Submitted:

02 December 2024

Posted:

03 December 2024

You are already at the latest version

Abstract

This comprehensive review paper explores the diverse landscape of cryptocurrency forecasting, tracing its evolution from an alternative to traditional monetary systems to its significant growth in the global financial arena. It consolidates existing research by categorizing and analyzing 234 scholarly articles, organizing them into machine learning, deep learning, deep reinforcement learning, and statistical methodologies, and evaluating the related metrics. The case study titled “Examining the performance differences between backtesting and forward testing” highlights the challenges investors face, as strategies that appear effective in backtesting often fail in practical use. Another case study, “Social Data Exploration in Cryptocurrency Trends,” examines how social media data can provide insights into market movements and investor sentiment, revealing the impact of social trends on cryptocurrency prices. The findings section provides a detailed view, illuminating trends such as yearly publication rates, methodological distributions, input features, training/testing splits, the total number of data samples considered, and forecasting time horizons. This survey paper serves as a valuable resource, providing researchers and investors with a solid foundation for understanding and navigating the dynamic field of cryptocurrency forecasting.

Keywords:

Bitcoin

; Cryptocurrency Forecasting

; Machine Learning

; Deep Learning

; Reinforcement Learning

; Statistical Models

; Time Series Analysis

; Social Data Analysis

; Market Sentiment Analysis

; Backtesting

; Forward Testing

; Financial Market Prediction

1. Introduction

In human history, currency systems have always played a vital role in shaping economies, societies, and the global financial landscape. The evolution of currency systems has been continuous, progressing from ancient barter systems to modern central banks and fiat currencies [1]. Traditional monetary systems are predominantly based on fiat currencies, characterized by government and central bank control over the issuance and regulation of money. However, this system faces several challenges, including inflation risk, dependence on intermediaries like banks, and centralization. Moreover, traditional currencies may not be accessible to unbanked individuals, limiting their ability to save money, make investments, or engage in financial activities. This exclusion underscores the importance of exploring alternative economic systems to address these limitations.

Figure 1.

From bartering shells to digital wallets: the journey of currency evolution in one glance.

Figure 1.

From bartering shells to digital wallets: the journey of currency evolution in one glance.

Table 1.

Abbreviations for AI models used in cryptocurrency forecasting literature.

| Name | Abbreviation | Type |

|---|---|---|

| Adaptive Neuro Fuzzy Inference System | ANFIS | Machine Learner |

| Advantage Actor-Critic | A2C | Deep Reinforcement Learner |

| Artificial Neural Network | ANN | Deep Learner |

| Asymmetric Power Autoregressive Conditional Heteroskedasticity | APARCH | Statistical Learner |

| Auto Regressive Integrated Moving Average | ARIMA | Statistical Learner |

| Bidirectional Long Short-Term Memory | BiLSTM | Deep Learner |

| Binary Auto Regressive Tree | BART | Statistical Learner |

| Convolutional Neural Network | CNN | Deep Learner |

| Convolutional Neural Network Long Short-Term Memory | CNN-LSTM | Deep Learner |

| Deep Feedforward Neural Networks | DFFNNs | Deep Learner |

| Deep Q-Network | DQN | Deep Reinforcement Learner |

| Exponential Generalized Autoregressive Conditional Heteroskedasticity | EGARCH | Statistical Learner |

| Exponential Smoothing | ES | Statistical Learner |

| Extreme Gradient Boosting | XGBoost | Machine Learner |

| Financial BERT | FinBERT | Deep Learner |

| Gated Recurrent Unit | GRU | Deep Learner |

| Generalized Autoregressive Conditional Heteroskedasticity | GARCH | Statistical Learner |

| Gradient Boosting Classifiers | GBC | Machine Learner |

| K-Nearest Neighbours | KNN | Machine Learner |

| Local Gaussian Mixture Model | LGTM | Machine Learner |

| Logistic Regression | LR | Machine Learner |

| Long Short-Term Memory | LSTM | Deep Learner |

| Naive Bayes | NB | Machine Learner |

| Neural Networks | NN | Deep Learner |

| Proximal Policy Optimization | PPO | Deep Reinforcement Learner |

| Random Forest | RF | Machine Learner |

| Recurrent Neural Network | RNN | Deep Learner |

| Support Vector Machines | SVM | Machine Learner |

| Support Vector Regression | SVR | Machine Learner |

| Temporal Convolutional Network | TCN | Deep Learner |

Digital currencies can be traced in 2008 when an anonymous figure using the pseudonym Satoshi Nakamoto published a groundbreaking whitepaper “Bitcoin: A Peer-to-Peer Electronic Cash System” [2]. This whitepaper introduced a decentralized digital currency system that operates independently of traditional financial intermediaries. The year 2009 marked the birth of the first cryptocurrency Bitcoin. Bitcoin was built upon blockchain technology which revolutionized the concept of trust by relying on cryptographic proofs rather than centralized authorities. Anyone can facilitate direct peer-to-peer transactions on a blockchain network without any processing times.

The cryptocurrency market experienced a significant surge in December 2017 [247], marked by Bitcoin’s price skyrocketing to nearly $20,000, garnering global attention. This period also witnessed the emergence of numerous alternative cryptocurrencies alongside Bitcoin. Among these, Ether stands out as a notable creation introduced by Vitalik Buterin and his team in July 2015 [248]. Ether, the native cryptocurrency of the Ethereum platform, introduced groundbreaking concepts such as smart contracts, enabling developers to build decentralized applications on its blockchain. In January 2018, Ether reached an all-time high of around $1,400 [247]. It’s crucial to note that while Bitcoin primarily serves as digital currency, Ethereum is a decentralized platform facilitating various applications beyond currency, making it a prominent player in the blockchain space.

The cryptocurrency market disrupted traditional financial systems. Investors, traders, businesses, and researchers seeking tools and technologies to know about the volatility of the cryptocurrency market and earn maximum profit. Researchers have recognized the importance of cryptocurrency forecasting to uncover underlying factors driving market dynamics, adoption, and liquidity. The cryptocurrency market operates 24/7 which allows traders and investors to take advantage at any time.

The cryptocurrency boom created new exciting opportunities for investors due to its high market volatility. This volatility is due to multiple factors like speculative trading, regulatory developments, market sentiment, and macroeconomic events. Therefore 24/7 trading environment causes market volatility as compared to traditional financial markets.

Table 2.

List of cryptocurrencies and their abbreviations.

| Name | Abbreviation | Name | Abbreviation |

|---|---|---|---|

| Avalanche | AVAX | Binance Coin | BNB |

| Bitcoin | BTC | Bitcoin Cash | BCH |

| Bitcoin SV | BSV | Cardano | ADA |

| Chainlink | LINK | Dogecoin | DOGE |

| Ether | ETH | Ethereum Classic | ETC |

| Litecoin | LTC | Maker | MKR |

| Monero | XMR | NEM | XEM |

| Polkadot | DOT | Polygon | MATIC |

| Ripple | XRP | Solana | SOL |

| Stellar | XLM | Tether | USDT |

| TRON | TRX | Zcash | ZEC |

This survey paper holds significant importance within the realm of cryptocurrency research and market analysis. It undertook a comprehensive examination of 234 scholarly articles about cryptocurrency forecasting. Given the inherent volatility of the cryptocurrency market, this survey offers a thorough exploration and data-driven analysis of recent research endeavors. By synthesizing a wide array of literature, this survey paper aims to furnish a comprehensive overview of prevailing trends, methodologies, and challenges in the domain of cryptocurrency forecasting. Its findings are poised to furnish invaluable insights to a diverse audience encompassing traders, investors, businesses, and researchers.

Moreover, this survey endeavors to arm its readership with a nuanced understanding of both the challenges and opportunities inherent in cryptocurrency forecasting. By serving as a conduit between academic research and practical applications, this paper endeavors to foster a deeper appreciation for the intersection of theoretical insights and real-world implementations in the cryptocurrency landscape.

2. Contribution of This Survey Article

This section highlights the significant contributions of this survey article to the field of cryptocurrency forecasting.

2.1. Existing Surveys

This survey paper highlights the lack of comprehensive surveys focused on cryptocurrency forecasting. Olvera et al. [3] conducted a study exclusively on Bitcoin price forecasting. However, their investigation was confined to Bitcoin price prediction and primarily relied on hybrid models such as ARIMA. Kervanci et al. [4] conducted a review encompassing both Machine Learning and Statistical methods for Bitcoin price forecasting, providing a broader scope compared to Olvera et al. [3] Fang et al. [5] undertook an extensive analysis of 146 research papers spanning from 2013 to June 2021, covering various aspects of cryptocurrency trading systems, crypto assets, forecasting volatility and returns, as well as addressing topics like bubbles and extreme market conditions. Their survey also delved into research trends and distributions among research objects and datasets.

Sina et al. [6] focused on forecasting cryptocurrency market volatility, albeit with a narrow emphasis on Artificial Neural Networks. Abubakar et al. [7] provided a survey specifically targeting the forecasting of digital assets using Machine Learning-based technologies from 2014 to 2022. Their review comprised 75 research articles focusing primarily on classification problems, covering aspects such as datasets, data sources, features, evaluation metrics, Machine Learning models, and model efficiency.

Biju et al. [8] conducted a bibliometric analysis of the financial sphere, specifically exploring the integration of Artificial Intelligence, Deep Learning, and Machine Learning. Utilizing the Web of Science bibliographic repository, they retrieved 723 publications from 1993 to 2022 indexed in the Social Sciences Citation Index. Their analysis revealed that institutions in the USA and China were at the forefront of applying AI and ML techniques in the financial domain. It is worth noting that they exclusively considered publications in the fields of ML and DL within the financial sphere.

2.2. Our Contributions

2.2.1. Comprehensive Coverage

One of the primary contributions of this survey is its comprehensive coverage. This survey conducted an extensive review of 234 research papers, encompassing various cryptocurrencies, including but not limited to Bitcoin, Ether, Ripple, Litecoin, and others. This broad coverage ensures that our survey provides insights into the latest developments and trends across multiple currencies.

2.2.2. Coverage of ML, DL, DRL, and Statistical Models

Our survey article covers a wide range of forecasting models, including Machine Learning, Deep Learning, Deep Reinforcement Learning, and Statistical Models. By exploring these different methodologies, this study offers readers a holistic understanding of the diverse approaches used in cryptocurrency forecasting.

2.2.3. Social Data Analysis

In addition to reviewing existing literature, this survey includes insightful case studies and analyses of social data. This study explores the impact of social media data, Google Trends, and other external factors on cryptocurrency price movements. These case studies provide practical examples and real-world insights into the complexities of cryptocurrency forecasting.

2.2.4. Investigation of Performance Disparities

This survey investigates the performance disparities between backtesting and forward-testing methodologies. By examining the effectiveness of these testing approaches, this survey sheds light on the challenges and limitations faced by cryptocurrency forecasters in practical settings.

2.2.5. Findings and Insights

Through comprehensive analysis, this survey extracts key findings and insights from the reviewed literature. These findings encompass Statistical analyses, trends, and patterns observed in cryptocurrency forecasting research. By synthesizing and presenting this information, this survey article contributes valuable knowledge to the field. Overall, this survey article offers a thorough examination of cryptocurrency forecasting, building upon existing literature and providing new insights into the field.

3. Background

In this survey paper, an exploration unfolds across key AI paradigms. Each subsection delves into the details of Machine Learning, Deep Learning, Deep Reinforcement Learning, and Statistical Learning. The goal is to break down these concepts for readers, whether new to the field or experienced, providing a clear understanding of different techniques in AI research. This paper aims to be a helpful resource, explaining how these methods work and their significance in the broader field of artificial intelligence.

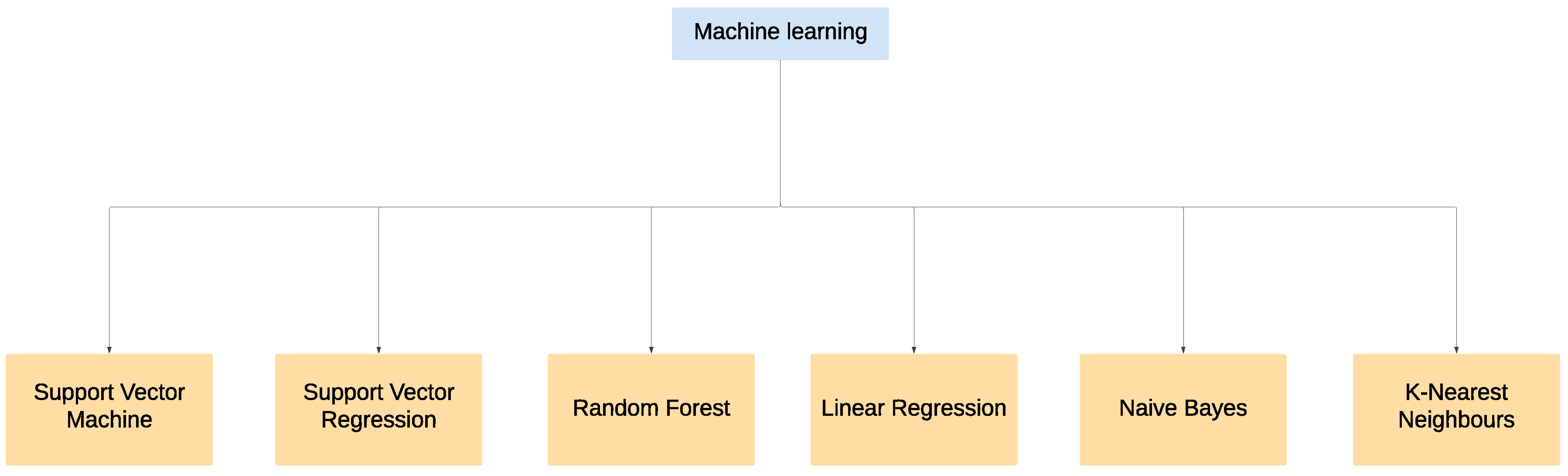

3.1. Machine Learning

Machine Learning is a diverse field with a variety of algorithms that serve as powerful tools in cryptocurrency forecasting. Each algorithm has distinct strengths, making them suitable for various tasks within the dynamic landscape of financial markets.

Figure 2.

Comprehensive overview of Machine Learning and its key algorithms. Machine Learning encompasses various algorithms including SVM, SVR, RF, LR, NB, and KNN, each representing distinct methodologies within the field.

Figure 2.

Comprehensive overview of Machine Learning and its key algorithms. Machine Learning encompasses various algorithms including SVM, SVR, RF, LR, NB, and KNN, each representing distinct methodologies within the field.

3.1.1. Support Vector Machines

Support vector machines [9] serve as robust classifiers in the ML toolkit. They excel in finding optimal decision boundaries within data, making them particularly useful for binary classification tasks in cryptocurrency analysis. SVM seeks to maximize the margin between different classes, ensuring a clear separation. In the context of cryptocurrency forecasting, SVM can effectively determine market trends, aiding traders and investors in decision-making. From a technological viewpoint, SVM employs a kernel trick to transform input data into higher-dimensional spaces, where complex relationships become more apparent. This transformation enables SVM to handle nonlinear relationships in the cryptocurrency data, providing a more nuanced understanding of market dynamics.

3.1.2. Support Vector Regression

Support vector regression [10] extends SVM’s capabilities into the realm of regression tasks. In cryptocurrency forecasting, SVR becomes a valuable ally for predicting numerical values, such as future price movements. Its ability to accommodate non-linear patterns in data makes SVR well-suited for capturing the complex dynamics of cryptocurrency markets. Technically, SVR employs support vectors and a specified epsilon-insensitive tube to guide the prediction process. The algorithm minimizes errors within this tube, allowing for flexibility in handling fluctuations in cryptocurrency prices. SVR’s adaptability and predictive accuracy make it a powerful tool for traders seeking precise forecasts.

3.1.3. Random Forest

Random forest [11] represents an ensemble learning technique in which multiple decision trees collaborate to make predictions. In the cryptocurrency realm, RF acts as a wise council of trees, each providing its opinion on potential market movements. This ensemble approach enhances prediction accuracy and robustness, making RF a reliable tool for understanding the complexities of cryptocurrency markets. At a technical level, RF constructs decision trees through a process called bagging (Bootstrap Aggregating). Each tree is trained on a subset of the data, and their collective wisdom is harnessed during the prediction phase. Moreover, RF introduces randomness during tree construction, further diversifying the perspectives considered in cryptocurrency forecasting.

3.1.4. Linear Regression

Linear regression [12] serves as a fundamental yet powerful tool for understanding the relationship between independent and dependent variables. In cryptocurrency analysis, LR becomes a guiding force in unveiling how specific factors influence market trends. For instance, it can elucidate how trading volume correlates with price movements. From a technological viewpoint, LR minimizes the sum of squared differences between observed and predicted values, finding the line (or hyperplane in multidimensional space) that best represents the relationship. This straightforward approach makes LR interpretable and valuable for identifying linear patterns in cryptocurrency data.

3.1.5. Naive Bayes

Naive Bayes [13] takes on the role of a probabilistic classifier, leveraging Bayesian principles for cryptocurrency sentiment analysis. In the vast sea of discussions surrounding cryptocurrencies, NB acts as a clever detective, discerning positive or negative sentiments from textual data. Technically, NB assumes that features are conditionally independent, simplifying the computation of probabilities. Cryptocurrency sentiment analysis processes textual data to estimate the probability of positive or negative sentiment. NB’s simplicity, efficiency, and effectiveness in handling large datasets make it a valuable asset in understanding market sentiment.

3.1.6. K-Nearest Neighbors

K-Nearest Neighbors [14] is a versatile algorithm employed in both classification and regression tasks. In the context of cryptocurrency forecasting, KNN acts as a neighborly guide, making predictions based on the majority class or average of its k-nearest data points. From a technological viewpoint, KNN relies on distance metrics, such as Euclidean or Manhattan distance, to determine the proximity of data points. The algorithm then classifies or predicts based on the collective behavior of its neighbors. KNN’s simplicity and adaptability make it a useful tool, especially in scenarios where local patterns in cryptocurrency data are crucial for accurate predictions.

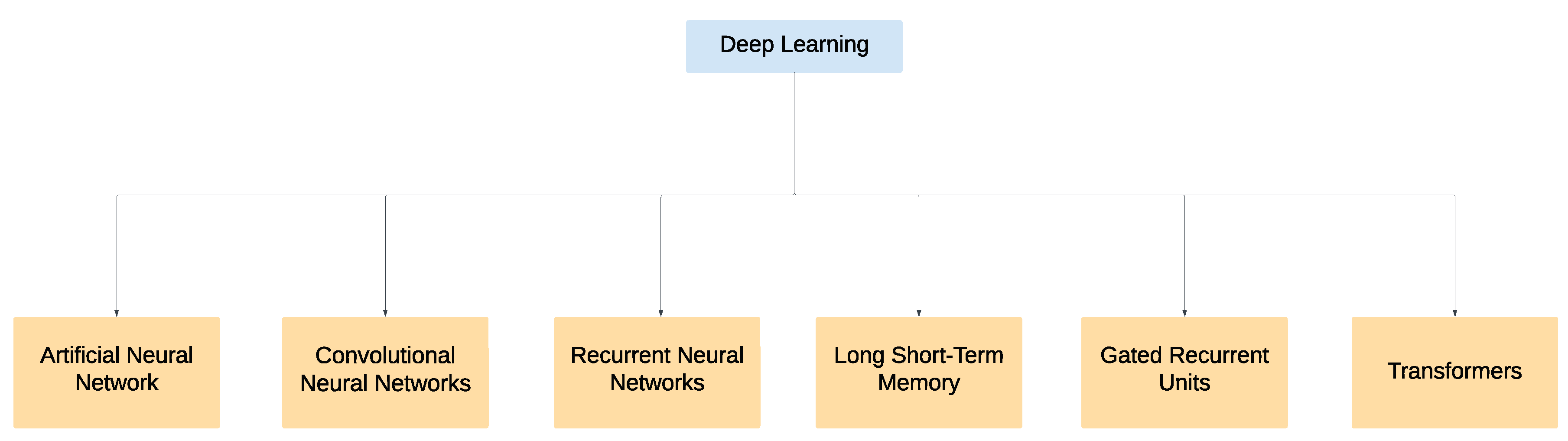

3.2. Deep Learning

Deep Learning [15] is a powerful tool in the world of cryptocurrency forecasting. It has lots of different methods, and each one is good at different tasks. They’re good at spotting tricky patterns in cryptocurrency data, which helps make better predictions about what might come next in the digital money world.

Figure 3.

Deep Learning encompasses a diverse array of architectures including artificial neural networks, Convolutional Neural Networks, Recurrent Neural Networks, Long Short-Term Memory networks, gated recurrent units, and transformers. Each architecture represents a unique paradigm within Deep Learning, collectively shaping the landscape of modern artificial intelligence.

Figure 3.

Deep Learning encompasses a diverse array of architectures including artificial neural networks, Convolutional Neural Networks, Recurrent Neural Networks, Long Short-Term Memory networks, gated recurrent units, and transformers. Each architecture represents a unique paradigm within Deep Learning, collectively shaping the landscape of modern artificial intelligence.

3.2.1. Artificial Neural Network

Artificial neural networks [16] are computational models inspired by the structure and functioning of the human brain. Comprising interconnected nodes organized into layers, ANNs are designed to process and learn from data, making them powerful tools for a diverse range of tasks. Each node takes in information, processes it, and gives an answer. When we train the network by showing it examples, it gets better at understanding complex patterns and connections in the data. ANNs can learn from one set of data and then use that knowledge to make predictions or sort things out in new, unseen data. They’re super versatile, helping with tasks like recognizing pictures, understanding language, looking at trends over time, and solving all kinds of tricky problems by learning and recognizing patterns.

3.2.2. Convolutional Neural Networks

A convolutional neural network [17] is a neural network that is specially designed for understanding image data. Imagine we have a picture of a cat and each small piece of image has some details like colors and shapes. Convolutional neural network process at each small piece and then put all these small pieces together to understand the whole image. Convolutional neural network uses special filters to understand specific parts of the image such as zooming in, sharpening, etc. Convolutional neural networks can be used in lots of places like recognizing faces, and in self-serving cars to figure out what is around them. CNN also has applications beyond visual data it can also be effectively implemented for time series analysis.

3.2.3. Recurrent Neural Networks

RNNs [18] are a class of artificial neural networks that is specifically designed to understand and work with data that comes in a specific order, making them particularly well-suited for tasks such as natural language processing, time series analysis, and speech recognition. The special thing about RNNs is that they remember stuff from the past and use it to make sense of what’s happening next. Imagine reading a story– you need to remember what happened in the beginning to understand the later parts. RNNs do something similar with data. This recurrent structure enables RNNs to capture sequential dependencies, making them particularly valuable in scenarios where the order of input data is crucial. Sometimes, they struggle to learn if the information is too far back in the past or if it becomes too big. We call these problems the vanishing and exploding gradient problems. It’s like trying to remember something from a really long time ago – it can be tough for the program. Even though there are challenges, RNNs are super useful. RNNs find application in a wide array of fields, including natural language processing, speech recognition, and time series analysis. This ability of RNNs to understand and remember sequential dependencies makes them valuable in tasks where understanding the context and order of input data is essential.

3.2.4. Long Short-Term Memory

A specialized variant of Recurrent Neural Networks is designed to address the challenges of modeling long-term dependencies in sequential data. LSTMs [18] have gained prominence in various applications due to their unique architecture, allowing for improved information retention and selective processing over extended time intervals. The key innovation of LSTMs lies in their ability to mitigate the vanishing gradient problem, a limitation in traditional RNNs. LSTMs achieve this through a more complex architecture involving specialized memory cells, and input, forget, and output gates. These components allow LSTMs to selectively retain or discard information over different time steps, facilitating the modeling of both short and long-term dependencies. The selective memory retention mechanism of LSTMs equips them with the ability to capture and remember patterns over extended time intervals. This feature makes LSTMs particularly well-suited for tasks where understanding long-term dependencies is essential, such as natural language processing, speech recognition, and time series analysis.

3.2.5. Gated Recurrent Units

Gated recurrent units [19] are a type of Recurrent Neural Network architecture, and they’re like smart memory systems for computers. Inspired by the way our brains remember and forget information, GRUs are designed to capture and store important details from past data. In a GRU, information is processed through special gates that decide what to keep and what to forget. These gates help the network learn and remember over time. This makes them useful for tasks like understanding the context in language, predicting future values in time series data, or anything where remembering and adapting to past information is important.

3.2.6. Transformers

Transformers [20] refers to a type of neural network architecture introduced to handle sequential data more efficiently, with a particular focus on natural language processing tasks. Transformers consist of an encoder-decoder structure, where the encoder processes input data and the decoder generates output. The Transformer architecture has been highly successful in tasks such as language translation, text summarization, various natural language understanding applications, and notably, time series analysis.

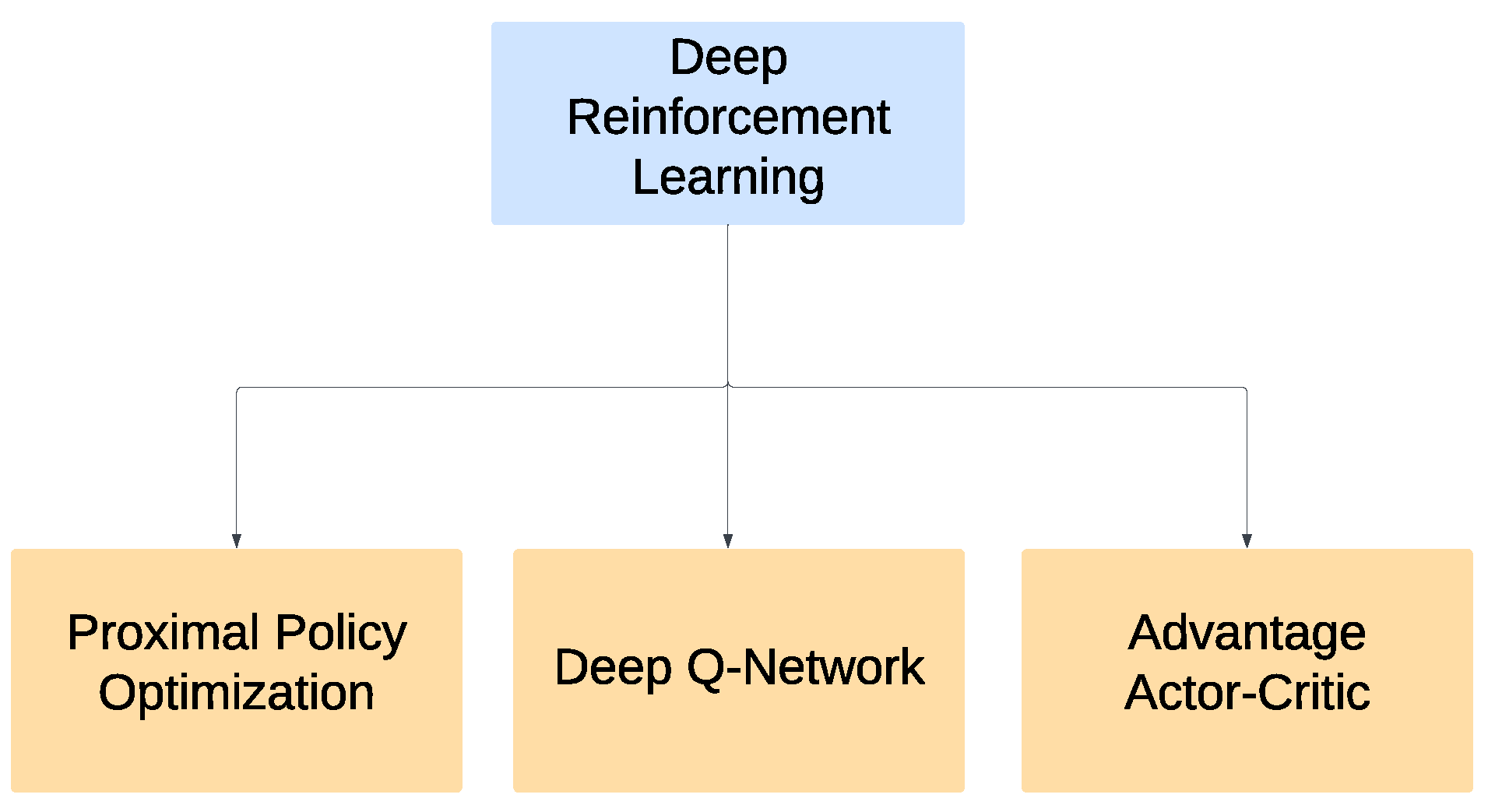

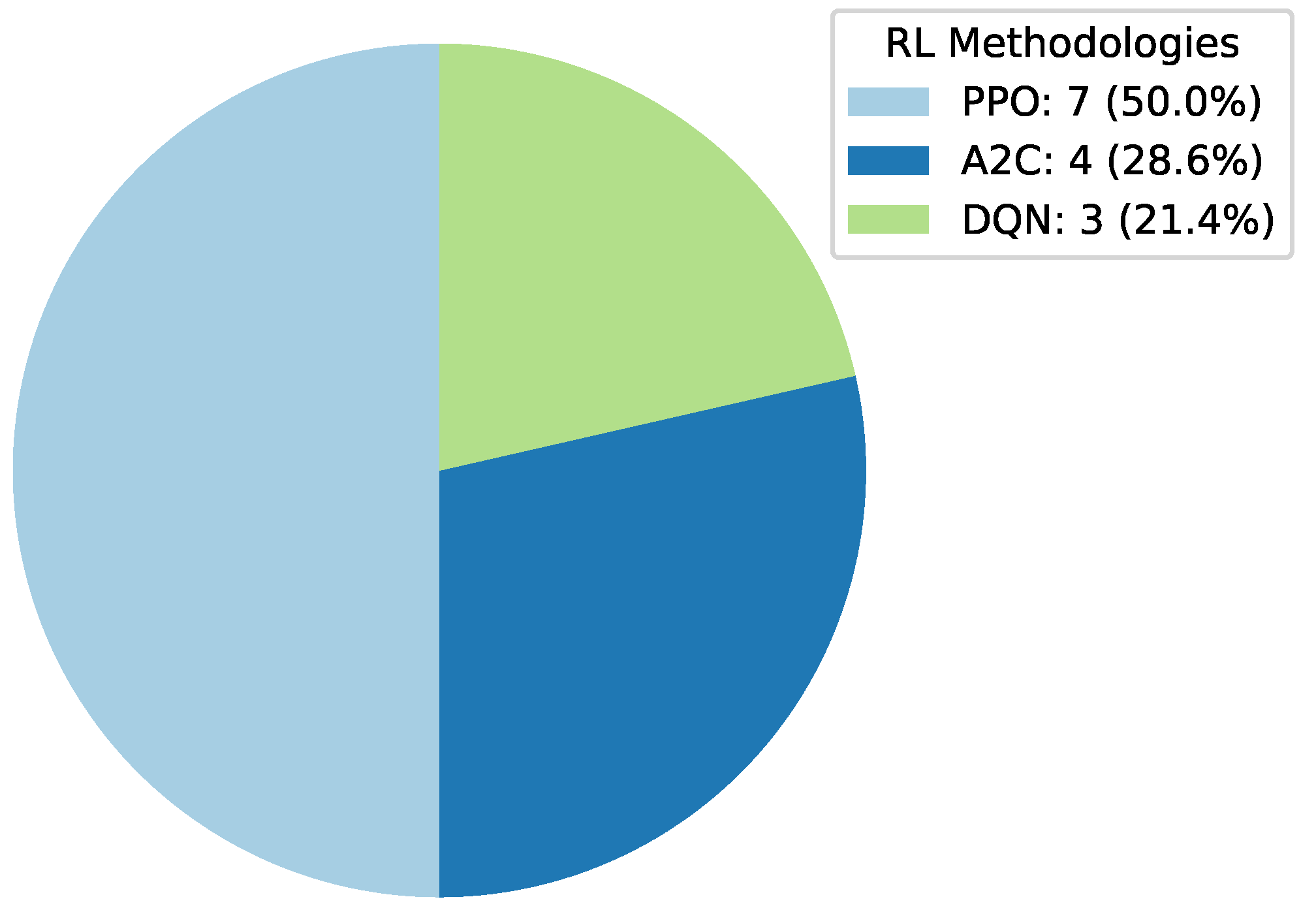

3.3. Deep Reinforcement Learning

Deep reinforcement learning! [21] brings a level of sophistication to cryptocurrency forecasting by combining neural networks with reinforcement learning principles. These algorithms learn optimal strategies through interactions with the environment, making them well-suited for dynamic and evolving cryptocurrency markets.

Figure 4.

Illustration demonstrating the breadth of Deep Reinforcement Learning algorithms, encompassing various techniques and methodologies.

Figure 4.

Illustration demonstrating the breadth of Deep Reinforcement Learning algorithms, encompassing various techniques and methodologies.

3.3.1. Proximal Policy Optimization

Proximal policy optimization [22] acts as a smart assistant in the DRL toolkit. It belongs to the family of policy optimization algorithms that focus on iteratively improving the policy governing an agent’s actions. In cryptocurrency trading, PPO continuously refines trading strategies by efficiently utilizing past experiences. Technically, PPO incorporates a clipped surrogate objective, preventing policy updates from deviating too far from the current policy. This stability ensures safer exploration and exploitation in the volatile cryptocurrency market. PPO’s adaptability and ability to handle continuous action spaces make it a valuable asset for refining trading strategies.

3.3.2. Advantage Actor-Critic

Advantage actor-critic [23] operates as a dynamic duo within DRL. This algorithm combines elements of policy iteration and value iteration, with an actor suggesting actions and a critic evaluating the quality of those actions. A2C’s collaborative approach enhances the learning process by providing a balance between exploration and exploitation. From a technological viewpoint, the actor determines the optimal policy, while the critic estimates the value of state-action pairs. By leveraging advantages (differences between actual and expected returns), A2C fine-tunes strategies for navigating the intricate landscape of cryptocurrency markets. The algorithm’s ability to adapt to changing conditions makes it a valuable tool for real-time decision-making.

3.3.3. Deep Q-Network

Deep Q-Network [21] stands out as a fearless explorer in the DRL domain. It operates on the principles of Q-learning [24], using a deep neural network to approximate the Q-function, which represents the expected cumulative reward for taking a particular action in a given state. Technically, DQN employs experience replay and target networks to stabilize training and improve sample efficiency. Experience replay involves storing and randomly sampling past experiences, facilitating better exploration and learning. DQN’s capacity to make decisions based on learned experiences makes it adept at navigating the intricate and ever-changing landscape of cryptocurrency markets.

3.4. Statistical Learning

Statistical models have a rich history in financial forecasting, and cryptocurrency markets are no exception. In this section, this survey reviews research that relies on Statistical models, such as autoregressive integrated moving averages, GARCH, and regression analysis, to predict cryptocurrency prices and trends. This survey analyzes the efficacy of Statistical approaches, their limitations, and their place in the landscape of cryptocurrency forecasting.

3.4.1. Autoregressive Integrated Moving Average

The Autoregressive integrated moving average [25] model is a fundamental Statistical method extensively applied in financial forecasting, including cryptocurrency markets. ARIMA models are particularly adept at analyzing and predicting time-series data by incorporating the autoregressive, differencing, and moving average components. The autoregressive facet elucidates the correlation between an observation and its preceding values, while differencing transforms non-stationary data into a stationary form to stabilize the mean. The moving average component captures the error of the model as a linear combination of past error terms. In cryptocurrency forecasting, ARIMA models excel at capturing short-term trends and patterns based on historical price data.

3.4.2. Generalized Autoregressive Conditional Heteroskedasticity

Generalized Autoregressive Conditional Heteroskedasticity [26] models are pivotal tools in financial time series analysis, renowned for their ability to model and forecast volatility, a crucial aspect of cryptocurrency markets. GARCH models extend the autoregressive conditional heteroskedasticity model by encompassing time-varying volatility dynamics. In cryptocurrency forecasting, where volatility fluctuations are prevalent, GARCH models provide invaluable insights into the evolving risk landscape. By capturing volatility clustering and persistence, GARCH models aid investors and analysts in comprehending and managing risk exposure within cryptocurrency portfolios.

4. Methodological Landscape in Cryptocurrency Forecasting Literature

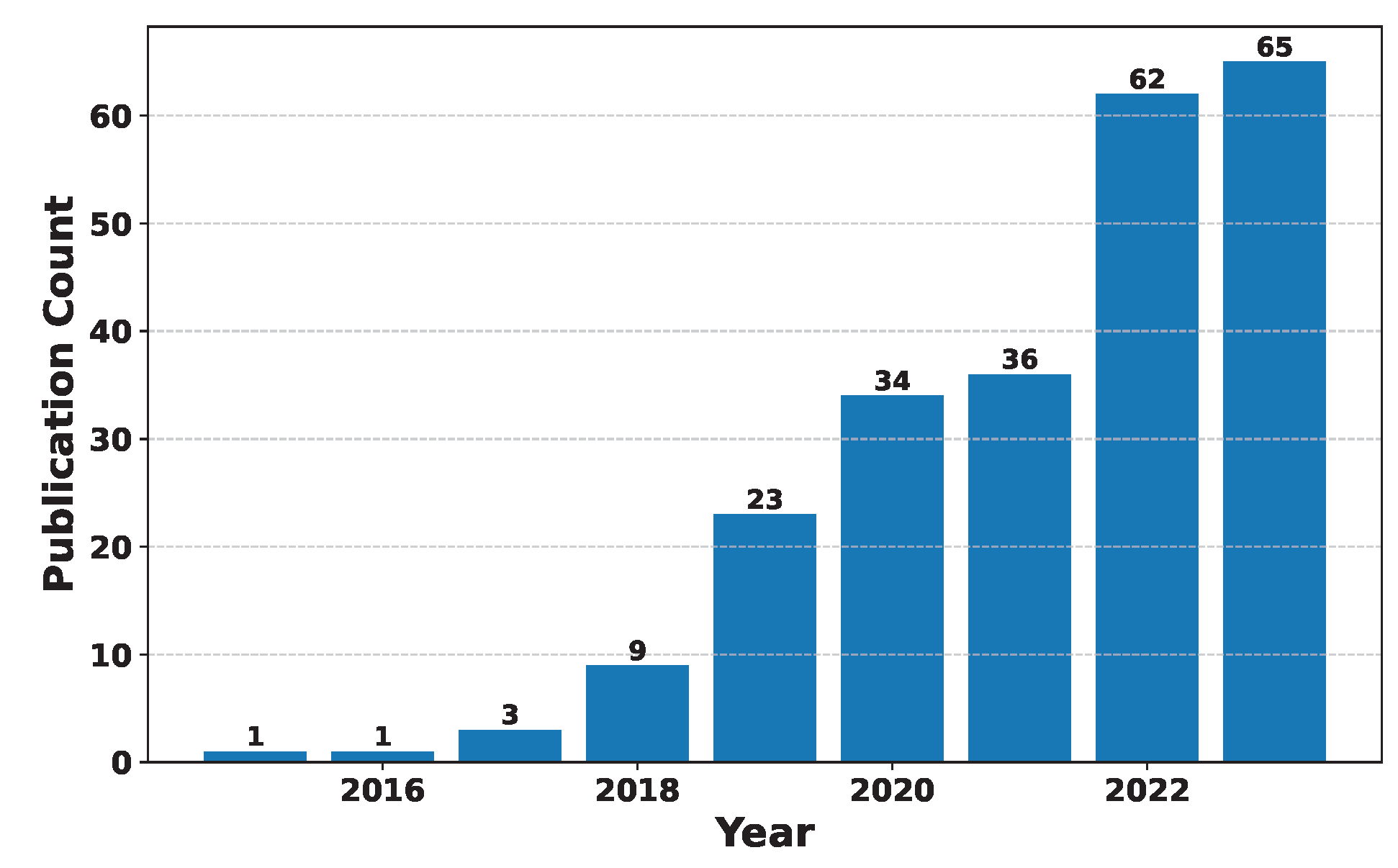

In cryptocurrency forecasting, the past decade has glimpsed an outbreak of research activity. As cryptocurrencies continue to reshape the financial sphere, scholars and practitioners alike have ventured into the depths of historical data, employing a diverse array of methodologies to decipher price trends, market dynamics, and investment opportunities.

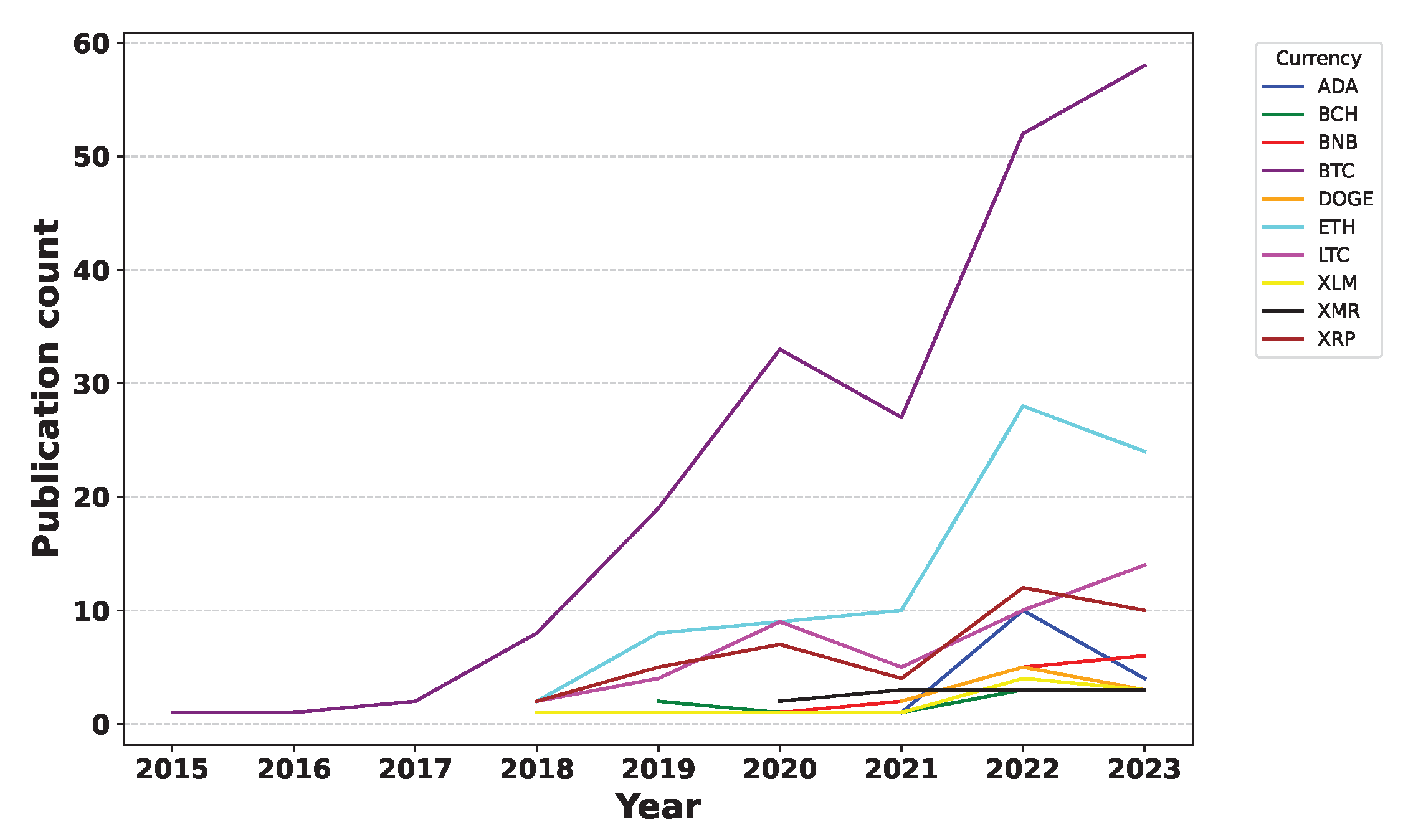

This comprehensive survey, containing a comprehensive analysis of 234 research papers, is poised to unravel the multifaceted landscape of cryptocurrency forecasting. The survey will systematically present the literature review, categorized by the methodologies employed, offering insights into the evolution and current state of this dynamic field. The approaches considered include Machine Learning, Deep Learning, Statistical Models, and Deep Reinforcement Learning. Each category represents a unique aspect of the methodologies adopted by researchers in their quest to forecast cryptocurrency movements.

As this study ventures on this journey through the cryptocurrency forecasting literature, this study will delve into the specific insights, trends, and challenges presented by each of these methodological approaches, providing readers with a holistic perspective on the vast and developing landscape of cryptocurrency prediction. Exploring the methodological landscape of Machine Learning literature further, this survey analyzes the distribution of publications across key methodologies.

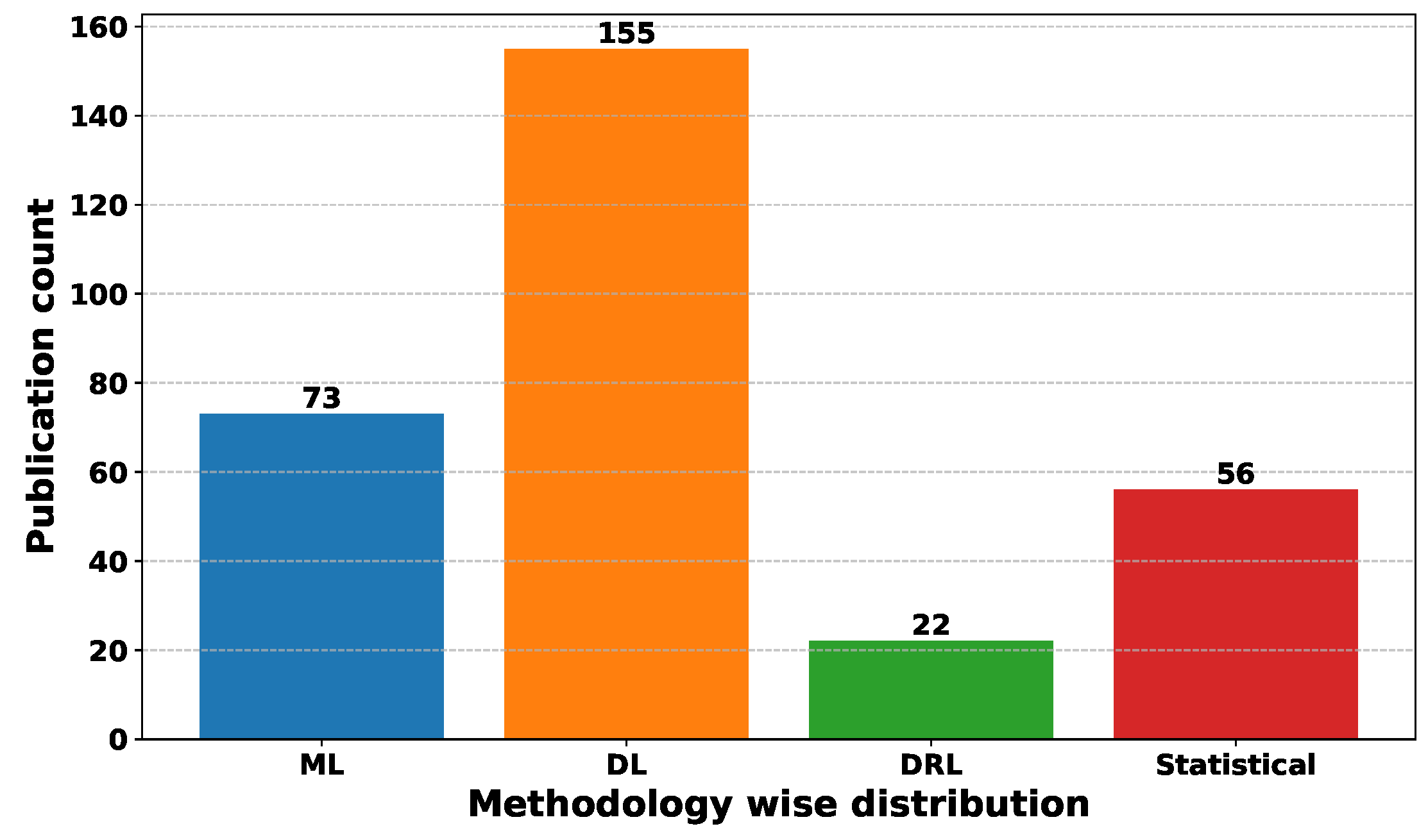

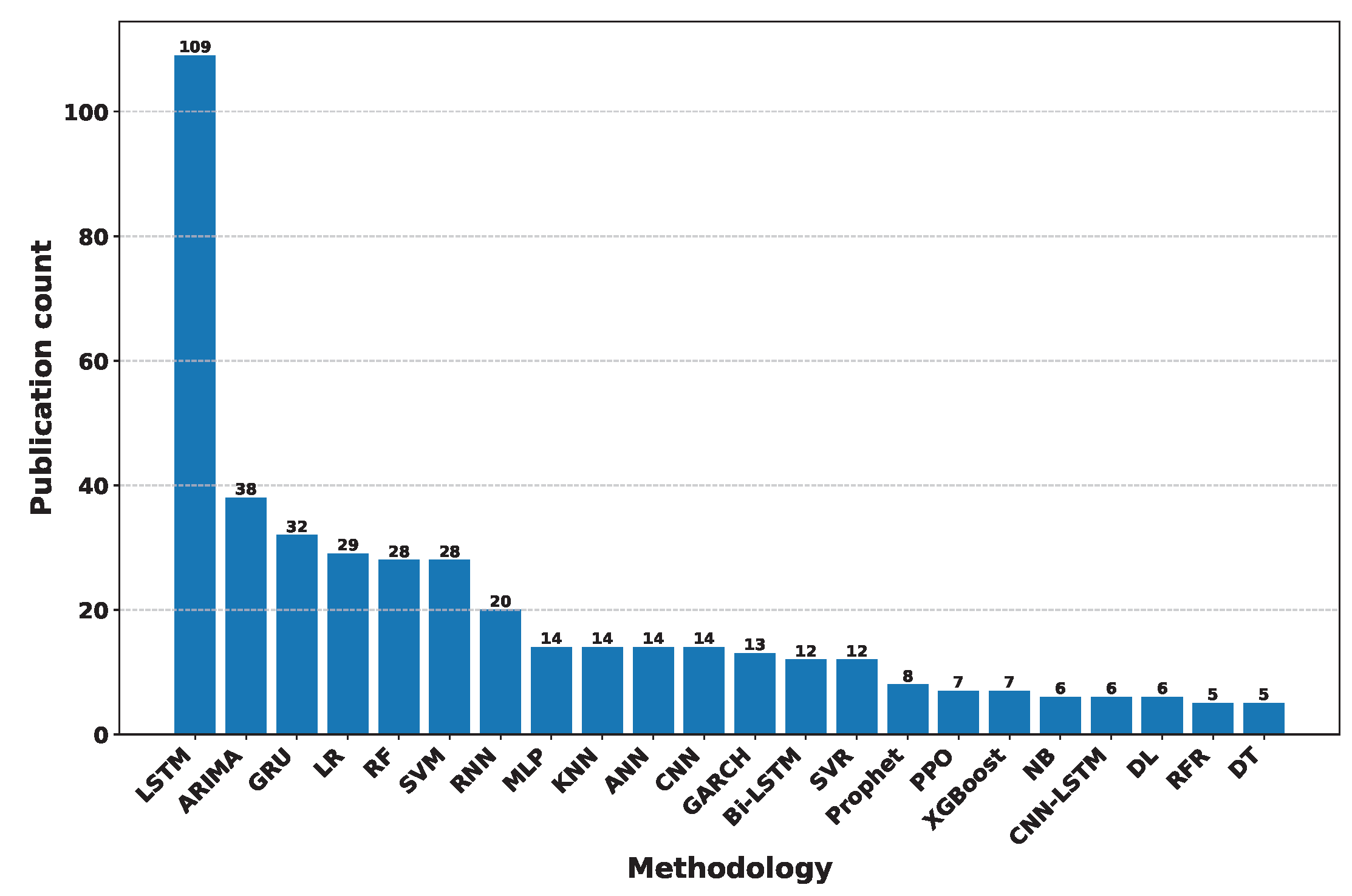

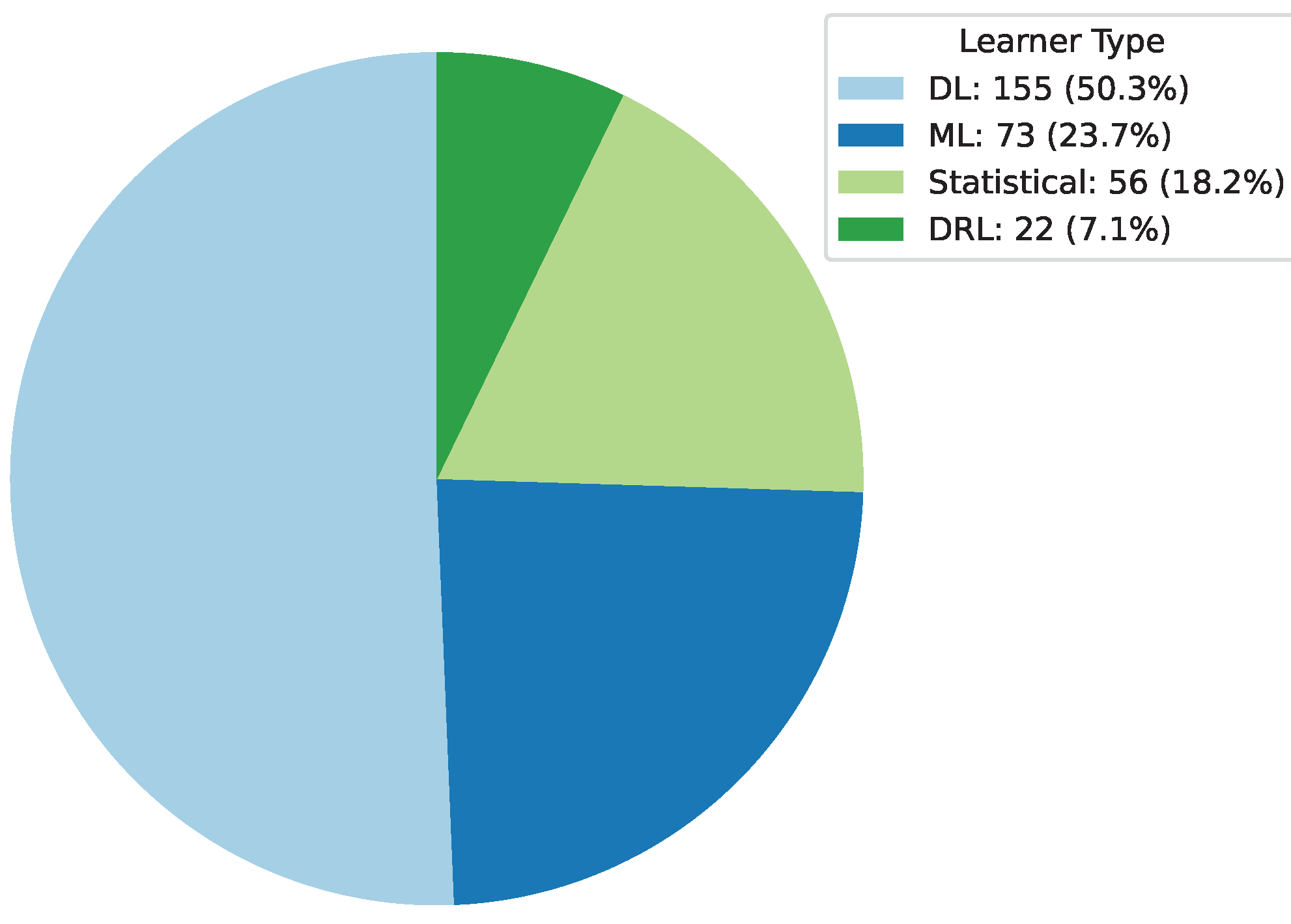

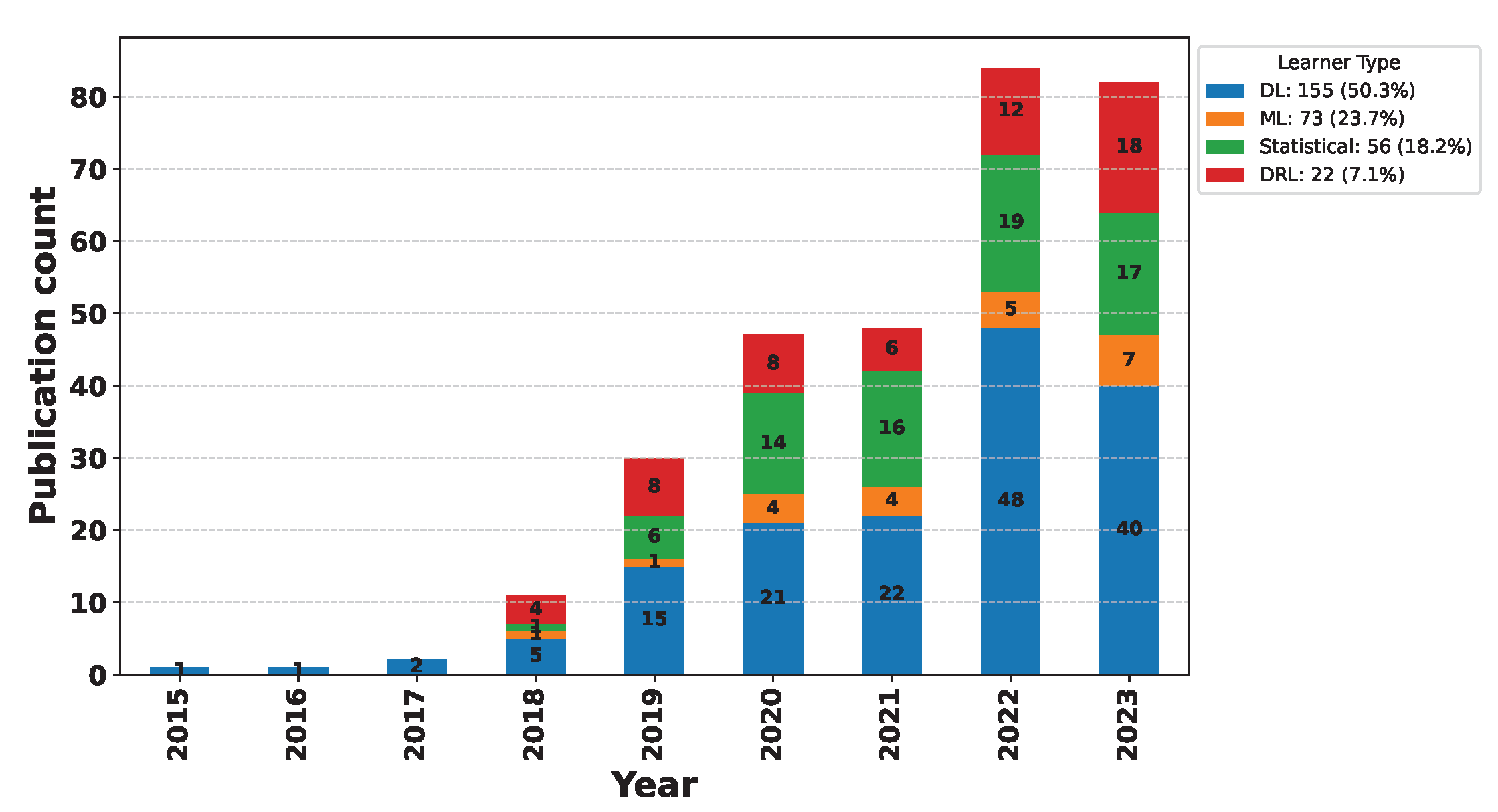

Figure 5 visualizes the prevalence of different approaches, with the y-axis indicating the count of publications and the x-axis representing categories including Deep Learning, Machine Learning, Deep Reinforcement Learning, and Statistical methods. Deep Learning emerges as the most frequently employed methodology, with the longest bar indicating its prevalence in current research. Machine Learning follows closely behind, reflecting its sustained relevance in the field. Statistical methods exhibit a significant presence, albeit less pronounced compared to DL and ML. Deep Reinforcement Learning shows the shortest bar, indicating its comparatively lesser utilization in recent literature. Figure 5 distribution sheds light on the dominant methodologies driving Machine Learning research, offering insights into the evolving landscape of techniques and approaches.

5. Use of ML in Cryptocurrency Forecasting

In this section, this survey will delve into the comprehensive body of research that harnesses machine-learning methodologies for cryptocurrency forecasting. ML, with its ability to identify patterns and relationships within vast datasets, has become a cornerstone of predictive analytics in the cryptocurrency domain. Machine Learning is a fascinating field in computer science that empowers computers to understand and make decisions from data, much like how humans learn from experience. At its core, ML is about building algorithms that can automatically identify patterns, make predictions, or take actions without being explicitly programmed to do so. It works by providing a computer with a large amount of data, allowing it to discover hidden insights and relationships within that data. Think of ML as teaching a computer to recognize cats in photos by showing it thousands of cat images until it learns the defining features of a cat. Once trained, an ML model can generalize its knowledge to identify cats in new, unseen images.

The Section 5 unfolds into three distinct categories, each offering a specialized perspective on the application and evolution of Machine Learning in cryptocurrency forecasting. Firstly, Section 5.1, the detailed analysis and trends in Machine Learning studies examine the methodological intricacies and emerging patterns prevalent in recent research endeavors. Secondly, Section 5.2, studies utilizing Machine Learning for cryptocurrency delve into specific case studies and methodologies employed to forecast digital asset prices. Lastly, Section 5.3, the summarized literature review of Machine Learning approaches encapsulates a synthesis of existing literature, distilling key insights and advancements in the field. Together, these subsections provide a comprehensive overview of the landscape, facilitating a deeper understanding of the complexities and innovations driving Machine Learning applications in cryptocurrency forecasting.

5.1. Detailed Analysis and Trends in Machine Learning Studies

In this dedicated section, the utilization of Machine Learning techniques to predict changes in the cryptocurrency market will be explored. Machine Learning involves the application of algorithms and Statistical models to analyze data, identify patterns, and make predictions without explicit programming. This study will delve into the specific methods used, the cryptocurrencies that are commonly analyzed, and how researchers consider time-related factors to improve prediction accuracy. By examining these aspects, this study aims to elucidate the significance of Machine Learning in comprehending and forecasting trends within the cryptocurrency market.

5.1.1. Methodological Trends in Machine Learning Literature

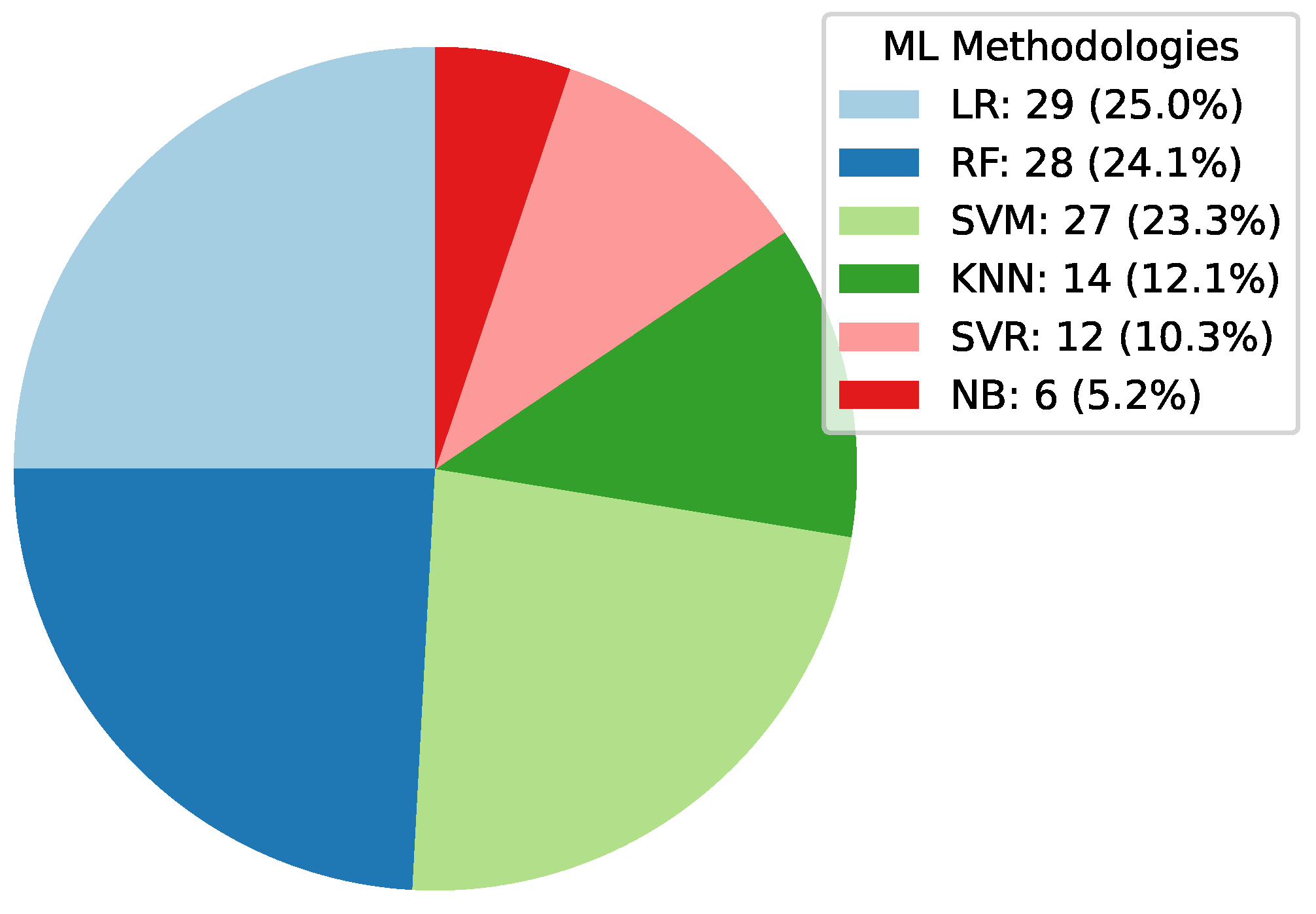

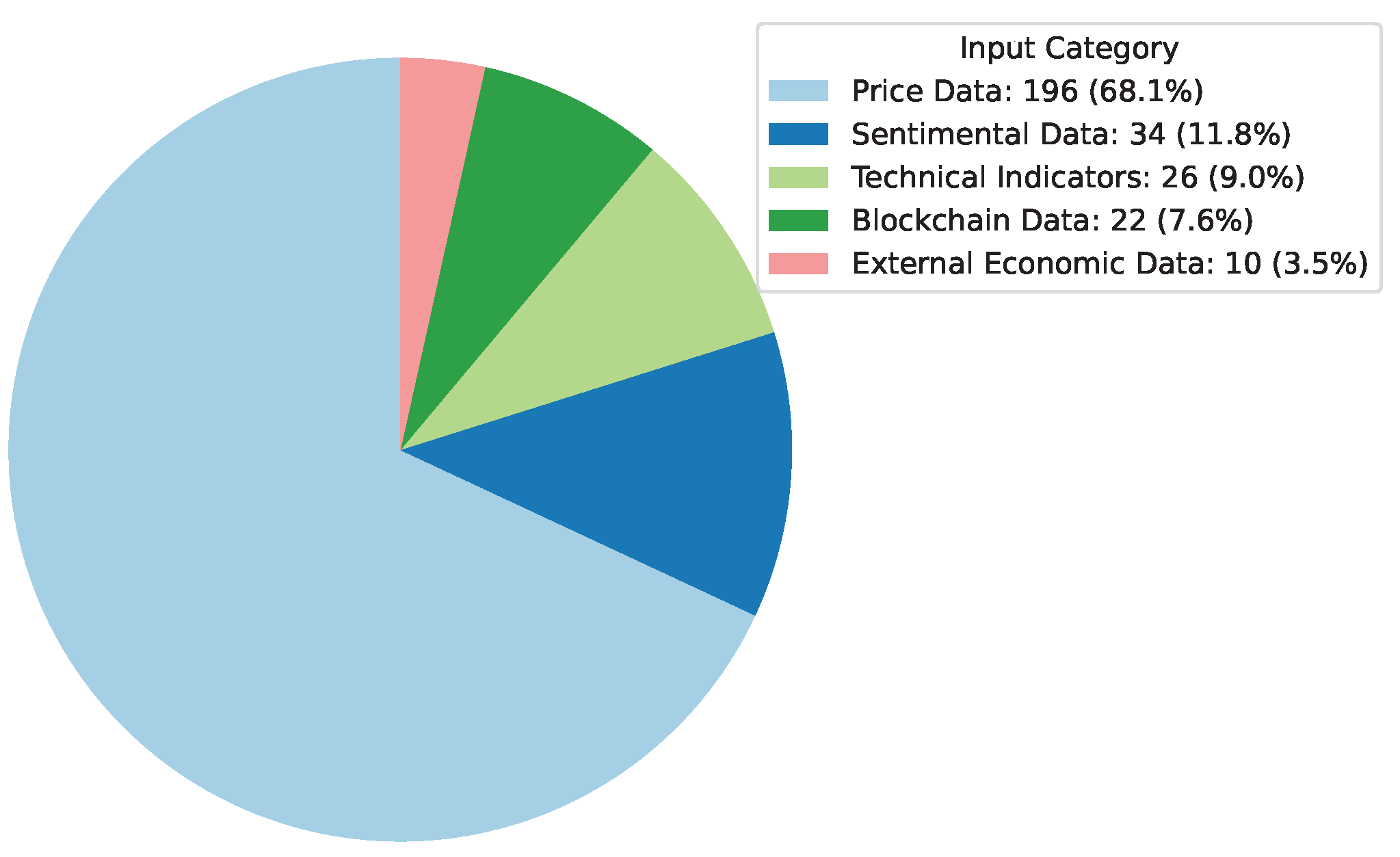

In investigating the methodological landscape of Machine Learning research, a comprehensive analysis reveals distinct patterns in the distribution of methodologies across the literature. A pie chart representation demonstrates the prevalence of various Machine Learning techniques utilized in recent research papers. Figure 6 illustrates that Linear Regression has been prominently featured in 29 research papers, closely followed by Random Forest with 28 instances. SVM techniques have been employed in 27 papers, while KNN has been utilized in 14 papers. This distribution not only reflects the popularity of certain methodologies within the Machine Learning domain but also provides insights into the preferences and trends shaping contemporary research practices.

5.1.2. Currency-Wise Distribution in Machine Learning Literature

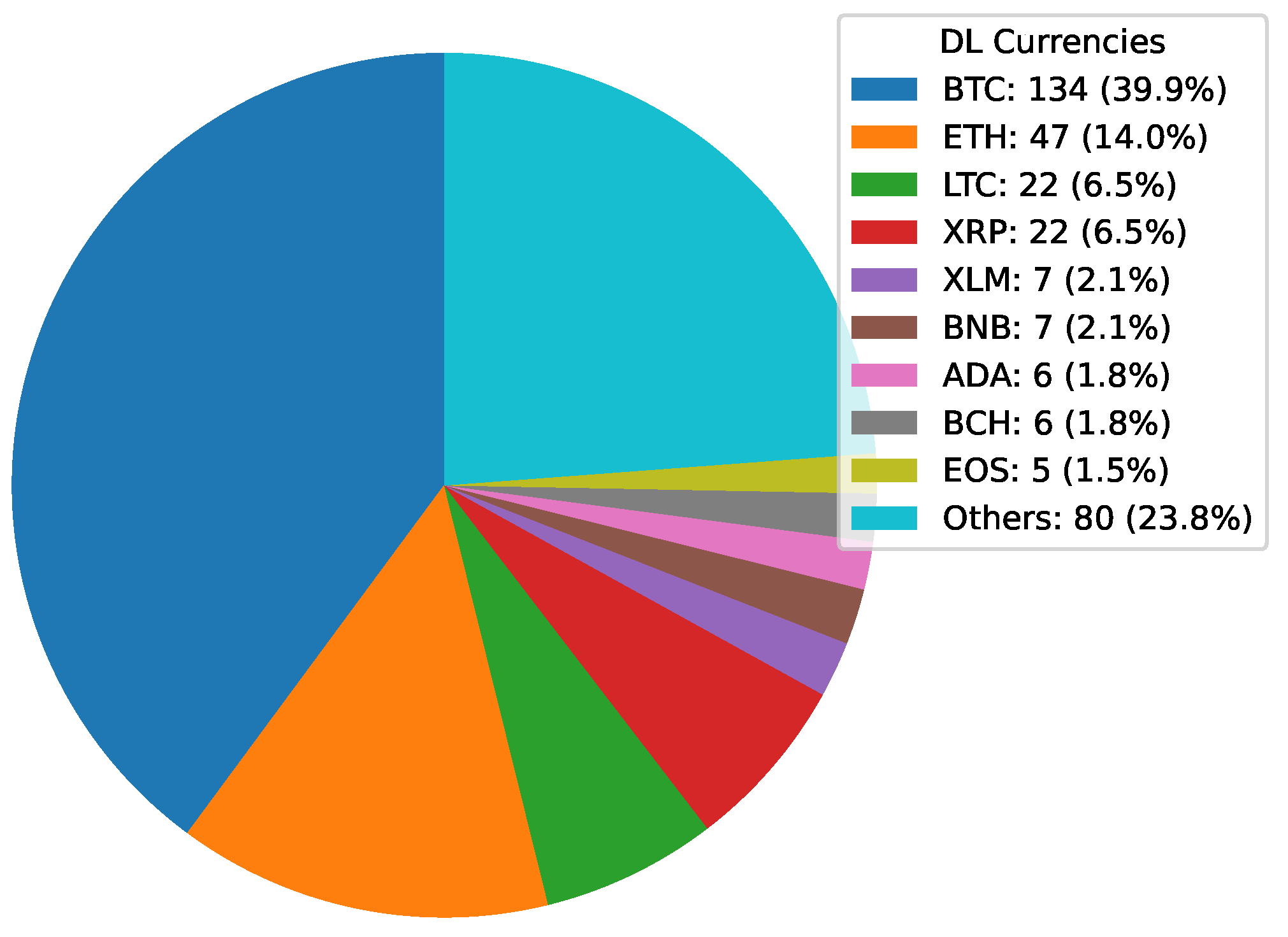

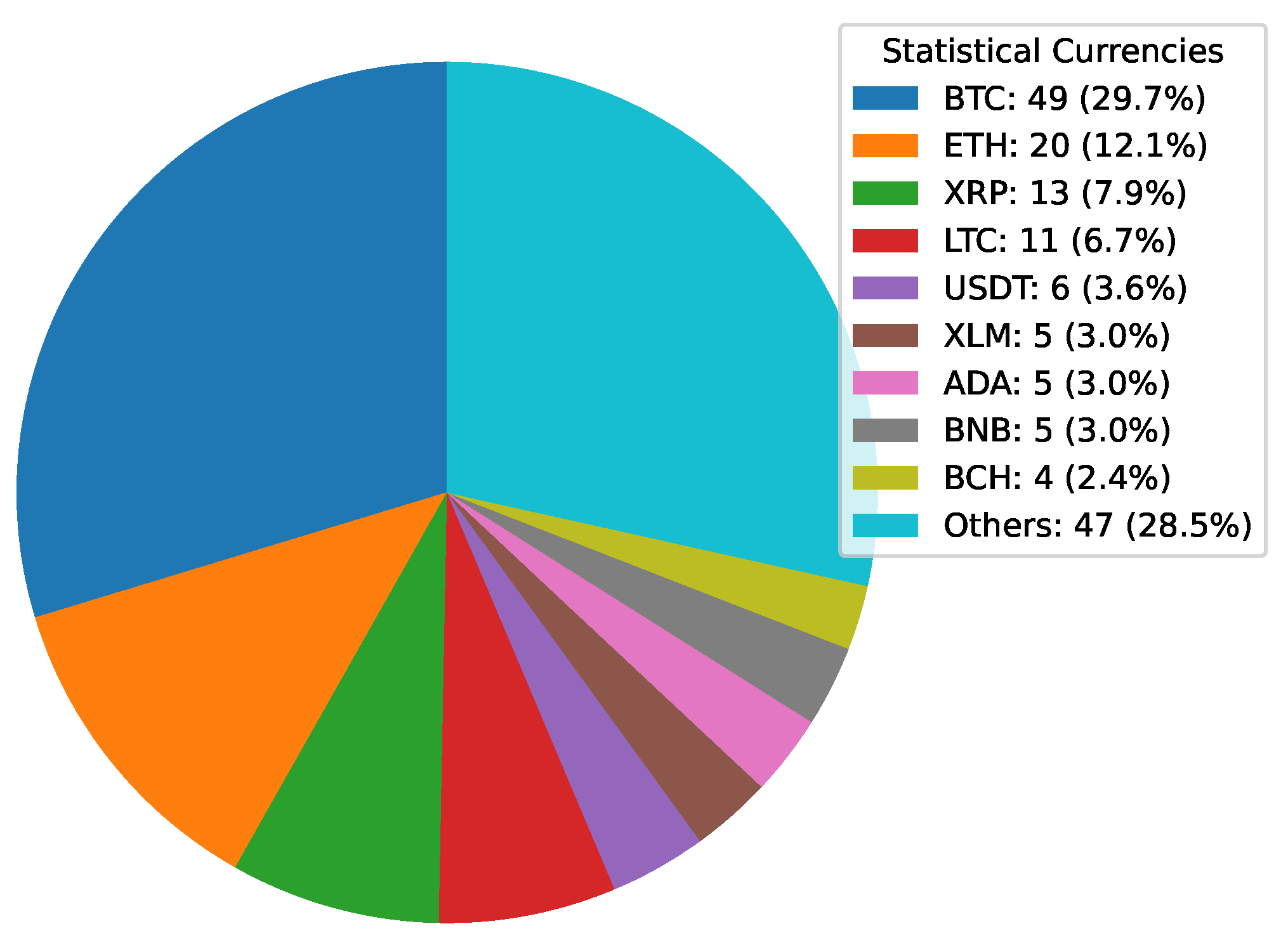

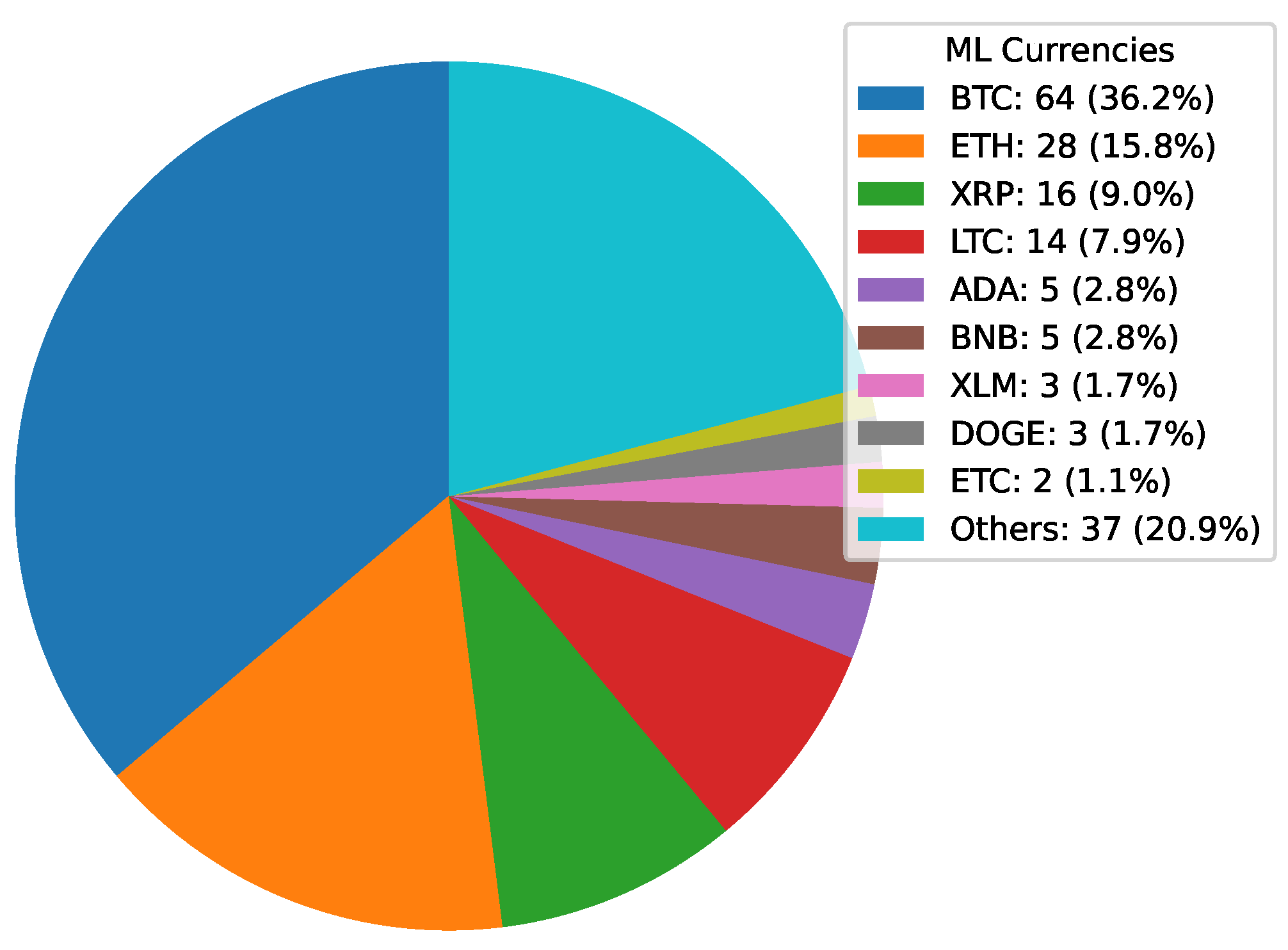

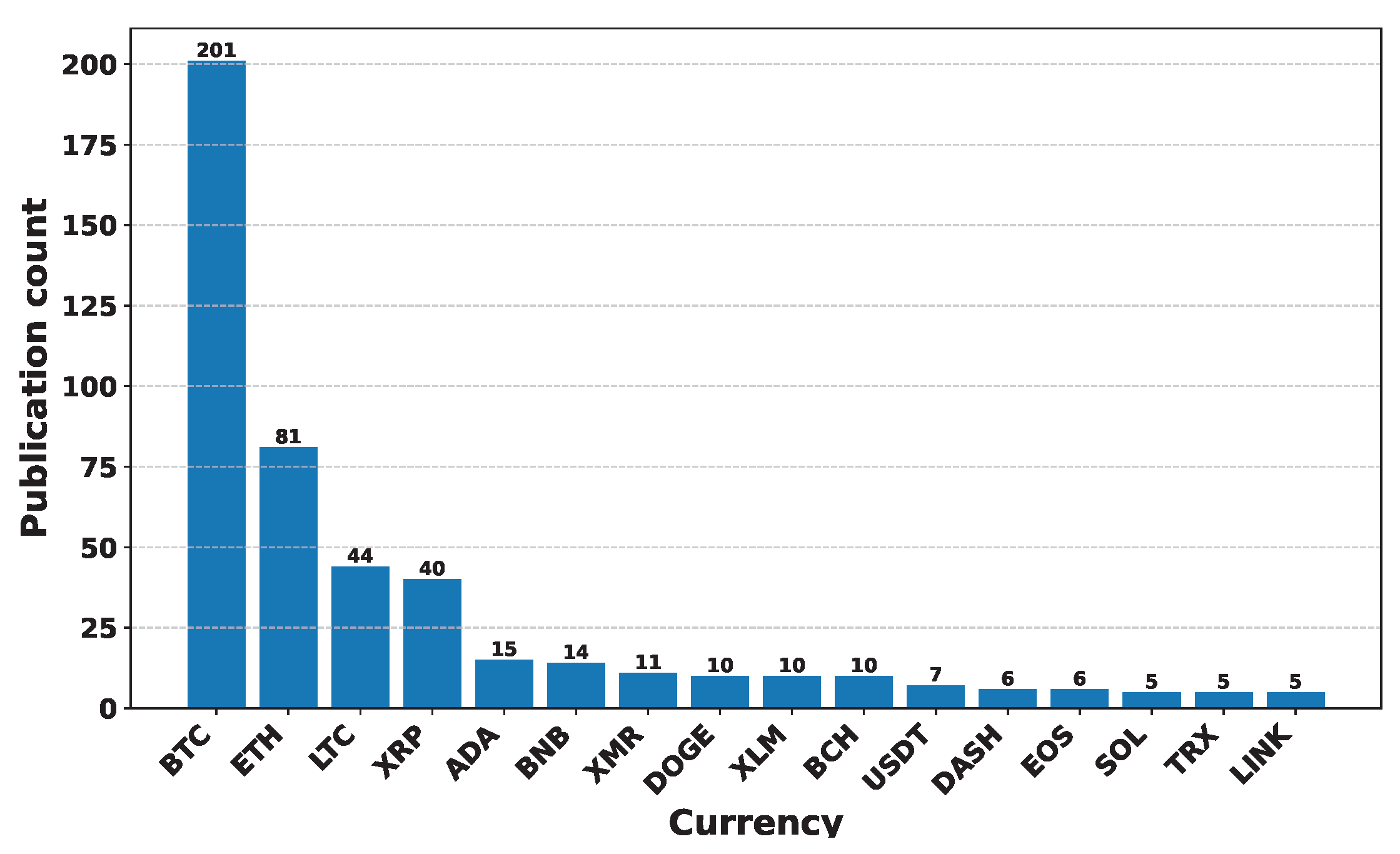

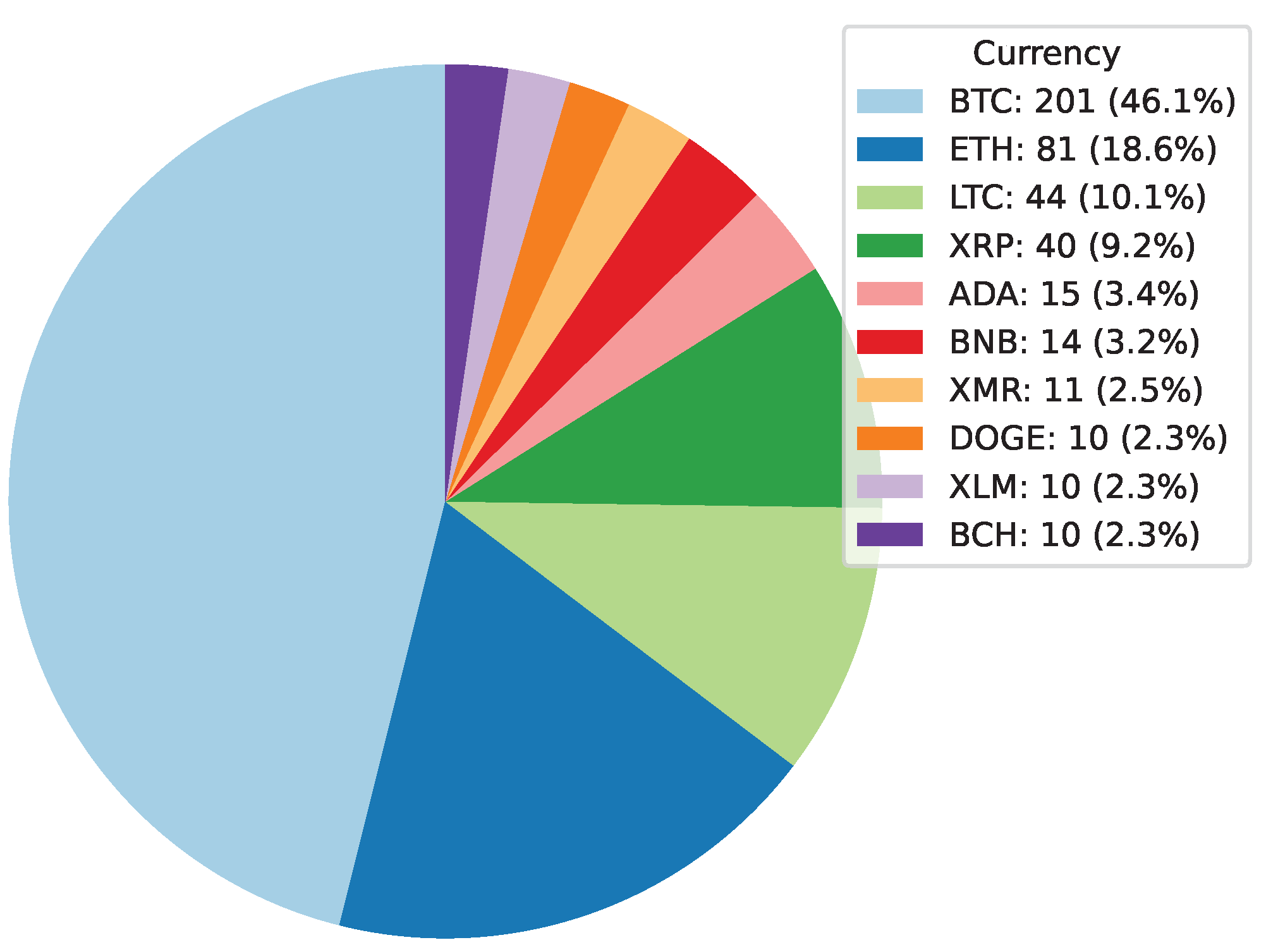

Examining the currency-wise distribution within Machine Learning literature provides valuable insights into the preferences and trends prevalent in the field. Figure 7 illustrates the proportional representation of various cryptocurrencies utilized in recent research papers. Bitcoin emerges as the dominant cryptocurrency, constituting 36.2% of the literature examined. Following BTC, Ether holds a significant share at 15.8%. Ripple and Litecoin account for 9% and 7.9% of the literature, respectively This distribution not only reflects the prevalence of specific cryptocurrencies within Machine Learning research but also highlights the diverse applications and interests within the intersection of cryptocurrency and Machine Learning domains.

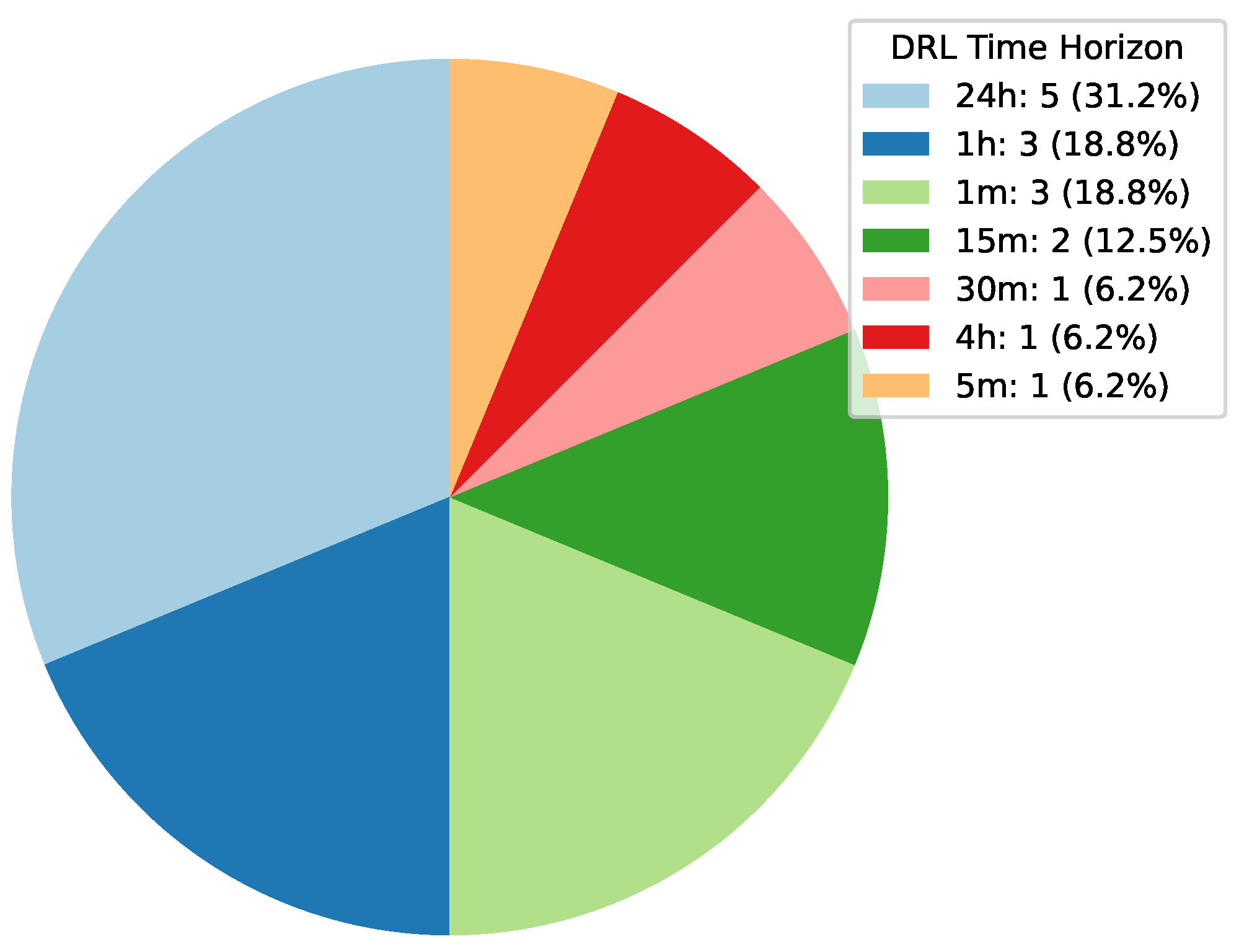

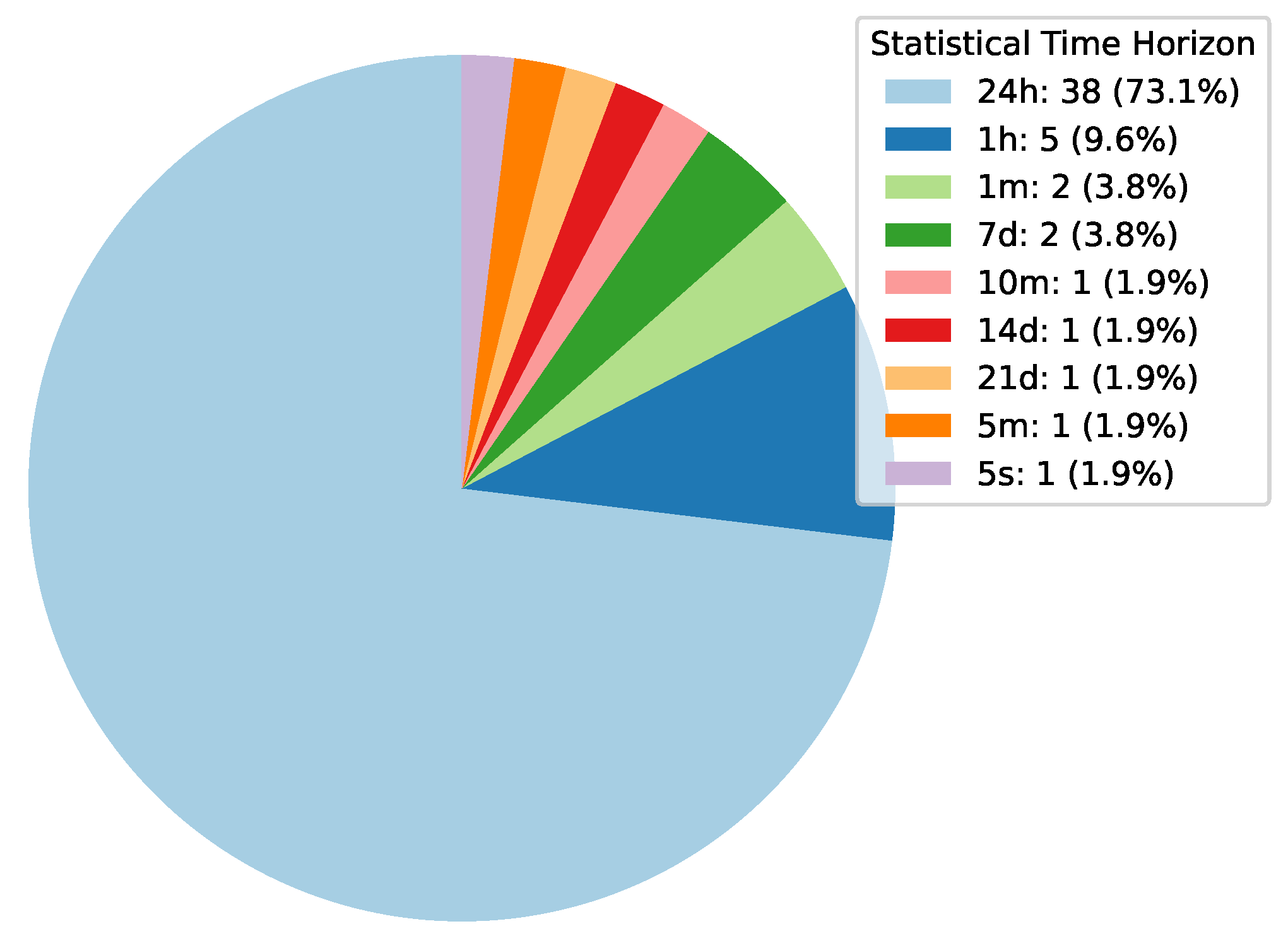

5.1.3. Time Horizon-Wise Distribution in Machine Learning Literature

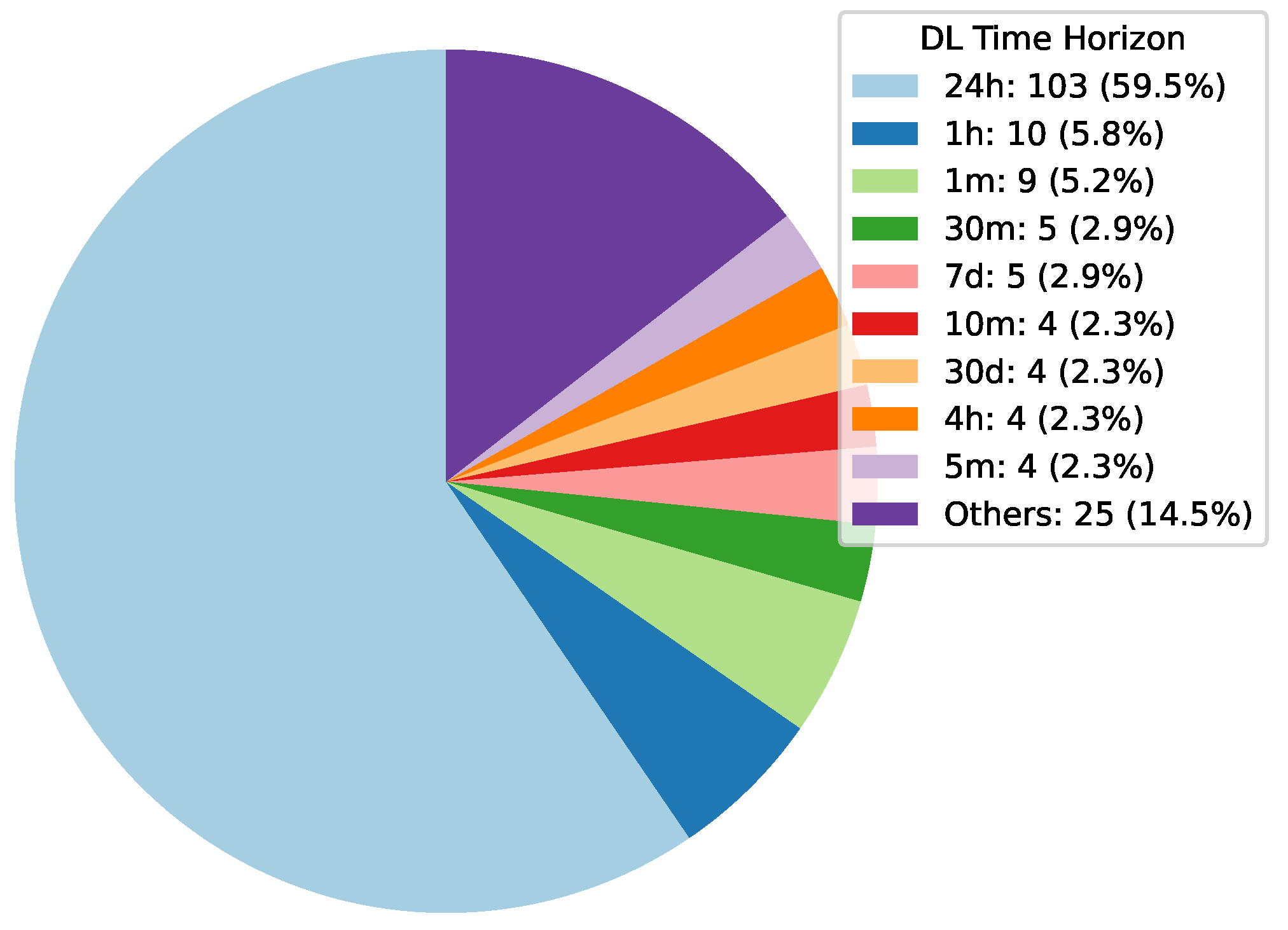

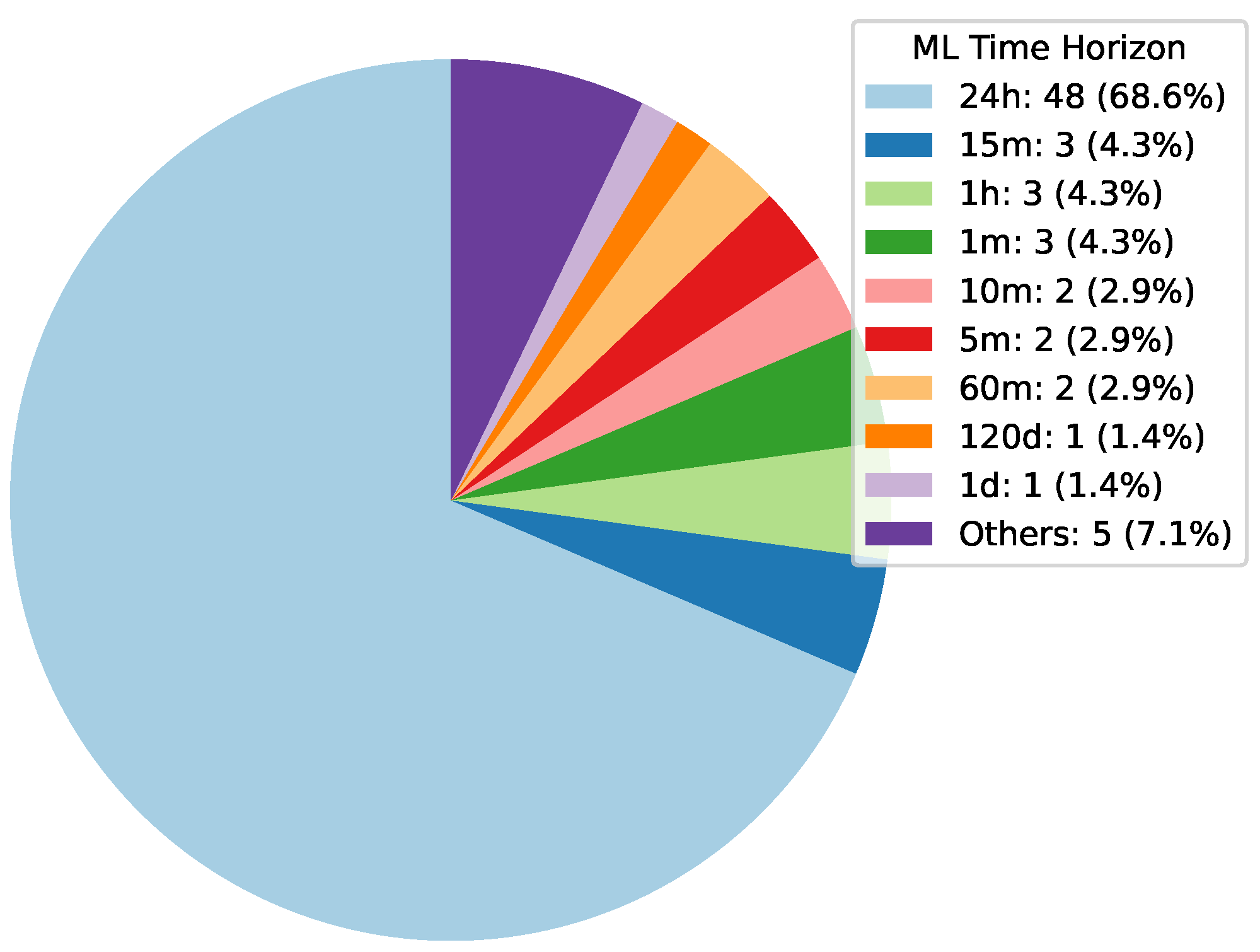

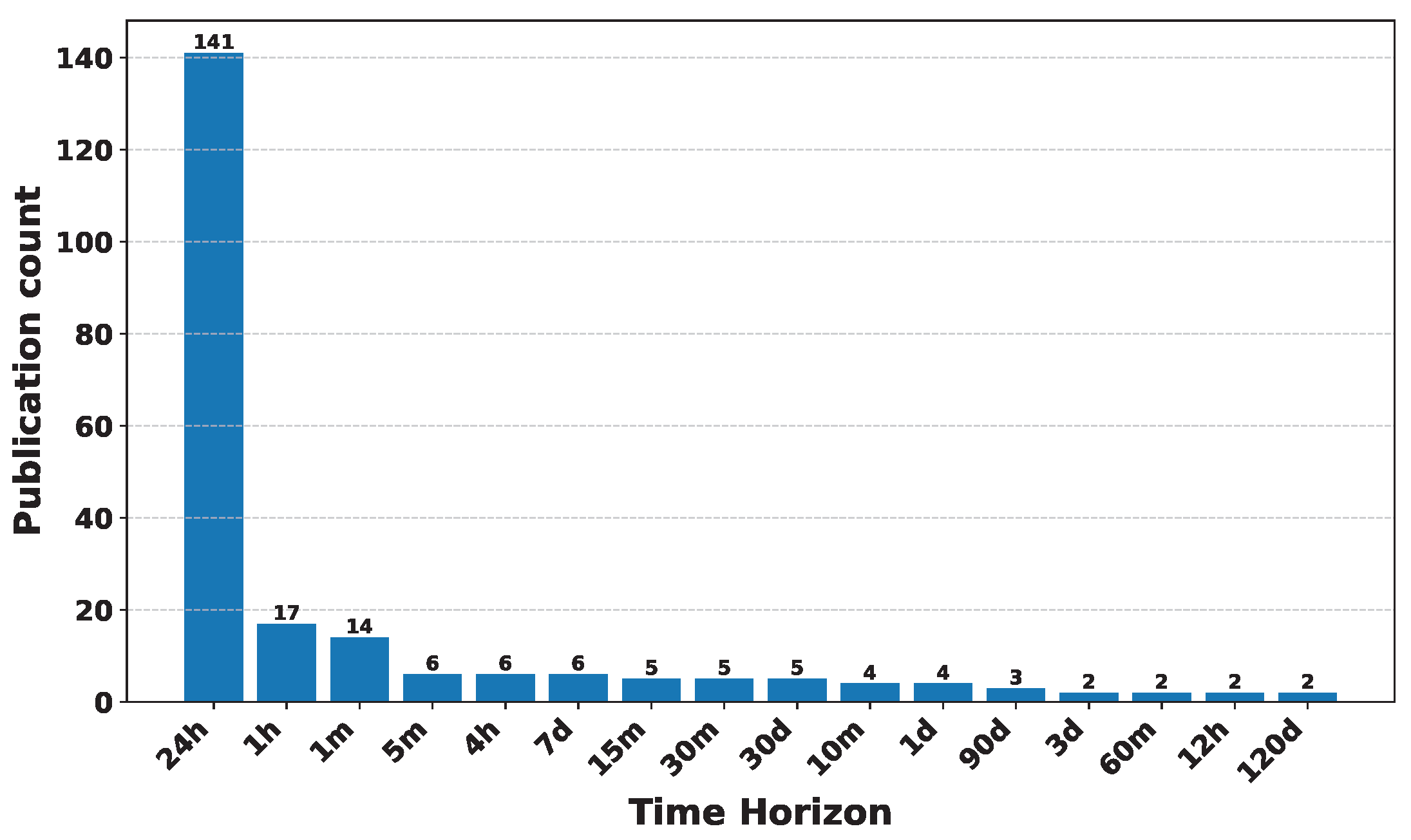

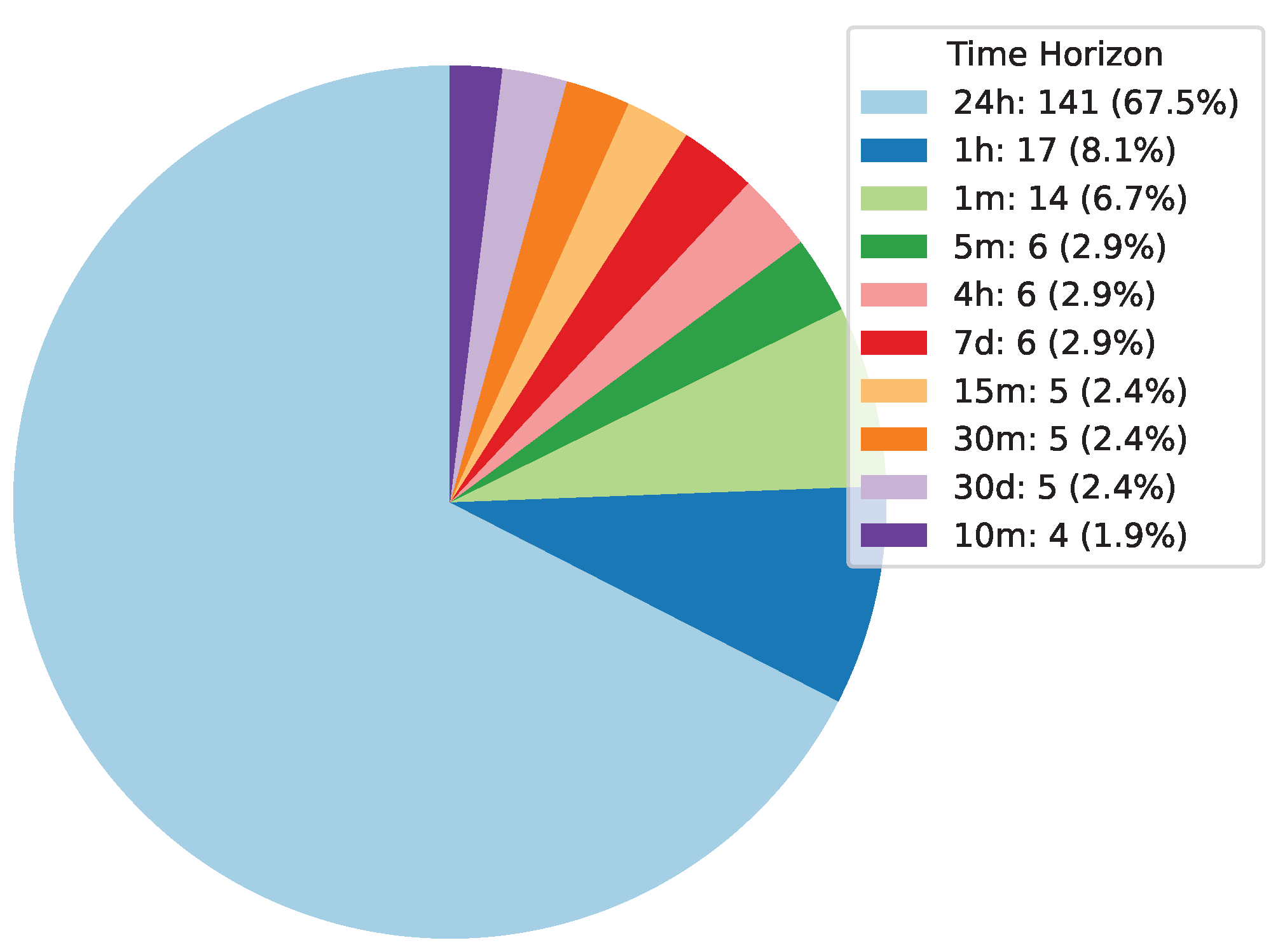

An examination of the time horizon-wise distribution within Machine Learning literature offers insights into the temporal aspects considered in research studies. A pie chart visually represents the prevalence of various time intervals utilized for analysis. Figure 8 reveals that the 24-hour time horizon dominates the distribution, constituting 68.6% of the literature surveyed. Meanwhile, shorter intervals such as 1 hour, 1 minute, and 15 minutes each represent 4.3% of the literature. This distribution underscores the significance of different time horizons in Machine Learning research and highlights the emphasis on analyzing data across various temporal scales.

5.2. Studies Utilizing Machine Learning for Cryptocurrency Forecasting

Cryptocurrency markets are known for their volatility and complexity, making accurate forecasting a challenging task. In recent years, researchers have turned to Machine Learning techniques to analyze historical data and predict future price movements in cryptocurrency markets. This subsection delves into a variety of Machine Learning methods applied in cryptocurrency prediction research. It covers traditional algorithms such as Support Vector Machine, Random Forest, linear regression, and Support Vector Regression models, alongside ensemble methods and time series prediction techniques like Prophet and boosting models. Researchers utilize a wide range of strategies to detect trends and patterns in cryptocurrency data. Exploring these methodologies helps develop reliable forecasting models that provide valuable insights into the ever-changing cryptocurrency markets, supporting investors and stakeholders in making well-informed decisions. This subsection highlights the complexities of Machine Learning applications in cryptocurrency forecasting and emphasizes the burgeoning trends in this swiftly advancing field.

5.2.1. Support Vector Machine, Random Forest, Linear Regression and Support Vector Regression Models

In the realm of cryptocurrency forecasting, a consistent thread weaves through several notable studies, offering a glimpse into the evolving landscape of predictive analytics. One such foundational study was conducted by Nor et al. [27] laid a sturdy foundation in 2018 by embarking on an extensive exploration encompassing seven major cryptocurrencies, such as Bitcoin, Ether, Litecoin, NEM, Ripple, and Stellar. Leveraging Machine Learning techniques, specifically Support Vector Machines, they examined daily trading data to predict price movements within a 24-hour horizon. Remarkably, their SVM-based classifier displayed exceptional performance, boasting a remarkable 95% accuracy rate—a testament to the power of ML. Furthermore, their commitment to robustness shone through their adaptation to varying data sample sizes for each cryptocurrency.

Shifting our focus exclusively to Bitcoin, Majid et al. [28] embraced both Statistical and Deep Learning methodologies in their 2019 cryptocurrency forecasting study. Centering their analysis on closing price data, they harnessed Support Vector Machines, Random Forest, and DL models, all within the familiar 24-hour prediction window. It’s noteworthy that the Random Forest model distinguished itself by yielding the smallest root mean square error and mean absolute percentage error values within their Bitcoin-exclusive dataset.

Building upon these insights, Franco et al. [29] ventured into cryptocurrency forecasting in 2019, echoing Nor et al.[27] temporal scope of a 24-hour prediction window. However, they introduced a unique twist by incorporating sentiment data alongside price data for Bitcoin, Ether, Ripple, and Litecoin. Employing support Vector machines and Random Forests as Machine Learning classifiers, supplemented by Deep Learning models, they conducted meticulous evaluations. While SVM and Random Forest excelled with price data, an intriguing revelation emerged—the Multi-Layer Perceptron model, asserting itself as the top performer with an impressive accuracy of 0.72 and a precision score of 0.76.

Support vector machines have been a prominent option among researchers for cryptocurrency price prediction. Ismail et al. [27] utilized SVM on price data for Bitcoin, Ether, Litecoin, and others, achieving forecasts with Mean Absolute Percentage Error metrics. Similarly, Cohen et al. [30] applied Support Vector Machines to cryptocurrency price forecasting, though specific cryptocurrencies and evaluation metrics are not mentioned. The time horizon is 24 hours. Alahmari et al. [31]applied Support Vector Regression for BTC, XRP, and ETH price predictions. Their evaluation criteria included mean absolute error, mean squared error, root mean squared error, and R-squared. The use of SVR is similar to previous studies.

Hakan et al. [32] conducted a cryptocurrency forecasting study centered on Bitcoin. Their approach incorporated price data, technical indicators, and various classifiers, including Support Vector Machines and Random Forests. They also assessed model performance using metrics like Accuracy, Mean Absolute Error, and Root Mean Square Error. Their research dataset encompassed a significant sample size, contributing to their findings.

Khedmati et al. [33] focused their study on Bitcoin, utilizing closing price data and Statistical models to predict price movements within a 24-hour time horizon. Their evaluation metrics included Root Mean Square Error and Mean Absolute Percentage Error, and despite a relatively small dataset, their study provided valuable insights into the accuracy of Bitcoin price predictions. In the year 2020, Saad et al. [31] included Bitcoin, Ripple, and Ether in their study on cryptocurrency forecasting. They exclusively utilized Support Vector Regression by integrating price data with external economic indicators. Their study used a 24-hour prediction horizon and evaluated performance using metrics like Mean Absolute Error, Mean Squared Error, Root Mean Square Error, and R-squared, which were consistent with previous studies.

In a unique departure from conventional methodologies, Alireza et al. [34] introduced sentimental data as input features exclusively for Bitcoin forecasting. Their Machine Learning-based neural network achieved impressive accuracy, contributing to a reduction in prediction errors.

Lokesh et al. [35] conducted a cryptocurrency forecasting study concentrating on Bitcoin. Their research encompassed Linear Regression and DL algorithms With a 24-hour time horizon, they emphasized the growing prominence of DL techniques in cryptocurrency forecasting.

In 2020, Vidyulatha et al. [36] undertook a comprehensive study in the domain of cryptocurrency forecasting, with a specific focus on Bitcoin. Their research incorporated historical price data and applied Linear Regression in conjunction with Statistical Models, extending the time horizon to 120 days for price prediction. Their dataset encompassed a substantial sample size of 2,191 data points for Bitcoin. Remarkably, the study aimed to leverage BTC information to enhance future price movement predictions. Notably, they introduced a time series analysis Statistical model to forecast Bitcoin prices over the subsequent four months. The study’s outcomes revealed the superior performance of Statistical models in comparison to the LR model, underscoring the efficacy of incorporating time series analysis techniques for accurate and robust cryptocurrency price predictions.

In 2021, Patrick et al. [37] conducted a focused study on Bitcoin price prediction. They used a wide range of input features, including technical indicators, blockchain data, and sentimental data, and applied Machine Learning models such as Random Forest, Gradient Boosting Classifiers, Logistic Regression, and Deep Learning models. The study assessed various time horizons, from 1 minute to 60 minutes. Their evaluation metric was accuracy, and they had an extensive dataset with 403,440 minute-level data points for Bitcoin. The findings revealed that Recurrent Neural Networks (RNNs) and Gradient Boosting Classifiers consistently provided more accurate predictions, with the choice between Gated Recurrent Unit and Long Short-Term Memory depending on the prediction horizon. Additionally, tree-based models, like GBC and Random Forest, showed notable differences in predictive accuracy primarily on the 5-minute prediction horizon, where GBC outperformed RF. These results highlight the importance of model selection and prediction horizon in cryptocurrency forecasting, especially for Bitcoin.

In 2021, Mohamed et al. [38] conducted a cryptocurrency prediction study, focusing on multiple cryptocurrencies, including BTC, ETC, and more. They employed price data as their primary input feature and utilized Support Vector Machines in conjunction with other Deep Learning models for a 24-hour time horizon. Their evaluation metric was accuracy, and for each cryptocurrency, they had a dataset comprising 1826 data samples. Notably, the paper introduced an enhanced Scatter Search Algorithm approach to optimize SVM. Through comprehensive experiments, the proposed SCA approach outperformed both the standard SVM method and the SVM-PSO method, achieving the highest accuracy among all methods analyzed. This highlights the effectiveness of their novel approach to cryptocurrency price prediction.

Table 3.

Comparison to find the best classifier [38].

Table 3.

Comparison to find the best classifier [38].

| Classifiers | BTC | ETH | LTC | XRP | XEM | XLM |

|---|---|---|---|---|---|---|

| SVM | 78.90 | 95.50 | 82.40 | 70.00 | 47.70 | 58.70 |

| SVM-PSO | 90.40 | 97.00 | 92.10 | 82.80 | 57.80 | 64.50 |

| SVM-eSCA | 91.21 | 97.44 | 92.31 | 84.07 | 58.86 | 66.23 |

In 2021, Erdinc et al. [39] focused on cryptocurrency price prediction, considering various cryptocurrencies including BTC, ETC, and more. Their study utilized price data as input features and employed a range of Machine Learning models, including SVM and other Deep Learning models, with a time horizon of 24 hours. Notably, the authors proposed an enhanced SCA (Sine Cosine Algorithm) approach to optimize SVM for cryptocurrency prediction. They compared this approach with the standard SVM method and the SVM-PSO (Particle Swarm Optimization) method. The experiments conducted indicated that the proposed SCA approach outperformed all other methods in terms of accuracy, highlighting its effectiveness in enhancing cryptocurrency price prediction [38].

In 2021, Mohamed et al. [39] conducted a comprehensive study on cryptocurrency price prediction. They considered several cryptocurrencies, including BTC, ETH, and more. They utilized price data as input features. The authors employed SVM along with other Deep Learning models and adopted a 24-hour time horizon for their predictions. Notably, they proposed an enhanced SCA (Sine Cosine Algorithm) approach to optimize SVM and compared it to the standard SVM method and SVM-PSO (Particle Swarm Optimization) method. The results of their experiments unequivocally demonstrated that the proposed SCA approach achieved the highest accuracy among all the methods considered in their analysis, highlighting its efficacy in enhancing cryptocurrency price prediction [39].

In 2021, Andrew et al. [40] conducted a cryptocurrency forecasting study focusing on three major cryptocurrencies: Bitcoin, Ether, and Ripple. They utilized price data as the primary input feature and considered a 24-hour time horizon for predicting price movements. To build predictive models, the researchers employed a diverse set of Machine Learning classifiers, including Linear Regression, Support Vector Machines, k-nearest Neighbors, Decision Trees, Random Forest, AdaBoost, and XGBoost, along with other Deep Learning models. The main evaluation metric used in their analysis was accuracy. Their dataset consisted of a total of 1579 data samples for each cryptocurrency. Interestingly, the study found that Support Vector Machines provided the most accurate classifications when forecasting the sign of next-day returns, achieving a log return of 3.72, which corresponds to a rate of return of approximately 41.3% on a $100 investment [40].

In 2021, Ashutosh et al. [41] conducted a cryptocurrency price prediction study with a focus on Bitcoin. Their analysis incorporated price data as input features and employed various regression models, including Linear Regression, Theil-Sen Regression, and Huber Regression, in addition to other Deep Learning models. The study utilized a 24-hour time horizon for predicting BTC prices and evaluated model performance using metrics such as accuracy, R-squared, and Mean Squared Error. Notably, the research found that all the models exhibited similar levels of accuracy, with Linear Regression standing out for its superior execution time. However, the authors acknowledged that factors such as Twitter sentiment analysis, gold price analysis, economic crises, parameter settings, and differing policies and laws across countries could potentially impact the results [41].

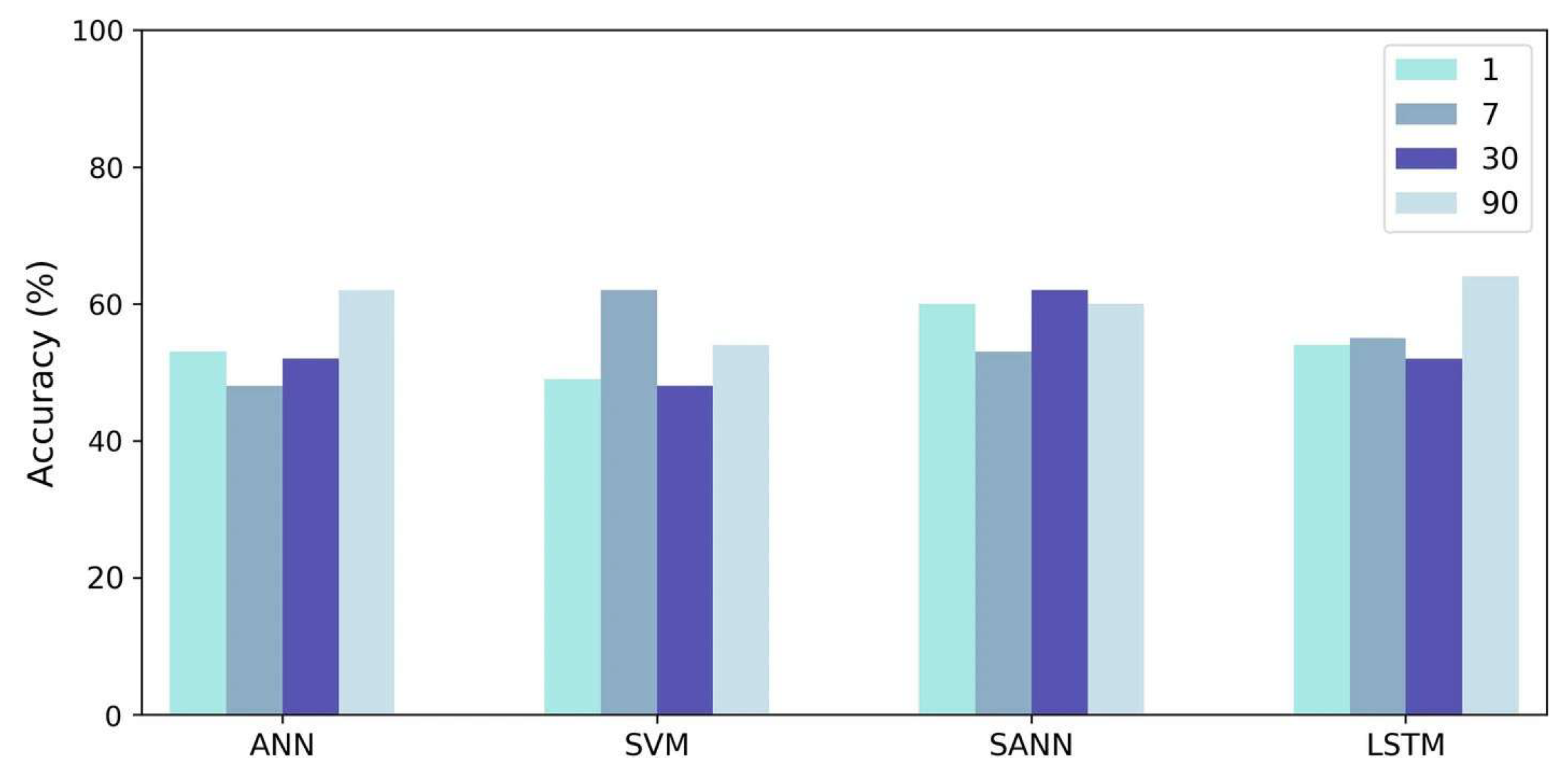

In a parallel effort, Mudassir et al. [42] delved into cryptocurrency forecasting, extending their analysis to various time horizons, including 1 day, 7 days, 30 days, and 90 days, exclusively focusing on Bitcoin. They employed Support Vector Machines and Deep Learning models while adopting metrics such as Mean Absolute Error and Root Mean Square Error for evaluation. Their dataset included a substantial sample size, enabling robust analysis.

Figure 9.

Accuracy of the classification models for nth day forecast in Interval III [42].

Figure 9.

Accuracy of the classification models for nth day forecast in Interval III [42].

Martin-Barreiro et al. [43] utilized Support Vector Machines for multi-cryptocurrency price forecasting, including Binance Coin, Bitcoin, Cardano, Dogecoin, Ether, and Ripple. The forecasting time horizon was 24 hours. Evaluation metrics included Mean Absolute Percentage Error, RMSE, and Normalized RMSE. The study did not specify the number of data samples used, and the training/testing split was 75/25. SVM proves to be a robust technique for devising profitable trading strategies, demonstrating its ability to provide accurate results both before and during the current pandemic. Our findings are valuable for stakeholders seeking to understand cryptocurrency dynamics and make informed investment decisions, particularly during periods of uncertainty such as the COVID-19 pandemic.

Rena et al. [44] conducted multi-currency forecasting, considering Bitcoin, Ether, Ripple, Cardano, Dogecoin, Polkadot, and Litecoin. Their approach involved Support Vector Machines for predictions with a 24-hour time horizon. Evaluation metrics included accuracy, precision, recall, F1-score, Sharpe Ratio, Sortino Ratio, Conditional Expected Quadratic Return, and Return Loss. The study reported 181 data samples for each currency but did not mention the training/testing split.The proposed multi-source data effectively aids in forecasting cryptocurrency price movements. Furthermore, the proposed portfolio strategy outperforms traditional approaches in terms of out-of-sample Sharpe ratio, Sortino ratio, and certainty equivalent return. Importantly, these conclusions are robustly verified in our testing. Valdés-Aguirre et al. [29] integrated price data and sentiment analysis using Support Vector Machines and Random Forest for forecasting BTC, ETH, XRP, and LTC prices. Their evaluation criteria included accuracy, precision, recall, and F1-score metrics. This approach extends the analysis to consider market sentiment alongside historical data.The MLP emerged as the top-performing model for BTC, achieving an accuracy exceeding 0.72 and a precision of 0.76, significantly outperforming random predictions. SVM and RF also demonstrated superior performance when utilizing market data. However, incorporating Twitter data alone did not contribute to predicting market movements across SVM and RF models; in fact, its inclusion appeared to degrade their performance. Nevertheless, it marginally enhanced precision in the MLP model.

Rabbania et al. [45] employed regression models, including Linear Regression, Gradient Boosting Regression, Support Vector Regression, and Random Forest Regression, for BTC, ETH, ZEC, and LTC price forecasting. They evaluated the models using metrics like Mean Squared Error, Mean Absolute Percentage Error, Mean Absolute Error, Akaike Information Criterion, and Bayesian Information Criterion (BIC).

Pinellas et al. (2020) explored Support Vector Regression, Linear Regression, K-nearest neighbors, and Decision Tree Regression for short-term cryptocurrency forecasting. They evaluated their models based on Root Mean Squared Error, Accuracy, Area Under the Curve, and F1-score metrics [46]. Azizi et al. (2020) and Azizi et al. (2019) explored Bayesian models alongside SVM and RF for BTC price prediction, with a focus on RMSE and MAPE metrics [28,33]. Their work is relevant to price prediction methodologies. Anbarasi et al. (2022) [47] adopted a straightforward Linear Regression model to predict cryptocurrency prices. Focusing on BTC, ETH, LTC, MKR, and BNB, this study targeted both short-term and long-term forecasting without specifying a time horizon. The evaluation was based on commonly used metrics, with a 70/30 training-testing data split.

Amirhosseini et al. [48] integrated sentiment data with Machine Learning, employing K-Nearest Neighbors, Logistic Regression, Gaussian Naive Bayes, Support Vector Machine, and Extremely Randomized Trees models to predict BTC prices over a 24-hour horizon. The F1 score served as the primary evaluation metric, emphasizing model precision and recall. They trained on 80% of the data, reserving 20% for testing.

Johari et al. [49] conducted research into cryptocurrency forecasting, concentrating on AVAX, XRP, SOL, DOGE, MATIC, and SHIB. Their approach involved utilizing Linear Regression, Stochastic Gradient Descent Regression, and Random Forest Regression as forecasting methodologies. The time horizon for predictions in this study was 24 hours. The models’ performance was assessed using multiple metrics, including Mean Absolute Error, Root Mean Squared Error, and Mean Percentage Error .

Godinho et al. [50] conducted multi-currency forecasting, considering BTC, ETH, and LTC. Their models included Linear Regression, Random Forest, and Support Vector Machine. With a 24-hour time horizon, their evaluation involved a variety of metrics, focusing on the accuracy of predictions.The trading strategies are constructed through model assembling. The ensemble approach, where five models generate identical signals (Ensemble 5), demonstrates the highest performance for Ethereum and Litecoin. It achieves annualized Sharpe ratios of 80.17% and 91.35%, along with annualized returns (after proportional round-trip trading costs of 0.5%) of 9.62% and 5.73%, respectively. Geetha et al. [51] explored an array of regression models for Bitcoin price prediction. These models included Linear Regression, Gradient Boosting Regression, Random Forest, Decision Trees, Adaboost Regression (AdaboostR), Ridge Regression (Ridge), and Lasso Regression (Lasso). This study did not specify a particular time horizon but evaluated predictions using metrics such as Root Mean Squared Error, R-squared, Mean Absolute Error, and E (unclear without further context). No details were provided regarding data samples and the training/testing split.

Arpitha et al. [36] utilized Linear Regression to predict Bitcoin prices over a 120-day time horizon. Although they didn’t specify the evaluation metric used, their dataset comprised 2,191 BTC data samples. Jatto et al. [52] focused on Bitcoin price forecasting using Support Vector Machines and K-Nearest Neighbors models. Their predictions had a 24-hour time horizon. Evaluation metrics included accuracy, standard deviation, mean, RMSE, ROC, and AUC. The study’s dataset consisted of 2,760 BTC data samples, with an 80/20 training/testing split. Bhat et al. [53] employed Linear Regression and Support Vector Regression for short-term Bitcoin price forecasting with a 1-hour time horizon. The primary evaluation metric used was accuracy. Their dataset encompassed 29,592 BTC data samples. Lee et al. [54] explored Bitcoin price prediction using various models, including Bayesian Neural Networks (BNN), Support Vector Regression, and Support Vector Machines. The forecasting time horizon was 24 hours. The evaluation focused on RMSE and Mean Absolute Percentage Error. They had access to 1,213 BTC data samples and did not mention a specific training/testing split.

Das et al. [55] investigated Bitcoin price forecasting using various models, including Adaptive Neuro-Fuzzy Inference System, Random Forest, Support Vector Regression, Multivariate Adaptive Regression Splines, and Lasso Regression. Their predictions were made with a 24-hour time horizon. The study did not provide specific evaluation metrics but reported a dataset size of 2,237 BTC data samples with an 80/20 training/testing split. Bhosale et al. [56] explored classification models, including Support Vector Machine, Linear Regression, K-Means Clustering, Naive Bayes, Random Forest, K-Nearest Neighbors, and Decision Trees, for Bitcoin price forecasting with a 1-minute time horizon. The study did not provide specific details on the dataset, data samples, or the training/testing split.

Qusef et al. [57] conducted multi-currency forecasting, encompassing Bitcoin, Ether, and Litecoin. Their approach involved Support Vector Machines, K-nearest neighbors, and Light Gradient Boosting Machines as forecasting methodologies. The time horizon for predictions was 24 hours, and the evaluation criteria included the F1 score and accuracy. They reported 17 data samples for each currency, although the training/testing split was not specified.

Vijayakumar et al. [58] employed Linear Regression models for cryptocurrency forecasting, covering Bitcoin, Dash, Litecoin, Dogecoin, Ether, and Monero. The time horizon for predictions was 24 hours. The evaluation was based on Mean Squared Error, but details about data samples and the training/testing split were not provided.

Neha et al. [53] cast an exclusive spotlight on Bitcoin, meticulously examining price data within a 1-hour prediction horizon. Their arsenal included Linear Regression, Support Vector Regression, and various Statistical models. Notably, their extensive dataset, exclusive to Bitcoin, marked a standout feature.

Prakash et al. [35] utilized price data and blockchain data as input for models. They used the LR model for BTC with a 24-hour time horizon, evaluating using Accuracy. Qusef et al. [57] used Price Data for BTC, ETH, and LTC, applying SVM, KNN, and LGBM models with a 24-hour time horizon. They evaluated using F1 and Accuracy. [59] focused on Price Data for ETH, LTC-BTC, and ZEC-BTC with a 4-hour time horizon. They used EGB, and RF models, evaluating using Accuracy.

Ioannis et al. [46] expanded their research to encompass BTC, ETH, and XRP. They employed a range of ML classifiers and assessed model performance with metrics including Root Mean Square Error and Accuracy. Their dataset consisted of a substantial number of data samples, enabling a comprehensive analysis of their models’ performance. In 2020, Lekkala et al. [60] conducted a comprehensive study focused on Bitcoin price prediction over a 24-hour time horizon. Their analysis encompassed the application of various Machine Learning algorithms, including LASSO, Decision Trees, and K-Nearest Neighbors, with the primary objective of enhancing predictive accuracy. Notably, they leveraged both price data and blockchain data as input features, ensuring a holistic approach to cryptocurrency forecasting. The evaluation of their models centered on the accuracy metric, facilitating rigorous performance assessment. Impressively, their findings highlighted that Linear Regression exhibited superior efficiency compared to other algorithms. Building on this insight, they successfully implemented the LASSO algorithm, emphasizing its effectiveness in reducing time complexity and further improving Bitcoin price prediction accuracy. This research by Lekkala et al. [60] contributes valuable insights into algorithm selection and its impact on cryptocurrency forecasting, particularly underscoring the significance of the LASSO algorithm in achieving superior predictive outcomes.

In 2020, several research studies focused on cryptocurrency forecasting, collectively contributing to a comprehensive understanding of this evolving field. Tri et al. [61] conducted a study that concentrated on predicting cryptocurrency prices, primarily Bitcoin, using the Adaptive Neuro-Fuzzy Inference System and Statistical models. Their research assessed model performance with metrics such as Root Mean Square Error and Mean Squared Error. Notably, they examined a 24-hour time horizon for forecasting BTC prices, similar to many prior studies. Afif et al. [61] utilized Price Data for BTC and employed the ANFIS model with a 24-hour time horizon. They evaluated using RMSE and MSE. Gessl et al. [62] incorporated RF on external economic, price, and blockchain data to predict BTC and LONA prices, emphasizing R-squared, Mean Absolute Error, and Mean Squared Error. Kaushik et al. [63] applied Random Forest for short-term price forecasting of BTC, emphasizing Mean Squared Error and R-squared as their evaluation metrics. KP et al. [64] employed the Random Forest model for short-term Bitcoin price forecasting with a 24-hour time horizon. Evaluation criteria included Mean Squared Error, Mean Absolute Error, and Root Mean Squared Error. The study had access to BTC price data and utilized 4,700 data samples.

5.2.2. Ensemble Strategies Based

Ensemble learning methods have shown promise in cryptocurrency forecasting, as evidenced by recent studies. For instance, the ensemble approach combines various models to enhance predictive accuracy. Gyameraha et al. (2019) [65] explored cryptocurrency price forecasting, particularly focusing on BTC. Their approach involved utilizing Random Forest and Support Vector Regression as forecasting methodologies. RF is an ensemble learning method known for its ability to handle complex relationships in data, while SVR is a powerful tool for regression tasks, often used in financial forecasting. The time horizon for predictions in this study was 24 hours. The models were evaluated using multiple metrics, including Mean Absolute Percentage Error, Root Mean Squared Error, Mean Absolute Error, and R-squared. Similarly, Ensemble techniques, including Random Forest, AdaBoost, XGBoost, and others, have been employed to improve prediction accuracy. The MAPE, RMSE, MAE, and R-squared values for the stacking ensemble model were 0.0191%, 15.5331 USD, 124.5508 USD, and 0.9967 respectively.

Lyu et al. [40] integrated multiple ensemble methods for forecasting BTC, ETH, and XRP prices, emphasizing accuracy . These ensemble models combine the strengths of various algorithms. Their analysis indicates that AdaBoost and XGBoost produce the most inaccurate classifications in the context of our study. In contrast, the Support Vector Machine (SVM) model, when utilized with a probability-based trading strategy, demonstrates a log return of 3.72. This translates to an approximate rate of return of 41.3%. Consequently, an initial investment of $100 would yield a profit of $41.30. Zhang et al.[66] harnessed ensemble models, including Logistic Regression, SVM, Random Forest, XGBoost, and LightGBM, while incorporating technical indicators for BTC price forecasting [66]. Their approach blends ensemble techniques and technical indicators. Balci et al.[67] explored a comprehensive set of Machine Learning models, including Support Vector Regression, Decision Tree Regression, Random Forest Regression, Linear Regression, Logistic Regression, and Gaussian Process Regression (GPR), to forecast the prices of major cryptocurrencies (BTC, ETH, ADA, XRP). Their analysis encompassed a 24-hour time horizon and utilized the Root Mean Squared Error as the evaluation metric. Remarkably, they trained individual models for each currency to capture unique market dynamics. The ARIMA model, commonly used by economists, is found to be unsuitable for cryptocurrency prediction. In contrast, the LSTM architecture, a deep learning model designed for time series prediction and classification, performs more effectively in this domain. Notably, the MM-LSTM architecture, an enhancement of LSTM, exhibits a lower RMSE value compared to traditional machine learning algorithms frequently employed in regression studies. However, machine learning methods such as Gaussian Process Regressor and Logistic Regressor demonstrate very successful results in cryptocurrency prediction. Similarly, Weinhardt et al. (2022) introduced lagged data analysis with Logistic Regression, Random Forest, and Gradient Boosting Classifier for predicting cryptocurrency prices. They employed a wide range of evaluation metrics, including Mean Return, Sharpe Ratio, and Value at Risk, demonstrating the versatility of ML in cryptocurrency forecasting [68]. All employed models produce statistically viable predictions, with average accuracy values across all cryptocurrencies ranging from 52.9% to 54.1%. These accuracy values increase to a range of 57.5% to 59.5% when calculated on the subset of predictions with the top 10% highest model confidence per class and day. Our analysis shows that a long-short portfolio strategy based on the predictions of the employed LSTM and GRU ensemble models yields an annualized out-of-sample Sharpe ratio of 3.23 and 3.12, respectively, after accounting for transaction costs. In comparison, the buy-and-hold benchmark market portfolio strategy yields a Sharpe ratio of only 1.33.

Similarly, Gregorio et al. (2023) integrated external economic data into their models, leveraging LR, SVM, and RF. They evaluated their approach using Recall, Accuracy, Precision, and F1-score metrics, concentrating on BTC price predictions [69]. The inclusion of external factors adds complexity to the forecasting process. Sentiment analysis and the incorporation of textual data have gained popularity. Souza et al. (2022) employed LightGBM, XGBoost, and LR models to predict BTC, ETH, BNB, ADA, and XRP prices, emphasizing accuracy, Sharpe Ratio, and Return on Investment [70]. Analyzing market sentiment provides a unique perspective on price movements. Technical indicators, coupled with ML, have been explored extensively. Ongan et al. (2020) employed Support Vector Machines, Naïve Bayes, Random Forest, and Logistic Regression on BTC price data, focusing on metrics such as F-statistic and AccuracyStat [32]. Technical indicators offer valuable insights into short-term price trends.

Uddin et al. (2021) utilized KNN, LR, Naïve Bayes, RF, SVM, and Ensemble Gradient Boosting with various time intervals for BTC price forecasting [39]. They evaluated models using the Sharpe Ratio and Mean Return. KNN, a distance-based method, allows for flexible predictions. Several studies have expanded their focus beyond a single cryptocurrency. Kate et al. [71] applied KNN, RF, and Support Vector Regression to predict the prices of XRP, BTC, LTC, ETH, and XMR. This multi-currency approach provides a broader view of the cryptocurrency market.

Table 4.

Average ensemble performance against individual models ranked by RMSE in ascending order [71].

Table 4.

Average ensemble performance against individual models ranked by RMSE in ascending order [71].

| Ensemble | RMSE | MAE | MAPE | R2 |

|---|---|---|---|---|

| LSTM | 0.0222 | 0.0173 | 3.86% | 0.73 |

| GRU, LSTM | 0.0225 | 0.0174 | 3.89% | 0.73 |

| HYBRID, LSTM | 0.0225 | 0.0174 | 3.89% | 0.73 |

| HYBRID, GRU, LSTM | 0.0226 | 0.0175 | 3.90% | 0.73 |

| LSTM, KNN | 0.0227 | 0.0175 | 3.92% | 0.73 |

| GRU, LSTM, KNN | 0.0227 | 0.0176 | 3.91% | 0.72 |

| GRU, LSTM, TCN | 0.0227 | 0.0176 | 3.92% | 0.72 |

| LSTM, TCN | 0.0227 | 0.0176 | 3.93% | 0.72 |

| HYBRID, LSTM, KNN | 0.0227 | 0.0175 | 3.92% | 0.72 |

| HYBRID, GRU and more | 0.0227 | 0.0175 | 3.91% | 0.72 |

Asgarim et al. (2022) [72] utilized a multi-model ensemble approach for Bitcoin price prediction, incorporating models such as Multilayer Perceptron, Linear Regression, Bayesian Ridge Regression (BRR), Random Forest Regression, Lasso Regression, Support Vector Regression, and Differential Evolution (DE). Their predictions had a 24-hour time horizon, with evaluation based on Mean Squared Error. The study reported 1,002 BTC data samples but did not specify the training/testing split. Many researchers have combined ML models with traditional technical indicators for cryptocurrency forecasting. Zhang et al. (2020) utilized Logistic Regression, Support Vector Machines, Random Forest, XGBoost, and LightGBM, while also considering technical indicators [66]. The inclusion of technical indicators adds a layer of insight into price predictions.

Samuel et al. [65] honed their research, concentrating solely on Bitcoin’s cryptocurrency forecasting. They introduced the concept of ensemble models, with a meta-learner encompassing two base learners: Random Forest and Generalized Linear Model via penalized maximum likelihood, alongside Support Vector Regression with a linear kernel. Their meticulous analysis, employing various evaluation metrics, unearthed the ensemble model’s prowess, yielding impressive MAPE, RMSE, MAE, and R2 values.

Further expanding the horizon, Kwon et al. [54], also in 2019, navigated cryptocurrency forecasting through the prism of Deep Learning and Machine Learning. Their Long Short-Term Memory DL model and Gradient Boosting ML classifier embraced a 10-minute prediction window, spanning multiple cryptocurrencies. Impressively, LSTM consistently demonstrated superior predictive capabilities across all cryptocurrencies.

Meanwhile, Malekia et al. [45] conducted a comprehensive study involving various cryptocurrencies, including BTC, ETH, ZEC, and LTC. Their research primarily employed price data and diverse Machine Learning classifiers, evaluating models with metrics such as Mean Squared Error and Mean Absolute Percentage Error. Notably, their innovative approach involved using the Lasso Regression algorithm to forecast BTC prices when direct price information was unavailable. Hammoudeh et al. (2020) [42] incorporated Blockchain Data and Price Data for BTC with various time horizons (1d, 7d, 30d, 90d) for SVM with other DL methods. They evaluated using MAE, RMSE, MAPE, Accuracy, F1, AUC, and ROC.

5.2.3. Time Series Forecasting with Prophet and Boosting Models

Time series forecasting, employing Prophet and boosting models, has emerged as a prevalent Machine Learning approach in cryptocurrency forecasting, showcasing promising results in recent studies. For instance, Iqbal et al. (2021) used Prophet and XG Boosting models for BTC price predictions, focusing on RMSE, Mean Absolute Error, and R-squared [73]. These models offer insights into short-term price fluctuations and trends. Their developed random forest model helps anticipate such regime changes by incorporating features from the analysis of user-generated data from Google Trends, Twitter, and Reddit. Similarly, Lim et al. (2022) utilized the Prophet and XGBoost models for BTC, ETH, and XRP price forecasting. Their evaluation criteria included RMSE [74]. The proposed 1DCNN-GRU model outperformed existing methods, achieving the lowest RMSE values of 43.933 on the BTC dataset, 3.511 on the ETH dataset, and 0.00128 on the XRP dataset. Han et al. (2019) [54] utilized gradient-boosting models for cryptocurrency forecasting, covering BTC, ETH, XRP, BCH, LTC, DASH, ETC, and KRW. Their evaluation criteria included accuracy, recall, precision, and F1-score, with a time horizon of 10 minutes. A substantial dataset with 48,816 samples per currency allowed for robust model training.

Sunny et al. (2021) [75] examined Time Series models, including Prophet, alongside XGBoost for Bitcoin price forecasting. The study did not specify the time horizon or evaluation metric but mentioned using Mean Absolute Percentage Error and R-squared. No information was given regarding data samples or the training/testing split. Dhawale et al. (2020) focused on sentiment analysis for BTC using XGBoost models. Their study delves into the role of sentiment data in predicting cryptocurrency price movements [76].

Abbasib et al. (2022) expanded their focus to BTC and utilized Random Forest, XGBoost, and LightGBM models. Their work is relevant to multi-currency forecasting, similar to Carraro et al. (2023) in the previous section [77]. Zhang et al. (2023) leveraged the Light Gradient Boosting Machine and XGBoost models for price predictions of BTC, ETH, BNB, AVAX, and SOL. Their focus was on accuracy, emphasizing the potential of gradient-boosting techniques in cryptocurrency forecasting [78]. Kolokotronis et al. (2021) used the XGBoost model for Ether price prediction, incorporating blockchain data and technical indicators. Their evaluation criteria included MAE, RMSE, Mean Absolute Percentage Error, and R-squared metrics [79]. This study is relevant to the integration of blockchain data and technical indicators mentioned earlier.

Khasteh et al. (2021) [59] conducted a study in cryptocurrency forecasting with a focus on multiple digital assets, including ETH, LTC-BTC, and ZEC-BTC. Their approach involved employing K-Nearest Neighbors, Extreme Gradient Boosting, and Random Forest as forecasting methodologies. The time horizon for predictions was 4 hours, providing insights into short-term cryptocurrency price movements. The models’ performance was assessed using accuracy as the primary evaluation metric.

Tapan et al. [76] concentrated on Bitcoin price prediction, utilizing sentimental data as input features and the XGBoost algorithm. Their study highlighted the efficacy of XGBoost in predicting Bitcoin price trends within a 24-hour horizon.

In 2021, Dimitrios et al. [79] conducted a cryptocurrency price prediction study focused exclusively on Ether. Their research integrated blockchain data and technical indicators as input features and applied the XGBoost Machine Learning classifier, alongside other Deep Learning models. The analysis was limited to a 24-hour time horizon, with an 80/20 training/testing data split. The study evaluated model performance using metrics such as Mean Absolute Error, Root Mean Squared Error, and R-squared. Notably, the research highlighted the significance of technological features in predicting ETH prices and suggested that Deep Learning approaches outperformed the XGBoost model in this specific forecasting context [79].

In 2021, Mahir et al. [73] conducted a cryptocurrency forecasting study exclusively focusing on Bitcoin. Their research centered on historical price data, employing Machine Learning models such as XGBoost and the Prophet model, alongside Statistical models, to predict BTC price movements within a 24-hour time horizon. For the evaluation of their predictive models, they utilized key metrics including Root Mean Squared Error, Mean Absolute Error, and R-squared. Notably, their study identified Statistical models as the most effective for forecasting BTC prices in the cryptocurrency market, achieving a notable RMSE score of 322.4 and an MAE score of 227.3. These results underscore the robustness and accuracy of Statistical approaches in predicting cryptocurrency prices, particularly for Bitcoin.

Han et al. (2019) [54] used Price Data for multiple cryptocurrencies with a 10-minute time horizon. They applied the GB model and evaluated using Accuracy, Recall, Precision, and F1. Iqbal et al. (2021) [73] focused on Price Data for BTC, using the Prophet and XG Boosting models with a 24-hour time horizon. They evaluated using RMSE, MAE, and R2. Gessl et al. In (2023) [62] incorporated External Economic Data, Price Data, and Blockchain Data for BTC and LONA. They employed the RF model with a 24-hour time horizon and evaluated using R2, MAE, and MSE. Sunny et al. (2021) [75] focused on BTC Price Data and Technical Indicators. They employed ARIMA, Prophet, and XGBoost models and evaluated using MAPE and R2. Lim et al. (2022) [74] used Price Data for BTC, ETH, and XRP, applying the Prophet and XGBoost models. They evaluated models using RMSE.

5.3. Summarized Literature Review of Machine Learning Approaches

In this section, this survey presents a summarized literature review of Machine Learning approaches utilized in cryptocurrency price prediction. The table A1 provides an overview of various methodologies, time horizons, currencies, evaluation metrics, data samples, and training/testing strategies employed in the literature. This summary aims to provide insights into the diverse range of machine-learning techniques applied to analyze cryptocurrency price movements and trends.

6. Use of DL in Cryptocurrency Forecasting