Submitted:

06 August 2024

Posted:

07 August 2024

You are already at the latest version

Abstract

This study offers an analysis of existing research on sustainability and its link to accounting and management control in the port sector. The existing studies do not provide a comprehensive discussion of management accounting and control tools in this context, despite recognizing the relevance of the issue. The Scoping Review was used as a methodological basis, with reference to the framework of Arksey and O’Malley [1], with the aim of mapping the literature on the role of ac-counting and management control, as well as their relationship with the Triple Bottom Line associated with the various levels of sustainability in this sector. The results point to a diversity of tools used essentially in developed countries, where the interest in efficiency, sustainability and strategic alignment stands out.

Keywords:

controle de gerenciamento

; portos marítimos

; sustentabilidade

; triplo resultado

1. Introduction

In recent years, the integration of sustainability into accounting and management control systems has emerged as a topic of growing importance, especially in the dynamic and complex context of the port sector. This article proposes a comprehensive review of studies exploring the intersection between sustainability, accounting and management control in the port context.

Although the literature on each of these topics is vast, the synchronic approach that examines the interaction between the three elements has been relatively underdeveloped in academia, an aspect that translates into an original challenge in this study, with a current and innovative approach that we intend to initiate. Therefore, the next section presents a review of the port literature, integrating the role of accounting and management control, as well as the three dimensions of the triple bottom line in the context of the port sector.

2. Literature Review

The active role of the port sector in the economic development of countries is widely recognized [2]. Traditionally seen as central infrastructures, ports have been key to integrating global and local markets, driving the process of globalization based on efficiency [3,4,5].

In addition to their economic function, maritime ports play a crucial role in promoting territorial cohesion and regional development, mitigating economic disparities. There is, however, a lack of studies looking at the economic impact of ports from a spatial econometric perspective [3].

In the context of global trade, maritime transport is essential for the flow of raw materials, products and consumer goods worldwide. To remain competitive, the sector has sought to increase its efficiency by reducing unit costs per transported commodity and modernizing processes at port terminals [6].

Faced with emerging challenges, such as the growth of port activity, it has become a priority to introduce new concepts and principles of sustainability [7,8], when especially combined with the expansion of port activity [8,9].

Today, this transport route is considered an efficient and economically viable option for large-scale transport [5], and is recognized for its ability to transport large volumes of cargo with lower fuel consumption compared to other means of transport. However, its impacts on sustainability in general and the environment in particular cannot be overlooked [9,10,11].

It is estimated that more than 80 per cent of global trade, by volume, is transported by sea, and that this percentage is even higher for most developing countries [12].

Despite the growing recognition of the importance of sustainability issues in achieving organizational success, research into management control and its relationship with sustainability is still an under-explored area in the academic context [13,14]. Therefore, the following section discusses the role of accounting and management control in the pursuit of good sustainable practices in the port context.

2.1. The Central Role of Accounting and Management Control

Nowadays, factors such as efficiency, transparency and informed decision-making play a few strategic roles. Alongside financial accounting, but in a collaborative way, control and management accounting focus on providing analyses, interpreting and accounting data through tools that enable managers to make strategic decisions in favor of sustainability and long-term success [15,16].

Consequently, the literature recognizes that accounting and management control systems align organizational and behavioral structures with the economic objectives of organizations, monitoring, evaluating and driving their performance, and are essential in promoting the integration of sustainable development and the dissemination of sustainable practices aligned with social, environmental and economic goals [17].

In the port context, these systems are seen as tools that support, improve and guide the strategic decision-making process [15,16,18], and their integration allows us to go beyond mere accounting, underpinning the strategic definition of port tariffs [19,20,21].

Accounting and management control, integrated into an efficient port system, play an essential role [15], for the operational and financial success of these vital infrastructures for socio-economic development. These areas are fundamental in assessing the performance of the resources used and supporting, improving and guiding the strategic decision-making process in the port context [15,16,18].

Management control systems support and optimize the decision-making process, especially when strategic decisions affect other entities for mutual competitive advantage [16]. Therefore, cost management and control are indispensable for the efficiency of the port system, along with regulation and price reductions [20].

2.2. Triple Bottom Line: The Dimensions of Sustainability

Sustainability is determined by various aspects, so there is no single agreed definition [22,23,24], insofar as its development process is intrinsic to the underlying change in organizational culture.

Organizations are currently facing growing internal and external pressures that encourage them to adopt sustainability practices, a behavior that is consistent with mimetic isomorphism [24]. Consequently, the measurement of organizational success, once based solely on profit, has in the last decade led to the use of a new framework based on sustainable development [25], based on three interconnected and overlapping pillars, the Triple Bottom Line (TBL) [25,26].

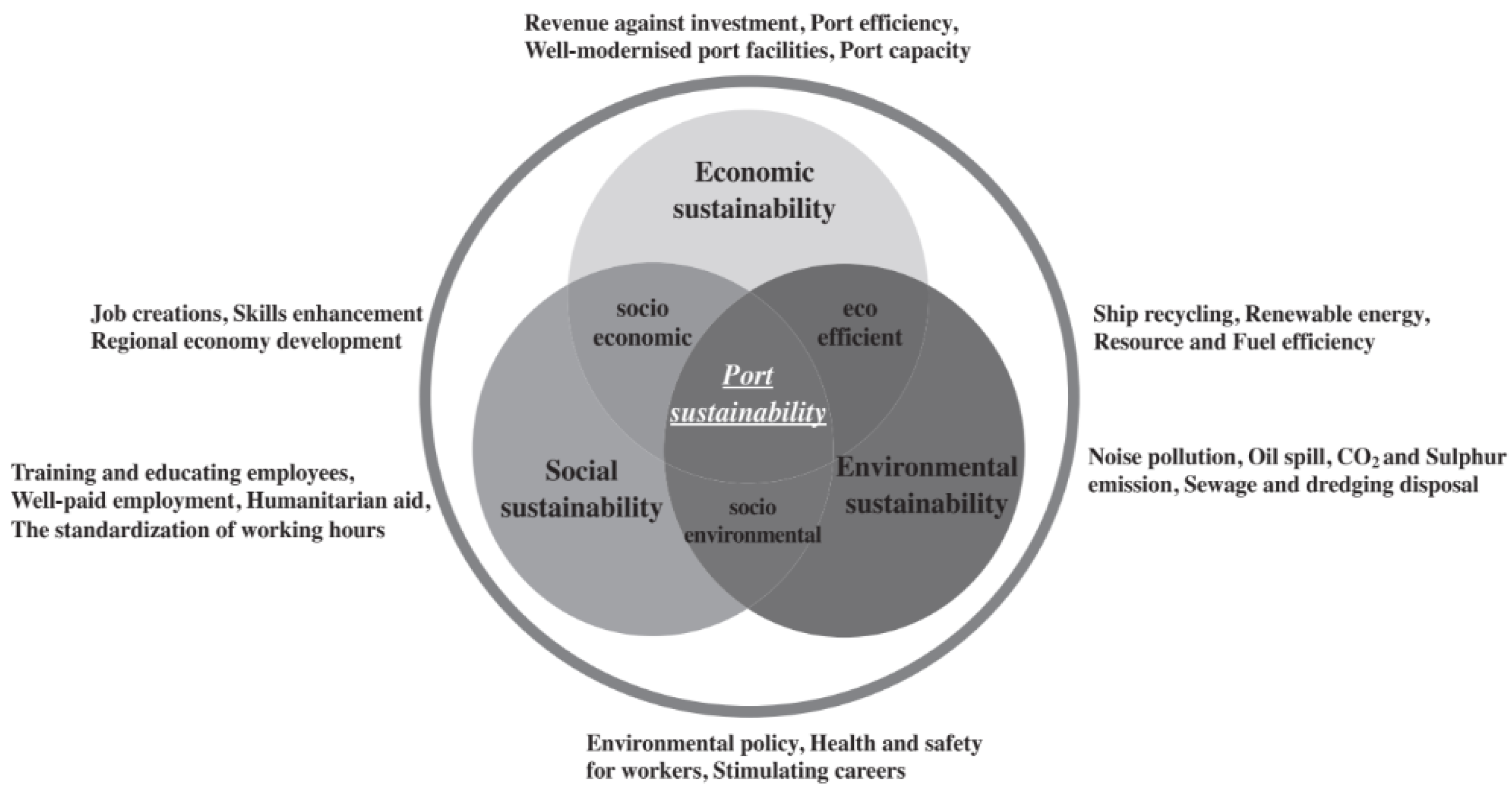

First proposed in 1994 and then in 1997 in his book "Cannibals with Forks: The Triple Bottom Line of 21st Century Business" [26], the TBL approach to evaluating business performance encompasses and seeks to promote socially responsible and environmentally sustainable business practices by balancing the social (people), environmental (planet) and economic (profit) dimensions. [9,25,26,27,28].

In the context of the global energy crisis and environmental degradation, sustainable development has emerged as the main strategic orientation for the port sector [29]. This approach consists of maintaining profitability while promoting sustainability through social responsibility and environment-related activities [9,30]. This focus has the potential to transform the port industry into a profitable and environmentally responsible industry in the coming decades, cultivating a commitment to environmental responsibility [31]. It is also recognized that when seaports operate to high sustainability standards, they are generally more likely to attract support from governments, local communities and potential investors [9].

Figure 1.

Triple Bottom Line integrated into the port context. Reproduced from Lim, S., Pettit, S., Abouarghoub, W., & Beresford, A. ,2019, Transportation Research Part D: Transport and Environment, 72, p.50 (https://doi.org/10.1016/j.trd.2019.04.009). © 2019 Elsevier Ltd.

Figure 1.

Triple Bottom Line integrated into the port context. Reproduced from Lim, S., Pettit, S., Abouarghoub, W., & Beresford, A. ,2019, Transportation Research Part D: Transport and Environment, 72, p.50 (https://doi.org/10.1016/j.trd.2019.04.009). © 2019 Elsevier Ltd.

2.2.1. Social Sustainability

Social sustainability has a positive impact on the quality of life of co-workers and consists of promoting well-being in favor of the surrounding community [11,31,32]. Factors such as ethics, labor conditions and corruption, among others, should be considered as guidelines with the aim of achieving stability from a social perspective.

In the last decade, maritime ports have excelled in a few areas, driving transformations and facing pressures, both socially and environmentally. In response to these pressures, Corporate Social Responsibility (CSR) has gradually been integrated into this sector [33,34]. The relationship between sustainable development and CSR is also showing an upward trend in academic research [35].

CSR involves the adoption of practices related to social, environmental and economic aspects which, in turn, is intrinsically linked to the concept of TBL, guiding organizations not to look exclusively at themselves, but also for the benefit of society in general [22] and to mitigate the negative impacts caused by seaport activity [36]. Vanelslander [33], investigated in which the importance of CSR objectives in the port context was assessed. In general, the results indicate a greater focus on social concerns, emphasizing the commitment to issues that have a direct impact on community and social relations.

2.2.2. Environmental Sustainability

Concern for the environmental dimension implies taking responsibility for its impacts and publicizing the efforts made to reduce the ecological footprint [11]. Environmental sustainability has emerged as a concern in various areas of society, especially those that have the greatest impact on economic growth, including seaports, which play a vital role as access points to globalization [34,37].

The core of sustainability in ports is the promotion of economic performance, the reduction of CO2 emissions, the search for safer methods in the provision of logistics services, environmental preservation and the reduction of consumption of natural resources for the benefit of present and future generations [33,38,39].

However, this sector still operates with old-fashioned fleets that predominantly use fossil fuels, so to tackle this issue, the UNCTD [12] advocates effective regulatory intervention together with stronger investment in green technologies and fleets, with the aim of achieving the goal of carbon neutrality by 2050. According to Acciaro [28], environmental responsibility in the port sector is driven by three factors:

- The need to comply with current and future regulations;

- The intention to identify efficiency gains by incorporating environmental aspects into the company's strategy;

- Establish an environmentally responsible image to gain a competitive advantage.

2.2.3. Economic Sustainability

Economic sustainability is related to economic performance, including profit, cost reduction, economic growth and organizational development, also covering financial information, but not limited to this. It also includes better and more responsible business practices, job creation, with the aim of achieving financial success through equitable and sustainable economic growth, from the perspective of the social and environmental dimension [11,32,40].

Triantafylli and Ballas [41] show that efficiency in the Greek port sector, especially through low-cost strategies, is an example of how economic sustainability can be achieved in port operations and investments.

Management accounting plays a crucial role in this process, providing a detailed analysis of costs and helping to identify opportunities for reducing expenses and optimizing resources. This is particularly relevant when we consider the observation of Zhao et al. [29], who associate an efficient customs process with improved port logistics performance, leading to an increase in trade volume and, consequently, sustainable economic development of the port.

In addition, the research by Batalha et al. [36] highlights the complex interrelationship between social and economic development in ports, thus making it difficult to separate these concepts. When assessing the impact of the socio-economic environment of ports, it's important to take into account the country's economic situation and its development prospects in light of the fact that the economic reality of maritime ports is intrinsically related to the development of the economy, both nationally and internationally, since demand conditions, cyclical economic development, inflation and unemployment are all variables that affect this market segment [42].

3. Methodology

The research adopts the Scoping Review methodology, based on the methodological structure proposed by Arksey and O´Malley [1], to map the literature relating management control and sustainability applied to the port sector. The main objective is to identify approaches, motivations and challenges underlying the research, establishing trends and identifying gaps in the integration of management control tools and sustainable practices in seaports.

The Scoping Review is a form of systematic unification of research and aims to structure the state of the art in a specific area of research [1,43]. In this methodology, the data is grouped to identify key concepts, possible research gaps and sources of evidence in the evaluation and formulation of policies, research and practice [43]. It is particularly relevant in areas that are complex or have not yet been comprehensively researched, and it is a methodology that translates into an interactive process in which researchers reflect on each stage and, when necessary, repeat some to ensure a comprehensive approach to the literature.

Considering the specificities underlying the methodology, we will describe the stages in the framework that lead to this Scoping Review:

- ❖ Stage 1: Identifying the research question;

- ❖ Stage 2: Identification of relevant studies;

- ❖ Stage 3: Study selection;

- ❖ Stage 4: Data mapping;

- ❖ Stage 5: Compiling, summarizing and presenting the results.

Stage 1: Identifying the research question

The formulation of research questions represents a guideline and a recurring point of reference in resolving uncertainties in the research process. This Scoping Review therefore seeks to answer the following question:

In the current panorama of research approaches, motivations and constant challenges, does accounting and management control influence the various dimensions of sustainability in the port context?

In this respect, this question is broad enough to enable a comprehensive understanding of the issue.

Stage 2: Identification of relevant studies

This stage, which focuses on identifying relevant studies, involves developing and applying specific criteria to determine the relevance of each study in congruence with the research question outlined in the previous stage.

The systematic search for relevant sources of information is carried out with precision and methodology, with the aim of ensuring that only relevant and significant studies are included, thus contributing to the robustness and relevance of the research. The following information sources were used to ensure a wide range of relevant articles and studies were captured: Scopus; Web of Science; Academic Search Complete; Business Source Complete; Google Scholar and the Snowball approach.

When identifying potentially relevant studies, the search terms were determined according to the subject being investigated. This critical choice and the adjacent criteria ensure that the research is comprehensive and aligned with the topics of interest. Thus, the search terms were defined according to the topic under study, incorporating various synonyms to ensure that we did not exclude relevant studies, even if they used different terms.

Management Control Systems

- Management Control Systems

- Management Control

- Management Control Tools

- Accounting and Management Control

- Managerial Accounting Instruments

- Cost Accounting

Maritime Sector

- Maritime Sector

- Ports

- Maritime ports

- Seaports

- Maritime Industry

- Shipping Marine Industry

- Green Ports

Sustainability

- Sustainability

- Sustainable Development

- Environmental Accounting

- Economic Sustainability

- Environmental Management Accounting Metrics

- Triple Bottom Line

- Environmental Cost Accounting

After determining the search terms, it was decided to set some limits. Generally, these limits (e.g. restricted time limit and articles published in other languages) are conditioned by budget and time constraints, although these search conditions are defined by practical terms, and the more conditions that are defined, the greater the likelihood of excluding appropriate studies [1].

The boundaries of this research include the period from 2000 to the present day. In addition, the delimitation of the study area was centered on the academic domains of “Business, Management and Accounting”.

As for the Snowball approach, as there are no limits, we are referring to a technique which, from an initial set of relevant articles, makes it possible to find others based on the references cited in those documents. What's more, as the name suggests, this methodology resembles a snowball that grows as new articles are discovered, thus guaranteeing comprehensive coverage of the state of the art to be investigated.

Stage 3: Study selection

The strategy of identifying relevant articles detected several studies that did not comply with the themes under analysis. To maintain methodological rigor, articles that did not directly address the research question in their abstract were thoroughly excluded. In addition, because various sources of information were used, some articles were also excluded because they were duplicates, to guarantee the integrity and impartiality of the results obtained.

- Titles and abstracts: initial selection

The titles and abstracts of potentially relevant articles went through an initial screening process, avoiding the misallocation of resources and effort in acquiring articles that did not fit in with the research [44]. In this process, if the information in the title and abstract is dubious in relation to the subject being analyzed, the researcher chooses to review the introduction and conclusion, requiring full access to the document.

About articles without access, efforts were made to contact the respective authors, explaining the purpose of the research and the potential importance of the article. Efforts were also made to contact the library services and try to obtain them through alternative access loans.

Once the articles had been identified and their accessibility confirmed, the next stage required reading them in their entirety, making sure that the inclusion was considered and conscious. In this study, it was not assumed that the abstracts were representative of the full article, but rather that they provided a quick overview of the overall content, helping those interested to decide whether the article was relevant to their needs. Aware of this limitation, we opted to read the whole article to capture all the nuances and details.

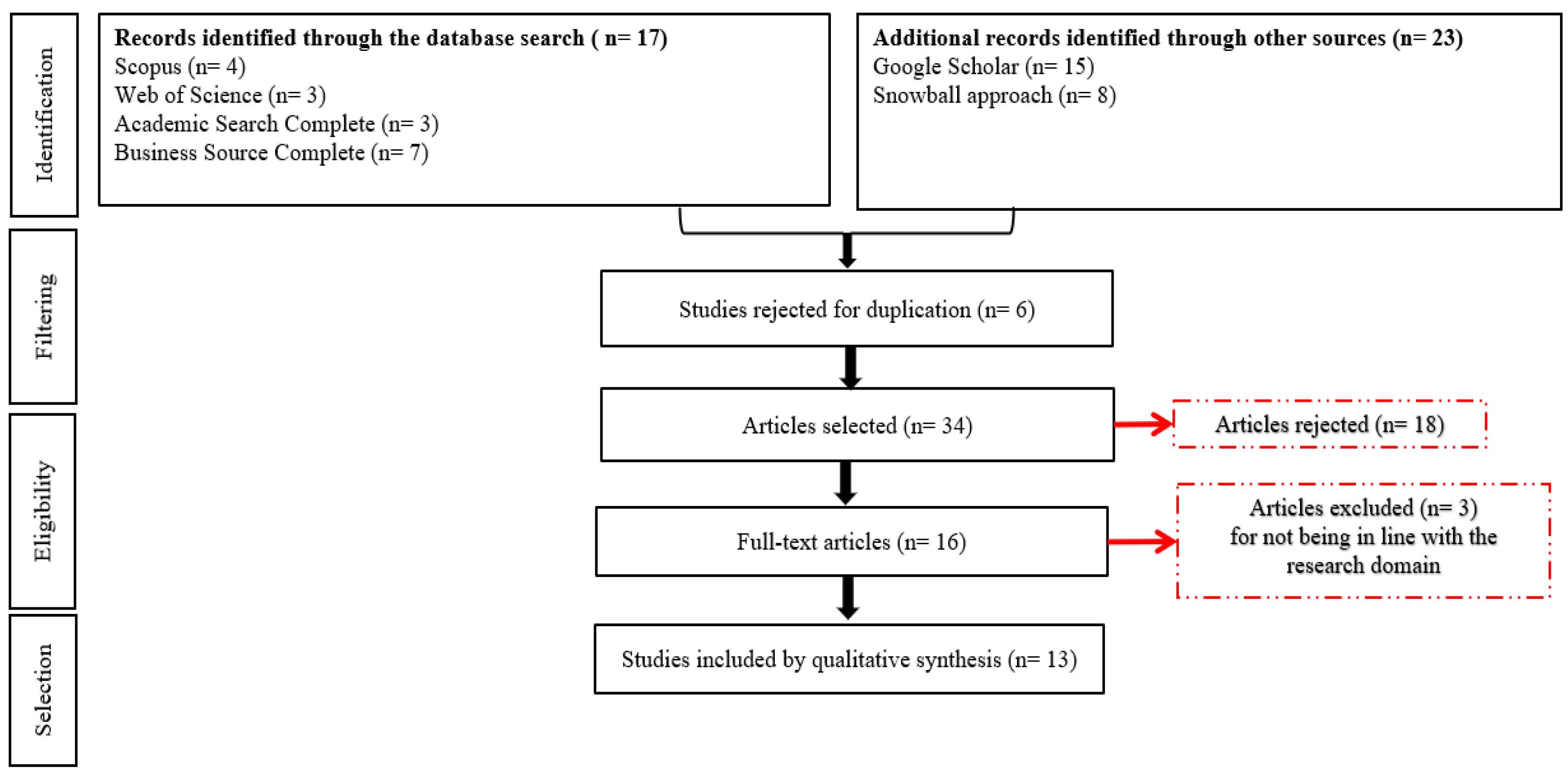

The process from Stage 2 to Stage 3 is represented in the following flow chart:

Stage 4: Data mapping

In the process of selecting the articles in an appropriate and methodological way, all potentially relevant articles were critically analyzed using a reading sheet model, allowing them to be grouped and mapped with all their relevant characteristics, keeping the researchers aligned with the issue under investigation.

At this stage, various eligibility and relevance criteria were also considered, providing a wide-ranging assessment that culminated in a well-founded decision on the inclusion or exclusion of each document, thus contributing to the rigor and robustness of this methodology.

Based on the reading sheet, which compiles the essential information extracted from the articles, the usefulness of the narrative review was considered using the descriptive-data analysis technique. This approach, which proved to be useful, made it possible to establish a uniform analytical structure for all the articles selected, incorporating the charting phase, which refers to a technique for synthesizing and interpreting qualitative data, involving various steps, such as sorting information, drawing up graphs/tables to visualize and organize this information. This organization technique, according to keywords and relevant themes, aimed to extract and visually represent the qualitative findings, thus contributing to the understanding and analysis of trends and patterns in the existing literature.

Figure 2.

Flowchart according to PRISMA flow chart of results.

Stage 5: Compiling, summarizing and presenting the results

At this stage, with a map of relevant information on the nu-clear articles intrinsic to the research, the information obtained is disseminated by presenting a narrative that elucidates the lessons learnt from this process, including the identification of gaps, as well as guidelines for future research with the aim of pointing in directions that will lead academia to new discoveries and insights.

4. Results and Discussion

Table 1.

Summary of the main characteristics of the studies analyzed.

| Author [Ref.] |

Objective(s) of the study | Methodology | Entity |

|---|---|---|---|

| [45] | Implementation of a strategic management system at the Valencia Port Authority. | Case study | Valencia Port Authority |

| [46] | Implementation of Lean Enterprise, principles, and tools in port activities. | Case study | Port of Mobile |

| [41] |

Explore the impact of management control systems (MCS) on the performance of shipping companies, analyze the relationship between business strategies and provide insights into the type of MCS to implement and the consequences of such choices on port performance. |

Case study | Shipping companies in Greece |

| [47] | Analysis of some definitions, advantages and an introduction to the use of the Balanced Scorecard (BSC) as a competitive advantage, business performance measure and port management techniques. |

Systematic literature review | N/A |

| [20] | To define a method to be applied in Portuguese port administrations to justify the tariffs to be charged for a variety of services. |

Case study | Portuguese Port Administrations |

| [48] | To analyze the role of MCSs in supporting the decision-making process of Port Authorities, maritime agents and cruise companies in preventing and reducing the negative environmental effects of maritime ports. |

Case study | Port of Naples |

| [49] | Develop a Sustainable Maritime Balanced Scorecard (SMBSC) considering economic, social and environmental indicators. |

Case study | Port of Alexandria |

| [16] | To investigate the SCG in support of decision-making processes, to prevent and reduce the negative environmental effects of seaports. |

Case study | Port of Naples |

| [50] | Modeling an integrated framework to boost port performance, which includes performance measurement using the BSC and PESTLE methods (analysis of political, economic, social, technological, legal and environmental factors) with the concepts of sustainability, smart port and green port. | Systematic literature review | N/A |

| [19] |

Understand and analyze modern cost accounting methods and their implications for planning, control and decision-making, identifying advantages and disadvantages, investigating implementation policies and highlighting the benefits of these systems for measuring costs. |

Case study |

Port of Sudan |

| [21] |

Revisiting the pricing of maritime services in South African ports. |

Case study |

Transnet National Port Authority |

| [18] | To analyze the development and implementation of the BSC/SBSC in the Cartagena Port Authority, providing relevant information for academic knowledge and exploring the fusion of the TBL concept within the SBSC. | Case study | Port of Cartagena |

| [51] | Identify and categorize the different Lean practices implemented in the maritime industry, as well as the main barriers and benefits of their implementation. | Systematic literature review | N/A |

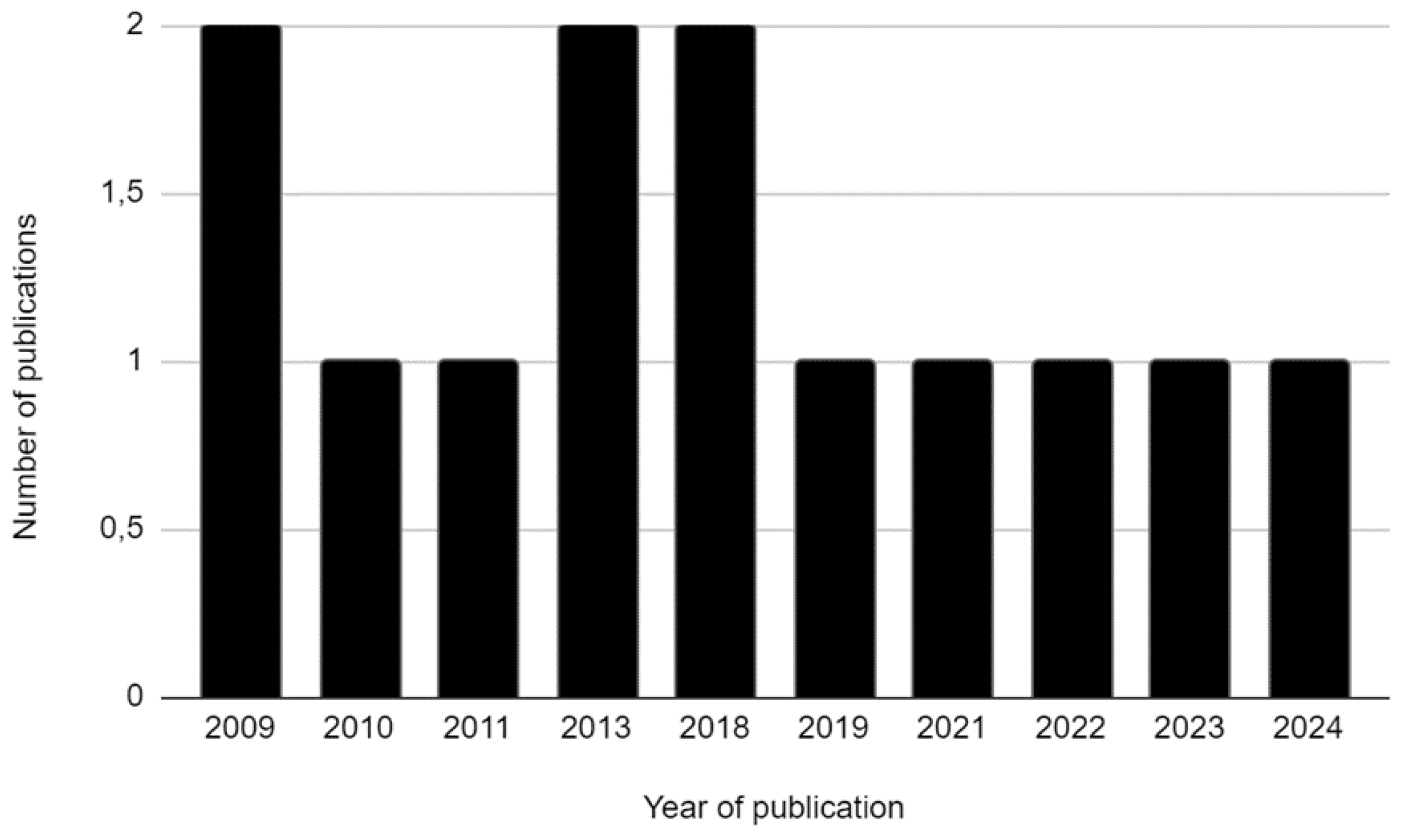

Figure 3 illustrates the number of articles published in the period defined by the research, which runs from 2000 to the present. It is important to note that no publications were found before 2009. The sample covers a total of 13 selected articles, indicating that this is a relatively under-researched topic, since the annual frequency of publications does not exceed two articles. However, the presence of publications in the last five years emphasizes the contemporary nature of the topic, suggesting that it continues to be relevant and discussed.

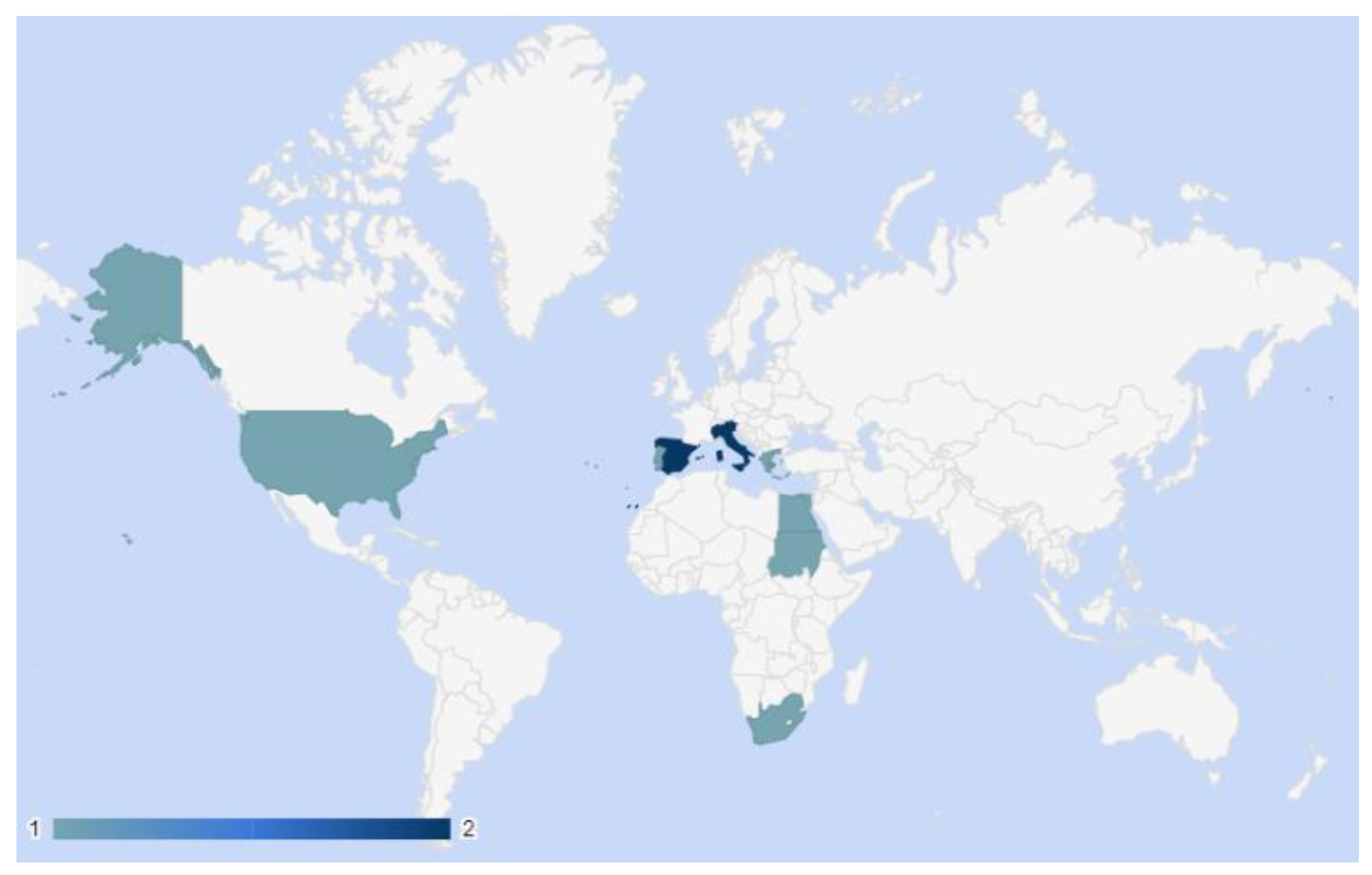

The predominant methodology among the articles analyzed is the case study, present in 10 of the 13 articles. This methodological approach aims to understand specific phenomena in one or more entities. The graph-map (Figure 4) provides a visual representation of the geographical regions covered in the articles, allowing a broader view of current research in the port field, from which Italy and Spain stand out as having the largest number of studies. These countries are classified as developed according to the Human Development Index [52], two of the articles identified focus on Italian ports and are co-authored by Assunta Di Vaio.

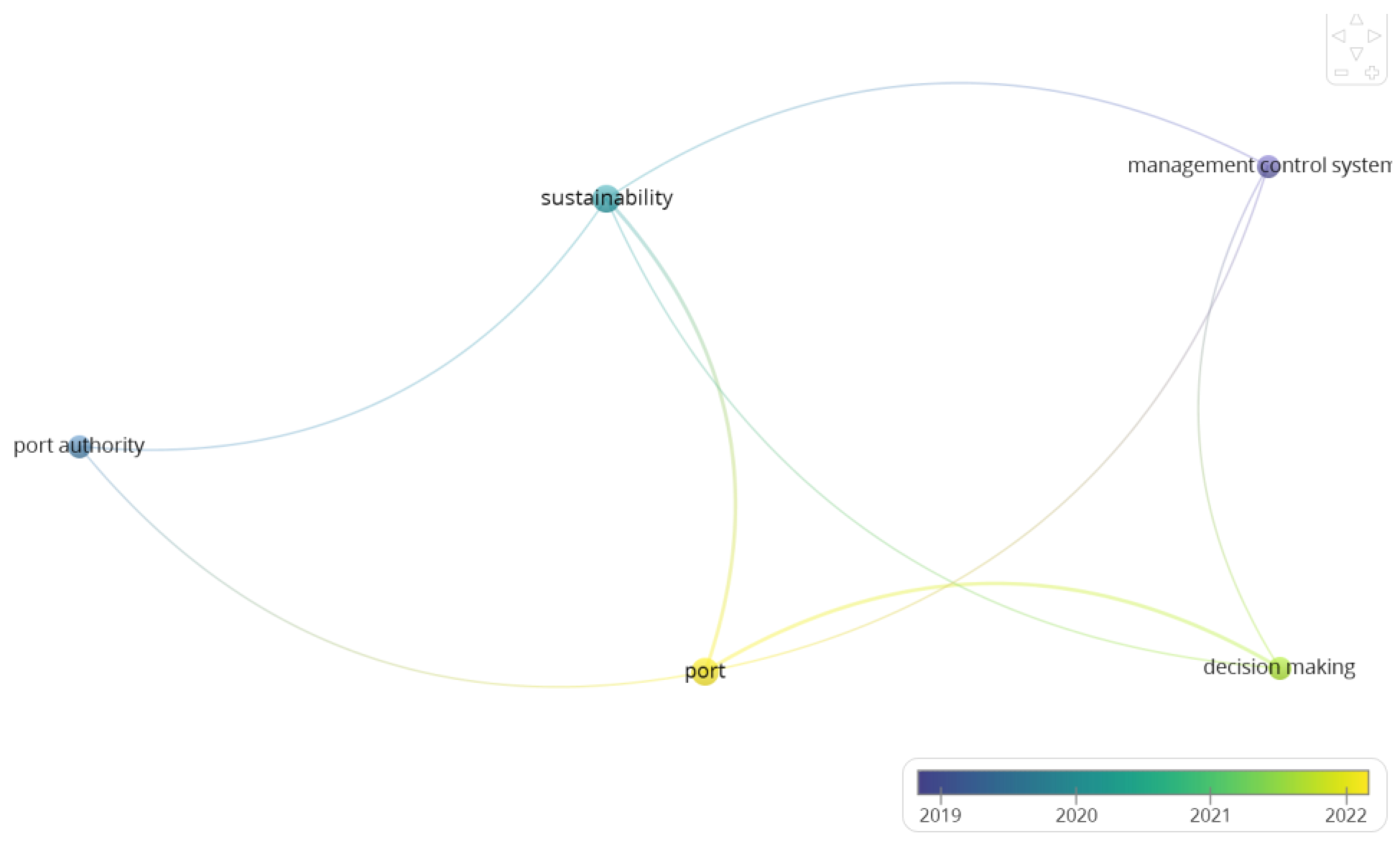

Analyzing the frequency of keywords in the articles found on Scopus revealed the relationship and connection between the concepts present in the titles, abstracts and keywords. Using VOSviewer software, all the keywords in the articles were collated and counted. The mapping considered a minimum of 5 occurrences of each keyword, resulting in 2 distinct clusters. The main cluster, which is more relevant, deals with themes related to ports, port authorities and sustainability. The secondary cluster emphasizes the interconnection between decision-making and management control systems. The size of the circle represents the weight of the item, indicating the frequency of occurrence of the keyword. The relationship between the nodes is stronger the closer they are, determining the central theme of the body of documents, i.e. their main lines of research.

4.1. Analyzing the Articles

The publications analyzed allowed us to identify a range of management control tools, from management control systems to more advanced tools, allowing us to understand how accounting and management control are intertwined in various dimensions with sustainability.

Port performance is intrinsically related to the choice of control systems aligned with the strategy, and there is no single universally successful control system. [41]. From this perspective, there is an urgent need for a balance between control, strategy and organizational culture.

Management Control Systems from a Generic Perspective

Taking the case of the port sector in Greece, studied by Triantafylli and Ballas [41] three types of MCS stood out:

- ∠

- Basic MCS: used to collect essential information for planning and establishing daily operations;

- ∠

- Cost MCS: implemented with a focus on minimizing costs. In the Greek example, the process of defining a low-cost strategy tends to favor this typology;

- ∠

- MCS of external information: used to gather information related to compliance with the requirements of the owners of the goods. Companies seeking differentiation prefer externally focused control systems.

The MCS can become a valuable tool for improving management and coordination in ports, favoring effectiveness and efficiency, regardless of the organizational model adopted by the seaport [48]. The scarcity of MCS related to environmental issues and the consequent activity in ports stands out, emphasizing the fact that the quality and quantity of information on environmental activities is insufficient.

Lean

The implementation of the Lean philosophy, specifically in the port sector, has proved useful in solving capacity problems related to expansion, as well as identifying and eliminating waste to meet customer needs, increasing efficiency and reducing costs and time in processes [51]. It should be noted that the main obstacles to implementation relate to a lack of know-how, employee training and a lack of management involvement and commitment.

Also in the context of Lean, the study of Loyd et al. [46] involved analyzing the Port of Mobile, located in Alabama, in the United States, where there was a significant increase in the capacity to manage more transport wagons, and a reduction in loading and unloading times, emphasizing that the change to a Lean approach is a gradual and constantly evolving process, rather than a final and definitive destination.

The successful implementation of this tool also predicted an increase in customers and organizational growth, with investment in continuous improvement in processes and investment in employees being considered essential response factors.

Activity-Based Costing (ABC)

Elyass et al. [19] carried out an analysis of the influence of contemporary accounting systems on the operations, planning, control and decision-making of seaport organizations, with an emphasis on ABC. It was found that this costing system, when integrated with the budgeting system, provided significant benefits to the port of Sudan.

Around 20% of the articles analyzed consider ABC to be the tool best suited to accurately determining the costs incurred for each activity, and therefore to supporting decisions on port tariffs [19,20,21].

Mthembu and Chasomeris [21] argue that the reform of maritime service prices should incorporate ABC, associated with the user-pays principle, considering it one of the best international practices. The authors also mention that this approach is recommended by several port users in South Africa.

Balanced Scorecard (BSC)

In the context of the fusion of techniques approach, considering integration with ABC, Divandri and Yousefi [47] point out that, together with the BSC, it is possible to drive the realization of strategy and achieve competitive advantage.

In the promotion of environmental performance, the importance of applying Key Performance Indicators (KPIs) when interlinked with the development of the BSC is identified in the measurement and control of effectiveness and efficiency in the port waste management process [16].

The BSC is highlighted as a valuable tool to guide companies in implementing sustainable strategies, however, the literature on this strategic tool in the port sector is still under development [53].

The benefits of the BSC include improvements in organizational culture, customer satisfaction orientation, teamwork, strategic goals [45], identification of environmental sustainability and energy efficiency strategies that result in effective and efficient solutions [16]. What's more, efficient use of this tool can optimize equipment scheduling, reducing the time ships spend in port and increasing terminal productivity [47].

With the aim of boosting port performance [50] propose the integration of the BSC and Political, Economic, Sociological, Technological, Legal and Environmental (PESTLE) (a strategic analysis tool used to assess the external environment) applied to sustainability. While the BSC is used as a tool to measure the port's internal performance, PESTLE measures external performance. The authors corroborate the fact that the fusion of these two tools is aimed at achieving greater production efficiency, reducing the time spent in ports and cutting labor costs, as well as improving environmental management and achieving port sustainability.

The BSC has also transformed port management in the port of Valencia, allowing it to evolve from a system of individualized objectives to a system of long-term strategic management with an emphasis on continuous improvement. This is why the authors see this tool more as a management approach aimed at global optimization and less as a financial instrument. Despite the benefits, there are limitations related to the complexity of implementation, and the continued need for research into the application of the BSC as a strategic management approach is also emphasized [54].

To simplify the implementation process, it was also considered important to secure the support of senior management as well as specialized external consultants [18].

Sustainable Maritime Balanced Scorecard (SMBSC)

Sislian and Jaegler [49] introduced new perspectives on the BSC in the port context by incorporating the TBL framework, thus constituting the SMBSC, based on the four perspectives, to include port sustainability in the Port of Alexandria, Egypt.

The SMBSC proved to be a useful and easy-to-implement tool, taking on the role of business partner by enabling higher levels of productivity and better financial results, along with the implementation of medium and long-term social and environmental sustainability indicators. Several factors stood out, particularly those based on the efficient scheduling of operations with a reduction in time spent in the port and an increase in terminal productivity with unequivocal impacts on the environment and society. By providing strategic information for emissions and fuel planning, the determination of efficiency also showed low administrative costs after investments in sustainable technologies, as well as real-time analysis of emissions-related data collection.

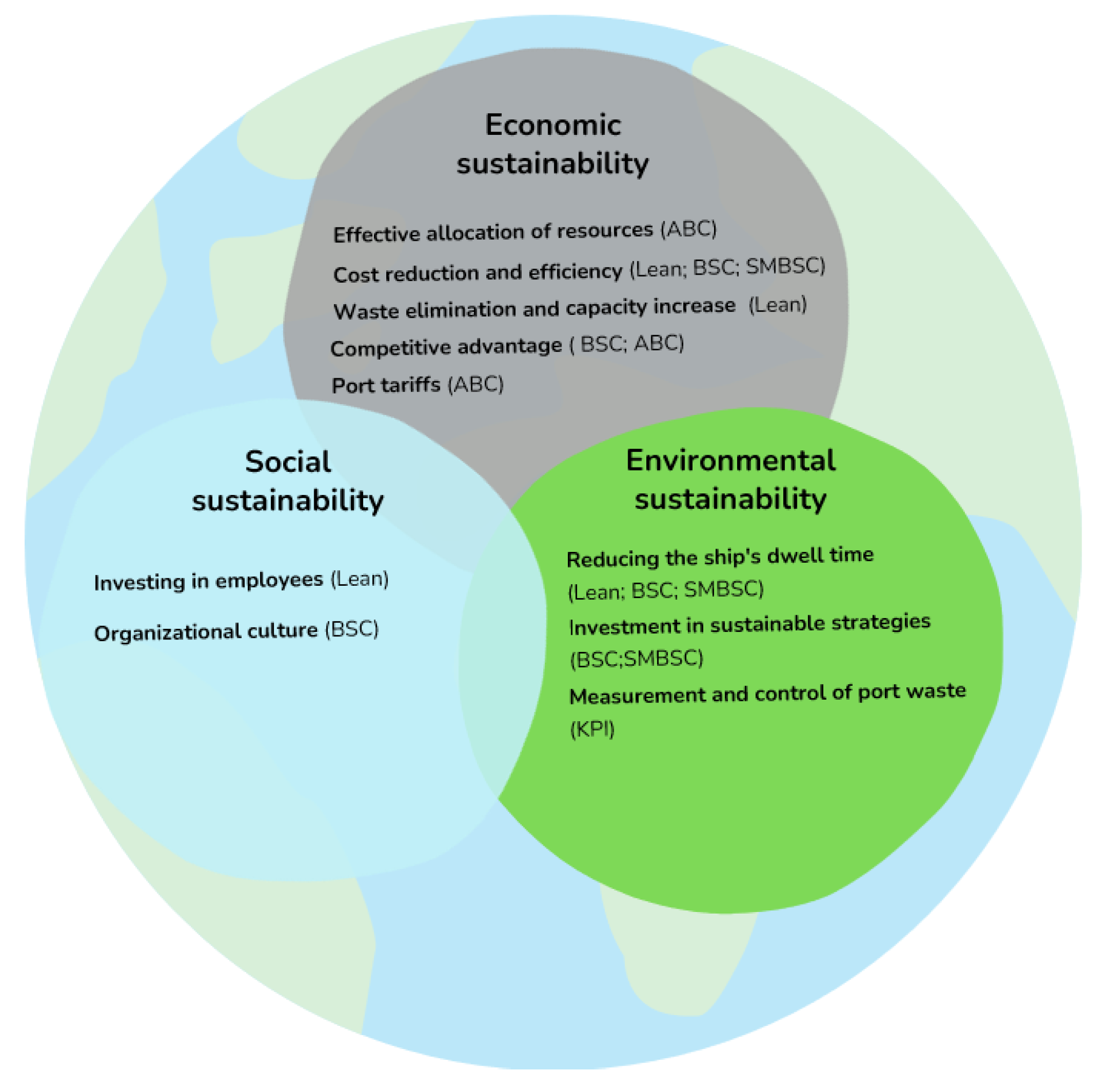

4.1.1. Critical and Multidimensional Reflection

To complement and provide an additional perspective on the integration of accounting and management control tools with sustainability in the port context, it was decided to carry out a multidimensional critical reflection mirrored in Figure 6.

Based on the potential impact factors and benefits mentioned in the previous section for each tool, we proceeded to integrate them into the various dimensions of sustainability.

As far as social sustainability is concerned, this research shows that Lean emphasizes the importance of investing in employees, with the aim of contributing to their professional development and well-being. This approach reinforces the organization’s social responsibility by promoting a healthy and fair working environment in the port sector. On the other hand, the implementation of the BSC has led to improvements in the organizational culture, thus influencing attitudes and behavior. An organizational culture aligned with sustainability spreads ethical practices, community integration and social responsibility.

Environmental sustainability is a fundamental principle in the search for a balance between human activities and the environment. It involves adopting practices that aim to preserve and regenerate natural resources, minimizing negative impacts on ecosystems and biodiversity. In this context, the BSC and SMBSC are tools that focus on sustainable strategies by implementing operational practices aimed at environmental sustainability, promoting environmental preservation and the conscious management of natural resources in the port context. In turn, KPIs allow for the measurement and control of port waste, efficient management of the waste generated in the port, making it possible to reduce the costs associated with handling waste and minimizing negative economic impacts. Lean, BSC and SMBSC, by demonstrating their effectiveness in reducing the length of time ships spend in port, provide the opportunity to reduce pollutant emissions and resource consumption during port operations. This efficiency contributes to reducing the carbon footprint and minimizing environmental impact.

Addressing the field of sustainability at an economic level, there are several areas where tools can have a positive impact in terms of reducing costs and increasing efficiency, namely Lean, BSC and SMBSC. In this context, increasing efficiency and reducing costs contributes to economic sustainability, allowing operations to be more profitable and viable in the long term. In addition, ABC offers the potential to maintain economic sustainability by maintaining competitive advantage and assisting in the process of setting port tariffs.

5. Conclusion

The results of this research have provided an in-depth understanding of the role of management control in the port context, with an emphasis on its interaction with sustainability at various levels that highlight the diversity of management control tools in seaports.

By applying the framework adopted from Arksey and O’Malley [1], the conclusions align with the strategic objectives, providing insights into the diversity of management strategies and exploring new ways to improve efficiency, sustainability and competitiveness. From a holistic perspective, the studies emphasize the importance of efficiency, sustainability and strategic alignment in port management, pointing to a future in which this sector stands out not only for its operational efficiency, but also for its commitment to practices associated with social and environmental responsibility.

Due to the small number of publications, it can also be concluded that this is an under-explored topic, thus recognizing the inherent limitations of this research with a possible impact on the results and interpretations. It should be emphasized that the specific approach of the literature review, although comprehensive, may not have captured all the recent developments in the field. In addition, the specific characteristics of the different ports should be considered in the conclusions drawn.

Also, the absence of few studies that address the synergistic interaction of management control systems and tools applied to the sector under study may translate into a gap in the comprehensive understanding of management control and accounting in their connection with sustainability, suggesting the need for a more in-depth analysis of how these areas can be effectively integrated.

However, the results obtained show synergistic links between accounting and management control with sustainability, with these areas effectively serving an effective strategy that drives sustainable performance in seaports. Port managers can use these findings to communicate practices and decisions to improve operational efficiency and promote sustainability.

Despite the contributions made, there is room for further research into the subject, and it is suggested that ABC be used to quantify the environmental costs associated with port operations, as well as to determine the cost of sustainable practices.

Finally, it should also be emphasized that this study contributes to a holistic understanding of the inherent concepts, offering a sufficiently robust conceptual basis for exploring the complex dynamics of the interconnections examined.

Author Contributions

Conceptualization, A.S. and I.F.; methodology, A.S. and I.F..; validation, A.C., C.C., J.M., I.F. and A.S.; formal analysis, A.C., C.C. and J.M.; investigation, A.C., C.C. and J.M.; writing—original draft preparation, A.S. and I.F.; writing—review and editing, A.C., C.C. and J.M.; visualization, A.S. and I.F.; supervision, A.C., C.C. and J.M.; project administration, A.C., C.C. and J.M.; funding acquisition, A.C., C.C. and J.M. All authors have read and agreed to the published version of the manuscript.

Funding

This study was funded by the PRR - Recovery and Resilience Plan and the NextGenerationEU funds at the University of Aveiro, as part of the Business Innovation Agenda "NEXUS: Innovation Pact - Green and Digital Transition for Transport, Logistics, and Mobility" (Project No. 53 with application C645112083-00000059) https://www.ua.pt/pt/projetos-id/1191.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Arksey, H.; O’Malley, L. Scoping Studies: Towards a Methodological Framework. International Journal of Social Research Methodology: Theory and Practice 2005, 8 (1), 19–32. [CrossRef]

- Chang, Y. T.; Shin, S. H.; Lee, P. T. W. Economic Impact of Port Sectors on South African Economy: An Input-Output Analysis. Transp Policy (Oxf) 2014, 35, 333–340. [CrossRef]

- Bottasso, A.; Conti, M.; Ferrari, C.; Tei, A. Ports and Regional Development: A Spatial Analysis on a Panel of European Regions. Transp Res Part A Policy Pract 2014, 65, 44–55. [CrossRef]

- Ha, M. H.; Yang, Z.; Notteboom, T.; Ng, A. K. Y.; Heo, M. W. Revisiting Port Performance Measurement: A Hybrid Multi-Stakeholder Framework for the Modelling of Port Performance Indicators. Transp Res E Logist Transp Rev 2017, 103, 1–16. [CrossRef]

- Hossain, T.; Adams, M.; Walker, T. R. Role of Sustainability in Global Seaports. Ocean Coast Manag 2021, 202, 1-10. [CrossRef]

- Marques, R. C.; Fonseca, Á. Market Structure, Privatisation and Regulation of Portuguese Seaports. Maritime Policy and Management 2010, 37 (2), 145–161. [CrossRef]

- Jeevan, J.; Mohd Salleh, N. H.; Abdul Karim, N. H.; Cullinane, K. An Environmental Management System in Seaports: Evidence from Malaysia. Maritime Policy and Management 2022, 1–18. [CrossRef]

- Lam, J. S. L.; Notteboom, T. The Greening of Ports: A Comparison of Port Management Tools Used by Leading Ports in Asia and Europe. Transp Rev 2014, 34 (2), 169–189. [CrossRef]

- Lim, S.; Pettit, S.; Abouarghoub, W.; Beresford, A. Port Sustainability and Performance: A Systematic Literature Review. Transp Res D Transp Environ 2019, 72, 47–64. [CrossRef]

- Hua, C.; Chen, J.; Wan, Z.; Xu, L.; Bai, Y.; Zheng, T.; Fei, Y. Evaluation and Governance of Green Development Practice of Port: A Sea Port Case of China. J Clean Prod 2020, 249, 1–10. [CrossRef]

- Cabezas-Basurko, O.; Mesbahi, E.; Moloney, S. R. Methodology for Sustainability Analysis of Ships. Ships and Offshore Structures 2008, 3 (1), 1–11. [CrossRef]

- United Nations Conference on Trade and Development. Review of Maritime Transport 2023 - Towards a Green and Just Transition; 2023.

- Crutzen, N.; Zvezdov, D.; Schaltegger, S. Sustainability and Management Control. Exploring and Theorizing Control Patterns in Large European Firms. J Clean Prod 2017, 143, 1291–1301. [CrossRef]

- Lueg, R.; Radlach, R. Managing Sustainable Development with Management Control Systems: A Literature Review. European Management Journal 2016, 34 (2), 158–171. [CrossRef]

- Di Vaio, A.; Varriale, L. Management Control Systems for the Water Concessionaires Governance: A Multiple Cases Study in the Italian Seaports. In Strengthening Information and Control Systems The Synergy Between Information Technology and Accounting Models; Mancini, D., Dameri, R. P., Bonollo, E., Eds.; Springer, 2016; Vol. 14, pp 145–156. [CrossRef]

- Di Vaio, A.; Varriale, L.; Trujillo, L. Management Control Systems in Port Waste Management: Evidence from Italy. Util Policy 2019, 56, 127–135. [CrossRef]

- Gond, J. P.; Grubnic, S.; Herzig, C.; Moon, J. Configuring Management Control Systems: Theorizing the Integration of Strategy and Sustainability. Management Accounting Research 2012, 23 (3), 205–223. [CrossRef]

- Suárez-Gargallo, C.; Zaragoza-Sáez, P. Port Authority of Cartagena: Evidence of a Sustainability Balanced Scorecard. Sustainable Development 2023, 3761–3785. [CrossRef]

- Elyass, M. A.; Elshareef, A. M.; Abdullah, Y. A. G. S. The Role of Contemporary Cost Accounting Systems in Planning, Decision-Making and Controlling, in Sudanese Sea Port Corporation. Journal of Science & Technology 2022, 3 (1), 1–20.

- Martins, A.; Jorge, S.; Sá, P. Price Regulation and Cost Accounting: The Case of the Portuguese Seaport Sector. International Journal of Law and Management 2013, 55 (6), 444–463. [CrossRef]

- Mthembu, S. E.; Chasomeris, M. Revisiting Marine Services Pricing in South Africa’s Ports. WMU Journal of Maritime Affairs 2023. [CrossRef]

- Glavič, P.; Lukman, R. Review of Sustainability Terms and Their Definitions. J Clean Prod 2007, 15, 1875–1885. [CrossRef]

- Rogers, K.; Hudson, B. The Triple Bottom Line The Synergies of Transformative Perceptions and Practices for Sustainability. Journal of the Organization Development Network 2011, 43 (4), 3–9.

- Corsi, K.; Arru, B. Role and Implementation of Sustainability Management Control Tools: Critical Aspects in the Italian Context. Accounting, Auditing and Accountability Journal 2020, 34 (9), 29–56. [CrossRef]

- Loviscek, V. Triple Bottom Line toward a Holistic Framework for Sustainability: A Systematic Review. Revista de Administracao Contemporanea 2021, 25 (3), 1–11. [CrossRef]

- Elkington, J. Enter the Triple Bottom Line. In The Triple Bottom Line: Does it All Add Up ?; Henriques, A., Richardson, J., Eds.; Routledge, 2004; pp 1–16. [CrossRef]

- Jaegler, A.; Sarkis, J. The Theory and Practice of Sustainable Supply Chains. Supply Chain Forum 2014, 15 (1), 2–5. [CrossRef]

- Acciaro, M. Environmental Social Responsibility in Shipping: Is It Here to Stay?; 2012.

- Zhao, C.; Wang, Y.; Gong, Y.; Brown, S.; Li, R. The Evolution of the Port Network along the Maritime Silk Road: From a Sustainable Development Perspective. Mar Policy 2021, 126, 1–9. [CrossRef]

- Di Vaio, A.; Varriale, L. Management Innovation for Environmental Sustainability in Seaports: Managerial Accounting Instruments and Training for Competitive Green Ports beyond the Regulations. Sustainability (Switzerland) 2018, 10 (3), 1–35. [CrossRef]

- Narula, K. Emerging Trends in the Shipping Industry –Transitioning Towards Sustainability. Maritime Affairs: Journal of the National Maritime Foundation of India 2014, 10 (1), 113–138. [CrossRef]

- Bahadur, W.; Waqquas, O. Corporate Social Responsibility for Sustainable Business Management. Journal of Sustainable Society 2013, 2 (4), 92–97. [CrossRef]

- Vanelslander, T. Seaport CSR: Innovation for Economic, Social and Environmental Objectives. Social Responsibility Journal 2016, 12 (2), 382–396. [CrossRef]

- Klimek, H.; Michalska-szajer, A.; Dąbrowski, J. Corporate Social Responsibility of the Ports of Szczecin and Świnoujście. Scientific Journals of the Maritime University of Szczecin 2020, 61 (133), 99–107. [CrossRef]

- Ye, N.; Kueh, T. B.; Hou, L.; Liu, Y.; Yu, H. A Bibliometric Analysis of Corporate Social Responsibility in Sustainable Development. J Clean Prod 2020, 272, 122679. [CrossRef]

- Batalha, E.; Chen, S. L.; Pateman, H.; Zhang, W. The Meaning of Corporate Social Performance in Seaports: The Managers’ Perspective. WMU Journal of Maritime Affairs 2020, 19 (2), 183–203. [CrossRef]

- Strupp, C. Seaports in Transition. Global Change and the Role of Seaports since the 1950s. Planning Perspectives 2016, 31 (1), 115–119. [CrossRef]

- Notteboom, T.; Lam, J. S. L. Dealing with Uncertainty and Volatility in Shipping and Ports. Maritime Policy and Management 2014, 41 (7), 611–614. [CrossRef]

- Gibbs, D.; Rigot-Muller, P.; Mangan, J.; Lalwani, C. The Role of Sea Ports in End-to-End Maritime Transport Chain Emissions. Energy Policy 2014, 64, 337–348. [CrossRef]

- Rounaghi, M. M. Economic Analysis of Using Green Accounting and Environmental Accounting to Identify Environmental Costs and Sustainability Indicators. International Journal of Ethics and Systems 2019, 35 (4), 504–512. [CrossRef]

- Triantafylli, A. A.; Ballas, A. A. Management Control Systems and Performance: Evidence from the Greek Shipping Industry. Maritime Policy and Management 2010, 37 (6), 625–660. [CrossRef]

- Gaidelys, V.; Benetyte, R. Analysis of the Competitiveness of the Performance of Baltic Ports in the Context of Economic Sustainability. Sustainability (Switzerland) 2021, 13, 1–23. [CrossRef]

- Daudt, H. M. L.; Van Mossel, C.; Scott, S. J. Enhancing the Scoping Study Methodology: A Large, Inter-Professional Team’s Experience with Arksey and O’Malley’s Framework. BMC Med Res Methodol 2013, 13 (1), 1–9. [CrossRef]

- Pham, M. T.; Rajić, A.; Greig, J. D.; Sargeant, J. M.; Papadopoulos, A.; Mcewen, S. A. A Scoping Review of Scoping Reviews: Advancing the Approach and Enhancing the Consistency. Res Synth Methods 2014, 5 (4), 371–385. [CrossRef]

- Aparisi-Caudeli, J. A.; Giner-Fillol, A.; Pérez-García, E. M. Evidence on Implementing a Balanced Scorecard System at the Port Authority of Valencia. Global Journal of Business Research 2009, 3 (2), 93–117.

- Loyd, N.; Jennings, L. C.; Siniard, J.; Spayd, M. L.; Holden, A.; Rittenhouse, G. Application of Lean Enterprise to Improve Seaport Operations. Transp Res Rec 2009, 2100 (1), 29–37. [CrossRef]

- Divandri, A.; Yousefi, H. Balanced Scorecard: A Tool for Measuring Competitive Advantage of Ports with Focus on Container Terminals. International Journal of Trade, Economics and Finance 2011, 2 (6), 472–477. [CrossRef]

- Di Vaio, A.; Varriale, L. Management Control Systems in Inter-Organizational Relationships for Environmental Sustainability and Energy Efficiency: Evidence from the Cruise Port Destinations. Lecture Notes in Information Systems and Organisation 2018, 24, 43–55. [CrossRef]

- Sislian, L.; Jaegler, A. A Sustainable Maritime Balanced Scorecard Applied to the Egyptian Port of Alexandria. Supply Chain Forum 2018, 19 (2), 101–110. [CrossRef]

- Praharsi, Y.; Hardiyanti, F.; Puspitasari, D.; Akseptori, R.; Maharani, A. An Integrated Framework of Balance Scorecard-PESTLE-Smart and Green Port for Boosting the Port Performance. In Proceedings of the International Conference on Industrial Engineering and Operations Management Monterrey, Mexico; 2021; pp 1643–1653.

- Neves, A.; Godina, R.; Erikstad, S. O. Enhancing Efficiency in the Maritime Industry Through Lean Practices: A Critical Literature Review of Benefits and Barriers. In FAIM - Flexible Automation and Intelligent Manufacturing; 2024; pp 1–14. [CrossRef]

- Conceição, P. Relatório Do Desenvolvimento Humano 2019: Além Do Rendimento, Além Das Médias, Além Do Presente: As Desigualdades No Desenvolvimento Humano No Século XXI; Camões – Instituto da Cooperação e da Língua, Ed.; Publicado pelo Programa das Nações Unidas para o Desenvolvimento (PNUD), 2019.

- Suárez-Gargallo, C.; Zaragoza-Sáez, P. Port Authority of Cartagena: Evidence of a Sustainability Balanced Scorecard. Sustainable Development 2023, 3761–3785. [CrossRef]

- Aparisi-Caudeli, J. A.; Giner-Fillol, A.; Pérez-García, E. M. Evidence on Implementing a Balanced Scorecard System at the Port Authority of Valencia. Global Journal of Business Research 2009, 3 (2), 93–117.

Figure 3.

Count of studies analyzed- Year of publication.

Figure 4.

Geographical distribution of the entities studied in the articles analyzed.

Figure 5.

Keyword network map. Data taken from the Scopus database and processed using the VOSviewer software.

Figure 5.

Keyword network map. Data taken from the Scopus database and processed using the VOSviewer software.

Figure 6.

Multidimensional critical reflection.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.