Submitted:

16 April 2025

Posted:

21 April 2025

You are already at the latest version

Abstract

This study presents the algorithm - Victoria - an approach that demonstrates there are parameters φ, k, j considered optimal that guarantee the player will always have an advantage over the house in sports betting field in the medium and long run with guaranteed satisfactory profits. After n Small Blocks (j n ) and Intermediate Blocks (IBs) containing k independent events with the same probability p, we conclude that the cost-benefit ratio over the value in a sequence of independent events β (success block) > ζ (failure block) is always the case. Taking into account the possible impacts of Victoria on Decision Theory as well as Game Theory, a function η(X t ) called “Predictable Random Component” was also observed and presented. The η(X t ) function (or fv(X t ) in the context of VNAE) refers to the fact that within a game in which the randomness factor in a uniform distribution is crucial to it, any player who has advanced knowledge of randomness added to other additional actions, whether with the support of statistics, mathematical, physical operations and/or other cognitive actions, will be able to determine an optimal strategy whose results of the expected value of the player's payoff will always be positive regardless of what happens after n sequences determined by the player. In addition, the possibility of the existence of a new equilibrium was also observed, thus resulting in the Victoria-Nash Asymmetric Equilibrium (VNAE) theorization. We develop a rigorous statistical foundation, incorporating Markov processes, Brouwer’s fixed-point theorem, and statistics convergence to validate the existence of asymmetrical advantages in structured random systems. And anchored by the Stirling Numbers, the Law of Large Numbers, the Central Limit Theorem, Kelly's Criterion, Renewal Theory, Unified Neutral Theory of Biodiversity, Nash Equilibrium and Monte Carlo simulation itself, for example, the proposed new equilibrium is expected to be a solid mathematical model suitable for modeling games in which one of the players tends to have asymmetric advantages. In this sense, VNAE is an extension of the classic Nash Equilibrium, Stackelberg Equilibrium, and Bayesian Equilibrium. Victoria has shown that by understanding the general behavior of randomness through statistics, we can, in a way, partially “predict” the future and shape it in our favor. Furthermore, in Game Theory, it is hoped that the impact could be relevant to better understanding and adapting concepts such as stochastic games, asymmetric games, zero-sum games, repeated games and imperfect information games, for example. By bridging gaps between theory and real-world applications, this work positions the VNAE as a foundational tool for interdisciplinary advancements in decision-making under uncertainty.

Keywords:

Randomness

; Sports Betting

; Decision Theory

; Game Theory

; Statistics

; Probability Theory

1. Introduction

The study of randomness and its application in different areas of knowledge has been a recurring theme in statistics, game theory and behavioral economics. Traditionally, games of chance and sports betting are structured in such a way as to guarantee a statistical advantage for the house, making overcoming this model a mathematical and theoretical challenge. However, this study presents the Victoria methodology, an approach based on statistics and the true nature of randomness that proposes a new paradigm: the possibility of achieving a sustainable advantage for the bettor in the long term.

The research assumes that it is possible to identify optimal configurations/parameters - φ, k and j - that will - at least theoretically - ensure a mathematical expectation for the gambler.

Through a rigorous probabilistic model, anchored in the convergence of probability, the Law of Large Numbers, the Central Limit Theorem and Monte Carlo simulations, the study shows that certain configurations allow the player to obtain a return greater than the risk involved in the long term.

In addition, the author, anchoring himself in the rich bibliography left by his colleagues over time, such as Stirling Numbers, Renewal Theory, Unified Neutral Theory of Biodiversity, Nash Equilibrium, Kelly Criterion, among other related topics, proposes the Predictable Random Component (η) function in game theory. This function η(Xt) (or fv(Xt), in VNAE) suggests that, even in scenarios dominated by randomness, advanced knowledge of probability distributions and randomness can significantly influence the expected results, even in a game whose basis is dominated by randomness in a uniform distribution.

This approach leads to the formulation of the Victoria-Nash Asymmetric Equilibrium (VNAE), a concept that is hoped to extend beyond the field of sports betting, with possible applications in cryptography, social and biological sciences as well as other academic domains.

In this way, this study not only challenges the traditional conception of randomness and the motto “the house always wins”, but also opens up new writing on the wall for the application of statistical techniques in strategic decision-making in probabilistic environments.

In addition, the author, aware of the controversies in the world of sports betting, has taken care to analyze the betting scenario in a way that encompasses different perspectives from mathematics, statistics, game theory, psychological biases according to psychology, as well as business practices in this market, analyzing the strengths and possible limitations found by the proposed model in the real world applications.

2. Methodology

The methodology employed consists of the fact that this study can be considered qualitative and quantitative at the same time.

Throughout this thesis, all of the content relating to the theoretical framework follows a logic that goes exclusively through areas such as Statistics and Probability, the world of gambling, Physics as well as approaches from Behavioral Economics, Decision Theory and Game Theory, in which the author after studies also aimed to raise possible impacts of Victoria as well as new approaches, reflections and possible contributions to these fields.

With regard to the quantitative aspect and sampling, we can say that it has been strongly influenced by Stirling Numbers and by Probability Theory itself. When analyzing duplicate values in random numbers sequence given an interval [0, 1], considering a uniform distribution, we will see that from a sample of n=100 we will find a tendency for the numbers to converge at 63.2%, which is increasingly clear as we increase our sample. In this sense, 100 or any other value close to 100 was chosen as the reference for the general blocks and intermediate blocks.

The author considered analyzing long-term profit and loss scenarios by considering two main groups of parameters: I. φ = 1.02, k = 50 e j = 2; II. φ = 1.04, k = 33 e j = 3. In addition, the author has also taken care to highlight other possible configurations as having the potential for positive mathematical expectation in the long run, for the author and/or the academic community to analyze.

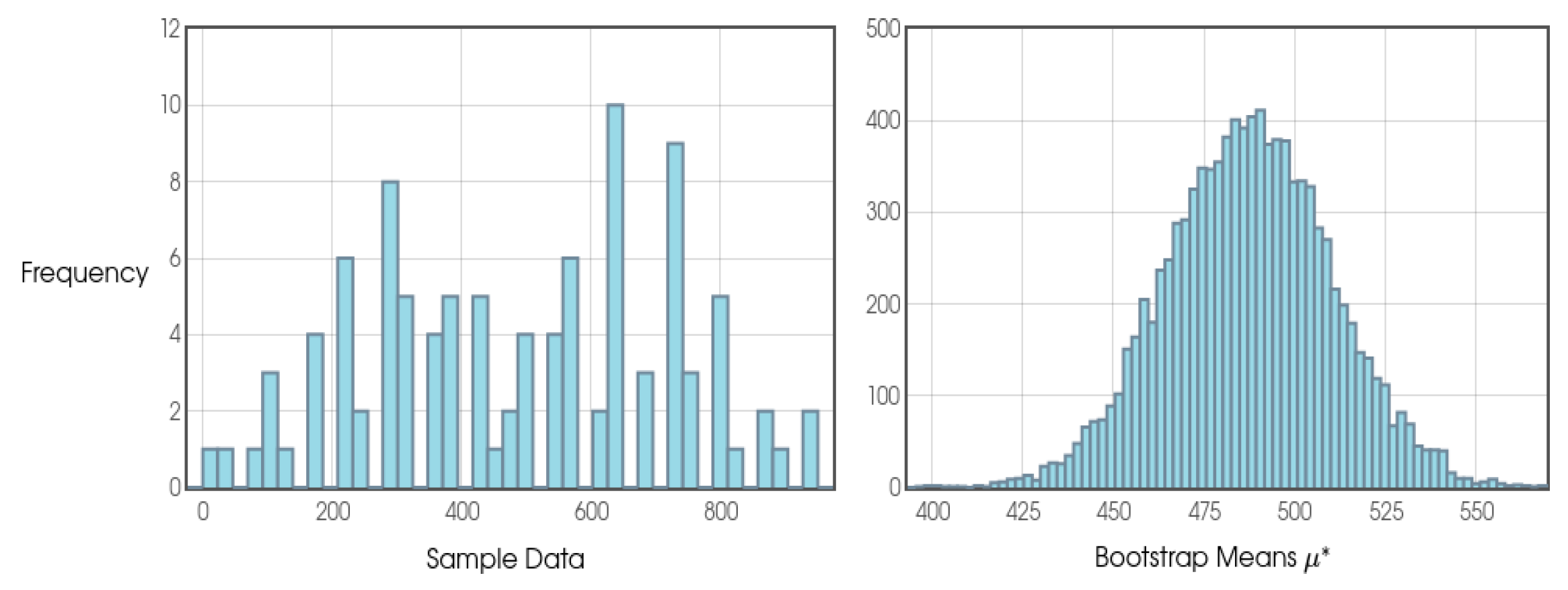

As this is a study with a new approach and, therefore, the probability distributions are not yet so clear and may be different according to different configurations of φ, k and j, the author opted to consider a frequentist approach and, therefore, due to the results presented in the Shapiro-Wilk tests, the use of the Bootstrap confidence interval presented by Efron and Tibshirani (1994) was considered the most appropriate model in all the analyses.

In addition, in order to state whether a given general or intermediate block was positive or negative in terms of profit for the bettor, the use of cumulative sum was considered, as well as graphical analysis (in which the author considered different sources in order to make it clearer) and the results on Return on Investment (ROI).

2. Theoretical Framework

2.1. Convergences in Probability

As Evans and Rosenthal (2004) pointed out, the concept of convergence is fundamental in mathematics. However, when we are dealing with random variables, it is very counterintuitive and more complex to understand, since if something converges to a certain result, how could it be random? Well, as a basic definition of convergence, which opens up countless other applications, we have:

Let X1... X2... be an infinite sequence of random variables, and let Y be another random variable. Then the sequence {Xn} converges in probability to Y , if for all  ϵ > 0, and we write Xn

ϵ > 0, and we write Xn Y.

Y.

ϵ > 0, and we write XnY.According to Talagrand (1996), if we were to ask ourselves which is the main theorem in the field of probability studies, we would probably say that a strong candidate would be: “in a long sequence of tossing a fair coin, it is likely that head will come up nearly half of the time”. This law is a fundamental theorem of probability that describes the behavior of the average of a sequence of repeated random experiments, i.e. the more experiments are carried out, the closer the average of the results is to the expected value. This question, as also corroborated by Packel (2006), serves as an intuitive introduction to the Law of Large Numbers.

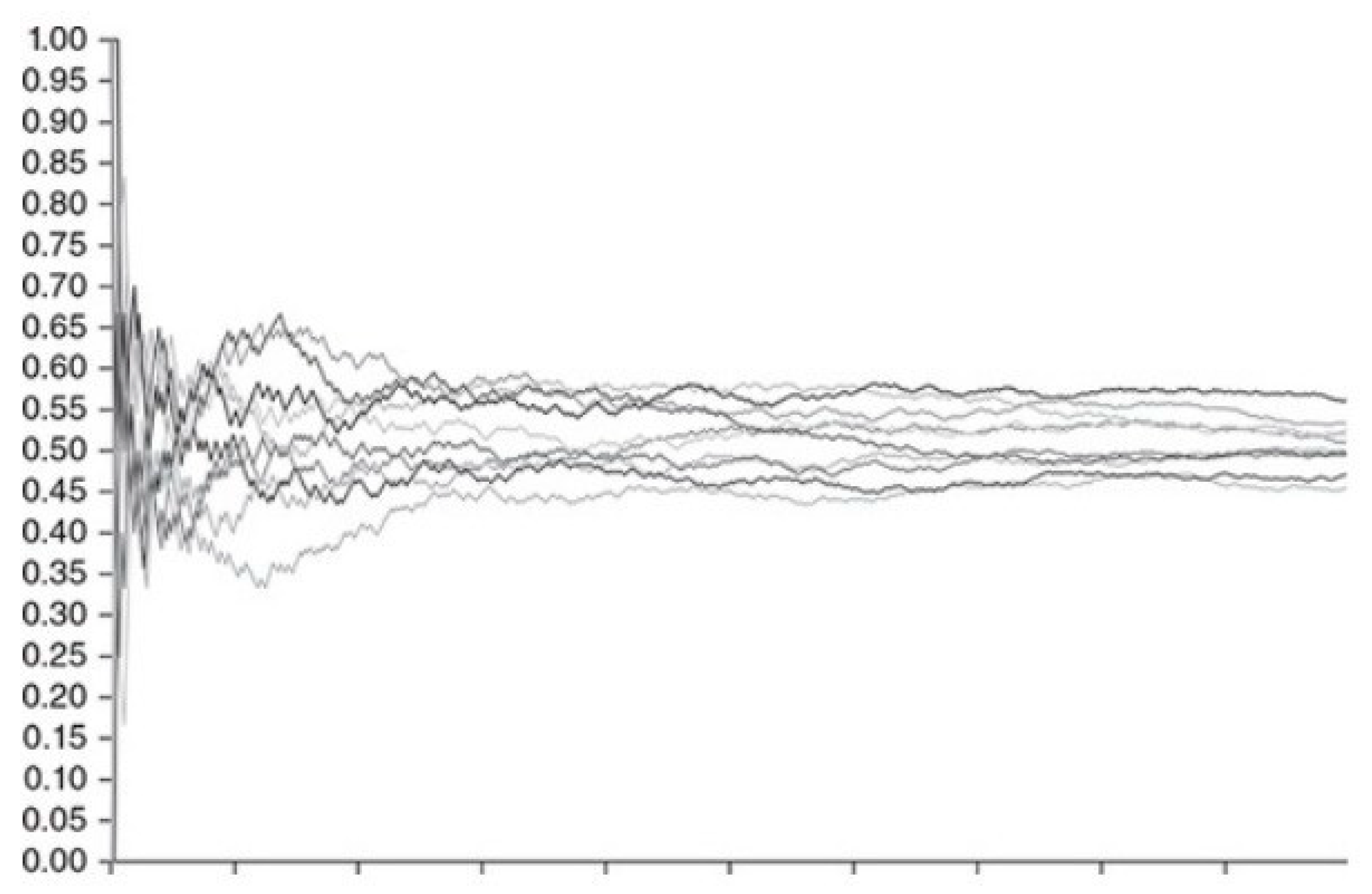

MacInnes (2022) shows us an example, considering the toss of 10 fair coins and analyzing the result of heads or tails in 10,000 tosses. It was observed that in a few tosses there was a large deviation up or down from the expected mean, however, with the increasing number of tosses we see the values of the proportion of heads and tails through the force of the law of large numbers converged to approximately 50%.

Through Figure 1 we can see that, as MacInnes (2022) rightly points out, although in the long term we expect the values to converge towards certain points, along the way we can observe various fluctuations in the sequence of heads or tails, and it is basically inconceivable to 'predict' in the short term the proportion of heads or tails to come out in such a way that a bettor has some kind of advantage.

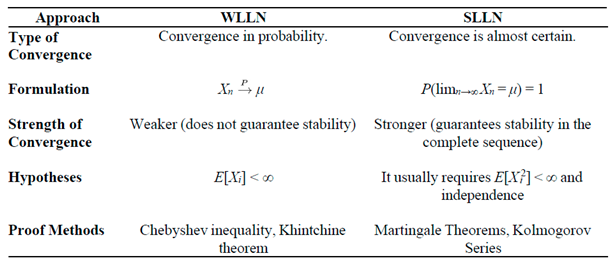

2.1.1. The Weak Law of Large Numbers (WLLN)

Let {Xi}i≥1 be a sequence of independent and identically distributed random variables with finite expected value E[Xi] = μ. Then, the sample mean:

converges in probability to μ, i.e.,

We can say that the probability of the sample mean deviating from μ by an amount greater than ϵ converges to zero as the sample size increases.

As Blitzstein and Hwang (2019) point out, convergence in probability by the weak law of large numbers does not guarantee that the sequence of sample averages will eventually stabilize around μ. It only ensures that, for sufficiently large sample sizes, the averages will be close to μ with high probability. Furthermore, the WLLN is usually demonstrated by applying Chebyshev's Inequality or through Khintchine's Theorem, which only requires the existence of a finite expected value.

2.1.2. The Strong Law of Large Numbers (SLLN)

SLLN establishes almost certain convergence (or convergence with probability 1), which is a stronger form of convergence:

this implies that the set of results in which the sample mean does not converge to μ has zero probability.

Almost certain convergence as highlighted in SLLN implies that over an infinite number of repetitions of the experiment, almost all sequences of sample means will converge to μ. In terms of comparison, this is a much stronger statement than convergence in probability in WLLN, as it implies stability over the complete sequence of observations. To arrive at a proof of SLLN we often use Martingale Convergence Theorems or the Kolmogorov Series, for example, which require stronger assumptions, such as the existence of second-order momentum (i.e., E[Xi2] < ∞).

For the purposes of differentiation, below is a table comparing the weak law and the strong law of large numbers:

Table 1.

Comparing the strong law of large numbers with the weak law of large numbers.

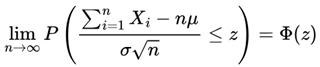

2.1.3. Central Limit Theorem

As Stevenson (1981) pointed out, the Central Limit Theorem probably represents the most important concept in statistical inference. This theorem states that, under certain conditions, the sum (or mean) of a large number of independent and identically distributed (i.i.d.) random variables tends to follow a normal distribution, regardless of the original distribution of these variables.

Consider a sequence of independent and identically distributed random variables X1, X2, ..., Xn, with expected mean μ and finite variance σ2. The Central Limit Theorem states that the standardized variable:

converges in distribution to a standard normal variable N(0,1) as n→∞. In mathematical notation:

As Blitzstein and Hwang (2019) highlighted, for the validity of the CLT, the following conditions are generally required:

- Independence: the variables Xi are mutually independent.

- Identically Distributed: all Xi have the same distribution with mean μ and variance σ2 < ∞.

- Finite Mean and Variance: the existence of a finite mean and variance is crucial to guarantee convergence to normality.

2.2. Monte Carlo Simulation

Simulation is an essential tool for understanding the phenomena of the world around us.

According to Fernandez-Granda (2017), Monte Carlo methods use simulation to estimate quantities that are difficult to calculate exactly. We can say that the Monte Carlo method was developed through Ulam and Metropolis (1949) as well as with significant contributions from John von Neumman, whose initial approaches began in 1946 and were later improved in the Manhattan Project and other subsequent years.

According to Kleiss (2019) Monte Carlo Simulation has been very important for scientific and industrial progress and its applications can be found in many other fields of study. According to Fernandez-Granda (2017), when we apply Monte Carlo Simulation we will also see natural convergences. As pointed out by Rajhans and Ahuja (2005), Monte Carlo simulation is characterized as a means of imitating the real world and has proved to be another case in which we can see that it has led to improvements in the industrial production process.

In the field of business administration, according to Nwafor (2023) Monte Carlo simulation is very useful in managerial decision-making processes. In the field of archaeology, McLaughlin (2023) raised the importance of adopting a more quantitative approach rather than verbal descriptions as a way of increasing precision and reducing human bias in certain activities.

When we look through the literature, we see that monte carlo simulation goes far beyond its original proposal and has a transversal character, covering basically all fields of science. In the field of computer science, Cunha Jr. et al. (2014) shows that parallelizing the Monte Carlo method in cloud computing environments, using the MapReduce paradigm, offers an efficient solution to overcome the method's computational limitations in complex simulations, thus reducing the time required as well as the processing cost.

Moreover, the results of Guatelli and Incerti (2017), show us the applicability of this technique to the field of medical physics by assisting in the decision-making process for the treatment of tumors in patients. Through Favaloro (1990) we can see that monte carlo simulation has been used to assess the variability in measurements made from angiograms and thus estimate the uncertainty associated with these variations, for example.

In addition to the micro world, Monte Carlo simulation is also very influential in the macro world, especially in helping scientists study the behavior of the universe, as presented by Trotta (2008) and Baratta et al. (2023).

2.3. Analysis of Duplicate Data in a Random Draw with Replacement and Uniform Distribution

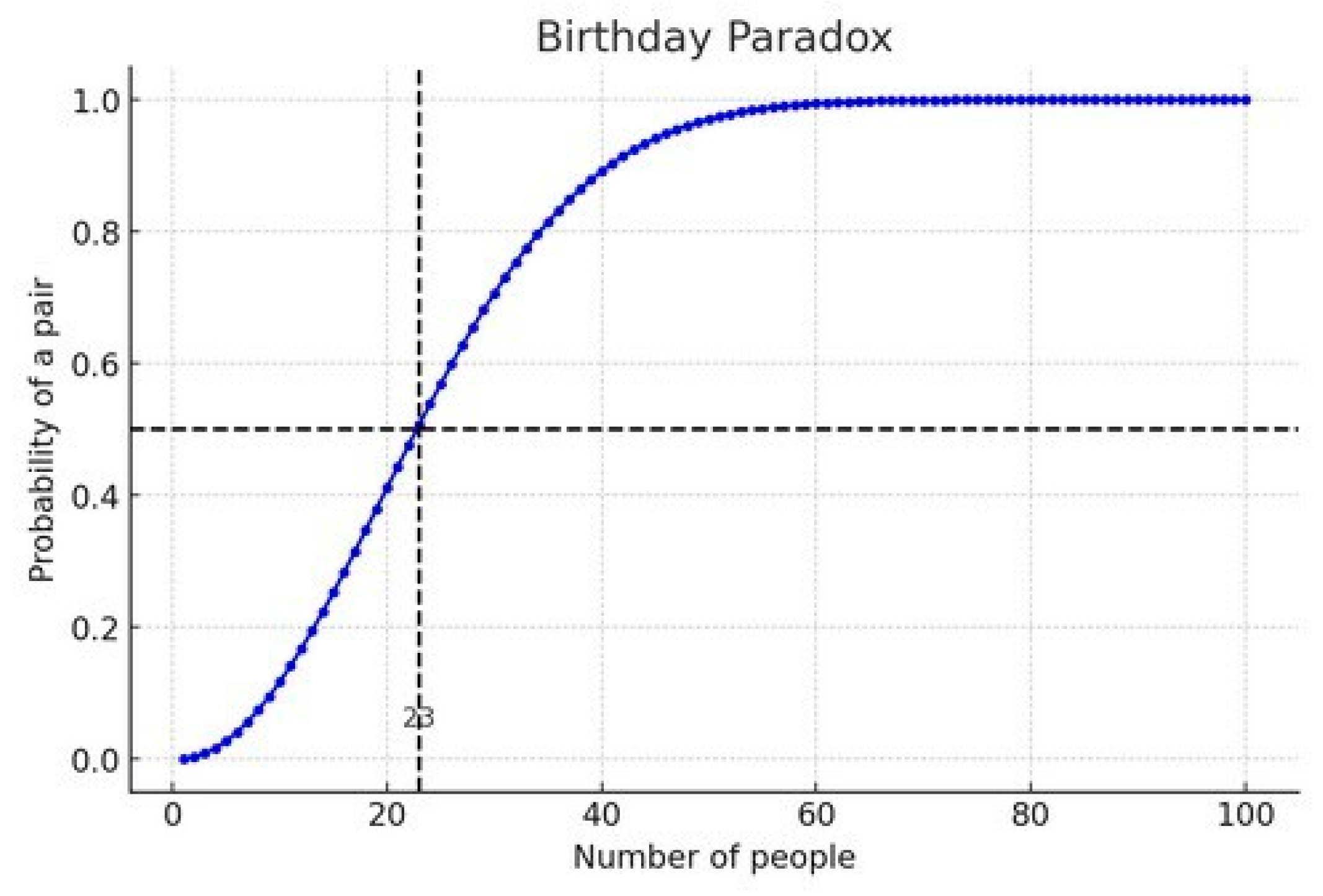

2.3.1. Birthday Problem and Stirling Numbers

The birthday problem is one of the best-known paradoxes within the field of statistics due to its counterintuitive results for the human mind. This paradox asks: how many people do we need to put together in a group so that the probability of two of them having a birthday on the same day is greater than 50%?

Well, below is one of the best-known formulations for dealing with this paradox:

When we apply the formula, the answer is somewhat surprising, since with only 23 people, the probability of at least two people having a birthday on the same day already exceeds 50%. This probability increases considerably as the number of people in the group grows, as we can see in the figure below.

Figure 2.

Graphical analysis of the birthday paradox.

The authors Yancey (2010), Mihailescu and Nita (2021), when dealing with the birthday paradox, are some of the examples of the connection between the Birthday Paradox and both first and second order Stirling Numbers to analyze the probability of occurrence of one or more conicidences of elements within a given set.

By delving into the topics of Stirling numbers, whether they are First Order or Second Order, we can be able to realize how powerful this set of techniques is for the field of mathematics and statistics and that, according to the authors Bagui and Mehra (2024), it is incredibly little debated within this universe of numbers. Likewise, through this paper, I hope to contribute to the propagation of this technique, which could be even more useful for new approaches in the field of studies on random variables and convergences in probability.

According to Riedel (2024), when dealing with scenarios in which we want to know the number of duplicate values in a list, we can simply apply the linearity of expectation and Stirling numbers, as shown below:

When dealing with Stirling numbers in duplicate data, we can see that if we only consider a sample of n = 100 numbers drawn with replacement, we will see that the numbers of duplicate data/values in a list will naturally converge to approximately 63.2%. This value becomes closer and closer as we increase our range of numbers drawn between a and b considering a uniform distribution.

2.4. On the Randomness Field

2.4.1. A Brief Historical Context and Its Meaning

Girolamo Cardano (1501-1574), through his paper written around 1526 and published posthumously in 1663, entitled “Liber de Ludo Aleae” which, translated into English, “The Book on Games of Chance”, took the first steps in the field of Probability Theory as a field of study.

After detailed analyses of various types of games of chance, Cardano translated by Sydney Gould (1965) developed and documented in his seminal work a systematization of probability calculations, highlighting the importance and influence of sampling on results as well as being one of the pioneers to raise the concept of expected value. As it was the Renaissance at the time, Cardano also left some reflections on the nature of uncertainty and its impact on human life and the world around us.

According to Chaparro (2023), in the field of studies on statistics and randomness, Jakob Bernoulli and Abraham de Moivre can be highlighted as having had the most outstanding work in the 18th century. Regarding Jakob Bernoulli - Swiss and the first mathematician in the Bernoulli family - we can mention that his main contributions came from his work entitled Ars Conjectandi “The Art of Conjecturing” (1713), which contains his theorizations on permutations and combinations, as well as establishing the central idea of Bernoulli's Law of Large Numbers and making it clear how he viewed probability through relative frequency, that is, if we repeat an experiment several times, the relative frequency of an event tends to approach the real probability of the event.

With regard to Abraham de Moivre (1738), who was a French mathematician who, in his paper entitled “The Doctrine of Chance” and especially its 1756 version, provided the academic community with the concept of statistical independence. As pointed out by Chaparro (2023), Moivre's other valuable contribution to Probability was through his other work entitled Miscellanea Analytica (1730). With this 1730 work, de Moivre deepens and expands concepts pioneered by Pascal and Fermat in 1654 among his famous letters, his main contributions being the first versions of what later became known as the Central Limit Theorem, on which Laplace (1810) continued this work, Binomial Approximation, as well as practical applications of probability calculus exploring concepts such as mathematical expectation aimed at games of chance as well as estimates of population parameters.

We can see that these aforementioned works were a great start in terms of mathematically formalizing the field of Probability Theory studies as well as randomness itself.

As Costa (2023) pointed out, the concept of “randomness” is too complex and all- encompassing. This is probably due, according to Chaparro (2023), to the fact that the study of randomness as a separate scientific field is relatively recent. However, in general, we consider something random to be anything that refers to the lack of pattern or predictability in an event or result. It is the characteristic of something that occurs by chance, without an apparent deterministic cause. In his study, Gödel (1940) made an interesting connection between randomness and the axioms of set theory. Gödel argues that all sets are expected to be “definable”, i.e. based in some way on some structure or rules. The problem arises from the fact that if all sets are definable, then the notion of randomness becomes empty, since something truly random could not follow a finite rule.

It is common to confuse and even use as synonyms the word “randomness” and random processes (also called stochastic processes). As we saw earlier, randomness refers to unpredictability as something general in its individual scope, a single event, while random processes are commonly related to a sequence of random events over a period of time t given a probability distribution.

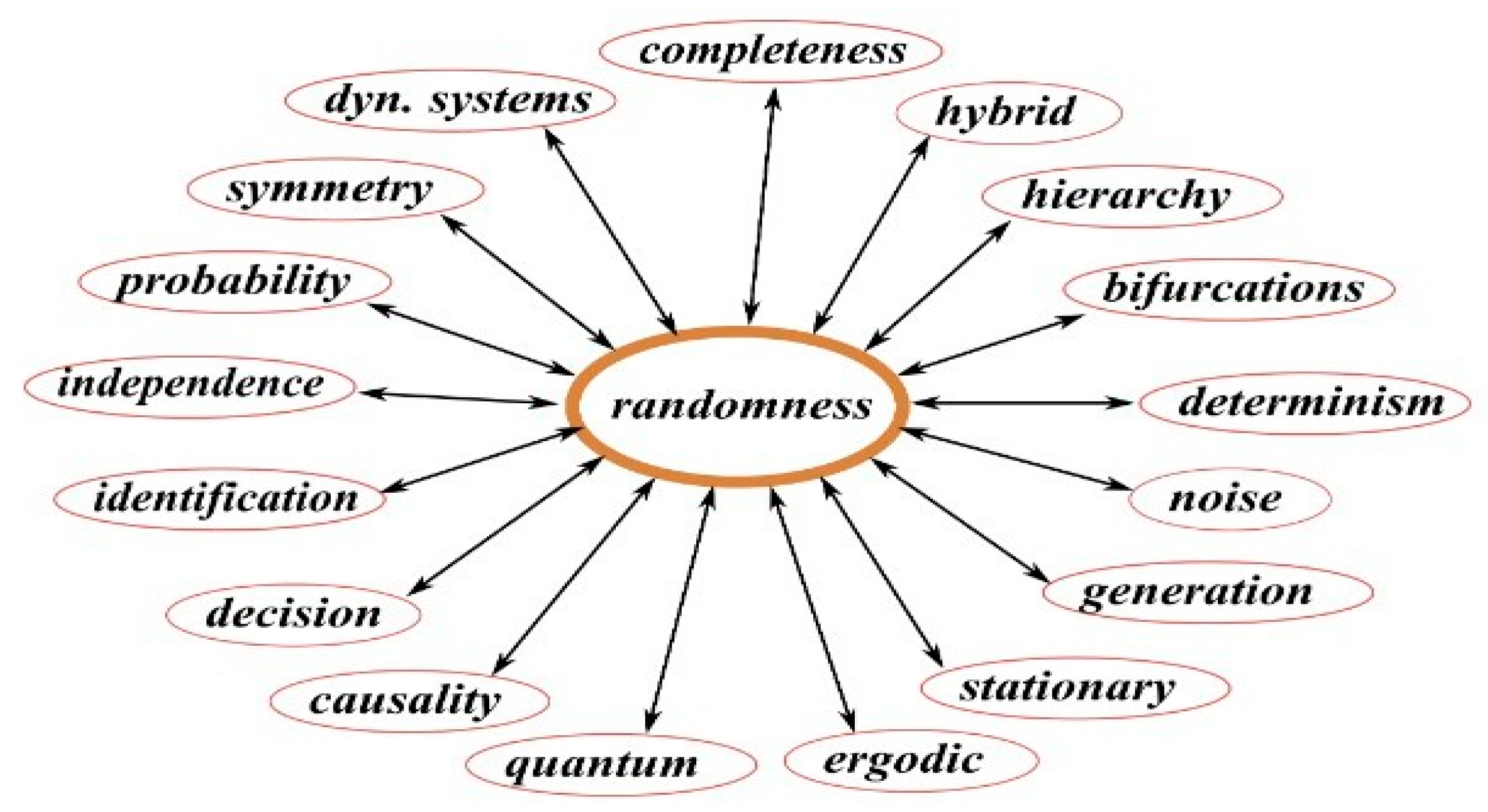

As you can see from the image, according to Costa (2023) within the field of study of randomness we can come across various other areas ranging from probability theory to dynamic systems and quantum physics. Therefore, we can infer that randomness is an interdisciplinary field, not only remaining within its core as it is usually related to statistics, mathematics and physics, but also being an integral part and/or of discussions in apparently “more distant” areas, such as Biological Sciences, Philosophy and Theology, for example.

Figure 3.

Ramifications of the field of study of randomness by Costa (2023).

Due to its scope, it is common for questions to arise within this field of study about the true nature of randomness, especially in theology and philosophy when addressing issues related to free will. Could randomness be completely random or is the randomness we consider purely due to our ignorance of all the variables that permeate the world and universe we know?

According to Chaparro (2023), these thoughts began to emerge in ancient times through philosophers such as Democritus, who firmly believed human beings consider something random simply because they are unaware of the universe and all its particularities as a whole. On the other hand, Aristotle raised the idea nature has patterns that could in no way have been part of chance alone.

Moving on to a time not so long ago, Albert Einstein also coined a well-known phrase in academic circles, stating that “God doesn't play dice” when referring to the probable non- existence of true randomness in the natural world.

The physicist Henri Poincaré, in his work “Science and Method” (1908), dedicated a chapter just to dealing with the profound complexity of chance/randomness and, according to the visions and studies shared by him, randomness is nothing more than the measurement of the ignorance of human beings.

As also discussed, Kucharski (2016) highlighted Poincaré's 3 degrees of ignorance, the first degree of ignorance being the act of knowing all the information about the variables behind a phenomenon considered random, so we could be fully able to represent mathematically through calculations what the expected final results could be, just as with established physical laws, for example.

In the second degree of ignorance, Poincaré makes us reflect even if we understand the laws that govern the universe, our ability to predict the future of an object is limited by two main factors: not knowing the exact initial states and the limitations of measurements. This means that no matter how precise our measuring instruments are, there will always be a degree of uncertainty about the initial state of an object.

This uncertainty, however small, can amplify over time, making future forecasts increasingly inaccurate, and this, for example, is easily verifiable and measurable through the Lyapunov time scale, which states that there is a time lapse in which a system becomes chaotic, that is, until the level of entropy increases considerably to the point of making any kind of long- term forecasting difficult.

Finally, the third degree of ignorance refers to the fact that we don't know the initial conditions or the physical laws behind the observed phenomena.

In addition, the field of study in Complex Dynamical Systems, according to Knill (2019) and corroborated by Akter and Ahmed (2019) aims to identify patterns through order in chaos (a deterministic system that is unpredictable) and the mathematical modeling of systems in motion in order to identify their behavior and make predictions of phenomena, whether physical, biological or financial, for example, as well as understanding the limitations of such predictions and their impacts.

These ideas about the possibility of the existence of “degrees of determinism” in the universe are also corroborated by Machicao (2018) and Costa (2023).

De Jouvenel (2017) shares a little about the myth of Cassandra and Oedipus as a form of representation of the deterministic world. Both share a central theme: the powerlessness of human beings in the face of fate. Both characters were aware of the future, but were unable to prevent it from being fulfilled. While Cassandra is an example of how knowledge of the future does not guarantee control over it, Oedipus illustrates how trying to avoid fate can lead to its fulfillment.

Normally, supporters of the “Deterministic School” such as neuroscientist Sapolsky (2023), apply arguments similar to those mentioned by Aristotle and Democritus and, in recent years, with the development of the field of study of Dynamic Systems, more specifically on the subfield called Chaos Theory, whose pioneers were Henri Poincaré (1854-1912) and Edward Lorenz (1917-2008) there are “patterns” that are present in nature that are undeniably fascinating both in mathematical and visual terms.

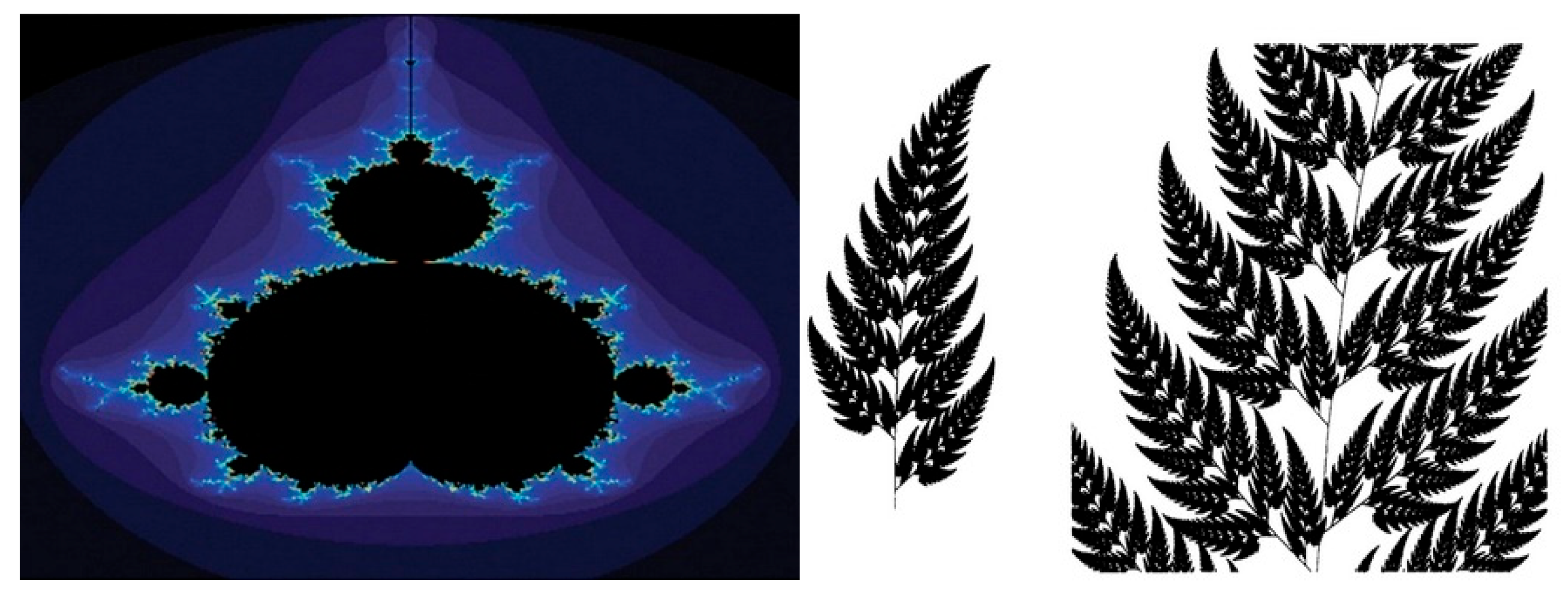

Other examples that can corroborate the thesis of the Deterministic School are the so- called Fractals. A Fractal, a word that comes from the Latin “Fractus” referring to something “broken” or “fragmented”, was first coined by Mandelbrot (1977). We can say that fractals are geometric patterns that present a repetitive pattern, what we can call “self-similarity”, which occur naturally, on different scales or not, in various phenomena from nature to art. We can see that, in particular, the property of self-similarity makes objects visually complex and fascinating.

We can say that there are several properties besides the remarkable self-similarity that make up a fractal, among which we can mention the main ones:

- Fractal dimension: while Euclidean geometric objects (lines, planes, solids) have integer dimensions (1, 2, 3...) fractals, on the other hand, have a “fractal dimension” which is a fractional number;

- Infinite Complexity: Fractals have infinite complexity, since their details can be repeated on smaller and smaller scales, i.e. by enlarging a small part of a fractal, we will always find new details and patterns;

- Irregularity: Fractals are generally irregular and do not follow Euclidean geometry;

- Self-organization: Many fractals can arise through simple processes of self-organization, in which patterns can occur through a set of rules;

- Scale invariance: in addition to self-similarity, some fractals can also have statistical scale invariance, i.e. their basic statistical properties can remain the same at different scales.

Furstenberg (2014) highlighted some of these aforementioned characteristics, especially by emphasizing the importance of “zooming in’’ on fractals to understand their properties in which this process of repeated magnification reveals the intricate self-similar patterns that characterize fractals. In addition, he highlights the significance of fractal dimension, which is a key concept in understanding the complexity of fractals. In his paper we can see that he suggests this dimension is closely linked to the study of ergodic averages in dynamical systems.

With regard to the presence of fractals and their properties in nature, we can easily give some examples such as snowflakes, river bends, lightning during a storm, in which, like branches of a tree, we can observe a series of repetitive patterns and ramifications similar to the “general structure”. Furthermore, in some flowers, plants and vegetables we can notice a pattern of self- similarity, such as Romanesco Broccoli, Succulents and Black spleenwort, for example, which we can see in the figure below by Barnsley (2014) to the right of the so-called mandelbrot set.

Figure 4.

Mandelbrot Set (1977) by Diehl et al. (2024) and Black Spleenwort by Barnsley (2014).

In order not to deviate from the main focus, which is to address randomness, issues related to Fractals as well as the field of Dynamical Systems itself can be further explored through some references such as Knill (2019), Machicao (2017), Barnsley (2014), Goufo et al. (2021), Diehl et al. (2024) and Youvan (2024), the latter four references addressing the concept of self-similarity and fractals with more emphasis. For a more in-depth look at ergodic theory, we recommend the paper by Viana and Oliveira (2014).

Another important point commonly discussed in the Deterministic School is the concept of self-organization. We say that self-organization is the ability of a complex system to structure itself without the need for external intervention or a predefined plan. In other words, self- organization occurs when the components of a system interact with each other and, through these interactions, patterns and structures emerge.

Sumpter (2005) argues that, despite the apparent complexity of many collective behaviours, such as the formation of shoals, flocks of birds or ant colonies, there are relatively simple principles that can explain their organization. The author also points out that simple mathematical models, based on these rules of interaction, can reproduce many of the patterns observed in real collective behaviors.

Although it doesn't have a well-defined name in the bibliographies, we can also mention the “School of Indeterminism”, which has a completely opposite approach to that of the Deterministic School, whose central idea is based on the principle that everything around us is governed purely by random factors, therefore, it is a game in which we cannot win, that is, by non-controllable and unpredictable factors. We can also say that among the main examples in which this approach is very present is through Quantum Physics and Quantum Computing.

Naturally, this school of thought is directly linked to the concept of the existence of free will. One of its proponents is the neuroscientist Nicolelis (2020) who noted that the brain shows electrical signals and/or readiness potential around 500 milliseconds before a voluntary movement takes place. At first glance, this seems to suggest that the brain “decides” before the person is aware of the decision. Despite this, the author states that there is not enough evidence since free will may have manifested itself before or during this process, even if the electrical activity precedes the physical movement.

We can also say about the possibility of a “Hybrid School” of thought in which it aims to unify parts of what we know about the universe being deterministic at the same time as free will is present in human beings.

2.4.2. Intuitions of Mises-Wald-Church

As pointed out by Terwijn (2016) and corroborated by Blando (2024), one of the first attempts to conceptualize the term Randomness mathematically was through von Mises (1919). We can say that it was von Mises who introduced the intuition that randomness must be something unpredictable. As such, he proposed a concept called Kollektiv to refer to an infinite sequence of events that satisfies certain statistical properties.

Of the two main features of the Kollektiv, we can say that the first is based on the central idea of the Law of Large Numbers, in which the relative frequencies of different events must converge on limit values. The second, however, is based on the idea that betting systems are impossible, i.e. it is hoped that there is no system that will allow someone to predict the next results with sufficient accuracy to guarantee a long-term gain. The latter is strongly related to the basis of the Efficient Markets Hypothesis, a theorization put forward by Fama (1998) that revolutionized the way investors and economists view the financial market.

A short time later, two other authors, Wald (1936) and Church (1940), also made important contributions to thinking about how we define randomness. Wald (1936) tried to analyze randomness from the point of view of random sequences as models and thus developed statistical methods for testing hypotheses by verifying, for example, whether a sequence was generated by a random process or whether there might be some underlying structure. Church (1940) revised and extended von Mises' theory by mentioning the concept of countable sets and recursive theory to rigorously formalize randomness, while at the same time being an important intuition for the emerging field of computing, above all by defining randomness from the perspective of algorithmic complexity.

As argued by Terwijn (2016, p. 5) “we thus arrive at the notion of Mises-Wald-Church randomness, defined as the set of Kollektiv's based on computable selection rules”. Thus, the concept of randomness as something unpredictable was derived through the intuitions of Mises- Wald-Church, and was therefore all too important for the progress of Randomness Theory in the following years.

2.4.3. From Absolute Randomness to Algorithmic Randomness

2.4.3.1. Kurt Gödel’s Incompleteness Theorems

Gödel's Incompleteness Theorems (1931) whose work was translated from German into English by Bauer-Mengelberg (1965) establishes two fundamental theorems. The first states that in any sufficiently powerful formal system, such as Peano's Arithmetic, there are propositions that are true but cannot be proved within that system. Therefore, we can say not all mathematical truths are accessible through axiomatic methods. The second theorem complements the first by saying that a consistent formal system cannot prove its own consistency.

We can say that, according Wolfram (2002) and corroborated by Terwijn (2016), Gödel's theory of Incompleteness (1931) was an important basis for the theory of computability as well as the theory of automata and the theory of complexity.

This connection to Gödel's work is strongly linked to the field of studying randomness, for example, due to the fact that the modeling of chaotic systems cannot be completely described and/or predicted. In this sense, systems that involve randomness can contain behaviors whose origin is not entirely deducible.

Furthermore, the idea that some logical sequences cannot be deduced refers to a type of logical randomness, as explored by Chaitin (1969) and (1975) in his theory of algorithmic complexity. In this sense, Gödel's Incompleteness Theorems (1931) show a form of fundamental limitation in mathematical knowledge, since they demonstrate that there are truths that cannot be proven within consistent formal systems. This limitation can be seen as a kind of “structural uncertainty” in the very foundations of mathematics, since not all truths are accessible by axiomatic methods. This perspective has implications both for formal logic and for computability theory and the modeling of complex systems.

2.4.3.2. Borel's Absolutely Normal Numbers and Alan Turing's Approach

We know that Alan Turing's focus was on the principles of computing, more specifically, intelligent systems. However, due to his strong interest in the field of cryptography, he was inevitably led to delve into the nature of randomness. According to Downey (2017), Turing became interested in the paper published by Emile Borel (1909) and the concept of normality.

As well documented by Downey (2017), Borel (1909) in his studies on the Law of Large Numbers arrived, among other results, at the so-called absolutely normal numbers. Formally, we can say that a number x is absolutely normal if, in any base b, each digit d in the set 0, 1, ..., b-1 appears with frequency exactly 1/b throughout the infinite expansion of the number.

As a classic example originating from the Copeland-Erdos theorem (1946), if we consider a base 10, each digit between 0 and 9 must appear with a frequency of exactly 10% in the decimal expansion. Therefore, for example, the combination of two digits such as “12” or “34” must appear with a frequency of 1% and so on.

Copeland-Erdös (1946), motivated by the papers of Borel (1909) and Champernowne (1933), showed that the sequence 0.p1p2p3,..., where pi is the i-th prime, is normal in base 10. This means that concatenating, in sequence, all the prime numbers expressed in decimal base generates a normal number that we can call the Copeland-Erdös constant, let's see:

0.2357111317192329313741…

In terms of cardinality, we can say that the set of absolutely normal numbers is “almost” the set of all real numbers. This means that if we choose a real number “at random”, the chance of it being absolutely normal is 1, i.e. it is practically certain that it will be absolutely normal. Despite its near certainty, proving that a number will be absolutely normal is too complex a task. This is because the definition of absolute normality is very demanding: it needs to apply to all bases, not just one specific base. It would be necessary to analyze the behavior of its expansions in all bases, which is a very complex task in both mathematical and computational terms.

From now on, as Downey (2017) rightly points out, instead of dealing with the metaphysical essence of absolute randomness, we will analyze randomness from now on through different levels and angles.

According to Downey (2017), Turing states that in mid-1938, in one of his many unpublished papers during his lifetime, he suggested an apparent connection between absolutely normal numbers and computable numbers. Turing (1936) states that a computable number is one whose decimals can be calculated by finite means, such as by a Turing machine or any other equivalent computational model.

The core idea is that the numbers we commonly use in mathematics are not just computable, but their computability might be a pathway to constructing normal numbers. Turing seems to be suggesting that the very process of computing a number’s digits could be a method for generating a normal number. We can say that this is a significant connection because explicitly constructing normal numbers is a difficult problem.

According to Downey (2017) and Becher (2012) Turing in his unpublished work “A Note on Normal Numbers” even proposed a theorem and proof for absolutely normal computable numbers. However, a few years later, in 1997, some disconnected points were found and, therefore, at first his proof was not fully accepted until Becher, Figueira and Picci (2007) reconstructed the model keeping Turing's original ideas and came to the conclusion that despite the fact of some disconnected points in the proof presented, Turing was right in his modeling thus confirming the existence of absolutely normal computable numbers.

2.4.3.3. Martingales

According to Terwjin (2016), an alternative way of formalizing the notion of unpredictability of an infinite sequence called martingale was presented by Ville (1939). We can say that a martingale is defined as a stochastic process X = (Xt)t∈T adapted to a filtration (Ft)t∈T, where T is a set of indices (usually discrete or continuous time), which satisfies the following conditions:

Integrability: ∀ t∈T, E[|Xt|] < ∞.

Martingale property: ∀ s, t ∈ T with s < t,

E[Xt | Fs] = Xs almost surely.

The martingale property means that, given knowledge of the past up to time s, the best prediction for the value of X at future time t is its current value Xs. In other words, there is no way to ‘predict the future’ of the martingale process based on the information available.

As presented above, Ville (1939) showed that the non-existence of an indefinitely growing martingale is equivalent to Kolmogorov's classical definition of probability, providing a basis for sequential statistical tests and probabilistic inference.

A classic example of a martingale is a symmetrical random walk on a discrete number line. Let Xn be a sequence of random variables representing the position of a player in a fair bet game. If in each round the player wins +1 with probability 0.50 and loses -1 with probability 0.50, then the sequence Xn, defined as the cumulative sum of these independent increments, forms a martingale with respect to the natural filtering Fn, because the conditional expectation of the future position, given the past history, is always equal to the current position:

E[Xn+1∣Fn] = Xn.

In addition to Ville (1939), Doob (1953) was another very important mathematician in the development of fundamental results, such as the martingale convergence theorem. Despite its strong relationship with the concept of randomness, we can see that there are some fundamental differences with the so-called martingales.

On the one hand, randomness is a broad concept that encompasses any process whose evolution over time is governed by uncertainty, and which may exhibit statistical trends, directional fluctuations or chaotic behavior. In contrast, a martingale is a specific stochastic process that satisfies the property that the conditional expectation of the next value, given the available history, is equal to the present value, implying the absence of a systematic upward or downward trend.

So, while randomness can manifest itself in a variety of formats, including processes with ‘bias’ or autocorrelation, a martingale represents a restricted subset of random processes in which, under a suitable probabilistic model, the best predictor for the future is always the current state, making it fundamental in probability theory. In summary, we can say that every martingale is random, but not every random process is a martingale.

Some of the areas where martingales are applied include finance through option pricing, statistics with sequential tests and physics through random walks, Brownian motion and superstring theory, for example.

2.4.3.4. Martin-Löf Randomness

As Terwijn (2016) pointed out, Martin-Löf's (1966) approach dealt with randomness from the perspective of classical probability theory and measurement theory.

In this sense, Martin-Löf (1966) proposed that an infinite sequence of bits S = s1, s2, s3, …, sn is considered random if it cannot be identified as non-random by any effective test of randomness.

A randomization test is a sequence of measurable subsets of the space of all bit sequences {0,1}∞, defined by

where each Un is a set of measure 2-n, representing subsets where the sequence is not random at an increasing level of precision. If a sequence belongs to all these Un sets, it is considered non-random.

U1⊇U2⊇U3⊇… Un

The Martin-Löf universal test can be seen as the “most powerful possible test” of randomness, because it encompasses all conceivable randomness tests that are computationally enumerable.

An S sequence is random in the Martin-Löf sense if it does not belong to the intersection

where Un is an effectively describable set with measure 2-n.

where Un is an effectively describable set with measure 2-n.

We say that these tests are related to the compressibility of the sequence by Turing machines, that is, if an infinite sequence S can be described by a short program, it is not random. If no compressed description is possible other than the sequence itself, S is random.

Martin-Löf's theorizing was surely one of the great revolutions in thinking about true randomness and in the deliberate search for how to measure it. In the following years, we saw the development of a set of statistical tests of randomness such as the Diehard test by Marsaglia (1996) and the battery of tests proposed by the National Institute of Standards and Technology, NIST, for example.

2.4.3.5. Algorithmic Randomness and Kolmogorov Complexity

The paper entitled “Grundbegriffe der Wahrscheinlichkeitsrechnung” by Andrey Kolmogorov (1933), translated into English as “Foundations of the Theory of Probability”, we can say was a milestone in the formalization of probability theory since Kolmogorov established the rigorous foundations of probability theory using an axiomatic approach based on David Hilbert's set theory and Lebesgue's integrals.

As we can see from Blitzstein and Hwang (2019), Kolmogorov defined probability as a function P that satisfies three main axioms:

- (1)

- P(A) ≥ 0 for all A⊂S

- (2)

- P(S) = 1

- (3)

- If A ∩ B = ∅,

Then (A∪ B) = P(A) + P(B).

In addition to the axiomatization of probability, we can also see that Kolmogorov in his seminal paper defined the concept of probability space, which consists of a sample space, i.e. the set of all possible outcomes of an experiment. He also defined an algebra of events, i.e. a set of subsets of the sample space, as well as a probability measure, which refers to a function that assigns probabilities to events.

Another notable contribution is the use of measure theory as a way of making it possible to deal with continuous probabilities and events with zero probability, which until then had not been possible using the classical approach to probability. For these reasons, Andrey Kolmogorov is often recognized as the “Father of Modern Probability Theory”.

We can say that the field of algorithmic randomness is a field of study that seeks to define and quantify the concept of randomness in data sequences. Unlike traditional probabilistic approaches which are based on statistical measures and probabilities, algorithmic randomness focuses on the inherent complexity of sequences. In short, algorithmic randomness can be defined in terms of computability and algorithms. Normally, this concept tends to become clearer when we talk about Kolmogorov Complexity. With regard to this concept, as Terwijn (2016) pointed out, it may be more appropriate to consider at least three authors: Kolmogorov (1965), Solomonoff (1964) and Chaitin, all of whom have made significant contributions to this seminal field of study.

Kolmogorov (1965) in his study provided the academic community with a model for quantifying a sequence of data. As Vadhan (2012) highlighted the Kolmgorov Complexity refers to the length of the shortest program, in a universal programming language, that generates a specific sequence that we called it as string. The Kolmogorov Complexity can be defined as:

where U is a universal Turing machine, an |p| is the length of the program p.

K(s) = min {|p| : U(p) = s}

We can that say there are two key properties: random strings and structured strings. We say a string s is considered structured when there are obvious patterns and, consequently, they are less complex and can be described using a short program.

Let's consider the following string s1 = 01010101010101010101. You can see that there is a clear pattern in this binary sequence - the repetition of “01”. In a compact program, we could easily write “write 01” and “repeat 10 times”.

On the other hand, a random string s is one that satisfies the following condition K(s) ≈ |s| in which, according to Campani and Menezes (2001), it is not possible to extract an obvious pattern in a given sequence of data by means of a Turing machine. Let's consider the following string s2 = 10110100101011010001. We can see that there is no obvious pattern that can be easily identified, so we can say that it has a higher level of Kolmogorov complexity than sequences that have some kind of pattern throughout the sequence.

In fact, not every string is comprehensible, which means that a random string has a Kolmogorov complexity close to its original size. This theorizing in the successful attempt to measure the level of randomness and compressibility of systems was very relevant to the field of studies on true randomness and, above all, to information theory.

2.4.3.6. Hardness vs Randomness

A few years later, another seminal paper in the field of algorithmic randomness and computational complexity entitled “Hardness vs Randomness” presented by Nisan and Wigderson (1994) explores the relationship between the difficulty of solving computational problems, i.e. “hardness”, and the ability to generate pseudo-random numbers efficiently, i.e. “randomness”.

The authors demonstrate that, under the assumption of the existence of computationally difficult functions, it is possible to construct efficient pseudo-random generators that reduce or eliminate the need for genuine randomness in probabilistic algorithms. This result establishes a relevant theoretical connection in the field of complexity class studies, suggesting that if sufficiently “hard” functions exist, then BPP = P.

The main implication of this paper lies in the possibility of transforming random problems into deterministic ones. Therefore, we can say that this paper was a major turning point for the development of optimization techniques as well as, among other examples, a more mature way of creating and accepting certain pseudo-random number generator algorithms (PRNGs) as an integral part for simulation and cryptography purposes.

The field of complexity theory usually unites the fields of computer science and pure mathematics. In this sense, it is often studied from different angles. As one of the most recent examples in the timeline, Vega (2022), Vega (2024), in addition to having worked continuously on the proof of P = NP in other manuscripts, has also contributed to advances in studies on Robin's divisibility criterion and other inherent topics to present a formulation for the proof of the Riemann Hypothesis.

2.5. From Entropy, Algorithmic Randomness to Structure in Randomness

The deliberate search for patterns and better measurement of randomness has always been the subject of curiosity and study over the years. However, we will only focus on the topics that have stood out the most.

The concept of entropy initially arose with the second law of thermodynamics through the German physicist Rudolf Clausius (1822-1888) in the mid-19th century, around 1865.

Clausius realized that the energy in a system is not completely converted into useful work, but there is always a portion that is lost in the form of heat. This energy “lost” or unavailable to do work was what he called entropy. Furthermore, the second law of thermodynamics states that the entropy of an isolated system, i.e. one with no exchange of energy with the outside world, tends to increase over time, i.e. disorder increases. To further his work, Clausius (1879) gave us his mechanical theory of heat.

Although this concept initially came from “pure physics”, it opened the door to the development and better understanding of many other academic areas, from statistical physics to information theory and cryptography, for example.

Shannon Entropy is a very relevant concept for the field of Information Theory. Its formulation was originated by Shannon (1948) through his work entitled “A Mathematical Theory of Information”.

Shannon entropy is a fundamental measure of the uncertainty or randomness associated with a random variable. In the context of Information Theory, it quantifies the average amount of information needed to describe an event or message. Mathematically, Shannon entropy is defined as the expected value of the negative of the logarithm of the probability of each possible outcome of the random variable. The higher the entropy, the greater the uncertainty or randomness of the system, and vice versa.

Below, we see its formulation:

Pi = Pr(X = xi).

A few decades later, Pincus (1991) took another major innovative step in the field of statistics with the so-called Approximate Entropy (ApEn), which is a statistical technique used to quantify the regularity and unpredictability of fluctuations in time series data. ApEn is, for example, particularly useful for analyzing non-linear and non-stationary data, where traditional methods of analysis may be inadequate.

This seminal study by Pincus (1991) inspired many studies in different areas of knowledge. As an example, we can mention Delgado-Bonal (2019) through his study with notable results in the field of the financial market and his approach of using Approximate Entropy (ApEn) as a way of measuring randomness and identifying patterns in the stock market. Below is some of what he described about Approximate Entropy:

“In this regard, Approximate Entropy (ApEn) is a statistical measure of the level of randomness of a data series which is based on counting patterns and their repetitions. Low levels of this statistic indicate the existence of many repeated patterns, and high values indicate randomness and unpredictability. Even though ApEn was originally developed after the entropy concept of Information Theory1 for physiological research2, it has been used in different fields from psychology3 to finance4”(Delgado-Bonal, 2019, p.1).

Mageed and Bhat (2022) revisited classical entropies such as Shannon's, Rényi (1961) and Tsallis (1988) and introduced the Generalized Z-Entropy (GZE), which is a generalization that includes these entropies as special cases. In addition, they discussed how the fractal dimension measures the complexity of patterns such as coastlines or Koch's snowflake and how it can be derived from entropies. The authors demonstrated that GZE offers a unified framework for studying fractal systems through generalized entropies, concluding that GZE is an important tool for exploring complex and fractal systems, paving the way for future applications in interdisciplinary areas.

Tao (2007) discusses the decomposition of combinatorial objects into three fundamental components: a structured (dominant) component, a pseudo-random component and a residual error term.

This approach has proved to be innovative and not restricted to the field of pure mathematics, as it allows predictable patterns to be isolated from chaotic elements, facilitating the analysis and resolution of problems involving large data sets with unspecified structures, and is therefore also an important contribution to the field of algorithmic complexity studies.

We can see that this approach by Tao (2007) was one of the notable studies on randomness from the perspective of combinatorial analysis. As such, it has influenced new studies such as the one carried out by Trevisan et al. (2009) when analyzing the relationship between high entropy distributions and efficiently sampled distributions, for example.

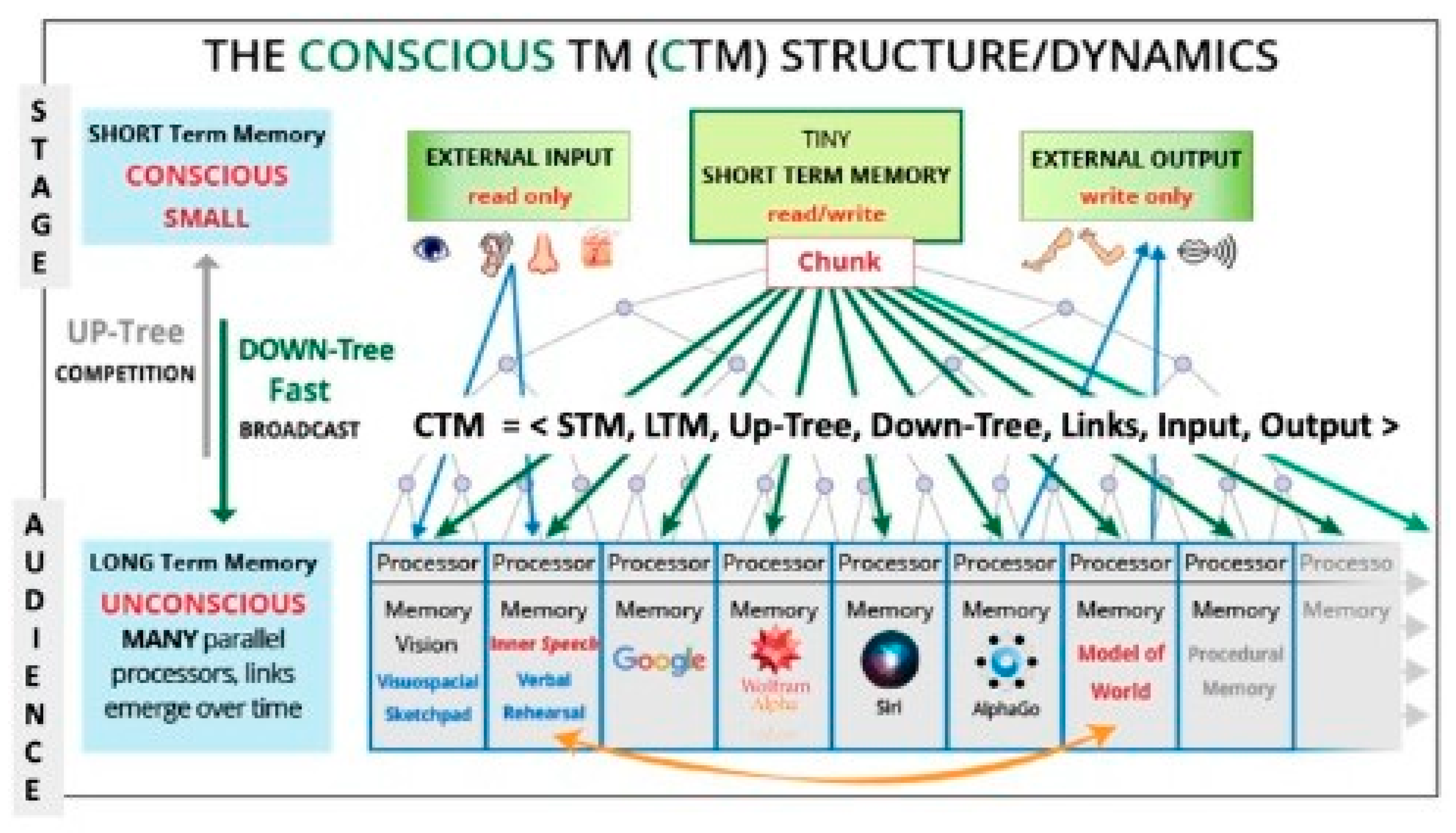

Blum and Blum (2022) propose an innovative approach to understanding consciousness based on the pillars of theoretical computer science, using tools from computational complexity theory and machine learning. The authors introduced a concept called the Conscious Turing Machine (CTM), that is, an abstract computational model inspired by the Turing Machine and the work of neuroscientist Baars (1997), but aimed at exploring consciousness through a formal machine model for consciousness. The structure of the CTM is shown below:

Figure 5.

The Conscious Turing Machine Structure by Blum and Blum (2024).

Furthermore, Blum and Blum (2024) in their most recent study in this direction concluded that consciousness in artificial intelligence will not only be possible, but also inevitable. The aim of these theorizations is to demonstrate how this perspective of theoretical computer science can contribute to research into consciousness and to encourage further studies in this direction.

2.6. Types of Random Number Generators: PRNG, Quasi-RNG, TRNG, QRNG

Informally, we say that an algorithm refers to any set of well-defined steps that leads to a certain end result. According to Cormen et al. (2022) an algorithm - in computing terms - can be defined as a computational procedure that uses a value or set of values as input, which in turn goes through an intermediate processing step that generates a value or set of values as output. An algorithm is usually designed to solve some computational problem. In this sense, as Baeza- Yates (1995) pointed out, algorithms are at the heart of computer science.

According to L'Ecuyer (2017) who was one of the authors of a relevant PRNG algorithm through Panneton et al. (2006), although they don't formally exist in the way we know them today, so-called random number generators and their role of providing “justice” and therefore serving as a means of decision-making and choice have always been present in people's lives since ancient times through other means such as through a coin and 6-sided dice, as we can read below:

“The Romans already had a simple method to generate (approximately) independent random bits. Flipping a coin to choose between two outcomes was then known as “navia aut caput”, which means “boat or head” (their coins had a ship on one side and the emperor’s head on the other). Dice were invented much earlier that that: some 5000-years ones have been found in Iraq and Iran”(L’Ecuyer, 2017, p.2).

Galton (1890) was one of the notable examples of scientists who used the 6-sided cubic dice as a tool in his research. As a result, he designed a method to sample a given probability distribution:

“He used cubic dice (with six faces) but after throwing the dice he was picking up each die by hand and placing it aligned in front of him, eyes closed, and considered the orientation of the upper face. This gives 24 possible outcomes per die (almost 4.6 random bits)”(L’Ecuyer, 2017, p.2).

In more recent times, we can say that the first RNG algorithm came from John von Neumann (1946) through the middle-square method (1951). For a more in-depth timeline on the history of Random Number Generators, we recommend following the paper by L'Ecuyer (2017).

Within the world of random number generators, we can say that there are 4 main branches: Pseudo-Random Number Generators (PRNGs); Quasi-Random Number Generators (QuasiRNGs); Truly Random Number Generators (TRNGs) and, more recently, taking into account concepts from quantum physics, Quantum Random Number Generators (QRNGs).

2.6.1. Pseudorandom Number Generators (PRNGs) e Quasi-Random Number Generators (Quasi-RNGs)

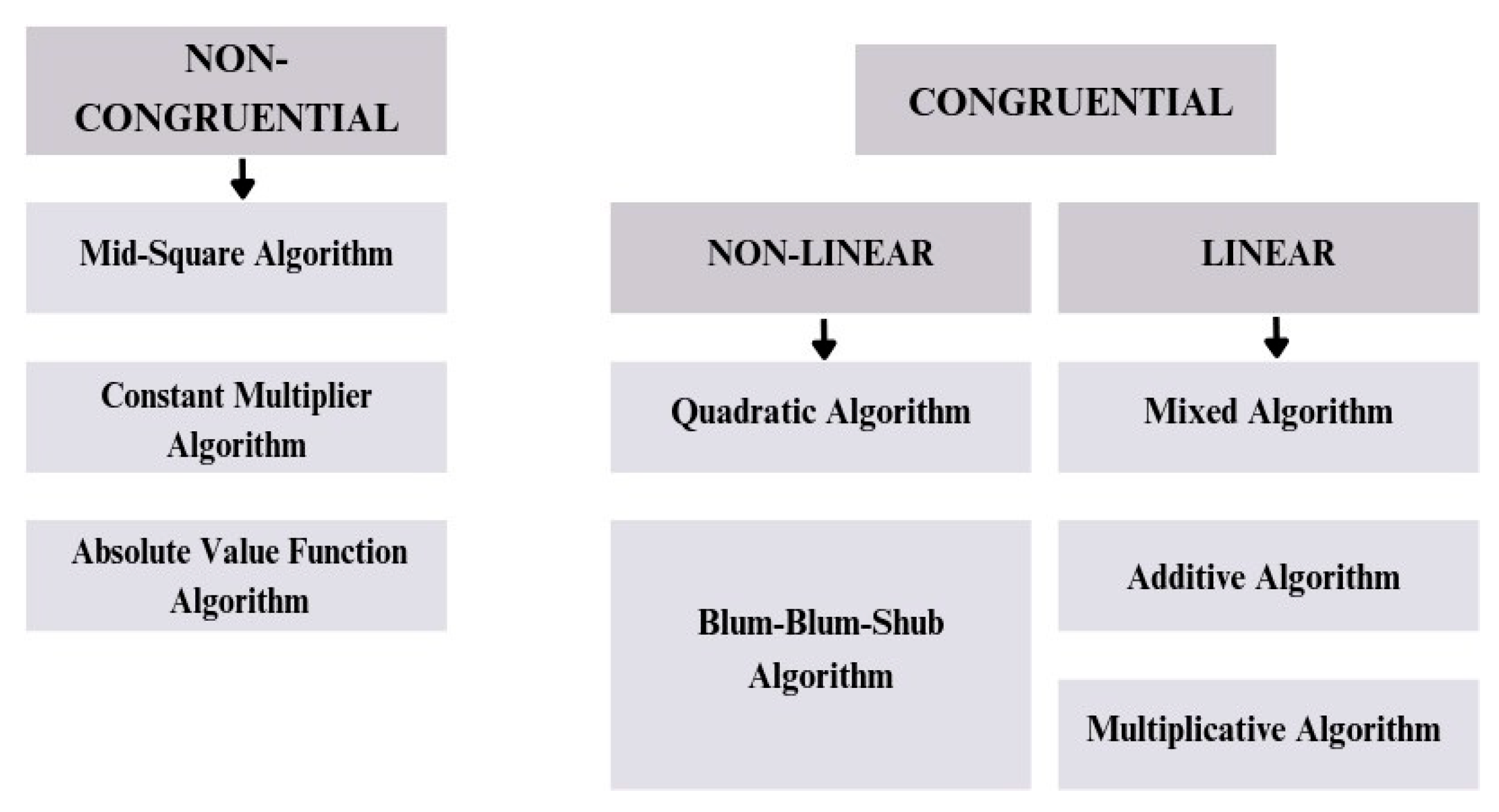

Bhattacharjee and Das (2022) argued that pseudo-random number generators (PRNGs) are a type of deterministic generator, i.e. derived from a mathematical function whose outputs appear to be random. According to Babaei and Farhadi (2011) it is desirable for PRNG algorithms to statistically satisfy certain requirements in order to be considered good, for example we can mention: uniform distribution, independence, large period and unpredictability.

We can also say that there are two main categories: Non-congruential and Congruential PRNG algorithms.

Figure 6.

“Types of PRNGs” by the author.

We say that a PRNG is congruent when it relies on a modular congruence relationship to generate the next sequence of numbers. A classic example of an algorithm with this structure is the LCG (Linear Congruential Generator) or DH Lehmer PRNG, which was one of the pioneering algorithms and therefore inspired the creation of many similar ones over time. Its formulation is shown below:

where:

Xn+1 = (a * xn + c) mod m

Xn+1 = next number of the sequence

Xn = the current number a = the multiplier

c = the increment m = is the modulus

mod = modulo operation.

It is common for there to be many models and algorithmic proposals, some of which may be better than others depending on the user's objectives. In this sense, like Machicao (2017), it is common to see scientific publications addressing the quality of PRNGs, as recently demonstrated by Boutsioukis (2023) in his article comparing models known as the Mersenne Twister by Matsumoto and Nishimura (1998), the Middle Square Method by John Von Neumann (1946) and the Linear Congruential Generator (LCG) by DH Lehmer and Thomson and Rotenberg (1958).

As Stinson (2005) points out we must emphasize although most pseudo-random algorithms are not the most suitable for the field of cryptography, there are some mathematical models of PRNGs that have historically been considered very good for information security, such as Blum-Blum-Shub by Blum et al. (1986) and Fortuna by Schneier and Ferguson (2003).

Although a pseudo-random function (PRF) is not exactly a PRNG due to some subtle differences that can be better explored through Vadhan (2012), we can say that the Naor and Reingold (1997) algorithm also has a strong structure for possible cryptographic applications.

Nowadays, we can mention some very promising new PRNGs in this field involving information security, such as Itamaracá PRNG by Pereira (2022) due to its results in statistical tests as well as the fact that its design employs the absolute value function as a form of "mirroring", making it even more difficult for someone malicious to take the path back and discover the initial seeds.

In addition, Itamaracá has been pointed out by Levina et al. (2022) and corroborated by Aslam and Arif (2024) because it is considered simple and practical, as well as because it generates aperiodic sequences, i.e. without having a cycle ending moment at first. In this sense, repetition will occur if and only if the values of the 3 initial seeds happen to appear in the middle of the sequence in exactly the same order, which, in probabilistic terms, will basically make it unlikely/impossible for a cycle to occur with repetition as we increase the maximum value of the interval and a uniform distribution.

Below, we can see the Itamaracá PRNG formulation:

As fixed parameters, we have:

M ∈ℝ+: a maximum positive value, representing the upper limit of the scale of the numbers generated.

λ∈ℝ+: a positive multiplicative constant whose values must be very close to 2 (1.97, 1.9886, 1.99545...).

As initial values, we have:

s1, s2, and s3 ∈ℝ+: three starting numbers called seeds, needed to start the random sequence.

As derived variables, or intermediate process ip, we have:

and the generated sequence can be represented by:

Δs : s3 – s1

xn : or nth pseudorandom number generated.

At each iteration n, the pseudo-random number xn is generated by the formula:

Δs = s3 – s1

s′1 = s2, s′2 = s3, s′3 = xn.

It is common that, due to the deterministic nature and the fragility that may exist in some PRNG algorithms, some scientists over time come to propose improved solutions to these classical models, such as the one proposed by Rahimov (2011), Widynski's “Squares” (2020) and the method of Padányi and Herendi (2022) with all of these with the proposal to improve the model of the Mean Square Method, proposed by John von Neumman (1946).

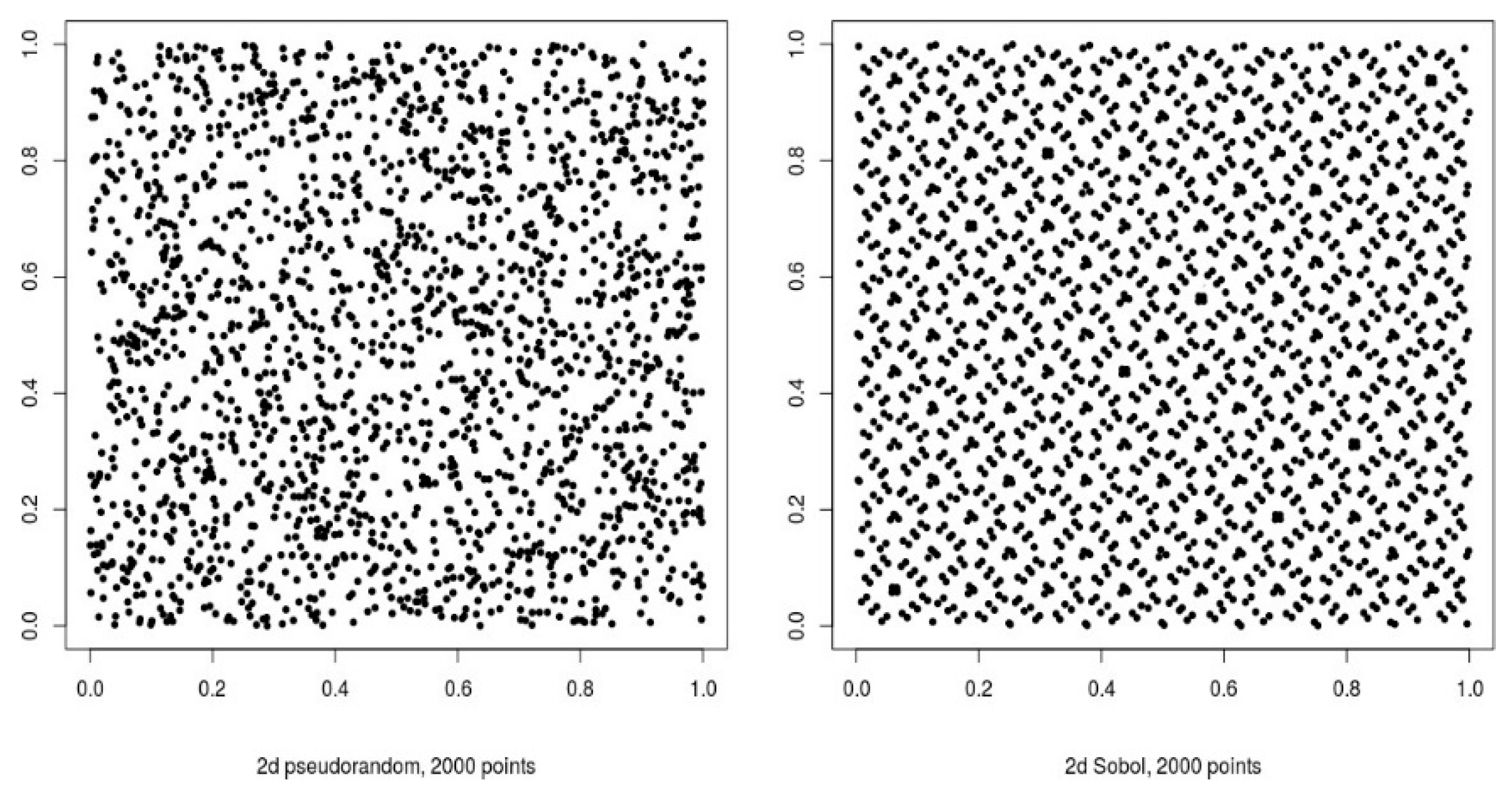

Quasi-RNGs, which stand for Quasi-Random Number Generators, are also deterministic in nature and very similar to PRNGs. However, according to Dutang and Wuertz (2009) and corroborated by Smith et al. (2017) the focus of Quasi-RNGs is more on creating a model that tries as much as possible to make each random number output equally (rather than approximately) distributed within the intervals considered.

Figure 7.

Bivariate uniform samples - pseudorandom (left) and quasirandom (right) Smith et al. (2017).

Figure 7.

Bivariate uniform samples - pseudorandom (left) and quasirandom (right) Smith et al. (2017).

It should be clear and understandable that pseudo-random number generators (PRNGs), despite their great relevance, are actually part of a larger scope of topics entitled “Pseudorandomness”. Due to its inherent particularities and rich extension, we see from Vadhan (2012) that other points are also important, such as the computational model and complexity classes, randomness extractors, expander graphs, list-decodable codes, derandomization techniques, among other topics. As such, this field of study should be seen as a separate field, deserving its own discipline for study.

2.6.2. True Random Number Generators (TRNGs), Quantum Random Number Generators (QRNGs) and Quantum Techniques

We also have TRNGs (Truly Random Number Generators) which, according to Herrero- Collantes and Garcia-Escartin (2016) are those designed to produce unique and unpredictable random sequences that normally use natural sources such as atmospheric noise and radioactive decay, for example. Sunar et al. (2006) presented their theoretical and practical approaches to a TRNG that has withstood adversarial attacks.

More recently, we have the so-called QRNGs, an acronym for Quantum Random Number Generators, which we can also say are part of the TRNG category, however, due to some particularities within quantum physics, it is preferable to classify them as a separate category.

As we can see from Herrero-Collantes and Garcia-Escartin (2016), Quantum Random Number Generators (QRNGs) exploit quantum mechanics phenomena to generate genuine random numbers. On the quantum mechanics, Avigliano (2014) explores the intersection of Rydberg atoms and superconducting cavities, focusing on manipulating and controlling these systems for quantum information processing. Uria et al. (2020) presented an innovative protocol to deterministically prepare a Fock state of a large number of photons in the electromagnetic field. Among these and other results, quantum algorithms can be developed over time that exploit the power of quantum computing to solve problems usually linked to optimization issues in different areas of knowledge, including cryptography, artificial intelligence and medicine.

Among the two main forms of QRNGs are those designed from the perspective of quantum optics (i.e. single photon emission, quantum interference, polarization of photons, understanding of light states, among others) and non-optical quantum (i.e. radioactive decay, thermal noise in electronic components, spin of subatomic particles, quantum vacuum fluctuations, among others).

Just as in the field of PRNGs TRNGs, where it is common to observe several different techniques behind their global developments, QRNGs are no different. As an example of its vast ramification, Contreras et al. (2021) introduced a robust and efficient iterative method for the reconstruction of multipartite quantum states from measurement data. The method shows fast convergence, especially in high-dimensional systems, and is applicable to any informationally complete set of generalized quantum measurements.

Furthermore, as demonstrated by the authors, its robustness against realistic errors in state preparation and measurement steps makes it a potentially valuable tool for quantum information processing and for emerging technologies such as Quantum Random Number Generators (QRNGs). This was just one of the papers included in more than 50 academic materials and publications carried out by a global project called “Quantum Random Number Generators: cheaper, faster and more secure” funded by the European Union.

Other outstanding works in this emerging field are Hensen et al. (2015) which reports a breaktrhough experiment on the Bell Inequality test, a fundamental concept in quantum mechanics that explores the nature of reality and locality. Among its main results, the data implied a statistically significant rejection of the local-realist null hypothesis, so the experiment provides strong evidence against local realism, strengthening the worldview of quantum mechanics. Through this and other experiments, Abellán (2018), Amaya, and Tulli et al. (2019) idealized Quside and, with it, developed technologies to strengthen information security as well as an important step towards new “quantum level” randomness certifications.

Meng et al. (2024) developed a GD-enhanced quantum RNG based on quantum walks of single photons in a linear optical system which, in addition to its good properties for uniform distributions, is also considered a flexible model for other probability distributions.

2.6.3. Other Categories of Random Number Generators

In addition to the categories mentioned above as the main ones, we can also say that there are other designs and ways of generating random numbers as well as forms of encryption for the information security area. Among these, we can highlight those derived from Chaotic Maps such as those worked on by Machicao (2018), Moysis et al. (2022) and Moysis et al. (2023).

There are some other PRNG algorithms whose design is also differentiated, such as Rule 30 developed by Wolfram (1983), whose main sources are techniques such as cellular automata, which, in turn, as also corroborated by Mariot el al. (2021), uses a set of rules similar to the so- called “Game of Life” within the field of study of mathematics with regard to evolutionary algorithms. In addition, another paper highlighted in the bibliography is that of Balková et al. (2016) who, through their studies, came up with an innovative technique for generating an aperiodic pseudo-random sequence using the infinite word technique.

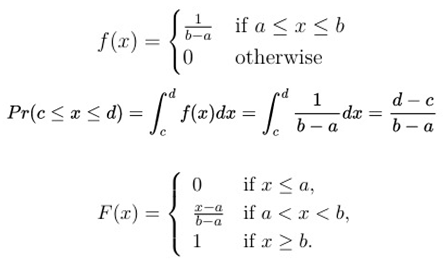

2.1. Uniform Distribution

We can say the uniform distribution is one of the main probability distributions in statistics, especially when it comes to the field of study of random variables. The authors Blitzstein and Hwang (2019) state this distribution assumes each element within an interval (a, b) has the same probability of occurrence, so we can say within this interval we can expect sequences of random numbers.

Below, for example, is the probability density function (PDF) of the uniform distribution for continuous values:

The expected value for a continuous uniform distribution is:

And its respective variance:

The PDF (Probability Density Function) represents the “density” of probability at each point in the interval. In the uniform distribution, the PDF is constant throughout the interval, indicating the probability of any value occurring within that interval is the same.

The CDF (Cumulative Distribution Function) of a uniform distribution can be said to increase linearly from 0 to 1 in the interval [a, b]. This means the cumulative probability grows proportionally as x moves from a to b.

Figure 8.

PDF and CDF graphical analysis by Blitzstein and Hwang (2019).

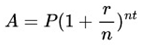

2.1. Compound Interest

As Campolieti and Makarov (2018) point out, compound interest is a way of calculating the interest on an investment or loan, where the interest for one period is added to the initial principal balance, and in the following periods, interest is calculated on this new total value (initial principal balance + accumulated interest). By this definition, and as also noted by Smart and Zutter (2020), it is “interest-on-interest” growing exponentially over time.

The following is the formulation of compound interest usually presented in financial mathematics bibliographies:

A = Final amount, resulting from the sum of the initial principal balance and Interest

P = Initial principal balance

r = interest rate, which must be on the same time basis as the period

n = number of times interest applied per period

t = number of time periods elapsed

Through Stojkovic et al. (2018) and Karn et al. (2024) we see that compound interest has always been a topic of debate throughout history by various mathematicians, from the studies of Jakob Bernoulli, Leon John Napier, and Leonhard Euler to the present day.

Nowadays, compound interest continues to be explored in various fields, including actuarial sciences, economic sciences, and even more specific areas like Computer Science through machine learning algorithms and algorithmic complexity. As Bartlett (1993) pointed out, it is also relevant in biology, where it is used to study population growth, from bacterial cultures to animal populations, and demographic growth. We can also observe this exponential behavior through Ma (2020) in his approach to dealing with epidemic scenarios as well as in Seshaiyer et al. (2020) when addressing the importance and limitations of mathematical models to model covid-19.

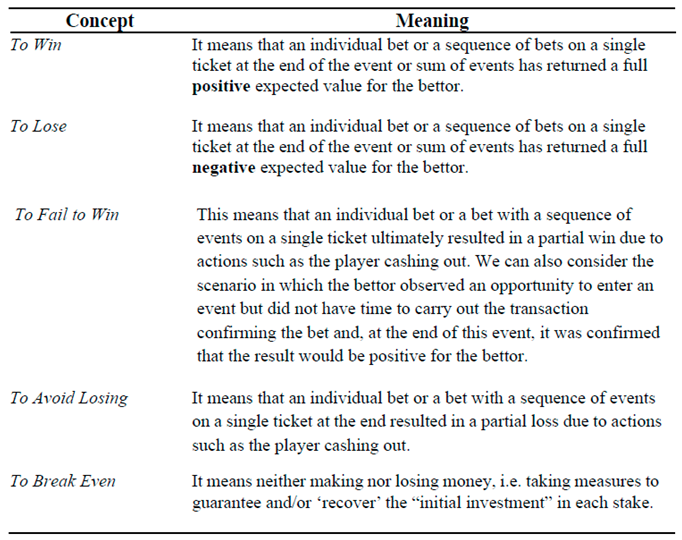

2.9. Sports Betting Universe

2.9.1. Understanding the Basics

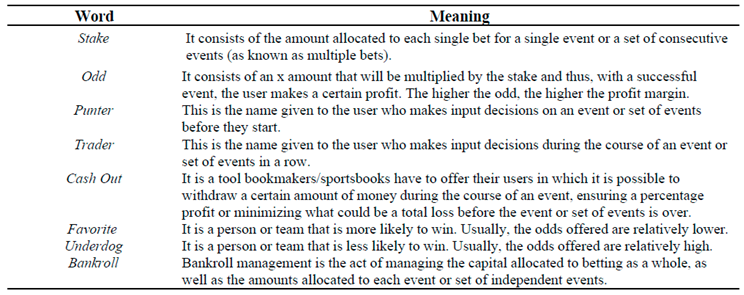

Within the world of sports betting, there are often very specific expressions inherent to this environment. Below we will look at the meaning of some of the most popular ones, which will be essential for a better understanding of this study.

Table 2.

Some basic concepts within the world of sports betting.

2.9.2. Sports Trading Market

According to Etuk et al. (2022) the world of sports betting has grown exponentially in recent years and reached the mark of more than 30,000 companies around the world with business models based on sports betting in 2019. In the same year, this market exceeded more than US$ 200 billion.

As Harris (2024) pointed out, through the repeal of the Professional and Amateur Sports Protection Act in 2018, sports betting was legalized and more than half of the states in the united states were covered by this law. According to the author, this field opens up new business opportunities and jobs, but also new challenges, both in terms of the illegality of certain platforms and the impact of betting on people's lives, especially in virtual environments. In this sense, it is necessary for government bodies, the academic community, and society as a whole to be in dialogue to debate this new business model that is here to stay.

2.9.3. The Mathematics Behind Sports Betting

2.9.3.1. Understanding Odds

The so-called “odds” refer to the probability of an event occurring. They are usually published by bookmakers (or sportsbooks, in a more modern term) in fractional or decimal form (which will be the focus of this study). As pointed out by Sladić and Tabak (2018), odds estimations by sportsbooks are carried out by experts who, in addition to relying on robust data structures, also factor in subjective analysis.

Table 3.

Probabilities of an event occurring in decimal representation by Buchdahl (2003).

| Decimal Odds | Probability | Decimal Odds | Probability |

|---|---|---|---|

| 1.1 | 0.91 | 3.25 | 0.31 |

| 1.11 | 0.9 | 3.4 | 0.29 |

| 1.13 | 0.89 | 3.5 | 0.29 |

| 1.14 | 0.88 | 3.6 | 0.28 |

| 1.15 | 0.87 | 3.75 | 0.27 |

| 1.17 | 0.86 | 3.8 | 0.26 |

| 1.18 | 0.85 | 4 | 0.25 |

| 1.2 | 0.83 | 4.33 | 0.23 |

| 1.22 | 0.82 | 4.5 | 0.22 |

| 1.25 | 0.8 | 5 | 0.2 |

| 1.3 | 0.77 | 5.5 | 0.18 |

| 1.33 | 0.75 | 6 | 0.17 |

| 1.44 | 0.69 | 6.5 | 0.15 |

| 1.5 | 0.67 | 7 | 0.14 |

| 1.53 | 0.65 | 7.5 | 0.13 |

| 1.57 | 0.64 | 8 | 0.13 |

| 1.62 | 0.62 | 8.5 | 0.12 |

| 1.67 | 0.6 | 9 | 0.11 |

| 1.73 | 0.58 | 9.5 | 0.11 |

| 1.8 | 0.56 | 10 | 0.1 |

| 1.83 | 0.55 | 11 | 0.09 |

| 1.9 | 0.53 | 12 | 0.08 |

| 1.91 | 0.52 | 13 | 0.08 |

| 2 | 0.5 | 15 | 0.07 |

| 2.1 | 0.48 | 17 | 0.06 |

| 2.2 | 0.45 | 21 | 0.05 |

| 2.25 | 0.44 | 26 | 0.04 |

| 2.38 | 0.42 | 34 | 0.03 |

| 2.5 | 0.4 | 51 | 0.02 |

| 2.62 | 0.38 | 67 | 0.01 |

| 2.88 | 0.35 | 151 | 0.01 |

| 3 | 0.33 | 201 | 0.01 |

| 3.2 | 0.31 | 501 | 0 |

As we can see from the table above, as the multiplicative values of the odds increase, the probability of success of the event also decreases. The probabilities of success and failure for an event can be determined using the following formulas:

2.9.3.2. Calculating the Odds

According to Buchdahl (2003), if we consider that a bettor enters a sporting event with an odd of 1.80, this means we can expect approximately 55.56% chances of success and 44.44% chances of failure. If this bettor places a stake of $10 he would recover his “investment” while making a further $8 profit if the event in question ended positively, thus totaling $18.

Considering that a bettor enters a sporting event with an odd of 1.25, this means we can expect approximately an 80% chance of success and a 20% chance of failure. Therefore, if this bettor places a stake of $10, in addition to recovering his “investment”, preferably saying “risk”, since if he loses the bet he loses all his money, of $10 he will make a profit of $2.50 if the event has a positive outcome in the end, leaving a result of $12.50.

Now, let's consider another scenario in which a bettor enters a sporting event with an odd of 2.5, which means we can expect approximately a 40% chance of success and a 60% chance of failure. Therefore, if this bettor places a stake of $10 in the event that he wins the bet, he will be able to recover the amount he already had and make a profit of $15, thus totaling a positive amount of $25.

2.9.3.3. Historically, Mathematics and Statistics Have Always Been in Favor of the House

It must be clear and understandable to each of us that the business model of sportsbooks, casinos, lotteries, among other gambling variations, is completely based on the main bibliographic bases within the field of mathematics and statistics. Among the main topics we could say that it is common to use Risk Management, Return on Investment, Rates, Break-even Point, Strong and Weak Law of Large Numbers, Time Series Analysis, Expected Value, Probability, Probability Distributions, Clustering, among others, for example.