Submitted:

22 May 2025

Posted:

23 May 2025

You are already at the latest version

Abstract

Financial Reporting Governance (FRG) encompasses the processes that ensure financial reporting is accurate, transparent, and compliant with regulations. A variety of models, policies, procedures, frameworks, and processes have been established to organize, manage, structure, share, and reuse knowledge within the FRG domain from multiple perspectives. However, these existing works are often tailored to specific scenarios, leading to a lack of a unified abstract model that organizes and structures FRG domain knowledge comprehensively. This paper aims to create a novel high-level abstract model for FRG domain knowledge, employing Model Driven Engineering (MDE) and metamodeling, which we refer to as the Financial Reporting Governance Model (FRGM). The FRGM comprises ten abstract components: corporate governance structures, auditing and financial controls, compliance and regulatory framework, transparency and accountability, risk management, stakeholder engagement and communication, performance measurement and financial reporting, cultural and ethical considerations, technology and innovation training and development. Each of these components represents a semantic knowledge area, complete with definitions, relationships, attributes, and operations. The capabilities and effectiveness of the FRGM are validated through vertical transformation, ensuring that solution models derived from the FRGM are practical and relevant. Ultimately, the FRGM addresses issues of heterogeneity and interoperability within the FRG domain.

Keywords:

finance report

; metamodel

; metamodeling

; governance

; model

; metamodel transformation

I. Introduction

Financial Reporting Governance (FRG) involves processes that guarantee financial reporting is accurate, transparent, and compliant with regulatory standards. Numerous models, policies, procedures, frameworks, and processes have been developed to organize, manage, structure, share, and reuse knowledge within the FRG domain from various perspectives. However, these existing approaches are typically designed for specific scenarios, resulting in a gap for a unified abstract model that comprehensively organizes and structures FRG domain knowledge [1].

The main contribution of this study is the development of FRGM. This metamodel provides a high-level, structured representation of the financial reporting governance process, encompassing key components such as roles, responsibilities, workflows, and decision-making hierarchies. By using a metamodeling approach, the FRGM enhances clarity and communication, facilitates better alignment among stakeholders, and streamline processes, leading to improved adherence to governance standards. The framework’s effectiveness is demonstrated through a real-world case study, highlighting its ability to identify inefficiencies, mitigate risks, and promote a culture of accountability.

The novelty of this research lies in its application of metamodeling to the complex domain of financial reporting governance. Unlike existing frameworks that often lack a structured, comprehensive approach, the FRGM offers a systematic and visual representation of the entire process. This allows for a more thorough analysis of interdependence and relationships between different governance components, enabling organizations to identify potential risks and areas for improvement. The use of metamodeling also facilitates easier documentation of processes, demonstrates compliance with regulations, and allows for greater adaptability to changing regulatory and technological landscapes. Thus, this study should answer these two questions:

What are the advantages and disadvantages of the current financial reporting governance models and frameworks?

Does the FRG domain have a structured and organized model to effectively represent its domain knowledge?

This paper is structured as follows: Section 2 presents related works, Section 3 describes the model-driven engineering methodology, Section 4 outlines the development process, Section 5 implements the developed FRGM, Section 6 presents findings and discussion, and Section 7 concludes with future work.

II. Related Works

Several works have been proposed in the literature for the FRG domain. This section discusses the advantages, disadvantages, methodologies, output and the contribution of the existing FRG works. For example, the incident response framework articulates the primary purpose of an integrated report as elucidating how an organization generates, sustains, or diminishes value over time to providers of financial capital. Consequently, it encompasses pertinent financial and non-financial information, offering a comprehensive view of the organization’s performance and strategic direction [2]. A risk management framework (RMF) is a set of guidelines and practices that help organizations identify, assess, and reduce risks. RMFs can help organizations protect themselves from cybersecurity threats, improve customer trust, and grow their business [3]. An Internal Audit Framework articulates the mission and goals of the internal audit function, highlighting its critical role in enhancing organizational governance and risk management. It also delineates the methods and guidelines that internal auditors follow to deliver objective and impartial evaluations of the organization’s processes and controls [4]. A data governance framework establishes a unified set of rules and procedures for the collection, storage, and utilization of data. Despite the continually expanding volume of data, this framework facilitates the streamlining and scaling of core data governance practices while ensuring adherence to policy and regulatory compliance requirements [5]. The COSO Framework is a comprehensive system designed to implement internal controls that are seamlessly integrated into an organization’s business processes [6]. Together, these controls offer reasonable assurance that the organization is operating ethically and transparently while adhering to established industry standards. COBIT (Control Objectives for Information and Related Technology) assists organizations in addressing business challenges related to regulatory compliance, risk management, and aligning IT strategy with broader organizational objectives [7]. International Financial Reporting Standards (IFRS) are a comprehensive set of accounting guidelines designed for the financial statements of public companies. These standards aim to ensure that financial statements are consistent, transparent, and easily comparable across the globe, facilitating greater understanding and trust among investors and other stakeholders [8]. The International Financial Reporting Standards (IFRS) are issued by the International Accounting Standards Board (IASB). Meanwhile, the Sarbanes-Oxley Act (SOX) is a U.S. federal law designed to regulate corporate financial reporting and record-keeping practices, ensuring accuracy and accountability in the preparation and disclosure of financial information [9]. The authors in [10] proposed a corporate governance structure that comprises seven interrelated mechanisms: oversight, managerial, compliance, audit, advisory, assurance, and monitoring functions. This comprehensive framework is designed to enhance organizational accountability and effectiveness. The well-balanced functioning of these seven interrelated functions can produce responsible corporate governance, reliable financial reports, and credible audit services. Based on the authors in [11], financial reporting can play a crucial role in reducing information asymmetries that exist between managers and both outside directors and shareholders, which are detrimental to the effectiveness of management. The authors in [12] examined the empirical and archival literature on Chinese corporate governance and financial reporting quality. However, despite the abundance of surveys on Chinese corporate governance, this study observed that there are no comprehensive surveys of corporate governance and financial reporting quality literature, so we have undertaken a systematic review. The authors in [13] examined the effectiveness of apparatus competence and internal control on financial reports and their impact on government governance. The study examined 70 working units and area devices in seven local governments in Jawa Tengah Province, Indonesia, as part of their research. The authors in [14] attempted to fill the gap by identifying specific characteristics of corporate governance that can contribute to reducing the possibility of fraud involving non-financial reporting that could assist in reducing the risk. The researchers in [15] examined the relationship between corporate governance and the quality of financial reporting, offering a thorough analysis of their findings on this important topic. Their study highlights key correlations and insights that underscore the influence of corporate governance practices on the integrity and reliability of financial reporting. The authors of [16] examined whether corporate governance components (board size, audit committee, board independence, non-audit service, multiple directorships) are related to instances of fraudulent financial reporting. The authors in [17] we examine the evolution of corporate governance in Japan since the 1990s, focusing specifically on financial reporting as a fundamental attribute of effective governance. As well as examining Japanese accounting practices, disclosure requirements, and reporting standards, the book presents an overview of the legal, institutional, and stakeholder dimensions of governance. In the paper, the authors argue that accurate financial reporting is essential to good corporate governance. According to the [18], various corporate governance indicators influence risk management practices differently at Islamic financial institutions compared to conventional financial institutions. This highlights the distinct approaches and considerations each type of institution employs in managing risk. Moreover, the study examined how institutional quality modifies practices’ impact on Pakistan’s financial institutions by moderating their impacts. The authors in [19] explored the intricate relationship between integrated reporting, corporate governance, and financial sustainability within the context of Islamic banking. The authors in [20] examined the intricate interplay between integrated reporting, corporate governance, and financial sustainability within the Islamic banking framework. Their research investigates how these elements interact and collectively enhance the effectiveness and ethical integrity of financial practices in Islamic financial institutions. The authors in [21] explained the concept of stories in organizations, discuss the characteristics and advantages of storytelling, and illustrate how stories can be created in organizations. A study reported in [22] investigated the relationship between the environmental, social, and governance performance of an organization and its quality of financial reporting with the assistance of data from the DataStream, Refinitiv Eikon, and ASSET4 databases. In the study [23], the authors examined the relationship between corporate governance and the internet financial reporting system in order to find out whether the two can be related. The authors in [24] examined the relationship between environmental and social reporting quality in favour of the impact that it has on these two variables in terms of their relationship. In their article [25], The authors examined the extent to which audit fees influence the independence of auditors in Nigeria, while also assessing the impact of independent non-executive foreign directors, foreign institutional ownership, and local institutional ownership on the quality of financial reporting. Their study provides valuable insights into these critical factors affecting audit integrity and financial transparency. As the authors of [26] stated, they examined the responses of 120 French listed companies to some corporate governance mechanisms used in integrated reporting in order to examine the effectiveness of such mechanisms. Table 1 displays the advantages, disadvantages, methodology, output and the contributions of the existing FRG works.

The studies cover diverse aspects of FRG, including corporate governance, financial reporting quality, integrated reporting, and the impact of regulations and technologies on FRG practices across different sectors and geographical regions. Each study employs various methodologies, such as literature reviews, regression analyses, case studies, and surveys, to examine the relationships between corporate governance and financial reporting quality. As a result, many entities struggle to implement a cohesive and efficient approach to managing their financial reporting processes. The absence of a comprehensive, unified model creates several challenges for organizations. It can lead to inconsistencies in reporting practices, difficulties in comparing financial information across different entities or time periods, and increased complexity in compliance efforts. Table 1 highlights the findings and contributions of each study, while also acknowledging limitations and suggesting areas for future research.

III. Model Driven Engineering

Model-Driven Engineering (MDE) is a sophisticated development approach designed to effectively create and model complex domains, enabling a structured and systematic way to address the intricacies of financial reporting and governance [30] at a high level of abstraction [31], where the metamodels are the central elements in the development process [32]. The primary goal of Model-Driven Engineering (MDE) is to offer solutions that address challenges related to interoperability, heterogeneity, and the complexities inherent in various domains [33]. The MDE methodology is built upon three foundational concepts: model, metamodel, and metamodel transformation. The following paragraphs provide a brief overview of these three key concepts of the MDE methodology. The first concept is a model, which serves as a representation layer that helps manage the complexity of real-world systems and processes [34]. It consistently organizes the core ideas of generic concepts that constitute the domain [35]. It aids designers in comprehending complex systems by breaking them down into smaller, manageable components known as solution models. Typically, a model comprises two fundamental elements: concepts and relationships [36]. A concept defines the entities within the domain, while relationships elucidate the connections between those entities [36]. A model conveys the structure, behaviours, and other properties across a variety of domains, including engineering, science, philosophy, mathematics, management, and medicine [37]. The behaviours of the model are governed by a metamodel, which is defined using a specialized metamodeling language. The following section provides a brief overview of metamodels.

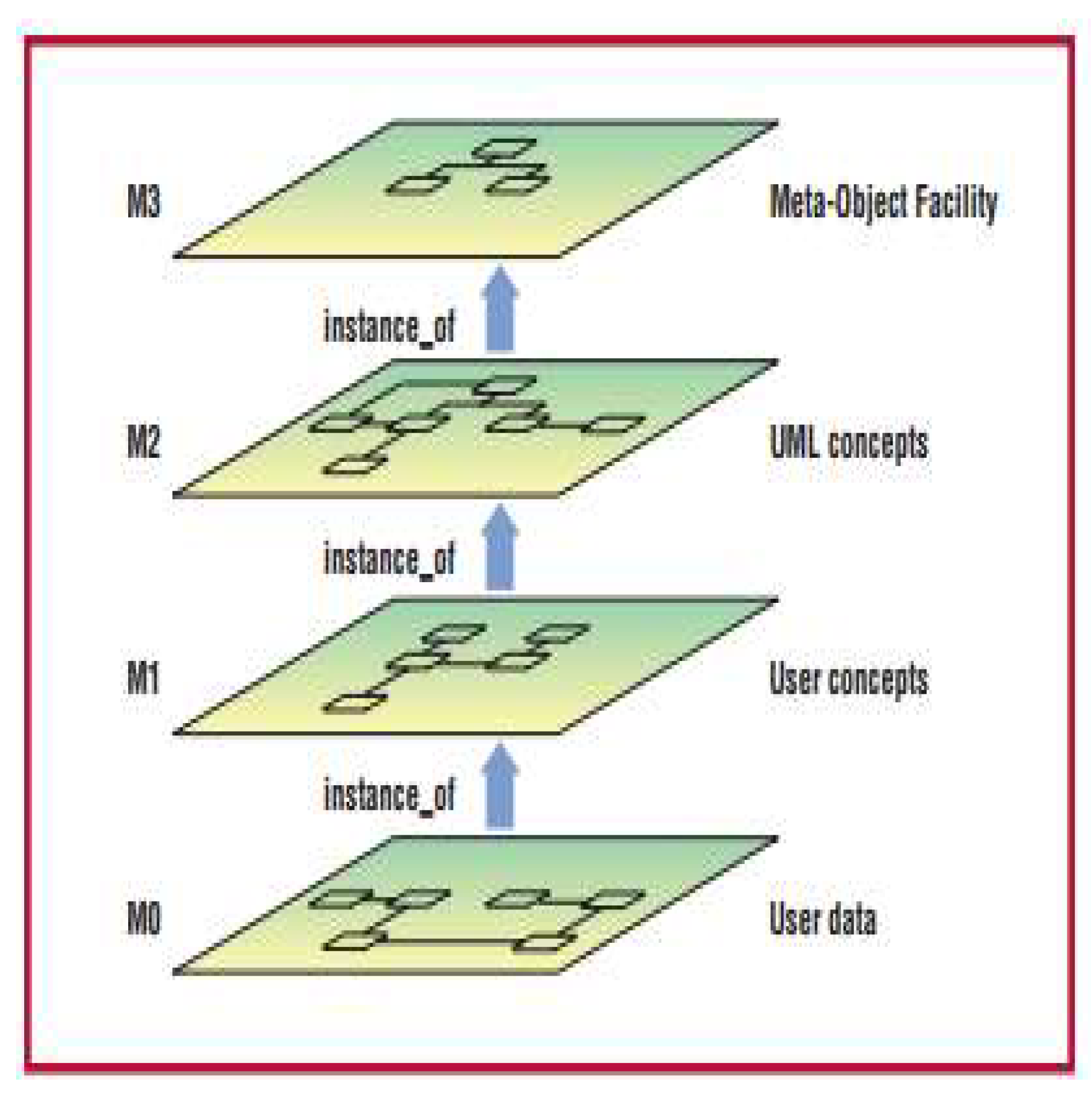

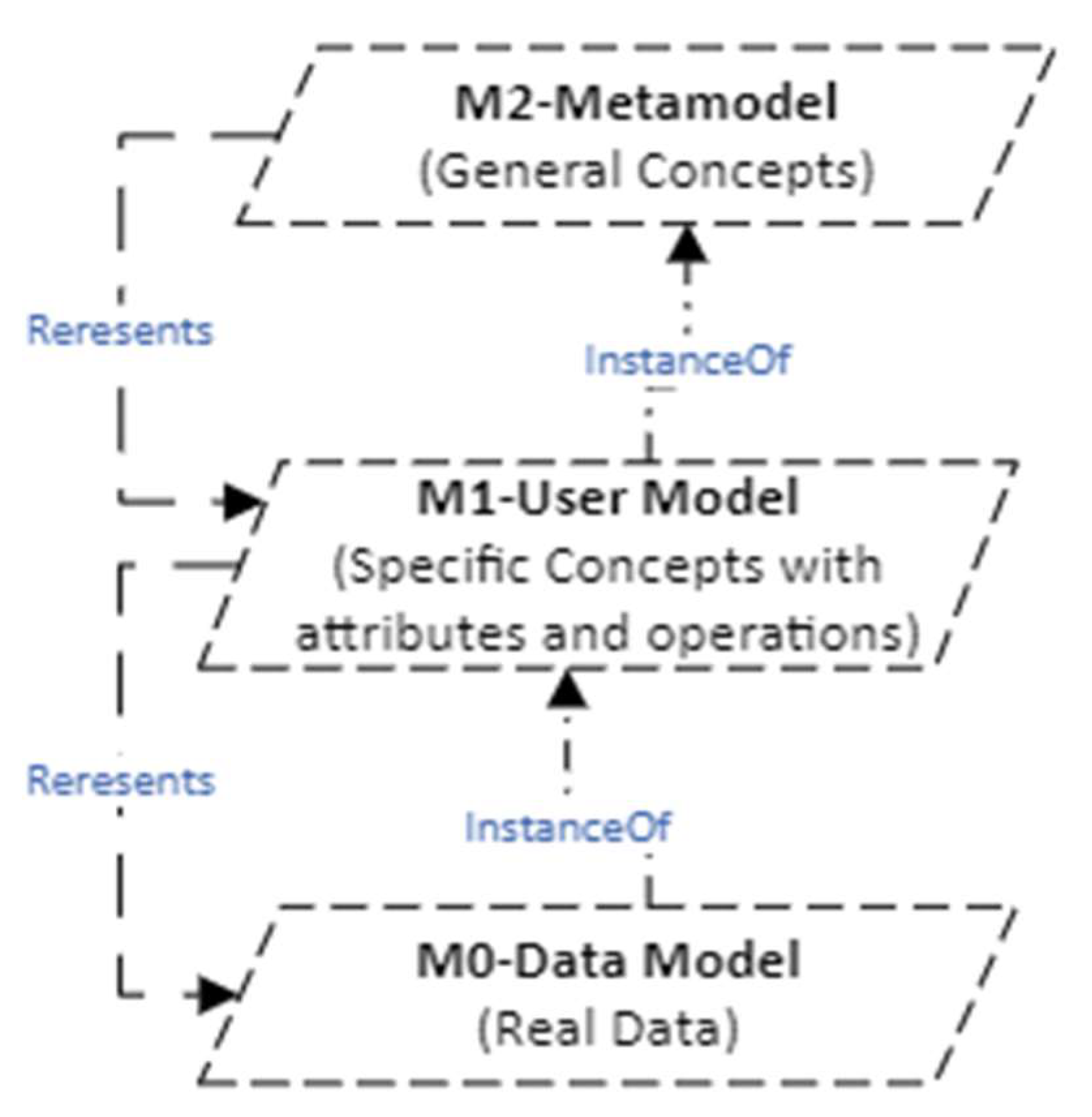

The second component is the metamodel, which serves as a model of a model, effectively providing a comprehensive explanation of the underlying structure of the model. It delineates the concepts, attributes, operations, and associations necessary to represent a specific domain accurately. Essentially, a metamodel offers a precise definition of the modeling elements such as concepts, attributes, operations, associations, and rules that are essential for constructing semantic models [38]. These elements are utilized to build a domain model. Therefore, a metamodel serves as both a prescriptive and descriptive framework for a modeling language. It addresses the ambiguity and heterogeneity present in complex domains by facilitating the generation of solution models that provide clarity and consistency [37]. The metamodel comprises four levels (M0, M1, M2, and M3), as illustrated in Figure 1, each providing a distinct perspective on modeling at varying levels of detail. Concepts at any level below M3 are derived from the concepts of the level immediately above. Furthermore, any concept at a given level (above M0) can be instantiated at the level below it. The M3 level is reserved for meta-metamodel components, which include explanations of the construction and semantics of the metamodel; however, this level is not a focus of this study. The M2 level represents instances of the meta-metamodel, detailing the construction and semantics of metadata, as illustrated through UML concepts such as classes, attributes, operations, relationships, and notations. The M1 level encompasses the model level and includes the metadata that defines data at the information level. Finally, the lowest level, M0, is dedicated to user models and is commonly referred to as the information level (or user data). In this study, the M0 level will address the data described by the FRG model at M1, while the M1 level will encompass the models outlined by the FRG metamodel at M2.

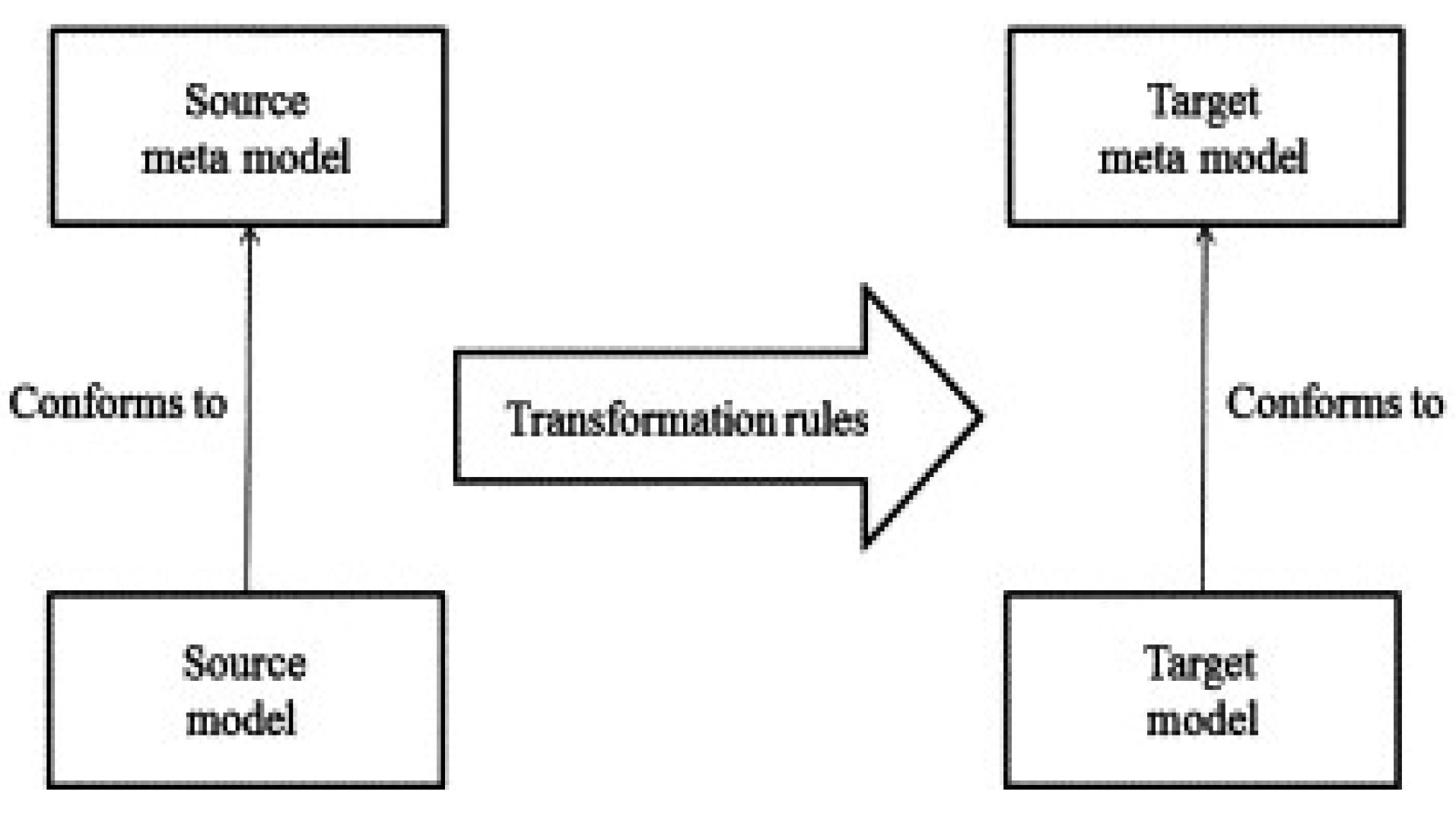

The transformation refers to the process of constructing a solution model from the underlying metamodel. This process entails interpreting the abstract constructs defined within the metamodel such as concepts, attributes, and relationships and applying them to create a specific, actionable solution model tailored to the needs of a particular domain. Through this transformation, developers can leverage the structured framework provided by the metamodel to ensure that the resulting solution model adheres to established guidelines and best practices, ultimately facilitating effective implementation and alignment with intended outcomes. This systematic approach enhances the capability to adapt and refine models as requirements evolve, promoting greater scalability and relevance in changing contexts [40]. The proposed FRGM must be transformed into multiple FRG solution models in a manner that ensures interoperability. In this study, we utilize the transformation methods introduced by the Meta Object Facility (MOF) to execute the transformation from metamodel to model for the FRGM. Within the MOF framework, model transformation can be viewed through both vertical and horizontal dimensions[41].

Figure 3.

Metamodel transformation mechanisms[31].

Figure 3.

Metamodel transformation mechanisms[31].

Vertical transformation refers to the process of converting models from one level of abstraction to another within a modeling hierarchy. This transformation can occur from a higher level to a lower level of abstraction, for example, transitioning from the metamodel (M2) level to the model (M1 and M0) levels. Additionally, the process of deriving individual concepts within the models is also considered a form of vertical transformation, as it involves breaking down higher-level abstractions into more specific, actionable representations that adhere to the defined structure of the modeling framework. As defined by [42], A model is said to conform to a metamodel when the metamodel defines every concept utilized in the instantiated model, and the model applies these concepts in accordance with the rules established by the metamodel. This relationship involves two key aspects of vertical transformation: Instantiation and Conformance. The Instantiation concept refers to the process of creating a specific instance of a concept from the metamodel, while the Conformance concept pertains to the instantiation of multiple concepts to derive a more complex concept or model object from the Financial Report Governance Model (FRGM) at the M2 level. While both Instantiation and Conformance are categorized as forms of vertical model transformation, conformance represents a broader application of instantiation.

In this study, this process elucidates how one or more concepts from the FRGM at the M2 level can derive one or more concepts in a model at the M1 level. Typically, concepts at the M1 level draw upon one or more concepts from the FRGM. Specifically, vertical transformation occurs when the M1-FRG Model and the M0-FRG User Data Model are derived from their conformant M2-FRGM. The detailed process of transforming the M1-FRG Model from the M2-FRGM will be elaborated upon in the following section through various case studies and scenarios.

IV. Methodology and Development Processs

The purpose of this study is to develop a Financial Reporting Governance Metamodel (FRPGM) based on the metamodeling approach [43,44,45]. Metamodeling is a kind of MDE. It is a powerful research methodology that focuses on the design, development, and evaluation of innovative solutions and artifacts to solve complex problems [46]. By combining theoretical insights and practical experience, researchers can create practical and meaningful solutions for real-world challenges. As a result, metamodeling is a valuable approach for creating impactful and practical solutions that can be applied to various domains [47].

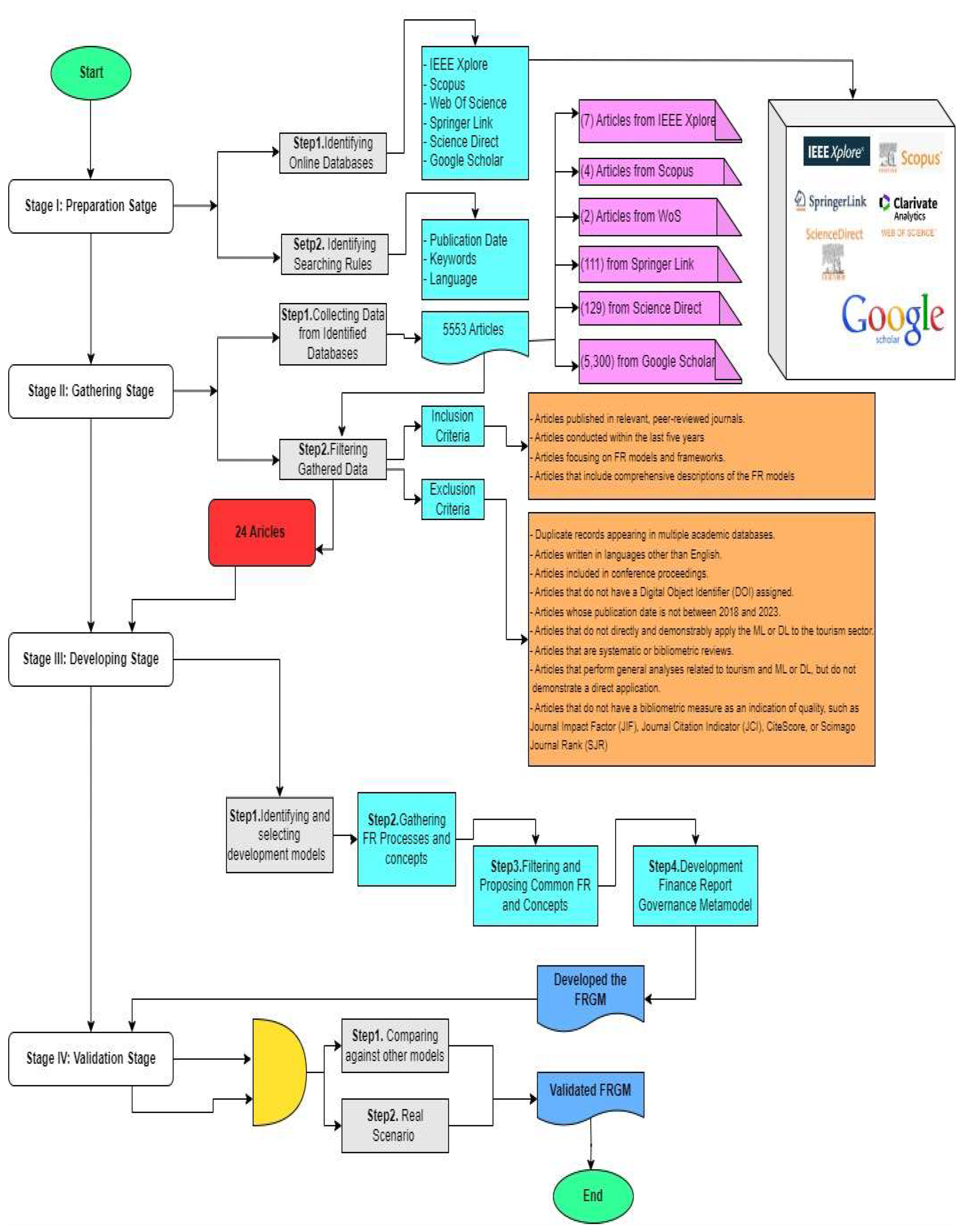

Stage I: Preparation Stage: The aim of this stage is to prepare the search controls that will be used to control the behaviour of the research in this study. It includes two controls: identifying online databases and identifying searching rules. This study identified six common online databases often used by researchers in academic fields: IEEE Xplore, Scopus, Web of Science, SpringerLink, ScienceDirect, and Google Scholar. Three search rules are identified in this study to guide the search in the commonly identified online databases: the publication date, keywords, and the language used to search. Generally, the publication date has been identified as between 2015 and 2025, and the keywords have been identified as “Finance Report” and “Governance” with the language restricted to English as the publication language. Table 2 summarize the results of searching. The next stage concentrates on gathering data from the identified online databases.

Stage II: Gathering stage: This stage consists of two steps: collecting data from identified databases, and filtering gathered data. During this phase, based on search rules that have been established, the data from the six online databases identified in the previous step will be gathered according to those rules. The online databases offered a total of 5,553 articles. More specifically, 4 articles were found on Scopus, 2 on WoS, 111 on Springer Link, 7 on IEEE Xplore, and 5,300 on Google Scholar. As a second step, all the articles that have been collected will filtered based on the inclusion and exclusion criteria offered in Table 3. Only 24 articles focused purely on finance reports and governance as shown in Table 4. The next stage concentrates of developing stage.

Stage III: Developing Stage: This stage focuses on developing a financial reporting governance metamodel to establish a comprehensive framework that encapsulates essential governance components, including roles, responsibilities, reporting lines, and decision-making processes. Adopting this approach enhances clarity and promotes more effective stakeholder communication, ultimately strengthening the governance structure. In this stage, the authors adapted metamodeling approach from [54]. It consists of four steps, as illustrated in Figure 4:

- 1.

- Identifying and selecting development models: In this step, the FRG already used in other studies for developing FRPGM were identified and selected. Among the existing models the ones that were focused solely on the FRG process were selected for this study. As a result, 24 FRG models and frameworks were selected as part of the process of developing the FRPGM.

- 2.

- Gathering FRG Processes and concepts: The aim of this step is to gather the main FRG processes and concepts from the 42 mobile forensic models, which could possibly be involved in the FRPGM. The processes and concepts are obtained from the textual contents (main body) of FRG models to prevent any omitted or irrelevant processes or concepts during the extraction process [55,56,57]. However, similar to the procedures in [54,55,57,58], the FRG processes and concepts were extracted manually from each model. Furthermore, this study adapted the concept mining process from [59,60]. As shown in Table 5, 202 FRG processes and concepts have been gathered from 42 FRG models. This step in the metamodeling approach is vital as it lays the groundwork for the development of the FRPGM. By determining essential FRG concepts and processes, we can make informed decisions regarding their inclusion in the metamodel. Next stage step is using to filter and propose the common FRG concepts and processes to develop the FRPGM.

- 3.

- Filtering and Proposing Common FR Processes and Concepts: This step involved filtering and combining the 202 concepts and processes collected in the previous step based on how similar their meanings and workings are [61,62,63]. For example, the Stakeholder Engagement [14,15,17,18,19,20,21,23,24,25,26,48,49,51,53], and Stakeholder Communication [11,50] mean the same function with different names. Both processes highlight the importance of interacting with various stakeholders (e.g., investors, customers, regulators) to understand their expectations and concerns, promoting transparency and trust. In addition, Sustainability Reporting [48] and Non-Financial have the same meaning; both refer to the disclosure of non-financial impacts or performance, including environmental, social, and governance factors that contribute to stakeholder decision-making. Therefore, the components that have similar semantic meaning or functional meaning are merged into one common category regardless of naming, and then each category is mapped, and the most frequent component of each category is. Therefore, 10 common components were proposed, as shown in Table 6. These components are used as the main inputs for the FRPGM. Table 7 displays the UML relationships among the proposed components.

- 4.

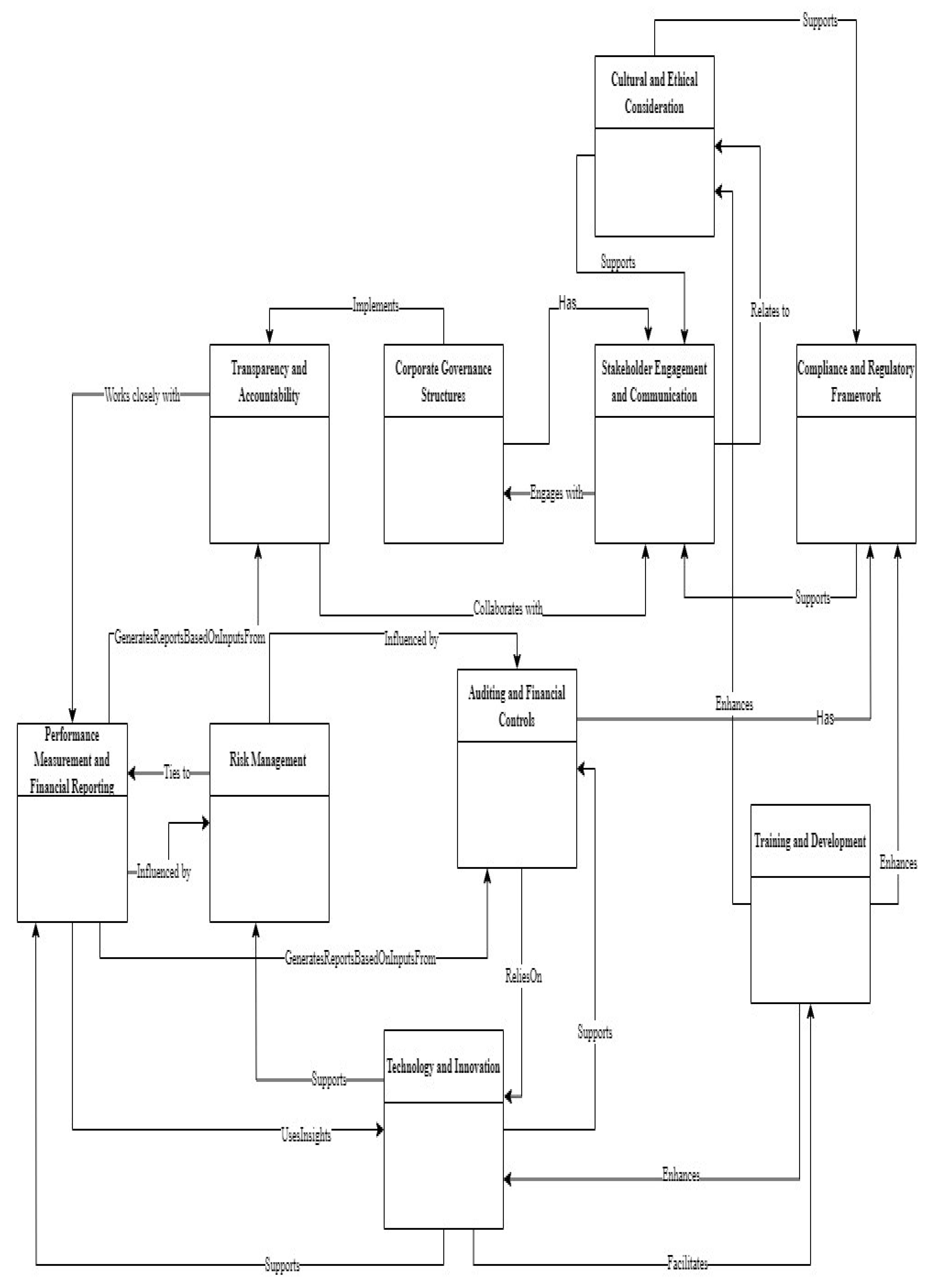

- Development Finance Report Governance Metamodel: This step aims to develop the FRGM. A unified modelling language (UML) relationship was adapted to develop the FRGM. This relationship refers to a link between metamodel components; it combines semantics, called the modelling language [64]. A modelling language is a set of concepts and constructs used to describe the underlying structure of a modelling language, which, if properly organized, allows for the creation of clear and concise representations [64]. As a result of this step, the finance report governance metamodel is developed and depicted in Figure 5.

The metamodel provides a standardized framework that clarifies roles, responsibilities, workflows, and decision-making hierarchies. By having a structured model, organizations can ensure consistency across departments and regions, improve communication among stakeholders, and enhance compliance with regulations. The metamodel also allows for flexibility and adaptability, which is crucial given the evolving regulatory and technological landscape.

Another key point is that the metamodel helps identify inefficiencies and risks by analysing interdependencies between components. For instance, Risk Management ties to Performance Measurement and Financial Reporting, which means that effective risk management can lead to better financial reporting. The use of technology and innovation supports various components like Auditing and Financial Controls, Risk Management, and Performance Measurement, indicating that integrating technology can streamline these processes.

It is important to recognize that the developed metamodel transcends being a simple diagram of the components and their interconnections; it functions as a semantic language that governs the behaviours of the domain. This metamodel provides a structured representation that facilitates a clear and precise definition of each component, along with their attributes and interactions.

By doing so, it empowers developers to design and implement applications that are not only domain-specific but are also fully compliant with the intricacies and requirements of the domain. Such clarity enables more effective communication among stakeholders and fosters better collaboration in the development process. In the next section, we will explore the architecture of the metamodel in greater detail, examining how it can be practically applied to enhance the development of domain-specific applications.

V. Implement the Developed FRGM in the FRG Domain

Based on the explanation about the metamodel in Section 3 and the model transformation from the source to the target, this section will explain in detail how can we instantiate the solution models (M1-FRG Model) from the (M2-FRGM Metamodel). Vertical transformations as mentioned in Section 3 refers to the process of elevating a model from one level to another. This transformation method is particularly useful for deriving specific concepts from a metamodel into derived models. A model adheres to a metamodel when the metamodel defines all the concepts utilized by the model, and the model aligns with these specified concepts. This alignment facilitates the transformation from a higher level to a lower level, such as from a metamodel (M2) to specific models (M1-User Model and M0 - Data Model), as illustrated in Figure 6. The M2 metamodel encompasses general concepts, relationships, and regulations that govern the functionalities of the M1 User Model. Figure 6 visually depicts the vertical transformation mechanism and the instantiation of models from the metamodel.

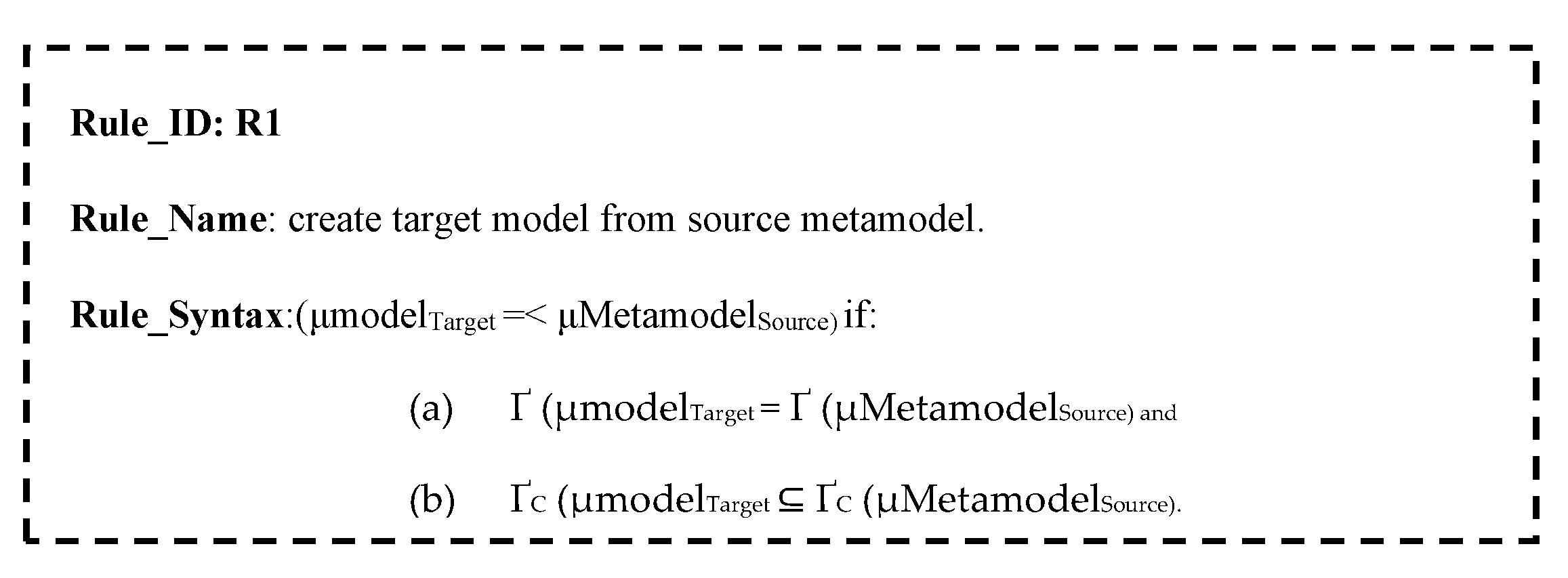

The vertical transformation mechanism must conform to the modelling rules adapted from [66] to effectively instantiate and derive solution models . Adhering to these rules ensures that the transformation process is systematic, reliable, and aligns with the underlying theoretical framework, ultimately enhancing the integrity and functionality of the resulting models. Figure 7 displays the rule which is used to create target model from source metamodel. Consequently, the M2-Finance Reporting Governance Metamodel (M2-FRGM) enables practitioners within the FRG domain to effectively instantiate the M1-Transparency and Accountability Model. This instantiation is guided by the established relationships (R1) that outline how the components and principles from the M2-FRGM translate into practical applications, as illustrated in Figure 8.

VI. Finding and Discussions

In this study the author developed a high abstract model to structure, organize, unify and manage the FRG domain called FRGM. The developed FRGM effectively captures and represents the essential components of the financial reporting governance process, including roles, responsibilities, workflows, and decision-making hierarchies. It encompasses ten primary components: corporate governance structures, auditing and financial controls, compliance and regulatory framework, transparency and accountability, risk management, stakeholder engagement and communication, performance measurement and financial reporting, cultural and ethical considerations, technology and innovation training and development. Thus, this section will try to answer the questions which highlighted in the Section 1:

- What are the advantages and disadvantages of the current financial reporting governance models and frameworks?

To explore the topic comprehensively, the author embarked on an extensive literature review, sourcing an initial pool of 5,553 articles from widely used search engines. This vast collection was aimed at capturing a broad spectrum of research perspectives and findings related to financial report governance. The sheer volume of articles underscores the complexity and multidisciplinary nature of the FRG domain, highlighting its importance in the contemporary financial landscape. Recognizing the need for a focused analysis, the author undertook a rigorous filtering process to distil the wealth of information down to the most pertinent studies. This process involved evaluating the relevance, credibility, and depth of each article with respect to financial report governance. The filtering criteria were designed to ensure that only the most insightful and impactful studies were retained for deeper examination. As a result, 31 articles were identified for their specific concentration on FRG, each offering unique insights into the domain’s intricacies. From this carefully curated selection, the author was able to identify and articulate the key advantages and disadvantages discussed within these studies. The advantages highlighted included improvements in compliance, accuracy, and transparency in financial reporting practices facilitated by effective governance mechanisms. Conversely, the disadvantages revealed challenges such as implementation complexity, costs, and resistance to change within organizations. This dual perspective provides a balanced understanding of the current state of FRG, offering valuable insights for future research and practical application.

- Does the FRG domain have a structured and organized model to effectively represent its domain knowledge?

Based on the literature review and analysis presented in the paper, the FRG domain previously lacked a comprehensive, structured, and organized model to effectively represent its domain knowledge. Existing frameworks and models (e.g., IFRS, GAAP, COSO, COBIT) addressed specific aspects of financial reporting governance but were fragmented, lacked standardization, and did not holistically integrate all critical components. These models often focused on isolated elements such as compliance, auditing, or risk management without clarifying interdependencies or providing a unified framework. Thus, the authors addressed this gap by developing the FRGM using a metamodeling approach as follow:

- -

- Unifies 10 core components (e.g., corporate governance structures, auditing, compliance, risk management, stakeholder engagement) into a single structured framework.

- -

- Standardizes relationships between components through UML modelling, enabling clarity, interoperability, and adaptability.

- -

- Resolves fragmentation by synthesizing processes and concepts from 24 existing models into a high-level abstract representation.

Thus, the FRGM serves as the first structured and organized model that systematically captures the complexity of FRG domain knowledge, addressing the limitations of prior frameworks. This metamodel enhances transparency, facilitates compliance, and enables dynamic adaptation to evolving regulatory and technological demands.

VII. Conclusions

Financial reporting governance (FRG) ensures that financial reporting is accurate, transparent, and compliant with regulations. Several models, policies, procedures, frameworks, and processes have been developed and proposed to organize, manage, structure, share, and reuse FRG knowledge from different perspectives. However, the proposed works are unique and developed to solve specific scenarios and cases. The FRG domain lacks a unified abstract model to organize and structure the domain knowledge. Thus, this paper aims to develop a novel high abstract model for the FRG domain knowledge using model derive engineering (MDE) and metamodeling called financial reporting governance (FRGM). The developed FRGM consists of ten abstract components: corporate governance structures, auditing and financial controls, compliance and regulatory framework, transparency and accountability, risk management, stakeholder engagement and communication, performance measurement and financial reporting, cultural and ethical considerations, technology and innovation training and development. Each abstract component represents semantic knowledge with definitions, relationships, attributes, and operations. The capabilities and effectiveness of the developed FRGM are validated using vertical transformation to ensure solutions models from the developed FRGM. The FRGM effectively addresses the issues of heterogeneity and interoperability within the FRG domain. Future work stemming from this study will focus on implementing the FRGM in real-world scenarios to enhance its effectiveness and applicability.

Funding

This work was supported and funded by the Deanship of Scientific Research at Imam Mohammad Ibn Saud Islamic University (IMSIU) (grant number IMSIU-DDRSP2502).

References

- Hasan, A.; Aly, D.; Hussainey, K. Corporate governance and financial reporting quality: a comparative study. Corp. Gov. Int. J. Bus. Soc. 2022, 22, 1308–1326. [Google Scholar] [CrossRef]

- Kılıç, M.; Kuzey, C. Assessing current company reports according to the IIRC integrated reporting framework. Meditari Account. Res. 2018, 26, 305–333. [Google Scholar] [CrossRef]

- RISK, C. Risk management framework. 2021.

- Hanson, D.; Straub, J. A Systematic Review of Cybersecurity Audit Frameworks for the Internet of Things. in 2024 IEEE International Conference on Cyber Security and Resilience (CSR), IEEE, 2024, pp. 133–138.

- Kim, H.Y.; Cho, J. Data governance framework for big data implementation with NPS Case Analysis in Korea. J. Bus. Retail Manag. Res. 2018, 12. [Google Scholar]

- Thabit, T.; Solaimanzadah, A.; Al-Abood, M.T. The effectiveness of COSO framework to evaluate internal control system: the case of kurdistan companies. Cihan Int. J. Soc. Sci. 2017, 1, 44. [Google Scholar]

- Ilori, O.; Nwosu, N.T.; Naiho, H.N.N. A comprehensive review of it governance: effective implementation of COBIT and ITIL frameworks in financial institutions. Comput. Sci. IT Res. J. 2024, 5, 1391–1407. [Google Scholar] [CrossRef]

- Ismail, R. An Overview of International Financial Reporting Standards (IFRS). Int. J. Eng. Sci. Invent. 2017, 6, 15–24. [Google Scholar]

- Obeng-Nyarko, J.K. Effects of Sarbanes-Oxley Act 2002 on the quality of corporate reporting by UK listed companies. 2023, University of Essex.

- Zabihollah, R. Corporate Governance Role in Financial Reporting. Res. Account. Regul. 2004, 17, 107–149. [Google Scholar]

- Armstrong, C.; Guay, W.R.; Mehran, H.; Weber, J. The role of information and financial reporting in corporate governance: A review of the evidence and the implications for banking firms and the financial services industry. Econ. Policy Rev. Forthcom. 2015.

- Habib, A.; Jiang, H. Corporate governance and financial reporting quality in China: A survey of recent evidence. J. Int. Accounting, Audit. Tax. 2015, 24, 29–45. [Google Scholar] [CrossRef]

- Rahmatika, D.N.; Afiah, N.N. Factors influencing the quality of financial reporting and its implications on good government governance. Int. J. Buainwaa, Econ. Law 2014, 5, 1552–2289. [Google Scholar]

- Persons, O.S. Corporate governance and non-financial reporting fraud. J. Bus. Econ. Stud. 2006, 12, 27. [Google Scholar]

- Cohen, J.R.; Krishnamoorthy, G.; Wright, A. The corporate governance mosaic and financial reporting quality. J. Account. Lit. 2004, 87–152. [Google Scholar]

- Rostami, V.; Rezaei, L. Corporate governance and fraudulent financial reporting. J. Financ. Crime 2022, 29, 1009–1026. [Google Scholar] [CrossRef]

- Rahman, K.M.; Bremer, M. EFFECTIVE CORPORATE GOVERNANCE AND FINANCIAL REPORTING IN JAPAN. Asian Acad. Manag. J. Account. Financ. 2016, 12. [Google Scholar] [CrossRef]

- Rashid, A.; Akmal, M.; Shah, S.M.A.R. Corporate governance and risk management in Islamic and convectional financial institutions: explaining the role of institutional quality. J. Islam. Account. Bus. Res. 2024, 15, 466–498. [Google Scholar] [CrossRef]

- Yusuf, M.; Dasawaty, E.; Esra, M.; Apriwenni, P.; Meiden, C.; Fahlevi, M. Integrated reporting, corporate governance, and financial sustainability in Islamic banking. Uncertain Supply Chain Manag. 2024, 12, 273–290. [Google Scholar] [CrossRef]

- Yetman, M.H.; Yetman, R.J. The effects of governance on the financial reporting quality of nonprofit organizations. in Conference on not-for-profit firms, Federal Reserve Bank, New York, 2004.

- Hassan, S.U. Corporate governance and financial reporting quality: A study of Nigerian money deposit banks. Chief Patron Chief Patron, 2011. [Google Scholar]

- Şeker, Y.; Şengür, E.D. The impact of environmental, social, and governance (esg) performance on financial reporting quality: International evidence. Ekonomika 2021, 100, 190–212. [Google Scholar] [CrossRef]

- Sanad, Z.; Al-Sartawi, A. Investigating the relationship between corporate governance and internet financial reporting (IFR): evidence from Bahrain Bourse. Jordan J. Bus. Adm. 2016, 12. [Google Scholar]

- Ghuslan, M.I.; Jaffar, R.; Saleh, N.M.; Yaacob, M.H. Corporate governance and corporate reputation: The role of environmental and social reporting quality. Sustainability 2021, 13, 10452. [Google Scholar] [CrossRef]

- Abdulmalik, S.O.; Ahmad, A.C. Audit fees, corporate governance mechanisms, and financial reporting quality in Nigeria. DLSU Bus. Econ. Rev. 2016, 26, 1. [Google Scholar]

- Hichri, A. Corporate governance and integrated reporting: evidence of French companies. J. Financ. Report. Account. 2022, 20, 472–492. [Google Scholar] [CrossRef]

- Zolfaghari, M.; Vaez, S.A.; Khodamoradi, M. Effect of the Corporate Governance Structure on the Performance of Banks in Financial Crises. Int. J. Financ. Manag. Account. 2025, 10, 133–140. [Google Scholar]

- Nguyen, T.T.H.; Phan, H.D. The Role of Governance and Digital Transformation in Enhancing Operational Sustainability of Non-Banking Financial Institutions.

- AGARWAL, Y. KPMG Global AI and Finance Report 2024: Transforming New Era with AI empowered Finance Functions1.

- Kent, S. Model driven engineering. in International conference on integrated formal methods, Springer, 2002, pp. 286–298.

- Muliawan, O.; Van Gorp, P.; Keller, A.; Janssens, D. Executing a standard compliant transformation model on a non-standard platform. in 2008 IEEE International Conference on Software Testing Verification and Validation Workshop, IEEE, 2008, pp. 151–160.

- Djeddai, S.; Strecker, M.; Mezghiche, M. Integrating a formal development for DSLs into meta-modeling. in Model and Data Engineering: 2nd International Conference, MEDI 2012, Poitiers, France, October 3-5, 2012. Proceedings 2, Springer, 2012, pp. 55–66.

- Benhlima, L.; Chiadmi, D. Vers l’interopérabilité des systèmes d’information hétérogènes. 2006.

- EdwardLee, H.G.; Schätz, B.R.B. Model-based engineering of embedded real-time systems. 2010.

- Hommes, B.-J. Evaluating conceptual coherence in multi-modeling techniques. in Information Modeling Methods and Methodologies: Advanced Topics in Database Research; IGI Global, 2005; pp. 43–62. [Google Scholar]

- Trabelsi, C.; Atitallah, R.B.; Meftali, S.; Dekeyser, J.-L.; Jemai, A. A model-driven approach for hybrid power estimation in embedded systems design. EURASIP J. Embed. Syst. 2011, 2011, 1–15. [Google Scholar] [CrossRef]

- Aßmann, U.; Zschaler, S.; Wagner, G. Ontologies, meta-models, and the model-driven paradigm. in Ontologies for software engineering and software technology, Springer, 2006, pp. 249–273.

- Koch, N.; Kraus, A. Towards a common metamodel for the development of web applications. in Web Engineering: International Conference, ICWE 2003 Oviedo, Spain, July 14–18, 2003 Proceedings 3, Springer, 2003, pp. 497–506.

- Atkinson, C.; Kuhne, T. Model-driven development: a metamodeling foundation. IEEE Softw. 2003, 20, 36–41. [Google Scholar] [CrossRef]

- Mens, T.; Van Gorp, P. A taxonomy of model transformation. Electron. Notes Theor. Comput. Sci. 2006, 152, 125–142. [Google Scholar] [CrossRef]

- Gardner, T.; Griffin, C.; Koehler, J.; Hauser, R. A review of OMG MOF 2.0 Query/Views/Transformations Submissions and Recommendations towards the final Standard. in MetaModelling for MDA Workshop, Citeseer Princeton, NJ, USA, 2003, p. 41.

- Rose, L.M.; Kolovos, D.S.; Paige, R.F.; Polack, F.A.C. Model migration with epsilon flock. in International conference on theory and practice of model transformations, Springer, 2010, pp. 184–198.

- Saleh, M.; et al. A Metamodeling Approach for IoT Forensic Investigation. Electron. 2023, 12. [Google Scholar] [CrossRef]

- Al-Dhaqm, A.; et al. Categorization and Organization of Database Forensic Investigation Processes. IEEE Access, 2020; 8. [Google Scholar] [CrossRef]

- Al-Dhaqm, A.; et al. CDBFIP: Common Database Forensic Investigation Processes for Internet of Things. IEEE Access, 2017; 5. [Google Scholar] [CrossRef]

- Alotaibi, F.M.; Al-Dhaqm, A.; Yafooz, W.M.S.; Al-Otaibi, Y.D. A Novel Administration Model for Managing and Organising the Heterogeneous Information Security Policy Field. Appl. Sci. 2023, 13. [Google Scholar] [CrossRef]

- Alotaibi, F.; Al-Dhaqm, A.; Al-Otaibi, Y.D. A Conceptual Digital Forensic Investigation Model Applicable to the Drone Forensics Field. Eng. Technol. Appl. Sci. Res. 2023, 13, 11608–11615. [Google Scholar] [CrossRef]

- Baker, C.R.; Wallage, P. The future of financial reporting in Europe: Its role in corporate governance. Int. J. Account. 2000, 35, 173–187. [Google Scholar] [CrossRef]

- Salehi, M.; Ajel, R.A.; Zimon, G. The relationship between corporate governance and financial reporting transparency. J. Financ. Report. Account. 2023, 21, 1049–1072. [Google Scholar] [CrossRef]

- Botti, L.; Boubaker, S.; Hamrouni, A.; Solonandrasana, B. Corporate governance efficiency and internet financial reporting quality. Rev. Account. Financ. 2014, 13, 43–64. [Google Scholar] [CrossRef]

- Dimes, R.; Molinari, M. Non-financial reporting and corporate governance: a conceptual framework. Sustain. Accounting, Manag. Policy J. 2024, 15, 1067–1093. [Google Scholar] [CrossRef]

- Van Frederikslust, R.A.I.; Ang, J.S.; Sudarsanam, P.S. Corporate governance and corporate finance: a European perspective; Routledge, 2007. [Google Scholar]

- Behbahaninia, P.S.; Safarzadeh, E.; Motahari, F. Corporate Governance, financial reporting quality and Performance in Tehran Stock Exchange with Emphasis on coronavirus. Appl. Res. Financ. Report. 2024, 12, 251–280. [Google Scholar]

- Al-Dhaqm, A.; Razak, S.; Othman, S.H.; Ngadi, A.; Ahmed, M.N.; Mohammed, A.A. Development and validation of a database forensic metamodel (DBFM). PLoS One 2017, 12. [Google Scholar] [CrossRef] [PubMed]

- Caro, M.F.; Josyula, D.P.; Cox, M.T.; Jiménez, J.A. Design and validation of a metamodel for metacognition support in artificial intelligent systems. Biol. Inspired Cogn. Archit. 2014, 9, 82–104. [Google Scholar] [CrossRef]

- Al-Dhaqm, A.; Razak, S.; Ikuesan, R.A.; Kebande, V.R.; Othman, S.H. Face validation of database forensic investigation metamodel. Infrastructures 2021, 6. [Google Scholar] [CrossRef]

- Gómez, A.A.; Caro, M.F. Meta-Modeling process of pedagogical strategies in intelligent tutoring systems. in 2018 IEEE 17th International Conference on Cognitive Informatics & Cognitive Computing (ICCI* CC), IEEE, 2018, pp. 485–494.

- Othman, S.H.; Beydoun, G. A metamodel-based knowledge sharing system for disaster management. Expert Syst. Appl. 2016, 63, 49–65. [Google Scholar] [CrossRef]

- Formica, A.; Missikoff, M. Concept similarity in SymOntos: an enterprise ontology management tool. Comput. J. 2002, 45, 583–594. [Google Scholar] [CrossRef]

- Frantzi, K.T. Automatic term recognition using contextual cues. in Proceedings of the 2nd Workshop on Multilinguality in Software Industry: the AI Contribution (MULSAIC’97), International Joint Conference on Artificial Intelligence (IJCAI), 1997.

- AL-DHAQM, A.M.R. SIMPLIFIED DATABASE FORENSIC INVETIGATION USING METAMODELING APPROACH. 2019, Universiti Teknologi Malaysia.

- Selamat, S.R.; Yusof, R.; Sahib, S. Mapping process of digital forensic investigation framework. Int. J. Comput. Sci. Netw. Secur. 2008, 8, 163–169. [Google Scholar]

- Ibrahim, R.; Leng, N.S.; Yusoff, R.C.M.; Samy, G.N.; Masrom, S.; Rizman, Z.I. E-learning acceptance based on technology acceptance model (TAM). J. Fundam. Appl. Sci. 2017, 9, 871–889. [Google Scholar] [CrossRef]

- Pilone, D.; Pitman, N. UML 2.0 in a Nutshell; O’Reilly Media, Inc., 2005. [Google Scholar]

- Alsulami, M.H. A Preservation Metamodel Based on Blockchain Technology for Preserving Mobile Evidence. IEEE Access 2024. [Google Scholar] [CrossRef]

- Alhussan, A.A.; Al-Dhaqm, A.; Yafooz, W.M.S.; Razak, S.B.A.; Emara, A.-H.M.; Khafaga, D.S. Towards development of a high abstract model for drone forensic domain. Electronics 2022, 11, 1168. [Google Scholar] [CrossRef]

Figure 1.

The levels of the metamodel [39].

Figure 1.

The levels of the metamodel [39].

Figure 4.

Instantiated M1-Collection Model from the preservation metamodel.

Figure 5.

Finance report governance metamodel (FRGM).

Figure 6.

Vertical transformation process for the metamodel [65].

Figure 6.

Vertical transformation process for the metamodel [65].

Figure 7.

Create target model from source metamodel.

Figure 8.

Instantiated M1-Transparency and Accountability Model from the FRGM.

Table 1.

Advantages and disadvantages of the existing works of the FRG domain.

| ID | Year | Ref | Advantages | Disadvantages | Methodology | Output | Contributions |

| 1. | 2004 | [10] | Strong corporate governance fosters enhanced investor confidence by ensuring transparency, accountability, and ethical decision-making within organizations | Merely complying with corporate governance measures may be insufficient to fully restore investor confidence. | The study used a descriptive approach to analyze existing literature and propose a new corporate governance structure. | The paper presented a holistic model of corporate governance consisting of seven interrelated functions and discusses their roles in financial reporting. | The paper offers a comprehensive framework for identifying and recovering corporate governance, particularly in the context of financial reporting. |

| 2. | 2004 | [15] | Enhances the quality of financial reporting and significantly decreases the risk of fraud and earnings manipulation. | Simply meeting regulatory requirements for corporate governance structures may not guarantee improved financial reporting quality or deter fraudulent activity. | The study synthesized prior research on corporate governance, focusing on the roles of the board of directors, audit committees, external and internal auditors. | The paper provided an overview of prior research on corporate governance and its impact on financial reporting, proposes a broader “governance mosaic” model, and identifies significant gaps in existing research | This research expands the understanding of corporate governance by examining the interactions among various stakeholders within a broader “governance mosaic” framework, highlighting the need for more research on the causal relationships between governance mechanisms and financial reporting quality. |

| 3. | 2004 | [20] | Stronger nonprofit financial reporting quality is associated with increased governance, particularly market-based governance from donors and lenders. | Regulatory-based governance measures show a less consistent effect on improving nonprofit financial reporting quality than market-based measures. | The study uses multiple measures of financial reporting quality from IRS Form 990 data, supplemented by a smaller hand-collected sample, and employs both cross-sectional and event study regression analyses to examine the relationship between governance and reporting quality. | The study finds that market-based governance measures are more consistently associated with higher-quality nonprofit financial reporting than regulatory measures, and that certain aspects of regulatory oversight may even negatively impact reporting quality. | This research provides evidence on the effectiveness of different governance mechanisms in enhancing nonprofit financial reporting quality, suggesting that market-based oversight may be more effective than regulatory approaches. |

| 4. | 2011 | [21] | The journal offers a diverse range of research articles on various topics related to computer applications, management, and allied fields, potentially providing valuable insights and knowledge for researchers and practitioners. | The journal’s scope is very broad, potentially leading to a lack of focus and in-depth analysis in specific areas. The small sample sizes in some studies may also limit the generalizability of findings. | The articles in this issue employ a variety of research methodologies, including surveys, experiments, archival data analysis, and case studies, applied to address different research questions across diverse fields. | This issue of IJRCM presents original research findings on various topics, including organizational storytelling, corporate governance, lean management, consumer preferences, and traffic management, along with recommendations for future research. | The collection of articles contributes to the body of knowledge in diverse fields by presenting original research, offering insights into current practices and problems, and proposing avenues for future investigation. |

| 5. | 2014 | [13] | High-quality financial reporting in local governments is crucial for effective resource allocation and good governance, fostering trust and accountability. | Widespread non-compliance with governmental accounting standards in Indonesian local governments, along with significant levels of corruption, highlight the need for improvements in both financial reporting and governance. | The study uses Partial Least Squares (PLS) to analyze primary data from a survey of 70 working units in seven Indonesian local governments to examine the impact of apparatus competence and internal control on financial reporting quality and good governance. | The findings reveal that apparatus competence and internal control significantly influence financial reporting quality, which in turn has a positive impact on good governance. However, no significant differences in these aspects were found across different local governments. | This research provides empirical evidence on the importance of competence and internal controls in achieving high-quality financial reporting and fostering good governance in the Indonesian context, offering insights for policy recommendations. |

| 6. | 2015 | [11] | Transparent financial reporting helps align the interests of managers, directors, and shareholders by reducing information asymmetry and facilitating more efficient contracting, contributing to financial stability. | The complexity of agency problems, along with the inherent costs and frictions of information transmission, means that even well-governed firms may still experience agency conflicts and variations in governance structures across firms and over time. | The paper reviews existing literature on corporate governance, focusing on the role of financial reporting in mitigating agency conflicts, and examines the distinction between formal and informal contracts. | The review highlights key themes such as information asymmetry, credible commitment to transparency, and the role of regulatory supervision, emphasizing that firms’ governance structures and information environments evolve to resolve agency conflicts. | This paper provides a valuable synthesis of existing research, offering a nuanced perspective on the role of financial reporting in corporate governance, and suggesting several avenues for future research, particularly concerning the unique governance challenges faced by banks and other financial institutions. |

| 7. | 2015 | [12] | This paper provides a comprehensive survey of empirical research on corporate governance and financial reporting quality in China, filling a gap in the existing literature. | The paper lacks a commonly accepted definition of financial reporting quality, which poses a challenge for synthesizing the research. | The study uses a systematic review methodology to analyse empirical archival literature on the effects of corporate governance on financial reporting quality in China. | The paper offers a systematic review of the empirical literature on the effects of corporate governance on financial reporting quality in China, identifying research gaps and suggesting areas for future research. | This paper contributes by offering a comprehensive review of the existing literature on corporate governance and financial reporting quality in China, highlighting the unique challenges and opportunities in this context. |

| 8. | 2016 | [17] | The paper provides a comprehensive survey of the empirical literature on corporate governance and financial reporting quality in China, highlighting unique governance factors and regulatory changes that offer valuable insights for regulators and investors. | The paper identifies shortcomings in the existing research, such as the lack of a commonly accepted definition of financial reporting quality and the limited exploration of the moderating role of financial reporting quality in the governance-performance relationship | The paper systematically reviews archival research from 2000 onwards, focusing on studies that examine the association between corporate governance (both internal and external) and financial reporting quality in China | The paper synthesizes findings on the effects of corporate governance mechanisms, such as ownership structure, board characteristics, and external auditing, on financial reporting quality, and provides a summary of key research findings in tabular form. | The paper contributes to the literature by offering a detailed review of the governance-reporting quality relationship in China, identifying gaps in the research, and suggesting directions for future studies, particularly in understanding the role of financial reporting quality in governance-performance outcomes. |

| 9. | 2016 | [23] | This study investigates the relationship between corporate governance and internet financial reporting (IFR) in Bahrain, a context not extensively studied before, adding to the existing literature on IFR | The study is limited by a relatively small sample size (38 companies) and the challenges of data collection from company websites | The study employs a multiple regression analysis of data gathered from company websites and the Bahrain Bourse to examine the relationship between corporate governance and internet financial reporting | The study finds a weak relationship between corporate governance and IFR in Bahrain, with board size and Big 4 auditors showing a positive association with IFR. It recommends guidelines for internet disclosure to enhance transparency | The research contributes original empirical evidence on the relationship between corporate governance and internet financial reporting in the Bahraini context, which has not been widely studied |

| 10. | 2016 | [25] | This study uses a robust methodology (GMM) to examine the impact of audit fees and corporate governance on financial reporting quality in Nigeria, controlling for endogeneity and unobserved heterogeneity. | The study combines audit and non-audit fees, limiting analysis of individual fee components. It only uses accrual earnings management as a measure of financial reporting quality | The study uses Generalized Methods of Moments (GMM) with dynamic panel data to address endogeneity and unobserved heterogeneity in examining the impact of audit fees and corporate governance on financial reporting quality in Nigeria | The study finds that abnormal audit fees in Nigeria do not impair auditor independence but may reflect effort; foreign directors and foreign institutional ownership improve financial reporting quality; local institutional ownership does not. | This study offers novel findings on the relationship between audit fees, corporate governance, and financial reporting quality in Nigeria, addressing limitations of previous studies by using GMM and considering the impact of regulatory changes |

| 11. | 2017 | [6] | This study addresses the lack of research on COSO framework application in Kurdistan, offering valuable insights into internal control system quality in this context | The study relies on a relatively small sample size (50 questionnaires) and uses subjective data from questionnaires, which might limit the generalizability and objectivity of the findings | The study uses questionnaires, Fuzzy Logic, and the Lean Diagnosis Tool (LDT) to analyze the effectiveness of the COSO framework in evaluating internal control systems in a sample of Kurdistan companies | The research reveals a gap between the internal control systems of Kurdistan companies and COSO framework requirements, highlighting areas needing improvement (leadership, culture, lean plant layout). It suggests that the COSO framework is applicable if companies strengthen their internal control | This study provides original research on applying the COSO framework and Lean Diagnosis Tool (LDT) to evaluate internal control systems in Kurdistan companies, filling a gap in the literature |

| 12. | 2017 | [8] | International Financial Reporting Standards (IFRS) offer increased transparency, accountability, and efficiency in global financial markets, facilitating easier comparison of financial statements across borders and potentially reducing costs for international businesses. | Implementing IFRS can be costly, and some believe that the standards may not fully benefit all economies, particularly developing ones, due to a lack of knowledge and appropriate training resources. | The paper offers an unbiased overview of IFRS, aiming to provide a balanced perspective, highlighting both the positive and negative impacts of IFRS adoption | The paper provides an overview of IFRS, including its history, key components, advantages, disadvantages, and its relationship with other accounting standards like GAAP, along with details on the G20 and IASB | The study uses a literature review of existing research, government and private organization reports, website information, and discussions with accounting professionals. |

| 13. | 2018 | [2] | Applying the IIRC integrated reporting framework enhances understanding of integrated reporting practices and evaluates the impact of corporate sustainability characteristics on integrated reporting disclosures | Current company reports mainly present generic rather than company-specific risks, focus on positive information while neglecting negative aspects, present financial and non-financial initiatives separately, lack a strategic focus, and primarily include backward-looking information. | The study uses a sample of non-financial companies listed on Borsa Istanbul, constructs a disclosure index based on IIRC framework elements, and employs statistical analyses to measure the integrated reporting disclosure score and test hypotheses. | The study analyzes the adherence level of current Turkish company reports to the IIRC integrated reporting framework and examines the impact of corporate sustainability characteristics on adherence | This research contributes by applying a checklist based on the IIRC framework to enhance understanding of integrated reporting and by evaluating the impact of corporate sustainability on integrated reporting |

| 14. | 2018 | [5] | A Big Data governance framework facilitates successful Big Data implementation by addressing data quality, personal information protection, and data disclosure/accountability, ultimately improving service quality and preventing problems. | Existing data governance models are insufficient for Big Data’s unique characteristics; challenges include data quality issues, data monopoly concerns, and the need for clear responsibility for data quality and service reliability | The research employs a case study approach analysing the NPS’s Big Data implementation in South Korea, using the proposed Big Data governance framework to identify issues, risks, and solutions | The paper proposes a Big Data governance framework, analyses its application in the National Pension Service (NPS) case study in South Korea, identifies vulnerabilities and risks, and offers recommendations for successful Big Data service implementation | The study develops and proposes a novel Big Data governance framework that considers the unique characteristics of Big Data and addresses issues of data quality, privacy, and accountability, contributing to a more robust approach to Big Data implementation. |

| 15. | 2021 | [3] | The document outlines a robust risk management framework encompassing credit, liquidity, market, and operational risks, ensuring stability and compliance. | The document does not explicitly state any disadvantages. The inherent risks themselves (credit, liquidity, market, and operational) are discussed, but not presented as disadvantages of the system itself. | The risk management methodology employs quantitative and qualitative measures, utilizing models like VAR and stress testing, combined with regular reviews and internal audits. | The document details HSBC Sri Lanka Branch’s risk management framework and capital structure, including policies, processes, and monitoring methods for various risk types. | The document contributes to understanding HSBC Sri Lanka’s comprehensive approach to risk management, ensuring regulatory compliance and financial stability. |

| 16. | 2021 | [22] | The study provides international evidence on the positive relationship between ESG performance and financial reporting quality. | The study’s findings on the social pillar of ESG are mixed, and the time frame is relatively short. | The study uses panel regression analysis on a large international sample of firm-year observations to investigate the relationship between ESG performance and financial reporting quality. | The study found a positive relationship between overall ESG performance and financial reporting quality, with significant positive effects for environmental and governance pillars but not the social pillar. | This study extends existing literature by providing international evidence on the relationship between ESG performance and financial reporting quality, including the impact of each ESG pillar. |

| 17. | 2021 | [24] | The study provides evidence of the positive impact of effective corporate governance and high-quality environmental and social reporting on corporate reputation in Malaysia | The study’s reliance on secondary data and the exclusion of certain industries limit the generalizability of the findings | The study used secondary data from multiple sources and employed multiple regression analysis to test hypotheses on the relationships between corporate governance, environmental and social reporting quality, and corporate reputation | The results showed positive relationships between corporate governance, environmental and social reporting quality, and corporate reputation, with environmental and social reporting quality mediating the relationship between corporate governance and reputation | The study bridges research gaps by providing evidence for the impact of effective corporate governance and environmental and social reporting quality on corporate reputation in Malaysia and the mediating role of reporting quality. |

| 18. | 2022 | [16] | Robust corporate governance significantly reduces fraudulent financial reporting. | The study’s findings may not be generalizable to other countries due to differences in regulations and economic environments | A linear regression model was used to analyze data from 187 listed Iranian companies from 2013-2019 to test the relationship between corporate governance and fraudulent financial reporting | The study found a significant negative relationship between robust corporate governance and fraudulent financial reporting, supporting the hypotheses | The research provides valuable insights into the importance of strengthening corporate governance to prevent fraudulent financial reporting |

| 19. | 2022 | [26] | Integrated reporting improves information quality, promotes compliance, and enhances stakeholder engagement | The study has limitations due to its short time frame, limited scope of governance mechanisms, and reliance on a single reporting medium | The study uses a quantitative, hypothetico-deductive approach with multiple linear regression analysis of 120 French companies’ data from 2016-2019 | The study reveals positive correlations between cognitive diversity, audit committees, and the level of integrated reporting, but not for board size or CEO duality | This research contributes significantly to the literature by empirically examining the influence of corporate governance on the determinants of integrated reporting within French listed companies |

| 20. | 2023 | [9] | The Sarbanes-Oxley Act (SOA) has had a favorable impact on UK corporate reporting quality, particularly for companies listed in the US, by improving transparency and reducing boilerplate language | The study’s relatively short timeframe (2000-2016) and focus on a limited number of companies may limit the generalizability of its findings | The study uses institutional theory to analyze the content of corporate governance, internal control, audit committee, and external auditor reports from UK companies listed in the US and UK-only listed companies, comparing pre- and post-SOA periods | he study finds that SOA compliance led to increased disclosure quantity and quality, changes in communication style (including increased use of pronouns and politeness), and a shift toward greater transparency in internal controls and audit reporting; effects also observed in non-compliant UK companies | This thesis contributes to the understanding of the SOA’s impact on UK corporate reporting and governance by utilizing institutional theory and a qualitative content analysis approach, addressing a gap in extant literature. |

| 21. | 2024 | [7] | Implementing COBIT and ITIL frameworks in financial institutions improves IT governance, enhances operational efficiency, and ensures regulatory compliance. | Challenges include organizational resistance to change, complexity of framework integration, and the need for continuous monitoring and adaptation. | The paper conducts a comprehensive literature review examining the effective implementation of COBIT and ITIL frameworks in financial institutions, supported by case studies | The review highlights the benefits and challenges of implementing COBIT and ITIL, suggesting synergistic application and strategies for overcoming implementation challenges | This research contributes by providing a comprehensive analysis of COBIT and ITIL implementation in financial institutions, offering valuable insights and recommendations for IT leaders and practitioners. |

| 22. | 2024 | [4] | The systematic review identifies gaps in current IoT security auditing practices and proposes areas for future research, leading to improved security standards and methodologies | A lack of widely adopted standards and insufficient research hinders the consistency and effectiveness of current IoT security audits | A systematic literature review of existing frameworks and research on IoT audit security was conducted using Google Scholar, focusing on risk-based approaches | The paper identifies areas of needed research in IoT security auditing, recommends practices for auditors and organizations, and suggests improvements in frameworks and standards | The review highlights the need for improved standards, methodologies, and automation in IoT security auditing, promoting more effective and consistent practices |

| 23. | 2024 | [18] | The study provides valuable insights into the impact of corporate governance on the financial performance of Islamic and conventional financial institutions in Pakistan, considering the moderating role of institutional quality | The study is limited to Pakistan’s financial sector and lacks a broader international comparison | A two-step system GMM analysis of a panel dataset of Pakistani financial institutions from 2006-2017 was used to examine the relationship between corporate governance, institutional quality, and financial performance | The study reveals the differential effects of corporate governance on Islamic and conventional financial institutions and highlights the significant moderating role of institutional quality | The research contributes to the existing literature by analysing the impact of corporate governance on the performance of both Islamic and conventional financial institutions in Pakistan, considering the moderating influence of institutional quality. |

| 24. | 2024 | [19] | This research offers valuable insights into the complex interplay between integrated reporting, corporate governance, and financial sustainability within Islamic banking, highlighting the importance of aligning banking practices with Sharia principles and emphasizing the significance of stakeholder engagement | The study’s scope is limited, focusing primarily on the literature related to Islamic banking and leaving out a broader financial sector comparison. Also, the reliance on a specific set of databases might limit the inclusiveness of the results | A systematic literature review employing bibliometric techniques and content analysis was used to analyze 30 studies selected from various databases based on predefined criteria, focusing on Islamic banks’ integrated reporting, corporate governance, and financial sustainability | The analysis reveals a positive correlation between integrated reporting, robust corporate governance, and strong financial sustainability in Islamic banking, suggesting that aligning operations with Sharia principles fosters these positive outcomes. Areas of high and low disclosure and potential areas for future research are also identified | This study expands the existing literature by providing a comprehensive overview of integrated reporting in Islamic banking, highlighting the importance of Sharia principles, emphasizing the need for stakeholder engagement, and identifying important areas for future research |

| 25. | 2025 | [27] | This study offers a unique perspective on the impact of corporate governance on bank financial performance in the MENA region during the COVID-19 pandemic, filling a gap in existing research. The two-stage least squares regression analysis provides robustness checks | The study is limited in scope (MENA region, one year of data, specific sample of banks), potentially affecting the generalizability of findings. Certain macroeconomic factors affecting bank performance may not be adequately considered | Financial and non-financial data from bank annual reports, Orbis Bank Focus, and World Bank reports were analysed using fixed effects regressions and two-stage least squares (2SLS) to assess the impact of internal and external corporate governance mechanisms on bank performance in the MENA region during the COVID-19 pandemic | The analysis reveals that the presence of independent board members, high ownership concentration, strong legal protection, and effective government oversight positively influence bank performance and reduce credit risk in the MENA region during the pandemic. Other governance mechanisms had no significant impact | This research expands the limited literature on corporate governance and bank performance in the MENA region during a pandemic. It contributes to both theoretical and practical understanding, offering insights for bankers, policymakers, and financial regulators. |

| 26. | 2025 | [28] | The study identifies the key drivers of operational sustainability in Vietnamese NBFIs, offering valuable insights for improving management practices and aligning with technological advancements | The research is limited to Vietnam’s NBFI sector, potentially limiting the generalizability of findings to other countries or financial context | Regression analysis of survey data from Vietnamese NBFI managers was used to examine the impact of governance, digital transformation, business model diversification, cost management, and macroeconomic factors on operational sustainability. Exploratory factor analysis was also conducted | Strong positive relationships were found between governance and digital transformation, and operational sustainability. Business model diversification had a moderate positive effect, while cost management’s impact was minimal. | This research contributes to the existing literature by validating the importance of governance and digital transformation in enhancing the operational sustainability of NBFIs while providing new insights into the dynamic interplay between business strategies and sustainability in this sector. |

| 27. | 2025 | [29] | The KPMG report provides a comprehensive overview of AI adoption in finance across major global markets, highlighting its benefits and potential for transforming financial functions. It offers practical recommendations for businesses | The report’s focus on a limited number of major economies might neglect the unique aspects of AI adoption in other regions. The review lacks critical discussion of the ethical considerations surrounding AI in finance | The KPMG report surveyed 1800 companies (expanded to 2900) across 10 major economies (and later 23) to assess AI adoption in finance, utilizing an AI Maturity Index to categorize companies into leaders, implementers, and beginners | The report indicates widespread AI adoption across various financial functions, with significant benefits observed in efficiency, accuracy, and decision-making. It identifies barriers to AI adoption and provides key recommendations for implementation and governance | The report contributes significantly to the understanding of AI’s impact on the finance industry, providing valuable insights and recommendations for businesses and highlighting the need for effective AI governance. |

Table 2.

Summary Of Searching on Online Databases.

| ID | Search Engine | Year | Keywords | Language | Content-Type | |||||

| Chapter | Article | Research Article | Reference Work Entry | Conference paper | Review Article | |||||

| 1 | Springer Link | 2015-2025 | “Finance Report”; “Governance” | English Language | 96 | 15 | 14 | 6 | 3 | 1 |

| 2 | Scopus | 2015-2025 | 0 | 3 | 0 | 0 | 0 | 1 | ||

| 3 | IEEE Xplore | 2015-2025 | 0 | 0 | 0 | 0 | 7 | 0 | ||

| 4 | Web Of Science | 2015-2025 | 0 | 0 | 2 | 0 | 0 | 0 | ||

| 5 | Science Direct | 2015-2025 | 6 | 3 | 107 | 4 | 1 | 6 | ||

| 6 | Google Scholar | 2015-2025 | 590 | 1550 | 835 | 0 | 2100 | 225 | ||

Table 3.

Inclusion And Exclusion Criteria.

| Inclusion Criteria | Exclusion Criteria |

|

|

Table 4.

Finance Reports Processes Governance Model.