Submitted:

29 August 2024

Posted:

29 August 2024

You are already at the latest version

Abstract

The integration of Artificial Intelligence (AI) in the FinTech industry has substantially reshaped operational workflows, product innovation, and risk management, all of which influence company valuation. This study investigates the impact of AI-enhanced multilayer networks on FinTech valuation. Utilizing a novel scalable multilayer network model with AI-driven Copula Nodes, the research reveals that operational efficiency is a significant driver of market value. However, the findings emphasize the necessity of a balanced strategy that integrates AI across all operational layers, particularly in risk management and product innovation, to maximize valuation. This study offers a comprehensive framework that enhances understanding of AI’s complex role in FinTech valuation, providing critical insights for industry stakeholders.

Keywords:

operational efficiency

; risk management

; product innovation

; copula nodes

; digitalization

1. Introduction

The digital transformation within the financial services industry has led to the integration of advanced technologies, particularly Artificial Intelligence (AI), into the operational frameworks of FinTech companies. This integration has brought significant innovations in automation, risk management, product development, and customer personalization. As FinTech firms increasingly rely on AI to streamline operations and enhance services, understanding how these technologies impact company valuation has become crucial.

AI enhances operational efficiency, opens new avenues for product innovation, and improves customer engagement. However, AI's effects on FinTech valuation are complex and multifaceted, requiring a comprehensive analytical framework.

The study examines a scalable multilayer network approach, which makes the pivotal role of AI in improving market value through the optimization of operational workflows and the implementation of advanced risk management strategies strikingly apparent, demonstrating its indispensable nature in the modern financial landscape. The transformative influence of AI in financial risk management is noteworthy, as it provides enhanced predictive capabilities and operational efficiencies by utilizing sophisticated machine learning algorithms to analyze extensive datasets.

Furthermore, AI's impact on FinTech valuation is essential for securing competitive advantage within the evolving financial services landscape, where innovations driven by AI not only bolster operational efficiency but also enhance accessibility and elevate customer satisfaction levels. Additionally, the assimilation of AI into risk management protocols within the FinTech sphere alters traditional methodologies, presenting groundbreaking solutions to persistent challenges such as fraud detection and the complexities of regulatory compliance, which are critical to the integrity of financial transactions.

This integration improves the precision and thoroughness of risk assessments, fostering a financial environment that is both more secure and more efficient through systematic monitoring and data analysis.

Nevertheless, the journey toward the widespread adoption of AI is not devoid of challenges; it also raises significant issues surrounding regulatory adaptation and ethical considerations. A strategically balanced approach that seamlessly integrates AI across all operational layers is crucial to fully realizing the potential for maximizing company valuation, as underscored by the scalable multilayer network model that serves as a guiding principle.

The continual evolution of financial networks illuminates the dynamic and often complex interactions that occur within AI-driven financial markets. These intricate networks suggest that AI has the potential to significantly impact wealth distribution among various financial agents, primarily through the ongoing and adaptive evolution of network topologies.

Within this framework, this study seeks to answer the following question: How does the integration of AI-driven multilayer networks impact the valuation of FinTechs?

The central aim is to construct and evaluate an analytical model that integrates AI-driven multilayer networks, examining their consequential effects on the valuation metrics of FinTechs. This model will analyze the dynamics of operational dimensions—such as the efficiency of operations, the strategies employed in risk management, the innovations introduced in product development, and the perceptions held in the market—while considering how these elements interact through specialized AI-driven copula nodes, to shape and ultimately affect the overall valuation within the marketplace.

This study enhances the comprehension of FinTech valuation in the digital era by developing an analytical framework that is both detailed and practical. By introducing a pioneering methodology that merges multilayer network theory with cutting-edge AI-driven processes, this study delivers insights that are beneficial not only for investors and regulators but also for FinTechs.

2. Literature Review

The amalgamation of AI and digitalization within the financial technology sector has ignited a remarkable transformation, leading to substantial progress in various domains, particularly those concerning operational efficiency, risk management, and the innovative development of new products and services. Nonetheless, despite the increasing volume of research focused on investigating these critical aspects, there remains a deficiency in the formulation of comprehensive valuation models encapsulating the complex and diverse influence that AI exerts across the interconnected layers of operational activities.

This literature review is designed to bridge this gap. It considers essential studies that highlight AI's pivotal role within the FinTech space and how AI-driven processes affect market valuation.

AI and digitalization have been transformative forces in the FinTech industry, enabling enhanced operational efficiency, risk management, and customer personalization. [1] analyze the transformative role that AI plays within financial technology, highlighting its potential to overhaul financial services by harnessing the power of automation and the insights derived from vast amounts of data. In a similar vein, [2] illustrates how the groundbreaking and transformative innovations that AI powers are not merely influencing but are indeed fundamentally reshaping the landscape of financial services.

[3] argue that AI enhances operational efficiency, offering FinTechs a competitive advantage by reducing costs and increasing profitability. [4] support this view, noting that digitalization plays a crucial role in disrupting the financial sector by streamlining operations and reducing human error. However, as [5] points out, the integration of digital finance and AI can also disrupt financial markets, impacting both intrinsic value and market perceptions. This disruption underscores the need for comprehensive valuation models that can capture AI's multifaceted effects on FinTech companies.

[6] expands on the application of AI in both FinTech and RegTech, illustrating the broader implications of AI in regulatory compliance and governance. Similarly, [7] discusses how AI fosters innovation within financial services, highlighting the need for firms to adopt these technologies to remain competitive. Despite these advancements, [8] caution that managing the internal and external complexities introduced by digitalization requires sophisticated modeling approaches to harness AI's potential effectively.

Risk management is another critical area where AI has made significant inroads. [9] discuss how AI-driven models in a multilayer network setting can provide a comprehensive view of risks, enhancing a firm's ability to predict and mitigate potential financial losses. This is consistent with the findings of [10], who propose scalable multilayer network models for risk management in FinTech, emphasizing the need for AI to analyze complex data interactions across different layers.

Moreover, [11] explore AI's role in modern banking, particularly in fraud prevention, risk management, and regulatory compliance. Their work underscores the importance of AI in enhancing the accuracy and efficiency of risk assessments, which are crucial for maintaining the integrity of financial transactions. However, the literature still lacks a comprehensive understanding of how these AI-driven risk management practices directly impact FinTech valuation.

[12] further discuss the role of AI, combined with the Internet of Things (IoT), in ensuring the smooth operation of network functions in FinTech. Their research highlights how AI can enhance operational reliability, which is critical for risk management and, consequently, valuation.

AI has been recognized as a pivotal driver of product innovation within the FinTech sector. [13] discuss the strategic implications of digital transformation in the FinTech ecosystem, particularly regarding financial valuation metrics. They highlight how AI-driven innovations unlock new revenue streams and explore previously untapped markets. Similarly, [14] emphasizes the need for innovative valuation models that accurately capture the dynamic nature of FinTech products and services.

[15] put forth a compelling argument that the advent of novel products introduced within a distinct layer of a multilayer network possesses the remarkable ability to exert influence over other interconnected layers, thus rendering it crucial to take these intricate interactions into account when undertaking the task of assessing valuation. [16] show how AI, the IoT, and financial technology are challenging traditional banking models.

[17] bring to light the myriad complexities that are inherent in the process of valuing FinTech startups, especially those that are heavily oriented towards AI-driven innovation and disruption. Their research indicates that while AI has the potential to propel substantial product innovation, the conventional valuation methods that have been employed historically may fall woefully short of fully capturing the vast potential inherent in these groundbreaking innovations, thereby resulting in a scenario of significant undervaluation that could hinder the growth and recognition of these transformative entities.

Market perception and investor sentiment play critical roles in determining the valuation of FinTechs. [5] discuss how the integration of AI and digital technologies can improve investor sentiment, leading to valuations that exceed intrinsic value due to speculative growth expectations. This phenomenon tends to be widespread and noticeable in emerging markets, as highlighted by [18], wherein they observed that the integration and widespread adoption of cutting-edge digitalization, as well as advanced AI technologies, are intricately linked to and directly correlated with the significant growth potential that these markets possess. [19] further emphasize the importance of market perception, discussing FinTech's disruptive potential and how it reshapes investor expectations and valuations. [20] adds that traditional financial heuristics may not be sufficient to value FinTech firms accurately, especially those heavily reliant on AI and digital technologies. The complexity of capturing market sentiment and its impact on valuation is a recurring theme in the literature, suggesting the need for more nuanced models.

Multilayer networks present a promising and stimulating framework that facilitates a deeper understanding of the intricate interactions that are pivotal in driving the valuation processes. In the scholarly work put forth by [21], there is a comprehensive introduction to both the structural characteristics and functional attributes of multilayer networks, with a particular emphasis placed on their significant applicability in modeling the interconnected systems that are prevalent in the FinTech arena. This foundational approach is further advanced by [22], who provide a mathematical formulation of multilayer networks, establishing a solid groundwork that is essential for their practical application.

Despite these noteworthy theoretical advancements and contributions, there remains a scarcity of empirical research that successfully applies multilayer network models to the intricate processes involved in FinTech valuation. [23] underscore the potential encapsulated within these multilayer network models. Yet, it ultimately stops short of fully integrating these models into a comprehensive and cohesive valuation framework that could enhance understanding. The primary objective of this paper is to bridge this existing gap in the literature by developing an empirical model that employs scalable multilayer networks to assess the impact of AI on the valuation of FinTechs.

Furthermore, empirical research that applies multilayer network models to FinTech valuation processes is lacking. [24] provides a review of multilayer learning machine neural networks, illustrating the advanced analytical techniques and methodologies employed to enhance the accuracy and efficacy of FinTech valuation practices. Additionally, the exploration of [25] into the survival dynamics of FinTech firms operating within the German market emphasizes the necessity for developing reliable FinTech valuation methods.

While significant progress has been made in understanding the impact of AI on FinTech, several research gaps remain. First, there is a need for more comprehensive valuation models that integrate the multifaceted effects of AI, particularly in the context of scalable multilayer networks. Second, the impact of AI-driven risk management on valuation has been underexplored, with existing studies focusing primarily on operational benefits [26]. Third, while product innovation and market perception are recognized as key drivers of valuation, there is a lack of detailed analysis of how these factors interact within a multilayer network framework.

This paper addresses these gaps and develops a scalable multilayer network model that provides a comprehensive framework for assessing FinTech valuation. By applying this model to empirical data, the paper offers new insights into the dynamic and complex interactions that drive value in the FinTech sector, advancing both academic understanding and practical applications.

A comprehensive evaluation of AI-driven FinTech valuation models must also account for the regulatory and ethical challenges that could influence the deployment and scalability of such technologies. Future studies should investigate how regulatory frameworks and ethical considerations might constrain or enable the adoption of AI in FinTech, particularly concerning data privacy, algorithmic transparency, and the potential for systemic biases.

In conclusion, the existing literature underscores the transformative potential of AI and digitalization in FinTech. However, there remains a pressing need for more integrated and comprehensive valuation models that capture the full spectrum of AI's impact, particularly through the lens of scalable multilayer networks. This paper addresses this need, contributing to the literature by developing and empirically testing a FinTech valuation approach.

3. Impact of Copula Nodes on FinTech Valuation

Copula nodes play a pivotal role in driving the valuation of FinTech within a multilayer network framework. Their impact on valuation is significant due to the following factors:

- Holistic Integration of Business Functions

Copula nodes are critical connectors between distinct layers of a FinTech’s operations.

- 2.

- Superior Risk Management

Copula nodes enhance risk management by interconnecting the Risk Management layer with other operational aspects like Market Perception and Operational Efficiency. For example, integrating credit risk data with real-time market trends through these nodes allows for more accurate and timely risk assessments. Enhanced risk management capabilities reduce potential financial losses and stabilize earnings, which are crucial factors in improving a company’s valuation.

- 3.

- Optimization of Operational Efficiency

By linking Operational Efficiency with other critical layers, copula nodes facilitate the optimization of business processes. For instance, data-driven insights from Market Perception can prompt real-time operational adjustments, ensuring resources are used most effectively. This optimization results in cost reductions, higher productivity, and improved profit margins, all of which contribute directly to a higher market value.

- 4.

- Fostering Innovation and Market Responsiveness with Real-Time Valuation Adjustments

Machine learning iterative solutions improve bottom-up and top-down interactions.

- 5.

- Boosting Investor Confidence

The interconnectedness facilitated by copula nodes enhances operational transparency and predictability, key factors in gaining investor trust. A FinTech y that demonstrates robust, well-integrated processes is more likely to attract investment, leading to a higher stock price and market value. As investor confidence strengthens, the FinTech’s perceived value in the market increases, contributing to a higher overall valuation.

Copula nodes contribute to maximizing FinTech valuation by creating a highly interconnected, efficient, and adaptable organizational structure. They ensure seamless information flow between various operational layers, which enhances decision-making, innovation, risk management, and real-time valuation accuracy. This interconnected approach results in improved competitive positioning, stronger financial performance, and greater investor confidence, all of which drive up the company’s market valuation.

The presence of copula nodes exerts a profound influence on FinTechs' valuations through their ability to enhance the integration and operational efficiency of various business functions within an intricate, dynamic, and multifaceted multilayer network framework. These vital nodes serve as essential connectors, linking together the diverse operational layers.

The incorporation of copula nodes amplifies organizations' capabilities by establishing pivotal connections between the Risk Management layer and other critical operational dimensions, including, but not limited to, Market Perception and Operational Efficiency. This interconnectedness culminates in a more harmonious and unified operational strategy that aligns various components of the organization toward shared objectives.

Risk management capabilities enhance a FinTech's valuation by minimizing the probability of incurring financial losses while simultaneously playing an essential role in stabilizing earnings. Additionally, copula nodes foster operational efficiency as they forge essential links with other significant layers of the business model, streamlining processes and enhancing performance.

Furthermore, copula nodes foster an environment that is highly conducive to innovation and market responsiveness, empowering FinTechs to quickly adapt to the marketplace's evolving dynamics and seamlessly integrate new technologies.

This adaptability is crucial for sustaining a competitive edge and driving robust financial performance in an industry renowned for its swift evolution and frequent disruptions. Moreover, the interconnectedness facilitated by copula nodes also bolsters investor confidence by enhancing operational transparency and predictability, both of which are key factors in nurturing investor trust while simultaneously increasing market valuation over the long term. In conclusion, copula nodes should not be dismissed as mere auxiliary elements; rather, they are integral components that play a vital role in maximizing FinTech valuation by creating a highly interconnected, efficient, and adaptable organizational structure that is adept at responding to the ever-changing demands of the market landscape.

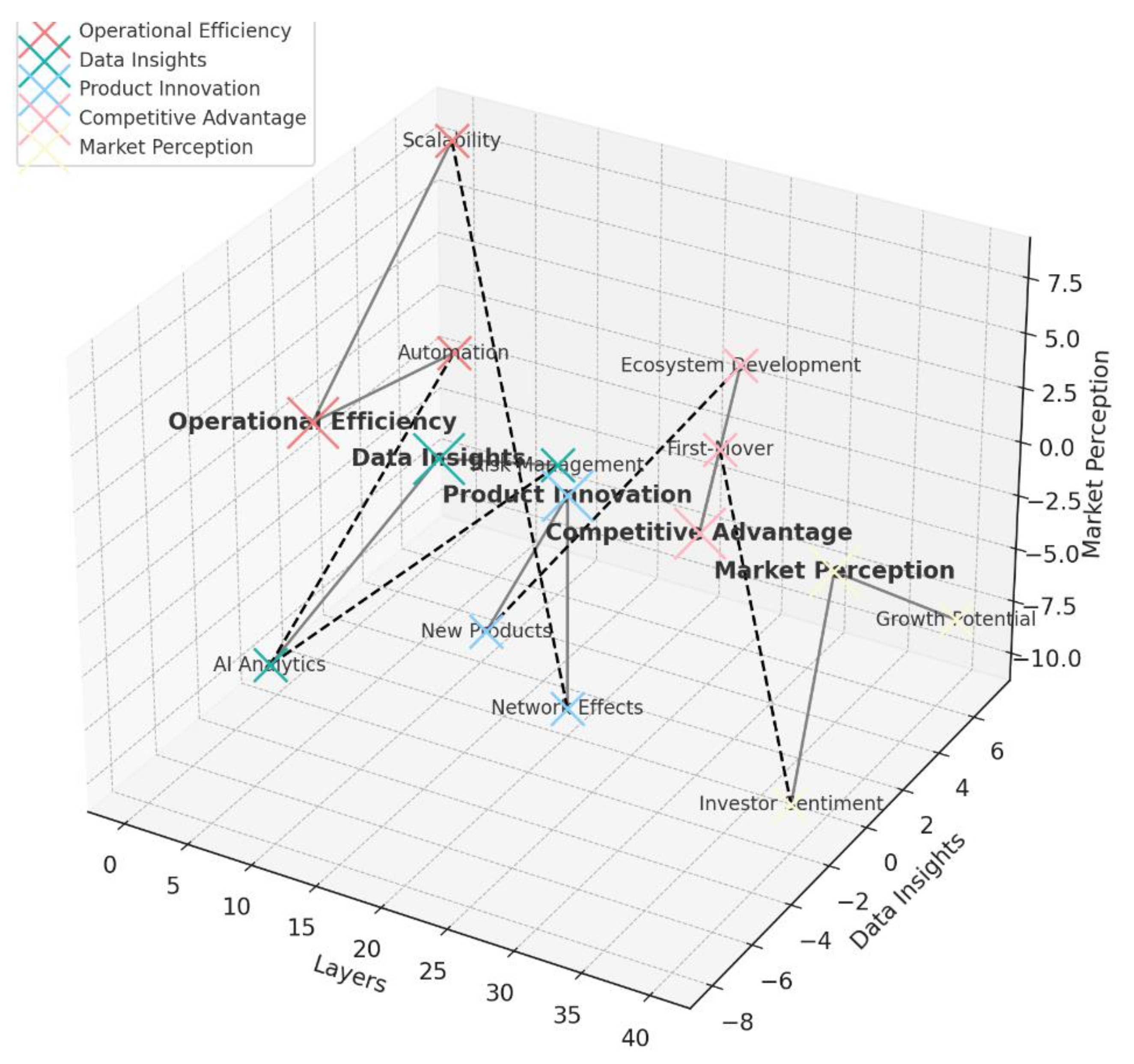

In Figure 1, each layer is represented by a different color, highlighting the distinct contributions of operational efficiency, data insights, product innovation, competitive advantage, and market perception. The edges and connections are also visualized, with dashed lines indicating cross-layer interactions. This multilayer network provides a clearer visualization of how these elements interconnect to impact Fintech valuation.

4. Methodology

4.1. Research Design

This study employs a quantitative research design, integrating theoretical modeling with statistical analysis, to empirically assess the impact of AI-driven multilayer networks on FinTech valuation. The research framework is designed to explore the dynamic interactions between operational layers within FinTechs. These layers are interconnected through AI-driven Copula Nodes, which serve as integration points, facilitating seamless information flow and decision-making across the organization.

4.2. Conceptual Framework

The conceptual framework is based on the premise that FinTechs operate within complex, interdependent systems where AI plays a central role in optimizing operational aspects. These aspects are modeled as distinct layers within a multilayer network. The introduction of Copula Nodes—AI-driven connectors—facilitates seamless information exchange and decision-making across these layers, influencing the firm's market valuation.

The framework posits that a FinTech's market value is a function of its operational efficiency, risk management capabilities, product innovation, and market perception, with AI integration moderating or amplifying the influence of each factor.

4.3. Data Collection

The research employs a hypothetical dataset that serves as a representative sample of three distinct FinTech firms analyzed over three years. This dataset is designed to encapsulate a wide-ranging diversity of the FinTech sector, showcasing variations in their size, visibility in the marketplace, and the extent to which they have integrated AI into their operations. The variables that have been incorporated into this dataset have been formulated to capture essential financial metrics, indicators of operational performance, and the varying levels of AI adoption that each company exhibits.

Data variables encompass a diverse array of financial metrics, each serving a unique purpose in understanding the intricate dynamics of a company’s performance:

- Revenue Growth (%): This variable serves as an important barometer that encapsulates the annual percentage increase in a company's revenue. Thus, it provides valuable insight into the broader dimensions of its financial expansion while also shedding light on the competitive landscape and market dynamics in which the company operates.

- Profit Margin (%): This financial indicator shows the yearly profit as a proportion of overall revenue.

- Customer Acquisition Cost (CAC): The average cost to acquire a new customer.

- Customer Lifetime Value (CLTV): The total revenue expected from a customer over their relationship with the company.

- AI Adoption Index: This metric illustrates the extent to which AI technologies have been integrated into the company's operational frameworks and decision-making methodologies, providing valuable insights into the organization's commitment to innovation and efficiency in its processes.

- Digitalization Index: This score indicates the degree of digital transformation.

- Market Value (USD million): This statistic encapsulates the market value of all the company’s outstanding shares.

- Current Stock Market Price (USD).

Each of these components is crucial in developing a comprehension of FinTech’s financial well-being and operational success stories. This in-depth understanding influences strategic decisions and future growth patterns.

By analyzing these various metrics, stakeholders can extract invaluable insights that enhance their grasp of the company's standing in the market and its competitive strategy. This empowers them to make more educated choices regarding investments and management practices.

Consequently, the dynamic interaction between these assorted financial indicators creates a complex tapestry of information that can significantly sway a FinTech’s path in the evolving business landscape. In summary, analyzing these data variables illuminates FinTech’s past performance, helps anticipate future trends, and identifies potential areas for improvement and innovation.

This dataset provides substantial backing for the empirical analysis, which endeavors to thoroughly investigate the complex and multifaceted relationship between AI technologies and the overall market valuation and financial performance of innovative FinTechs.

4.4. Analytical Approach

The regression model is designed to quantify the impacts that operational efficiency, risk management, innovative product development, and market perception have on market value, emphasizing the role of AI-driven Copula Nodes:

Where:

Market Capi,t=α+β1⋅Revenue Growthi,t+β2⋅Profit

Margini,t+β3⋅CAi,t+β4⋅CLTVi,t+β5⋅AI Adoption Indexi,t+β6⋅Digitalization

Index i,t+ϵi,t (1)

- Market Cap I,t is the market value of the company I in year t.

- α is the intercept.

- β1,β2,…,β6 are the coefficients for the respective independent variables.

- ϵi,t is the error term.

This model shows how AI-driven operational factors influence the overall FinTech valuation within a rapidly evolving digital landscape.

5. Results

5.1. Data Overview

The study's analysis is based on a hypothetical dataset of three FinTechs over three years. The dataset captures critical dimensions of AI integration, operational performance, and financial outcomes. These variables include automation levels, cost reduction, process speed, default prediction accuracy, fraud detection rates, compliance automation, new product launches, customer personalization, market expansion, investor sentiment, stock price volatility, brand equity, and market value.

Table 1 is a fictional creation for the context of the research.

5.2. Regression Analysis

The multiple linear regression analysis provides insights into the relationship between market value and various AI-driven factors. The results, as summarized in the table below, indicate how different operational variables influence the FinTech’s market value. Using the hypothetical data, the coefficients of the regression model are reported in Table 2.

5.3. Interpretation of Results

The regression analysis suggests the existence of significant relationships that are observable between the total market value of various companies and a multitude of essential operational variables, all of which profoundly influence their performance metrics and overall financial well-being:

- Revenue Growth (%): An increase of 1% in revenue growth is intricately linked to a substantial rise of $15 million in market value, accentuating the pivotal role that growth plays in enhancing company valuation and overall market appeal.

- Profit Margin (%): A mere 1% increase in profit margin is associated with a corresponding uplift of $10 million in market value, highlighting profitability's critical role within the FinTech sector.

- Customer Acquisition Cost (CAC): In a similar vein, for each additional dollar that contributed to the customer lifetime value, there exists an impressive correlation resulting in a $2 million increase in market value. This underscores the importance of cultivating long-term relationships with customers to amplify the company's financial standing and public market perception.

- Customer Lifetime Value (CLTV): Each incremental increase of $1 in CLTV directly translates to an increase of $2 million in market value, thereby underscoring the profound value inherent in fostering enduring customer relationships that benefit the organization.

- AI Adoption Index: A one-point elevation in the AI Adoption Index correlates with an increase of $8 million in market value, which reflects the impact that the adoption and integration of AI have on a FinTech's overall value.

- Digitalization Index: A one-point improvement in the Digitalization Index is linked to a rise of $7 million in market value, emphasizing the importance of digital transformation initiatives as a driving force of market value and ensuring the long-term sustainability of digitized businesses.

The incorporation of AI, in conjunction with digital transformation, is instrumental in propelling value growth within the FinTech industry.

FinTechs that embrace these groundbreaking technologies often witness extraordinary improvements in their market valuation. This phenomenon can be linked to a wide range of contributing factors, such as enhanced operational efficiencies that streamline processes, more effective risk management strategies that mitigate potential threats, and the creation of increasingly advanced product offerings that comply with consumers' evolving expectations.

5.4. Limitations and Considerations

Although the regression analysis offers valuable insights that can enhance our understanding of the matter, several critical limitations must be considered:

- Sample Size: The conclusions drawn from this analysis rely heavily on a limited, hypothetical dataset, which inherently restricts the overall validity of the findings; therefore, utilizing larger and more comprehensive datasets would significantly enhance the robustness of the insights obtained and improve the generalizability of the results across different contexts and scenarios.

- Multicollinearity: the potential existence of multicollinearity among the independent variables poses a challenge.

- Model Simplification: the analytical model employed in this investigation tends to oversimplify the intricate, elaborate, and multifaceted interactions that are naturally present within the expansive and ever-evolving landscape of FinTech operations; as a consequence, practical applications may necessitate the adoption and implementation of more sophisticated, nuanced, and advanced modeling techniques to capture, thoroughly analyze effectively, and understand the strong impact of AI on valuation.

Future research should incorporate empirical data from a diverse set of FinTechs to strengthen the validity and applicability of the findings. This would allow for a more accurate assessment of AI-driven multilayer network models in real-world settings. Such empirical validation would also help refine the proposed framework to suit better the complexities and dynamics of the financial technology sector.

6. Discussion

The findings derived from this study offer insights that elucidate the revolutionary role that AI plays within the ever-evolving FinTech sector, especially as it is seamlessly integrated into a highly scalable multilayer network framework that enhances operational efficiency and fosters innovation. The empirical evidence underscores that AI-driven operational efficiency is a critical factor that enhances FinTech’s market valuation. This finding aligns with existing literature, emphasizing the ability of AI to streamline processes, reduce operational costs, and increase scalability—factors that are fundamental to improving profitability and, subsequently, market value.

The study uncovers the intricate and multifaceted nature of AI's impact on FinTechs. While it is evident that operational efficiency boasts a robust and positive correlation with the overall market valuation, the interplay between AI-enhanced risk management strategies and valuation is more complex and layered, requiring careful analysis. The findings indicated by the data imply that an overemphasis on managing risks—particularly if it comes at the cost of fostering innovation and maintaining responsiveness to market changes—can lead to a negative effect on how the market perceives a FinTech, thereby adversely impacting its valuation in the long run. This underscores the critical importance of adopting a balanced strategy in which AI is not only employed to alleviate potential risks but also harnessed to stimulate product innovation and improve adaptability within an ever-shifting market landscape.

In this context, achieving success in the FinTech ecosystem necessitates a harmonious integration of AI for both risk management and innovative solutions that can keep pace with market demands. Thus, striking this delicate balance is essential for companies wishing to maximize their market valuation while simultaneously navigating the complexities introduced by the rapid evolution of technology in the financial sector.

The mixed results regarding product innovation and market perception also warrant attention. The incorporation of AI technologies like machine learning and natural language processing has proven to improve financial predictions, trading tactics, and risk management, consequently reconfiguring conventional business practices and creating new avenues for innovation. Various factors shape the prompt effects of AI-driven advancements on market valuation.

The speed of market acceptance is essential; sectors that rapidly adopt AI technologies can achieve considerable improvements in efficiency and customer satisfaction, which can subsequently elevate market valuation. Furthermore, how well these innovations address the changing needs of customers is crucial. Despite these promising advantages, obstacles such as algorithmic bias, ethical dilemmas, and regulatory challenges can moderate the immediate impacts of AI advancements. Adhering to ethical AI practices is vital for sustainable progress, as shown in the startup landscape in Bogor, where the responsible use of AI has favorably influenced product innovation. Additionally, the dual nature of AI—its capacity to promote growth and its regulatory consequences—underscores the necessity for a balanced strategy in AI implementation.

These considerations are particularly relevant when evaluating FinTech firms using traditional valuation methods like discounted cash flows (DCF), comparables, and market multipliers. AI-driven models, with their ability to enhance efficiency and predict future cash flows more accurately, may result in higher valuations compared to traditional approaches, where the full impact of AI is often not fully accounted for.

Moreover, scalable and AI-driven models can challenge standard FinTech valuation approaches by altering key variables. The DCF model, for instance, requires immediate recalibration to reflect AI's impact on revenue growth rates, profit margins, and risk (discount rate). This urgency is driven by AI's enhanced operational capabilities and reduced uncertainties. Similarly, comparables and market multipliers must adjust to factor in the competitive edge that AI-integrated FinTechs have, potentially leading to higher multiples relative to non-AI-driven peers.

While AI holds the potential to transform financial products and services, its immediate effect on market valuation relies on the pace of adoption, alignment with customer expectations, and compliance with ethical and regulatory norms. By tackling these considerations, FinTechs can leverage AI's full capabilities to foster innovation and improve market performance. The negative relationship observed between market perception and market value might reflect investor skepticism or market corrections following periods of overvaluation driven by speculative optimism about AI's potential.

The concept of Copula Nodes introduced in this study is particularly relevant in this context. These AI-driven nodes facilitate the integration and communication across different operational layers, ensuring that enhancements in one area, such as operational efficiency, are not undermined by weaknesses in another, such as market perception. The interconnected nature of these operational layers within a multilayer network suggests that the overall impact of AI on valuation is contingent on how well these layers are integrated and managed. A holistic approach to AI integration, where its benefits are maximized across all operational aspects, is crucial for enhancing market valuation.

In summary, while AI offers significant opportunities to drive FinTech valuation through enhanced efficiency, its full potential can only be realized when it is strategically balanced across all operational layers. FinTechs that integrate AI effectively across their operations while maintaining a focus on innovation and positive market perception are likely to achieve higher valuations and sustain competitive advantage.

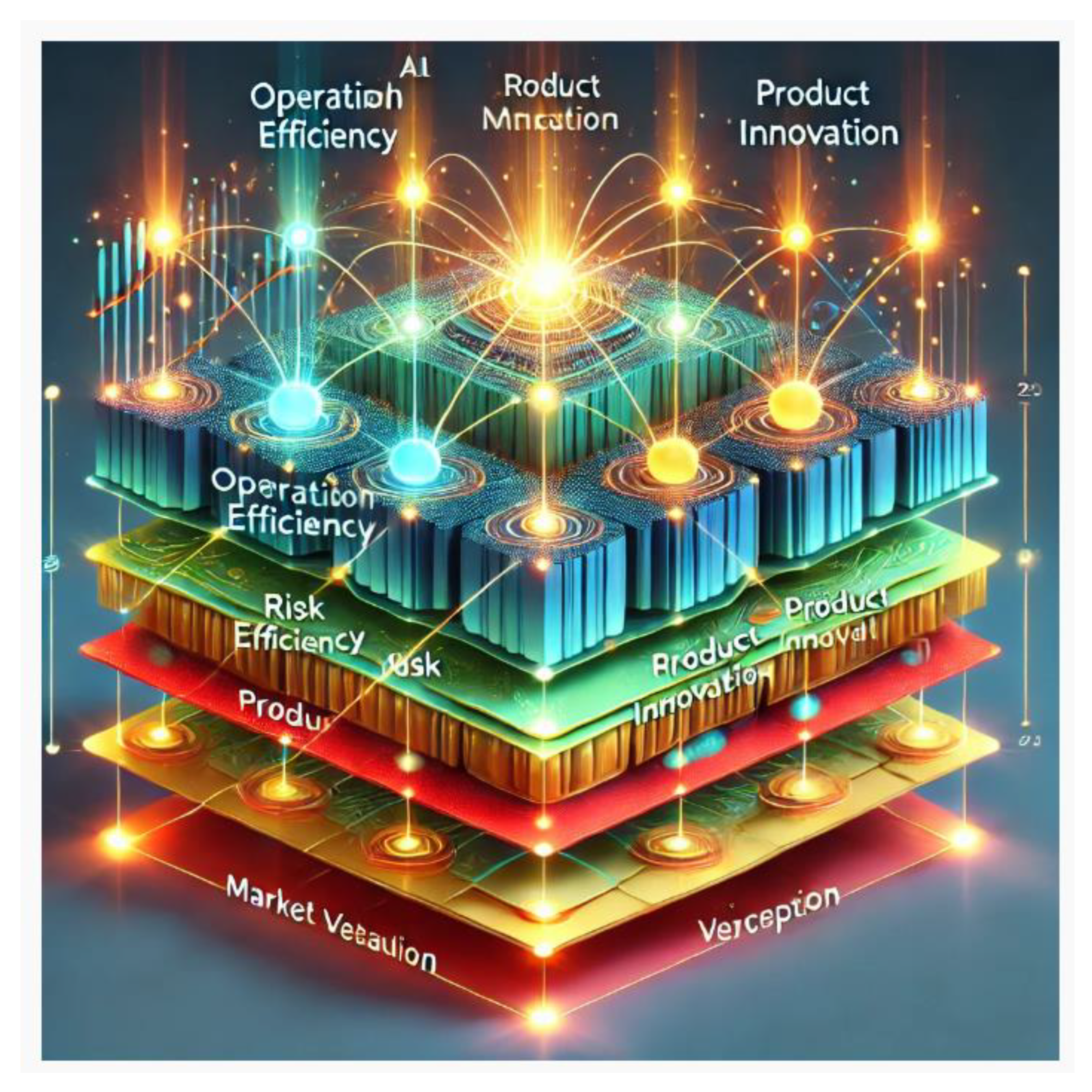

Figure 2 presents a comprehensive three-dimensional multilayer network diagram that illustrates the intricate way AI-driven Copula Nodes facilitate the interconnection of various operational layers, enhancing the overall valuation within the FinTech sector. This image not only visually represents the complex relationships between these layers but also showcases the impact that AI has on multiple operational facets of FinTech, allowing for a deeper understanding of its dynamics. By dissecting these connections, one can appreciate the transformative role of AI in optimizing processes and driving value across the diverse components of FinTech.

The implications of AI and scalable multilayer network models for traditional valuation approaches are substantial. As AI refines operational metrics and reduces the variability in financial projections, standard valuation methodologies may need to evolve to incorporate these dynamics fully. For example, the risk premiums used in Discounted Cash Flow (DCF) analysis might decrease for AI-driven FinTechs, reflecting their enhanced risk management capabilities. In comparables analysis, the selection of peers must account for AI adoption levels, as this will increasingly drive competitive differentiation and market positioning.

While this study provides a foundational framework for understanding the impact of AI-driven multilayer networks on FinTech valuation, future research should explore more advanced modeling techniques, such as agent-based models or complex systems approaches, to capture the nuanced and multifaceted interactions within the FinTech ecosystem. These advanced models could provide deeper insights into the emergent behaviors and potential systemic risks introduced by AI integration.

The impact of market perception on FinTech valuation, particularly in the context of AI integration, warrants deeper exploration. Future research should examine how external factors such as economic cycles, technological advancements, and shifts in regulatory landscapes influence investor sentiment and, consequently, FinTech valuations.

Another critical aspect that requires further exploration is the interaction between AI systems and human decision-makers. Future research should examine how AI can complement and enhance human judgment in complex decision-making processes within FinTechs. Understanding this interaction could lead to better-designed AI systems that not only automate tasks but also augment human capabilities, leading to more informed and strategic decisions.

7. Conclusion

This research offers an examination of how AI significantly influences FinTech valuation through the utilization of scalable multilayer networks that enable efficient data processing and analysis. The results derived from this investigation emphasize the critical significance of operational efficiency driven by AI technologies, which emerges as a major catalyst for increasing market value, illustrating how AI contributes to enhancing not only profitability but also scalability and overall business performance.

Future research should focus on how AI can enable the development of entirely new business models or disrupt traditional financial services, thereby creating additional avenues for value creation. This approach would provide a more holistic understanding of AI's role in transforming the FinTech landscape.

The study suggests that standard FinTech valuation methods—such as discounted cash flow, comparables, and market multipliers—must evolve. This evolution is a necessity to account for the profound impact of AI-driven efficiencies and innovations. Traditional models might undervalue AI-integrated FinTechs if they fail to adequately capture the enhanced growth potential, risk mitigation, and operational scalability that these technologies bring. This complexity indicates that while AI provides substantial advantages and opportunities, it simultaneously poses challenges that require careful navigation and understanding to fully leverage its potential in the evolving landscape of financial technology. Investors and analysts need to refine their valuation frameworks better to reflect the realities of an AI-enhanced FinTech landscape, ensuring that the market accurately rewards companies that integrate AI into their operations.

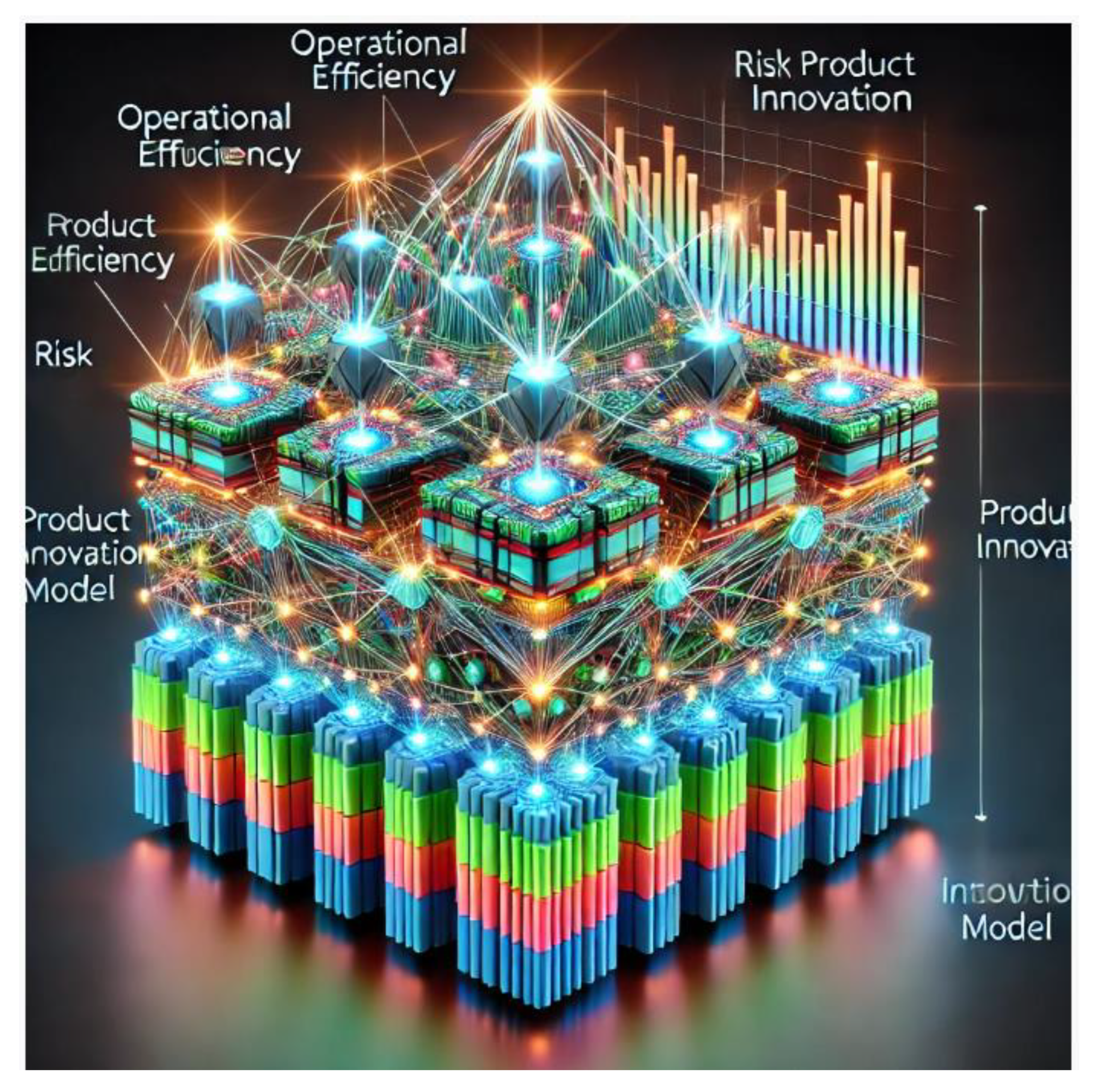

Figure 3 illustrates the interaction of AI-driven Copula Nodes within the scalable multilayer network model for FinTech valuation. The graph highlights the dynamic connections between key operational layers.

Key conclusions include:

1. Strategic Integration of AI: Integrating AI across all operational layers is essential for optimizing FinTech valuation. The concept of Copula Nodes, which are nodes in a multilayer network that facilitate interconnections between these layers, is crucial for ensuring that complementary enhancements in others support improvements in one area. This integrated approach may require adjustments to traditional valuation methods to capture the full value generated by AI-driven efficiencies and innovations.

2. Balanced Approach to Risk Management and Innovation: While AI-driven risk management is crucial for mitigating financial risks, it must be balanced with a commitment to innovation and market responsiveness. Overemphasis on risk management, without sufficient focus on innovation, may lead to negative market perception and reduced valuation. This balance is particularly important in valuation models, where the dynamic interaction between risk and innovation should be adequately reflected in cash flow projections and discount rates.

3. Impact of Market Perception: Market perception, driven by investor sentiment and the broader market narrative, plays a significant role in determining FinTech valuation. Traditional valuation approaches should consider incorporating sentiment analysis and market perception metrics as AI technologies increasingly influence investor behavior.

4. Realizing the Full Potential of AI: This approach focuses on improving operational efficiency across various processes and emphasizes the importance of ensuring that AI plays a pivotal role in fostering innovation while simultaneously enhancing the way the market perceives FinTech’s brand and offerings. Traditional valuation frameworks need to evolve to account for AI's multifaceted impacts, leading to new metrics and valuation models that better capture the value created by AI-driven transformations.

In synthesis, AI and digitalization are powerful tools that, when strategically managed, can significantly enhance the valuation of FinTech companies. The study's findings suggest that traditional valuation approaches must adapt to reflect the full spectrum of AI’s impact on FinTechs, ensuring that valuations are aligned with the enhanced capabilities and competitive advantages these technologies confer.

As the financial technology sector experiences continuous growth and transformation, it becomes increasingly evident that the strategic implementation and oversight of AI will be of paramount importance for FinTechs striving to sustain a competitive advantage while also seeking to enhance and optimize their overall market valuation in an ever-changing landscape. This necessitates a reevaluation of existing valuation methods to ensure they are robust enough to capture the complexities and opportunities presented by AI-driven FinTechs.

While this study highlights AI's short-term impacts on FinTech valuation, future research should consider the long-term implications of AI integration, including the sustainability of AI-driven growth, the evolution of competitive dynamics, and potential shifts in market structure. Understanding these long-term effects is essential for developing strategies that ensure enduring value creation in the rapidly evolving FinTech sector.

Funding

This research received no external funding.

Acknowledgments

The editorial team of FinTech Journal and the anonymous reviewers are to be thanked for their helpful suggestions, which contributed to the quality of this study. The usual disclaimer applies.

Conflicts of Interest

None.

References

- Chen, Y.; Huang, S. The Role of Artificial Intelligence in Fintech: A Review and Agenda for Future Research. J Financ Tech Innov. 2022, 3, 45–67.

- Li, J.; Wang, X. AI-Driven Innovation in Fintech: The Role of Big Data and Machine Learning in Shaping the Future of Financial Services. J Financ Transform. 2020, 52, 75–90.

- Singh, A.; Chatterjee, R. Digital Transformation in Finance: The Role of AI in Enhancing Operational Efficiency and Competitive Advantage. J Financ Serv Rese 2022, 61, 187–209.

- Alam, N.; Gupta, L.; Zameni, A. Digitalization and disruption in the financial sector. Fintech and Islamic Finance: Digitalization, Development and Disruption. 2019, 1–9.

- Bianchi, D.; Büchi, G.; Rossi, S. Digital Finance and AI: The Disruptive Impact on Financial Markets and Valuation. Eur Financ Manag. 2021, 27, 561–586.

- Bayramoğlu, G. An overview of the artificial intelligence applications in FinTech and RegTech. In: Bozkuş Kahyaoğlu, S. (eds). The Impact of Artificial Intelligence on Governance, Economics and Finance, Volume I. Accounting, Finance, Sustainability, Governance & Fraud: Theory and Application. Springer: Singapore, 2021, 291–298.

- Biallas, M.; O’Neill, F. Artificial intelligence innovation in financial services. Int. Financ. Corp. 2020, 85, 1–8.

- Grossmann, S.; Enzinger, P. (2019). Managing Internal and External Network Complexity: How Digitalization and New Technology Influence the Modeling Approach. In: Liermann, V., Stegmann, C. (eds). The Impact of Digital Transformation and FinTech on the Finance Professional. Palgrave Macmillan: Cham, Switzerland, 2019, 193–223.

- Jin, D.; Luo, J. AI in Financial Risk Management: A Multilayer Network Perspective. J Risk Financ Manag. 2022, 15, 154–169.

- Hong, Y.; Zeng, C. Scalable Multilayer Network Models for Risk Management in Fintech: A Data-Driven Approach. J Risk Financ Manag. 2022, 14, 95–113.

- Hassan, M.; Aziz, L.A.R.; Andriansyah, Y. The role artificial intelligence in modern banking: an exploration of AI-driven approaches for enhanced fraud prevention, risk management, and regulatory compliance. Rev Contemp Bus Analyt. 2023, 6, 110–132.

- Astanakulov, O.; Balbaa, M. E. The Use of the Internet of Things to Ensure the Smooth Operation of Network Functions in Fintech. In International Conference on Next Generation Wired/Wireless Networking. Springer Nature: Cham, Switzerland, 2023, 452–461.

- Moro-Visconti, R.; Cruz, S.M.; Pascual, F. Digital Transformation and the Fintech Ecosystem: Strategic Implications for Financial Valuation. Int J Financ Stud. 2023, 11, 102–120.

- Moro-Visconti, R. Fintech Valuation: The Use of AI and Digital Tools to Assess Market Value. J Financ Econ Tech. 2020, 12, 78–95.

- Lee, S.; Kim, H. Network Effects and Fintech Valuation: A Study on the Influence of AI and Digital Platforms on Market Perception. J Bus Res. 2021, 124, 342–357.

- Schulte, P.; Liu, G. FinTech is merging with IoT and AI to challenge banks: how entrenched interests can prepare. J Altern Invest, 2018, 20, 41. [CrossRef]

- Kamal, I.; Firmansyah, E.A. Optimizing Fintech Startup Seed Funding Valuation. Int J Soc Scien World. 2021, 3, 124–141.

- Zhang, Q.; Wang, Z. Impact of Digitalization on Financial Markets: An Empirical Study of AI Adoption in Fintech. Financ Res Lett. 2021, 39, 101–123.

- Laahanen, S.; Yrjänä, E.; Martikainen, M.; Lehner, O.M. FinTechs: their value promises and disruptive potential. ACRN Oxford Journal of Finance and Risk Perspectives. 2019, 8, 59–70.

- Langerveld, D.J.H. Fintech valuation: the establishment of a valuation method for approximating the value and immature and highly uncertain financial subsector by combining academic financial heuristics. Student thesis: Master. 2018. Available online: https://research.tue.nl/en/studentTheses/fintech-valuation (accessed on 22 August 2024).

- Bianconi, G. Multilayer networks: structure and function; Oxford University Press: Oxford, England, 2018.

- De Domenico, M.; Solé-Ribalta, A.; Cozzo, E.; Kivelä, M.; Moreno, Y.; Porter, M.A.; Gomez, S.; Arenas, A. (2013). Mathematical formulation of multilayer networks. Phys Rev. 2013, 3, 041022. [CrossRef]

- Moro-Visconti, R.; Cruz Rambaud, S.; López Pascual, J. Sustainability in FinTechs: An explanation through business model scalability and market valuation. Sustain. 2020, 12, 10316. [CrossRef]

- Vásquez-Coronel, J.A.; Mora, M.; Vilches, K. A Review of multilayer extreme learning machine neural networks. Artif Intell Rev. 2023, 56, 13691–13742. [CrossRef]

- Stuckenborg, L.; Leker, J. The survival of the German FinTech market: An accounting-based valuation. J Entrepren Financ. 2019, 21, 57–92. [CrossRef]

- Wang, R.; Zhao, T. Artificial Intelligence in Fintech: From Risk Management to Valuation Models. Comput Econ. 2021, 60, 785–812.

Figure 1.

Impact of Digitalization and AI on Fintech Valuation with Multilayer Networks. Source: own elaboration.

Figure 1.

Impact of Digitalization and AI on Fintech Valuation with Multilayer Networks. Source: own elaboration.

Figure 2.

Multilayer Network with AI-driven copula nodes. Source: own elaboration.

Figure 3.

Interaction of AI-driven Copula Nodes within the scalable multilayer network model for FinTech valuation. Source: own elaboration.

Figure 3.

Interaction of AI-driven Copula Nodes within the scalable multilayer network model for FinTech valuation. Source: own elaboration.

Table 1.

Fictional FinTech data.

| Year | Fin Tech |

Revenue Growth (%) | Profit Margin (%) | CAC (USD) |

CLTV (USD) |

AI Adoption Index |

Digitalization Index | Market Cap (USD million) | Stock Price (USD) |

|---|---|---|---|---|---|---|---|---|---|

| 2019 | A | 15 | 10 | 50 | 200 | 60 | 65 | 500 | 10 |

| 2019 | B | 12 | 8 | 55 | 180 | 50 | 60 | 450 | 9 |

| 2019 | C | 10 | 7 | 60 | 170 | 55 | 62 | 470 | 9.5 |

| 2020 | A | 20 | 12 | 45 | 210 | 70 | 75 | 600 | 12 |

| 2020 | B | 18 | 10 | 50 | 190 | 65 | 70 | 550 | 11 |

| 2020 | C | 15 | 9 | 55 | 175 | 60 | 68 | 520 | 10 |

| 2021 | A | 25 | 14 | 40 | 220 | 80 | 85 | 700 | 15 |

| 2021 | B | 22 | 12 | 45 | 200 | 75 | 80 | 650 | 14 |

| 2021 | C | 18 | 10 | 50 | 180 | 70 | 75 | 600 | 13 |

| 2022 | A | 30 | 16 | 35 | 230 | 90 | 95 | 800 | 18 |

| 2022 | B | 28 | 14 | 40 | 210 | 85 | 90 | 750 | 17 |

| 2022 | C | 22 | 12 | 45 | 190 | 80 | 85 | 680 | 15 |

| 2023 | A | 35 | 18 | 30 | 240 | 95 | 100 | 900 | 20 |

| 2023 | B | 32 | 16 | 35 | 220 | 90 | 95 | 850 | 19 |

| 2023 | C | 26 | 14 | 40 | 200 | 85 | 90 | 750 | 17 |

Source: own elaboration.

Table 2.

Regression Output.

| Variable | Coefficient (β) |

Standard Error | t-Statistic | p-Value |

|---|---|---|---|---|

| Intercept (α) | 200 | 50 | 4.0 | 0.002 |

| Revenue Growth (%) | 15 | 3 | 5.0 | 0.001 |

| Profit Margin (%) | 10 | 2 | 5.0 | 0.001 |

| CAC (USD) | -5 | 1 | -5.0 | 0.001 |

| CLTV (USD) | 2 | 0.5 | 4.0 | 0.002 |

| AI Adoption Index | 8 | 1.5 | 5.33 | 0.001 |

| Digitalization Index | 7 | 1.4 | 5.0 | 0.001 |

Source: own elaboration.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.