concerns | x | ||

| Circular Economy/Circularity | x | ||

| Waste management | x | ||

| Water management | x | ||

| Air pollution (emissions, GHG) | x | ||

| Responsible supply chain | x | x | |

| Economic impact | x | ||

| Human rights (diversity, inclusion, equal opportunities) | x | ||

| Employment (education, development, retention) | x | ||

| Health, safety and wellbeing (employees) | x | ||

| Local communities | x | ||

| Customer relations and satisfaction | x | ||

| Innovation and digital transformation |

x | ||

| Data privacy | x | ||

| Regulatory compliance | x | ||

| Business continuity | x | ||

| Business ethics and governance | x | ||

| Mobility | x | ||

| Economic Value Creation | x |

Table 25.

Material topics identified in the Materials sector with ESG categorization.

| Material issue | Environmental | Social | Governance |

|---|---|---|---|

| Climate concerns | x | ||

| Biodiversity | x | ||

| Energy concerns | x | ||

| Circular Economy/Circularity | x | ||

| Waste management | x | ||

| Water management | x | ||

| Raw materials (virgin, recycled, sustainable) | x | ||

| Air emissions (GHG, direct and indirect) | x | ||

| Pollution prevention and control | x | ||

| Decarbonization | x | ||

| Responsible sourcing | x | x | |

| Human rights (Diversity, inclusion, equal treatment and opportunities for all) | x | ||

| Employment (education, development, retention, working conditions) | x | ||

| Health, safety and wellbeing (employees, customers) | x | ||

| International presence | x | ||

| Local communities | x | ||

| Stakeholder engagement | x | ||

| Customers and end users | x | ||

| Product innovation | x | ||

| Product quality and safety | x | ||

| Digitalization | x | x | |

| Data privacy | x | ||

| Regulatory compliance | x | ||

| Corruption and bribery | x | ||

| Business continuity | x | ||

| Business ethics and governance | x | ||

| Strategy and investments | x | ||

| Anti-competitive behavior | x | ||

| Infrastructure | x | ||

| Economic Value Creation | x | ||

| Profitability | x | ||

| Extroversion and continuous growth | x |

Table 26.

Material topics identified in the Industrials sector with ESG categorization.

| Material issue | Environmental | Social | Governance |

|---|---|---|---|

| Climate concerns | x | ||

| Biodiversity | x | ||

| Energy concerns | x | ||

| Circular Economy/Circularity | x | ||

| Waste management | x | ||

| Water management | x | ||

| Air emissions (GHG, air quality) | x | ||

| Pollution prevention and control | x | ||

| Responsible sourcing | x | x | |

| Indirect social impacts | x | ||

| Human rights (equal opportunities, diversity) | x | ||

| Local communities | x | ||

| Employment (security, attraction, retention, education and development) | x | ||

| Health, safety and wellbeing (employees, customers) | x | ||

| Social dialogues | x | ||

| Product and service innovation | x | ||

| New technologies/ Digitalization | x | ||

| Risk management | x | ||

| Data privacy | x | ||

| Corruption and bribery | x | ||

| Transparency | x | ||

| Business continuity | x | ||

| Business ethics and governance | x | ||

| Infrastructure | x | ||

| Profitability | x |

Table 27.

Material topics identified in the Consumer Discretionary sector with ESG categorization.

| Material issue | Environmental | Social | Governance |

|---|---|---|---|

| Climate concerns | x | ||

| Energy concerns | x | ||

| Circular Economy/Circularity | x | ||

| Waste management | x | ||

| Natural resources management (raw materials) | x | ||

| Water management | x | ||

| Air emissions (GHG) | x | ||

| Sustainable supply chain | x | x | x |

| Stakeholder engagement | x | ||

| Human rights (Diversity) | x | ||

| Local communities | x | ||

| Education and development | x | ||

| Equal opportunities | x | ||

| Employment (engagement, retention) | x | ||

| Health, safety and wellbeing (employees, customers) | x | ||

| Positive social impact | x | ||

| Customer satisfaction | x | ||

| Product and service quality | x | ||

| Product and service innovation | x | ||

| New technologies/ Digitalization | x | ||

| Risk management | x | ||

| Strategy and investments | x | ||

| Data privacy | x | ||

| Corruption and bribery | x | ||

| Transparency | x | ||

| Regulatory compliance | x | ||

| Business continuity | x | ||

| Business ethics and governance | x | ||

| Economic Value Creation | x |

Table 28.

Material topics identified in the Consumer Staples sector with ESG categorization.

| Material issue | Environmental | Social | Governance |

|---|---|---|---|

| Climate change and stability | x | ||

| Energy management (energy consumption) | x | ||

| Biodiversity | x | ||

| Circular Economy/Circularity | x | ||

| Waste management | x | ||

| Natural resources management (raw materials, resource intensity) | x | ||

| Water management | x | ||

| Air emissions (GHG, air quality) | x | ||

| Supply chain management | x | x | x |

| Human rights (Diversity and inclusion | x | ||

| Socio-economic impact | x | ||

| Local communities | x | ||

| Employment (engagement, retention, education and development) | x | ||

| Health, safety and wellbeing | x | ||

| Customers and end-users | x | ||

| Product waste (food waste) | x | ||

| Product quality and safety | x | ||

| Product and service innovation | x | ||

| Strategy and investments | x | ||

| Data privacy | |||

| Transparency | x | ||

| Corporate citizenship | x | ||

| Business ethics and governance | x | ||

| Infrastructure | x | ||

| Economic Value Creation | x |

Table 29.

Material topics identified in the Health Care sector with ESG categorization.

| Material issue | Environmental | Social | Governance |

|---|---|---|---|

| Climate change | x | ||

| Energy management (energy consumption) | x | ||

| Waste management | x | ||

| Water management | x | ||

| Air emissions | x | ||

| Supply chain management | x | x | x |

| Human rights (diversity, equal opportunities) | x | ||

| Community support | x | ||

| Access to medical care | x | ||

| Employment (engagement, retention, education and development) | x | ||

| Health, safety and wellbeing | x | ||

| Customer satisfaction | x | ||

| Product quality and safety | x | ||

| Product and service innovation | x | ||

| Strategy and investments | x | ||

| Intellectual property | x | ||

| Digitalization | x | ||

| Data privacy | |||

| Transparency | x | ||

| Business ethics and governance | x | ||

| Infrastructure | x |

Table 30.

Material topics identified in the Financials sector with ESG categorization.

| Material issue | Environmental | Social | Governance |

|---|---|---|---|

| Climate concerns | x | ||

| Biodiversity | x | ||

| Energy concerns | x | ||

| Circular Economy/Circularity | x | ||

| Waste management | x | ||

| Water management | x | ||

| Pollution prevention and control (GHG reduction) | x | ||

| Sustainability integration into risk management | x | x | x |

| Responsible/sustainable banking | x | x | |

| Social contribution | x | ||

| Social impacts | x | ||

| Human rights (diversity, equal treatment and opportunities for all) | x | ||

| Cultural Heritage | x | ||

| Employment (longevity, satisfaction, education and development, work-life balance) | x | ||

| Health, safety and wellbeing | x | ||

| Workingconditions | x | ||

| x | |||

| Relationship with suppliers | |||

| Supporting young people | x | ||

| Social inclusion of consumers and/or end-users |

x | ||

| Customer/Investor/ Shareholder Satisfaction | x | ||

| Political engagement | x | ||

| Information-related Impacts for Consumers and/or End-users |

x | ||

| Equal access to banking/finance | |||

| Contact with the company | x | ||

| Product and service innovation | x | ||

| Providing modern and responsible products and services | x | ||

| New technologies/ Digitalization | x | ||

| Data privacy | x | ||

| Regulatory compliance | x | ||

| Corruption and bribery | x | ||

| Whistleblower protection | x | ||

| Business continuity | x | ||

| Corporate culture | x | ||

| Mobility/Infrastructure | x | ||

| Economic Value Creation | x | ||

| Solvency | x |

Table 31.

Material topics identified in the Information Technology sector with ESG categorization.

| Material issue | Environmental | Social | Governance |

|---|---|---|---|

| Climate change | x | ||

| Energy management (energy saving) | x | ||

| Environmental impacts of development projects | x | ||

| Waste management | x | ||

| Water management | x | ||

| Air emissions (GHG) | x | ||

| Responsible sourcing | x | x | |

| Ethical trade | x | ||

| Local communities | x | ||

| Equal opportunities | x | ||

| Employment (attraction, retention, education and development) | x | ||

| Diversity | x | ||

| Health, safety and wellbeing (employees and customers) | x | ||

| Product and service innovation (smart and safe cities) | x | ||

| Product security (cybersecurity) | x | ||

| New technologies/ Digitalization | x | ||

| Data privacy | x | ||

| Anticompetitive behavior | x | ||

| Corruption and bribery | x | ||

| Business continuity | x | ||

| Business Ethics | x | ||

| Risk management | x | ||

| Economic Value Creation | x |

Table 32.

Material topics identified in the Communication Services sector with ESG categorization.

| Material issue | Environmental | Social | Governance |

|---|---|---|---|

| Climate change | x | ||

| Energy | x | ||

| Air emissions (GHG) | x | ||

| Health, safety and wellbeing (employees) | x | ||

| Customer communication and satisfaction | x | ||

| Product and service safety (Electromagnetic field safety and management)/ | x | ||

| (Product security /cybersecurity) | x | ||

| Data privacy | x | ||

| Business continuity | x | ||

| Business Ethics | x | ||

| Risk management | x |

Table 33.

Material topics identified in the Utilities sector with ESG categorization.

| Material issue | Environmental | Social | Governance |

|---|---|---|---|

| Climate (climate change resilience, adaptation, mitigation) | x | ||

| Energy (management, efficiency, transition, green energy) | x | ||

| Biodiversity (Ecosystem protection) | x | ||

| Waste management | x | ||

| Water management | x | ||

| Circular economy | x | ||

| Natural resources management | x | ||

| Air emissions (GHG) | x | ||

| Responsible sourcing | x | x | |

| Local communities | x | ||

| Employment (attraction, retention, Education and development) | x | ||

| Working conditions | x | ||

| Health, safety and wellbeing (employees and customers) | x | ||

| Service accessibility | x | ||

| Customer satisfaction | x | ||

| Product and service innovation | x | ||

| Product security (network security, reliability) | x | ||

| New technologies/ Digitalization | x | ||

| Data privacy | x | ||

| Regulatory compliance | x | ||

| Corruption and bribery | x | ||

| Business continuity | x | ||

| Corporate culture | x | ||

| Business ethics and governance | x | ||

| Transparency | x | ||

| Economic Value Creation | x |

Table 34.

Material topics identified in the Real Estate sector with ESG categorization.

| Material issue | Environmental | Social | Governance |

|---|---|---|---|

| Climate change | x | ||

| Energy (efficiency, consumption) | x | ||

| Biodiversity (Ecosystem protection) | x | ||

| Decarbonization | x | ||

| Waste management | x | ||

| Water management | x | ||

| Circular economy | x | ||

| Resource management | x | ||

| Air emissions (GHG, air pollution) | x | ||

| Responsible procurement | x | x | |

| Affected communities | x | ||

| Human rights (diversity and inclusion, equal opportunities) | x | ||

| Employment (attraction, retention, education and development) | x | ||

| Health, safety and wellbeing (employees, customers) | x | ||

| Consumers and end-users (satisfaction) | x | ||

| Sustainable products (sustainable buildings) | x | x | |

| Data privacy | x | ||

| Risk management | x | ||

| Economic Value Creation | x |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.