1. Introduction

The study examines the influence of oil prices and economic policy uncertainty (hereafter EPU) on the stock market return of oil-importing and exporting countries. The focus is on five specific importing countries: China, India, Germany, Italy, and Japan. These countries have been selected based on their status as prominent oil importers, as indicated by their inclusion in the list of largest oil importers. The EPU index utilized in this research derives from the EPU Platform, a reliable and authorized source for measuring and analyzing policy-related uncertainty. Moreover, countries are selected based on their economic performance and annual oil consumption. Similarly, countries with a large proportion of oil exporting to the world are selected by the current study like Saudi Arabia, Russia, Iraq, Canada, and the United Arab Emirates, and depicted on the EPU index. In addition, these countries belong to the Organization of Petroleum Exporting Countries. (OPEC). These countries rely heavily on oil exports to generate revenue and fuel their economies. The amount of oil each country exports varies depending on the size of its oil reserves, the efficiency of its oil production processes, and the global oil demand.

Oil is considered one of the important raw materials used for the production of goods and services, and its demand is increasing day by day, approximately 3% of the GDP is spent by various oil-importing countries within a year. The increase in oil prices has a serious impact on micro and macro levels. At the micro level, it increases the cost of production, and prices of products, resulting in a consumption level decline, and at the macro level, it declines the productivity and growth of the overall economy, and a rise in import bills leads to a deficit balance of payments (Nazir et al., 2014, 2018).

Previous studies have mixed findings regarding the relationship between oil prices and stock returns, its direction, and sensitivity. Studies like Alamgir and Bin Amin's (2021) and Diaz and Perez de Gracia's (2017) have found a positive correlation between oil price swings and stock rates. However, other sources, like Civcir and Akkoc (2021), have documented a considerable adverse effect. Contrary to these findings, Henriques and Sadorsky (2008) explored the minimal impact of oil prices on stock rates. In addition, it has been noted that the effects of oil price shocks vary depending on whether the economy is oil-exporting or oil-importing. Hamilton (2009), Kilian (2009), Kilian and Park (2009), and Wang et al. (2013) specifically address the variation of impact on both economies. Similarly, the effects of demand and supply shocks are different for oil-importing and exporting countries (Wang et al. 2013).

However, some of the incidents had critical effects on oil prices and stock returns as an attack on the World Trade Center on September 11 led to a heavy decrease of 20% in oil prices, and as a result of this change, stock markets crashed (Synergen, 2020). Along the same lines, when the US economy was recovering from the recession during 2014-15, oil prices increased from USD 100 to USD 125 per barrel, consequently, this change had a significant impact on the US economy and other economies of the world as well. Once again, the stock markets were also affected by a massive fall in oil prices of USD 19.20 per barrel during the COVID-19 epidemic (Synergen, 2020). So, it is required to examine the impact of these factors along with other relevant factors affecting oil price shocks and their effects on stock returns.

The EPU index is used as a barometer to measure uncertainty about future economic policy that can impact investment decisions and economic activity in general. A rise in EPU leads to a reduction in investment, economic activity, and profitability, and as a result, the demand for and import of oil falls rapidly. Nusair and AL-Khasawneh (2022) and Batabyal and Killins (2021) documented the inverse effect of EPU on stock prices and stock returns. Moreover, it is widely recognized that EPU, along with fluctuations in oil prices, plays a significant role in influencing various commercial, economic, and monetary variables. These two factors are regarded as key determinants that can have profound effects on financial markets, investment decisions, and economic conditions. The interplay between EPU and oil price fluctuations creates a complex dynamic that shapes market sentiments and investor behavior, ultimately impacting share prices and other related variables. Thus, it is important to determine the factors behind the EPU index and how these factors can be managed to reduce the level of uncertainty in a country to boost the level of productivity, and efficiency of the overall economy.

The study investigates how changes in oil prices and EPU indices impact the stock returns of selected oil exporting and importing countries and develops an understanding of various factors and how they affect stock returns. Hence, it provides significant information for investors to manage the risks and predictability of oil prices. Categorizing fluctuations in the prices of oil and EPU into positive and negative highlights the asymmetries that arise due to the variations in oil prices. Determining the effect of the modifications in oil prices and EPU on oil importing and exporting countries will provide strategy-creating associations and suggestions for both capitalists and decision-makers about making policies.

Therefore, investors and policymakers will know where to pay close attention and how to respond to such changes. Also, it will provide notable information that will help policymakers determine and evaluate the consequences of oil prices and EPU indices on oil importing and exporting countries and how we should analyze these variables to avoid such destructive adverse impacts.

The study used asymmetric quantile regression to analyze and figure out the results of oil prices and EPU on the returns of the stock market will also identify the distributional heterogeneity of stock returns, which will help the researchers to evaluate different market conditions. The study is significant for investors, and it can lead to better asset allocation; along with this, it will help U.S. policy-making authorities to adjust their energy pattern, which helps manage the condition of the national economy.

Previous studies have not primarily focused on examining the oil price shocks on global EPU asymmetric effects and have not explored the co-integration relationship between these variables. Some studies have incorporated a short sample period of less than two months, which may not accurately capture potential nonlinearities in the data. It is important to consider longer timeframes to ensure a more comprehensive analysis of possible nonlinear relationships. (Jeris & Nath, 2020). Expanding the scope of analysis to include the examination of uncertainty arising from global economic policy is crucial. This can be accomplished by incorporating global uncertainty indices such as the global Economic Policy Uncertainty (EPU) index. By doing so, researchers can gain a broader understanding of the impact and dynamics of uncertainty on various aspects of the global economy. (Degiannakis et al., 2018).

The structure of this essay is as follows. The second portion includes a review of previous research on the relationship between oil price changes and the EPU on the return of both importing and exporting nations, as well as the conceptual and theoretical framework. The third section asses the methodology of the research. The fourth section shows the results and analysis of the data. The fifth section includes the final conclusion.

2. Literature Review

Previous studies related to economic research did not examine the non-linear and asymmetric dynamic relationship between the volatility of global monetary policy and the price of oil. Crude oil is the most important energy source because it produces fuel for industry, power vehicles, and delivers energy. Because of its value as a commodity, crude oil is in high demand and has a thriving financial trading market. Fluctuations in crude oil prices are eventually attached to changes in EPU.

Likewise, based on the monthly data analysis from 1973 to 2011, focusing on 12 oil-importing European nations, including Italy, Germany, France, and the UK, Cunado and Perez de Gracia (2014) identified a significant negative impact of oil price shocks on stock returns. Furthermore, they observed that oil supply shocks generally had more pronounced effects than demand shocks, suggesting that changes in oil supply exerted a greater influence on stock market performance. Along the same lines, Herrera (2015), empirically investigated that there is an asymmetric affiliation between the oil price shock and economic activity by collecting a long sample of monthly facts on industrial production and oil prices of countries including G-7, OECD- Europe, and OECD countries.

Economic policy uncertainty refers to the uncertainty surrounding government policies and their potential impacts on the economy. High levels of EPU can create uncertainty among investors and businesses, leading to cautious investment decisions and potential market volatility. When economic policies are unclear or uncertain, businesses may delay investment decisions, impacting corporate earnings and ultimately affecting stock prices. Some of the fresh past studies focus close attention on the effects of EPU and stock returns, and the majority of them discover that EPU and the American stock market have unfavourable correlations (Kang & Ratti 2013), G7 stock markets (Chiang, 2019), six Pacific Rim countries stock markets (Christou et al., 2017).

Similarly, employing a linear ARDL model and analyzing month-wise data from 1985 to 2016, a group of countries including Canada, Japan, the UK, and the USA, Bahmani-Oskooee and Saha (2019a) discovered that EPU had a short-run negative impact on stock prices. They also found that EPU did not have a significant long-run effect on stock prices. In other words, the negative effect of EPU on stock prices was observed in the short term, but it did not persist in the long run.

In contrast to previous findings, Bahmani-Oskooee and Saha (2019b) employed a nonlinear Autoregressive Distributed Lag model and analyzed monthly data covering from 1985 to 2018. Their study revealed that EPU exhibited a short-run effect on stock prices in Canada, the UK, and the US, but not in Japan asymmetrically. Additionally, they saw a major negative asymmetric long-run effect of EPU on stock prices across all the nations included in the study. This implies that the impact of EPU on stock prices was more pronounced and persistent in the long term, exhibiting a stronger negative relationship. EPU also harms purchasing power and some of the important economic decisions any oil-importing country makes (Al-Thaqeb and Algharabali, 2019). Moreover, Managi et al. (2022) found a negative association between oil price shocks and US stock returns by applying daily data from January 2018 to December 2020 and using a wavelet approach. They also noticed that the implementation of lockdown policies due to the outbreak of the COVID-19 pandemic, coupled with the subsequent oil price shock, led to an increase in the level of uncertainty. This suggests that these factors had a detrimental impact on the US stock market, contributing to decreased returns and heightened uncertainty.

The economic theory is a pertinent theory regarding the effects of oil prices. This theory proposes that variations in oil prices have an impact on supply and demand, which in turn affects economic activity. Oil's influence on the supply as a significant production component result in decreased output of businesses due to decreased productivity of other production input variables. Similar to the supply channel, the demand channel is equally impacted by changes in oil prices, which causes changes in consumption as a surge in oil prices moves money from oil-importing countries to oil-exporting countries. Moreover, Lin (2021) argued that the economic theory which suggests that the economy becomes more unreliable and then attracts the government's attention owing to such violent increases in crude oil prices has a detrimental influence on the economic policy uncertainty. Moreover, it will lead to a surge in economic policy uncertainty, also the consumers become very sensitive to the news that spreads to them when this oil price shock hits (Lin & Bai, 2021).

According to Rehman (2018), global oil price fluctuations affect every economy irrespective of the economic status of any nation, the energy demand is increasing day by day. There is an evident claim that the economic policy uncertainty of India, Spain and Japan respond highly to the price. However, oil is one of the most essential production elements, hence any increase in oil prices would result in increased production costs for countries that import oil (Backus & Crucini, 2000), and accordingly, stock markets would respond depressingly (Sadorsky, 1999). As a result, EPU has an inverse effect on stock returns, and fluctuations influence on the price of oil. Aloui et al. (2016) analyzed the influence of uncertainty on oil returns and discovered that a rise in EPU indices had a positive effect on oil returns before the shocks of the financial crisis. This finding was obtained using the structural Vector Auto regression framework (Rehman, 2018).

Later, Qin (2020) examined the time-varying interactions between the variables: oil price, monetary EPU, fiscal EPU, and trade EPU. The results depicted through the equilibrium model and wavelet analysis have depicted a certain impression of EPU on the prices of oil and further shown that there is a progressive result of oil prices on the EPU which indicates that the policy uncertainty increases when there is an oil bull market.

3. Methodology

3.1. Data and Variables

In this study, the sample end date for all countries is August 2023. The start dates vary, with the longest sample beginning in January 1997 for Canada, Germany, China, and Japan, and the shortest starting in April 2014 for Iraq. The dataset includes stock market price indexes obtained from Investing.com, representing start-of-month closing prices. Economic uncertainty is measured using the Economic Policy Uncertainty (EPU) index, developed by Baker et al. (2016) and Arbatli et al. (2019). The EPU index data is sourced from its official website,

www.policyuncertainty.com, which provides reliable and up-to-date information on economic policy uncertainty. Crude oil price data is obtained from a trusted financial platform, such as Investing.com, which offers accurate and comprehensive data on various financial instruments, including crude oil prices.

Table 1 summarizes the variables and their data sources.

3.2. Asymmetric Quantile Regression Model

We employ asymmetric quantitative regression analysis. QR analysis, developed by Koenker and Bassett in 1978, serves as a supplement to ordinary least squares (OLS) regression analysis. Unlike OLS, which only depicts the average relationship between a dependent variable and a set of independent factors based on the conditional median of the dependent variable's value, QR analysis reveals this relationship across multiple quantiles of the dependent variable. By representing the complete conditional distribution of the dependent variable, QR analysis overcomes the limitations of OLS analysis, which provides only a partial perspective, and offers a comprehensive viewpoint. Therefore, under various market situations, the impacts of the oil price and Economic Policy Uncertainty (EPU) on stock returns are shown using QR analysis. It records effects during periods of bullish market activity at the upper quantiles, bearish market activity at the lower quantiles, and normal market activity at the intermediate quantiles. In addition, QR analysis exhibits resilience to outliers, non-normal errors, deviation, and heterogeneity in the dependent variable, which makes it an important analytical tool (Neifer, 2015; Mensi et al., 2014; Zhu et al., 2016).

To perform the analysis, we adopt a methodology employed in previous studies (e.g., Arouri et al., 2016; Das and Kannadhasan, 2020; You et al., 2017) and estimate a sequence of models, commencing with the conventional ordinary least squares (OLS) model.

We utilize various variables to analyze the relationship between oil price shocks, Economic Policy Uncertainty (EPU), and stock returns where rst represents the real stock market return, calculated as the first difference of the natural logarithm of the real aggregate stock market price index. Specifically, it is obtained using the formula (rst = ln(SPt/SPt-1) * 100), where SPt refers to the aggregate stock price index at time t.and rot is a variable that represents the real oil return. It is figured out by taking the natural logarithm of the current real West Texas Intermediate (WTI) crude oil price and subtracting it first. While EPU, which stands for the uncertainty policy index, is a different variable in the study and aids in capturing the percentage change in the oil price over time, this transformation helps to capture it. The initial difference in the natural logarithm is used to calculate it. This index reflects changes in policy uncertainty over time and provides insights into the volatility or unpredictability of policy-related factors. The equation also contains the random error component, indicated by the letter €t.

The main focus of this study revolves around the parameters α2 and α3, which measure the effects of0changes in oil price (rot) and EPU on stock returns (rst), respectively. The inclusion of the lagged stock return (rst-1) enables us to investigate whether there is predictability in the stock markets of oil-importing and exporting countries based on previous returns, as explored in prior research (Arouri et al., 2016). Lastly, rst-1 is included as control variables to account for their potential influence on the relationship under investigation.

Equation (1) the assumption is that changes in the price of oil and EPU have a linear or symmetrical effect on stock returns. It implies that changes in oil prices and/or the EPU have different but similar effects on stock returns. Nevertheless, several studies have discovered empirical evidence supporting the notion that changes in oil prices exhibit an asymmetric impact on various economic and financial variables. (Cologni and Manera 2008; Hamilton 1996; Lee et al. 1995; Mork 1989). Mork (1989) research reveals the economic activity response of the US in an asymmetric manner to changes in oil prices. Specifically, it shows that the consequences of rising oil prices on the economy are different from those of falling prices. Sadorsky (1999). The findings suggest that favourable oil price movements have a greater impact on US stock returns than negative ones.

Similar to EPU, changes in stock returns could have an unbalanced impact. This disparity can be explained in part by traders' perceptions of how long-lived or short-lived fluctuations in EPU are. (Bahmani-Oskooee and Saha 2019b). When economic policy uncertainty (EPU) decreases, it may lead traders to make minimal or no adjustments to their stock portfolios by moving only a small portion of their investments into safer assets. However, if the decline in EPU is anticipated to be prolonged, traders may opt to allocate a significant portion of their holdings towards equities.

This behavior contributes to the existence of asymmetries in the impact of economic policy uncertainty (EPU) on stock returns. Additionally, another factor influencing these asymmetries is how traders respond to both good and bad market news. Growing research indicates that good and bad news exert uneven effects on individuals' perspectives, with bad news exerting a considerably stronger influence compared to good news. (Soroka 2006). For example, Zhou (2015) reveals that stock prices respond more strongly to unfavorable news updates than to good news, and Laakkonen and Lanne (2008) discover that negative news tends to boost volatility more than positive news.

We divide the effects of changes in the oil price and EPU into good and bad changes to account for asymmetry:

rot+ = max(rot,0), rot− = min(rot,0), epu+ = max(eput,0), and eput− = min(eput,0),

and include these changes in Eq. (1). This yields the asymmetric OLS model:

Where β2, β2, β3, and β3 evaluate the impact on stock returns of good and bad changes in the oil price and EPU, respectively.

Whereas the symmetric OLS model in Eq.(1) While it can give perceptivity on the impact of changes in oil return prices and profitable policy query EPU on stock request returns, it cannot determine whether these goods differ for requests with lower returns compared to those with advanced returns. Furthermore, it cannot ascertain how the state of the stock market, such as bearish, bullish, or normal conditions, influences the relationship between these changes and their impact on stock returns.

The asymmetric OLS model raises the same issues. (2); that is, while model (2) can answer the question of "whether changes in the oil price and the energy price index are significant for stock returns," but it is unable to answer the question of "whether these changes in the oil price and the energy price index affect stock market returns differently for markets with low returns than for markets with high returns." Utilising QR analysis, these problems are addressed. (Nusair and Al-Khasawenh 2018 and Nusair and Olson 2019).

On the bases of the Qr analysis modeling the unconfirmed

rth quantile of the dependent variable for some value of

r ∈ (0,1):

where Qrst (

r∕x) is the uncertain factor of

rth quantile of the variable factor of the (rst),

αr is the intercept which dependent on the ′

r,

βr is a vector of the coefficients associated with the factor

rth quantile, and the factor x changes in EPU, lagged real stock return, oil return prices make up the vector of explicatory factors. We employ QR analysis to look at how changes in real stock return and oil return price and EPU affect stock returns.

We use two QR models:

where equation (4) and equation (5) are the nine quantile which are estimated symmetric and asymmetric QR models. (= 0.10, 0.90).

These quantiles are then separated into three commands: low (r = 0.10 / 0.20 /0.30) equivalent to bear type market, medium (r = 0.40 / 0.50 / 0.60) consistent to normal market, and high (r = 0.70 / 0.80 / 0.90) which corresponds to strong market (Nusair and Olson 2019).

We pay attention on α2r and α3r in the symmetric QR model (4), which measure the dependence quality and degree of stock returns at the rth quantile to variations in oil return price and EPU in each nation. In the asymmetric QR model (5), we pay attention on β2r+, β2r−, β3r+, and β3r− we impose the grade to which changes in the oil return price and EPU have an approving and hostile concussion on stock returns at the rth quantile, independently.

4. Empirical Results

4.1. Descriptive Statistics

Table 2 provides descriptive statistics of returns of and provides important insights about GEPU, changes in crude oil prices, and returns of oil importing and exporting countries. and The Global GEPU shows a slight positive mean (1.0613) but exhibits substantial variability, as indicated by its high standard deviation (18.6052) and wide range, suggesting fluctuating uncertainty levels globally. Crude oil prices display notable volatility with a high standard deviation (13.8082) and extreme kurtosis (12.3161), reflecting large price swings and susceptibility to major shocks. Among the countries, developed economies like Japan and Canada exhibit relatively stable returns, with lower standard deviations and narrower ranges, while emerging markets such as UAE and India demonstrate higher volatility, wider ranges, and extreme kurtosis, pointing to greater investment risks. Countries like Germany and Japan generally experienced positive mean returns, indicating steady performance, while UAE and Iraq showed negative averages, highlighting underperformance. The data underscores the volatile nature of crude oil prices and economic uncertainty, the relative stability of developed markets, and the heightened risks in emerging economies, providing a comprehensive snapshot of variability, risks, and trends across global markets.

4.2. Asymmetric Quantile Regression

The results of Asymmetric Quantile Regression are shown below in

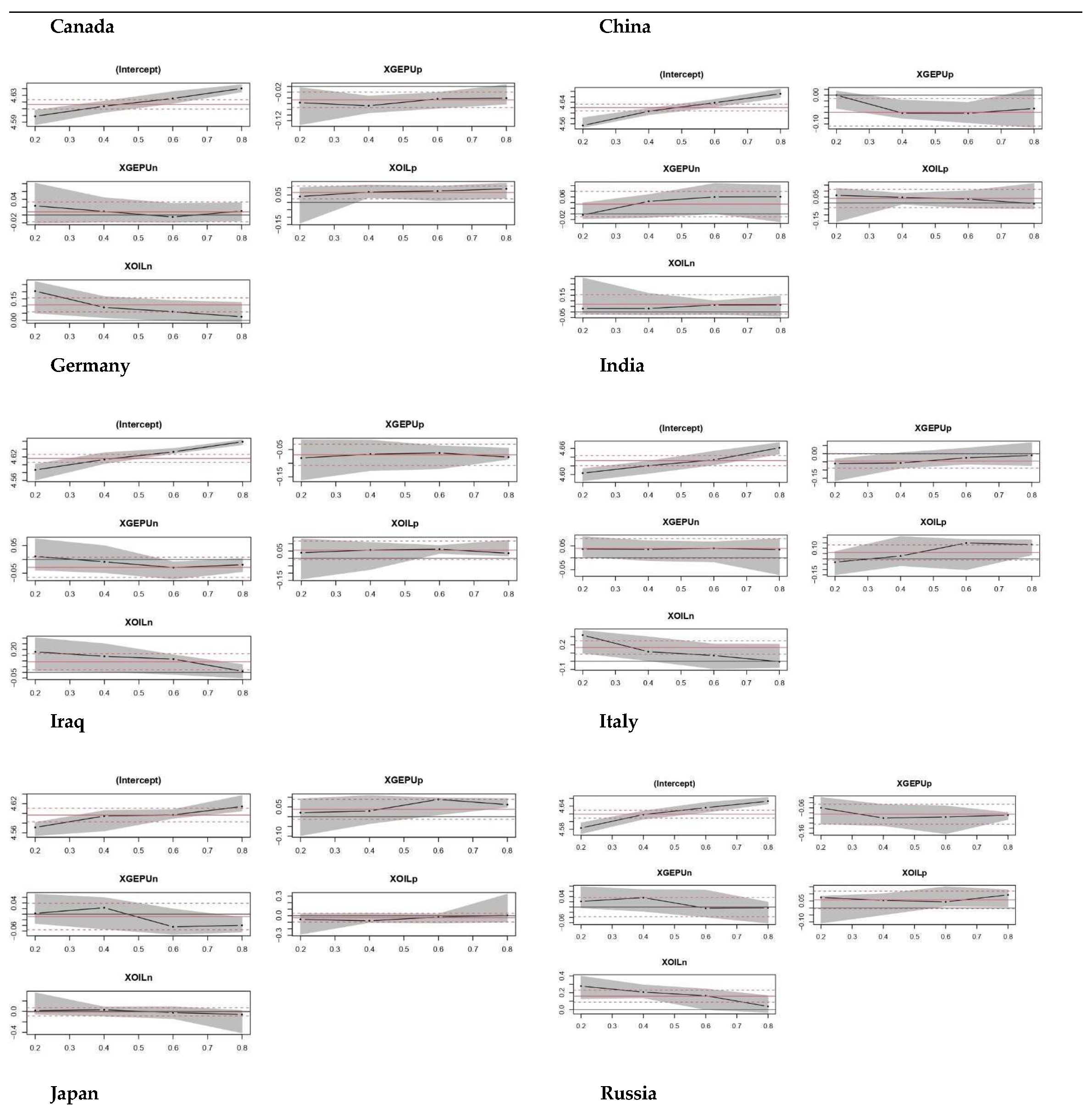

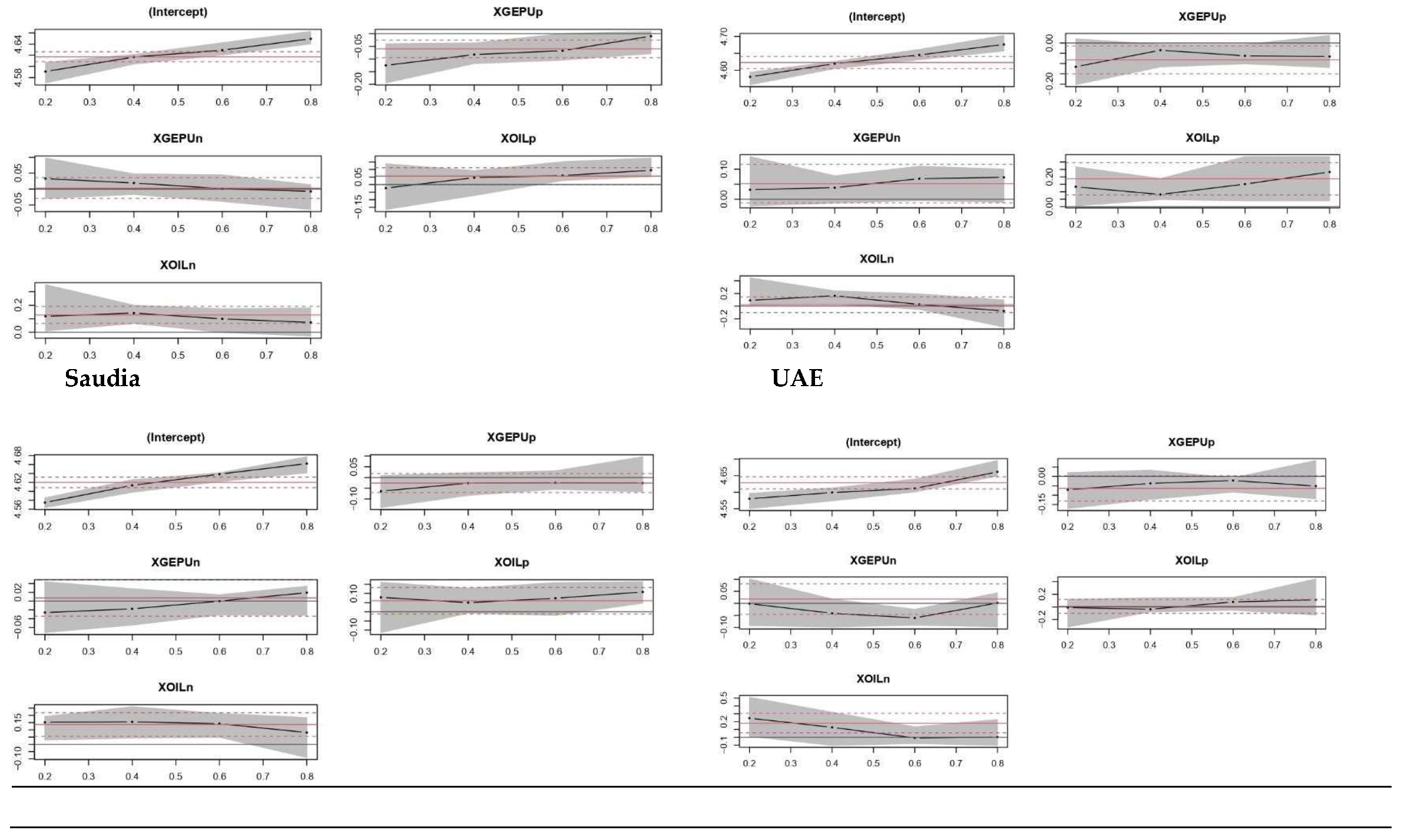

Table 3. As for Canada, the GEPUp shocks shows an increasing trend from -0.057 at 0.2 quantile to -0.041 at 0.8 quantile which shows that when GEPUp is at high quantile, we can see high market return and when GEPUp is at low quantile, we see low market return. GEPUn shows a decreasing trend. At 0.2 quantile, GEPUn is 0.023 which shows that when GEPUn is at lower quantile, we see higher market return. At 0.8 quantile, GEPUn is 0.010 which shows that when GEPUn is at higher quantile, we see lower market return. Coming to OILp (positive oil shocks), it shows an increasing trend moving from 0.040 at 0.2 quantile to 0.092 at 0.8 quantile which indicates a higher market return at high quantile and lower market return for lower quantile. Coming to OILn (negative oil shocks), a decreasing trend from 0.205 at 0.2 quantile to 0.025 at 0.8 quantile is observed. This indicates a high return at lower quantile and a low return at high quantile. In Asymmetric Quantile Regression of Iraq, the GEPUp shocks show an increasing trend which shows that when GEPUp is at high quantile, we can see higher market return and when GEPUp is at low quantile, we see lower market return.GEPUn shows a decreasing trend which indicates a higher market return at low quantile and a lower market return at high quantile. Coming to OILp (positive oil shocks), it shows an increasing trend which indicates a higher market return at high quantile and lower market return for lower quantile. Coming to OILn (negative oil shocks) a decreasing trend is witnessed which indicates a high return at lower quantile and a low return at high quantile.

In Asymmetric Quantile Regression of Russia, the GEPUp shocks shows an increasing trend from -0.116 at 0.2 quantile to -0.066 at 0.8 quantile which shows that when GEPUp is at high quantile, we can see high market return and when GEPUp is at low quantile, we see low market return. GEPUn shows an increasing trend. At 0.2 quantile, GEPUn is 0.032 which shows that when GEPUn is at lower quantile, we see lower market return. At 0.8 quantile, GEPUn is 0.073 which shows that when GEPUn is at higher quantile, we see higher market return. Coming to OILp ( positive oil shocks ), it shows an increasing trend moving from 0.133 at 0.2 quantile to 0.233 at 0.8 quantile which indicates a higher market return at high quantile and lower market return for lower quantile. Coming to OILn (negative oil shocks) a decreasing trend from 0.091 at 0.2 quantile to -0.076 at 0.8 quantile is observed. This indicates a high return at lower quantile and a low return at high quantile. In Asymmetric Quantile Regression of Saudia, the GEPUp shocks show an increasing trend which shows that when GEPUp is at high quantile, we can see higher market return and when GEPUp is at low quantile, we see lower market return. GEPUn shows an increasing trend which indicates a higher market return at high quantile and a lower market return at low quantile. Coming to OILp (positive oil shocks), it shows an increasing trend which indicates a higher market return at high quantile and lower market return for lower quantile. Coming to OILn (negative oil shocks) a decreasing trend is witnessed which indicates a higher return at lower quantile and a lower return at high quantile.

In Asymmetric Quantile Regression of UAE, the GEPUp shocks shows an increasing trend from -0.071 at 0.2 quantile to -0.052 at 0.8 quantile which shows that when GEPUp is at high quantile, we can see high market return and when GEPUp is at low quantile, we see low market return. GEPUn shows an increasing trend. At 0.2 quantile, GEPUn is -0.001 which shows that when GEPUn is at lower quantile, we see lower market return. At 0.8 quantile, GEPUn is 0.002 which shows that when GEPUn is at higher quantile, we see higher market return. Coming to OILp ( positive oil shocks ), it shows an increasing trend moving from -0.010 at 0.2 quantile to 0.113 at 0.8 quantile which indicates a higher return at high quantile and lower market return for lower quantile. Coming to OILn (negative oil shocks) a decreasing trend from 0.224 at 0.2 quantile to 0.003 at 0.8 quantile is observed. This indicates a higher market return at lower quantile and a lower market return at high quantile.

The results oil importing countries for Asymmetric Quantile Regression in

Table 4. Where for the results of China, the GEPUp shocks show an decreasing trend which shows that when GEPUp is at high quantile, we can see lower market return and when GEPUp is at low quantile, we see higher market return. GEPUn shows an increasing trend which indicates a higher market return at high quantile and a lower market return at low quantile. Coming to OILp (positive oil shocks), it shows a decreasing trend which indicates a lower market return at high quantile and higher market return for lower quantile. Coming to OILn (negative oil shocks) an increasing trend is witnessed which indicates a higher return at higher quantile and a lower return at lower quantile. In Asymmetric Quantile Regression of Germany, the GEPUp shocks shows an increasing trend from -0.081 at 0.2 quantile to -0.078 at 0.8 quantile which shows that when GEPUp is at high quantile, we can see high market return and when GEPUp is at low quantile, we see low market return. GEPUn shows a decreasing trend. At 0.2 quantile, GEPUn is 0.011 which shows that when GEPUn is at lower quantile, we see higher market return. At 0.8 quantile, GEPUn is -0.019 which shows that when GEPUn is at higher quantile, we see lower market return. Coming to OILp ( positive oil shocks ), it shows a decreasing trend moving from 0.039 at 0.2 quantile to 0.035 at 0.8 quantile which indicates a lower return at high quantile and higher market return for lower quantile. Coming to OILn (negative oil shocks) a decreasing trend from 0.179 at 0.2 quantile to 0.009 at 0.8 quantile is observed. This indicates a higher market return at lower quantile and a lower market return at high quantile.

In Asymmetric Quantile Regression of India, the GEPUp shocks show an increasing trend which shows that when GEPUp is at high quantile, we can see higher market return and when GEPUp is at low quantile, we see lower market return. GEPUn shows a decreasing trend which indicates a lower market return at high quantile and a higher market return at low quantile. Coming to OILp (positive oil shocks), it shows an increasing trend which indicates a higher market return at high quantile and lower market return for lower quantile. Coming to OILn (negative oil shocks), an decreasing trend is witnessed which indicates a lower return at higher quantile and a higher return at lower quantile.

Figure 1.

Plot for Asymmetric Quantile Regression.

Figure 1.

Plot for Asymmetric Quantile Regression.

In Asymmetric Quantile Regression of Italy, the GEPUp shocks shows a decreasing trend from -0.060 at 0.2 quantile to -0.089 at 0.8 quantile which shows that when GEPUp is at high quantile, we can see lower market return and when GEPUp is at low quantile, we see higher market return. GEPUn shows a decreasing trend. At 0.2 quantile, GEPUn is 0.022 which shows that when GEPUn is at lower quantile, we see higher market return. At 0.8 quantile, GEPUn is -0.003 which shows that when GEPUn is at higher quantile, we see lower market return. Coming to OILp ( positive oil shocks ), it shows an increasing trend moving from 0.074 at 0.2 quantile to 0.093 at 0.8 quantile which indicates a higher return at high quantile and lower market return for lower quantile. Coming to OILn (negative oil shocks) a decreasing trend from 0.279 at 0.2 quantile to 0.037 at 0.8 quantile is observed. This indicates a higher market return at lower quantile and a lower market return at high quantile.

In Asymmetric Quantile Regression of Japan, the GEPUp shocks show an increasing trend which shows that when GEPUp is at high quantile, we can see higher market return and when GEPUp is at low quantile, we see lower market return. GEPUn shows a decreasing trend which indicates a lower market return at high quantile and a higher market return at low quantile. Coming to OILp (positive oil shocks), it shows an increasing trend which indicates a higher market return at high quantile and lower market return for lower quantile. Coming to OILn (negative oil shocks), a decreasing trend is witnessed which indicates a lower return at higher quantile and a higher return at lower quantile.

4.3. Robustness Check: Standard Quantile Regression Model

The results in

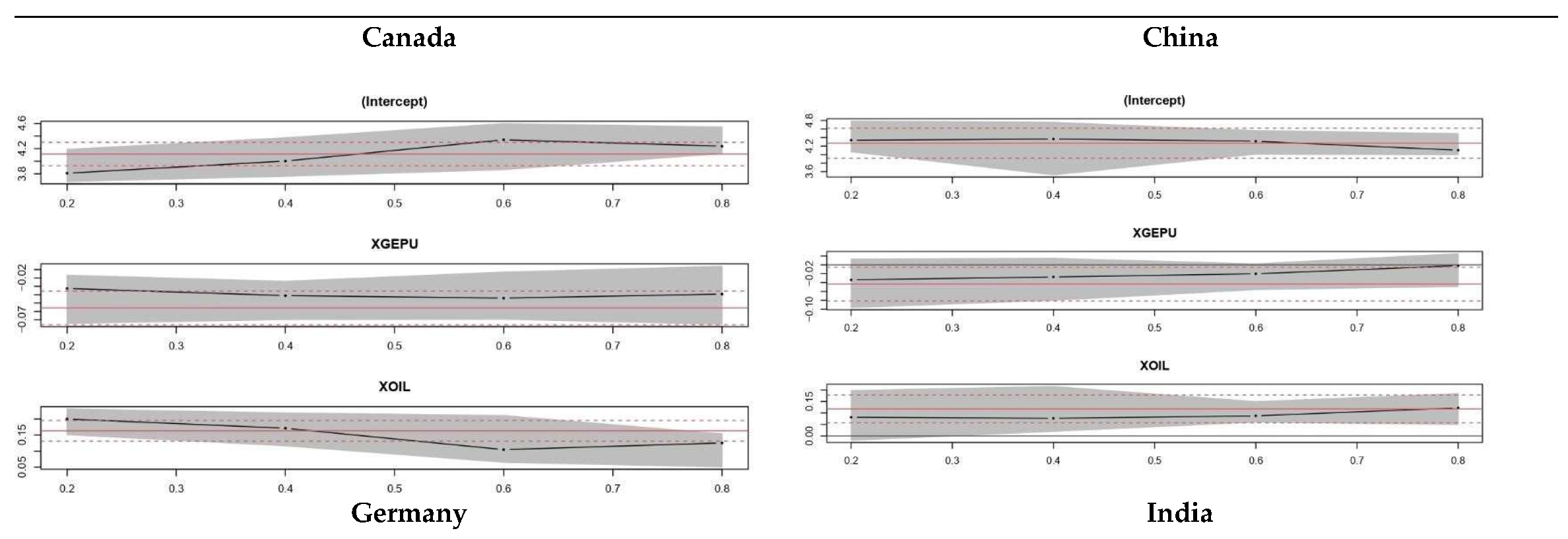

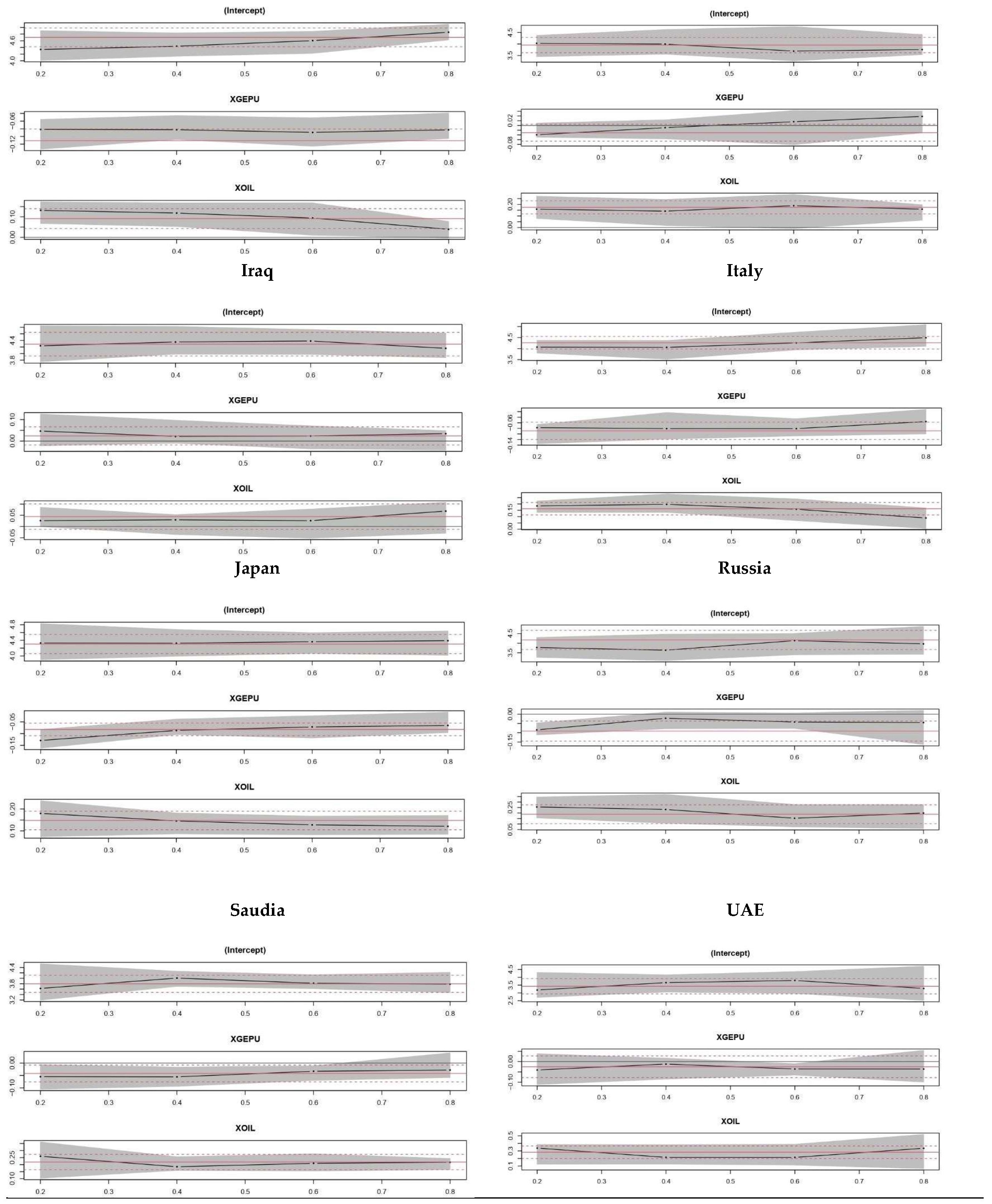

Table 5. shows that at 0.20 quantile of Canada, the GEPU value is -0.033 which is highly significant and is greater than -0.039 at 0.80 quantile which is also highly significant. For Canada, we can see that according to stock market returns, the GEPU shows a decreasing effect from 0.20 quantile to 0.80 and we witness the same for oil as well. It shows a decreasing trend from 0.200 at 0.20 quantile to 0.125 at 0.80 Quantile, both values being highly significant. At 0.20 quantile of Iraq, the GEPU value is 0.047 which is highly significant and is greater than 0.034 at 0.80 quantile which is also highly significant. For Iraq, we can see that according to stock market returns, the GEPU shows a decreasing effect from 0.20 quantile to 0.80. Oil shows an increasing trend from 0.026 at 0.20 quantile to 0.069 at 0.80 Quantile. Both of the values are insignificant showing that it has no real effect. At 0.20 quantile of Russia, the GEPU value is -0.084 which is highly significant and is less than -0.045 at 0.80 quantile which is insignificant showing no effect. For Russia, we can see that according to stock market returns, the GEPU shows an increasing effect from 0.20 quantile to 0.80. Oil shows a decreasing trend from 0.255 at 0.20 quantile to 0.200 at 0.80 Quantile. Both of the values are highly significant showing that it has an effect.

At 0.20 quantile of Saudia, the GEPU value is -0.055 which is moderately significant and is less than -0.028 at 0.80 quantile which is insignificant showing no effect. For Saudia, we can see that according to stock market returns, the GEPU shows an increasing effect from 0.20 quantile to 0.80. Oil shows a decreasing trend from 0.259 at 0.20 quantile to 0.217 at 0.80 Quantile. Both of the values are highly significant showing that it has an effect. At 0.20 quantile of UAE, the GEPU value is -0.041 which is less than -0.036 at 0.80 quantile both being insignificant showing no effect. For UAE, we can see that according to stock market returns, the GEPU shows an increasing effect from 0.20 quantile to 0.80. Oil shows a decreasing trend from 0.338 at 0.20 quantile to 0.335 at 0.80 Quantile. Both of the values are highly significant showing that it has an effect.

The results in

Table 6. Shows that at 0.20 quantile of China, the GEPU value is -0.034 which is less than -0.002 at 0.80 quantile both of values being insignificant. For China, we can see that according to stock market returns, the GEPU shows an increasing effect from 0.20 quantile to 0.80 and we witness the same for oil as well. It shows a decreasing trend from 0.081 being least significant at 0.20 quantile to 0.122 at 0.80 Quantile, being insignificant showing no true effect. At 0.20 quantile of Germany, the GEPU value is -0.082 which is greater than - 0.083 at 0.80 quantile both of values being highly significant. For Germany, we can see that according to stock market returns, the GEPU shows a decreasing effect from 0.20 quantile to 0.80. Oil shows an decreasing trend from 0.132 being highly significant at 0.20 quantile to 0.039 at 0.80 Quantile, being insignificant showing no true effect. At 0.20 quantile of India, the GEPU value is -0.039 which is less than 0.038 at 0.80 quantile both of values being least significant. For India, we can see that according to stock market returns, the GEPU shows an increasing effect from 0.20 quantile to 0.80. Oil shows no trend from 0.159 at 0.20 quantile to 0.159 at 0.80 Quantile, both values being highly significant.

At 0.20 quantile of Italy, the GEPU value is -0.077 which is less than -0.056 at 0.80 quantile both of values being highly significant. For Italy, we can see that according to stock market returns, the GEPU shows an increasing effect from 0.20 quantile to 0.80. Oil shows a decreasing trend from 0.185 at 0.20 quantile to 0.089 at 0.80 Quantile, both values being highly significant. At 0.20 quantile of Japan, the GEPU value is -0.129 which is less than -0.065 at 0.80 quantile both of values being highly significant. For Japan, we can see that according to stock market returns, the GEPU shows an increasing effect from 0.20 quantile to 0.80. Oil shows a decreasing trend from 0.180 at 0.20 quantile to 0.121 at 0.80 Quantile, both values being highly significant.

Figure 2.

Plot For Quantile Regression.

Figure 2.

Plot For Quantile Regression.

5. Conclusions

We employ quantile regression (QR) analysis to study the asymmetric effects of changes in oil price and EPU on the stock market returns of the Major oil importing and exporting countries. QR analysis provides information on the co-movement between stock returns and changes in oil price and EPU. We allow for asymmetries by differentiating between positive and negative changes in oil prices and EPU. We used monthly data from January 1997 to August 2023 and estimated four models for each country: symmetric and asymmetric OLS and QR models.

The symmetric OLS model for oil exporting countries shows that while changes in EPU hurt the stock returns in all countries except Iraq where it shows a positive but insignificant effect, and for oil price changes have a positive effect in all countries, whereas for oil exporting countries show that while changes in EPU have a negative effect on the stock market returns in all countries, more over for oil price changes have a positive effect on the stock returns in all countries and negative but insignificant effect for in the Iraq and UAE. In contrast, the asymmetric OLS model shows that while positive changes in EPU have a negative effect on the stock returns in all the countries, negative changes are insignificant in all the countries.

This indicates that positive and negative changes in EPU have asymmetric effects on stock returns since rising EPU lowers stock returns, whereas falling EPU is insignificant. We find that positive oil price changes have an insignificant effect for both oil importing and exporting countries except Canada and Russia where they show a significant effect. Moreover, we find that negative oil price changes have significant effect for all major oil importing and exporting countries except for Iraq, Russia and China. Similarly, the symmetric QR model for oil importing countries shows that while EPU harms the stock returns of all the countries except for Iraq, across the entire Quantile distribution on the stock returns and for oil price changes have a positive significant effect on the stock returns in all countries and insignificant effect in Iraq. Whereas for oil exporting countries it shows that while EPU has a negative effect on the stock returns of all the countries across the entire Quantile distribution on the stock returns and for oil price changes it also shows a positive significant effect on the stock returns in all oil importing countries.

On the other hand, for oil exporting countries the asymmetric QR models show that while positive changes in EPU have a negative effect on stock returns in Canada, Russia, Saudi Arabia and UAE across all of the Quantile, except for Iraq where it shows a positive effect. Negative changes are significant while positive changes in Iraq are insignificant. This shows that changes in EPU have an asymmetric effect on the stock market returns since rising EPU reduces stock market returns however decreasing EPU is insignificant in most of the Quantile for all the countries except it shows low and medium significance in medium Quantile of Iraq, Russia and UAE. As for oil it shows that while positive changes in oil prices show positive effect in all countries except for Iraq, and negative changes show positive but insignificant effect in all oil exporting countries. We find the decreasing oil prices reduce the stock market returns in all countries during almost all quantiles.

In contrast to that, for oil importing countries the asymmetric QR models show that positive changes in EPU have a negative effect on stock returns in all countries across all of the Quantile, where changes are significant. This shows that changes in EPU have an asymmetric effect on the stock market returns since rising EPU reduces stock market returns however decreasing EPU is insignificant in all of the Quantile for all the countries. As for oil it shows that while positive changes in oil prices show positive effect in all countries with insignificant values in low and medium quantile while significant values in the high qauntile, moreover we can see that some negative effect in the high quantile for china. The negative changes show positive effect in all oil importing countries, except china, where as all positive effects are significant and negative effects are insignificant.

6. Implications

Our research findings have some important policy implications. First, because the impacts of changes in oil price and EPU are not same and changes throughout the distribution of the stock returns, policy recommendations can be drawn based on the results of OLS since it can be misleading. Second, our results show that changes in oil price and EPU have massive effects on the stock returns of oil importing and exporting countries which seems to be asymmetric and changes according to the conditions of the market. Thus, policy makers should pay close to variations in oil price and EPU. They should be able to know how to respond to these changes in order to avoid adverse consequences. For instance, EPU shows a decreasing trend for Italy and India which means that the stock market return gets affected and decreases when there are fluctuations in the EPU, so investors are required to give full attention to such countries whereas countries like Canada and USA shows that increasing trend which gives insights to investors and policy makers not to respond to falling of EPU. Also, our results show that the influence of positive changes in EPU is more significant and larger than that of the negative changes. This indicates that policymakers and investors should devote more attention to rising EPU than falling EPU.

Lastly, positive changes in oil prices appear to carry more significance in most countries compared to negative changes. The resulting impact is generally positive, especially in the midst of extreme market conditions. As a consequence, policymakers are encouraged to allocate greater attention to the ascent of oil prices rather than their decline. It is advisable for policymakers to steer clear of uncertain information related to oil price shifts, as such ambiguity has the potential to induce heightened volatility in stock markets. A balanced approach to addressing both positive and negative changes in oil prices is crucial for comprehensive economic management. In addition, they may need to coordinate efforts internationally to manage the effects of oil price fluctuations on a global scale. To conclude, investors and policymakers need to come up with a holistic approach that takes into account both short term responses to extreme market conditions and long-term strategies for managing oil price fluctuations.

7.Limitations and Future Recommendations

This research has its own limitations as it is only restricted to the context of selected oil- importing and exporting countries. Future researchers can opt for conducting the same study for other oil imports and exports that are not selected in this research for comparative analysis. Another limitation of the study belongs to the insufficient data of 2023 makes it difficult for us to interpret the conclusion for the 2023 time period. In addition, as this study only focuses on macroeconomics factors like market returns, oil price, oil returns economic policy uncertainty so future researchers may add more factors such as unemployment rate, and political risk to more generalized the findings.

Author Contributions

Conceptualization, S.A. and H.Z..; methodology, A.B. ; software, H.N.; validation, E.T., and A.B.,; formal analysis, H.Z.; investigation, S.A.; resources, A.B.; data curation, E.T.; writing—original draft preparation, A.B.; writing—review and editing, H.Z..; visualization, E.T.; supervision, H.N..; project administration, S.A.; funding acquisition, A.B. All authors have read and agreed to the published version of the manuscript.

Data Availability Statement

Upon request from the corresponding author.

Acknowledgments

We thank the editor of the journal for the full fee waiver in the publication of this article.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Aloui, R., Gupta, R., & Miller, S. M. (2016). Uncertainty and crude oil returns. Energy Economics, 55, 92-100. [CrossRef]

- Al-Thaqeb, S. A., Algharabali, B. G., & Alabdulghafou, K. T. (2020, October 12). The pandemic and economic policy uncertainty. International Journal of Finance & Economics. [CrossRef]

- Alamgir, F., & Amin, S. B. (2021). The nexus between oil price and stock market: Evidence from South Asia. Energy Reports, 7, 693-703. [CrossRef]

- Arouri M, Estay C, Rault C, Raubaud D (2016) Economic policy uncertainty and stock markets: longrun evidence from the US. Financ Res Lett 18:136–141. [CrossRef]

- Arbatli E, Davus S, Ito A, Miake N, Saito I (2019) Policy uncertainty in Japan (August 5, 2019). Becker Friedman Institute for Research in Economics Working Paper No. 2017- 09. Available at SSRN: https://ssrn.com/abstract=2972891 or. [CrossRef]

- Bernanke B (1983) Irreversibility, uncertainty, and cyclical investment. Q J Econ 98(1):85– 106. [CrossRef]

- Backus, D. K., & Crucini, M. J. (2000). Oil prices and the terms of trade. Journal of international Economics, 50(1), 185-213. [CrossRef]

- Bahmani-Oskooee M, Saha S (2019a) on the efects of policy uncertainty on stock prices. J Econ Financ 43:764–778. [CrossRef]

- Bahmani-Oskooee M, Saha S (2019b) on the efect of policy uncertainty on stock prices: an asym- metric analysis. Quant Financ Econ 3(2):412–424. [CrossRef]

- Batabyal, S., & Killins, R. (2021). Economic policy uncertainty and stock market returns: Evidence from Canada. The Journal of Economic Asymmetries, 24, e00215. [CrossRef]

- Bjørnland H (2009) Oil price shocks and stock market booms in an oil exporting country. Scott J Polit Econ 56(2):232–254. [CrossRef]

- Bloom N (2014) Fluctuations in uncertainty. J Econ Perspect 28(2):153–176. [CrossRef]

- Baker S, Bloom N, Davis S (2016) Measuring economic policy uncertainty. QJ Econ 131(4):1593–1636. [CrossRef]

- Cologni A, Manera M (2008) Oil price, infation and interest rates in a structural cointegrated VAR model for the G-7 countries. Energy Econ 30:856–888.

- Christou, C., J. Cunado, R. Gupta, and C. Hassapis. 2017. “Economic Policy Uncertainty and Stock Market Returns in PacificRim Countries: Evidence Based on a Bayesian Panel VAR Model.”Journal of Multinational Financial Management40: 92–102. [CrossRef]

- Chiang, T. C. 2019. “Economic Policy Uncertainty, Risk and Stock Returns: Evidence from G7 Stock Markets.” Finance Research Letters 29 (C): 41–49. [CrossRef]

- Civcir, I., & Akkoc, U. (2021). Non-linear ARDL approach to the oil-stock nexus: Detailed sectoral analysis of the Turkish stock market. Resources Policy, 74, 102424. [CrossRef]

- Das D, Kannadhasan M (2020) the asymmetric oil price and policy uncertainty shock exposure of emerging market sectoral equity returns: a quantile regression approach. Int Rev Econ Finance 9:563–581. [CrossRef]

- Diaz, E. M., Molero, J. C., & de Gracia, F. P. (2016). Oil price volatility and stock returns in the G7 economies. Energy Economics, 54, 417-430. [CrossRef]

- Hamilton J (1996) this is what happened to the oil price-macroeconomy relationship. J Monet Econ 38(2):215–220. [CrossRef]

- Henriques, I., & Sadorsky, P. (2008). Oil prices and the stock prices of alternative energy companies. Energy Economics, 30(3), 998-1010. [CrossRef]

- Hamilton J (2009) Causes and consequences of the oil shock of 2007–08. Brookings Papers on Economic Activity, Spring, 215–261.

- Herrera, A. M., Lagalo, L. G., & Wada, T. (2015). Asymmetries in the Response of Economic Activity to Oil Price Increases and Decreases? Journal of International Money and Finance, 50(1), 108-133. [CrossRef]

- Kang, W., and R. A. Ratti. 2013. “Oil Shocks, Policy Uncertainty and Stock Market Return.” Journal of International Financial Markets, Institutions and Money 26: 305–318. [CrossRef]

- Kilian, L., & Park, C. (2009). The impact of oil price shocks on the US stock market. International economic review, 50(4), 1267-1287. [CrossRef]

- Kilian, L. (2009). Not all oil price shocks are alike: Disentangling demand and supply shocks in the crude oil market. American Economic Review, 99(3), 1053-1069. [CrossRef]

- Koenker R, Bassett G (1978) Regression quantiles. Econometrica 46(1):33–50. [CrossRef]

- Lee K, Ni S, Ratti R (1995) Oil shocks and the macroeconomy: the role of price variability. Energy J 16(4):39–56. [CrossRef]

- Laakkonen H, Lanne M (2008) Asymmetric news efects on volatility: good vs. bad news in good vs. bad times. Discussion Paper No. 207, Helsinki Center of Economic Research. ISSN 1795-0562.

- Lin, B., & Bai, R. (2021). Oil prices and economic policy uncertainty: evidence from global, oil importers, and exporters’ perspective. Research in International Business and Finance, 56, 101-357. [CrossRef]

- Mork K (1989) Oil and the macroeconomy when prices go up and down: an extension of Hamilton’s results. J Polit Econ 97(3):740–744.

- Mensi W, Hammoudeh S, Reboredo J, Nguyen D (2014) Do global factors impact BRICS stock markets? a quantile regression approach. Emerg Mark Rev 19:1–17. [CrossRef]

- Managi S, Yousf M, Ben Zaied Y, Ben Mabrouk N, Ben Lahouel B (2022) Oil price, US stock market and the US business conditions in the era of COVID-19 pandemic outbreak. Econ Policy Anal 73:129–139. [CrossRef]

- Narayan P, Narayan S (2010) Modelling the impact of oil prices on Vietnam’s stock prices. Appl Energy 97:356–361. [CrossRef]

- Nazir, Sidra, Qayyum, & Abdul. (2014). Impact of Oil Price and Shocks on Economic Growth of Pakistan: Multivariate Analysis. Munich Personal RePEc Archive.

- Neifer N (2015) Do global risk factors and macroeconomic conditions affect global Islamic index dynamics? a quantile regression approach. Q Rev Econ Financ. [CrossRef]

- Nusair S, Al-Khasawneh J (2018) Oil price shocks and stock market returns of the GCC countries: empirical evidence from quantile regression analysis. Econ Chang Restruct 51(4):339–372. [CrossRef]

- Nusair S, Olson D (2019) The efects of oil price shocks on Asian exchange rates: evidence from quantile regression analysis. Energy Econ 78:44–63. [CrossRef]

- Nusair, S. A., & Al-Khasawneh, J. A. (2022). Impact of economic policy uncertainty on the stock markets of the G7 Countries: a nonlinear ARDL approach. The Journal of Economic Asymmetries, 26, e00251. [CrossRef]

- Pastor, L., & Veronesi, P. (2012). Uncertainty about government policy and stock prices. The journal of Finance, 67(4), 1219-1264. [CrossRef]

- Rehman, M. U. (2018). Do oil shocks predict economic policy uncertainty? Physica A: Statistical mechanics and its applications, 498(1), 123-136. [CrossRef]

- Sadorsky, P. (1999). Oil price shocks and stock market activity. Energy economics, 21(5), 449- 469. [CrossRef]

- Soroka S (2006) Good news and bad news: asymmetric responses to economic information. J Polit 68(2):372–385.

- Synergen. (2020, May 3). Top 6 Events That Impacted Global Oil Prices. SynergenOG. Retrieved March 23, 2022.

- Wang, Y., Wu, C., & Yang, L. (2013). Oil price shocks and stock market activities: Evidence from oil-importing and oil-exporting countries. Journal of Comparative economics, 41(4), 1220-1239. [CrossRef]

- Yang T, Zhou F, Du M, Du Q, Zhou S (2021) Fluctuation in the global oil market, stock market volatility, and economic policy uncertainty. [CrossRef]

- You W, Guo Y, Zhu H, Tang Y (2017) Oil price shocks, economic policy uncertainty and industry stock returns in China: asymmetric efects with quantile regression. Energy Econ 68:1–18. [CrossRef]

- Zhou J (2015) The good, the bad, and the ambiguous: the aggregate stock market dynamics around mac- roeconomic news (24 Jan 2015).

- Zhu H, Guo Y, You W, Xu Y (2016) The heterogeneity dependence between crude oil price changes and industry stock market returns in China: evidence from quantile regression approach. Energy Econ 55:3. [CrossRef]

|

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).