Submitted:

18 April 2025

Posted:

21 April 2025

You are already at the latest version

Abstract

The increasing complexity of financial markets and the growing need for personalisation present significant challenges to the traditional investment advisory model. To address this issue, this paper puts forth a proposal for an investment advisor robot 2.0 system based on deep neural networks. This system is designed to offer bespoke investment recommendations aligned with the risk appetite, financial objectives, and market dynamics of individual investors. The proposed method employs a long short-term memory network (LSTM) to generate personalised investment strategies in real time through the analysis of historical market data, investor behaviour data and real-time financial information. The innovation lies in the introduction of a multi-objective optimisation mechanism, which automatically adjusts the allocation of the portfolio through deep learning algorithms, optimises the balance between risk and return, and significantly improves the accuracy and practicality of investment recommendations. The experimental results demonstrate that, in comparison to the conventional investment advisory model, the system exhibits enhanced resilience in responding to market volatility across a range of simulated scenarios. It is also evident that the system is capable of formulating more forward-thinking investment strategies, while simultaneously demonstrating heightened stability and yield.

Keywords:

Investment advisor

; Financial guidance

; Risk optimization

; Multi-objective optimization

1. Introduction

As the global economy becomes more complex and financial markets more volatile, individual investors will face challenges that we have never seen before. The traditional investment advisory model depends on the experience and judgment of human experts, but it learns to adapt to a fast-changing market environment and cannot meet needs for personalized investments through an adaptive system [1]. As globalization accelerates and information technology develops rapidly, the structure and operating mechanism of financial markets are increasingly complex and changeable.

The proliferation of financial products and investment vehicles — derivatives, index funds and exchange-traded funds (ETFs), among others has only added to the complexity of investment decisions. But on the other hand, investors' risk appetite and financial goals are highly individualized, which means that investment advisors need to offer more personalized and accurate services [2]. To tackle these challenges, the FinTech industry is quickly evolving to cater to the increasing demands of investors by transforming investment management into a more efficient and effective process through innovative technologies.

The latest developments in artificial intelligence (AI), particularly deep learning technology, have made great strides in financial application in the past few years. Deep neural networks have found extensive implementation in stock price prediction, risk management, and portfolio optimization owing to their powerful data processing and pattern recognition capabilities [3]. For instance, convolutional neural networks (CNNs), which are typical neural networks, work wonders for image and time series data; they are being used to analyze market movements and identify trading opportunities.

Generative adversarial networks (GANs) also have tremendous power when it comes to simulating market scenarios and generating synthetic data. LSTM, as an advanced RNN architecture, is superior in learning long-term dependencies in time series data and become a great instrument of financial time series analysis. LSTMs read financial information and able to remember past understandings of the market to make forecasts more precise and decision composition more rational. But turning these technologies to advance the financial sector is essential and pressing for development, implementing AI to personalized investment advisory system [4].

Additionally, traditional financial advisor robots might offer automated investment advice, but their algorithms are generally rule-based and simple optimization models which cannot fully elucidate investors' unique risk appetite and complicated financial goals [5]. Many existing robo-advisor systems, for example, using mainly static assessment of risk, and fixed ratio of asset allocation to formulate investment strategy, as well as the inability to react to the dynamic changes of the market and the behavior of investors in a timely manner.

Moreover, the traditional model lacks real-time response and high precision decision-making that can hardly fulfill investors' real-time response requirement under market emergency and high volatility. This not only undermines the performance of these investment strategies, but also diminishes the investor's confidence in these robo-advisor systems [6]. As a result, the traditional investment advisory system demands urgent improvement, with deep learning to fully take advantage of advanced means that can precisely respond to investment investors' personalized needs and quickly adapt to market changes.

This study has proposed the investment advisor robot 2.0 system that can use deep neural networks, in particular, the innovative long short-term memory network along with a multi-objective optimization mechanism to offer highly personalized and accurate investment suggestions. In addition to analyzing historical market data and investor behavioral data, the system also integrates real-time news, macroeconomic indicators, market sentiment, etc., to dynamically output the best investment strategies, maintaining efficient decision-making capabilities in the complex and volatile market environment [7]. In relation to the traditional robo-advisor system, the investment advisor bot 2.0 greatly enhances the accuracy and adaptability of investment recommendations by introducing a more complex, flexible model architecture, and addresses the needs of modern investors for personalized and real-time services.

We employ financial feature gating and adaptive attention mechanism for the iLSTM architecture to empower the model capability of learning complex financial data patterns. Financial feature gating enhances the model's sensitivity to market dynamics by incorporating multi-dimensional data, including macroeconomic indicators and industry trends, as well as sentiment provided by news sources. More specifically, financial feature gating can control the inflow amount of information into the model at any time according to the weight value of different financial features to better represent the current market from the practical level.

Meanwhile, its adaptive attention mechanism allows the model to adaptively balance the attention to historical information from different time dimensions based on the current market situation. For instance, in high volatility market condition, the model can give more weight to recent data so as to adjust in a timely manner; in relatively stable market condition, the model can focus more on the analysis of long-term trends. The iLSTM architecture show flexibility and robustness in processing financial time series due to these innovative designs, which tremendously improve forecast accuracy and strategy flexibility.

This system consists of extremely efficient multi-objective optimization mechanism. This is how the system can improve the overall portfolio performance by reducing the risk while at the same time improving the expected return by including regularization terms for avoiding overfitting and keeping within the risk appetite for individual investors. In particular, when it comes to risks of a portfolio, generally the variance or VaR (Value at Risk), while expected return is computed from past performance and future predictions of the asset.

Also the inclusion of regularization terms like L1 and L2 regularization will not only help with preventing overfitting of the model during training but also encourage sparsity and diversity of the portfolio and avoid concentration in high risk assets. Furthermore, the introduction of constraints such as full investment, no short selling, and a value-at-risk (VaR) limit guarantee that the optimization results are both feasible and useful. These constraints not only satisfy the needs of real investment operations, but also significantly improve the robustness and anti-risk capacity of the portfolio.

2. Preliminaries

In this section, we begin by reviewing the existing artificial intelligence-based methods used in financial investment advisory service system. Subsequently, we outline the primary parameters employed in our proposed model and provide a detailed explanation of how these parameters are utilized.

2.1. Related Work

Needhi and Manokar [8] discuss AI Robo-advisors for strategic investment decision-making, they propose a new cloud-based model using deep neural networks to achieve the purpose of providing better results in investment decisions with analysis on big data of financial information and market flow. They discusses the potential benefits of AI, namely that they can help process complex financial information faster than humans and that they can help generate real-time decisions, while also approaching the stability of models in the era of market volatility. Chacón et al. [9] implemented ensemble empirical modal decomposition (EEMD) to obtain the stationary series and used the output as input to the recurrent neural networks. After decomposing the original time series data and extracting multi-scale features by EEMD, they input the multi-scale characteristics into RNN to predict the results, which effectively improves the prediction performance of the model. There are some problems such as computational complexity and real-time performance of this method.

To provide investors with personalized investment recommendations using natural language processing technology, a conversational system-based robo-advisor was proposed by Day, Lin, and Chen [10] designed to have them interact with said investors. While the experiment shows an exciting potential to improve user experience and interaction efficiency, dialogue systems still require substantial upgrades in understanding and executing complex investment strategies.

Additionally, Shun [11] presents a stock market equity advisory neural network tool. The proposed tool implements a multilayer perceptron (MLP) model to investigate historical stock market price movements and predict short-term investment opportunities. While it has been found in studies that compared to traditional statistical methods, neural networks excel in short-term forecasting, the authors of previous studies acknowledged that the main drawback of this method is that neural networks only focus on investments with short time horizons and are not able to effectively capture the essence of long-term investment strategy formulations.

Shahani et al. [12] proposed a financial investment advisory system based on an intelligent cooperative paradigm integrating a long short-term memory network (LSTM) and a multi-objective optimization algorithm. The system assesses market data and investor interests in real-time, allowing it to make constant changes to portfolios. However, the system can process high-dimensional data and diversified investment objectives, which require high computing resources and affects the scalability of the system in its practical application.

Wang et al. [13] developed a robo-advisor using multi-objective RankNets integrated with gated neural network framework. The multi-objective portfolio is optimized via the RankNets of the model and the gating mechanism which underlies the model improves the trade-off ability of the model for different investment objectives. The experimental results demonstrate that the proposed method can be effectively used in multi-objective optimization, however, it is important to note that in an actual deployment, the training time of the model is significantly longer than where our customized model is possible to implement in short time, which results in greatly limiting the real-time application capabilities of the method.

Roy et al. [14] Used deep learning methods for mutual funds and stock price predictions. The methodology improves the forecasting accuracy of robo-advisors in price and portfolio management by having LSTM and Gated Recurrent Unit (GRU) networks. It has improved in prediction accuracy; however, the ability to adapt to abnormal market conditions is still quite weak. Day et al. this involves processing large amounts of financial data and user behavior data to make personalized investment advice. The study critically highlights the significance of big data in enhancing the intelligence level of robo-advisors, while still requiring more exploration on data privacy and security.

Méndez-Suárez and García-Fernández [15] created a framework of AI models for financial automated investment advisors focused on the copper market. Our framework employs deep neural networks to analyze real-time data and integrate it with the analysis of market trends to offer active, data-driven investment recommendations. The findings indicate the model performs well with precise performance and responsiveness in trade decisions in the copper sector, but it still requires additional tests in its scope and universality in different metal markets. Lynch [16] utilize artifical neural networks (ANNs) to allocate assets within diversified portfolios. Through the combination of data from both conventional site based investment advisors and the ANN model, the risk-return trade offs in the ANN model can be used to allocate the four key asset classes. Results show that ANN-based models achieve better performances than traditional asset allocations, while they still stay less adaptive and robust to changing environments.

2.2. Primary Parameters

Additionally, we explain the primary used parameters and functions in following Table 1.

3. Methodologies

3.1. iLSTM Architecture

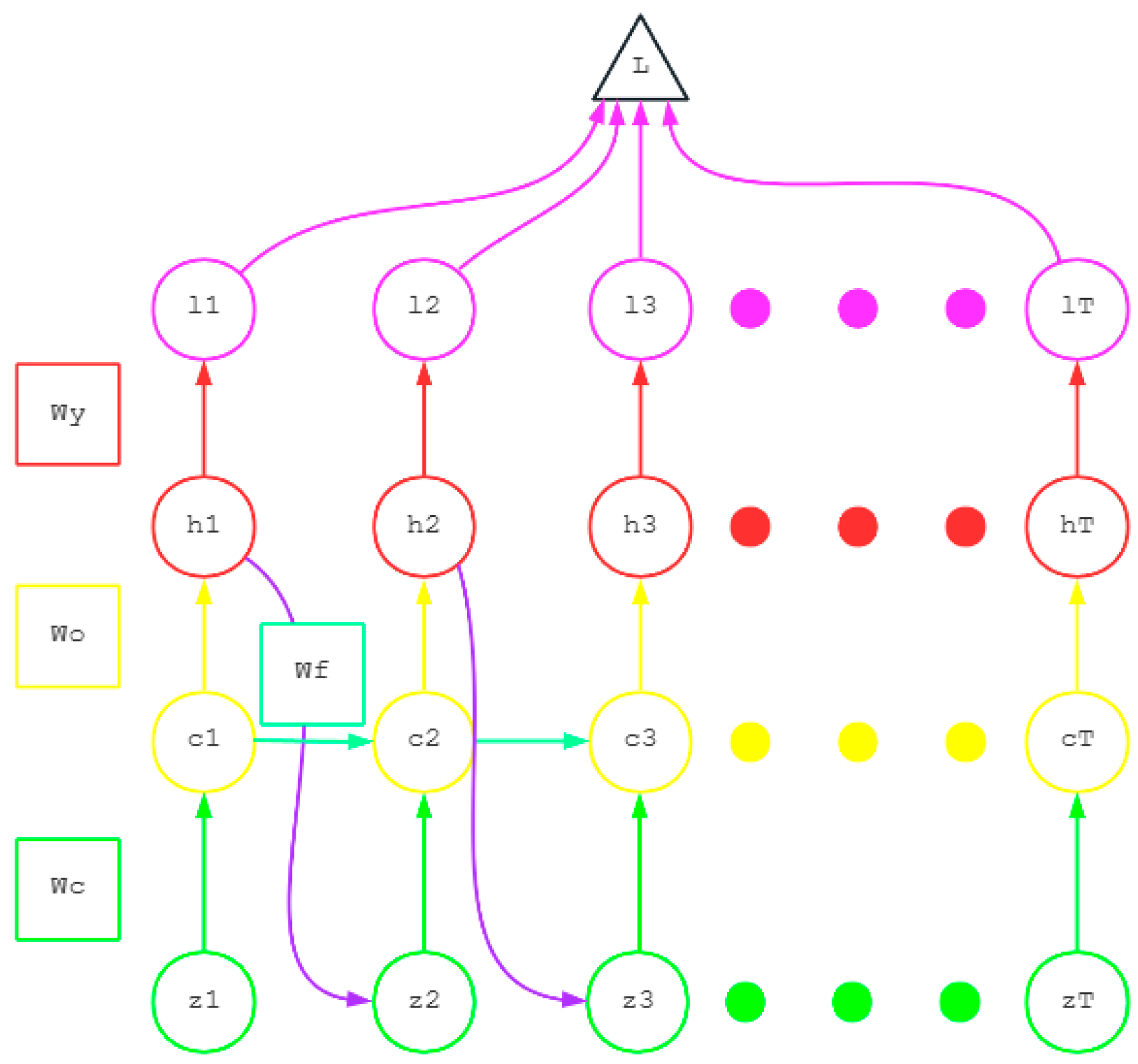

Since the traditional Long Short-Term Memory network is not adept at capturing the complex patterns that can be found in financial time series, a series of innovative improvements to it has led to the proposal of the iLSTM architecture. Based on the traditional LSTM, the iLSTM implements a Financial Feature Gate and multi-layer nonlinear transformations, reflecting the sensitivity of time-series financial data in the FFG. Subsequently, Equation 1 expands the formula of the input gate with additional nonlinear transformations and interaction terms.

where the sigmoid activation function is represented, with and denoting the weight matrices, whilst signifies the hidden state of the previous moment and represents the input of the current moment. denotes the financial feature vector at the current moment. The bias vector, , is also of significance. The symbol denotes the tensor product.

The term is introduced to facilitate the capture of the high-order interaction between the hidden state and the financial features, thereby enhancing the comprehension and processing capability of complex financial models. Subsequently, a time decay factor is incorporated into the forgetting gate to accommodate the information forgetting requirements of differing temporal increments, as illustrated in Equation 2:

where the quantity is defined as the weight matrix of the forgetting gate, the parameter is designated as the time decay factor, and the variable is denoted as the current time step. The memory effect of the financial market is known to dissipate over time. The integration of has been demonstrated to facilitate the dynamic adjustment of the forgetting gate, thereby optimising the adaptability to the time-varying characteristics of the market. In order to enhance the expression capacity of the cellular state, the iLSTM introduces helper cell state , as demonstrated in Equation 3:

In above given equation, The parameter known as is capable of being learned, whilst and represent the weight matrix and the bias vectors, respectively.

The integration of helper cell states within the model facilitates enhanced information integration, augmented memory capacity, and optimised processing of multi-dimensional financial data. The integration of the Adaptive Attention Mechanism within the model facilitates the dynamic allocation of attention to historical information at varying temporal intervals, as delineated in Equation 4,5:

where and denote the weight matrices of the attention mechanism, and signifies the number of historical steps considered.

By calculating the attention weight , the model is able to dynamically adjust the degree of attention to the hidden state of the past time steps based on the current input. This improvement in responsiveness to changes in market dynamics and the flexibility of the strategy is a result of the model's ability to make such calculations.

Finally, the output gate enhances its expressiveness through multi-layer nonlinear transformations, which are expressed as Equation 6:

The following elements are to be considered: and are the weight matrices of the output gates, while and represent an offset vector. The linear rectifier cell activation function is denoted by . It is through the implementation of multi-layer nonlinear transformation that the output gate is able to adjust the influence of cell state on the final output in a more complex manner, thereby enhancing the control and expression ability of the model in relation to complex financial models. Following Figure 1 shows the general framework of inner neural network.

3.2. Multi-Objective Optimization Mechanism

In the context of portfolio optimization, the primary objective is to achieve a balance between risk and return. To this end, a multi-objective optimization framework is employed, with the aim of minimizing portfolio risk while maximizing expected returns. To this end, a series of complex mathematical models and constraints are introduced. Firstly, the risk and expected return of the portfolio are defined, as expressed in Equations 7 and 8:

where denotes the portfolio weight vector, represents the covariance matrix of asset returns, signifies the expected return vector of the asset, and and are regularization parameters. The binary norm of the weight vector is denoted by . is a norm of the weight vector.

The incorporation of regularization terms within the risk-return function serves to impede overfitting and merging, thereby promoting the scarcity of the portfolio. This, in turn, enhances the generalisability and operational efficacy of the model in practical applications. The subsequent step is to define the objective of optimization, denoted as Equation 9:

It is important to note that and are the weight coefficients, satisfying the condition that . By weighting the risk-return objectives, the multi-objective optimization problem is transformed into a single-objective optimization problem, which is convenient to solve by optimization algorithms such as gradient descent. Constraints further refine the practicality of the portfolio, as demonstrated in Equation 10,11,12,13:

where denotes the number of assets, and represents the upper limit of the value at risk (). is the upper bound of the two norms of the weight vector.

These constraints play a critical role in keeping the workings of the portfolio as it ensures no wasted investment, no short selling, sane value-at-risk and constraints in terms of the size of the weight vector. This, in turn, increases the stability and operability of the portfolio. The Lagrange multiplier method is used to solve the above optimization problem, as shown in Equation 14:

Figure 2 illustrates the sequence of steps in the Advisor process, including the configuration phase, the matching phase, and the maintenance phase. In the allocation stage, it is responsible for providing corresponding investment advice to investors with different income-risk ratios; The matching stage is matched according to the correspondence between the type of customer and the type of investment proposal; The maintenance phase ensures the continuous optimization and adjustment of the portfolio by implementing the algorithm of the selected investment recommendations.

3.3. Real-Time Policy Adjustments

Following the completion of the design of the iLSTM architecture and the multi-objective optimization mechanism, the subsequent training process of the model and its application in real-time policy adjustment are introduced. A comprehensive loss function must be defined that combines the risks and benefits of multi-objective optimization, as illustrated in Equation 15:

where denotes the model parameter. denotes the total number of training samples. By calculating the mean of the losses for all time steps, the performance of the model on the entire training set is balanced, and the model's generalization ability is enhanced. The Adam optimization algorithm, a refined version of the original algorithm, is employed to minimize the loss function. This algorithm is updated according to the following formula, denoted as Equation 16:

where denotes the learning rate, and represent the first and second momentum estimates following bias correction, respectively, is the gradient adjustment factor, and is a small constant introduced to prevent the removal of the text.

The addition of a gradient adjustment factor to the momentum term enables the optimiser to adjust the learning pace with greater flexibility. This, in turn, has the effect of improving both convergence speed and stability, while also enabling adaptation to the high volatility characteristic of financial data. Moreover, in conjunction with Bayesian optimization methods, hyperparameters , , , and are automatically tuned, as expressed in Equation 17:

The parameter is a hyperparameter, is employed to balance expectation and variance. The employment of Bayesian optimization facilitates the identification of the optimal combination of hyperparameters within the efficient search space, thereby enhancing the performance of the model and the efficacy of the investment strategy.

4. Experiments

4.1. Experimental Setup

The data set consists of daily trading data of S&P 500 index constituents over the period of January 1, 2010 – December 31, 2023, and can be found on Yahoo Finance's S&P 500 historical information. The data is also broad based representative with high quality data sources for over 14 years of performance going through multiple economic cycles and major events minimizing the bias in the model training and testing underneaht different market conditions. The dataset is split 80%/20% to be used to train the novel Long Short-Term Memory Network (iLSTM) model and evaluate the model based on prediction accuracy, portfolio return, and risk control. Moreover, the optimization result is constrained by a multi-objective optimization mechanism to simultaneously minimize risk and maximize benefits, ensuring the feasibility and practicality of the optimization result.

In this study, various existing methods were selected as baselines: the traditional investment advisory model based on fixed rules and asset allocation strategy, the standard long short-term memory network (LSTM), the gated recurrent unit (GRU) model, the genetic algorithm (GA) for multi-objective optimization, the ensemble empirical modal decomposition combined with recurrent neural network (EEMD+RNN) as well as the use of generative adversarial network (GAN) in investment advisors. Advisor Bot 2.0 and its performance is portrayed across the comparison analyses as it highlights the difference between classical experience-based approaches to modern deep learning and optimization techniques in terms of new performance metrics such as forecast accuracy for up to 12 decades, portfolio optimization, risk management, and adaptability.

4.2. Experimental Analysis

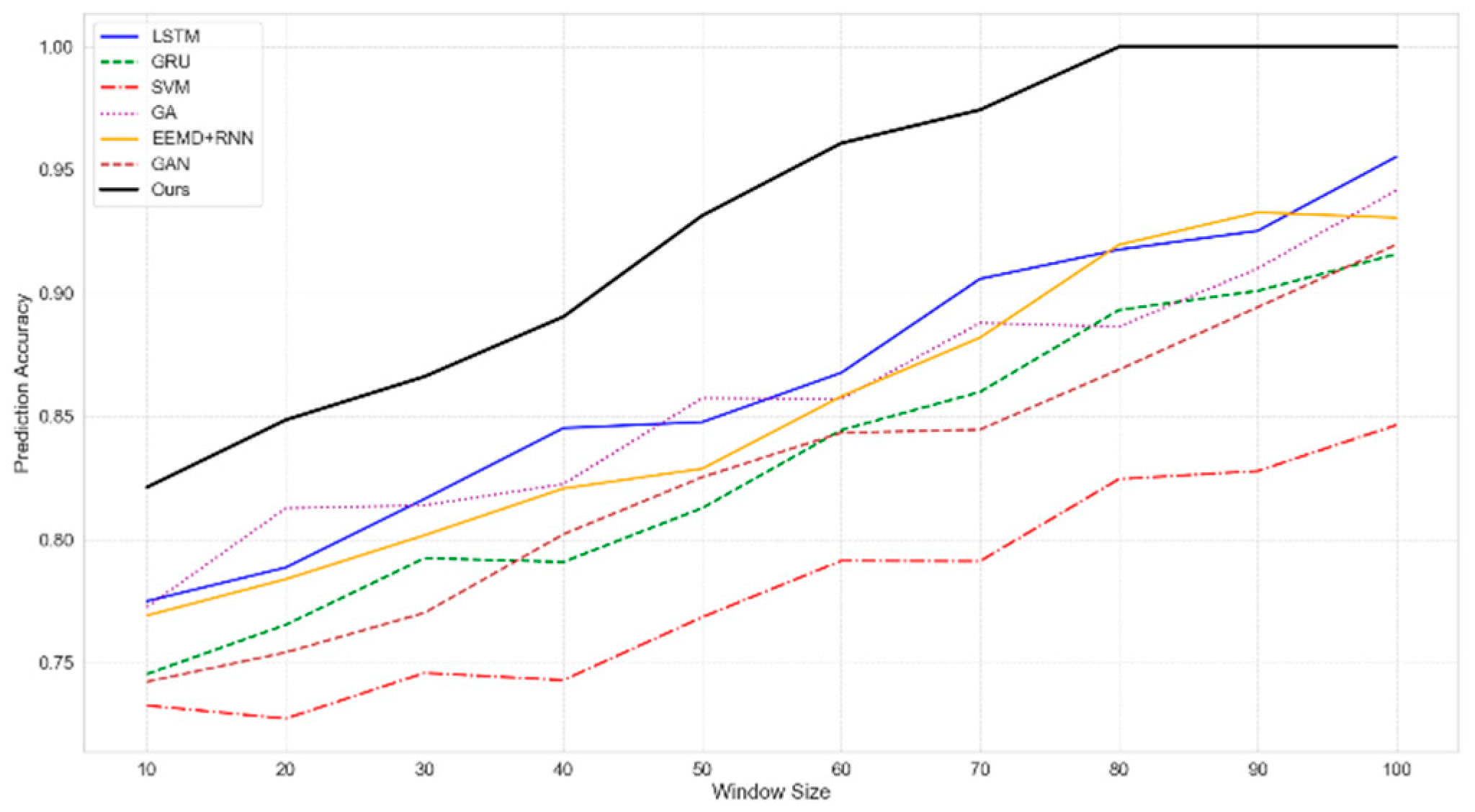

[Figure 3 here]Comparison of the prediction accuracy of different models with multi-parameter settings. The abscissa, for example, contains various parameter settings (e.g., 10 to 100 different sizes of time windows) that collectively indicate the ability of the model to make accurate spread predictions across multiple time frames. Methods used included: standard Long Short-Term Memory Network (LSTM), Gated Recurrent Unit (GRU), Support Vector Machine (SVM), Genetic Algorithm (GA) for multi-objective optimization, Ensemble Empirical Mode Decomposition Combined with Recurrent Neural Network (EEMD+RNN), Generative Adversarial Network (GAN), and the proposed "Ours" method.

As shown in Figure 3, the application of the "Ours" method achieves a high degree of accuracy in prediction at nearly all parameter settings and outperforms the other comparison models significantly. As a case in point, the "Ours" method shows its power for long-range time horizons where accuracy continues to ascend with larger other time windows, 80 and 100. On the other hand, the traditional models like SVM and GRU, have less prediction accuracy, especially when the parameters settings are higher. Moreover, though LSTM and EEMD+RNN outperform us in one or two parameters, they perform overall worse than "Ours", which reflects the adaptability and robustness of our method in the analysis of complex financial timeseries data.

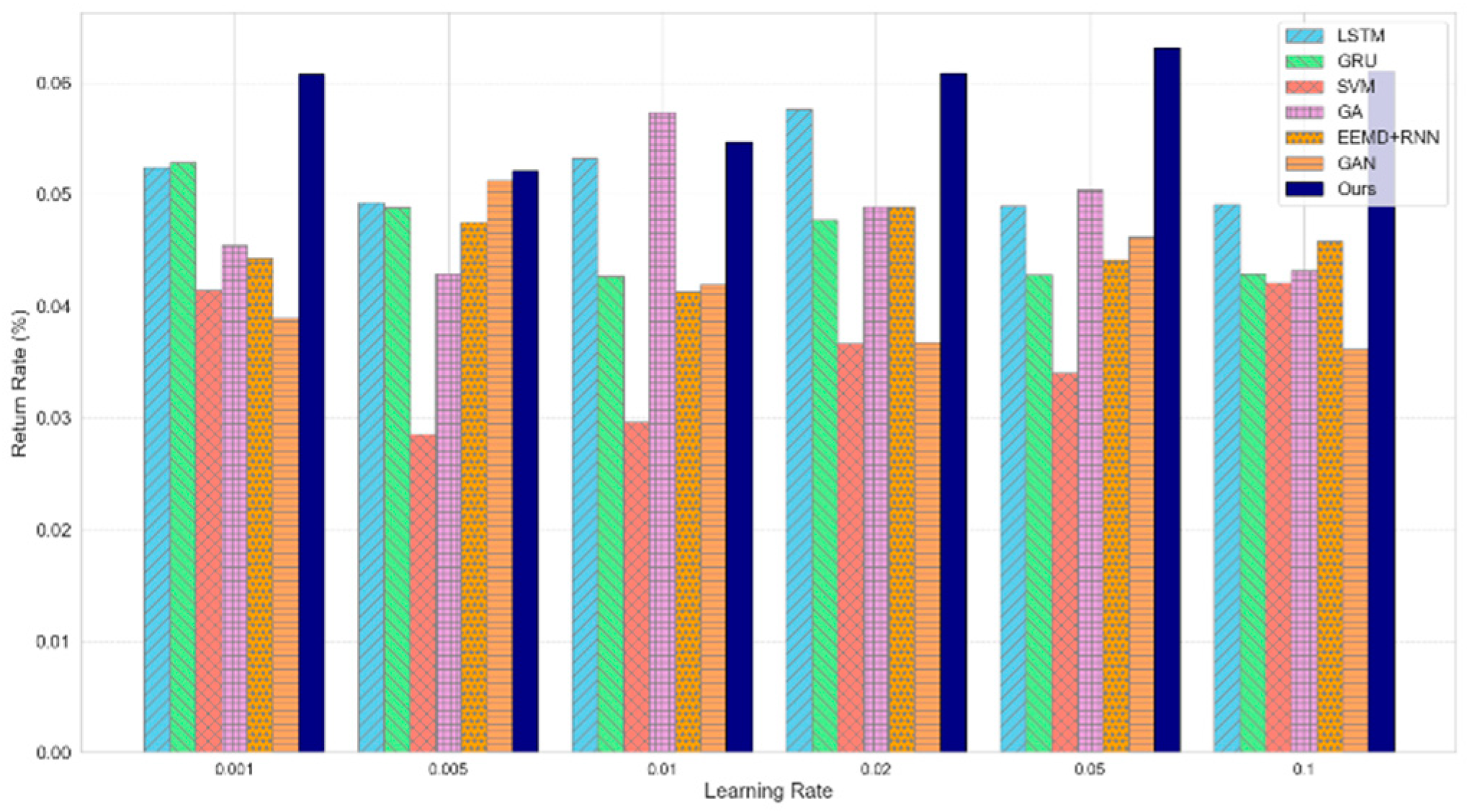

Figure 4 shows the portfolio return of each model at different learning rates. Figure 4 clearly shows that the "Ours" method achieves the highest rate of return at all learning rate settings, significantly outperforming the other comparison models. This suggests that our approach is more adaptable and stable under different learning conditions, and can effectively optimize portfolio returns. Figure 4 visually shows the relative performance differences of each model, which further verifies the advantages of iLSTM architecture and multi-objective optimization mechanism in improving the accuracy and efficiency of investment decision-making.

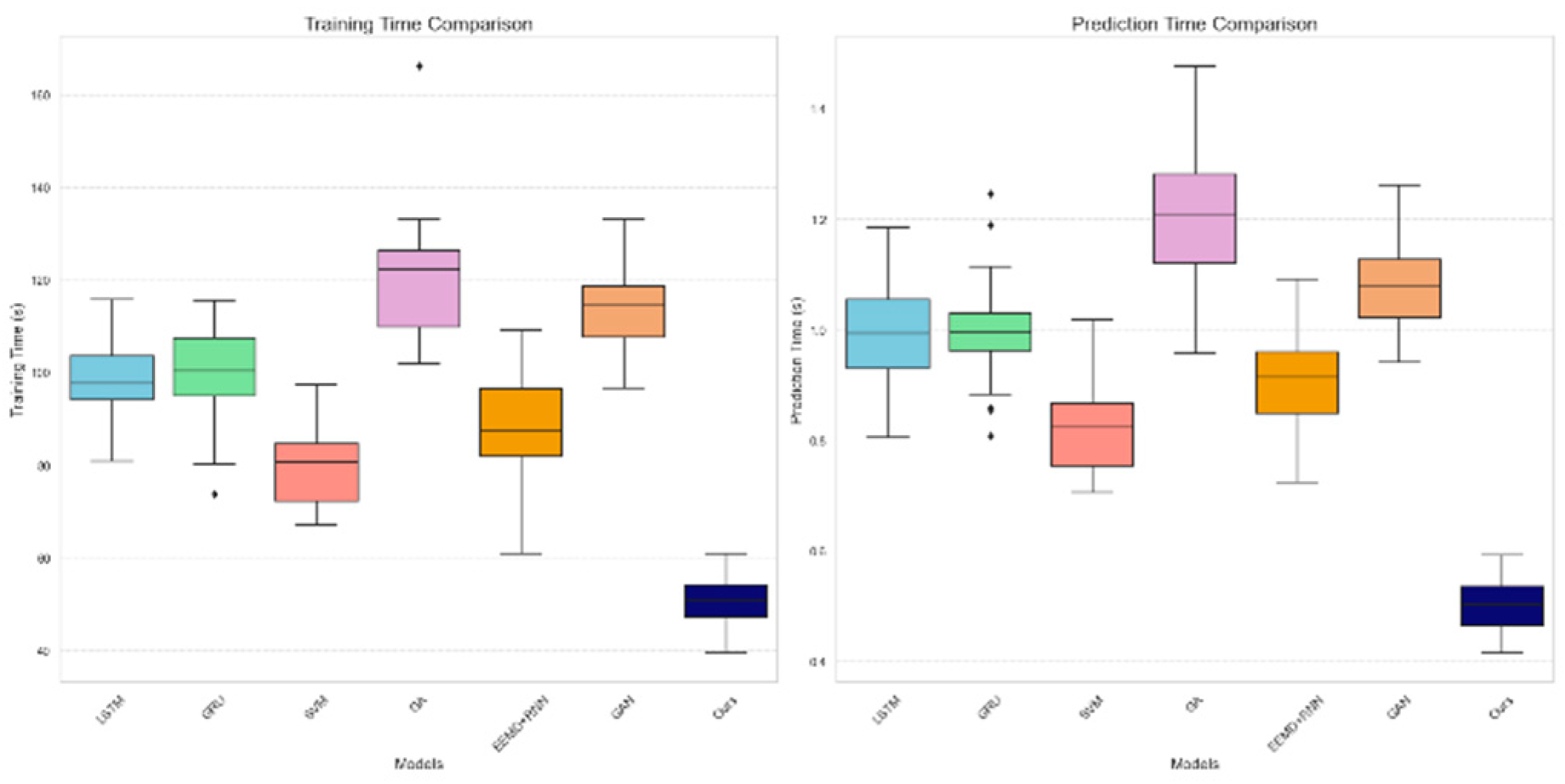

Another two major performance statistics were the training time and prediction time to comprehensively evaluate the Investment Advisor Robot 2.0 system performance. Training Time——It defines the overall duration needed for the model to accomplish the whole training on the training set, and displays the training efficiency of the model. Prediction time refers to how long it takes for the model to make predictions on the new data, summarizing the responsiveness of the model to real-world applications in terms of real-time. Boxplot comparison between all models selected in this work according to the training time and prediction time.

As shown in Figure 5, our method "Ours" has considerable advantages over others in terms of training time and prediction time. More specifically, the "Ours" method shows more concentrated, shorter training time distribution, which indicates its efficient training process. As for prediction time, the median of the "Ours" method not only reaches a lower level, but also has a small range of fluctuations, which shows that the proposed method has a faster response time and a higher stability for new data. On the contrary, several models, including GA and EEMD + RNN, have long training and prediction times with great variability in prediction time, limiting their application in real-time investment decisions.

5. Conclusions

In conclusion, the most prominent feature of this work is that it systematically designs experiments and comprehensively evaluates the performance of the Investment Advisor Robot 2.0 system with multidimensional evaluation indicators. Experimental results reveal that the proposed "Ours" method outperforms traditional models and other state-of-the-art deep learning methods in prediction accuracy, portfolio return, training efficiency and prediction response speed. In particular, the "Ours" method not only achieves a high prediction accuracy and return rate under different learning rates, but also achieves a significantly more efficient and stable performance regarding training time and prediction time, which illustrates its great potential and advantages in practical financial applications. Future research will focus on integrating more real-time data sources and advanced algorithms to improve their adaptability and decision-making capabilities in complex market environments.

References

- Qian, Hao, et al. "MDGNN: Multi-Relational Dynamic Graph Neural Network for Comprehensive and Dynamic Stock Investment Prediction." Proceedings of the AAAI Conference on Artificial Intelligence. Vol. 38. No. 13. 2024. [CrossRef]

- Lee, Woon Ming. Stock market equity advisory tool using analytic hierarchy process and single-layer perceptron neural network. Diss. UTAR, 2023.

- Nguyen, Minh. "AI-Powered Financial Advisory Services." Journal of AI-Assisted Scientific Discovery 4.2 (2024): 115-125.

- Asemi, Asefeh. A Novel Combined Investment Recommender System Using Adaptive Neuro-Fuzzy Inference System. Diss. Budapesti Corvinus Egyetem, 2023.

- Trivedi, Jeegar A., and Priti Srinivas Sajja. "Online Guidance for Effective Investment Using Type 2 Fuzzy-Neuro Advisory System." International Journal of Computer Science and Information Technologies (IJCSIT) 2.2 (2011): 799-803.

- Talwar, Shalini, et al. "Why retail investors traded equity during the pandemic? An application of artificial neural networks to examine behavioral biases." Psychology & Marketing 38.11 (2021): 2142-2163. [CrossRef]

- Shao, Qixiang, et al. "Toward intelligent financial advisors for identifying potential clients: a multitask perspective." Big Data Mining and Analytics 5.1 (2021): 64-78. [CrossRef]

- Needhi, Jeyadev, and S. Manokar. "Enhancing Financial Intelligence: AI Robo-Advisors for Strategic Investment Decisions." (2024).

- Day, Min-Yuh, Jian-Ting Lin, and Yuan-Chih Chen. "Artificial intelligence for conversational robo-advisor." 2018 IEEE/ACM International Conference on Advances in Social Networks Analysis and Mining (ASONAM). IEEE, 2018.

- Ng, Shun Yi. Stock market equity advisory tool by using of neural network method. Diss. UTAR, 2024.

- Shahani, M. N. A., et al. "INVESTOPAL-Smart Financial Investment Advisory System." 2023 7th International Conference On Computing, Communication, Control And Automation (ICCUBEA). IEEE, 2023.

- Wang, Pei-Ying, et al. "A robo-advisor design using multiobjective RankNets with gated neural network structure." 2019 IEEE international conference on agents (ICA). IEEE, 2019.

- Roy, Sunil K., et al. "Empowering Robo-Advisors: Data-Driven Mutual Fund and Stock Market Price Prediction with Deep Learning Techniques." 2024 Third International Conference on Electrical, Electronics, Information and Communication Technologies (ICEEICT). IEEE, 2024.

- Day, Min-Yuh, Tun-Kung Cheng, and Jheng-Gang Li. "AI robo-advisor with big data analytics for financial services." 2018 IEEE/ACM International Conference on Advances in Social Networks Analysis and Mining (ASONAM). IEEE, 2018.

- Méndez-Suárez, Mariano, Francisco García-Fernández, and Fernando Gallardo. "Artificial intelligence modelling framework for financial automated advising in the copper market." Journal of Open Innovation: Technology, Market, and Complexity 5.4 (2019): 81. [CrossRef]

- Lynch, Dustin Shane. Asset Allocation Technique for a Diversified Investment Portfolio Using Artificial Neural Networks. MS thesis. Ohio University, 2015.

Figure 1.

Framework of the proposed ILSTM neural network.

Figure 2.

Illustration of execution process of advisory robot.

Figure 3.

Prediction Accuracy Comparison Across Models.

Figure 4.

Investment Portfolio Return Comparison Results.

Figure 5.

Training and Prediction Time Comparison.

Table 1.

Notions.

| Notion symbols | Utilization |

|---|---|

| Sigmoid activation function | |

| Weight matrix of the forgetting gate | |

| Regularization parameters | |

| The fully invested Lagrange multiplier | |

| Weight coefficients | |

| Upper limit of the value | |

| Upper bound of the two norms of the weight vector | |

| The total number of training samples | |

| Small constant |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.