Submitted:

09 October 2024

Posted:

09 October 2024

You are already at the latest version

Abstract

The study focuses of analysis the impact of corporate social responsibility (CSR) on economic growth and reducing inequality, highlighting the importance of CSR in achieving sustainable development and social justice. The main aim is to analyze how different CSR initiatives contribute to economic development, social prosperity and the reduction of inequality, reviewing the methods used to assess their impact. The research methodology includes a detailed literature review, bibliometric analysis and scientific mapping, surveys of various business organizations and a Gap Analysis regarding the identification of gaps between the current state of CSR activities and the expected outcomes. The research shows that companies perceive CSR as a key tool for improving corporate image, responding to stakeholder expectations and investing in social justice. Despite positive intentions, challenges include the lack of clearly defined methodologies for measuring impact on economic inequality, as well as difficulties in assessing the long-term effects of CSR initiatives. Key conclusions highlight the need for more structured approaches to assessing the social and economic effects of CSR, recommending that companies improve their transparency and accountability, and implement clear indicators of success to achieve sustainable economic and social outcomes.

Keywords:

corporate social responsibility (CSR)

; sustainable development

; social justice

; economic growth and inequality

; strategic planning

; strategic management

1. Introduction

In the contemporary business world, Corporate Social Responsibility (CSR) plays an increasingly important role in defining companies’ strategies, pursuing sustainable development and social justice. CSR not only reflects on organizations’ ethical commitments to society, but also provides opportunities to reduce social and economic inequality. In the context of managing internal business processes, the implementation of CSR strategies promises significant benefits, including improving corporate reputation, increasing employee engagement and stimulating long-term economic growth.

The interest in CSR is based not only on ethical considerations, but also on the practical benefits it can bring to optimize operations and creating a fairer and more inclusive business environment. The application of CSR initiatives requires not only changes in the organizational structure but also in the work culture, focusing on the importance of social responsibility and ethical practices.

The focus of the study is on the methodological aspects of researching the trends and challenges faced by organizations in integrating CSR strategies and their impact on reducing inequality. The attitudes of business organizations towards these initiatives will be analyzed, focusing on the factors that influence their adoption and successful implementation. The analysis from a methodological point of view will be provided by a systematic literature review, bibliometric analysis with appropriate visualization, conducting a survey and Gap analysis.

This study defends that CSR has the potential to make a significant contribution to reducing economic and social inequality, but this potential often remains untapped due to various barriers. However, it is the authors’ position that overcoming these barriers is possible through individualized strategies, the establishment of ethical standards and active learning.

The object of study is CSR and the subject - its potential for improving social justice and reducing inequality. The main goal is to investigate the methodological aspects of the Analysis of attitudes and behavior towards the implementation of CSR as a means to reduce inequality. Specific sub-goals include approaches to measuring the degree of readiness and adoption of socially responsible practices by organizations, and the identification of factors influencing the success or failure of these initiatives.

The research has the ambition to improve the knowledge in the field of CSR and to serve as a basis for developing future strategies for successful implementation in business practices. Considering the current needs and challenges of organizations in this context, the study aims to provide concrete and relevant recommendations to promote a sustainable and equitable transition towards more responsible management of business processes.

2. Literature Review

CSR is a concept that emerged in the 20th century and has established itself as an important aspect of the management of contemporary organizations. CSR refers to the ethical responsibility of business towards society and the environment, transcending purely economic profit objectives. It includes a variety of activities such as voluntary initiatives that improve social welfare, environmental protection and the maintenance of ethical standards in business. The importance of CSR is supported by stakeholder theory (Freeman 1984; Freeman and McVea [2005] 2017; Katsoulakos and Katsoulacos 2007) which emphasizes that companies must consider the interests of all those affected by their activities, including employees, customers, suppliers and society as a whole (Ntiamoah et al. 2014).

Concerning CSR and economic inequality. Economic inequality is a serious social problem that is the subject of growing public and academic interest. Inequality refers to differences in income, wealth and access to resources between different segments of society (Bruton et al. 2021; Falkowski 2024; Koh 2020; Ravallion 2014; Schmidt and Juijn 2024; Simangunsong et al. 2023; Tweedie and Hazelton 2019; Voitchovsky 2011). In this context, CSR is being viewed as a tool to reduce inequalities through various mechanisms such as ensuring equal employment opportunities, fair payment and investment in public projects. According to some studies companies that invest in CSR can contribute to a fairer and more equitable society (Carroll 1991; Carroll 1999; Carroll 2009; Carroll 2016; Schwartz and Carroll 2003).

The literature review shows that the concept of CSR is based on several key theoretical frameworks:

- Stakeholder Theory. It presumes that companies must manage their activities in a way that satisfies not only shareholders but also all stakeholders (employees, customers, suppliers, local communities, etc.) (Freeman 2015; Friedman and Miles 2002; Jamali 2008; Kakabadse et al. 2005; Menezes et al. 2022; Pesqueux and Damak-Ayadi 2005);

- Social Contract Theory. It expresses the idea that there is an indirect social contract between business and society. Business has a responsibility to contribute to social welfare in return for the right to operate and earn a profit (Donaldson and Dunfee 2017; Inusah and Gawu 2021; Sequeira and Ward 2023; Wahlrab 2023; Windsor 2018);

- Corporate Legitimacy Theory. It considers CSR as a way of maintaining the legitimacy of the organization in the mind of the public. Legitimacy is ensured by demonstrating compliance with societal expectations and values (Cradden 2018; Janang et al. 2020; Olateju et al. 2021; Schiopoiu Burlea and Popa 2013; Stratling 2007; Zsolnai 2011); and

- Corporate Reputation Theory. CSR activities can improve corporate reputation, which can increase shareholder value and attract investment (Derevianko 2019; Esenyel 2020; Javed et al. 2020; Pires and Trez 2018; Rolf 2023; Yuncu and Koparal 2017).

As the theoretical framework and the essence of CSR has already been outlined, it is logical to pose the question of the methodological assessment of its impact in organizations on economic growth and inequality. This leads us to the need to identify key economic and social indicators that are influenced by CSR, on the one hand, and to develop approaches and tools in a corporate context to analyze and measure this influence. The results of such research will enrich the scientific knowledge in the outlined field and will provide valuable information for further development of research work. This will create a basis for a deeper understanding of the connections between corporate social responsibility, economic growth and social inequality, and will support future research on the topic.

Monitoring the relationship between CSR and corporate performance. Researching the relationship between CSR and corporate performance is diverse and often controversial. Some researchers (Deng et al. 2023; Fu et al. 2024; Orlitzky 2009; Orlitzky et al. 2003; Pekovic and Vogt 2021) have pointed to a positive correlation between CSR and financial performance, arguing companies that invest in social responsibilities often benefit from better reputations, customer loyalty and greater talent attraction. However, other researches (Kim et al. 2023; Margolis and Walsh 2003; Volchek et al. 2024) suggest that the relationship is not always direct and the benefits of CSR depend on the context and how these policies are implemented.

Regarding CSR and social justice. Social justice is a key element of CSR discussions (Balaceanu et al. 2012; Etikan 2024; Michelon et al. 2020; Newell and Frynas 2007). The concept of social justice in the context of CSR includes efforts to ensure equal opportunities, fair payment and working conditions, and to protect the rights of vulnerable groups. Companies can play an important role in promoting social justice by creating inclusive policies and supporting diversity and inclusion in the work environment.

Despite the potential benefits of CSR, there are also a number of challenges that can make its effective implementation difficult. These include (see Table 1):

The role of CSR in reducing inequality. CSR has the potential to be a powerful tool for reducing social and economic inequality. By supporting education, health and other social services, companies can improve the quality of life of their employees and communities. In addition, by creating skills development programs and encouraging minority participation, business organizations can play a key role in ensuring equal opportunities.

The theoretical framework of CSR highlights its multiple dimensions and its relevance for contemporary society. Despite the many challenges to its successful implementation, CSR remains a key instrument for achieving sustainable development and reducing inequalities.

3. Materials and Methods

The achievement of the research goals is realized through the application of a specific methodological apparatus that forms a multi-stage research design. This means that the results of one method are used as a basis or input for the next method, creating a cascade (chain reaction) of research steps.

First, a systematic review of the literature in accordance with the PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) protocol was used. Scientific publications were extracted from the Scopus database and appropriate inclusion and exclusion criteria were applied to the results. After conducting the systematic selection, the quantitative and qualitative analysis of the publications was performed using the Bibliometrix tool of R-Studio, including the Biblioshiny 4.1 application.

Second, several specific visualization tools were used in the analysis process, including Three-Field-Plot, which illustrates the relationships between authors, keywords and publication sources, as well as Thematic Map, which provides a graphical representation of the main themes and their evolution over time. These tools allow further analysis of thematic areas and support the extraction of scientific conclusions, trends and perspectives for future research. The research findings at this stage are the basis for continuing the process of research in the direction of constructing a questionnaire and generating conclusions.

Third, a sample survey was conducted. It covers 146 companies (including 32 small enterprises, 97 medium enterprises and 18 large enterprises) operating in Bulgaria and Romania, selected by the method of random non-recurrent selection. The sample is formed by enterprises from neighboring countries that have recently completed their transition. In terms of economic growth rates over the last 10 years, they are particularly similar. They are also similar in terms of prospects for joining the European area. The aim is to examine the attitudes of these companies regarding the impact of CSR on reducing economic inequality.

The survey contains 16 questions combining both closed and open formats. The questions cover topics such as the impact of CSR on social justice, the benefits and challenges for implementing CSR practices, the adoption of ethical standards, companies’ commitments to social and environmental issues, and opportunities for staff training and development. The surveys were distributed by email to the companies in the sample.

Fourth, in addition to the survey, a Gap Analysis is applied as a strategic tool to assess the gaps between the current condition of CSR initiatives and the targeted outcomes. The Gap Analysis identifies areas where existing practices are not meeting optimal standards and suggests opportunities for improvement. This enables organizations to formulate and implement effective strategies to integrate CSR better into their corporate policy and operational practice.

4. Results

The initial phase of the research process is the definition of keywords and terms and a search field in the Scopus database. It is the result of a panel discussion between academics and business in the field of CSR and sustainable business transformation. Search and information retrieval phase of data collection involves the use of various search techniques such as: Booleans, using parentheses, quotation marks and truncations. The selected keywords are in three directions: regarding CSR (“corporate social responsibility”, CSR), on economic growth (“economic grow*”), and, concerning the field of inequality – (inequalit*). The appropriate Booleans as OR and AND, quotation marks and truncations, are used. Querying the database for these keywords was performed on June 20, 2024, in a specifically selected field in Scopus – (All fields) and generated 4 430 documents as a result.

The selected PRISMA protocol provides additional search criteria to be defined to restrict the sample. The criteria were selected using the search filters suggested in the Scopus database. Depending on the number and type of documents in the sample, the criteria that delimit the sample can be inclusion and exclusion criteria.

The selected exclusion criteria options restrict the sample to the following:

- Open Access – all open access resulting in 1 574 documents;

- Year – a research publication period between 2015 and 2024 was selected, resulting in 1 504 documents;

- Subject area – the selected fields are Business, Management and Accounting; Social Sciences; Decision Sciences; Economics, Econometrics and Finance with a result of 1 152 documents;

- Document Type – only the articles with a result of 981 documents are of interest;

- Publication Stage – only fully completed articles with the Final option with a result of 946 documents are examined;

- Source Type – the selection of articles is of those published in journals with a result of 946 documents; and

- Language – the survey covers only articles in English with English option with a result of 932 documents.

The other filters as Author name, Source title, Keyword, Affiliation, Funding Sponsor and Country/territory, are not used. They function as inclusion criteria. Querying the database after applying these additional criteria sorts the data into a result and forms a sample size of 932 documents.

A very important part of the data processing process is the technical cleaning. It involves eliminating some of the records. The PRISMA protocol requires that the research materials (in our case, 932 scientific publications) are reviewed for duplicates in order to eliminate them. No duplicates were identified during the review.

The subsequent deep cleaning of the data consists in their full-text reading, which limits them to a sample of 531 scientific publications. The processed scientific information from the studied articles through a systematic literature review served as the basis for the construction of the conceptual framework of the study: the CSR of organizations has an impact on economic growth and inequality in society, and they should apply specific methodological tools to measure and evaluate these effects.

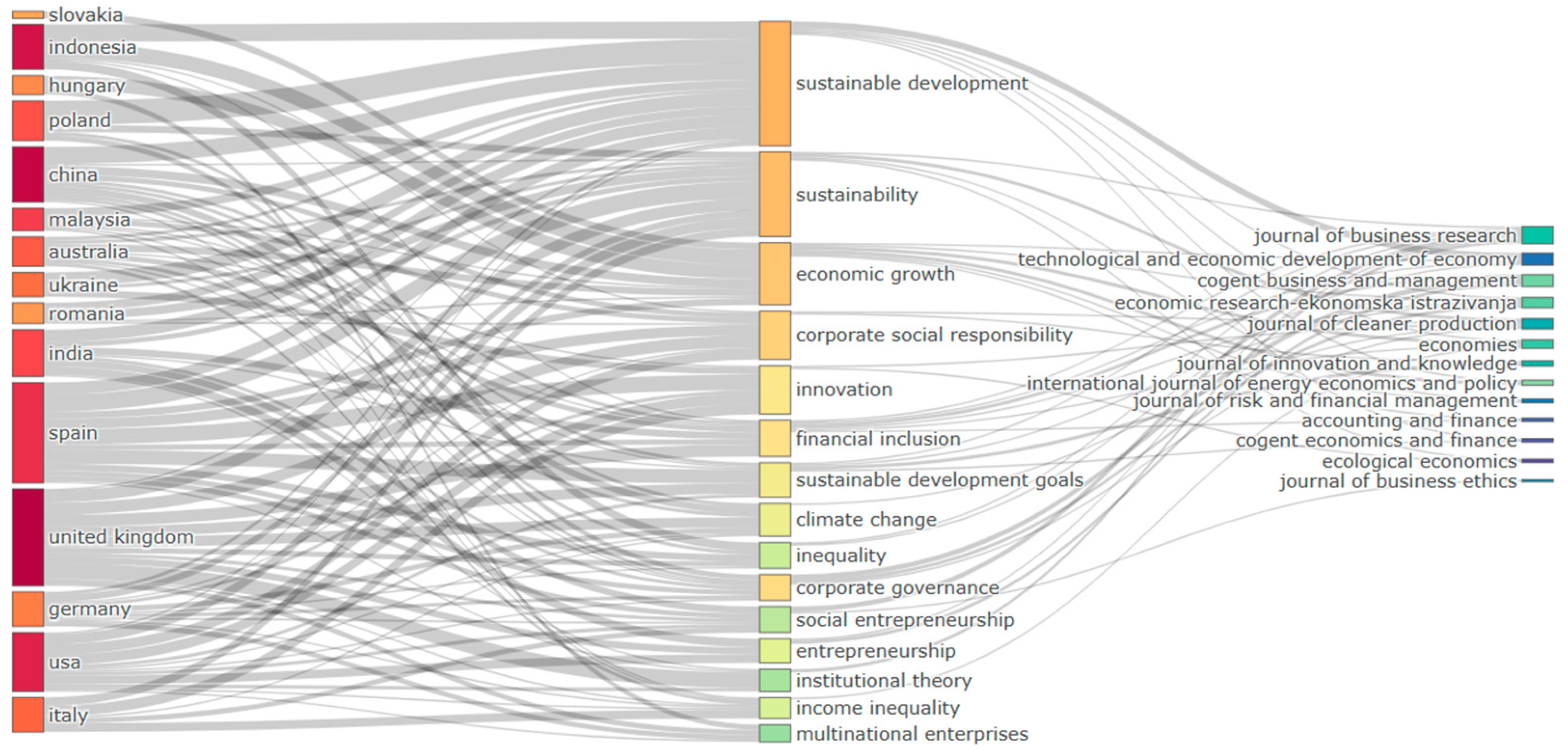

As a result of the systematic literature review, the relationship between keywords, countries and scientific journals was also researched. The visualization of these interrelationships is by the tool of Bibliometrix “Three Fields Plot” developed based on the Sankey diagram. The chart allows a user-defined number of values of a variable (e.g., keywords used to describe the research topic) to be placed in a central position, and then values of two other variables (e.g., authors, countries, universities, sources, etc.) to be placed on either side of it. The Three Fields Plot shows how interest in and/or activity of the side variables is relative to the central variable.

In this case, the keywords in the publications in the sample are set as the central variable and their number is set to 15, resulting in terms appearing in different colored and sized rectangles. These visually correspond to similar rectangles on both sides, which in the example are countries/regions and sources (see Figure 1).

This three-dimensional graph, reflecting the relationship between the main research themes, the geographical distribution of the research and the leading journals, provides the necessary basis for outlining the next research direction, i.e., the survey. Specifically, the diagram identifies three key directions:

- the indicators on which the CSR of the organizations has an impact, i.e., the economic inequalities in the society, including the impact of the CSR initiatives of the corresponding organization on them, the specific indicators and metrics to assess the contribution of the CSR initiatives to their reduction, and the methodological approaches to assess the long-term impact of the CSR initiatives on them;

- the territorial scope of the respondents in the survey, i.e., among the active countries, Romania was chosen as it is the only one neighboring Bulgaria;

- the relevant scientific journal to which this article will be directed for publication.

The next important research focus is to establish how the impact of an organization’s CSR initiatives on economic inequality in society is measured. Measuring this impact is pivotal to understanding the real contribution of organizations to social justice and the reduction of income and opportunity gaps. It allows companies to assess the effectiveness of their CSR programs and identify areas where improvements or adjustments can be made. In addition, clearly measuring impact provides actionable data that can be used to communicate with stakeholders and demonstrate a company’s commitment to sustainability and social responsibility.

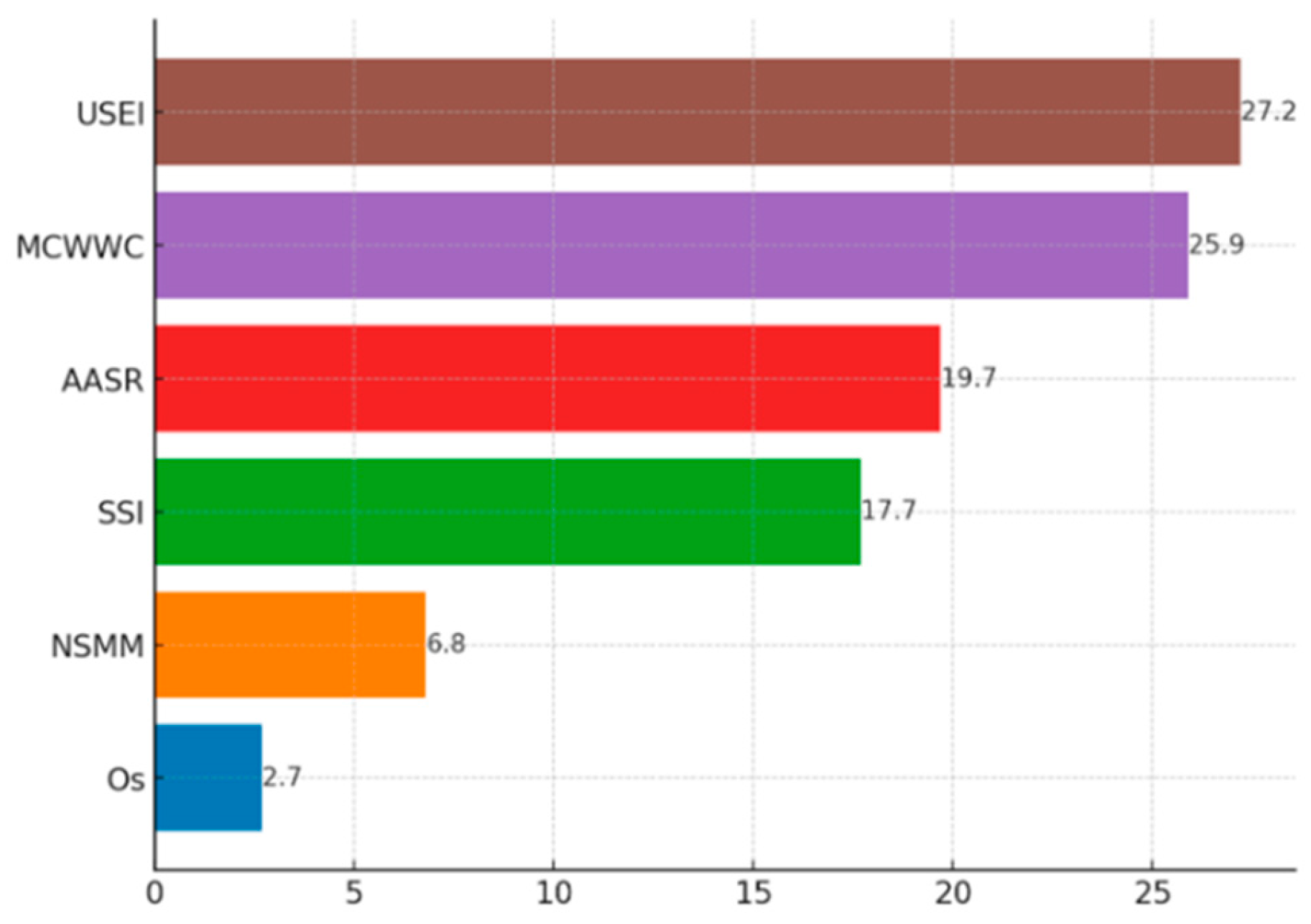

The results of the empirical research are as follows (see Figure 2):

The main conclusions are:

- • Monitoring changes in wages and working conditions (MCWWC). 25,9% show a strong focus on the internal aspects of employees and their rights. This measurement is directly linked to the assessment of income and working conditions as key factors of economic inequality;

- • Assessing access to services and resources (AASR). A significant proportion of companies (19,7%) are paying attention to access to services and resources, demonstrating a commitment to reducing social inequalities by improving accessibility to important services. This includes support for education, health and other social programs;

- • Stakeholder surveys and interviews (SSI). They are used by many organizations (17,7%), reflecting the importance of direct communication with those affected by CSR initiatives. This helps to understand the perception of the company’s efforts and the effect on the local community and employees;

- • Using social and economic indicators (USEI). The largest proportion is of organizations (27,2%) using social and economic indicators to assess impact, highlighting the need for objective and quantitative data for analysis. These indicators allow a broader view of the impact of CSR initiatives on economic inequality at national and local levels;

- • Others (Os). A small proportion of respondents (2,7%) use other measurement methods, indicating the diversity in approaches and the possibility of using alternative methods that may be specific to certain industries or companies; and

- • Lack of a systematic method of measurement (LSMM). Some organizations (6,8%) have not yet developed systematic methods to measure the impact of CSR initiatives. This points to the need to develop more structured evaluation and monitoring approaches.

These results highlight the diversity in the methods used by companies to measure the impact of CSR initiatives on economic inequalities. Although most organizations use structured and quantitative approaches, there are still gaps in systematic measurement, suggesting the need for development and standardization of methodologies.

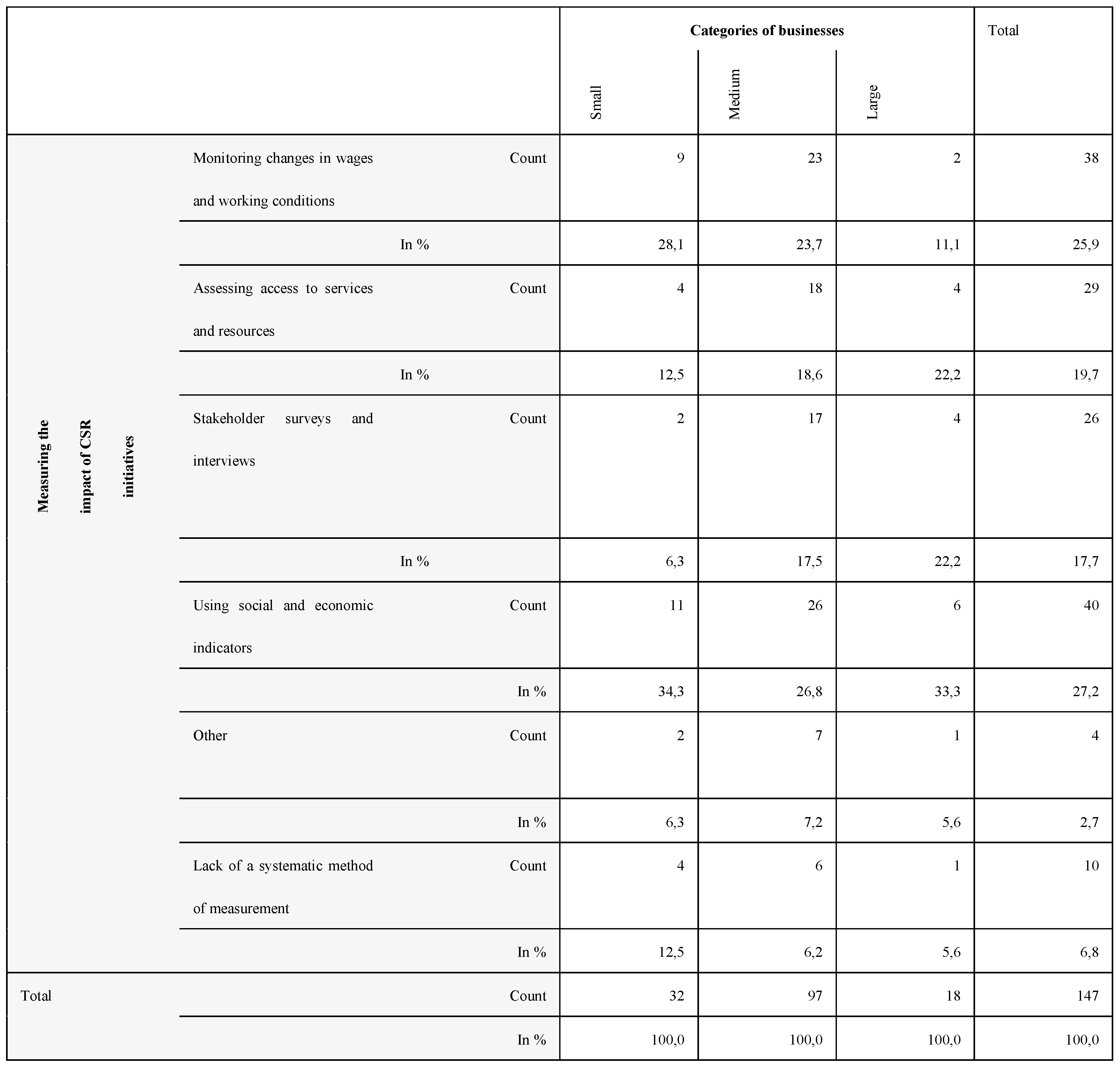

In an effort to deepen the analysis, we provide the bivariate distributions in Table 2 (cross-tabulation) below. The row “In %” refers to the % of the indicator Categories of businesses (Accountancy Act, am. SG/ 79 of 2024).

Researching the methods used by different business organizations to measure the impact of CSR initiatives on economic inequalities reveals interesting trends and differences between small, medium and large enterprises. For example, monitoring changes in wages and working conditions is the most popular method among small organizations (28,1%) choosing this approach. This is probably due to more limited resources and the need for direct control over internal working conditions and wages. Medium-sized companies (23,7%) and large companies (11,1%), demonstrating less emphasis on this method. This may reflect the complexity of internal structures and the presence of a variety of metrics that large companies use to assess.

Assessing access to services and resources is another important aspect (method), as it is used of 22,2% of large business organizations. This is likely a result of their broader scope of social initiatives, which include support for education, healthcare and other social programs. Medium sized businesses (18,6%) and small businesses (12,5%) demonstrate less focus on this approach, which may be due to limited resources and less engagement with a wide range of social services.

Stakeholder surveys and interviews also play an important role. 22,5% of large companies and 17,5% of medium-sized companies, significantly more than small companies (6,3%) use these methods to get direct feedback from stakeholders. This may be a result of the more structured and systematic communication processes available in larger companies.

Using social and economic indicators is most popular among small enterprises (34,3%) and large enterprises (37,3%). This highlights the need for objective data to assess the impact of CSR initiatives. Medium-sized enterprises (26,8%) also use social and economic indicators, but more limited, probably due to the more complex nature of evaluations and the need for different types of data.

A small percentage of companies surveyed (2,7%) use non-standard measurement methods, indicating that these approaches are not widespread and are likely specific to certain industries.

It is noteworthy that 6,8% of organizations still do not have a systematic method to measure the impact of CSR initiatives, which reveals the lack of readiness and the need to develop more structured and effective methods to assess the impact of social responsibility.

The differences in approaches between small, medium and large business organizations show how size and resources influence the choice of methods for measuring the impact of CSR initiatives. Small organizations tend to use simpler and more direct methods, while large companies rely on more complex and broad approaches that reflect their ability to manage and evaluate social responsibility on a broader basis.

These results provide a detailed analysis of the differences in approaches to measuring the impact of CSR initiatives depending on the categories of businesses (size of business organizations).

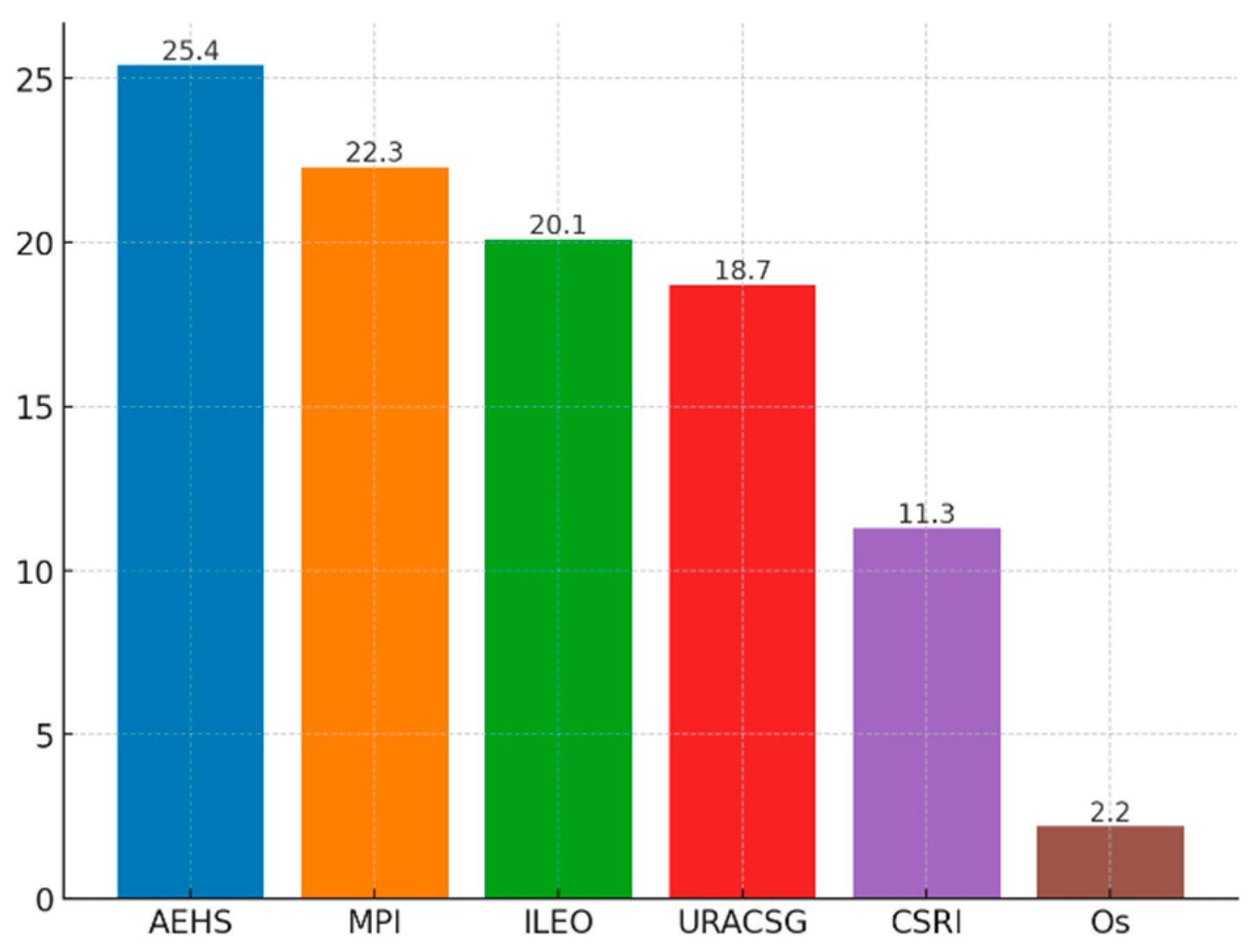

The other defining guideline of our study relates to which specific indicators and metrics a particular business organization uses to assess the contribution of CSR initiatives to reducing economic inequality. This aspect is essential for understanding the effectiveness and transparency of these initiatives. Choosing appropriate metrics allows companies to track and analyze specific aspects of economic impact, such as wage equality and access to resources. The question also provides valuable information on the level of commitment and accountability of organizations in measuring the long-term impact of their social commitments, which is very important for improving CSR policies and practices.

The data, collected from the survey, are presented in Figure 3:

The results regarding the indicators and metrics used to assess the contribution of CSR initiatives to reducing economic inequality indicate the following:

- • Multidimensional Poverty Index (MPI). A significant proportion of organizations (22,3%) use this index, indicating many aspects of poverty, including access to basic services, accommodation and education;

- • Unemployment rate among certain social groups (URACSG) – 18,7%. Using this indicator reflects companies’ interest in the impact of CSR initiatives on unemployment among vulnerable social groups;

- • Access to education and health services (AEHS). The highest proportion of organizations (25,4%) are monitoring access to education and healthcare, highlighting the importance of these essential services in reducing economic inequality;

- • Increase in local economic opportunities (ILEO). The indicator is used by a significant number of companies (20,1%) seeking to measure the effects of CSR initiatives on the creation of new economic opportunities locally;

- • Corporate social responsibility indicators (CSRI). Some organizations (11,3%) use specific CSR metrics, which may include internal metrics and standards for achieving social objectives; and

- • Others (Os). A small proportion of organizations (2,2%) use other indicators, which may suggest diversity in approaches or the availability of industry-specific assessment methods.

These distributions highlight differences in companies’ approaches to measuring the impact of CSR initiatives. The most commonly used indicators are those relating to access to basic services and socio-economic conditions, while specific CSR metrics and other indicators have less weight.

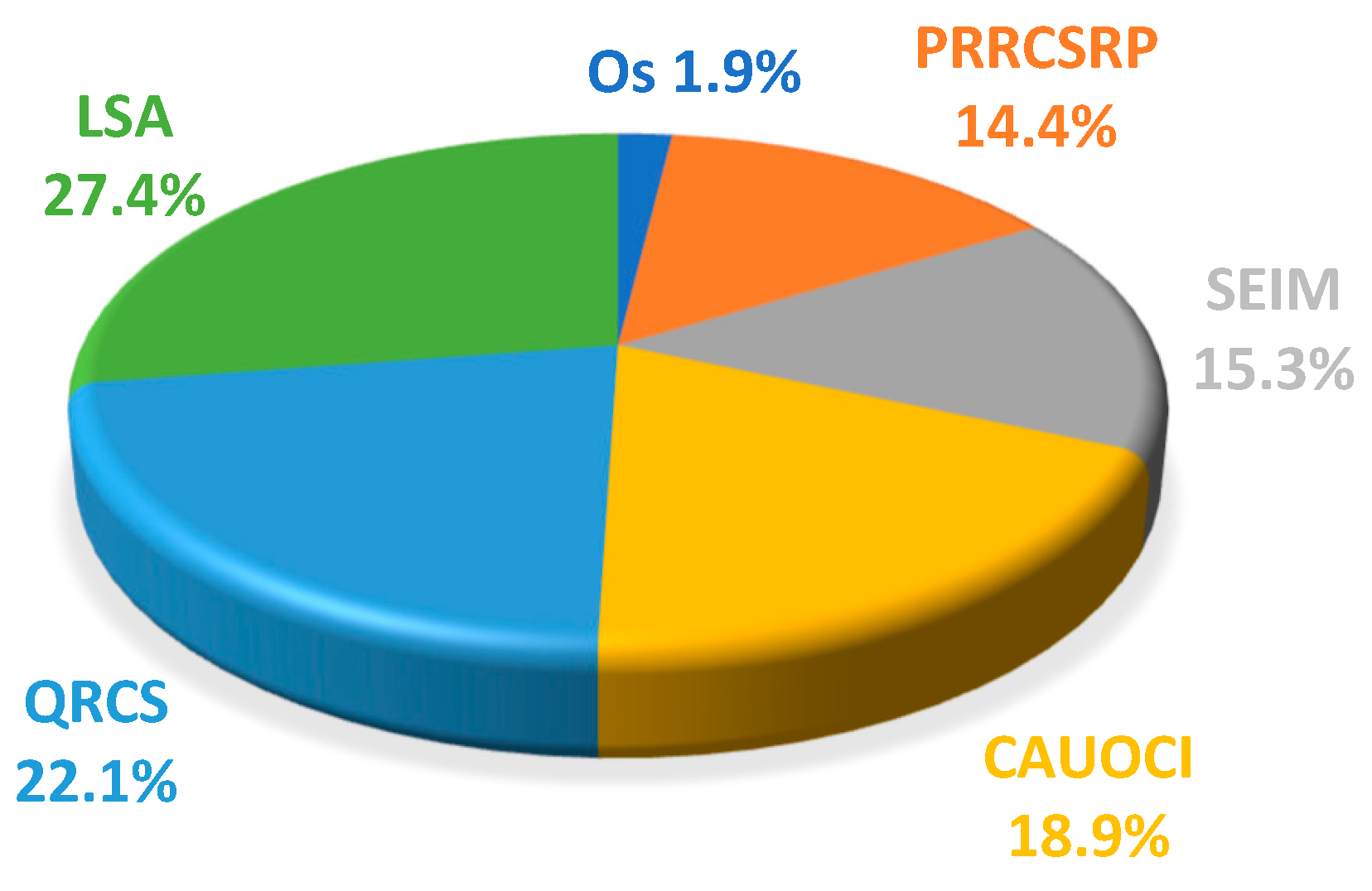

In addition, there is the question of the methodological approaches used to assess the long-term impact of CSR initiatives on economic inequality. It is essential to understanding the effectiveness and sustainability of organizations’ social commitments. It provides information on how companies systematically monitor and analyze the long-term impact of their initiatives, which is key to assessing their real contribution to social and economic justice. The right methodological approaches provide a deeper understanding of the effects on economic inequality and help organizations optimize their strategies and practices for maximum positive impact (see Figure 4).

The data collected reveal the following:

- • Longitudinal studies and analyses (LSA). The highest proportion of organizations (27,4%) use longitudinal research, indicating their commitment to long-term tracking of the impact of CSR initiatives. This allows monitoring changes over time and assessing the long-term effects on economic inequality;

- • Qualitative research and case studies (QRCS). Many companies (22,1%) are using qualitative research and case studies, which implies a focus on in-depth and contextualized case studies. This helps uncover specific effects and practices that cannot be fully captured through quantitative methods;

- • Comparative analysis using other companies or industries (CAUOCI). Comparative analysis has been chosen by 18,9% of organizations, reflecting the interest in comparing the effectiveness of CSR initiatives across companies and industries. This can provide useful insights into successful practices and areas for improvement;

- • Socio-economic impact modelling (SEIM). Socio-economic impact modelling is used by 15,3% of organizations, which implies an approach to quantifying complex social and economic interactions and consequences. It allows companies to predict and measure the impact of their initiatives in a detailed way;

- • Periodic reporting and revision of CSR programs (PRRCSRP) – 14,4%. Periodic reporting and revisions of CSR programs are important to monitor the progress and effectiveness of initiatives. They provide up-to-date information and help organizations make timely adjustments to their strategies; and

- • Others (Os). 1,9% of companies use other methodological approaches that may be specific to their needs. This highlights the diversity in methods and the scope for innovation in impact assessment approaches.

The decompositions above show that organizations use a combination of different methodological approaches to assess the long-term impact of CSR initiatives. Longitudinal studies and qualitative research are the most frequently chosen, demonstrating a commitment to in-depth and sustainable analysis. Comparative analysis and socio-economic impact modelling also play an important role, providing contextual and quantitative data to improve the effectiveness of CSR initiatives.

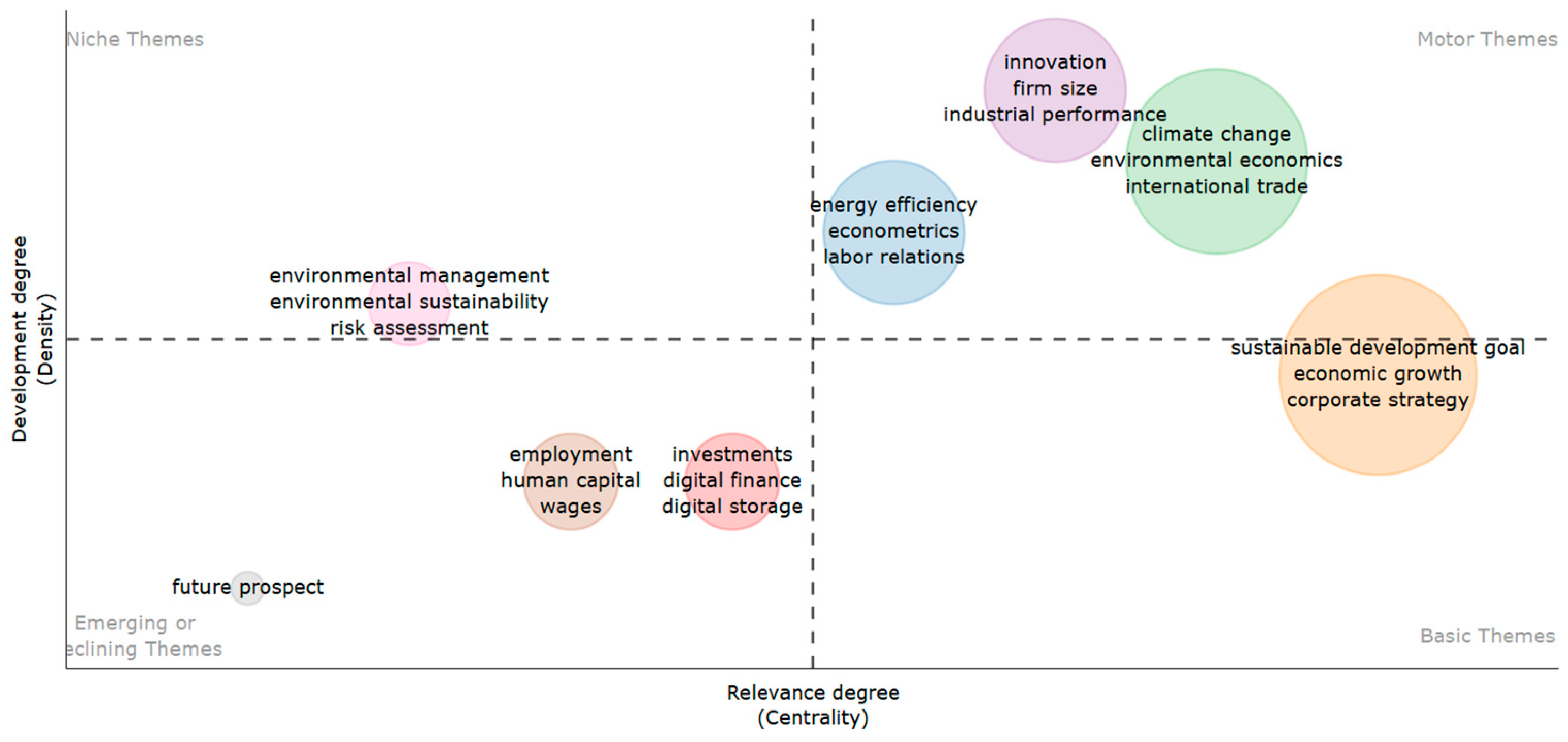

Special attention is paid to Bibliometrix potential for a deeper analysis of the terminology in the issues covered, by generating a so-called “thematic map”. The map is composed of four quadrants formed as a result of the intersection of the degree of development (density) and the degree of relevance (centrality) of the represented keywords, terms, concepts. As a result, the four quadrants contain information about the concepts that compose:

- • Basic themes (bottom right) – important but also very general themes that are not yet sufficiently developed in the research field;

- • Emerging or declining themes (bottom left) – themes with low density and low centrality represent barely perceptible, emerging or gradually declining themes;

- • Motor themes (top right) – well developed and important themes to structure the research area; and

- • Niche themes (top left) – very highly specialized and peripheral themes (Mühl and De Oliveira 2022).

The thematic map generates insights into the conceptual structure of the issues of methodological aspects of measuring the impact of CSR initiatives on economic growth and inequality in the economy and society (see Figure 5 and Table 3).

In the context of analyzing the impact of CSR on economic inequality, Gap Analysis provides a valuable perspective to reveal the gaps between the current status and the desired goals of CSR initiatives. It reveals key areas where organizations can improve their efforts to address economic inequality and achieve greater effectiveness in their social responsibilities (Table 4).

Gap analysis provides very useful information to identify differences and gaps in current approaches to measuring the impact of CSR initiatives on economic inequality. Addressing these gaps by applying systematic methods and expanding the indicators used will help to manage social responsibility more effectively and better achieve the goals of reducing economic inequality. Therefore, the implementation of the recommended measures from the Gap Analysis is key to optimize CSR strategies and achieve sustainable social outcomes.

5. Discussion

By examining the impact of CSR on economic inequality, the study reveals important aspects of current practices and approaches used by business organizations. By analyzing data from 146 companies based in Bulgaria and Romania, it identifies key gaps and areas where efforts to address economic inequality could be improved. These can be used to form the followingconclusions:

- Methodological differences according to the size of enterprises (categories of businesses). One of the key findings is that approaches to measuring the impact of CSR initiatives vary considerably depending on the scale of the work. Small companies often use simpler methods, such as monitoring changes in wages and working conditions, while large companies resort to more complex approaches such as social and economic indicators. This difference in approaches highlights the need for more tailored strategies, adapted to the resources and specific conditions of different sized companies;

- Lack of systematic methodologies. The survey reveals that a significant proportion of organizations (6,8%) do not have systematic methods for measuring the impact of CSR initiatives. This lack of structured approaches means that companies may not be completely aware of the impact of their efforts on economic inequalities, leading to inefficiencies and a lack of accountability;

- Using social and economic indicators. The most commonly used method for impact assessment is social and economic indicators (27,2%). These tools provide objective data and help monitor the long-term effects of CSR initiatives. However, there is potential to expand the range of indicators used, which could provide a more complete view of social and economic outcomes; and

- Variety of assessment methods. The analysis reveals that many organizations (17,7%) use stakeholder surveys and interviews, which indicates the importance of direct feedback from people covered by CSR initiatives. However, incorporating additional and more complex methods, such as qualitative research and socio-economic impact modelling, can improve the understanding and effectiveness of these initiatives.

Based on the results, the recommendations are focused on improving the methodology and effectiveness of CSR initiatives to better address economic inequality:

- • Development of systematic measurement methods. Organizations should develop and implement systematic methods to measure the impact of CSR initiatives. This includes establishing standardized evaluation procedures and indicators to enable more accurate and consistent assessment of social and economic outcomes. The development of structured methodologies will help to better understand the effects and to adequately correct strategies;

- • Customized approaches according to company size (categories of businesses). It is recommended to develop customized impact assessment strategies that reflect the size and resources of the business organization. Small companies can start with basic methods and gradually implement more complex approaches, while large organizations can focus on innovations in evaluation and the use of advanced indicators;

- • Integration of additional indicators. Due to the importance of social and economic indicators, it is important to consider integrating additional indicators and measurements to provide a more complete and justified view of impact. This could include new indicators specific to the industry or region and improving existing methods;

- • Supporting innovation and expanding methodology. Organizations should be open to innovation and new evaluation methods. Introducing new approaches such as qualitative research, socio-economic impact modelling and comparative analyses can provide a deeper and more comprehensive understanding of the effects of CSR initiatives. Investing in these areas will lead to more effective management and optimization of social responsibility; and

- • Periodic reporting and revisions. Regular reporting and revision of CSR programs is important to monitor long-term effects and ensure accountability. Periodic reviews will help organizations to identify problems and make necessary corrections in a timely manner, ensuring greater sustainability and effectiveness of initiatives.

The expectation is that by implementing these recommendations, organizations will significantly improve their CSR strategies and achieve more significant results in reducing economic inequality. Successful integration of innovation and systematic approaches will improve social equity and contribute to sustainable development of society.

6. Conclusions

Researching on the impact of CSR on economic inequality provides valuable insights into understanding current practices and methodologies used by business organizations. The results of the study highlight how different methodological approaches to evaluating the effectiveness of CSR initiatives can help reduce economic inequality and reveal areas where further development is needed.

Our study identified significant differences in approaches to measuring the impact of CSR initiatives depending on the size of enterprises (categories of businesses) and the resources available. Smaller companies often focus on simpler methods, such as monitoring changes in wages and working conditions, while larger organizations use more advanced social and economic indicators. This broadening of methodologies is essential to ensure accurate and consistent assessment of the impact of CSR initiatives.

The study also identified a lack of systematic methodologies in some organizations. The lack of structured approaches to measuring impact highlights the need to develop better methodologies and tools to enable companies to understand and maximize the impact of their social responsibility efforts.

The study also has some limitations. First, the limited representation of companies from Bulgaria and Romania only may limit the generalizations of the results to broader geographical and industry contexts. Second, survey data is only one of many possible sources of information and may not fully reflect the complexity of the issue. Third, the existence of different interpretations of impact measurement terms and methodologies may create difficulties in comparing results.

Despite these limitations, the survey results suggest significant opportunities for implementation and application of CSR initiatives. To successfully implement the proposed recommendations, companies need to adapt and increase their assessment methods, invest in innovation and develop customized strategies. Developing the indicators used and introducing new methods of analysis will allow organizations to gain a more complete and substantiated perspective on the effects of CSR initiatives.

The guidelines for future research include:

- Expanding the geographical and industrial scope of research. Studies that cover different countries and industries will provide a more complete view of the effectiveness of CSR initiatives in a global context;

- Integrating qualitative research. In addition to quantitative data, future research should include qualitative studies to provide a deeper understanding of the impact of CSR initiatives on different social groups; and

- The development of new measurement methodologies. Developing innovative methodologies for assessing the long-term impact of CSR initiatives can help organizations achieve more accurate and reliable results.

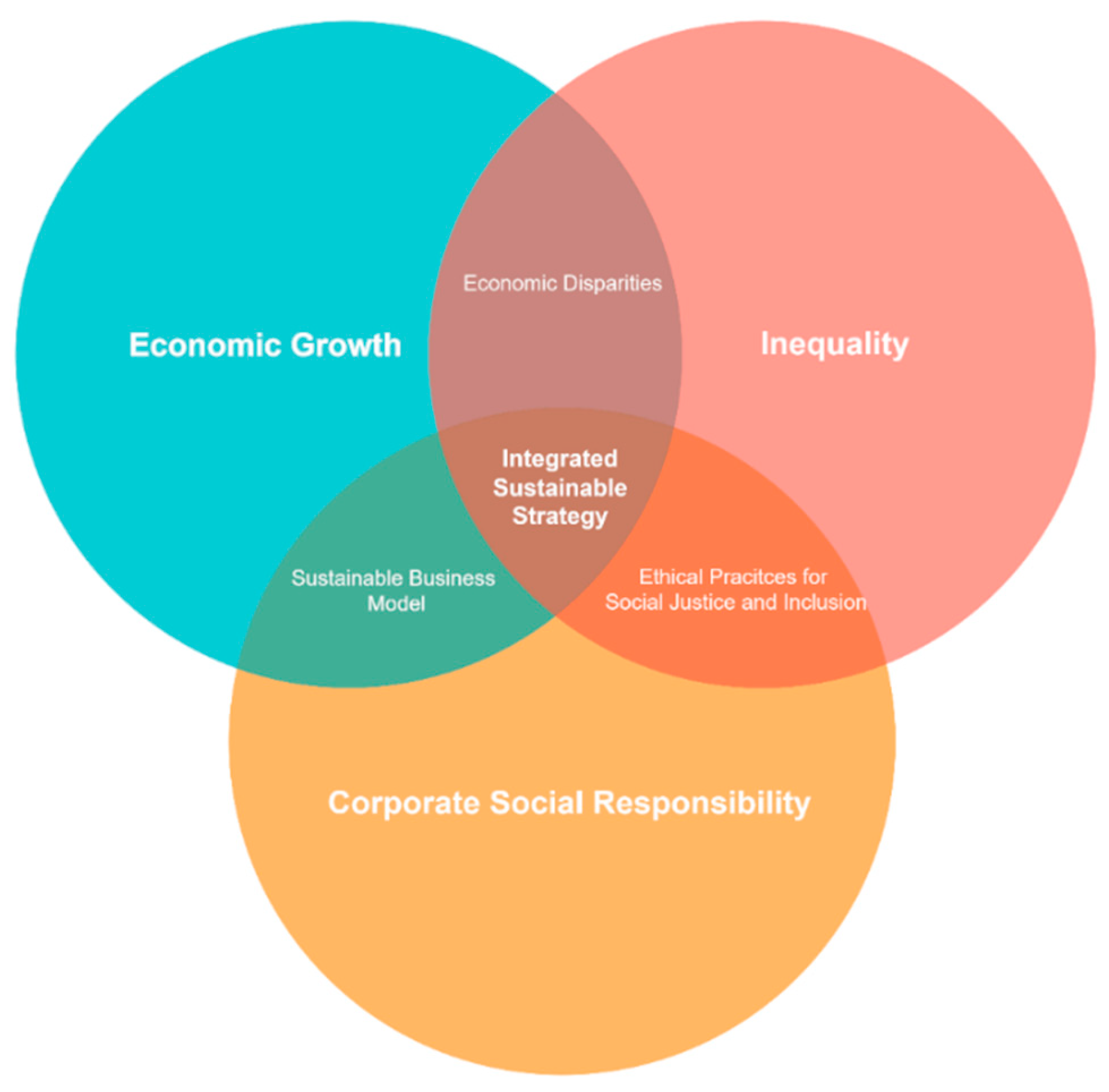

As a result of our research, we can conclude that the categories “Corporate Social Responsibility” (CSR), “Economic Growth” and “Inequality” interact in a specific way, generating added value and synergy, reflected in the following connections: between CSR and economic growth, a sustainable business model is formed, which not only improves the financial performance of companies but also contributes to their long-term stability. The relationship between CSR and inequality manifests in the development of ethical practices for social justice and inclusion, leading to a more equitable distribution of resources and opportunities in society. On the other hand, economic growth and inequality deepen economic disparities, potentially creating new social challenges.

Most significant, however, is the triple interaction between CSR, economic growth and inequality. This interaction is a key condition for building an integrated sustainable strategy. Such a strategy can successfully combine social, economic and environmental goals, contributing to the long-term sustainability of businesses and a fairer distribution of the benefits of economic growth (see Figure 6).

By actively implementing the proposed recommendations and guidelines, companies would improve their social responsibility strategies to make a significant contribution to reducing economic inequality. These efforts would not only improve social justice but also strengthen corporate image and contribute to the sustainable development of society. Investment in better working conditions, more equitable access to services and resources and innovation in evaluating CSR initiatives will lead to a fairer economy.

Author Contributions

Conceptualization, M.C. and G.C.; methodology, G.C. and R.K-H.; software, K.L.; validation, M.C., A.A. and K.L.; formal analysis, A.A.; investigation, M.C., G.C., A.A. and K.L.; resources, K.L.; data curation, R.K-H.; writing—original draft preparation, M.C.; writing—review and editing, G.C. and A.A.; visualization, R.K-H.; supervision, G.C.; project administration, M.C. and R.K-H.; funding acquisition, G.C., A.A. and K.L. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by Institute for Scientific Research of Tsenov Academy of Economics, Svishtov, Bulgaria.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Balaceanu, Cristina, Diana Apostol, and Daniela Penu. 2012. Sustainability and Social Justice. Procedia - Social and Behavioral Sciences. [CrossRef]

- Bruton, Garry, Christopher Sutter, and Anna-Katharina Lenz. 2021. Economic Inequality – Is Entrepreneurship the Cause or the Solution? A Review and Research Agenda for Emerging Economies. Journal of Business Venturing, 1060. [CrossRef]

- Carroll, Archie B. 1991. The Pyramid of Corporate Social Responsibility: Toward the Moral Management of Organizational Stakeholders. Business Horizons. [CrossRef]

- Carroll, Archie B. 1999. Corporate Social Responsibility: Evolution of a Definitional Construct. Business & Society. [CrossRef]

- Carroll, Archie B. 2009. A History of Corporate Social Responsibility: Concepts and Practices. In The Oxford Handbook of Corporate Social Responsibility, 1st ed. Edited by Andrew Crane, Dirk Matten, Abagail McWilliams, Jeremy Moon, and Donald S. Siegel. Oxford University Press, pp. 19–46. [CrossRef]

- Carroll, Archie B. 2016. Carroll’s Pyramid of CSR: Taking Another Look. International Journal of Corporate Social Responsibility. [CrossRef]

- Cradden, Conor. 2020. Repoliticizing Management: A Theory of Corporate Legitimacy, R: Social Responsibility Series. London New York.

- Deng, Dejun, Yi Wu, and Linyi Qin. 2023. CSR Preference, Market Competition, and Corporate Financial Performance. Managerial and Decision Economics, 1396. [CrossRef]

- Derevianko, O. H. 2019. Corporate Reputation Management: Theory and Applied Rating Approach. In Innovative Entrepreneurship: Approach to Facing Relevant Socio-Humanitarian and Technological Challenges. Publishing house “Liha-Pres.”, pp. 118-41. [CrossRef]

- Donaldson, Thomas, and Thomas W. Dunfee. 2017. Toward a unified conception of business ethics: Integrative social contracts theory. In Corporate Social Responsibility. London: Routledge, pp. 175–207.

- Esenyel, Vildan. 2020. Key elements of corporate reputation. Journal of Ekonomi 2020, 2, 76–79.

- Etikan, Julie. 2024. Corporate Social Responsibility (CSR) and Its Influence on Organizational Reputation. Journal of Public Relations. [CrossRef]

- Falkowski, Krzysztof. 2024. Economic Inequality and Its Relevance to Social and Economic Resilience in East Asia. In Regional Cooperation and Resilience in East Asia, 1st ed. Edited by Sebastian Bobowski. London: Routledge, pp. 101–27. [CrossRef]

- Freeman, R. Edward. 1984. Strategic Management: A Stakeholder Approach. Pitman series in business and public policy. Boston: Pitman, 276 p. [CrossRef]

- Freeman, R. Edward. 2015. Stakeholder Theory. In Wiley Encyclopedia of Management, edited by Cary L Cooper, 1st ed., 1–6. Wiley. [CrossRef]

- Freeman, R. Edward, and John McVea. 2017. A Stakeholder Approach to Strategic Management. In The Blackwell Handbook of Strategic Management, pp. 183–201. [CrossRef]

- Friedman, Andrew L., and Samantha Miles. 2002. Developing Stakeholder Theory. Journal of Management Studies. [CrossRef]

- Fu, Shuke, Mengxia Tian, Yingchen Ge, Tingting Yao, and Jiali Tian. 2024. Influencing Factors and Mechanisms of Corporate Social Responsibility Reputation under Green and Low-Carbon Transition: Evidence from Chinese Listed Companies. Energies, 2044. [CrossRef]

- Inusah, Husein, and Peter Sena Gawu. 2021. The Social Contract Theory and Corporation Moral Obligation. E-LOGOS. [CrossRef]

- Jamali, Dima. 2008. A Stakeholder Approach to Corporate Social Responsibility: A Fresh Perspective into Theory and Practice. Journal of Business Ethics. [CrossRef]

- Janang, Joanne Shaza, Corina Joseph, and Roshima Said. 2020. Corporate Governance and Corporate Social Responsibility Society Disclosure: The Application of Legitimacy Theory. International Journal of Business and Society. [CrossRef]

- Javed, Muzhar, Muhammad Amir Rashid, Ghulam Hussain, and Hafiz Yasir Ali. 2020. The Effects of Corporate Social Responsibility on Corporate Reputation and Firm Financial Performance: Moderating Role of Responsible Leadership. Corporate Social Responsibility and Environmental Management 27 (3): 1395–1409. [CrossRef]

- Kakabadse, Nada K., Cecile Rozuel, and Linda Lee-Davies. 2005. Corporate Social Responsibility and Stakeholder Approach: A Conceptual Review. International Journal of Business Governance and Ethics. [CrossRef]

- Katsoulakos, Takis, and Yannis Katsoulacos. 2007. Integrating Corporate Responsibility Principles and Stakeholder Approaches into Mainstream Strategy: A Stakeholder-oriented and Integrative Strategic Management Framework. The International Journal of Business in Society. [CrossRef]

- Kim, Byung-Jik, Youngkyun Chang, and Tae-Hyun Kim. 2023. Translating Corporate Social Responsibility into Financial Performance: Exploring Roles of Work Engagement and Strategic Coherence. Corporate Social Responsibility and Environmental Management 30 (5): 2555–73. [CrossRef]

- Koh, Sin Yee. 2020. Inequality. In International Encyclopedia of Human Geography. Elsevier, pp. 269–77. [CrossRef]

- Margolis, Joshua D., and James P. Walsh. 2003. Misery Loves Companies: Rethinking Social Initiatives by Business. Administrative Science Quarterly. [CrossRef]

- Menezes, David Curtinaz, Diego Mota Vieira, and Jessica Eloísa de Oliveira. 2022. Stakeholder Theory: Evolution and the Proposal of a Research Agenda. Revista Ibero-Americana De Estratégia. [CrossRef]

- Michelon, Giovanna, Michelle Rodrigue, and Elisabetta Trevisan. 2020. The Marketization of a Social Movement: Activists, Shareholders and CSR Disclosure. Accounting, Organizations and Society. [CrossRef]

- Mühl, Diego Durante, and Letícia De Oliveira. 2022. A Bibliometric and Thematic Approach to Agriculture 4.0. Heliyon. [CrossRef]

- Newell, Peter, and Jedrzej George Frynas. 2007. Beyond csr ? Business, Poverty and Social Justice: An Introduction. Third World Quarterly. [CrossRef]

- Ntiamoah, Evans Brako, Priscilla Oforiwaa Egyiri, and Michael Kwamega. 2014. Corporate Social Responsibility Awareness, Firm Commitment and Organizational Performance. Journal of Human Resource and Sustainability Studies. [CrossRef]

- Olateju, Dare John, Olakunle Abraham Olateju, Seyi Vincent Adeoye, and Idris Suleiman Ilyas. 2021. A Critical Review of the Application of the Legitimacy Theory to Corporate Social Responsibility. International Journal of Managerial Studies and Research. [CrossRef]

- Orlitzky, Marc. 2009. Corporate Social Performance and Financial Performance: A Research Synthesis. In The Oxford Handbook of Corporate Social Responsibility. Edited by Andrew Crane, Dirk Matten, Abagail McWilliams, Jeremy Moon, and Donald S. Siegel, 1st ed. Oxford University Press, pp. 113–34. [CrossRef]

- Orlitzky, Marc, Frank L. Schmidt, and Sara L. Rynes. 2003. Corporate Social and Financial Performance: A Meta-Analysis. Organization Studies. [CrossRef]

- Pekovic, Sanja, and Sebastian Vogt. 2021. The Fit between Corporate Social Responsibility and Corporate Governance: The Impact on a Firm’s Financial Performance. Review of Managerial Science, 1095. [CrossRef]

- Pesqueux, Yvon, and Salma Damak-Ayadi. 2005. Stakeholder Theory in Perspective. Corporate Governance: The International Journal of Business in Society. [CrossRef]

- Pires, Vanessa, and Guilherme Trez. 2018. Corporate Reputation: A Discussion on Construct Definition and Measurement and Its Relation to Performance. Revista de Gestão. [CrossRef]

- Ravallion, Martin. 2014. Income Inequality in the Developing World. Science. [CrossRef]

- Rolf, Skylar. 2023. Responding to a Societal Crisis: How Does Corporate Social Responsibility Engagement Influence Corporate Reputation? Journal of General Management. [CrossRef]

- Schiopoiu Burlea, Adriana, and Ion Popa. 2013. Legitimacy Theory. In Encyclopedia of Corporate Social Responsibility. Edited by Samuel O. Idowu, Nicholas Capaldi, Liangrong Zu, and Ananda Das Gupta. Berlin, Heidelberg: Springer Berlin Heidelberg, pp. 1579–84. [CrossRef]

- Schmidt, Andreas T., and Daan Juijn. 2024. Economic Inequality and the Long-Term Future. Politics, Philosophy & Economics. [CrossRef]

- Schwartz, Mark S., Archie B. Carroll. 2003. Corporate Social Responsibility: A Three-Domain Approach. Business Ethics Quarterly. [CrossRef]

- Sequeira, Lavina, and Stanley J. Ward. 2023. Social Contract Theory. In Ethical Leadership. Cheltenham, UK ; Northampton, MA: Edward Elgar Publishing, pp. 16–79. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85189581814&partnerID=40&md5=cdf21b0a0ff507732a96c7f279e3862f.

- Simangunsong, Humala, Baldry Pitre Stewart, and Debortoli Debortoli. 2023. The Impact of Economic Inequality on Social Disparities: A Quantitative Analysis. Jurnal Sosial, Sains, Terapan Dan Riset (Sosateris). [CrossRef]

- Stratling, Rebecca. 2007. The Legitimacy of Corporate Social Responsibility. Corporate Ownership and Control. [CrossRef]

- Tweedie, Dale, and James Hazelton. 2019. Economic Inequality: Problems and Perspectives for Interdisciplinary Accounting Research. Accounting, Auditing & Accountability Journal. [CrossRef]

- Voitchovsky, Sarah. 2011. Inequality and Economic Growth. In The Oxford Handbook of Economic Inequality. Oxford University Press. pp. 549-74. [CrossRef]

- Volchek, R, H Moskaliuk, L Halan, and O Dancheva. 2024. Implementation of Corporate Social Responsibility in the Context of Integration with the Enterprise Management Information System. Naukovyi Visnyk Natsionalnoho Hirnychoho Universytetu, no. 1 (February), 154–61. [CrossRef]

- Wahlrab, Amentahru. 2023. Social Contract Theory. In Handbook of the Anthropocene. Edited by Nathanaël Wallenhorst and Christoph Wulf. Cham: Springer International Publishing, pp. 1207–10. [CrossRef]

- Windsor, Duane. 2018. Dynamics for Integrative Social Contracts Theory: Norm Evolution and Individual Mobility. Journal of Business Ethics. [CrossRef]

- Yuncu, Volkan, and Celil Koparal. 2017. Fundamental Paradigms for Corporate Reputation. Annals of the University Dunarea de Jos of Galati: Fascicle: I, Economics & Applied Informatics 2017, 23, 60–65.

- Zsolnai, Laszlo. 2011. Corporate Legitimacy. SSRN Electronic Journal. [CrossRef]

Figure 1.

Three Fields Plot with data on keywords, country/region and source of publications in the sample. (Source: prepared by the authors with Bibliometrix).

Figure 1.

Three Fields Plot with data on keywords, country/region and source of publications in the sample. (Source: prepared by the authors with Bibliometrix).

Figure 2.

Measuring the impact of CSR initiatives in percentage. (Source: authors’ own research).

Figure 3.

Indicators used for identifying the contribution of CSR initiatives to reducing economic inequality in percentage. (Source: authors’ own research).

Figure 3.

Indicators used for identifying the contribution of CSR initiatives to reducing economic inequality in percentage. (Source: authors’ own research).

Figure 4.

Methodological approaches for assessing the long-term impact of CSR initiatives on economic inequality in percentage. (Source: authors’ own research).

Figure 4.

Methodological approaches for assessing the long-term impact of CSR initiatives on economic inequality in percentage. (Source: authors’ own research).

Figure 5.

Thematic map of conceptual structure in statics. (Source: prepared by the authors with Bibliometrix).

Figure 5.

Thematic map of conceptual structure in statics. (Source: prepared by the authors with Bibliometrix).

Figure 6.

Synergy between CSR, economic growth and inequality. (Source: authors’ own research).

Table 1.

Challenges for the implementation of CSR.

| Potential barriers | Specificity |

|---|---|

| Lack of commitment from senior management |

Senior management engagement is key to the successful implementation of CSR strategies. Without the support and active involvement of senior management, initiatives may remain a low priority. |

| Limited resources |

Small and medium-sized business organizations often have limited financial and human resources to invest in CSR. |

| Lack of transparency and measurement of results | Measuring the impact of CSR is a complex task that requires transparency and the availability of accurate data. |

| Conflict between economic and social goals | Companies sometimes face a dilemma between the pursuit of profit and a commitment to social responsibility. |

Table 2.

Estimates of how to measure the impact of CSR initiatives versus company size.

|

Table 3.

Keywords and terms grouped by themes, that compose the conceptual structure in statics.

| Basic themes | ||

|---|---|---|

| Sustainable development goal | Developing world | |

| Economic growth | Economic development | |

| Corporate strategy | Globalization | |

| Governance approach | Profitability | |

| Emerging/declining themes | ||

| Future prospect | Investments | |

| Employment | Digital finance | |

| Human capital | Digital storage | |

| Wages | ||

| Motor themes | ||

| Energy efficiency | Industrial performance | |

| Econometrics | Climate change | |

| Labor relations | Environmental economics | |

| Innovations | International trade | |

| Firm size | ||

| Niche themes | ||

| Environmental management | Risk assessment | |

| Environmental sustainability |

Table 4.

Gap analysis results (findings).

| Guidelines of the method application | Acquired results |

|---|---|

| Weaknesses in measurement methodologies | The initial Gap Analysis shows that a significant percentage of organizations (6,8%) still do not have a systematic method for measuring the impact of CSR initiatives. This reveals a major gap that needs to be addressed to achieve greater transparency and accountability. Developing structured and effective measurement methodologies will allow organizations to more accurately assess the effectiveness of their initiatives and adjust their strategies in line with actual results. |

| Difference in tools used | Gap analysis reveals differences in the use of assessment tools between small and large enterprises. Small companies prefer methods such as monitoring changes in wages and working conditions, while large business organizations tend to use more complex approaches such as social and economic indicators and qualitative research. This difference in approaches highlights the need to adapt the methodology depending on the size of the organization (categories of businesses), which can help to address identified gaps and achieve better results in addressing economic inequalities. |

| Extension of the indicators used | The research shows that the use of social and economic indicators is among the most popular methods for impact assessment. However, only 27,2% of organizations are using this approach, creating a Gap between current application and the potential opportunity for more detailed evaluation by including additional indicators. Integrating new and diverse indicators can provide a more complex and justified view of the impact of CSR initiatives, thereby improving the understanding and management of social and economic outcomes. |

| Availability of non-standard methods | The presence of a small percentage (2,7%) of organizations using non-standard measurement methods indicates the potential for innovation in the field of evaluating CSR initiatives. Although these methods are limited, they offer unique insights and opportunities to develop new approaches that can be adapted and applied on a broader basis. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.