Submitted:

09 February 2026

Posted:

10 February 2026

You are already at the latest version

Abstract

Emerging technologies are increasingly recognized as key drivers of sustainable man-agement, and Saudi Arabia presents a unique context in which digital transformation and sustainability have been strategically integrated under the Vision 2030 national reform agenda. While digitalization and sustainability have been examined inde-pendently in international scholarship, fewer studies have explored how emerging technologies enable sustainable management within national transformation contexts. This conceptual review synthesizes recent interdisciplinary literature to examine the enabling role of artificial intelligence (AI), blockchain, the Internet of Things (IoT), big data analytics, and cloud computing in advancing sustainability-oriented management practices in Saudi Arabia. Drawing on technology adoption and sustainability transition perspectives, the paper develops a conceptual framework linking technological capa-bilities to sustainability performance across environmental, social, economic, and gov-ernance (ESG) dimensions. The study outlines theoretical, managerial, and policy im-plications and proposes a future research agenda relevant to Saudi Arabia’s ongoing digital and sustainability transition. The paper contributes to bridging digital trans-formation and sustainability scholarship and provides a conceptual foundation for empirical studies within Gulf and emerging economy contexts.

Keywords:

emerging technologies

; sustainable management

; vision 2030

; Saudi Arabia

; digital transformation

; ESG

; sustainability transitions

; conceptual framework

1. Introduction

Digital transformation has increasingly reshaped how organizations and public institutions conceptualize management, moving sustainability from a peripheral concern toward a core strategic objective [1,2]. Rather than operating as a separate environmental agenda, sustainability is now intertwined with how resources are allocated, operations are coordinated, and stakeholders are engaged over the long term. This shift reflects a broader recognition that environmental stewardship, social responsibility, and economic resilience cannot be pursued independently of the digital infrastructures that support modern organizational systems [3,4].

Within this evolving landscape, emerging technologies—such as artificial intelligence (AI), blockchain, the Internet of Things (IoT), big data analytics, digital twins, and cloud computing—have expanded the managerial toolkit available for pursuing sustainability-oriented goals [5,6,7]. These technologies enable organizations to move beyond static reporting toward dynamic, data-driven decision-making, real-time monitoring, and predictive optimization. Their relevance is particularly pronounced as sustainability frameworks increasingly emphasize ESG performance, circular economy principles, and net-zero commitments, all of which depend on timely, reliable, and integrated data infrastructures.

Beyond firm-level dynamics, scholars have increasingly examined sustainability transitions through a socio-technical systems perspective, emphasizing that technological capabilities are deeply embedded within governance structures, regulatory frameworks, and cultural contexts [18,19]. Accordingly, the extent to which emerging technologies can support sustainability depends not only on their technical affordances, but also on how they are integrated into management systems, institutional arrangements, and decision-making processes [20,21]. This perspective highlights the need for integrative conceptual frameworks that link emerging technologies to sustainability-oriented management outcomes across environmental, social, economic, and governance dimensions.

Empirical research has consistently shown that Industry 4.0 technologies can enhance sustainability performance by improving resource efficiency, reducing emissions, and increasing transparency across organizational and supply chain processes [8,9,10]. AI-based systems, for instance, support energy optimization and environmental risk prediction in sectors such as manufacturing, logistics, and utilities [11]. Blockchain applications strengthen traceability and accountability in sustainability-oriented supply chains, thereby reinforcing the credibility of ESG disclosures [12,13]. At the same time, IoT-enabled sensing infrastructures facilitate continuous environmental monitoring and asset management, which are critical for circular economy and resource optimization initiatives [14,15]. Collectively, these developments suggest that emerging technologies increasingly function as strategic enablers of sustainable management rather than as isolated operational tools [16,17].

At the macro level, sustainability transitions are increasingly understood through a socio-technical systems perspective, which emphasizes that technological change is inseparable from governance arrangements, regulatory frameworks, and institutional contexts [18,19]. From this viewpoint, the sustainability impact of emerging technologies depends less on their technical sophistication alone and more on how they are embedded within managerial practices, decision-making structures, and institutional logics [20,21]. This insight underscores the need for integrative conceptual frameworks capable of linking technological capabilities with sustainability outcomes across environmental, social, economic, and governance dimensions.

Saudi Arabia offers a particularly salient context for examining this digital–sustainability nexus. Under the Vision 2030 agenda, sustainability and digital transformation are pursued as mutually reinforcing national priorities rather than as parallel policy tracks [22]. Digitalization has been positioned as a key driver of economic diversification, institutional modernization, and public sector efficiency, supported by comprehensive regulatory and strategic reforms [23,24]. The establishment of the Saudi Data and AI Authority (SDAIA) and the National Data Strategy further reflects a deliberate effort to treat data and artificial intelligence as strategic assets with direct implications for sustainable development and long-term economic resilience [25].

Beyond policy articulation, Saudi Arabia has operationalized technology-enabled sustainability through a range of governmental and sectoral initiatives. The Digital Government Authority (DGA) promotes digitally enabled sustainability by enhancing service efficiency, reducing administrative resource consumption, and strengthening transparency [26]. Large-scale smart city projects—most notably NEOM, The Line, and Oxagon—represent ambitious attempts to integrate AI-driven systems, IoT-based urban management, renewable energy, and circular resource models at an unprecedented scale [27]. In parallel, the Circular Carbon Economy (CCE) framework advanced by the Ministry of Energy provides a structured, technology-supported pathway toward low-carbon economic development [28].

The private sector has played a complementary role in translating these national priorities into operational sustainability practices. Leading Saudi organizations, including Saudi Aramco, SABIC, and the Saudi Electricity Company (SEC), have adopted advanced digital technologies to support ESG reporting, emissions management, and decarbonization strategies [29,30,31]. These organizational experiences illustrate how emerging technologies contribute not only to sustainability disclosure but also to measurable sustainability performance at the industry level.

Despite these developments, existing academic research remains fragmented in several respects [32,33,34]. Prior studies frequently focus on individual technologies or sector-specific applications without offering an integrated theoretical perspective. Moreover, much of the literature adopts technology adoption lenses while paying limited attention to managerial integration and institutional alignment [35]. Conceptual analyses that explicitly link emerging technologies to ESG-oriented management outcomes within the Vision 2030 context remain scarce [36].

In response to these gaps, this paper develops a conceptual framework that positions emerging technologies as enablers of sustainable management within Saudi Arabia’s national transformation context. By linking technological capabilities to ESG-oriented management practices and sustainability outcomes, the study seeks to bridge digital transformation and sustainability scholarship while offering a foundation for future empirical research in Gulf and emerging economy settings.

2. Background and Definitions

Digital transformation, emerging technologies, and sustainability were initially examined as largely independent research domains. Over time, however, these streams have converged as organizations and policymakers increasingly recognize that sustainability objectives cannot be achieved without digital capabilities that enable measurement, coordination, and governance. This convergence reflects a shift away from technology-driven digitalization toward sustainability-oriented organizational transformation, where digital systems function as enablers of long-term value creation rather than as efficiency-enhancing tools alone. To ground the conceptual framework proposed later in this paper, it is therefore necessary to clarify how emerging technologies and sustainable management are defined and how contemporary sustainability taxonomies structure these concepts.

2.1. Emerging Technologies: Definitions and Taxonomies

The concept of emerging technologies is widely used across innovation, management, and sustainability research, yet it remains fluid rather than fixed [37,38]. Rather than being defined solely by novelty, emerging technologies are commonly characterized by their developmental uncertainty, rapid evolution, and potential to reshape existing socio-economic and organizational arrangements [37]. These technologies are not fully institutionalized, but they exhibit strong growth trajectories and a capacity to alter established managerial practices and governance structures [39].

From a management and sustainability perspective, emerging technologies are increasingly distinguished by their ability to generate, process, and integrate large volumes of data, enable connectivity across organizational boundaries, automate complex processes, and support predictive and adaptive decision-making [40,41]. In this sense, their relevance extends beyond technical innovation to encompass managerial cognition, organizational coordination, and institutional transparency.

Over the past decade, academic literature has largely converged around a core group of technologies associated with Industry 4.0. These include artificial intelligence (AI), the Internet of Things (IoT), blockchain, big data analytics (BDA), cloud computing, digital twins, and cyber–physical systems (CPS) [42,43,44]. While these technologies are often discussed individually, recent research increasingly emphasizes that their transformative potential lies in their integration rather than in isolated deployment [20,58].

Artificial Intelligence (AI)

Artificial intelligence (AI) refers to computational systems capable of performing tasks that typically require human cognitive functions, such as learning, pattern recognition, and decision-making [45]. Within sustainability-oriented management, AI is increasingly applied to optimize resource utilization, reduce environmental impacts, and support strategic planning under conditions of uncertainty [11,46]. Rather than replacing human judgment, AI systems frequently operate as decision-support tools that enhance managerial capacity to interpret complex sustainability data and evaluate alternative courses of action.

Internet of Things (IoT)

The Internet of Things (IoT) describes interconnected networks of sensor-enabled physical objects capable of collecting, transmitting, and interacting with digital data streams [47]. In sustainability contexts, IoT infrastructures enable continuous monitoring of environmental conditions, asset performance, and resource flows, thereby transforming sustainability from a retrospective reporting exercise into a real-time management function [14,48]. Such capabilities are particularly critical for energy systems, industrial operations, and urban environments where dynamic feedback is essential for efficiency and risk mitigation.

Blockchain

Blockchain technology provides decentralized, tamper-resistant records of transactions and data exchanges, reducing reliance on centralized intermediaries [49]. Its relevance to sustainable management lies primarily in its capacity to enhance transparency, traceability, and accountability across organizational and supply chain boundaries [12,13,50]. By strengthening auditability and data integrity, blockchain supports governance-oriented sustainability objectives and reinforces trust in ESG disclosures.

Big Data Analytics (BDA)

Big data analytics encompasses analytical techniques designed to extract insights from large, heterogeneous, and high-velocity datasets [51]. In sustainability management, BDA enables evidence-based decision-making related to emissions accounting, environmental risk assessment, and ESG performance evaluation [35,52]. Importantly, BDA shifts sustainability from a compliance-driven activity toward a strategic intelligence function that informs long-term planning and resilience.

Cloud Computing

Cloud computing provides scalable, on-demand computing infrastructures that support data-intensive sustainability applications without requiring extensive physical IT assets [53,54]. Cloud platforms facilitate ESG data integration, digital government services, and cross-organizational collaboration, thereby lowering technological barriers to sustainability adoption and enhancing institutional interoperability.

Digital Twins and Cyber–Physical Systems

Digital twins enable the virtual representation and simulation of physical systems, allowing organizations to test alternative operational and environmental scenarios before implementation [7,55]. Cyber–physical systems (CPS) integrate sensing, computation, and actuation to enable real-time system control [56,57]. Together, these technologies support predictive optimization, reduce resource waste, and enhance operational sustainability across sectors such as manufacturing, energy, and infrastructure.

2.2. Sustainable Management Paradigms

Sustainable management has evolved from a predominantly environmental concern into a multidimensional organizational paradigm integrating environmental, social, economic, and governance considerations into managerial decision-making. Early approaches emphasized pollution control, resource efficiency, and environmental compliance [61]. However, as sustainability entered corporate strategy and public policy domains, its scope expanded in response to stakeholder pressures, regulatory demands, and globalized value chains [62,64].

Building on the Brundtland Commission’s definition of sustainable development as meeting present needs without compromising future generations [63], management scholarship increasingly conceptualizes sustainability as a systemic process that aligns organizational structures, incentives, and performance metrics with long-term societal goals [60,62]. From this perspective, sustainability is not an isolated function but a coordinating logic that shapes how organizations create value, manage risk, and engage stakeholders over time.

Recent literature further highlights the role of digital infrastructures and data-driven systems in operationalizing sustainable management. Advanced analytics, reporting platforms, and digital monitoring tools enable organizations to translate abstract sustainability commitments into measurable practices and outcomes [52]. The growing institutionalization of sustainability through reporting standards and rating systems has reinforced its managerial salience by linking sustainability performance to capital markets and regulatory oversight [67,71].

2.3. ESG, Triple Bottom Line, and SDGs: Toward Integrated Sustainability Taxonomies

Three major conceptual taxonomies now dominate sustainability discourse across corporate, academic, and policy domains: the Triple Bottom Line (TBL), the Environmental-Social-Governance (ESG) framework, and the United Nations Sustainable Development Goals (SDGs).

(a) Triple Bottom Line (TBL)

The Triple Bottom Line (TBL) framework introduced the idea that sustainability encompasses environmental, social, and economic dimensions rather than financial performance alone [59,66]. By emphasizing the interdependence of people, planet, and profit, TBL provided an early conceptual structure for integrating sustainability into organizational performance assessment [60]. Although later frameworks have expanded upon it, TBL remains influential as a foundational taxonomy that legitimized sustainability as a managerial concern.

(b) Environmental-Social-Governance (ESG)

The ESG framework emerged primarily from financial markets and investor communities, reflecting growing concern with long-term risk, transparency, and governance quality [65,67]. By explicitly incorporating governance, ESG extends earlier sustainability models and emphasizes accountability, ethical conduct, regulatory compliance, and disclosure integrity [71]. ESG has become particularly salient in national transformation contexts where governance reform and institutional credibility are central to economic diversification and sustainable development.

(c) Sustainable Development Goals (SDGs)

The United Nations Sustainable Development Goals (SDGs) provide a global policy framework consisting of 17 goals addressing environmental protection, social development, economic growth, and institutional capacity [68]. Although not originally designed for corporate reporting, SDGs are increasingly used by organizations and governments to signal alignment with global sustainability agendas and to benchmark progress across sectors [69].

Toward Convergence and Integration

Recent scholarship highlights increasing convergence among TBL, ESG, and SDGs [70]. TBL offers conceptual clarity regarding sustainability dimensions, ESG provides operational and governance-oriented metrics, and SDGs supply normative direction and societal benchmarks. In national transformation contexts such as Saudi Arabia’s Vision 2030, this convergence enables sustainability to be pursued simultaneously through corporate strategy, public policy, and institutional reform.

The integration of governance into sustainability taxonomies is particularly significant, as it aligns sustainability objectives with transparency, accountability, and regulatory modernization [65,71]. These dimensions are central to digitally enabled sustainability systems and directly inform the analytical framework developed in subsequent sections.

Why ESG + TBL + SDGs Integration Matters for Emerging Technologies

The convergence of these frameworks provides a conceptual foundation for analyzing how emerging technologies enable sustainable management. Specifically:

- TBL clarifies sustainability’s three core performance dimensions

- ESG operationalizes governance and investor relevance

- SDGs map sustainability to national and global development agendas

Emerging technologies interact with these frameworks in different but complementary ways. AI, BDA, IoT, and digital twins support environmental optimization; blockchain and cloud computing enhance transparency and governance; and CPS, automation, and data-driven models contribute to economic efficiency and social well-being 63,65. This multi-layered relationship will be elaborated in Section 2.4.

2.4. Emerging Technologies as Enablers of ESG-oriented Sustainable Management

The relationship between emerging technologies and sustainability performance can be understood through an ESG-oriented analytical lens. Rather than treating technologies as tools that merely enhance operational efficiency, the ESG perspective positions them as strategic enablers shaping transparency, environmental performance, social responsibility, and governance quality. Recent conceptual and empirical studies have highlighted the potential of digitalization to support ESG integration, accelerate sustainability reporting, and reduce information asymmetries [52,71].

(a) Environmental Dimension

Environmental sustainability focuses on minimizing ecological degradation, reducing carbon emissions, optimizing resource use, and supporting circular resource flows. AI, IoT, and digital twins enable environmental monitoring, emissions forecasting, predictive maintenance, and energy optimization [46,72]. IoT sensors embedded in industrial equipment and urban infrastructure generate real-time environmental performance data used to improve energy efficiency and waste management [48]. Digital twins enable simulation of environmental scenarios, allowing organizations to evaluate the environmental impacts of different configurations before real-world implementation [55,72]. Big data analytics enhances environmental planning by uncovering hidden patterns in consumption, emission, and waste data [52].

(b) Social Dimension

The social dimension addresses worker safety, human capital, community welfare, supply chain ethics, and labor conditions. IoT and CPS improve workplace safety through real-time hazard detection, while automation reduces exposure to high-risk environments [56]. Blockchain enhances ethical sourcing through traceability mechanisms, enabling verification of labor practices and provenance [50]. AI-driven analytics support workforce planning, training, and skills development, while digital platforms enhance community participation and service accessibility [54].

(c) Economic Dimension

Economic sustainability involves long-term viability, efficiency, productivity, innovation, and competitiveness. AI and BDA drive operational optimization and cost reduction, while cloud computing enables scalable business models, remote operations, and digital public services [52,53]. CPS and automation improve productivity, reduce downtime, and enhance asset utilization [56]. Together, these technologies support resilient value creation and long-term competitiveness, aligning economic sustainability with digital enterprise strategies [62].

(d) Governance Dimension

Governance is central to ESG and is increasingly viewed as the structuring mechanism through which sustainability commitments are translated into organizational processes. Blockchain enhances governance through tamper-resistant records, auditability, and data integrity [50]. Cloud-based digital platforms facilitate compliance, reporting, and risk management [53,71]. AI and analytics support governance by enabling regulatory monitoring and decision support systems [54,71]. The governance–technology nexus is particularly salient in emerging economies undergoing institutional modernization, where digital infrastructures can reduce corruption risks and enhance administrative transparency [54].

2.5. Alignment with Saudi Vision 2030 and National Digital Transformation

Saudi Arabia offers a distinctive national setting in which emerging technologies and sustainable management are integrated within a unified transformation agenda. Under Vision 2030, sustainability is positioned not merely as an environmental objective, but as a structural component of economic diversification, institutional reform, and long-term development [22]. Digital transformation functions as a central enabling pillar of this agenda, providing the technological and analytical infrastructure through which sustainability priorities can be translated into coordinated public- and private-sector action [23,24].

A defining feature of Vision 2030 is the strategic institutionalization of data and digital capabilities. The establishment of the Saudi Data and AI Authority (SDAIA), together with the National Strategy for Data and Artificial Intelligence, reflects a deliberate shift toward data-driven governance and evidence-based policymaking [25]. From an ESG-oriented perspective, these initiatives strengthen governance capacity and environmental oversight by improving data availability, interoperability, and coordination across institutions—conditions that are essential for effective sustainability-oriented management.

Digital government initiatives further demonstrate how emerging technologies are embedded within sustainability-oriented governance structures. Through the Digital Government Authority (DGA), Saudi Arabia has promoted digitally enabled public services designed to enhance administrative efficiency, reduce resource consumption, and increase transparency and accountability [26]. These initiatives align closely with the governance (G) dimension of ESG by embedding digital monitoring, reporting, and service delivery mechanisms into public sector operations, thereby reducing institutional fragmentation and information asymmetries.

Large-scale smart city and infrastructure projects provide concrete illustrations of how technology-enabled sustainability is operationalized at scale. Initiatives such as NEOM, The Line, and Oxagon integrate artificial intelligence, IoT-based urban management systems, renewable energy infrastructures, and circular resource models within their core design principles [27]. Beyond their technological ambition, these projects function as experimental platforms for ESG-oriented sustainable management, simultaneously addressing environmental optimization, social well-being, economic diversification, and digitally mediated governance.

In parallel, the Circular Carbon Economy (CCE) framework highlights how emerging technologies support environmentally focused sustainability strategies through data-driven measurement, optimization, and reporting mechanisms [28]. The CCE framework emphasizes emissions reduction, reuse, recycling, and removal pathways that rely on digital monitoring systems, advanced analytics, and predictive modeling. These mechanisms directly reinforce the environmental and governance dimensions of ESG by enabling continuous emissions tracking, policy evaluation, and institutional accountability.

The private sector complements these national initiatives by translating digital sustainability priorities into organizational practice. Major Saudi firms operating in energy, petrochemicals, and utilities have increasingly adopted ESG frameworks supported by advanced digital technologies. Saudi Aramco applies AI-based optimization, digital twins, and advanced analytics to improve energy efficiency and emissions management [29]. SABIC utilizes digital traceability and analytics platforms to support circular economy initiatives and sustainable supply chain management [30]. The Saudi Electricity Company (SEC) deploys smart grid technologies and digital platforms to enhance renewable energy integration and grid sustainability [31]. These cases illustrate how emerging technologies enable ESG-oriented management systems that extend beyond disclosure toward measurable operational sustainability outcomes.

Despite these advances, academic research examining the Saudi context remains limited and fragmented [32,33,34]. Much of the available evidence is derived from policy documents, corporate disclosures, and strategic roadmaps rather than from theory-driven conceptual or empirical studies. Moreover, prior research has rarely explored how emerging technologies interact with ESG-oriented management systems within the institutional architecture of Vision 2030 [35,36]. This gap highlights the need for integrative frameworks capable of explaining how national digital transformation agendas condition the sustainability impacts of emerging technologies.

Taken together, the Saudi context provides a valuable empirical and conceptual setting for examining technology-enabled sustainable management. The convergence of ESG adoption, digital government, institutional reform, and large-scale transformation initiatives creates conditions under which emerging technologies function not merely as operational tools, but as systemic enablers of sustainability-oriented governance and management. This alignment establishes a critical contextual foundation for the literature synthesis developed in the following section.

2.6. Corporate ESG Practices and Technology Adoption in Saudi Organizations

Governance constitutes the structuring backbone of ESG-oriented sustainable management, as it determines how sustainability commitments are translated into organizational rules, controls, and accountability mechanisms. Emerging technologies enhance governance quality by strengthening transparency, auditability, and compliance. Blockchain-based systems provide tamper-resistant records that improve data integrity and reduce opportunities for manipulation in ESG reporting and compliance processes [50].

Cloud-based digital platforms support governance by enabling standardized reporting, regulatory monitoring, and risk management across organizational boundaries [53,71]. AI and analytics further contribute by supporting fraud detection, regulatory oversight, and decision-support systems that enhance managerial and institutional accountability [54]. These governance-enhancing effects are particularly salient in emerging economies and national transformation contexts, where digital infrastructures can reinforce institutional credibility and public trust.

2.7. Analytical Bridge to the Conceptual Framework

The foregoing discussion suggests a structural pathway through which emerging technologies enable sustainable management:Emerging Technologies → ESG-oriented Management → Sustainability OutcomesThis pathway provides the analytical basis for the conceptual framework developed in later sections. It also highlights the multidimensional nature of digital sustainability, wherein technologies support not only environmental and economic performance but also social welfare and governance transparency—dimensions that are increasingly salient in national transformation contexts.

Integrative Interpretation

Taken together, the ESG-oriented perspective highlights that emerging technologies do not contribute to sustainability in isolation. Their impact depends on how they enable measurement, optimization, transparency, and institutionalization across environmental, social, economic, and governance dimensions. This integrative role positions emerging technologies as foundational components of sustainable management systems rather than as peripheral operational tools.

This interpretation provides a direct analytical bridge to the subsequent section, which examines how these technology-enabled ESG mechanisms align with national digital transformation agendas—particularly within the context of Saudi Arabia’s Vision 2030.

3. Literature Review

The body of literature examining the intersection of emerging technologies, digital transformation, and sustainable management has expanded substantially over the past decade. This expansion has been driven by escalating global sustainability challenges, increasing institutional investor pressure, and the rapid diffusion of digital technologies across industries and public-sector systems. Rather than forming a single coherent research tradition, this literature comprises multiple analytical streams that differ in theoretical orientation, technological emphasis, and interpretation of sustainability outcomes. This section synthesizes these streams to establish the theoretical grounding for the conceptual framework developed later in this study.

3.1. Technological Enablers of Sustainability: Global Theoretical and Empirical Insights

Early scholarly work linking digitalization to sustainability predominantly conceptualized emerging technologies as technical instruments for environmental efficiency. Research within this stream emphasized automation, optimization, and resource efficiency in industrial systems, framing sustainability largely in terms of emissions reduction, energy savings, and waste minimization [1,21]. With the emergence of Industry 4.0, this perspective expanded to examine how advanced digital technologies enable circular economy practices, smart manufacturing, and low-carbon production systems [3,4,5].

Systematic reviews have consolidated this body of work, demonstrating that technologies such as artificial intelligence (AI), the Internet of Things (IoT), blockchain, and big data analytics enhance sustainability by enabling data-driven control, process transparency, and coordinated resource management [6,7,8]. While these studies provide strong empirical evidence of environmental benefits, they tend to frame sustainability as a technical optimization problem rather than as a managerial or institutional process.

More recent research has broadened the sustainability construct by incorporating social and governance dimensions, leading to closer integration between digital transformation and ESG-oriented corporate strategies [9,10]. In this stream, digital technologies are shown to support ESG practices by improving data collection, disclosure accuracy, emissions monitoring, supply chain traceability, and stakeholder communication [11,12]. Empirical studies in logistics, manufacturing, and utilities further indicate that digital infrastructures can simultaneously reduce environmental externalities and enhance economic efficiency and operational resilience [13,14].

However, meta-analyses consistently highlight that sustainability outcomes are contingent not only on technological capabilities but also on organizational and institutional factors, including dynamic capabilities, governance arrangements, managerial cognition, and contextual conditions [15,17]. This insight aligns with sustainability transition theories that conceptualize digitalization as a socio-technical transformation requiring alignment across policy, technology, markets, and institutional logics [18,19]. Such multi-level perspectives are particularly relevant for emerging economies and national transformation programs, where digital and sustainability agendas often converge as part of broader industrial modernization strategies.

Emerging gap:Despite growing theoretical sophistication, much of this literature lacks integrative models that connect technological capabilities with ESG-oriented management systems in institutionally transforming contexts.

3.2. Technology-Specific Literature Streams

3.2.1. Artificial Intelligence (AI) and Sustainability

The AI–sustainability literature represents one of the most mature technology-specific streams. Research commonly clusters AI applications into four functional roles: optimization, prediction, automation, and decision support [6]. These functions underpin applications ranging from energy management and emissions reduction to climate forecasting and ESG analytics. Empirical studies demonstrate that AI can reduce energy waste and support renewable energy integration in energy systems [6,21], while supply chain applications improve forecasting, routing, and inventory management, thereby lowering carbon footprints and material waste [13].

Beyond operational domains, AI-enabled analytics increasingly contribute to sustainability governance by enhancing ESG disclosure quality, fraud detection, and risk assessment [24]. Collectively, this stream illustrates AI’s relevance across environmental, economic, and governance dimensions of sustainability. However, much of the literature remains functionally oriented, with limited attention to how AI capabilities are embedded within broader sustainability management systems.

3.2.2. Internet of Things (IoT) and Sensor-Based Sustainability

IoT-focused research emphasizes real-time sensing, monitoring, and automation of physical systems as foundational mechanisms for sustainability. Applications span smart agriculture, energy management, circular waste systems, and environmental monitoring [13,14]. In urban contexts, IoT is widely positioned as the backbone of smart city sustainability, enabling data-driven water management, intelligent lighting, traffic optimization, and pollution monitoring [14].

In industrial environments, IoT supports predictive maintenance and asset monitoring, reducing downtime and resource inefficiencies [13]. From a sustainability management perspective, a key contribution of IoT lies in its ability to make environmental performance continuously measurable and auditable—an essential prerequisite for ESG-oriented reporting and accountability. Nevertheless, IoT studies often focus on technical feasibility while underexploring governance integration and decision-making implications.

3.2.3. Blockchain and ESG Transparency

Blockchain research intersects strongly with sustainability through its emphasis on traceability, provenance, auditability, and trust. Scholars have identified blockchain as a promising enabler of ethical supply chains, fair labor verification, product provenance, and anti-counterfeiting systems [8,12]. A growing body of work connects blockchain to sustainability reporting and carbon markets, suggesting that distributed ledger technologies reduce data manipulation and enhance transparency in ESG disclosures [24].

In circular economy contexts, blockchain facilitates material tracking and reverse logistics, supporting recycling and reuse processes [7]. Governance-oriented studies further highlight blockchain’s capacity to reduce information asymmetries, enhance institutional trust, and strengthen compliance mechanisms—properties closely aligned with the governance pillar of ESG frameworks [9]. Despite these strengths, much of the blockchain literature remains fragmented across application domains, with limited synthesis at the management-system level.

3.2.4. Big Data Analytics and Data-Driven Sustainability

Big Data Analytics (BDA) plays a central role in transforming sustainability from a compliance-oriented activity into a data-driven strategic function. Research demonstrates that BDA supports emissions accounting, carbon risk analysis, renewable energy forecasting, waste management planning, and ESG data processing [15,16,17]. In energy-intensive sectors, predictive modeling enabled by BDA improves grid stability and reduces carbon intensity [20].

Within ESG reporting, BDA enhances disclosure accuracy, reduces estimation uncertainty, and improves data integrity, enabling organizations to respond to increasing stakeholder and regulatory expectations for transparency [24]. Scholars increasingly argue that BDA enables sustainability intelligence by linking environmental and social performance to strategic decision-making and long-term competitiveness [16]. However, empirical studies often examine analytics capabilities in isolation, without fully addressing their institutional embedding.

3.2.5. Cloud Computing and Digital Infrastructure for Sustainability

Cloud computing literature highlights the infrastructural foundations of digital sustainability. By providing scalable computing, storage, and analytics resources, cloud architectures reduce reliance on physical IT infrastructure and support remote collaboration and digital public services [43,44,45]. In sustainability contexts, cloud-native platforms facilitate ESG data aggregation, lifecycle assessment, traceability systems, and sustainability dashboards [46].

The integration of cloud computing with AI, BDA, and IoT strengthens organizational capacity to monitor and manage sustainability performance across geographically dispersed operations [47]. Despite its enabling role, cloud computing is often treated as a background infrastructure rather than as a strategic component of sustainability management systems.

3.2.6. Digital Twins and Cyber–Physical Systems for Sustainable Operations

Digital twins and cyber–physical systems (CPS) represent advanced architectures that tightly integrate digital models with physical processes. Digital twins enable real-time simulation, scenario testing, and predictive analysis, reducing material waste and resource inefficiencies in manufacturing, utilities, logistics, and infrastructure systems [20,21,22]. CPS extends these capabilities by enabling autonomous or semi-autonomous control loops that enhance operational precision and efficiency [19].

Sustainability applications include smart grids, microgrids, renewable energy integration, smart buildings, and low-carbon manufacturing systems [20]. Scholars emphasize that these technologies contribute not only to environmental performance but also to economic sustainability by extending asset lifecycles, reducing downtime, and improving productivity [17]. Nonetheless, their integration into ESG-oriented management frameworks remains underexplored.

3.3. Digital Transformation and Sustainable Management

An emerging stream of literature conceptualizes sustainability as a digital transformation challenge rather than solely an environmental or regulatory issue. From this perspective, sustainability-oriented management depends on the deployment of digital capabilities, data infrastructures, and algorithmic decision systems in addition to policy alignment and stakeholder engagement [23,25]. Digital transformation research identifies three interrelated pathways through which emerging technologies enable sustainability: datafication, automation, and institutionalization.

Datafication involves translating physical and organizational processes into measurable digital data that can be analyzed and optimized [15]. Automation leverages AI, IoT, CPS, and digital twins to optimize processes in real time and reduce human error [19,20]. Institutionalization embeds sustainability into governance structures, reporting systems, and organizational routines, often through ESG frameworks, SDG alignment, and standardized disclosure regimes [9,10].

From a managerial perspective, this literature emphasizes that sustainability outcomes depend on dynamic capabilities, organizational culture, and strategic intent rather than on technology adoption alone [17,26]. Firms that fail to align governance structures with digital capabilities often struggle to convert technological investments into sustained sustainability performance.

3.4. Emerging Technologies and ESG Performance: Integrative Evidence

A growing body of research directly examines the relationship between emerging technologies and ESG performance. Scholars argue that digital technologies reduce information asymmetries, enhance disclosure quality, and improve compliance monitoring across ESG dimensions [9,24]. Environmentally, AI, IoT, and digital twins support emissions monitoring, energy optimization, carbon forecasting, and environmental risk modeling [6,13,20].

Blockchain contributes primarily to governance and social dimensions by enhancing traceability, provenance, and accountability across supply chains [8,12]. In ESG reporting contexts, blockchain reduces fraud and improves assurance quality [24]. Big data analytics and cloud computing further institutionalize ESG practices by enabling large-scale data processing, visualization, and performance monitoring [15,43,46].

Importantly, finance and management literature increasingly positions ESG as a mechanism for managing long-term risk rather than as a purely ethical construct [11,16]. Digital infrastructures allow firms to quantify climate, social, regulatory, and reputational risks, linking ESG performance to enterprise risk management and investor decision-making [9,10].

3.5. Evidence from Saudi Arabia and Vision 2030

While much of the empirical literature originates from advanced economies, a growing body of research and corporate evidence has emerged from the Gulf region. In Saudi Arabia, sustainability and digital transformation are explicitly integrated under Vision 2030, which identifies digital government, industrial modernization, and economic diversification as enablers of sustainable development [30].

Policy initiatives emphasize data and AI as strategic assets, formalized through the establishment of the Saudi Data and AI Authority (SDAIA) [31]. Digital government platforms developed by the Digital Government Authority (DGA) support transparency, efficiency, and accessibility—key governance sustainability outcomes [32]. The Circular Carbon Economy (CCE) framework integrates technology-enabled pathways for emissions reduction, reuse, and recycling [33].

Smart city initiatives such as NEOM, The Line, and Oxagon further position Saudi Arabia as a testing ground for large-scale, digitally enabled sustainability transitions [34]. In the corporate sector, ESG adoption has accelerated, with firms such as Saudi Aramco, SABIC, Ma’aden, and the Saudi Electricity Company deploying digital twins, analytics, automation, and smart grid technologies to enhance sustainability performance [35,36,37,38]. Despite this progress, peer-reviewed academic research remains limited, reinforcing the need for conceptual synthesis.

3.6. Identified Research Gaps

Synthesizing the literature reveals six interrelated research gaps:

Gap 1: Fragmentation across technology streams.

Most studies examine individual technologies in isolation, despite evidence that sustainability outcomes arise from integrated digital infrastructures.

Gap 2: Underdeveloped ESG–technology integration.

The relationship between emerging technologies and ESG-oriented management systems remains weakly theorized.

Gap 3: Limited conceptualization of national transformation contexts.

Existing models rarely address state-led digital sustainability agendas such as Vision 2030.

Gap 4: Scarcity of empirical evidence from GCC economies.

Research remains concentrated in the U.S., EU, and China.

Gap 5: Narrow sustainability constructs.

Many studies focus on environmental outcomes, neglecting social, economic, and governance dimensions.

Gap 6: Absence of technology–institutional alignment models.

Governance and regulatory moderators are insufficiently incorporated into existing frameworks.

Synthesis of gaps.

These gaps collectively motivate the need for an integrative conceptual framework explaining how emerging technologies enable sustainable management across ESG dimensions within national transformation contexts. This synthesis directly informs the framework developed in Section 5.

4. Emerging Technologies Landscape

Emerging technologies can be understood as a foundational digital infrastructure layer that shapes how organizations, industries, and governments transition toward sustainability-oriented models. Unlike earlier phases of digital innovation—largely focused on operational efficiency and cost reduction—contemporary technologies provide cognitive, analytical, and integrative capabilities that enable advanced forms of sensing, prediction, coordination, and transparency. These capabilities are central to achieving performance across environmental, social, economic, and governance dimensions. Conceptualizing emerging technologies as a landscape, rather than as isolated tools, is therefore essential, as sustainability outcomes increasingly emerge from their interaction and integration rather than from individual technology adoption [1,3,18].

4.1. Technological Capabilities as Enablers of Sustainable Value Creation

Recent scholarship increasingly conceptualizes emerging technologies as bundles of interdependent capabilities embedded within broader socio-technical systems rather than as standalone artifacts [4,5,54]. From a sustainability-oriented management perspective, these capabilities can be organized into five mutually reinforcing clusters that collectively enable sustainable value creation:

(a) Sense → (b) Analyze → (c) Decide → (d) Act → (e) Verify

This capability-based framing shifts attention away from specific technologies toward the functional roles they perform within sustainability systems.

(a) Sensing Capabilities

Sensing capabilities are enabled primarily by IoT infrastructures, cyber–physical systems (CPS), and sensor platforms that transform physical, environmental, and social processes into measurable digital data [28,66]. These capabilities are foundational for sustainability management, as environmental variables such as emissions, energy use, air quality, resource consumption, and waste flows must first be rendered visible before they can be evaluated or optimized. Without reliable sensing, sustainability remains aspirational rather than actionable.

(b) Analytical and Cognitive Capabilities

Analytical and cognitive capabilities are primarily supported by artificial intelligence (AI) and big data analytics (BDA). These technologies interpret sensed data and generate predictive and diagnostic insights, including energy demand forecasting [7], logistics emissions optimization [8], environmental risk modeling [9], and climate scenario evaluation [10]. From a managerial perspective, these capabilities enable organizations to move from descriptive sustainability metrics toward anticipatory and evidence-based decision-making.

(c) Decision-Making and Optimization Capabilities

Decision-making capabilities leverage AI/ML engines, optimization algorithms, and rule-based control systems to translate analytical insights into actionable recommendations or automated interventions. Digital twins and CPS are particularly relevant at this stage, as they allow organizations to simulate alternative operational configurations, assess trade-offs, and optimize low-carbon or resource-efficient scenarios prior to physical implementation [11,12]. These capabilities reduce uncertainty and improve the robustness of sustainability decisions.

(d) Operational Execution Capabilities

Operational execution capabilities convert digital decisions into physical action. CPS, robotics, and automation systems play a central role by implementing optimized decisions in real time, reducing process inefficiencies, minimizing waste, and improving worker safety [13,14]. These capabilities are especially critical in asset-intensive sectors, where sustainability performance depends on consistent execution rather than isolated interventions.

(e) Verification and Assurance Capabilities

Verification capabilities are enabled by blockchain technologies and cloud-based infrastructures that support auditability, traceability, compliance verification, and assurance of ESG-related data [15,16,17]. These capabilities are essential for governance-oriented sustainability, as they ensure the integrity, credibility, and accountability of sustainability disclosures and performance claims.

Integrated Capability Loop:

Sense → Analyze → Decide → Act → Verify

This recursive loop aligns closely with sustainability governance frameworks and national digital transformation strategies, reinforcing sustainability as a continuous management process rather than a one-time outcome

4.2. Convergence and Synergy of Emerging Technologies

A defining characteristic of contemporary digital transformation is the increasing convergence of emerging technologies rather than their isolated deployment [20,21]. Scholars describe this phenomenon through concepts such as digital ecosystems, cyber–physical–social systems, and Industry 4.0 platforms, emphasizing the combinatorial nature of digital capabilities [22,24]. In sustainability contexts, performance gains arise from interactions among IoT, AI, cloud platforms, CPS, digital twins, and blockchain rather than from any single technology acting independently.

This technological convergence is reinforced by institutional convergence, whereby digital infrastructures become aligned with sustainability regulations, ESG reporting standards, and investor expectations [25,26,27]. As a result, emerging technologies increasingly function as integrated enablers of ESG-oriented governance and management systems.

4.3. Technology–Value Mechanisms for ESG Outcomes

The sustainability value created by emerging technologies can be analytically explained through four interrelated mechanisms:

(a) Measurement and Visibility

IoT, sensing platforms, digital twins, and BDA enable granular and continuous measurement of sustainability performance, making environmental and social impacts visible and traceable [28,30].

(b) Optimization and Control

AI, CPS, and digital twins support real-time optimization and control of resources, energy flows, and emissions, enabling organizations to reduce inefficiencies and environmental externalities [31,32,33].

(c) Transparency and Accountability

Blockchain and cloud platforms enhance traceability, provenance verification, and auditability, strengthening accountability across organizational and supply-chain boundaries [34,35,36].

(d) Reporting and Institutionalization

4.4. Cross-Sectoral Applications of Emerging Technologies

Emerging technologies support sustainability across multiple sectors:

(a) Energy Systems and Utilities

AI, IoT, digital twins, and CPS enable smart grid management, renewable energy integration, and real-time demand–supply optimization [40,42].

(b) Manufacturing and Industrial Production

Industry 4.0 technologies facilitate circular manufacturing, resource-efficient production, and traceable supply chains [43,44].

(c) Urban Infrastructure and Smart Cities

Smart city platforms leverage integrated digital infrastructures to improve mobility, water management, and air quality in urban environments [45,47].

(d) Logistics and Supply Chains

4.5. Institutional and Governance Dimensions in Digital Sustainability

Digital sustainability transitions reshape governance across three interconnected levels:

- Organizational governance: ESG metrics, internal controls, and sustainability dashboards

- Inter-organizational governance: Blockchain-enabled trust and coordination across supply chains

- Public governance: Digital government platforms and national sustainability monitoring systems

4.6. Alignment with National Transformation Contexts: The Case of Saudi Vision 2030

Saudi Arabia exemplifies the convergence of digital transformation and sustainability within a national transformation agenda. Under Vision 2030, national entities such as SDAIA, DGA, and MCIT position data and AI as strategic assets for sustainability-oriented governance and economic diversification [43,44,45]. Environmental initiatives, including the Circular Carbon Economy framework and large-scale smart city projects such as NEOM, embed AI, IoT, and digital twins into national sustainability infrastructures [46,47].

At the corporate level, ESG adoption by organizations such as Saudi Aramco, SABIC, Ma’aden, and the Saudi Electricity Company demonstrates how emerging technologies support emissions management, traceability, and ESG reporting in practice [48,49,50,51]. These developments illustrate how national transformation strategies condition the sustainability impacts of emerging technologies.

Analytical Bridge toSection 5

Section 4 demonstrates that sustainability outcomes emerge from the interaction of:

- Technological capabilities

- Value-creation mechanisms

- Institutional enablers

However, existing literature lacks a unified conceptual model explaining how these elements interact within national transformation contexts. Section 5 addresses this gap by developing an integrative conceptual framework that positions emerging technology capabilities as enablers of ESG-oriented sustainable management systems, moderated by institutional enablers and resulting in multi-dimensional sustainability outcomes.

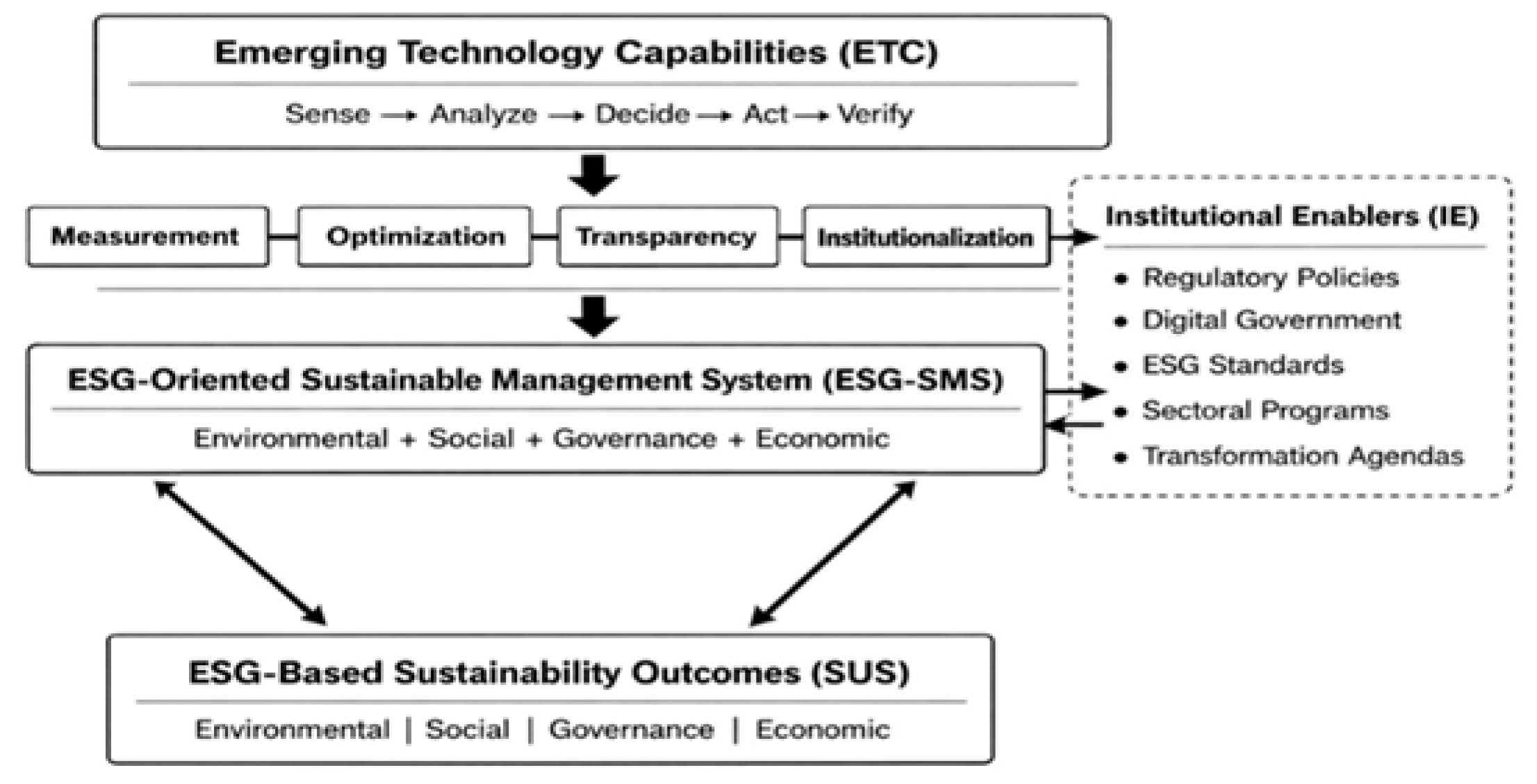

5. Conceptual Framework and Mechanisms of Digital Sustainability

5.1. Mechanisms of Influence

To explain how Emerging Technology Capabilities (ETC) translate into ESG-Oriented Sustainable Management Systems (ESG-SMS), the framework adopts a mechanistic perspective grounded in digital sustainability and socio-technical systems literature. Rather than assuming a direct or automatic impact of technology adoption, the model differentiates between four interrelated mechanisms through which technological capabilities are transformed into managerial sustainability practices:

Measurement → Optimization → Transparency → Institutionalization

These mechanisms are sequential in logic yet iterative in practice, reflecting the dynamic and recursive nature of sustainability management in digitally enabled environments.

Measurement represents the foundational mechanism through which sustainability performance becomes visible and actionable. Technologies such as IoT, cyber–physical systems (CPS), digital twins, and advanced analytics enable continuous data collection on environmental, social, and operational variables, thereby transforming abstract sustainability goals into measurable indicators [6,35]. Without measurement, sustainability remains a normative aspiration rather than a managerial practice.

Optimization builds upon measurement by leveraging artificial intelligence (AI), CPS, and digital twins to reduce inefficiencies, improve resource allocation, and support predictive decision-making [11,57]. Through optimization, organizations move from descriptive monitoring toward proactive sustainability management, enabling interventions that minimize waste, emissions, and operational risks.

Transparency mechanisms focus on governance and accountability. Blockchain technologies and cloud-based infrastructures enhance traceability, auditability, and data integrity across organizational and inter-organizational boundaries [12,50]. These mechanisms reduce information asymmetries, strengthen stakeholder trust, and improve the credibility of ESG disclosures.

Institutionalization represents the final mechanism through which sustainability practices are embedded into organizational routines, governance structures, reporting systems, and compliance architectures [71]. At this stage, sustainability becomes an integrated component of management systems rather than a standalone initiative, ensuring continuity and scalability over time.

Collectively, these mechanisms establish a structured causal pathway:

ETC → ESG-SMS → Sustainability Outcomes

5.2. Institutional Moderators: Vision 2030 as a National Transformation Context

Emerging Technology Capabilities do not operate in an institutional vacuum. Their effectiveness in shaping ESG-oriented management systems is contingent upon the broader regulatory, governance, and policy environment. Vision 2030 represents a policy-driven national transformation agenda in which digitalization, ESG integration, and sustainability governance are strategically coordinated [22,25].

In the Saudi context, digital transformation is orchestrated through national entities such as the Saudi Data and AI Authority (SDAIA), the Digital Government Authority (DGA), and the Ministry of Communications and Information Technology (MCIT), which collectively position data and digital infrastructure as strategic enablers of sustainable governance [23,25,26]. ESG integration is further reinforced through capital market reforms, disclosure standards, and regulatory initiatives that link sustainability performance to investment and accountability mechanisms [30,31].

Mega-projects such as NEOM operationalize digital sustainability at scale by embedding AI, IoT, and digital twins into urban and industrial systems [27]. In parallel, the Circular Carbon Economy framework institutionalizes emissions management through data-driven monitoring, optimization, and reporting infrastructures [28]. These initiatives exemplify how institutional arrangements amplify or constrain the translation of technological capabilities into ESG-oriented management practices.

Accordingly, the framework conceptualizes Institutional Enablers (IE) as moderating factors that shape the strength and effectiveness of the relationship between ETC and ESG-SMS:

ETC × IE → ESG-SMS

5.3. Conceptual Model Representation

The proposed conceptual model is structured as a multi-layered system reflecting the interaction between technology, management, and institutional context.

- Layer 1: Emerging Technology Capabilities (ETC)

- Represented by the integrated capability loop:Sense → Analyze → Decide → Act → Verify

- Layer 2: ESG-Oriented Sustainable Management System (ESG-SMS)

- Captures organizational processes that operationalize sustainability across environmental, social, governance, and economic dimensions.

- Layer 3: ESG-Based Sustainability Outcomes (SUS)

Institutional Enablers moderate the transition from Layer 1 to Layer 2, while feedback loops between ESG-SMS and Sustainability Outcomes reinforce learning and system adaptation over time.

5.4. Testable Propositions

Based on the theoretical constructs and mechanisms outlined above, the framework yields a set of testable propositions (P1–P6). While the wording of these propositions remains unchanged, their theoretical grounding is now explicitly anchored in:

- Emerging Technology Capabilities (ETC)

- Mechanisms of influence (measurement, optimization, transparency, institutionalization)

- ESG-oriented management systems

- Institutional moderators within national transformation contexts

5.5. Implications and Bridge to Section 6

The proposed framework advances sustainability and digital transformation theory by integrating technological capabilities, ESG-oriented management systems, and institutional governance within a unified analytical model [16,73]. Unlike linear technology–performance models, it emphasizes mediated and moderated relationships that reflect the complexity of sustainability transitions in digitally intensive environments.

From a managerial perspective, the framework highlights the importance of capability readiness, governance alignment, and investment in digital ESG infrastructures to translate technological potential into sustained sustainability performance [11,35]. For policymakers, the model underscores the strategic role of digital government, regulatory coherence, and ESG disclosure regimes in enabling technology-driven sustainability transitions [24,26].

These implications provide a natural bridge to Section 6, which elaborates on the research agenda, practical implications, and policy relevance of the proposed framework.

Figure 2 presents the proposed conceptual framework explaining how emerging technologies enable sustainable management through an ESG-oriented logic within national transformation contexts. The framework integrates technological capabilities, managerial systems, and institutional conditions to clarify the pathways through which sustainability outcomes are generated.

At the foundation of the framework, Emerging Technology Capabilities (ETC) are conceptualized as combinatorial digital capabilities enabled by artificial intelligence, the Internet of Things, big data analytics, blockchain, cloud computing, digital twins, and cyber–physical systems. These capabilities operate through a sequential yet recursive logic—Sense → Analyze → Decide → Act → Verify—reflecting how digital systems transform physical and organizational processes into actionable and verifiable sustainability practices.

The translation of ETC into management value occurs through four interrelated mechanisms: measurement, optimization, transparency, and institutionalization. Measurement renders sustainability performance visible through datafication and sensing technologies. Optimization leverages AI, CPS, and digital twins to improve resource allocation and reduce inefficiencies. Transparency is enabled by blockchain and cloud infrastructures that enhance traceability, auditability, and data integrity. Institutionalization embeds sustainability into governance routines, reporting systems, and compliance architectures. Together, these mechanisms explain how technological capabilities are converted into structured managerial practices rather than assuming a direct impact of technology adoption.

At the core of the framework, the ESG-Oriented Sustainable Management System (ESG-SMS) functions as a mediating system through which sustainability is operationalized across environmental, social, governance, and economic dimensions. ESG-SMS encompasses practices such as emissions monitoring, resource optimization, workforce safety management, supply chain traceability, and ESG disclosure and assurance.

Institutional Enablers (IE) moderate the relationship between ETC and ESG-SMS. These include regulatory policies, digital government platforms, ESG standards, sectoral programs, and national transformation agendas such as Vision 2030. Institutional Enablers shape the effectiveness with which technological capabilities translate into ESG-oriented management systems, highlighting the contingent nature of technology-driven sustainability.

At the outcome level, ESG-Based Sustainability Outcomes (SUS) capture multi-dimensional performance results, including environmental improvement, social well-being, governance quality, and economic resilience. The bidirectional relationship between ESG-SMS and sustainability outcomes emphasizes continuous learning and system adaptation.

Overall, the framework conceptualizes sustainability as a digitally enabled, institutionally moderated, and managerially embedded system. It underscores that sustainability outcomes emerge from integrated capabilities rather than isolated technologies, that ESG functions as a management system rather than merely a disclosure mechanism, and that national transformation contexts amplify technology-driven sustainability transitions.

6. Research Agenda

The conceptual framework developed in this study opens several interrelated research avenues for scholars examining how emerging technologies enable sustainable management within institutionally transforming national contexts. The intersection of digital transformation, ESG-oriented management systems, and national policy agendas—exemplified by Saudi Arabia’s Vision 2030—represents a critical yet under-theorized research domain that requires stronger conceptual integration and empirical validation [16,73]. Advancing this field requires multi-level analytical approaches that explicitly account for interactions among technological capabilities, managerial systems, institutional enablers, and national sustainability strategies. Accordingly, the research agenda is structured around five complementary themes.

Theme 1: Institutional and Policy Drivers of Technology-Enabled Sustainability

A first research direction concerns the institutional and policy conditions under which emerging technologies translate into sustainable management outcomes. While existing studies emphasize ESG disclosure regulations and sustainability reporting standards, limited attention has been given to how regulatory enforcement, digital government infrastructures, and national sustainability strategies interact with technological capabilities to shape ESG-oriented management systems [75,76]. Future research should examine how policy coherence, regulatory digitalization, and institutional capacity moderate the effectiveness of technology-enabled sustainability initiatives across sectors and governance regimes.

Theme 2: ESG Digitalization, Measurement, and Data Transparency

A second theme focuses on the digitalization of ESG practices. Technologies such as AI, blockchain, IoT, and big data analytics increasingly support ESG measurement, traceability, auditability, and disclosure [77]. However, the literature lacks integrated models explaining how digital infrastructures improve the accuracy, comparability, and institutional credibility of ESG metrics. Future studies may investigate how firms design digital ESG architectures, how sectoral characteristics influence ESG data practices, and how digital transparency affects investor confidence and sustainable finance outcomes, particularly in asset-intensive industries.

Theme 3: Technology-Enabled Governance and Managerial Decision-Making

A third research stream addresses the governance and managerial implications of digital sustainability systems. Emerging technologies reshape decision-making by enabling real-time monitoring, risk analytics, and compliance automation, thereby influencing sustainability strategy formulation and board-level oversight [78]. Future research could explore how digital governance infrastructures redistribute responsibilities across sustainability, strategy, and risk management functions, and how ESG-oriented decision processes are coordinated across multinational operations and complex supply chains.

Theme 4: Economic–Sustainability Trade-offs and Performance Dynamics

A fourth theme concerns the economic implications of technology-enabled sustainability. Although ESG performance is often associated with long-term competitiveness, the underlying mechanisms, contingencies, and temporal dynamics remain insufficiently understood. Empirical research may analyze how emerging technologies affect cost structures, productivity, resilience, and risk-adjusted performance, as well as how sectoral conditions and time horizons shape sustainability–economic complementarities. Longitudinal and comparative studies are particularly needed to distinguish short-term implementation costs from long-term sustainability payoffs.

Theme 5: Vision 2030 and National Sustainability Transformation Pathways

A final theme highlights the role of national transformation strategies in shaping digital sustainability transitions. Vision 2030 integrates sustainability, digital government, regulatory reform, and industrial policy within a unified national agenda. Future research may examine how such strategies function as institutional enablers that accelerate ESG-oriented management adoption, reshape industry ecosystems, and mobilize private sector participation. Comparative analyses between Vision 2030 and other national sustainability strategies (e.g., Net Zero roadmaps, Vision 2050 initiatives) represent a promising direction for theory development.

6.1. Practical Implications

The framework offers several implications for organizational practice. First, firms should recognize that technology adoption alone is insufficient to generate sustainability value; effective outcomes require ESG-oriented management systems capable of translating digital inputs into coordinated managerial actions [16]. This underscores the need for investments not only in digital tools, but also in governance structures, cross-functional coordination, and sustainability competencies. Second, organizations should leverage emerging technologies to enhance transparency, traceability, and auditability—capabilities increasingly demanded by investors, regulators, and global supply chains [77]. Finally, integrating digital transformation, sustainability, and risk management functions can strengthen ESG credibility and improve access to sustainable finance instruments.

6.2. Policy Implications

For policymakers, the framework emphasizes the importance of aligning digital transformation initiatives with ESG regulatory instruments. Governments can facilitate technology-enabled sustainability by standardizing digital ESG reporting formats, improving data interoperability, and deploying digital government platforms that automate monitoring and compliance [76]. Beyond regulation, industrial and innovation policies may incentivize private-sector adoption of digital ESG systems through targeted subsidies, procurement policies, and sustainability-linked financing. In institutionally transforming contexts such as Saudi Arabia, coordinated policy alignment under Vision 2030 plays a central role in orchestrating sustainability transitions across sectors.

6.3. Future Research Pathways

Methodologically, future research may empirically test the framework using structural equation modeling (SEM), PLS-SEM, hierarchical models, or longitudinal designs capturing time-varying sustainability effects. Qualitative approaches—such as case studies, comparative sector analyses, and institutional studies—can provide deeper insight into governance dynamics and contextual variation. Cross-country research is particularly valuable for assessing how national transformation agendas condition the diffusion and effectiveness of technology-enabled ESG systems. Further work is also needed to develop robust measurement models for ESG digitalization maturity, sustainability data governance, and institutional readiness.

6.4. Vision 2030 Alignment

The framework aligns closely with Saudi Arabia’s Vision 2030, which positions digital transformation, sustainability, and regulatory modernization as strategic national priorities. Vision 2030 introduces institutional enablers—including digital government infrastructures, ESG disclosure reforms, and green finance initiatives—that collectively accelerate the adoption of technology-enabled sustainable management systems. This context provides a fertile empirical setting for examining how national transformation agendas shape ESG performance and sustainability outcomes, while also offering a benchmark for comparative international research.

Conclusion

This study develops an integrative conceptual framework explaining how emerging technologies function as enablers of sustainable management within institutionally transforming national contexts. By synthesizing insights from sustainability transitions, digital transformation, ESG management, and institutional theory, the framework demonstrates that sustainability value does not arise from technology adoption alone. Instead, emerging technologies enable ESG-oriented management systems through capabilities of sensing, analysis, decision support, execution, and verification, operating via mechanisms of measurement, optimization, transparency, and institutionalization.

Beyond the organizational level, the framework highlights the critical role of institutional enablers—such as regulatory modernization, digital government, ESG standards, investor pressure, and national transformation agendas—in shaping technology-driven sustainability transitions. The Saudi Vision 2030 context illustrates how coordinated policy ecosystems amplify the sustainability impacts of digital capabilities. By emphasizing mediated and moderated causal relationships, the framework advances sustainability theory beyond linear technology–performance models and provides a foundation for future empirical research on digital ESG infrastructures, governance architectures, and national sustainability transformations.

Limitations and Future Extensions

Despite its contributions, this study has several limitations. First, the framework is conceptual and requires empirical validation to assess the strength and boundary conditions of the proposed relationships. Second, the focus on Saudi Arabia’s Vision 2030 may limit generalizability, suggesting the need for comparative cross-country research. Third, the analysis concentrates on firm-level outcomes and does not explicitly address system-level impacts such as sectoral decarbonization or national sustainability performance. Finally, future research should examine technological complementarities and trade-offs that may condition sustainability outcomes across different time horizons and institutional settings.

References

- Kraus, S.; Jones, P.; Kailer, N.; Weinmann, A.; Chaparro-Banegas, A. Digital transformation and sustainability: A review of research and implications for management. Technological Forecasting and Social Change 2021, vol. 171, 120987. [Google Scholar] [CrossRef]

- Barney, J. B. Firm resources and sustained competitive advantage. Journal of Management Foundational, cited conceptually. 1991, vol. 17(no. 1), 99–120. [Google Scholar] [CrossRef]

- A. B. L. de Sousa Jabbour et al., Industry 4.0 and the circular economy: A proposed research agenda and original roadmap. Journal of Cleaner Production 2020, vol. 277, 123226.

- Birkel, H.; Müller, J. M. Potentials of Industry 4.0 for supply chain sustainability. Journal of Manufacturing Technology Management 2021, vol. 32(no. 1), 135–163. [Google Scholar]

- C. J. C. Jabbour et al., Artificial intelligence and sustainable manufacturing. Journal of Cleaner Production 2021, vol. 278, 123377.

- Zhang, Y.; Ren, S.; Liu, Y.; Si, S. A big data analytics architecture for cleaner manufacturing. Journal of Cleaner Production 2017, vol. 142, 3075–3087. [Google Scholar] [CrossRef]

- Tao, F.; Qi, Q. Digital twin and big data towards smart manufacturing. IEEE Access 2019, vol. 7, 8456–8470. [Google Scholar]

- F. E. García-Muiña et al., The enabling role of Industry 4.0 technologies for sustainable performance. Sustainability 2020, vol. 12(no. 21), 8953.

- Awan, U.; Sroufe, R.; Shahbaz, M. Industry 4.0 and environmental sustainability. Journal of Cleaner Production 2021, vol. 318, 128451. [Google Scholar]

- Ibarra, D.; Ganzarain, J.; Igartua, J. Business model innovation through Industry 4.0. Sustainability 2020, vol. 12(no. 20), 8350. [Google Scholar] [CrossRef]

- S. Ren et al., Industrial AI and sustainability. Technovation 2023, vol. 125, 102628.

- M. Queiroz et al., Blockchain-driven supply chain sustainability. Transportation Research Part E 2022, vol. 157, 102524.

- Choi, T.-M. Blockchain technologies and sustainable supply chains. Sustainability 2021, vol. 13, 11941. [Google Scholar]

- A. Annunziata et al., The role of IoT in smart cities. Cities 2022, vol. 124, 103600.

- A. Kumar et al., IoT-enabled sustainable supply chains. International Journal of Production Economics 2022, vol. 250, 108637.

- Teece, D. J. Dynamic capabilities and sustainability. California Management Review 2020, vol. 62(no. 3), 94–117. [Google Scholar]

- J. W. Veile et al., Digital transformation and sustainability. Journal of Business Research 2022, vol. 145, 634–646.

- Geels, F. W. Socio-technical transitions. Research Policy 2020, vol. 49(no. 4), 103939. [Google Scholar]

- Markard, J. The next phase of sustainability transitions research. Environmental Innovation and Societal Transitions 2020, vol. 34, 1–32. [Google Scholar]