Submitted:

20 January 2025

Posted:

21 January 2025

You are already at the latest version

Abstract

Global CO2 concentrations keep rising despite all the efforts to decarbonize and limit the harmful emisions of Green House Gasses. This paper examines the role of sustainable business in reducing and limiting global CO2 concentrations based on daily CO2 data from Mauna Loa Observatory. Factors considered significant in determining global CO2 concentrations include economic variables like the Crude Oil Price and Dow Jones Sustainability Index but also astronomical variables such as Total Solar Irradiance and Cosmic Rays. Particular attention is drawn to the fact that in the COVID-19 pandemic while everyone was working from home, cars were not allowed on the roads and planes were not flying, the correlation between Dow Jones Sustainability Index and the global CO2 concentration was negative, what you could expect if business is to be the force for good, while before and after the pandemic, this correlation became positive. The final integrated model of global CO2 concentrations is built based on 2195 daily observations including all the variables outlined above. A range of policy conclusions is drawn.

Keywords:

Dow Jones Sustainability Index

; CO2 emissions

; ESG

; business sustainability

; econometric modelling

1. Introduction

Transformation of business models for sustainability, the role of impact investment as a transformational force and the role of business in driving sustainable progress have been embraced by a whole number of advocates including Cohen (2020) [8], Eccles, Ioannou, and Serafeim (2014) [13], and Elkington (2021) [16], Carney (2021) [4] and Polman (2022) [40]. In this paper we are going to establish if sustainable business performance as expressed in the Dow Jones Sustainability Index impacts the global concentrations of CO2 and can be ultimately considered the force for good. For the purposes of this paper, we define "force for good" as the ability of businesses to create measurable positive impacts on societal and environmental outcomes, beyond merely generating profit. This encompasses actions that contribute to reducing global CO₂ concentrations, fostering equitable economic development, and enhancing long-term sustainability. To this end, we will review recent contributions to the field of ESG investment, build a comprehensive econometric model of global CO2 concentrations and try to explain the variance in CO2 emissions based on a whole range of variables. By doing so, we aim to determine whether sustainable business practices, as reflected in the Dow Jones Sustainability Index (DJSI), can substantively reduce CO₂ levels and be considered a true "force for good”. Policy conclusions will follow.

2. Literature Review

Environmental, Social and Governance (ESG) investment has become an important player in the global financial markets. According to Bloomberg Intelligence, the projected ESG assets under management of $53 trillion would represent approximately 36.9% of the total global assets under management by 2025, assuming a steady growth rate of 6.5%. The UN Principles for Responsible Investment define ESG as “the key factors used to measure the sustainability and societal impact of an investment in a company or business” [75]. ESG factors are increasingly important for investors, companies, and other stakeholders to assess risks, opportunities, and long-term performance. Many studies examined various dimensions of ESG investing, reporting and have been predominantly focused on measuring the impact on financial performance. We have conducted a rigorous and structured literature review of the major contributions to the ESG field that you could see in Table 1. In the table, the major studies are described in terms of the country of focus, methodology used and the key findings. Below we will examine some of the contributions in more detail.

The findings indicate that ESG investing has, on average, performed similarly to conventional investing and sometimes even better. More specifically, recent research demonstrated that they found a positive relationship between ESG and financial performance for 58% of the studies focused on operational metrics such as ROE, ROA, or stock price with 13% showing neutral impact, 21% mixed results and only 8% showing a negative relationship. (Whelan et al, 2021) [66]. According to some studies ESG investing has been found to provide asymmetric benefits, particularly during social or economic crises, while in other studies it has been demonstrated that companies with high engagement with ESG managed to perform better in periods of crisis thanks to high levels of resilience and a lower volatility in the market (Broadstock et al., 2020). Overall, ESG integration as a strategy has been shown to be more effective than screening or divestment (Krosinsky and Purdom, 2016) [32].

ESG is clearly a strategic priority for many businesses and interested stakeholders nowadays; indeed, it has been found that many studies were focused on analyzing the internal and external drivers of ESG engagement. According to Crace and Gehman (2023), the most significant drivers came from within the firm and directly from the CEO. Furthermore, the authors indicate that negative ESG performance is usually correlated with external factors, whereas positive ESG performance has to deal with internal ones. These findings support previous analysis on internal drivers made by Eccles et al. (2011) who had stated the significant influence of the board of directors and firm’s governance on the level of ESG engagement. In more sustainably-minded corporations, boards are more keen on overseeing environmental and social issues, while management compensation may include sustainability metrics alongside financial ones.

Eccles and Serafim (2013) have provided a step-by-step approach that helps in defining materiality in the ESG context. To achieve this aim, companies need to take four steps: establish, which ESG issues are most important for their specific economic sector; estimate the potential financial savings stemming from resolving these issues; achieve the improvements, implement significant innovations in products, procedures, and, ultimately, business models and finally share the innovations with stakeholders. Naturally, integrated reporting, which combines financial and ESG performance data into a single document, is a powerful tool to assist in this process (Shmelev, 2012). Freiberg et al. (2020) investigated how ESG issues become material in the financial fields in the context of the Purdue Pharma business case. The authors designed a framework, which follows five steps on a journey that starts with the identification of a particular externality (related to an ESG issue) and reaches the disclosure of a specific regulation that tries to manage that specific ESG issue. Thus, the concept of materiality, as well as the level of impact, have a high relevance in this context.

Porter et al. (2019) [41] have indicated that investors must consider social factors alongside financial metrics, recognizing their influence on long-term competitive advantage (shared-value investing); but in the article they also criticize the efficiency of traditional ESG rankings and particularly its link with alpha generations, or those born in the 21st century. The importance of effective communication between companies and investors regarding the economic value of social impact has increased noticeably; examples of the success of this type of investments are Generation Investment Management and Summa Equity.

Several authors acknowledge, that investors should allocate capital towards companies driving social progress profitability, where capitalism is harnessed to address society’s most pressing needs while generating sustainable shareholder returns. The new movement called B-Corp movement is built entirely around the idea that business could be the force for good. By embracing shared-value thinking, investors can unlock growth, foster innovation, and contribute to a more equitable and prosperous future for all stakeholders. ESG scores have gained prominence as primary financial tools for constructing green portfolios and evaluating companies’ performances in the field of responsible investment as well as for enhancing transparency, trust and credibility among stakeholders (Suhita et al., 2020) (Linnenluencke, 2021) (Clement et al., 2023). ESG scores mitigate risks associated with environmental or social scandals by anticipating potential negative impact on investments. Companies that prioritize ESG considerations stand to gain not only enhanced market value but also improved financial performance and reduced risk exposure, which are, indeed, integral components of corporate strategy and value creation (Suhita et al., 2020) (Wang et al., 2022) (Clement et al., 2023). Friedea et al. (2015) have also discussed the evolving landscape of Environmental, Social and Governance criteria within investment decisions and highlight the slow adoption of sustainable investment practices among mainstream investors despite the significant assets managed under Principles for Responsible Investment signatories. Liennenluecke (2021) argues that even if there is a shift towards sustainable investments, there are many challenges in the market due to weaker institutions, less stringent regulatory environments and limited transparency.

Although there has been a higher interest in nonfinancial information (Shmelev, 2012) since the late 1990s (with the observed growth from 20 reporting organizations in 1999 to over 12,000 companies today), it has been noticed that the correlation between financial returns and such practices is not equivalent among environmental, governance and social issues. Indeed, Huang (2019) argues that environmental ESG measures tend to exhibit a stronger relationship with operational financial performace measures compared to social or governance ESG measures. Eccles et al. (2011) instead have stated that environmental and governance metrics are the ones on which investors are more interested in. Equity investors show more interest in ESG disclosure and GHG emissions data compared to fixed income investors. This study highlights also disparities between broker-dealers and money managers with the same distinction of the previous ones. Serafim and Yoon (2022) studied market reactions to diverse ESG news items and assesses the predictive power of ESG performance scores. Key findings reveal substantial market reactions to financially material ESG news, particularly positive news related to social capital issues like product impact. The study challenges traditional assumptions about investor responses to ESG news and underscores the evolving role of ESG considerations in investment strategies. Positive ESG news, especially regarding product quality and safety, drives significant market reactions, while negative news impacts market performance, particularly concerning customer welfare and GHG emissions. The research highlights the importance of unexpected news in influencing market dynamics and emphasizes the selective nature of market reactions to ESG news.

Menicucci and Paolucci (2022) have also pointed out the effects of ESG in the banking sector. They assessed the feasibility of enhanced corporate governance, reduced environmental impact, and social responsibility programs. Environmental commitments positively impact efficiency and trust, while social initiatives may challenge profitability. Corporate governance, especially board diversity and risk governance, correlates positively with performance. Empirical findings suggest varying impacts of ESG dimensions on bank performance, highlighting the complex relationship between ESG factors and profitability.

One of the consequences of the increase in engagement with ESG activities has been the development of ESG reporting and integration. Organizations like Global Reporting Initiatives (GRI), Sustainability Accounting Standard Board (SASB), International Integrated Reporting Committee (IIRC) and Carbon Disclosure Project (CDP) are playing a crucial role in promoting disclosure and accountability (Kotsantonis et al., 2016; Eccles et al., 2011). Efforts by organizations like the Global Sustainable Investment Alliance and sustainable stock exchanges aim to improve ESG data availability and quality. There is still skepticism about its accuracy, specifically in relation to data imputation methods that should be transparent as to ensure consistency and reliability to data (Kotsantonis et al., 2019). Linked to this trend, although there has been an increase in the number of sustainability reports published to enhance better transparency, there is still the need for improvement in ESG reporting: Arvidsson et al. (2021) underscore the importance of aligning ESG reporting with global standards and addressing sustainability challenges through proactive policies and enhanced reporting practices.

Eccles et al. (2014) have deeply studied the difference in performance between 90 high sustainability firms of the mis-1990s with similar low sustainability firms. The main conclusions of their research are that high sustainability firms exhibit a stronger governance structure, link executive compensation to sustainability metrics, engage stakeholders more proactively and disclose more nonfinancial data. This suggests that integrating social and environmental issues into business strategies may yield long-term financial benefits and improve stakeholder relationships. Regarding corporate performance, high sustainability firms tend to outperform low sustainability firms over the long term. Overall, the results show that High sustainability firms exhibit superior performance, with ESG activities as a source of competitive advantage which helps companies in SRI in the long term. (Eccles et al., 2011). However, Eccles et al. argue that High sustainability firms may underperform due to constraints imposed by their sustainability culture, or they may outperform due to better human capital, supply chains, community relations and innovation. However, in the study proposed, High sustainability firms significantly outperform Low sustainability firms, with annual abnormal performance higher by 4.8% on a value-weighted basis and 2.3% on an equal-weighted basis exhibiting also a lower volatility in their performance.

Serafim & Yoon (2011) studied the effects of sustainability disclosure regulations on corporate practices and valuations and they highlighted that while the disclosure of ESG information could enhance firm value through improved management practices and stakeholder perceptions, it also imposes potential costs and risks on firms. In fact, they have individualized positive aspects: improvement in management practices, operational efficiency, enhanced stakeholder trust, attraction of socially responsible investors and improved access to capital; and negative effects: compliance costs that could strain financial resources, mandatory disclosure may reveal proprietary or competitively sensitive information, potentially causing strategic risks or disadvantages negatively affecting firm value. In another study, Serafim and Yoon (2022) also investigated whether consensus ESG ratings predict future ESG-related news and how disagreement among raters affect this predictive ability. Despite challenges in assessing ESG rating quality due to disagreement among raters and the multidimensional nature of ESG issues, consensus ratings can forecast future news. Positive ESG news prompts a market response, although firms with high ESG ratings show smaller reactions, suggesting such news is already priced in. Firms with low rating disagreement experience stronger stock price reactions, indicating higher expectations for future news. ESG ratings from different providers vary in predictive ability, with the most predictive rating influencing future stock returns, particularly in cases of high disagreement. Overall, ESG ratings serve as proxies for market expectations and can forecast future news and stock returns, despite rating disagreement. While acknowledging that predictive ability is just one aspect of rating quality, the findings highlight the importance of ratings in reflecting organizational commitments to ESG outcomes. Furthermore, Broadsrock et al. (2020) found that firms with higher ESG ratings experience smaller stock price declines and lower volatility during period of crisis, with a specific study about stock prices during the pandemic period (COVID-19).

In contrast with the previous findings, Halbritter and Dorfleitner (2015) state that ESG portfolios do not exhibit significant return differences between companies with high and low ESG ratings; the study finds that the influence of ESG variables on returns is inconsistent across different ESG rating providers, indicating that the relationship is highly dependent on the specific rating methodology. Over time, there appears to be a diminishing impact of ESG variables on returns therefore suggesting a potential weakening of the relationship between CSP and CFP.

The article provided by Babynina et al. (2023) identifies significant ESG issues within the Russian business landscape, highlighting that the main challenges include a lack of understanding at the corporate level regarding the real impact of sustainable development projects, insufficient skills among employees and limited financial resources as well as external factors like geopolitical dynamics and regulatory frameworks; that’s why the solution proposed would be the creation of the National ESG Alliance and the development of an ESG Infrastructure Atlas.

The study of Sadiqa et al. (2022) explores global challenges arising from industrial expansion and the limited engagement in environmental and social initiatives despite increasing awareness. It discusses the 2030 Agenda for Sustainable Development, comprising 17 SDGs targeting environmental, social, and economic sustainability. ESG criteria are pivotal in evaluating firms' commitment to these goals, emphasizing environmental protection, social welfare, and corporate governance. Collaborative efforts from businesses are crucial to achieve SDGs, with effective environmental policies and social governance practices facilitating progress. Corporate governance ensures accountability and transparency, enhancing financial and social performance. In ASEAN countries, progress varies across social, environmental, and economic indicators. While strides have been made in poverty reduction and gender equality, environmental challenges persist. The article stresses the need for enhanced environmental, social, and corporate governance to accelerate SDG attainment (Sadiqa et al., 2022).

The Brazilian case studied by Miralles-Quirós et al. (2018) states that investors positively value CSR practices in Brazialian listed firms according to the value enhancing theory. However, while the market significantly values environmental practices, it does not equally value all three pillars of ESG. Specifically, social and corporate practices in environmentally sensitive industries generate significant added value in stock prices.

The analysis conducted by Strekalina et al. (2023) delves into the intricate dynamics between ESG performance and financial outcomes, reflecting the evolving landscape where businesses increasingly integrate sustainability into their operations pointing out that there is not a universally accepted positive/negative impact of ESGP on FP. Furthermore, the paper points out geographical variations in the ESG-FP relationships, noting difference between developed and emerging economies. While advanced economies may have stronger regulatory frameworks and shareholder activism, emerging markets face unique challenges related to institutional capacity and information dissemination. It is, therefore, important to study geographical influences on the ESG financial performance relationships, particularly within emerging markets like the BRICS countries, where each country adapts the sustainable development agenda differently. The studies reviewed here are summarized in Table 1.

3. Analysis

In this paper we will attempt to connect the global CO2 concentrations with a range of variables including corporate sustainability performance to understand if business could really be the force for good. CO₂ concentrations are defined as the amount of carbon dioxide present in a given volume of air, typically expressed in parts per million (ppm), representing the ratio of CO₂ molecules to every one million air molecules, providing a standardized metric for scientific, environmental, and industrial applications. We obtained the data on atmospheric CO₂ concentrations from the National Oceanic and Atmospheric Administration (NOAA) Global Monitoring Laboratory, specifically from their Mauna Loa Observatory dataset, which provides long-term measurements of monthly mean CO₂ levels [67].

The key hypothesis of our study H0 can be formulated as follows: sustainable business can be considered a force for good in relation to one of the key challenges of our time, climate change, expressed through the global CO2 concentrations in the atmosphere. The additional hypotheses H1 to be tested will address the feasibility of building an econometric model of global CO2 concentrations using daily data, ‘explaining’ these concentrations through a range of astronomical variables (total solar irradiance, cosmic rays), economic variables (oil price, Dow Jones Sustainability Index) and a possible autoregressive component.

3.1. Dow Jones Sustainability Index.

Dow Jones Sustainability Index (DJSI) is a global benchmark that tracks the performance of the top 10% of companies (325 companies in 2023) from various sectors based on their sustainability practices, evaluated using criteria such as economic, environmental, and social performance, corporate governance, and transparency.

The index is structured as follows: The Capital Goods sector represents 11.16% of the total, followed by Banks with 9.71%, Materials and Financial Services each at 8.63% and 6.12%, respectively. Pharmaceuticals, Biotechnology & Life Sciences also makes up 6.12%, while Equity Real Estate Investment Trusts (REITs) and Energy contribute 4.68% each. The Food, Beverage & Tobacco, Health Care Equipment & Services, Insurance, Semiconductors & Semiconductor Equipment, Technology Hardware & Equipment, Transportation, and Utilities sectors each represent 4.32%. Software & Services accounts for 5.76%, while Commercial & Professional Services, Consumer Discretionary Distribution & Retail, Consumer Staples Distribution & Retail, and Semiconductors & Semiconductor Equipment are each represented at 3.24%. Media & Entertainment has 3.96%, and Consumer Durables & Apparel stands at 2.88%, the same as Consumer Services and Consumer Staples Distribution & Retail. Automobiles & Components sector accounts for 2.16%, and Household & Personal Products is the smallest at 1.08%. The index represents companies headquartered in the following countries: USA (54), Japan (37), Taiwan (30), Republic of Korea (22), France (21), UK (16), Italy (15), Spain (15), Thailand (15), Germany (13), Australia (10), Brazil (8), Netherlands (8), Switzerland (8), Canada (4), Sweden (5), Colombia (4), Finland (4).

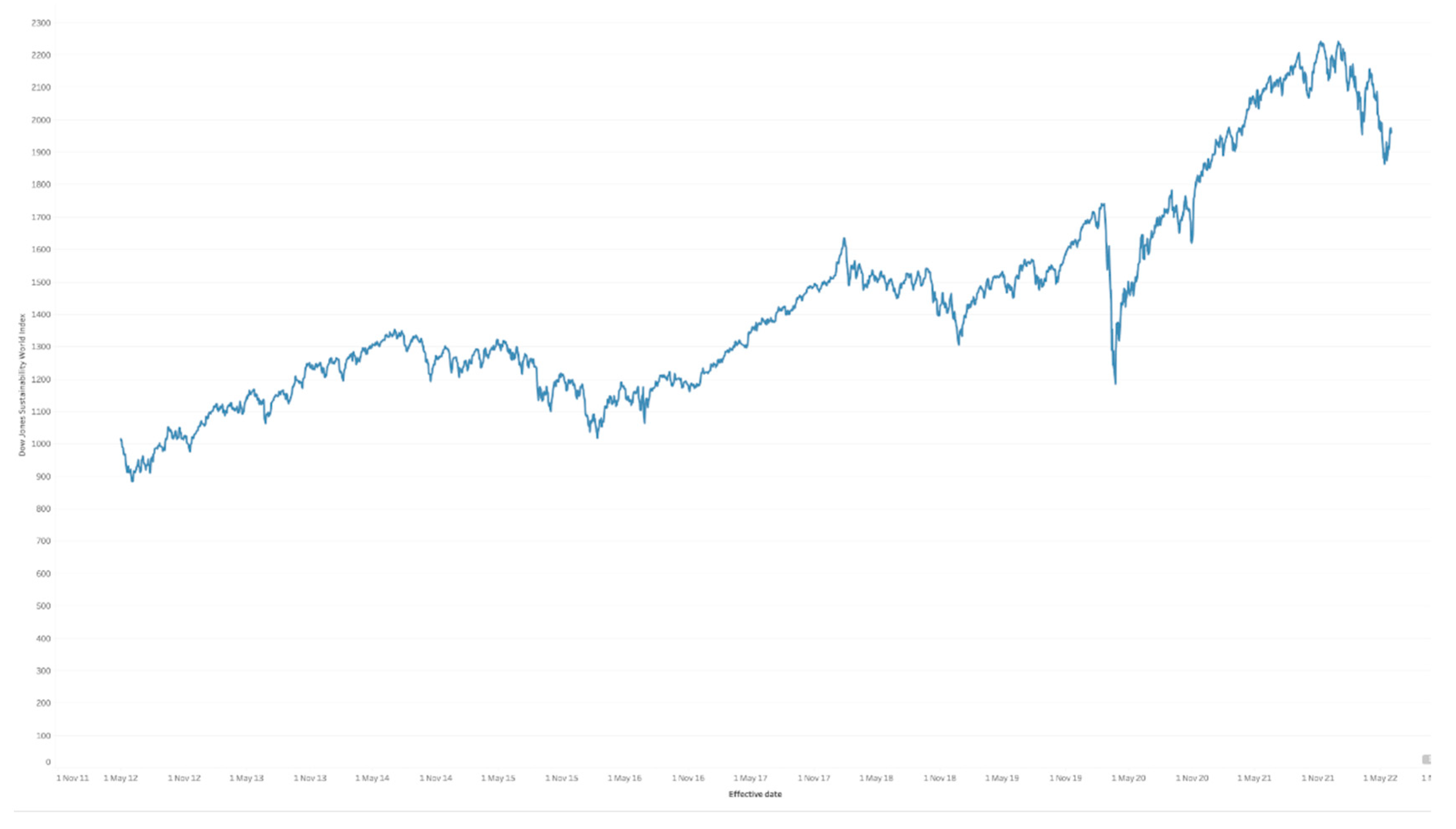

The index has been pioneered in 1999 and has become the benchmark for assessing sustainability of companies worldwide. Figure 1 presents the dynamics of the daily Dow Jones Sustainability Index between 2012 and 2021. We see an overall positive trend with downward spikes in the middle of the COVID-19 pandemic.

3.2. Brent Crude Oil Price.

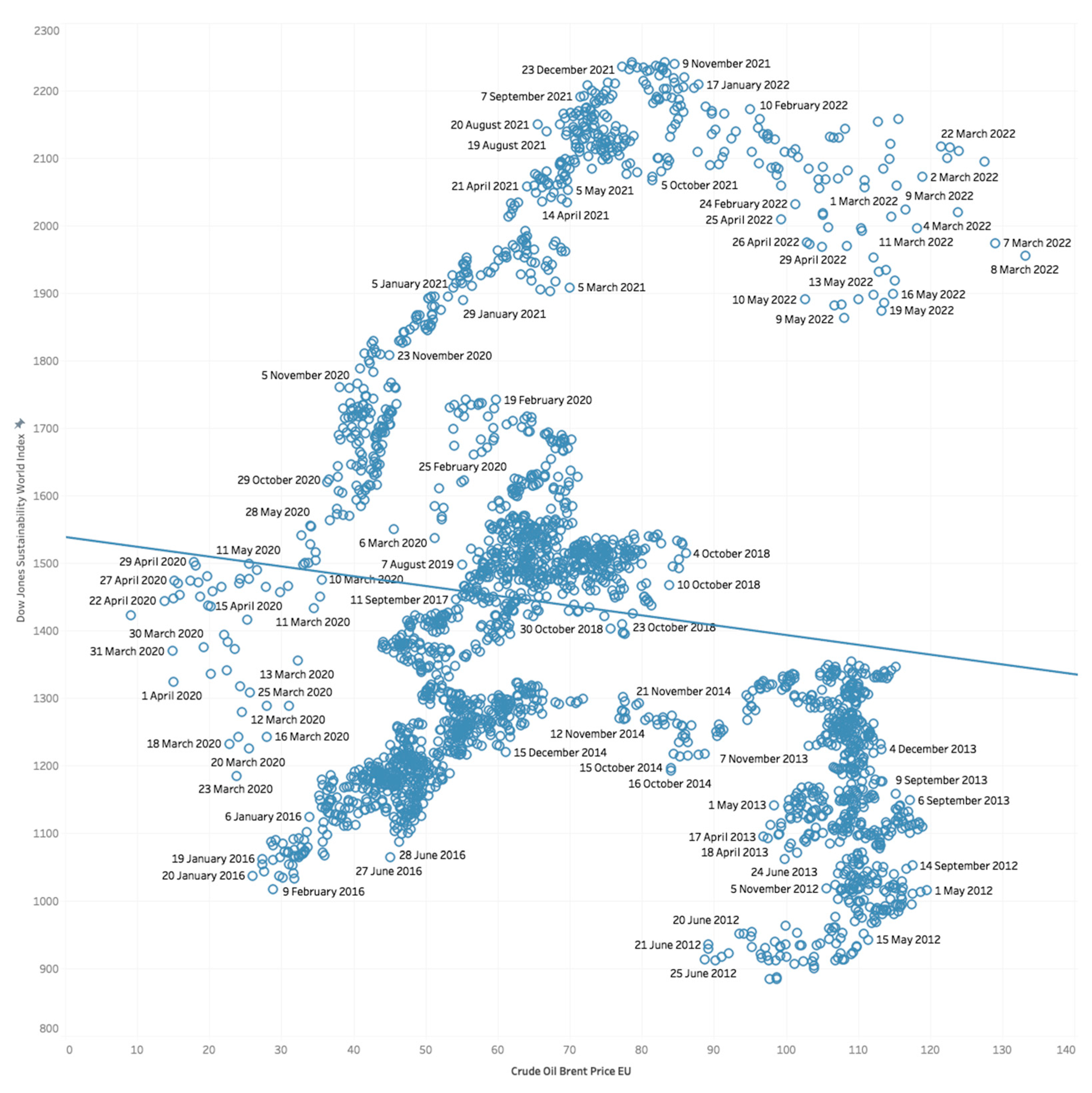

The dynamics of Brent crude oil prices are influenced by a range of factors, including the decisions made by OPEC (Organization of the Petroleum Exporting Countries) regarding production quotas, geopolitical events such as wars or crises like the Middle East Crisis of the 1970s and the Iranian Revolution, which can disrupt supply and lead to price volatility, as well as shifts in global demand and economic conditions that further impact the price of oil One can hypothesize that the DJSI would be positively correlated with the Oil Price, providing a safe haven for investors that experience oil price shocks.

Further analysis reveals that the Dow Jones Sustainability Index is inversely correlated with the Brent crude oil price (Figure 2) when the years 2012, 2013 and 2014 are taken into consideration and positively correlated when the years 2012, 2013 and 2014 are excluded (Figure 3). The regression model that describes the relationship between Crude Oil Price and the Dow Jones Sustainability Index with the years 2012, 2013 and 2014 taken into account (Figure 3) is statistically significant and the coefficient is negative. If the time horizon changes, however, the relationship becomes strongly positive as one would expect. This way, the companies are investing in sustainability to avoid the shocks of the high oil price. This is particularly relevant for the period 2014-2022 as the Figure 4 outlines.

So what is actually going on here? What makes the years 2012, 2013 and 2014 so different? In mid-2014 the hedge fund positions in Brent and WTI futures drop rapidly approximately around the month of July. At the same time, in the USA, 2013 and 2014 resulted in the fastest growth in the production of oil in history. The US output increased from 5mln bpd in 2008 to approximately 8.5 mln bpd in 2014 with output increasing by 160,000 bpd in 2011, 850,000 bpd in 2012, 950,000 bpd in 2013 and 1.2 mln bpd in 2014. On November 27, 2014, OPEC announced that it would keep its current production at 30mln pbd. The oil price by that time has already fallen to $77 per barrel, and dropped even further to $59.

3.3. Global CO2 concentrations

The Intergovernmental Panel on Climate Change (IPCC) has consistently highlighted the critical role of carbon dioxide (CO₂) concentrations in climate change. In its 2023 Synthesis Report, the IPCC states that "atmospheric CO₂ concentrations reached 410 parts per million (ppm) in 2019, higher than at any time in at least 2 million years”. The global concentrations of CO2 in the atmosphere continue to increase (Figure 6). This is a powerful illustration that the problem of climate change is far from being solved.

Global concentrations of CO₂ are primarily driven by human activities that release large amounts of carbon dioxide into the atmosphere. The major sources include the burning of fossil fuels for transportation (air, land, and sea), energy production, heating, industrial processes, and the agriculture sector, which contributes significantly through practices such as deforestation, livestock production, and the use of synthetic fertilizers. Additionally, resource-intensive sectors like manufacturing and construction further exacerbate CO₂ emissions through energy consumption and material extraction. These activities contribute to the accumulation of greenhouse gases, which trap heat in the atmosphere and drive climate change. Potential remedies to reduce CO₂ emissions include transitioning to cleaner energy sources such as nuclear and renewable technologies (wind, solar, hydro), adopting sustainable agricultural practices, embracing sustainability in production and consumption, and transforming business models to prioritize environmental responsibility. These measures aim to reduce dependence on fossil fuels, promote energy efficiency, and foster a more sustainable, low-carbon global economy.

When we explore the connections between Dow Jones Sustainability Index and the Global CO2 concentrations depicted in Figure 7, we clearly see that increases in the Dow Jones Sustainability Index have been associated with increases in global CO2 concentrations (Figure 7).

On the other hand, the correlation we see between the oil price and global CO2 concentrations is indeed very curious (Figure 8). What we see is a clear negative relationship where rising oil price implies a lower CO2 concentration in the atmosphere, which emphasizes the potential value of carbon and energy taxes, which we explored in Shmelev and Speck (2018). This is particularly striking because the data is collected on a daily basis.

During the pandemic, however, while nobody was allowed to use their private cars and the global travel industry collapsed, the situation has changed. During the months of the pandemic, the increases in the Dow Jones Sustainability Index were negatively correlated with the global CO2 emissions, confirming the role of sustainable business as a force for good, however only during the pandemic, while we didn’t consume petrol or flown across the oceans.

3.4. Total Solar Irradiance

Total Solar Irradiance (TSI) refers to the amount of solar energy that reaches the Earth's atmosphere per unit area, typically measured in watts per square meter (W/m²). It represents the total energy output of the Sun, including all wavelengths of electromagnetic radiation. TSI is not constant; it varies slightly over time due to solar cycles, with small fluctuations that can influence Earth's climate.

TSI is crucial for plant growth because it provides the energy necessary for photosynthesis, the process by which plants convert light energy into chemical energy to fuel their growth and development. Photosynthesis relies on light absorption by chlorophyll in plant cells, and TSI directly affects the intensity of this light. Higher solar irradiance typically leads to more efficient photosynthesis, promoting stronger plant growth. On a larger scale, variations in TSI can influence agricultural productivity, ecosystems, and the global carbon cycle, as plants play a vital role in carbon sequestration.

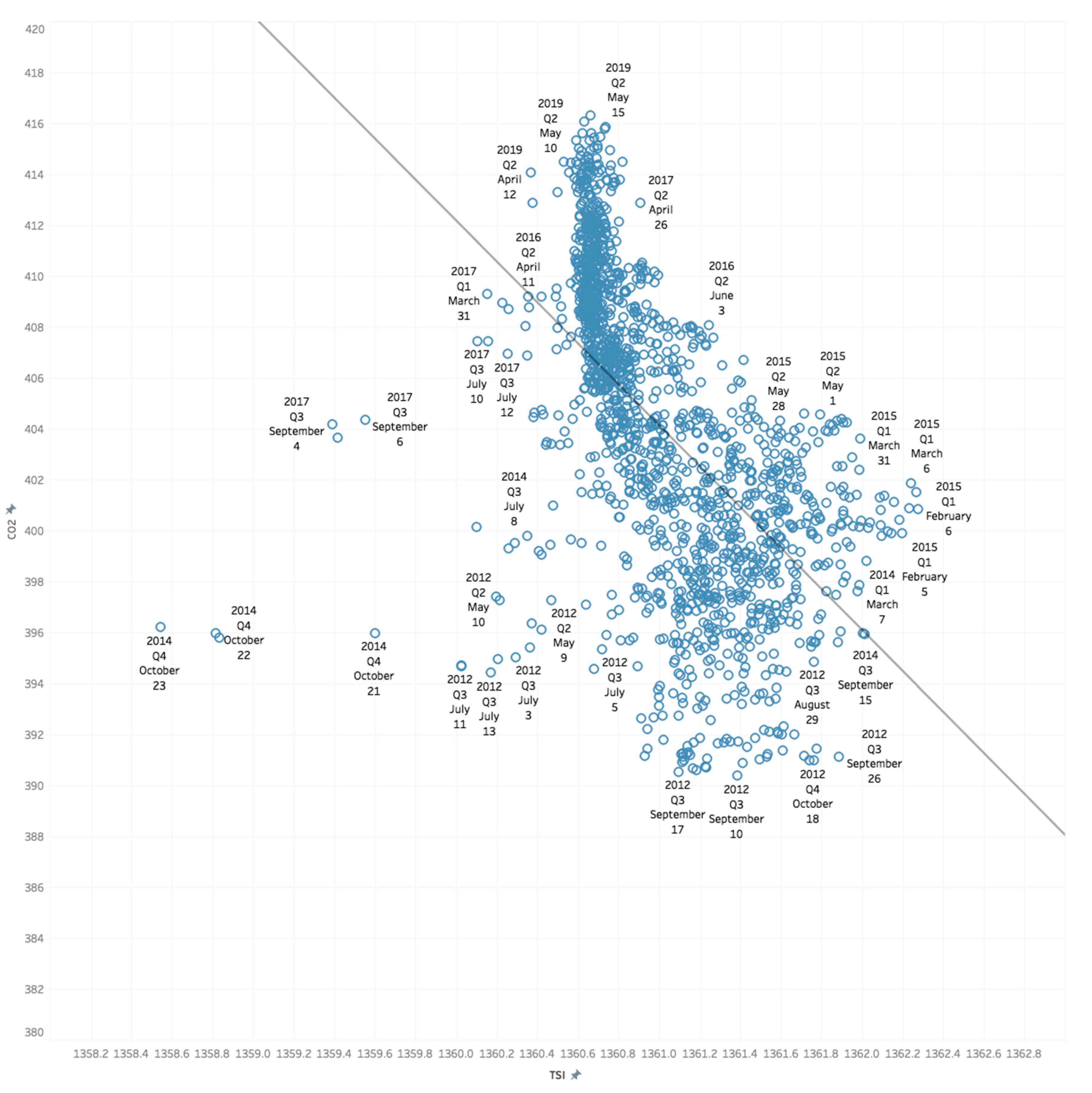

Figure 9 clearly illustrates a negative relationship between the Total Solar Irradiance and the CO2 concentrations in the atmosphere, which points towards the role of photosynthesizing biomass as decarbonization force.

3.5. Cosmic Rays

Cosmic rays are high-energy particles from outer space that reach Earth's surface and influence atmospheric and biological processes. According to Svensmark (2000), cosmic rays can help form cloud condensation nuclei, which influence cloud formation and precipitation patterns. This indirect effect on weather, particularly rain, is crucial for plant growth, as water is essential for seed germination and overall plant health. Research by Ormes (2018) also suggests that cosmic ray activity can influence long-term weather patterns, potentially altering rainfall and, thereby, affecting agricultural productivity.

Furthermore, cosmic rays have been shown to influence plant growth at the genetic level. Studies suggest that exposure to cosmic rays can enhance seed germination rates by inducing genetic mutations, which may improve stress resistance and growth in certain plant species. A study referenced in Frontiers in Plant Science (2023) supports this, showing that exposure to radiation, including cosmic rays, can trigger faster germination and stronger seedling development in certain plants.

Additionally, research by Dengel (2009) found that galactic cosmic rays could increase photosynthesis in tree canopies and affect tree ring growth, suggesting that cosmic rays can influence both tree vitality and long-term growth patterns. These effects, although subtle, demonstrate the potential role of cosmic rays in enhancing plant productivity, influencing genetic adaptations, and promoting healthier ecosystems over time.

As our previous research indicates (Shmelev et al, 2021), TSI and Cosmic Rays undoubtedly are connected with the global climate variables, and here we will try to establish if daily concentrations of CO2 emissions respond to these aggregates (Figure 10).

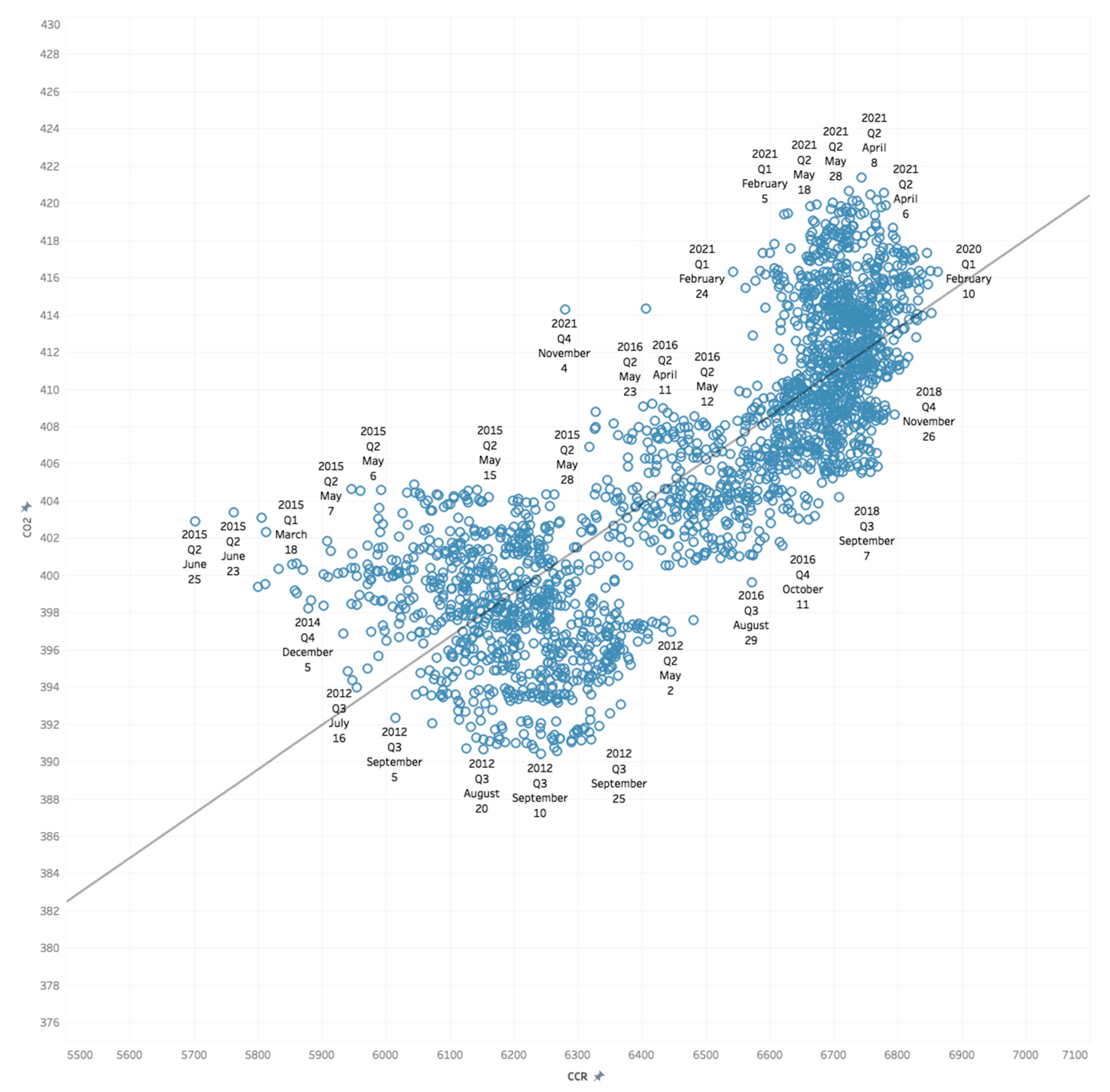

Figure 12 illustrates that there is an undoubted correlation between the Cosmic Rays and the global CO2 concentrations, and this correlation tends to be positive.

In order to understand all the potential factors involved, we are going to have to build a full-scale econometric model of global daily CO2 concentrations and examine the role of sustainable business as a force for good.

4. Model Building

4.1. Modelling CO2 Concentrations in Levels

We have built a dynamic econometric model aimed at explaining the daily fluctuations in global CO2 concentrations in the atmosphere. The model building rested on the theoretical understanding, which factors should affect CO2 concentration both at the level of emissions and at the level of absorption and this process combines two phases: modelling relationships in levels, modelling the relationships in differences and combining the models together following the so-called error-correction modelling (Engle and Granger, 1987; Hendry, 1995, Hendry & Nielsen, 2007, Hendry & Doornik, 2014).

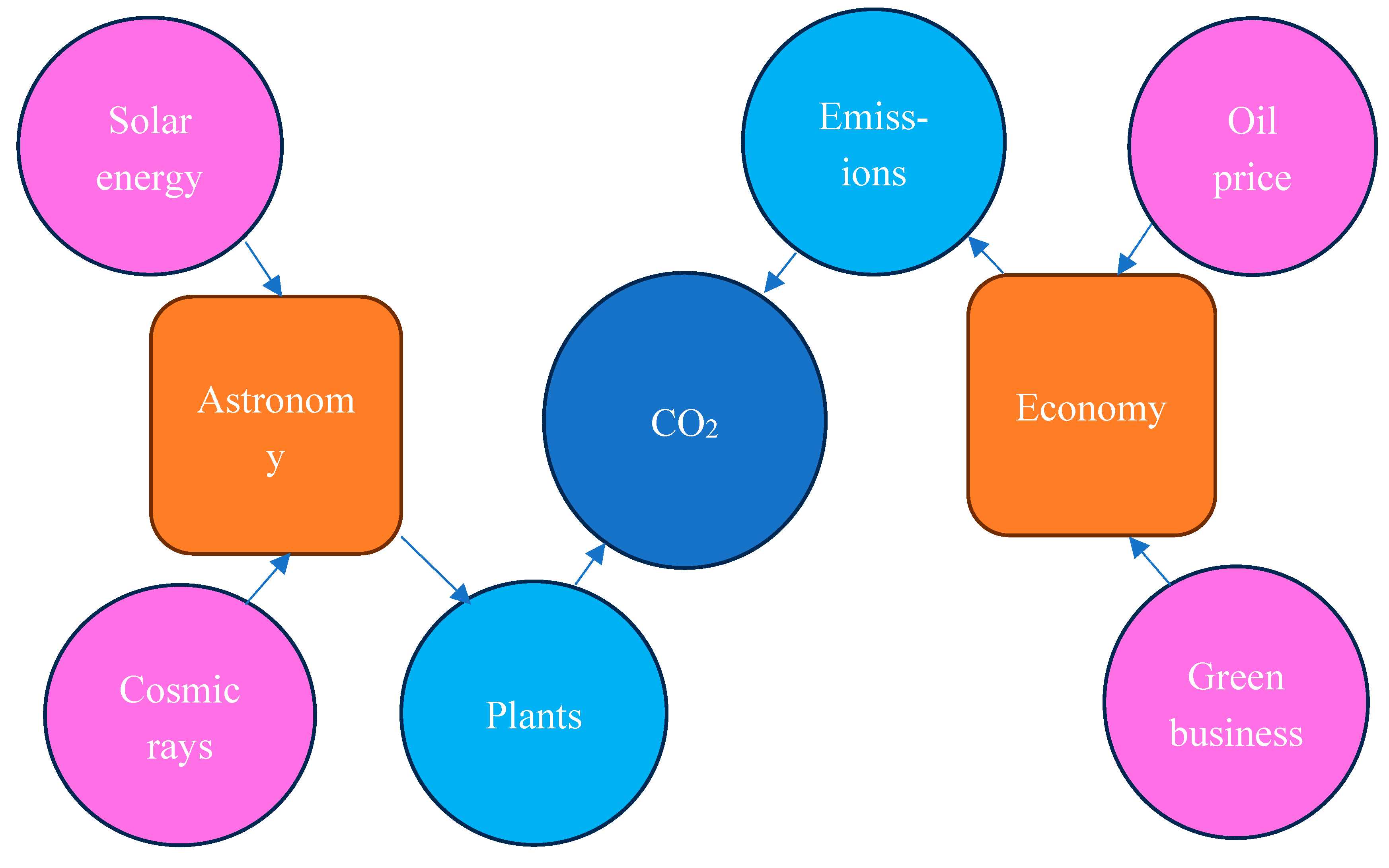

The methodological framework we used in our modelling (Figure 11) is largely based on the understanding of the carbon cycle. It is characterized by sources, represented by economy, which includes the Dow Jones Sustainability Index most sustainable companies and is also influenced by the oil price among other factors. The resulting emissions will be higher or lower depending on the combination of these factors, one of the crucial being the efforts by the largest companies to reduce their CO2 emissions. The opposite side of the equation affecting the concentrations of CO2 in a positive way, is the biomass represented by the Plants box. It is in turn influenced by astronomical factors such as solar energy and cosmic rays, which has already been illustrated in our previous works (Shmelev et al, 2021). Although this framework might be seen as a simplification of reality, every model is a reasonable simplification of reality with crucial elements and connections emphasized and less relevant omitted.

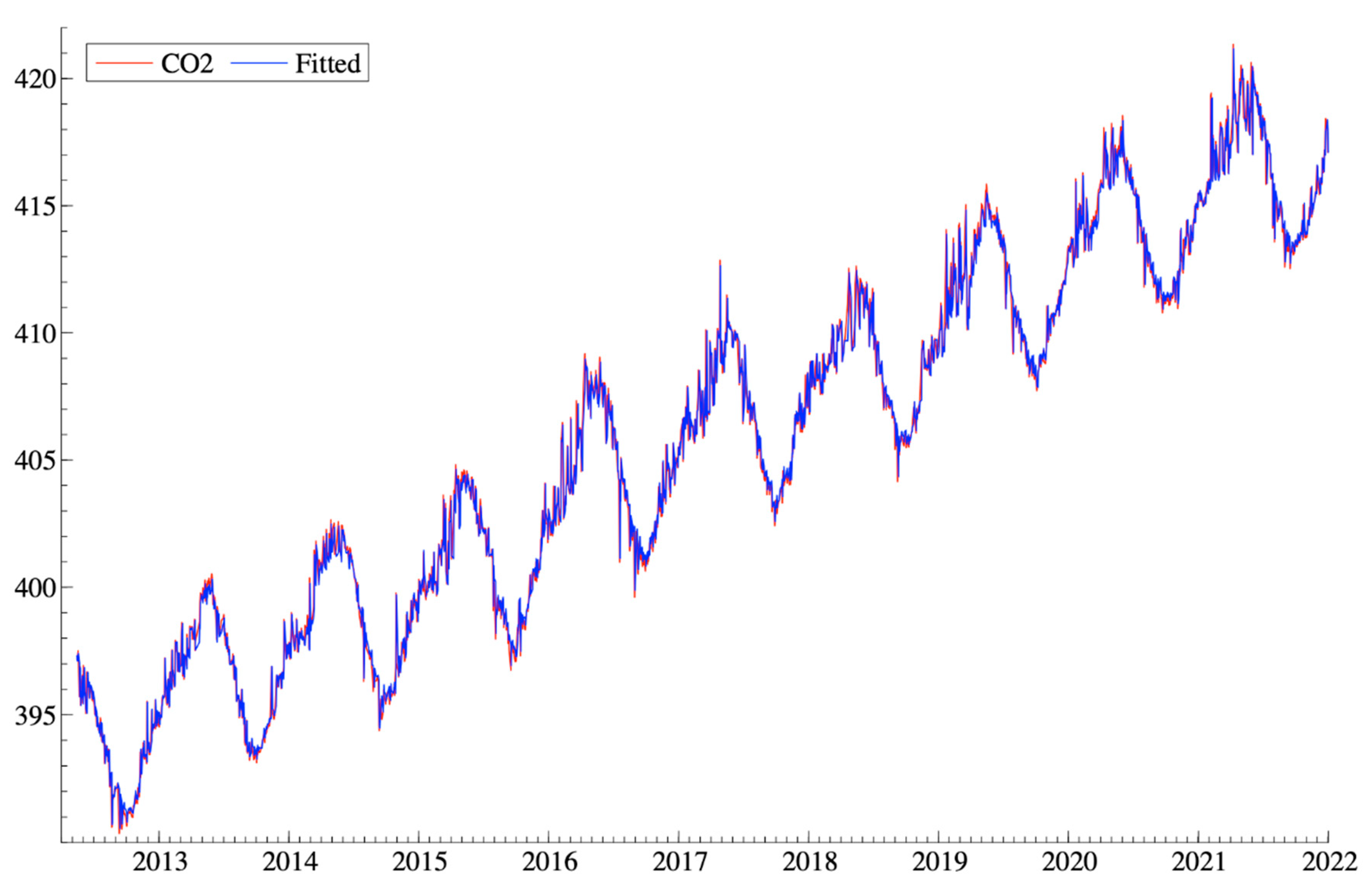

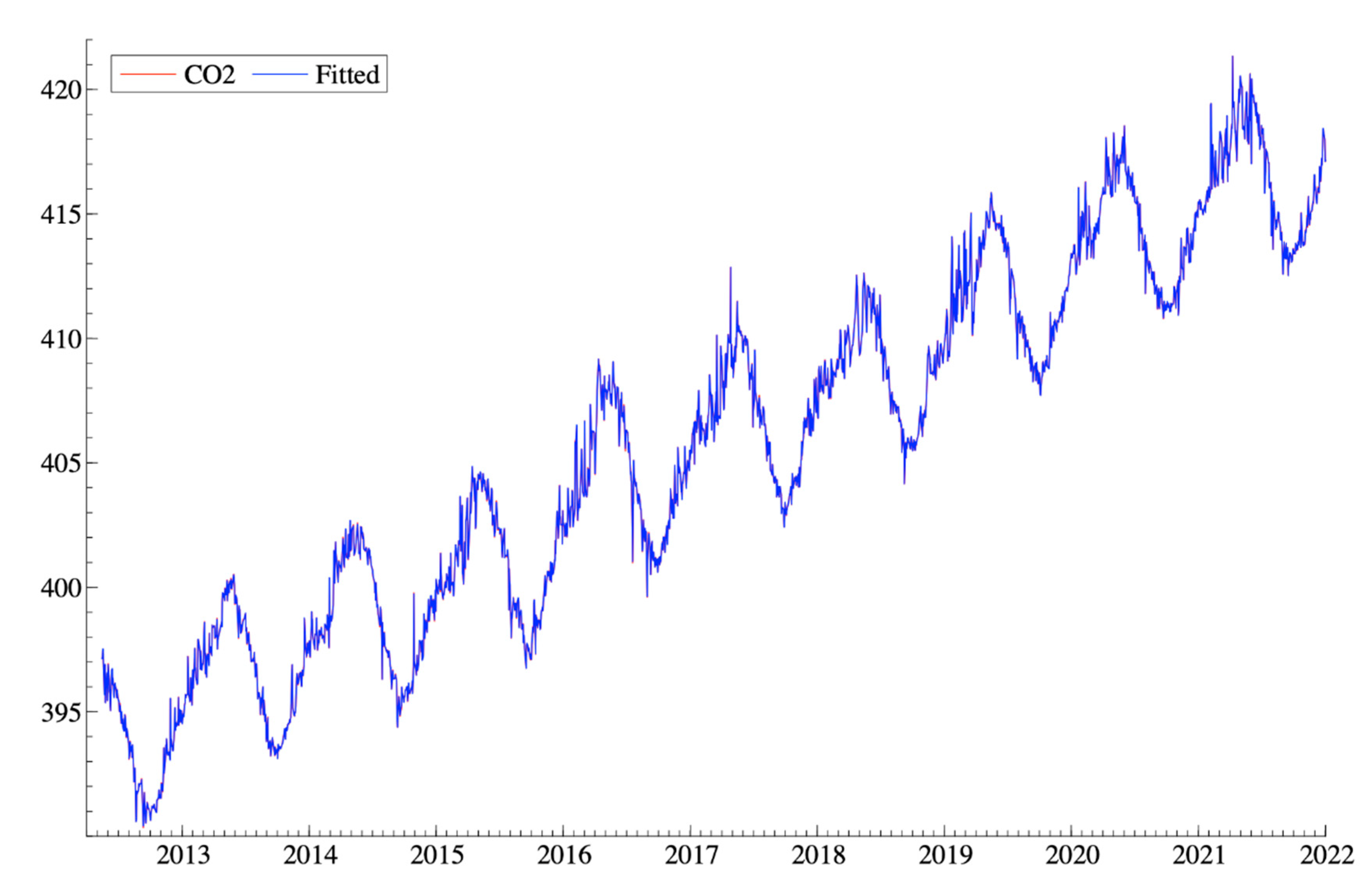

The modelling has been carried out with the help of advanced econometric analysis package OxMetrics. The first step in the modelling process has been to model the relationships in levels. This initial model is illustrated in Figure 14. We can see that the modelled CO2 concentrations follow the observed in quite a close way, the observed shown by the red line and the fitted by the blue. Based on 2195 observations, we establish that daily CO2 concentrations in the global atmosphere are very auto-correlated, have a positive impact from Dow Jones Sustainability Index, a negative impact from the oil price, a positive impact from Cosmic Rays, and a positive impact from Total Solar Irradiance (Table 2 and Figure 12).

Figure 12.

Model of CO2 concentrations in Levels, daily data.

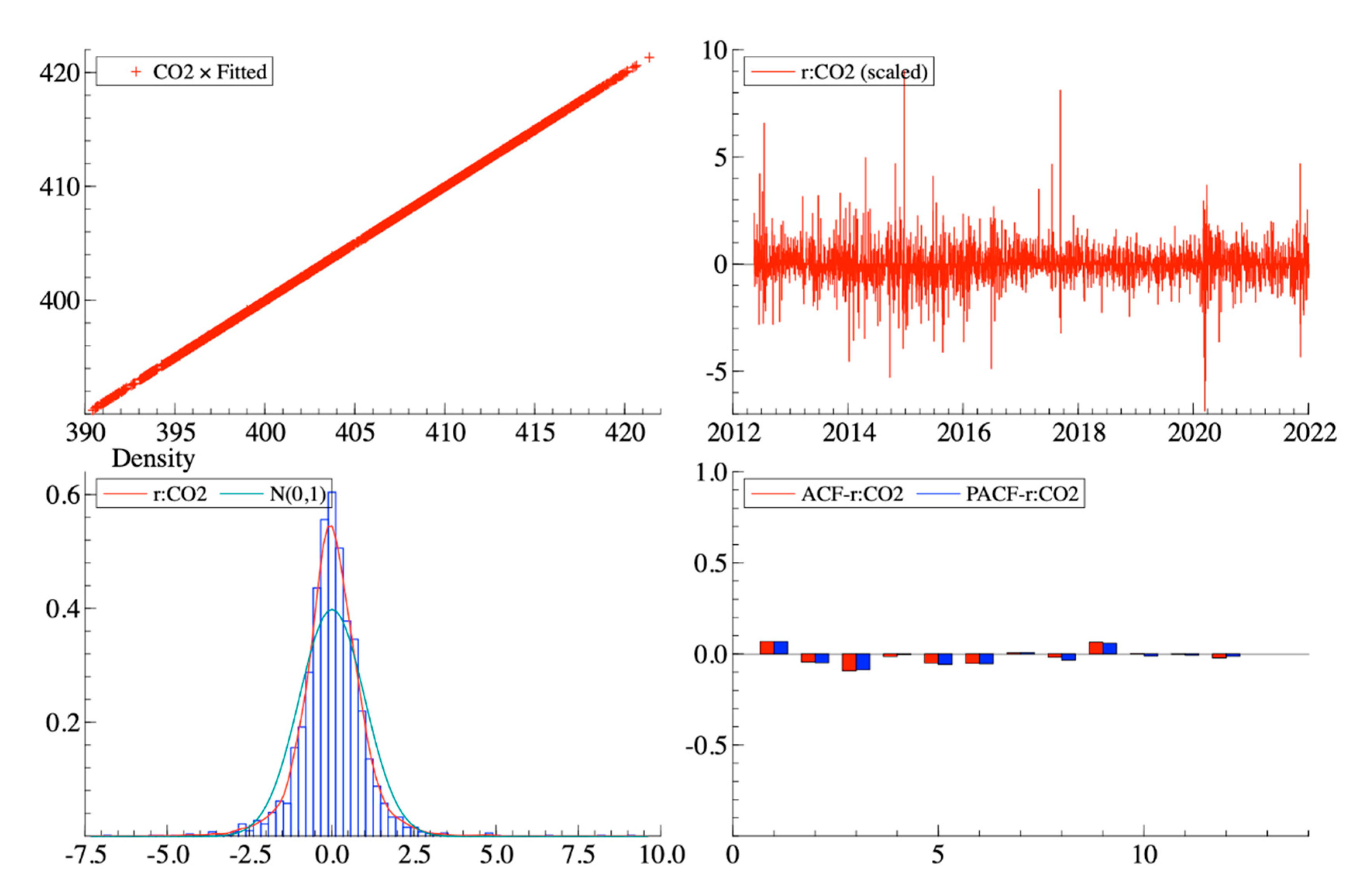

We note the good values of Adjusted R2 (0.990716), the AIC of -0.692693 and some issues with autocorrelation, normality and heteroskedasticity of residuals. We note that the Dow Jones Sustainability Index tends to contribute approximately 1% to the explanation of the variance in daily CO2 concentrations. Figure 13 presents the residuals in the levels model.

4.2. Modelling CO2 Concentrations in Differences

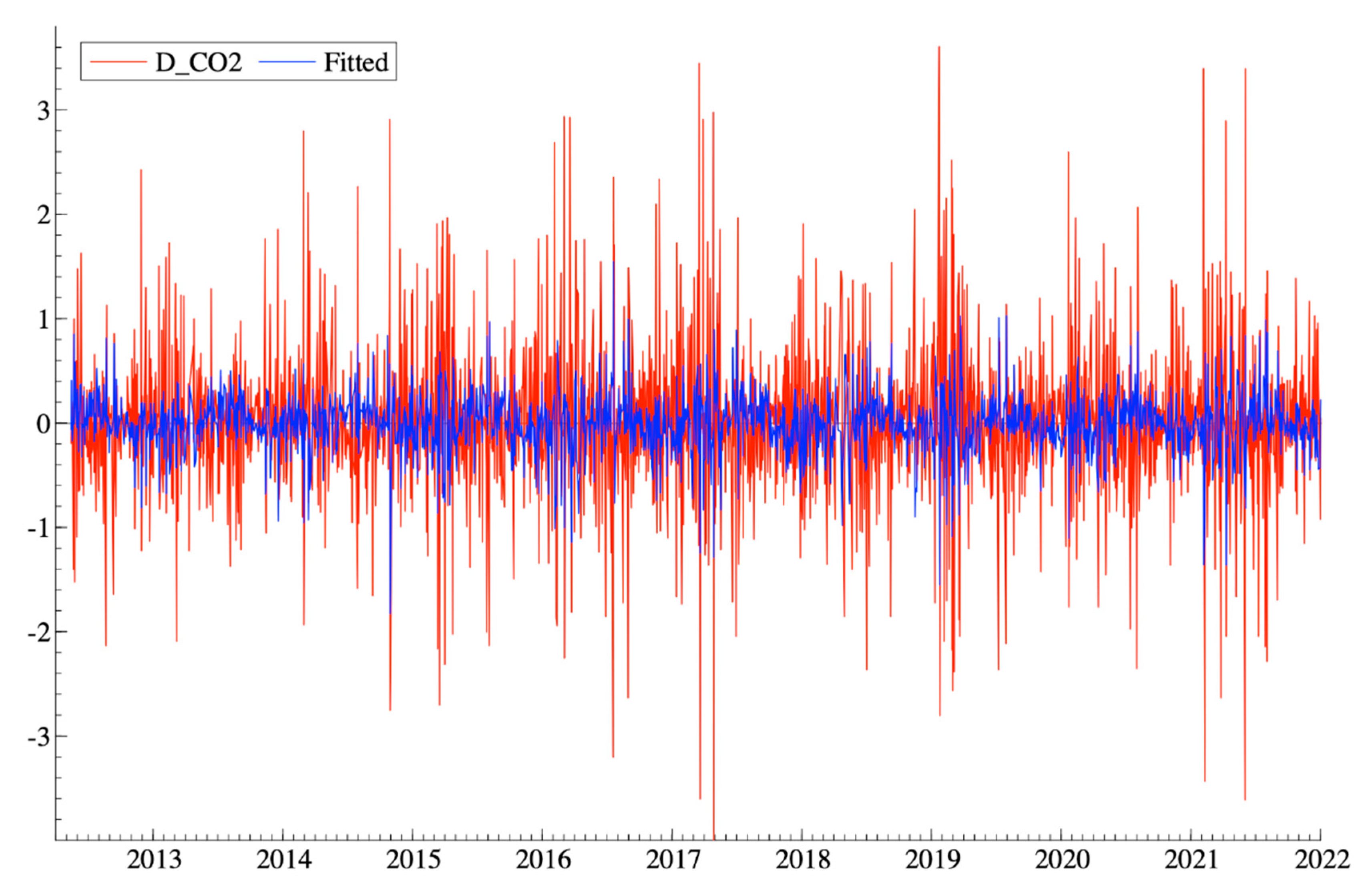

Modelling the process at hand in differences to examine the short-run dynamics, we obtain a model presented in Figure 14 and Table 3.

Figure 14.

Differences Model of D (CO2).

4.3. Final Combined Model

When we combine all the elements into the integrated model, to build a model examining both the long-run and the short-run, we obtain the model depicted in Figure 15 and Table 4. We can definitely observe a much closer fit between the actual CO2 concentrations data and the fitted data.

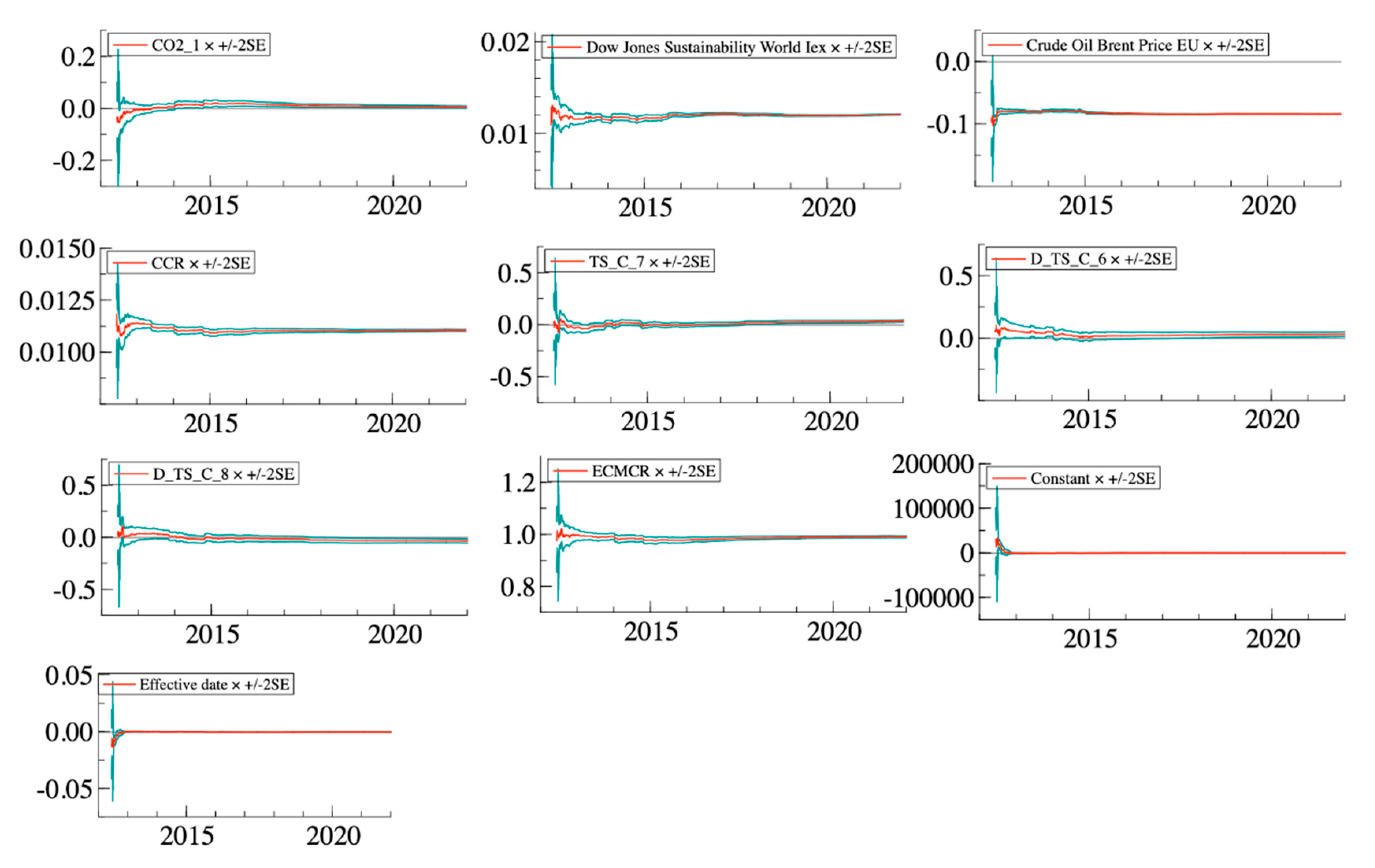

In the integrated model (Figure 15 and Table 4), we still observe autocorrelation of CO2 concentrations, which is to be expected, it represents the inertia in the system. Crude brent oil features now with a positive coefficient, the TSI square with the negative coefficient and CCR square with a negative coefficient, while Dow Jones Sustainability Index is also featured with a negative coefficient confirming our H0 hypothesis that the sustainable business can be the force for good. The inclusion of the decimal date variable allowed us to make sure that the model has much more stable coefficients than before (Figure 17) and we improved residuals (Figure 16) and our Adjusted R2 to 0.999993 and the AIC to -7.82265, which is excellent.

The reduction in the Akaike Information Criterion (AIC) from -0.692693 in the levels model to -7.82265 in the combined short-run and long-run final model indicates a substantial improvement in the model’s performance. AIC is a widely used metric for evaluating the quality of statistical models, balancing goodness of fit with model complexity. A lower AIC value reflects a model that better explains the observed data without overfitting.

The initial levels model, with an AIC of -0.692693, primarily captured the long-run relationships between variables. While this approach provided some insights, the relatively higher AIC suggests limitations in its ability to fully account for the dynamics of the system. By contrast, the final model incorporates both short-run dynamics and long-run relationships, leading to a significantly lower AIC of -7.82265. This marked reduction demonstrates that the inclusion of short-term adjustments, such as fluctuations or lagged effects, substantially enhances the explanatory power of the model.

Importantly, this improvement in AIC signifies that the added complexity of the combined model is justified by its ability to capture more of the variability in the data. The short-run components complement the long-run framework, allowing the model to better reflect real-world processes, such as immediate responses to external factors or transient deviations from equilibrium.

Overall, the reduction in AIC highlights the superior performance of the combined model, making it a more robust and reliable tool for understanding the dynamics of the system under study.

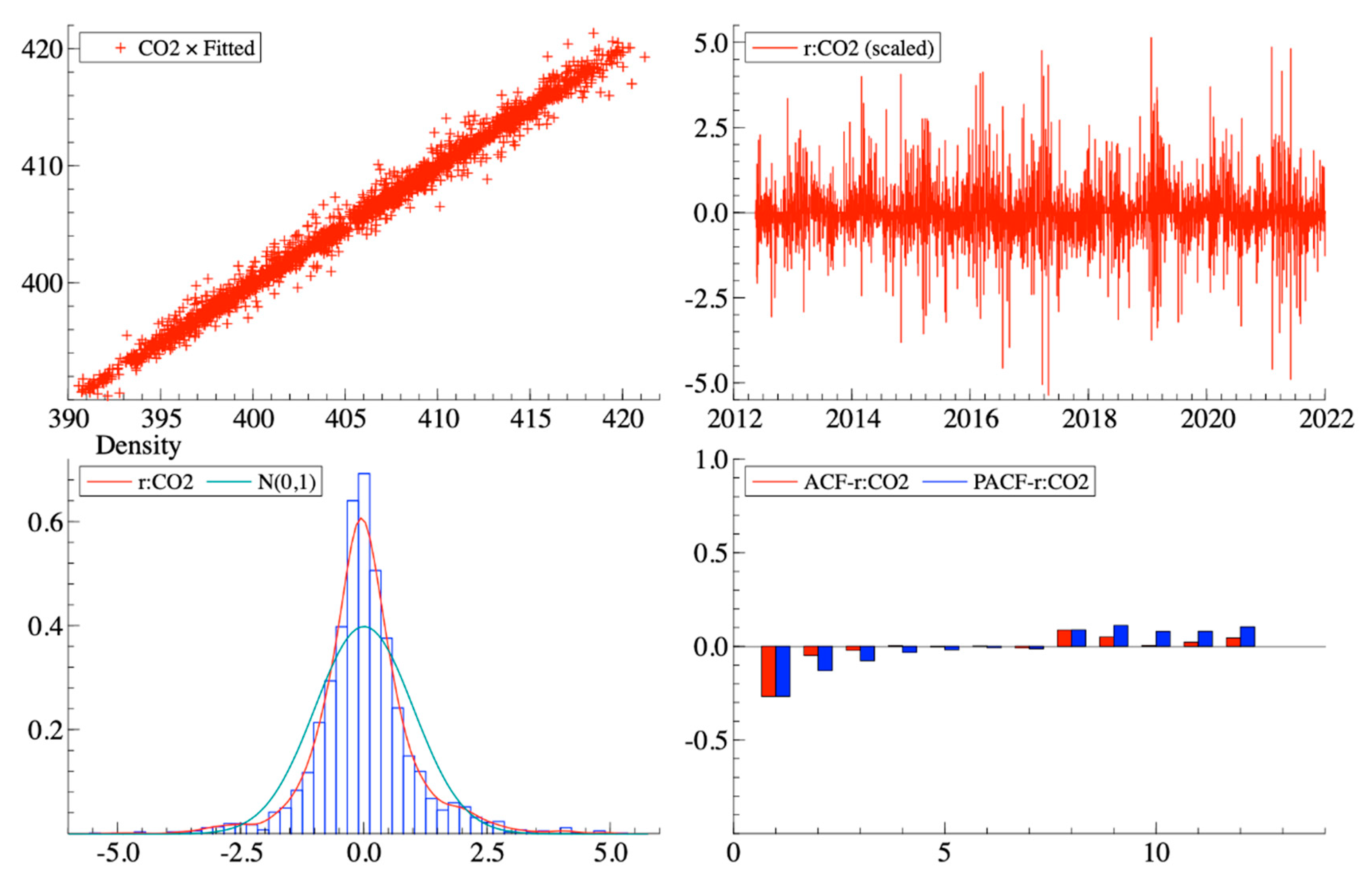

The residual analysis displayed in the top panels confirms that the model is highly robust and well-specified. The residual plot over time (top-right) exhibits no visible trends or patterns, indicating that the errors are randomly distributed and the model effectively captures the underlying data dynamics. The histogram of residuals (bottom-left) aligns closely with a normal distribution, centered at zero with minimal skewness, further validating that the model errors are unbiased and normally distributed. Additionally, the autocorrelation (ACF) and partial autocorrelation (PACF) functions (bottom-right) show no significant lags, suggesting that the residuals are not autocorrelated and the model has successfully accounted for time-dependent structures in the data.

The long-term stability of the model's coefficients, as illustrated in the bottom series of charts, underscores its reliability. All coefficients remain stable over the examined period, with confidence intervals tightly surrounding the point estimates. This stability signifies that the relationships captured by the model between predictors and the response variable are consistent over time, even in the presence of external variations. The absence of significant deviations or abrupt changes further confirms the robustness of the model, making it an excellent tool for forecasting and interpreting long-term dynamics.

5. Discussion

Let us take some steps to interpret the model that we managed to obtain, considering the meaning of each term in details and possible implications. To understand this model comprehensively, it is essential to consider the relationships between the variables, their statistical significance, and the underlying implications for atmospheric CO2 levels.

5.1. The Negative Constant

The negative constant of -6.17092 suggests an interesting starting point for the model. In the context of the equation, the negative constant can be seen as a baseline adjustment in the absence of all other influencing factors (e.g., CO2 from the previous day, economic activities, or commodity prices). This value may symbolize a potential long-term equilibrium in the Earth’s natural carbon cycle, one that existed before the rise of human industrialization.

Historically, before humans began significantly influencing the atmosphere, Earth’s natural processes maintained relatively stable CO2 levels. As the planet's ecosystems evolved, particularly with the rise of photosynthetic organisms, the amount of CO2 absorbed and emitted was approaching the state of dynamic equilibrium, creating a balance between carbon emissions and carbon sequestration. This natural equilibrium may be represented by the negative constant, signaling a period when nature operated in harmony, and the Earth’s biosphere and geosphere functioned to stabilize atmospheric CO2 concentrations.

However, the negative constant also reflects the fragility of this equilibrium. It indicates that while natural systems may have once been capable of absorbing more CO2 than they emitted, this balance is no longer in place due to human activities. The overwhelming emissions from fossil fuel combustion, industrial processes, deforestation, and other anthropogenic activities are now pushing CO2 levels far above this natural baseline.

5.2. DecimalDate

The DecimalDate coefficient (0.00387243) suggests a gradual increase in CO2 concentrations over time, where the passage of time itself (as represented by the date) is positively correlated with increasing CO2 levels. This could indicate that, over the period under study, global CO2 concentrations have been steadily rising due to long-term trends like industrialization, increased human activity, and fossil fuel consumption. The statistical significance (p-value = 0.0002) confirms the reliability of this relationship.

5.3. CO2(t-1) or Lagged CO2

The coefficient for CO2 (t-1): 1.00034 is striking in its magnitude and statistical significance, which shows a very strong autoregressive effect—meaning that today's CO2 concentrations are heavily influenced by the concentrations of the previous day. This makes sense given the nature of CO2 dynamics: concentrations do not change abruptly on a daily basis, and past emissions from human or natural sources influence present levels. The very high Part.R^2 (0.9999) suggests that past CO2 concentrations account for a substantial portion of today's CO2 levels, reflecting the inertia in the system and the persistence of atmospheric CO2.

5.4. Dow Jones Sustainability World Index (DJSI)

The Dow Jones Sustainability World Index coefficient (-1.60759e-05) shows a negative relationship with global CO2 concentrations. This means that as the DJSI rises, indicating improvements in sustainability practices by businesses, CO2 concentrations tend to decrease. This finding aligns with the idea that more sustainable business practices, such as increased energy efficiency, a shift toward renewable energy sources, and better waste management, may help mitigate CO2 emissions and confirms our H0 hypothesis. The statistical significance (p-value = 0.0047) further confirms that this relationship is meaningful, though the effect size is modest, as indicated by the Part.R^2 (0.0036).

This relationship suggests that a transition toward more sustainable business practices, transformation of the business models and the increased focus on ESG dimensions, as reflected in the DJSI, could have a tangible impact on reducing global CO2 levels, but it is not the sole factor influencing these concentrations.

5.5. Crude Oil Brent Price

The Brent Crude Oil Price coefficient (0.000110840) shows a positive relationship between oil prices and CO2 concentrations. This suggests that as oil prices increase, global CO2 concentrations also rise. This could be interpreted in two ways: higher oil prices might lead to greater investment in fossil fuel extraction and related activities, or they may reflect increased energy consumption due to global demand. The statistical significance (p-value = 0.0019) and moderate Part.R^2 (0.0044) suggest that this is a noteworthy, but not overwhelming, relationship.

This could be indicative of the economic structure, where fossil fuel reliance remains strong despite efforts to reduce emissions. Alternatively, this may point to a supply-demand effect in the energy markets, where higher prices lead to shifts in extraction and consumption behaviors.

5.6. CCR_SQUARE (Squared Terms of Cosmic Rays)

The coefficient for CCR_SQUARE (-2.62072e-09) reveals a significant nonlinear relationship between cosmic ray intensity and CO2 concentrations, with a highly significant t-value of -7.47 (p-value = 0.0000) and a Part.R^2 of 0.0249. This indicates that cosmic rays influence CO2 levels in a manner that is not strictly linear, likely due to their role in cloud formation, which has indirect effects on CO2 dynamics.

Cosmic rays are known to affect cloud nucleation, and in turn, this impacts rainfall patterns and atmospheric conditions favourable to plant growth. The negative sign of the coefficient suggests that increased cosmic ray activity could enhance cloud cover, leading to more favourable conditions for vegetation, which helps in reducing CO2 concentrations through increased photosynthesis and carbon sequestration. The squared term emphasizes that small changes in cosmic ray activity may have amplified effects on CO2 levels, possibly through the feedback loop where more cloud cover and rainfall lead to more plant growth, which in turn absorbs more CO2 from the atmosphere.

This result supports previous studies suggesting that cosmic rays, by influencing cloud formation and plant growth, can indirectly contribute to the reduction of atmospheric CO2 concentrations.

5.7. TSI_SQUARE (Squared Terms of Total Solar Irradiance)

The TSI_SQUARE coefficient (-8.90689e-07) is statistically insignificant (p-value = 0.1286) and has a very low Part.R^2 (0.0011). This suggests that, within the scope of this model, Total Solar Irradiance (TSI) does not have a strong influence on global CO2 concentrations when squared. However, the relationship might still warrant further investigation, especially when considering the cosmic ray effects that affect cloud formation and subsequent rainfall, which can indirectly impact plant growth and carbon sequestration.

5.8. D_CCR_4 (Differenced CCR Terms)

The D_CCR_4 coefficient (3.16413e-05) represents the differenced term for carbon cycle dynamics over a four-day lag, and it shows a positive relationship with CO2 concentrations. This suggests that short-term variations in the carbon cycle can influence CO2 concentrations in the immediate term. The statistical significance (p-value = 0.0012) and moderate Part.R^2 (0.0024) indicate that these short-term changes in the carbon cycle are relevant for daily CO2 dynamics.

5.9. ECM_DIFF (Error Correction Term)

The ECM_DIFF coefficient (0.999205) is highly significant (p-value = 0.0000) and demonstrates that error correction dynamics play a major role in the system. The coefficient’s value close to 1 indicates that the system is highly persistent, and deviations from the equilibrium state (whether caused by human activity or natural factors) are corrected very quickly. This suggests that global CO2 concentrations exhibit path dependence and tend to revert to a long-term trend or equilibrium once short-term disturbances are accounted for.

Conclusions

This model of global CO2 concentrations reveals several insightful relationships between human activity, economic variables, and natural processes. While the negative constant hints at a potential historical equilibrium in the carbon cycle, human-driven emissions have clearly disrupted this balance. The model suggests that business sustainability and oil prices play significant roles, but autocorrelation and cosmic rays dynamics have the most substantial impact on explaining daily CO2 concentrations. The presence of error correction mechanisms also reinforces the idea that, despite fluctuations, CO2 concentrations tend to revert to long-term trends influenced by natural and anthropogenic factors.

Our hypothesis H1 is, therefore, confirmed as well and we have been able to builds a comprehensive model of daily CO2 concentrations examining the role of multiple factors. One of these factors, and this confirms our H0 hypothesis, is sustainable business, expressed by the Dow Jones Sustainability Index. By improving sustainability practices, reducing fossil fuel reliance, and understanding the complexities of the carbon cycle, it is possible to mitigate the rise in CO2 concentrations and work towards restoring a more balanced and sustainable atmospheric state.

Discussing the ways to make sure that business makes an even greater contribution towards decarbonisation globally, we need to touch upon several interconnected issues. The first set of questions relate to what is actually inside the Dow Jones Sustainability Index and how truly sustainable these companies are. Estimating the market capitalization in brackets, we note that the index still includes oil giants like Total Energies ($158.64 bln), Exxon Mobil ($542.20 bln), Chevron Corporation ($305.93 bln), Rio Tinto ($104.73 bln), as well as truly more sustainable and lower impact companies like Apple ($2.76 trln), Microsoft ($2.45 trln), Salesforce ($186.75 bln), Alphabet Inc ($1.7 trln), Meta Platforms Inc ($779 bln), Tesla ($836.59 bln), SAP ($158.25 bln), Vestas Wind Systems A/S ($23.71 bln), NextEra Energy, Inc ($103.80 bln), Ørsted ($43.29 bln), Enel S.p.A. ($77.72 bln), JinkoSolar Holding Co., Ltd. ($2.90 bln), Iberdrola S.A ($90.03 bln) Munich Re ($32.7 bln), Zurich Insurance ($60.65 bln). So the biggest question is what are the criteria for inclusion of the companies into Dow Jones Sustainability Index, and should this be based on the Scope 3 CO2 emissions or emissions to turnover ratios, so that oil companies could not be part of the index? The performance of companies that could be considered as a backbone of sustainability transition, eg. Solar panels Jinko Solar or Ørsted has been less than spectacular, indicating the market myopy which is highly surprising.

The second issue in relation to how to make sure businesses are playing a larger role is regulation. Focusing on the subject of our paper, we can remark not all contries in the world have introduced a carbon tax, with only several countries fully embracing it like Sweden (Shmelev, Speck, 2018). The universal global carbon market has not yet been built. At the same time, there is no consistent regulation in the field of circular economy, with even European countries exhibiting conflicting signals. Many countries in Western Europe introduced landfill taxes, however many continue to export waste abroad, very few if at all supported them with incineration taxes to truly promote the circular economy. There is still very little in the way of regulation in the field of ecosystems and biodiversity impacts. In the EU there are some signs of a growing impact of new standards and EU cross-border regulations. In the United States there are multiple examples where whole states legislated against using ESG criteria for the assessment of investment fund performance, trying to defend the infamous quote from Milton Friedman that ‘the business of business is to do business’. Robert Eccles has discussed these instances at length: they seem to be clear violations of the principles of the free market because if the customers demand ESG focus, the investment community should follow.

A more general question could be posed regarding how markets really value sustainability and isn’t there an obstacle that we face there? How does business education embrace sustainability worldwide and how much do business leaders care? What could be said about the values and the deeply-held beliefs of the business leaders? There are, however, voluntary schemes like the B-Corp, which encourage its members to make a legal change in their statues to introduce the principle of respect to all stakeholders, not just the shareholders and, thereby, changing the nature of doing business itself. This example is very much in line with the sustainable business ideas presented by John Elkington, Ronald Cohen and Robert Eccles.

6. Conclusions

Examining the connection between the sustainable business expressed in the Dow Jones Sustainability Index and the global CO2 concentrations, we notice a high degree of auto-correlation in the global CO2 concentrations, some impact of the astronomical variables like the Cosmic Rays and Total Solar Irradiance and limited but statistically significant impact of the oil price and the Dow Jones Sustainability Index. The fact that the Dow Jones Sustainability Index comes with a negative coefficient gives us some hope that business could be a force for good, however many questions arise. The hypotheses we have formulated at the start of the paper, namely hypothesis H1 that business can be a force for good and make a positive contribution towards global decarbonization effort as well as H2 that it is feasible to build a dynamic econometric model based on daily data on atmospheric CO2 concentrations and a range of economic and astronomic factors have both been confirmed.

It is obvious that without the involvement of business, it is very unlikely that the sustainability transition will ever take place. If we are going to see the business as a true force for good, we will need clearer regulations, better sustainability education for top managers and a deep transformation of the business models addressing the most pressing issues of our time: climate change, biodiversity loss and the waste crisis.

References

- Arvidsson, s., & Dumay, J. (2022). Corporate ESG reporting quantity, quality and performance: Where to now for environmental policy and practice? 31: 1091-1110. [CrossRef]

- Babynina, L., Kartashova, L., Busalov, D., Chernitsova, K., & Akhmedov, F. (2023). Effective ESG Transformation of Russian Companies in the New Environment: Current Challenges and Priorities. Academic Journal of Interdisciplinary Studies. [CrossRef]

- Broadstock, D. C., Chan, K., Cheng, L. T.W., & Wang, X. (2021). The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Finance Research Letters 38, 101716 . [CrossRef]

- Carney, M. (2021) Value(s): The must-read book on how to fix our politics, economics and values, William Collins, 608 pp.

- Catalyst. (2020). The Bottom Line: Connecting Corporate Performance and Gender Diversity.

- Cheng, B., Ioannou, I. and Serafeim, G. (2104), ‘Corporate Social Responsibility and Access to Finance’, Strategic Management Journal, Vol. 35, Issue 1, pp. 1–23. [CrossRef]

- Clement, A., Robinot, E., & Trespeuch, L. (2023). The use of ESG scores in academic literature: a systematic literature review. Journal of Enterprising Communities: People and Places in the Global Econom. [CrossRef]

- Cohen, R. (2020). Impact: Reshaping Capitalism to Drive Real Change, Ebury Press, 256pp.

- Crace, L., & Gehman, J. (2023). What Really Explains ESG Performance? Disentangling the Asymmetrical Drivers of the Triple Bottom Line (Vol. 36). Organization & Environment 2023.

- Eccles, R. G., & Serafeim, G. (2013). The Performance Frontier: Innovating for a Sustainable Strategy, Harvard Business Review. https://hbr.org/2013/05/the-performance-frontier-innovating-for-a-sustainable-strategy.

- Eccles, R.G., Serafeim, G. and Krzus, M.P. (2011), Market Interest in Nonfinancial Information. Journal of Applied Corporate Finance, 23: 113-127. [CrossRef]

- Eccles, R. Ioannou, I. and Serafeim, G. (2011) The Impact of a Corporate Culture of Sustainability on Corporate Behaviour and Performance, National Bureau of Economic Research, Working Paper 17950 http://www.nber.org/papers/w17950.

- Eccles, R., Ioannou, I. and Serafeim, G. (2014), ‘The Impact of Corporate Sustainability on Organizational Processes and Performance’, Management Science, Vol. 60, Issue 11, pp. 2835–2857. Available at: . [CrossRef]

- El Ghoul, S., Guedhami, O., Kwok, C. and Mishra, D. (2011), ‘Does Corporate Social Responsibility Affect the Cost of Capital?’, Journal of Banking and Finance, Vol. 35, Issue 9, pp. 2388–2406. Available at: https://econpapers.repec.org/article/eeejbfina/v_3a35_3ay_3a2011_3ai_3a9_3ap_3a2388-2406.htm.

- Elkington, J. (2004). Enter the Triple Bottom line. In Henriques, A., Richardson, J., eds. (2004) The triple bottom line: does it all add up?, Routledge.

- Elkington (2021) Green Swans: The Coming Boom in Regenerative Capitalism, Fast Company Press.

- Ferri, G. and Pini, M. (2019) Environmental vs. Social Responsibility in the Firm. Evidence from Italy, Sustainability 2019, 11, 4277;. [CrossRef]

- Freiberg, D., Rogers, J., & Serafeim, G. (2020). How ESG Issues Become Financially Material to Corporations and Their Investors. Harvard Business School.

- Friede, G., Busch T. & Bassen, A. (2015) ESG and financial performance: aggregated evidence from more than 2000 empirical studies, Journal of Sustainable Finance & Investment, 5:4, 210-233. [CrossRef]

- Fulton, M., Kahn, B., & Sharples, C. (2012). Sustainable investing: Establishing long-term value and performance. Available at SSRN 2222740.

- Gabriel, V. (2019) Environmentally sustainable investment: Dynamics between global thematic indices, Cuadernos de Gestión Vol. 19-Nº1, 2019, pp. 41-62. [CrossRef]

- 22. GUIDO GIESE, LINDA-ELING LEE, DIMITRIS MELAS, ZOLTÁN NAGY, and LAURA NISHIKAWA Performance and Risk Analysis of Index-Based ESG Portfolios.

- 23. Guido Giese, Linda-ElingLee, Dimitris Melas, Zoltán Nagy, and Laura Nishikawa(2019) Foundations of ESG Investing: How ESG Affects Equity Valuation, Risk, and Performance, The Journal of Portfolio Management, 45 (5), pp.1-15.

- Guido Giese, Zoltan Nagy, Linda-Eling Lee (2020) Deconstructing ESG Ratings Performance Risk and Return for E, S and G by Time Horizon, Sector and Weighting, MSCI, June 2020.

- Halbritter, G., & Dorfleitner, G. (2015). The wages of social responsibility — where are they? A critical review of ESG investing. Review of Financial Economics, Volume 26, September 2015, Pages 25-35. [CrossRef]

- Hartzmar, S. M., Sussman, A.B. (2019) Do Investors Value Sustainability? A Natural Experiment Examining Ranking and Fund Flows, The Journal of Finance, Vol. LXXIV, No. 6, December 2019.

- Huang, D. Z. X. (2021). Environmental, social and governance (ESG) activity and firm performance: a review and consolidation. Accounting & Finance, vol. 61(1), pages 335-360. [CrossRef]

- Kell, G. (2018) The Remarkable Rise Of ESG, Forbes, https://www.forbes.com/sites/georgkell/2018/07/11/the-remarkable-rise-of-esg/#549a69021695.

- Khan, M., Serafeim, G. and Yoon, A. (2016), ‘Corporate Sustainability: First Evidence on Materiality’, The Accounting Review, Vol. 91, Issue 6, pp. 1697–1724. http://www.aaajournals.org/doi/abs/10.2308/accr-51383. [CrossRef]

- Kotsantonis, S., Pinne, C., & Serafeim, G. (2016). ESG Integration in Investment Management: Myths and Realities. Journal of applied corporate finance, 28, no. 2 (Spring 2016): 10–16. [CrossRef]

- Kotsantonis, S., Pinne, C., & Serafeim, G. (2019). Four things no one will tell you about ESG data. Journal of applied corporate finance, 31 (2), Spring 2019, pages 50-58, . [CrossRef]

- Krosinsky C., and Purdom, S. (2016) Sustainable Investing: Revolutions in theory and practice, Routledge.

- Linnenluecke, M. K. (2021). Environmental, social and governance (ESG) performance in the context of multinational business research. Multinational Business Review. [CrossRef]

- Maiti, M. (2020): Is ESG the succeeding risk factor?, Journal of Sustainable Finance & Investment. [CrossRef]

- McKinsey & Company. (2020). Diversity Wins: How Inclusion Matters.

- Menicucci, E., & Paolucci, G. (2022). ESG dimensions and bank performance: an empirical investigation in Italy. Emerald Publishing Limited. [CrossRef]

- Miralles-Quirós, M. M., Miralles-Quirós, J. L., & Valente Gonçalves, L. M. (2018). The Value Relevance of Environmental, Social, and Governance Performance: The Brazilian Case. Sustainability, 2018, 10(3), 574; [CrossRef]

- MSCI. (2021). MSCI World ESG Leaders Index.

- Nguyen-Taylor, K. and Martindale, M. (2018), Financial Performance of ESG Integration in US Investing (Principles for Responsible Investment, London). Available at: https://www.unpri.org/download?ac=4218.

- Polman, P. (2022) Net Positive: How Courageous Companies Thrive by Giving More Than They Take, Harvard Business Review Press.

- Porter, M. E., Serafeim, G., & Kramer, M. (2019). Where ESG fails? Institutional Investor, October 16: https://www.institutionalinvestor.com/article/2bswdin8nvg922puxdzwg/opinion/where-esg-fails.

- Sadiqa, M., Ngob, T. Q., Pantameec, A. A., Khudoykulovd, K., Ngane, T. T., & Tan, L. P. (2022). The role of environmental social and governance in achieving sustainable development goals: evidence from ASEAN countries. Economic Research-Ekonomska Istraživanja.

- Schoenmaker, D. & Schramade, W. (2019) Investing for longterm value creation, Journal of Sustainable Finance & Investment, 9:4, 356-377. [CrossRef]

- Serafeim, G., & Yoon, A. (2011). The Consequences of Mandatory Corporate Sustainability Reporting, Harvard Business School Working Paper, 11-110. https://www.hbs.edu/research/pdf/11-100.pdf.

- Serafeim, G., & Yoon, A. (2023). Stock price reactions to ESG news: the role of ESG ratings and disagreement. Review of Accounting Studies (2023), Springer, vol. 28(3), pages 1500-1530. [CrossRef]

- Serafeim, G., & Yoon, A. (2022). Which Corporate ESG News Does the Market React To? Financial Analysts Journal, Vol 72, Issue 1, Pages 59-78. [CrossRef]

- Setyahuni, S. W., Handayani, R. S. (2020). On the value relevance of information on environmental, social, and governance (ESG): an evidence from Indonesia. Journal of critical reviews, 7 (12), 50-58, 2020.

- Shmelev, S. E. (2012) Ecological Economics: Sustainability in Practice, Springer, 248pp.

- Shmelev S. E., Shmeleva I. A. (2018). Global urban sustainability assessment: A multidimensional approach. Sustainable Development, 26: 904–920. [CrossRef]

- Shmelev, S. E., Speck, S. U. (2018). Green fiscal reform in Sweden: Econometric assessment of the carbon and energy taxation scheme. Renewable and Sustainable Energy Reviews, 90, 969-98. [CrossRef]

- Shmelev, S. (Ed.). (2019). Sustainable Cities Reimagined: Multidimensional Assessment and Smart Solutions. Routledge. Retrieved from https://www.routledge.com/Sustainable-Cities-Reimagined-Multidimensional-Assessment-and-Smart-Solutions/Shmelev/p/book/9780367254209.

- Shmelev, S.E.; Salnikov, V.; Turulina, G.; Polyakova, S.; Tazhibayeva, T.; Schnitzler, T.; Shmeleva, I.A. (2021) Climate Change and Food Security: The Impact of Some Key Variables on Wheat Yield in Kazakhstan. Sustainability 2021, 13, 8583. [CrossRef]

- Sondre R. Fiskerstrand , Susanne Fjeldavli , Thomas Leirvik , Yevheniia Antoniuk & Oleg Nenadić (2020) Sustainable investments in the Norwegian stock market, Journal of Sustainable Finance & Investment, 10:3, 294-310. [CrossRef]

- Sparkes, R. (2002), Socially Responsible Investment: A Global Revolution (Wiley).

- Strekalina, A., Zakirova, R., Shinkarenko, A., & Vatsaniuk, E. (2023). The Impact of ESG Ratings on Financial Performance of the Companies: Evidence from BRICS Countries. Journal of Corporate Finance Research.

- 20 September 2019; 9, 56. UK Government Actuary’s Department (2019) Investment Bulletin, Issue 9, September 2019.

- UN Global Compact (2005) Who Cares Wins: Connecting Financial Markets to a Changing World.

- UNDESA (2015) A Briefing Note on Addis Ababa Agenda on Financing sustainable development and developing sustainable finance.

- UNDESA (2017) SDG Investing: Advancing a New Normal in Capital Markets.

- UNDP (2019) The SDG Impact Practice Standards for Private Equity Funds.

- UNEP FI (2019) SDG Investment Case.

- UNEP FI (2020) Fiduciary Duty in the 21st Century.

- University of Oxford and Arabesque Partners (2015), From the Stockholder to the Stakeholder: How Sustainability Can Drive Financial Outperformance (March 2015). Available at: https://arabesque.com/research/From_the_stockholder_to_the_stakeholder_web.pdf.

- Wang, N., Pan, H., & Du, S. (2022). How do ESG practices create value for businesses? Research review and prospects. Sustainability Accounting, Management and Policy Journal. [CrossRef]

- Stubbs, W. (2017). Sustainable entrepreneurship and B corps. Business Strategy and the Environment. [CrossRef]

- Whelan, T. Atz, U., Van Holt, T., and Clark, C. (2021) ESG and Financial Performance: Uncovering the Relationship by Aggregating Evidence from 1,000 Plus Studies Published between 2015 – 2020, NYU Centre for Sustainable Business, 19pp.

- NOAA (2025) National Oceanic and Atmospheric Administration. Trends in Atmospheric Carbon Dioxide: Mauna Loa CO₂ Monthly Mean Data. NOAA, https://gml.noaa.gov/ccgg/trends/mlo.html. Accessed 18 Jan. 2025.

- Engle, R. F., & Granger, C. W. J. (1987) Cointegration and Error Correction: Representation, Estimation, and Testing, Econometrica, 55(2), 251-276. [CrossRef]

- Hendry, D. (1995) Dynamic Econometrics. Oxford University Press.

- Hendry, D. Nielsen B. (2007) Ecomometric Modelling. A Likelihood Approach. Princeton University Press.

- Hendry, D., Doornik, J. (2014) Empirical Model Discovery and Theory Evaluation, MIT Press.

- Dengel, S.; Aeby, D.; Grace, J. A relationship between galactic cosmic radiation and tree rings. New Phytol. 2009, 184, 545–551. [CrossRef]

- Ormes, J.F. Cosmic Rays and Climate. Adv. Space Res. 2018, 62, 2880–2891. [CrossRef]

- Svensmark, H. Cosmic Rays and Earth’s Climate. Space Sci. Rev. 2000, 93, 175–185. [CrossRef]

- UN Principles for Responsible Investment (2025) https://www.unpri.org/.

Figure 1.

Dow Jones Sustainability Index, Daily, 2012-2021.

Figure 2.

Down Jones Sustainability Index and the Oil Price, Daily, 2012-2022.

Figure 3.

Brent Crude Oil price and Dow Jones Sustainability Index.

Figure 4.

Crude Oil Brent Price and the Dow Jones Sustainability Index (2014-2022).

Figure 5.

Dow Jones Sustainability and the Crude Oil Price (2012, 2013, 2014).

Figure 6.

Global CO2 concentrations, 1960-2025. Source: NOAA.

Figure 7.

DJSI and the CO2 concentrations.

Figure 8.

Oil price and CO2 concentrations at Mauna Loa Obsevatory.

Figure 9.

TSI Total Solar Irradiance and CO2 concentrations in 2012 to 2020.

Figure 10.

CO2 concentrations, daily and Cosmic Rays.

Figure 11.

Methodological Framework.

Figure 13.

Risiduals in the Levels model.

Figure 15.

Integrated model of global CO2 concentrations (2012-2022).

Figure 16.

Residuals in the final model.

Figure 17.

Coefficient Stability in the final model.

Table 1.

Literature Review Table.

| TITLE | AUTHORS | YEAR | REF | COUNTRY | METHODOLOGY | FINDINGS AND DISCUSSION |

| What Really Explains ESG Performance? Disentangling the Asymmetrical Drivers of the Triple Bottom Line | Crace, L., Gehman, J. | 2023 | [9] | CANADA | The study employs MSCI ESG KLD STATS dataset for its extensive coverage and historical evaluation. Variance partitioning analysis, using two samples from 2003 to 2010 and 1993 to 2010, examines categorical variables' impact on ESG performance. Multilevel modeling with cross-classified structures and MCMC estimation in MLwiN software ensure robust analysis. | The article examines ESG performance in strategic management, debating whether it's influenced more by external factors or internal traits. It highlights challenges in quantifying social impacts and suggests negative ESG indicators are driven by external factors while positive ones reflect internal strategies. Firm and CEO effects significantly shape ESG performance across dimensions. The article advocates for nuanced measures over aggregated indicators to capture true sustainability practices, contributing to a better understanding of ESG performance variation among firms. |

| The use of ESG scores in academic literature: a systematic literature review | Clement, A., Robinot, E., & Trespeuch, L. | 2023 | [7] | CANADA | The study followed Xiao and Watson's (2019) methodology for systematic qualitative systematic reviews. It collected and described definitions of ESG scores in academic literature using systematic meta-analysis. Initial data comprised 6,685 articles, narrowed down to 342 after systematic procedures and analysis of definitions. Various classification themes emerged from the analysis. | The reviewed article offers a qualitative systematic examination of environmental, social, and governance (ESG) scores in academic literature, focusing on their diverse definitions and applications. ESG scores serve as key financial tools for constructing green portfolios and evaluating companies' responsible performances, with investments projected to exceed US$53 trillion by 2025. ESG scores encompass environmental, social, and governance aspects, providing quantitative assessments through tangible and intangible data published by commercial firms. Initially tailored for financial companies, ESG scores have expanded to aid reputation enhancement and risk reduction. However, challenges persist in measuring sustainable practices, especially regarding community and environmental impacts. While significant for aligning with UN Sustainable Development Goals, ESG scores primarily focus on financial risk rather than comprehensive corporate social responsibility (CSR) performance. Academic research diverges across sustainability, CSR, disclosure, finance, and transdisciplinary analyses of ESG scores, revealing inconsistencies in definitions and utilization. The review underscores the necessity for cautious use of ESG scores beyond financial risk assessment and calls for improved methodologies to evaluate environmental and social impacts. It advocates for standardization and increased representation of small and medium-sized businesses in ESG assessments while suggesting a roadmap for future research to refine ESG score definitions and applications. |

| How do ESG practices create value for businesses? Research review and prospects | Wang, N., Pan, H., & Du, S. | 2022 | [64] | CHINA | Bibliometric method is used to analyze literature co-citation, burst detection and keyword co-occurrence, and literature review method is used to condense important ideas from the existing literature |

The text examines the rising importance of ESG (Environmental, Social, and Governance) factors in business, reflecting changing investor and stakeholder priorities. ESG criteria now gauge a company's sustainability and viability, influencing investment decisions and demanding transparency. Investors increasingly prefer firms with strong ESG performance, recognizing its significance for financial success. ESG practices extend beyond financial metrics, impacting societal resilience and market value while reducing risks. The text highlights theoretical frameworks explaining how ESG practices signal positive information, manage risks, and offer strategic advantages. It stresses the critical link between ESG performance and disclosure for transparency and accountability, despite challenges like greenwashing. External factors such as regulations and market dynamics, alongside internal factors like governance structures, shape ESG practices and corporate value. Embracing ESG as a strategic imperative is crucial for long-term value creation and stakeholder trust in businesses. |

| Effective ESG Transformation of Russian Companies in the New Environment: Current Challenges and Priorities | Babynina, L., Kartashov L., Busalov, D., ChernitsovK., & Akhmedov, F. | 2023 | [2] | RUSSIA | The article employs a comprehensive methodology, blending theoretical insights with empirical data to develop ESG-rating methodologies for businesses. | The article examines ESG (Environmental, Social, and Governance) awareness and transformation in Russian businesses, tracing its evolution from state-regulated to corporate norms. Despite economic shifts, ESG remains relevant as companies target Asian markets and restructure supply chains. Tasks include analyzing domestic and foreign studies on sustainable development, comparing Russian ESG rating methodologies, and assessing ESG factor significance. Benefits like risk reduction are acknowledged, but conflicting views exist on efficiency and reporting costs. Challenges include corporate understanding, skill shortages, and financial limitations, influenced by geopolitics and regulations. ESG disclosure is vital for confidence, but inconsistencies in rating agency practices persist. Proposed initiatives aim to promote collaboration and transparency, such as the National ESG Alliance and an ESG Infrastructure Atlas. The article calls for clearer regulations and increased stakeholder engagement to advance sustainable development in Russia. |

| Environmental, social and governance (ESG) performance in the context of multinational business research | Linnenluecke, M. K | 2021 | [33] | AUSTRALIA | The paper outlines emerging literature on global ESG ratings. It covers research on ESG-financial links in emerging markets, multinational ESG performance, and country-level ESG risks. | The article explores the complex landscape of monitoring firms' ESG performance, crucial in socially responsible investment strategies. It notes investors' shift towards aligning investments with societal values, necessitating robust ESG frameworks. Challenges arise when applying Western-centric ESG models to emerging markets due to weaker institutions and limited data. Research on ESG performance's financial impact yields varied results, especially in emerging markets, indicating nuanced patterns across jurisdictions. The text identifies diverse metrics and challenges in studying the ESG–financial performance relationship, including incomplete disclosures and cultural factors. Concerns also arise about the accuracy of ESG ratings, biases, and failures to capture material issues in emerging markets. The article suggests exploring supply chain analysis and incorporating local community concerns into ESG ratings for comprehensive sustainability assessments. In conclusion, it calls for enhanced research to address unresolved issues in ESG assessment, especially in emerging markets and multinational operations. It advocates for improved methodologies and stakeholder integration, emphasizing the importance of indigenous community perspectives in corporate sustainability evaluation. |

| ESG and financial performance: aggregated evidence from more than 2000 empirical studies | Friede, G., Busch T. & Bassen, A. | 2015 | [19] | GERMANY | Two methods aggregate primary and secondary study results, each with distinct calculation approaches. Analysis includes distributions, correlation effect sizes, and subgroup analyses. | The article analysis the evolving role of Environmental, Social, and Governance (ESG) criteria in investment decisions, noting slow mainstream adoption despite significant assets managed under Principles for Responsible Investment (PRI) signatories. It highlights limited integration of ESG information by investment professionals and minimal formal training in ESG analysis. Debates persist over the compatibility of ESG criteria with Corporate Financial Performance (CFP), with studies presenting ambiguous or contradictory results. A review of over 2,000 empirical studies since the 1970s reveals a positive correlation between ESG criteria and CFP across various assets and regions, except for portfolio-related studies. Using a two-step method, the authors analyze findings from 60 review studies, concluding empirical support for the business case for ESG investing. Despite limitations such as publication delays and diverse methodologies, ESG outperformance opportunities exist, particularly in non-equity assets and regions like North America and Emerging Markets. The article advocates deeper ESG integration into investment processes to align with broader societal goals, calling for further research into ESG criteria interaction and long-term performance impacts in portfolios. |

| ESG dimensions and bank performance: an empirical investigation in Italy | Menicucci, E., & Paolucci, G. | 2022 | [36] | ITALY | This study examines a sample of 105 Italian banks and develops three econometric models to verify the effect of ESG initiatives on BP indicators. The independent variables are the ESG dimensions collected from the Refinitiv database, whereas the explanatory variables are performance indicators measured through accounting and market variables | The article examines ESG integration in Italy's banking sector driven by client, investor, and regulatory pressures post-global financial crisis. It assesses the feasibility of enhanced corporate governance, reduced environmental impact, and social responsibility programs. Environmental commitments positively impact efficiency and trust, while social initiatives may challenge profitability. Corporate governance, especially board diversity and risk governance, correlates positively with performance. Empirical findings suggest varying impacts of ESG dimensions on bank performance, highlighting the complex relationship between ESG factors and profitability. The study contributes insights for practitioners and policymakers in sustainable finance and responsible banking. |