2.1. Key Features

The model features four types of agents: households, retail and wholesale banks and a regulator setting a prudential policy. There are two goods, a nondurable goods and a durable asset, which is capital. There is no capital’s depreciation, and the total supply of capital stock is normalized to unity. Wholesale and retail banks acquire capital through borrowed funds and their own equity. Households lend to banks and hold capital directly.

where

,

and

are the total capital held by wholesale and retail bankers, and households respectively.

Expenditure in terms of goods at time reflects the management cost of screening and monitoring investment projects. In the case of retail banks, the management costs might also reflect various regulatory constraints. We assume this management cost is increasing and convex in the total amount of capital, as given by the following quadratic formulation:

where type

and

represents wholesale banks, retail banks and households, respectively. The marginal cost from providing the management service is denoted by:

In addition, we assume the management cost is zero for wholesale banks and highest for households (holding constant the level of capital):

Assumption 1:

This assumption implies that wholesale bankers have an advantage over the other agents in managing capital. Retails banks in turn have a comparative advantage over households.

2.2. Households

Households consume and save either by lending funds to bankers or by holding capital directly in the competitive market. They may deposit funds in either retail or wholesale banks. In addition to the returns on portfolio investment, every period each household receives an endowment goods, that varies proportionately with the aggregate productivity shock .

Deposits held in a bank from to are one period bonds that promise to pay the noncontingent gross rate of return in the absence of a run by depositors. In case of a deposit run, depositors only receive a fraction of the promised return, where is the total liquidation value of retail banks assets per unit of promised deposit obligations.

In consequence, the household’s return on deposits, is expressed as follows:

If a deposit run occurs all depositors receive the same pro rata share of liquidated assets.

Household utility is given by:

where

is the household’s consumption and

The household chooses consumption, bank deposits and direct capital holdings to maximize expected utility subject to the budget constraint:

Consumption, saving, and management costs are financed by the endowment , the returns on savings, and the profits from providing management services to retail bankers. is the market price of capital.

The household chooses consumption and saving with the expectation that the realized return on deposits, equals the promised return with certainty, and that asset prices are those at which capital is traded when no bank run happens. (See Appendix B for the first-order conditions).

Moreover, the innovation shock follows an model:

where

is the autoregressive parameter,

the perturbation term and

is n.i.i.d process with variance

.

2.3. Banks

There are two types of bankers: retail and wholesale. Each type manages a financial intermediary. Banks fund capital investment, which refers to nonfinancial loans by issuing deposits to households, borrowing from other banks in an interbank market and using their own equity. Banks can also lend in the interbank market.

Bankers may be vulnerable to runs in the interbank market. In this case, creditor banks suddenly decide to not rollover interbank loans. In the event of an interbank run, the creditor banks receive a fraction of the promised return on the interbank credit, where is the total liquidation value of debtor bank assets per unit of debt obligations. Thus, the creditor bank’s return on interbank loans, is as follows:

where

. If an interbank run occurs, all creditor banks receive the same pro rata share of liquidated assets.

Due to financial market frictions, bankers may be constrained in their ability to raise external funds. To the extent they may be constrained, they will attempt to save their way out of the financing constraint by accumulating retained earnings in order to move towards 100% equity financing. To limit this possibility, we assume that bankers have a finite expected lifetime: specifically, each banker of type ( has an probability of surviving until the next period and a probability of exiting.

Every period new bankers of type enter with an endowment that is received only in the first period of life. This initial endowment may be thought of as the start up equity for the new banker. The number of entering bankers equals the number who exit, keeping the total constant.

To encourage the use of wholesale funding markets along with retail markets, we assume that the banker’s ability to divert funds depends on both the sources and uses of funds. The banker can divert the fraction of nonfinancial loans financed by retained earnings or funds raised from households, where . On the other hand, he/she can divert only the fraction of nonfinancial loans financed by interbank borrowing, where . Here, bankers lending in the wholesale market are more effective at monitoring the banks to which they lend than are households that supply deposits in the retail market.

For bankers that lend to other banks, we suppose that it is more difficult to divert interbank loans than nonfinancial loans. Specifically, we suppose that a banker can divert only a fraction of its loans to other banks, where . and are the parameters that govern the moral hazard problem in the interbank market.

The banker’s decision at reduces to comparing the franchise value of the bank , which measures the present discounted value of future payouts from operating honestly, with the gain from diverting funds. In this regard, rational lenders will not supply funds to the banker if he has an incentive to cheat. Thus, any financial arrangement between the bank and its lenders must satisfy the following set of incentive constraints:

Overall, there are two basic factors that govern the existence and relative size of the interbank market. First, the cost advantage that wholesale banks have in managing nonfinancial loans as in Assumption 1. Second, the size of the parameters and which govern the comparative advantage that retail banks have over households in lending to wholesale banks, as shown by Assumption 2.

Assumption 2:

.

This implies that and can be sufficiently small to permit an empirically reasonable relative amount of interbank lending.

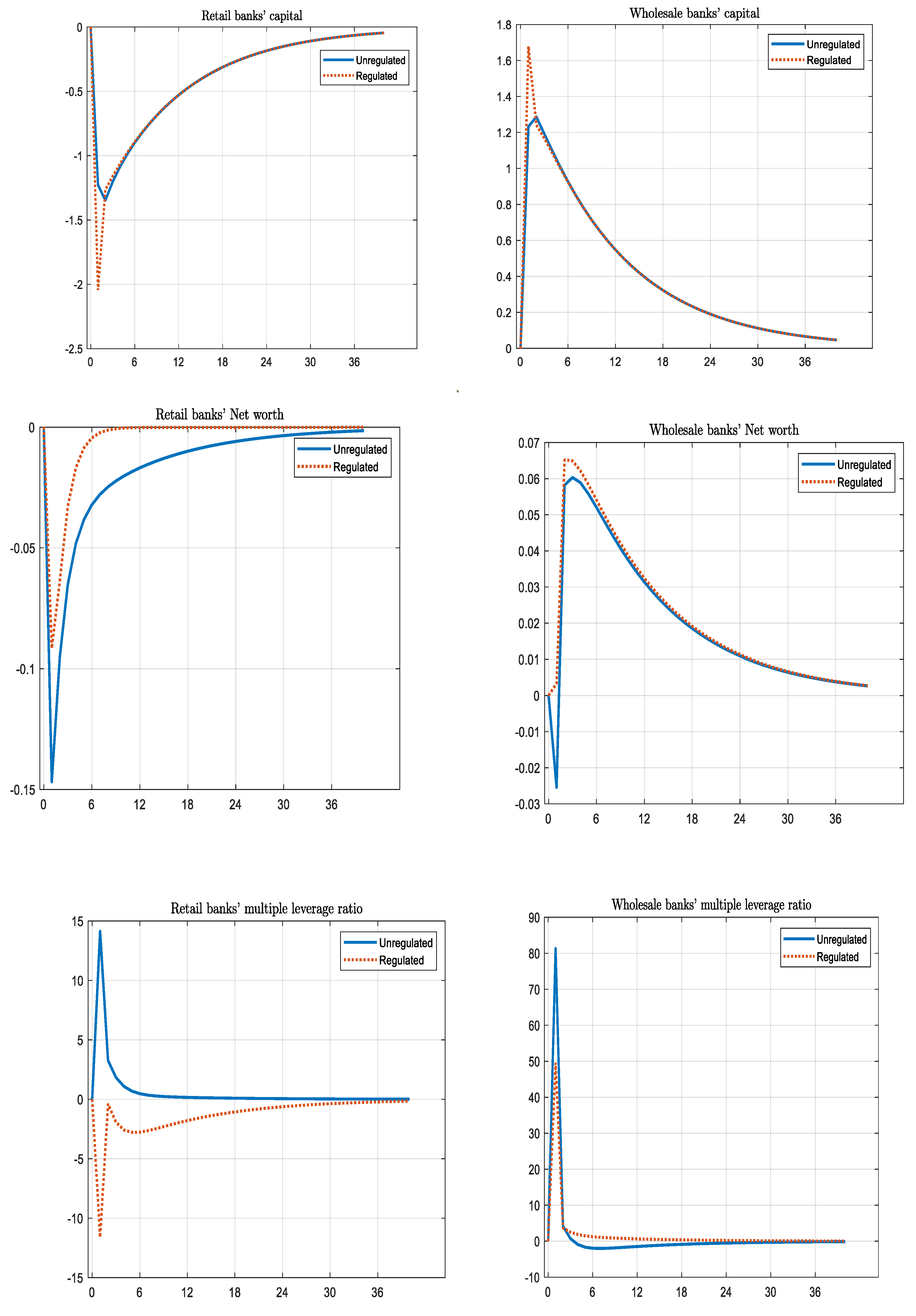

The banker’s evolution of net worth is thus:

where

is the rate of return on nonfinancial loans, given by:

The stochastic discount factor , which the bankers use to value is a probability weighted average of the discounted marginal values of net worth to exiting and continuing bankers at .

where

is the Tobin’s Q ratio.

The banker’s optimization problem then is to choose each period to maximize the franchise value subject to the incentive constraint and the balance sheet constraints and .

2.3.1. Wholesale Banks

Generally, wholesale banks may raise funds either from other banks or from households. Especially, the model focuses on wholesale funding markets equilibrium where the conditions for the Lemma 1 are satisfied:

Lemma 1: , and the incentive constraint is binding if and only if

Given Lemma 1 the evolution of bank net worth is:

where the multiple leverage ratio

is given by:

In turn, the wholesale banks optimization problem to choosing the leverage multiple to solve:

subject to the incentive constraint

Given the incentive constraint is binding under Lemma 1, the objective combines with the binding incentive constraint to obtain the following solution for

is increasing in

and decreasing in

. Intuitively, the franchise value

increases when returns on assets are higher and decreases when the cost of funding asset purchases rises as indicated by

. Increases in

loosen the incentive constraint, making lenders will, to supply more credit.

Likewise, is a decreasing function of both , the diversion rate on nonfinancial loans funded by net worth, and , the parameter that controls the relative ease of diverting nonfinancial loans funded by interbank borrowing relative to those funded by the other means: increases in either parameter tighten the incentive constraint, inducing lenders to reduce the amount of credit they supply.

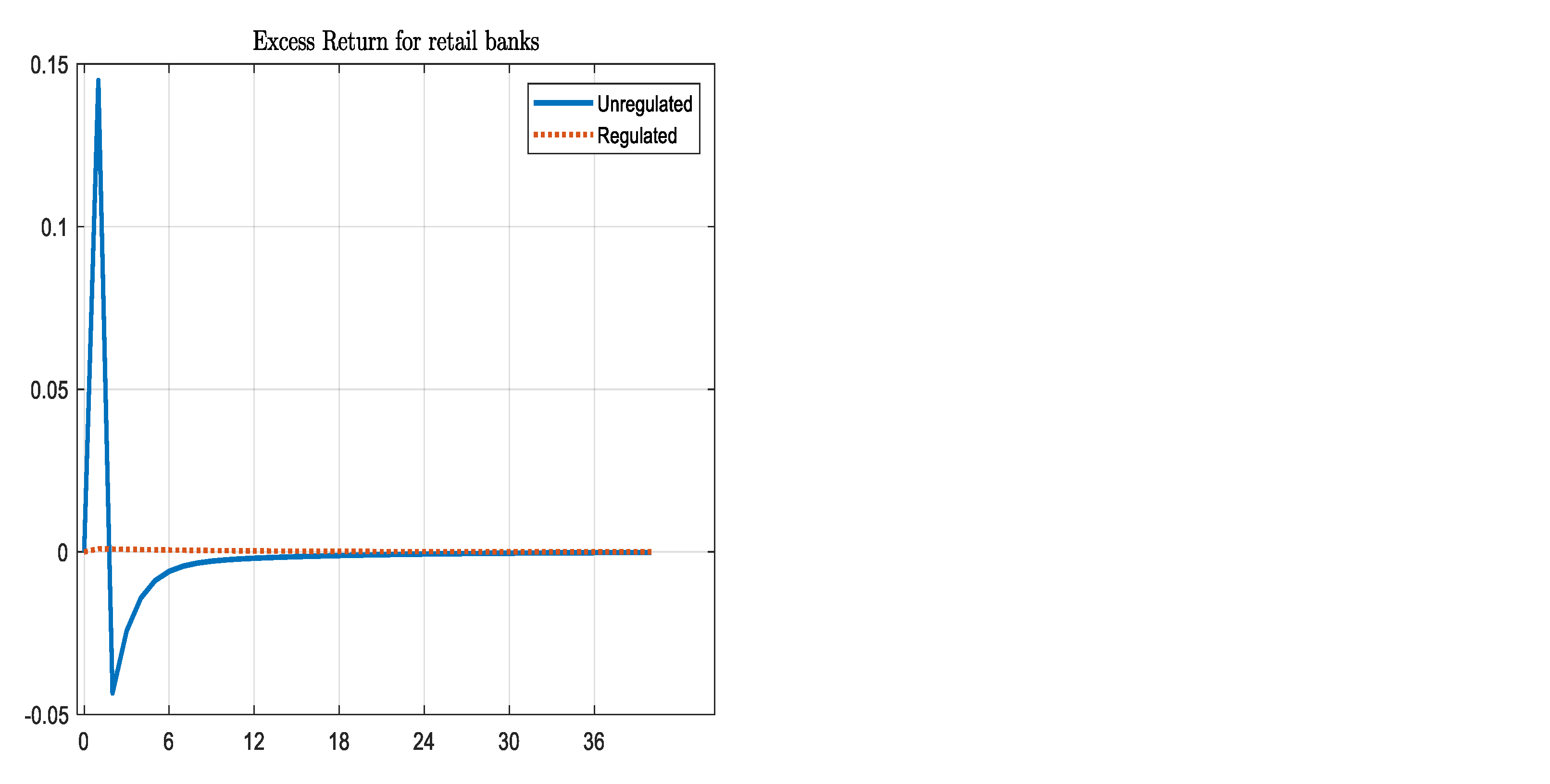

Lastly, from , an expression of the franchise value per unit of net worth or the shadow value of wholesale bank net worth, that we call is set as:

where

is given by

. The shadow value

is greater than 1 since extra net worth enables the bank to borrow more and invest in assets earning an excess return.

2.3.2. Retail Banks

As with wholesale banks, the model opts for a parametrization where the incentive constraint binds and narrows to the case where retail banks are holding both nonfinancial and interbank loans. Particularly, the model considers a parametrization where in equilibrium Lemma 2 is satisfied:

Lemma 2: and the incentive constraint is binding if and only if

For the retail bank to be indifferent between holding nonfinancial loans, the rate on interbank loans must be below the rate earned on nonfinancial loans in a way that satisfies the conditions for the lemma. Intuitively, the advantage for the retail bank to making an interbank loan is that households are willing to lend more to the bank per unit of net worth than for a nonfinancial loan. Therefore, to make the retail bank indifferent, must lie below .

Let be a retail bank’s effective leverage multiple, namely the ratio of assets to net worth, where assets are weighted by the relative ease of diversion:

The weight on is the ratio of how much a retail banker can divert from interbank loans relative to nonfinancial loans.

Given the restrictions implied by lemma 2, the same procedure is used as in the case of wholesale bankers to express the retail banker’s optimization problem as choosing to solve:

Given Lemma 2, imposing that incentive constraint binds, which implies:

As with the leverage multiple for wholesale bankers, is increasing in expected asset returns on the bank’s portfolio and decreasing in the diversion parameter.

At the end, from an expression for the franchise value per unit of net worth is as follows:

As with wholesale banks, the shadow value of a unit of net worth exceeds unity and depends only on aggregate variables.

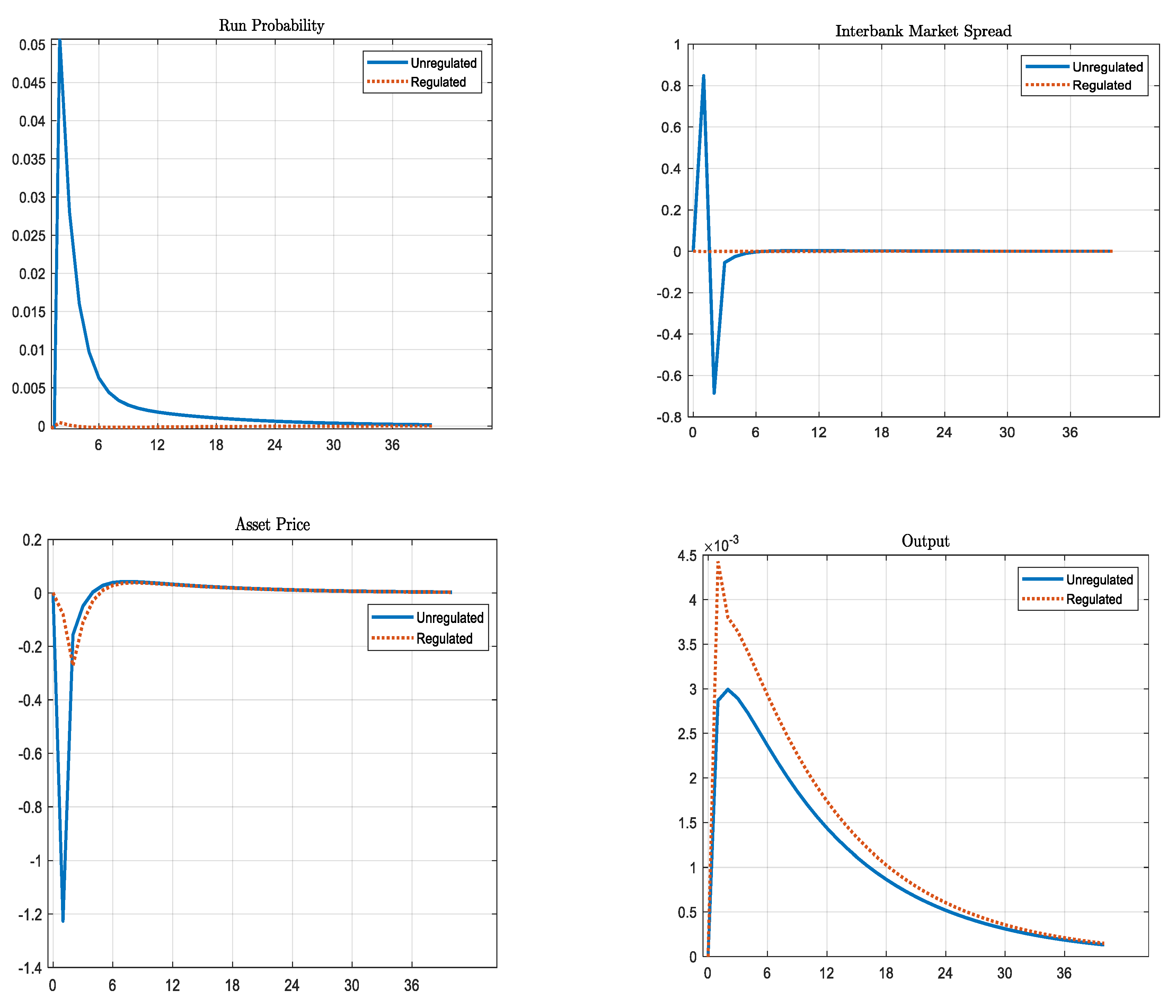

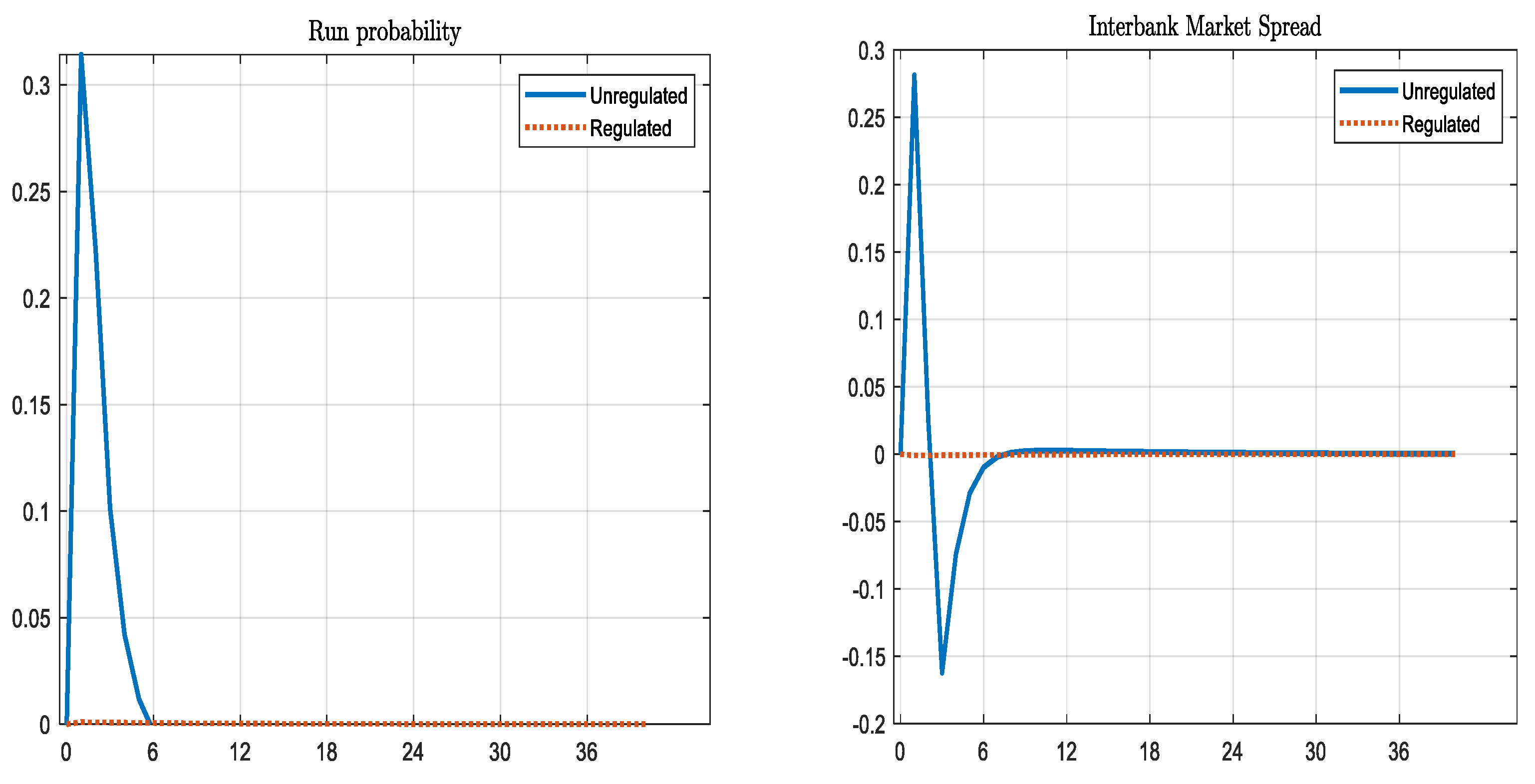

2.3.3. Recessions and Runs

This section deals with the scenario where the economy goes into recession, which involves a drop in , making a bank run equilibrium possible. In this instance, the run variable is defined as:

where

is the recovery rate on wholesale debt. Hence, for a run to exist the run variable must be positive or the recovery rate is less than unity, i.e., (see

Appendix C for the proof)

where

is the return on bank assets conditional on a run at

and

the liquation price expressed as below:

According to Gertler and Kiyotaki (2015) at each time , the probability of transitioning to a state where a run on wholesale banks occurs, is given by a reduced form decreasing function of the expected recovery rate as follows:

This formulation allows to capture the idea that as wholesale balance sheet positions weaken, the likelihood of a run increases. In the numerical simulations, is set to .