Submitted:

17 February 2025

Posted:

18 February 2025

You are already at the latest version

Abstract

Purpose/Originality: This study introduces a novel construct, Spendception, which conceptualizes the psychological impact of digital payment systems on consumer behavior, marking a significant contribution to the field of consumer psychology and behavioral economics. Spendception reflects the reduced psychological resistance to spending when using digital payment methods, as compared to cash, due to the diminished visibility of transactions and the perceived ease of payments. This research aims to explore the role of Spendception in increasing consumer purchase behavior whereas the role of impulse buying has been observed as mediator.

Method: To test the proposed model, an extensive survey has been done by collecting 1162 respondents from all walk of life to get the real picture. We employed Exploratory Factor Analysis (EFA) and Confirmatory Factor Analysis (CFA) to validate the measurement of key constructs. To test the hypothetical relations among all the variables, we employed Structural Equation Modelling (SEM). Furthermore, a machine learning technique has been used to test the robustness of the model.

Findings: Results shows that Spendception greatly boots the consumer purchase behavior with impulse buying partially mediates the relation. Gender was found to moderate the relationship, with female consumers being more susceptible to impulse buying caused by Spendception. The study shows that digital payment systems making buying feel less noticeable, which lead people spending more without realizing the financial impact.

Theoretical Contribution: This study introduces Spendception, a novel construct that extends existing consumer behavior theories by explaining how digital payment systems reduce psychological barriers to spending. It bridges the gap between mental accounting and the pain of paying, demonstrating that the lack of immediate visibility and physicality in digital payments alters consumers’ perceptions of spending, leading to increased impulse buying and higher purchase behavior. The findings also offer actionable insights for marketers in designing targeted campaigns that leverage the psychological effects of Spendception.

Keywords:

Spendception

; Impulse Buying

; Consumer Purchase Behavior

; Digital Payments

; Genders’ Moderation

; Mediation

; SEM

; EFA

; CFA

1. Introduction

Over the course of several decades, digital payments have brought about a revolution in global business (Zarco et al., 2024). This change began with the introduction of credit cards in the 1950s and 1960s, which let customers make transactions without the need for cash. With the advent of electronic fund transfers (EFTs), point-of-sale (POS) systems, and automated teller machines (ATMs) in the 1970s, transactions became more streamlined and secure (Mariana et al., 2025). The 1990s witnessed the proliferation of the internet, which resulted in the emergence of e-commerce and online payment systems, which were pioneered by software applications such as PayPal. Mobile payment systems and contactless technologies, such as near field communication (NFC), came into existence in the 2000s. Major players, such as Google Wallet and Apple Pay, revolutionized the way individuals conducted business(Cao et al., 2018; Humbani & Wiese, 2019; J. H. Kim et al., 2022; Lin et al., 2019; Mariana et al., 2025; Nan et al., 2020). The introduction of blockchain technology to the payment system was made possible by the emergence of cryptocurrencies, led by Bitcoin in 2009. In the 2010s, companies like Stripe and Venmo led a revolution in the financial technology industry, disrupting old systems and popularizing real-time payment systems globally(Gong et al., 2023; Monem et al., 2024; Samantray & Reddy, 2024). A significant acceleration of the use of digital payments was brought about by the COVID-19 epidemic, which led to the development of innovations like Buy Now, Pay Later (BNPL) services and the standardization of contactless transactions(Adams et al., 2021; Ahmadian, 2025; Niankara & Traoret, 2023; Xiong et al., 2024).

China's digital payments journey is unique due to its rapid adoption and general use. The decade of the 1990s saw the establishment of UnionPay, an interbank network that was supported by the government and used to create the framework for digital transactions (Guo et al., 2025; Liu et al., 2024; Wani et al., 2025). The beginning of the twenty-first century saw the proliferation of e-commerce platforms such as Alibaba, which introduced Alipay in 2004 as a safe and reliable online payment solution(T. Li et al., 2024; Zhao & Abeysekera, 2024). The year 2013 marked the beginning of the revolution in mobile payments, which was initiated by WeChat Pay. This application incorporated payment capabilities into Tencent's messaging service, utilizing QR codes to facilitate transactions in a simple manner. With Alipay and WeChat Pay controlling more than 90 percent of the market, China has transformed into a society that was almost entirely cashless by the late 2010s (Alrawad et al., 2023; X. Li et al., 2023; Mombeuil & Uhde, 2021; Pang & Ruan, 2023; Zarco et al., 2024). Beyond the realm of payments, these platforms have expanded their offerings to encompass services such as investments, loans, and payments for utility bills. A central bank digital currency (CBDC), also known as the digital yuan, was made available by the Chinese government in recent years with the intention of modernizing the country's financial system and decreasing its reliance on private platforms. Today, China is a global leader in digital technology. The country exports its technologies and incorporates them into global efforts, such as the Belt and Road Initiative. The country makes payments, exports its technologies, and integrates them into global initiatives such as the Belt and Road Initiative.

China has leapfrogged traditional payment systems by migrating directly to mobile payments powered by QR codes (Borzova, 2024). This is in contrast to the gradual growth of digital payments that globally followed, beginning with credit cards and progressing to mobile and real-time payments. In China, the government has taken a more aggressive role, as evidenced by the development of the digital yuan, making its system unique in terms of its scale and creativity. On the other hand, contactless cards and NFC continue to be the popular payment methods around the world.

The adoption of digital payment systems has reshaped consumer spending behavior by significantly altering how individuals perceive and interact with money. In traditional cash transactions, the physical exchange of money serves as a tangible reminder of spending, evoking what is often termed the "pain of paying." This physical and psychological visibility acts as a natural barrier to overspending. However, digital payment methods, such as mobile wallets, credit cards, and online banking, lack this tactile element, creating a psychological detachment from expenditures. This detachment not only reduces the perceived visibility of spending but also fosters behavioral and emotional changes that lead to increased purchases.

To encapsulate the psychological and behavioral shifts brought about by the invisibility and ease of digital payments, this study introduces Spendception as a novel construct. It is a blend of “spend” and “perception”. The term Spendception effectively combines the act of spending with the psychological perception of it. It is a unique terminology that encapsulates the behavioural and psychological aspects of spending through digital payments. The term is catchy, aligns with existing psychological constructs, and adds a modern, research-focused touch. Spendception serves as the central independent variable in this research, capturing the interplay of three critical dimensions: psychological visibility of spending, perceived spending control, ease of digital payment and emotional detachment.

2. Concept of Spendception

Spendception is conceptualized as a multidimensional framework that explains how digital payment systems influence consumer behavior. It reflects the diminished psychological resistance to spending when using digital payment methods compared to cash.

2.1. Psychological Visibility of Spending:

When we talk about psychological visibility of spending, we're talking about how we think about and feel about our financial transactions. When you pay with cash, the act of handing over the money provides a physical reminder of how much you spent. As cash in a wallet decreases, it serves as a clear and instant sign of spending, making people more aware and reinforcing the mental "cost" of purchases. This level of public awareness serves as a deterrent, making people think more carefully about their financial choices and supporting smart spending. Digital purchases, on the other hand, make this much harder to see. There is a feeling of being disconnected from real financial outflows when using credit cards, mobile apps, or online platforms to make purchases. This is because digital transactions are not tangible. People are less likely to feel the direct effects of their spending if they don't have to physically give up money. This loss of brain awareness can cause people to underestimate how much they've spent or not notice how the effects of multiple transactions add up. Since there aren't any obvious cues like a wallet or cash reserves running out, purchases don't carry as much emotional weight. This makes it easier for people to spend more without thinking about their spending limits. The ease and speed of digital payments, which allow transactions to be finished with little effort or thought, makes this psychological loss even stronger. Because of this, people are less likely to feel the cognitive friction they need to stop spending, which can make them consume more and buy things they don't need. Figuring out this effect makes me realise how important psychological exposure is in affecting how much people spend and how important it is to look at its effects in modern payment systems.

2.2. Perceived Spending Control:

Perceived Spending Control is the feeling that you have control over your money that comes from digital payments being so easy to use. When you pay with cash, you physically hand over the money and see your resources go down. With digital payments, you don't get that instant and tactile feedback. This separation weakens the mental link between spending and its results, which leads to a false sense of control. The speed and ease of digital transactions add to this impression, as the smooth process reduces the mental load that comes with making financial decisions. Also, the delayed financial impact, especially with credit-based payments, makes people less aware of the instant effects of their spending, which can make them overconfident in their money management skills. People who feel in charge tend to spend more because they don't realise how their actions add up over time, they break their budgeting habits, and they are more likely to buy things on the spot. This event makes it even more important to understand how digital payments affect how people spend their money and their overall financial health.

2.3. Ease of Digital Payment and Emotional Detachment:

Detachment is about the changes that happen in our minds and feelings because of how easy and intangible digital transactions are. Digital payments are quick and easy, and you don't even have to do anything to make them happen. You can pay with a card tap, an application clicks, or an automatic withdrawal from your digital bank. This smooth process gets rid of a lot of the problems that come with traditional cash payments, like having to count bills, get change, or hand over cash. This means that buying is less conscious and more automatic, which means that less thought is needed during a transaction. The fact that there is no physical exchange with digital purchases makes them even less personal. When you pay with cash, the act of handing over the money provides a physical link to the transaction that makes the emotional "cost" of spending stronger. Digital transactions, on the other hand, make the trade less clear, which makes it harder for people to connect the transaction with losing money. This generalisation lessens the "pain of paying," which is a psychological effect that happens when people have to part with money. Because digital payments don't have as much of an emotional effect, people are more likely to buy things without fully thinking about the financial implications. This feeling of ease and separation can make people buy things without thinking about it, because it weakens the mental walls that normally stop people from spending. Researchers can learn more about how modern payment methods affect customer behaviour and spending patterns by looking into how the ease of digital payments interacts with emotional distance.

3. Theoretical Support

There are several psychological and behavioural economic theories exists in the literature however, the Pain of Paying and Mental Accounting frameworks, provide a solid theoretical foundation for the concept of Spendception with which it is based. Both the conceptualisation of Spendception and the construction of its measurement dimensions are supported by these theories, which provide useful insights into the ways in which the shape and visibility of money influence consumer behaviour.

3.1. Pain of Paying

Ariely and Prelec (Ariely & Prelec, 2003) presented the idea of the "Pain of Paying," which is a term that defines the psychological discomfort that is linked with spending money. According to this hypothesis, different means of payment elicit different levels of cognitive and emotional participation during transactions and that these levels vary from person to person. Physical cash transactions include a concrete trade, in which persons physically part with money. Digital payments, on the other hand, require no money exchange at all. As a result of this visibility and tactility, the psychological pain of spending is amplified, and consumers become more conscious of the decisions they make regarding their finances. On the other hand, digital payment methods, such as credit cards or mobile wallets, abstract the process of spending, which lessens the emotional significance of the transaction and lessens the "pain." Similarly, the word Spendception is a concept that encompasses the lessened psychological visibility and emotional detachment that are inherent with digital payments. This concept aligns well with the Pain of Paying idea. The simplicity of digital payment and emotional detachment features, for instance, are clear reflections of the ways in which these systems eliminate the psychological barriers that prevent people from spending.

3.2. Mental Accounting

Mental accounting is a concept that was suggested by Thaler (Thaler, 1999) that investigates the ways in which individuals classify, assess, and keep track of their financial activities. Mental accounting describes the process by which individuals assign money to various mental "accounts" (such as savings, entertainment, and necessities) based on the source of the money, its intended use, or its shape. Because of the abstract nature of the transaction, individuals find it more difficult to effectively track or regulate their spending when they use digital payments. This might cause these mental accounts to get muddled. Psychological Control and Perceived Visibility: The cognitive processes that are engaged in mental accounting are undermined by the lowered psychological visibility that is associated with digital payments. In a similar vein, individuals are less inclined to put self-regulation on their spending when they sense that their spending is less tangible. This phenomenon is known as perceived spending control. Likewise, Spendception incorporates the ideas of mental accounting by addressing the ways in which digital payments blur the lines between mental accounts, lessen the perception of control, and undermine the psychological barriers that prevent people from spending.

3.3. The Role of Impulse Buying as a Mediator

The contemporary era of digital payments provides fertile ground for impulse buying, a phenomenon characterised by sudden, impulsive, and unplanned purchasing decisions (Kong et al., 2025). Spendception is a construct that is fundamental to this behaviour. It encompasses the convenience of digital payments, emotional detachment, perceived spending control, and diminished psychological visibility of spending. These dimensions collectively diminish the psychological barriers that have been traditionally associated with spending, thereby fostering an environment in which impetuous decisions are encouraged. Spendception modifies the manner in which consumers perceive, analyse, and react to their expenditures. Individuals are less inclined to actively monitor their spending due to the diminished visibility of expenditures in digital transactions. They engage with an abstract system in which money flows imperceptibly, rather than witnessing a wallet diminish with each payment. This psychological invisibility promotes a disconnection between financial consequences and expenditure. The act of making a purchase becomes nearly frictionless when combined with the perceived ease and convenience of digital payments, which necessitate minimal effort or contemplation. This frictionless experience reduces the cognitive and emotional defences that typically regulate consumer behaviour, thereby inducing impulse purchasing. In the absence of a tangible act of parting with currency or a visible depletion of resources, individuals are more susceptible to making spontaneous purchasing decisions. This tendency is further exacerbated by emotional detachment, as the absence of the "pain of paying" eliminates the natural distress or hesitation that might otherwise inhibit impulsive actions.

Consequently, impulse buying serves as a conduit between Spendception and an increase in purchasing behaviour. The psychological and emotional changes that Spendception introduces, such as reduced spending awareness and detachment, establish a favourable psychological environment for impulsive purchases. Consumers are not only more likely to purchase on impulse, but they are also more likely to justify these behaviours as insignificant or justified. This results in a cumulative increase in purchase behaviour over time, which is influenced by the emotional detachment, invisibility, and convenience of digital payments.

3.4. Consumer Purchase Behavior

Increased consumer purchasing behavior indicates the growing inclination of consumers to spend more frequently and in bigger amounts, affected by a number of psychological, technological, and situational factors (Karmaker et al., 2025). The idea of Spendception plays a major part in this phenomenon, as digital payment methods remove the psychological barriers to spending. With digital transactions, the immediate sight of spending lessens, establishing a sense of detachment from money outflows and encouraging consumers to make purchases more readily. Moreover, the seamless nature of digital payment methods generates an impression of control and comfort, leading to overconfidence in handling finances. This, paired with diminished emotional resistance to purchasing, results in heightened impulsivity and unplanned expenditures.

Impulse buying further amplifies increased purchase behavior by forcing consumers to make emotionally charged, unplanned purchases. The convenience of digital payments expedites this process by requiring minimal effort to complete a transaction, often bypassing the logical decision-making process. This behavior is also influenced by outside variables like convenience-driven incentives, special offers, and tailored marketing, which make it simpler for customers to defend more frequent and expensive purchases. This trend of rising purchasing behavior emphasizes how digital payment methods are changing consumer behavior, highlighting both company potential and financial responsibility problems.

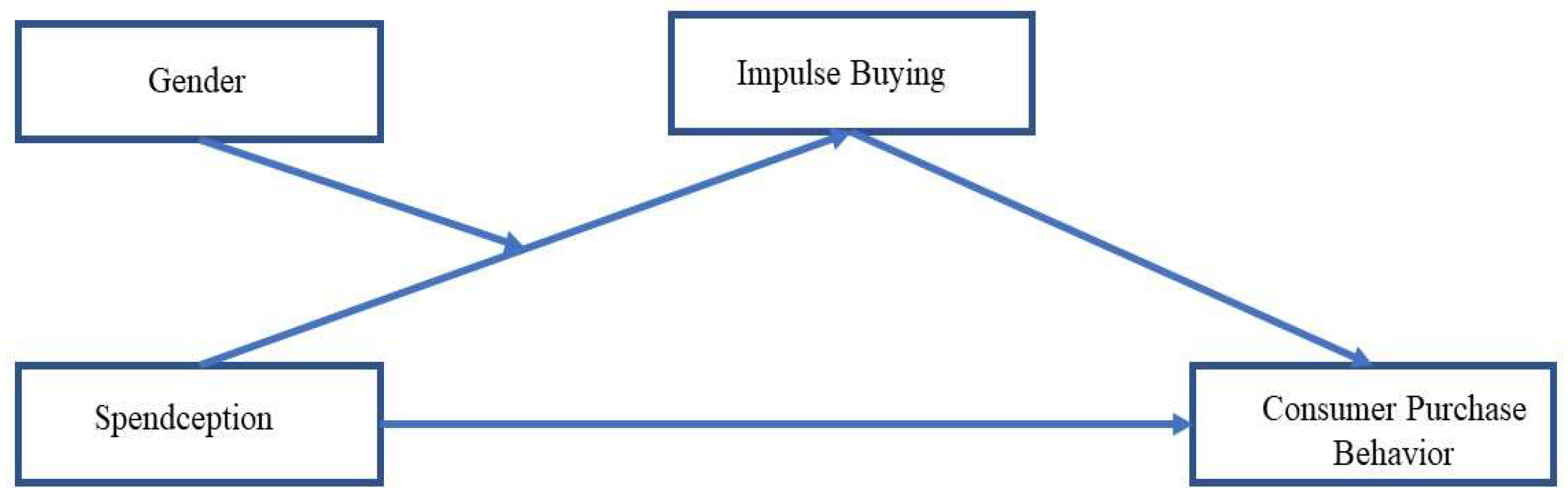

Figure 1.

Conceptual Model.

3.5. Significance of the Study

This research contributes to the emerging field of consumer psychology in the digital payment context by introducing and empirically validating the concept of Spendception. It underscores the psychological and emotional mechanisms that drive modern spending behavior, offering valuable insights for policymakers, financial institutions, and businesses. By understanding these dynamics, stakeholders can devise strategies to mitigate overspending while leveraging the benefits of digital payments to foster sustainable consumer habits.

3.6. Hypothesis

- H1: Spendception has significant and positive relation with increased purchase behavior

- H2: Impulse buying has significant and positive relation with increased purchase behavior.

- H3: Impulse buying mediates between Spendception and increased purchase behavior.

- H4a: Male Consumer moderates the relation between Spendception and Impulse buying so does Consumer Purchase Behavior

- H4b: Female Consumer moderates the relation between Spendception and Impulse buying so does Consumer Purchase Behavior

4. Methodology

4.1. Target Population

This study targeted 1,162 Shanghai residents who completed a digital payment usage questionnaire. The dense population and advanced digital infrastructure of Shanghai, with over 24 million citizens, make it ideal for investigating digital payment consumer behavior. With official encouragement and widespread acceptance of Alipay and WeChat Pay, the city has led the way in digital payment systems. These technologies have changed residents' payment patterns from cash to digital.

Using Shanghai as the study location reveals how metropolitan policies, technology, and consumer preferences influence the uptake of digital payments. Ages, genders, marital situations, and income are covered in the survey, from under 18 to 65 years.

4.2. Developing Questionnaire and Data Collection

We created an online questionnaire given in Table 1 to examine how Spendception and impulse buying affect digital payment users' shopping behavior. Spendception (psychological visibility of spending, perceived spending control, and simplicity of digital payments), impulse buying (Kong et al., 2025), and consumer purchase behavior were covered in the carefully crafted questions to meet research objectives (J. Kim & Park, 2013). The questionnaire also asked about consumers' emotional and psychological responses to digital payments and how these affect their purchases.

The questionnaire was developed to eliminate ambiguity and misleading statements. To accurately assess respondents' perspectives, a Likert scale from "strongly agree" (7) to "strongly disagree" (1) was used. This provided exact and comparative data collection on aspects of customer behavior, such as digital payment psychological effects, impulse buying triggers, and spending patterns.

Convenient sampling allowed the survey to reach a large audience quickly and cheaply. A small-scale presurvey refined the questionnaire's content and format to ensure its efficacy and feasibility before the main survey. To acquire a complete and timely overview of consumer behavior trends, data was collected from January 2025.

To improve collaboration and data quality, survey respondents were given extensive explanations of the questionnaire's goal, importance, and technique. A comprehensive data filtering process removed incomplete or inconsistent responses to assure authenticity and validity. The study of 1,162 valid questionnaires revealed a relationship between Spendception, impulse buying, and consumer purchase behavior. All participants supplied informed consent before participating in the study. The study followed the Declaration of Helsinki and was approved by the Ethics Committee of University of Shanghai for Science and Technology. The research was approved by an IRB on December 12, 2024. All participants gave written informed consent. Participants gave informed consent through voluntary and confidential responses

4.3. Data Analysis

This study conducted an in-depth investigation into the impact of Spendception on Consumer Purchase Behavior through a scientifically reasonable questionnaire design.

5. Results

Table 2 shows that the Cronbach's alpha coefficients (Becker, G. ,2000) for all constructs are above 0.9, indicating a high level of internal consistency reliability. The Cronbach's alpha coefficient of the overall scale is also high, at 0.953, indicating the reliability of the measurement results.

Table 3, shows the basic statistical characteristics of each variable. The minimum, maximum, mean and standard déviations are given. In data preprocessing, descriptive statistical analysis is performed on the data using SPSS. This helps to understand the basic characteristics and distribution of the data.

Table 4 presents an overview of the participants' basic information. Including age, gender, and marital status. In terms of age distribution, the proportion of participants aged 25-34 was the highest, reaching 41.73%; In terms of gender, 56.2% are women; Married accounted for 58.27% of the marital status

The Kaiser-Meyer-Olkin (KMO) (Cerny, C.A., & Kaiser, 1977; Shrestha, 2021). measure assessed sample readiness for factor analysis. Values closer to 1 indicate high variable correlations, indicating factor analysis suitability. This study's KMO value was 0.939, which is suggesting that the data is suitable for factor analysis.

Table 5 presents the factor loading, reliability and average variance extraction of each variable, which helps to evaluate the validity and reliability of the variable measurement.

Table 6 shows the correlations between the main components. The correlation between Spendception and Impulse Buying is 0.626, and CPB is 0.559, however correlation between Impulse Buying and CPB is 0.54, indicating that there is a positive correlation among components (Table 6).

Table 7 presents the common degree value of each variable, which is used to measure the degree to which the variance of a variable can be explained by common factors. The initial common degree of all three variables is 1, and the common degree of extraction is between 0.6481 and 0.798. It shows that these variables can be effectively explained by common factors to some extent.

Table 8 evaluates the goodness of fit of structural equation models. Several fit metrics such as CFI, NFI, IFI, TLI, GFI, RMSEA, Chi-square and were used (Rigdon, E. E. ,1996). The values of CFI, IFI and TLI were 0.95, 0.950 and 0.942, respectively, meeting the good fitting criteria of 0.9. NFI was 0.878, GFI was 0.858 and RMSEA was 0.061, which met the corresponding fitting criteria. Chi-square is 1.605, which also meets the good fitting requirement of 3, indicating that the overall fitting effect of the model is good. This indicates that the research is reasonable and effective in setting the relationship between the variables related to consumer behavior. Based on this model, the internal relationship among Spendception, Impulse Buying and Consumer Purchase Intention can be further analyzed and explained.

Table 9, presents the evaluation metrics for the model's performance on both the training and test data sets. The Mean Squared Error (MSE), Mean Absolute Error (MAE), and R-squared (R²) values are provided to assess the accuracy and generalization ability of the model. As shown in Table 8, the model demonstrates excellent predictive power with R-squared (R²) values of 0.9792 for both the training and test sets, indicating that the model explains approximately 97.92% of the variance in both datasets. The Mean Squared Error (MSE) for the training set (0.0092) is slightly lower than that for the test set (0.0123), which is typical and suggests the model's good generalization to new data. Similarly, the Mean Absolute Error (MAE) values for the training (0.0293) and test (0.0344) sets are close, supporting the conclusion that the model does not overfit and maintains accuracy across different data subsets. The low MSE and MAE values indicate that the model's predictions are close to the actual values, with only a slight increase in the error when applied to unseen test data, suggesting good generalization."

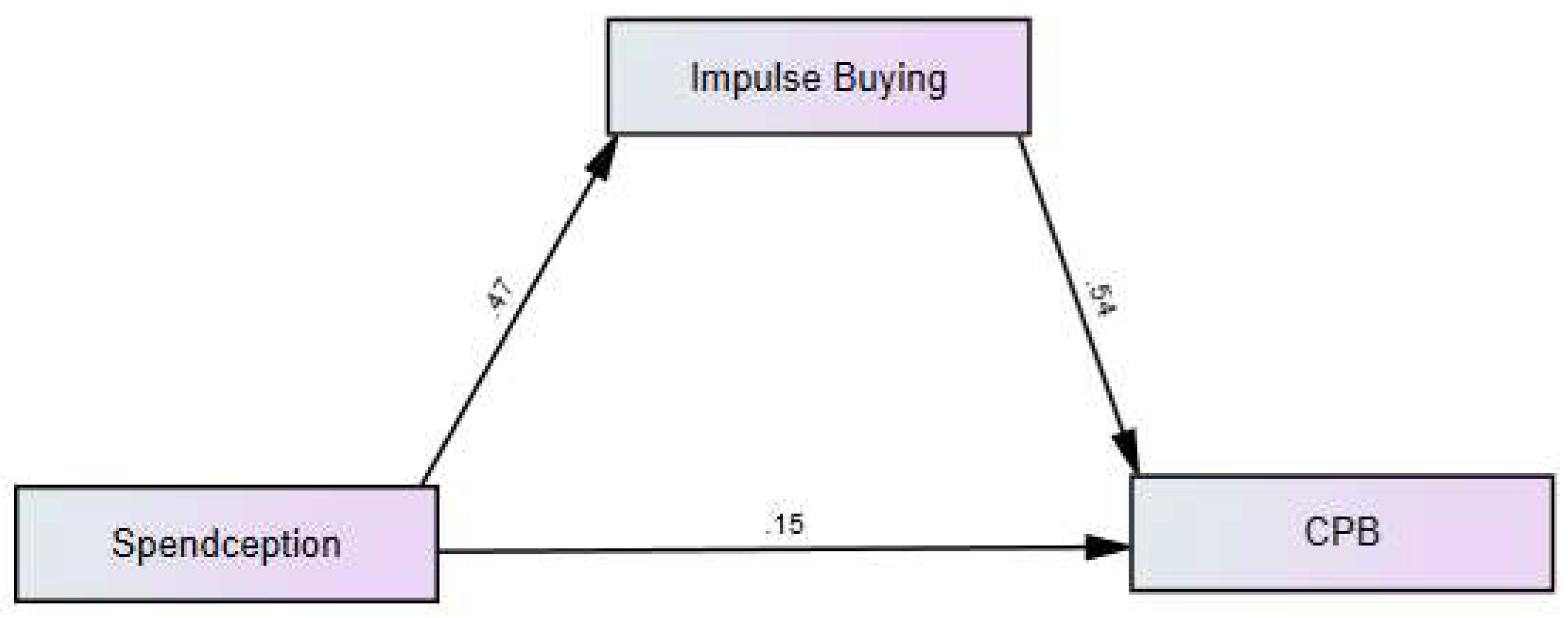

Figure 2 shows a direct and indirect path relationship model between Spendception, Impulse Buying, and Consumer Purchase Behavior.

Table 10 is presenting the direct effects of independent variables on dependent variable.

- H1: Spendception → Impulse Buying, the path coefficient (β-value) is 0.47, and the p-value is ***. The result is Accepted. This suggests that Spendception has a significant positive impact on Impulse Buying

- H2: Impulse Buying → Consumer Purchase Behavior, path coefficient is 0.544 and p-value is 0.029, and the result is accepted. This suggests that Impulse Buying has a significant positive impact on Consumer Purchase Behavior.

- H3: Spendception → Consumer Purchase Behavior, the path coefficient is 0.15, and the p-value is ***, and the result is accepted. This indicates that Spendception has significant positive impact on Consumer Purchase Behavior.

Table 11, shows SpendceptionIBCPB (indirect effect) path coefficient is 0.252, p-value is***, the result is accepted. This suggests that Impulse Buying plays a partial mediating role between Spendception and Consumer Purchase Behavior.

Direct Effect of Interaction term on IB is not significant. This implies that male has no direct moderating influence on the association between IB and Spendception. This Table 12 also examines how various degrees of male affect the indirect impacts of Spendception on CPB through IB:

Low male: The indirect impact is 0.087 with a SE of 0.086 at low levels of male, and it is significant at the p < 0.001 level (shown by ***). This indicates that when male is low, the relationship between Spendception, IB, and CPB is robust and substantial.

Medium male: The indirect impact rises marginally to 0.158 with a SE of 0.051 at medium levels of male, and it is still significant with a p-value of 0.003. This implies that, despite being weaker than at low male, the mediation pathway is nonetheless important even at medium male.

High male: The indirect impact is 0.23 with a SE of 0.099 and a p-value of 0.099 at high levels of male, which is insignificant. This suggests that the mediation pathway weakens and moderation is start playing its role however, Index of Moderate Mediation with p-value of 0.578, the SE is 0.035, and the Moderated Mediation Index is -0.003, all of which are not significant. This implies that this model does not support the idea of moderated mediation.

With an estimate of 0.034, SE of 0.014, and a critical ratio of 2.527, with a p-value of 0.012, the interaction between female consumer and Spendception has impact on Impulse Buying. This implies that there is a direct moderating influence when IB is decreased and both female consumer and Spendception are high.

Conditional Indirect Impacts:

The Table 13 also examines how varying degrees of female consumer affect the indirect impacts of Spendception on CPB through IB:

Low Female Consumer: The indirect impact is 0.055 at low levels of female consumer, with a SE of 0.023. It is significant at the p < 0.001 level, as shown by ***. This indicates that when female consumer level is minimal, there is a strong and significant pathway from Spendception to IB and ultimately to CPB.

Medium Female Consumer: With a p-value of 0.001, the indirect effect is still significant at medium levels of female consumer, rising to 0.77 with a SE of 0.047. This implies that the mediation pathway is still important at medium female consumer levels, but more so than at low risk.

High Female Consumer: The p-value is 0.71, the indirect impact is 0.087, and the SE is 0.099 for high levels of female consumer. This suggests that the mediation pathway become insignificant and it suggest moderated mediation.

Index of Moderate Mediation: The p-value is 0.019, the SE is 0.035, and the Moderated Mediation Index is -0.009. This index's significance suggests that there is moderated mediation, which means that the degree of female consumer influences the association between Spendception and CPB through IB.

The presence of moderated mediation suggests that Spendception have a direct impact on CPB, but that this influence is also influenced by female consumer, which in turn influences IB.

6. Discussion

A multifaceted paradigm known as "Spendception" was developed to describe the behavioural and psychological changes in consumer spending brought about by digital payment systems. The psychological visibility of spending, perceived control over spending, and the emotional separation that arises when consumers utilise digital payment systems instead of cash are the main concerns of Spendception, as this study makes clear. The results of this study have significant implications for comprehending how digital payment systems impact consumer behaviour in Shanghai, as these elements collectively impact consumer spending.

The data provided excellent support for hypothesis H1, which proposed that spending perception has a significant and positive relationship with increased purchasing behaviour. According to the study, digital payments—especially those made with credit cards, smartphone apps, and internet platforms—lessen the psychological visibility of spending. Because they physically transfer money and watch as their cash reserves decrease, customers who pay with cash experience an instant emotional connection to the transaction. Spendception reduces the mental friction related to spending because digital payments do not provide this instantaneous, tactile input. Because digital payments are so convenient, people tend to underestimate their total spending, which raises the possibility of impulsive purchases. This psychological effect is more pronounced in Shanghai's highly digitalised economy, where online purchasing platforms like Taobao, JD.com, and WeChat Pay rule the market. Shanghai's consumers, especially the younger ones, are used to the ease of quick transactions without the immediate repercussions. The impact of digital payment methods on consumer spending patterns is thus confirmed by the fact that "Spendception" leads to a notable rise in purchasing behaviour.

H2 proposes that impulse shopping has a significant and positive relationship with increased purchasing behaviours, and the results of this study support this hypothesis. Impulse buying, which refers to unplanned and spontaneous purchasing decisions driven by emotional or psychological triggers, was found to be a key driver of increased consumer purchase behaviour. Digital payment systems, such as mobile apps and credit cards, exacerbate this effect by diminishing the psychological visibility of spending. Unlike cash transactions, where consumers are physically aware of the money leaving their wallets, digital payments create a psychological detachment from the act of spending, making consumers less aware of the financial consequences of their purchases. In Shanghai, where e-commerce and mobile payments are ubiquitous, the ease and convenience of digital transactions encourage consumers to act on impulse more frequently. Furthermore, high exposure to advertisements, promotions, and limited-time offers on shopping platforms like Taobao and JD.com often triggers these impulse-buying behaviours. The study also highlights that consumers, especially in the 25-34 age group, are particularly susceptible to such influences, leading to increased purchase behaviour. Overall, impulse buying plays a crucial role in driving unplanned purchases in the digital age, especially when consumers are exposed to Spendception tactics that reduce the psychological barriers to spending.

H3, which examined the function of impulse buying as a mediator between Spendception and purchase behaviour, was also supported by the findings. As anticipated, the association between Spendception and increased consumer purchasing behaviour was largely mediated by impulse buying. The simplicity of digital payments eases the cognitive burden of decision-making, enabling customers to make impulsive purchases. Spendception makes spending less visible, which encourages people to make impulsive purchases without thinking through the long-term financial effects. In Shanghai's fast-paced consumption culture, where people are constantly exposed to online advertisements, promotions, and limited-time deals, this finding is consistent with the growing importance of impulse buying. Spendception in this context encourages impulsive buying, which contributes to higher consumer expenditure. The shift from Spendception cues to real purchase decisions is thus facilitated by impulse buying, which serves as a crucial mediator.

Gender moderates the association between spending perception, purchase behaviour, and impulse buying, according to the hypotheses of H4a and H4b. H4b was accepted, while H4a was not, and this disparity calls for a more thorough analysis of Shanghai's cultural and behavioural aspects. Spendception and Gender: The Reasons H4a Was Rejected According to H4a, the association between spending perception and both consumer purchasing behaviour and impulse buying would be moderated by male customers. The findings, however, indicated that this moderating impact was not statistically significant. There are a number of reasons for this, but in many Chinese households, men have traditionally been the breadwinners. Cultural Expectations: In Shanghai, men are frequently viewed as the main breadwinners and financial decision-makers. As a result, their spending tends to be more conservative and careful. Being responsible for providing for their family makes individuals more financially conscious and in control of their spending, which reduces their vulnerability to Spendception cues that drive impulsive purchases.

Psychological Resistance: Men tend to be more financially responsible and may be more resistant to overspending, especially those in older age groups. Men still have a stronger mental barrier against excessive spending, even though Spendception strategies may result in more purchases. Although they may still occasionally succumb to Spendception, their underlying financial prudence makes the moderating effect less noticeable. Economic Factors: Because they feel a sense of duty towards their families, men are more likely to budget or spend strategically. Compared to women, who are frequently more emotionally sensitive to purchasing impulses, this makes them less likely to engage in impulsive purchases. Spendception and Female Consumers (H4b) However, H4b was accepted, indicating that female consumers mitigate the association between Spendception and consumer purchasing behaviour and impulse buying. Women are more prone to being swayed by emotional cues in advertisements and promotions, especially in Shanghai, which increases their vulnerability to spending perception-induced impulse buying.

Emotional Spending: Ads and promotions typically have a greater emotional impact on women. Digital payment methods frequently target women with tailored marketing that elicits emotional buying in Shanghai, where online shopping is common. Spendception has a greater impact on women than on men since they are more prone to acting on impulsive urges.

Cultural and Social Norms: Women may feel less constrained in the Shanghai market when they spend money on goods that improve their own fashion, appearance, or way of life. Because of this propensity, they are more vulnerable to Spendception strategies, particularly on online platforms where spending is less genuine and less linked to actual financial repercussions.

Younger Demographics: Spendception tactics, including influencer promotions and flash deals, are widely employed on social media platforms, where the younger female demographic—particularly those between the ages of 18 and 34—is more active. These customers are more prone to acting on impulse and making more purchases as a result of digital indications.

7. Theoretical Contribution

Our study adds new ideas by combining Spendception with well-known concepts like the pain of paying and mental accounting. This helps us understand how digital payment systems affect how people buy things. Pain of Paying: This term describes the uncomfortable feeling people get when they spend money, particularly when using cash. Our study builds on this idea by showing how Spendception can lessen the mental distress of spending when using digital payment methods. Digital payments make it easier for people to spend money because they don't involve physically handing over cash. This can lead to more unplanned purchases since people feel less mental discomfort compared to when they use cash. This shows that we should think about how digital funds affect people's feelings when they decide what to buy. Mental Accounting: This idea means that people think of their money in different "accounts" in their minds, which can affect how they spend it. Our study builds on this by exploring how the separation of payment (i.e., digital payments) from instant financial consequences can distort mental accounting. Digital payments, like using credit cards or mobile apps, make it easy to lose track of how much money you’re actually spending. This can cause people to not realize how small purchases add up over time. This part of mental accounting is important when it comes to Spendception. Here, customers might not keep track of their total spending because digital transactions don’t provide clear feedback.

In summary, our study helps us understand consumer spending better by combining the ideas of pain of paying and mental accounting with the concept of Spendception. It creates new opportunities for future study on how digital payment systems influence how consumers make financial decisions, especially regarding impulse buying and controlling spending.

8. Conclusions

In conclusion, the research successfully validates all of the theories that were given, with the exception of the H4a hypothesis. More specifically, we discovered that the phenomenon known as "Spendception" greatly boosts the behavior of consumers who make purchases by lowering the psychological barrier to spending, and that the phenomenon known as "impulse buying" plays a key role in mediating the relationship between the two. Furthermore, it was discovered that gender has a moderating role in the connection between Spendception and impulse buying. Specifically, it was discovered that female consumers are more susceptible to the effects of these factors in comparison to male consumers. It is possible that the rejection of hypothesis H4a, which proposed that male consumers moderate the link between Spendception and impulse buying, can be attributable to the fact that males are traditionally more responsible with their finances and exhibit more cautious spending behavior. The findings, taken as a whole, demonstrate the intricate interplay that exists between digital payment methods, consumer behavior, and psychological aspects. Furthermore, they highlight the necessity of knowing how these elements influence purchasing decisions, particularly in the setting of modern payment systems.

9. Recommendations

9.1. Advice for Marketers:

Use Spendception in Marketing: Marketers can employ Spendception to boost impulse purchases. Their rapid, flawless, and psychologically detached purchasing procedure lowers the perceived cost of spending. One-click payments, mobile payment systems, and other payment methods should be prioritized by digital platforms to help consumers make faster purchases. They should guarantee these approaches are ethical to minimize consumer displeasure and reaction.Target Female Emotional Triggers: Since female consumers are more sensitive to Spendception and impulse buying, marketers should use emotional appeals and targeted offers. These may include limited-time deals, targeted discounts, or social proof (e.g., influencer endorsements) to attract female shoppers, who are more emotional about purchases. The rejection of H4a shows that males are less sensitive to Spendception, thus marketers should promote financial transparency and spending control options to men. For cautious and budget-conscious guys, campaigns could include financial management applications, spending alerts, or savings awards. Provide Digital Payment System Expense Tracking: Digital payment platforms should include expense tracking to assist users budget. Marketers can help consumers avoid overspending by presenting monthly expense summaries or spending categories. The moderating effect of Spendception may encourage more appropriate consumer behavior by making spending visible.

9.2. Advice for Consumers:

Beware Psychological Spending Traps: Customers should be informed of the psychological repercussions of digital payments, such as reduced payment pain and financial isolation. Understanding Spendception helps consumers set spending limits, use budgeting tools, and track financial objectives to avoid impulsive purchase. Digital solutions like expense tracking applications, budgeting tools, and spending limit alerts can help consumers cut back on spending. These tools can give them a more precise financial picture, enabling them make informed decisions without Spendception. Mindful Spending: Consumers should pause before buying, especially with online discounts. Set a monthly budget, manage expenditures, and limit impulse spending to reduce Spendception and help consumers reach their financial goals.

10. Future Research Directions

It is crucial to acknowledge the counterbalancing effect of the continuous tracking of expenditures made possible by digital payment systems, even though Spendception encourages increased consumer purchase behavior by lowering the psychological barriers related to spending. Digital payments give customers monthly expenditure records, which are frequently shown through mobile applications or online banking platforms, in contrast to cash payments, which are instantaneous and do not directly record previous transactions. As customers grow more conscious of their accrued expenses, this visibility of spending may operate as a moderating factor, possibly restricting buying behavior. As customers examine their monthly expenses, the ability to monitor spending trends over time may result in increased financial consciousness, which may drive them to revaluate their purchases. Therefore, the recording and visibility of these payments may serve as a moderating influence, encouraging more cautious spending behavior and thereby reducing impulsive purchases, even though Spendception may initially lessen the perceived cost of individual transactions. As a crucial element in comprehending consumer spending patterns, our future research will concentrate on the creation and investigation of cost tracking systems. We intend to examine how ongoing monitoring and visibility of spending can affect customers' decision-making processes, especially in reducing impulsive purchases, by utilizing the data offered by digital payment networks. In order to develop more effective strategies for controlling consumer spending behavior in the digital age, this field of study will help us better understand the balance between the psychological ease of digital payments, which is driven by Spendception, and the moderating effects of expense awareness.

11. Limitations of the Research

Limitations of the sample: The sample in this study is only from the Shanghai area and may not fully represent the situation of consumers in different regions of the country or even the world. Consumers in different regions have differences in culture, economic level, policy environment, and other factors, which may affect differently.

References

- Adams, M.; Boldrin, L.; Ohlhausen, R.; Wagner, E. An integrated approach for electronic identification and central bank digital currencies. Journal of Payments Strategy and Systems 2021, 15, 287–304. [Google Scholar] [CrossRef]

- Ahmadian, M. E-payments in the post-COVID-19: navigating uncertainty and forecasting trends. Journal of Economic Studies 2025. [Google Scholar] [CrossRef]

- Alrawad, M.; Lutfi, A.; Alyatama, S.; Al Khattab, A.; Alsoboa, S.S.; Almaiah, M.A.; Ramadan, M.H.; Arafa, H.M.; Ahmed, N.A.; Alsyouf, A.; Al-Khasawneh, A.L. Assessing customers perception of online shopping risks: A structural equation modeling–based multigroup analysis. Journal of Retailing and Consumer Services 2023, 71. [Google Scholar] [CrossRef]

- Ariely, D.; Prelec, D. Coherent arbitrariness”: Stable demand curves without stable preferences., 118, 73-106. The Quarterly Journal of Economics 2003, 118, 73–106. [Google Scholar] [CrossRef]

- Borzova, E. Global biotechnology leapfrogging during the COVID-19 pandemic: a trend to stay? Trends in Biotechnology 2024, 42, 1327–1330. [Google Scholar] [CrossRef] [PubMed]

- Cao, X.; Yu, L.; Liu, Z.; Gong, M.; Adeel, L. Understanding mobile payment users’ continuance intention: a trust transfer perspective. Internet Research 2018, 28, 456–476. [Google Scholar] [CrossRef]

- Cerny, C.A.; Kaiser, H.F. CA study of a measure of sampling adequacy for factor-analytic correlation matrices. Multivariate Behavioral Research 1977, 12, 43–47. [Google Scholar] [CrossRef]

- Gong, Y.; Chow, K.P.; Yiu, S.M.; Ting, H.F. Analyzing the peeling chain patterns on the Bitcoin blockchain. Forensic Science International: Digital Investigation 2023, 46, 301614. [Google Scholar] [CrossRef]

- Guo, R.; Liu, J.; Yu, Y. Digital transformation, credit availability, and MSE performance: Evidence from China. Finance Research Letters 2025, 72, 106552. [Google Scholar] [CrossRef]

- Humbani, M.; Wiese, M. An integrated framework for the adoption and continuance intention to use mobile payment apps. International Journal of Bank Marketing 2019, 37, 646–664. [Google Scholar] [CrossRef]

- Karmaker, S.; Oishi, M.E.F.; Qasem, A.; Sami, S.B.S.; Noor, J. Exploring influential factors of consumer purchase behavior on the adoption of digital payment apps in Bangladesh. Computers in Human Behavior Reports 2025, 17, 100587. [Google Scholar] [CrossRef]

- Kim, J.H.; Jang, J.; Kim, Y.; Nan, D. A Structural Topic Model for Exploring User Satisfaction with Mobile Payments. Computers, Materials and Continua 2022, 73, 3815–3826. [Google Scholar] [CrossRef]

- Kim, J.; Park, J. A consumer shopping channel extension model: Attitude shift toward the online store. Journal of Fashion Marketing and Management 2013, 17, 20–35. [Google Scholar] [CrossRef]

- Kong, X.; Wang, R.; Zhang, Y. Exploring the influence of “keeping consumers in suspense” in live streaming on consumer impulse buying behavior: A test of the mediating effects of consumer inner states. Acta Psychologica 2025, 253, 104762. [Google Scholar] [CrossRef]

- Li, T.; Jiang, Y.; Zhao, Y. Does mobile payment foster low-carbon lifestyles? Evidence from Alipay’s “collecting five blessings” campaign. Journal of Cleaner Production 2024, 463, 142513. [Google Scholar] [CrossRef]

- Li, X.; Zhu, X.; Lu, Y.; Shi, D.; Deng, W. Understanding the continuous usage of mobile payment integrated into social media platform: The case of WeChat Pay. Electronic Commerce Research and Applications 2023, 60, 101275. [Google Scholar] [CrossRef]

- Lin, X.; Wu, R.Z.; Lim, Y.T.; Han, J.; Chen, S.C. Understanding the sustainable usage intention of mobile payment technology in Korea: Cross-countries comparison of Chinese and Korean users. Sustainability (Switzerland) 2019, 11. [Google Scholar] [CrossRef]

- Liu, M.; Li, R.Y.M.; Deeprasert, J. Factors that affect individuals in using digital currency electronic payment In China: SEM and fsQCA approaches. International Review of Economics & Finance 2024, 95, 103418. [Google Scholar] [CrossRef]

- Mariana, C.D.; Husodo, Z.A.; Ekaputra, I.A.; Fahlevi, M. The advancement of digital payment ecosystem in metaverse: A literature review. Computers in Human Behavior Reports 2025, 17. [Google Scholar] [CrossRef]

- Mombeuil, C.; Uhde, H. Relative convenience, relative advantage, perceived security, perceived privacy, and continuous use intention of China’s WeChat Pay: A mixed-method two-phase design study. Journal of Retailing and Consumer Services 2021, 59, 102384. [Google Scholar] [CrossRef]

- Monem, M.; Hossain, M.T.; Alam, M.G.R.; Munir, M.S.; Rahman, M.M.; AlQahtani, S.A.; Almutlaq, S.; Hassan, M.M. A sustainable Bitcoin blockchain network through introducing dynamic block size adjustment using predictive analytics. Future Generation Computer Systems 2024, 153, 12–26. [Google Scholar] [CrossRef]

- Nan, D.; Kim, Y.; Park, M.H.; Kim, J.H. What motivates users to keep using social mobile payments? Sustainability (Switzerland) 2020, 12. [Google Scholar] [CrossRef]

- Niankara, I.; Traoret, R.I. The digital payment-financial inclusion nexus and payment system innovation within the global open economy during the COVID-19 pandemic. Journal of Open Innovation: Technology, Market, and Complexity 2023, 9, 100173. [Google Scholar] [CrossRef]

- Pang, H.; Ruan, Y. Determining influences of information irrelevance, information overload and communication overload on WeChat discontinuance intention: The moderating role of exhaustion. Journal of Retailing and Consumer Services 2023, 72. [Google Scholar] [CrossRef]

- Samantray, B.S.; Reddy, K.H.K. Blockchain enabled secured, smart healthcare system for smart cities: a systematic review on architecture, technology, and service management. Cluster Computing 2024. [Google Scholar] [CrossRef]

- Shrestha, N. Factor Analysis as a Tool for Survey Analysis. American Journal of Applied Mathematics and Statistics 2021, 9, 4–11. [Google Scholar] [CrossRef]

- Thaler, R.H. Mental accounting matters. Journal of Behavioral Decision Making 1999, 12, 183–206. [Google Scholar] [CrossRef]

- Wani, S.A.; Pani, A.; Mohan, R.; Bhowmik, B. Digital payment adoption in public transportation: Mediating role of mode choice segments in developing cities. Transportation Research Part A: Policy and Practice 2025, 191, 104319. [Google Scholar] [CrossRef]

- Xiong, Y.; Cui, X.; Yu, L. Impact of COVID-19 pandemic on online consumption share: Evidence from China’s mobile payment data. Journal of Retailing and Consumer Services 2024, 81, 103976. [Google Scholar] [CrossRef]

- Zarco, C.; Giráldez-Cru, J.; Cordón, O.; Liébana-Cabanillas, F. A comprehensive view of biometric payment in retailing: A complete study from user to expert. Journal of Retailing and Consumer Services 2024, 79. [Google Scholar] [CrossRef]

- Zhao, M.; Abeysekera, I. The behaviour of FinTech users in the Alipay Ant Forest platform towards environmental protection. Journal of Open Innovation: Technology, Market, and Complexity 2024, 10, 100201. [Google Scholar] [CrossRef]

Figure 2.

Direct and indirect path.

Table 1.

Statistics of the measurement items for consumer inner states.

| Variable | Coding | Measurement Items |

|---|---|---|

| Spendception | SP1 | When I pay with cash, I feel more aware of how much I am spending as compared to digital payment |

| SP2 | Digital payments make it harder for me to realize how much money I have spend | |

| SP3 | Seeing physical cash leave my hand makes me think twice before spending | |

| SP4 | Paying with digital methods feels less painful than paying with cash. | |

| SP5 | I feel like I spend more when I don’t see the money physically leaving my wallet. | |

| SP6 | Digital payments make spending feel easier and less stressful. | |

| SP7 | I don’t feel the pain of spending when I pay digitally compared to cash | |

| SP8 | When I pay with digital methods, it feels like I am not really spending money | |

| SP9 | I feel more in control of my spending when I pay with cash | |

| SP10 | I feel like I lose control over my budget when I rely on digital payments | |

| SP11 | Paying with cash helps me stick to my spending limits better than digital payments. | |

| SP12 | The convenience of digital payments makes me more likely to spend. | |

| Impulse Buying | IB1 | Digital currency makes it easier to buy items I hadn’t planned to purchase. |

| IB2 | I am more likely to make impulsive purchases when using digital payments | |

| IB3 | The convenience of digital currency encourages unplanned spending. | |

| IB4 | I tend to spend more on impulsive purchases with digital currency than with cash. | |

| IB5 | Digital payments reduce my hesitation to buy items on impulse | |

| Consumer Purchase Behavior | CPB1 | I purchase more frequently now because digital currency makes transactions easier. |

| I spend more on monthly purchases since adopting digital currency | ||

| I am more likely to purchase non-essential or luxury items because digital currency is convenient. | ||

| Digital currency has made me more confident in spending larger amounts | ||

| My shopping habits have changed significantly due to digital currency |

Table 2.

Cronbach’s Alpha Table.

| Construct. | Number of Items | Cronbach’s Alpha | High Reliability Interpretation |

| Spendception | 12 | 0.972 | High Reliability |

| Impulse Buying | 5 | 0.984 | High Reliability |

| Consumer Purchase Behavior | 5 | 0.903 | High Reliability |

| Total | 22 | 0.953 | High Reliability |

Table 3.

Descriptive statistics.

| Minimum | Maximum | Mean | Standard Deviation | |

| Spendception | 1 | 7 | 6.3704 | 0.70074 |

| Impulse Buying | 1 | 7 | 5.2457 | 0.666 |

| Consumer Purchase Behavior | 1 | 7 | 5.3292 | 0.60306 |

Table 4.

Participants' profiles (N=1162).

| Item | Description | Frequency | Percentage |

| Age | Under 18 | 4 | 0.3 |

| 239 | 20.5 | ||

| 485 | 41.73 | ||

| 309 | 26.6 | ||

| 85 | 7.3 | ||

| 40 | 3.57 | ||

| Gender | Male | 509 | 43.8 |

| Female | 653 | 56.2 | |

| Marital Status | Married | 677 | 58.27 |

| Unmarried | 485 | 41.73 |

Table 5.

Factor loadings and reliability analysis, Average variance extraction and composite reliability.

Table 5.

Factor loadings and reliability analysis, Average variance extraction and composite reliability.

| Variables | Items | Loading | Cronbach- | CR | AVE |

| Spendception | SP1 | 0.581 | 0.972 | 0.876 | 0.589 |

| SP2 | 0.766 | ||||

| SP3 | 0.841 | ||||

| SP4 | 0.784 | ||||

| SP5 | 0.837 | ||||

| SP6 | 0.876 | ||||

| SP7 | 0.747 | ||||

| SP8 | 0.720 | ||||

| SP9 | 0.683 | ||||

| SP10 | 0.909 | ||||

| SP11 | 0.788 | ||||

| SP12 | 0.459 | ||||

| Impulse Buying | IB1 | 0.742 | 0.972 | 0.880 | 0.556 |

| IB2 | 0.882 | ||||

| IB3 | 0.808 | ||||

| IB4 | 0.809 | ||||

| IB5 | 0.589 | ||||

| Consumer Purchase Behavior | CPB1 | 0.886 | 0.903 | 0.915 | 0.783 |

| CPB2 | 0.867 | ||||

| CPB3 | 0.901 | ||||

| CPB4 | 0.891 | ||||

| CPB5 | 0.786 | ||||

| Total | 0.953 |

Table 6.

Component correlation matrix.

| Components | Spendception | Impulse Buying | CPB |

| Spendception | 1 | ||

| Impulse Buying | 0.626 | 1 | |

| CPB | 0.559 | 0.540 | 1 |

Table 7.

Communality Values.

| Variables | Initials | Extraction |

| Spendception | 1 | 0.679 |

| Impulse Buying | 1 | 0.6481 |

| Consumer Purchase Behavior | 1 | 0.664 |

Table 8.

Goodness of fit.

| Fit Indices | Definition | Criteria | Values |

| CFI | Comparative fit index | 0.9 good fit | 0.95 |

| NFI | Normed fit index | 0.9 good fit | 0.878 |

| IFI | Incremental fit index | 0.9 good fit | 0.950 |

| TLI | Tucker-Lewis index | 0.9 good fit | 0.942 |

| GFI | Goodness of fit | 0.9 good fit | 0.858 |

| RMSEA | Root mean squared error of approximation | 0.08good fit | 0.061 |

| Chi-square | 3good fit | 1.605 |

Table 9.

Machine Learning Model Performance Evaluation: Training and Test Set Metrics.

| Metric | Train Set | Test Set |

| Mean Squared Error (MSE) | 0.0092 | 0.0123 |

| Mean Absolute Error (MAE) | 0.0293 | 0.0344 |

| R-squared | 0.9792 | 0.9792 |

Table 10.

Hypothesis results.

| Hypotheses | Path direction | -value | p-value | Result |

| H1 | SpendceptionImpulse Buying | 0.47 | *** | Accepted |

| H2 | Impulse BuyingConsumer Purchase Behavior | 0.54 | 0.029 | Accepted |

| H3 | SpendceptionConsumer Purchase Behavior | 0.15 | *** | Accepted |

Table 11.

Mediation Analysis.

| Hypotheses | Path direction | -value | p-value | Result |

| SpendceptionCPB | *** | |||

| SpendceptionCPB (Direct Effect) | 0.073 | |||

| IBCPB | 0.539 | *** | ||

| H4 | SpendceptionIBCPB | 0.252 | *** | Accepted |

Table 12.

Direct and Indirect moderating effect of Male Consumer through Hayes Process.

| Path | Estimate | SE | Critical Ratio | P-Value | Interpretation |

| Direct Effects | |||||

| SpendceptionIB | 0.382 | 0.101 | 3.773 | 0.020 | Spendception positively and significantly influences Male. |

| MaleIB | 0.149 | 0.147 | 3.049 | 0.002 | Male moderately enhances IB. |

| Interaction_Male_SpendceptionBC | -0.1 | 0.04 | 0..713 | 0.476 | Interaction effect is weak insignificant, indicating no direct moderation. |

| IB → CPB | 0.327 | 0.043 | 7.741 | *** | PBC drives BEIV |

| Spendception → CPB | 0.359 | 0.41 | 8.670 | 0.029 | Spendception also has a significant direct impact on CPB. |

| Conditional Indirect Effects | |||||

| Low Male | 0.087 | 0.086 | N/A | *** | The indirect pathway (Spendception →IB → CPB) is strong and significant at low Male. |

| Medium Male | 0.158 | 0.051 | N/A | 0.003 | The mediation pathway weakens but remains significant at medium Male. |

| High Male | 0.23 | 0.099 | N/A | 0.099 | At high Male, the mediation pathway becomes insignificant. |

| Moderated Mediation Index | -0.003 | 0.035 | N/A | 0.578 | The insignificant index indicates that moderated mediation does not exists. |

Table 13.

Direct and Indirect moderating effect of Female Consumer through Hayes Process.

| Path | Estimate | SE | Critical Ratio | P-Value | Interpretation |

| Direct Effects | |||||

| SpendceptionIB | 0.521 | 0.094 | 5.546 | *** | Spendception is significantly and positively influences IB. |

| FemaleIB | 0.732 | 0.150 | 4.892 | *** | Female significantly and positively influences IB |

| Interaction_Female_SpendceptionIB | 0.034 | 0.014 | 2.527 | 0.012 | Interaction term significantly influences IB, indicating direct moderation. |

| IB → CPB | 0.275 | 0.040 | 6.666 | *** | IB significantly and positively influences CPB. |

| Spendception → CPB | 0.451 | 0.036 | 12.406 | *** | Spendception significantly and positively influences CPB. |

| Conditional Indirect Effects | |||||

| Low Female | 0.055 | 0.023 | N/A | *** | The indirect pathway (Spendception→ IB →CPB) is strong and significant at low Male. |

| Medium Female | 0.77 | 0.047 | N/A | 0.001 | The mediation pathway weakens but remains significant at medium Female Consumer. |

| High Female Consumer | 0.087 | 0.099 | N/A | 0.07 | At high Female consumer levels, the mediation pathway weakens and insignificant, which suggest moderation. |

| Moderated Mediation Index | -0.009 | 0.035 | N/A | 0.019 | The significant index indicates that moderated mediation exists. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.