Submitted:

23 October 2023

Posted:

25 October 2023

You are already at the latest version

Abstract

Tax compliance is a problem in Bangladesh, despite the tax system’s importance to economic growth. This research aims to identify the causes of tax compliance behav- ior issues and design customer-centric marketing techniques to increase compliance. The two-fold research strategy began with exploratory and descriptive analysis of primary survey data. The findings revealed a knowledge gap, particularly among younger populations, and showed that public acknowledgment and gamification can improve compliance. Next, experimental and causal research was used. Direct com- munication with 1,000 people and Phase 1 outcomes-based treatments were imple- mented. The results were promising: 95.74% had never experienced tax-related edu- cational programs, and 87% lacked tax calculation knowledge. When offered incen- tives like a 2% tax decrease, 73% were willing to pay taxes immediately. This study shows customer-focused marketing methods can solve Bangladesh’s tax compliance problem. Bridging the information gap and implementing motivating mechanisms can make our nation more obedient and financially stable.

Keywords:

Tax Compliance

; Bangladesh Tax System

; Taxpayer Behaviors

; Tax Marketing

1. Introduction

Bangladesh, situated in the delta of the Padma (Ganges [Ganga]) and Jamuna (Brahmaputra) rivers, is a notable country in South Asia. Historically known as the eastern part of Bengal, it played a significant role in British India. Post the partition of India in 1947, it became East Pakistan under Pakistani rule, eventually gaining independence in 1971 and becoming the nation of Bangladesh. With its capital at Dhaka, Bangladesh shares its borders with multiple Indian states and Myanmar, with its southern region opening into the Bay of Bengal. Officially recognized as the People’s Republic of Bangladesh, the country functions as a unitary state with a parliamentary democracy. A rigorous election system ensures representation in its unicameral parliament, the Jatiya Sangsad. While the Prime Minister helms the government’s day-to-day operations, the President, a ceremonial post, represents the state. The highest judiciary power lies with the Supreme Court. An intricate three-tier local governance system further breaks the country into eight administrative divisions, which are subdivided into sixty-four districts. Historically, Bangladesh’s economy leaned heavily on agriculture, causing seasonal unemployment and a generally low standard of living. A shift towards industrialization was initiated in the mid-20th century, emphasizing industries relying on indigenous raw materials like jute and cotton (10). The country’s GDP has witnessed significant growth, especially in the 21st century, elevating Bangladesh to the ranks of the ’Asian Tigers’. From a modest GDP of 6.29 billion USD in 1972 (15), it soared to 416.3 billion USD in 2021. With a population exceeding 165 million, Bangladesh stands as the world’s 8th most populated country. Bengali dominates as the primary language, and Islam is the predominant religion, practiced by 91.04% of the population. The literacy rate has shown promising growth, reaching 74.66% in 2022. Bangladesh has strategically engaged in multinational diplomacy, with significant involvement in the United Nations and the Commonwealth of Nations. The economic landscape of Bangladesh has been dynamically evolving, with significant contributions from the private sector. The textile and garment industry has been a stalwart in the country’s exports, and other sectors like pharmaceuticals, shipbuilding, steel, electronics, and energy are rapidly growing.

While Bangladesh has made strides in modernizing its tax collection mechanisms, significant gaps in compliance and coverage persist. Traditional methods, though some- what effective, might not align with the evolving demographics, especially the digital- savvy younger generation. This mirrors a global challenge, where countries grapple with similar tax compliance issues. While traditional measures have often targeted systemic inefficiencies or punitive enforcement, there’s a burgeoning global recogni- tion of the role behavioral strategies can play. Notably, many nations are now turning to customer-centric marketing strategies—proven tools in the commercial sector—to influence tax-paying behavior. Such strategies prioritize understanding and address- ing taxpayers’ motivations, apprehensions, and needs, aiming for voluntary compliance over mere deterrence. Bangladesh, like many of its global counterparts, faces admin- istrative inefficiencies, public mistrust, and widespread evasion. In this context, the potential of customer-centric approaches in reshaping tax behavior presents itself as a promising, albeit largely unexplored, avenue. A deeper dive into their efficacy in the Bangladeshi context could reveal innovative solutions, potentially revolutionizing national revenue collection. This research study is based on two-fold objective,

The primary objective is:

- (1)

- To assess the effectiveness of customer-centric marketing strategies in improving the tax-paying behavior of the citizens of Bangladesh.

and the secondary objectives are:

- (1)

- To gauge the current tax-paying behavior of the citizens.

- (2)

- To understand the awareness level of citizens regarding their tax obligations and the benefits of compliance.

- (3)

- To analyze the potential and applicability of customer-centric marketing strate- gies in molding tax-paying attitudes and behaviors.

The outcome of this research holds significant implications for both policymakers and tax administrators in Bangladesh. By understanding the efficacy of customer-centric marketing strategies in the realm of tax collection, the government can potentially:

- (1)

- Increase its tax revenue without raising tax rates.

- (2)

- Enhance voluntary compliance, reducing the need for punitive measures.

- (3)

- Foster a culture of tax compliance among the citizens, aiding long-term fiscal sustainability.

This research focuses on the citizens of Bangladesh, spanning different income groups, professions, and regions. While the primary emphasis is on individual taxpay- ers, insights from businesses and tax professionals will also be considered to present a holistic view. The study will encompass both traditional and digital marketing strate- gies, examining their relevance and impact on different demographic groups.

2. Literature Review

2.1. Historical Overview of Taxation in Bangladesh

Bangladesh’s income tax system has evolved considerably from its early origins, re- flecting both the nation’s rich historical context and its contemporary economic pri- orities. The foundation of the income tax system in Bangladesh was laid in 1922 during the British colonial era (9). The British government, discerning the economic potential of the region, instituted an income tax regime that would set the course for future financial policies. This British-era income tax system persisted as East Pakistan, Bangladesh’s identity during its time as part of Pakistan, retained the core tenets of this system, albeit under a different administrative framework.

After gaining independence in 1971, Bangladesh embarked on a journey of redefining its income tax policies. In 1984, an army-backed government, recognizing the need for a robust and updated tax framework, introduced a comprehensive income tax law that would lay the groundwork for the nation’s fiscal policies for decades to come. Throughout the latter half of the 20th century, as the country’s economy expanded and diversified beyond its agrarian roots, there was an evident shift in the income tax policies to accommodate these changes.

The dawn of the 21st century brought with it renewed efforts to modernize and streamline the income tax system. With the rise of globalization and the digital econ- omy, Bangladesh undertook numerous reforms to adapt to the evolving economic land- scape. This encompassed broadening the income tax net, leveraging digital platforms for tax services, and addressing challenges posed by cross-border income sources.

However, the year 2023 marked a watershed moment in Bangladesh’s income tax history. The nation proudly introduced its first-ever income tax law, written in Ben- gali, the heart language of its people. This monumental step not only exemplifies Bangladesh’s commitment to its cultural and linguistic roots but also signifies its aim to render the income tax system more transparent, comprehensible, and citizen-centric.

Bangladesh’s journey in tax reforms can be demarcated into distinct phases, each addressing the unique challenges of its era. Some of the significant reforms include:

VAT Introduction (1991): Replacing a myriad of indirect taxes, VAT was introduced to simplify the tax structure and ensure better compliance. This move, while initially met with resistance due to its broad coverage, eventually contributed significantly to the national exchequer (17).

Direct Tax Code Reforms: Over the years, the direct tax codes have been revised to simplify provisions, rationalize tax rates, and provide incentives for industries and services crucial for national development (2).

Digital Initiatives: In alignment with global trends, Bangladesh has been making concerted efforts to digitize its tax administration. Initiatives like online tax return submission, A-challan, e-payment, e-TIN (Electronic Tax Identification Number), and digital tax clearance certificates have been introduced (1).

Taxpayer Services: Recognizing the importance of taxpayer education and facilitation, the National Board of Revenue (NBR) has over the years introduced taxpayer service zones, helplines, and awareness campaigns (9).

The impact of these reforms has been multifaceted. While they have led to an increase in tax-GDP ratio, indicating better compliance and collection, they have also highlighted areas that need further attention, especially in terms of administrative efficiency and tackling evasion.

2.2. Tax Compliance and Behavior in Bangladesh

Factors Influencing Tax Compliance Tax compliance, inherently multifaceted, is influenced by a complex interplay of factors in the context of Bangladesh (18):

- (1)

- Socio-cultural Norms: In many societies, including Bangladesh, tax compliance is often linked to prevailing social and cultural norms. Communities where paying taxes is considered a civic duty tend to have higher compliance rates (13).

- (2)

- Trust in Government: The level of trust citizens have in their government and its institutions plays a crucial role. If taxpayers believe that their contributions are being used efficiently for public welfare, they’re more likely to comply (19).

- (3)

- Economic Conditions: Economic stability and growth influence taxpayers’ ability and willingness to comply. During economic downturns, compliance rates may drop due to reduced incomes or business losses (12).

- (4)

- Administrative Efficiency: A streamlined and transparent tax administration can encourage compliance. Inefficiencies, bureaucratic hurdles, or perceptions of corruption can deter taxpayers.

- (5)

- Tax Rates and Complexity: High tax rates or a complex tax code can discour- age compliance. Simplified tax structures and reasonable rates can encourage voluntary payment (14).

- (6)

- Penalties and Enforcement: The probability of being detected for non- compliance, combined with the severity of penalties, can act as deterrents. Ef- fective enforcement mechanisms are vital for ensuring compliance.

2.3. Common Reasons for Evasion or Non-compliance

Despite efforts to increase tax compliance in Bangladesh, evasion remains a persistent challenge. Key reasons include:

- (1)

- Informal Economy: A substantial segment of Bangladesh’s economy operates informally, making it difficult to monitor and tax such entities (11).

- (2)

- Lack of Awareness: In rural and less urbanized areas, many taxpayers might not fully understand their tax obligations, resulting in unintentional non-compliance (6).

- (3)

- Perceived Inequity: A belief that the tax system is unfair or that others aren’t paying their due can deter compliance (7).

- (4)

- Corrupt Practices: Corruption within the tax administration can discourage hon- est taxpayers and perpetuate a culture of evasion. Additionally, there exists a segment of individuals who, driven by arrogance or a misguided belief in their cleverness, deliberately devise methods to evade paying income tax, thinking they can outsmart the system. Such attitudes further strain the system and undermine efforts to ensure fair and comprehensive tax compliance.

- (5)

- Complex Tax Procedures: Perceptions of cumbersome or intricate tax filing pro- cesses can deter or delay compliance.

- (6)

- Economic Hardships: Economic downturns or personal financial difficulties might drive individuals or businesses to evade taxes for financial relief.

- (7)

- Inadequate Resources of NBR: The National Bureau of Revenue (NBR), as the sole tax-collecting authority, faces significant challenges. The lack of resources for training and development, the absence of logistical support, and local offices operating in rented premises diminish its stature in the eyes of the public. Such operational constraints can cast a shadow over the NBR’s authority and efficacy.

- (8)

- Perception of NBR: The aforementioned operational challenges contribute to a psychological impact. The populace often doesn’t view the NBR with the same seriousness and reverence as other law enforcement agencies, undermining its authority and leading to reduced compliance.

- (9)

- Lack of penalty procedures.

2.4. Customer-Centric Marketing

2.4.1. Principles and Key Strategies

The term ”customer-centric marketing” was popularized by Philip Kotler (8), a renowned marketing guru. At its core, customer-centric marketing places the customer at the epicenter of all strategies and actions. It prioritizes understanding, catering to, and exceeding customer expectations, with the aim of fostering loyalty and advocacy. The foundational principles and strategies of this approach include understanding customer needs, personalization, consistent value delivery, feedback loops, building long-term relationships, and ensuring a holistic customer experience (3). Even though the National Bureau of Revenue (NBR) is a non-business entity, adopting a customer-centric marketing strategy is crucial (16). By understanding and addressing taxpayer needs, the NBR can enhance tax compliance, leading to increased tax collection and, subsequently, a boost in the nation’s GDP. Aligning with such strategies not only modernizes the tax collection process but also fosters a culture of voluntary compliance, which is instrumental in economic growth.

Customer-centric marketing places the customer at the epicenter of all strategies and actions. Its essence is to understand, cater to, and exceed customer expectations, fostering loyalty and advocacy. Here are the foundational principles and strategies:

- (1)

- Understanding Customer Needs: Before designing any marketing strategy, it’s imperative to understand what the customer wants. This involves collecting data, market research, and direct interactions (4).

- (2)

- Personalization: Tailoring messages and services to individual customer needs or segments ensures relevance and can enhance engagement (5).

- (3)

- Consistent Value Delivery: Customer-centricity involves not just attracting but retaining customers by consistently delivering value.

- (4)

- Feedback Loops: Actively seeking and responding to feedback helps in refining strategies and building trust.

- (5)

- Building Long-term Relationships: Rather than focusing on transactional inter- actions, a customer-centric approach prioritizes long-term relationship building.

- (6)

- Holistic Experience: This approach looks at the entire customer journey, ensuring a seamless and positive experience from the first interaction to post-purchase support.

2.4.2. Success Stories from Other Sectors or Countries

Customer-centric marketing has found immense success in various sectors, demon- strating its versatility and effectiveness:

- (1)

- E-commerce: Giants like Amazon and Alibaba prioritize customer experience. Their recommendation systems, easy return policies, and customer reviews are all tailored to enhance the customer journey.

- (2)

- Banking: Banks, especially in developed countries, have adopted customer- centric approaches to offer personalized financial products, enhance digital ex- periences, and improve customer support.

- (3)

- Telecom: Companies like T-Mobile in the U.S. have redefined their services around customer needs, leading to significant market share growth.

Internationally, countries like the UK have started adopting customer-centric strate- gies in public services. The UK’s tax authority, HMRC, for instance, has been working on improving the taxpayer experience by offering personalized online dashboards, sim- plifying communication, and proactively addressing taxpayer concerns.

2.5. Behavioral Economics and Tax Compliance

2.5.1. Psychological Factors Affecting Tax Behavior

Behavioral economics, which marries economics with psychology, offers profound in- sights into why people might or might not comply with tax obligations. Some pivotal psychological factors include:

- (1)

- Loss Aversion: People tend to prefer avoiding losses over acquiring equivalent gains. If taxpayers perceive tax payments as a ’loss’, they might be more inclined to evade.

- (2)

- Social Norms: Individuals often align their behavior with what’s perceived as ’normal’ or ’acceptable’ in their community. If tax evasion is rampant and socially acceptable, more might indulge in it.

- (3)

- Trust in Authorities: The belief that authorities will use the tax revenues for pub- lic good can influence compliance. Conversely, mistrust or perceived corruption can deter individuals from paying.

- (4)

- Anchoring: Taxpayers might anchor their tax decisions based on certain reference points, like past tax bills or anecdotal information, even if these aren’t relevant.

- (5)

- Prospect Theory: People make decisions based on potential gains or losses rela- tive to a specific reference point, rather than absolute outcomes. The framing of tax communications can thus influence compliance.

2.5.2. Potential Interventions to Improve Compliance

Drawing from behavioral economics, several interventions can be designed to nudge taxpayers towards better compliance:

- (1)

- Framing Effects: How tax information and obligations are presented can impact compliance. Emphasizing the public good achieved through taxes might motivate more people to comply.

- (2)

- Timely Reminders: Sending timely reminders, especially if personalized, can re- duce forgetfulness or intentional delays in tax payments.

- (3)

- Social Proof: Sharing data about how many people in a community or peer group comply with tax obligations can encourage others to follow suit.

- (4)

- Simplification: Reducing the cognitive load by simplifying tax forms, procedures, and communications can enhance voluntary compliance.

- (5)

- Feedback Loops: Informing taxpayers about how their previous year’s taxes were utilized can foster trust and a sense of contribution towards societal welfare.

Behavioral economics, by spotlighting the psychological underpinnings of decision- making, offers a treasure trove of strategies that tax authorities can employ. These interventions, if tailored to the specific nuances of the Bangladesh context, have the potential to revolutionize tax compliance.

2.6. Digital Interventions and Tax Collection

2.6.1. The Rise of Technology in Enhancing Tax Compliance

The digital age has ushered in a paradigm shift in how institutions, including tax authorities, operate and interact with their stakeholders. Here’s how technology is reshaping the tax landscape:

- (1)

- E-filing Systems: Digital platforms that allow taxpayers to file their returns on- line have made the process more convenient and efficient. Such systems reduce paperwork, human errors, and administrative burdens.

- (2)

- Digital Payment Gateways: The rise of digital payment solutions facilitates prompt and hassle-free tax payments, reducing delays and enhancing compli- ance.

- (3)

- Data Analytics: Tax authorities can leverage big data and analytics to identify patterns, forecast revenues, and detect potential cases of evasion or fraud.

- (4)

- Artificial Intelligence (AI) and Machine Learning: Advanced algorithms can be used to automate routine tasks, predict taxpayer behavior, and offer personalized services.

- (5)

- Mobile Apps: With the ubiquity of smartphones, tax authorities can engage taxpayers through mobile applications, offering services like payment reminders, tax calculators, and informational content.

2.6.2. Case Studies from Other Countries

Several countries have leveraged technology to revolutionize their tax systems:

- (1)

- Estonia: Known for its e-governance initiatives, Estonia’s e-Tax/e-Customs sys- tem allows citizens and businesses to declare taxes online. Nearly 95% of tax declarations in the country are filed electronically.

- (2)

- India: The introduction of the Goods and Services Tax Network (GSTN) has digitized tax filings and payments for businesses, providing a unified platform that integrates different state and central taxes.

- (3)

- Brazil: The country’s Receita Federal (tax authority) uses advanced data an- alytics to cross-reference taxpayer information, improving audit accuracy and reducing evasion.

- (4)

- South Africa: The South African Revenue Service (SARS) introduced eFiling, a digital platform enabling electronic submission of tax returns, payments, and other related services.

These case studies underscore the transformative potential of digital interventions. When tailored to the socio-cultural and economic context, such interventions can sig- nificantly boost compliance and streamline tax administration. Incorporating digital interventions in the realm of tax collection isn’t just about modernization; it’s about making the tax process more accessible, transparent, and efficient for all stakeholders involved. As Bangladesh continues its journey towards becoming a digitally empow- ered nation, embracing these technological advancements in the tax domain can be a game-changer.

Drawing from the provided paper and other sources, this section will offer an overview of the global landscape of tax collection, focusing on both the challenges faced by countries and their successes.

2.6.3. Challenges in Global Tax Collection

- (1)

- Economic Disparities: Nations with significant economic disparities often face challenges in tax collection, as large sections of the population might fall below the taxable income threshold.

- (2)

- Complex Tax Systems: Overly complex or frequently changing tax sys- tems can lead to confusion among taxpayers, resulting in unintentional non- compliance or evasion.

- (3)

- Informal Economies: Countries with large informal sectors face the challenge of bringing these segments into the tax net.

- (4)

- Cross-border Evasion: With globalization and the digital economy, cross- border tax evasion has emerged as a significant challenge, with entities leveraging tax havens or complex corporate structures to minimize tax liabilities.

- (5)

- Corruption and Trust Deficit: In countries where corruption within the tax administration is perceived to be high, voluntary compliance can be low due to a lack of trust in the system.

2.6.4. Successes in Global Tax Collection

- (1)

- Digital Transformation: Countries that have embraced the digital revolution, like Estonia and India, have witnessed improved compliance rates and streamlined tax administration processes.

- (2)

- Simplification of Tax Codes: Nations that have undertaken reforms to simplify their tax codes, making them more transparent and understandable, have ob- served better compliance.

- (3)

- Behavioral Interventions: Drawing from behavioral economics, countries like the UK have implemented ’nudges’ in their tax communications, resulting in im- proved taxpayer responses.

- (4)

- Broadening the Tax Base: By implementing policies that bring more entities into the tax net, especially from the informal sector, countries can enhance their revenue collections.

- (5)

- Strengthening International Cooperation: Global initiatives, like the Base Ero- sion and Profit Shifting (BEPS) project by the OECD, have aimed at ensuring that multinational enterprises pay their fair share of taxes, thereby addressing cross-border tax challenges.

By examining the global landscape, we can draw parallels with Bangladesh, noting both the common challenges and the unique intricacies faced by the country. This global perspective also offers insights into potential strategies or interventions that Bangladesh could consider enhancing its tax collection performance.

3. Methodology

3.1. Research Design

The research employs a twofold design, blending both exploratory/descriptive and experimental/causal components.

3.1.1. Exploratory, Descriptive, and Causal Aspects

Exploratory and Descriptive Research (Phase 1):

The initial phase leans on the data derived from a primary survey. This phase is geared towards uncovering preliminary patterns, tendencies, and taxpayer pain points. By assessing certain response frequencies and gauging the overall sentiment towards tax compliance, this phase sets the foundation for the formulation of targeted customer- centric marketing strategies. We will be calling the data from the survey as ’Taxpayer Survey Data’ from now on.

Experimental and Causal Research (Phase 2): In this second phase, we’ll put the marketing strategies we develop to the test. We’ll introduce these strategies to a specific group of people (known as the ’controlled group’) and see how effective they are in changing tax behaviors. By comparing this group with another group that hasn’t seen these strategies, we can better understand if our methods are truly making a difference.

3.2. Data Collection Methods

The multifaceted nature of the research necessitates the utilization of both qualitative and quantitative data collection techniques.

3.2.1. Qualitative and Quantitative Approaches (Phase 1)

Quantitative Approach: The Taxpayer Survey dataset stands as the linchpin for quantitative analysis. It supplies tangible data points reflecting respondents’ perspectives, behaviors, and tendencies. Future quantitative studies, especially those centered on experimental designs related to customer-centric strategies, will further fortify this approach.

Below are the questions asked in the survey:

- (1)

- Age RangeGender

- (2)

- Occupation

- (3)

- Annual Income Range

- (4)

- How frequently do you file your taxes?

- (5)

- Do you believe paying taxes is a civic duty?

- (6)

- On a scale of 1 to 5, how confident are you in your understanding of the tax regulations and procedures?

- (7)

- Have you ever received any formal information or training on tax filing?

- (8)

- How do you primarily pay your taxes?

- (9)

- Would you be motivated to pay taxes if you received some form of public recog- nition?

- (10)

- Do you believe there are significant benefits to being tax compliant?

- (11)

- How trustworthy do you find the tax system in Bangladesh?

- (12)

- Do you believe social proof (knowing others are paying their taxes) would influ- ence your behavior?

- (13)

- Would you be more likely to pay taxes if the process was gamified, offering rewards or points for timely compliance?

- (14)

- On a scale of 1 to 5, how responsive do you believe the tax department is to taxpayer needs?

3.2.2. Qualitative Approach:

Focus Group Discussions (FGDs) and in-depth interviews are the primary tools for this approach, aiming to dive deep into the intricacies of taxpayer sentiments, motivations, and perceptions. These mechanisms offer a granular understanding of taxpayer challenges and their perspectives on potential marketing interventions.

Business Goals:

- Tax Enrollment Boost: By providing a tax redemption of 2%, we aim to incen- tivize taxpayers to join the system and remain compliant.

- Awareness Drive: The initiative will focus on educating citizens about the im- portance of tax payments, how they are calculated, and the subsequent benefits for social and national development.

Target Audience Identification:

- Age: The core focus will be on individuals aged between 24-40 years. Gender: Both males and females are included in the target group.

- Occupation: The campaign will primarily target those in business services, gov- ernment services, and government employees.

- Income Bracket: The target audience has a monthly income ranging from 50,000 to 100,000 BDT.

- Location: The campaign will be concentrated on the outskirts of Dhaka, prefer- ably in areas like Savar or Gazipur.

- Challenges: One of the main challenges is the lack of comprehensive information available to this group about the importance of taxes, the tax calculation process, and the procedure for tax payments.

SWOT Analysis:

- Strengths: Being a government body, there’s no competition. Offering tax re- demption is an added advantage. Providing a reliable portal for instant tax payments and genuine information.

- Weaknesses: Limited resources available for the campaign. Focus restricted to a smaller area and group. Prevalent lack of information among the target audience. Opportunities: The younger demographic is more eager and concerned about tax obligations compared to the older generation. No competitors in the field, ensuring sole attention.

- Threats: Existing trust issues among potential taxpayers. Risks associated with misinformation and potential mistreatment by authorities.

Positioning & Differentiation:

- Unique Selling Proposition (USP): Authentic and reliable information on tax obligations.

- Offer of tax redemption.

- A trustworthy portal for instant tax payments.

Marketing Objectives:

- Data Collection: A registration log will maintain a record of all individuals suc- cessfully reached.

- Feedback Collection: Questionnaires will capture demographic details and gauge the perceptions of the target audience on government tax facilities.

- Outreach Target: The aim is to engage with 1000 individuals within a span of 3 days.

Budget Allocation:

An estimated budget of 30,000 BDT has been allocated. This will cover a team of 10 members, accounting for travel expenses, meals, accommodation, and other necessary materials for the campaign.

Marketing Channels:

The entire campaign is envisioned to be Face-to-Face (F2F), ensuring direct engage- ment and immediate feedback.

3.3. Sampling Techniques

Ensuring the reliability and validity of the research hinges on the meticulous appli- cation of sampling techniques. A total of 3239 people from different demographics responded to the primary survey (Exploratory and Descriptive Research (Phase 1)), the ’Taxpayer Survey’, and a Total of 1000 people participated in the Causal Research (Phase 2).

3.3.1. Criteria for Selecting Participants and Data Sources

Participants for the Taxpayer Survey dataset were emulated, reflecting the demo- graphic and behavioral tendencies of the original sample set. This approach guaran- tees a broad-based representation spanning various age groups, income levels, and sentiments.

For the experimental design in Phase 2, a random assignment methodology will be employed. Participants will be categorized into either the controlled group (those exposed to the marketing strategies) or the comparison group (those left unexposed). This stratification ensures an unbiased outcome, setting the stage for clear causal deductions.

3.41. Data Analysis Methods

A suite of tools and techniques will be deployed to distill meaningful insights from the amassed data.

3.4.1. Tools and Techniques for Analyzing Collected Data

- Descriptive Statistics: The preliminary analysis of the Taxpayer Survey dataset will focus on metrics of central tendency, dispersion, and frequency dis- tributions. These metrics will illuminate general trends and patterns.

- Inferential Statistics: To probe deeper, tools like T-tests, ANOVA, or regres- sion analyses may be invoked, especially when navigating the causal dynamics between marketing strategies and tax compliance.

- Qualitative Analysis: Data from FGDs and interviews will be subjected to the- matic analysis. Common themes, narratives, and sentiments will be spotlighted, serving as a qualitative counterpart to the quantitative findings, ensuring a com- prehensive grasp of taxpayer behaviors and motivations.

4. Result Analysis

4.1. Demographic Overview of Respondents

4.1.1. Age, Profession, Income Levels

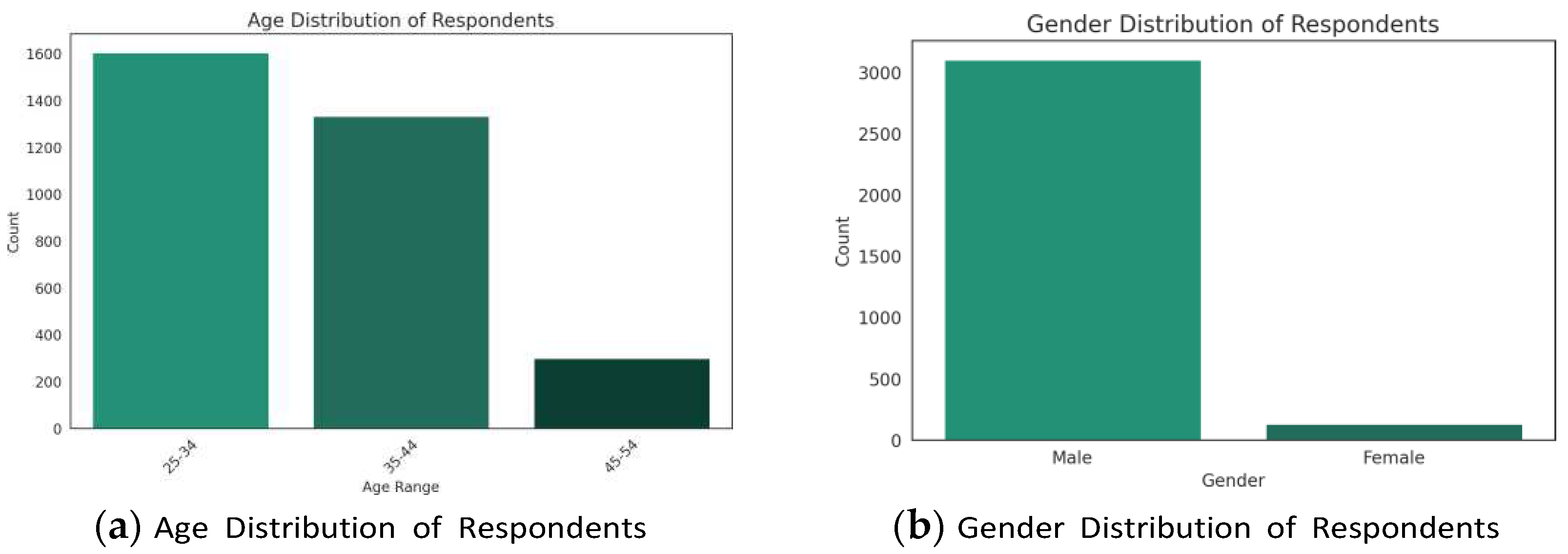

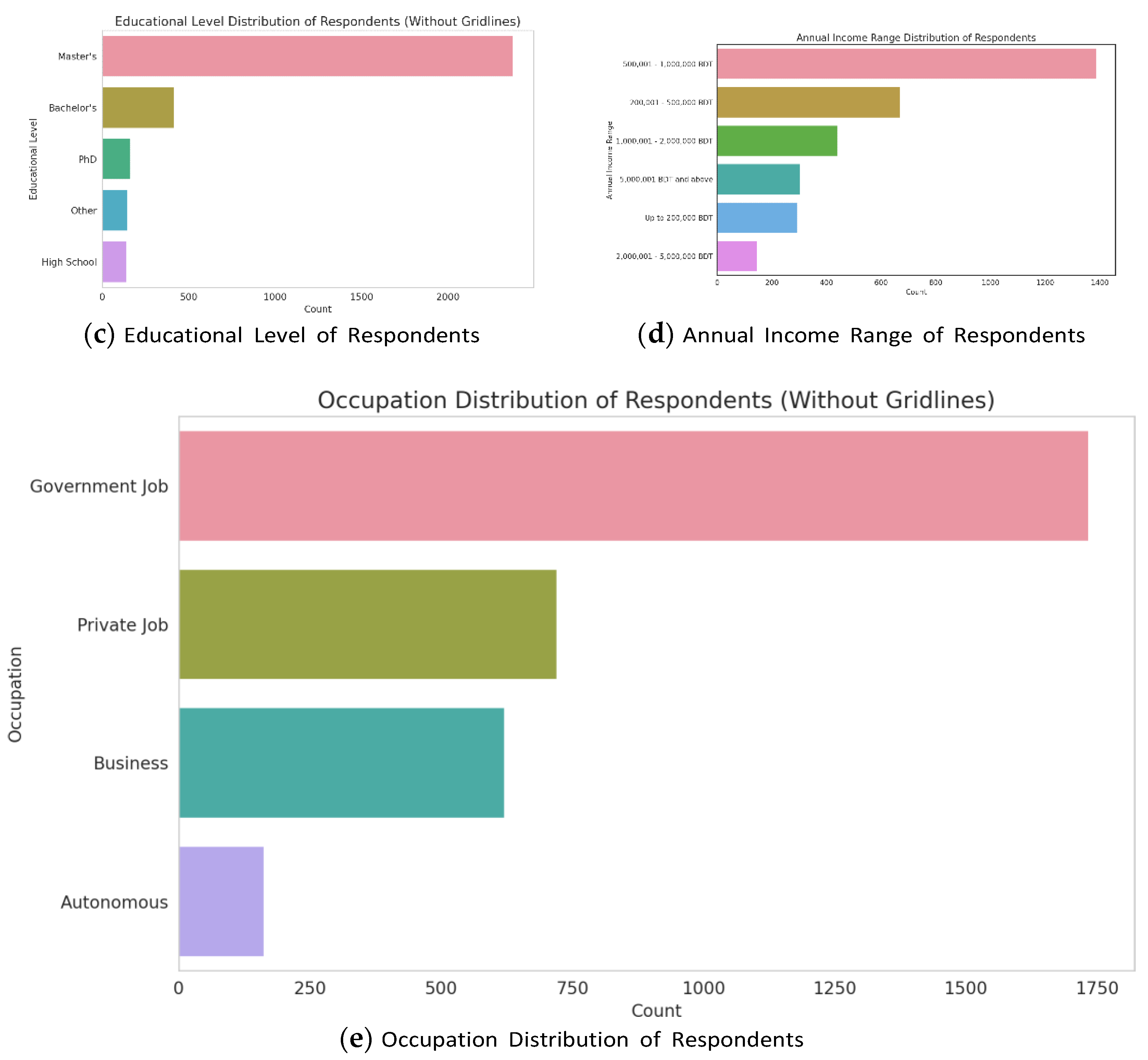

- Age Distribution: The majority of respondents fall within the age bracket of 25-34 years (1,605 respondents, 49.55% of total respondents) followed closely by the 35-44 age range (1334 respondents, 41.19%). This indicates that a signif- icant proportion of our sample represents the younger demographic, which is pivotal given their adaptability to newer tax compliance methods and digital innovations.

- Occupation Distribution: The predominant occupation among the respon- dents is ‘Government Job’ (1,734 respondents, 53.54%), followed by ’Private Job’ (721, 22.26%) and ’Business’ (621, 19.17%). This distribution provides insights into the earning patterns and potential tax liabilities associated with different professions.

- Income Distribution: The annual income distribution indicates that the largest group of respondents earns between BDT 500,001 - 1,000,000 BDT (Mid- dle income) (1387, 42.82%). The second largest group falls in the BDT 200,001 - 500,000 BDT range (665, 20.53%). This provides a perspective on the economic capacities of the respondents and the potential tax brackets they might belong to.

Figure 1.

Distribution of Demographics of Respondents.

4.2. Current Tax-Paying Behavior

4.2.1. Frequency, Amount, and Patterns

- Confidence in Understanding Tax Regulations: The majority of respon- dents indicate a low level of confidence in understanding tax regulations and pro- cedures, rating it as 1 out of 5. However, a notable percentage, nearly 18.86%, feel highly confident, rating their understanding as 5 out of 5. Additionally, about 18.34% of respondents have a moderate level of confidence, rating their understanding as 3 out of 5.

- Frequency of Seeking Tax Assistance: Most respondents seek assistance ’Sometimes’ when filing taxes, indicating some uncertainty or lack of clarity about the process. A noteworthy proportion of respondents seek assistance ’Of- ten’, highlighting the complexity of the tax filing process for a segment of the population.

- Primary Mode of Tax Payment: The vast majority of respondents, approx- imately 67.68%, primarily pay their taxes through manual or paper-based sub- missions, indicating a preference for traditional payment methods. However, a growing segment, nearly 12.99%, are adopting online or e-filing methods, show- casing the increasing trend and acceptance of digital payment avenues for tax compliance. Additionally, about 19.33% of respondents utilize tax agents for their tax payments.

4.3. Awareness and Perceptions

4.3.1. Knowledge about Tax Obligations

- (1)

- Receipt of Formal Information or Training on Tax Filing: A significant majority of respondents, approximately 68.54%, have not received any formal information or training on tax filing. This data highlights the critical need for increasing awareness initiatives and offering relevant training to taxpayers to potentially enhance tax compliance.

- (2)

- Confidence in Understanding Tax Regulations: While approximately 18.34% of respondents rate their confidence in understanding tax regulations as 3 out of 5, a combined 35.75% of participants rate their confidence as either 4 or 5. This suggests that, while many feel moderately confident about their understand- ing, there’s a significant segment that is highly confident in their grasp of tax regulations.

4.3.1. Attitudes Towards Taxation

- Trustworthiness of the Tax System: Trust is a critical factor in tax compli- ance. Approximately 36.46% of respondents perceive Bangladesh’s tax system as ”Trustworthy,” and an additional 4.82% regard it as ”Very Trustworthy.” Com- bined, this suggests that over 41% have a positive trust level towards the tax system. On the other hand, 26.18% of participants are neutral in their trust, in- dicating a moderate level of trust. However, it’s noteworthy that a sizable 32.54% find the system ”Distrustful,” pointing to areas that might need improvement to bolster public trust.

- Belief in Benefits of Being Tax Compliant: A substantial majority, cumu- latively 72% (48.75% who ”Agree” and 23.25% who ”Strongly Agree”), believe that there are considerable benefits to being tax compliant. This prevalent posi- tive perception can act as a driving force to boost tax compliance, as it signifies an inherent understanding and acknowledgment of the advantages linked with fulfilling tax responsibilities. However, it’s worth noting that a smaller segment, approximately 9.41%, either disagrees or strongly disagrees with the notion, sug- gesting areas that might require targeted awareness campaigns.

- Motivational Factors in Tax Compliance: The idea of public recognition as a reward for tax compliance resonates with a significant portion of respondents. Specifically, 40.32% are ”Highly Motivated” by such a proposition, and an ad- ditional 50.85% feel ”Motivated.” This suggests that a public acknowledgment system could be a potential strategy for enhancing tax compliance. On the topic of social proof, the data indicates that citizens are considerably influenced by the tax compliance behavior of their peers. A combined total of approximately 83% of respondents show varying degrees of positive influence when aware of others paying taxes, emphasizing the power of societal norms and peer behavior in this context. The concept of gamification in the tax payment process also emerges as a strong motivator. Over 53% are ”More Likely” to pay taxes if the process involves rewards or points for timely compliance, and 37.39% would be ”Much More Likely” motivated by such a strategy. This underscores the potential of integrating gamified elements into the tax filing system to boost participation and punctuality in tax payments.

4.4. Introduction to Causal Research (Phase 2)

After the initial exploratory research (Phase 1) that shed light on the existing tax behaviors and perceptions among the Bangladeshi citizens, Phase 2 was designed as an experimental approach to understand the effectiveness of certain strategies. This phase involved direct communication with a target group and the application of specific interventions based on the outcomes of Phase 1.

4.4.1. Results and Analysis

Awareness of Tax Educational Campaigns Upon inquiring whether the respondents had previously encountered tax-related educative campaigns, a staggering 95.70% (957 out of 1000) mentioned that they had never come across such initiatives. Only 31 individuals (3.1%) affirmed their exposure to such campaigns, while 12 respondents chose not to comment.

Knowledge of Income Tax Calculation The data revealed that a significant majority, 87% (870 respondents), lacked the knowledge to calculate income tax. While 8.6% (86 respondents) mentioned they would seek expert assistance for tax calculations, only 4.4% (44 respondents) expressed confidence in their ability to calculate income tax independently.

Inclination Towards Tax Payment with Incentives When presented with the prospect of a 2% reduction in their total tax amount, 73% of the respondents expressed willingness to pay their taxes instantly. In contrast, 23% were not influenced by the incentive, and 4% chose other options.

Perceived Value of the Information An overwhelming 98% of the respondents found the information shared during this phase beneficial. This suggests the effectiveness of the communication and the inherent value it holds for the target group.

Likelihood of Sharing Information Promisingly, 96% of the respondents were keen on sharing beneficial tax-related information with their friends and family, indicating the potential for organic dissemination of such knowledge. Only 4% opted for other responses.

Perception of Taxation on Quality of Living When queried about the impact of legitimate and fair taxation on their quality of living, 63% of respondents believed in a positive correlation. However, 14% did not see a direct link, and 23% were unsure, signifying the need for further awareness and education in this domain.

The results from Phase 2 underscore the significant knowledge gap among the citi- zens concerning taxation. The lack of prior exposure to tax educative campaigns and the high percentage of individuals unaware of tax calculations highlight the need for comprehensive awareness campaigns. The positive inclination towards tax payment when presented with incentives and the high likelihood of information sharing are promising indicators for future strategies.

5. Conclusion

Tax compliance, an issue that has significant socio-economic implications, is especially pertinent in a country like Bangladesh, with its diverse demographics and economic challenges. This research embarked on a detailed exploration to understand the land- scape of tax-paying behaviors, motivations, and perceptions among the citizens of Bangladesh. The first phase of the research highlighted that while a significant seg- ment of the younger population engages in tax-paying activities, there exists a palpable gap in their understanding of tax regulations. This raises questions about the current methods and mediums of information dissemination. Are they effective? Are they ac- cessible to all demographics? It underscores the importance of designing educational initiatives that cater to the diverse needs and literacy levels of the population. One of the most compelling findings from the causal research phase was the populace’s positive response to tangible incentives. The idea that a mere 2% reduction could sig- nificantly influence tax compliance behaviors is profound. It not only speaks to the economic motivations of individuals but also suggests that when the benefits of com- pliance are made explicit, people are more likely to engage. Trust, or the lack thereof, in the tax system emerged as a significant theme. The moderate trust levels indicate a need for transparency and accountability measures. Ensuring that taxpayers see where their money is going, perhaps through publicized infrastructural developments or com- munity projects funded by taxes, might bolster trust levels. While the preference for traditional tax payment methods was evident, there was a discernible interest in dig- ital methods among a segment of the population. Digitalization of payment systems can significantly enhance tax-paying behaviors. By offering a seamless, efficient, and user-friendly digital platform for tax payments, authorities can cater to the tech-savvy generation, reduce bureaucratic hurdles, and ensure timely compliance. Digital plat- forms also provide transparency, instant payment confirmations, and easy access to payment histories, further instilling confidence in taxpayers and promoting a culture of timely and consistent tax payments. This finding is especially pertinent in the age of digital transformation. It suggests that while face-to-face interactions and traditional methods remain important, there’s significant potential in developing user-friendly dig- ital platforms for tax compliance. The willingness of respondents to share tax-related information with friends and family is a testament to the power of community and word-of-mouth in shaping behaviors. It suggests that if individuals are equipped with the right information, they can become ambassadors of tax compliance in their own communities. The significant number of respondents who had never encountered tax- related educative campaigns paints a picture of missed opportunities. It’s imperative for relevant authorities to harness various communication channels, from community gatherings to digital platforms, to bridge this knowledge gap. In sum, this research presents a comprehensive view of tax compliance in Bangladesh, complete with its challenges and opportunities. The road to enhancing tax compliance is multifaceted, requiring a blend of traditional outreach, digital innovations, educational initiatives, and trust-building measures. As Bangladesh continues its journey of socio-economic development, ensuring a robust and compliant tax system will be paramount. The findings from this research provide a roadmap, highlighting areas of intervention and potential strategies to achieve this goal.

Conflicts of Interest

In the spirit of transparency, it is crucial to declare that there are no conflicts of in- terest associated with this research endeavor. The lead investigator and contributors affirmatively state that they have not received any external funding, financial support, or other affiliations that could potentially compromise the impartiality and objectiv- ity of the study. This absence of external influences underscores the commitment to conducting unbiased and independent research, ensuring the integrity of the findings presented in this article.

References

- Ahmed, S.U. Income visibility and tax compliance: Bangladesh perspective.

- Alam, M.F. Determinants of Tax Compliance Behavior in Bangladesh: The Case of Individual Tax Payers. PhD thesis, © University of Dhaka, 2021.

- Camilleri, M.A. The use of data-driven technologies for customer-centric marketing. International Journal of Big Data Management 1, 1 (2020), 50–63.

- Dadzie, K.Q., Dadzie, C.A., and Winston, E.M. The transitioning of marketing practices from segment to customer-centric marketing in the african business context: To- ward a theoretical research framework. In Contemporary Issues and Prospects in Business Development in Africa. Routledge, 2020, pp. 52–69.

- Habel, J., Kassemeier, R., Alavi, S., Haaf, P., Schmitz, C., and Wieseke, J. When do customers perceive customer centricity? the role of a firm’s and salespeople’s customer orientation. Journal of Personal Selling & Sales Management 40, 1 (2020), 25–42.

- Hossain, M.S., Ali, S., LING, D.C.C., and Fung, C.Y. Tax avoidance and tax evasion in bangladesh: Current insights and future research directions. Available at SSRN 4553962.

- Islam, T. Tax evasion by e-commerce businesses in bangladesh.

- Kotler, P., Kartajaya, H., and Setiawan, I. Marketing 5.0: Technology for human- ity. John Wiley & Sons, 2021.

- Mannan, D.K.A. Socio-economic factors of tax compliance: An empirical study of individual taxpayers in the dhaka zones, bangladesh. The cost and Management 48, 6 (2020).

- Miah, M.D., Hasan, R., and Uddin, H. Agricultural development and the rural economy: The case of bangladesh. Bangladesh’s Economic and Social Progress: From a Basket Case to a Development Model (2020), 237–266.

- Nurunnabi, M. Political influence and tax evasion in bangladesh: what went wrong? In Advances in Taxation. Emerald Publishing Limited, 2019, pp. 113–134.

- Rahaman, A., and Leon-Gonzalez, R. The effects of fiscal policy shocks in bangladesh: An agnostic identification procedure. Economic Analysis and Policy 71 (2021), 626–644.

- Rashid, M.H.U., and Ahmad, A. Business students’ perceptions of tax evasion: a study in bangladesh. International Journal of Accounting and Finance 10, 4 (2020), 233–247.

- Sadekin, M.N., Alam, M.M., Saha, S., et al. Analysis of trend and sources of government budget deficit financing in bangladesh. Journal of International Studies 16 (2020), 129–144.

- SARDER, M.F.R. The Tax Revenue Collection Performance Analysis in Bangladesh. PhD thesis, UNIVERSITY OF DHAKA, 2020.

- Saxena, D., Dhall, N., and Malik, R. Enhancing digital payments adoption through customer-centric marketing strategies: A conceptual framework. Manthan: Journal of Commerce and Management 8, 1 (2021), 60–78.

- Siddiquee, N., and Saleheen, A. Taxation and governance in bangladesh: a study of the value-added tax. International Journal of Public Administration 44, 8 (2021), 674–684.

- Submitter, G., and Alam, M.S. An examination of taxpayers attitude towards income tax: A case of bangladesh. Journals and Alam, Md Shahbub, An Examination of Taxpayers Attitude towards Income Tax: A Case of Bangladesh (September 30, 2021). Reference to this paper should be referred to as follows: Alam, MS (2021), 95–110.

- Titumir, R.A.M., and Titumir, R.A.M. Poverty and inequality in bangladesh. Numbers and narratives in Bangladesh’s economic development (2021), 177–225.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.