Submitted:

18 July 2025

Posted:

21 July 2025

You are already at the latest version

Abstract

The rapid digital transformation of the financial sector has prompted supervisory authorities worldwide to adopt new monitoring instruments for fintech innovation monitoring. Among these, Innovation Hubs have emerged as key institutional tools for enhancing regulatory accessibility, interpretive clarity and supervisory adaptation. This article explores the case of the Romanian Fintech Innovation Hub, launched by the National Bank of Romania as a non-binding consultation platform for FinTech and payment service providers navigating complex legal environments. Drawing on original research field, internal documentation and a conceptual framework that positions fintech innovation hubs as simultaneously outward-facing and inward-transformative, the paper assesses the Hub’s performance across several dimensions: stakeholder engagement, regulatory learning, policy calibration and institutional reflexivity. Findings reveal that while the Innovation Hub contributed significantly to internal capacity building and trust-based dialogue, its potential to inform rulemaking remained constrained by structural and procedural limitations. The study identifies best practices for optimizing Innovation Hubs in bank-dominated markets, including modular engagement pathways, AML/KYC guidance harmonization, pre-engagement diagnostics on ICT risk, and improved feedback loops into supervisory planning. The Romanian case illustrates both the functional value and the institutional boundaries of advisory-only innovation infrastructures in emerging fintech ecosystems. As such, it provides transferable lessons for jurisdictions aiming to reconcile innovation facilitation with prudential integrity and legal certainty.

Keywords:

Innovation Hub

; FinTech supervision

; regulatory innovation

; payment service providers

; institutional learning

; policy feedback

1. Introduction

The acceleration of financial innovation over the past decade has brought about a reconfiguration of supervisory practices and institutional mandates within the financial regulatory ecosystem. While traditional supervisory models were designed primarily for stable, vertically integrated financial intermediaries [1], the rise of FinTech1 actors, decentralized technologies and platform-based business models has prompted central banks and regulatory authorities to adopt new engagement and fintech monitoring instruments to understand and support. Among these, innovation facilitators such as innovation hubs and regulatory sandboxes and digital sandboxes or fintech accelerators that have emerged as key policy tools aimed at reconciling financial stability mandates with the objective of fostering responsible innovation [2,3,4].

In this context, the National Bank of Romania (NBR) launched its own Innovation Hub as a platform for engaging with entities developing new financial technologies, with a focus on understanding and clarifying applicable legal frameworks, fostering regulatory compliance, and facilitating internal supervisory learning. Unlike more interventionist tools such as Regulatory sandboxes, the Romanian Hub was conceived as a purely contact point as a consultative structure, without any derogation from applicable legal framework of compliance obligations.

The implementation of Innovation Hub offers an opportunity to examine how institutional design, engagement practices and regulatory communication evolve in response to the needs of a still-fragmented FinTech ecosystem worldwide [5].

Romania presents a particularly relevant case study given its bank-centric financial sector, a moderate FinTech penetration, and limited experience with formal innovation facilitation mechanisms. The Innovation Hub thus represents both a symbolic and functional entry point into a more adaptive and open to dialogue innovation monitoring posture.

This paper analyzes the implementation phase of the Romanian Innovation Hub, focusing on the nature of interactions, the institutional dynamics triggered by the initiative and the lessons that can be drawn for jurisdictions with similar characteristics. Drawing from internal documentation, stakeholder interviews and comparative information gathered from the working groups we take part in, this paper contributes to the literature on regulatory innovation by identifying the concrete mechanisms through which Innovation Hubs can support market access, enhance supervisory learning and inform future policy design.

Literature Review

The academic literature on regulatory innovation has expanded significantly in recent years, reflecting the increasing complexity of the interface between financial supervision and financial technological transformation. There are two competing regulatory imperatives: ensuring legal certainty and ICT risks mitigation, on the one hand, and facilitating innovation and market entry, on the other. Innovation hubs have been conceptualized as tools that seek to reconcile these goals by creating structured spaces for interpretive dialogue and supervisory learning, without offering legal exemptions or altering licensing conditions [6].

In comparative perspective, several typologies of innovation facilitators have been proposed. The Financial Stability Board (FSB) distinguishes between information-based, testing-based and hybrid models, placing innovation hubs in the first category—as mechanisms aimed at improving regulatory communication and interpretive clarity [7]. These instruments differ from regulatory sandboxes, which involve live testing under tailored conditions, and from accelerators, which often include commercial or funding components.

Innovation facilitation frameworks generally follow two models [8]. The authorization model requires firms to obtain individual approvals or waivers to test products within a controlled setting. While this allows for tailored regulatory approaches and may attract investment, it often involves a high administrative burden, is constrained by legal mandates, and excludes activities outside the regulator’s remit. In contrast, the notification model relies on firms merely informing regulators of their testing intentions. This model is less resource-intensive and does not require a bespoke sandbox structure, but it limits regulatory engagement and offers narrower flexibility through different types of financial services waivers, potentially reducing the depth of supervisory insight and support.

The concept of the Innovation Hub has gained increasing prominence across the European Union as a means to provide structured, non-binding dialogue between supervisory authorities and market innovators, particularly those navigating the licensing perimeter or seeking interpretive guidance on emerging business models [10]. The European Banking Authority and the Joint Committee of the European Supervisory Authorities have actively promoted the development of national innovation hubs as part of the broader FinTech Roadmap, emphasizing the need for consistency, transparency, and accessibility across jurisdictions [11].

In order to accommodate supervisory judgment and to reflect national particularities—such as the level of FinTech maturity, domestic market dynamics, or technological risk complexity—regulators have adopted proportionality-based frameworks. These allow for differentiated application of regulatory obligations depending on the nature and impact of the innovation in question. Combined with the enhanced role of the European Supervisory Authorities (ESAs) in promoting supervisory convergence across EU jurisdictions, this approach supports a more flexible and context-sensitive interpretation of licensing or authorization procedures for emerging FinTech solutions [12].

A growing body of empirical studies has examined the institutional design, effectiveness and limitations of national innovation hubs, which are increasingly viewed as institutional mechanisms that mediate between regulatory stability and technological change, enabling adaptive governance in complex and dynamic financial ecosystems [6,8,12,13,14,15,16,17]. The Financial Stability Board argues that the success of such initiatives depends not only on procedural access but also on the depth of feedback provided, the transparency of criteria, and the internal coordination within supervisory authorities [4]. Similarly, Omarova emphasizes the role of innovation hubs in building adaptive capacity within regulatory bodies, particularly in jurisdictions with legacy supervisory architectures [18].

In the European context, the European Banking Authority has issued detailed guidance on the features of effective innovation hubs, recommending clear application procedures, defined response timelines, public reporting and feedback loops into the policymaking process [19].

Over the past decade, the European Supervisory Authorities (ESAs) - including the European Banking Authority (EBA), the European Securities and Markets Authority (ESMA) and the European Insurance and Occupational Pensions Authority (EIOPA) - have intensified their efforts to monitor the emergence of innovative financial services and technologies, particularly in the field of payments [2]. This coordinated approach aims not only to identify regulatory risks, but also to foster safe experimentation and promote trust in digital financial services.

The European Supervisory Authorities’ Joint Committee highlights the importance of coordination across Member States to avoid fragmentation and regulatory arbitrage, particularly considering the cross-border aspect of some financial services, such as payments [9].

Within this institutional framework, EBA has developed a structured strategy for observing and analyzing innovation trends, with a focus on ensuring that regulatory and licensing frameworks remain both robust and adaptive [20,21]. One of the core messages articulated by the EBA is that financial innovation must be sustainable, inclusive and aligned with high standards of consumer protection and operational resilience [22]. As part of its thematic work, EBA has assessed the implications of FinTech developments on business models, initially focusing on credit institutions and subsequently extending its analysis to payment institutions and electronic money institutions. These assessments aim to capture how innovative technologies are transforming strategic positioning, compliance models and service delivery channels across the European financial ecosystem. In this context, open banking, payment initiation services and account information services have emerged as priority areas of observation, especially under the regulatory perimeter defined by PSD22 [23] and DORA3 [24]. Additionally, EBA has promoted the establishment of dedicated FinTech units and innovative working groups, both at its own level and within the national competent authorities. These structures collect and analyze information on technological developments (ex. artificial intelligence, blockchain, big data, IoT, machine learning etc.), supporting supervisory readiness and facilitating constructive engagement with market participants.

The SGIA (Sub-Group on Innovative Applications) operating within the EBA framework provides a platform for national experts to exchange information, share experiences and coordinate responses regarding innovation initiatives in financial services. During SGIA sessions, member authorities have discussed the risks and opportunities posed by emerging technologies, particularly in the context of payment services and financial system stability.

EBA has acknowledged the increasing reliance on automated and digital channels for consumer interaction, highlighting the expansion of digital finance tools for budgeting, price comparison, digital identity, and personal financial management. This growing digitalization trend has reinforced the need for harmonized supervisory responses and cross-border alignment [20].

To strengthen operational readiness and digital resilience, EBA has also contributed to developing regulatory frameworks such as the Digital Operational Resilience Act (DORA), which introduces harmonized ICT risk management requirements for financial entities and third-party providers, establishing a new regulatory layer for safeguarding systemic stability in the digital era.

In addition, the FinTech Knowledge Hub launched by EBA serves as a central node for disseminating knowledge, coordinating supervisory approaches, and providing visibility to national innovation efforts. According to available data , 18 Member States have already implemented national-level FinTech Innovation Hubs, aligned with EBA’s objective of enabling innovation while preserving prudential soundness and consumer trust [25].

These actions are part of a broader institutional commitment to support financial innovation through structured supervisory dialogue, proportional licensing frameworks, and enhanced regulatory clarity. The creation of FinTech innovation hubs at national level reflects the coordinated vision endorsed by the EBA in its 2018 FinTech Roadmap [11], which remains the strategic reference document for guiding supervisory adaptation in a rapidly evolving technological landscape.

The role of Innovation Hubs as learning facilitators has also gained prominence in policy-oriented literature. Such platforms contribute to supervisory modernization by surfacing novel risk configurations, enabling data-driven governance and supporting the evolution of rulemaking practices [14]. This perspective is particularly relevant in the context of the EU’s Digital Operational Resilience Act (DORA), which emphasizes the need for forward-looking supervisory tools in ICT-intensive financial environments [24].

According to this framework, Innovation Hubs serve not only as communication channels between regulators and market participants, but also as mechanisms for internal coordination, risk anticipation and feedback-driven policy refinement [9,25,26,27,28]. This multidimensional perspective informs the present analysis, which applies the framework to Romania’s national case and assesses the functional value of the Innovation Hub in terms of both market-facing and inward-facing impacts.

Innovation Centers stand at the crossroads of three key institutional functions: regulatory accessibility, institutional reflexivity and systemic calibration, creating an enabling environment for continuous adaptation and evolution. According to the FinTech Trend Report published by StartUs Insights, access to a global innovation ecosystem is increasingly critical for organizations seeking to maintain a competitive edge in the financial technology sector [29]. StartUs Insights provides instant access to over 4.7 million startups and 20,000 technologies worldwide, offering a strategic advantage through real-time, AI-powered insights. These capabilities enable fast and accurate identification of innovation opportunities, support data-driven decision-making, and foster long-term sustainable growth. Furthermore, leveraging these resources contributes to cost optimization and accelerates time-to-market, making them indispensable tools for navigating the complex and rapidly evolving fintech landscape.

Figure 1: Mapping Innovation in Financial Technology provides a visual overview of the current landscape of innovation within the fintech sector. It highlights key areas of digital transformation, major industry players, and the interconnections between various fintech verticals. The map showcases how emerging technologies—such as artificial intelligence, blockchain, open banking, and process automation—are driving new business models, financial products, and customer experiences. By organizing the fintech ecosystem in a clear and structured way, the figure helps illustrate the complexity, dynamics, and innovation pathways that are shaping the future of financial services.

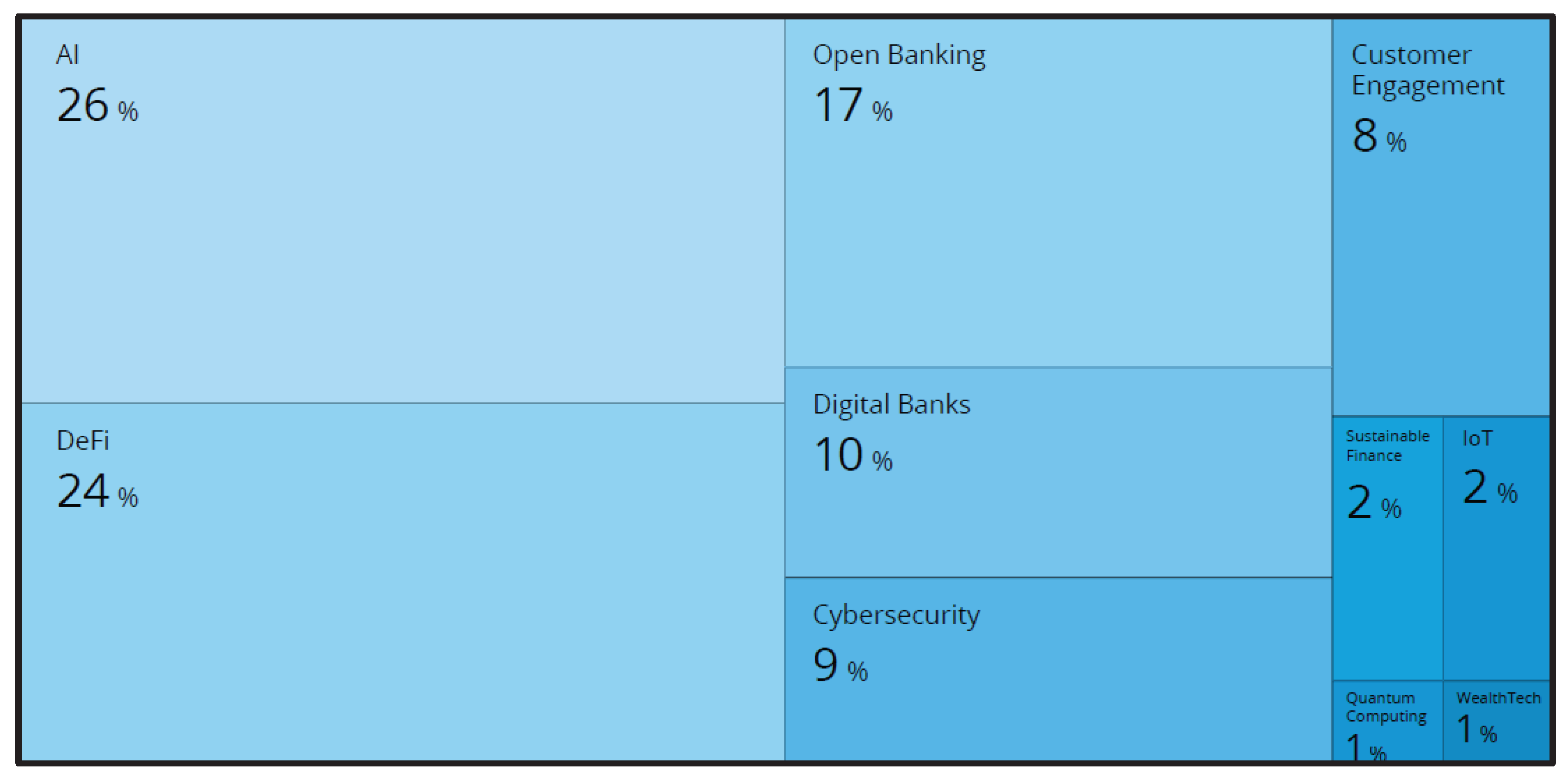

Figure 2: Top 10 Innovations in Financial Tech presents a visual breakdown of the most prominent innovative areas shaping the fintech landscape, based on their relative impact and industry focus. Leading the chart, Artificial Intelligence (26%) and Decentralized Finance (DeFi) (24%) dominate as the most influential drivers of change, powering automation, predictive analytics, and decentralized ecosystems. Open Banking (17%) and Digital Banks (10%) follow closely, reflecting the industry’s shift toward data-sharing, customer-centric platforms and embedded financial services. Other key areas include Cybersecurity (9%), addressing rising threats in digital finance and Customer Engagement (8%), emphasizing personalized experiences and interaction channels. Smaller but emerging domains such as Sustainable Finance (2%), IoT (2%), Quantum Computing (1%) and WealthTech (1%) hint at the future direction of innovation, highlighting a diverse and rapidly evolving financial technology ecosystem.

In the rapidly evolving fintech landscape, Artificial Intelligence (AI) plays a central role in automating processes, analyzing customer behavior and delivering personalized financial services [30]. AI-powered platforms enable financial institutions to better understand customer needs and deliver tailored experiences [31], thereby enhancing satisfaction and loyalty [30].

The rise of Digital Banks is redefining the banking experience by offering fully digital, fast, and accessible solutions that meet modern consumer demands [32]. These institutions leverage technology to eliminate traditional barriers, allowing customers to access banking services anytime and anywhere [32].

As digital ecosystems expand [7,33,34], cybersecurity becomes increasingly critical to safeguard sensitive data and protect against cyber threats [35]. Fintech companies implement advanced security measures such as data encryption and multifactor authentication to ensure confidentiality and data integrity [23,24,35].

Simultaneously, fintech firms enhance customer engagement through personalized, interactive technologies that improve user experience and loyalty [36]. Generative AI and machine learning enable faster and more accurate interactions, increasing customer satisfaction and reducing customer attrition4 [36].

Emerging technologies like the Internet of Things (IoT) allow financial services to be embedded into smart devices, creating new user touchpoints and transforming everyday interactions [37]. IoT devices collect real-time data that facilitates risk assessment, fraud detection, and personalization of financial offers [37].

There is also growing momentum around sustainable finance, which aligns financial strategies with environmental and social responsibility goals. Fintech plays a crucial role in integrating ESG (Environmental, Social, and Governance) factors into investment strategies [38], providing advanced tools to assess and manage impact [39].

On the frontier of innovation, quantum computing holds the potential to revolutionize data processing and risk modeling, offering unprecedented computational power for complex financial analyses. Although the technology is not yet widely available, ongoing research promises to transform the financial landscape [40].

Meanwhile, WealthTech is democratizing access to investment tools and financial planning through intelligent digital platforms, which allow users to access personalized financial services, lowering traditional barriers and offering more accessible investment opportunities [41].

2. Research Methodology

This article adopts a qualitative, case-based methodology, focusing on the institutional experience of the National Bank of Romania (NBR) with the implementation of its Innovation Hub. The research is structured around a single-country, single-institution case study design, consistent with the literature on regulatory innovation where national Innovation Hubs operate under national conditions and mandates, sometimes with different supervisory conditions.

The primary objective of the study is to identify and analyze the operational dynamics, institutional effects and policy-relevant lessons derived from the Romanian Innovation Hub. In particular, the paper seeks to examine the role of the Innovation Hub as a supervisory learning mechanism, the barriers faced by payment-focused innovators and the Hub’s capacity to alleviate them and the implications for regulatory design in bank-dominated financial systems.

The study is based on three primary types of data:

- ✓ institutional documentation, including public communications, published procedures and structured responses issued by the NBR Innovation Hub;

- ✓ evaluation materials from the NBR’s supervisory departments, accessed in anonymized format;

- ✓ interviews and direct observation from the authors’ own participation in the design and internal assessment of the Innovation Hub between 2019–2024.

The analysis does not evaluate its long-term impact on market entry, financial inclusion or regulatory harmonization. Moreover, due to confidentiality constraints, direct attribution of individual cases or feedback is not possible. The authors have sought to preserve analytical neutrality and ensure that institutional proximity does not bias interpretation, while leveraging insider knowledge for increased depth and contextual accuracy.

This study employs a mixed-methods approach, combining analysis of internal documentation from the Romanian FinTech Innovation Hub with original field research data, including interviews and participant observations. The research is framed by a conceptual model that positions FinTech innovation hubs as institutional tools with a dual role: externally facilitating dialogue with industry stakeholders and internally driving supervisory adaptation and transformation. Through this methodology, the Hub’s performance is assessed across several key dimensions: stakeholder engagement, regulatory learning, policy calibration and institutional reflexivity. This approach enables the identification of both the benefits and the structural and procedural limitations affecting Hub’s role in regulatory and supervisory processes.

Working Hypotheses

H1. Innovation Hubs enhance regulatory accessibility and foster trust-based dialogue between fintech stakeholders and supervisory authorities, contributing to internal capacity building within regulatory institutions.

H2. Despite their benefits in stakeholder engagement and regulatory learning, Innovation Hubs’ impact on formal rulemaking and policy development is limited by inherent structural and procedural constraints.

H3. Optimizing Innovation Hubs in bank-dominated markets requires modular engagement pathways, harmonized AML/KYC guidance, pre-engagement diagnostics on ICT risks and effective feedback mechanisms integrated into supervisory planning.

The findings generated through this methodology offer valuable insights into the dual role and institutional dynamics of the Romanian FinTech Innovation Hub. These results will be further examined in the Discussion section, where they will be interpreted in relation to the initial hypotheses, broader regulatory challenges in bank-dominated markets and comparative trends observed across the EU fintech landscape.

3. Results

In the context of accelerating digitalization and the increasing complexity of innovation in the financial sector, central banks are faced with the dual challenge of supporting technological progress while safeguarding financial stability and consumer protection. To respond to this dynamic, the National Bank of Romania (NBR) considered, as early as 2019, the strategic necessity of establishing a dedicated FinTech Innovation Hub. This initiative was aligned with the broader European trend of institutionalizing supervisory instruments aimed at monitoring and guiding innovation in the payment and financial services sectors.

Given the NBR’s statutory responsibilities, particularly those related to the oversight of payment service providers (including but not limited to credit institutions, payment institutions and electronic money institutions), the Innovation Hub was positioned under the coordination of the Oversight of financial market infrastructures and payments Department. The key objective was to offer a structured platform for dialogue with entities developing or deploying technological innovations in payment instruments, with a specific focus on areas such as strong customer authentication, secure communications, data protection, operational and ICT risk management, as well as continuity planning.

Engagement with market participants through the Innovation Hub enabled the NBR to assess the regulatory classification of new types of financial services and especially of payment services, understanding business models and identify associated risks and benefits. The increasing demand for such interaction reflected the growing number of FinTech entities exploring innovations such as artificial intelligence, data analytics and blockchain for the delivery of financial services. The implementation of the revised Payment Services Directive (PSD2) acted as a catalyst, prompting both incumbent and non-traditional actors to seek interpretive clarity on new regulatory obligations and opportunities.

The primary objectives of the FinTech Innovation Hub implemented by NBR are:

- to support and encourage innovation in payments and payment instruments, for the benefit of both service users and providers;

- to identify risks associated with technological developments and to provide supervisory feedback to help mitigate these risks;

- to foster the safe and inclusive growth of the payments market in line with EU regulatory developments and international best practices.

To achieve these goals, the Innovation Hub provides tailored guidance to both regulated and unregulated entities intending to introduce novel or significantly enhanced financial products. While the Innovation Hub does not issue binding opinions or authorizations, it plays a crucial role in helping entities navigate applicable regulatory frameworks and prepare for potential licensing procedures, thereby contributing to market transparency and compliance-readiness.

The Innovation Hub also seeks to increase regulatory flexibility by identifying implementation barriers and knowledge gaps, thus facilitating a more informed and proportionate regulatory stance. Importantly, the Innovation Hub serves as a monitoring mechanism for emerging risks, particularly in operational resilience and ICT security, and promotes the responsible adoption of innovation.

The Innovation Hub was also designed as a visible contact point, accessible through a dedicated section of the NBR website, offering resources such as guidance documents, summaries of relevant European initiatives and feedback channels for market participants.

Supervisory Methodology and Engagement Process

The NBR’s Innovation Hub operates on an open, continuous basis, without fixed deadlines for engagement, allowing for iterative assessment of ongoing developments. The methodology adopted comprises several sequential stages:

(a) submission of an “initial innovation form” through the web interface, containing essential information about the product/service, technology used and intended use cases;

(b) prioritization and screening by the Oversight Department, based on risk relevance and strategic potential;

(c) elaboration of a structured risk sheet and potential request for additional information;

(d) delivery of a reasoned, non-binding supervisory opinion regarding regulatory classification, potential authorization requirements and identified ICT/security risks.

Coordination with European institutions such as the EBA, the ECB, and the European Commission is considered essential in order to align supervisory interpretations and promote consistent regulatory practices across Member States.

The Role of the NBR’s FinTech Innovation Hub in Supporting Payment Innovation

In line with broader European efforts to promote safe and effective digital financial transformation, the National Bank of Romania (NBR) initiated the creation of a FinTech Innovation Hub (FIH) in 2019. This initiative was designed as a supervisory tool to monitor emerging technologies in the payment services ecosystem and to support the secure development of innovative financial solutions. The Hub serves as a national contact point for entities involved in developing new payment technologies and instruments, with the aim of identifying necessary regulatory or supervisory measures to ensure market safety, technological integrity and user trust.

FIHs have become a widespread supervisory instrument across the EU, with at least one such contact point established in every Member State, although regulatory sandboxes remain operational in only a limited number of jurisdictions [2,25]. Romania joined this collective European approach in September 2019, integrating its national efforts within the broader monitoring framework coordinated at EU level.

Through the Innovation Hub, the NBR continuously monitors the innovation environment in the payment domain, focusing on:

- -

- identifying and assessing innovative solutions in payment services and instruments;

- -

- evaluating ICT and cybersecurity risks and identifying appropriate mitigating measures;

- -

- determining proportional and adequate supervisory tools to guide FinTech firms in aligning with regulatory expectations.

Between its inception and the end of 2023, the Innovation Hub received 68 applications from various entities proposing innovative business models, primarily in the field of payments. Based on the maturity and development potential of the proposals, the Oversight Department conducted bilateral consultations to support implementation. In many cases, collaboration with internal authorization departments was required, as the proposed services fell within the scope of regulated activities.

Between 2019 and 2023, the Innovation Hub registered 66 unique submissions, with the following distribution:

- -

- 31%: entities seeking authorization as payment service providers (PSPs), including those offering account information services (AIS) or payment initiation services (PIS) under PSD2 or issuing electronic money;

- -

- 42%: technology providers supporting payment service providers (PSPs) through digital services, with potential for future regulatory authorization;

- -

- 4%: firms proposing crowdfunding or crowdlending platforms, typically within the remit of the national capital markets supervisor (ASF);

- -

- 3%: RegTech solutions aiming to support compliance and regulatory reporting through technology-driven frameworks;

- -

- 6%: solutions exploring central bank digital currency (CBDC) models or related infrastructure.

approximately two-thirds (66%) of all applications focused directly on payment-related innovations, confirming the sector’s leading role in FinTech development. These initiatives mirror European trends, where payment services represent the most dynamic and rapidly evolving segment of financial innovation [2,3,20,21,22]. All these data are summarized in Table 1.

Analysis of the submissions revealed several structural barriers to market entry for FinTech’s, including the need for greater flexibility in the secondary regulatory framework and increased clarity on supervisory expectations regarding licensing procedures. Based on these findings, the NBR initiated a revision of its internal rules concerning the assessment of documentation submitted during formal authorization processes, with particular attention to the principle of proportionality and the nature of the services proposed.

Furthermore, the Innovation Hub experience served as a basis for launching a broader institutional reflection on additional innovation-monitoring tools, including the potential design of a Regulatory or Digital Sandbox. This reflection aims to better understand the challenges faced by the Romanian FinTech ecosystem and to support a more agile regulatory environment.

The establishment of the Innovation Hub by the National Bank of Romania has fulfilled a dual institutional role: as an interface between regulators and market innovators and as a channel for regulatory introspection. While its operational scope has remained advisory, the initiative has produced tangible institutional effects and revealed the structural characteristics of Romania’s evolving FinTech landscape.

The role and impact of the Romanian Innovation Hub has been as a:

- facilitator of regulatory accessibility and institutional openness

One of the most visible effects of the Innovation Hub was the normalization of structured dialogue between authorities and non-bank innovators. In a jurisdiction where regulatory engagement had traditionally followed formal, document-based logic, the Hub introduced a more accessible, consultative model, without compromising legal consistency. This shift contributed to a reduced informational distance between supervisors and market actors.

Although the Innovation Hub did not issue formal opinions, its mere existence acted as a signaling mechanism indicating that the regulatory authority is willing to engage, listen and provide guidance (within defined limits). This reputational dimension is especially valuable in emerging markets where trust in regulatory and supervisory institutions may be unevenly distributed and access to interpretive clarity is often concentrated among incumbent actors (banks).

- non-disruptive path to modernization

Another lesson learned relates to the function of the Hub as a low-risk instrument for institutional modernization. In contexts where sandbox legislation or binding pilot regimes may be legally or politically sensitive, innovation hubs offer a gradual, reversible and cost-effective entry point into innovation governance. The Romanian case illustrates how such platforms can generate internal coordination effects and market outreach without requiring structural legal reform.

In practice, the Innovation Hub helped clarify internal roles, encouraged risk-based thinking in frontier areas and offered regulators a vantage point from which to observe innovation trajectories without assuming regulatory allowance. Its non-intrusive nature preserved supervisory independence while still promoting an open posture toward innovation, a balance that proved valuable in the absence of more complex experimentation frameworks.

- selective institutional impact and scalability limits

Despite its contributions, the Innovation Hub’s structural limitations must be acknowledged. Its nature limited public visibility and transparency related to the results, which may have reduced its reach among less connected or resource-constrained innovators. Additionally, the absence of direct policy feedback loops constrained its influence on long-term rulemaking.

Nevertheless, its implementation created institutional preconditions for future expansion, such as the development of the internal innovation analysis protocols, cross-functional training modules, which can support more ambitious frameworks in the future, such as structured sandboxes, cross-border pilot projects or DORA-compliant digital oversight modules.

- learning instrument for regulatory authorities

While its main role was to be a facilitation tool for innovators in the private sector, the Romanian Innovation Hub also functioned as a mirror for supervisory capacity. The diversity of topics submitted, ranging from digital wallets and biometric authentication to cross-border open banking schemes, revealed areas where internal expertise required updating or deeper coordination across departments.

Through its consultative practice, the Innovation Hub provided early signals on emergent market practices, legal ambiguities and technological adoption patterns in the national market. This knowledge was subsequently leveraged to inform supervisory training sessions and to adjust guidance in certain domains (such as in the application of the principle of proportionality in digital business models). These outcomes confirm international observations that innovation facilitators can strengthen supervisory preparedness, not only enable compliance dialogue [10,19].

Lessons Learned and Emerging Challenges

Since its establishment in 2019, the Romanian Innovation Hub has confirmed a growing mismatch between the pace of technological development and the capacity of regulatory frameworks to absorb and respond to innovation. This so-called “pacing problem” is not unique to Romania but reflects a wider structural issue affecting supervisory institutions globally. Several factors contribute to this gap:

- -

- the technical complexity of many new innovations makes rapid regulatory response difficult;

- -

- the exponential growth potential of FinTech models creates challenges in monitoring and enforcement;

- -

- the emergence of new business models and ecosystems raises novel questions regarding liability, data governance and systemic risks;

- -

- the increasing cross-border nature of innovation complicates the delineation of regulatory competences and demands deeper EU coordination.

In our opinion there might be some interrelated reasons that could explain why regulatory authorities are struggling to keep pace with changes arising from these innovations. The first one we appreciate is the degree of technical complexity associated with several innovations in the sector and, secondly, the astonishing pace at which FinTech can grow. All these data are summarized in Table 2.

Technology-driven innovation has been a constant feature of the financial sector for decades. At present, their pace and scope (potential applications of digital technologies spanning across areas such as payments and investment) is however leading to radical and far-reaching changes in traditional markets and thus several regulatory challenges. These challenges owe, among other phenomena, to the emergence of new business models, major impacts on competition and market efficiencies and implications for data security and privacy. Another significant challenge encountered by central banks in this context concerns the complexity of clearly attributing and distributing legal liability across actors involved in innovative financial ecosystems, coupled with the pressing need to prevent the escalation and systemic spread of fraudulent practices [1,4,7,27,42,43]. More generally, regulatory action needs to strike a balance between mitigating potential risks and enabling the development of innovations that can be beneficial for the economy and society as a whole.

We consider that, in this context of agile and intense developments of the FinTech innovation process there is also need for an innovative regulatory approach to support testing new technologies as an essential tool for central banks to better understand them. Regulatory sandboxes, for example, offer opportunities to implement and test disruptive technologies in a controlled regulatory environment while helping central banks to gain valuable insights to identify the right regulatory (or non-regulatory) approach.

Additional options worth exploring by the central banks include the need to develop new regulations that are outcome-oriented, allowing for the creation of testing spaces and innovation facilities and other related support mechanisms, as well as issuing specific guidelines. Furthermore, the rapid cross-border implications of Fintech innovations justify strengthening international and European regulatory cooperation and further developing anticipatory regulatory approaches.

From a central bank’s perspective, one of the most critical issues is balancing the need to protect financial stability and consumer interests, while avoiding the premature stifling of innovation. In this regard, the Innovation Hub has proven useful in identifying high-risk areas and guiding entities toward compliance, but further instruments may be required to test technologies in controlled environments.

One such tool is the regulatory sandbox, which allows authorities to observe real-world application of innovative models under limited, monitored conditions. This can yield valuable insights into the effectiveness of current regulations and inform the design of outcome-based rules. Beyond sandboxes, other approaches include the development of anticipatory regulatory strategies, soft-law instruments such as guidelines, and institutionalized cross-border collaboration frameworks [8,15].

We consider the main strategic challenges to be:

- technological complexity and operational resilience

The increasing reliance on advanced digital infrastructures has significantly raised the stakes for central banks in terms of supervisory obligations. New technological paradigms, such as real-time payment systems, distributed ledger technologies (DLT), cloud-based architectures and the integration of artificial intelligence and machine learning (AI/ML) into financial risk models, are reshaping the systemic relevance of core infrastructures. While these innovations promise greater efficiency and accessibility, they also introduce heightened exposure to cyber threats, operational disruptions and critical third-party dependencies. In this environment, ensuring the operational resilience of payment and settlement systems becomes not only a technical requirement, but a strategic priority for safeguarding trust and systemic integrity.

- evolving oversight perimeters and data governance imperatives

The traditional boundaries of the supervisory authority are increasingly blurred by the emergence of novel business models operating across regulatory domains and geographical borders. Entities such as platform-based financial intermediaries or digital conglomerates frequently operate beyond the reach of sector-specific prudential regulation, even though their cumulative activity may pose risks to financial stability. This raises questions about regulatory perimeter adequacy and supervisory reach. Furthermore, central banks face growing pressure to enhance their capabilities in data governance - namely, the ability to access, process and interpret high-quality supervisory data in real time - to enable informed oversight and agile intervention [7]. The strategic capacity to manage structured and unstructured data has become a foundational element of modern supervisory infrastructure.

- regulatory fragmentation and innovation asymmetries

Disparities in regulatory frameworks, divergent national approaches to data localization, and unequal technological capabilities across jurisdictions create an increasingly fragmented regulatory landscape. Such fragmentation complicates the development of consistent supervisory responses, especially in areas involving cross-border financial innovation. Moreover, these asymmetries are particularly acute in emerging and developing economies, which often struggle to align financial innovation with domestic objectives such as financial inclusion, consumer protection, cybersecurity and digital sovereignty. Without targeted support and coordination at the international level, there is a risk that technological progress may exacerbate rather than reduce structural inequalities across jurisdictions.

Ultimately, the effectiveness of central banks in supervising innovation will depend on their capacity to adopt agile, risk-sensitive and cooperative approaches, supported by continuous institutional learning and stakeholder engagement.

The operationalization of the Innovation Hub by the National Bank of Romania (NBR) marks a significant milestone in fostering dialogue between financial authorities and market innovators. This initiative aimed to create an accessible entry point for emerging financial service providers to better understand the regulatory perimeter, while facilitating the regulator’s understanding of novel business models, with a view toward inclusive innovation and systemic stability.

The implementation of the Innovation Hub by the National Bank of Romania has provided a valuable case study in regulatory engagement with emerging technologies, particularly in a jurisdiction characterized by a traditionally bank-centric financial ecosystem. A systematic analysis of the first operational cycle reveals several interrelated lessons relevant for both domestic regulatory design and the broader European conversation on innovation facilitation. The analysis of the Innovation Hub’s implementation revealed several key lessons:

- design and engagement: building regulatory openness and institutional credibility

The Romanian Innovation Hub was launched as a structured platform for regulatory consultation. Unlike more permissive or sandbox-based instruments, the Romanian Hub operates on an advisory basis without conferring preferential treatment or legal waivers, thereby maintaining regulatory neutrality. This structure proved particularly valuable in upholding trust from both incumbents and new entrants and avoiding asymmetric supervision.

A critical success factor was the clear internal delimitation of roles, whereby oversight, prudential and legal experts jointly assessed each submission that needed an authorization. This interdepartmental structure facilitated comprehensive evaluation of innovation proposals, while allowing the regulator to preserve its institutional boundaries.

Yet, an early challenge was the perceived complexity of procedures and the uncertainty regarding the outcome of engagement, particularly among smaller FinTech entities. To address this, the NBR introduced more transparent communication templates and clarified the scope of feedback that could be expected.

Despite the advisory nature of the Innovation Hub, participation offered an informal yet structured validation for innovators seeking funding or building compliance in the context of seeking a future authorization.

- institutional structuring: clarity, neutrality and internal coordination

Regulatory innovation initiatives require a clear institutional mandate and procedural predictability in order to gain market trust. The Romanian model, built around a cross-departmental review mechanism and without legislative amendments, succeeded in maintaining perceived neutrality and avoiding conflicts with formal supervisory procedures. However, the absence of legally binding outcomes initially limited its perceived utility among some FinTech actors, especially those unfamiliar with the functioning of regulatory institutions. This suggests that clarity of purpose, combined with transparent non-binding feedback protocols, is essential in the early phases.

Moreover, internal coordination proved critical to maintain consistency and avoid fragmentation in the response to inquiries. The centralized channeling of innovation-related queries through the Innovation Hub (rather than via informal departmental contacts) helped ensure that all queries received consistent consideration. This internal coherence also created an opportunity to identify systemic themes across seemingly disparate proposals.

- thematic and technological landscape: mapping the innovation perimeter

The Innovation Hub’s first years of activity revealed a concentration of interest around several recurring themes, including payment initiation services (PIS), account information services (AIS), electronic money issuance and smart contract-based automation. While some proposals focused on marginal improvements to existing services (such as customer experience optimization), others presented more transformative use-cases involving DLT-enabled settlement layers, biometric authentication and AI-driven credit scoring.

However, less than 20% of the inquiries were assessed as involving substantial regulatory uncertainty. A considerable share of applicants sought clarification on basic licensing thresholds, particularly in the context of the PSD2 and e-money regimes. This underscores the persistent information asymmetries and highlights the relevance of regulatory guidance even in the absence of new legal questions. It is worth mentioning that the role of national hubs is not just relevant for the national setting, but also in ensuring consistency and reducing cross-border regulatory arbitrage, as Romania is a member of the European Union and it ensures the application of the relevant European and national legal requirements.

From a technological perspective, the applications analyzed revealed certain maturity gaps. While the Romanian FinTech ecosystem displays high adaptability in user interface (UI) development and digital onboarding tools, there is limited in-house capacity of the FinTech’s to design back-end architectures with robust security layers. This imbalance translates into increased reliance on third-party providers for core functionalities, with implications for both operational resilience and oversight complexity under frameworks such as DORA ). This observation reinforces international findings regarding the uneven technological depth across innovation clusters in emerging markets [16].

- substance of inquiries: depth of uncertainty vs. basic regulatory navigation

Another significant lesson concerns the nature of the issues raised by applicants. Although the Hub’s mission was to assist with navigating regulatory complexity, a majority of queries did not involve high-consequence legal grey zones or legal innovation but rather requests stemming from limited regulatory literacy - basic requests for clarification regarding licensing thresholds, registration requirements or scope limitations under current legislation, such as PSD2 and the e-money directive.

From a supervisory perspective, this outcome underscores the persistent asymmetry in access to regulatory interpretation tools and reaffirms the need for public-facing guidance documents and simplified regulatory explainers. In addition, some inquiries revealed confusion about the relationship between national regulatory frameworks and EU-level directives, suggesting a need for better articulation of subsidiarity boundaries in public communication. This reflects the fact that innovation support mechanisms must be designed not only to address disruptive technologies but also to bridge routine informational gaps.

An additional point of interest is the temporal mismatch between the development cycle of FinTech solutions (if the commercial model had evolved or been withdrawn) and the institutional pace of regulatory clarification.

- institutional learning and supervisory reflexivity

A lesson learned from the Romanian experience relates to the internal value of the Innovation Hub as a driver of supervisory modernization. While originally conceived as a communication bridge toward the market, the platform also served as a mirror through which the authority identified areas of internal vulnerability. Therefore, a valuable effect of Romania’s Innovation Hub was its function as a trigger for institutional introspection. While its formal objective was to assist market actors navigating legal and procedural ambiguities, the platform also revealed gaps in regulatory preparedness related to some aspects of the emergent technologies. These learning effects are manifested across multiple dimensions: organizational, cognitive, procedural, and inter-departmental.

Firstly, the diversity of queries, ranging from biometric identity verification and API connectivity to AI-enabled credit scoring and token-based remuneration, surfaced supervisory knowledge asymmetries and limitations in interpretive agility. In particular, cases involving overlapping regulatory frameworks exposed the need for cross-functional collaboration and more granular internal guidance.

Secondly, the Hub functioned as a catalyst for internal training, prompting the development of thematic briefings, technology-specific checklists and inter-departmental knowledge-sharing sessions. These initiatives strengthened the internal supervisory capacity related to FinTech-specific risks, especially those related to outsourcing chains, real-time data flows and interfacing with non-bank platforms.

Thirdly, the Innovation Hub helped to institutionalize new modes of thinking about innovation - not as a marginal, optional dimension of supervision, but as a structural driver of change across all regulatory functions. Interviews with staff involved in the review process suggest that participation in the Innovation Hub prompted a reconsideration of how proportionality, risk-based assessment and regulatory neutrality are operationalized in emerging domains. This shift from rule-centric to context-sensitive supervision mirrors the broader evolution of financial oversight in data-rich environments.

Finally, the Hub enhanced interdepartmental reflexivity by facilitating the creation of common interpretive baselines across departments.

The NBR initiated targeted internal briefings and cross-functional workshops to build capacity in emerging domains. This learning-by-interaction model confirms the hypothesis that innovation engagement mechanisms contribute to institutional adaptability beyond their immediate consultative function.

- regulatory learning and policy insights

Beyond its role as a consultation platform, the Innovation Hub served as a monitoring tool for detecting different innovations development patterns into the financial market, risk propagation and innovation bottlenecks. The structured interaction between innovators and supervisors enabled the authority to early identify emerging risks—such as those related to digital identity, remote customer due diligence or the aggregation of financial data across institutions (open banking and eventually open finance market).

Several lessons emerged from this process. Firstly, innovation often outpaces legal clarity, especially when technological convergence blurs the boundaries between regulated and unregulated activities. Secondly, the degree of regulatory uncertainty varies by institutional profile: start-ups are often unsure about basic definitions and scope conditions, while established players may seek interpretative clarifications on advanced topics (ex. the regulatory perimeter of algorithmic decision-making). Thirdly, the absence of a national framework for innovation testing within certain rules, namely a legislative sandbox, limits the possibilities for supervised experimentation. However, the cost and legal complexity of such frameworks must be weighed against their marginal benefit in small, bank-dominated ecosystems, such as Romania [44].

The Romanian experience validates the hypothesis that Innovation Hubs can strengthen internal supervisory capacity. The cases reviewed revealed knowledge gaps that prompted the revision of written sectoral guidance to comply with the legislative requirements.

Regulatory authorities seek to strike a balanced approach that maximizes the benefits of financial innovation while safeguarding consumer interests and preserving systemic stability. One method for achieving this is by introducing transparent and consistent evaluation frameworks for emerging financial products and services. Such frameworks reduce the risk of regulatory arbitrage, whereby entities exploit inconsistencies or gaps in supervision to gain undue competitive advantages. Furthermore, regulators may employ tools such as stress testing and scenario analysis to examine the potential systemic implications of innovation and to enhance the financial system’s capacity to absorb external shocks.

Policy Feedback and Structural Constraints

While the Romanian Innovation Hub generated useful insights into regulatory friction points, the translation of these insights into systemic reform remained partial and under-institutionalized. In principle, one of the critical contributions of Innovation Hubs is to act as feeders into rule-making and supervisory modernization, transforming recurrent bottlenecks or thematic inconsistencies into agenda items for procedural or legislative adjustment.

In practice, however, several structural constraints limited the policy impact of Hub’s findings:

- the Innovation Hub operated without a dedicated innovation policy liaison unit, responsible for aggregating thematic trends, synthesizing engagement outcomes and informing institutional strategies. This lack of structured feedback loops limited the Hub’s influence beyond the boundaries of operational interaction;- the legislative environment in Romania, characterized by relatively prescriptive licensing conditions and limited flexibility in procedural interpretation reduced the space for policy experimentation or proactive adjustment, also taking into consideration the fact that most requirements applicable for the financial system are regulated at the European level, in order to provide harmonization within the European Union, with limited space for the implementation of national options. For example, while several Hub applicants identified barriers related to authorization process overall, cloud governance, experience requirements, interface standardization, anti-money laundering (AML), counter-financing of terrorism (CFT) requirements – with most stemming from known-your customer (KYC) requirements, the absence of a sandbox-like legal architecture meant that no temporary derogation or interpretive flexibility could be offered, even in cases when the risks involved would have been minimal or manageable;

- the low visibility of the Innovation Hub among other public authorities and its limited integration into national digital or FinTech strategies meant that cross-sectoral synergies were largely unexplored. This diminished the potential of the Hub to act as a node in broader regulatory innovation networks, a function increasingly recognized as essential in interconnected financial ecosystems.

Overall, while the Hub successfully performed its role as an interface and internal radar, its contribution to structural regulatory evolution remains contingent on the development of formal feedback instruments, cross-institutional coordination mechanisms and procedural flexibility in future legislative frameworks.

Policy Recommendations and Implementation Guidelines

Drawing from Romania’s Innovation Hub experience, several strategic recommendations can be formulated to enhance the operational, institutional and policy relevance of such innovation facilitation mechanisms. These insights are particularly important for authorities in bank-dominated markets where the innovation ecosystem remains emergent and risk-sensitive supervision must be preserved.

- establish a tiered engagement model

Innovation support should reflect the diversity of applicant profiles and the heterogeneity of regulatory complexity across proposals. A tiered approach -distinguishing between basic queries, interpretative uncertainties and strategic innovation with system-level relevance would allow more efficient resource allocation.

- strengthen procedural transparency and feedback traceability

While the Romanian Innovation Hub benefited from internal coordination, applicants frequently reported limited visibility regarding the review process and timelines. Publishing anonymized examples of past inquiries (with regulatory responses), alongside an indicative response timeframe, could enhance procedural trust without compromising confidentiality. Moreover, clear disclaimers regarding the legal nature of feedback should accompany all engagements.

- integrate innovation data into supervisory dashboards

Innovation hubs generate high-value, structured data on trends, technologies and regulatory frictions. However, in most cases, including Romania, such data remains underutilized institutionally. Authorities should consider embedding Innovation Hub outputs into their dashboards or cross-functional alert systems, particularly to track market entry patterns, technology adoption risks or cross-border regulatory pressures.

- formalize feedback loops between innovation and rulemaking units

An effective innovation strategy requires internal feedback mechanisms that link Innovation Hub activities with regulatory drafting units. In the Romanian case, while initial consultations influenced internal training and licensing practices, no structured pathway existed to channel recurring regulatory questions into forward-looking policy reform agendas. A dedicated Innovation Policy Liaison function could ensure institutional learning is captured and institutionalized.

- enhance regional cooperation and cross-border alignment

To mitigate regulatory arbitrage and promote consistency across EU jurisdictions, Romania’s Innovation Hub could be integrated more actively into cross-border frameworks such as the European Forum for Innovation Facilitators (EFIF). Joint consultations, shared registries of recurring themes and pilot testing of interoperable policy templates may increase efficiency and reduce duplication.

- consider a modular sandbox-like layer for high-impact use cases

While legislative constraints currently preclude the implementation of a formal sandbox in Romania, a modular, non-binding experimental interface could be piloted under the Innovation Hub for selected use cases with transformative potential. This model would allow testing supervisory approaches without committing to regulatory allowance.

In emerging ecosystems where regulatory complexity, legacy infrastructure and interpretive uncertainty combine to limit market access, Innovation Hubs can play a critical role in helping new entrants (particularly payment-focused FinTech’s, that the Romanian Innovation Hub focused on) overcome structural barriers. Drawing from both Romania’s experience and established international frameworks, several operational and policy-oriented practices can be identified to enhance the value of Innovation Hubs as enablers of inclusive financial innovation:

- modular support tailored to authorization complexity

One of the most cited challenges by payment innovators relates to the authorization process, particularly for entities unfamiliar with the financial sector. To address this, Innovation Hubs should adopt modular support schemes that segment applicants by their maturity level and regulatory proximity (ex. pre-licensing advisory, ongoing compliance dialogue, post-authorization adjustment). This approach, implemented by institutions such as the Dutch AFM and the UK FCA, helps reduce uncertainty while allocating supervisory resources proportionally.

- clarity on AML/KYC framework and identity verification tools

Difficulties in understanding and implementing AML/KYC requirements have been consistently reported by FinTech’s.

Innovation Hubs should develop clear guidance packages for payment service providers regarding acceptable digital onboarding procedures, risk-based customer due diligence models and the use of public or certified third-party identity validation tools. Additionally, Innovation Hubs can help bridge the information asymmetry regarding available national identity data sources, such as eID systems or public registries.

- preliminary assessments regarding ICT infrastructure, cloud governance frameworks and risks associated with the use of third-party service providers

A recurring obstacle is the regulatory ambiguity surrounding the use of cloud computing services, particularly in jurisdictions where supervisory guidance is limited or fragmented. To reduce friction, Innovation Hubs should offer pre-engagement diagnostics on cloud compliance, including documentation requirements, auditability expectations and data sovereignty implications. These consultations can reference DORA-compliant principles and should involve cross-departmental input from ICT risk units.

- proactive communication on licensing expectations and governance requirements

Innovation Hubs should play an active role in communicating clarified regulatory expectations concerning the licensing process for payment service providers, with particular emphasis on operational and security requirements, including those related to governance and internal control frameworks.

In Romania, the absence of consolidated public templates (other than the legal requirements which are public) and guidelines has contributed to perceived inaccessibility. Publishing past cases in the form of anonymized case studies, synthetic decision trees and a checklist of all requirements (documentation and implementation needed), that could be used for orientation, not binding interpretation, could reduce the cognitive compliance burden for first-time applicants.

- facilitating standardized technical solutions and sandboxed testing

Many applicants report a lack of access to standardized application programming interfaces (APIs), validation interfaces, or test environments needed to build PSD2-compliant solutions. Innovation Hubs should collaborate with central infrastructure providers (e.g., payment systems operators, ID issuers) to offer sandbox-like environments for testing onboarding flows, strong customer authentication, and consent mechanisms under supervised conditions. Such environments could accelerate product readiness and reduce regulatory friction.

- streamlining engagement for third party providers with limited market penetration

Given the limited and rather small number of third-party providers operating in several Member States — including Romania — Innovation Hubs could enhance their support function by establishing dedicated consultation tracks for specific categories such as account information service providers, payment initiation service providers and non-bank acquirers. These tracks should focus on identifying and addressing practical implementation challenges, particularly those related to access to bank APIs, the functionality of fallback mechanisms, and the availability and quality of data. Such an approach would be consistent with the recommendations set out by the European Forum for Innovation Facilitators [2].

- translating structural frictions into policy reform feedback loops

Finally, Innovation Hubs could act as conduits for regulatory improvement, not just interpretation. When recurring issues are identified, these insights must be translated into institutional feedback loops toward legislative or procedural reform, although the initiation of an update of the European legislation is not that fast (e.g., it requires consultation and negotiation between all member states). But the information about the national context and priorities is useful during the mentioned negotiations and review of the updated proposals.

4. Discussion

The findings derived from this study offer a nuanced understanding of the Romanian FinTech Innovation Hub’s institutional role, operational strengths and structural limitations. By evaluating the Hub’s performance against the three working hypotheses, this section interprets the empirical evidence through the lens of broader regulatory transformation processes. The discussion focuses on how Innovation Hubs function as adaptive supervisory instruments in evolving fintech ecosystems, particularly within bank-dominated regulatory environments. Each hypothesis is examined in relation to observed practices, stakeholder feedback and alignment with European-level trends.

4.1. Hypotheses Validation

Hypothesis 1: Innovation Hubs enhance regulatory accessibility and foster trust-based dialogue between fintech stakeholders and supervisory authorities, contributing to internal capacity building within regulatory institutions. Empirical findings support this hypothesis to a significant extent. The Romanian Innovation Hub has proven effective as a bridge-building mechanism, enabling fintech actors to engage in non-binding consultations with supervisory authorities in a relatively low-friction environment. Interviews with both public officials and private stakeholders suggest that the platform lowered perceived entry barriers to regulatory dialogue, especially for early-stage innovators and technology providers unfamiliar with financial regulation. Furthermore, the Hub has facilitated internal knowledge development by exposing supervisors to novel business models and technical architecture, which are often outside the scope of traditional prudential supervision. These interactions have played a key role in enhancing the institutional reflexivity and interpretive capacity of the National Bank of Romania (NBR), particularly in navigating evolving EU-level regulatory frameworks.

Hypothesis 2: Despite their benefits in stakeholder engagement and regulatory learning, Innovation Hubs’ impact on formal rulemaking and policy development is limited by inherent structural and procedural constraints. This hypothesis is strongly validated by research. While the Hub served as a valuable listening and learning interface, its advisory-only mandate limited its capacity to influence actual rulemaking. The absence of structured mechanisms for integrating insights from Innovation Hub consultations into formal supervisory planning or legislative drafting processes emerged as a recurring theme in interviews and internal documentation. In particular, the lack of regulatory follow-up or formal escalation pathways for issues raised during consultations suggests a disconnect between exploratory dialogue and concrete policy outcomes. Moreover, organizational silos and procedural rigidities within the central bank further reduced the likelihood of feedback from the Hub informing systemic regulatory change. This underscores the importance of institutional design in determining the effectiveness of innovative governance tools.

Hypothesis 3: Optimizing Innovation Hubs in bank-dominated markets requires modular engagement pathways, harmonized AML/KYC guidance, pre-engagement diagnostics on ICT risks, and effective feedback mechanisms integrated into supervisory planning. The research provides partial but meaningful support for this hypothesis. Several recommendations aligned with this statement emerged from stakeholder interviews and comparative analysis with similar hubs in the EU. Respondents consistently emphasized the need for more tailored and scalable engagement tracks—differentiated by innovation maturity, regulatory risk and business model complexity. Additionally, the lack of clear AML/KYC guidance was noted as a barrier to productive dialogue, particularly for cross-border platforms and RegTech providers. ICT-related risk diagnostics were only superficially addressed, despite being a major concern for both regulators and market participants. Importantly, the absence of institutionalized feedback loops from the Hub to supervisory planning processes limited the systemic utility of the initiative. These insights suggest that while the Hub has laid a strong foundation, further structural refinements are necessary to maximize its value in a heavily bank-centric and prudentially oriented regulatory context.

In summary, the Romanian Innovation Hub has shown clear value as a catalyst for regulatory dialogue and institutional learning, even as its influence on formal rulemaking remains limited. The evidence underscores the dual nature of such platforms: while effective in fostering engagement and interpretive flexibility, their long-term impact depends on their integration into broader supervisory and policy frameworks. This chapter has demonstrated that optimizing innovation hubs requires not only procedural enhancements, but also a deeper institutional commitment to iterative feedback, coordination and regulatory foresight. These insights provide a critical foundation for refining innovation governance models in Romania and other EU jurisdictions facing similar structural challenges.

4.2. Implications of Findings

The findings of this study have several important implications for both regulatory practice and institutional design in the context of financial innovation governance. Firstly, the Romanian case confirms that Innovation Hubs can serve as effective tools for enhancing regulatory accessibility and stakeholder trust, particularly in environments where traditional supervisory channels may appear opaque or rigid. This reinforces the argument that advisory platforms play a key intermediary role in facilitating early-stage compliance dialogue and reducing informational asymmetries between innovators and regulators.

Secondly, the limited policy impact of the Innovation Hub highlights a critical gap between exploratory consultation and formal regulatory adaptation. Without structured pathways for institutional learning to inform decision-making processes, Innovation Hubs risk becoming isolated mechanisms rather than integrated components of the regulatory cycle. This finding suggests that future reforms should prioritize building stronger internal feedback loops, formalizing escalation procedures and ensuring that innovation-related insights contribute meaningfully to supervisory planning and regulatory agenda-setting. Thirdly, the research points to the need for a more modular and risk-sensitive engagement model, particularly in jurisdictions with bank-dominated financial sectors. The adoption of differentiated consultation tracks, aligned with the complexity and maturity of innovations, could improve the relevance and efficiency of Hub’s activities. Moreover, standardized guidance on topics such as AML/KYC compliance and ICT risk assessment would enhance the predictability and utility of regulatory dialogue, especially for cross-border and technology-driven business models.

Finally, the broader institutional implication is that Innovation Hubs should not be viewed solely as external-facing instruments, but as platforms capable of catalyzing internal regulatory transformation. Their full potential can only be realized if supervisory authorities are willing to adapt governance structures and workflows to absorb, interpret and act upon the insights generated through these channels. In this regard, the Romanian case offers lessons that are transferable to other emerging fintech ecosystems seeking to balance innovation enablement with prudential oversight and legal certainty.

4.3. Policy Recommendations

Building on the findings and their implications, this section outlines several policy recommendations aimed at strengthening the institutional effectiveness and regulatory relevance of Innovation Hubs in Romania and similar bank-dominated markets.

Institutionalize feedback loops between the Hub and supervisory planning

To enhance the strategic value of insights generated through the Innovation Hub, supervisory authorities should establish formal mechanisms for transferring lessons learned into internal policy design, risk assessments and regulatory updates. This could include periodic reporting lines, thematic escalation channels, or a dedicated innovation liaison unit within supervisory structures.

Develop modular engagement pathways based on risk and innovation maturity

A one-size-fits-all model may limit the Hub’s capacity to respond to diverse stakeholder needs. Policymakers should consider tiered or modular interaction formats—such as basic orientation sessions, technical deep dives, or pre-authorization consultations—tailored to the complexity, business model and technological risk profile of participating firms.

Harmonize AML/KYC guidance to support consistent supervisory expectations

Given the recurring regulatory friction surrounding anti-money laundering and customer due diligence obligations, particularly for cross-border fintech’s, supervisory bodies should work toward clearer, standardized guidance. This would improve compliance predictability and reduce regulatory uncertainty for new market entrants.

Incorporate ICT risk diagnostics into early-stage fintech engagement

As digital infrastructure and cybersecurity risks become more prominent, pre-engagement ICT risk assessments should be integrated into the Hub’s methodology. This would allow regulators to address resilience issues early and support fintech firms in aligning with evolving supervisory expectations on digital risk governance.

Strengthen EU-level coordination and knowledge sharing

Given the increasingly cross-border nature of financial innovation, Romanian authorities should enhance alignment with EU innovation hub networks, including through participation in European forums, sharing anonymized case studies, and contributing to joint supervisory guidance initiatives. This would support regulatory consistency and knowledge transfer across jurisdictions.

4.4. Limitations and Future Research Directions

While this study offers valuable insights into the role and institutional dynamics of the Romanian FinTech Innovation Hub, several limitations should be acknowledged. Firstly, the empirical evidence is primarily qualitative and based on a limited number of interviews and internal documents. Although this approach allows for depth and contextual interpretation, it may not fully capture the diversity of perspectives across the broader fintech ecosystem. Future research could benefit from a larger, more representative dataset, including survey-based inputs from participating firms and non-participants alike.

Secondly, the analysis is context-specific and anchored in the Romanian regulatory environment. While the findings may be transferable to other EU jurisdictions, institutional variations—such as regulatory culture, market structure and supervisory mandates—may affect the generalizability of certain conclusions. Comparative studies across multiple innovation hubs, using a standardized analytical framework, would allow for a more robust assessment of institutional performance and policy effectiveness.

Thirdly, this study primarily focuses on the advisory and engagement functions of the Innovation Hub and does not fully examine its long-term impact on actual market outcomes, such as firm authorization rates, compliance quality, or innovation sustainability. Longitudinal studies tracking the regulatory trajectories of Hub participants could shed light on these dimensions and inform more targeted supervisory support mechanisms.