Submitted:

17 July 2025

Posted:

18 July 2025

You are already at the latest version

Abstract

Digital or Technology Strategies are the first step of a Digital Transformation. The main risk is that information and assessments not included in the Strategy and left to be confirmed and managed at later stages have the potential to negatively affect the successful implementation of the Digital Transformation, therefore, negating the sought after business benefits. To mitigate this risk, this article proposes DigStratCon, a Digital or Technology Strategy Framework that generalises the digital Transformation detaching it from its specific functional application, such as marketing, products, Information Technology (IT) and Operational Technology (OT). Therefore, DigStratCon applies to any area within an organisation or infrastructure including Data and Artificial Intelligence (AI). DigStratCon defines seven key components within a Digital or Technology Strategy, specifically 1) Market research, 2) Digital vision, 3) Current state, 4) Roadmap, 5) Risks, 6) Enablers, and finally 7) Supply Chain. A qualitative analysis of several United Kingdom (UK) government digital strategies assesses their completeness against the DigStratCon model. On average, UK digital strategies score 6/7 being innovative and ambitious in their vision; however, they generally lack a common or standardised structure and wider international benchmark and alignment.

Keywords:

digital strategy

; technology strategy

; digital transformation

; strategic consulting advisory

1. Introduction

Digital or Technology strategies are the starting step for a successful Digital Transformation. By following the strategy, stakeholders can rest assured the promised benefits will be delivered at the estimated price and following the planned schedule at a minimal risk of deviations. Decision makers are firmly guided by digital or technology strategies due to their definition of the overall direction of the asset or organisation, the inclusion of key and broad range focus areas or objectives and the prioritisation of initiatives, therefore ensuring alignment with the long term goals. However, Digital or Technology strategies may not deliver the expected benefits due to several risks.

1.1. Digital Transformation Risks

The strength of strategies is when they constitute the strategic case of an overarching business case. If the strategy is produced as an independent deliverable, then it needs to include the remaining elements of a business case, namely the economic, commercial, financial and management cases to ensure value for money, viability, affordability, and delivery, respectively. Digital Transformation risks arise from the lack of relevant specification on their scope, values and goals, management, governance, funding, change management, regulation, technical architecture, cybersecurity, and complexity within the digital strategy.

The scope of Digital Transformation ranges from rewiring existing processes to redefine client and supplier relationships beyond current boundaries [1]. In addition, distinct functions of the asset or organisation could commission independent digital strategies such as real estate, marketing, product, Information Technology (IT), and Operational Technology (OT), generating potential gaps and overlaps in scope and project interfaces. The effect is the detriment of the final business objectives and unnecessary additional costs, inefficient operations, and decision making, respectively.

An unclear vision and unfeasible goals lead to complete failure due to a waste of resources on unachievable results and ambiguous directions [2]. Digital or Technology strategies focused on technology without alignment to the business values and goals lack well defined and proven benefits, hindering the increase of revenue at the customer level or increasing its operating costs and detriment to the user or customer experience, therefore obstructing competitive advantage, growth, profit and business value.

Despite significant large scale investments, management errors can make Digital Transformation fall short of expectations in terms of service relevance and scalability, resulting in market decapitalisation [3]. The lack of agreed Key Performance Indicators (KPIs) and defined milestones triggers misalignment between activities. Furthermore, if stakeholders are not engaged before the initiation of digital strategies, sufficient project resources are not allocated, and testing and commissioning are not considered, the delivery of the Digital Transformation will be delayed, over budget, and misaligned with the strategy objectives.

Boards are normally focused on finance and legal for corporate governance, leaving Digital Transformation unaccountable [4]. The unclear definition of roles and responsibilities in the ownership, management and maintenance of the new digital systems, assets and associated services defined in the digital or technology strategy develops a lack of governance and accountability during the whole life cycle of the assets.

Financing constraints cause mediation between Digital Transformation and green innovation in organisations where the full benefits and main features, such as scalability, are inhibited [5]. Undetailed capital investments without scheduled cash flows and funding agreement generate Return on Investment (ROI) uncertainty as costs cannot be accurately accounted for, and the delivered benefits measured against them.

Digital Transformation programs fail to accomplish their goals due to inefficient change management, including inadequate management support, lack of clearly defined and achievable objectives and ineffective communication [6]. The existing culture and structure can present barriers and impede the Digital Transformation effort instead of fostering an environment that promotes change, innovation, pushing boundaries from comfort zones, and continuous learning. Siloed departments, functions, and teams working towards different goals hinder communication and collaboration. This issue also applies to leadership misalignment and inconsistent vision and support. Users can be voluntarily resistant or involuntarily able to change due to a lack of onboarding or training, therefore impeding user adoption. Moreover, users in an organisation can be unaware that there are already available digital tools, applications or features to enhance their productivity.

Regulatory frameworks lack the ability to adapt to the increasing pace of technological developments, generating regulatory risks due to the unknown type of regulatory change that will be established in response to digital innovation [7]. Currently, there is no single regulatory framework generally accepted for Digital Transformation and Industry 4.0, nor are there any universal international conventions. Instead, there are specific regulations for point applications.

Legacy servers and digital architecture reduce data interoperability, particularly at organisations with complex software systems, therefore increasing the costs of Digital Transformation as users need to develop more complicated processes to interact with technical systems [8]. The lack of interoperable and straight access to data, applications and systems reduces the functionality of digital applications, where non-standardised digital, technology, and data via proprietary and closed protocols, software, architecture, and standards disable seamless integrations.

The success of Digital Transformation depends on developing proactive and adaptive cybersecurity measures as digital technologies are increasingly incorporated into business operations [9]. Potential and new threats such as phishing, ransomware and insider attacks incur a digital loss of service and access to valuable data leading to substantial reputational and financial damage.

The progression of the relationships between the systems architecture and organisational structures after Digital Transformation has increased in complexity beyond human cognition due to the extended functionality, larger systems integration, and constant development [10]. Technical incompatibilities, system fragmentation and large volumes of data affect efficient operations.

1.2. Research Question and Proposal

The research question presented by this article is whether digital or technology strategies provide enough information to mitigate risks in Digital Transformation. These risks include scope, values and goals, management, governance, funding, change management, regulation, technical architecture, cybersecurity, and complexity.

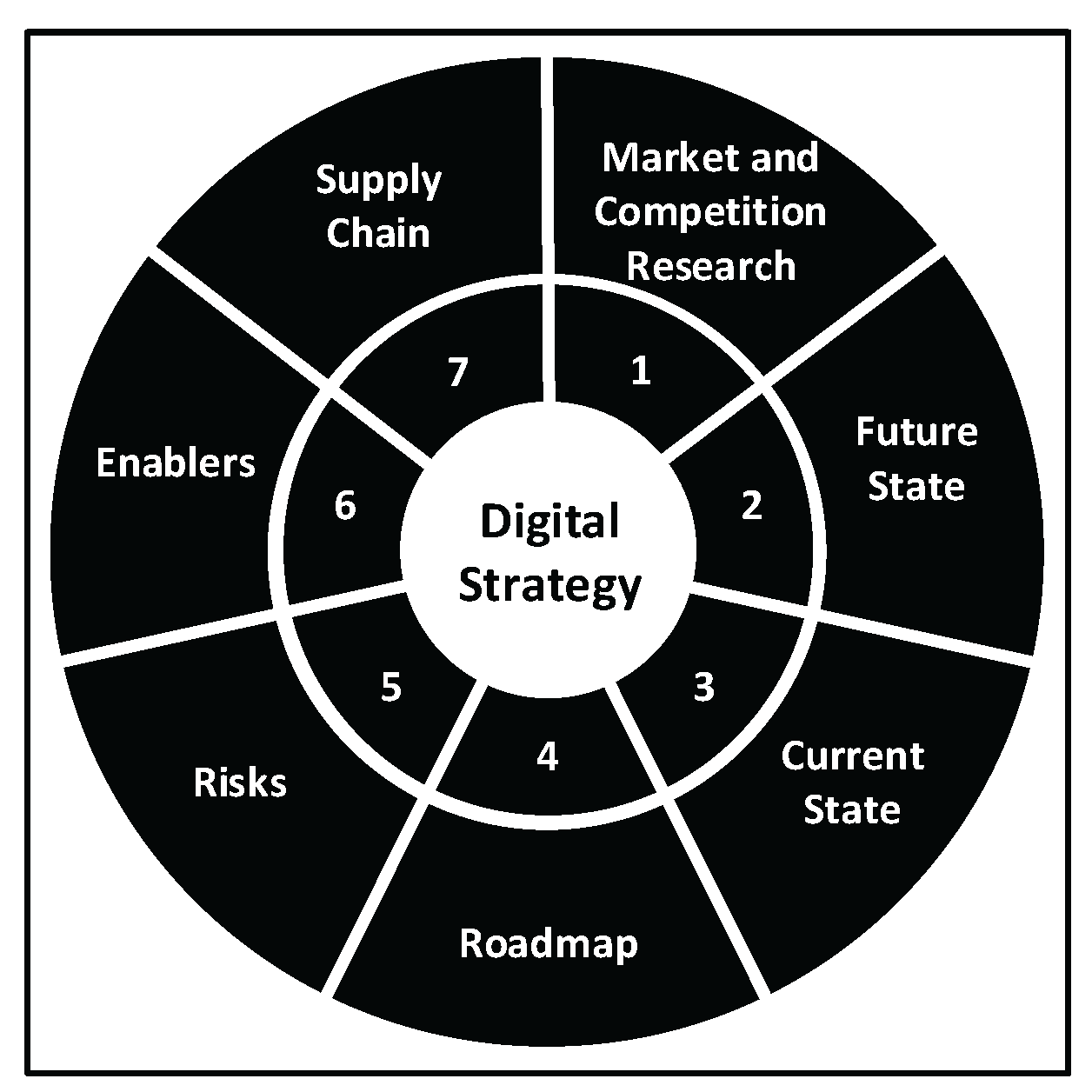

In addition, this article proposes DigStratCon as a digital or technology strategy framework that mitigates the presented risks in Digital Transformation by structuring the content and information. DigStratCon generalises the Digital Transformation, detaching it from its specific functional application, such as real estate, marketing, products, or Information Technology (IT). Therefore, DigStratCon applies to any area within a government, organisation or infrastructure, including Data and Artificial Intelligence (AI). DigStratCon defines seven components within a digital or technology strategy, specifically 1) Market and competition research of current applications of digital and technology, equivalent initiatives, standards and regulations, 2) Digital vision or future state, 3) Current state of the digital landscape, 4) Roadmap based on prioritisation based on benefits versus cost, dependencies, 5) Risk assessment based on their probability and impact with respective effective mitigations, 6) Enablers such as Project Management, Target Operational Model, Change Management, 7) Supply Chain that covers solution, service and asset providers.

To answer the research question, a qualitative analysis assesses whether digital strategies provide enough information to reduce the Digital Transformation risks based on the DigStratCon framework. Specifically, the selected digital strategies are from ten departments of the UK government, publicly available and retrieved from their respective websites.

This article is structured into Section 2, providing the research background and literature review for several digital directives, regulations, frameworks, and the different elements of the DigStratCon framework. Section 3 defines the DigStratCon model and its different components. Section 4 presents a qualitative analysis of ten departments of the UK government against the DigStratCon Model. Section 5 discusses the seven elements of the DigStratCon model in the UK digital strategies. Section 6 suggests further considerations based on the external consultants versus internal resources, artificial versus human intelligence, cost versus quality, tick in the box versus value added and strategy versus design. Finally, Section 7 shares the conclusions of this research.

2. Research Background

This section presents the literature review for UK and European digital directives, regulations and other proposed digital strategy frameworks. Moreover, this section includes specific research background which main topic specifically corresponds to a component of the proposed digital or technology strategy framework, DigStratCon; 1) Market and competition research, 2) Digital vision or future state, 3) Current state of the digital landscape, 4) Roadmap, 5) Risk, 6) Enablers such as Project Management, Target Operational Model, Change Management, and 7) Supply Chain.

2.1. Digital Directives and Regulations

There are several European digital directives and regulations. The Directive (EU) 2025/25 covers the use of digital tools and processes in company law, promotes trust and transparency in companies, and improves the reliability of company information to establish more connected public administrations [11]. The Directive (EU) 2022/2555 establishes a common cybersecurity regulatory framework based on cooperation, information sharing, supervision, and enforcement to enhance cybersecurity in the EU by strengthening cybersecurity capabilities, introducing cybersecurity risk management, and compulsory reporting in critical sectors [12]. The Regulation (EU) 2022/2065 Digital Services Act (DSA) creates a safer online environment for consumers and organisations by defining consumer rights, responsibilities for online platforms and social media, reporting, and oversight, and promoting innovation, growth, and competitiveness [13]. The Regulation (EU) 2016/679 General Data Protection Regulation (GDPR) protects the individuals’ information after its processing by the private and public sectors, enabling individuals to control their personal data and establishing independent supervisory authorities to monitor and enforce compliance [14].

The UK has a couple of sovereign acts for digital, where the British GDPR is adopted from the European Regulation. The UK Data Protection Act covers the processing of personal data, the definition of competent authorities for law enforcement, the implementation of the law enforcement directive, and the role of the Information Commissioner [15]. The UK Parliament. Data (Use and Access) Act regulates access to customer and business data, the determination and verification of individuals, the recording and sharing of information, privacy and electronic communications, and the establishment of the Information Commission [16].

2.2. Digital Strategy Frameworks

There are distinct theoretical frameworks already proposed for digital strategies and Digital Transformation in organisations, businesses, governments, assets, and products.

2.2.1. Organisations

An integrated approach for the development of a digital strategy is formed of six phases and four generic digital strategies [17]. The six phases include the external strategic analysis for the influencing factors from the macro and micro-environment, strategic forecasting from relevant environmental factors, internal strategic analysis of the company and its different divisions within the digital context, strategic principle to identify current and future fields of action, strategic options with evaluation and selection, and strategy formulation based on the strategic option selected. The four generic digital strategies cover the product provider, service provider, product platform operator and service platform operator. The macro-environment includes political, economic, sociocultural, technological, ecological, and legal dimensions, whereas the micro-environment covers potential new entrants, rivalry among competitors, substitution products and services, bargaining power of customers and bargaining power of suppliers.

A strategy framework for the Digital Transformation of any organisation comprises three stages with four core dimensions, namely positioning, business model, dynamic capabilities, and transformation roadmap [18]. The three stages cover the identification of Digital Transformation drivers from internal, external factors and consumer analysis. The development of a vision based, mission and objectives based on position, business model and dynamic capabilities, and the Digital Transformation roadmap covering customer aspects, organisational arrangements, business case, transformation approach and technology considerations.

A process model for the development of digital strategies consists of eight components, namely digital guiding principles, digital culture, digital competencies, strategic direction, Digital Transformation of products, services and value creation, IT/OT architecture, creation of value networks, and measurement and organisation [19]. An analysis of Digital Transformation strategies includes their components, success patterns, procedural factors, responsibilities, and the final integration of Digital Transformation strategies into organisations. These components divide Digital Transformation into four areas covering the application of technology, changes in the creation of value, changes in the structure of the organisation, and financial considerations [20].

An integrated methodological framework for Digital Transformation strategy is based on IT governance elements, namely business strategic planning, strategic planning, organisational structure, reporting, budgeting, investment decisions, steering committee, prioritisation process and reaction capacity [21]. In addition, the framework contains processes, goals, good practices, metrics, and evaluation parameters based on KPIs and Digital Transformation maturity levels.

2.2.2. Business

A digital business strategy framework is composed of eight critical success factors: sales and customer experience, organisation, culture and leadership, capabilities and HR competencies, foresight and vision, data and IT, operations, and partners [22]. The sales and customer experience covers the seamless integration of offline (physical) and online (digital) channels. Organisation includes the agility to reallocate resources and swift reorganisation. Culture and leadership create and foster a digital mindset with a digital agenda. The capabilities and HR competencies reinvent value chains and challenge the status quo, where employees identify value. Foresight and vision establish a clear vision with future positioning for the Digital Transformation. Data and IT use data and information from a central source. Operations create data driven and digitally automated processes for higher automation. Partners utilise network effects with open systems and partner integration.

An intelligence framework model for digital business strategies is based on four properties and seven dynamics [23]. 1) Layered to enable decision making for business, strategy, policy, and functional objectives, 2) Qualitative analysis to model uncertainty with hypotheses, 3) Sensitivity analysis, 4) Strategy evaluation and characterisation methodologies. In addition, the dynamics for digital disruption include threats, opportunities, digital marketplaces, current business model, transformed business model, digital business strategy, and Digital Transformation strategy.

A framework for a strategic Digital Transformation based on building a digital business by the digitisation of core and business processes to develop new digital products and service offerings is composed of several dimensions [24]. These dimensions cover organisational structure for the processes and skills; informational for the data and information management; environmental for the ICT integration; security for IT, data and human; quality for the products and services; financial for the investment and return on investment; cultural for the values and behaviors shared by a community; innovation for technology design, technology processes and ICT management; participative for collaboration and interaction of any stakeholder and user.

Four themes to guide digital business strategy in a Digital Transformation strategy framework consist of the scope, scale, speed, and the sources of business value creation and capture [25]. The scope includes the digitisation of products and services, the relationship with firms, industries as customers or supply chains, IT infrastructures, and the external environment. The scale covers the rapid digital deployment or disband as strategic dynamic capability, the network effects within multisided platforms, information abundance, alliances, and partnerships. The speed includes product launches, decision making, supply chain orchestration, network formation and adaptation. Sources of value creation consist of information, multisided business models, coordinated business models in networks, and the control of digital industry architecture.

Digital strategies for Small and Medium Enterprises (SMEs) and Large Sized Enterprises (LSEs) are structured based on the aim of Digital Transformation, the application of new technology, the creation of future value, the value added from changes, the future organisational structure, and the financing of digitalisation [26]. Furthermore, a transformational digital strategy in an SME covers the threat of new entrants, bargaining power of buyers, bargaining power of suppliers, threat of substitute products, intensity of competition, market differentiation, customer segmentation and targeting, brand positioning, pricing, and communications [27].

The digital readiness of emerging markets business is conceptualised as technological sensemaking, enterprise agility, and transformational implementation [28]. Technological sensemaking assesses the strategic capability for the implementation of new technology or the configuration of existing technology to adapt to market changes, including the understanding and interpretation of technological change, the elicitation of actionable insights, and the impact on business performance. Enterprise agility measures the speed of change management at which businesses adapt to market disruptions and respond for competitive advantage. Transformational implementation integrates digital technology entirely into the business to support strategic changes. The five factor model of digital readiness is composed of 1) Leadership in terms of millennial leadership and legacy employees, 2) Strategic focuses on operational efficiencies, rural market expansion and millennial customers, 3) Resource includes information availability and financial flexibility, 4) Customer covers expectations of personalised experience and readiness for digital technology and 5) Market includes the availability of specific platforms, and institutional support.

2.2.3. Assets

An asset omni-management framework for assets consists of the micro-management of services for the atomic functional functions [29]. These functions include users, spaces, management and technology. The standardisation of different assets or infrastructure supports the macro-functionality of the asset delivered by Distributed Ledger Technologies (DLT), Decentralised Autonomous Organisation (DAO) and their generated new business management with the effects for the role of intermediaries in asset management.

A Digital framework to deliver mega projects or digital strategies is based on a systems engineering methodology embedded into the business case [30]. Specifically, requirements management, interface management, systems architecture, the supply chain landscape, and Reliability, Availability, Maintainability, and Safety (RAMS) targets are included in the business case to provide a wider technical vision of the project or strategy. The approach reduces the risks of megaprojects or strategies composed of complex systems of systems in their earliest stage, when financial decisions based on cost estimations are made.

A strategy framework for Digital Transformation of the architectural, engineering, construction and operation and maintenance value chain consists of three pillars [31]. A simple, actionable and agile strategy centred on four areas, namely the identification of objectives, risk management, coordinated and team approach, and the achievement of value across the value chain. Strategy based on dynamic capabilities directed toward strategic change, at the organisational and individual unit levels. Strategy of transformation on the move, combining change and continuity in new business models, new services.

2.2.4. Governments

Adoption strategies of digital technology for local government follow the Preferred Reporting Items for Systematic Reviews and Meta Analyses (PRISMA) via the people, processes, and technology framework [32]. This framework includes the technology utilised for local government services, opportunities, challenges in implementing digital technology, and the final strategies to deliver digital technology. People strategies cover the building platform for public participation, employee skills, and a positive mindset of decision makers. Process strategies include recognising the roles of players, clear aims and procedures, appropriate regulation, and accepting user input. Technology strategies involve understanding the effect of technology, technology preparedness, and convenience adoption.

A conceptual model for Digital Transformation in governments combines the diamond, the technology enactment, and enterprise architecture frameworks [33]. The model covers technology, process, structure, and people areas, targeting flexibility via policy and technology throughout the digital progression within hierarchical and bureaucratic organisations. The diamond framework provides a conceptual view of the organisation as a system with four elements (actors, structure, tasks, and technology) to analyse the impact of technology on organisational changes. The technology enactment framework examines the effects of organisational structures and institutional arrangements on technology implementations in the public sector. The enterprise architecture framework develops an architecture description of a system based on domains, layers, views, matrices and diagrams to make systemic design decisions on components and long term decisions for new design requirements.

Digital innovation and transformation from an institutional perspective are divided into three digital institutional arrangements: organisational forms, institutional infrastructures, and institutional building blocks [34]. The digital organisational form is a digitally enabled configuration of practices, structures, and values that constitute the core of the organisation. The digital institutional infrastructure includes standardised digital technology that enables, constrains and coordinates numerous actions and interactions in sectors and industries. The digital institutional building blocks represent premade and customisable modules formed of digital technology for running or creating an organisation.

2.2.5. Products

A managerial framework for digital technology and digital innovation for product and service portfolio covers five areas [35]: 1) user experience including usability, aesthetics, and engagement, 2) value proposition covering segmentation, bundling and commissions, 3) digital evolution scanning including devices and channels, 4) behaviours and skills for learning, roles, and teams, and finally 5) improvisation in space, time, and coordination.

A Digital Transformation strategy for manufacturing products consists of six stages: the generation of a Digital Transformation vision and objectives, the assessment of the organisational capability for the Digital Transformation via digital maturity levels, the design of the end user and employee user experience, the assessment and selection of solutions and vendors, the creation of an implementation roadmap and the change of the organisation culture and infrastructure [36]. The Digital Transformation faces several challenges, including traditional analogue processes, resistance to change, legacy business models, limited automation, budget limitations, lack of relevant knowledge, rigid company structure, and security.

A framework to guide Digital Transformation in Industry 4.0 consists of capability maturity and alignment to support manufacturing companies in developing their products [37]. There are four maturity levels: No Industry 4.0 or only ad hoc, departmental level or isolated silos, organisational level or cross-departmental, and inter-organisational level or cross value chain/supply chain partners. The activities in the framework cover the establishment of the consultancy team, the assessment of the digitalisation, the benefit versus implementation effort analysis, the generation of ideas for use cases, and the estimation of the impact associated with the use cases.

2.3. Market and Competition Research

One of the options for the assessment of the market and competition research is its development as part of the digital strategy, although this activity is usually included in the marketing strategy of the organisation. The effect of digital marketing strategies on the buying behaviour of customers in online shopping is analysed via the rough set theory and decision tree rules [38]. These strategies include search engine optimisation, search engine marketing, social media marketing, content marketing, affiliate marketing, pay-per-click, recommender engine and email marketing. The five rules governing customer behaviour include cultural, social, individual, psychological, and marketing factors.

A hybrid knowledge automation system calculates, reasons and advises specific digital marketing strategies from various digital marketing strategy models, integrating several decision support methods based on Monte Carlo Simulation and fuzzy logic [39]. The Monte Carlo simulation captures the stochastic behaviour of the variables that influence digital marketing decision making. The fuzzy logic models the uncertainty of the input and strategic options, where “if-then” rules model and automate planning knowledge, analytical models and guidelines.

The dynamics of the evolution and adoption processes of digital strategies for public digital platforms in digital marketing depend on competitive market pressures and organisational readiness [40]. The evolution processes include the pressure from costs, performance and brand, response, effect path for startups, rapid growth, and mature organisations. Likewise, the adoption processes cover the evolutionary path of validation, cloning, and foresight path based on single, linear, and diverse capability readiness.

The impact of digital platforms on the performance of new startups and the influence of the digital strategy is based on broader market outreach, cost effectiveness and network effect [41]. The broader market outreach covers the growth of the market and the adaptation of the current business network, such as organisations, clients, suppliers, and competition, to gain new customers. Cost effectiveness maximises current resources to reduce labour costs for commercial processes, where business costs decrease as efficiency increases. The network creates strong circular feedback after the net worth of a product, service, or platform increases following an expansion in users.

A digital customer experience strategy includes management practices to provide direction and is divided into preservers, transformers and vanguards [42]. These practices are composed of the five dimensions, namely, definitions, scope and objectives, governance, management, policy development, and challenges. Preservers define customer experience management as an extension or development of existing service delivery practices while assessing its effectiveness via traditional customer outcome measures. Transformers acknowledge that customer experience is connected positively to the financial performance of the organisation. Vanguards present a clear strategic model of customer experience management, impacting all areas of the organisation, developing adequate business processes and practices and integrating functions into customer touch points to ensure consistency across their own business and their partners.

2.4. Digital Vision or Future State

The digital vision or future state is articulated following well defined and structured processes composed of several stages. Digital Transformation strategies are divided into two pillars: the vision and the readiness of a business model for digital operation [43]. These two dimensions create four generic Digital Transformation strategies: disruptive, business model led, technology led and proud to be analogue. These strategies differ in the digital vision, primary drive and target of the transformation, leadership style, creativity and entrepreneurial attitude between employees, risks and challenges, consequences of potential failure, and available methods for enhancement.

A model of alignment for a digital vision comprises five stages determined by combinations of sensing, seizing, and reorganising capabilities [44]. Sensing detects changes and learns quickly. Seizing addresses opportunities and captures value in the marketplace by the mobilisation of resources, the embracement of opportunities for innovation, and the execution of actions. Reorganising alters the company processes, leverages resources differently, accesses new resources to solve gaps, and releases resources to generate optimal arrangements. These five phases exhibit different visions for the technology applications (ad hoc vs. integrated) and methodologies for the adoption of technology (reactive vs. purposeful). 1) Passive acceptance uses limited digital technology, almost reluctantly, driven solely by external pressures. 2) Connection applies ad hoc, but voluntary, digital tools for both internal and external activities. 3) Immersion uses digital technology with proficiency and a growing dependency between business and technology, with some steps toward integration. 4) Fusion applies digital tools extensively, deployed to meet business objectives with a large alignment of the business to the digital strategy. 5) Transformation intentionally uses digital technology to transform the business.

Four visions for digital strategies, namely structural separation, strategic outsourcing, centralisation of decision making and the threat of digital disruption, are the inputs of a predictor for a digital service innovation [45]. This predictor applies a fuzzy set qualitative comparative assessment based on consistency, raw and unique coverage, solution consistency and coverage. Structural separation covers the distinction between innovation related activities and established organisational units. Strategic outsourcing measures the dependency of an organisation on external partnerships to develop service innovations. Centralisation of decision making includes the different levels within an organisation where power resides. The threat of digital disruption analyses the threat from new/established market entrants that apply digital technology to the core business of an organisation.

Digital Transformation visions and strategies for digital innovation based on AI are evaluated following an analytic hierarchical process and four criteria, namely subject, environment, resource, and mechanism [46]. Specifically, the subject is composed of the Chief Executive Officer, core talent, technical development, and business strategy. Environment consists of compliance and regulation, industry competition, market digitalisation, and social responsibility. The resource covers technology, big data infrastructure, capital and investment. The mechanism includes coordination, learning, selection, and change supervision.

2.5. Current State of the Digital Landscape

Some digital strategies prioritise the current state of the digital landscape as the starting point of the Digital Transformation. This is due to the organisations being heavily dependent on their current technologies, processes, management or having already started a Digital Transformation. Digital strategies continuously update and incorporate new learnings and insights from previous and ongoing implementation projects, like the physical transformation of an asset. The implementation of a digital strategy requires a balance between top-down and bottom-up approaches, where agile methodologies of trial and error are better suited than exhaustive analytical upfront planning processes [47]. To meet these requirements, a digital strategy is divided into seven phases focused on the underlying processes, strategising activities and current status: recognition of the need for Digital Transformation, setting the stages, initial formulation, preparation for the implementation, starting the implementation, establishment of a working mode and next enhancements.

A digital strategy for the city of Manchester promotes digital inclusion, industries and innovation [48] based on its current technology landscape. This Digital Transformation is then enabled by the city leadership, investment in new digital infrastructure and services, and an extensive exemplar of projects and activities. The transformational digital infrastructure includes access networks for businesses and citizens via fibre to the premises and wireless technology, digital hubs to connect these independent networks and backbone networks to connect the digital hubs to the Internet while hosting applications on services. Other initiatives include smart energy, smart health and wellbeing.

The role of high reliability organisational identity and value in Digital Transformation contrasts in terms of 1) tensions between innovation and transformation while maintaining the current reliable, secure and efficient operations, 2) dependency on established internal resources against recruiting external resources and 3) complexity versus transparency [49]. Failures or suboptimal outcomes on Digital Transformation are due to current misalignment in the IT workforce perception, which induces a threat perception followed by self protective behaviour.

A model for Digital Transformation evaluates the relationship between digital, corporate and business strategy stages against the current organisation leadership and management structure [50]. The management variables cover several leadership approaches characterised by the current perception of the autonomy provided to employees, the coherence of managers’ actions towards the mission of the organisation, and the effectiveness of the strategic management process. The Digital Transformation stages include the relevance of digital strategy to corporations, the business strategy, the level of innovations set by the digital strategy and the value of investment in digital strategies.

2.6. Roadmap

Roadmaps in digital strategies are based on the priorities an organisation sets to achieve from the vision, available funding, and their dependencies against the current state. A high level roadmap for Digital Transformation consists of three dynamic IT capabilities: digital platform, IT management, and IT knowledge management, which allow IT units to dynamically update their capabilities against variable business requirements and frequent technology releases [51]. This roadmap assists organisations in extracting business value from IT infrastructure and supports organisational sensing, seizing, and reconfiguring activities for the procurement, deployment, integration, and reconfiguration of IT resources to meet business objectives. Dynamic digital platform capability generates new value creation activities, enhances operational efficiency, enables access to external resources and capabilities, and supports participation and engagement, such as open innovation. Dynamic IT management capability designs and executes changes in processes that control IT resources and practices in alignment with the goals and priorities of the organisation. Dynamic IT knowledge management capability facilitates organisational IT technical knowledge creation, transfer, and retention; the deployment, coordination, and innovation of IT resources and practices; and the technical expertise and understanding of business staff to use IT in carrying out or refining daily operations.

Business process management implements Digital Transformation roadmaps based on six requirements: digital strategy, agility, digital expertise, IT innovation, collaboration and openness [52]. These requirements are then mapped into the six elements of a business process management roadmap: strategic alignment, governance, method, IT, people and culture. Based on these elements, three digital strategies for implementation are modelled as: communication/learning, unification/optimisation and automation/certification to cover six objectives: governance and compliance, management support, interaction model, education, tool support, conventions and guidelines.

The digital activities of strategists are represented in four stages of an open strategic roadmap, namely the broadcasting, soliciting, collaborating, and actioning stages. The broadcasting stage applies IT to describe the content of the proposed strategy and make it visible to stakeholders and the community while starting the engagement [53]. The soliciting stage generates and evaluates the content of the strategy with references to strategic plans while seeking views, thoughts, ideas, and deliberations from the community. The collaborating stage covers face to face discussions with the community to negotiate and refine the strategy while capturing emergent ideas. Finally, the actioning stage implements the acquired learning into the formal strategy and reprioritises the strategy via updates from promotion campaigns while defining a jointly developed membership model.

2.7. Risk Assessment

Although risk assessments follow a well stablished methodology based on the reduction of the probability and the mitigation of severity, there is specific research on several approaches to reduce the risks of Digital Transformation. The role of a sustainability strategy in a digital business strategy versus its financial performance and its capability to reduce sustainability risks is based on management and operational capabilities [54]. This sustainability strategy reduces the risk between managerial capability and financial performance; in contrast, it increases the risk among financial performance and operational capability.

An alignment process for a highly dynamic digital strategy reduces the risks of Digital Transformation based on an analysis of a Business to Business journey to enable the Business to Customer digital strategy [55]. This alignment process consists of several standardisable actions for the sensing, seizing, and transforming capabilities of the organisation that iteratively reconfigure and refine the resources to address changes in the external environment and internal issues. The sensing capacity focuses on opportunity identification and assessment; the seizing capacity covers the decisions and design of organisational components to capture opportunities, whereas the transforming capacity addresses the reconfiguration and redeployment of resources.

Three governance strategies that countries apply to reduce the risks derived from digitalisation, such as sustainability, social and environmental impact, while promoting private sector innovation, are divided into laissez faire, precautionary and preemptive, and stewardship with active surveillance [56]. The laissez faire governance approach requires limited government intervention or regulation and mostly depends on an industry driven and open market to recognise suitable strategies and manage the processes of digitalisation. The precautionary governance approach utilises regulation to confirm that the safe use of the strategy has been demonstrated and to prevent exposure to irreversible risk while mitigating short term risks after the revision of emerging and future threats and common themes. The stewardship governance approach supports the promotion of the digital economy while enforcing the government's prevention and mitigation of sustainability risks from future threats.

Digital technology supports organisations to enhance their resilience during a crisis based on a resilience capability model at the entrepreneur, organisational, and entrepreneurial ecosystem levels [57]. The entrepreneur level begins the resilience after understanding the crisis, its associated risks and then identifies relevant digital technology. The organisational level builds up this resilience as a dynamic capability, repurposing organisational resources. The entrepreneurial ecosystem develops the capabilities to have a transformational role via seamless integration with the organisation.

2.8. Enablers

Project management and Target Operating Models (TOM) are quite structured frameworks based on several standardised components; however, change management and user behaviour in Digital Transformation present more variability due to their human factor. A set of relevant organisational capabilities for managing Digital Transformation is divided into seven relevant themes [58]. 1) Strategy and ecosystem capabilities relate to the organisational strategy and ecosystem. 2) Innovation thinking capabilities cover the organisational need for innovation targeting open innovation and cocreation. 3) Technology capabilities include new disruptive technology. 4) Data capabilities provide the management, security, and capitalisation of data. 5) Operational capabilities consist of regular business and value creation activities. 6) Organisational design capabilities cover the design of the organisational structures and process. 7) Leadership capabilities provide the organisational management and culture.

Governments are investing large resources to develop an information society and close digital divides between regions based on broadband, Information Communication Technology (ICT) infrastructure, e-government services, e-health, access to public sector information, intelligent transport systems, smart energy, e-inclusion, ICT for SME, and ICT for rural agriculture for their citizens resulting in policies that include broadband infrastructures, the application of ICTs in the public sector, the digitalisation of SMEs, and digital inclusion [59]. A digital strategy aligns these policies and investment with the actual needs of local users while considering the factors that influence the strategic decisions between funding, investment and strategy.

There are several structural, cultural and social barriers against digital government, where digital champions need to navigate institutional frameworks to strategically deliver digital government solutions [60]. Structural barriers consist of technological infrastructure, institutional reliance on outdated technological platforms, technological resources, technical capacity and skills, human and financial resources, legal frameworks, privacy and security, rigid and siloed organisational structures, lack of organisational leadership, and outdated procurement processes. On the other side, cultural barriers cover political and management support and leadership, institutional habits and traditional processes, absence of engagement with and demand from users/citizens, risk aversion, hierarchical decision making, organisational vision and strategy, perceived legal barriers, organisational practice, finances, lack of awareness/strategic thinking, unclear definition of benefits, political alignment, workload and competing priorities, deficiency of evidence base and ethical concerns.

The role of proactiveness, risk taking, innovation, and relational capital in employee performance to achieve the digital strategy goals in a Digital Transformation is analysed via a four dimensional scale based on management, infrastructure, networking, and development [61]. The management capability plans and orchestrates digital resources to make strategic decisions aligned with the goals and vision of the organisation. The infrastructure capability identifies the human and technological digital assets and resources to assess the benefits of digital investments. The networking capability determines the speed and effectiveness of accessing, utilising, and exploiting external digital resources beyond the organisational boundaries. The development capability deploys digital resources to meet the current or emerging business, operational, and service requirements of the organisation.

The contribution of the Chief Digital Officer and its actions in the Digital Transformation within an organisation is modelled based on two variable design parameters [62]. On the vertical dimension, the Chief Digital Officer is vertically embedded in the structure of the organisation, following the Digital Transformation strategy and the responsibility for activities. On the horizontal dimension, the coordination mechanisms align employees working on Digital Transformation with formal and informal actions within different units at different hierarchical levels.

The rational and managerial practices of senior executives in a Digital Transformation, including their changing talent management role and the needs of individual employees, are categorised into four activities [63]: drive business change, master fluid and loose organisational structures, master talent complexity, and prioritise learning. These four activities are further divided into twelve subtasks. 1) switching from digital leader to business leader, 2) developing and promoting business experience in the digital function, 3) keeping updated on new developments, 4) encouraging and promoting dynamic and variable organisational structures, 5) integrating a mixture of formal and informal, internal and external and semi-permanent and temporary structures, 6) promoting mobility within the organisation, 7) managing new workforce needs for autonomy, purpose, ownership, and flexibility, 8) ensuring the required talent to digitally transform the business, 9) integrating and leveraging diverse teams, 10) deepening the talent pool, 11) making training a priority, 12) committing to personal permanent learning.

The effective Digital Transformation of organisations is based on the recent skills covering AI, IoT, nanotechnology, robotisation, augmented reality, and digitalisation [64]. These main digital learning contexts include participants, learning themes, learning processes, and learning facilitators via laptops, tablets, and smartphone applications.

2.9. Supply Chain

There are several strategies for digitalising the supply chain and digitally embedding them into an organisation. An approach to get competitive advantages in the digital supply chain includes Digital Transformation, smart technology and relationship performance [65]. Digital Transformation aims at the digitalisation of everything that can be digitalised, the collection of large amounts of data from different sources, the creation of stronger collaboration between the different business processes, and the enhancement of customer interfaces. Smart technology aims for all devices to be programmable, uniquely identified, alert to and adapt to changes within their environment, transmit and receive messages, record and store all information, and identify with other devices, places, or people. The relationship performance evaluates internal and external collaboration over the last three years.

Digital strategy developments for manufacturing supply chains are divided into three types: top-down, bottom-up and mixed approaches [66]. These three types are composed of several dimensions to include the company characteristics (revenue size and digital strategy adoption) and criteria (number of suppliers, product type and market demand. Top-down planning includes the strategic intentions of the top management, whereas bottom-up learning leverages practices and processes at an operational level.

The smart supply chain is delivered by Digital Transformation for flexible operational performance in uncertain environments with customers and suppliers across upstream and downstream relationships [67]. This supply chain flexibility is defined by three topics, namely sourcing, delivery, and manufacturing where information capabilities consist of three dimensions: Digital Transformation strategy, digital base technology, and digital front end technology. Base technology covers IoT, cloud, big data, AI, and blockchain, whereas front end technology includes robotics, 3D printing, simulation, and augmented reality.

Digital strategies focused on services transform processes that create value, therefore affecting relationships and power structures in supply chains [68]. These five strategies for industrial suppliers to keep access to critical resources while obtaining power within a digital services supply chain are based on a power constellation between supplier versus Original Equipment Manufacturer (OEM) dominated relationships and physical versus digitalised product service systems. Specifically, these strategies cover 1) the influence of digitalised product service systems in the knowledge of critical components 2) the facilitation of specific investments for the exchange of data 3) the commitment in the relationship of traditional service offerings, 4) the use of empowered end users to influence demand through the supply chain, 5) the downstream movement in OEM unserved markets.

Three generic digital strategies for shopping malls, namely digital awaiter, digital data gatherer, and digital embracer, include retailers and shoppers, the role of digital technology and their combination with physical devices into omnichannel strategies as supply chain [69]. These strategies are depicted from a constellation between the visionary role, type and services of digital technology, versus the centre of gravity in generating value, the supply side (retailers) and the demand side (shoppers). Digital awaiters use mature digital technology that is commonly accepted. Digital data gatherers apply increasingly sophisticated and complex digital technology to collect large amounts of big data from shoppers in the physical world to enable retailers the optimisation their business or operations. Digital embracers prioritise digital technology to generate advanced digital services to create their advanced digital services and offerings.

The value creation in digital business strategies is measured via three value networks in the supply chain: vertically integrated, loosely coupled and multisided platform [70]. Vertically integrated organisations have full and centralised control of their own value chains via vertical alliances. Loosely coupled organisations present more leadership, relevance and power obtained from their central position in the value network structure. Multisided platform organisations lead cross boundary industry disruptions, new business models, and innovative services in a common infrastructure platform, reducing distribution, transaction, and search costs.

3. DigStratCon: A Digital or Technology Strategy Framework

This article proposes DigStratCon as A Digital or Technology Strategy Framework that includes 1) Market and competition research of current applications of digital and technology, equivalent initiatives, standards and regulations, 2) Digital vision or future state, 3) Current state of the digital landscape, 4) Roadmap based on prioritisation based on benefits versus cost and dependencies, 5) Risks 6) Enablers including project management, target operational model, change management and finally 7) Supply chain.

Based on the gap identified within the research background, the innovation provided by DigStratCon consists of its generalisation of the Digital Transformation in seven stages, detaching it from specific functional applications, such as real estate, assets, marketing, products, IT or OT. Therefore, DigStratCon applies to any area within a government, organisation or infrastructure, including Data and AI. By following a standardised structure in the digital strategy, stakeholders are guaranteed that risks are mitigated, areas are holistically considered, and relevant information is easily identified by the next stage of the Digital Transformation, thus promoting digital and knowledge independence. In addition, this approach supports the Minimum Viable Product (MVP) approach in an agile methodology.

Figure 1.

DigStratCon Framework.

3.1. Market and Competition Research

Market and competition research is a vital component of a digital strategy as it provides insights into the current digital trends, user needs, business opportunities, competitor strategies and market landscape. This enhanced commercial understanding supports the development of informed decisions based on benchmark analysis. A useful approach is the assessment of previous and current issues affecting business and competition, and how technology has supported in addressing them, rather than directly recommending technology to be deployed in the market. Every organisation or asset is different; therefore, equivalent issues are normally solved via different solutions. In addition, technology evolves quite rapidly, therefore generating product obsolescence at the hardware and software levels.

Several methods provide research intelligence via the gathering of qualitative and quantitative data. These include direct online surveys to target audiences, interviews, focus groups and workshops, desktop analysis of information retrieved from the Internet, such as case studies or blogs, paid research reports by research and advisory organisations specialised in conducting them, or even hiring employees from the competition.

The data gathered from these methods is subsequently analysed and tailored to the organisation or asset requirements for trend identification, customer preferences, market opportunities, and regulatory updates. This research outcome identifies not only the strengths and weaknesses of the market and the competition based on comparable metrics, but also the organisation conducting the assessment, where weaknesses are then translated into opportunities. The impact of new technology on the customers, suppliers, partners, and competitors is also assessed. These gained insights inform the digital strategy supporting the business objectives and requirements.

3.2. Future State

The definition of the future state in a digital strategy for an asset or organisation involves envisioning where the asset or organisation wants to be in terms of digital capabilities and functionality. This clear and precise vision includes long term goals that align with the overall business strategy, such as environmental or sustainability, supported by Key Performance Indicators (KPIs) based on outcomes, rather than deployment progress, and measurable metrics like time or energy reduction, revenue generation or customer satisfaction. The alignment between business values, goals and technology delivers proactiveness in market opportunities and responsiveness against rapid market changes while staying ahead of the competition.

User centric digital strategies include simple user interfaces where users, including employees, are included in the process of developing the vision of the digital strategy vision. Another benefit of a user centric approach is users understand the benefits of the change.

The future state objectives are divided into smaller initiatives or use cases, according to an expandable Minimum Viable Product (MVP) and Specific, Measurable, Achievable, Relevant, and Time bound (SMART) definitions to provide clear direction. Furthermore, stakeholders covering leadership, team members, and external partners are consulted in the process to ensure their alignment and buy-in while avoiding scope gaps and overlaps.

Use cases relevant to the organisation or asset are enabled by digital systems, which in turn are dependent on the digital architecture or framework that hosts the software and information. These dependencies, therefore, generate a subset of foundational initiatives and use cases that require prioritisation for a successful orchestration of the digital strategy. Direct access to data, applications and systems enhances digital applications while enabling cross functional teams to innovate and improve continually. Modular technology architecture and Commercial Off the Shelf (COTS) applications with specific customisations, both at the cloud or premise level, reduce complexity and improve efficiency.

3.3. Current State

The assessment of the current state of a digital strategy involves a thorough analysis of the organisation or asset's existing digital infrastructure, with its associated management and utilisation processes. For a digital strategy, this includes the revision of the current systems, assets, platforms, applications, and capabilities, in terms of functionality, efficiency, scalability, and integration.

For enhanced user experience, current touch points such as websites, mobile apps or Graphical User Interfaces (GUIs), control panels, and data connectors are evaluated in terms of their performance and applicability. Feedback from customers, user engagement and direct stakeholder evaluations identify the strengths and weaknesses of the current digital use cases, applications and architecture. These current performance metrics are collected, analysed, and recorded to benchmark the effectiveness of the new digital applications and justify Return on Investment (ROI) challenges.

In addition to the current technology stack, its related asset management and processes are assessed and documented. This evaluation includes user team structures, workflows, resource allocation, asset manager and maintainer. Process inefficiencies and resource constraints are identified and their potential impact recorded in a risk register.

3.4. Roadmap

The digital roadmap is an essential tool to guide and align stakeholders throughout the Digital Transformation, ensuring collaboration while reducing conflicts. The different use cases are prioritised based on the quantitative and qualitative assessment of benefits and value to the organisation, including their alignment to the business strategy versus their cost of procurement, installation and maintenance. The technical dependencies between use cases are also accounted for to inject flexibility, agility and dynamism into the roadmap that enables possible future inclusions of changes from the evolution of the new technological advances and lessons learnt during the implementation of the digital strategy.

Gap analyses are conducted based on the target and the current state, and these gaps are accounted for via the use cases in the roadmap. Gaps include technical and organisational capabilities and skills to achieve the full benefits of the Digital Transformation. There are several tools to support the gap analysis elicitation, such as the Strengths, Weaknesses, Opportunities and Threats (SWOT) methodology. Strengths refer to the resources of an organisation that provide an advantage against the market, whereas weaknesses refer to the elements that induce disadvantages from the current state. Opportunities are features that can be exploited to the organisational advantage, while threats are characteristics that can cause issues from the market and competition research, respectively.

The roadmap is detailed with specific timelines, milestones, dependencies, key performance metrics, cash flows, resource allocation and Responsibility, Accountability, Consultation and Information (RACI) matrix for each digital initiative. These RACI roles in the project, system and asset levels are not limited to individuals but also include service providers, organisations or departments. This additional information, rather than a single list of use cases, ensures the successful orchestration of the Digital Transformation in alignment with the different functional units of the organisation and assets. Digital Transformation balances upfront Capital Expenditure (CAPEX) cost with ongoing Operational Expenditure (OPEX) cost based on service fees, cloud subscriptions and maintenance to keep the digital infrastructure up to date and secure, with the associated training and support. Capital investments follow scheduled cash flows for funding allocation and budget agreement for the programme, with contingencies for unexpected costs.

3.5. Risks

Digital Transformation is vulnerable to several risks that are identified, assessed and mitigated. These risks include every threat from the people, processes and technology dimension that has the potential to impact the successful implementation of a digital strategy. Once the risks have been identified via workshops or other research tools, the probability and impact are evaluated to generate a risk profile based on the likelihood and severity of the consequences. Solutions that minimise the probability of the risks while mitigating their impact are included in the roadmap. The residual risks are continuously monitored, and the effectiveness of the mitigation techniques is reviewed.

Risks normally include technology obsolescence, integration compatibility, gaps and overlaps in projects and use cases, organisational siloes, conflicting interests, funding for unplanned expenses, and availability of human and skilled resources.

Compliance with regulations, sustainability, directives and standards between different countries and regions is also incorporated into the risk register. This includes data privacy and protection at data collection, transmission and storage to ensure compliance with data governance policies. Potential changes in regulation, intellectual property infringements, the use of patented products, and antitrust monopolistic practices are also considered based on consultation with legal experts. Additional technology also brings cybersecurity risks that are efficiently mitigated via assessments and treatment plans to protect against data breaches and cyber attacks. Elicited cybersecurity requirements are fed into the overall strategy at the early stages.

3.6. Enablers

Enablers of digital strategies involve several essential methodologies that facilitate the successful Digital Transformation. These methods primarily include project management, change management and Target Operation Models (TOMs). Without these enablers, the application of technology will not directly integrate with the different functions and processes of the organisational or asset.

Project management regularly monitors the progress of the implementation of the digital strategy via its roadmap, releasing the budget when required, tracking risks and making adjustments to the schedule as required. Project management also addresses its governance of the strategy to establish the rules, policies, and controls to ensure compliance and effective implementation. Stakeholders are engaged and informed of the vision, reasons and benefits of the Digital Transformation. Delivery progress is continuously monitored and ready to adapt to deviations, where individuals are held accountable.

Change management supports the organisational transition to the future state, focusing on the skills, competencies, and culture that will successfully implement the digital strategy and drive its adoption among the different teams and users. Other elements to be considered include training, communication, and the address of any possible resistance to change. Change management covering users and processes is communicated and instructed to avoid misunderstandings and promote adoption.

The TOM includes the definition of the new teams, processes, asset capabilities and functions in alignment with the target operational state of the organisation to fully achieve the benefits of the Digital Transformation. The TOM defines and aligns the hierarchy, roles, responsibilities, reporting structure, workflows, and procedures covering the management and operation of the new digital assets delivered by the digital strategy while achieving operational efficiency.

3.7. Supply Chain

The supply chain has a fundamental role in successfully implementing digital strategies and delivering Digital Transformation. The supply chain can provide outsourced downstream services such as project, cost or design management as well as upstream digital assets comprising the manufacturing of hardware and software devices. Therefore, the mapping of the supply chain of different services and assets aligns with the digital strategy. Once the procurement, installation, commissioning and handover stages are accomplished, the supply chain can also provide services covering the maintenance and management of the digital assets that are accounted for.

4. Qualitative Research in Current Digital Strategies

Based on the previous research background and proposed sections for a Digital or Technology Strategy, DigStratCon, this section provides a qualitative assessment of alignment between several UK governments' digital strategies against the DigStratCon structure. These strategies have been chosen based on their public availability, retrieved from their websites and referenced accordingly. The information within this section has been extracted from these strategies. When the DigStratCon concept has been considered, the respective section is marked as “Provided” in the table; otherwise, the mark corresponds to “Lacking”.

Table 1.

Qualitative Analysis of DigStratCon sections in UK Government digital strategies.

| Strategy | Research | Digital vision | Current state | Roadmap | Risks | Enablers | Supply Chain | Score |

| DfT 2012 | Lacking | Provided | Provided | Provided | Lacking | Provided | Provided | 5/7 |

| DWP 2012 | Lacking | Provided | Provided | Provided | Provided | Provided | Provided | 6/7 |

| DCMS 2017 | Provided | Provided | Provided | Provided | Provided | Provided | Provided | 7/7 |

| DfE 2019 | Provided | Provided | Provided | Provided | Provided | Provided | Provided | 7/7 |

| MoD 2021 | Lacking | Provided | Provided | Provided | Provided | Provided | Provided | 6/7 |

| HMG 2021 | Lacking | Provided | Provided | Provided | Provided | Provided | Provided | 6/7 |

| DBEIS 2021 | Provided | Provided | Provided | Provided | Provided | Provided | Provided | 7/7 |

| DDCMS 2022 | Provided | Provided | Provided | Provided | Provided | Provided | Provided | 7/7 |

| HO 2024 | Lacking | Provided | Provided | Provided | Lacking | Provided | Lacking | 5/7 |

| MoJ 2025 | Lacking | Provided | Provided | Provided | Provided | Lacking | Lacking | 4/7 |

| Average | Lacking | Provided | Provided | Provided | Provided | Provided | Provided | 6/7 |

4.1. Department for Transport

The 2012 Department for Transport (DfT) digital strategy covers the scope, the digital aim, what has been delivered, how the DfT will become a more digital department, and the final monitoring of the delivery of the strategy [71].

Market and competition research: There are justifications for the reasons for going digital, with some research information that confirms the use of the Internet by businesses and online interaction with public sector bodies. However, there is no comparative study or benchmark against other national or international departments or trend analysis.

Digital vision or future state: There is a digital aim covering the provision of online self service, the collection of customer feedback, the use of digital tools to engage with customers, the support via digital help, the digital collaboration within the department and the improvement of DfT ICT systems and platforms. In addition, there are some high level KPIs without figures based on the reduction of the cost of delivery while improving the quality of services. There are no specific KPIs defined or an agile structure of the vision.

Current state of the digital landscape: The DfT has already delivered a list of thirty digital transactions and enquiry services, such as renewing car tax or booking driving tests, with services including Transport Direct, Web tools, computerised Ministry of Transport tests, and online blue badges. Opportunities are highlighted, such as some services not being online, the need to update technical platforms and the lack of systems integrations. In addition, some successful case studies include the DVLA Electronic Vehicle Licensing, The use of social media by the Driving Standards Agency to promote the Highway Code, The use of a web chat to engage with customers, the help of customers to get online via the Driver and Vehicle Licensing Agency silver surfer event, cost savings via YouTube, and engaging with younger drivers via social media. There are no details of the current ICT, technology infrastructure, service providers, or suppliers for these.

Roadmap: Initiatives are defined including the delivery of a common digital service standard across the department via Application Programming Interfaces (APIs), the creation of a common and simple user experience, the redesign of DfT contact centres, the provision of assisted digital services, the use of web chat, the migration of customer contacts to digital channels, the automation of the collection of digital performance data, the make of all new transactions digital by default, the definition of entry requirements for digital services to the minimum level required for cybersecurity, the development of a new identity assurance for DfT customers. There are no priorities on these activities, dependencies between them, nor an assessment of value versus cost.

Risks: There is no risk assessment or proposed mitigations to deliver this strategy.

Enablers: The removal of barriers that make it difficult for people to access, operate and pay digitally, the collaboration with the Government Digital Service to identify changes in legislation, the identification of individuals who have high end digital skills that could be deployed, the setup of digital skills training in place, the revision of the organisational boundaries. There are no estimated costs or cash flows. There is no TOM or changes to the organisational structure to embed the changes delivered by the strategy.

Supply chain: Third parties and intermediaries have a role to support DfT to deliver services digitally through their websites by providing them access via APIs and open data standards for all new procurements. The Cabinet Office will provide lean and lightweight procurement processes to incorporate more SMEs. There are no specific details about the services or assets that will be provided by the supply chain or delivered in-house.

4.2. Department for Work and Pensions

The 2012 Department for Work and Pensions (DWP) digital strategy includes its purpose, users, existing digital services, new services, the delivery of digital services, changing how policy is made and transforming the methods of work [72].

Market and competition research: There is no market analysis or competition assessment based on national or international case studies.

Digital vision or future state: High quality digital services built around the needs of users, the avoidance of duplication, the enablement of improved conversations between users and the department, the seamless integration with other digital and non-digital channels, the continuous improvement based on user feedback and analytics, working across different benefits, the engineered compatibility with a broad range of devices, the protection of personal data from cyber theft and taxpayers’ money from fraud, the simpler and faster access and use of services.

Current state of the digital landscape: The current welfare system is very complex and fragmented based on outdated legacy systems, leading to growing costs and established deprivation areas. Some current systems are already online, such as Jobseeker’s Allowance, State Pension, Carer’s Allowance, Benefits Adviser, My Benefits Online and Universal Jobmatch. On several occasions, even where a service has a digital front end interface, the underpinning back office processes are still manual.

Roadmap: The approach of agility, continuous improvement and user feedback to design services, the delivery of three exemplar services namely universal credit, personal independence payment and carer’s allowance; the redesign of services handling over 100,000 transactions a year, collaboration with Government Digital Service to create a digital standard for all services, the production of a standard for management information, alignment with policymakers and delivery experts. There are no dependencies or prioritisation on the activities arranged in a schedule.

Risks: The main threat identified is the time and cost to implement technology solutions in a complex organisation; however, new ways of working established in the government ICT and digital strategies enable faster development of new systems at a lower cost. In addition, other risks include the security of millions of citizens’ details, the protection of taxpayers’ money from fraud and theft based on identity and security and the dependence on obsolete legacy systems.

Enablers: Support staff and users with the required digital skills, partnerships with other government departments and organisations to enhance digital skills between disadvantaged users, the appointment of a digital champion at the board level to coordinate and direct the digital strategy, the assignation of accountability to skilled and experienced managers, the identification of digital gaps in the technical capabilities within the different departments and resolve these via external recruitment and internal development, the change of legislation and internal processes that stop the transformation of manual services into online. There are no details about costs or cash flows.

Supply chain: collaboration with a broad variety of suppliers including more SMEs, the reassessment of contracts to enable flexible services with a faster implementation, scalability and upgrade, the steer on providers to deliver better value, higher quality services, the use of common technology platforms and working with other departments for the development of combined services. There are two opportunities for DWP to potentially improve the user experience, subject to legal considerations: enabling the supply to access DWP data or enabling the supply chain to add to DWP databases.

4.3. Department for Digital, Culture, Media and Sport

The 2017 Department for Culture, Media and Sport (DCMS) Next Generation Mobile Technologies: A 5G Strategy for the UK covers the ambition, the development of the economic case, effective regulation, governance and local policy frameworks, coverage and capacity, safe and secure deployment of 5G, spectrum, technology and standards [73].

Market and competition research: Other countries are already providing 5G with an intrinsic lead in the development of some components of 5G, such as hardware. Tests and trials on 5G networks are already set in Japan, South Korea, the United States, China, Australia, and Sweden. The strategy leverages the UK’s existing strengths, focusing on systems integration, interoperability, and cybersecurity.

Digital vision or future state: The acceleration of the deployment of 5G networks, the maximisation of its associated productivity and efficiency and the creation of new national and international opportunities for UK businesses while promoting inward investment. The expected 5G capabilities are themed as massive machine type communications, ultra reliable and low latency communications, and enhanced mobile broadband. There are no specific KPIs for 5G coverage or fibre rollout.