Submitted:

16 May 2025

Posted:

19 May 2025

You are already at the latest version

Abstract

This study aims to investigate the short-run and long-run dynamics of the financial cycle in South Africa by identifying its key macroeconomic drivers and understanding their asymmetric effects across different phases of the cycle. The research addresses the persistent challenge in emerging market economies of achieving both financial development and stability amid volatile macroeconomic conditions. Using monthly data from 2002 to 2024, the study employs a Quantile Autoregressive Distributed Lag (QARDL) model to capture both the heterogeneity and persistence of macro-financial linkages across the distribution of the financial cycle. The findings indicate that the drivers of financial development in South Africa appear to be monetary policy and the housing sector, which have shown positive long-term effects. On the other hand, variables such as exchange rate movements, inflation, money supply, and macroprudential policy act as constraints on financial development. In terms of triggers of short-term financial booms and bursts, the evidence points to GDP growth, credit, share prices, and to some extent housing prices, as sources of temporary upswings in financial activity. Conversely, money supply and inflation are more closely associated with burst phases and financial volatility. These findings stress the importance of policy coordination—particularly between monetary and macro-prudential authorities—to strike a balance between promoting financial development and ensuring financial stability in emerging markets. This study contributes to the empirical literature on financial cycles in developing economies and offers practical insights for policymakers tasked with navigating complex financial environments.

Keywords:

financial cycles

; financial development

; quantile ARDL

; macroprudential policy

; South Africa

Introduction

For decades, the financial sector was considered peripheral to macroeconomic dynamics. However, the Global Financial Crisis (GFC) of 2007–2009 revealed its central role in driving economic growth and triggering widespread economic disruptions. It is increasingly clear that imbalances within the financial sector carry significant systemic consequences (Coimbra & Rey, 2024; Adarov, 2022; Miranda-Agrippino & Rey, 2022; Qin et al., 2021; Beirne, 2020; Aldasoro et al., 2020; Schuler et al., 2020; Ha et al., 2020). At the same time, when properly developed, the financial sector contributes meaningfully to economic development. However, the collapse of even a narrow segment of financial markets can induce deep recessions, with effects that reverberate nationally and globally (Kohler & Stockhammer, 2022; Borio et al., 2018; Kindleberger, 2016). Financial synchronization across countries can amplify the transmission of economic shocks, undermining domestic regulatory frameworks and importing risks from abroad (Magubane et al., 2024; Gammadigbe, 2022; Prabhesh et al., 2021). Nonetheless, a well-functioning financial system remains vital in supporting investment and spending, which in turn stimulate economic activity. Consequently, macroprudential policymakers have intensified efforts to monitor systemic risks within the financial sector (Epure et al., 2024; Vollmer, 2022).

This paper explores the persistent challenge faced by emerging market economies: the dual objective of achieving financial development and maintaining financial stability amid volatile macroeconomic conditions. In South Africa, this dual mandate is particularly complex due to enduring structural problems—high unemployment, limited financial inclusion, and pronounced income inequality. The country’s financial system is highly susceptible to external shocks such as capital flow reversals and commodity price volatility, which interact with internal vulnerabilities. In this context, financial cycles often magnify macroeconomic fragilities, particularly when policies prioritize short-term stability over long-term development. Addressing these challenges requires a coherent policy strategy grounded in a robust understanding of the drivers of financial fluctuations and development dynamics.

Financial cycles offer a systemic lens through which to assess the state of the financial sector. A widely cited definition describes them as self-reinforcing interactions between risk perceptions, asset valuations, and financing constraints—interactions that frequently result in boom-and-bust dynamics (Borio, 2014). Adarov (2022) recently defined financial cycles as cyclical deviations in financial market activity from long-run equilibrium, characterized by the build-up and subsequent correction of financial imbalances. This definition highlights two interrelated dimensions: the long-term trend of financial development and the shorter-term cyclical component. The trend reflects deeper financial intermediation that supports capital allocation and growth, while the cyclical component is essential for macroprudential surveillance and intervention (Skare & Porada-Rochoń, 2020; Yang, 2019; Borio et al., 2019; Ibrahim & Alagidede, 2018; Durusu-Ciftci et al., 2017).

Despite rising recognition of financial cycles post-GFC, the underlying drivers of financial cycle flctuations and their relationship with financial development remain poorly understood. Theoretically, this relationship is contested. Keynesian and debt-deflation views suggest a procyclical link between real and financial sectors (Bakar & Sulong, 2018; Chiarella & Guilmi, 2017; Hudson, 2012; Fink et al., 2004; Blum et al., 2002; Young, 1993; Robinson, 1979). In contrast, neoclassical business cycle models from the 1980s and 1990s view financial cycles as nominal frictions with limited macroeconomic relevance (Foroni et al., 2022; Giri et al., 2019; Christensen, 2008; Gilchrist et al., 1998; Bernanke et al., 1994). The Modigliani-Miller framework assumes a complete separation between financial and real sectors (Villamil, 2008; Stiglitz, 1969; Modigliani & Miller, 1958). Meanwhile, Minsky’s financial instability hypothesis emphasizes the inherently destabilizing nature of financial expansions (Knell, 2015; Vercelli, 2011; Minsky, 1992), while the efficient market hypothesis suggests financial fluctuations are limited and rational (Timmermann & Graner, 2004; Malkiel, 1989). These theoretical divergences underscore the need for empirical clarity—a gap this study aims to address.

Empirical research on financial cycles has also shown limitations. Most studies focus on documenting stylized facts—such as duration, amplitude, and synchronization—using statistical tools like bandpass filters, turning point algorithms, and wavelet methods (Borio, 2014; Schuler et al., 2020; Adarov, 2022; Beirne, 2020; Qin et al., 2021; Ha et al., 2020; De Wet & Botha, 2022; Oman, 2019; Skare & Porada-Rochoń, 2020; Yang, 2019; Adrian & Shin, 2010; Claessens et al., 2012; Drehmann et al., 2012; Jordà et al., 2013; Alessi & Detken, 2011; Rünstler & Vlekke, 2018; Krznar, 2017). Yet few delve into the structural causes of these fluctuations. Meanwhile, the financial development literature tends to emphasize the long-run growth effects of financial deepening, without engaging with short-run instability (Demetriades & Rousseau, 1992; King & Levine, 1993; Levine & Zervos, 1998; Rajan & Zingales, 1998; Beck et al., 2000; Hassan et al., 2011; Swamy & Dharani, 2019; Demetriades & Rewilak, 2020; Odhiambo, 2010; Rioja & Valev, 2004; Ang, 2008; Arellano & Bayoumi, 1993; Arestis & Demetriades, 1997; Fry, 1988; Greenwood & Jovanovic, 1990; McKinnon, 1973; Shaw, 1973; Aghion et al., 2005; Demirgüç-Kunt & Maksimović, 1998; Haber, 2003; Rousseau & Wachtel, 2000; Acemoglu et al., 2005; Arcand et al., 2015; Cecchetti & Kharroubi, 2012).

Thus, a significant gap persists in efforts to integrate the analysis of financial cycles and financial development. Policy actions designed to dampen cyclical volatility may inadvertently hinder long-term financial sector growth. Prolonged use of tight macroprudential policies, for example, can curb credit booms but also impede financial deepening. This trade-off between short-term stability and long-term development is especially pronounced in South Africa, where high poverty, inequality, and financial exclusion magnify the stakes of financial policy decisions. A unified analytical framework is therefore essential to inform policies that do not compromise one objective for the other.

To that end, this study develops a quantile autoregressive distributed lag (QARDL) model of South Africa’s financial cycle. It empirically investigates the short-term triggers of financial cycle deviations and the long-run drivers of financial development within a single framework that accommodates asymmetries across different phases of the financial cycle. The QARDL approach is well-suited to capture these nonlinearities and offers granular insights into the structural dynamics of the financial sector. South Africa provides a compelling case study: research on its financial cycle is limited, despite its exposure to volatile capital flows and the centrality of the financial cycle to domestic policy frameworks. Moreover, the prominence of its financial cycle among emerging markets—shaped by global liquidity, commodity price movements, and investor sentiment—makes the findings relevant for broader policy debates in similar contexts.

Materials and Methods

2.1. Data and variables

To represent the South African financial cycle, the following variables are used. Total domestic credit as percentage of GDP (CR), real house price index (HP), real all share price index (SHARE). The variables are selected because they are widely used in both global financial cycle literature and the South African literature on financial to represent financial cycles. The primary theoretical motivation for using these variables is that they drive financial market development, and they are strongly correlated with each other. Moreover, their peaks tend to coincide with system-wide fluctuations in the financial system. The practical consideration for these variables in the case of South Africa is that they represent the three largest financial sectors in the country: the credit sector which includes banks and insurers, the housing sector, and the equity market. In the country these sectors set the tone for the behavior of the overall financial system.

There are two important caveats regarding the use of these variables in the study. First, they are used to construct the financial cycle. This implies that they are aggregated into a single index, in the study the principal component analysis (PCA) is used to archive this task. For the purpose of this exercise, the variables are standardized using their mean and standard deviation. Second, the variables are also as explanatory variables in the QARDL of the estimated cycle. For this purpose, these variables are not standardized. However, in order to address the issue of multicollinearity, the lags of the variables and other explanatory variables were used. Accordingly, the Akaike Information Criteria is used to determine the optimal lag to be included in the QARDL. After determined the number of lags to be included, each variable is transformed to its optimal lag using the transformation (y=x[_- N-l], where y is the new transformed variable, x is the original variable, N is the current observation, and l is the optimal lag. The main motivation for including the credit, house prices, and share prices, in the QARDL is to uncover how the magnitude and direction of impact they have on the cycle, which cannot be robustly done in the PCA.

Other explanatory variables the real effective exchange rate (EXCH), GDP, inflation rate (INF), broad money supply (M3), the repo rate (REPO), and the macroprudential policy index (MPI). The inclusion of these variables in the model is justified by their significant roles in shaping the dynamics of the financial cycle and economic conditions in South Africa. Exchange rates are included because they capture the effects of the foreign exchange market, which are particularly relevant in South Africa due to its free-floating exchange rate system. This system makes the South African financial system more vulnerable to external shocks, such as fluctuations in global commodity prices and changes in international investor sentiment (Mlachila et al., 2013). Exchange rate volatility can directly impact inflation, external debt, and trade balances, all of which influence the broader economy and financial stability (Borio et al., 2012). GDP is incorporated as a key indicator because there is substantial evidence suggesting that the business cycle and the financial cycle are closely related, typically moving in tandem in a procyclical manner. In other words, periods of strong economic growth are often associated with financial booms, while economic downturns tend to coincide with financial contractions. Therefore, GDP serves as an essential driver in understanding both the short-term fluctuations and long-term trends within the financial cycle.

The inflation rate is included due to the significant threats that an unstable price environment poses to the financial system. High inflation can erode purchasing power, destabilize currency values, and increase uncertainty, which may prompt financial market volatility and disrupt investment decisions (Cecchetti et al., 2000). On the other hand, deflation can lead to reduced consumer demand, rising debt burdens, and greater risks of financial crises. Thus, inflation is a critical variable in analyzing financial cycles and their impact on economic stability. Monetary policy variables, such as interest rates, are essential in understanding the cost of borrowing, which directly affects financial activities such as lending, investment, and consumption (Bernanke & Gertler, 1995). Changes in the policy rate influence the level of credit in the economy and can exacerbate or dampen financial cycle fluctuations. As such, the repo rate, a key policy tool in South Africa, is included to reflect the central bank’s stance on liquidity and borrowing costs. Finally, macroprudential policy is included because it specifically targets the stabilization of the financial cycle. The goal of macroprudential measures is to mitigate systemic risks and enhance the resilience of the financial system, especially during periods of financial instability (Borio, 2011). By addressing imbalances and vulnerabilities within the financial sector, macroprudential policies aim to prevent the amplification of financial cycles and their detrimental effects on the broader economy. This makes the inclusion of the macroprudential policy index (MPI) crucial to understanding how regulatory actions influence the financial cycle. In addition to these key variables, the real effective exchange rate (EXCH), broad money supply (M3), and other monetary variables help provide a comprehensive picture of the financial cycle's drivers and the interactions between domestic and external economic conditions.

The data used in this study spans from 2000 to 2024 on a monthly basis. This period was specifically chosen for several reasons. First, it coincides with South Africa’s adoption of a flexible inflation targeting framework, which has shaped monetary policy decisions since its implementation. Second, the focus on macroprudential policy and financial stability concerns began around 2002, following the banking crisis in the country, marking a critical point in the evolution of financial regulation. The chosen period is also sufficiently long to capture both short-run and long-run effects of the financial cycle. The data for the variables CR, HP, REPO, EXCH, INF were obtained from the Bank for International Settlements statistics. The variables for GDP and Share Prices (SHARE) were collected from the SARB statical time series database. The MPI was sourced from the International Monetary Fund Integrated Macroprudential Policy database. These data sources provide reliable and consistent indicators crucial for understanding the dynamics of the South African financial cycle during this period.

The study applies the quantile ARDL model to examine the short-run and long-term impact of the exchange rate, gross domestic product, inflation rate, total domestic credit, house prices, share prices, money supply, repo rate, and macroprudential policy index on the South African financial cycle. The South African financial cycle has multiple phases, including expansions, contractions, peaks, and troughs which the model captures as per quantiles. The model was chosen because of its robustness to non-normal errors, as well as its ability to account for outliers, heterogeneity, and skewness in the dependent variable (Hashmi et al., 2022; Anwa et al., 2021; Sharif et al., 2020). Additionally, the model facilitates the examination of both short-run and long-run effects of independent variables on the dependent variable across different quantiles (Hashmi et al., 2023). It provides more reliable results when the sample size is small and, like the ARDL model, is particularly useful when the variables are integrated of either order zero I(0) or one I(1) (Mensi et al., 2019).

We start the following OLS specification as benchmark for estimating the impact of the afore-mentioned explanatory variables:

Where refers to the natural logarithm of variables. The QARDL model is not particularly robust when variables are integration order two (I). Therefore, for examining the order of integration of variables the Augmented Dickey-Fuller (ADF) unit root test is conducted. After the order of integration is determined, we proceed further and use the QARDL. The model estimated in the study is similar to Hashmi et al. (2022). An extension of the ARDL model into QARDL model leads to the following which is the standardized version of the OLS model in equation 1:

Where Y is the vector of financial explanatory variables, i.e., CR, HP, and SHARE which maintain the lag of dependent variable. X is a vector of real variables containing EXCH, GDP and INF. Z is a vector of policy variables which contains M3, REPO, and MPI. The parameter is the quantile measurement. In order to empirically investigate the impact of the above variables on the financial cycle, the study utilizes the following quantiles: . A Wald test is used to assess the short-run and long-run symmetry of parameters. For the short run, the symmetry is tested using the following null hypothesis:

In a similar fashion, the long-run symmetry is tested using the following null hypothesis:

At the end of estimation, several stability and diagnostic tests are conducted to assess the goodness of fit of the model in equation 2. Breusch-Pagan-Godfrey Heteroscedasticity test is employed to assess the residuals are homoscedastic. Breusch-Pagan LM test is employed to assess whether there is serial correlation in the lags of residuals. A Wald test is used the assess whether there should be variables that should be omitted. The Ramsey Reset test is employed to assess the robustness of the model specification. The CUSUM together with the Recursive coefficient’s tests are employed to assess the stability of the model and the estimated parameters.

Results and Discussion

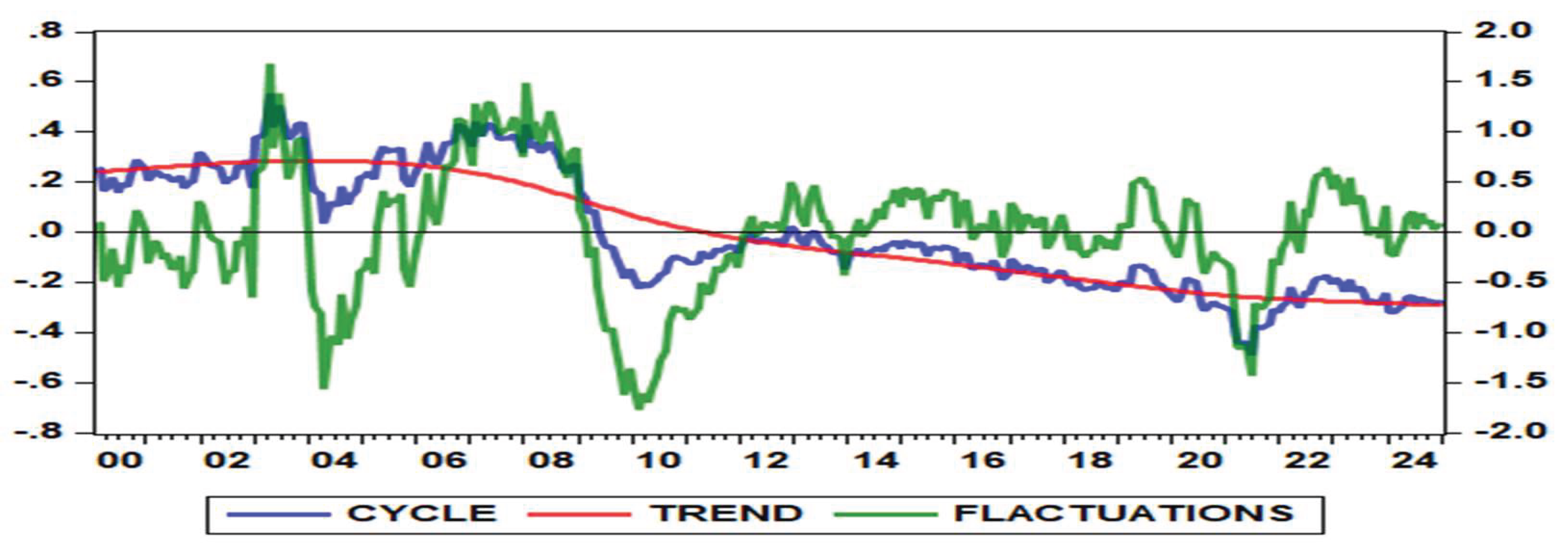

This section presents the key findings of the study. Figure 1 illustrates the South African financial cycle, decomposed into its long-term trend and short-term fluctuations. As shown in the figure, the long-term trend has been on a persistent downward trajectory since the early 2000s, indicating a gradual weakening in the underlying dynamics of financial development over time. A downward trend in financial development reflects a deterioration in the ability of the financial system to effectively support economic growth, allocate capital efficiently, mobilise savings, and extend credit to households and businesses. In developing economies like South Africa, this trend has serious implications—it may result in reduced access to financial services, lower investor confidence, and weaker economic performance. Financial development is critical in enabling productivity gains and supporting entrepreneurship and long-term investment. Therefore, when financial systems begin to contract or lose efficiency, the broader macroeconomic implications can be substantial. Beck and Levine (2004) argue that well-functioning financial systems play a vital role in fostering economic development by reducing transaction costs and improving risk-sharing. A downward trend thus signals the reversal of these gains.

Recent developments in South Africa mirror this concern. The South African rand (ZAR) has experienced significant depreciation and volatility over the past decade, driven by domestic political uncertainty, global monetary policy tightening, and episodes of capital flight. The “Nenegate” incident in 2015, in which a finance minister was unexpectedly replaced, led to a sharp fall in the rand and signaled weakening institutional credibility. Similar pressures resurfaced during the COVID-19 pandemic and again during the 2021 unrest, leading to further currency instability and capital outflows. These events discouraged long-term investment and undermined investor confidence, consistent with the findings of Aye et al. (2021), who note that currency volatility in South Africa is strongly associated with lower financial market efficiency and reduced private investment.

Stagnation in private sector credit extension also indicates a weakening financial system. According to the South African Reserve Bank, real growth in private sector credit extension has been below historical averages since 2020. Lending to households and corporates remains cautious amid high debt levels, weak consumer confidence, and rising interest rates. This stagnation restricts investment and consumption, ultimately constraining economic recovery. Mlachila, Tapsoba and Tapsoba (2020) similarly observe that in low- and middle-income economies, a reduction in credit growth often reflects deeper structural issues in financial intermediation, including risk aversion among lenders and lack of innovative financial products.

Further evidence of a downward trend is seen in South Africa’s housing market. House price growth has remained below inflation in many parts of the country, pointing to weak demand and affordability constraints. According to Lightstone Property (2024), real house prices have declined in several metropolitan areas, particularly where unemployment is high and credit access is limited. The housing sector is typically a driver of wealth accumulation and collateral formation, especially for middle-income households. Weakness in this sector constrains both consumer wealth and borrowing capacity, thereby limiting financial system depth and development. This observation is supported by Aron and Muellbauer (2016), who find that real house price stagnation has a negative feedback effect on consumption and loan demand.

Financial inclusivity, a key component of financial development, has also seen setbacks despite improvements in digital financial services. Many low-income households remain unbanked or underbanked, particularly in rural areas. The FinScope Consumer Survey (2022) revealed that significant segments of the population still lack access to formal savings instruments, credit facilities, and insurance products. These patterns highlight barriers such as limited financial literacy, high transaction costs, and weak infrastructure. Sahay et al. (2015) argue that financial inclusion is critical to achieving broader financial development and that exclusion undermines economic equality and limits the effectiveness of monetary policy transmission.

In sum, South Africa’s financial development trajectory has shown signs of decline, with multiple indicators reflecting reduced efficiency, inclusivity, and resilience of the financial sector. These findings align with empirical literature pointing to a growing disconnect between financial sector performance and real economic outcomes in emerging markets (De la Torre et al., 2017). Reversing this trend will require strengthening institutional frameworks, promoting financial literacy, improving credit infrastructure, and restoring macroeconomic stability.

The cyclical component of the South African financial cycle reveals several noteworthy dynamics with important implications for both academic inquiry and macroprudential policy design. Notably, the peaks of the financial cycle coincide with key periods of financial stress, underscoring the cycle's procyclical nature and its role in amplifying systemic risk. Three distinct episodes are aligned with these peaks. The first occurred in 2002–2003 during a domestic banking crisis that saw the collapse of institutions such as Saambou Bank and BOE Bank, precipitated by liquidity shortages, poor asset quality, and a loss of depositor confidence. Although the crisis was relatively contained, it led to significant consolidation in the sector and prompted enhanced supervisory frameworks (Van der Merwe, 2004; Padayachee, 2011).

The second major peak occurred during the global financial crisis of 2007–2009. While South Africa's banking system remained solvent, the economy experienced sharp declines in credit growth, portfolio investment, and consumer confidence. Asset prices fell markedly, and the rand depreciated significantly as global risk aversion surged (Aron, Muellbauer & Prinsloo, 2012; IMF, 2010). These events were mirrored in the financial cycle, which peaked prior to the crisis, providing early signals of the impending slowdown. This evidence supports the broader literature that views the financial cycle as a leading indicator of macro-financial vulnerabilities (Aikman et al., 2015; Drehmann et al., 2012).

The third peak of the financial cycle aligns with the 2019–2020 Covid-19 pandemic, which triggered a global economic shock. South Africa, already facing fiscal constraints and sluggish growth, experienced a sharp contraction in GDP, deterioration in household and corporate balance sheets, and a spike in financial market volatility. The South African Reserve Bank intervened through rate cuts and liquidity support, but financial conditions remained fragile (World Bank, 2021; SARB, 2020). The turning point in the financial cycle accurately captured this phase of financial distress, further validating its use as a real-time monitoring tool.

In addition to signalling crises, the cyclical component captures episodes of rapid financial expansion. Between 2004 and 2007, the South African economy experienced a credit and housing boom supported by accommodative monetary policy, strong global demand for commodities, and positive domestic sentiment. Household debt as a share of disposable income rose sharply, and residential property prices surged—developments that were clearly reflected in the steep upward trajectory of the financial cycle during this period. Similar, albeit more moderate, recoveries were observed in the post-GFC and post-Covid-19 periods, as indicated by the rebound in the cyclical component driven by policy stimulus and renewed credit demand.

These findings highlight the analytical value of the financial cycle as a medium-term macro-financial indicator. While traditional indicators such as GDP or inflation provide snapshots of economic conditions, they often fail to capture latent financial risks. The financial cycle, by aggregating information on credit volumes, asset prices, and leverage, offers a richer understanding of systemic dynamics (Borio, 2014; Claessens et al., 2011). Its historical alignment with crises in South Africa strengthens the case for its incorporation into early-warning frameworks and financial stability assessments.

From a policy perspective, these insights suggest that macroprudential authorities should closely monitor the financial cycle and calibrate their tools accordingly. Time-varying instruments—such as countercyclical capital buffers (CCyB), dynamic loan-to-value (LTV) ratios, and debt-to-income (DTI) caps—should be tightened during the upswing to contain excess credit growth and loosened during downturns to avoid credit crunches. This approach is consistent with international recommendations from the Basel Committee on Banking Supervision (BCBS, 2010) and empirical studies showing that pre-emptive tightening of macroprudential policy can reduce the probability and severity of financial crises (BIS, 2017; Cerutti, Claessens & Laeven, 2017).

Unit root tests using the Augmented Dickey-Fuller (ADF) method were employed to determine the stationarity properties of all variables. The results, presented in Table 1, reveal that the variables exhibit a mixed order of integration. Specifically, the financial cycle (CYCLE), share price index (SHARE), and the policy interest rate (Repo) were found to be stationary at level—indicating they are integrated of order zero, I(0). The remaining variables, namely the real effective exchange rate (EXCH), real GDP (GDP), inflation (INF), credit-to-GDP ratio (CR), house prices (HP), broad money supply (M3), and the macroprudential policy index (MPI), became stationary only after first differencing and are therefore classified as integrated of order one, I(1). None of the variables were found to be integrated of order two, I(2), thus satisfying a key prerequisite for applying the Autoregressive Distributed Lag (ARDL) modelling framework.

Econometric theory, as established by Pesaran and Shin (1999) and Pesaran, Shin, and Smith (2001), demonstrates that the ARDL bounds testing approach to cointegration is robust in the presence of a combination of I(0) and I(1) variables. Unlike traditional methods such as Johansen or Engle-Granger, which require all variables to be integrated of the same order, the ARDL method can accommodate regressors with differing levels of integration without compromising the validity of long-run relationships. Accordingly, this study proceeds to estimate the model using both I(0) and I(1) variables without transforming them to the same order of integration.

There are important theoretical and empirical advantages to this approach. First, keeping variables in their original form preserves the long-run economic relationships among the variables, which could otherwise be lost if stationary series were unnecessarily differenced. For example, modelling the financial cycle or monetary policy stance (repo rate) in levels allows for direct interpretation of their equilibrium relationships with GDP, credit, or inflation. Second, differencing I(0) variables, or over-differencing I(1) series, risks introducing misspecification and attenuating the signal-to-noise ratio, thereby weakening the explanatory power of the model (Nkoro & Uko, 2016). Third, the ARDL model’s flexibility enables it to simultaneously capture both the short-run dynamics and long-run equilibrium relationships in a single equation, making it particularly suited for macro-financial modelling in complex economies such as South Africa’s.

By using variables in their natural form, the model reflects the actual economic processes without imposing rigid assumptions. This approach improves empirical validity and enhances policy relevance—especially when evaluating the effects of monetary and macroprudential interventions on real and financial variables. Moreover, given the small-to-medium sample size typical of time series in emerging markets, the ARDL method is especially efficient, as it remains valid even in the presence of endogeneity among regressors and does not require pre-testing for cointegration (Narayan, 2005; Odhiambo, 2009).

To assess the existence of a long-run relationship between the financial cycle and the macroeconomic and financial variables, the ARDL bounds test for cointegration was conducted. Table 2 presents the findings. The results returned a highly significant F-statistic of 72.265 (***), which exceeds the critical upper bounds at the 1% level, confirming the presence of a long-run cointegrating relationship between the financial cycle (the dependent variable) and its regressors, including GDP, inflation, credit, house prices, monetary policy, and macroprudential policy. This result is consistent with the theoretical expectation that these variables share stable long-term relationships, despite short-term fluctuations (Pesaran et al., 2001; Narayan, 2005). The finding aligns with previous studies that emphasize the financial cycle as an important indicator of economic stability and financial health (Borio, 2012; Drehmann et al., 2012).

Several diagnostic tests were performed to ensure the robustness and validity of the ARDL model estimates (see Table 2). First, the Breusch-Pagan-Godfrey test for heteroscedasticity yielded an F-statistic of 1.265, which is not statistically significant. This suggests that the model does not suffer from heteroscedasticity, and the residuals have constant variance across observations. This result is crucial for ensuring that standard errors are consistent and reliable, which is essential for valid hypothesis testing and inference (Breusch & Pagan, 1979).

The Breusch-Godfrey LM test for serial correlation returned an F-statistic of 38.079 (***), indicating the presence of autocorrelation in the residuals. Autocorrelation is common in macroeconomic time series data and may arise due to omitted dynamics or lagged effects that are not captured in the model. To circumvent this issue, the study transformed the variables into their first lags, as suggested by the Akaike Information Criterion (AIC), which indicated that a one-lag structure was optimal. The transformation of variables into their one lags mitigated autocorrelation and ensured that the model's residuals were serially uncorrelated, enhancing the model's overall specification (Akaike, 1974). This adjustment helped to improve the reliability of the estimated coefficients and the consistency of the results.

The T Wald test for joint significance produced an F-statistic of 9.194, confirming that the explanatory variables in the model are jointly significant in explaining the variation in the financial cycle. This reinforces the empirical strength of the model and validates that the selected macroeconomic and financial variables collectively provide valuable information in understanding the behaviour of the financial cycle in South Africa.

Lastly, the Ramsey RESET test for functional form misspecification returned an F-statistic of 10.011, which is statistically insignificant. This result indicates no functional form concerns. In other words, the model appears to be correctly specified in terms of its functional form, and there is no evidence of omitted non-linearities or interactions between variables that would require adjustments to the model. This finding adds further confidence to the validity of the model, indicating that the estimated relationships are not misspecified or unduly influenced by incorrect functional form assumptions (Ramsey, 1969).

Despite the presence of autocorrelation, the model remains robust in terms of long-run relationships, absence of heteroscedasticity, and overall explanatory power. These findings support the use of the ARDL methodology to model the dynamics of the financial cycle and its interaction with macroeconomic and financial variables, such as monetary policy, credit, and house prices, in the South African context. This approach is particularly suitable for assessing the role of financial cycles in policy formulation, as it allows for the simultaneous estimation of both short-run and long-run effects, which is crucial for understanding the effectiveness of monetary and macroprudential policies in maintaining economic stability (Borio & Drehmann, 2009).

The main results of this study provide a comprehensive understanding of the long-run and short-run dynamics of the financial cycle in South Africa. Table 2 presents the results. By examining both the long-run and short-run impacts of various macroeconomic variables, we can better identify the drivers of financial development and those that trigger cyclical deviations. Notably, the results reveal that GDP growth exhibits a negative relationship with the financial cycle in the long run, despite its generally accepted positive role in financial development according to standard economic theory (Levine, 2005). This counterintuitive finding may be interpreted within the South African context, where prolonged periods of sluggish growth, coupled with high levels of public and household debt, have arguably limited productive investment and constrained financial intermediation (Adusei, 2013). However, GDP demonstrates a positive short-run effect on financial development, particularly at higher quantiles, suggesting that economic expansions may fuel financial booms in the late stages of the cycle, in line with the procyclical financial behavior documented in boom-bust literature (Claessens, Kose & Terrones, 2011).

The exchange rate shows a negative impact on the financial cycle in both the long and short run, especially at lower quantiles, though the short-run effect is not statistically significant at higher quantiles. This implies that currency depreciations are generally associated with financial instability and hinder long-term financial development. This finding is theoretically consistent with the view that exchange rate volatility undermines investor confidence, raises borrowing costs, and deters foreign capital inflows (Rancière, Tornell & Westermann, 2008). For instance, during the Asian Financial Crisis of 1997, severe currency devaluations in countries like Thailand and Indonesia led to banking collapses and reversed years of financial sector gains. In South Africa, the “Nenegate” incident of December 2015, when then-Finance Minister Nhlanhla Nene was abruptly fired, led to a sharp depreciation of the rand and a subsequent loss of market confidence, reflecting the vulnerability of financial development to currency shocks.

Similarly, inflation negatively affects the financial cycle throughout, reinforcing its destabilizing role. High inflation erodes the real value of financial assets and discourages long-term saving and lending, corroborating the classical view of inflation as a tax on financial intermediation (Boyd, Levine & Smith, 2001). This finding aligns with studies showing that inflation thresholds exist beyond which financial development deteriorates, particularly in emerging markets (Khan, Senhadji & Smith, 2006).

Contrary to the positive role of credit expansion in many development models, the results show that credit has a negative long-run effect on the cycle. This may reflect excessive household indebtedness and unproductive lending practices that fuel consumption rather than investment (Beck, Levine & Loayza, 2000). However, credit contributes positively to short-term financial booms across all quantiles, suggesting a cyclical pattern where credit expansions precede financial upswings. This finding is consistent with Schularick and Taylor (2012), who emphasize the role of credit booms in generating financial instability. A similar duality is observed with share prices and housing prices. While the long-run effect of share prices is negative—possibly due to speculative and volatile equity markets—their short-run impact is positive, consistent with the wealth effect and increased liquidity during market rallies (Mishkin, 2007).

In contrast, the housing sector appears to promote financial development in the long term, reflecting its role in asset-backed lending and capital formation (Green & Malppezi, 2003). Yet in the short run, rising housing prices can contribute to burst phases, consistent with the experiences of housing-led financial crises. For instance, the 2007–2008 Global Financial Crisis, which began in the U.S. subprime mortgage market, illustrates how housing bubbles can amplify credit booms and ultimately trigger systemic collapses. The empirical results here affirm this view by showing the negative short-run effect of housing prices, despite their long-run contribution to financial development.

Turning to policy variables, the repo rate exhibits a positive effect on the financial cycle in both the short and long term, although the short-run effect is not statistically significant. This suggests that tighter monetary policy—often aimed at controlling inflation and stabilizing macroeconomic conditions—supports financial development over time by fostering credibility and reducing volatility (Bernanke & Gertler, 1995). However, the insignificant short-term effect underscores the limitation of monetary policy alone in managing financial cycle fluctuations. In contrast, the macroprudential policy index consistently exerts a negative effect across all periods. While this supports the notion that strict macroprudential regulations may restrict credit and financial activity, they appear to play a stabilizing role by mitigating short-term fluctuations. This result aligns with Claessens (2015), who argue that macroprudential tools are designed more for financial stability than for promoting financial development per se.

From the combined interpretations and results, we learn that the drivers of financial development in South Africa appear to be monetary policy and the housing sector, which have shown positive long-term effects. On the other hand, variables such as exchange rate movements, inflation, money supply, and macroprudential policy act as constraints on financial development. In terms of triggers of short-term financial booms and bursts, the evidence clearly points to GDP growth, credit, share prices, and to some extent housing prices, as sources of temporary upswings in financial activity. Conversely, money supply and inflation are more closely associated with burst phases and financial volatility. These findings stress the importance of policy coordination—particularly between monetary and macroprudential authorities—to strike a balance between promoting financial development and ensuring financial stability in emerging markets.

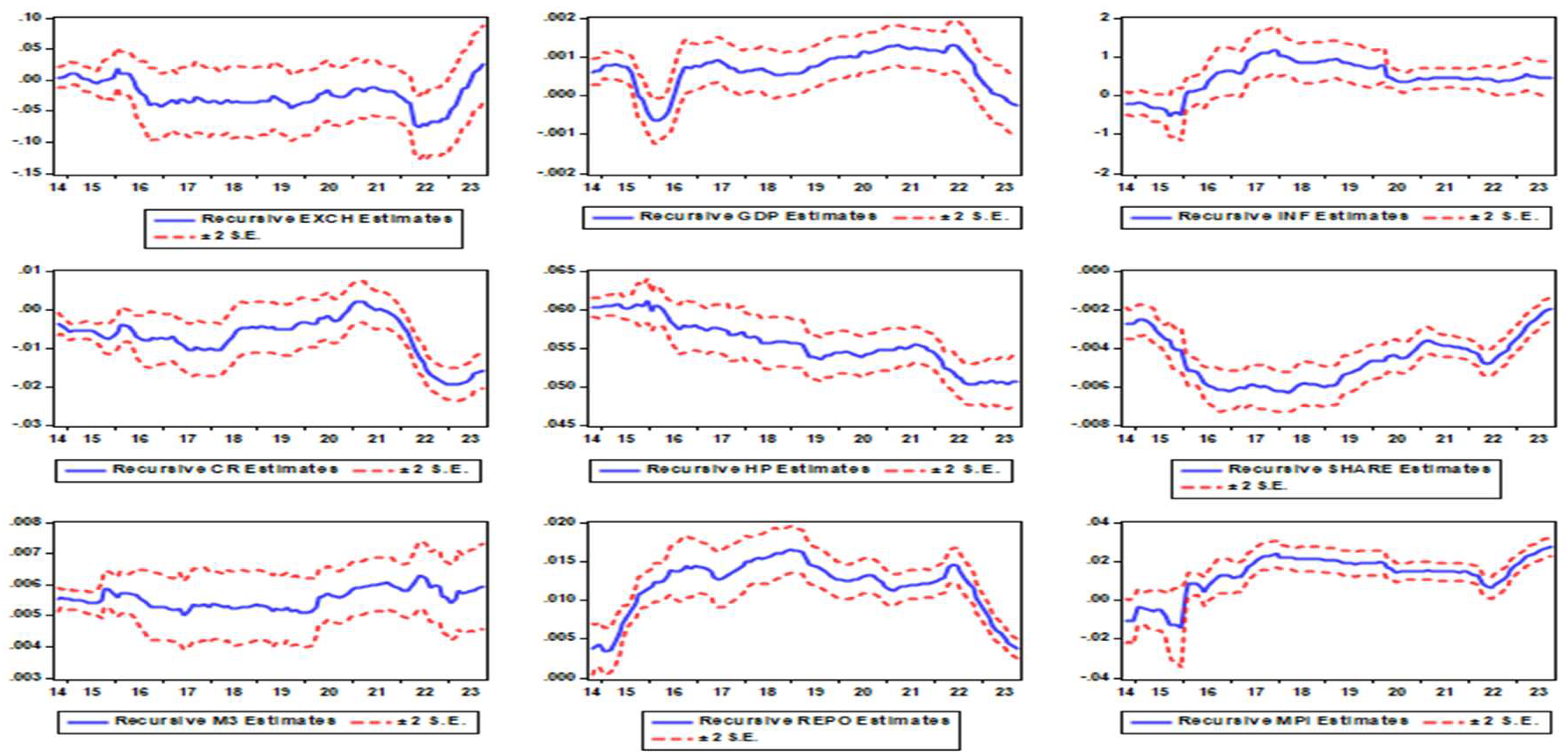

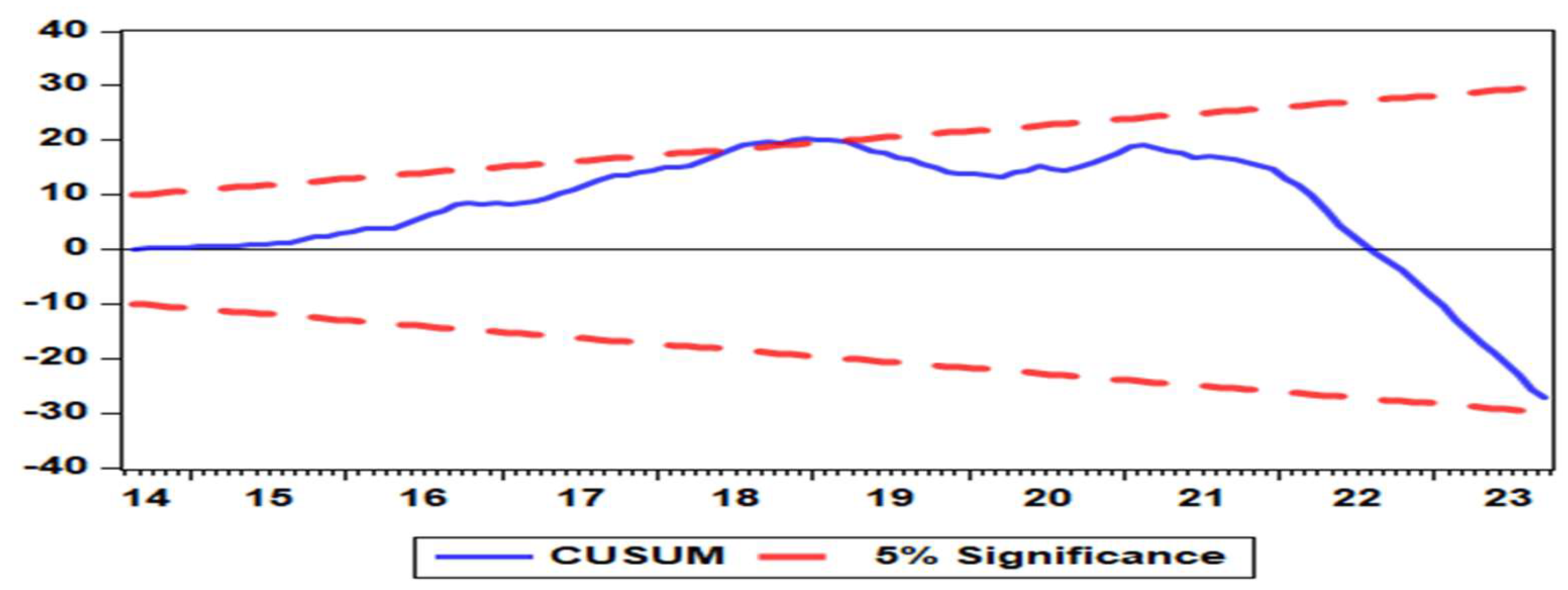

To assess the stability of the estimated parameters in Table 2, two diagnostic tools were employed. First, Figure 2 presents the recursive parameter estimates alongside their corresponding ±2 standard deviation bounds. Throughout the sample period, all estimated coefficients remained well within these confidence bounds, indicating that the parameters are stable over time. This implies that the long-run and short-run coefficients captured by the model are not affected by temporary shocks or sample-specific outliers, thereby confirming the temporal consistency of the model's structure. Second, Figure 3 displays the Cumulative Sum (CUSUM) test results. The CUSUM line remains within the 95% confidence interval throughout the period under analysis, which confirms the absence of significant structural breaks in the residuals and the overall stability of the model specification.

The stability evidenced in both Figure 2 and Figure 3 adds robustness to the study’s findings. It confirms that the relationships identified—namely the variables that drive long-term financial development and those that trigger short-run cyclical deviations—are not only significant but also stable across time. This enhances the utility of the model for policy analysis and forecasting, assuring macroprudential authorities that the estimated relationships can be relied upon when designing interventions aimed at managing financial cycles and promoting financial stability in South Africa.

Conclusions

This study set out to investigate the drivers and triggers of South Africa’s financial cycle, motivated by notable gaps in the empirical literature. As highlighted in the introduction, existing research tends to treat financial cycle development and financial cycle fluctuations as distinct areas of inquiry, often using disjointed empirical approaches. Furthermore, the theoretical literature provides conflicting perspectives on the relationship between the macroeconomy and financial cycles—ranging from procyclical to independent or even destabilizing interactions. In response, this study constructed a quantile autoregressive distributed lag (QARDL) model to empirically examine both the long-run determinants of financial development and the short-run triggers of cyclical fluctuations within a unified framework. The South African case, given its relatively large financial cycle and macroprudential policy relevance, provided an important and under-researched context for this analysis.

The study achieved its aims by using a quantile ARDL framework that accommodated both I(0) and I(1) variables without transforming them, consistent with the bounds testing procedure developed by Pesaran et al. (2001). The variables included in the model were selected based on economic theory and policy relevance, and their inclusion was validated through diagnostic testing. Importantly, the model's robustness was supported by several diagnostics: the Ramsey RESET test indicated that there were no functional form misspecifications, while the Breusch-Pagan-Godfrey test suggested the absence of heteroscedasticity. To address autocorrelation concerns—identified through the Breusch-Godfrey LM test—one lag of all variables was included, in accordance with the Akaike Information Criterion (AIC), which identified one lag as optimal. Furthermore, the model’s stability was confirmed by both recursive coefficient plots (Figure 2) and the CUSUM test (Figure 3), which demonstrated that the estimated parameters and overall model structure remained stable over time.

The findings reveal that financial development in South Africa is primarily shaped by long-run fundamentals such as inflation, credit growth, real house prices, money supply, and the repo rate, with varying significance across the distribution of the financial cycle. In contrast, short-run cyclical deviations were most strongly triggered by shocks to inflation, credit, house prices, and the macroprudential policy index—particularly during lower and middle quantiles of the financial cycle. Notably, the asymmetric effects captured through the quantile approach revealed that certain variables, such as the macroprudential index and money supply, exert a stronger influence during times of financial cycle contraction than expansion. These findings align partially with the Minsky hypothesis, which suggests that credit booms and asset price dynamics are key drivers of instability, while also supporting more recent empirical work emphasizing the dual role of inflation and interest rates in financial cycles (Claessens et al., 2011; Adarov, 2023).

The findings indicate that the drivers of financial development in South Africa appear to be monetary policy and the housing sector, both of which exhibit positive long-term effects. Conversely, variables such as exchange rate movements, inflation, money supply, and macroprudential policy act as constraints on financial development. Regarding short-term financial booms and bursts, GDP growth, credit, share prices, and, to some extent, housing prices, serve as triggers for temporary upswings in financial activity. On the other hand, money supply and inflation are more closely associated with burst phases and financial volatility. These results underscore the importance of policy coordination—especially between monetary and macroprudential authorities—in balancing the promotion of financial development with the maintenance of financial stability, particularly in emerging market economies like South Africa.

This study contributes to the literature in several important ways. First, it provides a rare empirical investigation that jointly models both short- and long-run financial cycle dynamics using a unified framework, something that has largely been absent in emerging market contexts (see Égert et al., 2017; Adarov, 2023). Second, it uses quantile techniques to uncover heterogeneous effects across different financial cycle conditions, offering nuanced insights that conventional mean-regression approaches cannot (Koenker & Bassett, 1978; Chen et al., 2020; Yin et al., 2023). Third, by focusing on South Africa, it enhances our understanding of financial cycle behavior in a systemically important emerging market, with direct implications for macroprudential surveillance and policy (see Alawadhi & Al Sadah, 2022; Ben Naceur et al., 2015; De Beer et al., 2020). Additionally, this study complements earlier findings by Claessens et al. (2011, 2012), Borio (2014), and Drehmann et al. (2012), who emphasize the importance of asset prices, credit, and macro-financial linkages in financial cycle analysis. The incorporation of a macroprudential policy index further aligns with the growing literature advocating for quantitative measures of regulatory stance to assess policy effectiveness (Cerutti et al., 2017; Budnik & Kleibl, 2018).

However, the research is not without limitations. The use of quarterly data, while appropriate for macro-financial analysis, may obscure high-frequency fluctuations and rapid policy reactions. Additionally, the macroprudential policy index used in the model—while novel and empirically tractable—may not capture all dimensions of regulatory tightening or loosening, particularly those related to institutional quality or regulatory enforcement. Future research could address these limitations by employing higher-frequency data, incorporating international spillover effects through global financial variables, or using machine learning methods to construct more granular macroprudential indices. Moreover, extending the QARDL approach to a panel of emerging markets could shed light on the extent to which these findings hold across different institutional and economic environments.

In sum, this study provides robust empirical evidence on the dual dynamics of financial cycles in South Africa. By identifying the key long-run drivers of financial development and the short-run triggers of cyclical disruptions, the findings offer important insights for policymakers aiming to foster financial stability while promoting sustainable economic growth. Future studies should build on this framework to further our understanding of financial cycle dynamics in an increasingly complex and interconnected global economy.

Funding

This research received no external funding

Data Availability Statement

The raw data supporting the conclusions of this article will be made available by the authors on request.

Acknowledgments

During the preparation of this manuscript/study, the author used ChatGPT, GPT-4-turbo for the purposes of improving spelling, grammar, language, and clarity. The author have reviewed and edited the output and take full responsibility for the content of this publication.

Conflicts of Interest

The authors declare no conflicts of interest.

Abbreviations

The following abbreviations are used in this manuscript:

| ADF | Augmented Dickey-Fuller |

| AIC | Akaike Information Criterion |

| ARDL | Autoregressive Distributed Lag |

| CUSUM | Cumulative Sum (of Recursive Residuals) Test |

| CR | Total Domestic Credit (as % of GDP) |

| EXCH | Real Effective Exchange Rate |

| GDP | Gross Domestic Product |

| GFC | Global Financial Crisis |

| HP | Real House Price Index |

| I(0) | Integrated of order 0 (stationary) |

| I(1) | Integrated of order 1 (non-stationary) |

| IMF | International Monetary Fund |

| INF | Inflation Rate |

| M3 | Broad Money Supply |

| MPI | Macroprudential Policy Index |

| OLS | Ordinary Least Squares |

| PCA | Principal Component Analysis |

| QARDL | Quantile Autoregressive Distributed Lag |

| REPO | Repo Rate |

| SARB | South African Reserve Bank |

| SHARE | Real All Share Price Index |

| VECM | Vector Error Correction Model |

References

- Adrian, T.; Shin, H.S. Liquidity, monetary policy, and financial cycles. Current issues in economics and finance 2008, 14. [Google Scholar]

- Adrian, T.; Boyarchenko, N.; Shin, H.-S. The cyclicality of leverage. Tech. rep.

- Adusei, M. Financial development and economic growth: Evidence from Ghana. The International Journal of Business and Finance Research 2013, 7, 61–76. [Google Scholar]

- Agénor, P.-R.; da Silva, L.A. (2019). Integrated inflation targeting-Another perspective from the developing world.

- Aikman, D.; Haldane, A. G. , & Nelson, B. D. Curbing the credit cycle. The Economic Journal 2015, 125, 1072–1109. [Google Scholar]

- Akaike, H. A new look at the statistical model identification. IEEE transactions on automatic control 1974, 19, 716–723. [Google Scholar] [CrossRef]

- Aldasoro, I.; Avdjiev, S.; Borio, C. E. , & Disyatat, P. (2020). Global and domestic financial cycles: variations on a theme.

- Amador-Torres, J. S. , Gomez-Gonzalez, J. E., Ojeda-Joya, J. N., Jaulin-Mendez, O. F., & Tenjo-Galarza, F. Mind the gap: Computing finance-neutral output gaps in Latin-American economies. Economic Systems 2016, 40, 444–452. [Google Scholar]

- Angelini, P.; Neri, S.; Panetta, F. The interaction between capital requirements and monetary policy. Journal of money, credit and Banking 2014, 46, 1073–1112. [Google Scholar] [CrossRef]

- Anwar, A.; Sharif, A.; Fatima, S.; Ahmad, P.; Sinha, A.; Khan, S. A. , & Jermsittiparsert, K. The asymmetric effect of public private partnership investment on transport CO2 emission in China: Evidence from quantile ARDL approach. Journal of Cleaner Production 2021, 288, 125282. [Google Scholar]

- Arcand, J.L.; Berkes, E.; Panizza, U. Too much finance? Journal of economic growth 2015, 20, 105–148. [Google Scholar] [CrossRef]

- Aron, J.; Muellbauer, J. Wealth, credit conditions, and consumption: Evidence from South Africa. Review of Income and Wealth 2013, 59, S161–S196. [Google Scholar] [CrossRef]

- Aron, J.; Muellbauer, J. Modelling and forecasting mortgage delinquency and foreclosure in the UK. Journal of Urban Economics 2016, 94, 32–53. [Google Scholar] [CrossRef]

- Aron, J.; Muellbauer, J.; Prinsloo, J. (2006). Estimating household-sector wealth in South Africa. Quarterly Bulletin (South African Reserve Bank).

- Aron, J.; Muellbauer, J.; Prinsloo, J. (2012). South African reserve Bank working paper.

- Bai, Y.; Kehoe, P. J. , & Perri, F. World financial cycles. 2019 meeting papers 2019, 1545. [Google Scholar]

- Bakar, H. O. , & Sulong, Z. The role of financial sector on economic growth: Theoretical and empirical literature reviews analysis. Journal of Global Economics 2018, 6, 1–6. [Google Scholar]

- Beck, R.; Georgiadis, G.; Straub, R. The finance and growth nexus revisited. Economics Letters 2014, 124, 382–385. [Google Scholar] [CrossRef]

- Beck, T.; Levine, R. Stock markets, banks, and growth: Panel evidence. Journal of Banking & Finance 2004, 28, 423–442. [Google Scholar]

- Beck, T.; Levine, R.; Loayza, N. Finance and the Sources of Growth. Journal of financial economics 2000, 58, 261–300. [Google Scholar] [CrossRef]

- Becker, M. C. , & Knudsen, T. Schumpeter 1911: farsighted visions on economic development. American Journal of Economics and Sociology 2002, 61, 387–403. [Google Scholar]

- Beirne, J. Financial cycles in asset markets and regions. Economic Modelling 2020, 92, 358–374. [Google Scholar] [CrossRef]

- Bernanke, B.S. The real effects of disrupted credit: Evidence from the global financial crisis. Brookings Papers on Economic Activity 2018, 2018, 251–342. [Google Scholar] [CrossRef]

- Bernanke, B. S. , & Gertler, M. Inside the black box: the credit channel of monetary policy transmission. Journal of Economic perspectives 1995, 9, 27–48. [Google Scholar]

- Bernanke, B. S., Gertler, M., & Gilchrist, S. (1994). The financial accelerator and the flight to quality. The financial accelerator and the flight to quality. National Bureau of Economic Research Cambridge, Mass., USA.

- Bertocco, G. The role of credit in a Keynesian monetary economy. Review of Political Economy 2005, 17, 489–511. [Google Scholar] [CrossRef]

- Blum, D. N. , Federmair, K., Fink, G., & Haiss, P. R. (2002). The financial-real sector nexus: Theory and empirical evidence. Research Institute for European Affairs Working Paper.

- Borio, C. Implementing a macroprudential framework: Blending boldness and realism. Capitalism and society 2011, 6. [Google Scholar] [CrossRef]

- Borio, C. (2014). The financial cycle and macroeconomics: what have we learned and what are the policy implications? In Financial Cycles and the Real Economy (pp. 10–35). Edward Elgar Publishing.

- Borio, C. E. , & Drehmann, M. (2009). Assessing the risk of banking crises–revisited. BIS Quarterly Review, March.

- Borio, C. E. , & Lowe, P. W. (2002). Asset prices, financial and monetary stability: exploring the nexus.

- Borio, C. E. , Drehmann, M., & Xia, F. D. (2018). The financial cycle and recession risk. BIS Quarterly Review December.

- Borio, C. E. , Drehmann, M., & Xia, F. D. (2019). Predicting recessions: financial cycle versus term spread.

- Borio, C.; Zhu, H. Capital regulation, risk-taking and monetary policy: a missing link in the transmission mechanism? Journal of Financial stability 2012, 8, 236–251. [Google Scholar] [CrossRef]

- Bosch, A.; Koch, S.F. The South African financial cycle and its relation to household deleveraging. South African Journal of Economics 2020, 88, 145–173. [Google Scholar] [CrossRef]

- Boyd, J. H. , Levine, R., & Smith, B. D. The impact of inflation on financial sector performance. Journal of monetary Economics 2001, 47, 221–248. [Google Scholar]

- Breusch, T. S. , & Pagan, A. R. J: for heteroscedasticity and random coefficient variation. Econometrica, 1979. [Google Scholar]

- Brunnermeier, M. K. , & Sannikov, Y. A macroeconomic model with a financial sector. American Economic Review 2014, 104, 379–421. [Google Scholar]

- Cecchetti, S.G. (2000). Asset prices and central bank policy. Centre for Economic Policy Research.

- Cecchetti, S. G. , & Kharroubi, E. (2012). Reassessing the impact of finance on growth.

- Cerutti, E.; Claessens, S.; Laeven, L. The use and effectiveness of macroprudential policies: New evidence. Journal of financial stability 2017, 28, 203–224. [Google Scholar] [CrossRef]

- Chiarella, C.; Di Guilmi, C. Monetary policy and debt deflation: some computational experiments. Macroeconomic Dynamics 2017, 21, 214–242. [Google Scholar] [CrossRef]

- Chorafas, D.N. Financial cycles. In Financial Cycles: Sovereigns 2015, Bankers, and Stress Tests (pp. 1–24). Springer.

- Christensen, I.; Dib, A. The financial accelerator in an estimated New Keynesian model. Review of economic dynamics 2008, 11, 155–178. [Google Scholar] [CrossRef]

- Cimoli, M.; Lima, G. T. , & Porcile, G. The production structure, exchange rate preferences and the short-run—Medium-run macrodynamics. Structural Change and Economic Dynamics 2016, 37, 13–26. [Google Scholar]

- Claessens, S. An overview of macroprudential policy tools. Annual Review of Financial Economics 2015, 7, 397–422. [Google Scholar] [CrossRef]

- Claessens, S.; Ghosh, S. R. , & Mihet, R. Macro-prudential policies to mitigate financial system vulnerabilities. Journal of International Money and Finance 2013, 39, 153–185. [Google Scholar]

- Claessens, S.; Kose, M. A. , & Terrones, M. E. Financial cycles: what? how? when? NBER international seminar on macroeconomics, 7, pp. 303–344.

- Claessens 2011, S.; Kose, M. A. , & Terrones, M. E. How do business and financial cycles interact? Journal of International economics, 87, 178–190.

- Coimbra, N.; Rey, H. (2024). Financial cycles with heterogeneous intermediaries. Review of Economic Studies 2012, 91, 817–857. [Google Scholar] [CrossRef]

- Corbet, S.; Hou, Y.; Hu, Y.; Lucey, B.; Oxley, L. Aye Corona! The contagion effects of being named Corona during the COVID-19 pandemic. Finance Research Letters 2021, 38, 101591. [Google Scholar] [CrossRef]

- Crockett, A. The theory and practice of financial stability. De Economist 1996, 144, 531–568. [Google Scholar] [CrossRef]

- De la Torre, A.; Gozzi, J. C., & Schmukler, S. L. (2017). Innovative Experiences in Access to Finance: Market-Friendly Roles for the Visible Hand? World Bank Publications.

- De Wet, M. C. , & Botha, I. Constructing and characterising the aggregate South African financial cycle: A Markov regime-switching approach. Journal of Business Cycle Research 2022, 18, 37–67. [Google Scholar]

- Detken, C. , Weeken, O., Alessi, L., Bonfim, D., Boucinha, M., Castro, C.,... others. (2014). Operationalising the countercyclical capital buffer: indicator selection, threshold identification and calibration options. ESRB: Occasional Paper Series.

- Drehmann, M.; Borio, C. E. , & Tsatsaronis, K. (2012). Characterising the financial cycle: don't lose sight of the medium term!

- Durusu-Ciftci, D.; Ispir, M. S. , & Yetkiner, H. Financial development and economic growth: Some theory and more evidence. Journal of policy modeling 2017, 39, 290–306. [Google Scholar]

- Epure, M.; Mihai, I.; Minoiu, C. ; Peydró; J-L Global financial cycle, household credit, and macroprudential policies. Management Science 2024, 70, 8096–8115. [Google Scholar] [CrossRef]

- Farrell, G.; Kemp, E. Measuring the financial cycle in South Africa. South African Journal of Economics 2020, 88, 123–144. [Google Scholar] [CrossRef]

- Fink, G.; Haiss, P.; Mantler, H. (2004). Financial sector macro-efficiency. Financial Markets in Central and Eastern Europe, London, 61–98.

- Fisher, I. The Debt-Deflation Theory of Great Depressions. Revue de l'Institut International de Statistique/Review of the International Statistical Institute 1934, 1, 48–65. [Google Scholar] [CrossRef]

- Fornari, F.; Lemke, W. (2010). Predicting recession probabilities with financial variables over multiple horizons. Tech. rep., ECB Working Paper.

- Foroni, C.; Gelain, P.; Marcellino, M.G. (2022). The financial accelerator mechanism: does frequency matter?

- Gammadigbe, V. Financial cycles synchronization in WAEMU countries: Implications for macroprudential policy. Finance Research Letters 2022, 46, 102281. [Google Scholar] [CrossRef]

- Gatti, D.; Gaffeo, E.; Gallegati, M.; Giulioni, G.; Palestrini, A. (2008). Emergent macroeconomics: an agent-based approach to business fluctuations. Springer Science & Business Media.

- Geanakoplos, J. The leverage cycle. NBER macroeconomics annual 2010, 24, 1–66. [Google Scholar] [CrossRef]

- Gertler, M.; Karadi, P. A model of unconventional monetary policy. Journal of monetary Economics 2011, 58, 17–34. [Google Scholar] [CrossRef]

- Gilchrist, S.; Bernanke, B.; Gertler, M. (1998). The financial accelerator in a quantitative business cycle framework. National Bureau of Economic Research.

- Giri, F.; Riccetti, L.; Russo, A.; Gallegati, M. Monetary policy and large crises in a financial accelerator agent-based model. Journal of Economic Behavior & Organization 2019, 157, 42–58. [Google Scholar]

- Gomez-Gonzalez, J. E. , Villamizar-Villegas, M., Zarate, H. M., Amador, J. S., & Gaitan-Maldonado, C. Credit and business cycles: Causal effects in the frequency domain. Ensayos sobre Polı́tica Económica 2015, 33, 176–189. [Google Scholar]

- Gorton, G.; Metrick, A. Securitized banking and the run on repo. Journal of Financial economics 2012, 104, 425–451. [Google Scholar] [CrossRef]

- Green, R. K. , & Malpezzi, S. (2003). A primer on US housing markets and housing policy. The Urban Insitute.

- Greenwood, J.; Jovanovic, B. Financial development, growth, and the distribution of income. Journal of political Economy 1990, 98, 1076–1107. [Google Scholar] [CrossRef]

- Gurley, J. G. , & Shaw, E. S. Financial aspects of economic development. The American economic review 1955, 45, 515–538. [Google Scholar]

- \, *!!! REPLACE !!!*. Ha, J.; Kose, M. A., Otrok, C., & Prasad, E. S. (2020). Global macro-financial cycles and spillovers. Tech. rep., National Bureau of Economic Research.

- Harun, C. A. , Taruna, A. A., Nattan, R. R., & Surjaningsih, N. (2014). Financial Cycle of Indonesia—Potential Forward Looking Analysis. Tech. rep.

- Hashmi, S. M. , & Chang, B. H. Asymmetric effect of macroeconomic variables on the emerging stock indices: A quantile ARDL approach. International Journal of Finance & Economics 2023, 28, 1006–1024. [Google Scholar]

- Hashmi, S. M. , Chang, B. H., Huang, L., & Uche, E. Revisiting the relationship between oil prices, exchange rate, and stock prices: An application of quantile ARDL model. Resources Policy 2022, 75, 102543. [Google Scholar]

- Hassan, M. K. , Sanchez, B., & Yu, J.-S. Financial development and economic growth: New evidence from panel data. The Quarterly Review of economics and finance 2011, 51, 88–104. [Google Scholar]

- Hiebert, P.; Jaccard, I.; Schüler, Y. Contrasting financial and business cycles: Stylized facts and candidate explanations. Journal of Financial Stability 2018, 38, 72–80. [Google Scholar] [CrossRef]

- Hudson, M. (2012). The road to debt deflation, debt peonage, and neofeudalism. Tech. rep., Working Paper.

- Ibrahim, M.; Alagidede, P. Effect of financial development on economic growth in sub-Saharan Africa. Journal of Policy Modeling 2018, 40, 1104–1125. [Google Scholar] [CrossRef]

- Immergluck, D. (2011). Foreclosed: High-risk lending, deregulation, and the undermining of America's mortgage market. Cornell University Press.

- Jordà; Ò; Schularick, M. ; Taylor, A.M. When credit bites back. Journal of money, credit and banking 2013, 45, 3–28.

- Jordà; Ò; Schularick, M. ; Taylor, A.M. The effects of quasi-random monetary experiments. Journal of Monetary Economics 2020, 112, 22–40. [Google Scholar] [CrossRef]

- Jordà, *!!! REPLACE !!!*; Ò, *!!! REPLACE !!!*; Schularick, M.; Taylor, A. M. Jordà; Ò; Schularick, M.; Taylor, A. M., & Ward, F. (2018). Global financial cycles and risk premiums. Tech. rep., National Bureau of Economic Research.

- Khan, M. S. , Senhadji, A. S., & Smith, B. D. Inflation and financial depth. Macroeconomic Dynamics 2006, 10, 165–182. [Google Scholar]

- Kim, S.; Mehrotra, A. Examining macroprudential policy and its macroeconomic effects–some new evidence. Journal of International Money and Finance 2022, 128, 102697. [Google Scholar] [CrossRef]

- Kindleberger, C.P. Manias, panics, and rationality. Eastern Economic Journal 1978, 4, 103–112. [Google Scholar]

- Kindleberger, C.P. Bubbles in history. Banking Crises: Perspectives from The New Palgrave Dictionary.

- King, R. G. , & Levine, R. Finance, entrepreneurship and growth. Journal of Monetary economics 1993, 32, 513–542. [Google Scholar]

- Kiyotaki, N.; Moore, J. Credit cycles. Journal of political economy 1997, 105, 211–248. [Google Scholar] [CrossRef]

- Knell, M. Schumpeter, Minsky and the financial instability hypothesis. Journal of evolutionary Economics 2015, 25, 293–310. [Google Scholar] [CrossRef]

- Kohler, K.; Stockhammer, E. Growing differently? Financial cycles, austerity, and competitiveness in growth models since the Global Financial Crisis. Review of International Political Economy 2022, 29, 1314–1341. [Google Scholar] [CrossRef]

- Krugman, P. (2001). Crises: the next generation. Conference Honoring Assaf Razin, Tel Aviv.

- Krznar, M. I., & Matheson, M. T. (2017). Financial and business cycles in Brazil. International Monetary Fund.

- Kunovac, D.; Mandler, M.; Scharnagl, M. (2018). Financial cycles in euro area economies: A cross-country perspective. Bundesbank Discussion Paper.

- Lane, P.R. The European sovereign debt crisis. Journal of economic perspectives 2012, 26, 49–68. [Google Scholar] [CrossRef]

- Lane, P. R. , & McQuade, P. Domestic credit growth and international capital flows. The Scandinavian Journal of Economics 2014, 116, 218–252. [Google Scholar]

- Lang, J. H. , & Welz, P. (2018). Semi-structural credit gap estimation. ECB Working Paper.

- Levine, R. Financial development and economic growth: views and agenda. Journal of economic literature 1997, 35, 688–726. [Google Scholar]

- Levine, R. Finance and growth: theory and evidence. Handbook of economic growth 2005, 1, 865–934. [Google Scholar]

- Magubane, K. Exploring causal interactions between macroprudential policy and financial cycles in South Africa. International Journal of Research in Business & Social Science.

- Magubane, K.; Nyatanga, P.; Nzimande, N. Financial cycle synchronization in the advanced and systemic middle-income economies: evidence from a dynamic factor model. International Journal of Research in Business & Social Science.

- Malkiel, B.G. (1989). Efficient market hypothesis. In Finance (pp. 127–134). Springer.

- McCulley, P. , & others. The shadow banking system and Hyman Minsky’s economic journey. Insights into the global financial crisis.

- McKinnon, R.I. The value-added tax and the liberalization of foreign trade in developing economies: a comment. The value-added tax and the liberalization of foreign trade in developing economies: a comment 1973, 11, 520–524. [Google Scholar]

- Mensi, W.; Shahzad, S. J. , Hammoudeh, S., Hkiri, B., & Al Yahyaee, K. H. Long-run relationships between US financial credit markets and risk factors: Evidence from the quantile ARDL approach. Finance Research Letters 2019, 29, 101–110. [Google Scholar]

- Merton, R. C., & Thakor, R. T. (2015). Customers and investors: A framework for understanding financial institutions. Tech. rep., National Bureau of Economic Research.

- Mian, A.; Sufi, A.; Verner, E. Household debt and business cycles worldwide. The Quarterly Journal of Economics 2017, 132, 1755–1817. [Google Scholar] [CrossRef]

- Minsky, H.P. (1970). Financial instability revisited: The economics of disaster. Financial instability revisited: The economics of disaster. Board of Governors of the Federal Reserve System St. Louis.

- Minsky, H.P. (1992). The financial instability hypothesis. Tech. rep., Working paper.

- Minsky, H.P. (1994). Financial instability and the decline (?) of banking: public policy implications. Tech. rep., Working Paper.

- Miranda-Agrippino, S.; Rey, H. (2022). The global financial cycle. In Handbook of international economics (Vol. 6, pp. 1–43). Elsevier.

- Mishkin, F.S. Global financial instability: framework, events, issues. Journal of economic perspectives 1999, 13, 3–20. [Google Scholar] [CrossRef]

- Mishkin, F.S. (2007). Housing and the monetary transmission mechanism. Housing and the monetary transmission mechanism. National Bureau of Economic Research Cambridge, Mass., USA.

- Mlachila, M.; Dykes, D.; Zajc, S.; Aithnard, P.-H.; Beck, T.; Ncube, M.; Nelvin, O. (2013). Banking in sub-Saharan Africa: Challenges and opportunities.

- Modigliani, F.; Miller, M.H. The cost of capital, corporation finance and the theory of investment. The American economic review 1958, 48, 261–297. [Google Scholar]

- Munk, C. (2018). Financial markets and investments. Copenhagen, Denmark: Lecture notes.

- Narayan, P.K. The saving and investment nexus for China: evidence from cointegration tests. Applied economics 2005, 37, 1979–1990. [Google Scholar] [CrossRef]

- Ng, T. (2011). The predictive content of financial cycle measures for output fluctuations. BIS Quarterly Review, June.

- Nkoro, E.; Uko, A. K. , & others. Autoregressive Distributed Lag (ARDL) cointegration technique: application and interpretation. Journal of Statistical and Econometric methods 2016, 5, 63–91. [Google Scholar]

- Nyati, M. C. , Tipoy, C. K., & Muzindutsi, P.-F. (2021). Measuring and testing a modified version of the South African financial cycle. Economic Research Southern Africa Cape Town.

- Odhiambo, N.M. Energy consumption and economic growth nexus in Tanzania: An ARDL bounds testing approach. Energy policy 2009, 37, 617–622. [Google Scholar] [CrossRef]

- Odhiambo, N.M. Finance-investment-growth nexus in South Africa: an ARDL-bounds testing procedure. Economic change and restructuring 2010, 43, 205–219. [Google Scholar] [CrossRef]

- Oman, W. The synchronization of business cycles and financial cycles in the euro area. International Journal of Central Banking 2019, 15, 327–362. [Google Scholar]

- Padayachee, V.; Sherbut, G. Ideas and Power Academic Economists and the Making of Economic Policy. The South African Experience in Comparative Perspective (1985-2007). Cahiers d’études africaines 2011, 51, 609–647. [Google Scholar] [CrossRef]

- Pagano, M. Financial markets and growth: An overview. European economic review 1993, 37, 613–622. [Google Scholar] [CrossRef]

- Parusel, M.; Viegi, N. (2009). Economic policy in turbulent times. Economic policy in turbulent times. Citeseer.

- Pesaran, M. H. , Shin, Y., & Smith, R. J. Bounds testing approaches to the analysis of level relationships. Journal of applied econometrics 2001, 16, 289–326. [Google Scholar]

- Pesaran, M. H. , Shin, Y., & Smith, R. P. Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American statistical Association 1999, 94, 621–634. [Google Scholar]

- Potjagailo, G.; Wolters, M.H. Global financial cycles since 1880. Journal of International Money and Finance 2023, 131, 102801. [Google Scholar] [CrossRef]

- Prabheesh, K. P. , Anglingkusumo, R., & Juhro, S. M. The dynamics of global financial cycle and domestic economic cycles: Evidence from India and Indonesia. Economic Modelling 2021, 94, 831–842. [Google Scholar]

- Qin, Y.; Xu, Z.; Wang, X.; Škare, M. ; Porada-Rochoń; M Financial cycles in the economy and in economic research: A case study in China. Technological and Economic Development of Economy 2021, 27, 1250–1279. [Google Scholar] [CrossRef]

- Ramsey, J.B. Tests for specification errors in classical linear least-squares regression analysis. Journal of the Royal Statistical Society Series B: Statistical Methodology 1969, 31, 350–371. [Google Scholar] [CrossRef]

- Ranciere, R.; Tornell, A.; Westermann, F. Systemic crises and growth. The Quarterly Journal of Economics 2008, 123, 359–406. [Google Scholar] [CrossRef]

- Robinson, J. (1979). The generalisation of the general theory. In The generalisation of the general theory and other essays (pp. 1–76). Springer.

- Rünstler, G. , Balfoussia, H., Burlon, L., Buss, G., Comunale, M., De Backer, B.,... others. (2018). Real and financial cycles in EU countries: Stylised facts and modelling implications. ECB Occasional Paper.

- Sahay, M. R. , Cihak, M., N'Diaye, M. P., Barajas, M. A., Pena, M. D., Bi, R.,... others. (2015). Rethinking financial deepening: Stability and growth in emerging markets. International Monetary Fund.

- Schularick, M.; Taylor, A.M. Credit booms gone bust: monetary policy, leverage cycles, and financial crises, 1870–2008. American Economic Review 2012, 102, 1029–1061. [Google Scholar] [CrossRef]

- Schüler, Y. S. , Hiebert, P. P., & Peltonen, T. A. Financial cycles: Characterisation and real-time measurement. Journal of International Money and Finance 2020, 100, 102082. [Google Scholar]

- Schüler, Y. S. , Hiebert, P., & Peltonen, T. (2017). Coherent financial cycles for G-7 countries: Why extending credit can be an asset.

- Sharif, A.; Godil, D. I. , Xu, B., Sinha, A., Khan, S. A., & Jermsittiparsert, K. Revisiting the role of tourism and globalization in environmental degradation in China: Fresh insights from the quantile ARDL approach. Journal of Cleaner Production 2020, 272, 122906. [Google Scholar]

- Shin, H.S. Global banking glut and loan risk premium. IMF Economic Review 2012, 60, 155–192. [Google Scholar] [CrossRef]

- Škare, M.; Porada-Rochoń, M. Forecasting financial cycles: can big data help? Technological and Economic Development of Economy 2020, 26, 974–988. [Google Scholar] [CrossRef]

- Stiglitz, J.E. A re-examination of the Modigliani-Miller theorem. The American Economic Review 1969, 59, 784–793. [Google Scholar]

- Stremmel, H. (2015). Capturing the financial cycle in Europe. ECB Working paper.

- Swamy, V.; Dharani, M. The dynamics of finance-growth nexus in advanced economies. International Review of Economics & Finance 2019, 64, 122–146. [Google Scholar]

- Tilly, C. Trust networks in transnational migration. Sociological forum 2007, 22, pp. 3–24. [Google Scholar] [CrossRef]

- Timmermann, A.; Granger, C.W. Efficient market hypothesis and forecasting. International Journal of forecasting 2004, 20, 15–27. [Google Scholar] [CrossRef]

- Tung, F. Financing failure: bankruptcy lending, credit market conditions, and the financial crisis. Yale J. on Reg. 2020, 37, 651. [Google Scholar]

- Van der Merwe, E.J. (2004). Inflation targeting in South Africa. South African Reserve Bank Pretoria.

- Vercelli, A. A perspective on Minsky moments: revisiting the core of the financial instability hypothesis. Review of Political Economy 2011, 23, 49–67. [Google Scholar] [CrossRef]

- Villamil, A.P. The Modigliani-Miller Theorem. The New Palgrave Dictionary of Economics, Second Edition. Eds. Steven N. Durlauf and Lawrence E. Blume. Palgrave Macmillan 2008, 6, 1–7. [Google Scholar]

- Vollmer, U. Monetary policy or macroprudential policies: What can tame the cycles? Journal of Economic Surveys 2022, 36, 1510–1538. [Google Scholar] [CrossRef]

- Yang, F. The impact of financial development on economic growth in middle-income countries. Journal of International Financial Markets, Institutions and Money 2019, 59, 74–89. [Google Scholar] [CrossRef]

- Young, G. Debt Deflation and the Company Sector: the economic effects of balance sheet adjustment. National Institute Economic Review 1993, 144, 74–84. [Google Scholar] [CrossRef]

Figure 1.

Evolution of the South African financial cycle.

Figure 2.

Recursive standard errors.

Figure 3.

CUSUM stability test.

Table 1.

ADF stationarity test.

| Level | First difference | |||

|---|---|---|---|---|

| t-Statistic | P-value | t-Statistic | P-value | |

| CYCLE | -3.753 | 0.004 | -8.291 | 0.000 |

| EXCH | -2.541 | 0.107 | -14.025 | 0.000 |

| GDP | -2.831 | 0.055 | -5.841 | 0.000 |

| INF | -2.664 | 0.082 | -6.575 | 0.000 |

| CR | -1.847 | 0.357 | -6.679 | 0.000 |

| HP | -1.927 | 0.320 | -2.818 | 0.057 |

| SHARE | -13.707 | 0.000 | -12.163 | 0.000 |

| M3 | 3.148 | 1.000 | -7.039 | 0.000 |

| Repo | -2.876 | 0.049 | -5.166 | 0.000 |

| MPI | -1.109 | 0.711 | -9.476 | 0.000 |

Table 2.

Quantile ARDL results.

| Long-run quantile ARDL results | |||||||||