Submitted:

14 January 2026

Posted:

15 January 2026

You are already at the latest version

Abstract

Over the past few years, the banking sector has undergone a rapid digital transformation. The combination of AI and ML is disrupting the old age systems and rule-based systems like anything. Various sectors are benefiting from implementing Artificial Intelligence (AI) and Machine Learning (ML) technologies to automate, personalise, and predict further changes in the customary banking model. In this paper, the study analyses the role of Machine Learning in improving customer experience and managing risk in the banking industry. Additionally, this paper discusses recent banking use-cases for chatbots, credit scoring systems, fraud detection systems, and anti-money laundering systems built using AI and ML. It also covers the ethical and regulatory aspects of AI and ML in the banking industry, including the concerns of privacy, algorithmic accountability, and algorithmic transparency. The report ends with a brief description of new technologies such as Explainable AI, Quantum Computing, and the use of Blockchain technology in financial systems. With the help of Artificial Intelligence and ML, customer experience has continued to improve, and risk management in the financial system is getting better. This study adopts a conceptual and literature-based analytical approach, and also makes an attempt to draw insights from recent empirical studies and industry reports are used to synthesise the applications of AI and ML in modern banking. The paper contributes by integrating dual perspectives, viz., customer experience and risk management, into a unified analytical framework. This study provides a structured understanding of how AI and ML combinedly enhance banking operations, offering theoretical and managerial insights for future empirical research.

Keywords:

artificial intelligence

; banking

; customer experience

; financial technology

; future of AI and ML

; machine learning

; risk management

Introduction

Artificial Intelligence and Machine Learning play a vital role in today’s modern banking system by managing the complicated tasks at lightning speed with utmost accuracy. The ability of these systems to learns from large data and make improved decision-making. This technology helps in identifying unusual things and also suggests solutions with utmost accuracy. This study also explores several recent studies that are going to shape the upcoming financial system.

According to the report given by McKinsey & Company (2024), which says that more than 60% of the financial institutions have already adopted AI-based systems globally for enhancing customer engagement and minimising risks. The increasing adoption of AI and ML in banks helps in changing the old traditional system into a higher level of intelligence. These ML systems basically learn from large data, and continuously they will improve their accuracy and adapt to it in real-time. This technology is not only helpful in improving efficiency, but it also helps in building prioritised strategies. Now banks are much focused on how to create more personalised data-driven customer experience and risk management frameworks to react with a more complex and dynamic environment.

Research Objectives:

- To examine how Machine Learning enhances the experience of customers in the banking industry.

- To analyse and interpret the role of AI and ML in strengthening the risk management frameworks of those systems.

- To identify the key challenges in the Implementation of AI and ML.

- To study the future implications of AI and ML adoption in the Banking industry.

Methodology:

This study adopts a conceptual and descriptive research design based on the secondary data. Data and insights are collected from the peer-reviewed journals, industry reports like Deloitte, McKinsey, WEF, etc., and also recent academic publications. This study applies a literature synthesis approach, organising the existing literature into two thematic dimensions: one is customer experience, another one is risk management. This analytical framework was developed by mapping the patterns across published papers and also identifying the conceptual linkages between technological and managerial applications in the banking industry. This qualitative synthesis gives rise to the conceptual model as presented in Figure 1.

Literature Review:

Artificial intelligence (AI) and Machine Learning (ML) have become an essential point for digital transformation in the banking sector. Over the past decade, the focus has shifted from technical modelling to exploring strategic and managerial implications. This section critically reviews existing studies and identifies how AI and ML have reshaped the customer experience and risk management in the banking industry.

AI, ML and Financial Services

Jordan and Mitchell (2015) gave a foundation for understanding Machine Learning by defining it as the ability of systems to improve performance through experience (learning). Their work established predictive analytics in finance. Later studies, by Hu et al. (2020) and Gao et al. (2024), expanded these discussions by highlighting the growing role of ML in automating bank operations and enabling accurate decision-making under uncertainties. Ghosh and Li (2022) emphasised ML’s superior capabilities in credit scoring, fraud detection accuracy and behaviour analytics, which are very important in banking operations.

Theoretical Perspectives on Customer Experience

The Technology Acceptance Model (TAM) provides the very foundation for understanding the interaction between customers and AI-driven banking systems. This model put forward the perceived usefulness and the ease of usage acceptance of the technology (Davis, 1989). This model puts forward the usefulness and ease of use that influence users’ acceptance of technology. In a similar way, the Customer Experience Management (CEM) framework emphasizes personalization, responsiveness, and trust as key determinants of satisfaction and loyalty in digital banking. AI-based tools such as chatbots, recommendation systems, and sentiment analysis platforms created for customers will improve the experience, encouraging further technology adoption and customer satisfaction. Studies by Deloitte (2023) and Fujitsu (2023) further support this view, emphasising that ML allows banks to design more responsive, data-driven customer service frameworks.

Improving Risk Management

Risk management is one of the most important areas where Machine Learning has shown great potential to transform the way banks handle risks. The traditional statistical models often fail to capture the complex relationships that exist in large datasets, whereas ML techniques such as Random Forest, Gradient Boosting, and Neural Networks help in improving the prediction accuracy and detection of fraud (Sharma & Tan, 2022; Gao et al., 2024). As mentioned by McKinsey & Company (2022), banks that have implemented ML-based fraud detection systems have reached almost 99% accuracy in identifying unusual transactions. Reports by Deloitte (2024) and the World Economic Forum (2022) also highlight that AI-based compliance models help in reducing false positives in Anti-Money Laundering (AML) processes and make regulatory activities more efficient. Overall, these developments show a clear shift from traditional reactive risk management towards a more proactive and intelligent risk management approach in the modern banking system.

Literature Gap:

The existing studies have explored AI and ML separately in banking, and there is limited research on the dual role in customer experience and risk management. However, most of the studies are focused more on technical aspects. There is no focus on the conceptual framework present holistically. This paper covers the conceptual framework aspects and fills the gap by offering a unified discussion that will connect technological innovation with the actual managerial application.

Meaning of AI and ML

AI (Artificial Intelligence) and ML (Machine Learning) are the two most powerful words that have come into mainstream recently, and revolutionised many industries in many ways. Their applications not only increased operational efficiency but also helped in rapid digitalisation.

- What is AI?

The AI simply means a machine, which is trained to behave like humans, and computers are empowered to learn many things and allowing computers to perform tasks that are done by human intelligence. To put into simple words. It is an intelligence created by human beings for machines by using data and programming. It mimics humans and thinks like humans. It makes improved decisions for a wide range of industries, such as healthcare to finance and retail, much more.

There are two types of AI.

| Weak AI | Strong AI |

| Works optimally for specific tasks and works within limitations for the mentioned parameters Ex: Alexa, Google Assistant, Apple’s Siri |

Learns continuously from data and improves accordingly Ex: Gen AI |

- What is ML?

ML is part of AI. Here the humans won’t write complex codes, explicit programmes, but instead the machine learns and makes decisions based on the large data, which is fed to the machine. These decisions are used to make better decisions, including the development of the desired algorithm or system, where it can find the patterns and make the predictions and give a report based on historical data (Jordan & Mitchell, 2015).

There are three types of ML.

| Supervised ML | Unsupervised ML | Reinforcement ML |

| It learns from labelled data, mapping on input and new data (output) | It learns from unlabelled data, without any guidance and understands from patterns. | It is trained on which actions to take for the reward; it is a reward-based learning of machines. (Goal-oriented learning) |

- The use of AI and ML in Financial Services

The availability of a large set of data and the advanced analytical systems have led to the adoption of ML in various sectors, which include banking and finance as well. Financial institutions make terabytes of transactions on an everyday basis, allowing ML systems to work and generate desired output in milliseconds with utmost accuracy. As observed in the study by Ghosh and Li (2022), ML offers great predictive capability compared to traditional statistical models due to the ability to learn complex relationships among different variables.

- Applications of Machine Learning in Enhancing Customer Experience

The customer experience and delight are increasingly becoming the key differentiator between modern and traditional banking. Machine learning empowers banks to deliver personalised, responsive, and seamless experiences to customers. Customer experience (CX) is increasingly becoming the key differentiator in the banking industry.

- Personalised Service and Recommendation Systems

An ML system can be used to understand the customer behaviour and spending patterns. Due to such ability, banks can offer individual recommendations based on their preference. This will give leverage to the banks to maintain long-term relationships with customers and make them spend more time on their platform. According to the report given by PwC (2023), the personalisation done through AI will increase customer interaction by 35%.

- 2.

- Chatbots and Virtual Assistants

Natural Language Processing (NLP) helps in focusing and understanding the interaction between customers and machines. Through this mechanism, the customer can interact with the machine in their natural language, which fills the gap between the machine and humans. This mechanism has revolutionised the customer experience and service. HDFC Bank’s EVA chatbot and SBI’s SIA are the best examples of AI systems that provide instant replies to customers. This helps in solving general and repetitive queries. This gives rise to improved customer satisfaction, faster responses and lowering human intervention in repetitive and manual tasks.

- 3.

- Sentiment Analysis and Customer Insights

Through the application of ML-integrated sentiment analysis to customer feedback, emails, social media handles, banks can uplift customer emotions and can improve existing customer emotions, and it can improve the services. ML systems can detect dissatisfaction trends and alert it, so that banks can frame corrective actions such as proactive outreach to customers or providing personalised offers to them.

- 4.

- Customer Retention Models

ML models can also predict customer dissatisfaction (leaving a platform) or deviation by the identification of behavioural patterns like reduced transactions and inactivity in a particular time period. This gives the power to banks to develop retention strategies before the customer is willing to leave. Predictive retention analytics can reduce the customer’s deviation by 20 to 25% (Accenture, 2023).

- Machine Learning in Risk Management

The management of risk is very necessary in banking to sustain for a longer period of time. The real-time activity of ML models analyses the variables and predicts the future risks. The effectiveness of risk management by ML will increase the trust of customers, and it will help in the prevention of fraudulent activities during regular banking operations.

- Assessment of Credit Risks

Traditional and old credit scoring models have limited financial indicators. In modern banking, supervised and unsupervised ML are popularly used for determining credit risks. A few models, like Random Forest and Gradient Boosting systems, can also be integrated into different data points, such as transaction history, spending behaviour, to evaluate the creditworthiness of customers. For example, ICICI Bank uses ML models for automated loan approvals that improve turnaround time also lower default risks.

- 2.

- Fraud Detection and Prevention

In the banking sector, for detecting fraud, ML helps a lot. It analyses the suspicious activities and user behaviour; it can detect the fraudulent activity. ML algorithms like Isolation Forest, Autoencoders, and Neural Networks can detect unusual things in transactions patterns within milliseconds. JPMorgan Chase’s COiN (Contract Intelligence) platform uses ML to process thousands of loan agreements and data and it is detecting unusual things with 99% accuracy. This will facilitate good competence between banks and customers.

- 3.

- ML in the analysis of cyber security attacks

Cyber-attack detection is awful challenge, because it takes months and years to detect cyber-attacks. In modern environment with large volume of data, the ML adoption makes the work easier, and is a powerful approach to improve cyber-attack detection. The cyber operations are increasing advance and these zero-day vulnerabilities will empower the cyber-attack defences.

- 4.

- Operational and Market Risk

The operational failures, market uncertainties and cybersecurity threats can be predicted by ML. It can also calculate the adverse changes in the economy helping banks to strengthen their capital adequacy planning. It not only minimizes risk; it also helps in governance and reporting to the authority.

Table 1.

Shows the synthesis of the results that are observed by different institutions after implementation of AI and ML in their managerial operations.

Table 1.

Shows the synthesis of the results that are observed by different institutions after implementation of AI and ML in their managerial operations.

| Area of Application | Technique Used in AI/ML | Results | Example |

| Personalized Banking | Recommendation Systems, Clustering | Enhanced engagement & loyalty | HDFC Bank – EVA chatbot |

| Fraud Detection | Anomaly Detection, Neural Networks | 99% accuracy in anomaly detection | JPMorgan COiN |

| Credit Risk Analysis | Random Forest, Gradient Boosting | Reduced default rates | ICICI Bank |

| AML & Compliance | Clustering, Pattern Recognition | Fewer false positives | HSBC |

| Customer Retention | Predictive Analytics | Reduced churn by 25% | Accenture report |

“Source:This table is created by synthesizing the literature and reports.”.

- Ethical, Regulatory, and Implementation Challenges

The findings can be interpreted by using well-established innovation theories. According to the Technology Acceptance Model (Davis, 1989), customer satisfaction and adoption depend on perceived usefulness and ease of use, which can both be enhanced by using AI. Similarly, Roger’s 2003 Diffusion of Innovation (DOI) theory explains that the banks adopting ML in the early stages will gain a competitive advantage through innovation diffusion. By integrating these theories, it provides a conceptual understanding of how technological adoption drives the outcomes in the banking industry. The adoption of AI and ML in Banking System will leads to a transformative opportunity along with that it also has many challenges, like

- Biasness and Fairness: The ML does not eliminate the bias from the existing data; instead, it carries forward the bias to the next phase. So that it leads to discrimination among the customers for classifications and credit scoring and eventually biasness will exist in lending services.

- Customer’s data privacy and trust: The banks should readily comply with the data protection regulations, provided by GDPR (General Data Protection Regulation), and banks should also comply with time-to-time guidelines released by RBI. For banks, it's hard to comply with those regulations regularly.

- Accountability: Many ML models work as “black boxes,” which means systems improve their performance by being exposed to a large data set rather than only explicit programming. It will be hard for regulators and policymakers to understand the decision-making logics and systems of ML.

- Adoption and interaction challenges: Traditional banking systems lack awareness; this will reduce the AI and ML adoption. The interaction between existing technology with the futuristic system will become very hard to implement.

- Skill Gaps: Banks face shortages of skilled professionals in AI, data science, and advanced financial analytics tools.

To minimise challenges, the banks must implement AI infrastructure, ethics and governance frameworks, and audit mechanisms, and invest heavily in training the employees.

Future Directions of AI and ML and their implications.

The future of ML in the Banking system is only possible through the perfect mixture of emerging technologies and responsible governance while keeping customers’ interests and trust intact.

- Quantum AI

Traditional AI robot checks the information or data one by one, and they find ways to complete that work efficiently. But in the case of Quantum AI, it can try many paths in a single moment at very high speed. And it helps in connecting information in smart ways that traditional robots are not able to do. Quantum AI mechanism gives the ability to execute complex problems more effectively by using the rules of quantum physics. It has the potential to increase the ML processing power exponentially, which helps in risk management modelling and portfolio management.

- 2.

- Blockchain and ML

The blockchain and ML have complementary capabilities, like secure, decentralised data management and identification of patterns out of large data. This practical application will increase efficiency, trust, automation, security, and build transparency in financial transactions with traceability.

- 3.

- Explainable AI (XAI)

The obvious dependency on technology will increase with the passing of time; along with that, regulatory things will also increase; in such a case, Explainable AI models play an important role for transparent and accountable decision making. Explainable AI is a group of methods and processes that make ML more transparent and predictable. This will allow humans to understand, trust and also help in validating the decisions made by the ML system.

- 4.

- Generative and Conversational AI

Advanced generative AI models will turn the normal equitable financial advice into very personalised financial advice relatable to each customer as per their needs, and the humanlike virtual assistants, AI chatbots, will enhance the digital banking experiences. It will also lower the operational costs, and it will lower the intervention of human resources in repetitive tasks. Due to these resources can be allocated to the main and severe problem-solving situations.

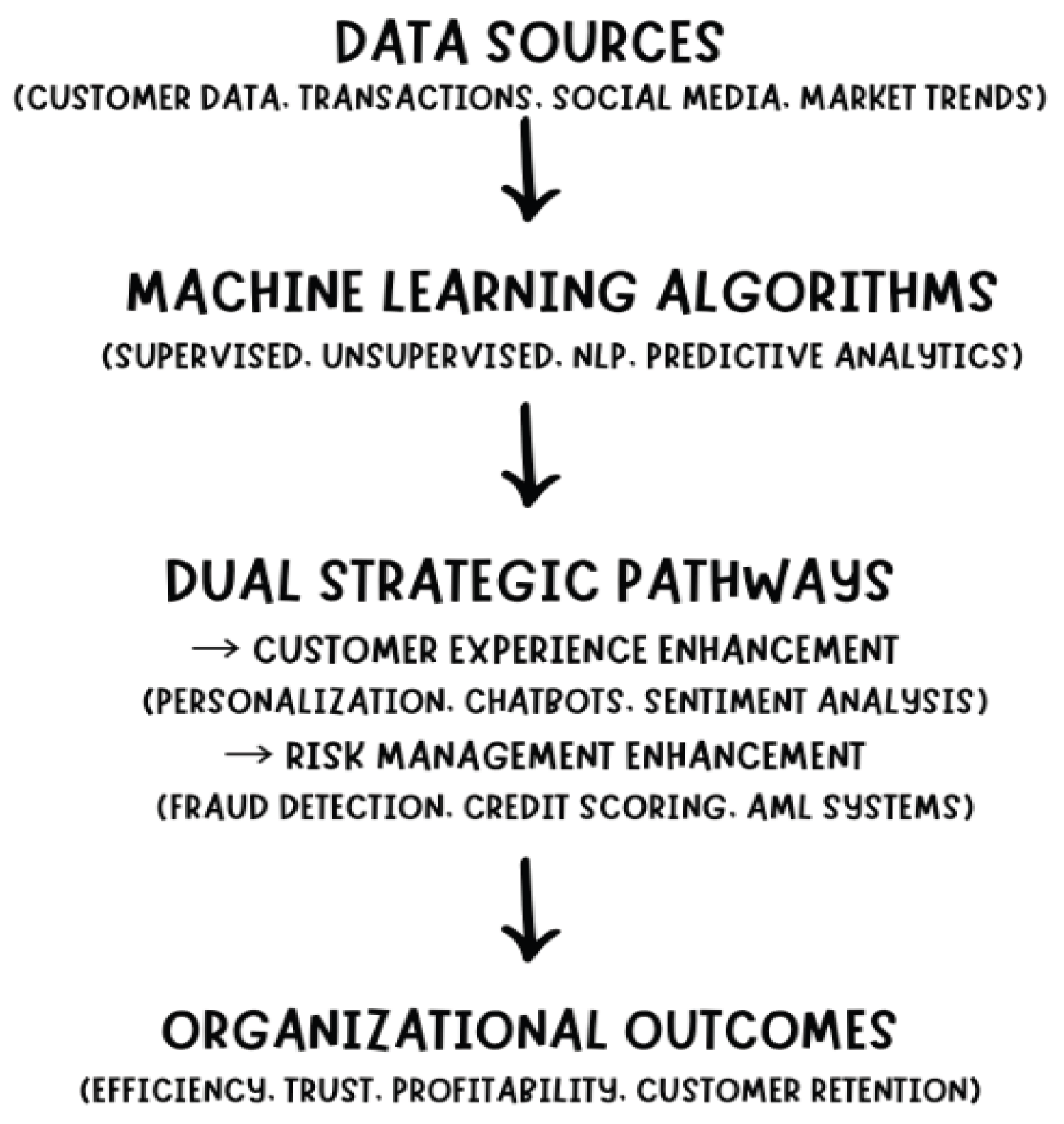

Below is a conceptual representation of how ML impacts both customer experience and risk management in banking.

- “Source: Self-created”

This framework is a simple flowchart on how ML-driven insights flow from the initial stage of data processing to the strategic outcomes, reinforcing that customer experience and risk management are interdependent goals.

Conclusion

To conclude that, AI and ML have the potential to devolatilise the banking industry, and it can shape the system as it used to work before. Machine Learning has come so far from the experimental stage to a precious strategic backbone to modern banking. The real-time learning intelligence system fills the gap between operational efficiency and customer needs. This increases personalisation, streamlines banking day-to-day operations and enhances the existing service quality and creates good and efficient technology for risk management. The regulation on such technology is also required, for which ethical governance, transparency with shareholders and human intervention to monitor this system becomes really important to keep the customer’s trust and believe system in the AI and ML-driven modern banking system. For policymakers, it is very important to understand the need to integrate data-driven personalisation and a robust mechanism for risk management. There should be encouragement to frame responsible frameworks that ensure transparency, explainability and accountability in banking algorithms.

The present technology is leading to Explainable AI, Blockchain adoption, and Quantum Analytics. In the near future, there will not only be automation, but it will be run by intelligent augmentation, where humans will focus only on leadership roles. Humans will become experts in ML and create good value. In the financial system, the ML will not only achieve great performance but also it will redefine the future.

This study contributes to the existing literature by synthesising AI and ML applications across two critical dimensions in the banking industry, one is enhancing the customer experience, and the one is improving risk management. It presents a conceptual study on dual aspects linking data-driven technology with customer and managerial outcomes. Future study can empirically validate this model using primary data from banks or conduct comparative case studies across developing and developed economies.

References

- Accenture. The age of AI: Banking’s new reality.; Accenture, 2023; Available online: https://www.accenture.com/content/dam/accenture/final/accenture-com/document-2/Accenture-Age-AI-Banking-New-Reality.pdf.

- Fujitsu. Transforming financial services with AI and automation. Fujitsu Technology Perspectives. 2023. Available online: https://www.fujitsu.com/global/vision/insights/ai-in-banking/.

- Gao, H.; Kou, G.; Liang, H.; et al. Machine learning in business and finance: a literature review and research opportunities. Financ Innov 2024, 10, 86. [Google Scholar] [CrossRef]

- Hu, J.; Zhang, T.; Wang, L. Supervised machine learning techniques: An overview with applications to banking. Expert Systems with Applications 142 2020, 112–128. [Google Scholar] [CrossRef]

- Jordan, M. I.; Mitchell, T. M. Machine learning: Trends, perspectives, and prospects. Science 2015, 349(6245), 255–260. [Google Scholar] [CrossRef] [PubMed]

- McKinsey & Company. Building the AI bank of the future. 2022. Available online: https://www.mckinsey.com/industries/financial-services/our-insights/building-the-ai-bank-of-the-future.

- Sharma, R.; Tan, Z. Artificial intelligence and cybersecurity in the banking sector: Opportunities and risks. Computers & Security 120 2022, 102784. [Google Scholar] [CrossRef]

- World Economic Forum. Artificial intelligence in financial services. World Economic Forum. 2022. Available online: https://www.weforum.org/reports/artificial-intelligence-in-financial-services.

- Lakhchini, Wassima; Wahabi, Rachid; Kabbouri, Mounime. Artificial Intelligence & Machine Learning in Finance: A literature review. 2022. [CrossRef]

- Davis, F. D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly 1989, 13(3), 319–340. [Google Scholar] [CrossRef]

- McKinsey; Company. The state of AI in banking 2024.; McKinsey Global Institute, 2024. [Google Scholar]

- Rogers, E. M. Diffusion of innovations, 5th ed.; Free Press, 2003. [Google Scholar]

- PwC. AI-driven personalization in banking.; PwC Research, 2023. [Google Scholar]

- Ghosh, R.; Li, M. Machine learning applications in retail banking. Journal of Financial Innovation 2022, 14(2), 45–62. [Google Scholar]

- Deloitte. AI in banking: Transforming the risk landscape. In Deloitte Insights; 2023. [Google Scholar]

- Accenture. AI for customer retention in financial services. In Accenture Insights; 2023. [Google Scholar]

- Deloitte. Systemic risk implications of AI in banking and finance. Deloitte Advisory Report. 2024. Available online: https://www.deloitte.com/content/dam/assets-zone3/us/en/docs/services/risk-advisory/2024/us-advisory-ai-systemic-risk-in-banking-june-2024.pdf.

Figure 1.

Showing a conceptual representation of how ML impacts both customer experience and risk management in banking.

Figure 1.

Showing a conceptual representation of how ML impacts both customer experience and risk management in banking.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.