Submitted:

31 December 2024

Posted:

03 January 2025

You are already at the latest version

Abstract

This paper examines the transformative effects of decarbonization on electricity market design, emphasizing the challenges and opportunities posed by the rapid integration of renewable energy sources such as wind and solar. It analyzes the evolution of key wholesale market segments—including day-ahead, real-time, capacity, long-term purchase agreements, ancillary services, and transmission markets—highlighting their critical roles in managing the variability of renewable energy generation through efficient price signals and resource coordination. Variable renewable energy integration introduces significant operational challenges, including overgeneration risks, ramping capacity demands, forecast inaccuracies, and transmission constraints. Addressing these issues requires enhanced market flexibility, dynamic pricing mechanisms, and advanced real-time balancing strategies. This paper assesses these challenges, offering strategies to align generation with demand and optimize market outcomes. As electricity systems evolve, legacy market structures must adapt to incorporate carbon-free resources while maintaining grid reliability and economic sustainability. By exploring case studies such as Chile and California, the paper demonstrates the importance of targeted innovations in market design, regulatory frameworks, and operational technologies. It advocates for a holistic approach to ensure a reliable, affordable, and equitable transition to a decarbonized energy future.

Keywords:

decarbonization

; renewable energy integration

; electricity market design

; resilient grids

; clean energy dynamics

; energy transition

; power shift

; future-proof energy

1. Introduction

The primary objective of decarbonization is to

significantly reduce CO2 equivalent emissions (CO2e) into the atmosphere,

recognizing them as the principal driver of climate change. Decarbonizing the

economy involves replacing conventional CO2-emitting fossil fuel (FF)

technologies with renewable energy (RE) technologies like solar, wind, nuclear,

and fossil fuel technologies equipped with carbon capture and storage (CCS).

It also demands energy efficiency and reduced CO2 emissions related to Land

Use, Land-Use Change and Forestry (LULUCF), and other human activities [1] 1

Decarbonization strategies shape energy markets in

a variety of impactful ways. Civil society and regulatory frameworks can play a

crucial role by leveraging public pressure and implementing mandatory

regulations, such as Renewable Energy Targets (RET), Renewable Portfolio

Standards (RPS), or Clean Electricity Standards (CES). These policies often

create markets for Renewable Energy Certificates (RECs) or Clean Electricity

Certificates (CECs) and push for the phased retirement of fossil fuel plants.

CO2 taxes, making FF-based energy more expensive, are strong incentives for

investing in cleaner energy technologies and energy efficiency. Similarly,

cap-and-trade systems create a market for carbon allowances, allowing emissions

reductions to happen where they are most economically viable. This top-down

approach helps guide the overall direction and pace of the transition to

sustainable energy.

On a more individualized level, CO2 quotas or

licenses make consumers and businesses directly accountable for their carbon

emissions, fostering energy-saving behaviors and cleaner energy choices.

However, such a system may be complex to administer. Mandated energy efficiency

improvements offer another path toward reduced emissions across various

sectors. Though they can be costly, subsidies for renewable energy, such as

feed-in tariffs or premiums, help lower the financial barriers to clean energy

adoption.

Finally, investments in research and development

are essential to spur innovation in energy generation, energy storage solutions

(ESS), systems integration and operation, and efficiency, unlocking long-term

solutions and accelerating the transition to a decarbonized future.

Each instrument’s impact varies, affecting market

dynamics, investment decisions, and the pace of transition towards a

decarbonized energy future.

The expected evolution of the power sector should

be characterized by the gradual substitution of FF generation, especially those

lacking CCS, with renewable sources like solar photovoltaic (PV), wind,

nuclear, and other low CO2e emission technologies.

Historically, the power system was designed for

baseload plants to meet demand on continuous high-output operations. Thermal

power stations, including coal, geothermal, and nuclear, typically exhibit

availability factors ranging between 70% and 90% or higher [2]. In contrast, renewables such as solar and wind

offer variable output contingent upon weather, daylight, and wind conditions,

resulting in minute, hourly, daily, seasonal, and yearly variations in energy

supply. The increasing variability and uncertainty in power generation—both

from utility-scale sources and a growing share of Distributed Energy Resources

(DERs)—across different geographic regions and temporal scales necessitates a

more adaptive and responsive power system infrastructure.

This transition also occurs with a growing

electrification trend across households, industry, and transportation. As

CO2-emitting technologies phase out, they are being replaced by cleaner

alternatives powered by electricity, as is happening with the introduction of

electric vehicles (EVs).

Thus, the primary challenges for power system

development and operation involve incorporating, integrating, and managing

increasing shares of variable renewable energy (VRE) and distributed generation

(DG) sources. While traditional market structures are centralized,

decentralization via DERs like rooftop solar, batteries, and microgrids

disrupts this model. This shift introduces a more sizable number of generation

units, several with small plate capacity and variable output profiles,

geographically dispersed and out of the reach of the System Operator (SO), all

while the SO (Independent Systems Operators -ISOs- and Regional Transmission

Organizations -RTOs-) - must ensure system reliability [3–6] 2

To address these challenges, expanding transmission infrastructure, ESS,

accommodating VRE, and implementing resource-enhancing technologies, such as

advanced communication and operational and control technologies that facilitate

the coordinated dispatch of all resources to match supply and demand in

real-time, are crucial. The historical baseload paradigm relying on large,

centralized plants has been challenged to evolve into a more flexible system

capable of adapting to demand and renewable generation variability.

Electricity markets are pivotal in facilitating

trade and resource allocation by providing a structured framework for valuing

and pricing tradable items. They can develop organically or designed to enable

the transfer of ownership rights. In the electric power industry, various

electricity market structures exist. Some rely on competitive bidding to

determine market-based prices, while others depend on administratively set

prices.

Physical and financial markets exist in electricity

and other markets. Physical electricity markets encompass the infrastructure,

institutions, and participants in, for example, trading energy and related

services like capacity and ancillary services. They are distinguished and

identified by location-based physical attributes and system conditions.

Locational Marginal Prices (LMPs) represent energy prices at specific grid

nodes and times (spatial distribution of electricity prices). Trades can occur

in real-time spot markets to balance instantaneous supply and demand of energy

and forward markets for future delivery, depending on market constructs

timeframes ranging from 30 minutes to multiple years. Market design aims to

efficiently manage grid constraints and electrical losses while matching

generation with load across the transmission system. Both spot and forward

physical markets are essential for reliable grid management, planning, and

investors’ decisions.

In contrast, financial electricity markets, also

known as futures and derivatives, center around trading financial instruments

whose values derive from underlying physical electricity prices. 3 A derivatives transaction doesn’t typically involve the transfer of any

physical product – just money. Electricity futures and similar derivatives

enable market participants to mitigate or hedge price risks, like LMPs, within

a competitive electricity market. These futures contracts, being legally

binding and negotiable, stipulate the future delivery of a commodity. In many

instances, physical delivery doesn’t occur, and the closure of the futures

contract is executed through buying or selling on or around the delivery date.

Financial instruments include derivatives, securities, options, swaps, forward

and futures, and insurance products linked to energy assets [7,8]. These markets have distinct structures,

institutions, participants, and products influenced by financial supply and

demand drivers. Participants may use financial markets for risk management,

speculation, or portfolio optimization without owning physical assets. These

markets provide flexibility and liquidity.

The key distinction between physical and financial

electricity markets remains in the nature of the traded products and

participants’ motivations. Recognizing this difference is vital for the

electricity market’s design and analysis. EIA data shows that 2021 US electric

industry sales to ultimate customers reached USD 422 billion, while for the

Americas, the energy derivative market size, mainly the US, by notional value,

registered by the World Federation of Exchanges for CME Group was USD 33

trillion, what underscores the difference in market size between the physical

market and the derivatives market, with the last being about 80 times bigger [9].

Flexibility has become essential in decarbonized

markets, as the fluctuating output from VRE sources requires energy storage

(ES), demand response (DR), and flexible generation to maintain grid stability.

To accommodate the growth of VRE and distributed energy resources (DERs),

significant investments in grid infrastructure, including transmission

upgrades, ES, more granular pricing, flexible markets, and advanced smart

metering and management technologies, are crucial.

Decarbonization also calls for comprehensive policy

and regulatory reforms, such as RPS, carbon pricing, and streamlined

permitting, to facilitate the efficient integration of renewable energy. These

regulatory shifts have and continue to influence market dynamics and investment

decisions, steering capital away from traditional FF infrastructure towards RE

projects and technologies.

The rise of decentralized energy producers,

prosumers, and smart grid technologies is disrupting traditional centralized

electricity markets, fostering competition and innovation. The need for

flexibility—through ES, DR, and adaptable generation—becomes critical as VRE

expands. This transition is poised to reshape industrial activity, job markets,

and the future of energy infrastructure.

To effectively navigate the complexities of

decarbonizing electricity markets, this paper adopts a conceptual framework

that integrates key components driving market evolution and operational

adaptation. The framework centers on three interconnected pillars: the

integration of VRE, the transformation of market structures, and the role of

policy and technological innovation. These pillars interact dynamically,

shaping how markets address challenges such as intermittency, grid flexibility,

and financial sustainability while pursuing decarbonization goals. By linking

operational challenges with economic and environmental objectives, this

framework provides a cohesive lens to analyze the evolving dynamics of

electricity markets, emphasizing the importance of holistic strategies to

ensure reliability, affordability, and sustainability in the energy transition.

This approach also highlights feedback loops where policy and technological

advancements influence market outcomes, fostering resilience in an increasingly

decentralized and renewable-powered energy landscape.

This paper analyzes trends on the impact of

decarbonization on wholesale electricity markets, on markets where supply and

demand dynamics, bilateral agreements, and administrative price-setting models

determine prices. However, the decarbonization of the energy matrix is not the

only driver of electricity markets [10]. As

economies worldwide transition toward low-carbon energy sources, electricity

markets must adapt to accommodate these new realities. While this analysis

primarily emphasizes the effects of decarbonization on competitive physical

wholesale electricity markets, it is essential to briefly mention the

interconnected nature of financial markets, given their significant role in

hedging risk and supporting investment in the evolving energy landscape.

The results emphasize that existing market designs,

pricing mechanisms, and grid infrastructure must adapt to integrate VRE while

ensuring reliability and affordability efficiently. DERs are disrupting market

structure, and price volatility is expected to increase, as VRE can cause

significant price drops during periods of overgeneration and low demand, as

well as sharp spikes during shortages. This volatility impacts power plant

revenues, with FF generators seeing reduced operating hours and declining revenues,

while VRE projects, supported by long-term contracts and evolving market

incentives, become more economically viable. The paper also underscores the

role of policy and regulatory frameworks, such as carbon pricing and RET, RPS,

REC, and CES, in shaping market dynamics and investment patterns. Additionally,

the transition towards a low-carbon energy system is introducing new market

players and creating opportunities for innovation. Still, it also poses

economic challenges, including the risk of stranded assets in the fossil fuel

sector.

To explore the transformative impact of

decarbonization on electricity market design, this paper adopts a mixed-methods

approach, combining qualitative and quantitative analysis within a cohesive

conceptual framework. The research draws on case studies to highlight regional

challenges and opportunities in integrating high shares of VRE. Pri-mary data

is sourced from open-access repositories, policy reports, and peer-reviewed

lit-erature from leading energy institutions. The analysis focuses on three interconnected

pil-lars: the integration of VRE, the transformation of market structures, and

the role of policy and technological innovation. These pillars interact

dynamically, addressing challenges such as intermittency, grid flexibility, and

financial sustainability while pursuing decar-bonization goals. The conceptual

framework synthesizes trends in market dynamics, op-erational challenges, and

policy adaptations, illustrating how market design, renewable integration, and

system flexibility interact to shape the future of decarbonized energy

sys-tems. This approach provides a comprehensive, evidence-based evaluation of

electricity market trends, emphasizing the importance of holistic strategies to

ensure reliability, af-fordability, and sustainability while fostering

resilience in an increasingly decentralized and renewable-powered energy

landscape.

2. Wholesale Electricity Markets

The design of electricity markets varies across

countries and regions, yet a common overarching framework prevails. This

framework typically encompasses energy, capacity, ancillary services,

transportation, storage, Long Term Purchase Agreements (LTPA) or Power Purchase

Agreements (PPA), and distribution markets, some of which operate at wholesale

and retail levels. Retail markets pertain to selling electricity directly to

consumers in distribution markets. In contrast, wholesale markets predominantly

revolve around electricity transactions among generation and transmission

sectors, electric utilities, and electricity traders before the final sale to

consumers or large consumers, typically at high voltages. In contrast, retail

electricity markets center around the sale of electricity within an electricity

distribution grid, often at lower voltages, targeting end consumers, including

households, commercial establishments, and smaller industrial consumers. The

local distribution company and third-party aggregators or suppliers utilizing

the distribution grid commonly manage this sale.

Historically, real-time operations in the energy

sector were defined by the constant variation of demand, where capable

generation units adapted their output in a process known as load following to

accommodate these ongoing demand shifts. ISO/RTOs utilize a centralized

economic dispatch based on generators/demand bids, or power plants' operational

costs merit order, to optimize the use of these generators and minimize

real-time operational costs.

Key wholesale market segments include bilateral

long-term contracting, day-ahead scheduling, real-time dispatch, capacity

auctions, ancillary services procurement [11],

and transmission markets. When the conditions enable competitive markets, each

segment establishes prices through competitive mechanisms based on supply and

demand fundamentals. Well-designed and complete markets provide incentives and

price signals to attract investment in a flexible, low-carbon resource mix

aligned with policy goals. Wholesale electricity markets are generally

organized into several segments where prices are determined:

- Electricity energy markets - Long-term power purchase agreements, day-ahead markets, and real-time/balancing markets facilitate the buying and selling of electricity for final consumption.

- Reliability/Capacity markets - Capacity obligations are purchased through centralized auctions and bilateral contracts to ensure adequate generation and demand-side resources are available to meet system reliability requirements.

- Ancillary services markets - Grid resources bid or agree on bilateral contracts to provide essential reliability services like frequency regulation, operating reserves, voltage support, and black start.

- Transmission markets - Prices for transmission networks, like access rights, are determined to efficiently manage grid congestion and losses.

2.1. Day-Ahead and Real-Time/Balancing Markets

Day-ahead and real-time wholesale electricity

markets facilitate reliable grid management and transparent pricing. In the

day-ahead market, generators offer their availability, and buyers bid on their

demands for the next day, resulting in financially binding schedules and

prices. Then, in real-time, actual generator dispatch and pricing are

determined every 5-15 minutes based on market design and precise system

conditions. The day-ahead projections provide price certainty for participants

to plan, while the real-time market ensures supply and demand are balanced.

These organized markets dynamically coordinate competitive resources on the

complex challenges of electric grid operations.

Some electricity systems that utilize day-ahead and

real-time market structures are: PJM - Covers parts of the Mid-Atlantic and

Midwest US states [12,13]; ISO New England

(ISO-NE) - Covers the six states in New England [14];

California ISO (CAISO) - Covers most of California [15];

New York ISO (NYISO) - Covers New York state [16]; Electricity Reliability Council of Texas

(ERCOT) - Manages most of Texas [17]; EU

European Union’s Day-ahead and intraday electricity markets,4 where Power Exchanges

organize trading and operate these markets [18];

Europe - Countries like Germany, the UK, and the Nordic [19]; Australia [20,21];5 Norway [22];6

Singapore [23];7

Canada, Alberta and Ontario [24–26];8 New Zealand [27,28]. In the US [29],

restructured competitive wholesale markets have dominated in the Northeast,

Mid-Atlantic, Texas, and parts of the Midwest.9

Meanwhile, traditional cost-based utility dispatch, explained below, continues

to be used across much of the Southeast, Southwest, and Northwest, as well as

some isolated systems where vertically integrated utilities have persisted

after deregulation. Thus, most utilities and retail choices have generally

embraced day-ahead and real-time market structures in large market-oriented

economies with larger interconnected systems and diverse resources.

While ISO/RTO runs day-ahead (or other time

intervals) and in real-time/balancing electricity markets, some general

features or main architectural characteristics, which vary according to market

design rules, are:

Day-Ahead Markets:

- Operate the day before electricity delivery (hence “day-ahead”).

- Participants submit bids to buy or offers to sell electricity for each hour of the next day.

- The system operator matches supply and demand for each hour to determine the market clearing price at the minimum cost, safeguarding system reliability and electricity transmission constraints.

- Provides price signals for generators and load-serving entities to plan their operations and bidding for the next day.

- Results in financial commitments to buy or sell electricity at the day-ahead price.

Real-Time/Spot Markets:

- Operate in real time as electricity is delivered, with intervals that can be 5 minutes.

- The ISO/RTO uses it to balance differences between day-ahead schedules and real-time demand/generation at the minimum cost, safeguarding system reliability and electricity transmission constraints.

- Prices fluctuate minute-to-minute based on actual system conditions.

- Generators are paid the real-time price for any extra electricity produced.

- Load-serving entities pay the real-time price for any extra electricity consumed.

- Provides price signals to incentivize generators to follow dispatch instructions.

Key Differences:

- Day-ahead prices are based on expected conditions and bids, whereas real-time prices reflect actual conditions.

- Day-ahead markets provide financial certainty, while real-time markets balance physical differences.

- Day-ahead markets have higher trade volumes, while real-time markets ensure reliability.

- Day-ahead prices are generally less volatile than real-time prices.

The actual physical operation of balancing

electricity supply and demand often deviates from the projections made in the

day-ahead electricity market. These disparities can arise due to unforeseen

shifts in supply or demand conditions that differ from the anticipated

scenarios envisioned during the day-ahead electricity market forecasting and

closure.

In summary, the day-ahead market facilitates

forward price discovery and financial commitments, while the real-time market

ensures the physical balance of supply and demand. Together, these markets

contribute to an efficient and reliable wholesale electricity market.

2.2. Capacity Market

A capacity market is a pivotal mechanism ensuring

an ample supply of future generation, encompassing potential demand-side

capacity aligned with projected needs. Its core mission is to stimulate

investments in new capacity and secure commitments through auctions, often

scheduled three or more years ahead. Participants receive capacity payments

for pledging their capacity, irrespective of actual energy dispatch.

In the United States, some ISOs/RTOs feature

capacity market mechanisms. However, it’s crucial to note that not all

ISOs/RTOs in the US adopt capacity markets; some rely solely on energy markets [30].10

PJM’s capacity market, known as the Reliability Pricing Model (RPM), stands out

prominently [31]. Operated by PJM

Interconnection, the largest wholesale electricity market operator in the US,

RPM plays a critical role in ensuring a reliable and secure electricity supply.

RPM operates through periodic auctions designed to

procure commitments from generators, load-serving entities, large consumers,

and other resources to provide a specific amount of generation capacity in the

future, typically three years ahead.

Participants in RPM auctions commit to delivering

capacity during specified future periods, assuring the grid operator of

sufficient resources, especially during peak periods. The RPM, as a capacity

market, serves to provide investment signals, with the auction process

intending to send price signals encouraging new investments where and when

needed for system reliability.

Generators that clear the auction and commit to

providing capacity receive compensation, regardless of whether they produce

electricity during the contracted period. In PJM, the RPM may also allow

demand-side resources, like demand response programs, to participate, offering

a comprehensive approach to meeting capacity needs.

Some ISO/RTOs, such as PJM, incorporate a penalty

structure enforcing capacity commitments. Resources committed to supply

capacity face financial penalties if unavailable during the delivery year.

This structure ensures resources meet their reliability obligations, with

potential penalties serving as a crucial incentive for standing behind auction

commitments [32].

The capacity mechanisms in the EU [33] have evolved as tools to ensure adequate

electricity generation capacity is available to meet demand, especially during

peak times. They have been a subject of regulatory development since the early

2000s, with key moments in 2003 and 2009 and a significant overhaul in the 2019

electricity market reform. Initially introduced to address the "missing

money" problem—where energy-only markets did not provide sufficient

incentives for investment in new capacity—the EU has progressively aimed to limit

their use on a perceived risk of potential market distortions. In response to

the energy crisis following Russia's invasion of Ukraine, the EU implemented

several emergency measures, and the European Commission proposed comprehensive

electricity market reforms in March 2023, which were agreed upon by EU member

states in December 2023, where among the Key elements is the support for

long-term capacity mechanisms aligned with decarbonization goals.

Chile, which pioneered the liberalization of

electricity markets in the 1980s [34],

established a payment mechanism for capacity, currently a power sufficiency

mechanism, to ensure sufficient generation capacity is available to satisfy the

maximum demand for the electrical system. This capacity payment is determined

based on each plant’s contribution to system reliability, availability during

peak demand periods, and the overall needs of the electrical system to maintain

an adequate reserve margin. However, the capacity payment is not made

irrespective of whether a generator unit is called in the day-ahead operations

planned dispatch. Instead, the system coordinator calculates the capacity

payment annually to adjust for changes in the electricity market, demand

forecasts, and the entry or exit of generation units [35].11

The debate over electricity market design

—specifically between energy-only models with scarcity pricing and

energy-plus-capacity markets—remains complex and contentious, with several

critical points of dispute [36–49]:

- Market Efficiency: Supporters of capacity markets argue that these mechanisms ensure sufficient generation capacity to meet peak demand, thereby maintaining grid reliability. Critics contend that capacity markets can distort price signals, potentially leading to costly overinvestment in unnecessary capacity.

- Cost to Consumers: Proponents believe capacity markets promote long-term price stability and secure supply, benefiting consumers in the long run. Detractors, however, argue that these markets increase consumer costs by compensating generators for potential capacity rather than actual production, which may not always be economically justified.

- Impact on Renewable Energy: Capacity markets can, some argue, facilitate renewable integration by ensuring a reliable backup capacity. Yet, others warn that capacity markets tend to favor traditional fossil fuel generators, potentially slowing the transition to cleaner energy sources.

- Complexity of Market Design: Advocates assert that capacity markets can be tailored to meet specific regional needs and policy goals, helping to stabilize prices that might otherwise become volatile under scarcity pricing alone. Conversely, critics argue that capacity markets add unnecessary complexity to electricity markets, creating opportunities for manipulation by market participants.

- Impact on Innovation: Capacity markets may provide revenue certainty, potentially encouraging investment in new technologies. However, some argue they may stifle innovation by favoring established technologies and existing market structures over more disruptive advancements.

While capacity markets may offer stability and

reliability, they also bring concerns about costs, complexities, and potential

drawbacks for market power, innovation, and renewable energy integration.

This controversy reflects broader debates about how

best to ensure electricity reliability, affordability, and sustainability in

evolving power markets. The appropriateness of capacity markets often depends

on specific regional circumstances and policy priorities, where we should

acknowledge that both energy-only and energy-plus-capacity markets are subject

to market power and imperfections, which need to be addressed in any market

design.

Notwithstanding, dynamic modeling that integrates

energy and capacity pricing can offer significant benefits, capturing the

effects of long-term investment decisions and technological advancements. While

simpler market structures have the advantage of lower transaction costs, they

often impose constraints, such as setting upfront capacity prices to zero,

which can reduce optimization variables and welfare compared to more flexible

systems that allow for dynamic energy and capacity pricing.

Innovation incentives and risk allocation are vital

considerations in any market design, whether it follows an energy-only or

energy-plus-capacity framework. These factors should be explicitly accounted

for, as they influence market adaptability and encourage new technologies.

Setting prices optimally in complex markets is

challenging, yet arbitrarily constraining prices—such as eliminating capacity

pricing—can lead to even more significant losses in welfare. Thus, with a

broader range of pricing options, the theoretical advantages of

energy-plus-capacity markets may yield tangible benefits if these market

designs can navigate real-world challenges effectively. In this way, markets

with greater flexibility and nuanced pricing mechanisms can better support

long-term goals of stability, innovation, and welfare.

While both market designs face challenges, a

well-designed market might aim to maximize social welfare, particularly when

considering long-term, dynamic effects. However, the effectiveness of either

approach ultimately depends on the specific implementation and how it addresses

real-world market complexities.

2.3. Long-Term Purchase Agreements

In general, Long-Term Purchase Agreements (LTPA)

are bilateral contracts between buyers and sellers, facilitating the purchase

of electricity over extended periods, typically one year or longer. These

agreements are voluntary and privately negotiated, existing externally to

ISO/RTO markets, where ISO/RTO does not have direct involvement.

Nevertheless, ISO/RTO considers the impact of LTPA

on scheduling, resource dispatch, and market prices. Load-serving entities and

large consumers utilize these agreements to secure generating capacity and

energy, aligning with their anticipated demand projections.

In PJM, generators engaged in the ISO/RTO capacity

market may offer surplus capacity not committed in LTPA to ISO/RTO Reliability

Pricing Model (RPM) auctions.

During day-ahead market scheduling, resources bound

by LTPA submit contracted MW amounts on their offers/bids, which ISO/RTO

utilizes for dispatch purposes. In real-time operations, resources under

long-term contracts can be self-scheduled or economically dispatched. LMPs

remain unaffected by the nature of bilateral transactions under long-term

agreements.

Thus, while the practice is that ISO/RTO

acknowledges the existence of LTPA, they refrain from direct negotiation or

regulation of these external transactions. However, ISO/RTO incorporates the

quantities from these agreements in its scheduling and dispatch processes to

uphold system reliability.

2.4. Ancillary Services Market

Ancillary Services (AS) help manage the various

technical challenges that arise in generating, transmitting, and distributing

electricity; the Ancillary Services Market, sometimes called the Reliability

Market,12

is a crucial component of electricity markets, providing essential support

services to ensure the power system’s reliability, stability, and flexibility.

The provision of AS is critical to real-time grid

operations. Operators continuously monitor the grid and, based on system

conditions, call upon resources that provide AS to address specific needs.

These services specifically target frequency control, voltage support, and grid

stability issues, operating within short timeframes, even microseconds,

extending beyond electricity generation and delivery. By swiftly addressing

sudden shifts in demand, like the loss of sizeable industrial consumption,

unforeseen outages, or disruptions, AS plays a pivotal role in averting voltage

instability, frequency deviations, and other potential challenges that might

escalate to a system-wide blackout, thereby enhancing grid reliability.

AS are typically acquired through auctions or

competitive bidding processes facilitated by ISO/RTO. The system operator

conducts competitive auctions to secure AS that align with operational

requirements. Participants, encompassing generators, demand response

providers, and resources such as energy storage facilities capable of instantly

or rapidly delivering energy, submit economic offers detailing the quantity and

price of their services. The operator compiles aggregate supply curves from

these offers and identifies clearing quantities and prices at the intersections

with demand requirements. Subsequently, service providers receive dispatch

instructions, prompting them to stand by or activate services based on

real-time system conditions.

Regulation resources respond to automated signals

to stabilize fluctuations, ensuring a continuous balance in the system. In

parallel, reserve resources stand ready for contingencies. Regulation markets

undergo frequent clearings with pricing dynamically adjusted in real-time,

whereas reserve markets generally feature longer clearing intervals with fixed

pricing. Payments are determined by both market clearing prices and the energy

supplied upon activation. Aligning AS commitments with energy market dispatch

enables the system operator to uphold reliability efficiently and

cost-effectively.

The specific payment structure is contingent on the

type of AS and the governing market rules. In some markets, participants

offering AS receive compensation for their contributions, possibly in capacity

payments, energy payments, or a combination of both.

AS are intricately linked with energy markets.

Resources such as flexible generators, energy storage facilities, or demand

response units can provide energy and AS. This integration fosters a more

streamlined and coordinated operation of the entire power system.

2.5. Cost Base Centralized Systems

In theory, a system with a centralized dispatch

based on reported marginal costs holds the potential to replace conventional

day-ahead and real-time electricity markets.

In this model, generators would submit their

short-run marginal costs directly to the system operator instead of

participating in market auctions. These declared costs reflect the expenses of

producing each facility’s next megawatt (MW) of power. An auditing process for

submitted generator marginal costs would be essential to ensure transparency

and prevent manipulation. Incentives and penalties based on accuracy would

guarantee the integrity of cost declarations.

The overarching goal of the ISO would be to

minimize total system production costs. This entails dispatching the

lowest-cost resources to meet demand requirements and ensure reliability. The

system operator would employ security-constrained unit commitment and economic

dispatch algorithms to schedule resources, aligning with forecasted load across

various time horizons and resource availability, from years and months to

day-ahead and real-time.

While generators undergo central dispatch in merit

order, prioritized by their declared marginal costs, ranging from the lowest to

the highest, market clearing prices would be removed, and generators would

receive compensation based on a price defined by the reported marginal costs of

the most expensive dispatched unit for the energy exchanged during the actual

dispatch. Depending on the design of government rules, load-serving entities,

and aggregators would then remit average rates to final consumers, encompassing

total production costs. Alternatively, prices for large energy consumers or

load-serving entities might be predetermined through bilateral contracts with

power generators or aggregators. In such cases, the real-time system marginal

cost, determined by declared costs, becomes the basis for the price on power

exchanges between producers facing deficits in their long-term agreements and

supply commitments with significant energy consumers or load-serving entities.

As crucial for grid stability, it could also be

procured based on systems costs, long-term auctions, central dispatch, and

energy. Competing investment in new resources could be achieved through

long-term planning processes, capacity payments, private investment

initiatives, auctions, and procurement mechanisms overseen by the SO or a

regulatory body.

Some countries and regions that use or have used

electricity dispatch systems based on declared marginal costs rather than

market pricing are France [50–52]; vertically

and former vertically integrated utilities in the US - like the Southeastern US

– Regions [53] served by utilities like

Southern Company [54], Duke Energy [55], and Tennessee Valley Authority [56], Western US [57]

including Colorado, Wyoming, and Montana, Hawaii [58,59]13 as an isolated

island system, Alaska [60,61], parts of the

Midwest [62] Missouri and Oklahoma; Chile [63];14

Argentina [64]; Peru [65]; 15

China, which has been transitioning from a planned dispatch approach to a more

market-oriented system but still relies heavily on a regulated cost-based

dispatch model in many regions [66,67].

In the past, some hydro-heavy systems have

effectively used centralized optimization relying on generator cost

submissions, as was the case of Norway, which later transitioned to a wholesale

market system. However, in the last three decades, a centrally optimized

security-constrained economic dispatch, relying on audited marginal cost

declarations, has led in many places to the new day-ahead and real-time market

price signals. Still, smaller systems use effective centralized dispatch based

on marginal costs. Nonetheless, large and diverse markets generally rely on

competitive day-ahead and real-time pricing, like the US, market-based pricing,

and Norway, which also depends on competitive pricing via Nord Pool’s

Day-ahead/Intraday markets.

2.6. Transmission Markets

The transmission market plays a critical role in

ensuring the efficient delivery of electricity, especially as renewable energy

sources become more integrated into the grid. Transmission facilitates the flow

of electricity from remote generation sites to consumption centers, maintaining

system reliability and market efficiency. By connecting renewable-rich regions

with consumption hubs, the transmission market enables the full utilization of

distant generation sources, such as hydro, wind, and solar. It reduces regional

price disparities by alleviating congestion and allowing electricity to flow to

areas of higher demand.

The classification and regulation of transmission

lines vary across jurisdictions and are influenced by several key factors.

Voltage levels and their impact on the system play a critical role, with

higher-voltage lines typically subject to stricter open-access regulations due

to their significant contributions to grid reliability and regional

connectivity. Investment structures also shape regulatory approaches, such as

the funding source—whether public or private—and the mechanisms for cost

recovery and risk allocation influence market dynamics and policy decisions.

Additionally, market design elements such as nodal versus zonal pricing,

congestion management strategies, and system operation requirements are pivotal

in determining how transmission networks are organized and managed, reflecting

each jurisdiction's unique needs and priorities.

Also, transmission lines are typically

characterized by their capacity, exclusivity, or shared usage and their role in

linking various regions or connecting major consumption hubs with significant

production centers.

- (a)

-

Open Access Interconnection Lines are essential infrastructure for interregional power exchanges and market integration. They provide non-discriminatory access to all qualified market participants, usually under regulated tariffs. Examples include:

- US interstate transmission lines under FERC Order 888 [68].

- European cross-border interconnectors are regulated by EU Regulation 714/2009 [69].

- Chile’s north-south interconnection system, Sistema Eléctrico Nacional (SEN) [70].

- Australian interstate connectors in the National Electricity Market (NEM) [71].

- (b)

- Dedicated Transmission Lines (Generator Lead Lines) connect specific generation facilities to the main grid or load centers. Usually funded and owned by the generator, these lines often have limited third-party access. Examples include lines that connect remote renewable projects, large thermal power plants, and mining operations.

- (c)

- Shared Access (Limited Participation) lines serve multiple users under restricted access schemes. Costs for these lines are typically shared among pre-defined users, and private agreements with possible regulatory oversight often govern them. Examples include shared infrastructure for mining companies or industrial parks.

- (d)

- Hybrid Access Lines: These lines blend dedicated use with open access requirements, where the primary capacity is reserved for an anchor user, but excess capacity is available for others through open access provisions. This often requires regulatory approval and may include compensation mechanisms for the original investor.

- Transmission Market Structures: Financial Instruments vs. Centralized Expansion

Energy markets utilizing Transmission Rights and

Financial Instruments, such as those in the US (PJM, ERCOT, CAISO, MISO), use

financial products like Congestion Revenue Rights (CRRs) or Financial

Transmission Rights (FTRs) to allow market participants to hedge against

congestion costs. The Nord Pool region in Europe uses similar mechanisms to

hedge against transmission congestion. This decentralized approach incentivizes

efficient grid use and encourages investment in reducing congestion.

Australia’s NEM operates with LMPs and is moving toward adopting financial

transmission rights.

In contrast, markets with Centralized Transmission

Expansion (Postage Stamp System), such as Chile, Brazil, and Mexico, manage

transmission centrally. A “postage stamp” system is used, where all users share

costs equally regardless of location or contribution to congestion. In these

systems, a central authority plans and oversees transmission expansion,

ensuring grid reliability and capacity for renewable integration.

Examples:

- Chile: The Coordinador Eléctrico Nacional (CEN) centrally plans transmission expansions, applying uniform tariffs across all users [72]Error! Reference source not found..

- Brazil: Transmission is centrally regulated by Agência Nacional de Energia Elétrica (ANEEL), with expansion carried out through public auctions [73].

- Mexico: Centro Nacional de Control de Energía (CENACE) manages grid operations and expansion, using a postage stamp system to allocate transmission costs [74].

Key Differences:

- Decentralized Markets: The US and parts of Europe use financial instruments (FTRs/CRRs) to manage congestion, offering flexibility for market participants to hedge against transmission risks.

- Centralized Markets: Chile, Brazil, and Mexico rely on centralized planning with uniform cost distribution and without financial tools for hedging congestion risks.

- System Reliability and Congestion Management

Tools such as congestion charges and LMPs manage

grid congestion, ensuring efficient use of transmission capacity. Financial

instruments like FTRs allow market participants to hedge against congestion

risks. Interregional coordination is critical in planning investments

supporting electricity flows across broader regions, facilitating RE

integration, and maintaining grid stability.

- Transmission Market Evolution

Technological advancements in transmission and

other technologies, such as DERs and ES, reshape the transmission market.

Future developments must incorporate smart grid technologies, adapt to the

changing energy mix, and improve planning for uncertainty and risk management.

Market operators are also considering cross-border integration to optimize

resources across wider areas.

Market structures vary globally, from decentralized

financial instruments like FTRs in the US to centralized planning and

cost-sharing models like Chile and Brazil.

3. Decarbonization in Electricity Market and Trends

The Energy Transition (ET) is producing comparable

trends across energy markets, which include increased plate capacity and

operational reserve requirements, greater demand for flexibility and ramping

capacity, changes in system demand, overgeneration curtailment risks, with

instances of zero or negative prices, forecast-increasing challenges, and risks

of increased price volatility. These challenges are becoming more prominent as

the integration of VRE accelerates.

- Larger Capacity and Operating Reserves per GWh

As VRE penetration increases, substantial capacity

and supporting infrastructure —and consequently significant investment— are

required to meet demand, underscoring the economic and infrastructural

challenges of integrating high levels of VRE. This situation necessitates

innovative policy design to avoid inefficiencies, excessive redundancies, and

unwarranted system costs.

OECD and NEA [75]

demonstrate that increasing shares of VRE, such as solar and wind, require

substantially higher capacity to produce the same electricity as conventional

thermal power plants due to lower load factors and capacity credits. As VRE

penetration increases to 10%, 30%, 50%, and 75%, the required installed

capacity and associated investments grow substantially. Total system costs,

encompassing grid infrastructure, balancing, and connection expenses, also

escalate with higher VRE shares, ranging from less than USD 10 per MWh at 10%

VRE to over USD 50 per MWh at 75% VRE. These costs can be significantly

influenced by the availability of system flexibility, such as interconnections

and flexible hydropower resources, which help mitigate the challenges

associated with VRE integration.

- Chile’s Case Study

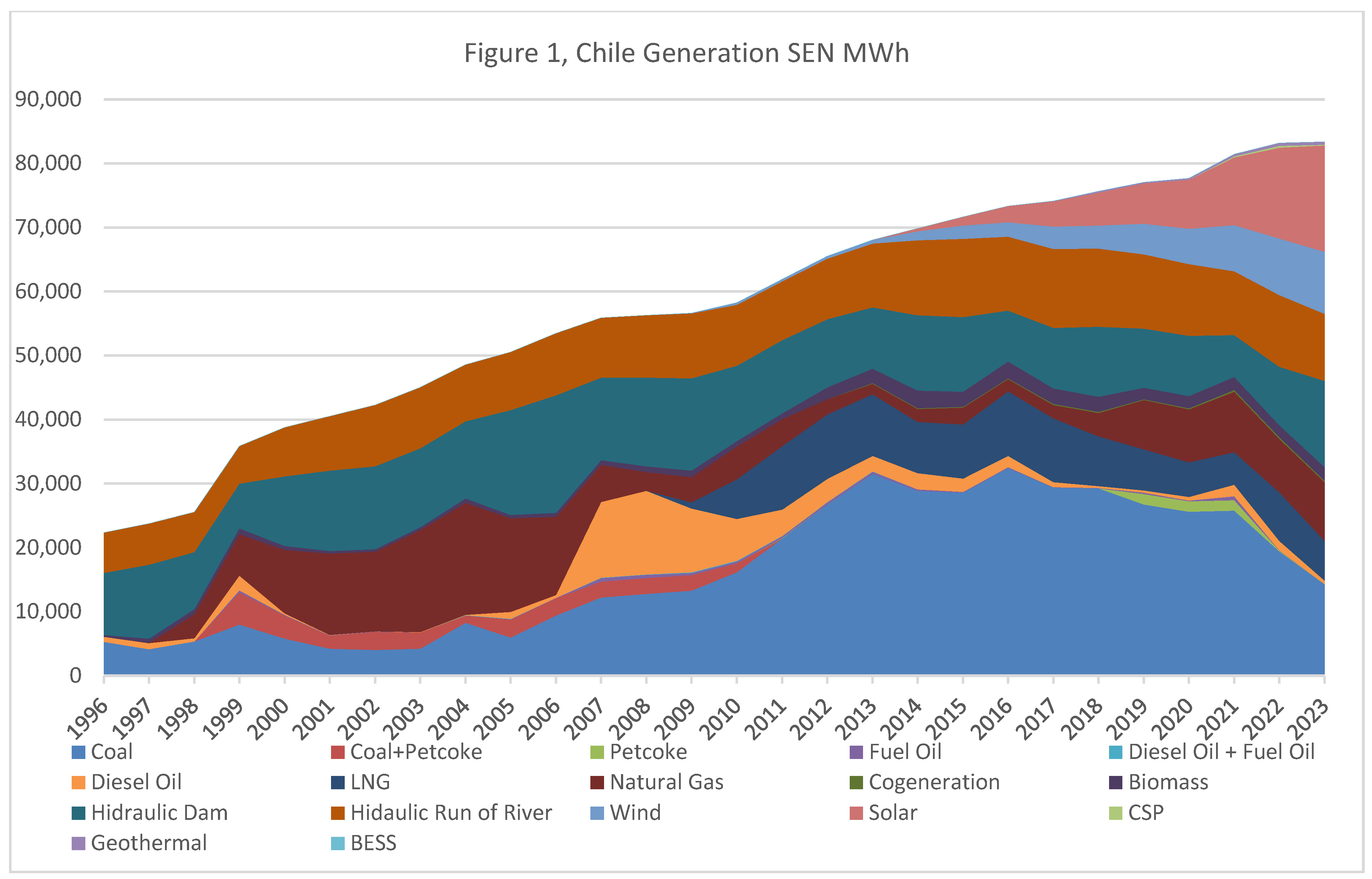

Chile has made significant strides in expanding its

VRE generation capacity over the past two decades. Installed plate capacity has

grown from around 10 GW in 2000 to 33 GW in 2023, a threefold increase

reflecting the country’s efforts to meet rising electricity demand and enhance

energy security while addressing climate change objectives with increasing

shares of VRE.

As of the first quarter of 2024, 66.1% of Chile’s

electricity comes from renewable sources, with renewable energy, different from

large hydropower plants, contributing 40.7%, up from 2% in 2010. In 2023, wind

and solar alone accounted for 40% of installed capacity and 28% of total

electricity generation, see Figures 1 and 2.

This substantial share highlights the effectiveness of policies and market

dynamics in promoting VRE, helping reduce greenhouse gas emissions, and

leveraging Chile’s abundant natural resources.

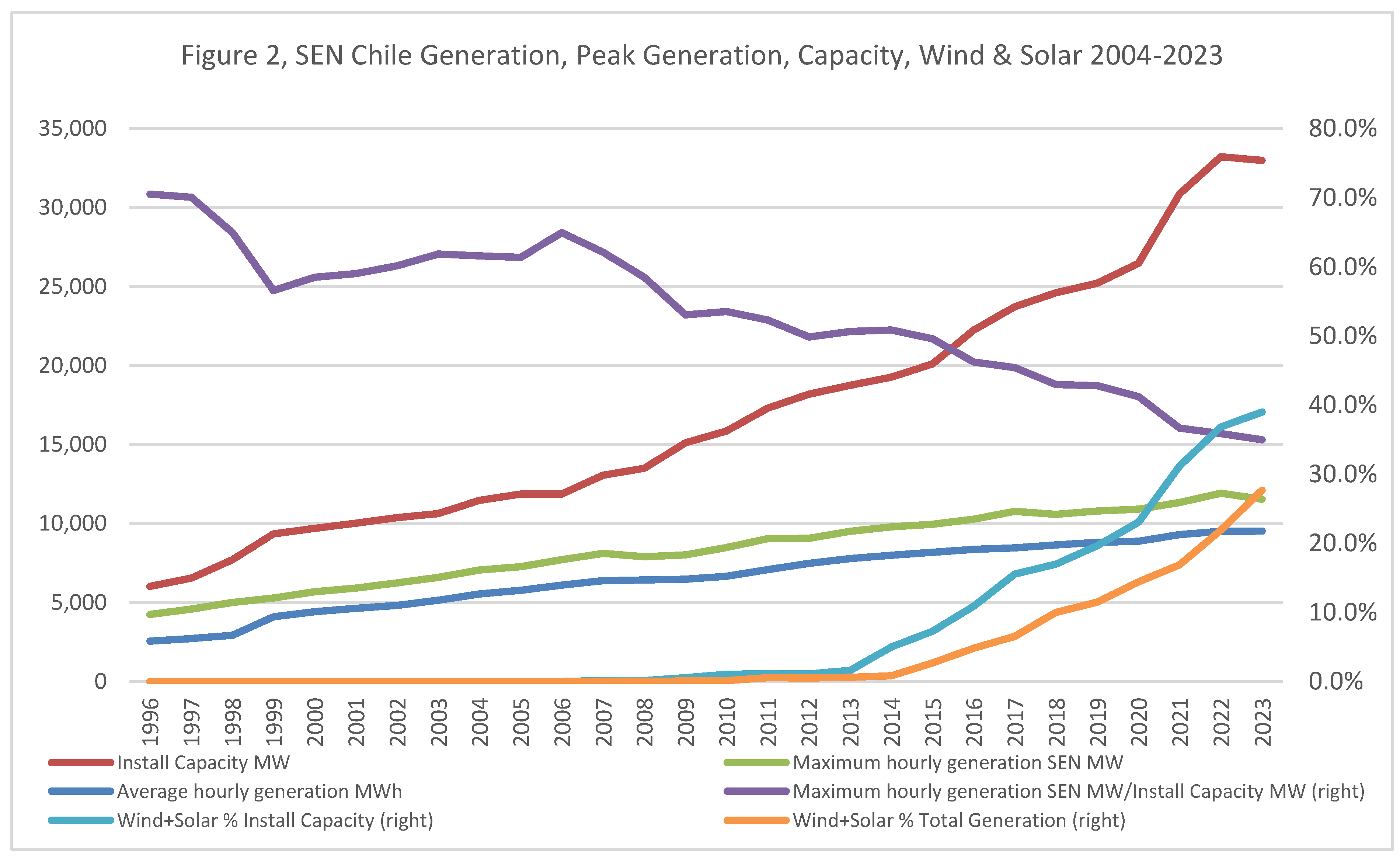

However, integrating these VRE sources into the

grid comes with challenges, particularly in ensuring the reliability and

stability of the power supply. Chile’s power system has experienced a

significant increase in spare capacity (Figure 3),

measured as the ratio of peak generation to installed capacity. This ratio has

climbed from approximately 40% in the early 2000s to 65% in 2023. Thus, while

peak generation has increased by 103% and annual generation by 115%, installed

capacity has grown by 254% since 2000 (or 36%, 43%, and 116%, respectively,

since 2010), indicating a growing buffer between plate capacity and peak demand

[76].

This capacity increase is primarily attributable to

the intermittent nature of wind and solar power, which is unavailable 24/7 and

must be complemented with other generation sources, storage, backup, or reserve

capacity to maintain grid stability. But the requirement for this complementary

capacity comes at a cost. While the naked average investment cost per MW of

installed capacity has decreased by 28% since 2000, when calculated at new

replacement value (NRV), the average investment cost to be amortized per MWh of

generation has increased by 26% over the same period. Interestingly, despite

this increase in investment cost per MWh, the weighted average of the Levelized

Cost of Electricity (LCOE) has decreased by 14% since 2000. The EIA has noticed

[77] that the LCOE is a limited measure

because it only reflects the cost to build and operate a plant, not the value

of the plant to the grid.

This scenario presents a growing challenge in many

markets. As the share of VRE increases, with its characteristic zero marginal

cost, it becomes increasingly difficult to secure a stable stream of revenues

to finance investment costs, and merchant power plants must increasingly shift

to revenues that need to be secured by AS markets, capacity markets, and LTPA.

This situation underscores the need for innovative market designs and policy

frameworks to ensure the long-term financial viability of the power system

while continuing to integrate higher proportions of VRE.

Source: Figure with open data from Comisión

Nacional de Energia (www.cne.cl) and Coordinador Eléctrico Nacional

(www.coordinador.cl), Chile.

Chile’s increasingly diverse electricity generation

mix, less reliant on imported FF, enhances its energy security from FF

geopolitical risks, like foreign FF market price manipulation, but requires

sophisticated grid management and operational strategies.

Source: Figure with open data from Comisión

Nacional de Energia (www.cne.cl) and Coordinador Eléctrico Nacional

(www.coordinador.cl), Chile.

Source: Figure with open data from Comisión

Nacional de Energia (www.cne.cl) and Coordinador Eléctrico Nacional

(www.coordinador.cl), Chile.

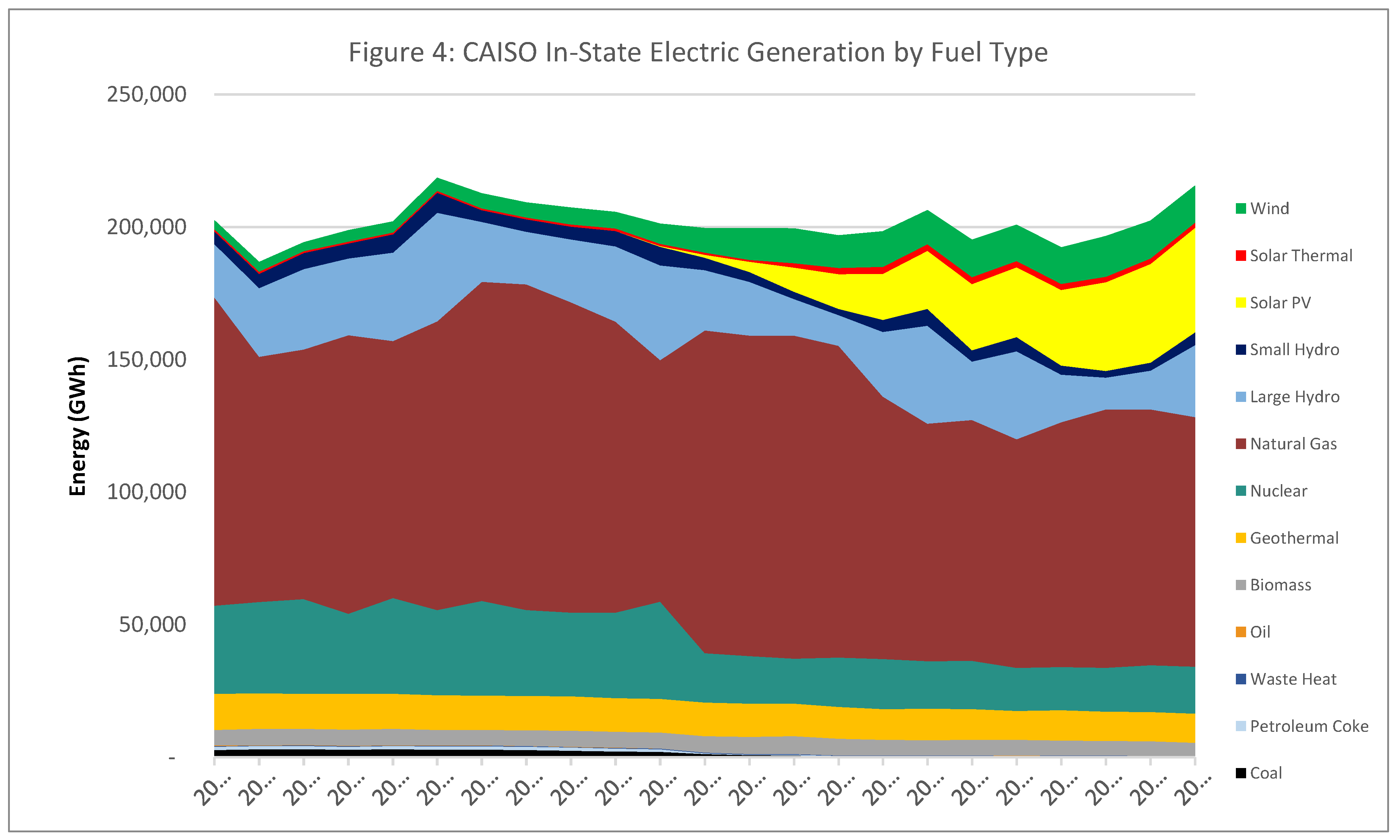

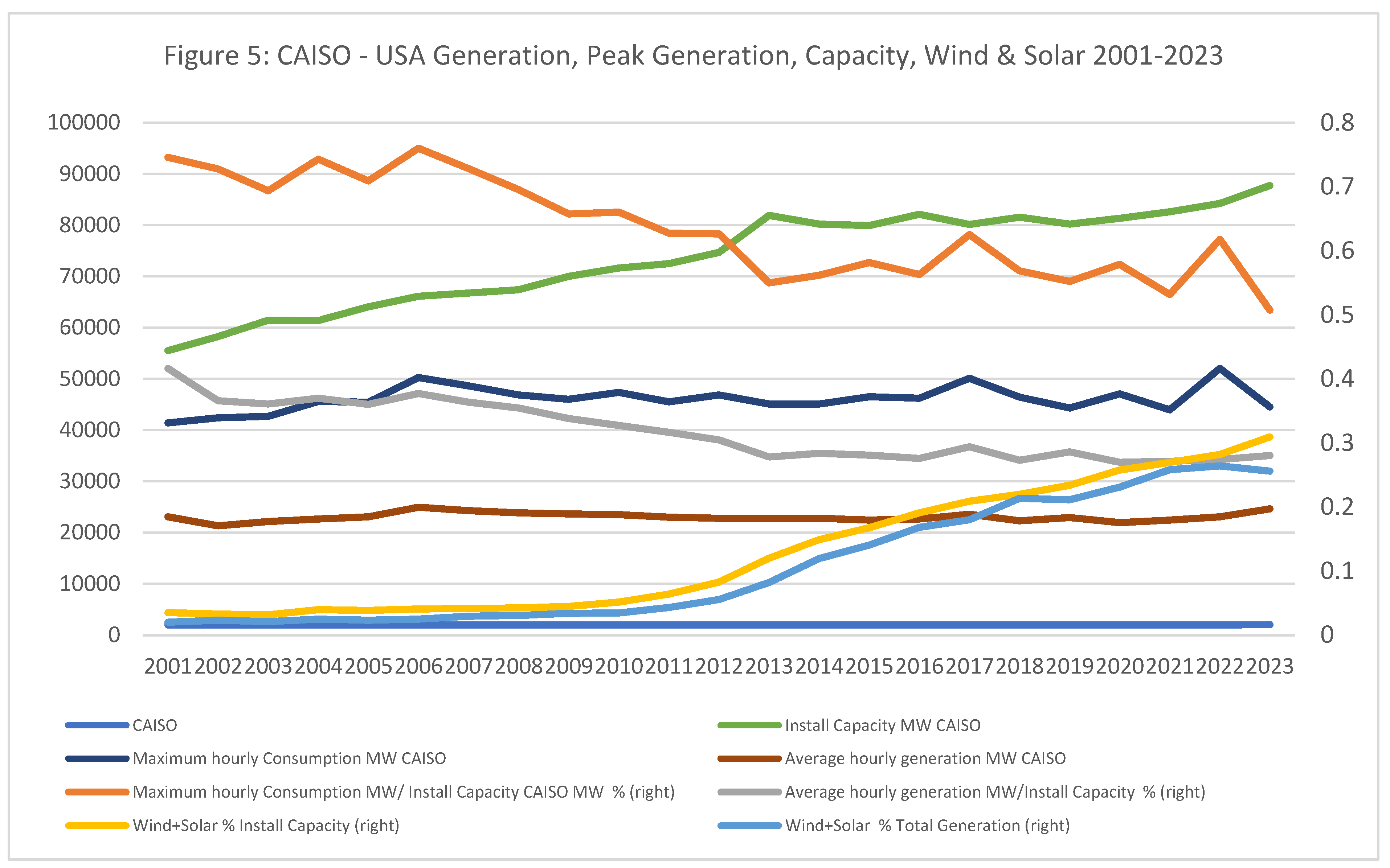

- CAISO Case Study

Over the past two decades, California has

significantly expanded its VRE capacity, reflecting global trends in

sustainable ET. Figure 4 shows that CAISO

installed capacity has grown from 55.5 GW in 2001 to nearly 88 GW in 2023, a

notable increase driven by the State’s ambition to meet electricity demand

while addressing climate objectives. The increasing share of solar and wind

explains this growth, which accounted for over 30% of installed capacity by

2023, compared to just 3.5% in 2001. Also, Figure

4 further illustrates the gradual reduction in the reliance on nuclear

and FF, with renewables, particularly solar PV, playing an increasing role in

CAISO’s energy mix.

Source: Figure with open data from CAISO Quarterly

Fuels and Energy Reporting Regulations, US.

As of 2023, wind and solar contributed 26% of total

electricity generation, marking a substantial shift from traditional FF

sources. Figure 5 further illustrates the

gradual reduction in the reliance on FF and nuclear, with renewables,

particularly solar PV, playing an increasing role in CAISO’s energy mix.

Source: Figure with open data from CAISO Quarterly

Fuels and Energy Reporting Regulations, US.

Despite the rise in VRE capacity, integrating these

resources into the grid remains challenging. CAISO’s power system requires

substantial backup and reserve capacity to compensate for the intermittent

nature of VRE, as illustrated by the increased spare capacity over time. Peak

generation as a percentage of installed capacity has decreased, signaling

growing buffer plate capacity —essential to ensure grid stability. In 2001, the

ratio of peak consumption to installed capacity was 75%, whereas by 2023, it had

dropped to 51%, reflecting significant capacity increases to accommodate VRE

intermittency.

As in Chile, California’s experience also provides

key insights for other regions seeking to diversify their energy mix and reduce

reliance on imported FF. However, SEN-Chile and CAISO, with different market

constructs, face similar challenges related to grid management, storage, and

flexible generation investment, as well as developing innovative market designs

to support continued growth in renewable energy.

- Ramping Capacity Needs and Operating Reserves

The increasing integration of VRE sources and DERs

introduces significant variability in energy production, demanding a more

flexible power system and better forecasting. While market designs are evolving

to accommodate VRE, new plants often benefit from existing system capabilities

without fully accounting for the additional costs they impose, such as expanded

operating reserves, transmission upgrades, and enhanced operational

capabilities to manage higher VRE penetration.

For example, some of these system costs associated

with VRE integration include:

- Balancing costs: The expenses for ancillary services needed to stabilize the grid include load-following and managing unforeseen fluctuations.

- Capacity costs: Backup generation and storage are required during low VRE output periods to ensure reliability.

- Transmission and distribution costs: Upgrading grid infrastructure to accommodate the increasing number of small power plants, DG systems, and behind-the-meter VRE sources.

- Operational costs: Coordinating a diverse and larger array of power generators, energy storage, prosumers, and demand management systems.

- Curtailment costs: Managing surplus generation when VRE output exceeds demand, leading to curtailment or the need for investment in energy storage.

Addressing these challenges requires thoughtful

planning and policy design to optimize renewable energy integration while

maintaining system reliability and controlling costs.

As a result, while increasing shares of VRE are

aimed at contributing to reducing greenhouse emissions, the stability and

security of energy supply, with characteristics of a public good, along with

the expansion of transmission lines and other services needed to operate an

electrical system, with an increasing share of VRE, are not always fully

compensated by VRE investors. These renewable sources, such as DERs, are

typically more dispersed and smaller than traditional energy sources, further

complicating system management.16

This new landscape necessitates crucial flexibility

and pricing schemes that assist with quickly ramping output up or down to

accommodate fluctuations in supply and demand, anticipated or not. Traditional

baseload power plants, designed to provide constant output, often struggle with

this requirement for rapid ramping. Consequently, there is a growing need for

flexible generation resources, ESS, DR programs, and adaptive grid

infrastructure.

[78] provides a

comprehensive analysis of thermal unit statistics in the United States,

examining historical operating costs of hundreds of conventional electrical

generation units and identifying key factors influencing costs associated with

providing flexibility services. These factors allow for estimating indirect

ignition costs, load following costs, and increased unit unavailability

resulting from more frequent cycling, focusing on coal and gas plants (combined

cycle, simple cycle, and aero-derivative). [79]

also review hydropower plants' start and stop costs by highlighting the

increased operational stresses and costs from frequent start and stop cycles

due to intermittent renewable energy sources. It categorizes cost estimation

approaches into economic and technical-economic types, emphasizing the need for

comprehensive, auditable models that integrate material and non-material costs.

Future research should aim to develop representative models for various

components and aggregate these to estimate system-level costs. [80] quantify the costs incurred by conventional

power plants in Germany due to increased VRE penetration, finding notable

increases in direct and indirect ignition costs with higher VRE penetration.

And, [81] examine the impact of greater VRE

penetration on the startup frequency of conventional thermal units, concluding

that total operating hours of thermal units decrease in scenarios with higher

renewable penetration, primarily due to changes in the generation portfolio,

such as the phase-out of nuclear plants. These studies collectively provide

valuable insights into the complex relationship between increasing VRE

penetration and conventional power plants' operational patterns and costs,

highlighting the need for a nuanced understanding of power system flexibility

in ET.

Table 1

highlights the operational characteristics of various power generation

technologies, showing significant differences in flexibility, start-up and

shut-down costs, and wear and tear costs.17

These differences influence their suitability for different roles within the

power grid, from steady baseload generation to dynamic peaking and backup

power.

As Table 1 illustrates, the flexibility and response time of the different technologies and start-up and shutdown costs vary significantly across technologies, with nuclear and coal having the highest due to their complexity and safety requirements. Natural gas, hydro, and diesel are lower, reflecting simpler and quicker processes. And, on Wear and Tear Costs, nuclear, wind, and solar have the lowest wear costs due to fewer mechanical stresses and steady operations. Hydropower has higher wear costs due to mechanical wear from water flow, while coal and natural gas have moderate wear costs due to thermal and mechanical stresses. This underscores the importance of considering system costs and operational flexibility when planning for a future of decarbonized energy.

Historically, baseload generation has relied on stable, continuous-output technologies like nuclear and coal, which efficiently meet the grid's constant demand but lack flexibility. In contrast, peaking power has been best served by flexible and fast-ramping technologies such as natural gas, hydro, and, recently, battery storage, which can quickly respond to demand spikes and shut down during low-demand periods. Diesel generators excel with their rapid start-up capabilities for backup and emergency power, providing immediate support during outages or unexpected demand surges. Each technology plays a distinct role in ensuring a balanced and reliable electricity supply.

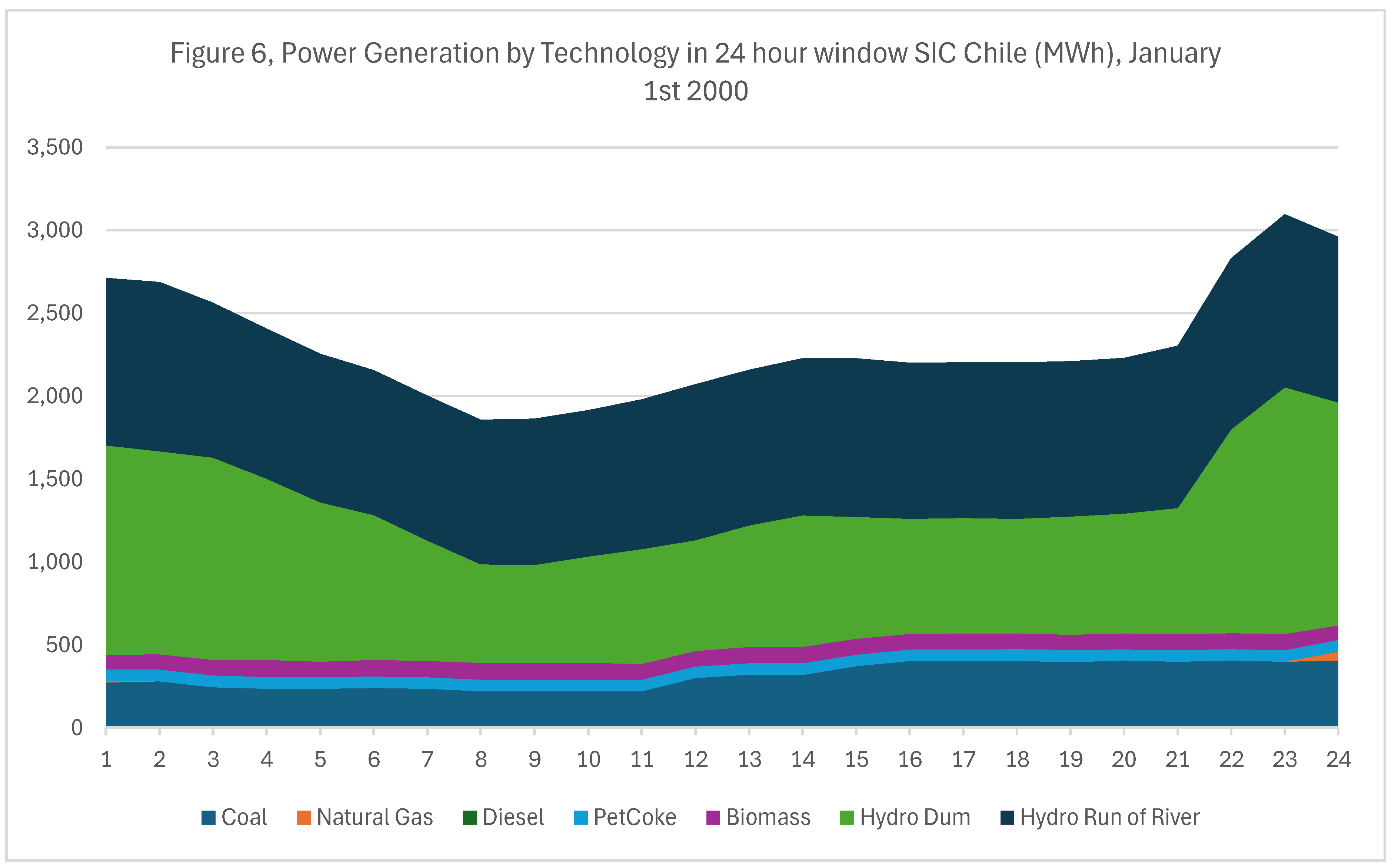

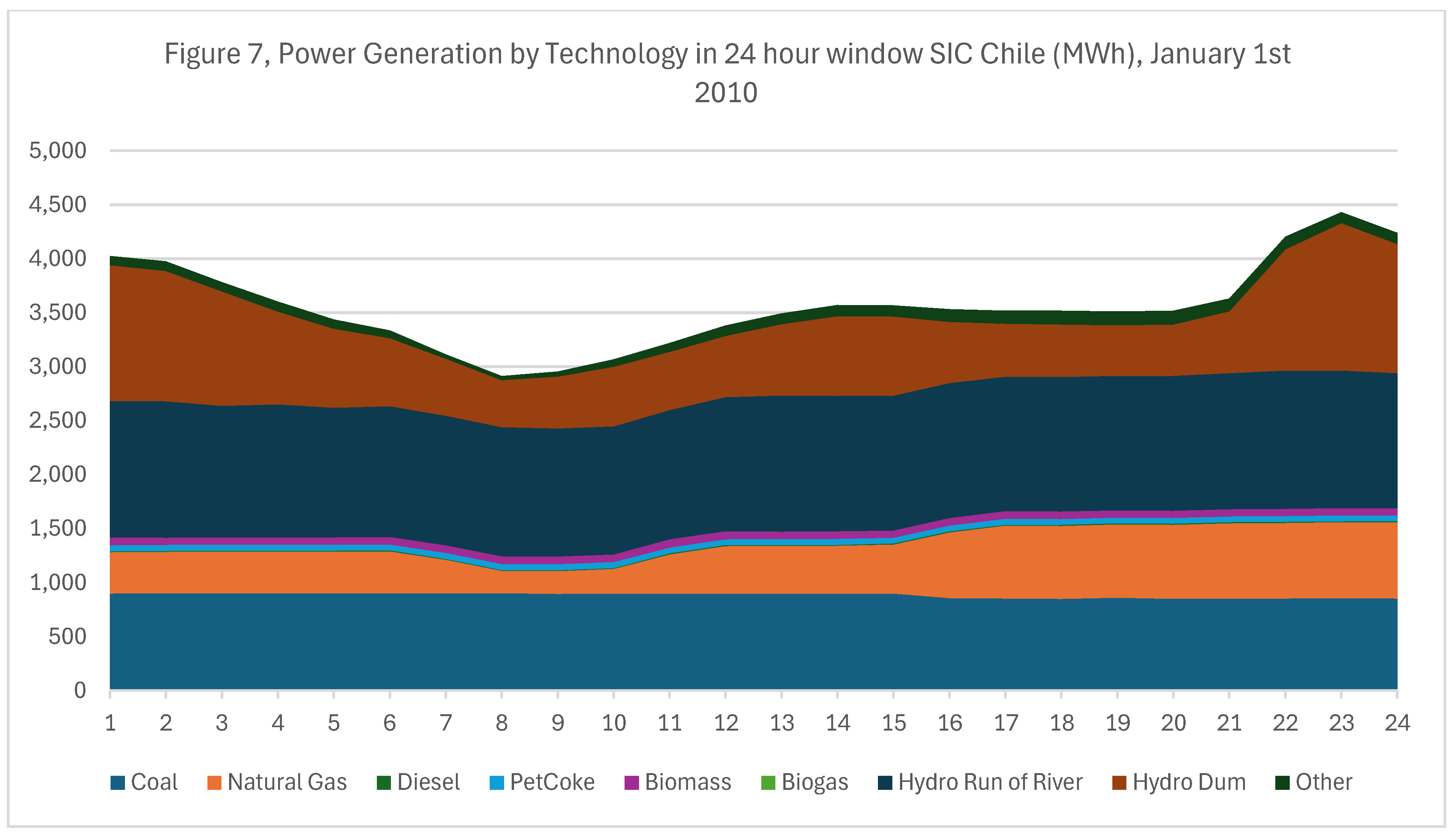

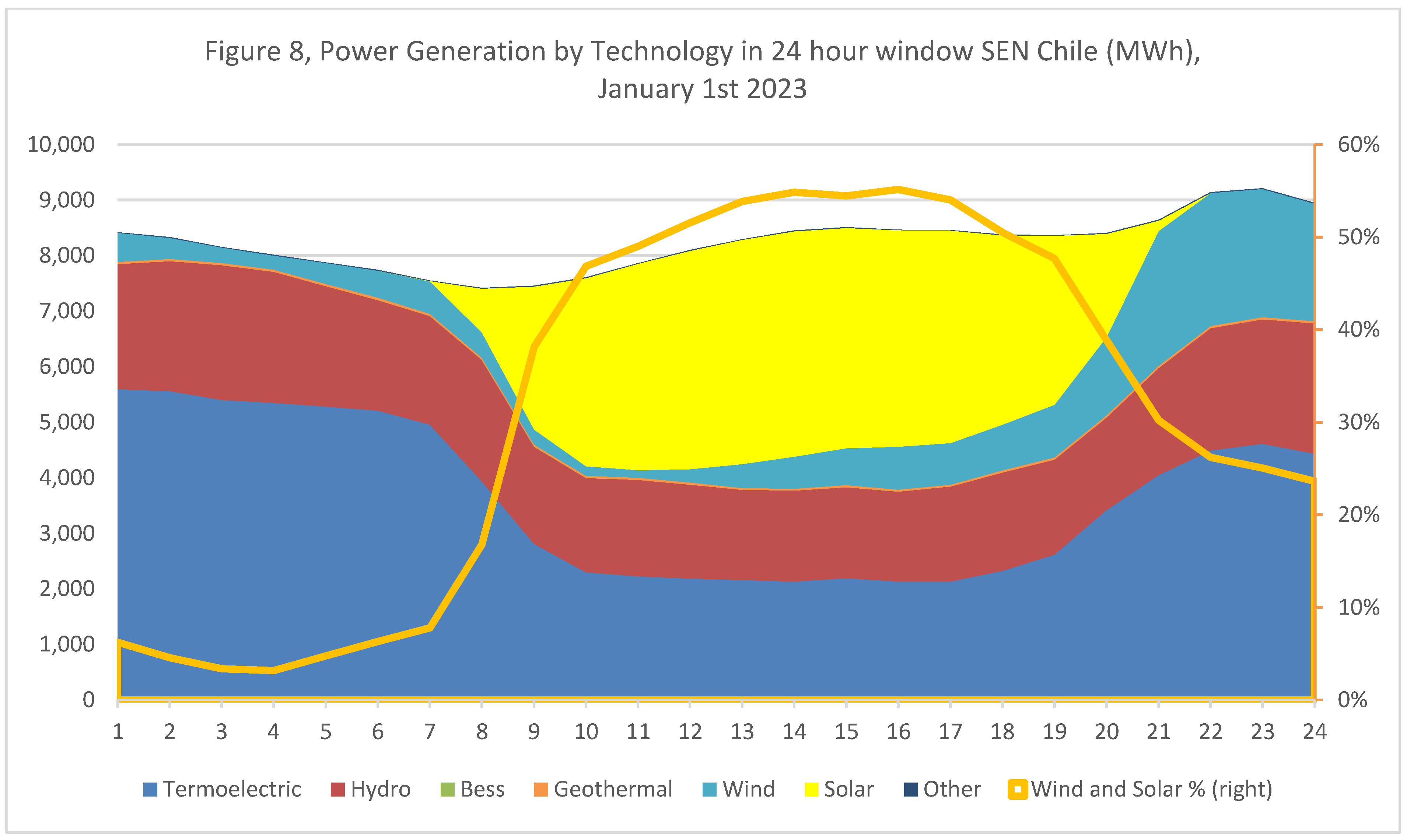

- Chile’s Case Study

For Chile, Figures 6, 7, and 8, on a 24-hour window time frame for January 1st, 2000, 2010, and 2023, depict the hourly electricity generation by technology. In 2000, the electricity generation mix was dominated by coal, hydro (dam and run-of-river), and natural gas, with relatively small contributions from other sources such as diesel and biomass. In 2010, the mix saw a significant increase in natural gas and a diversified contribution from coal, hydro, and a tiny but growing share of renewables like wind and biomass—when the transition towards increasing participation of VREs began. In 2023, the generation mix showed a substantial increase in solar and wind energy contributions alongside a significant presence of flexible generation and incipient BESS. Figures 6 to 8 illustrate that the demand for power sources that can quickly accommodate solar and wind generation variability in 2023 is evident.

Source: Figure with open data from Coordinador Eléctrico Nacional (www.coordinador.cl), Chile.

Source: Figure with open data from Coordinador Eléctrico Nacional (www.coordinador.cl), Chile.

Source: Figure with open data from Coordinador Eléctrico Nacional (www.coordinador.cl), Chile.

From the significant penetration of solar and wind energy, which creates pronounced fluctuations in the residual demand faced by natural gas, coal, and large hydropower plants, Figures 6 to 8 highlight the challenges faced in 2023 by the Chilean electric system. The system had to manage a morning ramp of 3,000 MW within 3 hours and an evening ramp of 2,000 MW as solar output decreased, partially offset by wind generation. On average, solar and wind contributed 52% of the electricity generation at 10:00 AM and 7:00 PM. Interestingly, while the system's peak daily demand between 8:00 PM and 10:00 PM necessitated an additional generation increase of 736 MW, the VRE ramping capacity needs exceeded the system ramping capacity needed to satisfy the system’s daily peak load.

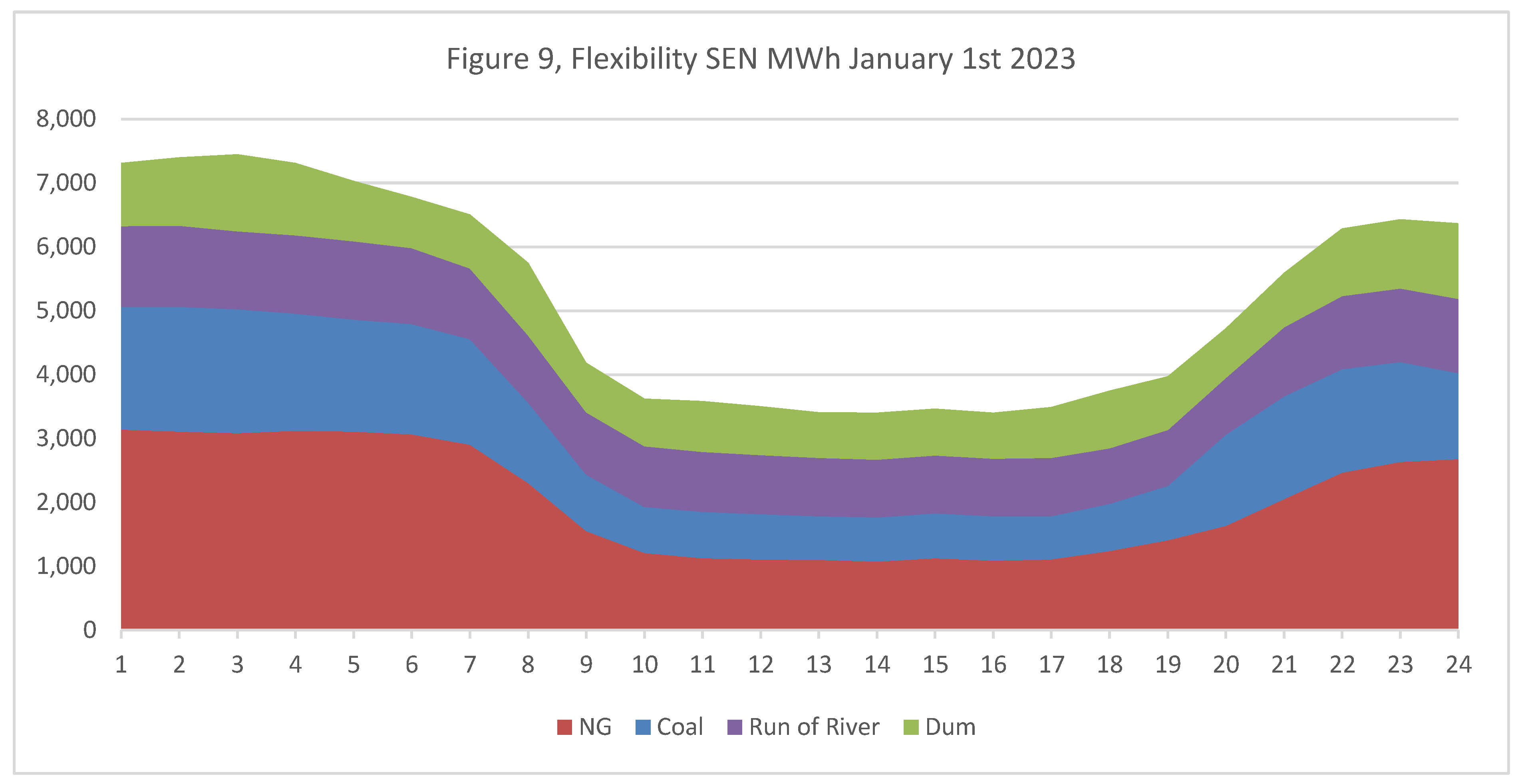

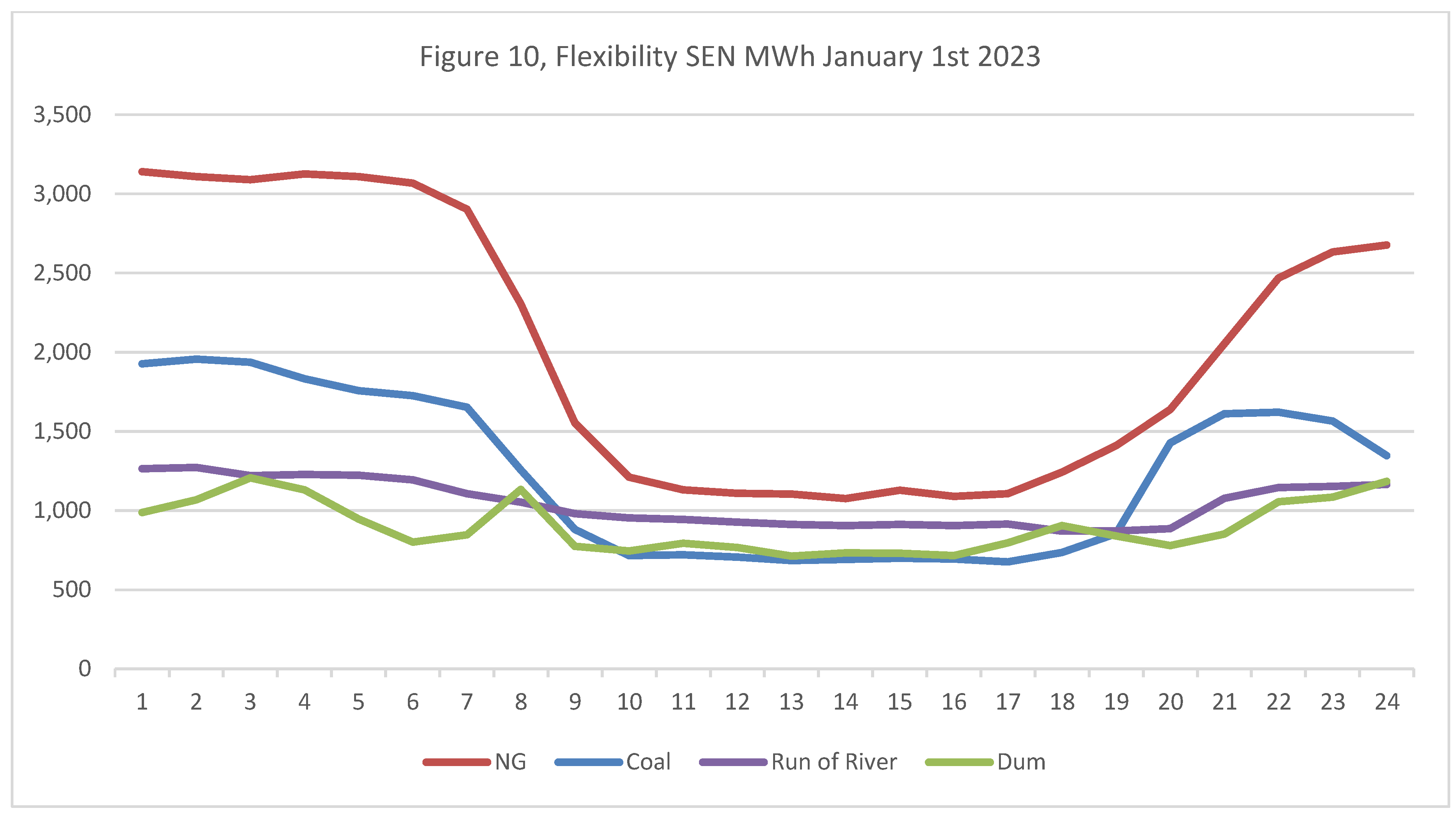

Figures 9 and 10 illustrate the daily variations in power generation by different technologies, reflecting the critical role of flexibility in maintaining grid stability amidst increasing renewable energy integration. To meet demand, peak load, VRE following, and ramping requirements, the system primarily relies on conventional FF technologies, including LNG power plants and, to a lesser extent, coal power plants and some hydropower plants. These conventional technologies are essential for providing flexibility to accommodate the variability in renewable energy production. The use of fast-response gas turbines, although effective, incurs high marginal costs, emphasizing the need for more sustainable flexibility solutions such as competitive BESS, and demand response mechanisms.

Source: Figure with open data from Coordinador Eléctrico Nacional (www.coordinador.cl), Chile.

Source: Figure with open data from Coordinador Eléctrico Nacional (www.coordinador.cl), Chile.

As net demand in Figure 9 illustrates, ramping capacity use has increased significantly in the Chilean electric system due to solar and wind power integration, following VRE supply fluctuations exceeding the resources needed to follow the daily system load fluctuations. VRE has created notable volatility in the net or residual demand curve faced by natural gas, coal, and hydropower plants, often called the "duck curve." The cost implications of this ramping are important.

- Caiso Case Study

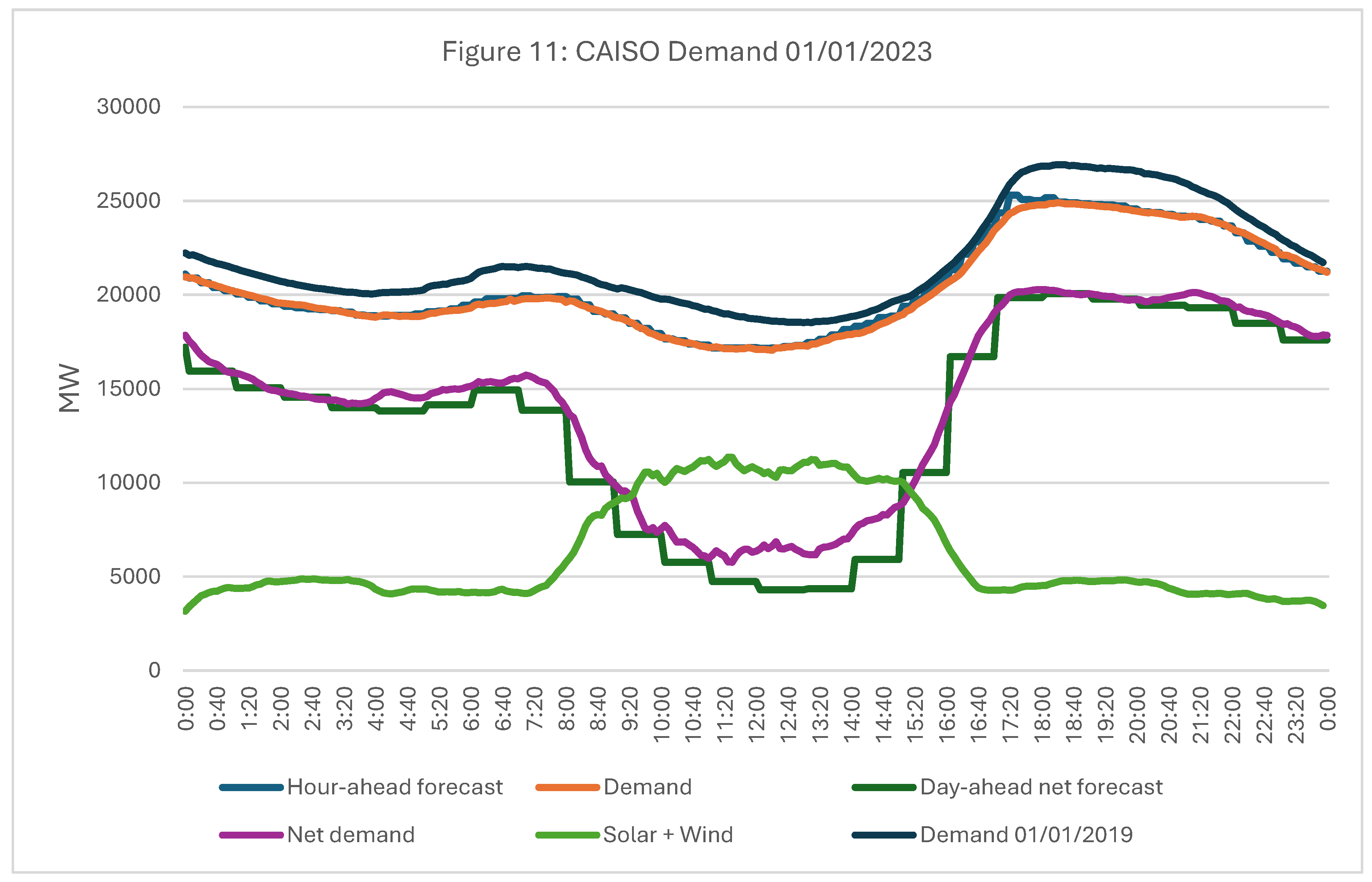

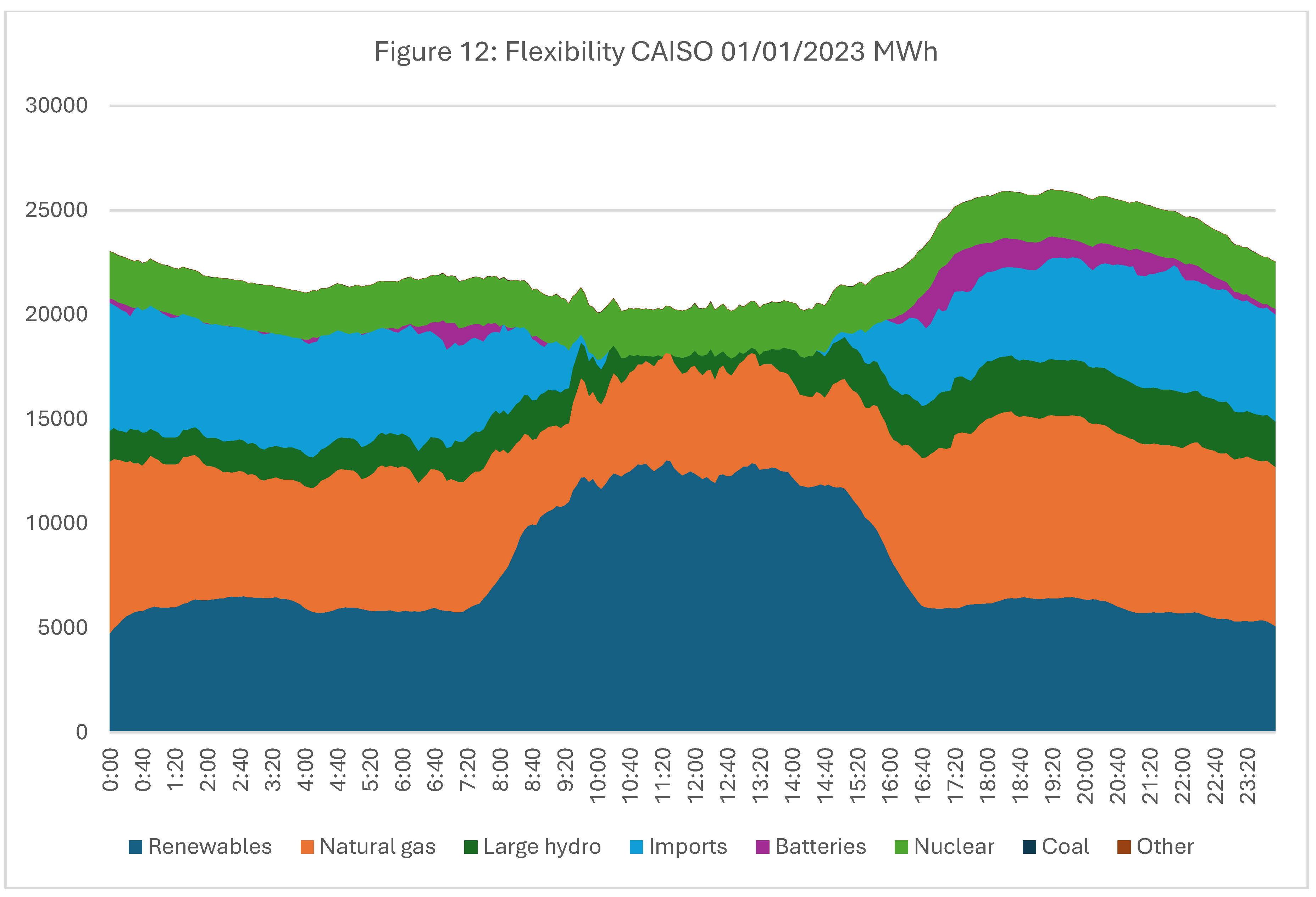

For CAISO, Figures 11 and 12, for January 1st, 2023, depict hourly electricity demand, forecasts, net demand, and flexibility providers by technology.

Source: Figure with open Net Demand 01/01/2023 data from CAISO, US.

CAISO demand has been steadily declining due to the increase in behind-the-meter (BTM) photovoltaic (PV) production, as shown in Figures 11 and 12. In the morning, the electric system faced a ramp-down of 8,000 MW in less than three hours, followed by a ramp-up of 11,000 MW in the evening as PV output decreased. Between 10:00 AM and 7:00 PM, solar and wind supplied an average of 52% of the electricity. These ramping capacity needs are further exacerbated by BTM PV production, which reduces demand during daylight hours, intensifying the need for ramping both in the morning and evening. At peak production, renewable sources like wind and solar can supply more than 65% of market demand.

Source: Figure with open Supply 01/01/2023 data from CAISO, US.

In CAISO, flexibility for ramping up and down is primarily provided by a combination of natural gas power plants, large hydropower, energy imports, and battery storage, as illustrated in Figures 11 and 12. These resources play a critical role in meeting fluctuating demand, particularly during rapid changes in renewable generation.

Fascinatingly, on April 8, 2024, a solar eclipse highlighted contrasting approaches to managing solar generation drops between California and Texas. In CAISO, battery storage systems played the primary role, switching from charging (2.6 GW) to discharging (2.7 GW) to compensate for the roughly 27% drop in solar output (from 14.5 GW to 9.1 GW), while curtailment of excess solar temporarily disappeared. In contrast, ERCOT, which experienced a more severe 94% solar reduction (13.8 GW to 0.8 GW), relied mainly on natural gas generation, which ramped up from 19 GW to 27+ GW. This difference exemplifies broader grid transition strategies: California leverages energy storage charged by excess renewables, while Texas and other regions depend primarily on natural gas for grid balancing.

As Chile, CAISO, and ERCOT cases illustrate, the dependency on conventional FF for flexibility further complicates the transition to a fully RE system, highlighting the importance of developing regulatory frameworks to manage new technologies, electronics, and storage costs efficiently, where ramping requirements with fast-response solutions can have high-levelized costs, impacting the overall economics of the power system [86,87].

Further, the transition from an electromechanical system to an electromagnetic one, especially in a system dominated by Inverter Based Resources (IBRs), indeed requires significant shifts across multiple levels of grid planning, operation, and regulatory frameworks. In electromechanical systems dominated by synchronous machines, conventional FF, or hydropower plants, the inherent physical characteristics of these machines, such as inertia, provide natural stability to the power grid. However, as the energy system integrates more power electronics and digital control through IBRs like solar PV, wind, and battery storage, the traditional methods for ensuring grid stability are no longer sufficient.

The transition towards a more renewable-based energy system highlights the need for a flexible and adaptive power grid. As VRE becomes more prevalent, the role of flexible generation resources, energy storage, demand response, and advanced grid infrastructure becomes increasingly important. These elements are crucial for ensuring grid reliability and resilience in the face of the inherent variability of renewable energy sources. Chile's 2000, 2010, and 2023 figures (Figures 6–10) and CAISO (Figures 11 and 12) vividly depict the significant shifts in the energy mix, emphasizing the growing need for technologies to support and stabilize VRE integration.

Ramping Capability and Risk of Market Power

The energy transition, characterized by increasing shares of VRE sources, leads to greater generation volatility— both anticipated and unanticipated—creating a critical need for technologies with ramping capabilities, much more significant than in systems primarily characterized by FFs, large hydro, and nuclear baseload generation. Units with ramping capabilities, such as natural gas turbines, hydroelectric plants, BESS, diesel generators, and, to a lower extent, coal plants, can adjust output in response to changes in residual demand through scheduled operations, on-the-spot adjustments or as ancillary services (e.g., a faster response such as frequency regulation and spinning reserves). Where demand response and, to some extent, VRE can also provide some of these adjustments. The residual or net demand for ramping and ancillary services that flexible power units and BESS face is the net demand, market demand minus the supply provided by VRE and other inflexible baseload generation or committed supply on the day ahead [88,89,90].18

In this context, flexible units with ramping capabilities can engage in a market where those who are unresponsive to price fluctuations or committed in advance to fixed outputs cannot participate. The elasticity of residual demand for these flexible power units is crucial, where the more significant the need for and the fewer the units capable of providing ramping—especially considering the inflexibility of VRE and other baseload generation—the more inelastic becomes the residual demand, enhancing the market power of flexible power units and BESS. A more significant and inelastic residual demand allows these units to influence market prices more effectively, as the grid has fewer alternatives when adjusting their output. Market power can be enhanced when demand and net demand are highly variable, and a VRE supply is hard to predict, where the influence of flexible power units and BESS can be more impactful on prices. Transmission constraints and conditions affecting demand and power equipment performance can further enhance local market power. Here, regulation is crucial in enabling as many technologies and agents to participate in ramp-following and ancillary services as possible [91].

Overgeneration and curtailment Risk

The increasing share of VRE, supported by economic incentives and limited transmission capacity and ES, introduces the risk of overgeneration and curtailment during high renewable output and low demand. Such conditions have resulted in zero or negative locational marginal prices (LMPs) where excess energy cannot always be immediately utilized. While this market response reflects the underlying incentives schemes and supply-demand dynamics, effective management strategies—including ES, curtailment mechanisms and rules, improved grid infrastructure, and well-designed VRE incentives—are essential to mitigate wasted energy and ensure grid reliability.

In the United States, overgeneration risk is observed, but with regional variations due to the diverse structure of US electricity markets. Some US markets, particularly those with high wind penetration, like the Midwest, have experienced negative pricing during periods of high renewable generation and low demand [92]. The frequency and impact of overgeneration vary significantly across different ISOs and RTOs [93]. Where VRE subsidies, state-level RPS, and federal tax incentives have all played a role in encouraging RE growth and contributing to these market dynamics for utility-scale and BTM solar PV and other RE deployment. According to [94], almost half of VRE generation capacity growth since 2000 is associated with state RPS requirements in the US, and the combined demand for clean electricity from RPS and Clean Energy Standards (CES) policies will grow from roughly 500 TWh in 2024 to 1700 TWh by 2050. Additionally, some markets have implemented or are reforming their AS and capacity markets to ensure sufficient flexible resources are available to manage variability [95].

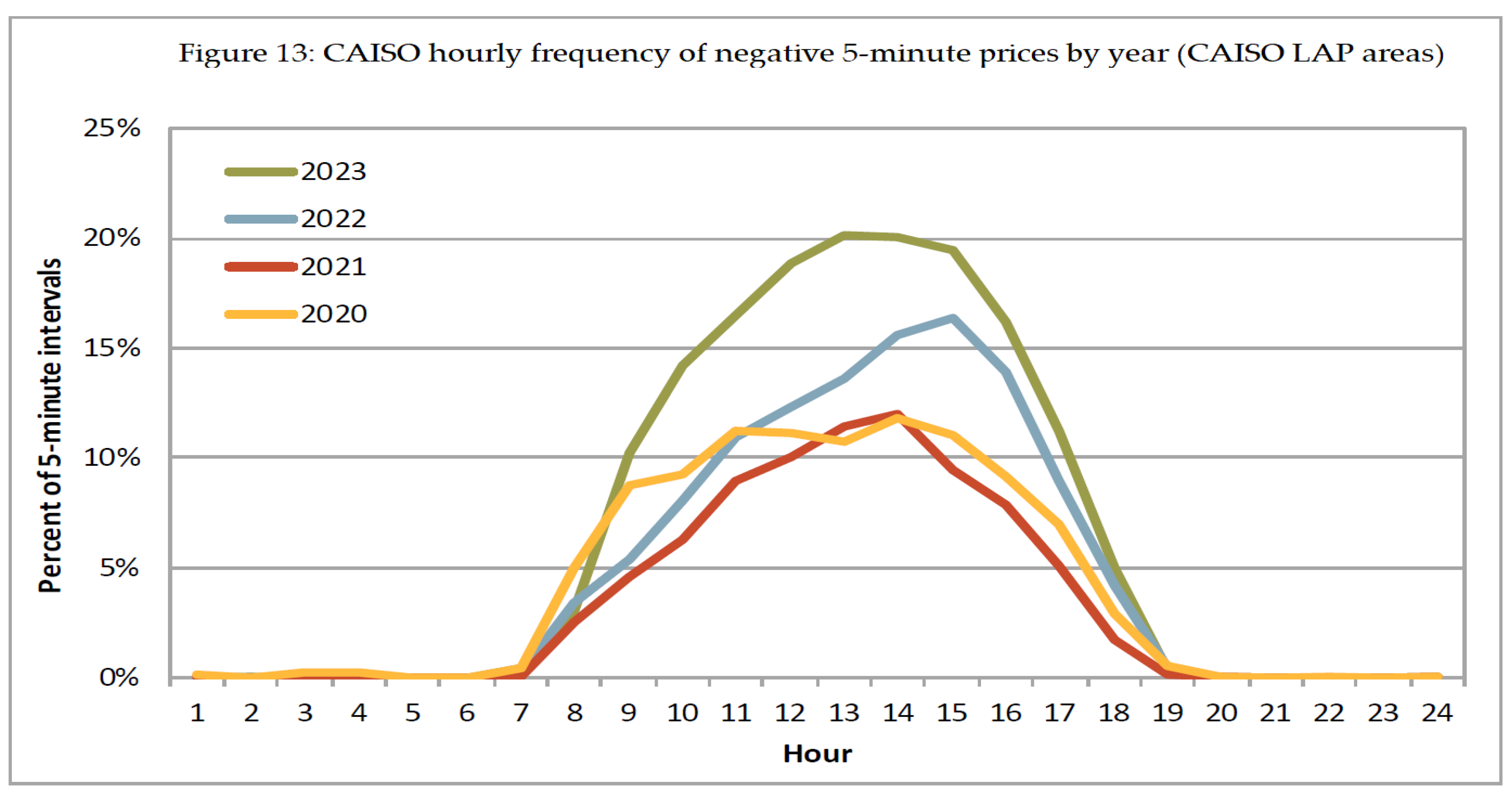

For example, CAISO has faced significant challenges with the "duck curve" phenomenon, leading to periods of potential overgeneration from solar during midday and steep ramp-up requirements in the evening [96].19 ERCOT has also experienced similar challenges with high wind penetration [97].

In 2023, CAISO faced increased price volatility, marked by a 73% rise in negative prices due to oversupply from growing solar and wind generation, while high price spikes diminished amid milder weather and fewer extreme demand events. Further, in the CAISO and WEIM areas, total downward dispatch in 2023 increased by 9.5 percent and 18.2 percent, respectively, relative to 2022. In both areas, most of the downward dispatch was economic. Economic downward dispatch accounted for about 2,688 GWh (95.5 percent) of curtailment during the year, while self-scheduled curtailment accounted for about 53 GWh (2 percent). Exceptional dispatch curtailments for self-scheduled and economic bid resources remained low at about 2.4 GWh (less than 1 percent). The roughly 70 GWh (2.5 percent) of remaining curtailment came from “other” economic and self-scheduled curtailment.

Source: [98] Figure 2.11 from “Annual Report on Market Issues and Performance,” Department of Market Monitoring, CAISO July 29, 2024.

The PJM Interconnection often commits more generation capacity than is ultimately needed, partly due to the Minimum Offer Price Rule (MOPR) and its interaction with the Variable Resource Requirement (VRR) curve in the Base Residual Auction (BRA). The MOPR, designed to mitigate buyer-side market power, establishes a price floor for specific resources, often clearing additional capacity beyond the VRR curve's target. When the MOPR sets the clearing price, PJM procures all resources subject to the MOPR at that price, even if their combined capacity exceeds system reliability needs. To respect lower-priced offers from non-MOPR resources, PJM further commits additional capacity, leading to over-procurement. While this ensures reliability and peak demand readiness, it can result in overgeneration during off-peak periods. During off-peak periods, the excess capacity procured in the capacity market might remain online due to inflexible generation commitments or economic pressures to operate.20 This oversupply can force grid operators to curtail renewable resources (e.g., wind or solar) due to their lack of dispatchability, as thermal generators may have minimum operating thresholds that require them to remain online. Thus, overgeneration pressures market prices downward and may force the curtailment of renewable resources due to their non-dispatchable nature, lack of ES, and transmission constraints, causing economic inefficiencies, such as higher consumer costs and underutilization of committed resources. This dynamic highlight the trade-off between ensuring reliability and avoiding the unintended economic consequences of excess capacity procurement [99,100,101,102,103,104,105,106].21,22

While facing overgeneration risk challenges, US markets have implemented various measures to address these issues, including improved forecasting, more flexible ramping products, and market rule changes to accommodate VRE [107]. Areas with transmission limitations exacerbate local overgeneration problems, particularly in regions with rapid RE growth, such as West Texas and the Southwest Power Pool (SPP) region. Such transmission constraints also affected the implementation and refinement of Ramp Products [108,109,110].