Submitted:

06 August 2024

Posted:

07 August 2024

You are already at the latest version

Abstract

Commercial banks are financial institutions that accept public deposits and provide loans for consumption and investment to generate profit. The term "bank" originates from the Italian word "banco," meaning "desk" or "bench," which was used by Florentine bankers during the Renaissance for conducting transactions. Banking activities, however, date back to ancient times. The primary objective of this study is to examine the impact of internal control components on the organizational performance of local commercial banks in Burao, Somaliland. A descriptive research design was employed, utilizing primary data collected from these banks to assess the role of internal controls on organizational performance.The findings indicate a strong influence of internal control systems on organizational performance, revealing a significantly positive relationship between the two. Effective internal control systems contribute to the administration, completeness, and accuracy of records, and provide a safeguard against fraud and collusion, particularly among those in positions of authority or trust. For optimal performance, internal control systems must be robust and well-implemented. It is recommended that local commercial banks conduct regular internal audits of their accounting systems to mitigate risk and enhance internal control measures. Strengthening internal control systems tailored to the organization's operations and ensuring strict authorization protocols for access to bank assets are essential for improving organizational performance.

Keywords:

role

; effects

; internal control

; organizational

; performance

; local

; commercial banks

; management

; reference

1.0. Introduction

Assessing organizational performance is a vital

aspect of strategic management by (Subramaniam, 2008) moreover, organizational

performance means the effectiveness of an organization in the achievement of

their desired goals (Henri, 2004) accordingly, and Richard, Organizational

performance involves the review of a firm against its goals and objectives. In

other words, as compared with expected outputs, organizational success requires

actual outcomes, The analysis focus on three mains out comes such as; total

shareholder return, sales and return on assets, and finally on a market share.

As well as that, the organizational performance including strategic planners,

operations, finance, legal and organizational development.

The purpose of this study is to assess role of

internal control on organizational performance of Local Banks at Burao district

especially; Dahabshiil bank, Dara-Salaam bank, Premier bank, and Amal bank.

Organizational performance includes; economic or financial performance and

non-financial or operational performance.

Theoretically; this study has utilized the fraud

triangle theory, which originated from sociological literature and was adopted

as an empirically valid explanation of fraud describing three necessary

conditions for crimes to occur: pressure; a non-shareable problem, opportunity;

lack of internal controls, and rationalization; the ability to justify one’s

actions. its founder, Donald Cressey in (1953), who modified it many times,

most recently in the early 1970s. Cressey's theory focused on the individual

and identified improving organizational internal control measures as the

deterrent for preventing fraud. (Poff, 2018)). the study relates to several

scientific theories, including fundamental accounting theories such as the cost

principal theory, among others. These theories provide a framework for

understanding the principles and practices that underpin effective internal

control systems in commercial banks. By examining these theories in the context

of internal control, the study highlights how adherence to established

accounting principles can enhance organizational performance and ensure the

accuracy, reliability, and integrity of financial records. (Danielle,

2018), Maslow’s hierarchy of needs theory (Kendra, 2022), and the job

characteristics model theory (Dr. Annette, 2020).

1.1. Problem Statement

Internal controls are typically established by an

organization to provide reasonable assurance regarding the achievement of its

objectives, including the reliability of financial reporting, the effectiveness

and efficiency of operations, and compliance with applicable laws and

regulations. These controls serve as mechanisms to ensure that the organization

operates in a manner that is consistent with its goals, mitigates risks, and

adheres to legal and regulatory requirements (Esther, 2021). In this regard,

internal controls, operates a healthy accountability system and promote

transparency and integrity. A sound internal control system helps an

organization prevent fraud and errors, minimize wastage, and positively

influence organizational performance. By implementing robust internal controls,

organizations can enhance the accuracy and reliability of their financial

reporting, improve operational efficiency, and ensure compliance with relevant

laws and regulations, ultimately contributing to overall organizational success.

Despite the implementation of internal controls,

local banks are often criticized for their failures, with many collapsing

within the first few years of operation. This may be due to the poor perception

of audits within the organization, which limits performance improvement,

creates tension, and results in negative returns. Weak or ineffective internal

control systems cause significant losses in many local banks and have

contributed to the failure of others globally. These losses could be prevented

or detected through effective internal control mechanisms before they occur.

Consequently, many local banks in Burao underperform if their internal control

systems are not strengthened. Thus, it is essential to study the impact of

internal control systems on the organizational performance of local commercial

banks in Somaliland.

2.0. Literature Review

2.1. Theoretical Prespectives

“Martin (1994), describes the internal control as

including internal checks and internal auditing, it projects the whole system

of controls to be applicable to sales, purchases, finance, cost, production,

and others. These controls provide safety and security to assets and continuous

checks on the day-to-day transactions” (Ayneshet, 2020). “According to

Jacksonville 2000, the internal control process, which historically has been a mechanism

for reducing instances of fraud, misappropriation and errors has become more

extensive, addressing all the various risks faced by organizations” (Ayneshet, 2020). “It is now recognized that a sound internal control process is critical

to the organization’s ability to meet its established goals. Internal control

consists of five interrelated elements: and these elements are explained with

it and of suitable principle to be followed by concerned people in an

organization and these elements are; Management oversight and the control

culture, Risk recognition and assessment, Control activities and segregation of

duties, Information, and communication; and Monitoring activities and

correcting deficiencies” (Ayneshet, 2020). "Sawyers (2002) guide for

internal Auditor pointed out the various internal controls and they are;

Documentation, Verification, supervision, safeguard assets, personal controls,

and reporting” (Ayneshet, 2020). “Accordingly, the effective functioning of

components of internal control provides a reasonable assurance regarding

achievement of one or more of the stated categories of objectives to ensure

high level of the organizational performance.

One of the five interrelated components of internal

control system is a control environment factor. It refers to the integrity,

ethical value and competence of the entity’s people (COSO, 1994). Internal

control should be viewed in a broader context for example it should as well be

reorganized as a function of people’s ethical values as it is of standards and

compliancy mechanisms” (Ayneshet, 2020). Internal controls ensure that a firm

complies with accounting laws and regulations. This helps a company identify

and correct accounting problems before an internal audit begins. Additionally,

internal controls ensure that the accounting or financial information presented

by a company manager is reliable, accurate, and free from fraud (Jason,

2022).

Mostly the internal control component of control

activities is used in sales process, so common internal controls over the sales

include; Establishment of sales responsibility, segregation of duties,

documentation procedure, physical controls, independent internal verification,

and human resource controls (Angie, 2019). Ting, Xiaotao, Chi and Yakun said

‘we find robust and consistent evidence that customer satisfaction is

negatively associated with internal control weaknesses and overall, our

findings provide the direct evidence that in-effective internal control compromises

customer satisfaction (Ting, Xiaotao, Chi and Yakun, 2021).

Control activities, monitoring and risk assessment

are positively and significantly impact on job satisfaction of employees in the

company and control environment is identified as the insignificant factor by

the study (A runa, 2019). Our research results show that detective controls

with more timely feedback improve employees’ performance without affecting

their intrinsic motivation. In contrast, the restriction of autonomy associated

with preventive controls, has no additional effect on employees’ performance

but significantly reduces employees’ motivation (Margaret, Scott A., Sott L.,

and David, 2009).

Marketing planning and marketing strategies are

integral to company planning and strategy. Marketing control, which is also

part of internal and financial control, assesses the degree of alignment

between planned and achieved marketing objectives and holds accountability for

undue costs and unused reserves. Similarly, marketing audits, as part of

internal audit activities, provide a continuous, independent, and objective

assessment of an organization's marketing activities and decisions (Plamen, 2019). Our research results indicate a significant positive correlation between

internal control and financial performance. Additionally, corporate social

responsibility (CSR) positively influences financial performance, and social

responsibility plays a strong intermediary role between internal control and

financial performance (Wang and Guan, 2017).

When internal control is effective, it can prevent

adverse events that damage social responsibility practices, thereby improving

corporate social responsibility performance. In other words, effective internal

control encourages business enterprises to fulfill their social

responsibilities (Xio, Zheng, Liu and Mohammed, 2018). However, as mentioned in

the conceptual framework and these theoretical perspectives, Internal control

components can take a role on each variables include; accounting and marketing.

“The study relates to a number of the scientific theories, include; basic

accounting theories which include the cost principle theory and others (Danielle, 2018), Maslow’s hierarchy of needs theory” (Kendra, 2022), and “the job

characteristics model theory” (Dr. Annette, 2020).

2.2. Organizational Performance

Organizational performance is defined as the

outcomes that indicate the organization's efficiencies or inefficiencies in

terms of corporate image, competencies, and financial results. Focusing on

organizational performance is essential as it involves processes aimed at

increasing the organization's effectiveness. Performance is essentially the

transformation of inputs into outputs to achieve specific outcomes. Performance

relates to the relationship between minimal and effective costs (economy),

effective costs and realized outputs (efficiency), and outputs and achieved

outcomes (effectiveness).

In this study, we examined the role of internal

control components on organizational performance, categorizing organizational

performance into two areas: financial performance and non-financial or

operational performance.

Financial performance is a subjective measure of

how effectively a firm uses its assets to generate revenue from its primary

business operations. It also serves as a general indicator of the firm's

overall financial health over a specified period. For the purposes of this

study, financial performance was refered to the steps and measures taken by

business organizations in the economic domain to achieve their goals, including

accounting procedures and sales processes.

Operational performance refers to the synergy

between various company units and their ability to collectively produce greater

output. It is the extent to which all business departments collaborate to

accomplish specific business goals. In this study, operational performance will

be understood as the steps and measures taken by business organizations that

are not directly related to finance but are crucial for achieving their goals,

such as customer and employee satisfaction, marketing, and social responsibility.

2.3. Review of Case Studies

Ayneshet Agegnew (2020) examined ‘the effect of

internal control on organizational performance in reference to Moha Soft Drinks

Company in Ethiopia’, using descriptive design in soliciting information, and

questionnaires in data collection. The results of his study showed that

internal control has an effect on organizational performance specially on

accounting procedures. The study recommended that management should develop

more effective strategies ensuring that internal control is effective and

efficient, also it recommended that the company should work to correct its

internal control system by periodic reconciliation (Ayneshet, 2020).

Esther Simon (2021) examined ‘the effect of

internal control on organizational performance in the Telecommunication

Industry in south and south-east Nigeria’, using a descriptive survey research

design, and questionnaire in addition with interview in data collection. The

study concluded that an organization's internal control environment and risk

assessment positively influence organizational performance. It recommended that

management should implement additional control activities to sustain and

enhance the effectiveness of internal controls, thereby improving overall

performance (Esther, 2021).

Hassan Mire (2016) investigated ‘effects of

internal control system on the organizational performance of remittance

companies in Mogadishu, Somalia’, using a descriptive research design, and

questionnaires in data collection. The study recommended that remittance

companies in Mogadishu should enhance their control environment, risk

assessment, and control activities. This recommendation is based on findings

that these variables positively impact the organizational performance of

remittance companies in Mogadishu (Mohamed, 2016).

Another study conducted (Oladele, 2010) Sought to

find out ‘the impact of the internal control system in the banking sector’. The

study classified controls into three main types: preventive controls, detective

controls, and corrective controls.

Data were gathered from both primary and secondary

sources, including interviews, structured questionnaires, journal publications,

textbooks, newspapers, and online resources. The findings indicate that the

primary cause of bank fraud in Nigeria is the absence of an effective internal

control system. Consequently, it is concluded that bank management should

develop and implement a robust internal control system capable of resisting

fraudulent activities. This will help ensure operational continuity, and maintain

the bank’s liquidity, solvency, and overall viability.

Qasim Ahmed (2021) examined ‘the effect of internal

control on employee performance of SMS enterprises in Jordan’ using survey

questionnaire to gather data. The results from the analyses in that research

provided that internal control system has a major effects and roles on employee

performance (Qasim, 2021).

Ting Chen and his friends (2021) investigated

‘customer satisfaction and internal control on Amazon.com’, using a large

sample of product rating data from Amazon.com. they found that customer

satisfaction is negatively associated with internal control weaknesses. In

other words, their findings provide the direct evidence that in-effective

internal control compromises customer satisfaction (Ting, Xiaotao, Chi and

Yakun, 2021).

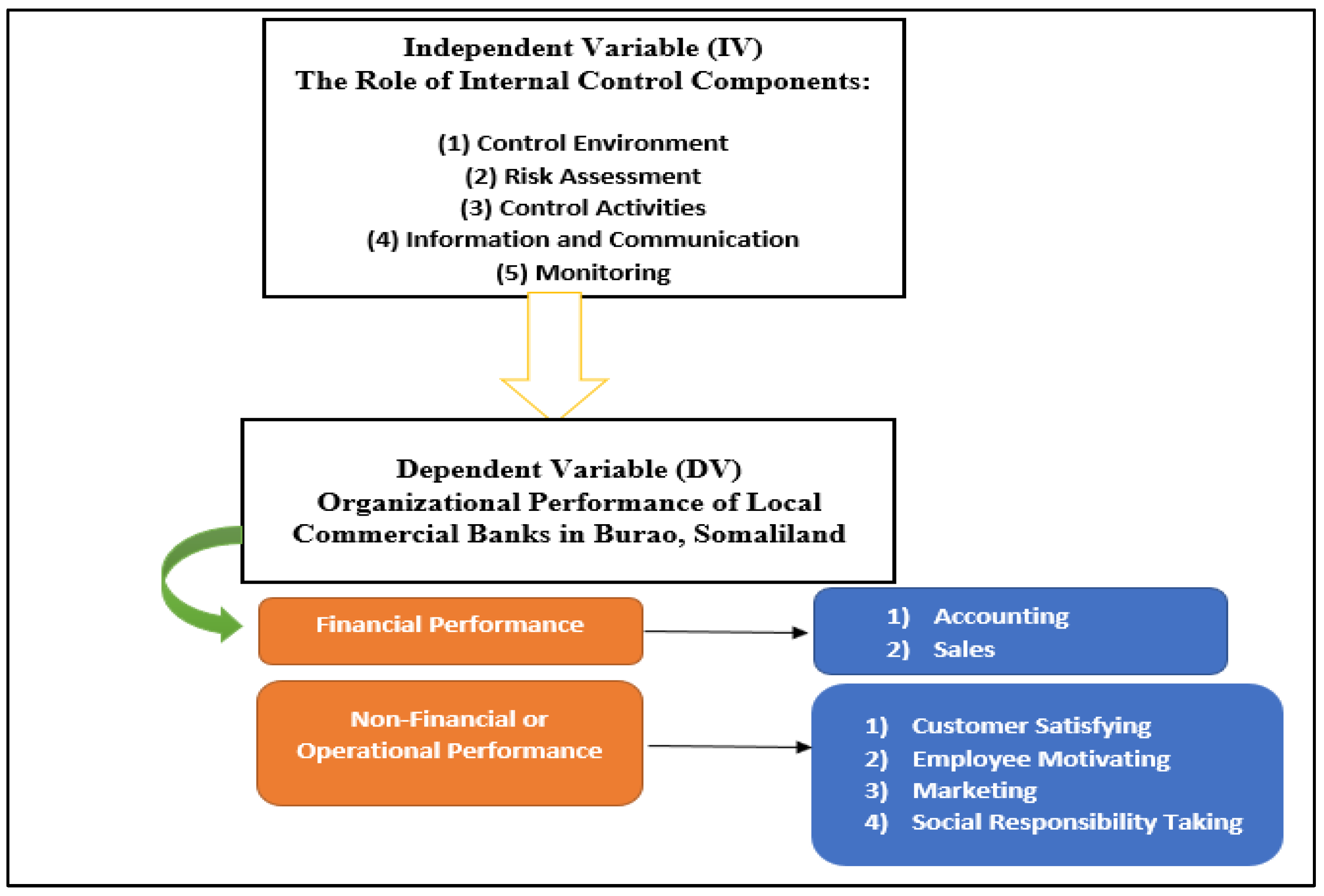

2.4. Conceptual Framework

The framework indicates the relationship between

the internal control components and the performance of local commercial banks

in Burao district. The frame (Figure 1)

is predicting direct effects from IV to DV thus neither moderating nor

mediating variable was considered.

Figure 1.

Coceptual Framework (Source: Researcher).

3.0. Methodologies

3.1. Summary

A descriptive research design was used, with

quantitative methods to collect numerical data from local banks in Burao,

Somaliland. The target population included 167 staff members, and a sample size

of 50 respondents was determined using a systematic random sampling technique.

Data were gathered through structured questionnaires and analyzed using SPSS

software. Validity and reliability were ensured through expert judgment and

Cronbach’s Alpha, respectively. Ethical considerations were observed by

obtaining informed consent, ensuring anonymity, and avoiding disruption during

data collection.

4.0. Data Presentation, Analysis, and Interpretation

4.1. Descriptive Analysis

Table 1.

Gender.

| Frequency | Percent | ||

| Valid | Male | 30 | 60.0 |

| Female | 20 | 40.0 | |

| Total | 50 | 100.0 | |

Source; Primary (2022).

The above table shows that 30 (60%) of the

respondents were male, and 20(40%) of them were female. this illustrates that

most of the respondents were male respondents, meaning that the number of males

working in commercial banks were more than the number of females working in

commercial banks.so in this table and chart we could see how that is possible.

Table 2.

What is your age?

| Frequency | Percent | ||

| Valid | 30-39 | 21 | 42.0 |

| 40-59 | 23 | 46.0 | |

| 60 and above | 6 | 12.0 | |

| Total | 50 | 100.0 | |

Source; Primary (2022).

As the above table shows age of 21(42%) of the

respondents were “between”, 30-39, 23 (46%) of the respondents were “between”

40-59, 6(12%) of the respondents were between 60-and above. This illustrates

that most of the respondents were ranged from 40-59. In that age is when person

he or she has the skills, experiences, and means necessary for an enjoyable

life and work.

Table 3.

What is your qualification?

| Frequency | Percent | ||

| Valid | Diploma | 7 | 14.0 |

| Bachelors | 35 | 70.0 | |

| Masters | 8 | 16.0 | |

| Total | 50 | 100.0 | |

Source; Primary (2022).

As the above table shows, 7(14%) of the respondents

were Diploma level, 35 (70%) of the respondents were Bachelors, 8(16%) of the

respondents was Masters, this illustrates that most of the respondents were

University level or bachelors. That means when we compare the number of

respondents were not in high school or less but they were university level and

graduated.

4.2. Variable Tests

4.2.1. Reliability Test:

The study assessed the reliability of the data

collected from 50 participants. The consistency of the responses was evaluated

empirically, with the calculated Cronbach’s alpha being 0.633, which indicates

a good level of reliability. This alpha value suggests that the responses from

interviews were largely consistent and interrelated. The analysis concluded

that the study's questionnaire was designed effectively, as responses from

participants were similar and logically organized. Additionally, test-retest reliability

was measured in the research. The results, as shown in the table, demonstrated

consistency and significance in the findings.

4.2.3. Correlation Tests:

Pearson’s Correlation Model: Role of Internal

Control on Organizational Performance in Local Commercial Banks in Burao

–Somaliland

Table 21.

Pearson Correlation.

| Internal Control Systems | Organizational Performance in Local Commercial Banks | ||

| Internal Control Systems | Pearson Correlation | 1 | 558** |

| Sig. (2 tailed) | 0.01 | ||

| N | 50 | 50 | |

| Organizational Performance in Local Commercial Banks | Pearson Correlation | 558** | 1 |

| Sig. (2 tailed) | 0.01 | ||

| N | 50 | 50 |

Source: Primary.

The table demonstrates a Pearson's correlation analysis exploring the relationship between Internal Control Systems and Organizational Performance in Local Commercial Banks in Burao, Somaliland. The analysis reveals a significant positive correlation coefficient of 0.558, suggesting that improvements in internal control systems are associated with enhancements in organizational performance. The statistical significance of this correlation is underscored by a p-value of 0.01, indicating that the observed relationship is highly unlikely to be due to chance. With a sample size of 50, the data robustly supports the conclusion that stronger internal control systems contribute positively to the performance of local commercial banks, affirming the critical role of these systems in ensuring financial stability and operational efficiency.

5.0. Conclusion and Recommendations

5.1. Conclusion

The researcher concludes that there is a significant positive relationship between internal control systems and organizational performance. Internal control systems are relatively effective and have a substantial impact on organizational performance. They ensure the proper administration, completeness, and accuracy of records and provide safeguards against fraud and collusion, particularly among those in positions of authority or trust. For optimal performance, internal control systems must be adequately robust in any organization.

The study also finds a moderate positive relationship between internal control systems and organizational performance. However, it reveals that the internal controls implemented in commercial banks in Burao, Somaliland, were ineffective and unsatisfactory. Consequently, the organizational performance was deemed inadequate. Despite this, a significant positive relationship between internal controls and organizational performance was established.

5.2. Recommendations

To enhance the performance and reduce risks in local commercial banks, it is essential to maintain regular internal audits of their accounting systems. Improvements should be made to internal control systems to align better with organizational operations, and robust authorization tools should be implemented to manage access to bank assets effectively. Strengthening internal control systems will contribute to increased profitability and overall bank performance. Additionally, close monitoring of employees is necessary to prevent the circumvention of established controls, ensuring the integrity of the system. To foster a diligent and honest workforce, employees should be motivated adequately, reducing the temptation to engage in fraudulent activities due to insufficient rewards.

References

- Wikipedia. (2022, January 1). Retrieved from Wikipedia: https://en.wikipedia.org/wiki/Organizational_performance.

- Wikipedia. (2022, june 24). Retrieved from Wikipedia: https://en.wikipedia.org/wiki/Bank.

- A runa, S. (2019). the impact of internal control on job satisfaction of female workers. international Journal of research in engineering, 1-8.

- Angie, M. (2019, January 28). Small Business Chron. Retrieved from Small Business Chron: https://smallbusiness.chron.com/audit-procedures-sales-collection-cycle-49846.html.

- Audit-Board. (2018, April 17). Audit Board. Retrieved from Audit Board: https://www.auditboard.com/blog/7-reasons-to-maintain-your-internal-controls-compliance-program/.

- Ayneshet, A. A. (2020). The Effect of Internal Control on Organization Performance in. International Journal of Research in Business Studies and Management, 1-10.

- Bhasin Hitesh. (2019). Internal Control: Meaning, Types, Components and objectives. marketing91.

- BPP, M. a. (1988). ICAN Study Test on Auditing and Investigation. oxford: Oxford: Oxford University Press.

- Brown, S. P. (Brown, S. P. ). A meta-analysis and review of organizational research on job involvement. Psychological Bulletin, 120(2),, 235–255.

- CFI Team. (2022, February 27). CFI. Retrieved from Corporate Finance Institute: https://corporatefinanceinstitute.com/resources/knowledge/finance/financial-performance/.

- Cornelius Kipkemboi Lagat¹, C. A. (2016). EFFECT OF INTERNAL CONTROL SYSTEMS ON FINANCIAL MANAGEMENT. Journal of Economics,, 162-186.

- Danielle, S. (2018, november 16). Retrieved from biz-fluent: www.bizfluent.com/about.

- Dr. Annette, T. (2020, may 30). Retrieved from ckju.net for management skills: www. ckju.net.

- Drupal. (2015).

- Esther, S. (2021). effect of internal control on organizational performance in the T.I in south and southeast Nigeria. International Journal of Social Science, 1-20.

- Forecast Academy team. (2021, August 20). Forecast. Retrieved from Forecast Platform: https://www.forecast.app/blog/operational-performance#:~:text=improve%20operational%20performance-,What%20is%20operational%20performance%3F,to%20accomplish%20specific%20business%20goals.

- Furlong, M. (January 25, 2019). What Are the Types of Internal Controls? bizfluent.

- Hackett, W. a. (1976). An auditing perspective of the Historical development of. Florida Agricultural and Mechanical University, 003-009.

- Henri, J. (2004). "Performance measurement and organizational effectiveness: bridging the gap". Québec City: 93-123.

- Ian Palmer, R. D. (1996). Reframing and organizational action: The unexplored link. Journal of Organizational Change, 12-25.

- James, A. H. (2008). Accounting information system. Mason, Ohio: Cengage Learning Academic Resource Center.

- Jamshidi-Navid, B. a. (2009). A Clear Look at Internal Controls: Theory and Concepts. Hamed: Social Science Research Network.

- Jason, G. (2022, April 07). the business Professor. Retrieved from the business Professor: https://thebusinessprofessor.com/en_US/accounting-taxation-and-reporting-managerial-amp-financial-accounting-amp-reporting/internal-controls-definition.

- Jonathan Duchac, J. M. (2007). financial accounting An Integrated Statements Approach. 0-324-37443-7: Cengage Learning.

- Julia Kagan. (2021, October 06). Investopedia. Retrieved from Investopedia: https://www.investopedia.com/terms/c/commercialbank.asp#toc-significance-of-commercial-banks.

- Katushabe, P. (2016). INTERNAL CONTROLS AND ORGANISATIONAL PERFORMANCE OF UNITED NATIONS ORGANISATION STABILISATION MISSION IN THE DEMOCRATIC, REPUBLIC OF THE CONGO, ENTEBBE BASE. Uganda management institute, 1-102.

- Kendra, C. (2022, January 26). Retrieved from verywell-mind: www.verywellmind.com.

- Kenton, W. (2019). Principles of Auditing & Other Assurance Services,. Sarbanes-Oxley (SOX).

- Margaret, Scott A., Sott L., and David. (2009). effectof preventive and defective controls on employee performance and motivation. Research-gate, 1-39.

- Martin. (1994). reports of tax cases. Northern Ireland: LNUK.

- Mohamed, A. M. (2016). EFFECTS OF INTERNAL CONTROL SYSTEM ON THE ORGANIZATOINAL PERFORMANCE OF REMITTANCE COMPANIES IN MODADISHU-SOMALIA. Journal of Business Management , 1-15.

- Noorbakhsh, F. a. (2001). Human Capital and FDI Inflows in Developing Countries: New Empirical Evidence. Journal of World Development, 1539-1610.

- Oladele, J. (2010). The Effect of Internal Control System on Nigerian Banks. International Journal of Accounting, 123-129.

- Oxford-Languages. (n.d.). Oxford University Press. Retrieved from Oxford Languages: https://languages.oup.com/google-dictionar-en/.

- Plamen. (2019). Pro-Quest Scholarly Journal. Control and Audit in Marketing, 1-5.

- Poff, D. C. (2018). Fraud triangle: Cressey's fraud triangle and alternative fraud theories. Springer, Cham, Switerland.: https://link.springer.com/referencework/10.1007/978-3-319-23514-1.

- Qasim, A. (2021). the effect of internal control on employee performance of SMS enterprises in Jordan. Jornal of Asian finance, economies, and Business, 1-9.

- Rae, K. a. (2008). Quality of internal control procedures : antecedents and moderating effect on organisational justice and employee fraud. Managerial auditing journal,, 104-124.

- Rae, Kirsten; Sands, John; and Subramaniam, Nava. (2017). Associations among the Five Components within COSO Internal Control-Integrated Framework as the Underpinning of Quality. Australasian Accounting, Business and Finance, 28-54.

- Richard, Pierre, Devinney, Timothy,Yip, George,Johnson, and Gerry. (2009). Measuring Organizational Performance: Towards Methodological Best Practice. Journal of Management, 35.

- Rynes, S. L. (1990). Applicant attraction strategies: An organizational perspective. Academy of Management Review, 286-310.

- Salah, S. (2012).

- Subramaniam, K. R. (2008). Quality of internal control procedures: Antecedents and moderating effect onorganisational justice and employee fraud. Managerial Auditing Journal, 104 - 124.

- Ting, Xiaotao, Chi and Yakun. (2021). Customer satisfaction and Internal Control. College of Management Journal, 1-53.

- Tipgos, M. A. (2002). Why Management Fraud Is Unstoppable. The CPA journal., 34-41.

- Uganda, B. o. (2011). BANK OF UGANDA FINANCIAL CONSUMER PROTECTION. Bank of Uganda, 1-18.

- Veyrat-Durebex, C. C. (2016). Disruption of TCA Cycle and Glutamate Metabolism Identified by Metabolomics in an In Vitro Model of Amyotrophic Lateral Sclerosis. Molecular Neurobiology, 6910–6924.

- Wang and Guan. (2017). Research on the relationship between internal control and financial performance. Advances in Economics, Business and Management Research Journal (Press Atlants), 1-6.

- Wikipedia. (2022, July O6). Retrieved from Wikipedia: https://en.wikipedia.org/wiki/Commercial_bank#Role.

- Wikipedia. (2022, April). Wikipedia. Retrieved from Wikipedia: https://en.m.wikipedia.org/wiki/Internal-control.

- Xio, Zheng, Liu and Mohammed. (2018). the effectiveness of Internal Control and Corporate Social Responsibility. MDPI Journal, 1-18.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.