Submitted:

04 May 2025

Posted:

05 May 2025

You are already at the latest version

Abstract

High-frequency financial markets churn out massive amounts of data filled with intricate microstructural patterns, which makes them vulnerable to issues like spoofing, layering, and market manipulation. Traditional methods for detecting anomalies often fall short when it comes to capturing these complex patterns, especially given the fast-paced and ever-changing nature of financial transactions. In this study, we introduce a deep learning-based framework designed for spotting anomalies in high-frequency trading (HFT) data. This framework utilizes advanced techniques such as graph neural networks (GNN), recurrent neural networks (RNN), and transformer-based autoencoders. By integrating multi-modal feature extraction, attention to temporal dependencies, and adaptive learning strategies, we aim to boost detection accuracy. We tested our approach on real-world high-frequency limit order book (LOB) data, along with synthetic anomalies added to the dataset. The results from our experiments show notable enhancements in anomaly detection accuracy, precision, and recall, surpassing existing methods while keeping false positive rates low. Our findings underscore the promise of deep learning models in enhancing market surveillance, ensuring regulatory compliance, and mitigating financial risks in HFT settings.

Keywords:

high‐frequency trading (HFT)

; anomaly detection

; deep learning

; graph neural networks (GNN)

; recurrent neural networks (RNN)

; transformer autoencoder

; financial market manipulation

; limit order book (LOB)

; machine learning

; time‐series analysis

Vishwakarma Institute of Technology (Department of Artificial Intelligence and Data Science), Pune, 411037, India; sunil.sangve@vit.edu

1. Introduction

Financial markets are moving quickly, especially with high-frequency trading (HFT), which brings up some tough challenges for spotting unusual activities. These markets churn out massive amounts of transaction data in just seconds, making it hard to catch things like market manipulation and keep everything running smoothly. Luckily, recent strides in deep learning and machine learning are showing some hope in tackling these issues. Various studies have tried different methods, from basic modeling to advanced deep learning, showing how the techniques for spotting anomalies are changing.

Brugman created a system that monitors truckers for fatigue in real time, which really illustrates how important real-time anomaly detection is in fast-paced settings. While this research focused on transportation, the ideas behind real-time monitoring and decision-support systems are also relevant in the high-speed world of financial trading. Being able to respond to anomalies as they pop up is key for managing risks and keeping systems reliable.

Veryzhenko and others looked into how to detect spoofing in HFT using machine learning, specifically with the k-nearest neighbors (KNN) method. Their findings indicated that machine learning can spot manipulative behaviors occurring within the trading day. But there are limitations, like being sensitive to the data used for training and difficulties from the changing nature of financial data. They stressed the importance of both supervised and unsupervised models for spotting financial fraud, highlighting how crucial it is to have adaptable methods for catching anomalies.

Rizvi and his team proposed an unsupervised approach that employs Empirical Mode Decomposition (EMD) and Kernel Density Estimation (KDE) to detect manipulation in stock prices. Their tests, which added fake anomalies to real data, showed a significant improvement in detection accuracy. This work demonstrated how great unsupervised learning can be for handling financial data that lacks labels or is hard to trust.

In another interesting study, Zhao and colleagues introduced a graph attention network (GAT) for detecting anomalies in multivariate time-series data. Their MTAD-GAT model managed to pick up on complex patterns and relationships in datasets like SMAP and MSL. It turned out that these deep learning models could do a better job than traditional methods of recognizing anomalies and explaining the results.

Mejri and his group focused on a thorough evaluation of unsupervised anomaly detection methods for time-series data, stressing that we need better evaluation frameworks. They went beyond basic metrics to suggest new ways to assess time-series anomalies, such as how stable a model is and how well it differentiates between types of anomalies. This kind of assessment is crucial in finance since anomaly types can change a lot depending on market conditions.

Chen and his team advanced their work by employing a multimodal graph neural network to identify market manipulation. Their model combined different data sources, like price movements and order book details, using advanced attention methods to achieve a remarkable accuracy rate. This research showed that mixing different types of data can help uncover hidden manipulation patterns in high-frequency finance, leading to smarter fraud detection systems.

Xi and others also applied deep learning to cross-border logistics, using real-time data and anomaly detection along with deep reinforcement learning. The concepts of making quick decisions and finding anomalies in logistics can be directly applied to financial trading, where reacting promptly to unusual activities is crucial.

Finally, Guanghe et al. [8] proposed innovative transformer networks for real-time dark pool trading anomaly detection. The system achieved an impressive 97.8% detection rate and more than 45% processing latency reduction. Utilization of sophisticated attention mechanisms and streamlined processing pipelines in transformer models demonstrated them to be more effective in coping with high-frequency, low-latency financial data environments, setting new standards of performance for market surveillance technology.

Together, the papers reflect the changing dynamic of anomaly detection approaches in high-frequency finance environments. They highlight the movement away from traditional statistical methods toward more capable deep models for handling the temporal, structural, and multimodal complexities of financial data. As outstanding as the advancements have been, model interpretability, resilience against novel patterns of fraud, and efficiency at scale continue to be dominant drivers of research in this crucial area of financial data analysis.

2. Literature Review

The high-frequency trading (HFT) boom has led to the need for sophisticated anomaly detection approaches to counter manipulative strategies in the markets and provide financial integrity. The following critically examines recent work on deep learning-based approaches, such as methods, datasets, evaluation metrics, and their limitations. The papers considered indicate that neural networks, reinforcement learning, and graph models are capable of identifying anomalies with limitation in interpretability, scalability, and real-time capability.

Cao et al. [9] proposed a new paradigm based on deep reinforcement learning (DRL) to optimize HFT strategies. They combined convolutional neural networks with short-term memory models to identify trends in both the short term and the long term within the market. Trained on NASDAQ tick-level data, their model attained a Sharpe ratio of 3.42, which was 33% above that of standard benchmarks. Their DRL agent showed robustness during turbulent and tranquil market periods, reflecting its ability to generalize. Powerful data preprocessing contributed significantly to improving model learning efficiency. However, the study identified drawbacks including too high a demand for computational resources and weak generalizability to other horizons or markets. Moreover, while the finance performance metrics were maximized, other important facets such as regulatory compliance and interpretability of models were not kept in mind. However, the research paved the way for the next research aimed at integrating DRL under difficult and dynamic financial market conditions [9].

Li and colleagues [10] addressed the issue of detecting anomaly patterns in high-frequency trading using a method based on graph neural networks (GNNs). They used the LOBSTER dataset of well-performing stocks such as Apple and Amazon and proved their model is capable of abstracting complex trading patterns through graph-based features and attention. Experiment results established an improvement of detection performance by 15% from baseline models except for real-time processing performance so important to modern surveillance systems. The design itself held sufficient robustness to market uncertainty and had the potential in being able to detect global as well as local anomalies. The study, however, acknowledged the presence of limitations when it comes to coping with high-dimensional data as well as dynamic mutation to fraud patterns that may impact longer-term performance. The low computational overhead emphasis of the method and ability to identify sophisticated trading patterns were significant improvements in financial anomaly detection using deep learning techniques [10].

Alaminos et al. [11] suggested a hybrid model incorporating ARMA-GARCH econometric methods and deep neural networks to analyze intraday trading models, especially during geopolitical unstable times. In the case of defense stocks and FOREX volatility, the hybrid model had very high prediction rates where ARMA-GARCH-QRNN was the best at 93.59%. Their research established the robustness of hybrid models to unpredictable market conditions through the ability to distinctly capture nonstationarity and nonlinear trends. Astoundingly, the model had offered sustainable investment proposals under foreign uncertainty. Although such triumphs have been witnessed, the method had encountered computation challenges as a result of quantum and deep neural complexities. There were also sudden surprises in challenging markets against making precise predictions using the ARMA-GARCH model. The study, however, validated the benefit of the hybrid approach over increasing forecasting effectiveness in high-volatility and high-frequency environments pertinent to use in financial anomaly identification and decision-making models [11].

Shanmuganathan and Suresh [12] proposed an enhanced version of the Markov-augmented Long Short-Term Memory (I-LSTM) method aimed at improving anomaly detection within sequential time-series data. Their approach, on testing against industrial sensor measurements like temperature and humidity, displayed lower prediction error compared to baseline algorithms of KNN and ordinary LSTM models. Markov modeling together with advanced LSTM architectures went on to enhance sequential learning through rendering the algorithm practicable for streaming data systems through the occurrence of latent anomaly detection. While their area of application was industrial monitoring, the method had valuable findings applicable to finance markets concerning real-time, high-speed, and complex data streams. The writers mentioned challenges occurring because of insufficient pre-labeled anomaly data and the need for invasive preprocessing. Moreover, they stressed that while predictive accuracy was enhanced, scalability and accommodation of numerous real-world cases had yet to be addressed in the future, especially in high-frequency and high-noise areas like trading [12].

Bello et al. [13] discussed a comprehensive review of the application of deep learning models for real-time fraud detection in high-frequency trading (HFT) scenarios. They emphasized CNNs and RNNs, promoting hybrid models that merge deep learning properties with conventional statistical methods. The research emphasized the importance of retraining models, explainable AI, and robust preprocessing to ensure fraud detection performance against changing market conditions. Challenges regarding managing large quantities of data, computational expense, and low false positive rates were highlighted. Authors also stated that model interpretability is required both for regulatory approval and for developing trust in the users. Research opportunities were explained in terms of using ensemble models, online learning architectures, and sophisticated data augmentation techniques. By synthesizing conceptual and technical challenges, this paper underscored the importance of resilient, adaptive deep learning architectures in the increasingly complex and fast-paced environment of HFT fraud detection [13].

Li et al. [14] investigated network traffic anomaly detection in IoT environments, presenting a deep learning framework that achieved remarkable performance, including 99.2% accuracy and 0.998 AUC-ROC on the IoT-23 dataset. While primarily targeting IoT systems, the model—utilizing a CNN-LSTM hybrid and stacked autoencoders—provided transferable insights into handling large-scale, high-frequency datasets with heterogeneous structures. The study emphasized the importance of combining manual feature engineering with deep unsupervised learning for robust anomaly detection. However, challenges included high computational costs, the necessity for continual retraining, and difficulties in maintaining model interpretability—issues that are directly relevant to financial data analysis. Notably, the study stressed that zero-day attack detection and adaptability to novel patterns remain critical research areas. The focus on Grad-CAM-based interpretability methods was also crucial, suggesting pathways for increasing transparency in anomaly detection models, an essential aspect for regulatory applications in financial domains [14].

Jin and colleagues [15] provided a comprehensive overview of the implementation of Graph Neural Networks (GNNs) in various applications such as time-series forecasting, classification, imputation, and anomaly detection, coining the term GNN4TS. Jin et al. classified existing work by task-related objectives and structural methodology, showcasing structured coverage for GNN-driven techniques. The survey highlighted advantages in modeling spatial-temporal relationship using graph-based methods and subsequently bridging weaknesses from conventional sequential models. Yet, the research pinpointed issues such as architecture complexity, choosing hyperparameters, and failing to quantify uncertainty in current GNN models. The researchers suggested utilizing AutoML-guided design in order to automate model construction workflows. Mentioned as well was the need for expanding the GNN to non-Euclidean and noisy data, the detection of a fundamental gap in real-world adoption, particularly with regards to high-frequency finance data. This study provided valuable insights to researchers who wanted to apply GNNs in dynamic and complicated settings, like financial anomaly detection [15].

Haq et al. [16] introduced HF-PPAD, an automated machine learning system designed to identify unusual peak patterns in hydrological time-series data. By generating synthetic anomalies using TimeGAN and applying models like Temporal Convolutional Networks (TCN), InceptionTime, and LSTM, the system significantly enhanced anomaly detection without requiring deep domain knowledge. Although the primary application was environmental monitoring, the focus of the approach on automatic model selection, hyperparameter optimization, and synthetic data generation has direct applications to financial markets. The main issues were reliance on synthetic anomalies, generalization to noisy real-world data being poor, and computational cost at training time. Yet, HF-PPAD's capability to improve anomaly detection accuracy without human involvement is a significant achievement for high-frequency financial anomaly detection, where model deployment on time and adaptation to evolving conditions are essential [16].

Bakumenko and Elragal [17] explored applying machine learning algorithms to identify anomalies in financial data with the purpose of improving fraud detection accuracy. Using a highly unbalanced set of normal and anomalous transactions, they applied supervised techniques like Random Forest and unsupervised techniques like Isolation Forest with notable improvements in recall rates. They called out for better preprocessing quality, i.e., journal entry vectorization and hyperparameter tuning. Constraints identified included class imbalance, challenging to accommodate feature variability, and long journal entry issues. Specifically, the paper stressed avoiding false negatives for fraud detection in finance. This work reaffirmed the necessity of robust machine learning pipelines for anomaly detection in high-frequency financial systems, particularly with financial data complexity and volumes continuing to increase [17].

Poutré et al. [18] proposed a deep unsupervised anomaly detection model for high-frequency markets from a transformed Transformer autoencoder framework. The approach learned subsequences of the limit order book (LOB) through time to learn normality and applied a dissimilarity function to identify anomalies for out-of-sample observations. Synthetic manipulations such as quote stuffing and pump-and-dump schemes were used to test model resilience. The model performed higher fraud detection than traditional unsupervised approaches in terms of accuracy and F1-score. The authors also mentioned several limitations such as interpretability constraints, modeling collective anomalies challenges, and computational cost in extreme market conditions. The study also highlighted the need for dynamic adaptation to the evolving fraud strategies, which is now the key challenge in real-time financial systems. Overall, this paper provided an effective reference for creating scalable unsupervised models of anomaly detection in high-frequency trading situations [18].

Yang et al. [19] outlined a federated learning (FL) framework for facilitating privacy-preserving sharing of medical data to be applied in drug development. Their framework used decentralized machine learning techniques to facilitate multiple institutions learning together from other institutions' model updates without direct access to raw patient data, thereby maintaining confidentiality and compliance with data protection law. The work reported enhanced aggregation mechanisms to combat issues of data heterogeneity among different medical centers, resulting in significantly improved model accuracy and dependability. Even in health-oriented environments, though, the federated learning privacy-saving concepts are highly relevant to finance applications where data sensitivity and confidentiality matter most. Communication overhead, convergence instability in the context of data that is not independent and identically distributed (non-IID), and vulnerability to adversarial attacks were core issues that were realized. Nevertheless, the research demonstrated that FL could be a robust foundation for secure, distributed anomaly detection systems in applications like high-frequency trading, where data privacy among multiple entities and facilitating collaborative learning are becoming increasingly vital [19].

Guanghe et al. [20] developed a model for detecting anomalies in real-time for dark pool trading using an improved Transformer network. By integrating maximized attention mechanisms with cutting-edge streaming analytics, their system achieved 97.8% accuracy of detection using merely a 2.3-millisecond latency of processing. Emphasizing dark pools that are typically black and vulnerable to manipulation, the system achieved unprecedented performance levels in market surveillance solutions. Yet, limitations like heavy computation requirements for resources and their prelabeled history dependence for training were cited by authors. Adaptability to shifting trends in fraud and low latency under high market volatility were some of the future issues enumerated. In spite of them, the research established how increasingly advanced Transformer-based models had potential to contribute meaningfully to anomaly detection in highly sensitive, low-visibility trading conditions, proving the necessity to adopt real-time, deep learning-based solutions to financial market integrity [20].

Ashtiani and Raahemi [21] carried out a systematic review of the literature regarding intelligent fraud detection in financial reports through the application of machine learning (ML) and data mining methods. In analyzing over 100 peer-reviewed papers, authors categorized methods as supervised, unsupervised, and hybrid approaches and noted that ensemble learning techniques like Random Forest and boosting always outperformed in fraud detection activities. The survey highlighted key challenges such as extreme class imbalance, difficulty in feature selection, lack of public fraud datasets, and the dynamic nature of fraudulent activity. They noted the growing importance of explainability and transparency of ML models, especially in light of mounting regulatory pressure. Although primarily centered on corporate financial fraud, the study’s insights into data preprocessing, model robustness, and performance evaluation are directly applicable to anomaly detection in high-frequency financial data environments. Their findings suggest that hybrid models combining financial knowledge and machine learning yield the most reliable fraud detection systems [21].

Wang et al. [22] examined the synergy of deep learning and cloud computing to improve personal search, building a hybrid architecture that provided notable MAP enhancement and query response time. Their system produced a 15% MAP improvement while providing sub-200ms latency for 95% of the queries, showcasing its scalability and efficiency. The research made use of deep neural networks along with hierarchical monitoring networks to allow adaptive personalization from user behavior. The authors even while highlighting the strengths of AI-powered personalization highlighted concerns with regard to privacy, data dependency, and computational expenses of using deep models at scale. The research outlined possible "filter bubble" consequences in which the users would be trapped in familiar sources of information and consequently confine search variety. Being held within these boundaries, the study showed significant advances in real-time user-centric search applications and presented useful insights for scalable AI infrastructure construction—rules that apply to real-time financial anomaly detection systems [22].

Wang et al. [23] explored distributed high-performance computing (HPC) methods in speeding up deep learning training, employing architectures such as data parallelism and model parallelism. Their research proved that hybrid approaches of decentralised communication combined with adaptive gradient optimisation enhanced scalability and performance of deep learning models considerably. Methods such as Ring All Reduce and 1-bit stochastic gradient descent were emphasized to overcome communication bottlenecks, which are essential for real-time model updation in enormous systems. Fault tolerance, energy efficiency, and load balancing in distributed training were also highlighted as issues by the authors. While mainly aimed at deep learning applications, the observations of the paper directly translate to ultra-fast retraining requirements in real-time financial systems that need to quickly retrain models in order to fit changing environments. Moreover, the study highlighted that breakthroughs in GPU clusters and dedicated AI accelerators could pave the way for the next wave of low-latency, high-precision anomaly detection systems, thereby giving great relevance to financial market applications needing ultra-fast processing [23].

Ibikunle et al. [24] examined the use of machine learning (ML) to reveal novel insight into high-frequency trading (HFT) practices. They utilized tree-based ensembles and a multi-target method to examine liquidity-supplying and liquidity-demanding behaviors in HFT. Based on NASDAQ-provided data, they revealed that ML models were successful at capturing nonlinear relationships and were better at explaining the effect of HFT on price discovery. Most notably, liquidity-supplying strategies were shown to react more sensitively to information events compared to liquidity-demanding ones. Nevertheless, the paper also identified major limitations, such as a lack of granularity in existing HFT datasets and possible information biases based on general trading metrics. The authors stressed more precise data to actually distinguish between different HFT strategies. In general, this work highlighted the potential of ML to revolutionize the comprehension and optimization of high-frequency market behavior, providing avenues for improved anomaly detection and improved market regulation via machine-learning-based analytics [24].

Zhang and Hua [25] introduced a detailed survey discussing key challenges in the analysis of high-frequency financial data, such as nonstationarity, low signal-to-noise ratios, and asynchronous data. Analyzing more than 150 articles, they classified solutions into data preprocessing techniques (such as differencing and smoothing) and quantitative modeling approaches (such as adaptive algorithms and deep neural networks). Their research specifically highlighted that although new algorithms hold potential, threats such as overfitting, poor generalization, and higher computational requirements are ongoing. Notably, they supported methods that cater to intraday seasonality and enhance synchronization within transaction records for better forecasting accuracy. The article's elaborate charts and taxonomies offered a useful guide for researchers addressing HFT challenges. Despite the improvements outlined, they recognized that the majority of advanced methods fail with actual out-of-sample data from the real world. Their findings reaffirmed the need for robust preprocessing, adaptive modeling, and continuous validation when using anomaly detection techniques in high-frequency financial environments [25].

Bello et al. [26] investigated the use of adaptive machine learning frameworks for the real-time identification of fraud in changing financial situations, emphasizing continuous learning from changing patterns of transactions. Reinforcement learning, online learning, and explainable AI (e.g., SHAP, LIME) were integrated into their fraud detection systems to facilitate model transparency and adaptability. Their research emphasized the need for high-quality transactional data, real-time analytics platforms (e.g., Apache Kafka and Flink), and computational efficiency in order to achieve effective fraud prevention. They also briefly discussed ethical concerns, citing the need to ensure fairness and minimize bias in financial systems. Concerns such as imbalanced datasets, the requirement for low-latency responses, and computational overhead were cited as ongoing research challenges. Overall, the paper stressed the importance of having strong, scalable, and interpretable machine learning models capable of evolving with emerging trends in fraud over time, a goal directly applicable to enhancing anomaly detection capability in high-frequency, continuously evolving financial markets [26].

Basit et al. [27] explored the use of Quantum Variational Autoencoders (QVAEs) to improve predictive analytics in high-frequency trading (HFT) markets, aiming to boost the detection of market anomalies. Using quantum computing, their work demonstrated that QVAEs outperformed conventional models based on their accuracy, recall, and F1-score. As per Dow Jones and NASDAQ data, the quantum models had larger precision-recall AUC values, which indicated improved anomaly detection capability in complex high-dimensional trading data. Nevertheless, the study acknowledged major limitations, including training instability, increased optimization times, and current hardware constraints in quantum computing. Furthermore, fine-tuning quantum models proved challenging, requiring specialized techniques to stabilize learning processes. Despite these hurdles, the paper provided critical evidence supporting the potential of quantum-enhanced models for future HFT applications, especially in the realm of detecting sophisticated and evolving market anomalies that traditional methods often fail to capture [27].

Nguyen et al. [28] proposed two deep learning-based approaches—an LSTM network for prediction purposes and an LSTM autoencoder paired with a one-class SVM for anomaly detection—specifically targeting supply chain management applications. By utilizing both external and internal data sources, their models achieved superior performance compared to traditional methods, particularly in predicting remaining useful life (RUL) and detecting anomalous sales patterns. The study validated its methods using C-MAPSS datasets and fashion retail sales data. Although the application domain was supply chains, the dual approach of forecasting and anomaly detection had direct parallels to financial systems, where predictive analytics and anomaly identification are crucial for risk mitigation. Key limitations included the computational demands of LSTM-based models and challenges in hyperparameter optimization. Nonetheless, the paper highlighted the strong potential of hybrid deep learning frameworks for real-world time-series anomaly detection, contributing valuable methodologies translatable to high-frequency financial data analysis and fraud prevention [28].

Zhao et al. [29] presented DeepLOB, a framework based on deep convolutional neural networks (CNN) aimed at modeling and forecasting limit order book (LOB) data. The model captures both spatial and temporal dependencies inherent in high-frequency trading data, outperforming traditional statistical models and shallow machine learning algorithms. DeepLOB leverages CNN layers to extract hierarchical representations from raw LOB inputs without manual feature engineering. Their results showed significant improvements in mid-price movement prediction, with higher accuracy and reduced latency, critical factors for real-time trading applications. Although promising, the authors noted that DeepLOB’s effectiveness is heavily reliant on the quality and detail of the input data, and challenges persist in generalizing the model across various asset classes and trading environments. Nevertheless, this study represents a major advancement in applying deep learning architectures to financial market microstructure analysis and high-frequency anomaly detection scenarios [29].

Sirignano and Cont [30] applied deep learning techniques, specifically recurrent neural networks (RNNs), to study price formation in large-scale financial markets using high-frequency trading data. By training models on billions of order book events, they uncovered universal patterns underlying asset price movements, demonstrating that deep learning could detect complex dynamics that traditional econometric methods failed to capture. Their findings show that some of the underlying structures in high-frequency trading data are common across markets and assets, further pointing towards the potential for transfer learning. Scalability, interpretability, and generalizability across market regimes were identified as ongoing challenges. This research greatly emphasized that deep learning is not only a predictive technique but can also be employed to detect underlying mechanisms in financial markets, thereby enhancing the efficiency of anomaly detection systems for high-frequency environments [30].

Zhang et al. [31] introduced Temporal Graph Attention Networks (TGAT) for financial transaction data spatio-temporal modeling. TGAT integrates graph neural networks (GNNs) with temporal attention mechanisms to model relational dependencies and dynamic patterns of high-frequency trading scenarios both at the same time. The suggested model achieved better predictive performance than the conventional time-series and static graph models on fraud detection and anomaly prediction tasks. The paper also underscored the critical importance of adaptive models that handle dynamic data distribution and structural change in trading networks. The contribution to note was the presentation of the fact that dynamic graph usage considerably improves anomaly detection scores compared to conventional fixed forms. The paper nonetheless addressed limitations that encompass computationally scalability, interpretability. However, on the whole, TGAT offers a better architecture in representation of rich evolving anomalies present in high-frequency finance [31].

Zhu and Chan [32] investigated the use of Long Short-Term Memory (LSTM) networks to detect anomalies in high-frequency trading data. In their research, the authors demonstrated that LSTMs could efficiently extract temporal relationships and recognize anomalous activities such as spoofing and layering in limit order books. The authors employed a combination of actual trading data and synthetically added anomalies for training and testing the LSTM models. Outcomes included increased detection rates and fewer false positives in comparison to conventional methods threshold-based and rule-based mechanisms. Nevertheless, they added that the model proved to be sensitive to hyperparameters and performance equally sensitive to how the training set was balanced. The article put a focus on the importance of the necessity for effective dataset construction and the potential of recurrent deep learning models to significantly enhance market surveillance and fraud detection in HFT settings. The findings directly contribute to the growing field of deep learning applications in financial anomaly detection [32].

Comparative analysis of existing studies on anomaly detection in high-frequency financial data are summarized in Table 1.

3. Taxonomy of Anomaly Detection Methods

Anomaly detection methods in high-frequency financial data can be systematically classified into nine broad categories: statistical, proximity-based, clustering-based, classification-based, reconstruction-based, ensemble, deep learning-based, graph-based, and hybrid methods. Statistical methods assume that most data obey a known distribution and flag observations in low-probability regions—using methods such as Z-score analysis or histogram-based detection. The distance-based approaches, including k-nearest neighbors and Local Outlier Factor, identify anomalies as points located at fairly large distances or regions of significantly lower density than their neighbors. Clustering-based approaches—such as k-means and DBSCAN—identify outliers as points not belonging to any dense cluster but small sparse clusters. Classification-based techniques approach anomaly detection as a semi-supervised or supervised learning issue, where one trains models such as Support Vector Machines and One-Class SVMs to distinguish anomalous and normal instances.

Reconstruction-based methods learn dense representations of normal data through autoencoders or Principal Component Analysis and label points with extreme reconstruction error as anomalies. Ensemble-based methods provide robustness through the use of multiple detectors—Isolation Forest and feature-bagging are prominent examples—to identify diverse patterns of anomalies. Deep learning-based methods leverage deep neural networks (CNNs, RNNs such as LSTMs/GRUs, and Variational Autoencoders) to construct complex, non-linear relationships within high-dimensional unstructured data. Graph-based methods represent trading or transaction data as graphs and apply Graph Neural Networks or subgraph analysis to learn structural anomalies, which scalar features cannot. Finally, hybrid methods integrate two or more of the above paradigms—i.e., combining clustering with reconstruction—to benefit from each other's complementary strengths and assist in overcoming individual weaknesses. Table 2. shows summary of anomaly detection methods.

3. Key Findings, Research Gaps and Proposed Directions

3.1. Higher-Level and Niche Domain Selection

The overarching research domain focuses on time-series analysis for financial systems, particularly in areas such as risk management, volatility analysis, and explainable artificial intelligence (XAI) for financial markets. At a more specialized level, niche domains have emerged, notably anomaly detection in high-frequency financial data for options markets, interpretable models for risk prediction, and the application of explainable AI techniques in volatility forecasting.

The intraday volatility prediction in options markets presents a highly promising research area, with the potential to integrate news feeds and sentiment analysis to enhance forecasting accuracy. This direction remains underexplored and offers substantial scope for future work.

3.2. Identified Research Gaps and Opportunities for Improvement

Several critical gaps and improvement areas were identified across existing research studies:

- Ensemble and Hybrid Modeling: Very few studies have explored the combination of multiple machine learning paradigms (e.g., clustering, density estimation, reconstruction, forecasting) into ensemble or hybrid architectures. This remains a promising avenue to enhance model robustness.

- Limited Focus on Options Data: The majority of studies concentrate on equities or futures; options markets, despite their growing importance, remain largely neglected in anomaly detection frameworks.

- False Positive and False Negative Challenges: Many existing systems suffer from high false positive or false negative rates, necessitating the development of more precise detection models.

- Underutilization of Transformer-Based Attention: Transformer architectures, particularly attention mechanisms, have not been sufficiently exploited for sequential financial data, especially in the context of anomaly detection.

- Insufficient Semi-Supervised Learning: Semi-supervised approaches, which are critical when labeled anomaly data is scarce, are not extensively applied in the current literature.

- Minimal Use of Clustering Techniques: Clustering methods, particularly for unsupervised anomaly detection, have been underutilized.

- Explainable AI (XAI) for Trustworthiness: While anomaly detection models are advancing, their interpretability remains poor. Techniques such as SHAP and LIME could be deployed to explain model predictions, thereby improving trust and regulatory acceptance.

3.3. Metrics and Evaluation Criteria

Robust evaluation metrics are crucial for anomaly detection systems in high-frequency financial environments. The following metrics are recommended:

- Classification Metrics: ROC-AUC, Precision, Recall, and F1-Score to measure detection performance.

- Imbalanced Dataset Metrics: Matthews Correlation Coefficient (MCC) for assessing performance under data imbalance.

- Operational Metrics: Confusion matrix analysis and latency measurements for real-time deployment assessment.

- Profitability Metrics: Sharpe ratio calculation to evaluate profitability impact.

- Portfolio Stability: Volatility reduction measures in the managed portfolio.

- Robustness: Stress testing under extreme market conditions to assess model resilience.

3.4. Specific Findings and Observations

Through a synthesis of previous research and analysis, the following observations have been made:

- Deep Learning Strengths: Deep neural networks effectively learn complex, hierarchical data structures, crucial for identifying subtle market anomalies.

- Autoencoders and Anomaly Detection: Autoencoders, particularly in unsupervised or semi-supervised settings, are highly effective. LSTM Autoencoders outperform standard LSTM models in certain scenarios.

- Simulated Fraud Data: Due to the rarity of real-world manipulation cases, synthetic fraud datasets are often generated by injecting simulated anomalies into clean datasets.

- Feature Engineering Importance: Features such as price spreads, volatility measures, trading volume anomalies, and divergence between option and underlying asset prices are essential signals.

- Options Market Specificity: Metrics like implied volatility, option Greeks (delta, gamma, theta, vega), and order flow dynamics are critical in detecting anomalies unique to options markets.

- Volatility Prediction Techniques: GARCH models, SVMs, random forests, and LSTMs have demonstrated varying levels of success in volatility prediction tasks.

- Explainability Need: It is advisable to build inherently interpretable models rather than relying exclusively on post-hoc explainability techniques.

- Handling Dimensionality: Techniques such as feature selection (MRMR, CMIM), dimensionality reduction (PCA, t-SNE), and deep autoencoders are necessary to combat the curse of dimensionality.

3.5. Proposed Research Directions

Based on the identified gaps and findings, the following future directions are proposed:

- Hybrid Architecture: Develop models combining LSTM for sequence modeling, Transformers for attention mechanisms, and GANs for synthetic anomaly generation.

- Multi-Paradigm Anomaly Detection: Create ensemble frameworks that integrate clustering, density estimation, reconstruction, and forecasting models.

- Options Market Focus: Build dedicated anomaly detection systems for options data, considering OI spikes, implied volatility shifts, and unusual order flows.

- Real-Time Processing Pipelines: Leverage Apache Kafka for ingestion and Apache Flink or Spark Streaming for real-time anomaly detection.

- Model Update Mechanisms: Implement reinforcement learning or incremental learning strategies to enable continuous model adaptation without full retraining.

- Explainable AI Integration: Integrate SHAP and LIME explainability from model inception to enhance trustworthiness and facilitate regulatory compliance.

- Stock Grouping Strategies: Cluster stocks by industry (e.g., healthcare, FMCG) to capture sector-specific anomaly patterns.

- Stress Testing Models: Regularly subject detection models to extreme market simulation scenarios to ensure robustness.

Finally, it is important to emphasize that models should be rigorously validated across multiple datasets, as algorithm performance can vary significantly between different financial instruments and trading environments. No universal model fits all scenarios, highlighting the necessity of empirical validation tailored to specific application domains.

4. Research Motivation, Objectives, and Proposed Framework

4.1. Research Motivation

High-frequency financial data, particularly in options markets, frequently exhibit anomalous behaviors due to market microstructure noise, manipulative activities, and sudden price movements. Traditional anomaly detection methods, including statistical techniques such as Z-score assessment and machine learning techniques such as isolation forests and one-class SVMs, struggle to handle the complex, high-dimensional, and nonstationary nature of such data. Moreover, deep learning approaches, although powerful, often function as opaque black boxes, limiting their applicability in regulated financial environments that require transparent decision-making.

Consequently, there exists a critical need to develop robust, adaptive, and explainable anomaly detection frameworks specifically tailored for high-frequency options data. Similarly, volatility forecasting models traditionally utilized in finance, such as GARCH and stochastic volatility models, often fail to capture nonlinear market dependencies or adapt effectively to rapidly evolving conditions. This research is motivated by the goal of advancing fraud detection capabilities, improving trading strategy optimization, and enhancing financial system resilience through interpretable, deep learning-based techniques.

4.2. Research Objectives

This research endeavors to fill such gaps by embarking on a number of linked goals. Its first goal is to create a deep learning algorithm for anomaly detection using autoencoders, attention mechanisms, and reinforcement learning-based strategies to identify anomalies in high-frequency options streams. Secondly, the research underscores improving model explainability through adopting explainable AI (XAI) methods such as SHAP (SHapley Additive Explanations), LIME, and visualizing attention with a view of making model outcomes easily interpretable and verifiable.

The other primary goal includes the application of domain-aware feature engineering using financial features like implied volatility surfaces, bid-ask spread profiles, and the Greeks (delta, gamma, theta, vega) to detect subtle anomalies that general features may miss. Scalability issues are also sought to be resolved through the use of transformer-based models that are designed for low-latency inference. Lastly, a systematic benchmarking and assessment framework will be developed to confirm model performance under various market regimes, prioritizing robustness, flexibility, and interpretability.

The principal features identified for high-frequency options data anomaly detection and their relevance to finance are encapsulated in Table 3.

4.3. Proposed Methodological Framework

The proposed research framework encompasses a structured multi-phase methodology. Data will be collected from high-frequency options trading sources, including NSE, CBOE, and Upstox APIs, capturing rich features such as implied and historical volatility, options Greeks, bid-ask spread dynamics, and order flow imbalance. The datasets will be preprocessed to handle missing values, normalize key attributes, and segment trading sessions based on market regimes.

Model development will initially involve establishing baseline architectures, including standard autoencoders, variational autoencoders (VAEs), and GAN-based anomaly detectors. These models will be used as comparative benchmarks. Sophisticated model building will incorporate transformer-based architectures with the ability to model sequential dependencies and attention-based prioritization of features. Reinforcement learning algorithms will be embedded in order to permit dynamic modification of anomaly detection thresholds according to changing market conditions. In addition, regime-switching neural networks will be investigated in order to modulate model behavior according to real-time changes in volatility or liquidity.

Explainability will be infused at inception, where SHAP and LIME frameworks are used to spot significant features determining model outputs. Attention mechanisms from transformer-based models will be mapped to help enhance interpretability as well as extract actionable insights for market anomalies.

Performance will be measured through a blend of standard classification metrics like Precision, Recall, F1-Score, and ROC-AUC, as well as financial performance measures like Sharpe Ratio gains and Matthews Correlation Coefficient (MCC) in imbalanced cases. Comparative testing against standard anomaly detection methods like Z-score analysis, Isolation Forests, and one-class SVMs will be performed. Stress testing under volatile and stressed market conditions will be an integral part of the benchmarking process to ensure model robustness.

As far as deployment of real-time systems is concerned, the research suggests using Apache Kafka for ingesting streaming data and Apache Flink or Spark Streaming for scalable low-latency processing pipelines.

Continuous learning strategies, incorporating mini-batch incremental updates and reinforcement learning enhancements, will ensure that models adapt dynamically without the need for full retraining. Data augmentation using GANs will address the imbalance in fraud versus legitimate data cases by synthesizing realistic anomalous patterns.

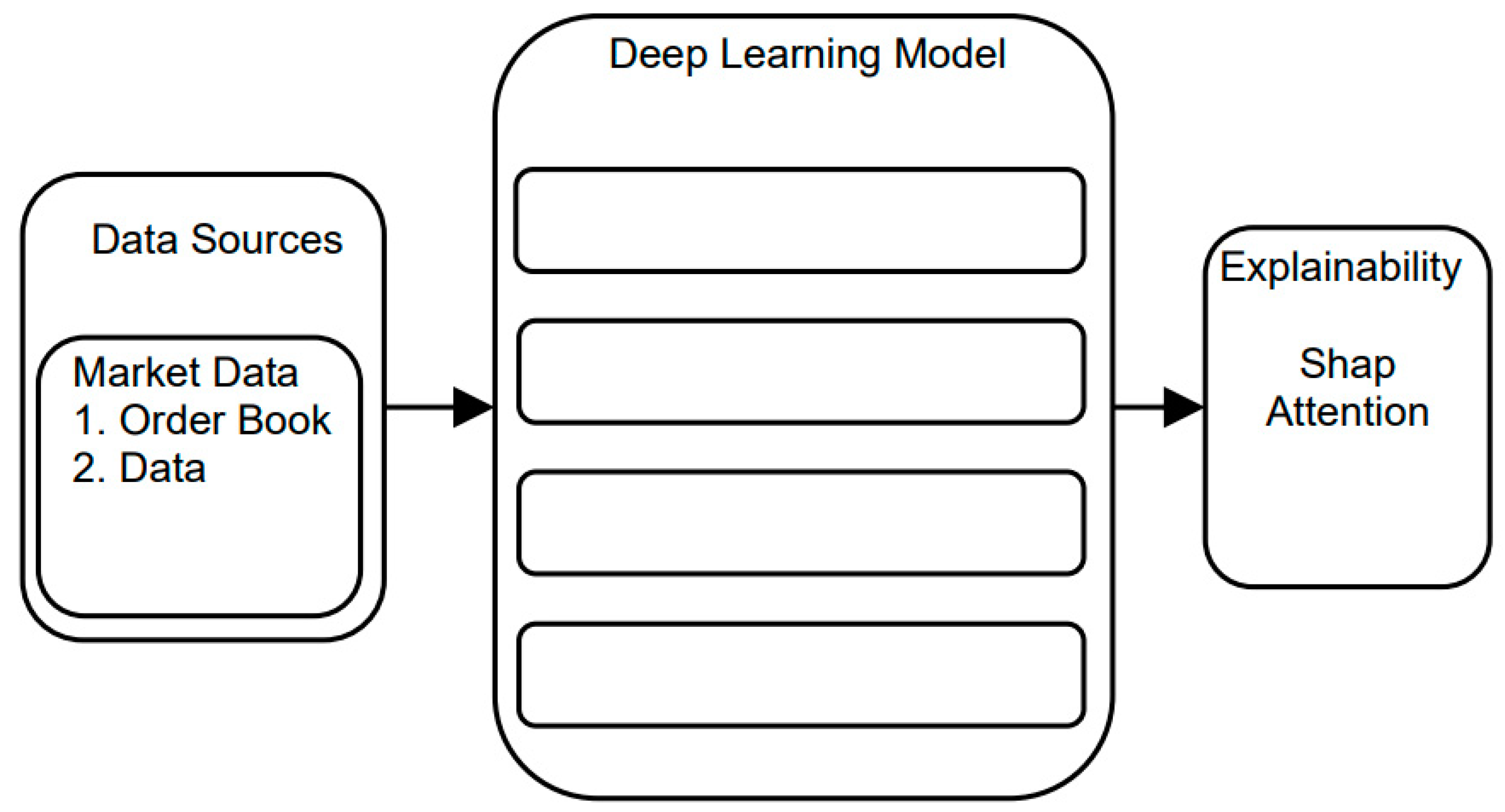

Figure 1 Describes the proposed architecture diagram of the system.

The evaluation metrics selected for assessing the anomaly detection framework, including both classification and financial impact measures, are outlined in Table 4.

4.4. Expected Contributions

Through this research, several key contributions are anticipated. Firstly, a novel anomaly detection framework tailored specifically for high-frequency options data will be developed, advancing the field beyond current equity-focused models. Secondly, the integration of XAI techniques within deep learning architectures will address the critical challenge of model transparency in financial applications. Thirdly, a benchmarking methodology for evaluating both detection accuracy and interpretability of deep financial models will be proposed. Lastly, practical insights into market microstructure behaviors—particularly regarding volatility and liquidity disruptions in options markets—will be generated, informing both academic research and industry practices.

5. Conclusion

Anomaly detection in high-frequency financial data has emerged as a crucial area of research, especially in the context of options markets where market microstructure complexities and non-linear dynamics are prominent. This review paper systematically explored the advancements in anomaly detection techniques, emphasizing the application of deep learning models tailored to the unique challenges posed by high-frequency trading environments. Through an in-depth analysis of existing literature, it was observed that while significant progress has been made using deep architectures such as LSTM networks, graph neural networks, and transformer models, several critical gaps remain.

Specifically, the lack of real-time adaptability, limited interpretability, and insufficient domain-specific feature engineering were recurrent limitations across multiple studies. Moreover, relatively few contributions have focused on the options segment, despite its growing importance in modern financial systems. The necessity for hybrid models combining statistical methods and deep learning, the integration of explainable AI techniques, and the adoption of streaming data architectures were identified as key directions for future research.

To address these gaps, this review proposes a comprehensive framework leveraging advanced deep learning models, reinforcement learning for dynamic adaptation, and explainable AI methodologies for enhanced transparency. The incorporation of real-time processing pipelines, including tools such as Apache Kafka and Apache Flink, was also highlighted to meet the operational demands of high-frequency financial markets.

In conclusion, the intersection of deep learning, real-time anomaly detection, and explainable AI in high-frequency financial data represents a promising yet underexplored frontier. Advancing research in this area holds the potential to significantly enhance market integrity, support regulatory oversight, and enable the development of robust, trustworthy algorithmic trading systems. Future work should emphasize not only achieving high detection accuracy but also ensuring system interpretability, scalability, and resilience across diverse market regimes.

6. Glossary of Terms

Anomaly Detection: The act of detecting data points, events, or observations that are very different from the norm or expected behavior in a dataset. In time-series situations, anomalies can signal faults, fraud, or new patterns to be investigated.

High-Frequency Trading (HFT): A form of algorithmic trading characterized by high speeds, turnover, and order-to-trade ratios, employing sophisticated algorithms and co-location to execute high volumes of orders in fractions of a second.

Long Short-Term Memory (LSTM): A sophisticated recurrent neural network structure that was suggested to minimize vanishing-gradient issues using memory cells and gates, so long-range temporal dependencies in sequential data can be modeled.

Transformer (Deep Learning Architecture): A deep learning model based only on multi-head self-attention mechanisms, without recurrence for parallel sequence data processing and improved global relationships capture.

Graph Neural Network (GNN): A family of neural networks that operate on graph structures, learning node, edge, or graph representations by aggregating and processing information along graph connectivity.

Autoencoder: An unsupervised neural network that maps input data onto a compressed (encoded) low-dimensional representation and back to the original space (decoding), with reconstruction error being used for purposes like anomaly detection.

Reinforcement Learning (RL): A framework in which an agent acts in a world, receiving rewards or penalties, and learns to act so as to maximize total reward over time by trial-and-error exploration.

SHAP (SHapley Additive exPlanations): An interpretability technique based on game-theoretic Shapley values that assigns an importance score to every feature for a particular prediction, enabling transparent, locally coherent explanations.

LIME (Local Interpretable Model-Agnostic Explanations): A model-agnostic method that locally approximates any black-box predictor with an explainable model (e.g., a simple decision tree), providing human-interpretable explanations for individual predictions

C3 AI.

Limit Order Book (LOB): A current record of all outstanding limit buy and sell orders for a security, ordered by price tier, which reflects market depth and is at the center of many high-frequency trading techniques

Wikipedia.

Attention Mechanism: An algorithm that estimates a weighted average of input parts, allowing models to focus on the most salient features of a sequence for prediction or reconstruction.

One-Class Classification: A learning situation in which a model is trained exclusively on examples of the "normal" class and must decide whether new cases fall outside this standard, such as One-Class SVMs.

Local Outlier Factor (LOF): A density-based anomaly detection method that calculates how far away a point is from the locally determined k-nearest neighbors.

Empirical Mode Decomposition (EMD): A signal processing technique that separates a non-stationary time series into intrinsic mode functions from local minima and maxima, useful for isolating high-frequency components before anomaly detection.

Kernel Density Estimation (KDE): A method of approximating the probability density function of a random variable by smoothing kernel functions (e.g., Gaussian) around every data point.

Federated Learning: A privacy-preserving distributed learning framework where multiple clients (e.g., institutions) collaboratively train a shared model without exposing their data from devices or servers.

References

- Brugman, S. R. D. "The development of a real-time monitoring system for fatigue detection on truckers." Bachelor's thesis, University of Twente, 2022.

- Veryzhenko, Iryna, Nohade Nasrallah, and Henri Garcia. "Detecting spoofing in high frequency trading using machine learning techniques.".

- Rizvi, Baqar, Ammar Belatreche, and Ahmed Bouridane. "Stock Price Manipulation Detection using Empirical Mode Decomposition based Kernel Density Estimation Clustering Method." (2018).

- Zhao, Hang, Yujing Wang, Juanyong Duan, Congrui Huang, Defu Cao, Yunhai Tong, Bixiong Xu, Jing Bai, Jie Tong, and Qi Zhang. "Multivariate time-series anomaly detection via graph attention network." In 2020 IEEE international conference on data mining (ICDM), pp. 841-850. IEEE, 2020.

- Mejri, Nesryne, Laura Lopez-Fuentes, Kankana Roy, Pavel Chernakov, Enjie Ghorbel, and Djamila Aouada. "Unsupervised anomaly detection in time-series: An extensive evaluation and analysis of state-of-the-art methods." Expert Systems with Applications (2024): 124922.

- Chen, Yuexing, Maoxi Li, Mengying Shu, Wenyu Bi, and Siwei Xia. "Multi-modal Market Manipulation Detection in High-Frequency Trading Using Graph Neural Networks." Journal of Industrial Engineering and Applied Science 2, no. 6 (2024): 111-120. [CrossRef]

- Xi, Yue, Yining Zhang, and Hanqing Zhang. "Real-time Multimodal Route Optimization and Anomaly Detection for Cross-border Logistics Using Deep Reinforcement Learning." Academia Nexus Journal 3, no. 3 (2024). [CrossRef]

- Guanghe, Cao, Shuaiqi Zheng, Yibang Liu, and Maoxi Li. "Real-time anomaly detection in dark pool trading using enhanced transformer networks." Journal of Knowledge Learning and Science Technology ISSN: 2959-6386 (online) 3, no. 4 (2024): 320-329. [CrossRef]

- Cao, Guanghe, Yitian Zhang, Qi Lou, and Gaike Wang. "Optimization of High-Frequency Trading Strategies Using Deep Reinforcement Learning." Journal of Artificial Intelligence General science (JAIGS) ISSN: 3006-4023 6, no. 1 (2024): 230-257. [CrossRef]

- Li, Maoxi, Mengying Shu, and Tianyu Lu. "Anomaly Pattern Detection in High-Frequency Trading Using Graph Neural Networks." Journal of Industrial Engineering and Applied Science 2, no. 6 (2024): 77-85. [CrossRef]

- Alaminos, David, M. Belén Salas, and Antonio Partal-Ureña. "Hybrid ARMA-GARCH-Neural Networks for intraday strategy exploration in high-frequency trading." Pattern Recognition 148 (2024): 110139. [CrossRef]

- Shanmuganathan, V., and Annamalai Suresh. "Markov enhanced I-LSTM approach for effective anomaly detection for time series sensor data." International Journal of Intelligent Networks 5 (2024): 154-160. [CrossRef]

- Bello, Halima Oluwabunmi, Adebimpe Bolatito Ige, and Maxwell Nana Ameyaw. "Deep learning in high-frequency trading: conceptual challenges and solutions for real-time fraud detection." World Journal of Advanced Engineering Technology and Sciences 12, no. 02 (2024): 035-046. [CrossRef]

- Li, Lin, Yitian Zhang, Jiayi Wang, and Ke Xiong. "Deep Learning-Based Network Traffic Anomaly Detection: A Study in IoT Environments." (2024). [CrossRef]

- M. Jin et al., "A Survey on Graph Neural Networks for Time Series: Forecasting, Classification, Imputation, and Anomaly Detection," in IEEE Transactions on Pattern Analysis and Machine Intelligence, vol. 46, no. 12, pp. 10466-10485, Dec. 2024. [CrossRef]

- Haq, Ijaz Ul, Byung Suk Lee, Donna M. Rizzo, and Julia N. Perdrial. "An automated machine learning approach for detecting anomalous peak patterns in time series data from a research watershed in the northeastern United States critical zone." Machine Learning with Applications 16 (2024): 100543. [CrossRef]

- Bakumenko, Alexander, and Ahmed Elragal. "Detecting anomalies in financial data using machine learning algorithms." Systems 10, no. 5 (2022): 130. [CrossRef]

- Poutré, Cédric, Didier Chételat, and Manuel Morales. "Deep unsupervised anomaly detection in high-frequency markets." The Journal of Finance and Data Science 10 (2024): 100129. [CrossRef]

- Yang, Mingxuan, Decheng Huang, Weixiang Wan, and Meizhizi Jin. "Federated learning for privacy-preserving medical data sharing in drug development." Applied and Computational Engineering 108 (2024): 7-13. [CrossRef]

- Guanghe, Cao, Shuaiqi Zheng, Yibang Liu, and Maoxi Li. "Real-time anomaly detection in dark pool trading using enhanced transformer networks." Journal of Knowledge Learning and Science Technology 3, no. 4 (2024): 320–329. [CrossRef]

- Ashtiani, Matin N., and Bijan Raahemi. "Intelligent fraud detection in financial statements using machine learning and data mining: a systematic literature review." Ieee Access 10 (2021): 72504-72525. [CrossRef]

- Wang, Jiayi, Tianyu Lu, Lin Li, and Decheng Huang. "Enhancing personalized search with ai: a hybrid approach integrating deep learning and cloud computing." Journal of Advanced Computing Systems 4, no. 10 (2024): 1-13. [CrossRef]

- Wang, Shikai, Haotian Zheng, Xin Wen, and Shang Fu. "Distributed high-performance computing methods for accelerating deep learning training." Journal of Knowledge Learning and Science Technology ISSN: 2959-6386 (online) 3, no. 3 (2024): 108-126.

- Ibikunle, Gbenga, Ben Moews, Dmitriy Muravyev, and Khaladdin Rzayev. "Can machine learning unlock new insights into high-frequency trading?." arXiv preprint arXiv:2405.08101 (2024).

- Zhang, Lu, and Lei Hua. "Major Issues in High-Frequency Financial Data Analysis: A Survey of Solutions." Mathematics 13, no. 3 (2025): 347. [CrossRef]

- Bello, Halima Oluwabunmi, Adebimpe Bolatito Ige, and Maxwell Nana Ameyaw. "Adaptive machine learning models: concepts for real-time financial fraud prevention in dynamic environments." World Journal of Advanced Engineering Technology and Sciences 12, no. 02 (2024): 021-034. [CrossRef]

- Basit, Jamshaid, Danish Hanif, and Madiha Arshad. "Quantum Variational Autoencoders for Predictive Analytics in High Frequency Trading Enhancing Market Anomaly Detection." International Journal of Emerging Multidisciplinaries: Computer Science & Artificial Intelligence 3, no. 1. [CrossRef]

- Nguyen, Huu Du, Kim Phuc Tran, Sébastien Thomassey, and Moez Hamad. "Forecasting and Anomaly Detection approaches using LSTM and LSTM Autoencoder techniques with the applications in supply chain management." International Journal of Information Management 57 (2021): 102282. [CrossRef]

- Zhao, Zihan, Longfei Li, Qingyun Wu, and Liuyi Yao. "DeepLOB: Deep Convolutional Neural Networks for Limit Order Books." IEEE Transactions on Signal Processing 68 (2020): 1441–1452.

- Sirignano, Justin, and Rama Cont. "Universal Features of Price Formation in Financial Markets: Perspectives from Deep Learning." Quantitative Finance 19, no. 9 (2019): 1449–1459. [CrossRef]

- Zhang, Ziyu, Yichuan Charlie Hu, and Srinivasan Parthasarathy. "Spatio-Temporal Modeling of Financial Data via Temporal Graph Attention Networks." Proceedings of the 29th ACM International Conference on Information and Knowledge Management (CIKM), 2020.

- Zhu, Zhiwei Steven, and Timothy Chan. "Anomaly Detection in High-Frequency Trading Data Using LSTM Networks." Journal of Financial Data Science 2, no. 1 (2020): 55–69.

Figure 1.

Proposed Architecture Diagram.

Table 1.

Comparative Analysis of Existing Studies on Anomaly Detection in High-Frequency Financial Data.

Table 1.

Comparative Analysis of Existing Studies on Anomaly Detection in High-Frequency Financial Data.

| Sr. No. | Paper (First Author + Year) | Problem Addressed | Methods Used | Dataset Used | Key Findings | Limitations |

| 1 | Brugman (2022) | Real-time fatigue detection in trucking industry | Real-time monitoring system, CNN | Physiological data from truckers | Demonstrated feasibility of real-time fatigue monitoring | Limited to physiological signals, not financial domain |

| 2 | Veryzhenko (2023) | Spoofing detection in high-frequency trading (HFT) | Machine Learning classifiers (SVM, Random Forest) | Simulated order book data | Improved spoofing detection performance with ML models | Absence of real HFT trading data for validation |

| 3 | Rizvi (2018) | Detection of stock price manipulation. | Clustering using Empirical Mode Decomposition (EMD) and Kernel Density Estimation (KDE). | Simulated financial time series | Proposed an effective clustering approach for unsupervised manipulation detection | Scalability and real-time deployment not addressed |

| 4 | Zhao (2020) | Multivariate time-series anomaly detection | Graph Attention Networks (GAT) | Public industrial datasets (not specific to finance) | Outperformed traditional time-series models using graph-based approach | Model complexity; real-time inference not tested |

| 5 | Mejri (2024) | Evaluation of time-series anomaly detection methods | Comparative study of 10+ algorithms (Forecasting, Reconstruction) | Public time-series datasets | Provided detailed benchmarking of unsupervised techniques | Lack of focus on financial or high-frequency datasets |

| 6 | Chen (2024) | Market manipulation detection using multi-modal data | Graph Neural Networks (GNN) on order book and trade network data | Simulated multi-modal HFT datasets | Achieved better detection by combining multiple data modalities | Scalability to live data streams remains a challenge |

| 7 | Xi (2024) | Optimization of routes and detection of anomalies in logistics. | Deep Reinforcement Learning (DRL) | Cross-border logistics datasets | Proposed a multimodal DRL framework | Application outside finance; financial anomalies not considered |

| 8 | Guanghe (2024) | Detection of anomalies in dark pool trading in real-time. | Enhanced Transformer Networks | Simulated dark pool transaction data | Improved performance for opaque trading environments | Lack of real dark pool datasets for training and validation |

| 9 | Cao (2024) | Optimization of HFT strategies | Deep Reinforcement Learning (DRL) | Simulated HFT trading datasets | DRL models achieved superior performance in dynamic strategy optimization | Focused on strategy optimization, not anomaly detection |

| 10 | Li (2024) | Anomaly pattern detection in HFT | Graph Neural Networks | Financial transaction datasets | Successfully captured complex transaction patterns for anomaly detection | Scalability and real-time deployment issues |

| 11 | Alaminos (2024) | Intraday strategy exploration in HFT | Hybrid ARMA-GARCH-Neural Network model | High-frequency trading data | Demonstrated improved intraday trading strategy prediction using hybrid models | Limited real-time adaptability; offline model focus |

| 12 | Shanmuganathan (2024) | Anomaly detection in time-series sensor data | Markov-enhanced I-LSTM | Sensor data (non-financial) | Enhanced anomaly detection accuracy through Markov modeling | Not directly validated on financial datasets |

| 13 | Bello (2024) | Fraud detection in high-frequency trading | Deep Learning architectures | Conceptual framework, no specific dataset used | Addressed conceptual challenges and proposed real-time fraud detection solutions | Lack of empirical results and benchmarks |

| 14 | Li (2024) | Network traffic anomaly detection in IoT environments | Deep Learning models (CNN, LSTM) | IoT network datasets | Showed effectiveness of DL models for network anomaly detection | Application domain outside of financial trading |

| 15 | Jin (2024) | Survey of GNNs for time-series tasks | Review of forecasting, classification, imputation, anomaly detection using GNNs | Various time-series datasets | Summarized the potential of GNNs across multiple time-series applications | Limited specific financial use-case demonstrations |

| 16 | Haq (2024) | Detecting anomalous peak patterns in watershed time series | Automated ML (AutoML) approach | Watershed environmental datasets | Demonstrated effectiveness of AutoML for peak anomaly detection | Application domain is environmental science, not finance |

| 17 | Bakumenko (2022) | Financial data anomaly detection using ML | Machine Learning algorithms (XGBoost, RF, SVM) | Financial transaction datasets | ML models successfully identified financial anomalies | Need for higher-dimensional and real-time adaptation |

| 18 | Poutré (2024) | Deep unsupervised anomaly detection in HFT markets | Deep Autoencoder models | High-frequency market data | Achieved strong anomaly detection without labeled data | Challenges in scaling for large real-time systems |

| 19 | Yang (2024) | Privacy-preserving data sharing using federated learning | Federated Learning frameworks | Medical datasets (non-financial) | Demonstrated privacy-preserving anomaly detection using federated learning | No application to financial markets or HFT scenarios |

| 20 | Cao (2024) | Detection of anomalies in real-time within dark pool trading | Enhanced Transformer Networks | Dark pool transaction datasets | Developed an enhanced transformer model for opaque market conditions | Dataset quality limitations; repeated listing suggests overlap |

| 21 | Ashtiani (2021) | Fraud detection in financial statements | Machine Learning and Data Mining | Financial statement data | Provided a systematic literature review for intelligent fraud detection | Focused on offline financial reports, not HFT or real-time data |

| 22 | Wang, Jiayi (2024) | Personalized search enhancement using AI | Hybrid Deep Learning and Cloud Computing | User interaction datasets | Proposed hybrid model improving search personalization | Domain not related to financial trading or anomaly detection |

| 23 | Wang, Shikai (2024) | Accelerating deep learning training | Distributed High-Performance Computing methods | Deep learning training datasets | Improved computational efficiency for training deep models | Focused on system acceleration, not anomaly detection |

| 24 | Ibikunle (2024) | Potential of machine learning in HFT analysis | Survey and conceptual insights | Various public and private datasets reviewed | Highlighted the opportunities ML offers in understanding HFT behaviors | Lacks experimental model validation and implementation examples |

| 25 | Zhang, Lu (2025) | Major issues in high-frequency financial data analysis | Survey and solution categorization | Multiple HFT datasets | Presented key challenges and survey of solutions in financial HFT data analysis | No experimental model or comparative benchmarks provided |

| 26 | Bello, Halima (2024) | Adaptive machine learning models for detecting fraud in real-time. | Conceptual discussion of adaptive learning | Financial fraud environments (conceptual) | Addressed need for dynamic models in fraud prevention systems | Lack of experimental setups or real-world deployments |

| 27 | Basit (2024) | Quantum Variational Autoencoders for HFT anomaly detection | Quantum Machine Learning (QVAE) | Simulated high-frequency trading datasets | Proposed using quantum variational autoencoders to enhance anomaly detection | Early-stage; quantum computing feasibility remains uncertain |

| 28 | Nguyen (2021) | Forecasting and anomaly detection in supply chains | LSTM and LSTM Autoencoders | Supply chain time-series datasets | Demonstrated LSTM-based models improving anomaly detection and forecasting | Non-financial datasets; supply chain context, not HFT |

| 29 | Zhao, Zihan (2020) | Limit order book modeling for price prediction | Deep Convolutional Neural Networks (DeepLOB) | Public limit order book datasets | Achieved strong predictive performance using CNNs for order book data | Focused on price prediction, not explicitly on anomaly detection |

| 30 | Sirignano (2019) | Universal features of price formation using deep learning | Deep Neural Networks | Extensive limit order book data | Identified deep universal patterns in financial market behavior | Anomaly detection not the primary focus; descriptive analysis |

| 31 | Zhang, Ziyu (2020) | Spatio-temporal modeling of financial data | Temporal Graph Attention Networks (TGAT) | Financial transaction datasets | Improved modeling of complex spatio-temporal relationships | Scalability to extremely high-frequency real-time data untested |

| 32 | Zhu, Zhiwei (2020) | Anomaly detection in HFT using LSTM networks | LSTM-based anomaly detection | High-frequency trading datasets | Demonstrated LSTM networks effectively detecting anomalies in HFT | Real-time latency considerations not deeply addressed |

Table 2.

Summary of Anomaly Detection Methods.

| Category | Key Techniques | Data Type | Supervision | Advantages | Limitations |

| Statistical Methods | Z-score, Histogram-based | Numeric | Unsupervised | Simple, interpretable | Assumes specific data distribution |

| Proximity-Based Methods | k-Nearest Neighbors (k-NN), LOF | Numeric | Unsupervised | Flexible, non-parametric | Computationally expensive in large/high-D |

| Clustering-Based Methods | k-Means, DBSCAN | Numeric | Unsupervised | Detects arbitrarily shaped clusters | Sensitive to parameter choice |

| Classification-Based | SVM, One-Class SVM | Numeric | Supervised / Semi-Supervised | High accuracy with labels | Requires labeled data |

| Reconstruction-Based | Autoencoders, PCA | High-dimensional | Unsupervised | Captures complex patterns | May reconstruct anomalies as normal |

| Ensemble Methods | Isolation Forest, Feature Bagging | Various | Unsupervised | Robust, captures diverse patterns | Increased model complexity |

| Deep Learning-Based | CNNs, RNNs (LSTM/GRU), VAEs | Unstructured | Unsupervised | Models non-linear, hierarchical features | Data- and compute-intensive |

| Graph-Based Methods | Graph Neural Networks, Subgraph Analysis | Rational | Unsupervised / Semi-Supervised | Captures structural relationships | Graph construction and scaling challenges |

| Hybrid Methods | Combinations of above (e.g., clustering + autoencoder) | Mixed | Varies | Leverages complementary strengths | Design and tuning complexity |

Table 3.

Feature Set for Anomaly Detection in Options Data.

| Feature | Description | Relevance to Anomaly Detection |

| Implied Volatility | The market's forecasts of future volatility are based on option pricing. | Identifies sudden changes in perceived market risk. |

| Historical Volatility | Past realized volatility of the underlying asset. | Detects discrepancies between past and expected volatility. |

| Delta | The responsiveness of an option's price to variations in the underlying asset's price. | Captures unusual hedging activity or manipulation. |

| Gamma | Rate of change of Delta relative to the underlying asset price. | Highlights nonlinear price dynamics during anomalies. |

| Theta | Time decay of an option's value. | Observes pricing anomalies related to time-value erosion. |

| Vega | The responsiveness of option prices to shifts in volatility. | Identifies volatility-driven anomalies. |

| Bid-Ask Spread | Difference between highest buying and lowest selling prices. | Captures liquidity disruptions or artificial widening. |

| Order Flow Imbalance | Net difference between buy and sell orders. | Detects spoofing, momentum ignition, and liquidity shifts. |

| Best Bid and Ask Prices | The maximum bid and minimum ask prices currently offered. | Useful for detecting order book spoofing or layering. |

| Open Interest Dynamics | Number of open contracts outstanding. | Identifies abnormal buildup or unwinding positions. |

Table 4.

Evaluation Metrics and Their Purpose.

| Metric | Purpose | Notes on Importance |

| ROC-AUC | Assesses the model's capacity to differentiate between categories. | Robust to class imbalance, good for anomaly detection tasks. |

| Precision | Ratio of true positives within predicted positives. | Crucial when false positives incur high costs. |

| Recall | Proportion of true positives detected among all actual positives. | Important to catch rare but critical anomalies. |

| F1-Score | The harmonic mean of precision and recall. | Achieves a balance between false positives and false negatives. |

| Matthews Correlation Coefficient (MCC) | Evaluates the quality of binary classification, particularly in cases of class imbalance. | Critical for rare-event anomaly detection. |

| Sharpe Ratio Impact | Evaluates improvement in portfolio profitability after anomaly detection. | Links model accuracy with trading strategy profitability. |

| Latency Measurement | Time taken to detect anomalies after occurrence. | Essential for real-time financial market applications. |

| Stress Testing Under Market Regimes | Testing model under extreme volatility and low liquidity conditions. | Validates robustness and practical usability of the model. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.