Submitted:

30 December 2025

Posted:

31 December 2025

You are already at the latest version

Abstract

Sustainability is now central to corporate legitimacy, yet its implementation remains uneven—particularly in emerging and fragile institutional contexts marked by weak enforcement, shifting stakeholder expectations, and fragmented governance. Although research acknowledges that senior executives shape sustainability outcomes, it often relies on structural or demographic proxies and overlooks how leaders actually interpret and address these demands. This conceptual, hypothesis-generating paper develops Executive Sustainability Cognition (ESC) as cognitive governance: the capability through which C-suite leaders select, frame, prioritise, and embed sustainability imperatives when formal institutional guidance is weak or ambiguous. Integrating Upper Echelons Theory, Institutional Theory, Stakeholder Theory, Strategic Leadership Theory, and sensemaking research, the paper proposes a four-stage ESC process: (1) attention and interpretation of sustainability cues, (2) framing and prioritisation of competing imperatives, (3) construction of sustainability vision, and (4) translation into structures, incentives, and culture. Eight testable hypotheses specify how ESC mediates between external pressures and organizational responses, and how institutional fragility, stakeholder fragmentation, and organisational learning orientation moderate these effects to produce symbolic versus substantive outcomes. By framing executive cognition as a substitute governance mechanism in fragile contexts, the paper offers a context-sensitive framework to guide research and improve sustainability practices in emerging and weak-governance markets.

Keywords:

executive sustainability cognition

; cognitive governance

; C-suite

; sustainability enactment

; institutional fragility

; emerging markets

; sensemaking

; Upper Echelons Theory

; strategic leadership

1. Introduction

Sustainability has become a central axis of corporate legitimacy worldwide. Firms are increasingly expected to manage environmental, social, and governance (ESG) responsibilities alongside financial performance, as capital markets, regulators, and civil society actors exert growing pressure for credible sustainability action [1,2,3]. Despite the rapid diffusion of ESG frameworks and the expansion of disclosure requirements, a persistent “implementation gap” remains: organizational sustainability commitments do not consistently translate into substantive changes in strategy, incentives, or operations. Evidence from emerging markets shows frequent symbolic adoption of ESG policies alongside limited transformation of core routines and governance practices, raising concerns about greenwashing and ceremonial compliance [4,5]. This pattern is especially pronounced in fragile institutional contexts where regulatory enforcement is inconsistent, governance systems are fragmented, and stakeholder expectations are fluid or contested [6,7].

There is broad agreement that senior executives play a decisive role in shaping sustainability trajectories, but less clarity on how this influence actually operates. Much of the literature associates ESG outcomes with governance structures, board characteristics, or CEO demographics, implicitly assuming that leadership effects flow primarily through formal mechanisms. More recent research suggests that executive cognition, professional experience, and values are central in orienting firms toward sustainability, showing that leaders with environmental or sustainability exposure are more likely to improve ESG performance and integrate sustainability into strategic priorities [8,9,10]. These findings imply that organizational differences in sustainability performance may originate not only in structural capabilities but also in how executives interpret, frame, and prioritize sustainability itself.

This issue becomes especially salient in African and other emerging-market environments characterized by institutional voids, policy discontinuity, political contestation, and volatile stakeholder pressures [6]. Firms in these settings face heightened risks linked to climate vulnerability, social inequality, resource governance, and energy transition challenges, while operating under regulatory regimes in which enforcement is uneven and expectations ambiguous. Under such conditions, executives frequently function as de facto sustainability governors, translating fragmented external expectations into internal priorities, narratives, and routines. At the same time, expanding sustainability reporting without commensurate behavioral change has sharpened concerns that ESG advances in such contexts may be largely symbolic rather than substantive, reinforcing the need to understand the cognitive processes through which executives distinguish between “compliance theatre” and authentic sustainability enactment.

Although research on corporate sustainability has advanced rapidly, three gaps remain insufficiently addressed. First, most studies infer executive influence on sustainability outcomes from demographic or structural proxies rather than examining the interpretive processes through which leaders make sense of sustainability demands. As a result, executive cognition remains theoretically under-specified. Second, dominant sustainability governance frameworks are largely derived from strong institutional environments and therefore do not fully explain how sustainability is enacted in environments where regulatory guidance is weak and enforcement is inconsistent. Third, while symbolic sustainability and greenwashing are widely documented, the cognitive mechanisms that enable symbolic responses to persist are rarely theorized. These gaps limit our understanding of how executives actually convert external sustainability pressures into organizational action in contexts of institutional fragility.

This paper addresses these gaps by developing the construct of Executive Sustainability Cognition (ESC) as a theoretical lens for explaining how C-suite executives interpret sustainability imperatives and convert them into organizational enactment under weak institutional conditions. ESC conceptualizes sustainability not merely as a structural compliance challenge but as a cognitive–institutional process grounded in attention, framing, prioritization, and translation into organizational systems. The central argument advanced in this paper is that, in fragile institutional environments, executive cognition functions as a form of cognitive governance. Where regulatory signals are ambiguous and institutional scaffolding is unreliable, ESC provides internal ordering, direction, and moral anchoring, shaping whether sustainability trajectories become substantive or remain symbolic.

The primary contribution of this paper is to articulate a conceptual model and a set of hypotheses that reposition executive cognition as a substitute governance mechanism in contexts with weak institutional foundations. The principal conclusion is that improving sustainability performance in emerging markets requires strengthening not only external regulatory systems but also the cognitive capabilities through which executives interpret sustainability demands, construct meaning, and translate commitments into practice.

2. Theoretical Foundations: Executive Cognition Under Institutional Fragility

2.1. Upper Echelons and Institutional Context: Why Executive Cognition Matters

Research on executive influence has long demonstrated that organizational outcomes reflect the values, experiences, and cognitive frames of top leaders [11,12]. At the core of Upper Echelons Theory (UET) lies a foundational proposition: strategic choices are not objective responses to external conditions but are filtered through the interpretive lenses of senior executives, who selectively notice, prioritize, and act upon issues based on their mental models, heuristics, and identities. Recent work reinforces this view by showing that executive cognitive attributes and green awareness significantly shape corporate environmental and social trajectories [13,14].

In the domain of sustainability, this insight carries particular significance because environmental and social challenges are inherently complex, future-oriented, and normatively contested [15,16]. Executives must interpret ambiguous signals, reconcile competing stakeholder expectations, and balance short-term performance pressures against long-term societal and ecological concerns in institutional environments where frameworks such as ESG and the SDGs are diffusing but remain unevenly embedded [1,17,18].

These tasks are not reducible to technical optimization or the mechanics of disclosure; they are fundamentally cognitive and interpretive acts of sensemaking, framing, and prioritization that determine whether sustainability is treated as a compliance burden, a reputational shield, or a strategic opportunity [19,20,21]. In practice, the way senior leaders construe sustainability shapes how far global imperatives and reporting regimes—such as ESG standards, EU-level disclosure directives, and ISO 26000—are translated into internal governance routines, performance systems, and incentive structures [22,23,24].

Where executive sensemaking remains narrow or instrumental, organizations are more likely to engage in symbolic ESG adoption and decoupled reporting. Where cognitive frames are broader, paradox-oriented, and value-driven, sustainability is more often substantively embedded into strategy, culture, and operations, narrowing the ESG implementation gap in fragile institutional contexts [25,26,27,28]. Empirical research demonstrates that differences in executive green cognition lead firms facing similar pressures to diverge in sustainability outcomes because leaders understand sustainability in qualitatively different ways [13,29].

Institutional Theory deepens this perspective by situating executive sensemaking within broader systems of legitimacy pressures, norms, and regulatory expectations [30,31]. In strong institutional environments, clear rules, credible enforcement, and active stakeholder scrutiny constrain executive discretion and reduce interpretive ambiguity, thereby making compliance pathways comparatively well-defined [27,32].

In fragile institutional contexts, however—characterized by regulatory inconsistency, overlapping mandates, weak monitoring capacity, and fragmented stakeholder demands—executives encounter contradictory or incomplete institutional signals [6,7,33]. Under such conditions, sustainability expectations are less clearly specified, enforcement is sporadic, and compliance-oriented cues provide limited guidance. These conditions enable the symbolic adoption of ESG and the decoupling of disclosure from substantive practice, as firms rely on reporting and legitimacy signaling rather than operational transformation [25,26,27,34].

As a result, executive cognition assumes a more central role. Senior leaders must not only respond to institutional pressures but also actively construct coherence by interpreting which sustainability demands matter, how they should be prioritized, and how they can be translated into organizational routines and governance systems [20,21,35]. In these contexts, the cognitive work of the C-suite effectively substitutes for missing or unreliable institutional scaffolds, shaping whether sustainability becomes symbolically acknowledged or substantively embedded in strategy [28,36,37].

Thus, Upper Echelons Theory and Institutional Theory demonstrate that executive cognition is not peripheral to corporate sustainability performance but constitutive of it—particularly where institutional guidance is weak, fragmented, or contested. Sustainability leadership in fragile contexts is therefore best understood as a cognitive–interpretive process through which executives mediate between ambiguous external pressures and internal organizational action, actively constructing meaning, legitimacy, and direction in the absence of strong institutional enforcement [1,27,38].

2.2. Strategic Leadership and Sensemaking: How Cognition Translates into Enactment

While Upper Echelons Theory and Institutional Theory clarify why executive cognition matters, Strategic Leadership Theory (SLT) and sensemaking scholarship illuminate how cognition becomes organizational action. Strategic leaders are responsible for articulating long-term direction, signaling priorities, mobilizing stakeholders, and adapting the organization in response to environmental complexity [39]. Each of these leadership functions is inherently interpretive: leaders must frame issues, assign meaning to uncertainty, and authorize strategic responses that reconcile competing organizational and societal demands [20,40].

Sensemaking research further underscores that organizational action emerges through iterative cycles of interpretation, framing, communication, and enactment [20,40]. In sustainability contexts, executives confront competing imperatives—financial performance, regulatory compliance, social legitimacy, and environmental responsibility—that cannot be resolved through simple optimization techniques. Rather than applying technical solutions alone, leaders must construct narratives and frames that render these tensions intelligible and actionable for organizational members [16,21].

Recent research reinforces this perspective by showing that sustainable leadership influences firms’ strategic adoption of environmental initiatives through psychological and interpretive mechanisms such as environmental identity and psychological ownership [41]. Similarly, studies on executive green cognition demonstrate that the way executives interpret environmental issues significantly shapes corporate environmental protection behavior and sustainable development outcomes, highlighting cognition as a pathway from interpretation to enactment [29]. Further work on executive green awareness reveals that cognition influences how firms configure global green value chains, demonstrating that framing at the top of the organization cascades into concrete strategic choices [13].

Prior sustainability research demonstrates that framing plays a decisive role in shaping enactment outcomes. Opportunity-oriented and paradoxical frames encourage innovation, integration, and long-term orientation, whereas narrow compliance-oriented frames tend to produce symbolic or superficial adoption [16,21,26]. These framing effects are not merely rhetorical devices; they shape the allocation of resources, the design of governance mechanisms, and the degree to which sustainability becomes embedded in core decision processes [19,42]. Evidence from recent research further supports this argument by showing that cognitive CEO attributes are associated with improved social and environmental performance, confirming that senior leaders’ cognitive orientations influence organizational sustainability trajectories [14].

Under conditions of institutional fragility, the importance of these interpretive functions is amplified. When regulatory signals are inconsistent and stakeholder expectations fragmented, executives cannot rely on external standards alone to guide action [6,7,33]. Instead, they draw more heavily on cognitive heuristics, experiential knowledge, and personal judgment to navigate uncertainty [43,44]. Decision-making under volatility heightens the salience of attention, framing, intuition, and prioritization, making executive cognition a primary determinant of sustainability outcomes.

Cumulatively, strategic leadership, sensemaking, and emerging cognitive research reveal that sustainability enactment is not the mechanical implementation of policies or frameworks. It is an ongoing process of meaning construction and translation through which executives render sustainability intelligible, legitimate, and actionable within the organization [20,40]. This process is deeply cognitive, socially embedded, and highly sensitive to institutional context—especially in emerging markets where formal governance systems provide incomplete guidance [26,27].

2.3. Executive Sustainability Cognition (ESC): From Fragmented Constructs to Cognitive Governance

Executive Sustainability Cognition (ESC) refers to the emergent, processual capacity through which senior executives interpret sustainability imperatives, frame their strategic significance, and translate these interpretations into coherent organizational practice. Although terminology varies across studies—encompassing labels such as executive green cognition, sustainability mindset, or attentional framing—a growing interdisciplinary literature converges on a shared insight: differences in how executives cognitively engage with sustainability decisively shape how it is prioritized, enacted, and sustained within organizations. Recent work demonstrates that executive green awareness influences firms’ integration into global green value chains by shaping how leaders construe environmental priorities [13], while CEOs with stronger cognitive and psychological engagement with environmental issues promote higher levels of social and environmental performance [14]. Firms facing similar ESG pressures therefore diverge sharply in sustainability trajectories because their leaders interpret and prioritize those pressures differently [10,45].

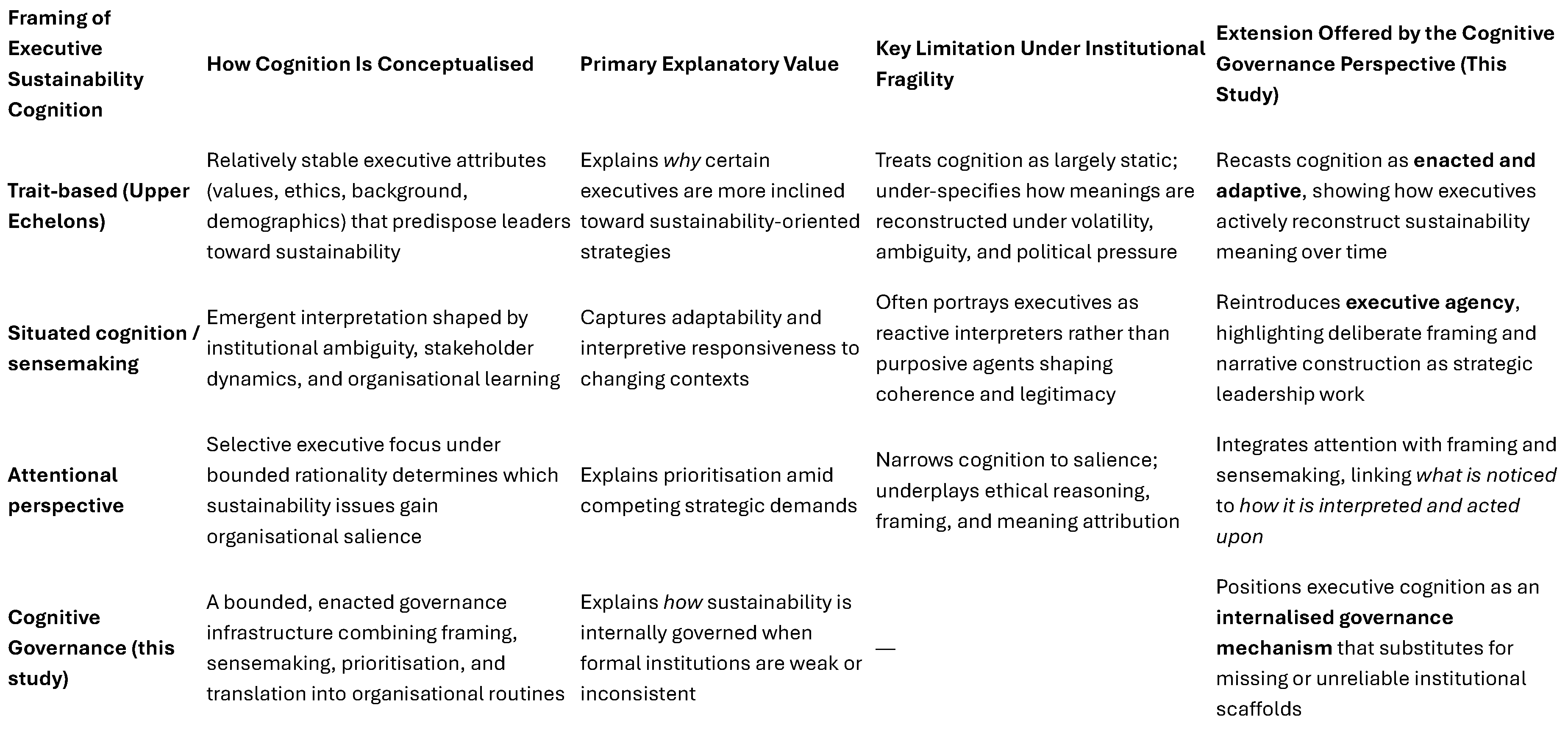

Despite this convergence on the importance of ESC, the literature remains theoretically fragmented. Existing work alternately conceptualizes executive cognition as (a) a relatively stable individual orientation, (b) a situated and adaptive interpretive process, or (c) a bounded attentional resource. Each perspective explains part of sustainability enactment, but none alone fully captures executive practice under fragile institutional conditions marked by weak enforcement, fragmented stakeholder expectations, and contested legitimacy [6,26]. This gap is particularly evident in emerging-market contexts, where symbolic adoption coexists with weak implementation, underscoring the need to understand how executives construct sustainability meaning, rather than merely whether structures exist.

Trait-based approaches, grounded in Upper Echelons Theory [11,12], view ESC as an outcome of relatively stable personal characteristics—values, ethical orientation, education, and demographic traits—that predispose certain executives toward sustainability-oriented decisions. Empirical studies show that executives with sustainability-oriented values or prior experience are more likely to support ESG integration, long-term investment, and stakeholder engagement [46,47]. Consistent with this line of thought, a recent study suggests that sustainable leadership influences strategic adoption through psychological mechanisms, such as environmental identity and psychological ownership [41]. These studies illuminate the origins of pro-sustainability orientations but risk essentializing cognition as static. In volatile environments, executive interpretations rarely remain fixed: sustainability meanings are continually renegotiated as leaders confront shifting political pressures, stakeholder conflict, and resource constraints.

A second body of literature conceptualizes ESC as situated and adaptive, emphasizing sensemaking processes through which leaders adjust their interpretations of sustainability in response to evolving institutional conditions [29,35,48]. From this perspective, cognition emerges through ongoing interaction with stakeholders, institutional ambiguity, and organizational learning. While this approach captures interpretive agility, it can underplay the discretionary leadership work of executives by portraying them primarily as reactive interpreters of context rather than as strategic agents who actively construct coherence and legitimacy amid fragmentation [20].

A third, increasingly influential perspective draws on the attention-based view of the firm, emphasizing selective focus under bounded rationality [49,50,51]. From this viewpoint, sustainability outcomes depend on which issues executives attend to—or ignore—amid competing strategic demands [52]. Attentional accounts thus explain which sustainability cues become salient, but they tend to underplay the ethical reasoning and framing work through which executives assign meaning and moral weight to sustainability priorities. Attention explains what is noticed, but not how sustainability is understood or why it is pursued substantively rather than symbolically.

These limitations become especially pronounced in fragile institutional contexts, where regulatory enforcement is inconsistent, stakeholder expectations are fluid, and legitimacy is persistently contested [7,33]. Under such conditions, executives cannot rely solely on inherited dispositions, contextual cues, or existing attentional routines. They must engage in sustained interpretive work—actively framing sustainability, mediating competing logics, and constructing organizational coherence in the absence of stable institutional guidance. In these settings, symbolic adoption and decoupling are common, and it is often the internal cognitive work of the C-suite that determines whether ESG commitments remain ceremonial or become substantively embedded [6,26].

This paper, therefore, reconceptualizes ESC as cognitive governance: an internalized capability through which sustainability is framed, prioritized, and enacted under institutional fragility. Rather than treating cognition as a fixed trait or purely reactive process, cognitive governance views executive cognition as an internal ordering mechanism—a bounded behavioral governance infrastructure— that substitutes for missing or unreliable institutional scaffolds [26,38]. In such contexts, executive cognition does not merely respond to governance; it performs governance by creating coherence, direction, and moral anchoring where formal systems fall short.

Within this framing, three interrelated cognitive mechanisms explain how ESC translates sustainability imperatives into organizational enactment:

- Framing sustainability’s meaning and boundaries, including whether executives adopt a narrow business-case logic or a paradoxical orientation that reconciles profit with planetary and social imperatives [16].

These mechanisms jointly shift the analysis from what ESC is to how ESC works. They integrate insights from trait-based, situated, and attentional perspectives while emphasizing sustainability leadership as enacted cognition—strategic judgement, ethical reasoning, and reflexive learning exercised under institutional fragility. By positioning ESC as cognitive governance, this section establishes the theoretical foundation for the conceptual model developed in Section 3. Sustainability enactment is understood not as a linear response to external mandates but as the outcome of executive interpretation operating through framing, sensemaking, prioritization, and translation into organizational structures and routines. Where formal institutions provide limited guidance or enforcement, executive cognition functions as the interpretive and steering architecture of sustainability, shaping whether ESG commitments remain symbolic or become substantively embedded.

Table 1 summarizes the dominant framings of executive sustainability cognition and clarifies how the cognitive governance perspective advanced here addresses their limitations under conditions of institutional fragility.

2.4. Approach to Theory Development and Conceptual Synthesis

This paper adopts a theory-building, conceptual-synthesis approach to develop the construct of Executive Sustainability Cognition (ESC) and specify its implications for sustainability enactment in fragile institutional contexts. Rather than testing predefined hypotheses empirically, the objective is to integrate existing but fragmented theoretical insights into a coherent model that can guide future empirical research.

The conceptual model was developed through an abductive, iterative engagement with multiple scholarly streams. Upper Echelons Theory provided micro-foundations for linking executive cognition to organizational outcomes; Institutional Theory foregrounded the role of fragility, weak enforcement, and legitimacy pressures; Strategic Leadership Theory highlighted how executives mobilize strategic direction; and sensemaking and behavioral strategy research illuminated the interpretive processes through which ambiguous signals become actionable organizational commitments. These literatures were examined not as competing explanations but as complementary lenses on how cognition shapes sustainability enactment.

The synthesis proceeded in three steps. First, recurrent cognitive mechanisms across the literature—attention, framing, prioritization, and translation—were identified. Second, evidence on the implementation of sustainability in weak-governance environments was reviewed to assess how these mechanisms operate under institutional fragility. Third, these insights were integrated into an overarching conceptual framework that theorizes ESC as a form of cognitive governance, and eight hypotheses were formulated to articulate empirically testable relationships.

The resulting model does not claim exhaustive coverage, but instead offers a theoretically grounded, context-sensitive foundation for subsequent qualitative and quantitative inquiry into how executives interpret and enact sustainability under conditions of institutional fragility.

3. Conceptual Model and Hypotheses

Building on the foregoing theoretical synthesis, this paper advances Executive Sustainability Cognition (ESC) as the core mechanism through which sustainability is interpreted, prioritized, and institutionalized in fragile institutional environments. Whereas much of the sustainability governance literature foregrounds formal structures, leadership competencies, or stakeholder pressures, these approaches often imply that enactment follows from rational–technical alignment. The ESC framework instead conceptualizes sustainability enactment as a cognitive–interpretive governance process through which executives stabilize meaning, set priorities, and authorize organizational responses when institutional signals are ambiguous, inconsistent, or weakly enforced.

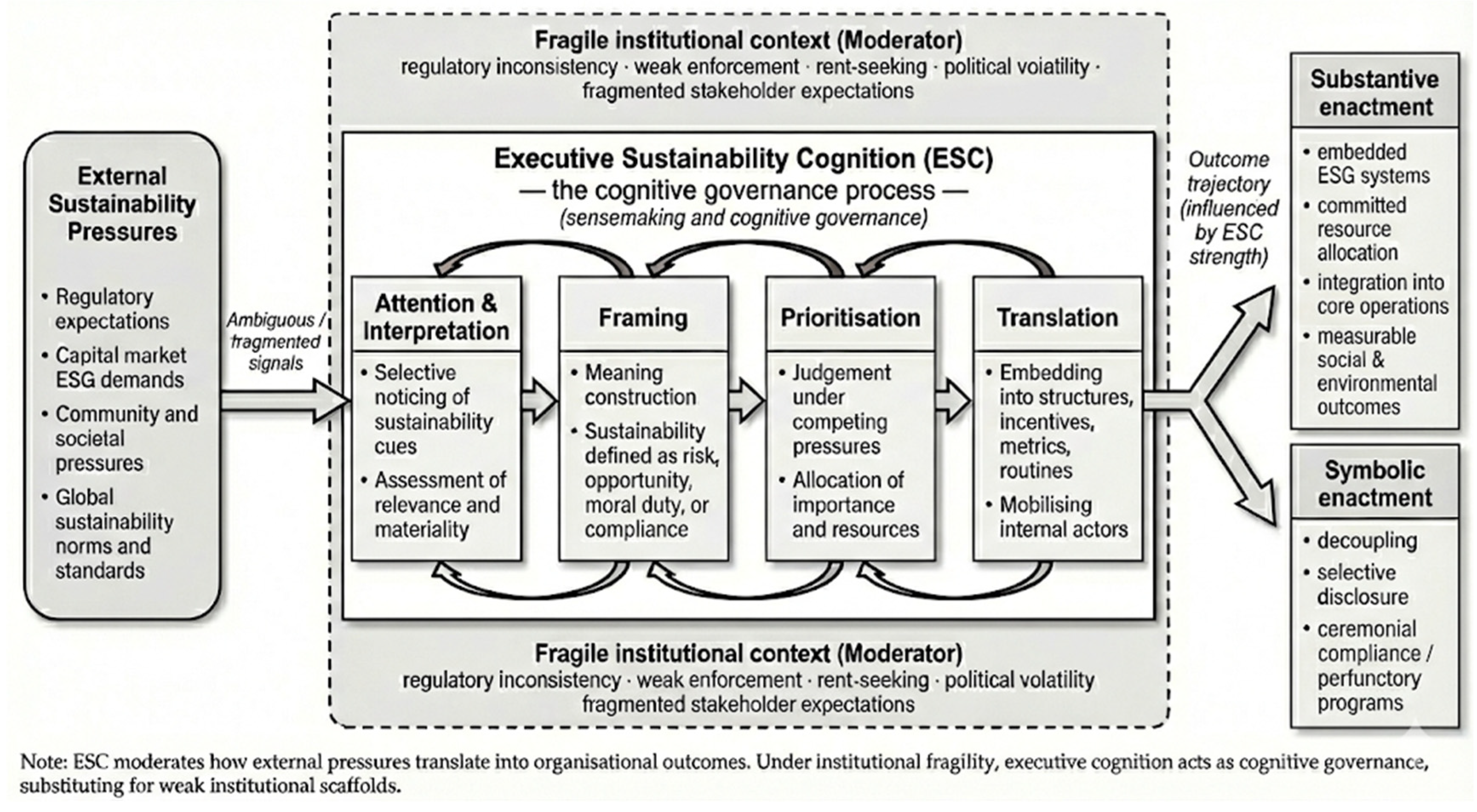

ESC is modelled as a dynamic, multi-stage process comprising four interrelated components—attention, framing, prioritization, and translation. Sensemaking is treated as the integrative interpretive work that links these stages: executives notice cues, construct meaning, adjudicate trade-offs, and convert commitments into routines and accountability. These processes collectively explain how sustainability imperatives are translated from contested external pressures into organizational agendas, decision-making processes, and institutionalized practices. To synthesize these relationships, Figure 1 presents the Executive Sustainability Cognition (ESC) framework, which models ESC as a multi-stage cognitive governance process linking external sustainability pressures to symbolic versus substantive sustainability enactment under varying conditions of institutional fragility.

The following subsections develop hypotheses linking the four ESC processes to sustainability enactment outcomes and identify institutional fragility, stakeholder fragmentation, and organizational learning orientation as key boundary conditions that condition these relationships.

3.1. Attention and Interpretation as an Interpretive Filter of Sustainability Signals

Attention determines which sustainability issues enter the strategic agenda and how they are initially rendered meaningful. Attention is selective rather than neutral; prior experience, cognitive biases, values, and the salience of external cues shape it. Consistent with Upper Echelons Theory, executives differ in their interpretations of sustainability, viewing it as a peripheral burden, an emerging risk, or a strategic opportunity, and these differences have downstream implications for organizational action.

In fragile institutional environments, attention and interpretation become especially consequential because external signals are often contradictory or underspecified. Limited enforcement, weak monitoring, and fluctuating stakeholder expectations necessitate that executives rely more heavily on judgment when determining which pressures warrant a response. Accordingly, attention and interpretation are not simply agenda-setting acts; they constitute the first step in cognitive governance, as they define what counts as “real” and actionable.

- Hypothesis (H1)

H1. In fragile institutional contexts, greater executive attention to sustainability-related cues is positively associated with the extent to which sustainability issues are integrated into the organization’s strategic agenda.

3.2. Framing and Strategic Orientation

Framing refers to the interpretive process through which executives assign meaning and urgency to sustainability issues. Frames shape whether sustainability is construed as compliance, reputational insurance, moral obligation, or strategic renewal. In environments characterized by ambiguity, framing becomes decisive because it establishes the organization’s posture toward uncertainty and competing demands.

Opportunity-oriented or paradoxical frames legitimize the simultaneous pursuit of economic and sustainability goals, supporting long-term commitment despite volatility. By contrast, narrow compliance or risk-avoidance frames stabilize short-term legitimacy but tend to produce symbolic adoption and minimal investment.

- Hypothesis (H2)

H2. Executives who adopt opportunity-oriented or paradoxical frames of sustainability are more likely to lead their organizations toward substantive sustainability enactment than executives who adopt compliance-driven or risk-avoidance frames.

3.3. Prioritization Under Competing Institutional Pressures

Sustainability enactment requires judgment about trade-offs among profitability, stakeholder legitimacy, regulatory demands, and long-term resilience. Prioritization captures how executives rank these claims and convert frames into strategic commitment.

Under institutional fragility, prioritization becomes both more complex and more powerful because stable external reference points are lacking. When guidance is inconsistent and sanctions uneven, executive prioritization logics—rather than institutional compulsion—determine whether sustainability is treated as a core strategy, a bounded initiative, or a rhetorical commitment. Prioritization, therefore, functions as a governance act because it allocates attention and authorizes trade-offs.

- Hypothesis (H3)

H3. The degree to which executives prioritize sustainability objectives over short-term financial pressures is positively associated with the depth of sustainability enactment within the organization.

3.4. Translation from Cognition to Organizational Action

Translation refers to embedding executive interpretations into strategies, resource allocations, governance arrangements, metrics, incentives, and routines. Many sustainability initiatives fail not because leaders lack intent but because translation mechanisms are weak.

In fragile institutional environments—where external enforcement is limited—translation depends heavily on leaders’ capacity to mobilize internal actors, maintain commitment, and construct accountability architectures independent of regulatory pressure. Translation, therefore, represents the decisive point at which cognition becomes institutional reality.

- Hypothesis (H4)

H4. Executive translation capability—reflected in the embedding of sustainability into structures, incentives, and organizational routines—is positively associated with the consistency and credibility of the organization’s sustainability performance.

3.5. Moderating Role of Institutional Fragility

Institutional fragility—manifested in regulatory inconsistency, weak enforcement, rent-seeking, and socio-political volatility—expands the role of ESC by increasing ambiguity and discretionary space. In such contexts:

- external guidance is unreliable,

- stakeholder expectations are fluid,

- monitoring systems are weak, and

- executive conviction substitutes for institutional mandate.

Accordingly, ESC becomes both a driving mechanism and a compensatory response to institutional voids.

- Hypothesis (H5)

H5. Institutional fragility positively moderates the relationship between Executive Sustainability Cognition and sustainability enactment, such that the positive effect of ESC on sustainability outcomes is stronger in more fragile institutional contexts than in more robust institutional environments.

3.6. ESC and the Boundary Between Symbolic and Substantive Enactment

Symbolic enactment occurs when attention, framing, prioritization, and translation are misaligned—such as when sustainability is rhetorically prioritized but not resourced. Substantive enactment requires coherence across these stages.

Where external monitoring of greenwashing is weak, internal cognitive coherence becomes particularly crucial for avoiding performative ESG behavior.

- Hypothesis (H6)

H6. The greater the alignment between executives’ framing of sustainability and the organizational structures and routines through which sustainability is implemented, the lower the likelihood of symbolic sustainability enactment and the higher the likelihood of substantive sustainability performance.

3.7. Stakeholder Fragmentation as a Cognitive Amplifier

Fragile institutional environments often exhibit fragmented and competing stakeholder expectations. This increases interpretive burden and magnifies the role of executive framing. Integrative frames help manage conflict among diverse claims; narrow frames, on the other hand, intensify short-termism.

- Hypothesis (H7)

H7. Stakeholder fragmentation positively moderates the relationship between executive framing and sustainability prioritization, such that the effect of integrative (opportunity/paradox) frames on sustainability prioritization is stronger under high stakeholder fragmentation than under low stakeholder fragmentation.

3.8. Organizational Learning Climate as an Enabler of Translation

The impact of ESC is conditioned by organizational receptivity. Learning-oriented cultures, cross-functional collaboration, and feedback systems enhance translation capability, whereas rigid cultures blunt it.

- Hypothesis (H8)

H8. Organizational learning orientation positively moderates the relationship between executive translation capability and substantive sustainability outcomes, such that the effect of translation capability on sustainability performance is stronger in organizations with stronger learning cultures than in those with weaker learning cultures.

3.9. Integrative Model

The ESC model brings together the preceding elements into an integrative account of how sustainability is enacted through cognitive governance. Sustainability enactment begins with executive attention and interpretation, through which leaders filter the multitude of sustainability signals surrounding the firm and determine what is considered salient or material. These interpretations provide the raw material for framing processes. Through framing, executives construct meaning around sustainability, define their organizational stance toward environmental and social tensions, and influence whether sustainability is viewed primarily as a risk, an obligation, or a strategic opportunity.

On this foundation, prioritization processes adjudicate among competing demands. Executives must decide which sustainability issues warrant resource allocation, which tensions can be deferred, and how trade-offs between economic and non-economic goals will be managed. These choices, in turn, must be translated into organizational reality. Translation refers to the institutionalization of sustainability commitments through governance structures, metrics, incentive systems, strategies, and everyday routines that embed executive cognition into practice.

Institutional fragility intensifies the consequences of each stage of this process. Weak enforcement, regulatory inconsistency, and political or stakeholder volatility expand executive discretion and increase ambiguity, making the quality of executive cognition more consequential for sustainability outcomes. Alignment across the ESC stages—attention, framing, prioritization, and translation—ultimately determines whether sustainability commitments remain symbolic or become substantively embedded in organizational action. Stakeholder fragmentation and organizational learning conditions further shape how ESC translates into outcomes, strengthening or weakening the pathway from cognition to enactment.

In this integrative model, sustainability enactment is not conceptualized as a simple compliance response to external rules. Rather, it is the product of executive interpretation within a specific context. Executive Sustainability Cognition operates as a cognitive infrastructure through which firms navigate uncertainty and volatility, particularly in emerging and fragile institutional environments, shaping whether ESG commitments are merely declared or meaningfully realized.

4. Discussion and Managerial/Policy Implications

The ESC model reframes sustainability enactment as a cognitively mediated process driven by how C-suite executives notice, interpret, prioritize, and institutionalize sustainability imperatives. This view departs from dominant frameworks that emphasize governance structures, technical ESG systems, or demographic proxies for leadership impact. Instead, it positions executive cognition as a decisive mechanism under institutional fragility, where formal guidance is weak and organizational action depends more heavily on interpretive ordering and internal accountability. This section outlines the model’s theoretical contributions and practical implications for leaders, boards, policymakers, and executive development in emerging and institutionally volatile contexts.

4.1. Theoretical Contributions

This paper makes three primary theoretical contributions to the research on sustainability leadership and governance.

First, it reframes sustainability enactment as fundamentally cognitive work rather than solely a structural or technical process. Much prior research emphasizes reporting systems, governance mechanisms, and organizational capabilities, implicitly assuming that action follows design. The ESC model instead highlights that sustainability outcomes are filtered through executive interpretation. What leaders notice, how they frame issues, and which priorities they construct determine what organizations come to regard as strategically material. By foregrounding cognition, the model expands the explanatory space of sustainability studies, suggesting that variations in sustainability performance often originate at the cognitive level rather than the structural level.

Second, the paper integrates multiple perspectives on executive influence at various levels. By drawing on Upper Echelons Theory, Institutional Theory, Strategic Leadership Theory, and sensemaking research, the ESC model shows how micro-level cognition interacts with macro-level institutional conditions. Sustainability enactment emerges not as a simple response to external mandates, but as an ongoing negotiation between institutional signals and executive judgement. This integration provides a theoretically grounded basis for analyzing sustainability strategies in volatile environments where institutions offer weak or inconsistent normative guidance.

Third, the paper extends sustainability research into fragile institutional contexts by conceptualizing ESC as a substitute governance mechanism. In environments characterized by inconsistent regulation, political interference, weak enforcement, and limited stakeholder scrutiny, formal institutions provide incomplete behavioral guidance. Under such conditions, executive cognition increasingly replaces formal governance systems as the primary driver of organizational behavior. This insight helps explain why firms operating within similar institutional environments nevertheless display widely divergent sustainability outcomes, offering a context-sensitive lens for understanding sustainability in emerging markets.

4.2. Managerial Implications for C-Suite Executives

The ESC model also carries significant implications for senior executives responsible for steering organizations through sustainability transitions. A first implication concerns executive attention and environmental scanning. In fragile institutional contexts, sustainability signals are often weak, inconsistent, or contradictory. Executives, therefore, need structured systems for noticing emerging issues early. Practices such as horizon scanning, ESG scenario analysis, and stakeholder-intelligence platforms can enhance attentional acuity, reduce blind spots, and ensure that weak sustainability cues are not ignored until they become crises.

A second implication concerns the organization’s framing of sustainability. How executives narrate sustainability—whether as an opportunity, a risk, or a mere compliance burden—strongly shapes employee engagement, resource allocation, and strategic orientation. Leaders operating in volatile contexts benefit from adopting opportunity-oriented and paradox-embracing frames that recognize constraints but emphasize long-term value creation and resilience. Through framing, executives influence not only what organizations do, but how organizational members think about why sustainability matters.

The model also highlights the importance of explicit prioritization in the face of competing demands. C-suite leaders routinely face tensions between short-term financial performance and long-term sustainability commitments. ESC highlights that these trade-offs are resolved cognitively before they are resolved structurally. Mechanisms such as integrating ESG criteria into capital budgeting processes, formalizing sustainability risk assessments, and routinely using sustainability scorecards in top-management meetings help anchor sustainability priorities in core decision-making processes, rather than merely making rhetorical statements.

Ultimately, the model highlights the significance of translating cognitive insights into organizational systems and routines. Executive awareness and intention are insufficient unless they are institutionalized through established structures, clear metrics, effective incentives, and a supportive culture. Practical steps include aligning executive compensation with ESG targets, embedding sustainability indicators into performance evaluation, creating cross-functional sustainability teams, and strengthening internal accountability architectures. Without this translation work, even a firm’s top-level commitment to sustainability risks remaining symbolic rather than substantive.

4.3. Implications for Boards and Governance Actors

Boards of directors have a powerful influence on the development and expression of executive sustainability cognition. The ESC model implies that governance actors should not only oversee sustainability performance, but also shape the cognitive conditions under which executives interpret sustainability demands. One important avenue is leadership selection. Boards can prioritize the recruitment of executives who demonstrate sustainability literacy, cognitive agility, and the ability to navigate complex socio-environmental issues rather than relying solely on traditional financial or operational track records.

Additionally, governance structures themselves can be recalibrated to support executive sense-making. Board-level sustainability committees should move beyond compliance monitoring to engage directly with strategic interpretation, scenario thinking, and longer-term societal implications of corporate action. Evaluation practices may also evolve: instead of focusing exclusively on ESG outcomes, boards can assess senior leaders based on their interpretive capacity — that is, their ability to attend to emerging sustainability issues, frame them rigorously, and integrate them into organizational priorities.

Finally, boards can institutionalize feedback loops that connect external stakeholders more directly to executive deliberation. Mechanisms such as structured stakeholder dialogues, board–community interfaces, and periodic sustainability hearings enrich the information environment in which executives operate, broadening the perspectives that inform their strategic judgment. Through these practices, boards do not simply monitor sustainability performance; they help cultivate the cognitive environment that enables executives to move from symbolic to substantive sustainability enactment.

4.4. Policy Implications for Emerging and Fragile Institutional Contexts

The ESC framework also has important implications for public policy in settings characterized by institutional fragility. Where regulatory systems are weak or inconsistently enforced, sustainability outcomes depend heavily on how executives interpret ambiguous signals. Strengthening sustainability performance in such environments, therefore, requires not only stricter rules but also a stronger cognitive infrastructure to support executive sensemaking. Policy interventions that provide more straightforward regulatory guidelines, accessible and reliable sustainability data, targeted capacity-building programs for senior corporate leaders, and multi-stakeholder platforms for dialogue can significantly enhance executives’ ability to interpret sustainability expectations and convert them into coherent action. Policy should not simply prescribe behavior; it should also enable leaders to understand what is expected and why it matters.

A second implication concerns the reduction of institutional ambiguity. Regulatory inconsistency remains a significant barrier to the enactment of sustainability in many emerging markets. When standards are fragmented or weakly enforced, executives receive contradictory signals and face substantial uncertainty regarding long-term investment decisions. Governments can play a central role by harmonizing ESG standards, signaling consistent enforcement, and providing incentive mechanisms that reward long-term sustainability commitments. Such actions reduce interpretive ambiguity and help align executive judgment with societal sustainability goals.

Finally, the model highlights the value of public–private partnerships as collective sensemaking arenas. In fragile contexts, no single actor possesses complete information or capacity. Collaborations among governments, firms, and civil society organizations can foster shared learning, diffuse best practices, and reduce the cognitive burden on individual executives facing complex sustainability dilemmas. Well-designed partnerships can thus compensate for weak formal institutions by creating spaces where sustainability expectations are jointly interpreted and translated into action.

4.5. Implications for Sustainability Practitioners and Educators

The ESC framework also carries practical implications for those involved in executive education, leadership development, and sustainability practice. Much of the current training architecture for sustainability leaders concentrates on technical ESG knowledge, reporting standards, and compliance tools. While these skills are essential, the ESC model suggests that they are insufficient in fragile institutional environments where executives must rely heavily on judgment and interpretation. Development initiatives should therefore focus more explicitly on strengthening the cognitive capabilities that underpin executive sustainability cognition. These include systems thinking, the ability to navigate paradox and tension, ethical reasoning, awareness of cognitive bias, values-based leadership, and sustainability sensemaking under uncertainty. Programs that cultivate these capabilities prepare executives not only to understand sustainability frameworks but to interpret ambiguous signals and translate them into coherent strategic action.

Beyond individual capability-building, the ESC perspective also underscores the importance of cultivating organizational learning. Consultants, sustainability officers, and educators can play a strategic role in creating structures that help organizations internalize sustainability knowledge over time. Examples include reflective-practice workshops, scenario simulations, peer-learning forums, and cross-functional platforms that encourage collaboration between strategy, finance, risk, and sustainability teams. Such mechanisms enable firms to treat sustainability not as an isolated function but as a shared cognitive resource. By strengthening both individual and collective sensemaking, these learning architectures enhance the likelihood that sustainability commitments will be translated into durable routines and consistently enacted in practice.

4.6. Overall Significance of the Model

The ESC model emphasizes that sustainability enactment is not merely a function of external pressure or formal governance; it is fundamentally shaped by how executives think, interpret, and decide—especially when institutions provide weak guidance. By articulating the pathways through which cognition influences sustainability outcomes, this paper offers a conceptual foundation for future empirical studies and provides practical direction for leaders navigating complex ESG landscapes.

5. Conclusion and Future Research

This paper advances a cognitively anchored understanding of sustainability leadership by introducing Executive Sustainability Cognition (ESC) as a central explanatory mechanism for how firms interpret and enact sustainability, particularly in fragile institutional environments. Departing from leadership models that emphasize formal governance structures, demographic proxies, or technical ESG capabilities, the ESC framework conceptualizes sustainability enactment as a layered process involving attention, interpretive framing, strategic prioritization, and organizational translation. This cognitive pathway becomes especially salient in emerging markets such as Nigeria, where inconsistent regulation, limited stakeholder scrutiny, and fluid institutional dynamics elevate the role of executive judgement in shaping organizational sustainability trajectories.

The conceptual model integrates insights from Upper Echelons Theory, Institutional Theory, Strategic Leadership Theory, and sensemaking to reveal how micro-level cognition interacts with macro-level institutional pressures. By doing so, it explains why firms operating under similar external conditions often exhibit divergent sustainability outcomes—differences rooted not primarily in resources or structures but in how executives perceive, ascribe meaning to, and act upon sustainability pressures. The related hypotheses suggest that sustainability leadership encompasses not only what executives do, but also how they think, particularly in uncertain situations. This cognitive emphasis offers a theoretical lens for understanding both high-performing sustainability exemplars and firms that exhibit symbolic or inconsistent ESG behaviors.

5.1. Contributions to Research and Practice

Conceptually, the paper contributes three key insights.

- First, it positions ESC as a substitute governance mechanism, extending sustainability scholarship into fragile institutional contexts where formal ESG infrastructures are weak or unreliable.

- Second, it bridges micro-cognitive processes with organizational and institutional analysis, offering a more integrated framework for studying sustainability leadership.

- Third, it provides a fine-grained basis for analyzing how sustainability strategies emerge, evolve, or stall within executive decision systems.

Practically, the model provides boards, policymakers, and organizational leaders with a framework for diagnosing and strengthening sustainability leadership. It suggests that enhancing sustainability outcomes requires not only governance reforms but also targeted development of executive cognitive capacities, strengthened organizational learning systems, and clearer regulatory signals that support coherent sensemaking.

5.2. Future Research Directions

As a conceptual contribution, the ESC model opens several avenues for empirical validation and theoretical refinement. A first priority is the empirical testing of the four ESC processes—attention, interpretation, prioritization, and translation—across different sectors and institutional environments. Operationalizing these processes and examining their links to sustainability outcomes would enable researchers to assess the explanatory power of ESC relative to more traditional governance or structural variables. Comparative studies between emerging and developed markets could also illuminate how institutional robustness moderates the effects of executive cognition.

Beyond testing relationships, future research would benefit from multi-method examinations of executive sensemaking in practice. In-depth qualitative approaches, such as cognitive interviewing, ethnography of top management teams, or executive diary studies, can capture how leaders interpret sustainability cues in real-time, while quantitative designs can develop measurement scales for ESC and subject the proposed hypotheses to longitudinal or multilevel testing.

Another promising line of inquiry concerns the interaction between ESC and organizational structures. Governance systems, sustainability committees, and digital ESG tools may either amplify or dampen the influence of executive cognition, particularly in data-poor or fragile institutional contexts. Understanding these interactions would clarify whether cognition substitutes for weak structures or is most effective when coupled with them.

A further research direction involves exploring the antecedents of ESC. Executive national culture, professional identity, ethical orientation, and exposure to sustainability discourses are likely to influence how leaders perceive sustainability. Explaining why cognition varies among executives facing similar external pressures would deepen the micro foundations of sustainability governance.

Finally, future work could examine ESC as a mechanism for cross-firm diffusion of sustainability practices. Investigating how cognitive frames travel across supply chains, industry networks, and public–private partnerships may reveal how shared meaning systems accelerate or impede collective sustainability action, particularly in emerging-market settings.

5.3. Conclusions

As global sustainability pressures intensify and institutional environments become increasingly heterogeneous, understanding how executives think about sustainability—not simply how they structure it—becomes essential. The ESC model provides a theory-driven foundation for analyzing this cognitive terrain, explaining variation in sustainability enactment where traditional models fall short. By shifting attention from structures and outputs to cognition and interpretation, the model offers scholars and practitioners a more nuanced lens for understanding the drivers of authentic, strategic, and context-sensitive sustainability leadership. It is hoped that this framework will catalyze new empirical work, inform executive development, and support more adaptive and meaningful sustainability transitions across diverse organizational and institutional settings.

Author Contributions

Conceptualization, P.O.U. and J.E.M.; methodology, P.O.U.; validation, P.O.U. and J.E.M.; formal analysis, P.O.U.; investigation, P.O.U.; resources, P.O.U.; data curation, P.O.U.; writing—original draft preparation, P.O.U.; writing—review and editing, P.O.U. and J.E.M.; visualization, P.O.U.; supervision, J.E.M.; project administration, P.O.U. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

During the preparation of this manuscript/study, the author(s) used ChatGPT 5.2 as a language and editing assistant to improve clarity, coherence, and structure, and to help rephrase and condense sections of the manuscript. The authors have reviewed and edited the output and take full responsibility for the content of this publication.

Conflicts of Interest

The authors declare that they have no conflicts of interest.

Abbreviations

The following abbreviations are used in this manuscript:

| CEO | Chief Executive Officer |

| ESC | Executive Sustainability Cognition |

| ESG | Environmental, Social, and Governance |

| EU | European Union |

| SDGs | Sustainable Development Goals |

| SLT | Strategic Leadership Theory |

| UET | Upper Echelons Theory |

References

- Eccles, R.G.; Klimenko, S. The investor revolution: Shareholders are getting serious about sustainability. Harvard Business Review 2019, 97(3), 106–116. [Google Scholar]

- Kotsantonis, S.; Pinney, C.; Serafeim, G. ESG integration in investment management: Myths and realities. Journal of Applied Corporate Finance 2016, 28(2), 10–16. [Google Scholar] [CrossRef]

- Kotsantonis, S.; Serafeim, G. Four things no one will tell you about ESG data. Journal of Applied Corporate Finance 2019, 31(2), 50–58. [Google Scholar] [CrossRef]

- Gonzaga, B.R.; et al. The ESG patterns of emerging-market companies: are there differences in their sustainable behavior after COVID-19? Sustainability 2024, 16(2), 676. [Google Scholar] [CrossRef]

- Nemes, N.; et al. An integrated framework to assess greenwashing. Sustainability 2022, 14(8), 4431. [Google Scholar] [CrossRef]

- Kolk, A.; Rivera-Santos, M. The State of Research on Africa in Business and Management: Insights From a Systematic Review of Key International Journals. Business & Society 2018, 57(3), 415–436. [Google Scholar]

- Nakpodia, F.; et al. Neither Principles Nor Rules: Making Corporate Governance Work in Sub-Saharan Africa. Journal of Business Ethics 2018, 151(2), 391–408. [Google Scholar] [CrossRef]

- Li, J.; Zhu, Y.; Ma, T. The Impact of the CEO’s Green Experience on Corporate ESG Performance: Based on the Upper Echelons Theory Perspective. Sustainability 2025, 17(15), 6859. [Google Scholar] [CrossRef]

- Deng, C.; et al. Environmental Background Directors and ESG Performance: A Perspective on Green Governance. Sustainability 2024, 16(23), 10559. [Google Scholar] [CrossRef]

- Zhang, Q.; Tan, L.; Gao, D. Leading Sustainability: The Impact of Executives’ Environmental Background on the Enterprise’s ESG Performance. Sustainability 2024, 16(16), 6952. [Google Scholar] [CrossRef]

- Hambrick, D.C. Upper echelons theory: An update. Academy of Management Review 2007, 32(2), 334–343. [Google Scholar] [CrossRef]

- Hambrick, D.C.; Mason, P.A. Upper echelons: The organization as a reflection of its top managers. Academy of Management Review 1984, 9(2), 193–206. [Google Scholar] [CrossRef]

- Huang, X.; Xie, J. Sustainability of Global Trade: The Impact of Executive Green Awareness on the Global Green Value Chain of Enterprises. Sustainability 2025, 17(4), 1510. [Google Scholar] [CrossRef]

- Wang, X.; et al. Can Cognitive Chief Executive Officers Revitalize Social and Environmental Performance? Assessing the Relation Under the Aegis of Innovation, the Moderating Role of Supervisors and Cash Holdings. Sustainability 2025, 17(13), 5752. [Google Scholar] [CrossRef]

- Bansal, P.; Song, H.-C. Similar But Not the Same: Differentiating Corporate Sustainability from Corporate Responsibility. Academy of Management Annals 2017, 11(1), 105–149. [Google Scholar] [CrossRef]

- Hahn, T.; et al. Cognitive frames in corporate sustainability: Managerial sensemaking with paradoxical and business case frames. Academy of Management Review 2014, 39(4), 463–487. [Google Scholar] [CrossRef]

- Pizzi, S.; Rosati, F.; Venturelli, A. The determinants of business contribution to the 2030 Agenda: Introducing the SDG Reporting Score. Business Strategy and the Environment 2021, 30(1), 404–421. [Google Scholar] [CrossRef]

- Van der Waal, J.W.; Thijssens, T. Corporate involvement in sustainable development goals: Exploring the territory. Journal of Cleaner Production 2020, 252, 119625. [Google Scholar] [CrossRef]

- Engert, S.; Rauter, R.; Baumgartner, R.J. Exploring the integration of corporate sustainability into strategic management: a literature review. Journal of Cleaner Production 2016, 112, 2833–2850. [Google Scholar] [CrossRef]

- Maitlis, S.; Christianson, M. Sensemaking in organizations: Taking stock and moving forward. Academy of management annals 2014, 8(1), 57–125. [Google Scholar] [CrossRef]

- Sonenshein, S. How Corporations Overcome Issue Illegitimacy and Issue Equivocality to Address Social Welfare: The Role of the Social Change Agent. Academy of Management Review 2016, 41(2), 349–366. [Google Scholar] [CrossRef]

- Christensen, H.B.; Hail, L.; Leuz, C. Mandatory CSR and sustainability reporting: Economic analysis and literature review. Review of accounting studies 2021, 26(3), 1176–1248. [Google Scholar] [CrossRef]

- Di Tullio, P.; Rea, M.A. Institutionalisation of sustainability in universities: insights from strategic planning and sustainability reporting practices in Italian universities. Meditari Accountancy Research 2025, 33(7), 338–368. [Google Scholar] [CrossRef]

- Kong, D.; Majhi, M. Integrating Social Responsibility into Business Strategy: a Roadmap for Sustainable Development. Journal of Lifestyle and SDGs Review 2025, 5(5), e06596–e06596. [Google Scholar] [CrossRef]

- Boiral, O. Accounting for the unaccountable: Biodiversity reporting and impression management. Journal of business ethics 2016, 135(4), 751–768. [Google Scholar] [CrossRef]

- Jamali, D.; Lund-Thomsen, P.; Khara, N. CSR institutionalized myths in developing countries: An imminent threat of selective decoupling. Business & Society 2017, 56(3), 454–486. [Google Scholar]

- Kolk, A. and M. Rivera-Santos, The social responsibility of international business: From ethics and the environment to CSR and sustainable development., in Multinationals, Poverty Alleviation and UK Aid: The Complex Quest for Mutually Beneficial Outcomes, J.A. Russon, Editor. 2023, Routledge.

- Su, L. Environmental regulation and corporate green innovation: evidence from the implementation of the total energy consumption target in China. Journal of Business Economics 2025, 95(4), 499–526. [Google Scholar] [CrossRef]

- Zhou, J.; Jin, S. Corporate Environmental Protection Behavior and Sustainable Development: The Moderating Role of Green Investors and Green Executive Cognition. International Journal of Environmental Research and Public Health 2023, 20(5), 4179. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American sociological review 1983, 48(2), 147–160. [Google Scholar] [CrossRef]

- Scott, W.R. Approaching adulthood: the maturing of institutional theory. Theory and society 2008, 37(5), 427–442. [Google Scholar] [CrossRef]

- Alsahali, K.; Malagueño, R.; Marques, A. Board attributes and companies’ choice of sustainability assurance providers. Accounting and Business Research 2024, 54(4), 392–422. [Google Scholar] [CrossRef]

- Adegbite, E. Good corporate governance in Nigeria: Antecedents, propositions and peculiarities. International business review 2015, 24(2), 319–330. [Google Scholar] [CrossRef]

- Meyer, J.W.; Rowan, B. Institutionalized organizations: Formal structure as myth and ceremony. American journal of sociology 1977, 83(2), 340–363. [Google Scholar] [CrossRef]

- Ahn, Y. A socio-cognitive model of sustainability performance: Linking CEO career experience, social ties, and attention breadth. Journal of Business Ethics 2022, 175(2), 303–321. [Google Scholar] [CrossRef]

- Ben Mahjoub, L. Greenwashing practices and ESG reporting: an international review. International Journal of Sociology and Social Policy 2024, 45(1-2), 173–188. [Google Scholar] [CrossRef]

- Gerged, A.M., K.M. Kehbuma, and E.S. Beddewela, Corporate social responsibility disclosure and corporate social irresponsibility in emerging economies: Does institutional quality matter? Business Ethics, the Environment & Responsibility, 2024.

- Greenwood, R., et al., The SAGE Handbook of Organizational Institutionalism. 2017: SAGE Publications.

- Ireland, R.D.; Hitt, M.A. Achieving and maintaining strategic competitiveness in the 21st century: The role of strategic leadership. The Academy of Management Executive 1999, 13(1), 43–57. [Google Scholar]

- Weick, K.E., Sensemaking in organizations. Vol. 3. 1995: Sage Publications Thousand Oaks, CA.

- Hu, L.; et al. How Does Sustainable Leadership Promote the Willingness to Adopt an Environmental Innovation Strategy? The Key Mediating Role of Environmental Value. Sustainability 2024, 16(7), 2988. [Google Scholar] [CrossRef]

- Hahn, T.; et al. Tensions in Corporate Sustainability: Towards an Integrative Framework. Journal of Business Ethics 2015, 127(2), 297–316. [Google Scholar] [CrossRef]

- Fagbemi, T.O.; et al. C-Suite bias, firm characteristics, and capital structure decisions of quoted industrial firms in Nigeria. Colombo Business Journal 2022, 13(2). [Google Scholar] [CrossRef]

- Gavetti, G.; et al. The behavioral theory of the firm: Assessment and prospects. Academy of Management Annals 2012, 6(1), 1–40. [Google Scholar] [CrossRef]

- Wu, L.; et al. How does executive green cognition affect enterprise green technology innovation? The mediating effect of ESG performance. Heliyon 2024, 10(14). [Google Scholar] [CrossRef] [PubMed]

- Pless, N.M.; Maak, T.; Waldman, D.A. Different approaches toward doing the right thing: Mapping the responsibility orientations of leaders. The Academy of Management Perspectives 2012, 26(4), 51–65. [Google Scholar] [CrossRef]

- Sarfraz, M.; He, B.; Shah, S.G.M. Elucidating the effectiveness of cognitive CEO on corporate environmental performance: the mediating role of corporate innovation. Environmental Science and Pollution Research 2020, 27(36), 45938–45948. [Google Scholar] [CrossRef]

- Zhou, S.; Jin, J. How executive cognitive styles influence corporate sustainability performance: The mediating role of dynamic capabilities. Journal of Cleaner Production 2023, 401, 136895. [Google Scholar]

- Brielmaier, C.; Friesl, M. The attention-based view: Review and conceptual extension towards situated attention. International Journal of Management Reviews 2023, 25(1), 99–129. [Google Scholar] [CrossRef]

- Ocasio, W. Towards An Attention-Based View Of The Firm. Strategic Management Journal 1997, 18(S1), 187–206. [Google Scholar] [CrossRef]

- Ocasio, W.; Laamanen, T.; Vaara, E. Communication and attention dynamics: An attention-based view of strategic change. Strategic Management Journal 2018, 39(1), 155–167. [Google Scholar] [CrossRef]

- Yu, K.; et al. CEO attention and sustainable development: An analysis of its influence on firm’s sustainability orientation. Sustainable Development 2024, 32(4), 4042–4056. [Google Scholar] [CrossRef]

- Andersén, J. An Attention-Based View on Environmental Management: The Influence of Entrepreneurial Orientation, Environmental Sustainability Orientation, and Competitive Intensity on Green Product Innovation in Swedish Small Manufacturing Firms. Organization & Environment 2022, 35(4), 627–652. [Google Scholar] [CrossRef]

- Eggers, J.P.; Kaplan, S. Cognition and capabilities: A multi-level perspective. Academy of Management Annals 2013, 7(1), 295–340. [Google Scholar] [CrossRef]

Figure 1.

Conceptual model of Executive Sustainability Cognition (ESC) as cognitive governance explaining the ESG implementation gap in fragile institutional contexts.

Figure 1.

Conceptual model of Executive Sustainability Cognition (ESC) as cognitive governance explaining the ESG implementation gap in fragile institutional contexts.

Table 1.

Competing framings of Executive Sustainability Cognition (ESC) and the added value of the cognitive governance perspective.

Table 1.

Competing framings of Executive Sustainability Cognition (ESC) and the added value of the cognitive governance perspective.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.