Submitted:

16 May 2025

Posted:

20 May 2025

You are already at the latest version

Abstract

This article examines how the Potential Payback Period (PPP) extends and surpasses the Gordon Growth Model (GGM) at the limits of financial theory. Both models rely on discounted future cash flows and assume growth and required return, yet diverge under edge-case conditions. As the growth rate nears the discount rate, the GGM becomes unstable, producing infinite valuations. In contrast, the PPP remains coherent, resolving indeterminate forms via L’Hôpital’s Rule. When both growth and discounting are zero, PPP reduces to the P/E ratio, affirming its role as a generalization of traditional metrics. These findings highlight PPP’s robustness and clarity where GGM fails.

Keywords:

potential payback period (PPP)

; Gordon growth model (GGM)

; equity valuation

; discounted cash flow

; valuation edge cases

; P/E ratio generalization

1. Introduction

The Gordon Growth Model (GGM), developed by Myron Gordon and Eli Shapiro in 1956, and the Potential Payback Period (PPP), introduced by Rainsy Sam (the author of this article), are two valuation frameworks that integrate assumptions about growth and discounting. The GGM — long a cornerstone of discounted cash flow analysis — estimates the present value of a perpetuity of dividends growing at a constant rate. The PPP, by contrast, is a more recent and evolving concept that estimates the time required for an investor to recover their initial investment through discounted, growing earnings. This paper compares the two models, with a particular focus on their behavior under limiting and edge-case conditions, where traditional valuation methods often break down.

2. Core Formulations

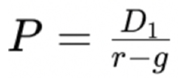

2.1. The Gordon Growth Model Is Expressed as

where:

- P is the stock price,

- D1 is next year's dividend,

- r is the required rate of return,

- g is the expected growth rate of dividends.

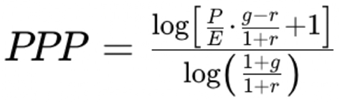

2.2. The Potential Payback Period (PPP) Is Defined as

where:

- P is the stock price,

- E is current earnings per share,

- g is the earnings growth rate,

- r is the discount rate.

Both models respond sensitively to the relationship between g and r , but their behavior near critical values diverges sharply.

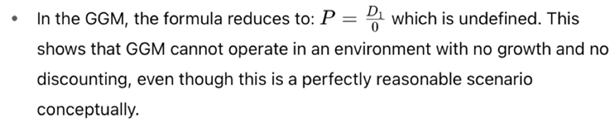

3. Limit Case: When g → r

In the GGM, as g → r, the denominator approaches zero, causing P to tend toward infinity. This result reflects a scenario in which future dividends are growing just fast enough to offset discounting, but it renders the model practically unusable.

In the PPP model, a similar issue arises: both the numerator and denominator of the formula approach zero, producing an indeterminate form 0/0 . However, applying L'Hôpital's Rule to resolve mathematical limits yields a meaningful and finite expression:

This outcome is intuitive: when growth exactly offsets the discount rate, the time required to recover the investment is equivalent to a discounted P/E ratio.

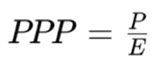

4. Extreme Case: When g = r = 0

The behavior of the models becomes even more revealing under the condition g = r = 0:

constant earnings is simply:

This is the classic P/E ratio. Hence the PPP reduces exactly and meaningfully to the static multiple it generalizes.

5. Interpretation and Implications

These comparisons yield several insights:

- Both models are built on the same valuation logic: future cash flows adjusted for time and growth.

- However, PPP demonstrates greater mathematical resilience and interpretive clarity near and at critical boundaries.

- The fact that PPP collapses to the P/E ratio when g = r = 0 reinforces its role as a generalization of static valuation multiples.

- Practically, PPP offers usable, consistent outputs in conditions where GGM fails — such as early-stage companies, low-growth environments, or when applying valuation to earnings rather than dividends.

6. Conclusions

While both the Gordon Growth Model and the Potential Payback Period model share a conceptual foundation, their behavior under edge cases reveals a key distinction: PPP remains robust and interpretable where GGM becomes unstable or undefined. This analytical flexibility underscores PPP's potential as a general-purpose valuation tool, particularly in dynamic or constrained financial environments. Its capacity to reduce to traditional metrics under simplifying assumptions further strengthens its theoretical legitimacy and practical appeal.

Remark

As the Potential Payback Period (PPP) is a concept solely initiated and developed by Rainsy Sam (the author of the above article), there are currently no other published books or articles on this methodology by other authors. The references listed below include essential works on fundamental financial theories and valuation principles — such as discounted cash flow, dividend discount models, and earnings-based valuation — from which the PPP concept is conceptually and mathematically derived. Each source is accompanied by a brief explanation of its relevance to the PPP framework.

References

- Gordon, M. J., & Shapiro, E. (1956). Capital Equipment Analysis: The Required Rate of Profit. Harvard Business Review, 34(5), 102–110.— Provides the foundation for the Gordon Growth Model (GGM), which the PPP extends and surpasses under limiting conditions.

- Gordon, M. J. (1962). The Investment, Financing, and Valuation of the Corporation. Richard D. Irwin, Inc.— Develops the dividend discount model that influenced PPP’s time-discounting structure.

- Sam, R. (2025). Proving that the P/E Ratio is Just a Limiting Case of the Potential Payback Period (PPP) When Earnings Growth and Interest Rate are Ignored. Preprints. — Provides the mathematical proof that PPP generalizes and reduces to the P/E ratio under static conditions. [CrossRef]

- Sam, R. (2025). How to Adjust the P/E Ratio for Earnings Growth in Equity Valuation: PEG or PPP? Preprints. — Compares PPP with PEG to show how PPP better integrates growth into valuation. [CrossRef]

- Sam, R. (2025). Revisiting the Gordon-Shapiro Model: How the Potential Payback Period (PPP) Refines and Operationalizes a Foundational Framework in Stock Valuation. Preprints. — Demonstrates how PPP refines the structure of the Gordon-Shapiro model by making it applicable in modern contexts. [CrossRef]

- Sam, R. (2025). Extending the P/E and PEG Ratios: The Role of the Potential Payback Period (PPP) in Modern Equity Valuation. Preprints. — Positions PPP as a superior alternative to both P/E and PEG ratios in dynamic valuation environments. [CrossRef]

- Sam, R. (2025). SIRRIPA: The Stock-Tailored Yield to Maturity (YTM) and the Emergence of a Cross-Asset Valuation Metric. Preprints. — Introduces SIRRIPA as a complement to PPP, bridging equity and fixed-income valuation methodologies. [CrossRef]

- Sam, R. (2025). How the Potential Payback Period (PPP) Bridges the Gap Between Stocks and Bonds — and Revolutionizes Portfolio Management. Preprints. — Expands on PPP’s role in creating a unified valuation framework across asset classes. [CrossRef]

- Sam, R. (2025). Why SIRRIPA is Set to Replace the P/E Ratio in Modern Equity Valuation. Preprints. — Advocates for a cross-metric valuation system that builds upon PPP-derived logic. [CrossRef]

- Sam, R. (2025). Challenging Conventional Wisdom in Stock Valuation with the Potential Payback Period (PPP). SSRN. https://ssrn.com/abstract=5248808 or. — Critiques legacy valuation metrics and positions PPP as a more rational, time-sensitive alternative. [CrossRef]

- Sam, R. (2025). Breaking the Valuation Deadlock: Replacing the P/E Ratio with the Potential Payback Period (PPP) for Loss-Making Companies – A Case Study on Intel (2025). SSRN. https://ssrn.com/abstract=5247858 or. — Applies PPP in contexts where P/E is inapplicable due to negative earnings, showing its practical advantages. [CrossRef]

- Damodaran, A. (2012). Investment Valuation: Tools and Techniques for Determining the Value of Any Asset (3rd ed.). Wiley.— Provides foundational DCF and risk-pricing frameworks that underpin PPP’s treatment of discounting.

- Penman, S. H. (2010). Financial Statement Analysis and Security Valuation (4th ed.). McGraw-Hill/Irwin.— Offers techniques for earnings-based valuation, aligned with PPP’s focus on EPS recovery.

- Brealey, R. A., Myers, S. C., & Allen, F. (2017). Principles of Corporate Finance (12th ed.). McGraw-Hill Education.— Covers key principles in financial theory including discounting, capital costs, and valuation logic integral to PPP.

- Bodie, Z., Kane, A., & Marcus, A. J. (2018). Investments (11th ed.). McGraw-Hill Education.— Discusses risk-return relationships and valuation methodologies that conceptually support PPP's discount-rate framework.

- Copeland, T. E., Koller, T., & Murrin, J. (2000). Valuation: Measuring and Managing the Value of Companies(3rd ed.). Wiley Finance.— Emphasizes practical DCF techniques and cost of capital, both central to PPP computation.

- Siegel, J. J. (2014). Stocks for the Long Run (5th ed.). McGraw-Hill Education.— Advocates for long-term valuation strategies, compatible with PPP’s time-recovery approach.

- Greenwald, B., Kahn, J., Sonkin, P. D., & van Biema, M. (2001). Value Investing: From Graham to Buffett and Beyond. Wiley.— Reinforces intrinsic value investing principles that PPP seeks to quantify more rigorously.

- Graham, B., & Dodd, D. L. (2008). Security Analysis (6th ed.). McGraw-Hill Education.— A foundational text on valuation that influenced PPP’s emphasis on earnings and intrinsic value.

- Miller, M. H., & Modigliani, F. (1961). Dividend Policy, Growth, and the Valuation of Shares. Journal of Business, 34(4), 411–433.— Established valuation equivalence principles that underlie PPP's sensitivity to growth and discounting.

- Fama, E. F., & French, K. R. (1992). The Cross-Section of Expected Stock Returns. Journal of Finance, 47(2), 427–465.— Provides empirical insights on return factors, supporting PPP’s incorporation of discount-rate-driven expectations.

- Arnott, R. D., & Bernstein, P. L. (2002). What Risk Premium Is “Normal”? Financial Analysts Journal, 58(2), 64–85.— Explores variability in equity risk premiums, essential for interpreting PPP's discounting logic.

- Koller, T., Goedhart, M., & Wessels, D. (2020). Valuation: Measuring and Managing the Value of Companies (7th ed.). McKinsey & Company / Wiley.— Offers contemporary valuation frameworks that PPP helps to extend under extreme or unconventional conditions.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.