Submitted:

02 February 2026

Posted:

03 February 2026

You are already at the latest version

Abstract

As the size of the Bitcoin market has expanded and trading activity has intensified, attention has increased toward its potential to substitute for or complement traditional safe-haven assets in financial markets. Despite this growing interest, there remains no unified empirical consensus on whether the relationship between gold and Bitcoin is stable across market conditions, nor on the circumstances under which directional information transmission emerges between the two assets. This study moves beyond mean-based dependence frameworks and examines the causal relationship between gold and Bitcoin at the intersection of return distribution quantiles, investment horizons, and changing market regimes. To this end, we employ a Causal–Frequency–Quantile–Regime (CFQR) framework that integrates frequency-domain causality, quantile-based dependence, and regime-conditioned dynamics. Using daily data spanning from 1 January 2013 to 31 December 2025, we analyze the logarithmic returns of Bitcoin and gold while controlling for broader financial market conditions. The empirical findings indicate that causal interactions between gold and Bitcoin are not persistent across states; instead, statistically meaningful causal structures emerge only within specific frequency–quantile–regime configurations. In particular, during stress regimes, information transmission from gold to Bitcoin becomes more pronounced at long investment horizons and within selected segments of the return distribution. In contrast, under normal market conditions, causal linkages appear weak and fragmented. Furthermore, regime-based hedging experiments reveal that although variance-based risk reduction remains limited, portfolios augmented with gold exhibit relatively more stable performance under stress when evaluated using downside-risk-sensitive measures. Taken together, these results suggest that gold does not serve as a uniformly effective haven for Bitcoin across all market environments but may function as a conditional hedge during periods of heightened uncertainty.

Keywords:

Bitcoin

; gold

; conditional safe-haven behavior

; causal analysis

; frequency-domain causality

; market regimes

; downside risk

; portfolio hedging

1. Introduction

In recent years, the Bitcoin market has expanded substantially, with a growing body of research documenting the increasing channels through which it interacts with traditional financial markets. Alongside this development, Bitcoin has frequently been portrayed as a gold-like defensive asset, often referred to as “digital gold.” Nevertheless, existing empirical evidence remains insufficient to support the view that this relationship is stable or uniform across all market conditions. Prior studies consistently emphasize that during periods of abrupt risk reappraisal, heightened systemic uncertainty, and regime transitions, the behavior of gold and Bitcoin may diverge rather than move in tandem, exhibiting patterns that are strongly contingent on prevailing market states (Baur & Lucey, 2010; Reboredo, 2013; Selmi et al., 2018; Bouri et al., 2020).

A substantial strand of the literature evaluates the gold–Bitcoin relationship using mean-centered approaches, such as correlation analysis, co-movement measures, or time-domain Granger causality tests. However, cryptocurrency returns are well known to exhibit non-normality, asymmetry, and heavy-tailed distributions. Under such conditions, dependence measures based on average behavior may fail to capture risk accumulation in the tails of the return distribution and the information transmission that arises during market regime shifts. Consequently, rather than addressing the broad question of whether gold serves as a safe-haven asset for Bitcoin in general, there is a growing need for empirical analyses that identify under which risk states, at which investment horizons, and within which segments of the return distribution, causal interactions between gold and Bitcoin are most likely to emerge.

This study examines the relationship between gold and Bitcoin from a directional and state-sensitive perspective. To achieve this objective, it adopts a CFQR framework that evaluates causal transmission at the intersection of investment horizons, quantile levels of the return distribution, and changes in market regimes. Importantly, this framework does not presume that causal dependence exists under all circumstances. Instead, it is designed to assess, in a data-driven manner, whether causal structures arise within specific combinations of frequency, risk states, and market conditions (Breitung & Candelon, 2006; Jeong et al., 2012; Baruník & Kley, 2019).

The empirical analysis uses daily data from 1 January 2013 to 31 December 2025 and examines the logarithmic returns of Bitcoin and gold, along with control variables capturing broader financial market conditions. Rather than asking whether the gold–Bitcoin causal relationship is uniformly present across all states, the analysis focuses on how this relationship evolves across different frequency, quantile, and regime configurations. This approach is consistent with the mixed and state-contingent empirical evidence documented in prior studies and aligns with recent methodological developments in time–frequency and tail-oriented financial analysis (Bouri et al., 2018; Maghyereh & Abdoh, 2020; Mensi et al., 2023).

To further assess whether the identified conditional causal patterns carry practical relevance for investment decisions, the study additionally incorporates hedging experiments conducted under market stress regimes. This approach is consistent with prior findings emphasizing that variance-based measures of risk reduction and downside-risk-sensitive metrics may yield materially different assessments of hedging effectiveness (Harris & Shen, 2006; Bouri et al., 2020). Accordingly, rather than concluding that gold provides a uniformly stable hedge for Bitcoin across all market environments, it becomes essential to carefully evaluate whether gold can serve a conditional protective role during periods of elevated uncertainty and financial stress.

In this way, the study seeks to demonstrate empirically that the gold–Bitcoin relationship should not be interpreted through a single-dimensional lens, but rather as a causal structure that evolves across the interaction of investment horizons, risk states, and market conditions. The application of the CFQR framework enables a more precise identification of directional information transmission, thereby offering a conditional and economically grounded interpretation of the relationship between cryptocurrencies and traditional safe-haven assets.

2. Literature Review

The classification of gold as a hedging or safe-haven asset is no longer understood as a property that holds uniformly across all market conditions. Instead, contemporary financial research widely recognizes that such protective characteristics emerge conditionally, particularly during abrupt risk reappraisal, heightened systemic uncertainty, and market regime transitions (Baur & Lucey, 2010; Reboredo, 2013). Within this framework, hedging behavior is typically associated with average or conditional co-movement. In contrast, safe-haven properties are defined by asset behavior during market crises, episodes of elevated uncertainty, and the tail regions of the return distribution where downside risk materializes.

Against this conceptual backdrop, efforts to empirically assess whether Bitcoin can be regarded as “digital gold” and to delineate the boundaries of such a characterization have intensified in recent years. Nevertheless, the existing literature has yet to reach a consensus on whether the relationship between Bitcoin and gold holds consistently across market environments (Selmi et al., 2018; Bouri et al., 2017; Ang & Bekaert, 2002; Bouri et al., 2020). Consequently, there is growing recognition that the Bitcoin–gold relationship should be examined within a multidimensional setting that accounts for risk states, investment horizons, and market regimes, rather than being generalized through mean-based measures of dependence.

2.1. Protective Roles of Bitcoin and Gold

Empirical studies assessing the hedging and safe-haven properties of Bitcoin have produced largely mixed results. In some settings, Bitcoin appears capable of partially mitigating risk during market disruptions, while in others its protective function is weak, unstable, or entirely absent (Bouri et al., 2017; Selmi et al., 2018). Comparative analyses involving Bitcoin, gold, and other traditional assets consistently demonstrate that Bitcoin’s defensive characteristics vary substantially with market conditions, the investment horizon under consideration, and the methodological framework employed, often leading to divergent empirical conclusions (Bouri et al., 2020; Bhuiyan et al., 2023).

Evidence from time–frequency-based studies further reinforces the state-dependent nature of this relationship. Analyses grounded in volatility connectedness reveal that financial stress affects Bitcoin and gold asymmetrically and horizon-dependently, with gold tending to exhibit a stronger response at medium-term horizons as uncertainty intensifies, whereas Bitcoin appears more sensitive in the short run (Zhang & Wang, 2021; Agyei et al., 2022). Consistent with this view, findings from ADCC-GARCH frameworks indicate that Bitcoin increasingly resembles a conventional risky asset at longer horizons, as co-movement with other markets rises sharply during crisis periods. This pattern provides additional evidence that Bitcoin’s hedging capacity is not uniform but depends critically on the investment horizon (Wang et al., 2022).

Using a Diagonal BEKK framework to examine how co-volatility spillovers intensify during shifts in market conditions, prior research shows that interlinkages among cryptocurrencies, currencies, and gold differ markedly between normal and extreme regimes. In particular, spillover asymmetries become substantially more pronounced following negative shocks, indicating that volatility transmission strengthens unevenly across assets during periods of stress (Hsu et al., 2021). These findings provide further evidence that Bitcoin’s hedging and safe-haven capacities are not stable features but are contingent on prevailing market regimes.

2.2. Tail Risk Across Investment Horizons

Cryptocurrency returns are well known to exhibit asymmetric and heavy-tailed distributions, implying that conventional correlation measures based on average behavior may fail to capture the true dynamics of risk (Koenker & Bassett, 1978). To address this limitation, quantile-based methodologies have been developed to examine dependence across different segments of the return distribution. Building on this line of research, the introduction of quantile coherency in the frequency domain has provided a foundation for tail-oriented time–frequency analysis, enabling a more nuanced assessment of dependence across both risk states and investment horizons (Baruník & Kley, 2019). In a related vein, asymmetric connectedness frameworks have enabled researchers to distinguish dependence patterns in the lower and upper tails of the return distribution (Baruník et al., 2016).

An influential empirical application of wavelet-based quantile methods is provided by Kumah and Mensah (2020), who decompose return series across multiple time scales and combine quantile and quantile-on-quantile regressions to examine cryptocurrency–gold linkages under bear and bull market conditions. Their findings suggest that cryptocurrencies may exhibit hedging properties relative to gold at medium- and long-term horizons; however, these relationships vary asymmetrically across quantiles and market states. This evidence underscores the importance of jointly accounting for tail behavior and investment horizons when evaluating protective asset characteristics.

Within a broader quantile–frequency framework, studies employing quantile cross-spectral analysis, quantile VAR models, and quantile connectedness measures document that the dependence between gold and leading cryptocurrencies is strongly conditioned on bearish versus bullish quantiles and on short-, medium-, and long-term horizons. Notably, during the COVID-19 period, gold appears to have played a more pronounced safe-haven and diversification role for cryptocurrencies (Mensi et al., 2023). Complementary evidence from wavelet–quantile correlations further indicates that gold may exhibit more stable protective properties than Bitcoin across multiple investment horizons (Kumar & Padakandla, 2022). Nevertheless, while these studies provide valuable insights into the structure of dependence, they do not explicitly address directional spillovers or directly evaluate causal mechanisms of transmission between gold and cryptocurrencies.

2.3. Non-Directional Interdependence and Spillovers

Alongside quantile–frequency approaches, VAR-based connectedness and spillover analyses consistently show that the relationship between Bitcoin and gold is asymmetric and intensifies depending on prevailing market conditions. Studies grounded in the Diebold–Yilmaz connectedness framework document that overall connectedness among Bitcoin, gold, oil, and equity markets is relatively modest on average, yet spillovers become substantially stronger during periods of negative returns, revealing a pronounced asymmetric transmission structure (Zeng et al., 2020).

Evidence from regime-switching and contagion-oriented models further indicates that the Bitcoin market is more exposed to transmission from traditional financial markets under adverse market states. Using a regime-switching skew-normal specification, prior research demonstrates that contagion from financial markets to Bitcoin intensifies during downturns and exhibits asymmetric patterns in correlation and co-skewness (Matkovskyy & Jalan, 2019). Risk-based evidence leads to similar conclusions, showing that hedging properties cannot be adequately assessed through mean dependence alone. In particular, studies combining copula-based dependence measures and Conditional Value-at-Risk with variational mode decomposition reveal that risk spillovers between Bitcoin and gold are asymmetric, time-varying, and strongly conditioned on both investment horizons and market regimes (Yu et al., 2021).

While these approaches provide valuable insights into the strength of interdependence and the transmission of shocks across markets, they remain limited in their ability to determine which asset predominates in directing information flows. In other words, although connectedness and spillover frameworks characterize the magnitude and asymmetry of linkages, they do not explicitly identify the direction of causal dominance between Bitcoin and gold.

2.4. Directional Causality Across Quantiles and Frequencies

Beyond measuring dependence, identifying which asset leads the other in terms of information transmission is central to studies of hedging and safe-haven assets. The frequency-domain Granger causality framework provides a methodological basis for distinguishing short-run from long-run causal effects (Breitung & Candelon, 2006). In parallel, quantile-based non-causality tests extend this framework by allowing causal transmission to be examined across different segments of the return distribution rather than being confined to average dynamics (Jeong et al., 2012). Importantly, the presence of causality does not necessarily imply dominance, as dominance is better characterized by persistent and asymmetric causal patterns that vary systematically across states, investment horizons, and market conditions.

Prominent empirical evidence on tail-oriented causality shows that global financial stress can exert directional effects on Bitcoin returns in both the lower and upper tails of the distribution. Using copula-based methods and cross-quantilogram analysis, prior studies document that stress indicators transmit information to Bitcoin primarily under extreme market conditions, highlighting the relevance of tail-dependent causal mechanisms (Bouri et al., 2018). Complementary findings from quantile cross-spectral approaches further reveal one-way tail dependence and causality running from traditional financial assets toward Bitcoin, suggesting that the diversification benefits of Bitcoin may arise only within specific quantile–frequency configurations (Maghyereh & Abdoh, 2020).

A systematic application of quantile-based causality to financial asset interactions is provided by Tiwari et al. (2019), who combine cross-quantilogram techniques with quantile-on-quantile regression to evaluate causal transmission between gold and equity markets in emerging economies across different segments of the return distribution and across pre-crisis and post-crisis regimes. Their results demonstrate that causal relationships can change markedly with market states, reinforcing the view that directional dependence in financial markets is inherently state-contingent rather than uniform.

2.5. Research Gap and the CFQR Framework

Although the existing literature has examined the relationship between Bitcoin and gold in considerable depth through dependence, spillover, connectedness, and regime-dependent dynamics, systematic evaluations of directional causal dominance remain limited. In particular, prior studies rarely assess causal dominance in a fully integrated manner across the joint intersection of quantiles, frequencies, and market regimes (Mensi et al., 2023; Hsu et al., 2021; Zeng et al., 2020; Matkovskyy & Jalan, 2019).

Wavelet–quantile and regime-based approaches have documented asymmetric and horizon-dependent responses in the interactions between Bitcoin and gold (Mejri et al., 2025; Colombage et al., 2025). However, these studies stop short of jointly identifying which asset leads information flows across different segments of the return distribution and across multiple investment horizons. Similarly, research examining the systemic effects of cryptocurrency price shocks has yet to establish causal dominance at the level of quantile–frequency intersections (Chen, 2025).

As a result, the existing body of research has not yet provided a comprehensive causal mechanism explaining when, under which conditions, and through which horizons either Bitcoin or gold assumes a leading role in transmitting market information. To address this gap, the present study investigates causal dominance between Bitcoin and gold within a CFQR framework that jointly captures conditional, horizon-dependent, and regime-dependent causal structures. Building on this conceptual foundation, the study advances a set of research questions and hypotheses that guide the subsequent empirical analysis.

RQ1. How does causal dominance between Bitcoin and gold manifest across different risk states represented by return distribution quantiles and across investment horizons defined in the frequency domain, and under which conditions does such dominance emerge in an economically meaningful manner? H1. Causal dominance between Bitcoin and gold does not appear uniformly across all quantiles and investment horizons; instead, statistically significant dominance arises only within specific quantile–frequency combinations.

RQ2. Does the quantile–frequency dependence of causal relationships differ systematically across endogenously identified market regimes, such as stress and normal states? H2. Quantile–frequency-based causal relationships between Bitcoin and gold are strongly regime-dependent: causal dominance becomes more pronounced under stress regimes, whereas it remains weak or fragmented under normal market conditions.

RQ3. Under lower quantiles associated with downside risk and during high-stress market regimes, which asset, gold or Bitcoin, predominates in directing market information flows? H3. Under high-stress regimes, gold exhibits stronger causal dominance over Bitcoin at longer investment horizons, with economically relevant implications for downside risk mitigation.

RQ4. Over which investment horizons, short, medium, or long, and under which market regimes, does Bitcoin exhibit characteristics consistent with the notion of “digital gold”? H4. The “digital gold” property of Bitcoin does not manifest uniformly across quantiles and horizons; rather, it emerges in a limited and conditional manner, primarily at longer investment horizons and during stress regimes, where Bitcoin’s behavior is shaped by the dominant causal influence of gold.

3. Methodology

3.1. Conceptual Foundations of the CFQR Framework

This study examines the relationship between Bitcoin and gold beyond conventional correlation, co-movement, or mean-based Granger causality frameworks by focusing on the conditions under which causal structures emerge, the investment horizons over which they operate, and the segments of the return distribution in which they become relevant. To achieve this objective, the analysis adopts a CFQR methodological framework that integrates directional causality with sensitivity to risk states, investment horizons, and market regimes.

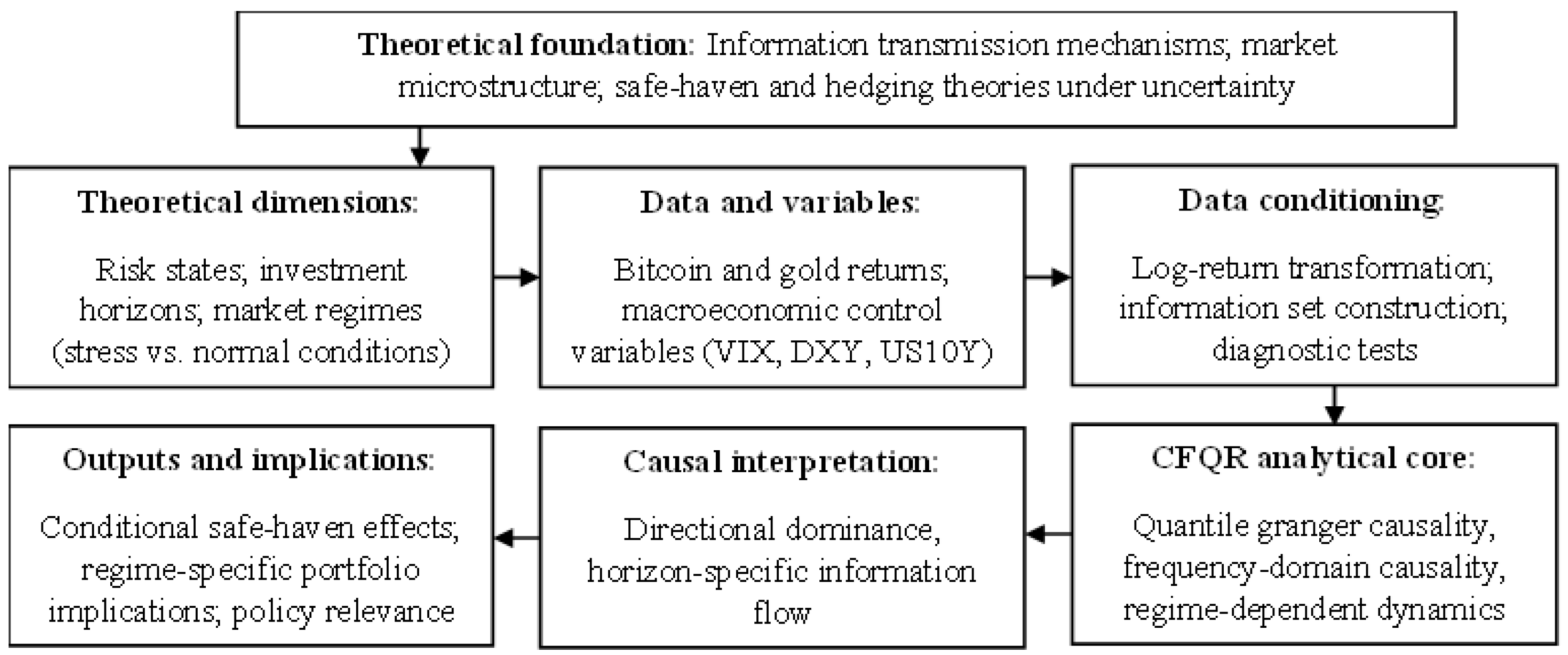

The primary strength of the CFQR framework lies in its ability to evaluate causal transmission without restricting analysis to a single dimension. Instead, it jointly assesses causality across the frequency domain, encompassing short-, medium-, and long-term horizons, across quantiles of the return distribution (including the lower, central, and upper segments), and across changing market regimes. Importantly, the CFQR framework does not presuppose the existence of causal relationships under all conditions. Rather, it is explicitly designed to test empirically whether causal structures arise under specific configurations of horizons, risk states, and market environments. The general architecture of the CFQR concept employed in this study is illustrated in Figure 1.

3.2. Multivariate VAR Baseline Model

The joint dynamics of the daily return series are represented by the following vector formulation:

Here, and denote the returns of Bitcoin and gold, respectively, while represents a vector of control variables capturing market risk and broader financial conditions. The dynamic interactions among these variables are modeled using the following VAR(p) process:

Here, denotes a vector of stochastic error terms with zero mean and finite variance. This multivariate VAR structure serves as the baseline model for evaluating the causal relationship between Bitcoin and gold while conditioning on common macro-financial influences.

3.3. Granger Causality in the Frequency Domain

Conventional time-domain Granger causality evaluates causal effects at an average temporal level and may therefore fail to capture heterogeneity in information transmission that can differ markedly across short- and long-run horizons. To address this limitation, the present study analyzes Granger causality within the frequency domain.

At a given frequency , Causality from X to Y is defined as:

This measure is designed not to quantify the magnitude of causal effects per se, but rather to distinguish the investment horizons over which information transmission predominantly occurs. Such a frequency decomposition enables a more refined interpretation of heterogeneous investor behavior across time horizons and the dynamic process through which market information is absorbed.

3.4. Quantile-Based Granger Causality

Financial data, particularly cryptocurrency returns, are well known to exhibit non-normality, asymmetry, and heavy-tailed distributions. As a result, causal relationships need not manifest uniformly across all segments of the return distribution. To account for this feature, the CFQR methodology defines Granger causality at the quantile level. For a given quantile , The conditional quantile of Bitcoin returns is specified as follows:

Here, denotes the information set available up to time t-1. If the coefficients are statistically significant, causality from gold to Bitcoin is inferred at the corresponding quantile q. An analogous procedure is applied to evaluate causal effects in the opposite direction.

This quantile-based approach allows the analysis to assess whether causal structures are confined to the lower tail of the return distribution or whether they extend across multiple segments, thereby revealing whether causality operates uniformly or varies conditionally across different market states.

3.5. Frequency–Quantile–Regime Integration in the CFQR Framework

The central component of the CFQR methodology lies in integrating causal relationships across the joint intersection of frequency and quantile dimensions. This integration can be formally expressed as follows:

This formulation identifies the segments of the return distribution, indexed by q, and the investment horizons, indexed by , at which causal transmission emerges. Because causal structures may evolve as market conditions change, market regimes are identified endogenously from the data. Specifically, market states are defined as follows:

Denoting market regimes in this manner, regime-conditioned causality is defined as follows:

In this way, the analysis systematically examines how the causal relationship between Bitcoin and gold varies across the joint interaction of risk states, investment horizons, and market conditions. To ensure reliable statistical inference in finite-sample settings and under non-normal return distributions, we employ bootstrap-based procedures and conduct robustness checks to assess whether results remain stable across lag lengths, quantile choices, frequency intervals, and market regime specifications.

4. Data and Variable Construction

4.1. Data Sources and Sample Coverage

To examine the causal relationship between Bitcoin and gold within the CFQR (Causal–Frequency–Quantile–Regime) framework, this study employs daily financial time-series data. Given that the proposed methodology simultaneously accounts for different segments of the return distribution, heterogeneity across investment horizons, and changes in market regimes, the analysis relies on high-frequency observations.

The sample period spans from 1 January 2013 to 31 December 2025. This interval begins with a phase in which Bitcoin market data becomes sufficiently continuous and trading activity relatively stabilized, and it encompasses multiple episodes characterized by alternating normal and turbulent market conditions. After aligning all variables to a daily frequency, the final balanced sample consists of 3,222 observations.

Bitcoin price data are obtained from daily closing prices widely used in international cryptocurrency markets, while gold price data are drawn from internationally recognized benchmark prices commonly employed by institutional investors. To control for broader financial conditions that may jointly influence both assets, the analysis incorporates a market uncertainty index, a broad U.S. dollar index, and yields on long-term U.S. government bonds.

4.2. Variable Definitions and Data Transformation

Because the CFQR analysis focuses on return dynamics rather than price levels, the Bitcoin and gold price series are transformed into logarithmic returns. Specifically, returns are defined as follows:

Here, and denote the daily price levels of Bitcoin and gold, respectively. Employing logarithmic returns eliminates scale differences while preserving abrupt price fluctuations and retaining information contained in the tail regions of the return distribution.

Prior to inclusion in the analysis, macro-financial control variables are transformed to ensure stationarity. Specifically, the U.S. dollar index is converted to returns, while the market uncertainty index and the yield on 10-year U.S. Treasury bonds are expressed in first differences. As a result, the vector of variables used in the empirical analysis is structured as follows:

4.3. Information Set and VAR Baseline Structure

To evaluate Granger causality in both the quantile and frequency domains, the information set conditioning each variable on its past realizations is defined as follows:

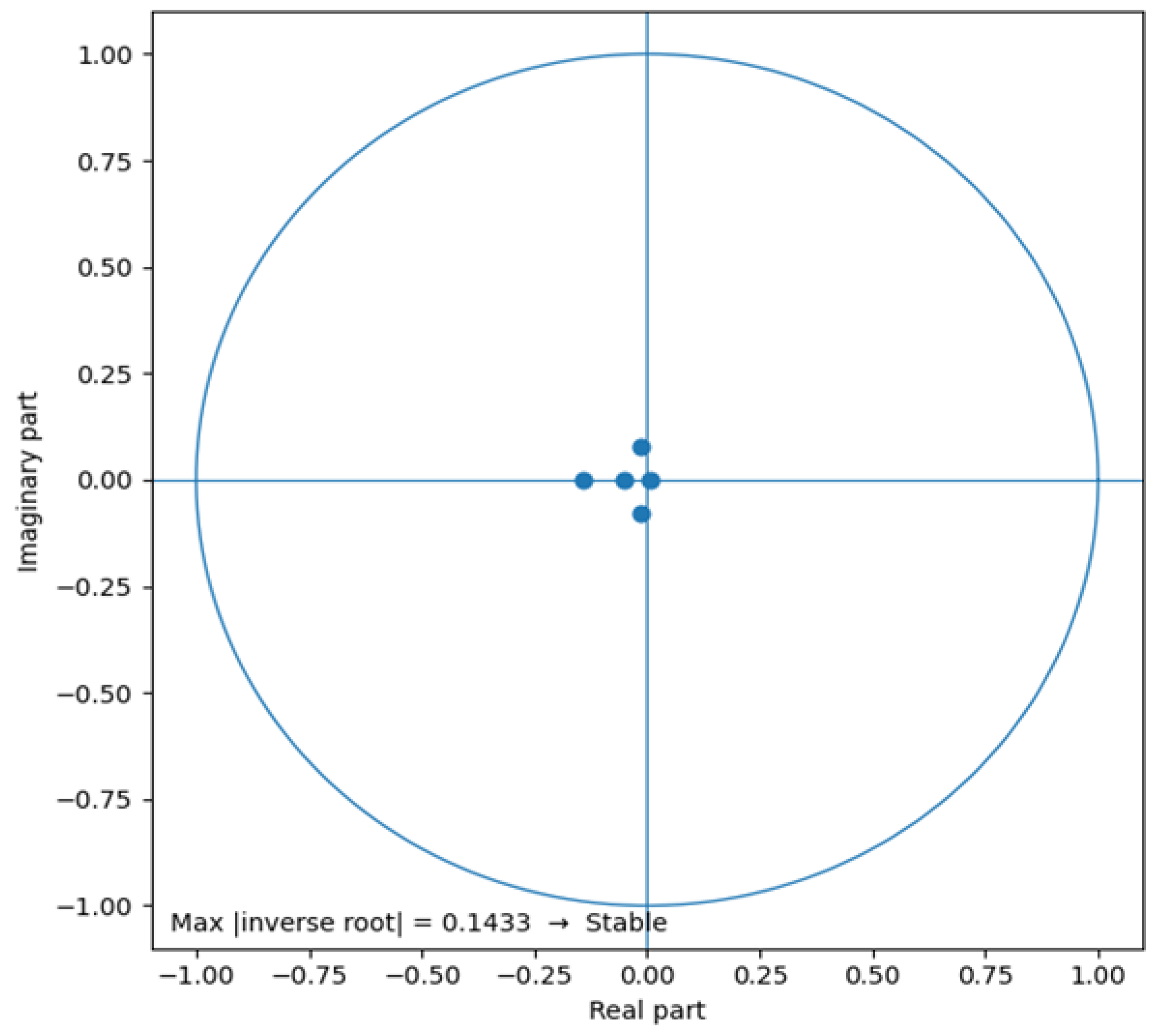

Here, p denotes the lag length selected using standard information criteria. Based on the lag selection results for the daily return data, a VAR(1) specification is identified as the most appropriate structure. An examination of the system’s dynamic stability confirms that all eigenvalues of the companion matrix lie within the unit circle, indicating that the VAR system satisfies the stability condition. Accordingly, this VAR specification serves as the baseline model for subsequent frequency- and quantile-based causality analyses.

4.4. Distributional Properties and Market Regime Classification

The CFQR methodology is particularly informative under conditions characterized by non-normal, asymmetric, and heavy-tailed distributions. Results from standard unit root tests indicate that all variables used in the analysis are stationary, while tests of distributional normality consistently reject the assumption of normality for the return series. These findings provide statistical justification for implementing quantile-based, tail-sensitive causality analyses.

Market regimes are identified using an endogenous approach based on the joint dynamics of returns and volatility. This procedure allows market conditions to be classified into stress and normal regimes, thereby establishing a framework for evaluating causal relationships conditional on prevailing market states. The resulting regime classification is validated against an exogenous proxy based on a market-uncertainty index, ensuring that the regime definitions remain data-driven while retaining economic interpretability.

5. Results

5.1. Descriptive Properties and Preliminary Validation

This subsection summarizes the key distributional characteristics of the data and the preliminary statistical validations required to evaluate the causal relationship between Bitcoin and gold across the joint intersection of risk states (quantiles), investment horizons (frequencies), and market regimes within the CFQR framework.

Table 1 presents the main descriptive statistics for the variables used in the analysis. The results indicate that Bitcoin returns exhibit substantially higher volatility than gold and the macro-financial control variables, as reflected in a larger standard deviation. Moreover, Bitcoin returns display pronounced asymmetry, with strong skewness and exceptionally high kurtosis, signaling a systematic departure from normality and a concentration of extreme observations in both the lower and upper tails of the distribution. In contrast, gold returns appear relatively more stable and less skewed; however, they also deviate from the normality assumption to a non-negligible extent.

These distributional features indicate that conventional approaches relying solely on average relationships are insufficient for capturing market interactions and underscore the need to investigate asymmetric and state-contingent dependence across different segments of the return distribution, particularly in the lower and upper quantiles. Moreover, because information transmission in financial markets may exhibit distinct dynamics over short- and long-term horizons, accounting for heterogeneity across investment frequencies is essential for empirical analysis.

Accordingly, the CFQR methodology, which jointly incorporates distributional asymmetry, horizon-specific dynamics, and regime-dependent market conditions, represents a theoretically and empirically well-founded choice for the present study. As part of the preliminary model validation, unit root tests (ADF), tests of distributional non-normality (Jarque–Bera), and lag selection and stability diagnostics for the VAR system underlying the CFQR analysis were conducted. Detailed results of these diagnostic checks are reported in Appendix A (Table A1 and Table A2, and A3; Figure A1), confirming that all variables are stationary at the 5 percent significance level and that the VAR system operates within the dynamically stable region. Consequently, the CFQR analyses presented in the subsequent subsections are based on data that satisfy the required statistical and dynamic conditions, ensuring the reliability of the empirical findings.

5.2. Frequency–Quantile Causal Dominance: Full Sample

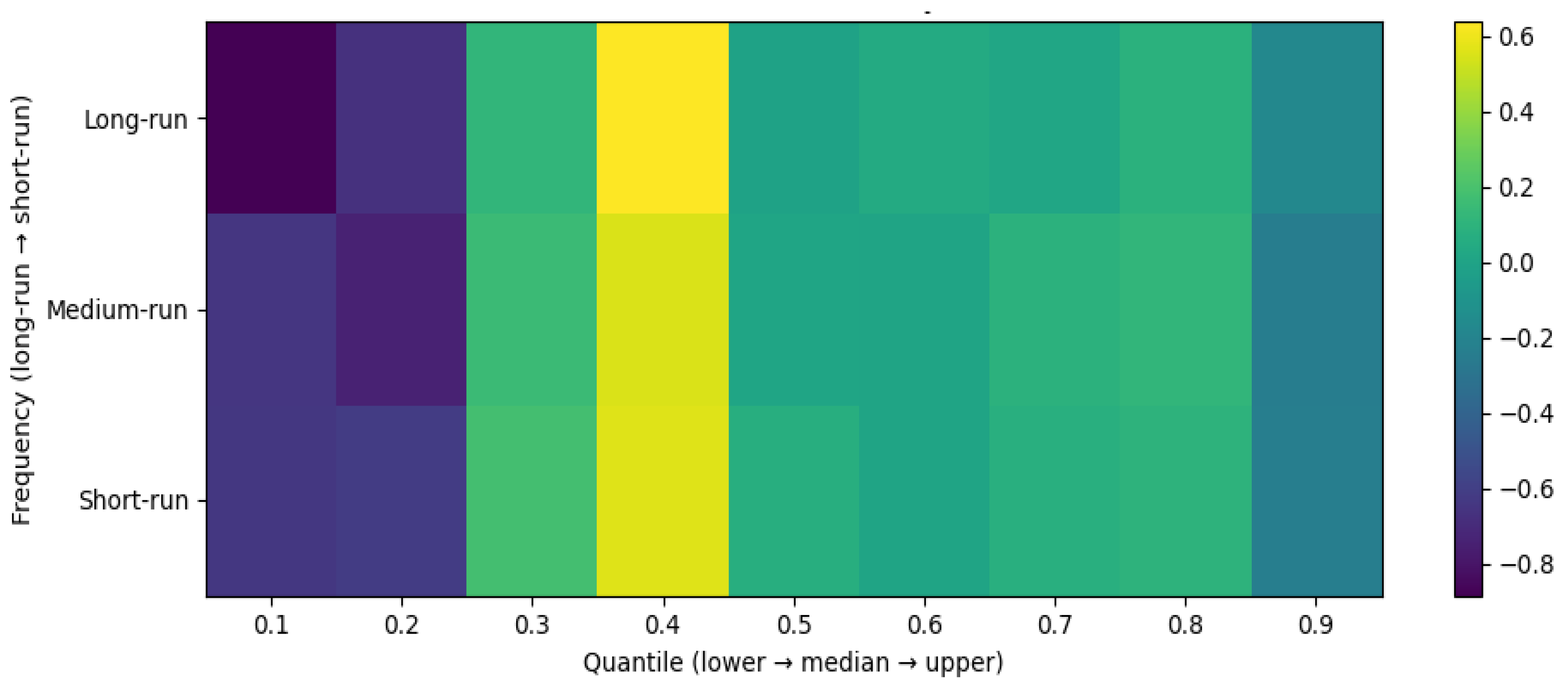

This subsection presents the results of the CFQR analysis evaluating frequency–quantile causal dominance between Bitcoin and gold over the full sample period. The findings are first illustrated visually and subsequently summarized using statistically validated quantitative measures. To avoid overly generalized interpretations, the results are discussed using conservative inference criteria. Figure 2 displays the frequency–quantile causal dominance map, where the horizontal axis represents return quantiles ranging from lower to median and upper segments, and the vertical axis denotes frequency bands corresponding to short-, medium-, and long-term horizons. Color intensity reflects the magnitude of net causal dominance, defined as the difference between the Wald-type quantile Granger causality statistic from gold to Bitcoin and the corresponding statistic from Bitcoin to gold.

Visual inspection of Figure 2 reveals patterns of both positive and negative dominance across certain regions of the frequency–quantile space. However, such visual patterns cannot, on their own, be interpreted as evidence of statistically significant causal relationships. Accordingly, to avoid reliance on purely descriptive impressions, we refrain from drawing inferences based solely on the heatmap and instead summarize only results confirmed using bootstrap-based significance criteria. The statistically validated outcomes are reported in Table 2.

Table 2 indicates that no statistically significant or systematic directional causal relationship is detected in the short- and medium-term frequency bands, nor within the lower and central quantiles of the return distribution. This finding suggests that information transmission between Bitcoin and gold is generally weak, unstable, or episodic across most market conditions.

In contrast, in the long-term frequency domain and at the upper quantiles of the return distribution, a statistically significant causal dominance of gold over Bitcoin is identified. This result implies that during prolonged expansionary market conditions, gold serves as an information leader in shaping Bitcoin’s dynamics. Visual fluctuations observed in other quantile–frequency combinations lack statistical validation and therefore cannot be interpreted as evidence of systematic causality.

Overall, the full-sample CFQR analysis demonstrates that the causal relationship between Bitcoin and gold is not uniformly present across all conditions. Instead, it emerges distinctly only within a specific configuration characterized by long investment horizons and upper-tail return states. This evidence provides a clear empirical rationale for the regime-dependent analysis pursued in the subsequent subsections.

5.3. Regime-Conditioned CFQR Results

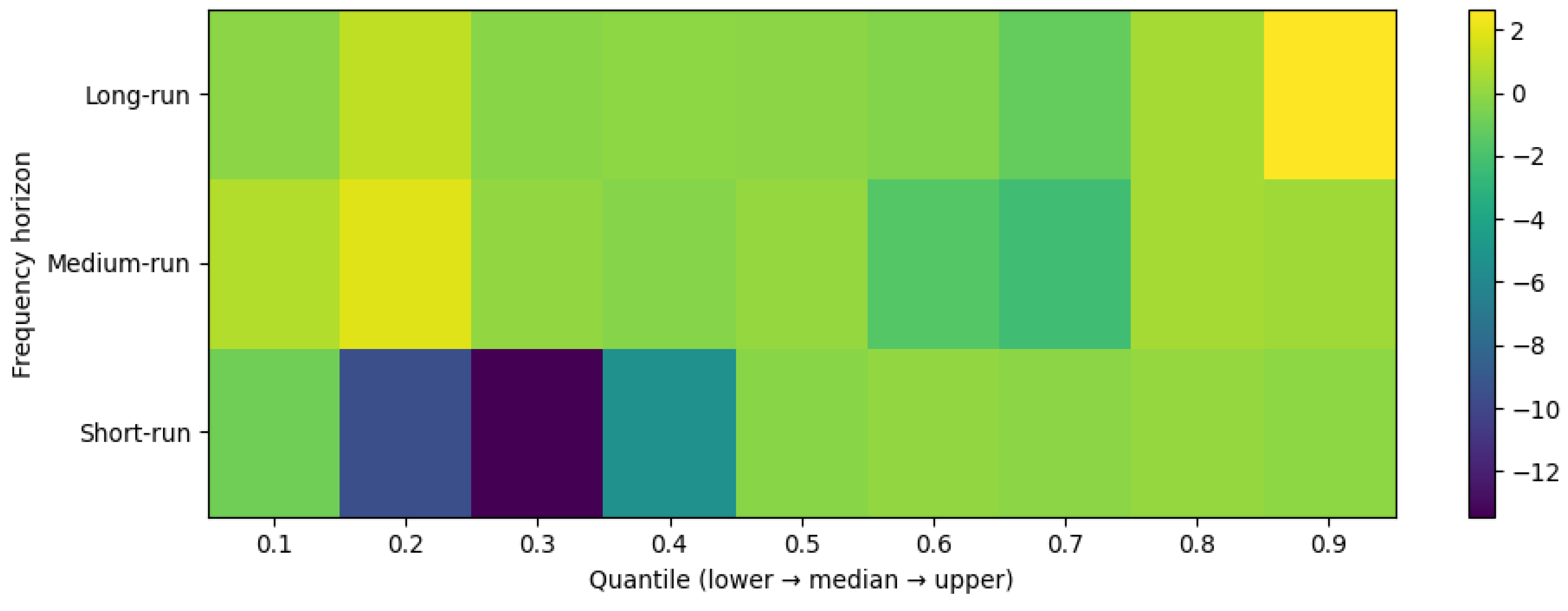

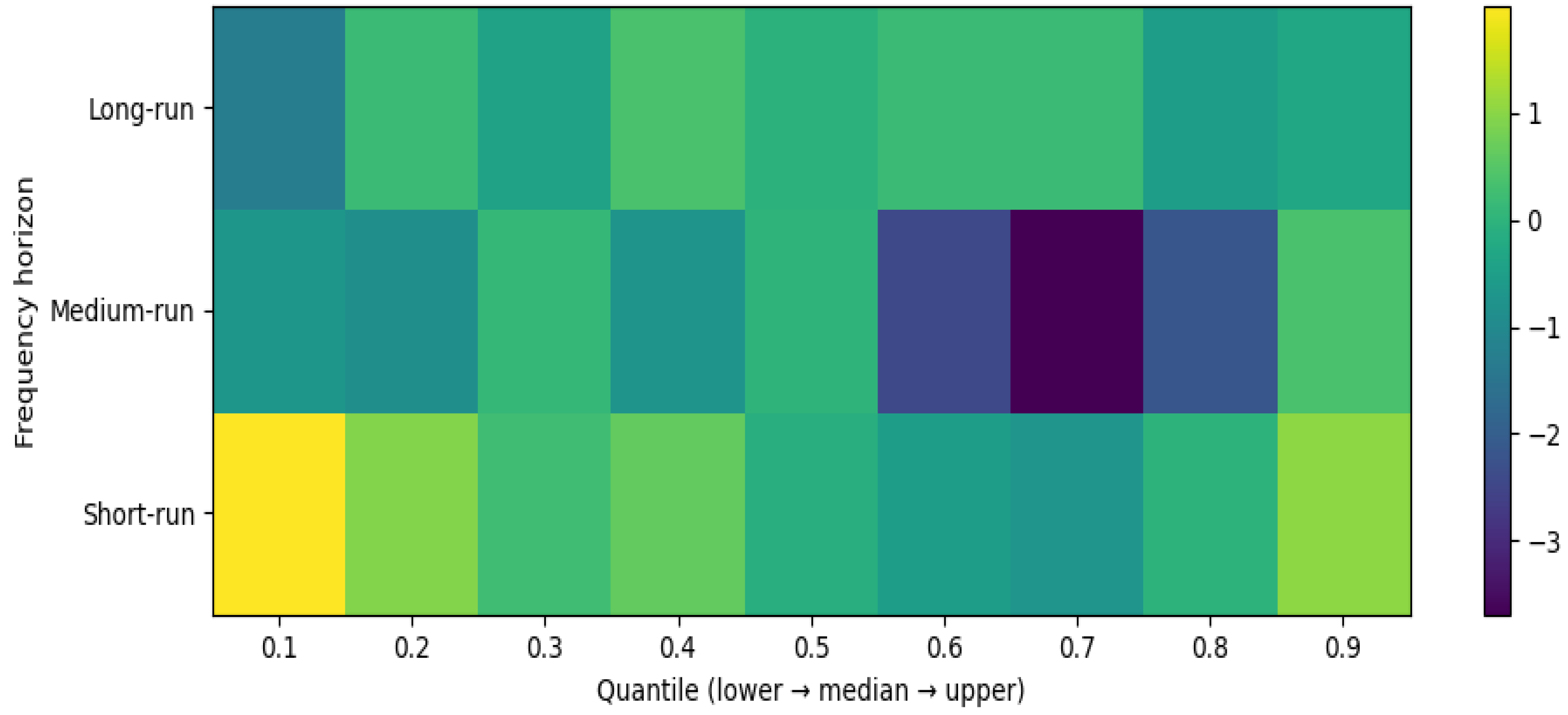

This subsection presents the CFQR results obtained by endogenously identifying market regimes from the data and classifying them into stress and normal states. The regime classification is based on the joint dynamics of returns and volatility, aiming to capture latent market conditions more accurately than approaches that rely on exogenous thresholds, such as fixed VIX cutoffs. Frequency–quantile causal dominance maps for the stress and normal regimes are illustrated in Figure 3 and Figure 4, respectively.

Figure 3 indicates that the causal structure becomes more pronounced and asymmetric under stress regimes. In particular, within the medium- and long-term frequency bands and across the upper quantiles of the return distribution, causal dominance from gold to Bitcoin emerges more systematically. This pattern suggests that during periods of heightened market instability and elevated risk, gold serves as an information leader, shaping Bitcoin’s price dynamics.

By contrast, at short investment horizons, the direction of causality appears unstable, with sporadic and short-lived fluctuations in the opposite direction observed in certain lower quantiles. These patterns may be associated with transient feedback effects arising during abrupt market downturns. However, given the lack of consistent statistical validation, such short-term reversals cannot be interpreted as evidence of stable or systematic causal dominance.

As illustrated in Figure 4, causal patterns observed across the frequency–quantile space under normal market conditions are relatively weak and fragmented. No asset exhibits stable dominance across all quantiles and investment horizons, and the direction of causality varies across different segments of the return distribution. This evidence indicates that during tranquil market phases, informational linkages between gold and Bitcoin are largely symmetric and episodic.

Interactions detected under normal regimes are therefore more likely to reflect short-term portfolio rebalancing and speculative trading activity rather than systematic hedging behavior or flight-to-safety dynamics. Consequently, there is insufficient empirical support to conclude that gold consistently acts as an information leader for Bitcoin under normal market conditions.

Taken together, the regime-conditioned CFQR results provide clear evidence that the causal relationship between Bitcoin and gold is fundamentally regime dependent. While gold’s dominance emerges primarily during stress regimes within specific frequency–quantile configurations, no comparable systematic structure is observed during normal market states. This contrast forms the empirical foundation for the hypothesis testing and economic interpretation presented in the subsequent subsection.

5.4. Validation and Characteristics of the Regime Classification

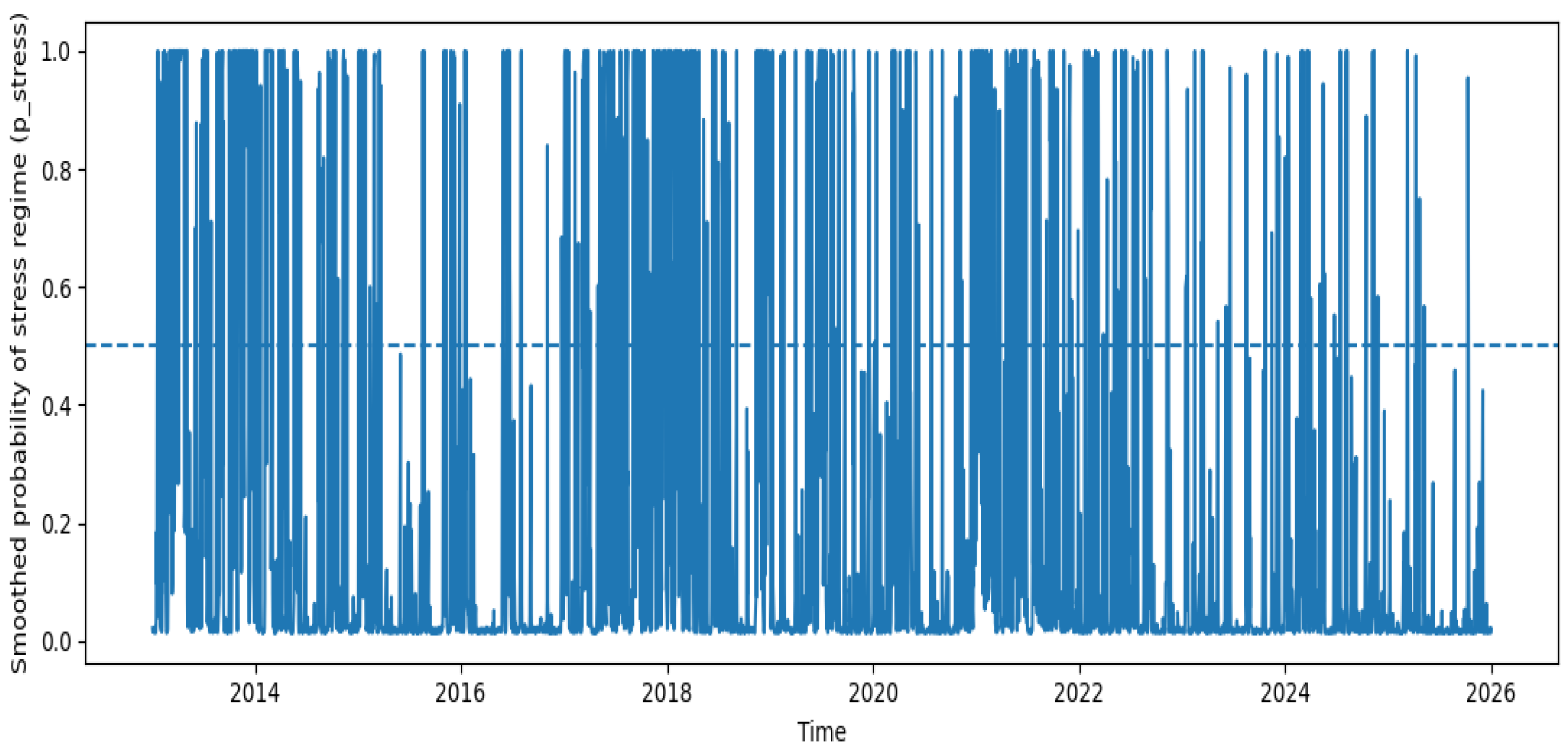

This subsection evaluates the economic interpretation, stability, and reliability of the endogenously identified market regime classification. In particular, we examine the time-varying dynamics of the stress-regime probabilities, the statistical characteristics associated with each regime, and validation results from comparisons with an exogenous benchmark based on the VIX. Figure 5 illustrates the temporal evolution of the stress-regime probability derived from the Markov-switching volatility model.

As shown in Figure 5, the probability of the stress regime exhibits sharp and short-lived transitions over time. This pattern reflects the highly volatile and nonlinear nature of the Bitcoin market and is consistent with stylized facts widely documented in the cryptocurrency literature. More specifically, periods characterized by a dominant stress regime systematically coincide with episodes of pronounced market turbulence and abrupt increases in uncertainty. The statistical characteristics associated with each market regime are summarized in Table 3.

Table 3 shows that, although the stress regime accounts for a relatively small proportion of the total observations, it is characterized by markedly higher volatility in both Bitcoin and gold returns. During stress periods, the average VIX is positive, while changes in the U.S. 10-year Treasury yield exhibit a negative mean. In addition, the relatively short average duration of the stress regime suggests that market shocks tend to be abrupt and intermittent. By contrast, under normal market conditions, return volatility is substantially lower, and regime durations are longer, reflecting a more stable market environment.

To further assess the reliability of the endogenously identified market regimes, we compare them with an exogenous stress indicator. The validation results based on a VIX-derived benchmark are reported in Table 4.

The confusion matrix reported in Table 4 evaluates the concordance between the endogenously identified market regimes and a stress indicator defined using the 80th percentile of the VIX. Although the overall agreement rate reaches 0.714, the Cohen’s kappa coefficient is notably low, indicating that the overlap between the two classifications does not substantially exceed what would be expected by random chance. This outcome should not be interpreted as evidence of misclassification. Rather, it reflects that the endogenous regime identification captures the internal volatility dynamics specific to the cryptocurrency market, whereas the VIX-based indicator proxies broader stress conditions in traditional financial markets.

Accordingly, the limited concordance between the two measures underscores their complementary nature rather than a methodological deficiency. The validation results, therefore, support the view that the endogenous regime classification provides economically meaningful information well aligned with the idiosyncratic characteristics of cryptocurrency markets.

5.5. Synthesis of CFQR Results and Economic Significance

This subsection synthesizes the results of the preceding CFQR analyses and evaluates whether the identified causal structures carry meaningful economic implications for real-world investment decisions through hedging experiments. The findings from earlier sections indicate that the causal relationship between Bitcoin and gold is not stable across all conditions. Instead, it exhibits an asymmetric and conditional structure that depends jointly on frequency, quantile, and market regime.

For the full sample, systematic causality is detected only within the configuration characterized by long-term investment horizons and upper-tail return states, with directional dominance running from gold to Bitcoin. When market conditions are explicitly accounted for, this dominance becomes markedly more pronounced under stress regimes. By contrast, under normal market conditions, causal effects remain weak and fragmented, suggesting that gold’s role as an information leader is not universal but rather contingent on adverse market environments.

To assess whether these conditional causal patterns translate into economically meaningful outcomes, we conduct a gold–Bitcoin hedging experiment during stress regimes, guided by the CFQR results. The performance of these regime-conditioned hedging strategies is summarized in Table 5.

Panel A of Table 5 reports the hedging results based on the minimum-variance hedge ratio (h*) computed under stress regimes (p ≥ 0.50). The inclusion of gold in the portfolio leads to a modest reduction in the variance of Bitcoin returns, indicating that variance-based hedging effectiveness is relatively limited under stressed market conditions.

In contrast, the downside risk measures presented in Panel B reveal a more pronounced economic significance. Both the semi-variance and the 5% Conditional Value-at-Risk (CVaR) decline more substantially for portfolios that include gold, providing clear evidence that, during stress regimes, gold plays a protective role by mitigating downside risk in Bitcoin returns.

Taken together, these findings corroborate the long-horizon × stress-regime dominance of gold identified by the CFQR analysis from an investment perspective. In other words, while gold does not serve as a stable hedge against Bitcoin under all market conditions, it delivers economically meaningful protection against downside risk during periods of heightened market instability and elevated risk.

6. Discussion

Authors should discuss the results and how they can be interpreted in light of previous studies and the working hypotheses. The findings and their implications should be discussed in the broadest context possible. Future research directions may also be highlighted.

6.1. Conditional and Directional Information Transmission

The results obtained from the CFQR framework clearly demonstrate that the relationship between Bitcoin and gold cannot be adequately explained by mean-based dependence or by assuming a constant hedging role. From the perspective of financial information transmission theory, asset interdependence should be characterized not merely by the magnitude of co-movement, but more fundamentally by which asset incorporates market-relevant information earlier and which asset responds conditionally to that information flow. Importantly, the CFQR framework does not increase model flexibility through additional parameters; instead, it decomposes the same underlying causal structure across multiple dimensions, thereby reducing aggregation bias rather than introducing overfitting.

This interpretation is consistent with prior evidence from time–frequency volatility connectedness studies, which show that the impact of financial stress is horizon-dependent and state-contingent rather than uniform across time and market conditions (Zhang & Wang, 2021). In other words, financial shocks do not propagate identically across short-, medium-, and long-term horizons, and during periods of heightened uncertainty, traditional safe-haven assets may assume a more prominent informational role in guiding market dynamics.

Our empirical findings indicate that causality running from gold to Bitcoin does not emerge uniformly across all conditions. Instead, it becomes statistically significant only at the intersection of long-term frequency horizons, specific segments of the return distribution, and stress market regimes. This pattern suggests that, under conditions of heightened uncertainty, gold may incorporate market-relevant information relatively earlier and exert a conditional influence on Bitcoin’s dynamics, thereby assuming an information leadership role.

Accordingly, interpreting hedging or safe-haven properties as time-invariant characteristics is theoretically inappropriate. Rather, protective and hedging attributes should be understood as state-contingent phenomena that may manifest differently across segments of the return distribution. This interpretation is consistent with evidence from studies linking asset behavior to shocks in economic policy uncertainty, which likewise document heterogeneous responses across quantiles (Wu et al., 2019).

By contrast, causality from Bitcoin to gold is observed primarily at short investment horizons and within limited quantile ranges, without forming a stable dominance structure. This pattern reflects the rapid information absorption and episodic nature of cryptocurrency markets, where informational effects tend to be conditional and short-lived. In comparison, gold’s informational influence appears more persistent during stress regimes, underscoring its relatively stable role in environments characterized by elevated risk and uncertainty.

6.2. From Dependence to Causal Dominance

Most prior studies examining the relationship between gold and Bitcoin rely on non-directional measures, including correlation, wavelet coherence, quantile correlation, and connectedness frameworks. While this literature documents that Bitcoin may exhibit gold-like behavior over certain horizons and under specific market conditions, it provides limited insight into the directional nature of information transmission, particularly in identifying which asset leads and which responds.

For instance, quantile–frequency and tail-based approaches suggest that gold may display stronger protective characteristics in lower quantiles and over medium- to long-term horizons. However, these studies do not systematically characterize causal dominance in a directional sense across different market conditions (Mensi et al., 2023). By explicitly decomposing causality across the quantile, frequency, and regime dimensions, the present study addresses this limitation and integrates prior empirical findings into a unified, logically consistent framework.

In addition, the endogenous identification of market regimes employed in this study allows for a more economically grounded interpretation than approaches relying on exogenous dummy variables. Unlike exogenously imposed thresholds, the endogenous regime classification enables market states to emerge from joint return–volatility dynamics, which is particularly relevant for cryptocurrency markets characterized by abrupt, non-linear stress episodes. Presenting causal dominance in a map-based format further avoids reliance on mean-based or aggregated conclusions and enables the analysis to capture heterogeneous, state-contingent dynamics that are typically obscured in conventional dependence-based studies.

6.3. A State-Contingent View of Digital Gold

The characterization of Bitcoin as “digital gold” is widely used in both academic and practitioner-oriented discussions. However, this concept is often implicitly treated as a time-invariant property that holds uniformly across market conditions. The CFQR results provide a more nuanced empirical interpretation, demonstrating that the “digital gold” attribute of Bitcoin is fundamentally state-contingent, emerging only under specific market environments.

In particular, at the intersection of stress market regimes, long-term investment horizons, and selected segments of the return distribution, Bitcoin’s dynamics become more sensitive to gold’s informational influence. This evidence indicates that Bitcoin does not consistently perform the same economic role as gold across all conditions. Instead, it converges toward the logic of a traditional safe-haven asset only within particular high-risk environments. This conclusion is consistent with wavelet-based evidence showing that gold and Bitcoin respond differently across frequencies and quantiles during periods of geopolitical and macroeconomic risk shocks (Mejri et al., 2025).

Importantly, the identification of causal dominance at longer horizons and specific quantile ranges does not contradict the relevance of gold for downside risk mitigation, as informational leadership and tail-risk protection operate through distinct but complementary channels. From a practical investment perspective, although variance-based risk reduction appears limited, portfolios that include gold exhibit markedly improved performance in downside risk measures during stress regimes. The superior performance of gold-augmented portfolios in mitigating tail risk supports the economic relevance of gold’s conditional protective role during periods of elevated uncertainty and instability.

6.4. Overall Theoretical and Methodological Contributions

This study makes several substantive contributions to the literature on financial interdependence. First, it demonstrates, both theoretically and empirically, that asset relationships should be interpreted not only through co-movement measures but also through the lens of directional information transmission. By shifting the focus from dependence to causality, the analysis highlights the importance of identifying which assets lead market information flows and under what conditions such leadership emerges.

Second, the CFQR framework, which integrates quantile, frequency, and regime dimensions with causality analysis, is shown to be a flexible and powerful methodological tool for examining the interactions between cryptocurrencies and traditional safe-haven assets. This framework allows researchers to move beyond mean-based, time-invariant representations and capture heterogeneous, state-dependent dynamics that are central to modern financial markets.

Third, the study provides a systematic empirical foundation for redefining “digital gold” as a conditional and dynamic phenomenon rather than a fixed or universal characteristic. By demonstrating that Bitcoin’s gold-like properties emerge only under specific combinations of market stress, investment horizons, and distributional states, the analysis offers a more precise and theoretically grounded interpretation of this widely used concept.

Finally, the mapped patterns of causal dominance reveal how the direction of information transmission can shift during periods of market stress. These findings are logically consistent with prior macro-level evidence documenting regime-dependent causality in financial markets (Colombage et al., 2025). Accordingly, the CFQR framework serves as a valuable analytical tool for explaining crypto–traditional safe-haven relationships at the level of directional information transmission rather than simple co-movement.

7. Conclusions

This study provides empirical evidence that the relationship between Bitcoin and gold cannot be adequately explained by mean-based dependence measures or by the assumption that gold consistently serves as a safe-haven asset under all market conditions. Instead, using the CFQR framework, we show that causality emerges conditionally at the intersection of risk states represented by return quantiles, investment horizons captured by frequency bands, and market regimes.

The CFQR results demonstrate that causality from gold to Bitcoin does not manifest uniformly across conditions. Statistically significant effects are observed only under stress market regimes, at long-term investment horizons, and within specific segments of the return distribution. By contrast, causality from Bitcoin to gold fails to form a stable dominance structure and appears primarily as short-lived and episodic effects concentrated in short horizons and limited quantile ranges. These findings indicate that the gold–Bitcoin relationship is inherently asymmetric and characterized by horizon-dependent and regime-dependent causal structures rather than symmetric or time-invariant interactions.

These findings indicate that the broad question of whether Bitcoin can be regarded as digital gold cannot be resolved through a universal or unconditional conclusion. Instead, the evidence suggests that Bitcoin’s digital-gold characteristic is inherently state-contingent. It becomes more closely aligned with the informational role of gold only under conditions of market stress, at longer investment horizons, and when downside risk dominates return dynamics. In this sense, Bitcoin does not perform the same economic function as gold across all environments, but it converges toward the logic of a traditional safe-haven asset only in specific high-risk settings.

From a practical perspective, the hedging experiment reveals that although the variance-based risk reduction achieved by adding gold to a Bitcoin portfolio is limited, portfolios incorporating gold exhibit substantially greater stability when evaluated using downside-risk-sensitive measures during stress regimes. This result confirms that gold does not constitute a universally effective hedge against Bitcoin fluctuations. Rather, it serves as a conditional protective asset that can meaningfully mitigate downside risk in environments characterized by heightened uncertainty and market instability.

From a methodological perspective, this study introduces the CFQR framework, which integrates quantile, frequency, and regime dimensions within a causality-based setting. By moving beyond co-movement analysis, the framework enables the examination of relationships between cryptocurrencies and traditional assets at the level of directional information transmission. As such, the CFQR approach constitutes a general and flexible analytical tool for investigating crypto–traditional safe-haven interactions in a conditional and dynamic manner.

Future research may extend the CFQR framework to other cryptocurrencies, alternative macroeconomic uncertainty indices, and international market data. Further scope also exists to examine policy-related shocks and geopolitical risk channels in greater detail within this unified causal structure. Notwithstanding these extensions, the present study provides one of the first systematic empirical assessments of when, over which horizons, and in which direction the relationship between Bitcoin and gold becomes economically meaningful.

Author Contributions

Conceptualization, T.S.; methodology, T.S.; software, T.S.; validation, T.S.; formal analysis, T.S.; investigation, T.S.; resources, T.S.; data curation, T.S.; writing—original draft preparation, T.S.; writing—review and editing, T.S.; visualization, T.S.; supervision, T.S.; project administration, T.S. The author has read and agreed to the published version of the manuscript.

Funding

This research received no external funding. The APC was funded by the author.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data used in this study are publicly available from the sources cited in the manuscript. Processed data supporting the findings of this study are available from the corresponding author upon reasonable request.

Acknowledgments

During the preparation of this manuscript, the author used ChatGPT (OpenAI) for language editing and clarity improvement. The author reviewed and edited the output and takes full responsibility for the content of this publication.

Conflicts of Interest

The author declares no conflicts of interest. The funders had no role in the design of the study, in the collection, analysis, or interpretation of data, in the writing of the manuscript, or in the decision to publish the results.

Abbreviations

| Abbreviation | Full Term |

| BTC | Bitcoin |

| CFQR | Causal–Frequency–Quantile–Regime |

| CVaR | Conditional Value-at-Risk |

| DXY | U.S. Dollar Index |

| IRB | Institutional Review Board |

| VIX | CBOE Volatility Index |

| VAR | Vector Autoregression |

Appendix A. Data Diagnostics and Model Validation

Table A1.

ADF Unit Root Test Results.

| Series | ADF statistic | p-value | Lags | N | 1% crit | 5% crit | 10% crit | Decision (5%) |

|---|---|---|---|---|---|---|---|---|

| r_BTC | -21.6693 | 0.0000 | 6 | 3215 | -3.4324 | -2.8624 | -2.5672 | Stationary |

| r_GOLD | -56.6950 | 0.0000 | 0 | 3221 | -3.4324 | -2.8624 | -2.5672 | Stationary |

| r_DXY | -15.7372 | 0.0000 | 12 | 3209 | -3.4324 | -2.8624 | -2.5672 | Stationary |

| d_VIX | -21.0192 | 0.0000 | 8 | 3213 | -3.4324 | -2.8624 | -2.5672 | Stationary |

| d_US10Y | -42.4732 | 0.0000 | 1 | 3220 | -3.4324 | -2.8624 | -2.5672 | Stationary |

Note: The ADF test is conducted with an intercept and lag length selected by AIC. The null hypothesis of a unit root is rejected at the 5% level for all series, indicating stationarity.

Table A2.

Jarque–Bera Normality Test Results.

| Series | JB statistic | p-value | Skewness | Kurtosis | N | Decision (5%) |

|---|---|---|---|---|---|---|

| r_BTC | 2,855,217.65 | 0.0000 | 3.9603 | 148.8483 | 3222 | Non-normal |

| r_GOLD | 3,920.46 | 0.0000 | -0.5272 | 8.3103 | 3222 | Non-normal |

| r_DXY | 1,362.15 | 0.0000 | 0.0814 | 6.1879 | 3222 | Non-normal |

| d_VIX | 153,396.04 | 0.0000 | 2.1597 | 36.5797 | 3222 | Non-normal |

| d_US10Y | 480.68 | 0.0000 | -0.0072 | 4.8970 | 3222 | Non-normal |

Note: The Jarque–Bera test strongly rejects the null hypothesis of normality for all series, confirming pronounced skewness and excess kurtosis.

Table A3.

VAR Lag Selection Criteria.

| Lag | AIC | BIC | HQIC | FPE |

|---|---|---|---|---|

| 1 | -31.542564 | -31.485959 | -31.522277 | 0.0 |

| 2 | -31.559471 | -31.455669 | -31.522268 | 0.0 |

| 3 | -31.560123 | -31.409099 | -31.505995 | 0.0 |

| 4 | -31.562915 | -31.364645 | -31.491852 | 0.0 |

| 5 | -31.555930 | -31.310388 | -31.467922 | 0.0 |

| 6 | -31.551526 | -31.258690 | -31.446566 | 0.0 |

| 7 | -31.543222 | -31.203060 | -31.421298 | 0.0 |

| 8 | -31.546332 | -31.158830 | -31.407437 | 0.0 |

| 9 | -31.545364 | -31.110493 | -31.389487 | 0.0 |

| 10 | -31.539366 | -31.057101 | -31.366498 | 0.0 |

| 11 | -31.531007 | -31.000423 | -31.340239 | 0.0 |

| 12 | -31.519346 | -30.942219 | -31.312468 | 0.0 |

| 13 | -31.510319 | -30.885724 | -31.286422 | 0.0 |

| 14 | -31.502603 | -30.830515 | -31.261678 | 0.0 |

| 15 | -31.490235 | -30.770630 | -31.232272 | 0.0 |

| 16 | -31.487303 | -30.720156 | -31.212293 | 0.0 |

| 17 | -31.480957 | -30.666424 | -31.188890 | 0.0 |

| 18 | -31.471321 | -30.609014 | -31.162188 | 0.0 |

| 19 | -31.460141 | -30.550217 | -31.133932 | 0.0 |

| 20 | -31.450396 | -30.492831 | -31.107103 | 0.0 |

Note: All information criteria (AIC, BIC, HQIC, and FPE) select a VAR(1) specification, indicating a parsimonious dynamic structure for daily return data.

Figure A1.

VAR Stability Check (Inverse Roots). Note: The inverse roots of the characteristic polynomial all lie strictly within the unit circle, confirming the stability of the VAR(1) system.

Figure A1.

VAR Stability Check (Inverse Roots). Note: The inverse roots of the characteristic polynomial all lie strictly within the unit circle, confirming the stability of the VAR(1) system.

These diagnostics confirm that the VAR(1) system is both optimally specified and dynamically stable, thereby providing a valid foundation for the subsequent frequency–quantile causality analysis.

Figure A2.

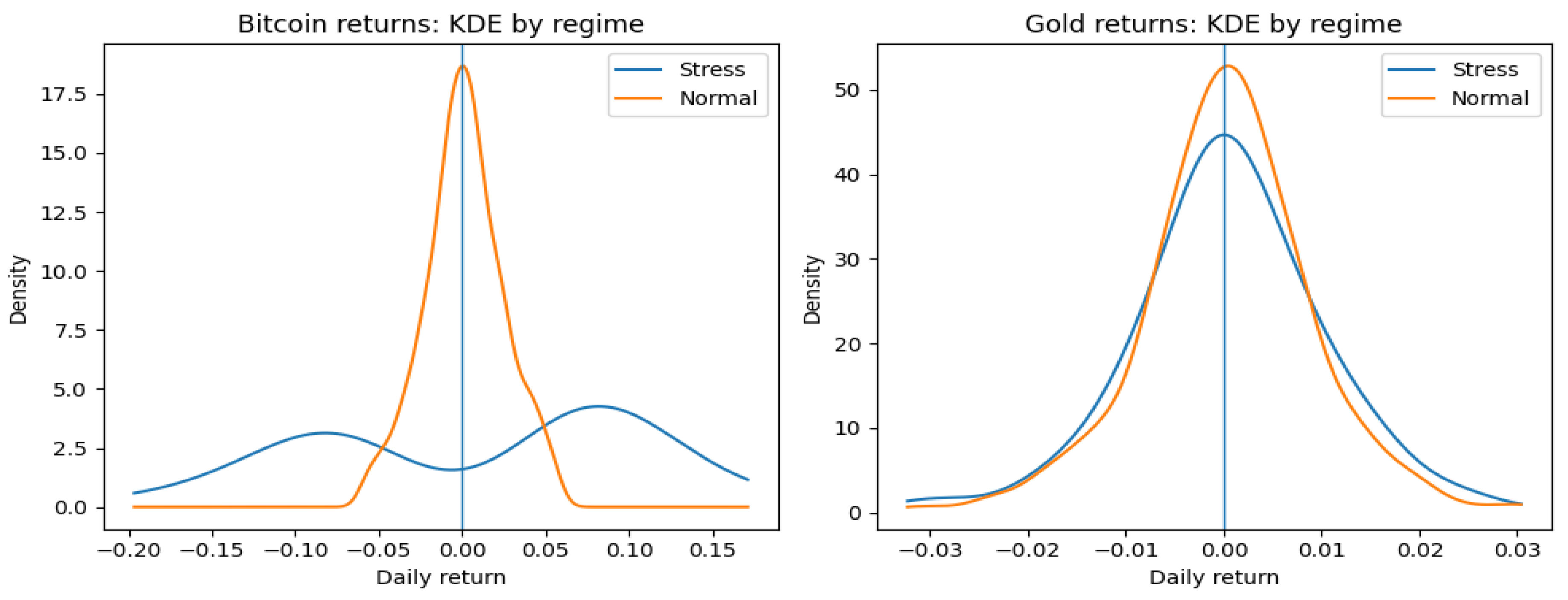

Regime-wise return distributions (Kernel density). Note: This figure presents kernel density estimates of Bitcoin and gold returns under stress and normal regimes identified by the endogenous Markov-switching model. Distributions in the stress regime exhibit wider dispersion and heavier tails, providing additional economic validation of the regime classification.

Figure A2.

Regime-wise return distributions (Kernel density). Note: This figure presents kernel density estimates of Bitcoin and gold returns under stress and normal regimes identified by the endogenous Markov-switching model. Distributions in the stress regime exhibit wider dispersion and heavier tails, providing additional economic validation of the regime classification.

References

- Agyei, S. K., Adam, A. M., Bossman, A., Asiamah, O., Owusu Junior, P., Asafo-Adjei, R., & Asafo-Adjei, E. (2022). Does volatility in cryptocurrencies drive the interconnectedness between the cryptocurrencies market? Insights from wavelets. Cogent Economics & Finance, 10(1). [CrossRef]

- Ang, A., & Bekaert, G. (2002). Regime Switches in Interest Rates. Journal of Business & Economic Statistics, 20(2), 163–182. [CrossRef]

- Baruník, J., & Kley, T. (2019). Quantile coherency: A general measure for dependence between cyclical economic variables. The Econometrics Journal, 22(2), 131–152. [CrossRef]

- Baruník, J., Kočenda, E., & Vácha, L. (2016). Asymmetric connectedness on the U.S. stock market: Bad and good volatility spillovers. Journal of Financial Markets, 27, 55–78. [CrossRef]

- Baur, D. G., & Lucey, B. M. (2010). Is Gold a Hedge or a Safe Haven? An Analysis of Stocks, Bonds and Gold. Financial Review, 45(2), 217–229. Portico. [CrossRef]

- Bhuiyan, R. A., Husain, A., & Zhang, C. (2023). Diversification evidence of bitcoin and gold from wavelet analysis. Financial Innovation, 9(1). [CrossRef]

- Bouri, E., Gupta, R., Lau, C. K. M., Roubaud, D., & Wang, S. (2018). Bitcoin and global financial stress: A copula-based approach to dependence and causality in the quantiles. The Quarterly Review of Economics and Finance, 69, 297–307. [CrossRef]

- Bouri, E., Molnár, P., Azzi, G., Roubaud, D., & Hagfors, L. I. (2017). On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Finance Research Letters, 20, 192–198. [CrossRef]

- Bouri, E., Shahzad, S. J. H., Roubaud, D., Kristoufek, L., & Lucey, B. (2020). Bitcoin, gold, and commodities as safe havens for stocks: New insight through wavelet analysis. The Quarterly Review of Economics and Finance, 77, 156–164. [CrossRef]

- Bouri, E., Hussain Shahzad, S. J., & Roubaud, D. (2020). Cryptocurrencies as hedges and safe-havens for US equity sectors. The Quarterly Review of Economics and Finance, 75, 294–307. [CrossRef]

- Breitung, J., & Candelon, B. (2006). Testing for short- and long-run causality: A frequency-domain approach. Journal of Econometrics, 132(2), 363–378. [CrossRef]

- Chen, Z. (2025). From Disruption to Integration: Cryptocurrency Prices, Financial Fluctuations, and Macroeconomy. Journal of Risk and Financial Management, 18(7), 360. [CrossRef]

- Colombage, S., Jayawardhana, A., & Oatley, G. (2025). Global Financial Stress and Its Transmission to Cryptocurrency Markets: A Cointegration and Causality Approach. Journal of Risk and Financial Management, 18(10), 532. [CrossRef]

- El Aoun, O. (2026). Market-specific connectedness behaviors across quantiles and frequencies connectedness patterns among G7 markets, commodities, bitcoin, and interest rate spread. Digital Finance, 8(1). [CrossRef]

- Hamilton, J. D. (1989). A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle. Econometrica, 57(2), 357. [CrossRef]

- Hsu, S.-H., Sheu, C., & Yoon, J. (2021). Risk spillovers between cryptocurrencies and traditional currencies and gold under different global economic conditions. The North American Journal of Economics and Finance, 57, 101443. [CrossRef]

- Jeong, K., Härdle, W. K., & Song, S. (2012). A CONSISTENT NONPARAMETRIC TEST FOR CAUSALITY IN QUANTILE. Econometric Theory, 28(4), 861–887. [CrossRef]

- Kayani, U., Ullah, M., Aysan, A. F., Nazir, S., & Frempong, J. (2024). Quantile connectedness among digital assets, traditional assets, and renewable energy prices during extreme economic crisis. Technological Forecasting and Social Change, 208, 123635. [CrossRef]

- Koenker, R., & Bassett, G. (1978). Regression Quantiles. Econometrica, 46(1), 33. [CrossRef]

- Kumah, S. P., & Mensah, J. O. (2020). Are cryptocurrencies connected to gold? A wavelet-based quantile-in-quantile approach. International Journal of Finance & Economics, 27(3), 3640–3659. Portico. [CrossRef]

- Kumah, S. P., & Odei-Mensah, J. (2022). Do cryptocurrencies and crude oil influence each other? Evidence from wavelet-based quantile-in-quantile approach. Cogent Economics & Finance, 10(1). [CrossRef]

- Lamine, A. (2025). G7 investors prefer cryptocurrencies, gold or digital gold to hedge their risk? Insights from quantile time frequency connectedness. International Review of Economics & Finance, 104, 104646. [CrossRef]

- Maghyereh, A., & Abdoh, H. (2020). Tail dependence between Bitcoin and financial assets: Evidence from a quantile cross-spectral approach. International Review of Financial Analysis, 71, 101545. [CrossRef]

- Matkovskyy, R., & Jalan, A. (2019). From financial markets to Bitcoin markets: A fresh look at the contagion effect. Finance Research Letters, 31, 93–97. [CrossRef]

- Mejri, S., Leccadito, A., & Yildirim, R. (2025). Dynamic responses of Bitcoin, gold, and green bonds to geopolitical risk: A quantile wavelet analysis. Borsa Istanbul Review, 25(6), 1183–1207. [CrossRef]

- Mensi, W., El Khoury, R., Ali, S. R. M., Vo, X. V., & Kang, S. H. (2023). Quantile dependencies and connectedness between the gold and cryptocurrency markets: Effects of the COVID-19 crisis. Research in International Business and Finance, 65, 101929. [CrossRef]

- Mensi, W., Gubareva, M., Ko, H.-U., Vo, X. V., & Kang, S. H. (2023). Tail spillover effects between cryptocurrencies and uncertainty in the gold, oil, and stock markets. Financial Innovation, 9(1). [CrossRef]

- Owusu Junior, P., Adam, A. M., & Tweneboah, G. (2020). Connectedness of cryptocurrencies and gold returns: Evidence from frequency-dependent quantile regressions. Cogent Economics & Finance, 8(1). [CrossRef]

- Reboredo, J. C. (2013). Is gold a safe haven or a hedge for the US dollar? Implications for risk management. Journal of Banking & Finance, 37(8), 2665–2676. [CrossRef]

- Selmi, R., Mensi, W., Hammoudeh, S., & Bouoiyour, J. (2018). Is Bitcoin a hedge, a safe haven or a diversifier for oil price movements? A comparison with gold. Energy Economics, 74, 787–801. [CrossRef]

- Wang, P., Liu, X., & Wu, S. (2022). Dynamic Linkage between Bitcoin and Traditional Financial Assets: A Comparative Analysis of Different Time Frequencies. Entropy, 24(11), 1565. [CrossRef]

- Wu, S., Tong, M., Yang, Z., & Derbali, A. (2019). Does gold or Bitcoin hedge economic policy uncertainty? Finance Research Letters, 31, 171–178. [CrossRef]

- Yu, J., Shang, Y., & Li, X. (2021). Dependence and Risk Spillover among Hedging Assets: Evidence from Bitcoin, Gold, and USD. Discrete Dynamics in Nature and Society, 2021, 1–20. [CrossRef]

- Zeng, T., Yang, M., & Shen, Y. (2020). Fancy Bitcoin and conventional financial assets: Measuring market integration based on connectedness networks. Economic Modelling, 90, 209–220. [CrossRef]

- Zhang, H., & Wang, P. (2021). Does Bitcoin or gold react to financial stress alike? Evidence from the U.S. and China. International Review of Economics & Finance, 71, 629–648. [CrossRef]

Figure 1.

Conceptual Research Framework of the CFQR Approach.

Figure 2.

Frequency–Quantile Causality Dominance Map (Full Sample).

Figure 3.

Frequency–Quantile Causality Dominance Map (Stress Regime).

Figure 4.

Frequency–Quantile Causality Dominance Map (Normal Regime).

Figure 5.

Time-Varying Probability of the Market Stress Regime (Endogenous Classification).

Table 1.

Descriptive Statistics of the Variables (n = 3,222).

| Variable | Mean | Std. Dev. | Min | Max | Skewness | Kurtosis |

|---|---|---|---|---|---|---|

| Bitcoin returns (r_BTC) | 0.0027 | 0.0585 | -0.8488 | 1.4744 | 3.960 | 148.848 |

| Gold returns (r_GOLD) | 0.0003 | 0.0097 | -0.0924 | 0.0487 | -0.527 | 8.310 |

| Change in VIX (d_VIX) | 0.0001 | 1.8586 | -18.7100 | 24.8600 | 2.159 | 36.579 |

| U.S. dollar index returns (r_DXY) | 0.0001 | 0.0313 | -0.0209 | 0.0187 | 0.081 | 6.188 |

| Change in U.S. 10-year yield (d_US10Y) | 0.0007 | 0.0522 | -0.3000 | 0.2900 | -0.007 | 4.897 |

Table 2.

Frequency–Quantile CFQR Dominance Summary (Full Sample).

| Frequency horizon | Low quantiles (0.1–0.3) | Mid quantiles (0.4–0.6) | High quantiles (0.7–0.9) |

|---|---|---|---|

| Short-run | None (Net = −0.360) | None (Net = 0.211) | None (Net = −0.020) |

| Medium-run | None (Net = −0.594) | None (Net = −0.112) | None (Net = −1.126) |

| Long-run | None (Net = −1.083) | None (Net = 0.730) | GOLD → BTC (Net = 2.891)* |

Note: “Net” denotes the average difference between gold-to-Bitcoin and Bitcoin-to-gold causality based on Wald-type quantile Granger tests. Significance is assessed at the 5% level.

Table 3.

Summary Statistics of Regime Characteristics.

| Regime | Observations share (%) | Avg duration (days) | BTC sd | GOLD sd | r_DXY mean | d_VIX mean | d_US10Y mean |

|---|---|---|---|---|---|---|---|

| Stress | 15.6735 | 1.6396 | 0.1373 | 0.0113 | 0.0003 | 0.2888 | −0.0014 |

| Normal | 84.3265 | 8.7929 | 0.0236 | 0.0094 | 0.0001 | −0.0536 | 0.0011 |

Table 4.

Validation of the Regime Classification (Endogenous vs. VIX-Based Indicator).

| Endogenous regime | Stress | Normal |

|---|---|---|

| Stress | 115 | 390 |

| Normal | 530 | 2187 |

| Agreement | 0.714 | |

| Cohen’s kappa | 0.029 | |

| VIX threshold (80th pct) | 21.596 | |

| Aligned N | 3222 |

Table 5.

Hedging Effectiveness of Gold against Bitcoin under Stress Regimes.

| Panel A. Variance-based hedging | ||||||||

|---|---|---|---|---|---|---|---|---|

| Regime | N | h* | Var(BTC) | Var(Hedged) | Reduction (%) | |||

| Stress (p ≥ 0.50) | 505 | 0.82 | 0.0188 | 0.01876 | 0.46 | |||

| Panel B. Downside risk hedging | ||||||||

| Measure | BTC | Hedged | Reduction (%) | |||||

| Semi-variance | 0.00779 | 0.00769 | 1.30 | |||||

| CVaR (5%) | −0.265 | −0.261 | 1.60 | |||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.