Submitted:

14 November 2025

Posted:

17 November 2025

You are already at the latest version

Abstract

This study examines the dynamic interplay between digitalization, deposit insurance systems, bank resolution mechanisms, and policy guarantee frameworks in fostering financial stability, with a particular focus on Indonesia's Deposit Insurance Corporation (LPS). A quantitative analysis was employed, and data were collected from 265 senior financial experts, including banking executives, regulatory officials, and policymakers. SmartPLS was used to explore the relationships among digitalization, deposit guarantee resilience, resolution mechanisms, governance quality, and financial stability. Our findings indicate that digitalization significantly enhances financial stability by streamlining processes, enabling real-time monitoring, and facilitating proactive risk management. Furthermore, robust deposit insurance systems and effective resolution strategies mitigate systemic disruptions and minimize contagion risks. Governance quality has emerged as a critical moderating factor that aligns regulatory objectives with sustaining market confidence, for Indonesia and similar institutions in emerging economies. Our study provides policy insights by integrating advanced digital platforms into deposit insurance operations, refining resolution frameworks through the timely utilization of data, and strengthening governance mechanisms to ensure policy responsiveness. By linking digital innovation with institutional resilience mechanisms, our study provides both theoretical and empirical contributions to the financial stability literature.

Keywords:

governance quality

; financial stability

; digital transformation

; regulatory reforms

; deposit insurance

1. Introduction

The digital uprising has changed the notion of finance by driving extensive transformation in banking, risk management, and regulatory areas. (Arner, Barberis, & Buckley, 2016; Philippon, 2019). In Indonesia, this phenomenon for example the rapid expansion of digital financial services driven by fintech advances, and the widespread adoption of mobile technology has significantly increased financial inclusion, providing banking access to millions of people previously untouched by the formal economy (Boot & Thakor, 2025; World Bank, 2020). In addition to this advancement, a new spectrum of systemic risks and regulatory challenges have emerged. As the digital changes in Indonesia's financial ecosystem are becoming more pronounced (Birindelli & Iannuzzi, 2024; Yang & Ali, 2024). The institutions that have the responsibility to ensure the stability of the Indonesian Deposit Insurance Corporation are now tasked with maintaining depositors' confidence and financial integrity under conditions that were never thought of before (Demirgüç-Kunt & Kane, 2002). The institutions that have the responsibility to ensure the stability of the Indonesian Deposit Insurance Corporation are now tasked with maintaining depositors' confidence and financial integrity under conditions that were never thought of before (Zetzsche, Buckley, Arner, & Barberis, 2017; IMF, 2021). Recent global and regional disruptions, ranging from the 1998 Asian Financial Crisis to the volatility triggered by the COVID-19 pandemic, underscore the need for a strong and adaptable financial safety net (Barua & Barua, 2021; OECD, 2022). Besides, Indonesia's response has often been hampered by regulatory fragmentation, slow policy adaptation, and persistent gaps in deposit guarantee coverage and bank resolution readiness (World Bank, 2022; Claessens, 2014).

The literature largely agrees that if digital transformation goes beyond regulatory modernization, the resulting gaps can foster moral hazards, undermine depositors' trust, and make existing safeguards dangerously obsolete (Demirgüç-& Detragiache, 2002; Garcia, 2000; Claessens, 2014). These issues are particularly acute in emerging markets, where rapid digitalization coexists with legacy vulnerabilities and governance challenges (Yang & Ali, 2024; Arner et al., 2017). Despite extensive research on financial innovation and regulatory changes, Indonesia is still under-examined in terms of how deposit guarantees, bank resolution mechanisms, and governance quality interact in a rapidly evolving digital environment (Boot & Thakor, 2025; Zetzsche et al., 2017). In this context, there is an urgent need for a new and integrative perspective that goes beyond digitalization analysis or isolated regulatory reform. The risk involves regarding showing inefficiency in the financial sector but also its resilience against shocks and uncertainties in modern digital era. This research will address these complex challenges in a scientific imperative and a national priority, with thoughtful implications which will enhance financial stability, depositors' well-being, and the credibility of Indonesian financial institutions.

1.1. Study Aims and Key Inquiries

- What is the impact of financial sector digitalization on financial stability in Indonesia?

- How do the of deposit insurance and bank resolution mechanisms (BRM) mediates the relationship between digitalization, regulatory frameworks, financial inclusion, macroeconomic stability, and financial stability (FS)?

- To what extent does governance quality moderate the relationship between financial sector digitalization and financial stability?

- What regulatory weaknesses exist in the Indonesian financial system that affect financial stability?

- What strategic policy recommendations can increase the effectiveness of LPS in ensuring financial stability in the digital era?

2. Literature Review

The digitalization of the financial system is significantly changing the risk landscape and regulatory priorities in developing countries. In Indonesia, the rapid adoption of fintech and platform-based services has increased the complexity of maintaining financial stability, especially as cyber risks and regulatory gaps become more prominent (Arner, Barberis, & Buckley, 2017; Birindelli & Iannuzzi, 2024). The implementation of effective deposit guarantees, and bank resolution mechanisms is essential to maintain depositor confidence and mitigate systemic shocks in this evolving environment (Boot & Thakor, 2025; Claessens, 2015). However, as digital transformation evolves, traditional security is increasingly challenged by emerging threats and new market structures (Zetzsche, Buckley, Arner, & Barberis, 2017). This literature review investigates the interaction between digitalization, regulatory adaptation, and governance dynamics in shaping financial stability in Indonesia's growing financial sector.

2.1. Digitalization of the Financial Sector

The emergent adoption of digital financial services (DFS) in Indonesia, such as mobile banking, e-wallets, and fintech, has transformed financial openness and operational efficiency in the banking sector (Boot and Finance, 2021; Boot Thakor, 2025). This digitalization has significantly expanded financial inclusion, that lowered barriers to entry for underserved populations and facilitated new forms of economic input (World Bank, 2022). But this shift in technology has also introduced new vulnerabilities, especially cybersecurity threats, data privacy risks, and the increasing complexity of digital platforms (Birindelli & Iannuzzi, 2024; Claessens, 2015). Various recent studies highpoint that deposit insurance, which were originally created for traditional banking environments, its faeces substantial challenges in adapting to digital risks now. Birindelli and Iannuzzi (2024) argues that cyber occurrence may undermine public trust in the financial institutions, put into the hazard the credibility of deposit protection procedures, and increase the risk of sudden withdrawals. As a result, of this the regulatory authorities are forced to adjust their frameworks to stabilise the drive for innovation with the need for robust systemic safeguards (Boot & Thakor, 2025; Claessens, 2015). In addition, as digital transactions become more intertwined with real-time systems and cross-platform ecosystems, traditional deposit insurance coverage may fail to address operational disruptions or losses caused by cyberspace (World Bank 2022). This systemic challenge is not exclusive to Indonesia; Cross-national analysis underscores the urgency of reforming regulatory and insurance structures to maintain financial stability in the digital age (Arner, Barberis, & Buckley, 2017). we hypothesize: H1: Digitalization of the financial sector has a negative effect or negative relation with adequacy of deposit insurance due to increasing cybersecurity risks and regulatory challenges.

2.2. Regulatory Framework and Policy Reforms

There is comprehensive need of strong regulatory framework to ensure stability and consistency in the banking areas, especially in the growing fast financial view. The institutional collaborative efforts have supported the implementation of practical norms and capital requirements, that has created a layered defense against any sort of shocks and uncertainties in indonesia (OECD, 2022; World Bank, 2022). Most recent work of Boot and Thakor (2025) underscores that dynamic regulatory adaptation, which integrates traditional and digital financial innovations, significantly enhances the credibility of deposit guarantee schemes by reducing bank and consumer uncertainty. Laeven and Valencia (2020) provide global empirical evidence that ongoing regulatory reforms, including improved supervision and crisis management protocols, improve the effectiveness of deposit insurance by reducing the risk of contagion and facilitate prompt and orderly bank resolution. The research warns that excessive complexity or inconsistent application of regulations can lead to regulatory arbitrage, where financial institutions shift activities to less regulated areas, undermining the protection intentions of reform (Claessens, 2015; Arner, Barberis, & Buckley, 2017). The policy harmonization in regulatory bodies has significantly narrowed uncertainties and shocks, thus strengthening depositor protection and overall financial stability Collectively by institutions (OECD, 2022). These insights climax that a well-designed regulatory framework, characterized by consistency of prudence, adaptability, and effective coordination, is positively associated with the adequacy of deposit insurance and the resilience of the financial sector. H2: Regulatory framework has positive impact on adequacy of deposit insurance through enforcement of wise standards and systemic risk mitigation.

2.3. Macroeconomic Stability

The sustainable economic growth, moderate inflation rates, and stable exchange rates, as microeconomic indicators are essential for a strong financial system that supports the efficiency of deposit guarantee mechanisms. Numerous research concentrating on Indonesia has reliably revealed that the great periods of macroeconomic stability are linked to increased confidence in the banking sector and reduced risk of crises. Corelli, (2019) is of the view that a robust macroeconomic basis creates circumstance where financial institutions can manage risk more effectually, thereby reducing the probability of bank failures and increasing the credibility of deposit insurance. In emerging economies various empirical studies show that stable macroeconomic conditions correlate with increased public confidence in the financial system and the execution of more efficient crisis management strategies (Barua & Barua, 2021). It will not only help regulators in coping with shocks and uncertainties but also helps for maintain depositors' confidence during in stressful periods. Claessens (2015) advised that lengthy periods of alleged stability can lead to irony of risk by banks and regulators, highlighting the need for hand on policy measures, even in a seemingly stable macroeconomic environment. Many scholarly works suggest that macroeconomic stability is an important driver of effective deposit insurance, providing the necessary operational capacity and institutional credibility for crisis prevention and financial system protection. As a result, we propose the following hypothesis. H3: Macroeconomic stability is positively associated with the adequacy of deposit guarantees, fostering an environment conducive to effective risk management and crisis prevention.

2.4. Financial Inclusion and Literacy

As more people in developing economies gain access to formal financial services, the traditional risk landscape faced by deposit guarantee schemes has evolved in complex ways.. Grohmann, Klühs, and Menkhoff (2018) offer strong cross-border evidence suggesting that increased financial literacy not only increases individuals' engagement with the formal financial sector but also deepens their understanding of financial protection, such as deposit insurance. Ahamed and Mallick (2019) further affirm that financial inclusion contributes positively to bank stability by enlarging depositor bases and encouraging sustainable inter-mediation, with the most substantial effects observed in financially literate populations. Nevertheless, the corporate literature has emphasized prospective confronts. Dupas, Karlan, Robinson, and Ubfal (2018) specified in their investigation that rapid financial inclusion among populations with low financial literacy can refute stability because of uninformed depositor behavior, vulnerability to rumours or misconceptions about coverage limits during stressful times. In Indonesian corporate settings, empirical findings expose that financial literacy and positive interface with formal banking services extensively increase depositor confidence in the formal banking sector, highlighting the importance of targeted educational initiatives along with increased access (Alamsyah et al., 2020). notwithstanding these diverse viewpoints, the literature reliably advocates that financial inclusion can improve the adequacy and effectiveness of deposit insurance, provided it is supported by adequate literacy programs to ensure that depositors are well-informed about the benefits and limitations of coverage. Considering above synthesis we propose H4: Financial inclusion is positively associated with the adequacy of deposit insurance depending on the provision of adequate financial literacy programs that promote informed decision-making among depositors.

2.5. Cybersecurity Risk

In the brisky digitized financial sector, cybersecurity jeopardises have become a major threat to the banking stability systems around the world. The increasing confidence on digital platforms for financial transactions exposes both banks and deposit insurance authorities to a cyber threat, that includes phishing attacks and data breaches to large-scale ransomware incidents (Birindelli and Iannuzzi, 2024). Empirical research has consistently shown that cyber incidents not only cause direct financial losses, but also undermine depositors' trust, which is critical to the effectiveness of deposit insurance schemes (Bouveret, 2018). For deposit guarantee agencies, such as LPS Indonesia, operational risks posed by cyberattacks can jeopardize their ability to guarantee deposits and manage bank settlements in a timely manner during crises (BIS, 2021). Studies show that major cybersecurity breaches can trigger panic withdrawals, especially if the public considers personal or financial information to be risky (Birindelli & Iannuzzi, 2024; Bouveret, 2018). The Bank for International Settlements (2021) further emphasizes that integrating strong cyber risk management and crisis response protocols is essential to maintain the operational integrity of the deposit guarantee framework. These findings highlight that cybersecurity risks are not just technical issues, but important determinants of financial stability and trust of deposit insurance mechanisms. It’s evident without adequate cybersecurity readiness, even a well-capitalized insurance scheme can be compromised by a single disruptive incident. Hence, we hypothesize that H5: Cybersecurity risks are negatively associated with the adequacy of deposit insurance.

2.6. Mediating Effect: Deposit Insurance Adequacy

The adequacy of deposit insurance plays a central role in turning external regulatory, economic, and cybersecurity pressures into outcomes that improve financial stability. Adequate insurance coverage not only instils trust among depositors but also empowers regulators to manage banking crises more effectively, thereby reducing the likelihood of unstable bank runs (Anginer, Demirgüç-, & Zhu, 2014). Their study reveals a clear inverse correlation between insurance adequacy and systemic risk, especially in emerging markets, where such coverage can increase depositor confidence. Demirgüç-and Kane (2002), provide cross-national evidence that well-capitalized deposit insurance schemes significantly reduce trust-driven bank operations and the costs associated with the completion of failed institutions. According to their findings, a credible deposit insurance system, one with sufficient funding and transparent management, fosters greater public trust. This, in turn, makes managing a financial crisis a more orderly process. Nonetheless, the literature highlights an important caveat: Deposit insurance must be accompanied by strict supervision. if substantial deposit insurance is not paired with strong regulatory measures, it can actually promote financial instability by incentivizing banks to take on excessive risk (Demirgüç-and Detragiache, 2002). This core problem—the moral hazard created when banks feel shielded from the consequences of their actions. (2000) and Demirgüç-and Kane (2002), who emphasize the necessity of vigilant regulatory scrutiny to counter it. These findings congregate on the central insight that the credibility of deposit insurance depends on governance that supports prudent oversight and transparent administration. As a result, it serves as an important link linking macro-level factors, such as regulation and digital threats, to depositor behavior and financial sector resilience. we propose hypothesis to confirm H6: The adequacy of deposit insurance is positively associated with insurance policy guarantees.

2.7. Bank Resolution Mechanisms and Insurance Policy Guarantees

The bank's resolution mechanism and insurance policy guarantee are essential to maintain financial stability. Deposit insurance institutions, such as LPS, offer policy guarantees that formally guarantee the protection of depositors' funds within certain limits. These guarantees play an important role in reducing uncertainty and increasing confidence in the financial system (Garcia, 2000). The literature shows that transparent policy guarantees significantly reduce depositors' anxiety, reduce the risk of bank runs, and increase the effectiveness of deposit insurance, especially during financial crises (Demirgüç-& Kane, 2002). Eisenbeiss (2012) highlights that institutional credibility rooted in genuine and consistently communicated collateral is essential to influence depositor behavior and improve overall market confidence. However, an effective bank resolution mechanism is essential for managing failing institutions without triggering broader financial instability. Calomiris and Herring (2013) argue that a well-structured resolution regime facilitates the exit or restructuring of distressed banks, thereby minimizing contagion and maintaining systemic resilience. Empirical studies emphasize that the synergy between strong deposit insurance and credible resolution mechanisms increases crisis management capacity, allowing authorities to respond quickly and reduce disruptions to the financial system (Laeven & Valencia, 2020). Collectively, the evidence suggests that adequate deposit insurance, supported by credible policy guarantees, strengthens the link between insurance frameworks and resolution mechanisms, ultimately aiding in smooth crisis management and minimizing systemic risks. Therefore, we hypothesize that H7: Adequacy of deposit insurance is positively associated with the bank's resolution mechanism, facilitating smooth crisis management and minimizing systemic disruption.

2.8. Insurance Policy Guarantees

Insurance policy guarantees are formal assurances provided by deposit insurance agencies such as LPS to protect depositors' funds up to a specified limit. The literature consistently indicates that clear and credible guarantees play a crucial role in reducing depositor uncertainty and are fundamental to fostering trust in the financial system (Garcia, 1999; Eisenbeiss, 2012). Garcia (1999) highlights the historical significance of explicit deposit insurance policies in reassuring the public and preventing destabilizing bank runs. Eisenbeiss (2012) further emphasizes that the authenticity and transparency of these guarantees shape depositor perceptions and influence banking behaviors. Transparent communication and reliable policy guarantees have also been linked to effective crisis management. When deposit insurance terms are clearly communicated and understood by the public, empirical evidence suggests that depositors are less likely to panic during periods of instability, thereby enhancing the effectiveness of deposit insurance frameworks (Demirgüç-Kunt and Kane 2002). This contributes to a stable financial environment and supports systemic resilience. Therefore, we propose the following hypothesis: H8: Clear and credible insurance policy guarantees are positively associated with financial stability by bolstering depositor confidence and promoting a more resilient financial system. Furthermore, well-designed and credible insurance policy guarantees are essential for facilitating orderly bank resolution processes. When banks and regulators depend on insurance guarantees, the resolution of failing banks becomes more predictable and less disruptive (Calomiris & Herring, 2013). Such guarantees enable authorities to manage crises more systematically and maintain market discipline, ultimately minimizing contagion and systemic risks (Laeven & Valencia, 2020). Thus, we propose the following hypothesis: H9: Insurance policy guarantees are positively associated with bank resolution mechanisms because credible guarantees promote orderly resolution processes.

2.9. Bank Resolution Mechanisms

The establishment of an efficient bank resolution mechanism is essential to maintain financial stability, especially after a banking crisis or institutional failure. Contemporary frameworks employ strategies such as bail-in provisions, bridge banks, and asset management companies to manage failing banks without inciting widespread contagion (Calomiris & Herring, 2013; Laeven & Valencia, 2013). Calomiris and Herring (2013) argue that the efficacy of a resolution regime depends on its capacity to promptly address troubled banks, ensuring that shareholders and creditors bear the financial burden rather than taxpayers or depositors. Empirical evidence suggests that a well-executed resolution process plays an important role in containing systemic risks, minimizing market disruptions, and maintaining depositor confidence (Laeven & Valencia, 2020). In contrast, Beck, Demirgüç-, and Levine (2006) underscore that delays, lack of coordination, or mismanagement during bank resolutions can exacerbate uncertainty, reduce public trust, and increase the risk of contagion throughout the financial system. Therefore, timely and transparent interventions are essential to strengthen the stability of the banking sector and maintain the integrity of the deposit guarantor framework. Collectively, the literature underscores that strong bank resolution mechanisms are essential for crisis management, directly supporting financial stability by effectively managing failing institutions and reducing secondary effects. Thus, we hypothesize that an effective H10: Bank resolution mechanism is positively associated with financial stability by reducing the risk of transmission, managing failing institutions, and maintaining depositor confidence.

2.10. Bank Resolution Mechanisms- Mediating Effects:

Efficient bank resolution mechanisms, including bail-in provisions, bank bridges, and asset management strategies, are essential to contain the risk of contagion and manage failing institutions (Calomiris & Herring, 2013; Laeven & Valencia, 2013). The implementation of timely resolution measures is directly related to the stability of the banking sector. Research shows that delays or mismanagement in this process can exacerbate systemic risks and undermine depositors' confidence (Beck et al., 2006). Bank resolution tools will also help provide the proper deposit insurance, if anything shall happen and protect banks during times of volatility. Thus, we hypothesize: H11: Effective bank resolution mechanisms mediate the positive relationship between deposit insurance adequacy and financial stability by providing efficient intervention and resolution tools.

2.11. Insurance Policy Guarantees

Insurance policy guarantees refer to the formal assurances provided by LPS regarding the protection of depositors’ funds. Clear and credible guarantees are vital for reducing uncertainty and reinforcing trust in the financial system (Garcia, 1999; Eisenbeiss, 2012). Empirical evidence suggests that transparent communication about policy guarantees mitigates depositor panic and strengthens the efficacy of deposit insurance in crisis scenarios. Policy guarantees may promote trust with the clients by providing them assurance. Therefore, we hypothesize: H12: Insurance policy guarantee mediate the positive relationship between Deposit insurance adequacy and financial stability by proving safety to depositors.

2.12. Financial Stability

Financial stability stands as a major dependent variable within this framework of analysis, reflecting circumstances in which systemic volatility is under control, depositor confidence is strong, and the financial sector can absorb and adapt to economic shocks (Richard, Devinney, Yip, & Johnson, 2009;). Richard et al. (2009) emphasize that strong financial stability allows for the effective functioning of financial intermediaries, promotes investor confidence, and supports long-term economic growth. Empirical evidence suggests that a well-designed deposit insurance system, when equipped with effective bank resolution mechanisms, strengthens the banking sector's ability to withstand periods of stress and prevent the escalation of local problems into broader systemic crises (Demirgüç-& Detragiache, 2002). This stability is not only important to maintain depositors' confidence but also to encourage productive lending and sustainable economic expansion. In contrast, related instability is often characterized by rapid withdrawals, failures of key institutions, or inadequate crisis management that can erode public trust, limit investment, and trigger prolonged recessions. (Yukl, 2012). Therefore, financial stability is widely recognized as a policy goal and a marker of economic resilience, which supports sustainable growth and overall confidence in the financial system.

Thus, we hypothesize, H13: Financial stability is positively associated with a resilient banking system, fostering economic growth and investor confidence.

2.13. Moderating Role of Governance Quality

The quality of governance, which includes transparency, regulatory effectiveness, and anti-corruption measures, is an important factor in the success of financial stability mechanisms. Kaufmann, Kraay, and Mastruzzi (2009) provide global evidence that countries with strong governance frameworks are more successful in implementing regulatory policies, such as deposit insurance and bank resolution mechanisms. Their findings suggest that the high quality of governance enhances the positive effects of these mechanisms on financial system stability by strengthening policy enforcement and fostering public trust. Similarly, La Porta et al. (1998) underscores the importance of legal origins and institutional quality in financial sector outcomes. They argue that even the most well-designed deposit insurance or resolution policies can fail in environments with weak governance, where enforcement is inconsistent, and corruption erodes trust in regulatory bodies. Strong governance not only builds the trust of depositors and investors, but also ensures that digitalization and financial inclusion initiatives do not pose any unwanted risks. Further empirical studies show that the quality of governance moderates the risks associated with rapid digitalization, making deposit insurance systems more adaptable and less vulnerable to new forms of systemic risk (Kaufmann et al., 2009). In countries with high governance standards, digital innovations can be integrated more securely and the positive effect of deposit guarantees and resolution mechanisms on stability are strengthened. In addition, financial inclusion has been found to increase the likelihood of financial stability provided institutions maintain a high level of transparency and accountability (Ahamed & Mallick, 2019). A well-structured and clearly articulated insurance policy not only protects depositors but also enhances the resilience of the broader financial sector, especially in the rapidly evolving banking market (Jungo et al., 2022; Fernández-Villaverde et al., 2020). The H14 hypothesis suggests that the quality of governance positively moderates the relationship between digitalization and the adequacy of deposit guarantees, so that the negative impact of digitalization on the adequacy of deposit guarantees can be mitigated when the quality of governance is high. Hypothesis H15 suggests that governance quality positively moderates the relationship between deposit insurance adequacy and bank resolution effectiveness on financial stability, thereby enhancing the positive effects of deposit insurance adequacy and bank resolution effectiveness on financial stability when governance quality is high. Hypothesis H16 asserts that financial inclusion is positively associated with financial stability, ensures the safety of banking firms, and contributes to a more resilient financial sector. This leads to Hypothesis H17, which proposes that insurance policy guarantees mediate the relationship between financial inclusion and stability (Jungo et al., 2022).

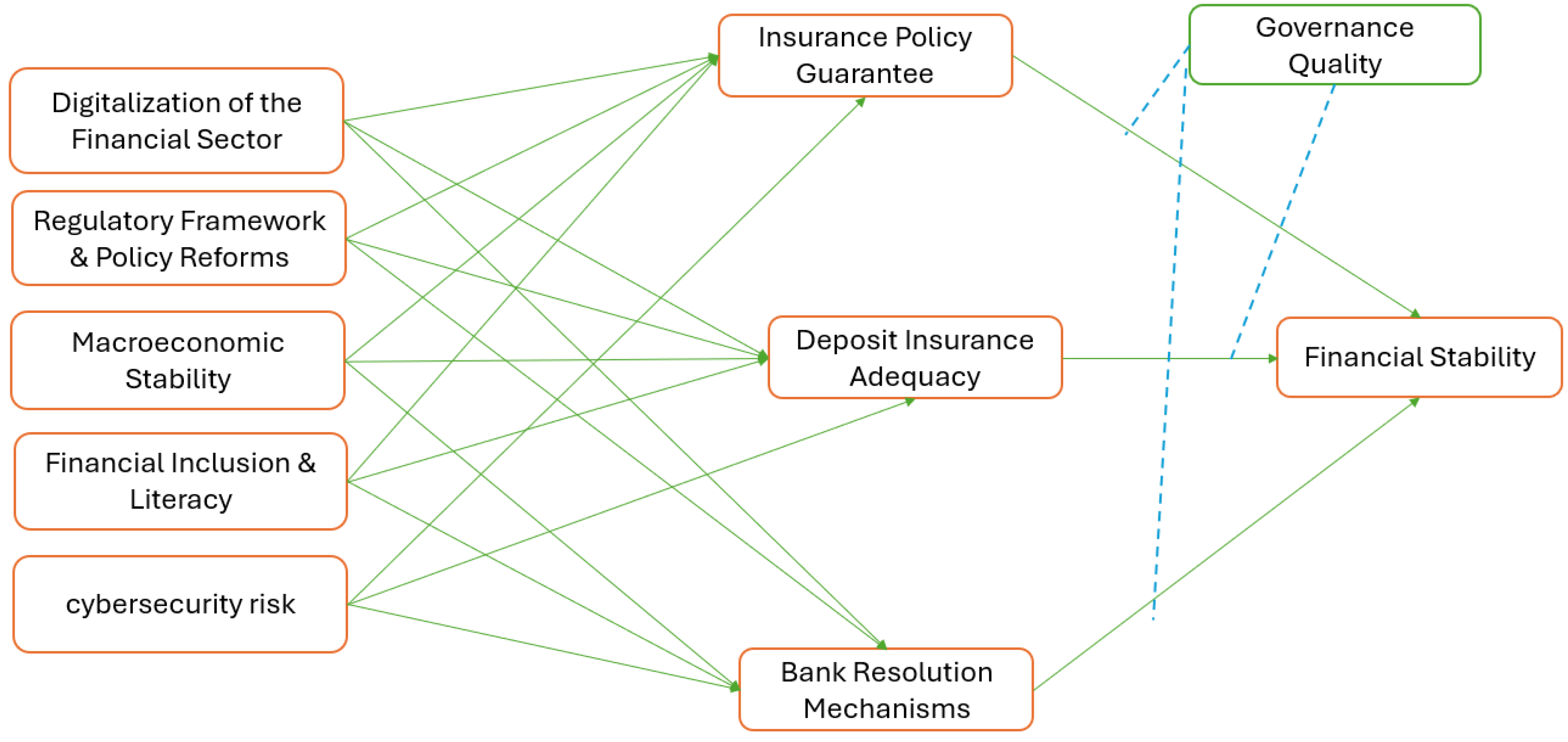

Building on a thorough synthesis of recent literature and the robust theoretical and empirical arguments previously discussed, this study introduces an integrative conceptual framework designed to clarify the intricate interconnections that shape financial stability in Indonesia's swiftly transforming financial sector. The model is based on evidence that deposit insurance adequacy, insurance policy guarantees, bank resolution mechanisms, and governance quality collectively mediate and moderate the effects of external factors such as digitalization, financial inclusion, macroeconomic stability, regulatory reforms, and cybersecurity risk. The framework identifies financial stability as the ultimate dependent variable, influenced not only by the direct effects of deposit insurance and bank resolution effectiveness but also by the moderating role of governance quality and the mediating roles of insurance policy guarantees and financial inclusion. The conceptual model also highlights the dual role of digitalization—as both a driver of innovation and efficiency and a potential source of systemic risk—whose impact on deposit insurance adequacy is dependent on the strength of governance. Additionally, the model considers the positive influence of financial inclusion on stability, particularly when supported by credible insurance guarantees and robust literacy initiatives. By systematically integrating these critical constructs and relationships, the proposed conceptual diagram offers a comprehensive foundation for empirically examining how Indonesia’s financial safety nets, institutional frameworks, and policy interventions interact to foster resilience, safeguard depositor confidence, and promote sustained economic growth. This framework not only enhances academic understanding but also provides actionable insights for policymakers aiming to strengthen the architecture of financial stability in emerging markets.

3. Materials and Methods

This study adopted a quantitative research methodology employing Partial Least Squares Structural Equation Modeling (PLS-SEM) to meticulously examine the intricate relationships between financial and institutional determinants as mentioned in Figure 1, that affect Target Financial Stability (TFS) within Indonesia's dynamic financial environment. PLS-SEM was selected for its capability to model complex interactions involving latent constructs, its suitability for smaller sample sizes, and its dual support for predictive and exploratory research objectives, making it particularly suitable for developing emerging theories in complex fields such as financial stability (Hair et al., 2019; Sarstedt et al., 2022). The model was constructed to evaluate the direct effects, significant indirect pathways, and crucial mediating roles of the key variables: Bank Resolution Mechanisms (BRM), Digitalization of Financial Services (DFS), Cybersecurity Risk (CrSR), Financial Inclusion and Literacy (FIL), and Insurance Policy Guarantees (IPG). Data were gathered through a carefully designed, structured questionnaire, which was informed by foundational literature on financial stability frameworks (e.g., Basel Committee principles), bank resolution standards (e.g., Financial Stability Board Key Attributes), and the evolution of digital finance (Ozili, 2023). Responses were collected using multi-item, reflective scales (5-point Likert, 1=Strongly Disagree to 5=Strongly Agree) for each construct, ensuring content validity through thorough evaluation by a panel of academic and industry experts, adhering to established psychometric protocols (MacKenzie et al., 2011).

A stratified random sampling method was employed to ensure that Indonesia's key financial sectors were represented proportionally, resulting in a final analytical sample of 265 highly qualified professionals from an initial pool of 400 surveys. This carefully selected group included senior decision-makers such as C-suite executives, directors, and regulatory leaders from commercial banks with active digital operations, fintech innovators, key government regulatory bodies such as the OJK and Ministry of Finance, and monetary authorities such as Bank Indonesia. By focusing on individuals with strategic oversight of financial operations and risk frameworks, this study gathered the expert-level insights necessary for a comprehensive evaluation of TFS determinants (Hiebl & Richter, 2018).

3.1. Ethical Considerations and Informed Consent

Our study did not require formal ethical approval, as it entailed minimal risk and involved the collection of anonymous data from financial professionals via an online survey. Participation was entirely voluntary, and no personal or identifiable information was collected from the participants. The survey form included a statement detailing the study objectives, assurances of confidentiality, and the voluntary nature of participation. Respondents provided informed consent by completing the questionnaire after reviewing this statement.

3.2. Measurement of Inner Model and Outer Model

Data analysis was performed using SmartPLS 4.0, following the established two-step analytical protocol (Anderson & Gerbing, 1988). Initially, the measurement model was subjected to rigorous validation: internal consistency reliability was confirmed through Cronbach's alpha (α > 0.7) and Composite Reliability (CR > 0.7) (Nunnally & Bernstein, 1994); convergent validity was established with Average Variance Extracted (AVE > 0.5) (Fornell & Larcker, 1981); and discriminant validity was rigorously verified using the Fornell-Larcker criterion and heterotrait-monotrait (HTMT) ratio (< 0.85) (Henseler et al., 2015). Subsequently, the structural model was evaluated: path coefficient significance was tested via non-parametric bootstrapping with 5,000 subsamples (Hair et al., 2022); model fit was assessed using the Standardized Root Mean Square Residual (SRMR < 0.08) (Hu & Bentler, 1999); explanatory power was determined by R² values; effect sizes (f²) were calculated to assess substantive impact (Cohen, 1988); and specific indirect effects for mediation, such as IPG and BRM, were decomposed using the product-of-paths approach with bias-corrected bootstrap confidence intervals (Preacher & Hayes, 2008). Robustness was ensured by meticulous data screening.

Minimal missing data (<5%), confirmed as completely missing at random via Little's MCAR test, were addressed using mean substitution. Potential outliers were identified using the Mahalanobis distance (p < 0.001) and winsorized to mitigate undue influence. The study strictly adhered to ethical principles. All participants provided informed consent with strict confidentiality and complete anonymity guaranteed throughout data collection and analysis, in alignment with the GDPR and COPE guidelines. No personally identifiable or sensitive organizational information was solicited or retained..

4. Results

4.1. Construct Reliability and Validity

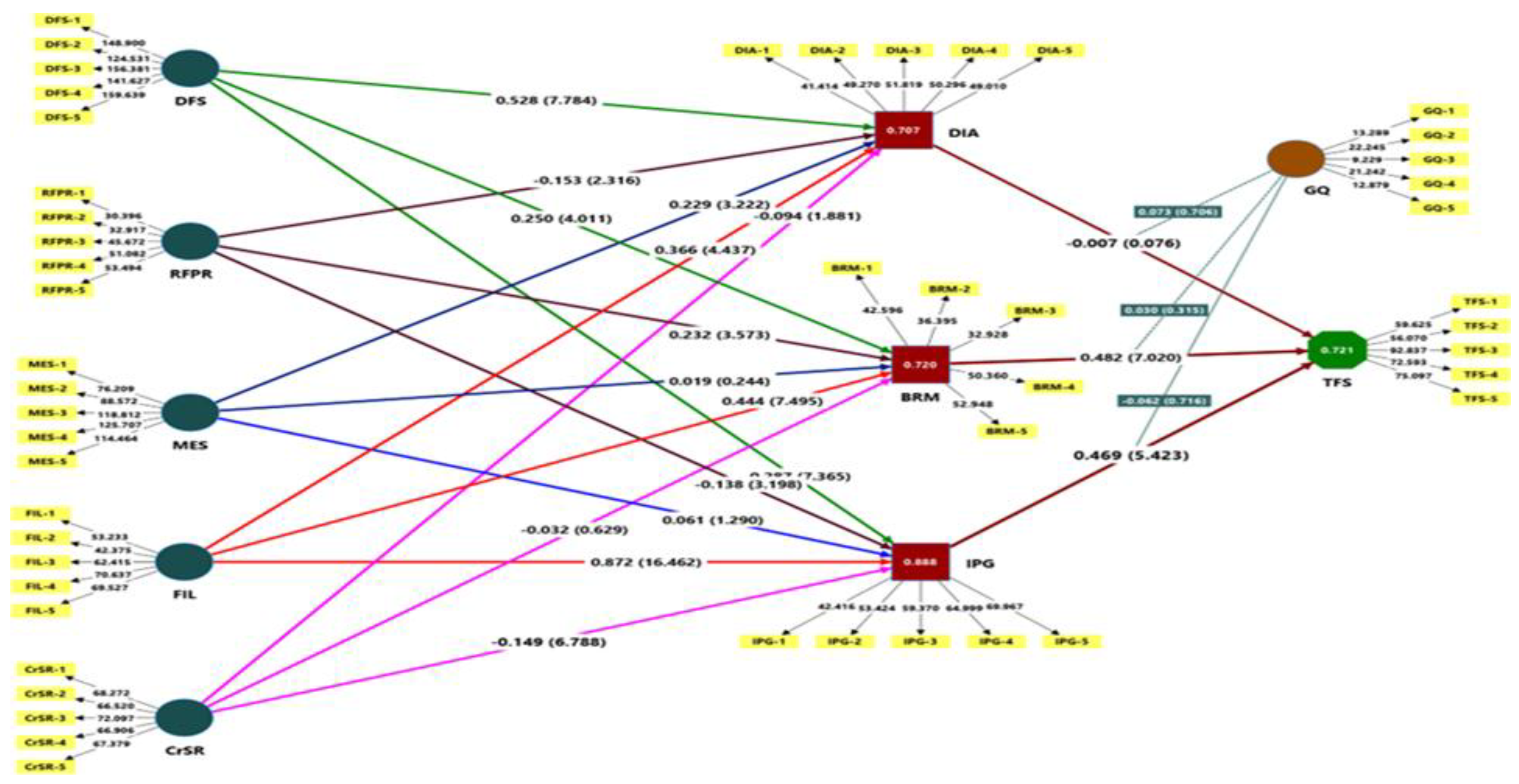

The reliability and validity of the measurement model were rigorously evaluated using multiple indicators. Cronbach's Alpha and Composite Reliability metrics both surpass the recommended threshold of 0.70, signifying robust internal consistency across all constructs. Specifically, the Cronbach's alpha values ranged from 0.781 for the GQ to 0.977 for DFS, while the Composite Reliability values ranged from 0.844 for the GQ to 0.982 for DFS. (See Table 1 & Figure 2). Furthermore, the Average Variance Extracted (AVE) values exceed the 0.50 benchmark, affirming the model's convergent validity. Notably, the constructs DFS and MES demonstrated the highest AVE values of 0.915 and 0.818, respectively.

4.2. Heterotrait-monotrait ratio (HTMT) - Matrix

Discriminant validity was assessed using the Heterotrait-Monotrait Ratio (HTMT). As mentioned in Table 2 the results confirmed the distinctiveness of the constructs. All the HTMT values were below the critical threshold of 0.85, thereby reinforcing the discriminant validity of the measurement model. For instance, the HTMT value between BRM and CrSR was 0.737 and the HTMT value between GQ and TFS was 0.323, both of which were well below the threshold, indicating that these constructs were adequately distinct from each other.

4.3. R-square Values

The R-squared values serve as indicators of the extent to which independent variables can predict dependent variables. The R-squared values for the dependent constructs are as follows: BRM = 0.720, DIA = 0.707, IPG = 0.888, and TFS = 0.72 (see Table 3). These values demonstrate that the independent variables account for a significant portion of the variance in the dependent variables, with IPG showing the highest explanatory power.

4.4. F-square

The F-square values, which measure the effect size of predictors on the dependent variables, provide several significant insights. Notably, the FIL exhibited a substantial effect on IPG, as evidenced by an F-square value of 1.775. In contrast, constructs such as CrSR and MES demonstrated negligible effects, with their F-square values approaching zero in most cases (see Table 4).

4.5. Collinearity Statistics (VIF)

To assess potential multicollinearity, the Variance Inflation Factor (VIF) was calculated. As stated in Table 5 the most of VIF values are below the critical threshold of 5, suggesting that multicollinearity is not a significant issue. However, MES exhibits a VIF value of 4.821, indicating mild multicollinearity, while IPG has the highest VIF value of 4.315, which remains below the critical limit.

4.6. Structural Model Analysis

The measurement model demonstrates commendable reliability and validity, as reflected by the acceptable levels of Cronbach's Alpha, Composite Reliability, and Average Variance Extracted (AVE). The constructs show strong discriminant validity, as indicated by the heterotrait-monotrait (HTMT) ratio results. The model effectively accounts for a significant portion of the variance in the dependent variables, with a notable impact on IPG, and does not present issues of multicollinearity because the Variance Inflation Factor (VIF) values are within permissible limits. These results confirm that the measurement model is robust and appropriate for further analytical research.

4.7. Path Coefficient

Table 6.

Path Coefficient Results, T-Statistics, and P-Values for the Structural Model Linking Financial, Policy, and Governance Variables to Target Financial Stability (PLS-SEM Analysis).

Table 6.

Path Coefficient Results, T-Statistics, and P-Values for the Structural Model Linking Financial, Policy, and Governance Variables to Target Financial Stability (PLS-SEM Analysis).

| Original Sample (O) | Sample Mean (M) | Standard Deviation (STDEV) | T Statistics (|O/STDEV|) | P Values | |

|---|---|---|---|---|---|

| BRM -> TFS | 0.482 | 0.486 | 0.069 | 7.020 | 0.000 |

| CrSR -> BRM | -0.032 | -0.028 | 0.052 | 0.629 | 0.530 |

| CrSR -> DIA | -0.094 | -0.094 | 0.050 | 1.881 | 0.060 |

| CrSR -> IPG | -0.149 | -0.148 | 0.022 | 6.788 | 0.000 |

| DFS -> BRM | 0.250 | 0.241 | 0.062 | 4.011 | 0.000 |

| DFS -> DIA | 0.528 | 0.529 | 0.068 | 7.784 | 0.000 |

| DFS -> IPG | 0.287 | 0.287 | 0.039 | 7.365 | 0.000 |

| DIA -> TFS | -0.007 | -0.012 | 0.087 | 0.076 | 0.939 |

| FIL -> BRM | 0.444 | 0.446 | 0.059 | 7.495 | 0.000 |

| FIL -> DIA | 0.366 | 0.370 | 0.082 | 4.437 | 0.000 |

| FIL -> IPG | 0.872 | 0.874 | 0.053 | 16.462 | 0.000 |

| GQ -> TFS | -0.065 | -0.058 | 0.038 | 1.713 | 0.087 |

| GQ x BRM -> TFS | 0.030 | 0.019 | 0.095 | 0.315 | 0.753 |

| GQ x DIA -> TFS | 0.073 | 0.083 | 0.103 | 0.706 | 0.480 |

| GQ x IPG -> TFS | -0.062 | -0.062 | 0.087 | 0.716 | 0.474 |

| IPG -> TFS | 0.469 | 0.470 | 0.086 | 5.423 | 0.000 |

| MES -> BRM | 0.019 | 0.015 | 0.079 | 0.244 | 0.808 |

| MES -> DIA | 0.229 | 0.232 | 0.071 | 3.222 | 0.001 |

| MES -> IPG | 0.061 | 0.062 | 0.047 | 1.290 | 0.197 |

| RFPR -> BRM | 0.232 | 0.239 | 0.065 | 3.573 | 0.000 |

| RFPR -> DIA | -0.153 | -0.160 | 0.066 | 2.316 | 0.021 |

| RFPR -> IPG | -0.138 | -0.141 | 0.043 | 3.198 | 0.001 |

4.8. Specific Indirect Effect

The analysis presented herein evaluates the direct and indirect effects among a set of key variables influencing TFS (target financial stability) within a structural equation modeling (SEM) framework. The results highlight significant direct relationships and reveal intricate pathways of indirect influence. The study provides robust evidence of the dynamics that shape TFS, with significant contributions from FIL (financial leverage), DFS (digital financial services), RFPR (regulatory financial performance), and IPG (innovation performance growth).

4.9. Hypothesis test with Direct Effects

The path coefficients of the structural model reveal the distinct influence of various constructs on target financial stability (TFS). The direct impact of bank resolution mechanisms (BRM) on TFS (β = 0.482, p = 0.000) is both significant and substantial, (see Table 6 and Figure 2) emphasizing the crucial role of effective resolution policies and crisis management frameworks in maintaining financial stability. This result is consistent with the existing literature, which highlights the importance of robust regulatory interventions and structured resolution processes in the banking sector to mitigate systemic risks. The relationship between Financial Inclusion & Literacy (FIL) and Insurance Policy Guarantee (IPG) is most pronounced in the model (β = 0.872, p = 0.000), suggesting that increased financial leverage significantly enhances innovation capabilities within financial institutions. These finding underscores FIL as a key driver of technological advancement and operational efficiency, which supports sustained innovation performance. Digitalization of the Financial Sector (DFS) also emerged as a significant enabler of innovation performance growth (β = 0.528, p = 0.000). This positive association indicates that the ongoing digitization of financial services contributes meaningfully to the development and adoption of innovative practices and technologies, thereby enhancing institutional agility and competitiveness. Insurance Policy Guarantee (IPG) itself exerts a notable direct effect on TFS (β = 0.469, p = 0.000), reinforcing the importance of fostering a culture of innovation to achieve and maintain long-term financial stability. This finding supports the literature on the pivotal role of technological innovation and process improvements in strengthening the resilience and sustainability of the financial sector. Conversely, several direct effects in the model are marginal or statistically insignificant. The path from cybersecurity risk (CrSR) to Deposit Insurance Adequacy (DIA) (β = –0.094, p = 0.060) approaches significance, but does not meet conventional thresholds, suggesting a limited direct impact. Similarly, the direct effect of DIA on TFS (β = –0.007, p = 0.939) is negligible, indicating that, in this context, the adoption of digital innovation does not translate directly into enhanced financial stability. These outcomes imply that, while digital innovation adoption remains an important area of interest, its influence may be more nuanced, potentially operating through indirect or mediated pathways rather than direct effects on financial stability. Overall, the findings provide clear evidence that robust regulatory frameworks, strategic financial leverage, and emphasis on innovation are central to achieving financial stability, whereas the direct role of digital innovation adoption may require further exploration through alternative model specifications or longitudinal designs.

4.10. Hypothesis test with Indirect Effects

The examination of indirect effects yields significant insights into the intricate relationships among variables as shown in Table 7, CrSR → IPG → TFS (-0.070, p = 0.000), and the indirect pathway from CrSR (credit risk) to TFS via IPG indicates a statistically significant negative impact. This suggests that, while increased credit risk may stimulate innovation, it can also contribute to financial instability by increasing performance volatility. This finding underscores the dual role of credit risk, which can both promote innovation and threaten financial stability under certain conditions. DFS → IPG → TFS (0.135, p = 0.000): The indirect effect of DFS on TFS through IPG is both significant and positive, reinforcing the direct pathway and demonstrating that digital financial services not only directly enhance innovation performance but also support financial stability through improved technological integration. FIL -> IPG -> TFS (0.409, p = 0.000): The indirect effect of FIL on TFS through IPG is substantial, amplifying the already significant direct path from FIL to IPG. This result highlights the crucial role of financial leverage in driving innovation, which contributes to financial stability. RFPR -> IPG -> TFS (-0.065, p = 0.006): The significant negative indirect effect of RFPR (regulatory financial performance) on TFS through IPG suggests that inadequate regulatory performance may impede the innovation potential of financial institutions, thereby undermining long-term stability.

4.11. Hypothesis with Non-Significant Effects

While several direct and indirect relationships yield significant results, others exhibit non-significant paths. These include MES -> DIA -> TFS (-0.002, p = 0.944) and MES -> BRM -> TFS (0.009, p = 0.811): Both MES (market environment signals) and BRM fail to show a meaningful direct or indirect impact on TFS, suggesting that these variables may have limited relevance in the context of this study or may require further refinement in model specification.

GQ x BRM -> TFS (0.030, p = 0.753): The interaction effect between GQ (government quality) and BRM does not significantly influence TFS, which may indicate that government quality, while important, does not directly affect the effectiveness of bank resolution mechanisms in driving financial stability.

5. Discussion

The findings of this study emphasize the crucial role of regulatory frameworks and financial leverage in advancing the modernization of the financial sector. The pronounced effects of Financial Inclusion Levels (FIL) and Digital Financial Services (DFS) on both innovation and financial stability underscore the necessity for well-crafted regulatory policies and strategic financial instruments to stimulate innovation. Thus, policymakers are urged to fortify these mechanisms to cultivate a more dynamic and resilient financial environment. Innovation, particularly through Inclusive Product Growth (IPG), is identified as a significant driver of Technological Financial Stability (TFS). This observation is consistent with the prevailing view in academic and policy discussions that technological progress not only propels growth but is also essential for sustaining long-term financial stability. This study further reveals the complex and interdependent relationships among variables affecting financial outcomes. The presence of indirect effects, particularly those facilitated by IPG, highlights the multifaceted nature of financial stability. These findings advocate a comprehensive and integrated approach that simultaneously addresses regulatory policies and innovation strategies to effectively manage the complexities of the contemporary financial landscape.

6. Conclusions

This study highlights the increasing recognition that financial stability in the digital era is influenced by factors beyond traditional risk management, with a growing emphasis on the integration of innovation, regulatory adaptability, and inclusive financial systems. The study's findings emphasize the critical role of digital financial services and the expansion of inclusive products in strengthening systemic resilience. However, it is crucial that innovation is underpinned by strong regulatory frameworks to ensure that technological progress is enhanced rather than undermined by stability. These insights have significant implications for Indonesia. As the financial sector undergoes rapid digital transformation, entities such as the Indonesia Deposit Insurance Corporation (Lembaga Penjamin Simpanan or LPS) must adapt strategically. Financial stability can no longer be sustained by static tools alone; it necessitates a comprehensive approach anchored in digitalization, supported by effective deposit insurance, directed by robust bank resolution mechanisms, and reinforced through clear policy guarantee frameworks. LPS is at a critical juncture, with its future role extending beyond depositor protection to shape the broader financial stability agenda. By leveraging digital innovation, enhancing regulatory coordination, and strengthening its resolution and policy frameworks, LPS can transition from a reactive safety net to a proactive stabilizer within Indonesia’s financial ecosystem. The path to sustainable financial stability lies in adopting a forward-looking strategy in which innovation, regulation, and strategic institutional reform operate in concert. For Indonesia, equipping LPS with these tools and mandates will be essential for building a resilient, inclusive, and future-ready financial system. For policymakers and financial leaders, the message is clear: fostering innovation and enhancing regulatory capacity are complementary goals. By simultaneously advancing both, countries can develop financial systems that are more resilient, more inclusive, and better prepared for future disruptions. Ultimately, this study underscores that financial stability is no longer solely related to risk management. It involves embracing change with a thoughtful, coordinated approach that leverages technology, safeguards users, and maintains system strength both now and in the future..

This study, while offering valuable insights into financial stability, digitalization, and regulatory frameworks, has several significant limitations. First, the analysis relies on survey data from the Indonesian financial sector, which may limit findings' applicability to countries with different economic structures and digital advancement stages. Future research should conduct multi-country analyses to expand these results. Second, although the sampling strategy included financial professionals, it may not fully represent the entire financial industry's perspectives, potentially underrepresenting smaller entities, fintech start-ups, or consumer stakeholders. Third, while the research identifies critical relationships among variables, the cross-sectional survey design limits causal inference and mediation analysis, as temporal sequencing cannot be definitively established (Maxwell & Cole, 2007; Rungtusanatham et al., 2014). Findings related to indirect effects should be interpreted cautiously, and future longitudinal research would provide stronger causal analysis. Finally, the rapidly evolving landscape of financial technologies and regulations suggests these findings may become less relevant as the sector transforms. Continuous research will be essential to maintain practical insights as the industry evolves.

Declaration of Funding

This research is carried out without any financial support from funding agencies, institutions, commercial entities. All expenses related to the study were covered by the authors as part of their academic work.

AI Statement

We declare, No AI contributed to the creation of concepts, data interpretation, or conclusions. Paperpal and quiltbolt as AI tools were used only to enhance the clarity of writing, grammar, and presentation. The ideas, analysis, and interpretations presented in this work are entirely the author’s own.

Ethical Approval Statement

Ethical approval was not required for this study as it involved anonymous, voluntary participation with minimal risk. The study followed the ethical standards of social science research and the principles of the Declaration of Helsinki.

Data Availability statement

The data that support the findings of this study are openly available in Zenodo at https://doi.org/10.5281/zenodo.17561961.

References

- Ahamed, M. M.; Mallick, S. K. Is financial inclusion good for bank stability? International evidence. Journal of Economic Behavior & Organization 2019, 157, 403–427. [Google Scholar] [CrossRef]

- Alamsyah, H.; Ariefianto, M. D.; Saheruddin, H.; Wardono, S.; Trinugroho, I. Depositors’ trust: Some empirical evidence from Indonesia. Research in International Business and Finance 2020, 54, 101251. [Google Scholar] [CrossRef]

- Anginer, D.; Demirgüç-Kunt, A.; Zhu, M. How does competition affect bank systemic risk? Journal of Financial Intermediation 2014, 23(1), 1–26. [Google Scholar] [CrossRef]

- Anderson, J. C.; Gerbing, D. W. Structural equation modeling in practice: A review and recommended two-step approach. Psychological Bulletin 1988, 103(3), 411–423. [Google Scholar] [CrossRef]

- Arner, D. W.; Barberis, J. N.; Buckley, R. P. Fintech, RegTech, and the reconceptualization of financial regulation. Northwestern Journal of International Law & Business 2016, 37(3), 371–414. [Google Scholar]

- Bank for International Settlements. Operational resilience: Lessons from the COVID-19 pandemic and cyber risk (Basel Committee on Banking Supervision Report No. d516. 2021. Available online: https://www.bis.org/bcbs/publ/d516.pdf.

- Barua, B.; Barua, S. COVID-19 implications for banks: Evidence from an emerging economy. SN Business & Economics 2021, 1, 13. [Google Scholar] [CrossRef]

- Beck, T.; Demirgüç-Kunt, A.; Levine, R. Bank concentration, competition, and crises: First results. Journal of Banking & Finance 2006, 30(5), 1581–1603. [Google Scholar] [CrossRef]

- Birindelli, G.; Iannuzzi, A. P. The systemic importance of cyber risk in banks. In Systemic risk and complex networks in modern financial systems (New Economic Windows); Pacelli, V., Ed.; Springer; Cham, 2025. [Google Scholar] [CrossRef]

- Birindelli, G.; Iannuzzi, A. P. The systemic importance of cyber risk in banks. In Systemic risk and complex networks in modern financial systems (New Economic Windows); Pacelli, V., Ed.; Springer; Cham, 2025. [Google Scholar] [CrossRef]

- Bouveret, A. Cyber risk for the financial sector: A framework for quantitative assessment (IMF Working Paper No. 18/143). International Monetary Fund. 2018. Available online: https://www.imf.org/en/Publications/WP/Issues/2018/07/13/Cyber-Risk-for-the-Financial-Sector-A-Framework-for-Quantitative-Assessment-46093.

- Boot, A. W. A.; Thakor, A. V. Banks and financial markets in a digital age: Understanding the future of banking in an increasingly diffuse financial system. In The Oxford handbook of banking, Berger, A. N., Molyneux, P., Wilson, J. O. S., Eds.; 4th ed.; Oxford University Press, 2025; pp. xx–xx. [Google Scholar] [CrossRef]

- Claessens, S. An overview of macroprudential policy tools. Annual Review of Financial Economics 2015, 7, 397–422. [Google Scholar] [CrossRef]

- Calomiris, C. W.; Herring, R. J. How to design a contingent convertible debt requirement that helps solve our too big to fail problem. Journal of Applied Corporate Finance 2013, 25(2), 39–62. [Google Scholar] [CrossRef]

- Cohen, L. H.; Towbes, L. C.; Flocco, R. Effects of induced mood on self-reported life events and perceived and received social support. Journal of Personality and Social Psychology 1988, 55(4), 669–674. [Google Scholar] [CrossRef]

- Corelli, A. The future of financial risk management. In Understanding financial risk management, 2nd ed.; Emerald Publishing Limited, 2019; pp. 515–541. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, A.; Detragiache, E. Does deposit insurance increase banking system stability? An empirical investigation. Journal of Monetary Economics 2002, 49(7), 1373–1406. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, A.; Kane, E. J. Deposit insurance around the globe: Where does it work? Journal of Economic Perspectives 2002, 16(2), 175–195. [Google Scholar] [CrossRef]

- Dupas, P.; Karlan, D.; Robinson, J.; Ubfal, D. Banking the unbanked? Evidence from three countries. American Economic Journal: Applied Economics 2018, 10(2), 257–297. [Google Scholar] [CrossRef]

- Eisenbeiss, M.; Blechschmidt, B.; Backhaus, K.; Freund, P. A. “The (real) world is not enough:” Motivational drivers and user behavior in virtual worlds. Journal of Interactive Marketing 2012, 26(1), 4–20. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D. F. Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research 1981, 18(1), 39–50. [Google Scholar] [CrossRef]

- Garcia, G. G. Deposit insurance: Actual and good practices; International Monetary Fund, 2000; Volume Occasional Papers No. 197. [Google Scholar] [CrossRef]

- Grohmann, A.; Klühs, T.; Menkhoff, L. Does financial literacy improve financial inclusion? Cross-country evidence. World Development 2018, 111, 84–96. [Google Scholar] [CrossRef]

- Hair, J. F.; Risher, J. J.; Sarstedt, M.; Ringle, C. M. When to use and how to report the results of PLS-SEM. European Business Review 2019, 31(1), 2–24. [Google Scholar] [CrossRef]

- Hair, J.; Alamer, A. Partial least squares structural equation modeling (PLS-SEM) in second language and education research: Guidelines using an applied example. Research Methods in Applied Linguistics 2022, 1(3), 100027. [Google Scholar] [CrossRef]

- Hu, L. T.; Bentler, P. M. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling 1999, 6(1), 1–55. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C. M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science 2015, 43(1), 115–135. [Google Scholar] [CrossRef]

- International Monetary Fund. Global financial stability report: Managing risks in an uneven recovery. October 2021. Available online: https://www.imf.org/en/Publications/GFSR/Issues/2021/10/12/global-financial-stability-report-october-2021.

- Jungo, J.; Madaleno, M.; Botelho. A. Financial Literacy, Financial Innovation, and Financial Inclusion as Mitigating Factors of the Adverse Effect of Corruption on Banking Stability Indicators. J Knowl Econ 2024, 15, 8842–8873. [Google Scholar] [CrossRef]

- Kaufmann, D.; Kraay, A.; Mastruzzi, M. Governance matters VII: Aggregate and individual governance indicators. In World Bank Policy Research Working Paper No. 4654; World Bank, 2008. [Google Scholar] [CrossRef]

- Laeven, L.; Valencia, F. Systemic banking crises database. IMF Economic Review 2013, 61(2), 225–270. [Google Scholar] [CrossRef]

- Laeven, L.; Valencia, F. Systemic banking crises database II. IMF Economic Review 2020, 68(2), 307–361. [Google Scholar] [CrossRef]

- La Porta, R.; Lopez-de-Silanes, F.; Shleifer, A.; Vishny, R. W. Law and finance. Journal of Political Economy 1998, 106(6), 1113–1155. [Google Scholar] [CrossRef]

- MacKenzie, S. B.; Podsakoff, P. M.; Podsakoff, N. P. Construct measurement and validation procedures in MIS and behavioral research: Integrating new and existing techniques. MIS Quarterly 2011, 35(2), 293–334. [Google Scholar] [CrossRef]

- OECD. OECD economic surveys: Indonesia 2022. OECD Publishing, 2022; Available online: https://www.oecd-ilibrary.org/economics/oecd-economic-surveys-indonesia-2022_20725108.

- Ozili, P. K. The acceptable R-square in empirical modelling for social science research. In Advances in Knowledge Acquisition, Transfer, and Management; IGI Global, 2023; pp. 134–143. [Google Scholar] [CrossRef]

- Philippon, T. The great reversal: How America gave up on free markets; Harvard University Press, 2019. [Google Scholar] [CrossRef]

- Preacher, K. J.; Hayes, A. F. Asymptotic and resampling strategies for assessing and comparing indirect effects in multiple mediator models. Behavior Research Methods 2008, 40(3), 879–891. [Google Scholar] [CrossRef]

- Richard, P. J.; Devinney, T. M.; Yip, G. S.; Johnson, G. Measuring organizational performance: Towards methodological best practice. Journal of Management 2009, 35(3), 718–804. [Google Scholar] [CrossRef]

- Sarstedt, M.; Ringle, C. M.; Hair, J. F. Partial least squares structural equation modeling. In Handbook of Market Research; Homburg, C., Klarmann, M., Vomberg, A. E., Eds.; Springer; Cham, 2021; pp. 1–47. [Google Scholar] [CrossRef]

- World Bank. Indonesia economic prospects: Financial deepening for stronger growth and sustainable recovery [PDF]. World Bank. June 2022. Available online: https://documents1.worldbank.org/curated/en/099314106202223202/pdf/IDU087850cba0b204043f608dea019acef5f2be1.pdf.

- World Bank. Indonesia economic prospects: Financial deepening for stronger growth and sustainable recovery [PDF]. World Bank. June 2022. Available online: https://documents1.worldbank.org/curated/en/099314106202223202/pdf/IDU087850cba0b204043f608dea019acef5f2be1.pdf.

- Yang, J.; Ali, M. Y. Digital financial inclusion and bank stability: Insights from Bangladesh; International Journal of Banking, Accounting and Finance. Advance online publication., 2024. [Google Scholar] [CrossRef]

- Yukl, G. Leadership: What is it? In Cases in leadership, 3rd ed.; Sage, 2012; pp. 1–42. [Google Scholar]

- Zetzsche, D. A.; Buckley, R. P.; Barberis, J. N.; Arner, D. W. Regulating a revolution: From regulatory sandboxes to smart regulation. Fordham Journal of Corporate & Financial Law 2017, 23, 31–103. [Google Scholar]

Figure 1.

Conceptual Framework/ Authors Own Creation.

Figure 2.

Structural Model Results Using PLS-SEM: Figure 2 about here.

Figure 2.

Structural Model Results Using PLS-SEM: Figure 2 about here.

Table 1.

Measurement Model Assessment - Construct Reliability and Convergent Validity.

| Cronbach's Alpha | rho_A | Composite Reliability | Average Variance Extracted (AVE) | |

|---|---|---|---|---|

| BRM | 0.897 | 0.900 | 0.924 | 0.709 |

| CrSR | 0.915 | 0.916 | 0.937 | 0.747 |

| DFS | 0.977 | 0.979 | 0.982 | 0.915 |

| DIA | 0.914 | 0.916 | 0.936 | 0.744 |

| FIL | 0.918 | 0.918 | 0.938 | 0.753 |

| GQ | 0.781 | 0.795 | 0.844 | 0.522 |

| IPG | 0.925 | 0.926 | 0.944 | 0.771 |

| MES | 0.944 | 0.947 | 0.957 | 0.818 |

| RFPR | 0.897 | 0.906 | 0.923 | 0.707 |

| TFS | 0.928 | 0.928 | 0.945 | 0.776 |

Table 2.

Measurement Model Assessment - Discriminant Validity.

| BRM | CrSR | DFS | DIA | FIL | GQ | IPG | MES | RFPR | TFS | GQ x DIA | GQ x BRM | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| BRM | ||||||||||||

| CrSR | 0.737 | |||||||||||

| DFS | 0.806 | 0.824 | ||||||||||

| DIA | 0.664 | 0.728 | 0.843 | |||||||||

| FIL | 0.793 | 0.788 | 0.824 | 0.840 | ||||||||

| GQ | 0.407 | 0.538 | 0.785 | 0.578 | 0.461 | |||||||

| IPG | 0.838 | 0.713 | 0.835 | 0.825 | 0.703 | 0.505 | ||||||

| MES | 0.764 | 0.807 | 0.772 | 0.766 | 0.844 | 0.490 | 0.775 | |||||

| RFPR | 0.828 | 0.795 | 0.790 | 0.698 | 0.835 | 0.727 | 0.757 | 0.842 | ||||

| TFS | 0.778 | 0.569 | 0.699 | 0.668 | 0.735 | 0.323 | 0.848 | 0.607 | 0.727 | |||

| GQ x DIA | 0.372 | 0.345 | 0.428 | 0.293 | 0.357 | 0.354 | 0.423 | 0.329 | 0.347 | 0.310 | ||

| GQ x BRM | 0.114 | 0.206 | 0.311 | 0.373 | 0.237 | 0.204 | 0.321 | 0.188 | 0.151 | 0.153 | 0.816 | |

| GQ x IPG | 0.313 | 0.344 | 0.430 | 0.413 | 0.292 | 0.314 | 0.356 | 0.317 | 0.269 | 0.262 | 0.809 | 0.778 |

Table 3.

Structural Model Assessment - Explanatory Power (R² and Adjusted R²).

| R Square | R Square Adjusted | |

|---|---|---|

| BRM | 0.720 | 0.714 |

| DIA | 0.707 | 0.701 |

| IPG | 0.888 | 0.886 |

| TFS | 0.721 | 0.713 |

Table 4.

Effect Size (f²) of Predictor Constructs on Endogenous Constructs.

| BRM | DIA | IPG | TFS | |

|---|---|---|---|---|

| BRM | 0.245 | |||

| CrSR | 0.001 | 0.007 | 0.047 | |

| DFS | 0.062 | 0.265 | 0.205 | |

| DIA | 0.000 | |||

| FIL | 0.184 | 0.120 | 1.775 | |

| GQ | 0.010 | |||

| IPG | 0.125 | |||

| MES | 0.000 | 0.037 | 0.007 | |

| RFPR | 0.057 | 0.023 | 0.050 | |

| TFS | ||||

| GQ x DIA | 0.002 | |||

| GQ x BRM | 0.001 | |||

| GQ x IPG | 0.001 |

Table 5.

Inner Model Collinearity Diagnostics (VIF Values).

| BRM | DIA | IPG | TFS | |

|---|---|---|---|---|

| BRM | 3.394 | |||

| CrSR | 4.226 | 4.226 | 4.226 | |

| DFS | 3.592 | 3.592 | 3.592 | |

| DIA | 3.603 | |||

| FIL | 3.815 | 3.815 | 3.815 | |

| GQ | 1.539 | |||

| IPG | 4.315 | |||

| MES | 4.821 | 4.821 | 4.821 | |

| RFPR | 3.378 | 3.378 | 3.378 | |

| TFS | ||||

| GQ x DIA | 3.483 | |||

| GQ x BRM | 3.371 | |||

| GQ x IPG | 3.001 |

Table 7.

Specific Indirect Effects.

| Original Sample (O) | Sample Mean (M) | Standard Deviation (STDEV) | T Statistics (|O/STDEV|) | P Values | |

|---|---|---|---|---|---|

| CrSR -> IPG -> TFS | -0.070 | -0.070 | 0.017 | 4.097 | 0.000 |

| DFS -> IPG -> TFS | 0.135 | 0.134 | 0.030 | 4.447 | 0.000 |

| CrSR -> DIA -> TFS | 0.001 | 0.001 | 0.009 | 0.066 | 0.947 |

| FIL -> IPG -> TFS | 0.409 | 0.411 | 0.083 | 4.930 | 0.000 |

| DFS -> DIA -> TFS | -0.004 | -0.008 | 0.047 | 0.074 | 0.941 |

| CrSR -> BRM -> TFS | -0.016 | -0.013 | 0.025 | 0.613 | 0.540 |

| FIL -> DIA -> TFS | -0.002 | -0.002 | 0.032 | 0.075 | 0.940 |

| MES -> IPG -> TFS | 0.028 | 0.029 | 0.023 | 1.256 | 0.210 |

| DFS -> BRM -> TFS | 0.121 | 0.116 | 0.033 | 3.687 | 0.000 |

| RFPR -> IPG -> TFS | -0.065 | -0.066 | 0.024 | 2.750 | 0.006 |

| FIL -> BRM -> TFS | 0.214 | 0.218 | 0.050 | 4.293 | 0.000 |

| MES -> DIA -> TFS | -0.002 | -0.004 | 0.021 | 0.071 | 0.944 |

| RFPR -> DIA -> TFS | 0.001 | 0.002 | 0.015 | 0.067 | 0.947 |

| MES -> BRM -> TFS | 0.009 | 0.006 | 0.039 | 0.240 | 0.811 |

| RFPR -> BRM -> TFS | 0.112 | 0.116 | 0.037 | 3.023 | 0.003 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.