Submitted:

24 February 2025

Posted:

26 February 2025

You are already at the latest version

Abstract

This study examines the influence of psychological biases on investment decision-making through the lens of behavioral finance, challenging the traditional assumption of investor rationality. By integrating psychological insights with economic principles, the research investigates how cognitive biases such as loss aversion, overconfidence, and herd behavior along with emotional factors, distort rational financial choices, leading to market inefficiencies and suboptimal outcomes. Employing a mixed-method approach, the study combines qualitative insights from interviews with financial experts and quantitative data from a survey of 398 retail investors in Jammu and Kashmir. The findings reveal the significant role these biases play in shaping risk perceptions, portfolio management, and market volatility. Furthermore, the research proposes practical strategies, including structured decision-making frameworks, professional guidance, and emerging technologies like AI, to mitigate the adverse effects of irrational behavior. By highlighting the interplay between human psychology and financial decision-making, this study contributes to a deeper understanding of investor behavior and offers actionable insights for improving investment performance in dynamic market environments.

Keywords:

1. Introduction

Behavioural Finance

Investment Decisions

- Risk-Seeking Investors: Also known as risk-takers, these investors prefer higher-risk options when presented with two investments offering the same rate of return but differing risk levels. They are inclined toward bold and high-risk investments in pursuit of potentially greater rewards.

- Risk-Neutral Investors: These investors require a proportional increase in return for any additional risk they assume. Highly adaptable, they often make strategic and well-calculated investment decisions.

- Risk-Averse Investors: Also referred to as risk avoiders, these investors prioritize safety and prefer the lower-risk option when faced with two investments offering the same expected return. They tend to make cautious, well-thought-out financial decisions.

2. Literature Review

Scope of the Study

Objectives of the Study

- To explore how cognitive biases and emotional triggers shape investment decisions, especially in volatile markets.

- To assess strategies that mitigate irrational decision-making and enhance portfolio performance.

Methodology

Research Design

Sample size and Data Collection Methods

Primary Data

Secondary Data

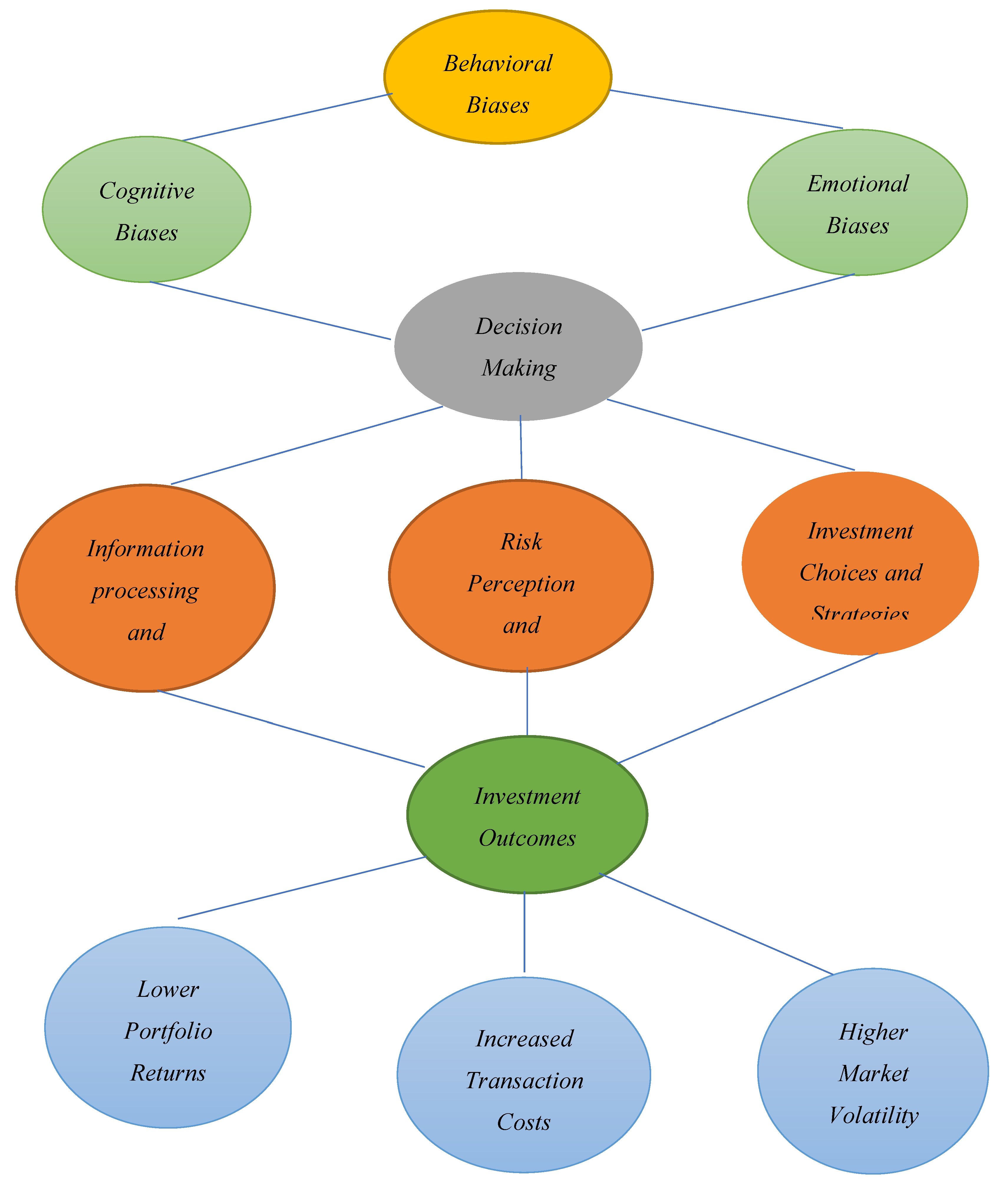

Theoretical Model of Behavioral Biases in Retail Investors' Decision-Making Process

| Investment Behaviour of Retail Investors | N | Mean | S. D |

|---|---|---|---|

| My sense of accomplishment and emotional well-being are closely tied to the profitability of my trades | 398 | 4.2940 | .51820 |

| Experiencing losses in trading significantly impacts my mood and confidence | 398 | 4.2764 | .51083 |

| I often exhibit a tendency toward risk aversion by securing profits prematurely. | 398 | 3.8166 | 1.00077 |

| Rather than closing trades early, I implement a trailing stop-loss strategy to manage risk and maximize gains. | 398 | 2.9472 | .97305 |

| I strictly follow predetermined stop-loss levels to mitigate losses and maintain discipline | 398 | 4.1533 | .47521 |

| I sometimes resist closing losing positions, expecting the market to eventually reverse in my favor | 398 | 3.0754 | 1.06435 |

| My approach to trading is structured around predefined profit targets. | 398 | 4.0101 | .63078 |

| My confidence in trading stems from my perception that my overall gains surpass my losses. | 398 | 2.7663 | .94598 |

| Past trading losses have triggered impulsive decision-making, leading to further financial setbacks. | 398 | 3.5126 | .96987 |

| My trading decisions are predominantly shaped by external information, such as market news and stock-related updates. | 398 | 4.1809 | .53815 |

3. Discussion

- Loss Aversion and Its Role in Portfolio Management

- 2.

- Overconfidence in Active Trading

- 3.

- Herd Mentality and the Formation of Market Bubbles

- 4.

- The Role of Behavioral Biases in Financial Crises

- 5.

- The Concept of Emotional Investing and Its Impact on Market Volatility

4. Conclusion

References

- Barberis, N., & Thaler, R. (2003). A survey of behavioral finance. Handbook of the Economics of Finance, 1, 1053-1128. [CrossRef]

- Bikas, E., Tiwari, R., & Sharma, N. (2013). Behavioral finance: A comprehensive review. International Journal of Economics and Financial Issues, 3(2), 588-596.

- Haroon, O., & Rizvi, S. A. R. (2020). Behavioral finance and investor psychology: A review. Journal of Behavioral and Experimental Finance, 25, 100285.

- Muhammad Atif Sattar, F., Rizvi, S. A. R., & Iqbal, M. Z. (2020). Behavioral biases in financial decision-making: A comprehensive review. Journal of Behavioral and Experimental Finance, 25, 100296.

- Bansal, A. (2015). Behavioral finance: An overview. Research Journal of Finance and Accounting, 6(9), 38-42.

- Roopadarshini, S. (2014). Behavioral finance: A study of behavioral biases in investment decisions. Indian Journal of Finance, 8(6), 42-53.

- Senthamizhselvi, A. V. (2020). Behavioral finance: Impact of psychological biases on investment decisions. Journal of Financial Planning and Analysis, 15(1), 11-16.

- Subashree, P. (2024). Behavioral finance and market anomalies: A critical review. International Journal of Finance and Banking Studies, 13(2), 118-130.

- Singh, R. (2009). Behavioral finance: The role of psychology in investment decisions. International Journal of Business and Management, 4(10), 21-30.

- Gill, M. S., & Bajwa, I. S. (2018). Behavioral finance and market anomalies: The impact of psychological biases on investor behavior. Journal of Financial Markets, 6(2), 103-118.

- Reilly, F. K., & Brown, K. C. (2011). Investment analysis and portfolio management (10th ed.). Cengage Learning.

- Brennan, M. J. (1995). The role of investment in a portfolio: A review. Journal of Finance, 50(3), 907-936.

- Tandelilin, E. (2001). Portfolios and risk management. Pustaka Pelajar.

- Kartini, K., & Nahda, K. (2021). Behavioral biases in investment decisions: Evidence from Indonesian stock market. Journal of Behavioral and Experimental Finance, 28, 100442.

- Muhammad Atif Sattar, F., Rizvi, S. A. R., & Iqbal, M. Z. (2020). Behavioral biases in financial decision-making: A comprehensive review. Journal of Behavioral and Experimental Finance, 25, 100296.

- N. Sathya, & R. Gayathir. (2024). Behavioral finance: A review of biases affecting financial decisions. International Journal of Finance and Banking Studies, 14(2), 92-105.

- Pandit, K. (2021). Cognitive biases and their impact on financial markets. Journal of Finance and Economics, 12(3), 210-225.

- Othman, N. N. (2024). Impact of cognitive biases on investment decisions in emerging markets. International Journal of Financial Planning and Analysis, 15(1), 57-68.

- Wang, Y. (2023). Cognitive biases in financial decision-making: A study on investor behavior. Journal of Financial Decision Making, 36(4), 467-480.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).