Submitted:

17 December 2025

Posted:

18 December 2025

You are already at the latest version

Abstract

The Regulation of Financial Service Authority Regulation (POJK 50/POJK/03/2017) regarding the obligation to fulfill the Net STABLE Funding Ratio (NSFR) aims to increase financial stability as well as to create Healthy banking System. Based on that regulation banks are required to meet an NSFR ratio of more than 100%. Islamic bank face challenges in complying with that regulation, because the funding instruments of Islamic Bank have shoter tenor compared to conventional ones, while sukuk as long-term instruments, still have limited liquidity in the Indonesian sukuk market. Based on agency theory, the preasure on profitability creates a stong incentif for managers to engage in earning management as strategic response. This study aims to investigate the impact of NSFR on Islamic Bank Margin (IBM) and also examine the impact of NSFR on Earning Management practices in Islamic Banking. This papaer also investigates the role of IBM in mediating relationship between NSFR and Earning Management. The data are collected from in Islamic Banking in Indonesia for the period of 2017 to 2024. Data processing technique used Panel Data Regression with Generalized Method of Moment (GMM). The result of this study shows that NSFR has a significant positive effect on IBM. Banks which have better liquidity tend to have better IBM. The second result is NSFR has a significant negative effect on EM practices. This funding shows that Islamic banks which have better liquidity tend to reduce EM practices. IBM play a partial mediating role in the relationship between NSFR and EM. IBM acts as a transmission mechanism between NSFR and EM.

Keywords:

net stable funding ratio (NSFR)

; islamic bank margin

; earning management

; Islamic bank

1. Introduction

The stability of the global financial sector has been a major concern for regulators in the wake of the 2008 financial crisis, prompting the finalization of the Basel III regulatory framework by the Basel Committee on Banking Supervision (BCBS) (Berg et al., 2025; Haqqi, 2017). One of the main pillars of this framework is the introduction of the Net Stable Funding Ratio (NSFR), which is designed to ensure that banks have a stable funding profile in relation to their off-balance sheet assets and activities over a one-year period (Siadat & Hammarlid, 2017).

Along with global implementation, the Islamic Financial Services Board (IFSB) has also adapted and issued guidelines for the application of NSFR for Islamic financial institutions, taking into account the unique characteristics of Islamic banking assets and liabilities (Krettek, 2025; Santillln-Salgado, 2015). Although aimed at strengthening stability, the implementation of NSFR presents significant challenges for Islamic banks, especially in Asia and the Middle East (Bitar et al., 2021). Indonesian Government through Financial Service Authority Regulation published POJK 50/POJK/03/2017. The implementation of NSFR required bank to think their financial strategies which can impact on their financial performance. Some of the prior studies found that liquidity effect on bank performance. In one view, it increases bank performance due to lower cost of capital (King, 2013), higher balanced growth (Grundke & Kühn, 2020), financial stability (Ashraf et al., 2016) and efficiency (Le et al., 2020). In other point of view, high liquidity lead to inefficiency (Le et al., 2020), lower lending rate (Acharya & Ryan, 2016) and lower net income (Grundke & Kühn, 2020). Other Studies of impact of liquidity on bank risk conducted by (Li et al., 2018) found that liquidity reduce risk because it lowers bank failure, default risk (Grundke & Kühn, 2020). On the other hand, an increase of liquidity related to higher bank risk (bank instability) and aggressive lending behavior (Acharya & Ryan, 2016).

A literature review on the impact of NSFR on Islamic banking shows mixed findings and highlights significant research gaps. A number of empirical studies indicate that compliance with NSFR obligations tends to have a negative impact on the long-term profitability of Islamic banks (Falikhatun et al., 2024; Salsabilla & Jaya, 2024). This is in line with the liquidity-profitability trade-off theory, which states that increasing liquidity through more stable and expensive funding will sacrifice potential profitability (Ashraf et al., 2016; Mohanty & Mehrotra, 2018)). For example, research by (Abbas et al., 2022; Ayub et al., 2023) found that NSFR has a significant negative effect on the profitability of Islamic banks in Pakistan and several other Asian countries (Ihsan et al., 2025). However, other studies, such as those conducted by (Alam et al., 2019) in Malaysia, show that NSFR can actually have a positive impact not only on stability but also on profitability, with the argument that a stronger funding structure reduces risk costs.

There is a limitation in studies that specifically examine the direct impact of NSFR on the main profitability component, namely bank margins, and how pressure on these margins could potentially trigger profit management practices. Agency theory provides a relevant framework for understanding this phenomenon, whereby managers (agents) may be incentivized to manipulate reported earnings to meet the expectations of principals (shareholders and depositors) when actual performance is constrained by regulation. Thus, a crucial research gap lies in the lack of integrated analysis between liquidity regulations (NSFR), their impact on financing margin structures, and strategic managerial behavior in the form of earnings management in the context of Islamic banking.

This study is different from previuous studies and offer new insight. Firstly, this study will investigate impact of NSFR on Islamic Bank Margin. Secondly, it will investigate impact of NSFR on Earning Management practices at Islamic Banks in Indonesia. Thirdly, the study examine the role of Islamic Bank Margin in mediating relationship between NSFR and Earning Management.

1.1. Literatur Review

1.1.1. Agency Theory

Agency theory explaines relationship between two parties within an organization, they are principals and agen. The pioner of agency theory is Jensen and Meckling. They defined Agency relationship as a contract under which one or more persons (the principals) engage another person (agent) to perform some service on their behalf which involves delegating some decision making authority” (Gumanti, 2000). The principal is the owner of the asets, while the agent is the one who manages the asset. Problems arise when both parties have different interest. This conflict of interest leads the agent (manager) try to exploit the situation by withholding information that benefits them, this resulting in asymetric information.

Agency theory in the banking sector has more complexs dynamics because it involves many parties and high level of risk. There are two types of agency relationships in the banking sector namely the relationship between banks and borrowers, which is reflected on the asset side of the balance sheet, and the relationship between banks and depositors, which is reflected on the liability side (A. Rahman, 2014; Huang & Song, 2006). Agency relationships in the banking sector also occur between banks and regulators (the Financial Services Authority/OJK and the Central Bank/BI), between banks and shareholders, and between shareholders and creditors. With the numerous agency relationships, the potential for conflicts of interest in the banking sector becomes greater.

Information asymmetry in the context of the relationship between banks and depositors may occur when depositors are unable to assess the capital strength of a bank and the likelihood of its bankruptcy. In contrast, in the context of the relationship between banks and borrowers, information asymmetry arises when banks do not possess accurate information regarding the reliability of borrowers, while borrowers have better knowledge of their own business conditions. Information asymmetry in the context of the relationship between banks and Financial Service Authority (OJK) may accur when banks have detail internal information, such as quality of credit portofolio, market risk exposure, liquidity, off balance sheet transaction, internal management practice. Meanwhile, OJK does not know the details of those information and it relies heavily on reports submitted by banks. Such problems may encourange banks to engage in earnings management practices, for example delaying the recognition of Non Performing Loans (NPL).

1.1.2. Implications of NSFR on Islamic Bank Margins

Literature that specifically examines the direct impact of NSFR on Islamic bank margins is still limited, but analysis can be drawn from studies that discuss margin components, such as profitability and funding costs. Bank profit margins, which are simply the difference between income from productive assets and funding costs incurred, will theoretically be affected by changes in the funding structure mandated by NSFR. Studies showing a negative or insignificant impact of NSFR on profitability in general, such as those reported by (Abbas et al., 2022) for Islamic banks in Asia and (Alhammadi et al., 2022) on a global scale, implicitly indicate pressure on margins. Increased reliance on stable and expensive long-term funding will increase the cost side of the margin equation. On the other hand, banks’ ability to increase income from the asset side may be limited due to competition and market conditions. A study of murabahah margin income in Indonesian Islamic commercial banks, while not directly testing the NSFR, highlights various factors that affect margins, indicating the sensitivity of margins to various internal and external variables (Akbary et al., 2025). High margins may also indicate inefficiency or higher risk, which highlights the complexity of interpreting margin movements in response to regulations.

The explanation for the mechanism of NSFR pressure on Islamic bank margins lies in shifts in the composition and cost of funding. To meet the NSFR ratio, banks must increase high- weighted Available Stable Funding (ASF), such as capital, long-term retail deposits, and long- term debt instruments (sukuk). These funding sources are inherently more expensive than short- term funds such as current accounts or interbank deposits, which have a lower ASF weighting. This increase in funding costs directly erodes the net income margin. On the other hand, Islamic banks have limitations in adjusting their assets. Financing instruments such as murabahah often have fixed profit margins, making it difficult to adjust in response to rising funding costs. In addition, competition with conventional banks limits the ability of Islamic banks to significantly increase financing prices without losing market share. The liquidity-profitability trade-off theory.

The relationship between pressure on Islamic bank margins and the reality of this research issue is very strong. Real phenomena show that since the implementation of NSFR, many Islamic banks, especially in competitive markets such as Southeast Asia and the Middle East, have faced a strategic dilemma. On the one hand, they must comply with regulations to maintain stability and regulator confidence. On the other hand, these compliance costs put pressure on profit margins, which are the main source of income and business sustainability. The decline in margins can have several impacts: first, it reduces the bank’s ability to generate retained earnings, which are important for strengthening internal capital; second, it reduces the bank’s competitiveness compared to conventional banks, which may have access to more diverse and cheaper sources of long-term funding; and third, it creates pressure on management to maintain the level of profitability expected by shareholders.

1.1.3. NSFR and Islamic Bank Margins

Literature that specifically examines the direct impact of NSFR on Islamic Bank Margins is still limited, but analysis can be drawn from studies that discuss margin components, such as profitability and funding costs. Bank profit margins, which are simply the difference between income from productive assets and funding costs incurred, will theoretically be affected by changes in the funding structure mandated by NSFR. Studies showing a negative or insignificant impact of NSFR on profitability in general, such as those reported by (Abbas et al., 2022) for Islamic banks in Asia and (Alhammadi et al., 2022) on a global scale, implicitly indicate pressure on margins. Increased reliance on stable and expensive long-term funding will increase the cost side of the margin equation. On the other hand, banks’ ability to increase income from the asset side may be limited due to competition and market conditions. A study of murabahah margin income in Indonesian Islamic commercial banks, while not directly testing the NSFR, highlights various factors that affect margins, indicating the sensitivity of margins to various internal and external variables. High margins may also indicate inefficiency or higher risk, which highlights the complexity of interpreting margin movements in response to regulations.

The explanation for the mechanism of NSFR pressure on Islamic bank margins lies in shifts in the composition and cost of funding. To meet the NSFR ratio, banks must increase high- weighted Available Stable Funding (ASF), such as capital, long-term retail deposits, and long- term debt instruments (sukuk). These funding sources are inherently more expensive than short-term funds such as current accounts or interbank deposits, which have a lower ASF weighting. This increase in funding costs directly erodes the net income margin. On the other hand, Islamic banks have limitations in adjusting their assets. Financing instruments such as murabahah often have fixed profit margins, making it difficult to adjust in response to rising funding costs. In addition, competition with conventional banks limits the ability of Islamic banks to significantly increase financing prices without losing market share. The liquidity-profitability trade-off theory.

The relationship between pressure on Islamic bank margins and the reality of this research issue is very strong. Real phenomena show that since the implementation of NSFR, many Islamic banks, especially in competitive markets such as Southeast Asia and the Middle East, have faced a strategic dilemma. On the one hand, they must comply with regulations to maintain stability and regulator confidence. On the other hand, these compliance costs put pressure on profit margins, which are the main source of income and business sustainability. The decline in margins can have several impacts: first, it reduces the bank’s ability to generate retained earnings, which are important for strengthening internal capital; second, it reduces the bank’s competitiveness compared to conventional banks, which may have access to more diverse and cheaper sources of long-term funding; and third, it creates pressure on management to maintain the level of profitability expected by shareholders.

1.1.4. Earnings Management

Academic literature has identified a relationship between regulatory pressure and earnings management practices in the banking sector. Studies show that when banks face pressure to meet capital requirements or when their profitability is threatened, managers may have incentives to manipulate accounting figures. Research by (Alam et al., 2019) found that although there were no significant differences in earnings management practices between Islamic and conventional banks, corporate governance factors played an important role. Another study focusing on Islamic banks globally found a significant negative impact of earnings management on internal performance (ROA/ROE) and stability (Z-score), indicating that this practice ultimately harms the bank itself (Haddou & Boughrara, 2025; Iqbal & Fikri, 2023; Ullah et al., 2023). Several studies also identify that Islamic banks tend to engage in lower profit management compared to conventional banks due to the Islamic principles that must be adhered to (Hatane et al., 2019). However, strong external pressures, such as the implementation of costly new regulations such as NSFR, can change these incentive dynamics. Various models for detecting earnings management, such as those applied to Islamic banks in Iran, show that this practice does exist and can be measured through discretionary accruals (Choi et al., 2018; Suripto, 2023).

A theoretical explanation for this behavior can be found in agency theory. This theory explains the potential conflict of interest between managers (agents) and shareholders (principals). In this context, managers, whose performance is often measured based on profitability, may face pressure to meet market and shareholder expectations, especially when real profitability is eroded by external factors such as NSFR regulations. The existence of information asymmetry, where managers have more complete information about the bank’s financial condition than external parties, provides them with the opportunity to engage in earnings management. This practice can be carried out for various purposes, such as income smoothing to show stable performance, avoiding debt covenant violations, or maximizing personal bonuses and compensation. The pressure of NSFR regulations on profit margins can be a strong trigger for managers to use accounting flexibility, for example through adjustments to financing loss provisions, to present a better picture of financial performance than is actually the case.

The implementation of NSFR creates real pressure on the profitability and margins of Islamic banks. Based on agency theory, this pressure can create incentives for management to engage in earnings management practices in order to maintain the company’s financial image in the eyes of investors, regulators, and the public (Rezki Zurriah et al., 2025; Widayawati, 2025). This is particularly relevant because Islamic banks are not only accountable to shareholders but also have a responsibility to adhere to Sharia principles, which prohibit deceptive or non-transparent practices. Therefore, the potential increase in earnings management in response to NSFR pressure poses a serious ethical and reputational dilemma for the Islamic banking industry. If Islamic banks respond to margin pressure by manipulating profits, this will not only undermine the quality of their financial statements but could also erode public confidence in the integrity of the Islamic banking model as a whole. Thus, understanding the relationship between NSFR regulatory pressure, its impact on margins, and the potential for earnings management behavior is crucial for regulators to design effective oversight and for bank management to develop compliant and ethical strategies.

1.2. Hypothesis

1.2.1. The Effect of NSFR on Islamic Bank Margin

The NSFR is one of the liquidity requirements within the Basel III regulatory framework, and in Indonesia, it is regulated under OJK Regulation No. 50/POJK/03/2017. The NSFR is intended to ensure that banks maintain more stable long-term funding to finance long-term assets. Although Islamic banks operate with different contracts and financing mechanisms, the principles of liquidity and funding remain applicable. Bank margins are often associated with the cost of funds and financing income derived from productive assets. To increase stable funding, Islamic banks may rely on more expensive funding sources, such as deposits with higher returns or the issuance of long-term financial instruments. Higher funding costs may reduce bank margins. A study on the impact of NSFR on bank performance in India found that NSFR has a negative effect on net interest margin (Sidhu et al., 2022). Other empirical studies also indicate that compliance with NSFR requirements negatively affects the long-term profitability of Islamic banks (Salsabilla & Jaya, 2024). These findings are consistent with the liquidity–profitability trade-off theory, which states that enhancing liquidity through more stable and costly funding will reduce potential profits (Ashraf et al., 2016). Studies conducted by (Abbas et al., 2022; Ayub et al., 2023) also found that NSFR has a significant negative effect on the profitability of Islamic banks in Pakistan and several Asian countries (Setiyono & Naufa, 2020). Based on the above explanation, the first hypothesis of this study is formulated as follows:

H-1 : NSFR has a negative effect on Islamic Bank Margin.

1.2.2. The Effect of NSFR Implementation on Earnings Management.

The obligation to comply with the NSFR may encourage banks to maintain more stable funding to meet long-term financing needs. Since the NSFR requires adjustments in the composition of funding and/or assets, it can affect profitability, thereby motivating management to adjust earnings in order to achieve performance targets. If the NSFR reduces short-term profitability, managers may manipulate provisions, revenue recognition, or expense timing to stabilize earnings, which is consistent with classical agency theory. The implementation of the NSFR creates pressure on the profitability and margins of Islamic banks. This pressure may create incentives for management to engage in earnings management practices in order to maintain the institution’s financial image in the eyes of investors, regulators, and the public (Rezki Zurriah et al., 2025; Widayawati, 2025). Based on the above explanation, the second hypothesis in this study is formulated as follows:

H-2: An increase in NSFR has a positive effect on earnings management.

1.2.3. Islamic Bank Margin Mediates the Effect of NSFR on Earnings Management.

Islamic Bank Margin reflects the ability of Islamic banks to manage funding efficiency and the distribution of financing. A high margin indicates that the bank has access to low-cost funding and productive financing, thus achieving efficiency, whereas a low margin implies that the bank bears higher funding costs or provides financing with lower yields. The study by (Setiyono & Naufa, 2020) found that a high NSFR decreases short-term profitability but enhances long-term stability. The liquidity–profitability trade-off theory explains that an increase in NSFR requires banks to secure more stable funding, which consequently raises funding costs and lowers bank margins. The implementation of Basel III regulations increases stability but exerts pressure on profitability, potentially creating incentives for earnings management (Alam et al., 2019; Setiyono & Naufa, 2020). According to agency theory, earnings serve as a key indicator of managerial performance; thus, when margins decline, managers have an incentive to adjust reported earnings to maintain stability. Conversely, when margins are high, the need for such manipulation is reduced. (Srairi, 2015) and (Mismiwati et al., 2022) conclude that profitability and margin are negatively associated with earnings management in Islamic banks, meaning that higher margins are associated with lower earnings management behavior.

Based on the above explanation, the third hypothesis in this study is formulated as follows:

H-3: Islamic Bank Margin mediates the effect of NSFR on Earnings Management.

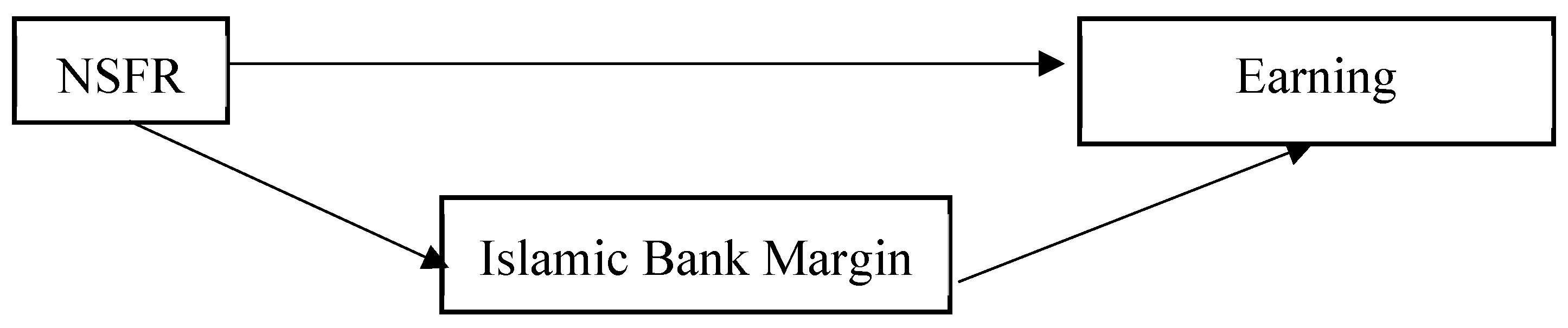

1.3. Conceptual Framework

This research examines the influence of the Net Stable Funding Ratio (NSFR) on Islamic Bank Margin and earnings management practices, as well as the mediating role of Islamic Bank Margin in the relationship between NSFR and earnings management. A higher NSFR indicates that the bank maintains more stable, long-term sources of funding relative to its funding needs.

Islamic Bank Margin reflects the bank’s ability to manage its funding and allocate resources to productive financing. A high margin indicates that the bank is able to utilize stable funding sources to generate profitable financing, while a lower margin may signal inefficiencies in funding costs or financing performance. Therefore, NSFR is expected to influence the level of Islamic Bank Margin.

Earnings management refers to the deliberate intervention in financial reporting to achieve certain performance targets or regulatory requirements. In the context of Islamic banks, earnings management may arise when management attempts to stabilize reported earnings or meet stakeholder expectations. NSFR can influence earnings management practices because banks with more stable funding conditions may have less pressure to manipulate earnings, while banks facing liquidity constraints may be more inclined to adjust earnings figures to present a stable financial performance. Therefore, the study examines whether NSFR has a direct association with earnings management behavior.

Furthermore, Islamic Bank Margin is proposed as a mediating variable in the relationship between NSFR and earnings management. When NSFR improves the stability of the bank’s funding structure, the bank may experience enhanced margins, strengthening its profitability and operational efficiency. Improved profitability may reduce the incentive for management to engage in earnings manipulation, as the bank can naturally meet performance and regulatory expectations. Thus, Islamic Bank Margin may serve as an intervening variable through which NSFR influences earnings management.

The conceptual framework of this research is described in the Figure 1 below:

2. Materials and Methods

This study uses data from eights Islamic Banks for the period of 2017 and 2024. The data are collected from the balance sheet and Income Statement. The data of Earning Management, Islamic Bank Margin and NSFR are calculated mannually, since some of banks did not publish NSFR report. Definition of variables are described in this table:

Table 1.

Definition of Variables.

| Variable | Definition | Formulation |

|---|---|---|

| Independent variable: Net Stable Funding Ratio (NSFR) |

NSFR is a liquidity ratio calculated by deviding the amount of Available Stable Funding (AFS) and Required Stable Funding (RSF) for one year time |

POJK 50/2017 |

| Dependent variable: Islamic Bank Margin (IBM) |

NSFR is a liquidity ratio calculated by deviding the amount of Available Stable Funding (AFS) and Required Stable Funding (RSF) for one year time IBM is a performance measure calculated by deviding of profit sharing rights owned by the bank and Earning Assets |

Beaver and Engel (1996) |

| Dependent variable: Descretionary Loan Loss Provision (DLLP) |

Deductible of Loan Loss Provision (LLP) and Non Descre-tionary Loan Loss Provision (NDLLP) | DLLP=LLP-NDLLP Beaver and Engel (1996) |

| Control variable: Capital Adequacy Ratio (CAR) |

CAR is ratio of a bank’s capital in relation to its risk weighted assets. |

Muhamad (2014) |

This study employ a quantitative approach to examine the dual impact of Net Stable Funding Ratio (NSFR) on Islamic Bank margin and earning Management practice in Indonesia Islamic Banking. Panel data regression analysis is utilized to capture both cross-sectionaland time series variation across the sampled banks fom 2017 to 2024. To adress potential endogeniety concern and accout for dynamic relationship among the variables, the Generalized Method of Moment (GMM) estimator is applied. This method is particulary suitable for financial panel data, as it controls for unobserved heterogeneity, mitigates autocorrelation and provides conistent estimate in the presence of heteroscedasity. The analyis incorporates bank-specific and time specific effect to ensure robustness. Two main regression models are specified to test the proposed hypotesis, with control variable include to isolate the effect of NSFR. The use ofthis econometric techniques allow for a comprehensive assesment of the regulatory impact on both performance and financial reporting behavior in Islamic Banking.

This study applied Panel Data Regression and GMM (Generalized Method of Moment) method to test the impact of NSFR on Islamic Bank Margin and the impact of NSFR on Earning Management practices.

The first Regression Model is used to examine the impact of NSFR on Islamic Bank Margin:

IBM_it = β0 + β1NSFR_it + β2CAR_it + μ_i + λ_t + ε_it

The second Regression Model is used to examine the impact of NSFR on Earning Management at Islamic Banks.

EM_it = β0 + β1NSFR_it + β2CAR_it + μ_i + λ_t + ε_it

3. Results and Discussion

3.1. Statistics Descriptive of the Variables

Statistics descriptive of these variables are described on the Table 2. The average of NSFR is 2.21 (221%), this figure indicates that banks have stable long term funding structure. The median is 1.66 (166%), this figure indicates that the most banks have an NSFR below the average, but there are few banks with very high NSFR. High standard deviation (2,54) indicates a very large variation or dispersion of data among banks and over time. The minimum value of NSFR 0,47 (47% comes from Mega Syariah Bank (2021) which is far below the regulator safety limit (minimum 100% or 1.00). It indicates a potential funding risk. The maximum value of NSFR (16.81) comes from BPD NTB Syariah (2017), it indicates a very conservative level of funding stability.

The average of Islamic Bank Margin is 0.064 (6.4%) The standard deviation (0.075) is relatively high compared to the mean; it indicates that a wide variation in margins among banks. The minimum value of IBM is 0.0003(0,03%) cames from BRK Bank (2020). It shows a period of very low profitability. The maximum value of IBM is 0.341 (34%) cames from BTPN Syariah Bank (2017), the figure indicates very strong margin performance (above the industry average).

Earning Management indicates the practice of income smoothing. The value of Positive/negative may indicate a bank’s tendency to increase or decrease reported earnings. The negative mean (-0.11) and median (-0.20) indicate that most banks tend to report lower profits. The large standard deviation (1.07) indicates very diverse earnings management behavior among Islamic banks. The minimum value (-5.16) from Bank Aceh Syariah (2017) shows a very significant decrease in profits for that year. The maximum value (1.80) from Bank BJB Syariah (2019) indicates a substantial increase in profits.

The average of Capital Adequacy Ratio (CAR) is 29,20%, CAR is above minimum regulation (12%), it indicates that islamic banks have a strong capital and are able to absorb potential risk.

3.2. Effect of Net Stable Funding Ratio (NSFR) on Islamic Bank Margin (IBM)

Output of panel data anaysis is described on the Table 3. The table reports the correlation between NSFR and IBM.

This Model is used to examine the impact of NSFR on Islamic Bank Margin:

IBM_it = 0.05183+ 0.00842NSFR_it + -0.02315CAR_it + μ_i + λ_t + ε_it

Net Stable Funding Ratio (NSFR), which is designed to ensure that banks have a stable funding profile in relation to their off-balance sheet assets and activities over a one-year period (Siadat & Hammarlid, 2017). Although the main objective of NSFR is to improve financial stability, NSFR can also have an impact on IBM.

Table 3 shows that coefficient of NSFR is 0.00842, it is indicates that NSFR has a positive and significant effect on IBM. Increase 1% of NSFR raises IBM by 0.842%. The results of this study shows that Islamic bank in Indonesia have NSFR of 221% (Table 2). Bank which have sufficient stable funds will reduce their dependence on more expensive and risky short term funding, this can reduce cost of fund and increase profit margin for islamic banks. NSFR encorages banks to manage their funding structure carefully and choose more stable fund and lower cost funding sources. Banks can improve efficiency and increase bank margins. Thus, the hypotesis that NSFR has a positive and significant effect on Islamic Bank Margin (IBM) is accepted.

This funding in line with study conducted by (Alam et al., 2019) in Malaysia, it showed that NSFR can actually have a positive impact not only on stability but also on profitability, with the argument that a stronger funding structure reduces risk costs. However, research by (Abbas et al., 2022; Ayub et al., 2023) found that NSFR has a significant negative effect on the profitability of Islamic banks in Pakistan and several other Asian countries (Ihsan et al., 2025). Other studies indicate that compliance with NSFR obligations tends to have a negative impact on the long-term profitability of Islamic banks (Falikhatun et al., 2024; Salsabilla & Jaya, 2024).

3.4. Effect of Net Stable Funding Ratio (NSFR) on Earning Management (EM)

Based on Table 4, this Model is used to examine the impact of NSFR on Earning Management (EM):

EM_it = 0.89263 − 0.42381NSFR_it -2.85624CAR_it + μ_i + λ_t + ε_it

Table 4 presents the results of the fixed effects regression analysis examining the relationship between NSFR and earnings management practices in Islamic banks. The coefficient of NSFR is -0.42381 (β = -0.42381, p < 0.05), indicating that NSFR has a significant negative influence on earnings management practices. This implies that an increase 1% of NSFR reduces earnings management practices by 0.424 Similarly, the Capital Adequacy Ratio (CAR) also exhibits a negative and significant relationship with earnings management (β = -2.85624, p < 0.05), suggesting that well-capitalized banks are less likely to engage in earnings manipulation.

Banks with higher NSFR possess more stable funding structures, which reduce liquidity risk and financial distress. Consequently, managers face less pressure to manipulate earnings to meet short-term performance targets or conceal financial weaknesses (Healy & Wahlen, 1999). Compliance with NSFR requirements often necessitates robust risk management and disclosure practices. This increased transparency limits opportunities for managers to engage in discretionary reporting behaviors (Dyreng et al., 2012).

Stable funding profiles lead to more predictable revenue streams, reducing the need for income smoothing through tools such as discretionary loan loss provisions Islamic banks are subject to additional ethical and Sharia governance standards, which discourage manipulative financial practices. A strong NSFR may reinforce this ethical stance by reducing liquidity-driven incentives for earnings management These findings align with studies linking strong liquidity management to higher financial reporting quality (Barth et al., 2017). However, they contrast with the view that stringent liquidity regulation may force banks into higher-risk asset portfolios or creative accounting to maintain profitability (Acharya & Ryan, 2016).

Based on the result of Hausman Test, both models are significant at α = 0.05, confirming that the use of fixed effects is more appropriate than random effects. The result of autocorrelation and heteroscedasticity tests prove that there is heteroskedasticity in both models and no significant serial autocorrelation was found in the model.

3.4. Panel Data Analysis with Robust Standard Errors

Then, we apply Panel Data Analysis with Robust Standard Errors to eliminate heteroskedasticity. The model used is Fixed Effects with Driscoll–Kraay Standard Errors. Result of the Analysis with Heteroskedasticity Correction presented on Table 5 and Table 6.

The Hypothesis to be tested is NSFR has an effect on Islamic Bank Margin. The results in Table 5 states that NSFR has a significant positive effect on Islamic Bank Margin. (β = 0.00792, p = 0.0012). A higher NSFR indicates that bank has stroger liquidity stability, dependence on stable, not valatile deposits and better long-term funding management. In Islamic banks, NSFR reflects the strenght of investment accounts (mudharabah) and other stable Sharia-compliant funding instruments

When banks maintain high NSFR it rely more stable deposits rather than expensive short-term funding. Stable funding sources such as saving account (wadiah), current account, and long-term investment deposits have lower relative cost. Study conducted by (Abbas et al., 2022; Le et al., 2020; Setiyono & Naufa, 2020) found that NSFR has a positive effect on Islamic bank funding efficiency.

CAR as an control variable does not have effect on the islamic bank margin. CAR is a safety buffer, it is not determinant of pricing or margin. The margin of Islamic banks mainly drivend by financing rates on mudharabah, musharakah and ijarah, cost of deposits and operatinal effeciency. Thus CAR does not directly affect Islamic Bank Margin.

Table 6 states that NSFR has a significant negative effect on Earning Management (β=-0.40163, p=0.0312). The NSFR reflects the stability of a bank’s long-term funding. When the NSFR increases, the bank possesses a healthier funding composition dominated by stable funding sources. The bank will have stronger liquidity, reducing the pressure on management to engage in earnings management in order to maintain the perceptions of investors or short-term fund providers. In the context of Sharia management, the NSFR enhances prudence, reduces uncertainty (gharar), and encourages safe funding activities. Islamic banks operating under the principle of risk sharing are not encouraged to manipulate earnings or pursue short-term gains. A high NSFR reinforces a Sharia-based culture of transparency, thereby reducing earnings-management practices. In relation to Agency Theory, when the NSFR is high, the risks associated with long-term funding become more manageable, liquidity pressures decrease, and regulatory monitoring mechanisms are strengthened. Such conditions reduce agency conflicts between managers and fund providers (depositors, investors, and shareholders), thereby weakening managerial incentives to engage in earnings management.

CAR has a sgnificant negative effect on Earning Management (β=-2.71485, p=0.0325). CAR measure the bank’s ability to absorb losses. A high CAR means the bank has strong capital, faces lower solvency risk. When the bank is well-capitelized, manajemen does not feel preasured to manipulate income in order to appear stronger. Bank with strong capital adequacy usualy adopt better corporate governance. Good corporate governance reduces the willingness of managers to manipulate earnings.

3.5. Analysis of Mediation: Islamic Bank Margin as Mediator

We apply (Baron & Kenny, 1986) approach and Sobel Test to test the role of Islamic Bank Margin as variable mediation. The mediation analysis framework are describeb below:

Path a: Effect of NSFR on Islamic Bank Margin

Path b: Effect of Islamic Bank Margin on Earning Management

Path c: Effect of NSFR on Earning Management (total effect)

Path c’: Effect of NSFR on Manajemen Laba (efek langsung)

The result of Mediation Regression Analysis presented on the tables below:

- Stage 1: Path a - Effect of NSFR on Islamic Bank Margin (Mediator)

Table 7.

Effect of NSFR on Islamic Bank Margin.

| Variable | Coefficient | Robust SE | t-stat | p-value |

|---|---|---|---|---|

| NSFR | 0.00792 | 0.00215 | 3.684 | 0.0012*** |

| CAR | -0.02148 | 0.01432 | -1.500 | 0.1473 |

| Intercept | 0.05216 | 0.00698 | 7.472 | 0.0000*** |

R-squared: 0.284; F-statistic: 15.82 (p-value: 0.0003)

The result of Path a: NSFR significantly effect on Islamic Bank Margin (β = 0.00792, p = 0.0012)

- Stage 2: Path b - Effect of Islamic Bank Margin on Earning Management

Fixed Effects Regression - Outcome Model presented on Table 8.

The result of Path b: Islamic Bank Margin significantly effect on Earning Management (β = -8.42361, p = 0.0121)

- Stage 3: Path c - Total Effect of NSFR on Earning Management (total effect)

Fixed Effects Regression - Total Effect

Table 9.

Total Effect of NSFR on Earning Management.

| Variable | Coefficient | Robust SE | t-stat | p-value |

|---|---|---|---|---|

| NSFR | -0.40163 | 0.17382 | -2.311 | 0.0282** |

| CAR | -2.71485 | 1.19245 | -2.277 | 0.0305** |

| Intercept | 0.84592 | 0.57284 | 1.477 | 0.1516 |

R-squared: 0.157; F-statistic: 6.24 (p-value: 0.0078)

- Stage 4: Path c’ – Direct Effect of NSFR Earning Management

Fixed Effects Regression - Direct Effect

Table 10.

Direct Effect of NSFR on Earning Management.

| Variable | Coefficient | Robust SE | t-stat | p-value |

|---|---|---|---|---|

| NSFR | -0.34582 | 0.16284 | -2.124 | 0.0426** |

| Islamic Margin Bank | -8.42361 | 3.12845 | -2.692 | 0.0121** |

| CAR | -2.89234 | 1.21543 | -2.380 | 0.0248** |

| Intercept | 1.29845 | 0.62384 | 2.082 | 0.0468** |

R-squared: 0.218; F-statistic: 8.73 (p-value: 0.0008)

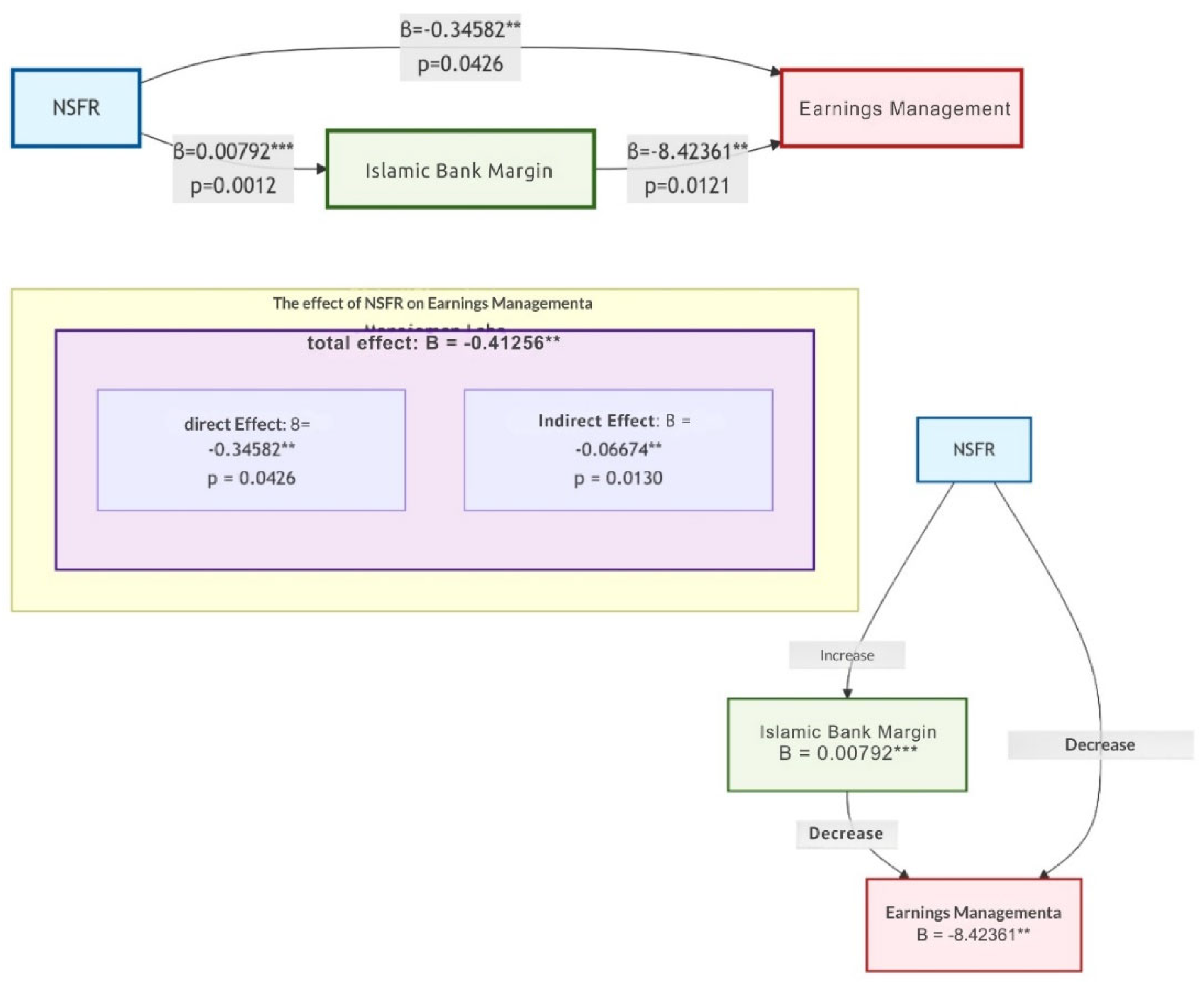

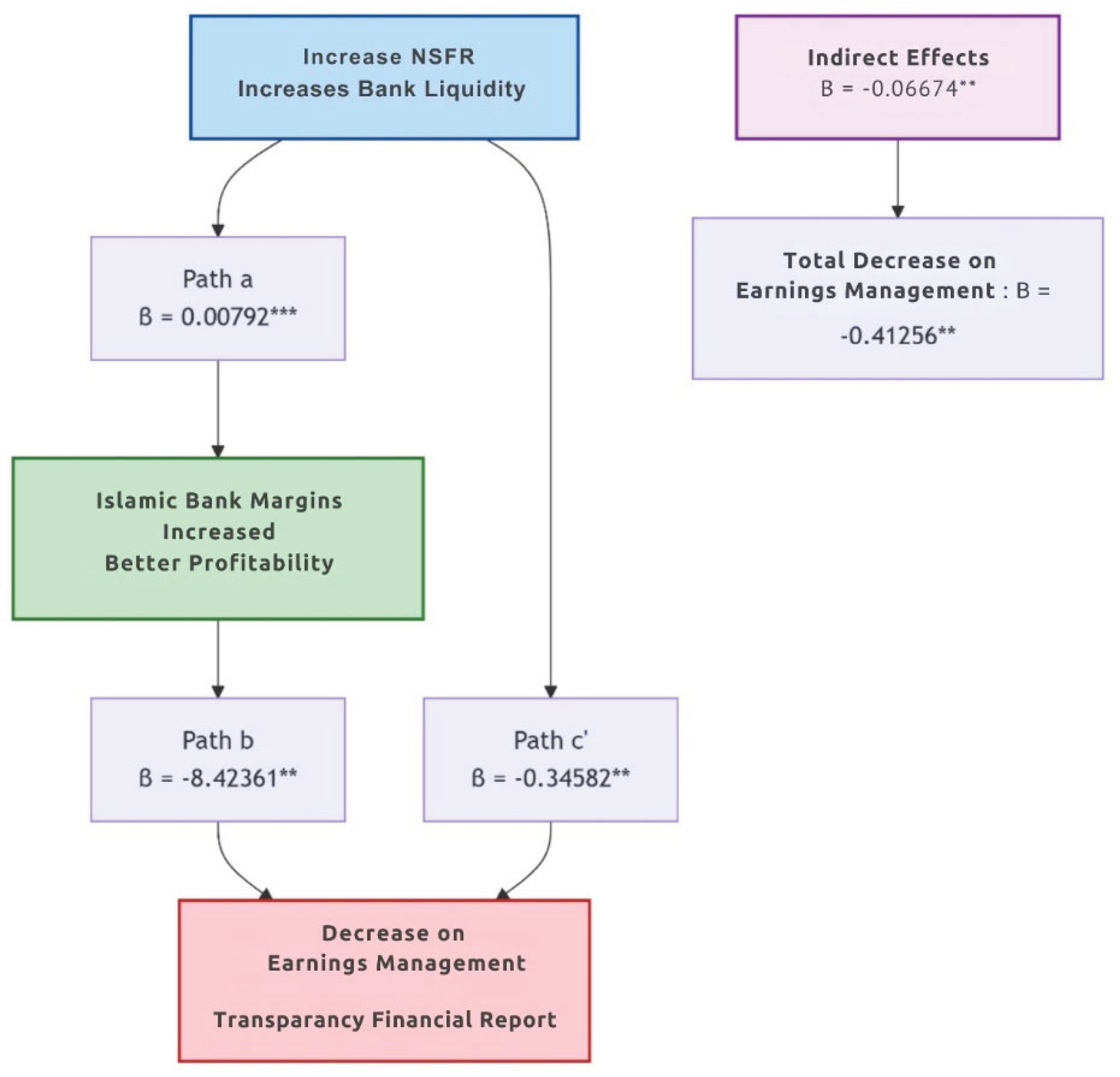

Figure 2.

Direct and Indirect Effecton NSFR on EM.

The above tables and figures show that NSFR has a significant direct effect on Earning management (β=-0.34582; p=0.0426). Islamic Bank Margin (IBM) mediates the relationship between NSFR and Earning Management (β=-0.06674; p=0.0130) in the other word NSFR affects Earnings Management both directly an indirectly through IBM. Total of effect NSFR on Earnings Management is -0.41256 and proportion of Islamic Bank Margin is 16.18% of total effect of NSFR on Earnings Management (partal mediation).

The figure below clarifies that NSFR directly and indirectly affects Earning Management.

An increase of NSFR means that the bank’s funding structure is more stable, allowing the bank to increase Islamic Bank Margin (IBM) and improve operational efficiency. Improved profitability (IBM) may reduce the incentive for management to engage in earnings manipulation, as the bank can naturally meet performance and regulatory expectations. The figure highlight the importance of stable funding in supporting profitability and maintainig transparent financial reporting practices in Islamic banking

4. Conclusions

This study examines the dual impact of Net Stable Funding Ratio (NSFR) implementation on Islamic banks in Indonesia, focusing on its relationship with Islamic Bank Margin (IBM) and earnings management practices. Firstly, the analysis reveals that NSFR has a positive and significant effect on Islamic Bank Margin. Banks with stronger liquidity positions tend to achieve higher profit margins. This suggests that stable funding structures contribute to cost efficiency and improved margin performance of Islamic banks. This finding contradicts the conventional liquidity-profitability trade-off theory in the context of Indonesian Islamic banking. Secondly, NSFR demonstrates a significant negative relationship with earnings management practices. Higher NSFR compliance is associated with reduced discretionary loan loss provisioning, indicating that banks with better liquidity management engage in less earnings manipulation. The last finding is IBM play a partial mediating role in the relationship between NSFR and EM.

The results contribute to agency theory by demonstrating how regulatory frameworks can align managerial incentives with transparent financial reporting. In the Islamic banking context, where ethical considerations are paramount, NSFR appears to reinforce Sharia principles by discouraging short-term earnings manipulation and promoting sustainable financial practices.

Furthermore, the study challenges the traditional view that liquidity regulations necessarily constrain bank profitability. Instead, it presents evidence that prudent liquidity management can coexist with, and even enhance, profit margin performance in Islamic banks.

Regulators and policymakers, particularly the Financial Services Authority (OJK), these findings support the continued enforcement of NSFR requirements. The regulation serves dual purposes, that are ensuring banking stability and promoting financial reporting integrity. Regulators may consider to Strengthen supervision of banks with consistently low NSFR levels, as they may present higher risks of both liquidity stress and earnings management, created specific NSFR implementation guidelines tailored to Islamic banks’ unique characteristics, mandate more detailed disclosures about funding stability and provisioning practices.

Islamic bank management is suggested to carry out Strategic Funding Management by Investing in stable funding sources can yield both stability and profitability benefits, incorporating liquidity management into overall corporate governance frameworks, and effectively communicating NSFR compliance as a marker of both financial strength and ethical operation.

This study has several limitations that present opportunities for future research, that are: the study covers only Indonesian Islamic banks. Future research could expand to multi-country comparisons across different regulatory environments, time period only six years, longer-term studies are needed to assess sustained impacts, while discretionary loan loss provisions are widely used, future studies could incorporate multiple earnings management measures, further research could explore the mediating role of bank margin in the relationship between NSFR and earnings management.

Author Contributions

Conceptualization, Y.I.H., M.D., H.M., and N.K.S.; methodology, M.D. and H.M.; software, M.D.; validation, Y.I.H. and N.K.S.; formal analysis, M.D.; investigation, Y.I.H., M.D., H.M., and N.K.S.; resources, Y.I.H., M.D., H.M., and N.K.S.; data curation, M.D. and H.M.; writing—original draft preparation, Y.I.H., M.D., H.M., and N.K.S.; writing—review and editing, Y.I.H., M.D., H.M., and N.K.S.; visualization, Y.I.H.; supervision, Y.I.H..; project administration, H.M.; funding acquisition, Y.I.H. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by Kemdiktisaintek Republik Indonesia, grant number 128/C3/DT.05.00/PL/2025.

Institutional Review Board Statement

Not applicable

Informed Consent Statement

Not applicable

Data Availability Statement

Not applicable

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Rahman, A. Combating money laundering and the future of banking secrecy laws in Malaysia. Journal of Money Laundering Control 2014, 17(2), 219–229. [Google Scholar] [CrossRef]

- Abbas, U.; Imran Farooq, M.; Noor, A.; Murtaza, S.; Waqas Ashraf, M. The Impact of Net Stable Funding Ratio (NSFR) Regulations of Basel-III on Financial Profitability and Stability: A Case of Asian Islamic Banks. In Indian Journal of Economics and Business; Copyright@ Ashwin Anokha Publications & Distributions., 2022; Vol. 21, Issue 1, Available online: http://www.ashwinanokha.com/IJEB.php.

- Acharya, V. V.; Ryan, S. G. Banks’ Financial Reporting and Financial System Stability. Journal of Accounting Research 2016, 54(2), 277–340. [Google Scholar] [CrossRef]

- Akbary, N. M. M.; Trinugroho, I.; Risfandy, T.; Pamungkas, P. Digital Transformation and Efficiency: Evidence From Indonesian Banks. International Journal of Business and Society 2025, 26(1), 135–150. [Google Scholar] [CrossRef]

- Alam, N.; Hamid, B. A.; Tan, D. T. Does competition make banks riskier in dual banking system? Borsa Istanbul Review 2019, 19, S34–S43. [Google Scholar] [CrossRef]

- Alhammadi, S.; Alotaibi, K. O.; Hakam, D. F. Analysing Islamic banking ethical performance from Maqāṣid al-Sharī‘ah perspective: evidence from Indonesia. In Journal of Sustainable Finance and Investment; Taylor and Francis Ltd, 2022; Vol. 12, Issue 4, pp. 1171–1193. [Google Scholar] [CrossRef]

- Ashraf, D.; Rizwan, M. S.; L’Huillier, B. A net stable funding ratio for Islamic banks and its impact on financial stability: An international investigation. Journal of Financial Stability 2016, 25, 47–57. [Google Scholar] [CrossRef]

- Ayub, R.; Musa, S.; Hasan, A. A.; Othman, A. MANAGING LIQUIDITY AND PROFITABILITY: A STUDY OF THE IMPACT OF BASEL III REGULATIONS ON ISLAMIC BANKS IN PAKISTAN; 2023; Vol. 6, Issue 2. [Google Scholar]

- Baron, R. M.; Kenny, D. A. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology 1986, 51(6), 1173–1182. [Google Scholar] [CrossRef]

- Barth, M. E.; Gomez-Biscarri, J.; Kasznik, R.; López-Espinosa, G. Bank earnings and regulatory capital management using available for sale securities. Review of Accounting Studies 2017, 22(4), 1761–1792. [Google Scholar] [CrossRef]

- Berg, J.; Boivin, N.; Geeroms, H.; Pinkus, D.; Veron, N.; Zenios, S.; Zettelmeyer Of Bruegel, J.; Overby, L. THE QUICKLY FADING MEMORY OF WHY AND WHEN BANK CAPITAL IS IMPORTANT. 2025. Available online: https://www.bis.org/baselframework/background.htm.

- Bitar, M.; Naceur; Ben, S.; Ayadi, R.; Walker, T. Basel Compliance and Financial Stability: Evidence from Islamic Banks. Journal of Financial Services Research 2021, 60(1), 81–134. [Google Scholar] [CrossRef]

- Choi, D. B.; Holcomb, M. R.; Morgan, D. P. Bank Leverage Limits and Regulatory Arbitrage: Old Question, New Evidence. 2018. Available online: https://ssrn.com/abstract=3199997Electroniccopyavailableat:https://ssrn.com/abstract=3199997.

- Dyreng, S. D.; Mayew, W. J.; Williams, C. D. Religious Social Norms and Corporate Financial Reporting. Journal of Business Finance and Accounting 2012, 39(7–8), 845–875. [Google Scholar] [CrossRef]

- Falikhatun, F.; Widaningrum, R.; Santoso, A. L. Do Islamic Financial Resources Affect Profitability Of Islamic Banking? JAS (Jurnal Akuntansi Syariah) 2024, 8(2), 438–458. [Google Scholar] [CrossRef]

- Grundke, P.; Kühn, A. The impact of the Basel III liquidity ratios on banks: Evidence from a simulation study. The Quarterly Review of Economics and Finance 2020, 75, 167–190. [Google Scholar] [CrossRef]

- Gumanti, T. A. Earnings Management: Suatu Telaah Pustaka. 2000. Available online: http://puslit.petra.ac.id/journals/accounting/.

- Haddou, S.; Boughrara, A. How diversification shapes full-fledged Islamic bank Stability? A causal inference approach. International Review of Economics & Finance 2025, 102, 104367. [Google Scholar] [CrossRef]

- Haqqi, A. R. A. Regulatory Regimes of Islamic Banking in ASEAN Economic Community (AEC): A Uniting Force in the Industry of the Region. Advances in Social Sciences Research Journal 2017, 4(13). [Google Scholar] [CrossRef]

- Hatane, S. E.; Octavia, F.; Florentina, J. The Comparison of Earnings Management Practices in Indonesia’s Islamic Banks and Conventional Banks. In Proceedings of the International Conference on Tourism, Economics, Accounting, Management, and Social Science (TEAMS 2018); 2019. [Google Scholar] [CrossRef]

- Healy, P. M.; Wahlen, J. M. A Review of the Earnings Management Literature and Its Implication for Standard Setting; 1999; Vol. 13, Issue 4. [Google Scholar]

- Huang, G.; Song, F. M. The determinants of capital structure: Evidence from China. China Economic Review 2006, 17(1), 14–36. [Google Scholar] [CrossRef]

- Ihsan, F.; Rivani, R.; Parlina, N. D. Analysis of Net Stable Funding Ratio (NSFR) in the Banking Sector Listed on the Indonesian Stock Exchange (IDX) on Financial Performance for the Period 2018-2023. Eduvest - Journal of Universal Studies 2025, 5(8), 9535–9546. [Google Scholar] [CrossRef]

- Iqbal, M. S.; Fikri, S. M. Title: Determinants of Growth in the Banking Sector: Time Series Analysis of Conventional and Islamic Banking in Pakistan History. Islamic Banking & Finance Review (IBFR) 2023, 10(1), 51–67. [Google Scholar] [CrossRef]

- King, M. R. The Basel III Net Stable Funding Ratio and bank net interest margins. Journal of Banking & Finance 2013, 37(11), 4144–4156. [Google Scholar] [CrossRef]

- Krettek, J. Market reactions to the Basel reforms: Implications for shareholders, creditors, and taxpayers. The Quarterly Review of Economics and Finance 2025, 101, 101990. [Google Scholar] [CrossRef]

- Le, M.; Hoang, V. N.; Wilson, C.; Managi, S. Net stable funding ratio and profit efficiency of commercial banks in the US. Economic Analysis and Policy 2020, 67, 55–66. [Google Scholar] [CrossRef]

- Li, J.; Wei, L.; Lee, C.-F.; Zhu, X.; Wu, D. Financial statements based bank risk aggregation. Review of Quantitative Finance and Accounting 2018, 50(3), 673–694. [Google Scholar] [CrossRef]

- Mismiwati, M.; Haryadi, H.; Arum, E. D. P.; Lubis, T. A. The role of profit management in mediation of financial performance and transparency towards profit distribution management in sharia commercial banks. International Journal of Research in Business and Social Science (2147- 4478) 2022, 11(1), 138–151. [Google Scholar] [CrossRef]

- Mohanty, B.; Mehrotra, S. Relationship between Liquidity and Profitability: An Exploratory Study of SMEs in India. Emerging Economy Studies 2018, 4(2), 169–181. [Google Scholar] [CrossRef]

- Zurriah, Rezki; Sembiring, Masta; Siregar, & Siti Aisyah. Real Earnings Management: Study on Manufacturing Sector. Jurnal Akuntansi 2025, 29(2), 359–376. [Google Scholar] [CrossRef]

- Salsabilla, L. Z.; Jaya, T. J. The impact of non-performing financing and operational efficiency on the stability of Islamic banks in Persian Gulf countries. Journal of Islamic Economics Lariba 2024, 10(2), 623–640. [Google Scholar] [CrossRef]

- Santillln-Salgado, R. J. Global Regulatory Changes to the Banking Industry after the Financial Crisis: Basel III. SSRN Electronic Journal 2015. [Google Scholar] [CrossRef]

- Setiyono, B.; Naufa, A. M. The impact of net stable funding ratio on bank performance and risk around the world. Buletin Ekonomi Moneter Dan Perbankan/Monetary and Banking Economics Bulletin 2020, 23(4), 543–564. [Google Scholar] [CrossRef]

- Siadat, M.; Hammarlid, O. Net Stable Funding Ratio: Impact on Funding Value Adjustment. 2017. Available online: http://arxiv.org/abs/1701.00540.

- Sidhu, A. V.; Rastogi, S.; Gupte, R.; Rawal, A.; Agarwal, B. Net Stable Funding Ratio (NSFR) and Bank Performance: A Study of the Indian Banks. Journal of Risk and Financial Management 2022, 15(11). [Google Scholar] [CrossRef]

- Srairi, S. Corporate Governance Disclosure Practices and Performance of Islamic Banks in GCC Countries. Journal of Islamic Finance 2015, 4(2). [Google Scholar] [CrossRef]

- Suripto. Earnings management determinants: Comparison between Islamic and Conventional Banks across the ASEAN region. Asia Pacific Management Review 2023, 28(1), 24–32. [Google Scholar] [CrossRef]

- Ullah, S.; Majeed, A.; Popp, J. Determinants of bank’s efficiency in an emerging economy: A data envelopment analysis approach. PLOS ONE 2023, 18(3), e0281663. [Google Scholar] [CrossRef] [PubMed]

- Widayawati, E. The role of corporate governance in moderating the influence of financial distress on earnings management. Jurnal Siasat Bisnis 2025, 250–264. [Google Scholar] [CrossRef]

Figure 1.

Conceptual Framework

Table 2.

Descriptive Statistics.

| Variable | Number of Data | Mean | Standard Deviation | Min | Max | Range |

|---|---|---|---|---|---|---|

| NSFR | 64 | 2,21 | 2,54 | 0,47 | 16,81 | 16,34 |

| Islamic Bank Margin (IBM) | 64 | 0,064 | 0,075 | 0,0003 | 0,341 | 0,341 |

| Earning Management (EM) | 64 | -0,11 | 1,07 | -5,16 | 1,8 | 6,96 |

| Capital Adequacy Ratio (CAR) | 64 | 29,20 | 10,67 | 12,34 | 58.27 | 45,93 |

Table 3.

Fixed Effects Regression Results.

| Variable | Coefficient | Std. Error | t-stat | p-value |

|---|---|---|---|---|

| NSFR | 0.00842 | 0.00231 | 3.642 | 0.0004*** |

| CAR | -0.02315 | 0.01587 | -1.459 | 0.1462 |

| Intercept | 0.05183 | 0.00762 | 6.802 | 0.0000*** |

R-squared: 0.284, F-stat 12.37 (p-value:0.0001)

Table 4.

Fixed Effects Regression Results.

| Variable | Coefficient | Std. Error | t-stat | p-value |

|---|---|---|---|---|

| NSFR | -0.42381 | 0.18734 | -2.263 | 0.0245** |

| CAR | -2.85624 | 1.28472 | -2.223 | 0.0273** |

| Intercept | 0.89263 | 0.61742 | 1.446 | 0.1498 |

R-squared: 0.157. F-statistic: 5.83 (p-value: 0.0036), p < 0.05

Table 5.

Effect of NSFR on Islamic Bank Margin (IBM).

| Variable | Coefficient | Std. Error | t-stat | p-value |

|---|---|---|---|---|

| NSFR | 0.00792 | 0.00215 | 3.684 | 0.0012*** |

| CAR | -0.02148 | 0.01432 | -1.500 | 0.1473 |

| Intercept | 0.05216 | 0.00698 | 7.472 | 0.0000*** |

*** p < 0.01, ** p < 0.05, * p < 0.1. R-squared: 0.284; F-statistic: 15.82 (p-value: 0.0003), Number of observations: 56. Number of groups: 7.

Table 6.

Effect of NSFR on Earning Management.

| Variable | Coefficient | Std. Error | t-stat | p-value |

|---|---|---|---|---|

| NSFR | -0.40163 | 0.17382 | -2.311 | 0.0312** |

| CAR | -2.71485 | 1.19245 | -2.277 | 0.0325** |

| Intercept | 0.84592 | 0.57284 | 1.477 | 0.1546 |

*** p < 0.01, ** p < 0.05, * p < 0.1; R-squared: 0.157; F-statistic: 6.24 (p-value: 0.0078); Number of observations: 56 Number of groups: 7; Number of groups: 7.

Table 8.

Effect of NSFR on Islamic Bank Margin on Earning Management.

| Variable | Coefficient | Robust SE | t-stat | p-value |

|---|---|---|---|---|

| Islamic Margin Bank | -8.42361 | 3.12845 | -2.692 | 0.0121** |

| NSFR | -0.34582 | 0.16284 | -2.124 | 0.0426** |

| CAR | -2.89234 | 1.21543 | -2.380 | 0.0248** |

| Intercept | 1.29845 | 0.62384 | 2.082 | 0.0468** |

R-squared: 0.218; F-statistic: 8.73 (p-value: 0.0008)

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.