Submitted:

03 January 2026

Posted:

05 January 2026

You are already at the latest version

Abstract

This empirical study examines how FinTech innovation is adopted, scaled, and sustained in a small and highly regulated market, such as Latvia. The triangulated analytical framework is applied in this study, integrating Rogers’ Innovation Diffusion Theory IDT [1], De Meyer’s Innovation Ecosystem framework [2], and the Value Chain Theory [3], [4]. This framework enables the exploration of the interaction between innovation characteristics, ecosystem relationships, and restructuring in the value chain. The data was collected from FinTech leaders, conventional financial institutions (banks), regulators, and associations, and it was analysed thematically. Based on the interviews with stakeholders, the relative advantage of Latvian FinTechs lies in their flexibility, speed, and trialability; however, the adoption barrier is the complexity of regulation and unevenness in infrastructure and institutional readiness. The authors found strong collaboration among the ecosystem's players but limited proactive regulatory engagement. This research provides a replicable model for cross-border or cross-sector analysis to assess the progress of innovation in regulatory and Environmental, Social and Governance ESG integration.

Keywords:

FinTech

; innovation ecosystem

; value proposition

; innovation diffusion

; sustainable business model

1. Introduction

FinTech disruption in the financial industry is driven by several factors, including its customer-centric approach, speed, and efficiency. Such traits of the FinTech solutions are due to Application Programming Interface APIs, FinTechs’ work, and partnerships with traditional financial institutions [5]. The smaller the economy, the greater the impact of FinTech on a country’s financial stability [6]. The ecosystem emerges more as a system of innovators and has a transformative impact on society [7]. Such is the case in Latvia, which has over 100 FinTech operating [8].

The primary research question for this study is: What roles do stakeholders in the FinTech Ecosystem Play in the diffusion, integration, alignment, and scaling of FinTech innovation in Latvia?

Roger’s Innovation Diffusion Theory is a foundational lens through which to analyse the growth and innovation of the FinTech sector. Prior studies have used this theory to determine the adoption of digital banking [5]. Also, to determine how FinTech businesses’ Innovation affects the value chain activities of micro and small enterprises (MSEs) [9].

The second analytical lens of this study is the De Meyer Innovation Ecosystem model, which conceptualises the stakeholders’ roles and their evolution from the niche innovator to the keystone player to the Orchestrator within the ecosystem’s development to co-create value through critical enablers like human capital, infrastructure, and regulatory coordination [10].

Value Chain Analysis is another lens through which to analyse FinTechs’ contribution to the financial industry, as they are both a disruptor and a crucial part. One example is that FinTech improves the risk assessment, reduces costs, and streamlines many operations, which leads to financial inclusion [11]. Also, in FinTech-driven ecosystems, supply chains tend to improve models’ financial efficiency, which aligns with Platform-based models [12].

Despite the global expansion of research on FinTech, the collective theoretical application of these three theories remains underexplored in small-market ecosystems, such as in Latvia. Smaller countries offer a unique innovation environment compared to large economies, due to their compact regulatory systems, limited talent pools, and export-oriented business models. Though these theories have been analysed separately before [5,10,11,13], they have not been examined from a singular analytical approach.

2. Literature Framework

The three theoretical business models, IDT, De Meyer’s Ecosystem Framework, and Value Chain Analysis, have not been studied together, but separately and independently in FinTech literature [5,10,11]. Therefore, this study addresses this gap and utilises the Latvian FinTech Ecosystem as the anchor for the empirical analysis.

Innovation Diffusion refers to the acceptance and eventual spread or diffusion of new products or services, ideas, or technologies [14]. The Innovation Diffusion Theory (IDT) by Rogers in 1962 suggested that five key attributes play a role in Innovation diffusion: Relative advantage, compatibility, complexity, trialability, and observability [1], to evaluate the acceptance and adoption of new technologies [15].

IDT has been used in prior studies for FinTech Innovation evaluation, for instance, for m-wallets [16,17], Near-field communication NFC payments [18,19], Mobile ticketing services [17], Open Data [20], commerce and payments [21], and digital banking [5].

In a volatile business environment, stakeholder collaboration is more important than competition [22], in terms of shared resources, knowledge spillovers, government support, local endowment, and network externalities [23]. Therefore, the ecosystem is the framework for elaborating, promoting, and persuading the stakeholders to collaborate [24], resulting in innovative capabilities creation [25] and attaining a complex value proposition [26] by their diversity [27], eventually benefiting the public [28] and attracting new entrants [29].

Tansley [30] coined the term Innovation Ecosystem, elaborated by Moore [31] on the competing players’ framework and by Basole & Karla [32] on their connectedness to co-develop, solve complex problems, and share knowledge for sustainable development [33] in a global perspective [25].

De Meyer Innovation Ecosystem has been used several times to explore the FinTech ecosystem’s maturity, stakeholders’ maturity, and different players’ roles [6,34,35]. Therefore, as the second lens, the De Meyer Innovation Ecosystem framework is valid and relevant for understanding the growth and evolution of FinTech, as well as its interactions with other stakeholders within an ecosystem.

Finally, the third lens is the Value Chain framework. Value chain refers to how businesses create, deliver, and capture value [3]. The value delivered by FinTech is a modular and network-based rather than firm-centric model, unlike traditional businesses [36,37]. Thus, emphasising or creating value for the partial process, which either improves or replaces traditional ways, for instance, FinTech creates value in onboarding (sign-up), compliance, payments, and scoring (credit) [38,39].

The value chain framework consists of three concepts: value proposition, value creation, and value capture [4,40]. Value proposition refers to the innovative products and services offered by companies that are aligned with customers’ needs offered by companies [40]. Value creation refers to how a company delivers its value propositions, for example, through the use of technology, people, and partnerships [4,41]. Value Capture refers to how businesses earn revenues and profit. For example, financial capture could be profit margins or data monetisation [42].

Therefore, Value Chain theory, as the third lens, enables the study of how and where Fintech contributes functionally to the financial services sector in a small market like Latvia, adding operational value.

3. Methodology

An empirical, qualitative, multiple-case study approach has been employed in this study, as it is an emerging topic that requires in-depth data for inductive exploratory research. It will explore how the FinTech sector in a small country like Latvia is innovating, how it collaborates and works within the ecosystem with its stakeholders, and its role in the Value Chain of financial services. This study employs semi-structured interviews with open-ended questions, grounded in a triangulated framework comprising IDT, De Meyer’s Innovation Ecosystem framework, and Value Chain theory. The interviewees were FinTech leaders from the most successful Latvian FinTech Subsector Lending, Payment, and Information Technology – Data – Know Your Customer IT-Data-KYC [8], Regulators, traditional financial institutions, and the associations for the multi-case design [43].

The authors employed a flexible and multimodal approach to collect data through interviews conducted from April to July 2025. Of the selected 15 FinTechs, 11 responded, yielding a 73% response rate. Additionally, all 8 of the other stakeholders responded, achieving a 100% response rate. All the responses were anonymised for Qualitative Content Analysis QCA. The questionnaires were designed to facilitate semi-structured interviews, incorporating all three theories within the triangulated theoretical framework: IDT [1], De Meyer’s Innovation Ecosystem [2], and Value Chain Theory [3,4]. There were 15 questions related to this theoretical framework, with five questions for each theory to explore the key components of these theories (see annexe no. A). IDT questions were based on the five attributes: relative advantage, complexity, compatibility, trialability, and observability; Innovation ecosystem questions were related to stakeholders’ role as orchestrators, enablers, or integrators; and Value chain’s questions emphasised the FinTech companies’ value proposition, value creation, and value capture. Also, there were two opening and three closing questions. The main questionnaire was created for FinTech firms, and a slightly modified version was administered to non-FinTech stakeholders, ensuring a theoretical context and allowing for cross-case analysis within the framework.

With transparent and systematic coding, the QCA was conducted, resulting in the integration of the evolving insights with the theory [44,45]. The codes were derived from the responses of FinTech ecosystem leaders, which were both deductive and inductive, providing a comprehensive picture of the FinTech ecosystem. Deductive codes were established based on academic theories, whereas inductive codes were derived from the collected data, helping to identify patterns or themes. In total, 177 codes were identified or generated inductively from the responses of FinTech leaders. These were the recurring themes, concepts, or ideas that were grouped into 78 sub-themes and further grouped into 41 grand themes. On the other hand, 183 initial codes were derived, grouped into 81 sub-themes, and subsequently into 42 grand themes, from the responses of non-FinTech stakeholders, as shown in Table 1.

Basic rules concerning the participants involved were adhered to for this research. Interviewee were informed about the purpose and context of this study, that their participation is voluntary, and they can step back whenever they wish. Everyone provided their informed decision, either verbally or in writing via email to the primary author of this research. The details of all interviewees, including their names, titles, and the names of their companies or institutions, are kept confidential to protect their privacy. However, all the interviews were recorded and stored safely, and only the researchers have access to them.

4. Findings & Analysis

4.1. Innovation Diffusion Theory (IDT)

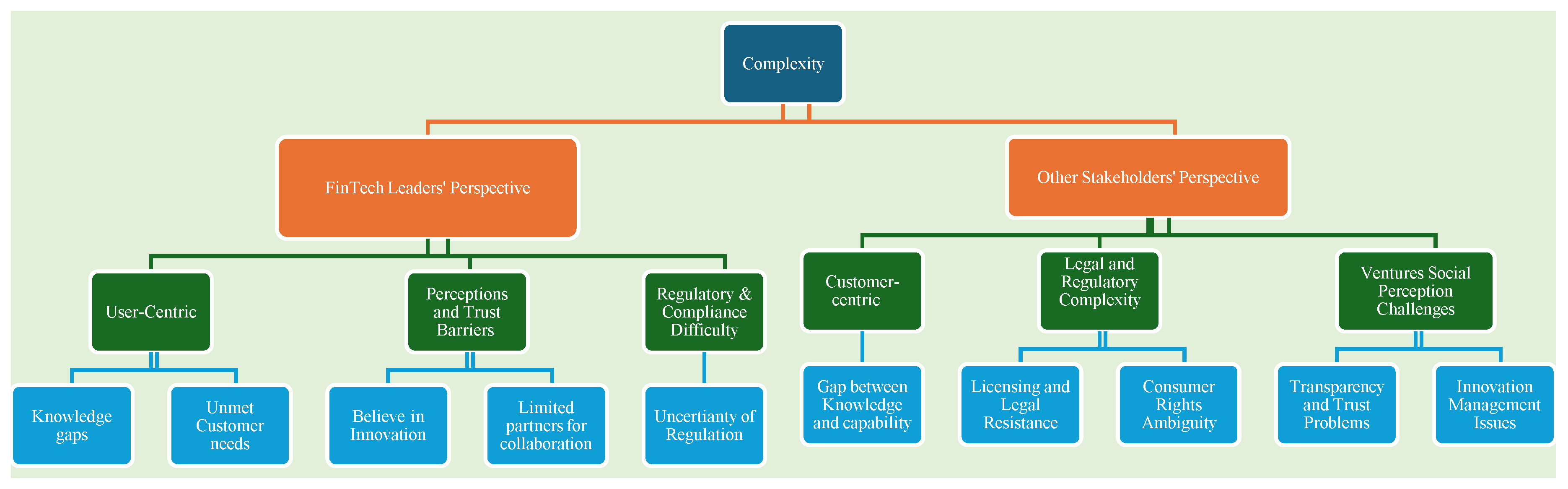

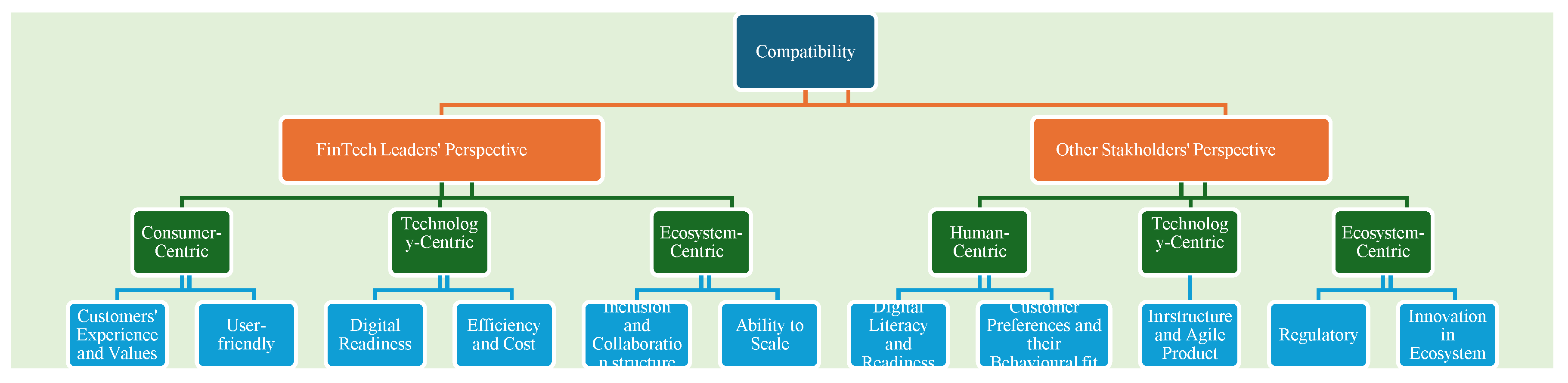

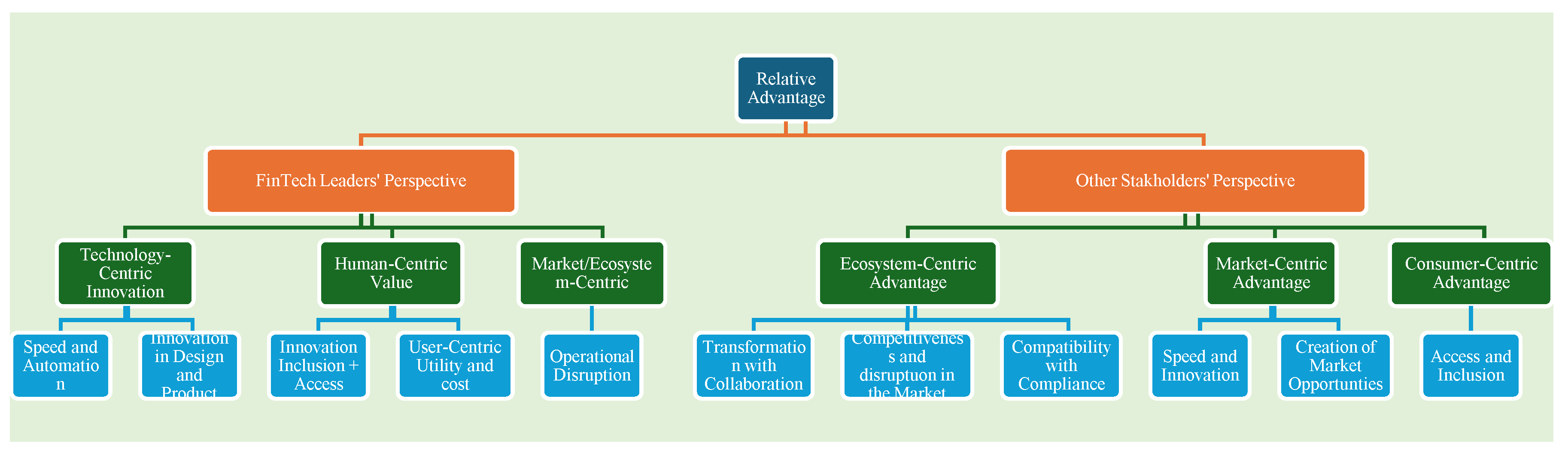

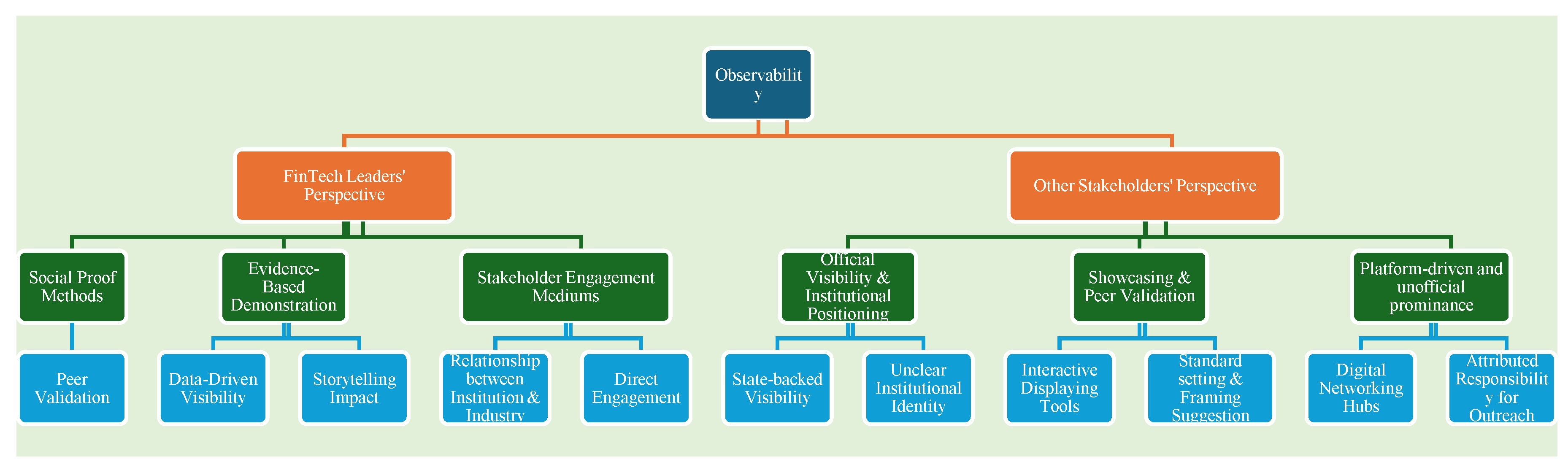

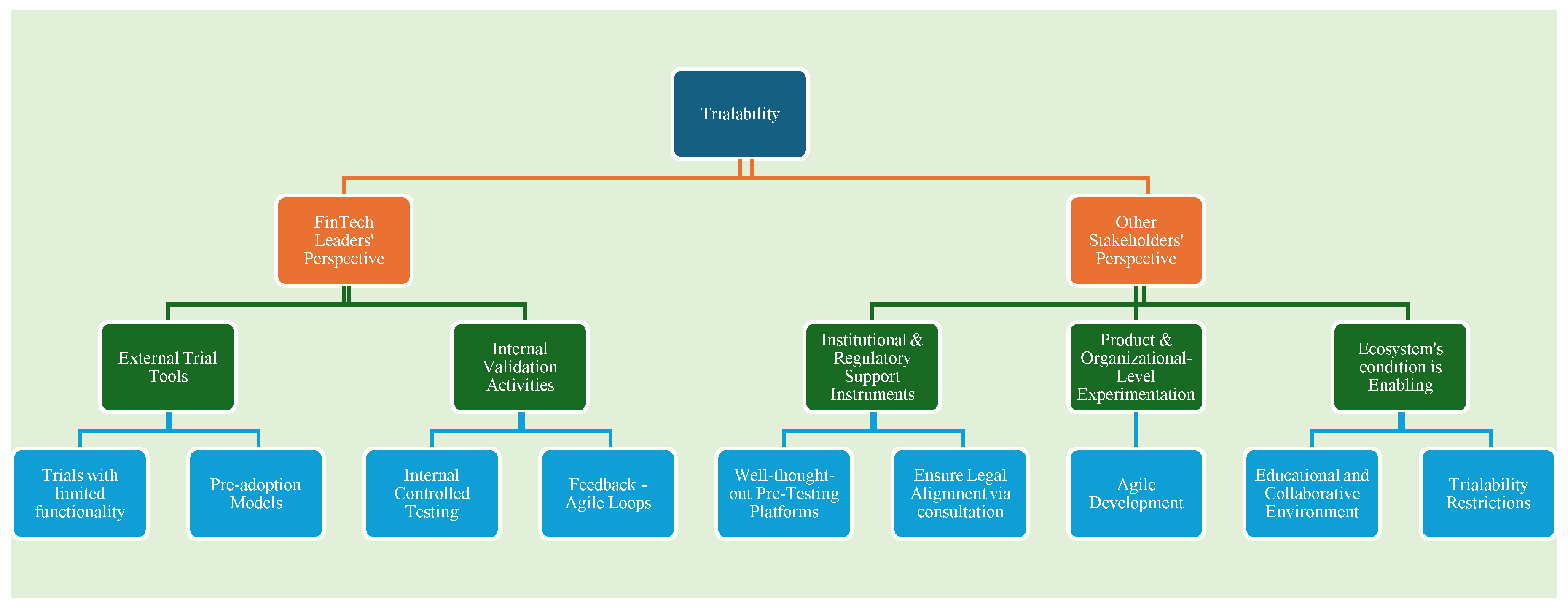

The summary in Table 2 and Figure B1, Figure B2, Figure B3, Figure B4 and Figure B5 in Appendix B illustrates the findings on how FinTech Innovation is diffusing according to Roger’s five attributes of IDT within the Latvian FinTech Ecosystem, as perceived by its FinTech Stakeholders. The Latvian FinTech sector exhibits a relative advantage through speed, customer-centricity, and automation, supported by technology, including white label and new Business-to-Business B2B business models. FinTech must be compatible with users’ digital expectations, market scalability, and continuous improvement of KYC. However, complexity increases due to the limited collaboration, trust gaps and regulatory ambiguity. Trialability can be achieved through both top-down processes, such as regulations implemented via innovation hubs and sandboxes, and bottom-up processes, including internal testing and freemium models. Observability is established through visibility provided by the regulator and association, as well as users’ testimonials and published success stories. Therefore, these approaches ensure that FinTech innovation diffusion aligns with Roger’s mentioned five attributes; however, they are limited due to the complexity of compliance and uneven infrastructure.

4.2. De Meyers’ Innovation Ecosystem Implications in the FinTech Sector

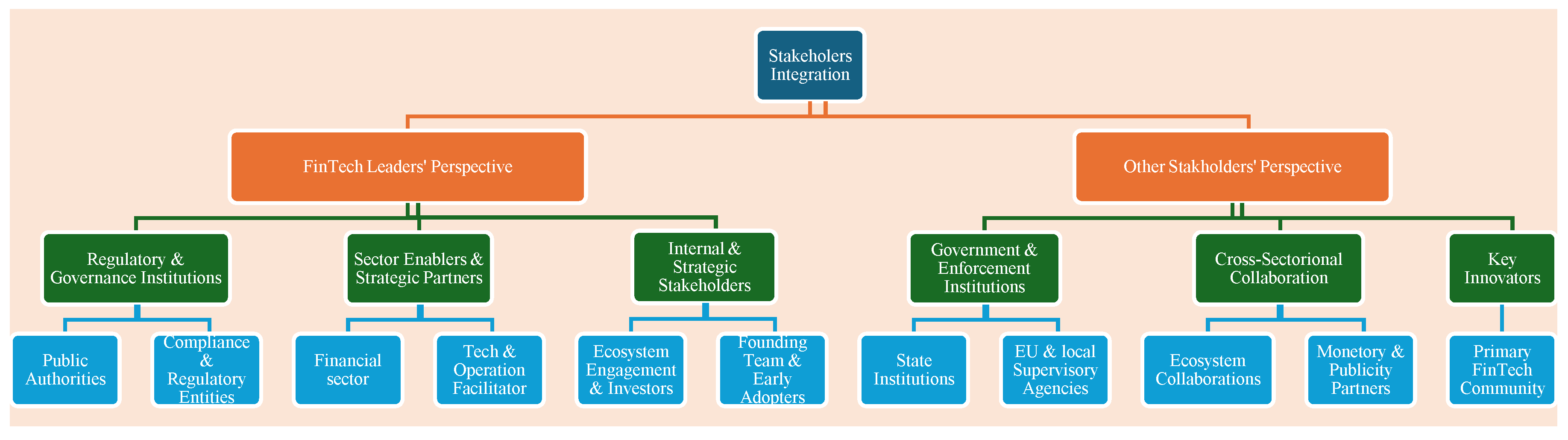

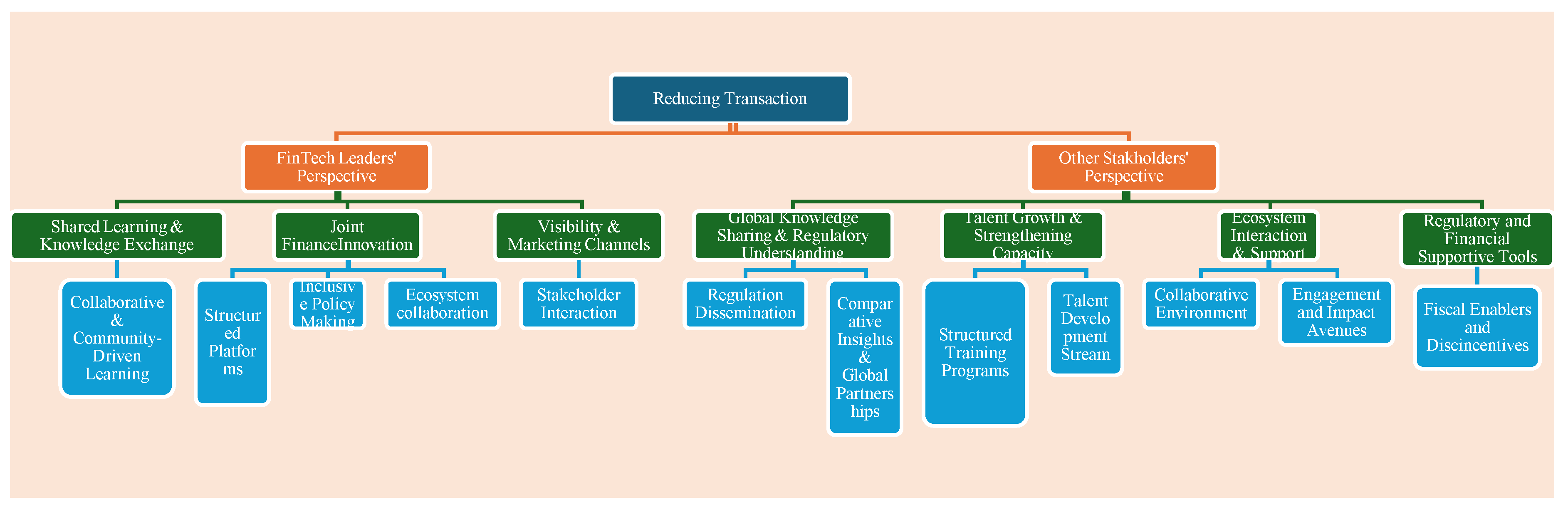

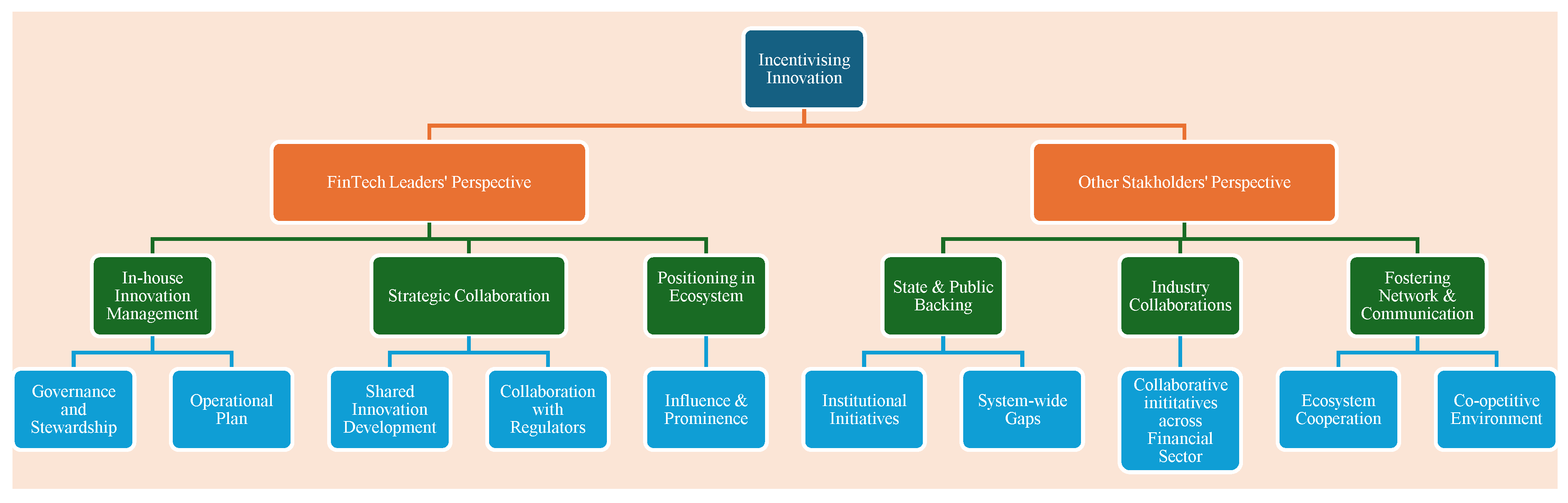

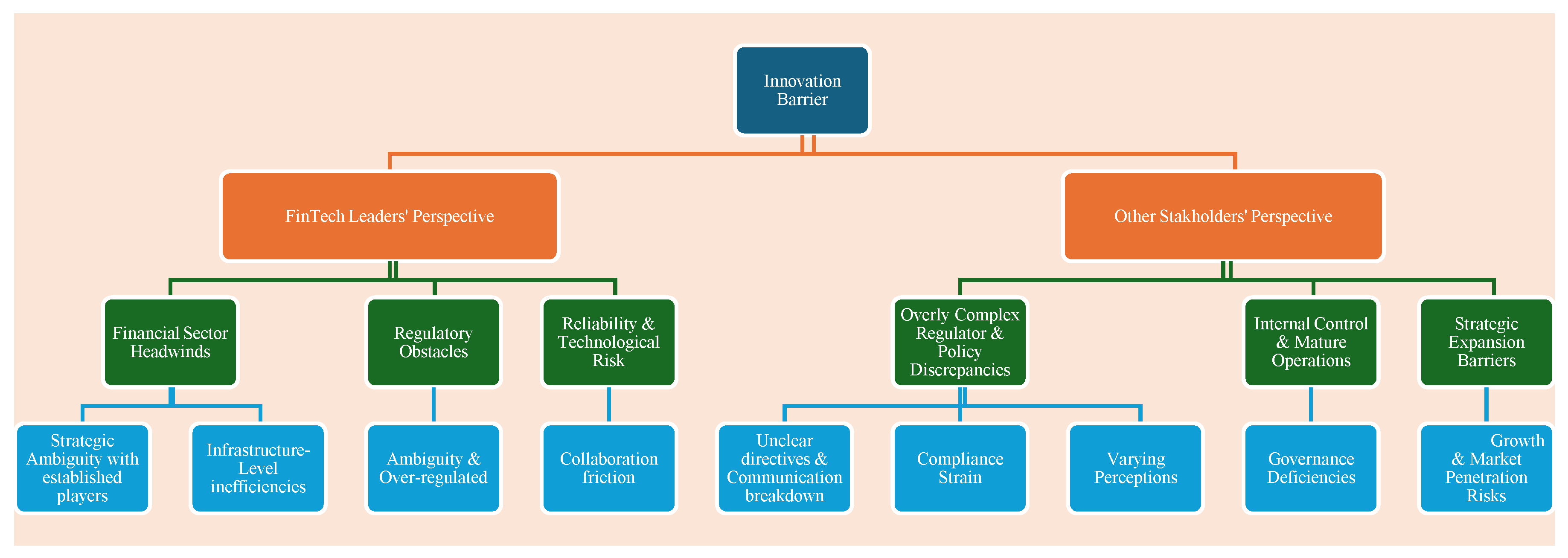

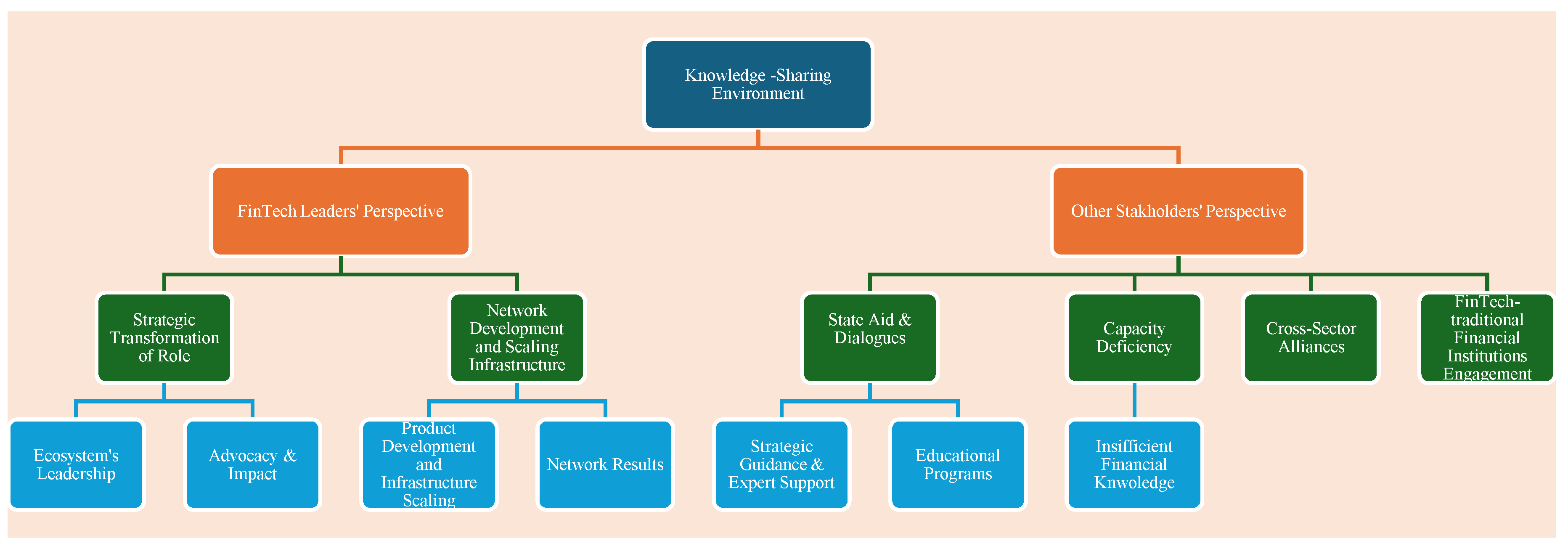

The summary in Table 3 and Figure B6, Figure B7, Figure B8, Figure B9 and Figure B10 in Appendix B presents the findings on how the Latvian FinTech Ecosystem’s stakeholders collaborate, interact, and co-create, as outlined in De Meyer’s innovation orchestration model. The results show that the Latvian FinTech Ecosystem are still on its ongoing journey to organised stakeholder orchestration. Regulators continue to be the primary players, and collaboration among associations, banks, and investors stays largely transactional. The major barriers are ambiguous regulations and low trust, which hinder scaling and lead to high integration costs. Regulator’s incentives remained slow and rigid; therefore, Latvian FinTechs rely on their own capabilities. According to the ecosystem’s leaders, clear communication, trained human capital, and shared Anti-Money Laundering AML/KYC measures may help reduce transactional costs. In Latvia, informal knowledge sharing occurs, which is mostly partner-driven and subsequently takes place within a limited loop of institutional feedback. Hence, overall, the Latvian FinTech Ecosystem tends to be more reactive than proactive, consequently reflecting the need for agile and structured co-creation policy instruments.

4.3. Value Chain Theory Implications/Mapping in the FinTech Sector

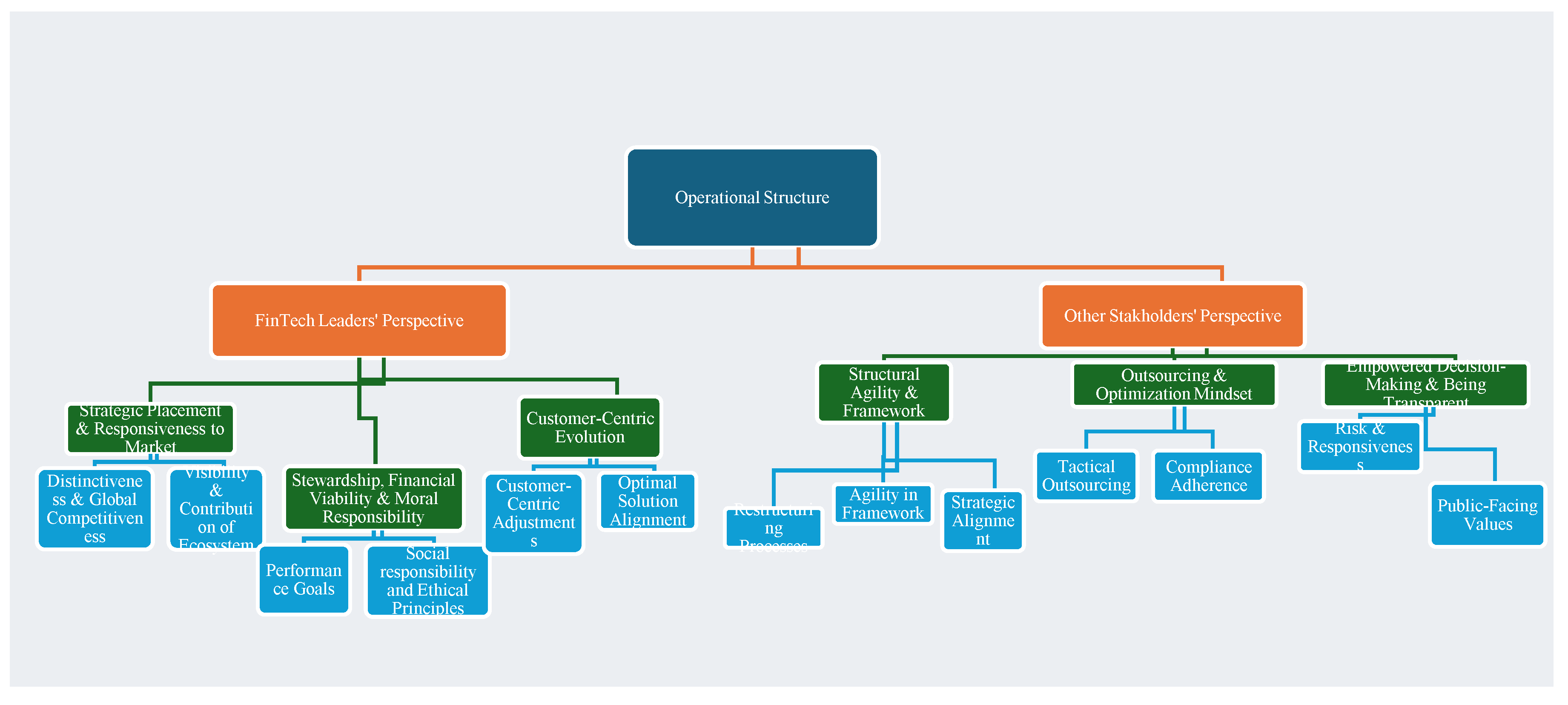

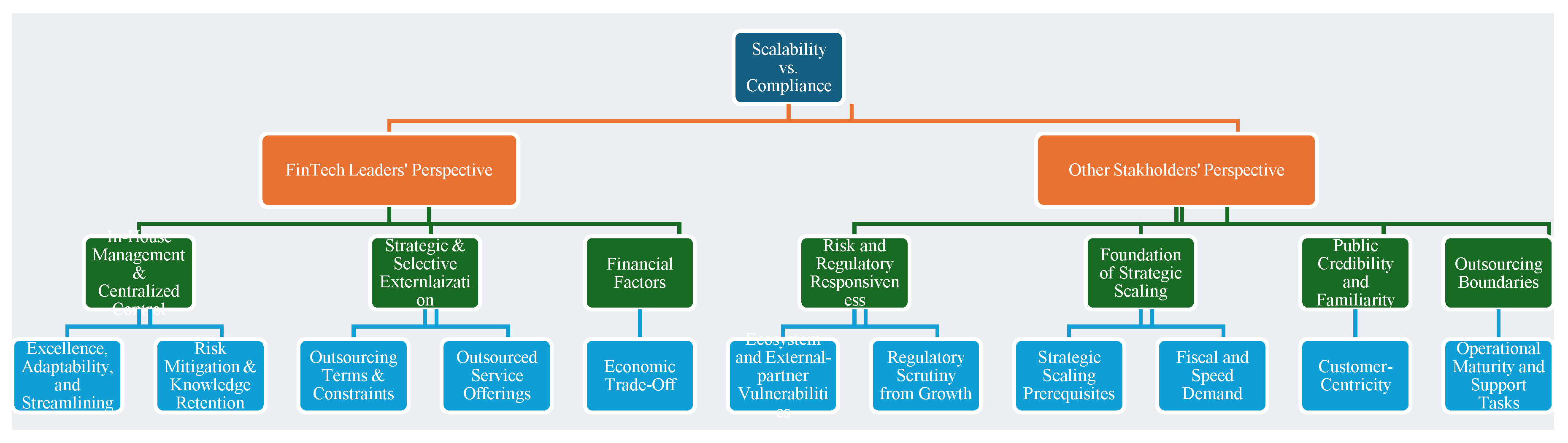

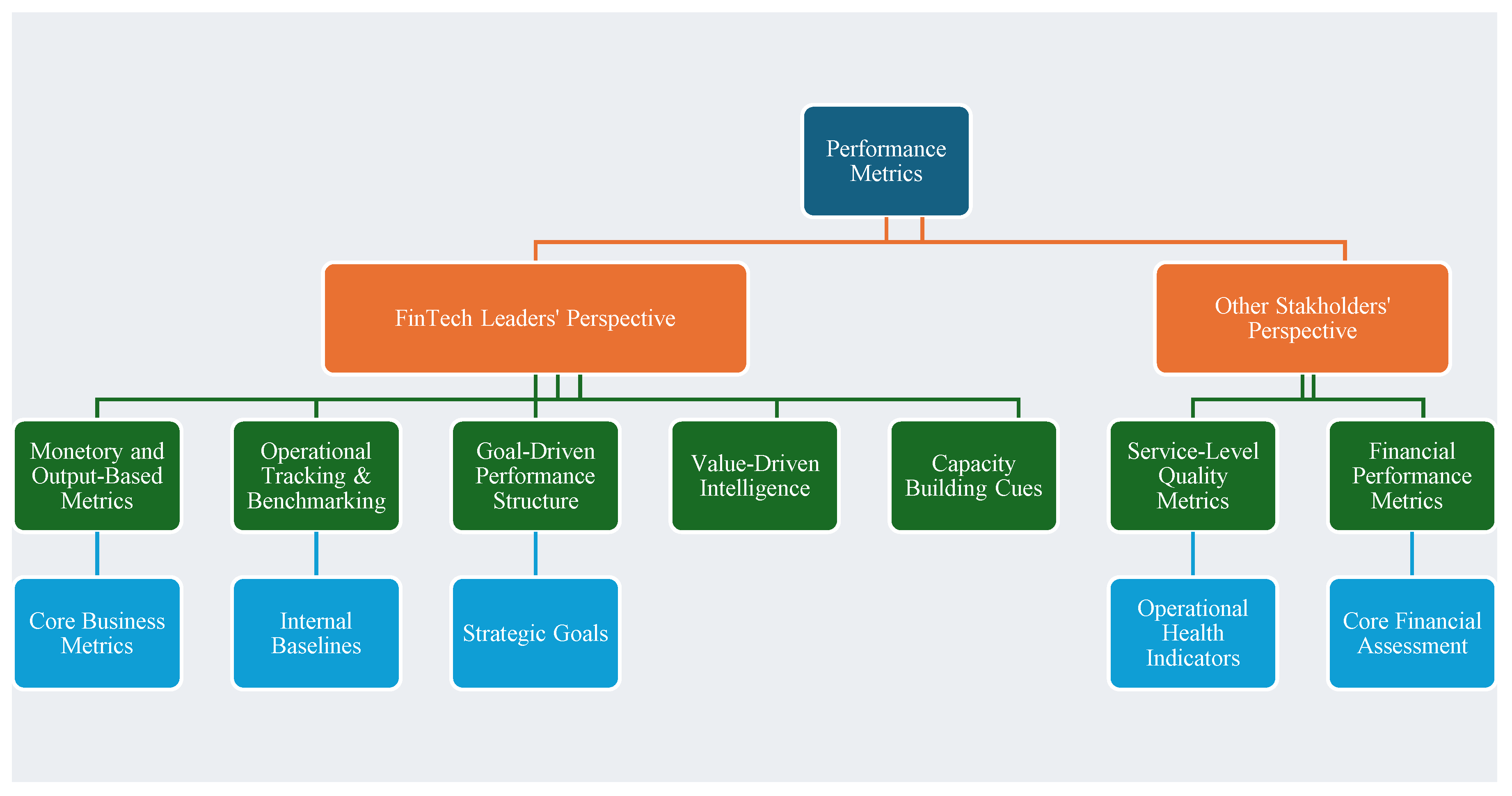

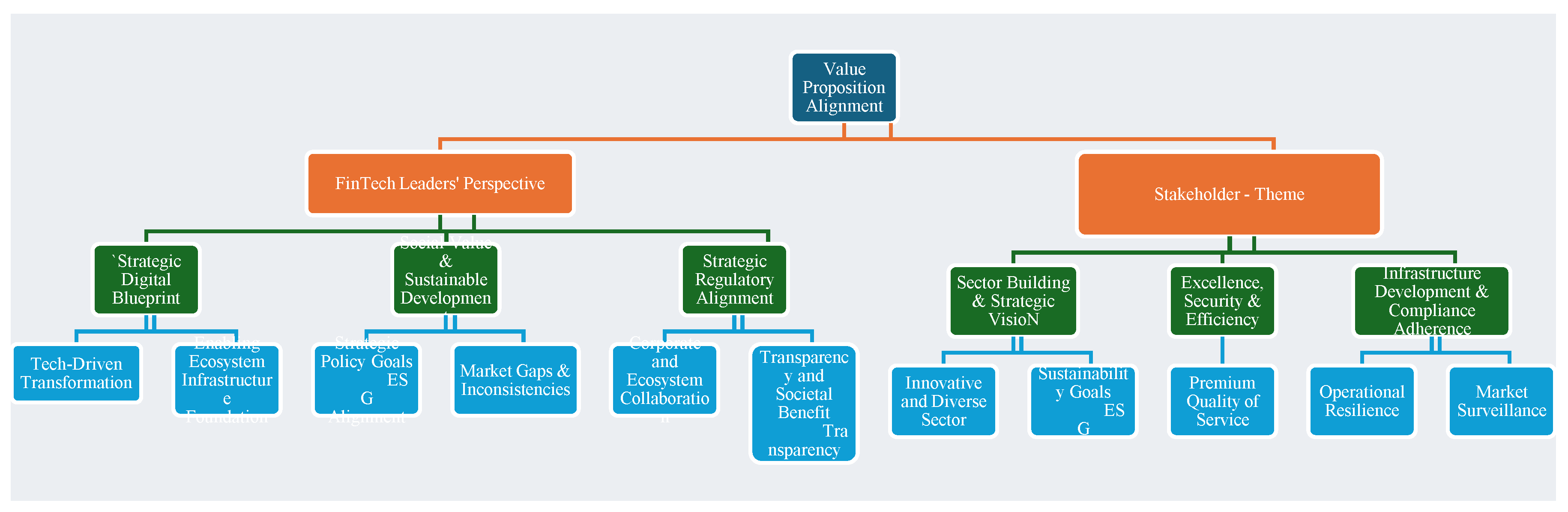

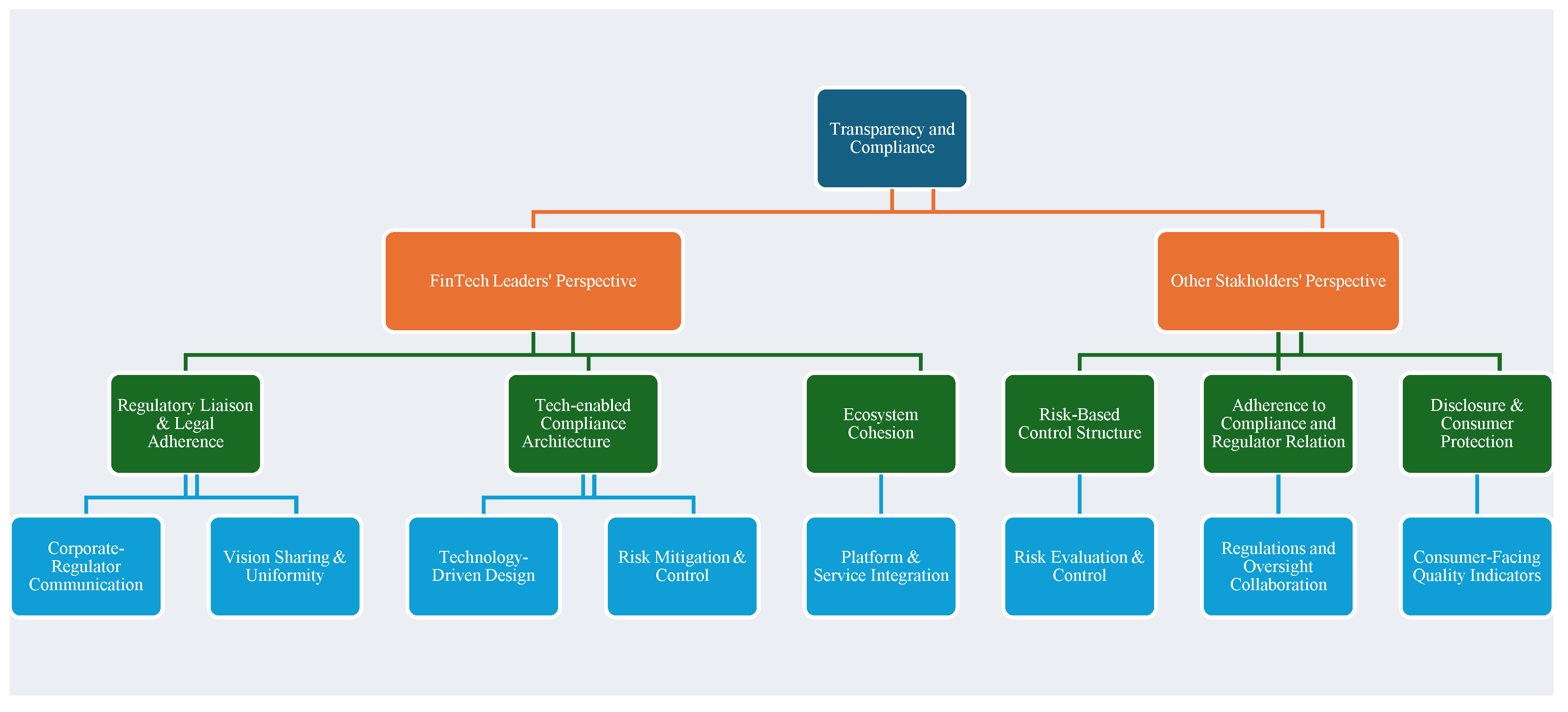

The summary in Table 4 and Figure B11, Figure B12, Figure B13, Figure B14 and Figure B15 in Appendix B illustrates the findings on how Latvian FinTechs and traditional financial institutions restructure and adapt their value chains to integrate innovation, thereby remaining compliant and scalable. FinTechs continue to maintain their customer-centric approach by diversifying their platforms, upholding ethical operations, and pursuing both profitability and inclusion. A selective outsourcing strategy, combined with In-house control, enables FinTech to achieve scalability. Automation, adaptive governance, and internal audits are used to integrate compliance and achieve transparency. FinTechs use Key Performance Indicators KPIs, Service Level Agreements SLAs, and the volume of client acquisition to track performance, which together signal their maturity level and signal trust in them. Lastly, Latvian FinTechs embed ESG goals, implement digital strategies and cooperate with policymakers to align with their value proposition. This way, Latvian FinTechs remain resilient and align with the European Union EU’s financial innovation goals.

5. Discussion

In this section, the research questions are answered based on the findings.

The research question was: What roles do stakeholders in the FinTech Ecosystem Play in the diffusion, integration, alignment, and scaling of FinTech innovation in Latvia?

The Latvian FinTech ecosystem stakeholders focus on innovation diffusion from the perspective of flexibility, speed, and digital-first capabilities. However, restricted due to a complex regulatory framework, uneven infrastructure, and institutional unreadiness. FinTech emphasised Agile modular product designs and embedded compliance, whereas non-FinTech stakeholders focused on consumer trust and compliance integration. Collaboration is strong except with regulators. The FinTech value chain maintains core operations in-house and selectively outsources. Innovation strength and strategic partnerships contribute to the scaling of FinTech.

Both FinTech and non-FinTech leaders agree that flexibility, speed, and customer-centric service are the relative advantages of FinTech services over traditional financial solutions, modular and API infrastructures. However, not all FinTech solutions are replacements; rather, they are supplements to conventional financial services. This viewpoint aligns with Roger’s concept of relative advantage [1], with Sharma et al. [46] on FinTech solutions’ adoption, and with Lee & Shin’s opinion on efficient solutions to remain competitive [39].

FinTechs meet the digital expectations of tech-savvy and younger users, as well as niche B2B markets, with strong compatibility; however, they are weak in Latvia due to a gap that exists between local consumer demand and innovative design, aligning with Sun et al. [47].

The success stories, events and testimonials enhance trust in FinTech, as stated by Zolkepli et al. [48]. Customers adopt user-friendly FinTech solutions. The complexity is a result of regulatory and compliance ambiguity, as well as associated costs. Demo or risk-free accounts, in addition to sandbox demos, increase FinTech adoption, lower perceived risk, and enhance trust and reputation, as stated by Sharma [46] and Thakur et al. [49].

FinTech private stakeholders synchronise their processes, collaborate with BaaS providers, payment processors, and card issuers, and engage in joint development Sprints and APIs. However, regulators tend to be reactive, extending guidance rather than providing structured facilitation with policy tools, contrary to the conclusions of Williamson et al. [2] and Fenwick et al. [50]. Fintechs partner with global partner networks to reduce operational costs and the burden of scaling. High compliance costs, lack of a sandbox, and ambiguity in regulations are key barriers to aligning with Adner’s [51] interdependence barrier.

There is a partial knowledge-sharing ecosystem in Latvia, which is unstructured and misaligned with the framework presented by Sangwa et al. [52]. However, the regional policies could enable FinTech to earn trust and integration.

FinTechs customised functions by reorganising compliance, partner integration and product development, and have transitioned from single-service models to a full-stack ecosystem. Banks also integrated APIs for alternative credit scoring. Most FinTechs consider that internal capabilities are vital, but external capabilities can also be leveraged through partnerships, helping to scale and mitigate risks, aligning with Williamson & De Meyer’s [2] and with Jangid et al. [53]. FinTech carefully scales, observing core functions in-house, to stay aligned with regulations. Regulators have stressed the importance of transparency and consumer protection for lasting viability. Financial innovation helps ESG goals [54] and AI solutions allow businesses to innovate faster if they follow the rules [55].

Throughout the analysis, FinTech leaders displayed a strong relative advantage provided by FinTechs. Nonetheless, the FinTech adoption barriers remained, with regulatory complexity and uneven readiness conditions. FinTech has well-developed observability and trialability, with strong Collaboration in the private sector. Based on these results, the authors conclude that advanced innovation diffusion and ecosystem growth rely heavily on institutional readiness, infrastructure capacity, and agile policy measures.

6. Conclusion and Contribution

The key goal was to understand how FinTechs and non-FinTech stakeholders perceive, develop, and scale their innovations. To explore this question, the authors have developed a triangulated analytical framework, Rogers’ IDT, Williamson’s and De Meyer’s Innovation Ecosystem and Value Chain Theory.

Results confirmed that speed and flexibility are significant relative advantages of FinTech. where infrastructure and institutional readiness affect compatibility, Complexity and regulation remained significant barriers. Stakeholders of the FinTech sector collaborate to co-create, with FinTechs acting as the Orchestrator; however, they require proactive regulatory commitment. Cross-border partnerships aid in scaling up. FinTech restructure to remain compliant, competitive, and digital-first. FinTechs combine in-house expertise alongside strategic partnerships.

This is the first study to combine IDT, De Meyer’s Ecosystem Framework, and Value Chain & Business Models theory into a single triangulated analytical framework; therefore. The framework can be replicated in small and highly regulated markets to analyse innovation in FinTech and other sectors with technology convergence, like health tech. The questionnaire to interview the FinTech Ecosystem leaders can be adapted and reused for further studies, such as cross-sector or cross-country studies.

In terms of limitations, this research is confined to one country (Latvia). Further, a comparative study of the EU FinTech Ecosystem can be conducted to gain more insights. A longitudinal study can be conducted to understand how the regulators’ role evolves. Moreover, further study is needed on how ESG elements are integrated into FinTech business models.

Author Contributions

Conceptualization, Z.S.; C.R.; methodology, Z.S.; software, Z.S.; validation, Z.S.; formal analysis, Z.S.; investigation, Z.S.; resources Z.S.; data curation, Z.S.; writing—original draft preparation, Z.S.; writing—review and editing, Z.S.; visualization, Z.S.; supervision, C.R.; funding acquisition, Z.S. amd C.R.. All authors have read and agree d to the published version of the manuscript.

Funding

This research was funded by project No. 5.2.1.1.i.0/1/23/I/CFLA/001 “Knowledge and Research Capacity Strengthening of Anti-Money Laundering, Financial Sector Technology and Analysis”.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The datasets are available upon request.

Acknowledgments

The Authors would like to thank RTU Riga Business School for its financial support in the writing of this paper.

Conflicts of Interest

The authors declare no conflicts of interest. The funders had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript; or in the decision to publish the results.

Abbreviations

The following abbreviations are used in this manuscript:

| IDT | Innovation Diffusion Theory |

| ESG | Environmental, Social and Governance |

| API | Application Programming Interface |

| MSE | Micro and Small Enterprises |

| NFC | Near-field communication |

| IT-Data-KYC | Information Technology – Data – Know Your Customer |

| QCA | Qualitative Content Analysis |

| B2B | Business-to-Business. |

| AML | Anti-Money Laundering. |

| KPI | Key Performance Indicator |

| SLA | Service Level Agreement |

| EU | European Union |

Appendix A

Appendix A.1. Stakeholder Questionnaire – FinTechs BOD

I appreciate your willingness to participate in this research. This questionnaire is part of a study exploring stakeholder perspectives on Latvia’s FinTech ecosystem. Please answer as thoroughly as you feel comfortable.

- What is your professional background, and how did you become a board member of this FinTech?

- How do you relate to the mission and vision of your FinTech company?

- What innovations does your firm offer that improve on traditional financial services?

- How do your products or platforms align with customer values and market needs? (Fit between the innovation and the target users’ lifestyles or expectations)

- What are the paramount usability or adoption challenges you’ve (or your users have) encountered?

- How do you allow customers to test or pilot your products before full use?

- What mechanisms help demonstrate the impact of your offerings (e.g., case studies, testimonials)?

- Who are the most critical partners in your business ecosystem (e.g., enablers, regulators, adopters)?

- What barriers have you encountered in navigating ecosystem relationships (e.g., with regulators or banks)?

- How do you foster trust, co-creation, or collaborative development with other ecosystem players? (Mutual development of innovation with partners)

- How does your firm contribute to or benefit from knowledge-sharing environments (events, consortia)?

- How has your role evolved—from a niche innovator to a keystone or Orchestrator (if applicable)? (Lifecycle progression within the ecosystem)

- How has your value proposition evolved since the company’s inception?

- What operational functions are handled in-house vs. outsourced, and why? (Internal capability vs. third-party reliance)

- How do you structure your company to ensure scalability while staying compliant?

- Do you track specific KPIs to evaluate business model performance?

- How does your business model align with national or EU-level goals for FinTech?

- What advice would you give to future FinTech board members or founders entering this space?

- Can you share an anecdote or memorable board discussion about innovation or transformation?

- How do you see your firm’s role evolving within the Latvian FinTech landscape in the next 5 years?

Appendix B

Appendix B.1. Emerging Concepts from the QCA of the Interviews

Figure B1.

Roger’s Innovation Diffusion Theory - Complexity - Developed by the author based on Interviews, 2025.

Figure B1.

Roger’s Innovation Diffusion Theory - Complexity - Developed by the author based on Interviews, 2025.

Figure B2.

Roger’s Innovation Diffusion Theory - Compatibility - Developed by the author based on Interviews, 2025.

Figure B2.

Roger’s Innovation Diffusion Theory - Compatibility - Developed by the author based on Interviews, 2025.

Figure B3.

Roger’s Innovation Diffusion Theory - Relative Advantage - Developed by the author based on Interviews, 2025.

Figure B3.

Roger’s Innovation Diffusion Theory - Relative Advantage - Developed by the author based on Interviews, 2025.

Figure B4.

De Meyer Innovation Ecosystem - Stakeholder Integration - Developed by the author based on Interviews, 2025.

Figure B4.

De Meyer Innovation Ecosystem - Stakeholder Integration - Developed by the author based on Interviews, 2025.

Figure B5.

Roger’s Innovation Diffusion Theory - Observability - Developed by the author based on Interviews, 2025.

Figure B5.

Roger’s Innovation Diffusion Theory - Observability - Developed by the author based on Interviews, 2025.

Figure B6.

Roger’s Innovation Diffusion Theory - Trialability - Developed by the author based on Interviews, 2025.

Figure B6.

Roger’s Innovation Diffusion Theory - Trialability - Developed by the author based on Interviews, 2025.

Figure B7.

De Meyer Innovation Ecosystem – Reducing Transaction - Developed by the author based on Interviews, 2025.

Figure B7.

De Meyer Innovation Ecosystem – Reducing Transaction - Developed by the author based on Interviews, 2025.

Figure B8.

De Meyer Innovation Ecosystem - Incentivising Innovation - Developed by the author based on Interviews, 2025.

Figure B8.

De Meyer Innovation Ecosystem - Incentivising Innovation - Developed by the author based on Interviews, 2025.

Figure B9.

De Meyer Innovation Ecosystem - Innovation Barrier - Developed by the author based on Interviews, 2025.

Figure B9.

De Meyer Innovation Ecosystem - Innovation Barrier - Developed by the author based on Interviews, 2025.

Figure B10.

Value Chain Contribution - Knowledge- Value Proposition - Developed by the author based on Interviews, 2025.

Figure B10.

Value Chain Contribution - Knowledge- Value Proposition - Developed by the author based on Interviews, 2025.

Figure B11.

Value Chain Contribution - Knowledge- Operational Model - Developed by the author based on Interviews, 2025.

Figure B11.

Value Chain Contribution - Knowledge- Operational Model - Developed by the author based on Interviews, 2025.

Figure B12.

De Meyer Innovation Ecosystem - Knowledge-Sharing Environment - Developed by the author based on Interviews, 2025.

Figure B12.

De Meyer Innovation Ecosystem - Knowledge-Sharing Environment - Developed by the author based on Interviews, 2025.

Figure B13.

Value Chain Contribution - Knowledge- Performance Metrics - Developed by the author based on Interviews, 2025.

Figure B13.

Value Chain Contribution - Knowledge- Performance Metrics - Developed by the author based on Interviews, 2025.

Figure B14.

Value Chain Contribution - Knowledge- Value Chain Alignment - Developed by the author based on Interviews, 2025.

Figure B14.

Value Chain Contribution - Knowledge- Value Chain Alignment - Developed by the author based on Interviews, 2025.

Figure B15.

Value Chain Contribution - Knowledge- Compliance and Scalability - Developed by the author based on Interviews, 2025.

Figure B15.

Value Chain Contribution - Knowledge- Compliance and Scalability - Developed by the author based on Interviews, 2025.

References

- E. M. Rogers, Diffusion of innovations, Fifth edition. New York London Toronto Sydney: Free Press, 2003.

- P. J. Williamson and A. De Meyer, ‘Ecosystem Advantage: How to Successfully Harness the Power of Partners’, California Management Review, vol. 55, no. 1, pp. 24–46, Oct. 2012. [CrossRef]

- D. J. Teece, ‘Business Models, Business Strategy and Innovation’, Long Range Planning, vol. 43, no. 2–3, pp. 172–194, Apr. 2010. [CrossRef]

- T. Clauss, ‘Measuring business model innovation: conceptualization, scale development, and proof of performance’, R & D Management, vol. 47, no. 3, pp. 385–403, June 2017. [CrossRef]

- I. M. Shaikh and H. Amin, ‘Influence of innovation diffusion factors on non-users’ adoption of digital banking services in the banking 4.0 era’, IDD, vol. 53, no. 1, pp. 12–21, Jan. 2025. [CrossRef]

- B. Koranteng and K. You, ‘Fintech and financial stability: Evidence from spatial analysis for 25 countries’, Journal of International Financial Markets, Institutions and Money, vol. 93, p. 102002, June 2024. [CrossRef]

- C. Yáñez-Valdés and M. Guerrero, ‘Assessing the organizational and ecosystem factors driving the impact of transformative FinTech platforms in emerging economies’, International Journal of Information Management, vol. 73, p. 102689, Dec. 2023. [CrossRef]

- Z. Siddiqui and C. A. Rivera, ‘MAPPING FINTECH LANDSCAPE IN LATVIA: TAXONOMY-BASED CLASSIFICATION AND ECONOMIC IMPACT ANALYSIS’, PJMS, vol. 30, no. 1, pp. 304–319, Dec. 2024. [CrossRef]

- S. Chen and Q. Guo, ‘Fintech and MSEs Innovation: an Empirical Analysis’, 2024, arXiv. [CrossRef]

- C. K. Takahashi, J. C. B. D. Figueiredo, and E. Scornavacca, ‘Investigating the diffusion of innovation: A comprehensive study of successive diffusion processes through analysis of search trends, patent records, and academic publications’, Technological Forecasting and Social Change, vol. 198, p. 122991, Jan. 2024. [CrossRef]

- G. Cornelli, J. Frost, L. Gambacorta, and J. Jagtiani, ‘The impact of fintech lending on credit access for U.S. small businesses’, Journal of Financial Stability, vol. 73, p. 101290, Aug. 2024. [CrossRef]

- Y. Guan, N. Sun, S. J. Wu, and Y. Sun, ‘Supply Chain Finance, Fintech Development, and Financing Efficiency of SMEs in China’, Administrative Sciences, vol. 15, no. 3, p. 86, Mar. 2025. [CrossRef]

- R. Rupeika-Apoga and S. Wendt, ‘FinTech in Latvia: Status Quo, Current Developments, and Challenges Ahead’, Risks, vol. 9, no. 10, p. 181, Oct. 2021. [CrossRef]

- K. K. Kapoor, Y. K. Dwivedi, and M. D. Williams, ‘Rogers’ Innovation Adoption Attributes: A Systematic Review and Synthesis of Existing Research’, Information Systems Management, vol. 31, no. 1, pp. 74–91, Jan. 2014. [CrossRef]

- A. Tarhini, N. A. G. Arachchilage, R. Masa’deh, and M. S. Abbasi, ‘A Critical Review of Theories and Models of Technology Adoption and Acceptance in Information System Research’:, International Journal of Technology Diffusion, vol. 6, no. 4, pp. 58–77, Oct. 2015. [CrossRef]

- P. Kaur, A. Dhir, R. Bodhi, T. Singh, and M. Almotairi, ‘Why do people use and recommend m-wallets?’, Journal of Retailing and Consumer Services, vol. 56, p. 102091, Sept. 2020. [CrossRef]

- K. K. Kapoor, Y. K. Dwivedi, and M. D. Williams, ‘Empirical Examination of the Role of Three Sets of Innovation Attributes for Determining Adoption of IRCTC Mobile Ticketing Service’, Information Systems Management, vol. 32, no. 2, pp. 153–173, Apr. 2015. [CrossRef]

- J.-P. Tsai and C.-F. Ho, ‘Does design matter? Affordance perspective on smartphone usage’, Industrial Management & Data Systems, vol. 113, no. 9, pp. 1248–1269, Sept. 2013. [CrossRef]

- X. Zhang, ‘Frugal innovation and the digital divide: Developing an extended model of the diffusion of innovations’, International Journal of Innovation Studies, vol. 2, no. 2, pp. 53–64, June 2018. [CrossRef]

- V. Weerakkody, Z. Irani, K. Kapoor, U. Sivarajah, and Y. K. Dwivedi, ‘Open data and its usability: an empirical view from the Citizen’s perspective’, Inf Syst Front, vol. 19, no. 2, pp. 285–300, Apr. 2017. [CrossRef]

- H. Sikandar, Y. Vaicondam, N. Khan, M. I. Qureshi, and A. Ullah, ‘Scientific Mapping of Industry 4.0 Research: A Bibliometric Analysis’, Int. J. Interact. Mob. Technol., vol. 15, no. 18, pp. 129–147, Sept. 2021. [CrossRef]

- A. MINÀ and G. B. DAGNINO, ‘Competition and cooperation in entrepreneurial ecosystems: a lifecycle analysis of a Canadian ICT ecosystem’, in Innovation, Alliances, and Networks in High-Tech Environments, 1st edn, Routledge, 2015, pp. 65–81.

- D. B. Audretsch, J. A. Cunningham, D. F. Kuratko, E. E. Lehmann, and M. Menter, ‘Entrepreneurial ecosystems: economic, technological, and societal impacts’, J Technol Transf, vol. 44, no. 2, pp. 313–325, Apr. 2019. [CrossRef]

- M. G. Colombo, G. B. Dagnino, E. E. Lehmann, and M. Salmador, ‘The governance of entrepreneurial ecosystems’, Small Bus Econ, vol. 52, no. 2, pp. 419–428, Feb. 2019. [CrossRef]

- E. B. Reynolds and Y. Uygun, ‘Strengthening advanced manufacturing innovation ecosystems: The case of Massachusetts’, Technological Forecasting and Social Change, vol. 136, pp. 178–191, Nov. 2018. [CrossRef]

- M. Talmar, B. Walrave, K. S. Podoynitsyna, J. Holmström, and A. G. L. Romme, ‘Mapping, analyzing and designing innovation ecosystems: The Ecosystem Pie Model’, Long Range Planning, vol. 53, no. 4, p. 101850, Aug. 2020. [CrossRef]

- H. Etzkowitz and L. Leydesdorff, ‘The dynamics of innovation: from National Systems and “Mode 2” to a Triple Helix of university–industry–government relations’, Research Policy, vol. 29, no. 2, pp. 109–123, Feb. 2000. [CrossRef]

- J. A. Cunningham, M. Menter, and C. O’Kane, ‘Value creation in the quadruple helix: a micro level conceptual model of principal investigators as value creators’, R & D Management, vol. 48, no. 1, pp. 136–147, Jan. 2018. [CrossRef]

- P. Ritala, V. Agouridas, D. Assimakopoulos, and O. Gies, ‘Value creation and capture mechanisms in innovation ecosystems: A comparative case study’, Int. J. of Technology Management, vol. 63, no. 3–4, pp. 244–267, Nov. 2013. [CrossRef]

- A. G. Tansley, ‘The Use and Abuse of Vegetational Concepts and Terms’, Ecology, vol. 16, no. 3, pp. 284–307, July 1935. [CrossRef]

- J. Moore, ‘Predators and Prey: A New Ecology of Competition’, Harvard business review, vol. 71, pp. 75–86, May 1999.

- R. C. Basole and J. Karla, ‘On the Evolution of Mobile Platform Ecosystem Structure and Strategy’, Bus Inf Syst Eng, vol. 3, no. 5, pp. 313–322, Oct. 2011. [CrossRef]

- O. Granstrand and M. Holgersson, ‘Innovation ecosystems: A conceptual review and a new definition’, Technovation, vol. 90–91, p. 102098, Feb. 2020. [CrossRef]

- V. Stefanelli, F. Manta, and P. Toma, ‘Digital financial services and open banking innovation: are banks becoming invisible?’, 2022, arXiv. [CrossRef]

- J. Kálmán, ‘The Role of Regulatory Sandboxes in FinTech Innovation: A Comparative Case Study of the UK, Singapore, and Hungary’, FinTech, vol. 4, no. 2, p. 26, June 2025. [CrossRef]

- C. Zott and R. Amit, ‘Business Model Design: An Activity System Perspective’, Long Range Planning, vol. 43, no. 2–3, pp. 216–226, Apr. 2010. [CrossRef]

- R. Adner, ‘Ecosystem as Structure: An Actionable Construct for Strategy’, Journal of Management, vol. 43, no. 1, pp. 39–58, Jan. 2017. [CrossRef]

- P. Gomber, R. J. Kauffman, C. Parker, and B. W. Weber, ‘On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services’, Journal of Management Information Systems, vol. 35, no. 1, pp. 220–265, Jan. 2018. [CrossRef]

- I. Lee and Y. J. Shin, ‘Fintech: Ecosystem, business models, investment decisions, and challenges’, Business Horizons, vol. 61, no. 1, pp. 35–46, Jan. 2018. [CrossRef]

- M. Morris, M. Schindehutte, and J. Allen, ‘The entrepreneur’s business model: toward a unified perspective’, Journal of Business Research, vol. 58, no. 6, pp. 726–735, June 2005. [CrossRef]

- M. W. Johnson, C. M. Christensen, and H. Kagermann, ‘Reinventing Your Business Model’, vol. 87, no. 12, pp. 52–60, 2008.

- A. Osterwalder and Y. Pigneur, Business model generation: a handbook for visionaries, game changers, and challengers. New York: Wiley&Sons, 2013.

- R. K. Yin, Case study research and applications: design and methods, Sixth edition. Los Angeles London New Delhi Singapore Washington DC Melbourne: SAGE, 2018.

- P. Mayring, ‘Qualitative Content Analysis’, Forum Qualitative Sozialforschung / Forum: Qualitative Social Research [On-line Journal]. https://qualitative-research.net/fqs/fqs-e/2-00inhalt-e.htm, vol. 1, no. 2, June 2000.

- M. Schreier, Qualitative Content Analysis in Practice, vol. 1. 1 Oliver’s Yard, 55 City Road London EC1Y 1SP: SAGE Publications Ltd, 2012. [CrossRef]

- V. Sharma, R. Rupeika-Apoga, T. Singh, and M. Gupta, ‘Sustainable Investments in the Blue Economy: Leveraging Fintech and Adoption Theories’, JRFM, vol. 18, no. 7, p. 368, July 2025. [CrossRef]

- H. Sun, Y. Fang, City University of Hong Kong, H. Zou, and City University of Hong Kong, ‘Choosing a Fit Technology: Understanding Mindfulness in Technology Adoption and Continuance’, JAIS, vol. 17, no. 6, pp. 377–412, June 2016. [CrossRef]

- I. A. Zolkepli and Y. Kamarulzaman, ‘Social media adoption: The role of media needs and innovation characteristics’, Computers in Human Behavior, vol. 43, pp. 189–209, Feb. 2015. [CrossRef]

- R. Thakur and M. Srivastava, ‘Adoption readiness, personal innovativeness, perceived risk and usage intention across customer groups for mobile payment services in India’, Internet Research, vol. 24, no. 3, pp. 369–392, May 2014. [CrossRef]

- M. Fenwick, E. P. M. Vermeulen, and M. Corrales, ‘Business and Regulatory Responses to Artificial Intelligence: Dynamic Regulation, Innovation Ecosystems and the Strategic Management of Disruptive Technology’, in Robotics, AI and the Future of Law, M. Corrales, M. Fenwick, and N. Forgó, Eds, in Perspectives in Law, Business and Innovation. Singapore: Springer Singapore, 2018, pp. 81–103. [CrossRef]

- R. Adner, ‘Match Your Innovation Strategy to Your Innovation Ecosystem’, HBR Spotlight, vol. 84, no. 4, pp. 98–107, 2006.

- S. Sangwa, S. Ndahimana, and F. Dusengumuremyi, ‘Diffusion of Innovation vs. Dependence Theory: FinTech Inclusion in the AfCFTA Era’, SSRN Journal, vol. 1, no. 3, pp. 45–107, 2025. [CrossRef]

- H. Jangid, D. P. Bal, and N. V. M. Rao, ‘Role of FinTech and technological innovation towards energy, growth, and environment nexus in G20 economies’, Sci Rep, vol. 15, no. 1, p. 20057, June 2025. [CrossRef]

- J. Y. Yong, M. Yusliza, T. Ramayah, C. J. Chiappetta Jabbour, S. Sehnem, and V. Mani, ‘Pathways towards sustainability in manufacturing organizations: Empirical evidence on the role of green human resource management’, Bus Strat Env, vol. 29, no. 1, pp. 212–228, Jan. 2020. [CrossRef]

- A. W. F. Kouam, ‘The Impact of Artificial Intelligence on Fintech Innovation and Financial Inclusion: A Global Perspective’, Nov. 15, 2024, In Review. [CrossRef]

Table 1.

QCA Coding Summary – by authors.

| Stakeholders’ Initial codes | FinTech Initial codes | Stakeholders sub-theme | FinTech sub-theme | Stakeholder Grand theme | FinTech Grand theme | |

| Total codes | 183 | 177 | 81 | 78 | 42 | 41 |

| Max | 21 | 25 | 12 | 9 | 4 | 4 |

| Min | 4 | 4 | 2 | 4 | 2 | 2 |

| Average | 12 | 12 | 5 | 5 | 3 | 3 |

Table 2.

Findings based on interviews on IDT– by authors.

| IDT Attribute | FinTech Key Responses | Non-FinTech Key Responses |

| Relative Advantage | • Technology-centric reasons: speed, automation, and product innovativeness. • Human-centric reasons: FinTech solutions serve underserved customers, increase end-user empowerment, provide digital platforms for accessibility, reduce costs through intermediary reduction, and supplement banks’ services. • Market-centric reasons: bring operational disruption through white-label strategy and new B2B models such as Platform as a Service (PaaS). |

• Ecosystem-centric advantage: transformation within collaboration. • Market-centric advantage: speed and innovation. • Consumer-centric advantage: access and inclusion. • Compliance with regulations is identified as a major concern, causing tension between regulators and FinTechs. |

| Compatibility | • Technology-centric reasons: FinTech services complement the digital readiness of its audience, requiring automated solutions and digital onboarding. • Human-centric reasons: FinTech services are customized to meet customers’ needs (individual and business, banked or unbanked). • Market-centric reasons: FinTech services serve the need for scalability of businesses. |

• Human-centric reasons: The Latvian market is prepared for digitalized financial services, but digital disparity persists across regions. • Technology-centric reasons: banks develop iterative and agile digital products to improve competitiveness. • Regulatory reasons: FinTechs must educate the public and businesses about innovation and digital security. |

| Complexity | • Technology-centric reasons: users prefer hybrid solutions combining new and familiar methods. • Human-centric reasons: tech-knowledge gaps among demographic groups create demand for simpler solutions. • Market-centric reasons: limited trust and regulatory uncertainty hinder collaboration. |

• Technology-centric reasons: strict regulations and licensing justified for consumer protection. • Human-centric reasons: lack of transparency leads to trust deficit and risk aversion. • Market-centric reasons: negative social responsibility perceptions reinforce risk aversion. |

| Trialability | • Technology-centric reasons: FinTech develops services in agile form based on user feedback to meet market needs. • Human-centric reasons: users test services internally and externally via freemium and pre-adoption models. • Market-centric reasons: bottom-up trialability reduces risk and increases adaptability. |

• Technology-centric reasons: sandboxes and innovation hubs enable pilot testing. • Human-centric reasons: regulators use experiments to educate and increase readiness. • Market-centric reasons: trialability is seen as a top-down mechanism, contrasting the FinTech approach. |

| Observability | • Technology-centric reasons: sandbox initiatives enhance visibility and trust. • Human-centric reasons: FinTech users are often unaware of the term “FinTech” despite using innovative services. • Market-centric reasons: FinTechs publish reports and share success stories to build relationships with businesses and regulators. |

• Technology-centric reasons: licensed public registries and documentation provide visibility. • Human-centric reasons: associations and events give FinTechs exposure. • Market-centric reasons: cross-stakeholder collaboration increases observability and credibility. |

Table 3.

Findings based on interviews on De Meyer’s Ecosystem– by authors.

|

Ecosystem Component |

FinTech Key Responses | Non-FinTech Key Responses |

| Stakeholder Integration | • Regulators are the most fundamental stakeholders for the guidelines structure and compliance testing. • In infrastructure development, traditional banks are perceived as both competitors and partners. • Friction continues on compliance interpretation. • Investors, boards and associations facilitate ecosystem growth. • Sustained FinTechs act as orchestrators via partnerships and co-creation. |

• Regulators are crucial in both the working groups and the coordination at the EU level. • Although the banks and Associations support FinTech integration, they remain transactional. • Slow collaboration is due to stricter bank rules. • Integration among stakeholders is limited to shallow operational links. • Focus on compliance is greater than co-creation. |

| Innovation Barrier | • Unclear relationships of FinTech with traditional businesses limit scaling. • Ambiguous regulations and their high integration costs result in slow innovation. • Regulatory ambiguity limits cross-border growth. • Lack of trust influences FinTech partnerships and reputation. • Compliance burden hinders new FinTech market entrants. |

• Uncertain and varying rules and their communication are highlighted by regulators. • Risk-averse approach of the regulators creates friction. • Compliance is perceived as expensive, time-consuming, and overwhelming. • Need for specialized compliance staff in FinTech increases costs. • Regulatory ambiguity is the prime barrier. |

| Incentivizing Innovation | • Most functions are maintained in-house to maintain speed and compliance. • External partnership restricted because of low trust in regulation. • Regulatory support, though, exists; nevertheless, it is slow and inflexible. • Industry recognition encourages continuity. • Mature FinTechs switch from niche innovators to the leaders of the ecosystem. |

• Collaborations are not enough to incentivize innovation. • Sandboxes tend to be more reactive rather than collaborative. • Supervisory focus confines co-creation. • Regulatory instruments are also reactive, not proactive. • Need for deeper industry partnerships. |

| Reducing Transaction Cost | • Shared systems are essential with banks and regulators to improve and synchronize AML / KYC functions. • Repetition and blurred rules waste resources. • FinTechs creäte joint templates and checklists to shorten onboarding processes. • Cross-institution co-operation helps in reducing duplication. • Efficiency leads to cost reduction. |

• to reduce errors, Clear rules, improved infrastructure and staff training are essential • Emphasis on clarity over cutting costs. • For smooth implementation, hiring expert staff is fundamental • Tax breaks reassure low-cost models. • Policy simplification is reviewed often at the institutional level. |

| Knowledge-Sharing Environment | • Knowledge exchange is largely informal and partner-driven; therefore, it has limited impact. • Systematic learning and institutional follow-up are limited. • Though events increase visibility, they do not increase infrastructure capacity. • Gaps exist in consistent learning platforms for FinTech. • Co-learning is essential with regulators. |

• Forums and working groups provide feedback and updates. • Institutions conduct the training in-house. • Sector-specific education programs are unavailable despite public education programs. • The sharing of Policy-driven knowledge is mostly top-down. • Iterative feedback loops are limited. |

Table 4.

Findings based on interviews on Value Chain Theory Implication– by authors.

| Value Chain Component | FinTech Key Responses | Non-FinTech Key Responses |

| Operational Structure | • Expand and diversify platforms for both global and local. • Trust and visibility are built by using awards and recognition. • The Main Aim is to increase profits and scalability, along with reducing costs. • Respect community-centric and ethical stewardship. • Emphasis on agility, which is customer-centric. |

• Adopting agile methods and AI tools to remain aligned with FinTech models. • To remain efficient and compliant, outsource non-core functions to FinTechs. • Cultural change in regards to customer focus. • Faster adoption is possible with reduced bureaucracy. • Encourage collaborative agility. |

| Scalability vs Compliance | • Core operations in-house to maintain control and efficiency. • Outsource specific tasks (like legal documentation) whilst preserving integrity. • Restrict over-dependence on third parties to restrict regulatory exposure. • Selective outsourcing maintains responsiveness. • Compliance rooted in growth strategy. |

• Unease regarding third-party risk and negative reputational exposure. • Regulators tightly supervise FinTech growth to ensure user protection. • FinTech maturity enhances trust and alignment. • Outsourcing oversaw for systemic risk. • Require a balance involving innovation and security. |

| Transparency & Compliance | • Compliance is a fundamental characteristic of FinTech products. • FinTechs use automation and architecture to internalize regulatory demands • adaptive governance supported by Internal audits and ecosystem co-operation. • Automation and AI enrich oversight efficiency. • Transparency enhances trust of the regulators in FinTech. |

• AI is designed for risk assessment and oversight Broader governance framework. • Associations observe inconsistent levels of compliance. • Emphasis on consumer protection and risk evaluation. • Mutual responsibility across institutions. • Culture of “doing things right.” i.e., risk-averse environment. |

| Performance Metrics | • Track volume and revenue regularly to evaluate health. • Non-financial metrics (For instance, testing, client acquisition) are linked to infrastructure needs and behaviour. • Strategic goals are data-driven and adaptable. • KPIs apprise partnership feasibility and trust. • Metrics indicate sustainability and maturity. |

• For partnership and governance, KPIs and SLAs are used. • Performance transparency builds trust. • Metrics demonstrate sustainability to partners and associations. • Indicators help to evaluate the health of the ecosystem. • It is encouraged to have shared benchmarking. |

| Value Proposition Alignment | • For modularity and quick market response, Digital strategies are embedded in core models. • Cloud-based structures, which are scalable, line up with ESG goals. • Co-operation with policymakers guarantees recognition along with compliance. • Alignment supports scalability and resilience. • Flexibility persists as a core differentiator. |

• For Digital Euro development and Open Finance, Operational infrastructure is prioritized. • Stability comes with policy alignment with policy and ESG frameworks. • Social fit and regulatory trust are vital for scaling. • FinTechs are presumed to be partners in the implementation of the policy. • Market access barriers lead to misalignment. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license.

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.