Submitted:

31 January 2026

Posted:

02 February 2026

You are already at the latest version

Abstract

This paper examines the expansion of bank lending in Kosovo during 2015–2025, using two primary indicators: (i) the annual value of newly originated loans and (ii) the effective interest rate charged on these loans. To provide additional context on financial deepening, the analysis also reports changes in the outstanding stock of loans over 2020–2025 and summarizes selected payment infrastructure indicators for 2024 (ATM/POS terminals and payment cards). The annual series indicates that new loan origination increased from €1.102 billion in 2015 to €2.684 billion in 2025, while effective interest rates declined from 8.3% toward a 6.0–6.5% range, with a modest uptick in 2025 relative to 2024. Methodologically, the paper combines descriptive statistics, year-on-year growth rates, compound annual growth (CAGR), correlation analysis, and an exploratory ordinary least squares (OLS) specification to characterize co-movements between borrowing costs and new lending volumes. The results point to sustained long-run lending expansion (CAGR ≈ 9.3% per year), whereas recent movements in effective rates may reflect gradual risk repricing and evolving funding conditions rather than a reversal of credit demand. The findings carry implications for financial stability surveillance, transparency of the total cost of credit, and macroprudential monitoring, and are discussed in light of CBK publications and the broader literature on the bank lending channel.

Keywords:

bank lending

; new loan origination

; effective interest rate

; credit growth

; financial stability

; Kosovo

1. Introduction

The banking sector in Kosovo plays a central role in financial intermediation. Lending to households and firms constitutes a primary channel through which consumption smoothing, business investment, and working-capital financing are supported. This role is especially pronounced in small, highly euroised economies with limited domestic capital market depth, where commercial banks remain the main conduit for allocating savings to productive economic activity.Recent developments suggest a notable acceleration in credit activity. In 2025, Kosovo reportedly recorded a historical high in newly originated loans, reaching €2.684 billion, which represents a 3.8% increase relative to 2024 (€2.587 billion). Over the same period, the effective interest rate on new loans increased modestly from 6.1% in 2024 to 6.4% in 2025, indicating a mild upward adjustment after several years of broadly stable or declining borrowing costs. The coexistence of expanding lending volumes with a slight increase in effective rates is analytically important: it raises questions about the relative strength of credit demand, the evolution of credit supply conditions, the role of competition in the banking sector, and the extent to which lending growth reflects changes in risk pricing or in the composition of borrowers and loan products.Beyond credit quantities and prices, payment infrastructure provides complementary evidence on financial modernisation and the diffusion of formal financial services. According to the Central Bank of the Republic of Kosovo (CBK), by end-2024 Kosovo had 635 ATMs and 20,913 POS terminals, alongside 1,401,086 debit cards and 194,667 credit cards. The expansion of electronic payment instruments can affect transaction formalisation, strengthen the information environment for lenders, and potentially influence household credit behaviour through greater integration into the formal banking system.Against this background, the aim of this paper is to: (i) document and interpret trends in new loan origination and effective interest rates in Kosovo over 2015–2025; (ii) assess their statistical co-movement using descriptive measures and exploratory econometric tools; and (iii) discuss implications for financial stability surveillance, cost-of-credit transparency, and policy. The paper contributes by providing a structured empirical synthesis of annual lending indicators and by interpreting the observed dynamics through a framework grounded in the literature on the bank lending channel and macro-financial linkages.The remainder of the paper is organised as follows. Section 2 reviews the relevant literature. Section 3 describes the data and methodology. Section 4 presents the empirical results and graphical evidence. Section 5 discusses the findings and their implications for financial stability and policy. Section 6 concludes and outlines directions for future research.

1.1. Research Objectives and Questions

The overarching objective of this study is to evaluate the evolution of new bank lending in Kosovo and the associated dynamics of borrowing costs, proxied by the effective interest rate on newly originated loans. The analysis is designed to provide an empirically grounded account of credit expansion and to clarify its relevance for financial stability and policy discussions.

Specifically, the study pursues four objectives:

(i) To document the trend in new loan origination over 2015–2025;

(ii) To compute annual growth rates and descriptive indicators that summarize the level and variability of new lending and effective interest rates;

(iii) To examine the statistical association between effective interest rates and new lending volumes using correlation measures and an exploratory linear specification; and

(iv) To discuss the implications of observed lending dynamics for financial stability surveillance and cost-of-credit transparency.

Accordingly, the paper addresses the following research questions:

RQ1: How has new loan origination evolved in Kosovo over the period 2015–2025?

RQ2: How has the effective interest rate on new loans changed over time, and what might the modest increase in 2025 indicate regarding risk pricing and funding conditions?

RQ3: Is there evidence of a measurable statistical relationship between effective interest rates and new lending volumes in the annual data?

RQ4: What are the implications of sustained lending expansion for financial stability monitoring and for improving transparency in the total cost of credit?

2. Literature Review

The literature relevant to this study can be organised into three complementary strands: (i) the bank lending (credit) channel and the role of interest rates in shaping credit supply and demand; (ii) credit cycles and macro-financial risks, including the rationale for macroprudential policy; and (iii) evidence from small and highly euroised economies, where banking systems tend to dominate financial intermediation and credit conditions can carry outsized macroeconomic implications.

2.1. The Credit Channel and Borrowing Costs

In the classic credit-channel framework, Bernanke and Blinder (1988) and Bernanke and Gertler (1995) argue that banks influence aggregate demand not only through the general level of interest rates but also via changes in credit supply and lending conditions. The effectiveness of this mechanism depends on how banks adjust their balance sheets and underwriting behavior in response to shocks. Empirically, Kashyap and Stein (2000) show that balance-sheet strength and liquidity conditions shape the transmission of monetary policy through bank lending, implying that loan supply is not frictionless and can amplify macroeconomic fluctuations.A related implication is that the headline or nominal interest rate alone does not fully describe borrowers’ financing costs. The effective interest rate, which incorporates fees and other charges embedded in loan contracts, is essential for measuring the total cost of borrowing and for ensuring transparency and comparability across loan products—particularly in consumer and mortgage lending, where pricing structures can differ materially across institutions.

2.2. Credit Cycles, Systemic Risk, and Macroprudential Policy

A second strand emphasizes the macro-financial consequences of sustained credit expansion. Borio (2014) argues that financial cycles can be longer and more pronounced than business cycles, reflecting persistent leverage dynamics and shifts in risk appetite, and therefore require dedicated macroprudential instruments to mitigate the build-up of systemic vulnerabilities. Historical evidence in Schularick and Taylor (2012) further indicates that rapid credit growth is strongly associated with subsequent banking crises, highlighting credit aggregates as key early-warning indicators for systemic risk monitoring. Consistent with this, Claessens and Kose (2018) stress the importance of macro-financial linkages and the need to integrate financial-sector analysis into broader macroeconomic policymaking and surveillance.

2.3. Small, Euroised Economies and the Kosovo Context

In small and highly euroised economies, the dominance of banks in financial intermediation often implies that credit conditions are tightly linked to both household welfare and firms’ investment capacity. For Kosovo, the Central Bank of the Republic of Kosovo (CBK)—particularly through its Financial Stability Reports—provides a risk-based assessment of the financial system, including liquidity conditions, portfolio quality, and resilience indicators. These sources are central for interpreting credit dynamics through a financial stability lens.A further dimension concerns financial inclusion and payment infrastructure (cards, POS terminals, ATMs), which can support financial modernisation, reduce transaction frictions, and strengthen the informational environment for lenders. Diffusion of electronic payment instruments may also affect consumer borrowing behavior, including demand for short-term credit products and broader engagement with formal banking services.

2.4. Micro-Level Mechanisms and Complementary Finance Literature

Finally, within the work of Rexhepi and co-authors, several themes are relevant for the micro-foundations of financial intermediation in Kosovo, including financial accounting management, professional ethics in accounting and auditing, and alternative financing instruments such as factoring. These contributions are useful for understanding informational quality, governance practices, and financing options that shape access to finance—especially for firms operating under constraints typical of bank-centered financial systems.

3. Data and Methodology

3.1. Data Sources and Coverage

The core dataset consists of annual observations for 2015–2025 on (i) the value of newly originated bank loans and (ii) the effective interest rate applied to these new loans. These figures are compiled from publicly reported series that reference statistics of the Central Bank of the Republic of Kosovo (CBK). To enrich the descriptive context on financial modernisation and inclusion, the paper additionally draws on CBK’s publication on payment card usage (data reported up to 31 December 2024), which provides indicators such as the number of ATMs, POS terminals, and the stock of debit and credit cards.Given that the primary lending series is annual and aggregated, the analysis is framed as a macro-descriptive and exploratory empirical assessment rather than a structural identification exercise. Where relevant, the discussion acknowledges that both credit volumes and borrowing costs may be jointly influenced by macroeconomic conditions and banking-sector dynamics over time.

3.2. Empirical Strategy

The empirical strategy combines graphical and statistical tools to summarise trends and to characterise the association between lending volumes and borrowing costs. Specifically, the analysis includes:

- Descriptive statistics (mean, dispersion, minimum/maximum) for new loans and effective interest rates.

- Growth accounting, including year-on-year (YoY) growth rates and compound annual growth rate (CAGR) for new lending over 2015–2025.

- Correlation analysis, using the Pearson correlation coefficient to assess linear co-movements between new loans and effective interest rates.

- Exploratory regression analysis, using a parsimonious ordinary least squares (OLS) specification of the form:

The OLS specification is interpreted as descriptive rather than causal. The relationship between lending volumes and effective interest rates may be confounded by omitted factors—such as income growth, inflation, expectations, loan composition, underwriting standards, funding conditions, and banking competition—which can affect both variables simultaneously. Moreover, both series exhibit time trends, which may mechanically influence correlation and regression estimates in small samples. For these reasons, regression outputs are treated as an empirical summary of co-movement rather than evidence of a structural lending relationship.

3.3. Variables

The study employs the following primary variables:

- New loans (EUR million): the annual value of newly originated loans granted by the banking sector in Kosovo.

- Effective interest rate (%): the annual average effective interest rate applied to newly originated loans, reflecting the aggregated total cost of borrowing.

In addition, the paper uses the following contextual indicators descriptively (where available): the stock of outstanding loans (EUR billion) and payment infrastructure indicators (number of ATMs, POS terminals, debit cards, and credit cards).

4. Results

4.1. Descriptive Analysis and Trends (2015–2025)

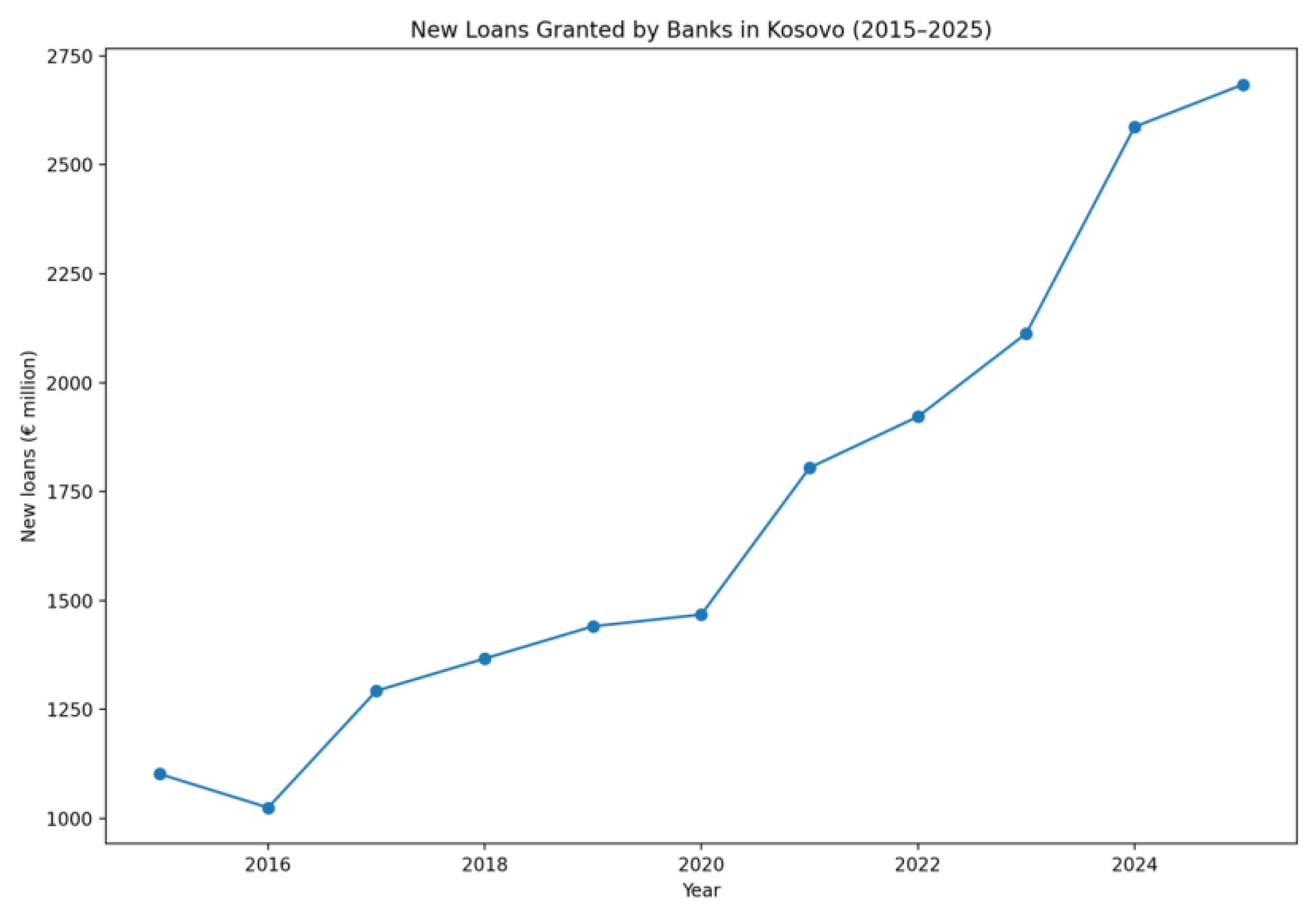

The annual series for 2015–2025 points to a sustained expansion in new bank lending in Kosovo. Over the full period, the value of newly originated loans rose from €1,102 million in 2015 to €2,684 million in 2025. This corresponds to an approximate cumulative increase of 143%, and implies a compound annual growth rate (CAGR) of about 9.3% per year. Taken together, these indicators suggest a substantial deepening of bank-based financial intermediation over the last decade.The growth pattern is not uniform across years, indicating phases of acceleration and moderation. Following a short-term contraction in 2016, new lending expanded strongly in 2017 and continued to increase at a steadier pace in 2018–2020. A notable acceleration emerges again in 2021 and 2024, when annual growth rates exceed 20%, consistent with episodes of intensified credit activity. By contrast, 2025 records a smaller year-on-year increase (despite reaching the highest observed level), suggesting a potential transition from rapid expansion to a more moderate growth phase—while still maintaining record-high origination volumes.From an interpretive standpoint, sustained growth in new loan origination can reflect several forces operating jointly: rising credit demand associated with household consumption and housing needs, improved access to finance for firms, competitive lending strategies among banks, and broad financial modernisation (including greater use of formal payment channels). At the same time, persistent credit expansion increases the importance of monitoring credit quality, borrower affordability, and pricing discipline—issues that are addressed later in the discussion through the lens of financial stability and cost-of-credit transparency.

Table 1.

New loans and effective interest rate in Kosovo (2015–2025).

| Year | New loans (€ million) | Effective rate (%) | YoY growth (%) |

|---|---|---|---|

| 2015 | 1,102 | 8.3 | — |

| 2016 | 1,025 | 7.5 | -6.99 |

| 2017 | 1,293 | 6.8 | 26.15 |

| 2018 | 1,367 | 6.6 | 5.72 |

| 2019 | 1,441 | 6.5 | 5.41 |

| 2020 | 1,468 | 6.2 | 1.87 |

| 2021 | 1,805 | 6.0 | 22.96 |

| 2022 | 1,922 | 6.0 | 6.48 |

| 2023 | 2,113 | 6.5 | 9.94 |

| 2024 | 2,587 | 6.1 | 22.43 |

| 2025 | 2,684 | 6.4 | 3.75 |

Table 2.

Descriptive statistics (2015–2025).

| Variable | Mean | Std. dev. | Minimum | Maximum |

|---|---|---|---|---|

| New loans (€ million) | 1709.73 | 565.29 | 1025.0 | 2684.0 |

| Effective interest rate (%) | 6.63 | 0.7 | 6.0 | 8.3 |

4.2. Figures

Figure 1.

New loans granted by banks in Kosovo (2015–2025).

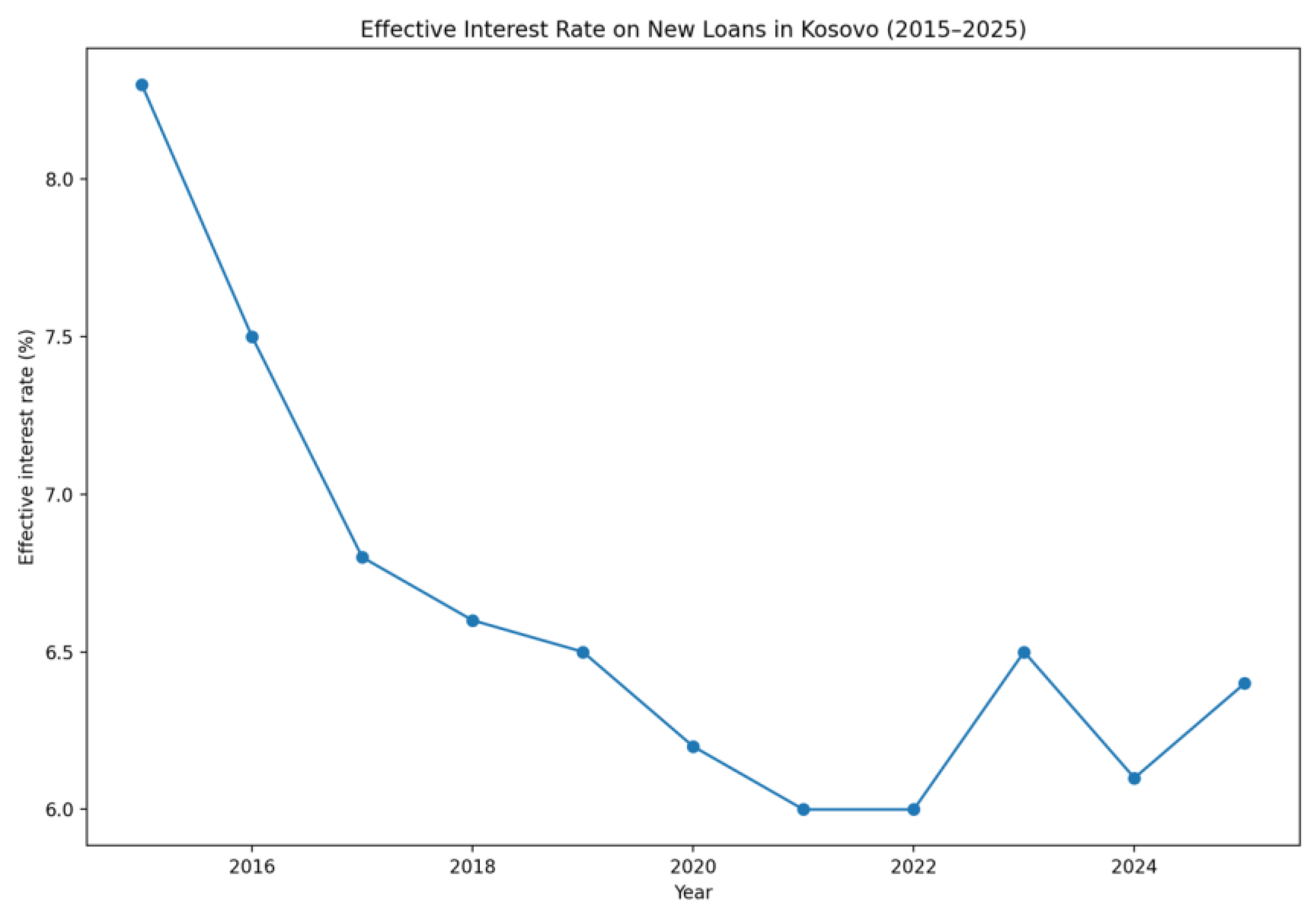

Figure 2.

Effective interest rate on new loans in Kosovo (2015–2025).

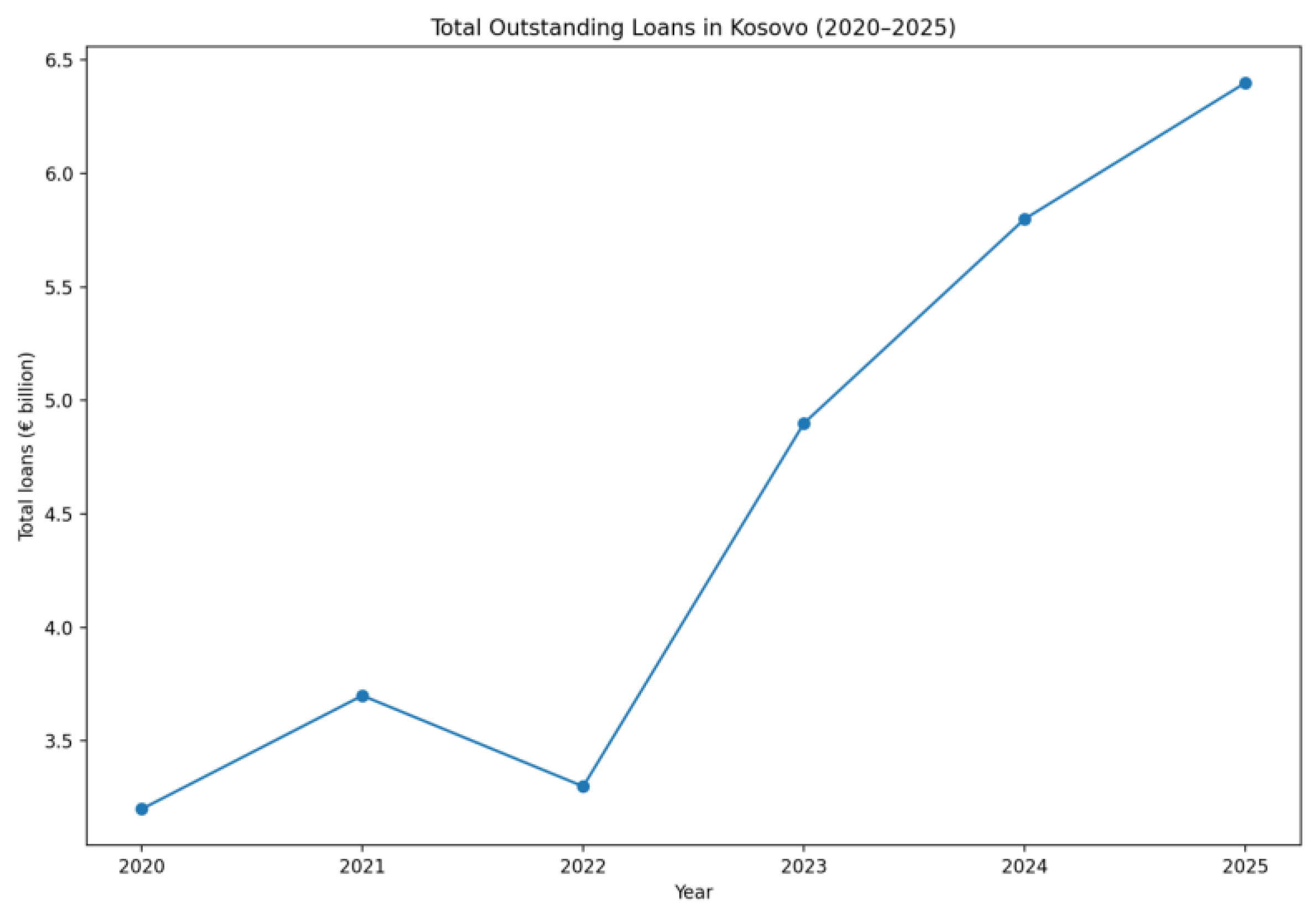

Figure 3.

Outstanding loan stock in Kosovo (2020–2025).

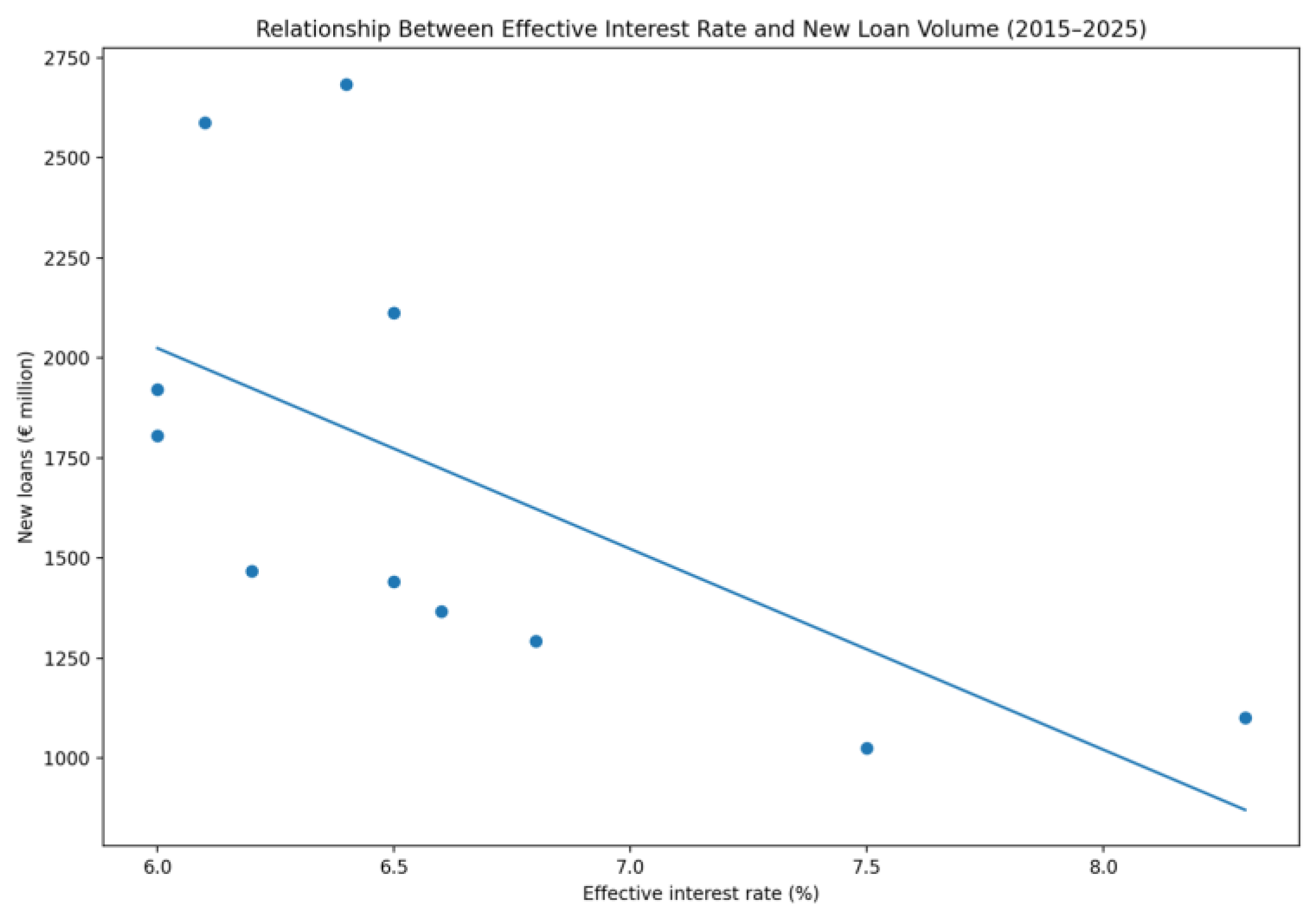

Figure 4.

Relationship between effective interest rate and new loan volumes (2015–2025).

4.2. Effective Interest Rate Dynamics (2015–2025)

The effective interest rate on newly originated loans displays a clear long-run downward trajectory over 2015–2025, followed by more visible short-run variation in the final years of the sample. In 2015, the effective rate stands at 8.3%, after which it declines to 7.5% (2016) and 6.8% (2017). This downward movement continues gradually through 2018–2022, reaching 6.6% (2018), 6.5% (2019), 6.2% (2020), and stabilising at 6.0% in both 2021 and 2022. Overall, these patterns indicate a substantial reduction in average borrowing costs compared with the beginning of the period, consistent with improved pricing efficiency and/or evolving market conditions in the banking sector.A notable departure from earlier stability occurs in the final part of the sample. The effective interest rate increases to 6.5% in 2023, then declines to 6.1% in 2024, before rising again to 6.4% in 2025. Although the magnitude of these changes is moderate, the sequence suggests that borrowing costs are no longer following a monotonic decline but have entered a phase of rate normalisation and repricing. This pattern is economically plausible in a highly euroised setting where external financial conditions—particularly euro-area interest rate movements—can affect banks’ funding costs and risk premia.Importantly, the effective interest rate is an aggregate indicator and may reflect composition effects as well as changes in the underlying price of credit. Shifts in the mix of household and corporate lending, maturities, collateralisation, and borrower risk categories can mechanically alter the annual average effective rate. For example, a higher share of consumer loans or longer-maturity lending may raise the aggregate effective rate even if pricing in other segments remains stable. Therefore, the 2025 uptick is consistent with (i) gradual risk repricing, (ii) shifts in the composition of new lending, and/or (iii) changing external funding conditions—rather than definitive evidence of broad tightening in credit supply.Graphical evidence supports these observations: Figure 2 illustrates the long-run decline from 2015 to the early 2020s, followed by greater fluctuation from 2023 onward. When considered jointly with the continued growth of new loan origination (Section 4.1), these interest-rate dynamics suggest that Kosovo’s credit expansion remained resilient while borrowing costs adjusted modestly in recent years.

4.3. Correlation and OLS Regression (Exploratory)

To characterise the association between borrowing costs and new loan origination, the analysis first computes the Pearson correlation between annual new lending volumes and the effective interest rate over 2015–2025. The estimated correlation is r = −0.622, indicating a moderately strong negative linear association: in this annual series, years with lower effective interest rates tend to coincide with higher volumes of newly originated loans. Importantly, this result should be interpreted with caution. Both variables evolve over time—most notably, new lending displays a pronounced upward trend—so the correlation may partly capture common time-related dynamics rather than a stable structural relationship.As a complementary descriptive exercise, an ordinary least squares (OLS) regression is estimated using the specification

NewLoanst=α+β ⋅EffectiveRatet + εt .

The estimated slope coefficient (β) is negative, consistent with the correlation result. The regression explains approximately 38.7% of the variation in new lending volumes (R² ≈ 0.387), and the coefficient is statistically significant at the 5% level (p ≈ 0.041) in this small annual sample. These findings should not be interpreted as causal. The specification omits potentially important determinants of lending (e.g., income growth, inflation, expectations, loan composition, underwriting standards, and funding conditions) and does not control for time trends or structural breaks. Accordingly, the OLS output is best viewed as a compact statistical summary that formalises the observed negative co-movement between effective rates and new lending volumes in the available annual data.Interpretive note. Given the strong time trend in lending volumes, future work could improve inference by estimating models in growth rates (e.g., YoY changes), adding time controls, or using higher-frequency data (monthly/quarterly) to better separate demand, supply, and pricing effects.

4.4. Outstanding Loan Stock Trends (2020–2025)

To complement the flow-based analysis of newly originated loans, this subsection considers the evolution of the outstanding stock of loans in Kosovo over 2020–2025, which provides a broader measure of financial intermediation and balance-sheet exposure in the banking sector. The reported figures indicate that the total loan stock increased from approximately €3.20 billion in 2020 to about €6.40 billion in 2025, implying that the stock of credit roughly doubled within five years. This expansion is consistent with the strong growth observed in annual new lending volumes and suggests a sustained accumulation of credit on bank balance sheets.The path of the loan stock also reveals changes in the pace of expansion. After rising from €3.20 billion (2020) to €3.70 billion (2021), the series shows a decline to €3.30 billion (2022), followed by a marked increase to €4.90 billion (2023) and continued growth to €5.80 billion (2024) and €6.40 billion (2025). The temporary decrease in 2022 may reflect measurement and timing effects (e.g., stock–flow differences, repayments, write-offs, or portfolio reclassification), highlighting the importance of interpreting stock-based indicators alongside new lending flows and portfolio-quality information.From an analytical standpoint, growth in the loan stock carries two main implications. First, it signals expanding credit intermediation capacity and potentially stronger financing support for households and firms. Second, it increases the relevance of financial stability surveillance, since a larger outstanding stock of loans implies greater exposure to credit risk and borrower affordability shocks. Consequently, the stock dynamics reinforce the need for monitoring loan composition, maturity structure, and repayment performance, particularly during periods of accelerated credit growth.Graphical evidence summarises this pattern. Figure 3 illustrates the trajectory of outstanding loans over 2020–2025, highlighting both the scale of expansion and the acceleration in the later years of the sample. When interpreted together with new loan origination trends (Section 4.1 and Section 4.2), the loan stock evidence suggests that Kosovo’s banking sector experienced a broad-based strengthening of credit activity, with implications for both economic financing and prudential oversight.

5. Discussion

The evidence presented in Section 4.1, Section 4.2 and Section 4.3 indicates a pronounced and persistent expansion in new bank lending in Kosovo over 2015–2025, alongside a long-run decline in effective borrowing costs relative to the beginning of the period. Interpreted jointly, these dynamics are consistent with deepening financial intermediation in a bank-centred system, where households and firms increasingly rely on formal credit to finance consumption, housing, investment, and working capital. The discussion below interprets these findings through four lenses: (i) structural drivers of lending growth, (ii) interest-rate dynamics and risk pricing, (iii) the role of payment infrastructure and information, and (iv) financial stability and policy relevance.

5.1. Credit Expansion as Deepening Intermediation (Levels and Phases)

The long-run increase in new loan origination—culminating in a record value in 2025—suggests that the banking sector has expanded its role in allocating savings toward the real economy. The time profile of growth is also informative: rather than a smooth linear increase, the data show episodes of acceleration (notably 2021 and 2024, with growth above 22%) followed by moderation in 2025. This pattern is compatible with a credit market transitioning from a “catch-up” phase (rapid financial deepening, product expansion, and broader access) toward a more mature phase where growth remains positive but becomes less explosive.Importantly, sustained credit growth in a small economy can be driven by both structural and cyclical factors. Structural drivers may include the expansion of banking networks and products, increased penetration of household lending (including housing-related credit), improvements in credit information systems, and stronger competition among banks. Cyclical drivers, by contrast, include fluctuations in income expectations, labour market conditions, and broader macroeconomic sentiment. Given the annual nature of the data, distinguishing these channels precisely is not possible here; however, the presence of sharp growth spikes in specific years suggests that cyclical elements likely interacted with longer-term structural deepening.

5.2. Borrowing Costs, Effective Rates, and the Meaning of the 2025 Uptick

The long-run decline in effective interest rates from the earlier years of the series toward the 6.0–6.5% range is consistent with a broad environment of falling borrowing costs and/or improved pricing efficiency. Several mechanisms plausibly contribute:

- Competitive dynamics: As competition strengthens, spreads can narrow and banks may price more aggressively to gain market share, particularly in standardised segments (e.g., consumer loans with predictable risk profiles).

- Improved borrower risk and screening: Better screening and underwriting technologies can reduce expected losses, allowing lower risk premia—especially if credit information becomes more reliable.

- Funding structure and liquidity conditions: A stronger deposit base and stable liquidity conditions tend to support lower loan pricing, because funding costs and liquidity premia are contained.

- Institutional/regulatory convergence: Gradual alignment with European-style disclosure and consumer protection norms can improve market discipline and reduce opaque fee structures, making borrowing costs more comparable.

Against this long-run decline, the modest increase in the effective rate in 2025 deserves attention. A mild uptick does not necessarily imply tightening credit conditions; it may reflect risk repricing or changes in the composition of new lending. For example, a higher share of consumer credit, longer maturities, or riskier borrower segments can raise the aggregate effective rate even if pricing in other segments remains stable. Similarly, external financial conditions—especially those influenced by euro-area monetary and financial developments—can affect bank funding costs and risk premia in euroised economies. Thus, the 2025 pattern (record lending volume with a small rise in effective rates) is consistent with a market where demand remains resilient and banks adjust pricing at the margin to reflect evolving cost-of-funds and risk considerations.

5.3. Payment infrastructure as an Informational and Behavioural Channel

The high number of POS terminals and ATMs, together with wide diffusion of debit and credit cards, is more than a “modernisation statistic.” In bank-based systems, payment infrastructure can influence credit outcomes through at least two channels:

- Formalisation and traceability: Greater electronic payment usage increases recorded transaction flows, which can improve banks’ ability to infer income stability, spending patterns, and repayment capacity. Better information typically supports more efficient credit allocation—either expanding access for creditworthy borrowers or tightening access where risk is elevated.

- Behavioural and product channels: Card usage can shape demand for consumer credit and short-term borrowing products, particularly when consumption is increasingly executed through electronic instruments. In such settings, credit growth can be partly driven by product innovation and distribution channels rather than purely by changes in macro fundamentals.

In Kosovo’s context, this suggests that payment system development may be reinforcing credit expansion by improving the informational environment and lowering frictions in accessing financial services. At the same time, it highlights the importance of monitoring consumer credit exposures and ensuring clear disclosure of total borrowing costs.

5.4. Financial Stability Interpretation: What Matters for Surveillance

Sustained credit expansion is not inherently problematic; it can support welfare and growth when credit is allocated efficiently and borrower debt burdens remain sustainable. However, financial stability concerns tend to rise when credit growth becomes rapid, broad-based, or concentrated in specific high-risk segments. The key issue is whether lending growth is accompanied by:

- Sound underwriting standards (income verification, realistic affordability assessments, prudent collateral valuation),

- Stable portfolio quality (non-performing loan dynamics and early warning indicators),

- Adequate capital and liquidity buffers to absorb shocks, and

- Transparent pricing, particularly via consistent disclosure of the effective interest rate and other cost components.

The empirical finding of a negative correlation and a negative OLS slope between effective rates and new loan volumes is informative as a descriptive co-movement, but it does not imply that rate movements “drive” lending in a mechanical way. For stability surveillance, the more relevant questions are whether debt service burdens increase, whether loan growth is increasingly concentrated in vulnerable borrower groups, and whether banks’ risk pricing remains consistent with underlying credit risk.

5.5. Implications for Future Research and Data Needs

The analysis also points to clear priorities for strengthening empirical inference in future Kosovo-focused work. Annual data are useful for documenting long-run trends, but stronger identification would benefit from: (i) higher-frequency series (quarterly or monthly), (ii) composition data (households vs. firms, maturity structure, sectoral allocation), and (iii) controls capturing macro conditions (income, inflation, labour market indicators) and bank-side variables (deposit growth, funding costs, NPL ratios, capital adequacy). Such data would allow more robust separation of credit demand, credit supply, and pricing effects—especially in years showing sharp accelerations.

6. Implications and Recommendations

The findings have clear implications for consumer protection, financial stability surveillance, and the longer-term development of Kosovo’s bank-centred financial system. Given sustained credit expansion alongside modest fluctuations in effective borrowing costs, policy priorities should focus on transparent pricing, risk-sensitive credit monitoring, and data infrastructure that enables evidence-based oversight. The recommendations below are formulated to be feasible within the institutional setting where commercial banks price loans individually and supervisory authorities rely primarily on prudential and macroprudential tools rather than direct price controls.

6.1. Strengthen Transparency and Financial Literacy Through Effective-Rate Disclosure

Recommendation 1: Promote the effective interest rate as the central and standardised disclosure metric for household and SME borrowers.

- Rationale: Effective rates better approximate the total cost of borrowing than nominal rates because they embed fees and other charges that materially affect affordability and comparability. Clear and consistent disclosure reduces information asymmetry, improves market discipline, and can foster healthier competition among banks on transparent terms.

- Implementation measures:

Require consistent presentation of effective rates in loan advertisements and pre-contractual information sheets, using harmonised templates.

Encourage “comparison tables” or publicly accessible calculators that translate effective rates into monthly instalments and total repayment amounts under standard assumptions (loan size, maturity).

Integrate effective-rate concepts into targeted financial literacy initiatives (e.g., for first-time borrowers, consumer credit users, and SMEs).

- Expected outcome: Better-informed borrowing decisions, improved comparability of products, and reduced likelihood of repayment stress linked to misunderstood credit costs.

6.2. Enhance Macroprudential Monitoring And Borrower Affordability Stress Testing

Recommendation 2: Expand macroprudential monitoring to track credit growth more granularly and routinely assess borrower resilience to adverse shocks.

- Rationale: Sustained or rapidly accelerating credit growth can increase cyclical vulnerabilities, especially when concentrated by sector, maturity, or borrower type. Monitoring should therefore move beyond aggregate volumes and incorporate composition and affordability.

- Implementation measures:

Monitor growth by households vs. firms, maturity buckets, and (where possible) sectoral allocation (e.g., construction, trade, services).

Institutionalise regular debt-service affordability stress tests, including scenarios with higher interest rates and income shocks.

Use early-warning dashboards incorporating indicators such as loan growth, delinquency transition rates, and concentration measures.

- Expected outcome: Earlier identification of risk build-up, improved calibration of supervisory attention, and stronger resilience in adverse macro-financial scenarios.

6.3. Improve data quality, accessibility, and research replicability

Recommendation 3: Expand open-format publication of time series for key lending indicators to support deeper empirical analysis and transparency.

- Rationale: Annual, aggregated series are useful for documenting long-run trends but limit inference on timing, composition, and the interplay between demand and supply. A stronger data infrastructure would improve surveillance, academic research, and public understanding.

- Implementation measures:

Publish machine-readable time series (CSV/Excel/API) for new lending flows, effective rates, and loan stock indicators.

Provide breakdowns by borrower segment, maturity, currency structure (where relevant), and credit purpose (e.g., housing vs. consumption vs. business investment), subject to confidentiality constraints.

Release metadata describing definitions, revisions, and methodology to ensure replicability.

- Expected outcome: Stronger evidence base for policy and research, easier cross-study comparability, and improved credibility of empirical results.

6.4. Diversify Financing Channels for SMEs and Support Alternative Instruments

Recommendation 4: Reduce exclusive dependence on traditional bank loans by developing complementary financing instruments for SMEs.

- Rationale: SMEs often face binding financing constraints due to limited collateral, informational opacity, and higher perceived risk. Diversifying instruments can ease constraints and improve allocation efficiency, especially during periods when banks tighten underwriting standards.

- Implementation measures:

Support the development of factoring and related receivables-based financing, which is particularly suitable for SMEs with stable invoices and trade relationships.

Explore targeted credit enhancement mechanisms (e.g., partial guarantees for eligible SME segments), while maintaining prudent risk-sharing to avoid moral hazard.

Encourage standardisation and legal clarity around receivables assignment and enforcement to reduce transaction costs in alternative financing markets.

- Expected outcome: Improved SME access to working capital, reduced credit concentration risk in bank balance sheets, and a more resilient financing ecosystem.

7. Study Limitations

This study has several limitations that should be considered when interpreting the empirical results and the associated policy implications.First, the analysis relies on an annual, aggregated time series for new loan origination and effective interest rates for 2015–2025, compiled from publicly reported figures that reference CBK statistics. Annual aggregation limits the ability to capture within-year dynamics, seasonality, and short-run adjustments in credit demand, credit supply, and pricing. It also reduces statistical power given the small sample size, which is particularly relevant for correlation and regression exercises.Second, the empirical design is intentionally parsimonious and does not include macroeconomic controls—such as GDP growth, inflation, remittances, unemployment, or broader measures of economic sentiment—that plausibly co-determine both borrowing costs and lending volumes. As a result, the OLS estimates should be interpreted as descriptive associations rather than causal effects. Relatedly, the analysis does not explicitly account for time trends, potential structural breaks, or regime shifts (e.g., changes in external financial conditions or domestic lending standards) that could influence both series and mechanically generate correlation.Third, the study does not incorporate bank-level supply indicators that are central to credit-supply interpretation, including deposits and funding conditions, net interest margins (NIM), non-performing loans (NPLs), capital adequacy, and liquidity buffers. Without such indicators, it is not possible to separate more precisely whether observed changes in lending volumes reflect shifts in credit demand, credit supply, or the composition of lending across borrower types and maturities.Fourth, the dataset does not provide detailed composition breakdowns (e.g., households versus firms, sectoral allocation, maturity structure, collateralisation, or loan purpose). Composition changes can materially affect the aggregate effective interest rate and the interpretation of lending growth, particularly if the mix of consumer lending, housing credit, and corporate lending changes over time.Future research can address these limitations by employing higher-frequency (monthly or quarterly) data, integrating macroeconomic and bank-level covariates, and adopting econometric designs that control for trends, structural breaks, and potential endogeneity (e.g., models in growth rates, time-series specifications, or bank-level panel approaches where available). Such extensions would allow more rigorous identification of the drivers of credit expansion and a clearer assessment of financial stability risks associated with rapid lending growth.

8. Conclusions

This paper examined the evolution of bank lending in Kosovo over 2015–2025, focusing on the annual value of newly originated loans and the effective interest rate as a proxy for the total cost of borrowing. The evidence documents a pronounced and persistent expansion in new loan origination across the period, culminating in a record level in 2025. In parallel, effective interest rates show a clear long-run decline relative to 2015, although the most recent years exhibit greater fluctuation, including a modest increase in 2025 compared with 2024. Considered jointly, these trends are consistent with deepening bank-based intermediation alongside gradual adjustments in risk pricing and/or changes in the composition of lending products and borrowers.The findings carry direct relevance for macro-financial surveillance in a bank-centred and highly euroised economy. Sustained credit expansion can support consumption smoothing, business activity, and investment; however, it also elevates the importance of monitoring cyclical vulnerabilities, borrower affordability, and the maintenance of prudent underwriting standards. In this context, strengthening the transparency of borrowing costs—particularly through consistent and prominent disclosure of the effective interest rate—remains essential for reducing information asymmetries, supporting informed borrower decisions, and improving comparability across loan products.From a methodological standpoint, the correlation and exploratory regression results provide a concise statistical summary of co-movement between effective rates and lending volumes in the available annual data, but they should not be interpreted as causal relationships. More rigorous inference will require higher-frequency data and richer covariates that capture macroeconomic conditions and bank-side supply factors. Accordingly, future research should prioritize: (i) monthly or quarterly series on new lending and interest rates, (ii) composition breakdowns (households versus firms, sectoral allocation, maturities, and loan purpose), and (iii) bank-level indicators (deposits, funding costs, NPLs, capitalization, and liquidity). Such extensions would enable stronger identification of credit demand and supply mechanisms and a more precise evaluation of macro-financial effects and financial stability implications.

References

- Bank for International Settlements. Credit-to-GDP gaps and the countercyclical capital buffer: Questions and answers; BIS, 2017. [Google Scholar]

- Bernanke, B. S.; Blinder, A. S. Credit, money, and aggregate demand. American Economic Review 1988, 78(2), 435–439, Working paper version: NBER Working Paper No. 2534. [Google Scholar] [CrossRef]

- Bernanke, B. S.; Gertler, M. Inside the black box: The credit channel of monetary policy transmission. Journal of Economic Perspectives 1995, 9(4), 27–48. [Google Scholar] [CrossRef]

- Borio, C. The financial cycle and macroeconomics: What have we learnt? Journal of Banking & Finance 2014, 45, 182–198. [Google Scholar] [CrossRef]

- Central Bank of the Republic of Kosovo. Statistical time series platform; CBK: Pristina, n.d. [Google Scholar]

- Central Bank of the Republic of Kosovo. Financial Stability Report No. 21; CBK: Pristina, 2025). Financial Stability Report No. 21 (January–December 2024. [Google Scholar]

- Central Bank of the Republic of Kosovo. Përdorimi i kartelave në Kosovë [Payment card usage in Kosovo] (data up to; CBK: Pristina, 2025. [Google Scholar]

- Claessens, S.; Kose, M. A. Frontiers of macrofinancial linkages. Journal of Financial Stability 2018, 40, 1–8. [Google Scholar]

- Demirgüç-Kunt, A.; Levine, R. Finance and inequality: Theory and evidence. Annual Review of Financial Economics 2009, 1(1), 287–318. [Google Scholar] [CrossRef]

- European Bank for Reconstruction and Development. Transition Report 2023–24; EBRD, 2024. [Google Scholar]

- European Central Bank. Financial integration and structure in the euro area (annual report); ECB, 2020. [Google Scholar]

- International Monetary Fund. Kosovo: Selected issues and country reports; n.d. [Google Scholar]

- Kashyap, A. K.; Stein, J. C. What do a million observations on banks say about the transmission of monetary policy? American Economic Review 2000, 90(3), 407–428. [Google Scholar] [CrossRef]

- Levine, R. Finance and growth: Theory and evidence. In Handbook of Economic Growth; Aghion, P., Durlauf, S., Eds.; Elsevier, 2005; Vol. 1A, pp. 865–934. [Google Scholar]

- McKinnon, R. I. Money and capital in economic development; Brookings Institution, 1973. [Google Scholar]

- Mishkin, F. S. The economics of money, banking, and financial markets, 12th ed.; Pearson, 2019. [Google Scholar]

- Monitor, et al. Kosova me rekord të ri kreditimi: 2.68 miliardë euro kredi të reja gjatë 2025. 2025. [Google Scholar]

- Murtezaj, I. M.; Rexhepi, B. R.; Xhaferi, B. S.; Xhafa, H.; Xhaferi, S. The study and application of moral principles and values in the fields of accounting and auditing. Pakistan Journal of Life and Social Sciences 2024, 22(2), 3885–3902. [Google Scholar]

- Rajan, R. G.; Zingales, L. Financial dependence and growth. American Economic Review 1998, 88(3), 559–586, Working paper version: NBER Working Paper No. 5758. [Google Scholar] [CrossRef]

- Rexhepi, B. R. Theory about factoring service. International Journal of Business and Technology 2021, 9(1), 26. [Google Scholar]

- Rexhepi, B. R. An outlook of the factoring industry in the world and in Kosovo. International Journal of Business and Technology 2022, 10(1), 1. [Google Scholar]

- Rexhepi, B. R. Developing factoring service for small and medium enterprises at Kosovo’s ProCredit Bank (Monograph); 2023. [Google Scholar]

- Rexhepi, B. R.; Rexhepi, F. G.; Xhaferi, B.; Xhaferi, S.; Berisha, B. I. Financial accounting management: A case of Ege Furniture in Kosovo. Quality – Access to Success 2024, 25, 200. [Google Scholar]

- Schularick, M.; Taylor, A. M. Credit booms gone bust: Monetary policy, leverage cycles, and financial crises, 1870–2008. American Economic Review 2012, 102(2), 1029–1061. [Google Scholar] [CrossRef]

- Schumpeter-style / development classics (as in your draft).

- Shaw, E. S. Financial deepening in economic development; Oxford University Press, 1973. [Google Scholar]

- Beck, T.; Demirgüç-Kunt, A.; Levine, R. Finance, inequality and the poor. Journal of Economic Growth 2007, 12(1), 27–49. [Google Scholar] [CrossRef]

- World Bank. Global Financial Development Report 2019/2020; World Bank, 2019. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.