Submitted:

16 January 2026

Posted:

19 January 2026

You are already at the latest version

Abstract

This study proposes a two-stage structural model that integrates financial literacy, educa-tion, attitudes, knowledge, behavior, advice, and financial stress as predictors of financial capabilities. It also examines the relationship between financial capabilities and financial well-being, highlighting financial resilience as a mediator. The main contribution is posi-tioning financial resilience as a central explanatory mechanism, challenging previous linear approaches. This holistic perspective addresses theoretical gaps and provides em-pirical evidence in an emerging economy context. A non-experimental, quantitative, cross-sectional design was used with a sample of 365 university students from Veracruz, Mexico. Data were collected through an online questionnaire and analyzed using explor-atory and confirmatory factor analysis, structural equation modeling (SEM), and media-tion analysis with bootstrap processing. Results show that financial literacy, education, attitude, advice, and behavior positively impact financial capabilities, with advice being the most significant predictor. Financial capabilities have a strong influence on financial well-being, while financial resilience does not act as a mediator. Study limitations include its cross-sectional design and non-probability sample, limiting generalizability. Future research could explore additional mediators and moderators and evaluate interventions tailored to different socio-economic contexts.

Keywords:

financial literacy-education

; financial advice

; financial capacities

; financial wellbeing

; financial resilience

1. Introduction

In the contemporary context, where the complexity of economic and financial systems

directly influences daily life, proper personal financial management has become an essential skill for individual and collective well-being. This need has fostered the development and evolution of key concepts such as financial literacy and financial education, which, while closely related, have distinct theoretical and practical nuances that must be distinguished. The term “literacy” initially refers to the process of acquiring basic reading and writing skills. However, educators like Paulo Freire broadened this concept, arguing that literacy is also an act of critical consciousness that enables individuals to “read the world,” equipping them to question and transform it. From this perspective, literacy implies empowerment, not merely the teaching of technical skills (Freire, 1968, 1970, 1985).

This pedagogical framework has been useful for understanding the emergence of new types of literacy. One of them is financial literacy, a concept that gained relevance in the late 20th century in response to the growing need for individuals to understand and manage saving, investing, borrowing, and budgeting. Authors such as Noctor, Stoney, and Stradling (1992) defined financial literacy as the ability to make informed financial decisions based on knowledge acquired in family or community contexts. The OECD (2005) expanded this definition, incorporating not only expertise but also responsible attitudes and behaviors toward finances. Furthermore, it evaluates the effectiveness of financial education programs and presents the OECD Council Recommendation on Principles and Good Practices for Financial Education and Awareness (OECD, 2005).

As educational strategies aimed at strengthening citizens’ financial literacy were formalized, a broader concept emerged: financial education. Unlike literacy, financial education is conceived as a structured learning process, both formal and informal, designed to equip individuals with the skills to understand financial products, make informed decisions, and develop sustainable financial behaviors. Formal financial education provides the necessary foundation for teaching individuals how to manage their money effectively, which, according to Bernheim, Garrett, and Maki (2001), has a positive impact on long-term financial management. Lusardi and Mitchell (2007, 2011) have emphasized that this approach involves not only the acquisition of knowledge, but also the evaluation of the processes by which this knowledge is taught and applied. This conceptual development finds support even in historical sources. In a letter from 1787, John Adams warned that many of the economic difficulties of his time were not due to structural flaws, but rather to widespread ignorance about currency, credit, and the circulation of money. This early observation highlights the importance of having basic economic knowledge to participate fully in social and political life (Adams, 1787).

However, access to financial information, while necessary, is not sufficient in itself. It is essential to develop an appropriate attitude towards money, which is known as financial literacy. Studies have shown that women are more likely to discuss financial matters with their parents, which is associated with a more positive attitude towards financial management (Edwards, Allen & Hayhoe, 2007). Furthermore, family involvement moderates the relationship between financial knowledge and attitudes towards debt (Koropp, Grichnik & Kellermans, 2013). Similarly, financial education programs for women promote changes in their attitudes, improving their ability to make more informed, sustainable financial decisions that support their families (Prandini & Baconguis, 2020). This financial literacy directly influences everyday financial decisions, planning capabilities, and, in the long term, economic stability. However, even with knowledge, financial decisions are not always rational.

Financial behavior is influenced by psychological and emotional factors, as explained by Kahneman (2011) and Thaler and Sunstein (2008), who demonstrate that people do not always make decisions logically but are influenced by cognitive and emotional biases. This is where financial attitude comes into play, a key component that influences how people approach economic decisions, whether in terms of saving, consumption, or investment.

Furthermore, financial advice plays a crucial role in decision-making, as professional guidance helps individuals better understand and manage complex financial matters, as emphasized by Lusardi and Tufano (2015). In this sense, financial advice appears to be a useful tool, but its effectiveness ultimately depends on the individual’s financial knowledge and behavior. Financial advice improves decision-making by enhancing confidence (Streich, 2021), encouraging participation in retirement plans (Fang, Hao, and Reyers, 2022), and influencing investment portfolio composition (Lei, 2018). Additionally, it can be beneficial in the early stages of financial planning (Allie, West, and Willows, 2016) and affects a client’s risk tolerance (Monne, Rutterford, and Sotiropoulos, 2023).

Often, a lack of education and preparation in these areas leads to financial stress, a growing phenomenon in modern societies. Its consequences are not limited to the economic sphere, but also affect mental health, quality of life, and overall well-being. Financial stress negatively impacts relationships, health, and work performance and is not simply a result of a lack of money; rather, it stems from structural, emotional, and social factors. It can be passed down through generations (Hubler et al., 2015), decrease productivity (Sabri and Aw, 2020), be exacerbated by certain types of debt in old age (Loibl et al., 2020), and affect the sense of purpose in young people (Goktan et al., 2025). While in some cases it can motivate work effort (Wei et al., 2024), in general it requires a comprehensive approach that combines financial education, psychosocial support, and life-cycle-sensitive public policies. Therefore, developing strong financial skills is crucial for promoting sustainable financial well-being and greater emotional stability. Financial literacy goes beyond technical knowledge; it encompasses attitudes, behaviors, self-confidence, and social context. Anders, Jerrim, and Macmillan (2023) show that the family environment has a greater influence on its development than formal education. In small businesses, responsible financial practices enhance sustainability (Babajide et al., 2021). Furthermore, financial self-efficacy is key to applying knowledge in practice (Çera et al., 2020; Rothwell, Khan, and Cherney, 2016).

Finally, training professionals to work effectively in vulnerable contexts also strengthens financial literacy (Sherraden et al., 2016). In this regard, evidence suggests that financial literacy is a multidimensional construct that requires support from family, education, and the workplace. These skills and knowledge, acquired through education and experience, constitute an individual’s financial literacy. According to Sherraden et al. (2016), financial literacy encompasses not only technical knowledge but also the ability to apply that knowledge in everyday situations. Individuals with higher levels of financial literacy manage their resources more effectively, make sound financial decisions, and adapt more easily to economic changes, thereby strengthening their financial resilience. García-Santillán et al. (2024) state that it not only depends on access to financial services, but also on education, personal confidence, and social support. Carton et al. (2024) add that beliefs, habits, and past experiences influence how people cope with uncertainty. Sakyi-Nyarko et al. (2022) emphasize that having a bank account, savings capacity, and support networks, such as remittances, improves resilience to crises, especially in rural areas.

For the reasons outlined above, this study examines how interrelated concepts, such as financial education, attitudes, and skills, influence financial behavior and quality of life. The objective is to bridge existing theoretical and empirical gaps by proposing an integrative framework that connects financial literacy, financial counseling, financial stress, financial capabilities, well-being, and financial resilience. In this context, the following question arises: How do financial literacy, financial education, financial attitudes and knowledge, financial behavior, financial counseling, and financial stress relate to financial capabilities, and how do these capabilities, in turn, relate to financial well-being, mediated by individuals’ financial resilience? Therefore, this research seeks to address an important theoretical gap based on the following arguments.

Despite growing interest in financial well-being, the academic literature presents a conceptual fragmentation, treating factors such as financial literacy, attitudes, knowledge, and financial behavior, among others, in isolation, as well as key variables such as financial stress, which also broadens the scope of analysis, providing a more complete view of the phenomenon. This holistic approach is crucial for designing educational interventions and public policies to improve financial well-being, addressing both technical and psychosocial factors that influence individuals’ economic stability.

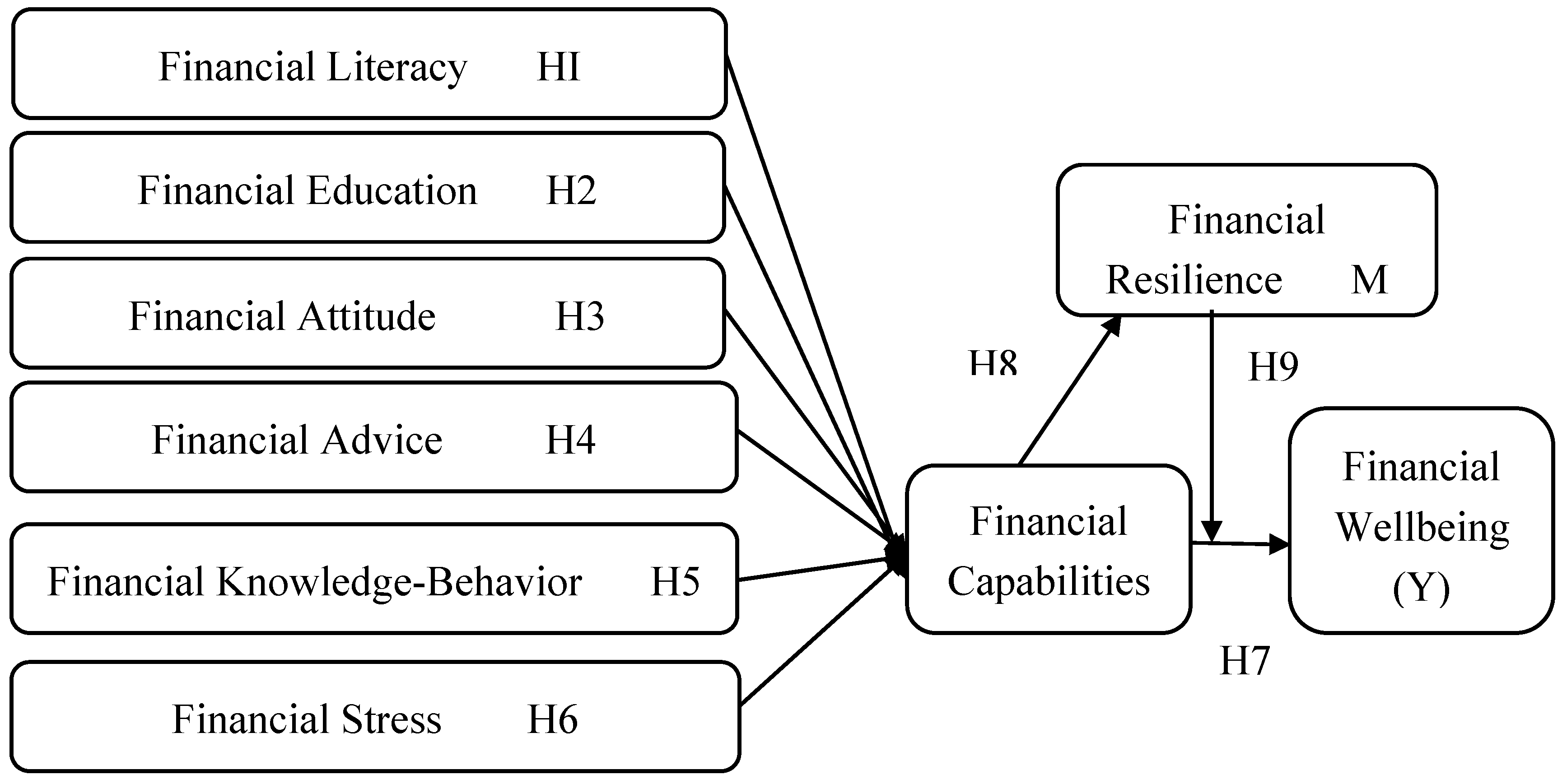

Based on the arguments presented in the literature review regarding the relevant variables, the conceptual model described in Figure 1 is shown below:

To validate the model shown in Figure 1, it is divided into two sections: one that examines the relationship between financial literacy (H1), financial education (H2), financial attitude (H3), financial advice (H4), financial knowledge and behavior (H5), and financial stress (H6), and their relationship with financial capabilities. The other section examines the relationships between financial capabilities and financial well-being and financial resilience (H7 and H8), as well as the mediating role of financial resilience in the relationship between financial capabilities and financial well-being (H9).

2. Literature Review

2.1. Theoretical Framework

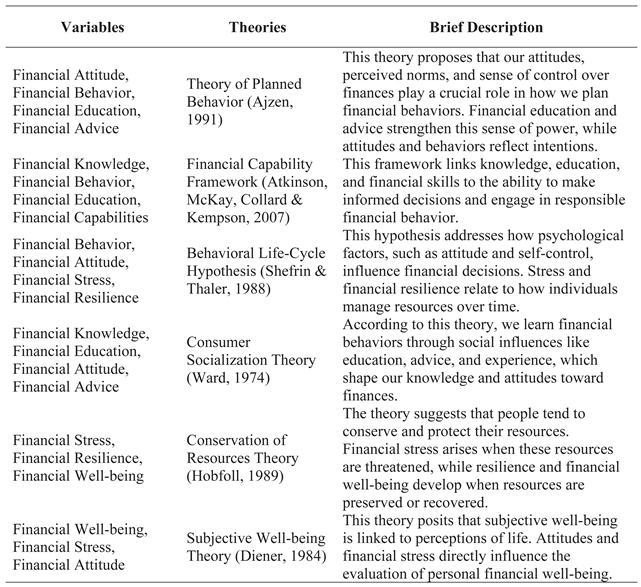

To situate this study within the theoretical framework that explains the relevant variables, this section presents a detailed analysis of the theories that underpin the key variables of the study. Following this, the latest state-of-the-art research on these variables is reviewed through a thorough examination of contemporary studies that explore and develop them. This approach helps us contextualize current perspectives, laying the foundation for a deeper understanding of the phenomenon we are investigating. The variables in the conceptual model: financial literacy, financial education, financial attitude, financial advice, financial knowledge and behavior, financial stress, financial skills, financial resilience, and financial well-being, are explained based on the theories described in Table 1.

2.1.1. Financial Education, Knowledge, and Capabilities

Financial education is widely recognized as a foundational element in developing the knowledge and skills required to make informed decisions. According to Atkinson, McKay, Collard, and Kempson (2007), financial capability extends beyond technical knowledge to include practical skills, motivation, and the confidence to apply learning in real-life situations. This holistic perspective is embodied in the Financial Capability Framework, which emphasizes that educational interventions should not only teach but also empower individuals to manage their finances responsibly. Consumer socialization theory (Ward, 1974) further illuminates how financial attitudes, values, and behaviors are shaped by environmental influences, particularly during childhood. Family, school, and media play a critical role in shaping financial knowledge and perceptions regarding money management.

2.1.2. Financial Attitudes and Behaviors

Financial attitudes and behaviors can be effectively understood through the Theory of Planned Behavior (Ajzen, 1991), which posits that an individual’s intention to perform a specific behavior is determined by attitudes toward the behavior, perceived social norms, and perceived control over it. In financial contexts, this framework helps explain why individuals with financial knowledge may still fail to act prudently, depending on their perspectives on saving, spending, and borrowing, as well as their perceived control over these actions. The Behavioral Life-Cycle Hypothesis (Shefrin and Thaler, 1988) adds that individuals often deviate from purely rational decision-making due to limited self-control and mental categorization of money. Understanding these behavioral tendencies is crucial for explaining why even financially literate individuals may exhibit impulsive or inconsistent financial behaviors.

2.1.3. Financial Advice and Decision-Making

The use and effectiveness of financial advice are closely linked to both financial education and personal attitudes toward money. From a social learning perspective, as suggested by consumer socialization theory, guidance from experts, parents, and institutions can strongly influence financial decision-making. However, the impact of such advice depends on an individual’s confidence and their ability to comprehend and apply the recommendations. Ajzen (1991) further notes that perceptions of social norms, such as beliefs about what constitutes a sound financial decision, can affect whether individuals seek professional advice.

2.1.4. Financial Stress and Economic Resilience

Financial stress is an emotional and behavioral response that arises when individuals perceive they lack sufficient economic resources to meet basic needs or achieve financial goals. According to Hobfoll’s Conservation of Resources Theory (1989), this type of stress occurs when a person perceives that they are losing, or are at risk of losing, their financial resources. The theory also introduces the concept of financial resilience, defined as the ability to cope with and recover from adverse situations by mobilizing and replenishing resources. Shefrin and Thaler (1988) extend this perspective by highlighting that a lack of self-control can exacerbate financial stress, as impulsive decisions often lead to negative long-term consequences.

2.1.5. Financial Well-Being and Subjectivity

Financial well-being refers to an individual’s perception of stability and security in relation to their personal finances. Subjective Well-Being Theory (Diener, 1984) posits that well-being is not solely determined by objective indicators such as income but also by the individual’s subjective evaluation of their situation. Consequently, two people with similar incomes may experience very different levels of financial well-being, depending on their expectations, goals, social context, and stress levels. Empirical studies have confirmed that financial well-being is closely linked to variables such as financial education, behavior, and resilience, demonstrating that higher financial literacy and better behavioral control are positively associated with perceived economic well-being.

2.2. State of the Art of Conceptual Model Variables

2.2.1. Financial Literacy and Financial Education

Recent studies have explored the relationship between financial education and financial literacy, revealing a positive but nuanced association. Zhang and Xiong (2020) found that financial education enhances literacy among rural residents in China, although methodological issues such as self-selection and endogeneity can reduce this effect. Individual factors, including education level, gender, age, and employment type, modulate this relationship. In a different context, Soejono et al. (2025) reported that young couples in Indonesia with higher prior financial education displayed better financial planning practices, highlighting the behavioral utility of literacy. Zhang and Fan (2024) showed that while education improves literacy, higher literacy may be negatively associated with mobile Fintech adoption but positively associated with healthy financial behaviors and well-being.

Ofori (2024) emphasized that formal education, age, and financial attitudes are key determinants of literacy among Ghanaian self-employed workers. Guerini, Masciandaro, and Papini (2024) examined financial education institutionally, noting its status as a credence good, whose effectiveness depends on public certification and political motivations, especially amid rapid financial innovation. Estelami and Estelami (2024) added a psychological perspective, demonstrating that cognitive styles (analytical, intuitive, adaptive) influence the impact of financial education on literacy. Taken together, these studies suggest that financial education effectively enhances financial literacy, though its effects vary across individuals, contexts, and structural factors. Higher literacy derived from education translates into better practical financial skills. Based on this evidence, we propose the following hypotheses: H1: Financial literacy positively influences individuals’ financial capabilities, and H2: Financial education positively influences individuals’ financial capabilities.

2.2.2. Financial Attitude

Financial attitudes play a critical role in decision-making and behavior. Mamo, Hassen, and Adem et al. (2021) found that higher education correlates with more responsible attitudes. Hassan, Prasad, and Meek (2020) highlighted that even limited knowledge combined with a positive learning attitude enhances financial decision-making. Obreja, Rughiniș, and Rosner (2023) showed that conservative attitudes toward science can limit the adoption of new financial tools. Kumar, Ahlawat, and Deveshwar et al. (2024) confirmed that financial attitude is a key determinant of behavior in periurban areas, while She, Ma, Pahlevan Sharif et al. (2024) found similar results among Malaysian millennials. Socialization within families significantly shapes young people’s attitudes (Abdul Ghafoor & Akhtar, 2024). Studies in India and Brazil (Nayak, Mahakud, & Mahalik et al., 2024; Bressan & Vieira, 2021) illustrate that positive attitudes improve resilience and long-term financial outcomes. Xu & Jiang (2024) and Ananda, Kumar & Dalwai (2024) emphasized the importance of risk-taking attitudes for entrepreneurship and savings behavior. Digital competencies further enhance positive attitudes toward financial technology (Marconi, Marinucci, & Paladino, 2024). Da Cunha et al. (2019) and Islam et al. (2023) confirmed that responsible attitudes toward resources and emerging technologies influence financial decisions. Therefore, we propose the following hypothesis: H3: Financial attitude positively influences individuals’ financial capabilities.

2.2.3. Financial Advice

Financial advisors play a vital role across contexts, from sustainability to retirement planning. De Jong and Wagensveld (2024) emphasized the role of advisors in promoting social and ecological value in SMEs. Staehelin, Dolata, and Schwabe (2024) demonstrated that hybrid interfaces combining paper and digital tools enhance client service. Schepen and Burger (2022) found that reliance on professional advice improves subjective well-being, particularly for households with rising income or low financial knowledge. Mustafa et al. (2025) highlighted the impact of advisors on retirement planning in Malaysia, moderated by financial literacy. Sun et al. (2024) examined advisors’ influence on risk investment decisions. Consequently, we hypothesize: H4: Financial advice positively influences individuals’ financial capabilities.

2.2.4. Financial Knowledge and Behavior

Studies have linked financial knowledge and behavior to skill development. Shanmugam, Chidambaram, and Parayitam (2022) found that access to financial information influences risk-taking and sustainable investments in India. Morris, Maillet, and Koffi (2022) highlighted the role of financial confidence in behavior. FINRA (2019) and Lee & Dustin (2021) emphasized the influence of behavior on financial satisfaction. Peter and Gupta (2024) showed that financial literacy and practical skills enhance women entrepreneurs’ decisions, while Rabbani, Heo & Lee (2021) identified profiles of knowledge linked to well-being and risk tolerance. She, Ma, Pahlevan Sharif et al. (2024) and Sabri, Anthony, Law et al. (2024) further demonstrated the mediating role of behavior between knowledge and financial well-being. Thus, we propose: H5: Financial knowledge and behavior influence individuals’ financial capabilities.

2.2.5. Financial Stress

Financial stress affects emotional, relational, and behavioral outcomes. Joseph & Peetz (2024) observed that financial anxiety predicts permissive attitudes toward financial monitoring in couples. Choi et al. (2025) and Heo, Liu & Park (2025) highlighted its impact on affect and self-esteem, with coping strategies moderating this effect. Sorgente, Zambelli & Lanz (2023) distinguished financial stress from subjective financial well-being, while Amonhaemanon (2024) emphasized literacy and advice as interventions for informal workers. Accordingly, we propose the following hypothesis: H6: Financial stress influences individuals’ financial capabilities.

2.2.6. Financial Capabilities, Financial Resilience, and Financial Well-Being

Financial well-being integrates economic, psychological, and contextual factors. Saeedi & Nishad (2024) highlighted the importance of disciplined financial behavior and gamification interventions. Weida, Carroll-Scott & Le-Scherban (2024) and Bhattacharya et al. (2025) stressed resilience and confidence. Sorgente, Atay & Aubrey (2024) validated multidimensional subjective well-being scales. Rai, Ahuja & Sharma (2025) and Wheeler & Brooks (2024) linked literacy, identity, and resilience to well-being. Sharma, Kumar & Sood (2025), Hernández-Pérez & Cruz Rambaud (2025), Du Plessis, Jordaan & van der Westhuizen (2025), and Kaur & Singh (2025) emphasized self-efficacy, self-control, and family socialization. Young (2024) underscored the role of cultural influences. Therefore, we propose: H7: Financial capabilities influence financial well-being; H8: Financial resilience influences financial well-being, and H9: The relationship between financial capabilities and financial well-being is mediated by financial resilience.

3. Methodology

3.1. Design Study

This study employs a non-experimental, quantitative, cross-sectional design to analyze a database to understand the interconnections among financial literacy, financial education, financial attitude, financial advice, financial knowledge and behavior, and financial stress, as well as their influence on financial capabilities. Additionally, it examines the mediating role of financial resilience in the relationship between financial capabilities and financial well-being.

3.2. Participants and Sample

The study population consists of individuals aged 18 or older with higher education. The aim is to explore their behavior in relation to the variables of the conceptual model and the applied instrument. A non-probability, self-selection sampling technique was employed, in which participants voluntarily chose to take part in the study. The questionnaire was distributed digitally through Google Forms to maximize response reach. Although this type of sampling does not allow for statistical generalization, it is considered appropriate for exploratory and validation purposes. As Bryman (2016) argues, non-probability sampling is particularly suitable in the early stages of research when the goal is to develop or test theoretical constructs rather than to ensure representativeness. Similarly, Saunders, Lewis, and Thornhill (2019) emphasize that self-selection sampling is valid when participants possess specific characteristics relevant to the research topic and when accessibility to the target population is limited.

Furthermore, Etikan, Musa, and Alkassim (2016) note that self-selected respondents often exhibit greater engagement and familiarity with the topic, which can enhance content validity in behavioral and attitudinal studies. In this first stage, 365 valid responses were collected, enabling an initial analysis of students’ financial behavior in the municipality of Veracruz. Since the purpose of this phase is not to generalize but to explore and validate the dimensions of financial behavior, the approach is both efficient and methodologically sound. Additionally, the open and ongoing design of data collection allows the inclusion of new participants over time, enriching the diversity and depth of responses. As Creswell and Creswell (2018) suggest, such a pragmatic approach aligns the research design with its exploratory objectives, strengthening the internal consistency and conceptual robustness of the study.

3.3. Ethical Code

This study was approved by the Ethics Committee of the Business School at the Universidad Cristóbal Colón (Project ID P-07/2025). The research adhered to the principles established in the Declaration of Helsinki. The study’s objectives and procedures were explained to participants during the administration of the questionnaire, ensuring their full confidentiality and anonymity. Informed consent was obtained from all participants after they had read and understood the provided instructions and statements.

3.4. Test Used

The instrument employed in this study was previously utilized by García-Santillán et al. (2024) and is structured as follows. The first section collects participants’ sociodemographic information. The second section comprises dimensions related to education and financial behavior, namely Financial Education, Financial Attitudes, Financial Advice, Financial Knowledge, and Financial Capabilities. These dimensions were adapted from the scale developed by Elrayah and Tufail (2024) -who refined earlier instruments- and assessed using items derived from recent empirical studies (Widyastuti et al., 2020; Khan et al., 2022; Çoşkun & Dalziel, 2020) through a five-point Likert-type scale. The third section includes eight indicators of financial well-being, based on frameworks proposed by BBVA (2020) and the Center for Financial Services Innovation (CFSI), complemented by sixteen items developed by Flores, Zamora-Lobato, and García-Santillán (2024).

Collectively, these items assess participants’ perceptions, lived experiences, and coping strategies in the face of economic crises. Furthermore, items assessing early financial literacy were incorporated, grounded in theoretical frameworks on financial socialization, observational learning, and the family environment. This section draws on the foundational contributions of Bandura (1986), Gudmunson and Danes (2011), Mandell (2008), and Lusardi and Mitchell (2011), as well as the recommendations of the OECD/INFE (2012, 2014). Finally, financial stress was measured through items adapted from internationally recognized instruments, including the Financial Stress Scale (Prawitz et al., 2006), the Financial Well-Being Scale (CFPB, 2015), and the Financial Anxiety Scale (Archuleta et al., 2013). These scales aim to examine economic pressure, the use of credit for basic needs, perceived financial control, and individuals’ ability to cope with adverse financial circumstances.

3.5. Statistical Procedure and Reliability and Validity Analysis

To validate the instrument and the data collected in this study, several statistical indicators were applied to assess the internal consistency and validity of the measurement model. Internal reliability coefficients, Cronbach’s alpha (α) and McDonald’s omega (ω), were calculated, along with Composite Reliability (CR) and Average Variance Extracted (AVE). The α and ω coefficients assess the internal consistency of the items within each scale, with ω considered a more robust indicator when variable factor loadings are present among items (Cronbach, 1951; McDonald, 1999; Tavakol & Dennick, 2011). Composite Reliability (CR), in turn, measures the internal consistency of the latent construct and is deemed acceptable when values exceed 0.70 (Fornell & Larcker, 1981). The AVE assesses the model’s convergent validity; values above 0.50 are considered adequate, indicating that the items adequately explain the variance of their corresponding constructs (Fornell & Larcker, 1981). The application of these indicators ensures that the scales used are statistically consistent and valid for the study.

Subsequently, multivariate normality of the data was evaluated. According to the theoretical criterion proposed by Kim (2013), a distribution can be considered normal if its skewness is between −2 and 2 and its kurtosis is between −7 and 7. Values outside these ranges indicate potential significant deviations, such as skewness or leptokurtosis, which may affect the analysis. George and Mallery (2010) recommend examining both indicators jointly, whereas Field (2013) emphasizes the need to verify normality before performing parametric tests. In this regard, Fisher’s criteria were applied to evaluate skewness and kurtosis in the data (Spiegel, Schiller, & Srinivasan, 2009). Table 2 presents the values proposed by Kim (2013).

3.5.1. Pearson Correlation

To test hypotheses H1 through H6, Pearson correlation analyses were initially conducted to examine the relationships among financial variables, specifically Financial Literacy, Financial Education, Financial Attitude, Financial Advice, Financial Knowledge–Behavior, and Financial Stress, and the dependent variable Financial Capabilities. This stage allowed for the assessment of the statistical significance and magnitude of association between each construct and financial capabilities, thereby distinguishing theoretical significance from practical relevance.

3.5.2. Exploratory and Confirmatory Factor Analysis (EFA and CFA)

To confirm the underlying structure of the previously defined construct, both an Exploratory Factor Analysis (EFA) and a Confirmatory Factor Analysis (CFA) were conducted, using Structural Equation Modeling (SEM) with AMOS v23. Before these analyses, data reliability, internal consistency, and normality were assessed. Additionally, Bartlett’s Test of Sphericity and the Kaiser-Meyer-Olkin (KMO) index were calculated to ensure the adequacy of the data for factor analysis (García-Santillán, 2017). In cases where significant deviations from normality were detected -such as excessive skewness or kurtosis- polychoric correlation matrices were employed (Muthén & Kaplan, 1985; Timmerman & Lorenzo-Seva, 2011).

The EFA was used to identify the latent structure of the variables and to reduce dimensionality, providing factor loadings that reflect the internal consistency of the constructs (Field, 2013). Based on the resulting factorial solution, a CFA was conducted to assess the factorial validity of the model, using indices of absolute fit, incremental fit, and parsimony (Hair et al., 1999). For absolute fit, indices such as the Comparative Fit Index (CFI > 0.90), Root Mean Square Error of Approximation (RMSEA < 0.08), and Normed Fit Index (NFI ≈ 0.90) were considered. Values for the Goodness-of-Fit Index (GFI) and Tucker-Lewis Index (TLI) were expected to be close to 1.0. Regarding structural fit, the Chi-square statistic was used, complemented by the RMSEA and the Standardized Root Mean Square Residual (SRMR < 0.08). Finally, to evaluate the parsimony of the model, the Akaike Information Criterion (AIC) and Bayesian Information Criterion (BIC) were examined, favoring simpler models that demonstrated adequate fit.

3.5.3. Mediation Model (Conceptual Procedure)

To test hypotheses H7 and H8, Andrew F. Hayes’ PROCESS macro for SPSS (version 5.0) was employed to examine the influence of Financial Capabilities on Financial Wellbeing and to determine whether Financial Resilience mediates this relationship. A bootstrap procedure with 5,000 samples was used to generate 95% confidence intervals for the indirect effect, and standardized coefficients were computed to facilitate interpretation. This approach allowed simultaneous assessment of the direct impact of Financial Capabilities on Financial Wellbeing and the indirect effect through Financial Resilience, providing robust empirical evidence for Financial Resilience as a potential mediator in the relationship between Financial Capabilities and Financial Wellbeing.

4. Data Analysis and Discussion

4.1. Reliability

The test validation was conducted using Cronbach’s alpha (α = .925) and McDonald’s omega (ω = .913), demonstrating satisfactory internal consistency and supporting the scales’ reliability (McDonald, 1999; Dunn, Baguley, & Brunsden, 2014). While Cronbach’s alpha assumes tau-equivalence among items, McDonald’s omega offers a more robust estimate by accounting for individual factor loadings, thereby minimizing potential over- or underestimations. After confirming internal consistency, multivariate normality was examined using the Kolmogorov–Smirnov and Shapiro–Wilk tests with the Lilliefors correction, complemented by skewness (±2) and kurtosis (±7) criteria, as recommended by Kim (2013). These procedures ensured compliance with the assumptions required for subsequent statistical analyses (see Table 3).

As shown in the previous table, the p-values from the Kolmogorov–Smirnov and Shapiro–Wilk tests indicate that some variables do not fully meet the assumption of normality. Nevertheless, the skewness and kurtosis values fall within the acceptable ranges proposed by Kim (2013) (skewness ±2, kurtosis ±7), indicating that the data are approximately normal for subsequent parametric analyses.

4.2. Hypothesis Test for H1 to H6

To test hypotheses H1 through H6 under the criteria Hₐ: r > 0.50; H0: r < 0.50, the following were proposed: H1: Financial literacy has a positive effect on individuals’ financial capabilities; H2: Financial education has a positive impact on individuals’ financial capabilities; H3: Financial attitude has a positive effect on individuals’ financial capabilities; H4: Financial advisory has a positive impact on individuals’ financial capabilities; H5: Financial knowledge and financial behavior influence individuals’ financial capabilities and H6: Financial stress influences individuals’ financial capabilities.

Table 4 presents the results of the Pearson correlation analysis. The findings show that financial literacy (FL) is positively associated with financial capability (FC) (r = .364, p < .01), theoretically supporting hypothesis H1. However, the effect size is moderate, suggesting limited practical relevance. Similarly, financial education (FE) and financial attitude (FAt) show positive correlations with FC (r = .435 and r = .566, p < .01, respectively), confirming H2 and H3, with effect sizes ranging from moderate to high in practical significance. Financial advisory (FA) exhibits the strongest correlation with FC (r = .586, p < .01), supporting H4 and indicating a considerable theoretical and practical impact. Collectively, the indicators of financial knowledge and financial behavior (FL, FE, FA, FAt) confirm H5, reflecting their influence on individuals’ financial capability. Conversely, financial stress (FS) is negatively associated with FC (r = –.193, p < .01), confirming H6; although theoretically significant, its practical effect is limited due to its low magnitude. In summary, while all correlations are statistically significant, only those with r > .50 are practically meaningful, underscoring the importance of distinguishing between theoretical and practical significance when interpreting results.

The Pearson correlation analysis indicates that financial literacy (FL) is positively associated with financial capability (FC) (r = .364, p < .01), theoretically supporting hypothesis H1. However, the effect size is moderate, suggesting that its practical relevance may be limited. Similarly, financial education (FE) and financial attitude (FAt) show positive correlations with FC (r = .435 and r = .566, p < .01, respectively), confirming H2 and H3, with effect sizes that reach moderate to high practical significance. Financial advisory (FA) exhibits the strongest correlation with FC (r = .586, p < .01), supporting H4 and demonstrating a substantial theoretical and practical impact. Taken together, the indicators of financial knowledge and financial behavior (FL, FE, FA, FAt) confirm H5, reflecting their influence on individuals’ financial capabilities. Conversely, financial stress (FS) is negatively associated with FC (r = –.193, p < .01), corroborating H6; although theoretically significant, its practical effect is limited due to its low magnitude. In summary, while all correlations are statistically significant, only those exceeding r > .50 are considered practically relevant, underscoring the importance of distinguishing between theoretical and practical significance when interpreting results.

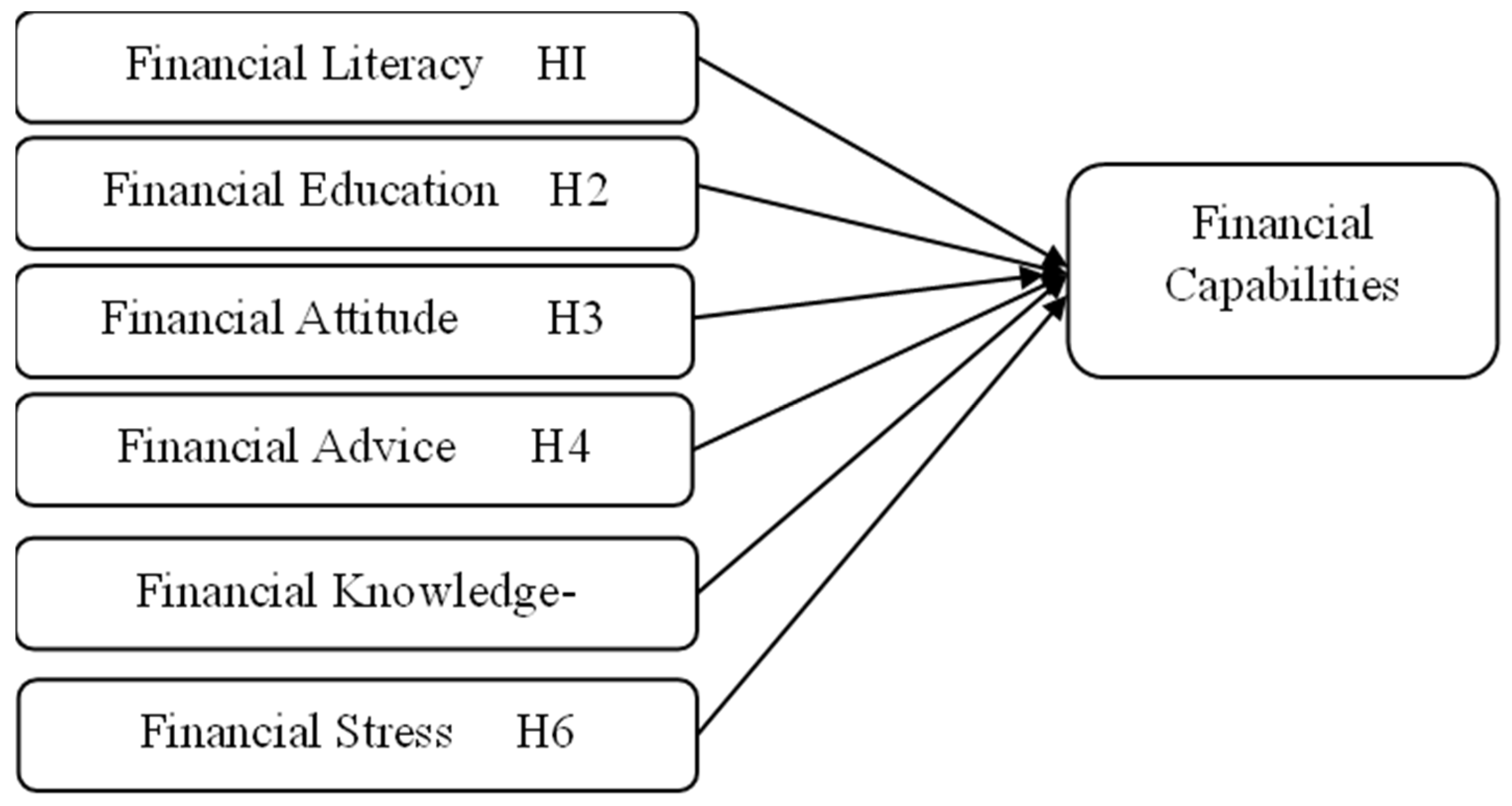

To validate the first block of the construct presented in Figure 2, the relationships between the following variables were tested: financial literacy (H1), financial education (H2), financial attitude (H3), financial advisory (H4), financial knowledge–behavior (H5), and financial stress (H6), with the dependent variable financial capabilities.

Sample Adequacy for Exploratory and Confirmatory Factor Analysis

Preliminary factor analysis indicated that the data were suitable for principal component analysis. The Kaiser-Meyer-Olkin (KMO) measure of sampling adequacy was .786, considered “acceptable to good.” Bartlett’s test of sphericity was significant (Chi2 (21, df) = 858.743, p < .001), indicating that the correlation matrix was significantly different from an identity matrix and that sufficient correlations existed among the variables to justify factor extraction. Two principal components were extracted, explaining 65.16% of the total variance. The first component accounted for 45.68% of the variance and primarily grouped variables related to financial education and capability, including FinLiteracy (.678), FinCapability (.763), FinAdvisory (.835), FinEducation (.484), FinAttitude (.806), and FinBehaviour (.741). The second component explained 19.48% of the variance. It was dominated by FinStress (.846), suggesting that this variable behaves relatively independently from the others and may represent a distinct construct related to financial stress.

Communalities indicate that most of the variance in the variables is well represented by the extracted components, with values ranging from .483 (FinEducation) to .760 (FinCapability), except for FinStress, which is mainly explained by the second component (.743). Overall, these results suggest that the study variables cluster into two meaningful dimensions: one focused on financial capability, education, and behavior, and another on financial stress, providing a robust factorial framework for subsequent analyses (see Table 5).

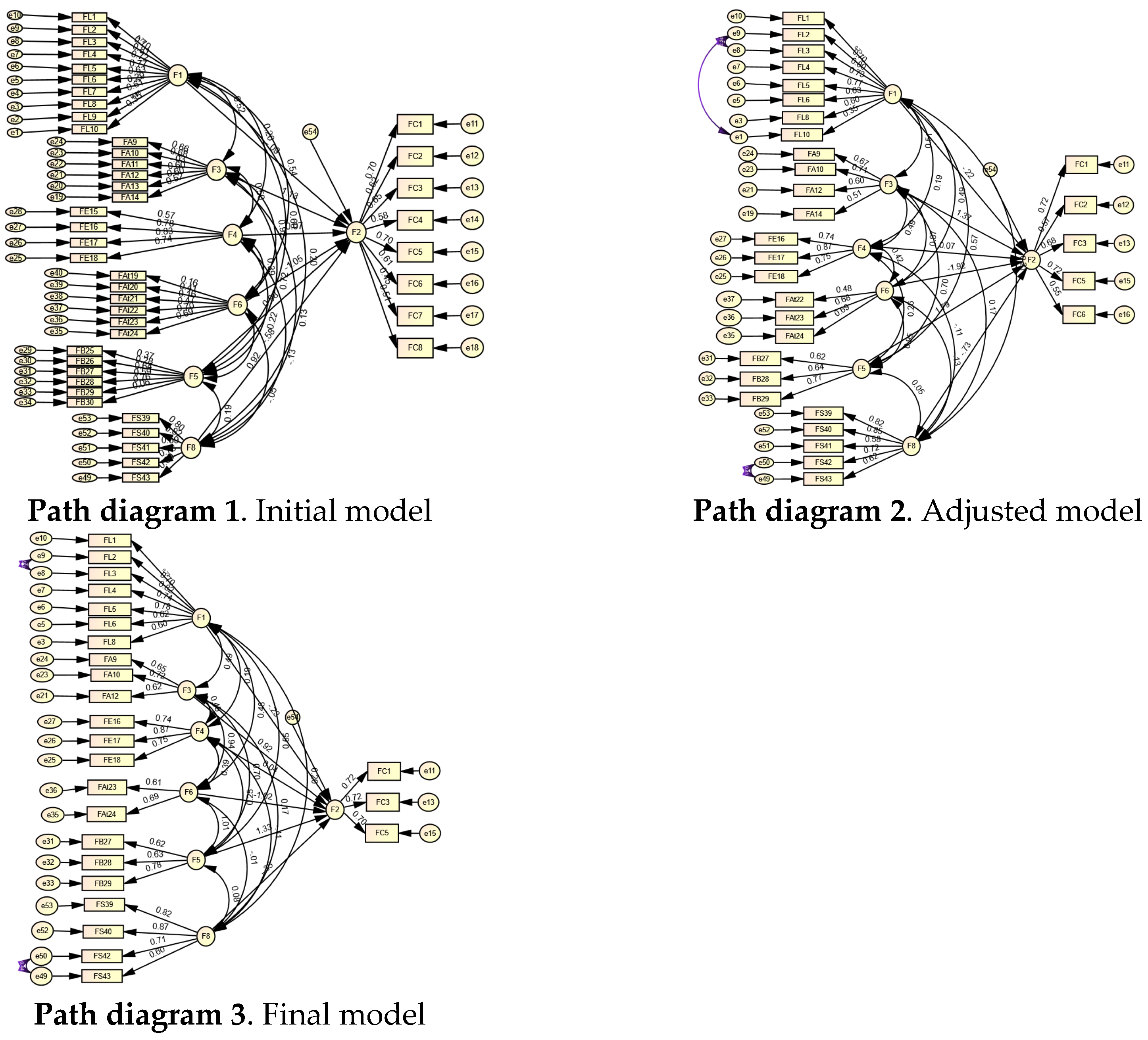

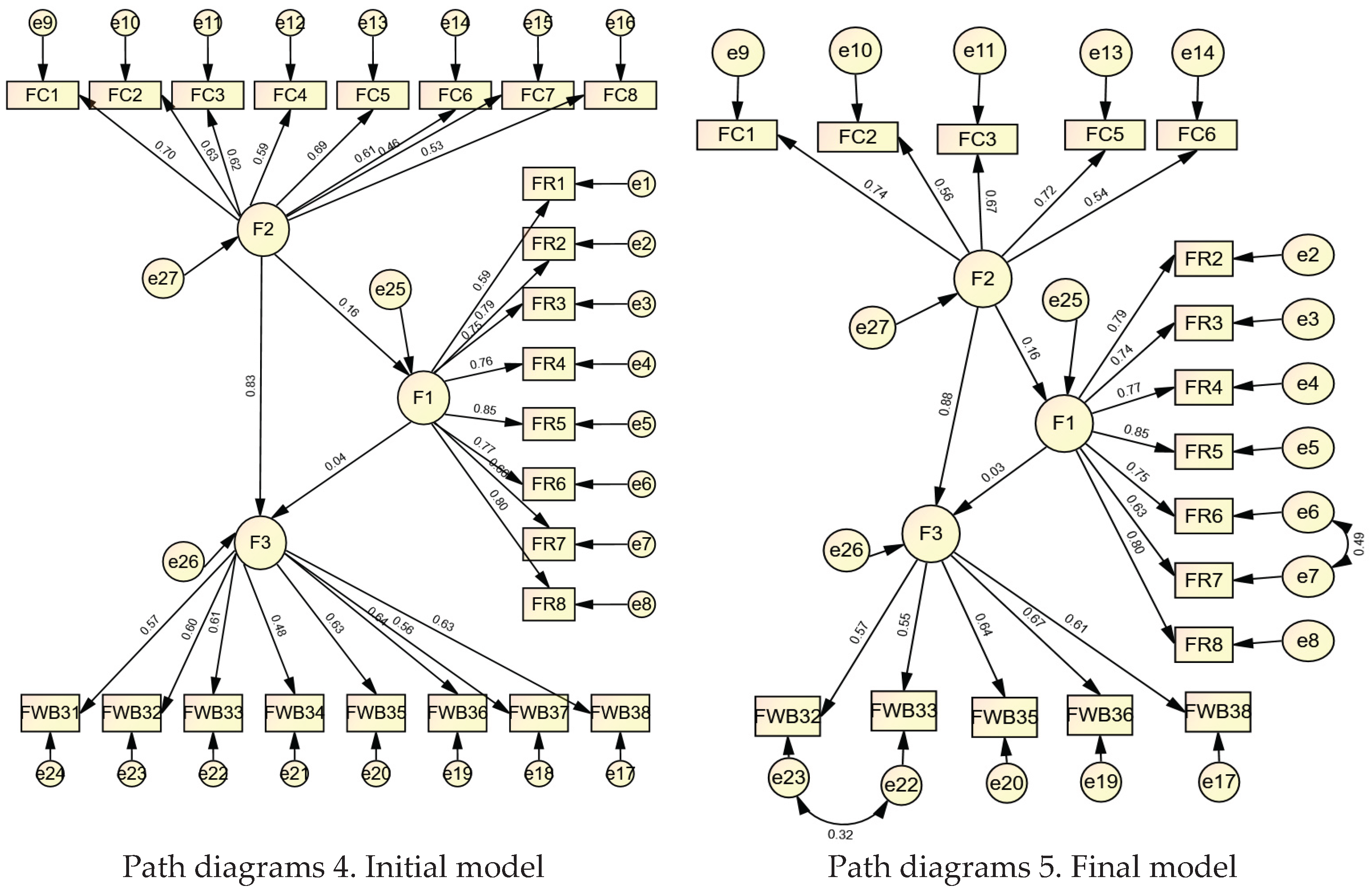

To validate the construct, Structural Equation Modeling (SEM) was employed. The structural pathways are illustrated in Path Diagrams 1, 2, and 3, Figure 3.

Model Fit Evaluation. The model fit was evaluated considering absolute, structural/relative, and parsimonious fit criteria, following the recommendations of Hu and Bentler (1999) and Kline (2016).

Absolute Fit: The relative Chi-square (CMIN/DF), Root Mean Square Residual (RMR), and general fit indices (GFI and AGFI) were examined. Commonly accepted reference values are: CMIN/DF < 2–3, RMR < 0.08, and GFI and AGFI > 0.90 (Bentler, 1990; Hooper et al., 2008). For the final model, the results were CMIN/DF = 1.890, RMR = 0.087, GFI = 0.907, and AGFI = 0.880, indicating good absolute fit.

Structural/Relative Fit: The Comparative Fit Index (CFI), Tucker-Lewis Index (TLI), Incremental Fit Index (IFI), and Normed Fit Index (NFI) were considered. Reference criteria are > 0.90 for adequate fit and > 0.95 for excellent fit. The final model yielded CFI = 0.945, TLI = 0.934, IFI = 0.945, and NFI = 0.891, suggesting a very satisfactory structural fit, approaching excellent levels.

Parsimony: Parsimonious fit was assessed using the Parsimony Goodness-of-Fit Index (PGFI), Parsimony Normed Fit Index (PNFI), and the Expected Cross-Validation Index (ECVI). Higher PGFI and PNFI values indicate a more parsimonious model, while lower ECVI values suggest greater replicability in other samples. In the final model, PGFI = 0.703, PNFI = 0.748, and ECVI = 1.710, reflecting a balanced model in terms of fit and parsimony.

Overall, the absolute, structural, and parsimonious fit indices indicate that the final model demonstrates satisfactory and reliable fit for the analyzed data. Table 6 presents a comparison of the models against the reference criteria.

The resulting Model 3 from the confirmatory analysis is the one that shows the best fit across its three blocks: absolute fit, structural fit, and parsimony. This can be explained as follows:

Regarding the Financial Literacy component, this construct captures individuals’ early experiences in handling money within the family context. The items illustrate how observing financial behavior at home, learning saving habits from parents or caregivers, and having conversations about money during childhood and adolescence contribute to the development of initial financial knowledge. They also highlight the importance of role modeling in acquiring financial habits, the early appreciation of money, and the distinction between needs and wants in consumption. Together, these indicators reflect how the family environment shapes early knowledge and attitudes toward finances. Concerning the Financial Advice component, this factor refers to individuals’ willingness to consider external opinions when making money-related decisions. The items capture openness to recommendations from others, trust in financial professionals, the perception that advice is a resource for those with greater capital, and the willingness to pay for advisory services if costs are reasonable. These elements reflect attitudes toward seeking and valuing specialized financial guidance.

For the Financial Education component, this construct focuses on formal or extracurricular training related to economic and financial topics. The items consider participation in university-level finance or economics courses, attendance in non-formal training programs, and exposure to economic content in other disciplines, such as political science or legal studies. The aim is to capture the individual’s level of engagement with structured educational processes that promote understanding of financial concepts. Finally, the Financial Attitude component reflects the degree of control and modernization in managing personal finances. The items address practices such as maintaining close oversight of financial matters and using technological tools—particularly mobile phones—to make or receive payments. This construct links the perception of individual responsibility with adaptation to new financial management methods.

Regarding the Financial Behaviour component, this factor focuses on practical habits in daily money management. The items indicate tendencies such as assessing one’s ability to pay before making purchases, having leftover funds at the end of the month, and maintaining discipline in meeting financial obligations on time. Together, they reflect observable behaviors associated with responsible financial management. For the Financial Stress component, this factor captures the perception of emotional tension related to one’s personal financial situation. The items include feelings of stress when thinking about finances, constant worry about being unable to cover basic expenses, the perception of money as a recurring source of anxiety, and the negative impact of financial circumstances on emotional well-being. This construct links the economic sphere with individuals’ psychological health.

Finally, the Financial Capabilities component can be described as follows. This construct reflects perceptions of the resources and skills available to meet the economic demands of daily life. The items address the ability to raise funds in an emergency, habitual use of electronic payment methods, and competence in managing routine financial matters, such as handling accounts, cards, and expense tracking. These indicators allow for evaluating individuals’ self-sufficiency and practical financial skills.

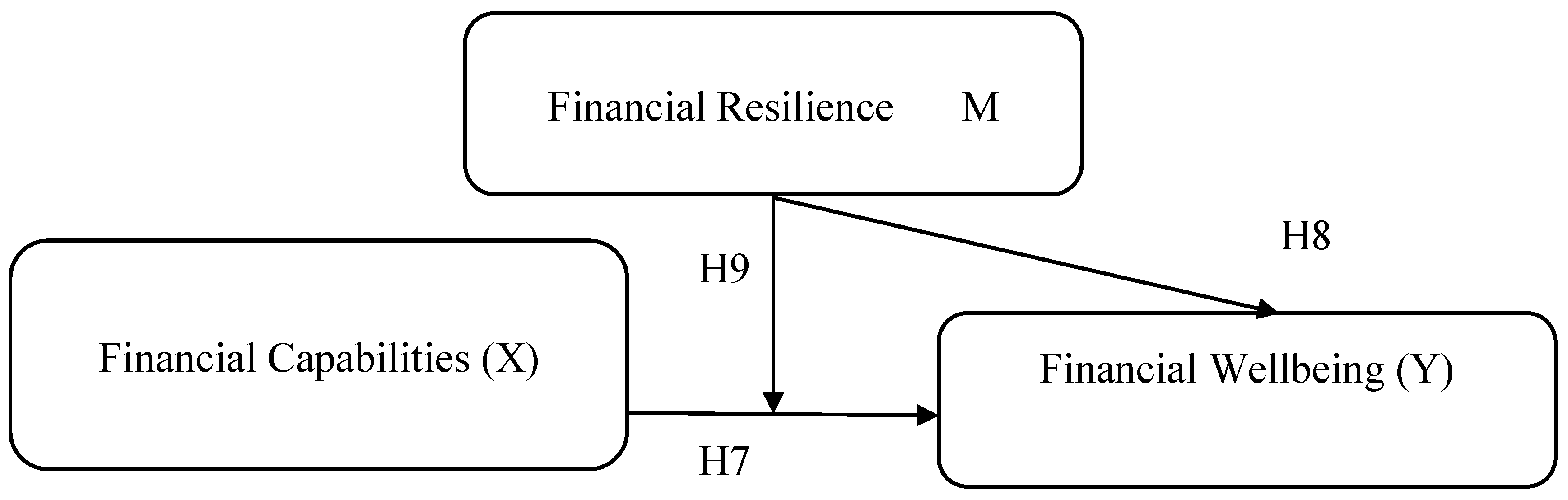

4.3. Hypothesis Test to H7 and H8

To test hypotheses H7 (financial capabilities influence financial well-being) and H8 (financial resilience influences financial well-being), a Pearson correlation was conducted between financial capabilities and financial well-being. The test is framed as follows: Alternative hypothesis (Ha): r > 0.5 and Null hypothesis (Ho): r < 0.5 (see Table 7)

As we can see in Table 7, the results of the Pearson correlation analysis show a positive and significant effect between financial capabilities and financial well-being (r = .679, p < .001), providing strong support for hypothesis H7 and suggesting that higher levels of financial capabilities are associated with greater perceived financial well-being. Likewise, a positive but weak correlation was found between financial resilience and financial well-being (r = .151, p = .004), confirming hypothesis H8 and indicating that resilience contributes, albeit to a lesser extent, to explaining financial well-being. Finally, the positive association between financial capabilities and financial resilience (r = .134, p = .011) further supports the relevance of exploring the mediating role of resilience in the relationship between financial capabilities and financial well-being. In summary, all correlations are statistically significant; however, only those with r > 0.5 are considered practically relevant, highlighting the importance of distinguishing between theoretical and practical significance when interpreting the results.

For the evaluation of the second block of the model described in Figure 4, the following results were obtained:

Sample Adequacy for Factorial and Confirmatory Analysis

The principal component analysis (PCA) was considered appropriate for the data, as indicated by the Kaiser–Meyer–Olkin (KMO) measure of sampling adequacy and Bartlett’s test of sphericity (Chi2, degrees of freedom, and p-value). In Table 8 show the KMO value (.521) was slightly acceptable, -just above the minimum threshold of .50, although it did not reach the ≥ .60 level generally considered acceptable for proceeding with factor analysis (≥ .70 = good; ≥ .80 = very good). The significance of Bartlett’s test indicated that the correlation matrix differed from the identity matrix, thereby justifying the extraction of a component. A single component was extracted, explaining 57.82% of the total variance. The variables Financial Capabilities (factor loading = .896; communality = .803) and Financial Well-being (factor loading = .900; communality = .811) showed very strong associations with this component, suggesting that they share a common latent basis. In contrast, Financial Resilience exhibited a low loading (.348) and a reduced communality (.121), indicating that the extracted factor does not adequately account for its variance. Taken together, these results demonstrate that the factorial structure consistently summarizes the dimensions of financial capability and well-being. In contrast, financial resilience behaves as a relatively independent dimension within the model.

To verify the construct, the Structural Equation Modeling (SEM) methodology was applied. The structural paths are described in Path Diagrams 4 and 5, Figure 5. In Table 9, the indices of absolute fit, structural fit, and parsimony are shown, which are compared with the reference criteria to determine the best-fitted model.

The principal component analysis conducted on the financial variables -Financial Capability (FinCapability), Financial Well-being (FinWellbeing), and Financial Resilience (FinResilience)-allowed for the extraction of a single component that explained 57.82% of the total variance. High communalities were observed for FinCapability (0.803) and FinWellbeing (0.811), whereas FinResilience showed a lower communality (0.121), indicating that it contributes less to the shared variance among the components. Sampling adequacy was moderate (KMO = 0.521), and Bartlett’s test of sphericity was significant (χ2 = 233.288, p < 0.001), justifying the application of the factor analysis. Subsequently, the evaluation of model fit through absolute, structural, and parsimony indices showed that Model 2 demonstrated a better overall fit, with CMIN/DF = 2.474, GFI = 0.920, RMSEA = 0.064, and CFI = 0.939, as well as good parsimony (PNFI = 0.756, PCFI = 0.787). Taken together, these results suggest that Model 2 efficiently captures the interrelationships among the financial variables considered and is more robust than Model 1 in explaining the data’s underlying structure.

2.4. Hypothesis Test for H9

Results of the Mediation Model for H9: The relationship between financial capabilities and financial well-being is mediated by financial resilience. In the Table 10 shows that financial capability (FinCap) positively and significantly predicts financial resilience (FinRes), with an unstandardized coefficient B = 0.111 (SE = 0.043, t = 2.57, p = .011, 95% CI [0.026, 0.197]), indicating that higher financial capability is associated with an increase in resilience; however, the model explains only a small proportion of the variance (R2 = 0.018). Subsequently, Table 11 presents the multiple regression model in which FinCap and FinRes are included as predictors of financial well-being (FinWB). In this analysis, FinCap maintains a strong and significant effect on FinWB (B = 0.570, SE = 0.033, t = 17.308, p < .001, 95% CI [0.505, 0.634]). In contrast, FinRes does not reach statistical significance (B = 0.063, SE = 0.040, t = 1.586, p = .114, 95% CI [-0.015, 0.140]), suggesting that the primary contribution to financial well-being comes from financial capability.

Finally, Table 12 presents the mediation analysis, in which the direct effect of FinCap on FinWB is significant (B = 0.570, SE = 0.033, t = 17.308, p < .001, 95% CI [0.505, 0.634]). In contrast, the indirect effect through FinRes (B = 0.007, BootSE = 0.006, 95% CI [-0.002, 0.021]) is not significant, as the confidence interval includes zero.

Taken together, these findings provide evidence that financial capability exerts a direct and substantial effect on financial well-being, whereas financial resilience does not play a significant mediating role. Consequently, the results suggest that financial well-being primarily depends on individuals’ financial capabilities, providing empirical support for the idea that interventions to improve financial well-being should focus on strengthening these capabilities. However, financial resilience may act as a complementary, non-determinant factor in this sample.

Discussion

The results of this study largely confirm the theoretical propositions underlying the proposed model, showing that financial literacy has a positive and significant effect on individuals’ financial capabilities (H1). This finding aligns with Lusardi and Mitchell (2014) and Atkinson and Messy (2012), who highlight literacy as a key determinant of the ability to manage economic resources. However, in contrast with some studies reporting stronger effects, such as Zhang and Xiong (2020), the effect size in the present study was moderate, suggesting that its practical relevance may be lower than expected. This indicates that contextual variables, such as socioeconomic environment or access to resources, may be moderating its impact, consistent with findings showing that individual and methodological factors can attenuate the relationship between education and financial literacy.

Similarly, financial education showed a positive effect on financial capabilities (H2), consistent with Remund (2010), Potrich et al. (2016), Guerini, Masciandaro, and Papini (2024), and Soejono et al. (2025), who emphasize the importance of structured formal and non-formal training to enhance financial competence. However, the effect size was moderate, suggesting that formal education and extracurricular courses do not always translate directly into practical skills, as noted by Zhang and Fan (2024). Financial attitude (H3) also showed a significant positive effect, corroborating the idea that psychological disposition and perceived control over finances are important determinants of economic management (Martino & Ventre, 2023; Kumar et al., 2024). While this relationship is consistent with studies reporting stronger effects of attitude on financial behaviors (She et al., 2024; Bressan & Vieira, 2021), our results suggest that attitude alone may not be sufficient to generate substantive improvements in financial capabilities if not combined with education and advice.

One of the most relevant findings concerns financial advice (H4), which showed the highest correlation with financial capabilities, confirming the arguments of Collins (2012), Stolper and Walter (2017), de Jong and Wagensveld (2024), and Mustafa et al. (2025) regarding the importance of professional advice for effective economic decision-making. This finding highlights the practical relevance of advice, especially when it integrates sustainability, retirement planning, and risk management. However, as noted by Staehelin et al. (2024), the effectiveness of advice also depends on personal interaction and the use of technology, which may explain variations in effect sizes across contexts.

Financial knowledge and financial behavior (H5) were positively related to financial capabilities, supporting the literature emphasizing the integration of information, practical skills, and self-control (Shanmugam et al., 2022; Morris et al., 2022). However, compared with studies reporting stronger effects of financial behavior on economic well-being (FINRA, 2018; Peter & Gupta, 2024), our results indicate that, although significant, this effect may be limited by contextual and cultural variables that affect the translation of knowledge into effective action.

Financial stress (H6) was negatively associated with financial capabilities, corroborating literature identifying economic tension as an inhibitor of decision-making and resource management (Joseph & Peetz, 2024; Choi et al., 2025; Netemeyer et al., 2018; O’Neill et al., 2005). Although statistically significant, the effect size was low, consistent with Sorgente et al. (2023), who note that financial stress and well-being are distinct constructs and that coping strategies and social support can moderate the influence of stress.

Regarding the relationship between financial capabilities and financial well-being (H7), the results show a positive and robust effect (r = 0.679, p < .001), consistent with research emphasizing the importance of practical skills in achieving economic stability and subjective satisfaction (Saeedi & Nishad, 2024; Rai et al., 2025; Kempson et al., 2017; Brüggen et al., 2017). Financial resilience also showed a positive, though weak, effect on financial well-being (H8; r = 0.151, p = .004), in line with Wheeler & Brooks (2024), Salignac et al. (2019), and Gerrans (2020), who recognize that resilience contributes to well-being, though not always decisively. The positive association between financial capabilities and resilience (r = 0.134, p = .011) supports the need to explore its mediating role.

However, the mediation analysis (H9) indicated that financial resilience does not mediate between capabilities and well-being, as the indirect effect was not statistically significant. This aligns with studies showing that direct financial capability is the main determinant of well-being (She et al., 2024; Sharma et al., 2025), while resilience may act as a complementary or moderating factor rather than a decisive mediator.

Overall, these findings align with the literature regarding the relevance of literacy, education, attitude, advice, and financial behavior for strengthening financial capabilities and economic well-being, while providing additional evidence on the distinction between statistical significance and practical relevance. They show that some effects, although significant, may be moderate or conditioned by contextual, individual, and cultural factors. This study also underscores the centrality of financial advice as a practical resource. It highlights the need to design educational and advisory interventions that consider these dimensions to maximize impact on financial well-being.

Theoretical Implications

This study provides robust evidence on the determinants of financial capabilities and their relationship with well-being and financial resilience, consolidating an integrative conceptual framework that encompasses financial literacy, education, attitudes, advice, knowledge, and financial behavior, as well as financial stress. The findings underscore the centrality of financial literacy and education as foundational constructs for the development of economic skills (Lusardi & Mitchell, 2014; Atkinson & Messy, 2012; Zhang & Xiong, 2020; Soejono et al., 2025; Guerini, Masciandaro & Papini, 2024; Zhang & Fan, 2024), highlighting that both individual and contextual factors can modulate their impact. Financial attitudes also emerge as a crucial determinant, consistent with recent studies emphasizing perceived control, future orientation, and self-regulation as facilitators of effective financial management (Martino & Ventre, 2023; Kumar et al., 2024; She et al., 2024; Bressan & Vieira, 2021).

Financial advice appears as a particularly strong predictor of capabilities, reinforcing recent evidence on the importance of professional guidance in retirement planning, risk management, and business sustainability (de Jong & Wagensveld, 2024; Mustafa et al., 2025; Staehelin et al., 2024; Sun et al., 2024). This underscores the need to integrate hybrid approaches—combining formal education, professional advice, and practical experience—to enhance financial development.

Moreover, the study confirms that financial stress inhibits financial capabilities (Joseph & Peetz, 2024; Choi et al., 2025; Sorgente et al., 2023), although its practical effects may be limited and modulated by coping strategies and social support. Finally, evidence regarding financial resilience and well-being suggests that, while resilience provides complementary support (Salignac et al., 2019; Wheeler & Brooks, 2024; Kempson et al., 2017; Brüggen et al., 2017), it does not significantly mediate the relationship between capabilities and well-being, indicating that practical skills and tangible resources are predominant in achieving economic well-being (She et al., 2024; Sharma et al., 2025).

Practical Implications

From an applied perspective, this study highlights the centrality of financial advice as a strategic resource for strengthening individual capabilities, even surpassing formal education and literacy, thereby providing concrete guidance for the design of effective public policy interventions, educational programs, and personalized financial services. The findings also underscore the importance of distinguishing between statistical significance and practical relevance, guiding financial education and economic well-being program managers to prioritize actions that generate measurable impacts in individuals’ daily lives. Furthermore, by linking financial capabilities with economic well-being and resilience, the study contributes to the global sustainability and financial development agenda, offering empirical evidence to inform strategies that promote economic stability, financial inclusion, and preparedness for personal and systemic shocks or crises.

Conclusions

In summary, this study makes a significant contribution to the literature by integrating multiple financial variables into a comprehensive, contextually grounded model. It confirms that literacy, education, attitudes, advice, and financial behavior are key determinants of financial capabilities, which in turn have a substantial impact on financial well-being. The study provides novel evidence on the limited mediating role of financial resilience, highlighting the predominance of practical capabilities in individual economic management. These findings consolidate a robust conceptual framework that is valuable both for academic research and professional practice, linking central financial topics on the current global agenda.

Limitations

The study’s limitations include its cross-sectional design, which precludes definitive causal inferences; the use of a non-probabilistic sample, which restricts the generalizability of the results; and the potential influence of unaccounted contextual variables, such as cultural, socioeconomic, or technological factors, which could modulate the observed effects.

Future Research Directions

Based on the findings, future research is suggested to explore: (i) the influence of cultural and socioeconomic contexts on the relationship between capabilities and financial well-being; (ii) the potential role of financial resilience in economic crises or emergencies, evaluating conditions under which its mediating effect may be more pronounced; (iii) the effectiveness of financial advice programs combined with formal education and practical experiences; and (iv) longitudinal studies that assess the evolution of these relationships over time, incorporating interactions with emerging financial technologies and economic inclusion tools.

Funding

Not applicable. This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

Institutional Review Board Statement

This study was approved by the Ethics Committee of the Business School at the Universidad Cristóbal Colón (Project ID P-07/2025). The research adhered to the principles established in the Declaration of Helsinki. The study’s objectives and procedures were explained to participants during the administration of the questionnaire, ensuring their full confidentiality and anonymity. Informed consent was obtained from all participants after they had read and understood the provided instructions and statements.

Informed Consent Statement

The instrument used to collect participants’ data included a statement of informed consent. By completing and submitting the questionnaire, each participant explicitly indicated their agreement to take part in the study, acknowledging the objectives and the intended use of the information provided.

Acknowledgments

I would like to express my sincere gratitude to UCC Business School for all the support to develop this research.

Conflicts of Interest

The author declares no competing interests.

References

- Abdul Ghafoor, K., Akhtar, M. (2024). Parents’ financial socialization or socioeconomic characteristics: which has more influence on Gen-Z’s financial wellbeing?. Humanit Soc Sci Commun 11, 522 (2024). [CrossRef]

- Adams, J. (1787, agosto 25). Carta a Thomas Jefferson. En L. J. Cappon (Ed.), The Adams-Jefferson Letters: The Complete Correspondence Between Thomas Jefferson and Abigail and John Adams (Vol. 1, pp. 194–195). University of North Carolina Press. https://uncpress.org/book/9780807842300/the-adams-jefferson-letters/.

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179–211. [CrossRef]

- Allie, J., West, D., & Willows, G. (2016). The value of financial advice: An analysis of the investment performance of advised and non-advised individual investors. Investment Analysts Journal, 45(sup1), S63–S74. [CrossRef]

- Amonhaemanon, D. (2024). Financial stress and gambling motivation: the importance of financial literacy, Review of Behavioral Finance, Vol. 16 No. 2, pp. 248–265. [CrossRef]

- Ananda, S., Kumar, R.P. & Dalwai, T. (2024). Impact of financial literacy on savings behavior: the moderation role of risk aversion and financial confidence. J Financ Serv Mark 29, 843–854 (2024). [CrossRef]

- Anders, J., Jerrim, J., & Macmillan, L. (2023). Socio-Economic Inequality in Young People’s Financial Capabilities. British Journal of Educational Studies, 71(6), 609–635. [CrossRef]

- Archuleta, K. L., Dale, A., & Spann, S. M. (2013). College students and financial distress: Exploring debt, financial satisfaction, and financial anxiety. Journal of Financial Therapy, 4(2), 1–15.

- Atkinson, A., McKay, S., Collard, S., & Kempson, E. (2007). Levels of Financial Capability in the UK. Public Money & Management, 27(1), 29–36. [CrossRef]

- Babajide, A., Osabuohien, E., Tunji-Olayeni, P., Falola, H., Amodu, L., Olokoyo, F., Adegboye, F., Ehikioya, B. (2021). Financial literacy, financial capabilities, and sustainable business model practice among small business owners in Nigeria. Journal of Sustainable Finance & Investment, 13(4), 1670–1692. [CrossRef]

- Bandura, A. (1986). Social foundations of thought and action: A social cognitive theory. Prentice-Hall.

- Bansal, D., Kaur, L. (2024). Financial literacy and gender gap: a study of Punjab state of India. J. Soc. Econ. Dev. 26, 77–101 (2024). [CrossRef]

- Bernheim, B. & Garrett, Daniel & Maki, Dean. (2001). Education and Saving: The Long-Term Effects of High School Financial Curriculum Mandates. Journal of Public Economics. 80. 435-465.

- Bhatia, S., Singh, S. (2024). Exploring financial well-being of working professionals in the Indian context. J Financ Serv Mark 29, 474–487 (2024). [CrossRef]

- Bhattacharya, R., Lobo, R., Barrows, J. et al. (2025). Financial education intervention to promote financial well-being among low-income mothers. Discov Educ 4, 101. [CrossRef]

- Brasil, C.V., Bressan, A.A., Vieira, K.M. et al. (2024). Financial Resilience, Financial Ignorance, and their impact on financial well-being during the COVID-19 pandemic: evidence from Brazil. Int Rev Econ 71, 273–299 (2024). [CrossRef]

- Bryman, A. (2016). Social research methods (5th ed.). Oxford University Press. https://ktpu.kpi.ua/wp-content/uploads/2014/02/social-research-methods-alan-bryman.pdf.

- Carton, F., Xiong, H., & McCarthy, J. B. (2024). Human-centred factors of decision-making for financial resilience. Journal of Decision Systems, 33(sup1), 311–321.

- Çera, G., Khan, K. A., Mlouk, A., & Brabenec, T. (2020). Improving financial capability: the mediating role of financial behaviour. Economic Research-Ekonomska Istraživanja, 34(1), 1265–1282. [CrossRef]

- Choi, S.L., Totenhagen, C.J., Tomeny, T.S. et al. (2025). Navigating Financial Storms: Does Dyadic Coping Buffer the Association Between Daily Financial Stress and Emotional Well-Being?. J Fam Econ Iss 46, 54–66 (2025). [CrossRef]

- Consumer Financial Protection Bureau (CFPB). (2015). Financial well-being: The goal of financial education. https://www.consumerfinance.gov/data-research/research-reports/financial-well-being/.

- Çoşkun, A., & Dalziel, N. (2020). Mediation effect of financial attitude on financial knowledge and financial behavior: The case of university students. International Journal of Research in Business and Social Science, 9(2), 1–8.

- Creswell, J. W., & Creswell, J. D. (2018). Research design: Qualitative, quantitative, and mixed methods approaches (5th ed.). SAGE Publications. https://www.ucg.ac.me/skladiste/blog_609332/objava_105202/fajlovi/Creswell.pdf.

- Cronbach, L.J. (1951). Coefficient alpha and the internal structure of tests. Psychometrika 16, 297–334. [CrossRef]

- Da Cunha, D.T., Antunes, A.E.C., Da Rocha, J.G., Dutra, T.G., Manfrinato, C.V., Oliveira, J.M. and Rostagno, M.A. (2019). “Differences between organic and conventional leafy green vegetables perceived by university students: Vegetables attributes or attitudinal aspects?”, British Food Journal, Vol. 121 No. 7, pp. 1579-1591. [CrossRef]

- de Jong, F., Wagensveld, K. (2024). Sustainable Financial Advice for SMEs. Circ.Econ.Sust. 4, 777–789 (2024). [CrossRef]

- Diener, E. (1984). Subjective Well-Being. Psychological Bulletin, 95(3), 542–575. [CrossRef]

- Du Plessis, L., Jordaan, Y. and van der Westhuizen, L.-M. (2025). Consumer spending self-control, financial well-being and life satisfaction: the moderating effect of relative deprivation from consumers holding debt, International Journal of Bank Marketing, Vol. ahead-of-print No. ahead-of-print. [CrossRef]

- Dunn, T. J., Baguley, T., & Brunsden, V. (2014). From alpha to omega: A practical solution to the pervasive problem of internal consistency estimation. British Journal of Psychology, 105(3), 399–412. [CrossRef]

- Edwards, R., Allen, M. W., & Hayhoe, C. R. (2007). Financial attitudes and family communication about students’ finances: The role of sex differences. Communication Reports, 20(2), 90–100. [CrossRef]

- Elrayah, M., & Tufail, B. (2024). Financial education, financial advice, financial attitude and financial literacy impact on university student’s financial behaviour through financial capabilities. Artseduca, 40, 193–207.

- Estelami, H., Estelami, N.N. (2024). The differential impact of cognitive style on the relationship between financial education and financial literacy. J Financ Serv Mark 29, 242–256 (2024). [CrossRef]

- Etikan, I., Musa, S. A., & Alkassim, R. S. (2016). Comparison of convenience sampling and purposive sampling. American Journal of Theoretical and Applied Statistics, 5(1), 1–4. [CrossRef]

- Fang, J., Hao, W., & Reyers, M. (2022). Financial advice, financial literacy and social interaction: what matters to retirement saving decisions? Applied Economics, 54(50), 5827–5850. [CrossRef]

- Field, A. (2013). Discovering statistics using IBM SPSS statistics (4th ed.). SAGE Publications.

- FINRA Investor Education Foundation. (2019). National Financial Capability Study (NFCS), 2018. Financial Industry Regulatory Authority. https://www.finrafoundation.org/nfcs.

- Flores, M., Zamora-Lobato, T. & García-Santillán, A. (2024). Three-dimensional model of financial resilience in workers: Structural equation modeling and Bayesian analysis. Economics and Sociology, 17(1), 69-88. doi:10.14254/2071- 789X.2024/17-1/5.

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. [CrossRef]

- Freire, Paulo. (1968). A alfabetizacao de adultos. CrÌtica de sua visao ingénua, compreensao de sua visao critica. Santiago de Chile.

- Freire, Paulo. (1968): La alfabetización funcional en Chile. UNESCO.

- Freire, Paulo. (1970). ¿Extensión o comunicación? La concientización en el medio rural. México, Siglo XXI Editores.

- Freire, Paulo. (1985): Pedagogía del oprimido. Montevideo, Tierra Nueva. México, Siglo XXI Editores.

- García-Santillán Arturo, Venegas-Martínez, Francisco & Mendoza-Rivera, Ricardo (2024). Structural equations model to explain financial knowledge on workers. Revista Mexicana de Economía y Finanzas Nueva Época REMEF, Volume 19 Issue 1, January–March 2024, pp. 1-15, . [CrossRef]

- García-Santillán, A. (2017). Measuring Set Latent Variables through Exploratory Factor Analysis with Principal Components Extraction and Validation with AMOS Software. (2017). European Journal of Pure and Applied Mathematics, 10(2), 167-198. https://www.ejpam.com/index.php/ejpam/article/view/2768.

- García-Santillán, A., Escalera-Chávez, M. E., & Santana, J. C. (2024). Exploring resilience: a Bayesian study of psychological and financial factors across gender. Cogent Economics & Finance, 12(1). [CrossRef]

- García-Santillán, Arturo, Zamora-Lobato Ma. Teresa, Tejada-Peña, Esmeralda y Valencia-Márquez, Liduvina (2025). Exploring the Relationship between Financial Education, Financial Attitude, Financial Advice and Financial knowledge: Insights through Financial Capabilities and Financial Well-being, Journal of Risk and Financial Management. 2025, 18(3), 151; [CrossRef]

- George, D., & Mallery, P. (2010). SPSS for Windows step by step: A simple guide and reference (10th ed.). Pearson.

- Goktan, A. J., Mitchell, A. M., Quirk, K., & Immekus, J. C. (2025). Emerging adults’ financial stress and self-rated health: Meaning in life as a moderator. Journal of American College Health, 1–12. [CrossRef]

- Gudmunson, C.G., Danes, S.M. Family Financial Socialization: Theory and Critical Review. J Fam Econ Iss 32, 644–667 (2011). [CrossRef]

- Guerini, C., Masciandaro, D. & Papini, A.(2024). Literacy and Financial Education: Private Providers, Public Certification and Political Preferences. Ital Econ J (2024). [CrossRef]

- Hair, J, Anderson, R., Tatham, R., Black, W. (1999). Análisis Multivariante. 5a ed. Madrid: Prentice Hall.

- Hassan T, Prasad B, Meek BP, (2020). Modirrousta M. Attitudes of Psychiatry Residents in Canadian Universities toward Neuroscience and Its Implication in Psychiatric Practice. The Canadian Journal of Psychiatry. 2020;65(3):174-183. doi:10.1177/0706743719881539.

- Heo, W., Liu, Y. & Park, H. (2025). Financial Stress, Psychological Factors, and Financial Knowledge on Life Satisfaction: A Comparative Pre- and Post-COVID Cross-Sectional Analysis in the United States. Applied Research Quality Life (2025). [CrossRef]

- Hernandez-Perez, J., Cruz Rambaud, S. (2025). Uncovering the factors of financial well-being: the role of self-control, self-efficacy, and financial hardship. Futur Bus J 11, 70. [CrossRef]

- Hobfoll, S. E. (1989). Conservation of Resources: A New Attempt at Conceptualizing Stress. American Psychologist, 44(3), 513–524. [CrossRef]

- Hu, L., & Bentler, P. M. (1999). Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling: A Multidisciplinary Journal, 6(1), 1–55. [CrossRef]

- Hubler, D. S., Burr, B. K., Gardner, B. C., Larzelere, R. E., & Busby, D. M. (2015). The Intergenerational Transmission of Financial Stress and Relationship Outcomes. Marriage & Family Review, 52(4), 373–391. [CrossRef]

- Islam, H., Rana, M., Saha, S., Khatun, T., Ritu, M.R. and Islam, M.R. (2023), “Factors influencing the adoption of cryptocurrency in Bangladesh: an investigation using the technology acceptance model (TAM)”, Technological Sustainability, Vol. 2 No. 4, pp. 423-443. [CrossRef]

- Joseph, M., Peetz, J. (2024). Financial Stress as an Antecedent of Financial Snooping Attitudes. J Fam Econ Iss 45, 786–799 (2024). [CrossRef]

- Kahneman, D. (2011). Thinking, Fast and Slow. Ed. Farrar, Straus and Giroux, Nueva York.

- Kaur, R. and Singh, M. (2025). Influence of family financial socialization on emerging adults’ financial well-being, LBS Journal of Management & Research, Vol. ahead-of-print No. ahead-of-print. [CrossRef]

- Khan, K. A., Çera, G., & Alves, S. R. P. (2022). Financial Capability as a Function of Financial Literacy, Financial Advice, and Financial Satisfaction. E&M Economics and Management, 25(1), 143–160. [CrossRef]

- Kim H. Y. (2013). Statistical notes for clinical researchers: assessing normal distribution (2) using skewness and kurtosis. Restorative dentistry & endodontics, 38(1), 52–54. [CrossRef]

- Koropp, C., Grichnik, D., & Kellermanns, F. W. (2013). Financial attitudes in family firms: The moderating role of family commitment. Journal of Small Business Management, 51(1), 114–137. [CrossRef]

- Kumar, P., Ahlawat, P., Deveshwar, A. et al. (2024). Do Villagers’ Financial Socialization, Financial Literacy, Financial Attitude, and Financial Behavior Predict Their Financial Well-Being? Evidence from an Emerging India. J Fam Econ Iss (2024). [CrossRef]

- Kumar, P., Ahlawat, P., Deveshwar, A. et al. (2024). Do Villagers’ Financial Socialization, Financial Literacy, Financial Attitude, and Financial Behavior Predict Their Financial Well-Being? Evidence from an Emerging India. J Fam Econ Iss. [CrossRef]

- Lee, Y. G., & Dustin, L. (2021). Explaining financial satisfaction in marriage: The role of financial stress, financial knowledge, and financial behavior. Marriage & Family Review, 57(5), 397–421. [CrossRef]

- Lei, S. (2018). Financial advice and individual investors’ investment decisions. Applied Economics Letters, 26(13), 1129–1132. [CrossRef]

- Loibl, C., Moulton, S., Haurin, D., & Edmunds, C. (2020). The role of consumer and mortgage debt for financial stress. Aging & Mental Health, 26(1), 116–129. [CrossRef]

- Lusardi, A & Tufano P. (2015). Debt literacy, financial experiences and overindebtedness. Journal of Pension Economics and Finance. 14(4): 332-368. [CrossRef]

- Lusardi, A., & Mitchell, O. S. (2007). Financial literacy and retirement preparedness: Evidence and implications for financial education. Business Economics, 42(1), 35–44. [CrossRef]