Submitted:

24 June 2025

Posted:

25 June 2025

You are already at the latest version

Abstract

This paper examines the impact of agent banking activities, a recent FinTech development, on the financial performance of commercial banks in Bangladesh, as agent banking has been receiving significant global attention due to its technology driven approach, cost-effective and easy accessibility and broader coverage to the unbanked population. Employing a panel data regression framework, the study estimates a random effect model using the bank-level quarterly data from nine commercial banks in Bangladesh that have been operating full-scale agent banking services including deposit mobilization and credit disbursement over the period from 2018Q1 to 2024Q4. The empirical findings indicate that credit disbursement by agent banks has a positive and statistically significant impact on bank profitability measures, return on asset (ROA) and return on equity (ROE). Similarly, the number of agent banking outlets has a significant positive impact on ROA. Therefore, an appropriate agent banking policy aimed at increasing agent banking outlets using digital platforms based on FinTech is vital for ensuring positive growth in credit disbursement in order to improve the financial performance of the banking sector in a developing country like Bangladesh.

Keywords:

Fintech

; Financial Performance

; Commercial Banks

; Panel data model

; Credit

1. Introduction

FinTech (Financial Technology) refers to the integration of technology into financial services to enhance accessibility, efficiency, security, and cost-effectiveness through software, mobile apps, and digital platforms. It has revolutionized financial services by providing greater accessibility to individuals and businesses, streamlining operations, and reducing costs. One of the most significant innovations within the FinTech sector is agent banking, which allows banks to extend financial services utilizing digital platforms through local agents in areas where conventional bank branches are not available [1]. This model has become increasingly prevalent in developing countries especially in Bangladesh, where it has been instrumental in addressing the challenges faced by underserved populations and promoting financial inclusion. Therefore, agent banking, being an innovative FinTech platform, facilitates digital financial solutions using advanced technology and eventually increases financial activities and employment generation in rural areas.

Agent banking model has been a major development in the financial landscape of Bangladesh. The agent banks act as small-scale representatives of commercial banks, equipped with point-of-sale (POS) devices, mobile phones, barcode scanners, computers, and biometric tools to facilitate a wide range of banking services. This innovative banking model is 86 percent more cost-effective than establishing a traditional bank branch, as it leverages existing business infrastructure reducing the need for significant investment in physical infrastructure and fixed operational costs [2]. Globally, various models of agent banking exist, with agents operating in diverse settings such as pharmacies, supermarkets, corner stores, and post offices. For example, post offices act as banking agents in Australia, while corner stores serve this role in France. Brazil delivers financial services through lottery outlets. Mobile-based branchless banking and agency banking are prominent in countries like Senegal, Pakistan, India, Kenya, Nigeria, the Democratic Republic of Congo, South Africa, and the Philippines [3,4,5,6,7,8]. Despite the varying models, agent banking is generally recognized as a cost-effective banking solution that offers greater accessibility to underserved market segments and thereby promoting broader financial inclusion.

In Bangladesh, agent banking has been a key tool in expanding financial services to rural and also remote areas, where traditional banking infrastructure is limited or non-existent. The scope of agent banking in Bangladesh was formalized in 2013 while Bangladesh Bank (BB), the central bank, introduced its agent banking guidelines.1 The full operation of agent banks began in 2016, aiming to enhance financial inclusion providing banking services to unbanked population. As of December 2024, 31 commercial banks in Bangladesh are operating agent banking services through a network of 16,021 agents and 21,248 outlets, with the majority of these agents and outlets located in rural areas [9]). In terms of banking service offerings, agent banking covers a wide range of financial services including cash deposits, withdrawals, account opening, utility bill payments, fund transfer and saving products. Unlike conventional banking, agent banking does not require the establishment of expensive brick-and-mortar branches, making it a more affordable and scalable solution for reaching the doorstep of unbanked population in rural underserved areas. The agent banking model conducts banking transactions on behalf of commercial banks (as mother bank) including deposit mobilization, loan disbursement, collection of utility bills, payments related to government programs, and handling domestic and international remittances. All transactions conducted through agents are recorded in the financial statements of the respective mother banks ensuring transparency and regulatory compliance.

Although customers have been significantly benefited from agent banking, the impact on the financial performance of commercial banks remains uncertain. Despite the recognized advantages of agent banking, such as expanding market reach and reducing operational expenses, a substantial research gap persists regarding its effect on the financial performance of commercial banks in Bangladesh. While existing literature largely emphasizes the benefits of agent banking for financial inclusion and service delivery, there is limited empirical evidence on how this FinTech based banking model influences the key financial performance metrics, including profitability, return on assets (ROA), return on equity (ROE), and overall financial stability. Addressing this gap is essential to uncover the strategic value of FinTech innovations for sustainable growth, profitability, and competitiveness of the banking sector in Bangladesh. These relationships also provide valuable insights into the broader economic impacts of FinTech adoption in emerging markets. This study, therefore, aims to investigate the effect of agent banking on the performance of commercial banks in Bangladesh. Based on the stated objective, the following research questions are outlined:

- RQ1:

- How does agent banking influence the accessibility and financial performance of commercial banks in Bangladesh?

- RQ2:

- What is the impact of agent banking outlets on the financial performance of commercial banks in Bangladesh?

- RQ3:

- How does deposit mobilization influence the financial performance of commercial banks in Bangladesh?

- RQ4:

- What is the effect of credit disbursement through agent banking on the financial performance of commercial banks in Bangladesh?

The remainder of the paper is organized as follows: Section 2 provides a brief literature review: theoretical and empirical literature. Section 3 constructs conceptual framework and develops hypotheses. Section 4 illustrates research design, data and methodology and model specification. Section 5 discusses empirical results. Section 6 checks the robustness of the empirical results and Section 7 concludes the paper.

2. Literature Review

This section briefly discusses both theoretical and empirical literature on agent banking models.

2.1. Theories on Agent Banking Model

The agent banking model is based on agency theory [10]. The model defines an agency relationship as a contract between a commercial bank (principal) and an agent hired to provide banking services on their behalf. Therefore, agent banking services are provided through agents under a valid agency service agreement with a commercial bank. An agent is the owner of an outlet who conducts banking transactions on behalf of a bank. These agents use FinTech platforms to process banking transactions, such as money transfer, bill payments, deposit mobilization and loan disbursement. The agent points are equipped with computers, biometric devices, mobile phones, point of sale (POS) devices and barcode scanners to provide banking services to unbanked populations of the remote areas in a cost-effective way. Therefore, commercial banks can reach the underserved or unbanked population through their agents utilizing advanced FinTech with less overhead costs instead of setting up a full-fledged bank branch. The model also allows the transaction software of any individual agent to be connected to the core software of the principal bank, so agent banking transactions are shown in the bank statement on real-time [11]. Agent banking model is beneficial for the mother bank in terms of larger customer base and market share, extended coverage with low-cost solution and increased revenue from additional investment, interest, and fee income.

Agent banking model also follows the theory of financial intermediation [12]. The theory reveals how agent banking strengthens the intermediation role of banks, i.e., mobilizing deposits and disbursing loans in remote areas and thus extends financial inclusion. The Technology Acceptance Model explains the impact of agent banking on key performance indicators including Return on Asset (ROA) and Return on Equity (ROE), operational efficiency (cost-to-income ratio), market expansion (customer acquisition) and risk management [13]. The framework offers a comprehensive understanding of how agent banking enhances financial performance in the digital economy.

[14] observe that agent banking offers banking and payment services through postal and retail outlets including grocery stores, pharmacies, seed and fertilizer retailers, and gas stations, among others instead of using bank branches and their own field officers. In India, under the Business Correspondent model, banks are entitled to engage intermediaries, for example, agents to disburse small value credits, recover principal and interest payments, collect small value deposits, sell micro insurance and/or pension products and receive or deliver small value remittances [5].

2.1. Empirical Literature

The impact of agent banking on the performance of commercial banks has attracted growing scholarly interest currently. Although several studies have been carried out but yet no unified conclusion has emerged. The literature on agent banking indicates that agent banking activities have a positive and significant impact on banks’ financial performance. Several studies on agent banking demonstrate that agent banking enhances accessibility, operational efficiency, and profitability [15,16,17,18,19]. [15] reveal that a larger agent network improves profitability by improving and expanding service reach, while [20] attributes performance gain in Kenyan banks with expanded market shares and lower transaction costs. [3] find that agent banking increases clients’ financial activities and thus contributes to increased savings. [6] argue that agent banking improves the business performance of commercial banks in terms of increased turnover, number of products, customers and transactions. [21] reveal that agency banking has a positive relationship with the growth of profits of commercial banks in Kenya. [7] examine the impact of agent banking on the performance of deposit money banks in Nigeria and find that banks’ profitability would be higher if banking services can be provided to grass root level people through agent banking.

The existing literature on agent banking also demonstrates mixed outcomes in regard to the influence of the number of agents on banks’ financial performance. While many researchers including [16,17,18,22,23,24,25,26,27] find a significant positive link between the number of agents and financial performance of banks, some other studies provide contrary evidence though. [16,28] find that more agents align with improved profitability (ROA/ROE) and financial inclusion. In contrast, [29] finds the coefficient for the number of agents negative and statistically significant for both ROA and ROE, and therefore, increasing the number of agents may not necessarily boost profitability. [30] finds similar negative relation between the number of agents, volume of deposit and bank profitability in terms of ROA, ROE and NIM.

A more consistent pattern emerges in studies focusing on deposit mobilization through agent banking and banks’ financial performance [16,23,24,29,31]. The authors have identified a positive and significant relationship between total deposits mobilized through agent banking and the financial performance of the mother bank in terms of ROA, ROE, and NIM. Agent banking has emerged as an effective channel for deposit mobilization, especially in underserved and rural regions, enabling banks to expand their customer base at a lower operational cost. [29] suggests that total deposits collected through agents have a statistically significant and positive impact on both ROA and ROE, attributing to improved financial inclusion and reduced overheads. Similarly, [16] finds that deposits collected through agents consistently enhance profitability metrics. The authors suggest that the financial performance of banks can be improved through deposit mobilization activity of agent banks as these deposits are used by the parent bank for investment and converting them into interest-earning assets, such as loans and advances, which in turn increase the profitability of the bank. Overall, deposit mobilization through agents plays a critical role in strengthening the financial performance of banks by improving resource mobilization and operational efficiency. Conversely, increased deposit mobilization through agent banking may not always enhance bank profitability. There is evidence of an inverse relationship between total deposits mobilization through agents and financial performance indicators such as Return on Assets (ROA) and Return on Equity (ROE). For example, [32] report that excessive liquidity, driven by unproductive deposits, can negatively impact profitability, while [24] warns that inefficient fund deployment, coupled with limited lending capacity through agents can lead to falling ROA and ROE. [33] demonstrate that short deposit maturities, high funding costs, and large foreign currency shares can lower ROA and undermine profitability despite deposit growth. Hence, while deposit growth through agent banking enhances outreach, its impact on profitability may depend on how effectively these deposits are utilized within the bank’s financial strategy.

The influence of agent outlets has yielded mixed results. Several studies on agent banking indicate that the number of agent banking outlets positively and significantly influences the financial performance (e.g., ROA) of commercial banks [16,24,34]. However, there are some other empirical studies that provide evidence of negative and statistically significant impacts on ROA suggesting diminishing returns or operational inefficiencies with excessive outlet expansion [28,29,35].

Credit disbursement via agents has also been found to have a positive and significant effect on key financial performance indicators. Many empirical studies suggest that lending activities of agents can increase both ROA and ROE of the mother commercial bank and, thus enhance financial inclusion, profitability, and operational efficiency [17,23,29,36,37,38]. The growing body of evidence indicates that agent-based credit delivery is rapidly expanding and contributes positively to overall bank performance. Conversely, [23] report that credit disbursement through agents has an insignificant effect on ROE. This finding is strongly supported by many empirical studies, for example, [16,22,31]. The authors argue that the effectiveness of credit disbursement through agent banking varies depending on institutional frameworks, regulatory environments, and the operational maturity of agent networks. Collectively, these studies underscore the importance of considering contextual and methodological differences when assessing the role of agent banking in driving financial performance across different regions and banking systems.

The literature further demonstrates the strategic role of remittances in bank performance. [23,29,30,39,40] agree that there is a positive impact of remittances on the financial performance of commercial banks. They argue that remittance inflows serve as a secure and resilient source of funds and increase banks’ deposit base which can be used for increasing credit and investment portfolios. [41,42,43] support the argument that remittances promote profitability, financial intermediation and financial inclusion. However, reliance on remittances also poses certain risks. Compliance and regulatory challenges related to anti-money laundering (AML) and combating the financing of terrorism (CFT) and the efficient integration of FinTech innovations are crucial. [44,45] argue that digital financial services platforms can mitigate transaction costs and foster formal banking habits among remittance recipients. Overall, the literature supports the view that remittances play a significant role in enhancing banks’ financial performance, particularly when integrated with robust regulatory frameworks and digital financial infrastructure. In regard to the number of accounts maintained with agents, the empirical findings remain inconclusive. Several studies reveal positive and significant relation between the number of agent accounts and the financial performance of the mother banks [4,22,28,31,46]. For example, [29] shows that the number of accounts has a significant positive effect on both ROA and ROE of commercial banks. Similarly, [22] finds that the growth in the number of accounts is significantly associated with increased profitability of the banks and customer satisfaction. [47] argues that more active accounts per agent network boosts financial intermediation, implying strengthened financial performance of banks. In contrast, several other studies find the opposite relationship between the number of agent accounts and financial performance of banks [29,30,32,33]. [29] found that for both ROA and ROE, the estimated coefficient for the number of agents is negative and statistically significant, indicates that an increase in the number of agents may not increase bank profit. Furthermore, [33] finds a negative relation between the number of agent accounts and return on assets (ROA), attributing a high maintenance costs and the short tenure of deposits. [24] also observes that an increase in agent accounts does not lead to higher profitability since banks were unable to allocate the funds effectively.

It is evident from the literature review above that no comprehensive study has been conducted so far to evaluate the performance of agent banking in Bangladesh since its inception in 2016. This notable gap in empirical research demonstrates the relevance and originality of the present study. Therefore, it is timely to assess the performance of FinTech based agent banking activities, with particular attention to how these activities have impacted the key financial performance metrics, including return on assets (ROA), and return on equity (ROE) of the parent commercial banks over time. As such, this study aims to investigate the impact of FinTech based agent banking operations on the financial performance of commercial banks in Bangladesh and thereby contributing to the limited body of empirical literature on the subject.

3. Conceptual Framework

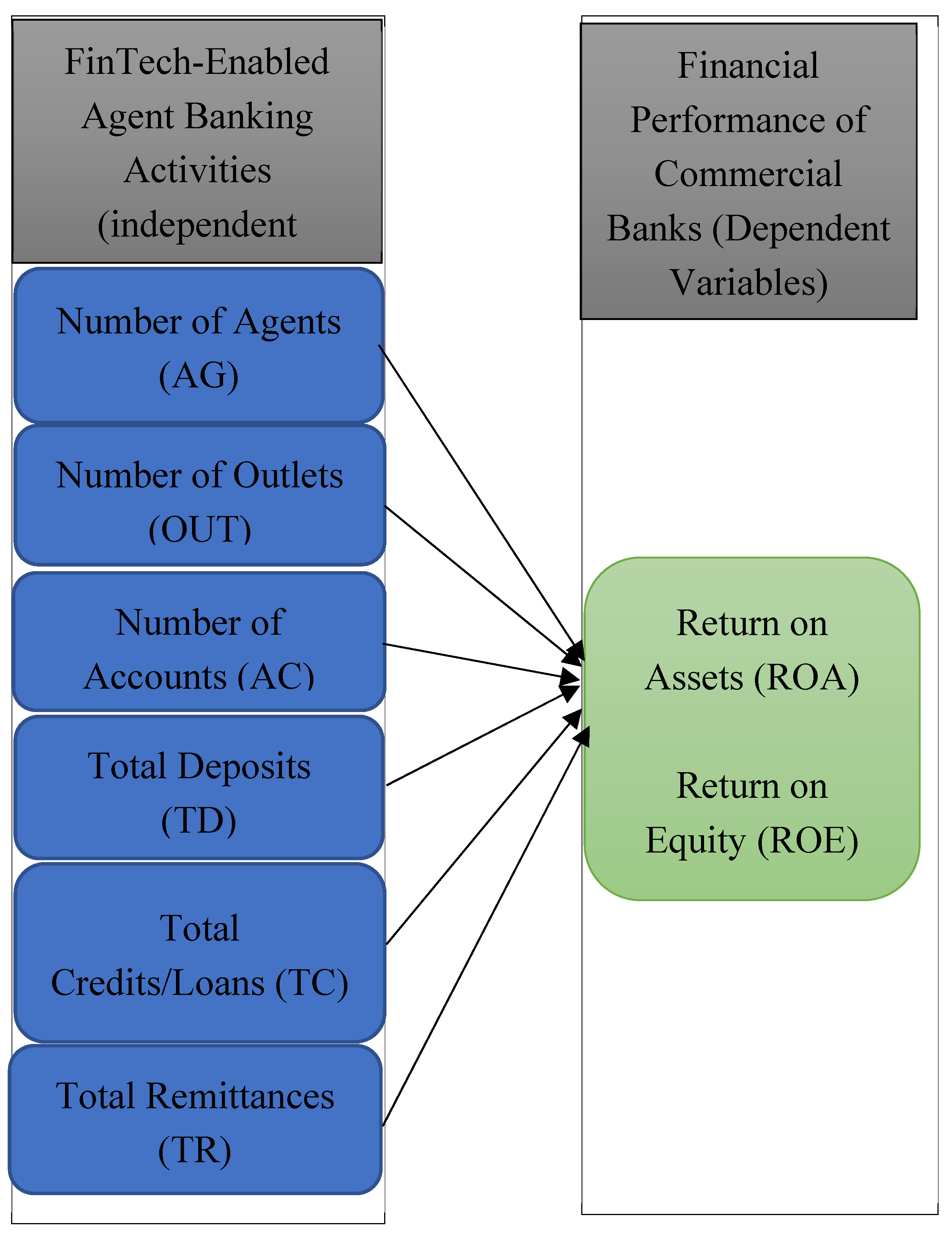

Based on the literature review presented in Section 2, this study develops the research framework illustrated in Figure 1, which hypothesizes a direct relationship between FinTech-based agent banking variables and the financial performance of commercial banks. The conceptual framework captures the core constructs of FinTech-driven agent banking and commercial bank performance, aiming to address the research questions outlined in Section 1.

3.1. Hypotheses Development

Based on the conceptual framework and existing literature, the following hypotheses are developed to examine the impact of FinTech-based agent banking on the financial performance of commercial banks in Bangladesh:

H1:

An increase in the number of agent banking agents (AG) is linked to a decline in both ROA and ROE for commercial banks in Bangladesh.

H2:

An increase in the number of agent banking outlets (OUT) is positively associated with both ROA and ROE for commercial banks in Bangladesh.

H3:

A higher number of agent banking accounts (AC) corresponds to lower financial performance, as reflected in both ROA and ROE, for commercial banks in Bangladesh.

H4:

Total deposit (TD) mobilized through agent banking is positively and significantly associated with both return on assets (ROA) and return on equity (ROE) for commercial banks in Bangladesh.

H5:

Total credit disbursement (TC) through agent banking has a significant positive effect on both ROA and ROE for commercial banks in Bangladesh.

H6:

Total remittance collection (REM) positively affects the financial performance, measured by ROA and ROE of commercial banks in Bangladesh.

4. Empirical Design: Methodology, Data and Variables

The study examines the effects of agent banking activities on the profitability of the sample commercial banks in Bangladesh. In the regression analysis, two different profitability measures, return on assets (ROA) and return on equity (ROE) of the sample banks are considered as dependent variables and, six agent bank specific independent variables are number of agents, number of agent banking outlets, number of total accounts with agent banks, total deposit collection and credit disbursement, and total remittance amount of agent banks. The detail definitions of the variables are presented in appendix A, Table A1.

The study estimates a panel data regression framework using bank level quarterly data of nine (09) commercial banks in Bangladesh that are operating full-fledged agent banking activities including both deposit mobilization and credit disbursement. The sample banks are Bank Asia, Dutch-Bangla Bank, Al-Arafah Islami Bank, Islami Bank Bangladesh, Mutural Trust Bank, The City Bank, Brac Bank, NRB Bank and Modhumoti Bank Limited (Appendix A, Table A2). Although 31 commercial banks are currently in agent banking operation in Bangladesh, only nine banks have transactions history with both deposit and loan products during the sample period 2018Q1-2024Q4. The study has constructed a unique balanced panel dataset with 234 observations for the period 2018Q1-2024Q4 and, estimated both Fixed Effect (FE) Model and Random Effect (RE) Model and also a pooled regression model (as robustness check) to examine the effects of agent banking activities on the financial performance of the sample commercial banks in terms of profitability measures, return on assets (ROA) and return on equity (ROE). Measuring the financial performance of commercial banks solely with ROA provides an incomplete picture of their financial health. The authors argue that relying solely on one metric (i.e., ROA) can be misleading as it may not capture the full scope of a bank’s financial health. They claim that return on equity (ROE) alongside ROA allows for a more comprehensive analysis that considers both operational efficiency and how well equity is being used, highlighting the impact of leverage and overall risk-return trade-off. This dual approach ensures that stakeholders, including investors and regulators, can better assess both profitability and financial stability.

The sample constitutes bank-level quarterly data of nine private commercial banks in Bangladesh for the period 2018Q1-2024Q4. The data has been collected from the balance sheet, income statement and other financial statements of the sample banks and from the central bank of Bangladesh (Bangladesh Bank).

4.1. Descriptive Statistics of the Variables

Table 1 presents the summary statistics of the variables considered for the empirical estimation.

4.1. Model Specification

The regression model is expressed as:

where Zit represents the profitability measures, ROA and ROE for banks i. Yit indicates the selected explanatory variables, Vit denotes the error term ꞵ is the constant term and γ is the vector of regression coefficients.

The empirical models to be estimated are as follows:

where, the explanatory variables are number of agents (AG), number of agent banking outlets (OUT) total credit disbursed by agent banks (TC), total deposit mobilization by agent banks (TD), number of accounts with agent banks (AC) and total remittances through agent banks (REM). is the constant term and is the vector of coefficients and e denotes the error term. Both random-effect (RE) and fixed-effect (FE) models are estimated for equation (2) and (3). The Hausman specification test is performed to choose which of the models is appropriate for representing the sample data. The results indicate the RE model is the appropriate one (the probability for the chi-square statistic is given in Appendix A, Table A2). The results for the RE model are presented in the text (Table 2). The full regression results for both the FE model and the RE model are presented in Appendix A, Table A3. To check the robustness of the RE model a pooled OLS regression model is estimated for equations (2) and (3). The estimated pooled regression model results are presented in Table 3.

𝑅𝑂𝐴𝑖𝑡 = 𝛽0 + 𝛾1𝐴𝐺 + 𝛾2𝑂𝑈𝑇 + 𝛾3𝑇𝐶 + 𝛾4𝑇𝐷 + 𝛾5𝐴𝐶 + 𝛾6𝑅𝐸𝑀 + 𝑒𝑖𝑡

𝑅𝑂𝐸𝑖𝑡 = 𝛽0 + 𝛾1𝐴𝐺 + 𝛾2𝑂𝑈𝑇 + 𝛾3𝑇𝐶 + 𝛾4𝑇𝐷 + 𝛾5𝐴𝐶 + 𝛾6𝑅𝐸𝑀 + 𝑒𝑖𝑡

5. Results and Discussion

Table 2 reports the results of the estimated random effect regression models for ROA (eq. 2) and ROE (eq. 3). The estimated positive and statistically significant coefficients of total credit (TC) for both ROA and ROE indicate that loan disbursement through agent banking has a positive impact on the profitability of a bank in terms of ROA and ROE which is in line with the hypotheses H5 (Section 3.1) and also strongly supported by the previous studies [17,23,29,36,37,38]. One possible reason for the increased profitability is the higher income earned from loan disbursement by agent banks. Since agent banking outlets are widely spread across the country, especially in the remote areas, clients prefer to do banking transactions with an agent rather than a formal bank branch due to closer travel distance, lower transaction cost and trustworthy personal relationship. Moreover, the same person (owner of the outlet) deals with clients who are small entrepreneurs within the locality and therefore, gradually, a trustworthy relationship is developed between them over time. Besides, the poorer section of clients lacking adequate financial transaction knowledge also depend on one-to-one relationship with the agent for their financial needs, such as loans. Furthermore, gender may play a significant role in building trust in financial transactions, for example, female clients may be more comfortable doing financial transactions with a female agent [4].

For both ROA and ROE, the estimated coefficient for the number of agents is negative and statistically significant, indicating that an increase in the number of agents does not necessarily increase bank profit. The findings is in line with the hypothesis H1 (Section 3.1) and also similar to the results outlined in the previous studies [29,30], while many researchers including [16,17,18,22,23,24,25,26], and [27] find a significant positive link between the number of agents and financial performance of banks.

The estimated coefficient for deposit mobilization by agent banks is positive for both ROA and ROE. However, the coefficient is not statistically significant. The positive magnitude of the coefficient supports the hypotheses H4 (Section 3.1) and also similar to the results reported in previous empirical studies [16,23,24,29,31]. The potential reasons for such positive magnitude could be that most of the commercial banks in Bangladesh utilize their agent banking network for deposit mobilization, especially from rural areas since agent banking has emerged as an effective channel for deposit mobilization, especially in underserved and rural regions, enabling banks to expand their customer base at a lower operational cost.

The estimated coefficients for total remittance collection are negative for both ROA and ROE where the result is statistically significant for ROA. The negative magnitude of the coefficient for total remittance is opposite to the hypotheses H6 (Section 3.1) and also dissimilar to the previous studies where the authors find a positive relation between remittance flow and the financial performance of commercial banks [23,29,30,39,40]. One possible reason for such negative coefficient may be because of the creation of liability against such remittance-related deposits and thus they cannot contribute to increasing profitability of a bank.

The estimated coefficient for the number of agent banking outlets is positive for both ROA and ROE and the coefficient is statistically significant for ROA but not for ROE. The findings support the hypotheses H2 (Section 3.1) and also similar results found in several empirical studies [16,24,34]. Both deposit mobilization and loan disbursement increase, and eventually, more financial intermediation is possible due to the increased number of agent banking outlets across the country. Therefore, bank profit increases due to more earnings from bank assets, i.e., loans and advances through agent banking services utilizing the bank deposit.

The estimated coefficient for the number of agent banking accounts is negative for ROA and positive for ROE. However, the coefficients are not statistically significant for both ROA and ROE. The findings support the hypotheses H3 (Section 3.1) for ROA. Several empirical studies also find significant negative relation between the number of agent banking accounts and bank profitability [29,30,32,33]. The reason for such negative relation could be high maintenance costs and the short tenure of deposits and also banks may not utilize or allocate the funds deposited in the agent banking accounts effectively.

6. Robustness Check

To check the robustness of the results demonstrated in Section 5, a pooled ordinary least square (OLS) regression model is estimated using the sample data. Table 3 reports the results obtained from the OLS regression. It is evident from Table 3 that the sign, magnitude and the level of statistical significance of the estimated coefficients are mostly very similar to the coefficients obtained from estimating the random-effect model demonstrated in Table 2.

7. Conclusions and Policy Implications

The paper evaluates the impact of agent banking service utilizing FinTech platforms on the financial performance of nine commercial banks in Bangladesh that have been operating full-fledged agent banking services. Employing a panel data regression framework, the study estimates a random effect model using the bank-level quarterly data for the period 2018Q1- 2024Q4. The empirical findings indicate that credit disbursement by agent banks have a positive and statistically significant impact on the bank profitability measures, return on assets (ROA) and return on equity (ROE). Similarly, agent banking outlets have a significant positive impact on ROA. However, the number of agents and deposit mobilization do not necessarily affect the profitability of the mother bank. The findings of this study would help the policy makers, bank management and other stakeholders for decision making and improving the performance of agent banking. Therefore, an appropriate agent banking policy aimed at increasing agent banking outlets using digital platforms based on FinTech is vital for ensuring positive growth in credit disbursement in order to improve the financial performance of the banking sector in a developing country like Bangladesh.

Author Contributions

Conceptualization, M.M.I. and I.A.R.; methodology, I.A.R.; software, I.A.R.; validation, I.A.R.; formal analysis, I.A.R.; investigation, I.A.R.; resources, I.A.R.; data curation, I.A.R.; writing—original draft preparation, M.M.I. and I.A.R.; writing—review and editing, M.M.I. and I.A.R.; visualization, M.M.I.; supervision, M.M.I. and M.A.; project administration, I.A.R., M.M.I. and M.A. All authors have read and agreed to the published version of the manuscript.

Funding

This study involved no external funding

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data sets that support the findings of this study are openly available on request. Data is available at: https://www.bb.org.bd/en/index.php/publication/publictn/2/68.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A

Table A1.

Variable definition.

| Variables | Definition/Measures |

|---|---|

| Dependent Variables | |

| ROA | Net Profit after tax/Total Assets |

| ROE | Net Profit after tax/Total Equity |

| Independent Variables | |

| AG | Number of Agents |

| AC | Number of accounts |

| OUT | Number of Outlets |

| TC | Total Credit/loans |

| TD | Total Deposits |

| REM | Total Remittance |

| Dependent Variables |

Table A2.

List of sample banks.

| Name of the sample banks | Sample period |

|---|---|

| Bank Asia PLC | 2018Q1-2024Q4 |

| Dutch-Bangla Bank PLC | 2018Q1-2024Q4 |

| Al-Arafah Islami Bank PLC | 2018Q1-2024Q4 |

| Islami Bank Bangladesh PLC | 2018Q1-2024Q4 |

| Mutual Trust Bank PLC | 2018Q1-2024Q4 |

| The City Bank PLC | 2018Q1-2024Q4 |

| Brac Bank PLC | 2018Q1-2024Q4 |

| NRB Bank PLC |

2018Q1-2024Q4 |

| Modhumoti Bank PLC | 2018Q1-2024Q4 |

Source: Authors’ compilation.

Table A3.

Fixed effect and Random effect model results: ROA & ROE.

| ROA | ROE | |||

|---|---|---|---|---|

| FE | RE | FE | FE | |

| Number of Agents (AG) | -0.001 (0.004) |

-0.003** (0.001) |

-0.003 (0.052) |

-0.036** (0.018) |

| Number of Outlets (OUT) | 0.002 (0.006) |

0.005*** (0.002) |

0.011 (0.073) |

0.028 (0.023) |

| Total Credit (TC) | -0.000 (0.001) |

0.001*** (0.009) |

-0.010 (0.009) |

0.011*** (0.004) |

| Total Deposit (TD) | 0.001 (0.002) |

0.002 (0.001) |

0.005 (0.022) |

0.005 (0.014) |

| Number of Accounts (AC) | 0.000 (0.001) |

-0.001 (0.001) |

0.011 (0.019) |

0.008 (0.012) |

| Total Remittance (REM) | 0.001 (0.002) |

-0.002** (0.001) |

0.019 (0.024) |

-0.003 (0.011) |

| Constant | -0.004 (0.006) |

0.001 (0.003) |

-0.096 (0.078) |

-0.005 (0.034) |

| R-squared | 0.005 | 0.123 | 0.037 | 0.113 |

| Hausman test | =0.003:RE | =0.000:RE | ||

| Total observations | 234 | 234 | ||

Source: Authors’ estimation using STATA. FE stands for fixed-effect model and RE is random-effect model. Standard errors are in parentheses. *** denotes statistical significance level at 1%; ** denotes the level of statistical significance at 5%; * denotes statistical significance level at 10%.

| 1 | PSD Circular No. 05: Guidelines on Agent Banking for the Banks dated 09 December 2013. |

References

- Gupta, R. & Gupta, A. (2020), Agent banking in the FinTech era: opportunities for financial inclusion, Journal of Financial Technologies, 15(2), 25-38.

- Veniard, C. (2010). How agent banking changes the economics of small accounts. Available online: https://docs.gatesfoundation.org/documents/agent-banking.pdf.

- Buri, S., Cull, R., Gine, X., Harten, S. & Heitmann, S. (2018). Banking with agents: experimental evidence from Senegal, Washinton, DC: World Bank.

- Cull, R., Gine, X., Harten, S., Heitmann, S. & Rusu, A. B. (2018). Agent banking in a highly under-developed financial sector: evidence from Democratic Republic of Congo. World Development, 107, 54-74.

- Kumar, A., Nair, A., Parsons, A. & Urdapilleta, E. (2006). Expanding bank outreach through retail partnerships: correspondent banking in Brazil, Washington, D.C.: World Bank.

- Margaret, K. G. & Ruth, N. K. (2019). The effect of banking services on the business performance of bank agents in Kenya. Cogent Business & Management, 6(1), 16844420. [CrossRef]

- Nezianya, N. P., & Izuchukwu, D.(2014). Impact of agent banking on the performance of deposit money banks in Nigeria, Research Journal of Finance and Accounting 5(9), 35-41.

- Zaffar, M. A., Kumar, R. L., & Zhao, K. (2019). Using agent-based modelling to investigate diffusion of mobile-based branchless banking services in a developing country. Decision Support Systems, 117, 62-74.

- Bangladesh Bank (2024). Quarterly Report on Agent Banking, October-December. Financial Inclusion Department: Bangladesh Bank.

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305-360. [CrossRef]

- Siddiquie, M. R. (2014). Agent banking, the revolution in financial service sector of Bangladesh. IOSR Journal of Economics and Finance, 5(1), 28-32.

- Diamond, D. W. (1984). Financial intermediation and delegated monitoring. The review of economic studies, 51(3), 393-414.

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS quarterly, 319-340.

- Lyman, T., Ivatury, G., & Staschen, S. (2006). Use of agents in branchless banking for the poor: rewards, risks, and regulation. Focus note, 38(1), 1.

- Ogoti, K.I., & Omwenga, Q.J. (2023). Influence of agency banking on the financial performance of commercial banks in kisii county, kenya. International Journal of Social Sciences and Information Technology. ISSN 2412-0294, Vol IX(V), 172-181.

- Alam, M.M., Bhowmik, D. & Bhowmik, D. (2020). The impact of agent banking on financial performance of commercial banks in Bangladesh, IOSR Journal of Economics and Finance, 11(3), 13-20.

- Karangwa, F. & Mulyungi, D.P. (2018), Effect of agency banking services on financial performance of commercial banks: a case of equity bank, International Journal of Management and Commerce Innovations, 6(1), 758-765.

- Ndambuki, D. (2016). The effect of agency banking on profitability of commercial banks in Kenya (Doctoral dissertation, University of Nairobi).

- Idoko, E. C., & Chukwu, M. A. (2022). Does Agency Banking Trigger Financial Inclusion? Perspective of Residents in Rural Setting. Sch Bull, 8(6), 180-188.

- Mwando, S. (2013). Contribution of agency banking on financial performance of commercial banks in Kenya, Journal of Economics and Sustainable Development, 20(4), 26-34.

- Aduda, J., Kiragu, P. & Ndwiga, J. M. (2013). The relationship between agency banking and financial performance of commercial banks in Kenya. Journal of Finance and Investment Analysis, 2(4), 97- 117.

- Ayadi, O. F., Oke, B., Oladimeji, A., & Aladejebi, O. (2023). Agency Banking in Nigeria: Impact and Impediments. SEDME (Small Enterprises Development, Management & Extension Journal), 50(3), 227-247.

- Hossain, M. I., Al-Amin, M., & Toha, M. A. (2021). Are commercial agent banking services worthwhile for financial inclusion? Business Management and Strategy, 12(2), 206-227.

- Hasan, Z. (2019). The effects of agent banking on the profitability of commercial banks in Bangladesh (Doctoral dissertation, Brac University).

- Seda, M. A. (2016). Effects of agency banking on the financial performance of commercial banks in Kenya (Doctoral dissertation, University of Nairobi).

- Waithanji, M. N. (2012). The impact of agent banking as a financial deepening initiative in Kenya (Doctoral dissertation, University of Nairobi, Kenya). Available online: https://erepository.uonbi.ac.ke/handle/11295/6933?utm_source=chatgpt.com.

- Kambua, B. D. (2015). The effect of agency banking on financial performance of commercial banks in Kenya (Doctoral dissertation). Available online: https://erepo.usiu.ac.ke/bitstream/handle/11732/3198/SIMBOLEY%20BRENDA%20CHEMUTAI%20MBA%202017.pdf?sequence=1.

- Nisha, N., Nawrin, K., & Bushra, A. (2020). Agent banking and financial inclusion: The case of Bangladesh. International Journal of Asian Business and Information Management (IJABIM), 11(1), 127-141.

- Hasan, M.K. (2023). Agent banks make a notable contribution. The Financial Express, Bangladesh. Available online: https://thefinancialexpress.com.bd/views/reviews/agent-banks-make-a-notable-contribution.

- Das, B. (2021). Impact of Agent Banking on Bank Profitability in Bangladesh (Master of Business Administration dissertation, University of Dhaka, Bangladesh). Available online: https://www.scribd.com/document/745526778/IMPACT-OF-AGENT-BANKING-ON-BANK-PROFITABILITY-IN-BANGLADESH?

- Dotun, O. V. & Adesugba, A. K.(2022). The impact of agency banking on financial performance of listed deposit money banks in Nigeria, Journal of Corporate Finance Management and Banking System, 2, 14-24.

- Pasiouras, F., & Kosmidou, K. (2007). Factors influencing the profitability of domestic and foreign commercial banks in the European Union. Research in international business and finance, 21(2), 222-237.

- Balaylar, N. A., Karımlı, T., & Bulut, A. E. (2025). The effect of non-interest income on bank profitability and risk: Evidence from Turkey. Revista galega de economía: Publicación Interdisciplinar da Facultade de Ciencias Económicas e Empresariais, 34(1), 1.

- Oburu, K. N. (2018). Effect of agency banking on the financial performance of commercial banks in Kenya, Doctoral dissertation, University of Nairobi. Available online: https://erepository.uonbi.ac.ke/bitstream/handle/11295/94726/Kambua%2CBelita%20D_The%20effect%20of%20agency%20banking%20on%20financial%20performance%20of%20commercial%20banks%20in%20kenya.pdf?sequence=1.

- Hirtle, B. (2007). The impact of network size on bank branch performance. Journal of Banking & Finance, 31(12), 3782-3805.

- Hasan, M. S. A., Manurung, A. H., & Usman, B. (2020). Determinants of bank profitability with size as moderating variable. Journal of applied finance and banking, 10(3), 153-166.

- Hasan, J. (2025). Agent banking lending up 56pc, deposit 15.4pc in Q4’24. The Financial Express, Bangladesh. Available online: https://thefinancialexpress.com.bd/economy/agent-banking-lending-up-56pc-deposit-154pc-in-q424.

- Khan, T.A. (2024). Agent Banking’s Impact on Financial Inclusion in Bangladesh. Asian Banking & Finance. Available online: https://asianbankingandfinance.net/retail-banking/commentary/agent-bankings-impact-financial-inclusion-in-bangladesh?utm_source=chatgpt.com.

- Aggarwal, R., Demirgüç-Kunt, A., & Pería, M. S. M. (2011). Do remittances promote financial development? Journal of Development Economics, 96(2), 255–264. [CrossRef]

- World Bank. (2020). Migration and Development Brief 32: COVID-19 Crisis Through a Migration Lens. Migration and Development Brief 32. Available online: https://documents1.worldbank.org/curated/en/989721587512418006/pdf/COVID-19-Crisis-Through-a-Migration-Lens.pdf.

- Giuliano, P., & Ruiz-Arranz, M. (2009). Remittances, financial development, and growth. Journal of Development Economics, 90(1), 144–152. [CrossRef]

- Demirgüç-Kunt, A., López Córdova, E., Martínez Pería, M. S., & Woodruff, C. (2011). Remittances and banking sector breadth and depth: Evidence from Mexico. Journal of Development Economics, 95(2), 229–241.

- Mundaca, B. G. (2009). Remittances, financial market development, and economic growth: The case of Latin America and the Caribbean. Review of Development Economics, 13(2), 288–303. [CrossRef]

- Ramadugu, R. (2023). Fintech, Remittances, And Financial Inclusion: A Case Study Of Cross-Border Payments In Developing Economies. Journal of Computing and Information Technology, 3(1).

- Zins, A., & Weill, L. (2016). The determinants of financial inclusion in Africa. Review of Development Finance, 6(1), 46–57. [CrossRef]

- Irura, N., & Munjiru, M. (2013). Technology Adoption and the Banking Agency in Rural Kenya. Journal of Sociological Research, 4(1), 249-266. [CrossRef]

- Darda, A. (2024). From Shops to Service Centers: The Rise of Agent Banking in Africa. Available online: https://amitdarda.com/from-shops-to-service-centers-the-rise-of-agent-banking-in-africa/?utm_source.

Figure 1.

Framework for the proposed model (Source: figure created by authors).

Table 1.

Summary statistics of the variables.

| Variable | Mean | S.E | Min | Max |

|---|---|---|---|---|

| Dependent Variables | ||||

| Return on Assets (ROA) | 0.005 | 0.004 | -0.011 | 0.019 |

| Return on Equity (ROE) | 0.061 | 0.055 | -0.149 | 0.323 |

| Independent Variables | ||||

| No. of Agents | 2.693 | 0.584 | 0 | 3.725 |

| No. of Outlets | 2.811 | 0.626 | 0 | 3.790 |

| Total accounts | 5.407 | 0.948 | 1.204 | 6.848 |

| Total Deposit | 4.177 | 0.872 | 1.079 | 5.905 |

| Total loans/credits | 3.058 | 1.268 | 0 | 5.409 |

| Remittance | 4.278 | 1.252 | 0.903 | 6.608 |

Source: Authors’ calculation.

Table 2.

Random effect model results: ROA and ROE as dependent variables.

| ROA | ROE | |||

|---|---|---|---|---|

| Coefficient | S.E. | Coefficient | S.E. | |

| No. of Agents (AG) | -0.003* | 0.001 | -0.036* | 0.018 |

| No. of Outlets (OUT) | 0.005** | 0.002 | 0.028 | 0.023 |

| Total Credit (TC) | 0.001*** | 0.000 | 0.011*** | 0.004 |

| Total Deposit (TD) | 0.002 | 0.001 | 0.005 | 0.014 |

| No. of Accounts (AC) | -0.001 | 0.001 | 0.008 | 0.012 |

| Total Remittance (REM) | -0.002* | 0.001 | -0.003 | 0.011 |

| Constant | 0.001 | 0.003 | -0.005 | 0.034 |

| R-squared | 0.123 | 0.113 | ||

| Wald Chi-square | 13.71 | 24.77 | ||

|

Prob |

0.033 |

0.000 |

||

| Total Observations | 234 | 234 | ||

Source: Authors’ estimation using STATA. ***, ** and * denote statistical significance level at 1%, 5% and 10% respectively.

Table 3.

Pooled regression results: ROA and ROE as dependent variables.

| ROA | ROE | |||

|---|---|---|---|---|

| Coefficient | S.E. | Coefficient | S.E. | |

| No. of Agents (AG) | -0.004*** | 0.001 | -0.038** | 0.017 |

| No. of Outlets (OUT) | 0.005*** | 0.002 | 0.029 | 0.024 |

| Total Credit (TC) | 0.001*** | 0.000 | 0.011*** | 0.003 |

| Total Deposit (TD) | 0.002 | 0.001 | 0.004 | 0.015 |

| No. of Accounts (AC) | -0.001 | 0.001 | 0.008 | 0.013 |

| Total Remittance (REM) | -0.002** | 0.001 | -0.003 | 0.010 |

| Constant | 0.001 | 0.003 | -0.004 | 0.037 |

| R-squared | 0.126 | 0.113 | ||

| Probability (F) | 0.000 | 0.000 | ||

| Total Observations | 234 | 234 | ||

Source: Authors’ estimation using STATA. ***, ** and * denote statistical significance level at 1%, 5% and 10% respectively.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.