Submitted:

16 January 2026

Posted:

19 January 2026

You are already at the latest version

Abstract

In emerging economies characterized by a predominance of the banking sector, the trans-mission of monetary policy to bank credit remains a central and ongoing topic of debate. Although the interest rate channel is the primary tool of central banks, numerous studies reveal persistent inertia in short-term bank credit, casting doubt on the effectiveness of monetary transmission. This study examines the transmission of monetary policy to bank credit for non-financial businesses in Morocco, adopting a dynamic, long-term approach.

The empirical analysis is based on monthly data covering 2006–2023 and uses an ARDL–ECM model that distinguishes short-term dynamics from long-term adjustment mecha-nisms and incorporates structural breaks. The results indicate that variations in the policy rate do not have a significant effect on short-term bank credit, which confirms the weaken-ing of the traditional rate channel. However, this inertia is accompanied by a strong long-term equilibrium relationship between credit, monetary policy, and risk conditions.

The results highlight a gradual monetary transmission, strongly influenced by credit risk and bank balance-sheet arbitrage. The apparent inefficiency of the short-term rate channel thus reflects a transmission modulated by prudential and structural constraints, rather than a breakdown of the monetary transmission mechanism.

Keywords:

monetary transmission mechanism

; bank credit

; credit risk

; portfolio adjustments

; balance‐sheet effects

; long‐run dynamics

; emerging markets

1. Introduction

In emerging economies characterized by a predominance of the banking sector, the transmission of monetary policy to the real economy is a significant challenge for macroeconomic stability and growth. The policy rate is the preferred conventional instrument of central banks to guide monetary conditions. However, the actual effectiveness of this tool in influencing bank credit to non-financial companies remains widely debated in academic literature and institutional analyses.

Monetary transmission is traditionally viewed as a relatively direct mechanism, in which changes in the policy rate quickly affect financing conditions and, consequently, bank credit volumes (Bernanke & Gertler, 1995). However, a growing number of empirical studies challenge this perspective, particularly in emerging economies. Several analyses demonstrate that bank credit adjustments are frequently weak, delayed, or even absent in the short term, even during prolonged periods of accommodative monetary policy (Tenreyro & Thwaites, 2016).

The literature offers divergent interpretations of this observation. Some authors consider it a structural weakening of the credit channel, attributable to strengthened prudential constraints, persistent risk aversion, or deep institutional rigidities. Others believe that this inertia does not constitute a failure of monetary transmission, but rather reflects adjustment delays inherent in risk assessment processes, bank portfolio arbitrations, and balance sheet constraints, particularly present in bank-dominated financial systems (Adrian & Shin, 2010; Gambacorta & Shin, 2018).

However, the relevant time horizon for evaluating the transmission of monetary policy remains insufficiently clearly defined in this debate. The empirical literature mainly focuses on short-term reactions to credit and often concludes that the transmission is weak or nonexistent. However, this focus on the immediacy of adjustments can obscure the existence of long-term equilibrium relationships, whose adjustments are slow, conditional, and heavily dependent on credit risk and the structure of bank balance sheets (Bernanke et al., 1999; Cloyne et al., 2023). Therefore, the lack of an immediate credit response does not necessarily constitute evidence of monetary policy ineffectiveness.

This issue is significant in the Moroccan context. Institutional analyses by Bank Al-Maghrib highlight a persistent dissociation between the relatively rapid adjustment of monetary conditions and the more rigid dynamics of bank credit granted to non-financial enterprises, notably due to the inertia of outstanding amounts, prudential constraints, and risk management mechanisms.

Generally speaking, the institutional literature on emerging economies shows that the transmission of monetary policy to bank credit often remains incomplete, variable, and dependent on the macro-financial context. A recent report from the International Monetary Fund indicates that international financial conditions, the evolution of risk spreads, and the structure and strength of bank balance sheets strongly influence monetary transmission channels. Thus, monetary policy measures most often lead to gradual adjustments in credit conditions and volumes, rather than immediate increases in bank financing to the private sector (IMF, 2024).

This study is set in this context. It aims to analyze how monetary policy is transmitted to bank credit intended for non-financial companies in Morocco, taking into account both short-term and long-term effects, as well as the role of credit risk and banks' portfolio choices. The analysis is based on monthly data from 2006 to 2023, which allows for the inclusion of different monetary regimes, periods of macro-financial stress, and phases of change in the structure of bank balance sheets.

Moreover, the choice to focus on bank credit in the non-financial sector is motivated by its dominant quantitative weight and its central role in macroeconomic transmission. According to the Bank Al-Maghrib Annual Report (2023), total outstanding bank credit reached 1,114.9 billion dirhams, equivalent to approximately 76.2% of GDP. In this total, the majority of the outstanding amount is allocated to the non-financial sector, which thus constitutes the main channel thru which the banking system finances real economic activity. Conversely, although loans to financial companies recorded a strong acceleration in 2023, their relative weight remains limited, and their dynamics are primarily determined by refinancing, liquidity management, and intra-financial arbitrage.

Moreover, recent developments confirm a structural divergence between the two credit segments. After an exceptional expansion in 2022, credit to the non-financial sector decelerated sharply in 2023, before embarking on a gradual recovery trajectory anticipated by Bank Al-Maghrib. This evolution contrasts with that of credit to the financial sector, whose high volatility reflects more balance-sheet adjustments and liquidity constraints than actual demand for financing from the real economy. Therefore, bank credit to the non-financial sector appears not only quantitatively dominant but also more economically relevant for analyzing the effective transmission of monetary policy in Morocco.

On the methodological front, this study uses an ARDL–ECM econometric model, adapted to the analysis of long-term relationships between integrated variables of different orders and likely to be influenced by structural breaks (Pesaran et al., 2001). This model clearly distinguishes short-term dynamics from long-term adjustments without imposing overly strict constraints on its structure.

The main results show that bank credit does not respond significantly to short-term variations in the policy rate, but this does not undermine monetary transmission. This exists with solid long-term equilibrium relationships. The results indicate that monetary transmission occurs mainly through gradual adjustments, influenced by credit risk and bank balance-sheet constraints, rather than through immediate reactions to monetary signals.

2. Literature Review

The transmission of monetary policy in emerging economies with strong banking dominance has long been the subject of a theoretical consensus, but remains empirically controversial. If traditional models posit that the policy rate influences the real economy through the bank credit channel, empirical results suggest that this relationship is far from mechanical. In many emerging countries, changes in the policy rate do not translate into immediate adjustments or proportional quantitative responses in bank credit, particularly for financing non-financial companies.

A first reading of this literature highlights a persistent inertia in short-term bank credit, often interpreted as a structural weakening of the credit channel. Several studies document the lack of significant credit expansion following episodes of monetary easing, suggesting that lending decisions would be dominated by non-monetary factors, such as risk, solvency, or institutional constraints (Mishra et al., 2014). However, this interpretation remains incomplete, as it relies on a contemporary reading of credit adjustments.

A second approach, stemming from the foundational works of Bernanke and Gertler (1995) and Bernanke et al. (1999), challenges this view by emphasizing that the lack of immediate credit response should not be equated with the ineffectiveness of monetary policy. According to this perspective, transmission depends closely on the financial situations of banks and borrowers, as well as on the balance sheet constraints to which intermediaries are subject. Bank credit can thus react with a delay, once risk and balance sheet structure adjustments have been made.

This logic is further developed in the literature on the bank balance sheet channel and portfolio arbitrages. The work of Adrian and Shin (2010) shows that banks adjust their leverage and asset composition in response to monetary and financial conditions, which can, in specific contexts, lead to a reallocation toward liquid, low-risk assets, such as government securities. The empirical results of Acharya and Steffen (2015) and Gambacorta and Shin (2018) confirm that these arbitrages can temporarily neutralize the expected effect of the policy rate on bank credit, without breaking the long-term relationship between monetary policy and the financing of the real economy.

At the same time, the credit risk literature emphasizes that asset quality is a central determinant of monetary transmission. The credit rationing framework (Stiglitz & Weiss, 1981) suggests that when perceived risk increases, banks primarily adjust credit quantities rather than prices. The empirical work of Jiménez et al. (2012) shows that the deterioration of non-performing loans limits banks' ability to amplify monetary impulses through credit expansion, particularly in emerging economies where risk-sharing mechanisms are incomplete.

These microeconomic analyses extend into international institutional assessments. Reports from the Bank for International Settlements and the International Monetary Fund highlight that, in many emerging countries, monetary transmission to bank credit is filtered mainly through capital constraints, balance sheet quality, and prudential requirements (BIS, 2019; IMF, 2019). More recently, Checo et al. (2024) show that monetary policy shocks are mainly absorbed through balance sheet adjustments and risk revaluations, while credit volumes respond gradually and heterogeneously, depending on the macro-financial regime.

The case of Morocco fits this issue perfectly. Despite several phases of monetary easing, the evolution of bank credit to non-financial enterprises remains marked by significant inertia and structural breaks related to economic cycles and prudential reforms (Bank Al-Maghrib, 2021). Recent studies by Boutfssi and Zizi (2025) show that access to bank financing depends less on contemporary variations in the key interest rate than on prudential constraints, risk perception, and institutional hedging mechanisms. Similarly, Boutfssi and Quamar (2026) highlight a dissociation between the rapid reaction of financial conditions and the inertia of credit volumes, emphasizing the central role of portfolio arbitrages and progressive correction mechanisms.

On the institutional front, the progressive strengthening of the prudential framework, notably through Bank Al-Maghrib's circular no. 1/W/16 has increased the resilience of the banking system while altering the conditions for the transmission of monetary policy. Recent supervision and financial stability reports confirm that credit supply is now conditioned mainly by loss-absorption capacity and balance-sheet structure, rather than by a mechanical response to the sole signal of the policy rate.

Despite these advances, the literature remains fragmented. Few studies simultaneously integrate the non-stationarity of macro-financial series, structural breaks, and delayed credit adjustment mechanisms within a unified econometric framework. In particular, the articulation between long-term relationships, short-term dynamics, and changes in prudential regimes remains insufficiently explored in the context of bank-dominated emerging economies.

It is precisely from this perspective that the present study is situated, employing an ARDL–ECM framework that allows for the identification of both long-term equilibrium relationships and conditional adjustment mechanisms governing the transmission of monetary policy to bank credit in the non-financial sector.

3. Conceptual Framework and Research Hypothesis

This study falls within the literature on the transmission of monetary policy within bank-dominated financial systems, with a focus on emerging economies. In this context, bank credit to the non-financial sector serves as a central channel for the transmission of monetary impulses to the real economy. However, the theoretical and empirical literature indicates that this transmission is neither immediate nor uniform over time, and that it can be influenced by financial frictions, balance sheet constraints, and institutional characteristics specific to the banking system.

In this context, the policy rate is a central monetary policy instrument capable of influencing financing conditions. However, its effect on bank credit supply results from the interaction among interest rate signals, credit risk conditions, and banks' portfolio arbitrages. Short-term changes in credit can thus exhibit a certain inertia, attributable to contractual rigidities, internal risk assessment processes, and prudential requirements. Conversely, long-term dynamics can highlight stable relationships between credit and its macro-financial determinants.

The adopted conceptual framework thus distinguishes short-term mechanisms from long-term relationships, while accounting for the possibility that transmission mechanisms may vary over time. Changes in the macro-financial context, the regulatory framework, or the operating conditions of the banking sector are likely to alter the transmission of monetary policy to credit, without necessarily questioning the existence of a long-term equilibrium. The proposed empirical analysis aims to examine the nature of these relationships, their adjustment modalities, and their temporal stability, within a unified econometric framework.

Research hypothesis:

H1:

Short-term monetary transmission

Changes in the policy rate have a statistically significant effect on the short-term dynamics of bank credit to the non-financial sector.

H2:

Long-term relationship

Bank credit to the non-financial sector maintains a statistically significant long-term relationship with monetary policy and macro-financial conditions.

H3:

Adjustment mechanism toward equilibrium

The deviations of bank credit from its long-term equilibrium level are gradually corrected over time, reflecting a dynamic adjustment mechanism.

H4:

Non-invariance of transmission mechanisms

The mechanisms through which monetary policy and macro-financial conditions influence bank credit to the non-financial sector are not time-invariant and can undergo structural changes as the macro-financial and institutional environment evolves.

4. Methodology

4.1. General Empirical Strategy

This study uses a time series econometric method to analyze how monetary policy is transmitted to bank credit for non-financial companies in an emerging economy dominated by banks. This choice is based on the tradition of dynamic macro-financial analysis, which shows that bank credit adjustments are often slow, depend on risk conditions, and take time due to balance sheet constraints and prudential rules (Bernanke & Gertler, 1995; Bernanke et al., 1999).

Unlike static approaches or models that assume the policy rate immediately, symmetrically, and linearly influences credit volumes, this study assumes that credit dynamics depend on complex interactions among the monetary signal, perceptions of credit risk, and banks' portfolio choices. This idea aligns with the literature on bank balance sheets and risk channels, which explains that credit decisions depend primarily on the financial soundness of banks, asset quality, and applicable regulations, and not solely on the cost of liquidity (Adrian & Shin, 2010; Gambacorta & Shin, 2018).

From an econometric perspective, this approach assumes that monetary policy can have different effects across time horizons. There may be little or no impact in the short term, but gradual adjustments toward a long-term equilibrium. The analysis must therefore use a framework that clearly distinguishes short-term dynamics from long-term relationships, while accounting for the statistical properties of macro-financial series, which are often non-stationary and prone to structural breaks (Lütkepohl, 2005).

The methodology is structured sequentially and cumulatively, in accordance with best practices in time series econometrics applied to macro-financial data (Pesaran et al., 2001; Banerjee et al., 1993). It aims to successively examine:

- (i)

- the statistical properties of the series in order to identify their order of integration and avoid any spurious regression (Phillips & Perron, 1988);

- (ii)

- (the possible presence of structural breaks or changes in the macro-financial regime, apprehended thru structural controls and stability tests (Brown et al., 1975);

- (iii)

- the existence of a long-term equilibrium relationship between bank credit and its determinants, a prerequisite for identifying a sustainable monetary policy transmission mechanism (Pesaran et al., 2001);

- (iv)

- short-term adjustment mechanisms, analyzed within an error correction framework allowing for the measurement of the speed of convergence toward long-term equilibrium after a shock (Banerjee et al., 1993);

- (v)

- the temporal stability of these mechanisms, in order to evaluate the robustness of the estimated relationship in the face of changes in the macro-financial and regulatory context (Brown et al., 1975).

This empirical strategy thus allows for the analysis of monetary transmission within a dynamic and institutionally coherent perspective, adapted to the specificities of emerging economies dominated by the banking sector, without presupposing a priori the speed or intensity of bank credit adjustments.

4.2. Data

The empirical analysis is based on monthly data from January 2006 to September 2023. This period encompasses several monetary policy regimes, significant prudential developments, and various macro-financial shocks, all of which are likely to have influenced banks' credit supply behavior.

The data comes exclusively from official institutional sources. Credit aggregates, risk indicators, and balance sheet variables are sourced from the consolidated statistics of the banking system. In contrast, monetary and macro-financial variables are sourced from the official publications of the competent authorities. The use of these sources ensures the reliability, consistency, and reproducibility of the analysis.

Volume variables are expressed in natural logarithms to stabilize the variance and facilitate the economic interpretation of the coefficients, while rates and ratios are kept at levels.

4.3. Transmission Variables and Channels

The dependent variable is bank credit granted to the non-financial corporate sector, denoted as ,,expressed in logarithmic form:

Three main explanatory variables are introduced, each corresponding to a specific transmission channel:

- Monetary channel: the policy rate (), representing the conventional signal of monetary policy.

- Risk and prudential channel: the non-performing loan ratio (), used as a proxy for perceived risk and prudential constraints weighing on credit supply.

- Portfolio and liquidity arbitrage channel: the outstanding amount of public securities held by banks, expressed in logarithm (), reflecting asset allocation choices and balance sheet management.

This specification allows for a joint analysis of the effects of the monetary signal, risk conditions, and balance-sheet arbitrages on the dynamics of bank credit.

4.4. Properties of Series, Unit Root Tests, and Collinearity

Before undertaking dynamic modeling, the stationarity properties of the series are evaluated using the Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) unit root tests. This step aims to identify the order of integration of the variables and to prevent the risks of spurious regressions, common in the analysis of macro-financial series.

Unit root tests are conducted, accounting for the possibility of structural breaks to limit biases arising from unacknowledged regime changes. This approach ensures that the conditions for applying the ARDL–ECM framework are met.

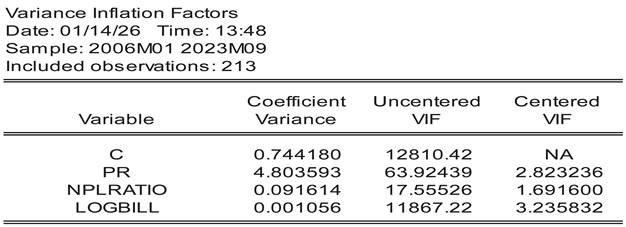

Furthermore, a collinearity test is conducted before estimating the model to ensure that the explanatory variables are not excessively interdependent. Collinearity is assessed using variance inflation factors (VIFs), which help ensure the stability of the estimated coefficients and the robustness of subsequent econometric inferences.

4.5. Control of Structural Breaks

Given the length of the studied period and the likelihood of regime changes that may affect the dynamics of bank credit, the analysis explicitly incorporates a control for structural breaks.

To this end, structural break detection tests are employed to identify statistically significant discontinuities in the analyzed series. Based on these tests, exogenous dummy variables are introduced as structural controls at all empirical stages, including stationarity tests and ARDL and ECM model estimations.

The introduction of these variables aims to neutralize the potential impact of statistically identified regime changes, which could undermine the stability of the estimated relationships over the long term. These dummy variables are not interpreted as economic transmission mechanisms but are used solely as control variables to ensure the robustness of the estimates.

4.6. Choice of the ARDL Model and General Specification

Given the presence of integrated variables of mixed orders I(0) and I(1), the strong inertia of bank credit, and the need to incorporate structural break controls, the study adopts an Autoregressive Distributed Lag (ARDL) model.

The ARDL approach allows for the simultaneous identification of a long-term equilibrium relationship and short-term adjustment mechanisms, while remaining suitable for the analysis of monthly series exhibiting slow dynamics.

The general specification estimated is as follows:

4.7. Cointegration Test and Long-Term Relationship

The existence of a long-term equilibrium relationship between bank credit and its determinants is tested using the bounds cointegration test associated with the ARDL approach. The rejection of the null hypothesis of no cointegration indicates that the variables share a stable long-term relationship.When cointegration is established, the long-term relationship is estimated in the form:

4.8. Short-Term Dynamics

The ARDL model is reparametrized as an error-correction model (ECM) to analyze short-term adjustments while maintaining consistency with the long-term equilibrium. The error correction term measures the speed of adjustment of credit toward its equilibrium level following a shock.

4.9. Tests de Diagnostic et Stabilité Des Paramètres

The statistical validity of the model (Error Correction Model, ECM) is evaluated using standard diagnostic tests. The autocorrelation of residuals is examined using the Breusch–Godfrey LM test, heteroscedasticity by the White test, and parameter stability by the CUSUM and CUSUM of Squares tests.

4.10. Endogenous Rupture and Potential Change in Transmission Mechanisms

To evaluate the potential for a dominant reconfiguration of credit adjustment mechanisms during the studied period, an endogenous Quandt–Andrews-type breakpoint test is applied to the ECM equation. This test allows for the identification of potential structural instability affecting short-term dynamics.

When relevant, the model is enriched by interaction terms between a post-break dummy variable and the main explanatory variables, and a joint Wald test is used to assess whether the transmission mechanisms differ significantly between regimes.

5. Preliminary Tests

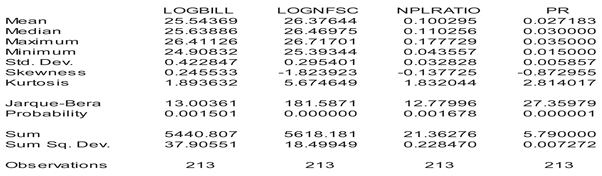

5.1. Descriptive Analysis

Table 1 presents the descriptive statistics for the main macro-financial variables studied, based on 213 monthly observations. The volume variables, such as credit to the non-financial sector and the outstanding amount of Treasury bills, are expressed in logarithms to reduce their asymmetry and facilitate the interpretation of relative variations.

The variables LOGNFSC (credit to the non-financial sector) and LOGBILL (outstanding Treasury bills held by banks) exhibit moderate dispersion, with standard deviations of 0.295 and 0.423, respectively. This stability corresponds to the cumulative nature and institutional inertia of these aggregates. The distribution of LOGNFSC is very leptokurtic (kurtosis = 5.67) and left-skewed, indicating periods of slowdown or credit contraction, often observed during macro-financial tensions.

The non-performing loan ratio (NPLRATIO) varies more than its average, with a standard deviation of about 0,0328, for an average of 0.10. This reflects the cyclical nature of credit risk and its sensitivity to macroeconomic conditions. Its distribution is not normal, as is typical for banking risk indicators, which are often influenced by one-off adjustments and threshold effects.

The policy rate (PR) exhibits low absolute dispersion but a highly asymmetric, leptokurtic distribution. This reflects the discretionary nature of monetary policy, which is adjusted in steps and rarely continuously.

The Jarque–Bera normality tests reject the normality assumption for all variables. This result is expected for long-term monthly macro-financial series and justifies the use of robust methods based on time-series dynamics rather than strict assumptions of normality.

5.2. Correlation Test

The correlation matrix reveals significant co-movement among the main macro-financial variables, highlighting economic regularities consistent with a financial interpretation of monetary transmission.

First, the positive and relatively high correlation between credit to the non-financial sector (LOGNFSC) and outstanding Treasury bills held by banks (LOGBILL), at 0.684, indicates a strong co-evolution of these two aggregates in the sample. On the economic front, this relationship suggests that phases of credit expansion coincide with an increase in public securities portfolios, which corresponds more to a simultaneous expansion of bank balance sheets and favorable liquidity conditions than to a simple mechanism of private credit displacement.

Secondly, the policy rate (PR) shows a negative correlation with bank balance sheet variables. The correlation between PR and LOGNFSC is −0.535, while that between PR and LOGBILL is even more pronounced (−0.801). These coefficients show that higher policy rates are associated with lower levels of bank credit and public securities holdings. This relationship primarily reflects the fluctuations of the monetary cycle and overall financial conditions, without necessarily implying a direct and immediate causal effect of the policy rate on credit volumes.

Thirdly, the correlation between credit risk (NPLRATIO) and credit volume (LOGNFSC) is very weak and slightly negative (−0.050). This coefficient, close to zero, indicates that the impact of risk on credit supply does not manifest immediately, but rather through delayed adjustments, in accordance with prudential mechanisms and bank decision-making timelines. On the other hand, NPLRATIO shows a negative correlation with the policy rate (−0.560), which reflects the cyclical nature of credit risk.

Finally, no bilateral correlation exceeds absolute values close to unity, which excludes severe multicollinearity and confirms the feasibility of multivariate estimation. Overall, these descriptive results justify the use of a dynamic ARDL–ECM approach, which distinguishes short-term co-movements from long-term equilibrium relationships.

Table 2.

Correlation matrix (Pearson).

| Variable | LOGBILL | LOGNFSC | NPLRATIO | PR |

| LOGBILL | 1,000 | 0,684 | 0,633 | −0,801 |

| LOGNFSC | 0,684 | 1,000 | −0,050 | −0,535 |

| NPLRATIO | 0,633 | −0,050 | 1,000 | −0,560 |

| PR | −0,801 | −0,535 | −0,560 | 1,000 |

Source: Authors’ calculations.

The results indicate that all centered VIFs remain well below the usual threshold of 5, which suggests the absence of problematic multivariate collinearity among the explanatory variables. Therefore, the multivariate estimates can be interpreted without a significant risk of distorting standard deviations or instability in coefficients due to collinearity.

Table 3.

Variance Inflation Factors (VIF).

| Explanatory Variable | Centered VIF |

| PR | 2,823 |

| NPLRATIO | 1,692 |

| LOGBILL | 3,236 |

Source: Authors’ calculations.

5.3. Stationarity Tests

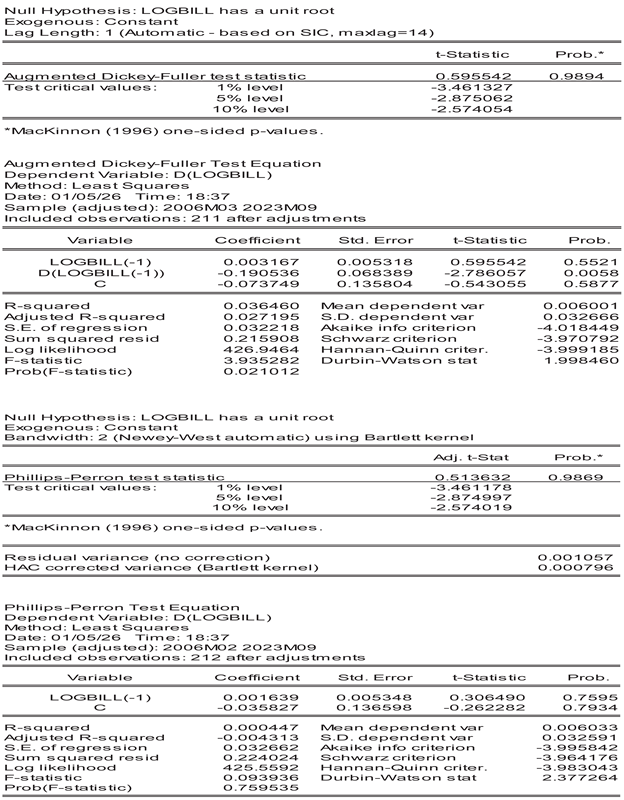

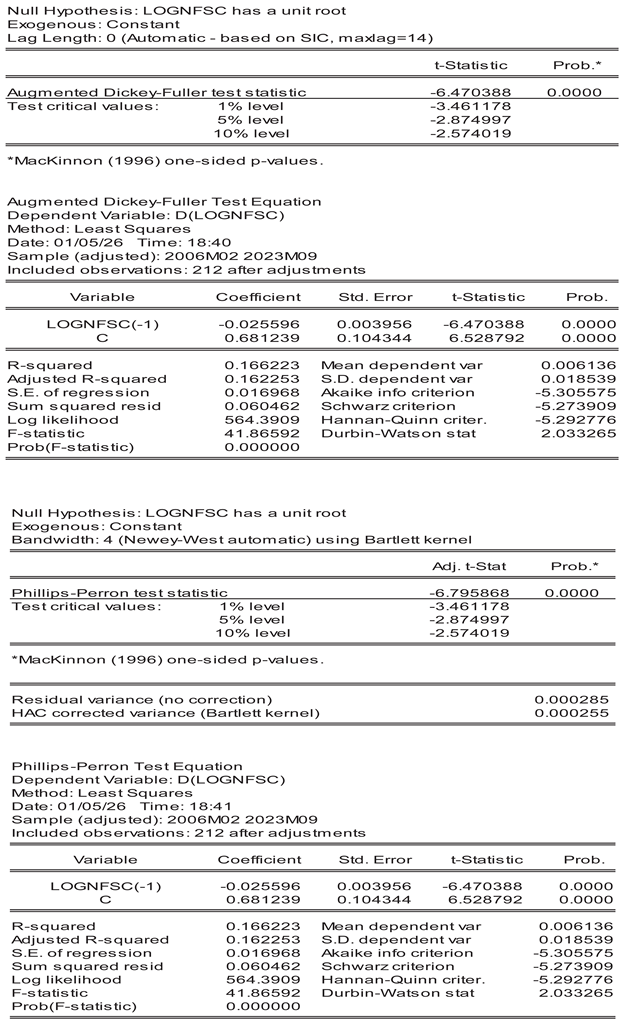

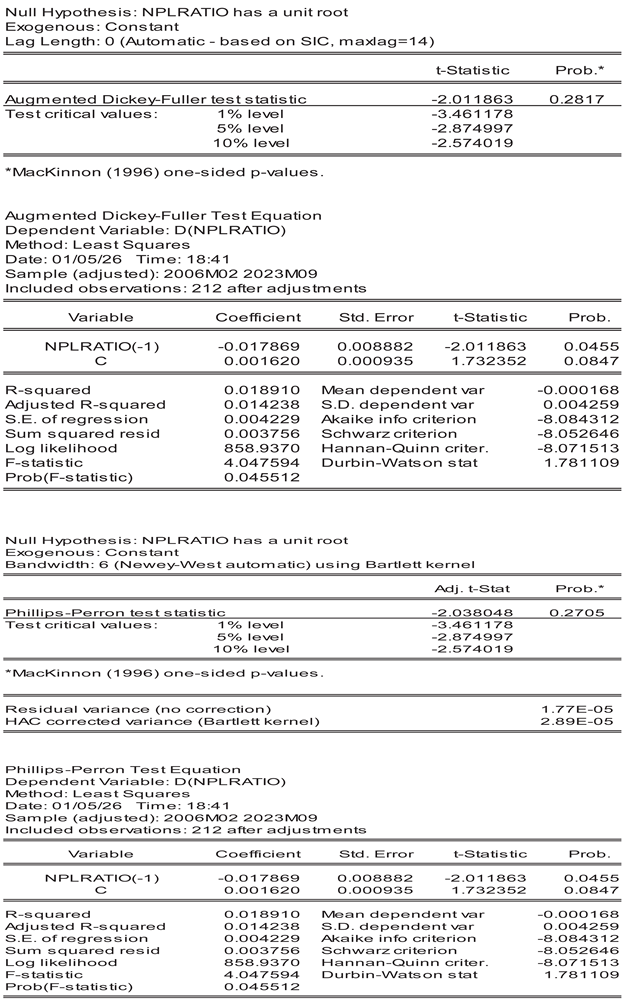

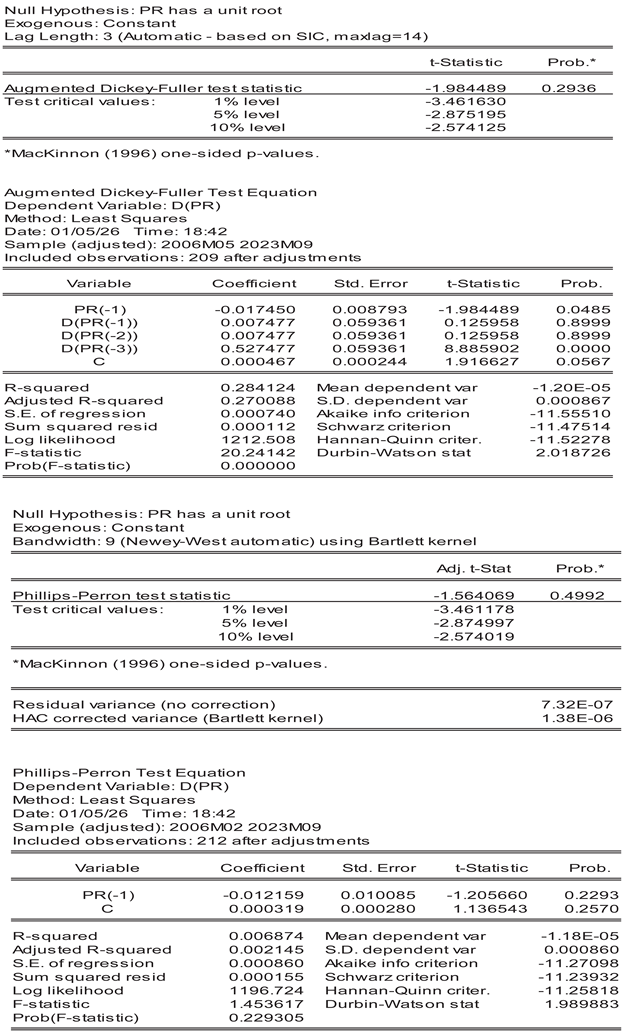

The ADF and Phillips-Perron tests give consistent and reliable results. LOGBILL, NPLRATIO, and PR do not reject the null hypothesis of a unit root at the level (p-values between 0.27 and 0.99), indicating non-stationarity due to their cumulative, cyclical, or discretionary nature. On the other hand, LOGNFSC clearly rejects the unit root hypothesis, with ADF statistics = −6.47 and PP statistics = −6.80 (p-values at 0.000), well below the 1% critical threshold, confirming its stationarity at the level (I(0)).

This difference in the orders of integration, with LOGNFSC in I(0) and the other variables in I(1), is logical in a regulated banking system. Institutional and prudential rules limit credit, while monetary instruments, risk, and public securities evolve more sustainably. Moreover, none of the variables is I(2), confirming that the ARDL–Bounds model is suitable for studying both long-term relationships and short-term adjustments.

Table 4.

Unit root tests (ADF and Phillips–Perron).

| Variable | Test | Statistic | p-Value | Order of Integration |

| LOGBILL | ADF | 0,596 | 0,989 | I(1) |

| PP | 0,514 | 0,987 | I(1) | |

| LOGNFSC | ADF | −6,470 | 0,000 | I(0) |

| PP | −6,796 | 0,000 | I(0) | |

| NPLRATIO | ADF | −2,012 | 0,282 | I(1) |

| PP | −2,038 | 0,271 | I(1) | |

| PR | ADF | −1,984 | 0,294 | I(1) |

| PP | −1,564 | 0,499 | I(1) |

Source: Authors’ calculations.

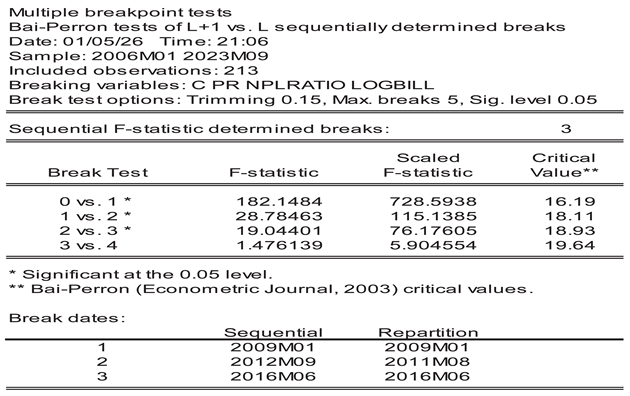

5.4. Structural Ruptures

The Bai–Perron test highlights three statistically significant structural breaks in the relationship between credit to the non-financial sector and its macro-financial determinants. The sequential F statistics exceed the 5% critical values for the 0 vs 1, 1 vs 2, and 2 vs 3 tests, leading to rejection of the null hypothesis of coefficient stability. On the other hand, the 3 vs 4 test is not significant, which indicates that three breaks constitute the optimal specification.

On a methodological level, these results confirm that credit dynamics cannot be correctly analyzed under the assumption of parametric stability over the entire period. They fully justify the introduction of dummy variables or stability tests in the ARDL model, as well as the differentiated analysis of macro-financial regimes. The identified break dates, 2009M01, 2012M09, and 2016M06, correspond to macro-financial regime changes likely to affect credit transmission mechanisms, without presuming a priori the exact nature of the shocks. It is important to emphasize that the Bai–Perron test does not identify temporary shocks, but rather lasting changes in the structural relationships between credit, risk, and bank portfolio arbitrages.

Thus, the 2009 break is consistent with a phase of global macro-financial stress, the 2012 break with a period of prolonged tensions affecting risk quality and the economic environment, while the 2016 break suggests a more profound and more persistent reconfiguration of credit adjustment mechanisms. This last break is significant because it concerns the coefficients themselves, and not just a simple level effect.

Table 5.

Test of multiple structural breaks (Bai–Perron).

| Sequential Test | F-Statistic | F-Statistic Adjusted | Critical Value | Decision |

| 0 vs 1 | 182,15 | 728,59 | 16,19 | Rejet H₀ |

| 1 vs 2 | 28,78 | 115,14 | 18,11 | Rejet H₀ |

| 2 vs 3 | 19,04 | 76,18 | 18,93 | Rejet H₀ |

| 3 vs 4 | 1,48 | 5,90 | 19,64 | Non rejet |

Source: Authors’ calculations.

6. Estimation of the Dynamic Model

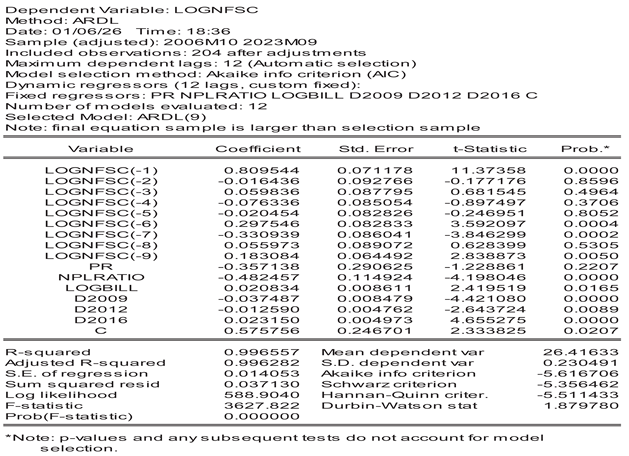

6.1. Estimation of the ARDL Model

The ARDL estimation reveals strong persistence in the dynamics of credit to the non-financial sector. The coefficient for the first credit lag, LOGNFSC(−1), is 0.8095 and highly significant (p < 0.01), indicating that approximately 81% of the current credit level is explained by its previous value. This observation confirms the marked inertia of bank credit, consistent with its nature as a stock variable and the presence of contractual and institutional rigidities.

Several higher-order credit lags are also significant, with alternating signs. Lags 6 and 9 show positive effects, while lag 7 (LOGNFCS -7) shows an adverse effect. This configuration suggests a delayed, non-monotonic adjustment dynamic, reflecting progressive mechanisms of balance-sheet reallocation and risk reassessment rather than an immediate adjustment to cyclical shocks. The lack of significance of the intermediate lags supports the hypothesis of a gradual adjustment.

The coefficient of the policy rate (PR) is negative (−0.3571) but not statistically significant (p = 0.221). Although the sign is consistent with the theoretical mechanisms of monetary transmission, this result indicates that, in the short term, changes in the policy rate do not lead to a significant quantitative adjustment in bank credit. Monetary policy thus seems to act indirectly, with a delay, and without an immediate effect on credit volumes.

On the other hand, credit risk conditions exert a decisive influence. The coefficient associated with the non-performing loan ratio (NPLRATIO) is negative, high, and highly significant (−0.4825; p < 0.01). A one percentage point increase in this ratio, on average, leads to a contraction of about 0.48% in bank credit, highlighting the primacy of prudential considerations and asset quality in lending decisions.

The outstanding Treasury bills (LOGBILL) show a positive and significant coefficient (0.0208; p < 0.05). Although this effect is quantitatively limited, it suggests that investments in public securities are accompanied by favorable liquidity conditions and an overall expansion of bank balance sheets, rather than a credit eviction mechanism for the non-financial sector.

Finally, the dummy variables capturing major macro-financial stocks are all statistically significant. The negative coefficients for the years 2009 and 2012 indicate notable contractions in bank credit during periods of economic stress, while the positive coefficient for the period after 2016 reflects a phase of expansion and gradual normalization of credit. These results confirm the sensitivity of bank credit to macroeconomic cycles and systemic shocks.

Table 6.

ARDL estimation of non-financial sector credit.

| Variable | Coefficient | Standard Error | t-Statistic | p-Value |

| LOGNFSC(−1) | 0,809544 | 0,071178 | 11,37358 | 0,0000 |

| LOGNFSC(−2) | −0,016436 | 0,092766 | −0,177176 | 0,8596 |

| LOGNFSC(−3) | 0,059836 | 0,087795 | 0,681545 | 0,4964 |

| LOGNFSC(−4) | −0,076336 | 0,085054 | −0,897497 | 0,3706 |

| LOGNFSC(−5) | −0,020454 | 0,082826 | −0,246951 | 0,8052 |

| LOGNFSC(−6) | 0,297546 | 0,082833 | 3,592097 | 0,0004 |

| LOGNFSC(−7) | −0,330939 | 0,086041 | −3,846299 | 0,0002 |

| LOGNFSC(−8) | 0,055973 | 0,089072 | 0,628399 | 0,5305 |

| LOGNFSC(−9) | 0,183084 | 0,064492 | 2,838873 | 0,0050 |

| PR | −0,357138 | 0,290625 | −1,228861 | 0,2207 |

| NPLRATIO | −0,482457 | 0,114924 | −4,198046 | 0,0000 |

| LOGBILL | 0,020834 | 0,008611 | 2,419519 | 0,0165 |

| D2009 | −0,037487 | 0,008479 | −4,421080 | 0,0000 |

| D2012 | −0,012590 | 0,004762 | −2,643724 | 0,0089 |

| D2016 | 0,023150 | 0,004973 | 4,655275 | 0,0000 |

| Constante | 0,575756 | 0,246701 | 2,333825 | 0,0207 |

Source: Authors’ calculations.

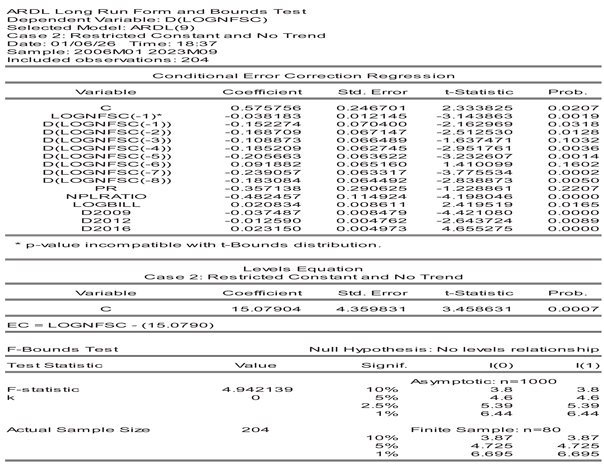

6.2. Cointegration Test

6.2.1. ARDL Bounds Cointegration Test

The bounds cointegration test associated with the ARDL approach indicates an F statistic of 4.942. This value is higher than the upper critical bound at the 5% level (I(1) = 4.725), but lower than the critical value at the 1% level.

As a result, the null hypothesis of no long-term relationship is rejected at the 5% significance level, confirming the existence of a stable cointegration relationship between credit to the non-financial sector and the model's variables.

The parameter k = 0 indicates that, in the chosen specification, no explanatory variable is explicitly integrated into the long-term equation, apart from the constant. This result means that the identified cointegration must be interpreted as the existence of a long-term equilibrium level of credit, rather than as a structural relationship directly linking credit to its observed determinants.

Table 7.

ARDL cointegration test using the bounds method (Bounds Test).

| Test | Value |

| F-statistic | 4.942 |

| Number of variables (k) | 0 |

Source: Authors’ calculations.

Table 8.

Critical values.

| Threshold | I(0) | I(1) |

| 10 % | 3.87 | 3.87 |

| 5 % | 4.725 | 4.725 |

| 1 % | 6.695 | 6.695 |

Source: Authors’ calculations.

6.2.2. Long-Term Relationship (Levels Equation)

The cointegration test indicates that the long-term relationship reduces to a positive, highly significant constant (15.079; p = 0.0007). This coefficient indicates the long-term equilibrium level of the logarithm of credit to the non-financial sector, around which short-term dynamic adjustments take place.

The statistical significance of this constant indicates that there is a stable anchor for long-term bank credit, despite temporal fluctuations. Since there are no explanatory variables in the long-term equation (k = 0), this means that the economic factors of credit do not structurally appear in the long term in this model, but rather mainly through the short-term adjustments captured by the error correction model (ECM).

The long-term relationship thus serves as a reference point for equilibrium and ensures the model's dynamic coherence. The analysis of factors explaining credit focuses mainly on short-term dynamics.

Table 9.

Level estimation of the long-term relationship (ARDL).

| Variable | Coefficient | Standard Error | t-Statistic | p-Value |

| Constant | 15.07904 | 4.359831 | 3.458631 | 0.0007 |

Note: The long-term relationship is represented here solely by a constant (k = 0), indicating the existence of a long-term equilibrium level of credit, without explicit identification of structural determinants. Source: Authors’ calculations.

6.2.3. ARDL–ECM Error Correction Model (Short-Term Dynamics)

The coefficient of the error correction term ECM(−1) is negative and statistically significant (−0.038; p = 0.0019), which confirms the existence of a long-term equilibrium return mechanism. This result shows that approximately 3.8% of the deviation from the equilibrium level of credit is corrected each period, indicating a slow but stable adjustment speed. This slowness is explained by the nature of bank credit, which involves long-term commitments, contractual rigidities, and prudential constraints.

The delayed variations in credit (ΔLOGNFSC) have significant effects at various horizons. The negative and significant coefficients at lags 1, 2, 4, 5, 7, and 8 indicate that credit expansion phases are followed by short-term corrective movements, reflecting gradual adjustment mechanisms related to risk management and balance sheet arbitrations. On the other hand, lags 3 and 6 are not statistically significant, indicating the absence of an autonomous effect at these intermediate horizons. These results reveal a short-term dynamic that is non-linear and irregular, rather than an instantaneous adjustment.

The policy rate (PR) has a negative coefficient (−0.357) but is not statistically significant (p = 0.221). This result suggests that, in the short term, variations in the policy rate do not lead to a significant quantitative adjustment in bank credit, confirming the absence of an immediate rate channel in credit dynamics.

Conversely, risk conditions play a decisive role. The coefficient associated with the non-performing loan ratio (NPLRATIO) is negative, high, and highly significant (−0.482; p < 0.01). An increase of 1 percentage point in the non-performing loan ratio leads, on average, to a contraction of about 0.48% in bank credit, underscoring the primacy of prudential considerations and asset quality in credit-granting decisions.

The outstanding Treasury bills (LOGBILL) have a positive and significant effect (0.021; p < 0.05). Although quantitatively modest, this effect suggests that higher levels of public securities holdings are associated with favorable liquidity conditions and an overall expansion of bank balance sheets, rather than a credit displacement mechanism for the non-financial sector.

Finally, the dummy variables capturing macro-financial shocks are all statistically significant. The negative coefficients for 2009 and 2012 reflect significant contractions in bank credit during periods of economic stress, while the positive coefficient in 2016 reflects a phase of expansion and gradual normalization of credit. These results confirm the high sensitivity of bank credit to macroeconomic cycles and systemic shocks.

The results of the ARDL–ECM model indicate that, in the short term, the dynamics of bank credit are dominated by risk conditions and balance sheet adjustments. At the same time, the policy rate does not play a significant immediate role. The error-correction mechanism confirms a slow but stable convergence toward long-term equilibrium, highlighting that monetary transmission to credit operates indirectly and gradually, rather than through rapid quantitative adjustments

Table 10.

Short-run dynamics.

| Variable | Coefficient | Erreur-Type | Stat. t | p-Value |

| ECM(-1) | -0.038183 | 0.012145 | -3.143863 | 0.0019 |

| ΔLOGNFSC(-1) | -0.152274 | 0.070400 | -2.162969 | 0.0318 |

| ΔLOGNFSC(-2) | -0.168709 | 0.067147 | -2.512530 | 0.0128 |

| ΔLOGNFSC(-3) | -0.108873 | 0.066489 | -1.637471 | 0.1032 |

| ΔLOGNFSC(-4) | -0.185209 | 0.062745 | -2.951761 | 0.0036 |

| ΔLOGNFSC(-5) | -0.205663 | 0.063622 | -3.232607 | 0.0014 |

| ΔLOGNFSC(-6) | 0.091882 | 0.065160 | 1.410099 | 0.1602 |

| ΔLOGNFSC(-7) | -0.239057 | 0.063317 | -3.775534 | 0.0002 |

| ΔLOGNFSC(-8) | -0.183084 | 0.064492 | -2.838873 | 0.0050 |

| PR | -0.357138 | 0.290625 | -1.228861 | 0.2207 |

| NPLRATIO | -0.482457 | 0.114924 | -4.198046 | 0.0000 |

| LOGBILL | 0.020834 | 0.008611 | 2.419519 | 0.0165 |

| D2009 | -0.037487 | 0.008479 | -4.421080 | 0.0000 |

| D2012 | -0.012590 | 0.004762 | -2.643724 | 0.0089 |

| D2016 | 0.023150 | 0.004973 | 4.655275 | 0.0000 |

Source: Authors’ calculations.

6.3. Model Stability Tests

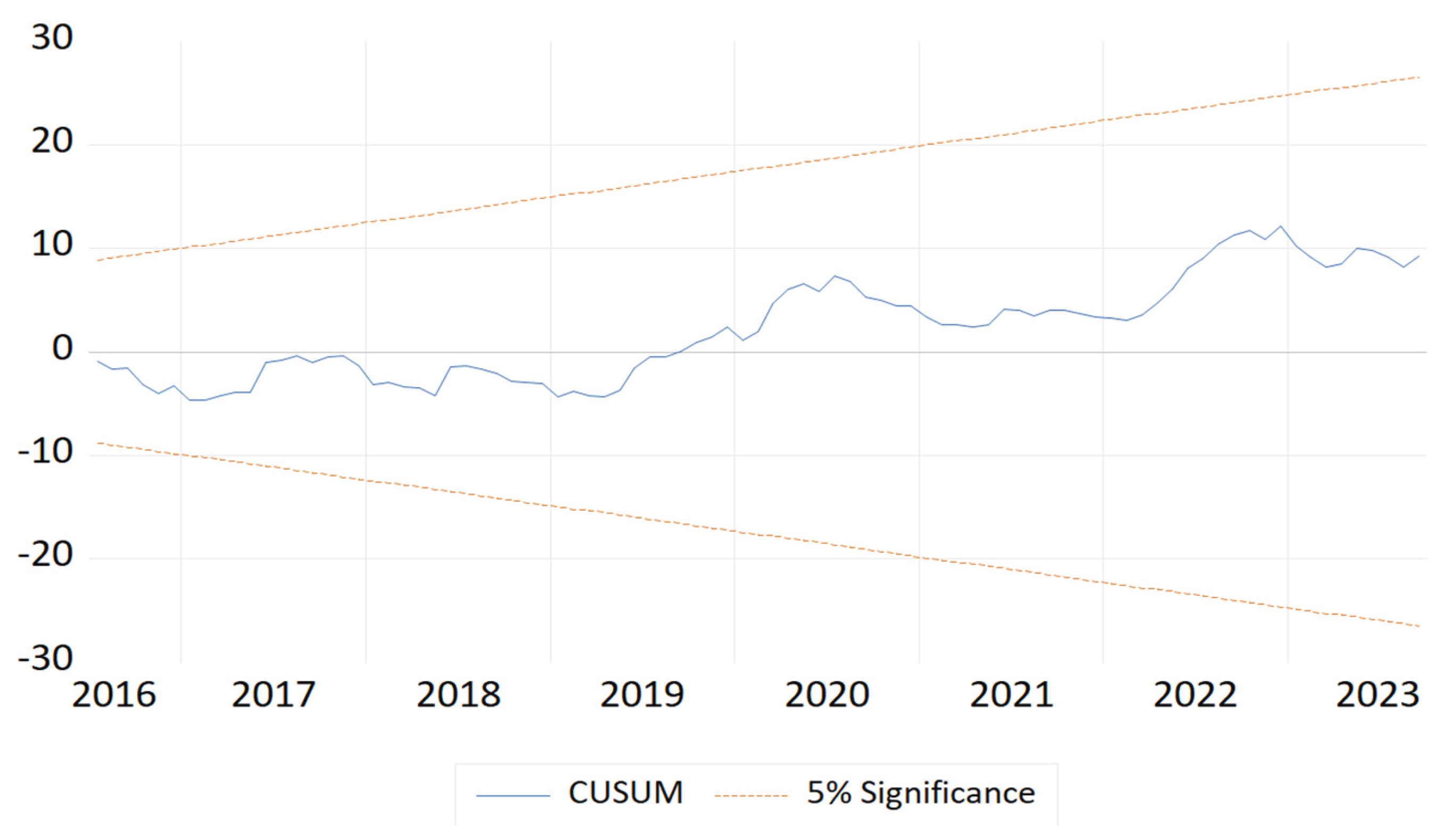

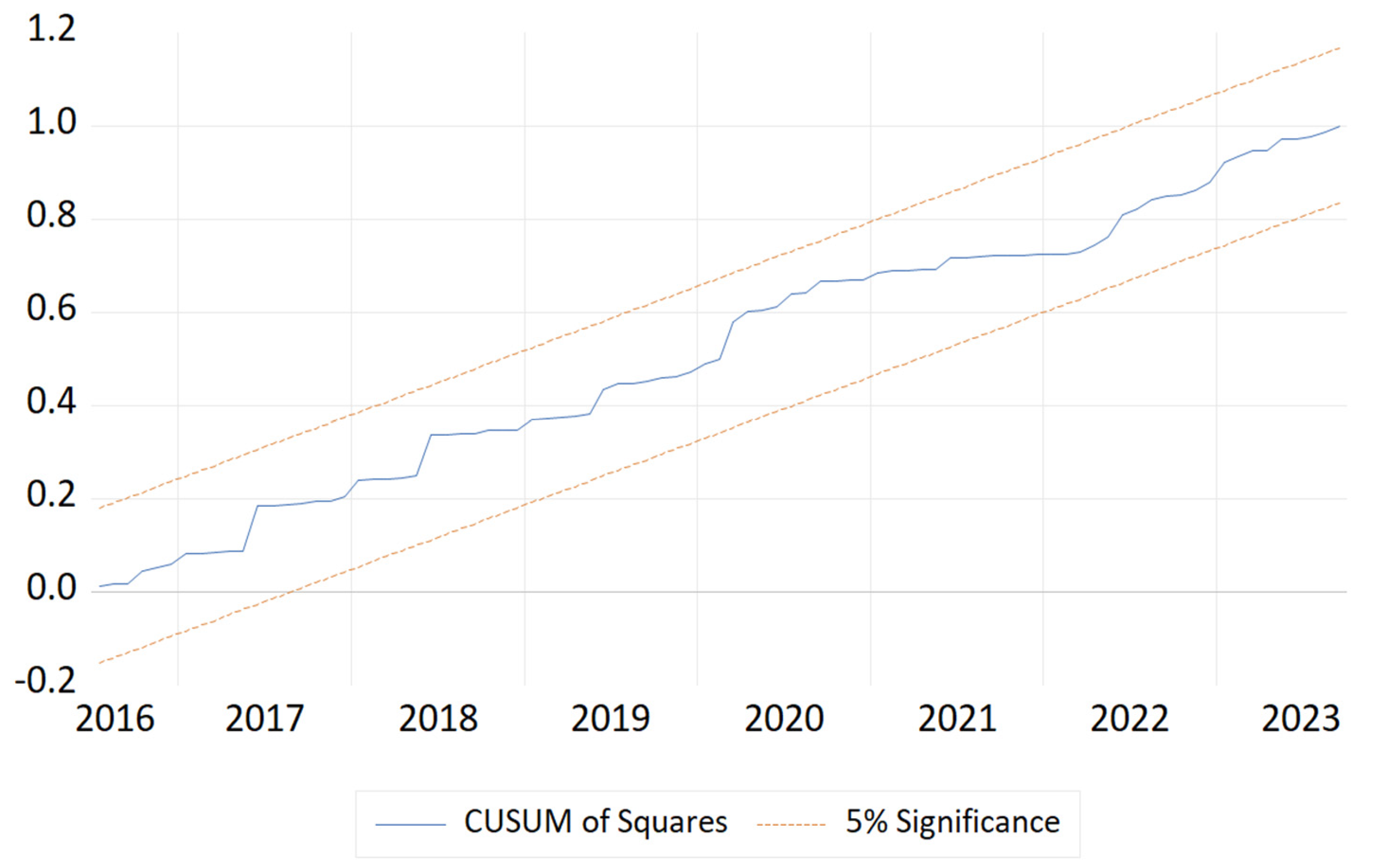

The stability of the coefficients of the ARDL-ECM model was evaluated using the CUSUM and CUSUM of Squares tests, applied to the error-correction version estimated by least squares. These tests, based on recursive residuals, apply only to the sub-period during which all model parameters are correctly identified, due to the model's complex dynamic structure and the high number of lags. Therefore, the stability graphs do not cover the entire 2006-2023 sample, but only the relevant recursive period.

During this sub-period, the CUSUM and CUSUM of Squares statistics remain within the critical bands at the 5% threshold, indicating the absence of structural instability in the estimated coefficients. This result suggests that, once the model's dynamics are established, the observed relationships, such as the speed of adjustment toward long-term equilibrium and the influence of risk conditions on credit dynamics, remain stable over time. The fact that the critical bands are never crossed, even during recent macroeconomic shocks, confirms the robustness of the parameters estimated over the analyzed period.

It should be noted that this temporal limitation is inherent to the CUSUM test methodology and does not affect the validity of the stability analysis. This constraint indicates that the test evaluates the recursive stability of the coefficients once the model is fully specified. In this context, the results provide robust empirical evidence of the stability of the ARDL–ECM model and enhance the credibility of conclusions regarding monetary transmission and the risk mechanisms influencing credit to the non-financial sector.

Figure 1.

Parameter stability test – CUSUM (ECM equation). Note: The CUSUM statistic remains within the 5% confidence bands, indicating the stability of the parameters over the studied period. Source: Authors’ calculations.

Figure 1.

Parameter stability test – CUSUM (ECM equation). Note: The CUSUM statistic remains within the 5% confidence bands, indicating the stability of the parameters over the studied period. Source: Authors’ calculations.

Figure 2.

Parameter stability test – CUSUM of Squares (ECM equation). Note: The CUSUM of Squares statistic remains within the critical bounds at 5%, confirming the absence of progressive structural instability. Source: Authors’ calculations.

Figure 2.

Parameter stability test – CUSUM of Squares (ECM equation). Note: The CUSUM of Squares statistic remains within the critical bounds at 5%, confirming the absence of progressive structural instability. Source: Authors’ calculations.

6.4. Diagnostic Tests for the ARDL–ECM Model

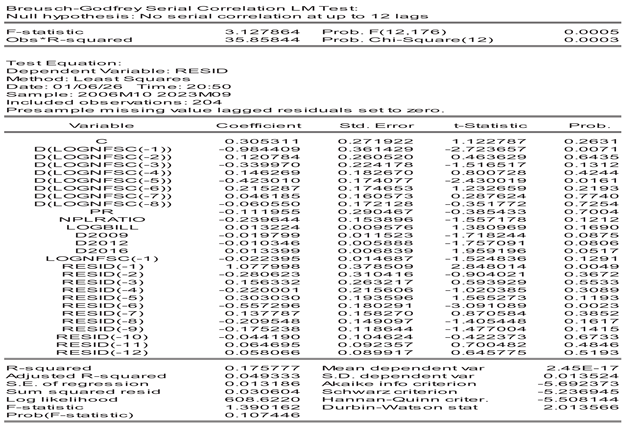

6.4.1. Diagnosis of Autocorrelation of Residuals

The Breusch–Godfrey test applied to the ECM residuals indicates statistically significant autocorrelation at the monthly horizon. Indeed, the LM statistic based on F is equal to 3.1279 with a p-value of 0.0005, and the Obs*R² statistic reaches 35.8584 with a p-value of 0.0003; in both cases, the null hypothesis of no autocorrelation up to 12 lags is rejected at the 5% level. This result is consistent with the strong persistence of credit series and the slow dynamics observed by the ECM. In order to ensure the validity of the inferences, the model results are interpreted using robust standard deviations of the HAC/Newey–West type (with a setting consistent with the monthly frequency, typically 12 lags), which allows for the correction of the impact of autocorrelation on standard errors without modifying the estimated coefficients.

Table 11.

Diagnostic of autocorrelation of residuals (Breusch–Godfrey LM).

| Test | Statistic | Df | p-Value | Decision (5%) |

| LM (F-statistic) | 3,1279 | (12, 176) | 0,0005 | Rejet de H0 |

| LM (Obs*R-squared) | 35,8584 | 12 | 0,0003 | Rejet de H0 |

Source: Authors’ calculations.

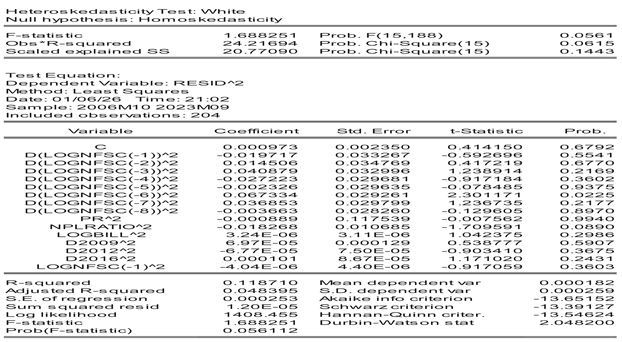

6.4.2. Test for Heteroscedasticity

The White heteroscedasticity test applied to the residuals of the ARDL–ECM model does not reveal non-constant conditional variance at the 5% threshold. Indeed, the F statistic is equal to 1.688 with a p-value of 0.056, while the Obs*R² statistic reaches 24.217 with a p-value of 0.062; in both cases, the null hypothesis of homoscedasticity cannot be rejected at the conventional threshold of 5%. These results indicate that the errors' variance remains generally stable over the studied period. Out of caution, and given the model's monthly dynamics and the previously detected residual autocorrelation, statistical inferences are nevertheless based on robust standard deviations of the HAC/Newey–West type, ensuring robust conclusions.

Table 12.

Test of heteroscedasticity of residuals (White).

| Statistic | Valeur | df | p-Value | Decision |

| F-statistic | 1,6883 | (15, 188) | 0,0561 | H₀ non rejetée (5 %) |

| Obs*R-squared | 24,2169 | 15 | 0,0615 | H₀ non rejetée (5 %) |

| Scaled explained SS | 20,7709 | 15 | 0,1443 | H₀ non rejetée |

Source: Authors’ calculations.

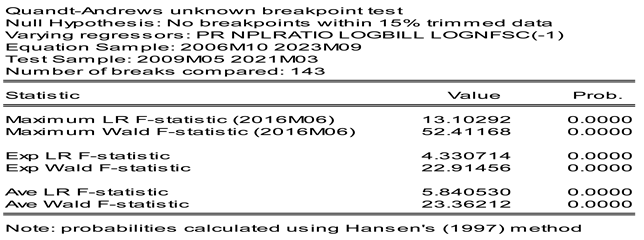

6.5. Structural Break Tests

The Quandt–Andrews test with unknown breakpoint unambiguously rejects the null hypothesis of no structural break in the dynamics of credit to the non-financial sector. All the statistics (Maximum, Exponential, and Average, both LR and Wald) are significant at the 1% threshold, confirming a robust regime change. The break is endogenously located in June 2016, at which point the coefficients associated with the policy rate, credit risk, portfolio arbitrages, and the error-correction term change significantly. This result indicates that, from 2016 onward, the relationship between monetary policy, prudential conditions, and credit adjustment underwent a structural reconfiguration, compatible with a change in the monetary and financial framework. The break thus affects the transmission mechanisms rather than simple cyclical volatility, which reinforces the interpretation in terms of a long-term regime conditioning the short-term dynamics of credit.

Table 13.

Quandt–Andrews Structural Break Test.

| Statistic | Date of Rupture | Value | p-Value |

| Maximum LR F-statistic | 2016M06 | 13,103 | 0,000 |

| Maximum Wald F-statistic | 2016M06 | 52,412 | 0,000 |

| Exp LR F-statistic | — | 4,331 | 0,000 |

| Exp Wald F-statistic | — | 22,915 | 0,000 |

| Average LR F-statistic | — | 5,841 | 0,000 |

| Average Wald F-statistic | — | 23,362 | 0,000 |

Note.probabilities calculated using Hansen’s 1997 method. Source: Authors’ calculations.

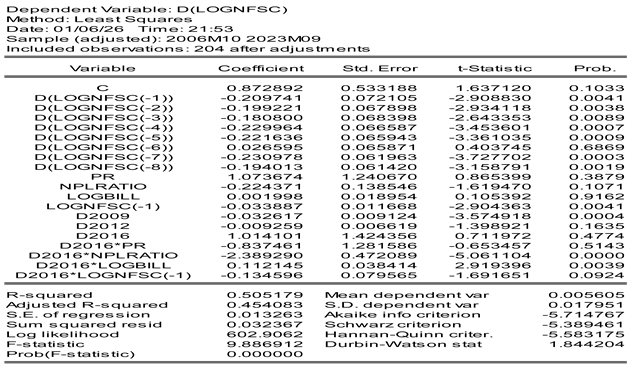

6.6. Analysis of the Change in Mechanisms (ECM with Interactions)

6.6.1. ECM with Regime Interactions

The results confirm that the structural break identified in 2016 corresponds to a change in transmission mechanisms rather than a level shock. Before 2016, the policy rate had little influence on credit dynamics, and this observation holds after the break, as indicated by the lack of a significant interaction between D2016 and PR. In contrast, the prudential channel is profoundly altered; indeed, the D2016×NPLRATIO interaction is strongly negative and highly significant, showing that after 2016, a deterioration in credit risk leads to a much sharper contraction in credit growth. Moreover, the positive and significant interaction between D2016 and Treasury bill holdings suggests an increased role for liquidity conditions and balance sheet arbitrage in post-2016 credit dynamics. Finally, the error-correction term remains negative and significant, confirming the existence of a long-term equilibrium, with a slight indication of acceleration in adjustment after the break. Overall, the disruption of 2016 reflects a shift towards a credit dynamic more governed by prudential constraints and balance sheet management than by the direct transmission of monetary policy.

Table 14.

Test of mechanism changes after 2016.

| Variable | Coefficient | t-stat | p-Value |

| PR | 1.0737 | 0.865 | 0.388 |

| NPLRATIO | −0.2244 | −1.615 | 0.107 |

| LOGBILL | 0.0020 | 0.105 | 0.916 |

| ECM (LOGNFSC(-1)) | −0.0339 | −2.904 | 0.004 |

| D2016 | 1.0141 | 0.712 | 0.477 |

| D2016 × PR | −0.8375 | −0.653 | 0.514 |

| D2016 × NPLRATIO | −2.3893 | −5.061 | 0.000 |

| D2016 × LOGBILL | 0.1121 | 2.919 | 0.004 |

| D2016 × ECM | −0.1346 | −1.692 | 0.092 |

Source: Authors’ calculations.

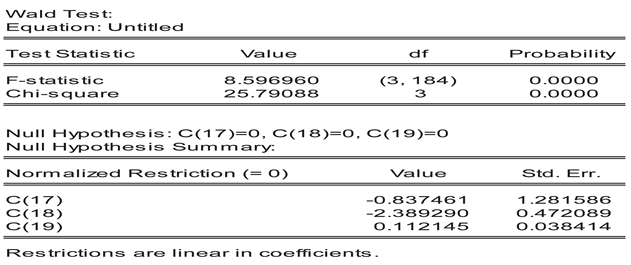

6.6.2. Joint Stability Test of the Mechanisms

The joint Wald test significantly rejects the hypothesis of stability of transmission mechanisms from 2016 onward. The simultaneous significance of the interactions among the post-2016 dummy variable, the policy rate, the non-performing loan ratio, and outstanding Treasury bills indicates a structural reconfiguration of credit dynamics in the non-financial sector from that date onward. This observation confirms that the identified break is not limited to a simple level shift but reflects a change in the economic channels governing credit adjustment. More specifically, the transmission becomes more sensitive to risk conditions and liquidity arbitrages, while the policy rate channel remains secondary.

It is important to note that an additional disruption was also anticipated for the 2020–2021 period, in connection with the pandemic crisis. This period was characterized by a major exogenous macro-financial shock, likely to influence both the supply and demand for credit. However, the absence of a dominant structural break during this phase suggests that the observed mechanisms mainly involve a temporary intensification of existing constraints, rather than a lasting change in transmission channels. As a result, the health crisis constitutes a cyclical shock, addressed by exceptional and transitional measures, without a profound questioning of the structural regime established since 2016.

Thus, the post-2016 period is characterized by a credit dynamic permanently constrained by prudential requirements, risk management, and bank balance-sheet trade-offs. The subsequent crisis episodes, including the pandemic, fit within this already modified structural framework, without fundamentally altering its operational logic.Tableau 14. Test de Wald conjoint – Rupture structurelle postérieure à 2016

Table 15.

Joint Wald Test – Stability of Coefficients (Post-Break Period).

| Statistique | Valeur | ddl | p-Value |

| F-statistic | 8,597 | (3, 184) | 0,000 |

| Chi-square | 25,791 | 3 | 0,000 |

Note.The test statistics confirm the rejection of the null hypothesis at the 1% level, indicating that the coefficients associated with the interaction variables are jointly significant. The restrictions are linear in the coefficients. Source: Authors’ calculations.

Table 16.

Linear restrictions tested (normalized coefficients).

| Coefficient | Estimated Value | Standard Error |

| C(17) | −0,837461 | 1,281586 |

| C(18) | −2,389290 | 0,472089 |

| C(19) | 0,112145 | 0,038414 |

Source: Authors’ calculations.

7. Results, Economic Policy Implications, and Recommendations

The empirical results of this study highlight a transmission of monetary policy to bank credit to the non-financial sector, marked above all by strong short-term inertia. However, this inertia does not indicate a lack of transmission but instead fits within a well-identified long-term equilibrium relationship, accompanied by dynamic adjustment mechanisms strongly conditioned by credit risk and bank balance-sheet trade-offs. By combining an ARDL–ECM approach with stability and structural break tests, the analysis goes beyond a strictly instantaneous reading of monetary transmission. It highlights a process dependent on the macro-financial regime, characteristic of bank-dominated emerging economies.

On the empirical front, the lack of a statistically significant effect of the short-term policy rate first confirms the weakening of the traditional interest rate channel. Nevertheless, this result should not be interpreted as an indication of monetary policy ineffectiveness. It rather reflects the existence of institutional rigidities, long-term contracts, and prudential constraints that limit the immediate adjustment of credit volumes. In this context, the policy rate primarily serves as a macro-financial signal rather than as a direct short-term quantitative lever. On the other hand, the significance of the error-correction term confirms the existence of a gradual adjustment mechanism toward long-term equilibrium, attesting that monetary policy effectively influences the credit trajectory, albeit with a differentiated timeline.

Moreover, the results highlight that risk conditions are the central determinant of short-term credit dynamics. The dominant role of the non-performing loan ratio indicates that prudential and informational considerations, consistent with the theoretical frameworks of credit rationing and the risk channel, primarily guide lending decisions. Thus, banks primarily adjust credit volumes in response to deteriorating perceived risk, which explains the apparent inertia of credit in the face of contemporary monetary impulses, even in the presence of a stable long-term relationship.

Moreover, bank portfolio arbitrages appear as a structuring mechanism of monetary transmission. The positive effect associated with public securities holdings suggests that these assets primarily serve a liquidity management and balance sheet stabilization function, rather than a role in systematically displacing private credit. However, this result highlights an essential intermediate channel: the allocation of balance sheets between sovereign securities and credit to the non-financial sector directly conditions the adequate sensitivity of credit supply to monetary impulses. Thus, monetary transmission is filtered by portfolio arbitrages, particularly in a context where government securities hold a structural place on bank balance sheets.

Moreover, the structural break and joint Wald tests confirm the time-varying nature of transmission mechanisms. This break does not correspond to a simple change in the level of credit, but to a deeper reconfiguration of the adjustment channels, marked by a strengthening of the role of risk and balance sheet constraints. This evolution is consistent with the transformations of the institutional and prudential framework, notably the progressive tightening of requirements for equity and risk management in line with international standards. Therefore, if the long-term equilibrium relationship remains intact, the adjustment dynamics toward this equilibrium are profoundly altered, reflecting a change in the macro-financial regime.

On this basis, the empirical results allow explicit testing of the formulated research hypotheses. First, the absence of a statistically significant effect of the short-term policy rate leads to the rejection of hypothesis H1, which posits that monetary transmission occurs immediately through the interest rate channel. Secondly, the existence of a long-term equilibrium relationship between bank credit, as indicated by the cointegration test, validates hypothesis H2. Thirdly, the significance and negative sign of the error correction term confirm the existence of a dynamic adjustment mechanism toward equilibrium, thereby validating hypothesis H3. Finally, the structural break tests and the joint Wald test reject the hypothesis of coefficient stability, confirming the time-varying nature of transmission mechanisms and thus validating hypothesis H4.

Implications of Economic and Prudential Policy

These results have several important implications for monetary authorities, prudential supervisors, and banking institutions.

First, the evaluation of monetary policy transmission to credit cannot be limited to a short-term analysis based solely on the interest rate channel. It must explicitly integrate risk mechanisms and balance sheet adjustments, which condition the effective response of credit supply. In this regard, the analytical frameworks for monetary policy would benefit from closer alignment with prudential supervision tools.

Secondly, although Moroccan banks already have advanced risk management and stress-testing systems, the results highlight the value of more systematically integrating credit risk dynamics into macro-financial analysis of monetary transmission. Thus, stress tests can be mobilized not only as instruments of regulatory compliance but also as analytical tools to anticipate the impact of monetary impulses on credit supply in different macro-financial regimes.

Thirdly, the slow adjustment toward long-term equilibrium argues for evaluating the effectiveness of monetary policy over a medium- to long-term horizon. Indeed, an exclusive focus on the immediate reactions of credit would risk underestimating the cumulative and indirect effects of monetary policy, mediated by risk conditions and prudential constraints.

Fourthly, the results highlight the need for greater monitoring of banks' government securities portfolios. These portfolios should not be viewed solely as liquidity reserves or low-risk assets, but also as key variables conditioning monetary transmission and credit allocation to the non-financial sector. In particular, an excessive accumulation of sovereign bonds can strengthen balance sheets' short-term resilience while altering the sensitivity of credit supply to monetary signals.

Finally, the overall results highlight the importance of close coordination between monetary policy and prudential policy. In a banking system dominated by balance-sheet constraints, the transmission of monetary impulses depends closely on the regulatory framework, portfolio quality, and liquidity trade-offs. Therefore, a coherent articulation between monetary orientation, prudential requirements, and macro-financial supervision appears essential to ensure an effective and stable transmission of monetary policy to the non-financial sector.

8. Conclusions

The findings of this study indicate that the transmission of monetary policy to bank credit for the non-financial sector in Morocco does not occur immediately, nor does it primarily operate through the conventional interest rate channel. Instead, robust empirical results demonstrate that short-term credit inertia coexists with a long-term equilibrium relationship and a statistically significant dynamic adjustment mechanism. Therefore, the effectiveness of monetary policy can only be assessed by considering different time horizons, rather than relying solely on a contemporaneous analysis of credit volumes.

This article makes a scientific contribution by identifying credit risk and bank balance-sheet arbitrage as key elements in the transmission of monetary policy in a bank-dominated emerging economy. The absence of a direct short-term effect on the policy rate does not imply monetary policy neutrality. Instead, transmission occurs indirectly, shaped by prudential constraints, information asymmetry, and risk management practices. Banks primarily adjust credit volumes based on portfolio quality and perceived risks, rather than solely in response to interest rate changes.

Furthermore, the analysis highlights the structuring role of government securities portfolios in the monetary transmission process. Rather than merely serving as a mechanism for crowding out private credit, these portfolios function as tools for balance sheet stabilization and liquidity management, while also influencing the adequate sensitivity of credit supply to monetary impulses. In this context, the interaction between sovereign asset allocation and the financing of the non-financial sector represents an intermediate channel that remains underexplored empirically in emerging economies, constituting an original contribution of this study.

Moreover, structural break tests confirm that monetary transmission mechanisms are not time-invariant. The identified break reflects a shift in the macro-financial regime, characterized by a strengthened role for prudential constraints and balance sheet arbitrage in lending decisions. While the long-term equilibrium relationship remains stable, the adjustment dynamics toward this equilibrium are significantly reconfigured. This finding underscores the importance of explicitly incorporating institutional and regulatory developments into analyses of monetary transmission.

From an economic policy perspective, these results demonstrate that the effectiveness of monetary policy cannot be evaluated solely by the immediate responses in bank credit. It is also necessary to consider risk indicators, the structure of bank balance sheets, and the composition of sovereign securities portfolios. To ensure stable and coherent transmission to the non-financial sector, coordination between monetary and prudential policies is essential.

Overall, this study contributes to the literature by demonstrating that, in bank-dominated emerging economies, monetary transmission is a gradual, indirect process dependent on the macro-financial regime. It is primarily structured by credit risk and balance-sheet arbitrage rather than solely by the interest rate channel. In doing so, the article provides a relevant analytical framework for understanding both the limitations and the conditions for monetary policy effectiveness across comparable institutional contexts.

Author Contributions

Conceptualization, A.B.; methodology, A.B.; software, A.B.; validation, A.B., Y.Z., and T.Q.; formal analysis, A.B.; investigation, A.B.; resources, A.B.; data curation, A.B.; writing original draft preparation, A.B.; writing review and editing, A.B., Y.Z., and T.Q.; visualization, A.B.; supervision, Y.Z. and T.Q.; project administration, A.B.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

https://data.gov.ma/data/fr/group/finance; https://www.bkam.ma/Publications-et-recherche/Publications-institutionnelles/Rapport-annuel-presente-a-sm-le-roi; https://www.bkam.ma/Politique-monetaire/Cadre-strategique/Decision-de-la-politique-monetaire/Historique-des-decisions; https://www.bkam.ma/Marches/Principaux-indicateurs/Marche-obligataire/Marche-des-bons-de-tresor/Marche-secondaire/Taux-de-reference-des-bons-du-tresor

Appendix

The empirical results are presented in the form of screenshots because the Student Version of EViews 12 does not permit the direct export or downloading of estimation outputs in editable formats (such as Excel, or Word tables). As a result, it is not technically possible to transfer the original output tables directly from the software into the manuscript.

Accordingly, all reported tables in the paper were carefully reconstructed and formatted based on the original EViews output displayed in the screenshots. Each coefficient, test statistic, and p-value was transcribed faithfully from the software results, ensuring full consistency between the presented tables and the underlying estimations. The screen-shots are provided for transparency and verification purposes, allowing readers and re-viewers to cross-check the reported values against the original software output.

Importantly, this limitation is purely technical and does not affect the estimation procedures, the validity of the econometric methods employed, or the robustness of the results. All estimations were conducted using standard econometric routines in EViews, and the reported findings can be fully replicated using the same dataset and model specifications in any unrestricted version of the software.

Appendix A. Descriptive Analysis and Preliminary Tests

Reproduction at the level ofTable 1.

Appendix A.1. Data Description

Appendix A.2. Collinearity Test

VIF

Appendix A.3. ADF and PP Tests: Stationary Result

Reproduction at the level ofTable 3

Appendix A.3.1. ADF and PP Tests: Stationary Result of LOGBILL

Appendix A.3.2. ADF and PP Tests: Stationary Result of LOGNFSC

Appendix A.3.3. ADF and PP Tests: Stationary Result of NPLRATIO

Appendix A.3.4. ADF and PP Tests: Stationary Result of PR

Appendix A.4. Multiple Structural Fracture Test (Bai–Perron)

Reproduction at the level ofTable 5.

Appendix B. Estimation du Modèle ARDL

Reproduction at the level ofTable 6

Appendix C. Cointegration Test and ARDL-ECM Error Correction Model (Short-Term Dynamics)

Appendix D. ARDL–ECM Diagnostic Test

Reproduction at the level ofTable 11(Breusch–Godfrey LM)

Appendix E. Heteroscedasticity Test of Residues (White)

Reproduction at the level ofTable 12

Appendix E. Structural Failure Tests

Reproduction at the level ofTable 13

Appendix F. Analyse du Changement des Mécanismes

Reproduction at the level ofTable 14

Appendix J. Joint Stability Test of Mechanisms

References

- Acharya, V. V., & Steffen, S. (2015). The “greatest” carry trade ever? Understanding eurozone bank risks. Journal of Financial Economics, 115(2), 215–236. [CrossRef]

- Adrian, T. and Shin, H.S. (2010) Liquidity and Leverage. Journal of Financial Intermediation, 19, 418-437. [CrossRef]

- Banerjee, et al. (1993) Panel Data Unit Roots and Cointegration: An Overview. Oxford Bulletin of economics and Statistics, 61, 607-629. [CrossRef]

- Bank al-maghrib.(2021). Rapport annuel. https://www.bkam.ma/Publications-et-recherche/Publications-institutionnelles/Rapport-annuel-presente-a-sm-le-roi/Rapport-annuel-2021.

- Bank al-maghrib.(2022). Rapport annuel. https://www.bkam.ma/Publications-et-recherche/Publications-institutionnelles/Rapport-annuel-presente-a-sm-le-roi/Rapport-annuel-2022.

- Bank al-maghrib.(2023). Rapport annuel. https://www.bkam.ma/Publications-et-recherche/Publications-institutionnelles/Rapport-annuel-presente-a-sm-le-roi/Rapport-annuel-2023.

- Bank Al-Maghrib. (2016). Circulaire n° 1/W/16 relative au dispositif de gouvernance et de gestion des risques des établissements de crédit. Rabat: Bank Al-Maghrib.

- Bank for International Settlements. (2019). Global liquidity: Vulnerabilities, risks, and spillovers. BIS Annual Economic Report. Basel: BIS.https://www.bis.org/publ/arpdf/ar2019e.htm.

- Bernanke, B. S., Gertler, M., & Gilchrist, S. (1999). The financial accelerator in a quantitative business cycle framework. In J. B. Taylor & M. Woodford (Eds.), Handbook of Macroeconomics (Vol. 1, Part C, pp. 1341–1393). Amsterdam: Elsevier. [CrossRef]

- Bernanke, B.S., & Gertler, M. (1995). Inside the black bo x: The credit channel of monetary policy transmission. Journal of Economic Perspectives, 9(4), 27–48. [CrossRef]

- Boutfssi, A., & Quamar, T. (2026). Short-run monetary policy transmission, credit risk, and bank portfolio adjustments: Evidence from the non-financial corporate sector in an emerging economy (Preprint). Preprints. [CrossRef]

- Boutfssi, A., & Zizi, Y. (2025). Macro and micro-institutional determinants of VSMEs’ access to bank financing in Morocco: An empirical analysis of monetary policy, prudential risk, and public support (2014–2024). Prague Economic Papers, 2025(3), 408–441. [CrossRef]

- Brown, R. L., Durbin, J., & Evans, J. M. (1975). Techniques for Testing the Constancy of Regression Relationships over Time. Journal of the Royal Statistical Society. Series B (Methodological), 37(2), 149–192. http://www.jstor.org/stable/2984889.

- Checo, A., Grigoli, F., & Sandri, D. (2024). Monetary policy transmission in emerging markets: Proverbial concerns, novel evidence (IMF Working Paper No. 24/093). International Monetary Fund. [CrossRef]

- Cloyne, J., Ferreira, C., Froemel, M., & Surico, P. (2023). Monetary policy, corporate finance, and investment. Journal of the European Economic Association, 21(6), 2586–2634. [CrossRef]

- Gambacorta, L., & Shin, H. S. (2018). Why bank capital matters for monetary policy. Journal of Financial Intermediation, 35, 17–29. [CrossRef]

- International Monetary Fund. (2019). Global Financial Stability Report: Lower for Longer. Washington, DC: International Monetary Fund.https://www.imf.org/en/Publications/GFSR/Issues/2019/10/01/global-financial-stability-report-october-2019.

- International Monetary Fund. (2024). Global Financial Stability Report: Financial Tightening amid Global Uncertainty. Washington, DC: International Monetary Fund.https://www.imf.org/en/Publications/GFSR.

- Jiménez, G., Ongena, S., Peydró, J.-L., & Saurina, J. (2012). Credit supply and monetary policy: Identifying the bank balance-sheet channel with loan applications. American Economic Review, 102(5), 2301–2326. [CrossRef]

- Lütkepohl, H. (2005). New introduction to multiple time series analysis. Springer Science & Business Media. [CrossRef]

- Mishra, P., & Montiel, P. (2013). How effective is monetary transmission in low-income countries? A survey of the empirical evidence. Journal of Economic Surveys, 27(2), 211–235. [CrossRef]

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds Testing Approaches to the Analysis of Level Relationships. Journal of Applied Econometrics, 16(3), 289–326. http://www.jstor.org/stable/2678547.

- Phillips, P.C.B. and Perron, P. (1988) Testing for a Unit Root in Time Series Regression. Biometrika, 75, 335-346. [CrossRef]

- Stiglitz, J.E., & Weiss, A. (1981). Credit rationing in markets with imperfect information. The American Economic Review, 71(3), 393–410. https://www.jstor.org/stable/1802787.

- Tenreyro, S., & Thwaites, G. (2016). Pushing on a string: US monetary policy is less powerful in recessions. American Economic Journal: Macroeconomics, 8(4), 43–74. [CrossRef]

Table 1.

Descriptive statistics.

| Variable | Mean | Standard Deviation | Skewness | Kurtosis | Jarque–Bera | Observations |

| LOGBILL | 25,5437 | 0,4228 | 0,2455 | 1,8936 | 0,0015 | 213 |

| LOGNFSC | 26,3764 | 0,2954 | −1,8239 | 5,6746 | 0,0000 | 213 |

| NPLRATIO | 0,1003 | 0,0328 | −0,1377 | 1,8320 | 0,0017 | 213 |

| PR | 0,0272 | 0,0059 | −0,8730 | 2,8140 | 0,0000 | 213 |

Note: LOGNFSC denotes the logarithm of bank credit to the non-financial sector; LOGBILL the logarithm of outstanding Treasury bills held by banks; NPLRATIO the ratio of non-performing loans; PR the policy rate. The Jarque–Bera tests indicate a rejection of normality for all variables, which is common for monthly macro-financial series. Source: Authors’ calculations.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license.

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.