Submitted:

20 May 2024

Posted:

21 May 2024

Read the latest preprint version here

Abstract

This study investigates the impact of General Government Final Consumption Expenditure (GC) on GDP growth in Saudi Arabia during major economic crises from 1990 to 2022, focusing on periods marked by fluctuations in oil and non-oil revenues. By integrating these revenue streams, the research provides a more comprehensive analysis of fiscal policy effectiveness during economic downturns. Using an Autoregressive Distributed Lag (ARDL) model, the study reveals that Government Consumption significantly stabilizes and stimulates the Saudi economy amidst revenue volatility. Key findings highlight the dual role of Government Consumption (GC) as both a buffer against immediate economic shocks and a stimulus for economic recovery. The study contributes to the discourse on fiscal policy in oil-dependent economies by demonstrating the critical role of diversified revenue strategies in enhancing economic resilience. Recommendations are offered for policymakers to optimize fiscal strategies, ensuring robust economic recovery and long-term stability in volatile markets. This research underscores the necessity for Saudi Arabia to refine its fiscal policies towards greater economic diversification and stability.

Keywords:

Saudi Arabia

; oil revenues

; economic resilience

; fiscal policy

; oil-dependent economies

; economic diversification

1. Introduction

In countries heavily reliant on oil revenues, the dynamics of fiscal policy are critically influenced by fluctuations in global oil prices, making fiscal planning and stability more complex. This theoretical understanding is especially pertinent to Saudi Arabia, an economy where oil revenues form the backbone of government income and are thus highly sensitive to market volatilities.

Economic stability and growth remain pivotal concerns for such national economies, particularly during periods marked by significant geopolitical and economic disruptions. Historical events such as the 1990-1991 Gulf War, various oil price crashes (1998, 2008, 2014-2016), and the 2020 coronavirus pandemic have tested Saudi Arabia’s economic resilience. Each of these events has underscored the vulnerabilities inherent in an oil-dependent economy and has catalyzed various efforts towards economic diversification. For instance, the Gulf War highlighted geopolitical risks that impacted oil production and prices, leading to broader economic implications. Similarly, severe drops in oil prices due to global oversupply and diminished demand in 1998 and 2008 severely impacted Saudi Arabia’s fiscal position, prompting the kingdom to earnestly pursue economic reforms and diversification strategies.

The 2014-2016 oil price slump further exacerbated these challenges, leading to significant budget deficits and catalyzing substantial economic reforms under Vision 2030. This strategic initiative aims to diversify the economy and reduce oil dependency through comprehensive socio-economic reforms across various sectors such as health, education, infrastructure, recreation, and tourism. However, the sudden economic shock brought by the COVID-19 pandemic tested the resilience and efficacy of these ongoing economic transformations, impacting not only the oil sector but also the nascent tourism industry.

During such times, the role of fiscal policies, especially Government Consumption (GC), becomes crucial in mitigating economic downturns. This study aims to extend beyond the traditional scope of GC analysis by incorporating oil and non-oil revenues, significant drivers of economic activity, to dissect their combined impact on GDP. By doing so, it connects the specific historical and economic challenges faced by Saudi Arabia with the broader theoretical discourse on the role of fiscal policy in oil-dependent economies, highlighting how strategic fiscal management and diversification are essential for stabilizing and stimulating economic growth amidst external shocks and market fluctuations.

High oil prices typically lead to budget surpluses, while low prices can swiftly turn these into significant deficits. To manage these fluctuations, oil-dependent countries often establish stabilization funds, also known as sovereign wealth funds, which are crucial for maintaining economic stability during periods of low oil prices by enabling the government to sustain spending without drastic cuts.

Moreover, the implementation of counter-cyclical fiscal policies—where savings are made during boom periods and spent during downturns—is considered ideal for such economies. However, the practical application of these policies can be challenging due to political pressures to increase spending or reduce taxes when oil revenues are high, often leading to pro-cyclical fiscal behaviors that exacerbate economic fluctuations rather than stabilizing them.

The theoretical backdrop of fiscal policy in oil dependent economies is directly relevant to the aims of this study, which seeks to analyze how these policies influence economic stability and growth in Saudi Arabia.

Research Objectives

The primary aim of this study is to assess the role of fiscal policies, specifically government consumption (GC), in mitigating the adverse effects of economic fluctuations and enhancing economic recovery. Aligned with the stated objectives, this study addresses the following research questions:

Research Questions

- How does Government Consumption (GC) influence GDP growth in Saudi Arabia during significant fluctuations in oil and non-oil revenues?

- Are the existing fiscal policies effective in stabilizing the economy during downturns and stimulating recovery post-crisis?

- What strategic fiscal policy recommendations can be derived from the analysis to enhance economic resilience and stability in Saudi Arabia?

The discussion on the role of fiscal policies in stabilizing and diversifying the economy, as well as managing public debt and addressing social and political challenges, forms a critical theoretical foundation for understanding the complex interplay between fiscal management and economic performance in oil-dependent countries. By examining these aspects, this study aims to contribute valuable insights into the formulation of more resilient economic strategies for Saudi Arabia, echoing the broader discourse on economic management in similar geopolitical and economic contexts.

2. Literature Review

Theoretical Backdrop of Counter-Cyclical Fiscal Policies

Counter-cyclical fiscal policies are rooted in Keynesian economic theory, which emphasizes the role of government intervention in stabilizing the economy. These policies are designed to counterbalance the business cycle by adjusting government spending and taxation in a manner that is opposite to the prevailing economic trend. The primary objective is to mitigate the adverse effects of economic fluctuations, thus promoting economic stability and growth (Keynes, 1936).

Managing Aggregate Demand

In Keynesian theory, managing aggregate demand is central to stabilizing economic output and employment levels. Counter-cyclical fiscal policies serve as a tool to regulate aggregate demand, ensuring economic stability across business cycles. During recessions, governments can stimulate demand by increasing spending. This boosts economic activity, creates jobs, and offsets the decline in private sector demand. Conversely, during periods of economic expansion, reducing government spending helps prevent overheating and inflation. Additionally, tax policies can be used to manage aggregate demand. Lowering taxes during downturns increases disposable income, stimulating spending and investment. Conversely, raising taxes during economic booms helps reduce excessive demand and control inflationary pressures. By adjusting government spending and tax policies in a counter-cyclical manner, policymakers can effectively manage aggregate demand, contributing to overall economic stability and growth.

Automatic Stabilizers

Automatic stabilizers are fiscal mechanisms that naturally counterbalance economic fluctuations without additional government action. Examples include unemployment insurance, which increases government spending during downturns as more people become eligible for benefits, and progressive taxation, where tax revenues fall during recessions as incomes drop, cushioning disposable incomes.

Smoothing the Business Cycle

Counter-cyclical fiscal policies are designed to smooth the business cycle and promote economic stability. During recessions, these policies aim to mitigate economic downturns by boosting aggregate demand. This helps reduce the depth and duration of recessions, limiting the negative impacts on employment and output. Conversely, during periods of economic expansion, counter-cyclical fiscal policies work to prevent overheating. By curbing demand through measures such as reducing government spending or increasing taxes, these policies help prevent the economy from reaching unsustainable levels of growth that can lead to inflation and asset bubbles. Overall, the goal of counter-cyclical fiscal policies is to maintain a stable economic environment by moderating the extremes of the business cycle and promoting sustainable growth over the long term.

Fiscal Multipliers

The effectiveness of these policies is influenced by fiscal multipliers, which measure the impact of government spending or tax changes on overall economic output. Fiscal multipliers tend to be larger during recessions due to a higher marginal propensity to consume and underutilized resources. Increased demand during downturns can more readily translate into higher output.

Long-term Fiscal Sustainability

While counter-cyclical fiscal policies aim to stabilize the economy in the short term, they must be designed with long-term fiscal sustainability in mind. This involves accumulating surpluses during booms to build a buffer for future downturns and avoiding excessive debt to maintain investor confidence and the ability to respond to future crises.

Influence on Economic Stability and Growth

Fiscal policy, encompassing government spending and taxation decisions, plays a pivotal role in influencing national economic stability and growth. Foundational economic theories posit that through adept manipulation of these fiscal tools, governments can mitigate the effects of economic downturns and foster conditions conducive to growth during recovery periods. A substantial body of literature has examined the dual role of fiscal policy in both stabilizing economies during recessions and stimulating them during expansions.

Counter-cyclical fiscal policies significantly influence economic stability and growth, particularly in oil-dependent economies like Saudi Arabia. By managing aggregate demand, these policies help mitigate the volatility caused by fluctuations in oil prices. During periods of low oil prices, increased government spending and reduced taxes can sustain economic activity, prevent severe recessions, and promote recovery. Conversely, during periods of high oil prices, reducing spending and increasing taxes can prevent overheating and maintain economic stability.

In the context of Saudi Arabia, where oil revenues form the backbone of government income, counter-cyclical fiscal policies are crucial. Establishing stabilization funds, such as sovereign wealth funds, allows the government to sustain spending during periods of low oil prices without drastic cuts. Implementing counter-cyclical measures ensures that savings are made during boom periods and spent during downturns, helping to stabilize the economy.

The Role of Fiscal Policies in Managing Public Debt

Fiscal policies play a pivotal role in managing public debt, particularly in oil-dependent countries where revenue volatility can significantly affect fiscal stability. Strategic fiscal management involves setting fiscal rules, such as debt ceilings or balanced budget requirements, which constrain excessive borrowing and promote prudent fiscal behavior. For example, Saudi Arabia and the UAE have adopted fiscal rules to manage their debt levels more effectively, enhancing their fiscal resilience and stability. Blanchard and Leigh (2013) suggest that counter-cyclical fiscal policies can mitigate the adverse effects of revenue volatility by smoothing out public spending and avoiding pro-cyclical fiscal behavior that exacerbates economic fluctuations. These policies help stabilize the economy by saving surplus revenues during booms and using these reserves during downturns, ensuring consistent public services and avoiding drastic spending cuts.

Fiscal policies play a critical role in addressing social and political challenges, particularly in oil-dependent economies like Saudi Arabia. Beyond economic stabilization, these policies can help mitigate social inequities and foster political stability. By allocating resources towards social welfare programs, education, healthcare, and infrastructure, fiscal policies can improve the quality of life for citizens, thereby reducing social unrest and enhancing public trust in government institutions. Additionally, targeted fiscal measures can address regional disparities and promote inclusive growth, ensuring that the benefits of economic development are more evenly distributed across different segments of the population. The implementation of counter-cyclical fiscal policies, such as those supported by the Public Investment Fund (PIF), not only cushions the economy against oil price volatility but also allows the government to maintain essential public services during economic downturns. This approach can prevent the exacerbation of social tensions that often accompany economic hardships. Moreover, transparent and accountable fiscal governance is crucial for maintaining political stability. Effective management of public finances, including anti-corruption measures and fiscal transparency, can strengthen institutional trust and support for government policies. In the context of Saudi Arabia, the strategic use of the PIF to fund diverse economic sectors and social programs aligns with the broader objectives of Vision 2030, aiming to create a more equitable, resilient, and politically stable society. Through these measures, fiscal policies become instrumental in not only driving economic growth but also in fostering social cohesion and political stability.

This theoretical backdrop provides a foundation for understanding the complex interplay between fiscal management and economic performance in oil-dependent countries. By examining these aspects, this study aims to contribute valuable insights into the formulation of more resilient economic strategies for Saudi Arabia, echoing the broader discourse on economic management in similar geopolitical and economic contexts.

According to Keynesian theory, recent studies have highlighted the importance of these policies in mitigating the impacts of economic fluctuations and promoting stability and growth. For instance, Luan, Man, and Zhou (2021) emphasize that fiscal policy can effectively complement monetary policy to stabilize macroeconomic conditions . Similarly, Shaheen (2019) discusses the impact of fiscal policy on private consumption and labor supply, illustrating how government expenditure and tax policies influence economic variables through their effects on aggregate demand .

According to Keynesian theory, aggregate demand plays a crucial role in determining economic output and employment levels. Counter-cyclical fiscal policies manage aggregate demand by increasing government spending and reducing taxes during economic downturns to boost demand and by decreasing spending and increasing taxes during economic expansions to prevent overheating (Bravo & Ayuso, 2021).

Moreover, automatic stabilizers are fiscal mechanisms that naturally counterbalance economic fluctuations without additional government action. Examples include unemployment insurance, which increases government spending during downturns as more people become eligible for benefits, and progressive taxation, where tax revenues fall during recessions as incomes drop, cushioning disposable incomes (Bongers & Díaz-Roldán, 2019). These mechanisms help smooth out the economic cycle, providing a buffer during economic shocks.

Bongers and Díaz-Roldán (2019) as well as Buendía-Martínez, Álvarez-Herranz, & Moreira Menéndez (2020) highlight the significance of counter-cyclical fiscal policies in maintaining economic stability and fostering sustainable growth. These policies, which address economic fluctuations through deliberate fiscal interventions, play a crucial role in smoothing the business cycle, contributing to overall economic resilience and long-term prosperity. By boosting aggregate demand during downturns, they aim to reduce the depth and duration of recessions, while curbing demand during booms helps to prevent inflation and asset bubbles. These fiscal mechanisms include automatic stabilizers such as unemployment insurance and progressive taxation, which operate without additional government action. For instance, unemployment insurance increases government spending automatically during economic downturns as more people become eligible for benefits, while progressive taxation reduces tax revenues during recessions as incomes drop, thereby cushioning disposable incomes and helping to stabilize the economy.

Recent studies have emphasized the critical importance of designing fiscal policies with long-term sustainability in mind, complementing short-term counter-cyclical measures. Piroli and Calderón (2021) underscored this point in their analysis of fiscal sustainability in Central and Eastern European countries, highlighting the need to accumulate surpluses during economic booms to prepare for future downturns.

Studies such as those by Auerbach and Gorodnichenko (2012) have demonstrated the variability of fiscal multipliers, showing that government spending can have different impacts on the economy depending on the state of the economic cycle. During recessions, fiscal multipliers are typically larger due to increased idle capacity and higher marginal propensities to consume among households. Conversely, in boom times, the impact of fiscal expansion might be more subdued or even counterproductive, leading to overheating of the economy.

These insights reinforce the foundational principles of Keynesian economics and the practical importance of counter-cyclical fiscal measures in achieving economic stability.

However, the effectiveness of these fiscal tools often depends on the economic context, the structural characteristics of the economy, and the initial fiscal position of the government. For example, high levels of public debt can constrain a government’s ability to implement expansive fiscal policies due to the increased cost of borrowing and potential impacts on investor confidence. Thus, while the theoretical benefits of fiscal policy are widely recognized, its practical implementation and outcomes can vary significantly across different economic environments.

Fiscal policy in oil dependent economies

Fiscal policy in oil dependent economies is characterized by its heavy reliance on oil revenues to fund government expenditures and stimulate economic growth. These economies often face unique challenges and vulnerabilities due to the volatility of oil prices, which can lead to fluctuations in government revenues and budget deficits.

In such economies, fiscal policy plays a crucial role in managing the impacts of oil price volatility. Governments typically use fiscal policy to stabilize their economies, especially during periods of low oil prices. This can involve adjusting government spending and taxation to maintain fiscal sustainability and economic stability.

However, the effectiveness of fiscal policy in oil-dependent economies can be limited by several factors. These include a lack of economic diversification, which makes these economies overly reliant on oil revenues, as well as institutional weaknesses, such as poor governance and corruption, which can undermine the efficiency and effectiveness of fiscal policy measures.

To address these challenges, policymakers in oil-dependent economies often seek to diversify their economies away from oil, strengthen fiscal institutions, and improve the transparency and accountability of fiscal policy decisions. By doing so, they aim to reduce their economies’ vulnerability to oil price volatility and promote sustainable economic growth.

Venezuela presents a stark example of the risks associated with high oil dependency. As detailed by Su et al. (2020), Venezuela’s economic crises have been exacerbated by fiscal mismanagement and an inability to stabilize or diversify the economy away from oil. The result has been hyperinflation, soaring public debt, and severe social and economic dislocations, illustrating the consequences of not adhering to counter-cyclical fiscal policies. The situation in Venezuela illustrates a compelling case of how heavy reliance on oil revenues, combined with fiscal mismanagement, can lead to significant economic instability. Venezuela possesses one of the world’s largest oil reserves, and historically, the country’s economy has been highly dependent on oil revenues. This dependency meant that the government’s spending was closely tied to the fluctuations of global oil prices. When prices were high, the country experienced substantial government spending and economic growth. However, the lack of diversification in its economy made it highly vulnerable to oil price shocks. The Venezuelan government, under various administrations, increased public expenditures significantly during periods of high oil prices without sufficient savings for future downturns. This fiscal policy was not sustainable and was compounded by a lack of transparency and accountability in managing public funds. Investments in other sectors of the economy were neglected, and over time, the non-oil economic infrastructure deteriorated. As oil prices began to fall after 2014, Venezuela’s government faced enormous fiscal deficits. In response, rather than implementing counter-cyclical fiscal policies, which would involve cutting expenditures or increasing savings, the government financed the deficit by printing money, leading to hyperinflation. According to Su et al. (2020), these actions were a primary driver behind the economic instability that followed.

Contrasting with the previous study on Venezuela, where fiscal mismanagement amidst resource dependency precipitated severe economic disruptions, the case of Russia presents a different scenario. A study conducted by Antonio Spilimbergo (2007) analyzed the performance of fiscal policy in Russia, particularly its role in stabilizing the economy post-1998 crisis. This analysis highlighted effective fiscal management as crucial during this period. Unlike Venezuela, the subsequent oil price boom enabled the Russian government to maintain a sustainable fiscal balance. However, significant oil revenues since 2003 have raised concerns regarding the underdevelopment of non-oil sectors, capable of absorbing this increased fiscal capacity. The study also credited the Oil Stabilization Fund (OSF) with successfully managing the surge in oil revenues in 2004, mitigating the potential for fiscal imbalances.

Byiabani and Mohseni (2014) explored the impact of fiscal policy on Iran’s economic growth from 1974 to 2007. Utilizing co-integration techniques and a vector error correction model, their empirical analysis indicated that Iran’s long-term economic performance was influenced by various factors, including labor force and physical capital, alongside proactive fiscal measures such as tax reductions and increased government spending on development. This approach starkly contrasts with the Venezuelan experience, highlighting the significance of strategic fiscal management in avoiding economic volatility.

Aghilifar, H., Zare, H., Piraei, K., & Ebrahimi, M. (2023) demonstrated that although Iran heavily relies on oil for its revenue, making it susceptible to global price fluctuations, effective fiscal policies have been crucial in mitigating the impact of these external shocks and maintaining macroeconomic stability.

Similarly, in a study conducted by Khosravi and Karimi (2010), the relationship between fiscal and monetary policy and economic growth in Iran was examined. The bounds testing (ARDL) approach to cointegration was used to analyse the long-term and short-term relationships between fiscal policy, monetary policy, and economic growth. Their findings revealed that while government expenditure, as a fiscal policy, had a significant positive impact on GDP growth, inflation, and exchange rates, as components of monetary policy, had a negative impact.

These case studies underscore the critical importance of strategic fiscal management and the necessity for oil-dependent economies to diversify their revenue bases. Implementing counter-cyclical fiscal policies could potentially mitigate the adverse effects of revenue volatility. Moreover, research by Schmidt-Hebbel and Marshall (2007) demonstrates how effectively integrating oil and non-oil revenue streams into the fiscal policy framework can help stabilize the economy and reduce dependence on oil.

The comprehensive review underscores the necessity for oil-dependent economies to pursue diversified economic strategies, enhancing non-oil exports and developing industrial and service sectors to foster economic resilience. These integrated studies enrich the context of fiscal policy effectiveness, particularly in economies undergoing significant structural transformations.

Economic Diversification as a Necessity for Fiscal Resilience in Oil Dependent Countries

Economic diversification stands as a crucial imperative for nations heavily reliant on oil revenues. The vulnerability of oil-dependent economies to price volatility has been starkly demonstrated in recent years, emphasizing the urgent need for these countries to broaden their economic bases. This section explores the concept of economic diversification as a fundamental strategy for enhancing fiscal resilience in oil-dependent countries. By reducing dependence on oil revenues and fostering a more diversified economic structure, these nations can mitigate the risks associated with volatile oil markets and build a more sustainable foundation for economic growth and stability. The following discussion examines the key principles and benefits of economic diversification, highlighting its importance in the context of fiscal policy and long-term economic development.

Diversifying revenue sources is also crucial for managing public debt in oil-dependent economies. Saudi Arabia’s Vision 2030 aims to develop sectors such as tourism, entertainment, and renewable energy, reducing dependence on oil revenues and creating a more balanced economic structure. By broadening the tax base and developing non-oil sectors, governments can achieve more stable and predictable fiscal outcomes. Maintaining fiscal discipline and managing public expenditures effectively are fundamental to controlling public debt. Cavallo (2005) and Tulsidharan (2006) highlight the importance of efficient government spending in maintaining economic stability and growth. Prioritizing essential expenditures and avoiding wasteful spending improve fiscal balance and reduce debt levels.

Structural reforms and institutional strengthening are vital for effective public debt management. Fatai et al. (2017) emphasize that institutional quality, including effective governance and anti-corruption measures, significantly influences fiscal outcomes. Strong fiscal institutions provide a stable framework for policy implementation, ensuring sustainable debt management. Empirical studies, such as those by Aslam and Shastri (2019) and Hamdi & Sbia (2013), demonstrate the long-term benefits of strategic fiscal planning and diversification in countries like Oman, Saudi Arabia, and Bahrain. These studies show that well-managed fiscal policies can help stabilize economies and reduce debt burdens, even in the face of oil revenue volatility.

Building on the discussion of fiscal responsiveness, the literature also delves into the significant impact of oil revenue volatility on the fiscal policies of oil-dependent countries. A pivotal study by Sohag, Kalina, and Samargandi (2024) explores this dynamic interplay between oil price fluctuations and fiscal policies in OPEC+ member countries. The authors employ advanced econometric tools such as Hodrick-Prescott and Hamilton filters to isolate cyclical components of oil prices, enhancing the analysis through a Panel VAR approach under a system GMM framework. This methodology addresses potential issues of endogeneity, heterogeneity, and cross-sectional biases.

Their findings reveal that cyclical oil price shocks have an immediate, positive impact on the fiscal stances of these countries, though the effects tend to diminish over the medium to long term. Interestingly, gradual oil price trends show an insignificant impact on fiscal policies, suggesting that OPEC+ countries’ fiscal strategies are more responsive to abrupt changes rather than gradual shifts in the oil market. The study highlights the disparate capabilities among OPEC+ countries, such as Gabon, Iraq, Russia, Saudi Arabia, the UAE, and Kazakhstan, to leverage these shocks for economic advantage. This differentiation is critical as it illustrates the varied economic resilience within the alliance, informing tailored policy formulations aimed at enhancing fiscal stability and growth.

Further contributing to our understanding of the fiscal dynamics in oil-dependent economies, Fatai, Liu, Adeniyi, and Kabir (2017) utilize a panel dataset from 2000 to 2015 to empirically examine the relationship between crude oil rents and fiscal balance, controlling for various covariates. Employing several econometric techniques, including pooled OLS, LSDV fixed effects, and instrumental variable approaches like IV/2SLS, their analysis underscores the limitations of the General Method of Moments (GMM) due to the small sample size. Their findings suggest that in countries with fiscal rules, the reaction of fiscal balance to oil rent shocks is weak and statistically insignificant. They also highlight thoes factors such as welfare spending, the debt-to-GDP ratio, and the government’s effectiveness in curbing corruption and mismanagement significantly influence fiscal balance. These insights are invaluable for policymakers within the OPEC+ alliance, providing empirical evidence that can guide strategic fiscal planning in the face of oil market volatility.

Economic diversification has been widely advocated in the literature as a crucial strategy for oil-dependent economies to mitigate the risks associated with volatile oil markets. This approach involves expanding the economic base to include a broader array of sectors beyond the dominant oil and gas industry, thereby reducing the economy’s vulnerability to global oil price fluctuations. In exploring the trajectories of economic development and diversification, Gelb (2010) highlights the significant shift from primary commodity exports to industrial products in developing countries. Originally, these countries exported primarily commodities, but now, industries such as manufacturing have come to dominate their export structures. This evolution has been crucial to their transformation into major industrial economies, with nations like China, India, and Brazil becoming central players in global production networks. The diversification into various industrial sectors not only stabilized their national incomes but also reduced economic volatility, contributing substantially to sustainable growth. This shift, according to Gelb, is indicative of successful integration into South–South trade and continuous enhancement of export sophistication.

Parallel to Gelb’s findings on economic diversification, Richard M. Auty (2001) has extensively explored the role of resource abundance in enhancing economic performance. Auty’s work emphasizes that while resource wealth can lead to economic advantages, strategic diversification is crucial to harness these benefits effectively and sustainably. His analysis suggests that countries with abundant resources can leverage this advantage to fuel broader economic development, but this requires deliberate policy efforts aimed at diversification into non-resource sectors to avoid the pitfalls of over-reliance on volatile resource markets. This perspective is crucial for understanding the complex dynamics between natural resource wealth and long-term economic stability.

Fiscal policies play a fundamental role in supporting diversification efforts, as noted by the World Bank (2019). Strategic government spending and tax incentives can encourage investments in non-oil sectors like manufacturing, agriculture, and services, thus broadening the economic landscape. Countries such as Saudi Arabia and the UAE have utilized fiscal initiatives like the development of economic cities, investment in renewable energy projects, and labor law reforms to promote economic diversification. These policies aim to attract foreign direct investment, stimulate private sector growth, and create a more resilient economic environment.

The literature also suggests that while the immediate benefits of diversification may be gradual, the long-term effects are significantly positive. Diversified economies tend to exhibit more stable economic conditions during oil downturns. However, the effectiveness of these strategies often relies on the consistent implementation of supportive fiscal policies and the overall political and economic stability of the country. Therefore, policymakers are encouraged to consider comprehensive fiscal reforms that align with broader economic diversification goals to ensure sustainable development and economic stability.

Case studies highlight the importance of strategic fiscal management and the necessity for oil-dependent economies to diversify their revenue bases. Implementing counter-cyclical fiscal policies, such as those proposed by Blanchard and Leigh (2013), could potentially mitigate the adverse effects of revenue volatility. Additionally, integrating oil and non-oil revenue streams effectively into the fiscal policy framework, as shown in VAR models by Schmidt-Hebbel and Marshall (2007), can help stabilize the economy and reduce dependence on oil.

The interplay between fiscal policies and their economic impacts is critical, with government expenditures significantly shaping economic outcomes. Foundational studies by Cavallo (2005) and Tulsidharan (2006) examine the effects of government expenditure on economic stability and growth, particularly in India, setting the stage for a detailed exploration of General Government Final Consumption Expenditure (GC) and its role during financial crises. Similarly, Kira (2013) highlights the significant role of government and household consumption in influencing GDP in developing countries like Tanzania, underscoring the importance of fiscal measures in driving economic output.

Empirical studies illustrate that General Consumption (GC) acts as a stabilizer during downturns by buffering cyclical fluctuations and supporting demand. For instance, Auerbach and Gorodnichenko (2012) demonstrate the variability of fiscal multipliers of GC across business cycles, highlighting increased effectiveness during recessions. This is particularly notable in sectors directly linked to government spending, such as healthcare and infrastructure, where Blanchard & Leigh (2013) observed enhanced benefits.

Drawing on historical crises, the literature suggests prioritizing GC in fiscal strategies for rapid and effective economic recovery, supported by empirical evidence from past events like the 2008 financial crisis (Bernanke, 2015).

This section synthesizes findings from countries like Oman, Saudi Arabia, and Bahrain, focusing on the long-term and short-term impacts of oil revenues on GDP, demonstrated through studies by Aslam and Shastri (2019) and Hamdi & Sbia (2013). The need for strategic economic planning and diversification away from oil-dependence is emphasized. Khayati (2019) provides insights into the differential impacts of oil and non-oil exports on Bahrain’s economic growth, advocating for economic diversification to reduce volatility and promote sustainable development. Azmi (2013) supports this view by demonstrating the significant impact of government spending on economic metrics like GDP, interest rates, and unemployment in Malaysia, further reinforcing the multifaceted role of fiscal policies in economic management.

Building on this discussion, the literature further explores the relationship between national oil revenues and economic growth across various countries. A pivotal study conducted by Al Rasasi, Qualls, and Alghamdi in 2019 illustrates a strong link between oil revenues and both the short- and long-term growth in Saudi Arabia, emphasizing the promotion of the private sector outside the traditional oil industry. This study highlights the importance of effectively harnessing oil wealth to foster economic growth and development, particularly in the non-oil private sector.

Similarly, in 2017, Nwoba and Abah examined the impact of oil revenues and the presence of multinational oil companies on economic growth in Nigeria. Their findings suggest that these factors play a vital role in driving economic growth, particularly through job creation. Furthermore, a study by Hassan and Abdullah in 2015 investigated the impact of oil revenues on the output of the service sector in Sudan between 2000 and 2010, finding that oil revenues positively affected the sector’s output.

These studies collectively provide robust evidence of the diverse effects of oil revenues on economic growth in regions like Saudi Arabia, Nigeria, and Sudan. They underscore the nuanced ways in which oil-dependent economies can leverage their natural resources to achieve broader economic objectives, highlighting the need for carefully crafted fiscal policies that support sustainable development and diversification.

In conclusion, while oil revenues can provide substantial funding for government budgets, their volatility demands a sophisticated approach to fiscal policy that emphasizes stability, diversification, and long-term economic planning. The experiences of Saudi Arabia, Russia, and Venezuela offer valuable lessons on the potential pitfalls and strategic necessities in managing economies with significant oil revenues.

3. Methodology

In this study, the selection of variables such as Government Consumption (GC), oil revenues, and non-oil revenues is grounded in both theoretical and empirical considerations of fiscal policy impact on economic performance. The theoretical framework is informed by Keynesian economic principles, which postulate that GC can play a stabilizing role in the economy, especially during periods of downturn. This effect is potentially magnified in an oil dependent economy like Saudi Arabia, where revenue streams are highly volatile and susceptible to external shocks in the global oil market.

GC is expected to counteract economic fluctuations by directly injecting funds into the economy, thus sustaining employment and consumption during downturns. The role of GC becomes particularly critical in managing the cyclical nature of oil revenues, which are prone to cause economic instability due to their sensitivity to global oil price fluctuations. Moreover, the inclusion of non-oil revenues, which may arise from sectors such as tourism, manufacturing, and services, helps to assess the effectiveness of economic diversification efforts and their role in fiscal stability. These revenues, often promoted through fiscal incentives, exhibit different dynamics from oil revenues and contribute to overall economic resilience, balancing the instability of oil-dependent financial streams.

Analytically, this study employs an Autoregressive Distributed Lag (ARDL) model to explore the short-term and long-term relationships among these variables. The ARDL model is chosen for its ability to handle the integration properties of the series, whether they are I(0) or I(1), and to reveal both immediate and equilibrium impacts of fiscal policy changes. This choice facilitates a detailed examination of how relationships among these key economic variables evolve over time, offering a nuanced understanding of how immediate shocks to oil revenues can affect government spending decisions and GDP in the short term. Additionally, the model facilitates the examination of the convergence of these variables towards a long-term equilibrium state, providing insights into both transient and enduring economic phenomena. This capability is essential for evaluating the effectiveness of fiscal policies during periods of significant economic upheaval and for informing strategic economic planning and policy formulation in response to future challenges.

The primary data, collected annually, is sourced from World Bank and Ministry of Finance This ensures a robust dataset that reflects the key economic activities impacting the Saudi economy. The dependent variable, GDP, reflects the overall economic health and performance of the nation. The independent variables specifically include Government Consumption (GC), Oil Revenues(OR), Non-Oil Revenues(NOR).

Data analysis begins with descriptive statistics that outline the central tendencies and dispersions within the data. Correlation analysis preliminarily identifies relationships between GDP and the independent variables. After this, the ARDL bounds test approach is employed to verify the existence of long-term relationships among the studied variables. An Error Correction Model (ECM) is then applied to describe short-term dynamics and the adjustment process towards long-term equilibrium.

To ensure analytical rigor, the study conducts various diagnostic tests including checks for serial correlation, heteroskedasticity, and stationarity of residuals. These tests are essential to affirm the model’s suitability and the reliability of the findings, providing a solid foundation for drawing conclusions about the impact of fiscal policies and economic structure on Saudi Arabia’s GDP.

3.1. Justification for the Selected Variables

In this study, the selection of variables was strategically chosen to evaluate the impact of General Government Final Consumption Expenditure (GC) on GDP during economic downturns, specifically during the 2008 Financial Crisis and the 2020 Coronavirus Pandemic. The inclusion of oil and non-oil revenues additionally offers a broadened perspective on the various economic activities that influence GDP. Here is the justification for each selected variable:

3.1.1. General Government Final Consumption Expenditure (GC)

GC is a core component of government expenditure that directly affects the current consumption of goods and services. It excludes capital expenditures, providing a clear measure of government consumption’s immediate impact on economic activity. GC is particularly relevant for analysing fiscal policy’s effectiveness in stimulating the economy during downturns, aligning with Keynesian economic theory, which posits that government spending can act as a stabilizer in fluctuating economic cycles.

3.1.2. Gross Domestic Product (GDP)

GDP represents the total market value of all final goods and services produced within a country in a given period and is a primary indicator of economic health. It serves as the dependent variable in this study, with the impacts of GC, oil, and non-oil revenues being gauged against it. Understanding the dynamics that influence GDP is crucial for assessing economic policies’ efficacy and for strategic economic planning.

3.1.3. Oil Revenue (OR)

Oil revenue is included due to its significant impact on the economies of oil-exporting nations. Fluctuations in oil prices and production levels can have profound effects on these countries’ economic stability and growth. By analysing oil revenue, the study can identify how dependencies on such volatile economic factors influence the broader economic stability and the buffering role of fiscal policies like GC.

3.1.4. Non-Oil Revenue (NOR)

Non-oil revenue encompasses income from sectors other than oil, including manufacturing, services, and agriculture. This variable is essential for assessing economic diversification and stability in countries that are less reliant on oil. It provides insights into how non-oil sectors contribute to the economy, particularly how these sectors fare during economic crises and their role in recovery processes.

4. Results and Discussion

4.1. Results

4.1.1. Descriptive Statistics and Correlation Analysis

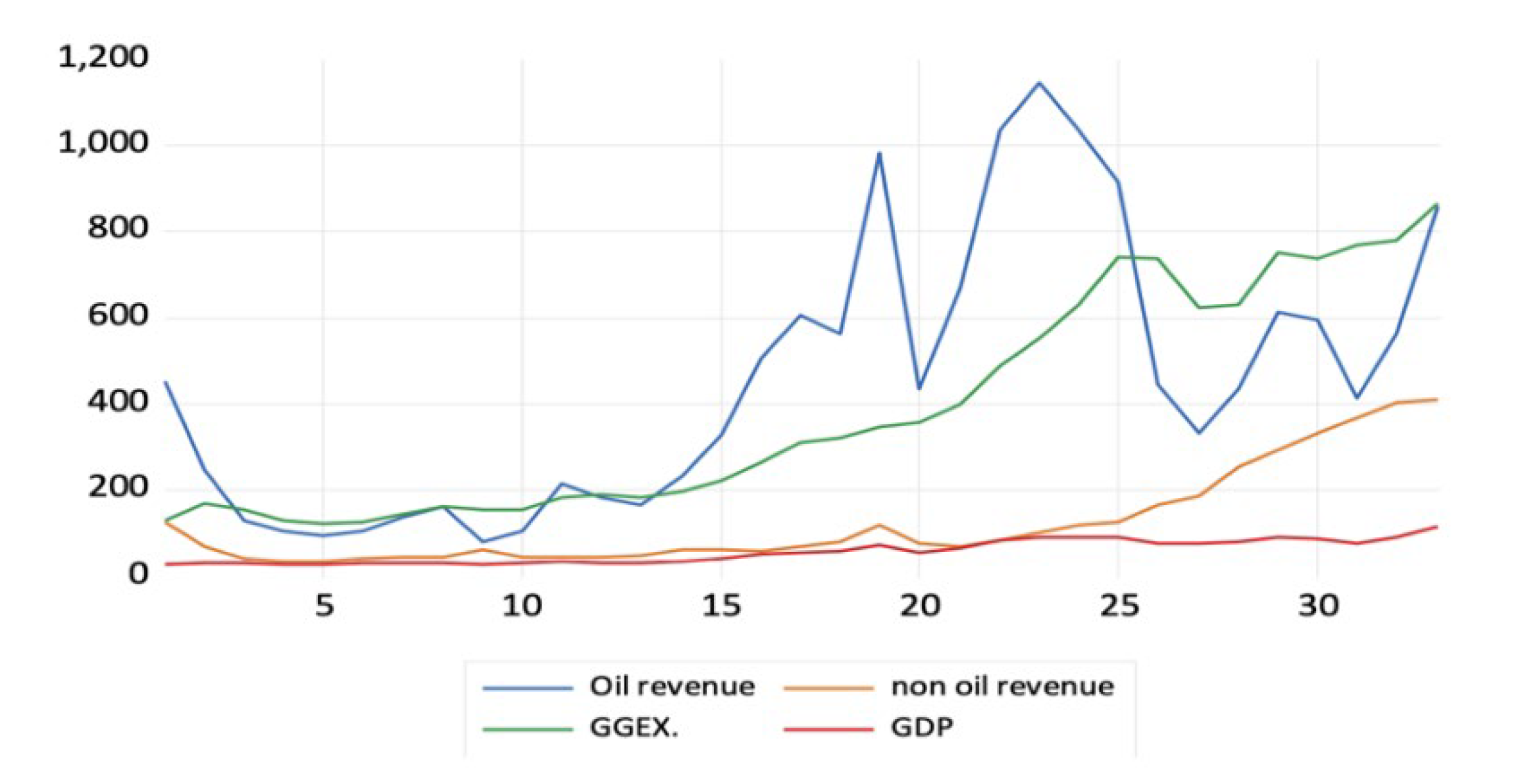

The analysis begins with the descriptive statistics for GDP, Government Consumption (GC), oil revenue, and non-oil revenue. The data reveals higher mean values for GC, and oil revenue compared to GDP and non-oil revenue, suggesting their significant roles in the economy. A particularly high correlation coefficient of 0.950 between GDP and GC underscores the strong influence of government expenditure on economic output.

4.1.2. Correlation Matrix

Table 2 shows the correlation coefficients between the dependent variable, Gross Domestic Product (GDP), and the independent variables: Government Consumption (GC), Oil Revenues (OR), and Non-Oil Revenues (NOR). The analysis reveals a pronounced and positive correlation between GDP and GC, with a coefficient of 0.950, indicating the pivotal role of government spending in stimulating economic activity, particularly during economic downturns. This supports the research objective of quantifying the immediate effects of GC on economic output, answering the first research question regarding the influence of GC on GDP growth during major downturns. Similarly, the correlation between GDP and OR is strongly positive, with a coefficient value of 0.826, suggesting that oil revenues account for approximately 82.6% of the variations observed in GDP. Moreover, the relationship between GDP and NOR is also significantly positive, evidenced by a coefficient of 0.752, which implies that non-oil revenues contribute to 75.2% of GDP’s variability.

Inter-variable correlations among the independent factors reveal insightful dynamics (Table 2); GC and OR exhibit a positive and substantial correlation, marked by a coefficient of 0.645, demonstrating a 65% common variance. Furthermore, an even stronger relationship is observed between GC and NOR, with a correlation coefficient of 0.852, indicating that 85.2% of the variability in GC can be linked to changes in NOR. Conversely, the correlation between OR and NOR, while still positive, is comparatively lower, with a coefficient of 0.369, highlighting a 36.9% shared variance.

These correlation findings underscore the intricate relationships that exist among the economic indicators studied, illustrating the substantial impact of government expenditure and revenue sources on Saudi Arabia’s GDP. The strength of these correlations not only reflects the interdependent nature of these variables but also sets a foundation for further regression analysis to elucidate the direct impacts and predictive capacities of GC, OR, and NOR on the nation’s economic growth.

4.1.3. Regression Analysis

The regression results demonstrate Table 3 a significant positive relationship between GDP and both GC and oil revenue, highlighting their pivotal roles within the economic framework. GC, in particular, shows a substantial positive effect on GDP (coefficient = 0.070939, t-cal = 9.926155, p < 0.001), underscoring the effectiveness of government spending in stimulating economic growth. Similarly, oil revenue shows a significant positive relationship with GDP (B = 0.032003, p < 0.001), although less pronounced than GC. Conversely, non-oil revenue does not exhibit a statistically significant impact on GDP. The adjusted R2 values of 0.978 indicate that the model explains nearly all the variability in GDP.

4.1.4. Stationarity and Cointegration Tests

Tests confirm the stationarity of GDP, GC, OR, and NOR, validating the regression model’s suitability. Furthermore, ARDL Bound tests indicate a cointegrating relationship among these variables, suggesting a long-term equilibrium relationship consistent with economic theory.

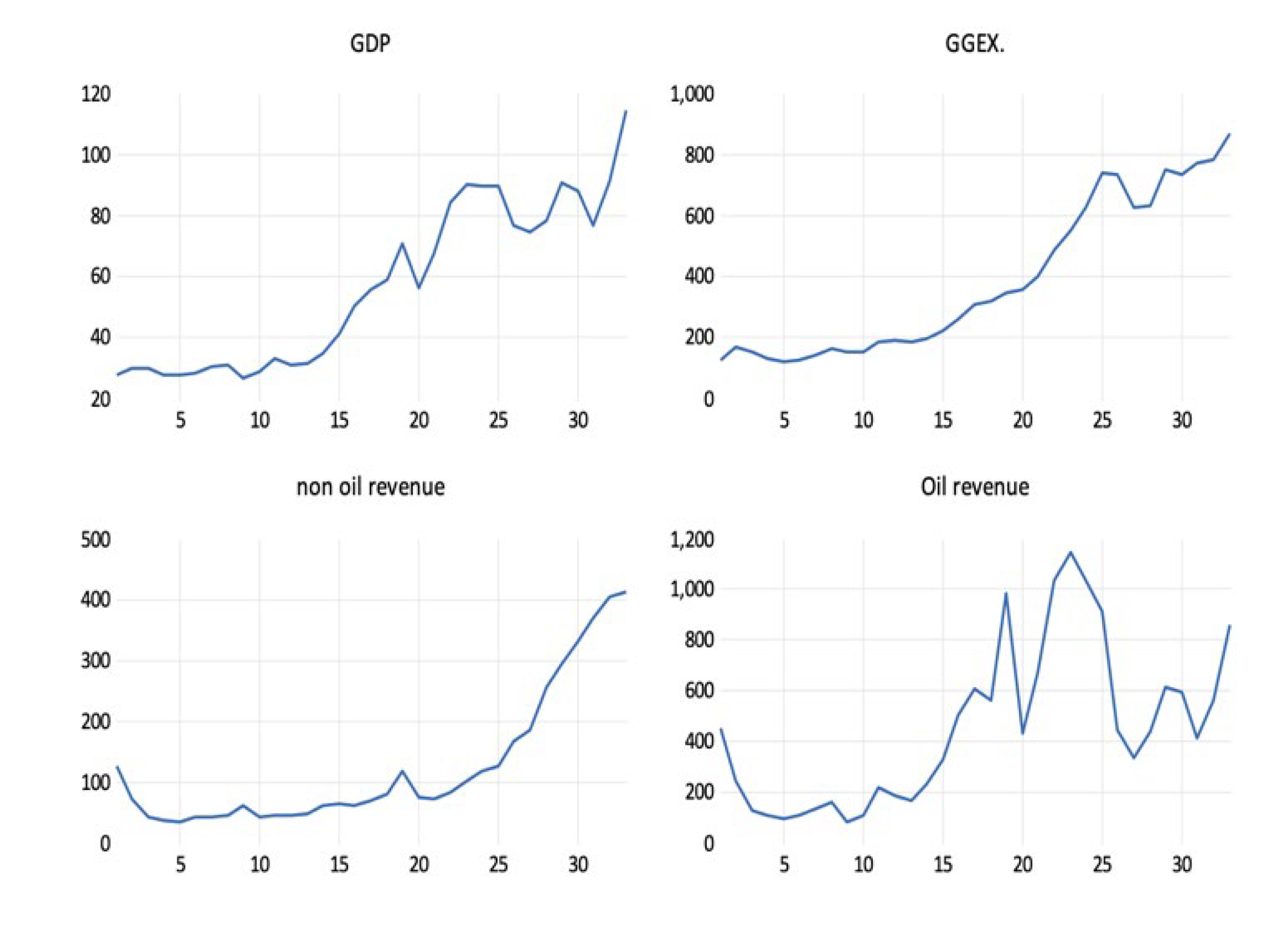

The above Figure 2 show that the time series do not have a general trend over time. We use Unit root test to find stationary of these variables for each variable as follows:

4.1.5. Time Series Analysis

The ARDL model captures both short and long-term impacts, with significant lagged variables indicating the historical persistence on current GDP. This provides insights into the economic inertia and the adjustment speeds towards equilibrium, underlining the effectiveness of fiscal and monetary policies over various periods.

4.1.6. Diagnostic Checks

The diagnostic tests conducted as part of the analysis serve to validate the reliability and appropriateness of ARDL model used in the study. These tests include the Breusch-Godfrey Serial Correlation LM Test, the Heteroskedasticity Test (ARCH), and a Bounds Test to assess the presence of cointegration among the variables.

4.1.7. Serial Correlation LM Test

The Breusch-Godfrey Serial Correlation LM Test results (Table 7) indicate no evidence of serial correlation in the model residuals. The F-statistic of 0.173 with a probability of 0.842 and an Obs*R-squared value of 0.636 with a Chi-Square probability of 0.7275 both confirm the absence of autocorrelation up to 2 lags. This suggests that the residuals are independently distributed, supporting the model’s specification and enhancing confidence in the regression analysis.

4.1.8. Heteroskedasticity Test (ARCH)

The Heteroskedasticity Test results (Table 8) also affirm the model’s robustness, indicating constant variance among the residuals. The F-statistic of 0.147 with a probability of 0.7039 shows no significant heteroskedasticity effects, implying that the variance of the residuals is stable and does not depend on the level of the dependent variable, which is crucial for reliable statistical inference.

4.1.9. Bounds Test for Cointegration

The Bounds Test (Table 5) explores the long-term relationships among the variables. The F-statistic of 14.329494 significantly exceeds the upper bounds I(1) values across all significance levels (1%, 5%, and 10%), indicating the presence of a cointegrating relationship among the variables. This suggests that the variables move together in the long run, providing further validity to the ARDL model’s capability to capture both short-term and long-term dynamics.

These diagnostic checks—confirming no serial correlation, no heteroskedasticity, and the presence of cointegration—substantiate the ARDL model’s suitability for this analysis. They provide strong evidence that the model is well-specified and that the analytical inferences drawn from this study are reliable. The tests affirm that the model adequately captures the dynamics among GDP, oil revenue, non-oil revenue, and government expenditure, making it a robust tool for policy analysis and economic forecasting.

Table 6. ARDL Correlation.

| Dependent Variable: D(Y) | |

| Method | ARDL |

| Date | 04/06/24 |

| Time | 11:00 |

| Sample | 4 33 |

| Included observations | 30 |

| Dependent lags | 4 (Automatic) |

| Automatic-lag linear regressors (4 max. lags) | X11 X22 X33 |

| Deterministics | Restricted constant and no trend (Case 2) |

| Model selection method | Akaike info criterion (AIC) |

| Number of models evaluated | 500 |

| Selected model | ARDL(2,3,1,2) |

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| COINTEQ* | -1.111586 | 0.118787 | -9.357838 | 0.0000 |

| D(Y(-1)) | 0.543237 | 0.137107 | 3.962144 | 0.0007 |

| D(X11) | 0.011987 | 0.008700 | 1.377925 | 0.1821 |

| D(X11(-1)) | -0.043489 | 0.010619 | -4.095530 | 0.0005 |

| D(X11(-2)) | -0.054899 | 0.009758 | -5.626075 | 0.0000 |

| D(X22) | -0.069815 | 0.015875 | -4.397785 | 0.0002 |

| D(X33) | 0.040275 | 0.002206 | 18.25773 | 0.0000 |

| D(X33(-1)) | -0.017486 | 0.005052 | -3.460963 | 0.0022 |

| Model Fit | ||||

| R-squared | 0.969565 | |||

| Adjusted R-squared | 0.959881 | |||

| S.E. of regression | 1.661787 | |||

| Akaike info criterion | 4.076843 | |||

| Sum squared resid | 60.75380 | |||

| Log likelihood | -53.15264 | |||

| Hannan-Quinn criter. | 4.196377 | |||

| F-statistic | 100.1213 | |||

| Prob(F-statistic) | 0.000000 |

p-values are incompatible with t-Bounds distribution.

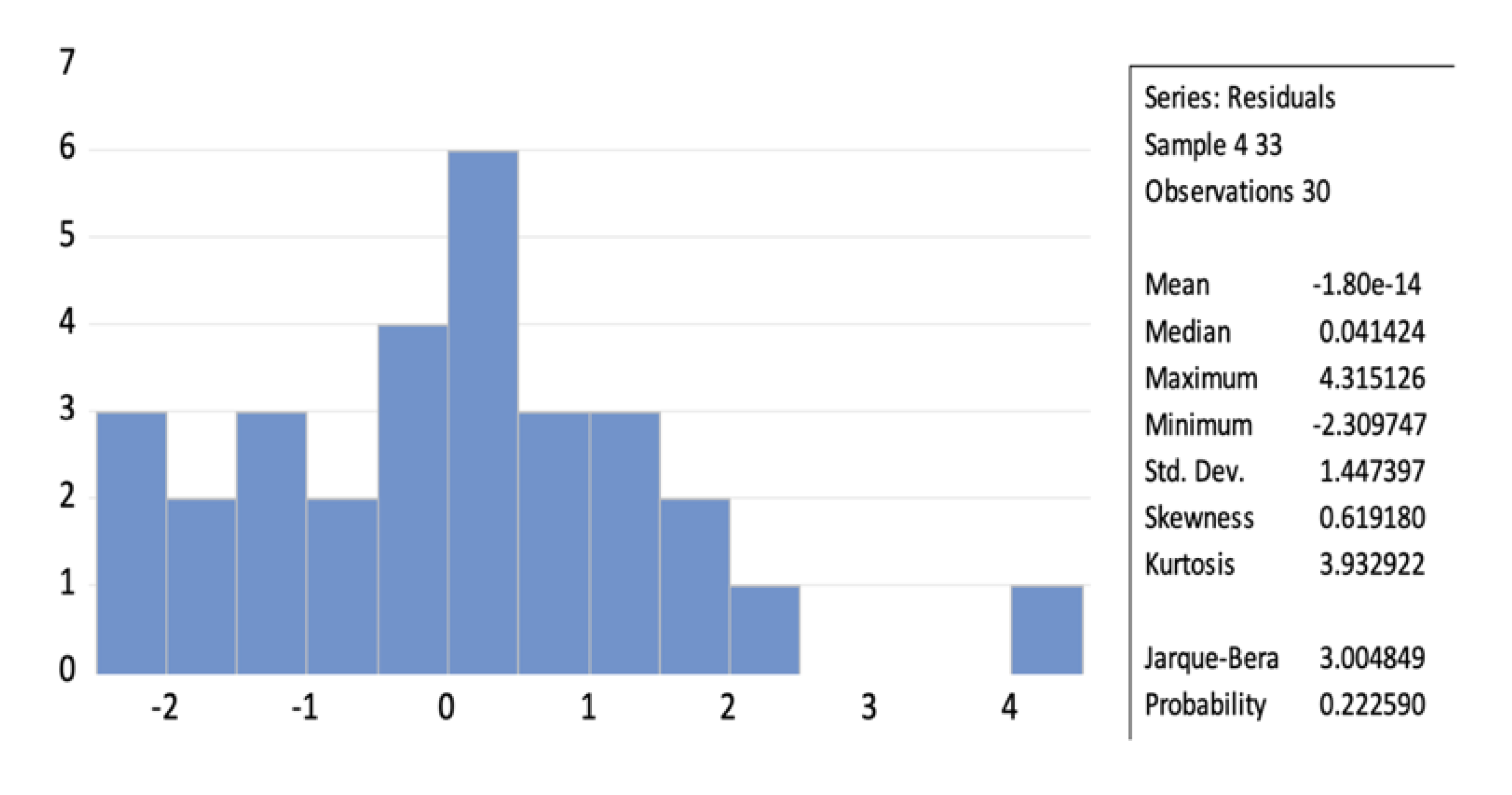

Figure 3 shows the extent to which the errors are normally distributed. Based on the p-value of the Jarque-Bera test, which is 0.222590 and greater than 0.05, we can conclude that the errors are not statistically significant.

4.2. Discussion

The ARDL model results provide empirical evidence to the theoretical premise that fiscal policy, particularly Government Consumption (GC), plays a critical role in stabilizing and stimulating the Saudi economy during periods of economic fluctuations. This section discusses the implementation of these fiscal policies, examining the extent to which they align with the theoretical expectations of counter-cyclical measures and how they have impacted economic stability and growth in the context of Saudi Arabia’s oil-dependent economy.

4.2.1. Counter-Cyclical Measures and Public Investments:

the Saudi government’s approach to fiscal policy has traditionally aimed to leverage oil revenues to fund substantial public investments in infrastructure, healthcare, education, and new economic cities. These investments are intended to stimulate economic activity and diversify the sources of income. The ARDL results indicate that increases in GC typically lead to short-term boosts in GDP, supporting the Keynesian view that government spending can activate economic growth. However, the counter-cyclical potential of these fiscal measures has often been undermined by timing and the scale of implementation. During periods of high oil revenue, the tendency has been towards increased spending, which is theoretically appropriate. Yet, the reduction in expenditure during low oil price periods suggests a pro-cyclical retreat, which may exacerbate economic downturns rather than mitigating them.

4.2.2. Challenges of Pro-Cyclical Spending

The analysis highlights a critical challenge in the form of pro-cyclical fiscal behaviour, where government spending intensifies the economic booms and busts instead of smoothing them. This tendency has been particularly problematic in the context of recent oil price volatilities, where necessary fiscal contractions have been delayed, leading to increased borrowing and public debt. The social and political repercussions of these adjustments have been significant, manifesting in public discontent and pressure on the government to maintain subsidies and public spending levels, even when economically unsustainable.

4.2.3. Social and Political Impacts of Fiscal Adjustments:

The ARDL model results also shed light on the broader social and political impacts of fiscal adjustments. Reductions in subsidies and public spending during economic downturns have often led to public unrest and dissatisfaction, which poses a risk to social stability. The empirical evidence suggests that while fiscal tightening might be necessary from an economic standpoint, the timing and manner of implementation require careful management to mitigate adverse social impacts.

4.2.4. Linking Theory to Practice

The practical outcomes observed through the ARDL model underscore the complex interplay between theory and practice in fiscal policy implementation. While the theoretical framework supports the use of counter-cyclical fiscal policies as an effective tool for managing economic fluctuations, the actual application in Saudi Arabia illustrates the challenges of adhering to these principles in an oil-dependent economy characterized by high revenue volatility. The findings highlight the need for more consistent and carefully calibrated fiscal policies that not only aim to stabilize the economy but also consider the socio-political context within which these policies are implemented.

In conclusion, the discussion reveals that while Saudi Arabia has made strides in implementing expansive fiscal policies aimed at economic diversification and stability, there remains a significant gap in achieving the ideal counter-cyclical fiscal approach. This gap points to the need for continued reforms and strategic fiscal management to ensure that fiscal policies effectively contribute to sustainable economic growth and stability.

The findings of this study, provide a comprehensive examination of the critical role that Government Consumption (GC) plays during periods of economic turmoil in Saudi Arabia. The use of ARDL model has allowed for a detailed analysis of how GC, in conjunction with oil and non-oil revenues, influences GDP growth, especially during significant economic crises that have historically impacted the Saudi economy.

4.2.5. Economic Impacts and Fiscal Response

Throughout the observed periods, such as the Gulf War, various oil price crashes, and the COVID-19 pandemic, Saudi Arabia faced severe economic downturns that were effectively mitigated by strategic increases in GC. The ARDL model’s results indicate that GC not only provides an immediate boost to economic output but also plays a stabilizing role, buffering the economy against external shocks. The significant positive relationship between GC and GDP growth highlights the effectiveness of fiscal policy as a tool for economic stabilization and recovery. Which supports Keynesian principles advocating for active government intervention during downturns. The ARDL model’s findings that GC effectively stimulated economic activity during both crises corroborate the importance of fiscal tools in managing economic stability.

4.2.6. Role of Oil and Non-Oil Revenues

The interaction between GC and oil revenues revealed an expected dependency where high oil revenues generally reduce the urgency for high government spending, whereas low oil revenues lead to increased GC to maintain economic stability. This dynamic underscore the challenges of an oil-dependent economy, where fiscal policies must be adaptable to fluctuations in oil market conditions. Additionally, the analysis showed that non-oil revenues are becoming increasingly significant, reflecting the gradual success of economic diversification efforts under Vision 2030. The positive correlation between non-oil revenues and GC suggests that as the economy diversifies, fiscal policy can increasingly rely on more stable income sources, reducing vulnerability to oil price volatility.

4.2.7. Policy Implications

The findings underscore the necessity for Saudi Arabia to continue its efforts in economic diversification. The strong correlation between GC and GDP growth during downturns supports policies aimed at enhancing the efficiency and responsiveness of fiscal interventions. It is crucial for policymakers to ensure that GC is not only sufficient but also timely and well-targeted to the sectors most in need during economic crises.

Moreover, the relationship among GC, oil revenues, and non-oil revenues offers vital insights for managing future economic challenges. An integrated fiscal strategy that leverages all available economic levers will be essential for enhancing economic resilience and recovery capabilities.

4.2.8. Long-Term Strategic Planning

The sustained impact of GC on GDP underscores the importance of long-term fiscal planning. The government should consider establishing fiscal buffers during periods of high oil revenue that can be deployed in times of economic distress. Additionally, continuous investment in non-oil sectors should be pursued to reduce the economic reliance on oil, thereby fostering a more stable and diversified economic environment.

The ARDL analysis has provided robust empirical evidence supporting the strategic use of GC in managing economic downturns effectively. By maintaining flexible and robust fiscal policies, Saudi Arabia can better navigate future economic fluctuations, ensuring sustainable growth and stability. The study highlights the necessity for policymakers to prioritize GC in their fiscal strategies, ensuring rapid and effective responses to both current and future economic challenge.Top of FormBottom of Form

4.2.9. The Public Investment Fund (PIF)

The Public Investment Fund (PIF) plays a crucial role in stabilizing the economy of Saudi Arabia. As a sovereign wealth fund, the PIF enables the government to implement counter-cyclical fiscal policies, which are essential for managing the inherent volatility of oil revenues. During periods of high oil prices, surplus revenues are saved in the PIF, creating a financial buffer that can be utilized during economic downturns. This mechanism allows the government to sustain public spending and avoid drastic budget cuts when oil prices fall, thus stabilizing the economy.

The strategic use of the PIF aligns with Saudi Arabia’s Vision 2030, which aims to diversify the economy and reduce dependence on oil. By investing in various sectors such as infrastructure, renewable energy, and technology, the PIF supports economic diversification and long-term sustainable growth. This approach not only mitigates the risks associated with oil revenue fluctuations but also promotes economic stability and resilience.

The effectiveness of the PIF in stabilizing the economy is underscored by research on counter-cyclical fiscal policies. Blanchard and Leigh (2013) highlight the importance of such policies in mitigating revenue volatility and fostering fiscal stability. By adopting a strategic approach to managing its financial resources through the PIF, Saudi Arabia can ensure continuous development and economic stability despite external economic shocks. This proactive fiscal management is essential for achieving the goals outlined in Vision 2030 and ensuring a sustainable future for the Saudi economy.

5. Conclusion and Recommendation

This study has examined the dynamics between fiscal policy, specifically Government Consumption (GC), and its impact on GDP growth in Saudi Arabia, set against the backdrop of oil and non-oil revenue fluctuations. The findings from the ARDL model analysis reveal significant insights into how the kingdom’s fiscal policy has interacted with economic variables within the context of an oil-dependent economy. These findings allow us to draw several important conclusions about the efficacy of fiscal policy design and implementation in Saudi Arabia.

5.1.1. Alignment with Theoretical Expectations

Theoretically, fiscal policies in oil-dependent economies should be counter-cyclical, aimed at stabilizing the economy by smoothing the fluctuations caused by volatile oil prices. In practice, however, Saudi Arabia’s fiscal policy has often been pro-cyclical, with government spending ramping up when oil revenues are high and contracting sharply during downturns. This approach aligns only partially with Keynesian principles, which advocate for increased spending during downturns to stimulate the economy. The results indicate that while GC has had a positive effect on GDP, the overall fiscal strategy has not fully mitigated the economic instability that arises from oil revenue volatility.

5.1.2. Deviations from Theoretical Expectations

The pro-cyclical nature of spending highlighted by the study underscores a significant deviation from theoretical expectations. Such spending patterns exacerbate economic peaks and troughs, thereby increasing the vulnerability of the Saudi economy to global oil price shocks. This deviation suggests a critical area for policy reform, emphasizing the need for more robust counter-cyclical measures that not only stabilize the economy during downturns but also build fiscal buffers during periods of high oil prices.

5.1.3. From Venezuela to Saudi Arabia: Lessons in Fiscal Management

The Venezuelan experience underscores the critical importance of prudent fiscal management, especially in countries that rely heavily on commodity exports like oil. Economists and policymakers argue for the necessity of establishing stabilization funds, diversifying the economy to reduce dependency on a single commodity, and implementing counter-cyclical fiscal policies to buffer against economic downturns. As oil prices began to fall after 2014, Venezuela’s government faced enormous fiscal deficits. In response, rather than implementing counter-cyclical fiscal policies, which would involve cutting expenditures or increasing savings, the government financed the deficit by printing money, leading to hyperinflation. According to the findings of Su et al. (2020), these actions were a primary driver behind the economic instability that followed. Venezuela’s situation remains a stark warning of the risks associated with high oil dependency, particularly when combined with poor fiscal management. The lessons from Venezuela highlight the need for comprehensive fiscal reforms and economic diversification strategies to prevent similar crises in other nations reliant on commodities.

Similarly, Saudi Arabia, another nation heavily reliant on oil, finds itself at a crossroads. While it has not faced the severe economic crises of Venezuela, the potential risks are evident. The implications for future policy formulation in Saudi Arabia are clear: the kingdom must refine its fiscal strategies to better harness the stabilizing potential of fiscal policy. This involves enhancing the capacity of the government to implement more disciplined and responsive fiscal measures. Additionally, the Saudi experience points to the need for continued efforts in economic diversification, reducing the economy’s reliance on oil revenues, and thereby diminishing the amplitude of economic fluctuations tied to external market conditions. By learning from Venezuela’s pitfalls, Saudi Arabia can aim to fortify its economic framework against future shocks, ensuring more sustainable economic growth and stability.

5.1.4. Implications for Future Policy Formulation

To achieve strategic economic objectives, several recommendations are put forward for Saudi Arabia. Firstly, it is vital to enhance the efficiency of public spending. By ensuring that investments are directed towards sectors that promote sustainable growth, the country can improve its economic stability and potential for long-term development.

Secondly, the development of more sophisticated fiscal rules is crucial. These rules should enforce budget discipline across economic cycles, ensuring that any increases in spending during economic downturns are timely, targeted, and reversible. This approach will provide a buffer that mitigates the impacts of economic fluctuations.

Thirdly, Saudi Arabia should accelerate its policies aimed at economic diversification, with a particular focus on non-oil sectors. Expanding into these areas will help create a more balanced and less volatile economic base, reducing the country’s reliance on oil revenues and fostering a more resilient economy.

Lastly, the establishment and maintenance of sovereign wealth funds or stabilization funds are recommended. These funds would provide a financial reserve that can be utilized during economic downturns to support public spending, thereby avoiding drastic cuts that could further destabilize the economy. Such funds are integral to maintaining economic stability and ensuring that financial resources are available in times of need.

In conclusion, while Saudi Arabia has made some progress in aligning its fiscal policy with economic stabilization objectives, significant challenges remain. The findings of this study reinforce the importance of effective fiscal policy design and implementation, as advocated by fiscal policy theory. For Saudi Arabia, adhering more closely to these theoretical principles could lead to greater economic stability and a more resilient economic structure capable of withstanding global economic shocks.

This study embarked on a rigorous analysis to assess the comprehensive effects of Government Consumption (GC) on GDP growth, particularly during significant economic downturns like the 2008 financial crisis and the 2020 coronavirus pandemic. Incorporating the influences of oil and non-oil revenues, the research aimed to:

- Quantify the impact of GC alongside oil and non-oil revenues on national economic output.

- Evaluate the effectiveness of fiscal policies in stabilizing and stimulating the economy during and after major economic crises.

- Provide policy insights for crafting resilient economic strategies for future crises.

5.1.5. Key Findings

The research successfully addressed the formulated questions, revealing that:

- The combined effect of GC, oil, and non-oil revenues on GDP during economic downturns is significantly positive, indicating that these variables collectively play a crucial role in driving economic activity and recovery.

- Fluctuations in oil and non-oil revenues significantly influence the effectiveness of GC in economic stabilization and recovery, highlighting the need for adaptive fiscal policies that can respond to dynamic economic conditions.

- The relationships among GC, oil revenues, and non-oil revenues provide vital insights for managing future economic challenges, emphasizing the importance of an integrated fiscal strategy that leverages all available economic levers

5.1.6. Implications for Economic Policy

The findings from this study underscore the critical role of GC as a stabilizing force during economic crises, reinforcing the need for robust, flexible fiscal policies that can be swiftly adapted to changing economic conditions. The significant relationships identified among GC, oil, and non oil revenues advocate for a holistic approach to fiscal policy, which considers multiple revenue streams to enhance economic resilience and recovery.

5.2. Recommendations for Future Crises

Policymakers are advised to prioritize GC in fiscal strategies to ensure rapid and effective economic recovery during future crises. Strategic planning should incorporate the volatility of oil and non-oil revenues to tailor fiscal responses that optimize short-term relief and promote long-term stability. Investments in non-oil sectors and infrastructure, supported by stable non-oil revenues, should be intensified to reduce dependency on oil and diversify economic bases.

5.2.1. Future Research Directions

To further enhance the understanding of fiscal policy effectiveness, future studies should explore:

- The impact of GC under various economic conditions and policy environments, using more granular data such as quarterly or monthly figures.

- The role of additional variables such as foreign direct investment and technological advancements in shaping economic responses to fiscal measures.

- Comparative analyses of different countries to validate the generalizability of the findings and refine policy recommendations based on regional economic characteristics.

5.2.2. Concluding Thoughts

This study has not only confirmed the pivotal role of GC during economic downturns but also highlighted the nuanced contributions of oil and non-oil revenues to economic stability and growth. The insights derived are intended to guide effective policy formulation, offering a comprehensive framework for leveraging fiscal policies to achieve rapid and sustainable economic recovery. By prioritizing strategic fiscal interventions and diversifying economic strategies, nations can better prepare for and respond to future economic challenges.

These datasets were integral to our analysis, enabling a comprehensive examination of the Fiscal Resilience in Times of Crisis: The Impact of Government Consumption Alongside Oil and Non-Oil Revenues on Saudi Arabia’s GDP Growth. The accessibility of these data in public repositories ensures that our research adheres to the principles of transparency and reproducibility, aligning with the open scientific inquiry standards advocated by MDPI.

- All co-authors have been informed and consent to the open access posting of the manuscript on Preprints.org.

- The manuscript has been submitted to Sustainability.

- All authors are aware of and understand the Preprints.org withdrawal policy, acknowledging that preprints cannot be completely removed once posted online.

- Ethical approval for experiments involving animals, humans, or plants is not applicable.

- No copyright permissions are required.

- Research data supporting the findings of this manuscript are available upon request.

Appendix A

Table A1.

Unit Root Test Results for GDP Growth Rate in Saudi Arabia.

| Test | Statistic | Critical Values | Result |

| Elliott-Rothenberg-Stock DF-GLS test statistic | -4.454874 | 1%: -3.770000 <br> 5%: -3.190000 <br> 10%: -2.890000 | Reject Null Hypothesis (Unit Root) |

| DF-GLS Test Equation on GLS Detrended Residuals | -0.857422 | - | Significant at 1% level (p < 0.01) |

Table A2.

Unit Root Test Results for Government Consumption in Saudi Arabia.

| Test | Value |

| Null Hypothesis | D(GG_) has a unit root |

| Test Statistic | -4.955707 |

| Critical Values | |

| - 1% level | -3.770000 |

| - 5% level | -3.190000 |

| - 10% level | -2.890000 |

| Result | Reject the null hypothesis |

| Coefficient | Std. Error | t-Statistic | Prob. |

| GLSRESID(-1) | -1.111459 | 0.224278 | -4.955707 |

| D(GLSRESID(-1)) | 0.377074 | 0.177452 | 2.124940 |

| Model Fit | |||

| R-squared | 0.483162 | ||

| Adjusted R-squared | 0.464704 | ||

| S.E. of regression | 39.99909 | ||

| Akaike info criterion | 10.27993 | ||

| Sum squared resid | 44797.95 | ||

| Log likelihood | -152.1990 | ||

| Durbin-Watson stat | 1.938520 |

Table A3.

Unit Root Test Results for Non-Oil Revenue in Saudi Arabia.

| Test | Value |

| Null Hypothesis | D(NON_OIL_REVENUE) has a unit root |

| Test Statistic | -4.648893 |

| - 1% level | -3.770000 |

| - 5% level | -3.190000 |

| - 10% level | -2.890000 |

| Result | Reject the null hypothesis |

| Coefficient | Std. Error | t-Statistic | Prob. |

| GLSRESID(-1) | -0.839274 | 0.180532 | -4.648893 |

| Model Fit | |||

| R-squared | 0.418742 | ||

| Adjusted R-squared | 0.418742 | ||

| S.E. of regression | 18.55557 | ||

| Akaike info criterion | 8.711143 | ||

| Sum squared resid | 10329.27 | ||

| Log likelihood | -134.0227 | ||

| Durbin-Watson stat | 1.967910 |

Table A4.

Unit Root Test Results for Oil revenue in Saudi Arabia.

| Test | Value |

| Null Hypothesis | D(OIL_REVENUE) has a unit root |

| Test Statistic | -5.406359 |

| Critical Values | |

| - 1% level | -3.770000 |

| - 5% level | -3.190000 |

| - 10% level | -2.890000 |

| Result | Reject the null hypothesis |

| Coefficient | Std. Error | t-Statistic | Prob. |

| GLSRESID(-1) | -0.995692 | 0.184171 | -5.406359 |

| Model Fit | |||

| R-squared | 0.492892 | ||

| Adjusted R-squared | 0.492892 | ||

| S.E. of regression | 205.1555 | ||

| Akaike info criterion | 13.51714 | ||

| Sum squared resid | 1262663 | ||

| Log likelihood | -208.5157 | ||

| Durbin-Watson stat | 1.977099 |

References

- Aghilifar, H., Zare, H., Piraei, K., & Ebrahimi, M. (2023). Does the type of government expenditure affect the cyclicality of fiscal policy? (Case study: Iran). International Journal of Nonlinear Analysis and Applications, 14(4), 139-150.

- Al Rasasi, M., Qualls, J., & Alghamdi, B. (2019). Oil revenues and economic growth in Saudi Arabia. International Journal of Economics and Financial Research, 5(3), 49-55.

- Aslam, N., & Shastri, S. (2019). Relationship between oil revenues and gross domestic product of Oman: an empirical investigation. International Journal of Economics and Financial Issues, 9(6), 195.

- Auerbach, A. J., & Gorodnichenko, Y. (2012). Measuring the output responses to fiscal policy. American Economic Journal: Economic Policy, 4(2), 1-27. Economic Policy.

- Auty, R. M. (2001). Resource Abundance and Economic Development. Oxford University Press. Retrieved from https://www.ageconsearch.umn.edu/record/295339/files/rfa44.pdf.

- Azmi, F. (2013). An empirical analysis of the relationship between GDP and unemployment, interest rate and government spending. Interest Rate and Government Spending (June 10, 2013). 10 June.

- 7. Blanchard, O., & Leigh, D. (2013). Fiscal consolidation: At what speed. VoxEU. org, 3.

- Bongers, A., & Díaz-Roldán, C. (2019). Stabilization policies and technological shocks: towards a sustainable economic growth path. Sustainability, 11(1), 205.

- Bravo, J. M., & Ayuso, M. (2021). Linking Pensions to Life Expectancy: Tackling Conceptual Uncertainty through Bayesian Model Averaging. Mathematics, 9(24), 3307. https://doi.org/10.3390/math9243307. [CrossRef]

- Byiabani, J., & Mohseni, R. (2014). Fiscal Policy and Economic Growth A Case Study of IRAN. Kuwait Chapter of Arabian Journal of Business and Management Review, 4(1), 48-57.

- Buendía-Martínez, I., Álvarez-Herranz, A., & Moreira Menéndez, M. (2020). Business Cycle, SSE Policy, and Cooperatives: The Case of Ecuador. Sustainability, 12(13), 5485. [CrossRef]

- Cavallo, M. P. (2005). Government employment and the dynamic effects of fiscal policy shocks. Federal Reserve Bank of San Francisco.

- Fatai, A. F., Liu, C., Adeniyi, O. A., & Kabir, M. (2017). Oil rents and fiscal balance in oil-dependent economies: do fiscal rules matter? Asian Journal of Empirical Research, 7(8), 176-201. Retrieved from http://aessweb.com/journal-detail.php?id=5004.