Submitted:

02 September 2025

Posted:

03 September 2025

You are already at the latest version

Abstract

This study investigates the influence of contingency factors on Enterprise Risk Management (ERM) implementation and its impact on firm sustainability performance in Southeast Asia's mining sector. Green Intellectual Capital (GIC) serves as a moderator, addressing the gap in understanding the role of firm-specific characteristics in enhancing the ERM-sustainability relationship amid environmental uncertainty and industry competition. Using a quantitative approach with Structural Equation Modeling (SEM) based on Partial Least Squares (PLS-SEM), the study analyzes data from 205 mining companies listed on Southeast Asian stock exchanges between 2016 and 2023. Findings reveal that factors such as firm complexity, leverage, size, industry competition, and international diversification influence ERM implementation and corporate performance. ERM acts as a facilitator connecting contingency factors to sustainability, while GIC enhances ERM effectiveness, fostering improved competitiveness. The study recommends sector-specific ERM policies, incentives for GIC adoption, and further research on mediation models. It highlights that ERM, supported by GIC, can help companies address social and environmental issues, contributing to operational sustainability and enhancing stakeholder relationships. This research fills a gap in the application of ERM in Southeast Asia’s mining sector and explores the critical role of GIC in strengthening the link between ERM and sustainability firm performance.

Keywords:

enterprise risk management

; green intellectual capital

; sustainability

; firm performance

; contingency factors

1. Introduction

The mining industry in Southeast Asia has been shown to contribute significantly to the GDP of the region's countries. For example, Indonesia, the Philippines, Cambodia, Vietnam, and Malaysia contribute between 2.1% and 5.8% to their respective GDPs. In Indonesia, the coal industry is the preeminent sector, contributing between 5-8% of the nation's total GDP over the past decade. The industry has set a target of over 700 million tons of coal production by 2024, primarily intended for export to China and India (iesr.or.id). Concurrently, Indonesia exhibited a comparatively elevated level of profitability in its mining sector, with an annual return of 13.99% in 2023 (ima-api.org). However, the industry is confronted with numerous challenges, including the volatility of global commodity prices, environmental concerns that give rise to stringent regulations, social conflicts with local communities, and escalating operational costs (bimashabartum.co.id). A comprehensive risk management strategy is imperative for companies to adhere to mounting environmental regulations and effectively address social concerns, while concurrently maximizing growth prospects through enhanced operational efficiency and cost management. The mining sector requires a robust risk management strategy to maximize growth potential in the face of global market volatility and internal challenges (lngrisk.co.id).

In recent decades, the Enterprise Risk Management (ERM) approach has increasingly become the focal point of global business management. Large companies in various sectors have transitioned from conventional risk management systems to ERM-based strategic approaches to enhance resilience to increasingly intricate uncertainties. Concurrently, the significance of Green Intellectual Capital (GIC)—a synthesis of environmentally oriented knowledge, skills, and innovation—is also rising in response to the demands of sustainability and green innovation (Shah et al., 2025). A synthesis of extant literature reveals an intricate interconnection between three elements — ERM, green intellectual capital, and firm performance — in the creation of long-term competitive advantage (Hitt et al., 2001; Kianto et al., 2013). A multitude of global studies have demonstrated that enterprises that proactively oversee risk management and cultivate environmentally oriented intellectual capacity frequently exhibit superior performance in comparison to their competitors (Subramaniam et al., 2015; Uwuigbe & Uwuigbe, 2015).

In the Southeast Asian context, concerns regarding sustainability, industry competition, and the volatile business environment have prompted companies to enhance their risk management systems and cultivate green intellectual assets. In the mining and energy sectors, particularly, commodity price volatility, regulatory pressures, and social and environmental complexities require companies to transform their management and strategy (Pangestuti et al., 2024). Recent studies indicate that companies in Southeast Asia are beginning to adopt the 2017 COSO-based ERM framework, while concurrently modifying the ERM evaluation index to align with the local context. This adaptation has led to the emergence of novel indices, such as the Modified ERM Index (MERMi) (Pangestuti et al., 2023). In this context, the integration of environmental, social, and governance (ESG) considerations with green intellectual capital becomes imperative in supporting sustainable firm performance amid external pressures (Riaz et al., 2024; Sohu et al., 2024).

Despite the extensive implementation of ERM and its acknowledged advantages, including comprehensive risk management, enhanced decision-making processes, and augmented strategic adaptability (Resende et al., 2024; Horvey & Odei-Mensah, 2023) the application of ERM in the mining sector, particularly in developing countries, remains a relatively under-researched area. While ERM has been demonstrated to enhance profitability and align with corporate social responsibility (CSR) strategies (Resende et al., 2024), challenges persist in evaluating its effectiveness, particularly when relying on proxies such as the appointment of a Chief Risk Officer (Horvey & Odei-Mensah, 2023). Furthermore, the diverse outcomes of ERM implementation in various industries underscore the necessity for context-specific studies, particularly in sectors such as mining that encounter distinctive risks and uncertainties (Amoah & Eweje, 2023; Dashwood, 2007; Frolova, 2019). Mining companies in Southeast Asia, for instance, are particularly vulnerable to significantly different environmental and regulatory risks compared to developed countries (Zungu et al., 2018).

The implementation of ERM in the mining sector in Southeast Asia indicates that while ERM implementation has occurred in certain companies, the level of implegmentation remains comparatively low. This observation aligns with the findings of Resende et al., (2024), who contend that the scope of ERM implementation is typically confined to the disclosure level, with limited integration into the broader framework of corporate governance. While approximately 50% of Southeast Asian mining companies have appointed a Chief Risk Officer (CRO) or established a risk committee, factors such as board involvement and the presence of an effective CRO have been identified as crucial to enhancing the effectiveness of ERM implementation (Horvey & Odei-Mensah, 2023). Furthermore, incidents of substantial environmental degradation, such as those observed at tin mines in Bangka Belitung and nickel mines in Raja Ampat Indonesia, underscore the persistent challenges confronting the region's mining sector in effectively managing environmental risks. This phenomenon is further compounded by the inadequate quality and depth of emerging ESG reporting. However, regulatory developments in certain countries, such as Singapore and Malaysia, are beginning to promote the disclosure of environmental risks. Consequently, the enhancement of risk governance, the augmentation of transparency in GRI/ESG-based reporting, and the implementation of more stringent oversight of illegal mining are projected to enhance ERM effectiveness and forestall subsequent environmental incidents in the sector (Chlopecký, 2018)

While GIC is acknowledged as a pivotal element in augmenting firm value, its function as a moderator in the association between ERM practices and firm performance remains under-researched, particularly within the mining sector. Green institutional capital, comprising green human capital, green structural capital, and green relational capital, has been demonstrated to enhance environmental performance and exert a favorable influence on firm value (Alnaim & Metwally, 2024; Ericho & Amin, 2024). However, the effect of GIC as a moderator may vary depending on factors such as firm size, industry sector, as well as other mediating variables such as environmental management accounting and green human resource management (Andini & Harsono, 2024; Martínez-Falcó et al., 2025). In the mining sector, which faces more complex environmental and regulatory uncertainties, the utilization of GICs to moderate the effect of ERM on firm performance is still limited, especially in developing countries that have challenges in effectively utilizing and integrating GIC resources (Ahmed, 2016; Kianto et al., 2013). This discrepancy underscores the necessity for additional research that is more specifically oriented towards the mining sector. Such research could examine the extent to which GICs can influence the effectiveness of ERM practices and firm performance, particularly in developing countries that face different economic and environmental conditions (Kujansivu & Lonnqvist, 2007). While ERM and GIC have been the focus of numerous studies, research that explicitly examines the role of GIC as a moderator in the relationship between ERM influenced by contingency factors, especially in developing countries such as Southeast Asia, remains scarce. Furthermore, a substantial research gap persists concerning the impact of ERM implementation on firm performance in the Southeast Asian mining sector, moderated by GIC. GIC has the potential to enhance the relationship between ERM and firm performance by accelerating the adoption of sustainability strategies and reducing environmental risks, particularly in the mining sector, which faces environmental challenges such as natural disasters and sustainability issues that are unique to Southeast Asia(Asiaei et al., 2022). The variability of ERM's impact on firm performance, which differs across industries and countries, adds to the complexity of this relationship. ERM can improve performance through better risk management, but it can also have a negative impact if not managed properly (Hoang Thanh & Truong Cong, 2024). Consequently, further research is necessary to investigate the impact of integrating ERM with GICs on risk management in the mining sector and to provide practical guidance for effective implementation in the Southeast Asian region.

The implementation of GIC in the Southeast Asian mining sector exhibits considerable variation in terms of disclosure and implementation across different countries, with Indonesia being a notable leader in this regard. A study of 51 Indonesian mining companies from 2016 to 2020 revealed that 65.86% of the companies attained the highest level of disclosure for GICs, emphasizing green human capital, green structural capital, and green relational capital. These elements have been incorporated into the sustainability reports mandated by the OJK (Financial Services Authority) for listed companies since 2020 (Resende et al., 2024). The positive impact of GIC on the environmental performance of mining companies in Indonesia has also been significant, in line with the integration of green accounting and material flow cost accounting (Rajesh & Rajendran, 2020). Conversely, countries such as Malaysia and Thailand demonstrate that, despite the pivotal role of GIC in catalyzing green innovation, its direct impact on sustainability performance remains multifaceted (Liu & Liu, 2014). Singapore and Vietnam have instituted regulations mandating ESG disclosures, though specific GIC disclosures are less subject to regulation, and the quality of ESG reporting in Singapore is comparatively superior to that of other countries in the region. Nevertheless, significant challenges persist throughout Southeast Asia, including the absence of comprehensive disclosure and the underutilization of GICs in the mining sector. Additionally, there is a necessity to enhance the implementation and transparency of GRI and TCFD-based reporting to ensure more consistent sustainability performance across the region.

To address these issues, a more strategic and contextualized approach to risk management is required. One effective solution is to make green intellectual capital a moderating variable that can strengthen the relationship between ERM implementation and improved corporate performance. Consequently, the integration of contingency factors ERM, and green intellectual capital can serve as a pivotal strategy to enhance the competitiveness and performance of mining companies in Southeast Asia.

The present study endeavors to address the extant research gap concerning the influence of ERM on sustainable firm performance in the Southeast Asian mining sector. By underscoring the benefits of ERM in holistic risk management and strategic flexibility supporting decision-making (Horvey & Odei-Mensah, 2023; Resende et al., 2024), this study seeks to contribute to the body of knowledge in this area, although it recognizes that challenges remain in its measurement and implementation. Furthermore, this study will examine the role of GIC, which includes green human, structural, and relational capital, as a moderator variable affecting the relationship between ERM and firm performance. This study's objective is twofold: first, to analyze the impact of contingency factors on ERM implementation and sustainable firm performance, and second, to provide theoretical contributions in building a relevant green intellectual-based risk management strategy for firms in developing and high-risk regions, such as Southeast Asia. Moreover, it is anticipated that this research will yield a pragmatic contribution by way of formulating more adaptive and data-driven ERM implementation policies and strategies. Additionally, it is expected to support the GIC's role as a catalyst to optimize the achievement of corporate sustainability goals in the Southeast Asia region, which faces significant environmental challenges.

2. Literature Review and Hypothesis Development

2.1. Contingency to ERM

Enterprise Risk Management (ERM) is an integrated approach to risk management that is increasingly regarded as strategic to enhance firm performance. In the context of contingency theory, the effectiveness of ERM implementation is largely determined by contextual factors inherent in firm characteristics, such as organizational complexity, financial leverage, firm size, industry complexity, and international diversification (Gordon et al., 2009). Contingency in ERM signifies the notion that the conceptualization and execution of an ERM system should be customized to the distinct conditions and attributes of an organization. This approach acknowledges the absence of a universally applicable solution for risk management and recognizes that various factors can influence the effective implementation of ERM in different organizational contexts. A contingency-based framework for ERM posits that factors such as organizational size, structure, strategy, and the external environment play a pivotal role in shaping ERM practices. These factors have the potential to influence the effectiveness of ERM in managing risks and improving organizational performance (Mikes & Kaplan, 2013; Silva, 2019). Large organizations require more formal and complex risk management systems, while small organizations benefit more from a more flexible and adaptive approach (Dashwood, 2008). Furthermore, the effectiveness of risk management within organizations is influenced by factors such as decentralization and the distribution of control rights (Lee et al., 2020). The integration of Enterprise Resource Planning (ERP) systems with information technology has been demonstrated to enhance risk management capabilities (Nedaei et al., 2015). Consequently, organizations are obliged to perpetually evaluate and recalibrate their risk management methodologies to sustain efficacy in the face of evolving environmental dynamics (Lamptey, 2018). In the view of the Resource-Based View and Knowledge-Based View theories, the customization of ERM systems to the internal characteristics of the firm is crucial to create sustainable competitive advantage and performance improvement (Barney, 2001; Subramaniam et al., 2015).

A multitude of contingencies have been demonstrated to promote the implementation of more advanced ERM due to the necessity of overseeing interconnected and extensive risk profiles (Pangestuti et al., 2024). These contingencies encompass organizational complexity, signifying the extent of diversity in organizational processes, structures, and operations. This finding aligns with the observation that organizations with intricate structures often implement more extensive risk management systems (Liebenberg & Hoyt, 2003). Conversely, the contingency factor, firm leverage, exhibits a negative relationship with ERM because financial pressures from high debt usage can impede the effectiveness of risk management system implementation (Razali & Tahir, 2011). Another salient factor in the adoption of ERM is firm size. Larger firms possess the greater resources necessary for developing a comprehensive ERM framework (Pagach & Warr, 2010). However, the extant literature indicates that firm size is not always directly proportional to the level of disclosure of ERM practices. Furthermore, the presence of contingency factors and the inherent complexity of various industries, such as the intense competition and regulatory pressures characteristic of certain sectors, necessitate the formulation of responsive and adaptive ERM strategies by companies. However, it should be noted that such strategies do not invariably exert a direct and significant impact on company performance (Chang & Yoo, 2023). Concurrently, the international diversification contingency factor introduces risk dimensions in the form of currency fluctuations, political instability, and regulatory differences. These factors necessitate a more holistic and strategically integrated ERM system (Lechner & Gatzert, 2018). The explanation of the contingency factor demonstrates that ERM implementation is contingent on firm-specific characteristics and conditions, including organizational complexity, financial leverage, firm size, industry complexity, and international diversification. It is imperative for each organization to implement a risk management approach that is customized to the specific situation and challenges it faces. In light of the aforementioned rationale, the hypotheses postulated in this study are as follows:

H1: contingency factors affect ERM implementation.

2.2. Contingency on Sustainability Firm Performance

Contingency theory elucidates the interplay between specific factors and firm performance, contingent upon the presence of certain conditions (Otley, 2016). Barki et al., (2001) underscored the notion that organizations adapt to internal and external influences in order to maximize performance. He further elaborated that each organization employs unique strategies and decision-making processes to align with its goals and gain a competitive advantage. The relationship between contingency theory and sustainability in firm performance has attracted significant academic attention, revealing the various dynamics that companies face when integrating sustainability into their strategic framework. Contingency theory posits that a uniform managerial approach is nonexistent; rather, the optimal strategy is contingent upon the external and internal scenarios confronting the firm (Gordon et al., 2009). Specifically, sustainability practices can vary significantly based on the contextual environment, including legal, cultural, and industry factors that influence a firm's behavior and its performance metrics (Chairani & Siregar, 2021).

The sustainability performance of firms in the Southeast Asian mining sector is influenced by a number of contingent factors. These factors include firm complexity, financial leverage, firm size, industry competition, and international diversification. The presence of high firm complexity, characterized by a diversity of operations and a geographical spread, has been demonstrated to exert a positive influence on the sustainability performance of firms operating within the mining sector. This phenomenon can be attributed to the ability of complex firms to leverage a diverse array of resources and capabilities, thereby facilitating the enhancement of sustainability outcomes (Amoah & Eweje, 2023). High financial leverage has been shown to have a negative impact on sustainability performance, as it limits a firm's financial flexibility to invest in sustainability initiatives. In contrast, firms with lower leverage have greater capacity to invest in long-term sustainability strategies (Razak et al., 2024). Firm size has been demonstrated to exert a positive influence on sustainability performance. This is due to the fact that larger firms possess greater resources with which to invest in sustainability initiatives. However, these firms may encounter bureaucratic challenges that impede expeditious implementation (Sevil et al., 2022). In the context of high industry competition, firms are often compelled to adopt sustainability practices as a strategy for distinguishing themselves in the market and achieving competitive advantage. Conversely, firms operating in industries with low competition levels tend to exhibit less motivation to prioritize sustainability, potentially leading to suboptimal sustainability performance (Gold et al., 2022). International diversification has been shown to have a positive effect on the sustainability performance of firms in the mining sector. This is due to the fact that it allows firms to adopt best practices from different regions and to reduce risks associated with local environmental regulations (Capar et al., 2015).

In order to enhance their performance through the leveraging of sustainability, companies must give careful consideration to the interaction of multiple contingent factors. Companies that align their sustainability practices with these contextual elements are likely to achieve a stronger and more favorable impact on their performance metrics. The relationship between contingency factors and corporate sustainability performance also suggests that companies with certain characteristics, such as organizational complexity or larger size, are better able to integrate sustainability in their strategy. The adoption of long-term oriented sustainability practices is influenced by a variety of external factors, including industry competition and environmental regulations. In light of the aforementioned explanations, the hypotheses proposed in this study are as follows:

H2: contingency factors affect sustainability firm performance.

2.3. ERM on Sustainability Firm Performance

The evolution of risk management has led to the development of ERM, which is characterized by an integrated and holistic approach. According to the Risk and Insurance Managers Society (RIMS), ERM is a strategic business discipline that aims to achieve organizational objectives by addressing multiple risks and managing their combined impact as a portfolio of interconnected risks. Business risk is defined as the potential for organizational failure, which has the capacity to impair profitability and overall performance. According to the principles of agency theory, the application of ERM has been demonstrated to enhance corporate performance and maximize shareholder value (Beasley et al., 2005; Gordon et al., 2009; Hoyt et al., 2009). According to Lechner & Gatzert, (2018), ERM accomplishes this objective through a multifaceted approach, including the mitigation of stock price volatility, the reduction of the cost of external capital, the enhancement of capital efficiency, and the curtailment of the risk of catastrophic failure. In the context of industries characterized by elevated inherent risks, such as finance, banking, energy, oil, and gas, the adoption of ERM has been observed to be a prevalent practice aimed at sustaining performance (Golshan & Rasid, 2012). This finding aligns with the conclusions of previous studies (Lechner & Gatzert, 2018; Lee et al., 2020; Malik et al., 2020) which have demonstrated the efficacy of ERM in reducing the overall risk of the firm and enhancing performance.

ERM has evolved into an integrated risk management system that serves not only to identify and control risks, but also to improve a company's sustainable performance (Ai & Brockett, 2014; Gordon et al., 2009). In the mining industry, which is characterized by high and complex risks, including commodity price fluctuations, environmental damage, and social pressure, the implementation of ERM becomes even more crucial (Pangestuti et al., 2024). According to Ardian & Kumral, (2021) findings, the implementation of mature ERM systems has been demonstrated to enhance financial performance by increasing profitability and decreasing exposure to market risks. This enhancement is particularly evident in the domains of supply chain management and production stability. This finding suggests that ERM functions not only as a protective measure, but also as an enabler of operational efficiency and financial resilience.

In addition to enhancing financial aspects, ERM contributes substantially to the company's strategic alignment with sustainability objectives (Chang & Yoo, 2023). When ERM is integrated with strategic planning, organizations can identify risks relevant to business continuity, including environmental, social, and governance (ESG) risks, and actively respond to them through corporate social responsibility (CSR) policies. In the context of the mining industry, the integration of ESG factors, namely environmental, social, and corporate responsibility (ESCR), has been demonstrated to enhance corporate reputation and cultivate stakeholder trust, consequently generating long-term value and supporting the sustainability of a social license to operate (Nurcahyo, 2024; Sarwar & Mustafa, 2024). This approach validates that effective risk management, when integrated with sustainability initiatives, will augment corporate competitiveness through reputation, innovation, and efficiency.

However, the effectiveness of ERM in promoting sustainability firm performance is not uniform and is contingent on contextual factors, including firm size, industry complexity level, geographic location, and digital infrastructure readiness (Jabbour & Crawford, 2024). In a broader context, ERM has the potential to generate competitive advantage when integrated with information technology and intellectual capital, thereby facilitating data-driven decision-making and prompt responsiveness to external dynamics (Yuniarti et al., 2022). Consequently, it is imperative for mining companies to adopt ERM not solely as a compliance measure, but to integrate it strategically as an integral component of their sustainability value system. A comprehensive approach to ERM can serve as a significant catalyst in achieving overall sustainability performance.

In terms of ESG performance, this study corroborates the notion that ERM is not merely a risk management instrument, but rather a pivotal catalyst for enhancing sustainable financial and operational performance, particularly within high-risk sectors such as mining. The effective integration of risk management strategies, including environmental and social risk management, has been demonstrated to have a positive impact on long-term sustainability performance. In light of the aforementioned explanations, the hypotheses proposed in this study are as follows:

H3: ERM affects sustainability firm performance

2.4. Green Intellectual Capital (GIC), on Sustainability Firm Performance

A number of theoretical frameworks have been developed to elucidate the relationship between intellectual capital and firm performance. The Resource-Based View (RBV) theory posits that distinctive and valuable resources, including green intellectual capital, contribute to sustainable competitive advantage and superior performance (Hitt et al., 2016; Kianto et al., 2013). According to the RBV theory, intellectual capital serves as a source of differentiation and innovation, enabling organizations to create value and achieve higher performance outcomes (Subramaniam et al., 2015). The Knowledge-Based View (KBV) theory perspective underscores the significance of knowledge creation, transfer, and utilization within organizations (Wang, 2018). Green intellectual capital, defined as knowledge assets, has been shown to facilitate organizational learning, innovation, and improved decision-making processes (Edvinsson & Kivikas, 2007). The utilization of green intellectual capital has been demonstrated to enhance organizational performance by facilitating adaptation to dynamic environments, the identification of opportunities, and the development of competitive strategies (Komara et al., 2020).

Green Intellectual Capital, comprising green human capital, structural capital, and relational capital, has been demonstrated to exert a significant influence on the enhancement of corporate performance within the mining industry, particularly with regard to innovation, sustainability, and corporate value. According to the Resource-Based View (RBV) and Knowledge-Based View (KBV) theories, GICs are regarded as intangible assets with the potential to generate sustainable competitive advantage through environmentally friendly innovation and knowledge-based decision-making processes (Hitt et al., 2001; Subramaniam & Youndt, 2005). In the context of the mining industry, which is significantly impacted by environmental concerns, GIC promotes green innovation practices and the integration of environmental management accounting. This, in turn, enhances financial performance metrics such as return on assets (ROA) and augments firm value (Alnaim & Metwally, 2024; Yuniarti et al., 2022). Moreover, green intellectual capital fosters organizational reputation and environmental performance achievement through synergies between green process strategies and relational capital (Jirakraisiri et al., 2021; Yadiati et al., 2019).

While GICs have been shown to positively contribute to performance, their effectiveness is influenced by a number of external and internal factors. Firm size, for instance, functions as a moderating variable that determines the extent to which GICs can be optimized to increase firm value. Large firms tend to be better able to utilize GICs effectively (Ericho & Amin, 2024). The utilization of GICs is influenced by a number of factors, including technological turbulence and stringent environmental regulations, which may either hinder or encourage their use(Shehzad et al., 2023). The extant body of empirical research also confirms that firms with high GIC capacity are more adaptive to market changes and more strategically competitive (Ahmed, 2016; Kianto et al., 2013; Marr, 2008). Consequently, it is imperative for mining companies to formulate contextual and quantifiable strategies, thereby enabling GICs to optimally contribute to the attainment of overall company performance.

The study also emphasizes the significance of GICs in promoting ERM and sustainability performance. GICs, through the utilization of green human, structural, and relational capital, provide intellectual resources that enable firms to address sustainability challenges more effectively. GICs have been shown to promote green innovation and knowledge-based decision-making, which in turn has been linked to enhanced competitiveness and performance in the mining sector. In light of the aforementioned explanations, the hypotheses proposed in this study are as follows:

H4: Green Intellectual Capital (GIC) affects sustainability firm performance.

2.5. Green Intellectual Capital Moderates the Effect of ERM on Sustainability Firm Performance

Green intellectual capital, as defined by Edvinsson & Kivikas, (2007), encompasses knowledge, applied experience, organizational technology, customer relationships, and professional skills that provide a competitive advantage. As Yusoff et al., (2019) underscores, this concept serves as a valuable repository of knowledge, comprising human capital, structural capital, and customer capital. The optimal alignment and balancing of these components has the potential to generate financial value. Ni & Cheng, (2019) posited that innovation in green intellectual capital enables firms to explore new areas and maintain sustainable growth while gaining a competitive advantage. According to the resource-based theory, the possession of sustainable advantages by firms leads to the development of unique and inimitable resources. These resources, in turn, are used effectively to improve performance and value creation (Subaida et al., 2018). Green intellectual capital has been demonstrated to enhance productivity and performance, particularly when integrated with ERM, as evidenced by previous studies (Al-Nimer, 2024; Khan & Ali, 2017).

ERM has been recognized as a strategic management framework capable of improving the sustainable performance of companies, particularly in high-risk sectors such as the mining industry (Florio & Leoni, 2017; Pangestuti et al., 2024). ERM facilitates the comprehensive management of environmental, social, and governance (ESG) risks, in addition to enhancing operational stability and financial resilience (Shah et al., 2025). However, the effectiveness of ERM in driving sustainable performance is contingent upon an organization's capacity to absorb, leverage, and internalize sustainability strategies into its culture and operational systems. In this context, green intellectual capital (GIC)—comprising green human capital, green structural capital, and green relational capital—functions as a catalyst in fortifying the relationship between ERM and sustainability firm performance (Jirakraisiri et al., 2021; Sarwar & Mustafa, 2024).

GIC provides the intellectual and organizational foundation that enables the implementation of ERM to be more effective in the context of sustainability. Green human capital, defined as employees' knowledge and skills in environmental issues, assists companies in identifying and responding innovatively to ESG risks (Yadiati et al., 2019). Green structural capital, encompassing green systems, organizational culture, and technology, facilitates the integration of ERM strategies into sustainable operational practices. Concurrently, green relational capital fortifies relationships with stakeholders and engenders collaborative opportunities to enhance corporate environmental and social performance (Jirakraisiri et al., 2021). Consequently, when GIC is elevated, the firm's capacity to translate ERM policies into sustainability outcomes is considerably augmented.

A substantial body of research supports the notion that GIC may function as a moderating variable, thereby amplifying the impact of ERM on firm sustainability performance (Alnaim & Metwally, 2024; Faedfar et al., 2022). For instance, firms with robust green organizational capital demonstrate an enhanced capacity to leverage risk information during the process of green innovation and strategic decision-making. Furthermore, GIC has the capacity to facilitate the alignment between ERM compliance and the realization of sustainability objectives by integrating sustainability principles into fundamental business processes (Shehzad et al., 2023). However, the efficacy of this moderation may vary depending on the industry, the scale of the company, and the readiness of human resources and technology. Therefore, it is imperative to investigate how GIC functions as a moderator in the relationship between ERM and sustainability performance, particularly in environmentally stressed sectors such as mining.

The relationship between ERM, GIC, and sustainability performance is further elucidated by the role of GIC as a moderator in the relationship. The relationship between ERM, GIC, and corporate sustainability performance is interdependent. ERM provides a framework for managing risks in an integrated manner, while GICs offer intellectual resources that enable firms to respond to sustainability risks in innovative and proactive ways. The integration of these two factors enables companies to enhance their sustainability performance, encompassing financial, environmental, and social dimensions. In light of the aforementioned explanations, the hypotheses proposed in this study are as follows:

H5: Green Intellectual Capital moderates the effect of ERM on sustainability firm performance.

2.6. The Moderating Role of ERM in the Relationship of Contingency Factors to Sustainability Firm Performance

Contingency theory posits that no control system is universally applicable, a notion that has been previously emphasized by Fisher (1992), Otley (2016), Reid, (2005). Gordon et al., (2009), Hoque, (2004), Otley, (2016) have demonstrated that optimal performance is attained when control systems are aligned with the organizational context. Consequently, a universally ideal ERM system does not exist; various ERM approaches are more appropriate for different circumstances, as COSO (2004) has demonstrated. The paucity of a unifying theoretical framework to predict the factors that influence the relationship between ERM and firm performance necessitates the utilization of contingency theory, as articulated by Gordon et al., (2009).

A comprehensive review of the extant literature reveals that five contingent factors—firm complexity, firm leverage, firm size, industry complexity, and international diversification—create different risk profiles and demand different ERM responses (Florio & Leoni, 2017; Hamzah & Febriansyah, 2023). Organizational complexity, defined as the presence of numerous business units and interconnected processes, has been identified as a key factor in encouraging companies to develop comprehensive ERM frameworks. The implementation of sustainability initiatives across the entity is a primary objective of these frameworks, ensuring uniformity in their application (Pangestuti et al., 2024). Conversely, high leverage introduces financial pressure, prompting ERM to function as a balancing mechanism to ensure that sustainability projects are selected based on the optimal risk-adjusted return (Ibrahim & Esa, 2017). Furthermore, firm size contributes to resource capacity and data analytics, thereby enhancing the efficacy of ERM-sustainability implementation (Lechner & Gatzert, 2018).

Cross-industry studies demonstrate that regulatory intricacy and competition in risk-intensive industries, such as mining and manufacturing, heighten the urgency of ERM in responding to ESG demands and preserving a social license to operate (Razak et al., 2024; Chang & Yoo, 2023). In the context of multiple countries, the diversification of international operations can amplify the heterogeneity of risk factors, including exchange rates, political instability, and compliance regulations. Consequently, companies must implement global ERM standards that incorporate sustainability practices throughout the supply chain (Fremeth & Richter, 2011). Recent research has also noted the contribution of ERM in mediating the influence of contingent factors on financial and nonfinancial performance, such as increased carbon efficiency, reputation, and green innovation (Faedfar et al., 2022; Resende et al., 2024). ERM functions as a strategic conduit, translating the heterogeneity of contingent factors into coordinated sustainability actions.

Despite the prevalence of inconsistent direct contingency factor-sustainability performance relationships, extant literature corroborates the indirect-only mediation pattern, indicating that significant effects emerge exclusively when ERM is utilized as an intermediary variable (Khan et al., 2020; Sax & Andersen, 2019). For instance, company complexity does not invariably enhance sustainability performance in the absence of an integrated risk control system (Anggraini & Hidayat, 2025) and leverage, in fact, diminishes environmental performance if ERM is not sufficiently developed (Raharjo & Hasnawati, 2022). In light of the aforementioned explanation, the hypothesis proposed in this study is as follows:

H6. ERM moderates the relationship between contingency factors on sustainability firm performance.

3. Method

This study employs a quantitative approach to assess the indirect impact of contingency factors on corporate sustainability performance through ERM, with the moderating influence of GIC. The population under study consists of mining sector companies that are listed on the stock exchanges of Southeast Asian countries, namely Indonesia, Malaysia, Singapore, Thailand, Vietnam, and the Philippines. The sampling technique employs purposive sampling, predicated on the criteria for the availability of the requisite data during the observation period and consistency in annual reporting. The sample of this study comprised 205 mining companies in Southeast Asia during the 2016-2023 time period. The dependent variable is sustainability firm performance, measured using Tobins Q. The independent variables are contingent factors (firm complexity, financial leverage, firm size, industry competition, and international diversification). The intervening variable is ERM. The moderating variable is GIC, which consists of green human capital, green structural capital, and green relational capital.

The measurement of each variable in this model is achieved through the utilization of indicators that have been previously validated in extant literature. The complexity of a firm is measured by the number of business segments (Ge & McVay, 2005; Gordon et al., 2009). The leverage of a firm is calculated by the ratio of the book value of debt to the market value of equity (Hoyt et al., 2009). The size of a firm is measured by the natural logarithm of total assets (Razali & Tahir, 2011). The level of industry competition is measured by the Herfindahl-Hirschman index (Chang & Yoo, 2023; Madobi & Umar, 2021). International diversification is measured dichotomously (1 if there is international diversification, 0 if not) (Capar et al., 2015; Espinosa-Méndez et al., 2021; Karthik, 2015). The classification of ERM variables is predicated on a quantitative (score 2), qualitative (score 1), or no ERM (score 0) approach, as developed by (Pangestuti et al., 2024). Green Intellectual Capital (GIC), calculated using MVAIC (Modified Value Added Intellectual Capital), is the sum of Human Capital Efficiency (HCE), Structural Capital Efficiency (SCE), and Relational Capital Efficiency (RCE), which describe the contribution of each element to the intellectual value of the company with a focus on green sustainability aspects (Jirakraisiri et al., 2021; Yadiati et al., 2019).

Table 1.

Summary of Variable Measurements.

| Variable | Measurements | References |

|---|---|---|

| Sustainability Firm Performance | Tobin's Q = (Market value of equity + Book value of liabilities) / Book value of assets |

(Gordon et al., 2009) ; (Hoyt & Liebenberg, 2011) ; |

| Enterprise Risk Management | a quantitative (score 2), qualitative (score 1), or no ERM (score 0) approach | (Pangestuti et al., 2024) |

| Green Intellectual Capital | MVAIC (Modified Value Added Intellectual Capital) = Human Capital Efficiency (HCE) + Structural Capital Efficiency (SCE) + Relational Capital Efficiency (RCE) | (Jirakraisiri et al., 2021; Yadiati et al., 2019). |

| Contigency Factors | ||

|

number of business segments | (Ge & McVay, 2005; Gordon et al., 2009) |

|

ratio of the book value of debt to the market value of equity | (Hoyt et al., 2009) |

|

natural logarithm of total assets | (Razali & Tahir, 2011) |

|

the Herfindahl-Hirschman index | (Chang & Yoo, 2023; Madobi & Umar, 2021). |

|

dichotomously (1 if there is international diversification, 0 if not) | (Capar et al., 2015; Espinosa-Méndez et al., 2021; Karthik, 2015). |

The hypothesis testing was carried out using a Structural Equation Modeling (SEM) approach based on Partial Least Squares (PLS-SEM), with the help of the latest version of SmartPLS software. The selection of PLS-SEM was predicated on its aptitude for conducting exploratory and predictive studies, in addition to its capacity to manage intricate models encompassing latent variables and measurement indicators (Hair et al., 2019; Benitez et al., 2020). The model analysis was conducted in three stages:(1) Outer model testing was performed to measure construct validity using the outer loading value (>0.70) and Average Variance Extracted (>0.5); (2) Inner model testing was conducted to assess the significance of the relationship between constructs by looking at the t value (>1).The statistical analysis was conducted using a bootstrapping technique, which yielded a p-value of 0.05, indicating a 96% confidence level. The goodness of fit was evaluated using the SRMR (0.08) and NFI (>0.90) metrics, along with the f² effect size value and Q² predictive relevance.

Subsequent analyses were conducted to assess the mediating and moderating effects. The mediating effect of ERM was evaluated through a statistically significant indirect effect approach. Concurrently, the moderating role of GIC is analyzed using the interaction effect approach constructed in the structural model. The model is deemed appropriate if it fulfills the predictive criteria (Q² > 0.02) and effect size (f² > 0.15), indicating a moderate to strong influence (Hair et al., 2019). It is hypothesized that this research will provide theoretical contributions that will expand the ERM contingency framework and practical contributions that will encourage GIC integration as a driver of extractive sector sustainability in emerging markets.

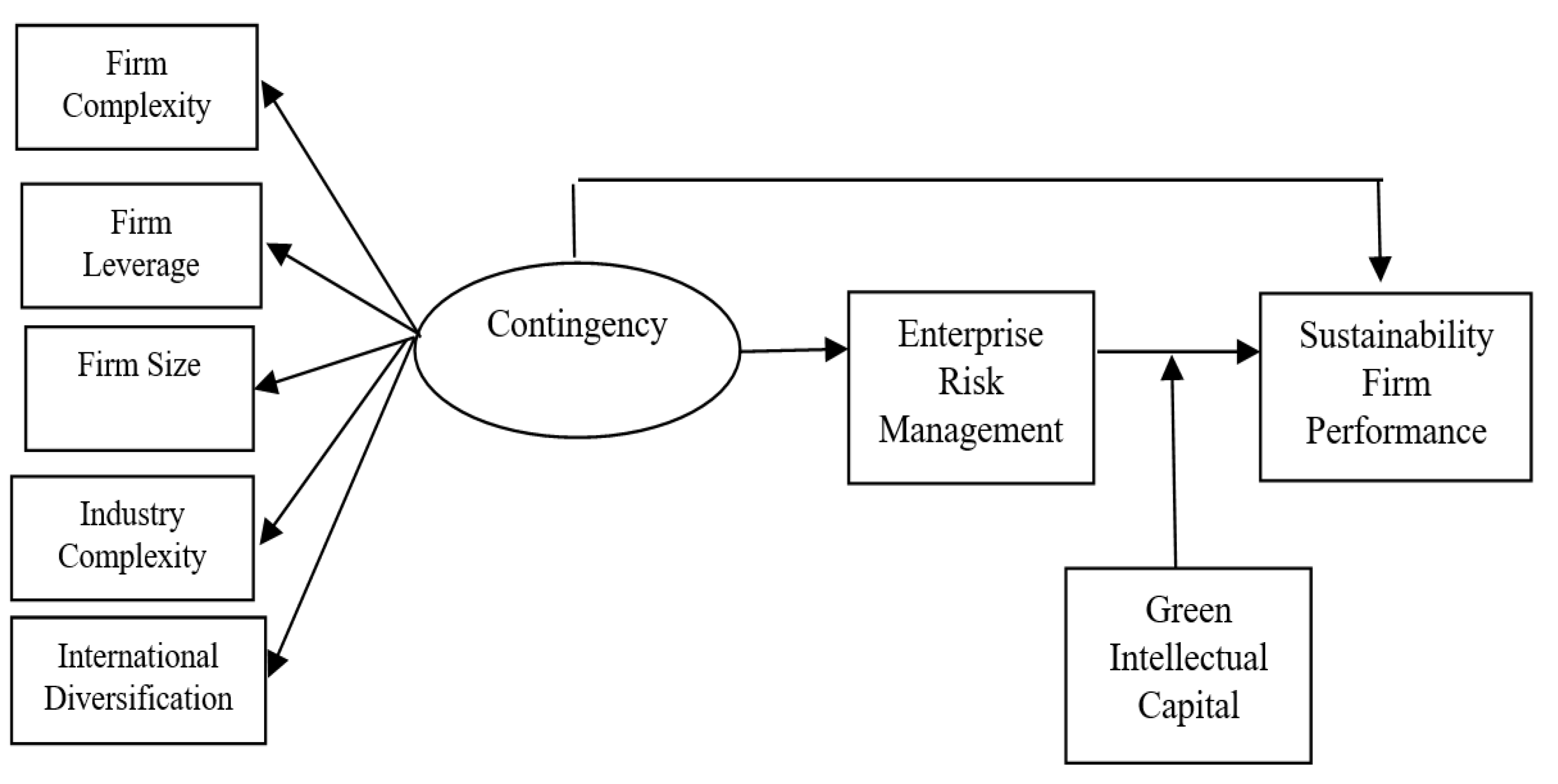

Figure 1.

Research Model.

Structural Equation Model (SEM)

- Exogenous Variables (Independent Variables): Firm Complexity (FC), Firm Leverage (FL), Firm Size (FS), Industry Complexity (IC), International Diversification (ID)

-

Contingency (C):The central mediator that connects the exogenous variables to the dependent variables.Equation for Contingency (C):C = β1.FC + β2. FL + β3.FS + β4. IC + β5 .ID + ϵCWhere:

- -

- β1,β2,β3,β4,β5 are the coefficients to be estimated.

- -

- ϵC is the error term for the contingency variable.

-

Endogenous Variables (Dependent Variables): Sustainability Firm Performance (SFP), Enterprise Risk Management (ERM), and Green Intellectual Capital (GIC)The relationships can be formulated as:ERM=γ1⋅C+ϵERMSFP=γ2⋅C+γ3⋅GIC+ϵSFPGIC=γ4⋅C+ϵGICWhere:

- -

- γ1,γ2,γ3, are the coefficients to be estimated.

- -

- ϵERM,ϵSFP,ϵGIC are the error terms for each endogenous variable.

The entire system of equations captures the relationships between firm’s characteristics (Firm Complexity, Firm Leverage, Firm Size, Industry Complexity, International Diversification), contingency (mediator), and the outcomes (ERM, sustainability, and intellectual capital). This model suggests that the firm’s characteristics impact contingency, which then affects both enterprise risk management and sustainability firm performance, with green intellectual capital acting as an additional determinant for sustainability.

4. Results and Discussion

4.1. Results

This descriptive statistical method is employed to ascertain the mean, median, maximum, minimum, and standard deviation values of each variable utilized in the study. This enables a more comprehensive comprehension of the data's distribution and central tendency.

Table 2.

Descriptive Statistic of Variables.

| Variables | Mean | Median | Max | Min | Std. Dev. | N |

|---|---|---|---|---|---|---|

| Sustainability Firm Performance | 1.218930 | 1.018572 | 5.331107 | 0.204720 | 0.742213 | 1640 |

| Enterprise Risk Management | 0.019919 | 0.020000 | 0.031250 | 0.003750 | 0.003252 | 1640 |

| Green Intellectual Capital | 15.62967 | 15.91114 | 23.83971 | 5.129380 | 3.465822 | 1640 |

| Contingency factor: | 1640 | |||||

| a. Firm Complexity | 2.937979 | 3.000000 | 10.00000 | 1.000000 | 1.211141 | 1640 |

| b. Financial Leverage | 1.715193 | 0.860262 | 22.74331 | 0.000650 | 2.648160 | 1640 |

| c. Firm Size | 17.12995 | 16.83968 | 25.60336 | 1.609438 | 4.177361 | 1640 |

| d. Industry Competition | 0.015813 | 0.004204 | 0.182923 | 0.000052 | 0.026769 | 1640 |

| e. International Diversification | 0.565157 | 1.000000 | 1.000000 | 0.000000 | 0.495909 | 1640 |

Source: data processed.

A thorough examination of descriptive statistics reveals substantial variability among mining companies in Southeast Asia with respect to the various factors that influence their performance and strategies. The companies' sustainability performance is generally suboptimal, with an average score of 1.219. However, there are a number of companies that demonstrate significantly higher levels of performance. The average enterprise risk management level is 0.0199, indicating a uniform implementation of risk management policies across a significant proportion of companies. Green intellectual capital demonstrates greater variability, with more advanced companies exhibiting higher values (average 15.63), reflecting differences in the adoption of environmentally friendly technologies. Contingency factors, including firm complexity, financial leverage, firm size, industry competition, and international diversification, also demonstrate significant variation. For instance, financial leverage exhibits a substantial standard deviation of 2.648, suggesting the presence of companies with notably elevated debt levels. Additionally, company size displays a range from large to small enterprises. The degree of industry competition is comparatively minimal; however, there are certain industries that exhibit notably elevated levels of competition. The extent of international diversification exhibited by companies also varies, with the majority demonstrating higher levels of diversification. The findings reveal a wide array of structures and strategies employed by mining companies in Southeast Asia, thereby underscoring the influence of these factors on their capacity to manage risk and attain sustainability objectives.

Table 3.

Descriptive Comparison Between Countries.

| Variable | Singapura | Indonesia | Malaysia | Filipina | Thailand | Vietnam | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Std. Deviasi | Mean | Std. Deviasi | Mean | Std. Deviasi | Mean | Std. Deviasi | Mean | Std. Deviasi | Mean | Std. Deviasi | |

| Sustainability Firm Performance | 1.29380 | 0.64236 | 1.28537 | 0.86521 | 1.14556 | 0.62131 | 1.08231 | 0.57111 | 1.07125 | 0.80116 | 1.05262 | 0.26532 |

| Enterprise Risk Management | 0.02087 | 0.00396 | 0.01975 | 0.00178 | 0.01949 | 0.00309 | 0.01692 | 0.00285 | 0.01969 | 0.00290 | 0.01668 | 0.00258 |

| Green Intellectual Capital | 18.44682 | 2.26274 | 16.19979 | 3.39349 | 17.86967 | 0.74554 | 13.25275 | 2.24093 | 14.10909 | 1.96921 | 11.01591 | 1.97871 |

| Contingency factor : | ||||||||||||

| a. Firm Complexity | 2.75862 | 1.01272 | 2.89237 | 1.40244 | 3.37912 | 1.33966 | 2.09524 | 1.18749 | 3.11290 | 0.84267 | 1.90476 | 0.82075 |

| b. Financial Leverage | 1.28537 | 1.48850 | 2.24372 | 3.46274 | 2.75468 | 3.26826 | 0.57457 | 0.77335 | 1.00865 | 1.27427 | 1.86974 | 1.87111 |

| c. Firm Size | 16.18664 | 1.77063 | 21.55927 | 1.71069 | 20.44412 | 0.80649 | 12.90114 | 3.80365 | 13.95157 | 1.70048 | 11.47333 | 1.39545 |

| d. Industry Competition | 0.02686 | 0.04114 | 0.01114 | 0.01709 | 0.01502 | 0.01760 | 0.03998 | 0.03869 | 0.00873 | 0.01958 | 0.05969 | 0.03345 |

| e. International Diversification | 0.81281 | 0.39103 | 0.75147 | 0.43259 | 0.32967 | 0.47139 | 0.73016 | 0.44744 | 0.35023 | 0.47759 | 0.09524 | 0.29710 |

Source: data processed.

A comparative analysis of the mining sectors in six Southeast Asian countries reveals significant variations in terms of corporate sustainability performance, risk management, green intellectual capital, and contingency factors. Singapore's performance is noteworthy, with slightly higher corporate sustainability performance (average 1.29) and exceptional green intellectual capital (average 18.45), despite its relatively low firm complexity and financial leverage. Meanwhile, Indonesia has a sustainability performance that is analogous to that of Singapore, yet with slightly greater variability (standard deviation of 0.865) and higher financial leverage (average of 2.24), indicative of a riskier industry. Malaysia demonstrates exceptional green intellectual capital (mean 17.87), characterized by elevated levels of corporate complexity (mean 3.38), indicative of a more intricate sector. Conversely, the Philippines and Vietnam exhibit lower sustainability performance metrics (averaging 1.08 and 1.05, respectively), accompanied by less international diversification, indicative of smaller and less developed markets. Despite its relatively low sustainability performance (averaging 1.07), Thailand demonstrates a higher level of industry competition (averaging 0.06), reflecting a more competitive sector. In the context of Vietnam, factors such as firm size and financial leverage tend to be lower, indicating that smaller companies generally have less debt. In contrast, Singapore and Malaysia tend to have larger companies and more moderate leverage. International diversification indicates that Singapore and Indonesia have higher levels of diversification, while other countries, such as Vietnam, demonstrate lower levels of diversification. The mining sector in these countries is influenced by a variety of factors, including corporate structure, competition levels, and the presence of diverse sustainability policies.

In order to fortify the conclusions of this study, additional analysis was undertaken employing Structural Equation Modeling (SEM-PLS). This approach entailed the assessment of the outer model, inner model, and model feasibility. The objective of this comprehensive evaluation was to furnish a more profound understanding of the interrelationships between the variables.

The inner model analysis, also referred to as the hypothesis test, has been observed through the magnitude of path coefficients derived from bootstrapping procedures. The primary indicators employed in this analysis include the T-test value greater than 1.96 and the p-value less than 0.05 for a significance level (α) of 5%. An examination of Table 4 will reveal the test results.

The analysis of the results of this study utilizes the inner model test, also known as the hypothesis test. This test is conducted by measuring the path coefficient through the bootstrapping procedure. The findings of this study demonstrate that contingency factors exert a substantial influence on ERM, as evidenced by the remarkably high T-statistics value (15.271) and the low p-value (0.003). This observation signifies a considerable impact on the implementation of risk management strategies. Furthermore, the positive effect of contingency on sustainability firm performance (SFP) is more pronounced, although less significant, as evidenced by the T-statistics value of 3.476 and a p-value of 0.041. The findings of this study demonstrate that ERM exerts a substantial positive influence on corporate sustainability performance, as evidenced by T-statistics of 5.498 and p-values of 0.027. Similarly, GIC has been found to have a significant positive effect on corporate sustainability performance, as indicated by T-statistics of 9.460 and p-values of 0.012. These results underscore the pivotal role of green intellectual capital in enhancing sustainability performance. The interaction between GIC and ERM has been shown to exert a positive effect on corporate sustainability performance, although with a smaller path coefficient (0.015), the significant T-statistics (3.515) and p-value of 0.035 indicate that combining the two strengthens their impact. The mediation path analysis demonstrates that contingencies can influence corporate sustainability performance through ERM, as evidenced by T-statistics of 5.217 and p-values of 0.034. This finding underscores the significance of external factors in enhancing corporate performance. The Adjusted R² (Adj. R²) value of 0.753 indicates that 75.3% of the variation in corporate sustainability performance (SFP) can be explained by the model involving the independent variables in this study, namely ERM, GIC, and contingency factors. This figure suggests that the model employed is quite adept at predicting corporate sustainability performance, as evidenced by an Adjusted R² greater than 0.7, which is indicative of a model with considerable predictive capability. ERM and GIC have a significant influence on corporate sustainability performance, both directly and through interactions with other factors. Similarly, contingency factors also influence ERM implementation and corporate sustainability performance. These findings indicate that mining companies in Southeast Asia need to integrate effective and sustainability-oriented risk management strategies to achieve better long-term performance.

4.2. Discussion

4.2.1. The Effect of Contingency on ERM

The findings of the statistical analysis demonstrate that contingency factors exert a substantial influence on the implementation of ERM in the Southeast Asian mining sector. This finding lends further support to contingency theory, which posits that the efficacy of management systems—in this case, ERM—is contingent upon the alignment between organizational conditions and the approach employed (Otley, 2016). The collective influence of organizational complexity, financial structure, firm size, industry dynamics, and international diversification has been demonstrated to drive mining companies to establish adaptive and structured ERM systems. In the context of an industrial environment characterized by substantial external pressures, including environmental regulations and stakeholder expectations, ERM emerges as a pivotal mechanism for achieving corporate sustainability and resilience.

This finding aligns with the ERM Theory framework (Mikes & Kaplan, 2015), which states that companies facing high risk and structural complexity tend to adopt a more formal and integrated risk management system. In the context of high leverage and cross-border operations, for instance, the implementation of proactive risk controls becomes imperative for the management of financial and geopolitical exposures. Conversely, large-sized companies possess the requisite resource capacity to implement a comprehensive ERM system. The present study corroborates the findings of Gordon et al., (2009) and Farrell & Gallagher, (2015), which demonstrate that the congruence between firm characteristics and ERM exerts a substantial influence on sustainable performance.

This finding underscores the impact of contingency factors on the performance of mining companies in Southeast Asia, which is consistent with prior research (Pangestuti et al., 2024). Contingency theory, a framework developed to elucidate the relationship between a firm and its environment, underscores the significance of aligning management practices with the distinct characteristics of the situation (Hanisch & Wald, 2012). The theory acknowledges the absence of a universally optimal approach to firm management, emphasizing that its efficacy is contingent on factors such as firm complexity, leverage, size, market uncertainty, and dynamics (Volberda et al., 2012). Contingency theory posits that the adaptation of organizational structures and managerial approaches to environmental demands can enhance performance. In highly uncertain and dynamic markets, for instance, decentralized and flexible organizational structures enable firms to respond quickly to changes. Conversely, in stable and predictable markets, centralized and hierarchical structures may be more suitable (Otley, 2016).

ERM is regarded as a vital component of an organization's management control system, which facilitates performance enhancement through the effective management of risks (Nedaei et al., 2015). The implementation of risk management is critical in a dynamic business environment, where contingent variables significantly affect firm performance, thus requiring appropriate internal controls (Khan, 2016). Adopting ERM as a comprehensive strategy facilitates effective risk management, safeguarding organizational and stakeholder value (Shatnawi & Eldaia, 2020). This finding aligns with the prevailing notion that organizations endeavor to optimize their performance by calibrating internal and external factors in accordance with their objectives and operations (Gordon, 2009). In the pursuit of competitiveness, organizations implement strategies and policies that are customized to their distinct circumstances(Lamptey, 2018). Consequently, a universally applicable solution for managing companies is lacking. To maintain competitiveness and business continuity, strategies must be tailored to specific circumstances.

In terms of practical contributions, this research provides strategic guidance for mining industry players in designing ERM systems that are tailored to the internal characteristics of the company. It is imperative to acknowledge that not all companies necessitate a uniform ERM approach. For instance, enterprises operating within highly competitive industry landscapes should adopt ERM as a strategic innovation instrument to ensure the preservation of a competitive advantage (Phương et al., 2022). Conversely, enterprises characterized by elevated operating complexity stand to benefit from the integration of information technology and data analytics, a strategy that has been demonstrated to enhance the responsiveness of ERM to operational and environmental risks (Radebe & Chipangamate, 2024). This suggests that ERM functions not only as a risk mitigation instrument, but also as a catalyst for long-term value creation.

This study contributes to the extant literature by positing that ERM is contextual and dynamic, as articulated in the Contingency-Based Risk Management Framework (Nedaei et al., 2015). It is incumbent upon companies to adjust their ERM systems on an ongoing basis as contingency factors, both internal and external, evolve. The model utilized in this study corroborates the notion that the greater the level of contingency faced by the company, the more pressing the need to implement ERM as an integrative strategy becomes. These findings give rise to policy implications, particularly for regulators and industry associations, who are tasked with encouraging ERM standards that are adaptable yet grounded in the specific context of each sector and firm size. Therefore, the present study offers theoretical contributions through the empirical validation of contingency theory and practical contributions through data-driven recommendations for decision-makers in the Southeast Asian mining industry.

4.2.2. Effect of Contingency on Sustainability Firm Performance

Contingency theory offers profound insights into how particular factors can influence firm performance, particularly within the context of sustainability in the Southeast Asian mining sector. The findings of this study indicate that contingency factors, including firm complexity, financial leverage, firm size, industry competition, and international diversification, play a pivotal role in shaping firm sustainability performance.

Firm complexity, defined by the diversity of its operations and geographical dispersion, has been shown to positively impact corporate sustainability performance. More complex firms have the potential to utilize diverse resources and capabilities to improve sustainability outcomes, even though they face challenges in implementing sustainability practices uniformly across their operations (Amoah & Eweje, 2023). Conversely, firms with lower complexity levels tend to demonstrate more efficient implementation of sustainability policies and strategies. The positive impact of firm complexity on sustainability performance is driven by the need for sophisticated management systems to handle diverse operations, which in turn can lead to better sustainability outcomes (Anggraini & Hidayat, 2025).

High financial leverage has been demonstrated to have a detrimental effect on a company's capacity to allocate financial resources toward sustainability initiatives. This is due to the fact that highly leveraged companies generally possess limited financial flexibility for such resource allocation. It has been demonstrated that high leverage has the potential to exert a detrimental influence on environmental performance. Companies characterized by high leverage appear to place a higher priority on financial stability than on sustainability initiatives. This tendency can impede long-term sustainability performance (Raharjo & Hasnawati, 2022). Conversely, firms with low leverage demonstrate a superior capacity to allocate funds toward long-term sustainability strategies (Razak et al., 2024) . These findings suggest that financial leverage plays an important role in determining the extent to which firms can implement and utilize sustainability initiatives to improve their performance.

Firm size has been demonstrated to exert a positive influence on sustainability performance, as larger firms generally possess greater resources to allocate toward sustainability initiatives. However, large companies often encounter bureaucratic challenges that can impede the rapid and agile implementation of these systems (Sevil et al., 2022). Larger companies tend to possess a greater quantity of resources and capabilities for implementing sustainability measures, which, in turn, can lead to improvements in performance. The extensive operations of prominent corporations frequently necessitate a more systematic management framework to ensure sustainability (Esmailikia, 2023; Maharani & Pangestuti, 2024). Furthermore, firm size has been shown to positively impact non-financial sustainability performance. Large firms are more likely to engage in social and environmental activities driven by greater public scrutiny and stakeholder expectations (Esmailikia, 2023). In contrast, smaller companies with less bureaucratic structures can more easily adapt to sustainability demands, allowing them to innovate and adapt more quickly in a dynamic market.

The presence of industry competition has been demonstrated to enhance the efficacy of environmental management practices, thereby contributing to the enhancement of sustainability performance. Companies operating in complex industries have the opportunity to leverage their environmental management capabilities to gain a competitive advantage, thereby improving their sustainability outcomes (Hartmann & Vachon, 2018). The adoption of sustainability practices is also influenced by industry competition. In industries characterized by high levels of competition, firms are more motivated to implement sustainability practices as a means of differentiation and gaining competitive advantage (Gold et al., 2022). Conversely, in industries characterized by minimal competitive pressures, corporate entities may prioritize other factors over sustainability, potentially leading to suboptimal sustainability performance.

International diversification has been shown to offer both opportunities and challenges for firm performance. While the process of international diversification has been shown to improve performance by facilitating access to new markets and resources, it also introduces additional risks that necessitate the implementation of effective ERM practices (Karthik, 2015). The relationship between international diversification and performance is contingent upon product diversification, suggesting that firms with high levels of international and product diversification possess the capacity to effectively manage the intricacies of international operations and attain superior sustainability performance (Karthik, 2015). International diversification has been shown to have a positive impact on sustainability performance (Tongli et al., 2005). This is due to the fact that it allows firms to adopt best practices from different regions and reduce risks associated with local environmental regulations. As demonstrated in the research by Capar et al., (2015), internationally diversified firms possess a distinct advantage in terms of environmental risk management and capital utilization within the global market. This capacity to navigate and leverage diverse market opportunities is a hallmark of such firms, underscoring their strategic agility in navigating complex and dynamic global economic landscapes.

Contingency theory posits that a uniform managerial approach does not exist for all firms. Conversely, the efficacy of strategic initiatives is contingent upon the congruence between the organizational framework and the external environment encountered by the enterprise. In the challenging mining sector, characterized by market uncertainty and strict regulations, companies must adjust their approach to achieve optimal sustainability performance (Otley, 2016; Volberda et al., 2012). This strategic adjustment to external and internal environmental factors has been demonstrated to enhance a firm's competitiveness and improve its sustainability performance (Gordon et al., 2009; Nedaei et al., 2015).

From a pragmatic standpoint, these findings convey a salient signal to policymakers and corporate leaders that a uniform sustainability approach is unfeasible. It is incumbent upon companies to proactively map the contingency factors relevant to their business models and to establish adaptive sustainability governance systems. This study makes a theoretical contribution to the strengthening of contingency theory in the context of sustainability firm performance. It also makes a practical contribution in the form of adaptive strategies that align with the structure and challenges of mining companies in Southeast Asia. This study emphasizes that in the face of economic, regulatory, and environmental pressures, it is imperative for firms to navigate contingency factors through a holistic and dynamic management system.

4.2.3. The Effect of ERM on Sustainability Firm Performance

The implementation of ERM in the Southeast Asian mining sector has been demonstrated to exert a positive influence on corporate sustainability performance. ERM is an integrated and holistic strategic framework that focuses not only on financial risk management but also on ESG risk management. This is particularly relevant in the context of the mining industry, which has high inherent risks and strict regulatory pressures. This finding aligns with the conclusions of Razak et al., (2024) and Amoah & Eweje, (2023), who underscore the significance of integrating ERM with sustainability practices for achieving operational efficiency and long-term sustainability in industries that are particularly susceptible to external risk exposures.

In the context of stakeholder theory, ERM can function as a mediator between corporate social responsibility (CSR) and firm performance. When companies are able to manage ESG risks systematically, it has been demonstrated to increase stakeholder trust, which in turn strengthens firm value and market competitiveness (Resende et al., 2024). In the mining sector, which faces complex challenges such as social conflict, environmental degradation, and local community resistance, ERM serves as an adaptive mechanism to respond to external pressures and maintain the license to operate. The success of sustainability programs in this sector is determined by strategic intentions and the resilience of the risk management system embedded in the organizational structure.

From an empirical perspective, the present research aligns with prior studies demonstrating that ERM implementation can enhance operational efficiency, reduce stock price volatility, and decrease the cost of external capital. These factors collectively contribute to enhanced corporate sustainability performance (Gordon et al., 2009; Lechner & Gatzert, 2018). In the mining sector, which is highly affected by environmental uncertainty and stringent regulations, a comprehensive ERM system acts as a substantial performance differentiator, minimizing the risks faced by the company and increasing the transparency and accountability of the company to external stakeholders.

The implementation of ERM has been demonstrated to be associated with enhanced sustainability reporting quality, a phenomenon that has been empirically linked to an increase in firm value (Nguyen & Vo, 2020). This phenomenon is especially salient in the mining sector, where stakeholder expectations of companies are perpetually escalating, particularly with regard to social and environmental sustainability. Integrating ERM into management strategies can enhance sustainability performance, ensure financial stability, and align with stakeholder expectations.

The findings of this study demonstrate that ERM plays a substantial role in the sustainability performance of companies in the Southeast Asian mining sector. The application of effective risk management practices, as facilitated by ERM, empowers firms to adapt to the dynamic environmental and regulatory shifts that characterize contemporary business environments. This adaptation, in turn, contributes to the enhancement of performance, resulting in sustainable outcomes (Beasley et al., 2005; Moeller, 2007). The theoretical contribution of this study is twofold. Firstly, it contributes to the construction of ERM as a multidimensional strategic variable by linking risk management theory, sustainability, and agency theory. This research also promotes a novel understanding that sustainability success cannot be separated from the context of the operational environment and the design of an adaptive risk management system. The findings of this study indicate that mining companies are designing ERM systems that are not only compliance-based, but also proactive and dynamic. This approach will enable companies to survive market turbulence and to grow sustainably in an increasingly complex business ecosystem. This is due to the fact that the ecosystem demands greater social and environmental responsibility.

4.2.4. The Effect of Green Intellectual Capital on Sustainability Firm Performance

The findings of the research indicate GIC exerts a substantial influence on the performance of mining companies in Southeast Asia. This outcome serves to substantiate the notion that GIC is not merely an intangible asset, but rather, it functions as the primary catalyst in propelling sustainable performance through augmented innovation, enhanced operational efficiency, and strategic adaptability. This finding aligns with the Natural Resource-Based View (NRBV), which posits that rare, valuable, and inimitable resources—such as GICs—can serve as a source of sustainable competitive advantage (Sohu et al., 2024). In the context of the capital-intensive and risk-intensive mining industry, the existence of GICs enables companies to navigate ESG challenges more strategically.

Conceptually, the components of GIC—namely, Green Human Capital (GHC), Green Structural Capital (GSC), and Green Relational Capital (GRC)—have complementary functional roles. GHC provides the foundation of competence and environmental orientation in human resources. GSC supports green knowledge infrastructure and systems that enable knowledge diffusion internally, while GRC expands an organization's ability to collaborate with external stakeholders critical to sustainability (Kianto et al., 2013; Marr et al., 2003). When these three dimensions are effectively integrated, organizations can create dynamic capabilities that are relevant in the context of market turbulence, strict regulations, and civil society demands.

From an empirical perspective, the role of GICs is crucial in accelerating the transformation of green technology in the mining sector. The successful adoption of green technology, such as automation, sensor-based mining, and real-time environmental monitoring, is strongly influenced by the quality of intellectual resources owned by the company (Riaz et al., 2024; Subaida et al., 2018). This assertion is further substantiated by the tenets of Resource Orchestration Theory (Ireland et al., 2003) which posits that competitive advantage is contingent not solely on resource ownership, but also on the organization's capacity to orchestrate, integrate, and configure these resources in a dynamic manner in accordance with strategic imperatives. GICs play an instrumental role in orchestrating environmental and social assets into outputs that contribute to business value-added and corporate reputation.