Submitted:

15 August 2025

Posted:

15 August 2025

You are already at the latest version

Abstract

The digital transformation of financial services has emerged as a strategic pathway to bridge economic inclusion gaps in historically marginalized urban areas. This study examines the structural barriers faced by micro and small enterprises (MSEs) in the Historic Center of San Salvador, particularly regarding access to traditional financial services and the adoption of digital technologies. Using a qualitative, exploratory-descriptive approach, the research combines documentary analysis and a comparative review of FinTech ecosystems in Latin America and Spain to identify key components and enabling conditions. Findings highlight persistent challenges in access to financing, financial literacy, digital infrastructure, and regulatory adaptation, which hinder financial inclusion for MSEs. In response, the study proposes an integrated FinTech ecosystem model that connects public institutions, private actors, academia, and end-users to foster innovation, intersectoral collaboration, and economic resilience. Although grounded in the Salvadoran context, the model offers a replicable framework for other urban regions facing similar constraints. The research contributes to ongoing debates on digital inclusion and provides actionable insights for designing public policies that promote inclusive and sustainable digital transformation in emerging economies.

Keywords:

FinTech ecosystem

; digital financial inclusion

; micro and small enterprises

; digital transformation

; financial innovation

; inclusive public policy

1. Introduction

Micro and small enterprises (MSEs) play a fundamental role in job creation, local development, and economic resilience, particularly in emerging economies where informal business activity predominates [1,2]. In countries such as El Salvador, these units account for over 90% of the business sector and contribute significantly to GDP and both formal and informal employment [12]. However, many of these businesses, especially those located in historically marginalized urban areas, face persistent structural barriers that hinder sustainable growth. The most critical challenges include limited access to formal financial services, lack of technological training, weak digital skills, and the absence of a regulatory framework that fosters innovation [3,4]. In this context, the digital transformation of financial services—commonly referred to as FinTech—has emerged as a strategic solution to expand financial inclusion and improve the operational efficiency of MSEs. Academic literature has highlighted FinTech’s potential to reduce transaction costs, democratize access to credit, strengthen value chains, and promote financial transparency in excluded populations [5,6,7]. In structurally unequal societies, FinTech ecosystems provide key platforms for integrating public and private actors, fostering not only access but also technological ownership [8,9]. However, adoption across Latin America has been fragmented and uneven, partly due to low digital literacy, limited system interoperability, and institutional resistance to change [10,11].

1.1. Literature Review

The concept of an ecosystem, originally developed in the field of ecology, has been adopted by social and economic sciences to describe complex and interconnected environments where multiple actors interact dynamically [13,14]. In the business context, this concept has evolved into entrepreneurial ecosystems, which integrate factors such as access to finance, digital infrastructure, entrepreneurial culture, public policies, and support networks [15,16]. In particular, the financial ecosystem for entrepreneurs has gained relevance by connecting traditional institutions with alternative financing mechanisms such as crowdfunding, venture capital, and flexible regulatory instruments [1,17,18]. The introduction of FinTech technologies has substantially transformed these environments, allowing for scalable, user-centered, and personalized financial services [6].

Various studies identify the FinTech ecosystem as a catalyst for financial innovation, capable of articulating technology startups, banking institutions, software developers, investors, regulatory bodies, universities, and financial consumers into a collaborative network [8,20,21,22]. This complex institutional architecture depends on enabling conditions such as skilled human capital, access to seed capital, regulatory sandbox frameworks, public–private partnerships, and resilient digital infrastructure [10,19]. In Latin America, these dynamics have taken shape in cities like Bogotá, Santiago, Mexico City, and São Paulo, where FinTech ecosystems have rapidly scaled and generated positive impacts in terms of financial access, credit efficiency, and informal market digitalization.

In the Salvadoran context, however, specific challenges remain. Although the National FinTech Strategy recognizes the importance of building an inclusive digital financial ecosystem, implementation has been limited. Barriers include weak inter-institutional coordination, dominance of traditional banking, urban–rural technology gaps, and the lack of a dynamic regulatory framework [11,12]. In the Historic Center of San Salvador, where informality, social exclusion, and urban decay converge, MSEs represent both a source of livelihood for thousands of families and an opportunity for economic regeneration. Yet these enterprises operate in conditions of high vulnerability, without access to financial services adapted to their needs or support for digital transformation.

1.2. Research Question

In light of these challenges, this study is guided by the following research question:

What are the essential components of a FinTech ecosystem adapted to the Historic Center of San Salvador to promote the digital financial inclusion of MSEs?

This article aims to identify and systematize those components by conducting a comparative review of international experiences, a critical analysis of the national institutional framework, and a synthesis of key enabling elements to propose a replicable model. The proposed framework is grounded in intersectoral collaboration, territorial relevance, and operational sustainability, bringing together public, private, and academic stakeholders. In doing so, this study contributes to the global debate on inclusive digital transformation and provides valuable insights for public policymaking aimed at promoting local economic development and financial equity in emerging economies like El Salvador.

2. Materials and Methods

This study adopts a qualitative, exploratory, and descriptive approach, aligned with the need to understand how a FinTech ecosystem can be designed to respond to the real conditions of micro and small enterprises (MSEs) in the Historic Center of San Salvador. The methodology integrates documentary analysis, comparative case studies, and theoretical modeling to construct a replicable framework for digital financial inclusion. Ethical considerations were addressed by ensuring the use of publicly available data and institutional sources, and digital tools such as ATLAS.ti and Excel were employed for data coding and thematic categorization. The research adheres to the MDPI guidelines for methodological transparency and rigor.

2.1. Methodological Design and Information Sources

The methodological design was structured on three levels: (1) a review of academic literature on FinTech ecosystems, digital transformation, and MSEs; (2) an examination of technical reports, regulatory frameworks, and national and international public policies; and (3) a comparative case study analysis of FinTech ecosystems in Latin America and Europe. Selection criteria for authors included peer-reviewed publications indexed in Scopus and Web of Science from the last five years (2018–2024), with emphasis on empirical studies and theoretical contributions to financial inclusion and digital innovation. Case selection was based on relevance to urban MSE contexts, availability of institutional data, and documented outcomes in financial ecosystem development. Key sources included ASAFINTECH, the Financial Innovation Office (OIF), the Central Reserve Bank (BCR), and El Salvador’s National FinTech Strategy [1,2,3].

2.2. Comparative Analysis and Model Construction

The comparative analysis was guided by a theoretical framework grounded in the concept of innovation ecosystems and inclusive digital transformation [4,5]. The analytical process focused on identifying structural patterns, key actors, functional relationships, and enabling conditions that support the development of FinTech ecosystems in vulnerable urban contexts. Thematic matrices and comparative schemes were used to synthesize findings and construct an integrated model. Digital tools such as Excel and ATLAS.ti facilitated the coding and categorization of data. The model construction was informed by the works of Danladi et al. (2023), Ajouz et al. (2023), and Bamidele et al. (2024), which emphasize collaborative governance, adaptive regulation, and technological infrastructure as pillars of financial inclusion [6,7,8].

Table 1.

Key Elements of the FinTech Ecosystem (Comparative Summary).

| Elements | González (2019) | Lee & Shin (2018) | Rubaceti (2022) | Bencomext (2019) | EY Ecuador (2022) | OIF (2023) | ASAFINTECH (2024) |

| FinTech Startups | x | x | x | x | x | x | x |

| Government | x | x | x | x | x | x | x |

| Traditional Financial Institutions | x | x | x | x | x | x | x |

| Financial Consumers | x | x | x | x | x | x | |

| Technology Developers | x | x | x | x | x | ||

| Venture Capital & Accelerators | x | x | x | x | |||

| Consumer Protection Agencies | x | ||||||

| Insurance Companies | x | ||||||

| Academia | x | x | x | ||||

| Investors | x | x | |||||

| Venture Capital Institutions/Funds | x | ||||||

| Investment Facilitators | x | ||||||

| Professional Service Providers | x | ||||||

| Professional Associations | x | ||||||

| Regulators/Supervisory Entities | x |

3. Results and Discussion

3.1. Results

The findings of this study reveal that the development of a FinTech ecosystem tailored to the needs of micro and small enterprises (MSEs) in the Historic Center of San Salvador requires an integrated articulation of actors, capacities, and regulatory frameworks. Based on a comparative analysis of cases in Latin America and Europe, as well as the systematization of documentary sources and contextual data, five key dimensions were identified that structure an inclusive FinTech ecosystem: (1) diversity of actors, (2) technological infrastructure, (3) financing mechanisms, (4) institutional capacities, and (5) adaptive regulatory frameworks. These dimensions are synthesized in Table 2.

a- Diversity of Actors and Collaborative Governance

One of the most consistent findings across the analyzed models is the need for collaborative governance involving FinTech startups, traditional financial institutions, regulators, academic institutions, financial consumers, MSE support agencies, and investors. In the Salvadoran context, this articulation remains in an early stage, limiting innovation flows and the creation of solutions tailored to MSE needs.

b- Technological Infrastructure and Digital Gaps

The analysis showed that the lack of technological infrastructure in historically marginalized urban areas, such as the Historic Center, is a critical structural barrier to financial digitalization. Low connectivity, limited access to digital devices, and poor interoperability among financial systems hinder the effective implementation of FinTech solutions.

c- Alternative Financing Mechanisms

The study found that the most successful models of financial inclusion for MSEs incorporate non-traditional financing schemes such as crowdfunding platforms, digital microcredits, and impact investment funds. In El Salvador, these mechanisms remain largely inaccessible to MSEs due to banking concentration and the absence of regulatory frameworks that promote inclusive financial innovation.

d- Institutional Capacities and Financial Literacy

The comparative review demonstrated that sustainable FinTech ecosystems integrate programs for technical training, financial literacy, and the development of digital skills for entrepreneurs. In the Salvadoran case, this dimension is underdeveloped and requires multisectoral strengthening coordinated by public, private, and academic actors.

e- Adaptive Regulation and Regulatory Environment

The study found that the most effective regulatory environments combine flexibility, innovation, and consumer protection. Initiatives such as regulatory sandboxes, progressive licensing frameworks, and collaborative monitoring platforms have been essential in ecosystems like those of Spain and Colombia. In El Salvador, although some initial efforts exist, regulatory instruments that foster the safe development of FinTech services have yet to be consolidated. These results not only enhance the theoretical understanding of FinTech ecosystems in emerging contexts but also provide a practical foundation for the design of public policies and interventions aimed at territorial economic development and financial justice.

The triangulation of these findings supports the proposal of a FinTech ecosystem model oriented toward MSEs in vulnerable urban contexts. This model is based on intersectoral collaboration, recognizes the structural conditions of the territory, and integrates governance, financing, training, and regulatory mechanisms to foster sustainable digital financial inclusion. The discussion highlights that the digital transformation of MSEs depends not only on technological adoption but on the creation of an enabling environment that aligns capacities, policies, and local financial culture.

3.2. Discussion

The proposed FinTech ecosystem model tailored to the Historic Center of San Salvador directly addresses gaps identified in both the literature and the empirical findings. Unlike fragmented approaches that tackle financial inclusion from a single dimension—technological, institutional, or regulatory—this model integrates five key dimensions that interact synergistically: collaborative governance, technological infrastructure, alternative financing mechanisms, institutional capacities, and adaptive regulation.

From a theoretical standpoint, the model responds to the limitations highlighted by Ajouz et al. (2023) and Danladi et al. (2023), who emphasize the need for flexible and collaborative institutional frameworks to scale FinTech solutions in emerging economies. Likewise, Bamidele et al. (2024) underscore the importance of integrating technological innovation with microfinance to improve credit access for MSMEs, which is reflected in the model’s emphasis on alternative financing mechanisms.

In terms of contribution to the Sustainable Development Goals (SDGs), the model aligns with SDG 8 (Decent Work and Economic Growth) by promoting access to financial services for urban entrepreneurs; SDG 9 (Industry, Innovation and Infrastructure) by strengthening digital infrastructure and fostering financial innovation; and SDG 10 (Reduced Inequalities) by facilitating equitable access to financial services in historically excluded areas. The integration of these goals into the model’s design reinforces its relevance for public policy aimed at sustainable development.

In summary, the discussion demonstrates that the model not only addresses local challenges but also offers both theoretical and practical contributions to the field of digital financial inclusion. Its multisectoral and territorial approach makes it a useful tool for replication in other Latin American cities with similar socioeconomic conditions.

4. Conclusions

4.1. Findings

This study highlights the importance of designing contextualized FinTech ecosystems that respond to the territorial, institutional, and technological realities of micro and small enterprises (MSEs) in vulnerable urban contexts. Specifically, the analysis identified five fundamental dimensions that must be integrated synergistically to create an enabling environment for digital financial inclusion: diversity of actors, technological infrastructure, alternative financing mechanisms, institutional capacities, and adaptive regulation.

4.2. Contributions

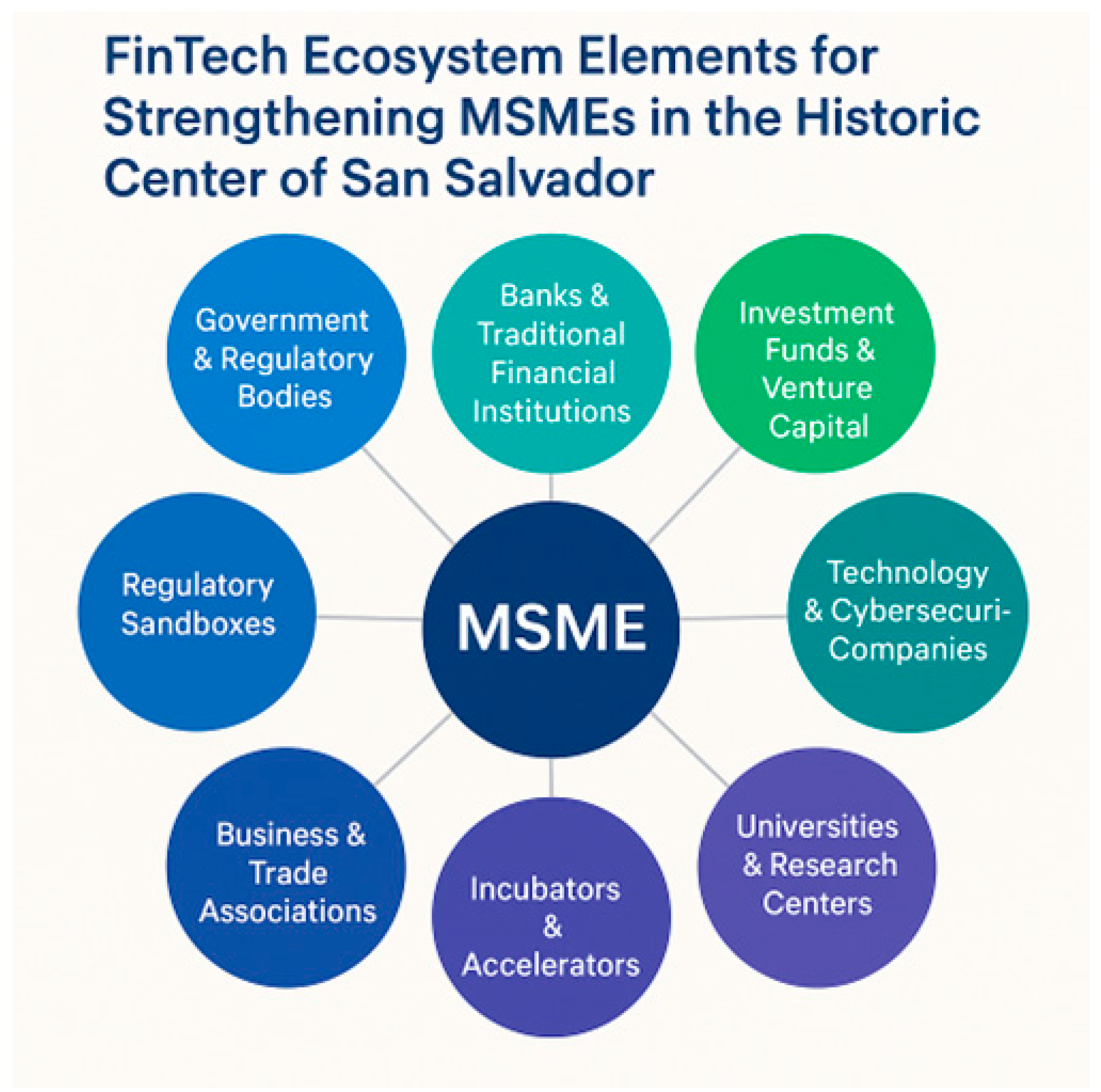

From a theoretical perspective, the main contribution of this study is the proposal of an integrated FinTech ecosystem model focused on urban MSEs. The model connects concepts from the literature on innovation ecosystems, financial inclusion, and territorial economic development, adapting them to underexplored subnational realities in Central America. The research expands the conceptual framework of FinTech by linking it to local dynamics, intersectoral relations, and structural barriers, offering a more complex and situated understanding of the phenomenon (Table 3, Figure 1).

On a practical level, the findings offer guidance for the formulation of public policies and institutional interventions aimed at strengthening the digital transformation of MSEs. The proposed model can serve as input for local economic development strategies, financial literacy programs, inclusive regulatory frameworks, and alternative financing schemes that promote economic sustainability in traditionally excluded sectors.

Figure 2.

Readiness of FinTech Ecosystem Dimensions in San Salvador.

4.3. Limitations

Among the limitations of the study is its reliance on secondary sources and the absence of direct fieldwork with ecosystem actors in El Salvador. Although previous research findings were incorporated, future studies should adopt mixed-methods approaches that combine document analysis with interviews, surveys, or empirical case studies to deepen understanding of institutional dynamics and MSE experiences in adopting FinTech solutions.

4.4. Future Research

Advancing toward truly inclusive digital transformation requires more than just technology; it demands enabling environments that acknowledge structural inequalities and foster innovation through a logic of multisectoral collaboration and financial justice.

The following are suggested as future lines of research:

- Assessing the effectiveness of pilot FinTech ecosystems implemented in mid-sized cities with similar characteristics.

- Exploring cultural perceptions and adoption barriers among MSE users regarding digital technologies.

- Investigating the role of universities and innovation centers as key drivers of technological financial inclusion.

- Analyzing the impact of adaptive regulation on the sustainability and scalability of FinTech solutions for low-income segments.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Banco Centroamericano de Integración Económica. El estado de la Mype 2024. 2024. Available online: https://www. bcie. org/novedades/noticias/articulo/el-informe-el-estado-de-la-mype-2024-indica-que-las-micro-y-pequenas-empresas-de-el-salvador-aportan-mas-del-35-al-producto-interno-bruto (accessed on 10 March 2024).

- Vaquerano Benavides, J. R. Aporte de las MYPES a la generación de empleo en Zona Oriental de El Salvador. Entorno 2024, 1, 11–17. https://camjol.info/index.php/entorno/article/view/18428.

- Bruton, G. ; Khavul, S. ; Siegel, D. ; Wright, M. New Financial Alternatives in Seeding Entrepreneurship: Microfinance, Crowdfunding, and Peer–to–Peer Innovations. Entrep. Theory Pract. 2015, 39, 9–26. [CrossRef]

- Bromley, R. D. F. Informal Commerce: Expansion and Exclusion in the Historic Centre of the Latin American City. Int. J. Urban Reg. Res. 1998, 22, 245–263. [CrossRef]

- Gai, K. ; Qiu, M. ; Sun, X. A Survey on FinTech. J. Netw. Comput. Appl. 2018, 103, 262–273. [CrossRef]

- Gomber, P. ; Kauffman, R. J. ; Parker, C. ; Weber, B. W. On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services. J. Manag. Inf. Syst. 2018, 35, 220–265. [CrossRef]

- Bamidele, M. O. ; Urefe, O. ; Mokogwu, C. ; Ewim, S. E. Integrating Fintech and Innovation in Microfinance: Transforming Credit Accessibility for Small Businesses. Int. J. Front. Res. Rev. 2024, 3, 90–100. [CrossRef]

- Danladi, S. ; Prasad, M. S. V. ; Modibbo, U. M. ; Ahmadi, S. A. ; Ghasemi, P. Attaining Sustainable Development Goals through Financial Inclusion: Exploring Collaborative Approaches to Fintech Adoption in Developing Economies. Sustainability 2023, 15, 13039. [CrossRef]

- Zhang-Zhang, Y. ; Rohlfer, S. ; Rajasekera, J. An Eco-Systematic View of Cross-Sector Fintech: The Case of Alibaba and Tencent. Sustainability 2020, 12, 8907. [CrossRef]

- Puschmann, T. ; Hoffmann, C. H. ; Khmarskyi, V. How Green FinTech Can Alleviate the Impact of Climate Change—The Case of Switzerland. Sustainability 2020, 12, 10691. [CrossRef]

- Banco Interamericano de Desarrollo. Ecosistema Fintech en América Latina y el Caribe supera las 3. 000 startups. 2024. Available onlinehttps://www.finnosummit.com/wp-content/uploads/2024/06/Comunicado-Final-IV-Informe-Fintech-BID-Finnovista.pdf (accessed on 10 March 2024).

- Banco Central de Reserva. Encuesta de competitividad e innovación financiera en El Salvador. 2022. Available online: https://www.bcr.gob.sv/documental/Inicio/vista/566cfa120c155ccdf979b4bdb9d46d75.pdf (accessed on 10 March 2024).

- Holling, C. S. Understanding the Complexity of Economic, Ecological, and Social Systems. Ecosystems 2001, 4, 390–405. [CrossRef]

- O’Connor, A. ; Stam, E. ; Sussan, F. ; Audretsch, D. B. Entrepreneurial Ecosystems: The Foundations of Place-Based Renewal. In International Studies in Entrepreneurship; Springer: Cham, Switzerland, 2018; Volume 38, pp. 1–21. https://link.springer.com/chapter/10.1007/978-3-319-63531-6_1.

- Isenberg, D. J. How to Start an Entrepreneurial Revolution. Harv. Bus. Rev. 2010. Available online: https://hbr. org/2010/06/the-big-idea-how-to-start-an-entrepreneurial-revolution (accessed on 10 March 2024).

- Stam, E. The Dutch Entrepreneurial Ecosystem. SSRN Electron. J. 2014. [CrossRef]

- Beck, T. ; Demirguc-Kunt, A. Small and Medium-Size Enterprises: Access to Finance as a Growth Constraint. J. Bank. Financ. 2006, 30, 2931–2943. [CrossRef]

- Mollick, E. The Dynamics of Crowdfunding: An Exploratory Study. J. Bus. Ventur. 2014, 29, 1–16. [CrossRef]

- Lee, I. ; Shin, Y. J. Fintech: Ecosystem, Business Models, Investment Decisions, and Challenges. Bus. Horiz. 2018, 61, 35–46. [CrossRef]

- Ajouz, M. ; Abuamria, F. ; Zeer, I. A. ; Salahat, M. ; Shehadeh, M. ; Binsaddig, R. ; Al-Sartawi, A. ; Al-Ramahi, N. M. Navigating the Uncharted: The Shaping of FinTech Ecosystems in Emerging Markets. Cuad. Econ. 2023, 46, 189–201. https://cude.es/submit-a-manuscript/index.php/CUDE/article/view/469.

- Barrera Rubaceti, N. A. ; Robledo Giraldo, S. ; Zarela Sepulveda, M. Una revisión bibliográfica del Fintech y sus principales subáreas de estudio. Econ. CUC 2021, 43, 83–100. [CrossRef]

- Cohen, S. ; Hochberg, Y. V. Accelerating Startups: The Seed Accelerator Phenomenon. SSRN Electron. J. 2014. [CrossRef]

Figure 1.

Proposed FinTech Ecosystem Model.

Table 2.

Summary of Key Dimensions and Case Examples.

| Dimension | Key Findings | Case Example |

| Diversity of Actors | Collaborative governance among FinTechs, banks, regulators, academia | Colombia: Ruta N Medellín [1] |

| Technological Infrastructure | Connectivity, interoperability, and digital access | Mexico: FinTech Law and infrastructure expansion [2] |

| Alternative Financing Mechanisms | Crowdfunding, microcredits, impact funds | Chile: Cumplo platform [3] |

| Institutional Capacities | Training, digital literacy, entrepreneurship support | Brazil: SEBRAE digital programs [4] |

| Adaptive Regulation | Regulatory sandboxes, progressive licensing | Spain: CNMV sandbox [5] |

Table 3.

Proposed FinTech Ecosystem Model.

| Component | Function |

| Government and Regulatory Bodies | Establish a flexible and secure regulatory framework that fosters financial innovation. Includes FinTech legislation, regulatory sandboxes, tax incentives, and public policies aimed at financial inclusion. |

| Banks and Traditional Financial Institutions | Act as strategic allies of FinTechs, facilitating interoperability, access to payment networks, and co-creation of digital financial products. May also invest in startups or integrate them into their platforms. |

| Investment Funds and Venture Capital | Provide funding to early-stage and scaling FinTech startups. Also offer mentorship, strategic advice, and access to networking opportunities to strengthen the ecosystem. |

| Technology and Cybersecurity Companies | Develop the digital infrastructure required for FinTech platforms, ensuring data security, interoperability, and service scalability. |

| Universities and Research Centers | Generate knowledge, train specialized talent, and promote innovation through academic programs, incubators, hackathons, and partnerships with the productive sector. |

| Incubators and Accelerators | Offer technical, legal, and financial support to FinTech startups, facilitating their validation, growth, and scalability. Also connect entrepreneurs with investors and potential clients. |

| Business and Trade Associations | Represent sector interests, promote collaboration among actors, and facilitate dialogue with government. Also drive financial education and technological adoption among MSEs. |

| Regulatory Sandboxes | Supervised testing environments where FinTechs can experiment with new products and business models in a controlled setting, reducing risks and fostering innovation. |

| Financial Consumers (MSEs) | The core of the ecosystem. Their active participation, feedback, and adoption of FinTech technologies are key to validating and scaling solutions. Require financial and digital education to fully benefit from the ecosystem. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.