Submitted:

04 November 2025

Posted:

04 November 2025

You are already at the latest version

Abstract

This study examines the impact of Environmental, Social, and Governance (ESG) strategies on reducing air pollution in the West Kazakhstan region, a major hub for Kazakhstan's oil and gas industry. A spatial analysis of atmospheric emissions reveals an uneven distribution of emission sources, predominantly concentrated in the northern industrialized part of the region, where the Karachaganak oil and gas condensate field is located. The ESG model of Karachaganak Petroleum Operating b.v. (KPO), implemented as an integrated management system based on Global Reporting Initiative (GRI) standards, is compared with the ESG strategies of leading oil and gas companies in Kazakhstan and globally, aligning with current international research trends. The analysis underscores the interdependence of technological and social aspects in the transition to a low-carbon economy, confirming the importance of integrating the environmental, social, and governance components of ESG into a unified strategic planning framework for sustainable development. Using econometric modeling, the study establishes a relationship between ESG indicators and the reduction of atmospheric pollution and provides a forecast for emission reductions by 2030. The key measures proposed to improve regional air quality are linked to long-term decarbonization strategies within the context of the sustainable development of the entire region. The proposed algorithm for implementing ESG principles helps to identify the concentration of functions and associated risks at different management levels within Highly Polluting Enterprises (HPEs) and optimizes business processes by focusing efforts on air pollution mitigation. The findings are applicable to other countries, as oil and gas producers worldwide face a number of common air pollution challenges.

Keywords:

air pollution

; ESG strategy

; sustainable development

; energy efficiency

; best available techniques

; corporate social responsibility

1. Introduction

Highlights

-This study investigates the impact of ESG principles on air pollution reduction in the West Kazakhstan region. Spatial analysis of atmospheric emissions reveals an uneven distribution of pollution sources, with the highest concentration observed in the northern part of the region.

-The relationships between key ESG indicators and reductions in air pollution were identified using econometric modeling.

-The findings demonstrate that the implementation of ESG strategies effectively reduces atmospheric emissions by promoting the adoption of best available techniques and enhancing corporate environmental responsibility.

Fossil fuel pollution represents a fundamental challenge for the modern economy, with detrimental impacts on the climate, environment, and human health [1]. Intensive oil and gas production is a primary source of carbon dioxide and other greenhouse gas (GHG) emissions, which are major drivers of climate change. The world’s 60 largest oil and gas companies were responsible for over 40% of global cumulative industrial emissions from 1988 to 2015 [2], a trend that continued as global fossil fuel emissions reached a record high in 2023 [3].

The scientific concept of sustainable development is now operationalized through more specific ESG standards, which encompass environmental, social, and governance dimensions. Integrating ESG criteria into decision-making, alongside traditional economic metrics, has emerged as a promising mechanism for advancing the green economy and enabling low-carbon development [4].

As governments worldwide establish net-zero emissions targets, energy companies face increasing pressure to incorporate ESG principles into their business models. Effectively reducing atmospheric emissions within an ESG framework requires an integrated approach and continuous monitoring to achieve set goals and generate a positive environmental impact.

The substantial impact of the oil and gas sector on atmospheric pollution necessitates a shift in strategic management approaches, extending beyond individual companies to encompass the entire industry. Integrating the environmental aspects of the sector’s development into a national socio-economic strategy is a critical tool for addressing ecological challenges and achieving broader socio-economic objectives [5]. Research on strategic management increasingly emphasizes the implementation of sustainable management principles, as traditional strategic management alone is insufficient to meet contemporary demands.

Consequently, these findings underscore the importance of incorporating social and technological dimensions into corporate carbon reduction strategies. They further validate the strategic value of investing in renewable energy and fostering a gender-sensitive corporate environment as integral components of a comprehensive ESG approach.

This study aims to analyze pathways for reducing air pollution in the West Kazakhstan region by applying novel environmental assessment approaches grounded in ESG principles. To achieve this aim, the following objectives are established:

- To assess the impact of ESG adoption on air pollution reduction in the West Kazakhstan region, a key oil and gas producing area in Kazakhstan.

- To perform a spatial analysis of atmospheric emissions in the region to evaluate the environmental impact of the KPO company, which develops the Karachaganak oil and gas condensate field.

- To analyze the effectiveness of ESG strategy implementation at KPO, benchmarking its performance against leading national and international oil and gas companies within a sustainable development framework.

- To develop an ESG algorithm for evaluating recurring functions and identifying operations with concentrated ESG risks. This algorithm will integrate the environmental, social, and governance components of ESG into a unified strategic planning system for sustainable development.

- To perform a correlation-regression analysis examining the relationship between atmospheric emission levels and the E, S, and G factors of the ESG model for the selected oil and gas companies, and to provide a predictive assessment of ESG’s influence on emission reduction.

The research questions and problem statement led to the formulation of the following hypothesis:

H1:

The implementation of ESG principles in corporate operations contributes to a reduction in regional air pollution.

This study posits that integrating ESG principles into the corporate governance of oil and gas companies facilitates the reduction of GHG and pollutant emissions. The effectiveness of these strategies is hypothesized to depend on the level of institutional maturity, the robustness of ESG reporting mechanisms, and specific geographic factors.

In Kazakhstan, the national low-carbon development strategy and the country’s commitments under the Paris Agreement have heightened the focus on regulating greenhouse gas emissions [6]. Given that KPO is a significant source of national GHG emissions, this research examines how the company’s ESG strategy can inform effective management decisions to reduce air pollution and advance decarbonization goals, thereby contributing to the sustainable development of the region.

The novelty of this study lies in the integrated application of econometric modeling and spatial analysis within a comprehensive framework. This approach examines the reduction of air pollution through an ESG strategy in the context of sustainable development for the entire region. While most research assesses the impact of ESG principles either on corporate financial performance—such as profit and market value—through social and governance indicators, or on environmental metrics solely through environmental indicators, this study adopts a distinct perspective. Its methodological significance stems from assessing the sensitivity of atmospheric emissions to the influence of indicators from all three ESG components simultaneously.

Furthermore, the experience of KPO holds practical relevance for other countries, as oil and gas companies worldwide face similar air pollution challenges. This is particularly applicable in regions with significant hydrocarbon reserves, such as Central Asia [7].

2. Materials and Methods

2.1. Object of the Study

This study focuses on companies classified within the HPE category, which are characterized by their industrial operations and significant environmental impact. The analysis specifically centers on KPO, one of the principal sources of air pollution in the West Kazakhstan region.

2.2. Research Methodology

This research employs an interdisciplinary methodology, integrating cartographic and statistical modeling with a comparative analysis of socio-economic, energy, and environmental indicators. It also includes a systematic review of atmospheric impact reduction policies in global and Kazakhstani contexts.

A comprehensive analysis was conducted on representative data from the Scopus database, covering air pollution issues and ESG trends from 2012 to 2024. Consistent with the study’s objectives, particular emphasis is placed on the environmental (E) component of the ESG triad.

Building on an examination of current practices in HPE-type companies, an algorithm was developed for an ESG strategy aimed at reducing air pollution through the implementation of Environmental Impact Assessment (EIA) principles.

Data were collected and selected based on comparability, relevance, and materiality criteria. To ensure systematic and objective analysis, the study benchmarks KPO’s performance against leading global oil and gas companies—Shell, Eni S.p.A., BP, and the Kazakh company KMG—examining their sustainable development goals, key trends, and ESG implementation challenges. The selection of these companies is justified by their participation, along with Chevron, in the KPO production sharing agreement (with BP included as an additional comparator). Chevron was excluded from detailed analysis due to largely unstandardized or unavailable ESG data, particularly for social (S) and governance (G) indicators. The collected data, covering the period 2019–2023, were systematized into panel data for analyzing ESG parameters.

Based on the theory of Lawrence D. Miles [8], “Algorithm of ESG Strategy for Reducing Air Pollution” maps were developed for each ESG component. These maps utilize color coding to facilitate the inventory and optimization of key functions during the implementation of an ESG strategy in oil and gas companies.

The relationships between ESG indicators and air pollution reduction were identified using econometric modeling in R. An element-by-element approach was applied to isolate the key factors driving emission reductions. Initial integration of all factors into a single model revealed the dominant influence of environmental (E) factors. Consequently, following the precedent of similar studies, social (S) and governance (G) factors were integrated for analysis, while environmental factors were evaluated independently. This methodological distinction yielded critical insights that form the basis for the presented practical recommendations.

This research builds upon the authors’ prior work [9], which analyzed the impact of KPO on regional development and the formation of a circular economy between 2012 and 2022. The current study continues this line of inquiry by focusing on the implementation of ESG strategies and enhancements in energy efficiency.

2.3. Data sources

This study utilizes three primary datasets. The key indicators are derived from internationally recognized frameworks, including GRI, ISO 14001:2015, ISO 50001:2018, ISO 26000, ISO 45001:2018, and standards from the International Association of Oil and Gas Producers (IOGP) [10,11,12,13,14,15]. These frameworks were selected for their global recognition, cross-industry applicability, user-friendly templates, and ongoing updates [16]. The first datasets comprise:

- 1.

- Environmental indicators.

- 2.

- Economic and energy indicators.

- 3.

- Social (S) and governance (G) performance indicators for the companies under study.

Data were collected from annual environmental bulletins of Kazakhstan for 2019–2023 [17,18]. The analysis of ESG factors relied on sustainability reports from KPO, Shell, Eni S.p.A., BP, and KMG for the same period [19,20,21,22,23,24], supplemented by GRI reports and Sustainability Reporting Guidelines [10,25].

Spatial analysis of air pollution was conducted using ArcMap 10.8. with data sourced from the Emissions Database for Global Atmospheric Research (EDGAR) [26]. The data processing involved spatial interpolation via spherical kriging, selected for its efficacy in smoothing regional data. A spherical and isotropic variogram model was applied to ensure a uniform and accurate representation of pollution distribution across the region. Map construction employed kriging interpolation, with the specific method—Ordinary Kriging or Universal Kriging—chosen based on data characteristics and spatial distribution.

The second dataset comprises economic and energy indicators for the aforementioned companies from 2019 to 2023, sourced from fact sheets, sustainability reports, and the Emissions Database for Global Atmospheric Research (EDGAR) [26]. Key metrics included the average annual emission growth rate, specific energy intensity (GJ/t), specific CO₂ emissions (t/1000t of extracted raw materials), and the share of renewable energy sources (%) in the energy balance, which characterizes production carbon intensity.

The third dataset encompasses social (S) and governance (G) indicators that reflect corporate performance. This information was extracted from the sustainability reports of KPO, Shell, Eni S.p.A., BP, and KMG for the period 2019–2023 (KPO, 2019-2023; SHELL, 2019-2023; ENI, 2019-2023; BP, 2019-2023; KazMunayGas, 2019-2023) [20,21,22,23,24].

The study faced several limitations in parameter selection:

- Varying reporting timelines: The sustainability reports of the analyzed companies covered different periods. To ensure comparability, the earliest common year for all five companies—2019—was selected as the baseline.

- Evolving reporting standards: Although the Sustainable Development Goals (SDGs) were adopted in 2015, the companies implemented GRI standards in different years. Furthermore, standardized requirements for the circular economy within ESG frameworks remain under development.

- Lack of standardized disclosure: Sustainability reports lack strict formatting requirements, allowing companies significant discretion in data presentation. Established practice shows that environmental (E) criteria are relatively standardized for indicators such as greenhouse gas emissions, net carbon intensity, energy consumption, and waste management. In contrast, no consensus exists regarding social (S) and governance (G) indicators, which complicates their analysis, comparative assessment, and interpretation.

Literature Review

ESG principles are increasingly recognized as a catalyst for technological innovation aimed at mitigating environmental pollution and addressing the drivers of climate change. While a substantial body of research has been dedicated to this field, the present study seeks to contextualize its relevance by systematically reviewing and classifying the existing literature into distinct thematic areas. This classification helps to identify prevailing research trends, gaps, and central debates.

Table 1.

Systematization of the results of the literature review in the direction of “The impact of ESG on reducing air pollution”.

Table 1.

Systematization of the results of the literature review in the direction of “The impact of ESG on reducing air pollution”.

| Direction | Works (authors) | Conclusions | Field of knowledge / application |

|---|---|---|---|

| The relevance of ESG application | [3,4,27,28,29,30,31,32,33,34,35,36,37] | ESG is seen as a tool for implementing the concept of sustainable development, a driving force for technological development that can help reduce environmental pollution and eliminate factors influencing climate change. | Economic research |

| Justification of the relevance of the research topic | |||

| Assessment of global, regional, and national greenhouse gas emissions | [2,38,39,40,41,42,43,44,45,46,47] | Growing global carbon emissions from fossil fuels are becoming one of the fundamental problems of the modern economy and require a comprehensive ESG approach that includes political regulators, technological, organizational, economic and social aspects. | Environmental research |

| Identification of factors, independent variables | |||

| Studying the best global practices of ESG transformation | [48,49,50,51,52,53,54,55] | The study of the best global practices in ESG transformation and sustainable development around the world has shown that ESG strategies are supported at the legislative level | Interdisciplinary research |

| Rationale for recommendations | |||

| Implementing ESG principles into the strategy of oil and gas companies | [56,57,58,59,60] | By integrating ESG principles, oil and gas companies can significantly improve their energy efficiency, which in turn helps reduce air pollution. | Economic research |

| Identification of factors, independent variables | |||

| Development of green technologies, sustainable and responsible investment | [61,62,63,64,65,66,67,68,69,70,71,72,73,74,75,76,77,78,79,80,81] | The applicability of ESG strategies is discussed from a macroeconomic perspective of regulatory policy. Due to the dominance of the climate and environmental components of ESG, insufficient attention is paid to the disclosure of environmental S.G. components. | Economic research |

| Justification of the relevance of the research topic Identification of factors, independent variables |

The preceding analysis identifies critical gaps in the literature on corporate ESG strategy implementation.

First, departing from prior research, this study employs non-financial performance indicators to conduct a pioneering comparative analysis of ESG strategy effectiveness in reducing air pollution. By benchmarking leading global and Kazakhstan’s oil and gas companies within a sustainable development framework, it integrates environmental, social, and governance indicators—constituting its primary novelty. While ESG has gained prominence in corporate sustainability discourse, scholarly focus has remained predominantly on its impact on economic metrics such as productivity, financial costs, risk, and foreign direct investment [54,55,62,64]. Although studies confirm significant indirect benefits from improved profitability and operational efficiency [68], the direct environmental impact of ESG in specific regional contexts remains underexplored.

The relevance of this approach is underscored by the limited research on ESG strategies for improving air quality in Kazakhstan. This study thus complements international scholarship by evaluating ESG efficacy in a context of high energy intensity and hydrocarbon dependency.

Second, a notable scarcity of data exists on how natural resource companies successfully integrate all three ESG components into a unified strategic planning system for sustainable development. The literature frequently addresses ESG from a macroeconomic and regulatory perspective [58,59], yet companies often lack the operational tools for practical implementation.

Third, this paper introduces a novel methodology for assessing ESG initiatives in Kazakhstan’s oil and gas sector through the integration of econometric modeling and spatial analysis. Furthermore, by examining current practices in High Polluting Enterprises (HPE), it develops an algorithm for an ESG air pollution reduction strategy incorporating Environmental Impact Assessment (EIA) principles.

Fourth, investigating the contribution of ESG indicators to emission reduction holds profound practical and strategic importance. Based on a correlation-regression analysis of the relationship between atmospheric emissions and the E, S, G factors for the selected companies, this article provides an emissions forecast up to 2030. The results confirm the positive role of ESG indicators in reducing emissions, demonstrating that by actively fulfilling their environmental, social, and governance responsibilities, companies can enhance their sustainability and significantly contribute to regional and national carbon reduction goals.

KPO was selected as a case study to analyze the applicability of ESG principles in reducing air pollution. The company, located in the West Kazakhstan Region, was among the first in Kazakhstan to formulate a comprehensive environmental policy vision as an initial step in implementing an ESG system and adopting a “green economy” concept.

The West Kazakhstan Region is of particular interest due to its favorable geographical location and substantial resource potential, accounting for 97% of the republic’s gas condensate production and 37% of its gas production. KPO, established at the world’s largest Karachaganak oil and gas condensate field [9], serves as both a supplier and consumer of fuel and energy resources. A distinctive feature of the field is the high hydrogen sulfide content in its natural gas (4–4.3%), which is classified as a Class I hazard [82].

KPO’s mission centers on developing gas condensate fields through principles that balance environmental respect with economic profitability while fostering socio-economic growth [20]. The company has demonstrated a longstanding commitment to sustainability reporting, becoming the first in Kazakhstan in 2009 to issue an independently verified sustainability report meeting international requirements, and adopting GRI guidelines by 2014. This commitment has been recognized in the PwC Kazakhstan rating, where KPO’s reporting is ranked among the best non-financial companies for ESG disclosure [83]. Following assessments of reports for 2022 and 2023 based on completeness, quality, and availability of ESG information, the company secured a position among the top five leaders in Kazakhstan with a B+ rating [83,84]. Notably, GRI standards are actively utilized by leading global oil and gas companies, including Eni S.p.A, Shell, and BP, to enhance the transparency and quality of their sustainability reporting.

3. Results

The study is based on the task of constructing an algorithm for an ESG strategy to reduce air pollution, which includes a number of sequential steps (Figure 1).

The ESG strategy for reducing air pollution is grounded in Environmental Impact Assessment (EIA) principles and a comprehensive analysis of representative literature on air pollution issues and ESG trends from 2012 to 2025. The algorithm was developed considering recommendations for implementing the ESG agenda from various professional associations and international organizations. It constitutes a structured system of functional actions in the areas of environmental, social, and governance responsibility for High Polluting Enterprises (HPE).

3.1. Implementation of the Environmental (E) Component of the ESG Strategy

The proposed algorithm for an ESG strategy to reduce air pollution involves a sequence of steps (Figure 1). At the initial stage of assessing and monitoring the ESG ecosystem, it is prudent to begin with an analysis of the Environmental (E) component by identifying sources of environmental impact, the affected receptors, and the composition and volume of emitted pollutants.

Environmental Impact Assessment of KPO Operations

Hydrocarbon production at KPO affects nearly all components of the biosphere, with the most significant impact on the atmosphere and soil, which subsequently affects flora, fauna, and human populations. Primary sources of environmental impact at KPO include:

- Flares for gas and condensate combustion during well development and testing.

- Open tanks and storage facilities.

- Warehouses and storage areas for reagents.

- Boiler house operations.

- Drilling and cement solutions.

- Solid drilling waste and drilling wastewater.

- Heavy-duty vehicle fleet.

Air pollutants are generated throughout the entire production cycle—extraction, treatment, storage, and transportation of gas and condensate. Twenty-two types of pollutants spanning hazard classes 1-4 are emitted into the atmosphere.

The chemical composition of the atmospheric air at the field is characterized by greenhouse gas emissions (nitrogen oxides, carbon dioxide, and methane), non-greenhouse pollutants (sulfur dioxide), and specific pollutants such as hydrogen sulfide, volatile organic compounds (VOCs), and particulate matter (PM) originating from oil and gas facilities. Leaks in process equipment are a significant source of specific emissions, including hydrogen sulfide and mercaptans.

Sources of hydrocarbon emissions encompass pumping stations, petroleum condensate storage tanks, diesel fuel storage tanks, and equipment leaks. The majority of emissions are generated by gas combustion in flares (37%), waste incinerators (21%), gas turbine units (20%), with boilers, process furnaces, and compressors contributing 12%, and fugitive sources accounting for 10%. The primary combustion products are sulfur dioxide, carbon monoxide, and nitrogen oxides.

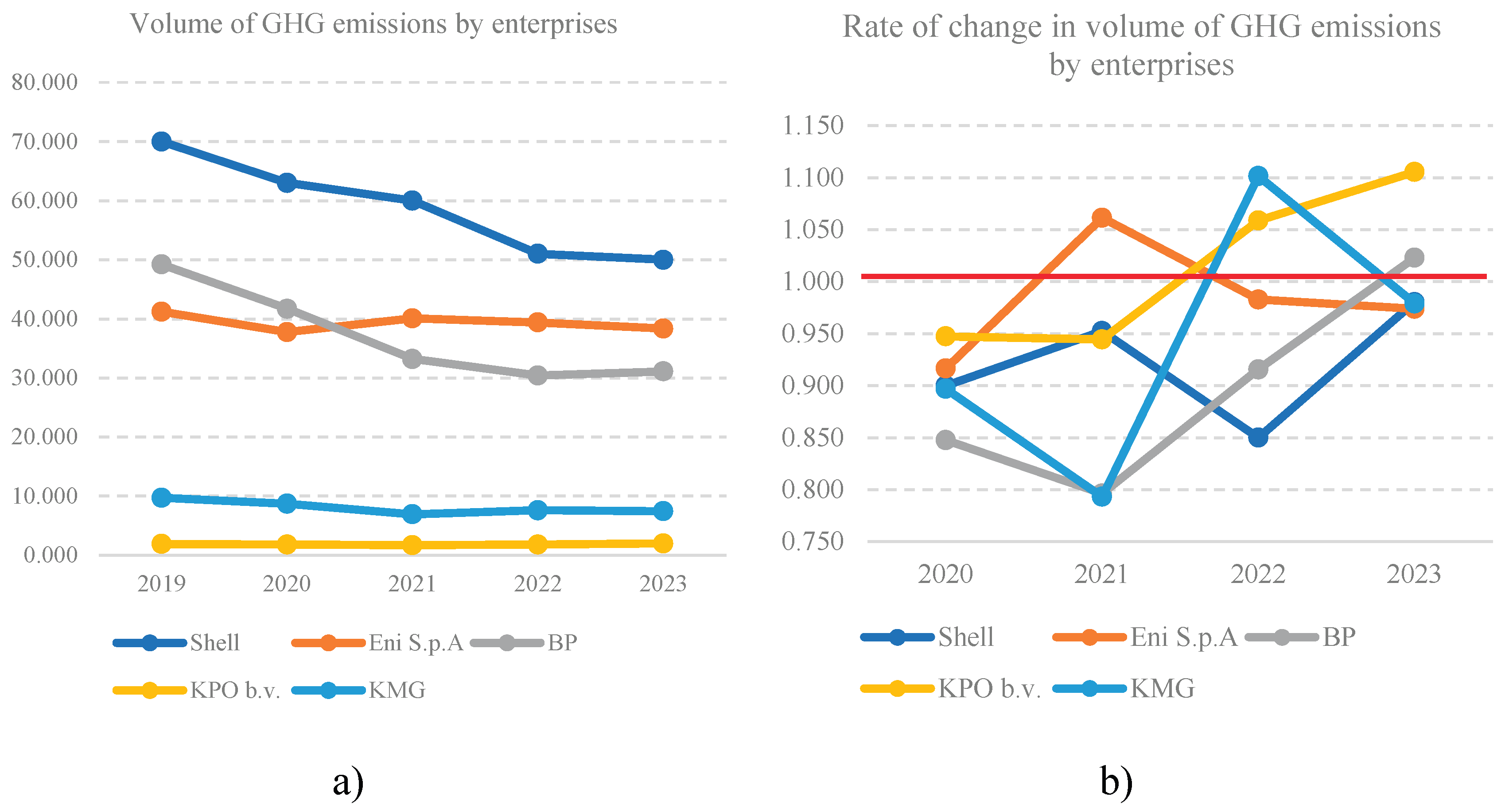

Based on the analysis of KPO’s sustainable development reports for 2019–2023, key ESG metrics were selected in accordance with GRI standards and are presented in a comparative analysis with leading global and Kazakhstani oil and gas companies (Figure 2).

KPO’s GHG emissions (in CO₂ equivalent) are significantly lower than those of the other companies analyzed (Figure 2a). Furthermore, a comparative analysis of specific greenhouse gas emission dynamics against International Association of Oil & Gas Producers (IOGP) benchmarks reveals that KPO’s actual specific emissions are 15% lower than European averages and 44% below IOGP figures.

However, a comparison of absolute GHG emissions (Figure 2a) with their annual growth rates (Figure 2b) yields more nuanced insights. While standard practice expects a steady year-on-year decline in emissions, the data reveals a more complex picture. Figure 2a indicates that only Eni S.p.A. exhibited a temporary increase in emissions between 2020–2021, while other companies generally followed a linear decreasing trend. In contrast, the analysis of annual growth rates in Figure 2b shows a cyclical pattern across all companies throughout the study period, deviating from the linear decline observed in absolute terms. Among the companies, only Shell demonstrated a consistent downward trend (with all growth rate values below 1.0), while others displayed periodic increases. Eni S.p.A. has achieved a sustained reduction over the past three years. KPO, despite its low absolute emissions, shows steady growth in the emission rate. This assessment of emission dynamics sustainability reveals that the overall downward trend is often accompanied by periodic deviations, likely attributable to seasonality, fluctuations in production activity, or external economic factors.

Previous studies concluded that the impact on water, soil, and vegetation quality in the Karachaganak field area was negligible [87]. Air pollution studies conducted at the field analyzed four components: hydrogen sulfide, sulfur dioxide, nitrogen dioxide, and carbon monoxide. These studies indicated that while emissions lead to air pollution at the border of the sanitary protection zone, no significant deterioration of ambient air quality was reported [88,89]. Health risk assessments for the nearby population suggested that under normal operating conditions, concentrations of these priority pollutants do not pose a health hazard, though strict emission regulation was emphasized as necessary [90,91,92].

It is important to note that these studies were conducted more than 7–14 years ago and lacked a detailed geographical analysis of the regional impact. Our previous research identified two distinct zonal sectors in the West Kazakhstan region: an industrial north, responsible for the majority of atmospheric emissions, and an agricultural south [9]. To address this gap, we deemed it essential to conduct a contemporary geospatial assessment of emissions in the region.

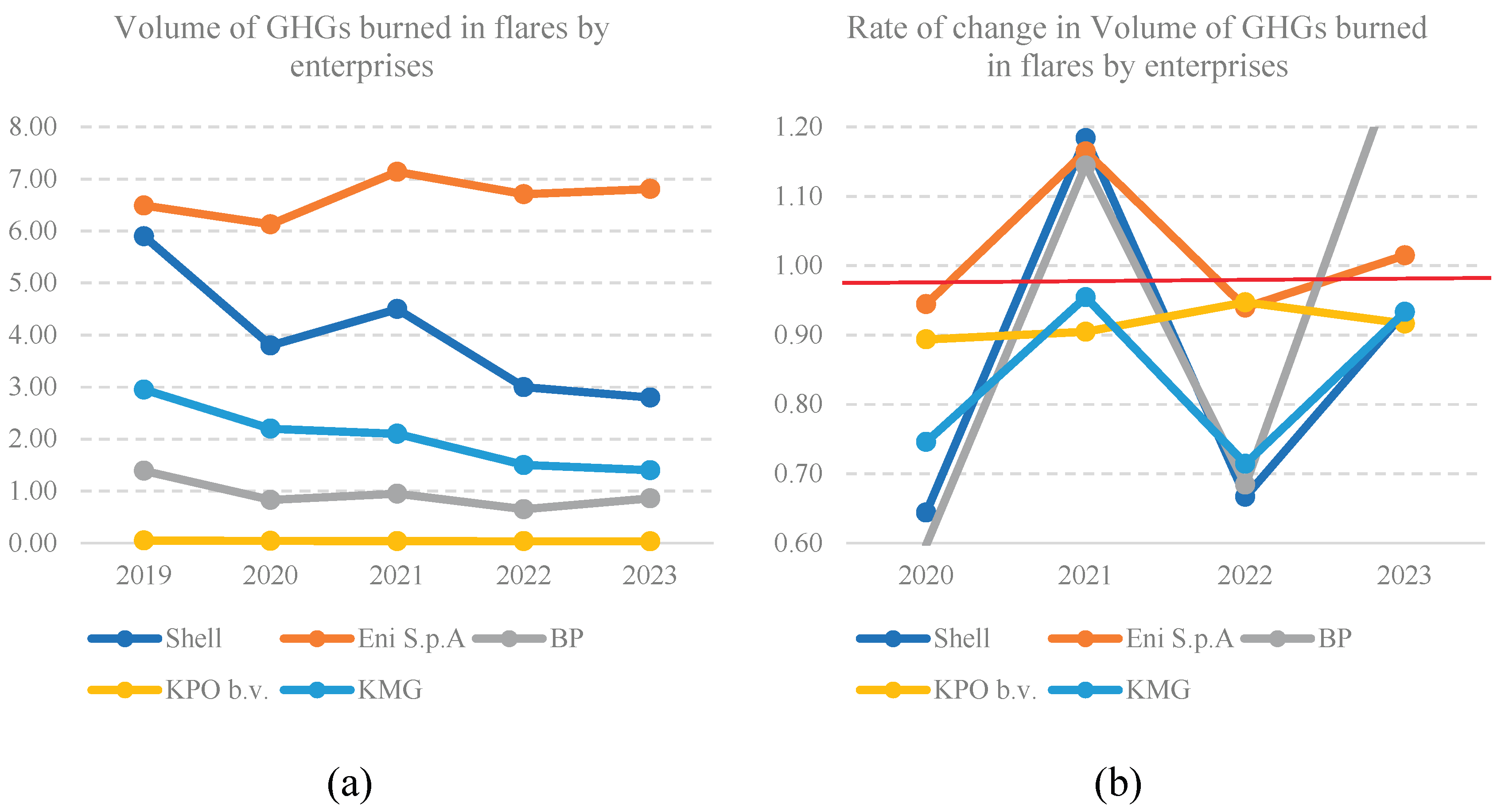

The spatial maps presented in this study (Figure 3) serve to identify areas with the highest environmental burden, determine spatial pollution patterns, and assess the impact of industrial facilities, particularly KPO. Given that 2022 was identified as a period of increasing GHG emissions for KPO in Figure 2b, the spatial analysis was conducted using data from this specific period to capture the associated environmental footprint.

Thus, the spatial analysis of atmospheric pollutant emission sources (Figure 3a) and emission volumes (Figure 3b) for 2022 revealed an uneven distribution, with sources heavily concentrated in the northern industrial zone of the West Kazakhstan region. Key areas include Borly (the location of KPO), the city of Oral, and Baiterek. In the Borly area, gaseous and liquid marker emissions constitute the majority (86% of the region’s total), while particulate matter (PM) accounts for the remaining 14%. The primary pollution sources in these zones are oil and gas extraction facilities, power generation plants, and main pipeline compressor stations. The interpolation results effectively visualize these pollution hotspots, and the maps (Figure 3) clearly illustrate the spatial disparity between emission sources and concentration levels.

KPO has implemented an integrated management system that incorporates control and monitoring mechanisms for all environmental parameters, aligned with the Global Reporting Initiative (GRI). This system forms the foundation for defining energy policy and establishing goals, objectives, and measures for energy conservation and efficiency improvement. It is noteworthy that KPO has published its Sustainability Development Report (SDR) since 2008, with reports from 2017 onward prepared in accordance with contemporary GRI standards.

An analysis of the company’s sustainability reports from 2019–2023 identified ESG strategies where environmental commitments are focused on the following GRI 3-3 objectives: pollution prevention, GHG emission reduction, biodiversity and ecosystem conservation, protection of natural resources, and the continuous improvement of environmental performance (Figure 4). The inclusion of emission data and reduction progress in KPO’s ESG reporting fosters public transparency regarding the company’s contributions to the objectives of the Paris Agreement.

A comparison of the indicators in Figure 4a,b reveals that, in contrast to overall emissions, KPO demonstrates the most effective performance in reducing the volume of gases flared among the studied companies. The data for the period shows a generally stable downward trend (average value of 0.9). For the other companies, discrepancies between linear and cyclical trends are again observed.

While absolute emission volumes (Figure 4a) show a steady and consistent decline, indicating successful implementation of environmental mitigation plans, the stability of this trend (Figure 4b) reveals fluctuations. Periods of rapid decline alternate with short-term plateaus, suggesting that the overall positive trajectory is influenced by factors such as seasonal patterns, the phased introduction of new technologies, and global economic conditions. Consequently, a robust long-term climate strategy must aim not only for cumulative emission reductions but also for greater stability and predictability in the rate of change.

The heightened focus on the climate and environmental components of ESG has, however, led to an increase in “greenwashing”—the dissemination of misleadingly positive reports about a company’s environmental impact. The flexible selection of ESG criteria can result in the overstatement or understatement of reported metrics, with studies showing that various ESG ratings are consistent in only six out of ten cases [71]. In response, major asset managers (e.g., BlackRock) and key industry players (e.g., Bloomberg) are advocating for mandatory ESG disclosures [16]. Consequently, the European Union is actively developing regulatory frameworks, including new rules to enhance the transparency and reliability of ESG ratings. These stringent regulations compel companies to disclose emissions and implement reduction measures, creating direct incentives for businesses to improve their environmental performance and reduce their carbon footprint [73].

According to external audits, the environmental monitoring system for air quality developed and implemented by KPO complies with international standards ISO 14001:2015, GRI, and the national legislation of the Republic of Kazakhstan [10,11,82].

KPO manages its direct GHG emissions within the framework of the national emissions trading system, adhering to the limits set in its environmental permits. This is achieved through systematic sampling and analysis by an accredited laboratory, supported by 18 stationary automatic monitoring stations. These stations operate continuously around the perimeter of the facility, within sanitary protection zones, and along the export pipeline, and are equipped with an alert system for when pollutant concentrations exceed permissible levels. This integrated approach has enabled the company to achieve a systematic reduction in atmospheric emissions. KPO’s technological targets include ensuring that the residual hydrogen sulfide content in fuel gas does not exceed 0.02 g/m³ and mercaptans do not exceed 0.036 g/m³. During the treatment of stable condensate, the company guarantees a hydrogen sulfide content of no more than 20 ppm and a mercaptan content of no more than 40 ppm in commercial crude oil.

During the study period, KPO achieved a 44.9% reduction in gross atmospheric emissions, with the most significant decreases observed for sulfur dioxide (59.3%), nitrogen dioxide (38.1%), and volatile organic compounds (40.3%). Specific pollutant emissions decreased by 51.3%. This reduction, and the corresponding decrease in ground-level pollutant concentrations, is attributed to a comprehensive set of technological and organizational measures implemented through an energy conservation-focused ESG strategy.

Applying Lawrence D. Miles’ theory [8] as a framework for developing a color-coded ESG algorithm has helped identify recurring functions and pinpoint operations with concentrated ESG risks. The analysis of KPO’s environmental and energy management systems shows that the achieved emission reductions can be attributed to the implementation of a structured algorithm (Table 2).

Thus, in the domain of accountability and transparency, KPO’s reporting is verified by audit firms for data reliability, and its environmental and energy management systems undergo regular audits. Since 2014, with the adoption of GRI standards, ESG strategies have been progressively integrated. Under the areas of “Environmental Management System, Waste Management, and Energy Efficiency,” KPO has deployed continuous monitoring systems for air, surface water, and groundwater. Strategies for water resource management, wastewater reuse, material recycling in production, and waste disposal have been established.

Pollutant concentrations in emissions are monitored in real-time. A Leak Detection and Repair (LDAR) system is utilized to identify and mitigate methane leaks, and international standards ISO 14001:2015 and ISO 50001:2018 are implemented [11,12]. The adoption of ISO 50001:2018 [12], in particular, has facilitated the optimization of energy consumption and enhanced energy efficiency in hydrocarbon production and processing.

As part of its “Innovation and Research: Using the Best Available Technologies” program, atmospheric emissions have been reduced through high-pressure (550 bar) gas re-injection technology. Since 2024, KPO has participated in the UN-led Oil and Gas Methane Partnership 2.0 (OGMP 2.0) under its Carbon Footprint initiative.

3.2. Implementation of the Social (S) and Governance (G) Components of the ESG Strategy.

Karachaganak, as the region’s largest enterprise, plays a pivotal role in its social, economic, and cultural development. An analysis of the company’s socially responsible business strategy reveals a comprehensive set of measures focused on improving working and living conditions, healthcare, collaboration with trade unions, enhancing industrial safety, providing social guarantees, supporting education and internships, fostering university partnerships, maintaining dialogue with local communities, and developing social and infrastructure projects for the region.

Concurrently, an analysis of institutional and legislative differences between Kazakhstan and oil-producing nations with more advanced institutional frameworks (e.g., Norway, the USA, Canada) indicates that the latter manage natural resource revenues more effectively, achieving superior results in economic growth and social development [81]. For instance, unlike Norway, Kazakhstan’s National Fund has not attained a similarly advanced level of sovereign wealth fund management, which has contributed to its depletion, low long-term investment efficiency, and limited signs of sustainable development [93].

A review of global best practices in ESG transformation demonstrates that in the EU, ESG strategies are legislatively supported through initiatives like the European Green Deal, which aims for carbon neutrality by 2050 [48]. Governments of OECD member and partner countries have developed and are implementing numerous specific measures to stimulate the green economy [62].

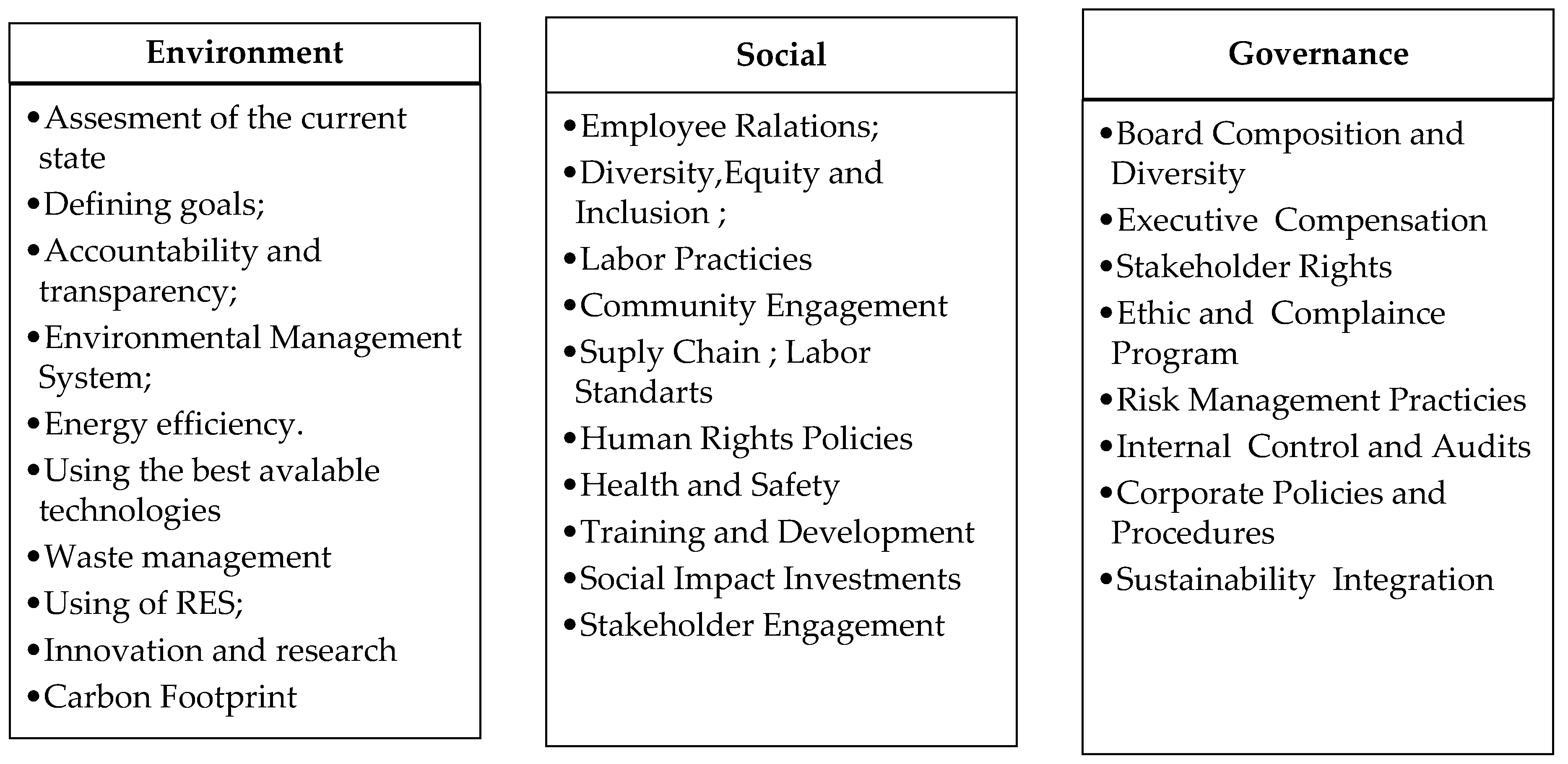

An assessment of measures supporting KPO’s social responsibility implementation and their impact on sustainable development underscored the need to systematize these actions using the proposed algorithm (Figure 1). This analysis resulted in the development of a structured action algorithm (Table 3).

As part of its commitment to balancing corporate and employee interests through a healthy work environment, KPO has increased the proportion of local hires over the past three years under its “Employee Relations, Diversity, Equity, and Inclusion, Labor Practices, Supply Chain, and Labor Standards” program. Local citizens now constitute 98% of the total workforce and 86% of management personnel.

To advance Sustainable Development Goal (SDG) 16.b, KPO has implemented the “KPO 365” Corporate Strategy, which focuses on preventing major incidents and mitigating risks to personnel, the environment, assets, and corporate reputation. The company’s social responsibility policies, procedures, and standards align with International Financial Reporting Standards (IFRS).

Within the “Human Rights Policies, Health and Safety, Training and Development” framework, KPO has amended internal documents to ensure compliance with labor legislation, Kazakhstan’s Environmental Code, and ISO 26000 guidelines. A Safety Management Center, involving all employees, was established to implement process safety fundamentals, enhance industrial safety protocols, and conduct regular training. The introduction of health, safety, and environmental protection cards facilitated the identification of 125 potentially hazardous incidents. In 2023, the lost-time injury rate for KPO and contractor employees was 0.05. The company allocated over $240 million for local workforce development between 1999 and 2023, including the introduction of the Udemy e-learning platform in 2023. Security systems undergo regular audits, with new technologies continuously integrated for risk monitoring and management [83].

The “Community Engagement, Stakeholder Engagement, Social Impact Investments” program maintains dialogue through advisory council meetings with residents, forums, conferences, public hearings, surveys, and audits. A direct communication channel with the company has been established, and KPO’s social project portfolio is coordinated with regional authorities.

Social investment has increased from $10 million in 2012 to $30 million in 2023. Eighteen social infrastructure projects worth $43.2 million have been completed, including the construction of 13 schools, two sports complexes, a visitor center, and road repairs in the West Kazakhstan region.

KPO actively engages Kazakhstani suppliers and manufacturers in its development process. The local content indicator for procurement of goods, works, and services reached 63.24% ($756.1 million) in 2023. During 2022–2023, 30 contracts totaling $107 million were awarded to domestic companies for locally produced goods.

Since 1998, the company has financed over 250 social and infrastructure facilities. These social responsibility initiatives contribute directly and indirectly to reducing air pollution by fostering sustainable community development and enhancing operational accountability.

An analysis of processes, case studies, and documentation related to KPO’s corporate governance implementation and its impact on sustainable development highlighted the value of structuring these efforts using the proposed algorithm (Figure 1). This analysis resulted in the development of a corresponding action algorithm (Table 4).

Under the “Board Composition and Diversity, Executive Compensation” guidelines, KPO implements ESG best practices, including ensuring board independence and conducting regular performance assessments. The company adheres to principles of equal opportunity and non-discrimination, with all compensation, hiring, evaluation, and promotion decisions based on objective criteria such as merit, qualifications, and performance.

The “Stakeholder Rights, Ethics and Compliance Program” operates within the framework of applicable legislation and internal corporate procedures. By transparently disclosing emissions data and reduction progress in its ESG reporting, KPO enables stakeholders and interested parties to assess the strategy’s effectiveness and its environmental impact.

Furthermore, adherence to business ethics, compliance with GRI standards, and the digital transformation of production and safety operations collectively contribute to reducing the company’s environmental footprint. In accordance with “Risk Management Practices, Internal Control, and Audits,” a systematic approach and continuous assessment are employed to develop optimal business strategies and manage organizational change.

KPO is continuously enhancing its methods for assessing environmental risks and incidents, including those related to oil spills and hazardous substances. The implementation of GRI standards facilitates a more structured approach to risk management. The “Goal Zero” principle underscores the company’s commitment to personnel and environmental safety.

The company has launched an enhanced methane emissions monitoring program for 2024–2029, making transparent reporting a key priority. Internal audits are regularly conducted in high-risk operational areas. The ESG report is approved by the Company’s Board of Directors and, during its preparation, is coordinated with members of the Sustainability Subcommittee representing the partner companies. Prudent resource management within a stable budgetary framework, aligned with strategic management approaches and sustainability targets, has become a cornerstone of corporate governance. An electronic procurement and work permit system was launched in 2024.

In line with “Corporate Policies and Procedures, Sustainability Integration,” KPO is developing and implementing the “KPO-365 Business Strategy.” This strategy integrates sustainable development principles into business operations, investment planning, and decision-making processes, supported by a comprehensive digitalization strategy and production forecasting using advanced analytical tools [20].

4. Modeling

In accordance with the adopted research methodology, the subsequent stage involved econometric modeling to explain variations in GHG emissions and to assess the impact of environmental, social, and governance factors on air pollution levels through a staged approach.

This process yielded three separate models for a single dependent variable—the volume of GHG emissions by enterprises. All generated indicators were consolidated into panel data series for the companies under study. Given the previously noted limitation of non-uniform ESG reporting requirements for the social (S) and governance (G) components, the number of independent variables collected for these dimensions was smaller than for the environmental (E) component (Appendix A).

In the next step, the factors identified through regression analysis were integrated into a single aggregate regression model to assess the collective impact of oil and gas companies’ ESG strategies on emission reductions. The results of the econometric modeling necessitated the evaluation of ESG factor influence using two distinct models: a comprehensive ESG model and a combined S+G model.

4.1. Modeling of GHG Emissions Based on Environmental Factors in the Oil and Gas Industry

A total of 16 factors were collected for the five companies covering the period from 2019 to 2023. This timeframe was selected because comprehensive sustainability reporting has been consistently compiled and published by companies for a relatively short duration, particularly considering the Sustainable Development Goals (SDGs) were adopted in 2015. It should be noted, however, that some companies have published reports in various forms significantly earlier. For example, Shell has formally reported on sustainability-related performance for over 25 years, aiming to maintain transparency regarding activities relevant to investors, governments, and civil society [21]. Nevertheless, disparities in the calculation and measurement methodologies for certain indicators made it feasible to generate systematic and comparable data only from 2019 onward.

During the model construction, explicit linear relationships (aliases) were identified:

- X13 and X14 in KMG: close values - minimal difference → high multicollinearity → alias).

- X1 and X2: In some companies, they move in parallel (correlation ≈ 1).

- X6 and X7: At Shell, BP, and EniS.p.A, the indicators often move in sync (the same trend).

- X9 and X10: The variables are “scaled,” but proportional to each other.

- X11 and X12: Often nearly proportional (all years rise/fall together).

Based on this, in order to obtain a reliable model, the following predictors were excluded from the equation: X2, X6, X10, X12, X14 - they were the ones that caused the alias error when calculating vif ().

Rationale for this choice:

- X2 is a strong duplicate of X1 → makes the X matrix undefined.

- X6 and X7 — in small samples, it’s better to leave only one (X7 is more informative).

- X10 is almost always linearly dependent on X9 (all observations are nearly proportional).

- X12 is very close to X11 (a scale factor, duplicates).

- X14 ≈ X13 (in some rows, the difference is 0 → complete collinearity).

After removing them, alias() will return an empty result, and vif() will be calculated without error.

The following results were obtained as a result of the transformations:

- Coefficients: Estimate Std. Error z-value Pr(>|z|)

- (Intercept) 10.94087567 5.83964695 1.8736 0.0609924 .

- X1 0.85999310 0.47076372 1.8268 0.0677292 .

- X3 -2.11488142 4.04309198 -0.5231 0.6009150

- X4 0.05534474 0.02754940 2.0089 0.0445448 *

- X5 -9.11477183 4.74350876 -1.9215 0.0546655 .

- X7 0.03013069 0.04034971 0.7467 0.4552214

- X8 0.03668248 0.01007773 3.6400 0.0002727 ***

- X9 -2.17414745 1.96847151 -1.1045 0.2693828

- X11 -0.00389659 0.00178096 -2.1879 0.0286754 *

- X13 0.00253414 0.00098908 2.5621 0.0104039 *

- X15 -0.18348608 1.15986542 -0.1582 0.8743023

- X16 0.06956297 0.01750540 3.9738 7.074e-05 ***

Of all the indicators, X8, X11, X13, X16 turned out to be significant, and when testing for fixed and random effects, the Hausman test [94] determined that the model with random effects is more acceptable.

Coefficients:

- Estimate Std. Error z-value Pr(>|z|)

- (Intercept) 5.38069167 3.55208454 1.5148 0.12982

- X8 0.05288441 0.00222165 23.8041 < 2.2e-16 ***

- X11 -0.00636748 0.00152916 -4.1640 3.127e-05 ***

- X13 0.00261056 0.00083545 3.1247 0.00178 **

- X16 0.10166146 0.01319440 7.7049 1.310e-14 ***

ŷ = 5.3807 + 0.05288·X₈ − 0.00637·X₁₁ + 0.00261·X₁₃ + 0.10166·X₁₆

The resulting regression model allows us to identify the influence of key factors X8, X11, X13, and X16 on the performance indicator and understand their uniqueness. To forecast future performance indicators, Holt’s exponential smoothing model and the ARIMA model [95] will be used, as they allow for the trend and seasonality of time series.

In the next step, we apply RW+drift, the addition of which allows us to reflect the average annual decline. ARIMA models over short time periods can be sensitive to recent changes, so for conservative predictions, a random walk model with trend accounting is preferable.

Negative results should be considered a side effect of econometric analysis; to avoid their influence, the parameter “level = 0” is set and special attention is paid to the range of possible values rather than to a specific point.

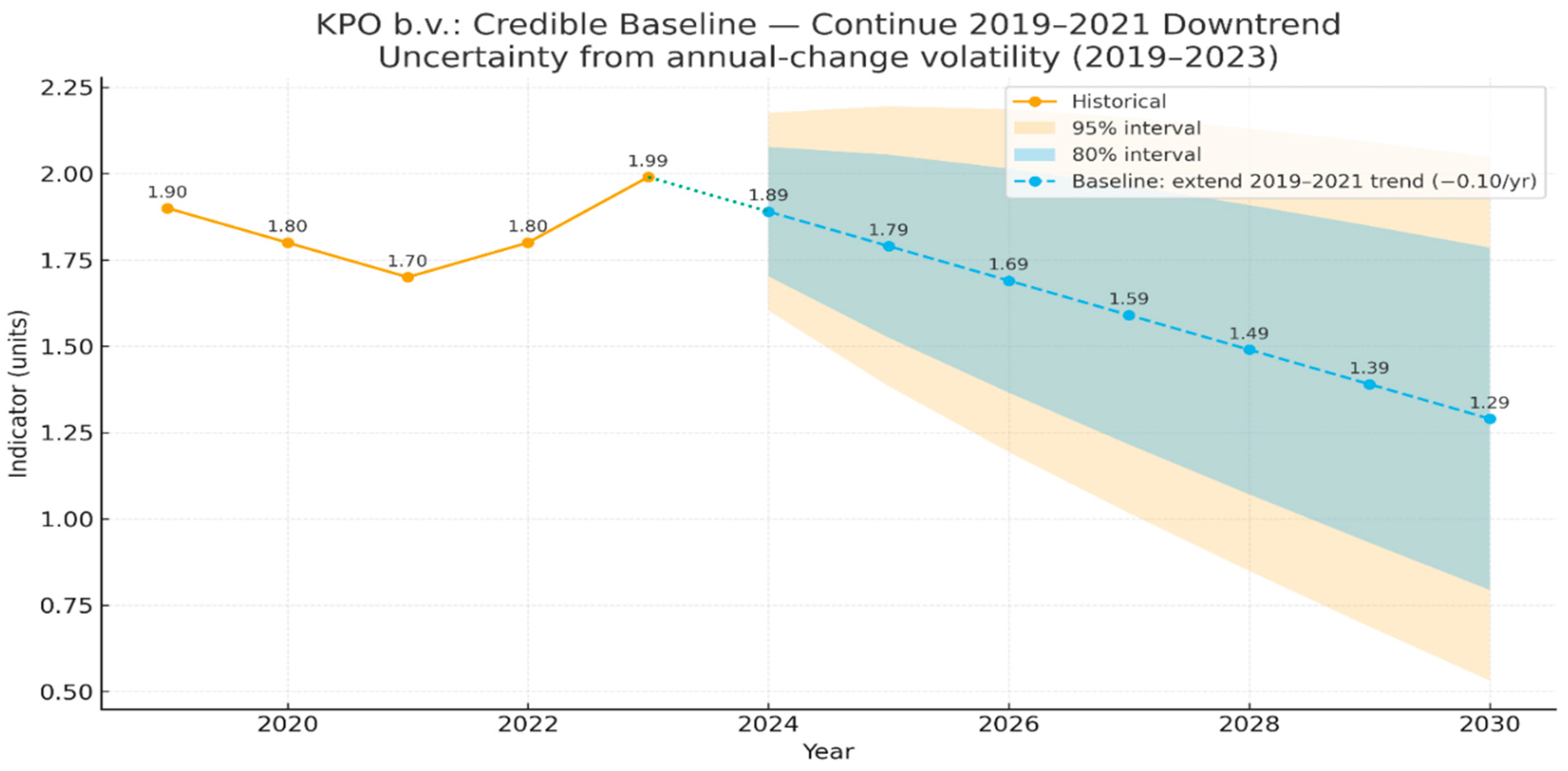

Thus, using RW+drift with “level = 0” generates a conservative, replicable baseline for gradual reduction of cumulative emissions by 2030, which should be regularly updated as new data becomes available. The RW+drift model is based on recent data, taking into account that a new year may slightly shift the average rate of decline (Appendix B).

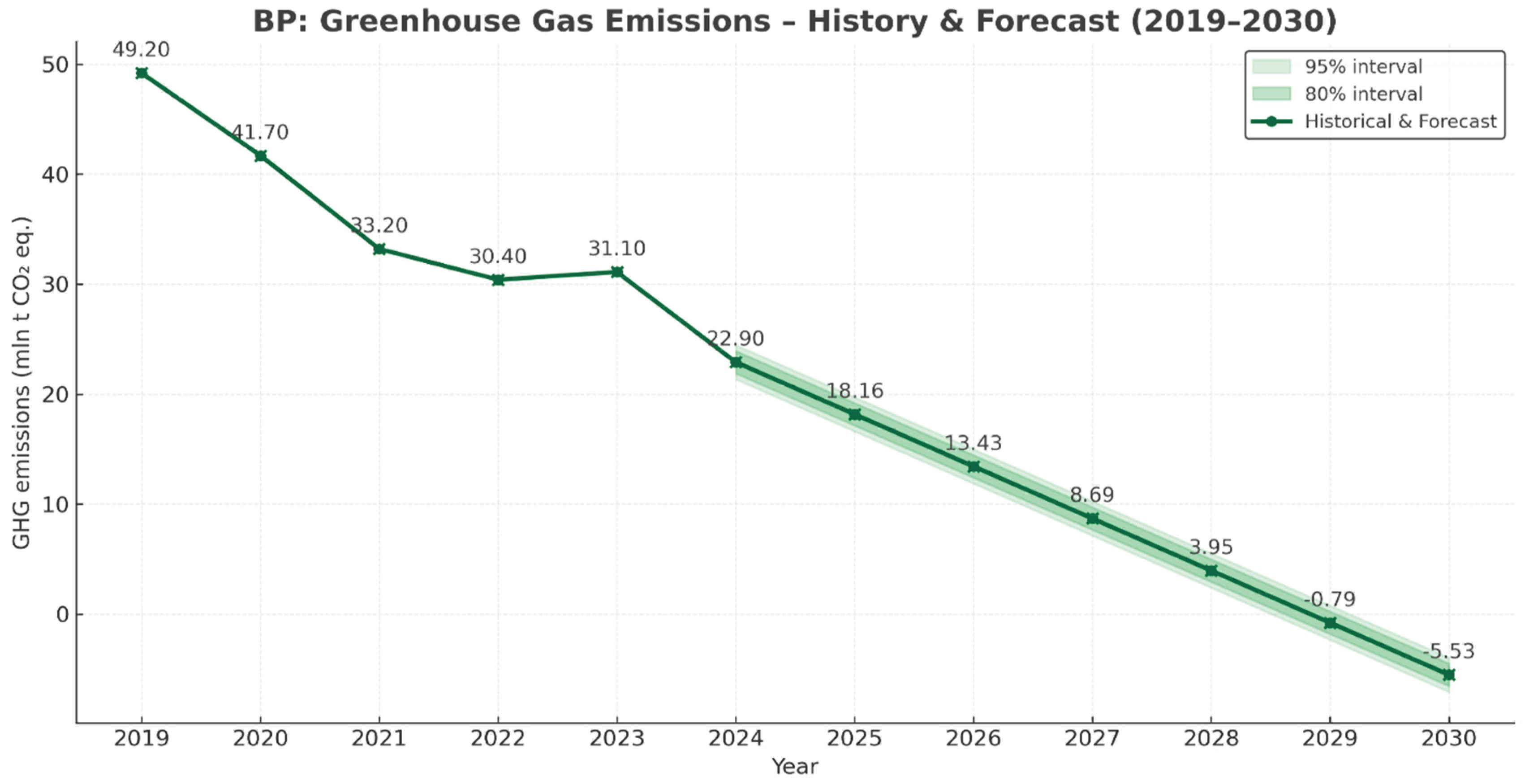

Figure 5.

Forecasting RW+drift of GHG emissions at KPO (mil.t CO2 equivalent) taking into account the impact of factors demonstrating the company’s environmental responsibility.Note: constructed using R.

Figure 5.

Forecasting RW+drift of GHG emissions at KPO (mil.t CO2 equivalent) taking into account the impact of factors demonstrating the company’s environmental responsibility.Note: constructed using R.

As part of the study, an ARIMA (1,1,0) model was constructed for the time series of KPO’s greenhouse gas emissions for 2019–2023. The Ljung–Box test [95] yielded a p-value of 0.5462, which significantly exceeds the critical significance level of 0.05.

This allows us to conclude that the model residuals do not contain statistically significant autocorrelation, and the model itself adequately describes the dynamics of the original time series and can be used for forecasting. Analysis of the resulting forecast values for GHG emissions shows that, all other things being equal, the implementation of the KPO environmental strategy to reduce environmental pollution will lead to a reduction in emissions.

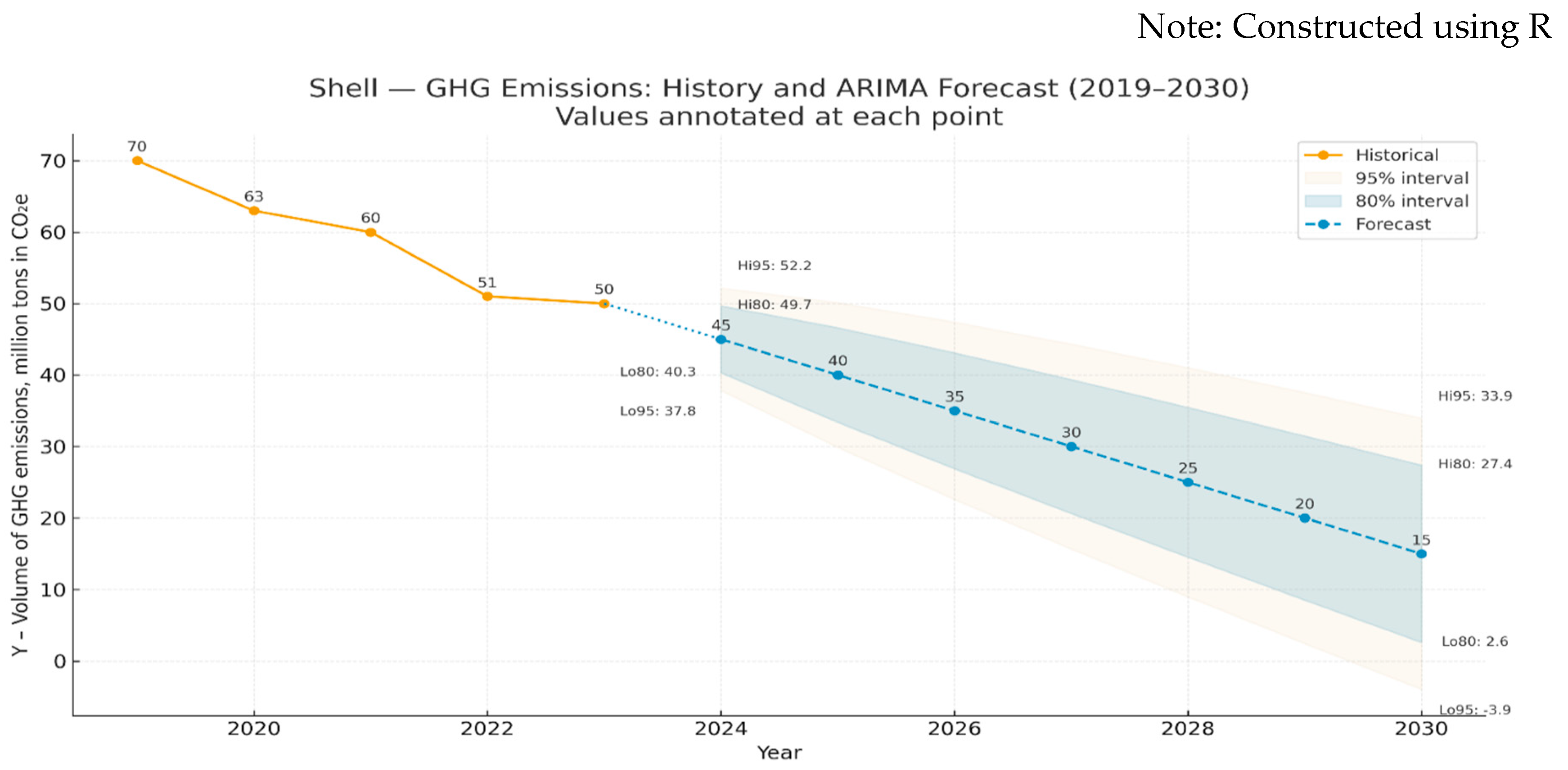

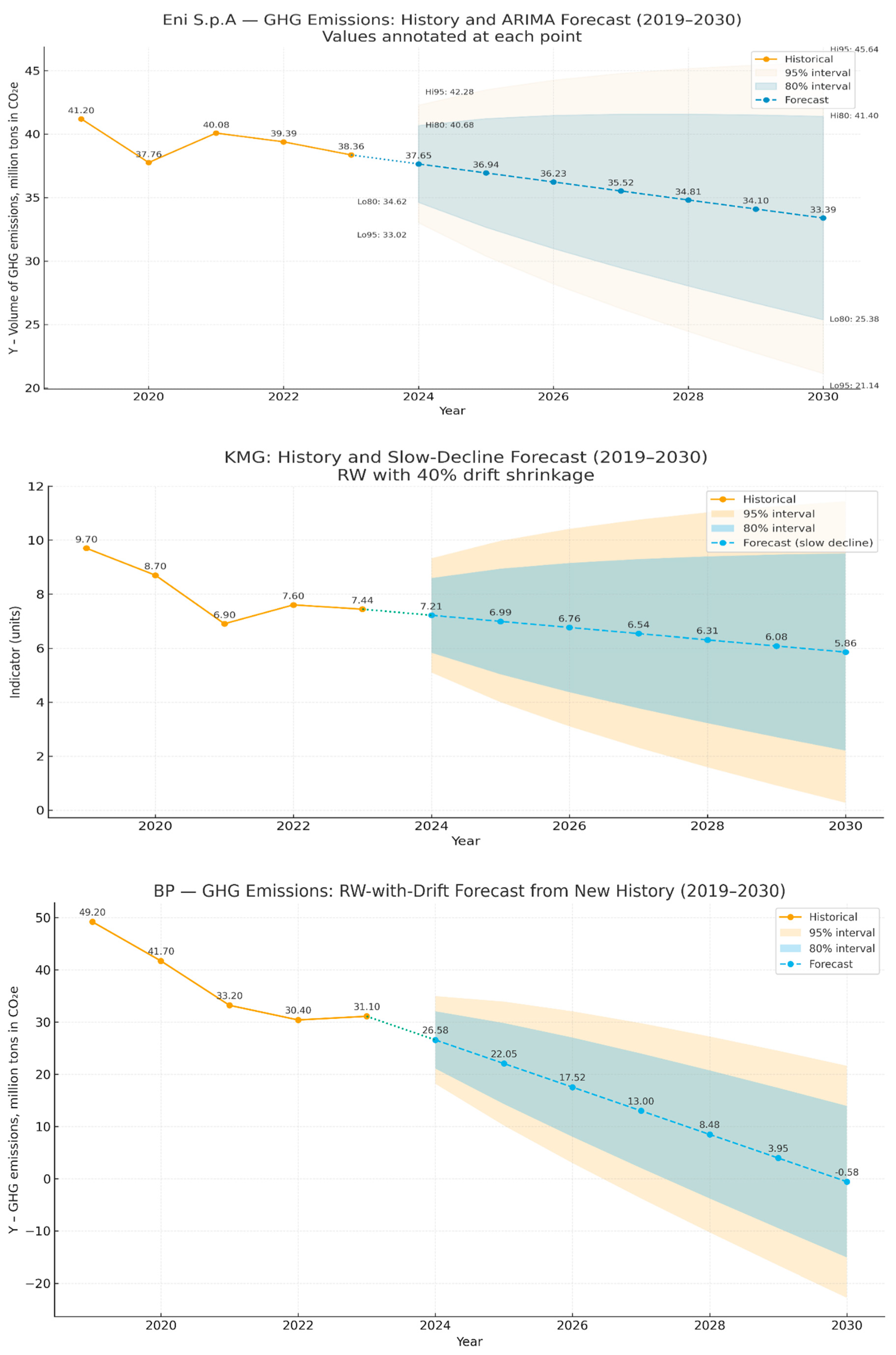

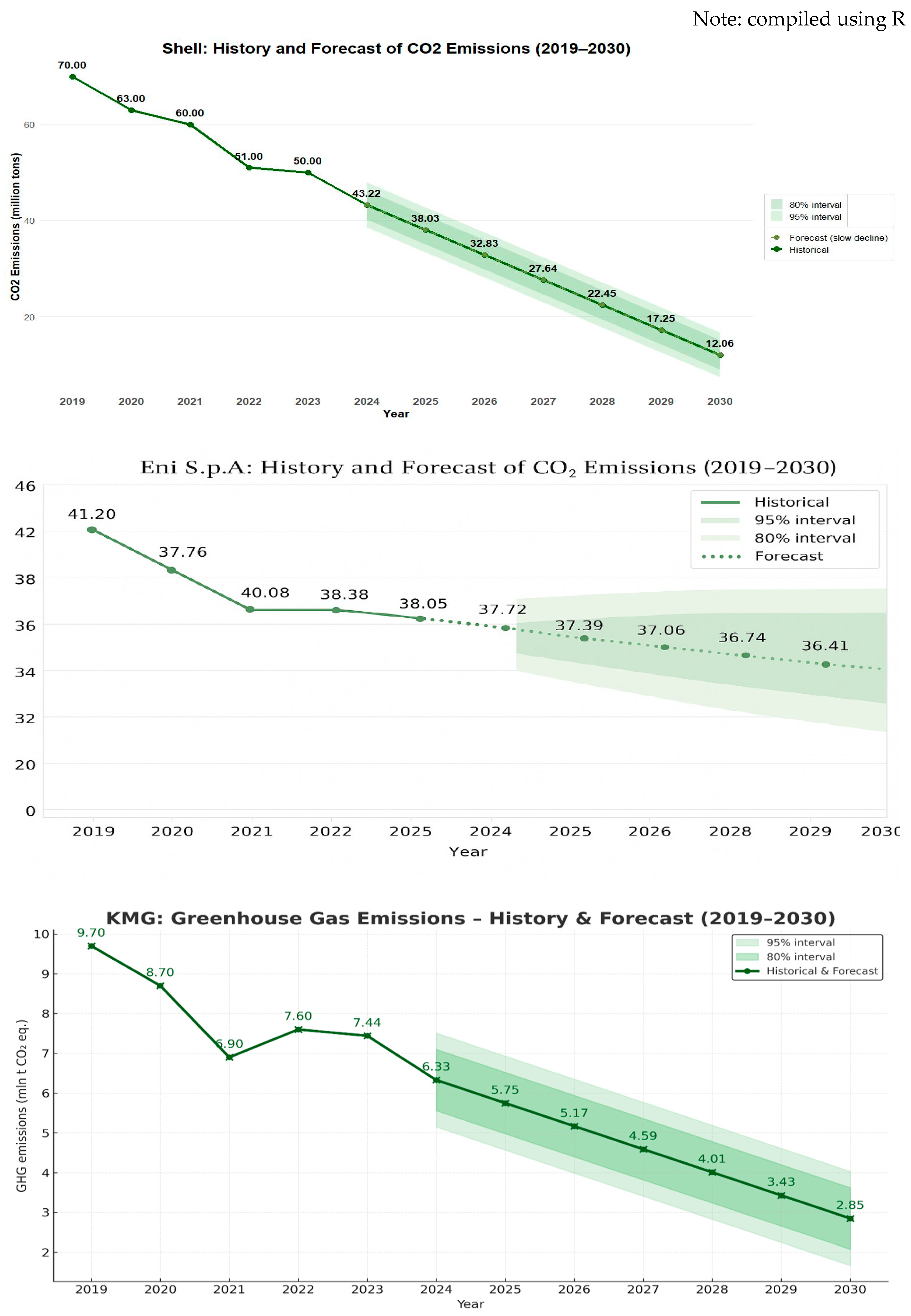

A review of forecasts for Shell, Eni S.p.A., BP, and KMG revealed the following. For Eni S.p.A., maintaining its ESG principles implementation approaches will result in a 13% reduction in pollutant emissions by 2030 (compared to 2023). Similarly, at Shell, we achieved a 70% reduction in emissions, and at BP, we are seeing a complete elimination of emissions and the achievement of complete decarbonization of oil and gas production technologies. For the Kazakh company KMG, the forecast model shows a 22% reduction in emissions. All these findings indicate that environmental management in oil and gas companies demonstrates varying levels of effectiveness, suggesting the value of studying the experiences of leading companies.

4.2. Modeling of GHG Emissions Based on Factors Demonstrating the Social Responsibility of Companies in the Oil and Gas Industry

A total of 11 factors were collected for five companies for the period from 2019 to 2023, demonstrating corporate social responsibility (Appendix A). The results of the panel regression analysis are presented, including the coefficients for the independent factors, their corresponding errors, significance criteria, and probability (p-values).

Coefficients:

- Estimate Std. Error z-value Pr(>|z|)

- (Intercept) 1.0275e+02 3.1881e+01 3.2228 0.001270 **

- Xs1 1.0166e+01 9.9885e+00 1.0178 0.308781

- Xs2 -3.6245e-01 1.3573e+00 -0.2670 0.789440

- Xs3 3.2524e-02 2.0996e-02 1.5491 0.121368

- Xs4 -3.7928e-02 3.2649e-02 -1.1617 0.245362

- Xs5 9.4815e-03 9.5502e-03 0.9928 0.320804

- Xs6 4.8436e-01 4.1010e-01 1.1811 0.237568

- Xs7 -3.2479e-03 1.6184e-03 -2.0069 0.044760 *

- Xs8 -2.3854e+00 7.4694e-01 -3.1936 0.001405 **

- Xs9 -1.6766e-03 5.3711e-03 -0.3122 0.754925

- Xs10 -9.6529e-02 1.4743e-01 -0.6547 0.512644

- Xs11 -1.8208e-05 1.3603e-04 -0.1338 0.893521

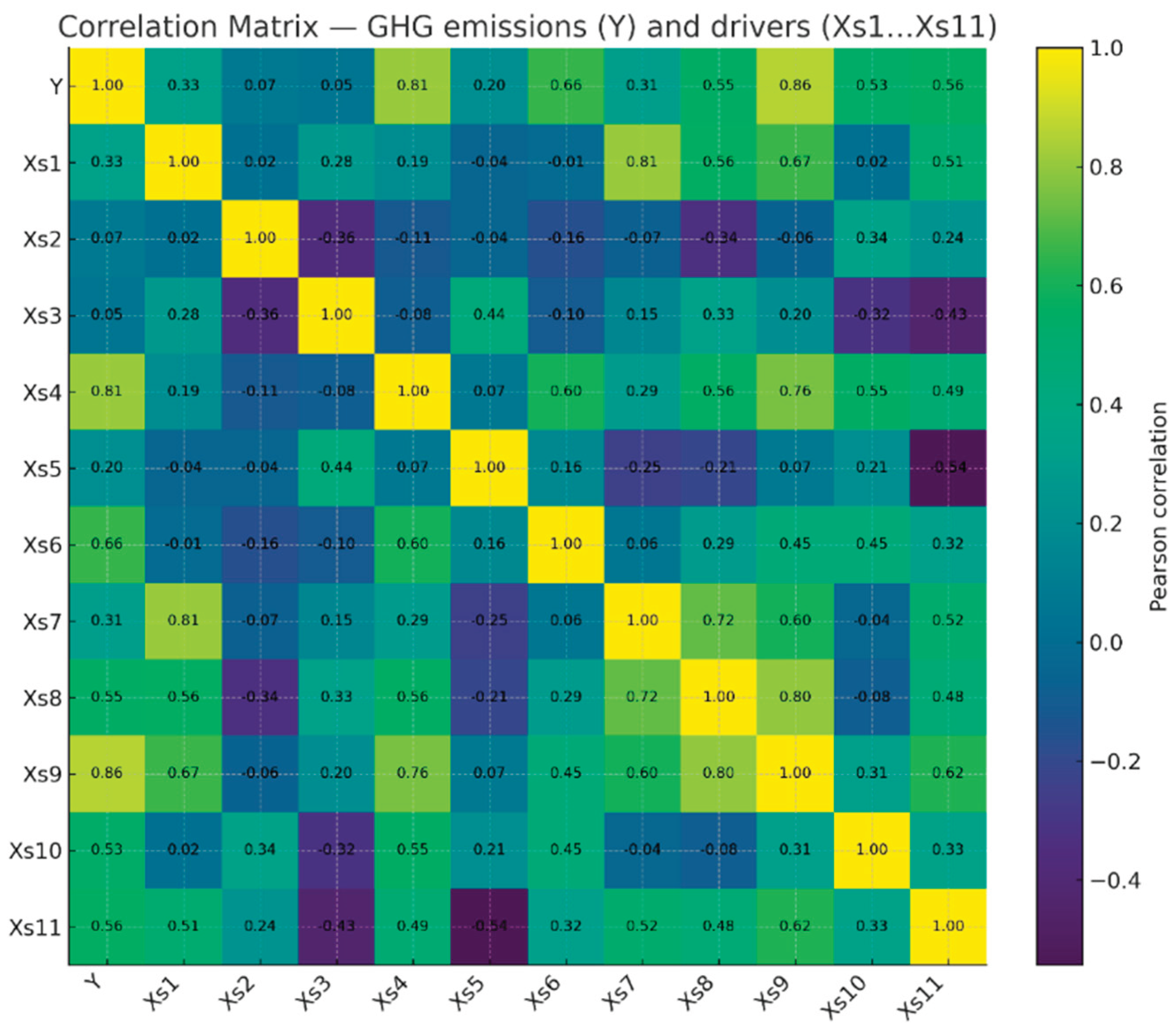

According to the results of the analysis of the correlation matrix (Figure 6), the most pronounced positive relationship was recorded with the variables Xs4 (r = 0.81), Xs7 (r = 0.81) and Xs9 (r = 0.86), indicating a close relationship between emissions and these indicators.

A moderately positive correlation can be observed for Xs6 (r = 0.66), Xs8 (r = 0.60), and Xs11 (r = 0.56). In turn, variables Xs2, Xs3, Xs5, and Xs10 showed an insignificant or negative correlation with emission volumes, indicating a minor influence of these factors. It was also established that there are strong relationships between the independent variables themselves, such as Xs4–Xs7 (r = 0.81) and Xs8–Xs9 (r = 0.80), which can create a problem of multicollinearity when constructing regression models. After checking for multicollinearity, Xs7 (Low carbon development, Renewable Energy Investments) and Xs8 (Diversity and Inclusion (women in the company), %) were found to be significant in the model. Furthermore, the Hausman test confirmed the use of the random-effects model.

Coefficients: Estimate Std. Error z-value Pr(>|z|)

(Intercept) 94.3244368 23.3562504 4.0385 5.379e-05 ***

Xs7 -0.0034038 0.0008342 -4.0803 4.498e-05 ***

Xs8 -2.1699157 0.5438818 -3.9897 6.616e-05 ***

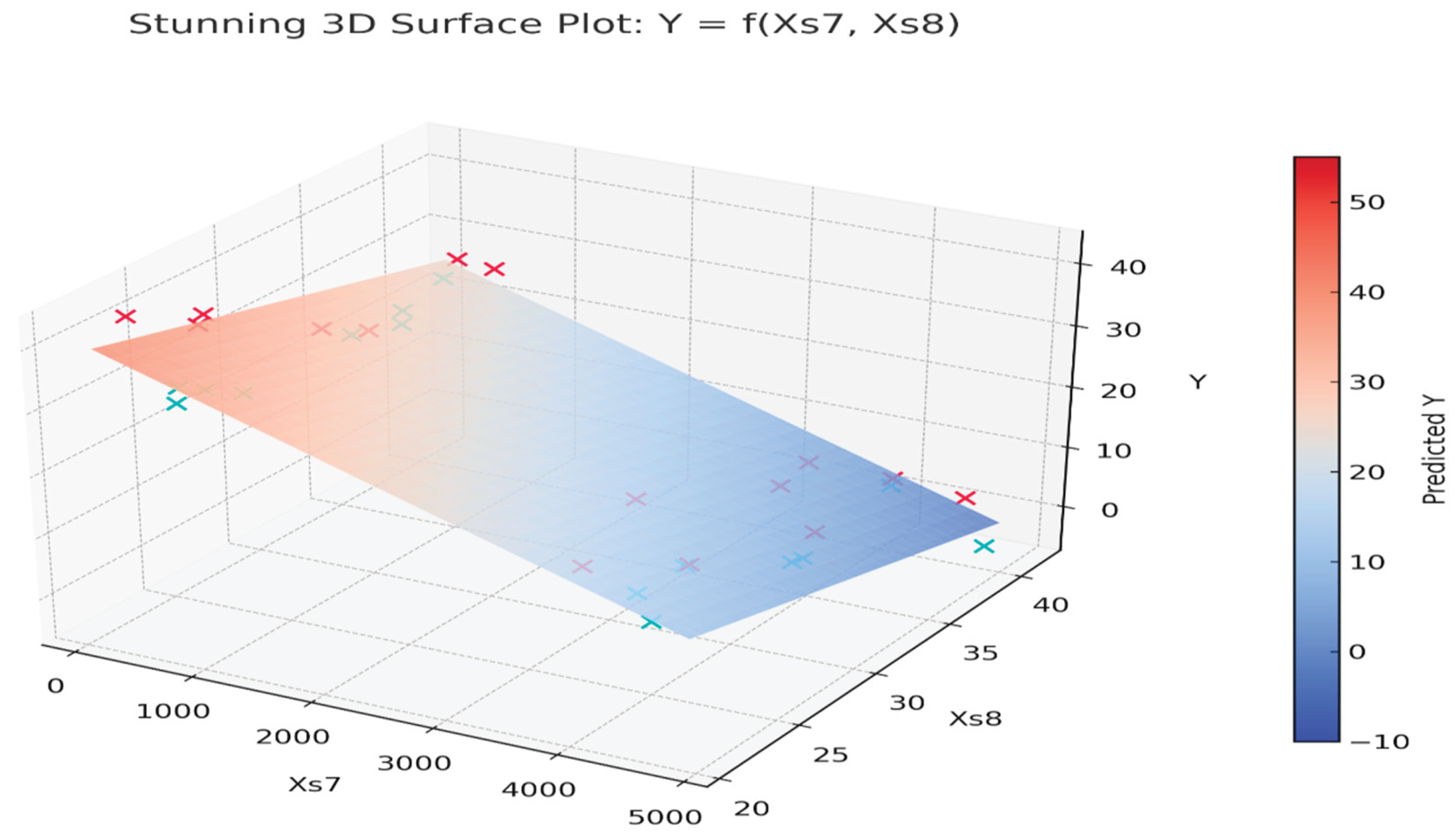

Y = 94.3244368 - 0.0034038·Xs7 - 2.1699157·Xs8

The results of the autocorrelation test are presented in Figure 7.

Surface visualization (Y = 94.3244368 - 0.0034038•Xs7 - 2.1699157•Xs8) Y=f(Xs7, Xs8) shows that the slope of the plane clearly indicates a negative influence of both factors. The red dots (real data) fit well on the theoretical surface, confirming the adequacy of the model.

Turquoise projections onto the Xs7–Xs8 plane allow us to see the distribution of factors without taking Y into account. Thus, a regression analysis of the impact of the ESG strategy of oil and gas companies in the context of their social responsibility on the reduction of GHG emissions showed that investments in renewable energy sources as a criterion for low-carbon development (Xs7) and the share of women in the company (Xs8) are significant.

Negative coefficient values for both variables indicate an inverse relationship: increased investment in renewable energy and increased representation of women in the workforce lead to a decrease in GHG emissions. The coefficient Xs7=−0.0034 demonstrates that each additional investment in renewable energy sources is accompanied by an average reduction in GHG emissions by 0.0034 conventional units, which is a manifestation of the transition to production with a smaller carbon footprint.

This is in line with the principles of sustainable development, where the introduction of innovative and environmentally friendly technologies helps to reduce the intensity of carbon use. The coefficient Xs8=−2.1699 indicates that a one percent increase in the share of women leads to a reduction in emissions of approximately 2.17 units, which can be seen as a beneficial effect of gender diversity on environmental management performance.

4.3. Modeling GHG Emissions Based on Factors Demonstrating the Management Responsibility of Companies in the Oil and Gas Industry

As a result of the study, data were generated from ten indicators characterizing the implementation of corporate governance principles of five enterprises in the period from 2019 to 2023 (Appendix A). The results of the analysis conducted using the panel regression method include data on the coefficients of influence of independent variables, as well as estimates of their errors, statistical indicators of reliability and p-values.

Coefficients: Estimate Std. Error z-value Pr(>|z|)

(Intercept) 6.2275986 21.4709182 0.2900 0.7717795

X1G -0.0257988 0.1362364 -0.1894 0.8498044

X2G -0.0039458 0.0165425 -0.2385 0.8114743

X3G 0.1576491 0.0493119 3.1970 0.0013888 **

X4G 0.1908606 0.1126435 1.6944 0.0901935

X5G -0.0127722 0.0097460 -1.3105 0.1900261

X6G -0.5811444 0.1746336 -3.3278 0.0008754 ***

X7G 0.4129630 0.2531780 1.6311 0.1028656

X8G 0.0079756 0.0098253 0.8117 0.4169409

X9G 0.0026412 0.0078205 0.3377 0.7355720

X10G 0.1565727 0.1182101 1.3245 0.185

The indicators X3G (number of violations of corporate ethics) and X6G (amount of taxes paid) were determined as the indicators.

Coefficients:

Estimate Std. Error z-value Pr(>|z|)

(Intercept) 30.162609 15.225108 1.9811 0.047579 *

X3G 0.147488 0.032621 4.5212 6.148e-06 ***

X6G -0.529817 0.163269 -3.2451 0.001174 **

ŷ = 30.1626 + 0.1475·X₃G − 0.5298·X₆G

The presence of coefficients of different signs allows us to identify two opposing influencing factors. First, the positive value of the X3G variable (0.1475) demonstrates that an increase in the number of business ethics violations leads to an increase in GHG emissions.

The presence of coefficients of different signs allows us to identify two opposing influencing factors. First, the positive value of the X3G variable (0.1475) demonstrates that an increase in the number of business ethics violations leads to an increase in greenhouse gas emissions.

This fact points to a link between corporate governance effectiveness and environmental performance. An increase in ethical violations indicates deficiencies in the internal control system, a lack of concern for the environment, and unclear corporate policies.

Thus, the study’s results support the hypothesis that an organization’s honest behavior is an indicator of its commitment to environmentally friendly development. On the other hand, the negative coefficient for X6G (-0.5298) indicates that increasing the amount of taxes paid leads to a reduction in GHG emissions. This can be seen as a sign of financial discipline and corporate social responsibility: companies that meet their tax obligations on time tend to be more mindful of environmental issues and implement carbon footprint reduction technologies. Furthermore, full tax payment may indicate a high level of transparency and stability in company management, which is linked to environmental compliance (Figure 8).

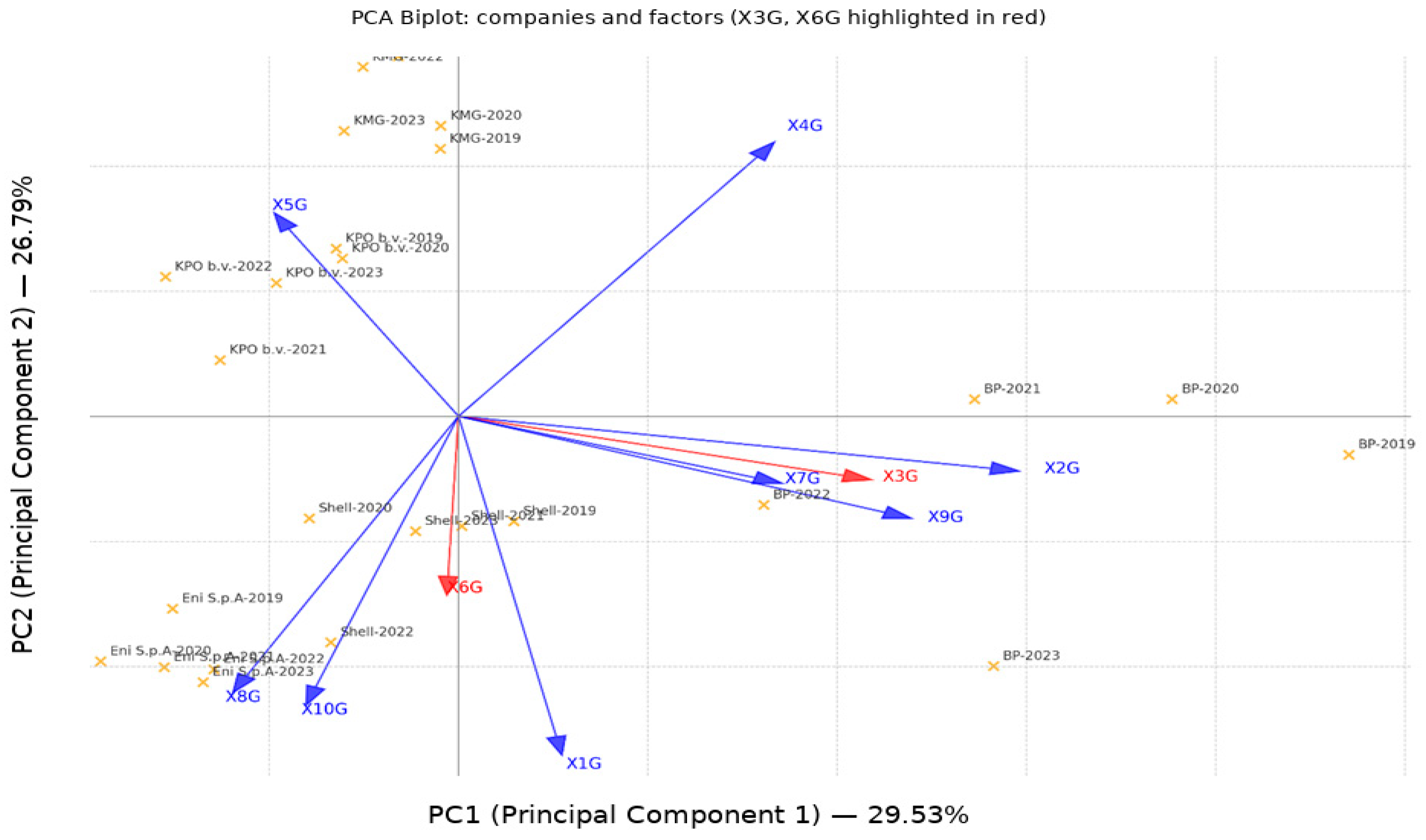

The graph represents the result of a principal component analysis (PCA) for variables X1G–X10G. The PC1 axis (Principal Component 1) explains approximately 29.53% of the total data variance. The PC2 axis (Principal Component 2) explains approximately 26.79% of the variance. Together, the two components explain approximately 56.32% of the total variance—a good result for a multivariate set of factors. The PC1 axis runs from left to right and reflects the main direction of data variation. The X3G and X6G factors highlighted in red contribute the most to it. The analysis demonstrates that corporate governance practices (the G aspect of ESG) directly impact companies’ environmental performance.

Failure to comply with business ethics principles leads to an increase in environmental threats, while honest financial management (including tax issues) helps to reduce these risks. The proposed model indicates that ethical and open governance are important not only from a moral point of view, but also serve as economic and environmental factors for sustainable progress, strengthening the connection between the elements of Environmental and Governance in the context of ESG.

4.4. Modeling GHG Emissions Based on Factors Demonstrating the Integrated Impact of ESG Responsibility of Oil and Gas Companies

At the initial stage of the integration process, indicators identified as significant based on the component-by-component impact assessment were included in the model. A panel regression analysis revealed the overwhelming influence of the Environment group of factors, which largely offset the impact of Social and Governance.

Coefficients: Estimate Std. Error z-value Pr(>|z|)

(Intercept) 12.74279814 9.60857607 1.3262 0.184777

X8 0.04606081 0.00548540 8.3970 < 2.2e-16 *** Nitrogen oxides (NOx), thousand t,

X11 -0.00789834 0.00172348 -4.5828 4.588e-06 *** Production volume, thousand tons

X13 0.00272337 0.00086318 3.1550 0.001605 ** Total waste disposal volume, thousand tons

X16 0.10795273 0.02153480 5.0129 5.360e-07 *** Oil spills and environmental incidents, volume

Xs7 -0.00027363 0.00035034 -0.7810 0.434791 Investments in renewable energy sources, $ million

Xs8 -0.11803320 0.22847358 -0.5166 0.605424 Share of women in the company, %

X3G 0.00977672 0.01048735 0.9322 0.351213 Violations of corporate ethics, number

X6G -0.05641341 0.04350179 -1.2968 0.194698 Taxes, $ million

In addition to the traditional ordinary least squares (OLS) method, new regression analysis approaches were used to ensure the stability of the created model and identify the most determining factors: partial least squares (PLS) and LASSO regression.

The use of these tools helps to increase the reliability of conclusions by reducing the influence of multicollinearity between variables, and also helps to identify those parameters that have the greatest impact on the indicator under study.

According to the results of PLS and LASSO testing, only four main factors continue to have a significant impact on the amount of GHGs emitted.

This allows us to conclude that the analysis of the relationship between eight sustainability indicators – four environmental, two social and two governance-related – and GHG emissions, carried out within a single model, showed a significant impact mainly of environmental aspects.

To study in detail the nature of this influence, an independent model was developed, focusing exclusively on social and managerial factors.

This methodology is consistent with common principles of empirical analysis and is used in particular in the work of [96] to assess the stability of the obtained data (robustness check). Thus, according to experts, comparing the results obtained using full and simplified versions of the model helps determine the stability of the impact of individual parameters and avoid a situation where strong predictors obscure the effect of other variables.

This approach is common in studies addressing multicollinearity and factor dominance. In complex models [97,98] that incorporate ESG factors, environmental parameters often have the most significant and direct impact on emissions, which can obscure or mask the contribution of social and governance indicators.

In fundamental works on the application of the LASSO method, this approach is explained through the application of the principle of model parsimony [99]. In his works, the selection of individual influencing parameters corresponds to sequential regression and regularization approaches, which strive to create the most concise and understandable structure.

According to methods for assessing mediation effects, within the framework of the ESG integration concept, governance and social aspects can influence environmental performance indirectly, but rather through organizational systems or internal company policies. The S+G model makes it possible to measure precisely this indirect effect [100].

Thus, the creation of an isolated model that includes social and governance variables allows us to assess the independent contribution of these factors to reducing greenhouse gas emissions.

At the same time, it provides a detailed explanation of the ways in which they are impacted through management and social instruments. The construction of an S+G model allows for the mitigation of the overwhelming influence of environmental factors during the modeling process.

At the same time, this approach improves understanding of the model and provides greater clarity to scientific conclusions.

Regression analysis results: Coefficients: Estimate Std. Error z-value Pr(>|z|)

(Intercept) 75.28376991 23.77155120 3.1670 0.001540 **

Xs7 -0.00195038 0.00095936 -2.0330 0.042051 *

Xs8 -1.55417944 0.57401770 -2.7075 0.006778 **

X3G 0.08223244 0.03425467 2.4006 0.016367 *

X6G -0.24491608 0.16967034 -1.4435 0.148885

Ŷ = 75,2838 − 0,00195·Xs7 − 1,5542·Xs8 + 0,0822·X3G

At the next stage, the model was tested for heteroscedasticity of residuals and autocorrelation.

bptest(model_re)

studentized Breusch-Pagan test

data: model_re

BP = 3.5702, df = 3, p-value = 0.3118, the p-value confirmed the null hypothesis that there is no heteroscedasticity, and the constancy of variance is confirmed.

pbgtest(model_re)

Breusch-Godfrey/Wooldridge test for serial correlation in panel models

chisq = 4.9697, df = 5, p-value = 0.4196, in the autocorrelation test, the p-value also confirmed the hypothesis of no autocorrelations, which indicates that the model does not suffer from residual autocorrelation, meaning that its estimates are efficient and unbiased.

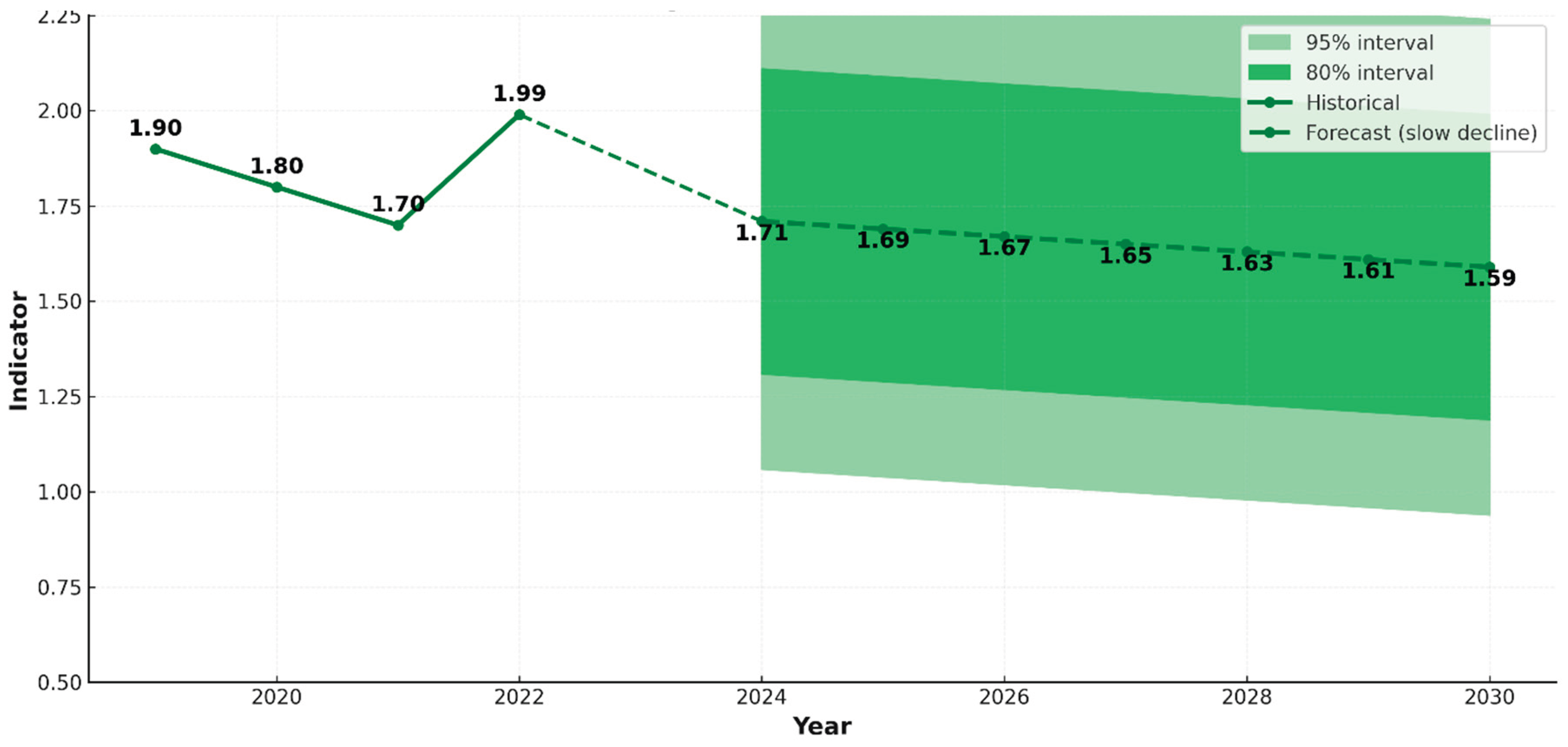

The next step involved forecasting greenhouse gas emissions, taking into account socio-governance factors. To ensure methodological rigor and consistency in the study, the ARIMAX model was used, accounting for both the internal dynamics of the time series and the impact of controllable ESG factors.Unlike basic autoregressive models, ARIMAX integrates exogenous variables reflecting investments in low-carbon development, gender diversity, and corporate ethics, making the model more managerially realistic (Figure 9, Appendix C).

The forecast presented in Figure 9 (model of the dependence of GHG emissions into the atmosphere on social and management factors of KPO activities) shows that according to the geometric interpretation of the linear trend of emission reduction, the trend slope angle is -10 over a 7-year period (tan(α)=∆Y/∆X; α=arctan(−0.01714) = - 0.9820). From an econometric perspective, this amounts to 7% over a seven-year period, or an estimated 1% per year. Meanwhile, the forecast compiled for the KPO model of GHG emissions dependent on environmental management factors (Figure 5) shows a slope of almost 60 (-5.710), or a sixfold greater effect. From an econometric perspective, the reduction rate is 35% over a seven-year period, or 5% per year—five times higher. A geometric interpretation of the linear trend in emissions reduction is more accurate for management decision-making. This comparison once again confirmed the powerful impact of environmental management on reducing greenhouse gas emissions. However, it also demonstrated that measures to demonstrate ESG commitment within the social and governance component also have an impact.

Forecasts for other companies, compiled using the S+G model, are presented in Appendix C. Thus, the forecasted reduction of GHG emissions into the atmosphere from social and management factors of the activities of BP, Shell, and Eni S.p.A. is more effective than that of KPO Moreover, while Eni S.p.A.’s forecast for component E showed a 13% reduction, the integrated S+G model showed only an 8% reduction. Conversely, KMG’s implementation of ESG principles in the social and governance responsibility components shows a greater impact on reducing atmospheric emissions – 55% versus 22% for component E. The results are consistent with the findings of the IOGP Energy Efficiency Expert Group, which found that leading global companies such as BP, ExxonMobil and Shell are actively implementing various strategies to improve energy efficiency by investing in new technologies and innovations [15,101]. Clearly, KPO faces limitations in funding and access to modern foreign technologies, which may limit flexibility in applying international practices and technologies used in Western companies.

The overall conclusion indicates that the hypothesis put forward in the study has thus been tested and confirmed: the use of ESG principles in companies’ activities contributes to the reduction of air pollution.

5. Suggestions for Improving the ESG Strategy for Reducing Atmospheric Emissions

The econometric analysis identified key ESG factors in the performance of oil and gas companies that contribute to addressing the important issue of maintaining air quality in the context of global climate commitments.

An empirical analysis of environmental, social, and governance (ESG) performance indicators yielded findings relevant to management recommendations. According to the analysis of the Environmental component, the relationship between energy consumption (X₈), the number of environmental deviations (X₁₆), and greenhouse gas emissions is direct, while water use (X₁₁) has an inverse effect: more efficient water use is associated with reduced emissions.

Hazardous waste disposal (X₁₃) shows a small but positive effect, consistent with the growth of industrial production and the need for efficient waste management. Such findings are confirmed by international studies: for example, [102] found that reducing water losses and introducing energy-saving technologies significantly reduce GHG emissions in water supply and sanitation systems. The work [103] highlights the high energy costs of wastewater treatment processes, particularly aeration, and points to a direct link between reduced energy consumption and reduced emissions. Based on the model data and similar international studies, the following management recommendations can be formulated:

Implement programs to improve energy efficiency at enterprises, paying particular attention to areas with the highest consumption (e.g., resource provision, production, waste disposal). An important area is improving the rational use of water resources and improving wastewater treatment methods as part of sustainable development policies, which simultaneously reduce emissions and save resources. Now KPO is taking steps to improve energy efficiency, most notably through an innovative high-pressure gas re-injection system, which not only increases production volumes but also minimizes environmental impacts by achieving 99.94% associated gas utilization. To effectively manage waste at KPO in accordance with GRI standards, it is proposed to integrate AI-based waste monitoring systems with other corporate management systems, such as Enterprise Resource Planning (ERP) and supply chain management systems [104]. This will provide a more comprehensive understanding of the environmental impact of operations and improve reporting according to GRI standards. Furthermore, the use of Artificial Intelligence (AI) to analyze waste data will enable waste volume forecasting and the development of waste minimization strategies.

Continue improving the atmospheric air monitoring systems as part of the region’s ESG strategy. As noted above, the system for industrial environmental monitoring of industrial emissions at KPO facilities is ongoing. Furthermore, it should be noted that the region has currently established a regional geoportal developed within the framework of the national scientific program, which serves as a key platform for integrating real-time environmental data into decision-making processes [105]. In addition, within the framework of the scientific program for Western Kazakhstan, a methodology for comparing Sentinel-5P/TROPOMI data and ground-based measurements was developed [106]. The patterns of formation of atmospheric air pollution at various levels in the region were studied based on an analysis of the features of the formation of the atmospheric mixing layer in the region under consideration, as well as scenarios for changes in atmospheric air quality. In the context of Compliance with Environmental Regulations, conducting further systematic research at the KPO will help identify patterns in the distribution of pollutants in the atmospheric boundary layer and create a modern pollutant database using GIS technologies, allowing for the prediction of atmospheric air quality, taking into account the socio-economic development of the region. The results obtained can serve as a basis for subsequent modeling based on best international practices for the future.

To establish the objective impact of the deposit on biotic communities and agrocenoses, it is necessary to conduct comprehensive in-depth monitoring studies using GIS technologies. Current climate change trends require more frequent biodiversity monitoring in areas where oil and gas operations operate. Unlike the approach used at KPO, where satellite imagery is conducted once every ten years, it is recommended to conduct such surveys more frequently. Although the company has developed regulatory actions for sensitive coastal ecosystems and created a database of flora and fauna species, analysis has shown that the data has not yet been systematized, and the results are unclear. At the same time, there is study, the results of which showed a high level of impact on living organisms [107]. Modern remote sensing technologies, including hyperspectral imaging and machine learning algorithms, allow for more accurate and effective analysis of ecosystem and biodiversity status, further necessitating more frequent surveys.

The data obtained for the assessment of the Social component is in harmonious agreement with global scientific research devoted to issues of social responsibility and sustainable development.

Considering that there is still no practical use of renewable energy sources at KPO and no significant investments in renewable energy sources are planned, it is proposed to increase funding for RES. The negative value of the coefficient for the variable X₇ indicates a genuine impact of the move towards a low-carbon economy, which is noticeable even with a small increase in the volume of “green” investments in total capital investments.

As numerous studies show [34,36,108,109,110], increasing funding for renewable energy sources stimulates the restructuring of production processes, the introduction of resource-saving technologies and the reduction of greenhouse gas emissions by companies. Thus, PwC, among the key trends influencing global oil and gas production, emphasizes the importance of switching to renewable energy sources to reduce atmospheric emissions. Therefore, companies must balance traditional operations with increasing investment in low-carbon technologies. In the context of increasing investment in renewable energy sources, biogas production from agricultural raw materials in the West Kazakhstan region (the total volume of agricultural waste in the West Kazakhstan region was 162,200 tons per year) at KPO appears entirely feasible, given the availability of suitable resources and the growing interest in renewable energy sources. This will provide economic benefits by complementing existing energy sources and reducing the region’s dependence on electricity imports from Russia.

In terms of the Governance component, it is recommended to increase the representation of women among the organization’s employees, since the impact of the social aspect - the representation of women among KPO employees - demonstrates a significant and inverse correlation. An analysis of the application of ESG principles [111,112], according to scientific data [113,114,115], shows that women’s participation in corporate governance and decision-making increases attention to environmental issues, stimulates the creation of an ethical management style and optimizes resource consumption. This indicates that gender diversity can be considered not only as an important social factor, but also as a significant element influencing environmental stability.

Furthermore, the inverse relationship between the size of tax payments and the level of pollution obtained in the study demonstrates that financial honesty and transparency are key indicators of business environmental awareness. The negative value of the coefficient for the tax payments indicator (−0.5298) indicates that further improvement of corporate governance and openness of the information provided is necessary. This finding is consistent with a number of studies that show that financial integrity and transparency have a positive impact on emissions reduction, while non-compliance with business ethics standards is associated with increased environmental threats and deterioration in the performance of internal control systems. This trend is supported by studies [116,117,118,119,120,121] (indicating that ineffective corporate governance and limited information transparency exacerbate carbon footprints and negatively impact organizational image. Emissions and corporate ethics are interrelated in the context of ESG analysis, where compliance with ethical standards and emission reduction are key factors for achieving sustainable development and enhancing a company’s reputation. This is consistent with the principles of good governance, according to which compliance with tax legislation is a sign of maturity of management practices, accountability and a high level of trust in institutions.

Research shows that companies with high levels of emissions often experience downgrades to their ESG scores. This is because pollutant emissions can be perceived as a breach of social and environmental responsibility, negatively impacting the company’s reputation and sustainability scores [122]. Research by the OECD (2023) and the World Economic Forum (2023) [117] highlights the link between tax transparency and sustainable business development, as organizations operating within the legal framework are more likely to invest in emission reduction technologies and publish ESG reports.