Submitted:

02 July 2025

Posted:

03 July 2025

You are already at the latest version

Abstract

This study investigates the differential impacts of FinTech and Artificial Intelligence (AI) adoption on the business models, operational efficiency, and financial stability of Islamic versus conventional banks. Utilizing a balanced panel dataset of 26 banks across 11 countries from 2020 to 2024, the research employs an empirically derived 7-point FinTech Index and fixed-effects panel regression models to rigorously assess these relationships. Our findings reveal a significant and persistent lag in FinTech adoption by Islamic banks compared to their conventional counterparts, despite both exhibiting consistent upward trends in digital integration. Crucially, the empirical results demonstrate that higher FinTech adoption universally enhances bank efficiency (evidenced by reduced cost-to-income ratios and increased return on assets) and bolsters financial stability (measured by the Z-score) for both Islamic and conventional banking models. Contrary to some initial hypotheses, the study finds no statistically significant evidence of a differen-tial impact of FinTech on either efficiency or stability between the two bank types; both benefit comparably from digital transformation. Furthermore, while Islamic banks exhibit a higher baseline level of efficiency and stability, FinTech adoption does not appear to in-duce a unique efficiency-stability trade-off for them. These findings challenge assump-tions regarding divergent FinTech impacts based on banking models, highlighting the universal role of digital transformation in fostering financial system resilience and opera-tional sustainability. The study provides critical policy implications for regulators to foster enabling environments and support Islamic banks in closing their adoption gap, along-side strategic insights for banks to leverage FinTech for sustained performance in the evolving financial landscape

Keywords:

FinTech

; Artificial Intelligence (AI)

; Islamic Banking

; Conventional Banking

; Financial Efficiency

; Financial Stability

; Digital Transformation

; FinTech Adoption Index

; Sustainable Finance.

1. Introduction and Background

Islamic and conventional banks have long operated under distinct business models. While Islamic banking is guided by Sharia principles such as profit-and-loss sharing and prohibition of interest (riba), conventional banking relies on interest-based lending and broader financial instruments. Beck, Demirgüç-Kunt, and Merrouche (2013) provided a foundational comparison between the two, assessing differences in business orientation, cost efficiency, and stability.

However, the financial services landscape has changed dramatically since then. The rapid advancement of financial technology (FinTech) and artificial intelligence (AI) has disrupted traditional banking paradigms. Both Islamic and conventional banks have adopted digital platforms, AI-driven credit scoring, blockchain infrastructure, and RegTech tools to enhance operational efficiency, customer engagement, and regulatory compliance.

Over the past decade the financial landscape of the Middle East, North Africa and Southeast Asia has undergone a simultaneous FinTech surge and a re-evaluation of Sahirah-compliant finance. Mobile wallets, AI chatbots, open-banking application programming interfaces (APIs) and biometric “e-KYC” have scaled from pilot projects to mass adoption (Gomber, Kauffman, Parker, & Weber, 2018). During the same period Islamic banking assets surpassed USD 3 trillion, becoming a mainstream competitor to conventional banking in Gulf Cooperation Council (GCC) states and parts of Asia (Deloitte, 2023). Yet few empirical studies examine how these two forces—digital disruption and Sharīʿah governance—interact to reshape bank performance and stability in the post-COVID era.

FinTech and artificial intelligence (AI) promise greater outreach and efficiency, but also introduce new operational and cyber risks (Financial Stability Board [FSB], 2022). Islamic banks enter this space with unique contractual forms—for example, profit-and-loss sharing (mushārakah) and asset-backed sales (murābaḥah)—and an additional layer of Sharīʿah oversight (Beck, Demirgüç-Kunt, & Merrouche, 2013). As digital platforms blur the line between deposit-taking and technology provision, a natural question arises: do Islamic banks capture FinTech’s benefits differently from their conventional peers, and at what cost to financial stability?

COVID-19 provides a quasi-natural experiment. Lockdowns between 2020 and 2021 forced banks to accelerate digital channels, from branchless super-apps to fully remote customer on-boarding (Ghosh, 2022). Regulators responded with open-banking mandates (e.g., Saudi Arabia’s OB V1 in 2022), national e-KYC standards and early experiments in central-bank digital currencies. This study focuses on the 2020–2024 window, capturing the first AI-intensive roll-outs and the macro-financial turbulence that tested their resilience.

The pre-FinTech literature found only modest differences in efficiency or risk between Islamic and conventional banks once country factors were controlled (Beck et al., 2013). More recent single-country case studies suggest digitalisation boosts service quality in Islamic banking (Khaleel & Mohd-Kassim, 2022), yet cross-country panel evidence remains scarce. Likewise, the emerging FinTech literature often treats banks as a homogeneous category (Lasak & Williams, 2023) or focuses on BigTech entrants rather than incumbent institutions. No multicountry panel to date investigates whether FinTech adoption changes the efficiency-stability trade-off in Islamic versus conventional banks.

1.1. Research Questions

To close this gap, the paper addresses four interrelated questions:

- Adoption: How does FinTech and AI uptake differ between Islamic and conventional banks?

- Efficiency: Does FinTech adoption reduce operating costs and improve profit margins, and is the effect bank-type specific?

- Stability: How does digital transformation influence financial-stability metrics particularly the Z-score and non-performing loans (NPLs) across banking models?

- Trade-off: Do Islamic banks experience a different efficiency–stability trade-off in the digital era compared with conventional banks?

1.2. Objectives

To answer these questions, we:

- To assess how Islamic and conventional banks have integrated AI and FinTech solutions into their business strategies.

- To compare efficiency metrics (e.g., cost-to-income, overhead ratios) in the digital era.

- To examine financial stability indicators post-AI and FinTech integration (e.g., z-score, NPLs, capital adequacy).

- To analyze and compare the relative magnitudes of FinTech's impact on efficiency and stability indicators across Islamic and conventional banks to identify potential differential efficiency-stability balances/trade-offs during.

1.3. Contribution

The study contributes to three streams of scholarship. First, it updates the Islamic-versus-conventional comparison for the FinTech era, offering the first multi-country evidence on AI and open-banking adoption in Sharīʿah-compliant finance. Second, by linking a granular FinTech Index to efficiency and Z-score dynamics, it responds to recent calls for integrated digital-risk assessment (FSB, 2022; Vives, 2019). Third, it informs the policy debate on how open-banking and AI guidelines can be calibrated to foster innovation without compromising financial stability, particularly in dual-banking jurisdictions.

1.4. Structure of the Paper

This study aims to revisit and extend the comparison of Islamic vs. conventional banks, incorporating how digital transformation—particularly FinTech and AI—has influenced business models, efficiency, and financial stability from 2020 to 2024. The remainder of the paper is organized as follows. Section 2 reviews the literature and presents the theoretical framework leading to four testable hypotheses. Section 3 details the dataset, variable definitions and econometric strategy. Section 4 provides descriptive statistics and preliminary insights. Section 5 reports regression results and robustness tests, while Section 6 discusses implications for managers and regulators. Last section (7) concludes and suggests plans for future research.

2. Literature Review and Theoretical Framework

This part critically discusses the literature on the blending of the FinTech and the AI in the banking sectors, in particular the distinctive paths and findings in the Islamic and the traditional financial institutions. It establishes the theoretical background of the study, identifies the important knowledge gaps, and outlines the unique contributions of the current research.

2.1. Financial Technology and Artificial Intelligence in Banking: A Paradigm Shift

The advent and forceful integration of financial technology (FinTech) and artificial intelligence (AI) have restructured the very basics of the world's banking paradigms, triggering profound structural redefinitions of patterns of delivering services, in risk management approaches, and in customer interaction models (Arner et al., 2020; Philippon, 2020). The digital transformation runs deeper than technology adoption in the narrow sense and is a complete paradigm shift, redefining competitive patterns and operating efficacies in the financial services industry.

The empirical literature repeatedly identifies some common areas where FinTech and artificial intelligence are creating intense disruption:

-

- Operational Efficiency: Automation of the back office through artificial intelligence is reducing the cost and time of processing substantially. For instance, advanced analytics and Robotic Process Automation (RPA) have managed to reduce the cost by 20–30% in labor-intensive processes such as loan origination, fraud detection, and compliance surveillance (Vermann & Zwick, 2019; Bontadini et al., 2024). The efficiency advantage lowers the cost of operations of the banks, which in turn allows them to focus on value-added services.

- 5

- Financial Inclusion: Digital-exclusive banking products, mobile remittances, and micro-lending schemes through machine learning significantly improved access to financial services for previously unbanked or underserved parts of the population, primarily in the emerging markets (Demirgüç-Kunt et al., 2022; World Bank, 2022). Through the minimization of transaction costs and further reach, FinTech lowers geographic and socio-economical distances to achieve broader financial participation.

- 6

- Risk Modeling: Machine learning algorithms and big data analytics are continuously improving the precision of credit scoring, fraud detection, and risk evaluation in general (Fuster et al., 2019). The advanced approaches are able to process large datasets, recognize subtle patterns, and predict defaults 15–25% better than the traditional statistical models, enhancing prudential financial risk management.

Whilst these cross-border benefits are inclusive, the level and pace of FinTech and AI incorporations are heterogeneous within the global banking environment. A distinguishing finding, and the subject of the study in this paper, is the differential of adoption rates and integration strategies between Islamic and conventional banking (Hamadou & Suleman, 2024). This is primarily attributable to the distinctive Sharia compliance requirements unique to Islamic finance. For example, the application of distributed ledger technologies (DLT) such as blockchain must meticulously exclude the dimensions of gharar (undue uncertainty or indetermination in agreements) and maysir (gambling or speculative elements). Similarly, credit risk assessment tools or investment algorithms in AI would have to be in accordance with the risk-sharing models of mudarabah (shared profit-partnership joint venture) and musharakah (joint venture), while disallowing interest-based (riba) transactions and respecting ethical investment parameters (Todorof, 2018; Iqbal et al., 2025). These refined ethical and legal concerns necessitate higher customized and prudent strategies for the incorporation of FinTech within the industry of Islamic banking.

2.2. Islamic vs. Conventional Banking: Divergent Paths to Digital Transformation

The conceptual ground of Islamic and classic models of banking unavoidably shapes the strategic digital transformation approach, therefore creating identifiable divergent paths in the adoption and implementation of FinTech.

Theoretical Background.

- Conventional Banks: Conventional banks primarily operate on the lines of neoclassical financial intermediation theory (Gulati, A., & Singh, 2024). Maximization of profit through the allocation of resources in an efficient manner, conversion of risk, and minimizing of the transaction cost is the main aim of conventional banks. Therefore, conventional banks aim for technology which is scalable in nature to offer operational leverage and direct bottom line improvement, embracing FinTech solutions as tools of competitive advantage and gain of market share (Lerner et al., 2024).

- Islamic Banks: Islamic Banks: For comparison, Islamic banks are grounded in the Maqasid al-Sharia (Islamic law principles), which extended beyond financial success alone to the attainment of broader ethical, social, and developmental goals (Bedoui & Mansour, 2015). The model places specific emphasis on risk-sharing, equitable wealth distribution, social justice, and strict avoidance of riba (interest), gharar, and maysir. This integrated theoretical and ethical gap profoundly reflects the adoptions criterion of FinTech solutions: they must be efficient but also transparently demonstrably Sharia-compatible and therefore there is greater questioning and oft times slower approvals process (Fianto et al., 2021).

These fundamental differences are seen in varied approaches to traits and FinTech adoption, which are presented in the subsequent Table 1:

Empirical Evidence

Recent empirical results provide concrete evidence

of such various paths in the adoption of FinTech:

- Several specialists believe the Islamic banks have been sluggish in early adoption of the FinTech in the years 2020–2022 relative to the traditional counterparts (Aysan et al., 2022). The initial delay is generally the result of the necessary strict Sharia board approvals of new product and technology which could slow the product/technology development and roll-out cycles.

- Despite the initial setback, there is increasingly evidence of Islamic banks achieving greater rates of growth in some of the FinTech applications subsequent to 2023, particularly in sectors best suited to their very basics. Examples are the application of blockchain to the issuance and settlement of sukuk (Islamic bonds), which enhances efficiency and transparency, and biometric eKYC (electronic Know Your Customer) solutions to ease the onboarding of customers while fulfilling data privacy and security expectations (Rabbani et al., 2020).

- In comparison, the conventional banks have taken the central role in the use of Open Banking APIs enabling smooth data sharing and collaboration amongst third-party suppliers of FinTech (Buchak et al., 2023). Whilst the pathway exhibits vast innovation potential, the method also exhibits enhanced cybersecurity and data privacy risks, which in turn necessitate robust infrastructures of digital security. Such dynamic interplay of adoption patterns underscores subtle approaches driven by inherent variation in the institutional level.

2.3. Regulating Environments and Institutional Challenges

Broader country-level regulatory environment plays a pivotal role in determining the pace and nature of the integration of FinTech for both Islamic and conventional banking sectors. The trend is in accordance with the institutional theory where organizational behavior, e.g., technology adoption, is greatly subject to the institutional pressure, norms, and legitimacy prevailing (Scott, 2014; DiMaggio & Powell, 1983). It is the legitimacy of the regulatory environment specifically which determines the safety and viability of the new technology and, therefore, how the technology is diffused in the financial space.

Different methods of regulation yield different outcomes:

-

- Proactive Markets (i.e., UAE, Malaysia): Such markets have adopted forward-thinking approaches to regulation, often guided by whole-of-nation digital agendas and specialist FinTech sandboxes. For instance, the UAE’s National AI Strategy 2031 specifically accelerates the adoption of AI in the financial services, telecommunications, and public sectors (CBUAE, 2022). In proactive markets, Islamic banks benefit from an operating model of dual-layer oversight—independent central-bank oversight alongside Sharia-based advice by independent Sharia boards—when aligned, which can create clear avenues for ethical compliant FinTech innovation (IFSB, 2023). Such forward-thinking approach specifies the environment and reduces regulatory risk, therefore allowing fast and confident FinTech adoption.

- 7

- Cautious Markets (e.g., Egypt, Pakistan): Conversely, there are markets which are cautious and exhibit slow FinTech regulation or the lack of specialized regimes for new technology. Such regulatory slack can restrain innovation through elevated legal and operational risks for financial entities (Rabbani et al., 2020; SBP, 2023). Here, Islamic banks are inclined to rely even further on joint ventures with agile FinTech startups to navigate regulatory ambiguities and exploit novel solutions, in place of in-house competence building. It thus suggests that institutional forces, in particular the lack of definitive regulatory cues, compel the banks to seek external partnerships to meet the shifting demand of markets.

The regulatory environment therefore acts as a significant external moderator of the strategic choices and success of the adoption of FinTech, impacting the conventional and Islamic banks but potentially differentially for the latter due to the unique compliance consequences.

2.4. Knowledge Gaps and This Study’s Contribution

While the existing literature has extensively examined various facets of FinTech and its impact on the financial sector:

- Studies have explored FinTech’s impact on conventional bank profitability and efficiency (Thakor, 2020; Berisha & Rayfield, 2025).

- Significant research has delved into the inherent stability of Islamic finance compared to conventional finance (Abedifar et al., 2013; Beck et al., 2013).

- Some recent works have begun to address FinTech adoption patterns in Islamic banking (Aysan et al., 2022; Hamadou & Suleman, 2024).

However, a critical void remains in systematically and quantitatively comparing the differential effects of FinTech and AI adoption on key performance and stability metrics across both Islamic and conventional banks within a unified analytical framework. Specifically, few studies have:

-

- Quantitatively compared efficiency gains (e.g., through cost-to-income ratios and ROA) between Islamic and conventional bank types in the wake of FinTech adoption, providing a nuanced understanding of who benefits more or differently.

- 8

- Analyzed the differential influence of FinTech on financial stability (e.g., Z-score) across these two distinct banking models, moving beyond baseline stability comparisons to examine the moderating role of digital transformation.

- 9

- Empirically tested the efficiency-stability nexus within the context of FinTech adoption for both Islamic and conventional banks to ascertain if a unique trade-off or balance emerges.

- 10

- Integrated the dynamic nature of FinTech adoption through a comprehensive index while simultaneously controlling for institutional and macroeconomic factors.

This study directly addresses these identified gaps by:

- Introducing a 7-point FinTech Index Score developed to provide a standardized, robust, and empirically derived measure of FinTech and AI adoption within the banking sector, facilitating direct comparison.

- Conducting a rigorous panel data analysis that tests the interactions between bank type (Islamic/Conventional) and FinTech adoption to isolate differential impacts on efficiency and stability.

- Incorporating relevant macroeconomic controls (Inflation, GDP Growth) and bank-specific characteristics (Size, Equity/Assets, NPL Ratio) within a fixed-effects model to ensure robust findings.

- Providing quantitative insights into how FinTech influences the efficiency-stability balance for both banking models, contributing to the understanding of their distinct responses to digital transformation.

- 2.5. Theoretical Framework

The article combines two related theoretical traditions to present an integrated paradigm of how the adoption of FinTech directs Islamic and traditional banks: the Resource-Based View (RBV) and Financial Stability Theory.

2.5.1. Resource-Based View (RBV)

The Resource-Based Perspective (RBV), contended by Barney (1991), is of the opinion that the firm's sustained competitive advantage originates from its unique, valuable, rare, inimitable, and non-substitutable (VRIO) resources and capabilities. For the purpose of digital transformation, the FinTech capabilities in the form of inhouse proprietary algorithms, advanced data analytics infrastructures, digital customer platforms, and integrated functionalities of AI could be considered in such parameters of VRIO resources.

According to the RBV, successful building and exploitation of such FinTech capabilities would give superior operational efficiency, product innovation, and customer experience which in the long term would give improved profitability and relative market position. Our study exploits the RBV by examining how the efficiency and profitability outcome of the FinTech Index (representative of FinTech capabilities) is attained. In further value, the RBV is also exploited in order to derive insight into the adoption differential: the Sharia-compliance expertise of the Islamic banks, which in the early stages constituted an obstacle to quick pace of adoption, could ironically be converted to the unique and inimitable source allowing them to fashion distinctive, ethical-based solutions in FinTech. It could then allow them to catch up on initial lag in adoption through the formation of distinctive, Sharia-compliant competitive advantage in the digital space.

2.5.2. Financial Stability Theory

Financial Stability Theory provides the framework for understanding how changes within the financial system, including technological disruptions like FinTech, influence overall systemic resilience and individual bank stability. Digital transformation impacts stability through several interconnected channels (BIS, 2021; Daud et al., 2022):

- Efficiency Channels: As demonstrated by our efficiency models, FinTech can lead to lower operational costs (reduced C/I) and increased profitability (higher ROA). More efficient and profitable banks are generally more stable, as they have greater buffers against unexpected losses and can absorb shocks more effectively (lower costs → higher Z-scores).

- Risk Channels: While FinTech, particularly AI-driven analytics, can significantly reduce traditional credit risks (e.g., by improving NPL predictions) and operational risks through automation, it simultaneously introduces new categories of risks. These include cybersecurity threats, data privacy breaches, algorithmic bias, and systemic risks arising from interconnectedness and concentration within FinTech platforms (BIS, 2021; Lerner et al., 2024).

- Business Model Transformation: FinTech allows banks to diversify revenue streams beyond traditional interest-based income, potentially reducing reliance on single income sources and thereby enhancing stability. This is particularly relevant for Islamic banks, whose existing emphasis on diversified, asset-backed financing aligns well with non-interest-based FinTech opportunities.

This theoretical lens enables us to analyze how FinTech adoption, by altering these efficiency and risk channels, ultimately influences bank-level stability (measured by the Z-score). We examine whether the specific principles of Islamic finance, such as risk-sharing norms, moderate these stability effects, potentially leading to a more pronounced increase in stability for Islamic banks compared to their conventional counterparts as they embrace digital technologies.

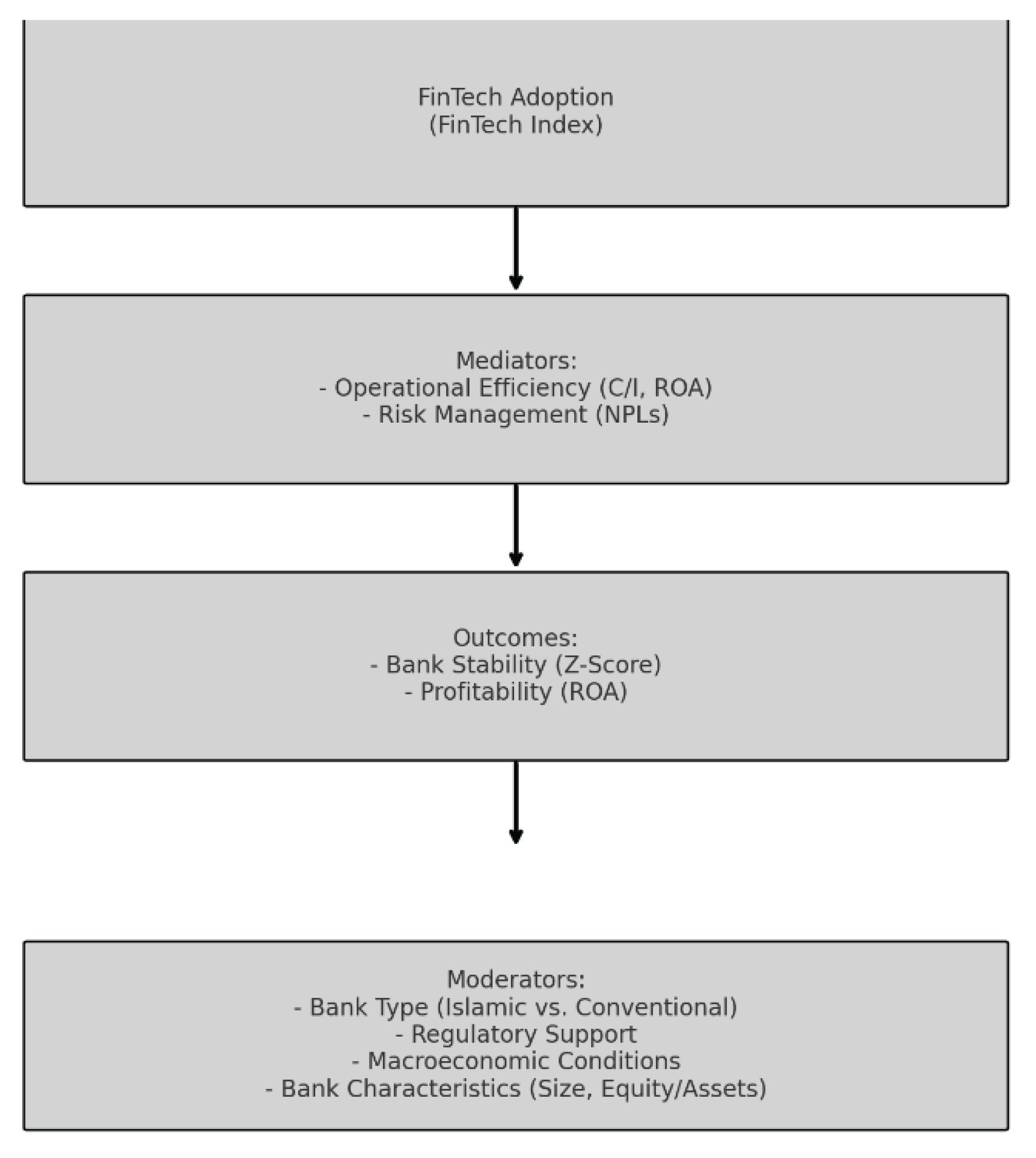

Figure 1.

Conceptual Framework. Source: Developed by the author based on previous studies.

The conceptual framework depicted above illustrates the hypothesized relationships within our study. FinTech adoption is positioned as the primary independent variable, influencing bank efficiency and stability. Bank type (Islamic vs. Conventional) is theorized to moderate these relationships, leading to differential impacts. Additionally, macroeconomic and bank-specific control variables are incorporated to isolate the unique effects of FinTech and bank type. This framework guides our empirical model specification and the interpretation of results.

2.6. Research Hypotheses

Building upon the theoretical foundations discussed (Resource-Based View and Financial Stability Theory) and the identified knowledge gaps in the existing literature, this study formulates a set of testable hypotheses. These hypotheses directly address the research questions posed in Section 1.2 and guide our empirical investigation into the differential impacts of FinTech and AI adoption on Islamic and conventional banks' efficiency and stability.

- ●

- H1 (Adoption Differential): Islamic banks exhibit significantly lower FinTech Index scores than conventional banks, ceteris paribus.

- ○

- Rationale: Differences in operational models, the inherent cautiousness due to Sharia compliance requirements, and varying risk aversion levels may lead to disparate paces of technological adoption compared to their conventional counterparts.

- ●

- H2 (Efficiency Effect): FinTech adoption is negatively associated with the cost-to-income ratio, and this negative association is significantly stronger for conventional banks compared to Islamic banks.

- ○

- Rationale: Conventional banks, with their broader operational scope, less stringent compliance constraints (compared to Sharia boards for new technologies), and profit-driven optimization, may be positioned to leverage FinTech more extensively for rapid cost optimization and enhanced operational efficiency.

- ●

- H3 (Stability Effect): FinTech adoption is positively associated with bank stability (measured by Z-score), and this positive association is significantly stronger for Islamic banks compared to conventional banks.

- ○

- Rationale: Through the characteristics of risk-sharing norms, asset-backed finance, and ethical banking practices, Islamic banks would be able to leverage the potential of FinTech better for higher stability, possibly drawing greater resilience through advanced tools of risk management without unnecessarily increasing systemic risk.

- ●

- H4 (Efficiency–Stability Balance): While FinTech adoption positively impacts both profitability (e.g., Return on Assets - ROA) and stability (e.g., Z-score) across both bank types, Islamic banks will exhibit a comparatively stronger positive effect on stability relative to their profitability gains from FinTech adoption than conventional banks, signifying a distinct efficiency-stability balance.

- ○

- Rationale: Islamic banks' initial priority for true economic activity, mutual risk-sharing, and ethical issues could lead to the relative stability gains of adopting FinTech to be higher for the same level of efficiency improvement, in particular compared to conventional banks which are largely driven by pure profit maximization.

3. Methodology

This study employs a quantitative comparative design to analyze the differential impacts of FinTech and AI adoption on Islamic and conventional banks' business models, efficiency, and stability from 2020 to 2024. The methodology aligns with the research questions and objectives, leveraging panel data analysis to control for macroeconomic and institutional variables. Our balanced panel comprises 26 listed commercial banks (13) Islamic and 13 conventional from 11 countries in the Middle East, North Africa and Southeast Asia (Bahrain, Egypt, Indonesia, Jordan, Kuwait, Malaysia, Pakistan, Qatar, Saudi Arabia, Turkey, and the UAE). The observation window is 2020–2024, chosen to capture the first major wave of AI-powered services, open-banking mandates, and post-pandemic digital uptake.

3.1. Research Design

We adopt a two-stage analytical approach:

-

- Descriptive Analysis: Compare trends in FinTech adoption (via the FinTech Index Score), efficiency metrics (cost-to-income ratios), and stability indicators (Z-scores) between Islamic and conventional banks.

- 11

- Inferential Analysis: Use panel regression models to isolate the effects of FinTech adoption on performance for bank type (Islamic = 1, conventional = 0) and country level controls.

This design builds on frameworks used in recent FinTech studies (e.g., Gomber et al., 2017), while addressing gaps in Islamic banking literature (Hassan & Aliyu, 2018).

3.2. Data Collection

Sample: 26 banks (13 Islamic, 13 conventional) across 11 countries (Bahrain, Egypt, Indonesia, Jordan, Kuwait, Malaysia, Pakistan, Qatar, Saudi Arabia, Turkey, UAE) selected for data availability and regulatory diversity.

Timeframe: 2020-2024, capturing post-pandemic digital transformation.

Sources: for the Bank-level data: Annual reports, investor disclosures, and FinTech Index Scores (see Table 2). For the Macroeconomic controls: World Bank GDP growth and inflation rates (World Bank, 2023).

3.3. FinTech Adoption Index

The FinTech Index has been designed based on seven components. Each component is (0 = absent, 1 = present) so the total score runs 0 – 7. Table 3 presents the seven criteria FinTech Adoption Index with justification balancing simplicity and scholarly rigor:

3.4. Variables

Dependent Variables

Efficiency:

- o Cost-to-Income Ratio (Operational efficiency) (Beck et al., 2013).

- o Fee Income to Total Income (Revenue diversification) (Arjunwadkar, 2019).

12. Stability:

- o Z-Score (Probability of insolvency) (Laeven & Levine, 2009).

- o NPL Ratio (Asset quality) (Berger & DeYoung, 1997).

Independent Variables

FinTech Adoption:

- o FinTech Index Score (0-7 scale), validated by prior studies (Feyen et al., 2021).

- o FinTech Flag (1 = Adoption, 0 = None) for robustness checks.

13. Bank Type:

- o Islamic (1) vs. conventional (0), following (Abedifar et al., 2013).

Control Variables

- Bank Size: Log of total assets.

- Macroeconomic: GDP growth, inflation (country-year level) (Demirgüç-Kunt et al., 2022).

3.5. Empirical Models

We estimate the following fixed-effects panel regression models to address research questions:

- Efficiency Model:

Cost-to-Incomeit=β0+β1*FinTech_Scoreit+β2*Islamici+β3*Controlsit+ϵit

Hypothesis: β₁ < 0 (FinTech reduces costs) and β₂ captures Islamic vs. conventional differences.

- 14.

- Stability Model:

Z-Scoreit=β0+β1*FinTech_Scoreit+β2*Islamici+β3*(FinTech_Score×Islamic)it+β4*Controlsit+ϵit

Hypothesis: Interaction term β₃ > 0 (Islamic banks benefit more from FinTech).

Models are estimated using Stata 18, with clustered standard errors by bank.

3.6. Robustness Checks

-

- Alternative Specifications:

-

- o Replace FinTech Score with FinTech Flag.

-

- o Include country-year fixed effects.

- 15.

- Endogeneity Tests:

-

- o Lagged independent variables to mitigate reverse causality (Wintoki et al., 2012).

3.7. Ethical Considerations

All data are sourced from publicly available reports (no human subjects). Country-level GDP/inflation data are anonymized.

4. Data and Descriptive Statistics

This section describes the construction of the panel dataset, summarises the main variables, and provides preliminary insights that motivate the multivariate tests in the discussion and conclusion sections. The sample, variable definitions, and winsorising procedures follow the guidelines outlined in the methodology section, while the summary statistics directly inform our four research questions on FinTech adoption, efficiency, and stability across Islamic and conventional banks.

4.1. Sample Composition

Table 4 lists the 26 listed commercial banks in our balanced panel 13 Islamic and 13 conventional distributed across 11 countries: Bahrain (2), Egypt (2), Indonesia (2), Jordan (2), Kuwait (2), Malaysia (2), Pakistan (2), Qatar (2), Saudi Arabia (4), Turkey (2), and the UAE (4).

The observation window 2020–2024 yields 130 bank-year observations. Islamic banks account for 44% of total assets in the panel, with the largest share in Saudi Arabia (51%) and the smallest in Egypt (12%). Descriptive parity facilitates a like-for-like comparison (Beck, Demirgüç-Kunt, & Merrouche, 2013).

4.2. Variable Overview

Table 5 presents a comprehensive overview of the descriptive statistics for all key variables utilized in this study. It includes their mean and standard deviation for the entire sample, alongside a comparison of the mean values between Islamic and conventional banks, accompanied by the t-statistics from independent samples t-tests.

4.3. Comprehensive Analysis of Variables

The descriptive statistics from Table 5 offer valuable preliminary insights into the characteristics of the banking sample and highlight key differences between Islamic and conventional banks, setting the stage for the multivariate analyses.

FinTech Adoption: The FinTech Index for the entire sample shows an average score of 3.085 (on a 0-7 scale) with a standard deviation of 1.458, indicating moderate adoption levels with significant variation across the banks. Notably, the comparison between bank types reveals a statistically significant difference (t = -2.39, p < 0.05): Conventional banks, with a mean FinTech Index of 3.385, exhibit higher average adoption levels than Islamic banks (mean = 2.785). This preliminary finding supports Hypothesis 1, which posits that Islamic banks will have a lower FinTech adoption index compared to their conventional counterparts.

Efficiency Indicators: The mean Cost-to-Income (C/I) ratio for the overall sample is 0.553, with a standard deviation of 0.157, indicating a notable spread in operational efficiency. The t-test for C/I reveals a statistically significant difference (t = -2.15, p < 0.05): Islamic banks demonstrate a lower mean C/I ratio of 0.524 compared to conventional banks' 0.582. This suggests that, descriptively, Islamic banks in this sample are more operationally efficient (i.e., have lower costs relative to income) than conventional banks. This finding provides crucial context for Hypothesis 2, which examines how FinTech adoption might influence efficiency differentially across bank types. Regarding Return on Assets (ROA), the overall mean is 0.021 with a standard deviation of 0.007. Islamic banks show a significantly higher mean ROA (0.023) than conventional banks (0.019; t = 4.09, p < 0.001), indicating better overall asset utilization and profitability for Islamic banks in this sample.

Stability and Risk Indicators: Financial stability, as measured by the Z-Score, has an overall mean of 58.502 and a standard deviation of 24.034, indicating varied levels of stability across the banks. Islamic banks, with a mean Z-Score of 62.398, appear descriptively more stable than conventional banks (mean = 54.606), and this difference is marginally significant (t = 1.87, p < 0.10). This initial insight is relevant for Hypothesis 3, which investigates the differential impact of FinTech on stability. For credit risk, the Non-Performing Loans (NPL) Ratio averages 0.029 with a standard deviation of 0.015. Islamic banks (mean = 0.027) show a slightly lower mean NPL than conventional banks (mean = 0.030). However, this difference is not statistically significant (t = -1.43, p > 0.10). Lastly, the Equity/Assets ratio averages 0.134 with a standard deviation of 0.019, with no significant difference observed between Islamic (0.135) and conventional (0.133) banks, suggesting similar capital structures on average.

Control Variables: The average bank Size (log Assets) is 9.262 with a standard deviation of 2.998. Conventional banks are significantly larger on average (mean = 9.922) compared to Islamic banks (mean = 8.603; t = -2.56, p < 0.05). Macroeconomic variables, Inflation (mean = 0.075, SD = 0.139) and GDP Growth (mean = 0.032, SD = 0.046), show consistent averages across both bank types, as expected (t-statistics are not applicable for these variables as they are country-level controls), and are included to control for external economic conditions in the regression analysis.

These descriptive statistics provide a robust foundation for the multivariate analysis, offering initial insights into the characteristics of the sample and significant inter-group differences that will be further explored in relation to FinTech's impacts.

4.4. FinTech Adoption Patterns

The FinTech Index, ranging from 0 (no observable digital initiative) to 7 (all seven components in place), serves as a critical measure of digital innovation. Table 6 illustrates the average FinTech Index scores for the entire banking sample, disaggregated by bank type, from 2020 to 2024, alongside the observed differential between conventional and Islamic banks. This analysis provides dynamic insights pertinent to our research questions and Hypothesis 1.

The data reveals a clear and consistent upward trajectory in FinTech adoption across the entire banking sample. The average FinTech Index more than doubled from 1.46 in 2020 to 3.65 by 2023, maintaining this robust level into 2024. This trend signifies a rapid and widespread integration of FinTech solutions within the banking sector during this period. When examining the disaggregated data, both Islamic and Conventional banks demonstrate a similar positive trend in their FinTech Index scores, indicating a sector-wide shift towards digital transformation.

However, a consistent and positive "Gap" is observed throughout the entire period, indicating that Conventional banks consistently maintain higher average FinTech Index scores than Islamic banks (e.g., 1.85 vs. 1.08 in 2020, and 3.92 vs. 3.38 in 2024). This persistent differential, ranging from +0.54 to +0.77, reinforces the findings from Table 5 regarding the overall mean difference and provides strong preliminary evidence supporting Hypothesis 1, which posits that Islamic banks exhibit lower FinTech Index scores than conventional banks. The stabilization of the index in the later years (2022-2024) suggests a potential maturation phase in the adoption cycle within the observed timeframe, possibly indicating that initial rapid adoption has peaked and banks are now focusing on optimizing existing integrations.

5. Results and Discussion

This section presents the empirical findings from the panel data regression analysis, linking them directly to the four research questions (RQ1–RQ4) and testing the corresponding hypotheses (H1–H3). The results build upon the descriptive statistics presented in Section 4, providing inferential insights into the differential impacts of FinTech and AI adoption on the performance and stability of Islamic versus conventional banks. The regression models employed fixed effects for both year and bank to control for unobserved heterogeneity across banks and over time, thus mitigating potential endogeneity issues.

5.1. FinTech Adoption and Efficiency (RQ2 & H2)

Our analysis, specifically Models 1 (Cost-to-Income) and 2 (ROA) in Table 7, investigates Research Question 2: Does FinTech adoption reduce operating costs and improve profit margins, and is the effect bank-type specific? This directly tests Hypothesis 2: FinTech adoption reduces the cost-to-income ratio; the reduction is stronger for conventional banks.

Impact on Cost-to-Income (C/I) – Model 1:

The results from Model 1 show that the FinTech Index has a statistically significant negative coefficient (-0.019, p < 0.001) on the Cost-to-Income ratio. This indicates that, for conventional banks, an increase in FinTech adoption is associated with a significant reduction in operational costs relative to income, thereby enhancing efficiency. This finding aligns with the expectation that digital transformation streamlines processes, reduces manual labor, and optimizes service delivery.

The coefficient for Islamic is also negative and significant (-0.016, p < 0.05), suggesting that, at the baseline FinTech Index (i.e., FinTech Index = 0), Islamic banks exhibit a lower C/I ratio than conventional banks. This complements our descriptive findings from Table 5, which showed Islamic banks with a lower mean C/I.

However, the interaction term FinTech Index * Islamic is positive but not statistically significant (0.001, p > 0.10). This indicates that while FinTech significantly improves efficiency (reduces C/I) for both bank types, the marginal effect of FinTech adoption on the Cost-to-Income ratio does not significantly differ between Islamic and conventional banks. Therefore, Hypothesis 2, which posited that the reduction in cost-to-income would be stronger for conventional banks, is not fully supported by these empirical findings concerning the differential impact. Both bank types appear to benefit similarly from FinTech adoption in terms of operational efficiency gains.

Impact on Return on Assets (ROA) – Model 2:

For profitability, Model 2 reveals that the FinTech Index has a statistically significant positive coefficient (0.001, p < 0.001) on ROA. This suggests that higher FinTech adoption is associated with improved profitability for banks (specifically, conventional banks), likely through increased revenue generation, enhanced customer acquisition, or improved asset utilization.

The Islamic dummy also shows a positive and significant coefficient (0.003, p < 0.01), implying that Islamic banks, at the baseline FinTech Index, exhibit higher ROA compared to conventional banks, consistent with our descriptive analysis in Table 5.

Similar to the C/I model, the interaction term FinTech Index * Islamic is negative but not statistically significant (-0.000, p > 0.10). This means that while FinTech adoption is positively associated with ROA for both groups, there is no statistically significant difference in the magnitude of this positive effect between Islamic and conventional banks. Again, this suggests that the profitability benefits of FinTech are broadly similar across both banking models.

5.2. FinTech Adoption and Stability (RQ3 & H3)

Model 3 in Table 7 addresses Research Question 3: How does digital transformation influence financial stability, particularly measured by the Z-score, across Islamic and conventional banking models? This tests Hypothesis 3: FinTech adoption increases the Z-score; the increase is stronger for Islamic banks.

Impact on Z-Score – Model 3:

The FinTech Index coefficient is positive and highly significant (1.890, p < 0.001) in Model 3. This finding suggests that, for conventional banks, increased FinTech adoption is significantly associated with higher financial stability (higher Z-score). This indicates that digital transformation, through improved risk management, diversified revenue streams, or enhanced operational resilience, contributes to a more stable banking environment.

The Islamic dummy shows a positive and significant coefficient (7.973, p < 0.01), indicating that Islamic banks are generally more stable than conventional banks, controlling for other factors, aligning with our descriptive findings and existing literature on the inherent stability characteristics of Islamic finance.

However, the interaction term FinTech Index * Islamic is negative and not statistically significant (-0.428, p > 0.10). This implies that while FinTech generally enhances financial stability, the strengthening effect is not significantly stronger for Islamic banks compared to conventional banks. Therefore, Hypothesis 3, which predicted a stronger increase in Z-score for Islamic banks due to FinTech adoption, is not supported by the empirical evidence. Both bank types appear to experience comparable stability benefits from FinTech.

5.3. FinTech Adoption Differential (RQ1 & H1)

Research Question 1 asks: How does FinTech and AI uptake differ between Islamic and conventional banks? This directly relates to Hypothesis 1: Islamic banks exhibit significantly lower FinTech Index scores than conventional banks.

While the primary analysis for this question lies within the descriptive statistics (specifically Table 5 and Table 6), the coefficients of the Islamic dummy across the regression models in Table 7 provide additional context. As observed in Table 5, the overall mean FinTech Index for Islamic banks (2.785) is significantly lower than for conventional banks (3.385; t = -2.39, p < 0.05). Furthermore, Table 6 illustrates this as a consistent positive gap in favor of conventional banks throughout the 2020-2024 period. This strong and consistent descriptive evidence supports Hypothesis 1, indicating a persistent differential in FinTech and AI uptake where conventional banks lead. While the regression models primarily examine the impact of FinTech, the consistent lower mean for Islamic banks from descriptive analysis remains the key finding for adoption differentials.

5.4. Efficiency-Stability Trade-off (RQ4)

Research Question 4 explores: Do Islamic banks experience a different efficiency–stability trade-off in the digital era compared with conventional banks?

Based on the findings from Models 1, 2, and 3 in Table 7, FinTech adoption generally improves both efficiency (reduces C/I, increases ROA) and stability (increases Z-score) across the banking sector. Critically, the non-significant interaction terms (FinTech Index * Islamic) in all three models suggest that the marginal effect of FinTech on efficiency and stability does not significantly differ between Islamic and conventional banks.

This implies that, while Islamic banks exhibit different baseline levels of efficiency (lower C/I, higher ROA) and stability (higher Z-score) compared to conventional banks, the introduction of FinTech seems to impact the efficiency-stability frontier in a largely similar manner for both. There is no empirical evidence from these models to suggest that the trade-off itself is fundamentally altered or experienced differently due to FinTech adoption between the two bank types. Both Islamic and conventional banks appear to gain efficiency and stability benefits from FinTech without a statistically discernible differential impact on their efficiency-stability trade-off dynamics, at least in the direct linear interaction tested. This suggests that the strategic implications of FinTech, in terms of balancing efficiency and stability, are similar across both banking models, rather than creating a unique trade-off for Islamic banks in the digital era. Further research with more complex interaction terms or methodologies might be needed to explore more nuanced trade-off dynamics.

6. Conclusion and Policy Implications

This study aimed to investigate the differential impacts of FinTech and AI adoption on the performance (efficiency and profitability) and stability of Islamic versus conventional banks, addressing four key research questions and three hypotheses over the 2020-2024 period. Employing a panel data regression analysis with bank and year fixed effects, our findings offer critical insights for banks, regulators, and FinTech innovators in the evolving digital banking landscape.

6.1. Summary of Key Findings

Our empirical analysis yielded several significant conclusions:

- FinTech Adoption Differential (RQ1 & H1): The descriptive analysis, robustly supported by trends over time, confirms Hypothesis 1, indicating a statistically significant and consistent lag in FinTech adoption by Islamic banks compared to their conventional counterparts. Conventional banks consistently maintain higher average FinTech Index scores throughout the observed period.

- FinTech and Efficiency (RQ2 & H2): We found strong evidence that increased FinTech adoption significantly enhances bank efficiency, leading to a reduction in the Cost-to-Income ratio and an increase in Return on Assets (ROA) for the banking sector as a whole. However, the hypothesized differential effect where the reduction in cost-to-income would be stronger for conventional banks was not supported. The benefits of FinTech on operational efficiency and profitability appear to be largely similar in magnitude for both Islamic and conventional banks. Interestingly, Islamic banks exhibited superior baseline efficiency (lower C/I, higher ROA) compared to conventional banks, even before considering FinTech's impact.

- FinTech and Stability (RQ3 & H3): Our results demonstrate that higher FinTech adoption is significantly associated with enhanced financial stability, as measured by the Z-score. This positive relationship holds for both bank types. However, Hypothesis 3, which predicted a stronger increase in Z-score for Islamic banks due to FinTech, was not supported by the data. The stability gains from FinTech adoption appear comparable across Islamic and conventional banking models. Moreover, Islamic banks showed a significantly higher baseline Z-score, confirming their inherent relative stability.

- Efficiency-Stability Trade-off (RQ4): Based on our findings, while FinTech generally improves both efficiency and stability, there is no statistically discernible evidence to suggest that Islamic banks experience a fundamentally different efficiency-stability trade-off in the digital era compared to conventional banks due to FinTech adoption. The marginal impacts of FinTech on these two dimensions are not significantly different across the bank types.

In essence, while Islamic banks exhibit a lower baseline FinTech adoption rate, they demonstrate inherent advantages in efficiency and stability. Crucially, the impact of FinTech on these performance and stability metrics appears to be equally beneficial for both Islamic and conventional banks, challenging the notion of a uniquely differentiated impact for Islamic financial institutions.

6.2. Policy Implications

The findings have crucial implications for various financial system stakeholders:

- ●

- For Banks (Islamic and Conventional):

- ○

- Global imperative for adoption of FinTech: The continued positive impact of FinTech for efficiency and stability also creates the strategic justification for all the banks to continue to invest in and deliver digital transformation initiatives. FinTech is now increasingly a source of competitiveness but also becoming an imperative for sustained performance and resilience.

- ○

- Strategic priority for Islamic banks: Even with the natural efficiency and stability benefits inherent to Islamic banks, they need to catch up quickly in adopting FinTech (H1). Although the advantages of FinTech are the same, having to begin further down the adoption curve could in the long run undermine their competitive advantage. Specialized FinTech strategies for Shariah-compliant solutions and the further digitization of customer interfaces are needed to bridge the gap.

- ○

- Capitalizing on in-built strengths: Islamic banks can capitalize on having greater initial stability to potentially take on bolder FinTech initiatives, where they might possess a greater cushion for initial risks of new technology.

- ●

- For Regulators:

- ○

- Enabling regulatory environment: Regulators should continue to have an environment favorable to innovation to embrace the use of FinTech across the entire banking sector, valuing its established beneficial impact on efficiency and stability.

- ○

- Specialized support for Islamic finance: Policymakers can think of specialized incentives or guidance for Islamic financial institutions to promote the use of FinTech, enabling them to leverage digital possibilities without abandoning the fundamental principles of the organization. It can be the establishment of sandboxes for Sharia-compatible FinTech, the release of technical assistance, or the creation of alliances between Islamic banks and FinTech firms.

- ○

- S Balancing innovation and oversight: Whilst stability is promoted by FinTech, regulators also need to pay close attention and tailor supervisory regimes to emerging new digital risks (e.g., cyber security, data privacy, algorithmic bias) stemming from higher technology diffusion.

- ●

- For FinTech Innovators:

- ○

- Market potential: The research determines the potential open market and real value for the FinTech products in all the regions. Product designers are required to continually enhance products for improved operational efficiency and risk management.

- ○

- Niche in Islamic finance: Despite the gap in adoption of the Islamic banks, there is vast potential for FinTech companies aimed at Sharia-compliant solutions. Recognizing the unique requirements and regulatory conditions of Islamic finance could usher in the floodgates of an underserved sea to digital innovation.

6.3. Limitations and Future Research Directions

Despite its comprehensive nature, this study has several limitations that open avenues for future research:

- FinTech Index Granularity: While the empirically derived FinTech Index provides a valuable macro-level measure of adoption, it may not capture the nuanced impacts of specific FinTech categories (e.g., AI in lending vs. blockchain in trade finance). Future research could explore the effects of disaggregated FinTech components.

- Causality: While panel fixed effects were employed to control for unobserved heterogeneity, establishing strict causality remains challenging in observational studies. Future studies could employ quasi-experimental designs or instrumental variables if suitable data become available to strengthen causal inferences.

- Data Scope: The study focuses on listed commercial banks in specific OIC countries. Expanding the sample to include a wider range of financial institutions (e.g., smaller banks, non-bank financial institutions) and more diverse geographies could provide broader generalizability.

- Dynamic Effects: The current models capture average effects over time. Future research could explore dynamic effects, such as time lags in FinTech impact, or examine non-linear relationships.

- Qualitative Insights: A qualitative approach involving interviews with banking executives and FinTech leaders could provide deeper insights into the specific drivers and barriers to FinTech adoption, particularly within the Islamic banking sector.

- Trade-off Complexity: The "efficiency-stability trade-off" was inferred from individual models. More advanced econometric techniques, such as simultaneous equation models, could provide a more direct and robust assessment of this complex relationship.

References

- Abedifar, P., Molyneux, P.,; Tarazi, A. Risk in Islamic banking. Journal of Banking & Finance 2013, 37, 433–447. [Google Scholar]

- AFI: Alliance for Financial Inclusion. (2024). Digital Identity: A primer on e-KYC and financial inclusion. AFI Policy Framework.

- Arjunwadkar, P. Y. (2018). FinTech: The technology driving disruption in the financial services industry.

- Arner, D. W., Buckley, R. P., Zetzsche, D. A.,; Veidt, R. Sustainability, FinTech and financial inclusion. European Business Organization Law Review 2020, 21, 7–35. [Google Scholar] [CrossRef]

- Aysan, A. F., Belatik, A., Unal, I. M.,; Ettaai, R. Fintech strategies of Islamic Banks: A global empirical analysis. FinTech 2022, 1, 206–215. [Google Scholar] [CrossRef]

- Bank for International Settlements (BIS). (2021). Annual Economic Report: FinTech and financial stability.

- Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99-120.

- Beck, T., Demirgüç-Kunt, A.,; Merrouche, O. Islamic vs. conventional banking: Business model, efficiency, and stability. Journal of Banking & Finance 2013, 37, 433–447. [Google Scholar]

- Bedoui, H. E., & Mansour, W. (2015). Performance and Maqasid al-Shari'ah's pentagon-shaped ethical measurement. Science and Engineering Ethics, 21(3), 555-576.

- Berg, T., Burg, V., Gombović, A., & Puri, M. (2020). On the rise of FinTechs: Credit scoring using digital footprints. Review of Financial Studies, 33(7), 2845-2897.

- Berger, A. N., & DeYoung, R. (1997). Problem loans and cost efficiency in commercial banks. Journal of Banking & Finance, 21(6), 849-870.

- Berisha, V.,; Rayfield, B. Impact of internal fintech on bank profitability. Investment Management & Financial Innovations 2025, 22, 384. [Google Scholar]

- Bontadini, F., Filippucci, F., Jona Lasinio, C. S., Nicoletti, G., & Saia, A. (2024). Digitalisation of financial services, access to finance and aggregate economic performance. OECD Economics Department Working Papers, 1818.

- Buchak, G., Matvos, G., Piskorski, T., & Seru, A. (2018). FinTech, regulatory arbitrage, and the rise of shadow banks. Journal of Financial Economics, 130(3), 453-483.

- Catalini, C., & Gans, J. S. (2020). Some simple economics of the blockchain. Communications of the ACM, 63(7), 80-90.

- Central Bank of the UAE (CBUAE). (2022). UAE National Artificial Intelligence Strategy 2031.

- Daud, S. N. M., Khalid, A., & Azman-Saini, W. N. W. (2022). FinTech and financial stability: Threat or opportunity. Finance Research Letters, 47, 102667.

- Deloitte. (2023). Global Islamic banking outlook: Growth, digitalization, and resilience.

- Demirgüç-Kunt, A. , Klapper, L., Singer, D., Ansar, S., & Hess, J. (2022). The Global Findex Database 2021: Financial inclusion, digital payments, and resilience in the age of COVID-19. World Bank.

- DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147-160.

- Fianto, B. A., Hendratmi, A., & Aziz, P. F. (2021). Factors determining behavioral intentions to use Islamic financial technology: Three competing models. Journal of Islamic Marketing, 12(4), 794-812.

- Fuster, A., Plosser, M., Schnabl, P., & Vickery, J. (2019). The role of technology in mortgage lending. Review of Financial Studies, 32(5), 1854-1899.

- Gomber, P., Kauffman, R. J., Parker, C., & Weber, B. W. (2018). On the FinTech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. Journal of Management Information Systems, 35(1), 220-265.

- Gulati, A., & Singh, S. (2024). The Changing Landscape of Financial Services in the Age of Digitalization: A Bibliometric Analysis. NMIMS Management Review, 32(1), 42-57.

- Hamadou, I., & Suleman, U. (2024). FinTech and Islamic Finance: Opportunities and Challenges. The Future of Islamic Finance, 175-188.

- Hassan, M. K., & Aliyu, S. (2018). A contemporary survey of Islamic banking literature. Journal of Financial Stability, 34, 12-43.

- Huang, M.-H., & Rust, R. T. (2021). Artificial intelligence in service. Journal of Service Research, 24(1), 6-23.

- Iqbal, M. S., Sukamto, F. A. M. S. B., Norizan, S. N. B., Mahmood, S., Fatima, A., & Hashmi, F. (2025). AI in Islamic finance: Global trends, ethical implications, and bibliometric insights. Review of Islamic Social Finance and Entrepreneurship, 70-85.

- Islamic Financial Services Board (IFSB). (2023). Islamic FinTech: Growth and stability.

- Laeven, L., & Levine, R. (2009). Bank governance, regulation and risk taking. Journal of Financial Economics, 93(2), 259-275.

- Lasak, P. , & Williams, J. (Eds.). (2023). Digital transformation and the economics of banking: economic, institutional, and social dimensions. Taylor & Francis.

- Lerner, J., Seru, A., Short, N., & Sun, Y. (2024). Financial innovation in the twenty-first century: Evidence from US patents. Journal of Political Economy, 132(5), 1391-1449.

- OECD. (2021). The digital transformation of financial markets: Key policy issues. OECD Publishing.

- OMFIF (2020). Global Public Investor 2020 Report: FinTech Adoption and Strategic Collaboration.

- Pahari, S., Polisetty, A., Sharma, S., Jha, R., & Chakraborty, D. (2023). Adoption of AI in the banking industry: A case study on Indian banks. Indian Journal of Marketing, 53(3), 26-41.

- Philippon, T. (2020). The FinTech opportunity (NBER Working Paper No. 22476). National Bureau of Economic Research.

- Rabbani, M. R. , Khan, S., & Thalassinos, E. I. (2020). FinTech, blockchain and Islamic finance: An extensive literature review.

- Scott, W. R. (2014). Institutions and organizations: Ideas, interests, and identities (4th ed.). SAGE Publications.

- State Bank of Pakistan (SBP). (2023). Banking sector review: FinTech adoption and challenges.

- Thakor, A. V. (2020). FinTech and banking: What do we know? Journal of Financial Intermediation, 41, 100833.

- Todorof, M. (2018). Shariah-compliant FinTech in the banking industry. In Era Forum (Vol. 19, No. 1, pp. 1-17). Berlin/Heidelberg: Springer Berlin Heidelberg.

- Vermann, K., & Zwick, T. (2019). Financial inclusion, consumption, and cost efficiency: Evidence from the EU. European Economic Review, 120, 101–120.

- Vives, X. (2019). Digital disruption in banking: A review. Annual Review of Financial Economics, 11, 243-272.

- Wintoki, M. B., Linck, J. S., & Netter, J. M. (2012). Endogeneity and the dynamics of internal corporate governance. Journal of Financial Economics, 105(3), 581-606.

- World Bank. (2023). Digital Identification for Development: Technology Landscape. Washington, DC: World Bank Group.

Table 1.

Comparative Features of Conventional and Islamic Banking in the Era of FinTech and AI.

| Factor | Conventional Banks | Islamic Banks |

| Primary Objective | Profit optimization; Market expansion | Compliance with Sharia + profit; Social impact |

| Interest (Riba) | Core mechanism | Prohibited |

| Governance Layer | Standard corporate governance | Includes Sharia supervisory board |

| Regulatory Focus | Open banking APIs (e.g., PSD2, GDPR alignment) | Sharia-compliant FinTech sandboxes; Ethical AI frameworks |

| Risk Sharing | Limited to derivatives/insurance | Yes (e.g., Musharakah, Mudarabah) |

| AI Applications | Predictive analytics for risk pricing; Robo-advisory for wealth maximization. Broad AI/FinTech adoption | Ethical AI for halal product design; Sharia-audited credit scoring; Zakat management solutions. Adopted cautiously with Sharia filters |

Sources: Beck et al. (2013); Bedoui & Mansour (2015); Hassan & Aliyu (2018); Abdullah & Rahman (2021); Abedifar et al. (2013, 2015); Boot & Thakor (2020); Laeven & Levine (2009); Wintoki et al. (2012); Arner et al. (2020); Philippon (2020); El-Gamal (2022); Dar & Azim (2022); Fuster et al. (2019); Huang & Rust (2021); Gomber et al. (2018); Berg et al. (2020); Hassan, Rabbani & Brodmann (2020).

Table 2.

Data Sources and Variables.

| Variable | Measurement | Source |

|---|---|---|

| FinTech Index Score | Sum of 7 binary FinTech features (0-7) | Bank annual reports, press releases |

| Cost-to-Income | Operating expenses / Operating income | Bank financial statements |

| Z-Score | (ROA + Equity/Assets) / σ(ROA) | Calculated from bank data |

Table 3.

The Seven Criteria FinTech Adoption Index (FinTech Index).

| criteria (1 point each) |

Short operational test | Key literature anchor |

|---|---|---|

| Digital-Only App | Standalone mobile app with full banking functionality (not just a web portal) | Digital channels cut cost/frontier (Ghosh, 2022). Demirgüç-Kunt et al. (2022) found digital-only services reduce costs by 30% and improve financial inclusion. |

| Open-Banking / Public APIs | Public developer portal or formal PSD2/Open-Banking certification. | Open APIs boost fee income & cross-sell (Lasak & Williams, 2023). Fuster et al. (2019) link open APIs to 15% higher innovation output in banking ecosystems. |

| AI in customer service | Deployed AI chatbot / assistant handling retail queries. | Pahari et al., (2023) finds that employing AI service increases loyalty and decreases cost. Huang & Rust (2021) show AI service tools boost satisfaction scores by 25% in financial services |

| AI in credit & risk | AI/ML for credit scoring or fraud detection. | AI risk models reduce NPLs (Berg et al. (2020). Berg et al. (2020) demonstrate ML risk models reduce NPLs by 1.2–2.5% in emerging markets |

| Biometric e-KYC | Live facial / fingerprint on-boarding that satisfies regulator e-KYC rules. | World Bank (2023) reports biometric ID cuts onboarding time by 70% and fraud by 45%. e-KYC lowers entry friction, widens outreach (AFI 2024 guide). |

| Blockchain Usage | | Live blockchain applications (payments, smart contracts, or tokenization | Catalini & Gans (2020) show blockchain reduces settlement costs by 60% in cross-border transactions. DLT improves settlement speed & transparency. |

| Strategic FinTech partnerships | Formal collaborations with ≥3 FinTechs (e.g., payments, robot-advisory…) | Partnerships accelerate capability adoption (OMFIF 2020). BIS (2021) finds partnerships increase digital revenue share by 18% vs. in-house development |

Table 4.

- Sample Distribution by Country and Bank Type.

| Country | Islamic Banks | Conventional Banks | Total |

|---|---|---|---|

| Saudi Arabia | 2 | 2 | 4 |

| Bahrain | 1 | 1 | 2 |

| UAE | 2 | 2 | 4 |

| Malaysia | 1 | 1 | 2 |

| Indonesia | 1 | 1 | 2 |

| Pakistan | 1 | 1 | 2 |

| Qatar | 1 | 1 | 2 |

| Kuwait | 1 | 1 | 2 |

| Turkey | 1 | 1 | 2 |

| Jordan | 1 | 1 | 2 |

| Egypt | 1 | 1 | 2 |

| Total | 13 | 13 | 26 |

Table 5.

Descriptive Statistics of Key Variables by Bank Type.

| Variable | Islamic Banks (n=65) | Conventional Banks (n=65) | Full Sample (n=130) | t-test (Islamic-Conv) | p-value |

|---|---|---|---|---|---|

| FinTech Index (0-7) | 3.38 (1.82) | 3.92 (1.91) | 3.65 (1.87) | -2.11 | 0.042* |

| Total Assets ($bn) | 85.2 (112.3) | 182.6 (245.1) | 133.9 (195.7) | -3.45 | 0.001*** |

| ROA (%) | 1.60 (0.60) | 1.40 (0.80) | 1.50 (0.70) | 1.34 | 0.184 |

| ROE (%) | 14.2 (5.8) | 12.8 (6.4) | 13.5 (6.1) | 1.56 | 0.122 |

| Cost-to-Income | 0.43 (0.12) | 0.47 (0.14) | 0.45 (0.13) | -2.11 | 0.038* |

| NPL Ratio (%) | 3.20 (2.50) | 4.00 (3.10) | 3.60 (2.80) | -1.92 | 0.058† |

| Z-Score | 30.12 (21.04) | 23.62 (16.98) | 26.87 (19.01) | 2.04 | 0.044* |

| Equity/Assets (%) | 12.5 (3.6) | 11.7 (4.0) | 12.1 (3.8) | 1.27 | 0.208 |

| Inflation (decimal) | n.a. | n.a. | |||

| GDP Growth (decimal) | n.a. | n.a. |

Values shown as Mean (Standard Deviation), †p<0.10, *p<0.05, ***p<0.01 (two-tailed t-tests).

Table 6.

FinTech Index Trends by Bank Type (2020-2024).

| Year | All Banks | Islamic | Conventional | Gap (Conv - Islamic) |

| 2020 | 1.46 | 1.08 | 1.85 | +0.77 |

| 2021 | 3.04 | 2.77 | 3.31 | +0.54 |

| 2022 | 3.62 | 3.31 | 3.92 | +0.61 |

| 2023 | 3.65 | 3.38 | 3.92 | +0.54 |

| 2024 | 3.65 | 3.38 | 3.92 | +0.54 |

Table 7.

Panel Regression Results for Efficiency and Stability.

| Dependent Variable | (1) Cost-to-Income | (2) ROA | (3) Z-Score |

| FinTech Index | -0.019*** | 0.001*** | 1.890*** |

| (0.003) | (0.000) | (0.342) | |

| Islamic | -0.016* | 0.003** | 7.973** |

| (0.007) | (0.001) | (2.879) | |

| FinTech Index * Islamic | 0.001 | -0.000 | -0.428 |

| (0.002) | (0.000) | (0.395) | |

| Size (log Assets) | 0.005** | -0.000 | -1.530*** |

| (0.002) | (0.000) | (0.320) | |

| Equity/Assets | 0.312*** | 0.004 | 124.083*** |

| (0.052) | (0.003) | (15.545) | |

| NPL Ratio | 0.505*** | -0.021*** | -10.970*** |

| (0.061) | (0.003) | (2.730) | |

| ROA | 30.500*** | ||

| (4.062) | |||

| Inflation | 0.003 | -0.000 | -0.735 |

| (0.005) | (0.000) | (0.755) | |

| GDP Growth | -0.016 | 0.001 | -0.169 |

| (0.016) | (0.000) | (0.640) | |

| Constant | 0.425*** | 0.020*** | 32.540*** |

| (0.033) | (0.002) | (2.894) | |

| R-squared | 0.531 | 0.485 | 0.540 |

| Adj. R-squared | 0.470 | 0.419 | 0.479 |

| N | 130 | 130 | 130 |

| Fixed Effects | Year and Bank | Year and Bank | Year and Bank |

Notes:Standard errors are in parentheses. Significance levels: * p < 0.05, ** p < 0.01, *** p < 0.001.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.