Submitted:

14 August 2024

Posted:

15 August 2024

You are already at the latest version

Abstract

Financial technologies (Fintech) have become an indispensable part of most of the business infrastructure around the world. The Fintech ecosystem provides this solution by providing a suitable environment for all financial techno services to synergize. The objective of this paper is two folds; first, it aims to investigate & summarize Fintech programs products, and services in Saudi Arabia. Second, it maps the sustainable development goals (SDG) and indicators of the Fintech programs in Saudi Arabia. Secondary data was collected from published reports, institutional & governmental websites, official portals, and research papers focusing on the companies operating in Saudi Arabia. In the second step, the content analysis method was employed to investigate the features and characteristics of each program to map it to the sustainable development goals (SDGs). It was found that Fintech in Saudi Arabia is addressing SDGs goals 1, 2, 5 8 & 17. The paper also attempted to map further the SDG indicators with the products and services which Fintech companies are offering. This study will be beneficial for the institutions and policymakers of the Fintech industry to fill the gaps in addressing SDG goals which is a global agenda for eradicating poverty and offering sustainable development opportunities.

Keywords:

Fintech

; SDGs

; Content analysis

; Fintech ecosystem

1. Introduction

Today’s business world is challenged by many technological, economic, and social factors. Digital transformation is one of the most important which imposes additional pressure on investors, businesses, entrepreneurs, policymakers, and all stakeholders. Among the technological improvements, financial technology (Fintech) has recently emerged as a critical tool for financial institutions to be competitive in the face of global competition and contributes towards the development of any country. According to Wikipedia, Fintech is defined as “A financial technology, which is used by firms to replace the old technology in the delivery of financial services”. The key areas of financial technology include Artificial Intelligence, Blockchains, Cloud Computing, and Big data. Fintech firms, which include both new and old financial institutions and technology firms, aim to replace or improve upon the use of the financial services offered by conventional financial firms. Therefore, Fintech is not regarded as an important tool of the financial markets to bring the change in the mode of business but it also improves and increases the efficiency and performance of the firm, which overall enhances the economic condition of any country.

Fintech opens new doors of prosperity for financial institutions and the banking sector. Huang (2020) highlights the importance of Fintech that, due to Fintech, the goal of financial inclusion was achievable, which enhances the overall financial ecosystem. Therefore, Financial institutions have an additional responsibility to not only provide techno-friendly solutions to their users but also address sustainability. The precedent of millennium development goals (MDGs), which focused on developing countries, sustainable development goals stress the role of developed countries to achieve the goals (Biermann et al., 2017; Kroll, 2015) and the role of financial institutions in the economy is detrimental to achieve SDGs.

Sustainable development goals were first introduced and presented at the United Nations conference on the topic of sustainable development in 2012 in Rio de Janeiro. Sustainable development goals address the world’s real issues like environmental, political, and economic. These challenges are faced by almost every country in the world, even after COVID-19, these issues are at their peak in third-world countries. Now it is the need of time to introduce different strategies including technology to achieve sustainable goals. There are seventeen sustainable goals presented at the conference of the united nations that are: no poverty, zero hunger, good health and well-being, quality education, gender equality, clean water and sanitation, affordable and clean energy, decent work and economic growth, industries innovation, and infrastructure, reduced inequalities, sustainable cities, and communities, responsible consumption and production, climate action, life below water, life on land, peace, justice, and strong institutions and partnerships for the goals.

It is desired by every country to have a stable financial system and nowadays, Fintech gives an opportunity and helps to achieve a stable and technologically enriched financial ecosystem. In the past decades, countries did not have resources in terms of technology, so it is regarded as the hurdle to the prosperity of the financial sector. The traditional finance theories, including the efficient market hypotheses stress the role of increasing profits and do not include the sustainable development aspect. The paradigm shift of the finance world is redirected to include the well-being and welfare of society and hence the global economy. Social, economic, and environmental factors have become significantly important in the changing economy. Therefore, it is not adequate and coherent for the financial world to compete without addressing these challenges. Not to forget the risks which these (social, economic & environmental) factors bring along. Fullwiler (2016) argues that sustainable finance calls for the inclusion of technological, economic, and social factors which correlate with the major themes of SDG goals.

There has been tremendous research on technological advancement in the business and finance industry, however, little is known about the impact of social, economic, technological, and environmental factors on the Fintech ecosystem (Puschmann, 2017). The current study has tried to fill this gap by exploring the Fintech companies and how they are making a difference in the achievement of SDGs.

2. Literature Review

The literature review is divided into two parts: the first is related to the previous studies of the Fintech and sustainable development goals and the second part highlights the overview of the Fintech ecosystem in Saudi Arabia.

Around the world, special attention has been given to the usage of financial technology in all sectors where it is possible to attain sustainable development goals. About 194 countries around the world passed the sustainable development goals in September 2015(Hoang et al.,2022). Many economists, policymakers, authors, researchers, scholars, practitioners, and standard setters believe that financial technology, which leads to financial innovation helps to face the challenges and remove the hurdles, which are on the way to attaining sustainable development (Allen et al., 2016). Moreover, Digital finance is progressively proving its ability to overcome challenges affecting the expansion of finance for sustainable development. It has been observed that Automated technologies and transformation have significantly improved performance in the banking sector over the past 20 years (Collste et al., 2017; Hinson et al., 2019).

Farahani et al. (2020) studied the issues like digitalization, green finance, climate change, big data, sustainable development parameters, etc which impact Fintech and artificial intelligence during COVID-19. The findings indicate that Fintech and artificial intelligence can be useful in attaining sustainable development goals and that they can be crucial in reducing the negative effects of COVID-19 in a variety of areas, including the economy, social health, environment, and others. Zhang et al. (2021) found that Fintech contributes to sustainable development in respect of forest and land restoration in China. In northern China, we discovered that the Ant Forest has made significant strides in land restoration, carbon abatement, and socioeconomic betterment. Its effectiveness is dependent on several variables, including technical development, process transparency, and its ability to promote public participation. Additionally, it influences people’s lifestyles and heightens their understanding of low-carbon living while promoting individual and corporate social responsibility.

Mhlanga (2022) addressed the connection between Fintech and financial inclusion with climate change issues. The findings suggested that financial inclusion through FinTech could improve people’s homes, and businesses’ resilience in the event of a sudden climate event or the more gradual consequences of altered rainfall patterns, increasing sea levels, or saltier water intrusion. The study, therefore, suggests promoting financial inclusion through FinTech as one of the avenues that can help in mitigating the risks of climate-related problems and achieving sustainable development goals through development patterns, governments, and civil society. Ye et al. (2022) highlight the importance of Fintech in alleviating poverty. The impact of Fintech on reducing poverty in Chinese provinces is examined in this study. Data for 31 provinces from 2011 to 2020 are included in the sample. The empirical findings of this study demonstrate that, despite regional differences in the development of the Fintech index, Fintech has a significant impact on reducing poverty across all provinces. Additionally, low-income provinces experience the benefits of Fintech in reducing poverty considerably more strongly than high-income provinces. Therefore, additional digital financial technology platforms should be built by policymakers and practitioners, particularly in China’s low-income provinces (Lee et al.,2022).

Poverty and hunger are one of the major issues faced by third-world countries. According to the world bank report, by the end of 2022, 685 million people living below the poverty line, and it will be expected these figures reaches their peak by 2030. Therefore, it is added as one of the crucial sustainable development goals that to eradicate poverty throughout the world and make the policies in such a way that there will be no hunger. This sustainable goal would be achieved by using financial technology. Several research presented and addressed this issue and given the way outs for the eradication of poverty. Emara and Mohieldin (2021) employed the technique of General Methods of Moments by taking the data from 12 Middle East and North Africa (MENA) and 45 Sub-Saharan Africa (SSA) countries. It is observed that people from SSR countries faced the issue of poverty more than the other countries of the world. the findings of this study conclude that Fintech brings breakthroughs in MENA as compared to the SSA countries. Therefore, special intention has been given by the policymakers and government for the provision of financial services in these regions so that they do not go beyond the poverty line.

Nasution et al. (2022) investigated the impact of financial inclusion and Fintech on economic factors and poverty growth in five developing countries in ASEAN. It concludes that financial inclusion and Fintech introduction in different shapes like credit availability, number of ATMs, etc play an important role in boosting the economy while reducing poverty in these countries. Hudaefi et al. (2020) and Zuliansyah et al. (2022) also stress the role of Fintech in the alleviation of poverty in Indonesia. It is a qualitative study and highlights the role of Fintech in the management of Zakat which leads to the eradication of poverty in the state. Emara (2022) and Khaki et al. (2022) explore the dynamic relationship between financial technology adoption and poverty alleviation by gathering data from the Sub-Saharan Africa (SSA) region over the period from 2004 to 2020. In his research, he confirmed the results of the previous research on how Fintech helps in the eradication of poverty and hunger throughout the world.

Decent work and economic growth, gender equality, and corporation and partnership for attaining these goals are important parts of the sustainable development goal. Fintech also plays an important role in the economic growth of Indonesia. Moreover, Fintech has a positive impact on economic growth (Narayan, 2019). Panjwani and Shili (2020) compared Fintech with the traditional financial ecosystem in Islamic banking and give the Fintech new directions by explaining the role of Fintech in financial services. Lukonga (2021) talked about the connection between the Fintech and economic growth of the Middle East, North Africa, Afghanistan, and Pakistan (MENAP) Region. It emphasizes the increased setup of small and medium-sized enterprises and easy access to credit. This will only be possible by proper induction of financial technology.

The researchers also address the connection between Fintech and Islamic banking. Financial technology works in developing countries not only to boost economic growth but also to increase the burden on the regulators as they ensure the stability of the financial ecosystem. (Saba et al.2019). Barata (2019) also found the Indonesian economy also transformed from a traditional setting to a digital setting and gives a special focus on information communication and technology (ICT). As it is observed that the Fintech in Indonesia is in its initial stages, even then shows the impact on economic growth which leads to the increase in income, which reduces inequality and poverty. Zhou et al. (2022) explore financial technology and green finance in achieving green growth in the Chinese economy. Song and Otoo (2022) also confirmed the results of previous studies in respect of China. This study also recommends institutional reforms which help to achieve the goal of sustainable development.

Shin and Choi (2019) found that Fintech plays an important in the fourth industrial revolution in Korea. The Fintech acts as a growth simulator and plays an important role in uplifting the national economy. Akmal et al. (2023) talked about the perception of Fintech in the Middle East region. They surveyed between November 2021 and February 2022 and asked questions to the respondents about the usage and performance of financial technology. The findings suggest that digital banking is Fintech’s most advantageous characteristic for all customer types and improves the performance of financial institutions.

2.1. An Overview of the Fintech Ecosystem in Saudi Arabia

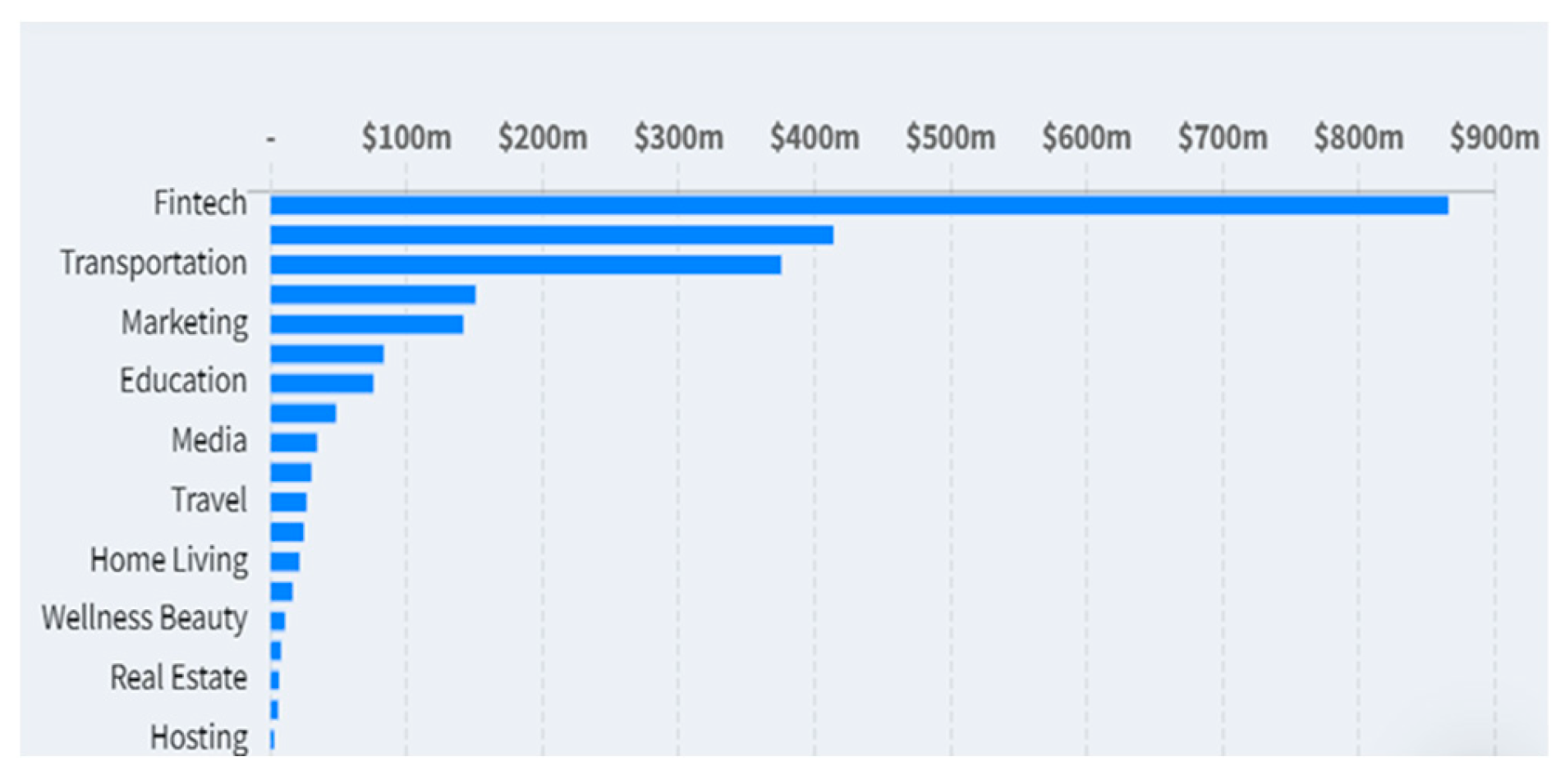

Saudia Arabia has an important position among the Arab countries of its location. It is one of the biggest oil-producing and exporter countries in the world. Fast pace tech ecosystem in Saudi Arabia has urged businesses for digital transformation due to increasing demand for technology. Nowadays businesses are serological-based alternatives for better quality products and efficiency. The government of Saudi Arabia has been highly supportive of the progression of the tech ecosystem since there is an availability of talent and high demand for technological solutions. Figure 1 shows the amount of dollars invested in financial technology by the Saudi government.

2.2. Saudi Arabia’s Strategy towards Sustainable Development Goals

Saudia Arabia is recognized as one of the biggest exporters of oil and oil products around the world. Therefore, the major revenue earned by the government of Saudia Arabia is from oil exporting and giving the Haj and Umrah services to Muslim countries all over the world. So, these are two basic sources of income in Saudi Arabia. Now the Saudi Vision 2030 will be to reduce the dependency on the income/revenue earned from oil exporting and they try to come up from this dependency and start focusing on the other sectors of the economy. The vision especially gives attention to the development of financial and fiscal sustainability programs.

The 2030 vision of Saudi Arabia will also link with the sustainable development goals and this vision and sustainable development goals are achieved by using financial technology (Fintech) in different sectors of the economy. One of the themes, in the 2030 vision is to prosper the economy by making investments for the future like starting different projects for the wellbeing of the people as well as overall for the country. Under this theme, the Financial Sector Development Program (FSDP) introduces the Fintech programs, which make the economy innovative and competitive. The overall satisfaction index of Fintech coincides with the Kingdom of Saudi Arabia’s Fintech ecosystem. Moreover, Saudi Arabia introduces venture capital funding in different sectors by taking Fintech into account(FSDP,2020). Therefore, Saudia Arabia initiates Fintech startup in industries and generate a major portion of the venture capital which is 36% from food tech and 45% from the transportation industry. According to the data of Dealroom.co, In August 2022, the capital venture funding covers the regions in three different rounds and exceeds $100 million sum.

The venture capital funding indicates that the investors are interested to invest in the technology sector which has the potential for the growth and overall uplifting of the Saudi economy. The Saudi businesses raised slightly shy of $1B for the year in 2022, setting a new milestone for the country’s digital economy in terms of VC investment.

3. Materials & Methods

The main aims of this study are to investigate & summarize Fintech programs products and services in Saudi Arabia. Second, it maps the sustainable development goals (SDG) and indicators of the Fintech programs in Saudi Arabia. To fulfil these purposes, the qualitative approach was used to explore Fintech and its relationship with sustainable development goals, particularly in the region of Saudi Arabia. Therefore, data were taken from published reports, institutional & governmental websites, official portals, and research papers focusing on the companies operating in Saudi Arabia. In the second step, the content analysis method was employed to look into the features and characteristics of each program to map it to the sustainable development goals (SDGs). There are different thirteen websites and seventeen published reports are used for the gathering and analyzing of data. It was found that Fintech in Saudi Arabia is addressing SDG’s goals 1, 2, 5 8 & 17. Therefore, the data was divided into four different SDGs which are linked with Fintech.

The details of the SDG’s goals linked to financial technology (Fintech) are presented in the following table:

Table 1.

Sustainable Development Goals Linked to FinTech.

| Sr. No | Sustainable Development Goals |

|---|---|

| 1 | No Poverty |

| 2 | Zero Hunger |

| 5 | Gender Equality |

| 8 | Decent work and economic growth |

| 17 | Strong Global partnership and cooperation for the goals |

4. Results and Discussions

The results of the study are presented in Table 2. It gives the overall Fintech programs which help attain the SDG. This study explored the five sustainable goals with their indicators and presents the Fintech program product and services which help to achieve that sustainable goal.

5. Conclusions

Fintech is the need of every business setup. By using the financial technology in different sectors of the economy, it results in the innovation and increased growth. Likewise, there are 17 sustainable goals approved in the conference of the United Nations for all the countries of the world and countries are striving to attain or achieve the sustainable development goals by designing and implementing different strategies at local and national levels. Saudi Arabia is one of the amongst which work hard for achieving these goals.

This qualitative type of study explores the link between Fintech and five different sustainable goals. We used the different indicators of the sustainable goals and identify the industries where Fintech is applied by attaining these goals. The latest Data was collected from different reports and institutional and government websites and exploratory data analysis. It was found that Saudi Arabia attempted to map Fintech with sustainable development goals. They are striving to achieve it in different industries and sectors also. Furthermore, this study identifies the SDGs indicators with the products and services which Fintech companies are offering. This study will be beneficial for the institutions and policymakers of the Fintech industry to fill the gaps in addressing SDG goals which is a global agenda for eradicating poverty and offering sustainable development opportunities. This study recommends further research by exploring the relationship between Fintech and other sustainable development goals in the region of Saudi Arabia. Another recommendation will be that this study should be applied to other countries of the world.

References

- Akmal, S.; Talha, M.; Faisal, S.M.; Ahmad, M.; Khan, A.K. Perceptions about FinTech: New evidences from the Middle East. Cogent Economics & Finance 2023, 11, 2217583. [Google Scholar]

- Allen, F.; Demirguc-Kunt, A.; Klapper, L.; Peria, M.S.M. The foundations of financial inclusion: Understanding ownership and use of formal accounts. Journal of financial Intermediation 2016, 27, 1–30. [Google Scholar] [CrossRef]

- Arestis, P. 21 Financial liberalization and the relationship between finance and growth. In A handbook of alternative monetary economics; Edward Elgar Publishing: Cheltenham; UK; Northampton, MA, USA, 2006; pp. 346–364. [Google Scholar]

- Barata, A. Strengthening national economic growth and equitable income through sharia digital economy in Indonesia. Journal of Islamic Monetary Economics and Finance 2019, 5, 145–168. [Google Scholar] [CrossRef]

- Biermann, F.; Kanie, N.; Kim, R.E. Global governance by goal setting: The novel approach of the UN Sustainable Development Goals. Current Opinion in Environmental Sustainability 2017, 26, 26–31. [Google Scholar] [CrossRef]

- Collste, D.; Pedercini, M.; Cornell, S.E. Policy coherence to achieve the SDGs: Using integrated simulation models to assess effective policies. Sustainability science 2017, 12, 921–931. [Google Scholar] [CrossRef]

- Emara, N. Asymmetric and threshold effects of FinTech on poverty in SSA countries. Journal of Economic Studies 2022. [Google Scholar] [CrossRef]

- Emara, N.; Mohieldin, M. Beyond the Digital Dividends: Fintech and Extreme Poverty in the Middle East and Africa. Topics in Middle Eastern & North African Economies: Proceedings of the Middle East Economic Association 2021, 23. [Google Scholar]

- Farahani, M.S.; Esfahani, A.; Moghaddam, M.N.F.; Ramezani, A. The impact of Fintech and artificial intelligence on COVID 19 and sustainable development goals. International Journal of Innovation in Management, Economics and Social Sciences 2022, 2, 14–31. [Google Scholar]

- Fullwiler, S. Sustainable finance: Building a more general theory of finance. In Routledge handbook of social and sustainable finance; Routledge: 2016; pp. 17–34.

- Hinson, R.; Lensink, R.; Mueller, A. Transforming agribusiness in developing countries: SDGs and the role of FinTech. Current Opinion in Environmental Sustainability 2019, 41, 1–9. [Google Scholar] [CrossRef]

- Hoang, T.G.; Nguyen, G.N.T.; Le, D.A. Developments in financial technologies for achieving the Sustainable Development Goals (SDGs): FinTech and SDGs. In Disruptive technologies and eco-innovation for sustainable development; IGI Global: 2022; pp. 1–19.

- Hudaefi, F.A.; Zaenal, M.H.; Farchatunnisa, H.; Junari, U.L. How does zakat institution respond to fintech? Evidence from BAZNAS Indonesia. Journal website: Journal. zakatkedah. com. My 2020, 2. [Google Scholar]

- Khaki, A.R.; Messaadia, M.; Jreisat, A.; Al-Mohammad, S. Fintech Adoption for Poverty Alleviation in African Countries: Application of Supervised Machine Learning Approach. In Africa Case Studies in Operations Research: A Closer Look into Applications and Algorithms; Springer International Publishing: Cham, 2022; pp. 197–210. [Google Scholar]

- Kroll, C. spotlight europe, August 2015: Sustainable Development Goals: Are the rich countries ready? 2015.

- Lukonga, I. Fintech and the real economy: Lessons from the Middle East, North Africa, Afghanistan, and Pakistan (MENAP) region. The Palgrave handbook of fintech and blockchain 2021, 187–214. [Google Scholar]

- Lee, C.C.; Lou, R.; Wang, F. Digital financial inclusion and poverty alleviation: Evidence from the sustainable development of China. Economic Analysis and Policy 2023, 77, 418–434. [Google Scholar] [CrossRef]

- Mhlanga, D. The role of financial inclusion and FinTech in addressing climate-related challenges in the industry 4.0: Lessons for sustainable development goals. Frontiers in Climate 2022, 4, 949178. [Google Scholar] [CrossRef]

- Narayan, S.W. Does fintech matter for Indonesia’s economic growth? Buletin Ekonomi Moneter Dan Perbankan 2019, 22, 437–456. [Google Scholar] [CrossRef]

- Nasution, L.N.; Sadalia, I.; Ruslan, D. Investigation of Financial Inclusion, Financial Technology, Economic Fundamentals, and Poverty Alleviation in ASEAN-5: Using SUR Model. ABAC Journal 2022, 42, 132–147. [Google Scholar]

- Panjwani, K.; Shili, N. The impact of fintech on development of islamic banking sector in the contemporary world. Saudi Journal of Economics and Finance 2020, 4, 346–350. [Google Scholar] [CrossRef]

- Puschmann, T. Fintech. Business & Information Systems Engineering 2017, 59, 69–76. [Google Scholar]

- Saba, I.; Kouser, R.; Chaudhry, I.S. FinTech and Islamic finance-challenges and opportunities. Review of Economics and Development Studies 2019, 5, 581–890. [Google Scholar] [CrossRef]

- Shen, Q. Investment Analysis on Precision Medicine Project in Saudi Arabia. Highlights in Business, Economics and Management 2023, 8, 385–395. [Google Scholar] [CrossRef]

- Shin, Y.J.; Choi, Y. Feasibility of the FinTech industry as an innovation platform for sustainable economic growth in Korea. Sustainability 2019, 11, 5351. [Google Scholar] [CrossRef]

- Song, N.; Appiah-Otoo, I. The impact of fintech on economic growth: Evidence from China. Sustainability 2022, 14, 6211. [Google Scholar] [CrossRef]

- Ye, Y.; Chen, S.; Li, C. Financial technology as a driver of poverty alleviation in China: Evidence from an innovative regression approach. Journal of Innovation & Knowledge 2022, 7, 100164. [Google Scholar]

- Zhang, Y.; Chen, J.; Han, Y.; Qian, M.; Guo, X.; Chen, R.; Chen, Y. The contribution of Fintech to sustainable development in the digital age: Ant forest and land restoration in China. Land use policy 2021, 103, 105306. [Google Scholar] [CrossRef]

- Zhou, G.; Zhu, J.; Luo, S. The impact of fintech innovation on green growth in China: Mediating effect of green finance. Ecological Economics 2022, 193, 107308. [Google Scholar] [CrossRef]

- Zuliansyah, A.; Pratomo, D.; Supriyaningsih, O. The Role of Financial Technology (Fintech) in ZIS Management to Overcome Poverty. Indonesian Interdisciplinary Journal of Sharia Economics (IIJSE) 2022, 5, 203–224. [Google Scholar] [CrossRef]

Figure 1.

Investment in Fintech in terms of dollars.

Table 2.

Mapping of Fintech Programs with SDGs.

| SDG Goals & Indicators | Fintech Program Helping to Achieve SDG | Fintech Program Product & Services | References |

|---|---|---|---|

| Goal 1. End Poverty in All its Forms Everywhere | |||

| Indicator 1.1.1. The proportion of the Population Below the International Poverty Line Indicator 1.4.1 The proportion of the population living in households with access to basic services |

Lendo: Digital Lending for Information Technology (Debt – CrowdFunding Platform) SURE (Digital Payments) |

Invoice financing, A relatively new method for SMEs to borrow money directly from investors is through invoice financing, also known as receivables financing. This method allows SMEs to borrow money against the payments they are expected to receive from their clients or customers. Peer-to-peer (P2P) Lending, commonly referred to as social lending or crowd lending, is a form of alternative financing that enables people to borrow money from other people. When compared to conventional finance (like banks), this approach is becoming more and more popular because it: the inconvenience of a middleman (financial institution) is reduced requires neither party to physically inconvenience themselves makes the waiting period shorter, from weeks to only a few days allows for more flexible terms than banks offers a wide range of interest rates based on the applicant’s creditworthiness. Fandaqah a comprehensive hotel management program for hotels, resorts, and furnished flats. It’s simple, and you may use it right away and without any difficulties. gives management complete control over all lease requirements, stages, and alternatives. The system may be accessed from anywhere using a mobile phone, allowing the owner to track the facility and receive complete reports at any time. Sure Pay No matter the type of transaction—unattended, in-store, outdoor, or mobile—our smart payment systems can handle it. They support all forms of cashless payment and adhere to the strictest security standards. Many industries, such as hotels, retail, banks, and transportation, benefit from their multimedia possibilities, which can provide a rich user experience. |

https://lendo.sa/about-lendo/?lang=en https://www.sure.com.sa/en/ https://surepay.sa/ |

| Haseel App Fruits, vegetables, and other catering services are all provided by Haseel. |

https://haseelapp.com/ |

||

| Majles tech The Majles Tech platform is a system that can control general assemblies and administrative councils to provide best practices in line with established governance systems. Majles Tech’s jobs encompass all needs and procedures and shift them away from paper and files to the digital world rather than being restricted to a single sort of operation. |

https://site.majles.tech/ |

||

|

Goal 2. End hunger, achieve food security and improved nutrition, and promote sustainable agriculture. | |||

| 2.1.1 Prevalence of undernourishment 2.3.2 Average income of small-scale food producers ) |

Foodies |

Point of Sale Solution Foodics is a complete point-of-sale system and restaurant management program that can be customized to meet all of your requirements. Use a single platform to control all restaurant operations, including orders and inventory. Foodics Pay is a payment method that is incorporated into your Foodics Cashier App. Accept all card payments safely and sync your bank accounts every day. |

https://www.foodics.com/rms-pos/ https://www.foodics.com/pay/ |

| Foodics Online store You may quit paying third-party commission costs by offering straightforward self-ordering directly from your website, mobile application, and QR menu. |

https://www.foodics.com/online/ |

||

| Self-Ordering Increase the average order size per customer to increase average sales while reducing costs in the restaurant by enhancing operational effectiveness. |

https://www.foodics.com/self-ordering/ |

||

| All You Get Is One Device Easily manage your business with just one device that includes a built-in cashier, quick printer, and secure payment gateway. businesses including flower shops, vehicle washes, and hair salons |

https://www.foodics.com/one/ |

||

|

Goal 8. Promote sustained, inclusive, and sustainable economic growth, full and productive employment, and decent work for all | |||

| 8.2 Achieve higher levels of economic productivity through diversification, technological upgrading, and innovation, including through a focus on high-value-added and labor-intensive sectors |

Saudi Fintech Company (Alinma Pay) (Digital Payments) |

AlinmaPay Fund When you enrolled for AlinmaPay, an IBAN was generated for you and may be used to transfer money from any domestic or international bank account. Digital Card from AlinmaPay AlinmaPay provides you with a digital card that can be used for online shopping and is compatible with various payment methods like ApplePay and Mandalay. Buying You can use a digital card to pay for all of your purchases from stores, eateries, and online. Money Transfer on a Local and Global Scale Your preferred choice for quick local or international money transfers is AlinmaPay. You can also use a few of the well-known services for sending money abroad, such Western Union and AlinmaPay Direct. SADAD: Paying Services Bills Utilize AlinmaPay, which includes all SADAD and government payments, to pay your expenses quickly. |

https://www.alinmapay.com.sa/ |

| Zain Payments (Limited) (Consumable Micro-lending) |

Tamam offers instant financing without complicated documentation or visiting bank branches. Loans comply with the Shariah Tawaruq model. The product has been approved and certified by a well know Shariah Committee. |

https://tamam.life/ |

|

| Money Loop (Digital Savings Association) |

Investing Money Funded Forex Account Money Invest |

http://ww7.moneyloop.org/ |

|

|

Goal 5. Achieve gender equality and empower all women and girls | |||

| 5.1.1 Whether or not legal frameworks are in place to promote, enforce and monitor equality and non-discrimination based on sex |

Noon Hakbah Co for Information Technology (Digital Savings Association) |

By providing a full one-stop-shop solution for Savings Groups to begin, administer, join, and pay directly within the mobile app, Hakbah is modernizing financial saving through its intelligent platform. Customers are given a practical and straightforward technique for Savings Groups’ habits by the solution. It intends to help close the gender savings gap and expand financial inclusion for all people. |

https://hakbah.sa/?lang=en |

| Savings Circles company for Information Technology (Digital Savings Association) |

At Circles, we organize the circles by opening new circles monthly and supervising each circle as we make sure to obtain guarantees to avoid stumbling, and this process lasts until the circle expires. Additionally, we work to verify the eligibility of each member who enters the circle through several entities. | https://circlys.com/#who-we-are | |

| Business research storming company (Digital Savings Solutions) |

Without the need for manual entry, you can automatically and intelligently track your spending and get complete summaries of your purchases and payments. Wafer makes it simple to manage your finances, grow your savings, and improve your expenditures. | https://wafeer.net/ | |

|

Goal 17. Strengthen the means of implementation and revitalize the Global Partnership for Sustainable Development | |||

| 17.1 Strengthen domestic resource mobilization, including through international support to developing countries, to improve domestic capacity for tax and other revenue collection 17.3 Mobilize additional financial resources for developing countries from multiple sources |

Nayifat Finance Company (Debt – CrowdFunding Platform) |

SME Finance enables SMEs to finance their business needs through different structured financing programs including working capital financing, Trade Financing, and lease financing to expand and grow their business in the kingdom. Financing several industries such as Healthcare, Accommodation & Food services, Real estate, Education, Electricity, Gas, Steam & Air Conditioning supply, and Manufacturing. Consumer Finance: Enables consumers to instantly finance their personal needs and repay the amount through flexible repayment solutions. Personal finance programs are available for individuals in public and private sectors up to SR 300,000 and an instant smart loans program enables the customer to avail of financing facilities up to SR 100,000 without salary transfer or personal guarantor in line with Shari’a principles such as (Tawaruq, Murabaha, Ijarah) Credit Card Nayifat VISA Card brings you a growing range of benefits. Say goodbye to your worries, with immediate acceptance at all VISA Card merchants & ATMs All over the world. Live comfortably with stress-free and safe transactions 24/7, and provide SMS alerts for every transaction, giving you total control. |

https://www.nayifat.com https://www.nayifat.com/sme-finance/overview-4/ https://www.nayifat.com/consumer-finance-3/overview-consumer-finance/ https://www.nayifat.com/home/credit-cards/overview-2/ |

| Platform Company Ltd. Tameed Financing (Debt – CrowdFunding Platform) |

Performance Bond and PO Financing Comprehensive financing solutions to all of your PO needs from performance bond to PO needs, all in one financing package! Debt-Based Crowd Lending For Government Purchase Orders As the first Debt Based Crowd Lending Platform specializing in financing Purchase Order licensed by Saudi Central Bank, Tameed offers fast financing for your PO E-Invoicing Free E-invoice service for B2B which is compliant with Zatca and will ease the organization’s relationship with their customers |

https://www.ta3meed.com/en https://www.ta3meed.com/en/get-funding |

|

| Manafa capital (Debt – CrowdFunding Platform) |

Proprietary Platform Equity crowdfunding is your ideal and fastest destination to enable your project. Religious PlatformIt helps you, as a financing student, to obtain immediate cash liquidity and achieve attractive returns for investors in short-term investment Financing solutions compatible with Islamic Shariah |

https://manafa.co/ https://manafa.sa/shariah |

|

| Funding Souq Company (Debt – CrowdFunding Platform) |

Funding Souq company helps in investing and borrowing Earn regular income. Up to 13%per year. Grow your wealth by financing small and medium-sized businesses. |

https://www.fundingsouq.com/en/ | |

| Raqamyah Platform (Debt- Crowdfunding Platform) |

Finance enables established companies of all sizes to achieve their next business objective or stage. To choose the best SMEs, Get Financed combines the best in technology and financial research. Applications are chosen and presented to financiers only if they are creditworthy. Finance POS Raqamyah’s point of sale (POS) finance is a quick funding option that satisfies your funding requirements. Your POS sales will determine how much financing you receive. By taking a certain proportion from each swipe made on the POS Machines, automatic payback is made possible with POS finance. The funding options for SMEs include term financing, POS financing, invoice financing, and inventory financing. |

https://www.raqamyah.com/en/Finance https://www.raqamyah.com/en/Get_financed https://www.raqamyah.com/en/Pos_Finance https://www.raqamyah.com/en/Smes |

|

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.