Submitted:

23 April 2025

Posted:

24 April 2025

You are already at the latest version

Abstract

This paper examines the macroeconomic implications of unrealistic optimism, a psychological bias that has been largely overlooked in economic models. While traditional models often link optimism to speculative bubbles and excessive risk-taking, this study challenges that view by demonstrating that unrealistic optimism may rather accelerate recessions. Specifically, we develop a model in which consumers, under the influence of unrealistic optimism, believe that negative aggregate shocks will affect others but not themselves. This misjudgment leads to a premature fall in output prices, reducing production and triggering recessions. Additionally, we show that government intervention, when optimally timed, can mitigate the adverse effects of unrealistic optimism, offering important policy implications for stabilizing economies. By highlighting the possibility of optimism-induced downturns, this paper provides new insights into behavioral macroeconomics and offers a novel perspective on policy design.

Keywords:

unrealistic optimism

; recessions

; market collapse

; government intervention

1. Introduction

Understanding how behavioral or cognitive biases affect economic decisions and outcomes is central in modern economics because traditional models based on the assumption that agents are fully rational struggle to explain a wide range of economic phenomena. For instance, the recurrent occurrence of bubbles and crashes in financial markets poses a challenge to classical models with agents who have unbiased beliefs and always make rational decisions. To overcome these limitations, researchers have been seeking alternative explanations to better understand various abnormal economic phenomena, especially employing experimental and psychological approaches. Some of the groundbreaking work that spawned this relatively new field includes, not limited to, Kahneman and Tversky [1], who introduced prospect theory to explain decision-making under risk; Thaler [2], who developed the concept of mental accounting to describe how people categorize economic outcomes; Fehr and Schmidt [3], who provided evidence for fairness and reciprocity in economic interactions; and Loewenstein et al. [4], who emphasized the role of emotions in risk perception and decision-making. Additional recent studies that investigate how cognitive biases affect economic and financial decisions include Exler et al. [5] and Sharma et al. [6].

While many different types of cognitive biases have been explored in this growing literature, one that has recently attracted particular interest in psychology is unrealistic optimism. According to the formal definition provided by Weinstein [7], unrealistic optimism means that people tend to erroneously believe that negative outcomes are less likely to occur to themselves than to others. In other words, unrealistic optimism indicates the tendency that people typically perceive themselves as less vulnerable to misfortune while believing others as more prone to bad luck.

Specifically, Weinstein [7] shows that individuals perceive their own chance of developing lung cancer as significantly lower than the true average likelihood of being diagnosed with that disease. Weinstein [8] extends this study and shows that this phenomenon is ubiquitous regardless of which type of disease is considered, including diabetes, heart attack, drug addiction, and insomnia. Moreover, Burger and Palmer [9] find that while individuals tend to lose their optimism about the likelihood of a specific negative event after experiencing that event, those people typically do not change their perceived vulnerablity to other negative events. In addition, a recent study by Gassen et al. [10] shows that people continue to exhibit this type of cognitive bias, using the survey data on the risk perceptions of individuals on the likelihood of being infected by COVID-19. However, as argued by Coelho [11], the potential impact of unrealistic optimism on economic and business outcomes has been largely ignored by economic researchers, practitioners in corporate sectors, and policymakers, despite the prevalence of unrealistic optimism among individuals in various situations, as seen above. In a related critique, Rizzo and Whitman [12] emphasize the broader challenges that behavioral economics faces in incorporating context-dependent cognitive biases like unrealistic optimism into policy-making, due to persistent knowledge limitations regarding individual preferences and situational heterogeneity.

This paper sheds new light on the potential economic consequences of unrealistic optimism by examining how this type of optimistic beliefs influences individual decision-making and market dynamics. Specifically, we develop an economic model to show that when people hold unrealistic optimism, the economy is more likely to enter into recessions earlier and face underinvestment rather than experiencing bubbles and overinvestment. This result challenges conventional wisdom because optimism or overconfidence is generally considered a behavioral bias that generates economic booms, excessive risk taking, and overinvestments. In particular, Malmendier and Tate [13], Gervais et al. [14], Hirshleifer et al. [15], and Lee et al. [16] empirically show that overconfident corporate managers often overestimate the profitability of new projects and thereby invest more aggressively in new investment opportunities. Malmendier et al. [17] explores this issue further by analyzing how managerial overconfidence varies across different hierarchical levels within firms. Moreover, Harrison and Kreps [18] and Scheinkman and Xiong [19] develop theoretical models to show that asset markets tend to experience speculative bubbles when investors have time-varying heterogeneous beliefs on assets because assets are usually owned by those investors with the most optimistic view at any given point in time. Our paper, however, shows that the conceptually opposite outcomes may occur by particularly examining unrealistic optimism, a form of optimism intensively studied in psychology but largely overlooked in economics.

Our model consists of producers and consumers. Producers produce output goods to maximize their profits, taking the output price and production costs as given. Initially, each consumer values one unit of the output as 1 in terms of the consumption goods. However, in the future, an aggregate shock may hit all existing consumers. Upon the arrival of the shock, each consumer will assign a value of less than 1 to one unit of the output. That is, the aggregate shock can be categorized as a preference shock, while another interpretation is possible. However, each consumer is assumed to hold unrealistic optimism in this model. Specifically, as briefly mentioned above, every consumer incorrectly believes that the aggregate shock will hit all other consumers, but not herself. In other words, each consumer considers that she will not be the victim of the adverse event unlike all other consumers. For instance, if we interpret the aggregate shock as income shocks, we can say that consumers incorrectly believe that all other consumers will experience a wage cut if a crisis hits the economy, but such a bad event would not occur to themselves.

In the benchmark economy, in which each consumer correctly believes that nobody, including herself, can avoid the aggregate shock, the output price stays at 1 today but will drop in the future exactly when the aggregate shock occurs. In this case, every consumer makes zero profits at every date. However, when consumers hold unrealistic optimism, the output price falls today even before the aggregate shock actually hits the economy.

To see the underlying mechanism behind this outcome, note that when consumers exhibit unrealistic optimism, each of them wrongly believes that she can make arbitrage profits in the future if she waits until the aggregate shock occurs, instead of purchasing output goods today. Thus, if the output price does not fall today, the output goods market cannot clear today because all consumers with unrealistic optimism would choose to buy the goods in the future in this case. Therefore, the output price must fall immediately to clear the market. Further, once the output price plummets, producers will lose incentives to produce output goods to some extent, leading to underinvestment. Through this mechanism, unrealistic optimism can trigger early recessions and underinvestment even before the aggregate shock occurs rather than causing expansions or bubbles.

Our paper also investigates whether the government can effectively prevent or mitigate economic crises arising from the aforementioned mechanism driven by unrealistic optimism. It is well known that when all agents have the correct beliefs about the impact of the aggregate shock in a canonical setting, the government cannot enhance welfare or may even hurt welfare by providing subsidies to consumers or directly purchasing the output goods. However, when the economy experiences recessions due to the unrealistic optimism of agents, there is room for the government to intervene in the market and improve welfare of the economy. Specifically, suppose that the government provides subsidies to all consumers, who intend to purchase the output goods today, in order to lift the output price to 1. Then the utility level of some consumers, who would otherwise purchase the goods in the future in the case without subsidies, increases because they can buy the output goods, which they value as 1, at a price lower than 1 due to the subsidies. Thus, this increment in their utility offsets the amount of money paid by taxpayers. But when the output price increases, producers produce more outputs, eventually leading to the welfare improvement. This argument can be used to support the effectiveness of a number of government intervention policies implemented during the 2008 financial crisis and 2020 COVID-19 crisis, such as stimulus packages and direct financial aid to consumers and businesses.

Despite the positive effects of government subsidies, the government must be able to choose the right timing for intervention. We show that if the government intervenes in the market after the aggregate shock hits the economy, the government subsidies would make no difference or would be less effective, compared to the case where the government takes the action preemptively. Specifically, suppose the government provides subsidies right after the occurrence of the aggregate shock. Then, at that date, consumers can still buy the output goods by spending the same amount of money as before due to the subsidies. As such, at the beginning, consumers with unrealistic optimism will again falsely expect to exploit the arbitrage opportunity unless the output price remains at a low level as before. As a result, the output price will still stay at the low level in the first period, which means that the government has failed to prevent the early occurrence of the recession. In this regard, we see that the government can improve welfare to the maximum capacity only when it chooses the right timing for intervention.

The rest of the paper is organized as follows. In Section 2, we provide the literature review. In Section 3, we develop the model and discuss the main results of the model. In Section 4, we discuss the welfare implications of government intervention. In Section 5, we extend the model into a dynamic setup. In Section 6, we discuss the limitations and the directions for future research. In Section 7, we conclude.

2. Related Literature

Understanding the causes and consequences of economic fluctuations has been a central focus in economic research. Traditional macroeconomic theories mainly attribute economic fluctuations to various factors, including productivity shocks, liquidity constraints, and financial frictions. For instance, Kydland and Prescott [20] show that time lags in production and investment decisions, driven by exogenous technology shocks, can generate persistent and empirically plausible aggregate fluctuations in output. Kiyotaki and Moore [21] demonstrate how credit constraints can amplify and propagate shocks, leading to prolonged recessions. Bernanke et al. [22] highlight the role of financial accelerator mechanisms, where deteriorating balance sheets exacerbate downturns by tightening borrowing conditions. Brunnermeier and Sannikov [23] extend these insights by incorporating liquidity constraints and fire sales into macroeconomic models, showing how financial instability can lead to severe economic contractions. Furthermore, Guerrieri and Lorenzoni [24] show that credit market frictions can exacerbate economic downturns by limiting firms’ access to external financing, leading to constrained investment and prolonged recessions.

Another strand of the economics literature attempts to explain economic fluctuations using information-based mechanisms. For instance, Veldkamp [25] studies why financial markets tend to exhibit sudden crashes and slow recoveries by developing information-based models. More specifically, Veldkamp [25] shows that during economic booms, public information about economic conditions is more abundantly produced and so, prices and economic activities adjust more rapidly during booms, which can potentially trigger a sudden crash when the economic conditions start to make a downturn. In addition, Ordonez [26] incorporates financial frictions and agency costs into the model by Veldkamp [25] to show that this asymmetric phenomenon generally occurs because monitoring costs for lenders are more likely to increase during recessions and crisis periods, hindering the lenders from identifying the best timing for re-entering the market, compared to the boom periods. Ordonez [26] further shows that such an asymmetric outcome would be more likely to occur in countries with poor financial systems.

While these traditional approaches have substantially enhanced our understanding of the mechanism behind economic fluctuations, whether these theories are supported by data is inconclusive. Specifically, Altug [27] finds that the model by Kydland and Prescott [20] struggles to account for observed aggregate fluctuations, particularly regarding the persistence and volatility of output. Gali [28] also presents empirical evidence suggesting that technology shocks alone cannot explain observed business cycle patterns. Regarding the model with financial frictions, while Christiano [29] provide evidence supporting the idea that financial frictions play a crucial role in explaining the depth and persistence of recessions, Boehl and Strobel [30] show that the ability of these models to explain the macroeconomic dynamics of the real economy is limited. Also, the mechanisms proposed by Veldkamp [25] and Ordonez [26] are theoretically compelling, measuring the precise role of informational frictions in market crashes and recoveries remains challenging due to the lack of detailed micro-level data. In addition, Shiller [31] also argues that severe fluctuations in stock prices are hard to justify from the rational forecasts of firms’ future cash flows.

Due to the shortcomings of these conventional macroeconomic models, researchers have started exploring alternative theories to explain economic booms and crises. Among those recent approaches, the approach incorporating insights from behavioral psychology has gained significant attention. For example, Shiller [31] shows that an excessive volatility of stocks is hard to justify from rational forecasts of future cash flows of firms, suggesting that psychological factors, such as overreaction to market news, must be considered to account for large fluctuations in asset prices. Thaler [2] shows how individuals systematically deviate from rational decision-making, which in turn leads to bubbles and crashes, providing a cornerstone for the later development of behavioral economics models. Banerjee [32] shows how herd behavior can arise when individuals make decisions based on the observed actions of the crowd rather than on their own private information, which can potentially lead to bubbles and crashes in financial markets. Bordalo et al. [33] explore the role of diagnostic expectations, a belief formation mechanism based on the representativeness heuristic proposed by Kahneman and Tversky [34], in shaping boom-and-bust cycles in the economy.

In addition, Kaizoji and Sornette [35] propose a mechanism in which optimism drives asset bubbles that eventually collapse, triggering recessions. Bianchi et al. [36] explore how belief distortions, driven by subjective expectations about economic fundamentals, amplify macroeconomic fluctuations and business cycle dynamics. Song [37] incorporates investor sentiment into a dynamic capital mobility model to unravel the role of investtor sentiment in causing market crashes. Relatedly, researchers have also analyzed the role of pessimistic biases such as ambiguity aversion in driving significant discounts in asset prices, a phenomenon commonly called the equity premium puzzle; see, for instance, Gilboa and Schmeidler [38], Hansen and Sargent [39], and Epstein and Schneider [40], and Ju and Miao [41], and Bao et al. [42].

Despite the growing interest in psychology-based explanations, few studies have examined the role of unrealistic optimism in macroeconomic outcomes, although this specific type of optimism has been extensively studied in the psychology literature, as mentioned above. To the best of our knowledge, our paper is the first to incorporate unrealistic optimism into an economic framework and sheds new insights into the economic role of this type of behavioral bias. Specifically, our paper demonstrates that unrealistic optimism can accelerate recessions, while previous papers typically link optimism to speculative bubbles or explain market crashes as correction of preceding booms driven by optimism. This unique feature of our paper underscores the need for further empirical research to differentiate between optimism-driven booms and optimism-induced downturns. By highlighting this mechanism, our study contributes to the literature on behavioral macroeconomics and provides new insights for government policy design as well.

3. Model and Main Results

In this section, we develop a simple model with unrealistic optimism and examine how such a cognitive bias influences output prices and production decisions.

3.1. Simple Model with Unrealistic Optimism

Consider a simple model with a representative producer and a continuum of infinitely many consumers who are prone to a certain type of cognitive bias, which will be described later. There are only two dates indexed by . All agents are risk neutral and discount future consumptions at a rate normalized to 0.

At each date t, the producer can produce units of the output at costs of by taking the output price as given, where represents the marginal cost per unit of output. Although the main results of this paper continue to hold with a more general form of the cost function, we adopt this quadratic cost function for simplicity. Let be the output price at date t. Then the producer decides to produce at each date t. Here, although we interpret the output goods as the real goods for convenience, the main implications of the model can be certainly applied to a setup where investors trade financial assets such as stocks or bonds instead of real goods.

We now consider the behavior of consumers. Each consumer is initially endowed with a certain unit of the consumption goods, which is normalized to 1. For simplicity, we assume that consumption goods are perfectly storable. As such, in this model, each risk-neutral consumer only needs to decide when to buy the output goods between date 0 and date 1. Although we can relax the assumption that consumption goods are perfectly storable, considering such a more general setup would not yield any additional important implications.

At date 0, all consumers value one unit of the outputs as 1 in terms of the consumption goods. At date 1, an aggregate preference shock will hit the economy with a probability . Upon the arrival of the shock, each consumer will value one unit of the outputs as . Here, we can interpret this preference shock in many different ways. For example, if we regard the producer as an input supplier and the consumers as the producers of the final goods, we can interpret the preference shock as a productivity shock to those final goods producers. Or, if we alternatively assume that consumers receive an exogenous amount of income at every date, we may say that the amount of income at date 1 will drop with a certain probability.

Before introducing the unrealistic optimism held by consumers, we first consider the canonical case where all consumers have correct beliefs about the potential impact of the aggregate shock. In this benchmark economy, due to market competition, the price of the output goods at date t, denoted by , will be equal to

That is, in equilibrium, the output price is determined in a way that all consumers earn zero profits at each date. For the latter purpose, we refer to the state where the aggregate shock does not occur as the good state and the other state as the bad state.

Regarding the production and consumption decisions, suppose that all agents expect that the output price will be given in the above way. Then, at date 0, (i) the producer produces units of the output, (ii) any consumer who wishes to buy the outputs at date 0 can buy one unit of the output, (iii) the total measure of consumers who buy the outputs at date 0 is equal to , and (iv) the other consumers decide to consume at date 1. At date 1, if the aggregate shock occurs, (i) the producer produces units of the output, (ii) any consumer who wishes to buy the outputs at date 0 can buy units of the output, (iii) the total measure of consumers who buy the outputs is , and (iv) the other consumers consume their own endowment. If the aggregate shock does not occur at date 1, the economic outcomes remain the same as in date 0.

Now, we assume that each consumer is susceptible to a certain type of cognitive bias. Specifically, we assume that each consumer incorrectly believes that the aggregate shock will hit all other consumers, but not herself. But the truth is that the aggregate shock will actually hit all existing consumers, including herself, and each consumer will eventually learn this fact once the shock indeed occurs at date 1. For instance, if we interpret the aggregate shock as an income shock, we can say that consumers believe that all other consumers will face a wage cut when the economy enters a recession, while believing such a bad shock would not hit themselves. In the psychology literature, this form of optimism, which states that people tend to underestimate the chances of negative outcomes occurring to themselves compared to others, is widely called unrealistic optimism, optimism bias, or comparative optimism; see, for instance, Weinstein [8], Weinstein and Klein [43], Hoorens et al. [44], Jefferson et al. [45], and Gassen et al. [10].

Using this model, we show that the unrealistic optimism can cause an earlier market collapse and underinvestment. To this aim, first recall that every consumer believes the aggregate shock to hit all other consumers, but not herself. As such, every consumer expects that the output price will drop to A at date 1 if the aggregate shock actually occurs, because she believes that the shock will at least hit all other consumers. But then, from the date-0 perspective, each consumer believes that she can make positive profits equal to in expectation if she purchases the output goods at date 1 rather than at date 0. Hence, for the output market to clear at date 0, the output price must drop to some extent at date 0 so that each consumer would be indifferent between purchasing the outputs at date 0 or date 1. For clarification, note that no consumers can actually earn positive profits in the end because the truth is that the aggregate shock will actually hit all consumers as mentioned above.

Accordingly, in the presence of unrealistic optimism, the output price at date 0 is determined so as to satisfy the following indifference condition:

which implies

The left-hand side of (2) indicates the immediate profits that each consumer can earn if she buys the output goods at date 0. The right-hand side denotes the present value of the profits that each consumer expects to earn if she buys the output goods at date 1, as discussed above. Then, since these two terms must be equal to each other for the output market at date 0 to clear, the output price at that date is given by the expression in (3). This result implies that the output price will be more depressed due to the unrealistic optimism if the aggregate shock is more likely to occur or the magnitude of the shock, measured by , is larger, both of which are intuitive.

In addition, the above result also implies that the unrealistic optimism causes underinvestment. Specifically, since the output price falls below 1 at date 0, which is the intrinsic value of the output, the producer decides to produce only units of the output rather than as in the case without the unrealistic optimism.

These results sharply contrast with our common intuition because optimism is generally viewed as a cognitive bias that leads to bubbles in financial markets or overinvestment in the production side. For instance, Harrison and Kreps [18] and Scheinkman and Xiong [19] show that when investors have heterogeneous beliefs and short selling is not allowed, markets exhibit bubbles not only because assets are priced by those investors who have the most optimistic view on given assets but also because those investors can resell their assets when their own valuation drops relative to the valuation of other investors. Also, Malmendier and Tate [13], Gervais et al. [14], and Hirshleifer et al. [15] provide empirical evidence that overconfident managers tend to overvalue their investment projects and thus invest more aggressively in new projects than other managers without overconfidence, especially when firms have abundant internal capital.

The type of optimism considered in this paper is different from the types of optimism considered in the above papers. In our paper, each consumer correctly estimates the impact of the aggregate shock on all other consumers but incorrectly estimates the impact of the aggregate shock on herself. When agents have this type of optimism, our model shows that markets can rather experience an early downturn and firms underinvest in new projects. In this regard, our paper sheds new light on the true sources of economic recessions and investment distortions through the lens of behavioral bias.

4. Government Intervention and Welfare

In this section, we examine whether the government can increase the welfare of the economy by providing subsidies to consumers exhibiting unrealistic optimism. Throughout the model, we define the welfare at each date as the sum of the consumer surplus and the producer surplus, created from production at that date, minus the amount of government subsidies, which come from taxpayers. We first consider the benchmark model in which consumers do not exhibit unrealistic optimism. We then analyze the impact of subsidies in the model with unrealistic optimism.

4.1. Without Unrealistic Optimism

In the benchmark model without unrealistic optimism, we show that the government cannot improve welfare by providing subsidies when the aggregate shock occurs at date 1. Specifically, at date 0, the consumer surplus is 0 because the outputs are sold at a price that is equal to the true valuation of consumers. The producer surplus is equal to

where 1 is the output price at date 0 and is the marginal cost of production. Hence, the welfare is also equal to , as consumer surplus is 0. The welfare in the good state at date 1 is equal to the welfare at date 0. If the bad state occurs at date 1, a similar argument shows that welfare is equal to , which is the area of the triangle, denoted by R, in the left panel of Figure 1.

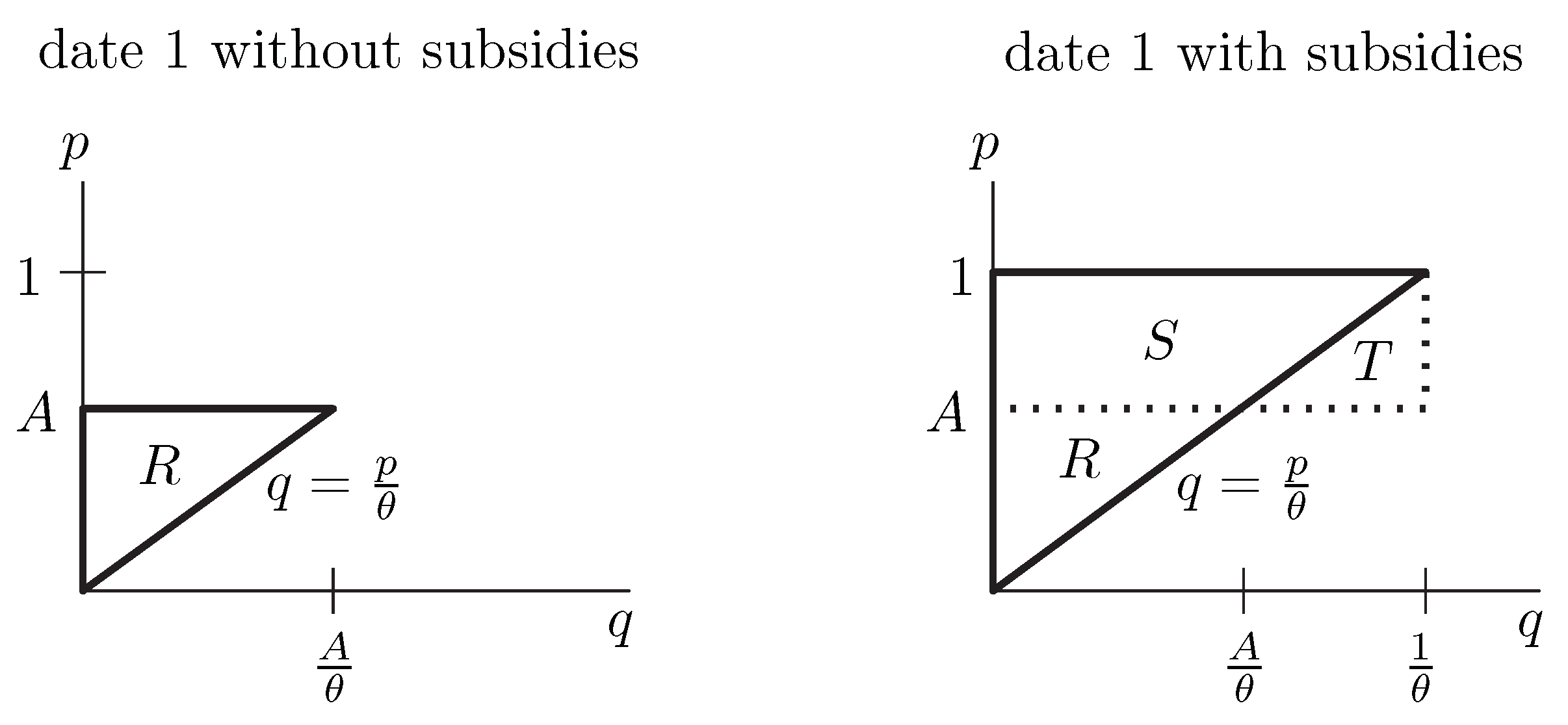

Now, suppose the government aims to raise the output price from A to 1 in the bad state at date 1 by providing subsidies of per unit output to every consumer who buys the outputs. Then, the consumer surplus is still 0 because each consumer, who values one unit of output as A, still pays A from her own pocket. The producer surplus, however, increases from to because the output price has been raised to 1 due to subsidies. That is, the producer surplus increases by when the government provide subsidies, as illustrated in the right panel of Figure 1. However, the amount of subsidies provided by the government is equal to which corresponds to , because the total units of outputs sold are and the amount of subsidies per unit output is . As a result, welfare of the economy decreases by , compared to the case with subsidies, when consumers do not exhibit unrealistic optimism.

For robustness, note that even if the government intervenes in the market by directly purchasing the output goods using the money of taxpayers, the welfare cannot be improved. Specifically, suppose that the government directly purchases the output goods at the price of 1 in the bad state at date 1 and then distributes those output goods to consumers. Then, the utility of those consumers who receive the output goods from the government increases by A. But the amount of subsidies spent for one unit of the output was 1. Thus, the welfare actually drops as in the previous case even if the government adopts this alternative intervention policy. In this regard, in what follows, we will focus on the intervention policy presented above, which aims at providing subsidies to consumers. Also, note that this type of intervention policy is more realistic because we can interpret such a policy as tax cuts on consumer goods.

4.2. With Unrealistic Optimism

When consumers hold unrealistic optimism, we show that government subsidies, if carefully designed, can effectively improve welfare of the economy. We first consider the case without government subsidies. In this case, at date 0, the consumer surplus is equal to because (i) consumers can now purchase one unit of the output goods at the price of , which is given by (3), while the true value of the output goods is 1 to those consumers, and (ii) the total units of outputs produced is equal to . The producer surplus is equal to , similar to the case in the benchmark model. Thus, the welfare at date 0 is

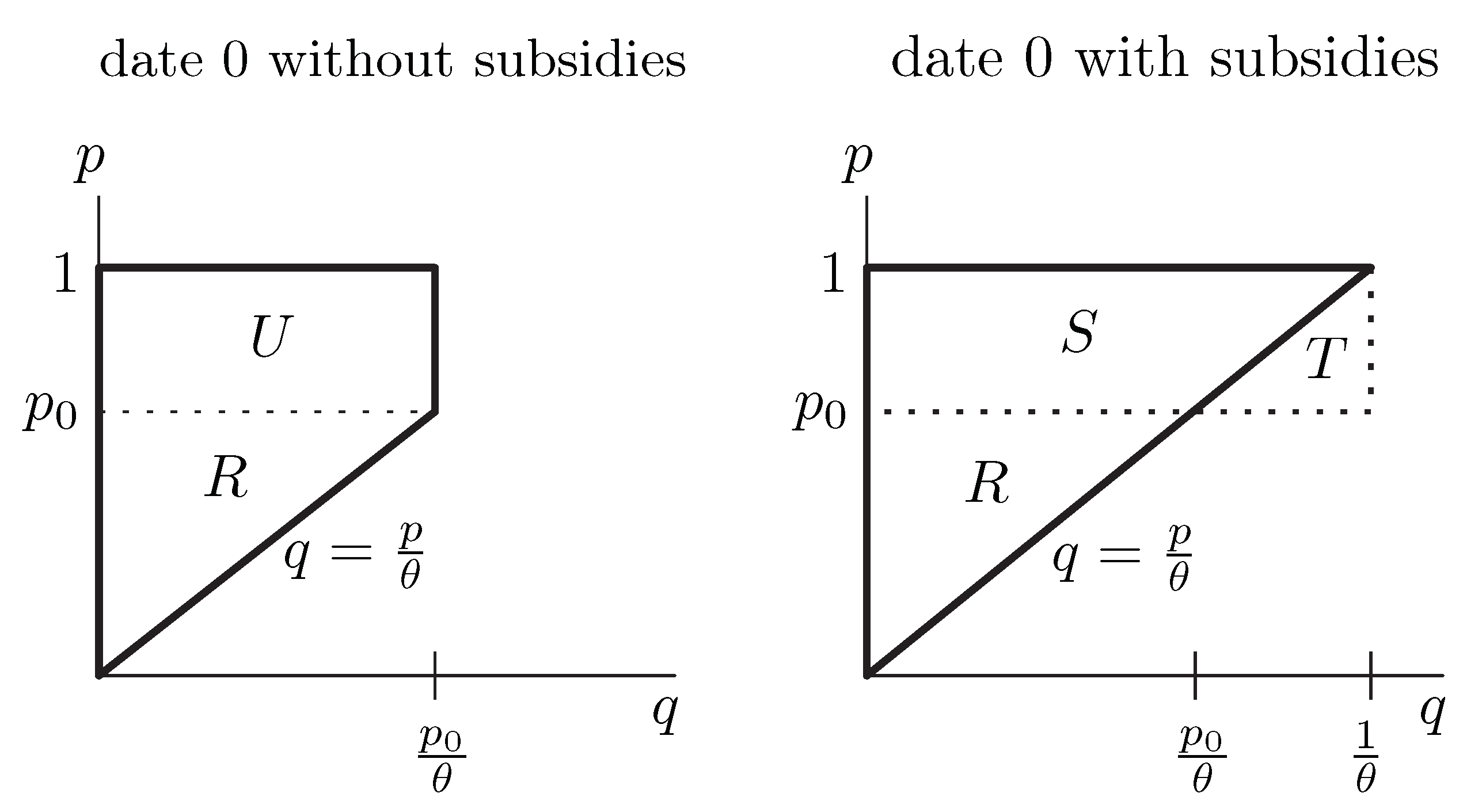

as illustrated by the left panel of Figure 2, where U indicates the consumer surplus and R denotes the producer surplus. At date 1, the welfare is the same as that in the benchmark model regardless of whether the aggregate shock hits the economy or not. So, we have omitted to plot this case in Figure 2.

Now, we consider two possible government intervention policies: one is to provide subsidies at date 0 and the other is to provide subsidies in the bad state at date 1. Under the first policy, the welfare of the economy is equal to

The consumer surplus increases to because each consumer still needs to pay only from her own pocket to purchase one unit of the output at date 0, but the total units of the outputs produced increases from to . This consumer surplus corresponds to the area in the right panel of Figure 2. The producer surplus is equal to , which corresponds to in the same panel, because the price has been raised to 1. Now, note that the amount of subsidies is equal to because the government subsidizes per unit of output and the total units of the output produced is . The amount of subsidies also corresponds to in the above panel. That is, when the output price is pushed down due to unrealistic optimism, the consumer surplus is the same as the amount of subsidies provided by the government, as shown in the figure.

Then, the fact that implies that the welfare increases if the government provides subsidies at date 0, that is, before the aggregate shock occurs. This result is intuitive because when the output price is suppressed due to the cognitive bias of consumers, there is room for the government to intervene in the market and improve welfare. Of course, in the real world, the government should be more cautious because providing subsidies through tax collections may incur some deadweight losses. In this regard, the government must compare the increase in welfare resulting from subsidies to the deadweight losses associated with subsidies and choose to intervene in the market only when the benefits outweights the costs.

Meanwhile, we now show that if the government provides subsidies at date 1 rather than date 0, the welfare will decline as in the benchmark economy without unrealistic optimism. Interestingly, when the government subsidizes consumers at date 1, the output price at date 0 will remain unchanged at as described in (3). The reason for this outcome is that each consumer can still pay A from her own pocket to buy one unit of the output in the bad state at date 1. So, from the date-0 perspective, each consumer still incorrectly believes that she could make profits of in the bad state at date 1. Hence, the output price at date 0 must stay unchanged at for the market to clear at date 0. Then, as we have already seen that if the government intervenes in the market at date 1, the welfare will decrease at that date, such an intervention policy cannot improve welfare at any date.

The above two results imply that the government must take the action early, that is, before the aggregate shock hits the economy, to enhance welfare of the economy. Otherwise, the government would only waste the money of taxpayers. In this regard, investigating an optimal timing of the government intervention should be very critical for the entire economy.

5. Extensions

In this section, we extend the above model into a dynamic setup with infinite horizons to show the main result of our model continues to hold in a more general setting. Specifically, we incorporate the unrealistic optimism into the neoclassical investment model developed by Hayashi [46].

To begin, consider a firm that produces stochastic outputs over time, where the output level is determined by the investment decisions of the firm. Specifically, the time-t output level, denoted by , evolves according to

where is the investment rate at time t, is a constant volatility, and is a standard Brownian motion. To choose the investment level of at time t, the firm has to spend as the convex adjustment costs, where is a constant that measures the size of investment costs. At each point in time, the firm makes the investment decisions to maximize the present value of its future profits. We assume that all agents are risk neutral and discount future consumptions at a constant risk-free rate of r.

Initially, the firm can sell one unit of the outputs at the normalized price of 1. But an aggregate preference shock may hit the firm’s consumers in the future. Specifically, the preference shock will arrive at a Poisson rate of . Upon the arrival of the shock, all consumers will value one unit of the outputs as . In this regard, we can also interpret the preference shock to consumers as the profitability shock to the firm. We call the periods with the high profitability the normal times and the periods with the low profitability the bad times. Also, as in the previous model, each consumer can buy at most one unit of the outputs throughout her life due to some budget constraints.

If consumers have correct beliefs about the impacts of the aggregate shock, the price of the output will stay at 1 during the normal times and will fall right after the aggregate shock hits the economy. However, as in the above simple model, we assume that consumers incorrectly believe that the aggregate shock will hurt only other consumers, but not herself. In this case, we will show that the output price will not stay at 1 during the normal times. Specifically, let P denote the per-unit output price during the normal times. We will later verify that the output price should be a constant during the normal times due to the stationary structure of the model.

To pin down the output price during the normal times, we consider two strategies regarding when to buy the product. The first strategy is that a consumer buys the product just today. The second possible strategy is that a consumer waits until the aggregate shock hits the economy. Under the strategy, the consumer will immediately earn as profits, while under the second strategy, she expects to earn

in terms of the time-t present value value. Then, for the output market to clear at each point in time, each consumer must be indifferent between those two strategies, which implies

This result first means that the output price lies between A and 1 as expected. From this expression, we can also see that the output price falls more due to the unrealistic optimism when the discount rate is lower, the aggregate shock is more likely to occur, and the magnitude of the shock is larger. All these results are intuitive.

For clarification, in the above argument, we have used the fact that consumers do not have any incentives to buy the product after the aggregate shock hits the economy because of discounting. Further, we can actually consider other more general strategies in addition to the above-mentioned two strategies. Specifically, let denote the arrival time of the aggregate shock. Then consider a consumer who aims to buy the product at time , where is any specific date. That is, this consumer will buy the product at time T if the aggregate shock has not occurred until then, but will buy the product right after the aggregate shock hits the economy if that event happens before time T. Under this strategy, the consumer expects to earn the profits of

by definition. Then we see that the amount of these profits does not depend on the specific time T if the output price P is given by (5). In fact, this argument can be further extended to the case where the target purchasing time T is a random stopping time that is independent of the arrival time of the aggregate shock. Therefore, we confirm that P expressed in (5) is indeed an equilibrium price.

We now calculate the present value of the firm. We first pin down the firm value during the bad times. During this period, the firm value denoted by satisfies the following Hamilton-Jacobi-Bellman equation:

The left-hand side is the required return. The first term on the right-hand side is the amount of cash flows produced by the firm, the second term is the adjustment costs, and the remaining terms represent the changes in the firm value due to the growth and fluctuations in the output level. We conjecture that is equal to for some constant , which is called Tobin’s Q. Then, using the first-order condition that , we see that must satisfy

Hence, we find that Tobin’s Q and the optimal investment level during the bad times are respectively given by

where we have excluded the other possible choice for and to ensure that the growth rate should not exceed r in the risk-neutral measure. We also impose the parameter condition that to ensure that the investment rate is positive.

During the normal times, the firm value denoted by satisfies the following differential equation:

We again conjecture that for some constant q. Then, proceeding similarly as above, we find that Tobin’s Q and the optimal investment level during the normal times are respectively given by

From this result, we clearly see that the optimistic bias causes underinvestment rather than overinvestment because the socially optimal level of investment is equal to

We have therefore characterized a dynamic model with infinite horizons, in which consumers display unrealistic optimism. This model shows that even if the aggregate shock is expected to hit the economy in the far future, the output price must drop to some extent immediately today. This result therefore confirms that recessions or market crashes can be precipitated by unrealistic optimism.

6. Limitations and Future Research

While this study provides novel insights into the economic implications of unrealistic optimism, several limitations warrant further investigation. First, the model assumes that all consumers exhibit identical degrees of unrealistic optimism. In reality, cognitive biases vary across individuals, as shown in Rabin [47] and Berthet [48], and thus, incorporating heterogeneous beliefs could yield richer dynamics and more nuanced policy implications. In this regard, future research could explore how varying levels of optimism among consumers affect aggregate economic outcomes.

Second, our model considers a simplified setting in which the economy consists of a single representative producer and consumers who face an exogenous aggregate shock. Extending the framework to a multi-sector economy or incorporating endogenous belief formation could enhance our understanding of how unrealistic optimism interacts with broader economic forces, including labor markets, financial intermediation, and global trade. In particular, Agranov et al. [49] provide experimental evidence that individuals’ cognitive levels and beliefs are shaped endogenously by their environment and strategic context, suggesting that belief formation is a dynamic process rather than a fixed trait. Incorporating such mechanisms into macroeconomic models could yield more realistic predictions about behavior under uncertainty.

Third, while the model emphasizes the role of government intervention in mitigating the adverse effects of premature recessions, the analysis does not account for potential distortions arising from policy implementation. Investigating how different forms of intervention, such as monetary policy or regulatory measures rather than fiscal subsidies, affect the inefficiencies stemming from unrealistic optimism would be a valuable avenue for future research. Relatedly, Krokida et al. [50] examine the interactions between monetary policy and herd behavior in stock markets.

Finally, empirical validation remains an essential step in furthering this line of inquiry. Developing robust empirical methodologies to distinguish the effects of unrealistic optimism from those of traditional pessimism would significantly contribute to our understanding of behavioral biases in macroeconomic settings. A recent approach adopted by Liu et al. [51], who examine how distinct aspects of behavioral biases, such as bounded rationality, myopic behavior, prospect-biased behavior, optimism, and pessimism, differently affect decision-making, could be useful for this task. In addition, future studies could also leverage survey data or experimental methods to identify the prevalence and economic consequences of unrealistic optimism in different contexts.

7. Conclusion

This paper examines how unrealistic optimism, where individuals underestimate their own exposure to negative shocks while overestimating others’ risks, can contribute to premature recessions and underinvestment. Unlike traditional perspectives that associate optimism with economic booms, we show that unrealistic optimism can depress output prices before an aggregate shock occurs, leading to early downturns and inefficient investment decisions. By developing a theoretical framework, we highlight a novel mechanism through which this cognitive bias distorts market dynamics. In particular, our results demonstrate that when consumers incorrectly believe they can exploit future arbitrage opportunities, the market-clearing price must decline in advance, triggering an early contraction in economic activity. We also explore the role of government intervention, showing that well-timed subsidies can mitigate the adverse effects of unrealistic optimism. However, the effectiveness of such policies crucially depends on their timing, in the sense that intervening before an aggregate shock occurs is more beneficial than reacting afterward. Overall, our findings offer fresh insights into the behavioral foundations of economic recessions. They underscore the importance of integrating cognitive biases into macroeconomic models and highlight potential policy measures to counteract their negative effects. Future research should further investigate the empirical prevalence of unrealistic optimism and its broader implications for financial markets and economic stability.

Author Contributions

Conceptualization, HD; Modeling, JP; Model analysis, JP; Writing, HD and JP; Funding acquisition, HD; All authors have read and agreed to the published version of the manuscript.

Funding

This research was supported by Hanyang University, ERICA Campus, under the grant HY202400000003411.

Informed Consent Statement

Informed consent was obtained from all subjects involved in this study.

Data Availability Statement

No new data were created or analyzed in this study. Data sharing is not applicable to this article.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Kahneman, D.; Tversky, A. Prospect theory: An analysis of decisions under risk. Econometrica 1979, 47, 263–292. [CrossRef]

- Thaler, R. Mental accounting and consumer choice. Marketing science 1985, 4, 199–214. [CrossRef]

- Fehr, E.; Schmidt, K.M. A theory of fairness, competition, and cooperation. The quarterly journal of economics 1999, 114, 817–868.

- Loewenstein, G.F.; Weber, E.U.; Hsee, C.K.; Welch, N. Risk as feelings. Psychological bulletin 2001, 127, 267. [CrossRef]

- Exler, F.; Livshits, I.; MacGee, J.; Tertilt, M. Consumer credit with over-optimistic borrowers. Journal of the European Economic Association 2024, p. jvae057. [CrossRef]

- Sharma, A.; Hewege, C.; Perera, C. Exploring the Relationships Between Behavioural Biases and the Rational Behaviour of Australian Female Consumers. Behavioral Sciences 2025, 15, 58. [CrossRef]

- Weinstein, N.D. Unrealistic optimism about future life events. Journal of personality and social psychology 1980, 39, 806. [CrossRef]

- Weinstein, N.D. Unrealistic optimism about susceptibility to health problems: Conclusions from a community-wide sample. Journal of behavioral medicine 1987, 10, 481–500. [CrossRef]

- Burger, J.M.; Palmer, M.L. Changes in and generalization of unrealistic optimism following experiences with stressful events: Reactions to the 1989 California earthquake. Personality and Social Psychology Bulletin 1992, 18, 39–43. [CrossRef]

- Gassen, J.; Nowak, T.J.; Henderson, A.D.; Weaver, S.P.; Baker, E.J.; Muehlenbein, M.P. Unrealistic optimism and risk for COVID-19 disease. Frontiers in Psychology 2021, 12, 1–16. [CrossRef]

- Coelho, M.P. Unrealistic optimism: Still a neglected trait. Journal of business and psychology 2010, 25, 397–408. [CrossRef]

- Rizzo, M.J.; Whitman, G. The unsolved Hayekian knowledge problem in behavioral economics. Behavioural Public Policy 2023, 7, 199–211. [CrossRef]

- Malmendier, U.; Tate, G. CEO overconfidence and corporate investment. The journal of finance 2005, 60, 2661–2700. [CrossRef]

- Gervais, S.; Heaton, J.B.; Odean, T. Overconfidence, compensation contracts, and capital budgeting. The Journal of Finance 2011, 66, 1735–1777. [CrossRef]

- Hirshleifer, D.; Low, A.; Teoh, S.H. Are overconfident CEOs better innovators? The journal of finance 2012, 67, 1457–1498. [CrossRef]

- Lee, J.M.; Park, J.C.; Chen, G. A cognitive perspective on real options investment: CEO overconfidence. Strategic Management Journal 2023, 44, 1084–1110. [CrossRef]

- Malmendier, U.; Pezone, V.; Zheng, H. Managerial duties and managerial biases. Management Science 2023, 69, 3174–3201. [CrossRef]

- Harrison, J.M.; Kreps, D.M. Speculative investor behavior in a stock market with heterogeneous expectations. The Quarterly Journal of Economics 1978, 92, 323–336. [CrossRef]

- Scheinkman, J.A.; Xiong, W. Overconfidence and speculative bubbles. Journal of political Economy 2003, 111, 1183–1220. [CrossRef]

- Kydland, F.E.; Prescott, E.C. Time to build and aggregate fluctuations. Econometrica: Journal of the Econometric Society 1982, pp. 1345–1370. [CrossRef]

- Kiyotaki, N.; Moore, J. Credit cycles. Journal of political economy 1997, 105, 211–248.

- Bernanke, B.S.; Gertler, M.; Gilchrist, S. The financial accelerator in a quantitative business cycle framework. Handbook of macroeconomics 1999, 1, 1341–1393. [CrossRef]

- Brunnermeier, M.K.; Sannikov, Y. A macroeconomic model with a financial sector. American Economic Review 2014, 104, 379–421. [CrossRef]

- Guerrieri, V.; Lorenzoni, G. Credit crises, precautionary savings, and the liquidity trap. The Quarterly Journal of Economics 2017, 132, 1427–1467. [CrossRef]

- Veldkamp, L.L. Slow boom, sudden crash. Journal of Economic theory 2005, 124, 230–257. [CrossRef]

- Ordonez, G. The asymmetric effects of financial frictions. Journal of Political Economy 2013, 121, 844–895. [CrossRef]

- Altug, S. Time-to-build and aggregate fluctuations: some new evidence. International Economic Review 1989, pp. 889–920. [CrossRef]

- Gali, J. Technology, employment, and the business cycle: do technology shocks explain aggregate fluctuations? American economic review 1999, 89, 249–271. [CrossRef]

- Christiano, L. Financial frictions in macroeconomics. Journal of International Money and Finance 2022, 122, 102529. [CrossRef]

- Boehl, G.; Strobel, F. The empirical performance of the financial accelerator since 2008. Journal of Economic Dynamics and Control 2024, 167, 104927. [CrossRef]

- Shiller, R.J. Do stock prices move too much to be justified by subsequent changes in dividends? American Economic Review 1981, 71, 421–436.

- Banerjee, A.V. A simple model of herd behavior. The quarterly journal of economics 1992, 107, 797–817.

- Bordalo, P.; Gennaioli, N.; Shleifer, A. Diagnostic expectations and credit cycles. The Journal of Finance 2018, 73, 199–227. [CrossRef]

- Kahneman, D.; Tversky, A. Subjective probability: A judgment of representativeness. Cognitive psychology 1972, 3, 430–454. [CrossRef]

- Kaizoji, T.; Sornette, D. Bubbles and Crashes. Encyclopedia of Quantitative Finance 2010.

- Bianchi, F.; Ludvigson, S.C.; Ma, S. Belief distortions and macroeconomic fluctuations. American Economic Review 2022, 112, 2269–2315. [CrossRef]

- Song, G.H. Unraveling stock market crashes: insights from behavioral psychology. Review of Behavioral Finance 2025, 17, 217–233. [CrossRef]

- Gilboa, I.; Schmeidler, D. Maxmin expected utility with non-unique prior. Journal of mathematical economics 1989, 18, 141–153. [CrossRef]

- Hansen, L.P.; Sargent, T.J. Robust control and model uncertainty. American Economic Review 2001, 91, 60–66.

- Epstein, L.G.; Schneider, M. Ambiguity and asset markets. Annu. Rev. Financ. Econ. 2010, 2, 315–346. [CrossRef]

- Ju, N.; Miao, J. Ambiguity, learning, and asset returns. Econometrica 2012, 80, 559–591. [CrossRef]

- Bao, T.; Duffy, J.; Zhu, J. Information Ambiguity, Market Institutions, and Asset Prices: Experimental Evidence. Management Science 2024. [CrossRef]

- Weinstein, N.D.; Klein, W.M. Unrealistic optimism: Present and future. Journal of Social and Clinical Psychology 1996, 15, 1–8. [CrossRef]

- Hoorens, V.; Van Damme, C.; Helweg-Larsen, M.; Sedikides, C. The hubris hypothesis: The downside of comparative optimism displays. Consciousness and Cognition 2017, 50, 45–55. [CrossRef]

- Jefferson, A.; Bortolotti, L.; Kuzmanovic, B. What is unrealistic optimism? Consciousness and cognition 2017, 50, 3–11.

- Hayashi, F. Tobin’s marginal q and average q: A neoclassical interpretation. Econometrica: Journal of the Econometric Society 1982, pp. 213–224. [CrossRef]

- Rabin, M. Psychology and economics. Journal of economic literature 1998, 36, 11–46.

- Berthet, V. The measurement of individual differences in cognitive biases: A review and improvement. Frontiers in psychology 2021, 12, 630177. [CrossRef]

- Agranov, M.; Potamites, E.; Schotter, A.; Tergiman, C. Beliefs and endogenous cognitive levels: An experimental study. Games and Economic Behavior 2012, 75, 449–463. [CrossRef]

- Krokida, S.I.; Makrychoriti, P.; Spyrou, S. Monetary policy and herd behavior: International evidence. Journal of Economic Behavior & Organization 2020, 170, 386–417. [CrossRef]

- Liu, P.; Dwarakanath, K.; Vyetrenko, S.S.; Balch, T. Limited or Biased: Modeling Subrational Human Investors in Financial Markets. Journal of Behavioral Finance 2024, pp. 1–24. [CrossRef]

Figure 1.

The Effect of Subsidies on Welfare in the absence of Unrealistic Optimism. The left panel depicts the welfare in the bad state at date 1 in the absence of government subsidies, which corresponds to the area of the triangle, denoted by R. The right panel shows that with government intervention, the producer surplus increases by S, but the total amount of subsidies becomes , implying that welfare declines by T, compared to the case without subsidies.

Figure 1.

The Effect of Subsidies on Welfare in the absence of Unrealistic Optimism. The left panel depicts the welfare in the bad state at date 1 in the absence of government subsidies, which corresponds to the area of the triangle, denoted by R. The right panel shows that with government intervention, the producer surplus increases by S, but the total amount of subsidies becomes , implying that welfare declines by T, compared to the case without subsidies.

Figure 2.

The Effect of Subsidies on Welfare in the presence of Unrealistic Optimism. This figure depicts the effects on welfare when the government provides subsidies at date 0 in the presence of unrealistic optimism. The left panel depicts welfare in the absence of subsidies, where U denotes the consumer surplus and R denotes the producer surplus. The right panel depicts welfare in the presence of subsidies, where denotes the consumer surplus, denotes the producer surplus, and denotes the amount of subsidies provided.

Figure 2.

The Effect of Subsidies on Welfare in the presence of Unrealistic Optimism. This figure depicts the effects on welfare when the government provides subsidies at date 0 in the presence of unrealistic optimism. The left panel depicts welfare in the absence of subsidies, where U denotes the consumer surplus and R denotes the producer surplus. The right panel depicts welfare in the presence of subsidies, where denotes the consumer surplus, denotes the producer surplus, and denotes the amount of subsidies provided.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.