Submitted:

24 July 2025

Posted:

24 July 2025

You are already at the latest version

Abstract

The behavioral theory of the firm offers a robust framework for explaining how firms react to performance feedback. However, less is known about how firms integrate backward-looking performance feedback with forward-looking assessments of market opportunity when making market retrenchment decisions. To address this gap, this study investigates how the interaction between market share performance and market attractiveness shapes retrenchment decisions, using prefecture-level data from Japanese life insurance companies (2006–2019). The findings reveal that market attractiveness substantially moderates a firm's response to gaining or losing market share. In attractive markets, share gains and losses alike are associated with reduced retrenchment, as firms are motivated to invest in addressing challenges or capitalizing on success. Conversely, in unattractive markets, either outcome is linked to greater retrenchment, indicating a strategy of withdrawal. The paper contributes to the behavioral theory of the firm by demonstrating that market attractiveness acts as a cognitive filter. This filter shapes the interpretation of performance feedback, ultimately determining whether a firm responds to performance changes by increasing or decreasing its market withdrawal. The results also suggest a structured way for managers to approach retrenchment, prompting critical questions about resource allocation that help distinguish rational analysis from common behavioral biases.

Keywords:

bounded rationality

; cognitive filter

; resource allocation

; attention-based view

; performance feedback

; regional market

; Japanese life insurance companies

1. Introduction

Managers frequently make strategic resource

allocation decisions by choosing from multiple options under conditions of

uncertainty. The behavioral theory of the firm offers valuable insights into

these processes (Cyert & March, 1963). Some research within this framework

conceptualizes market share as an indicator of overall firm performance,

demonstrating that deviations from aspiration levels influence subsequent

corporate actions such as inter-firm network formation (Baum et al., 2005),

firm growth (Greve, 2008), and new product introduction (Joseph & Gaba,

2015). Separately, Greve (1998) treated regional market share as a reflection

of market position, showing that changes in this position relative to

aspiration levels drive subsequent organizational change. Such responses occur

because boundedly rational managers often simplify their assessment of market

performance, frequently converting it into measures of market share gains or

losses (Cyert & March, 1963). Consequently, firms tend to be more motivated

to initiate organizational change when their market share falls below their

aspiration levels. Conversely, exceeding these aspirations can lead to

satisficing with the current situation and reduced extent of change (Jordan

& Audia, 2012). In parallel, research has indicated that shifts in regional

market attractiveness can stimulate subsequent market expansion efforts by

firms (Barreto, 2012).

While grounded in the behavioral theory of the

firm, prior research has primarily focused on how backward-looking performance

feedback, such as a change in market share, triggers problem-driven search and

organizational change. A complementary perspective suggests that firms are also

guided by opportunity-driven search, where forward-looking assessments of a

market's potential shape strategic choices. Although Barreto (2012)

demonstrated that market attractiveness stimulates expansion, this perspective

has not been applied to retrenchment decisions, and the interaction at the

market level between attractiveness and performance feedback remains

underexplored.

This separation in the literature creates a

theoretical tension and a practical dilemma. Managers rarely evaluate

performance feedback in isolation. Instead, they must reconcile conflicting

signals: does a loss in market share signal a need to maintain its commitment

in a promising market, or does it confirm the wisdom of market retrenchment

from an unpromising one? Similarly, does a gain in market share signal an

opportunity to capitalize on success, or does it present a strategic window to

harvest profits before exiting the market? The behavioral theory of the firm

currently offers insufficient guidance on how managers resolve this ambiguity.

This study addresses this gap by developing and

testing a model that examines how the interplay between these two signals

influences a firm's market retrenchment decisions. Research grounded in the

behavioral theory of the firm has largely focused on proactive behaviors such

as risk-taking, innovation, mergers and acquisitions, and strategic change

(Shinkle, 2011). However, the dynamics of market retrenchment remain less

understood, with a few notable exceptions. For instance, Shimizu (2007)

analyzed the divestment of previously acquired units, and Vidal and Mitchell

(2015) examined how performance feedback influences divestitures. This

theoretical lens has recently been applied to other forms of strategic

withdrawal, such as the reshoring of manufacturing activities, demonstrating

that non-financial metrics like environmental performance can also trigger

these decisions (Zhang et al., 2023). Although allocating excessive resources

to a market can lead to inefficiencies (Arrfelt et al., 2013), managers may

hesitate to withdraw because such actions compel them to acknowledge prior

human or financial losses (Staw, 1976). This managerial tension highlights the

need for a clearer theoretical framework. Accordingly, this study investigates

which market signals managers focus on, how they interpret these signals, and

how the interaction between these interpretations shapes market retrenchment

decisions.

The analysis reveals that the influence of changes

in market share on market retrenchment is not uniform but contingent on the

level of market attractiveness. This interplay leads to distinct market retrenchment

under varying market appeal and performance conditions. For example, in markets

of average attractiveness, neither a market share gain nor loss had a clear

effect on retrenchment decisions. Large losses and gains in market share are

associated with less retrenchment in highly attractive markets. Conversely, in

markets with low attractiveness, substantial losses and gains are associated

with more retrenchment. These findings underscore that life insurance

companies, when evaluating regional market retrenchment, consider not only

changes in their market share but also the attractiveness of the specific

region, leading to complex decision-making patterns.

2. Theory and Hypotheses

2.1. The Behavioral Theory of the Firm

The behavioral theory of the firm provides a

foundational framework for understanding how organizations make strategic

decisions under conditions of uncertainty. At its core, the theory posits that

managers operate with bounded rationality, simplifying complex problems and

often converting performance assessments into straightforward metrics like

market share gains or losses to guide their actions. Central to the behavioral

theory of the firm is the concept of "performance feedback," where

firms evaluate their actual performance against aspiration levels—defined as

"the smallest outcome that would be deemed satisfactory by the decision

maker" (Schneider, 1992, p. 1053). These aspirations can be historical

(based on the firm's own past performance) or social (based on the performance

of competitors). Deviations from these aspiration levels are primary drivers of

organizational change and resource allocation strategies.

When performance falls below the aspiration level,

it triggers a "problemistic search" for solutions. This

dissatisfaction motivates firms to undertake change and corrective actions to

improve performance. Recent research has further disentangled this search

process, distinguishing between "problem-defining" search, aimed at

diagnosing the cause of a shortfall, and "solution-generating"

search, focused on finding remedies (van der Voet, 2023). Conversely, when

performance exceeds the aspiration level, it can lead to

"satisficing," where managers are content with the current situation,

reducing the impetus for significant change. Exceeding targets can also generate

organizational slack, which may enable "slack-driven

search"—experimentation and the pursuit of novel opportunities.

This framework applies to both broad, overall firm

goals, such as return on assets (ROA) and firm size, and more specific action

goals (Kim et al., 2015), such as performance in a particular business unit or

regional market. According to the attention-based view, an extension of the

behavioral theory of the firm, organizations simplify decision-making by

selectively focusing managerial attention on salient issues, such as

performance shortfalls or significant market opportunities. While much research

has used the behavioral theory of the firm to explain proactive behaviors like

innovation and strategic change, its application to retrenchment and strategic

reduction is a growing area of inquiry. For example, recent studies have

applied the theory to explain firms' decisions regarding the reshoring of

manufacturing activities based on environmental performance feedback (Zhang et

al., 2023) and the reduction of environmental, social, and governance (ESG)

disclosures in response to negative financial performance (Seow, 2025). This

study applies these core principles to understand the decision-making processes

behind market retrenchment.

2.2. Market Attractiveness as a Cognitive Heuristic: An Attention-Based View

To understand how market

attractiveness influences market retrenchment, this study draws on the

attention-based view of the firm, which posits that managerial attention is a

scarce resource and that organizational actions are a function of where

decision-makers focus their attention. In a multi-market environment,

managers cannot attend to all stimuli equally; they rely on simplifying

cognitive heuristics to determine which issues are most salient. Following Barreto (2012),

this study posits that market attractiveness serves as such a heuristic. High

attractiveness makes a regional market highly salient and frames it as a

valuable, goal-congruent opportunity worthy of attention and resources. Low

attractiveness, in contrast, frames a market as a less promising opportunity,

prompting consideration for resource reallocation.

More critically, the study extends this logic by

proposing that market attractiveness functions as a cognitive filter that

contextualizes the interpretation of performance feedback. It alters the

meaning of market share gains and losses. A performance shortfall in a market

perceived as highly attractive and aligned with firm objectives is likely to

trigger a problem-solving response aimed at recovery. The same shortfall in a

market deemed unattractive and less aligned with strategic goals is more likely

to be interpreted as a confirmatory signal to withdraw. Thus, attractiveness

does not merely moderate the relationship between performance and retrenchment;

it shapes the fundamental cognitive process by which managers evaluate and act

upon performance signals, as developed in the subsequent hypotheses.

In summary, the theoretical framework of this study

posits that market retrenchment decisions result from managers interpreting

backward-looking performance signals through the lens of forward-looking market

attractiveness. The following hypotheses test this overarching argument by

examining the direct effects of these factors and, more critically, their

interactive effects in markets of varying attractiveness.

2.3. Research Context: The Japanese Life Insurance Industry

The Japanese life insurance industry offers an

instructive context for examining market retrenchment decisions. Historically,

life insurance distribution in Japan has centered on face-to-face interactions.

During the country’s period of high economic growth, major insurance companies substantially

expanded their physical presence by establishing extensive nationwide networks

of sales offices.

However, the economic landscape changed

significantly following the collapse of Japan’s asset bubble in the early

1990s. This economic shift, coupled with long-term demographic trends,

accelerated depopulation in rural regions. The nation’s working-age population

peaked in 1995 and has since declined due to an aging society and a low

birthrate. This demographic trend has been more pronounced in rural areas than

in urban centers. Life insurance products primarily provide financial

protection for bereaved families. Therefore, a shrinking customer base,

particularly the decline in households with children—a core market

segment—diminishes the attractiveness of a regional market.

Consequently, life insurance companies that had

previously invested heavily in extensive national networks began to

strategically consolidate or close sales offices in these less profitable

regional markets to improve operational efficiency. This strategic

consolidation, a key form of market retrenchment, presents a compelling

empirical setting for analyzing how declining regional market attractiveness

and firm performance influence retrenchment strategies.

2.4. Market Attractiveness and Market Retrenchment

Building on the principles of the behavioral theory

of the firm, particularly the role of managerial attention, market

attractiveness is a crucial factor in strategic decisions. Barreto (2012)

integrated insights from the behavioral theory of the firm and the

attention-based view to emphasize the importance of market attractiveness in

organizational decisions regarding market expansion. In this context, market

expansion refers to the scope and selection of multiple market opportunities

that competing firms pursue. Barreto’s empirical findings demonstrate that

market attractiveness, defined by regional demographic characteristics and the

market presence of competitors, significantly drives a bank’s decisions to open

new branches. Critically, this relationship exists independently of

market-level performance considerations, underscoring that organizational

search and selection behaviors are also stimulated by exogenous environmental

factors.

Applying this logic to retrenchment decisions,

organizations simplify complex decision-making processes by selectively

focusing managerial attention on salient environmental cues that align with

their core objectives (Cyert & March, 1963; Ocasio, 1997). Barreto (2012),

building upon this foundation, emphasized that market attractiveness plays a

crucial role in guiding organizational attention and strategic decisions.

Specifically, firms are likely to allocate greater attention and resources to

markets perceived as highly attractive because these markets align closely with

a firm’s primary objective of profit maximization (Greve, 2008; Joseph &

Gaba, 2015). Conversely, when market attractiveness diminishes, managerial

attention is often drawn to the challenges posed by these less attractive

markets (Ocasio, 1997), leading to strategic retrenchment and resource

reallocation (Kuusela et al., 2017; Vidal & Mitchell, 2015). Therefore, a

high level of market attractiveness acts as a strong incentive to maintain or

enhance market presence, whereas a low level of market attractiveness prompts

market retrenchment. Accordingly, the following hypothesis is proposed:

Hypothesis 1.

The higher the market attractiveness, the lower a firm’s market retrenchment.

2.5. Market Share Changes in Markets with Average Attractiveness

Some studies in the behavioral theory have used

market share as a measure of overall firm performance (Baum et al., 2005;

Joseph & Gaba, 2015). For instance, Baum et al. (2005) explored syndicate

underwriting by investment banks. They found that organizations engage in

problem-driven search when their market share falls below their aspiration

level. Under these conditions, firms recognize that current approaches are

insufficient to achieve their market share goals, prompting them to undertake

riskier and more novel actions. Consequently, they tend to establish syndicate

relationships with nonlocal banks in their social networks.

Baum et al. (2005) also demonstrated that

surpassing market share aspiration levels leads organizations to engage in

slack-driven search. Exceeding performance targets generates additional

resources or organizational slack, allowing firms to tolerate higher risks and

experiment with new approaches rather than strictly adhering to existing

practices. This slack facilitates the formation of syndicate relationships with

nonlocal banks, reflecting willingness to pursue novel opportunities and

innovative behaviors.

Particularly relevant to the present study’s focus

on firms operating in multiple local markets, Greve (1998) reported that radio

stations were less likely to change their formats when their market share

exceeded their aspiration level. When market share exceeds the aspiration

level, radio stations tend to be satisfied with their performance. This

satisfaction, in turn, increases participants’ incentive to maintain the status

quo, diminishing their perceived need and motivation to undertake risky format

changes. Conversely, when market share falls below the aspiration level,

dissatisfaction with the current situation typically intensifies, thereby

strengthening firms’ motivation to make changes to improve performance.

Building on these insights, this study investigates

how year-over-year changes in market share—specifically, market share losses

and gains—influence a firm’s retrenchment decisions in markets with average

attractiveness. One perspective, drawing from the behavioral theory of the firm

and research on organizational problem-solving (Cyert & March, 1963; Greve,

1998), suggests that a market share loss is likely to be perceived by managers

as a significant performance shortfall—a deviation from aspirations that

demands corrective action. According to Greve (1998), managers often interpret

such losses as problems localized to a specific market, prompting them to

intensify efforts to regain their footing. This can manifest as increased

investment, renewed marketing initiatives, or other forms of market expansion

activities aimed at recovering the lost share. From this viewpoint, a market

share loss would motivate actions contrary to retrenchment, thereby leading to

a decrease in market retrenchment or even a renewed commitment to expansion.

This response might be particularly salient if managers are influenced by loss

aversion, becoming more risk-seeking in their attempts to recover previous

losses (Kahneman & Tversky, 1979).

Conversely, an alternative perspective posits that

a loss in market share can serve as a stark indicator to managers that the firm

is facing a competitive disadvantage relative to its rivals in that particular

market (Porter, 1980). This loss may be interpreted as evidence that the firm’s

offerings are less appealing, its cost structure is uncompetitive, or its

strategic positioning has weakened. In such a scenario, particularly in a

market that offers only average attractiveness—meaning it lacks strong growth

prospects or high profit potential to justify a difficult turnaround

battle—managers might conclude that further investment would be uneconomical

(Harrigan, 1980). Prudent resource allocation would then dictate a strategy for

conserving resources by scaling back operations in underperforming markets.

These resources could then be redeployed to more attractive or promising

markets where the firm has a stronger competitive standing or perceives better

opportunities (Bettis & Mahajan, 1985). Consequently, this interpretation

would lead to an increase in market retrenchment as the firm seeks to cut

losses and optimize its overall portfolio.

Considering the interplay between the

forward-looking assessment of market opportunity (i.e., attractiveness) and the

backward-looking feedback on performance (i.e., share change), markets of

average attractiveness present a unique decision-making context. In these

markets, the forward-looking signal from market attractiveness is neither

strong enough to compel major new investment, nor is it weak enough to demand

immediate exit. Without this strong contextual guidance, the interpretation of

a performance signal like a market share loss becomes unclear.

As the behavioral theory of the firm suggests, a

performance shortfall typically triggers problemistic search. However, the

urgency and direction of that search are often shaped by the perceived

importance of the context. In a market of only average attractiveness, managers

lack a strong strategic imperative. Some may interpret a share loss as a

localized problem to be fixed, prompting actions to reduce retrenchment, while

others may view the same signal as evidence of competitive disadvantage in a

market not worth fighting for, thus increasing retrenchment. With no clear

guidance from the market’s strategic value, these competing managerial

interpretations are likely to be inconsistent across firms and time. On

average, these opposing responses may counteract each other, leading to no

systematic, predictable change in retrenchment. Therefore, the following

hypothesis is proposed:

Hypothesis 2.

When market attractiveness is at an average level, a loss in market share relative to the previous year leads to no change in market retrenchment.

Continuing this line of inquiry, the focus now turns

to the implications of a firm experiencing a gain in market share relative to

the previous year, specifically within markets of average attractiveness. While

market share losses in such contexts may elicit divergent managerial

interpretations and thus ambiguous effects on retrenchment, it is proposed that

a market share gain generates more consistent motivations that collectively

argue against market retrenchment. This proposition is supported by two primary

theoretical perspectives.

First, drawing upon the behavioral theory of the

firm (Cyert & March, 1963) and the work of Greve (1998), a market share

gain is likely to engender managerial satisfaction. In his study of radio

stations, Greve (1998) found that organizations with market share above their

aspiration levels were less likely to change their formats. This reluctance to

change when performing well, a core tenet of aspiration-level adaptation,

indicates that satisfaction with the current state and strategy is often

fostered by exceeding performance targets. Managers content with their firm’s

performance in a specific market would perceive less need for substantial

strategic retrenchment. They are likely inclined to maintain the status quo to

preserve the favorable performance trajectory. In a market with average

attractiveness, incentives for aggressive expansion or immediate retrenchment

are typically not overwhelming. In such settings, this satisfaction with a

positive trend becomes particularly influential, reinforcing the decision to

continue current operations rather than pursue the disruptive and

resource-diverting act of market retrenchment.

Second, managers can interpret a gain in market

share as a clear signal of a firm’s competitive advantage in that particular

market (Porter, 1980). This improved standing relative to competitors might

stem from more effective sales proposals, higher personnel efficiency in sales

activities, stronger brand recognition in the region, and more effective

strategic positioning. Even in a market that only has average attractiveness

and lacks exceptional growth prospects or high profit potential, a demonstrated

and growing competitive advantage is a valuable capability. Managers would

likely view this as an opportunity to consolidate their position and further

leverage their strengths. The positive performance signified by the market

share gain may also generate organizational slack in the focal market (Cyert

& March, 1963). In the context of a recognized competitive advantage, this

slack is more likely to be reinvested to fortify the current market position

rather than to fund retrenchment or geographic diversification away from a

proven area of success, thereby enhancing profitability or stability. From this

perspective, a reasonable response would be to reinforce success through

continued commitment or even cautious expansion, rather than initiating market

retrenchment and ceding hard-won ground.

Unlike the conflicting pressures potentially arising

from market share loss, these two managerial responses to a market share

gain—satisfaction derived from surpassing aspirations (Greve, 1998) and the

recognition of a competitive advantage (Porter, 1980)—are not contradictory.

The desire to maintain satisfactory performance, which is rooted in the

behavioral theory of the firm, and the strategic imperative to capitalize on an

evident competitive strength converge. This convergence provides robust

motivation for managers to resist market retrenchment. In markets of average

attractiveness, where the strategic path is not always clear, a positive

performance signal, such as a market share gain, provides a compelling

rationale to stay the course or even deepen commitment, thereby reducing the extent

of retrenchment. Therefore, the following hypothesis is advanced:

Hypothesis 3.

When market attractiveness is at an average level, a gain in market share relative to the previous year decreases market retrenchment.

2.6. Market Share Changes in Markets with High and Low Attractiveness

This subsection focuses on markets at the high or

low ends of attractiveness, because extremes materially alter how share changes

are interpreted for retrenchment decisions. Attractiveness is conceptualized as

a heuristic that functions as a cognitive filter translating raw performance

signals into strategic meanings.

First, consider a firm that has experienced a loss

in market share in a highly attractive market. As discussed in relation to

Hypothesis 1, high market attractiveness provides a strong incentive for firms

to maintain or strengthen their market presence, driven by factors such as

favorable growth prospects and high profit potential. Building on the

attention-based view (Ocasio, 1997, 2011), Barreto (2012) emphasized that attractive

market opportunities can prompt forward-looking organizational actions

independent of traditional performance feedback. The identification and

assessment of such opportunities are central to strategic decision-making (Christensen

& Bower, 1996; Shane & Venkataraman, 2000). When an insurance company

loses market share in such an environment, the strong forward-looking signal of

opportunity provided by the market's high attractiveness is likely to outweigh

the backward-looking signal of a performance shortfall. Consequently, managers

are unlikely to interpret the loss as a signal to withdraw, but rather as a

localized problem that must be solved to protect a valuable market position. As

a result, a loss in market share is expected to decrease market retrenchment in

such valuable and opportunity-rich markets.

In contrast, consider a firm that loses market

share in a market with low attractiveness. As suggested by the logic underlying

Hypothesis 1, low market attractiveness naturally orients firms toward market

retrenchment. These markets often provide limited growth potential, low profit

margins, or declining strategic value, making continued investments less

appealing (Porter, 1980). The loss in market share in such contexts reinforces

the rationale for withdrawal. It serves as further evidence of a competitive

disadvantage or an eroding position in a market that already lacks strategic

value (Harrigan, 1980).

Moreover, managers may pay less attention to such

markets because of their low attractiveness (Ocasio, 1997; Barreto, 2012),

making withdrawal an even more likely outcome. Allocating resources to defend

or regain market share in these contexts is likely to be seen as inefficient,

particularly when more promising alternatives are available (Bettis &

Mahajan, 1985). As such, resource reallocation favors market retrenchment to

optimize the overall portfolio. Thus, loss in market share is expected to

increase market retrenchment in low-attractiveness markets.

These contrasting responses indicate that the

effect of market share loss on market retrenchment is systematically shaped by

the market context. In highly attractive markets, strategic importance and

potential returns motivate firms to persist. In contrast, in less attractive

markets, particularly when performance declines, market retrenchment becomes a

more reasonable and urgent course of action. Therefore, the following

hypothesis is put forward:

Hypothesis 4.

When market attractiveness is at a high (low) level, a loss in market share relative to the previous year decreases (increases) market retrenchment.

Building on the logic that market attractiveness

moderates a firm’s response to market share changes, this study examines how a

gain in market share affects market retrenchment under conditions of high or

low market attractiveness.

First, when a firm gains market share in a highly

attractive market, the rationale for decreasing market retrenchment is

strengthened. High market attractiveness already provides a strong incentive

for continued—or even increased—commitment (Porter, 1980; Barreto, 2012). A

gain in market share further reinforces managerial perceptions of success and

competitive advantage (Greve, 1998). This convergence of positive signals—an

attractive market and improved firm performance—likely strengthens managerial

confidence and increases their willingness to invest further to solidify or

expand their position. Managers would have little reason to scale back

operations and may instead pursue aggressive growth. Therefore, in highly attractive

markets, a gain in market share is expected to significantly decrease market

retrenchment, potentially more so than in markets with average attractiveness.

The situation differs significantly when a firm

gains market share in a market with low attractiveness. While such a gain is a

positive performance signal, its implications for retrenchment are more complex

and may follow two distinct, though not mutually exclusive, managerial logics.

One possibility is that managers interpret the gain through a harvest strategy

lens (Harrigan, 1980). Acknowledging the market’s limited long-term prospects

(Porter, 1980), firms may view the improved position as an opportunity to

maximize short-term cash flows with minimal additional investment or to exit

the market in a more controlled and profitable manner (Bettis & Mahajan,

1985). In this view, the gain does not signal a renewed commitment but rather

facilitates a strategic withdrawal.

Alternatively, managers—constrained by bounded

rationality and limited organizational resources (Cyert & March, 1963)—may

reach a similar retrenchment decisions through different rationales. They

conclude that the fundamental market outlook remains poor despite recent gains

(Harrigan, 1980). If maintaining or building on this gain requires

disproportionate effort or investment, the gain may highlight the opportunity

cost of remaining in the market when more promising alternatives exist (Bettis

& Mahajan, 1985). Rather than encouraging further investment, the gain

could trigger increased market retrenchment to redirect resources to more

attractive markets and avoid deeper involvement in a low-potential environment.

Therefore, the following hypothesis is proposed:

Hypothesis 5.

When market attractiveness is at a high (low) level, a gain in market share relative to the previous year decreases (increases) market retrenchment.

Table 1

summarizes the hypotheses regarding the effects of market share changes and

market attractiveness on market retrenchment. "Increases" and "Decreases"

respectively indicate a hypothesized increase and decrease in market

retrenchment. "No changes" indicates the hypothesis 2 that market

retrenchment will not change under specific conditions.

3. Methods

3.1. Data and Sample

Data on sales activities in the 47 prefectures and

firm-level data were obtained from the annual editions of the Statistics of

Life Insurance Business, published by Hoken Kenkyujo Ltd. Because this

publication is sold only in print, the author manually digitized the data. In

addition, demographic data for each prefecture were obtained from a database

provided by the Ministry of Internal Affairs and Communications.

The initial dataset was acquired from 2006 to 2019.

Data from boundary years 2006 and 2019 were used exclusively to calculate

independent and dependent variables derived from year-over-year differences.

This study investigates the extent to which life insurance companies, already

established in a regional market, reduced their number of sales offices. To

operationalize this focus on adjustments by incumbent firms with ongoing

operations, Firm-prefecture-year observations were excluded if a company had no

sales offices in a given prefecture in year t or no sales offices in that same

prefecture in year t+1. The latter condition includes instances of complete

withdrawal from the prefecture. Given these criteria, the final analytical

sample comprises firms that maintained at least one sales office in a specific

prefecture in both year t and the subsequent year t+1. This sample consists of

4,223 firm-prefecture-year observations, representing 16 life insurance

companies across Japan’s 47 prefectures, covering the period from 2007 to 2018.

3.2. Variables

The dependent variable in this study is market

retrenchment, measured as the decrease in the number of sales offices (a

positive integer) operated by the focal life insurance company within each

focal prefecture from year t to year t+1.

The independent variables are market

attractiveness, share gain, and loss. Following Barreto (2012), market

attractiveness is calculated based on the ratio of demand to supply in each

prefecture. For the demand side, the number of households (in thousands) was

used. The number of households is a more appropriate measure than population

when assessing the demand for life insurance across prefectures. Life insurance

policies are typically purchased at the household level, primarily by

breadwinners who seek to provide financial protection for their dependents.

Furthermore, households better represent the decision-making unit for financial

products such as life insurance. In contrast to population figures, which

include children and other individuals who generally do not make purchasing

decisions, household counts more accurately reflect the number and

characteristics of potential life insurance customers. For the supply side, the

number of sales offices operated by all competing life insurance companies

(i.e., all life insurance companies excluding the focal firm) was used. This

market attractiveness variable was then standardized to facilitate the

interpretation of the analysis results.

To construct the two independent variables related

to market share, the market share (%) of the focal life insurance company in

each prefecture was first calculated. This was done by dividing the number of

insurance contracts by the total number of insurance contracts held by all life

insurance companies in that prefecture and then multiplying the result by 100. Market

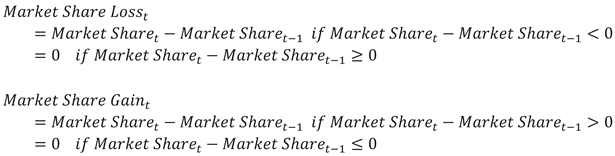

share gain and loss are derived from a spline function of the change

in market share from year t-1 to year t. These can be represented by the

following equations (Marsh & Cormier, 2001):

This spline function approach allows for separate

examination of the effects of positive changes (gains) and negative changes

(losses) in market share. Using the previous year's performance as a reference

point is consistent with the operationalization of the historical aspiration

level within the behavioral theory of the firm. While many studies in this area

adopt an exponentially weighted moving average of past performance, some

research uses the previous year’s performance as a simpler variable for the

historical aspiration level (e.g., Audia & Brion, 2007; Iyer & Miller,

2008). For reasons of parsimony and in line with this latter approach, this

study adopts the previous year’s market share as the reference point to explore

how boundedly rational managers perceive gains and losses in market share.

The behavioral theory of the firm also identifies

another key benchmark: the social aspiration level, which is typically the

average performance of competing firms. A robustness check was conducted using

the deviation from the average market share of competitors as an alternative

reference point; however, the results were not significant. This finding

suggests that when making market retrenchment decisions, managers in the

context of this study focus more on their own firm’s performance than on their

relative standing against competitors.

Several control variables at the firm-prefecture

level are included to control for the competitive environment of the local

market. Market households represent the number of households (in

thousands) in the focal prefecture. Market competition density is the

number of sales offices maintained by competing life insurance companies in a

prefecture. Own local density is the number of focal life insurance company

sales offices in the focal prefecture. Prefecture size is measured as

the land area of the prefecture (in square kilometers) divided by 100,000.

To control for individual firm characteristics,

several firm-level variables are also incorporated. ROA is calculated as

the current year’s surplus divided by total assets. Firm slack is

measured as the average of three standardized slack variables: absorbed

slack, unabsorbed slack, and potential slack (Greve, 2003). Absorbed

slack is the ratio of operating expenses to premium income. Unabsorbed

slack is the ratio of cash, deposits, and call loans to total liabilities. Potential

slack is the ratio of debt to equity. Firm size is the natural

logarithm of total premium income, which is an appropriate measure of firm size

for insurance companies (Greve, 2008). Geographic diversification is

measured as one minus the Herfindahl-Hirschman Index (HHI). The HHI is a common

measure of market concentration calculated by squaring the market share of each

firm operating in a market and then summing the resulting numbers. A higher HHI

indicates greater market concentration; consequently, a lower value for the

geographic diversification measure indicates less diversification.

The initial strategy for managing time-specific effects

was to incorporate a full set of year dummy variables. However, this approach

resulted in Stata not reporting the Wald chi-squared statistic for overall

model significance. This is a common issue when the estimated parameters are

numerous relative to the data clusters and is a documented concern with

clustered standard errors (Cameron & Miller, 2015). In this study,

employing numerous year dummies with the chosen panel data model and 16 firm

clusters substantially increased the parameter count. This compromised the

asymptotic Wald test’s reliability, a known issue for statistical methods that

account for within-cluster data correlation (Liang & Zeger, 1986; Hardin &

Hilbe, 2002).

This high parameter count, which led to the

unreported Wald chi-squared statistic, prompted a more parsimonious approach to

modeling temporal trends. Consequently, the individual year dummies are

replaced with a continuous industry clock variable (a linear time trend

variable) constructed by subtracting the base year 2007 from the year variable.

This reduces the model parameters while controlling for secular time trends.

Dowell and Killaly (2009), who analyze similar firm-market-year observations,

also use an industry clock.

Similarly, including firm-specific dummies to

control for unobserved time-invariant firm heterogeneity also led to the

non-reporting of the Wald chi-squared statistic, likely because these

additional dummies substantially increased the number of parameters relative to

clusters. Consequently, firm-specific dummies were excluded from the final

model. The model uses standard errors clustered by firm to address potential

within-firm error correlation and heteroskedasticity (Liang and Zeger, 1986).

However, excluding firm-specific dummies means that estimated coefficients may

suffer omitted variable bias if unobserved time-invariant firm characteristics

correlate with the included explanatory variables (Wooldridge, 2010). This

limitation warrants consideration when interpreting the results.

3.3. Model

To address potential multicollinearity within the

dataset, the variance inflation factors (VIFs) were calculated using ordinary

least squares (OLS) models, consistent with Barreto (2012). The analysis

identified one pair of control variables for which the VIFs (36.93 and 29.85,

respectively) significantly surpassed the commonly accepted benchmark of 10

(Kennedy, 2008). Therefore, an orthogonalization technique was applied to this

pair. This set of variables exhibited strong intercorrelation, which introduced

multicollinearity issues. Specifically, a modified Gram-Schmidt procedure was

employed using the orthog command in Stata. After this procedure, the dataset

was reevaluated for multicollinearity. Subsequent VIF calculations confirmed

that all variable VIFs in the model were then reduced to acceptable levels,

with the maximum VIF being 5.14.

The dependent variable in this study is a count

variable. While the Poisson distribution is a common starting point for

modeling count data, it assumes that the mean and variance of the distribution

are equal (equidispersion) (Cameron & Trivedi, 2013). However, count data

in practice often exhibit overdispersion (variance greater than the mean) or

underdispersion (variance less than the mean). In the analysis, the Stata

output for the Generalized Estimating Equations (GEEs) model indicated that the

dispersion parameter, estimated at 0.915, was less than unity, suggesting that

the equidispersion assumption of the Poisson model was not met. This finding

indicates a potential underdispersion of the data. The negative binomial

distribution provides a more flexible alternative as it can account for such

departures from equidispersion by including an additional parameter to model

the dispersion (Hilbe, 2011). Following Barreto (2012), to appropriately model

the count nature of the dependent variable and address the observed dispersion,

a negative binomial distribution was employed for the analysis.

This research uses panel data on insurance company

market retrenchment across multiple prefectures and employs negative binomial

regressions with GEEs (Hubbard et al. 2010). While various control variables

are incorporated, it is crucial to address potential remaining within-firm

correlations across prefectures. GEEs are well-suited for this because they

allow for an estimated, rather than assumed, error-term correlation matrix,

unlike models that assume an identity matrix typical of independent

observations (Liang & Zeger, 1986); this approach also helps in considering

spatial dependence. Following previous studies (Barreto, 2012; Rhee &

Haunschild, 2006), negative binomial regressions with GEEs were conducted, specifying

an exchangeable correlation matrix (Ballinger, 2004). This approach manages any

remaining nonindependence of errors across markets for the same insurance

company, reflecting the potential correlation of observations for the same

insurance company within a given year. Furthermore, the Huber-White robust

variance estimator ensures valid standard errors even if the specified

correlation structure does not perfectly capture actual within-group

correlations (Huber, 1967; White, 1980).

In the analysis of panel data using GEE via Stata's

xtgee command with the options family(nbinomial), link(log), and i(firm), an

exchangeable working correlation structure specified by corr(exchangeable) was

initially considered. This choice is based on the theoretical expectation that

observations within the same firm over time are likely to exhibit some degree

of consistent, nonzero correlation. However, the model that employed the

corr(exchangeable) structure failed to converge. To address this issue, a

simplified working correlation structure specified as corr(independent) was adopted, assuming no correlation

between observations within the same firm after accounting for covariates. This

specification allowed the model to converge.

The vce(robust) option was employed to obtain the

robust standard errors based on the Huber-White sandwich estimator (Huber,

1967; White, 1980). The use of robust standard errors in the GEE provides valid

inferences for the estimated coefficients and their standard errors even if the

chosen working correlation structure is misspecified, provided that the mean

model itself is correctly specified. Therefore, although the corr(independent)

structure assumes no within-firm correlation, the inferences are robust to

potential deviations from this assumption. Although the vce(robust) option

ensures the consistency of the parameter estimates and the validity of the

standard errors, the choice of a working correlation structure can affect the

estimation efficiency. If the true underlying correlation structure is indeed

closer to corr(exchangeable), using corr(independent) might result in less

efficient estimates (that is, larger standard errors) compared to what could

have been achieved with a correctly specified and converged corr(exchangeable)

model. Nevertheless, achieving model convergence is a prerequisite for

obtaining interpretable results, and the corr(independent) structure, in

conjunction with robust standard errors, provides a valid and practical

approach in this instance.

4. Results

Table 2

presents the descriptive statistics and Pearson’s correlations for all

variables (N = 4223). The average market retrenchment was 0.763 (standard

deviation SD = 2.065), indicating varied retrenchment activity. Market

retrenchment shows significant correlations (p < 0.05, |r| >

0.029). It is positively correlated with market households (r = 0.412), own

local density (r = 0.617), and market attractiveness (r = 0.083).

Conversely, it is negatively correlated with market share loss (r =

−0.073), market competition density (r = −0.219), and industry clock

(r = −0.109). The correlation with market share gain (r = −0.028) is not

statistically significant.

Table 3

presents the results of the negative binomial regression models with GEEs used

to predict market retrenchment. Model 1 only included control variables

(Wald chi-squared = 3337.23). Model 2 introduces only market attractiveness

as an independent variable, showing a statistically significant improvement in

model fit (Wald chi-squared = 3687.22; the change in Wald chi-squared, ΔWald

chi-squared = 350.00, for Δdf = 1, is significant, p < 0.01) compared

to Model 1. Model 3 adds only the two independent variables from the spline

function related to market share change (market share loss and gain)

to Model 1, also demonstrating a statistically significant improvement in fit

(Wald chi-squared = 5318.94; ΔWald chi-squared = 1981.72, for Δdf = 2, is

significant, p < 0.01). Model 4 includes market attractiveness and

share change variables. This model shows a statistically significant

improvement in fit over Model 2 (to which market share change variables

were added: ΔWald chi-squared = 2300.67, for Δdf = 2, is significant, p

< 0.01) and over Model 3 (to which market attractiveness was added:

ΔWald chi-squared = 668.95, for Δdf = 1, is significant, p < 0.01),

with a Wald chi-squared of 5987.89. Finally, Model 5, the full model, includes

the interaction terms between market share change and market

attractiveness. The addition of these interaction terms resulted in a

statistically significant improvement in model fit compared to Model 4 (Wald

chi-squared = 92977.05; a joint Wald chi-squared test of the interaction terms,

Wald chi-squared(2) = 19.41, p < 0.01, confirms this improvement).

The Wald chi-squared statistics were significant for all models (p <

0.01), indicating good overall model fit and progressive improvement as key

variables and interactions are added (Jaccard & Turrisi, 2003).

Hypothesis 1 predicts that higher market

attractiveness is associated with lower market retrenchment. This

hypothesis was tested using Models 2 and 4. In Model 2, the coefficient for market

attractiveness is positive and statistically significant (β = 0.124, p

< 0.05). Similarly, in Model 4, the coefficient for market attractiveness

remained positive and statistically significant (β = 0.123, p <

0.05). This positive main effect suggests a counterintuitive relationship where

higher attractiveness is associated with greater retrenchment. However, this

finding must be interpreted with caution, as subsequent analysis reveals that

this effect is highly dependent on performance feedback. The interaction with

market share changes, detailed in the tests of Hypotheses 4 and 5,

fundamentally alters this relationship. Therefore, Hypothesis 1 is not

supported.

Hypothesis 2 proposes that when market

attractiveness is at an average level, a previous-year loss in market share

leads to no change in market retrenchment. This hypothesis concerns the

effect of market share loss when market attractiveness is at its

mean. In Model 4, the coefficient for market share loss is 0.059 and is

not statistically significant (p > 0.10). For confirmation, Model 3,

which does not include market attractiveness, also shows a

nonsignificant coefficient for market share loss (β = 0.064, p

> 0.10). In Model 5, which includes the interaction term, the main effect of

market share loss (−0.038, p > 0.10) specifically represents

this effect at average market attractiveness (where the standardized market

attractiveness variable is 0). Although a nonsignificant result does not

formally prove the null hypothesis, it accords with the prediction of no

change. Accordingly, the result is consistent with Hypothesis 2 within the

scope of this sample.

Hypothesis 3 posits that when market

attractiveness is at an average level, a previous-year gain in market share

decreases market retrenchment. This hypothesis concerns the effect of market

share gain when market attractiveness is at its mean. Model 4, which

includes market attractiveness as a control, shows that the coefficient

for market share gain is −0.202 and statistically significant (p

< 0.01). Model 3, which does not include market attractiveness, also

shows a significant negative coefficient for market share gain (β =

−0.204, p < 0.01). However, in Model 5, which includes the

interaction term, the main effect of market share gain (−0.073, p

> 0.10) represents this effect at average market attractiveness

(where the standardized market attractiveness variable is 0), and this

specific coefficient is not significant. Although Models 3 and 4 (which do not

account for interaction effects) suggested a significant negative relationship,

the findings from Model 5, which is more comprehensive as it accounts for

interaction effects, do not provide clear support for a direct negative effect

of market share gain on average market attractiveness. Therefore,

it is concluded that Hypothesis 3 is not supported.

Hypothesis 4 concerns the moderating effect of market

attractiveness on the relationship between market share loss and market

retrenchment. It was predicted that when market attractiveness is

high, a loss in market share decreases market retrenchment, and when it

is low, a loss in market share increases market retrenchment. This

hypothesis was tested using Model 5. The interaction term market share loss

× market attractiveness in Model 5 is positive and significant (β =

0.135, p < 0.01). To interpret this interaction, for high market

attractiveness (e.g., +1 SD), the effect of a one-unit loss in market share

(represented by a value of −1 for the market share loss variable) on market

retrenchment is calculated as (−0.038 * −1) + (0.135 * −1 * 1) = 0.038 + (−0.135) = −0.097. This negative

effect indicates that in highly attractive markets, loss of market share

decreases market retrenchment, supporting the first part of Hypothesis

4. Conversely, for low market attractiveness (e.g., −1 SD), the effect

of a one-unit loss in market share on market retrenchment is (−0.038 *

−1) + (0.135 * −1 * −1) = 0.038 + 0.135 = 0.173. This positive effect indicates

that in markets with low market attractiveness, loss of market share

leads to an increase in market retrenchment, supporting the second part

of Hypothesis 4. Collectively, these findings support Hypothesis 4. The

collective significance of these interaction terms, confirmed by the joint Wald

test noted earlier when discussing Model 5, lends overall support to the

hypothesized moderating role of market attractiveness.

Hypothesis 5 addresses the moderating effect of market attractiveness on the relationship between market share gain and market retrenchment. It was predicted that when market attractiveness is high, a gain in market share decreases market retrenchment, and when it is low, a gain in market share increases market retrenchment. This hypothesis was tested using Model 5. The interaction term market share gain × market attractiveness in Model 5 is negative and significant (β = −0.115, p < 0.01). To interpret this interaction, for high market attractiveness (e.g., +1 SD), the effect of a one-unit gain in market share (represented by a value of +1 for the market share gain variable) on market retrenchment is (−0.073 * 1) + (−0.115 * 1 * 1) = −0.073 − 0.115 = −0.188. This negative effect indicates that in highly attractive markets, a market share gain decreases market retrenchment, supporting the first part of Hypothesis 5. Conversely, for low market attractiveness (e.g., −1 SD), the effect of a one-unit gain in market share on market retrenchment is (−0.073 * 1) + (−0.115 * 1 * −1) = −0.073 + 0.115 = 0.042. This positive effect indicates that in markets with low market attractiveness, a market share gain leads to an increase in market retrenchment, supporting the second part of Hypothesis 5. Thus, Hypothesis 5 is supported. As mentioned under Hypothesis 4, the joint Wald chi-square test of the interaction terms further supports the overall significance of these moderating effects.

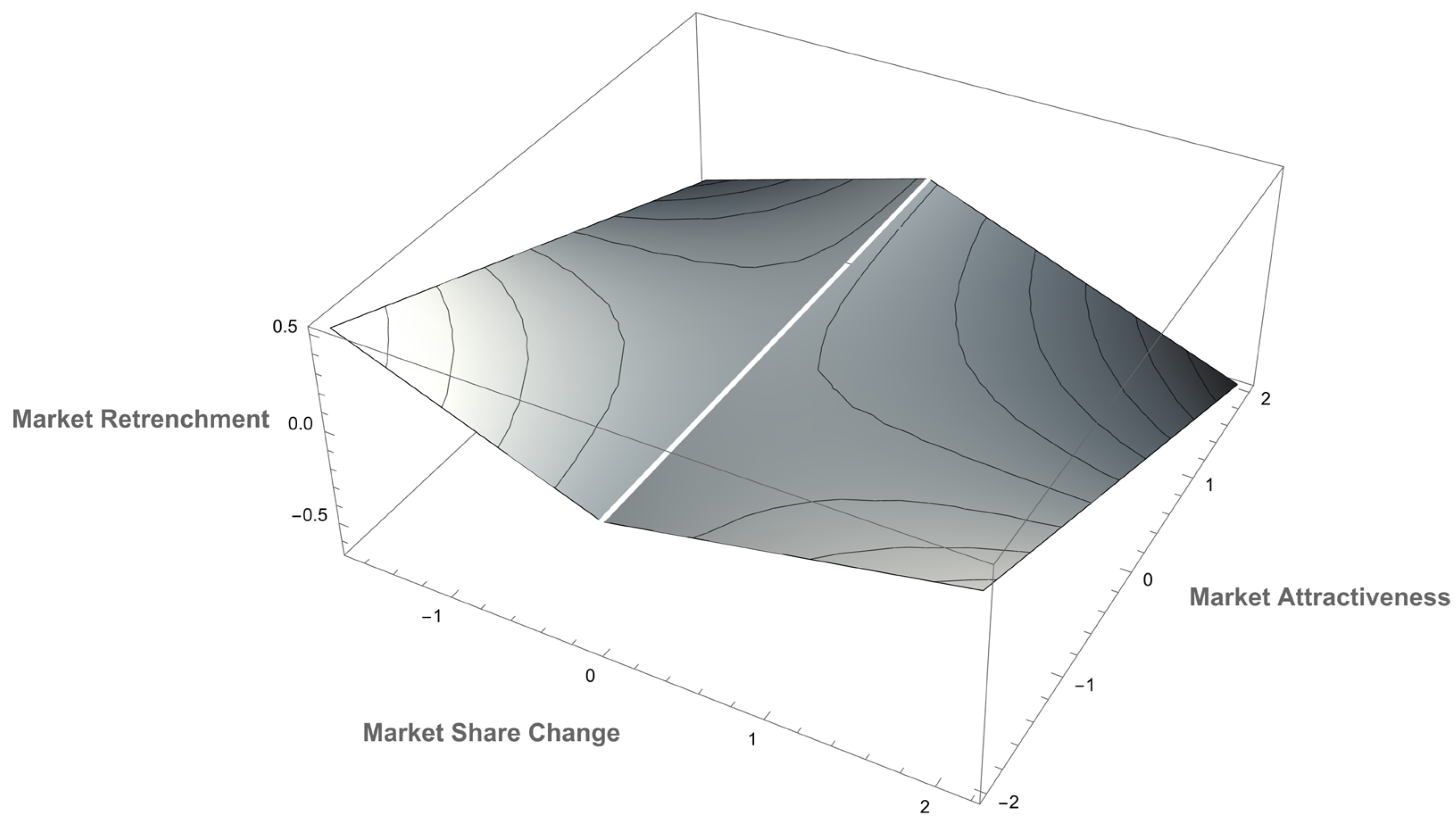

Figure 1 visually represents the interactive effects of market share change and attractiveness on market retrenchment, as detailed in the results for Hypotheses 4 and 5. The three-dimensional plot illustrates how the predicted values of market retrenchment (vertical axis) are shaped by the interplay of two horizontal axes: market share change and market attractiveness. The "market share change" axis (one horizontal dimension) distinguishes between market share losses (negative values) and gains (positive values). This axis covers a range of approximately ±2 SD of market share change, where a value of 0 indicates no change in market share from the previous year. For example, a value of −1 signifies a 1% decrease in market share from the previous year. The "market attractiveness" axis (the other horizontal dimension) indicates the SD from the mean. A value of 0 represents average market attractiveness, whereas values such as +2 or −2 indicate market attractiveness with two SD above or below the average, respectively. In the context of this study, higher attractiveness thus signifies a market with a more favorable ratio of potential customers (households) to competing sales offices.

Specifically, the plot’s surface demonstrates that when market attractiveness is high (e.g., at +2 SD), loss and gain in market share (e.g., moving toward −2 SD or +2 SD on the market share change axis) are associated with a decrease in predicted market retrenchment. This trend is shown by the downward slope of the surface as changes in market share move away from zero at high levels of market attractiveness. Therefore, in highly attractive markets, a larger magnitude of market share change (either loss or gain) corresponds to less market retrenchment. Conversely, when market attractiveness is low (e.g., at −2 SD), both loss and gain in market share are associated with an increase in predicted market retrenchment. This trend is depicted by the upward slope of the surface as changes in market share move away from zero at low attractiveness levels. Consequently, in markets with low attractiveness, a larger magnitude of market share change (either loss or gain) leads to more market retrenchment.

At average levels of market attractiveness (i.e., 0 SD from the mean), the relationship between market share change and market retrenchment appears nearly flat. This observation aligns with the statistical analysis, which indicates that in markets with average attractiveness, neither market share losses nor gains significantly influence market retrenchment decisions.

Finally, when the change in market share is near zero, the plot surface reveals a subtle but important trend. As one moves along the axis of zero share change from low to high market attractiveness, the surface tilts slightly upward, indicating a marginal increase in market retrenchment. This upward tilt visually represents the positive main effect of market attractiveness that led to the rejection of Hypothesis 1, showing that the direct influence of attractiveness is most apparent when the moderating effect of performance feedback is minimal. This corresponds to the conditional main-effect coefficient for market attractiveness at a near-zero share change in the interaction model (β = 0.216, p < 0.01). As the magnitude of market share change increases, this direct positive effect is negated and even reversed by the interaction.

Overall, Figure 1 encapsulates the core finding that the predicted level of an insurance company’s market retrenchment is contingent upon the combined influence of market share changes and the attractiveness of the market in question.

5. Discussion

5.1. Theoretical Contributions and Implications

This study contributes to the behavioral theory of the firm by conceptualizing market retrenchment as a decision process in which managers integrate two distinct informational cues: backward-looking feedback on past performance and forward-looking assessments of future opportunities. While the behavioral theory of the firm has traditionally emphasized problem-driven search triggered by historical performance shortfalls, the study incorporates a complementary, opportunity-driven perspective wherein cognitive representations of future potential guide strategic action. Whereas Barreto (2012) applied this forward-looking perspective to explain market expansion, this study extends the same logic to the context of market retrenchment. The findings empirically demonstrate that retrenchment decisions are not driven by performance or attractiveness independently, but by their interplay, providing a more comprehensive understanding of strategic decision-making in declining industries.

Second, the study advances the behavioral theory of the firm by theorizing and demonstrating the role of market attractiveness as a key cognitive filter. This study moves beyond viewing attractiveness as a simple moderator and instead frames it as a heuristic that shapes managerial attention and, more critically, contextualizes the meaning of performance feedback. A performance loss is interpreted differently—as a problem to be solved in an attractive market versus a confirmatory signal to exit in an unattractive one. This filtering mechanism explains not only how performance feedback is interpreted but also resolves the apparent puzzle of the main effect of market attractiveness. The counterintuitive positive association between attractiveness and retrenchment, which runs contrary to baseline assumptions, is shown to be an incomplete picture. The interaction analysis demonstrates that this main effect is largely an artifact of situations with minimal performance change and is either reversed or rendered irrelevant by significant gains or losses in market share. This filtering effect also clarifies the finding, where the seemingly direct effect of a market share gain on reducing market retrenchment becomes non-significant once the interaction with attractiveness is accounted for. It demonstrates that the performance signal alone carries an ambiguous meaning until it is interpreted through the lens of the market's potential. This cognitive reframing directly explains the study's key empirical results for the interactive hypotheses: in highly attractive markets, a substantial loss triggers intensive problemistic search aimed at recovery, while a gain reinforces the market’s perceived value, both of which discourage retrenchment decisions. Conversely, in markets with low attractiveness, a significant loss accelerates withdrawal, while even a gain may be treated as an opportunity to "harvest and exit," both of which encourage retrenchment.

Finally, by focusing on a specific action goal—performance within a regional market—the paper offers a more granular application of the principles of the behavioral theory of the firm. In doing so, it complements recent work that has expanded the theory's application to non-financial metrics, such as environmental performance driving reshoring decisions (Zhang et al., 2023), and to other forms of strategic reduction, like scaling back ESG disclosures (Seow, 2025). Much of the prior literature has tested the behavioral theory of the firm using broad, firm-level goals. This study, however, demonstrates that the core mechanisms of performance feedback operate at a more operational, market-specific level. This helps explain the seemingly contradictory behavior of a single firm simultaneously pursuing different strategies in different markets, highlighting that organizational action is a localized response to specific performance-context combinations rather than a monolithic reaction to overall corporate performance.

5.2. Practical Implications

The findings of this study suggest a more structured and analytical approach to decision-making, particularly regarding resource allocation across multiple regions. This framework allows managers to use the interplay of market attractiveness and performance as a diagnostic tool. This enables them to move beyond intuitive responses and ask more disciplined, strategic questions. Specifically, the approach involves plotting each regional market based on its attractiveness and performance to formulate critical questions that guide a systematic assessment of the firm's portfolio.

For example, in a highly attractive market where market share has been lost, a common bias is to escalate commitment to avoid acknowledging a potential failure. A more systematic approach would be to ask: Have we thoroughly analyzed the root causes of this share loss? Is it a correctable operational issue (e.g., sales coverage, local marketing), or a more fundamental misalignment between our offerings and market needs? This line of questioning shifts the focus from defending past decisions to a forward-looking analysis of recovery potential.

Conversely, in a low-attractiveness market where market share has been gained, the intuitive response might be a reflexive "harvest and exit" strategy. A more strategic question would be: Have we analyzed why we are gaining share while others may be struggling? Does this signal an opportunity to serve a profitable niche at a low cost as competitors withdraw? Answering these questions requires a data-driven assessment of the emerging competitive landscape.

This analytical discipline applies to all scenarios. In a highly attractive market with a market share gain, a key risk is complacency or "satisficing." The strategic question becomes: Beyond celebrating success, have we analyzed the source of our advantage and considered how to best leverage this success? Options include reinvesting to solidify our lead, attempting to replicate the advantage in other markets, or reallocating the generated resources to another strategic priority. For a low-attractiveness market with a market share loss, the bias might be a hasty exit. A more disciplined process would ask a series of questions: First, could the withdrawal of competitors transform this into an attractive market with potential for survivor gains? Second, if an exit is still the best course of action, have we developed an orderly withdrawal plan that is explicitly linked to the reallocation of freed-up resources to a specific, higher-value opportunity elsewhere? By systematically asking these action-oriented questions, managers can better navigate behavioral traps and optimize resource allocation for the entire firm.

5.3. Limitations and Future Research

The findings of this study are subject to certain limitations, which in turn suggest avenues for future research. First, the analysis relies on data from a single industry in a single country: Japanese life insurance companies. Although this context provides a clear empirical setting for observing market retrenchment driven by historical and demographic shifts, it limits the generalizability of the findings. The institutional, regulatory, and cultural factors specific to Japan likely influence how firms interpret market signals and formulate strategic responses. For instance, strong norms promoting employment stability and a long-term orientation, which are characteristic of Japanese corporate governance, may encourage firms to persist in attractive markets even when facing performance losses.

Although the specific parameters and thresholds for such decisions are likely context-dependent, the underlying theoretical mechanism proposed in this study appears to be more universal. The core finding—that managers use forward-looking assessments of market attractiveness as a cognitive filter to interpret backward-looking performance feedback—represents a fundamental process. This process aligns with the propositions of the behavioral theory of the firm, specifically regarding bounded rationality and managerial attention. This theory posits that managers in any context rely on such heuristics to simplify complex decisions; however, the specific cues they prioritize and the weight they assign to them may differ across contexts.

Therefore, an important avenue for future research is to test the robustness of the proposed model across different contexts. Replicating this study in different industries (e.g., retail banking, manufacturing) or in other national contexts with different corporate governance logics (e.g., shareholder-centric economies in North America or Europe) would offer valuable insights. Such comparative research could disentangle the universal behavioral mechanisms of retrenchment decisions from their context-specific manifestations, thereby enhancing the broader generalizability of the proposed framework.

Second, the analytical model in this study does not include firm fixed effects due to statistical estimation challenges. Consequently, the possibility that the results are biased by unobserved, time-invariant firm heterogeneity cannot be fully ruled out, as acknowledged in the methods section. This represents an important limitation of the study. Future research should seek to overcome this by employing alternative estimation methods that can robustly account for such firm-specific effects.

Third, a limitation stems from the counterintuitive main effect observed for market attractiveness. Although the interaction analysis clarifies that this direct positive effect on market retrenchment is conditional and largely superseded by performance feedback, the underlying reason for this main effect remains a puzzle. The finding that, in the absence of significant performance change, firms may engage in slightly more retrenchment in more attractive markets contradicts established logic. The scope of the data used in this study does not permit a definitive explanation for why this underlying direct effect is positive, suggesting its influence is more complex than theorized. Therefore, this unresolved issue represents a critical avenue for future research. Future inquiry is needed to verify whether this finding holds in other contexts—such as different industries or countries—and to re-evaluate the relationship with different measures of market attractiveness.

6. Conclusions

By integrating backward-looking performance feedback with forward-looking assessments of opportunity, this study extends the behavioral theory of the firm to explain the complex dynamics of market retrenchment. The analysis of Japanese life insurance companies demonstrates that market attractiveness is not merely a contextual factor but a crucial cognitive filter. It determines whether performance signals are interpreted as problems to be solved within a valuable market or as confirmations to exit a less promising one. These findings underscore that managers’ responses to performance feedback are not uniform; they are highly contingent on the perceived strategic value of the market, leading to complex and sometimes counterintuitive strategic choices. While the study provides valuable insights, future research should aim to validate these findings across different industries and national contexts, explore the underlying reasons for market share changes, and examine varied forms of market retrenchment. Practically, the interaction pattern distilled here provides a diagnostic lens for portfolio-level decisions. By considering how each market's situation impacts resource allocation, managers are better equipped to pose action-oriented questions, challenge behavioral traps, and select a strategic path with clearer justification.

Author Contributions

hidden due to double-blind peer-review.

Funding

This work was supported in part by JSPS KAKENHI Grant Number 21K13364 and the KAMPO Foundation.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data analyzed in this study were manually digitized from 14 volumes of Statistics of Life Insurance Business in Japan (インシュアランス生命保険統計号), covering fiscal years 2006–2019. While the publisher, Hoken Kenkyujo Ltd., has ceased operations, the original printed volumes remain accessible through selected public and university libraries in Japan. The digitized dataset supporting the findings of this study is available from the author upon reasonable request for the purpose of reproducing the analyses and verifying the results. Separately, the author welcomes inquiries regarding potential research collaborations.

Acknowledgments

The author also wishes to recognize the invaluable publishing contribution of Hoken Kenkyujo Ltd.—now, regrettably, no longer in operation—whose publication Statistics of Life Insurance Business served as a crucial data source for this study.

Conflicts of Interest

The author declares no conflict of interest.

Abbreviations

The following abbreviations are used in this manuscript:

| ESG | Environmental, Social, and Governance |

| GEE | Generalized Estimating Equations |

| HHI | Herfindahl-Hirschman Index |

| OLS | Ordinary Least Squares |

| ROA | Return on Assets |

| SD | Standard Deviation |

| VIF | Variance Inflation Factor |

References

- (Arrfelt et al., 2013) Arrfelt, M., Wiseman, R. M., & Hult, G. T. M. (2013). Looking Backward Instead of Forward: Aspiration-Driven Influences on the Efficiency of the Capital Allocation Process. Academy of Management Journal, 56(4), 1081-1103. [CrossRef]

- (Audia & Brion, 2007) Audia, P. G., & Brion, S. (2007). Reluctant to change: Self-enhancing responses to diverging performance measures. Organizational Behavior and Human Decision Processes, 102(2), 255-269. [CrossRef]

- (Ballinger, 2004) Ballinger, G. A. (2004). Using Generalized Estimating Equations for Longitudinal Data Analysis. Organizational Research Methods, 7(2), 127-150. [CrossRef]

- (Barreto, 2012) Barreto, I. (2012). A Behavioral Theory of Market Expansion Based on the Opportunity Prospects Rule. Organization Science, 23(4), 1008-1023. [CrossRef]

- (Baum et al., 2005) Baum, J. A. C., Rowley, T. J., Shipilov, A. V., & Chuang, Y.-T. (2005). Dancing with Strangers: Aspiration Performance and the Search for Underwriting Syndicate Partners. Administrative Science Quarterly, 50(4), 536-575. [CrossRef]

- (Bettis & Mahajan, 1985) Bettis, R. A., & Mahajan, V. (1985). Risk Return Performance of Diversified Firms. Management Science, 31(7), 785-799. [CrossRef]

- (Cameron & Miller, 2015) Cameron, A. C., & Miller, D. L. (2015). A practitioner’s guide to cluster-robust inference. Journal of human resources, 50(2), 317-372. [CrossRef]

- (Cameron & Trivedi, 2013) Cameron, A. C., & Trivedi, P. K. (2013). Regression analysis of count data. Cambridge university press.

- (Christensen & Bower, 1996) Christensen, C. M., & Bower, J. L. (1996). Customer power, strategic investment, and the failure of leading firms. Strategic Management Journal, 17(3), 197-218. [CrossRef]

- (Cyert & March, 1963) Cyert, R. M., & March, J. G. (1963). A behavioral theory of the firm. Englewood Cliffs, NJ: Prentice-Hall.

- (Dowell & Killaly, 2009) Dowell, G., & Killaly, B. (2009). Effect of Resource Variation and Firm Experience on Market Entry Decisions: Evidence from U.S. Telecommunication Firms' International Expansion Decisions. Organization Science, 20(1), 69-84. [CrossRef]

- (Greve, 1998) Greve, H. R. (1998). Performance, Aspirations, and Risky Organizational Change. Administrative Science Quarterly, 43(1), 58-86. [CrossRef]

- (Greve, 2003) Greve, H. R. (2003). A Behavioral Theory of R&D Expenditures and Innovations: Evidence from Shipbuilding. Academy of Management Journal, 46(6), 685-702. [CrossRef]

- (Greve, 2008) Greve, H. R. (2008). A Behavioral Theory of Firm Growth: Sequential Attention to Size and Performance Goals. Academy of Management Journal, 51(3), 476-494. [CrossRef]

- (Hardin & Hilbe, 2002) Hardin, J. W., & Hilbe, J. M. (2002). Generalized estimating equations. Chapman and Hall/CRC.

- (Harrigan, 1980) Harrigan, K. R. (1980). Strategy Formulation in Declining Industries. Academy of Management Review, 5(4), 599-604. [CrossRef]

- (Hilbe, 2011) Hilbe, J. M. (2011). Negative binomial regression. Cambridge University Press.