Submitted:

11 August 2024

Posted:

14 August 2024

You are already at the latest version

Abstract

It’s very well known that the world's attention is currently focused on the energy transition. The energy security, in addition to the drive to reduce greenhouse gas emissions in order to limit global warming, and the generalization of the access to energy, have contributed to adoption of the Moroccan Energy Strategy with a strong focus on Renewable Energies (RE). Morocco is notoriously poor in conventional fossil primary energy resources with an energy dependence on the order of 90%. The energy crisis and that resulted from Covid-19 pandemic and the geopolitical conflicts, combined compounded with steady increase in demand have heavily affected the security and the stability of the country's energy situation. The transition to RE, by strongly engaging in the implementation of several solar, wind and hydro energy projects benefiting from the country's excellent solar and wind energy potential, has made the country the leader in RE in Africa. By 2030, the share of RE in the installed capacity is expected to reach 52%. In this work, an overview of the current situation of RE (particularly solar energy) in Morocco is provided, including, the potentials, obstacles and challenges, and future perspectives. Thanks to its high solar potential location, it’s predictable that Morocco effort will be focused on this field: the Erasmus Plus Innomed Project is a virtuous example of international cooperation, aiming at create a Solar Energy Network, in synergy with EU Partners.

Keywords:

Solar Energy

; Photovoltaic

; CSP

; solar thermal

; Morocco

; Renewable Energy

; sustainable development

; strategic investment

1. Introduction

Population growth, urbanization and global economic development are gradually increasing the demand for energy. Historically, fossil fuels, particularly coal, natural gas and oil, have been the main sources of energy to meet these needs. However, fossil fuel resources are limited, and their exploitation leads to greenhouse gas emissions (CO2) which contribute directly to global warming causing devastating effects on a global scale [1].

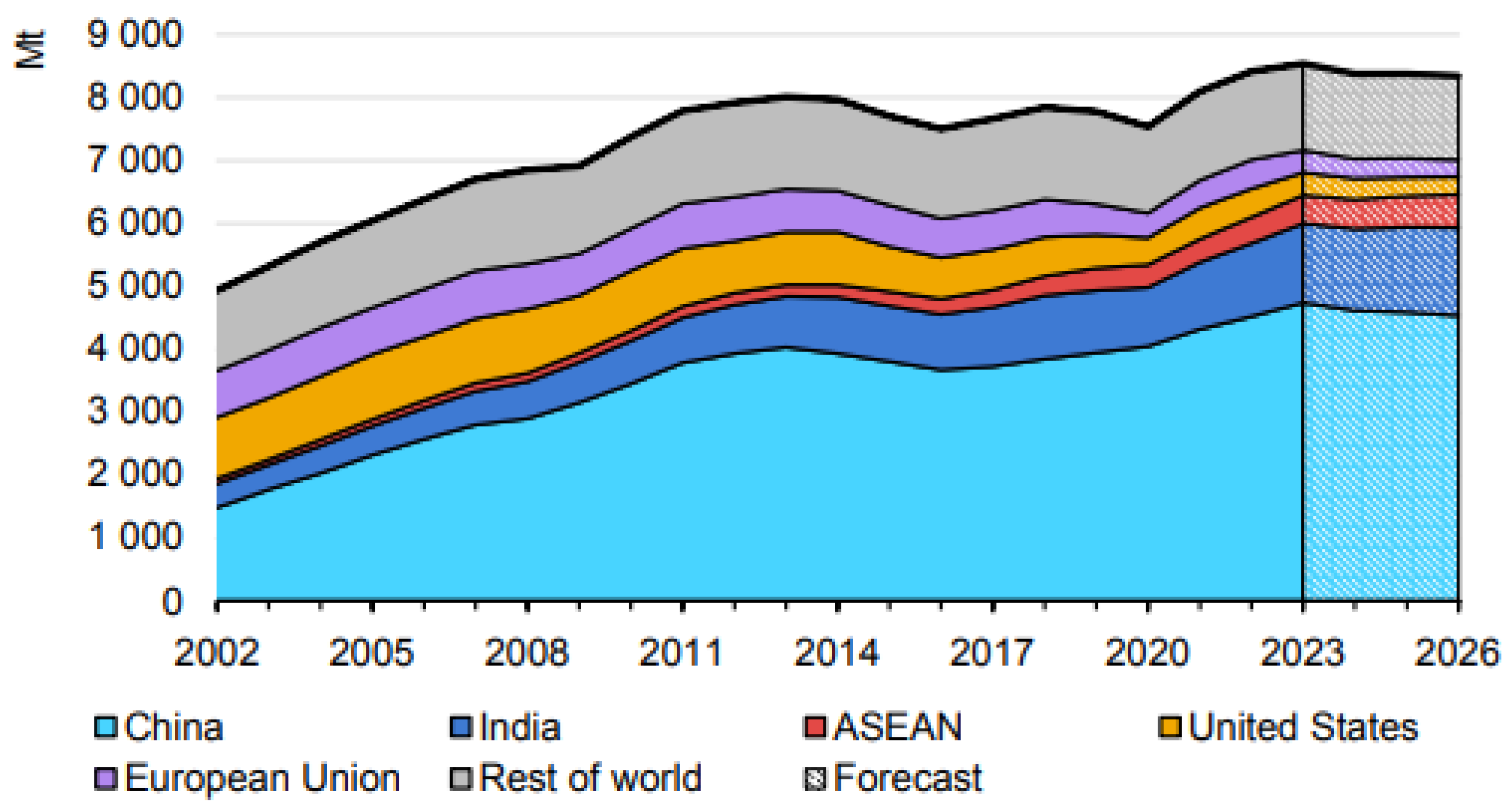

Coal is the most dominant irreversible energy source worldwide, with a global reserve estimated at 1,150 billion tons in 2022. Coal consumption has reached 8.4 billion tons (Bt), of which 5.68 Bt is required for electricity production, while the rest is destined for non-electric uses [2]. Figure 1 summarizes the International Energy Agency’s (IEA) analysis and prediction of global coal consumption between 2002 and 2026. The IEA has estimated a 1.4% increase in coal demand by 2023, as China, India and the ASEAN countries accounted for three quarters of global demand. Significant declines are also expected in the European Union and the United States between 2024 and 2026, due to the rapid transition to renewable electricity, as well as a reduction in industrial activity. Moreover, coal consumption in China accounts for more than half of global demand, which is still rising [2]. High dependence on coal for power generation and industrial activities, combined with the country’s vast coal reserves, justify this trend. However, coal is a major contributor to greenhouse gas emissions, so that China claims to be the world’s largest emitter of the latter [3].

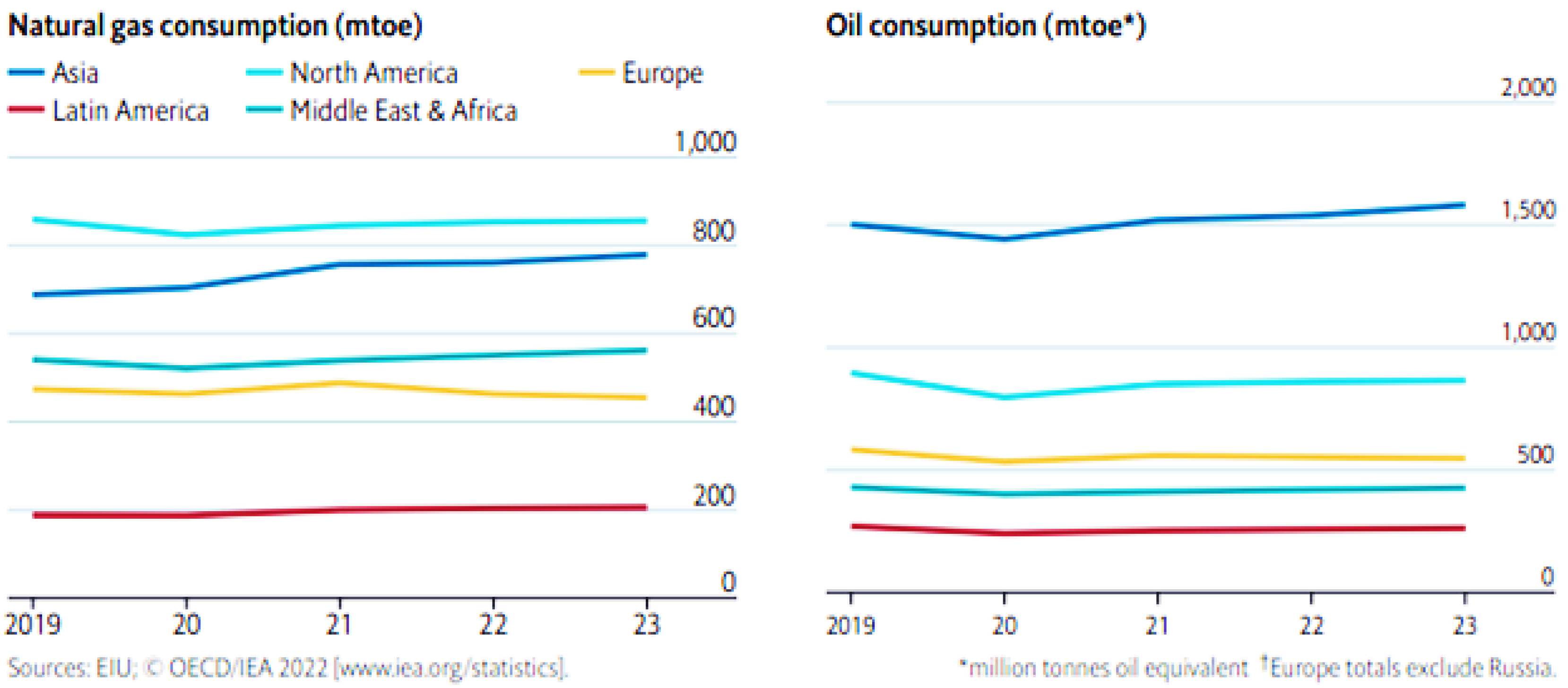

Natural gas and oil are two other irreversible energy sources concentrated in certain regions of the world and used for electricity generation, heating, transport, and as primary materials in some industrial sectors. The variation in natural gas and oil consumption from 2019 to 2023 for the various regions of the world, are illustrated in Figure 2 [4]. This figure indicates that the total average annual consumption grew by 1.3% in 2023 compared with 2.2% in 2022, marking a slowdown for the second year running after the recovery in 2021. This trend is explained by the slowdown in the global economy and volatile energy prices observed after the COVID19 pandemic and the energy crisis. Additionally, volatile fuel costs could lead to economic uncertainty and imbalances in global energy markets. In light of these effects, it is imperative to diversify the energy mix, encourage the adoption of alternative and sustainable energy sources and accelerate the electrification process worldwide [4]. Investments in RE such as solar, wind, hydro and geothermal are necessary to reduce the dependency on fossil fuels and mitigate the effects of climate change. Effective supply and demand side energy management as well as energy efficiency measures will also contribute to reducing the overall energy demand. In addition, the General Assembly of the United Nations adopted a development program for the period 2015-2030 in order to ensure access to reliable, sustainable, modern and affordable energy services for all. It aims to significantly increase the share of RE in the energy mix.

The world’ss attention is currently focused on the energy transition, characterized by the rise of the share of RE for electricity production with an additional emphasis on energy efficiency. According to the International Renewable Energy Agency (IRENA), the world’s average renewable electricity capacity rose to 3865 GW in the end of 2023, an increase of almost 14% compared with the end of 2022 [5]. In 2023, a significant increase in the installed capacity was recorded. This is attributable to the adoption of new systems and technologies [5]. The solar and wind power sectors have enjoyed increased growth, driven by high energy prices and favorable government policies. In addition, carbon capture and storage (CCS) technologies have gained in interest in recent years, thanks to the commitment of several companies and the political support of the government. In particular, several decarbonization projects will be commissioned thus increasing carbon capture and storage by 2.3 million tons per year [4,6]. At the same time, the production of green hydrogen has gained in strength, particularly in Europe following the REPOWEREU strategy, as well as in developing countries such as Morocco [4] and will certainly boost the share of renewables in the energy mix.

At a continental level, Africa remains the least electrified region globally, with certain areas still grappling with electrification challenges compounded by the effects of climate change. According to IRENA, the total RE capacity in Africa reached 62.1 GW in 2023, marking a 4.6% increase from 2022. This capacity accounts for a mere 1.6% of the world’s installed renewable electricity generation capacity [5]. Despite these challenges, the efforts of African nations in energy development show promise and perseverance amidst increasing demographic pressures, the urgency of climate change, and the need for substantial investment.

According to the African Union Commissioner for Infrastructure and Energy, Morocco is positioning as the African leader in RE and an increasingly important actor on the world stage [6]. Taking advantage of its vast potential in sustainable resources, particularly solar and wind, Morocco initiated RE projects as early as 2009 and 2010 with the launch of two national programs aimed at integrating solar (2 GW) and wind (2 GW) electricity by 2020. It has heavily invested in RE infrastructure such as the Noor Ouarzazate complex, with a capacity of 580 MW, representing one of the world’s largest CSP power plants. REs have increasingly become the focal point of strategic and policy discussions in the Morocco. The country reinforces these efforts by accelerating the energy transition by various reliable and competitive technologies to address energy security and environmental protection.

Overall, since the adoption of the Moroccan Energy Strategy (MES) in 2009, the installed electrical power capacity has grown at a global growth rate of 74.2%, increasing from 6.34 GW in 2010 to 11.05 GW in 2022 (Figure 3). This growth is partly attributable to the share of RE, accounting for 37.6% of the total installed capacity in 2022, which is equivalent to 4154 MW (including wind, solar, hydro, and pumped hydro storage technologies) [7]. Wind and solar capacity installed in 2022 represent 37.4% and 20% respectively in the RE mix [7]. By 2030, Morocco aims to raise the share of RE to 52% of the installed capacity with a reduction in greenhouse gas emissions by 18% [8,9]. In parallel, the gradual liberalization strategy of the electricity sector (since 1994) and the establishment of a favorable regulatory and institutional framework for RE development encourage public-private investment at both national and international levels. The country also launched the National Investment Pact, aimed at enhancing private sector involvement in investment and reaching 550 billion dirhams (equivalent to approximately to 53.9 billion US$) by 2026 [7]. This initiative will undoubtedly intensify and accelerate the energy transition by supporting RE development projects, seawater desalination, and the emerging green hydrogen sectors, which are promising sectors requiring substantial investments. However, the large-scale integration and development of solar energy in Morocco faces a number of challenges. Indeed, massive deployment of intermittent RE sources into the electricity grid requires investment in power system flexibility, including energy storage, grid management and eventually cross-sector coupling through the development of Power-to-X in order to mitigate the effects of uncertainty in supply (intermittence) and demand (absence of demand side management). Financing solar energy projects is also still a challenge, particularly for developing countries [10].

Since the launch of renewable energies in Morocco, several articles have delved into the country’s energy potential, emphasizing the development of the national energy strategy as well as the outlook and barriers to be addressed [11,12]. A more recent analysis of energy sources (including solar, hydroelectric, tidal, wave, and geothermal) and their potential in Morocco is presented by Nakach et al. [13]. Additionally, Boulakhbar et al. [14] examined a scenario for 2030 regarding the Moroccan electrical system and identified challenges to accelerate the integration of renewable energies into the Moroccan energy mix. Kettani et al. [15] highlighted ambitious prospects in solar energy that will enable the country to become a regional leader and proposed a typology of possible trajectories.

The wide exploitation of RE and solar in particular represents a significant opportunity for Morocco to reduce its reliance on fossil fuels, contribute to combating climate change, and foster sustainable economic development. The present paper provides an in-depth overview of the current status of renewable energy, particularly solar energy, in Morocco. An assessment is carried out of its positioning within the Moroccan’s energy strategy and its ambitions to achieve future targets. In addition, the paper analyzes closely existing policies and regulations, the current state of installed capacity and investments, upcoming challenges, and promising prospects. It is organized as follows: Section two presents an overview of Morocco’s energy landscape. Section three presents the solar resources potential in Morocco. Section four gives the current state of solar energy in Morocco, including the policies and regulations, the installed capacity, the investments, and the challenges. Section five, presents a future outlook of solar energy in Morocco.

2. Overview of Morocco’s Energy Landscape

In the absence of yet to be exploited major fossil fuel reserves in the country, Morocco’s energy sector heavily depends on imported fuels. As such, the Moroccan government endeavors to increase security of supply by reducing its dependency on energy imports, primarily through increasing use of renewables for electricity generation as stressed in the MES put forward in 2009.

2.1. Moroccan Energy Sector in Numbers

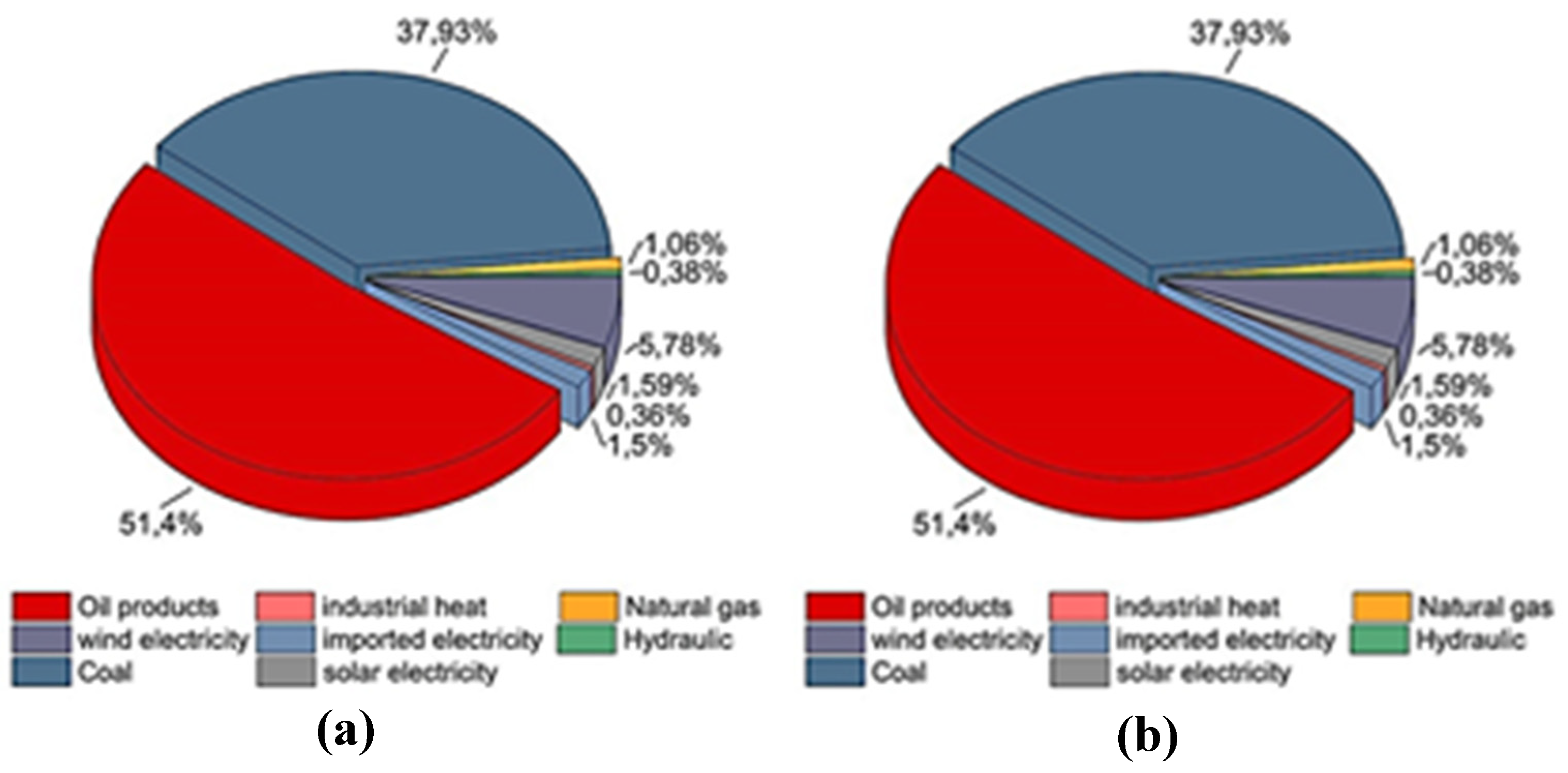

With limited domestic oil and natural gas resources, Morocco is considered energy-poor in terms of fossil fuels, a situation that poses a significant threat to the country’s energy security and independence. According to the World Bank and the HCP, approximately 90% of the Morocco’s energy primary energy relies heavily on imported fossil fuels (refined oil, gas, and coal.) The total primary energy consumption has been increasing at a rate of approximately 5% per year since 2004 [16]. Total primary energy demand in 2022 was 23.37 million tons of oil equivalents (Mtoe), a significant increase of 35.3% compared to 2009 (15.1 Mtoe). Oil products dominate with a 51 % of demand (12,237 Mtoe), closely followed by coal with 38% (9,031 Mtoe), while primary energy from renewable sources accounts for 8.8% of the total. Total energy produced was 41.41 TWh, of which 22% was generated from renewable sources. The distribution of national primary energy demand and the total energy consumption, electricity is shown in Figure 4a and Figure 4b respectively. A detailed analyses of total energy consumption in Morocco for 2021/2022, as well as forecasts for 2023 is provided by [17,18,19]. Recent figures can be found in the annual reports of the National Office of Electricity and Drinking Water (ONEE) and the High Commission in Planning [20].

To meet growing electricity demand and address challenges posed by expanding RE, Morocco aims to diversify its energy sources by increasing the use of Liquefied Natural Gas (LNG). In May 2021, the Moroccan Office of Hydrocarbons and Mines (ONHYM) started plans for an integrated Floating Storage Regasification Unit (FSRU) terminal. ONHYM intends to issue tenders or explore Public Private Partnership (PPP) options in the future. The initial goal of the FSRU project in Morocco is to meet an annual natural gas requirement of 1.1 billion cubic meters (bcm) by 2025, rising to 1.7 bcm in 2030 and 3 bcm in 2040. Additionally, a roadmap for natural gas development (2021-2050), unveiled by the Moroccan Ministry of Energy, Mines, and the Environment in August 2021, prioritizes industrial needs while gradually integrating domestic and electricity generation requirements. As a net energy importer, Morocco seeks to reduce reliance on foreign oil and coal by attracting investment in oil and gas exploration [21].

RE will provide the solution for ensuring Moroccan energy independence while reducing CO2 emissions. The government has proactively embarked on a series of long-term and medium-term strategic plans. These plans prioritize exploring all available RE sources to enhance energy security by reducing dependence on imported fuels and safeguarding the environment.

2.2. Moroccan Energy Strategy

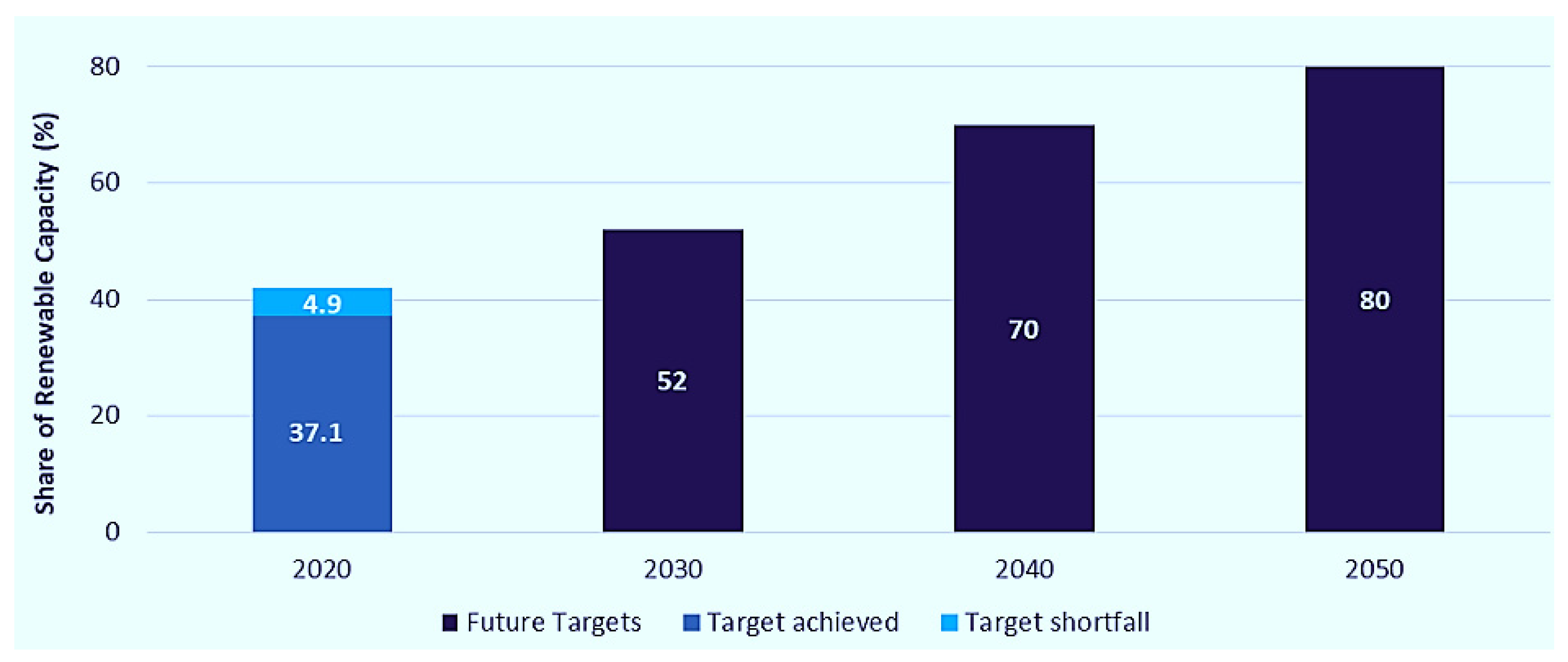

The Moroccan Energy Strategy launched in 2009 is one of the main sectorial strategies based on the development of RE as a national priority, the improvement of energy efficiency and regional integration. The strategy’s four principal objectives are to strengthen the security of supply, generalize access to energy at competitive prices, demand control and, lastly, preserve the environment. One of the strategy’s orientations towards large-scale development of RE is the ambition to contribute 42% by 2020, 52% by 2030 and 70% by 2040 in the national electrical capacity mix [22]. It’s a roadmap towards energy independence based largely on RE.

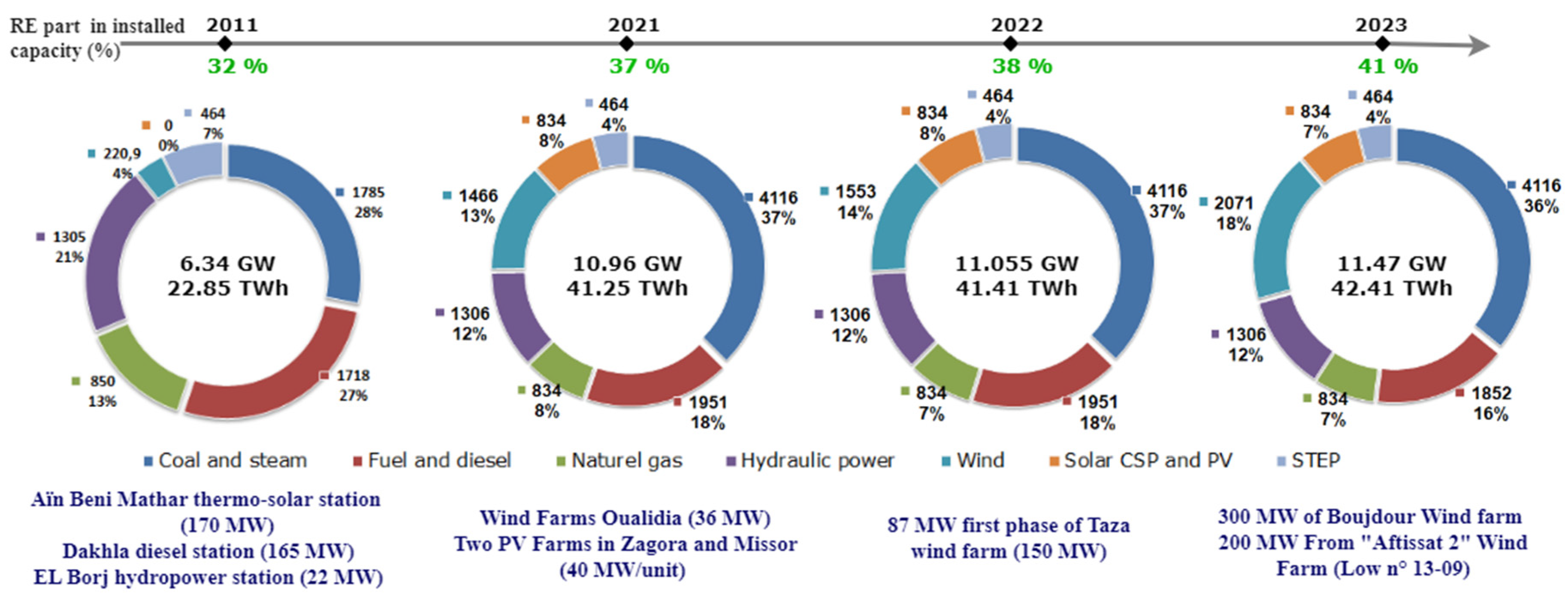

The first objective has not yet been achieved, as the share of RE capacity installed and connected to the grid by the end of 2021 stands at of 37.08% of the country’s total electricity mix, which is 5% below the target set [23]. This is justified by the impact of Covid-19 on Morocco’s energy sector, as well as on the rest of the world. Confinement and curtailment of industrial and tourist activities has led to disruption of supply chains. Rising prices of fossil fuels and energy equipment have contributed to inflation and stagnation in investment and RE projects deployment. As a consequence, the demand for electricity in 2020 fell by 8.5% compared to 2019. However, the installed capacity remained almost the same (10.6 GW), distributed as follows: 1,430 MW of wind capacity, 751 MW of solar capacity, 464 MW pumped hydro capacity, 6,974 MW of thermal capacity and 1,306 MW of hydroelectric capacity. In addition to this pandemic, the geopolitical crisis (the war in Ukraine) has highlighted the risk of fossil fuel supply, which underlines the importance of accelerating the transition to RE [24].

Moroccan energy sector began to show signs of recovery in 2021, with electricity production increasing by 6.5% after a 3.9% decline in 2020. Moreover, there was a 19.6% decrease in the volume of imports alongside a 36.5% increase in exported volume [23]. Additionally, it is noted that the share of RE in the national electricity mix reached 38% in 2022 and surpassed 40% in 2023. By the end of 2023, the total installed capacity reached 11.47 GW, representing an increase of approximately 400 MW compared to 2022 [25]. This increase includes the commissioning of 500 MW wind energy, including 300 MW from the Boujdour wind farm (as part of the integrated wind energy program of 850 MW) and 200 MW from the “Aftissat 2” project (under Law No. 13-09).

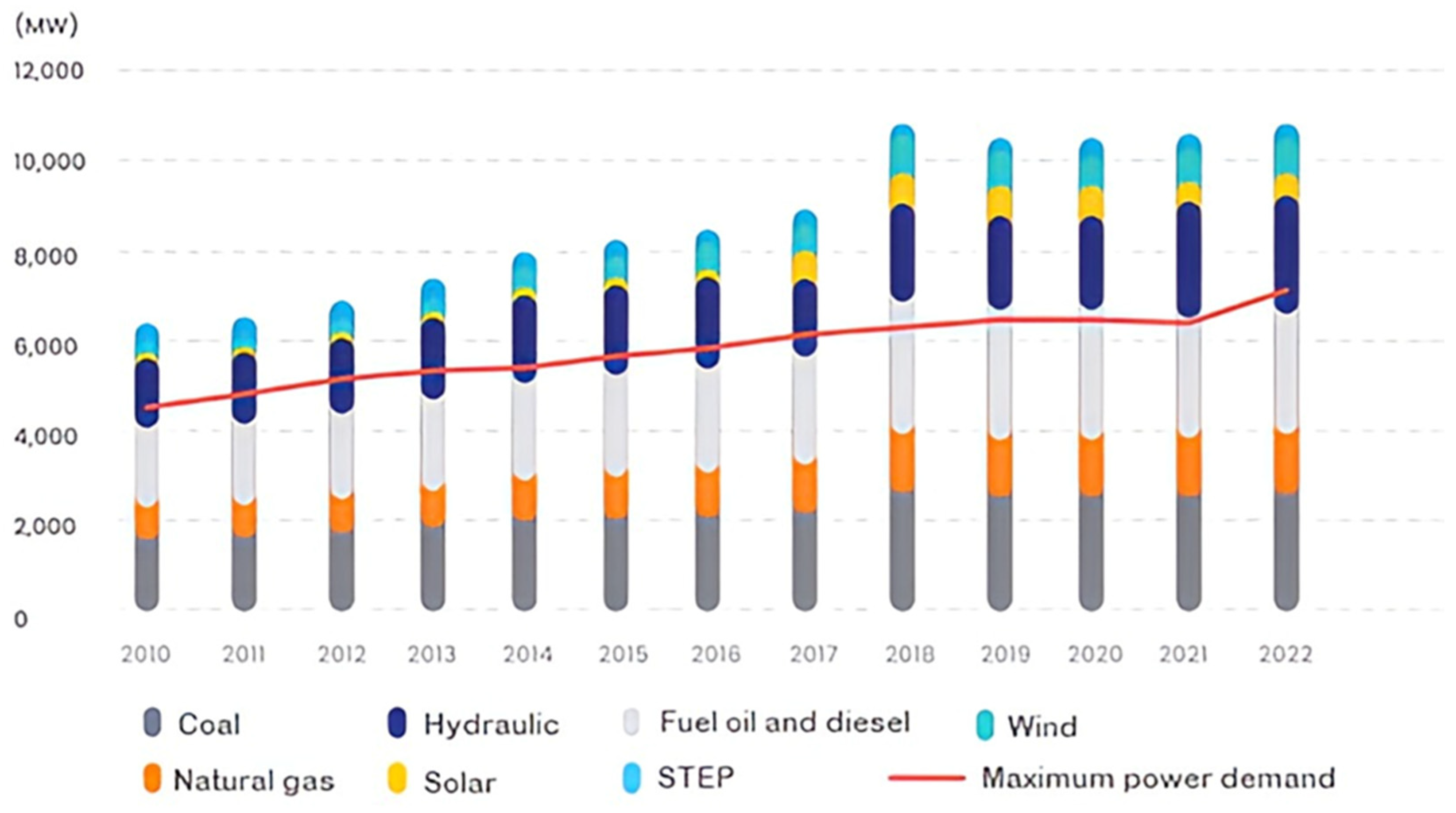

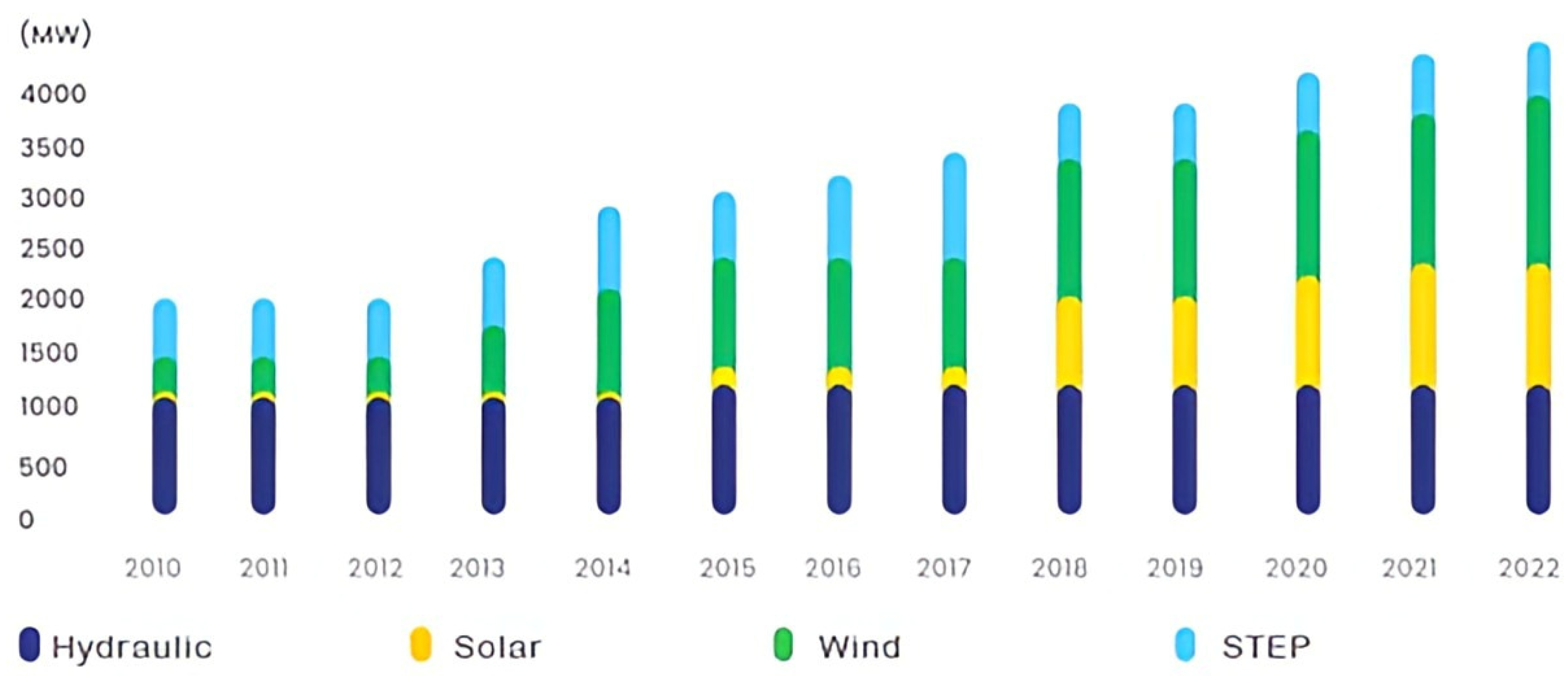

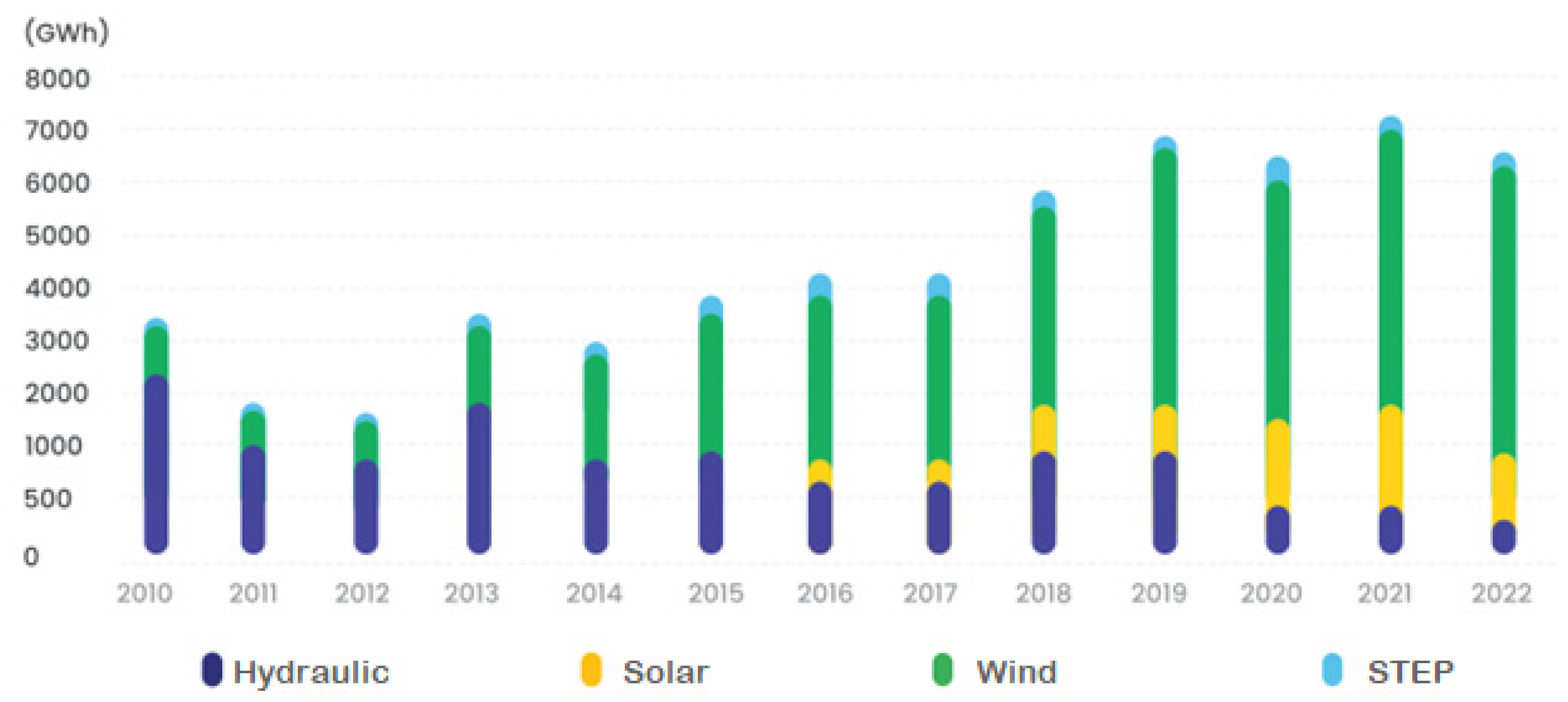

Overall, it can be observed that the MES led to an 80.9% increase in total installed capacity in 2023, compared to 2010, and a 7.97% increase compared to 2020. The maximum power demand reached 7400 MW in 2023, marking a 2% increase over the year. Total electricity production amounted to 42.409 TWh, with 9.2 TWh originating from ONEE facilities. RE accounted for 20.9% of national demand satisfaction, equivalent to nearly 8863 GWh. Figure 5 summarizes the development of the Moroccan electricity sector in terms of installed capacity in GW, total electricity production in TWh, and the share of RE in total installed capacity, spanning from 2010 to the last three years after the global energy crisis. The figure illustrates the main projects contributing to progress each year.

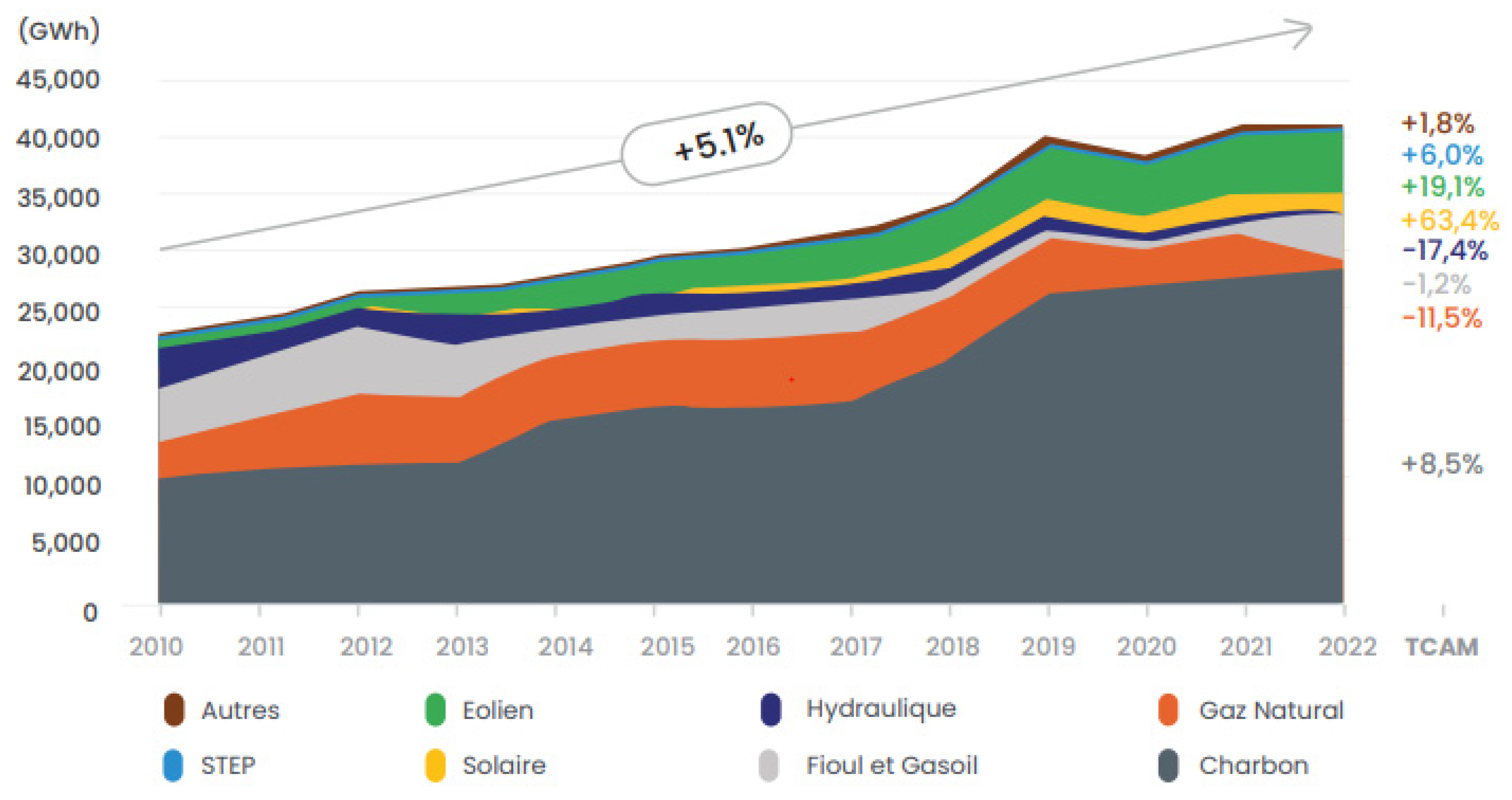

The National Electricity Regulatory Authority (ANRE) has examined the evolution of national production by energy sources between 2010 and 2022, as depicted in Figure 6. The use of coal has experienced a continuous rise with an annual growth rate of 8.5%. Conversely, electricity production from natural gas has seen a decline of 11.5% on average annually over the same period, with a sharp and significant drop of 80.3% noted between 2021 and 2022. This can be attributed to the end of the Maghreb Europe gas pipeline contract at the end of 2021 and the global crisis affecting the natural gas sector. To address the resulting security of supply in the electricity sector, the use fuel oil and diesel in electrify production was intensified.

Figure 6 depicts the significant evolution of RE’s contribution to national electricity production. Notably, solar energy has achieved the most substantial growth rate at 63.4%, followed by wind energy at 19.1%. This is attributed to the success of MES in harnessing the countries solar and wind potential through the development and investment in many projects (detailed in Section 3). The country hosts one of the largest solar complexes, NOOR, spanning an area of 6000 hectares, which required investments exceeding 24 billion MMDH (equivalent to approximately 2,303 milliards US$). It is divided into four stations where large scale photovoltaic (PV) and concentrated solar power (CSP) technologies are used with a total installed capacity of 580 MW. The first plant NOOR 1of this series was launched in 2016, followed by the others two years later. Regarding wind energy, several projects have been implemented, particularly in southern regions, where the largest wind farm in Africa (300 MW) is located in Tarfaya and became operational in 2014. Currently, wind power is considered the champion among RE, surpassing solar energy. Both sectors foresee continuous future advancements, particularly with the development of other scheduled projects such as the Nour Midelt solar projects with storage (1600 MW), the six plants under the Noor Atlas solar program (300 MW), and the completion of the Nassim Koudia Al Baida wind farm (100 MW). With these considerations, significant efforts have yet be deployed to achieve the government’s target of raising the share of RE to 52% by 2030. It’s noteworthy that solar and wind projects are distributed across various regions of the country. This ensures sustainable regional development, leading to increased electrification rates and a fair distribution of socio-economic impacts. The report from ONEE indicates the success of the overall Rural Electrification Program (PERG), which electrified 99.88% of rural areas by the end of 2023 [25]. The program used individual photovoltaic kits to electrify approximately 51,599 households in villages far from the electrical grid.

Furthermore, the building sector stands out as the largest consumer of energy, followed by the industrial sector and then agriculture. It consumes approximately 36% of the total energy, with the residential sector alone accounting for 25% [26]. Consequently, Morocco has shown its commitment to energy efficiency as a cornerstone of its adopted energy strategy. It aims for a 20% energy savings by 2030, including action plans to reduce energy consumption in the transportation (-24%), buildings (-14%), industry (-22%), agriculture, and public lighting (-13%) sectors [27].

The electricity sector is the leading emitter of greenhouse gases in Morocco [28]. These emissions are primarily due to the significant dependence of the electricity sector on thermal power plants (coal, natural gas, fuel oil, and diesel). However, the rapid transition from fossil fuels to RE is an imperative that Morocco has already begun, along with the development of de-carbonization strategies for its industry. As a result, the Kingdom has secured the first place in Africa and the 9th in the European Union countries in the 19th Climate Change Performance Index 2024 (CCPI). This report allows for the visualization and comparison of the climate protection efforts and progress made by the countries. It is based on scores in greenhouse gas emissions, RE, energy consumption, and climate policy [29].

The country’s determination and rigor to promote the development of RE, energy efficiency and energy security are reflected in the implementation of several energy plans and strategies [30]. Alongside this, the government is pursuing a continuous evolution of the regulatory and institutional framework of the energy sector (particularly laws and regulations related to RE integration) in order to facilitate integration into the national grid and improve private sector investment in RE projects in a secure and viable manner (the main RE laws and amendments are detailed in Section 4.1) [31]Morocco has stepped up its efforts as part of its national energy strategy by investing 54 billion dirhams (≈5,184 milliards US $) in RE projects by 2030 [10]. Furthermore, the launch of the National Investment Pact, aimed at boosting the private sector’s contribution to investment to 550 billion dirhams (≈ 52,782 milliards US $) by 2026 was also launched [7].

2.3. Moroccan Green Hydrogen Strategy

Through its ambitious energy strategy, Morocco has emerged as a regional leader in RE over the past decade, contributing to their competitiveness. Due to its optimal geographical position and abundant resources in RE, Morocco has also the potential to become a key player in the development of the green hydrogen sector regionally and could capture up to 4% of the global demand for green molecules [32]. The objective is to position Morocco today as a green hydrogen technological hub. The establishment of economic and industrial sectors around green molecules, particularly hydrogen, ammonia, and methanol, will contribute to reducing greenhouse gas emissions (up to 20%) and support the de-carbonization efforts of the country and other partner countries. In the reference scenario, domestic demand for green hydrogen and its derivatives is estimated to reach 4 TWh in 2030, 22 TWh in 2040 and 40 TWh in 2050. Export demand is estimated at 10 TWh in 2030, 46 TWh in 2040, and 115 TWh in 2050. The RE capacity required to meet these demands is estimated at 8 GW for 2030, 36.7 for 2040 and 78.2 for 2050. This will require a cumulative investment of 90 billion dirhams (8.6 mile M$) by 2030 and 762 billion dirhams (73.13 mile M$) by 2050. This roadmap presents significant prospects for industrialization across the entire value chain, including desalination, RE (photovoltaic and wind), electrolysis, and green chemistry. A National Hydrogen Commission involving all stakeholders will coordinate the implementation of this roadmap through technological development, investments, infrastructure, and markets. The Commission will also contribute to structuring the optimal deployment of the hydrogen sector within the country by facilitating investment inflows and the development of PtX (Power to X) projects through the establishment of favorable regulatory, legislative, and fiscal measures.

As Morocco is one of the largest importers of ammonia, the country also endeavors to become a leader in the production of green ammonia to fulfill long-term demands of its domestic and foreign fertilizer markets. To this end, OCP (Office Cherifienne des Phosphates), which is in charge of the phosphate industry, has setup the new green investment plan with two targets: a) Green ammonia: the OCP Group aims to produce 1 million tons by 2027 and 3 million tons by 2032. b) Green energy: the OCP Group intends to install 5 GW of clean energy by 2027 and no less than 13 GW by 2032.

Furthermore, exporting methanol and other synthetic fuels will meet the demand of several European partner countries. In the long term, sectors such as heavy transportation, maritime, and aviation can also be decarbonized through the utilization of green hydrogen. Other applications such as urban mobility, industrial heat, energy storage, and methane substitution for cooking can be decarbonized in the medium-term through the use of synthetic fuels. A capacity building program, research, and innovation in the field of green hydrogen will accompany industrial integration and enhance the competitiveness of national enterprises through the formation of qualified human capital, the preparation of local subcontracting, and the development of national champions. Power-to-X and cross-sector coupling will therefore play a major role in the massive deployment of intermittent RE sources into the electricity grid.

The action plan of the hydrogen roadmap includes the following 8 measures: a) Cost reduction throughout the value chain of green hydrogen and its derivatives, b) Creation of a Moroccan and regional research and innovation hub, c) Promoting measures to ensure local industrial integration, d) Establishment of an industrial cluster and development of a master plan for corresponding infrastructure, e) Ensuring financing for the hydrogen sector, f) Creation of favorable conditions for the export of green molecules, g) Development of a storage plan, h) Development of domestic markets [MEM ].

2.4. Electricity Sector Organization

Morocco’s electricity sector has been progressively liberalized since the 1990s. This liberalization laid the foundations for investment by independent power producers, in accordance with Decree-Law 2-94-503. Subsequently, Law 16-03 introduced self-generation, thus enabling large industrial users to generate their own electricity for internal consumption, notably for power plants with a capacity of less than 50 MW, and to sell a limited surplus of electricity to National Office of Electricity and Drinking Water (ONEE). In 2009, the government launched the process of creating a competitive market for RE, now open to private investors under the Law 13-09. This law authorizes electricity transactions between private individuals for RE projects and requires third-party access to ONEE’s transmission network. In addition, the self-generation was extended with the removal of the 50 MW limit, thus integrating this sector into the new open market. Law 13-09 also allows small-scale renewable projects to sell their surplus electricity to ONEE and large industrial customers, either through a consortium of consumers with access to extra-high voltage (EHV) and high voltage (HV) transmission lines, or through public distribution utilities [33].

The Moroccan government has prioritized the growth of the RE sector by strengthening the role of the Moroccan National Agency for Solar Energy (MASEN) (now National Agency for Sustainable Energy) in developing and implementing RE projects, as well as streamlining the authorization process for these projects. MASEN operates as a public limited company with a Board of Directors and a Supervisory Board, created under Law 57-09 in 2010, and placed under the administrative and technical supervision of the Ministry of Energy Transition and Sustainable Development. It provides a “one-stop shop” for private project developers, covering all aspects of permitting, land acquisition and financing, as well as a state guarantee for the investment [34].

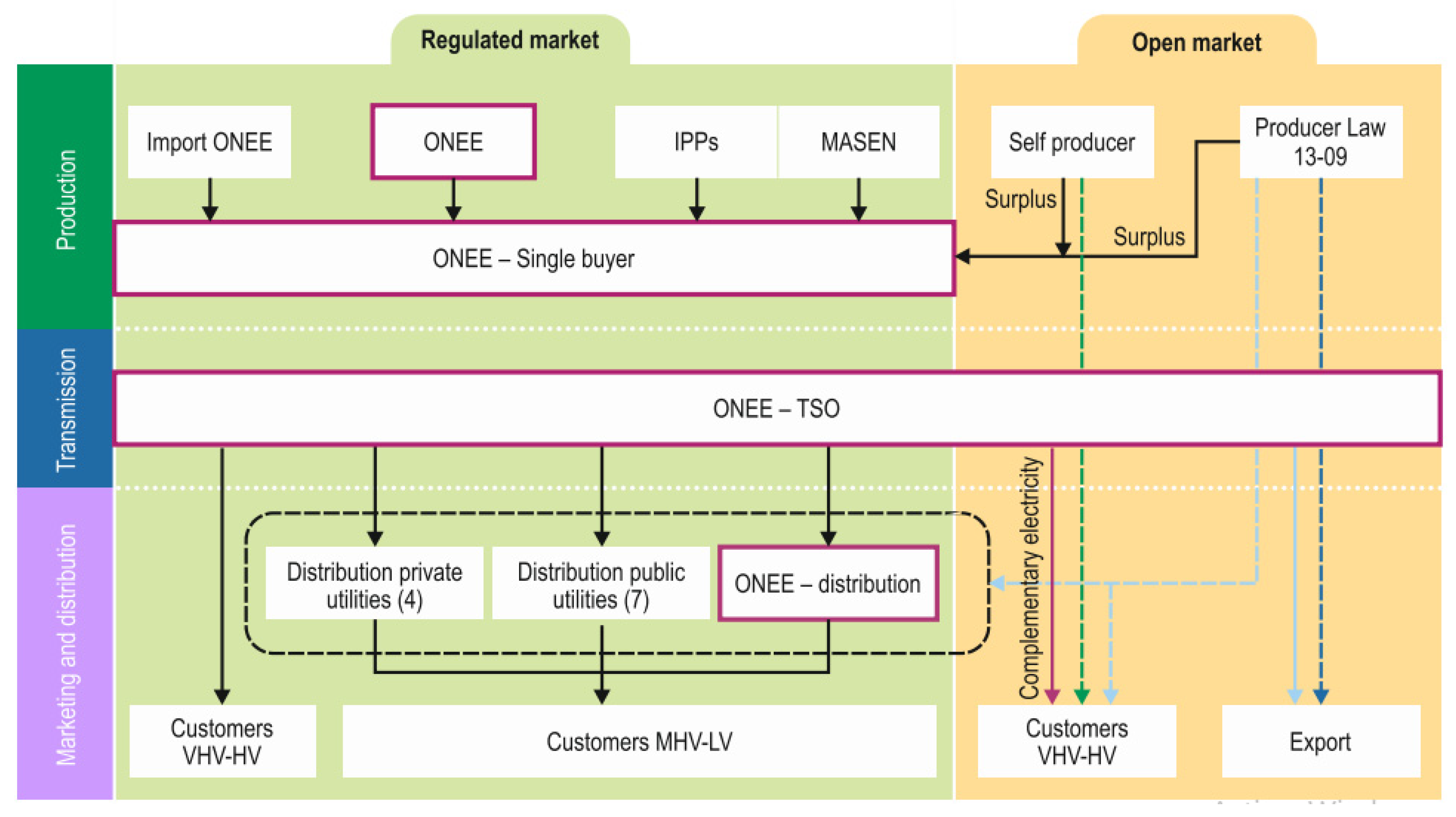

Nowadays, Morocco’s electricity market has a hybrid structure, combining a regulated market dominated by ONEE, independent power producers (IPPs) and MASEN’s public-private partnerships, with an open market welcoming RE producers and self-generators. The various public and private players involved in various activities, such as generation, transmission and distribution, to meet electricity needs, as illustrated in Figure 6 [33].

ONEE is the central player in Morocco’s electricity sector. It is the only authorized wholesale buyer and the only authorized reseller to distribution companies. ONEE is also responsible for grid management, planning and maintenance of the Moroccan electricity system, ensuring that electrical energy is transported from production plants to consumption centers under the best conditions of safety and efficiency.

Independent power producers (IPPs) can also sell RE electricity to a consumer or consortium of consumers through access to extra-high voltage (EHV), high voltage (HV) and, under certain conditions, medium voltage (MV). IPPs are linked to ONEE through long-term power purchase agreements. The concessionary power producers include Jorf Lasfar Energy Company (JLEC) with a capacity of 2080 MW, Compagnie Eolienne du Détroit (CED) with 54 MW and SAFI Energy Company (SAFIEC) with 1386 MW.

A list of the various actors presents and active in the development of the energy sector in Morocco is presented in Appendix A.

Figure 7.

Current organization of Morocco’s electricity sector. Source:[33].

Figure 7.

Current organization of Morocco’s electricity sector. Source:[33].

3. Solar Resources Potential in Morocco

The performance of a solar system is closely linked to the characteristics of solar radiation in a specific location. These are figured out from the solar resources which are influenced by factors such as latitude, climatic conditions, topography, season and time of day [35]. Typically, a horizontal surface will receive two main components of solar irradiance: the direct component and the diffuse component. The direct component, particularity the DNI (Direct Normal Irradiance), comes directly from the sun. This component is particularly useful in concentrated solar power (CSP) or concentrated photovoltaic systems, where it can be focused to maximize energy production. The diffuse component, known as DHI (Horizontal Diffuse Irradiance), corresponds to the irradiance received on the horizontal plane from all other directions in the sky. Global Horizontal irradiance (GHI) is the sum of the direct and diffuse components of solar radiation. A thorough understanding of these components is crucial to the efficient design and optimal management of solar systems [35].

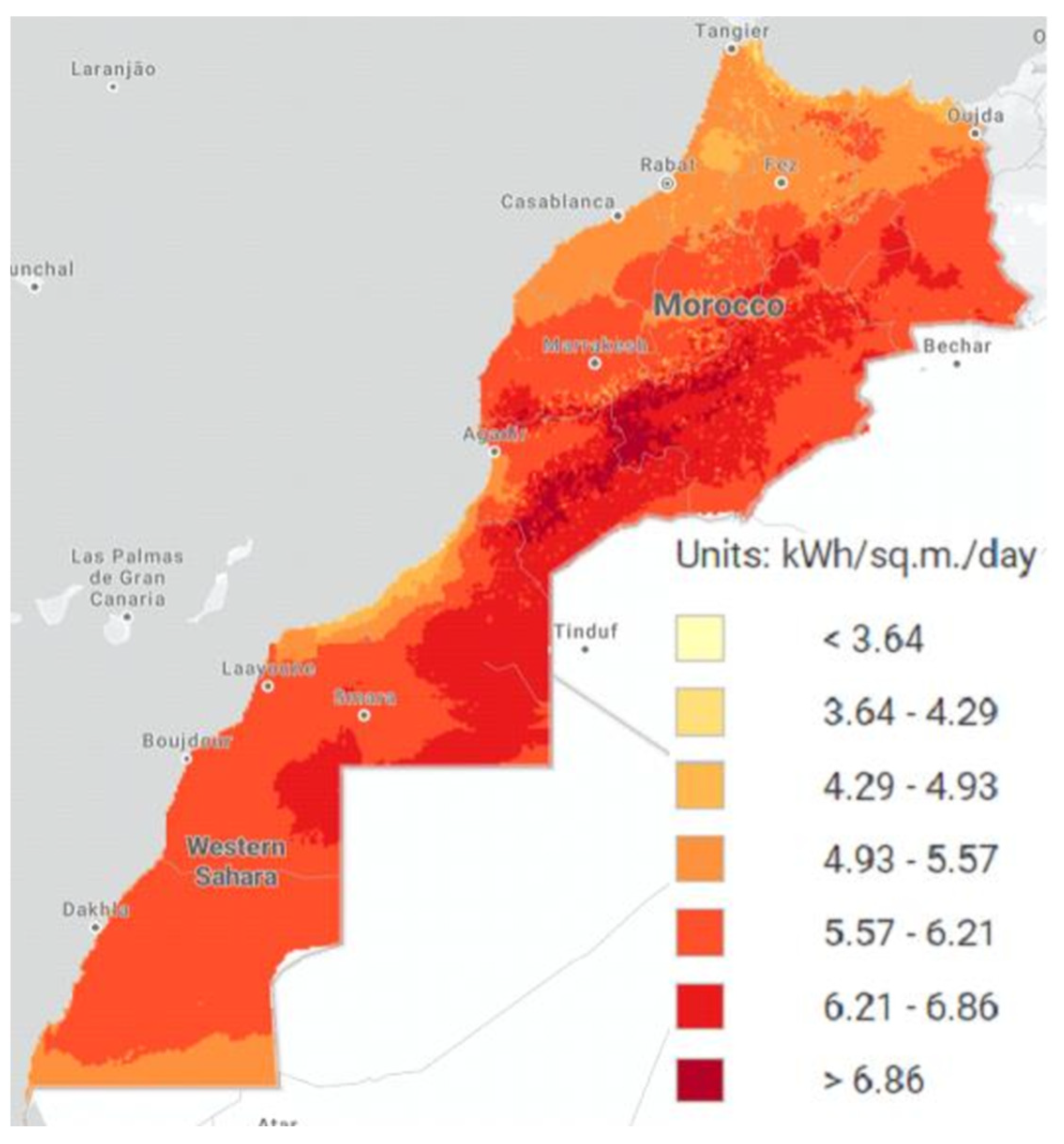

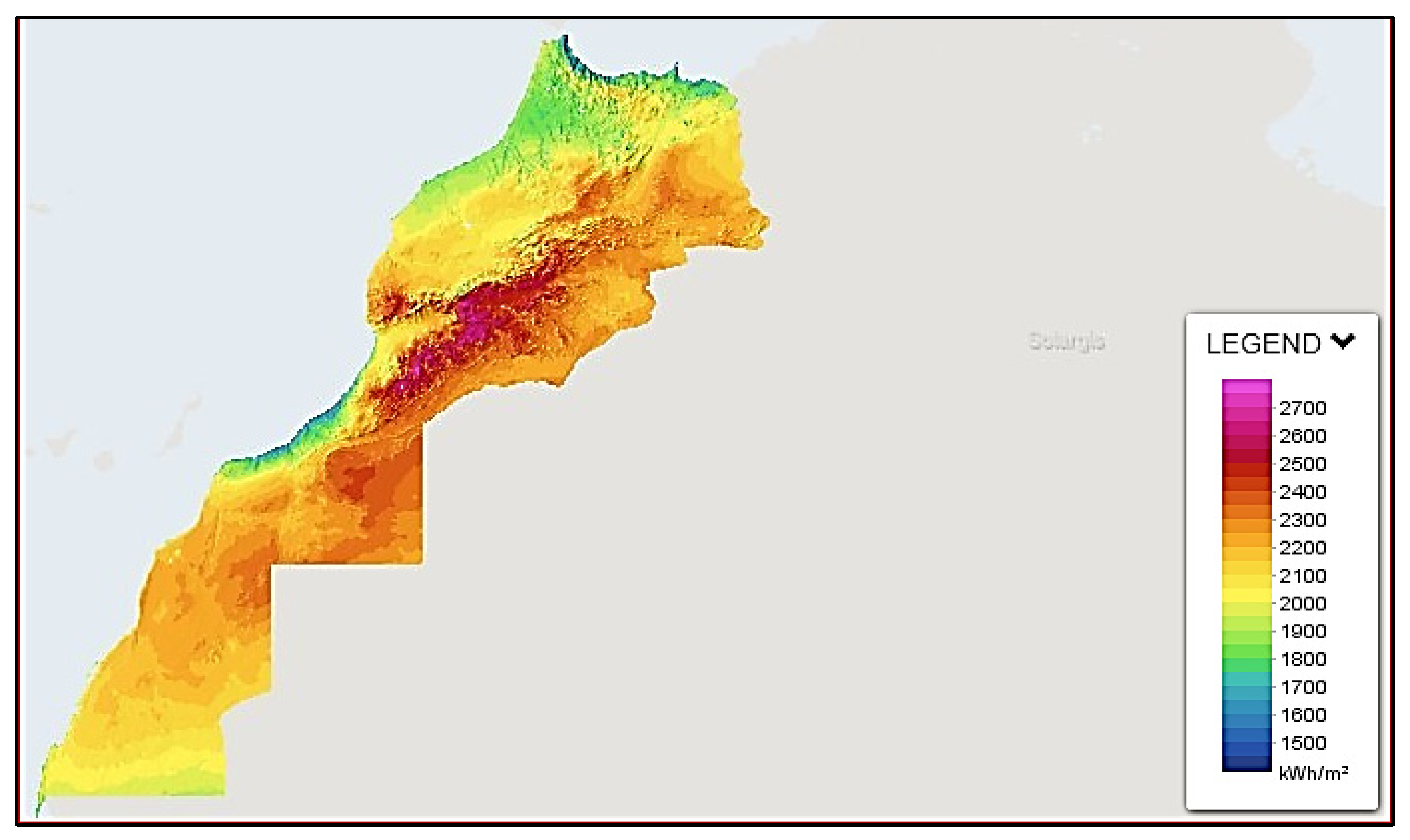

Indeed, Morocco is located in a high solar potential position. Its territory benefits from an average of 3000 hours of sunshine a year, with up to 3600 hours in the desert. This corresponds to a GHI of a daily average of 5.8 kWh/m²/day, with an annual global irradiance between 1800 and 2000 kWh/m² (said HIDANE and al.2023) (Figure 8). The lowest values are found in some coastal areas, while the highest values are found in the south of the country. From Figure 8, seven climatic zones can be distinguished, each zone receives approximately the same amount of irradiation, same altitude and other performances indicators [37]. Bouhal el al. have mapped Morocco in accordance with climate zoning, in order to compare the energy generated by concentrating solar power (CSP) systems, particularly parabolic through systems. The results confirm the cost-effectiveness of this technology on a large scale (less expensive and more productive). The best results were obtained in the zone with GHI levels of over 5.57 kWh/m2/day, which includes Errachidia, Taroudant, Ouarzazate, Smara and Bouarfa [37]. In addition, this area offers a high abundance of direct solar irradiation (DNI), making these regions attractive potential destinations for concentrated solar power (CSP) technologies, such as those employed in Ouarzazate. Morocco ranks among the top five countries in the world in terms of the highest DNI, with an annual average of more than 2200 kWh/m² in the southern regions and exceeding 2500 kWh/m² in some areas (Figure 9).

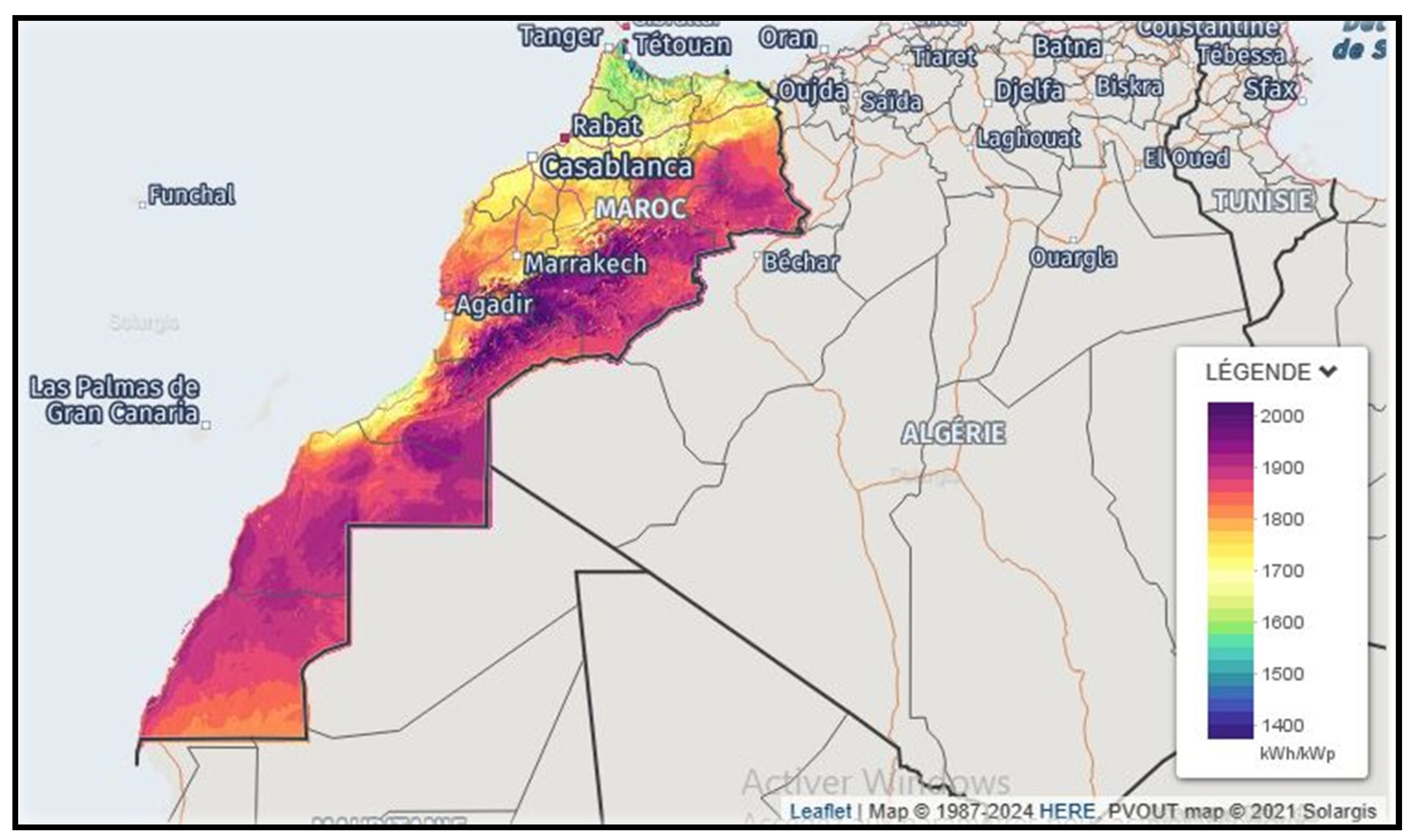

Figure 10 shows the significant potential for photovoltaic energy (PVOUT) in most regions of Morocco. PVOUT (photovoltaic Output) is an indicator that evaluates potential solar energy production per unit of solar panel capacity installed over a long period, expressed in kWh/kWp. The average annual PVOUT in Morocco reaches from 1600 to 1900 kWh/kWp/yr according to the different location. Consequently, a solar system with a capacity of 1 kWp can produce around 4.4 to 5.5 kWh of electricity per day in average.

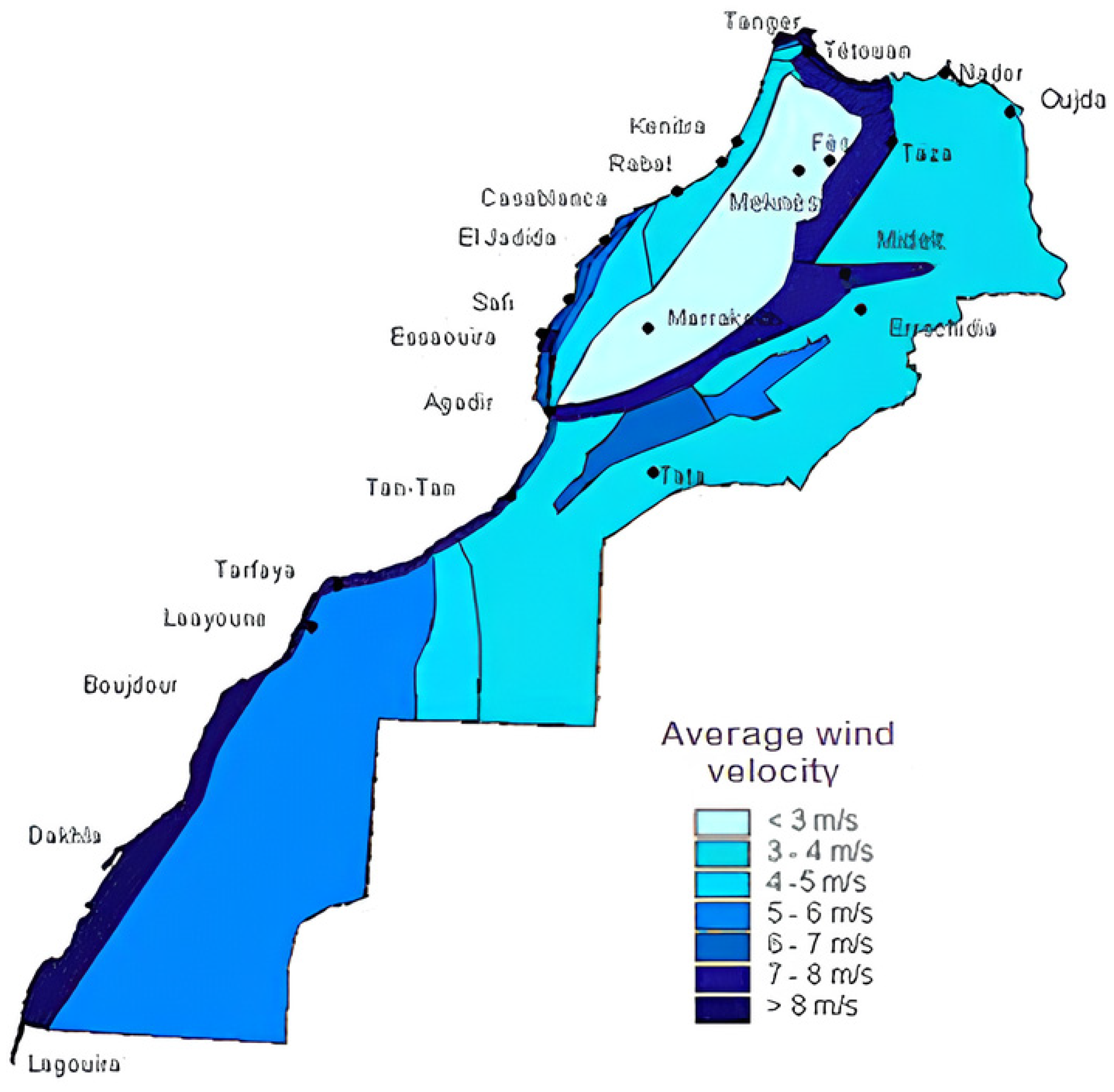

Therefore, it can be seen that Morocco has the resources for sustainable energy options that can address the two challenging issues that the country faces: electricity availability and global warming mitigation. Indeed, the country has a huge technical capacity in sustainable resources, primarily solar and wind, with generation potential varying from 20 to 25 GW. On a worldwide scale, the Moroccan sustainable energy agency-MASEN indicates that the country ranks 9th in terms of solar radiation, and 31st in terms of wind energy potential. The 3500 km of Atlantic coastline record wind speeds of between 7.5 and 11 m/s, representing an estimated technical potential of 25,000 MW. Figure 11 illustrates the wind power potential in Morocco [36] (said HIDANE and al.2023).

4. Current State of Solar Energy in Morocco

4.1. Policies and Regulations

The electricity sector in Morocco has undergone a remarkable transformation, transitioning from a vertically integrated monopoly to a more open and competitive market. During the first phase of the monopoly from 1963 to 1994, the Office National of Electricity (ONE), which was established in 1963, was in charge of electricity production, transmission, and distribution, thereby laying a solid foundation for the country’s electricity system [39]. The second phase, which started in 1994, marked a shift towards liberalization, with Morocco encouraging private operators to take part in electricity production through contracts offering purchase guarantees or as independent power producers (IPPs). Since then, there have been consistent efforts to foster private sector involvement in electricity generation and distribution while promoting investment in the energy sector and ensuring the stability of the electricity grid [39].

Morocco operates under a specific regulatory framework tailored to facilitate the development of RE within the electricity sector. Institutional and legislative measures have continuously evolved since the inception of the energy strategy in 2009, aiming to create an environment conducive to sustainable growth and innovation in the energy sector. These are based mainly on three framework laws. Law N° 13-09 on RE (amended and supplemented by Law N° 58-15), Law N° 47-09 on energy efficiency, and Law N° 54-14 on producers to supply medium voltage end-user. Table 1 summarizes the main laws relating to the RE sector, as well as the texts creating the dedicated institutions, in particular AMEE, MASEN and ANRE.

For further details, laws and regulation texts are available for download from the website of the Ministry for Energy Transition and Sustainable Development, and on the AMEE Website.

4.2. Installed Capacity

Solar energy is harvested through three primary technologies. Firstly, Photovoltaic (PV) systems directly convert solar radiation into electricity through solar cells made of semiconductor materials. These systems are widely used due to their simplicity of operation and efficiency, especially for small and medium-scale applications. Their continual advancement has led to reasonable costs in the market. The second technology involves solar thermal systems, where solar energy is used to heat water or air for residential, commercial, or industrial applications. The third technology is the Concentrated Solar Power (CSP) systems. They employ mirrors to reflect solar rays towards a focal point (solar Towers and Dish-Sterling systems) or focal line (as in the case of Fresnel or Parabolic Trough systems), thereby heating a heat-transfer fluid to elevated temperatures which is subsequently used in the power block of the power plant to produce steam which powers turbines and generates electricity. CSP systems allow the storage of heat by passing part of the heated fluid into the large tanks filled with molten salts or other storage media. This is one of the major advantages of this technology since it has a storage capacity greater than that of batteries. This allows the stabilization of electricity production, thus limiting the intermittency of solar energy and facilitating its integration into the grid. However, the Levelized cost of CSP derived electricity is generally higher than of PV systems. Despite this, their higher efficiency and reduced intermittency ease of storage of heat, makes them well-suited for large-scale power generation.

Development of manufacturing and technologies has led to a significant drop in LCOE. Over the 2010 to 2022 period, LCOE dropped from 0.445 to 0.049 $/kWh for PV and from 0.380 to 0.118 $/kWh for CSP [40]. At national scale, a lower LCOE of 0.05 $/kWh is obtained for photovoltaic plant NOOR IV, while an LCOE of 0.14 $/kWh is obtained for CSP plant NOOR I [33]. We should highlight that the cost of PV electricity becomes higher that of CSP when batteries are used for energy storage (discussed in Section 5). For international and national scale, detailed analysis about the cost of electricity production, installation and maintenance for different renewable energy sources (solar, wind, geothermal, hydropower, …), are available in IRENA reports [40,41,42] and other reference [13,33,43].

All these technologies are making a major contribution to the exploitation of solar energy and the development of RE on various scales in Morocco’s private and public sectors. Concentrated photovoltaic (CPV) is another technology based on a solar radiation for direct electricity generation, with a conventionally higher efficiency than any other technology (around 39%) [44]. Its operating principle involves the use of optical devices (mirrors or Fresnel lenses) to concentrate the radiation on the PV cells. This structure makes it possible to reduce the surface area occupied by a project, as well as the number of cells and thereby the quantity of semiconductor materials used, which is one of the most expensive element in a photovoltaic cell. Due to the significant intensity of direct normal irradiation (DNI) in Morocco, CPV is potentially attractive as it offers higher efficiency compared to other PV technologies [45]. However, this technology presents added investments for optical devices, solar tracking systems in addition to cooling systems to evacuate heat that could affect solar cell efficiency. These constraints explain the limitations of this technology to an experimental scale in Morocco. CPV projects in Morocco are limited to a few pilot projects and trails led primarily by research institution and technology companies such as IRESEN, MASEN and AMEE. For example, MASEN adopted the world’s first CPV pilot plant (Sumitomo Electric) in 2016, with an installed capacity of 1 MWe and the ability to generate over 1 GWh of electricity, enabling large-scale testing of CPV systems [33]. In addition, pilot systems are installed at various universities, such as the AL Akhawayn University in Ifrane, which has installed a 30 kW CPV system (with three two-axis sun trackers) [44], and the Mohamed V University in Rabat, which installed a CPV system (Beghelli HCPV technology) with a state of the art two-axis tracking systems with azimuthal rotation and zenithal elevation [45].

The Moroccan solar energy plan (MSP) which is one of the pillars in the implementation of the MES aims to increases the share of solar energy in the electricity production [46,47]. The main expected outcomes of the MES include:

- RE will account for 52% of total installed electrical capacity before 2030, and 70% by 2040.

- By 2030, solar, wind and hydropower are expected to account for 20%, 20% and 12% respectively in the energy mix.10GW of RE must be add between 2018 and 2030: 4560 MW of solar, 4200 MW of wind and 1330 MW of hydropower [33], including those to be carried by the private sector within the framework of Law No. 13-09.

- Investment: 9 billion USD for solar projects

- Reduction in greenhouse gas emissions by 42% in 2030

- Creation of an industrial base for the solar technologies

- Promotion of capacity building and applied research in PV and CSP technologies (particularly parabolic through and solar tower) and related disciplines.

In addition, for the year 2030, energy savings by sector would be 17% for industry, 24.5% for transport, 14% buildings and 13.5% for agriculture and sea fishing which will amount to 1 million toe.

In the framework of the MSP, Morocco has completed one of the largest solar complexes of the word which aims to contribute to meeting domestic and European green energy demands. The Noor Ouarzazate complex extends over 6,000 acre and consists of four power plants each using different technologies. Noor I (160 MW), and Noor II (200 MW), use parabolic through mirrors while Noor III (150 MW) uses heliostats technology which directs the sun to a collector on top of a tower. Each of these power plants uses a thermal storage system to store the heat obtained by the concentrated radiation in a large tank filled with molten salt. Storage capacities in the three plants are different, as Noor I have a three-hour storage capacity, while Noor II and Noor III each have a seven-hour storage capacity [48]. Meanwhile, Noor IV plant (72 MW) employs polycrystalline photovoltaic modules with tracking system. Noor I was commissioned in 2016 and the other plants in 2018 [33]. MASEN is leading the complex, while construction, operation and maintenance were awarded to a consortium led by Saudi company ACWA Power. The project was co-financed by the World Bank and the European Investment Bank.

At the present date, the CSP technology is predominant in Morocco, with 510 MWe installed at the Nour Ouarzazate complex and 20 MWe (Parabolic Through) at the Ain Beni Mathar plant. Ain Beni Mathar consists of a 470 MWe hybrid plant integrated Solar Combined-Cycle (ISCC) [49].

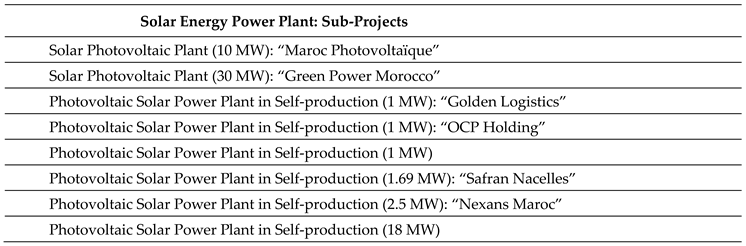

Other utility scale solar projects are still in the pipe or under testing such as Noor Midelt (800 MWe), Noor Tata (800 MWe), in addition to the ONEE Noor projects (Noor Atlas, Noor Tafilalt, Noor Argana) totaling 400 MW. The Noor Midelt project involves a hybrid technology combining CSP (600 MWe) and PV (1000 MWe), which will be realized in two phases (Noor Midelt I and Noor Midelt II). Midelt I combined 300 MWe of Parabolic troughs CSP and 500 MWe of PV system, taking the advantage of a storage option offered by CSP technology with a much lower cost per kWh for photovoltaic technology. As a result, this project will supply electricity 5 hours after sunset with a cost 0.068 US$/kWh. Morocco is among the first countries to adopt such a hybrid solution. Table 2 summarizes all solar projects in operation and under construction as part of Morocco’s large-scale solar strategy. In addition, other solar projects are implanted by self-producers and according to the law 13-09 and the law 16-08 related to auto production (Table 3).

Several other small scale solar energy projects and/or sub-projects were implemented in the framework of the MSP by ONEE:

- Small PV plant in Tit Mellil: 46 kW

- Small PV plant in Ouarzazate: 120 kW

- PV plant in Assa: 800 kW

- PV plant in Kénitra: 2 MW

Two photovoltaic solar power plants are being built under Law 13-09 related to RE. “Maroc Photovoltaïque”, which consists of implementing a PV system with a capacity of 10 MW in the province of Jerada, scheduled for commissioning in 2024. In addition, “Green Power Morocco” with a capacity of 30 MW, developed by the company Green Power. The electricity generated will be used exclusively by the delegated operator Amendis-Tanger to meet its ancillary service’s needs. Furthermore, the other projects are being developed within the framework of law 16- 08, where the electrical energy produced by the power stations is intended entirely for the producer’s own use.

The geographical locations of the installed and planned solar energy plants are shown in Figure 12 (source MASEN).

These projects combined with other planned wind and hydro projects will greatly contribute to the attainment of the national RE target of 52% of installed capacity by 2030.

In addition, there has been a significant increase in the use of PV in solar water pumping (SWP) either for the supply of drinking water or for irrigation. These systems are widely used in the agricultural sector as a means to promote RE and energy efficiency in this vital sector. The first program “The Moroccan’s National Solar Pumping program” was launched in 2013 under the responsibility of The Ministry of Energy, Mines, Water and Environment, and the Ministry of Agriculture. The government aimed to install 3000 SWPs with an approximate capacity of 15MW [50]. Given the limited results achieved by this program, an additional one was launched in 2016 under the title “The United Nations Development Program: Promotion of the development of photovoltaic pumping systems for irrigation”[51]. In collaboration with the Agricultural Development Fund (FDA), an envelope of 2.5 billion DH was divided between subsidizing photovoltaic systems and subsidizing irrigation, and is intended to support 4450 SWPs for small and medium-scale farmers. Statistically, 10 000 SWPs were installed in the agricultural sector between 2019 and 2020 SWP system lead to a competitive cost pumped water of 0.44 DH/m3 compared to the price of 0.76 and 1.67 DH for butane and diesel respectively [52].

The use of solar water heating systems (SWH) has also noticeably increased. SWH has a height potential in Morocco and in other countries in the MENA region, since it plays a crucial role in the development of energy efficiency and the reduction of the greenhouse gases. Morocco promotes the use of thes systems in administrative touristic buildings, schools, collective and individual housing. To this end, it has developed various programs such as the PROMOSOL (programme de développement du marché marocain des chauffe-eau solaires) program carried out by the Ministry of Energy, Mines and the Environment (MEMEE) in two phases (2000 - 2008) with the aim of promoting the use of solar water heaters and improving their quality. In addition, the SHEMSI program set up by AMEE was designed to encourage the development of SWHs. It aimed to install 1.7 million m² of SWH by 2020 and 3 million m² by 2030, which will save 920,000 tons of CO2 per year [53]. The first launched project aimed at promoting the Moroccan solar thermal market, although it failed to produce a significant result. The second one, launched to present a new Moroccan SWH with an accessible price and a technology adapted to the economic and climatic conditions of the country [54].

The Moroccan SWH market is based on imports of over 120,000 solar water heaters annually mainly from Turkey and China. Morocco will also be able to produce 40,000 units of solar water heaters locally, thanks to the construction of a large “MySol CES” unit in Tafilalet, scheduled to come on stream in the second half of 2023. In addition, a scientific and technological partnership is included with universities to support process development, ensure continuous innovation of solar water heaters and guarantee better quality and competitiveness in the long term [55].

Furthermore, the private sector is also increasingly using PV technologies to offset some of its conventional electricity consumption. However, official statistics of the overall installed power in these cases are yet to be performed as mentioned in Section 2, the installed capacity of RE connected to the transmission grid in 2023 increased by 500 MW, reaching a total capacity of 4672 MW by the end of 2023, compared to 4154 MW at the end of 2022. This increase is attributed to the commissioning of 300 MW from the Boujdour wind farm (as part of the 850 MW wind farm project) and 200 MW from the “Aftissat2” wind farm under the provisions of Law 13-09. The share of RE in the total energy mix rose from 4% in 2010 to 41% in 2023. These remarkable achievements during this period are attributed to the development of solar and wind energies, as illustrated in Figure 13. The installed capacity of hydroelectric and pumped hydro storage plants connected to the transmission grid has remained stagnant over the past two years at 1306 MW and 464 MW respectively [25]. The Pumped Hydro Storage (PHS or STEP) power plants consists of a pump-turbine system for energy storage and generation two water reservoirs located at different altitudes. Energy is stored by pumping water from the lower reservoir to the upper reservoir when demand is low, and then released from the upper reservoir through hydraulic turbines to supply the electricity grid when demand is high. This process allows for the storage and regulation of energy production while preserving the environment (no CO2 emissions and no pollution). The first PHS plant commissioned in Morocco in 2011 was the Afourer plant, with an installed capacity of 464 MWe [56]. STEP plants have become a strategic priority for Morocco to achieve its ambitious renewable energy (RE) targets. As such, several other STEP plants (STEP El Menzel 300 MW, STEP Abdelmoumen 350 MW, IFAHSA 300 MW and Many small hydroelectric power plant projects [57]) are under construction, with the aim of adding 1,330 MW of installed capacity by 2030 [56]. Benefiting from a 3,500 km coastline, Morocco is also exploring solutions for marine PSH plants with an artificial waterfall between an elevated reservoir and sea level. This approach, combined with wind power, would represent a promising solution to smooth load curves and make the national power system independent of fossil-fuel-based power plants [48].

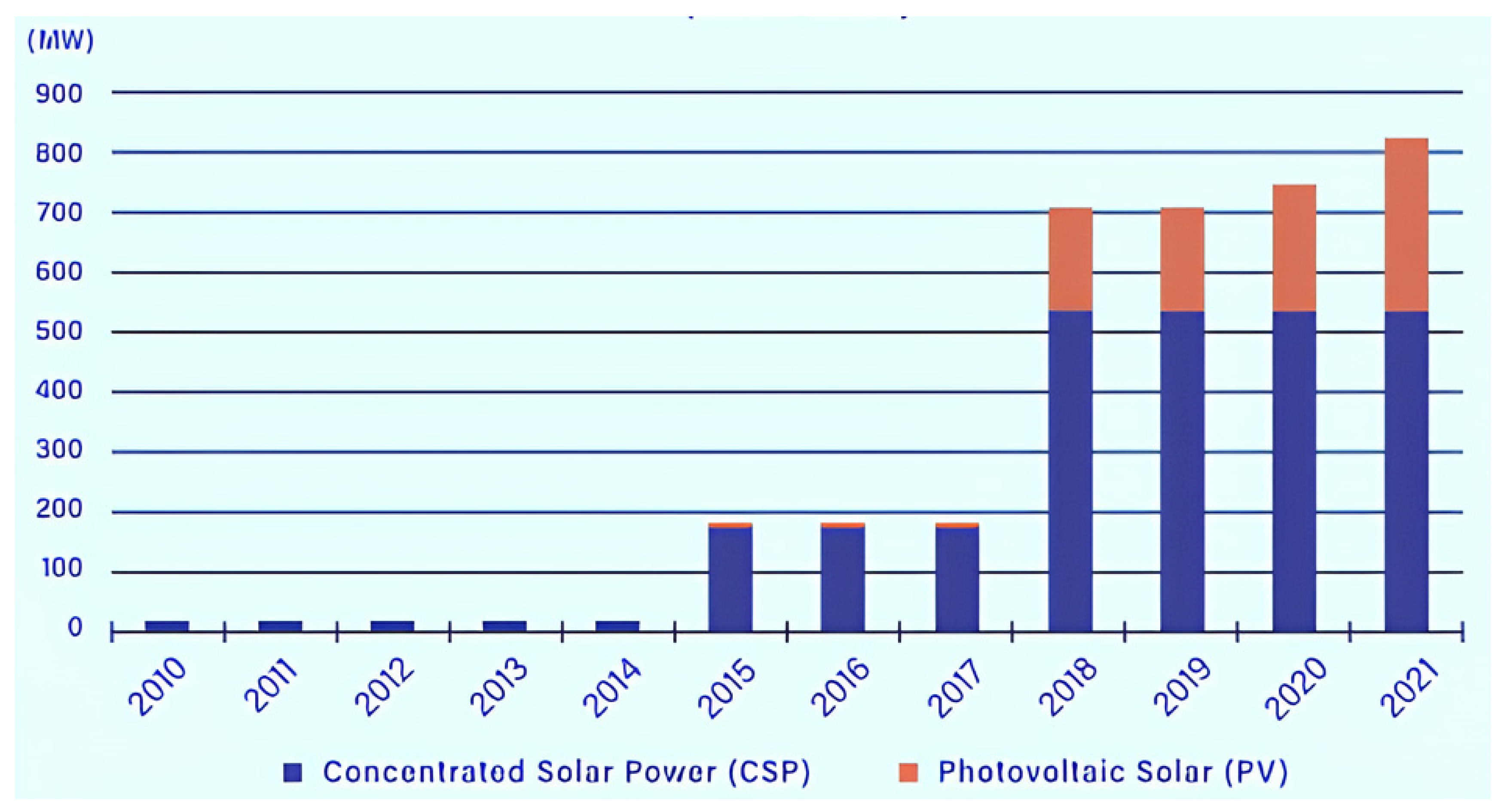

Solar energy has transitioned from an installed capacity of 20 MW originating from the Ain Beni Mathar CSP project in 2010 to 831 MW from both solar thermal and photovoltaic sources in 2023 (still being constant since the end of 2021). According to statistics from 2022 and 2023, the installed capacity of solar energy is 7.5% and 7.2% of the total national capacity respectively, and 20% and 18% of the installed capacity in the RE mix. Consequently, it has contributed 3.5% to national production. This breakdown includes 13.3% from concentrated solar power and 7.2% from photovoltaic sources, with 85% supplied by MASEN production and 15% by ONEE plants. However, no solar projects connected to the transmission grid were developed under Law No. 13.09 due to delays in the publication of the decree specifying the areas suitable for hosting solar power plants. This decree was published in the Official Gazette on September 25, 2022. This step aims to facilitate the development of large-scale solar energy, using the national grid to deliver the produced energy to consumers. Figure 15 and Figure 16 respectively illustrate the evolution of installed solar capacity and solar energy fed into the grid in Morocco between 2010 and 2021.

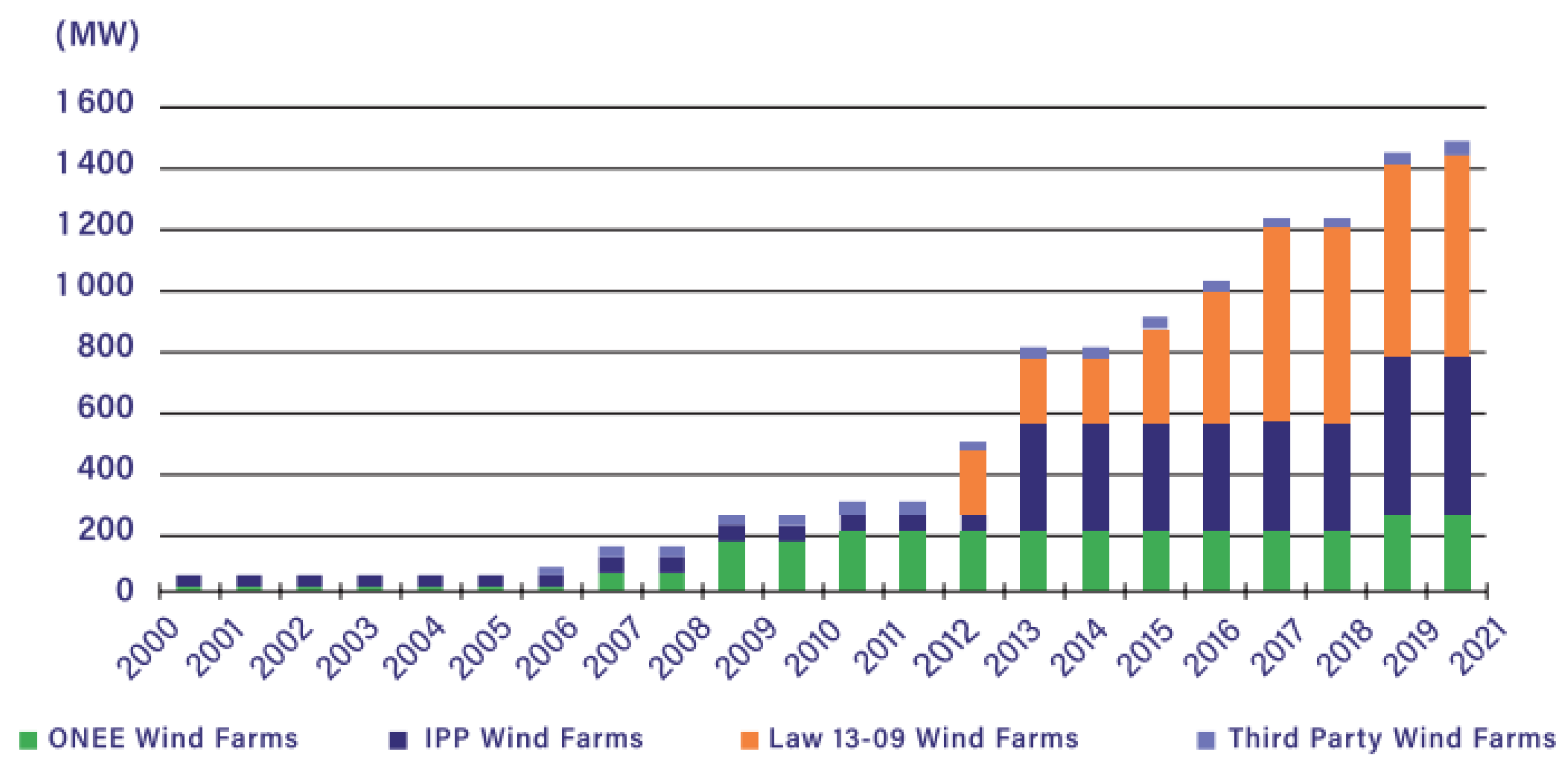

In addition, the installed wind energy capacity has increased significantly during this period, from 222 MW in 2010 to an installed capacity of 2071 MW in 2023. Figure 16 illustrates the evolution of installed wind energy capacity in the country between 2000 and 2021.

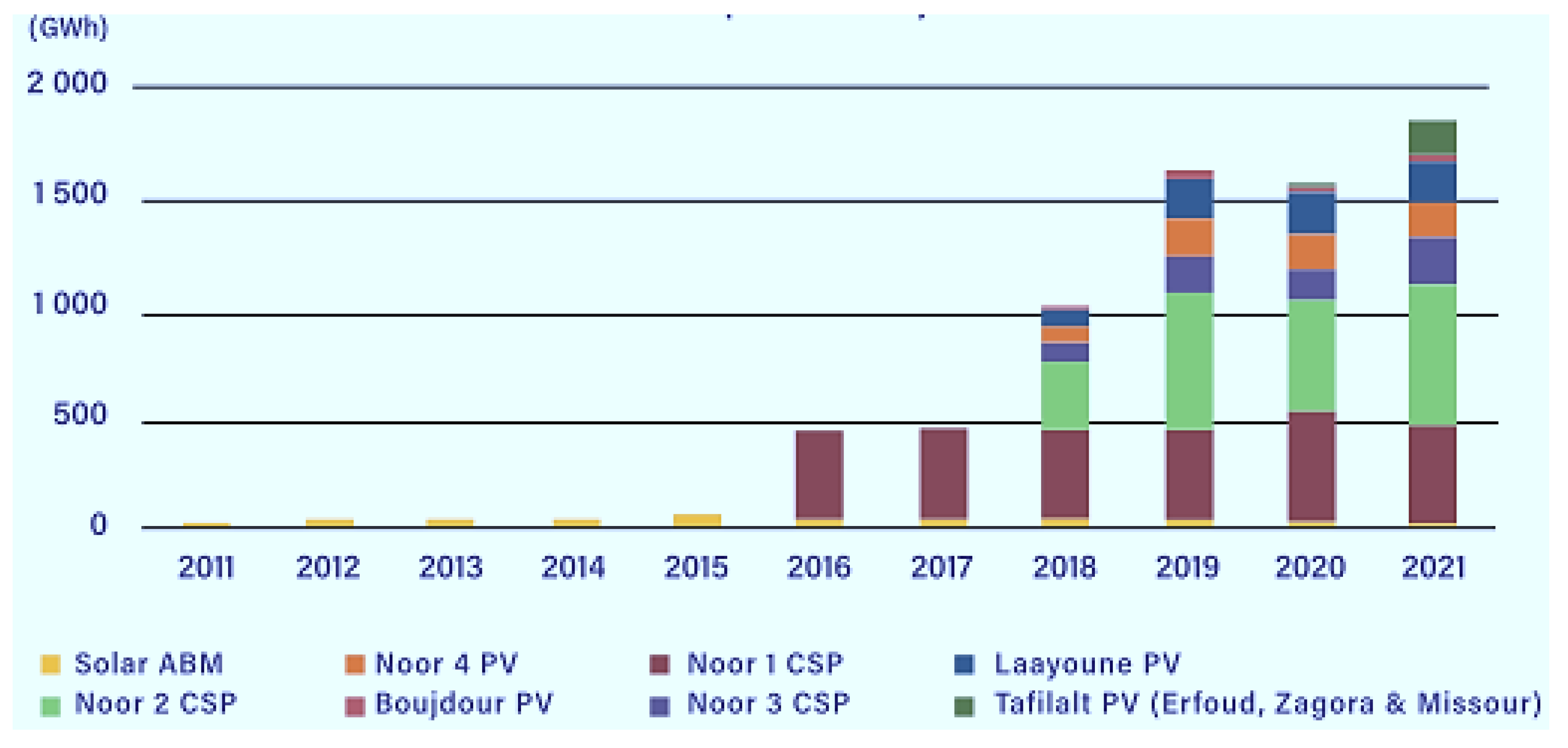

In terms of energy, electricity generated from RE sources and fed into the national transmission grid in 2022 amounted to 7421 GWh instead of 7972.8 GWh in 2021 (Figure 17). This represents a -7.8% annual variation compared to 2021. This decrease can be attributed to a reduction in hydroelectric, pumped hydro storage and solar productions, which account for -57.2%, -16.5%, and -20.3% respectively of the decrease [7].

4.3. Investment and Funding

Morocco stands out among the MENA countries for its steadfast commitment to developing RE, aimed at enhancing energy security through the reduction of its dependency on imported fossil fuels and curbing greenhouse gas emissions. Leveraging its abundant solar and wind energy potential, Morocco has successfully implemented many projects. Furthermore, the country’s enhanced regulatory and institutional framework concerning RE makes it an attractive destination for both national and international investments.

To meet the objectives outlined in its energy plan and programs, the Moroccan government estimated a minimum investment of eight and six billion dollars for the implementation of solar and wind energy projects, respectively. Moreover, it anticipated a total investment of 45 billion dollars to implement strategies aimed at reducing greenhouse gas emissions by 32% from 2015 to 2030 [30]. Additionally, an investment of 2.3 billion dollars is planned between 2023 and 2027 for the green hydrogen project [58]. Consequently, the funding and realization of RE projects rely on various actors, including government’s political and financial backing, involvement of national public-private institutions, collaboration with international organizations and foreign governments, and engagement of the private sector.

MASEN was established specifically to implement RE projects, particularly solar energy initiatives. Its mandate encompasses the entire project lifecycle, including coordination and supervision of related activities. Actors of the agency include the Hassan II Fund for Economic and Social Development, the Energetic Investment Company, and the National Office of Electricity (ONEE). The solar plan receives support from Germany, with funding provided by the German Federal Ministry for the Environment (BMU) and KfW Development Bank, while GIZ engages in enhancing industry skills and capabilities. For instance, the first project executed under the Moroccan solar plan, the Noor Ouarzazate Complex, required an investment of $3.9 billion, including $1 billion from the German investment bank KfW, $596 million from the European Investment Bank, and $400 million from the World Bank [59].

Furthermore, the acceleration of MES orientations and the encouragement of Moroccan companies can be further developed through the mobilization of financing within the framework of the green financing concept. This concept gained momentum in Morocco in 2016 during the COP22 held in Marrakech [60]. Green finance relies on various instruments and mechanisms, such as green bonds, ISR labels, green or environmental funds, regulation, as well as monetary and financial policies. In collaboration with the Solar Cluster, AMEE (Moroccan Agency for Energy Efficiency) has developed a financing and support guide for Moroccan businesses [61]. These financing instruments revolve around two main axes. The first axis of this guide focuses on financing and supporting green investments by businesses, including financial support from national organizations (such as Tatwir Croissance Vert and subsidies for resource protection in agriculture), co-financing offers like Green Invest in partnership with Moroccan banks, and offers in partnership with international financial institutions (such as Cap Blue, Green Economy Financing Facility (GEFF), Green Value Chain, and Istidama). The second axis concerns investment funds (such as AZUR, Maroc Numeric Fund II, and SEAF) and programs for the development of green entrepreneurship.

On the other hand, there are other financing options available to businesses, including the following:

- MORSEFF, a financing line for energy efficiency and RE projects, which allows Moroccan companies to access loans (or leasing) for the acquisition of equipment or the realization of major sustainable energy projects of up to € 4.5 million in financing, an investment subsidy of 10% of the credit, as well as a free energy audit for the evaluation, implementation and verification of the project. MORSEFF’s services are accessible locally thanks to distribution through partner banks such as Banque Populaire with Eco Energy Invest credit, BMCE with Cap Énergie or Maghrebail with Energy Lease. For example, a loan of 75 million dirhams has been granted to Moroccan companies to improve their energy efficiency, thanks to the BMCE and BCP banks.

- Standard credits from a local bank such as BMCI’s Green Credit or Attijariwafa Bank’s Effinergie.

- Imtiaz-Croissance to strengthen the support system for SMEs, VSEs and auto-entrepreneurs. It targets: SMEs operating in industry and activities integrated into industry that meet the following criteria: i) Turnover of the last financial year between 10 MDH and 200 MDH. ii) Having a development project promoting growth, the creation of added value and the creation of jobs likely to accelerate the change of scale and the emergence of new business models.

- The Moussanada program aims to support 700 companies per year in their process of modernization and improvement of their productivity to: i) strengthen their competitiveness factors in terms of reducing costs and lead times and improving quality. ii) Improve their performance and productivity. iii) Support them to access new markets.

- FODEP aims to encourage industries to invest in depollution or saving resources and to introduce the environmental dimension into their activities to deal with the regulatory framework in preparation to the globalization of trade.

- The Small Business Support (SBS) program launched by the European Bank for Reconstruction and Development (EBRD) and financed by a grant from the European Union and other donors, to support Moroccan SMEs through appropriate advice and international industrial expertise coupled with grant mechanisms.

- The establishment of energy performance contracts with an Energy Service Company (ESCO), which allows the financing of investment and maintenance costs, and the guarantee of savings. Download here an explanatory brochure of a typical green electricity supply and energy efficiency improvement project.

- Companies can also finance their green energy projects through funds dedicated to improving the competitiveness of companies in general, as part of Morocco SMEs programs for example.

4.5. Main Challenges and Barriers

According to the 2020 diagnostic of the Moroccan economic model carried by the government, it was stated that the challenges facing the Moroccan energy sector are key factor that could accelerate the Moroccan energy transition. Resolving these issues can provide pathways that will stimulate resilient and sustainable growth of the country.

One of the challenges is that in the electricity sector Morocco still relies heavily on coal despite the increase in the installed RE capacity. Indeed, in 2020, about 68% of electricity was generated using imported coal. RE sources only represented 19% of the overall electricity production.

Furthermore, the barriers to the development of solar energy in Morocco can be overcome by improving the institutional and regulatory frameworks including those related to low-voltage grid access (net metering), completing the liberalization of the renewable electricity sector. In addition, enacting National Electricity Regulatory Authority and an effective coordination between the different actors in this field (ONEE, MASEN, and Ministry of Energy and Mines.) will accelerate the implementation of the transition.

Furthermore, as recent studies showed that the de-carbonization pathways of Morocco call for an attractive policy framework to encourage private investments and to promote private-public partnership to scale-up investments in this sector. Some of the challenges that need to be resolved include:

High capital of the systems (PV or water heaters) especially for public. The initial cost of purchasing a solar system is still fairly high, especially with the existence of subsidies for butane (Water heating, pumping, …)

Weak industrial base in Morocco for solar energy systems (PV modules, BOS, solar water heaters, concentrators, monitoring systems, …)

Energy storage, especially for PV electricity. The development of large-scale storage (pumped hydro) and/or fast response time power (e.g.,. natural gas) is required for large scale integration of solar energy. Additional sources of flexibility of the national electric power system should be reinforced for large scale integration of intermittent RE sources, including demand side management, smart grids, cross-sector coupling through the development of power-to -X.

Grid instability, especially when the Low Voltage Grid (LV) grid access is granted. Laws and regulations and enforcing agencies, certification bodies need to be established before granting wide access to LV grid

Innovative R&D in the solar energy sector needs to be further stimulated by reinforcing collaboration between HEIs and research institutes and the private sector.

Absence of certified installers and OM operators which can be overcome by the capacity building.

Land usage: which requires to further increase the efficiency of the systems (promote R&D)

Lack of government incentives and subsidy policy for RE systems (PV, water heating…)

G. Vidican et al. have confirmed that the deployment of RE in the MENA region faces difficulties due to reluctance to invest in such projects, primarily because of lower profitability and higher risks. RE projects are often more costly and involve longer payback periods than traditional energy sources. Additionally, low electricity prices and high subsidies for fossil fuels in the region exacerbate profitability issues. Furthermore, RE projects require significant initial investments and are subject to various risks, including political and regulatory uncertainties. As a result, commercial banks and private investors hesitate to finance these projects. Despite these challenges, Morocco has implemented measures to attract private investments and ensure adequate financing for RE projects [50]. However, investors still express concerns, especially regarding the uncertainty surrounding investments in solar energy. Similarly, A. Šimelytė conducted detailed research on persistent obstacles in the Moroccan energy sector, highlighting challenges in terms of financing, institutional coordination, technical capacity, and social acceptance. She identified various obstacles at the commercial, political, and market levels [10]. These challenges require concerted action to overcome barriers and accelerate the energy transition towards renewable sources. There is enormous global potential for using solar energy to meet the rising demand. In addition to being eco-friendly, solar energy and its applications (electricity generation, water pumping, desalination, green hydrogen production, integration in buildings,) can stimulate economic growth, create new jobs, and become a pillar for the growth of manufacturing and service industries. M. Said Hidane et al. have proposed several recommendations regarding the photovoltaic (PV) and wind sectors to address challenges and strengthen the emergence of a competitive industrial ecosystem [36]

5. Future Outlook of Solar Energy in Morocco

Morocco currently is steadily working on increasing the share of renewables in its electricity mix and has set up very ambitious targets of reaching an RE share in the installed capacity of 52% by 2030, 70% by 2040 and 80% by 2050 (Figure 18 and Figure 19). These targets will be achieved thanks to the technological advances in energy storage and green hydrogen productions, as well as decreasing costs. The country is actively engaged in its 2030 renewable capacity target and will reduce its dependence on fossil-fuel-based power plants (oil and coal). The share of coal in the installed capacity is expected to decrease from 38.8% in 2020 to 22% by 2030 and that of oil will drop to 9.2% by 2030 from 16.2% in 2020.

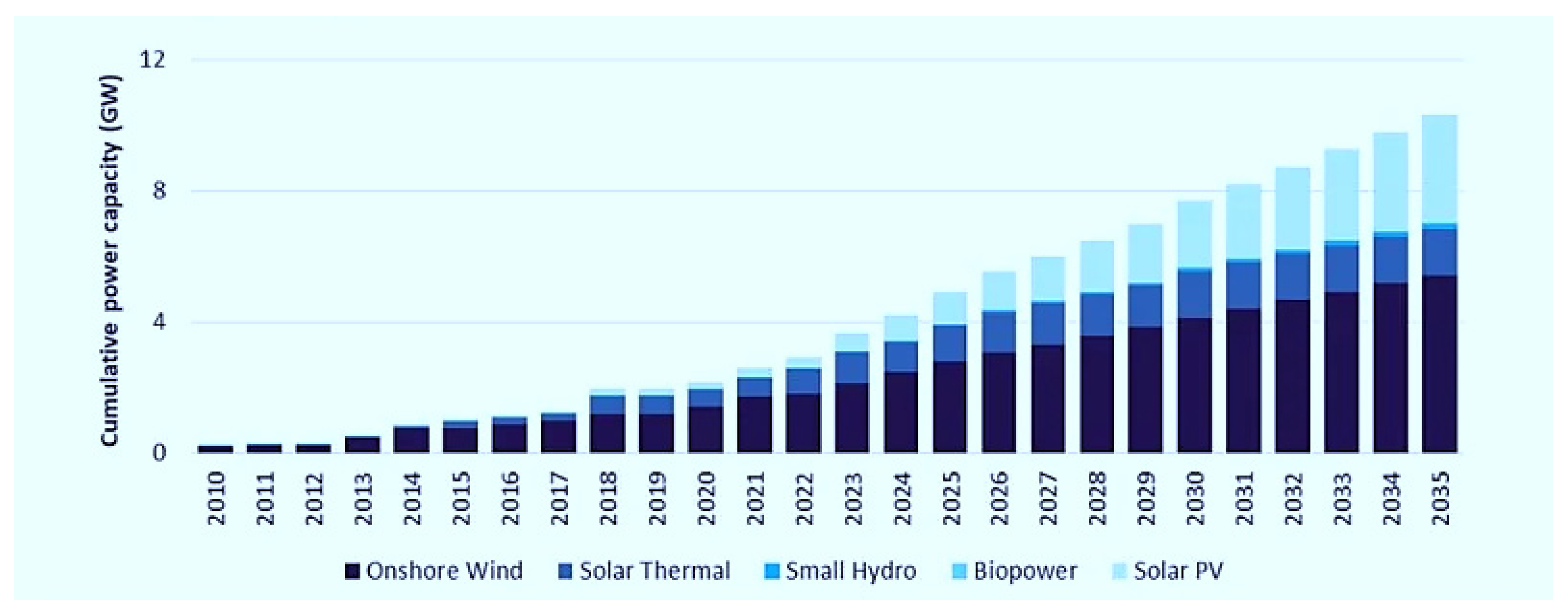

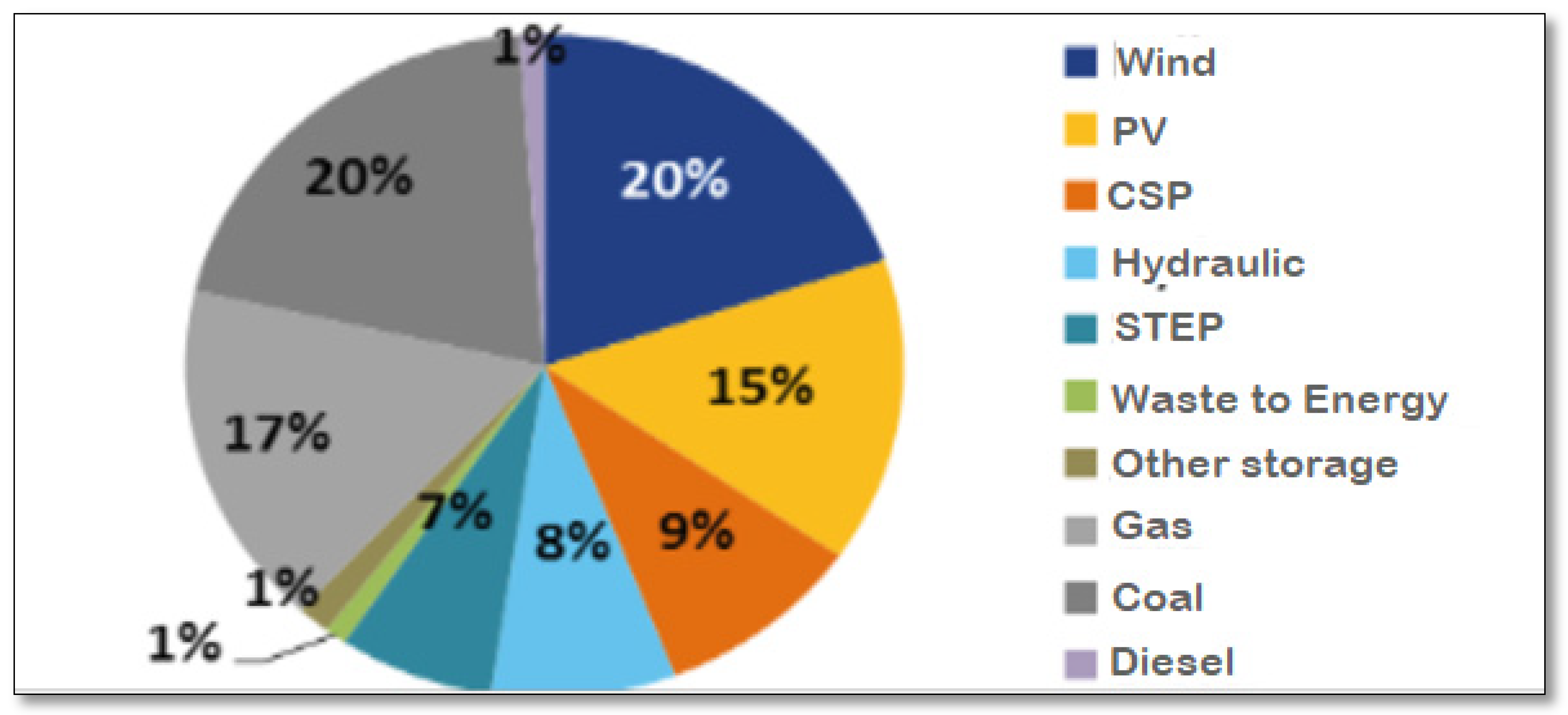

Morocco’s renewable installed capacity is expected to increase at an average rate of 9.3% between 2020 and 2030. Wind power is expected to surpass hydroelectricity. The installed capacity for wind will increase from 1.4 GW in 2020 to 4.3 GW in 2030 at an average growth rate of 11.5%. On the other hand, solar power capacity (both PV and CSP) will increase from 734 MW in 2020 to 2.1 GW in 2030 at rate of 11%, while hydropower capacity (including PHS) will go from 1.8 GW in 2020 to 3.3 GW in 2030. An actionable plan determining the share of various sources in the energy mix is proposed by MASEN as illustrated in Figure 20 Compared to the initial orientations of the National Energy Strategy (NES), which focused on large-scale projects considering CSP systems as the first choice, the new forecasts express the kingdom’s orientation towards more PV (15% by 2030) against CSP (9 % by 2030) through projects at various scales.

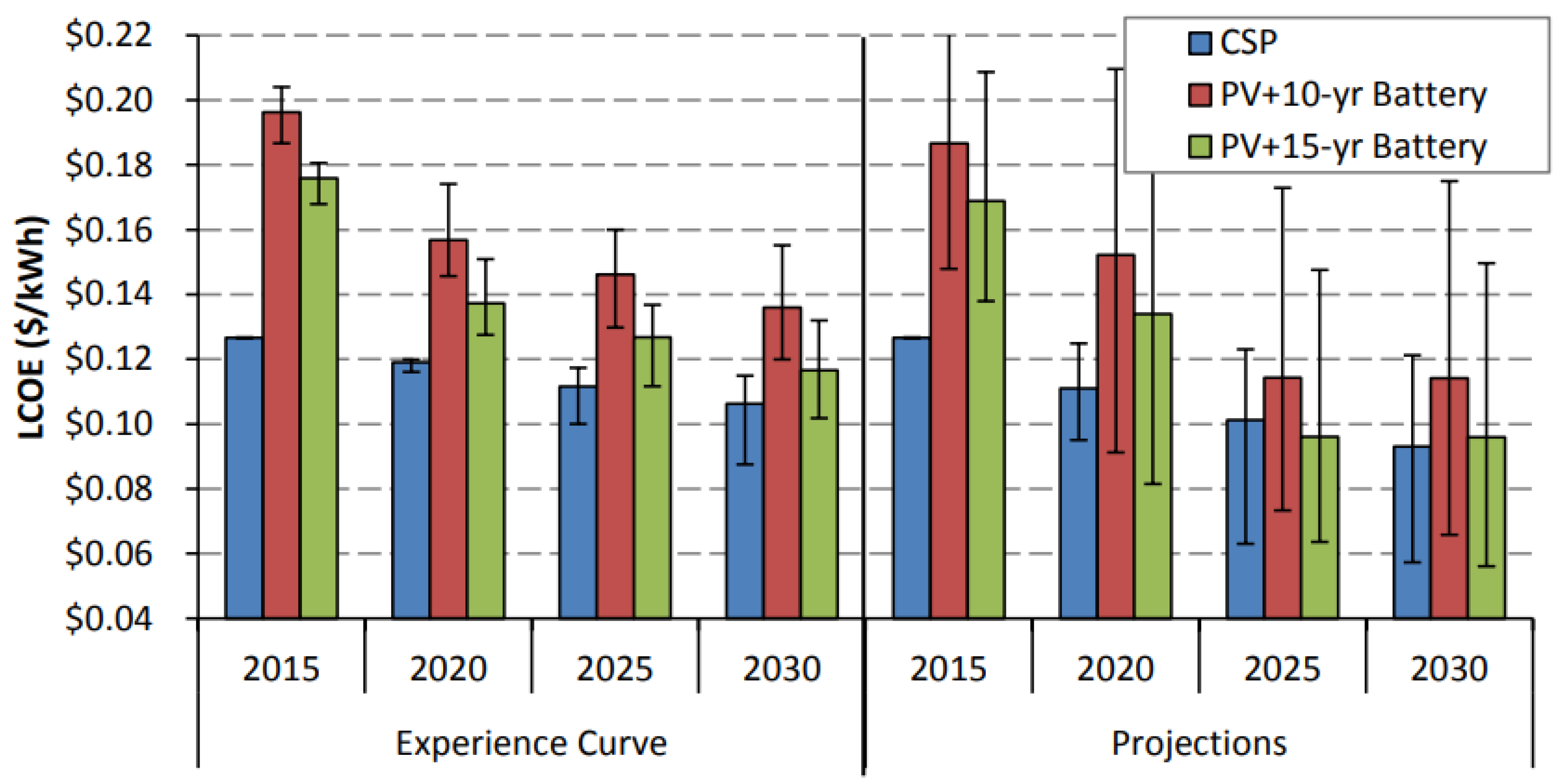

The choice to develop PV technology can be explained by its continuous advancement in terms of efficiency and durability, alongside low installation costs and a low Levelized Cost of Energy (LCOE). PV module prices have dropped by over 80% globally in less than ten years. It is worth noting that PV technology requires the use of storage systems (often batteries), which significantly increases the LCOE. Conversely, CSP technology allows for storage (latent or sensible), justifying its efficiency in large-scale projects connected to the national electrical grid. Estimates conducted by NREL suggest that a PV system with six hours of storage tends to produce a projected LCOE lower than CSP by 2030 (Figure 21). Additionally, MASEN has demonstrated through a comparative study of various technologies that a CSP/PV hybrid system is the optimal solution for a predefined production profile.

Furthermore, the solar sector has seen considerable development. Table 2 summarizes the various projects constructed and scheduled for commissioning by 2030. Particularly, the Noor ATLAS project led by ONEE involves installing 200 MW of PV distributed across eight plants. MASEN has launched various projects including the multi-site solar program “Noor PV II” with a capacity of 800 MW, the Noor Midelt I project (800 MW) using a hybrid system (CSP/PV), and the Noor Midelt II project designed to provide a total grid-fed power of around 230 MW (190 MW during peak hours) by allowing private developers to propose optimal configurations combining PV, CSP, thermal storage, or battery storage. Moreover, other projects are programmed under the framework of private very high voltage (VHV) and high voltage (HV) production, as well as projects of photovoltaic solar power plants intended for consumers connected to medium voltage (Table 3). However, self-production projects can only contribute 20% of their annual production to the grid.

Alongside the development of these projects, solar energy will contribute to several of the country’s sustainable strategies to strengthen the energy transition, reduce electricity consumption by improving energy efficiency, and preserve the environment.

Indeed, the residential sector is a major consumer of energy. Projections indicate an interesting increase in the next decade, surpassing 30% to 70% by 2030 [15]. This trend presents a compelling opportunity for self-production using photovoltaic (PV) systems to supply households. Studies suggest that the residential sector could see installations ranging from 100 MW to 250 MW of PV capacities by 2030. This translates to a potential generation of 0.2 to 0.4 TWh of solar energy. In a high-case scenario, this would equip 160,000 households with an average system size of 1.5 kWp, representing roughly 2% of all households by 2030. Looking towards 2040, the high-case scenario suggests installations could even surpass 1 GW. However, the adoption of photovoltaic in the residential sector is facing some challenges. These include variations in household energy consumption and equipment levels and the complexity of adapting the current tariff structure implemented by ONEE and other utilities [15]

Furthermore, PV systems are recommended to ensure self-production for public administrations and companies while maximizing energy efficiency measures. With the support of the AMEE and the Investment Company (SIE), the total installed capacity on residential, public, and industrial rooftops is estimated at 210 MW. Thus, PV technology development has been addressed in the national public lighting program (2020-2040) with the aim of reducing electricity consumption in the public lighting network [48].

According to the World Resources Institute (WRI), Morocco is facing a major water deficit, with an extremely high level estimated by 2040 [63]. According to 2022 statistics, irrigation consumes 89.26% of the available water volume [64]. In this regard, the country has prepared a National Program for Drinking Water Supply and Irrigation 2020-2027 (PNAEPI 2020-2027) presenting various solutions aimed at irrigation water management, wastewater reuse, and desalination. In particular, PV and CSP technologies hold promising potential in the desalination strategy. The cost of desalinated water as a function of different energy sources between 2017 and 2030 has been studied by [65]. This analysis demonstrates that solar energy is a competitive option for large-scale reverse osmosis desalination plants. Prospective results until 2030 suggest that CSP + Storage + Grid and PV + Storage + Grid solutions offer potential benefits, but PV + Grid remains the most competitive solution. This research demonstrated the capacity of photovoltaic (PV) and concentrated solar power (CSP) technologies to be rapidly integrated into the reverse osmosis desalination process. Moreover, the capacity of CSP to store heat at low cost offers significant flexibility, thereby considerably reducing dependence on the electrical grid, if necessary. Consequently, this work advocates for the integration of PV and CSP technologies to meet the energy needs of desalination. Within 10 years, desalination in Morocco could require between 40 MW and 200 MW of installed solar capacity. By 2040, this demand could significantly increase, surpassing 500 MW, to meet government objectives of desalinating several million cubic meters per day. Achieving this goal would require energy production on the order of terawatt-hours (TWh) [15]

Building on the return of experience of the last two decades, Morocco is committed to give new impetus to the energy transition and to play a vital role in the fight against Global Warming and the resulting climate changes in Africa. The country has revised and submitted its Nationally Determined Contribution (NDC) to the United Nations Framework Convention on Climate Change in June 2021. In its new NDC, Morocco has revised its emissions reduction targets to 45.5%, from the value of 42% by 2030 of the business-as-usual scenario.

Morocco has the potential to be a role model in decarbonized energy production and, as such, expand, its experience to neighboring markets. In addition, Morocco ambitions to become a world leader in the new clean technologies, including green hydrogen. Despite, encouraging prospects and ambitious roadmaps are being developed, technical limitations such as production technologies, transport/storage infrastructures, loss of ecological value in addition cost reduction, need to be overcome before Morocco will be able to export green hydrogen. Further the large scale integration of intermittent RE energies required for the decarbonization of the economy compounded by the uncertainty in the demand call for greater flexibility in the power system. Supply side flexibility, transmission/distribution reinforcement, energy storage; both large and small scale (e.g., Electric vehicles), demand side management, Advanced grid management (Smart grid), and sector coupling through power-to-X should be promoted for proper balancing of the grid at different time scales.

A strong focus should also be put on improving the existing laws relative to the development of small-scale grid-connected renewable systems. Legislation as well as incentive mechanisms promoting investments in rooftop PV and small-scale renewable systems other than for self-generation should be developed. These distributed systems will play a significant role in the future grids as they reduce transmission and distribution losses, improve grid stability and security and reduced the GHG emissions.

6. Conclusion

The development of RE in Morocco is a national priority to ensure energy security and preserve the environment by reducing dependence on fossil fuels. Consequently, the energy sector has made significant progress since 2009, following the implementation of the Moroccan Energy Strategy. This strategy aims to strengthen supply security and energy availability by promoting the participation of RE in the national electricity mix to reach 42% by 2020 and 52% by 2030. Despite missing the first target because of the pandemic and the energy crisis, Morocco has accelerated its progress to achieve the second aims.

Positive trends are observed, as the share of RE in the electricity mix has increased from 24% in 2009 to 41% in 2023. Until 2022, wind energy occupies the first place in installed capacity (1553 MW), accounting for 12.9% of the total national electricity production capacity. The second place is for solar energy with a capacity of 831 MW, contributing to 3.5% of the national production. Morocco has fully invested in the world’s largest solar complex (Noor Ouarzazate), which was fully commissioned in 2018 using primarily concentrated solar power systems. A new hybrid project (CSP/PV) is planned for 2024, while the government is more inclined to photovoltaic in other projects.

Overall, Morocco has successfully overcome the consequences of the pandemic and the energy crisis and has continued to pursue the goals of its energy strategy. The liberalization of the electricity sector and the continuous improvement of the regulatory and institutional framework for RE encourage private sector participation and financing in various projects. Given Morocco’s abundant solar and wind potential, it offers a suitable ground for both national and international investments. The Country has recently emphasized accelerating the energy transition towards RE through the development of green hydrogen production, desalination and de-carbonization of the economy. Morocco is involved in Innomed (Boosting Innovative Solar Energy Technologies and Application in Mediteranean Countries Education) an Erasmus Plus Project based on virtual classrooms, which aims to promote innovative technologies and applications of solar energy in Mediterranean countries. Funded by the European Union, Innomed brings together the University of Jordan, Cyprus, Morocco, Austria, Greece and Italy.

The development of RE has faced certain obstacles and barriers, particularly in terms of financing, institutional coordination, technical capacity, and social acceptance. There is enormous global potential for using solar energy to meet the rising demand. In addition to being eco-friendly, solar energy and its applications (electricity generation, water pumping, desalination, green hydrogen production, integration in buildings) can stimulate economic growth, create new jobs, and become a pillar for the growth of manufacturing and service industries.

Disclaimer “Funded by the European Union. Views and opinions expressed are however those of the author(s) only and do not necessarily reflect those of the European Union or the European Education and Culture Executive Agency (EACEA). Neither the European Union nor the granting authority can be held responsible for them.”

Acknowledgments

This work is financially supported by Boosting Innovative Solar Energy Technologies and Applications in Mediterranean Countries Education project (INNOMED) (Grant Agreement 101092041).

Conflicts of Interest

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Appendix A. Acronyms

- Ministry for Energy Transition and Sustainable Development (MTEDD). www.mem.gov.ma

- Direction Générale des Collectivités Territoriales (Directorate-General for Local Authorities);

- Moroccan Agency for Energy Efficiency (AMEE) http://www.amee.ma/index.php/en/

- Office National de l’électricité et de l’Eau Potable (Water Branch / Electricity Branch) http://www.one.org.ma

- National Office for Hydrocarbons and Mines (ONHYM)

- ANRE - l’Autorité Nationale de Régulation de l’Électricité: https://anre.ma/en/

- Moroccan Agency for Sustainable Energy (MASEN), http://www.masen.ma/fr/masen/

- National Inventory Commission (CNI)

- Moroccan Energy Observatory (OME)

- Moroccan Agency for Nuclear and Radiological Safety and Security (AMSSNur)

- National Centre for Nuclear Energy, Science and Technology (CNESTEN)

- Energy Investment Company (SIE), https://www.siem.ma/ which offers consultancy services and assists in project development (energy efficiency, RE) through several actions such as identification of needs, choice of appropriate technologies, financing options, project implementation arrangements, and assessment of the project profitability.

- Société Chérifienne des Pétroles (SCP)